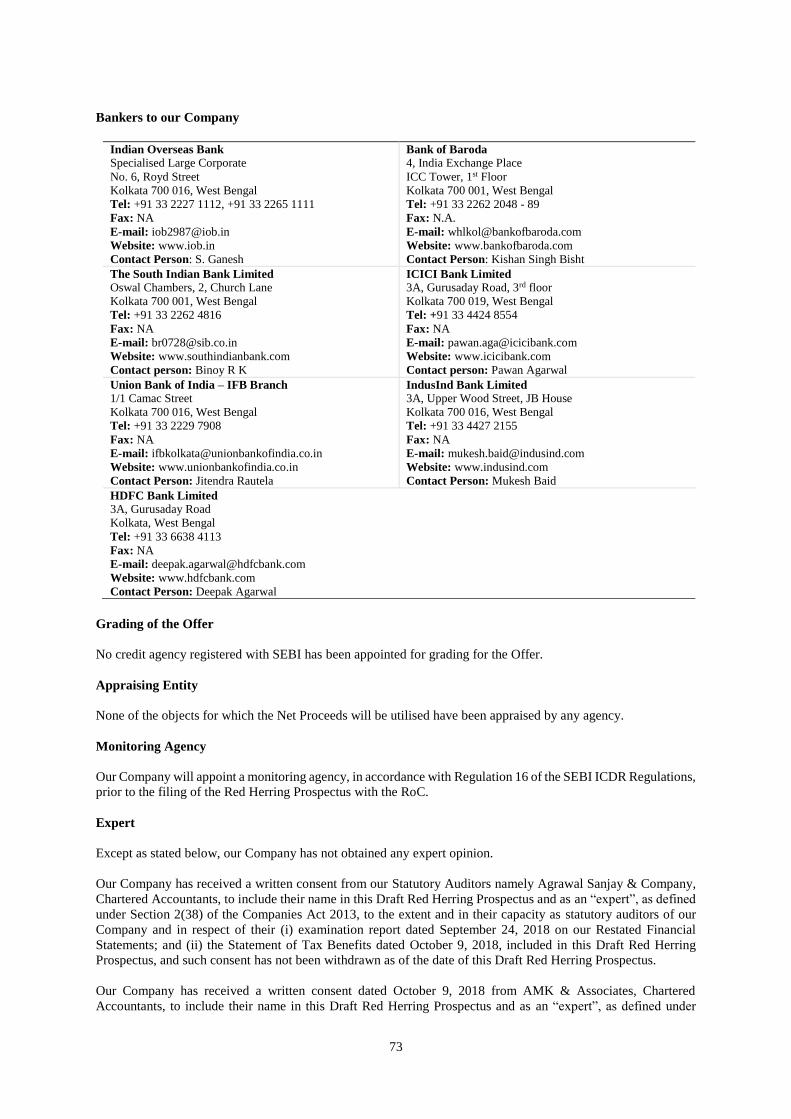

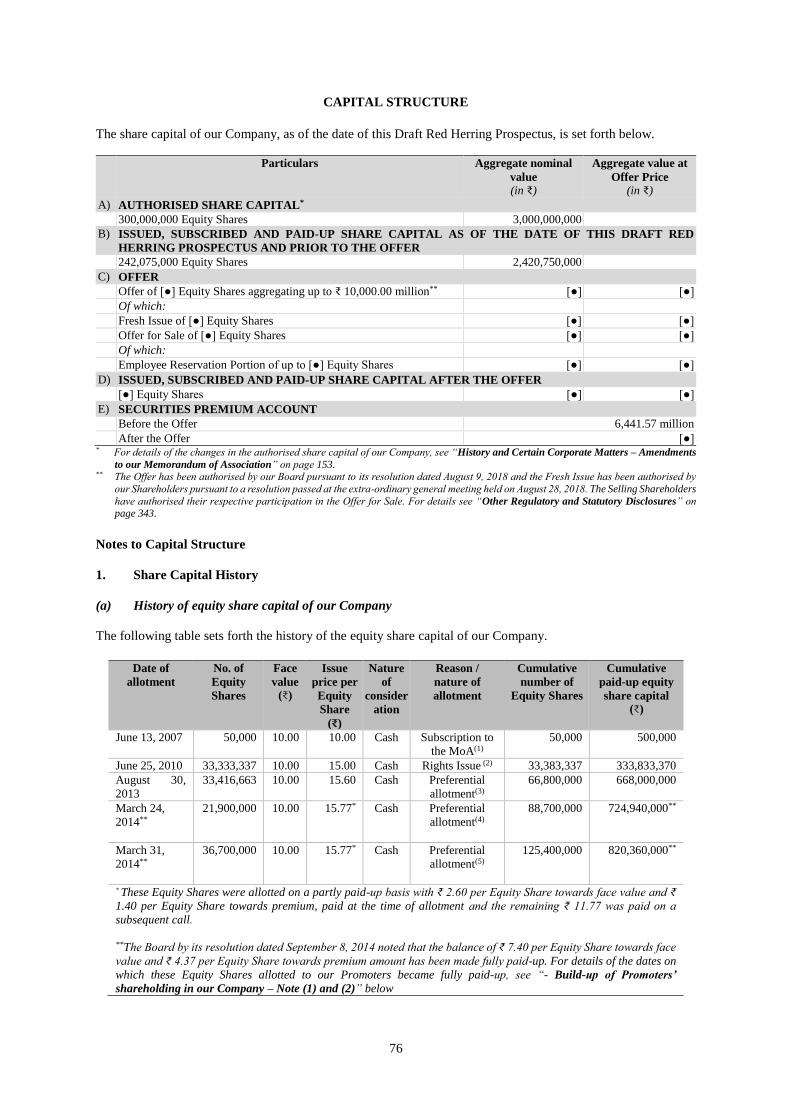

emami cement limited - sebi

TRANSCRIPT

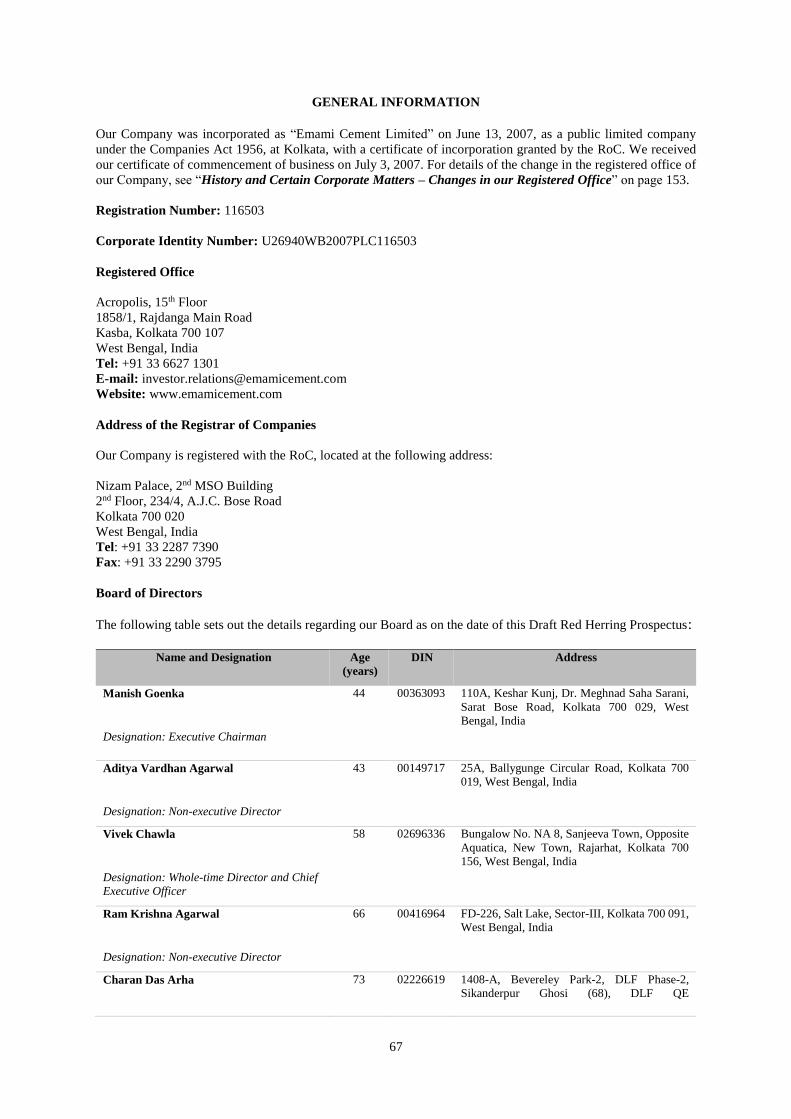

Our Company was incorporated as “Emami Cement Limited” on June 13, 2007, as a public limited company under the Companies Act 1956, at Kolkata, West Bengal with a certificate of incorporation

issued by the Registrar of Companies, West Bengal, at Kolkata (the “RoC”). We received our certificate of commencement of business on July 3, 2007. For details of the change in the registered office

of our Company, see “History and Certain Corporate Matters” on page 153.

Corporate Identity Number: U26940WB2007PLC116503

Registered Office: Acropolis, 15th Floor, 1858/1, Rajdanga Main Road, Kasba, Kolkata 700 107, West Bengal, India

Tel: +91 33 6627 1301; Fax: N.A. E-mail: [email protected]; Website: www.emamicement.com

Contact Person: Debendra Banthiya, Company Secretary and Compliance Officer; Tel: +91 33 6627 1301

OUR PROMOTERS: DR. RADHE SHYAM AGARWAL, DR. RADHE SHYAM GOENKA, MANISH GOENKA, ADITYA VARDHAN AGARWAL, HARSH VARDHAN AGARWAL, MOHAN

GOENKA, BHANU VYAPAAR PRIVATE LIMITED, DIWAKAR VINIYOG PRIVATE LIMITED AND SUNTRACK COMMERCE PRIVATE LIMITED INITIAL PUBLIC OFFERING OF [●] EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (THE “EQUITY SHARES”) OF EMAMI CEMENT LIMITED (OUR “COMPANY” OR THE “COMPANY” OR THE “ISSUER”) FOR

CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (INCLUDING SHARE PREMIUM OF ₹ [●] PER EQUITY SHARE) (THE “OFFER PRICE”) AGGREGATING UP TO ₹ 10,000.00 MILLION (THE “OFFER”) COMPRISING

A FRESH ISSUE OF [●] EQUITY SHARES BY OUR COMPANY AGGREGATING UP TO ₹ 5,000.00 MILLION AND AN OFFER FOR SALE OF [●] EQUITY SHARES AGGREGATING UP TO ₹ 5,000.00 MILLION,

COMPRISING AN OFFER FOR SALE OF [●] EQUITY SHARES BY DR. RADHE SHYAM AGARWAL, [●] EQUITY SHARES BY DR. RADHE SHYAM GOENKA, [●] EQUITY SHARES BY ADITYA VARDHAN AGARWAL,

[●] EQUITY SHARES BY HARSH VARDHAN AGARWAL, [●] EQUITY SHARES BY BHANU VYAPAAR PRIVATE LIMITED, [●] EQUITY SHARES BY DIWAKAR VINIYOG PRIVATE LIMITED, [●] EQUITY SHARES BY

SUNTRACK COMMERCE PRIVATE LIMITED (COLLECTIVELY, THE “PROMOTER SELLING SHAREHOLDERS”) AND [●] EQUITY SHARES BY THE OTHER SELLING SHAREHOLDERS (AS DEFINED

HEREINAFTER) (TOGETHER WITH THE PROMOTER SELLING SHAREHOLDERS, THE “SELLING SHAREHOLDERS” AND SUCH OFFER, THE “OFFER FOR SALE”). THE OFFER INCLUDES A RESERVATION OF

[●] EQUITY SHARES AGGREGATING UP TO ₹ [●] MILLION FOR SUBSCRIPTION BY THE ELIGIBLE EMPLOYEES (AS DEFINED HEREINAFTER) (WHICH SHALL NOT EXCEED 5% OF THE POST-OFFER EQUITY

SHARE CAPITAL OF OUR COMPANY) (“EMPLOYEE RESERVATION PORTION”). THE OFFER LESS THE EMPLOYEE RESERVATION PORTION IS HEREINAFTER REFERRED TO AS THE “NET OFFER”,

AGGREGATING UP TO [●] EQUITY SHARES. THE OFFER AND THE NET OFFER SHALL CONSTITUTE [●]% AND [●]%, RESPECTIVELY OF THE POST-OFFER PAID-UP EQUITY SHARE CAPITAL OF OUR

COMPANY.

THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS (“BRLMS”) AND WILL BE ADVERTISED IN [●]

EDITIONS OF [●] (A WIDELY CIRCULATED ENGLISH NATIONAL DAILY NEWSPAPER), [●] EDITIONS OF [●] (A WIDELY CIRCULATED HINDI NATIONAL DAILY NEWSPAPER) AND [●] EDITIONS OF [●] (A

WIDELY CIRCULATED BENGALI NEWSPAPER, BENGALI BEING THE REGIONAL LANGUAGE OF WEST BENGAL, WHERE OUR REGISTERED OFFICE IS LOCATED) AT LEAST FIVE WORKING DAYS PRIOR

TO THE BID/OFFER OPENING DATE (OR SUCH OTHER TIME PERIOD AS PRESCRIBED UNDER THE APPLICABLE LAW) AND SHALL BE MADE AVAILABLE TO BSE LIMITED (“BSE”) AND NATIONAL STOCK

EXCHANGE OF INDIA LIMITED (“NSE” AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR THE PURPOSES OF UPLOADING ON THEIR RESPECTIVE WEBSITES.

THE FACE VALUE OF THE EQUITY SHARES IS ₹ 10 EACH AND THE OFFER PRICE IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES

In case of a revision in the Price Band, the Bid/Offer Period will be extended for at least three additional Working Days after such revision of the Price Band subject to the Bid/Offer Period not exceeding a total of 10 Working

Days. Any revision in the Price Band and the revised Bid/Offer Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by indicating the change on the websites

of the BRLMs, and at the terminals of the members of the Syndicate.

The Offer is being made in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended (the “SCRR”), read with Regulation 41 of the Securities and Exchange Board of India (Issue of Capital and

Disclosure Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”), through the Book Building Process and in compliance with Regulation 26(2) of SEBI ICDR Regulations, wherein at least 75% of the

Net Offer shall be Allotted to Qualified Institutional Buyers (“QIBs”) on a proportionate basis (the “QIB Category”), provided that our Company may, in consultation with BRLMs, allocate up to 60% of the QIB Category to

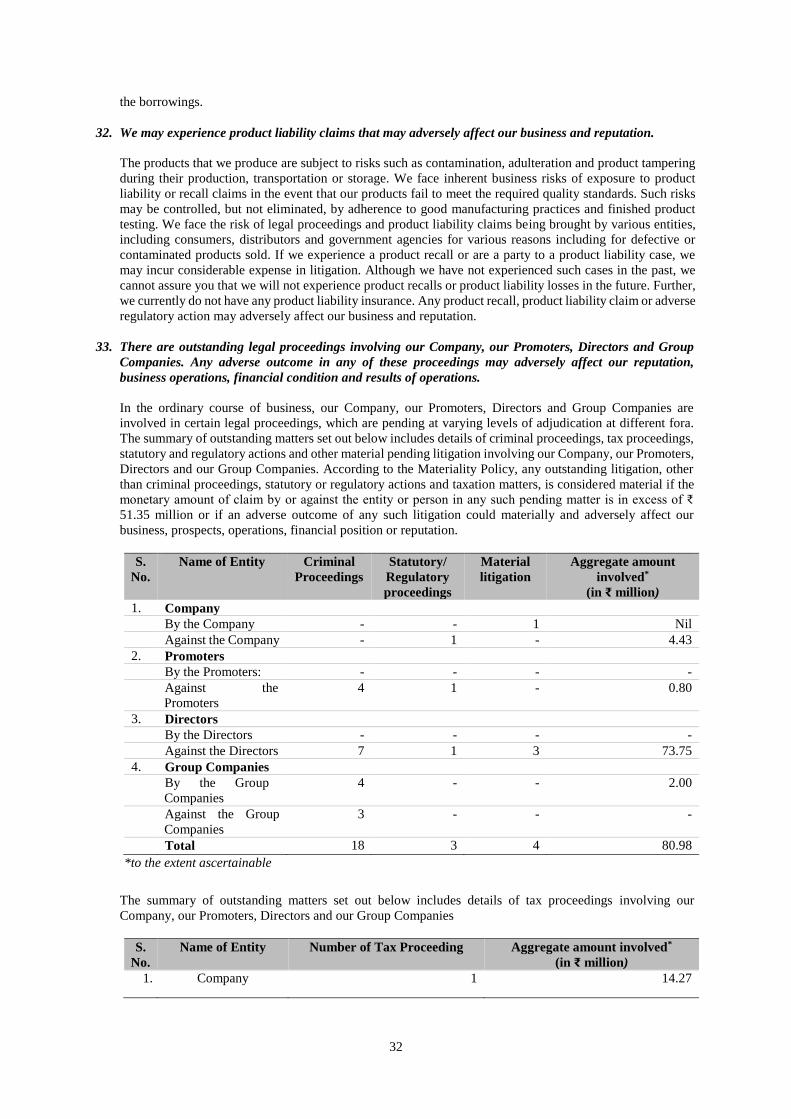

Anchor Investors on a discretionary basis in accordance with the SEBI ICDR Regulations (the “Anchor Investor Portion”), of which one-third is to be reserved for domestic Mutual Funds, subject to valid Bids being received

from domestic Mutual Funds at or above the price at which allocation is made to Anchor Investors. Further, 5% of the QIB Category (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate

basis only to Mutual Funds, and the remainder of the QIB Category shall be available for allocation on a proportionate basis to all QIBs (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received

at or above the Offer Price. If at least 75% of the Net Offer cannot be Allotted to QIBs, the entire application money shall be refunded forthwith. Further, not more than 15% of the Net Offer shall be available for allocation on a

proportionate basis to Non-Institutional Investors and not more than 10% of the Net Offer shall be available for allocation to Retail Individual Investors, in accordance with the SEBI ICDR Regulations, subject to valid Bids being

received at or above the Offer Price. All Investors (except Anchor Investors) shall mandatorily participate in this Offer only through the Application Supported by Blocked Amount (“ASBA”) process, and shall provide details of

their respective bank account in which the Bid Amount will be blocked by the SCSBs. Anchor Investors are not permitted to participate in the Anchor Investor Portion through the ASBA process. For details, see “Offer Procedure”

on page 368.

RISKS IN RELATION TO THE FIRST OFFER

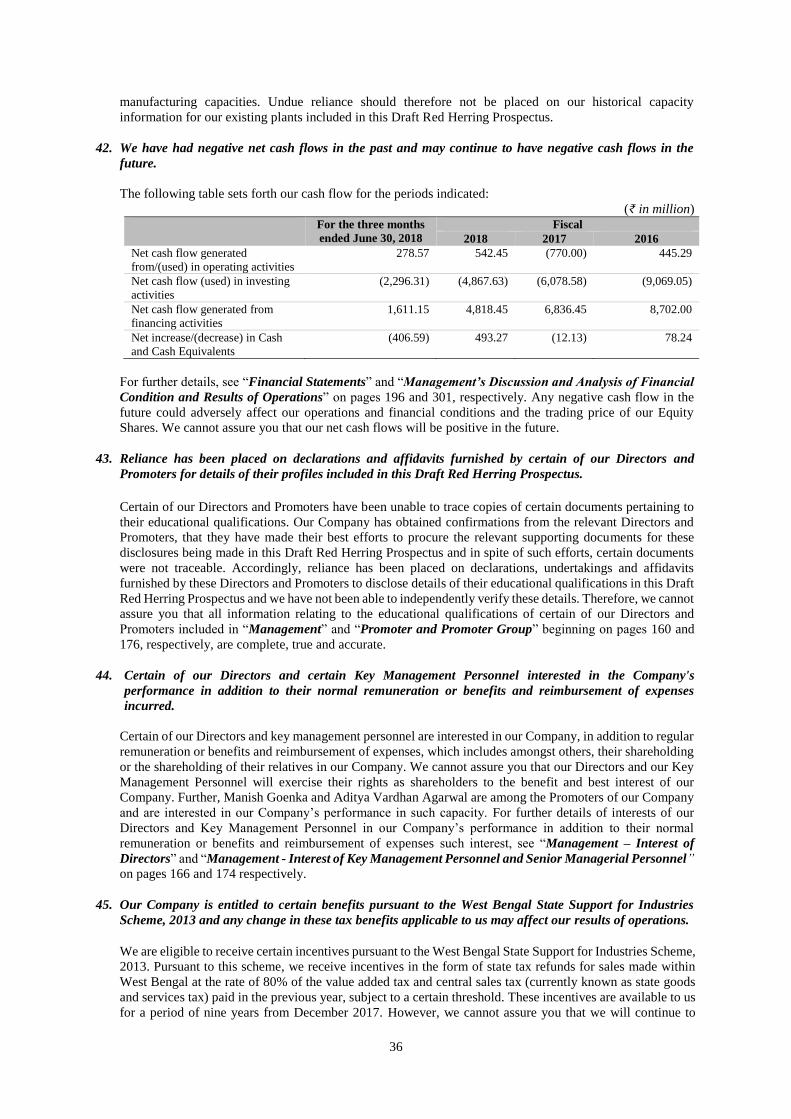

This being the first public issue of the Equity Shares, there has been no formal market for the Equity Shares. The face value of our Equity Shares is ₹ 10 and the Floor Price and Cap Price are [●] times and [●] times of the face

value of the Equity Shares, respectively. The Offer Price (as determined and justified by our Company, in consultation with the BRLMs, in accordance with the SEBI ICDR Regulations, and as stated in “Basis for Offer Price” on page

94) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active and/or sustained trading in the Equity Shares or regarding the price at which

the Equity Shares will be traded after listing.

