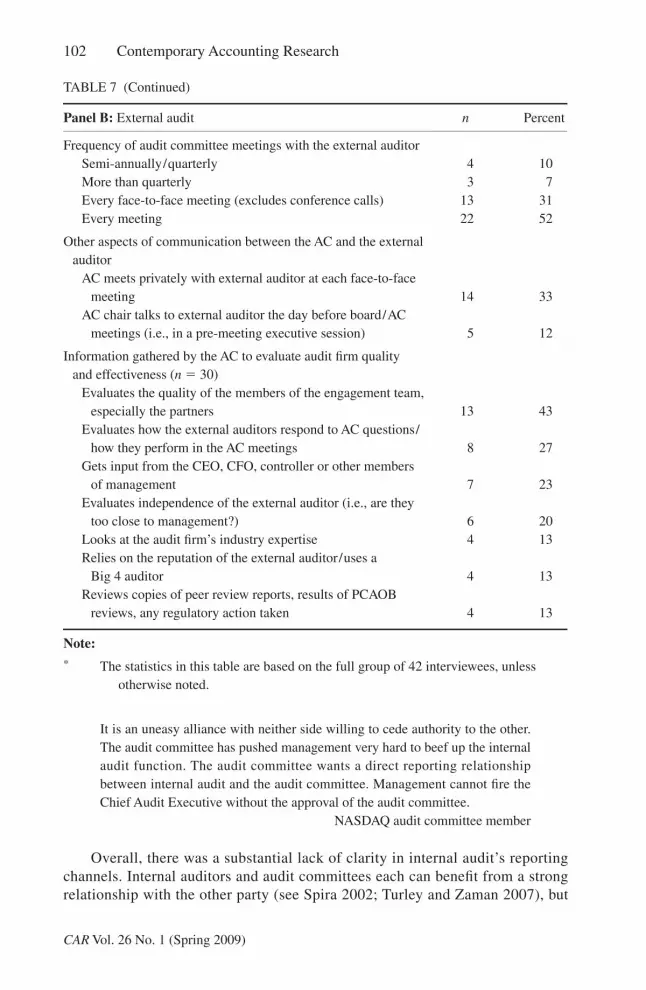

the audit committee oversight process

TRANSCRIPT

The Audit Committee Oversight Process*

MARK S. BEASLEY, North Carolina State University

JOSEPH V. CARCELLO, University of Tennessee

DANA R. HERMANSON, Kennesaw State University

TERRY L. NEAL, University of Tennessee

1. IntroductionNo one really understands how limited an audit committee is in its work. Inbig companies it is virtually impossible to know what is going on without rely-ing on management, the internal auditor, and the external auditor.

NYSE audit committee chair

Audit committees are increasingly responsible for the quality of financial reportingand oversight of the audit processes in U.S. public companies (e.g., Blue RibbonCommittee [BRC] 1999; New York Stock Exchange [NYSE] 2004; Sarbanes-Oxley Act [SOX] 2002), but as noted in the quote above, it is often challenging toprovide effective oversight, especially in large, complex organizations. The intensefocus on greater audit committee responsibility has led to a number of studies onaudit committee performance (for reviews of the academic literature on audit com-mittees, see Cohen, Krishnamoorthy, and Wright 2004; DeZoort, Hermanson,Archambeault, and Reed 2002; and Turley and Zaman 2004). Much of this

Contemporary Accounting Research Vol. 26 No. 1 (Spring 2009) pp. 65–122 © CAAA

doi:10.1506/car.26.1.3

* Accepted by Michel Magnan. An earlier version of this paper was presented at the 2007 Contem-porary Accounting Research Conference, generously supported by the Canadian Institute ofChartered Accountants. We thank Peter Gleason, Chuck ReCorr, and Hal Shear from theNational Association of Corporate Directors, Ellen Richstone from Financial Executives Interna-tional, Warren Neel from the University of Tennessee’s Corporate Governance Center, and ChrisRossie and Patrick Taylor from Oversight Systems, Inc. for their help in arranging many of ourinterviews. In addition, we appreciate suggestions on the paper and/or interview design fromLarry Abbott, Joe Brazel, Rich Clune, Jeff Cohen, Todd DeZoort, Yves Gendron, Rich Houston,Lisa Koonce, Paul Lapides, Michel Magnan (editor), John McAllister, John Olson, Gary Peters,Steve Salterio, Hal Shear, James Tompkins, Arnie Wright, two anonymous reviewers, and partici-pants at the 2007 Contemporary Accounting Research Conference. We also thank Doug Car-michael, Tom Ray, and other members of the Office of the Chief Auditor at the Public CompanyAccounting Oversight Board for their feedback on the interview questions. We thank Scott Bron-son, Jon Hansen, Katherine Hansen, Beverly Hudler, Shelly Kane, Stacy Mastrolia, FredMuchunu, Hazel Ryon, and Beth Swang for their assistance in transcribing, tabulating, and cod-ing the interview data. Finally, we thank KPMG’s Audit Committee Institute for sponsoring thisstudy, and Scott Reed and Mark Terrell of KPMG for their unwavering support and encourage-ment during the process. Most of all, we thank the audit committee members who were extremelygenerous with their time in talking with us.

66 Contemporary Accounting Research

research examines the relation between audit committee inputs (e.g., characteris-tics such as audit committee member independence, expertise, and diligence) andfinancial reporting outputs (e.g., restatements, fraud, and auditor going-concernreporting).

Although audit committee inputs and their relation to various outputs areimportant, the extant literature largely fails to examine the process used by auditcommittees as a whole or by individual audit committee members when fulfillingtheir oversight responsibilities (Cohen et al. 2004; Gendron, Bédard, and Gosselin2004; Turley and Zaman 2004, 2007). Turley and Zaman (2004, 324) state, “Whilethere is some evidence of a correlation between financial reporting characteristicsand governance arrangements, further research is needed to establish issues relatingto the processes and impact unique to [audit committees].” The authors specificallycall for audit committee research using the interview method to better understandaudit committees’ activities. Cooper and Morgan (2008) note that case studyapproaches are especially well suited to examining complex behavioral processesand addressing questions of how and why, and Ahrens and Chapman (2006) discussthe potential for qualitative research to contribute to theory. Through interviews ofaudit committee members, our study directly responds to such calls for qualitativeaudit committee research and offers the advantage of gathering more detailedinformation than typically is collected in quantitative research (Patton 1990).

To enhance our understanding of audit committee oversight, this paper pro-vides extensive information about the audit committee process obtained throughin-depth interviews of 42 individuals actively serving on U.S. public companyaudit committees. Our evaluation of the interview results is framed in part by thetension between the agency theory (e.g., Fama and Jensen 1983; Jensen and Meck-ling 1976) view of the audit committee as an independent monitor of managementversus the institutional theory view that audit committees may often be primarilyceremonial in nature, with a focus on providing symbolic legitimacy but not neces-sarily vigilant monitoring (Cohen, Krishnamoorthy, and Wright 2007b; Spira2002). This study addresses these often competing theories by examining the ques-tion “Do audit committees appear to provide substantive oversight of financialreporting, or do they appear to be primarily ceremonial bodies designed to createlegitimacy?”

We find that many audit committee members strive to provide effective monitor-ing of financial reporting and seek to avoid serving on ceremonial audit committees.However, within six specific audit committee process areas we find evidence ofboth substantive monitoring and ceremonial action, such that neither agency theorynor institutional theory fully explains our results. We also find that many responsesvary with personal and company characteristics, with particularly notable differ-ences related to audit committee members’ accounting expertise and time ofappointment to the audit committee (pre-SOX versus post-SOX).

This paper is organized as follows. The next section provides backgroundinformation and the motivation for the present study. We describe our researchmethod in section 3. Section 4 presents our overall findings, and section 5 describesthe supplemental analyses. In section 6 we provide discussion and conclusions.

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 67

2. Background and motivation

The role of the audit committee

The Sarbanes-Oxley Act (SOX 2002, section 2) defines an audit committee as “acommittee (or equivalent body) established by and amongst the board of directorsof an issuer for the purpose of overseeing the accounting and financial reportingprocesses of the issuer and audits of the financial statements of the issuer”. A com-petent, committed, independent, and tough-minded audit committee has beendescribed as “one of the most reliable guardians of the public interest” (Levitt2000, 5).

