ec securities regulation paola lucantoni economic and financial market law

TRANSCRIPT

EC Securities Regulation

Paola LucantoniEconomic and Financial Market Law

First phaseEfforts were directed towards the construction of

a single deep and liquid securities market which issuers across the EC could access for their financing needs.

The regulatory focus was on harmonization of member States’ rules on the

admission to official listing process and on disclosure required when an issuer makes

a public offer or officially lists securities.

First phase

1966/1985

1966 Segré Report marked the first significant foray by EC into securities regulation and identified many of the market-integration and regulatory themes

which continue to preoccupy the regulation regime some 40 years later and highlighted the poor condition of the EC capital or securities market

and the benefits which could follow from the integration of capital markets

and identified the obstacles to integration, chief among them the imposition by Member States of diverging ad duplicative rules on market participants

and proposed remedial measurers with respect to the capital-raising process and the harmonization of disclosure standards

Phase two1985/1992

Attention shifted to the construction of a single market in investment services.

The regulatory touchstones were mutual recognition minimum standards home country control

But a number of core areas were not addressed and others were not subject to harmonization at a level sufficient to support home-country control and mutual recognition.

Phase twoThe second phase can be traced to 1985 and

the presentation of the Commission’s White Paper on the Internal Market which set out a programme of measures designed to deliver the single market by 1992 and the Commission’s intention to accelerate the harmonization/home Member State control device.

Phase three

1993/2005

A dramatic increase in the scope and sophistication of EC securities regulation

Financial Services Action Plan (FSAP)

Phase four

2005/ nowadaysThe Reform of

EU Financial Market Supervision

The EU’s Role in the Regulation of Financial Markets (1985-2011)

1985: European Commission White Paper on reform of the internal market proposed measures for the purpose of creating a Single Market in financial service

Three basic principles to be followed in the free movement of financial services across the EU: the harmonisation of essential standards; mutual recognition amongst the regulatory authorities; and home country control (that is a financial institution’s branches

would be regulated by the authorities in the Member State where it had its registered offices)

The EU’s Role in the Regulation of Financial Markets (1985-2007)

Banking The First Banking Directive of 1977 had applied the principle of non-

discrimination against businesses from other Member States to the banking sector – i.e. a bank from one Member State that wished to operate in another Member State had to be able to do so on equal terms to domestic banks.

The Second Banking Directive of 1989 provided for minimal capital requirements for all retail banks and set out the procedure under which home country regulators would control branches of an institution in another Member State ("European Passport“).

Insurance The Single Market for insurance services was developed using the same

principles that applied to the banking sector - harmonisation and mutual recognition. A 1973 directive had abolished restrictions on EU companies establishing non-life insurance businesses in other Member States. Later directives extended the scope of the Single Market in insurance.

Investment services The approach to investment services was similar to that of the other two

sectors. The Investment Services Directive provided for a system of regulation based on single authorisation, reciprocity with third countries, common prudential rules and co-operation amongst the various national regulators.

The EU’s Role in the Regulation of Financial Markets (1985-2007)

The Financial Services Action Plan (FSAP, 1999)

The FSAP sought a fully integrated financial services marketthe elimination of disparities in the tax treatment of savings,and better co-ordination between national regulators.

FSAP in four strategic objectives:a single EU wholesale market;open and secure retail markets;state of the art prudential rules and supervision;and wider conditions to create an optimal single financial market.

The EU’s Role in the Regulation of Financial Markets (1985-2007)

The Lamfalussy process is a regulatory strategy launched in 2001 for the purpose of strengthening the European regulatory and financial sector supervision framework. It consists of four levels:

Level 1: adoption of the framework legislation;

Level 2: detailed implementing measures. For the technical preparation of the implementing measures, the

European Commission was advised by committees, made up of representatives of national supervisory bodies, which exist in three sectors: banking, insurance and occupational pensions, and the securities markets (Lamfalussy committees)

The EU’s Role in the Regulation of Financial Markets (1985-2007)

Level 3: the Lamfalussy committees contributed to the consistent implementation of EU directives in the Member States, ensuring effective cooperation between national supervisory authorities and convergence of their practices.Lamfalussy committees (or level three committes):

Committee of European Banking Supervisors (CEBS); Committee of European Insurance and Occupational Pensions

Supervisors (CEIOPS); Committee of European Securities Regulators (CESR)

Level 4: the EU Commission’s enforcement of the timely and correct transposition of EU legislation into national law.

