future of payments colloquium - filene research institute · number 16 march 2013 mckinsey on...

TRANSCRIPT

Agenda & Pre-Reading

Future of Payments Colloquium

At Filene we appreciate the generosity of all our

benefactors. We particularly wish to thank CO-OP Financial Services for its support of this and all of the colloquia in Filene's 2013 series.

Mountain America Credit Union 7167 S. Center Park Drive West Jordan, Utah 84084 801-325-6228

Future of Payments Colloquium

May 30, 2013

Agenda 8:00 – 9:00 Registration/Breakfast

9:00 – 9:30 Welcome/Introductions

Mountain America Credit Union | Utah’s Credit Unions | Filene

9:30 – 10:45 Emerging Payments Showcase and Digital Wallet Overview McKinsey

10:45 – 11:00 Break

11:00 – 11:30 Credit Unions in the Canadian Payments Milieu Credit Union Central of Canada

11:30 – 12:15 Lunch/Networking

12:15 – 1:45 Service Provider Panel and Audience Discussion CO-OP FS | CSCU | Fiserv | PSCU – Moderated by McKinsey

1:45 – 2:00 Break

2:00 – 3:30 Payments Scenarios for Credit Unions with Open Discussion and Breakouts Presented/Moderated by McKinsey

3:30 – 3:45 Closing Remarks Filene

Logistics

Directions to H. Floyd Tanner Building Mountain America Credit Union 7167 S. Center Park Drive West Jordan, Utah 84084

• Take I-‐15 to the 7200 South Exit. • Head west. • This street eventually turns into 7000 South. • Proceed west to Bangerter Highway. • Proceed through intersection—the street becomes Jordan Landing Boulevard. • Continue on Jordan Landing Blvd. past Carl’s Jr. • Go to next stoplight and turn right onto Center Park Drive. • Drive about one block to Campus View Drive, turn right. • You will see two, tan-‐colored Mountain America buildings. • The H. Floyd Tanner Building is on the west side of the street. • Go about ½ block and turn left into the parking lot. Use this parking lot ONLY. • Enter the building— the Tanner Auditorium is located to the left of the reception desk.

Please DO NOT park in the lot on the east side of the street—this is Mountain America’s Corporate Headquarters Building, and the parking lot is reserved for that building ONLY. Your vehicle may be towed.

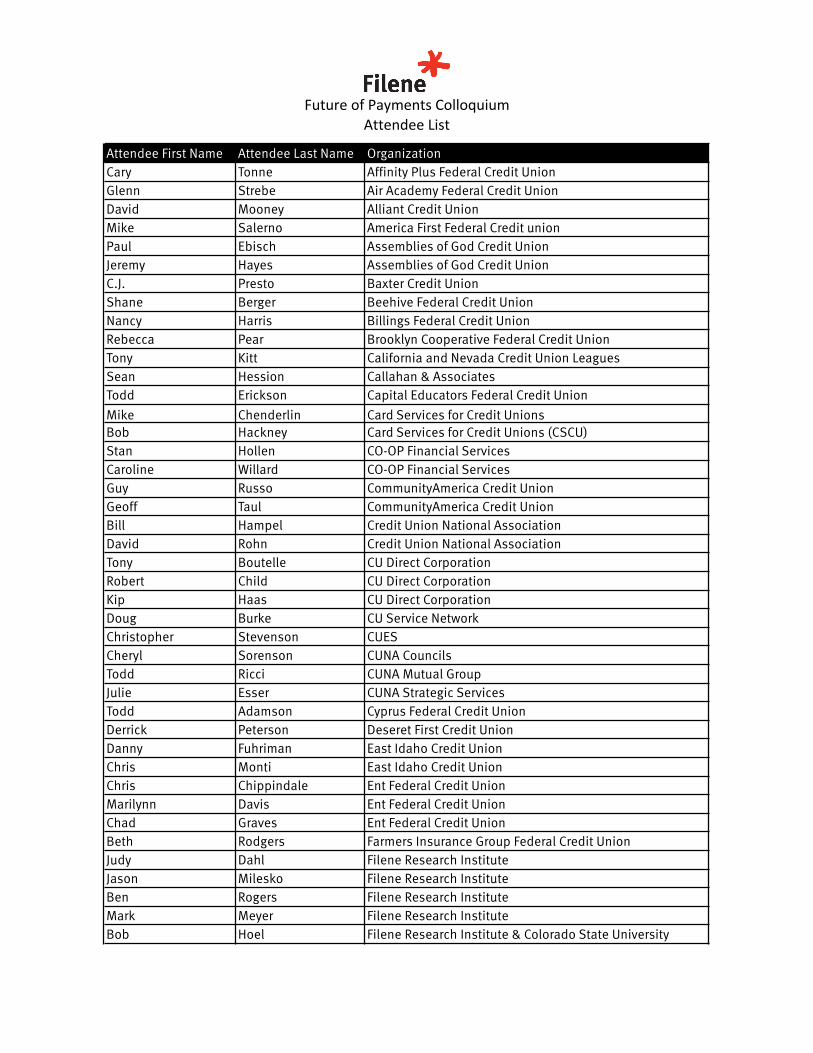

Future of Payments ColloquiumAttendee List

Attendee First Name Attendee Last Name Organization Cary Tonne Affinity Plus Federal Credit UnionGlenn Strebe Air Academy Federal Credit UnionDavid Mooney Alliant Credit UnionMike Salerno America First Federal Credit unionPaul Ebisch Assemblies of God Credit UnionJeremy Hayes Assemblies of God Credit UnionC.J. Presto Baxter Credit UnionShane Berger Beehive Federal Credit UnionNancy Harris Billings Federal Credit UnionRebecca Pear Brooklyn Cooperative Federal Credit UnionTony Kitt California and Nevada Credit Union LeaguesSean Hession Callahan & AssociatesTodd Erickson Capital Educators Federal Credit UnionMike Chenderlin Card Services for Credit UnionsBob Hackney Card Services for Credit Unions (CSCU)Stan Hollen CO-OP Financial ServicesCaroline Willard CO-OP Financial ServicesGuy Russo CommunityAmerica Credit UnionGeoff Taul CommunityAmerica Credit UnionBill Hampel Credit Union National AssociationDavid Rohn Credit Union National AssociationTony Boutelle CU Direct CorporationRobert Child CU Direct CorporationKip Haas CU Direct CorporationDoug Burke CU Service NetworkChristopher Stevenson CUESCheryl Sorenson CUNA CouncilsTodd Ricci CUNA Mutual GroupJulie Esser CUNA Strategic ServicesTodd Adamson Cyprus Federal Credit UnionDerrick Peterson Deseret First Credit UnionDanny Fuhriman East Idaho Credit UnionChris Monti East Idaho Credit UnionChris Chippindale Ent Federal Credit UnionMarilynn Davis Ent Federal Credit UnionChad Graves Ent Federal Credit UnionBeth Rodgers Farmers Insurance Group Federal Credit UnionJudy Dahl Filene Research InstituteJason Milesko Filene Research InstituteBen Rogers Filene Research InstituteMark Meyer Filene Research InstituteBob Hoel Filene Research Institute & Colorado State University

Future of Payments ColloquiumAttendee List

Brian Bodell Finivation on behalf of CUNA Tech CouncilSteve Shaw FiservLindsay Beyer Fox Communities Credit UnionDavid Thone Fox Communities Credit UnionFernando Ortega GECU Kerstin Plemel Greater Nevada Credit UnionBrad Sears Grow Financial Federal Credit UnionRandy Gailey Horizon C.U.Michael Spink Local Government Federal Credit UnionCJ Daiker Maps Credit UnionDavid Deckelmann Maps Credit UnionChris Giles Maps Credit UnionMark Zook Maps Credit UnionMichael Hanson Massachusetts Credit Union Share Insurance CorporationAmy Cohen McKinsey & Co.Sean Sims McKinsey & CompanyGlen Sarvady McKinsey & Company (alumni)Tony Rasmussen Mountain America Credit UnionSterling Nielsen Mountain America Federal Credit UnionDrew Kishbaugh MYCU Services / Mid-Atlantic Corporate Federal Credit Jerald Garner National Credit Union Administration (NCUA)Steve Schexnayder Neighbors Federal Credit UnionRobert Morgan NorthCountry Federal Credit UnionPete Jenkins One Nevada Credit UnionLaura Thompson Orange County's Credit UnionMike Kenzie Patriot Federal Credit UnionAlisha Johnson Postal Credit UnionRoxanne Sonnek Postal Credit UnionFredda McDonald PSCURandy Stolp PSCUEvelyn Royer Purdue Federal Credit UnionHeather Moshier San Diego County Credit UnionGulshan Garg SchoolsFirst Federal Credit UnionGulshan Garg SchoolsFirst Federal Credit UnionTammy Fleiger Spokane Teachers Credit UnionChris Ayer State Employees' Credit UnionSue Douglas State Employees' Credit UnionBelinda Caillouet STCULily Newfarmer Tarrant County Credit UnionShazia Manus The Members GroupJim Giacobbe United Solutions CompanyJeffrey Goff University Federal Credit UnionSteve Kubala University Federal Credit Union

Future of Payments ColloquiumAttendee List

Bill Raker US Federal Credit UnionMarilyn Pearson Utah Credit Union AssociationRob Van Nevel UW Credit UnionChristopher Saneda Virginia Credit UnionDeb Wreden Virginia Credit UnionSteve Salazar Warren Federal Credit UnionWalter Cunningham Washington State Employees Credit UnionBen Morales Washington State Employees Credit UnionBrock Mortensen Weber State Credit UnionVickie van der Have Weber State Credit UnionMark Chamberlain Weber State Federal Credit UnionJohn Best Wescom Credit UnionRyan Frank World Council of Credit Unions

March 2013Number 16

McKinsey on Payments

Foreword

Forging a path to payments digitizationThe social cost of cash is high wherever it predominates. Moving to a digital paymentsmarket can stimulate economic growth and facilitate financial transparency.