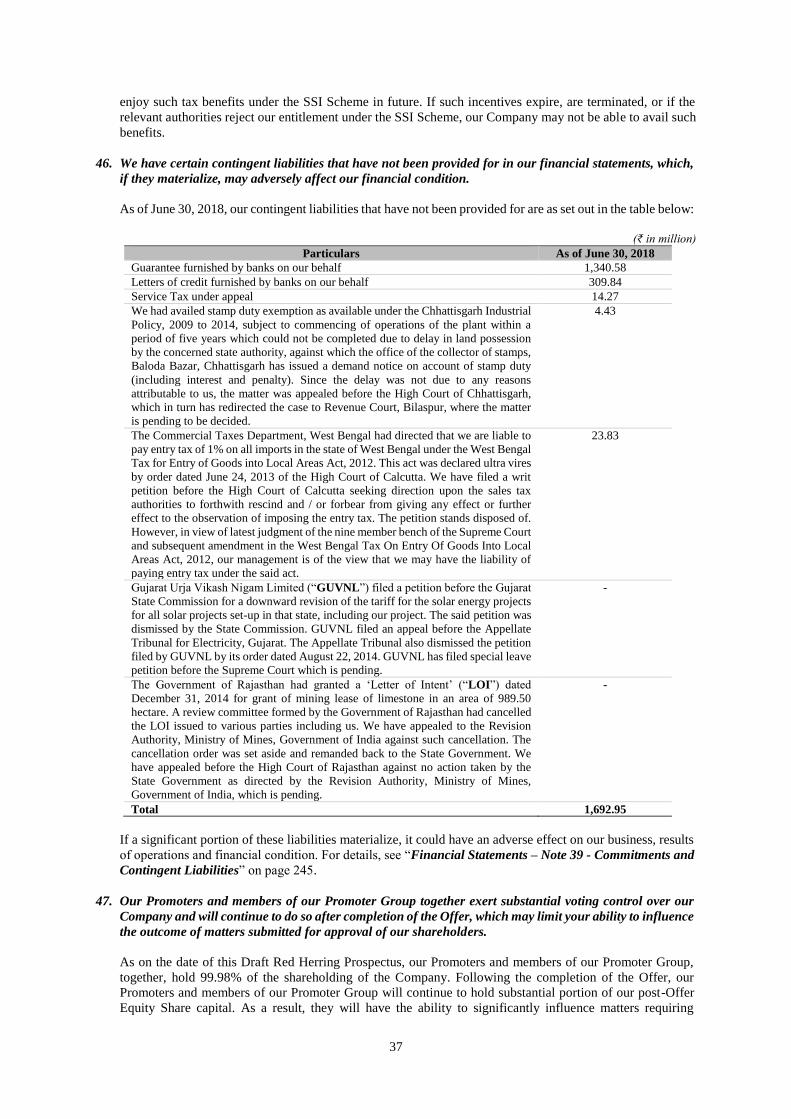

GENERAL RISKS

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors are advised to read

the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer including the risks involved. The Equity

Shares have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does the SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific

attention of the investors is invited to “Risk Factors” on page 16.

ISSUER’S AND SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Offer, which is material in the

context of the Offer, and that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein

are honestly held and that there are no other facts, the omission of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions, misleading in any

material respect. Each Selling Shareholder, severally and not jointly, assumes responsibility only for statements made by such Selling Shareholder in this Draft Red Herring Prospectus to the extent that such statements contain

information in relation to the Selling Shareholder and its respective portion of the Equity Shares being offered by it in the Offer and confirms that such statements are true and correct in all material respects and not misleading in

any material respect.

LISTING

The Equity Shares issued though the Red Herring Prospectus are proposed to be listed on the Stock Exchanges. We have received in-principle approvals from BSE and NSE for the listing of the Equity Shares pursuant to letters

dated [●] and [●], respectively. For the purposes of this Offer, [●] is the Designated Stock Exchange. A copy of the Red Herring Prospectus and the Prospectus shall be delivered for registration to the RoC in accordance with

Section 26(4) of the Companies Act 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring Prospectus up to the Bid/ Offer Closing Date, see “Material Contracts and

Documents for Inspection” on page 424.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER

IIFL Holdings Limited

10th Floor, IIFL Centre

Kamala City, Senapati Bapat

Marg, Lower Parel (West)

Mumbai 400 013, Maharashtra

India

Tel: +91 22 4646 4600

Fax: +91 22 2493 1073

E-mail:

Investor grievance e-mail:

Website: www.iiflcap.com

Contact person: Sachin Kapoor/

Devendra Maydeo

SEBI Registration No.:

INM000010940

Axis Capital Limited

1st Floor, Axis House

C-2, Wadia International

Centre, P.B. Marg, Worli

Mumbai 400 025

Maharashtra, India

Tel: + 91 22 4325 2183

Fax: +91 22 4325 3000

E-mail:

Website:

www.axiscapital.co.in

Investor grievance E-mail:

Contact person: Sagar

Jatakiya

SEBI Registration No.:

INM000012029

CLSA India Private Limited

8/F Dalamal House

Nariman Point

Mumbai 400 021, Maharashtra

India

Tel: +91 22 6650 5050

Fax: +91 22 2284 0271

E-mail: [email protected]

Website: www.india.clsa.com

Investor grievance e-mail:

Contact person: Prachi

Chandgothia

SEBI Registration No.:

INM000010619

Edelweiss Financial Services

Limited

14th Floor, Edelweiss House, Off

C S T Road, Kalina

Mumbai 400 098

Maharashtra, India

Tel: +91 22 4086 3535

Fax: +91 22 4086 3610

E-mail:

Website: www.edelweissfin.com

Investor Grievance E-mail:

customerservice.mb@edelweissfi

n.com

Contact Person: Shubham

Mehta/ Mohit Kapoor

SEBI Registration No.:

INM0000010650

Nomura Financial Advisory and

Securities (India) Private Limited

Ceejay House, Level 11, Plot F

Shivsagar Estate, Worli

Mumbai 400 018, Maharashtra, India

Tel: +91 22 4037 4037

Fax: +91 22 4037 4111

Email:

Investor grievance e-mail: [email protected]

Website:www.nomuraholdings.com/c

ompany/group/asia/india/index.html

Contact person: Vishal Kanjani/

Srishti Tyagi

SEBI Registration No.:

INM000011419

Karvy Computershare Private

Limited

Karvy Selenium Tower – B

Plot 31 and 32, Gachibowli

Financial District, Nanakramguda

Hyderabad 500 032

Telangana, India

Tel: +91 40 6716 2222

Fax: +91 40 2343 1551

E-mail: [email protected]

Website: www.karisma.karvy.com

Investor Grievance E-mail:

Contact Person: Murali Krishna M

SEBI Registration No.:

INR000000221

BID/OFFER PERIOD

BID/OFFER OPENS ON* [●] BID/OFFER CLOSES ON ** [●] * Our Company in consultation with the BRLMs, may consider participation by the Anchor Investors, in accordance with the SEBI ICDR Regulations. The Anchor Investor Bidding Date shall be one Working Day prior to the

Bid/Offer Opening Date. ** Our Company in consultation with the BRLMs, may decide to close the Bid/Offer Period for QIBs one Working Day prior to the Bid/Offer Closing Date, in accordance with the SEBI ICDR Regulations.

DRAFT RED HERRING PROSPECTUS

Dated October 12, 2018

Please read Section 32 of the Companies Act 2013

(This Draft Red Herring Prospectus will be updated upon filing with the RoC)

100% Book Building Offer

EMAMI CEMENT LIMITED

TABLE OF CONTENTS

SECTION I - GENERAL ..................................................................................................................................... 3

DEFINITIONS AND ABBREVIATIONS ..................................................................................................... 3 CERTAIN CONVENTIONS, USE OF FINANCIAL INFORMATION AND MARKET DATA AND

CURRENCY OF PRESENTATION ............................................................................................................ 12 FORWARD-LOOKING STATEMENTS ................................................................................................... 15

SECTION II - RISK FACTORS ....................................................................................................................... 16

SECTION III – INTRODUCTION ................................................................................................................... 46

SUMMARY OF INDUSTRY ........................................................................................................................ 46 SUMMARY OF BUSINESS ......................................................................................................................... 50 SUMMARY FINANCIAL INFORMATION .............................................................................................. 56 THE OFFER .................................................................................................................................................. 65 GENERAL INFORMATION ....................................................................................................................... 67 CAPITAL STRUCTURE .............................................................................................................................. 76 OBJECTS OF THE OFFER ......................................................................................................................... 88 BASIS FOR OFFER PRICE ........................................................................................................................ 94 STATEMENT OF TAX BENEFITS ............................................................................................................ 97

SECTION IV: ABOUT THE COMPANY ....................................................................................................... 99

INDUSTRY OVERVIEW ............................................................................................................................. 99 BUSINESS .................................................................................................................................................... 128 KEY REGULATIONS AND POLICIES IN INDIA................................................................................. 147 HISTORY AND CERTAIN CORPORATE MATTERS ......................................................................... 153 MANAGEMENT ......................................................................................................................................... 160 PROMOTER AND PROMOTER GROUP .............................................................................................. 176 GROUP COMPANIES................................................................................................................................ 186 RELATED PARTY TRANSACTIONS ..................................................................................................... 194 DIVIDEND POLICY ................................................................................................................................... 195

SECTION V – FINANCIAL INFORMATION ............................................................................................. 196

FINANCIAL STATEMENTS..................................................................................................................... 196 SELECTED FINANCIAL INFORMATION ............................................................................................ 299 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS

OF OPERATIONS ...................................................................................................................................... 301 FINANCIAL INDEBTEDNESS ................................................................................................................. 327

SECTION VI – LEGAL AND OTHER INFORMATION ........................................................................... 330

OUTSTANDING LITIGATION AND OTHER MATERIAL DEVELOPMENTS .............................. 330 GOVERNMENT AND OTHER APPROVALS ........................................................................................ 338 OTHER REGULATORY AND STATUTORY DISCLOSURES ........................................................... 343

SECTION VII – OFFER RELATED INFORMATION ............................................................................... 361

OFFER STRUCTURE ................................................................................................................................ 361 TERMS OF THE OFFER ........................................................................................................................... 365 OFFER PROCEDURE................................................................................................................................ 368

SECTION VIII – MAIN PROVISIONS OF ARTICLES OF ASSOCIATION .......................................... 415

SECTION IX – OTHER INFORMATION .................................................................................................... 424

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ................................................ 424 DECLARATION ......................................................................................................................................... 427

3

SECTION I - GENERAL

DEFINITIONS AND ABBREVIATIONS

Unless the context otherwise indicates or implies, the following terms shall have the meanings provided below in

this Draft Red Herring Prospectus, and references to any statute, regulation, rule, guideline, circular, notification

or clarification or policy will include any amendments or re-enactments thereto, from time to time and any

reference to a statutory provision shall include any subordinate legislation made from time to time under that

provision. Notwithstanding the foregoing, terms in “Statement of Tax Benefits”, “Industry Overview”, “Basis for

Offer Price”, “Key Regulations and Policies in India”, “Capital Structure”, “History and Certain Corporate

Matters”, “Financial Statements”, “Outstanding Litigation and Other Material Developments”, “Government

and Other Approvals” “Offer Procedure” and “Main Provisions of Articles of Association”, will have the

meaning ascribed to such terms in these respective sections.

Unless the context otherwise indicates, all references to “the Company” and “our Company” are references to

Emami Cement Limited, a company incorporated in India under the Companies Act 1956 with its registered office

at Acropolis, 15th Floor, 1858/1, Rajdanga Main Road, Kasba, Kolkata 700 107, West Bengal, India, and

references to “we”, “us” and “our” are references to our Company.

In case of any inconsistency between the definitions given below and the definitions contained in the General

Information Document (as defined below), the definitions given below shall prevail.

