estate planning issues in pre- and post ... planning issues in pre- and post-nuptial agreements...

TRANSCRIPT

ESTATE PLANNING ISSUES IN PRE- AND POST-NUPTIAL AGREEMENTS

First Run Broadcast: March 5, 2013

1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes)

Martial agreements – both in pre- and post-nuptial forms – have lost their stigma and are

frequently used as estate planning tools. But they are not simple documents, either to plan or

draft, or to integrate with other estate documents. Martial agreements involve complicated issues

surrounding retirement account assets – IRAs, 401(k)s, and other qualified plans – life insurance

policies, personal residences, the allocation of debts, and the rights of former spouses and

children form prior marriages. In addition, if proper disclosures are not made, the agreements

are subject to challenge by one of the parties or by third parties. There are many planning traps

in martial agreements. This program will provide you with a practical guide to major estate and

trust issues in planning and drafting pre- and post-nuptial agreement, including retirement assets,

life insurance policies, personal residences, debts and expenses and more.

Estate and trust issues in martial agreements

IRA, 401(k) and retirement account issues

Life insurance policy considerations

QTIP planning and personal residences

Protecting trust assets in a divorce

Issues involving former spouses and children from prior marriages

Integrating martial agreements and estate planning documents

Speakers:

Bridget Sullivan is a partner in the Denver office Sherman & Howard, LLP, where her practice

focuses on estate planning, wealth transfer planning, estate administration, trust administration,

and litigation related to trusts and estates. Ms. Sullivan has extensive experience with

sophisticated estate planning techniques for prenuptial agreements, and has written and lectured

on the topic for numerous bar and other organizations. She has counseled clients on a variety of

wealth transfer strategies and charitable giving techniques to accomplish family giving

objectives while minimizing the impact of gift, estate, generation-skipping transfer, and income

taxes. Ms. Sullivan received her B.A. from Regis College and her J.D. from Yale Law School.

Jennifer A. Pratt is a partner in the Baltimore office of Venable, LLP, where she has assists

client with estate planning, charitable giving, and estate and gift tax controversy matters. She

has extensive experience with estate administration, the preparation of federal estate and gift tax

returns, as well as fiduciary income tax returns. Earlier in her career, she worked with a major

national bank and has particular expertise in adapting financial products to the estate planning

needs of clients. Ms. Pratt received her B.A., summa cum laude, from the University of

Baltimore, her J.D., magna cum laude, from the University of Baltimore School of Law, and her

LL.M. in taxation from the University of Baltimore.

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name: _____________________ Middle Initial: _____Last Name: __________________________

Firm/Organization:____________________________________________________________________

Address:___________________________________________________________________________

City:__________________________________ State: _________ ZIP Code: ______________

Phone #:________________________ Fax #:________________________

E-Mail Address: ____________________________________________________________________

I will be attending:

Estate Planning Issues in Pre- & Post-Nuptial Agreements

Teleseminar March 5, 2013

Early Registration Discount By 02/26/13 Registrations Received After 02/26/13

VBA Members: $70.00 Non VBA Members/Atty: $80.00

VBA Members: $80.00 Non-VBA Members/Atty: $90.00

NO REFUNDS AFTER February 26, 2013

PLEASE NOTE: Due to New Hampshire Bar regulations, teleseminars cannot be used for New Hampshire CLE credit

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association): $________________ Credit Card (American Express, Discover, MasterCard or VISA) Credit Card # ________________________________________Exp. Date_______ Cardholder: ________________________________________________________

Vermont Bar Association

ATTORNEY CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: March 5, 2013 Seminar Title: Estate Planning Issues in Pre- & Post-Nuptial Agreements Location: Teleseminar Credits: 1.0 General MCLE Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

TAX/1324233.1

ESTATE PLANNING ANDPRENUPTIAL AND POSTNUPTIAL AGREEMENTS

BY

BRIDGET K. SULLIVAN, ESQ.1

SHERMAN & HOWARD L.L.C. – DENVER, COLORADO(o) (303) [email protected]

AND

JENNIFER A. PRATT, ESQ.2

VENABLE, LLP – BALTIMORE, MARYLAND(o) (410) 528-2883

1 Bridget Sullivan is the Department Manager of the Tax & Probate Department Sherman &Howard L.L.C. in Denver. She practices in the areas of estate planning, wealth transferplanning, estate administration, trust administration, and litigation related to trusts and estates.Ms. Sullivan focuses on sophisticated estate planning techniques and prenuptial agreements. Shehas counseled clients on a variety of wealth transfer strategies and charitable giving techniques toaccomplish family giving objectives while minimizing the impact of gift, estate, generation-skipping transfer, and income taxes.

Ms. Sullivan graduated from Yale Law School in 1990. She is named in Best Lawyers inAmerica for Trust and Estates and is named as a Colorado Super Lawyer.

2 Ms. Pratt is a Partner at Venable LLP in Baltimore. She assists clients with estate planning,charitable giving, and business continuity planning while minimizing estate, gift and generation-skipping transfer tax exposure. She is experienced in the administration of decedent’s estates andthe preparation of estate planning documents and the incorporation and application forexemption for Private Foundations. Ms. Pratt assists clients and business owners with businesssuccession planning and business tax planning. Ms. Pratt is also experienced in drafting Pre-Marital Agreements and Post-Marital Agreements.

Ms. Pratt graduated with an LL.M. in Taxation from the University of Baltimore in 2006 andwith a JD from the University of Baltimore School of Law in 2000. She is listed in Best Lawyersin America for Taxation and is named as a Maryland Super Lawyers Rising Star.

2TAX/1324233.1

I. INTRODUCTION: ESTATE AND TRUST ISSUESIN MARITAL AGREEMENTS

Discussion By: Bridget Sullivan

The principal purpose of a marital agreement is to alter the rights otherwise provided bylaw of one or both spouses to the property of the other spouse, whether upon termination of themarriage by divorce or by death or both. Many states have a marital agreement act, whichdetermines the rights of parties who have entered a marital agreement, the types of matters thatparties may agree to and the enforceability of marital agreements.3 In most states, maritalagreements are enforceable under the terms of state law unless a party did not execute theagreement voluntarily or was not provided full and fair financial disclosure prior to signing theagreement.

This outline will focus on the trusts and estates, tax law, and estate planning techniquesas they relate to marital agreements. The state laws governing the property rights of a survivingspouse in and to the “estate” of the deceased spouse is a wholly distinct body of law from the lawgoverning property rights in divorce. The concepts of “marital property” and “separateproperty,” while central concepts to divorce law, have no application in the context of thetermination of marriage by the death of one spouse. When parties to a marital agreement intendto alter some of all of the rights and obligations arising as a result of death, the marital agreementshould set forth these death provisions separately from the divorce provision of the agreement.This outline is not intended to provide a discussion of divorce laws and the alteration of spousalrights in relation to a divorce by use of a marital agreement.

