fraud+and+auditevidence (1).ppt

TRANSCRIPT

5-1

Chapter 5

Audit Evidence and the Auditor’s Responsibility for Fraud Detection

5-2

Audit Evidence and its Role in the Audit Process

Auditing Standards require the auditor to obtain sufficient appropriate evidence sufficient appropriate evidence to reach a conclusion about whether the financial statements have been prepared in accordance with the applicable financial reporting framework– Process relies on professional judgment of auditor– Evidence provides the basis for the audit opinion

issued– Auditor must be familiar with documentation

requirements of the auditing standards

5-3

Evaluating the Sufficiency and Appropriateness of Evidence

SufficiencySufficiency of audit evidence is a measure of the quantity of evidence needed

AppropriatenessAppropriateness is a measure of the quality of audit evidence needed. Quality is measured by:– Relevance – related to the connection between the

audit procedure’s purpose and the evidence; it is often related to the assertion being tested

– Reliability - related to its source and nature and the circumstances under which it is obtained

5-4

What are the components of good judgment?

Logical Flexible Unbiased Consistent and reliable Appropriately balances experience with knowledge,

intuition, and emotion Uses the right amount of relevant information, including

professional literature and evidence

4

5-5

Environmental factors affecting judgment

– External Factors: Time pressure Limited resources Client, regulatory,

industry

5

– Internal Factors: Judgment traps

– Rush to solve– Judgment triggers

Judgment shortcuts Bias caused by self -

interest

© 2010 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The KPMG Professional Judgment Framework

6

5-7

Documentation Requirements for Audit Evidence

Working papers Working papers or work papers work papers include a record of the audit procedures performed, audit evidence obtained and conclusions reached by the auditor.

Audit documentationAudit documentation, which is the auditor’s property, should be retained for at least seven years from the report release date (five years for private companies). It is confidential information, but may be subject to subpoena.

5-8

FRAUD: These Are Interesting Times

More than half of US organizations have experienced fraud in last 2 years.

54% of fraud over $100,000; 8% over $5Mill

Financial statement up to 23% (2014) from 16% (2011), bribery/corruption (14% vs. 7%), and cybercrime moving to forefront.

54% of fraud committed by middle management.

Profile: male, 31 to 40yrs old, employed 3-5 yrs, and a college graduate.

5-9

Auditor’s Responsibility- Fraud Dectection

Auditors are responsible for “obtaining reasonable assurance that the financial statements as a whole are free from material misstatement, whether caused by fraud or error”

– Primary responsibility for fraud prevention rests with company management

– Auditor’s responsibility is to plan the audit to plan the audit to gather sufficient appropriate evidence to determine whether the financial statements are free of material misstatement from fraud or error

5-10

The Audit Team’s Fraud Discussion

Auditing Standards require the audit team to discuss the susceptibility of the financial statements to fraud. It should be documented and include:

– A discussion of management’s involvement in supervising employees with access to cash or other assets susceptible to misappropriation

– A consideration of unusual or unexplained changes in the behavior or lifestyle of employees that have come to the auditor’s attention

– A consideration of the types of circumstances that indicate the possibility of fraud

– A discussion of how an element of unpredictability can be built into the nature, timing, and extent of audit procedures

– A consideration of the types of audit procedures that could be effective in responding to the susceptibility of the company’s financial statements to material misstatement and whether some of the audit procedures can be more effective than others

– A discussion of any allegations of fraud that have come to the auditor’s attention

