2022 march 3 audit committee meeting

TRANSCRIPT

2022 March 3 Audit Committee Meeting

March 3, 2022 at 12:30 PM (EST)

Keene State College

Young Student Center

Keene, NH 03431

If you need assistance or have trouble connecting please call 603-862-0918 or [email protected]

A. Approve Minutes of October 22, 2021 Meeting

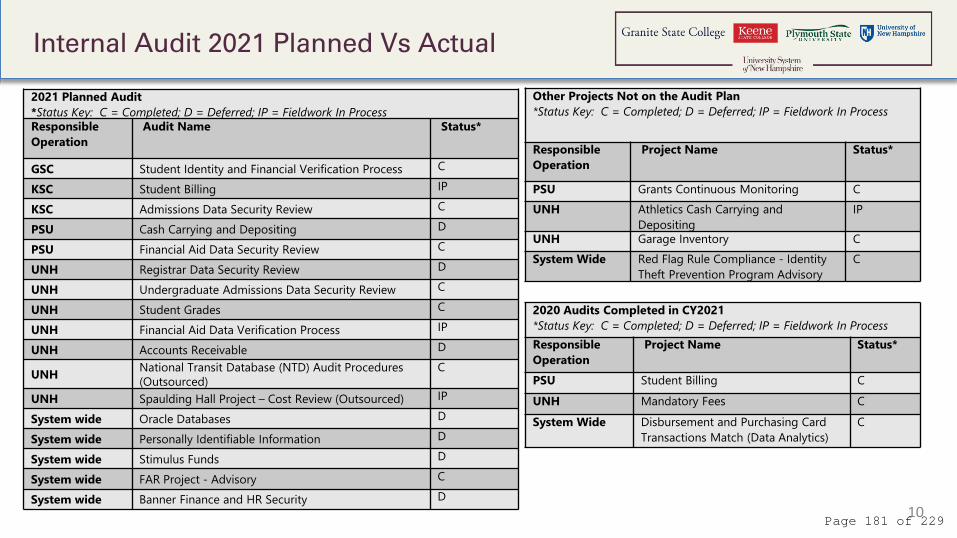

1. UNH Spaulding Hall Project Cost Review Report.pdf - 11

2. UNH Student Grades Audit Report.pdf - 18

3. UNH Garage Inventory Audit Report.pdf - 47

4. GSC Student Identity and Financial Verification Audit Report.pdf- 61

B. Accept Internal Audit Reports Issued

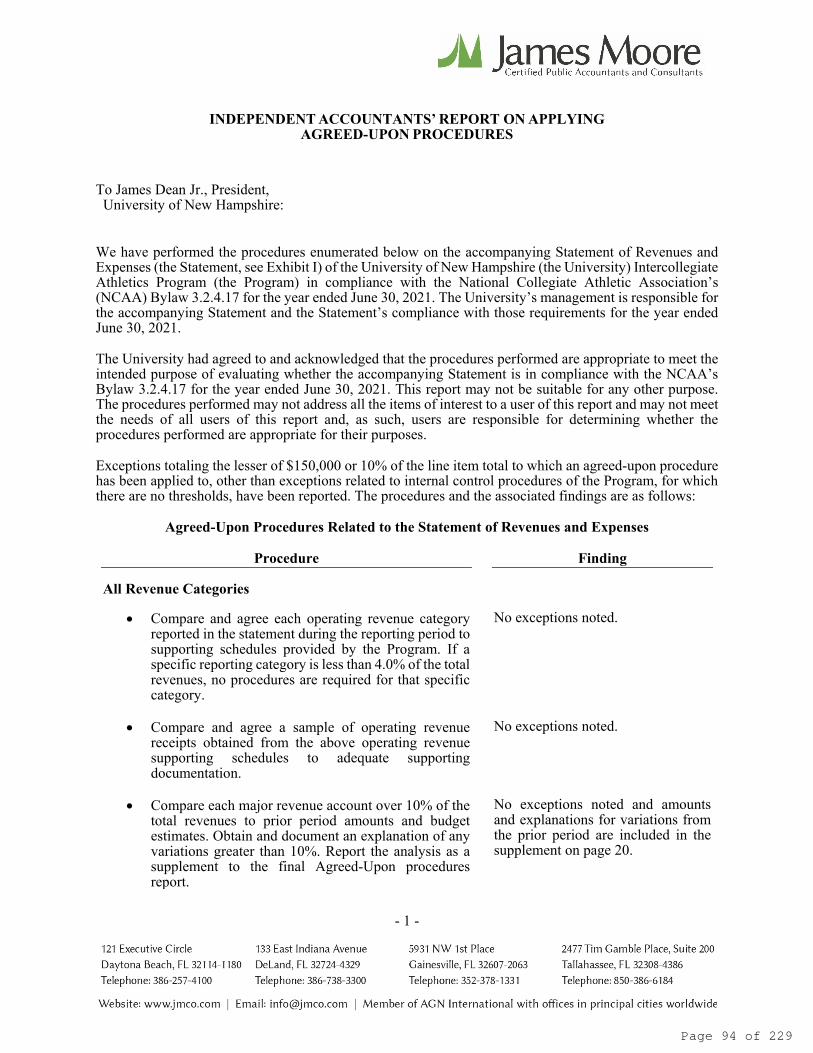

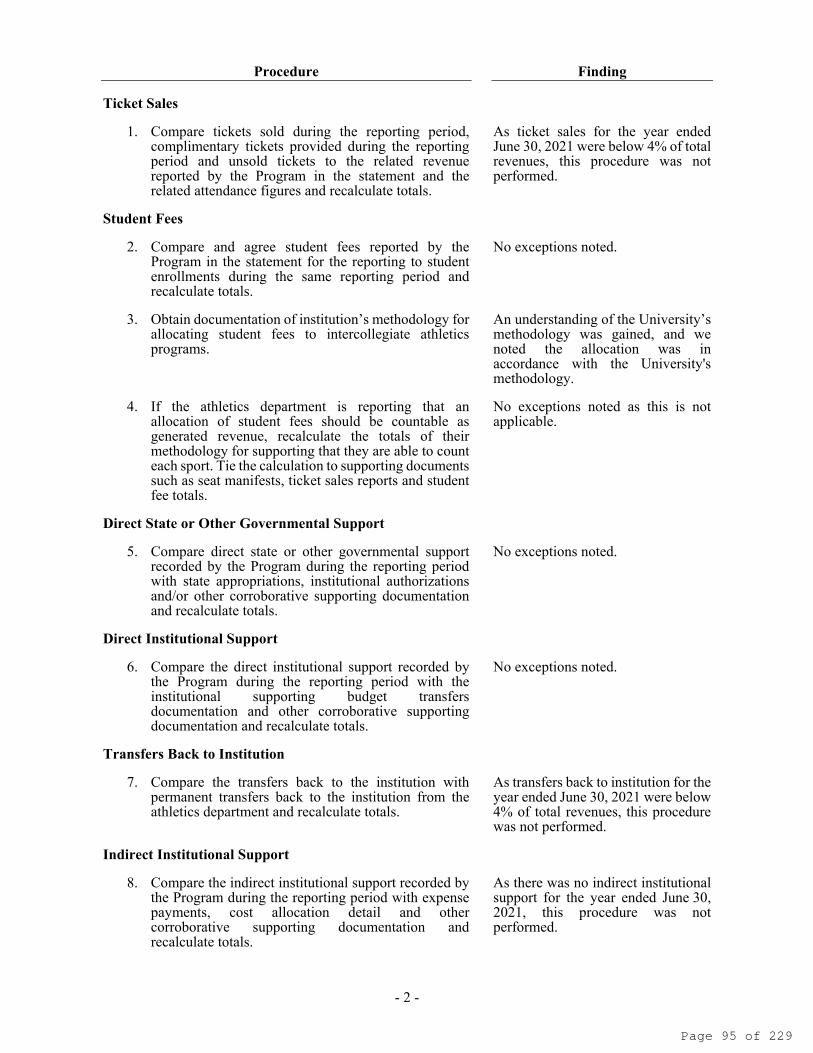

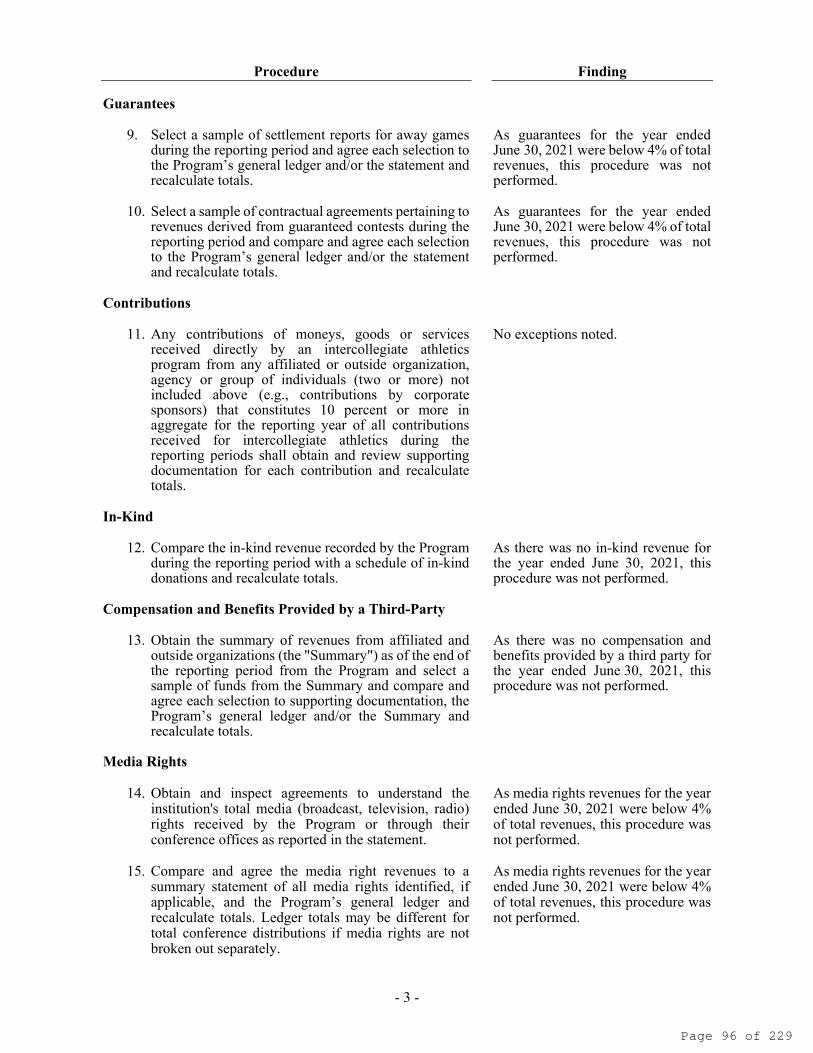

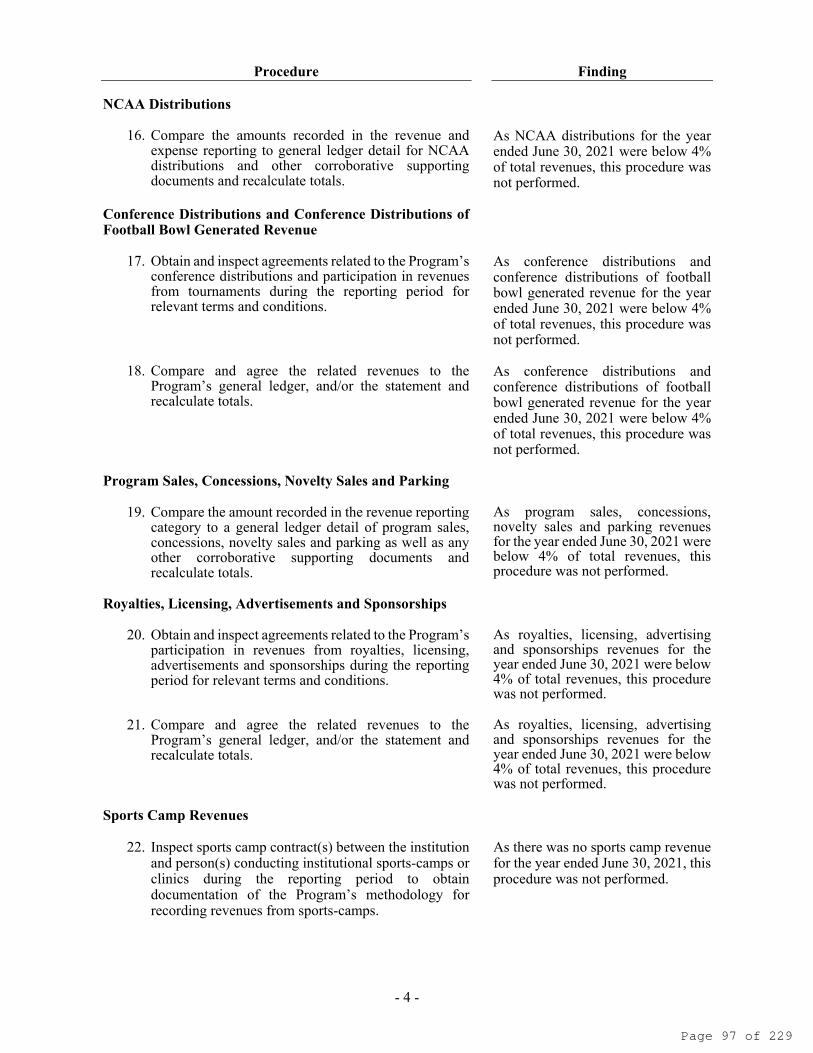

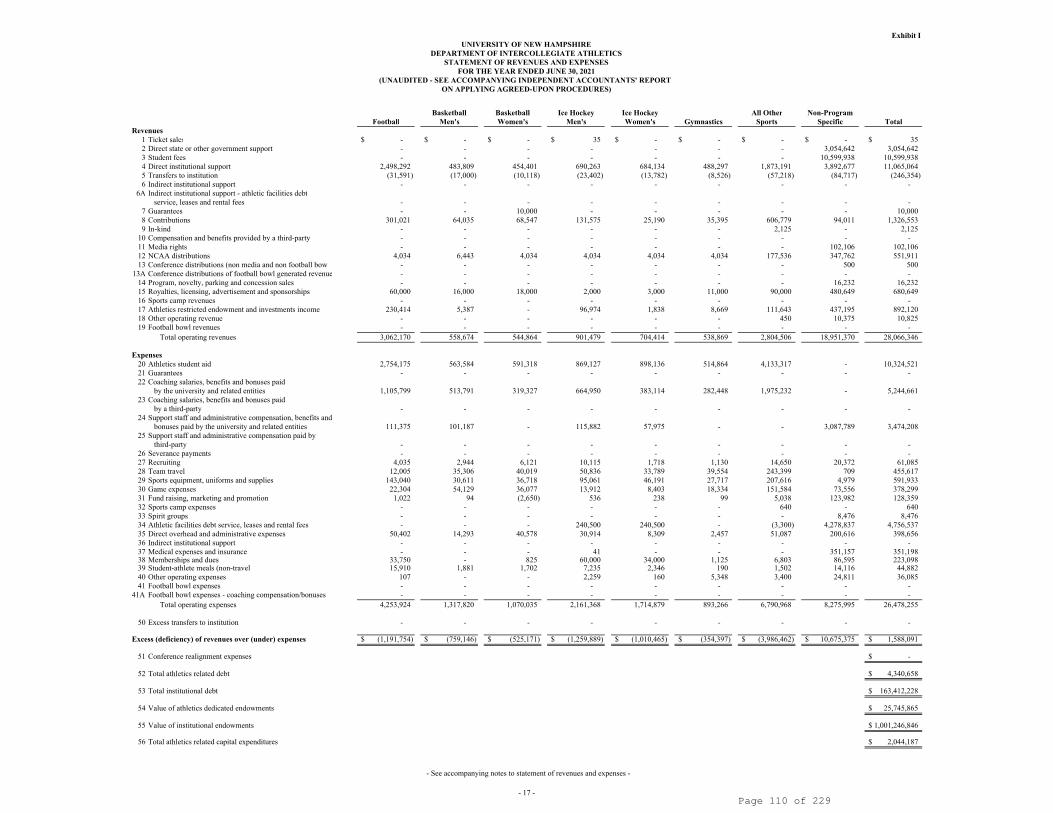

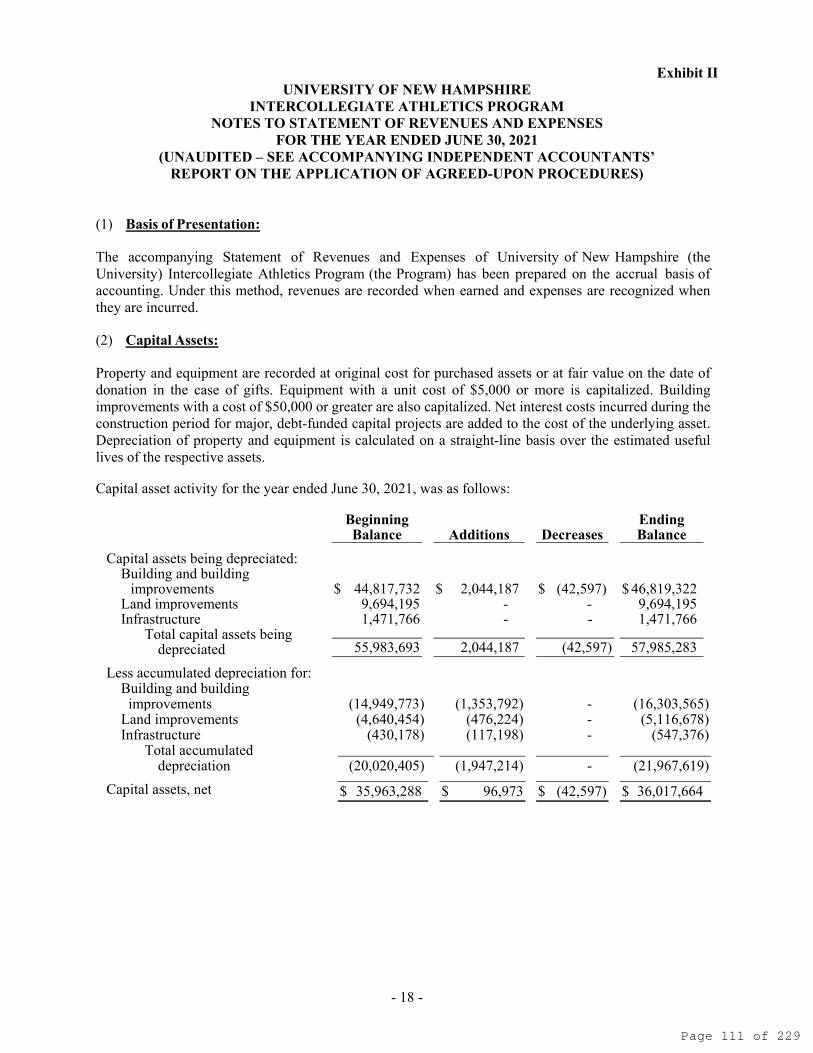

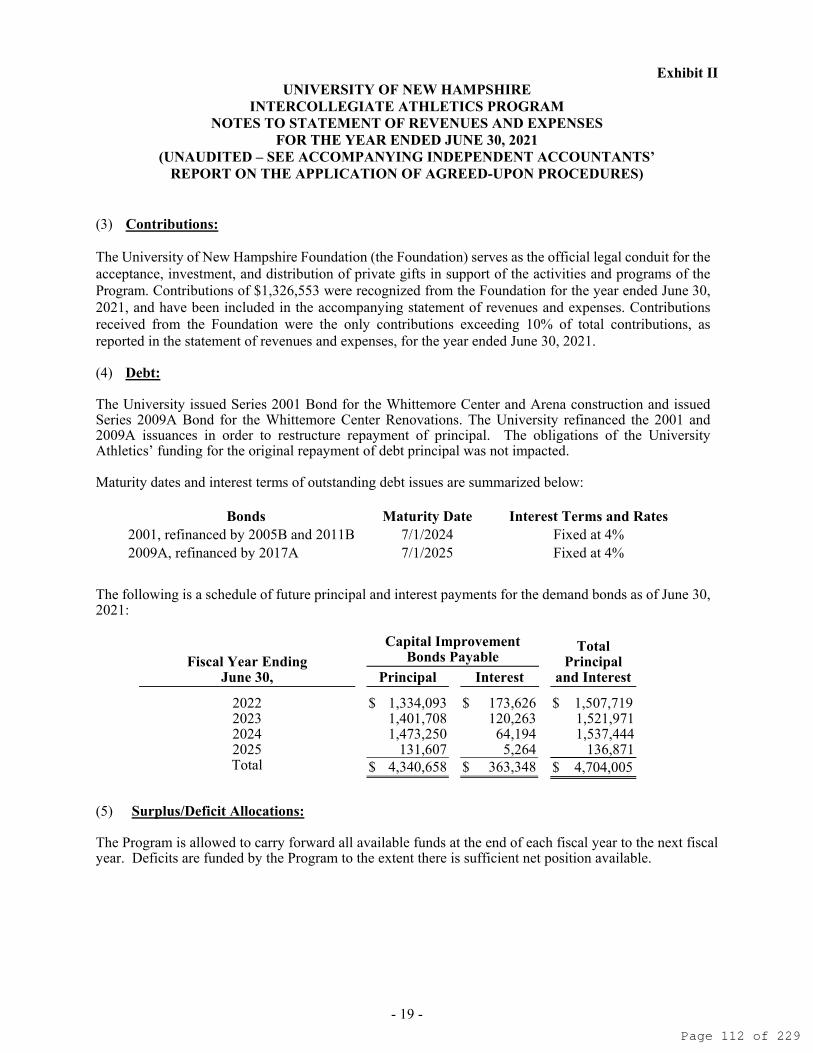

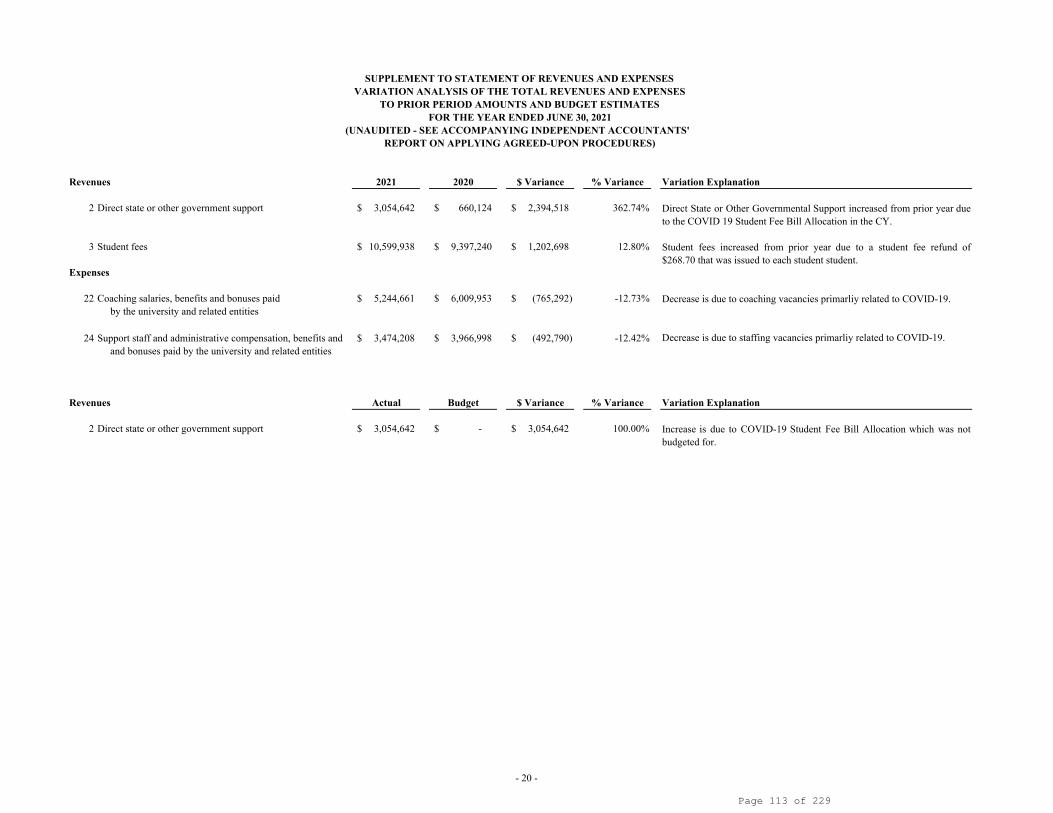

C. Accept UNH NCAA Agreed Upon Procedures Report

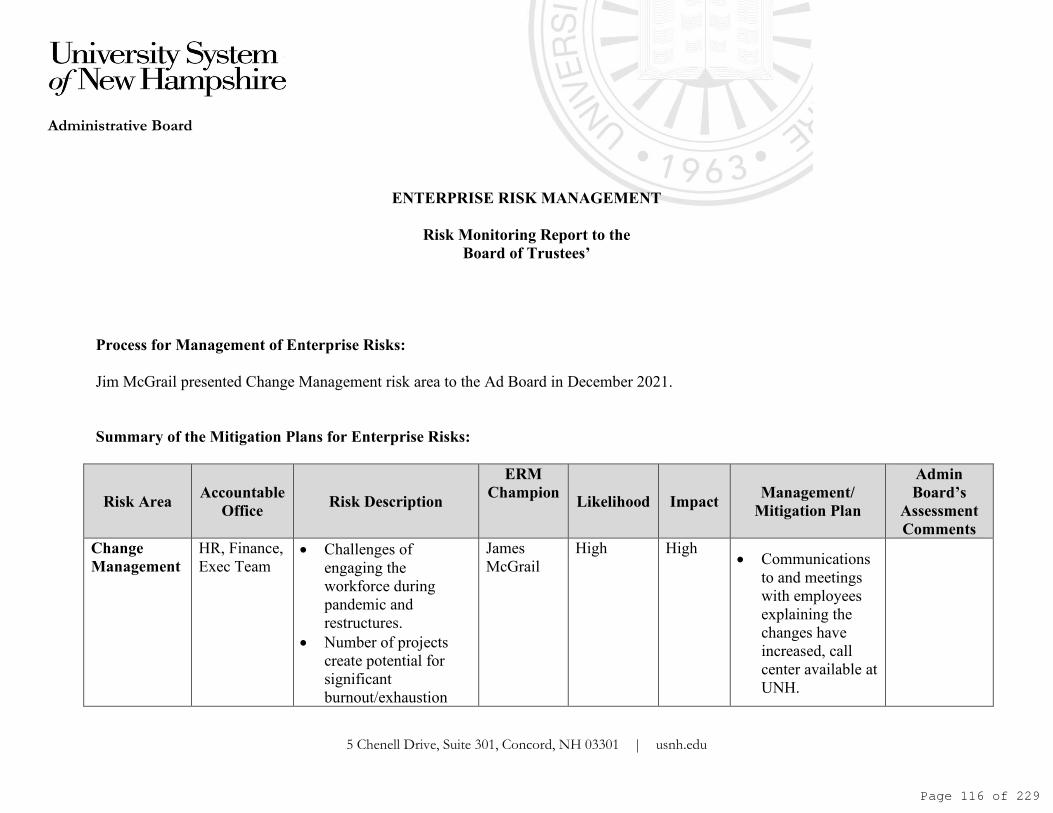

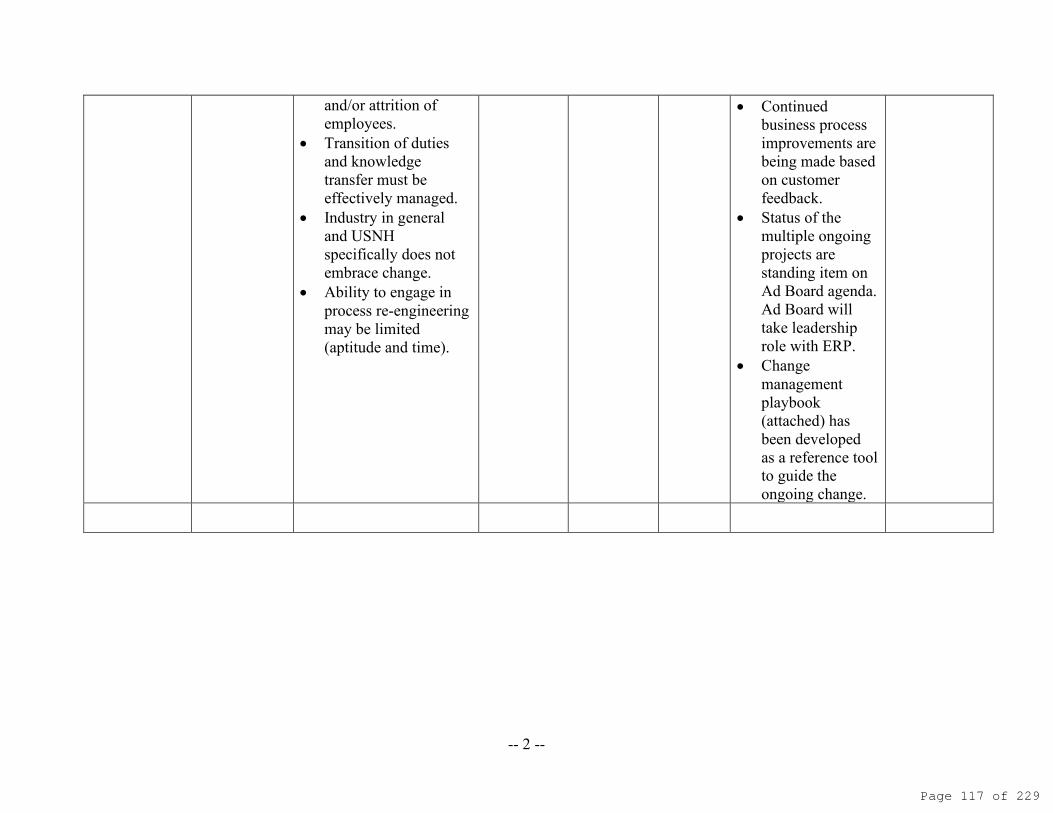

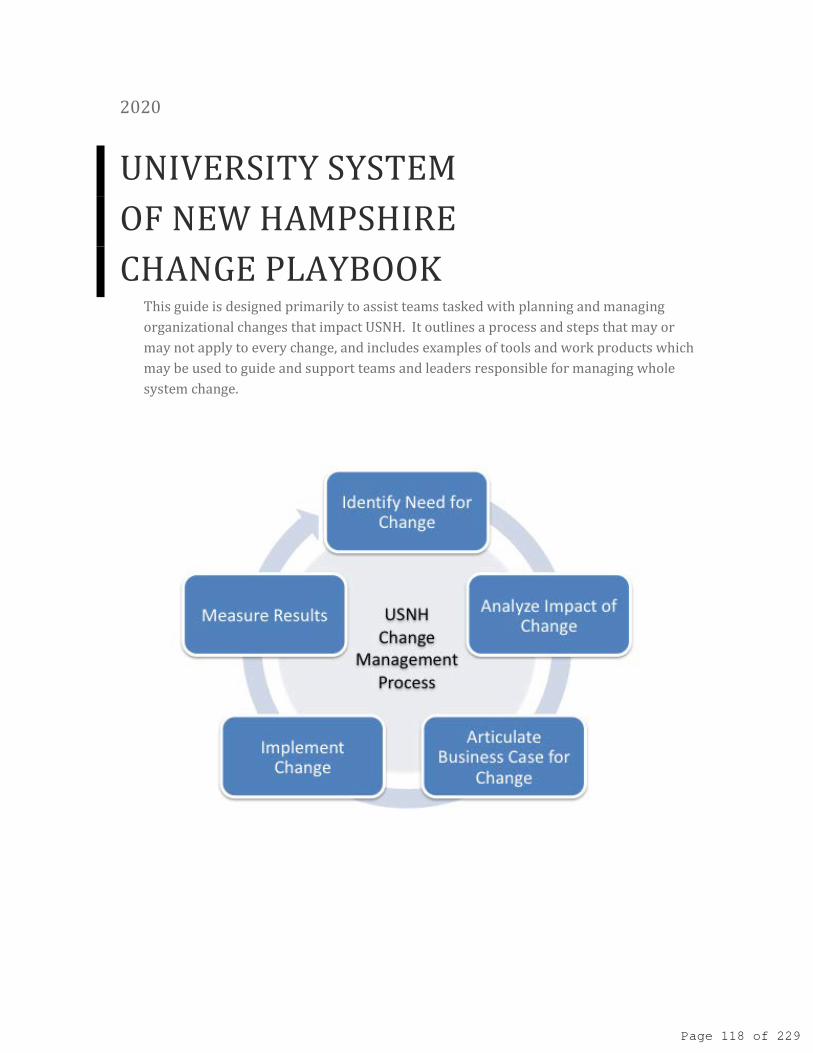

D. ERM Update on Change Management, Campus Safety, andCompliance

1. AC 10-22-2021 DRAFT minutes.pdf - 4

5. PSU Financial Aid Data Security Review Report.pdf - 80

1. UNH NCAA AUP Report.pdf - 92

12:30-12:35 pm VV. . Approval of Consent Agenda ItemsApproval of Consent Agenda ItemsMOVED, that the Consent Agenda Items be approved.

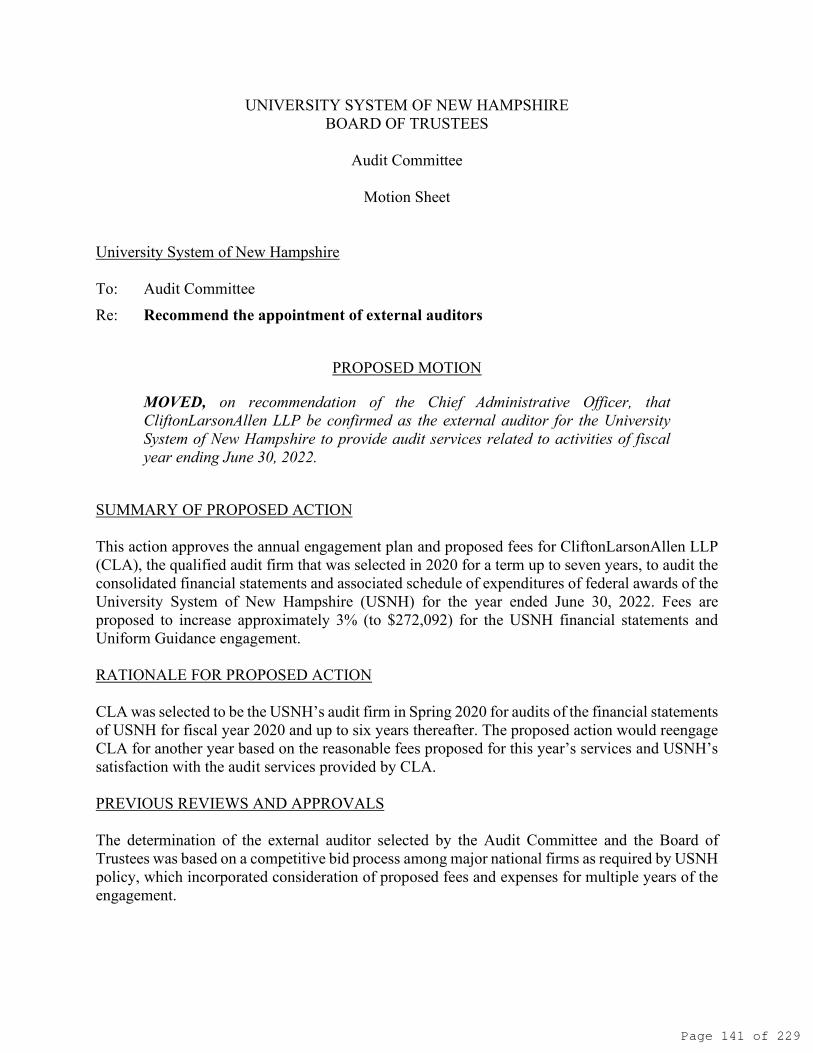

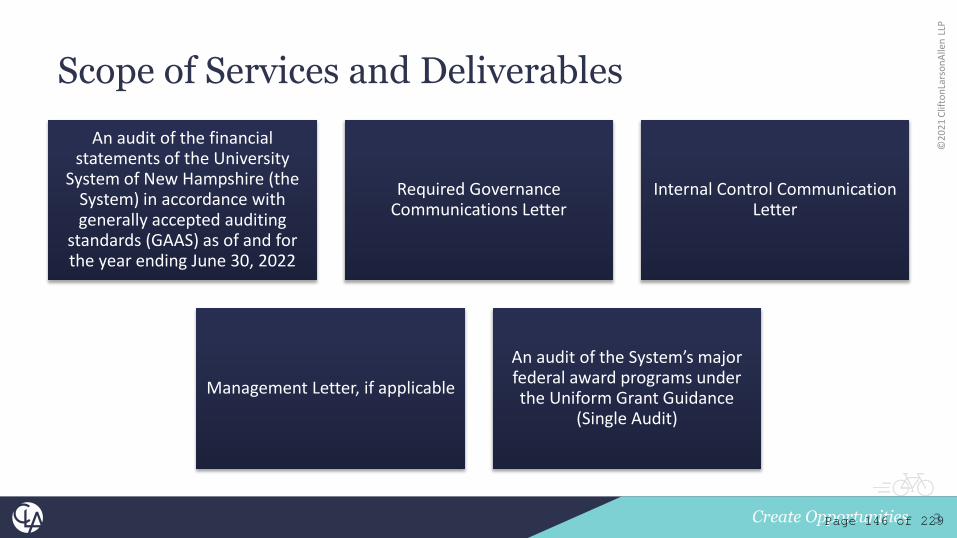

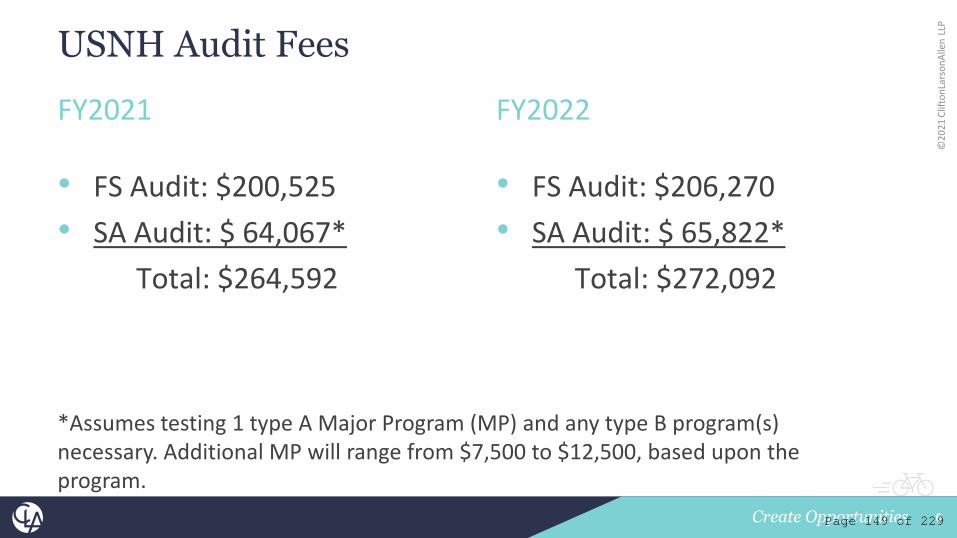

