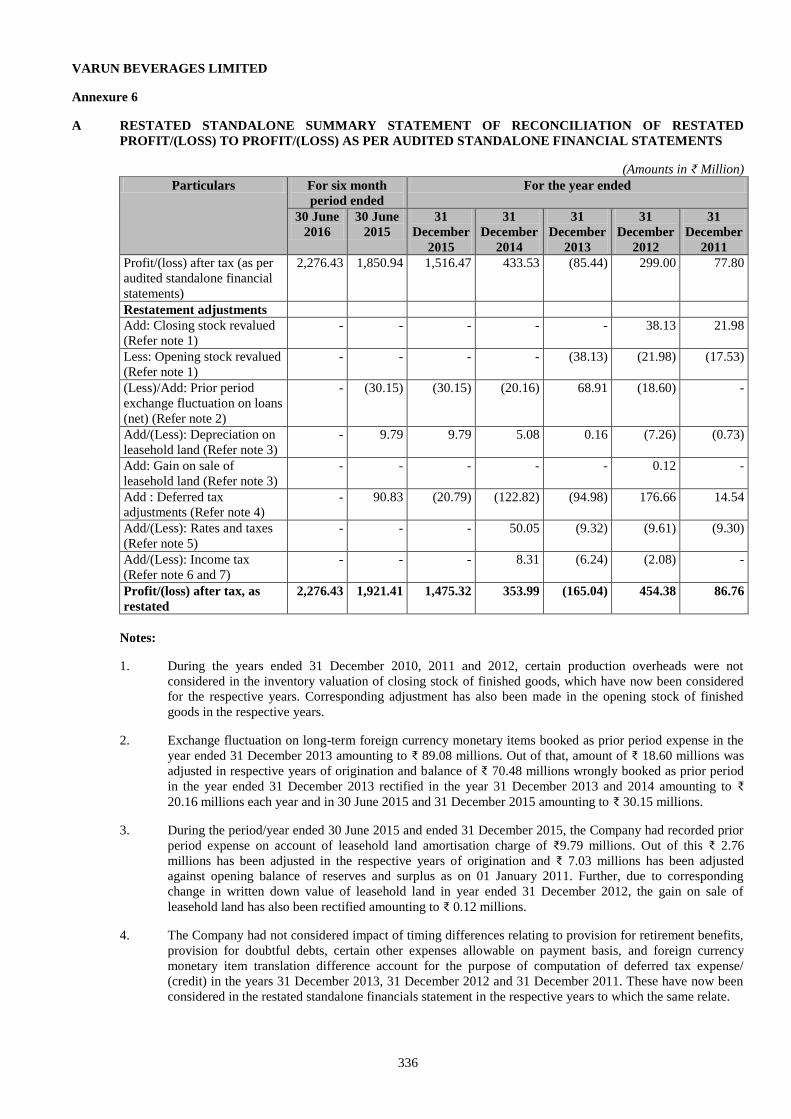

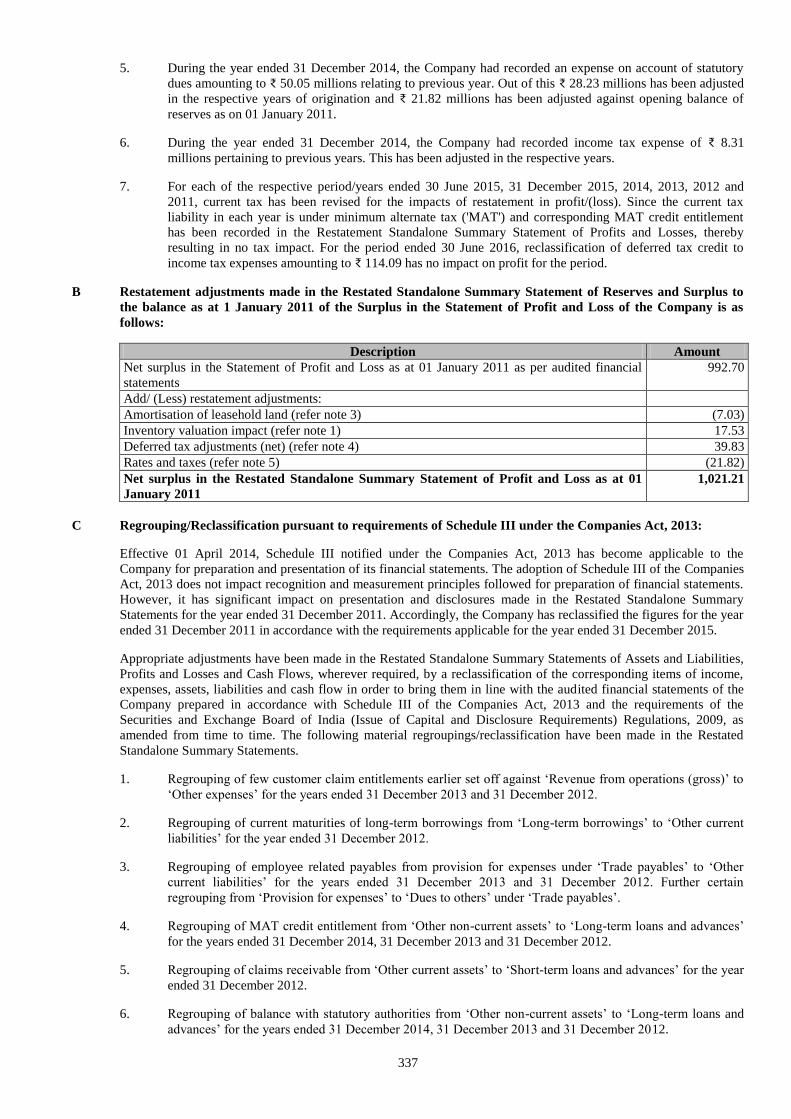

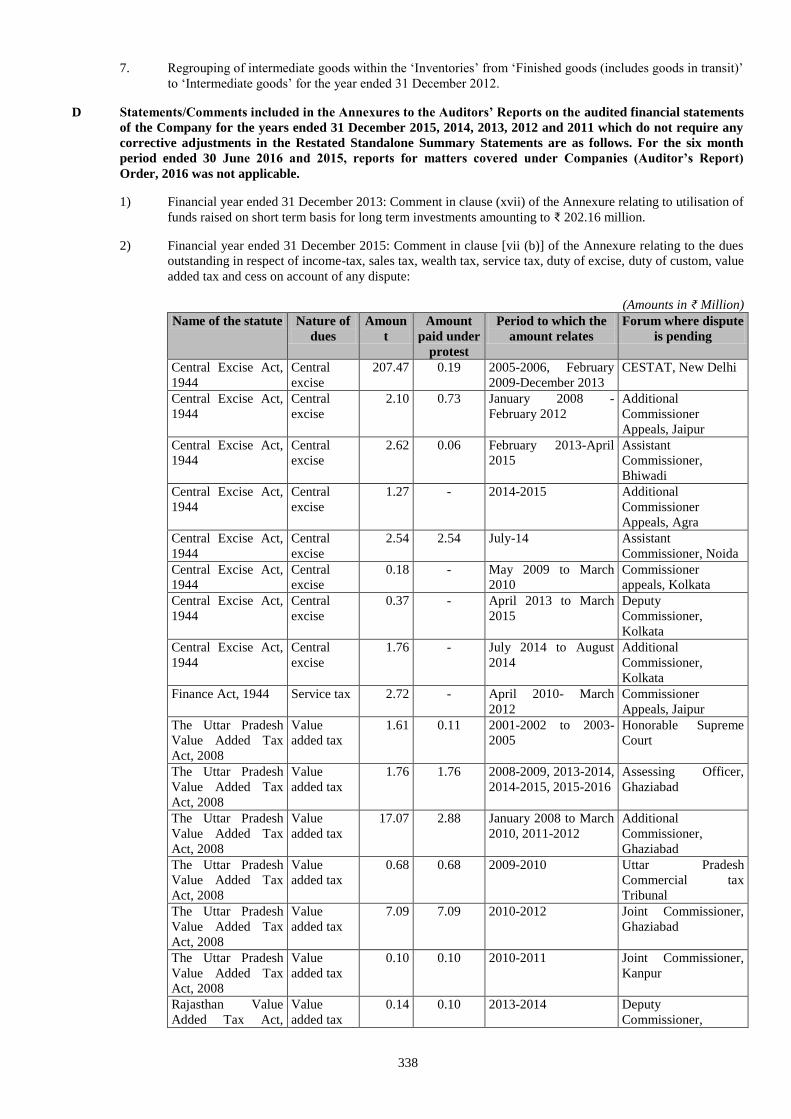

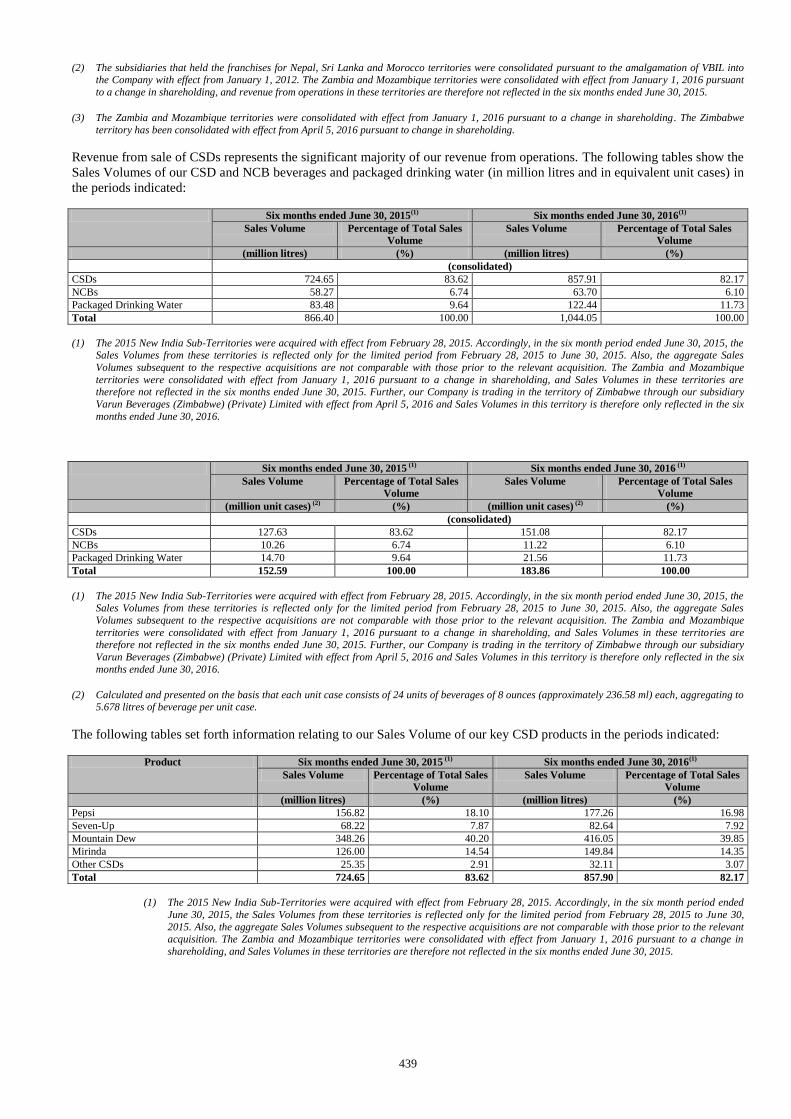

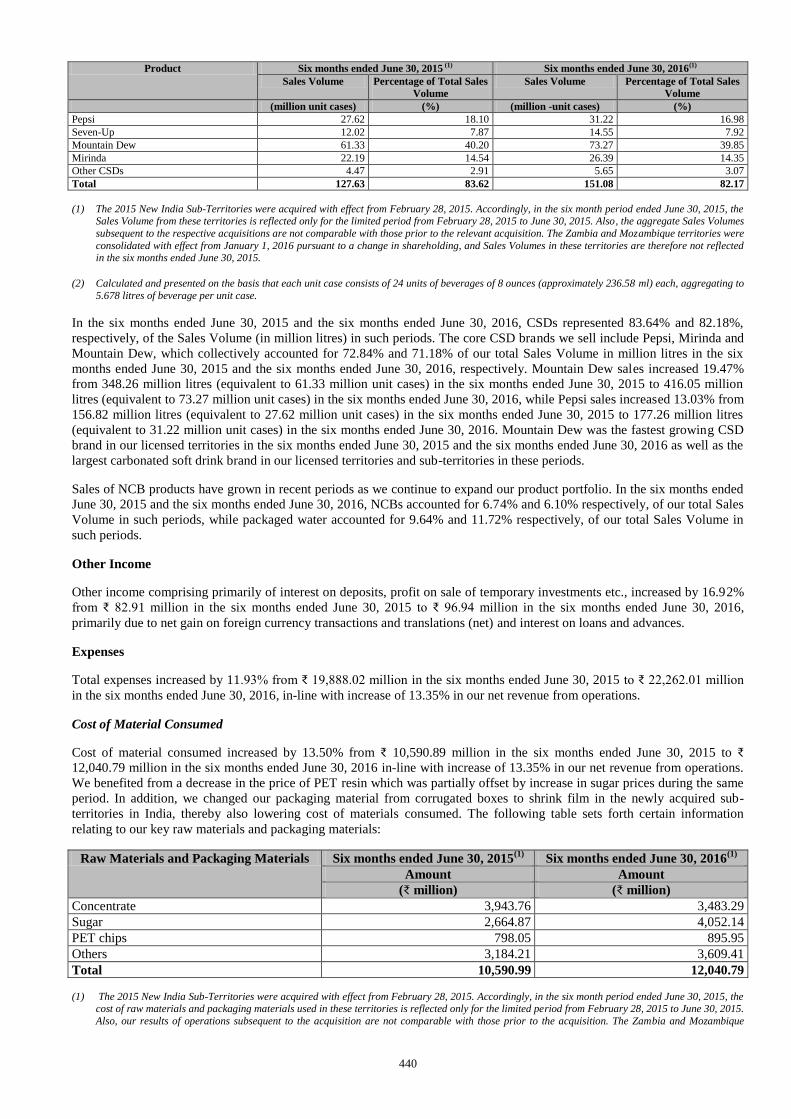

varun beverages limited - sebi

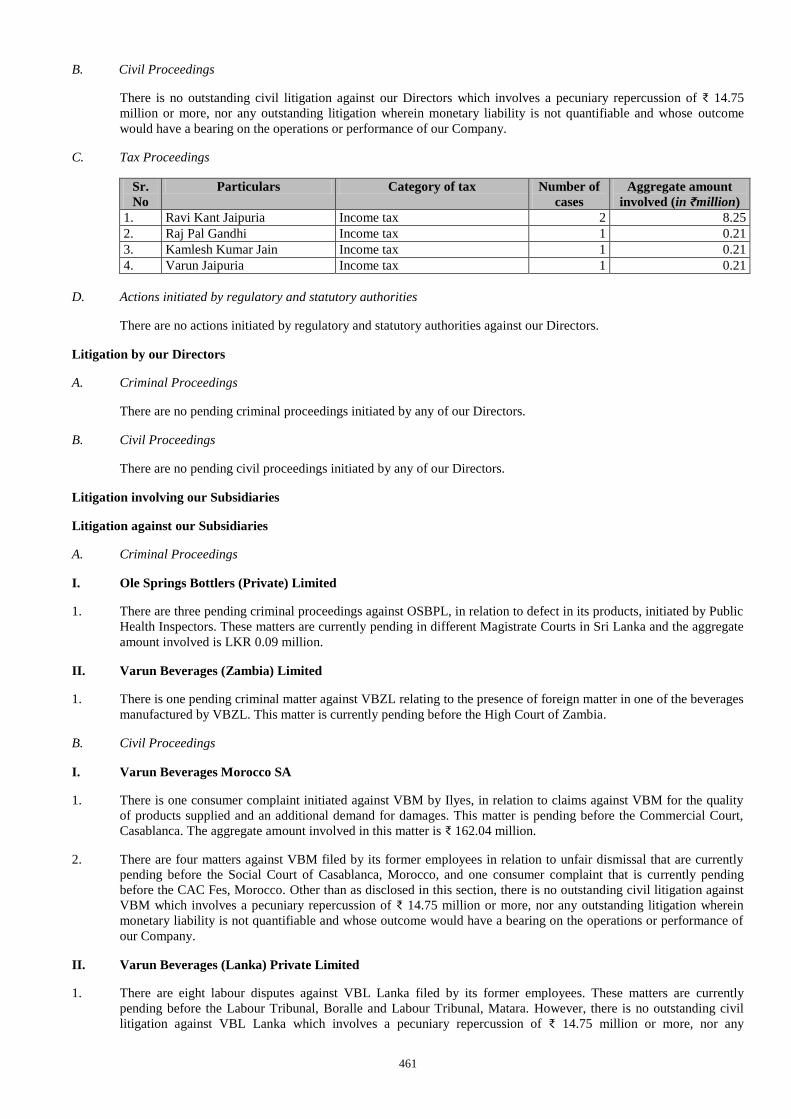

TRANSCRIPT

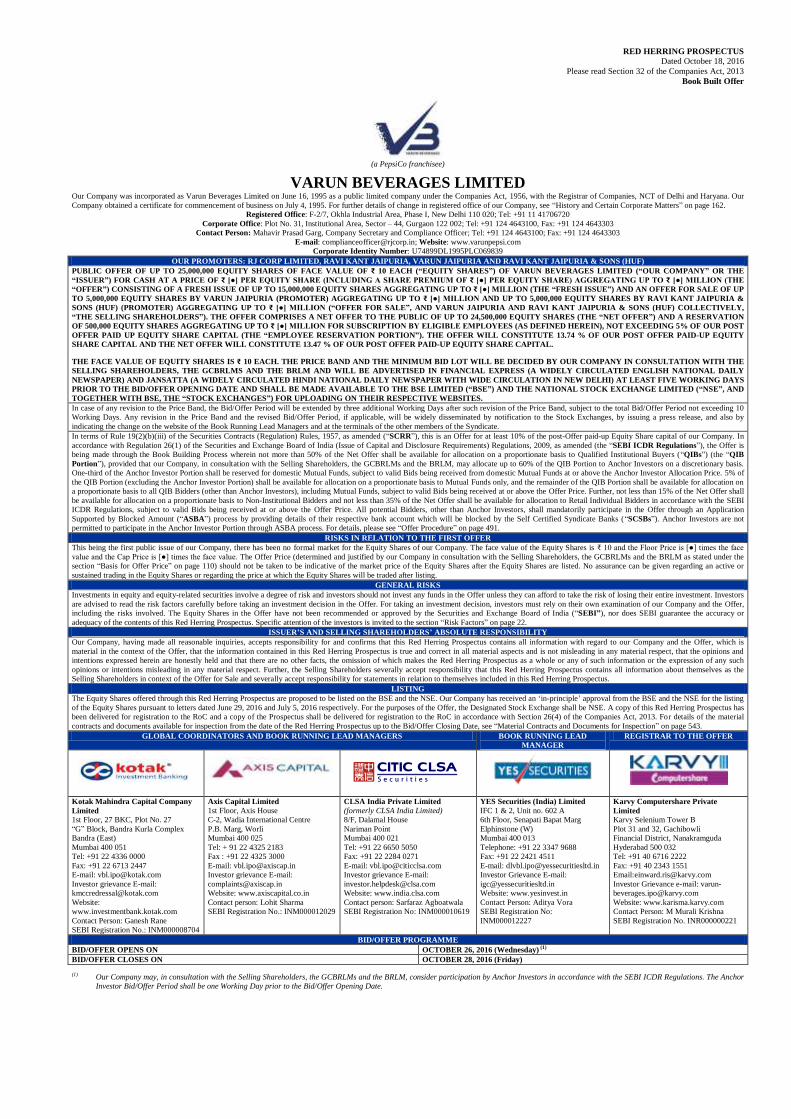

RED HERRING PROSPECTUS

Dated October 18, 2016

Please read Section 32 of the Companies Act, 2013

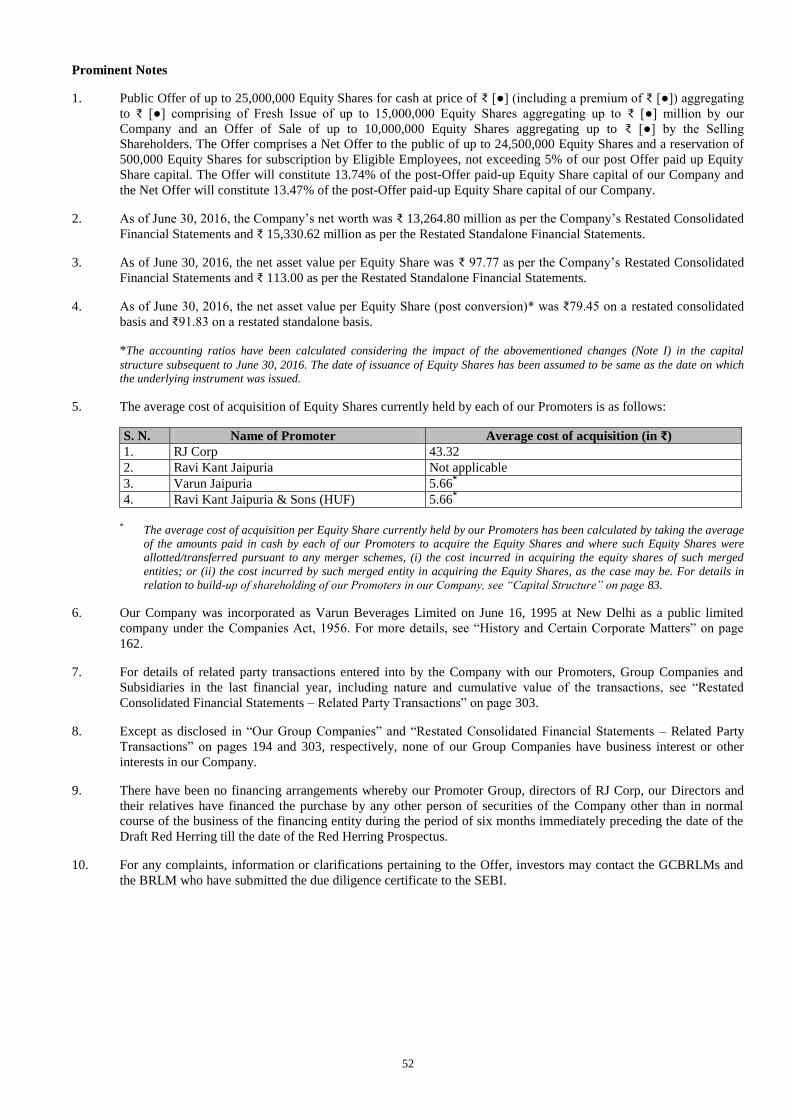

Book Built Offer

(a PepsiCo franchisee)

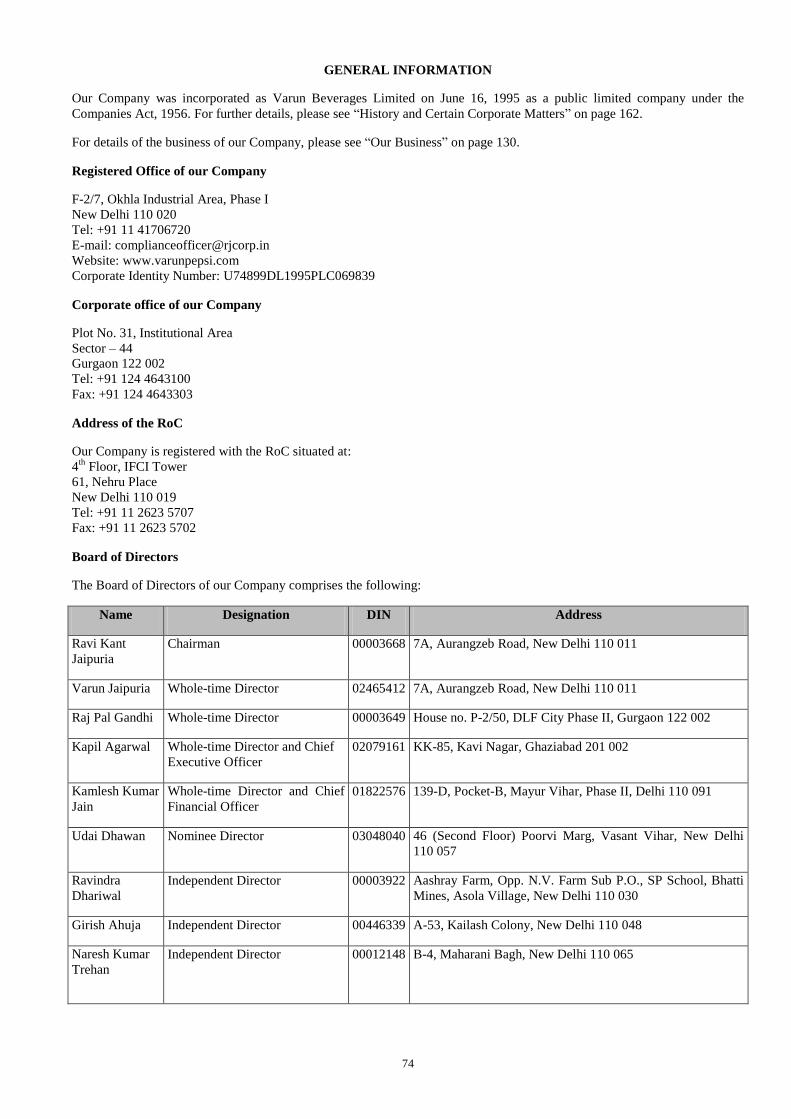

VARUN BEVERAGES LIMITED Our Company was incorporated as Varun Beverages Limited on June 16, 1995 as a public limited company under the Companies Act, 1956, with the Registrar of Companies, NCT of Delhi and Haryana. Our

Company obtained a certificate for commencement of business on July 4, 1995. For further details of change in registered office of our Company, see “History and Certain Corporate Matters” on page 162.

Registered Office: F-2/7, Okhla Industrial Area, Phase I, New Delhi 110 020; Tel: +91 11 41706720

Corporate Office: Plot No. 31, Institutional Area, Sector – 44, Gurgaon 122 002; Tel: +91 124 4643100, Fax: +91 124 4643303

Contact Person: Mahavir Prasad Garg, Company Secretary and Compliance Officer; Tel: +91 124 4643100; Fax: +91 124 4643303

E-mail: [email protected]; Website: www.varunpepsi.com

Corporate Identity Number: U74899DL1995PLC069839

OUR PROMOTERS: RJ CORP LIMITED, RAVI KANT JAIPURIA, VARUN JAIPURIA AND RAVI KANT JAIPURIA & SONS (HUF)

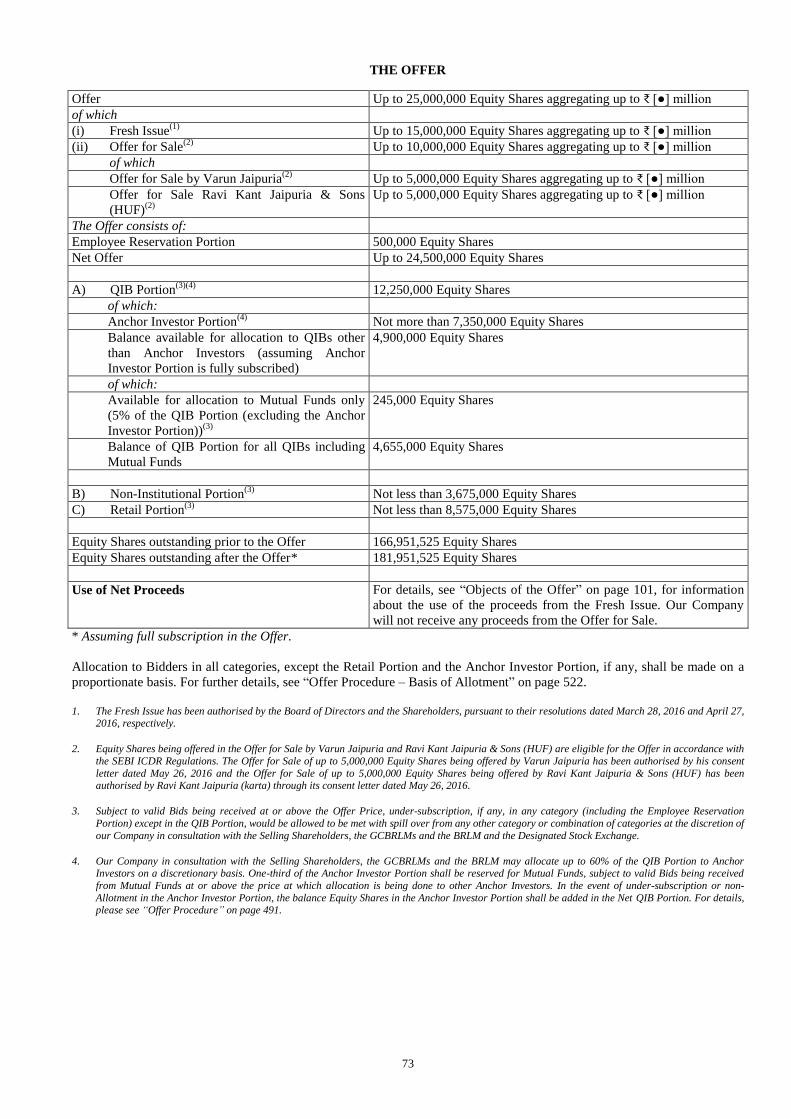

PUBLIC OFFER OF UP TO 25,000,000 EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (“EQUITY SHARES”) OF VARUN BEVERAGES LIMITED (“OUR COMPANY” OR THE

“ISSUER”) FOR CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹ [●] PER EQUITY SHARE) AGGREGATING UP TO ₹ [●] MILLION (THE

“OFFER”) CONSISTING OF A FRESH ISSUE OF UP TO 15,000,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION (THE “FRESH ISSUE”) AND AN OFFER FOR SALE OF UP

TO 5,000,000 EQUITY SHARES BY VARUN JAIPURIA (PROMOTER) AGGREGATING UP TO ₹ [●] MILLION AND UP TO 5,000,000 EQUITY SHARES BY RAVI KANT JAIPURIA &

SONS (HUF) (PROMOTER) AGGREGATING UP TO ₹ [●] MILLION (“OFFER FOR SALE”, AND VARUN JAIPURIA AND RAVI KANT JAIPURIA & SONS (HUF) COLLECTIVELY,

“THE SELLING SHAREHOLDERS”). THE OFFER COMPRISES A NET OFFER TO THE PUBLIC OF UP TO 24,500,000 EQUITY SHARES (THE “NET OFFER”) AND A RESERVATION

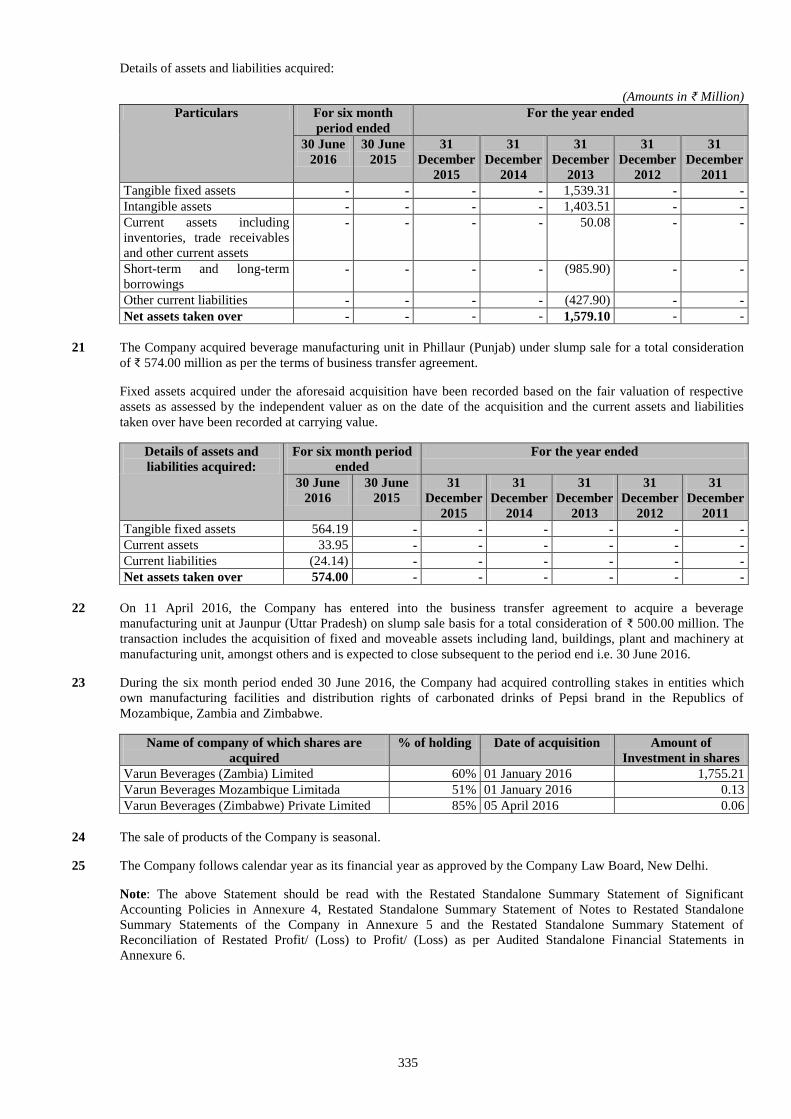

OF 500,000 EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION FOR SUBSCRIPTION BY ELIGIBLE EMPLOYEES (AS DEFINED HEREIN), NOT EXCEEDING 5% OF OUR POST

OFFER PAID UP EQUITY SHARE CAPITAL (THE “EMPLOYEE RESERVATION PORTION”). THE OFFER WILL CONSTITUTE 13.74 % OF OUR POST OFFER PAID-UP EQUITY