1. RIGHTS OF SURVIVING SPOUSE UPON DEATH OF OTHER SPOUSE

a. Waivers of Surviving Spouse Rights

A marital agreement may govern the rights of the parties in the event of thetermination of the marriage by death of either party. The agreement may include a partial orcomplete waiver of property rights arising at death. The agreement may also include a promiseto provide for a substitute transfer of property to the waiving spouse. While both parties to amartial agreement may agree to waive – in whole or in part – their respective property rightsarising at death, each party remains free to leave more property to the other than would berequired by the agreement. In other words, the marital agreement may limit the right to inheritfrom a spouse without imposing a ceiling on the potential of one spouse to provide voluntarilyfor the surviving spouse in excess of the rights granted by the agreement.

A release and waiver of “all rights upon death” or equivalent language in a maritalagreement encompasses the waiver of several statutorily granted spousal rights and priorities.

3 The following states have adopted the Uniform Premarital Agreement Act or some variation ofit: Arizona, Arkansas, California, Connecticut, Delaware, District of Columbia, Florida, Hawaii,Idaho, Illinois, Indiana, Iowa, Kansas, Maine, Montana, Nebraska, Nevada, New Jersey, NewMexico, North Carolina, North Dakota, Oregon, Rhode Island, South Dakota, Texas, Utah, andVirginia.

3TAX/1324233.1

These statutory rights and priorities include the right to a spouse’s elective share (sometimesreferred to as the statutory or forced share), the right to receive the family allowance and exemptproperty allowance, and the priority to serve as personal representative, executor oradministrator.

b. Status as Surviving Spouse

A person who is divorced from a decedent or whose marriage has been annulled isnot a surviving spouse. However a decree of separation does not terminate the status of husbandand wife for death purposes. A husband and wife are considered married regardless of whether adivorce action has been instituted. So, if one spouse dies after a decree of separation has beenentered or after a divorce action has been initiated, the survivor will likely have rights as asurviving spouse under most state laws.

A marital agreement can modify these provisions, stating specifically that aseparation decree or the filing of an action for divorce terminates all surviving spouse rights.

c. Intestate Share of Surviving Spouse

If a person dies without a will, the decedent’s property will be distributed inaccordance with the applicable statute of intestate succession. Under many states, the survivingspouse’s share of the intestate estate is dependent upon the circumstances of the parties,including whether there are adult or minor children of the marriage, whether the decedent hasadult or minor children from another relationship, and whether the decedent is survived by one orboth parents. Under the law of many states, the surviving spouse receives the entire intestateestate (1) when the decedent has no surviving descendants or ancestors or (2) when all of thedecedent’s surviving descendants are also descendants of the surviving spouse and there are notother descendants of the surviving spouse who survive the decedent (i.e., it was likely a firstmarriage for both spouses). The surviving spouse’s share tends to be diminished if the decedenthad children from other marriages.

d. Spouse’s Elective or Statutory Share

At common law, dower refers to the legal right or interest that a wife acquired inthe estate of her husband. It consists of the right to one-third of the husband’s real property.Curtesy is the common law life estate given to a husband in the real property of a deceased wife.Many states have abolished dower and curtesy, replacing these common law rights with statutoryrights to an elective or forced share.

Absent a marital agreement, the surviving spouse has the right to an elective shareof the augmented estate. Uniform Probate Code states have adopted a right to elect an amountnot greater than 50% of the “augmented estate”).4 Under the Uniform Probate Code, thepercentage of the augmented estate to which the surviving spouse is entitled is determined by thelength of time the spouses were married, but is essentially as follows:

4 The following states have adopted the Uniform Probate Code: Alaska, Arizona, Colorado,Florida, Hawaii, Idaho, Maine, Massachusetts, Michigan, Minnesota, Montana, Nebraska, NewJersey, New Mexico, North Dakota, South Carolina, South Dakota and Utah.

4TAX/1324233.1

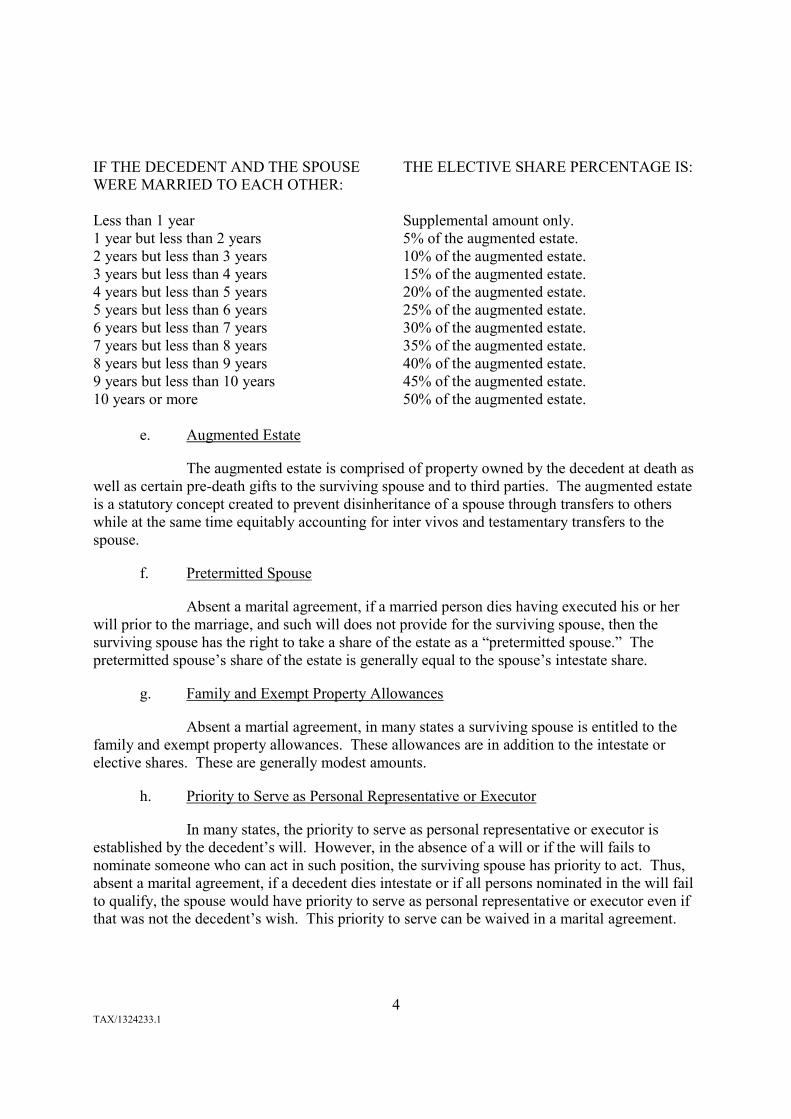

IF THE DECEDENT AND THE SPOUSEWERE MARRIED TO EACH OTHER:

