audit committee - meetings, agendas, and minutes

TRANSCRIPT

AUDIT COMMITTEEAUDIT COMMITTEEAUDIT COMMITTEEAUDIT COMMITTEE

10.00 AM

ON

MONDAYMONDAYMONDAYMONDAY

18 APRIL 201118 APRIL 201118 APRIL 201118 APRIL 2011

IN

MEETING ROOM 1 - SHIRE HALL,

GLOUCESTER

MEETING PAPERS

Public Document Pack

Audit Committee

Monday 18 April 2011 10.00 am

Meeting Room 1 - Shire Hall, Gloucester

AGENDA

Item CONTACT

1 Apologies for Absence Andrea Griffiths Tel: 01452 425006

2 Declaration of Interest

Please refer to note 1 at the end of the agenda

Andrea Griffiths Tel: 01452 425006

3 Minutes (Pages 1 - 8)

(a) To consider any issues arising from the meeting held on 24th January 2011.

(b) To confirm and sign the minutes as a correct record.

Andrea Griffiths Tel: 01452 425006

4 Internal Audit Plan (Pages 9 - 34) Mark Spilsbury Tel: 01452 426127

5 External Audit Progress Report (Pages 35 - 48) Peter Barber

6 Reports on actions taken in relation to key issues (Pages 49 - 60)

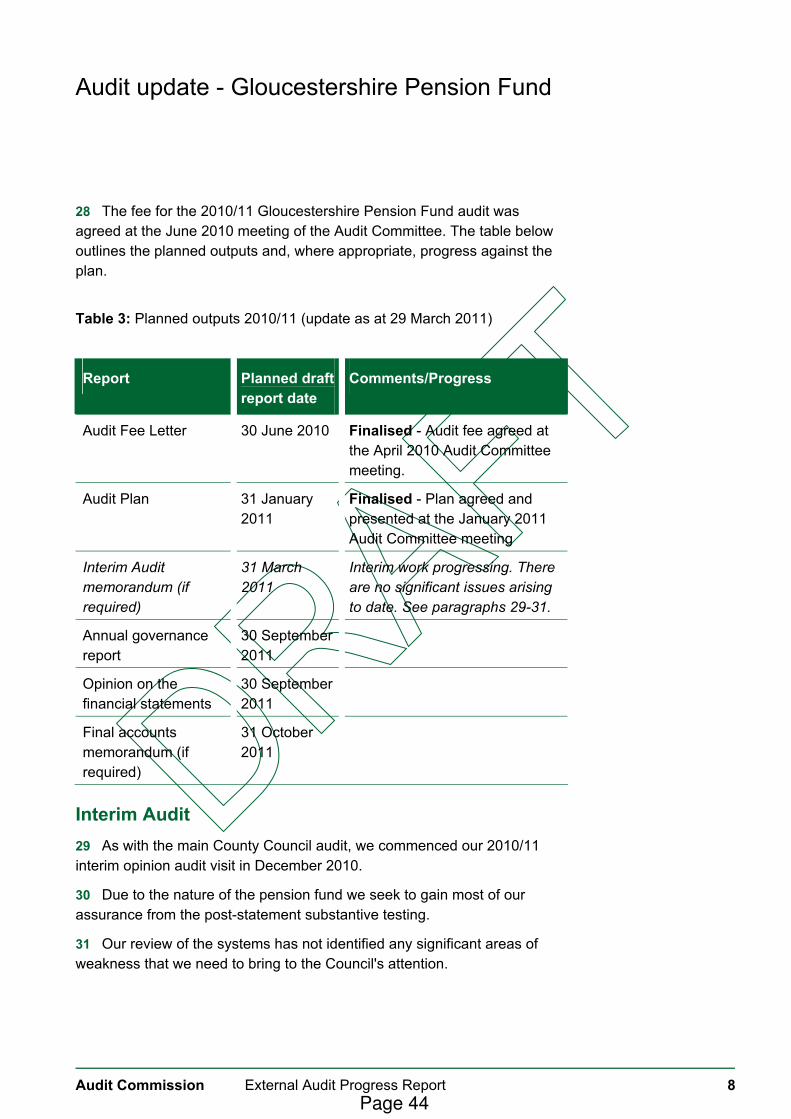

(a) Domiciliary Care – Contract re-negotiation and the monitoring of

care provision – Presented by Mark Branton (b) School Deficit Budgets – Presented by Jo Grills (c) Major Transport Contracts – Presented by Philip Williams

Jo Grills, Mark Branton, Philip Williams

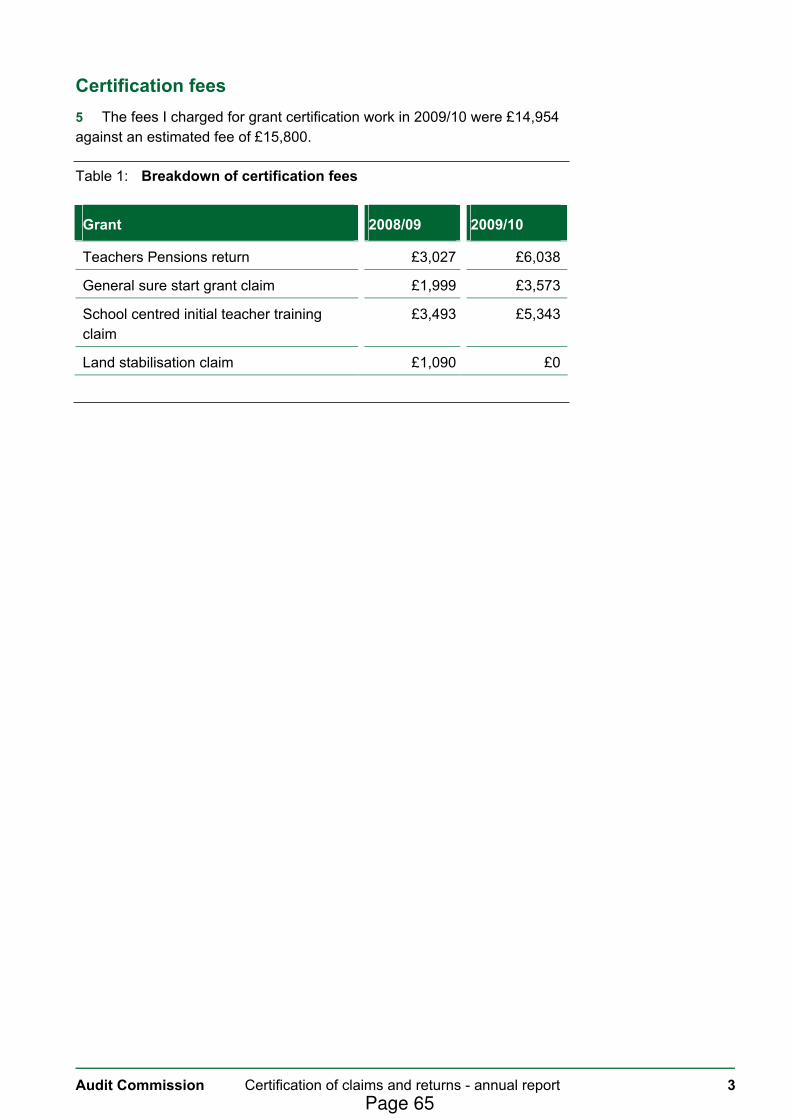

7 Certification of Claims and Returns - Annual Report 2009/10 (Pages 61 - 72)

Peter Barber

8 Effectiveness of the Audit Committee (Pages 73 - 92) Mark Spilsbury Tel: 01452 426127

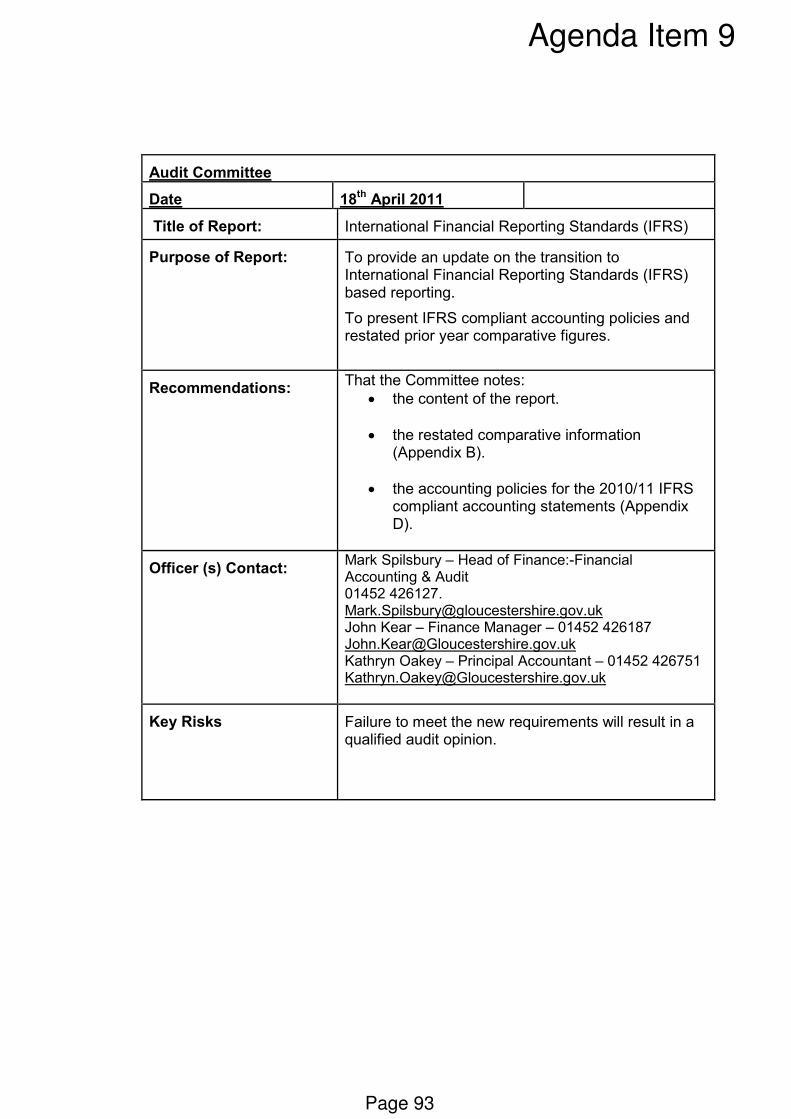

9 IFRS - Restatement of opening balances (Pages 93 - 112) Mark Spilsbury Tel: 01452 426127

10 Audit & Inspection of Local Authorities (Pages 113 - 124)

The full consultation report referred to within the report relating to this item

can be accessed at

http://www.communities.gov.uk/documents/localgovernment/pdf/1876169.pdf

Mark Spilsbury Tel: 01452 426127

11 Accounts & Audit Regulations (Pages 125 - 130)

For information purposes: The full regulations can be accessed at http://www.legislation.gov.uk/uksi/2011/817/made/data.pdf

Mark Spilsbury Tel: 01452 426127

12 Annual Report of the Audit Committee (Pages 131 - 132)

Annual Report of the Audit Committee as prepared by the Chairman, for agreement prior to presentation to County Council

Cllr Philip McLellan

13 Date of next meeting

The next meeting will be held on 28th June 2011

Cllr Philip McLellan

The Audit Committee

Cllr Ron Allen, Cllr John Burgess, Cllr Gerald Dee, Cllr Philip McLellan (Chair), Cllr Mike Sztymiak and Cllr Brian Tipper

NOTES

1. DECLARATIONS OF INTEREST – Members requiring advice or clarification about whether to make a declaration of interest are invited to contact the Monitoring Officer (Nigel Roberts�01452 425201/fax: 426790/e-mail: [email protected]) prior to the start of the meeting.