SHARE CAPITAL AND THE NET OFFER WILL CONSTITUTE 13.47 % OF OUR POST OFFER PAID-UP EQUITY SHARE CAPITAL.

THE FACE VALUE OF EQUITY SHARES IS ₹ 10 EACH. THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY IN CONSULTATION WITH THE

SELLING SHAREHOLDERS, THE GCBRLMS AND THE BRLM AND WILL BE ADVERTISED IN FINANCIAL EXPRESS (A WIDELY CIRCULATED ENGLISH NATIONAL DAILY

NEWSPAPER) AND JANSATTA (A WIDELY CIRCULATED HINDI NATIONAL DAILY NEWSPAPER WITH WIDE CIRCULATION IN NEW DELHI) AT LEAST FIVE WORKING DAYS

PRIOR TO THE BID/OFFER OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (“BSE”) AND THE NATIONAL STOCK EXCHANGE LIMITED (“NSE”, AND

TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR UPLOADING ON THEIR RESPECTIVE WEBSITES.

In case of any revision to the Price Band, the Bid/Offer Period will be extended by three additional Working Days after such revision of the Price Band, subject to the total Bid/Offer Period not exceeding 10

Working Days. Any revision in the Price Band and the revised Bid/Offer Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by

indicating the change on the website of the Book Running Lead Managers and at the terminals of the other members of the Syndicate.

In terms of Rule 19(2)(b)(iii) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”), this is an Offer for at least 10% of the post-Offer paid-up Equity Share capital of our Company. In

accordance with Regulation 26(1) of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”), the Offer is

being made through the Book Building Process wherein not more than 50% of the Net Offer shall be available for allocation on a proportionate basis to Qualified Institutional Buyers (“QIBs”) (the “QIB

Portion”), provided that our Company, in consultation with the Selling Shareholders, the GCBRLMs and the BRLM, may allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis.

One-third of the Anchor Investor Portion shall be reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price. 5% of

the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on

a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Net Offer shall

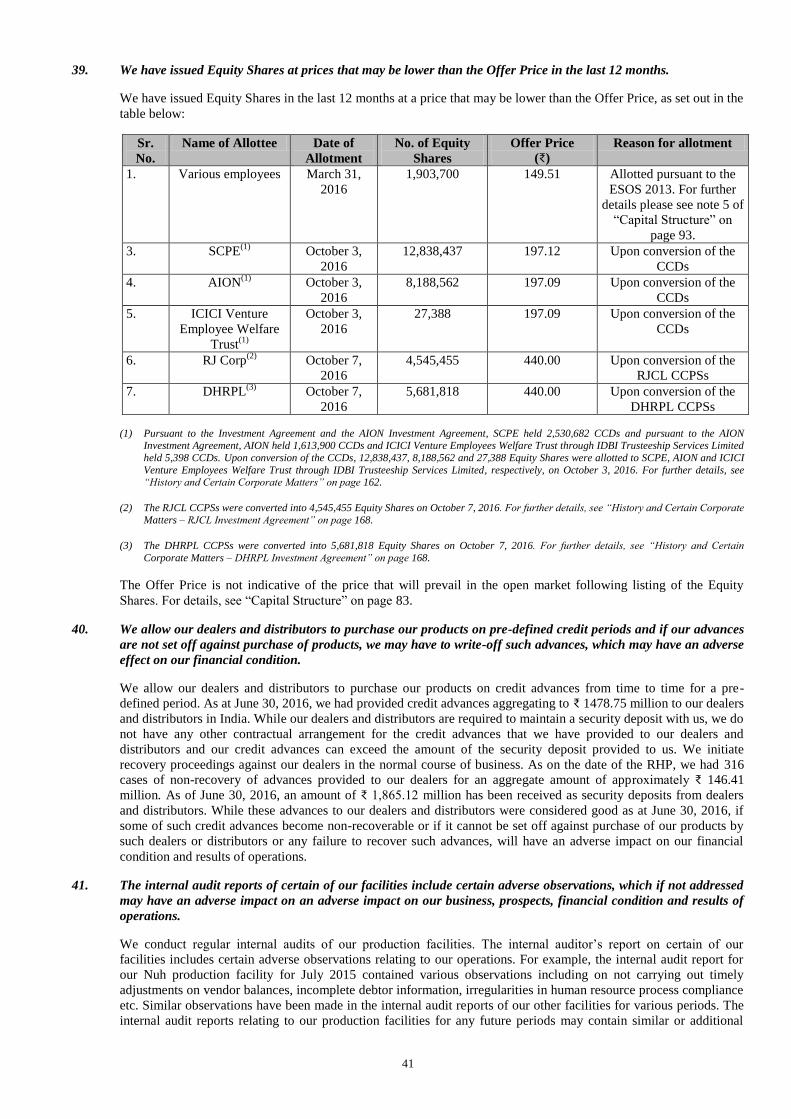

be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Net Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI

ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All potential Bidders, other than Anchor Investors, shall mandatorily participate in the Offer through an Application

Supported by Blocked Amount (“ASBA”) process by providing details of their respective bank account which will be blocked by the Self Certified Syndicate Banks (“SCSBs”). Anchor Investors are not

permitted to participate in the Anchor Investor Portion through ASBA process. For details, please see “Offer Procedure” on page 491.