THE ELECTIVE SHARE PERCENTAGE IS:

Less than 1 year Supplemental amount only.1 year but less than 2 years 5% of the augmented estate.2 years but less than 3 years 10% of the augmented estate.3 years but less than 4 years 15% of the augmented estate.4 years but less than 5 years 20% of the augmented estate.5 years but less than 6 years 25% of the augmented estate.6 years but less than 7 years 30% of the augmented estate.7 years but less than 8 years 35% of the augmented estate.8 years but less than 9 years 40% of the augmented estate.9 years but less than 10 years 45% of the augmented estate.10 years or more 50% of the augmented estate.

e. Augmented Estate

The augmented estate is comprised of property owned by the decedent at death aswell as certain pre-death gifts to the surviving spouse and to third parties. The augmented estateis a statutory concept created to prevent disinheritance of a spouse through transfers to otherswhile at the same time equitably accounting for inter vivos and testamentary transfers to thespouse.

f. Pretermitted Spouse

Absent a marital agreement, if a married person dies having executed his or herwill prior to the marriage, and such will does not provide for the surviving spouse, then thesurviving spouse has the right to take a share of the estate as a “pretermitted spouse.” Thepretermitted spouse’s share of the estate is generally equal to the spouse’s intestate share.

g. Family and Exempt Property Allowances

Absent a martial agreement, in many states a surviving spouse is entitled to thefamily and exempt property allowances. These allowances are in addition to the intestate orelective shares. These are generally modest amounts.

h. Priority to Serve as Personal Representative or Executor

In many states, the priority to serve as personal representative or executor isestablished by the decedent’s will. However, in the absence of a will or if the will fails tonominate someone who can act in such position, the surviving spouse has priority to act. Thus,absent a marital agreement, if a decedent dies intestate or if all persons nominated in the will failto qualify, the spouse would have priority to serve as personal representative or executor even ifthat was not the decedent’s wish. This priority to serve can be waived in a marital agreement.

5TAX/1324233.1

i. Federal Law Rights to Retirement Plan Assets

The survivorship rights in and benefits under qualified retirement plans aregoverned by federal law, including ERISA and other provisions of the Internal Revenue Code, itis federal law, and not state law, that governs when and how a participant may obtain a validwaiver of survivorship rights and interests in such plans. A participant in a retirement plancannot obtain a valid waiver of spousal survivorship rights prior to the parties’ marriage. Thus,the general waivers of “all rights upon death” or even a specific waiver of rights to a retirementplan, will not constitute an effective waiver of spousal survivorship rights in a retirement plan.Notwithstanding this fact, marital agreements often include waivers of surviving spouse rights toretirement assets. These waivers must be coupled with mutual promises to execute separateretirement plan waivers after the parties are married. Such a waiver might read as follows:

“Each party hereby waives any and all rights to any pension plan, profit sharingplan, deferred compensation plan or retirement benefits and cash accumulationsin life insurance which have or might have accrued for the benefit of the other,unless specifically designated as beneficiary. Each party agrees to execute thedocuments necessary to effectuate that waiver as required by the terms of thepension plan, profit sharing plan, deferred compensation plan or retirementbenefit plan, state law or federal law.”

2. WAIVERS OF SURVIVING SPOUSE ENTITLEMENTS IN MARITALAGREEMENTS

a. Waiver of statutory and common law rights upon death.

A release and waiver of “all rights upon death” or equivalent language in a maritalagreement encompasses the waiver of statutorily granted spousal rights and priorities. Suchwaivers can be done in a general waiver or in a more specific laundry list of waivers. I generallyprefer the laundry list, as it serves as an educational template, generating questions from theclient and a detailed discussion of spousal rights upon death. My laundry list (covering Coloradolaw) generally appears as follows:

“Specific Waiver. Upon the death of either of us, the other waives the following:

i. The right to take an intestate share under Colo. Rev. Stat. 15-11-102 or 15-11-301;

ii. The right to an elective share under Colo. Rev. Stat. 15-11-201,and to take any interest in the augmented estate under Colo. Rev. Stat. 15-11-202;

iii. The right to an exempt property allowance under Colo. Rev. Stat.15-11-403;

iv. The rights of an omitted spouse under Colo. Rev. Stat. 15-11-301;

v. The right to a family allowance under Colo. Rev. Stat. 15-11-404;

6TAX/1324233.1

vi. The right to a homestead interest under Colo. Rev. Stat. 38-41-201and 38-41-204 (as to each other, but not as to third parties);

vii. The right to act as a personal representative or trustee of the estateor trust of the other, unless specifically nominated or designated by the other;

viii. All rights to any pension plan, profit sharing plan, deferredcompensation plan or retirement benefits and cash accumulations in lifeinsurance which have or might have accrued for the benefit of the other, unlessspecifically designated as beneficiary; each of us agrees to execute the documentsnecessary to effectuate that waiver as required by the terms of the pension plan,profit sharing plan, deferred compensation plan or retirement benefit plan, statelaw or federal law ;

ix. Any rights to contest any disposition of property by the other byany inter vivos trust;

x. Any provisions of the Colorado Marital Agreement Act, Colo. Rev.Stat. 14-2-301 through 310 in conflict with this Agreement; and

xi. Any rights either of us might have to claim any portion of theestate of the other under the laws of any jurisdiction other than Colorado whichare of like or similar purpose to the enumerated Colorado statutes that providedower, curtesy, forced heirship, community property or marital property interestsor any other right to claim against the estate of a deceased spouse by a survivingspouse.”

b. Limitations on Waivers If There Are Children of the Marriage

Note, in cases of young couples marrying with family wealth who do not havechildren from previous marriages, sometimes these waivers of rights upon death are appropriateonly if there are no children of the marriage. In such circumstances, if the marriage produces nochildren and the wealthier parties dies, the waivers are intact, and the family wealth passes backto the family, subject to any provisions made for the surviving spouse, whether pursuant to theprovisions of the marital agreement or made voluntarily pursuant to the estate plan. However, ifthere are children of the marriage, it may not make sense to have the less wealthy spouse waive“all rights upon death.” If the wealthier spouse fails to follow up with estate planning or withproper estate planning, the less wealthy spouse, now the parent of the children of the marriage,may be disinherited.

c. Community Property Waivers

I practice in Colorado, which has adopted the Uniform Probate Code state and isnot a community property state. An exhaustive discussion of community property is outside thescope of this outline.

Generally, community property is owned by both spouses equally. Communityproperty does not include property owned by a spouse prior to marriage, property gifted from

7TAX/1324233.1

one spouse to the other, property inherited by a spouse or property which was separate propertyprior to the time the spouses moved to the community property jurisdiction. The titling ofproperty is not determinative of its status. Earned income of the spouses is community property.Income from separate property is community property in some jurisdictions and not in others.

