forecasting using - rob j hyndman · outline 1stationarity 2ordinary differencing 3seasonal...

TRANSCRIPT

Forecasting using

8. Stationarity and Differencing

OTexts.com/fpp/8/1

Forecasting using R 1

Rob J Hyndman

Outline

1 Stationarity

2 Ordinary differencing

3 Seasonal differencing

4 Unit root tests

5 Backshift notation

Forecasting using R Stationarity 2

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

A stationary series is:

roughly horizontal

constant variance

no patterns predictable in the long-term

Forecasting using R Stationarity 3

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

A stationary series is:

roughly horizontal

constant variance

no patterns predictable in the long-term

Forecasting using R Stationarity 3

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

A stationary series is:

roughly horizontal

constant variance

no patterns predictable in the long-term

Forecasting using R Stationarity 3

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

A stationary series is:

roughly horizontal

constant variance

no patterns predictable in the long-term

Forecasting using R Stationarity 3

Stationary?

Forecasting using R Stationarity 4

Day

Dow

−Jo

nes

inde

x

0 50 100 150 200 250 300

3600

3700

3800

3900

Stationary?

Forecasting using R Stationarity 5

Day

Cha

nge

in D

ow−

Jone

s in

dex

0 50 100 150 200 250 300

−10

0−

500

50

Stationary?

Forecasting using R Stationarity 6

Annual strikes in the US

Year

Num

ber

of s

trik

es

1950 1955 1960 1965 1970 1975 1980

3500

4000

4500

5000

5500

6000

Stationary?

Forecasting using R Stationarity 7

Sales of new one−family houses, USA

Tota

l sal

es

1975 1980 1985 1990 1995

3040

5060

7080

90

Stationary?

Forecasting using R Stationarity 8

Price of a dozen eggs in 1993 dollars

Year

$

1900 1920 1940 1960 1980

100

150

200

250

300

350

Stationary?

Forecasting using R Stationarity 9

Number of pigs slaughtered in Victoria

thou

sand

s

1990 1991 1992 1993 1994 1995

8090

100

110

Stationary?

Forecasting using R Stationarity 10

Annual Canadian Lynx trappings

Time

Num

ber

trap

ped

1820 1840 1860 1880 1900 1920

010

0020

0030

0040

0050

0060

0070

00

Stationary?

Forecasting using R Stationarity 11

Australian quarterly beer production

meg

alite

rs

1995 2000 2005

400

450

500

Stationary?

Forecasting using R Stationarity 12

Annual monthly electricity production

Year

GW

h

1960 1970 1980 1990

2000

6000

1000

014

000

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

Transformations help to stabilize the

variance.

For ARIMA modelling, we also need to

stabilize the mean.Forecasting using R Stationarity 13

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

Transformations help to stabilize the

variance.

For ARIMA modelling, we also need to

stabilize the mean.Forecasting using R Stationarity 13

Stationarity

DefinitionIf {yt} is a stationary time series, then for

all s, the distribution of (yt, . . . , yt+s) does

not depend on t.

Transformations help to stabilize the

variance.

For ARIMA modelling, we also need to

stabilize the mean.Forecasting using R Stationarity 13

Non-stationarity in the mean

Identifying non-stationary series

time plot.

The ACF of stationary data drops to

zero relatively quickly

The ACF of non-stationary data

decreases slowly.

For non-stationary data, the value of r1is often large and positive.

Forecasting using R Stationarity 14

Non-stationarity in the mean

Identifying non-stationary series

time plot.

The ACF of stationary data drops to

zero relatively quickly

The ACF of non-stationary data

decreases slowly.

For non-stationary data, the value of r1is often large and positive.

Forecasting using R Stationarity 14

Non-stationarity in the mean

Identifying non-stationary series

time plot.

The ACF of stationary data drops to

zero relatively quickly

The ACF of non-stationary data

decreases slowly.

For non-stationary data, the value of r1is often large and positive.

Forecasting using R Stationarity 14

Non-stationarity in the mean

Identifying non-stationary series

time plot.

The ACF of stationary data drops to

zero relatively quickly

The ACF of non-stationary data

decreases slowly.

For non-stationary data, the value of r1is often large and positive.

