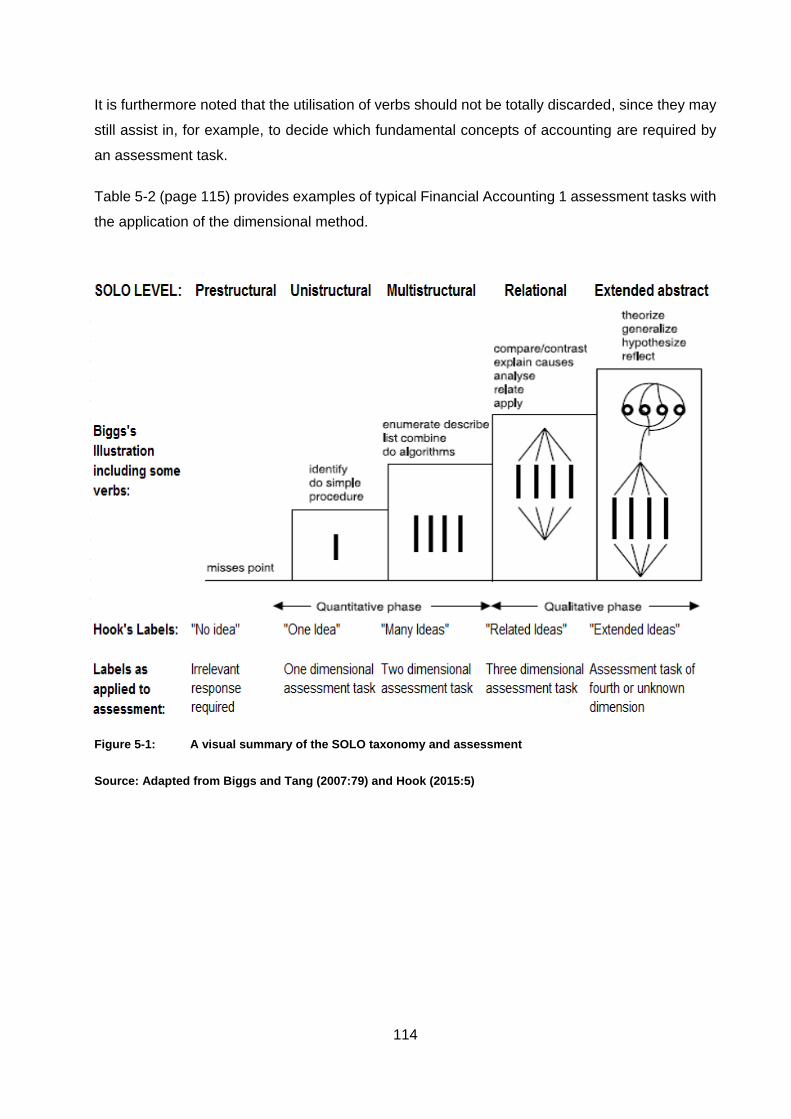

the application of the solo taxonomy in evaluating the level

TRANSCRIPT

The application of the SOLO taxonomy in evaluating the level of introductory financial accounting assessments

G von Benecke

orcid.org/0000-0003-3480-8801

Dissertation accepted in fulfilment of the requirements for the degree Master of Commerce in Accountancy at the North-West

University

Supervisor: Prof S van Rooyen

Graduation: June 2021

Student number: 23227389

i

ACKNOWLEDGEMENTS

I would like to express my sincere gratitude and appreciation towards the following persons for

their support of this study:

My Heavenly Lord and Father, Jesus our Christ and Redeemer and the Holy Ghost. The

most merciful and Almighty. May I never forget that my purpose on this earth is to do all

for Your glory alone.

My wife Aletta, for her love, support and patience and the many cups of coffee along this

journey. I love you so much.

My broader family for their love, support and listening to many stories about SOLO even

when we were on holiday. I love all of you.

Prof Surika van Rooyen for her guidance, provision of reference material, patience and

above all the motivation she has given me. You were always friendly and reasonable. You

are a special person.

The universities that provided the data for this study. Thank you so much.

My NWU colleagues for their support and reference material.

The NWU bursaries department for funding my study.

The language editor, Mrs Ann-Lize Grewar, for her professional assistance.

ii

ABSTRACT

Key terms: Accounting education, assessment, constructive alignment, cognitive level,

professional accounting programmes, SOLO taxonomy

There is wide consensus that assessment drives student behaviour and that assessment needs

to be fair. In terms of a financial accounting module pitched at NQF level 5, universities

predominantly used the revised Bloom’s taxonomy to demonstrate an approximate cognitive

demand level for their summative assessments. This process remains largely subjective, since

the use of a verb (e.g. “apply”) to indicate a Bloom level is not particularly suited to financial

accounting, where one verb may imply different levels in different contexts. This pertinent issue,

together with the fact that a gap was found in the literature, leads to the primary objective of this

study, i.e. to provide a framework for the application of the SOLO taxonomy in evaluating the

standard of summative assessment of an introductory professional financial accounting module.

As part of achieving the study’s primary and secondary research objectives, a systematic

literature review was undertaken, which included contextualising summative assessment (dealing

with issues such as principles of assessment and stakeholders) as well as conceptualising the

application of the SOLO taxonomy as well as summarising and building on the work of other

scholars.