Frequently, parties execute a marital agreement in one state and move to anotherjurisdiction. All practitioners should be careful to draft waivers of rights upon death broadlyenough to cover rights granted in any jurisdiction. A well drafted waiver of rights upon deathwill include a specific waiver of any property rights based on the laws of community property.(See the waiver in 3.a, xi, supra.)

California and Texas are both community property states that permit spouses tocontract with respect to their rights and obligations in property whenever and wherever acquiredor located. See CAL. FAM. CODE § 1612; TEX. FAM. CODE ANN. § 4.003. Thus, spouses mayagree, either in a prenuptial or postnuptial agreement, which property acquired during theirmarriage will constitute separate property and which will constitute community property.

In Texas, for example, spouses may agree that the income arising from onespouse’s employment will continue to be that spouse’s separate property. TEX. FAM. CODE ANN.§ 4.103. Spouses may also, at any time, partition or exchange between themselves all or part oftheir community property. § 4.102. Similarly, in California, spouses may agree, with or withoutconsideration, to transmute community property to separate property, and vice versa. CAL. FAM.CODE § 850.

From an estate planning perspective, one benefit of preserving communityproperty is that the entire property receives a step-up in basis at the death of the first spouse.I.R.C. 1014 (b)(6). Under Section 1014(b)(6), even though only the decedent spouse’s one-halfinterest is includable in his gross estate, the entire community property obtains a stepped upbasis. This is perhaps the greatest advantage of community property. Because of this advantage,a lawyer preparing a marital agreement for clients in a community property state or clients whohave migrated from a community property state will want to consider whether to retain thecommunity property character of certain assets.

3. SUBSTITUTE TRANSFERS IN EXCHANGE FOR WAIVERS OF SURVIVINGSPOUSE RIGHTS

It is common for parties who enter into mutual waivers of rights upon death toagree to make substitute transfer to each other, either during the marriage or at the time of death.Like most provisions of a marital agreement, the wealthier party may seek complete waiversfrom the less wealthy party in exchange for certain promised gift transfers during marriageand/or certain transfer upon death. The amount, timing and manner of fulfilling the substitutetransfers is subject to negotiation.

a. Federal Gift Tax Marital Deduction Issues

(a) Gifts to a Spouse During Marriage. Transfers to the spouse duringthe marriage will qualify for the unlimited deduction for gift tax purposes, so long as suchtransfers are made outright to the surviving spouse or to a qualifying trust. I.R.C. § 2523. A gift

8TAX/1324233.1

of a life estate or terminable interest will not qualify for the gift tax marital deduction, unlesssuch transfer is a qualified terminable interest as described in I.R.C. § 2523(f). Outright gifttransfers are obviously simplest from the perspective of qualifying for the gift tax exclusion.However, clients may be adverse to such outright transfers and may wish to make transfers intrust for the spouse.

(b) Inter Vivos QTIP Trust. If an inter vivos trust is created for thespouse, be sure the trust qualifies as a QTIP trust. If a QTIP trust is created and funded duringthe marriage, be sure to make a timely QTIP election. The IRS provides no relief for a late filedQTIP election for an inter vivos QTIP trust.

There are several significant advantages of a lifetime QTIP trust in amarital agreement setting. First, it allows the wealthier spouse to provide an income stream tothe less wealthy spouse during the marriage and after the wealthier spouse’s death. Second, atthe death of the beneficiary spouse, regardless of the order of deaths, the trust assets will pass tothe beneficiaries selected by the wealthier spouse (presumably the children from the firstmarriage). The unified credit and GST exemption of the less wealthy spouse can be fullyutilized, saving the wealthier spouse’s beneficiaries estate tax.

(c) Cautions. Be wary of drafting provisions which require thewealthier spouse to make transfers during the marriage or upon termination of the marriage tothe children of the less wealthy spouse. Such contemplated gifts should qualify for the gift taxannual exclusion (currently $12,000 or $24,000 if the spouses will gift split) or the exclusion forpayment of certain educational or medical expenses. I.R.C. § 2503.

(d) Gift Splitting. A marital agreement may request the less wealthyspouse to agree to gift splitting during the marriage, thereby allowing the wealthier spouse tomaximize gifting to descendants. Be specific about whether the less wealthy spouse isconsenting to gift splitting for annual exclusion gifts only or whether he/she is also consenting touse of his or her lifetime gift tax exemption. I.R.C. § 2513.

b. Federal Estate Tax Marital Deduction

The substitute transfer of property described in a marital agreement should qualifyfor the federal estate tax marital deduction. If the form of the transfer qualifies for the unlimitedmarital deduction, the property transferred will pass free of the federal estate tax at thetransferring party’s death. When a martial agreement provides for a marital deduction qualifyingtransfer, such as a QTIP trust, the agreement should explicitly allocate liability for the estate taxarising at the survivor’s death (presumably, but not necessarily, from the assets of the QTIPtrust). The following common forms of testamentary spousal transfers will qualify for theunlimited marital deduction.

i. An outright, unrestricted transfer of property;

ii. A transfer for a qualified terminable interest property (QTIP) trust;

9TAX/1324233.1

iii. A transfer to an estate trust or a power of appointment trust5;

iv. A transfer to a qualified domestic trust (QDOT) for a non-citizensurviving spouse;

v. A transfer of the right to unitrust or annuity payments from a charitableremainder trust.

c. QTIP Trusts

Estate planners frequently use QTIP trusts to provide for a second spouse,particularly when a party wishes to preserve wealth for children of a prior marriage. Atestamentary marital trust, created under the decedent’s will or revocable trust will qualify for themarital deduction as a QTIP trust if:

i. Property passes from the decedent to the QTIP trust;

ii. The governing instrument requires all income to be distributed at leastannually to the surviving spouse;

iii. No other beneficiary may have any rights in the trust during the survivingspouse’s lifetime; and

iv. The personal representative or executor makes the corresponding electionon the federal estate tax return filed for the decedent’s estate. I.R.C. § 2056(b)(7).

The obvious benefit of the QTIP trust is that the surviving spouse need not begiven a general power of appointment over the trust and therefore may be prevented fromdisinheriting the remainder men of the trust (presumably, the deceased spouse’s children from aprior marriage). This is the best method of “handcuffing” the inheritance of the surviving spousewhile at the same time qualifying the transfer for the marital deduction.