5-11

Rationalization Opportunity

Pressure

Why does Fraud Happen-Fraud Triangle

5-12

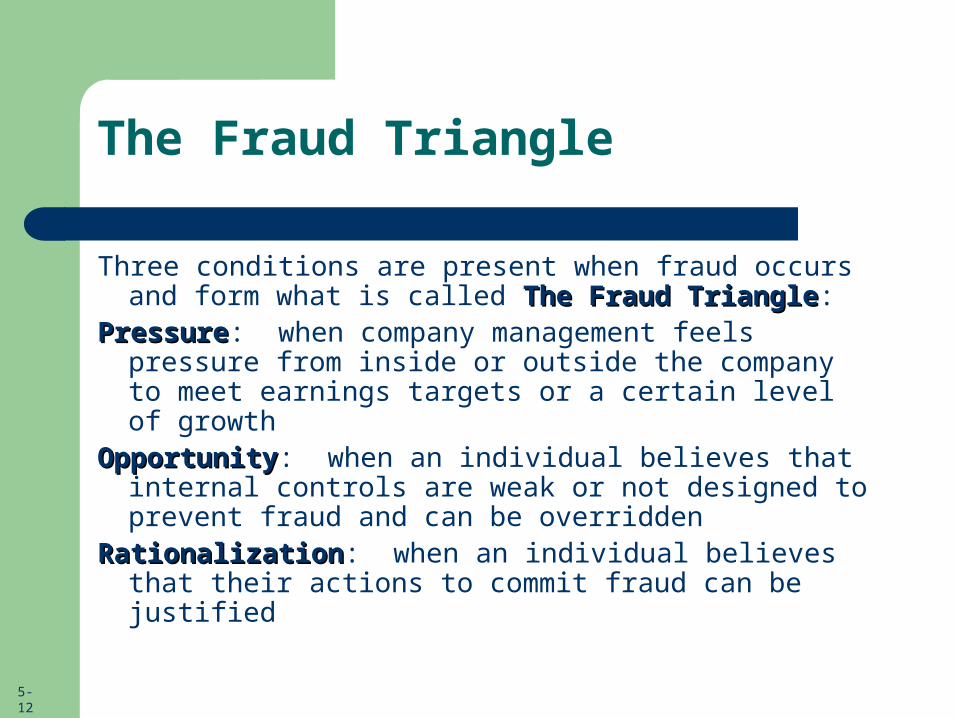

The Fraud Triangle

Three conditions are present when fraud occurs and form what is called The Fraud TriangleThe Fraud Triangle:

PressurePressure: when company management feels pressure from inside or outside the company to meet earnings targets or a certain level of growth

OpportunityOpportunity: when an individual believes that internal controls are weak or not designed to prevent fraud and can be overridden

RationalizationRationalization: when an individual believes that their actions to commit fraud can be justified

5-13

Fraud Detection

Misstatements in the financial statements can be caused by errors or fraud– Errors – unintentional acts of the company– Fraud – intentional acts of the company and may

be from. 2 Types:

1. Fraudulent financial reporting – occurs when a company prepares financial statements that are materially misstated

2. Assets that are misappropriated – occurs when employees in a company steal its assets

5-14

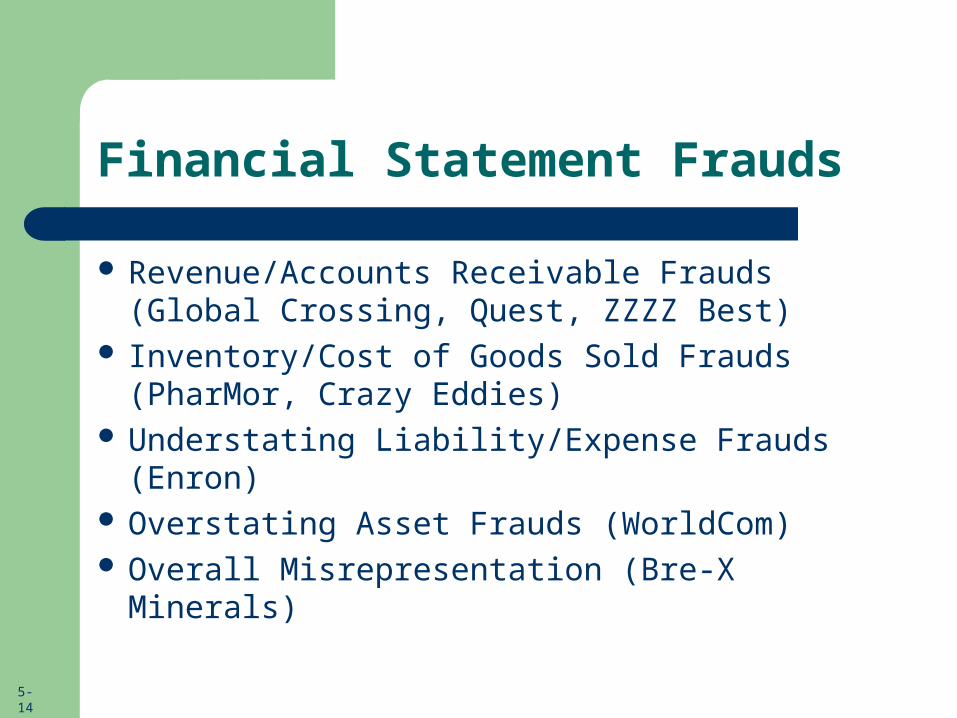

Financial Statement Frauds

Revenue/Accounts Receivable Frauds (Global Crossing, Quest, ZZZZ Best)