2. INSPECTION OF PAPERS AND GENERAL QUERIES - If you wish to inspect Minutes or Reports relating to any item on this agenda or have any other general queries about the meeting, please contact: Andrea Griffiths, Democratic Services Officer �:01452 425006/fax: 425850/e-mail:[email protected]

3. GENERAL ARRANGEMENTS (a) Will Members please sign the attendance list.

(b) Please note that substitution arrangements are in place.

EVACUATION PROCEDURE - in the event of the fire alarms sounding during the meeting please leave as directed in a calm and orderly manner and go to the assembly point which is outside the main entrance to Shire Hall in Westgate Street. Please remain there and await further instructions.

This page is intentionally left blank

- 1 -

AUDIT COMMITTEE

MINUTES of the meeting of the Audit Committee held on Monday 24th January, 2011 commencing at 10.00 am.

PRESENT MEMBERSHIP:

Cllr Ron Allen Cllr John Burgess Cllr Gerald Dee

Cllr Philip McLellan (Chair) Cllr Mike Sztymiak Cllr Brian Tipper

Substitutes:

1. APOLOGIES FOR ABSENCE

2. MEMBERSHIP The chairman wished to recognise the valuable contribution Councillor Glanfield had made to this committee, his valuable knowledge would be sadly missed. The chairman also welcomed Councillor Ron Allen to the meeting.

3. DECLARATIONS OF INTEREST BOTH CLLR BURGRESS AND CLLR DEE DECLARED A PERSONAL NON-PREJUDICIAL INTEREST IN RESPECT OF THEM RECEIVING A LOCAL GOVERNMENT PENSION FROM GLOUCESTERSHIRE COUNTY COUNCIL. Both the Chairman and Cllr Mike Sztymiak declared a personal non-prejudicial interest in respect of them being a member of the Pensions Committee. It was duly noted that Cllr Sztymiak was employed by Capita.

4. MINUTES All matters arising had been dealt with and communicated to members of the committee.

Resolved

THAT PAGE 1, MINUTE 38, READ AS “RECEIVING A LOCAL GOVERNMENT PENSION FROM GLOUCESTERSHIRE COUNTY COUNCIL” AND WITH THIS AMENDMENT THE MINUTES OF THE MEETING HELD ON 22 SEPTEMBER 2010 BE SIGNED AS A CORRECT RECORD BY THE CHAIRMAN.

5. ANNUAL AUDIT LETTER - 2009/10 - GLOUCESTERSHIRE COUNTY COUNCIL

Agenda Item 3

Page 1

Minutes subject to their acceptance as a correct record at the next meeting

- 2 -

Martin Robinson presented this report that summarised the findings from the 2009/10 audit. It included messages arising from the audit of the council’s financial statements and the results of the work that had been undertaken to assess the Council’s arrangements to secure value for money in its use of resources. The Auditor had given an unqualified opinion on the accounts and an unqualified value for money opinion. It was noted that a decision was still awaited with regard to whether Local Authorities would be a preferred creditor in the Icelandic Banks situation. RESOLVED THAT the report be noted.

6. AUDIT COMMISSION PROGRESS REPORT Peter Barber presented the regular update report showing work to be undertaken by the Audit Commission in relation to the Council and progress made on Audits already been undertaken. RESOLVED That the report be noted.

7. AUDIT COMMISSION UPDATE ON PLANNING FOR AN AGEING POPULATION REPORT Peter Barber presented the report. It was evident that Gloucestershire would have an increasing older population which would place increased financial pressure on the medium term financial strategies of public sector bodies involved. He explained that the proportion of older residents living in the county was high and was expected to increase at a faster rate than the national average over the next 20 years.

Members agreed there was a risk to Gloucestershire’s public services and the task of balancing the growing demand for services against financial constraints would be difficult. The report highlighted a number of challenges that were fundamental to ensure the future service delivery, thus making it effective and affordable in Gloucestershire. It was noted that the report had been shared with the Primary Care Trust and other partners. Mark Spilsbury explained there was currently a £1.5 million overspend and every effort was being made to reduce the deficit. As such a review team was being established to look individual cases and care packages on offer. As part of the ongoing review process, different panels would be established to ensure

Page 2

Minutes subject to their acceptance as a correct record at the next meeting

- 3 -

robustness and that the appropriate packages would be offered to the people who needed them. The committee felt that the report should be discussed in more detail by providers of the service, so that an informed response could be collated. After some discussion it was agreed that the report would be referred the Health & Overview Scrutiny Committee who would report back to the September 2011 Audit Committee. RESOLVED (i) That the Committee noted the report (ii) That the report would be referred to the Health & Overview Scrutiny

Committee, to report on responses received from care providers. (iii) That a report on the responses be submitted to the September 2011

Audit Committee

8. COMPLIANCE WITH INTERNATIONAL AUDITING STANDARDS Mark Spilsbury presented the report, he explained that in order to comply with International Auditing Standards the Audit Commission was required to obtain an understanding of how those charged with governance (the Audit Committee) exercised oversight of management processes for identifying and reporting the risk of fraud and possible breaches of internal control in respect of the Council and Gloucestershire Pension Fund.

RESOLVED

(i) That the Committee noted the report (ii) That a response would be collated on behalf of the Chairman and

emailed to him for approval.

9. AUDIT PLAN 2010/11 Martin Robinson, Audit Commission, presented the reports which informed the Committee of the audit work to be undertaken for the 2010/11 financial year for Gloucestershire County Council, the Gloucestershire Pension Fund and the fee involved.

It was explained that because the 2010/11 audit was not yet complete, the audit

planning process for 2011/12, including the risk assessment would continue as the year progressed and the fees would be reviewed and updated as necessary.

The total indicative fee for the audit for 2010/11 was £242,000 which was 1.9per

cent above the scale fee. It was reported this was due to additional audit work associated with the small number of County Councils with integrated fire services.

RESOLVED

Page 3

Minutes subject to their acceptance as a correct record at the next meeting

- 4 -

THAT the reports be noted.

10. INTERNAL AUDIT MONITORING REPORT Mark Spilsbury presented this report that provided the Committee with an update on key findings emanating from Internal Audit reports issued since the last audit monitoring report to the Committee. Members scrutinised the report content in detail and after some discussion it was agreed that the committee would request reports on the three areas where limited assurance had been given.

RESOLVED That the Committee (i) Notes the key findings. (ii) Notes the actions proposed in relation to the audits reported. (iii) Notes the overall progress made against the plan. (iv) Notes the changes made to the plan. (v) School Deficit Budgets – Director, Learning and Development (CYP)

report back to the Audit Committee in April 2011 on the progress made in relation to the actions being taken

(vi) External Care for Older People & Income Collection - A senior officer from CACD report back to the Audit Committee in June 2011 on the progress made in relation to the actions being taken

11. REPORT ON ACTIONS TAKEN IN RELATION TO KEY ISSUES (a) Complex needs (Social Care) Budget – CYPD Andy Ray, Head of Children in Care gave a detailed presentation of the report’s findings. He explained that since his appointment in June 2010 the system had undergone a review process and any care placements made had to be authorised by himself or a delegated officer in his absence. Members were informed that different cost options were now available for different rationales, and as such all children in care were reviewed on a regular basis to ensure their needs were being met. It was reported that in 2009/10 there was an overspend of £7 million, however as such significant improvements had been made, this was somewhat of a success story and there was no longer an overspend. Members were informed that a profile was sent to all service providers for costing, Andy explained that this ensured an appropriate match for the child’s needs, as it was not possible to sit in an office and make an informed judgment on a child, when they had never met them, as sometimes there needs were more specific.

Page 4

Minutes subject to their acceptance as a correct record at the next meeting

- 5 -

A panel made up of approximately 13 members from across the services, reviewed cases on a regular basis to ensure quality of care and consistency in the approach used. As such it was reported that there was now a £500,000 under spend. RESOLVED

That the report be noted (b) Information Security Dave Badham, Head of ICT and Heather Forbes, Head of Information Management & Archives presented the report which detailed action and progress made since April 2010. In response to a question, members were informed that the appropriate safeguards would be installed on photo copier hard drives as standard. So when a copier was due to be disposed off the appropriate deletion programme would be applied to wipe the hard drive of all data. RESOLVED

That the report be noted

12. MEETING THE CHALLENGE Andrew McCartney gave a verbal report to the committee. Members were interested to know what affect Meeting the Challenge may have on the Audit Plan.

RESOLVED

(i) That a verbal report would be given at the June Committee meeting, regarding the affects of Meeting the Challenge on the Audit Plan

(ii) It was also agreed that a report detailing Corporate Risk & Governance would be presented at the June committee meeting.