The role of data analytics companies in mobile commerceData-rich companies—including banks and retailers—can use their assets to addvalue and secure their competitive position in the new digital order.

Disruption brings opportunity in merchant paymentsAs the payments environment evolves, financial institutions and merchants will havemany options for collaborating on approaches that create real value.

The battle for the point of salePayments service providers are offering an array of products that are reinventing thepoint-of-sale experience.

Driving merchant services and digital commerce: Findings fromMcKinsey’s 2012 U.S. Small Business Acquiring PanelSmall merchants not only account for the largest portion of merchant acquiring, theyalso play a major role in the current trend toward digital payments.

Payments regulation: A catalyst for innovationPayments regulators are beginning to recognize their role in attaining a balancebetween protection and growth.

The U.S. payments industry at a glance

1

3

10

17

24

30

38

46

The stiff headwinds that continue to confront the U.S. payments industry are evident in the latest release of McKinsey’s U.S.Payments Map, which reveals a second consecutive year of revenue decline—the first two in the profit pool model’s 20-yearhistory. McKinsey forecasts continued rough waters, but our model identifies opportunities for payments providers to opti-mize their returns in a difficult environment, and to target still-meaningful areas of growth.

A look at 2011• U.S. payments providers earned revenue of $280 billion in 2011, down nominally from 2010 and continuing a retrench-ment from a high-water mark of $294 billion in 2009.

• Net interest declines were the primary cause of 2011’s revenue weakness. The historically low rate environment continuedto depress demand deposit account (DDA) net interest margins (NIMs) despite all-time high consumer and commercialDDA balances. Consumer credit cards absorbed the largest hit to net interest income, due in large part to a 5 percent dropin average card balances.

• Nonetheless consumer credit cards remain the largest revenue product, comprising more than 40 percent of overall rev-enue. The product has returned to pre-recession profit margins, albeit on a smaller business. Outstanding card balanceshave stabilized but remain 17 percent percent below the highs established in 2008. Delinquency rates continue to improve,and are now at all-time lows.

• Consumer DDA—the second-largest product—faces multiple challenges. Along with the NIM environment, overdraft regu-lations continue to suppress fee income, and debit interchange regulations that took effect in late 2011 will have greater im-pact in 2012. Profitability fell slightly, as cost savings from branch reductions (over 1,800 closed in 2011) did not fully offsetthe billions of dollars in foregone overdraft income.

• Cash remains the vehicle for nearly half of transactions, primarily small value consumer point-of-sale transactions. How-ever, 80 percent of the dollar value is carried by check and ACH—the primary vehicles for larger-ticket business payments.

Looking ahead• Over the next five years the longstanding declining trend in check volumes will continue, albeit at a slower rate. By 2015,business checks will provide the majority of remaining paper.

• Double-digit growth rates in prepaid and debit cards will moderate, consistent with the products’ maturation curves. PINdebit will gain share relative to signature as a result of debit interchange regulation (Reg II).

• The rapidly evolving mobile e-wallet space could comprise as much as 7 percent of point-of-sale volume by 2016.

• The industry will generate $60 billion to $70 billion of new revenue by 2016. A meaningful share will stem from an interest raterecovery, placing a premium on balances. Transaction fees and credit cards (both consumer and business) offer significantgrowth opportunities. Banks will struggle to replace past revenue opportunities in penalty and account fees, however.

• The fastest-growing revenue segment is money services (primarily products like prepaid and check cashing services ad-dressing needs of the underbanked), which is expected to grow by over 35 percent between 2011 and 2016, with generalpurpose reloadable prepaid and payroll cards leading the way.

The U.S. payments industry at a glance

Consumer credit card 116

U.S. payments industry 280

Money services1

Business/government DDA 36

Other2 5

12

15Merchant acquiring

Business/government card issuing 23

Consumer DDA 7267%

27%

NII

Fees

2011 U.S. payments industry revenuesU.S.$ billions

Consumer general purpose credit card issuing and consumer checking account for most payments industry revenues

Commercial payments services generate 27% of revenues

Money services, typically products for underserved customers, is a small but growing segment

1 Includes prepaid cards, electronic money transfer (EMT), non-bank check cashing and money orders.

2 Includes armored transport, check verification/guarantee, travelers checks and ISO ATM fees.

Source: McKinsey U.S. Payments Map, Release Q4-2012

Financial institutions and other providers earn $280 billion in fees and net interest income from payments services to U.S. payers and payees

For more information on McKinsey’s U.S. Payments Map, please contact Ryan Cope ([email protected]) or David Stewart ([email protected]).

2 (0%)

11,876 (13%)

47 (0%)

215 (0%)

662 (1%) 42,721 (48%)

28,680 (32%)

2,217 (2%)

1,070 (1%)

2,043 (2%) Cash

Credit card

Signature debit

Check1

ACH

Prepaid

Book entry transfers

Wire transfer2

Other3

PIN debit

Cash

Credit card

Signature debit

Check1

ACH

Prepaid

Book entry transfers

Wire transfer2

Other3

PIN debit

0.4 (0%)

8.8 (4%)

16.3 (7%)

20.2 (9%)

21.7 (9%) 23.5 (10%)

29.1 (13%) 109.6 (48%)

0.1 (0%)

0.2 (0%)

2011 U.S. transactions230 billion total

2011 U.S. dollar flows$89.5 trillion total, $ billions

1 Reflects checks paid, not checks written. Checks converted to ACH are counted in ACH.

2 Excludes vast majority of wire transfer dollars in an effort to approximate customer payments activity rather than financial institution settlement.

3 Includes deferred payments services (e.g., Bill Me Later) and cell phone/other bill charges.

Source: McKinsey U.S. Payments Map, Release Q4-2012

Cash dominates transaction counts, while ACH represents most dollar flows

1-3

1-5

1-5

5-10

10-15

10-15

15-20

Other2 5

Money services1 12

Acquiring 15

Business/government credit card

23

Business/governmentDDA

36

Consumer DDA 72

Consumer credit card

Transaction fees

Penalty fees

Account fees

Net Interest Income

116 = Decline

2011 U.S. payments revenuesU.S.$ billions

Net new revenue 2016 versus 2011U.S.$ billions

1 Includes prepaid cards, EMT, non-bank check cashing and money orders.

2 Includes armored transport, check verification/guarantee, traveler’s checks, ISO ATMs, deferred payments and phone/other bill charges

Source: McKinsey U.S. Payments Map, Release Q4-2012, base case scenario

Growth in U.S. banking revenues will rely increasingly on deposits, credit card transactions and prepaid cards

2011-16

20%14%

6% 5% 5%

4% 4%

2% 2%

-2% -5%

Other1 86% PIN debit 12% Wire transfer 3% Signature debit 13% Prepaid 20% ACH 7% Credit card 2% Book entry transfers 20% Total 2% Cash -1% Check -7%

2006-11

U.S. payment transaction growthCAGR, base case scenario

1 Includes deferred payments services (e.g., Bill Me Later), and cell phone/other bill charges.

Source: McKinsey U.S. Payments Map, Release Q4-2012, base case scenario

Check decline will decelerate and ACH and signature debit growth will mature, while PIN debit will gain from Reg. II

June 2012Number 14

McKinsey on Payments

Foreword

The evolving mobile payments consumer: Strategic insights fromaround the globeAs mobile commerce and mobile payments gain footholds around the globe, a newMcKinsey survey identifies emerging themes and important differences betweenmarkets.

Pathways to growth in mobile paymentsWorldwide mobile payments transaction volume is expected to grow from $60billion this year to $545 billion in 2015. But achieving significant growth in widelydiffering markets will require special measures.

Mobile money: Getting to scale in emerging marketsOnly a handful of mobile-money deployments in emerging markets have managedto reach sustainable scale. McKinsey research with on-the-ground players points tothree keys to success. In a related interview, Michael Joseph talks about his role inthe launch of the highly successful mobile money venture, Kenya’s M-Pesa.

Innovation and the future of credit cardsThe short-term performance and long-term health of the global credit card industryare on divergent paths. The good news is that the industry appears to be reboundingto profitable growth. The longer-term outlook, however, poses greater challenges.

Card processing in Europe: Dead or alive?Core processing for the European card market appears strong by a number ofmeasures, but other indicators suggest the industry model is at risk. Processors facedifficult choices about where to focus their investment and development efforts.

