forums on issues and innovations in real estate global products and sources for real estate capital...

TRANSCRIPT

Forums on Issues and Innovations in Real Estate

Global Products and Sources for Real Estate Capital

October 2006

Tommy Brown

Agenda

Global real estate capital flows

Real estate products

Tommy Brown

Agenda

Global real estate capital flows

Real estate products

Tommy Brown

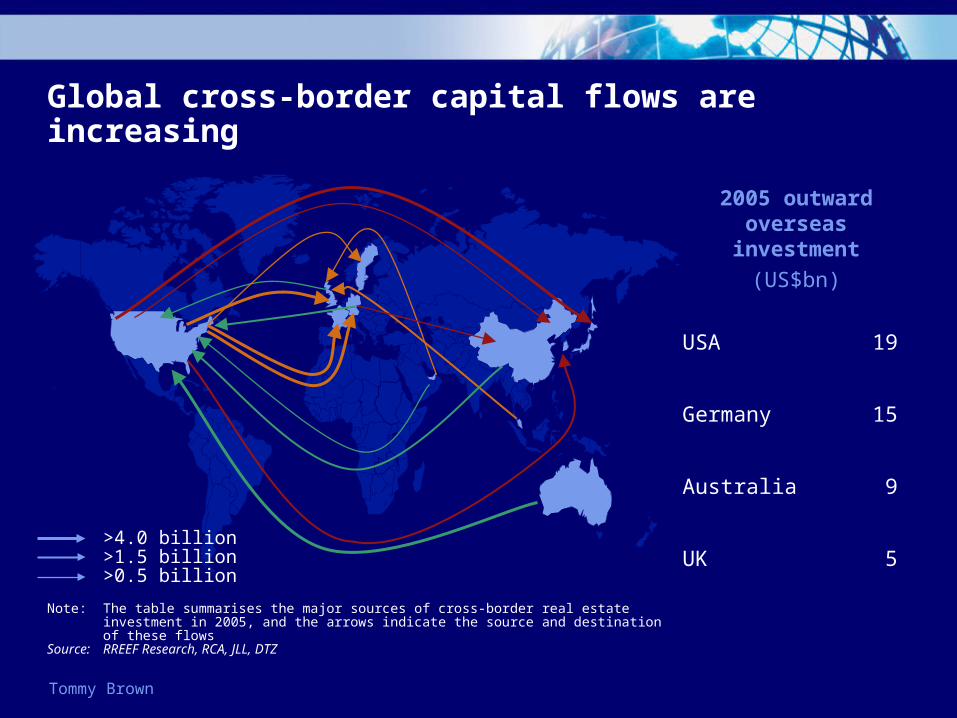

Global cross-border capital flows are increasing

Note: The table summarises the major sources of cross-border real estate investment in 2005, and the arrows indicate the source and destination of these flows

Source: RREEF Research, RCA, JLL, DTZ

>4.0 billion>1.5 billion>0.5 billion

2005 outward overseas investment

(US$bn)