Forecasting using R Stationarity 14

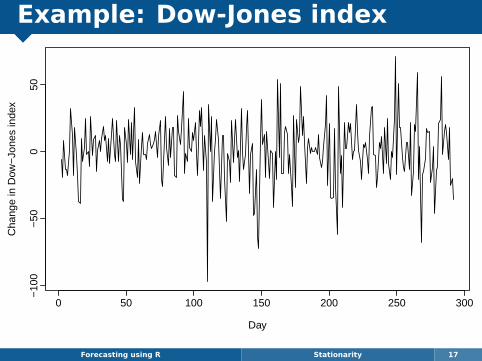

Example: Dow-Jones index

Forecasting using R Stationarity 15

Dow Jones index (daily ending 15 Jul 94)

0 50 100 150 200 250

3600

3700

3800

3900

Example: Dow-Jones index

Forecasting using R Stationarity 16

−0.

20.

00.

20.

40.

60.

81.

0

Lag

AC

F

1 2 3 4 5 6 7 8 9 10 12 14 16 18 20 22

Example: Dow-Jones index

Forecasting using R Stationarity 17

Day

Cha

nge

in D

ow−

Jone

s in

dex

0 50 100 150 200 250 300

−10

0−

500

50

Example: Dow-Jones index

Forecasting using R Stationarity 18

−0.

15−

0.05

0.05

0.10

0.15

Lag

AC

F

1 2 3 4 5 6 7 8 9 10 12 14 16 18 20 2211 13 15 17 19 21 23

Outline

1 Stationarity

2 Ordinary differencing

3 Seasonal differencing

4 Unit root tests

5 Backshift notation

Forecasting using R Ordinary differencing 19

Differencing

Differencing helps to stabilize the

mean.

The differenced series is the change

between each observation in the

original series: y′t = yt − yt−1.

The differenced series will have only

T − 1 values since it is not possible to

calculate a difference y′1 for the first

observation.

Forecasting using R Ordinary differencing 20

Differencing

Differencing helps to stabilize the

mean.

The differenced series is the change

between each observation in the

original series: y′t = yt − yt−1.

The differenced series will have only

T − 1 values since it is not possible to

calculate a difference y′1 for the first

observation.

Forecasting using R Ordinary differencing 20

Differencing

Differencing helps to stabilize the

mean.

The differenced series is the change

between each observation in the

original series: y′t = yt − yt−1.

The differenced series will have only

T − 1 values since it is not possible to

calculate a difference y′1 for the first

observation.

Forecasting using R Ordinary differencing 20

Example: Dow-Jones indexThe differences of the Dow-Jones index

are the day-today changes.

Now the series looks just like a white

noise series:no autocorrelations outside the 95% limits.Ljung-Box Q∗ statistic has a p-value 0.153 forh = 10.

Conclusion: The daily change in the

Dow-Jones index is essentially a

random amount uncorrelated with

previous days.Forecasting using R Ordinary differencing 21

Example: Dow-Jones indexThe differences of the Dow-Jones index

are the day-today changes.

Now the series looks just like a white

noise series:no autocorrelations outside the 95% limits.Ljung-Box Q∗ statistic has a p-value 0.153 forh = 10.

Conclusion: The daily change in the

Dow-Jones index is essentially a

random amount uncorrelated with

previous days.Forecasting using R Ordinary differencing 21

Example: Dow-Jones indexThe differences of the Dow-Jones index

are the day-today changes.

Now the series looks just like a white

noise series:no autocorrelations outside the 95% limits.Ljung-Box Q∗ statistic has a p-value 0.153 forh = 10.

Conclusion: The daily change in the

Dow-Jones index is essentially a

random amount uncorrelated with

previous days.Forecasting using R Ordinary differencing 21

Example: Dow-Jones indexThe differences of the Dow-Jones index

are the day-today changes.

Now the series looks just like a white

noise series:no autocorrelations outside the 95% limits.Ljung-Box Q∗ statistic has a p-value 0.153 forh = 10.

Conclusion: The daily change in the

Dow-Jones index is essentially a

random amount uncorrelated with

previous days.Forecasting using R Ordinary differencing 21

Example: Dow-Jones indexThe differences of the Dow-Jones index

are the day-today changes.

Now the series looks just like a white

noise series:no autocorrelations outside the 95% limits.Ljung-Box Q∗ statistic has a p-value 0.153 forh = 10.

Conclusion: The daily change in the

Dow-Jones index is essentially a

random amount uncorrelated with

previous days.Forecasting using R Ordinary differencing 21

Random walk modelGraph of differenced data suggests model

for Dow-Jones index:

yt − yt−1 = et or yt = yt−1 + et .