Another advantage of the QTIP trust is that if the surviving spouse has a minimalestate of his or her own, the unified credit of that less wealthy surviving spouse can be utilizedfor the benefit of the wealthier spouse’s beneficiaries. The same is true of the less wealthysurviving spouse’s generation skipping transfer tax (GST) exemption. Since the beneficiaryspouse is considered the transferor of the QTIP trust for estate tax purposes, that surviving

5 Because the QTIP trust is the most commonly favored modern form of marital trust, estateplanners don’t often use the estate trust or power of appointment trust in a marital agreementcontext. However, both of these trust forms qualify for the marital deduction. They aregenerally not favored in a marital agreement context where the deceased spouses wishes for theremaining trust to pass to his or her selected beneficiaries, because the estate trust must be paidto the spouse’s estate at death and the power of appointment trust requires that the survivingspouse must have a general power of appointment over the trust property at death. Both of theserequirements can defeat the protection provided to the children of the decedent spouse affordedby the QTIP trust.

10TAX/1324233.1

spouse’s GST exemption may be allocated to the trust thereby insulating the trust (or asubdivided portion of the trust) from GST tax.

(a) Standards and Guidelines for Principal Distributions. Providedthat the surviving spouse is entitled to the income from the trust, at least annually, the survivingspouse need not be given any other beneficial interests to the principal of the trust. Additionalaccess to principal, however, is frequently given to the surviving spouse for health, support, andmaintenance. Many times the marital agreement will specify under what circumstances principalmay be accessed by the surviving spouse.

(b) Selection of Trustees. The marital agreement may specify that athird party will serve as sole trustee or as co-trustee with the surviving spouse to ensure betterprotection to the trust assets for the remainder beneficiaries. “Neutral” trustees and successortrustees are generally advisable. The surviving spouse as sole trustee generally provides lessprotection to principal than the deceased spouse may want. On the other hand, a child of thedecedent (the step-child of the surviving spouse) as trustee may cause family discord. Asurviving spouse might be allowed to select a trustee among a group of mutually agreeablepotential trustees. Or, a surviving spouse could be authorized to appoint an institutional trustee.

(c) Selection of Assets. The marital agreement may provide specificdirections with regard to what assets will be directed into the QTIP trust for the benefit of thesurviving spouse. If there is a closely held business, both spouse’s may favor terms prohibitingsuch closely held stock from passing to the QTIP trust. If the wealthier spouse holds promissorynotes from children, the less wealth spouse may want to include a provision specificallyprohibiting those types of assets from being used to fund the QTIP trust.

(d) Further Examples of QTIP Trust Provisions.

Example 1 – Standard QTIP Provisions:

If our marriage terminates by virtue of Ann’s death, Ann agrees to makeprovisions by will, trust, beneficiary designation or other dispositive instrument toprovide Sam with a disposition of property in a Marital Trust of two milliondollars ($2,000,000) which is intended to qualify as a Qualified Terminal InterestProperty (“QTIP”) trust under Section 2056 of the Internal Revenue Code. Noestate or death taxes shall be allocated to any amount passing to the MaritalTrust at Ann’s death. The trustee of the Marital Trust shall pay to Sam thegreater of all income or a five percent (5%) unitrust payment at least annually forlife. In addition, the trustee in his or her discretion may distribute principal toSam for his health, support and maintenance. The trustee shall be a corporatetrustee designated by the terms of Ann’s estate planning document or anindividual trustee designated by the terms of Ann’s estate planning document andapproved by Sam. At Sam’s death, the balance of the trust principal remaining, ifany, shall be distributed to Ann’s chosen beneficiaries in accordance with her willor trust. Sam acknowledges that Ann’s personal representative may elect QTIPtreatment of the Marital Trust under Section 2056 of the Internal Revenue Code.

11TAX/1324233.1

At Sam’s death, the Marital Trust shall bear any and all estate or death taxesattributable to the inclusion of the trust in Sam’s estate.

Example 2 – Directions with Regard to Specific Assets:

Jim agrees that if the marriage terminates by his death, he shall make provisionsin his will, revocable trust or other dispositive estate planning instrument toprovide Sally with the following:

1. An outright disposition of Jim’s general partner interest in Jim-Sally Family Partnership.

2. A lifetime interest in a Marital Trust which shall meet therequirements of a Qualified Terminal Interest Property Trustunder Section 2056 of the Internal Revenue Code. The MaritalTrust for Sally shall be composed of cash or marketable securitieshaving a fair market value on Jim’s date of death of $3,000,000.Under the terms of the Marital Trust, Sally shall receive thegreater of all net income from the trust or four percent (4%) of thenet fair market value of the assets (calculated excluding the valueof non-productive real property)of the trust valued as of the lastbusiness day of the first calendar month of each taxable year of thetrust ("unitrust amount"). The net income or 4% unitrust amountshall be paid to Sally in payments which are made at least quarter-annually. In addition, the trustee of the Marital Trust shalldistribute to or for the benefit of Sally so much of the principal asthe trustee, in its sole discretion, shall consider necessary oradvisable for the support, health, and maintenance of Sally. Sallyshall be named as co-trustee of the Marital Trust, and her rights asa co-trustee under Colorado law shall not be limited by the termsof the Marital Trust. At Sally's death, the balance of the trustprincipal remaining shall be distribute in equal one-thirds to Jim’stwo daughters and Sally’s daughter (“our daughters”), or if anyone of our daughters is not then living, her share shall pass to herdescendants, by representation, or if one of our daughterspredeceases Sally leaving no descendants, the balance of the trustprincipal shall be distributed in equal shares to our daughters,then living. At Sally’s death, if none of our daughters nor anydescendants of our daughters are then living, then Sally mayappoint 20% of the trust principal by a testamentary power ofappointment among any persons, and the remaining 80% shallpass to Jim’s contingent beneficiaries as determined by his will orrevocable trust document.

12TAX/1324233.1

d. Credit Shelter Trust

Now that the federal estate tax exemption is set at $5,000,000 and indexed toinflation ($5,250,000 in 2013), the provisions for the less wealthy spouse upon the death of thewealthier spouse may include an agreement to make the less wealthy spouse the only beneficiaryor the primary beneficiary of the credit shelter trust.

If the less wealthy spouse is the survivor and is made sole beneficiary of the creditshelter trust, the same issues arise with a QTIP trust, namely: (1) trustee selection, and (2)language regarding distribution of principal to the surviving spouse.

If the credit shelter trust will allow additional beneficiaries, such as children of thedeceased spouse, the terms of the distribution provisions should be carefully detailed in themarital agreement, to avoid conflict between the surviving spouse and the children of thedeceased spouse.

e. Use of Life Insurance in Conjunction with a Marital Agreement

Some parties to a marital agreement favor a waiver by the less wealthy spouse ofall rights upon death of the wealthy spouse coupled with a death benefit paid to the survivingspouse pursuant to a life insurance policy. If the wealthy spouse owns the policy and designateshis or her spouse as the beneficiary, the policy proceeds will be included in the decedent’s estate,by will qualify for the estate tax marital deduction. If the surviving spouse is both the owner andthe beneficiary of the policy, the policy proceeds will not be included in the decedent’s grossestate.