1

3

12

18

28

36

To develop a perspective on how consumerattitudes and usage vary by market, in 2011McKinsey initiated its Global Mobile Pay-ments Consumer Survey. Spanning six lead-ing national markets, the survey explorescurrent and anticipated consumer use ofmobile devices, commerce and payments inseveral categories.

At the broadest level, the research confirmsthat mobile commerce has become a world-wide reality. Roughly two-thirds of respon-dents indicated they purchase mobilecontent and applications, and more thanhalf of this group believe that within threeto five years mobile payments will be widelyavailable at merchants. The study’s findingsalso suggest that growth in mobile com-merce will promote the growth of mobilepayments at brick-and-mortar retailers.The results show as well that the drivers of

consumer behavior differ substantially be-tween developed and emerging markets,and that customers everywhere have con-cerns about the security of their data andpersonal information. Overall, the findingsindicate that issuers, networks, telecommu-nications operators, merchants and otherpayments players need to make their strate-gies more reflective of local market differ-ences, and more relevant to consumers.

Consumers’ responses also show that smart-phone adoption is a major catalyst for bothmobile commerce and mobile payments.Meanwhile, owners of basic and featurephones are increasingly open to using thosemore-limited devices for mobile commerceand payment transactions. In many markets,these non-smartphone users are generatingan increasing flow of mobile purchases andmoney transfers.

3The evolving mobile payments consumer

Dan Ewing

Dan Leberman

James Mendelsohn

James Milner

The evolving mobile paymentsconsumer: Strategic insights fromaround the globe

Mobile commerce and mobile payments are advancing in many international

markets. But, while consumer behaviors and preferences in various markets

share many similarities, there are also important differences. Creating the right

mobile strategy for a market demands an understanding of how consumer

drivers differ and how they are evolving.

Emerging mobile commercethemes

The survey provides insights in three criti-cal areas: current usage, key market drivers,and the outlook for mobile payments. Whilethe findings on both mobile commerce andmobile payments are diverse, several trendsare evident, and the outlook for adoptionand usage is strong (Exhibit 1).

Mobile commerce

Smartphone users across the income spec-trum are actively buying mobile content,purchasing apps and engaging in otherforms of mobile commerce, generating sig-nificant sales volumes (Exhibit 2). Typically,mobile commerce refers to diverse activities

that include product searches, comparisons,purchases and delivery (including down-loading), while mobile payments refers morenarrowly to payment transactions.

Although less popular, point-of-sale (POS)mobile payments and person-to-personmoney transfers are also growing, possiblyspurred in part by growth in mobile com-merce. Increasing consumer familiaritywith both mobile commerce and mobilepayments will likely drive increased use ofmobile payments in brick-and-mortarstores. And growing consumer familiaritywith other types of mobile transactions mayeven become a productive source of lever-age for expanding on-site mobile payments.

4 McKinsey on Payments June 2012

Frequency of mobile payments1

Percent

U.S.

U.K.

Brazil

India

Hong Kong

China

23

19

7

32

13

3

49

8

1

Once a week

Once to several times a day

Do not use mobile payments

18

27

8

26

17

3

45

9

2

15

27

15

30

16

6

32

15

7

30

11

30

13

5

35

15

4

27

12

1222

8

17

20

6

10

32

24

211513

25

10

10

Last year

Last year

This year

This year

Next year Last year This year Next year

Last year This year Next year

Last year This year Next year

Next year

Last year This year Next year

10

8

1 Population-weighted responses; survey results were weighted based on the market penetration of mobile device types.

Source: McKinsey Global Mobile Payments Consumer Survey

Exhibit 1

In all surveyed markets, consumers plan to increase their use of mobile payments

Value propositions

McKinsey research confirms that presentingconsumers with compelling value proposi-tions is a key driver of mobile paymentsadoption, but what consumers considercompelling differs substantially by market.No single approach resonates across allcountries (Exhibit 3, page 6). Two proposi-tion archetypes have emerged to date. Thefirst is rewards-driven. In developed mar-kets, making offers directly to consumers,such as coupons, rewards and related valuepropositions, increases adoption. Consumersin these markets view mobile phones as toolsthat enhance their shopping experience. So,Google Wallet, PayPal, Visa and other play-ers rely on deal and offer strategies in these

markets. In the U.S., for example, offers de-livered via mobile channels were the leadingdriver of consumer interest, with 25 percentof respondents noting they were “very ex-cited” about this feature. The other arche-type is convenience-driven. This is mostvisible in emerging markets where con-sumers are broadly enthusiastic about mo-bile commerce and most excited about valuepropositions that favor convenience andease-of-use, along with rewards. The differ-ence could be due to the level of payments-infrastructure development in emergingmarkets and, in some of the markets, to mo-bile payments enabling consumers to go be-yond bank cards, which have relatively lowpenetration. In all markets, however, con-

5The evolving mobile payments consumer

Mobile paymentactivities

15

4

15

38

4

24

31

6

39 30 9

46

18

15

58

11

20

11 9

46

2

23

39

5

34

35

8

47

26

12

53

18

14

66

7

20

36

39

10

43

41

16

44

30

13

43

31

13

71

27

30

61

26

22

44

37

17

51

39

22

48

39

21

61

27

22

72

29

33

65

27

28 Buy applications

Buy mobile content

Conduct mobile commerce

Perform remote payments

Send personal payments

Transact at point of sale 35

40

10

43

40

10

43

36

10

46

33

10

57

33

17

64

25

24 35

44

35

14

63

33

31

57

34

23

74

34

40

65

32

32

70

30

Smartphone users in category1,2 Percent

U.S. U.K. Brazil India Hong Kong China

FrequentlyOccasionally

1 Only owners of smartphones included in analysis

2 Question: “How frequently have you performed these types of mobile payments (never, rarely, occasionally, frequently)?”

Source: McKinsey Global Mobile Payments Consumer Survey

Exhibit 2

Smartphone respondents show heavy usage of mobile commerce

sumers’ security concerns present the great-est barrier — one that seems likely to growwith scale.

Behavioral change

When consumers use mobile devices to shopin new ways, they disrupt the retail shop-ping paradigm. Today, shoppers can re-search products, compare competitors’prices, and buy goods from online sellers —all while standing in the aisles of brick-and-mortar competitors. Consumers in all sur-veyed markets reported using mobilephones to inform their purchase decisions,both at home and in stores. Product re-search and price comparisons were commonin both locations (Exhibit 4).

Some payments players are already creatingintegrated solutions that merge customers’most preferred shopping-related services. InChina, for example, AliPay is developing aservice suite that will enable shoppers to in-stantly compare prices, search for bargainsand share purchase decisions with friendsand other shoppers. While mobile paymentsis still the least common type of in-storetransaction, strong consumer interest sug-gests that it could become a disruptive forcefor brick-and-mortar retailers. Google andApple already appear committed to findinginnovative POS solutions, and other playersare following suit. By keeping pace with thistrend retailers can constructively influencein-store purchasing, for instance by con-

6 McKinsey on Payments June 2012

Less excited More excited

Key drivers

Pay for anything, anywhere (online, mobile, POS)

Deals and offers sent to me

More convenient way to purchase

Integrated payments and coupons in e-wallet

Integrate payments with other apps (e.g., email, banking)

Leave my wallet at home

38

36

36

34

37

35

20

20

19

16

16

25

18

14

13

13

13

15

35

25

26

26

30

29

32

29

28

26

31

30

8

10

8

7

8

11

Respondents who selected “very excited” as response1

Percent

U.S. U.K. Brazil India Hong Kong China

1 Questions “Thinking about the future bene�ts of mobile payments, what things are most exciting for you (1=not excited, 3=somewhat excited, 5=very excited)?”

Source: McKinsey Global Mobile Payments Consumer Survey

Exhibit 3

The drivers of mobile payments usage vary across countries

tributing to the design and implementationof new search-and-compare shopping tools.

Market segmentation

The survey data shows that while basic mar-ket segments tend to be common amongcountries, segment composition varies signif-icantly. In fact, two critical insights emergedregarding mobile-commerce shoppers.

First, these consumers adopt differentstances toward mobile commerce and mo-bile payments. For example, while youngearly-adopters enjoy exploring new tech-nologies, many other consumers are reluc-tant to take advantage of mobile offerings,believing that they add complications with-out adding corresponding value. Impor-

tantly, between these groups is a broad seg-ment of consumers that is open to mobilepayments wherever there is a convenientand secure infrastructure. Attracting thisgroup will require simple, safe solutionsthat are easy to learn and work seamlesslyacross multiple platforms. This mass-mar-ket segment presents the greatest potentialfor profits.