“Random walk” model very widely used

for non-stationary data.

This is the model behind the naïve

method.

Random walks typically have:long periods of apparent trends up or downsudden and unpredictable changes in direction.

Forecasting using R Ordinary differencing 22

Random walk modelGraph of differenced data suggests model

for Dow-Jones index:

yt − yt−1 = et or yt = yt−1 + et .

“Random walk” model very widely used

for non-stationary data.

This is the model behind the naïve

method.

Random walks typically have:long periods of apparent trends up or downsudden and unpredictable changes in direction.

Forecasting using R Ordinary differencing 22

Random walk modelGraph of differenced data suggests model

for Dow-Jones index:

yt − yt−1 = et or yt = yt−1 + et .

“Random walk” model very widely used

for non-stationary data.

This is the model behind the naïve

method.

Random walks typically have:long periods of apparent trends up or downsudden and unpredictable changes in direction.

Forecasting using R Ordinary differencing 22

Random walk modelGraph of differenced data suggests model

for Dow-Jones index:

yt − yt−1 = et or yt = yt−1 + et .

“Random walk” model very widely used

for non-stationary data.

This is the model behind the naïve

method.

Random walks typically have:long periods of apparent trends up or downsudden and unpredictable changes in direction.

Forecasting using R Ordinary differencing 22

Random walk modelGraph of differenced data suggests model

for Dow-Jones index:

yt − yt−1 = et or yt = yt−1 + et .

“Random walk” model very widely used

for non-stationary data.

This is the model behind the naïve

method.

Random walks typically have:long periods of apparent trends up or downsudden and unpredictable changes in direction.

Forecasting using R Ordinary differencing 22

Random walk modelGraph of differenced data suggests model

for Dow-Jones index:

yt − yt−1 = et or yt = yt−1 + et .

“Random walk” model very widely used

for non-stationary data.

This is the model behind the naïve

method.

Random walks typically have:long periods of apparent trends up or downsudden and unpredictable changes in direction.

Forecasting using R Ordinary differencing 22

Random walk with drift model

yt − yt−1 = c + et or yt = c + yt−1 + et .

c is the average change between

consecutive observations.

This is the model behind the drift

method.

Forecasting using R Ordinary differencing 23

Random walk with drift model

yt − yt−1 = c + et or yt = c + yt−1 + et .

c is the average change between

consecutive observations.

This is the model behind the drift

method.

Forecasting using R Ordinary differencing 23

Random walk with drift model

yt − yt−1 = c + et or yt = c + yt−1 + et .

c is the average change between

consecutive observations.

This is the model behind the drift

method.

Forecasting using R Ordinary differencing 23

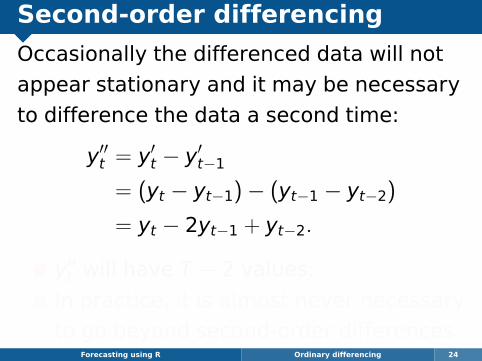

Second-order differencing

Occasionally the differenced data will not

appear stationary and it may be necessary

to difference the data a second time:

y′′t = y′t − y′t−1

= (yt − yt−1)− (yt−1 − yt−2)

= yt − 2yt−1 + yt−2.

y′′t will have T − 2 values.

In practice, it is almost never necessary

to go beyond second-order differences.Forecasting using R Ordinary differencing 24

Second-order differencing

Occasionally the differenced data will not

appear stationary and it may be necessary

to difference the data a second time:

y′′t = y′t − y′t−1

= (yt − yt−1)− (yt−1 − yt−2)

= yt − 2yt−1 + yt−2.

y′′t will have T − 2 values.

In practice, it is almost never necessary

to go beyond second-order differences.Forecasting using R Ordinary differencing 24

Second-order differencing

Occasionally the differenced data will not

appear stationary and it may be necessary

to difference the data a second time:

y′′t = y′t − y′t−1

= (yt − yt−1)− (yt−1 − yt−2)

= yt − 2yt−1 + yt−2.

y′′t will have T − 2 values.