The words and expressions used but not defined in this Draft Red Herring Prospectus will have the same meaning

as assigned to such terms under the Companies Act, the SEBI Act, the SEBI ICDR Regulations, the SCRA, the

Depositories Act and the rules and regulations made thereunder.

Company Related Terms

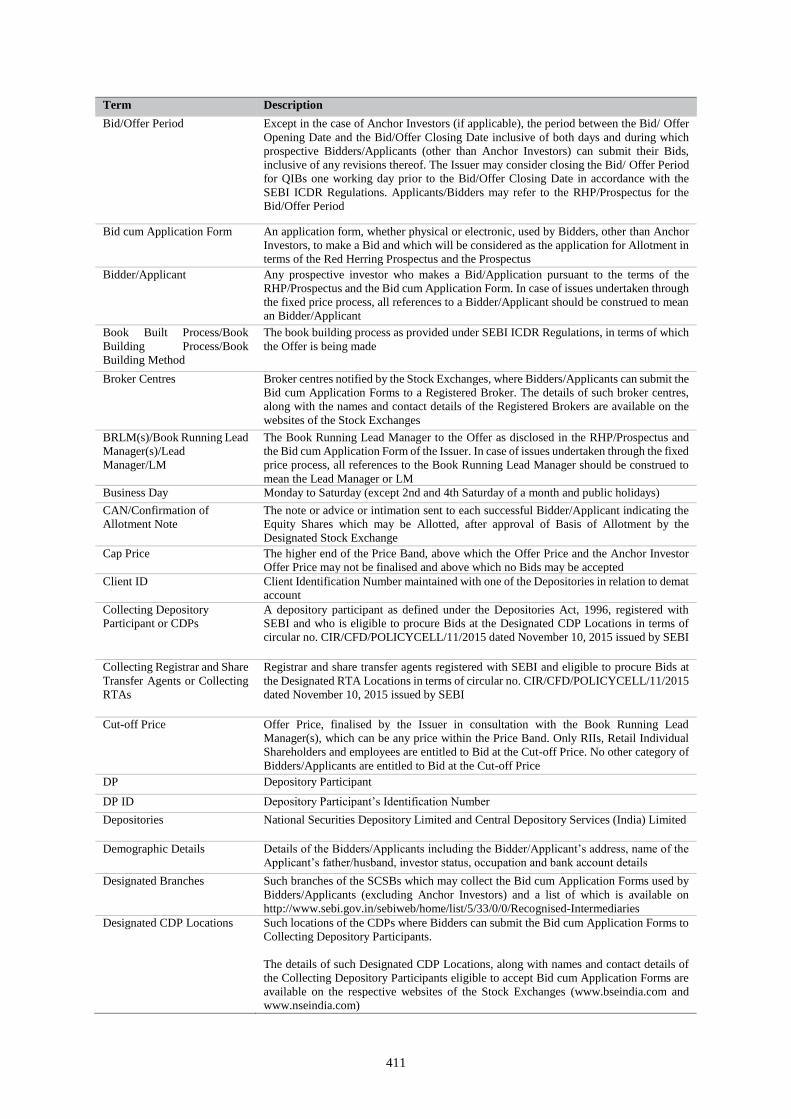

Term Description

AoA/Articles of Association

or Articles

The articles of association of our Company, as amended

Audit Committee The audit committee of our Board

Auditors/ Statutory Auditors The statutory auditor of our Company, being Agrawal Sanjay & Company, Chartered

Accountants

Bhabua Manufacturing

Plant

Cement grinding plant located at Bhabua, Bihar

Bhanu Vyapaar Bhanu Vyapaar Private Limited

Board/ Board of Directors The board of directors of our Company, or a duly constituted committee thereof

Chief Financial Officer The chief financial officer of our Company, Rajiv Ranjan Thakur

Chief Marketing Officer The chief marketing officer of our Company, Vinit Tiwari

Company Secretary and

Compliance Officer

The company secretary and compliance officer of our Company, Debendra Banthiya

CRISIL Report Report titled “Cement Market Assessment for India and Eastern Region” dated October 2018

prepared by CRISIL

CSR Committee The corporate social responsibility committee of our Board

Demerger Scheme The scheme of demerger filed by our Company and Emami Power in respect of the Proposed

Demerger

Director(s) The director(s) on our Board

Diwakar Viniyog Diwakar Viniyog Private Limited

Eco Cements Eco Cements Limited

Emami Natural Resources Emami Natural Resources Private Limited

Emami Paper Mills Emami Paper Mills Limited

Emami Power Emami Power Limited

Equity Shares The equity shares of our Company of face value of ₹ 10 each

Executive Chairman The chairman of our Board of Directors, Manish Goenka

Group Companies The group companies of our Company, as covered under the applicable accounting

standards and other companies as considered material by our Board and described in “Group

Companies” on page 186

Guntur Mining Unit Limestone mining unit in Guntur, Andhra Pradesh, which is under development

Independent Director(s) The independent Director(s) on our Board

IPO Committee The IPO committee of our Board constituted to facilitate the process of the Offer, comprising

Manish Goenka, Aditya Vardhan Agarwal and Vivek Chawla

Kalinganagar

Manufacturing Plant

Cement grinding unit under construction at Kalinganagar, Odisha

4

Term Description

KMP/ Key Management

Personnel

Key management personnel of our Company in terms of Regulation 2(1)(s) of the SEBI ICDR

Regulations being the ‘key managerial personnel’ of our Company in terms of Section 2(51)

of the Companies Act 2013 and as disclosed in “Management – Key Management Personnel

and Senior Management Personnel” on page 173

Manufacturing Plants Collectively, the Risda Manufacturing Plant, the Panagarh Manufacturing Plant, the Bhabua

Manufacturing Plant and the Kalinganagar Manufacturing Plant

Materiality Policy The policy adopted by our Board on September 24, 2018 for identification of Group

Companies, material outstanding litigation and outstanding dues to material creditors in

accordance with the requirements under the SEBI ICDR Regulations

MoA/Memorandum

of Association

The memorandum of association of our Company, as amended

Mining Units Collectively, the Risda Mining Unit, the Guntur Mining Unit and the Proposed Nagaur Mining

Unit

New Way New Way Constructions Limited

Nomination and

Remuneration Committee

The nomination and remuneration committee of our Board

Other Selling Shareholders Collectively, Indu Goenka, Jyoti Goenka, Magnificent Vyapaar LLP, Mansi Agarwal,

Prabhakar Viniyog, Priti A Sureka, Puja Goenka, Rachana Goenka, Rashmi Goenka,

Raviraj Viniyog, Richa Agarwal, Raj Kumar Goenka, Santosh Goenka, Shruti Goenka,

Suraj Viniyog and Usha Agarwal

Panagarh Manufacturing

Unit

Cement grinding unit located at Panagarh, West Bengal

Prabhakar Viniyog Prabhakar Viniyog Private Limited (formerly Emami High Rise Private Limited)

Promoters The promoters of our Company, namely, Dr. Radhe Shyam Agarwal, Dr. Radhe Shyam

Goenka, Manish Goenka, Aditya Vardhan Agarwal, Harsh Vardhan Agarwal, Mohan

Goenka, Bhanu Vyapaar, Diwakar Viniyog and Suntrack Commerce

Promoter Group Persons and entities constituting the promoter group of our Company, pursuant to Regulation

2(1)(zb) of the SEBI ICDR Regulations and as disclosed in “Promoter and Promoter Group”

on page 176

Proposed Demerger The proposed demerger of the solar power business of our Company, as described in

“History and Certain Corporate Matters - Details regarding acquisition of

business/undertakings, mergers, amalgamation, revaluation of assets, etc. - Proposed

Scheme of Demerger” on page 156

Proposed Nagaur Mining

Unit

Limestone mining units proposed to be set up by our Company at Nagaur, Rajasthan

Promoter Selling

Shareholders

Collectively, Dr. Radhe Shyam Agarwal, Dr. Radhe Shyam Goenka, Aditya Vardhan

Agarwal, Harsh Vardhan Agarwal, Bhanu Vyapaar, Diwakar Viniyog and Suntrack

Commerce

Raviraj Viniyog Raviraj Viniyog Private Limited (formerly Emami Enclave Markets Private Limited)

Registered Office The registered office of our Company, located at Acropolis, 15th Floor, 1858/1, Rajdanga Main

Road, Kasba, Kolkata 700 107, West Bengal, India

Restated Financial

Statements

The restated financial statements of our Company, which comprise the restated balance

sheet, the restated profit and loss and the restated cash flow statement as at and for the three

months ended June 30, 2018 and the financial years ended March 31, 2018, 2017, 2016,

2015 and 2014, together with the annexures and the notes thereto, which have been prepared

in accordance with the Companies Act and restated in accordance with the SEBI ICDR

Regulations

Risda Manufacturing Plant Integrated cement manufacturing plant comprising inter alia a grinding and clinkering unit

located at Risda in Chattisgarh

Risda Mining Unit Limestone mining unit located at Risda, Chhattisgarh

Sapphire Merchants Sapphire Merchants Private Limited

Selling Shareholders Together, the Promoter Selling Shareholders and the Other Selling Shareholders

SMP/ Senior Management

Personnel

Senior management personnel of our Company as disclosed in “Management – Key

Management Personnel and Senior Management Personnel” on page 173

Shareholders The holders of the Equity Shares from time to time

Stakeholders Relationship

Committee

The stakeholders’ relationship committee of our Board

Suntrack Commerce Suntrack Commerce Private Limited

Suraj Viniyog Suraj Viniyog Private Limited

5

Offer Related Terms

Term Description

Acknowledgment Slip The slip or document issued by the Designated Intermediary(ies) to a Bidder as proof of

registration of the Bid cum Application Form

Allotment Advice The note or advice or intimation of Allotment, sent to each successful Bidder who has been or

is to be Allotted the Equity Shares after approval of the Basis of Allotment by the Designated

Stock Exchange

Allotted/Allotment/Allot Unless the context otherwise requires, the issue, allotment and transfer of the Equity Shares to

successful Bidders pursuant to the Offer

Allottee A successful Bidder to whom the Equity Shares are Allotted

Anchor Investor A qualified institutional buyer, who applies under the Anchor Investor Portion in accordance

with the requirements specified in the SEBI ICDR Regulations and the Red Herring

Prospectus

Anchor Investor Bidding

Date

The date, one Working Day prior to the Bid/Offer Opening Date, on which Bids by Anchor

Investors shall be submitted and allocation to the Anchor Investors shall be completed

Anchor Investor Offer Price The final price at which the Equity Shares will be Allotted to Anchor Investors in terms of

the Red Herring Prospectus and the Prospectus, which will be a price equal to or higher than

the Offer Price and/ or the price at which Equity Shares are allocated to Anchor Investors on

the Anchor Investor Bidding Date as determined by the Company in consultation with the

BRLMs, but not higher than the Cap Price.