The second important insight is that marketsegments and drivers appear to be corre-lated. Since the same fundamental segmentswere found in each of the markets surveyed,certain market drivers may also be common.For example, each country has significantearly-adopter and active-resister segments,and members of mass-market segments de-

7The evolving mobile payments consumer

Activity

Less excited More excited

41 42 37 42 50Research products before store visits

44 38 36 40 54In-store, compare prices

37 35 32 35 59Inform purchase decisions using consumer ratings

35 29 27 28 37In-store, research products

27 26 22 20 45Shop directly on my phone at retailer Web sites

25 30 16 29 27Check local store stocks before shopping

21 12 30 23 24“Follow” my favorite stores and merchandisers

16 17 14 25 19Collect rewards from checking in to stores

15 13 22 24 34Seek input on purchase before shopping

9 7 20 19 21In-store, make purchases on my phone

Respondents indicating given activity1

Percent

U.S. U.K. Brazil Hong Kong China

1 Question: “How do you use your mobile device when shopping (select “yes” if you do the following activity)?”

Source: McKinsey Global Mobile Payments Consumer Survey

Exhibit 4

Mobile shopping approaches vary by market

fined themselves as likely to be interested inmobile payments when it becomes available.Mass-market opportunities, therefore, prob-ably exist in most countries.

Consumer outlook

Consumers generally believe that mobile pay-ments will become mainstream within threeto five years. Consumers in emerging marketsexhibit the greatest enthusiasm for itsprospects, whereas those in the U.S., the U.K.and other developed markets have a moresubdued outlook. Developed-market con-sumers nonetheless expect mobile paymentsto grow and to eventually alter how they payfor purchases. Few shoppers in any marketforesee an end of cash transactions, so multi-ple payment forms will likely remain the rule.While there is some potential for loweringtotal checkout costs, actual cost savings willdepend on several factors — such as capitaland operating costs, transaction volume andfraud risk — that affect players across thepayments and financial value chain.

How national markets differ

Generally, consumers in emerging marketsshow high levels of engagement with mobilecommerce and strong positive outlooks to-ward it. Although this may seem counterin-tuitive, developed markets face the greatest

adoption challenges because of their highlyentrenched payments infrastructures. Inthese markets, more consumers say they areunlikely to adopt mobile payments.

Survey highlights by market include the fol-lowing:

• Brazil. Brazilian consumers include thelargest proportion of early adopters, sug-gesting a dynamic marketplace. There isstrong interest in offers delivered via mo-bile channels and in mobile payments ca-pabilities: value and convenience areimportant to both. Brazilians show strongregard for local market players, such as OiPaggo and mopay.

• China. This is the largest pre-paid marketand one in which smartphone usage isgrowing rapidly. Chinese consumers areactive buyers of mobile content, includingmobile commerce and apps. They arehighly optimistic about the future of mo-bile commerce. They are also frequentusers of mobile phones in retail stores,using them to rate products, compareprices and make e-wallet and POS pay-ments. Chinese shoppers expect that re-tailers will offer them the mobilepayments option.

• Hong Kong. Among the countries sur-veyed, Hong Kong reports the highestlevel of mobile payments usage. Surpris-ingly, however, its consumers are also themost skeptical that their market will expe-rience widespread adoption of mobilepayments within the next three to fiveyears. In fact, they are generally less en-thusiastic about mobile payments thanconsumers in most of the other marketssurveyed. Hong Kong may therefore be a

8 McKinsey on Payments June 2012

Consumers in emerging marketsexhibit the greatest enthusiasm

for mobile payments, whereas those in the U.S., the U.K. and other

developed markets have a moresubdued outlook.

more challenging market to penetrateprofitably, unless players find ways to turnconsumer interest around.

• India. Of the markets surveyed, India hasmore owners of non-smartphones thanany other, yet it is also the most optimisticregarding mobile payments adoption.Consumers appear strongly biased towardmobile commerce. The ability to “leave mywallet at home” is a powerful consumerincentive. India’s market leaders include ablend of global players and such localleaders as mChek and Paymate.

• U.K. Usage and outlook dynamics in theU.K. are similar to those observed in theU.S.: consumers’ primary interest is in thevalue of related offers. Of the six countriessurveyed, British consumers exhibit theleast enthusiasm for mobile payments,

which may stem from their heightenedconcerns about data security and privacy.However, given a widely deployed infra-structure many British consumers remainopen to mobile payments. A focus on ac-ceptance infrastructure will therefore bekey to overcoming consumer barriers.

• U.S. The U.S. is the largest post-paidsmartphone market in which digital offersdrive adoption. A broad and diverse mar-ket, it nonetheless has a significant num-ber of consumers who expressindifference to mobile commerce becausethey see it as being of limited value (Ex-hibit 5). The data nonetheless show thatshoppers here are indeed using their mo-bile phones for commerce, but whenasked about usage they tend to think onlyof POS payments. In any case, U.S. con-

9The evolving mobile payments consumer

50 40 30 20 10 30

35

40

45

0

Resistant

Completely indifferent

Skeptical

Open

Selective

Early adopter

Relative share of respondents

N=1000 survey respondents

Average ageYears

Estimated number of purchasesPurchases/Year

Source: McKinsey Global Mobile Payments Consumer Survey

Exhibit 5

In the U.S., segment affiliation correlates significantly with number ofpurchases and level of engagement

Consumer self-identified segments

“I’m an early adopter. I enjoy trying new things with my mobile phone and payments is a big part of that.”

“I’m selective. If mobile payments delivers value to me I’ll embrace it.”

“I’m open. If my phone has it and merchants accept it then I’ll give it a try.”

“I’m skeptical. This is still new and I think there are risks in making the transition.”

“I’m indifferent. My current bank cards work fine. Mobile payments doesn’t help me.”

“I’m resistant. I like the way I pay today and don’t want to change anything.”

sumers generally expect that mobile pay-ments will be widely available in three tofive years. Given this market’s size, is-suers, network operators and other play-ers should focus on motivating earlyadopters while developing strategies forsubsequent broad marketing efforts onceadoption rates accelerate.

Strategic implications

In light of current consumer sentiments,there are several strategic actions that willbe vital for mobile payments success. Aboveall, rapid change and broad global diversitymean that participants will need to carefullycalibrate their marketing strategies. Keyconsiderations should include the following:

• Value propositions. Tailor consumervalue propositions to local market charac-teristics. In the U.S. and U.K., for exam-ple, offer compelling deal and rewardprograms; in emerging markets, focus onspeed and convenience. In all markets,participation should be easy and conven-ient. Brand positioning should flexibleand tailored to local market needs, evenwhen underlying offers are similar.

• Security and privacy. In all markets, in-vest sufficiently in transaction and iden-tity security, to minimize both fraud andconsumer anxiety.

• Payment forms. Offer multiple paymentoptions. PayPal, for example, is developingmobile-phone-number and card-based so-lutions that will enable POS terminals tohandle alternative payment forms.

• Partnerships. Strategic alliances will becritical, as few players have the widerange of capabilities that mobile com-merce and payments demand. From mar-keting to security, success will requirecreating bundled consumer offers – achallenging task in markets where players’capabilities vary greatly.

• Merchant acceptance. Gaining broadmerchant acceptance will be crucial tothe growth of mobile payments. New en-trants may look to leverage existing dis-tribution channels (e.g., acquirers,independent sales organizations) to growquickly. Speed of adoption is a focus asplayers seek to reach a tipping pointwhere broad acceptance drives customer

10 McKinsey on Payments June 2012

The McKinsey Global Mobile Payments Consumer Survey

In December 2011, McKinsey surveyed members of an online consumer research panel to better

understand current usage of mobile commerce services and the likely drivers of adoption. The

research spanned six major markets – U.S., U.K., Hong Kong, China, India and Brazil – and included

500 to 1,000 consumers from each market who access financial services via their mobile devices.

The results were not adjusted to reflect the general population of the respective markets, and the

responses therefore specifically reflect the views of these consumers. McKinsey will update the survey

every few months. Other countries may be included in future surveys.

For more information about the survey please contact Dan Ewing ([email protected]) or James Mendelsohn ([email protected]).

interest. But rushing is risky: Consumerengagement with any end-state model ofmobile commerce and payments is con-tingent on both the ubiquity and ease-of-use of POS networks.

* * *

The Global Mobile Payments Consumer Sur-vey underscores an important point: stan-dardized approaches rarely succeed in thedevelopment of global capabilities. Whilemarkets frequently exhibit common traits,global success in mobile payments will de-mand close attention to local differences in

established infrastructure, consumer behav-ior patterns, market trends and in regulatoryand competitive environments. Players mustalso take considerable care in selecting part-ners with the commitment and capabilitiesto create and sustain broad mobile paymentsnetworks. While time-to-market is impor-tant, so too is building a solid foundationthat can efficiently and effectively scale upover the years to come.

Dan Ewing is an associate principal, Dan Leberman

is a consultant and James Milner is an associate, all

based in McKinsey’s San Francisco office. James

Mendelsohn is an associate principal in the

Washington, D.C. office.

11The evolving mobile payments consumer

March 2013Number 16

McKinsey on Payments

Foreword

Forging a path to payments digitizationThe social cost of cash is high wherever it predominates. Moving to a digital paymentsmarket can stimulate economic growth and facilitate financial transparency.

The role of data analytics companies in mobile commerceData-rich companies—including banks and retailers—can use their assets to addvalue and secure their competitive position in the new digital order.

Disruption brings opportunity in merchant paymentsAs the payments environment evolves, financial institutions and merchants will havemany options for collaborating on approaches that create real value.

The battle for the point of salePayments service providers are offering an array of products that are reinventing thepoint-of-sale experience.