The parties to the marital agreement may want to address specifically what typeof policy is to be acquired to satisfy the provisions of the agreement. Term insurance willobviously be less expensive, but if the marital agreement requires the insured spouse to maintainsuch insurance until death, a term policy may become impractical or unaffordable at some point.If the marital agreement requires the insured spouse to carry insurance until death, the agreementshould require that permanent insurance be acquired.

The parties to the agreement also may want to specify that the beneficiary spousebe the owner of the policy. This will prevent the insured spouse from changing the beneficiary,cancelling the policy or borrowing against the policy without the beneficiary spouse’s consent.

The agreement should specifically address which party will have the obligation topay the premiums.

If you represent the beneficiary spouse, consider drafting a backstop provisionwhich will give the surviving spouse a right to claim against the decedent’s estate if, for anyreason, such insurance is not in place at the death of the spouse whose life was to be insured.

Consider using a QTIP trust or an irrevocable life insurance trust as thebeneficiary of the insurance policy if the wealthy spouse wishes to have the policy proceedsremaining after the surviving spouse’s death pass to his or her children from a previous marriage.

13TAX/1324233.1

f. Joint Tenancy

Clients should be advised regarding the implications of joint tenancy and thepossibility of defeating all of the careful planning for death in the marital agreement by holdingproperty as joint tenants with rights of survivorship.

Consider including a provision in the marital agreement which gives the wealthierspouse credit for joint tenancy transfers against any required devises to the surviving spouse. Igenerally include the following language:

“Effect of Jointly Held Property, Beneficiary Designation Property, or Transfer onDeath Property Payable to Joe. If Jane predeceases Joe, the obligation to provideJoe with an outright disposition of cash or marketable securities having a fairmarket value of $500,000 under paragraph ______ shall be deemed satisfied tothe extent of the date of death value of any cash or marketable securities passingby beneficiary designation or transfer on death designation and to the extent ofone-half of the date of death value of cash or marketable securities passing byjoint tenancy or tenancy by the entireties as a result of Jane’s death. If Janepredeceases Joe, the obligation to provide Joe with $2,000,000 in a marital trustunder paragraph ____ shall be deemed satisfied to the extent of the date of deathvalue of any property passing by beneficiary designation or transfer on deathdesignation and to the extent of one-half of the date of death value of jointtenancy or tenancy by the entireties property passing to Joe as a result of Jane’sdeath. If the value of property passing to Joe by beneficiary designation, transferon death designation, joint tenancy or tenancy by the entireties should exceed therequired amount payable to Joe pursuant to paragraphs _____, then Jane’s estateshall have no further obligation to Joe under this Agreement, nor shall Joe haveany obligation to return funds to Jane's estate.”

g. Tenancy by the Entirety

As with joint tenancy, clients must be wary of the implications of holdingproperty in this manner. Tenancy by the entirety resembles joint tenancy in that upon the deathof either the husband or wife, the survivor automatically acquires title to the share of thedeceased spouse. In states that recognize tenancy by the entirety, it may exist only between ahusband and a wife, and can only be terminated by death, divorce, or mutual agreement. Thus, itmight be wise to include a provision similar to the one above whereby the wealthier spouse isgiven credit for transfers of property held in tenancy by the entirety against any required devisesto the other spouse.

4. COORDINATION OF ESTATE PLANNING DOCUMENTS WITH THEMARITAL AGREEMENT

a. Maintenance of Testamentary Documents

If the marital agreement requires that wills, trusts, beneficiary designations, deeds,or other documents be prepared to reflect the agreement reached, this can be done by one of twomethods: (1) the marital agreement can be drafted as a specific roadmap which will contain the

14TAX/1324233.1

essential terms of the documents that will be prepared at a later date, or (2) the marital agreementcan include concurrently prepared and executed documents as exhibits to the agreement.

If the parties execute a marital agreement which provides a general waiver or “allrights upon death” or similar language, be sure to advise your client to maintain updated estateplanning documents after the marriage if your client does in fact wish to leave property to thespouse.

b. Enforcement for Breach

If the marital agreement requires a spouse to devise property to the survivingspouse, the agreement constitutes a contract to devise property. Be sure to consult your statelaws regarding contracts to make a will or devise to ensure that the marital agreement satisfiesany specific requirements. Assuming the marital agreement also qualifies as a contract to make awill or devise, the terms of the agreement will be enforceable notwithstanding the decedent’sfailure to make the devise required by the contract. The surviving spouse would then be treatedas a claimant against the decedent’s estate and would have to comply with the claims statutes. Ifyou represent the spouse who is to receive the devise in accordance with the marital agreement,consider including language which extends the surviving spouse’s time for making a claim andwhich reimburses the surviving spouse for attorney’s fees incurred in connection with the claim.I use the following language:

“Provisions Binding on John’s Estate. John intends to make provisions in hiswill, revocable trust or other dispositive estate planning instrument which willprovide Sally with the benefits described in paragraph ___. However, if no suchwill, revocable trust or other dispositive estate planning instrument provisionshave been executed, or if purported will or revocable trust provisions or otherdispositive estate planning instrument provisions should be ineffective or onlypartially effective, or if for any reason provisions made by John do not secure forSally the benefits described in paragraph ___, John agrees and specificallydirects that if Sally survives him, she shall have a claim against his estate oragainst any other assets, or the transferee of any other assets, passing as a resultof his death, for the benefits described in paragraph ___ or for so much of suchbenefits as are not otherwise provided for her, and for Sally’s reasonableattorneys' fees incurred to present such claim. If John predeceases Sally, Johnintends and directs that his estate, fiduciaries, beneficiaries, and transferees shallbe bound by this Agreement and direction, and John further agrees that if Sally’srights under paragraph ___ are created by John’s agreement and direction in thisparagraph that Sally shall have a claim for them, rather than by specificprovisions in John’s will, revocable trust, beneficiary designation or by non-testamentary provisions, and if for any reason Sally fails to file her claim duringthe period in which a claimant may file such a claim against John’s estate, Johndirects his fiduciaries, beneficiaries and transferees to refrain from asserting thatfailure as a defense to Sally’s claim, so long as such claim is made within oneyear of John’s death.”

15TAX/1324233.1

c. New Estate Planning Clients – Verify Whether a Marital Agreement Exists

New estate planning clients may not mention the existence of an old maritalagreement. Estate planning attorneys should specifically confirm with clients whether or nor amarital agreement exists, and if one does, obtain a copy.

d. Estate Planning Clients with Grown Children

When preparing estate planning documents for wealthy clients with grownchildren, consider having a discussion with those clients regarding whether the children have orshould have marital agreements in place. This may affect whether a client decides to leaveproperty outright or in a lifetime trust to an adult child.