13. TREASURY MANAGEMENT STRATEGY 2011/12 Mark Spilsbury, Head of Finance, explained that the council had adopted the CIPFA Code of Practice for Treasury Management in Public Services which required an annual strategy in advance of the year to be prepared. The report provided gave details of the borrowing and lending activities that may take place during 2011/12. It was duly noted that this was a prudent strategy to follow given the financial constraints.

The Committee noted the revised treatment of the Icelandic Bank impairments as

outlined in the report.

Page 5

Minutes subject to their acceptance as a correct record at the next meeting

- 6 -

RESOLVED

THAT the Committee noted the Treasury Management Strategy for 2011/12.

14. DATE OF NEXT MEETING The Committee noted that its next meeting would take place on 18 April 2011.

CHAIRPERSON

Meeting concluded at 12:20

Page 6

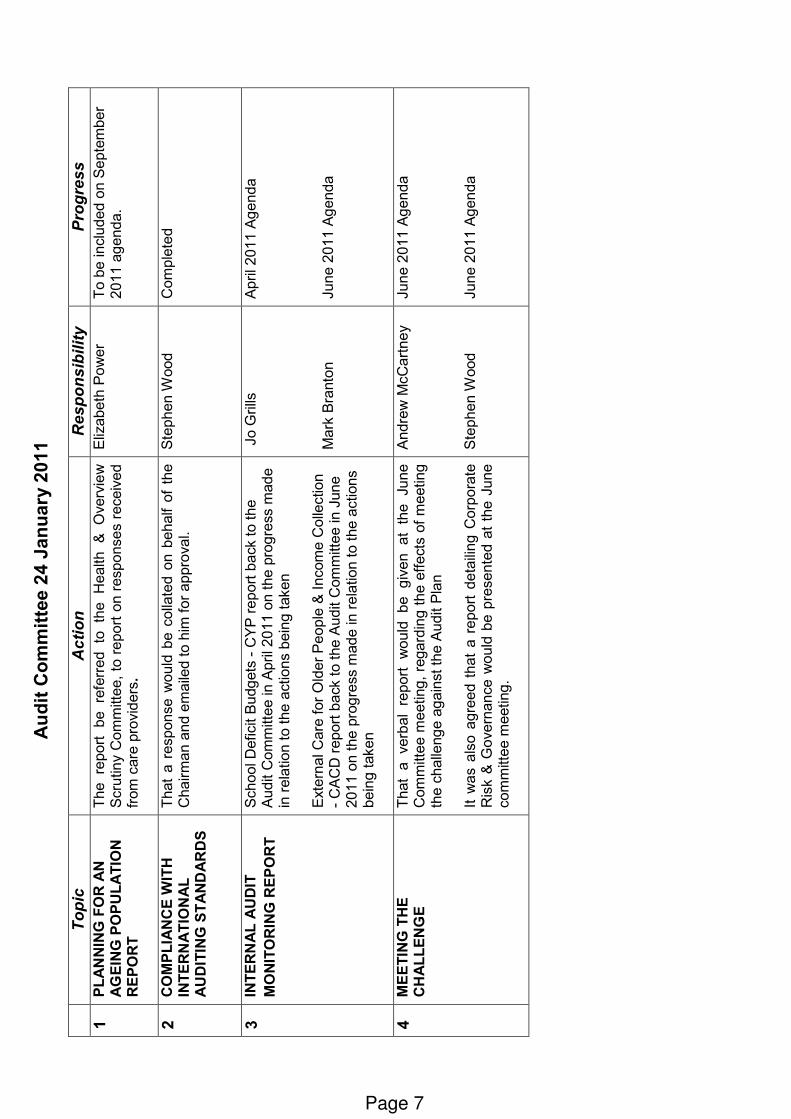

Audit Committee 24 January 2011

Topic

Action

Responsibility

Progress

1 PLANNING FOR AN

AGEING POPULATION

REPORT

The report be referred to the Health & Overview

Scrutiny Committee, to report on responses received

from care providers.

Elizabeth Power

To be included on September

2011 agenda.

2 COMPLIANCE WITH

INTERNATIONAL

AUDITING STANDARDS

That a response would be collated on behalf of the

Chairman and emailed to him for approval.

Stephen W

ood

Completed

3 INTERNAL AUDIT

MONITORING REPORT

School Deficit Budgets - CYP report back to the

Audit Committee in April 2011 on the progress made

in relation to the actions being taken

External Care for Older People & Income Collection

- CACD report back to the Audit Committee in June

2011 on the progress made in relation to the actions

being taken

Jo Grills

Mark Branton

April 2011 Agenda

June 2011 Agenda

4 MEETING THE

CHALLENGE

That a verbal report would be given at the June

Committee m

eeting, regarding the effects of meeting

the challenge against the Audit Plan

It was also agreed that a report detailing C

orporate

Risk & G

overnance would be presented at the June

committee m

eeting.

Andrew McCartney

Stephen W

ood

June 2011 Agenda

June 2011 Agenda

Page 7

Page 8

This page is intentionally left blank

1

Audit Committee

18th April 2011

Internal Audit Work Plan – 2011/12

SUMMARY

This report provides the Committee with details of the Internal Audit Plan for 2011/12. CONTEXT

The Internal Audit plan is submitted to the Committee for approval, in its capacity as the Audit Committee for the Authority. COMMENTARY The plan has been formulated taking account of the key business risks, and following discussion with and/or feedback from :-

• The Corporate Management Team;

• Strategic Finance Director;

• Other Directors;

• The Meeting the Challenge Team; and

• External Audit. ACTION

To consider and approve the Internal Audit plan for 2011/12.

Contact Officers: Mark Spilsbury – Head of Finance – Tel 01452 426127 Pam Jell – Audit / Fraud Manager – Tel 01452 425919 Theresa Mortimer – Audit / Risk Manager – Tel 01452 427013

Agenda Item 4

Page 9

2

Introduction

This report details the work planned for the Internal Audit service within Gloucestershire County Council in 2011/12. The starting point for the plan was to establish the key strategic priorities of the Council and prepare an outline plan, which ensures that we cover the key risks associated with the achievement of those priorities, and provide independent assurance that those risks are being controlled effectively. The Council’s priorities as detailed with the Council Strategy 2011 - 2014 are as follows:

♦ Getting our own house in order

o The overall savings delivered through Meeting the Challenge

o Total funds generated through sale of assets

♦ Protecting Vulnerable People

o The percentage of social care clients being given control of their own budgets

o A reduction in children returning into the Child Protection system for a second or subsequent time

♦ Supporting Active Communities

o Total funding provided to community groups through our small grants scheme o The number of buildings transferred to community ownership

♦ Building a Sustainable County

o The number of potholes and road defects repaired o The reduction in the amount of waste going into landfill o An increase in the renewable energy generated from the Council’s estate over

the lifetime of this strategy o The reduction in carbon emissions from Council buildings and transport

Many of the key systems and processes within the authority impact on a number, or indeed all of these priorities, therefore the plan has been developed to reflect these priorities and to enable Internal Audit to provide an independent, objective opinion to the Council on the effectiveness of the control environment, comprising risk management, control and governance, in their achievement. The annual plan also reflects national and local circumstances, and specifically takes account the views of:

• The Corporate Management Team;

• The Strategic Finance Director;

• Other Directors who were consulted as part of the formulation of the annual internal audit plan;

• The Meeting the Challenge Team; and

• External Audit.

Page 10

3

In terms of the key national and local factors which have been taken into account during the formulation of the plan, the key factors are:-

• The Meeting the Challenge agenda, and particularly the importance of ensuring that there are robust governance arrangements to ensure the effective delivery of the required MtC savings whilst minimising service implications;

• The need to continue with a high level of coverage of key financial systems, as dictated by International Accounting Standards, and relied upon by the External Auditors;

• The requirement under Risk Based Internal Auditing (RBIA) for internal audit to be strategically and operationally linked to business risk and assurance frameworks;

• Internal Audit certification requirements;

• High risk budget areas, particularly in the context of underlying budget pressures experienced in 2010/11 and forecast for 2011/12 onwards;

• Contractual arrangements, in the context of the increasing movement towards a commissioning authority with increased partnership working; and

• The need to publish a control assurance statement (Annual Governance Statement), as required by the Accounts and Audit Regulations 2003 and the CIPFA Code of Practice for Internal Audit 2006.

In accordance with these key factors, the audit plan, as set out in Appendix A, directs more resources in 2011/12 to certain high priority areas, particularly aimed at :-

• Ensuring that adequate governance arrangements are in place, particularly in relation to “Meeting the Challenge” projects.

• Building on the audit work undertaken in 2011/12, at the request of senior management within the Community and Adult Care Directorate, to ensure that high risk areas receive audit coverage in 2011/12, including the implementation of personal budgets, direct payments to adults, home care contracts and top up payments to adults. This input, together with follow up reviews of the external care budget and service user contributions, will ensure that the controls operating in these high risk areas are robust and effective, providing assurance, as requested, to senior managers within the Directorate;

• Undertaking a detailed review of partnerships, shared services and third party governance arrangements;

• Directing school audit resources to an examination of the processes in place within deficit schools which are designed to deliver on budget recovery plans, and an examination of additional payments to Headteachers;

• Continuing to provide information management and security consultancy, at the direct request of senior management;

• Continuing to audit major financial systems on a cyclical basis in accordance with an agreed strategic plan (Appendix C); and

• Providing adequate resources for the identification and/or investigation of areas of suspected fraud.

Page 11

4

It should be noted that Internal Audit work very closely with the External Auditors in accordance with a Joint Working Agreement, under which the External Auditors rely on the work of Internal Audit in certain key areas, particularly the key Financial systems audits, and any audits which help to inform their Value for Money opinion which, in the case of the planned audits for 2011/12 are likely to include the effectiveness of governance arrangements regarding the Meeting the Challenge projects and all of the Commissioning audits. The plan is intended to be flexible. Whilst we intend to complete the majority of audits outlined here, there may be circumstances where we will have to amend the programme, e.g. when a major irregularity investigation is required or a specific project becomes a matter of priority/risk, or audit findings warrant the investment of increased time.

In order to monitor performance in relation to the 2011/12 plan, all suggested amendments to the plan, in terms of new or deleted audits, will be reported to the Audit Committee within the regular internal audit monitoring reports.

The detailed plan for 2011/12 is attached at Appendix A, from which it can be seen that the plan will be delivered using 1804 chargeable days input by just over 10 fte staff.