USA 19

Germany 15

Australia 9

UK 5

Tommy Brown

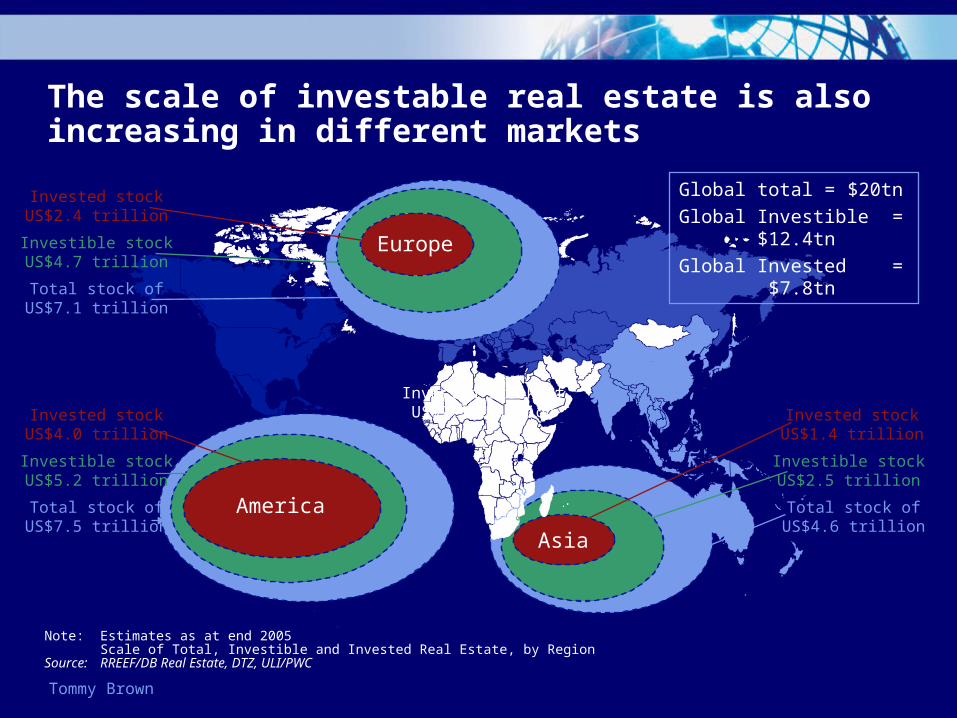

The scale of investable real estate is also increasing in different markets

Note: Estimates as at end 2005Scale of Total, Investible and Invested Real Estate, by Region

Source: RREEF/DB Real Estate, DTZ, ULI/PWC

Asia

America

Europe

Invested stockUS$2.4 trillion

Invested stock ofUS$7.1 trillion

Total stock ofUS$7.1 trillion

Investible stockUS$4.7 trillion

Invested stockUS$4.0 trillion

Total stock ofUS$7.5 trillion

Investible stockUS$5.2 trillion

Invested stockUS$1.4 trillion

Total stock ofUS$4.6 trillion

Investible stockUS$2.5 trillion

Global total = $20tn

Global Investible = $12.4tn

Global Invested = $7.8tn

Tommy Brown

Additionally, overall capital to real estate is increasing

Pubic equity Public debt

Private debt Private equity

Note: Size of global listed real estate marketSource: UBS

Note: Issuance of CMBSSource: Deutsche Bank Securitisation Research

Note: Bank lending to commercial real estateSource: RREEF Research, DTZ

Note: Direct real estate investment activitySource: RREEF, DTZ, JLL, RCA

0

400

800

2001 2002 2003 2004 2005

(US

$b

n)

REIT Non-REIT

0

150

300

2001 2002 2003 2004 2005

(US

$b

n)

US Non-USA

0

2,250

4,500

2001 2002 2003 2004 2005

(US

$b

n)

US Europe Asia-Pacific

0

250

500

2001 2002 2003 2004 2005

(US

$b

n)