Inventory/Cost of Goods Sold Frauds (PharMor, Crazy Eddies)

Understating Liability/Expense Frauds (Enron)

Overstating Asset Frauds (WorldCom) Overall Misrepresentation (Bre-X Minerals)

5-15

Financial Statement Fraud

Financial statement fraud causes a decrease in market value of stock of approximately 500 to 1,000 times the amount of the fraud.

$7 million fraud $2 billion drop in stock value

5-16

Fraud Cost….Two Examples

General Motors– $436 Million Fraud– Profit Margin = 10%– $4.36 Billion in

Revenues Needed– At $20,000 per Car,

218,000 Cars

Bank– $100 Million Fraud– Profit Margin = 10 %– $1 Billion in Revenues

Needed– At $100 per year per

Checking Account, 10 Million New Accounts

Detecting Financial Statement Detecting Financial Statement FraudFraud

Detecting Financial Statement Fraud

1. Management & Board 2. Relationships With Others

3. Organization & Industry 4. Financial Results & Operating Characteristics

Transaction Accounts Involved Fraud Schemes

1. Estimate all uncollectible accounts receivable

Bad debt expense, allowance for doubtful accounts

1. Understate allowance for doubtful accounts, thus overstating receivables

2. Sell goods and/or services to customers

Accounts receivable, revenues (e.g. sales revenue) (Note: cost of goods sold part of entryh is included in Chapter 5)

2. Record fictitious sales (related parties, sham sales, sales with conditions, consignment sales, etc.)3. Recognize revenues too early (improper cutoff, percentage of completion, etc.)4. Overstate real sales (alter contracts, inflate amounts, etc.)