The plan provided at Appendix A, excludes non-chargeable audit time such as time spent on administration and developing the internal audit service, and a contingency provision for unplanned items.

The planned audits are all linked in to the key risks of the authority as contained in the Strategic and Operational Risk Registers. The Strategic Risks are cross referenced as per the examples below:-

SRR1 Strategic Risk Register 1 Finance SRR3 Strategic Risk Register 3 Partnerships SRR6 Strategic Risk Register 6 MtC - Programme SRR10.1 Strategic Risk Register 10.1 Safeguarding - Adults SRR10.2 Strategic Risk Register 10.2 Safeguarding - Children Detailed terms of reference will be drawn up for every audit and will be agreed with appropriate management at the commencement of each of the audits. However, in summary, the main audit areas included within the plan are detailed by audit category in Appendix B. Finally, to ensure that key financial systems are audited at an appropriate frequency, as dictated by International Accounting Standards, and relied upon by the External Auditors, a rolling 5 year strategic plan for such systems has been produced, which is provided at Appendix C to this report.

Page 12

5

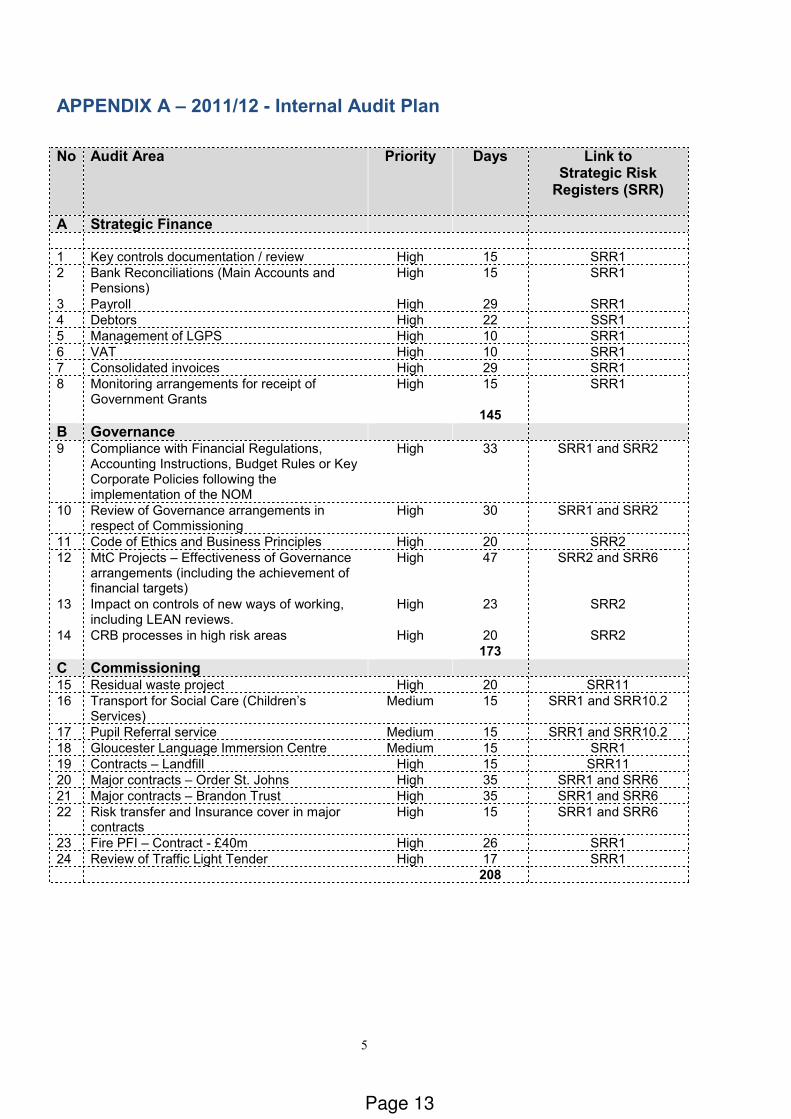

APPENDIX A – 2011/12 - Internal Audit Plan

No Audit Area Priority Days

Link to Strategic Risk Registers (SRR)

A Strategic Finance

1 Key controls documentation / review High 15 SRR1

2 Bank Reconciliations (Main Accounts and Pensions)

High 15 SRR1

3 Payroll High 29 SRR1

4 Debtors High 22 SSR1

5 Management of LGPS High 10 SRR1

6 VAT High 10 SRR1

7 Consolidated invoices High 29 SRR1

8 Monitoring arrangements for receipt of Government Grants

High 15 SRR1

145

B Governance 9 Compliance with Financial Regulations,

Accounting Instructions, Budget Rules or Key Corporate Policies following the implementation of the NOM

High 33 SRR1 and SRR2

10 Review of Governance arrangements in respect of Commissioning

High 30 SRR1 and SRR2

11 Code of Ethics and Business Principles High 20 SRR2

12 MtC Projects – Effectiveness of Governance arrangements (including the achievement of financial targets)

High 47 SRR2 and SRR6

13 Impact on controls of new ways of working, including LEAN reviews.

High 23 SRR2

14 CRB processes in high risk areas High 20 SRR2

173

C Commissioning 15 Residual waste project High 20 SRR11

16 Transport for Social Care (Children’s Services)

Medium 15 SRR1 and SRR10.2

17 Pupil Referral service Medium 15 SRR1 and SRR10.2

18 Gloucester Language Immersion Centre Medium 15 SRR1

19 Contracts – Landfill High 15 SRR11

20 Major contracts – Order St. Johns High 35 SRR1 and SRR6

21 Major contracts – Brandon Trust High 35 SRR1 and SRR6

22 Risk transfer and Insurance cover in major contracts

High 15 SRR1 and SRR6

23 Fire PFI – Contract - £40m High 26 SRR1

24 Review of Traffic Light Tender High 17 SRR1

208

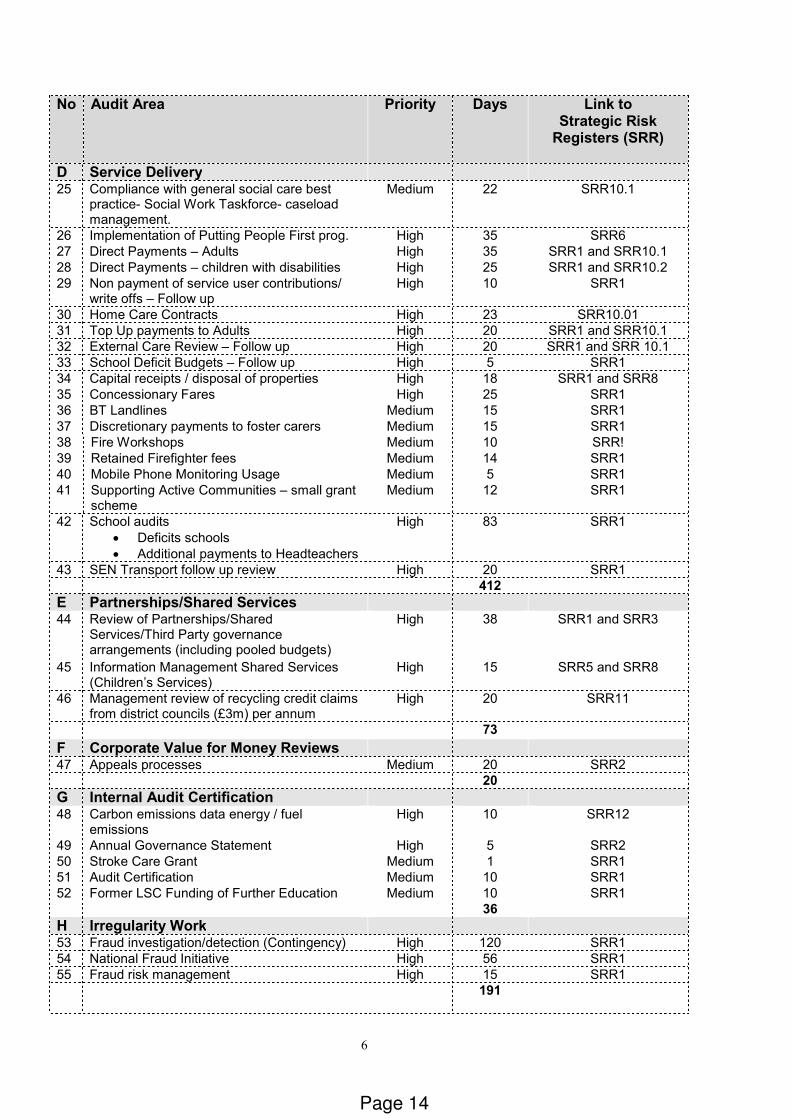

Page 13

6

No Audit Area Priority Days

Link to Strategic Risk Registers (SRR)

D Service Delivery

25 Compliance with general social care best

practice- Social Work Taskforce- caseload management.