US Europe Asia-Pacific

Tommy Brown

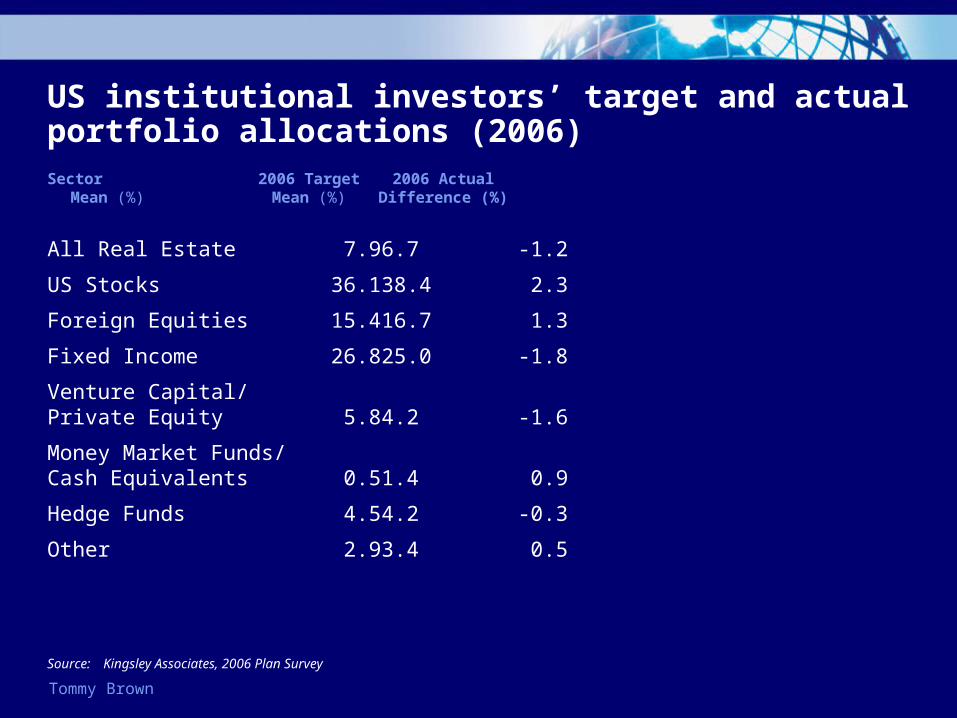

US institutional investors’ target and actual portfolio allocations (2006)

All Real Estate 7.9 6.7 -1.2

US Stocks 36.1 38.4 2.3

Foreign Equities 15.4 16.7 1.3

Fixed Income 26.8 25.0 -1.8

Venture Capital/Private Equity 5.8 4.2 -1.6

Money Market Funds/Cash Equivalents 0.5 1.4 0.9

Hedge Funds 4.5 4.2 -0.3

Other 2.9 3.4 0.5

Sector 2006 Target 2006 ActualMean (%) Mean (%) Difference (%)

Source: Kingsley Associates, 2006 Plan Survey

Tommy Brown

US institutional investors’ over/Under allocation

Source: Kingsley Associates, 2006 Plan Survey

1.5 1.4

-0.9-1.5

2.2

0.8

-1.3

0.7

-1.2

1.3

-1.8

-0.5

-1.7

-0.1

0.4

-0.7

-0.1

2.3

-1.6

-0.3

0.9

-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.53.0

All RealEstate

US Stocks ForeignEquities

All FixedIncome

VC/PrivateEquity

Cash HedgeFunds

% o

ver/

un

de

r ta

rge

t

2004 2005 2006

Investors remain challenged to

meet real estate targets.