RISKS IN RELATION TO THE FIRST OFFER

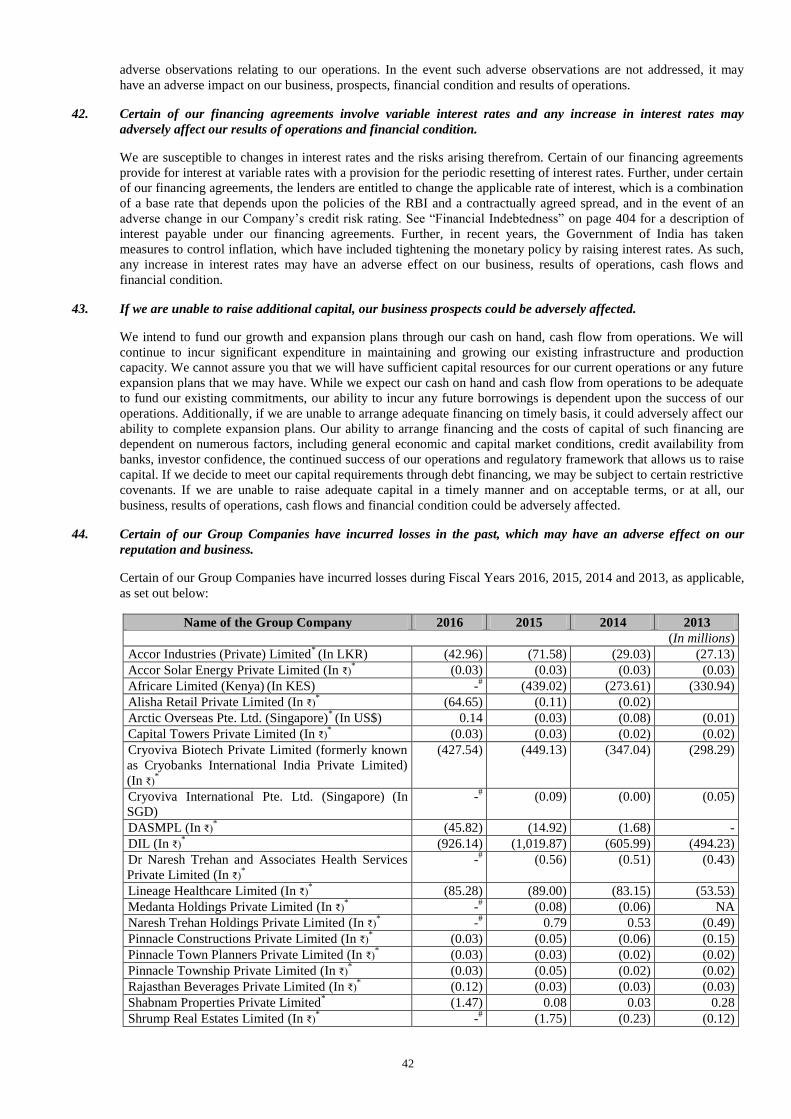

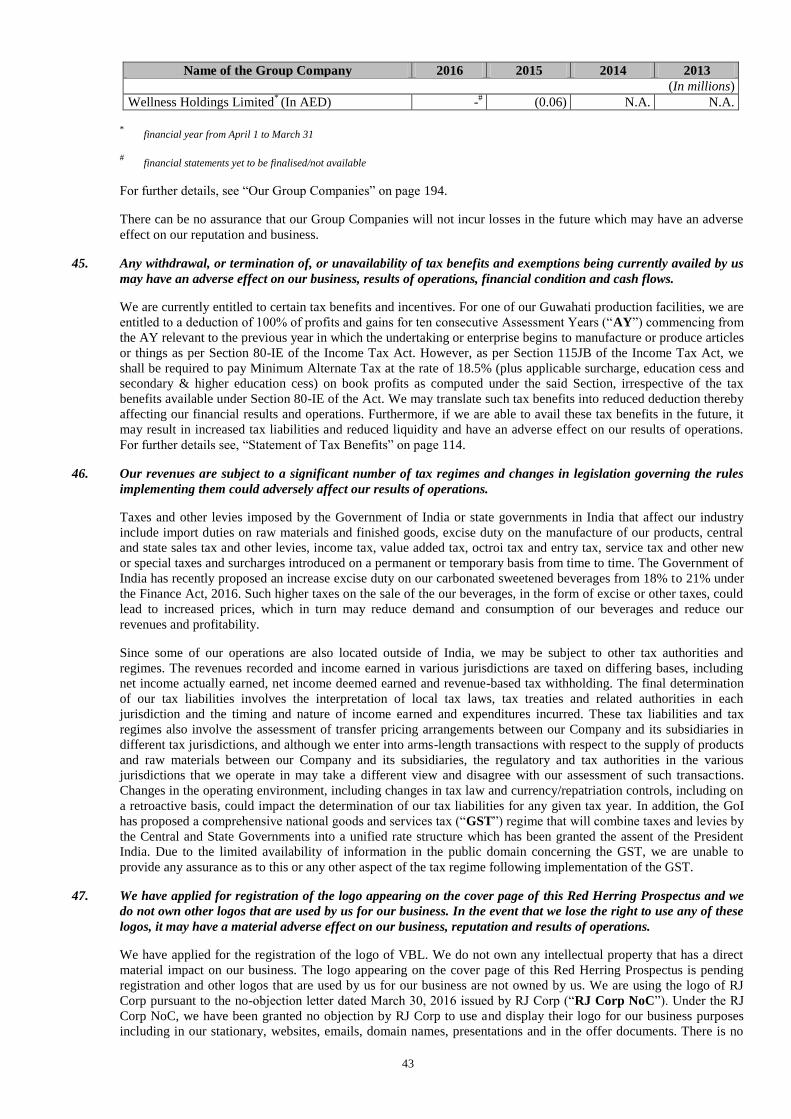

This being the first public issue of our Company, there has been no formal market for the Equity Shares of our Company. The face value of the Equity Shares is ₹ 10 and the Floor Price is [●] times the face

value and the Cap Price is [●] times the face value. The Offer Price (determined and justified by our Company in consultation with the Selling Shareholders, the GCBRLMs and the BRLM as stated under the

section “Basis for Offer Price” on page 110) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or

sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors

are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer,

including the risks involved. The Equity Shares in the Offer have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or

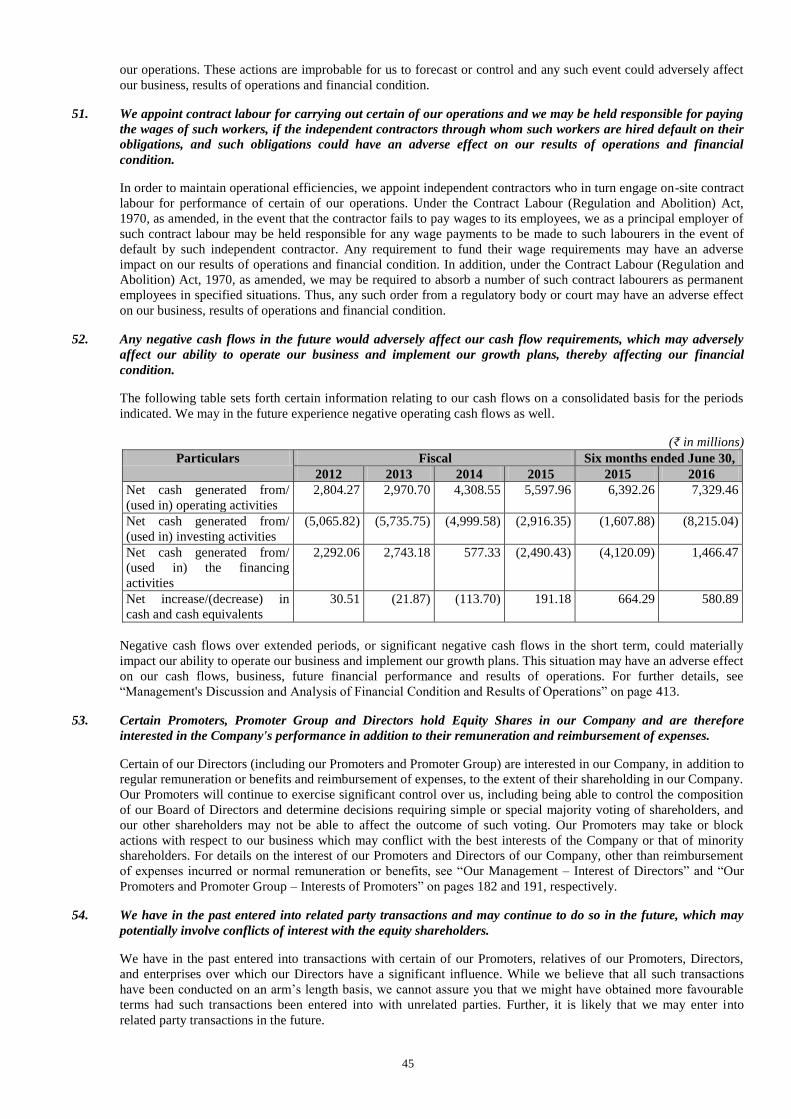

adequacy of the contents of this Red Herring Prospectus. Specific attention of the investors is invited to the section “Risk Factors” on page 22.

ISSUER’S AND SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Red Herring Prospectus contains all information with regard to our Company and the Offer, which is

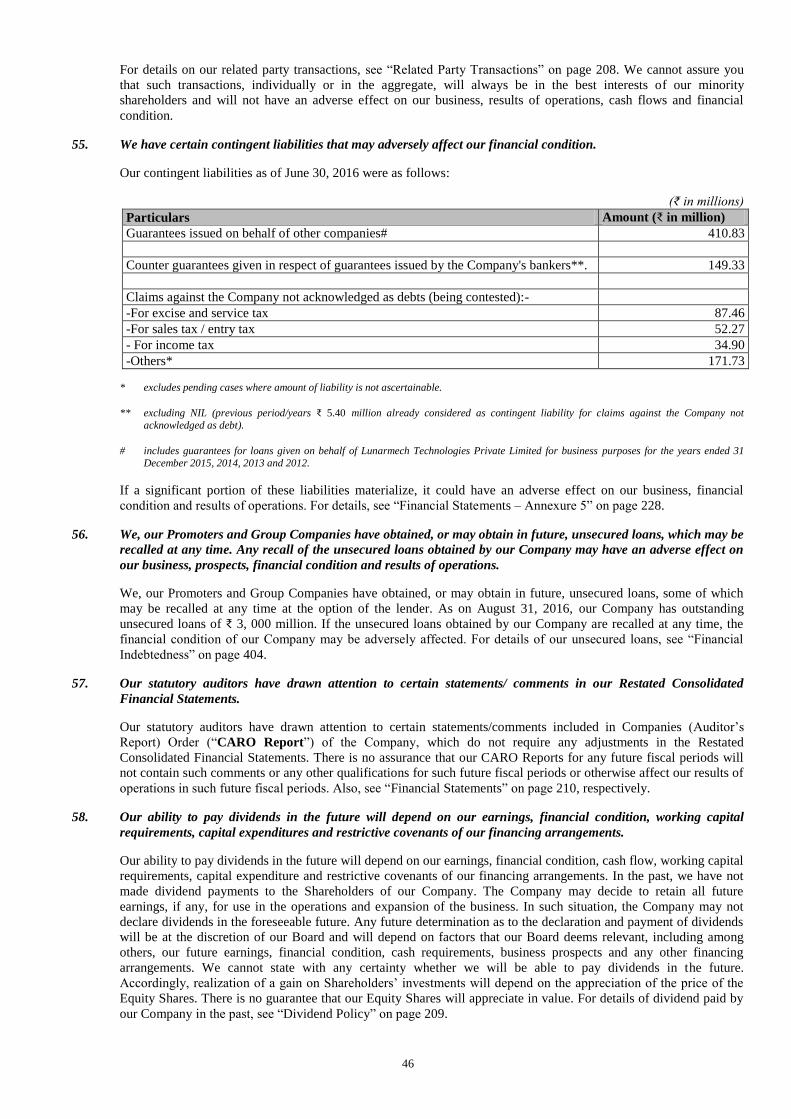

material in the context of the Offer, that the information contained in this Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and

intentions expressed herein are honestly held and that there are no other facts, the omission of which makes the Red Herring Prospectus as a whole or any of such information or the expression of any such

opinions or intentions misleading in any material respect. Further, the Selling Shareholders severally accept responsibility that this Red Herring Prospectus contains all information about themselves as the

Selling Shareholders in context of the Offer for Sale and severally accept responsibility for statements in relation to themselves included in this Red Herring Prospectus.

LISTING

The Equity Shares offered through this Red Herring Prospectus are proposed to be listed on the BSE and the NSE. Our Company has received an ‘in-principle’ approval from the BSE and the NSE for the listing

of the Equity Shares pursuant to letters dated June 29, 2016 and July 5, 2016 respectively. For the purposes of the Offer, the Designated Stock Exchange shall be NSE. A copy of this Red Herring Prospectus has

been delivered for registration to the RoC and a copy of the Prospectus shall be delivered for registration to the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material

contracts and documents available for inspection from the date of the Red Herring Prospectus up to the Bid/Offer Closing Date, see “Material Contracts and Documents for Inspection” on page 543.

GLOBAL COORDINATORS AND BOOK RUNNING LEAD MANAGERS BOOK RUNNING LEAD

MANAGER

REGISTRAR TO THE OFFER

Kotak Mahindra Capital Company

Limited

1st Floor, 27 BKC, Plot No. 27

“G” Block, Bandra Kurla Complex

Bandra (East)

Mumbai 400 051

Tel: +91 22 4336 0000

Fax: +91 22 6713 2447

E-mail: [email protected]

Investor grievance E-mail:

Website:

www.investmentbank.kotak.com

Contact Person: Ganesh Rane

SEBI Registration No.: INM000008704

Axis Capital Limited

1st Floor, Axis House

C-2, Wadia International Centre

P.B. Marg, Worli

Mumbai 400 025

Tel: + 91 22 4325 2183

Fax : +91 22 4325 3000

E-mail: [email protected]

Investor grievance E-mail:

Website: www.axiscapital.co.in

Contact person: Lohit Sharma

SEBI Registration No.: INM000012029

CLSA India Private Limited

(formerly CLSA India Limited)

8/F, Dalamal House

Nariman Point

Mumbai 400 021

Tel: +91 22 6650 5050

Fax: +91 22 2284 0271

E-mail: [email protected]

Investor grievance E-mail:

Website: www.india.clsa.com

Contact person: Sarfaraz Agboatwala

SEBI Registration No: INM000010619

YES Securities (India) Limited

IFC 1 & 2, Unit no. 602 A

6th Floor, Senapati Bapat Marg

Elphinstone (W)

Mumbai 400 013

Telephone: +91 22 3347 9688

Fax: +91 22 2421 4511

E-mail: [email protected]

Investor Grievance E-mail:

Website: www.yesinvest.in

Contact Person: Aditya Vora

SEBI Registration No:

INM000012227

Karvy Computershare Private

Limited

Karvy Selenium Tower B

Plot 31 and 32, Gachibowli

Financial District, Nanakramguda

Hyderabad 500 032

Tel: +91 40 6716 2222

Fax: +91 40 2343 1551

Email:[email protected]

Investor Grievance e-mail: varun-

Website: www.karisma.karvy.com

Contact Person: M Murali Krishna

SEBI Registration No. INR000000221

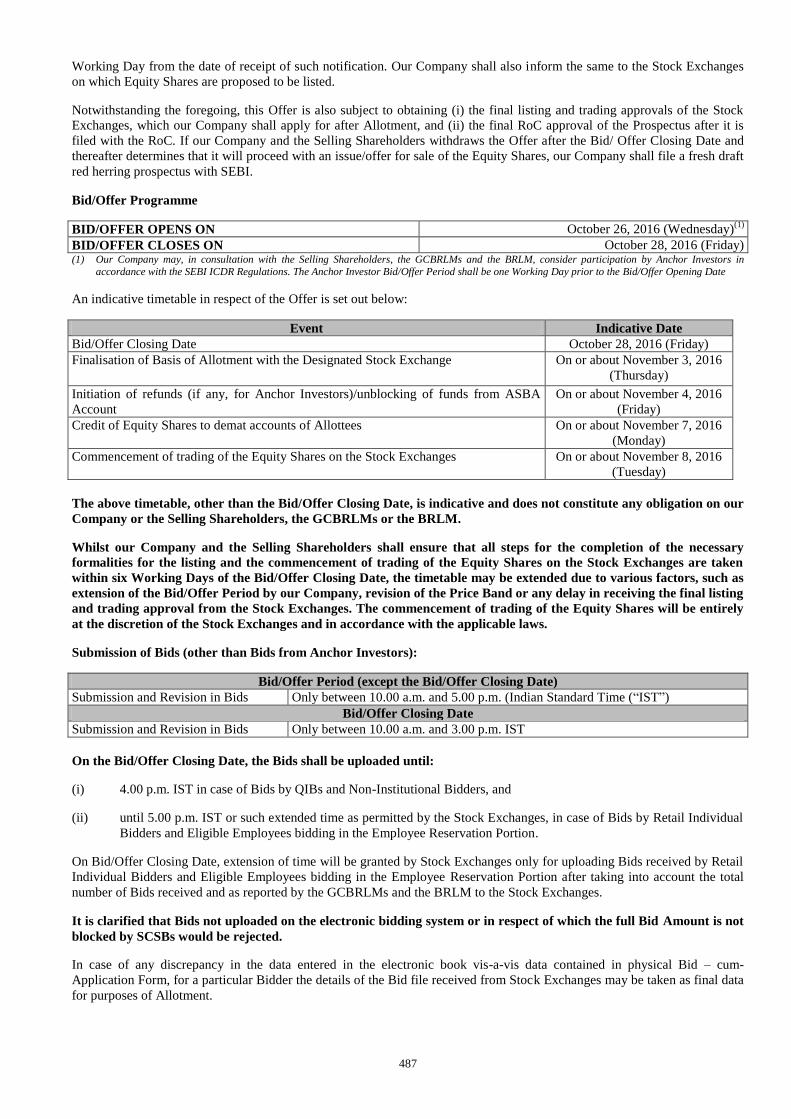

BID/OFFER PROGRAMME

BID/OFFER OPENS ON OCTOBER 26, 2016 (Wednesday) (1)

BID/OFFER CLOSES ON OCTOBER 28, 2016 (Friday) (1) Our Company may, in consultation with the Selling Shareholders, the GCBRLMs and the BRLM, consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor

Investor Bid/Offer Period shall be one Working Day prior to the Bid/Offer Opening Date.