Medium 22 SRR10.1

26 Implementation of Putting People First prog. High 35 SRR6

27 Direct Payments – Adults High 35 SRR1 and SRR10.1

28 Direct Payments – children with disabilities High 25 SRR1 and SRR10.2

29 Non payment of service user contributions/ write offs – Follow up

High 10 SRR1

30 Home Care Contracts High 23 SRR10.01

31 Top Up payments to Adults High 20 SRR1 and SRR10.1

32 External Care Review – Follow up High 20 SRR1 and SRR 10.1

33 School Deficit Budgets – Follow up High 5 SRR1

34 Capital receipts / disposal of properties High 18 SRR1 and SRR8

35 Concessionary Fares High 25 SRR1

36 BT Landlines Medium 15 SRR1

37 Discretionary payments to foster carers Medium 15 SRR1

38 Fire Workshops Medium 10 SRR!

39 Retained Firefighter fees Medium 14 SRR1

40 Mobile Phone Monitoring Usage Medium 5 SRR1

41 Supporting Active Communities – small grant scheme

Medium 12 SRR1

42 School audits

• Deficits schools

• Additional payments to Headteachers

High 83 SRR1

43 SEN Transport follow up review High 20 SRR1

412

E Partnerships/Shared Services 44 Review of Partnerships/Shared

Services/Third Party governance arrangements (including pooled budgets)

High 38 SRR1 and SRR3

45 Information Management Shared Services (Children’s Services)

High 15 SRR5 and SRR8

46 Management review of recycling credit claims from district councils (£3m) per annum

High 20 SRR11

73

F Corporate Value for Money Reviews 47 Appeals processes Medium 20 SRR2

20

G Internal Audit Certification 48 Carbon emissions data energy / fuel

emissions High 10 SRR12

49 Annual Governance Statement High 5 SRR2

50 Stroke Care Grant Medium 1 SRR1

51 Audit Certification Medium 10 SRR1

52 Former LSC Funding of Further Education Medium 10 SRR1

36

H Irregularity Work 53 Fraud investigation/detection (Contingency) High 120 SRR1

54 National Fraud Initiative High 56 SRR1

55 Fraud risk management High 15 SRR1

191

Page 14

7

Audit Area Priority Days

Link to Strategic Risk Registers (SRR)

I Information Systems 56 BT Billing Data Network Service Medium 15 SRR8

SAP Specific

New Systems/Consultancy/Advice

57 Information Management /Security consultancy

High 50 SRR5

58 New projects (system acquisitions/implementation controls) – Integrated Children’s system

High 10 SRR8

59 ICT Consultancy, advice on risk and control Medium 30 SRR5 and SRR8

Technical Areas

60 Penetration testing, vulnerability scanning and internal health check.

High

20 SRR8

61 Transactional Website High 25 SRR8

62 Back up and restoration of systems applications, and data including ICT BCM arrangements

High 25 SRR8

63 Secure disposal of hardware/confidential waste

High 20 SRR5 and SRR8

64 User Information Security Review High 20 SRR5

215

J Other

65 Provision of internal control/general advice Medium 48 SRR2

66 Audit Systems and processes review Medium 21 SRR2

67 Accounts and Audit Regulations Review of the Effectiveness of Internal Audit

High 10 SRR2

68 Audit Committee/Member reporting/CFO reporting/Planning / Head of Finance input

High 40 SRR2

69 External audit liaison High 7 SRR2

70 Internal Working Groups Medium 21 SRR2

71 External Auditing Groups Medium 9 SRR2

72 Benchmarking Medium 3

73 Recommendation Monitoring Medium 8

74 Contingency for unplanned and/or additional high priority/risk work and/or planned carry forward audits

High 164 SRR2

331

Total GCC Per Plan 1804

Page 15

8

APPENDIX B – Summary Scope for Main Audits

A Strategic Finance - 145 days Audits 1 to 8 1. Key controls documentation / review

The County Council’s external auditors are required to sign off the Annual Statement of Accounts. In order to do this they need to gain assurance that the financial information emanating from the main accounting system is accurate. Internal Audit will work with the Audit Commission on an annual basis to identify key financial systems where Internal Audit will provide the assurance that is required. Internal Audit will carry out walkthrough testing, in-house testing of manual controls, and testing of the effectiveness of the implementation of key controls. This allocation allows for Internal Audit to continue with this work in respect of both the 2010/11 accounts and the 2011/12 accounts. 2. Bank Reconciliations (Main Accounts and Pensions)

This is an audit of a key financial system. The balancing of accounting general ledger records to bank account statements must be undertaken at frequent and regular intervals in order to prove the integrity of financial systems. This audit will examine the bank reconciliation processes in operation to verify their accuracy, completeness, frequency and regularity. 3. Payroll

Staff costs make up a significant proportion of the County Council’s expenditure with over £400 million of staff related payments (42% of annual gross expenditure), including salaries, superannuation and national insurance payments, being made via the payroll system every year. As a result of the scale of payments made it is very important that this key financial system is audited on a regular basis. This audit will review a sample of the high risk processes that form part of the overall payroll system to ensure that risks are being identified and managed, and that adequate controls continue to operate in this very high risk area.

4. Debtors A key financial system, which controls the credit and cash income of the authority, to ensure that all income due is recognised, accounted for and collected in full and on a timely basis. The system is reviewed on a regular cyclical basis. This review will focus on ensuring that debtors are all raised on a timely basis and that there are robust follow up procedures for the collection of debt and adequate reporting of debts outstanding to the originating service areas and on the overall position to senior management.

5. Management of LGPS

The audit will utilise the assurance methodology produced by the County Auditors Network and endorsed by the Society of County Treasurers, which was designed to provide sources of assurance on the adequacy of governance and control arrangements in relation to fund management and custodian arrangements.

Page 16

9

Suitable sources of assurance will be obtained in order to provide adequate evidence to support the Statement on Internal Control in relation to the Pension Fund.

6. VAT

The County Council processes some £32m worth of VAT each year. It is essential that procedures for accounting for this are sound in order to minimise the risk of penalties and the Council’s tax liability. This audit will examine those processes.

7. Consolidated invoices The Council have contracts in place for advertising (Thirty Three), mobile phones (Vodafone), energy (West Mercia Supplies), agency staff (Comensura) and hotels (Capita). All of these bodies supply the Council with consolidated bills. This audit will review the system in place, in relation to a sample of these contracts, for authorisation and reconciliation of the invoices, and ensure that managers are able to understand and challenge charges made to their cost centres. 8. Monitoring Arrangements for receipt of Government Grants This audit will review the monitoring arrangements for the receipt of government grants ensuring that:

• a central register which identifies all sources of grant, the amounts and their expected frequencies is maintained;

• forecasting of expected levels of grant income, is accurate and complete;

• monitoring of the receipt of grant against the register and forecasts is undertaken; and

• that there is a formal procedure to follow up any discrepancies, trends, or unexpected patterns; including bringing such instances to the attention of senior finance managers.

B Governance - 173 days Audits 9 - 14 9. Compliance with Financial Regulations, Accounting Instructions, Budget Rules or

Key Corporate Policies following the implementation of the New Operating Model As the Council moves through a period of considerable change, with the implementation of the new operational model, the cessation of the traditional directorates, and downsizing in staff numbers, there is an increased risk that the underlying financial policies and procedures may not be adhered to. This review will test the level of compliance to these policies within the organisation. (The review of compliance in relation to commissioning will be undertaken as a separate piece of work, as detailed separately in this plan). This is a pure probity review which will undertake test checks to ensure that agreed control processes are being adhered to, particularly with regard to the ordering, receipt and payments of goods, and the authorisation of payroll changes, to ensure that rules and procedures set out in the accounting instructions covering these areas are being adhered too.

Page 17

10

10. Review of Governance arrangements in respect of Commissioning

Commissioning is the key vehicle through which to deliver timely quality services in a cost effective way. It is paramount that the Council procures all goods, works, and services in the most economic, efficient and effective way, and that the Council’s internal systems and processes that underpin sound procurement throughout the “procurement lifecycle” are robust, and have been disseminated/are accessible to all relevant staff. This review will look at the adequacy of the current internal arrangements, and planned arrangements under the new organisational model, i.e. regulatory governance, guidance, policies; documents etc, and undertake sample compliance testing to ascertain the level of adherence to these within the Council.

11. Code of Ethics and Business Principles

The purpose of a Code of Ethics and Business Principles is to give all stakeholders (i.e. Members, Staff, Volunteers, Third Parties) responsible for delivering services on behalf of the Council, guidance on how the Council and the public in general expects them to behave. If the Code is followed then the stakeholders should not find themselves in a situation where their conduct could create an impression of conflict of interest, pose a reputational risk to the Council or corruption in the minds of the public.

Compliance with the Code is an essential element in the Council’s success particularly during periods of significant change. This audit will review the adequacy of the guidance and frameworks in place and related mechanisms to manage and monitor ethical performance.

12. Meeting the Challenge Projects – Effectiveness of Governance arrangements (including the achievement of financial targets)

Following the issue of the financial settlement issued in January 2011, it is clear that GCC, in line with all other parts of the public sector, will experience significant reductions in funding levels going forward which will necessitate major changes to service delivery.

This is a challenge which involves the whole council and our partners across the public sector. To respond to this challenge, the 'Meeting the Challenge' programme was launched in September 2010 - a programme to change the way services are provided in Gloucestershire.

As Council resources become tighter, it is vital that we have effective portfolio, programme and project management in place, including robust financial monitoring and challenge, so that we can gain the most from our investment. It will also help to improve our capacity to manage change across the organisation and reduce the number of projects and programmes that fail.

The council has adopted the Office of Government Commerce approved Managing Successful Programmes (MSP) framework as the basis for our approach to programme and project management. A set of tools and guidance to help programme and project managers with their work have been developed.

Page 18

11

An approval process has been agreed for programmes and projects and the rules that programmes and projects need to adhere to are captured in eight minimum standards.

The purpose of this audit is to review the adequacy and effectiveness of the:

• Portfolio Office’s role in quality assuring MtC projects in terms of: § Milestones § Risks & issues § Project plans § Product documentation

• Current governance arrangements in place re: § Appropriate and robust management Information § Decision making § Adequate scrutiny

• Financial forecasting, costing and monitoring of MtC savings, ensuring that finance adopt an independent role in highlighting potential savings shortfalls as early as possible.

Following this review Internal Audit will make recommendations, as deemed appropriate, to enhance the existing arrangements, to enable the Council to efficiently and effectively achieve its MtC planned objectives. 13. Impact on controls of new ways of working, including LEAN reviews LEAN reviews, undertaken as part of the Meeting the Challenge Programme, concentrate on streamlining processes and procedures, eliminating unnecessary tasks and thereby delivering efficiencies. This allocation is to allow Internal Audit to input into these reviews to ensure that key controls are not taken out of systems which mitigate key risk exposures. 14. CRB processes in high risk areas Gloucestershire County Council employs around 17,000 staff. Getting the right staff in post is critical to the achievement of the Council’s strategic objectives. Vetting staff is a high-risk activity and, wherever appropriate, the risks should be minimised. Recruiting the “wrong” staff can involve exposure to various risks, particularly when working with the most vulnerable members of the community. These risks can be mitigated using a range of checks to vet the suitability of applicants and existing employees. This audit will review the effectiveness of the new CRB checking processes operating within the authority.