3. Accept returned goods from customers

Sales returns, accounts receivable

5. Not record returned goods from customers6. Record returned goods after the end of the period

4. Write off receivables as uncollectible

Allowance for doubtful accounts, accounts receivable

7. Not write off uncollectible receivables8. Write off uncollectible receivables in a later period

5. Collect cash after discount period

Cash, accounts receivable

9. Record bank transfers as cash received from customers10. Manipulate cash received from related parties

6. Collect cash within discount period

Cash, sales discounts, accounts receivable

11. Not recognize discounts given to customers

Revenue-Related Transactions and Frauds

Transaction Accounts Involved Fraud Schemes

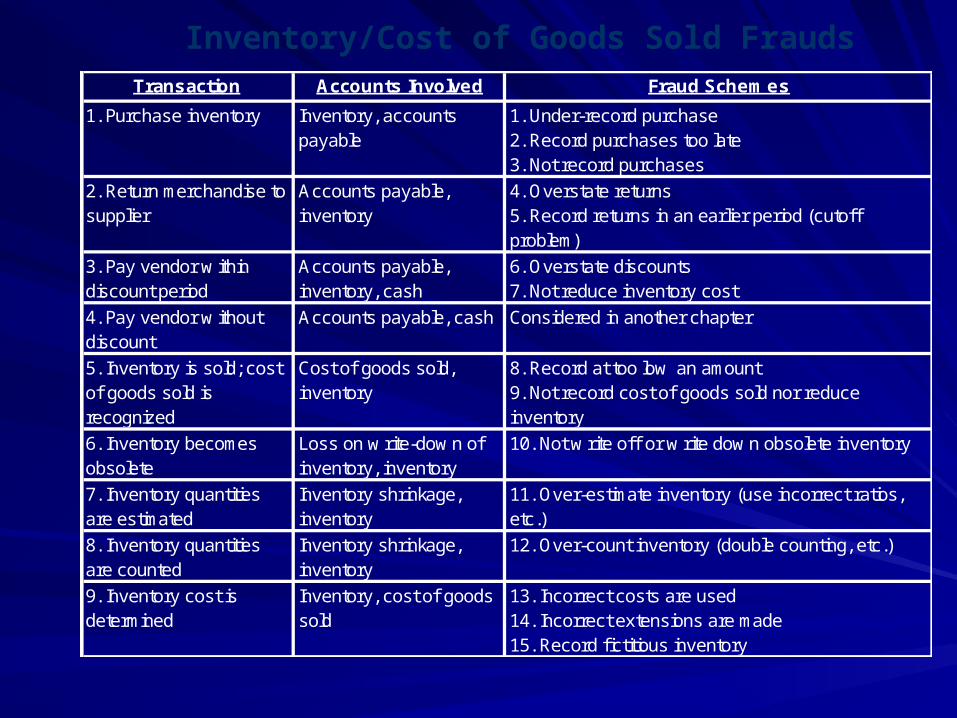

1. Purchase inventory Inventory, accounts payable

1. Under-record purchase2. Record purchases too late3. Not record purchases

2. Return merchandise to supplier

Accounts payable, inventory

4. Overstate returns5. Record returns in an earlier period (cutoff problem)

3. Pay vendor w ithin discount period

Accounts payable, inventory, cash

6. Overstate discounts7. Not reduce inventory cost

4. Pay vendor w ithout discount

Accounts payable, cash Considered in another chapter

5. Inventory is sold; cost of goods sold is recognized

Cost of goods sold, inventory

8. Record at too low an amount9. Not record cost of goods sold nor reduce inventory

6. Inventory becomes obsolete

Loss on w rite-dow n of inventory, inventory

10. Not w rite off or w rite dow n obsolete inventory

7. Inventory quantities are estimated

Inventory shrinkage, inventory

11. Over-estimate inventory (use incorrect ratios, etc.)

8. Inventory quantities are counted

Inventory shrinkage, inventory

12. Over-count inventory (double counting, etc.)

9. Inventory cost is determined

Inventory, cost of goods sold

13. Incorrect costs are used14. Incorrect extensions are made15. Record f ictitious inventory

Inventory/Cost of Goods Sold Frauds

5-20

Professional Skepticism

The auditor is expected to conduct the audit with an attitude of professional skepticism professional skepticism when considering a company’s risk of fraud.– It is an attitude or a state of mind– It involves having a questioning mind questioning mind and making

a critical assessment critical assessment of the evidence, especially the reliability of the evidence gathered and the controls over the company’s preparation of the statements

5-21

Auditor Tools- Skepticism!

Six Characteristics of Skepticism

➤ Questioning Mind—A disposition to inquiry, with some sense of doubt

➤ Suspension of Judgment—Withholding judgment until appropriate evidence is obtained

➤ Search for Knowledge—A desire to investigate beyond the obvious, with a desire to corroborate

➤ Interpersonal Understanding—Recognition that people’s motivations and perceptions can lead them to provide biased or misleading information

➤ Autonomy—The self-direction, moral independence and conviction to decide for oneself, rather than accepting the claims of others

➤ Self-Esteem—The self confidence to resist persuasion and to challenge assumptions or conclusions

5-22

Auditor Tools- Data Analysis

Build a profile of potential frauds, obtain data, verify data, cleanse and analyze data

Regression Analysis to find relationships in large data pools

Calculate ratio of maximum to minimums- can be used to verify accuracy of unit product prices or areas where large variations not expected

