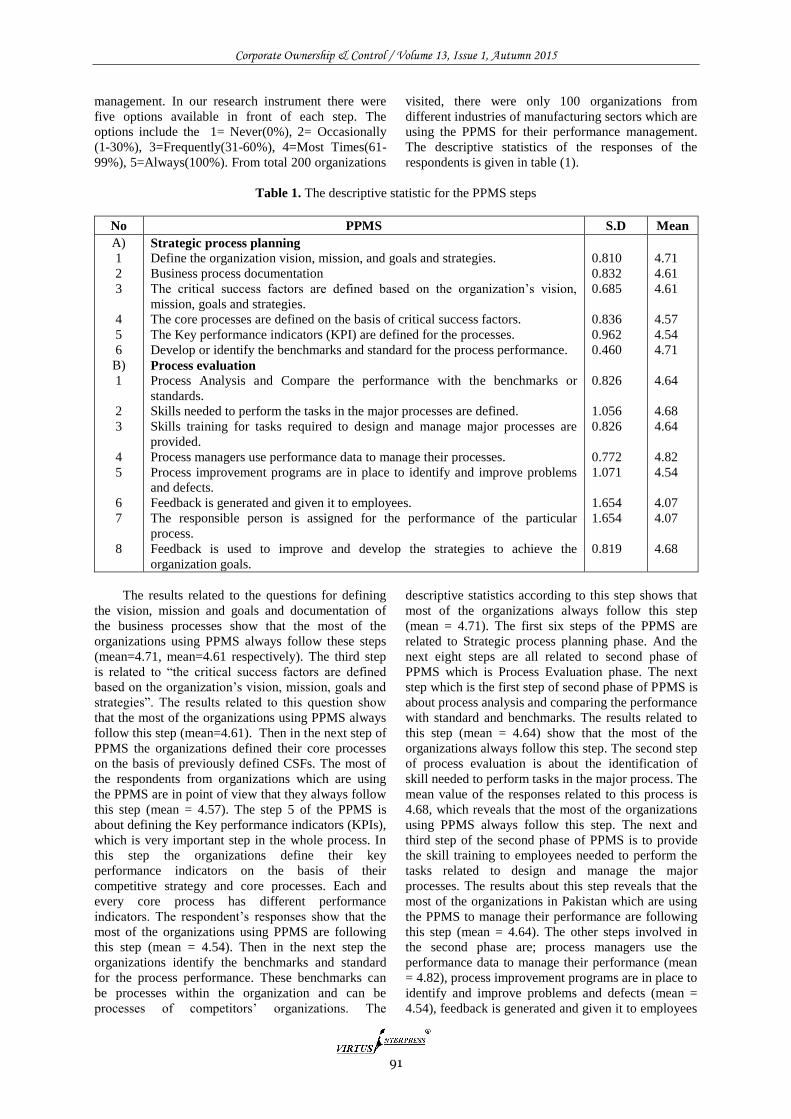

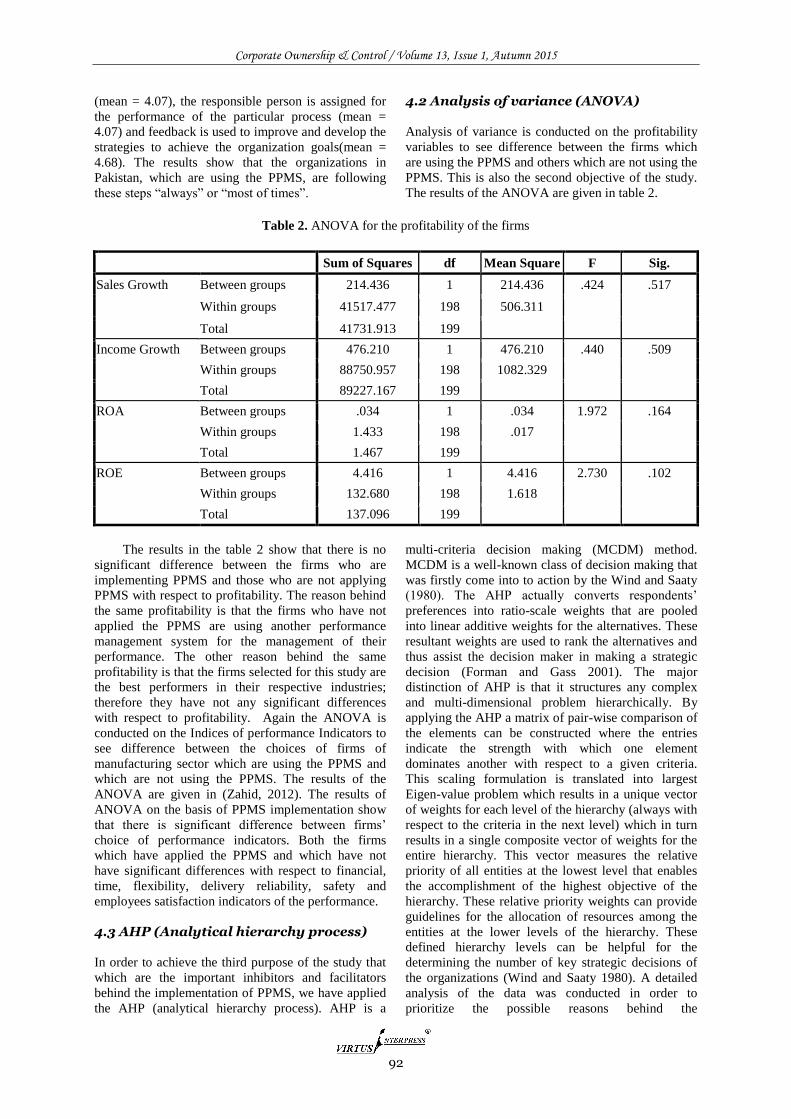

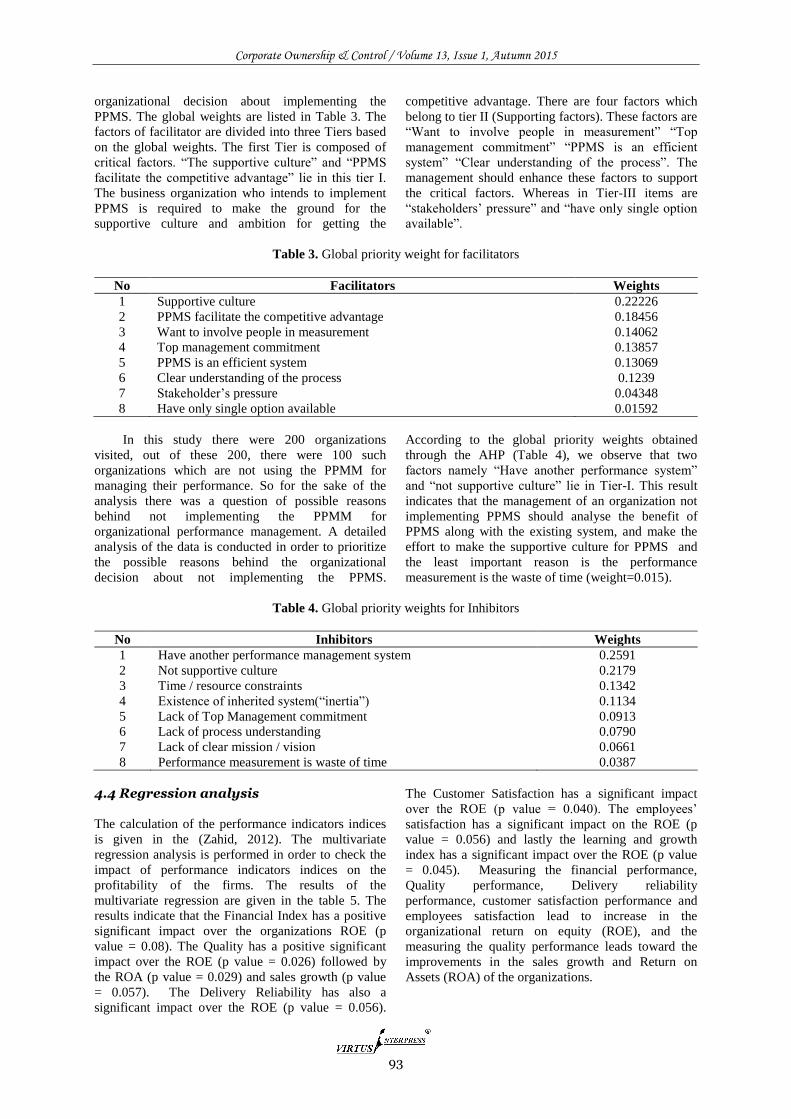

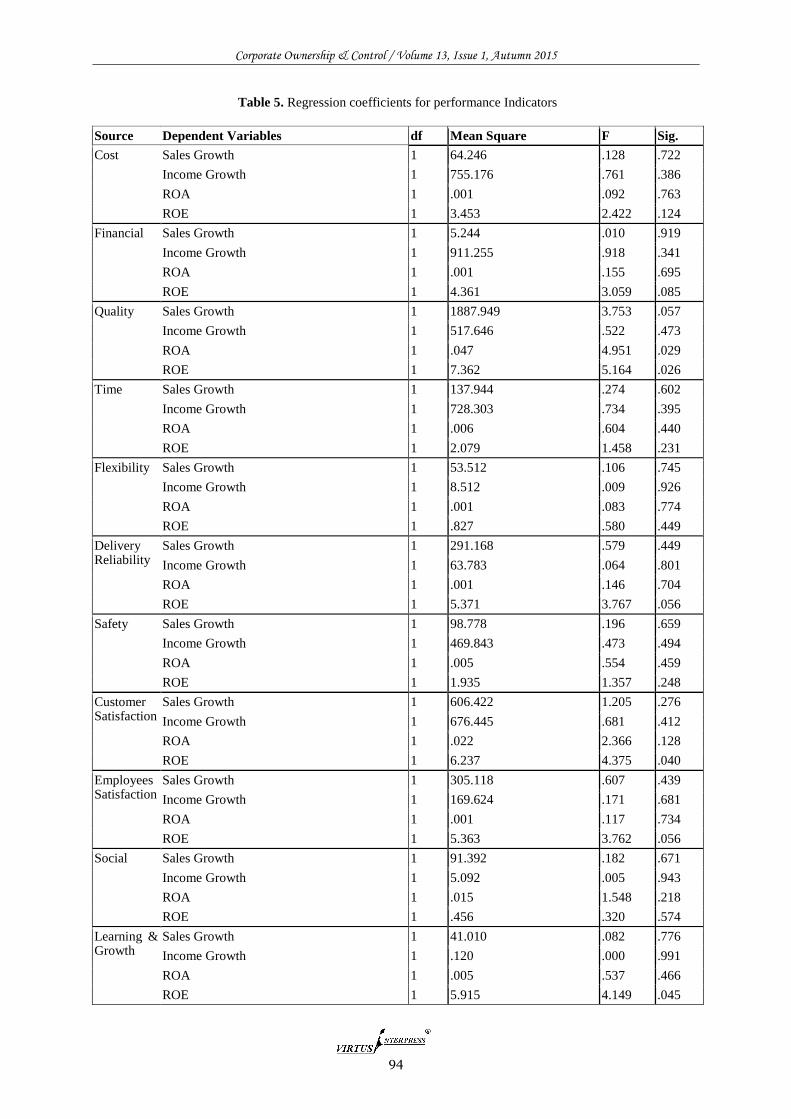

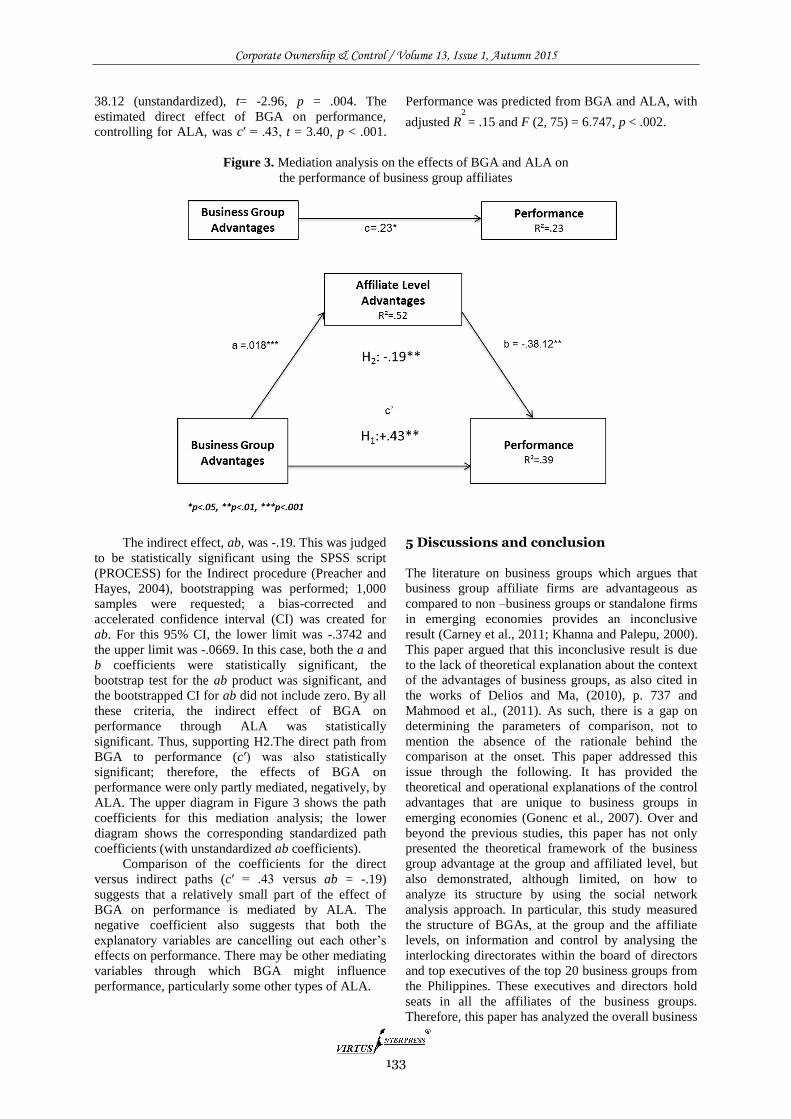

theoretical foundation of diversification decisions: - virtus

TRANSCRIPT

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

3

CORPORATE

OWNERSHIP & CONTROL

Postal Address:

Postal Box 36

Sumy 40014

Ukraine

Tel: +380-542-698125

Fax: +380-542-698125

e-mail: [email protected]

www.virtusinterpress.org

Journal Corporate Ownership & Control is published four times a year, in September-November, December-

February, March-May and June-August, by Publishing House “Virtus Interpress”, Kirova Str. 146/1, office 20,

Sumy, 40021, Ukraine.