Page 19

12

C Commissioning - 208 days Audits 15 - 24 15. Residual Waste Project Gloucestershire County Council is engaged in procuring a major facility for the treatment of residual waste for the county for the next 25 years. Internal Audit will continue to review this former PFI project and challenge the processes and management as it moves through to the selection of the final tender stage and the signing of the contract. 16. Transport for Social Care (Children’s Services)

This audit will review transport arrangements for children in receipt of social care. It will not include Special Educational Needs (SEN) or Home to School transport. Currently the budget is held in the Children and Young People’s Directorate (CYPD). A mixture of voluntary drivers (through Cheltenham Voluntary Service) and taxis are used. The audit will include a review of the following:

• Whether there are any policies in place;

• How the services are procured;

• How transport is allocated;

• Whether the allocations are equitable; and

• How journeys are authorised.

17. Pupil Referral service GCC delegates funding to establishments who then use this to commission places and services for pupils. This can often be on a spot purchase basis rather than block purchasing and may result in poor value for money. This audit will review policies and procedures in place for commissioning and procurement to establish whether there is scope for GCC to procure more strategically, e.g. when pupils are excluded from school and/or educated by the Pupil Referral Service. 18. Gloucester Language Immersion Centre The project for the creation of a Language Immersion centre has been approved with funding from the DCSF (£5m), SWRDA (£780,850) and English Heritage (£180,850) and GCC Capital (£400,000). Once complete the centre will be operated by a newly constituted body formed by Gloucestershire Association of Secondary Heads (GASH), Gloucestershire Initial Teacher Training Partnership (GITEP), consortium of schools and colleges in the City of Gloucester (G15) and specialist Language Schools and International Awards Schools. This review will look at the risks to GCC associated with the project to ensure that they have been properly identified and are being appropriately managed. The review will include an examination of terms and conditions attached to grant funding.

Page 20

13

19. Contracts – Landfill

The County Council has a contract with Cory Environmental Gloucestershire Limited to provide waste management services at the two landfill sites. The contract value is in the region of £15m per annum. This audit will aim to confirm that the contractor is complying with the main terms and conditions of contract and that the payments made to them are correct.

20. Major contracts – Order of St. Johns The Gloucestershire Care Partnership (GCP) is a single purpose vehicle set up and funded by contributions from the Order of St John (OSJ) and the Bedford Pilgrims Housing Association (BPHA). The Partnership arrangement allows for OSJ to provide care under a sub let arrangement as it is to GCP that the County has let its former Elderly People’s Homes and with whom it has contracted the refurbishment of the properties under an agreed strategy. This review will look at the effectiveness of the current systems and processes in place for reconciling the financial payments for the provision of care under the terms of the contract.

21. Major contracts – Brandon Trust The Council currently contracts with Brandon Trust to provide care services to people with Learning Disabilities. It is a long term arrangement over the term of approximately 25 years, and payments made under the contract amount to approximately £11million per annum. This review will look at the effectiveness of the deliverables under the current contract in relation to the Council’s future business needs. 22. Risk transfer and Insurance cover in major contracts As the Council moves towards a commissioning model, it is imperative that the contractual arrangements consider and adequately reflect the risk transfer arrangements and insurance liabilities. This audit will review the following:

• To ascertain the level of Legal Services support in the development of the contract;

• To ascertain the level of input / consultation on specific clauses, indemnity limits, transfers of risk from the relevant experts;

• To review the amount of time given to experts to obtain their input prior to contracts being signed; and

• To ascertain the change management and monitoring arrangements relating to risk and insurance.

23. Fire PFI – Capital Build Contract - £40m In March 2008 Gloucestershire Fire & Rescue gained Government approval and outline funding approval through the Private Finance Initiative (PFI) to commence with a '£40 million project to build four new Community Fire Stations within Gloucester and Cheltenham and a Life Skills Centre. Following a lengthy bidding process, cabinet awarded Blue 3 (a consortium of contractors) with the Private Finance Initiative (PFI) contract.

Page 21

14

Following the recent final confirmation of the full award of the PFI credits, construction will take place during 2011 with the stations and Life Skills Centre planned to become operational between November 2011 and March 2012. This review will look at the contract monitoring arrangements during the construction phase of the project, and the proposed on-going monitoring arrangements. 24. Traffic Light Tender As a result of a complaint received by an unsuccessful tenderer into the evaluation process used for this tender, Internal Audit has been asked by senior management to undertake a review of the processes followed.

D Service Delivery - 412 days Audits 25 - 43 25. Compliance with general social care best practice – Social Work Taskforce –

caseload management The General Social Care Council Code of Practice for Employers of Social Care Workers sets down the responsibilities of employers in the regulation of social care workers. The code requires that employers adhere to the standards set out in their code, support social care workers in meeting their code and take appropriate action when workers do not meet expected standards of conduct. This review, included at the direct request of senior management within the Directorate, will look at the Council’s arrangements for compliance to the code. 26. Implementation of Putting People First Programme Putting People First is a nationwide change programme for adult social care which aims to give people more choice and control over their lives and will put them at the centre of the support services they require. This review will look at the effectiveness of the implementation of the PPF programme within the Council and how this is to be managed in the future as the initial programme team’s work comes to an end and the personalisation agenda is incorporated into the ongoing management of adult social care. 27. Direct Payments – Adults The aim of personal budgets is to give power to a person to decide the nature of their own support. Having a transparent allocation of money and the right to choose how this money is spent and managed is central to the personalisation agenda set out in the Putting People First national programme. The personal budget may be taken in the form of:

• A direct (cash) payment held directly by the person or where they lack capacity, by a suitable “person”;

• By way of an “account” held and managed by the Council in line with the person’s wishes to pay for community care services which are commissioned by the Council, or as an account placed with a third party (provider) and “called-off” by the user in direct negotiation with the provider; and

Page 22

15

• As a mixture of the above two.

This review will look at the effectiveness of the current governance, monitoring and risk management arrangements for direct payments, including an examination of the procedures in place which are designed to ensure that vulnerable adults are protected from potential financial mismanagement in this high risk area. 28. Direct Payments – Children with Disabilities A direct payment is money that the County Council gives to an individual to buy the services or equipment that they need following an assessment rather than providing or arranging the services or equipment. Parents of, or people with parental responsibility for, disabled children, are entitled to receive a direct payment for services to meet the child’s needs. The audit will review the decision making processes that are in place to agree and make direct payments for children with disabilities and how much of the decision making is or should be influenced by the parents. The audit will also examine whether the direct payments appear to be delivering value for money. 29. Non payment of service user contributions / write offs – Follow up

During 2010/11 we carried out a brief review to examine the area of non-payment of Service User Contributions as we had previously identified this as an area of risk. During the 2010/11 audit we concluded that there was a significant risk that not all income due from service users was being invoiced and collected. As a result we made two fundamental recommendations to address the weaknesses identified. As part of this year’s audit we will check that these recommendations have been fully implemented, the weaknesses addressed and identified increased income realised. 30. Home Care contracts The Council contracts with 14 external care providers under a Framework Agreement for domiciliary care services. These providers supply approximately 80% of the external domiciliary care service, and the Council also places “spot” contracts with up to as many as 55 other providers. This review will look at the adequacy of the current and future contract monitoring arrangements. 31. Top Up payments to Adults To undertake a review of the use of Local Authority “top ups” (the amount paid over and above the standard contract price), and extra payments for younger adults to ensure that these are being applied consistently and appropriately, and provide for best value.

Page 23

16

32. External Care Review Follow up The External Care Budget outturn for 2009/10 reported a £9.3 million overspend. During 2010/11 Internal Audit conducted a review of the reasons contributing to the current in-built budget problem, working with CACD management, and made a number of fundamental recommendations to strengthen further the control environment to address the weaknesses identified. Although significant improvements have been made, this follow-up review will look to establish whether all of the key recommendations made have now been fully addressed. The review will also examine the effectiveness going forward of the new panel procedures in financial monitoring arrangements. 33. School Deficit Budgets Follow up For 2010/11 there were 34 schools requiring Licensed Deficit Agreements (LDAs) totalling £5,044,000. The audit undertaken during 2010/11 examined the processes in place for identifying, monitoring and controlling school deficits, with particular reference to ensuring that all schools had entered into deficit agreements and had robust budget recovery plans in place. The audit also examined the monitoring and reporting arrangements in relation to recovery plans. As only limited assurance could be given over the control environment, the 2010/11 audit will be formally followed up during 2011/12 to ensure that the agreed recommendations have been implemented. 34. Capital receipts / disposal of properties During the course of the next four years it is planned that capital receipts in the order of £44m will be generated. Target receipts for 2011/12 are £10m. This audit will review the controls in the system for effecting such disposals, testing transactions on a sample basis, with the Authority’s disposal policy and legislative requirements. 35. Concessionary Fares The scheme introduced in 2006, provides free local bus travel for the over 60’s and eligible disabled people throughout England. In Gloucestershire, currently each district council operates a different scheme, which means eligibility varies from area to area. However, from April 2011, Gloucestershire County Council will take over the responsibility from the district councils to provide the concessionary fares service with a budget for 2011/12 of £5.9m. A concessionary fares policy is being prepared and a contract has been awarded with an external organisation to produce and issue the passes. This review will examine the arrangements for the management of the scheme and compliance with policy/eligibility criteria. It will also aim to provide assurance that the contract awarded to the external organisation has been let in compliance with EU Legislation and the Council’s Contract Standing Orders.

36. British Telecom landlines In 2010/11 Internal Audit reviewed payments made under the council’s mobile phone contract with Vodafone. This review will look at payments made to BT for landlines, it will include a review of charges made, monitoring of expenditure, reimbursement of private telephone call income and a review of the charging mechanism to see if this could be more cost effective.

Page 24

17

37. Discretionary Payments to foster carers The budget for discretionary payments to foster carers is in the region of £300,000. This audit will review the following areas:

• To ensure that there is a policy in place for making discretionary payments to foster carers;

• To ensure that payments made have not already been included in the fostering contracts and should therefore be borne by the foster carers;

• To ensure that the payments made are equitable;

• To establish the effectiveness of the authorisation of payment processes; and

• To establish the effectiveness of the budget management arrangements.