(i)

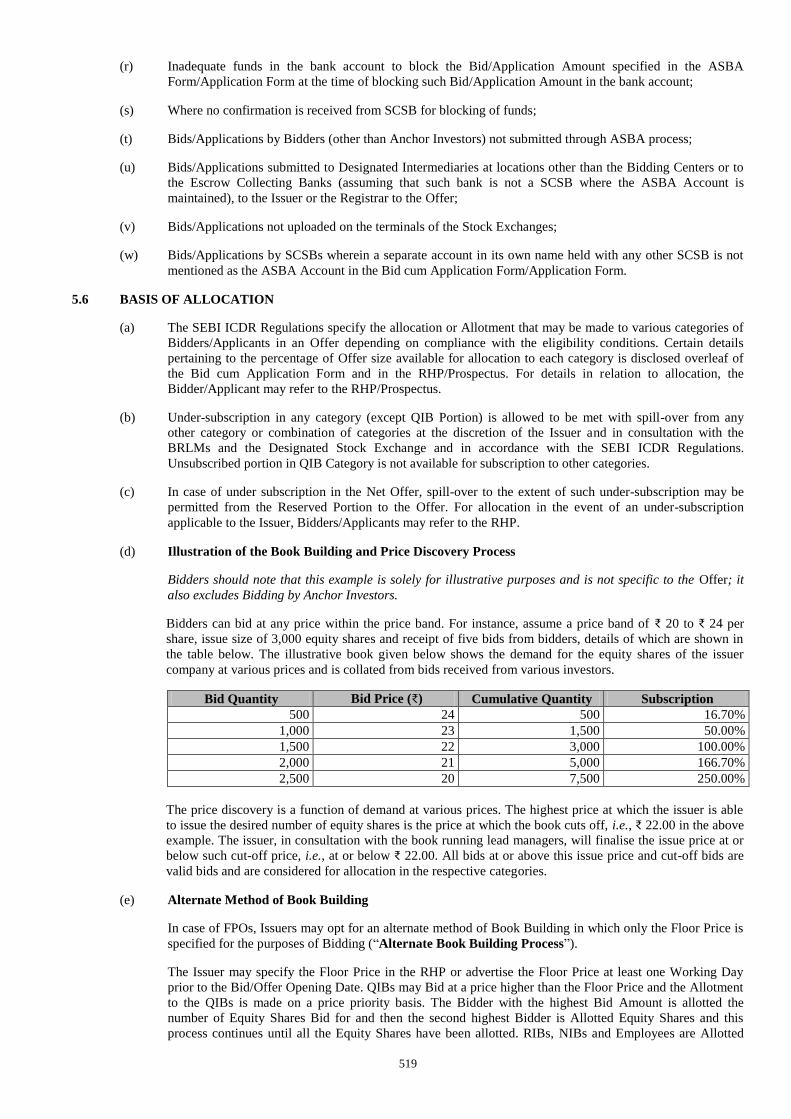

TABLE OF CONTENTS

SECTION I: GENERAL ........................................................................................................................................................ 1 DEFINITIONS AND ABBREVIATIONS ............................................................................................................................. 1 PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA ........................................................................ 17 FORWARD-LOOKING STATEMENTS ............................................................................................................................ 20

SECTION: II RISK FACTORS .......................................................................................................................................... 22

SECTION III: INTRODUCTION ....................................................................................................................................... 53 SUMMARY OF INDUSTRY ............................................................................................................................................... 53 SUMMARY OF BUSINESS ................................................................................................................................................ 57 SUMMARY FINANCIAL INFORMATION ....................................................................................................................... 64 THE OFFER ......................................................................................................................................................................... 73 GENERAL INFORMATION ............................................................................................................................................... 74 CAPITAL STRUCTURE...................................................................................................................................................... 83 OBJECTS OF THE OFFER ................................................................................................................................................ 101 BASIS FOR OFFER PRICE ............................................................................................................................................... 110 STATEMENT OF TAX BENEFITS................................................................................................................................... 114

SECTION IV: ABOUT THE COMPANY ....................................................................................................................... 116 INDUSTRY OVERVIEW .................................................................................................................................................. 116 OUR BUSINESS ................................................................................................................................................................ 130 REGULATIONS AND POLICIES ..................................................................................................................................... 157 HISTORY AND CERTAIN CORPORATE MATTERS .................................................................................................... 162 OUR SUBSIDIARIES ........................................................................................................................................................ 170 OUR MANAGEMENT ...................................................................................................................................................... 174 OUR PROMOTERS AND PROMOTER GROUP ............................................................................................................. 189 OUR GROUP COMPANIES .............................................................................................................................................. 194 RELATED PARTY TRANSACTIONS ............................................................................................................................. 208 DIVIDEND POLICY .......................................................................................................................................................... 209

SECTION V: FINANCIAL INFORMATION ................................................................................................................. 210 RESTATED CONSOLIDATED FINANCIAL STATEMENTS ........................................................................................ 210 RESTATED STANDALONE FINANCIAL STATEMENTS ............................................................................................ 310 FINANCIAL INDEBTEDNESS......................................................................................................................................... 404 SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND IND AS ........................................ 406 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.................................................................................................................................................................... 413

SECTION VI: LEGAL AND OTHER INFORMATION ............................................................................................... 457 OUTSTANDING LITIGATION AND OTHER MATERIAL DEVELOPMENTS ........................................................... 457 GOVERNMENT AND OTHER APPROVALS ................................................................................................................. 467 OTHER REGULATORY AND STATUTORY DISCLOSURES ...................................................................................... 471

SECTION VII: OFFER INFORMATION ....................................................................................................................... 485 TERMS OF THE OFFER ................................................................................................................................................... 485 OFFER STRUCTURE ........................................................................................................................................................ 489 OFFER PROCEDURE ....................................................................................................................................................... 491 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES .................................................................... 531

SECTION VIII: MAIN PROVISIONS OF ARTICLES OF ASSOCIATION .............................................................. 532

SECTION IX: OTHER INFORMATION ........................................................................................................................ 543 MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ............................................................................ 543 DECLARATION ................................................................................................................................................................ 545

1

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

This Red Herring Prospectus uses certain definitions and abbreviations which, unless the context otherwise indicates or

implies, shall have the meaning as provided below. References to any legislation, act, regulation, rule, guideline or policy

shall be to such legislation, act, regulation, rule, guideline or policy, as amended, supplemented or re-enacted from time to

time.

The words and expressions used in this Red Herring Prospectus but not defined herein, shall have, to the extent applicable,

the meaning ascribed to such terms under the Companies Act, the SEBI ICDR Regulations, the SCRA, the Depositories Act or

the rules and regulations made there under.

Notwithstanding the foregoing, terms used in of the sections “Statement of Tax Benefits”, “Restated Consolidated Financial

Statements”, “Restated Standalone Financial Statements” and “Main Provisions of Articles of Association” on pages 114,

210, 310 and 532, respectively, shall have the meaning ascribed to such terms in such sections.

General Terms

Term Description

“our Company”, the “Company”,

or the “Issuer”

Varun Beverages Limited, a company incorporated under the Companies Act, 1956,

having its registered office at F-2/7, Okhla Industrial Area, Phase I, New Delhi 110 020

we/us/our Unless the context otherwise indicates or implies, our Company, its Subsidiaries and its

associate, on a consolidated basis

Company Related Terms

Term Description

2015 Existing India Sub-Territories Delhi, Rajasthan, West Bengal, Goa, Arunachal Pradesh, Assam, Meghalaya, Manipur,

Mizoram, Nagaland, Tripura as well as certain designated parts of the following sub-

territories: Madhya Pradesh, Uttar Pradesh, Uttarakhand, Haryana and Maharashtra.

2015 New India Sub-Territories Punjab, Himachal Pradesh, Chandigarh UT, as well as the remaining parts of the

following sub-territories: Haryana, Uttarakhand and Uttar Pradesh.

ADBL Aradhana Drinks and Beverages Private Limited

AION AION Investments II Singapore Pte. Ltd.

AION Investment Agreement Securities purchase cum investment agreement dated September 18, 2015 between our

Company, AION Investments II Singapore Pte. Ltd. and Standard Chartered Private

Equity Mauritius II Limited

Articles of Association/AoA The articles of association of our Company, as amended

Audit Committee The audit committee of the Board of Director described in the section “Our

Management” on page 174

Board/Board of Directors The board of directors of our Company or a duly constituted committee thereof

Compulsorily Convertible

Debentures or CCDs

Compulsorily convertible debentures issued by our Company of face value of ₹ 1,000

each

CMCI Concentrate Manufacturing Company of Ireland

Compulsorily Convertible

Preference Shares or CCPSs

Compulsorily convertible preference shares of our Company of a face value of ₹ 100

each

Corporate Office Plot No. 31, Institutional Area, Sector – 44, Gurgaon 122 002

DBL Devyani Beverages Limited

2

Term Description

DASMPL Devyani Airport Services (Mumbai) Private Limited

DEPL Devyani Enterprises Private Limited

DexPL Devyani Exim Private Limited (formerly Rajputana Stores (Jaipur) Private Limited)

DHRPL Devyani Hotels and Resorts Private Limited

DIL Devyani International Limited

DHRPL CCPSs 25,000,000 CCPSs issued to DHRPL at par pursuant to the DHRPL Investment

Agreement and converted into 5,681,818 Equity Shares on October 7, 2016

DHRPL Investment Agreement Investment agreement dated February 16, 2015 between our Company and DHRPL

Director(s) The director(s) of our Company

Equity Shares The equity shares of our Company of face value of ₹ 10 each

ESOS 2013 Employee Stock Option Scheme 2013

ESOS 2016 Employee Stock Option Scheme 2016

Group Companies Companies which are covered under the applicable accounting standards and other

companies as considered material by our Board. For details, please see “Our Group

Companies” on page 194

Investment Agreement Investment agreement dated July 18, 2011 between VBIL, SCPE, RJ Corp, Ravi Kant

Jaipuria & Sons (HUF) and Varun Jaipuria as amended by an amendment and

supplemental agreement dated September 29, 2012 and an amendment agreement dated

June 13, 2016

Key Management Personnel Key management personnel of our Company in terms of section 2(51) the Companies

Act, 2013, the SEBI ICDR Regulations and as disclosed in the section “Our

Management” on page 174

Memorandum of Association/MoA The memorandum of association of our Company, as amended

Non-Convertible Debentures or

NCDs

Unsecured redeemable non-convertible debentures of our Company (denominated in

rupees) of a face value of ₹ 10,000,000 listed on the wholesale debt market segment of

NSE

OSBPL Ole Spring Bottlers (Private) Limited

PepsiCo Refers to PepsiCo Inc., PepsiCo India, Seven-Up International, a division of CMCI,

Tropicana Products Inc. and/ or their affiliates, as applicable

PepsiCo India PepsiCo India Holding Private Limited (formerly known as PepsiCo India Holding

Limited)

PepsiCo India Agreements Refers collectively to the four bottling appointment and trademark license agreements,

two dated October 3, 2012 executed between our Company and PepsiCo Inc., one dated

October 3, 2012 between our Company and PepsiCo India and another effective from

June 13, 2016 between Tropicana Products Inc. and our Company, as amended from

time to time, as applicable

PepsiCo International Agreements Refers collectively, to the 12 bottling agreements entered into by our Company in

relation to our international operations and specifically, the (i) exclusive bottling

appointment agreement dated November 7, 2013 between PepsiCo Inc. and VBL

Lanka; (ii) exclusive bottling appointment agreement dated August 1, 2011 between

PepsiCo Inc. and VBL Lanka; (iii) exclusive bottling appointment agreement dated

August 1, 2011 between Seven-Up International, a division of CMCI and VBL Lanka;

(iv) bottling appointment and trademark license agreement dated October 30, 2013

3

Term Description

between Tropicana Products Inc and VBL Lanka; (v) exclusive bottling appointment

agreement dated December 1, 2011 between PepsiCo Inc. and VBNPL, (vi) exclusive

bottling appointment agreement dated December 1, 2011 between Seven-Up

International, a division of CMCI and VBNPL; (vii) exclusive bottling appointment

agreement dated September 1, 2010 between Seven-Up International, a division of

CMCI and VBZL; (viii) exclusive bottling appointment agreement dated September 1,

2010 between PepsiCo Inc. and VBZL; (ix) exclusive bottling appointment agreement

dated February 1, 2011 between PepsiCo Inc. and VBM; (x) exclusive bottling

appointment agreement dated February 1, 2011 between Seven-Up International, a

division of CMCI and VBM; (xi) exclusive bottling appointment agreement dated

December 18, 2008 between PepsiCo Inc. and VBML effective from January 25, 2009;

and (xii) exclusive bottling appointment agreement dated December 18, 2008 between

Seven-Up International, a division of CMCI and VBML effective from January 25,

2009, as amended from time to time, as applicable

PepsiCo International Entities Refers to PepsiCo Inc., Seven-Up International, a division of CMCI, Tropicana

Products Inc. and/ or their affiliates, as applicable, with whom our Company through its

Subsidiaries has entered into the PepsiCo International Agreements

Promoter Group Persons and entities constituting the promoter group of our Company in terms of

Regulation 2(1)(zb) of the SEBI ICDR Regulations, but excluding any persons and

entities apart from the following: (i) Accor Developers (Private) Limited, (ii) Accor

Industries (Private) Limited, (iii) Accor Solar Energy Private Limited, (iv) Africare

Limited, (v) Agarwal Cold Drinks Private Limited, (vi) Alisha Retail Private Limited,

(vii) Angelica Technologies Private Limited, (viii) Anuj Traders Private Limited, (ix)

Arctic International Private Limited, (x) Arctic Overseas Pte. Limited, (xi) Capital

Infracon Private Limited, (xii) Capital Towers Private Limited, (xiii) Cryoviva

International Pte. Ltd., (xiv) Cryoviva Singapore Pte. Ltd., (xv) D.J. Agri Industries

Private Limited, (xvi) Devyani Enterprises Private Limited, (xvii) Devyani Food

Industries Limited, (xviii) Devyani Hotels & Resorts Private Limited, (xix) Devyani

International Limited, (xx) Devyani Overseas Private Limited, (xxi) Diagno Labs

Private Limited, (xxii) Empire Stocks Private Limited, (xxiii) Farm2Plate Dairy

Produce Private Limited (formerly known as ABInbev India Private Limited), (xxiv)

Lineage Healthcare Limited, (xxv) Lunarmech Technologies Private Limited, (xxvi)

Modern Montessori International (India) Private Limited, (xxvii) Mumbai Rockets

Sports Private Limited, (xxviii) Parkview City Limited, (xxix) Pinnacle Constructions

Private Limited, (xxx) Pinnacle Infracon Limited, (xxxi) Pinnacle Town Planners

Private Limited, (xxxii) Pinnacle Township Private Limited, (xxxiii) Rajasthan

Beverages Private Limited, (xxxiv) Ratnaker Foods & Beverages Private Limited,

(xxxv) S V S India Private Limited, (xxxvi) Sellwell Foods and Beverages Private

Limited, (xxxvii) Shabnam Properties Private Limited, (xxxviii)Universal Dairy

Products Private Limited, (xil) Wellness Holdings Limited, (xl) Mr. Ravi Kant Jaipuria,

(xli) Ms. Dhara Jaipuria, (xlii) Mr. Varun Jaipuria, (xliii) Ms. Devyani Jaipuria, (xliv)

RJ Corp Limited, (xlv) Ravi Kant Jaipuria & Sons (HUF), (xlvi) Mr. Vivek Gupta,

(xlvii) Ms. Bela Jyoti Kumar Saha, (xlviii) Ms. Madhu Rajendra Prasad Jindal, (xlix)

Alaknanda Traders Private Limited, (l) Avni Securities Private Limited, (li) Chanda

Exports Private Limited, (lii) Gee Kay Builder & Development Services Private

Limited, (liii) Manog Securities Private Limited, (liv) Ragini Advisors Private Limited,

(lv) Stallion Advisors Private Limited, (lvi) Geld Consultancy Services Private Limited,

(lvii) Saha Sprague Limited, (lviii) Sara Ferrous Private Limited, (lix) SFT Syscon

Private Limited, (lx) SFT Technologies Private Limited, (lxi) Sankalp Lifespaces

Private Limited, (lxii) Dr. Naresh Trehan and Associates Health Services Private

Limited; and (lxiii) Lemon Tree Hotels Limited. For details, please see “Our Promoters

and Promoter Group” on page 189

Promoters The promoters of our Company namely, RJ Corp Limited, Ravi Kant Jaipuria, Varun

Jaipuria and Ravi Kant Jaipuria & Sons (HUF). For details, please see “Our Promoters

and Promoter Group” on page 189

Registered Office F-2/7, Okhla Industrial Area, Phase I, New Delhi 110 020

4

Term Description

Restated Consolidated Financial

Statements

The consolidated financial statements of our Company’s assets and liabilities as at June

30, 2016, June 30, 2015, December 31, 2015, 2014, 2013 and 2012 and the consolidated

statements of profit and loss and cash flows for the six months periods ended June 30,

2016 and June 30, 2015 and for the years ended December 31, 2015, 2014, 2013 and

2012 of our Company prepared in accordance with Indian GAAP and the Companies

Act and restated in accordance with the SEBI ICDR Regulations and the Revised

Guidance Note on Reports in Company Prospectuses (Revised) issued by the ICAI,

together with the schedules, notes and annexures thereto

Restated Financial Statements Collectively, the Restated Consolidated Financial Statements and the Restated

Standalone Financial Statements

Restated Standalone Financial

Statements

The standalone financial statements of our Company’s assets and liabilities as at June

30, 2016 and June 30, 2015, December 31, 2015, 2014, 2013, 2012 and 2011 and the

standalone statements of profit and loss and cash flows for the six months periods ended

June 30, 2016 and June 30, 2015 and for the years ended December 31, 2015, 2014,

2013, 2012 and 2011 of our Company prepared in accordance with Indian GAAP and

the Companies Act and restated in accordance with the SEBI ICDR Regulations and the

Revised Guidance Note on Reports in Company Prospectuses (Revised) issued by the

ICAI, together with the schedules, notes and annexures thereto

RJCL CCPSs 20,000,000 CCPSs issued to RJCL at par pursuant to the RJCL Investment Agreement

and converted into 4,545,455 Equity Shares on October 7, 2016

RJCL Investment Agreement Investment agreement dated October 20, 2014 between our Company and RJ Corp

RJ Corp RJ Corp Limited (formerly Arctic Drinks Private Limited)

RoC Registrar of Companies, NCT of Delhi and Haryana at 4th

Floor, IFCI Tower; 61, Nehru

Place, New Delhi 110 019

Sales Volume(s) Represents sales volume (in million litres and / or million unit cases) of our PepsiCo

products to our customers but does not include any sales to PepsiCo and/or any other

franchisees of PepsiCo.

SCPE Standard Chartered Private Equity (Mauritius) II Limited

Shareholders Shareholders of our Company

Statutory Auditors The statutory auditors of our Company, Walker Chandiok & Associates and O.P. Bagla

& Co.