Information for subscribers: New orders requests should be addressed to the Editor by e-mail. See the section

"Subscription details".

Back issues: Single issues are available from the Editor. Details, including prices, are available upon request.

Advertising: For details, please, contact the Editor of the journal.

Copyright: All rights reserved. No part of this publication may be reproduced, stored or transmitted in any form

or by any means without the prior permission in writing of the Publisher.

Corporate Ownership & Control

ISSN 1727-9232 (printed version)

1810-0368 (CD version)

1810-3057 (online version)

Certificate № 7881

Virtus Interpress. All rights reserved.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

4

EDITORIAL

Dear readers!

The recent issue of the journal Corporate Ownership and Control pays attention to issues of corporate

social responsibility, risks management, audit issues, corporate codes etc. More detailed issues are

given below.

Sujani Thrikawala, Stuart Locke, Krishna Reddy examine the impact of corporate governance

practices of microfinance institutions (MFIs) on outreach to the poor people in Sri Lanka by using

three outreach variables. Ziad Mohammad. Zurigat, Nadia Jawdat aim at testing the partial adjustment

model of cash holdings to investigate whether Jordanian industrial firms have a target cash holdings

and how fast they move toward that target when any target deviation exists. The results of the research

of Turki Al-Sabah signify a negative relationship between the firm’s financial leverage and dividend

payout ratio. Samer Khalil, Assem Safieddine examines governance-related issues within Middle East

family businesses. They construct a governance index and use a probit model to examine whether

family-related variables can explain the level of corporate governance.

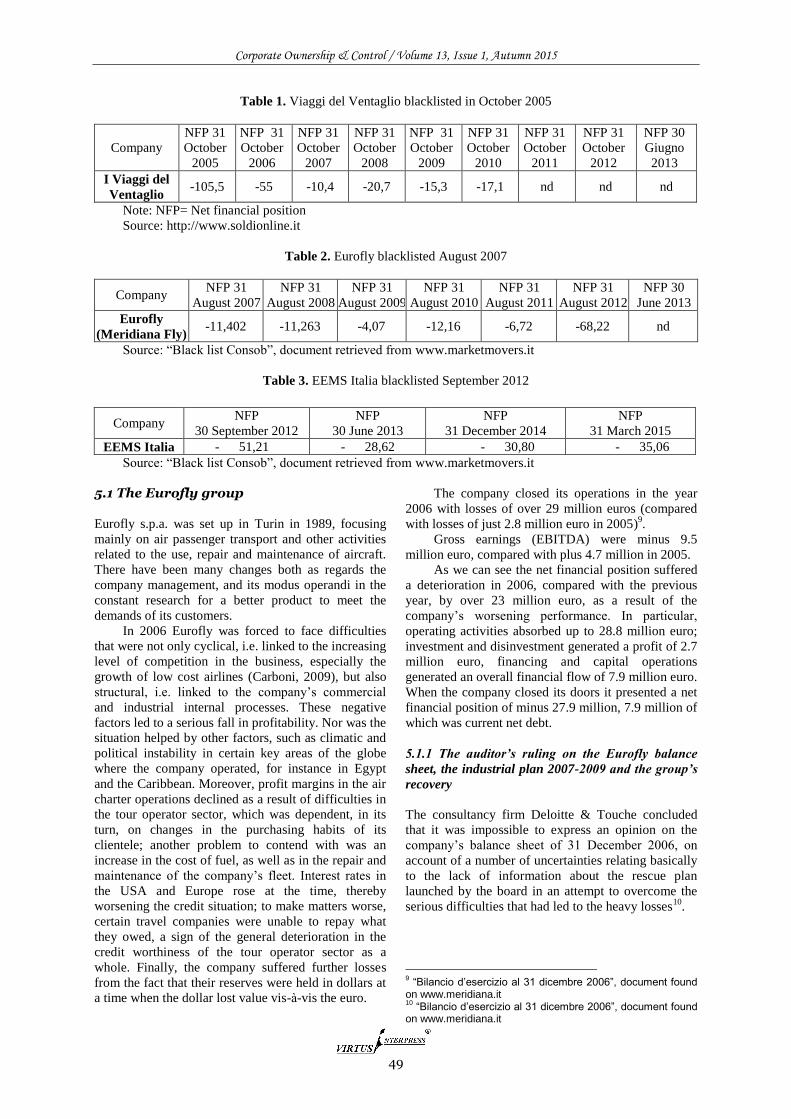

Graziella Sicoli, Paolo Tenuta analyse the concept of going concern on the one hand, through a case

study of three companies which have recently come under observation of the CONSOB and have been

inserted in the so-called “black list” and, on the other, the consequences that the removal of the

presumption of continuity can have on the kind of assessment the auditors make. Rajni Mala, Parmod

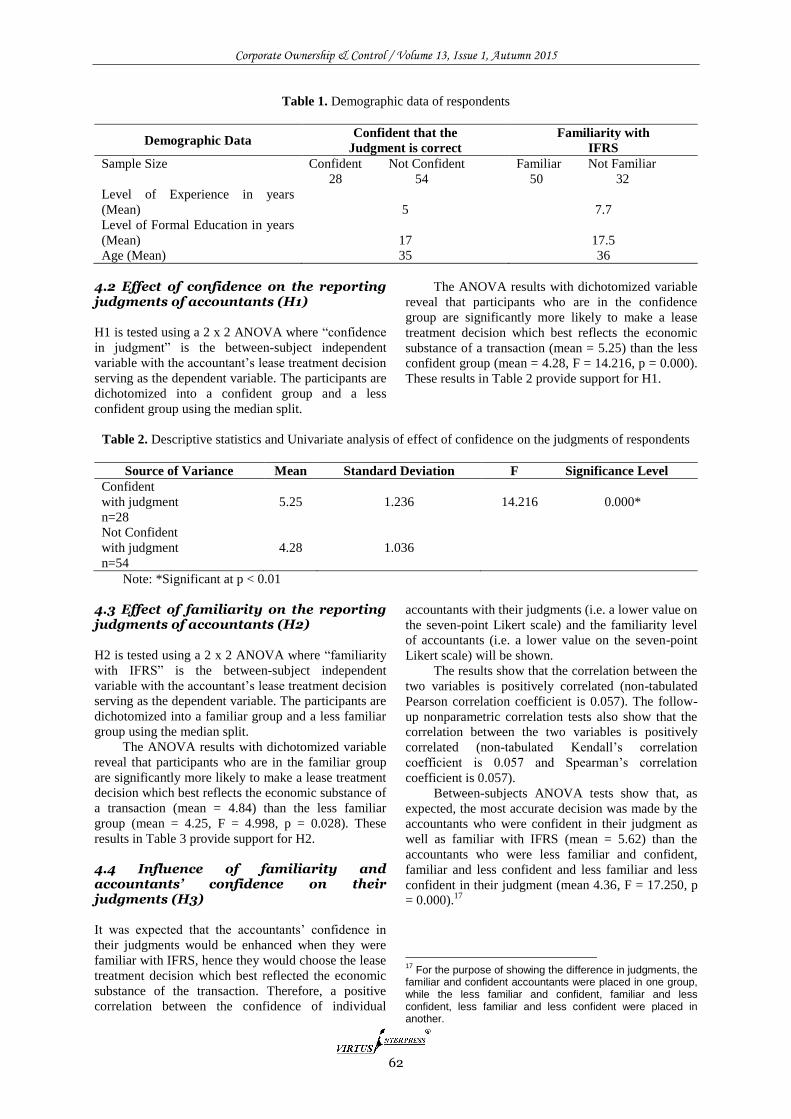

Chand examine whether the accuracy of judgments made by accountants varies as a consequence of

their level of confidence, and whether their confidence in exercising judgments could be enhanced by

greater familiarity with IFRS. Sutaryo Sutaryo, Yediel Lase

investigate the effects of auditor

characteristics on local governments’ audit delay by studying 127 Indonesian local governments.

Agung Nur Probohudono, Eko Arief Sudaryono, Nurmadi Harsa Sumarta, Yonatan Ardilas examine

the impact of ownership, corporate governance and mandatory tax disclosure on voluntary financial

disclosure in Indonesia using 102 Indonesian listed companies in the period of 2009 to 2012.

Hayat M. Awan, M. Ishaq Bhatti, Zahid Razaq investigate the financial management performance

involved in increasing the firms’ profitability. Reem Khamis, Wajeeh Al-Ali, Allam Hamdan examine

the relation between ownership structure and corporate performance; the sample of the study included

42 out of 48 companies (resembling 87.5% of the population) of all sectors in Bahrain Stock Exchange

in five years from 2007-2011. Mahlomola Khumalo, Andries Masenge investigate the relationship

between CEO remuneration and firm performance. Roderick Bugador views the network of control in

a corporate business group as its source of competitive advantages.

We hope that you will enjoy reading the journal and in future we will receive new papers, outlining

the most important issues and best practices of corporate governance!

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

5

CORPORATE OWNERSHIP & CONTROL VOLUME 13, ISSUE 1, AUTUMN 2015

CONTENTS

EDITORIAL 4

ACADEMIC NVESTIGATIONS & CONCEPTS AN EMPIRICAL ANALYSIS OF CORPORATE GOVERNANCE IMPACT ON OUTREACH OF MICROFINANCE INSTITUTIONS (MFIS) 8 Sujani Thrikawala, Stuart Locke, Krishna Reddy This study examines the impact of corporate governance practices of microfinance institutions on outreach to the poor people in Sri Lanka. The findings of this study revealed several significant relationships: Breadth of outreach in Sri Lankan MFIs improve when they have a female chair on the board but decreases when they have more female directors and client representation on the board, and female borrowers get more loans when the firm has women representation and international/donor directors on the board, but less loans if they have a female chair. TESTING THE PARTIAL ADJUSTMENT MODEL OF OPTIMAL CASH HOLDING: EVIDENCE FROM AMMAN STOCK EXCHANGE 15 Ziad Mohammad. Zurigat, Nadia Jawdat This study aims at testing the partial adjustment model of cash holdings to investigate whether Jordanian industrial firms have a target cash holdings and how fast they move toward that target when any target deviation exists. The study uses the estimated fitted values from the conventional cash equation as a proxy for the target cash holding. The study provides evidence suggesting that cash flows, net working capital, leverage and firm size significantly affect the cash holdings of Jordanian firms. THE EFFECT OF THE FIRM’S AGE AND FINANCIAL LEVERAGE ON ITS DIVIDEND POLICY – EVIDENCE FROM KUWAIT STOCK EXCHANGE MARKET (KSE) 24 Turki Al-Sabah In this research, the effect of the firms’ financial leverage and age on their dividend policy has been explored. Two hypotheses were formulated, where the first focused on examining the effect of the firms’ financial leverage and the second concentrated on investigating the effect of the firms’ age on their dividend policy. The hypotheses were tested using ordinary least square and fixed-effect panel regression. The results signify a negative relationship between the firm’s financial leverage and dividend payout ratio. CORPORATE GOVERNANCE IN MIDDLE EAST FAMILY BUSINESSES 32 Samer Khalil, Assem Safieddine This study examines governance-related issues within Middle East family businesses. The absence of proper external monitoring mechanisms – governmental or other – to protect shareholder rights, and

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

6

the absence of any pre-existing literature on the Middle East market provides the motivation to evaluate the corporate governance practices of Middle East family businesses. Authors construct a governance index and use a probit model to examine whether family-related variables can explain the level of corporate governance. It is found that the majority of boards had a prevalence of family members and a low proportion of independent directors.

AUDIT, ACCOUNTING & REPORTING THE IMPACT OF THE “GOING CONCERN” ON AUDITORS’ JUDGEMENT. ANALYSIS OF THE ITALIAN CONTEXT FROM AN INTERNATIONAL PERSPECTIVE 44 Graziella Sicoli, Paolo Tenuta The present work aims to analyse the concept of going concern on the one hand, through a case study of three companies which have recently come under observation of the CONSOB and have been inserted in the so-called “black list” and, on the other, the consequences that the removal of the presumption of continuity can have on the kind of assessment the auditors make. The aim of the present work is twofold: the first part analyses the principle of going concern from a business and economic perspective. Once this has been completed, the work will go on to offer an overview of the dynamics that can bring a company to a crisis point, and how these affect the judgments expressed by the auditors. CONFIDENCE OF ACCOUNTANTS IN APPLYING INTERNATIONAL FINANCIAL REPORTING STANDARDS 56 Rajni Mala, Parmod Chand Research on how accountants could increase their confidence in interpreting and applying IFRS is lacking. This study examines whether the accuracy of judgments made by accountants varies as a consequence of their level of confidence, and whether their confidence in exercising judgments could be enhanced by greater familiarity with IFRS. The results of the study support that accountants who are more confident make judgments that better reflect the economic substance of a transaction than accountants who are less confident. The results further indicate that familiarity with IFRS enhances the confidence of accountants and the most accurate judgments are made by those accountants who are not only familiar with IFRS but also have confidence in their judgments. AUDITORS CHARACTERISTICS AND AUDIT DELAY: EVIDENCE FROM INDONESIAN REGIONAL GOVERNMENTS 66 Sutaryo Sutaryo, Yediel Lase