Anchor Investor Portion Up to 60% of the QIB Category, which may be allocated by our Company, in consultation

with the BRLMs, to Anchor Investors, on a discretionary basis, in accordance with SEBI

ICDR Regulations. One-third of the Anchor Investor Portion is reserved for domestic Mutual

Funds, subject to valid Bids being received from domestic Mutual Funds at or above the price

at which allocation is made to Anchor Investors

Application Supported by

Blocked Amount/ ASBA

The application (whether physical or electronic) by a Bidder (other than Anchor Investors) to

make a Bid authorizing the relevant SCSB to block the Bid Amount in the relevant ASBA

Account

ASBA Account A bank account maintained with an SCSB and specified in the Bid cum Application Form

which will be blocked by such SCSB to the extent of the appropriate Bid Amount in relation

to a Bid by a Bidder (other than a Bid by an Anchor Investor)

ASBA Form An application form, whether physical or electronic, used by Bidders bidding through the

ASBA process, which will be considered as the application for Allotment in terms of the Red

Herring Prospectus and the Prospectus

Axis Axis Capital Limited

Banker(s) to the Offer The Escrow Bank(s), Refund Bank(s) and Public Offer Account Bank(s), as the case may be

Basis of Allotment The basis on which the Equity Shares will be Allotted to successful Bidders under the Offer,

described in “Offer Procedure” on page 368

Bid An indication to make an offer during the Bid/Offer Period by a Bidder (other than an Anchor

Investor), or on the Anchor Investor Bidding Date by an Anchor Investor, pursuant to

submission of a Bid cum Application Form, to subscribe for or purchase our Equity Shares at a

price within the Price Band, including all revisions and modifications thereto, to the extent

permissible under the SEBI ICDR Regulations, in terms of the Red Herring Prospectus and the

Bid cum Application Form. The term ‘Bidding’ shall be construed accordingly

Bid Amount The highest value of the optional Bids as indicated in the Bid cum Application Form and

payable by the Bidder or as blocked in the ASBA Account of the Bidder, as the case may be,

upon submission of the Bid in the Offer. However, for the Retail Individual Investors and

Eligible Employees Bidding under the Employee Reservation Portion applying at the Cut-Off

Price, the Bid Amount shall be calculated at the Cap Price multiplied by the number of Equity

Shares Bid for by such Retail Individual Investors and Eligible Employees Bidding under the

Employee Reservation Portion and mentioned in the Bid cum Application Form

Bid cum Application Form The form in terms of which the Bidder shall make a Bid, including an ASBA Form, and which

shall be considered as the application for the Allotment pursuant to the terms of the Red Herring

Prospectus and the Prospectus

Bid Lot [●] Equity Shares

Bid/Offer Closing Date Except in relation to any Bids received from the Anchor Investors, the date after which the

Designated Intermediaries shall not accept any Bids for the Offer, which shall be published in

[●] editions of [●] (a widely circulated English national daily newspaper), [●] editions of [●] (a

widely circulated Hindi national daily newspaper) and [●] editions of [●] (a widely circulated

Bengali newspaper, Bengali being the regional language of West Bengal, where our

Registered Office is located) and in case of any revisions, the extended Bid/Offer Closing Date

will be widely disseminated by notification to the Stock Exchanges, by issuing a press release,

and also by indicating the change on the websites of the BRLMs, and at the terminals of the

members of the Syndicate. Our Company, in consultation with the BRLMs, may decide to close

6

Term Description

the Bid/ Offer Closing Date for QIBs one Working Day prior to the Bid/Offer Closing Date, as

required under the SEBI ICDR Regulations

Bid/Offer Opening Date Except in relation to Anchor Investors, the date on which the Designated Intermediaries shall

start accepting Bids for the Offer, which shall be published in [●] editions of [●] (a widely

circulated English national daily newspaper), [●] editions of [●] (a widely circulated Hindi

national daily newspaper) and [●] editions of [●] (a widely circulated Bengali newspaper,

Bengali being the regional language of West Bengal, where our Registered Office is located)

Bid/Offer Period The period between the Bid/Offer Opening Date and the Bid/Offer Closing Date, inclusive of

both days during which prospective Bidders (excluding Anchor Investors) can submit their Bids,

including any revisions thereof, in accordance with the SEBI ICDR Regulations and the terms

of the Red Herring Prospectus

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring Prospectus

and the Bid cum Application Form and unless otherwise stated or implied, includes an Anchor

Investor

Bidding Centres Centres at which the Designated Intermediaries shall accept the Bid cum Application Forms,

being the Designated Branches for SCSBs, Specified Locations for the Syndicate, Broker

Centres for Registered Brokers, Designated RTA Locations for CRTAs and Designated CDP

Locations for CDPs.

Book Building Process The book building process as described in Schedule XI of the SEBI ICDR Regulations, in terms

of which the Offer is being made

Book Running Lead

Managers/ BRLMs

The book running lead managers to the Offer, namely, IIFL, Axis, CLSA, Edelweiss and

Nomura

Broker Centres Broker centres of the Registered Brokers, where Bidders (other than Anchor Investors) can

submit the Bid cum Application Forms. The details of such Broker Centres, along with the

names and contact details of the Registered Brokers are available on websites of the Stock

Exchanges and updated from time to time

CAN / Confirmation of

Allocation Note

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors, who have been

allocated the Equity Shares, after the Anchor Investor Bidding Date

Cap Price The higher end of the Price Band above which the Offer Price and Anchor Investor Offer Price

will not be finalized and above which no Bids will be accepted, including any revisions thereof

Client ID Client identification number of the Bidder’s beneficiary account

CLSA CLSA India Private Limited

Collecting Depository

Participants/ CDPs

A depository participant, as defined under the Depositories Act, 1996 and registered under

Section 12 (1A) of the SEBI Act and who is eligible to procure Bids at the Designated CDP

Locations in terms of circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015

issued by SEBI

Collecting Registrar and

Share Transfer Agents /

CRTAs

Registrar and share transfer agents registered with SEBI and eligible to procure Bids at the

Designated RTA Locations in terms of circular no. CIR/CFD/POLICYCELL/11/2015 dated

November 10, 2015 issued by SEBI

Cut-off Price The Offer Price, finalized by our Company, in consultation with the BRLMs, which shall be

any price within the Price Band. Only Retail Individual Investors and Eligible Employees

Bidding under the Employee Reservation Portion are entitled to Bid at the Cut-off Price. QIBs

(including Anchor Investors) and Non-Institutional Investors are not entitled to Bid at the Cut-

off Price

Demographic Details The details of the Bidders including the Bidders’ address, names of the Bidders’ father/husband,

investor status, occupation and bank account details

Depository Participant A depository participant, as defined under the Depositories Act, 1996

Designated Branches Such branches of the SCSBs which may collect the Bid cum Application Form used by Bidders

(other than Anchor Investors), a list of which is available at the website of the SEBI

(https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=34)

and updated from time to time or at such other website as may be prescribed by SEBI from time

to time

Designated CDP Locations Such centres of the Collecting Depository Participants where Bidders (except Anchor Investors)

can submit the Bid cum Application Forms. The details of such Designated CDP Locations,

along with the names and contact details of the CDPs are available on the websites of the Stock

Exchanges and updated from time to time

Designated Date The date on which the funds from the Escrow Accounts are transferred to the Public Offer

Account or the Refund Account(s), as appropriate, and the relevant amounts blocked by the

SCSBs are transferred from the ASBA Accounts, to the Public Offer Account and/or are

unblocked, as applicable, in terms of the Red Herring Prospectus, following which the Board

of Directors may Allot Equity Shares to successful Bidders in the Offer.

Designated Intermediaries Collectively, the members of the Syndicate, sub-syndicate members/agents, SCSBs,

Registered Brokers, CDPs and CRTAs, who are authorized to collect Bid cum Application

Forms from the Bidders (other than Anchor Investors), in relation to the Offer

7

Term Description

Designated RTA Locations Such centres of the CRTAs where Bidders (except Anchor Investors) can submit the Bid cum

Application Forms. The details of such Designated RTA Locations, along with the names and

contact details of the CRTAs are available on the websites of the Stock Exchanges and updated

from time to time

Designated Stock Exchange [●]

Draft Red Herring

Prospectus/ DRHP

This draft red herring prospectus dated October 12, 2018, issued in accordance with the SEBI

ICDR Regulations, which does not contain complete particulars of the price at which our Equity

Shares will be Allotted and the size of the Offer and includes any addenda or corrigenda thereto

Edelweiss Edelweiss Financial Services Limited

Eligible Employee All or any of the following:

(a) a permanent and full time employee of our Company (excluding such employees not eligible

to invest in the Offer under applicable laws, rules, regulations and guidelines) as of the date of

filing of the Red Herring Prospectus with the RoC and who continues to be an employee of our

Company until the submission of the Bid cum Application Form, and is based, working and

present in India as on the date of submission of the Bid cum Application Form; and

(b) a director of our Company, whether a whole time director, part time director or otherwise,

(excluding such directors who are not eligible to invest in the Offer under applicable laws, rules,

regulations and guidelines) as of the date of filing the Red Herring Prospectus with the RoC and

who continues to be a director of our Company, as applicable until the submission of the Bid

cum Application Form and is based and present in India as on the date of submission of the Bid

cum Application Form.

An employee, who is recruited against a regular vacancy but is on probation as on the date of

submission of the Bid cum Application Form will also be deemed a ‘permanent and a full time

employee’. The maximum Bid Amount under the Employee Reservation Portion by an Eligible

Employee cannot exceed ₹ 500,000.

Employee Reservation

Portion

The portion of the Offer, being [●] Equity Shares aggregating up to ₹ [●] million (which shall

not exceed 5% of the post-Offer equity share capital of our Company), available for allocation

to the Eligible Employees

Eligible NRI An NRI, resident in a jurisdiction outside India where it is not unlawful to make an offer or

invitation under the Offer and in relation to whom the Red Herring Prospectus and the Bid cum

Application Form constitute an invitation to subscribe to or purchase for the Equity Shares

Escrow Account Account to be opened with the Escrow Bank and in whose favour the Anchor Investors will

transfer money through direct credit or NACH or NEFT or RTGS in respect of the Bid Amount

when submitting a Bid

Escrow Agreement The agreement to be entered into among our Company, the Selling Shareholders, the Registrar

to the Offer, the BRLMs and the Banker(s) to the Offer for collection of the Bid Amounts and

where applicable remitting refunds, if any, on the terms and conditions thereof

Escrow Bank A bank, which is a clearing member and registered with SEBI as a banker to an issue under the

SEBI BTI Regulations and with whom the Escrow Account will be opened, in this case being

[●]

First Bidder The Bidder whose name appears first in the Bid cum Application Form or the Revision Form

and in case of joint Bidders, whose name appears as the first holder of the beneficiary account

held in joint names

Floor Price The lower end of the Price Band, and any revisions thereof, at or above which the Offer Price

and the Anchor Investor Offer Price will be finalized and below which no Bids will be accepted

and which shall not be less than the face value of the Equity Shares

Fresh Issue Fresh issue of [●] Equity Shares aggregating up to ₹ 5,000.00 million to be issued by our

Company as part of the Offer, in terms of the Red Herring Prospectus and Prospectus.