Subsidiaries Subsidiaries of our Company (including any step-down subsidiary) set out in the section

“Our Subsidiaries” on page 170

VBIL Varun Beverages (International) Limited

VBL Lanka Varun Beverages Lanka (Private) Limited

VBM Varun Beverages Morocco SA

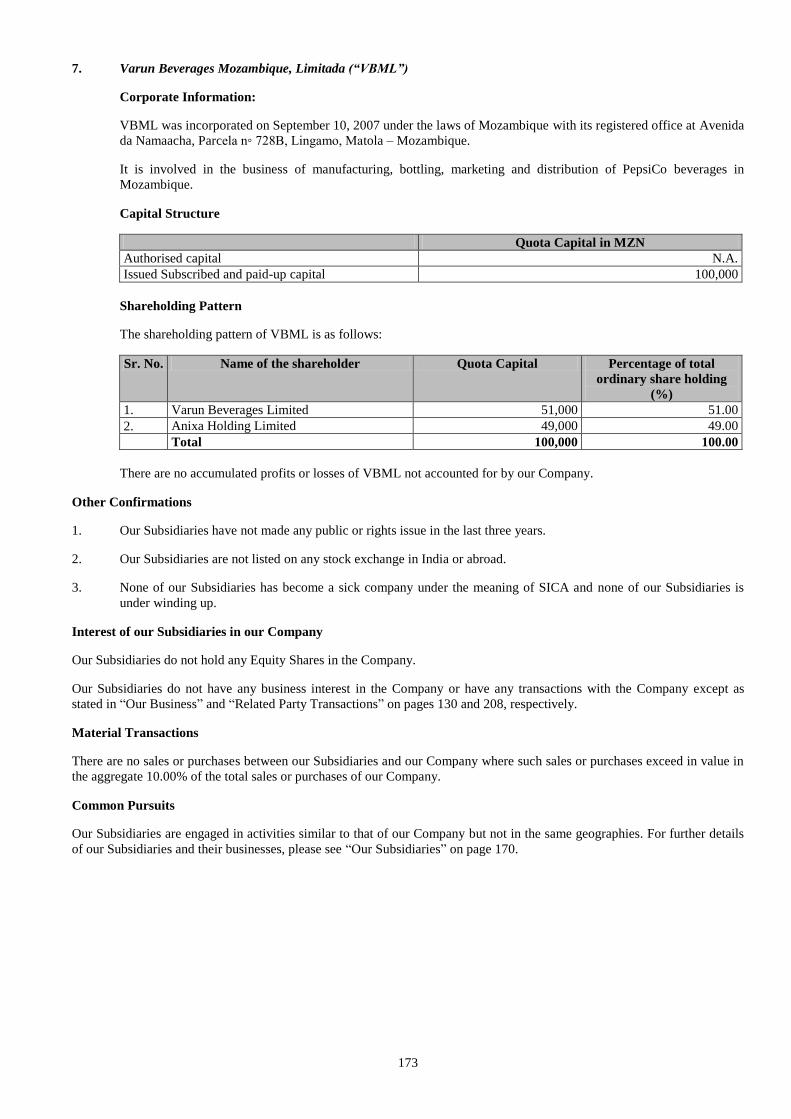

VBML Varun Beverages Mozambique, Limitada

VBNPL Varun Beverages (Nepal) Pvt. Ltd.

VBZL Varun Beverages (Zambia) Limited

VBZPL Varun Beverages (Zimbabwe) (Private) Limited

5

Offer Related Terms

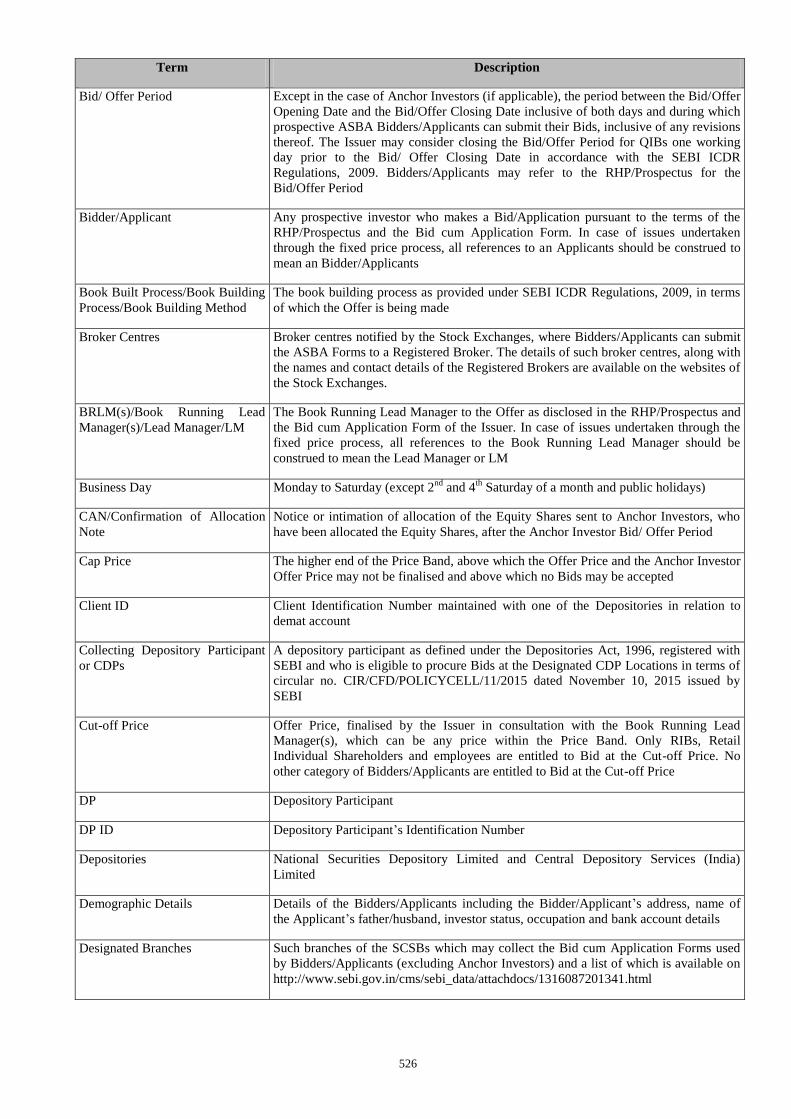

Term Description

Acknowledgement Slip The slip or document issued by the Designated Intermediary to a Bidder as proof of

registration of the Bid cum Application Form

Allot/Allotment/Allotted Unless the context otherwise requires, allotment of the Equity Shares pursuant to the

Fresh Issue and transfer of Equity Shares offered by the Selling Shareholders pursuant

to the Offer for Sale, to the successful Bidders

Allottee A successful Bidder to whom the Equity Shares are Allotted

Allotment Advice Note, advice or intimation of Allotment sent to the Bidders who have been or are to be

Allotted the Equity Shares after the Basis of Allotment has been approved by the

Designated Stock Exchange

Anchor Investor A Qualified Institutional Buyer, applying under the Anchor Investor Portion in

accordance with the requirements specified in the SEBI ICDR Regulations and the Red

Herring Prospectus

Anchor Investor Allocation Price The price at which the Equity Shares will be allocated to Anchor Investors in terms of

the Red Herring Prospectus and the Prospectus which will be decided by our Company

in consultation with the Selling Shareholders, the GCBRLMs and the BRLM

Anchor Investor Application Form The form used by an Anchor Investor to make a Bid in the Anchor Investor Portion and

which will be considered as an application for Allotment in terms of the Red Herring

Prospectus and Prospectus

Anchor Investor Bid/Offer Period The day which is one Working Day prior to the Bid/Offer Opening Date, on which Bids

by Anchor Investors shall be submitted and allocation to the Anchor Investors shall be

completed

Anchor Investor Offer Price Final price at which the Equity Shares will be Allotted to Anchor Investors in terms of

the Red Herring Prospectus and the Prospectus, which price will be equal to or higher

than the Offer Price but not higher than the Cap Price

The Anchor Investor Offer Price will be decided by our Company in consultation with

the Selling Shareholders, the GCBRLMs and the BRLM

Anchor Investor Portion Up to 60% of the QIB Portion consisting of up to 7,350,000 Equity Shares which may

be allocated by our Company in consultation with the Selling Shareholders, the

GCBRLMs and the BRLM to Anchor Investors on a discretionary basis

One-third of the Anchor Investor Portion shall be reserved for Mutual Funds, subject to

valid Bids being received from Mutual Funds at or above the Anchor Investors

Allocation Price

Application Supported by Blocked

Amount or ASBA

An application, whether physical or electronic, used by an ASBA Bidder, to make a Bid

and authorize a SCSB to block the Bid Amount in the ASBA Account

ASBA Account A bank account maintained with a SCSB and specified in the ASBA Form submitted by

Bidders for blocking the Bid Amount mentioned in the ASBA Form

ASBA Bid A Bid made by an ASBA Bidder including all revisions and modifications thereto as

permitted under the SEBI ICDR Regulations

ASBA Bidder All Bidders other than Anchor Investors

ASBA Forms An application form, whether physical or electronic, used by an ASBA Bidder and

which will be considered as an application for Allotment in terms of the Red Herring

Prospectus and the Prospectus

Axis Capital Axis Capital Limited

6

Term Description

Banker to the Offer/Escrow

Collection Bank

Bank which is a clearing member and registered with SEBI as banker to an issue and

with whom the Escrow Account will be opened, in this case being HDFC Bank Limited

Basis of Allotment The basis on which the Equity Shares will be Allotted to successful Bidders under the

Offer and which is described in the section “Offer Procedure” on page 491

Bid An indication to make an offer during the Bid/Offer Period by an ASBA Bidder

pursuant to submission of the ASBA Form, or during the Anchor Investor Bid/Offer

Period by the Anchor Investors pursuant to submission of Anchor Investor Application

Form, to subscribe to or purchase the Equity Shares of our Company at a price within

the Price Band, including all revisions and modifications thereto as permitted under the

SEBI ICDR Regulations

The term Bidding shall be construed accordingly

Bid Amount The highest value of optional Bids indicated in the Bid cum Application Form and

payable by the Bidder or as blocked in the ASBA Account of the Bidder, as the case

may be, upon submission of the Bid

Bid cum Application Form The Anchor Investor Application Form or ASBA Form, as the context requires

Bid/Offer Closing Date Except in relation to any Bids received from the Anchor Investors, the date after which

the Designated Intermediaries will not accept any Bids, which shall be published in all

editions of Financial Express (a widely circulated English national daily newspaper) and

all editions of Jansatta (a widely circulated Hindi national daily newspaper with wide

circulation in Delhi)

Our Company may, in consultation with the Selling Shareholders, the GCBRLMs and

the BRLM, consider closing the Bid/Offer Period for QIBs one Working Day prior to

the Bid/Offer Closing Date in accordance with the SEBI ICDR Regulations

Bid/Offer Opening Date Except in relation to any Bids received from the Anchor Investors, the date on which the

Designated Intermediaries shall start accepting Bids, which shall be published in all

editions of Financial Express (a widely circulated English national daily newspaper) and

all editions of Jansatta (a widely circulated Hindi national daily newspaper with wide

circulation in Delhi)

Bid/Offer Period Except in relation to Anchor Investors, the period between the Bid/Offer Opening Date

and the Bid/Offer Closing Date, inclusive of both days, during which prospective

Bidders can submit their Bids, including any revisions thereof

Bid Lot [●] Equity Shares

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring

Prospectus and the Bid cum Application Form and unless otherwise stated or implied,

includes an Anchor Investor

Bidding Centers Centers at which the Designated Intermediaries shall accept the Bid cum Application

Forms, i.e, Designated SCSB Branch for SCSBs, Specified Locations for Syndicate,

Broker Centres for Registered Brokers, Designated RTA Locations for RTAs and

Designated CDP Locations for CDPs

Book Building Process Book building process, as provided in Schedule XI of the SEBI ICDR Regulations, in

terms of which the Offer is being made

Broker Centres Broker centres notified by the Stock Exchanges where Bidders can submit the ASBA

Forms to a Registered Broker

The details of such Broker Centres, along with the names and contact details of the

Registered Brokers are available on the respective websites of the Stock Exchanges

(www.bseindia.com and www.nseindia.com)

7

Term Description

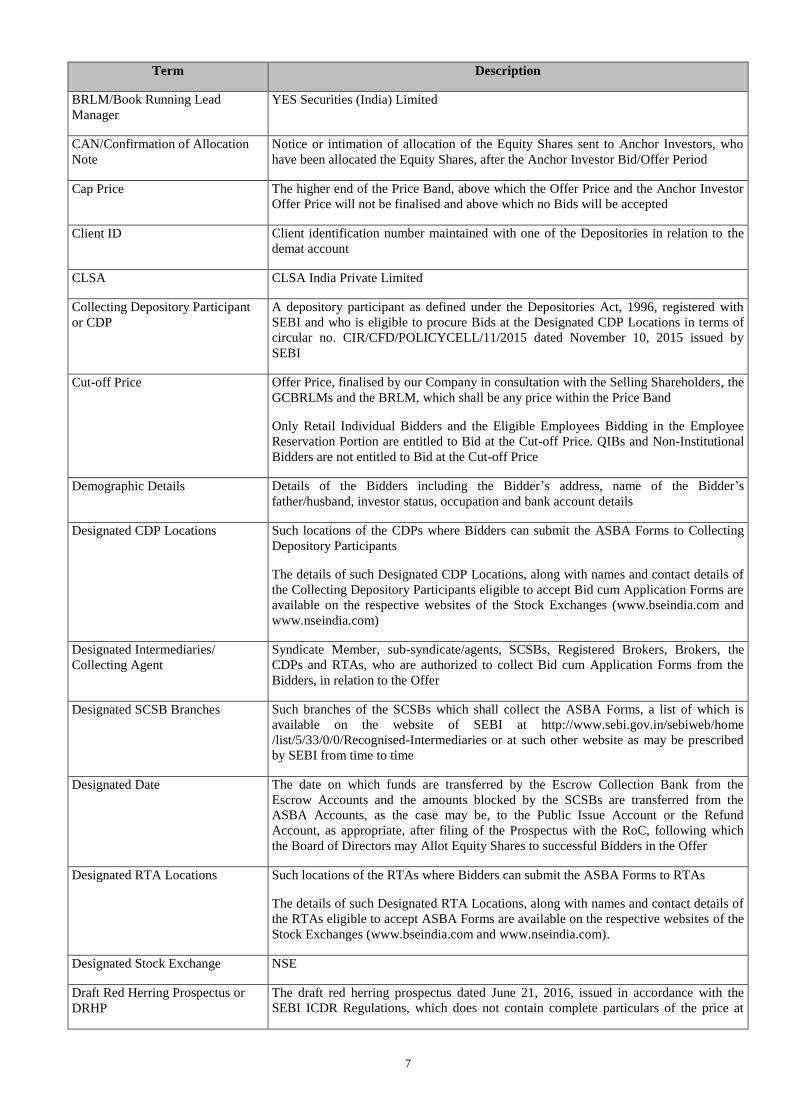

BRLM/Book Running Lead

Manager

YES Securities (India) Limited

CAN/Confirmation of Allocation

Note

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors, who

have been allocated the Equity Shares, after the Anchor Investor Bid/Offer Period

Cap Price The higher end of the Price Band, above which the Offer Price and the Anchor Investor

Offer Price will not be finalised and above which no Bids will be accepted

Client ID Client identification number maintained with one of the Depositories in relation to the

demat account

CLSA CLSA India Private Limited

Collecting Depository Participant

or CDP

A depository participant as defined under the Depositories Act, 1996, registered with

SEBI and who is eligible to procure Bids at the Designated CDP Locations in terms of

circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by

SEBI

Cut-off Price Offer Price, finalised by our Company in consultation with the Selling Shareholders, the

GCBRLMs and the BRLM, which shall be any price within the Price Band

Only Retail Individual Bidders and the Eligible Employees Bidding in the Employee

Reservation Portion are entitled to Bid at the Cut-off Price. QIBs and Non-Institutional

Bidders are not entitled to Bid at the Cut-off Price

Demographic Details Details of the Bidders including the Bidder’s address, name of the Bidder’s

father/husband, investor status, occupation and bank account details

Designated CDP Locations Such locations of the CDPs where Bidders can submit the ASBA Forms to Collecting

Depository Participants

The details of such Designated CDP Locations, along with names and contact details of

the Collecting Depository Participants eligible to accept Bid cum Application Forms are

available on the respective websites of the Stock Exchanges (www.bseindia.com and

www.nseindia.com)

Designated Intermediaries/

Collecting Agent

Syndicate Member, sub-syndicate/agents, SCSBs, Registered Brokers, Brokers, the

CDPs and RTAs, who are authorized to collect Bid cum Application Forms from the

Bidders, in relation to the Offer

Designated SCSB Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of which is

available on the website of SEBI at http://www.sebi.gov.in/sebiweb/home

/list/5/33/0/0/Recognised-Intermediaries or at such other website as may be prescribed

by SEBI from time to time

Designated Date The date on which funds are transferred by the Escrow Collection Bank from the

Escrow Accounts and the amounts blocked by the SCSBs are transferred from the

ASBA Accounts, as the case may be, to the Public Issue Account or the Refund

Account, as appropriate, after filing of the Prospectus with the RoC, following which

the Board of Directors may Allot Equity Shares to successful Bidders in the Offer

Designated RTA Locations Such locations of the RTAs where Bidders can submit the ASBA Forms to RTAs

The details of such Designated RTA Locations, along with names and contact details of

the RTAs eligible to accept ASBA Forms are available on the respective websites of the

Stock Exchanges (www.bseindia.com and www.nseindia.com).

