economics chapter 11.2

TRANSCRIPT

ECONOMICSApril 15, 2015

Chapter 11: Financial Markets

Section 11.2: Bonds and Other

Financial Assets

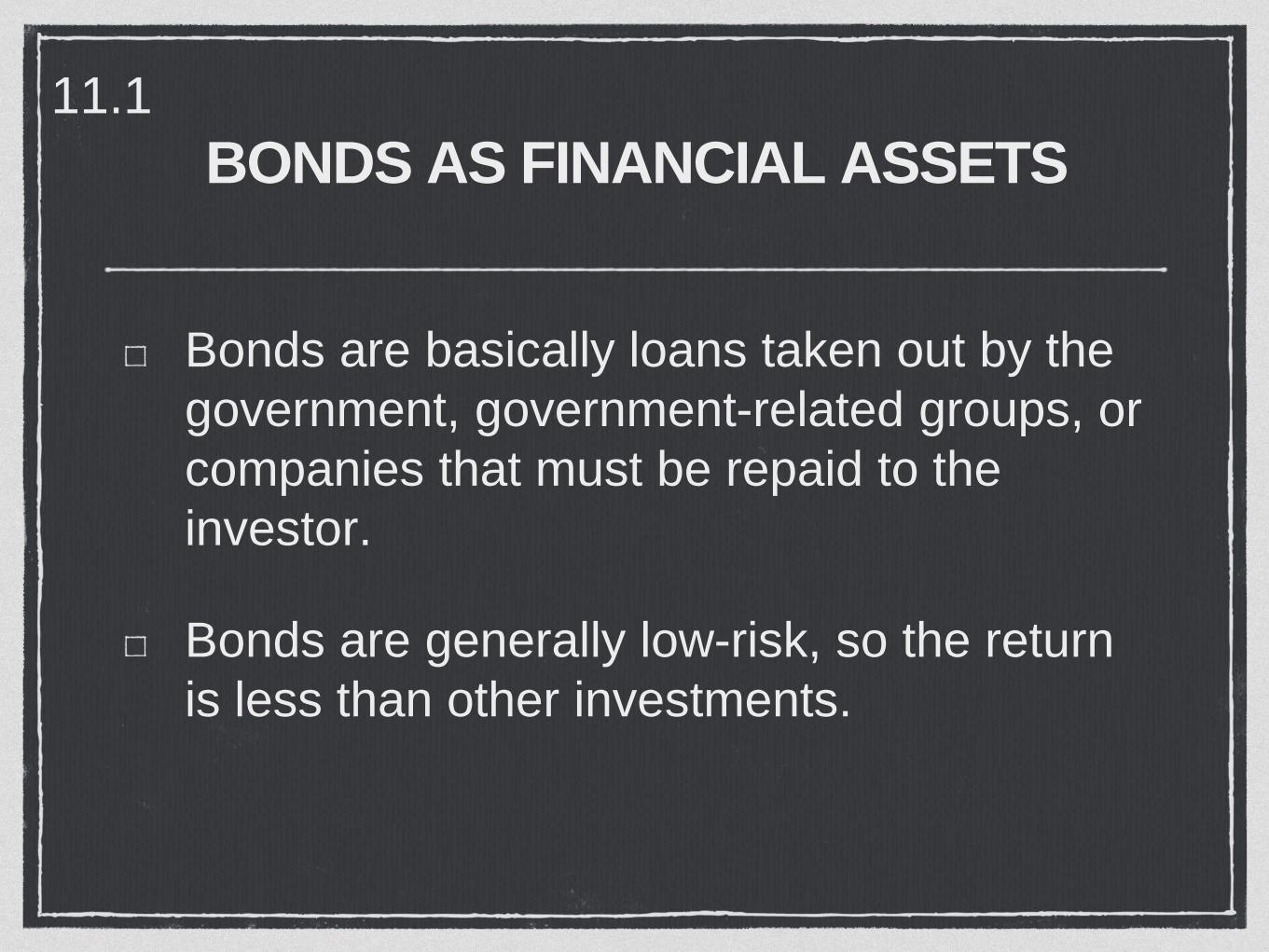

BONDS AS FINANCIAL ASSETS

Bonds are basically loans taken out by the

government, government-related groups, or

companies that must be repaid to the

investor.