In practice, it is almost never necessary

to go beyond second-order differences.Forecasting using R Ordinary differencing 24

Second-order differencing

Occasionally the differenced data will not

appear stationary and it may be necessary

to difference the data a second time:

y′′t = y′t − y′t−1

= (yt − yt−1)− (yt−1 − yt−2)

= yt − 2yt−1 + yt−2.

y′′t will have T − 2 values.

In practice, it is almost never necessary

to go beyond second-order differences.Forecasting using R Ordinary differencing 24

Outline

1 Stationarity

2 Ordinary differencing

3 Seasonal differencing

4 Unit root tests

5 Backshift notation

Forecasting using R Seasonal differencing 25

Seasonal differencing

A seasonal difference is the difference

between an observation and the

corresponding observation from the

previous year.

y′t = yt − yt−m

where m = number of seasons.

For monthly data m = 12.

For quarterly data m = 4.Forecasting using R Seasonal differencing 26

Seasonal differencing

A seasonal difference is the difference

between an observation and the

corresponding observation from the

previous year.

y′t = yt − yt−m

where m = number of seasons.

For monthly data m = 12.

For quarterly data m = 4.Forecasting using R Seasonal differencing 26

Seasonal differencing

A seasonal difference is the difference

between an observation and the

corresponding observation from the

previous year.

y′t = yt − yt−m

where m = number of seasons.

For monthly data m = 12.

For quarterly data m = 4.Forecasting using R Seasonal differencing 26

Seasonal differencing

A seasonal difference is the difference

between an observation and the

corresponding observation from the

previous year.

y′t = yt − yt−m

where m = number of seasons.

For monthly data m = 12.

For quarterly data m = 4.Forecasting using R Seasonal differencing 26

Antidiabetic drug sales

Forecasting using R Seasonal differencing 27

Antidiabetic drug sales

Year

$ m

illio

n

1995 2000 2005

510

1520

2530

> plot(a10)

Antidiabetic drug sales

Forecasting using R Seasonal differencing 28

Log Antidiabetic drug sales

Year

1995 2000 2005

1.0

1.5

2.0

2.5

3.0

> plot(log(a10))

Antidiabetic drug sales5

1015

2025

30

Sal

es (

$mill

ion)

1.0

1.5

2.0

2.5

3.0

Mon

thly

log

sale

s

−0.

10.

00.

10.

20.

3

1995 2000 2005Ann

ual c

hang

e in

mon

thly

log

sale

s

Year

Antidiabetic drug sales

Forecasting using R Seasonal differencing 29

> plot(diff(log(a10),12))

Electricity production

Forecasting using R Seasonal differencing 30

Year

Bill

ion

kWh

1980 1990 2000 2010

150

200

250

300

350

400

> plot(usmelec)

Electricity production

Forecasting using R Seasonal differencing 31

Year

Logs

1980 1990 2000 2010

5.0

5.2

5.4

5.6

5.8

6.0

> plot(log(usmelec))

Electricity production

Forecasting using R Seasonal differencing 32

Year

Sea

sona

lly d

iffer

ence

d lo

gs

1980 1990 2000 2010

−0.

050.

000.

050.

100.

15

> plot(diff(log(usmelec),12))

Electricity production

Forecasting using R Seasonal differencing 33

Year

Dou

bly

diffe

renc

ed lo

gs

1980 1990 2000 2010

−0.

10−

0.05

0.00

0.05

0.10

> plot(diff(diff(log(usmelec),12),1))

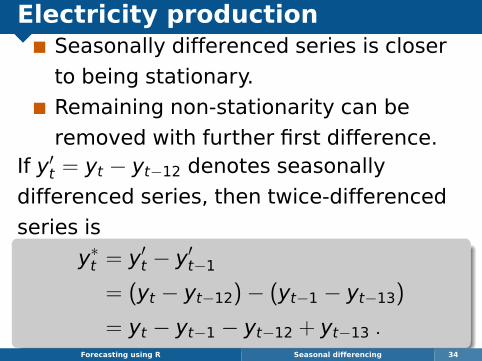

Electricity productionSeasonally differenced series is closer

to being stationary.

Remaining non-stationarity can be

removed with further first difference.If y′t = yt − yt−12 denotes seasonally

differenced series, then twice-differenced

series is

y∗t = y′t − y′t−1

= (yt − yt−12)− (yt−1 − yt−13)

= yt − yt−1 − yt−12 + yt−13 .Forecasting using R Seasonal differencing 34

Seasonal differencing

When both seasonal and first differences areapplied. . .

it makes no difference which is done first—theresult will be the same.