A. Approve appointment of CliftonLarsonAllen (CLA) as external auditorsand CLA’s Fiscal Year 2022 audit plan covering USNH financialstatements and federal awards under the Uniform Guidance (15 min)MOVED, on recommendation of the Chief Administrative Officer, thatCliftonLarsonAllen LLP be confirmed as the external auditor for theUniversity System of New Hampshire to provide audit services relatedto activities of fiscal year ending June 30, 2022.

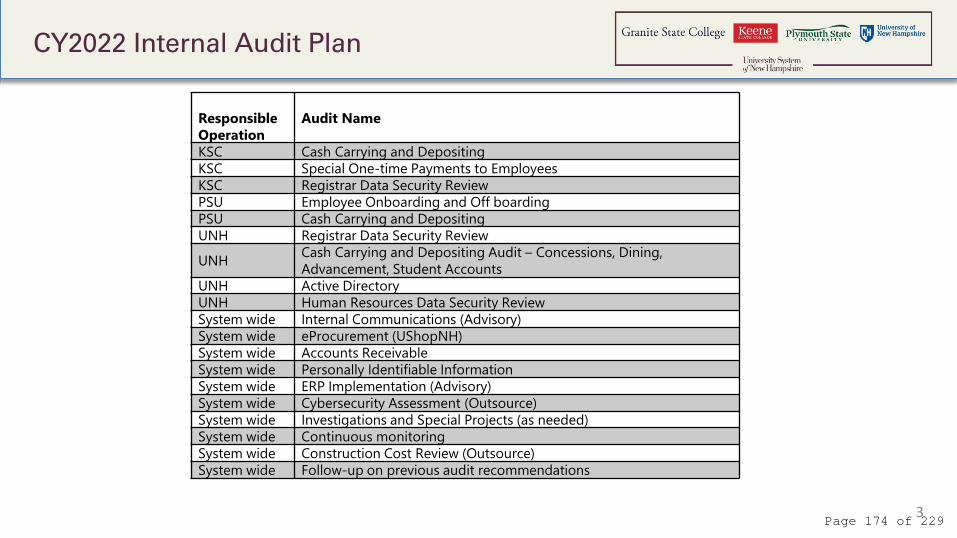

B. Approve CY22 Internal Audit Plan/Review Internal Audit's CY21Annual Report (20 min)

1. CLA appointment-audit plan-engagement letter.pdf - 141

12:35-1:10 pm VIVI. . Items for Committee Consideration and ActionItems for Committee Consideration and Action

II. . Meeting InformationMeeting InformationPhysical location:Keene State College (masks required for all indoor spaces)Young Student CenterMabel Brown RoomKeene, NH 03431

Call in: 1 301 715 8592Meeting URL: https://unh.zoom.us/j/91662457599Meeting ID: 916 6245 7599

IIII. . Audit Committee MembersAudit Committee MembersAlexander Walker, Chair, Gregg Tewksbury, Vice Chair, M. JacquelineEastwood, Shawn Jasper, Mackenzie Murphy, Governor Sununu

IIIIII. . In the Unlikely Event of a Zoom Call FailureIn the Unlikely Event of a Zoom Call FailureCall: 1 877 228 3100Participant Code: 638408

IVIV. . Call to OrderCall to Order

1. ERM Update - Change Management, Campus Safety, andCompliance.pdf - 114

Meeting Book - 2022 March 3 Audit Committee Meeting

MEETING AGENDA - March 3, 2022 at 12:30pmMEETING AGENDA - March 3, 2022 at 12:30pm

Page 2 of 229

MOVED, on recommendation of the Chief Administrative Officer, thatthe proposed Internal Audit Plan for CY22 be approved.