Designated Stock Exchange NSE

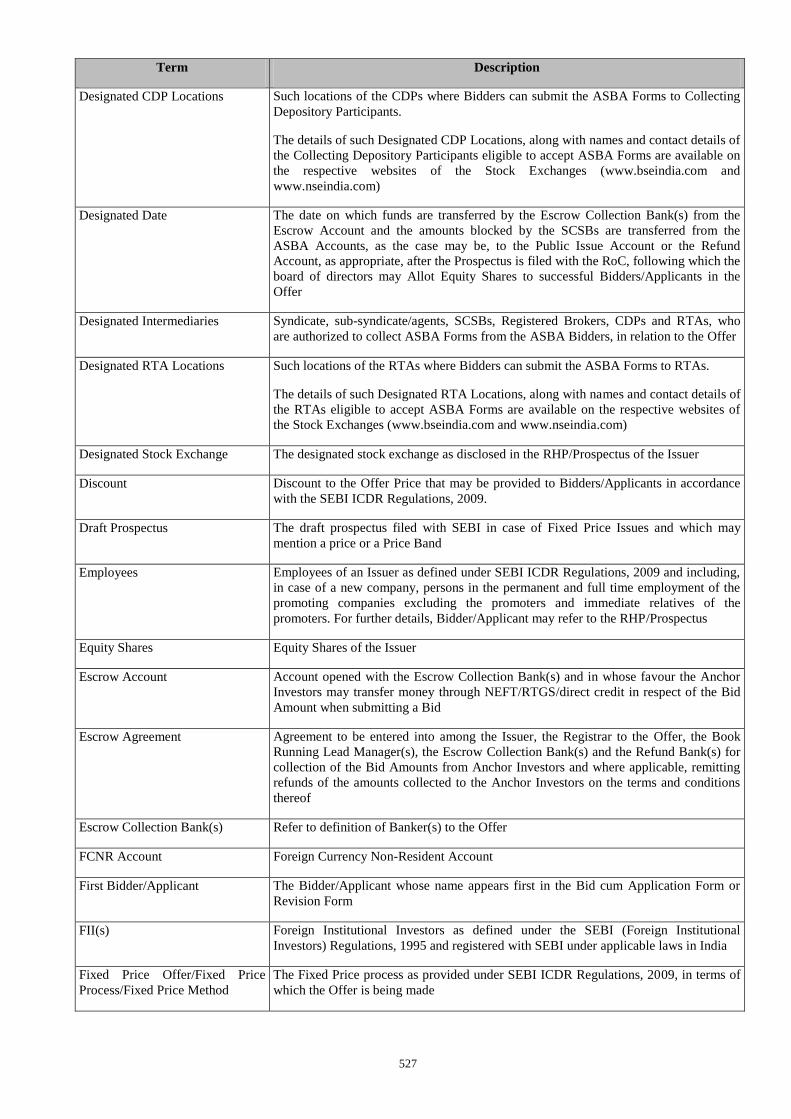

Draft Red Herring Prospectus or

DRHP

The draft red herring prospectus dated June 21, 2016, issued in accordance with the

SEBI ICDR Regulations, which does not contain complete particulars of the price at

8

Term Description

which the Equity Shares will be Allotted and the size of the Offer

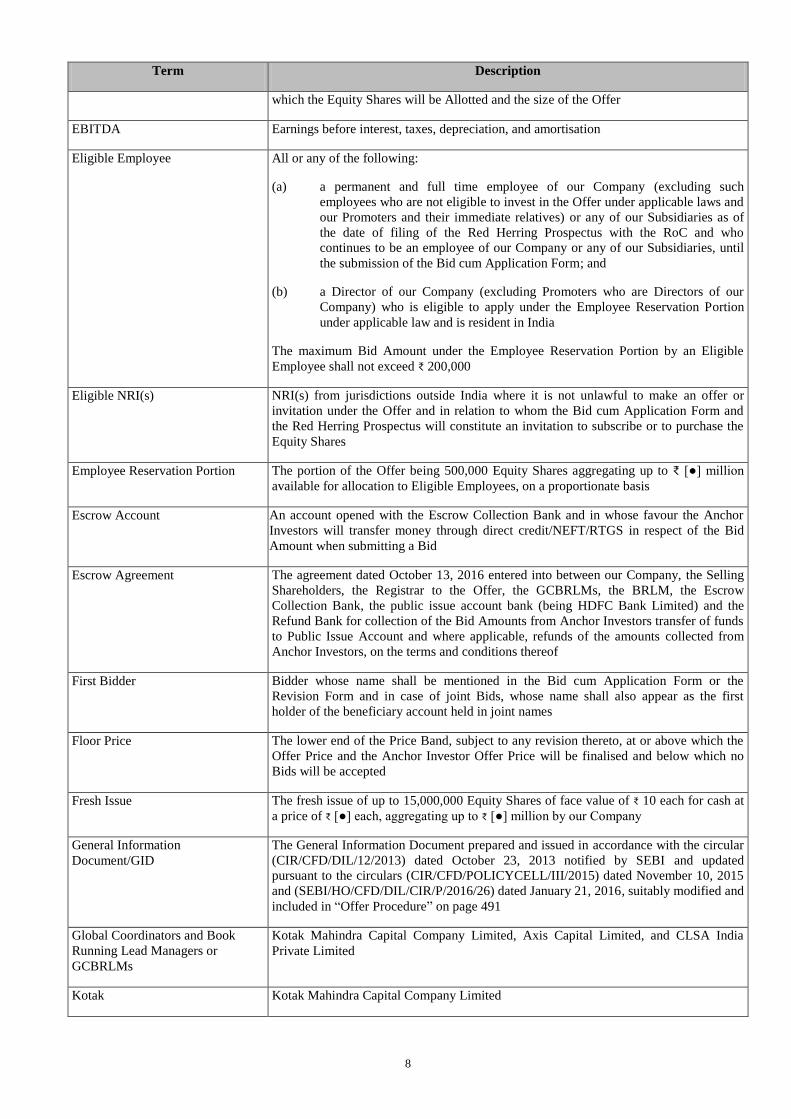

EBITDA Earnings before interest, taxes, depreciation, and amortisation

Eligible Employee All or any of the following:

(a) a permanent and full time employee of our Company (excluding such

employees who are not eligible to invest in the Offer under applicable laws and

our Promoters and their immediate relatives) or any of our Subsidiaries as of

the date of filing of the Red Herring Prospectus with the RoC and who

continues to be an employee of our Company or any of our Subsidiaries, until

the submission of the Bid cum Application Form; and

(b) a Director of our Company (excluding Promoters who are Directors of our

Company) who is eligible to apply under the Employee Reservation Portion

under applicable law and is resident in India

The maximum Bid Amount under the Employee Reservation Portion by an Eligible

Employee shall not exceed ₹ 200,000

Eligible NRI(s) NRI(s) from jurisdictions outside India where it is not unlawful to make an offer or

invitation under the Offer and in relation to whom the Bid cum Application Form and

the Red Herring Prospectus will constitute an invitation to subscribe or to purchase the

Equity Shares

Employee Reservation Portion The portion of the Offer being 500,000 Equity Shares aggregating up to ₹ [●] million

available for allocation to Eligible Employees, on a proportionate basis

Escrow Account An account opened with the Escrow Collection Bank and in whose favour the Anchor

Investors will transfer money through direct credit/NEFT/RTGS in respect of the Bid

Amount when submitting a Bid

Escrow Agreement The agreement dated October 13, 2016 entered into between our Company, the Selling

Shareholders, the Registrar to the Offer, the GCBRLMs, the BRLM, the Escrow

Collection Bank, the public issue account bank (being HDFC Bank Limited) and the

Refund Bank for collection of the Bid Amounts from Anchor Investors transfer of funds

to Public Issue Account and where applicable, refunds of the amounts collected from

Anchor Investors, on the terms and conditions thereof

First Bidder Bidder whose name shall be mentioned in the Bid cum Application Form or the

Revision Form and in case of joint Bids, whose name shall also appear as the first

holder of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, subject to any revision thereto, at or above which the

Offer Price and the Anchor Investor Offer Price will be finalised and below which no

Bids will be accepted

Fresh Issue The fresh issue of up to 15,000,000 Equity Shares of face value of ₹ 10 each for cash at

a price of ₹ [●] each, aggregating up to ₹ [●] million by our Company

General Information

Document/GID

The General Information Document prepared and issued in accordance with the circular

(CIR/CFD/DIL/12/2013) dated October 23, 2013 notified by SEBI and updated

pursuant to the circulars (CIR/CFD/POLICYCELL/III/2015) dated November 10, 2015

and (SEBI/HO/CFD/DIL/CIR/P/2016/26) dated January 21, 2016, suitably modified and

included in “Offer Procedure” on page 491

Global Coordinators and Book

Running Lead Managers or

GCBRLMs

Kotak Mahindra Capital Company Limited, Axis Capital Limited, and CLSA India

Private Limited

Kotak Kotak Mahindra Capital Company Limited

9

Term Description

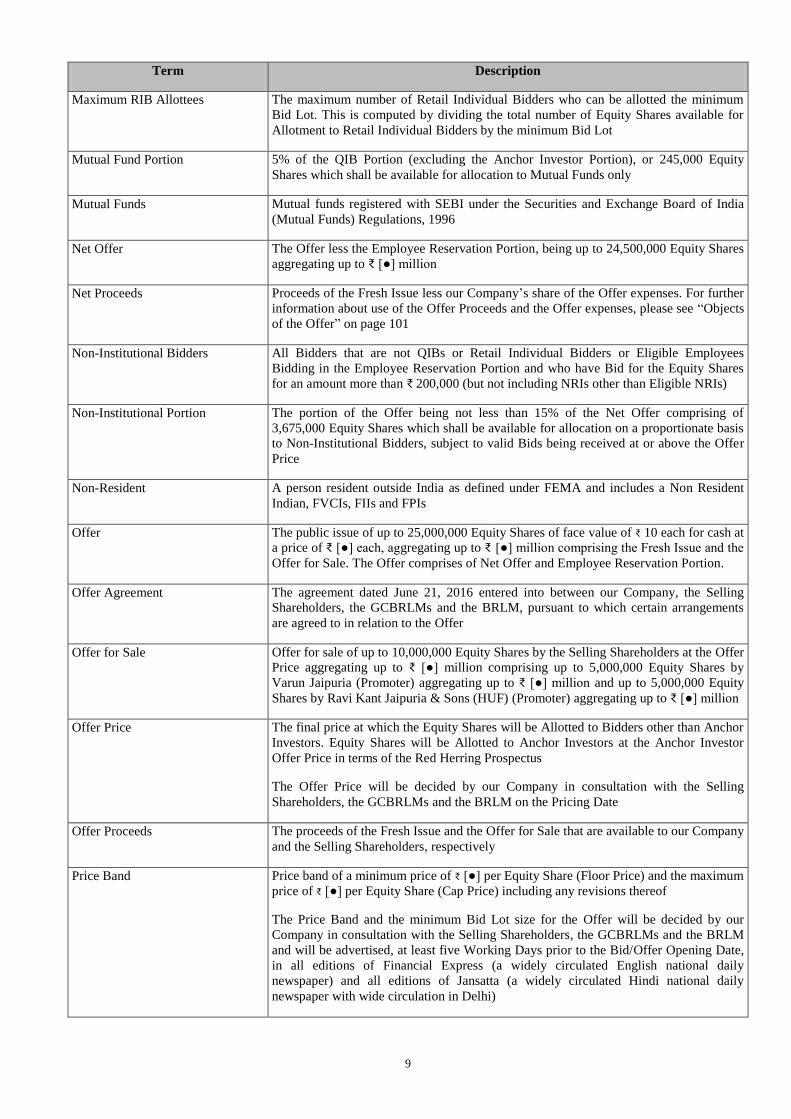

Maximum RIB Allottees The maximum number of Retail Individual Bidders who can be allotted the minimum

Bid Lot. This is computed by dividing the total number of Equity Shares available for

Allotment to Retail Individual Bidders by the minimum Bid Lot

Mutual Fund Portion 5% of the QIB Portion (excluding the Anchor Investor Portion), or 245,000 Equity

Shares which shall be available for allocation to Mutual Funds only

Mutual Funds Mutual funds registered with SEBI under the Securities and Exchange Board of India

(Mutual Funds) Regulations, 1996

Net Offer The Offer less the Employee Reservation Portion, being up to 24,500,000 Equity Shares

aggregating up to ₹ [●] million

Net Proceeds Proceeds of the Fresh Issue less our Company’s share of the Offer expenses. For further

information about use of the Offer Proceeds and the Offer expenses, please see “Objects

of the Offer” on page 101

Non-Institutional Bidders All Bidders that are not QIBs or Retail Individual Bidders or Eligible Employees

Bidding in the Employee Reservation Portion and who have Bid for the Equity Shares

for an amount more than ₹ 200,000 (but not including NRIs other than Eligible NRIs)

Non-Institutional Portion The portion of the Offer being not less than 15% of the Net Offer comprising of

3,675,000 Equity Shares which shall be available for allocation on a proportionate basis

to Non-Institutional Bidders, subject to valid Bids being received at or above the Offer

Price

Non-Resident A person resident outside India as defined under FEMA and includes a Non Resident

Indian, FVCIs, FIIs and FPIs

Offer The public issue of up to 25,000,000 Equity Shares of face value of ₹ 10 each for cash at

a price of ₹ [●] each, aggregating up to ₹ [●] million comprising the Fresh Issue and the

Offer for Sale. The Offer comprises of Net Offer and Employee Reservation Portion.

Offer Agreement The agreement dated June 21, 2016 entered into between our Company, the Selling

Shareholders, the GCBRLMs and the BRLM, pursuant to which certain arrangements

are agreed to in relation to the Offer

Offer for Sale Offer for sale of up to 10,000,000 Equity Shares by the Selling Shareholders at the Offer

Price aggregating up to ₹ [●] million comprising up to 5,000,000 Equity Shares by

Varun Jaipuria (Promoter) aggregating up to ₹ [●] million and up to 5,000,000 Equity

Shares by Ravi Kant Jaipuria & Sons (HUF) (Promoter) aggregating up to ₹ [●] million

Offer Price The final price at which the Equity Shares will be Allotted to Bidders other than Anchor

Investors. Equity Shares will be Allotted to Anchor Investors at the Anchor Investor

Offer Price in terms of the Red Herring Prospectus

The Offer Price will be decided by our Company in consultation with the Selling

Shareholders, the GCBRLMs and the BRLM on the Pricing Date

Offer Proceeds The proceeds of the Fresh Issue and the Offer for Sale that are available to our Company

and the Selling Shareholders, respectively

Price Band Price band of a minimum price of ₹ [●] per Equity Share (Floor Price) and the maximum

price of ₹ [●] per Equity Share (Cap Price) including any revisions thereof

The Price Band and the minimum Bid Lot size for the Offer will be decided by our

Company in consultation with the Selling Shareholders, the GCBRLMs and the BRLM

and will be advertised, at least five Working Days prior to the Bid/Offer Opening Date,

in all editions of Financial Express (a widely circulated English national daily

newspaper) and all editions of Jansatta (a widely circulated Hindi national daily

newspaper with wide circulation in Delhi)

10

Term Description

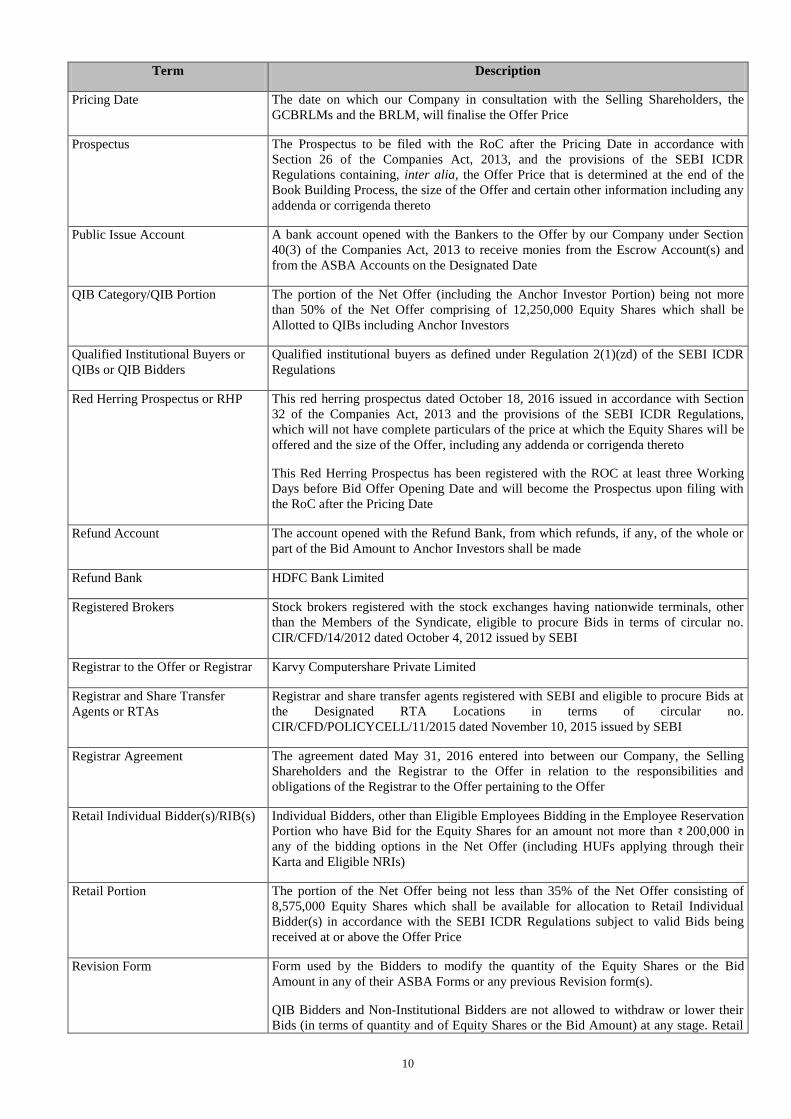

Pricing Date The date on which our Company in consultation with the Selling Shareholders, the

GCBRLMs and the BRLM, will finalise the Offer Price

Prospectus The Prospectus to be filed with the RoC after the Pricing Date in accordance with

Section 26 of the Companies Act, 2013, and the provisions of the SEBI ICDR

Regulations containing, inter alia, the Offer Price that is determined at the end of the

Book Building Process, the size of the Offer and certain other information including any

addenda or corrigenda thereto

Public Issue Account A bank account opened with the Bankers to the Offer by our Company under Section

40(3) of the Companies Act, 2013 to receive monies from the Escrow Account(s) and

from the ASBA Accounts on the Designated Date

QIB Category/QIB Portion The portion of the Net Offer (including the Anchor Investor Portion) being not more

than 50% of the Net Offer comprising of 12,250,000 Equity Shares which shall be

Allotted to QIBs including Anchor Investors

Qualified Institutional Buyers or

QIBs or QIB Bidders

Qualified institutional buyers as defined under Regulation 2(1)(zd) of the SEBI ICDR

Regulations

Red Herring Prospectus or RHP This red herring prospectus dated October 18, 2016 issued in accordance with Section

32 of the Companies Act, 2013 and the provisions of the SEBI ICDR Regulations,

which will not have complete particulars of the price at which the Equity Shares will be

offered and the size of the Offer, including any addenda or corrigenda thereto

This Red Herring Prospectus has been registered with the ROC at least three Working

Days before Bid Offer Opening Date and will become the Prospectus upon filing with

the RoC after the Pricing Date

Refund Account The account opened with the Refund Bank, from which refunds, if any, of the whole or

part of the Bid Amount to Anchor Investors shall be made

Refund Bank HDFC Bank Limited

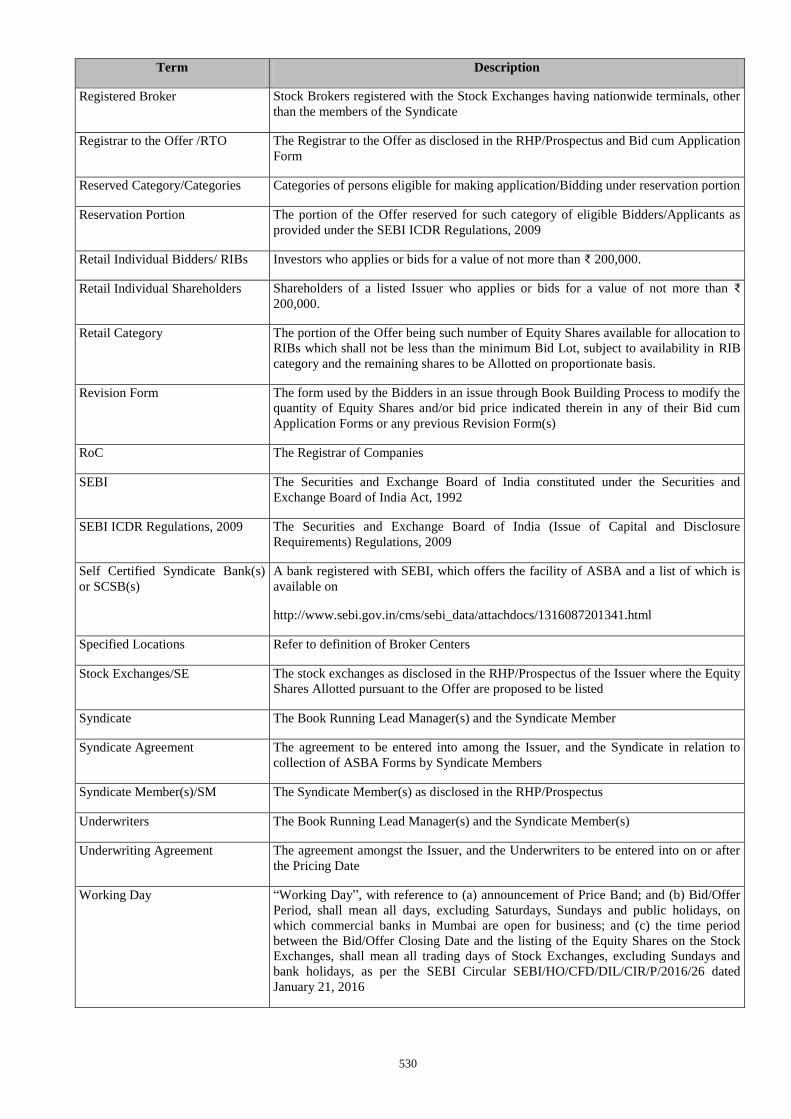

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals, other

than the Members of the Syndicate, eligible to procure Bids in terms of circular no.