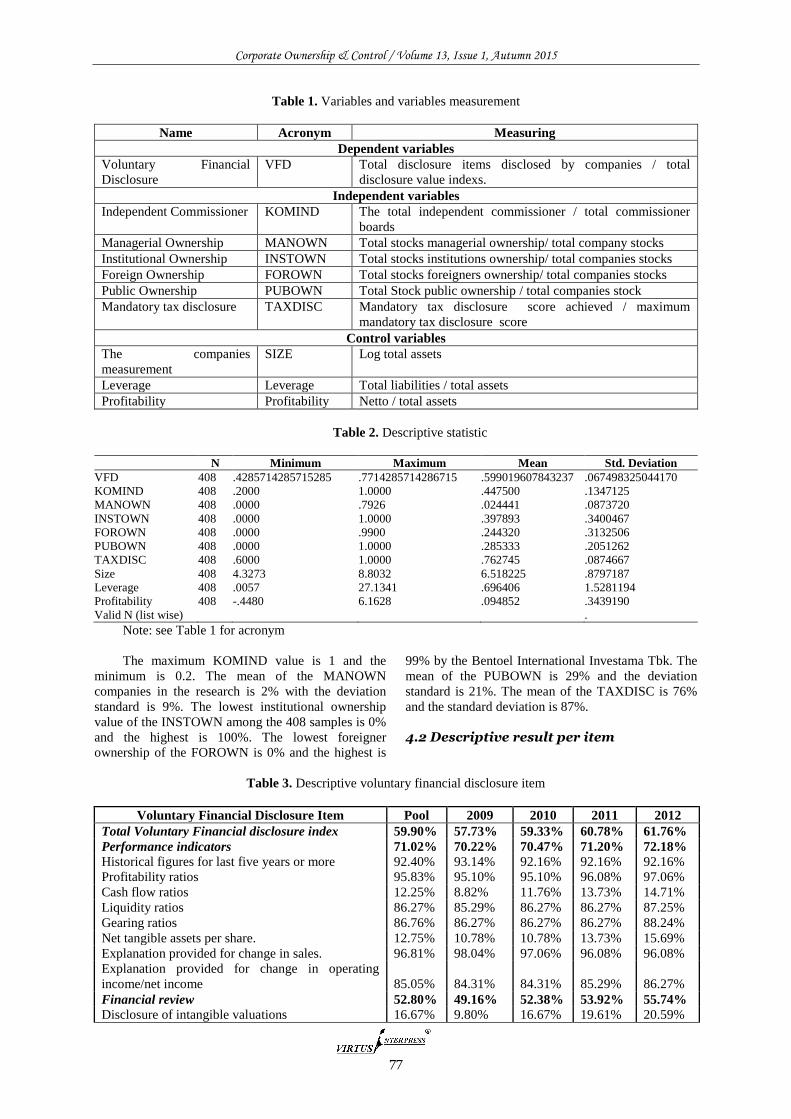

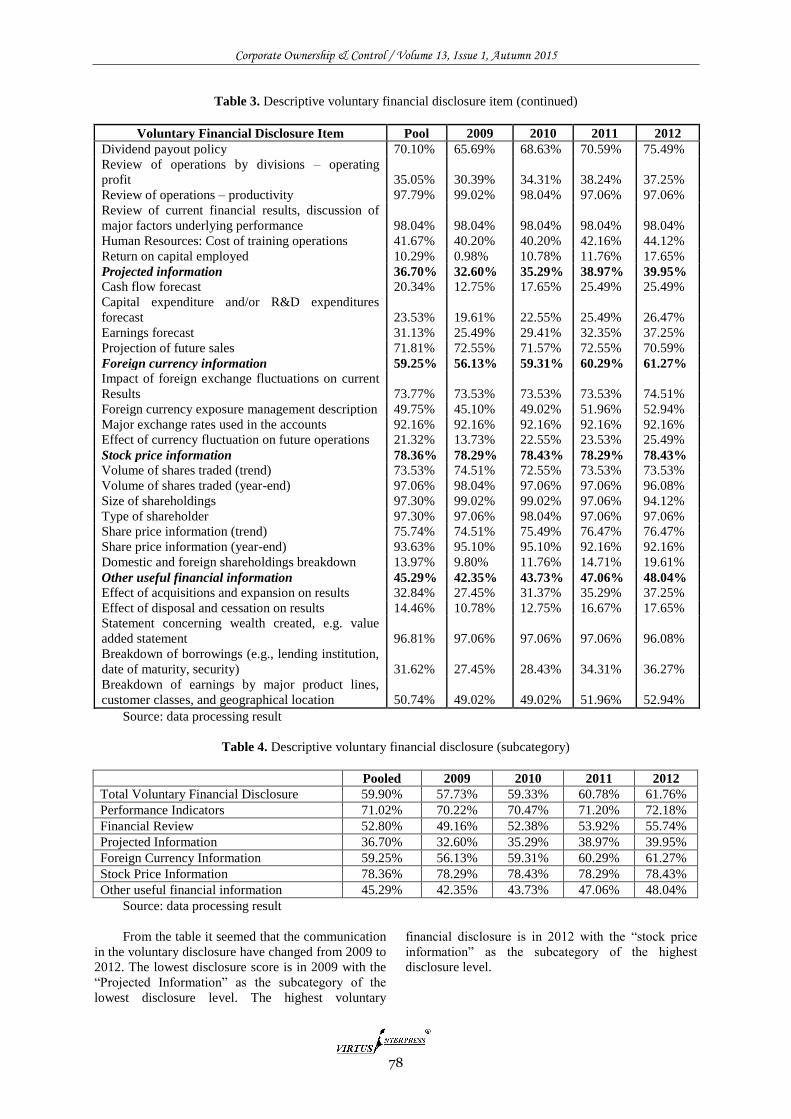

Overdue financial statements reporting, more specifically audit delay, can cause losses in its capacity in decision making. We investigate the effects of auditor characteristics on local governments’ audit delay. We find that auditor professional proficiency and auditor educational background have significant effect on the audit delay of local government financial statements. Our results also indicate the intersection of some auditor characteristics in affecting audit delay. Our findings mainly suggest that the auditor professional proficiency should be improved to shrink audit delay. OWNERSHIP, CORPORATE GOVERNANCE AND MANDATORY TAX DISCLOSURE INFLUENCING VOLUNTARY FINANCIAL DISCLOSURE IN INDONESIA 74 Agung Nur Probohudono, Eko Arief Sudaryono, Nurmadi Harsa Sumarta, Yonatan Ardilas This study examines the impact of ownership, corporate governance and mandatory tax disclosure on voluntary financial disclosure in Indonesia. The results show that proportion of independent director, managerial ownership, institutional ownership, foreign ownership and mandatory tax disclosure are assosiated with voluntary financial disclosure. Analysis reveals a moderate level of 59,90% score of disclosure in the period of 2009 to 2012 in Indonesian listed companies.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