A. Internal Audit Charter Review (5 min)

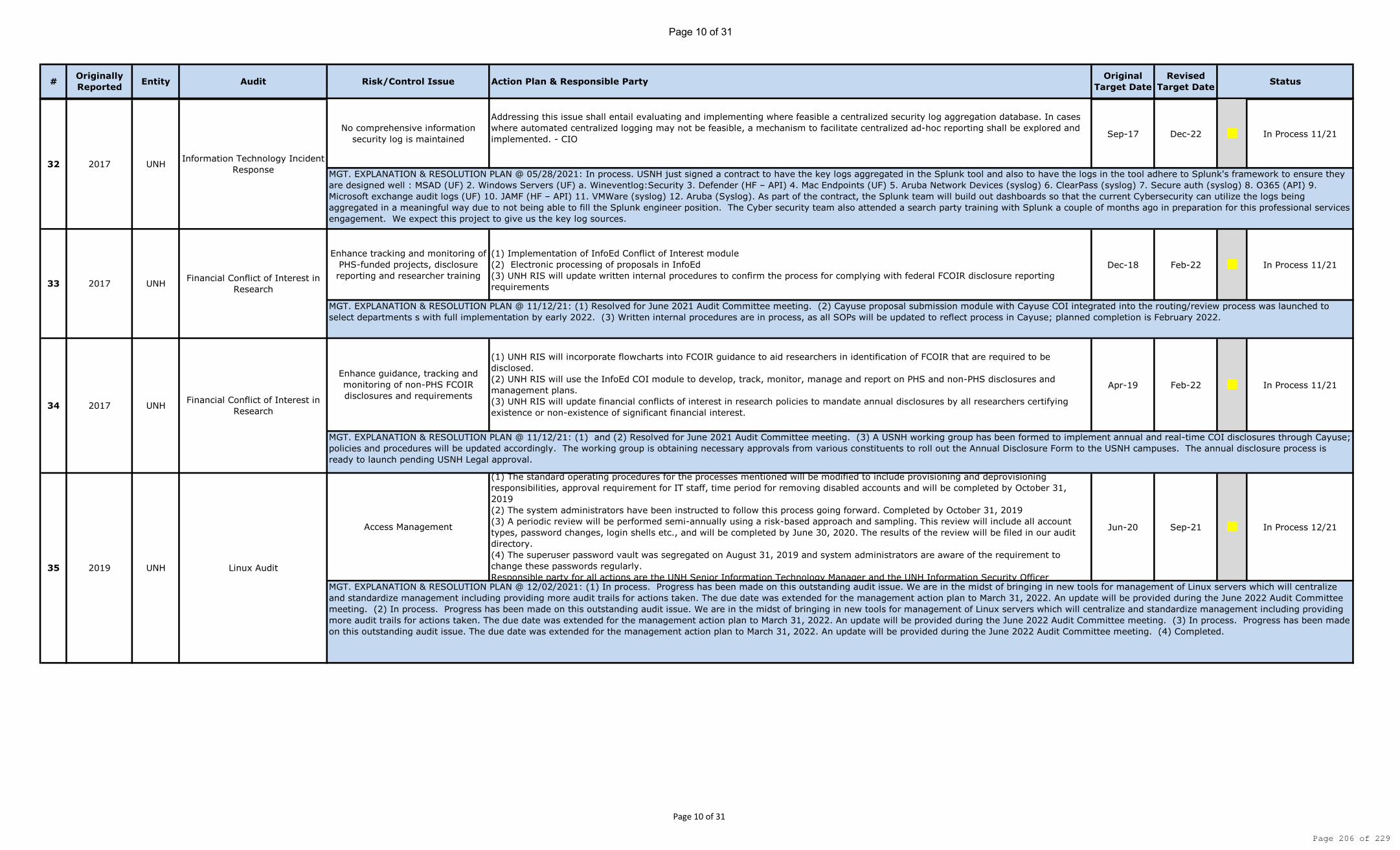

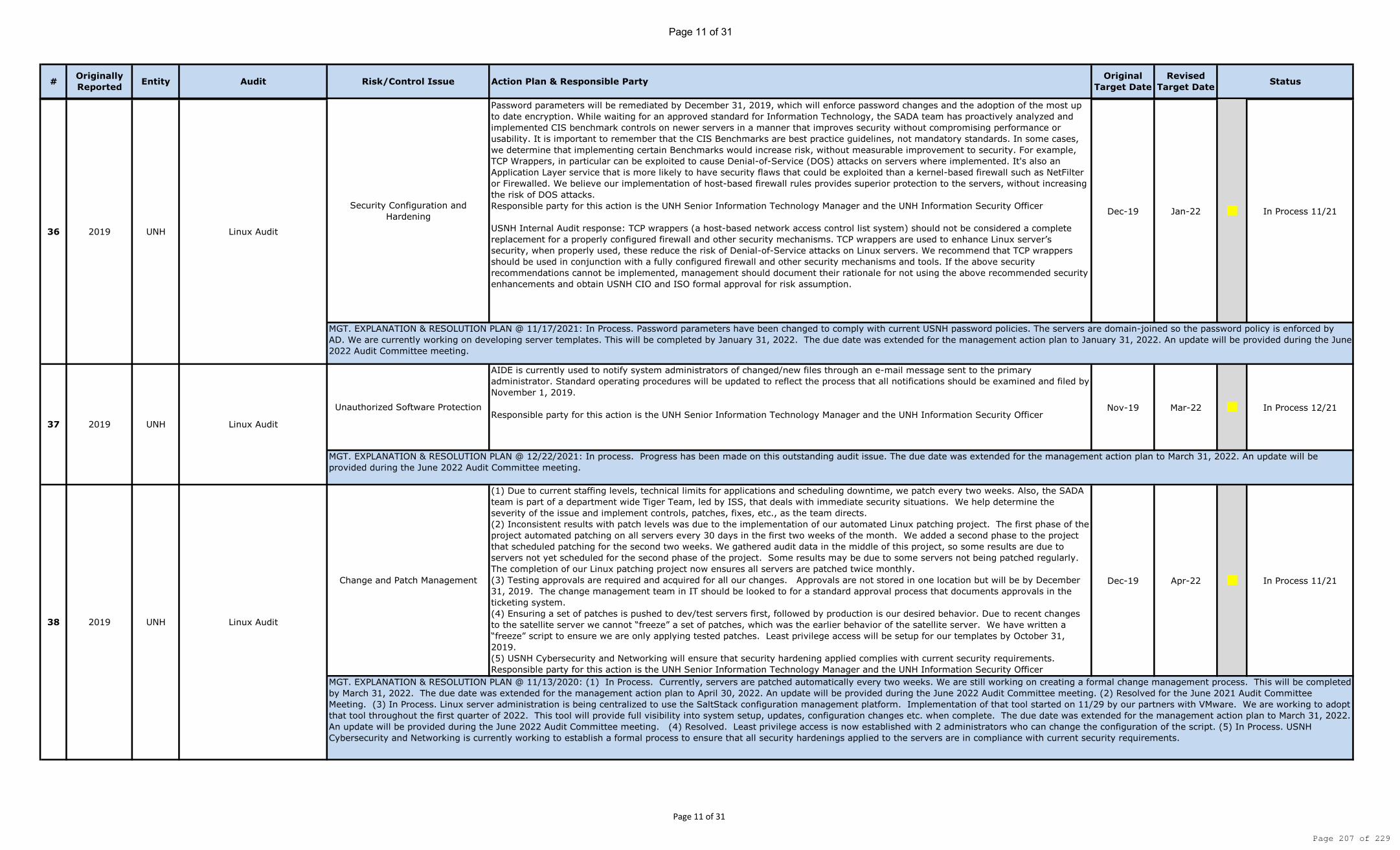

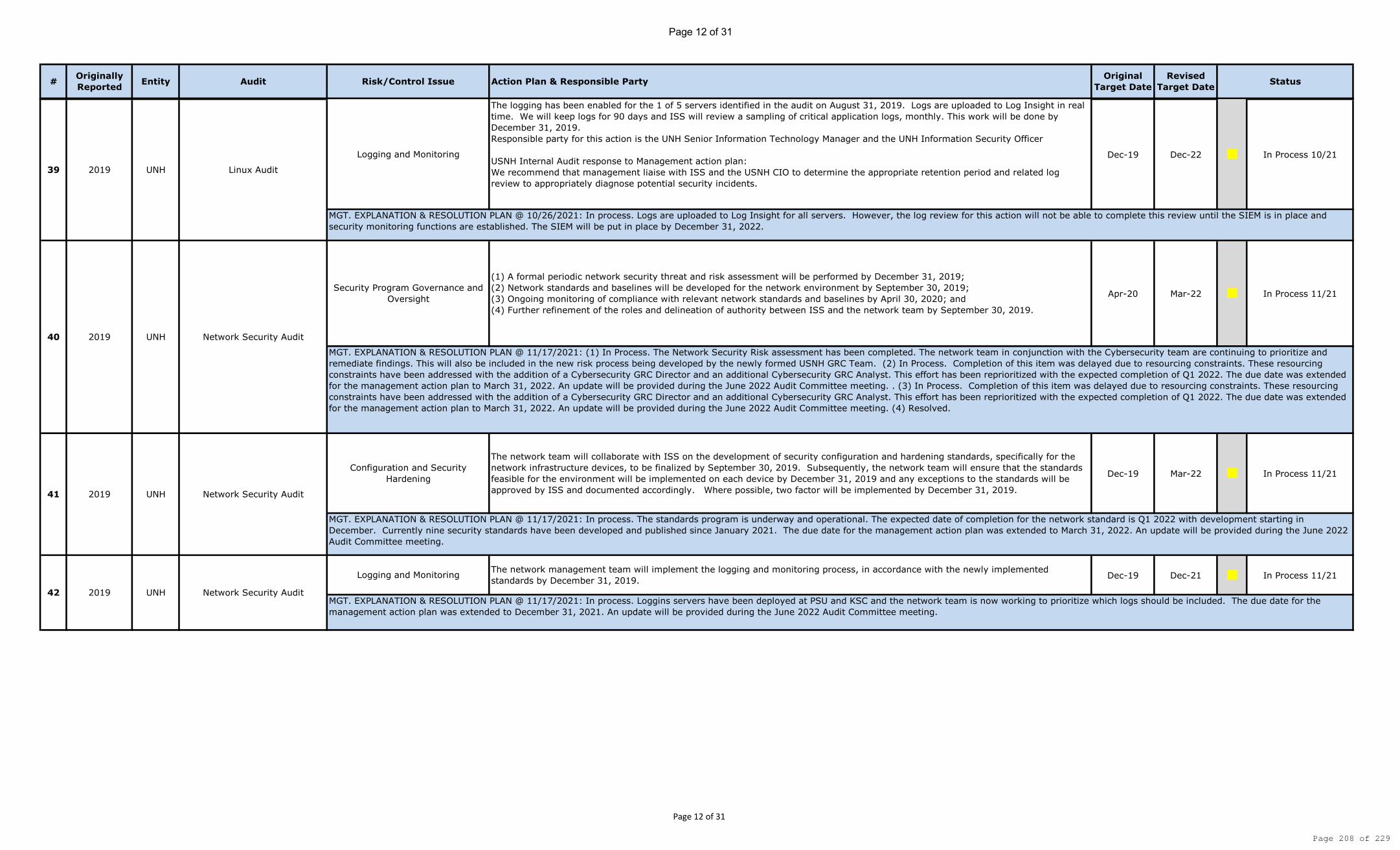

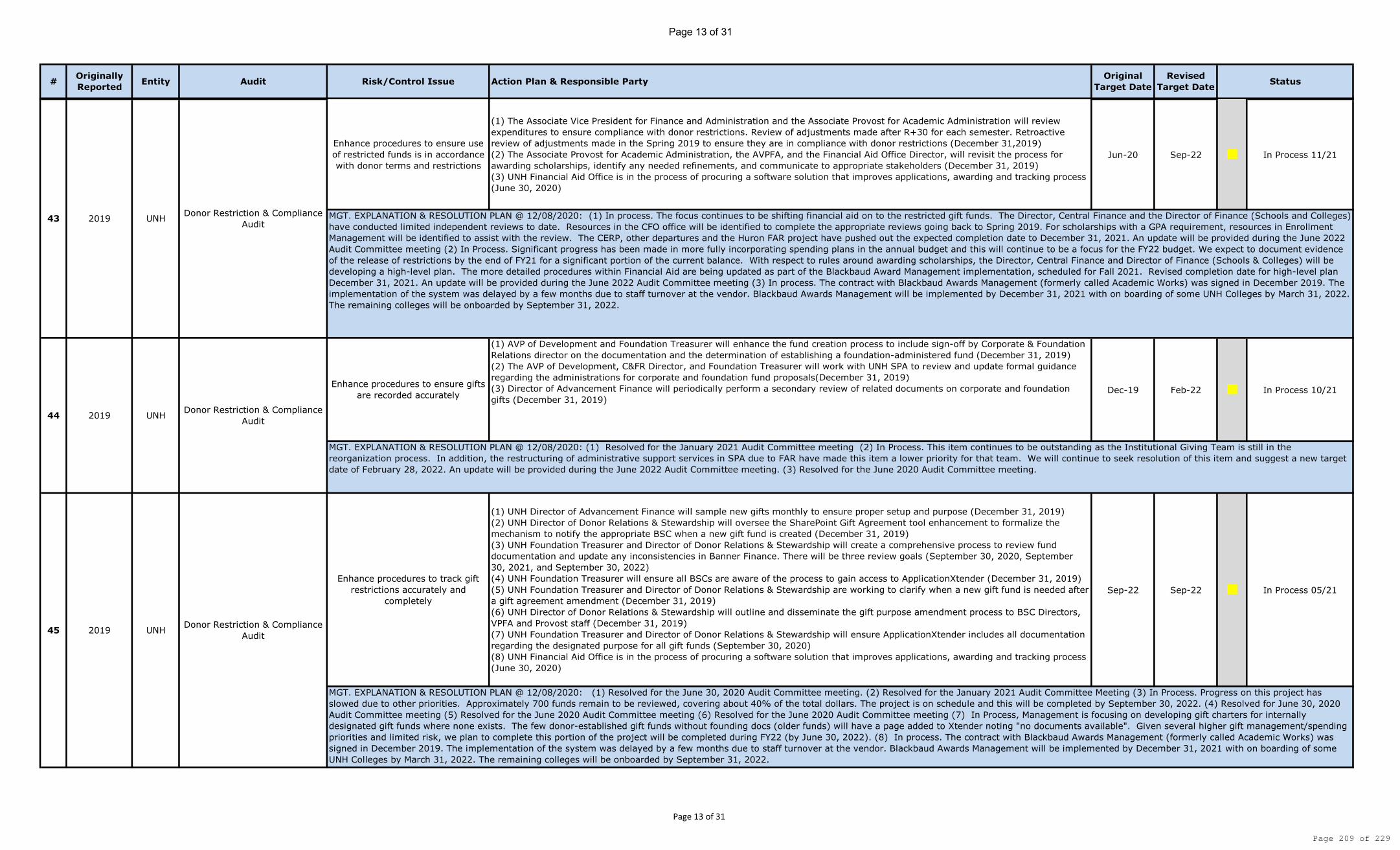

B. Review status of outstanding audit issues (5 min)

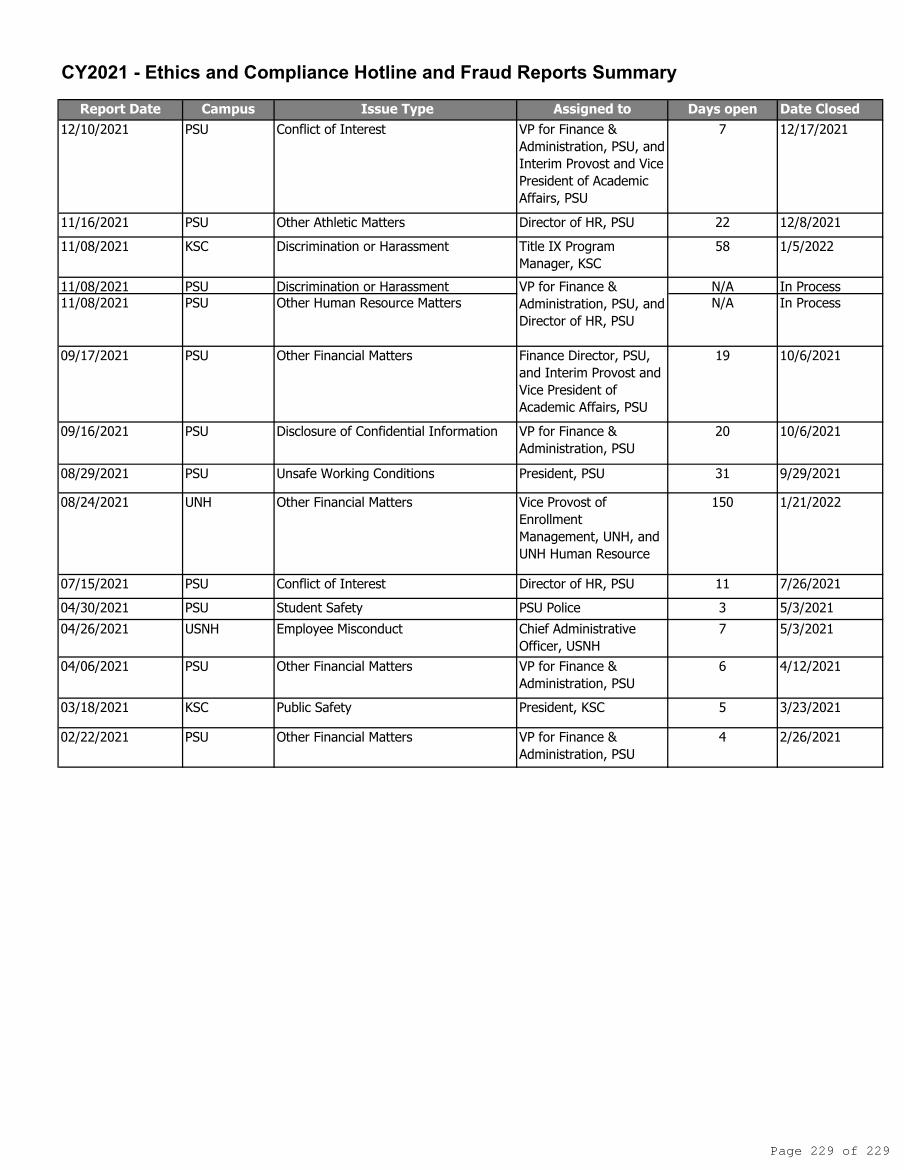

C. Ethics and Compliance Hotline and Fraud Reports Summary (5 mins)

1. IA charter and summary sheet.pdf - 192

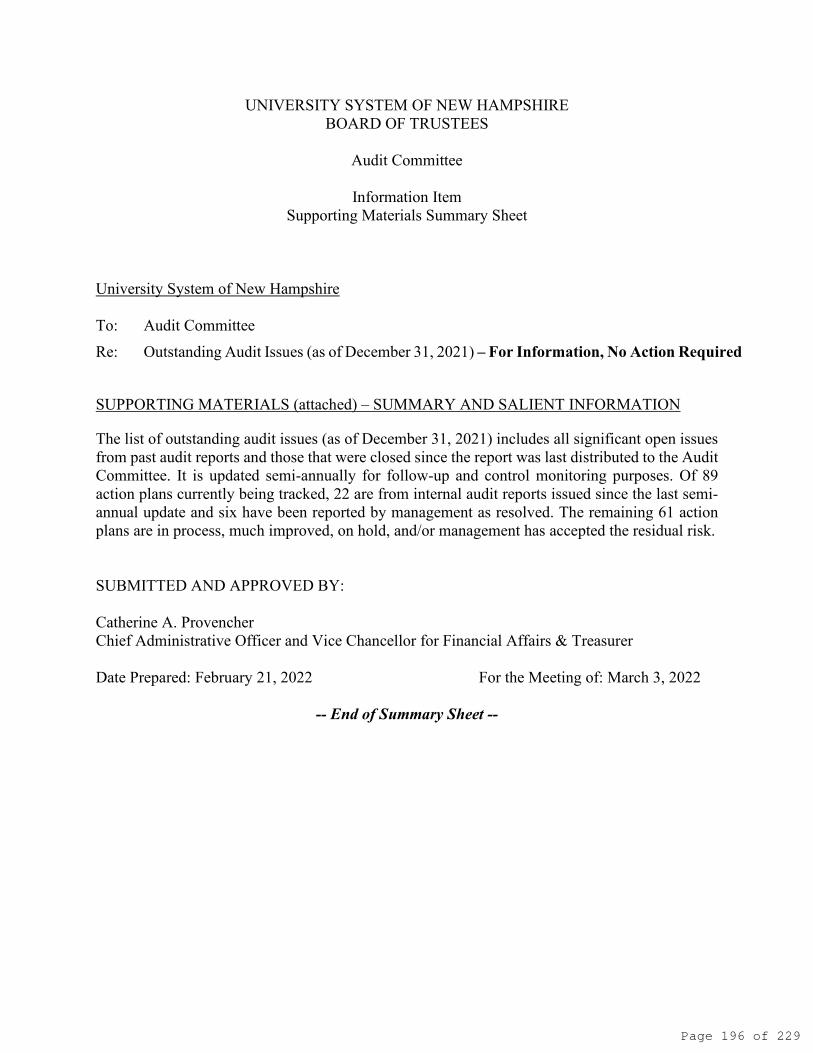

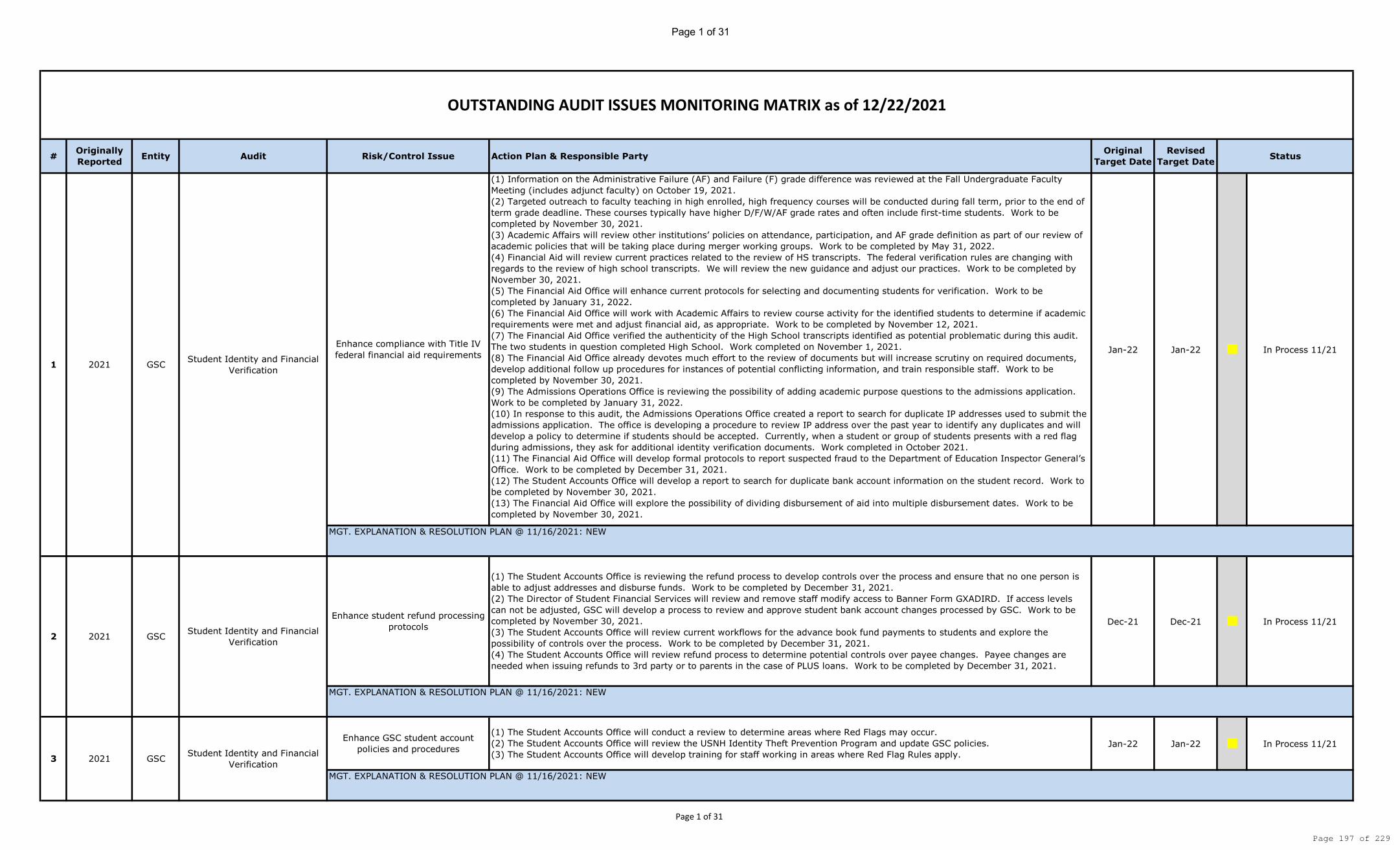

1. Status of outstanding audit issues with summary sheet.pdf - 196

1:10-1:25 pm VIIVII. . Items for Committee Consideration and DiscussionItems for Committee Consideration and Discussion

A. Chair or Committee comments

B. Next scheduled meeting: June 23, 2022 at the University of NewHampshire in Durham

IXIX. . Other BusinessOther Business

1. CY22 IA Plan-IA CY21 Annual Report.pdf - 170

1. Hotline and fraud summary 02-01-2022.pdf - 228

VIIIVIII. . Non-Public Session (if needed)Non-Public Session (if needed)

C. Adjourn

Page 3 of 229

BOARD OF TRUSTEES

p. 1 of 7

AUDIT COMMITTEE OCTOBER 22, 2021

PLYMOUTH STATE UNIVERSITY PLYMOUTH, NEW HAMPSHIRE

and BY ZOOM MEETING:

HTTPS://UNH.ZOOM.US/J/92467918189

MEETING MINUTES Draft for Approval

Committee members physically present: Chair Alexander Walker, Wallace R. Stevens, M. Jacqueline Eastwood, Shawn Jasper, Mackenzie Murphy Other Trustees physically present: Melinda Treadwell, Sen. James Gray Other participants participating by videoconference: (USNH) Karyl Martin, Ashish Jain, Kara Bean, Francine Ndayisaba; (GSC) Tiffany Doherty; (PSU) Janette Wiggett; (KSC) Jeffrey Maher, Kelli Jo Harper; (USSB) Reshma Giji, Ty Gioacchini, Jacob Riley, Christian Merheb; (CLA) Andy Lee, Luke Winter Other participants participating in person: (USNH) Tia Miller; (UNH) Wayne Jones; (Governor’s Office) Jonathan Melanson I. Call to Order At 10:32 a.m., Committee Chair Walker called the meeting to order. Chair Walker called the roll and noted the presence of a quorum sufficient for the conduct of business. On a question regarding committee membership, Chair Walker declared that he has made Trustee Stevens’ resignation from the committee effective end of day on Friday, October 22, 2021. II. Approval of Consent Agenda Items Chair Walker asked the committee members if they had any comments or questions about the consent agenda items; there were none. On motion offered by Trustee Eastwood and duly seconded, the committee voted to approve the consent agenda.

Page 4 of 229

Audit Committee p. 2 of 7

Items on the consent agenda appear below:

A. Minutes of April 15, 2021 Meeting B. FY21 Financial Statements and audit report/comments for UNH Foundation C. ERM Update on Information Technology and Security D. Internal Audit Reports Issued:

1. KSC Admissions Data Security Review Report 2. PSU Student Billing Audit Report 3. UNH Undergraduate Admissions Data Security Review Report

Chair Walker noted that the UNH Foundation financial statements were approved by the Foundation’s Board and the ERM update for Information Technology and Security was reviewed by the Administrative Board at their August meeting. III. Items for Committee Consideration and Action

A. Approve FY21 University System of New Hampshire Financial Statements B. Review FY21 audit report and comments from CLA

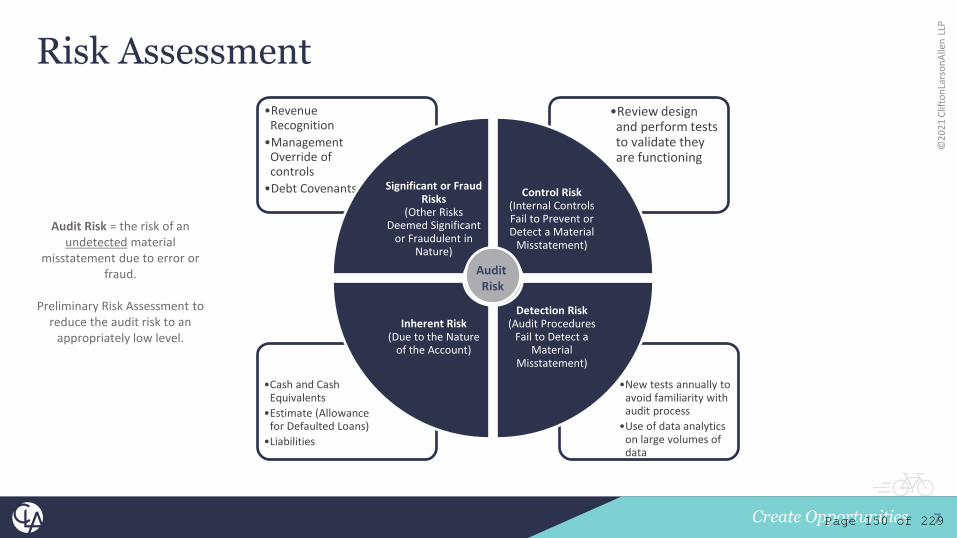

Mr. Jain introduced Francine Ndayisaba, USNH Director of the Financial Operations Center and Controller, and Andy Lee and Luke Winter from CLA. Ms. Ndayisaba noted that the audit went well and there were no concerns. She discussed financial highlights including statements of revenues, expenses, and changes in net position since FY17, statements of net position since FY17, and statements of cash flows since FY17. Financial highlights in FY21 include:

• USNH had an unprecedented net loss of $44M. The results reflect the impact of Covid-19 related costs of $64M of which approximately $50M were in surveillance testing, offset by $20M in HEERF institutional support and $33M in GOEFFER state support. In addition, the Covid Enhanced Voluntary Separation Incentive Program (CERP) had a cost of $56M. There were 485 participants in the program.

• There were healthy returns on endowment investments which increased the market value of total endowments by $211M over the prior year

• There was a $39M net increase of UFR. The increase in endowment returns drove this increase.

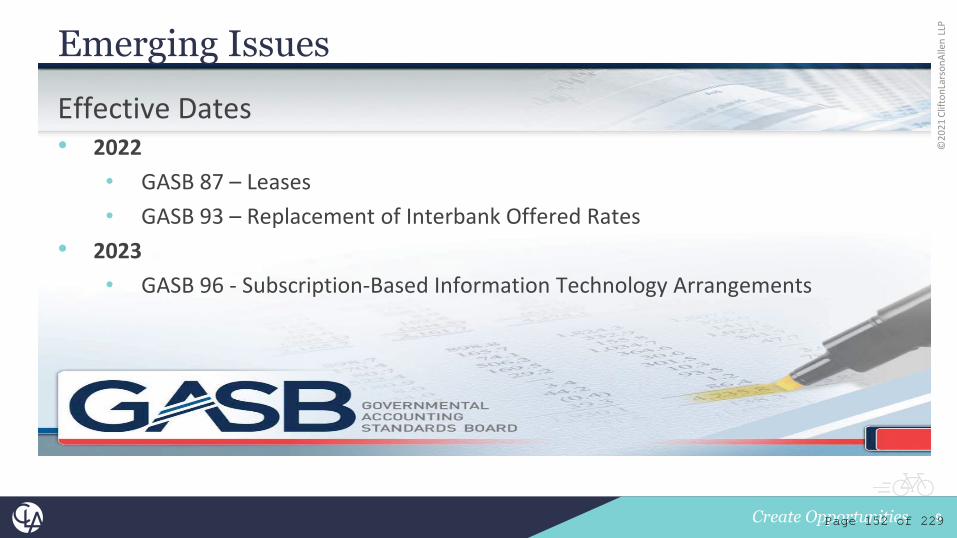

• USNH adopted three new accounting standards. The most notable standard adopted was GASB 84 regarding fiduciary activities which affects reporting of the Operating Staff Retirement Plan (OSRP). However, USNH has historically presented these funds in the notes to the financial statements so no further compliance was necessary. The remaining two accounting standards had no effect on the financial statements.

Ms. Ndayisaba drew the committee’s attention to net tuition and fees, employee compensation and supplies and services on the statements of revenues, expenses and changes in net position. Net tuition and fees decreased due to a decrease in enrollment and an increase in financial aid.

Page 5 of 229

Audit Committee p. 3 of 7

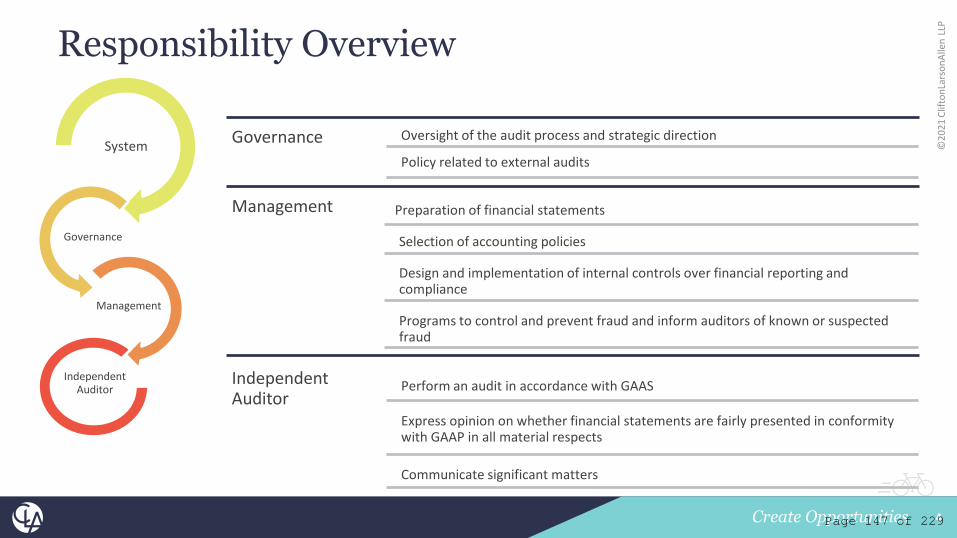

Employee compensation increased in large part because of the CERP. The supplies and services cost increased due to Covid expenses. On the statements of net position, Ms. Ndayisaba highlighted the increase in endowment and similar investments due to healthy returns and the increase in other liabilities and deferred inflows of resources again due to the CERP. Finally, Ms. Ndayisaba discussed receipts from tuition and fees (net), noncapital gifts, grants and other receipts, and net cash (used in)/provided by investing activities on the statements of cash flows. There was a decrease in net tuition and fees due to FY20 student refunds which remained in student accounts. USNH received grants such as CARES and GOEFFER grants which contributed to the increase in grant funds. Net cash increased due in part to an investment liquidation. Chair Walker expressed his appreciation for the work of Ms. Ndayisaba and her team. There were no questions or comments from the committee. Mr. Lee briefly reviewed the engagement scope and deliverables which includes issuance of the following reports: required governance communications letter, internal control communication letter, and a management letter, if necessary. Mr. Lee noted that a management letter was not necessary this year. The Uniform Guidance Audit is in progress. CLA is expecting one compliance supplement. They will perform Major Program Determination and Risk Assessment to identify other major programs for testing. The results are typically provided at the January Audit Committee meeting. Mr. Lee reviewed the responsibility overview of governance, management and the independent auditor, and audit focus areas. He noted that the focus areas did not deviate from the plan discussed at the April Audit Committee meeting. Finally, Mr. Lee stated that the USNH Financial Statement audit resulted in an unmodified opinion (“clean opinion”) on the financial statements, noting his appreciation to the USNH Accounting and Finance team. Regarding internal controls, Mr. Winter stated that CLA found no material weakness or significant deficiencies, no non‐compliance with laws and regulations regarding internal controls over financial reporting, compliance and other matters. He reminded the committee that CLA does not express an opinion on the effectiveness of the System’s internal controls because it is not required under GAAS. Mr. Winter briefly discussed the footnotes in the financial statements, specifically management’s significant accounting policies (Note 1) and disclosure around the COVID‐19 pandemic (Note 15).