General Information

Document

The General Information Document for investing in public issues prepared and issued in

accordance with the circular (CIR/CFD/DIL/12/2013) dated October 23, 2013, notified by

SEBI and updated pursuant to the circular (CIR/CFD/POLICYCELL/11/2015) dated

November 10, 2015 and (SEBI/HO/CFD/DIL/CIR/P/2016/26) dated January 21, 2016

notified by SEBI and included in “Offer Procedure” on page 368

Gross Proceeds Gross proceeds from the Fresh Issue that will be available to our Company

IIFL IIFL Holdings Limited

Maximum RII Allottees The maximum number of RIIs who can be allotted the minimum Bid Lot. This is computed

by dividing the total number of Equity Shares available for Allotment to RIIs by the minimum

Bid Lot

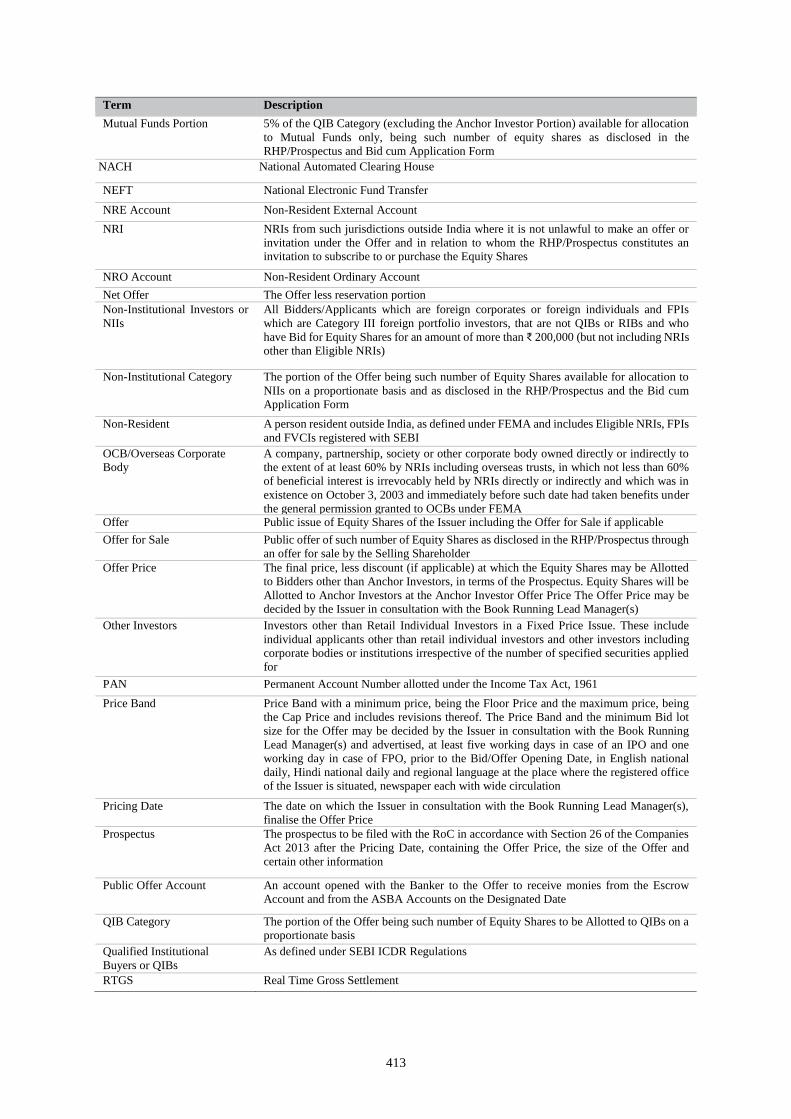

Mutual Fund Portion 5% of the QIB Category (excluding the Anchor Investor Portion) or [●] Equity Shares which

shall be available for allocation to Mutual Funds only, on a proportionate basis, subject to valid

Bids being received at or above the Offer Price

Net Offer The Offer less the Employee Reservation Portion, aggregating up to [●] Equity Shares

8

Term Description

Net Proceeds Proceeds of the Fresh Issue that will be available to our Company, i.e., Gross Proceeds, less

Offer Expenses to the extent applicable to the Fresh Issue

Nomura Nomura Financial Advisory and Securities (India) Private Limited

Non-Institutional Category The portion of the Offer, being not more than 15% of the Net Offer or [●] Equity Shares,

available for allocation on a proportionate basis to Non-Institutional Investors subject to valid

Bids being received at or above the Offer Price

Non-Institutional

Investors/NIIs

All Bidders, including Category III FPIs that are not QIBs (including Anchor Investors), Eligible

Employees Bidding under the Employee Reservation Portion or Retail Individual Investors, who

have Bid for Equity Shares for an amount of more than ₹ 200,000 (but not including NRIs other

than Eligible NRIs)

Offer Public issue of up to [●] Equity Shares of face value ₹ 10 each for cash at a price of ₹ [●]

including a premium of ₹ [●] per Equity Share aggregating up to ₹ 10,000.00 million comprising

the Fresh Issue and the Offer for Sale. The Offer comprises the Net Offer and the Employee

Reservation Portion

Offer Agreement The agreement dated October 12, 2018 entered into among our Company, the Selling

Shareholders and the BRLMs, pursuant to which certain arrangements are agreed to in relation

to the Offer

Offer for Sale Offer of [●] Equity Shares for cash aggregating up to ₹ 5,000.00 million to be offered for

sale/transfer by the Selling Shareholders pursuant to the Offer in terms of the Red Herring

Prospectus and the Prospectus

Offer Price The final price at which Equity Shares will be Allotted to the successful Bidders (except Anchor

Investors), as determined in accordance with the Book Building Process and determined by our

Company, in consultation with the BRLMs in terms of the Red Herring Prospectus on the

Pricing Date.

Price Band Price band of the Floor Price of ₹ [●] and a Cap Price of ₹ [●], including any revisions thereof.

The Price Band and the minimum Bid Lot size for the Offer will be decided by our Company,

in consultation with the BRLMs, and advertised in [●] editions of [●] (a widely circulated

English national daily newspaper), [●] editions of [●] (a widely circulated Hindi national daily

newspaper) and [●] editions of [●] (a widely circulated Bengali newspaper, Bengali being the

regional language of West Bengal, the place where our Registered Office is located) at least

five Working Days prior to the Bid/Offer Opening Date (or such other period as prescribed

under the applicable law), with the relevant financial ratios calculated at the Floor Price and at

the Cap Price and shall be made available to the Stock Exchanges for the purpose of uploading

on their websites

Pricing Date The date on which our Company, in consultation with the BRLMs, shall finalize the Offer Price

Prospectus The Prospectus to be filed with the RoC for this Offer on or after the Pricing Date in accordance

with Section 26 of the Companies Act 2013 and the SEBI ICDR Regulations, containing, among

others, the Offer Price, the size of the Offer and certain other information, including any addenda

or corrigenda thereto

Public Offer Account The bank account(s) to be opened with the Banker(s) to the Offer under Section 40(3) of the

Companies Act 2013 to receive monies from the Escrow Account(s) and the ASBA Accounts

on the Designated Date

Public Offer Account Bank The bank(s) with whom the Public Offer Account will be opened for collection of Bid Amounts

from Escrow Account and ASBA Account on the Designated Date, in this case being [●]

QIB Category The portion of the Offer, being at least 75% of the Net Offer or [●] Equity Shares to be Allotted

to QIBs on a proportionate basis, including the Anchor Investor Portion (in which allocation

shall be on a discretionary basis, as determined by our Company in consultation with the

BRLMs), subject to valid Bids being received at or above the Offer Price

Qualified Institutional

Buyers/ QIBs

A qualified institutional buyer as defined under Regulation 2(1)(zd) of the SEBI ICDR

Regulations

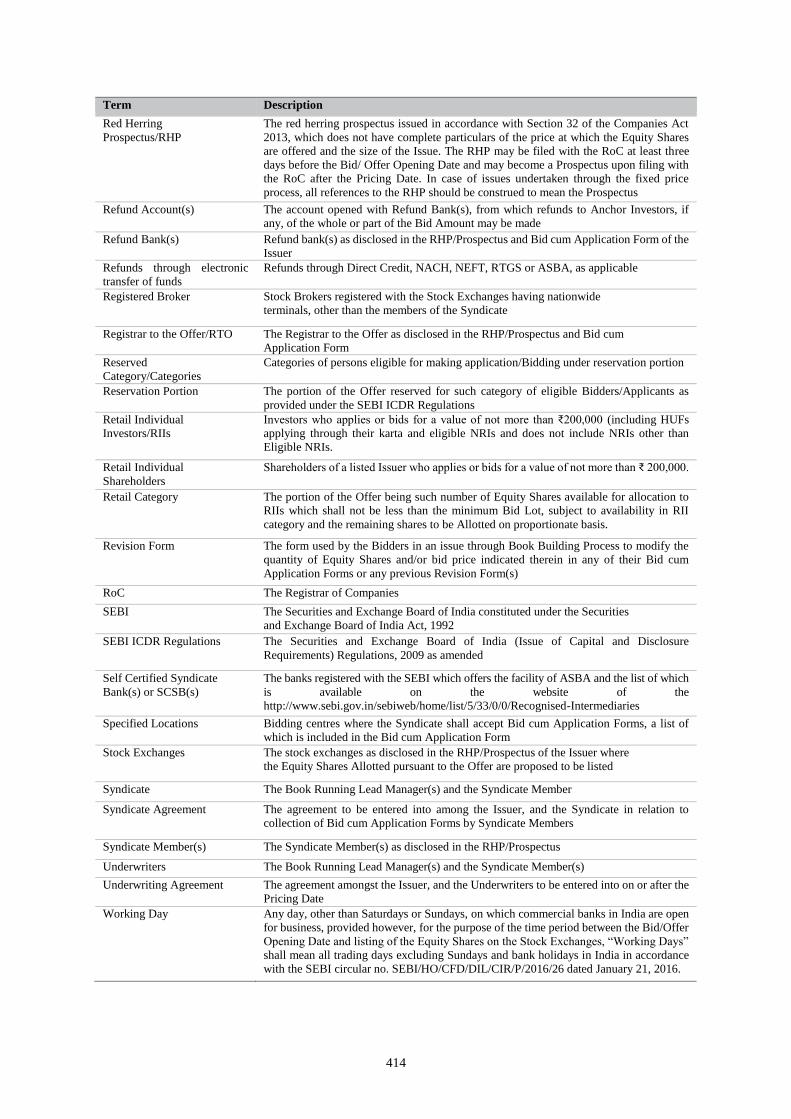

Red Herring Prospectus/

RHP

The red herring prospectus to be issued in accordance with Section 32 of the Companies Act

2013 and the SEBI ICDR Regulations, which will not have complete particulars of the price

at which the Equity Shares shall be Allotted and which shall be filed with the RoC at least

three Working Days before the Bid/Offer Opening Date and will become the Prospectus after

filing with the RoC after the Pricing Date, including any addenda or corrigenda thereto

Refund Account(s) The account(s) opened with the Refund Bank(s) from which refunds, if any, of the whole or part

of the Bid Amount shall be made to Anchor Investors

Refund Bank(s) The Banker(s) to the Offer with whom the Refund Account(s) will be opened, in this case

being [●]

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals, other than the

members of the Syndicate and eligible to procure Bids in terms of circular number

CIR/CFD/14/2012 dated October 14, 2012, issued by SEBI

Registrar Agreement The agreement dated October 10, 2018, entered into among our Company, the Selling

Shareholders and the Registrar to the Offer in relation to the responsibilities and obligations of

the Registrar to the Offer pertaining to the Offer

9

Term Description

Registrar to the Offer Karvy Computershare Private Limited

Retail Category The portion of the Offer, being not more than 10% of the Net Offer or [●] Equity Shares,

available for allocation to Retail Individual Investors, which shall not be less than the minimum