Tommy Brown

Agenda

Global real estate capital flows

Real estate products

Tommy Brown

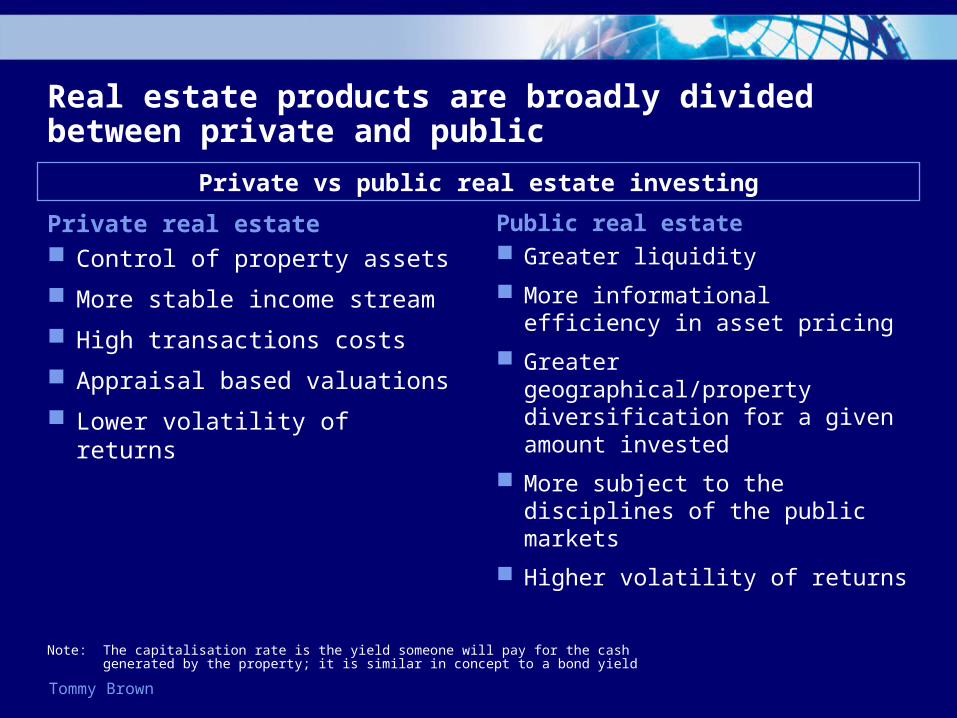

Real estate products are broadly divided between private and public

Private real estate Control of property assets

More stable income stream

High transactions costs

Appraisal based valuations

Lower volatility of returns

Public real estate Greater liquidity

More informational efficiency in asset pricing

Greater geographical/property diversification for a given amount invested

More subject to the disciplines of the public markets

Higher volatility of returns

Private vs public real estate investing

Note: The capitalisation rate is the yield someone will pay for the cash generated by the property; it is similar in concept to a bond yield

Tommy Brown

Several questions need to addressed when investing in real estate

Investment process

Strategic asset allocation

Real Estate

Equity

Debt

Cash

Other

How much to invest in Real Estate? Where to invest?

What’s The Risk/Reward balance?

What type of property?

What format? How much

liquidity is required?

Who is performing mgmt/ oversight of investment?

Str

ate

gic

ass

et

allo

catio

n

Geographic allocation

Domestic

Europe

US

Asia

Other

Investment strategy

Core

Core plus / Value add

Opportunistic

Sector allocation

Office

Retail

Industrial

Residential

Special property(1)

Investment vehicle

Private equity direct(2)

Private equity indirect(3)

Private debt

Public equity(4)

Public debt(5)

Real estate investment

(1) Includes self storage, care homes and medical labs(2) Real Private equity direct (buildings)(3) Private equity indirect (funds)(4) Public equity (REITS / Mutual funds)(5) Public debt (CMBS / Mezzanine)

Private real estate investing

Public real estate investing

Tommy Brown

The real estate universe has matured to provide an array of investment alternatives

Low Risk (and leverage) High

Breakdown of universe of real estate investment products

Private

Core Value-added returns Opportunistic(up to 8%) (up to 14%) (+18%)

Direct

Indirect

Note: The above illustration can be further segmented by geography and property type. The returns shown are for illustrative purposes only and are indicative IRRs (internal rate of return) without regard to the duration of the investment.

Source: Deutsche Bank

Public

Equity

Debt

Debt

Equity

Direct investments in existing assets

Funds

Real estate operating companies

Opportunity funds

Direct property development

Mortgage lending Mezzanine debt

CMBS

Unsecured debt of real estate companies

Real estate companies

Mutual funds

Structured products

Debt /Mezzfunds

Tommy Brown

European market for private real estate funds is achieving scale and positioned to increase substantially

Non-listed institutional real estate funds

Source: INREV, Quarterly Report, Issue No,12

0

50

100

150

200

250

300

350

Au

g 0

3

De

c 0

3

Ma

r 0

4

Jul 0

4

No

v 0

4

Jan

04

Ap

r 0

5

Jul 0

5

Oct

05

Jan

06

Ap

r 0

6

Jul 0

6Siz

e o

f E

uro

pe

an

ma

rke

t (€

bn

)

0

100

200

300

400

500

GAV (€bn) Number of funds

Tommy Brown

There has been significant new public real estate equity issuance

0

10,000

20,000

30,000

40,000

50,000

60,000

2001 2002 2003 2004 2005

De

al v

alu

e (

$m

)