7

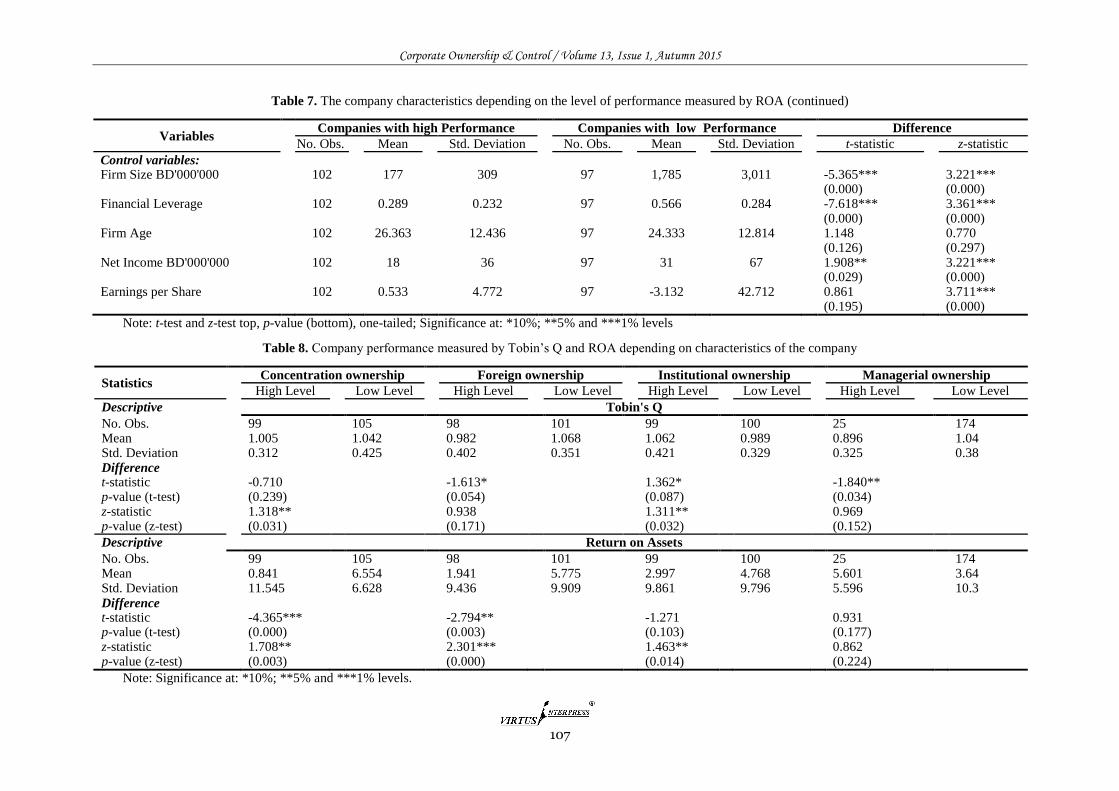

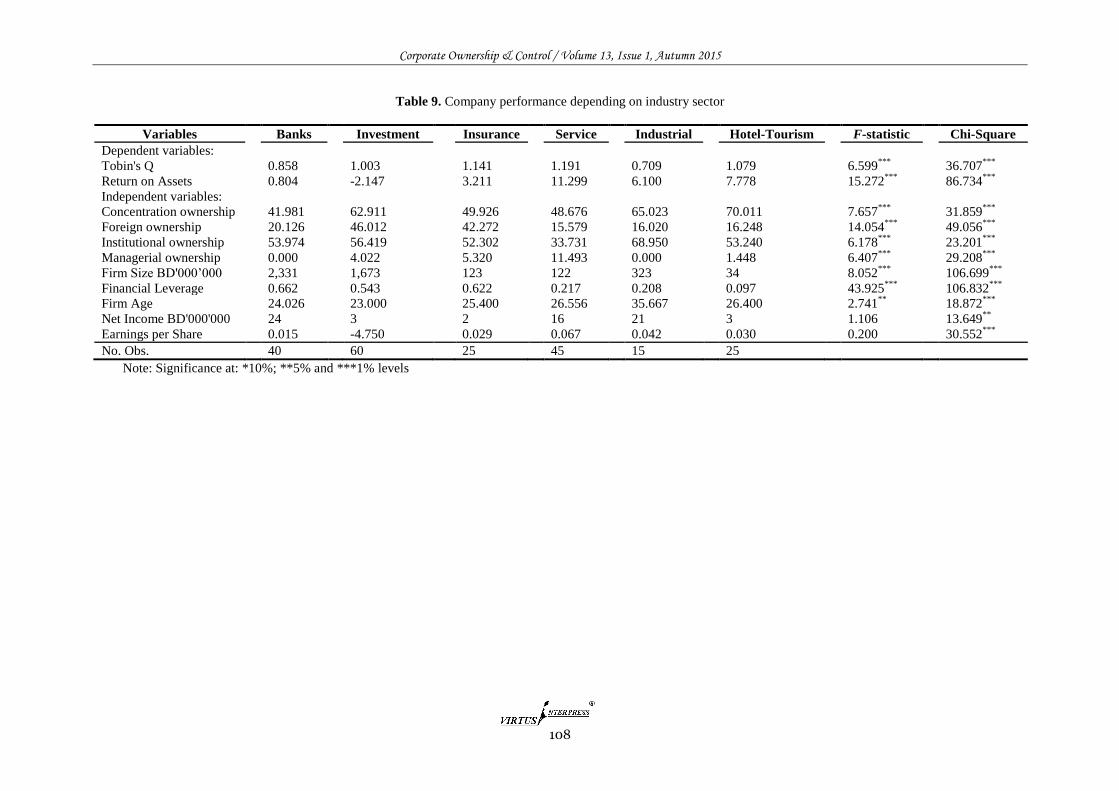

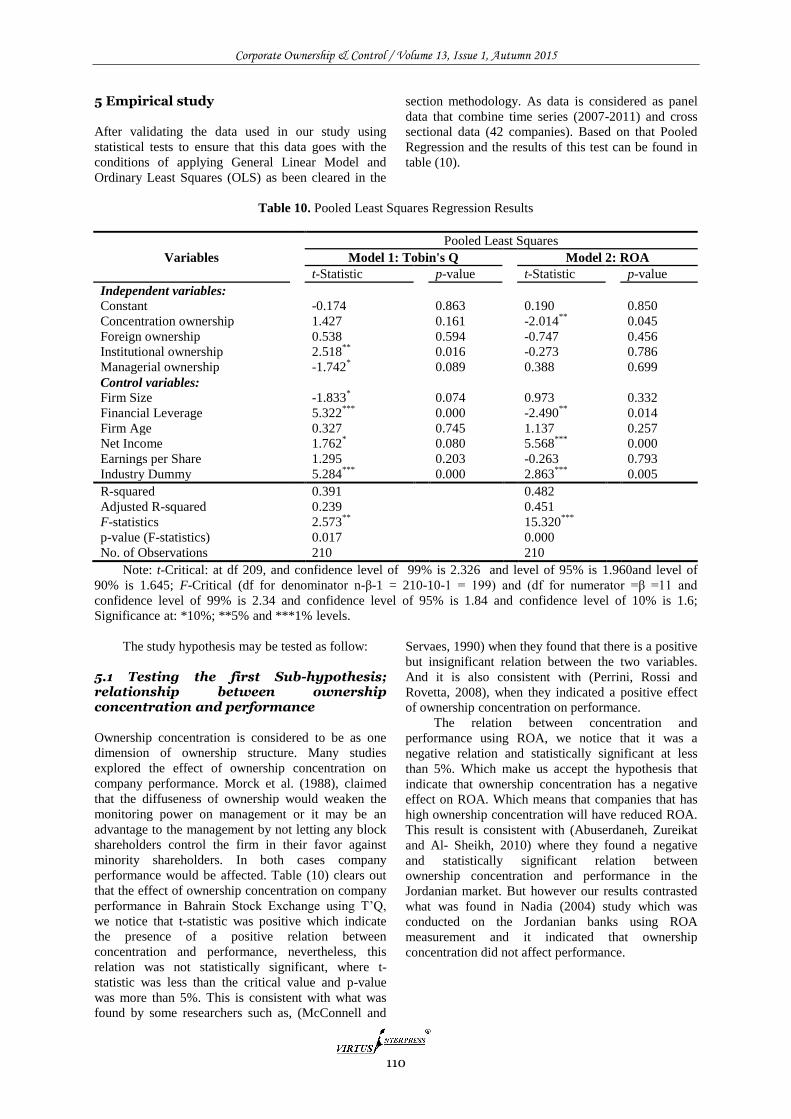

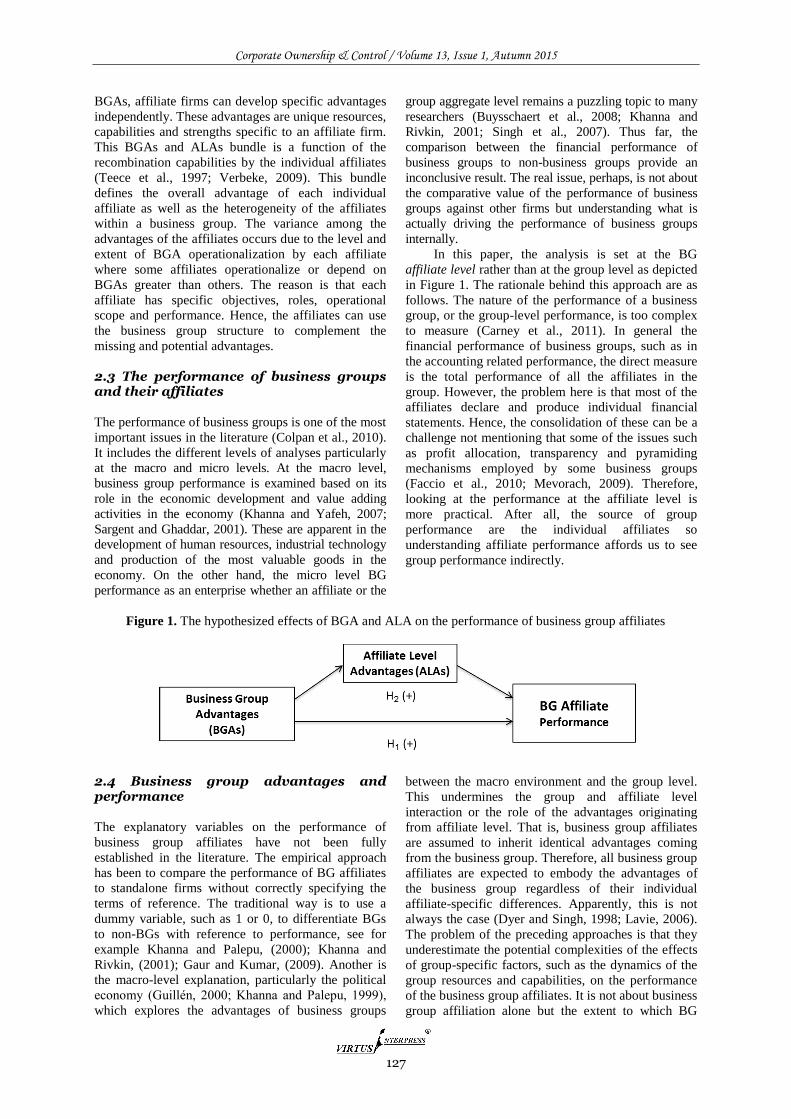

CORPORATE GOVERNANCE & PERFORMANCE FINANCIAL MANAGEMENT: THE IMPACT OF PERFORMANCE INDICATORS ON THE ORGANIZATIONAL PROFITABILITY 84 Hayat M. Awan, M. Ishaq Bhatti, Zahid Razaq This paper investigates the financial management performance involved in increasing the firms’ profitability. Stratified random sampling technique was used to select a sample of 200 manufacturing firms with process performance management system (PPMS) criteria to check the impact of performance indicators on the overall business performance index using ROE, ROA. The results of AHP analysis show that the “Supportive Culture” and “PPMS facilitate the competitive advantage” are the major facilitators for those organizations who have implemented the PPMS whereas firms without implementation of PPMS have major inhibitors as “ Non supportive culture” and ”Have another Performance System”. THE RELATIONS BETWEEN OWNERSHIP STRUCTURE AND CORPORATE PERFORMANCE: EVIDENCE FROM BAHRAIN STOCK EXCHANGE 97 Reem Khamis, Wajeeh Al-Ali, Allam Hamdan In this article we examine the relation between ownership structure and corporate performance; the sample of the study included 42 out of 48 companies of all sectors in Bahrain Stock Exchange in five years from 2007-2011. Several dimensions of ownership structure were studied and two different measurements of performance were used to capture the different results from using each one of them and to assess the relevance of each measurement to performance and to justify the conflicting results found by previous studies. Another objective of this study was to explore the patterns of ownership structure found in Bahraini market. EXAMINING THE RELATIONSHIP BETWEEN CEO REMUNERATION AND PERFORMANCE OF MAJOR COMMERCIAL BANKS IN SOUTH AFRICA 115 Mahlomola Khumalo, Andries Masenge The relationship between CEO remuneration and firm performance continues to receive much attention. Although the focus of most of the studies is across sectors, attention is increasingly being directed towards the banking industry. At the same time, controversy around what is deemed excessive remuneration of CEOs in the light of not so impressive firm performance across sectors continues. The 2008 global financial crisis and subsequent problems in the banking industry have increased interest in the dynamics of CEO remuneration and bank performance. This study, which examines the relationship between CEO remuneration and bank performance in South Africa, aims to bring a new perspective to the on-going research and debate. THE EFFECTS OF BUSINESS GROUP CONTROL ADVANTAGES AND AFFILIATE LEVEL ADVANTAGES ON AFFILIATE PERFORMANCE 125 Roderick Bugador This study views the network of control in a corporate business group as its source of competitive advantages. These control advantages are distributed among the business group affiliates and eventually influence their performance. This paper examines this by providing a reconceptualization of both the nature of business group and affiliate level advantages using the data of the top 20 Philippine corporate groups. The study found out that the group level control advantage affects the affiliate performance more than their individual level advantages. This result confirms the capability of business groups to influence and control their group internal market. This also implies that the business group affiliates have not yet developed significant capabilities which are independent to that of their business group. SUBSCRIPTION DETAILS 136

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

8

ACADEMIC INVESTIGATIONS

& CONCEPTS

SECTION 1

AN EMPIRICAL ANALYSIS OF CORPORATE GOVERNANCE IMPACT ON OUTREACH OF MICROFINANCE

INSTITUTIONS (MFIS)

Sujani Thrikawala*, Stuart Locke**, Krishna Reddy**

Abstract This study examines the impact of corporate governance practices of microfinance institutions (MFIs) on outreach to the poor people in Sri Lanka by using three outreach variables: Breadth of outreach, percentage of women borrowers and depth of outreach. Data for 54 MFIs are analysed using regression analysis of unbalanced panel data from 2007 to 2012. The findings of this study revealed several significant relationships: Breadth of outreach in Sri Lankan MFIs improve when they have a female chair on the board but decreases when they have more female directors and client representation on the board, and female borrowers get more loans when the firm has women representation and international/donor directors on the board, but less loans if they have a female chair. This study provides a direction for future researchers to explore more, and recommend good corporate governance practices for MFIs to reach more poor clients. Keywords: Microfinance Institutions (MFIs), Corporate Governance, Outreach, Sri Lanka, Panel Data *Corresponding author. Department of Finance, Waikato management School, University of Waikato, Private Bag 3105, Hamilton 3240, New Zealand Tel: +647 838 8182 **Department of Finance, Waikato Management School, University of Waikato

1 Introduction

Microfinance institutions (MFIs) emerge as an

important provider of microcredit to under-served

people and an instrument to combat extreme poverty

in developing nations (Hermes & Lensink 2007).

Widespread public enthusiasm for microcredit has

generated a dramatic increase in the number of MFIs

operating in developing countries. It is estimated that

in 2007 there was a total of around 10,000 MFIs in the

world (Ming-Yee 2007), serving over 113 million

clients. Due to the high profits and public perception

of social responsible investment, this sector has grown

commercially and now concerns itself only with

profitability. Unlike other firms, MFI performance

encompasses both financial profitability and outreach.

However, many MFIs are now drifting from their

original mission of alleviating poverty. Accordingly,

among policy makers there is a hefty debate on the

compatibility or trade-off between financial

sustainability and outreach of microfinance sector

(Hermes et al. 2011). Muhammad Yunus, the

foremost pioneer of the microfinance movement, also

expressed the opinion that MFIs must protect the poor

from loan sharks and not give rise to their own breed

of loan sharks. As a result, extant studies have

identified that good corporate governance practices

can improve the MFIs’ outreach to poor people

because sound corporate governance practices can

help MFIs to operate effectively and efficiently.

However, currently available measurements of MFIs

indicate an overriding concern with the profitability of

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

9

MFI activities and less with outreach. Therefore, it is

important to identify which corporate governance

practices are helping MFIs to reach more clients.

The motivation to examine the impact of

corporate governance on outreach of MFIs in Sri

Lanka is based on the following: First Sri Lanka has

been recovering after 30 years of war and terrorism

and enjoying peace and harmony for about four years

since the war. It is imperative to boost the economic

development of such a suffered country. As a result,

enhancement of microfinance activities became one of

the major economic development goals in Sri Lanka

(Central Bank of Sri Lanka 2012). However, there is

lack of formal governance guidelines for Sri Lankan

MFIs to improve their service in a broader context

(Modoran & Grashof 2009), particularly code of best

practice on corporate governance is not mandatory for

MFIs in Sri Lanka. Therefore, the findings of this

study will contribute to the existing literature relating

to corporate governance practices in MFIs in the Sri

Lankan context and boost the economic development

of a recovering country. From a policy perspective,

Kumar and Zattoni (2013, p. 199) stated that “firm-

level corporate governance performance affects the

development of national governance institutions”.

The remainder of this paper is structured as

follows: Section 2 provides a brief review of the

literature relating to corporate governance. Data

collection and research methods used are described in

section 3. Section 4 discusses the empirical research

results. Finally, the paper concludes with implications

of the study.

2 Literature review

Only a handful of studies have been done to test the

impact of corporate governance on outreach of MFIs.

The empirical analysis of good corporate governance

practices in relation to MFIs is still at an immature

stage and it is important to conduct more studies in

this field to enhance MFIs’ development (Hartarska

2005; Cull et al. 2007; Hartarska & Nadolnyak 2007;

Bassem 2009; Hartarska 2009; Mersland 2009;

Mersland & Strøm 2009). However, there is plenty of

empirical evidence in the financial literature that

supports the view that good corporate governance

enhances the performance of a firm. The same

rationale recommends that good governance practices

of MFIs would enhance their performance and reduce

risk. Therefore, it is important to examine the

empirical evidence of corporate governance

mechanisms in for-profit firms that improve firm

performance.

Previous studies undertaken by different scholars

have recognised certain aspects, such as board

composition and characteristics, and their impact on

firm performance (Lorsch & MacIver 1989; Daily &

Dalton 1997; Muth & Donaldson 1998; Bhagat &

Black 1999; Kula 2005; Roberts et al. 2005). They

revealed many factors to measure the corporate

governance practices of a firm, such as board size,

proportion of non-executive directors, stakeholder

representation on board, gender diversity,

CEO/chairman duality, education qualifications of

board members and number of board meetings

(Lorsch & MacIver 1989; Daily & Dalton 1997;

Bhagat & Black 1999; Roberts et al. 2005; Huse &

Solberg 2006; Kyereboah-Coleman & Biekpe 2006;

Solomon 2007).

However, the researchers that have tested the

relationship between corporate governance practices

and firm performance in the for-profit companies have

reported inconclusive evidence (Bhagat & Black

1999; Weir et al. 2002; Bathula 2008). Some have

reported evidence of a positive relationship between

corporate governance and firm performance (Gompers

et al. 2003; Kyereboah-Coleman & Biekpe 2006),

while others have reported evidence of a negative

relationship between governance and performance

(Hambrick et al. 1996; Sheridan & Milgate 2005;

Rose 2007). In addition, some studies found no

evidence to support the link between corporate

governance and firm performance (Baliga et al. 1996;

Dalton et al. 1998; Abdullah 2004), whereas Dalton

et al. (1998) and Weir et al. (2002) reported that there

is little evidence to support the view that board

characteristics have an impact on firm performance.

The appropriate corporate governance practices

have been a matter of continuing debate and

researches give mixed results. Inconsistent findings of

prior studies and lack of empirical results for the

microfinance industry have led to unclear ideas about

corporate governance influence on firm performance.

However, based on the indication given by many

empirical studies in developed and developing

countries around the world, it is important to further

explore the impact of corporate governance on

outreach of MFIs, as it leads to better service to the

poor people in these countries. Therefore, this study

argues that MFI boards need to have a high standard

of governance practices to deliver better outreach to

the poor.

3 Research methodology

Sample and sample period were constrained by the

data availability, accessibility and validity. Therefore,

our panel was comprised of 300 firm-year

observations over the period of 2007 to 2012. This

study collected data from the MFIs that are registered

with MIX market and Lanka Microfinance

Practitioners' Association (LMFPA), the Sri Lankan

microfinance network. Recent studies (Bassem 2009;

Cull et al. 2011; Lin & Ahlin 2011; Shahzad et al.

2012) have used MIX market database for their

empirical studies as MIX collects its data mainly

through the contracted consultants and the country

level networks that are based in each country

(Lafourcade et al. 2006). The director information has

been collected from the individual institutions by

going through their websites and by individually

contacting them.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

10

Table 1. Dependent and independent variable definitions

Variables Acronym Definition

Dependent Variable

Breadth of outreach Breadth The natural logarithm of the number of active borrowers

in the MFI

Percentage of female borrowers FemBorr The ratio of female borrowers to total number of active

borrowers

Depth of outreach Depth

The natural logarithm of average loan balance per

borrower/adjusted gross national income (GNI) per

capita

Independent Variables

Percentage of female directors FemDir The ratio of female directors to total number of

directors on the board

Female CEO FemCEO Dummy variable that takes a value of 1 if the CEO of

the firm in a female

Female chairperson FemChair Dummy variable that takes a value of 1 if the

chairperson of the firm in a female

Duality Duality Dummy variable that takes a value of 1 if the firm’s

CEO and chairperson are same

Board of directors who represent

international/donors agencies of the

firm

IntdorDir

Dummy explanatory variable that takes a value of 1 if

the firm has at least one international/donor agency

representative on board.

Board of directors who represent

clients of the firm Clientdir

Dummy variable that takes a value of 1 if the firm has at

least one director representing clients of the firm.

Independent directors on board IndDir Dummy variable that takes a value of 1 if the firm has at

least one independent director on board.

Board size Bsize The natural logarithm of the total number of directors

on the board

Internal auditor IntAudit Dummy variable that takes a value of 1 if the firm has

an internal auditor reporting to the board

Control Variables

Regulated by banking authority Regbank Dummy variable that takes a value of 1 if the firm

regulated by banking authority in the country

Firm Age Fage The natural logarithm of the number of years from the

date of establishment

Firm size Fsize The natural logarithm of the firm’s total assets

Leverage Lev The ratio of the firm's total debt to its total assets

Year dummy variables year Six year dummies for each of the years from 2007 to

2012

Organisation type dummy variables otype

Dummy variables for each of the organisation type:

NGO, Company, NBFI, Specialised Licenced Bank,

Cooperatives and Credit Unions

Table 1 depicts the definitions of dependent and

independent variables in the study. Breadth of

outreach is measured by the number of clients that

MFIs has provided loans to, or the number of

borrowers over a specific period of time who currently

have an outstanding loan balance with the MFI

(Microfinance Consensus Guidelines 2003; Quayes

2012). Since the inception of the Grameen bank

concept, outreach to women has been a priority

because compared with men, women face greater

problems in accessing loans. According to Quayes

(2012), outreach to female borrowers (FemBorr) is

measured by the number of women borrowers as a

fraction of the total number of borrowers. With the

development of the microfinance sector, Depth of

outreach has become an important measure that

concerns with the overall social outreach of the

microfinance sector. It measures the access of credit

disbursement to poor people; that is, poorer borrowers

will lead to greater depth of outreach (Quayes 2012).