Driving merchant services and digital commerce: Findings fromMcKinsey’s 2012 U.S. Small Business Acquiring PanelSmall merchants not only account for the largest portion of merchant acquiring, theyalso play a major role in the current trend toward digital payments.

Payments regulation: A catalyst for innovationPayments regulators are beginning to recognize their role in attaining a balancebetween protection and growth.

The U.S. payments industry at a glance

1

3

10

17

24

30

38

46

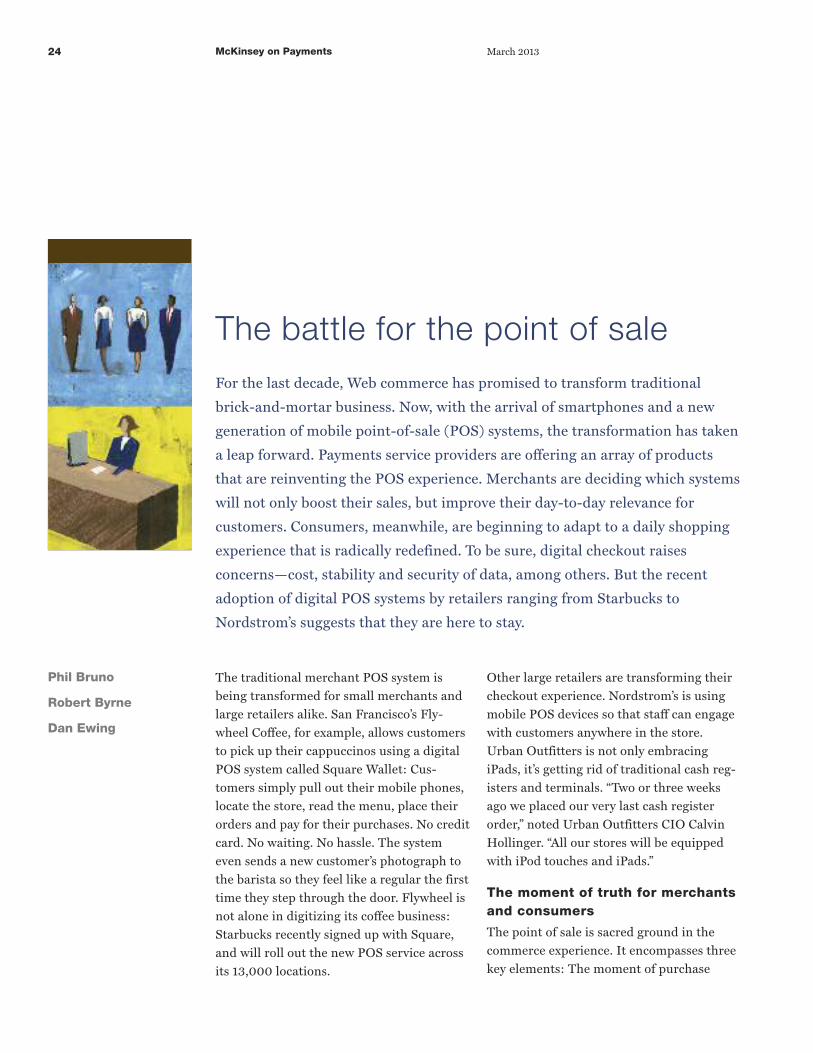

24 McKinsey on Payments March 2013

The traditional merchant POS system isbeing transformed for small merchants andlarge retailers alike. San Francisco’s Fly-wheel Coffee, for example, allows customersto pick up their cappuccinos using a digitalPOS system called Square Wallet: Cus-tomers simply pull out their mobile phones,locate the store, read the menu, place theirorders and pay for their purchases. No creditcard. No waiting. No hassle. The systemeven sends a new customer’s photograph tothe barista so they feel like a regular the firsttime they step through the door. Flywheel isnot alone in digitizing its coffee business:Starbucks recently signed up with Square,and will roll out the new POS service acrossits 13,000 locations.

Other large retailers are transforming theircheckout experience. Nordstrom’s is usingmobile POS devices so that staff can engagewith customers anywhere in the store.Urban Outfitters is not only embracingiPads, it’s getting rid of traditional cash reg-isters and terminals. “Two or three weeksago we placed our very last cash registerorder,” noted Urban Outfitters CIO CalvinHollinger. “All our stores will be equippedwith iPod touches and iPads.”

The moment of truth for merchantsand consumers

The point of sale is sacred ground in thecommerce experience. It encompasses threekey elements: The moment of purchase

The battle for the point of saleFor the last decade, Web commerce has promised to transform traditional

brick-and-mortar business. Now, with the arrival of smartphones and a new

generation of mobile point-of-sale (POS) systems, the transformation has taken

a leap forward. Payments service providers are offering an array of products

that are reinventing the POS experience. Merchants are deciding which systems

will not only boost their sales, but improve their day-to-day relevance for

customers. Consumers, meanwhile, are beginning to adapt to a daily shopping

experience that is radically redefined. To be sure, digital checkout raises

concerns—cost, stability and security of data, among others. But the recent

adoption of digital POS systems by retailers ranging from Starbucks to

Nordstrom’s suggests that they are here to stay.

Phil Bruno

Robert Byrne

Dan Ewing

(time); the transaction between merchantand consumer (relationship); and the equip-ment that facilitates and completes thetransaction (the device). The critical shiftnow is in the technology of the device—which in turn changes the purchase experi-ence for the consumer and the merchant.

Two major trends are reshaping the POS.First, the systems themselves are being radi-cally redefined by new technology, openplatforms and cloud computing. Second, awave of commerce innovators are battling toget access to these systems. Together, thesetwo trends are transforming the traditionalcheckout experience.

Trend 1: Transforming the POS

Until recently, most POS systems were de-signed to have tightly focused functionalityand a high degree of dependability (Exhibit1). The market was led by equipment makersincluding VeriFone and Ingenico (makers ofcard swiping devices); software systemproviders like Micros (which makes inte-grated systems for restaurants, hotels, etc.);and payments processors like First Data(whose systems make credit and debit pay-ments swift and secure). It was a tightlymanaged ecosystem, with a few “gatekeeper”players controlling POS access—much likethe telecom industry before the iPhone.

25The battle for the point of sale

POS system – software & hardware diagram

Hardware (e.g. VeriFone, Ingenico)

Terminal OS (e.g. Windows Compact, Windows POSReady, Linux)

Point of sale software solution (e.g. JPMA, Microsoft Dynamics)

Presentation to the cashier on the cash register screen

Data presentation to back end systems/servers

Presentation to the consumer on the POS terminal

Terminal provider applications

(e.g., encryption, receipt printing, register interface)

Merchant acquirer applications

(e.g., trxn routing, chargeback management)

Back-office applications

(e.g., inventory management pricing, supply)

Specialized software solutions

(e.g. restaurant tables and kitchen management)

Third party applications

(e.g., bill payment prepaid card activation/reload)

IngenicoVeriFoneSZZT and others

First DataVantivGlobal Payments and others

Retail PlusAccuPOSMerchantOSand others

AlohaSquirrelSableand others

InCommBlackHawkNetspendand others

Internet and internal network

Other POS devices

Source: McKinsey analysis

Exhibit 1

Service providers that have point-of-sale real estate have a head start in introducing new services

26 McKinsey on Payments March 2013

If that closed system was POS 1.0, open,cloud-based platforms are now leading thetransition to POS 2.0. These open plat-forms not only allow integration across de-vices and channels (e.g., enabling on- andoffline commerce), but give POS entrepre-neurs the ability to develop new servicesthat tie into the merchant’s existing pay-ments, marketing and back-office account-ing systems. As Leonard Speiser,co-founder of POS start-up Clover noted,“The moment you open a system up, youenable new innovations and get productsright to your customers.”

Now that smartphones and tablets are pow-erful enough to serve as POS platforms, the“sacred” POS commerce experience is po-

tentially open to anyone seeking to reinventthe merchant-customer interaction.“[We’re] concerned with design,” JackDorsey, the founder and CEO of Square, re-marked recently, pointing to a photo of theGolden Gate Bridge and using it as a refer-ence to the merchant payments experience.“This is what I want to build. This is classy.This is inspiring. This is limitless. Everysingle aspect of this is gorgeous.”

The playing field has been leveled so thatnew entrants, be they Clover or ShopKeepPOS (another tablet-based system), can cre-ate new, open platforms that allow develop-ers to build new services. Notably, newentrants may have the ability to drive downprices in this arena, in service of adjacent

Read-only NFCPhone or sticker touch at POS to send customer payment information One tag always transmits the same message

Read-write NFCPhone or smart-card touch at POS to send customer information and receive merchant information/offers

QR-codeCustomer generates or receives QR-code on phone and scans phone into QR readerCode may contain different information each time

mPOSMerchant’s phone or tablet (with additional peripherals) swipes customer’s card or reads through direct NFC or Bluetooth

Apps in terminalTerminal software upgrade allows customer to pay at a terminal using a unique identifier (e.g., phone number + PIN)

In-person e-commerceMerchant recognizes customer (with geo-locating), and merchant completes transaction “in the cloud” while authentication and inventory-check occur in person

SMSAny two phones with SMS send value directly to each other

Self-checkoutCustomer “scans” items themselves throughout location, and completes transaction on phone “in the cloud”

Source: McKinsey Payments Practice; expert interviews

Exhibit 2

Transaction models for mobile payments at the POS

revenues from other business. Established

leaders like First Data and VeriFone are re-

sponding with enhanced, app-driven strate-

gies for their own devices. The new world of

POS is open to any number of players.