Bonds are generally low-risk, so the return

is less than other investments.

11.1

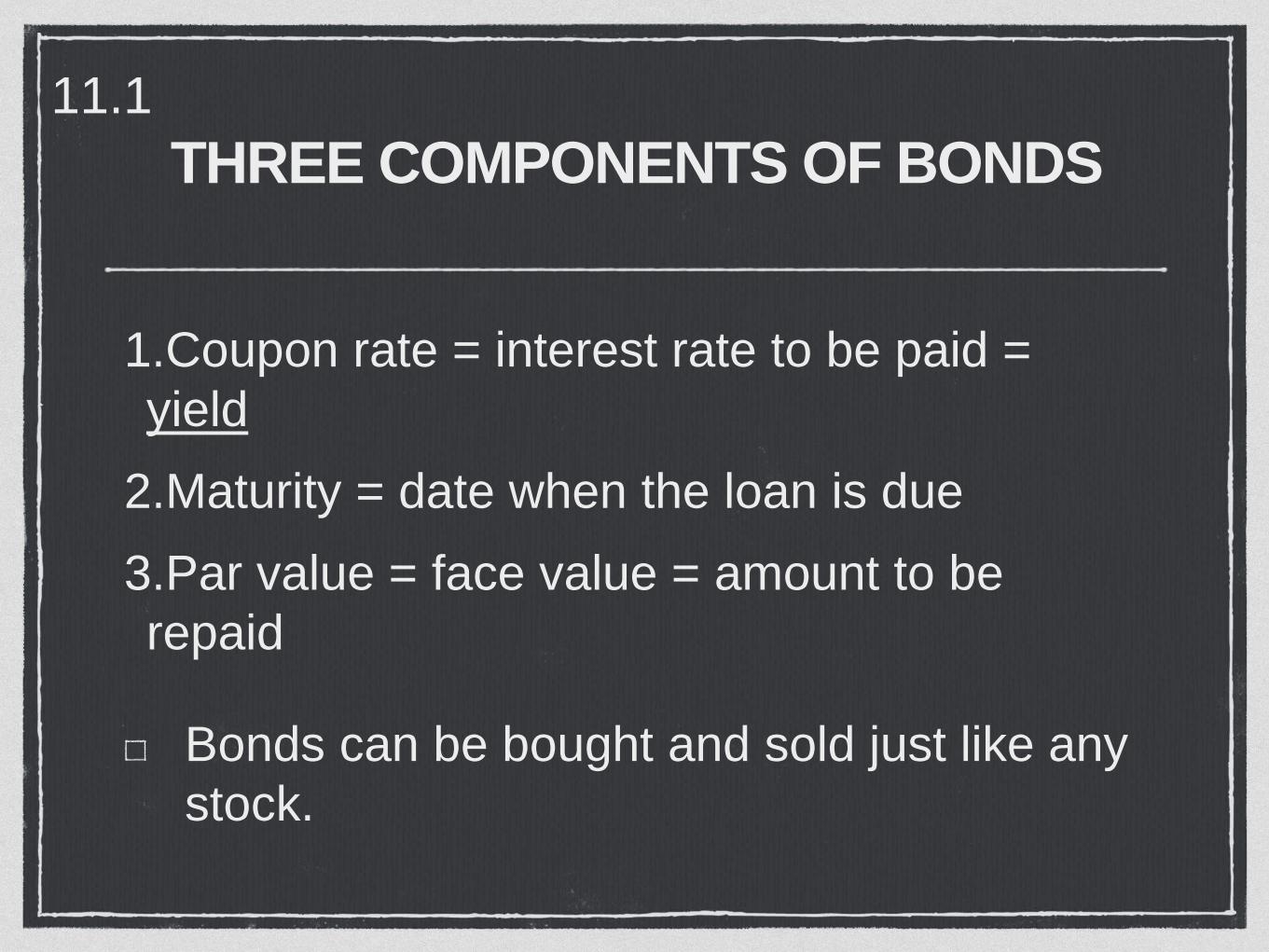

THREE COMPONENTS OF BONDS

1.Coupon rate = interest rate to be paid =

yield

2.Maturity = date when the loan is due

3.Par value = face value = amount to be

repaid

Bonds can be bought and sold just like any

stock.