Pre-crisis financial market regulationThe Lamfalussy Level 3 Committees

The three pan-European committees of financial market supervisors that operated until 2011: CESR, CEBS and CEIOPS.

Established by the European Commission between 2001 and 2003.

They became known, collectively, as the “Lamfalussy” or “Level 3” Committees.

As from January 2011, the Level 3 Committees are transformed into the ESAs.

Level 3 Committees’ charachteristics Committee of national regulatory/supervisory authorities from member States and other EEA

countries

Bodies without legal personality

Based in Paris (CESR), London (CEBS), Frankfurt (CEIPS) and chaired by the representative of a member State competent authority

Modest financial resources

At least four plenary sessions a year

Making decision process operated on the basis on consensus

Level 3 Committees’ general tasks and powers

fostering consistent, cooperative practices and open relations among the national supervisors

Lack of binding regulating

Lack of power to impose binding decisions on the member States' competent authorities

No direct supervisory powers in relation to individual market participants

Committee of European Securities Regulators (CESR)

Advising the Commission on policy and on draft implementing (secondary) legislation in the field of securities

Issuance of non-binding "Level 3" interpretative guidance, recommendations and standards

Day-to-day co-ordination in supervision and enforcement: CESR-Pol standing committee as a forum in which CESR members could share their experiences

concerning market surveillance and enforcement activities; the multilateral Memorandum of Understanding between CESR Members (a general framework

for cooperation and consultation between the supervisory authorities); protocols relating to home-host supervisory cooperation in key areas

(i.e. supervision of branches under MiFID and passport notifications) improvement of market transparency by mantaining a variety of databases.

(i.e. the CESR-MiFID database containing information on shares admitted to trading on EU regulated markets, systematic internalisers, multilateral trading facilities, regulated markets and central counterparties)

Committee of European Banking Supervisors (CEBS)

Like CESR in the securities field, CEBS’s responsibilities were to advise the European Commission on banking policy issues and legislation to contribute to the consistent application and implementation of EU law and to the convergence

of supervisory practices, and to enhance supervisory cooperation and the exchange of information between national

supervisors.

CEBS provided non-binding Level 3 standards, guidance and recommendations (since 2008 adopted on the basis of qualified majority)

CEBS Level 3 measures could be divided broadly into four sub-categories: guidelines relating to supervisory processes, including guidelines on cross-border supervisory

cooperation for banking and investment firm groups; guidelines relating to model validation, external credit assessment institutions, and prudential

filters; guidelines on the supervisory review process under the Capital Requirements Directive (CRD); and guidelines on financial reporting.

Committee of European Insurance and Occupational Pensions Supervisors

(CEIOPS)

giving of technical advice to the Commission with respect to the legislative framework (in particular the Solvency II Directive, which stipulates solvency requirements for the

insurance sector)

Cooperation with CEBS in relation to financial conglomerates

Point of contact for regulatory dialogues with third countries (dialogues with international standardsetting bodies).

Monitor and report periodically on main market trends within the insurance and occupational pensions sectors

The Financial crisis Main causes:

overextension of credit due to very low interest rates for a long period of time;

the overleveraging of many financial institutions directly or through derivative techniques;

the existence of several asset bubbles, in the real estate sector, in commodities and in the equity markets, leading to over-optimism and relaxing of risk management standards;

underestimation by CRAs of the credit default risks of instruments collateralised by subprime mortgages

The Financial crisis/2

The traditional regulation of equity markets – in Europe mainly on the basis of ISD and later of Mifid – had become obsolete in two respects:

trading in derivatives has increasingly replaced trading in equities; and

trading on regulated markets is being taken over by trading on OTC markets, including dark pools of liquidity and crossing networks, that are subject to different, or often non-comparable regulations

Shortcomings of the previous system Lack of adequate macro-prudential supervision;

Lack of early warning mechanisms;

No means for national supervisors to take common decisions;

Lack of frankness and cooperation between national supervisors;

Failures to challenge supervisory practices on a cross-border basis;

Lack of consistent supervisory rules, powers and sanctions across member States (EU based regulation vs member State based supervision)

Lack of resources in the Level 3 committees.