Trend 2: New payments servicescompeting for limited access

While the POS is being transformed, an

array of new payments solutions and appli-

cations are also competing for access to mer-

chant terminals (Exhibit 2). Google Wallet

has been advancing NFC-based payments.

PayPal is leveraging its software applications

on existing terminals to connect to the Inter-

net. Apple is pioneering self-checkout op-

tions with EasyPay and open-store formats.

Looking beyond payments, new entrants

such as CardSpring (a platform that allows

card-linked loyalty apps); POS LAVU (pro-

viding payments and management apps for

restaurants); and LevelUp (acquisition and

loyalty programs) are reinventing mer-

chant rewards programs linked to check-

out. Considering that mobile devices are

proliferating and that writing a mobile

phone app takes a couple of smart entre-

preneurs and very little money, it is easy to

see why the POS 2.0 industry is bursting

with possibilities.

Success is not easy, however. To achieve

mass usage, digital payments entrepreneurs

must win over both the consumer and the

27The battle for the point of sale

Would you consider using an alternative POS system?Percentage respondents

No“My current system works fine”“It needs to integrate into my other systems”“They are not durable enough”“iPads are too expensive…easy to steal”

Yes“If it is simple and saves me money, sure”“Better display and interface”“If it saves me money”“Becoming more popular and would be easier to update in the future.”

“Seems like it would be simple and save space on the counter”

Already use it“Works with our software”“Ease of use, simple setup, maintenance free, easily replaced, takes up very little space on the counter”

Smartphone POS Tablet POS

63

34

60

47

50

100100

Source: McKinsey Small Business Panel – June 2012

Exhibit 3

Small businesses are largely open to alternative POS systems

28 McKinsey on Payments March 2013

merchant. Thus far, none of the players—

merchant acquirers, device manufacturers or

software providers—have a lock.

The merchant perspective

Merchants have particular concerns aboutPOS 2.0. Security and stability are para-mount. They don’t want to invest in fly-by-night POS schemes that may not be aroundin a few months. Also, they need partners

who can help them scale their solutions.POS applications must be appropriate forthe merchant. For instance, retailers likeNordstrom’s, Sears and Macy’s—those withcheckouts distributed throughout the storesand a consultative sales approach—want amulti-device strategy, with both traditionalregisters and iPad-equipped POS. Smallerretailers, with a single location, may preferlighter, more flexible POS solutions. Thenthere are food trucks, taxis and other mobilebusinesses, with different needs. Still otherstores, such as high-volume, multi-lane re-tailers, may require another approach.

Regardless of the complexities, merchantsare intrigued. According to McKinsey’sSmall Business Acquiring Panel, roughlyhalf of small businesses are willing to con-sider alternate POS models if the particularmodel delivers value (see Exhibit 3, page 27

and “Driving merchant services and digitalcommerce,” page 30).

Competitive implications

The merchant POS system, therefore, is thenarrow gateway that must be unlocked to ac-cess to the consumer’s “moment-of-truth.”Here are a few of the considerations:

• Secure merchant trust: Merchants don’twant to turn their POS into a test lab forevery start-up with a new payments solu-tion. They have to balance experimenta-tion with running their day-to-daybusiness. As a result, they are selectingpartners carefully.

• Ensure integration: Offering successfulapplications will hinge on the deploymentmodels for merchants. Integrating appli-cations into a seamless solution is com-plex and will be a critical differentiator.

• Build scale and momentum: The mer-chant landscape is highly fragmented andpopulated with legacy systems. So con-verting a critical mass of businesses is ex-tremely challenging. Players should lookfor merchant partners or niches to gaintraction and scale

• Evaluate partnerships: Due to the scalingchallenges, many players will look tostrategic partnerships to drive adoption.For example, Heartland Payments hasteamed up with LevelUp to bring newcheckout options to merchants; PayPal isworking with large companies (VeriFone)and small players (ShopKeep POS). Fur-ther alliances are expected.

* * *

Who will rise to the top in merchant POS?No one has fully broken out of the pack, and

Merchants don’t want to turn their POS into a test lab

for every start-up with a new payments solution. They have to

balance experimentation with runningtheir day-to-day business.

even if one does, a major system failure, asecurity breach or just customer confusioncould derail the leader. POS 2.0, after all, isa platform. Whichever system climbs to thetop will subsequently affect terminal manu-facturers, software providers, business solu-tion providers, marketing companies, retaillogistics providers and everyone else. And

whatever the outcome, one thing is clear:Tomorrow’s shopping experience will lookvery different from today’s.

Phil Bruno is a principal in the New York office.

Robert Byrne is a principal, and Dan Ewing is a

senior expert, both in the San Francisco office.

29The battle for the point of sale

June 2012Number 14

McKinsey on Payments

Foreword

The evolving mobile payments consumer: Strategic insights fromaround the globeAs mobile commerce and mobile payments gain footholds around the globe, a newMcKinsey survey identifies emerging themes and important differences betweenmarkets.

Pathways to growth in mobile paymentsWorldwide mobile payments transaction volume is expected to grow from $60billion this year to $545 billion in 2015. But achieving significant growth in widelydiffering markets will require special measures.

Mobile money: Getting to scale in emerging marketsOnly a handful of mobile-money deployments in emerging markets have managedto reach sustainable scale. McKinsey research with on-the-ground players points tothree keys to success. In a related interview, Michael Joseph talks about his role inthe launch of the highly successful mobile money venture, Kenya’s M-Pesa.

Innovation and the future of credit cardsThe short-term performance and long-term health of the global credit card industryare on divergent paths. The good news is that the industry appears to be reboundingto profitable growth. The longer-term outlook, however, poses greater challenges.

Card processing in Europe: Dead or alive?Core processing for the European card market appears strong by a number ofmeasures, but other indicators suggest the industry model is at risk. Processors facedifficult choices about where to focus their investment and development efforts.

1

3

12

18

28

36

Structural changes that will impact creditcard profitability and the business model,especially in the U.S. and Europe, includeconservative lending policies, tighter regula-tory controls on products, and higher capitalrequirements.

The biggest challenge is in the customer re-lationship itself. New entrants and substi-tute products, both in-store and online, areoffering more features and flexibility thantraditional credit cards – and at lower cost.Transactions are already starting to move tothese new types of payments, raising thethreat that traditional players will lose di-rect contact with their customers, as portalsand apps take the place of cards and state-ments. Issuers must innovate to stay rele-vant to the consumer and avoid becoming abackground utility.

There is a great risk that traditional creditcard issuers will act too late to address thesechallenges. This article describes the four

major catalysts that are likely to redefine theglobal credit card industry over the next fiveyears, then presents a set of imperatives thatissuers must act on to thrive in the trans-formed credit landscape.

Catalysts

If the credit card industry is to continue togrow, it must respond to four catalysts: therenewed importance of lending, the rise ofthe interactive shopping experience, thepower of big data, and the need for betterand more flexible infrastructure.