CIR/CFD/14/2012 dated October 4, 2012 issued by SEBI

Registrar to the Offer or Registrar Karvy Computershare Private Limited

Registrar and Share Transfer

Agents or RTAs

Registrar and share transfer agents registered with SEBI and eligible to procure Bids at

the Designated RTA Locations in terms of circular no.

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Registrar Agreement The agreement dated May 31, 2016 entered into between our Company, the Selling

Shareholders and the Registrar to the Offer in relation to the responsibilities and

obligations of the Registrar to the Offer pertaining to the Offer

Retail Individual Bidder(s)/RIB(s) Individual Bidders, other than Eligible Employees Bidding in the Employee Reservation

Portion who have Bid for the Equity Shares for an amount not more than ₹ 200,000 in

any of the bidding options in the Net Offer (including HUFs applying through their

Karta and Eligible NRIs)

Retail Portion The portion of the Net Offer being not less than 35% of the Net Offer consisting of

8,575,000 Equity Shares which shall be available for allocation to Retail Individual

Bidder(s) in accordance with the SEBI ICDR Regulations subject to valid Bids being

received at or above the Offer Price

Revision Form Form used by the Bidders to modify the quantity of the Equity Shares or the Bid

Amount in any of their ASBA Forms or any previous Revision form(s).

QIB Bidders and Non-Institutional Bidders are not allowed to withdraw or lower their

Bids (in terms of quantity and of Equity Shares or the Bid Amount) at any stage. Retail

11

Term Description

Individual Bidders cannot revise their Bids after the Bid/Offer Closing Date

Self Certified Syndicate Bank(s) or

SCSB(s)

Banks registered with SEBI, offering services in relation to ASBA, a list of which is

available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries and

updated from time to time

Selling Shareholders Varun Jaipuria and Ravi Kant Jaipuria & Sons (HUF)

Share Escrow Agent Share escrow agent appointed pursuant to the Share Escrow Agreement namely Karvy

Computershare Private Limited

Share Escrow Agreement The agreement dated October 13, 2016 entered into between the Selling Shareholders,

our Company and the Share Escrow Agent in connection with the transfer of the

respective portion of Offered Shares by each of the Selling Shareholders and credit of

such Equity Shares to the demat account of the Allottees

Specified Locations Bidding centres where the Syndicate shall accept ASBA Forms, a list of which is

available on the website of SEBI at

www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised-Intermediaries and updated

from time to time

Stock Exchanges BSE Limited and the National Stock Exchange of India Limited

Syndicate Agreement The agreement dated October 13, 2016 entered into between, the GCBRLMs, the

BRLM, the Syndicate Member, our Company, the Selling Shareholders and Registrar to

the Offer in relation to the collection of Bid cum Application Forms by the Syndicate

Member

Syndicate Member Intermediary registered with SEBI who is permitted to carry out activities as an

underwriter, in this case, Kotak Securities Limited

Syndicate or Members of the

Syndicate

The GCBRLMs, the BRLM and the Syndicate Member

Underwriters [●]

Underwriting Agreement The agreement dated [●] to be entered into among the Underwriters, our Company and

the Selling Shareholders on or after the Pricing Date

Working Day “Working Day”, with reference to (a) announcement of Price Band; and (b) Bid/Offer

Period, shall mean all days, excluding Saturdays, Sundays and public holidays, on

which commercial banks in Mumbai are open for business; and (c) the time period

between the Bid/Offer Closing Date and the listing of the Equity Shares on the Stock

Exchanges, shall mean all trading days of Stock Exchanges, excluding Sundays and

bank holidays, as per the SEBI Circular SEBI/HO/CFD/DIL/CIR/P/2016/26 dated

January 21, 2016

YES Securities YES Securities (India) Limited

Technical/Industry Related Terms/Abbreviations

Term Description

CSD Carbonated Soft Drinks

CSO Central Statistics Office

CSR Corporate and social responsibility

F&B Food and Beverages

12

Term Description

GBO Global Brand Owner

GPRS General Packet Radio Services

IMF International Monetary Fund

LBN Local Brand Network

NBO National Brand Owner

NCB Non-Carbonated Beverages

Off-trade sales Sales that take place at retail outlets such as grocery stores, hypermarkets, super markets

etc.

On-trade sales Sales through consumer foodservice outlets that serve the general public in a non-

captive environment.

PET Polyethylene terephthalate

RGB Returnable Glass Bottles

RTD Ready-to-drink

SAMNA Sales Automation Management for the New Age

SKU Stock Keeping Unit

Conventional and General Terms or Abbreviations

Term Description

₹/Rs./Rupees/INR Indian Rupees

AGM Annual General Meeting

AIF Alternative Investment Fund as defined in and registered with SEBI under the Securities

and Exchange Board of India (Alternative Investments Funds) Regulations, 2012

AS/Accounting Standards Accounting Standards issued by the Institute of Chartered Accountants of India

BIS Act The Bureau of Indian Standards Act, 2016

Bn/bn Billion

Boilers Act Indian Boilers Act, 1923

BSE BSE Limited

C.P.C Civil Procedure Code, 1908

CAGR Compounded Annual Growth Rate

Category I Foreign Portfolio

Investors

FPIs who are registered with SEBI as “Category I foreign portfolio investors” under the

SEBI FPI Regulations

Category II Foreign Portfolio

Investors

FPIs who are registered with SEBI as “Category II foreign portfolio investors” under the

SEBI FPI Regulations

Category III Foreign Portfolio

Investors

FPIs who are registered with SEBI as “Category III foreign portfolio investors” under the

SEBI FPI Regulations

13

Term Description

CCI Competition Commission of India

CDSL Central Depository Services (India) Limited

CENVAT Central Value Added Tax

CESTAT Customs, Excise and Service Tax Appellate Tribunal

CGWA Central Ground Water Authority

CIN Corporate Identity Number

CIT Commissioner of Income Tax

Client ID Client identification number of the Bidders beneficiary account

CLRA Contract Labour (Regulation and Abolition) Act,1979

Companies Act Companies Act, 1956 and/or the Companies Act, 2013, as applicable

Companies Act, 1956 Companies Act, 1956, as amended (without reference to the provisions thereof that have

ceased to have effect upon the notification of the Notified Sections)

Companies Act, 2013 The Companies Act, 2013, to the extent in force pursuant to the notification of the

Notified Sections

COPRA Consumer Protection Act, 1986

Cr.P.C Criminal Procedure Code, 1973

Depositories NSDL and CDSL

Depositories Act The Depositories Act, 1996

DIN Director Identification Number

DIPP Department of Industrial Policy and Promotion, Ministry of Commerce and Industry,

Government of India

DP ID Depository Participant’s Identification

DP/Depository Participant A depository participant as defined under the Depositories Act

DTC Direct Taxes Code

EC Act Essential Commodities Act, 1955

ECB External commercial borrowing

EGM Extraordinary General Meeting

Environment Act Environment Protection Act, 1986

EPS Earnings Per Share

Equity Listing Agreement Listing Agreement to be entered into with the Stock Exchanges on which the Equity

Shares of our Company are to be listed

ESI Act Employees State Insurance Act, 1948

FCNR Foreign Currency Non-Resident

FDI Foreign Direct Investment

14

Term Description

FDI Policy Consolidated Foreign Direct Investment Policy notified by DIPP by notification D/o IPP

F. No. 5(1)/2016-FC-1 dated June 7, 2016 effective from June 7, 2016

FEMA Foreign Exchange Management Act, 1999, read with rules and regulations thereunder

FEMA Regulations Foreign Exchange Management (Transfer or Issue of Security by a Person Resident

Outside India) Regulations, 2000, as amended

FII(s) Foreign Institutional Investors as defined under the SEBI FPI Regulations

Financial Year/FY/Fiscal Unless stated otherwise, the period of 12 months ending December 31 of that particular

year

FIPB Foreign Investment Promotion Board

FIR First Information Report

FPI(s) A foreign portfolio investor as defined under the SEBI FPI Regulations

FSSA Food Safety and Standards Act, 2006

FSSAI Food Safety and Standards Authority of India

FSSR Food Safety and Standards Rules, 2011

FVCI Foreign venture capital investors as defined and registered under the SEBI FVCI

Regulations

GAAR General Anti Avoidance Rules

GDP Gross Domestic Product

GIR General Index Register

GoI or Government Government of India

GST Goods and services tax

HUF Hindu Undivided Family

ICAI The Institute of Chartered Accountants of India

ICDS Income Computation and Disclosure Standards

IFRS International Financial Reporting Standards

Income Tax Act The Income Tax Act, 1961

Ind AS Indian Accounting Standards

Ind AS Rules Companies (Indian Accounting Standards) Rules, 2015

India Republic of India

Indian GAAP Generally Accepted Accounting Principles in India

IPC Indian Penal Code, 1860

IPO Initial Public Offering

IRDAI Insurance Regulatory and Development Authority of India

IST Indian Standard Time

15

Term Description

IT Information Technology

Legal Metrology Act Legal Metrology Act, 2009

LIBOR London Interbank Offered Rate

MICR Magnetic Ink Character Recognition

Mn Million

MV Act Motor Vehicles Act, 1988

N.A./NA Not Applicable

NAV Net Asset Value

NECS National Electronic Clearing Services

NEFT National Electronic Fund Transfer

NI Act Negotiable Instruments Act, 1881

Notified Sections The sections of the Companies Act, 2013 that have been notified by the Ministry of

Corporate Affairs, Government of India

NRE Account Non Resident External Account

NRI A person resident outside India, who is a citizen of India or a person of Indian origin, and

shall have the meaning ascribed to such term in the Foreign Exchange Management

(Deposit) Regulations, 2000

NRO Account Non Resident Ordinary Account

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

OCB/Overseas Corporate Body A company, partnership, society or other corporate body owned directly or indirectly to

the extent of at least 60% by NRIs including overseas trusts, in which not less than 60%

of beneficial interest is irrevocably held by NRIs directly or indirectly and which was in

existence on October 3, 2003 and immediately before such date had taken benefits under

the general permission granted to OCBs under FEMA. OCBs are not allowed to invest in

the Offer

p.a. Per annum

P/E Ratio Price/Earnings Ratio

Packaged Commodities Rules Legal Metrology (Packaged Commodities) Rules, 2011

PAN Permanent Account Number

PAT Profit After Tax

PFA Prevention of Food Adulteration Act, 1954

RBI The Reserve Bank of India

RoNW Return on Net Worth

RTGS Real Time Gross Settlement

SCRA Securities Contracts (Regulation) Act, 1956

16

Term Description

SCRR Securities Contracts (Regulation) Rules, 1957

SEBI The Securities and Exchange Board of India constituted under the SEBI Act

SEBI Act Securities and Exchange Board of India Act, 1992

SEBI AIF Regulations Securities and Exchange Board of India (Alternative Investments Funds) Regulations,

2012

SEBI FII Regulations Securities and Exchange Board of India (Foreign Institutional Investors) Regulations,

1995

SEBI FPI Regulations Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2014

SEBI FVCI Regulations Securities and Exchange Board of India (Foreign Venture Capital Investor) Regulations,

2000

SEBI ICDR Regulations Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements)

Regulations, 2009

SEBI Listing Regulations Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015

SEBI VCF Regulations Securities and Exchange Board of India (Venture Capital Fund) Regulations, 1996

Securities Act United States Securities Act of 1933

SICA Sick Industrial Companies (Special Provisions) Act, 1985

Sq. ft. Square feet

State Government The government of a state in India

Stock Exchanges The BSE and the NSE

STT Securities Transaction Tax

Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and

Takeovers) Regulations, 2011

U.K. United Kingdom

U.S./U.S.A/United States United States of America

US GAAP Generally Accepted Accounting Principles in the United States of America

USD/US$ United States Dollars

VAS Value Added Services

VAT Value Added Tax

VCFs Venture Capital Funds as defined in and registered with SEBI under the SEBI VCF

Regulations or the SEBI AIF Regulations, as the case may be

17

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

Certain Conventions

All references in this Red Herring Prospectus to “India” are to the Republic of India and all references to the “U.S.”, “U.S.A”

or “United States” are to the United States of America. Further, all references to following countries are:

S.N. Reference Country

1. Kenya Republic of Kenya

2. Morocco Kingdom of Morocco

3. Mozambique Republic of Mozambique

4. Nepal Federal Democratic Republic of Nepal

5. Singapore Republic of Singapore

6. Sri Lanka Democratic Socialist Republic of Sri Lanka

7. Zambia Republic of Zambia

8. Zimbabwe Republic of Zimbabwe

Unless stated otherwise, all references to page numbers in this Red Herring Prospectus are to the page numbers of this Red

Herring Prospectus.

Financial Data

Unless stated otherwise, the financial information in this Red Herring Prospectus is derived from our Restated Financial

Statements prepared in accordance with the Companies Act and Indian GAAP and restated in accordance with the SEBI

ICDR Regulations.

Our Company did not have a Subsidiary in Fiscal 2011 and hence financial information included herein is derived from our

Restated Standalone Financial Statements for Fiscal 2011. Following the consolidation of certain of our Subsidiaries from

Fiscal 2012 onwards, pursuant to the amalgamation of Varun Beverages International Limited into the Company with effect

from January 1, 2012, the financial information included herein is derived from our Restated Consolidated Financial

Statements for Fiscal 2012, 2013, 2014 and 2015.

In this Red Herring Prospectus, any discrepancies in any table between the total and the sums of the amounts listed are due to

rounding off. All figures in decimals have been rounded off to the second decimal and all percentage figures have been

rounded off to two decimal places and accordingly, there may be consequential changes in this RHP.

Historically, under the Companies Act, 1956, companies had the freedom to fix any annual period as their Financial Year,

however, with the introduction of the Companies Act, 2013, the Financial Year of company is required to be from April 1 to

March 31 each year. Our Company’s financial year commences on January 1 and ends on December 31; accordingly, all

references to a particular financial year, unless stated otherwise, are to the 12 month period ended on December 31 of that

year. Our Financial Year ending of December 31 was approved pursuant to an order dated December 15, 2015 issued by the

Company Law Board, New Delhi.

There are significant differences between Indian GAAP, U.S. GAAP and IFRS. Our Company does not provide reconciliation

of its financial information to IFRS or U.S. GAAP. Our Company has not attempted to explain those differences or quantify

their impact on the financial data included in this Red Herring Prospectus and it is urged that you consult your own advisors

regarding such differences and their impact on our financial data. Accordingly, the degree to which the financial information

included in this Red Herring Prospectus will provide meaningful information is entirely dependent on the reader’s level of

familiarity with Indian accounting policies and practices, the Companies Act, the Indian GAAP and the SEBI ICDR

Regulations. Any reliance by persons not familiar with Indian accounting policies and practices on the financial disclosures

presented in this Red Herring Prospectus should accordingly be limited.

Unless the context otherwise indicates, any percentage amounts, as set forth in the sections “Risk Factors”, “Our Business”,

“Management’s Discussion and Analysis of Financial Conditional and Results of Operations” on pages 22, 130 and 413,

respectively, and elsewhere in this Red Herring Prospectus have been calculated on the basis of our Restated Financial

Statements prepared in accordance with Companies Act and Indian GAAP and restated in accordance with the SEBI ICDR

Regulations.

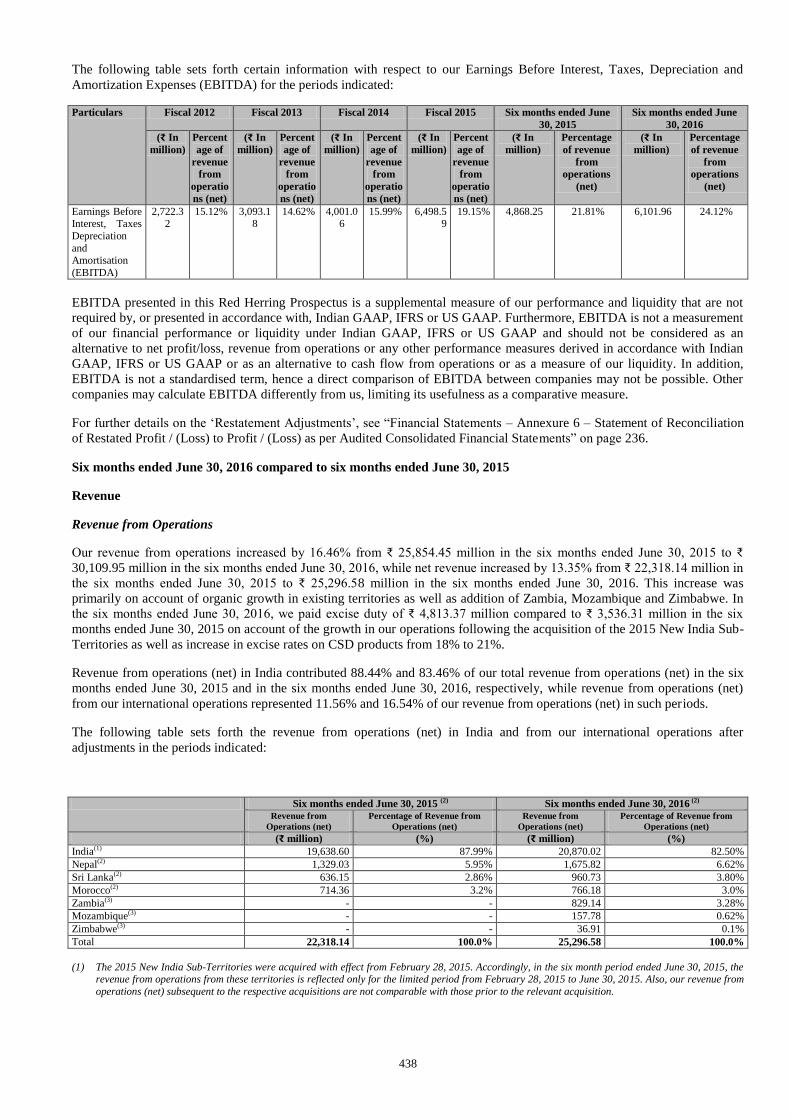

EBITDA presented in this Red Herring Prospectus is a supplemental measure of our performance and liquidity that is not

required by, or presented in accordance with, Indian GAAP, IFRS or US GAAP. Furthermore, EBITDA is not a measurement

of our financial performance or liquidity under Indian GAAP, IFRS or US GAAP and should not be considered as an

alternative to net profit/loss, revenue from operations or any other performance measures derived in accordance with Indian

GAAP, IFRS or US GAAP or as an alternative to cash flow from operations or as a measure of our liquidity. In addition,

EBITDA is not a standardised term, hence a direct comparison of EBITDA between companies may not be possible. Other

companies may calculate EBITDA differently from us, limiting its usefulness as a comparative measure.