Page 6 of 229

Audit Committee p. 4 of 7

CLA concluded that management has a reasonable basis for significant judgements and estimates for items including Net Pension Asset & Net OPEB Liability and noted that they are in agreement with management. There were no corrected misstatements, errors or adjustments noted. There was one uncorrected misstatement regarding Investment FMV Appreciation. Mr. Winter emphasized that this was not an error; the confirmations revealed that there was a higher threshold than shown. There were no disagreements with management on accounting/auditing matters. Emerging issues include GASB 84, 87, 93 and 96. GASB 84 regarding Fiduciary Activities (any funds owned by other parties) was adopted in FY21. CLA concluded that OSRP funds are immaterial to USNH and subsequently a separate statement is unnecessary. GASB 87 regarding Leases is effective in 2022 and will be a significant workload. Management is working with an accounting firm to comply with the standard. Also effective in 2022 is GASB 93 regarding replacement of interbank offered rates; however, it should have no major effect on USNH. GASB 96 regarding cloud-based subscription information technology arrangements is effective in 2023. In response to a question from Chair Walker, Mr. Lee stated that much of the audit work was done virtually. CLA and management will revisit this arrangement for next year’s audit. Mr. Lee noted that CLA is comfortable with that approach. Mr. Winter mentioned that CLA will be on site at UNH next week for the single audit. The following motion was made by Trustee Eastwood, duly seconded, discussed, and approved with no votes abstained or dissenting.

VOTED, on recommendation of the Chief Administrative Officer, that the USNH Financial Statements for the fiscal year ended June 30, 2021 be approved and forwarded to the Board of Trustees with the following recommended action: MOVED, on recommendation of the Audit Committee, that the USNH Financial Statements for the fiscal year ended June 30, 2021 be accepted and forwarded to the Governor, the Legislative Fiscal Committee, and others as specified in state law RSA 187-A:22. C. Approve Audit Committee FY22 Meeting Schedule and Work Plan

Mr. Jain noted that the work plan is being presented at this meeting due to the cancellation of the June 2021 meeting. Items expected to be on the January agenda include the Single Audit report, Internal Audit’s annual plan and report, and ERM updates as presented to Administrative Board. The Title IX report is on the agenda for the January 2022 meeting; however, the Title IX Coordinators have proposed to present the next report at the January 2023 meeting because of changes in the state law. The timing can be adjusted based on the committee’s expectations. The following motion was made by Trustee Eastwood, duly seconded, discussed, and approved with no votes abstained or dissenting.

Page 7 of 229

Audit Committee p. 5 of 7

VOTED, on recommendation of the Chief Administrative Officer, that the Audit Committee FY22 Meeting Schedule and Work Plan be approved.

V. Items for Committee Consideration and Discussion

A. Title IX Annual Report Chair Walker introduced the Title IX staff present at the meeting. Jeffrey Maher discussed the update and report. He noted that the report was scheduled for the June 2021 meeting, and that the reporting period covers from July 2020 through May 2021. Mr. Maher briefly explained the term “disclosure.” There was a decrease in the total number of disclosures (including pre-affiliation) to 201. These trends are consistent with prior years though the number of incidents is lower due in part to the impact of COVID-19. Sexual harassment and sexual assault with penetration (27% each) were the highest reported types of misconduct, followed by dating violence (12%). Overall, there were approximately 21% fewer disclosures across the University System compared to 2019-2020 (pandemic shutdown) and 31% fewer than 2018-19 (pre-pandemic). Reduced on-campus density, social gathering restrictions, and remote/hybrid classes all contribute to these trends. The new Title IX regulations were effective in August 2020 so this was the first academic year under the new regulations, which require a formal complaint to initiate an institutional investigation of misconduct. Of 182 affiliated disclosures, 14 parties chose to initiate formal complaints. The high number of formal complaints was unexpected but Title IX Coordinators were able to process them using tools such as shared resources and Zoom. RSA 188-H was effective in January 2021. Title IX Coordinators are actively working to meet the law’s requirements which include development of policies, climate surveys, awareness campaigns, and data reporting to the NH Department of Education (DOE). A state-wide Task Force, on which USNH is participating, is the vehicle for these requirements. There are also a number of sub-committees being formed. A Confidential Resource Advisor has been designated and protocols regarding investigations and prosecution of sexual misconduct incidents have been updated. All NH institutions must conduct a climate survey (due in March) and provide annual data concerning allegations of sexual misconduct to the DOE, Department of Health and Human Services (DHHS), NH House and Senate (due annually on October 1). A standardized climate survey was recently released. Data required for DOE reporting include allegations of dating and domestic violence, sexual assault, stalking, concurrent law enforcement investigations, and student conduct outcomes. Important to note is that the data will be comparative to other NH institutions outside of USNH. Trustee Eastwood inquired whether the state data excluded data that has previously been reported. Attorney Martin noted that at a minimum the USNH reports will be supplemented with information concerning 3rd party reports. She also confirmed that data and climate surveys regarding other institutions will be included for the committee.

Page 8 of 229

Audit Committee p. 6 of 7

Chair Walker asked whether there were inconsistencies or redundancies between State and Federal law. Mr. Maher stated there are some inconsistencies because the state law was passed before the Title IX rules were finalized. He noted that the DOE is using the rulemaking process to clarify the requirements for the climate survey. For consistency and data analysis purposes, USNH Title IX Coordinators proposed to consolidate the Board of Trustees report with the annual State reporting. Title IX Coordinators would like to submit their next annual report to the Audit Committee in January 2023 which would cover the data from the prior academic year, and every January thereafter. The committee agreed with this approach. Chair Walker thanked the Title IX coordinators for their valuable work.

B. Results of Audit Committee's Self-assessment Mr. Jain noted that there was low survey participation. Mr. Jain requested members to provide feedback/comments/questions, which can be incorporated into the upcoming meetings. If necessary, committee members can contact him with any feedback. In response to a question from Chair Walker regarding suggestions for “deeper dive” items, Trustee Stevens emphasized the importance of Title IX and campus culture. He also encouraged USSB representatives to attend meetings. Lastly, he noted the value of USNH financial staff.