Expectations related to audit committees continued to expand throughout the1990s and early 2000s as financial reporting scandals unfolded. Many believethose expectations have sky-rocketed as a result of SOX 2002 and through subse-quent changes in audit committee regulations (e.g., NYSE 2004). KPMG’s AuditCommittee Institute (2003a, 2) states:

Today, as never before, the role, responsibility, and accountability of the auditcommittee continue to be the focus of lawmakers, regulators, and shareholders.The audit committee’s role in overseeing a company’s financial reporting pro-cess, including the audits (and auditors) of the financial statements, is morevisible and demanding.

The importance of process: The Hollinger case

Because we seek to provide insight into the audit committee process, an importantquestion is, “Does the audit committee process truly matter?” We believe that therecent corporate governance disaster at Hollinger International Inc. provides com-pelling anecdotal support for the importance of the audit committee process.Hollinger’s audit committee had three financially literate members, each with signif-icant public company director experience and impressive professional credentials.The members included a former governor/law firm chairman, a former ambassador/investment banking and consulting firm chairman, and a senior fellow of an institute.According to recent trial testimony (United States v. Conrad Black, John Boultbee,Peter Atkinson, and Mark Kipnis [Hollinger case] 2007), each of the audit committeemembers was considered “independent”, and the audit committee met several timeseach year (typically at least four times in person, with additional meetings by phone).

Despite the impressive audit committee membership and meeting schedule, trialtestimony (Hollinger case) and the Hollinger board’s special investigation report(Paris, Savage, and Seitz [Paris report] 2004) reveal apparent deficiencies in the auditcommittee’s oversight process. These deficiencies allowed key executives to “linetheir pockets at the expense of Hollinger almost every day, in almost every way theycould devise” (Paris report 2004, 2). The Paris report (2004, 4) asserts that two keyexecutives stole essentially all of the company’s profits over a seven-year period.

The trial testimony and the Paris report reveal numerous apparent concernsregarding the audit committee process that are relevant to certain audit committeeprocess areas examined in the present study (see section 3, “Method”):

CAR Vol. 26 No. 1 (Spring 2009)

68 Contemporary Accounting Research

1. Acceptance and continuance of due diligence processes: According to trial tes-timony, the Hollinger chief executive officer (CEO) “bumped into” an individualhe knew on a New York City street and invited him to the join the Hollingerboard. That person joined the board and audit committee. As part of the subse-quent Hollinger trial, that audit committee member testified that before joiningthe board, he did “not really” receive any information about what his boardduties would entail. The Paris report (2004, 28) asserts that the board wasselected by the CEO and “functioned more like a social club or public policyassociation”.

2. Selection of audit committee nominees: According to trial testimony, althoughall three audit committee members were financially literate, no committeemember was considered to be an audit committee financial expert.

3. Audit committee meeting processes: According to trial testimony, (a) in oneinstance, the portion of an audit committee meeting devoted to complexrelated-party transactions lasted for only a few minutes, and the committeemembers had no comments or questions whatsoever; (b) audit committee meet-ing agendas were not always prepared, and if they were, they were prepared bya member of management; (c) one audit committee member testified that thecommittee did not always receive materials before an audit committee meet-ing; and (d) the audit committee relied on management to bring related partytransactions to the committee’s attention. The audit committee chair reliedheavily on management, testifying that he relied “on the members of manage-ment who dealt with the Audit Committee to advise us of anything that shouldbe brought to our attention” (Thompson testimony, May 1, 2007, 30). Anothermember testified, “we would really rely to a great deal on management in dis-cussing [public filings] with management to point out important elements ofthose disclosures to us” (Burt testimony, April 24, 2007, 9). The audit commit-tee chair testified that he reviewed draft financial filings by “skimming” themand admitted that he should have read the filings. Similarly, the Paris report(2004, 14–5) asserts that the audit committee approved management fees with-out understanding the effect on top executives’ compensation, yet the auditcommittee failed to demand the information necessary to evaluate the situation.The audit committee failed to ask questions, failed to be skeptical, and failedto gather independent information (Paris report 2004, 33–4).

4. Audit committee oversight of the financial reporting process: The audit com-mittee chair testified that he “trusted” management. Another member testified,“It never occurred to me to check [the truthfulness of management’s state-ments] … I always assumed … that management was giving us a full andcomplete description of the affairs of the company” (Burt testimony, April 24,2007, 10). The Paris report (2004, 36) asserts that the audit committee put toomuch faith in management’s integrity and did not “Trust, but verify”. The auditcommittee continued to rely on management’s assertions even after there wasevidence of questionable management integrity (Paris report 2004, 505).

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 69

On the basis of the information above, it appears that the Hollinger audit com-mittee, despite its impressive membership and meeting schedule, had a deficientprocess in place. Specifically, there are fundamental concerns with the selection ofaudit committee members (the role of the CEO, the lack of accounting expertise),the audit committee meeting process (time spent on important issues, agenda set-ting, information flow, reliance on management, and review of information), andthe propensity to trust management. We believe that such process characteristicscan contribute to corporate disasters, and each of these process elements isaddressed in our interviews with audit committee members.

Theoretical foundations

There are several, often competing but sometimes complementary, theories withregard to corporate governance and audit committees (e.g., Cohen, Krishnamoor-thy, and Wright 2002, 2007b; Kalbers and Fogarty 1998). The finance (agency)view (e.g., Fama and Jensen 1983; Jensen and Meckling 1976) holds that the boardand audit committee are in place to monitor management, who otherwise may actin their personal best interest and not in the interests of the principal (e.g., share-holders). Thus, the board and audit committee’s independent members monitormanagement to prevent opportunistic behavior by management. This perspective isthe predominant view of the role of corporate governance in the academic account-ing literature.

Alternatively, an institutional theory (e.g., Scott 1987) view of governance inthe academic accounting literature considers changes in organizational processesover time (Cohen et al. 2002, 2007b) and how governance structures “fulfill ritual-istic roles that help legitimize the interactions among the various actors within thecorporate governance mosaic” (Cohen et al. 2007b, 11). Under this view of gover-nance, audit committee processes may become more similar over time (Barretoand Baden-Fuller 2006; Dacin 1997; DiMaggio and Powell 1983), as organizationsare coerced to become similar through regulation (such as SOX), by following“best practices”, or by mimicking other organizations to enhance their legitimacy(Cohen et al. 2007b).

Kalbers and Fogarty (1998, 131) state that under this view, “organizationalstructures … become symbolic displays of conformity and social accountability”(also see Spira 1999 and DiMaggio and Powell 1983). In other words, some gover-nance activities and structures may be primarily driven by a desire to fosterlegitimacy; therefore, the activities and structures are primarily ceremonial andserve as symbols of effective oversight. Cohen et al. (2007b) note that the auditorbears great responsibility for reliable financial reporting when the audit commit-tee’s role is primarily ceremonial, although the committee’s symbolic efforts canlead to effective questioning of management.

Ceremonial efforts may not be closely related to how a given task is actuallyaccomplished (e.g., to the extent that true monitoring and oversight take place,these activities may not occur during the ceremonial meetings) — that is, there isonly a “loose coupling” between the ceremonial actions and claims of audit com-mittee effectiveness (see Fogarty and Rogers 2005). Scheid-Cook (1990, 189)

CAR Vol. 26 No. 1 (Spring 2009)

70 Contemporary Accounting Research

states, “Loose coupling in organizations implies that structure and process areloosely connected with organizational goals.” Scheid-Cook (1990, 190) also statesin her study of ritual conformity in community mental health centers, “any controlsover the output of [community mental health centers] that do exist are largely ritual.That is, existing output controls serve to legitimate the [community mental healthcenter’s] use of [outpatient commitment], but have little or no bearing on organiza-tional effectiveness.” In other words, the formal control structures of the commun-ity mental health center are only loosely coupled with its technical activities.Returning to the audit committee setting, under the institutional theory view, auditcommittee activities may be only loosely coupled with claims of audit committeeeffectiveness, such that the formal audit committee activities are primarilyceremonial/ritualistic and designed to create legitimacy outside the organization.