US Non-US

Historical public real estate equity issuance

Source: Equityware

Tommy Brown

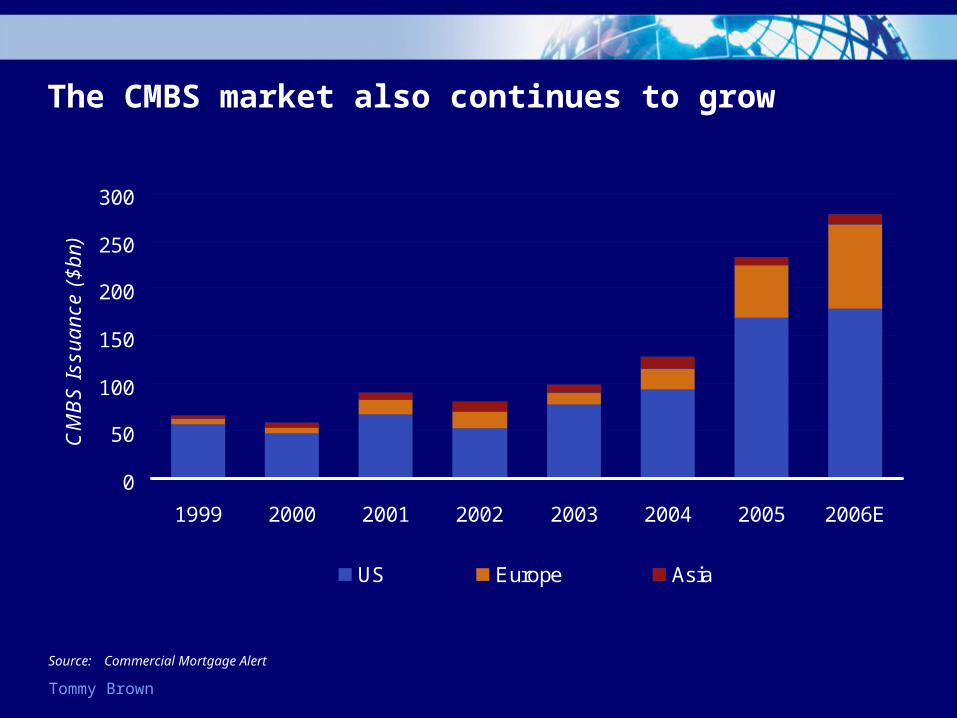

The CMBS market also continues to grow

0

50

100

150

200

250

300

1999 2000 2001 2002 2003 2004 2005 2006E

CM

BS

Iss

ua

nce

($

bn

)

US Europe Asia

Source: Commercial Mortgage Alert

Tommy Brown

Disclaimer

THIS PRESENTATION CONTAINS INFORMATION WHICH HAS BEEN PROVIDED BY A NUMBER OF SOURCES. WHILE THE INFORMATION HEREIN IS BELIEVED TO BE RELIABLE, NO REPRESENTATION IS MADE HEREIN BY DEUTSCHE BANK OR ANY OF ITS AFFILIATES, AS TO THE ACCURACY OR COMPLETENESS OF SUCH INFORMATION.

THIS PRESENTATION HAS BEEN PREPARED FOR INFORMATIONAL AND DISCUSSION PURPOSES ONLY AND DOES NOT CONSTITUTE AN OFFER, OR AN INVITATION TO OFFER, OR A RECOMMENDATION TO ENTER INTO ANY TRANSACTION. DEUTSCHE BANK IS NOT ACTING AS YOUR FINANCIAL ADVISOR OR IN A FIDUCIARY CAPACITY IN RESPECT OF ANY TRANSACTION WITH YOU UNLESS EXPRESSLY AGREED BY DEUTSCHE BANK IN WRITING. BEFORE ENTERING INTO ANY TRANSACTION YOU SHOULD TAKE STEPS TO ENSURE THAT YOU UNDERSTAND THE TRANSACTION AND HAVE MADE AN INDEPENDENT ASSESSMENT OF THE APPROPRIATENESS OF THE TRANSACTION IN THE LIGHT OF YOUR OWN OBJECTIVES AND CIRCUMSTANCES, INCLUDING THE POSSIBLE RISKS AND BENEFITS OF ENTERING INTO SUCH TRANSACTION. YOU SHOULD ALSO CONSIDER SEEKING ADVICE FROM YOUR OWN ADVISORS IN MAKING THIS ASSESSMENT. NEITHER DEUTSCHE BANK OR ANY OF ITS AFFILIATES ACCEPT ANY LIABILITY WHATSOEVER WITH RESPECT TO THE CONTENT OF THIS DOCUMENT, ITS USE OR ANY LOSS ARISING FROM IT.

Forums on Issues and Innovations in Real Estate

Global Products and Sources for Real Estate Capital

October 2006