C. Review Audit Committee Charter The Audit Committee has the responsibility to review and assess the adequacy of the Audit Committee Charter on an annual basis and recommend any changes to the Board. No changes to the Audit Committee Charter are recommended by USNH staff at this time. Mr. Jain asked the Committee members to provide suggestions. If necessary, committee members can contact him with any feedback. There were no questions from the committee.

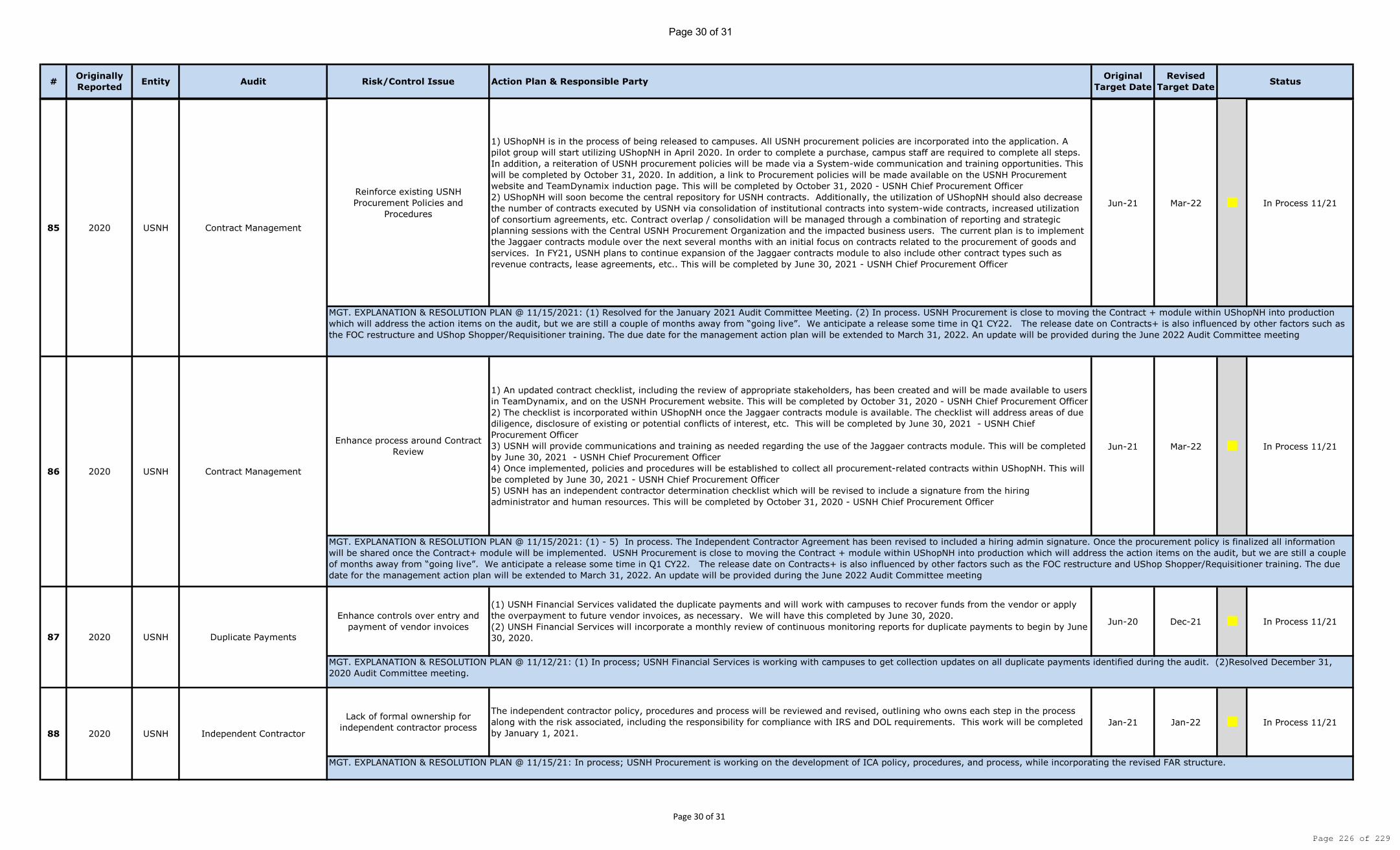

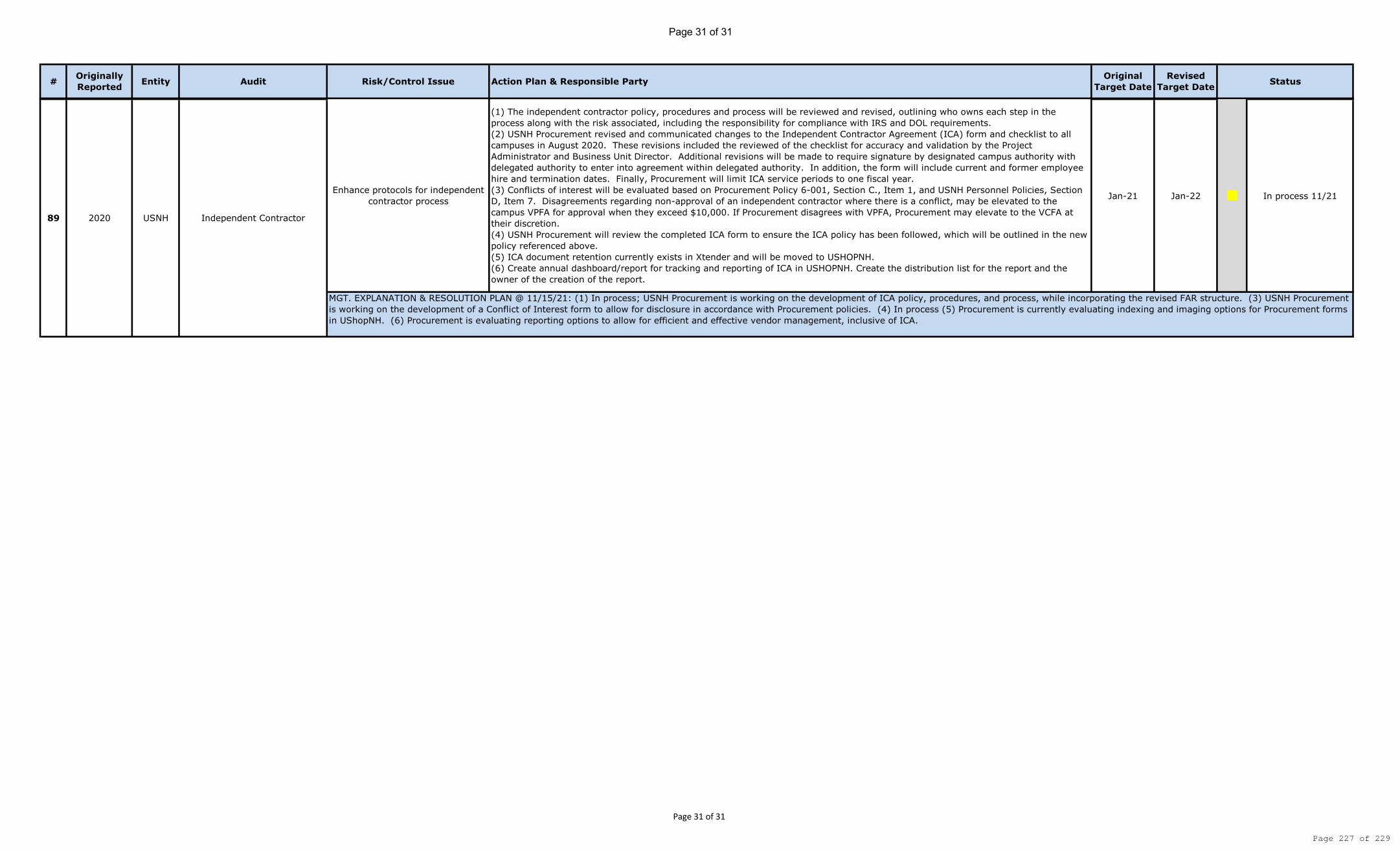

D. Status of Outstanding Audit Issues Mr. Jain noted that the list of outstanding audit issues (as of June 9, 2021) includes all significant (high risk) open issues from past audit reports and those that were closed since the report was last distributed to the Audit Committee. It is updated semi-annually for follow-up and control monitoring purposes. Of 78 action plans currently being tracked, including nine from internal audit reports issued since the last semi-annual, 11 of the underlying risk/control issues have been reported by management as resolved and the remaining 67 are in process, much improved, on hold, and/or management has accepted the residual risk.

Page 9 of 229

Audit Committee p. 7 of 7

In response to a question from Trustee Eastwood, Mr. Jain noted that Information Technology related risks are most concerning. He and his team work closely with staff responsible for monitoring these items. Much progress has been made to mitigate these risks such as MFA (multi-factor authentication), encryption, etc. Some solutions may require resources and/or technology which delay progress. Trustee Treadwell expressed her appreciation to Mr. Jain and his team for their diligent work. VI. Other Business Trustee Jasper expressed his concern regarding inclusion of Cooperative Extension positions in the CERP. He noted that there were approximately 17 positions approved for reinstatement over a 2-3-year period. The departure of these employees and the extended period of time to refill these positions will have a negative effect on farmers in NH, who rely heavily on the Cooperative Extension. Provost Jones agreed with Trustee Jasper’s concern and acknowledged the error and mitigation efforts, noting that there are ongoing efforts to accelerate the reinstatement process. Trustee Eastwood suggested that this topic be added as a formal agenda item for the next Educational Excellence Committee meeting. This is Trustee Stevens’ last Audit Committee meeting, on which he has served for many years. Chair Walker thanked Trustee Stevens for his gracious and wise guidance over the years and expressed appreciation for all of his accomplishments on the committee. He will be missed. Mr. Jain also expressed his appreciation for Trustee Stevens noting that he has been an integral contributor to the committee and USNH. Mr. Jain stated that Trustee Stevens always understood the challenges faced by management and Internal Audit and provided valuable support. Lastly, he stated that the contributions of Trustee Stevens can never be overstated. Trustee Stevens thanked them for their kind words. There being no further business, the meeting adjourned at 11:42 a.m.

-- End of Audit Committee Meeting Minutes --

Page 10 of 229

Page 11 of 229

Page 12 of 229

Page 13 of 229

Page 14 of 229

Page 15 of 229

Page 16 of 229

Page 17 of 229

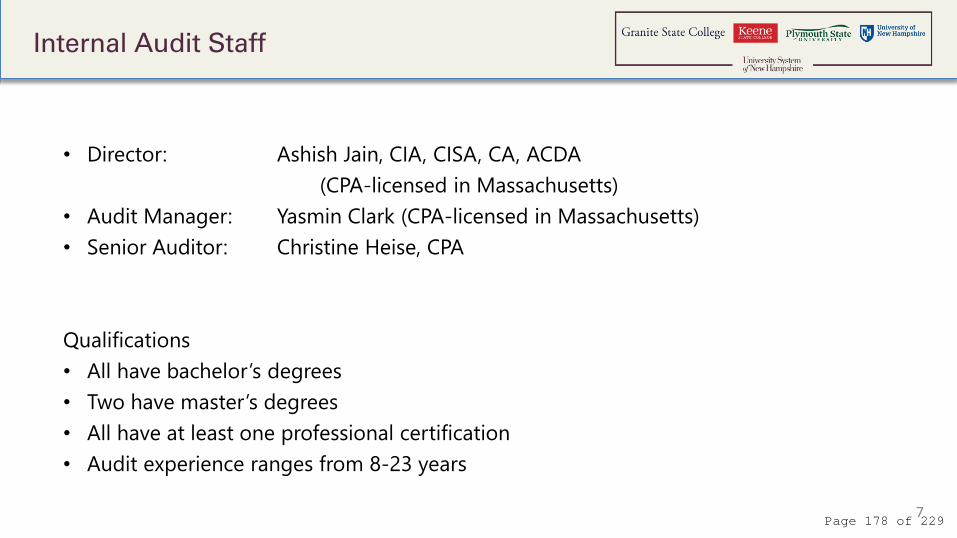

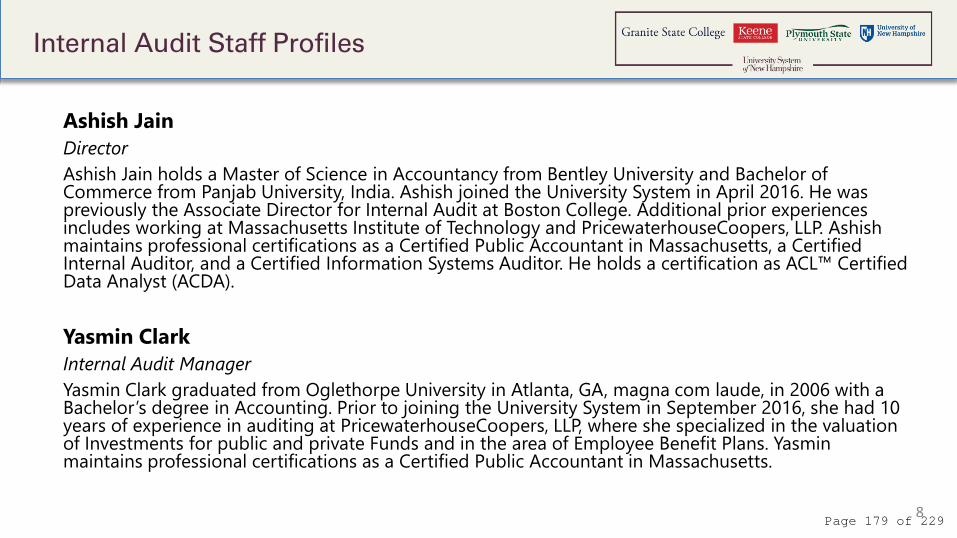

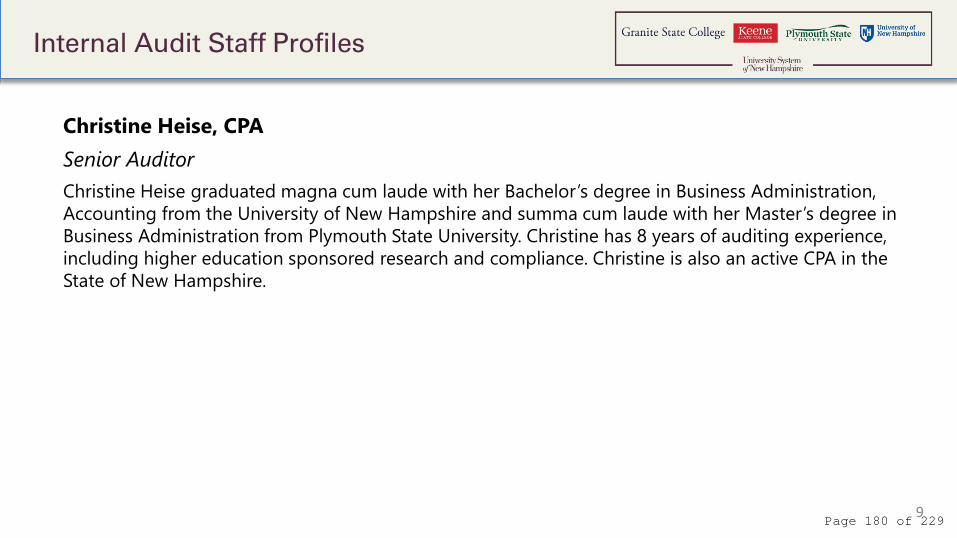

Internal Audit | 5 Chenell Drive, Suite 301, Concord, NH 03301 | usnh.edu

University of New Hampshire

Student Grades Audit

Report issued November 9, 2021

Page 18 of 229

Internal Audit | 5 Chenell Drive, Suite 301, Concord, NH 03301 | usnh.edu

November 9, 2021 James W. Dean Jr., President University of New Hampshire Durham, New Hampshire 03824

Dear President Dean: This letter conveys our report on the audit on the University of New Hampshire Student Grades. As communicated in our engagement letter of March 5, 2021, the primary objective of the audit is to obtain reasonable assurance on the effectiveness on internal controls over the integrity and security of the student grades, adequacy of oversight over the process, and control override possibilities to evaluate whether the risks are appropriately identified and managed and whether the existent internal controls are efficient, effective, and operate as expected. This report reflects our observations, which were discussed with members of UNH management, and their action plans in response to our recommendations. It is being distributed to the individuals listed below and will be presented to members of the Audit Committee of the University System of New Hampshire (USNH) at its next scheduled meeting. It is also available for review by external auditors of USNH. We appreciated the full cooperation and assistance we received from Liz Smith, Associate Registrar of Records and Matthew Grady, Assistant Dean for Registration and Records and Registrar with whom Christine Heise, Senior Internal Auditor, worked most closely as she conducted the fieldwork for this audit. Please feel free to contact me with any comments, questions, or suggestions you may have. Sincerely,

Ashish Jain Director of Internal Audit

Distribution: Andy Colby, University Registrar, UNH Pelema Ellis, Vice Provost of Enrollment Management, UNH Matthew Grady, Registrar and Assistant Dean for Registration and Records, UNH Law Wayne Jones, Provost and Vice President for Academic Affairs, UNH Bill Poirier, Chief Information Officer, USNH Catherine Provencher, Chief Administrative Officer and Vice Chancellor for Financial Affairs and Treasurer, USNH

Page 19 of 229

University of New Hampshire Student Grades Audit

3

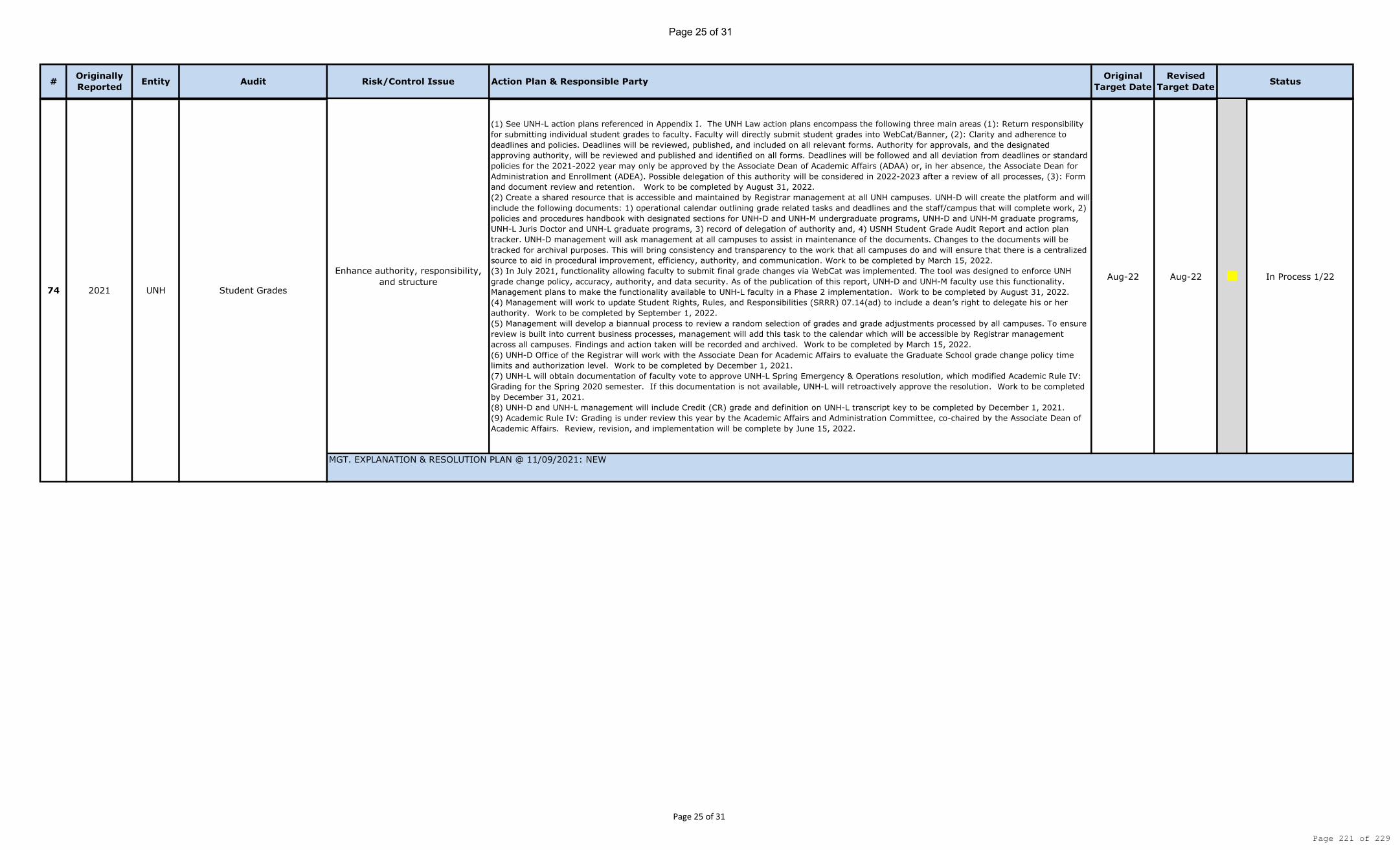

I. Executive Summary We performed an audit of the University of New Hampshire student grade process. We noted that the control structure, authority, and responsibility over student grades could be enhanced. UNH student grade responsibilities are distributed across UNH campuses. Student grade related processes and systems, including grade entry, grade adjustments, grade monitoring, and academic policy exceptions, are inconsistent and not standardized across UNH campuses and student levels resulting in inaccurate grades assigned, inaccurate grade modes assigned, missing or incomplete supporting documentation, and inappropriate authorization of student grade adjustments. We also noted lack of segregation of duties over student grade transactions. We recommend that management evaluate the reporting structure, authority, and responsibilities of the campus Offices of the Registrar for standardization and process alignment, including the formal documentation of roles and responsibilities between campus Offices of the Registrar. Management should monitor grade entry and adjustments for accuracy and authorization, develop policies and procedures for grade adjustment authority and academic policy exceptions, and develop supporting documentation retention protocols. Also, instructors at all campuses should be required to enter and submit final grades in Canvas to streamline the process. We noted that the Canvas and WebCat grade entry interfaces are not consistently reconciled. The systems are not configured or designed with edit input controls and permissions to ensure valid and consistent application of student grades. We also noted inconsistent access between Canvas and WebCat. Management should develop policy and protocols that provide a framework that guides grade access and authorization for Canvas and WebCat. Management should also enhance the configuration of Canvas and WebCat grading systems to provide consistent grade scale menus that align with course grade modes. We also noted that the change management process for Canvas superuser accounts is ad-hoc and lacks key components, including review and approval. We recommend that formal protocols should be developed for the management and monitoring of admin superuser accounts, privileges, and activity. Management should periodically review Canvas and Banner Student grade access for appropriateness. We recommend that management enhance monitoring of transfer credits and repeat courses to ensure compliance with UNH policy. Finally, we recommend for management to enhance the monitoring of Parchment (third party vendor used for transcript processing) for compliance with data security requirements and contract terms. II. Background UNH Faculty Senate is responsible for UNH undergraduate and graduate grading policies. Any modifications to UNH Durham (UNH-D) and UNH Manchester (UNH-M) grading policies are proposed and approved by the UNH Faculty Senate. UNH Law Faculty are responsible for UNH Law grading policies and proposed to the UNH Law faculty for approval. UNH Law Academic Affairs & Administration Committee (AAAC) is responsible for updating and amending academic rules. UNH undergraduate, graduate, UNH-Law masters and UNH-Law Juris Doctor have different grading policies and grade scales for their programs.