A third view of governance, resource dependence, asserts that the board’sprimary role is to assist management with strategy and resource acquisition(Cohen et al. 2007b; Nicholson and Kiel 2007). The board’s role is that of helper orpartner, rather than monitor of management. Cohen, Krishnamoorthy, and Wright(2007c) find that auditors consider both traditional agency variables and resourcedependence variables when evaluating corporate governance for the purpose ofaudit planning.

Fourth, stewardship theory presumes that managers are honest, capable stew-ards of the company’s resources (Nicholson and Kiel 2007). Accordingly, the focusis on inside directors’ ability to promote shareholder value through their superiorknowledge of the company.

Finally, the managerial hegemony theory asserts that management simplychooses friends to serve as passive directors who derive all of their informationfrom management (Cohen et al. 2007b). The board then becomes purely symbolicand consistently supportive of management, even when the members appear to beindependent directors. Under such a view, the audit committee is completely undermanagement’s control and offers virtually no monitoring at all.

To summarize, agency theory emphasizes directors as independent, vigilantmonitors of management; institutional theory emphasizes the symbolic/ceremonialrole of governance structures where legitimacy is paramount and formal processesare only loosely coupled with true monitoring; resource dependence theory focuseson the board’s efforts to assist management with strategy and resources; steward-ship theory presumes that managers are honest; and managerial hegemony assertsthat the audit committee will be weak and under management’s control. Consistentwith Kalbers and Fogarty 1998, of primary interest as we consider the interviewresults below, are agency theory (the audit committee as a strong, substantive, activemonitor) and institutional theory (the audit committee as a ceremonial entity withless substantive monitoring). Given the nature of the audit committee’s oversightrole (SOX 2002), we expect the audit committee to be most heavily focused onactual monitoring (agency theory) or on creating legitimacy by engaging in appro-priate ceremony and ritual (institutional theory, Spira 2002).1

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 71

Research on audit committees

Much of the research on audit committees examines the relation between auditcommittee inputs (e.g., independence, expertise, or diligence) and financial report-ing outputs (e.g., abnormal accruals) (Klein 2002; Bédard, Chtourou, and Courteau2004); restatements (Abbott, Parker, and Peters 2004; Agrawal and Chadha 2005);fraudulent financial reporting (Beasley, Carcello, Hermanson, and Lapides 2000);going-concern reports (Carcello and Neal 2000); auditor changes (Carcello andNeal 2003); and stock price reaction (DeFond, Hann, and Hu 2005)). These studiesgenerally find that a more independent, expert, and diligent audit committee isassociated with higher quality financial reporting and auditing. However, becausethese studies examine publicly available measures of audit committee inputs(mainly through corporate proxy statements) and outputs (available in publishedfinancial statements, Securities and Exchange Commission [SEC] filings andenforcement actions, or quoted stock prices), the process by which the audit com-mittee contributes to improvements in financial reporting and auditing has beenlargely unexamined.

To the best of our knowledge, the only studies that examine audit committeeprocesses for overseeing financial reporting are Gendron et al. 2004; Gendron andBédard 2006; Spira 1999, 2002; Turley and Zaman 2007; and Cohen, Krishna-moorthy, and Wright 2002, 2007a. Gendron et al. (2004) examine the activities inaudit committee meetings for three Canadian public companies by interviewingnine audit committee members and 13 other individuals in 2000 and 2001 (e.g.,CEO, chief financial officer [CFO], internal auditor, external auditor). They findthat audit committee members place significant attention during their meetings onfinancial statement accuracy and appropriate wording, internal controls, and auditquality. They also conclude that a key role of the audit committee is to ask chal-lenging questions of management and auditors.

Gendron and Bédard (2006) explore the process by which audit committeemembers develop a definition of “audit committee effectiveness”. The authors sup-plement the data from Gendron et al. 2004 with interviews of three audit committeechairs in 2004. Gendron and Bédard (2006) find that audit committee members’notions of effectiveness come from their reflecting on audit committee processesand results, with variation across individuals in the definition of effectiveness andin the confidence that effectiveness is being achieved in a certain area. The authorsalso find that post-SOX, the “chairpersons’ sense of audit committee effectivenesswas not fundamentally fractured” (2006, 235).

Spira (1999, 2002) interviews 21 individuals, including audit committeechairs, finance directors, and auditors, in the United Kingdom during 1994–96.She focuses particular attention on the ceremonial nature of audit committee activ-ities and on the audit committee as a seeker and provider of comfort regardingfinancial reporting. Comfort is obtained from various parties, such as the financedirector and auditors, and comfort is provided to financial statement users.

Turley and Zaman (2007) use a case study approach, interviewing nine indi-viduals at one U.K. company, including the audit committee chair, internal andexternal auditors, and management. They find that the audit committee’s greatest

CAR Vol. 26 No. 1 (Spring 2009)

72 Contemporary Accounting Research

impact comes through informal processes and the committee’s effect on powerrelationships among other governance participants. For example, this particularaudit committee tends not to ask difficult, probing questions during committeemeetings, but it influences governance outcomes through informal meetings withauditors and through serving as an ally to the auditors.

Cohen et al. (2002) interview 36 auditors regarding the influence of corporategovernance on the audit process, including the role played by the audit committee.They find that auditors perceive management to be “the primary driver of corporategovernance” (573). Many of the auditors view audit committees as weak and inef-fective.2 Cohen et al. (2007a) update their 2002 study by interviewing 38 auditorsin the post-SOX period. They find that auditors perceive audit committees to bemore diligent, active, expert, and powerful post-SOX.

Motivation

Spira (2002) and Turley and Zaman (2004, 2007) specifically call for additionalqualitative research on the audit committee process to increase our understandingof the linkages between audit committee inputs and outcomes, particularly thoserelated to financial reporting and internal control. Patton (1990, 14) states that rela-tive to large-sample quantitative research, “[Q]ualitative methods typically pro-duce a wealth of detailed information about a much smaller number of people andcases. This increases understanding of the cases and situations studied.”

Gendron et al. (2004), Gendron and Bédard (2006), Spira (1999, 2002), andTurley and Zaman (2007) offer important insights into the audit committee process(and Cohen et al. (2002, 2007a) examine auditor perceptions of audit committees),and many of these studies are based on pre-SOX data from Canadian or U.K. compa-nies. Our paper is based on interviews with 42 U.S. public company audit committeemembers in the post-SOX environment. DeZoort, Hermanson, and Houston (2008)indicate that certain audit committee members in the post-SOX period are moreconservative (more supportive of the auditor in auditor–management disagree-ments) and more concerned about financial reporting accuracy than in the pre-SOXperiod. In addition, Cohen et al. (2007a) find that auditors believe that audit commit-tee members are more diligent, active, expert, and powerful post-SOX. As a result,the nature of audit committee oversight may be different post-SOX than pre-SOX.

3. Method

The goal of our study is to provide detailed insights into the audit committee pro-cess. We use the interview method to gather such insights, because this methodallows us to explore issues that are difficult to examine using archival methods. Forexample, archival research provides insights into obvious threats to audit committeemember objectivity, such as those revealed by the member’s employment history.However, the interview method can reveal more subtle threats to objectivity, suchas those arising from personal friendships with management that may not be iden-tified through archival methods.

We organized our interviews around six audit committee process areas (see theappendix for the six areas and for the specific research questions). These process

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 73

areas are consistent with several elements of the KPMG Audit Committee Insti-tute’s Building a Framework for Effective Audit Committee Oversight 2003b.3 Weexplore audit committee member responses to specific questions surrounding thesix audit committee process areas. We used several sources of information todesign our questions, including (a) our prior experiences working with auditorsand audit committees, (b) the professional literature (e.g., auditing standards, SOX,SEC rules), (c) the academic literature (e.g., DeZoort et al. 2002), (d) discussionswith two sitting members of one or more public company audit committees, and(e) discussions with standard-setters and regulators.4

Following the approach used in Graham, Harvey, and Rajgopal 2005, wesolicited feedback on our interview questions from several academic researchersand current audit committee members. We pilot tested the questions and our inter-view approach on three sitting audit committee members. We modified theresearch instrument and our interview approach on the basis of feedback from ourpre-test and our pilot testing.