In other words, it indicates how well MFIs have

reached the very poor clients, and focuses on poverty

lending. It can be measured by comparing the loan

size to the Gross National Income (GNI) per capita of

a country.

Percentage of female directors on the board,

female CEO, female chairperson, duality,

international/ donor representation on boards, client

representation on boards, outside/independent

directors on board, board size and internal auditor are

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

11

employed as the proxies for corporate governance

variables. Regulated by central bank of Sri Lanka,

firm age, firm size, leverage, year dummy variables

and organisation type dummy variables are treated as

control variables in line with previous studies

(Hartarska 2005; Kyereboah-Coleman 2006;

Hartarska & Nadolnyak 2007; Kyereboah-Coleman &

Osei 2008; Reddy et al. 2008; Bassem 2009;

Hartarska 2009; Hartarska & Mersland 2009;

Mersland & Strøm 2009; Mersland et al. 2011;

Galema et al. 2012; Hewa-Wellalage et al. 2012;

Strøm et al. 2014).

This study employed different statistical methods

to analyse panel data. Under univariate analysis,

descriptive statistics including mean, standard

deviation, minimum and maximum values were

computed to identify the overall behaviour of the data.

In particular, the data was normally distributed so that

parametric form of statistical modeling could be

employed. Pearson’s correlation matrix and variance

inflation factor (VIF) were used to determine whether

there were multicollinearity issues in our dataset. The

strength of correlation between dependent variables

and explanatory variables suggests that independent

variables should be included in our regression. Our

results show that the correlation coefficients among

the regressors are below the threshold of 0.80

suggested by Gujarati and Porter (2009). Even though

the multicollinearity is not a serious problem, VIF was

used to do a further test for multicollinearity.

According to Myers (1990), VIF value of 10 or above

is a good indicator that multicollinearity is present

among independent variables and therefore, is a cause

for concern. The results of this study indicate that all

the independent variables had VIF values of less than

3. Therefore, the above evidence leads us to conclude

that there is no multicollinearity issue in our

estimations, as all the values are well below the

thresholds.

Under inferential statistics, we have used a

multiple linear regression model to estimate the

unknown parameters of corporate governance and

outreach of MFIs in Sri Lanka. The two methods,

fixed-effect and random-effect, were used to diagnose

the unobserved factors in the panel regression model.

The main difference between these two methods lies

with the treatment of the dummy variables. Both

fixed-effect and random-effect have their own strength

and weakness. According to Greene (2012), in both

models the explanatory variables tend to be

uncorrelated to the observed firm heterogeneity term

ui and suggest using the Hausman test to choose

between fixed-effect and random-effect model

(Hausman 1978). The test examines whether the

individual effects are uncorrelated with other

regressors in the model. The null hypothesis of the

Hausman test assumes that individual effects are

random, therefore estimators for both models should

be consistent (Cameron & Trivedi 2010, p. 266). The

Hausman test result suggests that it is important to

employ a fixed effect model for Depth variable, due to

the rejection of the null hypotheses where p-values are

significantly lower than the 0.05 level but employed a

random effect model for Breadth and FemBorr

variables due to the acceptance of the null hypotheses.

4 Discussion of empirical findings

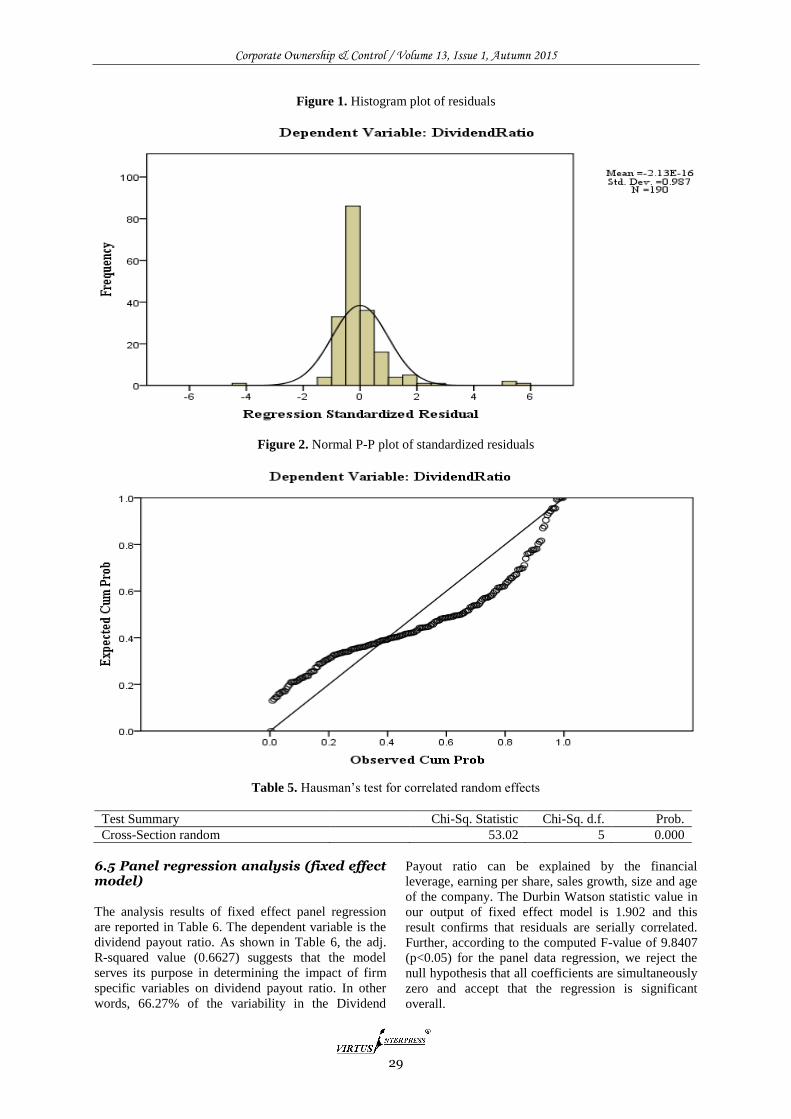

Table 2 provides descriptive statistics for major

variables in the study. Due to the huge dispersion in

the number of active clients in the sample, this study

used natural logarithm transformation to condense the

dispersion, as a result the mean and the median values

are 8.16, 7.70 respectively. In Sri Lanka, the average

number of female borrowers represents 81% of the

total number of credit clients. The median value of

88% indicates that fifty percent of the MFIs have less

than 12% of male clients. Average depth of outreach

in Sri Lankan MFIs is Rs.0.14 where the median is

Rs.0.10. This is a relatively weak value when

compared with other studies, and these lower values

indicate that the poor borrowers are very well served

in Sri Lanka, because a higher value would mean that

fewer poor clients are being served (Hartarska 2005;

Bassem 2009). The percentage of women directors on

the board is approximately 43%, which is higher than

the value obtained by Hewa-Wellalage et al. (2012)

for listed companies in Sri Lanka (7.4%). MFIs with

female CEOs are 34% in Sri Lanka, while on the other

hand, 66% of the MFIs have male counterparts as their

CEOs. Findings of this study show that in Sri Lanka,

40% of MFIs have female chairpersons which is a

fairly high figure when compared with a global study.

Out of the total MFIs in the sample, 26% of them have

a CEO who is doubling the role as chairperson of the

board, and this value is relatively high when compared

with the global sample (12%-15%) but low with

Ghana (50%). Sri Lankan MFI boards have around

7.4% of directors who represent international/donor

directors which is a very insignificant representation

when compared with literature (Mersland & Strøm

2009; Galema et al. 2012). As found by Hartarska

(2005) and Mersland and Strøm (2009), Sri Lankan

MFIs also have very small numbers of directors (7%)

on their boards who represent the clients. Around 67%

of the board members in Sri Lankan MFIs are

independent directors. The number of board members

in Sri Lankan MFIs is around 9. On average, 31% of

MFIs have an internal auditor reporting to the board.