Page 20 of 229

University of New Hampshire Student Grades Audit

4

UNH Offices of the Registrar The UNH Durham (UNH-D) Office of the Registrar serves the students, faculty, staff, and alumni of the University of New Hampshire through registration, maintenance, and security of students’ educational records as well as student data that feeds the academic, reporting, and financial needs for the institution; course and classroom management; graduation, catalogs, and academic support. As part of record keeping, the Office of the Registrar is responsible for grade entry, grade adjustments, grade publishing, and transcript processing. The UNH Manchester (UNH-M) Registration Office manages course registration, classroom scheduling, and faculty relations for the UNH-M campus. The Registration Office is responsible for several UNH-M functions that are typically under the authority of UNH-D Dean Offices. The UNH Law (UNH-L) Office of the Registrar is responsible for maintaining student’s official academic records, course scheduling and registration, exam scheduling and administration, bar certification, and veteran certification. The UNH-L Office of the Registrar is also responsible for grade entry, including the processing of student withdrawal requests. Student Grade Entry The UNH-D Office of the Registrar is responsible for the publishing of all final grades for all UNH campuses. For UNH-D and UNH-M, all teachers assigned to a course in Banner can enter final grades directly into WebCat. Student grades can also be entered by faculty in the learning management software, Canvas. Both WebCat and Canvas have grade scale drop-down menus for faculty to select the grade to be awarded to the student. Canvas teacher and student access is granted through a daily feed from Banner to Canvas. All instructors denoted in Banner Student form SSASECT are assigned teacher access in Canvas. Teachers and course designers have the ability to assign other Canvas users’ roles to access their course. Course designer roles are assigned to department administrative assistants for courses to facilitate the setup of courses in Canvas when the instructor has not yet been determined. See the chart below for commonly used Canvas roles that provides access to student grade information: Canvas Roles Permissions TA Teacher Designer Add/remove other teachers, course designers or TAs to course

No Yes Yes

Add/remove students Yes Yes Yes Edit grades Yes Yes No Moderate grades No Yes No View grades Yes Yes Yes

Faculty designated as the primary instructor in Banner are authorized to submit final grades in Canvas. Grades entered in Canvas are transferred to WebCat through the grade passback process. UNH has developed code to validate grades submitted in Canvas for publishing in WebCat. If any grade errors exist, the faculty member will receive an email notifying them of the error in publishing grades. The types of errors that the rules will check for include: (1) grades were submitted for students not registered for the course, (2) final grade does not equal the current grade, (3) person who submitted grades is not the instructor of record, (4) grade not valid for course, (5) grading period is closed, and (6) student is not an active UNH student. For

Page 21 of 229

University of New Hampshire Student Grades Audit

5

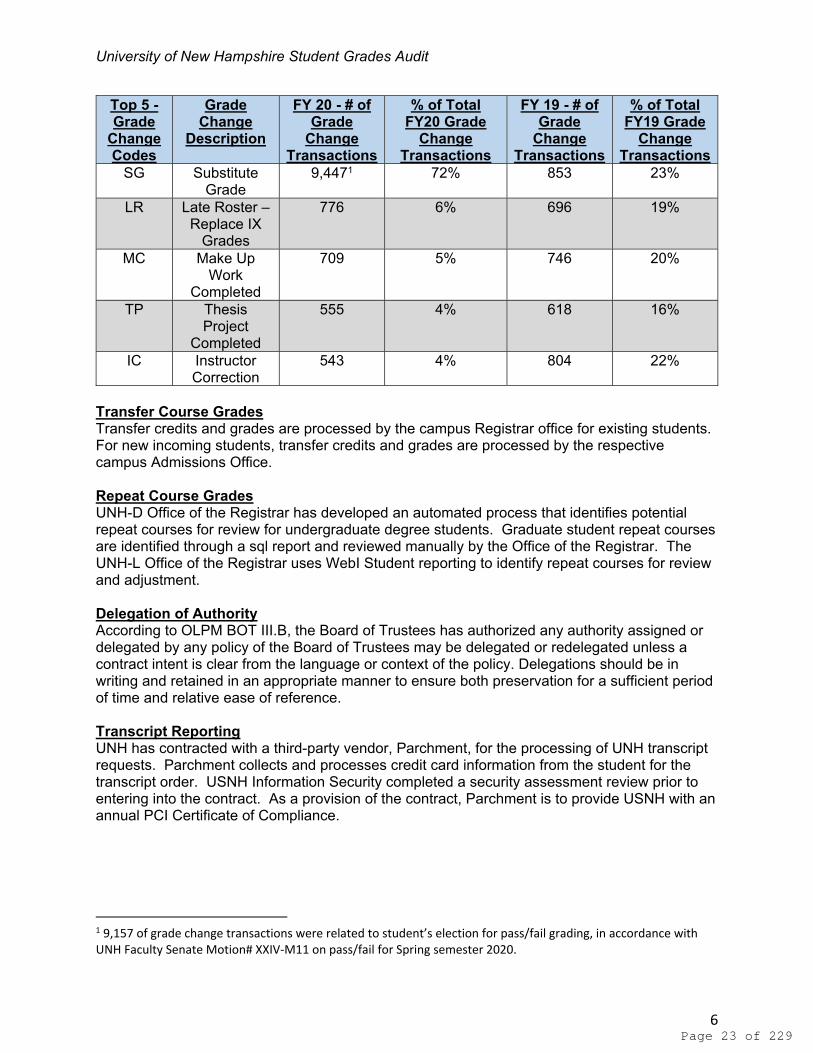

UNH-L, grades are entered into Banner Student by the UNH-L Office of the Registrar staff. Banner Student is the system of record for student grades. UNH-D and UNH-M share the same grade scale; whereas UNH-L has their own grade scale which is different for UNH-L JD major and other UNH-L Master’s program majors. The grade mode is the grading schema assigned to a course. Undergraduate students may elect to take a limited number of elective courses pass/fail. Grade mode options are coded on each course, and student registrations reflect grade mode when a choice is relevant. At UNH, the following grade modes are used: letter grade, pass/fail, credit/no credit, satisfactory/unsatisfactory, and audit. In addition, UNH-D and UNH-M use the grade mode to denote students who have elected to take a course as pass/fail. The WebCat and Canvas grade dropdown menus available for grade entry populates grades associated with a course. UNH-D Office of the Registrar runs periodic grade monitoring reports to identify potential issues in grades assigned to UNH-D and UNH-M undergraduate and graduate students. These error reports include: (1) letter grades entered for credit/fail courses, (2) credit/fail grade entered for letter grade course, (3) AF* or F* grades entered for letter grade course, (4) withdrawn students with an incomplete grade, (5) withdrawn students with a letter grade, (6) withdraw grades that have not been published to academic history, and (7) letter grade for an audit course. Student Grade Adjustments For undergraduate student grade changes submitted before the middle of the semester immediately following the one in which the grade was granted may be approved by the Dean of the College. After mid-semester, students must petition the Academic Standards and Advising Committee (ASAC) for any grade changes. For graduate student grade changes, after consulting the instructor, if a student still believes that the grade is unfair, the student has the right to seek redress from the chairperson of the department or program in which the course is offered. Under exceptional circumstances, a final appeal may be made to the Dean of the College or School in which the program is offered. For UNH-L JD student grade changes, a student desiring to appeal an instructor’s final grade should do so to the Associate Dean of Academic Affairs at UNH School of Law. A written appeal must be delivered to the Associate Dean of Academic Affairs no later than the fifth week of the fall semester in the case of grades from spring or summer courses or the fifth week of the spring semester in the case of grades from fall courses. Student grade adjustments are requested through the completion of the Special Grade Report (SGR). This form is initiated by the instructor and is approved by the respective UNH College Dean. In July 2021, functionality allowing faculty to submit grade adjustments via WebCat was implemented. Grade adjustments for all UNH campuses and students are processed through the UNH-D Office of the Registrar. During FY20 and FY19, there were 13,136 and 5,376 student grade changes processed. The FY20 grade changes related to academic terms ranging from Fall 2001 to Summer 2020, with 88% of grade changes related to FY20 academic terms. The top five grade change codes for FY20 and FY19 represented 91% and 69% of the total of grade changes.

Page 22 of 229

University of New Hampshire Student Grades Audit

6

Top 5 - Grade

Change Codes

Grade Change

Description

FY 20 - # of Grade

Change Transactions

% of Total FY20 Grade

Change Transactions

FY 19 - # of Grade

Change Transactions

% of Total FY19 Grade

Change Transactions

SG Substitute Grade

9,4471 72% 853 23%

LR Late Roster – Replace IX

Grades

776 6% 696 19%

MC Make Up Work

Completed

709 5% 746 20%

TP Thesis Project

Completed

555 4% 618 16%

IC Instructor Correction

543 4% 804 22%

Transfer Course Grades Transfer credits and grades are processed by the campus Registrar office for existing students. For new incoming students, transfer credits and grades are processed by the respective campus Admissions Office. Repeat Course Grades UNH-D Office of the Registrar has developed an automated process that identifies potential repeat courses for review for undergraduate degree students. Graduate student repeat courses are identified through a sql report and reviewed manually by the Office of the Registrar. The UNH-L Office of the Registrar uses WebI Student reporting to identify repeat courses for review and adjustment. Delegation of Authority According to OLPM BOT III.B, the Board of Trustees has authorized any authority assigned or delegated by any policy of the Board of Trustees may be delegated or redelegated unless a contract intent is clear from the language or context of the policy. Delegations should be in writing and retained in an appropriate manner to ensure both preservation for a sufficient period of time and relative ease of reference. Transcript Reporting UNH has contracted with a third-party vendor, Parchment, for the processing of UNH transcript requests. Parchment collects and processes credit card information from the student for the transcript order. USNH Information Security completed a security assessment review prior to entering into the contract. As a provision of the contract, Parchment is to provide USNH with an annual PCI Certificate of Compliance.

1 9,157 of grade change transactions were related to student’s election for pass/fail grading, in accordance with UNH Faculty Senate Motion# XXIV‐M11 on pass/fail for Spring semester 2020.

Page 23 of 229

University of New Hampshire Student Grades Audit

7

III. Scope

The audit focused on key controls surrounding the student grade process and compliance with policies. We performed an audit to obtain reasonable assurance whether the risks associated with the integrity and security of student grades are appropriately identified and managed, internal controls are in place, and the established internal controls are designed effectively and operating as expected. Specifically, we performed the following procedures:

Reviewed a sample of UNH grade entry transactions assigned for approval, authorization, and compliance with UNH grading policies;

Reviewed a sample of UNH transfer and repeat course grade transactions for compliance with UNH policies;

Reviewed a sample of grade adjustment transactions for authorization and compliance with UNH grading policies;

Reviewed grades assigned for students in a sample of undergraduate, graduate, and JD majors for Fall 2020, Spring 2020, and Summer 2020 semesters to determine if grade assigned aligned with grade mode;

Reviewed UNH Spring 2020 grading policy resolutions for authorization and approval; Reviewed modify access to Banner Student Grade Entry Form SFASLST, Banner Grade

Adjustment Form SHATCKN, and Banner Grade Process SFUIXGR; Review view access to student grades in Banner Student Forms SFARHST, SFASLST,

SHACRSE, SHATERM, and SHATRNS; Reviewed Canvas access for users assigned course roles with edit and moderate grade

permissions; Reviewed WebCat access for faculty assigned access to courses; Reviewed modify access to UNH code server; Interviewed personnel in the UNH-D Office of the Registrar, UNH-L Office of the

Registrar, Enterprise Technology and Services, and Teaching and Learning Technologies and met with management to confirm test results.

Internal Audit noted that UNH Teaching and Learning Technologies staff made changes to Canvas admin accounts and Canvas role permissions during the information gathering phase of the audit. As a result, for purposes of the audit, we relied on Canvas role, user, and access reports provided to Internal Audit, and our audit procedures may not fully identify control issues with Canvas roles and access. Student grade data security elements were presented in this audit report but were not the primary objective of the audit. The compliance with student program requirements for degree completion was outside the scope of this audit. Access to systems maintaining grade data e.g., WebI were not considered in scope of this audit. IV. Report Structure The seven observations in Section V of this report outline internal control issues for management’s attention and consideration. The order of the comments is based on their relative importance in terms of potential risk to UNH or foregone effectiveness if not addressed. The observations marked with an asterisk indicates the significance for management attention and resolution, which will be tracked for the USNH Audit Committee’s monitoring until resolved. The report contains recommendations that management has considered and incorporated the

Page 24 of 229

University of New Hampshire Student Grades Audit

8

management action plans indicated below. The business process improvement observations in Section VI are strongly recommended but do not require a management action plan. V. Observations

*1. Enhance authority, responsibility, and structure We noted that UNH student grade responsibilities are distributed across the campus UNH Offices of the Registrar. We noted that there is no formal documentation of roles and responsibilities among the campus Offices of the Registrar. We also noted that student grade related processes and procedures, including grade entry, grade adjustments, grade monitoring, and academic policy exceptions, are inconsistent and not standardized between UNH campuses and student levels (i.e., undergraduate, graduate, masters, and JD). Finally, we noted that the level of authority and time limits for grade adjustment transactions is not consistent among UNH programs. Due to inconsistencies in grade related processes and procedures, we noted inaccurate grades assigned, inaccurate course grade modes, inaccurate student grade modes, missing or incomplete supporting documentation, and inappropriate authorization of student grade adjustments. We also noted lack of segregation of duties over student grade transactions and inadequate review of grade entry. There is the risk that student grades are inaccurate or invalid and are not in compliance with UNH policies, resulting in reputational loss. Refer to Appendix I for detailed observations and recommendations. We noted that UNH-Law grade adjustments were initiated (on behalf of the instructor) and approved by the UNH Law Assistant Registrar. The Assistant Registrar combined her own authority with the informal Registrar’s delegated authority, to process these transactions, which resulted in a lack of review over the grade adjustments. We noted that the UNH Law Assistant Registrar authorized special grade report forms on behalf of the UNH Law Registrar. Through inquiry, the UNH Law Assistant Registrar indicated that the Registrar verbally delegated authority replicating her signature on various forms, including special grade reports. We noted that there was no documentation to support this delegation. The delegation of authority by the UNH Law Registrar is not in compliance with OLPM BOT III.B, which requires the delegation to be in writing and retained. There is the risk that student grade adjustment transactions are not properly reviewed, approved, and authorized, resulting in the loss of reputation. Finally, we noted that UNH-L proposed a modification to Academic Rule IV (Grading) applicable to the Spring 2020 semester. This modification intended to allow instructors to award only credit/no credit (CR/NCR) grades in certain circumstances. Although CR/NCR grades were awarded, we were unable to obtain documentation to support the review and approval of underlying modification. Also, we noted that CR/NCR grades are not currently defined in UNH-L Academic Rule IV. We have the following recommendations with regards to this observation:

Refer to Appendix I for detailed recommendations related to student grade entry and adjustment testing.

Management should evaluate the reporting structure, authority, and responsibilities of the campus Offices of the Registrar for standardization and process alignment.

UNH should consider standardized student grade processes across UNH campuses.

Page 25 of 229

University of New Hampshire Student Grades Audit

9

Management should formalize the documentation of roles and responsibilities for UNH campus registrar operations.

Management should review grade change procedure time limits and authorization protocols for student grade adjustments for UNH programs for appropriateness and determine if in alignment with management expectations.

Management should develop procedures for the documentation, tracking, and monitoring of delegation of authority for UNH Office of the Registrar forms.

Management should formally approve the UNH Law Spring Emergency & Operations resolution (which modified Academic Rule IV: Grading for Spring 2020 semester) and for authority and compliance with academic rule modification procedure.

Management should formally define UNH Law grades awarded to students in Spring 2020 semester.

Management Action Plan The following actions will be taken to address the above observation: 1. See UNH-L action plans referenced in Appendix I. The UNH Law action plans encompass

the following three main areas (1): Return responsibility for submitting individual student grades to faculty. Faculty will directly submit student grades into WebCat/Banner, (2): Clarity and adherence to deadlines and policies. Deadlines will be reviewed, published, and included on all relevant forms. Authority for approvals, and the designated approving authority, will be reviewed and published and identified on all forms. Deadlines will be followed and all deviation from deadlines or standard policies for the 2021-2022 year may only be approved by the Associate Dean of Academic Affairs (ADAA) or, in her absence, the Associate Dean for Administration and Enrollment (ADEA). Possible delegation of this authority will be considered in 2022-2023 after a review of all processes, (3): Form and document review and retention.

Responsible Party: UNH-L Associate Dean of Academic Affairs and UNH-L Assistant Dean for Registration and Records, unless otherwise noted in Appendix I Due Date: August 31, 2022, unless otherwise noted in Appendix I

2. Create a shared resource that is accessible and maintained by Registrar management at all UNH campuses. UNH-D will create the platform and will include the following documents: 1) operational calendar outlining grade related tasks and deadlines and the staff/campus that will complete work, 2) policies and procedures handbook with designated sections for UNH-D and UNH-M undergraduate programs, UNH-D and UNH-M graduate programs, UNH-L Juris Doctor and UNH-L graduate programs, 3) record of delegation of authority and, 4) USNH Student Grade Audit Report and action plan tracker. UNH-D management will ask management at all campuses to assist in maintenance of the documents. Changes to the documents will be tracked for archival purposes. This will bring consistency and transparency to the work that all campuses do and will ensure that there is a centralized source to aid in procedural improvement, efficiency, authority, and communication.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

3. In July 2021, functionality allowing faculty to submit final grade changes via WebCat was implemented. The tool was designed to enforce UNH grade change policy, accuracy, authority, and data security. As of the publication of this report, UNH-D and UNH-M faculty use this functionality. Management plans to make the functionality available to UNH-L faculty in a Phase 2 implementation.

Page 26 of 229

University of New Hampshire Student Grades Audit

10

Responsible Party: UNH-L Registrar and Assistant Dean for Registration and Records and UNH-D Associate Registrar of Records Due Date: August 31, 2022

4. Management will work to update Student Rights, Rules, and Responsibilities (SRRR) 07.14(ad) to include a dean’s right to delegate his or her authority.

Responsible Party: University Registrar Due Date: September 1, 2022

5. Management will develop a biannual process to review a random selection of grades and grade adjustments processed by all campuses. To ensure review is built into current business processes, management will add this task to the calendar which will be accessible by Registrar management across all campuses. Findings and action taken will be recorded and archived.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

6. UNH-D Office of the Registrar will work with the Associate Dean for Academic Affairs to evaluate the Graduate School grade change policy time limits and authorization level.

Responsible Party: UNH-D Associate Registrar of Records Due Date: December 1, 2021

7. UNH-L will obtain documentation of faculty vote to approve UNH-L Spring Emergency & Operations resolution, which modified Academic Rule IV: Grading for the Spring 2020 semester. If this documentation is not available, UNH-L will retroactively approve the resolution.

Responsible Party: UNH-L Associate Dean of Academic Affairs Due Date: December 31, 2021

8. UNH-D and UNH-L management will include Credit (CR) grade and definition on UNH-L transcript key.

Responsible Party: UNH-L Registrar and Assistant Dean for Registration and Records, and UNH-D Associate Registrar of Records Due Date: December 1, 2021

9. Academic Rule IV: Grading is under review this year by the Academic Affairs and Administration Committee, co-chaired by the Associate Dean of Academic Affairs. Review, revision, and implementation will be complete before the end of the academic year.