11.1

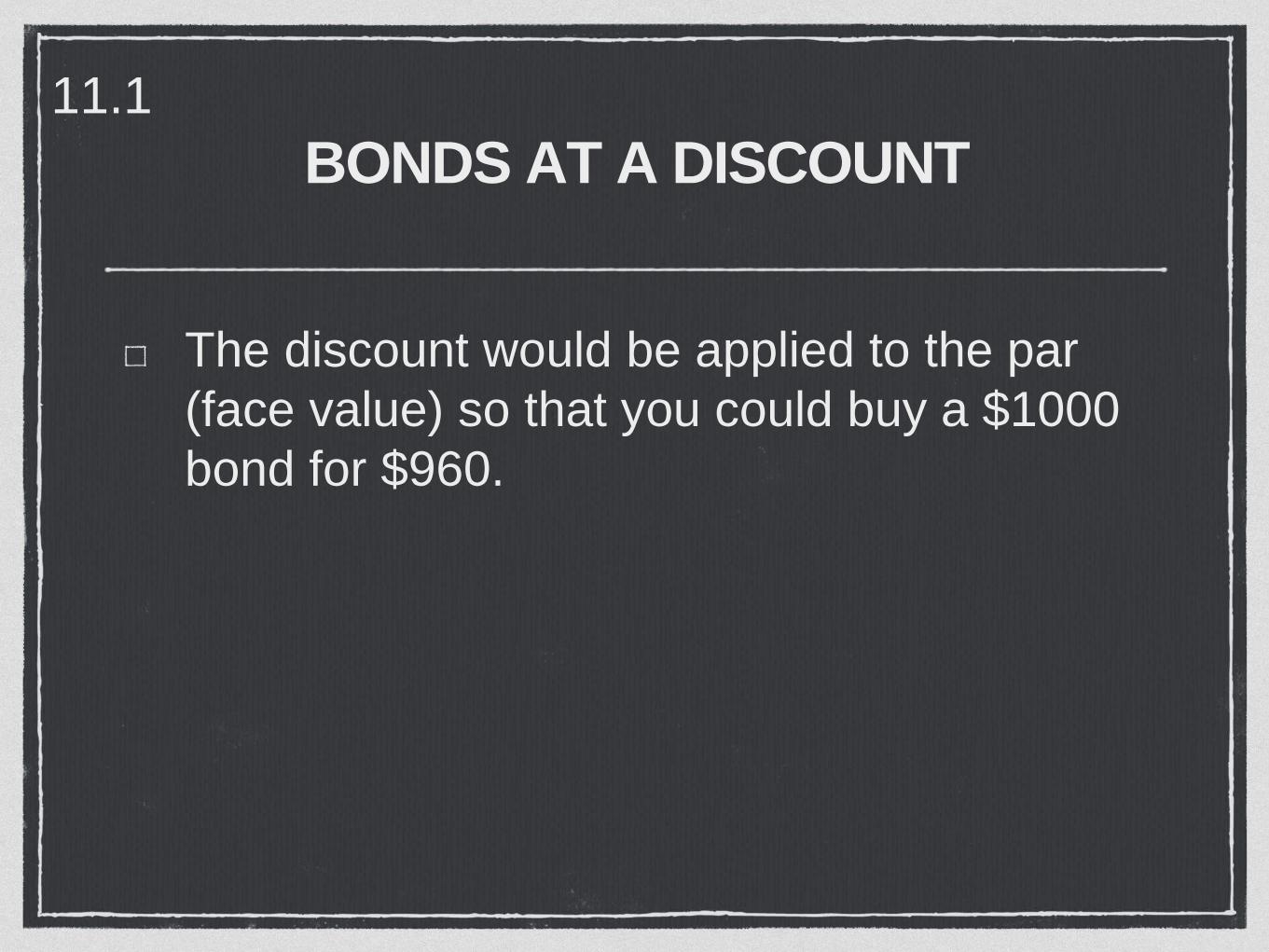

BONDS AT A DISCOUNT

The discount would be applied to the par

(face value) so that you could buy a $1000

bond for $960.

11.1

BOND RATINGS

Because bonds are formed of loans taken

out, the company or government issuing

the bonds are subject to ratings just like

other borrowers.

Just like your personal credit rating, your

government wants the highest possible

(AAA, Standard and Poor’s).

11.1

BONDS AT A DISCOUNT

A higher rating on the bonds might mean

you would pay more than the par value for

that bond.

The higher the rating, the higher the price

of the bond. This is good for the company

selling the bonds and for the individual

selling their bonds.

11.1

ADVANTAGES AND

DISADVANTAGES OF BONDS

Once the bond is issued, the coupon rate

will not change.

Bondholders do not own a part of the

company, only a part of the company’s

debt.

If the company does poorly, the bonds

could be downgraded and be harder to sell

or liquidate.

11.1

TYPES OF BONDS

Savings Bonds: bonds sold by the US

government; interest is paid when bond

matures; original bond is discounted

Treasury Bonds, Bills and Notes: issued by

the US Treasury; backed by the “full faith

and credit” of the US government

11.1

TYPES OF BONDS

Municipal Bonds: same type of bonds, but

sold by city governments, as well as state

and county governments

Corporate Bonds: sold by corporations;

have higher risks than those issued by

governments; backed by “future profits”;

regulated by the Securities and Exchange

Commission (SEC).

11.1

TYPES OF BONDS

Junk Bonds: have the highest return of any

bonds, but also the higher risk of default on

payments.

11.1

OTHER TYPES OF FINANCIAL

ASSETS

Certificates of Deposit: a contract with a

financial institution for a depositor to leave

a certain amount of money on deposit for a

specified time in order to earn a specified

interest rate.

11.1

OTHER TYPES OF FINANCIAL

ASSETS

Money Market Mutual Funds: money is

collected from a group of investors and is

invested by a financial institution to buy

stocks, bonds or other financial assets;

investors receive higher returns; deposits in

mutual funds are NOT covered by the

FDIC.

11.1

FINANCIAL ASSET MARKETS

Financial asset markets can be described

based on the length of the investment or

based on whether the asset can be resold.