Post-crisis reform of the structure of EU financial market supervision: overview

The de Larosière Report, published in February 2009, marked the start of the new bolder phase in the organisation of EU-wide financial market supervision. Proposal: to establish a macro-prudential supervisor (“ESRB”) for the purpose

of monitoring systemic risk to replace Level 3 Committees with new EU Supervisory Authorities

(“ESAs”) and to confer on those latter certain powers:to give binding directions to national supervisors, to make decisions that would be binding on firms directly, to draft binding technical standards, and to be responsible for the licensing and direct supervision of some

specific EU-wide institutions (i.e. Credit Rate Agencies)

The new supervisory architectureThe European Parliament and the Council adopted legal texts setting up a reform of

the EU framework for regulation/supervision of the financial system, aimed at eliminating deficiencies that were exposed during the financial crisis

The regulations established:

● the European Systemic Risk Board (ESRB), which will provide macro-prudential oversight of the financial system,

● and three new supervisory authorities at the micro-financial level:

European Banking Authority (EBA);

European Insurance and Occupational Pensions Authority (EIOPA);

European Securities and Markets Authority (ESMA).

The ESRB and the EIOPA will be sited in Frankfurt, the EBA in London and the ESMA in Paris

The new system is operational since 1 January 2011.

European System of Financial Supervision (ESFS) formed by the ESAs, their

Joint Committee, the ESRB and the national supervisors

The European Systemic Risk Board (ESRB)

ESRB Regulation (EU) No 1092/2010:

“The ESRB shall be responsible for the macro-prudential oversight of the financial system within the Union in order to contribute to the prevention or mitigation of systemic risks to financial stability in the Union that arise from developments within the financial system and taking into account macro-economic developments, so as to avoid periods of widespread financial distress. It shall contribute to the smooth functioning of the internal market and thereby ensure a sustainable contribution of the financial sector to economic growth.”

ESRB’s tasks/1 determining and/or collecting and analysing all the relevant and necessary

information;

identifying and prioritising systemic risks;

issuing early warnings where such systemic risks are deemed to be significant and, where appropriate, make those warnings public;

issuing recommendations for remedial action in response to the risks identified and, where appropriate, making those recommendations public;

when the ESRB determines that an emergency situation may arise issuing a confidential warning addressed to the Council and providing the Council with an assessment of the situation, in order to enable the Council to adopt a decision addressed to the European Supervisory Authorities (ESAs) determining the existence of an emergency situation;

ESRB’s tasks/2 monitoring the follow-up to warnings and recommendations;

cooperating closely with all the other parties to the European System of Financial Supervision (ESFS); where appropriate, providing the ESAs with the information on systemic risks required for the performance of their tasks; and, in particular, in collaboration with the ESAs, developing a common set of quantitative and qualitative indicators (risk dashboard) to identify and measure systemic risk;

coordinating its actions with those of international financial organisations, particularly the International Monetary Fund (IMF) and the Financial Stability Board (FSB) as well as the relevant bodies in third countries on matters related to macro-prudential oversight;

carrying out other related tasks as specified in Union legislation.

ESRB’s organization and structure The European Systemic Risk Board has:

a General Board The General Board takes the decisions necessary to ensure the performance of the tasks

entrusted to the ESRB. It consists of the following members with voting rights: (i) the President and the Vice-President of the ECB; (ii) the Governors of the national central banks of the Member States; (iii) one member of the European Commission; (iv) the Chairperson of the European Banking Authority (EBA); (v) the Chairperson of the European Insurance and Occupational Pensions Authority (EIOPA); (vi) the Chairperson of the European Securities and Markets Authority (ESMA)

the Chair and the two Vice-Chairs of the Advisory Scientific Committee (ASC) the Chair of the Advisory Technical Committee (ATC) a Steering Committee a Secretariat an Advisory Scientific Committee an Advisory Technical Committee

Accountability and reporting obligations

At least annually the Chair of the ESRB si invited to an annual hearing in the European Parliament, marking the publication of the ESRB’s annual report to the European Parliament and the Council.