Bid Lot, subject to availability in the Retail Category

Retail Individual Investors/

RIIs

Bidders (other than Eligible Employees Bidding in the Employee Reservation Portion)

(including HUFs and Eligible NRIs) whose Bid Amount for Equity Shares in the Offer is not

more than ₹ 200,000 in any of the bidding options in the Offer (including HUFs applying

through their karta and Eligible NRIs and does not include NRIs other than Eligible NRIs)

Revision Form The form used by the Bidders to modify the quantity of Equity Shares or the Bid Amount in any

of their Bid cum Application Forms or any previous Revision Form(s), as applicable. QIBs

bidding in the QIB Category and Non-Institutional Investors bidding in the Non-Institutional

Category are not permitted to withdraw their Bid(s) or lower the size of their Bid(s) (in terms of

quantity of Equity Shares or the Bid Amount) at any stage. Retail Individual Investors and

Eligible Employees Bidding under the Employee Reservation Portion can revise their Bids

during the Bid/ Offer Period and withdraw their Bids until the Bid/ Offer Closing Period

Self Certified Syndicate

Banks/ SCSBs

The banks registered with the SEBI which offer the facility of ASBA and the list of which is

available on the website of the SEBI

(https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&intmId=35)

and updated from time to time and at such other websites as may be prescribed by SEBI from

time to time

Share Escrow Agent The share escrow agent appointed pursuant to the Share Escrow Agreement, namely [●]

Share Escrow Agreement The agreement to be entered into among our Company, the Selling Shareholders and the Share

Escrow Agent in connection with the transfer of the respective portion of the Equity Shares

offered by each Selling Shareholder and the credit of such Equity Shares to the demat account

of the Allottees

Specified Locations Bidding centres where the Syndicate shall accept Bid cum Application Forms, a list of which

is included in the Bid cum Application Form

Syndicate Agreement The agreement to be entered into among our Company, the Selling Shareholders, the members

of the Syndicate and the Registrar to the Offer in relation to the collection of Bid cum

Application Forms by the Syndicate

Syndicate Members Intermediaries registered with the SEBI and permitted to carry out activities as an underwriter,

in this case being [●]

Syndicate/ members of the

Syndicate

Together, the BRLMs and the Syndicate Members

Underwriters [●]

Underwriting Agreement The agreement to be entered into among our Company, the Selling Shareholders, the

Underwriters and the Registrar to the Offer, to be entered into on or after the Pricing Date but

prior to filing of the Prospectus

Working Day(s) Any day, other than the second and fourth Saturdays of each calendar month, Sundays and

public holidays, on which commercial banks in India are open for business, provided

however, for the purpose of announcement of the Price Band and the Bid/ Offer Period,

“Working Day(s) shall mean all days on which commercial banks” in Mumbai, Maharashtra

are open for business, excluding all Sundays, Saturdays and public holidays and with

reference to the time period between the Bid/Offer Opening Date and listing of the Equity

Shares on the Stock Exchanges, “Working Days” shall mean all trading days of the Stock

Exchanges excluding Sundays and bank holidays in India in accordance with the SEBI

circular no SEBI/HO/CFD/DIL/CIR/P/2016/26 dated January 21, 2016

Conventional and General Terms and Abbreviations

Term Description

AIF(s) Alternative Investment Funds, as defined and registered with SEBI under the SEBI AIF Regulations

BIS Act Bureau of Indian Standards Act, 2016

Bn Billion

BSE BSE Limited

CAGR Compounded Annual Growth Rate

Category I FPIs FPIs registered as category I FPIs under the SEBI FPI Regulations

Category II FPIs FPIs registered as category II FPIs under the SEBI FPI Regulations

Category III FPIs FPIs registered as category III FPIs under the SEBI FPI Regulations, which shall include all other

FPIs not eligible under Category I and II foreign portfolio investors, such as endowments, charitable

societies, charitable trusts, foundations, corporate bodies, trusts, individuals and family offices

CDSL Central Depository Services (India) Limited

CSE The Calcutta Stock Exchange Limited

Companies Act Together, the Companies Act 1956 and the Companies Act 2013

10

Term Description

Companies Act 1956 The Companies Act, 1956 (without reference to the provisions thereof that have ceased to have

effect upon notification of the Notified Sections)

Companies Act 2013 The Companies Act, 2013, to the extent in force pursuant to the notification of the Notified

Sections, read with the rules, regulations, clarifications and modifications thereunder

Copyright Act The Copyright Act, 1957

Depositories Act The Depositories Act, 1996

Depository A depository registered with the SEBI under the Securities and Exchange Board of India

(Depositories and Participants) Regulations, 1996

DIN Director Identification Number

DP ID Depository Participant’s identity number

EBITDA Earnings Before Interest, Tax, Depreciation and Amortization

EPF Act The Employees’ Provident Fund and Miscellaneous Provisions Act, 1952

EPS Earnings per share

Factories Act The Factories Act, 1948

FCNR Account Foreign Currency Non Resident (Bank) account established in accordance with the FEMA

FDI Foreign direct investment

FEMA The Foreign Exchange Management Act, 1999 read with rules and regulations thereunder

Financial Year/ Fiscal/

Fiscal Year

The period of 12 months commencing on April 1 of the immediately preceding calendar year

and ending on March 31 of that particular calendar year

FPIs A foreign portfolio investor who has been registered pursuant to the SEBI FPI Regulations

FVCI The Foreign Venture Capital Investors (as defined under the Securities and Exchange Board of

India (Foreign Venture Capital Investors) Regulations, 2000) registered with SEBI

GDP Gross Domestic Product

GoI/ Central Government The Government of India

GST Goods and services tax

GUVNL Gujarat Urja Vikash Nigam Limited

HUF(s) Hindu Undivided Family(ies)

IAS Rules The Companies (Indian Accounting Standards) Rules, 2015

ICAI Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

IFSC Indian Financial System Code

IPO Initial Public Offering

Income Tax Act The Income Tax Act, 1961

Ind AS The Indian Accounting Standards referred to in the IAS Rules

Indian GAAP Generally Accepted Accounting Principles in India

INR/ Rupee/ ₹/ Rs. Indian Rupee, the official currency of the Republic of India

IRDA Insurance Regulatory and Development Authority

IT Information Technology

MAT Minimum Alternative Tax

MCA The Ministry of Corporate Affairs, GoI

MOEFCC Ministry of Environment, Forest and Climate Change, Government of India

Mn Million

Mutual Funds Mutual funds registered with the SEBI under the Securities and Exchange Board of India (Mutual

Funds) Regulations, 1996

NA/ N.A. Not applicable

NACH National Automated Clearing House

NAV Net asset value

NCLT National Company Law Tribunal, Kolkata, West Bengal

NEFT National Electronic Fund Transfer

Notified Sections The sections of the Companies Act 2013 that have been notified by the MCA and are currently in

effect

NR/ Non-resident A person resident outside India, as defined under the FEMA and includes an NRI

NRE Account Non-Resident External Account

NRI Non-Resident Indian

NRV Net realizable value

NSDL National Securities Depository Limited

NSE National Stock Exchange of India Limited

OCB/ Overseas

Corporate Body

A company, partnership, society or other corporate body owned directly or indirectly to the

extent of at least 60% by NRIs including overseas trusts, in which not less than 60% of beneficial

interest is irrevocably held by NRIs directly or indirectly and which was in existence on October

3, 2003 and immediately before such date had taken benefits under the general permission

granted to OCBs under FEMA. OCBs are not allowed to invest in the Offer

P/E Ratio Price/earnings ratio

11

Term Description

PAN Permanent account number allotted under the Income Tax Act

Payment of Bonus Act The Payment of Bonus Act, 1965

Payment of Gratuity Act The Payment of Gratuity Act, 1972

PPE Property, plant and equipment

RBI The Reserve Bank of India

Regulation S Regulation S under the Securities Act

RoC or Registrar of

Companies

The Registrar of Companies, West Bengal, at Kolkata

RoNW Return on net worth

RTGS Real Time Gross Settlement

Rule 144A Rule 144A of the Securities Act

SCRA The Securities Contract (Regulation) Act, 1956

SCRR The Securities Contracts (Regulation) Rules, 1957

SEBI The Securities and Exchange Board of India constituted under the SEBI Act

SEBI Act The Securities and Exchange Board of India Act, 1992

SEBI AIF Regulations The Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012

SEBI BTI Regulations The Securities and Exchange Board of India (Bankers to an Issue) Regulations, 1994

SEBI FPI Regulations The Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2014

SEBI FVCI Regulations The Securities and Exchange Board of India (Foreign Venture Capital Investors) Regulations,

2000

SEBI ICDR Regulations The Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements)

Regulations, 2009

SEBI Listing Regulations Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements)

Regulations, 2015

Securities Act U.S. Securities Act of 1933, as amended

State Government The government of a state in India

STT Securities Transaction Tax

Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers)

Regulations, 2011

Trademarks Act Trademarks Act, 1999

U.S. GAAP Generally Accepted Accounting Principles in the United State of America

U.S. QIBs “qualified institutional buyers” as defined under Regulation 144A under the Securities Act

US$/ USD/ US Dollar United States Dollar, the official currency of the United States of America

USA/ U.S./ US United States of America, its territories and possessions, any state of the United States of America

and the District of Columbia

VAT Value Added Tax

VCFs Venture capital funds as defined in and registered with the SEBI under the Securities and Exchange

Board of India (Venture Capital Fund) Regulations, 1996 or the Securities and Exchange Board of

India (Alternative Investment Funds) Regulations, 2012, as the case may be

WBIDC West Bengal Industrial Development Corporation Limited

Wilful Defaulter Wilful Defaulter as defined under Regulation 2(zn) of the SEBI ICDR Regulations

Industry Related Terms

Term Description

BIS Bureau of Indian Standards

CAGR Compounded Annual Growth Rate

CRISIL CRISIL Research, a division of CRISIL Limited

GDP Gross Domestic Product

MMT Million Metric Tonnes

MMTPA Million Metric Tonnes Per Annum

MT Metric Tonnes

OPC Ordinary Portland Cement

PPC Portland Pozzolana Cement

PSC Portland Slag Cement

RCC Reinforced cement concrete

12

CERTAIN CONVENTIONS, USE OF FINANCIAL INFORMATION AND MARKET DATA AND

CURRENCY OF PRESENTATION

Certain Conventions

All references in this Draft Red Herring Prospectus to “India” are to the Republic of India and all references to

the “U.S.”, “U.S.A” or “United States” are to the United States of America.

Unless indicated, all references to page numbers in the Draft Red Herring Prospectus are to the page numbers of

this Draft Red Herring Prospectus.

Financial Data

Unless indicated otherwise, the financial data in this Draft Red Herring Prospectus is derived from our Restated

Financial Statements.

Unless the context otherwise requires, any percentage, amounts, as set forth in “Risk Factors”, “Summary of

Business” “Business”, “Management’s Discussion and Analysis of Financial Conditions and Results of

Operations” on pages 16, 50, 128 and 301, respectively and elsewhere in this Draft Red Herring Prospectus have

been calculated on the basis of our Restated Financial Statements unless otherwise stated.”