38. Fire & Rescue workshops The workshops are based in the Tri-Service building located at Waterwells. The Fleet presently consists of some 108 vehicles (69 Appliances and 39 vans and cars) plus 2 Hovercrafts, 2 Boats and 24 Contract Hire cars utilised personally by Uniformed Officers. The servicing of the appliance type vehicles is mainly undertaken in-house with the majority of the smaller vehicles serviced through the GCC contract with Ryder. This audit will review the:

• Control of stores;

• Ordering and receiving spares;

• Use of pool cars over hire cars;

• Use of demonstration vehicles;

• Emergency call out payments made to technicians;

• Use of the Fleet Management System (TRANMAN); and

• Purchasing & Sales of Fleet Vehicles.

39. Retained Fire-fighter fees Gloucestershire Fire & Rescue Service employs a group of 300 men and women who in addition to their normal jobs or careers, are on call in their free time or will respond to emergency calls from their place of employment. These individuals are paid a retaining fee of £2,116 to £2,821 per annum depending on experience, rank and length of time within the retained fire service. They are also paid for each incident attended and to attend the two hour weekly training sessions. The budget for the service is close to £2.4 m and this audit will review the arrangements for controlling how payments are made to the individuals within the retained fire service, and how performance / attendance is being monitored. 40. Mobile Phone Monitoring Usage Vodafone provide mobile phones for staff at GCC. Whilst the mobile phone policy allows staff to use their phones for private calls, they are required to reimburse the council for such usage. The Vodafone system allows Internal Audit to view reports of the most expensive calls made, the phones with the highest call charges and call charges incurred during evenings and weekends. Internal Audit use these reports to check compliance with policy.

Page 25

18

41. Supporting Active Communities – small grant scheme This audit will review the system of allocation and monitoring of this grant funding. 42. School audits In 2011/12 audit resources on school audits will be targeted at these two areas, with schools being selected for audit based on these criteria. The areas to be audited in relation to each area are summarised below:-

Deficit Schools

School deficit budgets are worsening both in terms of the number of schools setting deficit budgets as well as the cumulative value of deficit budgets set. Currently there are 51 schools in deficit.

In 2010/11 we reviewed how these deficits were monitored centrally and made recommendations to improve this process. This year as part of our regular programme of school audits we will focus on 20 schools in a deficit position reviewing the steps they are taking to address the situation at the school. In addition to individual reports to schools, which will be copied to CYPD Management, a composite report will be produced highlighting examples of best practice, for circulation to all schools in deficit positions.

Additional payments to Headteachers

Cases of additional payments being made to Headteachers will be identified centrally via payroll records. Where significant additional payments are identified, schools will be audited, with this area being covered. Discussions will take place at the schools to determine the reason for the additional payments and to ensure that the rules governing such payments, recently highlighted to schools, are being adhered to.

43. SEN Transport To undertake a follow up audit of procedures following an investigation into weaknesses identified in 2010/11.

E Partnership / Shared Services - 73 days Audits 44 - 46 44. Review of Partnerships/Shared Services/Third Party governance arrangements

(including the management of pooled budgets) The Council is now increasingly entering into a broad range of relationships across the public, private and third sectors. Many of these relationships will underpin the operations and future service delivery of the entire local authority. This way of working is much more than simply subcontracting or logistics management as services will be delivered in a completely different way. This raises a wide range of risks, opportunities and control issues, these include:

• Human resource issues;

Page 26

19

• Cultural differences;

• Communications between all parties;

• Technology;

• Funding arrangements and good financial management;

• Liability issues (including insurable risk);

• Crisis management;

• Assets (including intellectual assets);

• The impact on the control environment and potential gaps in obtaining the relevant assurances;

• Performance and risk management processes and attitudes;

• Legality and compliance; and

• Information management and security. This audit will review the adequacy of the governance frameworks that have been put in place i.e. clearly defined governance documents including delegated authorities and clearly defined roles and responsibilities in respect of key areas such as performance, financial and risk management arrangements. 45. Information Management Shared Services (Children’s Services) GCC works in partnership with the NHS. One of the areas that has been highlighted is record keeping across the partnership. Records need to be kept as evidence of decision making and service delivery and this includes appraisals and 121s. This audit will follow the trail of evidence and records that should be in place to support safe effective quality care. 46. Management review of recycling credit claims from district councils The six district councils (and to a much lesser extent – charitable organisations) receive payments from the County Council based on the amount of tonnage collected at the kerbside or from collection points, e.g. supermarket car parks and then sent to the recycling processing centres. For each tonne they will receive a payment of £47.17 costing the Council some £2.3m per annum. This audit will aim to provide assurance that the credits claimed by the organisations’ can be substantiated, and assess whether the checks made by the service to verify the numbers claimed are in place and operating effectively.

F Corporate Value for Money Reviews - 20 days Audit 47 47. Appeals processes The Appeals process covers areas such as transport, SEN tribunals, Home to School transport etc. This audit will review the following:

• The robustness of the appeals process;

• The effectiveness of the decision making processes;

• How successful appeals are authorised; and

• Scope for minimising additional transport costs emanating from successful appeals.

Page 27

20

G Internal Audit Certification - 36 days Audits 48 - 52 48. Carbon emissions data energy / fuel emissions The Carbon Reduction Commitment Energy Efficiency Scheme (CRC EES) came into force in April 2010 and aims to significantly reduce UK carbon emissions not covered by other pieces of legislation. CRC EES is a mandatory carbon emissions reporting and pricing scheme to cover all organisations using more than 6,000MWh per year of electricity (equivalent to an annual electricity bill of about £500,000). Participants in the CRC EES will need to measure and report their carbon emissions annually following a specific set of measurement rules with the first annual report of emissions due in July 2011. Starting in 2012, participants will buy allowances from Government each year to cover their emissions in the previous year which means that organisations that decrease their emissions can lower their costs under the CRC EES. This audit will review the methodology used to collect the sources of data, assess its accuracy and confirm this is in line with the agreed set of measurement rules.

49. Annual Governance Statement This allocation is to produce the 2010/11 Annual Governance Statement to be included with the annual accounts. 50. Stroke Care Grant Each local authority in England was allocated grant for each of the three years 2008/09 to 2010/11, ring fenced for the purpose of providing support services to stroke survivors and their carers. The funding is to help support the implementation of the National Stroke Strategy, within which high quality social care is recognised to be of fundamental importance. The allocation to Gloucestershire for 2010 - 11 was £114,000 and in accordance with the Department of Health requirement the final statement prepared by the Local Authority (at the end of each financial year), requires certification as correct by the LA’s Internal Audit section.

51. Audit Certification

This allocation is to allow for the formal Internal Audit certification of grant expenditure which may be required during 2011/2012.

52. Former LSC Funding of Further Education This audit, to be undertaken at the year end, will examine whether adequate checking procedures have been implemented to meet national guidelines following the transfer of responsibilities in this area from the former Learning and Skills Council to GCC. The audit will particularly concentrate on guidance issued regarding checking expected to verify the accuracy of sixth form funding (SSF). This assurance will be used to support the Grant Return that has to be submitted to the Young Peoples Learning Agency (YPLA).

Page 28

21

H Irregularity work – 191 days Audits 53 - 55 53. Fraud investigation / detection (Contingency) In recent years Internal Audit has developed considerable expertise in investigating cases of suspected irregularity. This contingency has been set aside in order to allow time to conduct these investigations, without impacting on the remainder of the audit plan. It is difficult to predict the number and complexity of this work. This year we have reduced the allocation to this contingency, however based on past experience if there are no major investigations then we anticipate that this contingency will be sufficient to enable staff to carry out both the investigations and some fraud detection work, focusing resources on areas where the risk of fraud is high. However if a major investigation takes place then we may have to revise the overall plan. 54. National Fraud Initiative The NFI is a national data matching exercise that compares records (payroll, pensions, care home residents, blue badge holders, insurance and creditors) for a wide range of local authorities and public bodies under the auspices of the Audit Commission (AC). The exercise is biannual; data was collected in October 2010 and matches were received in late January. The matches are individually investigated, with the outcome of the investigation being reported back on the NFI website. This allocation is to enable as many of the high (and in some cases medium) matches to be investigated and the findings reported back to the AC, in the areas which are felt to have the highest probability of delivering benefits to GCC, i.e. private residential care home matches, payroll matches, pensions matches, creditors matches and insurance claimants matches. In addition this allocation allows for the provision of information to District Councils following up possible housing benefit fraud.

Any suspected fraudulent activity could result in criminal or disciplinary proceedings.

55. Fraud risk management Good governance requires that the Council assess its counter fraud arrangements and performance against professional guidance, best practice and the findings of its own reviews; it strengthens its systems and procedures in response. The CIPFA Better Governance Forum has issued a guide recommending actions to be taken to counter fraud and corruption within an organisation.

This allocation is to undertake a self assessment against the guidance and following this assessment, to direct its counter fraud audit resources accordingly.

Page 29

22

I Information Systems – 215 days Audits 56 - 64 56. BT Billing Data Network Service The data network support budget is in the region of £1,000,000 of which the BT circuits account for around 50%. As the Council reduces in size, it is important that the BT One Bill for the data network circuit is managed effectively by Capita (formerly Sungard). This audit will review the processes in place to monitor and manage the BT One Bill to ensure that we do not pay for circuits that have been ceased. 57. Information Management / Security consultancy Information security is an essential component in facilitating efficient and effective service delivery, and protecting the Council’s reputation. A successful information security programme includes:

• Developing and maintaining security policies, and supporting standards, procedures, and guidelines;

• Assigning roles and responsibilities;

• Managing information security incidents; and

• Raising awareness, and educating users and managers about information security.

Recognising this the Council’s Interim Chief Information Officer enlisted additional information security expertise and support from Internal Audit (Principal IT Auditor), to update the Council’s Information Security Policy to take account of changes introduced by the Government, and to develop a framework of supporting policies, standards, procedures and guidelines. These will provide a basis for delivering information security council-wide, and integrating information security in to day-to-day operations. 58. New projects (system acquisitions / implementation controls) – Integrated

Children’s system Successful systems acquisition and implementation projects must have appropriate arrangements in place for: oversight by the project board/committee, including effective risk management, cost management, planning and dependency management, reporting, change control, requirements definition and software testing and implementation. This time allocation is for audit to provide advice and guidance, to officers involved in new system replacement projects, including the new Integrated Children’s system, and to highlight to management any audit concerns identified during the implementation process. 59. ICT Consultancy, advice on risk and control In view of the very fast pace of change in the areas of Information Technology, Information Systems and Information Security and increasing demand for associated knowledge and skills, this allocation has been included to provide advice to business managers, audit management and other auditors regarding issues that arise throughout the year.