Our study is based on interviews with 42 individuals currently serving on at leastone public company audit committee.5 Several individuals were identified throughthe assistance of the KPMG Audit Committee Institute, the National Association ofCorporate Directors, and the Boston chapter of Financial Executives International(sometimes through emailed solicitations to their members). Others were identifiedthrough our personal and university-related contacts.6

Interviewees are located in cities across the United States. As a result, 20 ofthe interviews were conducted in person, while 22 interviews were conducted bytelephone.7 We used a standardized interview script to guide all of the interviews:this script was designed so that questions were asked in relatively short parts, thusmaking it easy to record the details of the responses. There were no differences ininterview questions for those conducted in person versus those conducted bytelephone.

In performing the interviews, we drew heavily from the approaches used byHirst and Koonce 1996 and Cohen et al. 2002. Generally, one member of ourauthor team made the inquiries and took detailed notes of responses, while a secondauthor or graduate student created a separate set of detailed notes (Nicholson andKiel 2007).8 The audit committee members were told that their responses would beheld in strict confidence. In order to encourage candid responses and to fully protectthe anonymity of the interviewees, we did not tape record the interviews (consistentwith Nicholson and Kiel 2007), nor did we record the names of the audit committeemembers or the companies they serve in our data set. We believe that these measureswere necessary to allow us access to public company audit committee members inthe immediate post-SOX period, a time of great focus on audit committees and sig-nificant concerns about audit committee member liability. All of the intervieweesprovided their informed consent. Given the specificity of many of the responses wereceived, we believe that the audit committee members were candid in theirresponses.

Despite the use of a script to guide our interviews, the interview approach wassemi-structured — that is, “when questions took us down an important path, we

CAR Vol. 26 No. 1 (Spring 2009)

74 Contemporary Accounting Research

pursued them before returning to the planned interview materials” (Hirst andKoonce 1996, 460). We began by collecting demographic data and then proceededwith questions related to our six process areas. Our first set of questions addresseddue diligence processes performed by individuals before they agreed to join orstand for reelection to a board, given that board and audit committee service areinterconnected. The second set of interview questions was specific to a particularaudit committee and addressed the other five areas of audit committee processexamined in this study. For this set of research questions, we generally asked theaudit committee members to base their responses on the largest public company auditcommittee on which they currently serve (and had served for at least one year).

The interviews were conducted from February 2004 through February 2005and lasted approximately 90 minutes on average, with the shortest interview being45 minutes and the longest 180 minutes. After each interview, one of the authorstranscribed (typed) our notes. The other author present at the interview checked thetranscription of the notes and compared them with the other set of notes (see Salte-rio and Denham 1997).9

We borrowed heavily from parts of Gibbins, Richardson, and Waterhouse1990 (139–40) in developing a coding scheme to categorize and summarize theinformation gathered during the interviews. We analyzed the interview transcriptsto create a vocabulary for discussing audit committee activities and processes.More specifically, we (a) selected one of the typed transcripts as the first case to beanalyzed, (b) highlighted significant words or phrases in the transcript,10 (c) sortedthe highlighted words or phrases into categories on the basis of similarity, and(d) iterated through the accumulated categories to identify more general categoriespermitting us to combine certain initially identified categories. Using this codingscheme (which was influenced by the nature of the responses we received), we devel-oped 438 unique categories that captured the audit committee members’ responses.Two different graduate students assigned the audit committee members’ responses tothese categories, each working independently. The mean intercoder agreement forthese 438 items is 94 percent, and the mean Kappa statistic is 0.78 (p � 0.01).11

4. Findings

Table 1 presents background information on the interviewees, who have extensivefinancial and public company audit committee (AC) experience. The intervieweesserve on audit committees across a broad range of company sizes (median revenuesare $1.5 billion) and industries.12

To provide an initial overview of the results, Table 2 presents information onthe range of responses within each of the six process areas. Within each of theareas, we find responses reflecting activities that range from substantive, meaning-ful oversight to less substantive, ceremonial action that is only loosely coupledwith claims of audit committee effectiveness.

The remainder of this section provides detailed analyses of audit committeeresponses to our interview questions related to the six key audit committee processareas. The amount of data we obtained through these interviews is quite extensive.As a result, we describe key findings related to each of the six process areas, and

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 75

we encourage readers to carefully examine the tables. Where possible, we supple-ment the results with insights from individual audit committee members, relate ourfindings to previous research, and assess whether the results are consistent withagency theory (substantive audit committee monitoring) or institutional theory (theaudit committee as a ceremonial entity whose activities are loosely coupled withclaims of audit committee effectiveness).

TABLE 1Background information on interviewees*

GenderMale 31 74Female 11 26

Professional certificationCertified public accountant 15 36

Professional experience in finance or accountingChief financial officer 19 45Public accounting experience 19 45General management 8 19Accounting professor 4 10Controller 4 10Regulator 4 10

Age 58.5 48 73

Cumulative governance experienceYears of corporate audit committee experience 8.2 1 20Corporate audit committees served in career 3.2 1 9

Current service on public company auditcommittees (ACs)

Number of public company audit committeesnow served 1.8 1 5

Number of audit committees where they are afinancial expert 1.5 0 5

Number of audit committees where they arethe chair 1.1 0 4

Number of years serving as the AC chair(n � 27) 4.4 1 18

Revenues (in millions) of audit committeecompany (n � 41) $6,688 $15 $130,000

(The table is continued on the next page.)

Panel A: Percentages n Percent

Panel B: Means Mean Minimum Maximum

CAR Vol. 26 No. 1 (Spring 2009)

76 Contemporary Accounting Research

AC process area 1: Acceptance and continuance due diligence processes

Given the legal risk (Veasey 2005) and reputational risk (Srinivasan 2005) faced byboard and audit committee members in the current environment, we examine duediligence processes performed by potential audit committee members in evaluatingtheir decision to serve on a board. As shown in panel A of Table 3, we find thataudit committee members generally perform significant due diligence beforeaccepting a board / audit committee position. Audit committee members oftenreview documents, conduct interviews, and carefully assess management integrityand their personal comfort level:13

Always do some form of due diligence. I first want to determine if I have theknowledge necessary to serve on that particular company’s board (e.g., indus-try) and whether I have the capacity (time) to be able to serve effectively.Often my involvement starts because of some relationship I have with a largeinvestor or senior executive — that is often what initiates contact with me. Iwant to be knowledgeable about senior management — want to know whothey are and what they are like. I want to gain some sense of management’sethical makeup. I also examine recent public filings of the company and talk toone or two other directors currently serving — to gain a sense for the companyand management style as well as how the board actually operates. I also try totalk with large investors.

NASDAQ audit committee chair

I am constantly going through the due diligence process — every meeting, filing,and transaction is a learning process. I ask: (1) Is this a company that I want tobe associated with?, (2) Am I adding value and serving the shareholders well?and (3) Do I want to continue my association with this company?

NASDAQ audit committee chair

TABLE 1 (Continued)

Packaging, logistics, and transportation 6Retail 6Technology 6Financial services 4Media and telecommunications 4Health care 3Manufacturing 3Other 10Total 42

Note:* The statistics in this table are based on the full group of 42 interviewees, unless

otherwise noted.

Panel C: Industry distribution n

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 77

These perspectives are consistent with Spira’s 2002 (156) notion of audit com-mittee members’ “continuing preoccupation with the provision and maintenance ofcomfort”. In addition, regarding integrity, a NYSE audit committee member toldus that a prospective board member “better have faith in management’s integrity,especially that of the CEO. Otherwise, the liability risk is just too great.”