Certain data included in this Draft Red Herring Prospectus in relation to certain operating metrics, financial and

other business related information not otherwise included in the Restated Financial Statements has been reviewed

and verified by (i) S.K. Bhatia, Chartered Engineer; (ii) AMK & Associates, Chartered Accountants; (iii) Global

Environment and Mining Services (Consulting Engineers, Mine Designers, Geologists and Surveyors); (vi)

Synergy Geotech Private Limited; (v) Sripad Pujar and BVR Achar, on behalf of Chaithanya Geo Lynx, Mining,

Geology, Survey and Environmental Consultants; (vii) Shailendra Singh Bisht, on behalf of Udaipur Mi-Tech

Private Limited; (viii) S.K. Soni; and (ix) Agrawal Sanjay & Company, Chartered Accountants.

Our Company’s financial year commences on April 1 of the immediately preceding calendar year and ends on

March 31 of that particular calendar year, so all references to a particular financial year are to the 12 month period

commencing on April 1 of the immediately preceding calendar year and ending on March 31 of that particular

calendar year. Reference in this Draft Red Herring Prospects to the terms Fiscal or Fiscal Year or Financial Year

or FY is to the 12 months ended on March 31 of each year, unless otherwise specified.

On February 16, 2015, the Ministry of Corporate Affairs issued the Companies (Indian Accounting Standards)

Rules, 2015 (“IAS Rules”) for the purpose of enacting changes to Indian GAAP that are intended to align Indian

GAAP further with IFRS. The IAS Rules provide that the financial information of the companies to which they

apply shall be prepared and audited in accordance with the Ind AS. We have transitioned to the Ind AS accounting

standards with effect from April 1, 2015 and have prepared our Restated Financial Statements for (i) the three

months ended June 30, 2018 and Fiscals 2018, 2017 and 2016 in accordance with Ind AS; and (ii) Fiscals 2015

and 2014 in accordance with Indian GAAP.

In accordance with the SEBI circular no. SEBI/HO/CFD/DIL/CIR/P/2016/47 dated March 31, 2016 and Ind AS

101, First-time Adoption of Indian Accounting Standard, we have presented reconciliation from Indian GAAP to

Ind AS in “Financial Statements – Note 49 – First Time Adoption of IND AS - Reconciliations between previous

Indian GAAP and Ind AS” on page 255. Except such reconciliation, we have not made any attempt to quantify

the impact of the differences between Indian GAAP and Ind AS as applied to our financial information and it is

urged that you consult your own advisors regarding the impact of difference, if any, on financial data included in

this Draft Red Herring Prospectus. Potential investors should consult their own advisers for an understanding of

the principal differences between the existing Indian GAAP and the Ind AS, and how these differences might

affect the financial statements appearing in this document. See “Risk Factors – Significant differences exist

between Ind AS and other accounting principles, such as Indian GAAP, IFRS and U.S. GAAP, which may be

material to investors’ assessment of our financial condition.” on page 41.

Indian GAAP and Ind AS differ from accounting principles with which prospective investors may be familiar in

other countries, including IFRS and US GAAP and the reconciliation of the financial information to other

accounting principles has not been provided. Our Company has not attempted to explain those differences or

13

quantify their impact on the financial data included in this Draft Red Herring Prospectus and investors should

consult their own advisors regarding such differences and their impact on our Company’s financial data. The

degree to which the financial information included in this Draft Red Herring Prospectus will provide meaningful

information is entirely dependent on the reader’s level of familiarity with Indian accounting policies and practices,

Ind AS, Indian GAAP, the Companies Act and the SEBI ICDR Regulations. Any reliance by persons not familiar

with Indian GAAP, Ind AS, the Companies Act, the SEBI ICDR Regulations and practices on the financial

disclosures presented in this Draft Red Herring Prospectus should accordingly be limited and we urge you to

consult your own advisors regarding such differences and their impact on our financial data. See “Risk Factors –

Significant differences exist between Ind AS and other accounting principles, such as Indian GAAP, IFRS and

U.S. GAAP, which may be material to investors’ assessment of our financial condition.” on page 41.

Certain figures contained in this Draft Red Herring Prospectus, including financial information, have been subject

to rounding adjustments. All decimals have been rounded off to two decimal points. In certain instances, (i) the

sum or percentage change of such numbers may not conform exactly to the total figure given; and (ii) the sum of

the numbers in a column or row in certain tables may not conform exactly to the total figure given for that column

or row. However, where any figures that may have been sourced from third-party industry sources are rounded

off to other than two decimal points in their respective sources, such figures appear in this Draft Red Herring

Prospectus as rounded-off to such number of decimal points as provided in such respective sources.

Industry and Market Data

For the purpose of confirming our understanding of the industry in connection with the Offer, we have

commissioned a report titled “Cement Market Assessment for India and Eastern Region” dated October 2018

prepared by CRISIL (“CRISIL Report”). CRISIL has included the following disclaimer as part of such report:

“CRISIL Research, a division of CRISIL Limited (CRISIL) has taken due care and caution in preparing this report

(the “Report”) based on the Information obtained by CRISIL from sources which it considers reliable (the

“Data”). However, CRISIL does not guarantee the accuracy, adequacy or completeness of the Data / Report and

is not responsible for any errors or omissions or for the results obtained from the use of Data / Report. This Report

is not a recommendation to invest / disinvest in any entity covered in the Report and no part of this Report should

be construed as an expert advice or investment advice or any form of investment banking within the meaning of

any law or regulation. CRISIL especially states that it has no liability whatsoever to the subscribers / users /

transmitters/ distributors of this Report. Without limiting the generality of the foregoing, nothing in the Report is

to be construed as CRISIL providing or intending to provide any services in jurisdictions where CRISIL does not

have the necessary permission and/or registration to carry out its business activities in this regard. Emami Cement

Limited will be responsible for ensuring compliances and consequences of non-compliances for use of the Report

or part thereof outside India. CRISIL Research operates independently of, and does not have access to information

obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions Ltd (CRIS), which may, in their

regular operations, obtain information of a confidential nature. The views expressed in this Report are that of

CRISIL Research and not of CRISIL’s Ratings Division / CRIS. No part of this Report may be

published/reproduced in any form without CRISIL’s prior written approval.”

Aside from the above, unless stated otherwise, industry and market data used throughout this Draft Red Herring

Prospectus has been derived from certain industry sources. Industry publications generally state that the

information contained in such publications has been obtained from sources generally believed to be reliable, but

their accuracy, adequacy or completeness and underlying assumptions are not guaranteed and their reliability

cannot be assured. Accordingly, no investment decisions should be made based on such information. Although

we believe that the industry and market data used in this Draft Red Herring Prospectus is reliable, it has not been

independently verified by us, the Selling Shareholders, the BRLMs, or any of our or their respective affiliates or

advisors, and none of these parties makes any representation as to the accuracy of this information. The data used

in these sources may have been re-classified by us for the purposes of presentation. Data from these sources may

also not be comparable. The extent to which the industry and market data presented in this Draft Red Herring

Prospectus is meaningful depends upon the reader’s familiarity with and understanding of the methodologies used

in compiling such data. There are no standard data gathering methodologies in the industry in which we conduct

our business and methodologies and assumptions may vary widely among different market and industry sources.

Such data involves risks, uncertainties and numerous assumptions and is subject to change based on various

factors, including those discussed in “Risk Factors” on page 16.

In accordance with the SEBI ICDR Regulations, “Basis of Offer Price” on page 94 includes information relating

14

to our peer group companies. Such information has been derived from publicly available sources and neither we

nor the BRLMs have independently verified such information.

Currency and Units of Presentation

All references to “Rupees” or “₹” or “Rs.” or “INR” are to Indian Rupees, the official currency of the Republic

of India. All references to “US$”, “U.S. Dollar”, “USD” or “US Dollars” are to United States Dollars, the official

currency of the United States of America.

In this Draft Red Herring Prospectus, our Company has presented certain numerical information. Unless otherwise

indicates, all figures have been expressed in millions. One million represents ‘10 lakhs’ or 1,000,000. However,

where any figures that may have been sourced from third-party industry sources are expressed in denominations

other than millions in their respective sources, such figures appear in this Draft Red Herring Prospectus expressed

in such denominations as provided in such respective sources.

Exchange Rates

This Draft Red Herring Prospectus contains conversions of U.S. Dollars into Indian Rupees that have been

presented solely to comply with the requirements of the SEBI ICDR Regulations. These conversions should not

be construed as a representation that such currency amounts could have been, or can be converted into Indian

Rupees, at any particular rate, or at all.

The exchange rates of the currencies used in this Draft Red Herring Prospectus into Indian Rupees are provided

below.

(in ₹)

Currency June 30, 2018* March 31,

2018**

March 31, 2017 March 31, 2016 March 31,

2015

March 31,

2014#

1 USD^ 68.5753 65.0441 64.8386 66.3329 62.5908 60.0998 ^Source: RBI Reference Rate * Exchange rate as on June 29, 2018, as RBI Reference Rate is not available for June 30, 2018 being a Saturday. ** Exchange rate as on March 28, 2018 as RBI Reference Rate is not available for March 29, 2018, March 30, 2018 and March 31, 2018 being public holidays and a Saturday, respectively. #Exchange rate as on March 28, 2014, as RBI Reference Rate is not available for March 31, 2014, March 30, 2014 and March 29, 2014 being

a public holiday, Sunday and Saturday, respectively.

15

FORWARD-LOOKING STATEMENTS

This Draft Red Herring Prospectus contains certain “forward-looking statements”. These forward looking

statements include statements which can generally be identified by words or phrases such as “aim”, “anticipate”,

“believe”, “expect”, “estimate”, “intend”, “likely to”, “objective”, “plan”, “propose”, “will continue”, “seek to”,

“will pursue” or other words or phrases of similar import. Similarly, statements that describe our strategies,

objectives, plan, prospects or goals are also forward looking statements.

These forward-looking statements are based on our current plans, estimates and expectations and actual results

may differ materially from those suggested by such forward-looking statements. All forward-looking statements,

whether made by us or any third party, are subject to risks, uncertainties and assumptions about us that could

cause actual results to differ materially from those contemplated by the relevant forward-looking statement. This

may be due to risks or uncertainties associated with our expectations with respect to, but not limited to, regulatory

changes pertaining to the industries in India in which we have our businesses and our ability to respond to them,

our ability to successfully implement our strategy, our growth and expansion, technological changes, our exposure

to market risks, general economic and political conditions in India, which have an impact on our business activities

or investments, the monetary and fiscal policies of India, inflation, deflation, unanticipated turbulence in interest

rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in

India and globally, changes in domestic laws, regulations and taxes, changes in competition in our industry and

incidence of any natural calamities and/or acts of violence. Important factors that could cause actual results to

differ materially include, including, but not limited to:

A relatively short operating history of our business.

Any adverse development affecting eastern India where our operations are concentrated.

A slowdown or shutdown in our manufacturing operations or under-utilization of our manufacturing

plants.

Our inability to mine sufficient limestone for our operations or failure to comply with the terms of the

mining lease.

A shortage or non-availability of labour, power, fuel or water .

Inability to source adequate raw materials at acceptable costs.

Inability to continue to use the ‘Emami’ brand name or any negative impact on the ‘Emami’ brand name.

Delays in the construction of our new and proposed manufacturing plants.

Failure to yield the benefits of our planned capital expenditure.

For a further discussion of factors that could cause our actual results to differ, see “Risk Factors”, “Business” and