If seasonality is strong, we recommend thatseasonal differencing be done first becausesometimes the resulting series will bestationary and there will be no need for furtherfirst difference.

It is important that if differencing is used, thedifferences are interpretable.

Forecasting using R Seasonal differencing 35

Seasonal differencing

When both seasonal and first differences areapplied. . .

it makes no difference which is done first—theresult will be the same.

If seasonality is strong, we recommend thatseasonal differencing be done first becausesometimes the resulting series will bestationary and there will be no need for furtherfirst difference.

It is important that if differencing is used, thedifferences are interpretable.

Forecasting using R Seasonal differencing 35

Seasonal differencing

When both seasonal and first differences areapplied. . .

it makes no difference which is done first—theresult will be the same.

If seasonality is strong, we recommend thatseasonal differencing be done first becausesometimes the resulting series will bestationary and there will be no need for furtherfirst difference.

It is important that if differencing is used, thedifferences are interpretable.

Forecasting using R Seasonal differencing 35

Seasonal differencing

When both seasonal and first differences areapplied. . .

it makes no difference which is done first—theresult will be the same.

If seasonality is strong, we recommend thatseasonal differencing be done first becausesometimes the resulting series will bestationary and there will be no need for furtherfirst difference.

It is important that if differencing is used, thedifferences are interpretable.

Forecasting using R Seasonal differencing 35

Seasonal differencing

When both seasonal and first differences areapplied. . .

it makes no difference which is done first—theresult will be the same.

If seasonality is strong, we recommend thatseasonal differencing be done first becausesometimes the resulting series will bestationary and there will be no need for furtherfirst difference.

It is important that if differencing is used, thedifferences are interpretable.

Forecasting using R Seasonal differencing 35

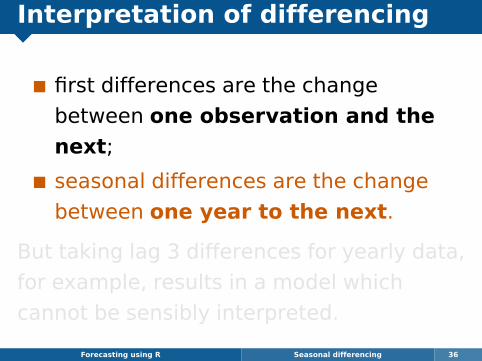

Interpretation of differencing

first differences are the change

between one observation and the

next;

seasonal differences are the change

between one year to the next.

But taking lag 3 differences for yearly data,

for example, results in a model which

cannot be sensibly interpreted.

Forecasting using R Seasonal differencing 36

Interpretation of differencing

first differences are the change

between one observation and the

next;

seasonal differences are the change

between one year to the next.

But taking lag 3 differences for yearly data,

for example, results in a model which

cannot be sensibly interpreted.

Forecasting using R Seasonal differencing 36

Interpretation of differencing

first differences are the change

between one observation and the

next;

seasonal differences are the change

between one year to the next.

But taking lag 3 differences for yearly data,

for example, results in a model which

cannot be sensibly interpreted.

Forecasting using R Seasonal differencing 36

Interpretation of differencing

first differences are the change

between one observation and the

next;

seasonal differences are the change

between one year to the next.

But taking lag 3 differences for yearly data,

for example, results in a model which

cannot be sensibly interpreted.

Forecasting using R Seasonal differencing 36

Outline

1 Stationarity

2 Ordinary differencing

3 Seasonal differencing

4 Unit root tests

5 Backshift notation

Forecasting using R Unit root tests 37

Unit root tests

Statistical tests to determine the

required order of differencing.

1 Augmented Dickey Fuller test: null

hypothesis is that the data are

non-stationary and non-seasonal.

2 Kwiatkowski-Phillips-Schmidt-Shin

(KPSS) test: null hypothesis is that the

data are stationary and non-seasonal.

3 Other tests available for seasonal data.Forecasting using R Unit root tests 38

Unit root tests

Statistical tests to determine the

required order of differencing.

1 Augmented Dickey Fuller test: null

hypothesis is that the data are

non-stationary and non-seasonal.

2 Kwiatkowski-Phillips-Schmidt-Shin

(KPSS) test: null hypothesis is that the

data are stationary and non-seasonal.