Page 30

23

60. Penetration testing, vulnerability scanning and internal health check

As the size and complexity of the network grows, vulnerability testing should be one element of the Council’s overall security testing strategy, to provide assurance about the security of the Council’s network, and ensure due care for the protection of the Council’s information and infrastructure. This audit will review the arrangements in place to ensure regular vulnerability testing is undertaken, and appropriate controls are in place for reporting, risk assessment, and remediation. 61. Transactional Website

The implementation of a transactional website is one of the cross cutting “Meeting the Challenge” projects. This audit allocation is to provide advice in relation to this website and to ensure that adequate consideration is given to the security implications regarding the implementation of such a system, particularly security and confidentiality of data input and access controls. 62. Back up and restoration of systems applications, and data including ICT BCM

arrangements Business continuity planning is intended to minimise disruption to business critical systems from the effects of major failures or disasters. The Council is due to lose its recovery site (Hucclecote Centre) which is currently used for the secure storage of backup media. Also, the removable media policy requires all RESTRICTED information stored on removable media to be encrypted (this would include that on backup tapes). Currently data on backup tapes isn’t encrypted but are informed that compensating physical controls are in place. The audit will review the effectiveness of the controls put in place to respond to a major incident following the loss of the recovery site. 63. Secure disposal of hardware/confidential waste There has been a lot of work recently to ensure that personal/sensitive information on removable media is encrypted. However a proportion of the assets currently being disposed will not have encryption, the Council does not encrypt information on PCs, and equally as important is the process for disposal of confidential paper waste. Therefore this audit would review processes for secure disposal of information (i.e. hardware and paper), and would include looking at the processes for:

• return of assets to Capita SIS;

• Capita SIS receipt and storage of returned assets, and processes for hand over to the third party contracted to dispose of the Council’s hardware assets;

• The third parties processes/assurance processes; and

• The processes within the Council for the disposal of confidential paper waste.

Page 31

24

64. User Information Security Review

Following the information security policy development and dissemination, and user education/awareness it is important to ascertain the extent to which users understand their responsibilities e.g.

• Do users understand the differences between unclassified, protect, restricted and handling requirements?

• How do they protect information at work?

• How do they protect information when working remotely?

• How do they secure email? Questions generally designed to assess the extent to which people take personal responsibility for data.

J Other - 331 days Audits 65 - 74 65. Provision of internal control/general advice This allocation allows auditors to facilitate the provision of advice which is regularly requested by officers within the authority, including school based staff. 66. Audit Systems and processes review To ensure the Internal Audit function continually improves the quality of the service provided to the Council (in compliance with regulatory requirements), it is essential that internal audit’s own operational systems and processes are operating efficiently and effectively. Although each audit review is unique, for most engagements the audit process is similar and normally consists of four stages: Planning, Fieldwork, Audit Report, and Follow-up Review. Client involvement is critical at each stage of the audit process. One of Internal Audit’s key objectives is to minimise the time spent on pure systems and process, to enable the audit resources to be spent on its core function which is to provide independent objective assurance to members and management that the key risks which are material to the achievement of the Council’s objectives are being adequately controlled. This allocation is to review the current systems and processes in operation and streamlining them where deemed appropriate. 67. Accounts and Audit Regulations Review of the Effectiveness of Internal Audit Regulation 4(2) of the Accounts and Audit Regulations 2003, as amended by the Accounts and Audit (Amendment) (England) Regulations 2006 states that internal audit should conform to ‘proper practices’ and it is advised that proper practice for internal audit is set out in the Code of Practice for internal audit in local government in the UK published in 2006 by the Chartered Institute of Public Finance and Accountancy (CIPFA).

Page 32

25

The current regulations require the council to annually review the effectiveness of its system of internal audit. Clarification has previously been sought on the meaning of the term ‘system of internal audit’, as opposed to a review of the effectiveness of the internal audit function. CLG now recognises the confusion and proposes to clarify the requirement by requiring an annual review of the effectiveness of internal audit. This allocation is to undertake a self assessment against the Code of Practice in order to comply with the Accounts and Audit Regulations. 68. Audit Committee/Member reporting/CFO reporting/ Head of Finance input

This allocation covers member reporting procedures, mainly to the Audit Committee, plan formulation and monitoring, and regular reporting to and meeting with, the Chief Financial Officer. In addition this allocation includes the input from the Head of Finance into the delivery of the audit plan for 2011/12. 69. External audit liaison The External Audit Manager, the Chief Internal Auditor and the Internal Audit Managers regularly meet to discuss plans and audit findings, to ensure that a “managed audit” approach is followed in relation to the provision of internal and external audit services. 70. Internal Working Groups

Internal Audit is frequently asked to nominate representatives for working groups. 71. External Audit Groups Attendance / work in relation to the Midland Counties Chief Internal Auditors Group, the County Council Audit Network (national group) and the Midland Contract Auditing Group. 72. Benchmarking This allocation is to enable Internal Audit to take part in the annual CIPFA Benchmarking exercise. 73. Recommendation Monitoring This allocation allows Internal Audit to monitor the progress with implementation of fundamental recommendations. 74. Contingency for unplanned and/or additional high priority/risk work and/or

unplanned carry forward audits This allocation is to allow for the completion of various 2010/11 audits, which require the odd day to finalise in 2011/12 and hence are not restated in the plan and to allow for any unplanned or unforeseen work arising.

Page 33

26

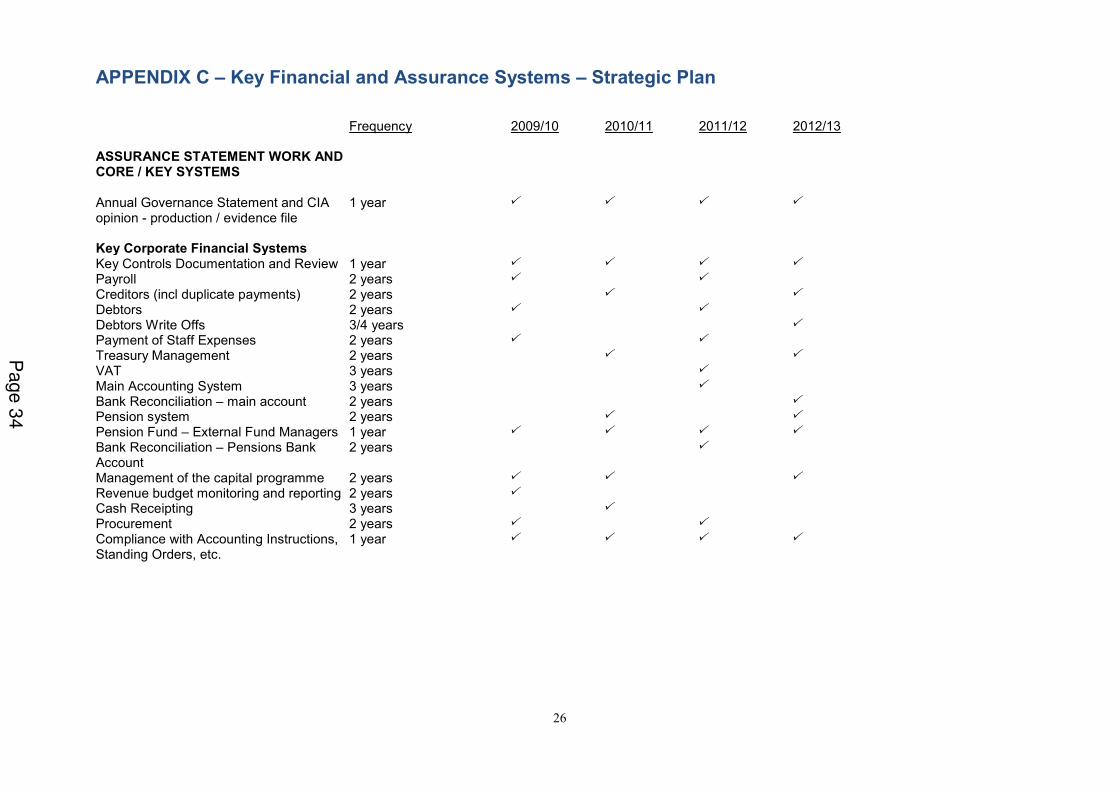

APPENDIX C – Key Financial and Assurance Systems – Strategic Plan

Frequency 2009/10 2010/11 2011/12 2012/13 ASSURANCE STATEMENT WORK AND CORE / KEY SYSTEMS

Annual Governance Statement and CIA opinion - production / evidence file

1 year � � � �

Key Corporate Financial Systems

Key Controls Documentation and Review 1 year � � � �

Payroll 2 years � �

Creditors (incl duplicate payments) 2 years � �

Debtors 2 years � �

Debtors Write Offs 3/4 years �

Payment of Staff Expenses 2 years � �

Treasury Management 2 years � �

VAT 3 years �

Main Accounting System 3 years �

Bank Reconciliation – main account 2 years �

Pension system 2 years � �

Pension Fund – External Fund Managers 1 year � � � �

Bank Reconciliation – Pensions Bank Account

2 years �

Management of the capital programme 2 years � � �

Revenue budget monitoring and reporting 2 years �

Cash Receipting 3 years �

Procurement 2 years � �

Compliance with Accounting Instructions, Standing Orders, etc.

1 year � � � �

Page 3

4

External Audit Progress Report Gloucestershire County Council

Audit 2010/11

Agenda Item 5

Page 35

The Audit Commission is an independent watchdog,

driving economy, efficiency and effectiveness in local

public services to deliver better outcomes for everyone.

Our work across local government, health, housing,

community safety and fire and rescue services means

that we have a unique perspective. We promote value for

money for taxpayers, auditing the £200 billion spent by

11,000 local public bodies.

As a force for improvement, we work in partnership

to assess local public services and make practical

recommendations for promoting a better quality of life

for local people.

Page 36

Audit Commission External Audit Progress Report 1

Contents

Introduction ........................................................................................................2

Audit update - Gloucestershire County Council .............................................3

Interim Audit..................................................................................................4

Value for money conclusion..........................................................................4

International Financial Reporting Standards.................................................5

Audit Fees 2011/12.......................................................................................5