TABLE 2Summary of substantive versus ceremonial activities

Process area 1: Acceptance and continuance due diligence processes• Substantive: extensive due diligence before joining the board and audit committee• Ceremonial (5%*): very little due diligence before joining the board and audit

committee

Process area 2: Selection of audit committee nominees• Substantive: chosen for audit committee due to accounting expertise and belief that

person would be outspoken• Ceremonial (19%): chosen for board/audit committee due to personal relationship

with management

Process area 3: Audit committee meeting processes• Substantive: risk-driven agendas set by audit committee chair, heavy audit committee

involvement in information packet development, information packet received well in advance of each meeting, frequent interaction between meetings

• Ceremonial (43%): agendas driven by management, little audit committee involvement in information packet development, information packet received just prior to each meeting, little interaction between meetings

Process area 4: Audit committee oversight of the financial reporting process• Substantive: heavy audit committee involvement in accounting policy choice and

accounting alternatives, extensive audit committee analysis of estimates and judgments, audit committee responsible for fraud risk assessment, active audit committee assessment of fraud risk and management integrity

• Ceremonial (31%): minimal audit committee involvement in accounting policy choice and accounting alternatives, no audit committee analysis of estimates and judgments, audit committee not responsible for fraud risk assessment, audit committee complete reliance on auditors for assessment of fraud risk

Process area 5: Oversight of the internal and external audit processes• Substantive: audit committee truly oversees the internal audit function and has

extensive formal and informal contact with internal audit, audit committee has extensive contact with and oversight of external audit, including gathering significant information to evaluate auditor performance

• Ceremonial (31%): internal audit really reports to management and has little or no contact with the audit committee outside of audit committee meetings, audit committee has limited contact with and oversight of external audit and gathers no information to evaluate auditor performance

(The table is continued on the next page.)

CAR Vol. 26 No. 1 (Spring 2009)

78 Contemporary Accounting Research

A number of audit committee members indicated that some companies arelooking for independent directors in name only. The executives want to be able topoint to their independent directors, but they do not really want vigilant monitoringof their actions:

The big question is are there any integrity issues? Any baggage? Do they wantto do things right? Will management and the board be stable? I want to avoidshow and tell meetings. Avoid cases where they want your name, but nosubstance.

NYSE audit committee chair

This audit committee member is trying to avoid situations where management wantsthe audit committee to be merely ceremonial. As a NYSE audit committee chairsaid, “I will only go on the board if the CEO and CFO take governance seriously.”

We also asked why a prospective board member would decline to serve on aboard or would resign from a board where he or she was already serving. Our find-ings are presented in panel B of Table 3. Management integrity issues dominate,followed by time constraints, inability to contribute, and concerns about manage-ment’s commitment to sound governance. A NASDAQ audit committee chairstated:

If management’s attitude toward the role of the board and the attitude of otherboard members regarding the board’s responsibility are not acceptable, Iwould decline or leave. I don’t want to be the Lone Ranger on the board. …I left a board due to not feeling like other board members felt like their respon-sibility was as serious as I felt it should be — they appeared too self-serving. Ialso left because I didn’t think I made a good match for the board. I havedeclined several invitations. For some, I felt I wasn’t qualified. For others, Ideclined because I felt like management didn’t get what board responsibilities

TABLE 2 (Continued)

Process area 6: Other audit committee activities• Substantive: audit committee formally benchmarks against leading practices, audit

committee is heavily involved in the code of conduct, audit committee does not get too comfortable

• Ceremonial (19%): audit committee does not benchmark against leading practices, audit committee is not involved in the code of conduct, audit committee is too comfortable with management

Note:* The frequency information for ceremonial activity is based on the percentage of

participants indicating a ceremonial approach to at least one of the listed activities within a process area. Within process areas 4 and 5, some questions were not asked of all participants (see Tables 6 and 7).

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 79

TABLE 3AC process area 1: Acceptance and continuance due diligence processes*

Steps taken before agreeing to join the board or audit committeeMeet with or talk to the following people

Existing board members 23 55CFO 17 40External auditor 17 40CEO 16 38Unspecified senior management 16 38In-house counsel 11 26

Read/review the following documentsSEC filings (including financial statements) 26 62Directors’ and officers’ insurance 10 24Litigation 8 19Company websites 6 14

Take the following actionsTalk to colleagues, including assessing reputation of

company and management 16 38Understand the company’s business and industry 10 24Analyze financial health of the company 4 10Analyze long-term strategic plan of the company 4 10Assess composition and reputation of the current board 4 10Make sure board service poses no conflict with employer 4 10

Make the following assessmentsCan he or she make a contribution to the board? 12 29Are there any integrity issues with management or the

board? 10 24

Steps taken when agreeing to continue on the board or auditcommittee

Make the following assessmentsAre there any integrity issues with management or the

board? 14 33Does he or she still have a good comfort level? 11 26Is he or she still making a contribution to the board? 11 26How has management handled board suggestions/advice? 7 17How effective is the board and its committees? 6 14Is the time commitment required still acceptable given his

or her schedule? 5 12No specific actions taken 7 17

How often does he or she make this evaluation regarding continuedservice (n � 37)?

Continuously 29 78Periodically (e.g., when up for reelection) 6 16As needed (e.g., when an issue arises) 2 5

(The table is continued on the next page.)

Panel A: Acceptance and continuance n Percent

CAR Vol. 26 No. 1 (Spring 2009)

80 Contemporary Accounting Research

really were — they didn’t take board responsibility seriously. I also havedeclined when I felt like management’s attitude for what they were looking forin a board member was primarily driven by their desire for form over substance.

Overall, the interviewees appear quite committed to due diligence efforts sothat they can avoid being associated with a problem company. It appears to us thatmany prospective audit committee members approach a board invitation with adefault response of “no” and must be convinced to say “yes”. Thus, most of theaudit committee members we interviewed apparently favor an agency view ofthe audit committee, where they are engaged to provide monitoring of manage-ment, as opposed to serving only in a ceremonial role reflective of institutionaltheory. (Similarly, Spira (2002, 69) notes that participants in her interviews “didnot want audit committee meetings to be described as ceremonial”.) However, itappears that the audit committee members we interviewed have encountered man-agement teams with a loosely coupled view of governance (ceremonial boards andaudit committees), and they try to avoid such managers.

TABLE 3 (Continued)

Reasons he or she would decline to serve or leave a position onthe board or AC

Management issuesConcerns about management credibility and/or integrity or

witnessed fraud, illegal acts, or unethical conduct 24 57Lack of open/honest communication between management

and the board 7 17Independent directors are not desired and the corporate

governance system is not taken seriously 6 14Top management is not supportive of financial reporting or

controls 5 12Individual director issues

Excessive time and/or travel demands 13 31Inability to contribute 10 24Lack of business and industry knowledge 7 17

Number of directors who have declined an invitation to serveon a board 15 36

Number of directors who have resigned from a board 11 26

Reasons given for why they resigned from a board (n � 11)Time demands 4 36Board is not effective 3 27Lack of compatibility with the CEO 2 18

Note:* The statistics in this table are based on the full group of 42 interviewees, unless

otherwise noted.

Panel B: Declining or leaving n Percent

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 81

AC process area 2: Selection of audit committee nominees

Because we are interested in learning about company-specific audit committeeprocesses, we generally asked the interviewees to describe processes related to thelargest public company audit committee where the interviewee had served for atleast one year. The remainder of this paper addresses the interviewees’ experienceswith one public company audit committee.

Table 4 presents information on how the audit committee member was identifiedfor board service and why he or she was asked to serve on the audit committee.Many audit committee members were identified for audit committee servicebecause of their previous contact with management or other directors.14 Considerthe following perspectives that raise questions about the degree of arms-lengthmonitoring that may take place:

I was friendly with the CEO of the company. Our kids were in the sameschools, and our wives were friends. The previous CEO perpetrated a majorfraud in this company. My friend became the new CEO, and he had to rebuildthe board. I was asked to join the board.

NYSE audit committee member (joined board pre-SOX)

The CFO suggested that I join the board. The CFO is a personal friend. Longago I served on the company’s audit engagement (35 years ago). The CFOwanted my financial expertise.

NASDAQ audit committee chair (joined board post-SOX)

In some cases, the selection of directors is consistent with managerial hegemony(get friends on the board) or institutional theory (have independent directors forlegitimacy, but the directors’ true objectivity is suspect).