Analyze transactions during non-business hours and weekends

5-23

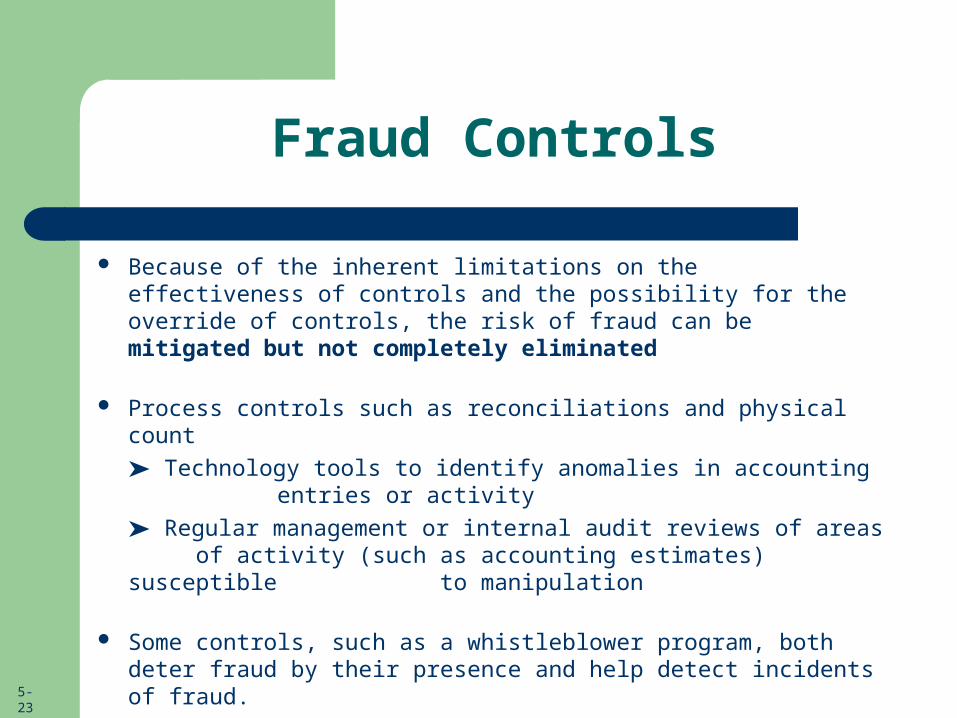

Fraud Controls

Because of the inherent limitations on the effectiveness of controls and the possibility for the override of controls, the risk of fraud can be mitigated but not completely eliminated

Process controls such as reconciliations and physical count

➤ Technology tools to identify anomalies in accounting entries or activity

➤ Regular management or internal audit reviews of areas of activity (such as accounting estimates)

susceptible to manipulation

Some controls, such as a whistleblower program, both deter fraud by their presence and help detect incidents of fraud.

5-24

Evidence to Assess the Risk of Material Misstatement because of Fraud

The auditor’s assessment of fraud determines the nature, extent, and timing of audit procedures. If the risk of fraud is high, the auditor can:– Change the naturenature of audit testing and obtain

more reliable evidence– Change the timingtiming of audit tests and perform

substantive tests at year-end– Change the extentextent of audit tests and gather more

audit evidence

5-25

Reporting of Fraud to Management and the Audit Committee

An auditor who believes that misstatements in the financial statements can be the result of fraud must consider its impact on other aspects of the audit and they may consider withdrawing from the engagement.

The auditor needs to bring the fraud to the attention of the appropriate level of management, usually, one level above where the fraud occurred, as soon as possible. Fraud involving management and that materially misstates the financial statements should be reported to the audit committee.

5-26

Reporting of Fraud to Management and the Audit Committee

PCAOB auditing standards require the external auditor to communicate various matters to the audit committee, including, but not limited to, the following:

➤ Significant accounting policies, management judgments, and accounting estimates

➤ The auditor’s judgments about the quality, not just the acceptability, of the company’s accounting principles

➤ Significant difficulties, if any, encountered during the audit

➤ Uncorrected misstatements that were determined by management to be immaterial, individually and in the aggregate

➤ Audit adjustments arising from the audit, either individually or in the aggregate, that in the auditor’s judgment could have a significant effect on the entity’s financial reporting process

➤ Significant internal control deficiencies or material weaknesses and disagreements with management

5-27

Documentation Regarding the Consideration of Fraud

The auditor is required to documentdocument in the work papers their understanding of:

Significant decisions Significant decisions made during the audit team’s discussion regarding the susceptibility of the company’s financial statements to material misstatement because of fraud

How and when the fraudfraud discussion discussion occurred and the audit team members who participated

The identified and assessed risks of material risks of material misstatements due to fraud misstatements due to fraud at both the financial statement level and the relevant assertion level as well as the procedures performed to obtain the information

5-28

Documentation Regarding the Consideration of Fraud

The auditor is required to document in the work papers their response response to:

The assessed risk of material misstatement due to fraud at the financial statement level; the nature, timing, and extent of audit procedures at the assertion level; and a linkagelinkage between the audit procedures and the assessed risk of material misstatement

The results of the audit procedures results of the audit procedures including those designed to address the risk of management override of internal controls

Other conditions and analytical procedures conditions and analytical procedures that cause the auditor to believe that additional auditing procedures were appropriate to address the risk of material misstatement because of fraud

5-29

Documentation Regarding the Consideration of Fraud

NEW DEVELOPMENTS:

AntiFraudCollaboration.org: provides resources to help audit committees, executives, internal and external auditors defer and detect financial reporting fraud.

Dodd-Frank Act- new whistleblower program allows SEC to pay financial awards up $1M to whistleblowers who provide information that leads to successful SEC enforcement action