5. PORTABILITY AND THE DECEASED SPOUSAL UNUSED EXLCUSIONAMOUNT

Portability of a deceased spouse’s estate tax exemption was made permanent on January2, 2013, with the American Taxpayer Relief Act. Now, Code Section 2010(c)(4) which allowsthe surviving spouse of a deceased spouse dying after December 31, 2010, to use the deceasedspouse’s unused exclusion amount (DSUE) as an exemption against estate tax in the survivingspouse’s estate, is a permanent part of the estate tax law.

In order for the surviving spouse to obtain the deceased spouse’s DSUE amount, anelection must be made on a timely filed Form 706, Federal Estate Tax Return, at the firstspouse’s death.

With the estate tax exemption now set at $5 million, plus inflation adjustment, theportable DSUE amount should be viewed as a valuable asset of the less wealthy spouse. Forexample, if the prospective wife has an estate of $10 million, and her prospective husband has anestate of $1 million, if the husband predeceases wife, his unused exemption amount or DSUEcould be ported to the wife’s estate at her second death, allowing her to shelter at least $4 millionof additional assets at her death.

Because the portability election must be made by the Executor or Personal Representativeof the first spouse’s estate, the parties should agree in the Marital Agreement that the lesswealthy spouse will leave instruction in his or her estate planning document directing his or herExecutor or Personal Representative to file the Form 706 and make the portability election. Inthe absence of such a filing, the children of the less wealthy spouse may not want to file theForm 706, because it would otherwise be unnecessary if the less wealthy spouse’s estate is wellunder the estate tax exemption amount. Because of the added costs of preparation of the Form706 for the less wealthy spouse’s estate, which filing benefits only the wealthier spouse’s estate,the marital agreement should obligate the wealthier spouse to pay for the preparation of the Form706.

Please see the article entitled “Portability and Prenuptials: A Plethora of Preventative,Progressive and Precautionary Provisions,” by George D. Karibjanian, published in the 2012Tax Management Memorandum by Tax Management Inc, for numerous examples of samplelanguage for marital agreements dealing with the portability issues.

16TAX/1324233.1

II. PROTECTING TRUST ASSETS IN A DIVORCE

Discussion By: Jennifer Pratt

If the marital agreement does not specifically address trust assets, then whether trustassets will be subject to distribution upon a dissolution of the marriage, and if so to what extentthe trust assets could be invaded are subject to litigation at the time of the dissolution proceeding.This litigation is costly and time consuming.

a. State Law Concerns. Each state has different rules regarding the criteria whichresults in trust assets being subject to distribution upon dissolution. Although the parties mayenter into marriage in one state where the laws are known and aligned with the partiesexpectations, the parties could later move to another state whose laws are very different,therefore the marital agreement should detail the expectations of each party with respect to trustassets.

b. Trust Assets: Marital Property or Separate Property. The marital agreement needsto specify whether certain trust assets will be included in the definition of marital property or beexcluded and treated as sole and separate property, including the criteria for possible future trustscreated by the spouse, the spouse’s family members, etc. The marital agreement should alsospecify how distributions from any trusts during the parties’ marriage will be treated, will they beconsidered marital property once distributed from the trust or are distributions intended to remainsole and separate property.

c. Powers of Appointment/Powers of Withdrawal. The marital agreement needs tospecify exactly what is intended with respect to any powers of appointment or powers ofwithdrawal over trust assets. Many times trusts are created by parents or grandparents allowingan invasion of principal at stated times during the trust terms. The parties need to thoroughlystate what their intentions are with respect to withdrawals that have not yet been taken by thepermitted party or how powers of appointment should be exercised. Is it intended that the spousethat is a beneficiary will take the permitted distributions, or is it left to that spouse’s solediscretion to decide.

III. ISSUES INVOLVING FORMER SPOUSES AND CHILDREN FROM PRIORMARRIAGES

Discussion By: Jennifer Pratt

Second marriages and children from first marriages result in significantly morecomplexity for negotiating the marital agreements. There may be prior requirements that are yetto be satisfied from the first marriage. There may be ongoing support obligations to the priorspouse and children that need to be addressed in the marital agreement for the second marriage.

a. Prior Marital Home. The spouse may own a residence that is his sole asset, yet theprior spouse and children are now living in that residence. The spouse may be required toprovide for the payment of the mortgage or maintenance expenses on the prior marital home for

17TAX/1324233.1

a period that continues until his youngest child graduates from college. In the event of death ofthe spouse, the residence would be considered an asset, yet without an agreement, the estate maybe faced with raising cash to buy out the new spouse’s interest in the home occupied by the firstspouse. Additionally, if the second marriage ends in divorce, should the prior marital home beconsidered marital property, the appreciation on the home’s value? What about improvements tothat home made with contribution from wages? Without a properly drafted marital agreement,there could be significant issues.

b. Estate Benefits to Prior Spouse or Children. The second spouse and children fromthe first marriage are wrought with concerns that need to be negotiated by the parties. Thespouse may have an obligation to provide for a specific death benefit to the children from thefirst marriage, how does that impact the planning with the second marriage. Additionally, thetime assets could remain in trust for a surviving spouse’s lifetime could be affect by a secondmarriage to a much younger spouse. If the plan was to fund a trust for surviving spouse’slifetime, then remainder to children from the first marriage, the children could be waiting manymore years before distributions are coming to them. This could cause tension between secondspouse and children. The marital agreement will spell out what the intentions of the parties arefor estate benefits for the second spouse and will make it clear the natural parent’s objectives andgoals. Absent a marital agreement, these issues could be fought in courts expended much timeand proving to be costly.

IV. PERSONAL RESIDENCE ISSUES

Discussion By: Bridget Sullivan

Frequently, the marital agreement will address the use and disposition of the primaryresidence during the marriage, upon a divorce, or after the death of the owner spouse. Inaddition, the marital agreement frequently addresses secondary residences as well.

a. Definitions. First, it is important to define the primary residence, so that formulti-residence couples, there will be no room for ambiguity.

“The primary residence where the parties intend to reside following theirmarriage is located at _________________. In the future, if the parties choosean alternate residence as the parties’ primary residence, such primary personalresidence shall be defined as that residence in which the parties jointly spentmore nights than any other residence owned by either or both of the parties in thetwelve months immediately prior to [dissolution of the marriage or death of oneparty].”

b. Expenses of Residences. In many cases, it may be important to clarify whoshould pay for expenses of the parties during the marriage.

“Joint Living Expenses. John will pay for our reasonable and customary jointliving expenses incurred during the marriage and prior to the filing of a petition,at a standard of living which Steve determines reasonable in his sole discretion.Joint living expenses shall include, but not be limited to, the following: (a) allexpenses incurred in maintaining all residences of the parties; (b) all reasonable

18TAX/1324233.1

expenses incurred for our support and maintenance; (c) all expenses related toour health and medical care; (d) all expenses incurred in procuring, maintaining,and insuring automobiles for each of us; (e) all expenses incurred for our jointtravel, recreation, and entertainment; and (f) all joint debt. Joint living expensesincurred after the date of a separation but prior to the date a petition is filed shallbe reasonable and customary and consistent with past practices. Use of separateproperty or income from separate property by Steve to pay joint living expensesshall not cause his separate property, or any portion of it, to be recharacterizedas marital property.”