18

Important Note on Sales Volume Information

The Sales Volume information presented in this Red Herring Prospectus represents sales to our customers in our licensed

territories but does not include any sales to PepsiCo or any other franchisees of PepsiCo. Sales to PepsiCo and / or other

PepsiCo franchisees are reflected in our revenues from operations. However, such sales have not been significant in the last

five Fiscals and in the six months ended June 30, 2016. We do not make any such sales other than in India. Sales Volume

information in any Fiscal period included in this Red Herring Prospectus cannot be directly correlated to our revenues from

operations in the respective Fiscal.

Important Note on Introduction of Ind AS and its Impact on Preparation and Presentation of our Historical and

Future Financial Statements

The Ministry of Corporate Affairs (“MCA”) has notified the Companies (Indian Accounting Standards) Rules, 2015 on

February 16, 2015 providing revised roadmap on implementation of Indian Accounting Standards (“Ind AS”) which

stipulates implementation of Ind AS in a phased manner beginning from accounting period 2016 – 2017 (“MCA Roadmap”).

Our Company’s debt securities are listed and it had a net worth of less than ₹ 5,000 million as at December 31, 2014 and a net

worth of more than ₹ 5,000 million as at December 31, 2015.

Pursuant to the clarification provided by Bulletin 1 issued by the Ind AS Transition Facilitation Group (ITFG) if the net worth

of a company has or is expected to exceed ₹ 5,000 million after March 31, 2014, such company will be required to apply Ind

AS from the immediate next accounting year in the manner specified in sub-rule (1). Since the net worth of our Company

exceeded ₹ 5,000 million in the year ended December 31, 2015, Ind AS shall be applicable from the year ended December 31,

2017, with comparatives for the periods ended December 31, 2016. The transition date of convergence with Ind AS shall be

January 1, 2016.

Given that Ind AS differs in many respects from Indian GAAP, our financial statements relating to any period subsequent to

January 1, 2017 (and for any prior comparative periods) may not be comparable to our historical financial statements

prepared under Indian GAAP. There can be no assurance that the adoption of Ind AS will not materially affect the preparation

and presentation of our financial statements in the future. In addition, there can be no assurance that if Ind AS were to be

applied to our historical financial statements prepared under Indian GAAP, there will not be material differences in applicable

accounting policies and standards that will require material adjustments to our historical financial statements prepared under

Indian GAAP.

We have not completed the preparation of any of our financial statements in accordance with Ind AS, and are in the process

of evaluating the difference in accounting policies and practices under Ind AS and Indian GAAP that may be reasonably

expected to impact the preparation and presentation of our future financial statements, and, to the extent applicable, our

historical financial statements, in accordance with Ind AS. The preparation of our standalone and consolidated financial

statements in accordance with Ind AS may require our management to make judgments, estimates and assumptions based

upon management’s evaluation of the relevant facts and circumstances as on the date of the relevant financial statements, and

such estimates and underlying assumptions may be reviewed in the future on an on-going basis. For further information, see

“Risk Factors - Our Company, will be required to prepare financial statements under Ind AS (which is India’s convergence to

IFRS). Additionally, Ind AS requires Indian companies to compute Income Tax under the Income Computation and

Disclosure Standards (the “ICDS”). The transition to Ind AS in India is very recent and there is no clarity on the impact of

such transition on our Company. Ind AS also differs from IFRS and US GAAP. The introduction of Ind AS and other

regulatory developments affecting fiscal matters in India may significantly affect preparation and presentation of our financial

statements in the future and such financial statements prepared in accordance with Ind AS may differ from the Restated

Standalone Financial Statements and the Restated Consolidated Financial Statements included in this Red Herring Prospectus.

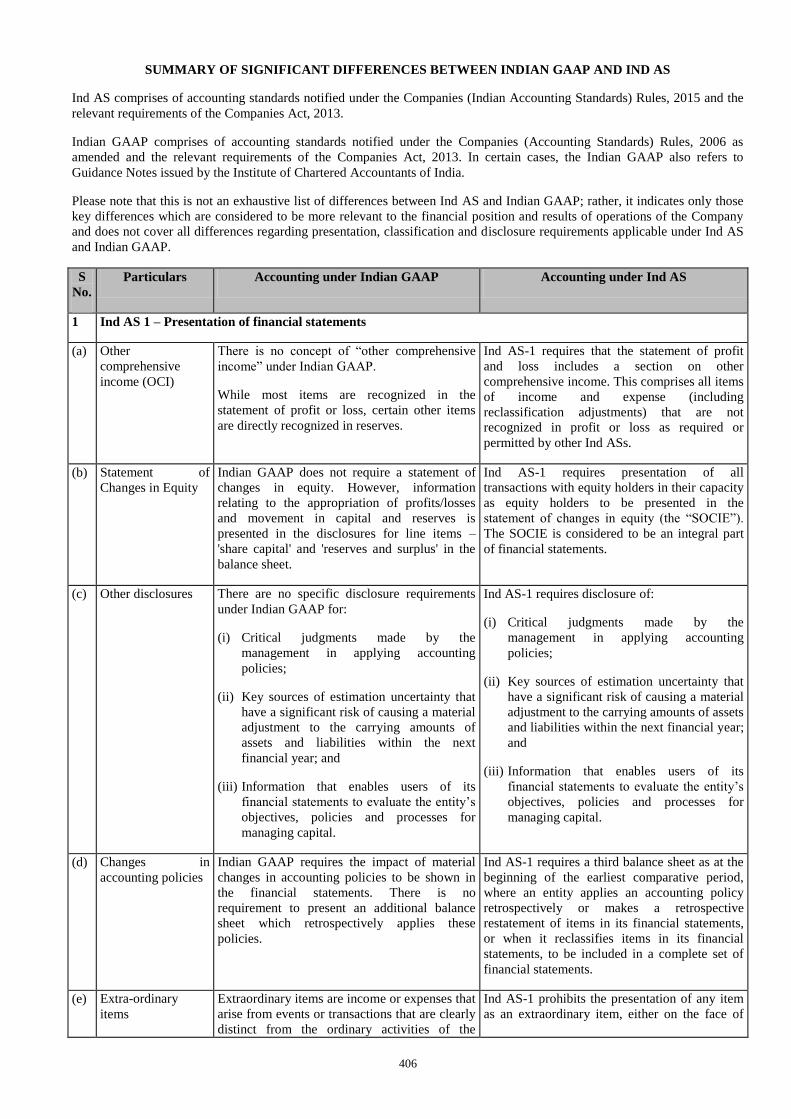

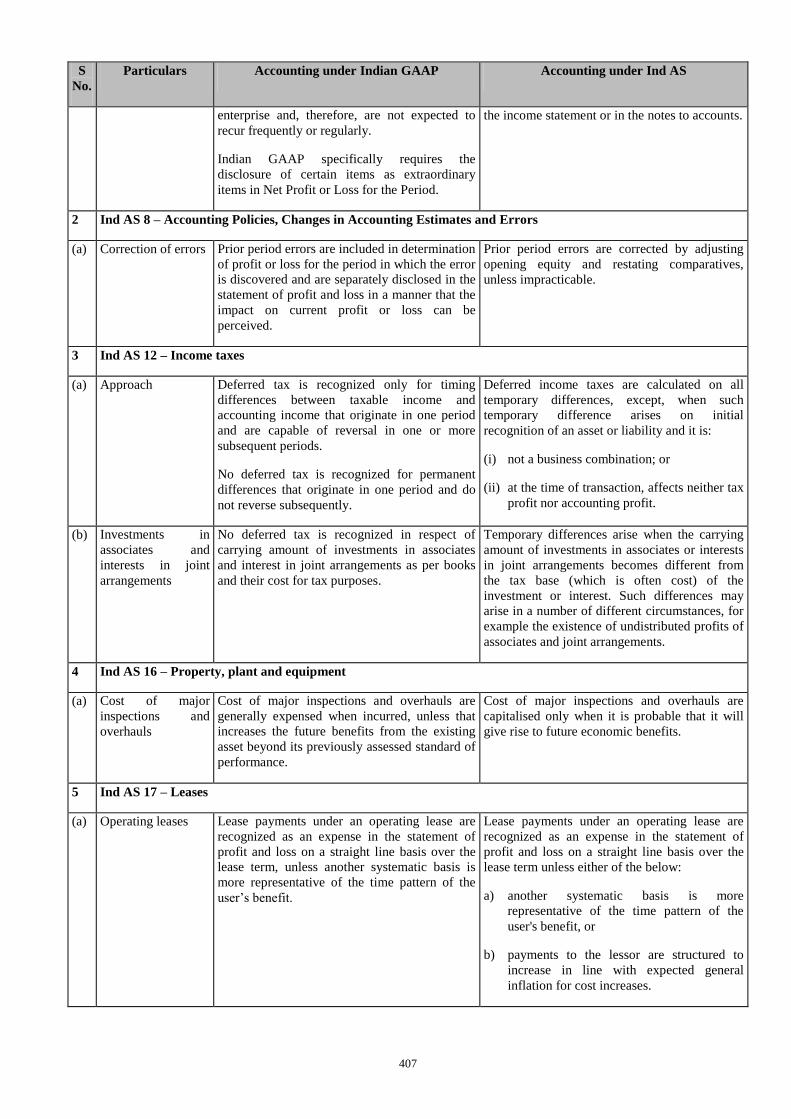

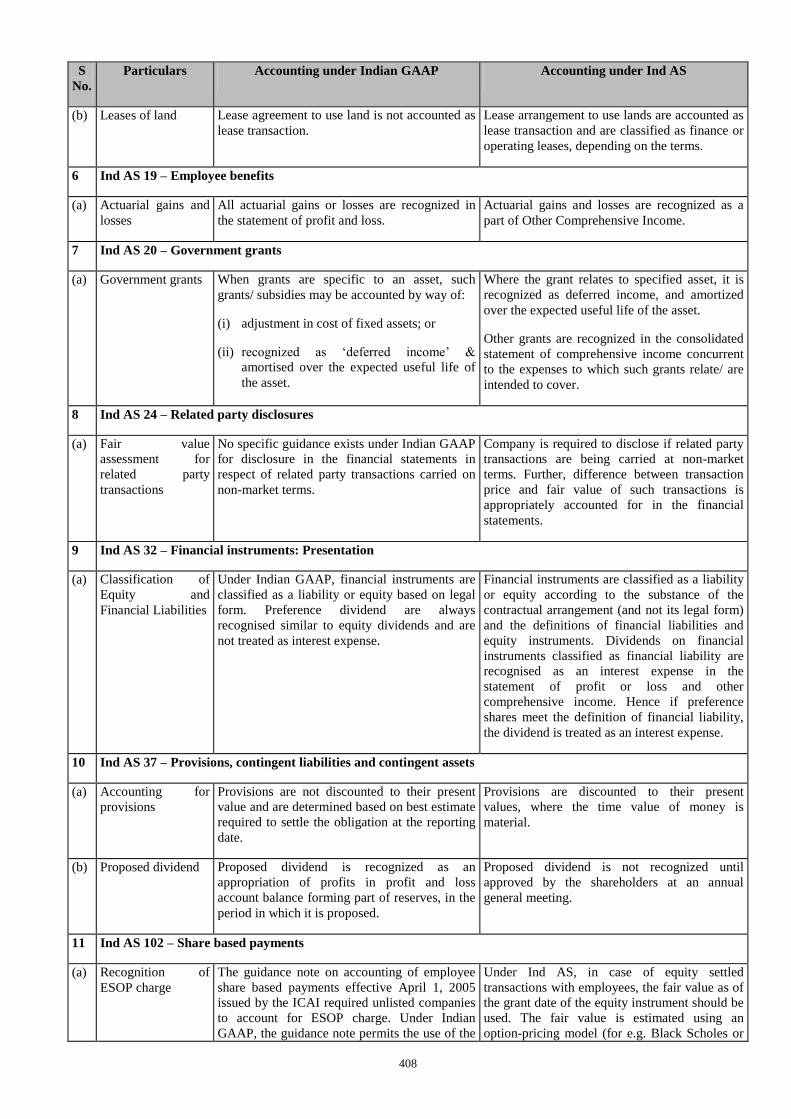

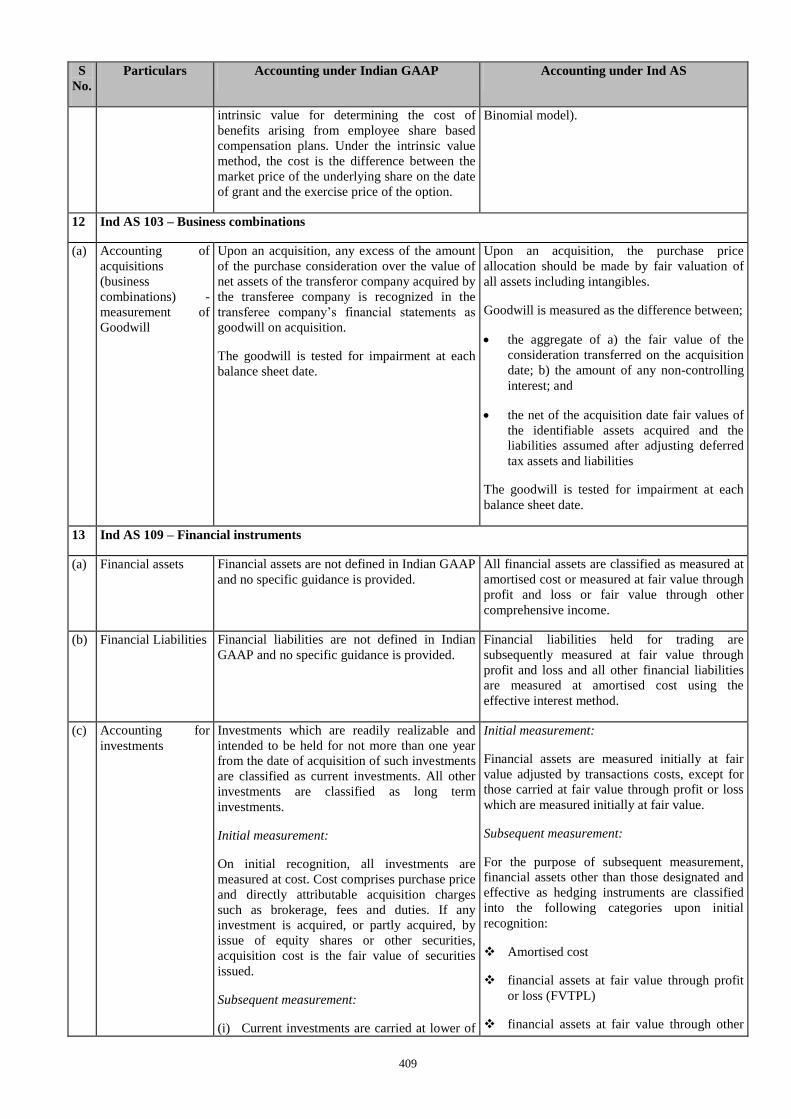

Please see “Summary of Significant Differences between Indian GAAP and Ind AS” and “Management’s Discussion and

Analysis of Financial Condition and Results of Operations – Introduction of Ind AS and Impact on Preparation and

Presentation of our Historical and Future Financial Statements” on pages 406 and 415, respectively.

Currency and Units of Presentation

All references to:

“KES” are to Kenyan Shilling, the official currency of Kenya;

“LKR” are to Sri Lankan Rupees, the official currency of Sri Lanka;

“MAD” are to Moroccan dirham, the official currency of Morocco;

“MZN” are to Metical, the official currency of Mozambique;

“NPR” are to Nepalese Rupee, the official currency of Nepal;

19

“Rupees” or “₹” or “INR” or “Rs.” are to Indian Rupee, the official currency of the Republic of India;

“SGD” are to Singapore Dollar, the official currency of Singapore;

“USD” or “US$” are to United States Dollar, the official currency of the United States; and

“ZMK/ZMW” are to Zambian kwacha, the official currency of Zambia.

Our Company has presented certain numerical information in this Red Herring Prospectus in “million” units. One million

represents 1,000,000 and one billion represents 1,000,000,000.

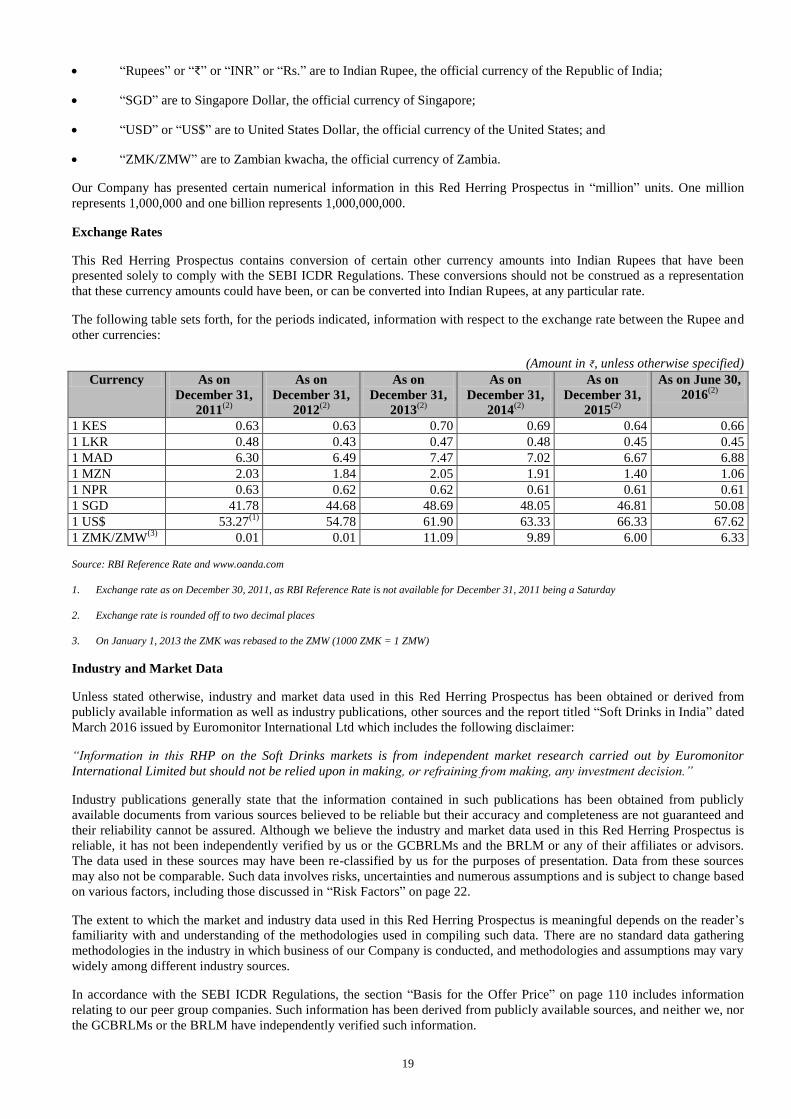

Exchange Rates

This Red Herring Prospectus contains conversion of certain other currency amounts into Indian Rupees that have been