3 Other tests available for seasonal data.Forecasting using R Unit root tests 38

Unit root tests

Statistical tests to determine the

required order of differencing.

1 Augmented Dickey Fuller test: null

hypothesis is that the data are

non-stationary and non-seasonal.

2 Kwiatkowski-Phillips-Schmidt-Shin

(KPSS) test: null hypothesis is that the

data are stationary and non-seasonal.

3 Other tests available for seasonal data.Forecasting using R Unit root tests 38

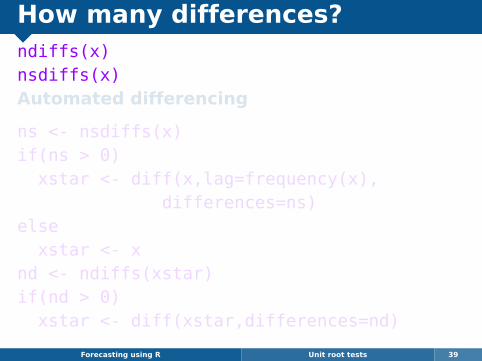

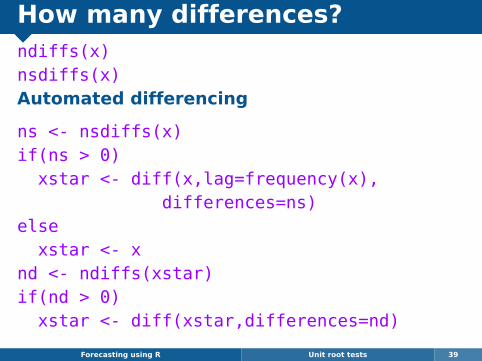

How many differences?ndiffs(x)nsdiffs(x)Automated differencing

ns <- nsdiffs(x)if(ns > 0)

xstar <- diff(x,lag=frequency(x),differences=ns)

elsexstar <- x

nd <- ndiffs(xstar)if(nd > 0)

xstar <- diff(xstar,differences=nd)

Forecasting using R Unit root tests 39

How many differences?ndiffs(x)nsdiffs(x)Automated differencing

ns <- nsdiffs(x)if(ns > 0)

xstar <- diff(x,lag=frequency(x),differences=ns)

elsexstar <- x

nd <- ndiffs(xstar)if(nd > 0)

xstar <- diff(xstar,differences=nd)

Forecasting using R Unit root tests 39

Outline

1 Stationarity

2 Ordinary differencing

3 Seasonal differencing

4 Unit root tests

5 Backshift notation

Forecasting using R Backshift notation 40

Backshift notationA very useful notational device is the backward shiftoperator, B, which is used as follows:

Byt = yt−1 .

In other words, B, operating on yt, has the effect ofshifting the data back one period. Twoapplications of B to yt shifts the data back twoperiods:

B(Byt) = B2yt = yt−2 .

For monthly data, if we wish to shift attention to“the same month last year,” then B12 is used, andthe notation is B12yt = yt−12.

Forecasting using R Backshift notation 41

Backshift notationA very useful notational device is the backward shiftoperator, B, which is used as follows:

Byt = yt−1 .

In other words, B, operating on yt, has the effect ofshifting the data back one period. Twoapplications of B to yt shifts the data back twoperiods:

B(Byt) = B2yt = yt−2 .

For monthly data, if we wish to shift attention to“the same month last year,” then B12 is used, andthe notation is B12yt = yt−12.

Forecasting using R Backshift notation 41

Backshift notationA very useful notational device is the backward shiftoperator, B, which is used as follows:

Byt = yt−1 .

In other words, B, operating on yt, has the effect ofshifting the data back one period. Twoapplications of B to yt shifts the data back twoperiods:

B(Byt) = B2yt = yt−2 .

For monthly data, if we wish to shift attention to“the same month last year,” then B12 is used, andthe notation is B12yt = yt−12.

Forecasting using R Backshift notation 41

Backshift notationA very useful notational device is the backward shiftoperator, B, which is used as follows:

Byt = yt−1 .

In other words, B, operating on yt, has the effect ofshifting the data back one period. Twoapplications of B to yt shifts the data back twoperiods:

B(Byt) = B2yt = yt−2 .

For monthly data, if we wish to shift attention to“the same month last year,” then B12 is used, andthe notation is B12yt = yt−12.