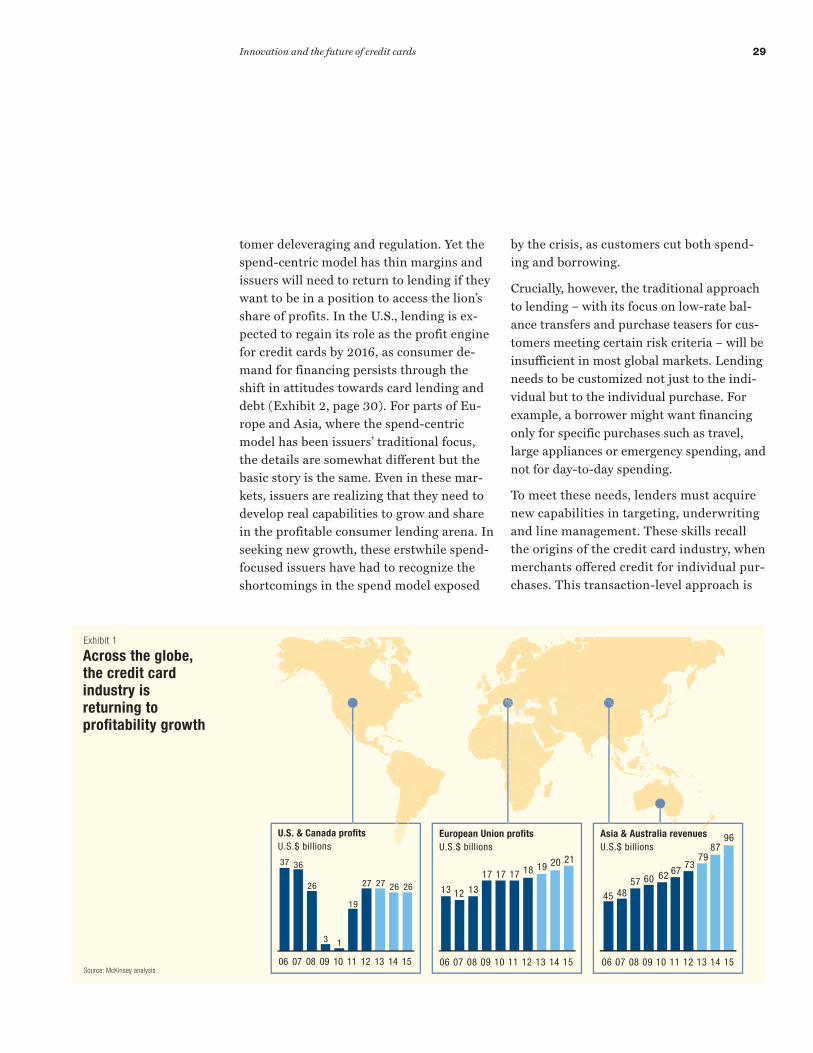

The renewed importance of lending

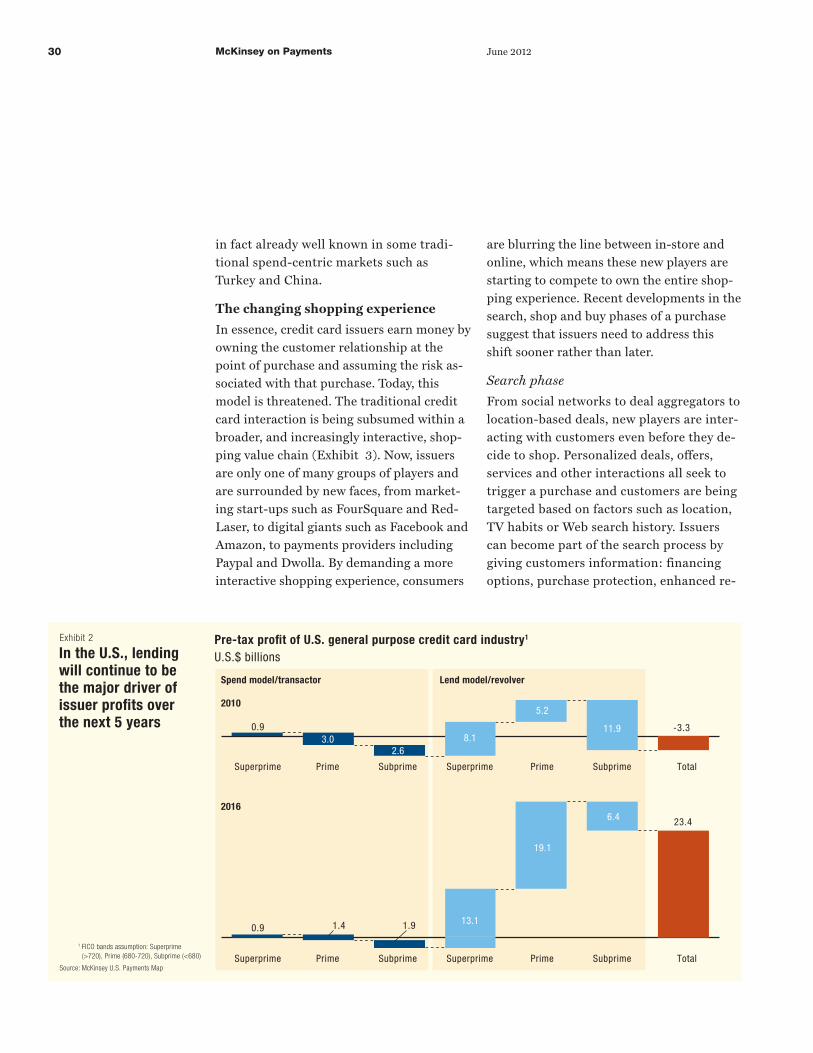

In recent years, common wisdom has heldthat a spend-centric business model is nec-essary for success. Obviously, many issuerssaw their lending business model fallthrough the floor during the crisis. Butspend-centric advocates believe that lendingeconomics will remain problematic due toan uncertain economic environment, cus-

28 McKinsey on Payments June 2012

Innovation and the future of credit cardsThe short-term performance and long-term health of the global credit card

industry are on divergent paths. The good news is that the industry appears to

be rebounding to profitable growth in major markets driven by a return to

spending and financing by customers (Exhibit 1). The outlook, however, is not

perfectly rosy. Several threats and challenges face the industry that may affect

issuers’ long-term profitability unless action is taken now.

Philip Bruno

JJ Kasper

Maria Martinez

Robert Mau

tomer deleveraging and regulation. Yet thespend-centric model has thin margins andissuers will need to return to lending if theywant to be in a position to access the lion’sshare of profits. In the U.S., lending is ex-pected to regain its role as the profit enginefor credit cards by 2016, as consumer de-mand for financing persists through theshift in attitudes towards card lending anddebt (Exhibit 2, page 30). For parts of Eu-rope and Asia, where the spend-centricmodel has been issuers’ traditional focus,the details are somewhat different but thebasic story is the same. Even in these mar-kets, issuers are realizing that they need todevelop real capabilities to grow and sharein the profitable consumer lending arena. Inseeking new growth, these erstwhile spend-focused issuers have had to recognize theshortcomings in the spend model exposed

by the crisis, as customers cut both spend-ing and borrowing.

Crucially, however, the traditional approachto lending – with its focus on low-rate bal-ance transfers and purchase teasers for cus-tomers meeting certain risk criteria – will beinsufficient in most global markets. Lendingneeds to be customized not just to the indi-vidual but to the individual purchase. Forexample, a borrower might want financingonly for specific purchases such as travel,large appliances or emergency spending, andnot for day-to-day spending.

To meet these needs, lenders must acquirenew capabilities in targeting, underwritingand line management. These skills recallthe origins of the credit card industry, whenmerchants offered credit for individual pur-chases. This transaction-level approach is

29Innovation and the future of credit cards

U.S. & Canada pro�tsU.S.$ billions

13 06 07 14 08 09 10 11 15 12

27

37 36

2626

3 1

19

2627

European Union pro�tsU.S.$ billions

13 06 07 14 08 09 10 11 15 12

19

13 12

20

13

17 17 17

2118

Asia & Australia revenuesU.S.$ billions

13 06 07 14 08 09 10 11 15 12

79

45 48

87

57 60 62 67

96

73

Source: McKinsey analysis

Exhibit 1

Across the globe, the credit card industry is returning to pro�tability growth

in fact already well known in some tradi-tional spend-centric markets such asTurkey and China.

The changing shopping experience

In essence, credit card issuers earn money byowning the customer relationship at thepoint of purchase and assuming the risk as-sociated with that purchase. Today, thismodel is threatened. The traditional creditcard interaction is being subsumed within abroader, and increasingly interactive, shop-ping value chain (Exhibit 3). Now, issuersare only one of many groups of players andare surrounded by new faces, from market-ing start-ups such as FourSquare and Red-Laser, to digital giants such as Facebook andAmazon, to payments providers includingPaypal and Dwolla. By demanding a moreinteractive shopping experience, consumers

are blurring the line between in-store andonline, which means these new players arestarting to compete to own the entire shop-ping experience. Recent developments in thesearch, shop and buy phases of a purchasesuggest that issuers need to address thisshift sooner rather than later.

Search phase

From social networks to deal aggregators tolocation-based deals, new players are inter-acting with customers even before they de-cide to shop. Personalized deals, offers,services and other interactions all seek totrigger a purchase and customers are beingtargeted based on factors such as location,TV habits or Web search history. Issuerscan become part of the search process bygiving customers information: financingoptions, purchase protection, enhanced re-

30 McKinsey on Payments June 2012

Spend model/transactor Lend model/revolver

8.1 0.9

0.9

3.0 2.6

5.2

11.9 -3.3

23.4

1.4 13.1 1.9

6.4

19.1

Pre-tax pro!t of U.S. general purpose credit card industry1

U.S.$ billions

Superprime Prime TotalSubprime Superprime

2010

2016

Prime Subprime

Superprime Prime TotalSubprime Superprime Prime Subprime 1 FICO bands assumption: Superprime

(>720), Prime (680-720), Subprime (<680)

Source: McKinsey U.S. Payments Map

Exhibit 2

In the U.S., lending will continue to be the major driver of issuer pro!ts over the next 5 years

ward offers and other purchase-specific de-tails that are critically important whileshopping but have not been typically avail-able until after a purchase.

Shop phase Lines are already blurring between onlineand physical shopping. PayPal sees a futurewhere shoppers browse the aisles with asmartphone and shop physically and elec-tronically at the same time. Best Buy alreadyencourages in-store smartphone research,and provides kiosks where customers cancomplete an order and arrange for delivery.

For issuers, this is a fight over mind share. Ifa merchant or online service owns all otheraspects of the shopping experience it couldalso own the checkout and payment process.Issuers need to be relevant in their cus-tomers’ shopping journey and offer features

and services that bring the card to top ofmind at the right moment. They might in-clude warranty offers, service plans, pricematch guarantees or special offers from mer-chant partners. Imagine buying a TV andthe card issuer instantly sends you a dis-count coupon for a new couch, directions tothe nearby furniture store and even offers toredeem your rewards for three months of anonline movie service (Exhibit 4, page 32).