The ESRB shall also examine specific issues at the invitation of the European Parliament, the Council or the Commission.

The European Parliament may request the Chair of the ESRB to attend a hearing of the competent Committees of the European Parliament.

Regulations establishing the ESAs

Regulation (EU) 1093/2010 of the European Parliament and of the Council of 24 November 2010 establishing a European Supervisory Authority (European Banking Authority)

Regulation (EU) 1094/2010 of the European Parliament and of the Council of 24 November 2010 establishing a European Supervisory Authority (European Insurance and Occupational Pensions Authority),

Regulation (EU) No 1095/2010 of the European Parliament and of the Council of 24 November 2010 establishing a European Supervisory Authority (European Securities and Markets Authority)

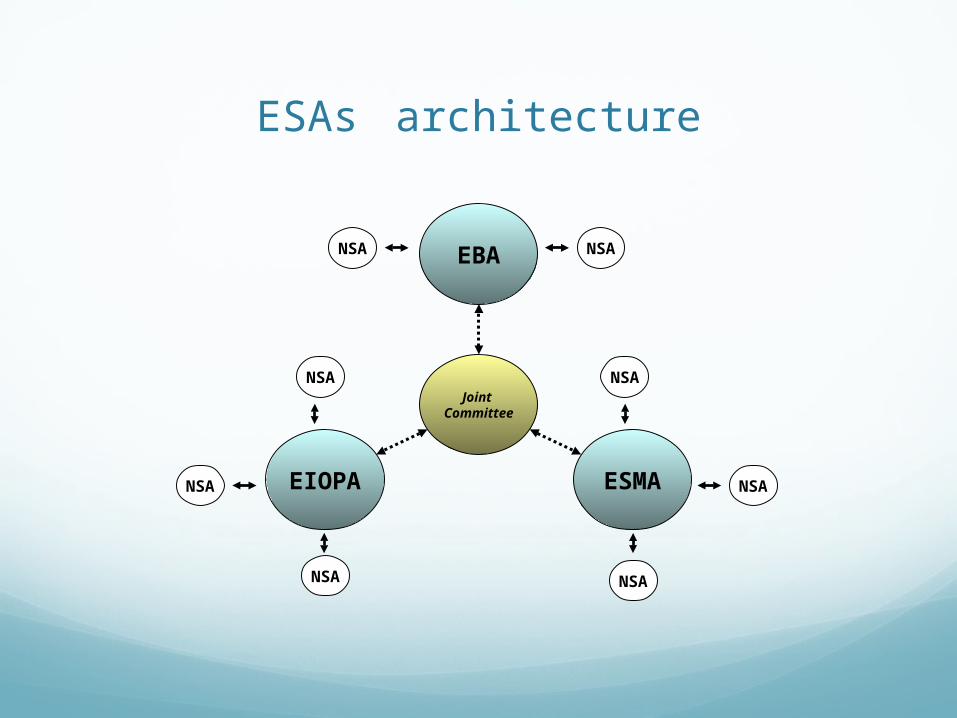

ESAs architecture

EIOPA ESMA

EBA

Joint Committee

NSA

NSA

NSA

NSA

NSA

NSA

NSA

NSA

ESAs, overview Bodies with legal personality under EU law.

Each ESA has its head office in the same place as its predecessor Level 3 Committee (London (Banking), Frankfurt (Insurance and Occupational Pensions) and Paris (Securities and Markets).

Each ESA has a Chairperson and an Executive Director (full-time professionals) Board of Supervisors and a Management Board The ECB is also represented (in a non-voting capacity) on the EBA

The main decision-making body of each ESA will be its Board of Supervisors, consisting of the heads of the relevant national supervisors as well as the Chairperson of the respective Authority

The ESAs are accountable to the EU Institutions via annual reporting obligations (in addition, annual and multi-annual workprogrammes must be transmitted to the EU Institutions and be made public)

ESAs: level 3 Committes successors The ESAs inherit all the functions that were performed by the Level 3

Committees.