11.1

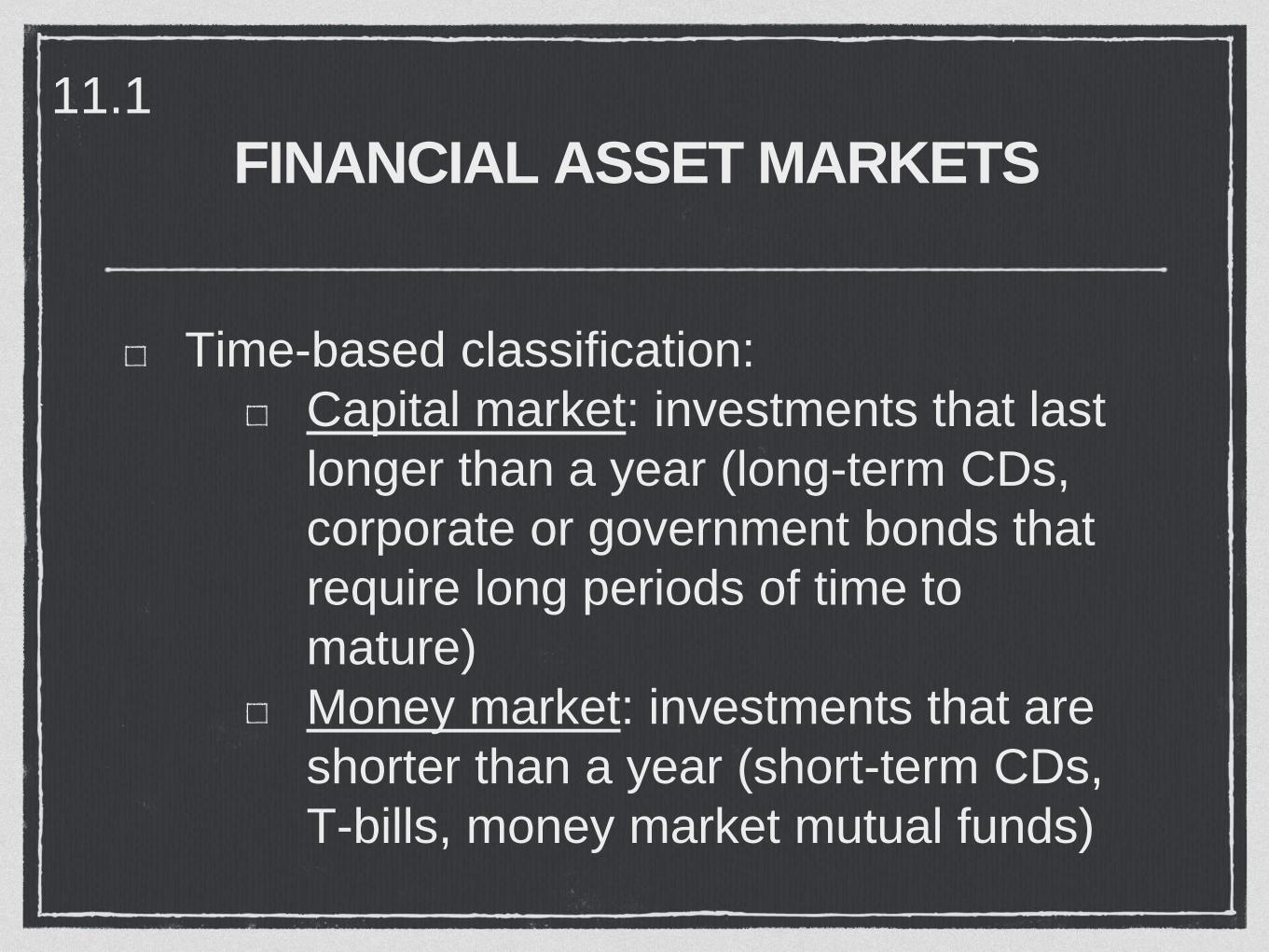

FINANCIAL ASSET MARKETS

Time-based classification:

Capital market: investments that last

longer than a year (long-term CDs,

corporate or government bonds that

require long periods of time to

mature)

Money market: investments that are

shorter than a year (short-term CDs,

T-bills, money market mutual funds)