Thus, there is an interesting contrast in the first two process areas. Audit com-mittee members appear to want to engage in meaningful monitoring (they want thecompany to take governance seriously); however, many of them were selected forboard service due to previous relationships that may call their objectivity into ques-tion. In addition, some prospective board members gain comfort from knowingcurrent board members. A NASDAQ audit committee chair stated, “If you don’tknow people on the board, it is not possible to do enough due diligence.”

By far the most common reason for being asked to serve on the audit commit-tee is the interviewees’ financial or accounting expertise.15 This is consistent withGendron and Bédard’s 2006 finding that financial and accounting backgrounds areconsidered critical to audit committee effectiveness (also see Spira 2002). Also,some interviewees were appointed to the audit committee because of their industrybackground or expertise. The following perspectives elaborate:

My background as a CFO and auditor led to my audit committee service. Inaddition, no other board member wanted to serve on the audit committee.

NASDAQ audit committee chair

CAR Vol. 26 No. 1 (Spring 2009)

82 Contemporary Accounting Research

I was the only person on the board with financial experience and with experi-ence in the industry. I was operationally stronger in finance and with industryknowledge. Knowledge of the industry was a big plus.

NASDAQ audit committee chair

AC process area 3: Audit committee meeting processes

Audit committee meeting number and length

Panel A of Table 5 presents information about the number and length of typicalaudit committee meetings. Meeting frequency now averages approximately 10meetings per year.16 One audit committee member stated:

CAR Vol. 26 No. 1 (Spring 2009)

TABLE 4AC process area 2: Selection of audit committee nominees

Did the nominee have significant previous contact with executivemanagement before being approached to serve on the board?

No 25 60Yes 17 40

Did the nominee have any personal ties to management orboard members?

No 28 67Yes 14 33

Identified to serve on the board because of financial expertise 6 14

Identified to serve on the board because of industry expertise 5 12

How was the nominee identified to serve on the board?Previous interaction with management of the company

Management (including the CEO) knew the nominee 9 21Chair of the board knew the nominee 3 7Founder of the company knew the nominee 2 5

Previous experience with other board membersSome of the other board members knew the nominee 5 12Served on another board with members of this board 3 7

Identified by the governance committee or by an outsidegroup

Identified by an executive search firm 5 12Representing a large investor in the company or a creditor’s

committee 4 10Recommended by an accounting firm and/or law firm 3 7

Factors that led to being appointed to the audit committeeFinancial or accounting background/expertise 28 67Industry background/expertise 6 14

n Percent

The Audit Committee Oversight Process 83

We meet 12 times in total plus two or three miscellaneous calls. Four times ayear we hold conference calls with CEO, CFO, external auditor, GeneralCounsel, and full audit committee. The primary purpose of these calls is to goover the press release before it is released. We usually get a draft of the pressrelease in advance of the call. Four times a year we meet face-to-face or viateleconference to review the 10-Q and 10-K prior to their issuance. Four timesa year we meet as an audit committee in conjunction with a full board meetinggenerally in the afternoon or evening preceding the full board meeting. Gener-ally the external auditor is always a part of these meetings.

NASDAQ audit committee chair

A number of audit committee members told us that meeting length hasincreased dramatically post-SOX. For example, one NYSE audit committee memberindicated that the meetings used to last for 90 minutes; however, recently the meet-ings have lasted for approximately five hours, an experience the committee memberdescribed as “awful” (apparently due to the extreme length of the meetings). Someaudit committee members told us that they hold their meetings the night beforeboard meetings so that no artificial limits are placed on the length of the commit-tee’s meeting (consistent with Spira 2002), and many audit committees often meetwithout management present.

Given that we did not attend audit committee meetings, we cannot assess thesubstance of the meetings. However, it appears to us that many of the audit com-mittee members are committed to meaningful, substantive meetings, consistentwith an agency perspective. Similarly, Gendron et al. (2004, 168) conclude, “auditcommittee meetings are not mere rituals devoid of interest to managers and auditors”(also see Gendron and Bédard 2006).

Audit committee meeting agenda setting

Most proponents of audit committee reform argue that effective boards and auditcommittees should set their own agendas and determine the types of informationthat they want to review before meetings (National Association of Corporate Direc-tors [NACD] 1996). In fact, some have noted that the usurpation of these responsi-bilities by senior management at Enron and WorldCom contributed to the financialfrauds at those entities (Batson 2003; Breeden 2003). A similar concern was notedat Hollinger International Inc. (Paris report 2004), and Gendron and Bédard (2006)and Spira (2002) note that management can influence the agenda or informationflow to its advantage. We asked a series of questions to learn more about theagenda-setting processes for audit committee meetings (see panel B of Table 5).

Agendas typically are set well in advance of the meeting, and the audit com-mittee chair often sets the agenda, with input from the CFO and other committeemembers, consistent with Spira’s 2002 finding that the agenda is driven by thefinance director and audit committee chair. Three individuals described this processas follows:

CAR Vol. 26 No. 1 (Spring 2009)

84 Contemporary Accounting Research

TABLE 5AC process area 3: Audit committee meeting processes*

Number of audit committee meetings each year 10.1 4 30Face-to-face meetings 5.1 3 11Telephone meetings 5.0 0 20

Length of typical audit committee meeting(in minutes)

Normal face-to-face meetings 197.5 90 420Special face-to-face meetings (n � 6) 177.5 90 360Telephone meetings (n � 21) 85.0 30 270

How often does the audit committee meetwithout management present (n � 41)? n Percent

Every AC meeting 16 39Every face-to-face AC meeting 19 464–6 times per year 5 12Less than 4 times per year 1 2

Setting the agenda for audit committee meetingsWhen is the agenda set? (n � 27)

5–7 days before the meeting 4 158–14 days before the meeting 10 3715–28 days before the meeting 8 301 year in advance of the meeting 5 19

Individual with primary responsibility for putting the agendatogether (n � 40)

Audit committee chair 32 80CEO or CFO 5 13

Other individuals with input on the agendaCFO 26 62Other audit committee members 25 60Internal auditor 10 24General counsel 9 21External auditor 8 19CAO/controller 7 17CEO 7 17

Method used to put the agenda togetherA detailed calendar of what is covered at each committee

meeting 12 29A matrix that maps audit committee responsibilities to

specific committee meetings per the charter 10 24

(The table is continued on the next page.)

Panel A: Number and length Mean Minimum Maximum

Panel B: Agenda n Percent

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 85

TABLE 5 (Continued)

Type of information received in advance of AC meetingsDraft regulatory filings, including financial statements 32 76Reports and other forms of communication from the external

auditor 21 50Reports from internal audit 19 45Draft press releases 12 29Reports from counsel and other attorneys 7 17

When is the information packet received (n � 41)?1–3 days before the meeting 3 74–7 days before the meeting 16 391–2 weeks before the meeting 19 46Varies depending on the type of information received 3 7

Role of the AC in determining type of information included inthe packet (n � 39)

Information is jointly determined by AC and another party(typically management) 16 41

Information is primarily determined by the AC 14 36Information is primarily determined by others (i.e., not by

the AC) 9 23

What the AC member does when he or she receives (reviews) thepacket

Assesses whether disclosures are full, complete, and accurate 8 19Reviews external auditor comments/audit plans/management

letters 7 17Compares financial results with the past 5 12Reviews special risk areas 5 12Reviews management’s analysis of the financial statements 4 10Reviews presentations for upcoming meeting to develop

questions and comments 4 10Reads draft of earnings release and other outside

communications 3 7

What the AC member looks for when he or she receives (reviews)the packet

Unusual things/trends, including the reasonableness ofexplanations 18 43

Reasonableness of margins, other F/S indicators, and financialmetrics 13 31

Consistency of actual performance vs. expectations 5 12Status of litigation involving the entity 5 12Status of the 404 compliance project 5 12

(The table is continued on the next page.)

Panel C: Information packet n Percent

CAR Vol. 26 No. 1 (Spring 2009)

86 Contemporary Accounting Research

We redid the charter in 2002 — it now drives the audit committee agenda (wewant to be sure that we cover what we said we’d do). We also hit additionalrisk areas — litigation, patents, et cetera. We keep a matrix of three years ofsubjects down the left side and time across the top. Each topic is hit at leastonce every 24 months, although some topics are addressed at every audit com-mittee meeting.