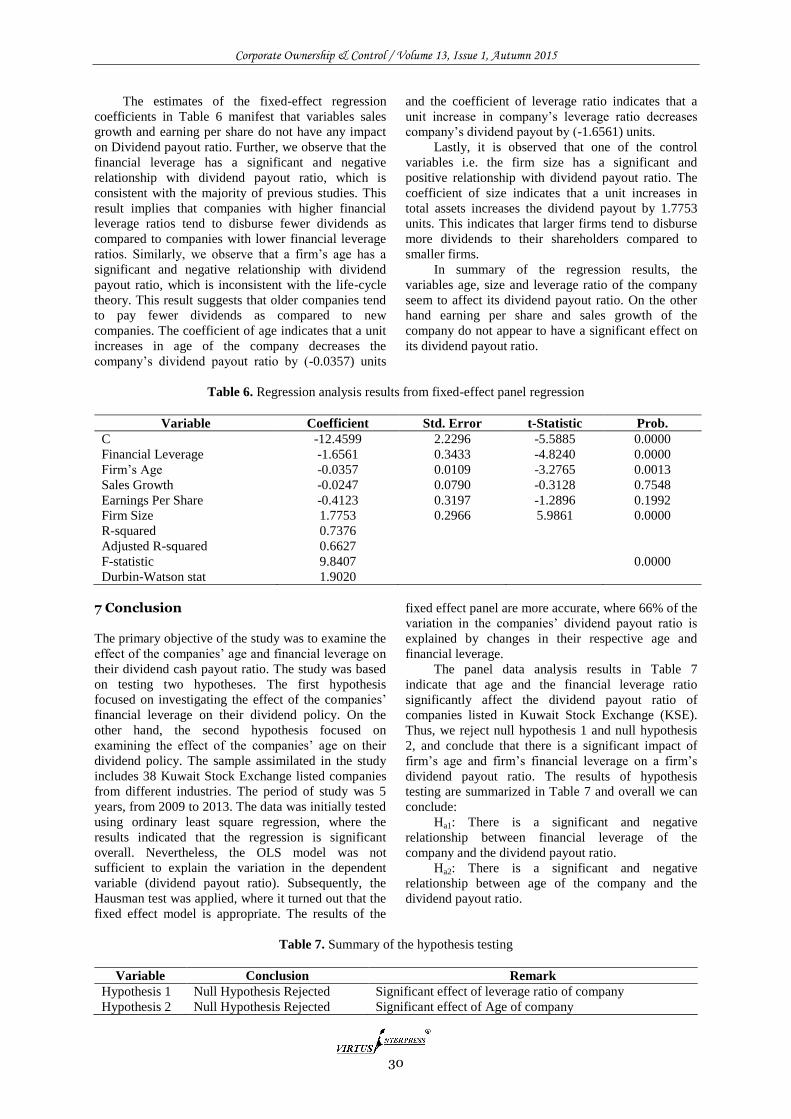

Table 3 illustrates the empirical results of

multivariate analysis of outreach variables in this

study. The study comments on the regression result as

a whole by controlling the unobserved heterogeneity

in the panel model. Even though most of the expected

signs of the coefficients are generated from the

regression, only very few of them are significant for

Sri Lankan MFIs. However, interesting results appear

in both of these significant and non-significant

regression results.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

12

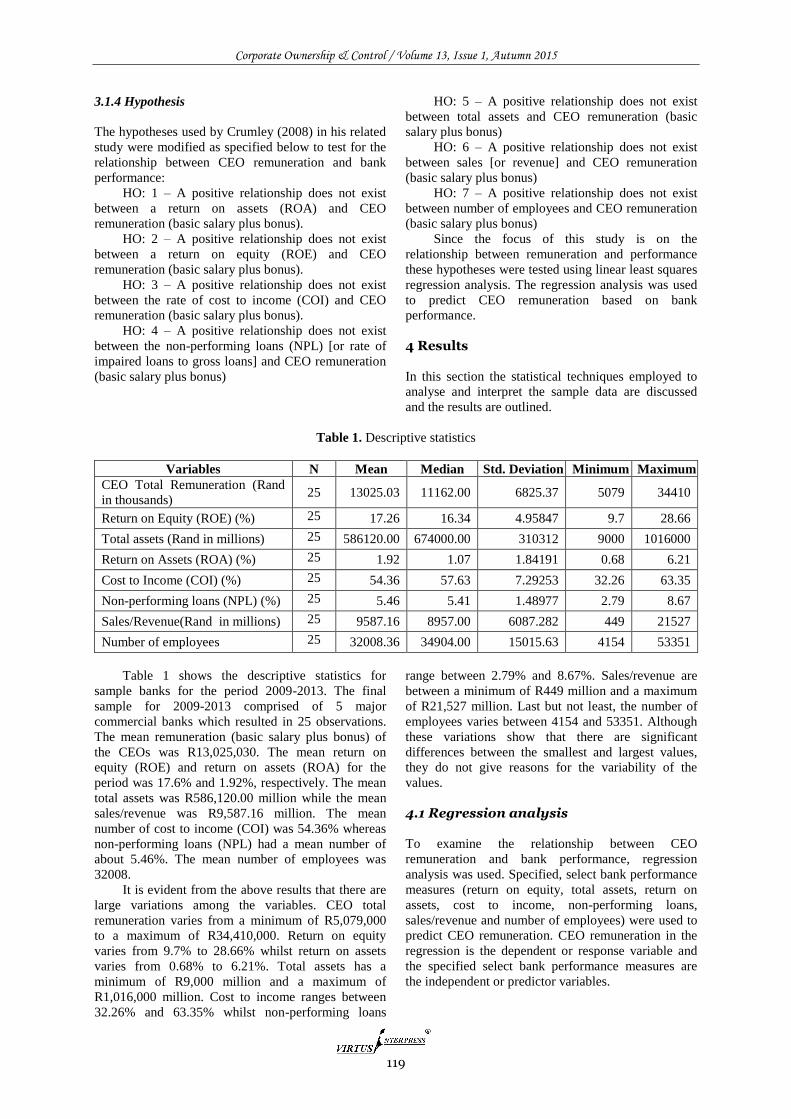

Table 2. Descriptive statistics

Variables Mean Median Std. Dev. Min Max

Outreach Variables

Breadth of outreach [LN(Active Borrower)] 8.16 7.70 2.03 3.22 13.7

Female borrowers on active borrowers (%) 0.81 0.88 0.19 0.30 1

Depth of outreach (Average loan balance per

borrower/GNI per capita) 0.14 0.10 0.13 0 0.89

Explanatory Variables

Female directors on board (%) 0.43 0.33 0.33 0 1

Female CEO 0.34 0 0.47 0 1

Female chairman 0.4 0 0.49 0 1

Duality 0.26 0 0.44 0 1

International/donor directors on board (%) 0.074 0 0.21 0 1

Directors representing clients (%) 0.071 0 0.16 0 0.8

Independent directors on board (%) 0.67 0.71 0.22 0 1

Board size (No. of board members) 8.47 8 4.44 1 30

Internal auditor reporting to board 0.31 0 0.46 0 1

Control Variables

Regulated by banking authority 0.13 0 0.34 0 1

Firm age 12.8 12 8.05 1 41

Firm size [LN(Total assets)] 18.1 17.7 2.41 12.7 25

Leverage 0.69 0.77 0.25 0 1.1

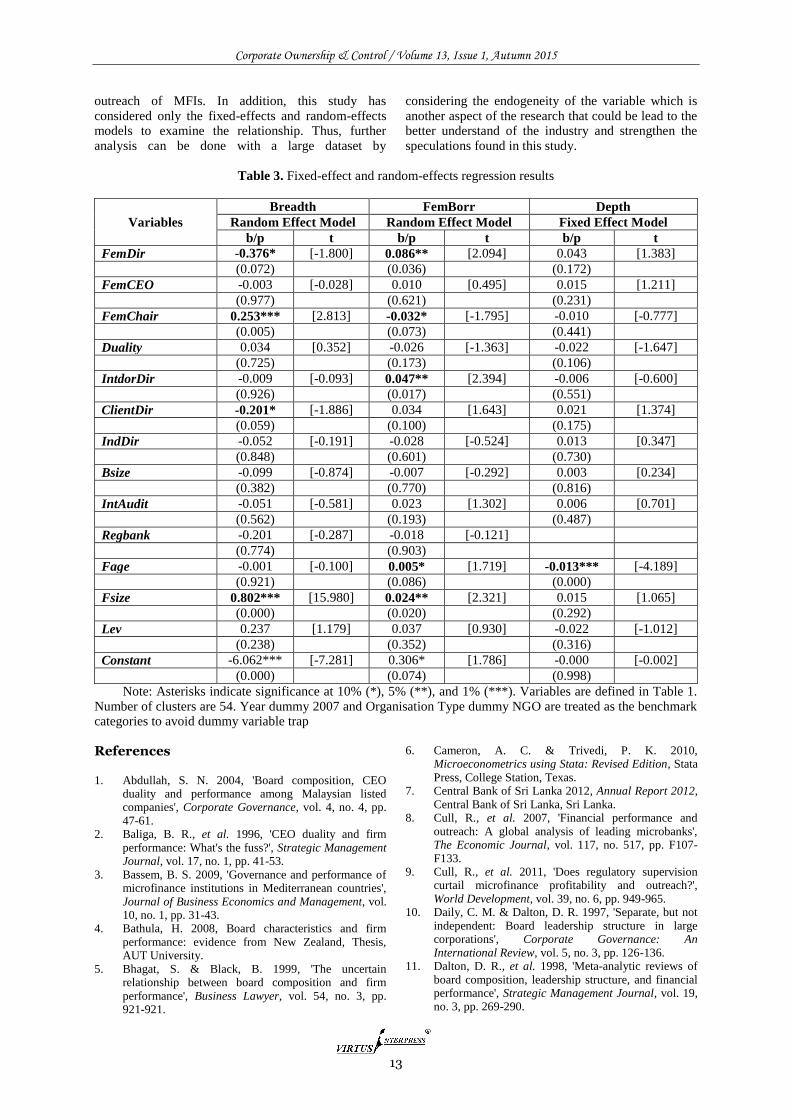

Female directors on the board are significantly

negatively correlated only with breadth of outreach and positively correlated with percentage of female borrowers in total active borrows in Sri Lankan MFIs. The findings of this study indicate that the number of female directors on boards is highly concentrated on gender inequality in the country, and they promote microfinance loans to more female clients. This result is vice versa for female chairperson on board. The female chairperson on board is significantly positively correlated to breadth of outreach but negatively correlated with female borrowers from MFIs in Sri Lanka. Even though they are female leaders they highly concentrate on increasing the number of active borrowers overall, rather than increasing the number of women borrowers only.

The international/donor directors have a significant positive correlation with female borrowers which shows that directors who represent international/donor agencies are highly concerned about providing microcredit to women in Sri Lanka. However, our results show that directors who represent clients are statistically significantly negatively associated with the number of active clients (breadth) in MFIs in Sri Lanka. Interestingly, depth of outreach does not have any significant relationship with corporate governance variables in this study. 5 Conclusion Based on the indication given by many empirical studies in developed and developing countries around the world, it is important to further explore the impact of corporate governance on outreach of MFIs as it enhances the financial services to the poor people in these countries. Inconsistent findings of prior studies

and lack of empirical results for the microfinance industry have led to unclear ideas about corporate governance influence on outreach. Therefore, this study expands the understanding of the corporate governance practices in MFIs and its impact on outreach for poor in Sri Lanka. This study has employed Sri Lankan data, to investigate the relationship between established internal corporate governance practices as independent variables and outreach as dependent variable for MFIs for the period 2007 to 2012.

Our results are robust with respect to controls for legal status, firm age, firm size, leverage and organisation type. However, our findings are mixed depending on the depended variables that we have examined. In spite of the mixed results, a number of interesting results have emerged from the study. The results of this study are appropriate for both individual MFIs and policy makers in the country, as they indicate that firms can perform better when they comply with good corporate governance practices, and invisible hands in the industry can direct MFIs to improve their corporate governance. The microfinance sector needs to be more effective if it wants to become the miracle cure for poverty and economic development. Now the sector is attempting to reinvent itself. This study points to the need for further empirical research into MFIs using more outreach measures to strengthen the speculations found in this study.

This study has a number of limitations that may pave the way for the further research. Since our focused was on only one country, further research could be undertaken by using more corporate governance variables and/or more countries to check the relationship between corporate governance and

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

13

outreach of MFIs. In addition, this study has considered only the fixed-effects and random-effects models to examine the relationship. Thus, further analysis can be done with a large dataset by

considering the endogeneity of the variable which is another aspect of the research that could be lead to the better understand of the industry and strengthen the speculations found in this study.

Table 3. Fixed-effect and random-effects regression results

Variables

Breadth FemBorr Depth

Random Effect Model Random Effect Model Fixed Effect Model

b/p t b/p t b/p t

FemDir -0.376* [-1.800] 0.086** [2.094] 0.043 [1.383]

(0.072) (0.036) (0.172)

FemCEO -0.003 [-0.028] 0.010 [0.495] 0.015 [1.211]

(0.977) (0.621) (0.231)

FemChair 0.253*** [2.813] -0.032* [-1.795] -0.010 [-0.777]

(0.005) (0.073) (0.441)

Duality 0.034 [0.352] -0.026 [-1.363] -0.022 [-1.647]

(0.725) (0.173) (0.106)

IntdorDir -0.009 [-0.093] 0.047** [2.394] -0.006 [-0.600]

(0.926) (0.017) (0.551)

ClientDir -0.201* [-1.886] 0.034 [1.643] 0.021 [1.374]

(0.059) (0.100) (0.175)

IndDir -0.052 [-0.191] -0.028 [-0.524] 0.013 [0.347]

(0.848) (0.601) (0.730)

Bsize -0.099 [-0.874] -0.007 [-0.292] 0.003 [0.234]

(0.382) (0.770) (0.816)

IntAudit -0.051 [-0.581] 0.023 [1.302] 0.006 [0.701]

(0.562) (0.193) (0.487)

Regbank -0.201 [-0.287] -0.018 [-0.121]

(0.774) (0.903)

Fage -0.001 [-0.100] 0.005* [1.719] -0.013*** [-4.189]

(0.921) (0.086) (0.000)

Fsize 0.802*** [15.980] 0.024** [2.321] 0.015 [1.065]

(0.000) (0.020) (0.292)

Lev 0.237 [1.179] 0.037 [0.930] -0.022 [-1.012]

(0.238) (0.352) (0.316)

Constant -6.062*** [-7.281] 0.306* [1.786] -0.000 [-0.002]

(0.000) (0.074) (0.998)

Note: Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). Variables are defined in Table 1. Number of clusters are 54. Year dummy 2007 and Organisation Type dummy NGO are treated as the benchmark categories to avoid dummy variable trap

References 1. Abdullah, S. N. 2004, 'Board composition, CEO

duality and performance among Malaysian listed companies', Corporate Governance, vol. 4, no. 4, pp. 47-61.

2. Baliga, B. R., et al. 1996, 'CEO duality and firm performance: What's the fuss?', Strategic Management Journal, vol. 17, no. 1, pp. 41-53.

3. Bassem, B. S. 2009, 'Governance and performance of microfinance institutions in Mediterranean countries', Journal of Business Economics and Management, vol. 10, no. 1, pp. 31-43.

4. Bathula, H. 2008, Board characteristics and firm performance: evidence from New Zealand, Thesis, AUT University.

5. Bhagat, S. & Black, B. 1999, 'The uncertain relationship between board composition and firm performance', Business Lawyer, vol. 54, no. 3, pp. 921-921.

6. Cameron, A. C. & Trivedi, P. K. 2010, Microeconometrics using Stata: Revised Edition, Stata

Press, College Station, Texas. 7. Central Bank of Sri Lanka 2012, Annual Report 2012,

Central Bank of Sri Lanka, Sri Lanka. 8. Cull, R., et al. 2007, 'Financial performance and

outreach: A global analysis of leading microbanks', The Economic Journal, vol. 117, no. 517, pp. F107-F133.

9. Cull, R., et al. 2011, 'Does regulatory supervision curtail microfinance profitability and outreach?', World Development, vol. 39, no. 6, pp. 949-965.

10. Daily, C. M. & Dalton, D. R. 1997, 'Separate, but not independent: Board leadership structure in large corporations', Corporate Governance: An International Review, vol. 5, no. 3, pp. 126-136.

11. Dalton, D. R., et al. 1998, 'Meta-analytic reviews of board composition, leadership structure, and financial performance', Strategic Management Journal, vol. 19, no. 3, pp. 269-290.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

14

12. Galema, R., et al. 2012, 'Do powerful CEOs determine microfinance performance?', Journal of Management Studies, vol. 49, no. 4, pp. 718-742.

13. Gompers, P., et al. 2003, 'Corporate governance and equity prices', The Quarterly Journal of Economics, vol. 118, no. 1, pp. 107-156.

14. Greene, W. H. 2012, Econometric Analysis, Pearson Prentice Hall, Upper Saddle River, NJ.

15. Gujarati, D. N. & Porter, D. C. 2009, Basic econometrics, McGraw-Hill, Boston.

16. Hambrick, D. C., et al. 1996, 'The influence of top management team heterogeneity on firms' competitive moves', Administrative Science Quarterly, vol. 41, no. 4, pp. 659-684.

17. Hartarska, V. 2005, 'Governance and performance of microfinance institutions in Central and Eastern Europe and the newly independent states', World Development, vol. 33, no. 10, pp. 1627-1643.

18. Hartarska, V. 2009, 'The impact of outside control in microfinance', Managerial Finance, vol. 35, no. 12, pp. 975-989.

19. Hartarska, V. & Mersland, R. 2009, 'Which governance mechanisms promote efficiency in reaching poor clients? Evidence from rated microfinance institutions', European Financial Management, vol. 18, no. 2, pp. 218-239.

20. Hartarska, V. & Nadolnyak, D. 2007, 'Do regulated microfinance institutions achieve better sustainability and outreach? Cross-country evidence', Applied Economics, vol. 39, no. 10, pp. 1207-1222.

21. Hausman, J. A. 1978, 'Specification tests in econometrics', Econometrica, vol. 46, no. 6, pp. 1251-1271.

22. Hermes, N. & Lensink, R. 2007, 'The empirics of microfinance: What do we know?', The Economic Journal, vol. 117, no. 517, pp. F1-F10.

23. Hermes, N., et al. 2011, 'Outreach and efficiency of microfinance institutions', World Development, vol. 39, no. 6, pp. 938-948.

24. Hewa-Wellalage, N., et al. 2012, 'Does one size fit all? An empirical investigation of board structure on family firms' financial performance', Afro-Asian Journal of Finance and Accounting, vol. 3, no. 2, pp. 182-194.

25. Huse, M. & Solberg, A. G. 2006, 'Gender-related boardroom dynamics: How Scandinavian women make and can make contributions on corporate boards', Women in Management Review, vol. 21, no. 2, pp. 113-130.

26. Kula, V. 2005, 'The impact of the roles, structure and process of boards on firm performance: Evidence from turkey', Corporate Governance: An International Review, vol. 13, no. 2, pp. 265-276.

27. Kumar, P. & Zattoni, A. 2013, 'Editorial: How much do country-level or firm-level variables matter in corporate governance studies?', Corporate Governance: An International Review, vol. 21 no. 3, pp. 199–200.

28. Kyereboah-Coleman, A. 2006, 'Corporate board diversity and performance of microfinance institutions: The effect of gender', Journal for Studies in Economics and Econometrics, vol. 30, no. 3, pp. 19-33.

29. Kyereboah-Coleman, A. & Biekpe, N. 2006, 'The relationship between board size board composition, CEO duality, and firm performance: experience from Ghana', Corporate Ownership and Control, vol. 4, no. 2, pp. 114-122.

30. Kyereboah-Coleman, A. & Osei, K. A. 2008, 'Outreach and profitability of microfinance institutions: the role of governance', Journal of Economic Studies, vol. 35, no. 3/4, pp. 236-248.

31. Lafourcade, A. L., et al. 2006, Overview of the outreach and financial performance of microfinance institutions in Africa, Feature Articles, Microbanking Bulletin, Washington, DC.

32. Lin, J. & Ahlin, C. 2011, 'Where does microfinance flourish?: Microfinance institution performance in macroeconomic context', Journal of Development Economics, vol. 95, no. 2, pp. 105-120.

33. Lorsch, J. W. & MacIver, E. 1989, Pawns or Potentates: The Reality of America's Corporate Boards, Harvard Business School Press, Boston, Mass.

34. Mersland, R. 2009, Corporate governance and ownership in microfinance organizations, Thesis, University of Agder.

35. Mersland, R., et al. 2011, 'The impact of international influence on microbanks’ performance: A global survey', International Business Review, vol. 20, no. 2, pp. 163-176.

36. Mersland, R. & Strøm, R. Ø. 2009, 'Performance and governance in microfinance institutions', Journal of Banking and Finance, vol. 33, no. pp. 662-669.