Responsible Party: UNH-L Associate Dean of Academic Affairs Due Date: June 15, 2022

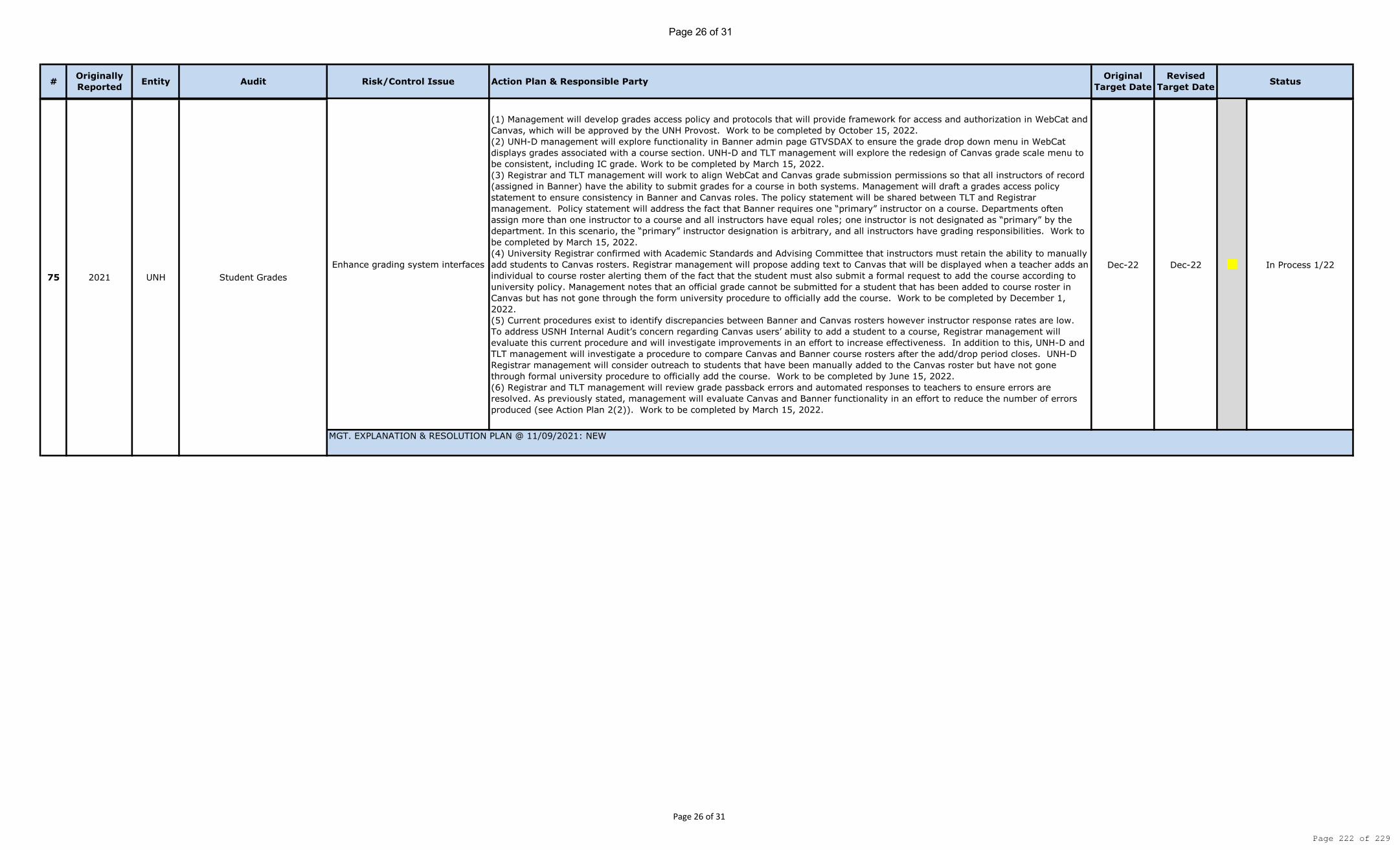

*2. Enhance grading system interfaces We noted that the Canvas and WebCat systems have not been designed with edit input controls and permissions to ensure valid and consistent application of student grades. We noted that the grade menu in the Canvas and WebCat system are not configured to the course grade mode. We also noted that the grade scale menus in Canvas and WebCat are not consistent. As an example, instructors must enter incomplete (IC) grades in WebCat, as the Canvas grade scale menu does not have this grade available. Also, we noted that final grade submittal permissions vary between WebCat and Canvas. All course instructors listed in Banner Student can submit grades in WebCat; whereas only the primary instructor can submit final grades in Canvas. Finally, we noted that select Canvas roles’ have the ability to add students to a course in Canvas, bypassing the automated control of registered students being assigned the student role via a feed from Banner Student to Canvas. Due to the above system configuration, UNH-D has developed grade passback code and grade reporting error reports (for UNH-D and UNH-M students) to identify exceptions, rather than designing the system to not allow for invalid grade

Page 27 of 229

University of New Hampshire Student Grades Audit

11

entries or grade submittals. Also, system interface errors noted are not managed and reconciled to ensure that error resolved, and grades are appropriately transferred from Canvas to the WebCat system. Instead, numerous manual and time-consuming workarounds are created, which still does not provide reasonable assurance that the data is appropriately transferred from Canvas to WebCat. There is the risk that the invalid or improper grades are posted to student academic records. We have the following recommendations with regards to this observation:

Policies and protocols should be developed to guide grades setup, access, and authorization of WebCat and Canvas.

Management should redesign Canvas and WebCat grade scale menus to be consistent and align with course grade modes.

Grade submittal authorization should be evaluated and applied consistently in WebCat and Canvas.

Canvas user roles should be updated to not allow for Canvas users to manually add a student to a course.

Interface between Canvas and WebCat should be reconciled and Canvas grade passback errors should be tracked and managed to ensure resolution.

Management Action Plan The following actions will be taken to address the above observation:

1. Management will develop grades access policy and protocols that will provide framework for access and authorization in WebCat and Canvas, which will be approved by the UNH Provost.

Responsible Party: UNH-D Associate Registrar of Records and University Registrar Due Date: October 15, 2022

2. UNH-D management will explore functionality in Banner admin page GTVSDAX to ensure the grade drop down menu in WebCat displays grades associated with a course section. UNH-D and TLT management will explore the redesign of Canvas grade scale menu to be consistent, including IC grade.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

3. Registrar and TLT management will work to align WebCat and Canvas grade submission permissions so that all instructors of record (assigned in Banner) have the ability to submit grades for a course in both systems. Management will draft a grades access policy statement to ensure consistency in Banner and Canvas roles. The policy statement will be shared between TLT and Registrar management. Policy statement will address the fact that Banner requires one “primary” instructor on a course. Departments often assign more than one instructor to a course and all instructors have equal roles; one instructor is not designated as “primary” by the department. In this scenario, the “primary” instructor designation is arbitrary, and all instructors have grading responsibilities.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

4. University Registrar confirmed with Academic Standards and Advising Committee that instructors must retain the ability to manually add students to Canvas rosters. Registrar management will propose adding text to Canvas that will be displayed when a teacher adds

Page 28 of 229

University of New Hampshire Student Grades Audit

12

an individual to course roster alerting them of the fact that the student must also submit a formal request to add the course according to university policy. Management notes that an official grade cannot be submitted for a student that has been added to course roster in Canvas but has not gone through the form university procedure to officially add the course.

Responsible Party: UNH-D Associate Registrar of Records Due Date: December 1, 2022

5. Current procedures exist to identify discrepancies between Banner and Canvas rosters however instructor response rates are low. To address USNH Internal Audit’s concern regarding Canvas users’ ability to add a student to a course, Registrar management will evaluate this current procedure and will investigate improvements in an effort to increase effectiveness. In addition to this, UNH-D and TLT management will investigate a procedure to compare Canvas and Banner course rosters after the add/drop period closes. UNH-D Registrar management will consider outreach to students that have been manually added to the Canvas roster but have not gone through formal university procedure to officially add the course.

Responsible Party: UNH-D Associate Registrar of Records Due Date: June 15, 2022

6. Registrar and TLT management will review grade passback errors and automated responses to teachers to ensure errors are resolved. As previously stated, management will evaluate Canvas and Banner functionality in an effort to reduce the number of errors produced (see Action Plan 2(2)).

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

Internal Audit Response to above Management Action Plan:

Manual processes are inefficient, prone to human error, and a waste of limited UNH resources and consequently should not be considered a replacement for automated system control. This way the University can leverage technology while having a better control environment. We recommend that the interface reconciliation verification process should be implemented to confirm that the data extracted from Canvas is accurately and completely reflected in WebCat.

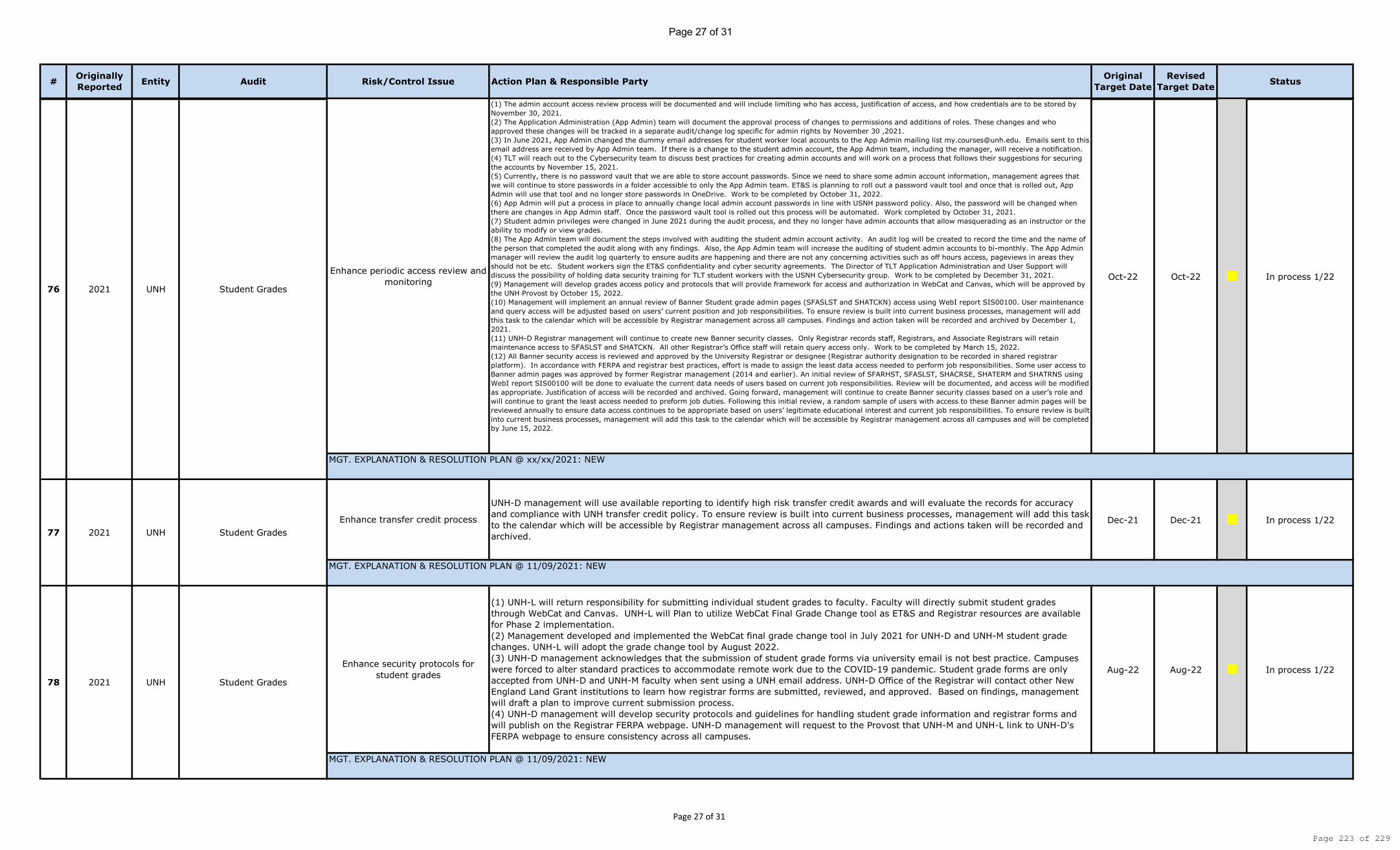

*3. Enhance periodic access review and monitoring

a. Canvas admin accounts are highly privileged accounts primarily used for system administration. During the audit, we noted that the Canvas admin account access modification process is ad-hoc and lacks key components including, appropriate review and approval. In addition, we noted that the semi-annual review of admin accounts for appropriateness is informal and ineffective. Finally, we noted that admin account activity is not periodically reviewed for appropriateness. Specifically, we noted the following with regards to Canvas admin accounts:

i. One shared superuser admin account, for which the credentials are saved on the shared drive in a folder accessible to the Teaching and Learning Technology staff

ii. Two superuser admin accounts had non-USNH email addresses iii. 15 superuser admin accounts had dummy/invalid email addresses. We noted

that these accounts were associated with student workers employed by UNH Teaching and Learning Technology department to provide customer support to

Page 29 of 229

University of New Hampshire Student Grades Audit

13

Canvas users. These students are assigned student admin access to Canvas. This access allows students to impersonate an instructor allowing them to enter or modify grades and submit final grades. We noted that there was no documented periodic review of student admin account activity. To protect the integrity and confidentiality of student data, student workers must be assigned carefully defined roles and responsibilities and provided data security training. There is the risk that a student worker can access or modify student grade information for unauthorized purposes, which can result in the loss of reputation to the University.

These conditions exist because there are no formal protocols for the granting of access to grades and the management and monitoring of admin accounts and for reviewing admin user activity. There is a risk that unauthorized or accidental modifications are made to the Canvas system which could go undetected, resulting inaccurate grade entry, modifications, or submittals.

We have the following recommendations with regards to this observation:

Management should develop formal procedures for the review and approval of changes to system administration users, permissions, and roles. The review and approval should be tracked, documented, and communicated.

Management should periodically review Canvas admin account activity for appropriateness.

Management should implement and document the periodic review of Canvas admin user access for appropriateness and alignment with job responsibilities.

Admin account credentials should not be shared. Alternatively, management should document how and when the shared admin account should be used, which users can use the account, and change the password periodically.

Management should discontinue the practice of storing admin credentials in electronic shared files.

Management should develop and assign student workers carefully defined role and responsibilities limiting their access to sensitive data, including student grades. In addition, management should extend data security training to student workers.

Management should consider modifying the Canvas student admin account role to exclude view and modify access to student grades. Alternatively, management should periodically monitor and document the review of Canvas student admin account activity.

Management Action Plan

The following actions will be taken to address the above observation:

1. The admin account access review process will be documented and will include limiting who has access, justification of access, and how credentials are to be stored. Responsible Party: AT Application Administrator

Due Date: November 30, 2021 2. The Application Administration (App Admin) team will document the approval

process of changes to permissions and additions of roles. These changes and who

Page 30 of 229

University of New Hampshire Student Grades Audit

14

approved these changes will be tracked in a separate audit/change log specific for admin rights.

Responsible Party: AT Application Administrator Due Date: November 30, 2021

3. In June 2021, App Admin changed the dummy email addresses for student worker local accounts to the App Admin mailing list [email protected]. Emails sent to this email address are received by App Admin team. If there is a change to the student admin account, the App Admin team, including the manager, will receive a notification.

4. TLT will reach out to the Cybersecurity team to discuss best practices for creating admin accounts and will work on a process that follows their suggestions for securing the accounts.

Responsible Party: Director, Teaching and Learning Technologies Due Date: November 15, 2021

5. Currently, there is no password vault that we are able to store account passwords. Since we need to share some admin account information, management agrees that we will continue to store passwords in a folder accessible to only the App Admin team. ET&S is planning to roll out a password vault tool and once that is rolled out, App Admin will use that tool and no longer store passwords in OneDrive.

Responsible Party: AT Application Administrator Due Date: October 31, 2022

6. App Admin will put a process in place to annually change local admin account passwords in line with USNH password policy. Also, the password will be changed when there are changes in App Admin staff. Once the password vault tool is rolled out this process will be automated.

Responsible Party: AT Application Administrator Due Date: October 31, 2021.

7. Student admin privileges were changed in June 2021 during the audit process, and they no longer have admin accounts that allow masquerading as an instructor or the ability to modify or view grades. Responsibility Party: AT Application Administrator Due Date: June 30, 2021

8. The App Admin team will document the steps involved with auditing the student admin account activity. An audit log will be created to record the time and the name of the person that completed the audit along with any findings. Also, the App Admin team will increase the auditing of student admin accounts to bi-monthly.

Responsible Party: Director, Academic Application Administration & Support Due Date: December 31, 2021.

9. The App Admin manager will review the audit log quarterly to ensure audits are happening and there are not any concerning activities such as off hours access, pageviews in areas they should not be etc.

Responsible Party: Director, Academic Application Administration & Support Due Date: December 31, 2021.

10. Student workers sign the ET&S confidentiality and cyber security agreements. The Director of TLT Application Administration and User Support will discuss the possibility of holding data security training for TLT student workers with the USNH Cybersecurity group.

Responsible Party: Director, Academic Application Administration & Support Due Date: December 31, 2021

Page 31 of 229

University of New Hampshire Student Grades Audit

15

b. We noted that Canvas users and course role access is not periodically reviewed for appropriateness. During our review of Fall 2020 Canvas course enrollments, we noted the following:

20 course teacher roles assigned to non-employees 61 course TA roles assigned to non-employees 151 course teacher roles assigned to students 580 course TA roles assigned to students 12 courses had no teacher assigned, but had TA, Learning Assistant, Observer

and Academic Advisor roles assigned 55 courses that had both the designer and teacher role assigned

These conditions exist because there is no formal review and approval process or policy for the granting of access to student grades. There is the risk that sensitive student information is not protected; inappropriate users are assigned access to the course; and grade entry and modifications are not authorized.

We have the following recommendations with regards to this observation:

Management should develop protocols for the granting, review, and approval of Canvas access.

Management should disable non-employees Canvas access unless justification is documented and appropriately approved.

Management should consider limiting the ability of the teacher role to be assigned by Canvas users. Management should require teacher roles to be approved by the department head and entered in Banner Student Course Registration Form by the Registrar’s Office to be incorporated in the feed process to Canvas for course role assignment.

Management should consider restricting access to grades for designer roles who remain active once course has commenced.

Management Action Plan

Management will develop grades access policy and protocols that will provide framework for access and authorization in WebCat and Canvas, which will be approved by the UNH Provost.

Responsible Party: UNH-D Associate Registrar of Records and University Registrar Due Date: October 15, 2022

c. We noted that access to sensitive Banner Student grade forms is not appropriately restricted. Furthermore, a review of the appropriateness of user roles and access based upon job responsibilities is not performed on a periodic basis. Specifically, we noted that modify access to Banner Student Form SFASLST (student grade entry form) was granted to 39 individuals within 17 UNH departments who do not have student grade entry responsibilities. Also, we noted that 14 Office of the Registrar staff members had modify access to the SFASLST form but did not have original grade entry or withdrawal processing responsibilities. We also noted that modify access to Banner Student Form

Page 32 of 229

University of New Hampshire Student Grades Audit

16

SHATCKN (student grade adjustment form) was granted to nine individuals within five UNH departments who do not have student grade adjustment responsibilities. Also, we noted that seven Registrar’s Office staff members had modify access to the SHATCKN form but are not responsible for processing student grade adjustments. There is the risk that inappropriate users can enter or adjust student grades, which can result in inaccurate grade reporting. We also noted that view access to Banner Student Forms SFARHST, SFASLST, SHACRSE, SHATERM, and SHATRNS (which all display student grades) is not restricted. Grade view access was granted to 438 individuals from 165 different UNH departments.

We recommend that a formal process is established for the periodic review of Banner Student grade form access for appropriateness and alignment with job responsibilities. Management Action Plan The following actions will be taken to address the above observation: 1. Management will implement an annual review of Banner Student grade admin pages

(SFASLST and SHATCKN) access using WebI report SIS00100. User maintenance and query access will be adjusted based on users’ current position and job responsibilities. To ensure review is built into current business processes, management will add this task to the calendar which will be accessible by Registrar management across all campuses. Findings and action taken will be recorded and archived.

Responsible Party: UNH-D Associate Registrar of Records Due Date: December 1, 2021

2. UNH-D Registrar management will continue to create new Banner security classes. Only Registrar records staff, Registrars, and Associate Registrars will retain maintenance access to SFASLST and SHATCKN. All other Registrar’s Office staff will retain query access only.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

3. All Banner security access is reviewed and approved by the University Registrar or designee (Registrar authority designation to be recorded in shared registrar platform). In accordance with FERPA and registrar best practices, effort is made to assign the least data access needed to perform job responsibilities. Some user access to Banner admin pages was approved by former Registrar management (2014 and earlier). An initial review of SFARHST, SFASLST, SHACRSE, SHATERM and SHATRNS using WebI report SIS00100 will be done to evaluate the current data needs of users based on current job responsibilities. Review will be documented, and access will be modified as appropriate. Justification of access will be recorded and archived. Going forward, management will continue to create Banner security classes based on a user’s role and will continue to grant the least access needed to preform job duties. Following this initial review, a random sample of users with access to these Banner admin pages will be reviewed annually to ensure data access continues to be appropriate based on users’ legitimate educational interest and current job responsibilities. To

Page 33 of 229

University of New Hampshire Student Grades Audit

17

ensure review is built into current business processes, management will add this task to the calendar which will be accessible by Registrar management across all campuses.