NASDAQ audit committee chair

The agenda is set weeks in advance by the independent audit committee chair-man. There are no restrictions on adding items before the meeting or during it.Often an item discussed at meeting #1 is put on the agenda for follow-up atmeeting #2.

NASDAQ audit committee member

The audit committee builds a calendar at the beginning of the year to serve asits agenda for the committee meetings appended to the board meeting. Theaudit committee together identifies a “top 10” list of issues. This top 10 listhelps the audit committee focus on gaining a better understanding of the

TABLE 5 (Continued)

Communications received between AC meetingsFrequency of communications (n � 34)

Daily 3 9Weekly 7 21Semi-monthly 2 6Monthly 22 65

Parties from whom oral communication is receivedCFO 8 19CEO 6 14Internal audit 6 14Unspecified management 4 10External audit partner 3 7

Nature of written communication receivedMonthly financial statements 17 40Research reports (e.g., analysts) 8 19Press releases 6 14Press coverage 5 12Updates on changes in the regulatory environment 4 10

Note:* The statistics in this table are based on the full group of 42 interviewees, unless

otherwise noted.

Panel D: Between meetings n Percent

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 87

business and underlying accounting issues. The top 10 list also includes a listof compliance issues to be covered each year by the audit committee. Compli-ance issues include evaluating auditor independence, the audit committeecharter, proxy disclosures, and identification of the financial expert of the auditcommittee.

NASDAQ audit committee chair

This focus on agenda formality is consistent with Gendron and Bédard 2006,who find a strong emphasis on consistent, mechanistic agenda setting (also seeTurley and Zaman 2007). Without access to audit committee meetings, it is diffi-cult to determine whether the audit committee agenda-setting process results insubstantive monitoring or is simply ceremonial. It is clear that many audit commit-tees devote significant effort to ensuring that the agenda is responsive to the auditcommittee charter and to company risks. In other cases, however, it appears thatmanagement still drives the agenda.

Pre-meeting flow of information to the audit committee

As shown in panel C of Table 5, the audit committee members described pre-meetinginformation packets that typically contain draft filings and various audit reportsand include a substantial amount of information (Gendron et al. 2004; Spira 2002).One interviewee described the information packet:

The audit committee receives a spiral-bound notebook. The notebook containsall reports prepared by internal audit since the last meeting (10–15 reports).The audit committee also receives internal audit’s plan and a status report onits progress in meeting that plan. In addition, the audit committee receivesreports from the external auditor and a separate internal compliance group.The audit committee also gets press releases.

American Stock Exchange [AMEX] audit committee chair

The packets typically are received at least four days before the meeting, butinformation timeliness can be a significant issue and may reduce the audit committeeto a ceremonial role:

We get the packet in advance, but not as far as we’d like — usually 5–6 daysahead of a meeting. This is a major improvement — used to be one day before.The new Corporate Secretary has done a super job on this.

NASDAQ audit committee chair

We get the packet about two days in advance. It turns into panic reading.NYSE audit committee chair

Contrary to the more passive audit committee in Turley and Zaman 2007,many of these audit committees appear to drive much of the content of the infor-mation packet:

CAR Vol. 26 No. 1 (Spring 2009)

88 Contemporary Accounting Research

Guidelines of what the audit committee wanted were given to management.Management gave the audit committee content following those guidelines.The audit committee often asks for changes, and management then makes thechanges. Management exhibits a good deal of flexibility and responsiveness.

Mutual fund audit committee chair

Over time the content of the information in the packet has evolved. It used tobe determined by the various service providers (counsel, external auditor,investment advisor).

NYSE audit committee member

We also inquired about the nature of the audit committee member’s review ofthe packet and what the audit committee member looks for when he or she reviewsthe information packet. Some audit committee members assess the adequacy offinancial disclosures, while others review external auditor comments, audit plans,and management letters. However, each of the reported percentages is low (allunder 20 percent), reflecting a lack of consensus on how to review the informationpacket. Such a lack of consensus could be positive because different audit commit-tee members may approach issues in nonoverlapping ways.

Many committee members look for unusual results or unexpected trends, andthey evaluate the explanations provided by management for these unusual items.Many evaluate the reasonableness of reported margins, other financial statementindicators, and financial metrics. Several audit committee members described theirprocess:

I read the entire packet carefully. I look for things to concentrate on — what’smost important? There is a lot of boilerplate external auditor communications,and I ask them [the external auditor] to highlight things that are important.There is lots of external auditor butt-covering now (trying to reduce liability). Icompare across my three audit committees to identify things to focus on and tobenchmark company practices — there are great spillover benefits of servingon three audit committees.

NASDAQ audit committee chair

Look for certain things in the financial statements (e.g., inventory by location,bank borrowings). Look at margins, income elements, Selling, General &Administrative expenses (a dozen or so indicators). Look at internal auditreports for failures that have been “glossed over”. Look at litigation issues.Must be careful to not become complacent when looking at the same stuff eachtime! The questions and answers can become similar and boring. What couldhappen that we need to ask about? Better to find it now than later.

NYSE audit committee chair

I don’t necessarily look at “management’s answer”. Rather, I try to evaluatewhether there is an ongoing disciplined process that management is doing to

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 89

do its job. I don’t think our role is to solve the problem. Instead, our role isto determine if there is a process in place that we are comfortable with. Wemight occasionally get involved in a specific litigation issue to ensure it mapscorrectly to the footnote disclosure.

NASDAQ audit committee chair

I particularly look at estimates, judgments, follow-up items, anything fromprior discussions — anything that revolves around management’s judgmentsand how well it was disclosed to determine if that disclosure is robust enough.I assess information we are given and information we are putting out (e.g., inthe 10-K) to be sure it fairly reflects the situation.

NASDAQ audit committee chair

I am looking for surprises from anything. Looking for inconsistencies and forinformation about future risks. Looking for things we need to take action on.Assessing whether information is telling you what you expect or whether youare surprised by it.

NASDAQ audit committee chair

It appears that most of the audit committee members quoted above attempt toengage in rigorous, meaningful analysis of the information provided to them, con-sistent with the “smell test” highlighted by Gendron et al. 2004 and with an agencytheory view of an audit committee’s responsibility. However, these efforts are limitedby the timeliness and quality of the information packet. In cases where the informa-tion packet arrives just prior to the meeting or does not contain useful information,the audit committee may be reduced to a ceremonial role.17

Communications between meetings

Gendron and Bédard (2006), Spira (2002), and Turley and Zaman (2007) find thata great deal of audit committee activity occurs outside of formal meetings. Simi-larly, our interviewees describe frequent, ongoing substantive communicationswith management, internal auditors, and external auditors between scheduledmeetings (see panel D of Table 5; also see text under the heading “AC ProcessArea 5: Oversight of the Internal and External Audit Processes”, below, regardinginteractions with auditors). However, there are notable differences in informationflow between meetings:

Every month I get a sales report, and every 4–6 weeks I get market information(what the market is saying about us). I have lots of contact with managementand others — CFO (twice per month), Controller (once per month), ChiefAudit Executive (twice per month), external audit partner (once per quarter),and counsel (once per month).

NYSE audit committee chair

I don’t get information that frequently. As audit committee chairman, I occa-sionally call the CFO and chat about recent events or issues. I’m trying to

CAR Vol. 26 No. 1 (Spring 2009)

90 Contemporary Accounting Research

determine if there are new issues that have arisen that require the audit commit-tee’s involvement. We do not receive monthly financial statements or budget-to-actual comparisons.

NASDAQ audit committee chair

It’s becoming almost excessive. We get press releases almost weekly to review.It’s becoming a burden on my email at home. Earnings releases, litigationinformation, and acquisition information — something seems to always becoming my way.

NYSE audit committee member

It depends. The external auditor sends stuff. We give the auditor two standards:(1) you need to have read it yourself, and (2) you need to have thought aboutand summarized the application of the information to this company. This is avery good discipline to follow. We get other stuff sent to the full board — ana-lyst reports, governance reports, monthly financial statements, public relationsinformation, clippings, et cetera.