37. Microfinance Consensus Guidelines 2003, Definitions of Selected Financial Terms, Ratios, and Adjustments for Microfinance, CGAP, The World Bank Group, Washington, DC.

38. Ming-Yee, H. 2007, The International Funding of Microfinance Institutions: An Overview, LuxFLAG,

39. Modoran, C. & Grashof, L. 2009, Microfinance Institutions in Sri Lanka, Ministry of Finance & Planning with GTZ-ProMiS, Colombo, Sri Lanka.

40. Muth, M. & Donaldson, L. 1998, 'Stewardship theory and board structure: a contingency approach', Corporate Governance: An International Review, vol. 6, no. 1, pp. 5-28.

41. Myers, R. H. 1990, Classical and Modern Regression with Applications, PWS-Kent, Boston.

42. Quayes, S. 2012, 'Depth of outreach and financial sustainability of microfinance institutions', Applied Economics, vol. 44, no. 26, pp. 3421-3433.

43. Reddy, K., et al. 2008, 'Corporate governance practices of small cap companies and their financial performance: An empirical study in New Zealand', International Journal of Business, Governance and Ethics, vol. 4, no. 1, pp. 51-78.

44. Roberts, J., et al. 2005, 'Beyond agency conceptions of the work of the non-executive director: Creating accountability in the boardroom', British Journal of Management, vol. 16, no. s1, pp. S5-S26.

45. Rose, C. 2007, 'Does female board representation influence firm performance? The Danish evidence', Corporate Governance: An International Review, vol. 15, no. 2, pp. 404-413.

46. Sheridan, A. & Milgate, G. 2005, 'Accessing board positions: A comparison of female and male board members’ views', Corporate Governance: An International Review, vol. 13, no. 6, pp. 847-855.

47. Solomon, J. 2007, Corporate Governance and Accountability, John Wiley & Sons Ltd, England.

48. Weir, C., et al. 2002, 'Internal and external governance mechanisms: Their impact on the performance of large UK public companies', Journal of Business Finance & Accounting, vol. 29, no. 5-6, pp. 579-611.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

15

TESTING THE PARTIAL ADJUSTMENT MODEL OF OPTIMAL CASH HOLDING: EVIDENCE FROM AMMAN

STOCK EXCHANGE

Ziad Mohammad. Zurigat*, Nadia Jawdat**

Abstract This study aims at testing the partial adjustment model of cash holdings to investigate whether Jordanian industrial firms have a target cash holdings and how fast they move toward that target when any target deviation exists. A sample of 57 industrial firms listed in the Amman Stock Exchange (ASE) over the period 2001-2013 is used. The study uses the estimated fitted values from the conventional cash equation as a proxy for the target cash holding. Using pooled and panel data analysis, the study provides evidence suggesting that cash flows, net working capital, leverage and firm size significantly affect the cash holdings of Jordanian firms. Moreover, it reveals that Jordanian industrial firms have a target cash level and make a target reversion whenever needed. However, Jordanian industrial firms adjust their actual cash holdings to its target level too slowly. Keywords: Cash Holdings, Trade-off Theory, Pecking Order Theory, Agency Theory of Free Cash Flow, Partial Adjustment Model *Department of Banking and Finance, Yarmouk University **Department of Islamic economy, Yarmouk University

1 Introduction The perfection assumption of capital market suggests

that firms should not show any preferences of internal

over external financing. Both internal and external

financing are perfectly substitute for each other.

Consequently, there is no need for holding cash to

meet any shortage in external financing as long as

external funds can be raised at any time needed. On

the other hand, when frictions exist, capital markets

are no longer perfect. This may restrict the firm's

ability to generate funds externally. Hence, external

and internal financing are not perfect substitutes for

each other. Consequently the need for holding cash

increases in order to avoid under investment problem

that might arise because of the presence of agency and

bankruptcy costs of using external financing (Jensen

& Meckling 1976). Consistent with this argument,

Acharya et al. (2005) argue that, in the presence of

financing frictions, cash plays a separate role and

should therefore be managed and studied in its own

right. The main problem in developing countries in

general is the lack of sources of funds and the reliance

on internal financing to take the advantages of

investment opportunities. In Jordan, the capital market

has been described as imperfect, less developed and

all frictions are relevant and may affect the firm's

investment, financing and dividend policy decisions.

This, along with the fact that banks credit policy is

largely affected by the uncertainty condition in the

world and the region. Such conditions make Jordanian

firms show a preference of internal over external

financing and increase the need for holding cash.

The most relevant theoretical models that can

explain determinants of the cash holding level are the

trade-off theory, the pecking order theory and the

agency theory. According to the trade off theory, firms

trade off the costs and benefits of cash holdings to

maximize the value, implying that the presence of

cash holding costs may outweigh its benefits.1 This

suggests that there is some threshold level of cash

holdings under which the firm’s value is maximized.

This threshold of cash is generally called the optimal

(target) level of cash holdings. Hence, the observed

cash holding is not always the optimal level which

increases the necessity of target adjustment when

deviation from that target exists.

With respect of pecking order theory, issuing

new equity is very costly for firms because of

information asymmetries. Therefore, firms finance

their new investment opportunities primarily with

internal funds, then with debt and finally with equities

as the last resort. Extending the pecking order theory

of Myers & Majluf (1984) and Myers (1984) to

explain what determine cash holdings leads to the

conclusion that there is no optimal cash level but cash

is used as a buffer between retained earnings and

1 The benefits of holding cash are the reduction of transaction

cost for precautionary needs and the cash allowance for speculation, while, the costs are the opportunity cost and liquidity premium.

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

16

investment needs, implying that cash level would just

be the result of financing and investment decisions.

Few studies provide evidence supporting the

prediction of pecking order theory such as Kalcheva &

Lins (2003) who conclude that cash is positively

related to the growth opportunities of the company, its

size and cash flow. Whilst, negatively related to the

level of debt and capital expenditures.

The agency theory of Jensen & Meckling (1976)

provides another explanation as to why firms hold

cash. It states that managers hold cash and other liquid

assets in order to minimize the cost of external

finance. Dittmar et al. (2003) find evidence suggesting

that firms hold more cash in countries with greater

agency problems. Dittmar & Mahrt-Smith (2007) and

Pinkowitz et al. (2006) find that cash is worth less,

when agency problems between insiders and outside

shareholders are greater.

According to Alles et al. (2012), tradeoff model,

pecking order theory and agency theory of free cash

flow complement each other and work together to

explain the existence of target cash level. Although a

cash holding is considered as one of the most

important topics of corporate finance, there are few

studies that focus on the partial adjustment of

corporate cash holding. Most of the studies focused on

investigating the determinants of firms' cash level,

mainly of large public and private firms in developed

economies (i.e. Ozkan & Ozkan, 2004 and Alles et al.,

2012) with less attention is paid to this topic in less

developed countries including Jordan.

In Jordan, where the capital market is imperfect,

market frictions such as information asymmetry

agency and bankruptcy costs are applicable and

influence a firm's investment and financial decisions

and thereby its value. Moreover, it is a thin and a

small market, making the cost of raising external

funds in primary market relatively high which

increases the reliance on internally generated funds.

However, information asymmetries and agency costs

restrict the firms’ ability not only to raise funds

externally, but also to raise funds internally,

supporting the information content of dividend

payment ( see, Baskin, 1989). This makes cash

management decisions too important for Jordanian

listed companies in Amman Stock Exchange(ASE).

Therefore, this study tries to investigate whether

Jordanian industrial companies have target cash

holdings and how fast do they move towards that

target if any deviations exist by testing the partial

adjustment model of cash holding using a sample of

57 Jordanian Industrial firms listed in the ASE over

the period of (2001- 2013). For this purpose, the

current study uses fitted values estimated by using the

conventional cash equation as a proxy for target cash

holdings level.

This paper is organized as follows. Section 2

presents theoretical framework and a related literature

review. Section 3 discusses the research methodology.

Section 4 presents the estimation results with some

conclusions and recommendations.

2 Theoretical framework and literature review

The theoretical background of cash holdings refers to

Modigliani & Miller (1958) who stated that, under the

perfection assumption of capital market, holding large

amounts of cash is irrelevant because all companies

can borrow and lend at the same rate and can easily

finance their profitable investment projects at

negligible transaction costs. The absence of market

frictions such as transaction, bankruptcy, agency and

information costs makes firms show no preferences of

internal financing over external financing. Hence, the

firm's decision to hold cash is not related to, or

affected by other financial decisions.

However, when transaction costs, agency costs

and information asymmetries are considered, firms'

investment decisions become highly sensitive to the

cash holdings. This suggests that the firm's decision to

hold cash is largely affected by capital market

frictions. More precisely, it is largely affected by the

costs and benefits of cash holding when firms are

restricted to raise funds externally, implying that there

is an optimal cash level that balances costs and

benefits and thus maximizes the firm's value (Garcia-

Teruel & Martinez-Solano, 2008). Moreover,

empirical evidence shows that any deviations from the

optimal level reduce firm value. This implies that

firms can increase their market value merely by being

around the optimal level of cash, which seems

consistent according to the trade-off between benefits

and cost of cash holdings.

In the absence of adjustment cost and the costs of

liquidating assets, firms would always have and

maintain their target cash ratio by changing its

existing ratio to equal its target cash ratio. On the

other word, each firm’s observed cash ratio should be

its optimal ratio. However, the presence of adjustment

costs may restrict the firm’s ability to back

immediately to its target level. Thus, when the

observed level of cash deviates from its optimal level,

firms will gradually adjust that level to the optimal

level in a process referred to as the partial adjustment

process (Jalilvand & Harris, 1984; Taggart, 1977).

The partial adjustment mechanism allows for firms’

observed cash ratio not always to be equal to their

optimal level. Hence, the dynamic trade-off theories,

not the static trade-off theory, will be able to capture

the dynamic change in firms cash holdings. Dynamic

behavior exists because the presence of market

frictions may limit the firm's ability to manage their

cash level, causing them to deviate from optimal

levels and consequently increasing the need for target

reversion to maximize value (Kim et al., 2011).

Moreover, it may not be appropriate for firms to

immediately adjust their target deviations when the

cost of moving toward target level is higher than that

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

17

of being away from the target (Alles et al., 2012). This

suggests that firms will make target-reversion when

the benefit of moving toward the target level is higher

than the cost of being away from the target. In

addition, Bruinshoofd (2009) found that firms increase

their level of cash holdings from an insufficient level

to a target level more rapidly than they decrease their

level from an excessive level to a target level.

Therefore, firms are very concerned about the speed

by which they move toward their target cash levels

because of high adjustment costs. Few studies

recognize and incorporate the dynamic nature of cash

holdings.

Therefore another trend of research appears to

examine the existence of partial adjustment model of

cash holding. Whether adjustment frictions, such as

those that affect capital structure decisions, influence

cash holding decisions is an important research

question because of their consequences on the

shareholder wealth which associated with deviating

from optimal levels of liquid assets, especially for

financially constrained firms (Denis & Sibilkov,

2010).

Bruinshoofd and Kool (2004) collect data from

Dutch firms and investigate the existence of long-run

liquidity targets. Depending on the empirical

methodology, they document that the rates of annual

target convergence range from 20 percent to over 60

percent which supports the dynamic nature of the

cash-holding decision, which is characterized by a

trade-off between the costs of deviation from the

target and the costs of adjustment. Slow adjustment

process is attributed to adjustment cost and therefore a

firm’s actual cash level is not necessarily identical to

the desired cash holding level.

Ozkan and Ozkan (2004) estimate a partial

adjustment model of cash holdings for a sample of

U.K. firms and find that a dynamic model of cash

holding behavior is better suited than the static models

employed in the extant literature. They find that the

estimated target-adjustment coefficient has a positive

value of 0.54, implying that UK companies adjust

their target deviation too quickly and supporting the

view that firms always adjust towards a target cash

ratio. Drobetz and Grüninger (2006) analyze Swiss

firms’ speed of adjustment towards an endogenous

target cash ratio, using dynamic panel estimation.

They find that the speed of target adjustment of Swiss

firms is between 0.35 and 0.5, indicating that Swiss

firms adjust their liquidity holdings more slowly

towards an endogenous target cash ratio than firms in

other countries. They suspect that the most reasonable

explanations are based on the strong influence of

banks in Switzerland and/or the unfavorable economic

conditions during the sample period that entail low

costs of deviation from the target.

Guney et al.(2006) investigate corporate cash

holding behavior in Japan, France, Germany, and the

UK using data for 3,989 companies over the period

1983-2000. Their findings reveal that the dynamic

cash holding analysis indicates that firms tend to

adjust their cash levels towards a target cash structure.

The speed of adjustment of cash holdings for France,

Germany and Japan is found to be similar (adjustment

coefficient is approximately 0.5),while firms in the

UK seem to adjust to the target cash level more

quickly. This possibly, may suggest that when

adjustment costs are higher, resulting in lower speeds

of adjustment. According to their study, the lower

speed of adjustment for Japan and Germany can be

explained by the fact that German firms and Japanese

firms have close ties with their banks and depend on

them for external financing. It is feasible for them to

adjust slowly towards their target level without

incurring a high level of agency cost. Overall, the

results lend strong support to the dynamic nature of

the cash holding decision of firms. Firms tend to

trade-off between costs of speedy adjustment and

costs of delay in achieving the target cash structure.

Empirical studies also indicate that the speed of

adjustment towards target levels varied among

different samples with different firm characteristics

and at different cash positions. For example, using a

dynamic adjustment model to analyze the cash-

holding behavior of small and medium-sized firms

(SMEs) in Spain, Garcia-Teruel and Martinez-Solano

(2008) find that SMEs aim to achieve a target level of

cash holdings and that they adjust their actual level

towards the target level more rapidly than large firms

do in developed countries.

Another related study by Jiang and Lie (2010)

estimates that firms close about 36% of the gap

between actual and target cash ratios each year. They

further document that across all sample firms, the

adjustment speed is slower if the cash level is above

the target than if it is below. They interpret this as

evidence that self-interested managers are reluctant to

disburse excess cash, and will allow cash levels to

remain high unless they are subject to external

pressure and this is consistent with the argument of

Opler et al. (1999).

Using a sample of U.S. manufacturing firms,

Venkiteshwaran (2011) estimates a dynamic model

that allows firms to adjust their cash holding levels

over time and find evidence consistent with trade-off

type behavior in cash holding levels. He finds a very

strong mean reversion in cash holding levels to

optimal levels and that any deviations from optimal

cash levels are rapidly corrected, typically within two

years for the average firm in the sample. He also finds

that this adjustment rate is faster for small, financially

constrained firms than for larger firm consistent with

the expectation that constrained firms may find it

more costly to operate at sub-optimal levels of cash.