Responsible Party: UNH-D Associate Registrar of Records Due Date: June 15, 2022

*4. Enhance transfer credit process During our testing, we noted that two out of 10 selected transfer credits were inappropriately coded to include the transfer grade in the overall UNH GPA calculation. We also noted that there is no review, approval, or monitoring of transfer credits processed by UNH. There is the risk that a student’s academic ranking and performance does not meet UNH academic policy and standards, resulting in reputational loss for the University. We recommend that management should periodically review transfer credits processed for compliance with UNH policy. Management Action Plan UNH-D management will use available reporting to identify high risk transfer credit awards and will evaluate the records for accuracy and compliance with UNH transfer credit policy. To ensure review is built into current business processes, management will add this task to the calendar which will be accessible by Registrar management across all campuses. Findings and actions taken will be recorded and archived.

Responsible Party: UNH-D Associate Registrar of Records Due Date: December 1, 2021

*5. Enhance security protocols for student grades During our testing of UNH Law grade entry, we noted that instructors submit grades to the UNH Law Office of the Registrar through email for entry into Banner Student. We also noted that student grade forms are submitted to the campus Registrar’s Offices through email. Sensitive data delivered via email increases the risk of data loss, as emails are not a secure medium to transmit sensitive information and are frequently subject to phishing attacks. Sensitive personally identifiable information should be protected under various legal requirements and USNH Information Classification Policy USY VIII.C.4. The loss of data may result in financial and reputational loss for the University. We have the following recommendations with regards to this observation:

Management should develop and communicate security protocols and guidelines for handling of student grade information and forms.

Student grades should be entered directly into WebCat or Canvas by instructors. Management should explore the development of a secure submission system for student

grade related forms.

Page 34 of 229

University of New Hampshire Student Grades Audit

18

Management Action Plan The following actions will be taken to address the above observation: 1. UNH-L will return responsibility for submitting individual student grades to faculty. Faculty

will directly submit student grades through WebCat and Canvas. UNH-L will Plan to utilize WebCat Final Grade Change tool as ET&S and Registrar resources are available for Phase 2 implementation.

Responsible Party: Associate Dean of Academic Affairs and UNH-L Assistant Dean for Registration and Records Due Date: August 31, 2022

2. Management developed and implemented the WebCat final grade change tool in July 2021 for UNH-D and UNH-M student grade changes. UNH-L will adopt the grade change tool by August 2022.

Responsible Party: University Registrar and UNH-D Associate Registrar of Records Due Date: Completed – July 2021

3. UNH-D management acknowledges that the submission of student grade forms via university email is not best practice. Campuses were forced to alter standard practices to accommodate remote work due to the COVID-19 pandemic. Student grade forms are only accepted from UNH-D and UNH-M faculty when sent using a UNH email address. UNH-D Office of the Registrar will contact other New England Land Grant institutions to learn how registrar forms are submitted, reviewed, and approved. Based on findings, management will draft a plan to improve current submission process.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

4. UNH-D management will develop security protocols and guidelines for handling student grade information and registrar forms and will publish on the Registrar FERPA webpage. UNH-D management will request to the Provost that UNH-M and UNH-L link to UNH-D's FERPA webpage to ensure consistency across all campuses.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

6. Enhance repeat course process We noted that the identification, review, and adjustment of grades for students taking repeat courses is a manual process and is inconsistent for different student types (i.e., undergraduate, graduate, Law). Based upon discussion with management, the automation of this process has been challenging due to the course coding of special topics courses and course repeat rule exceptions denoted in the course catalog. Also, during testing, we noted that an instructor requested a grade and registration change through the special grade report form. The UNH-D Office of the Registrar adjusted the grade for the student but did not correct the course registration error. As a result, the student received credit and grades for the same course in the Spring 2018 and Spring 2019 semesters. These conditions exist because course repeat rules are not listed in Banner Student and special topics courses do not have unique course code numbering. There is the risk that a student receives GPA credit for the same course more than once, which is not in compliance with UNH policies, resulting in the inaccurate reporting of a student’s academic record.

Page 35 of 229

University of New Hampshire Student Grades Audit

19

We have the following recommendations with regards to this observation:

Management should document, review, and approve exceptions for courses identified as repeat courses in periodic monitoring reports.

Management should evaluate course code numbering methodology for special topics courses.

Management should evaluate the use of Banner Student to manage course repeat rule exceptions.

Management Action Plan The following actions will be taken to address the above observation: 1. Management will continue to work towards the use of Banner Student to manage course

repeat policy and automated records maintenance. Responsible Party: UNH-D Associate Registrar of Records Due Date: October 15, 2022

2. Management will discuss and explore the course code numbering methodology for special topics courses as well as the standardization of special topic titles with college divisions when sufficient resources are available.

Responsible Party: UNH-D University Registrar Due Date: October 15, 2022

7. Enhance controls over monitoring of Parchment contract We noted that UNH uses Parchment for the processing of UNH transcript requests. We noted that UNH does not obtain periodic SOC reports or PCI-DSS compliance reports. In addition, UNH does not periodically monitor the vendor for compliance with contract provisions. There is the risk that UNH student grade data and sensitive student information is not properly secured to ensure integrity and security of student grades, resulting in loss of reputation. We recommend that UNH should develop a service provider monitoring plan. As part of monitoring, UNH should obtain and review periodic SOC reports and PCI-DSS compliance certificates to ensure that Parchment is meeting data security requirements. Management Action Plan The following actions will be taken to address the above observation: 1. Management will ask USNH IT if there are any plans to implement a service provider

monitoring plan. Responsible Party: University Registrar Due Date: February 1, 2022

2. UNH-D Registrar management will request and review SOC reports and PCI-DSS compliance certificates annually. To ensure this is built into current business processes, management will add this task to the calendar which will be accessible by Registrar

Page 36 of 229

University of New Hampshire Student Grades Audit

20

management across all campuses. Parchment reports and certificates will be archived in a secure location accessible by appropriate managers.

Responsible Party: UNH-D Associate Registrar of Records Due Date: March 15, 2022

VI. Business Process Improvements 1. Enhance course schedule development and entry process The UNH-D Office of the Registrar coordinates the course schedule process with each individual UNH department. The individual UNH department downloads the prior semester schedule via a WebI report and then edits the schedule to reflect course subject, sections, instructors, days, times, and room location for the new semester. The course schedule information is manually entered into the Banner Student Form SSASECT by staff. There are two more iterations of the course schedule development process, whereby departments are responsible for downloading the course schedule WebI report and submitting any changes to the Scheduling department, prior to the semester schedule going live on the UNH Course Registration website. We noted that the development of the course schedule is manual. Manual course schedule development is inefficient, a waste of staffing resources, and can be prone to error. There is the risk that course information listed on the website is inaccurate, resulting in students enrolling in courses that may not meet student expectations or requirements. We recommend that management should automate the course schedule development and entry process. Management should consider course scheduling software options that integrate with Ellucian Banner Student. 2. Enhance grade definition documentation

During the audit, we noted that the UNH Offices of the Registrar assign various symbols to student grades, which appears on the student record and/or academic transcript. There is no internal grade definition key to document how the symbol should be applied and interpreted. There is the risk that a grade assigned may be incorrect, resulting in the loss of reputation. We recommend that management should consider developing a grade definition key for symbols used in the assignment of student grades. 3. Enhance transfer credit policy During our testing of transfer credits, we noted that SRR 05.33(fs) states that grades earned in the 200-level Thompson School courses will be recorded on the student’s transcript but will not be included in the student’s GPA. The policy does not explicitly address the treatment of non-200-level courses. There is the risk that Thompson School credits for non-200 level courses are not recorded and in accordance with expectations. We recommend that management should update SRR 05.33(fs) to address the treatment of all Thompson School level courses.

Page 37 of 229

University of New Hampshire Student Grades Audit

21

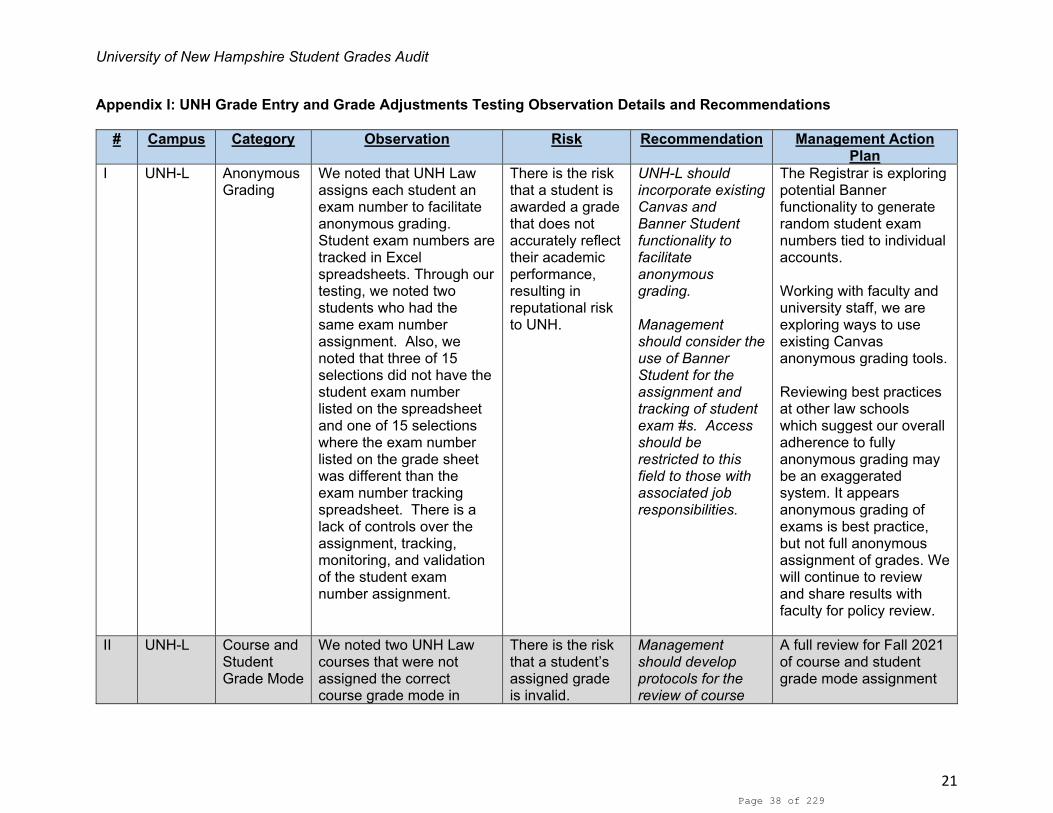

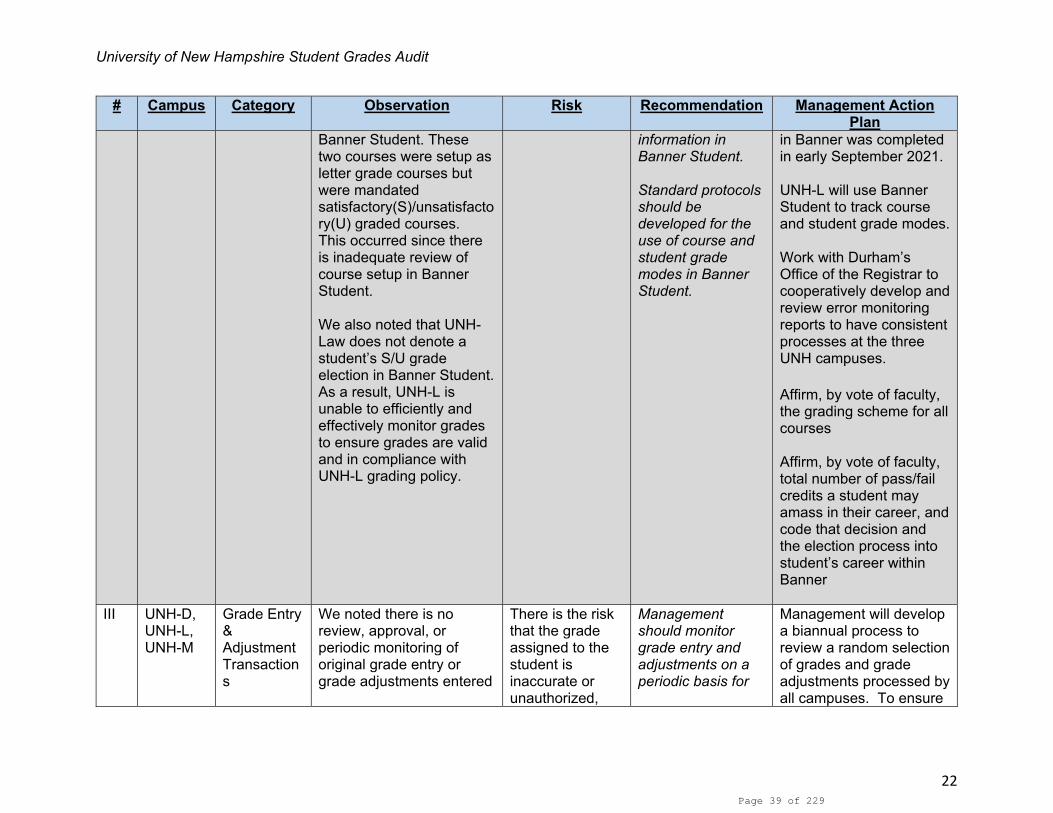

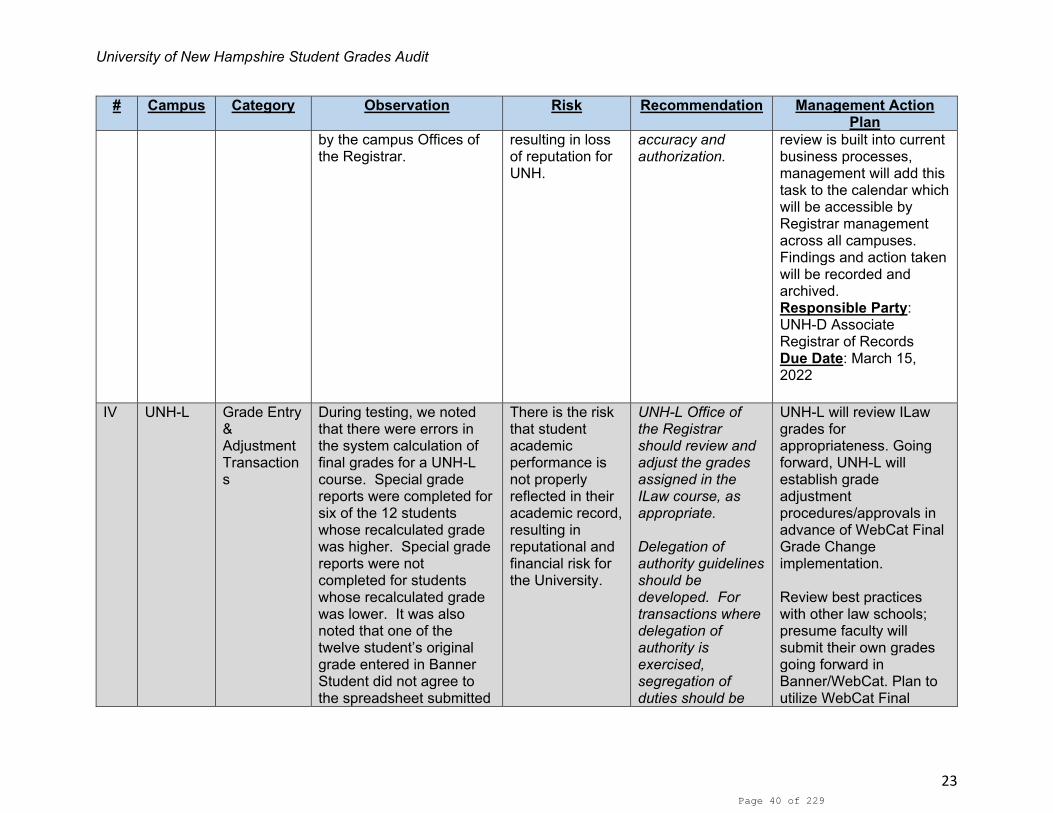

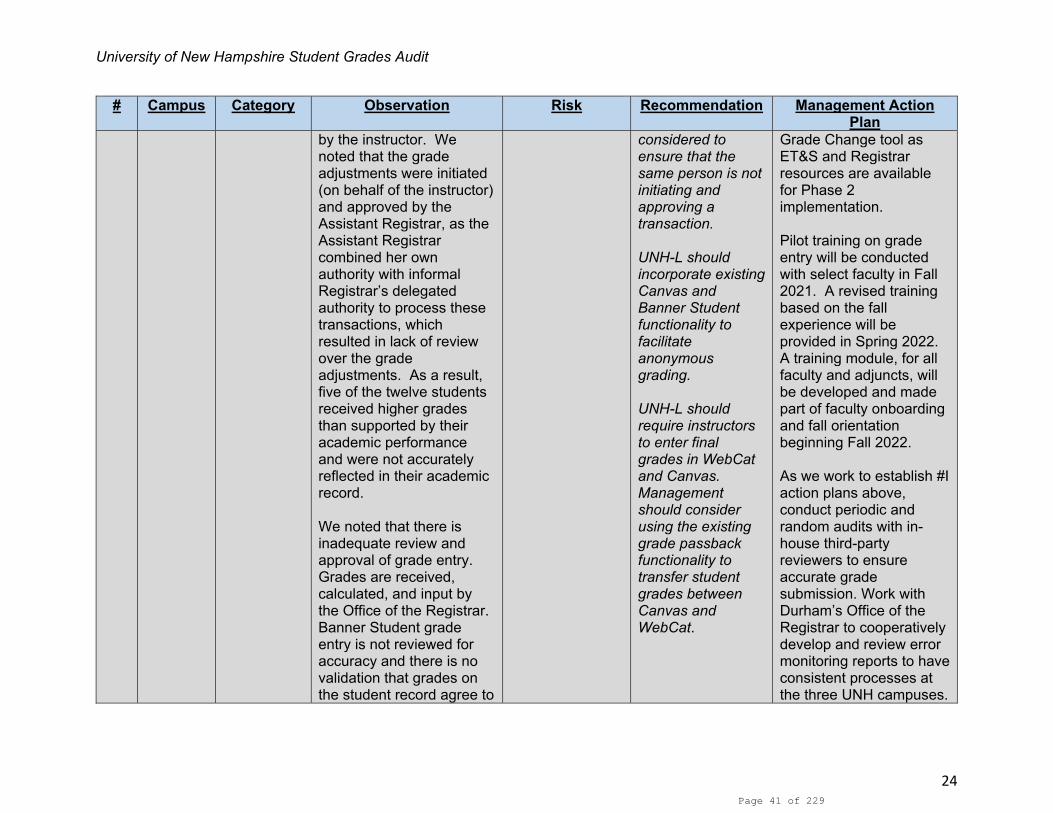

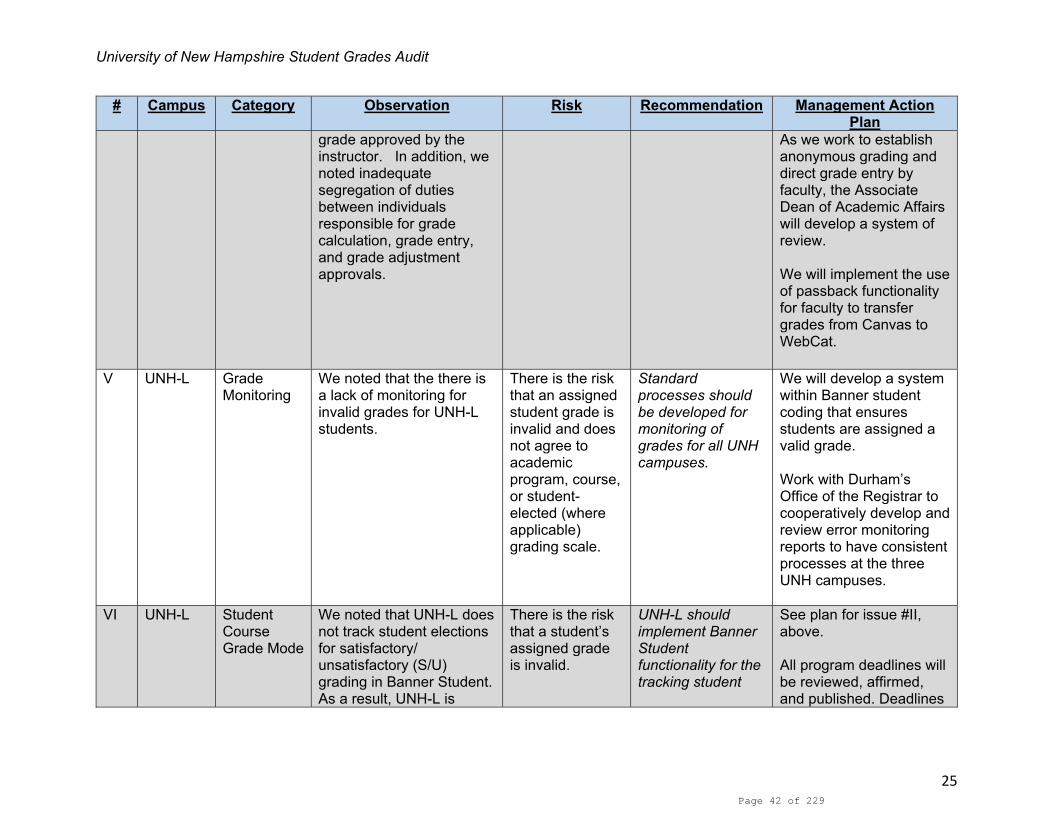

Appendix I: UNH Grade Entry and Grade Adjustments Testing Observation Details and Recommendations

# Campus Category Observation Risk Recommendation Management Action Plan

I UNH-L Anonymous Grading