Their responsibilities and powers thus include: writing non-binding guidelines and recommendations, conducting peer reviews, mediating disputes between supervisors on a non-binding

basis, promoting supervisory cooperation, convergence and coordination, facilitating home/host MS relations, including fostering the coherent functioning of

colleges of supervisors, collecting information, establishing central databases, providing standard reporting formats, monitoring market developments and conditions generally, and providing opinions to the Union Institutions.

Like the Level 3 Committees before them, the ESAs have a role in external relations

ESAs: new powers It is in respect of their entirely new powers to take action with binding legal

effect that the ESAs differ most from the predecessor Level 3 Committees

development of binding technical standards in specified EU financial markets legislation

enforcement of EU law

action in emergency situations

resolution of disputes between supervisors in cross-border situations

direct supervision of financial market participants and direct control over market activity

ESAs’ binding technical standards Drafting technical standards requires the qualified majority vote from an

ESA’s Board of Supervisors and acquires binding force through endorsement by the Commission

Their adoption implies a rather complicated procedure (in order to comply with the prohibition in EU constitutional law against the

delegation to agencies of the general regulatory powers that have been conferred by Treaty on the EU Institutions)

Once endorsed by the Commission, binding technical standards have the status of Regulations or Decisions in EU law (which means that they apply directly to financial firms and other private

actors as well as to member States and their public authorities)

The direct effect of binding technical standards has implications for ESAs enforcement

Procedure for the adoption of binding technical standards (Artt. 10-15 ESAs Reg.) Drafting binding technical standards

Public consultations on draft regulatory technical standards

Submission of the draft standards to the Commission for endorsement

Within 3 months of receipt of a draft regulatory technical standard, the Commission shall decide whether to endorse it (the Commission may amend the draft, but in such case must previously liaise with the ESAs)

ESA enforcement of EU law (Art. 17, ESAs’ Regulations)

In case of an alleged breach of, or failure to apply, specified EU financial market laws (including binding technical standards) by a national supervisor: ESA enforcement process.

The ESA may act on its own initiative or upon request from one or more national supervisors, the European Parliament, the Council, the Commission or the relevant Stakeholder Group. The stages of the process are as follows:

ESA investigation (can take up to two months);

ESA compliance recommendation addressed to the national supervisor; national supervisor must give its initial response within 10 days and comply within one month;

Commission compliance formal opinion addressed to the national supervisor; formal opinion to be issued within 3 months (extendable to 4) of the ESA’s adoption of a recommendation; national supervisor has 10 working days to respond to the Commission’s formal opinion and must comply within period specified in that opinion;

ESA compliance decision in conformity with the Commission’s formal opinion addressed directly to financial market participant; decision to be made public unless such publication would be in conflict with the legitimate business interests of financial market participants in the protection of their business secrets or could seriously jeopardise the orderly functioning and integrity of financial markets or the stability of the EU’s financial system.

Action in emergency situations (Art. 18, ESAs’ Regulations)

This new power is triggered by a determination by the Council in consultation with the Commission, ESRB and, where appropriate, the ESAs, that an emergency situation is in existence (ESA Regs, art 18.2)

Where the Council has declared that an emergency situation is in existence, the ESA may adopt individual decisions requiring national supervisorsto take the necessary action in order to ensure that operators and competent authorities comply with EU financial market laws

There is some overlap between this procedure and the direct enforcement under art. 17 of the Regs.: the key difference is that in an emergency situation ESA can intervene on a more expedited basis and without the need to go through the Commission

Resolution of disputes between supervisors in cross-border situations

(“Binding mediation”, Artt. 19 - 20 ESA Regs.) The mediation function that was performed by the Level 3 Committees is

reinforced: the ESAs are granted a new power allowing them in certain cross-border situations: to impose a binding settlement decision on national supervisors if attempts to resolve

a disagreement through conciliation fail; and, to direct a decision to a financial market participant.