- or -

“Living Expenses Related to Residences. Each party will pay all expenses formaintaining all residences titled in that party’s name. For any jointly titledresidences, all expenses of maintaining such joint residences shall be split equallybetween the parties.”

c. Transfer of Interest in Residence as Gift During Marriage

“Gifts During Marriage. John agrees that as a gift to Jane, no later than sixtydays after the Marriage Date, she will cause to be delivered and recorded a deedtransferring to Jane a one-half interest in John’s residence located at_______________, Colorado. Title shall be held by both parties as equal tenantsin common. This gift is contingent upon the occurrence of our marriage.”

- or -

“Use and Possession of Primary Residence After Filing of Petition. During thependency of the petition, John shall have the exclusive right to the use andpossession of the parties’ primary residence. John shall have a right of firstrefusal to purchase Jane’s ownership interest in our primary residence. In orderto exercise such right of first refusal, John must give written notice to Jane withintwo months of the filing of a petition that she will exercise her right. John willthen have an additional two months to complete the purchase of Jane’s interest inthe residence at fair market value less Jane’s share of debt encumbering theproperty, if any, and refinance any mortgage so that she is solely responsible forany mortgage on the residence. If John does not exercise her right of first refusalwithin two months of the date a petition is filed, then Jane shall have a right offirst refusal to purchase John ’s interest under the same terms. Jane’s right offirst refusal shall last for two months from the time John fails to exercise herright of first refusal. The fair market value of the residence shall be determinedby the average of two appraisals performed by qualified residential appraisersand based on comparable sales; one obtained by John and one obtained by Jane.That average appraised value shall then be multiplied by the seller’s ownershipinterest as set forth on the title to determine the gross purchase price. The debtencumbering the property, if any, shall also be multiplied by the seller’sownership interest as set forth on the title to determine the seller’s share of debt.

19TAX/1324233.1

The seller’s share of debt shall then be subtracted from the gross purchase priceto determine the net purchase price. If both John and Jane decline theirrespective right of first refusal, the house shall be placed on the market for sale assoon as possible. If the house is placed on the market for sale, mutually agreedupon expenses incurred in preparing the house for sale and all costs of the saleshall be paid by the parties in proportion to their respective ownership interestsas indicated on the instrument of title. John shall pay all maintenance expenses,including the mortgage (if any), taxes, and insurance, from the time a petition isfiled until the residence is sold, unless Jane exercises his right of first refusal, inwhich case he shall pay all maintenance expenses from the time he gives Johnwritten notice that he is exercising such right.”

Be wary of provisions which transfer a property to the less wealthy spouse during themarriage, such as title to a residence, but provide that if a divorce were to occur the residenceshall revert to the wealthier spouse. This may be attractive from an estate planning perspectiveand it may be attractive to the less wealthy spouse because she will hold the residence outright(rather than in a marital trust) at the wealthier spouse’s death. However, this arrangement maynot qualify for the gift tax deduction as an outright transfer to the less wealthy spouse. Rather itwill likely be treated as a terminable interest because the interest transferred to the less wealthyspouse will terminate or fail upon an event (the divorce) and because the donor retains in himselfan interest in such property (the right of the property to revert to the donor upon a divorce).I.R.C. § 2523(b).

d. Transfers of Residence Upon Death of One Spouse

“Provisions for John as Mary’s Surviving Spouse. If our marriage terminates byMary’s death and if John survives Mary by at least 90 days, Mary agrees that shewill make provisions by will, trust or other dispositive instrument to provide Johnwith a Marital Trust which shall be funded with Mary’s entire ownership interest,if any, in the parties’ primary residence free and clear of all encumbrances, plusfurniture and furnishings in the parties’ primary residence. The trustee shall bedesignated by the terms of Mary’s estate planning document.”

If the residence is transferred to the QTIP trust, it will be important to include provisionsin the QTIP trust so that the surviving spouse’s rights to the residence will constitute thenecessary qualifying income interest (i.e., the surviving spouse must have the right to demandthat unproductive property be made productive). Consider the following provision:

“Following the settlor’s death and during the surviving spouse’s remaininglifetime, the real property that was used by the parties as their primary residenceshall be distributed to the marital trust. The trustee shall accord to the survivingspouse the free use and enjoyment of such real property as one of the benefits ofthis trust. The trustee shall also be authorized, in its discretion, to sell orexchange such residential real property held as a trust asset, and to invest theproceeds in other residential real property, or to hold any residential realproperty acquired by exchange, supplying to the surviving spouse the free use andenjoyment of such newly acquired real property, so that she shall be afforded a

20TAX/1324233.1

satisfactory home during her lifetime. Such use and enjoyment shall be accordedas the surviving spouse’s sole responsibility, but the trustee may utilize so much ofthe net income of the trust or, if the net income is insufficient, the principal, as itshall determine to be necessary or advisable to discharge the cost ofmaintenance, upkeep, insurance, and taxes on such property. At such time as thesurviving spouse ceases to use such residential real property and has no use forother residential real property for her personal use, the trustee shall be free tosell the residential real property that is an asset of the trust and add the proceedsfrom such sale to the principal of the trust. The trustee always shall have fullauthority to carry such insurance on such real property, and in such amount andform, as it may require for its own protection, as an expense of administering thetrust. The trustee shall not be accountable for any loss sustained by reason of anyaction taken under the provisions of this paragraph.”

V. IRA, 401(K) AND RETIREMENT ACCOUNT ISSUES & LIFE INSURANCEPOLICY CONSIDERATIONS

Discussion By: Jennifer Pratt

a. Retirement Accounts. Retirement accounts like 401(k), IRAs, 403(b) or similarqualified plans provide many unique concerns. These assets pass by beneficiary designations soit is important to be sure that what was agreed to in a marital agreement actually gets filed withthe plan administrators. Furthermore, there are specific rules with qualified plans that requireconsents if the spouse is not the named beneficiary. It is important to get the proper waivers andconsents during the time you are signing the marital agreement so that there are no problemsdown the road. Additionally, there are tax implications to who is the beneficiary of the qualifiedretirement accounts and those need to be negotiated as well.

b. Insurance Policies. Insurance policies are similar to retirement accounts in the factthat they too pass by contract beneficiary designation. Insurance policies are a terrific way tofund some of the obligations that incur under the marital agreement, but this also creates therequirement to maintain insurance. There are some considerations if you have a policy which isintended to be split among different beneficiaries. What happens if the policy is cancelled ordoes not perform, is there another plan in which to fund the obligations. Again here it isimportant to be sure to correctly complete the insurance designation forms so that the formsmatch what was agreed to in the marital agreement.