NASDAQ audit committee chair

Assuming meaningful interactions and review of information, such extensivecontact and information flow between meetings may be consistent with substantiveaudit committee monitoring, although perhaps in an informal manner (Turley andZaman 2007). In many cases, we see evidence of such contact; however, in othercases, it appears that the audit committee’s efforts are almost exclusively centeredaround formal meetings and, therefore, may be more ceremonial.

AC process area 4: Audit committee oversight of the financial reporting process

Review of financial reporting risk areas

In terms of specific risk areas, one clearly stands out in panel A of Table 6: revenuerecognition, which is specifically reviewed by almost half of the audit committees(some of those who did not list revenue recognition as a risk area felt compelled toexplain why not). Several audit committee members described their efforts regard-ing revenues, all of which signal fairly vigilant monitoring by the audit committee,consistent with agency theory:

Revenue recognition is the biggest, since it’s software. We go through deal-by-deal [sale-by-sale each quarter], and the external auditor shares their view(using the deal documents) on revenue recognition.

NASDAQ audit committee chair

There is a heavy focus on revenue recognition given the company sells a soft-ware product plus services. There are lots of issues that can be affected by thesales staff that might dictate revenue recognition terms. We also discuss issuesrelated to materiality.

NASDAQ audit committee member

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 91

Revenue recognition is very hard in the medical device industry. It’s very diffi-cult to predict demand, and it’s very difficult to establish the revenue cut-off.Hospitals are bad at documenting when things (e.g., surgery) happen. That makesit difficult to establish revenue cutoff — in essence our products are at hospitalson consignment until pulled from shelf to be inserted inside a patient (becauseof the way contracts are written). The company is trying to work better withhospital partners to do a better job of this — building in contract incentives toimprove information reliability. The audit committee’s primary concern is basedon management’s confidence in the quarterly numbers. As we sense manage-ment is more confident about its numbers and cutoff, the more confident we are.

NYSE audit committee member

The company uses an outside firm to do our internal audit work. This outsidefirm reviews revenue recognition at every subsidiary (and every type of con-tract) and reports back to the audit committee chair on whether revenue isbeing recognized correctly.

NASDAQ audit committee chair

Other key risk areas examined include reserves, fixed assets (primarily relatedto asset impairment), inventory (primarily related to the obsolescence reserve), andreceivables. For example, three audit committee members described financialreporting risks and monitoring efforts:

I want to understand how we’ve done and apply technical knowledge to makesure we’ve done things correctly (e.g., new standards). I focus on properdisclosure/communication to shareholders. In terms of specific areas, there isa major focus on fraud (to never let it happen again in this company). I some-times ask myself, “Would I have caught the fraud [that occurred before thisperson’s term on the board]?” The honest answer is probably not. It wouldhave required someone to step back from the details and understand thatratios/analytics that appeared okay should not have appeared okay due to whatwas happening in the industry.

NASDAQ audit committee chair

Our company is merger and acquisition driven. We focus on revenue recognitionissues, tone at the top at acquired companies, and how acquired companiestreat contracts. I am very concerned about anything done to inflate earnings/revenues. I review whether the company is in compliance with EmergingIssues Task Force pronouncements on revenue recognition.

NASDAQ audit committee chair

We focus on subjective areas of accounting that affect income. I ask the auditpartner about the five most subjective areas of income determination. Examplesinclude warranty reserves, post-retirement benefits, income taxes, impairmentof long-lived assets, and journal entries at period end.

NYSE audit committee chair

CAR Vol. 26 No. 1 (Spring 2009)

92 Contemporary Accounting Research

These perspectives all suggest substantive monitoring on the part of someaudit committees.

Review of accounting policies and estimates

Panel B of Table 6 provides information about processes performed by audit com-mittees related to their review of accounting policies and estimates, which rangefrom extensive to minimal. Two audit committee members described their extensiveinvolvement with accounting policies; the second description may reflect a mana-gerial role for the audit committee:

TABLE 6AC process area 4: Audit committee oversight of the financial reporting process*

Financial reporting risk areas reviewed by the audit committeeRevenue recognition 19 45Reserves 12 29Fixed assets, including asset impairment 9 21Inventory, including obsolescence 9 21Receivables, including allowance for doubtful accounts 8 19Critical accounting policies 7 17Litigation 6 14Management judgments/estimates 6 14Mergers and acquisitions 6 14Regulatory compliance concerns 6 14Taxes 6 14Debt, including covenants 5 12

Audit committee involvement in setting/reviewing specificaccounting policies (n � 37)

Reviews policies 28 76Not currently involved, but would be if a major change

occurred 7 19Minimal involvement 2 5

Audit committee discussion of specific judgments/estimates/assumptions involved in implementing an accounting policy(n � 31)

Yes, involved 24 77Involved to some extent 7 23

Audit committee review of accounts dependent on assumption/estimates (n � 11)

Audit committee reviews assumptions/management judgments 9 82Audit committee relies on the external auditor 2 18

(The table is continued on the next page.)

Panel A: Financial reporting risks n Percent

Panel B: Accounting policies and estimates n Percent

CAR Vol. 26 No. 1 (Spring 2009)

The Audit Committee Oversight Process 93

Our review of accounting policies is extensive. We are trying to make sure thatthe message gets through that the audit committee is not tolerant of GAAPnon-compliance due to immateriality. We are looking for the right tone in thecompany and to set the right tone. We aim to set high expectations and we havean aggressive attitude in setting this tone — no sloppiness.

Mutual fund audit committee chair

The audit committee actually sets the policies and reviews them annually. Theaccounting practices and financial practices of the company are reviewed andapproved on an annual basis.

NYSE audit committee member

Two others discussed their very limited role with accounting policies:

The audit committee has minimal involvement in setting and reviewing account-ing policies. The audit committee relies on the external auditor to identify areaswhere a change is needed. Also, the audit committee feels that they are only usedfor oversight. We do not have active involvement in setting these policies.

NYSE audit committee chair

TABLE 6 (Continued)

Audit committee discussion of alternative accountingtreatments available under GAAP (n � 30)

Always discuss 20 67Sometimes discuss 5 17Discussions have been held in the past 2 7No discussion 3 10

Does the AC ask the external auditor which treatment theywould use (n � 27)?

Yes 24 89No 3 11

Form of external auditor’s communication regarding alternativetreatments (n � 30)

Oral 18 60Both oral and written 11 37Written 1 3

Is management present for the discussion of alternativeaccounting treatments (n � 30)?

Sometimes 10 33Yes 9 30Yes, followed by a separate executive session without

management 11 37

(The table is continued on the next page.)

Panel C: Alternative accounting treatments n Percent

CAR Vol. 26 No. 1 (Spring 2009)

94 Contemporary Accounting Research

The audit committee’s involvement in setting policies is close to zero. Man-agement will discuss a policy and get the concurrence of the audit committee.

NYSE audit committee chair

Overall, there is some lack of consensus on the audit committee’s role in thisarea. Many audit committees approach accounting policies with the goal of providingvigorous monitoring, while others appear to do very little, serving more of a cere-monial role by simply relying on the auditors with minimal audit committee analy-sis of the issues (also see Pomeroy 2007 for post-SOX evidence on auditcommittee members’ evaluation of accounting decisions).

The audit committee’s involvement in reviewing management estimates, judg-ments, and assumptions often is quite extensive. All of the audit committee members

TABLE 6 (Continued)

Audit committee involvement in assessing financial statementfraud risks

Audit committee’s own actions 32 76Reliance on the external auditor 16 38Reliance on the internal auditors 14 33Little involvement 2 5

Audit committee’s own actions in assessing financial statementfraud risks

Closely analyze reserves and other financial statement areaswhere fraud could occur 6 14

Assess character of management 4 10Regular interaction with management 4 10Actively promote the company’s hotline 3 7Actively search for fraud risks 3 7Review officers’ expenses (annually) 3 7

Assessing and monitoring management’s integrityHow does the audit committee assess management’s integrity?

Evaluate management’s body language 7 17Observe management’s transparency/openness, especially