Forecasting using R Backshift notation 41

Backshift notationThe backward shift operator is convenient fordescribing the process of differencing. A firstdifference can be written as

y′t = yt − yt−1 = yt − Byt = (1− B)yt .

Note that a first difference is represented by (1−B).Similarly, if second-order differences (i.e., firstdifferences of first differences) have to becomputed, then:

y′′t = yt − 2yt−1 + yt−2 = (1− B)2yt .

Forecasting using R Backshift notation 42

Backshift notationThe backward shift operator is convenient fordescribing the process of differencing. A firstdifference can be written as

y′t = yt − yt−1 = yt − Byt = (1− B)yt .

Note that a first difference is represented by (1−B).Similarly, if second-order differences (i.e., firstdifferences of first differences) have to becomputed, then:

y′′t = yt − 2yt−1 + yt−2 = (1− B)2yt .

Forecasting using R Backshift notation 42

Backshift notationThe backward shift operator is convenient fordescribing the process of differencing. A firstdifference can be written as

y′t = yt − yt−1 = yt − Byt = (1− B)yt .

Note that a first difference is represented by (1−B).Similarly, if second-order differences (i.e., firstdifferences of first differences) have to becomputed, then:

y′′t = yt − 2yt−1 + yt−2 = (1− B)2yt .

Forecasting using R Backshift notation 42

Backshift notationThe backward shift operator is convenient fordescribing the process of differencing. A firstdifference can be written as

y′t = yt − yt−1 = yt − Byt = (1− B)yt .

Note that a first difference is represented by (1−B).Similarly, if second-order differences (i.e., firstdifferences of first differences) have to becomputed, then:

y′′t = yt − 2yt−1 + yt−2 = (1− B)2yt .

Forecasting using R Backshift notation 42

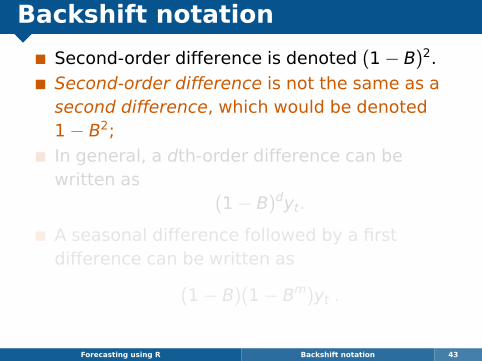

Backshift notation

Second-order difference is denoted (1− B)2.

Second-order difference is not the same as asecond difference, which would be denoted1− B2;

In general, a dth-order difference can bewritten as

(1− B)dyt.

A seasonal difference followed by a firstdifference can be written as

(1− B)(1− Bm)yt .

Forecasting using R Backshift notation 43

Backshift notation

Second-order difference is denoted (1− B)2.

Second-order difference is not the same as asecond difference, which would be denoted1− B2;

In general, a dth-order difference can bewritten as

(1− B)dyt.

A seasonal difference followed by a firstdifference can be written as

(1− B)(1− Bm)yt .

Forecasting using R Backshift notation 43

Backshift notation

Second-order difference is denoted (1− B)2.

Second-order difference is not the same as asecond difference, which would be denoted1− B2;

In general, a dth-order difference can bewritten as

(1− B)dyt.

A seasonal difference followed by a firstdifference can be written as

(1− B)(1− Bm)yt .

Forecasting using R Backshift notation 43

Backshift notation

Second-order difference is denoted (1− B)2.

Second-order difference is not the same as asecond difference, which would be denoted1− B2;

In general, a dth-order difference can bewritten as

(1− B)dyt.

A seasonal difference followed by a firstdifference can be written as

(1− B)(1− Bm)yt .

Forecasting using R Backshift notation 43

Backshift notation

The “backshift” notation is convenient because theterms can be multiplied together to see thecombined effect.

(1− B)(1− Bm)yt = (1− B− Bm + Bm+1)yt= yt − yt−1 − yt−m + yt−m−1.

For monthly data, m = 12 and we obtain the sameresult as earlier.

Forecasting using R Backshift notation 44

Backshift notation

The “backshift” notation is convenient because theterms can be multiplied together to see thecombined effect.

(1− B)(1− Bm)yt = (1− B− Bm + Bm+1)yt= yt − yt−1 − yt−m + yt−m−1.

For monthly data, m = 12 and we obtain the sameresult as earlier.

Forecasting using R Backshift notation 44