the cross-border disagreement must relate to the procedure followed by or the content of the action/inaction required of a national supervisor in particular cases identified in specified EU financial markets law

the final decision is made by the Board of Supervisors on the basis of a one-Member, one-vote simple majority

the creation of a binding mechanism to resolve disagreements between supervisors means that a supervisor’s judgment on what EU law requires could be overridden, potentially even on a matter in which the relevant EU legislation confers supervisory discretion

ESA’s assessment of market developments (Art. 32 ESAs Regs)

although the ESRB will be responsible for macro-prudential analysis of the EU financial sector, the ESAs should continue the work of the Level 3 Committees in this area as:

the focus of their analysis is different, i.e., micro-prudential analysis provides a bottom-up analysis, rather than macro-prudential analysis which is top-down, and;

their analysis may serve as helpful input into the work carried-out by the ESRB.

ESAs joint bodies (Art. 54 ss. f the ESAs Regs): Joint Committee

The Joint Committee of the ESAs is the body that will take forward cross-sectoral work under the new arrangements.150 It is the Joint Committee that will settle cross-sectoral disagreements. It serves as a forum in which the ESAs cooperate and ensure cross-sectoral consistency on the following matters: financial conglomerates, accounting and auditing, micro-prudential analyses of

cross-sectoral developments, risks and vulnerabilities for financial stability, retail investment products, measures combating money laundering; and, information exchange with the ESRB and developing the relationship between the ESRB and the ESAs

The Joint Committee have a dedicated staff provided by the ESAs

In the event that a financial market participant reaches across different sectors, the Joint Committee shall resolve disagreements

ESAs joint bodies (Art. 58 ss. f the ESAs Regs): Board of Appeal

An appeal system will ensure that any person, including national supervisory authorities, may in first instance appeal to a Board of Appeal against a decision by the ESAs to ensure the coherent application of EU rules, action in emergency situations, and the settlement of disagreements;

Proceedings may be brought before the Court of Justice of the European Union, in accordance with Article 263 TFEU, contesting a decision taken by the Board of Appeal or, in cases where there is no right of appeal before the Board of Appeal, by the Authority.

BudgetThe transformation of the Level 3 Committees into effective

ESAs, enhanced resources are needed - both personnel and budgetary.

For the EBA, the total operational expenditure from the EU budget in commitment and payment appropriations for the years 2011-2013 is EUR 21.527 million.

In addition, member States (national supervisory authorities or ministries of finance) will contribute EUR 32.290 million over the three year period.

This gives a total of EUR 53.816 million from 2011 to 2013.

ESMA’s powers in relation to CRA Regulation (EC) No 1060/2009 on credit rating agencies

Regulation (EC) No 513/2011 amending Regulation (EC) No 1060/2009 on credit rating agencies and conferring powers to ESMA

ESMA is exclusively responsible for the registration and supervision of Credit Rating Agencies registered in the European Union.

To the above end, a registry of all CRAs currently registered in the EU is kept by the ESMA

In addition, ESMA also carries out policy work to prepare future legislation (such as regulatory technical standards and guidelines). This work is undertaken through the CRA technical committee, which has representatives from all the national competent authorities

CRAs’ RegulationsOn 30 May 2012, four Commission Delegated Regulations

establishing regulatory technical standards for credit rating agencies have been published. These technical standards set out (Regs 446/2012; 447/2012; 448/2012; 449/2012): the information to be provided by a CRA in its application for

registration to the ESMA; the presentation of the information to be disclosed by credit rating

agencies in a central repository (CEREP) so investors can compare the performance of different CRAs in different rating segments;

how ESMA will assess rating methodologies; the information CRAs have to submit to ESMA and at what time

intervals in order to supervise compliance.

ESMA Reg. on short selling and CDSRegulation on short selling and certain aspects of credit

default swaps (EU) No 236/2012 will become applicable from 1 November 2012

According to the provisions of the Regulation, ESMA will have to provide for public access to certain types of information: Significant net short position notification thresholds for each

sovereign issuer (Article 7(2)); Links to central websites operated or supervised by competent

authorities where the public disclosure of net short positions is posted (Article 9(4));

The list of shares for which the principal trading venue is located in the third country (Article 16(2));

A list of market makers and authorised primary dealers (Article 17(3));

A list of existing penalties and administrative measures applicable in Member States (Article 41).