Buy phase

Even at the buy phase, where card issuershave dominated, new players are attemptingto plant a flag. TabbedOut is a smartphoneapp that lets users enter their payment in-formation and open a tab at a partnerrestaurant. They can then pay, include a tipand leave without waiting for the server tobring a bill or having to swipe a card, be-

31Innovation and the future of credit cards

Search Shop Buy

Revenues at stake (U.S. example)U.S.$ billions

NetworkIssuer Acquirer

$

$10$5$100

$250

Generate demand

Find local merchant

Compare local merchants

Contact/arrive at store

Decide on purchase

PayShopping value chain

New players

Traditional credit card value chain

Value-added services leveraging digital info to aid merchants (e.g., marketing)

Integration with the consumer’s “search, shop, buy” experience

Source: McKinsey U.S. Payments Map

Exhibit 3

The traditional value chain in which issuers have played is only one piece of a broader shopping value chain for consumers and merchants

cause the stored payment information isshared with the merchant. This new technol-ogy cuts out the terminal, network and po-tentially also the card. Issuers must findways to keep pace with third-party innova-tion and should start by developing dynamiccredit offers at the point of sale, transaction-level financing for specific purchases andflexible payment options.

Big Data allows real-time interactionwith customers

The credit card industry is focusing on howBig Data can drive more granular ap-proaches to the existing business model andimprove targeting, underwriting and seg-mentation. (See “The impact of big data onpayments,” McKinsey on Payments, March2012.) There is another element just as im-

portant for issuers: Big Data enables real-time interaction between issuers and cus-tomers — a key ingredient of the shoppingexperience outlined above and a source ofdifferentiation in credit decision-makingaround line assignment and pricing.

The need for flexible systems

The last major catalyst for change will be theactions of issuers themselves as they seek toovercome the limitations of their own sys-tems. Most issuers’ systems and infrastructureare unsuitable for engaging with consumers ina digitally enabled shopping experience. Inthe depths of the financial crisis, saving thefranchise took priority over meeting the needfor systemic change. Now, however, issuerscannot compete against the alternatives with-out modifying their current systems.

32 McKinsey on Payments June 2012

20% off

CAMERAS

2011

30

2012

60

2013

110

2014

245

Inside store

Interactive product info

Interactive offers

Customer service/sales

In-aisle checkout Digital signage

Offers Analytics

Outside store

Offers based on browsing patterns

At-hand product information

Self-scan and pay in-aisle

Geo-located personalized support

Shelf labeling product information

Offers pushed to customers

Sophisticated targeting of customers

Source: McKinsey analysis

Exhibit 4

A new interactive shopping experience is now emerging

Consider that most issuers take nine monthsto a year to launch a simple new productwhereas it takes just one or two months todevelop an app. New systems need to enablereal-time interaction with customers, rapidproduct development, true integration intothe shopping value chain, and expansionacross channels. We see a wave of systemsdevelopment coming, with successful issuersacting early, before the wave breaks.

Imperatives

The catalysts detailed above are alreadychanging the competitive landscape forcredit cards. To prepare, traditional card is-suers must make definitive strategic choicesand commitments.

1. Embrace and stick to a businessmodel

To maximize the opportunities created by thischanging marketplace, issuers will need to se-lect the right business model. The imperativeto act is there and, with the move to lendingand profits, so is the income to reinvest. Fourgeneral business models can be identified forissuers around the globe. Issuers will need toanchor their approach by adopting one ofthese models, even when particular strategiesmight cut across the models.

The bank relationship play

This model is common in Europe and tosome extent in Latin America, but is seen far

less in the U.S. or Asia. Customers choosethe credit card because it is fully integratedinto an overall banking relationship, withbenefits that outweigh the benefits of havinga card from another provider. These cus-tomers typically enjoy an integrated view offinances and reporting, better pricing, extrarewards, easier payment choices and moreflexible credit terms. Some U.S. issuers havealready made moves in this direction: PNC’sCashbuilder product, for example, increasesthe reward if the customer has a currenthigher-spending checking account. Underthis model, the overall customer relationshipcan be far more rewarding for the customerand profitable for the bank when comparedwith a less integrated approach.

The economies of skill play

Scale can sometimes be a burden for largeissuers. New regulations, such as Dodd-Frank in the U.S., impose greater constraintson larger issuers. More pertinently, many is-suers have found that scale has introducedonly greater complexity and costs: more cus-tomer segments, products, systems andchannels. Issuers should use “bulk” to gener-ate economies of skill not scale. They mustfind ways to develop centers of competencyand capabilities that are truly distinctive.Multinational card issuers may have an ad-vantage in creating skill centers for analyt-ics, systems development and partneringcapabilities that can be used across regions,while still allowing for locally tailored solu-tions. Issuers will need to work morequickly, intelligently and effectively thancompetitors in terms of marketing, risk andservice. Meanwhile, centers of excellenceacross major functions can drive the wide-spread use of advanced capabilities, such asthose required by Big Data.

33Innovation and the future of credit cards

Customers choose the credit cardbecause it is fully integrated into an

overall banking relationship, withbenefits that outweigh the benefits of

having a card from someone else.

The partnership play

In this model, issuers seek out new partnersamong digital and physical retailers, mar-keting technology companies and social net-working players. The partner relationshipwill not be characterized by the typical co-branded arrangement. Rather, new partner-ships will be deeply connected and requirenew ways of thinking about profit sharing,loyalty program interactions, and coordi-nated and integrated marketing systems andservices. Issuers need to start thinkingstrategically about the partnerships neces-sary for success and begin to develop apipeline of high-potential partnership op-portunities.

The “card in the cloud” play

Banks have yet to fully exploit the power of“digital.” (See “The future of payments:Markers for success,” McKinsey on Pay-ments, June 2011.) This shortcoming is be-coming more glaring as the online world

goes ever more mobile. The fully digitalmodel captures the benefits of cost reduc-tion that accrue from eliminating bricks,mortar and paper, while engaging the cus-tomer in ways highly beneficial to the issuer.The digital model gives the issuer a dispro-portionate share of wallet, and puts it frontof mind when customers look for new serv-ices. The most concrete example of this isPayPal’s recent venture with Home Depot inthe U.S. to bring online transactions to thephysical store. Watch for online giants suchas Google and Facebook to drive further in-novation in this space.

2. Embrace infrastructure and systemschange as a competitive differentiator

Issuers need to begin what is likely to be amultiyear journey to upgrade systems and in-frastructure. Getting started requires under-standing what platforms can be integratedinto existing business processes while stillmeeting tomorrow’s needs. Issuers should

34 McKinsey on Payments June 2012

New players looking to expand into payments can leverage an existing bank’s licensing and infrastructure instead of building it from scratch

1. Licensing

Integrating with a bank’s online and mobile services would provide a seamless interface enabling payments in addition to any services players are already offering

2. Consumer interface

Some companies may need physical outlets for deposits, payments and redemptions – traditional issuers can supply these

3. Access to funds

New players may soon need a co-brand, prepaid and virtual debit card4. Traditional Products

There are a number of functions that traditional players can do better than emerging players: fraud detection, card ful!llment, customer service, dispute resolution and other back-of!ce functions

5. Infrastructure

Source: McKinsey analysis

Exhibit 5

There are a number of ways an emerging player can partner with an issuer in the broader shopping value chain

have two goals in mind: first, more flexibilityto set up and manage products, channels andcustomer interactions; and second, a data ar-chitecture that allows for flexible real-timeanalytics. Issuers could choose to stick withtraditional data structures but may benefitfrom new approaches to data managementsuch as Apache Hadoop to lower costs andincrease flexibility.

Issuers will also need to begin thinking morestrategically about their HR and talent strat-egy. A shift has already been observed in theprofiles being sought by issuers in the jobmarket, with a move towards talent withdeep retail experience, digital marketing ex-pertise from other consumer industries andadvanced analytics capabilities.

3. Embrace Big Data

Finally, tomorrow’s winners will be thosewho can collect, store and process huge vol-umes of data. For example, an issuer mayfind that just the mention of the words “in-terest rate” on a service call is predictive of amove to a competitor in the next 12 months.They may want to mine all their calls andmake selective proactive counteroffers. How

many issuers have the capability to watchand process non-card data sources or areprepared to permanently store recordings ofall customer calls? Issuers have a lot to learnin this area and need to build partnershipsand alliances quickly with emerging playersto jump-start their progress (Exhibit 5).

* * *

The challenges facing the credit card indus-try are formidable but they also present is-suers with an opportunity to re-inventthemselves and enjoy a strong future. De-spite the new entrants in the paymentsecosystem, traditional card issuers still oc-cupy the envied “pole position”: they stilldominate the buying experience and owncustomer relationships around the world.This industry has thrived in the past thanksto innovation; once again, innovation is theway to a secure future.

Philip Bruno is an expert principal, JJ Kasper

is an associate principal and Robert Mau

is a Payments Practice knowledge expert, all in

McKinsey’s New York office. Maria Martinez is a

principal in the Madrid office.

35Innovation and the future of credit cards