11.1

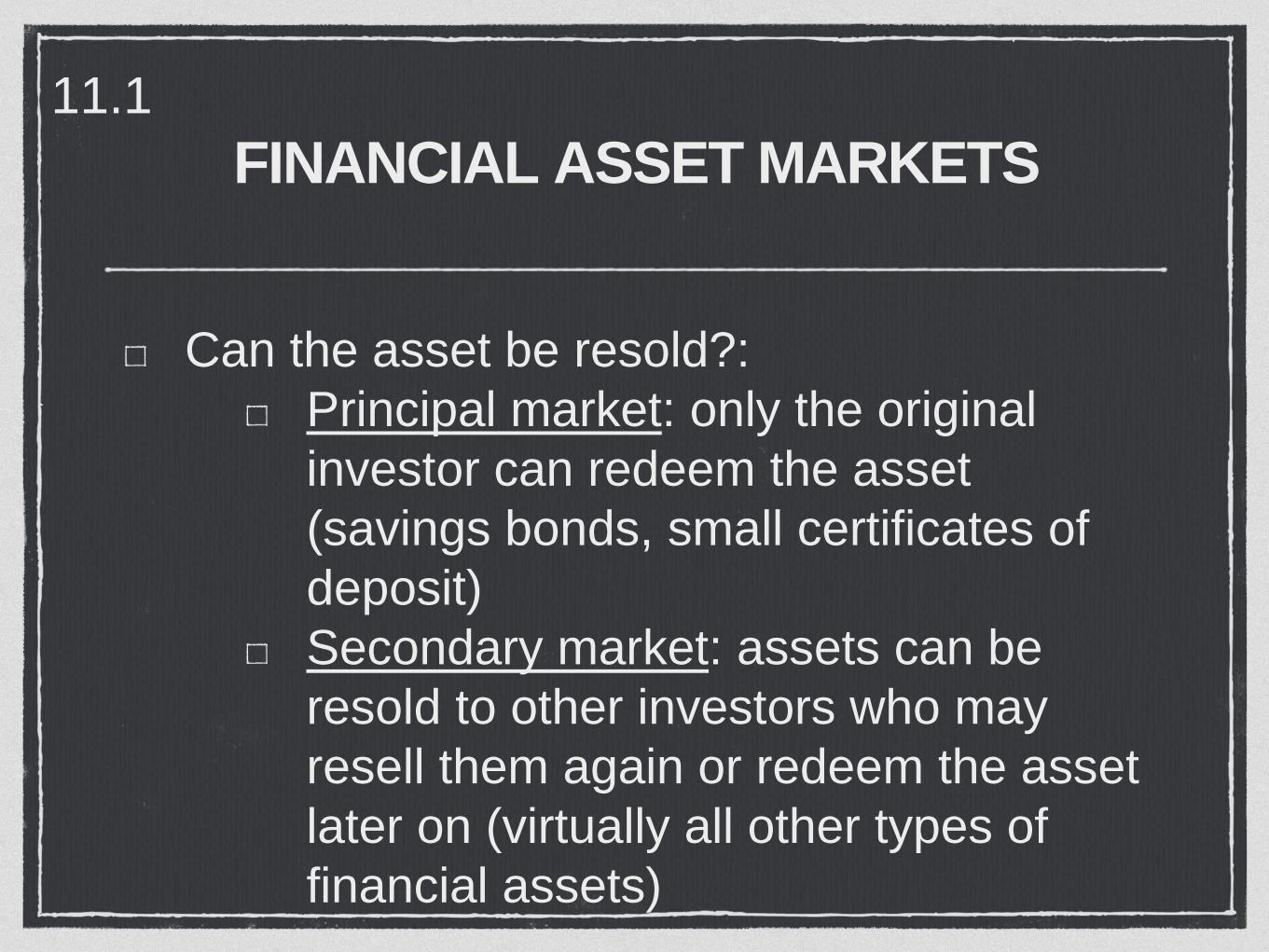

FINANCIAL ASSET MARKETS

Can the asset be resold?:

Principal market: only the original

investor can redeem the asset

(savings bonds, small certificates of

deposit)

Secondary market: assets can be

resold to other investors who may

resell them again or redeem the asset

later on (virtually all other types of

financial assets)

11.1

CHECK QUESTION 11.2

Write complete question and answer on your Bell Ringer form.

Describe five different types of bonds.