Further, he finds that firms with excess cash are

slower to return to optimal levels than firms that have

cash deficiencies. His findings are similar to those

reported in Ozkan and Ozkan (2004) for a sample of

U.K. firms, but inconsistent with the finding reported

by Dittmar and Duchin(2011) for U.S. firms who

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

18

report a slower adjustment rates for a broader sample

of firms; firms need three to six years to correct any

deviations from optimal levels. They also find that, on

average, cash deficient firms are slower to adjust to

optimal levels compared to firms with surpluses and

attribute this finding to asymmetric adjustment costs

associated with building versus spending cash

reserves.

3 Research methodology

The study uses pooled and panel data analysis which

is usually estimated by either fixed effect or random

effects technique.

As the current study aims at investigating the

target adjustment path of Jordanian firms, the

conventional cash equation is used to estimate the

target cash holding. This is because the target cash

holding itself is unobservable. Previous studies have

analyzed determinants of cash holdings assuming

implicitly the existence of optimal cash holding (Opler

et al., 1999; Kim et al., 1998).In addition, Opler et

al.(1999) estimate the optimal cash holding as a

moving average of past cash holding levels.

Consistent with the majority of previous studies

(e.g. Opler et al., 1999, Dittmar et al., 2003, Kalcheva

& Lins, 2003, Ferreira & Vilela, 2004 and Bates et al.,

2009) which have identified a set of firm specific

characteristics that influence the target level of cash

holdings of firms, the current study uses firm specific

characteristics as predictors for target cash holdings of

listed Jordanian firms.

It is worth noting that the selection of

explanatory variables in the current study is based on

alternative theories that might be responsible for the

corporate cash holdings and can be found in the

literature. However, the choice is sometimes limited,

due to lack of relevant data. Following Opler et al.,

(1999) and Bates et al., (2009) in the selection of

independent variables, the following variables are

selected; firm size, growth opportunity (the market to

book ratio), cash flow, net working capital, capital

expenditure, leverage ratio and profitability.

The current study employs the following static

model to investigate the determinants of optimal cash

holding of listed Jordanian industrial firms in the

Amman Stock Exchange. In this model, the observed

cash holding is modeled as a function of the various

firm-specific factors has been discussed above.

ititit

itititititit

CExpCflow

LevprofNWCFSizGrthCash

1716

15141312110 (1)

Where Cash: is the dependent variable and measured by the ratio of cash and cash equivalent to total assets (e.g.

Kim et al., 1998; Opler et al., 1999; Ozkan and Ozkan, 2004; Bruinshoofd and Kool, 2004).

Grth is the Growth opportunity and measured by market to book ratio.

FSiz is the Firm size, and measured by the natural logarithm of total assets.

NWC is Net working capital and measured by current assets minus current liabilities minus cash.

Prof is the firm's profitability and measured as the ratio of earnings before interest and tax (EBIT)

divided by total assets.

Lev is the leverage ratio and measured by the ratio of total liabilities to total assets.

Cflow is the cash flows. Operating cash flows are calculated by EBIT+ Depreciation- Taxes.

CExp is the firm's capital expenditure is measured as the yearly change in fixed assets added to

depreciation.

ε is the error term which represents all random variables that are not included in the model.

3.1 Target adjustment model of cash holding

To investigate whether Jordanian listed industrial

firms have targeted cash ratio and move gradually

toward their target ratio when any deviations exist, the

static-partial adjustment models are adopted. Prior

studies have used several methods to estimate the

adjustment speed for cash levels. This study will

follow the theoretical framework developed by Opler

et al. (1999), who argue that firms' optimal cash

holdings are determined by the tradeoff between the

marginal costs and benefits of holding liquid assets.

They emphasize the persistence of cash holdings and

the existence of implicit target cash levels. They test

the validity of the static trade-off theory, using a

partial adjustment model to provide evidence for the

presence of target level of cash holdings. The

underlying assumption of this model is that, firms

optimally balance the costs and benefits of cash

holdings to maintain their target level of cash reserves.

Moreover, firms may not be always in equilibrium at

their target level of cash holdings. A delay in target

adjustment exists because of its adjustment costs

(Nicolusc, 2005). The presence of adjustment costs

may restrict the firms’ ability to make target reversion

immediately, suggesting the occurrence of partial

adjustment toward the target level (Opler et al., 1999;

Kim et al., 1998).

Hence, the firms’ observed cash ratio will be at

their target level only if no adjustment costs exist.

The speed of target adjustment, when target reversion

exists, depends on the adjustment cost as well as on

the cost of being away from the target level (the

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

19

benefits of moving back towards the target level). In

reality firms may not completely close the gap

between their actual and target levels of cash holdings

because it may not be effective to do due to the

existence of market friction (Alles et al., 2012). More

precisely, firms may keep the gap between their

observed cash holding and target level if the cost of

being away from the target is lower than that of

moving toward the target and vice versa (Dittmar &

Duchin, 2011).

Following Ozkan & Ozkan (2004) and Garcia-

Teruel & Martinez-Solano (2008), the partial

adjustment model of cash holding can be formalized

as follows:

11

itititit CBCBCBCB (2)

Where, *

ititandCBCB denote the actual cash

holding and the target cash holdings for firm i at time

t. 1 itit CBCB is the difference between a firm's

actual or observed cash holdings between year t and

year t-1. The expression 1

*

itit CBCB is the

deviation of a firm’s cash holdings from its target

level of cash holdings indicating that the target

adjustment is required to reach the optimal level.

Finally, estimating dynamic panel data model of

cash holdings taking into account the dynamic nature

of cash level, will help to analyze the speed of

adjustment of Jordanian firms towards an endogenous

target cash ratio. Unlike the static model that

implicitly assumes that firms can instantaneously

adjust their cash holdings toward the target levels, the

dynamic model recognizes that an adjustment process

may take place and there are some lags for firms to

adjust their cash holdings to their target levels (Gao et

al., 2012). By extending the static model, the study

estimates the speed of adjustment towards an

endogenous target cash ratio in a dynamic panel

model.

For the purpose of target adjustment estimation,

model 2 will be re-formalized as follows:

ititit TRDCBCB 10 (3)

Where itCB is 1 itit CBCB , itTRDCB

is 1

*

itit CBCB and used to measure how far the

actual cash ratio deviates from the target cash ratio.

it is the error term and assumed to be independently

distributed with zero mean.

In this study, 1 is used to capture a firm’s

ability to adjust to its target cash holdings, 1 should

be statistically significant and between zero and one,

not zero nor one (0 < < 1) implying that the

movement toward the target is not a costless process.

At one extreme, when 1 = 1, the model implies that

firms can immediately adjust to their target levels.

Such immediate adjustment is possible only in

frictionless perfect capital markets that impose no

adjustment costs. At the other extreme, when 1 = 0,

the model implies that adjustment costs are so large

that firms cannot adjust their actual level of cash

reserves (Alles et al.,2012).

In general, this class of model is used to describe

the adjustment process toward target levels of

corporate cash holdings taking in to account that the

deviations from target cash ratio are not necessarily

offset quickly. This implies that value-maximizing

firms will gradually adjust their actual cash holding

toward their target level (Garcia-Teruel & Martinez-

Solano, 2008). The reason for this is that cash holding

decisions may be affected by the existence of market

imperfections such as information asymmetry, agency

conflicts or the existence of transaction costs incurred

by accessing the capital markets (Garcia-Teruel &

Martinez-Solano, 2008).

It worth's noting that the conventional cash

equation will be used to estimate the target cash

holdings level that will be used to calculate the target

deviation and then estimating the target adjustment

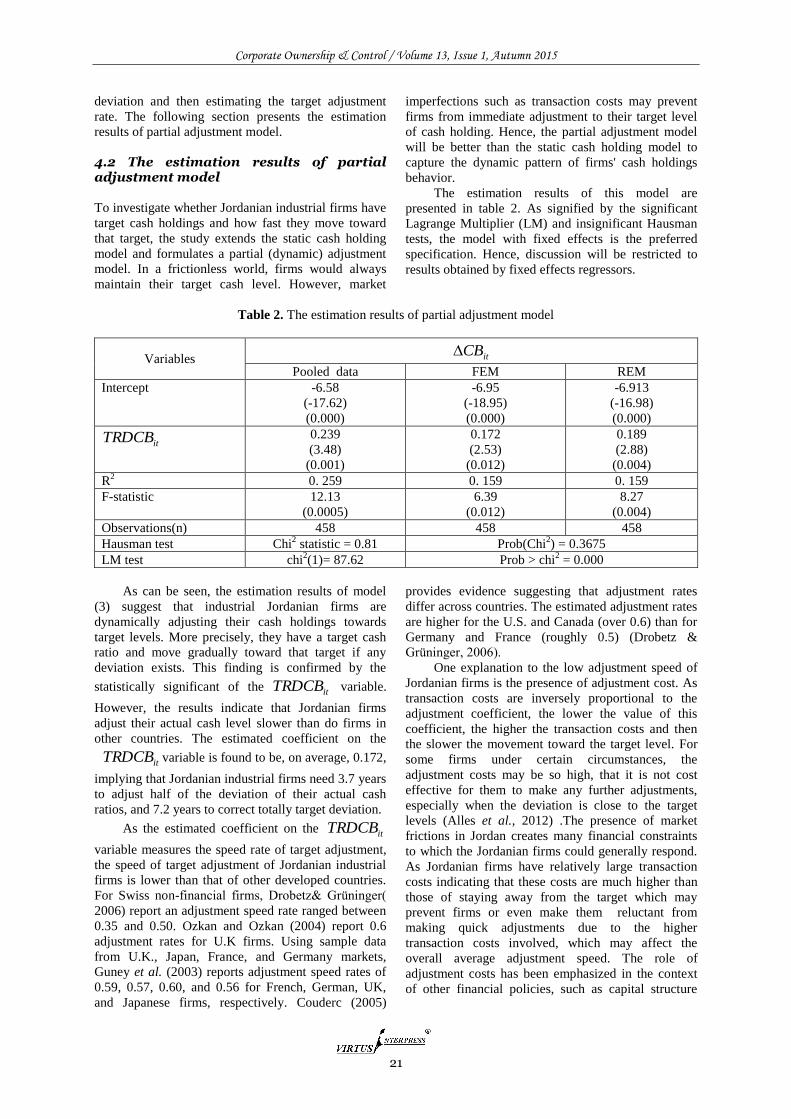

rate. The following section presents the estimation

results of partial adjustment model.

4 Regression results

This section consists of two sub-sections. The first one

presents the estimation results of conventional cash

holding equation; the equation that has been used in

the current study to estimate the fitted values of cash

holdings as a proxy for the target cash level. The

second one presents the estimation results of partial

adjustment model.

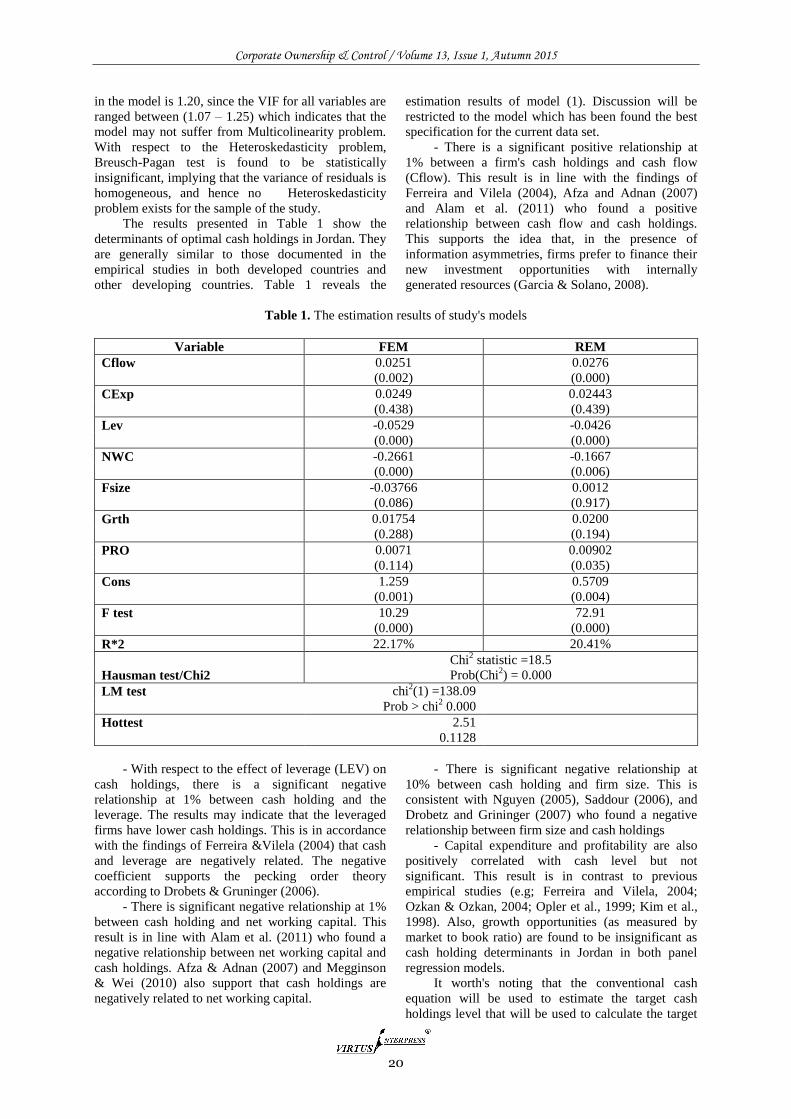

4.1 Estimation results of conventional cash equation

The result presented in table (4-1) suggests that the

fixed effect model is found to be the best specification

of the study's data set. The significant Lagrange

Multiplier (LM) test implies that the panel data

analysis is better than pooled OLS analysis,

suggesting the presence of firm and time specific

effect, and hence, OLS regression will not be efficient

to estimate study empirical model. The Ch2 value of

LM test is estimated to be 138.09 with p-value of

0.000. However, Hausman test suggests that the fixed

effects regressors will be better than random effect

regressors to greater efficient estimation results. This

finding is confirmed by the insignificant value of

Hausman CH2. It is found to be 18.5 with a p-value of

0.000. Moreover, the results of diagnostic tests for

Multicolinearity and Heteroskedasticity indicate that

the empirical models have no Multicolinearity and

Heteroskedasticity problems. The results of VIF show

that the mean value of VIF for all variables included

Corporate Ownership & Control / Volume 13, Issue 1, Autumn 2015

20

in the model is 1.20, since the VIF for all variables are

ranged between (1.07 – 1.25) which indicates that the

model may not suffer from Multicolinearity problem.