The chosen design and methodology of the study was driven by the research objectives as

underpinned by an overall philosophy of pragmatism. The nature of the research objectives and

data (being the financial accounting examinations) lead to a methodological choice of mixed

methods research, with the qualitative research design being dominant. The qualitative design

type is a document analysis specifically set in an interpretative paradigm mainly relying on the

technique of thematic analysis. The quantitative part of the study utilises content analysis and

basic descriptive statistics as part of the overall pragmatic approach to achieving the research

objectives.

The results of the study showed that the fundamental concepts of financial accounting (such as

recognition, measurement, etc.) as well as the applicable topics (as driven by the intended

learning outcomes and typically including assets, liabilities, income, expenses, etc.) can be used

as a proxy for cognitive demand induced by the assessment tasks. The combination of these

concepts and topics, together with the requirement (or lack thereof) of material relational activity

or extended abstract, can then be used to set a SOLO level for the assessment task. The SOLO

level of an assessment task may also be materially disrupted (or even set) by the themes of “time

allowed”, “layout” or “conventional wisdom”. A framework, which includes examples of

iii

assessment tasks as evaluated through the SOLO taxonomy, is given as the final product of the

research objectives being achieved.

iv

LIST OF ABBREVIATIONS

CAQDAS Computer-assisted qualitative data analysis software

CRA Criterion-referenced assessment

HEI Higher Education Institution

HEQSF Higher Education Qualifications Sub-Framework

IAESB International Accounting Education Standards Board

IES International [Accounting] Education Standard

IFAC International Federation of Accountants

IFRS International Financial Reporting Standards

ILO Indented learning outcome

NRA Norm-referenced assessment

NQF National Qualifications Framework

NQF Act National Qualifications Framework Act 67 of 2008

SAQA South African Qualifications Authority

SOLO Structure of the Observed Learning Outcome taxonomy

TLA Teaching and learning activities

USAf Universities South Africa (formerly known as Higher Education South Africa or

HESA)

v

TABLE OF CONTENTS

ACKNOWLEDGEMENTS ............................................................................................................. I

ABSTRACT .................................................................................................................................. II

LIST OF ABBREVIATIONS ....................................................................................................... IV

CHAPTER 1 INTRODUCTION ................................................................................................. 13

1.1 INTRODUCTION ................................................................................................. 13

1.1.1 Background ......................................................................................................... 13

1.1.2 Motivation of the study and previous research .................................................... 15

1.1.3 The context of the study ...................................................................................... 18

1.2 PROBLEM STATEMENT ................................................................................... 18

1.3 OBJECTIVES OF THE STUDY .......................................................................... 19

1.3.1 Primary objective/s .............................................................................................. 19

1.3.2 Secondary objectives .......................................................................................... 19

1.4 RESEARCH DESIGN AND METHODOLOGY ................................................... 20

1.4.1 Literature review .................................................................................................. 20

1.4.2 Empirical study .................................................................................................... 21

1.4.2.1 Target population and sampling frame ................................................................ 21

1.4.2.2 Sample method ................................................................................................... 22

1.4.2.3 Sample size ......................................................................................................... 22

1.4.3 Paradigmatic assumptions and perspectives ...................................................... 22

1.4.3.1 Ontological assumptions ..................................................................................... 22

1.4.3.2 Epistemological assumptions .............................................................................. 22

vi

1.4.3.3 Rhetorical assumptions ....................................................................................... 23

1.4.3.4 Methodological assumptions ............................................................................... 23

1.4.3.5 Theoretical framework ......................................................................................... 24

1.5 ETHICAL CONSIDERATIONS ........................................................................... 24

1.6 CHAPTER CLASSIFICATION ............................................................................ 25

1.7 SUMMARY .......................................................................................................... 26

CHAPTER 2 CONTEXTUALISING SUMMATIVE ASSESSMENT .......................................... 27

2.1 INTRODUCTION ................................................................................................. 27

2.2 CONSTRUCTIVE ALIGNMENT ......................................................................... 27

2.3 PRIMARY STAKEHOLDERS ............................................................................. 29

2.3.1 Students .............................................................................................................. 29

2.3.2 The Government of South Africa ......................................................................... 30

2.3.3 Professional bodies ............................................................................................. 31

2.3.4 Universities .......................................................................................................... 32

2.4 FUNDAMENTAL CONCEPTS OF ASSESSMENT ............................................ 32

2.4.1 Definitions of assessment ................................................................................... 33

2.4.2 Kinds of knowledge ............................................................................................. 34

2.4.3 Forms of assessment .......................................................................................... 35

2.4.4 Taxonomies ......................................................................................................... 36

2.4.5 Principles of credible assessment ....................................................................... 36

2.5 CONCEPTUALISING THE APPLICATION OF THE SOLO TAXONOMY IN

EVALUATING THE LEVEL OF SUMMATIVE ASSESSMENTS ....................... 38

2.5.1 Exploring the concept of SOLO ........................................................................... 38

vii

2.5.1.1 Origination of the SOLO taxonomy ..................................................................... 38

2.5.1.2 The meaning of the SOLO taxonomy .................................................................. 39

2.5.1.3 The SOLO taxonomy’s levels .............................................................................. 40

2.5.2 Review of other scholarly research on SOLO ..................................................... 44

2.5.2.1 Lucas and Mladenovic’s study ............................................................................ 44

2.5.2.2 Newton and Martin’s study .................................................................................. 45

2.5.2.3 Other studies ....................................................................................................... 46

2.6 SUMMARY .......................................................................................................... 47

CHAPTER 3 RESEARCH DESIGN AND METHODOLOGY .................................................... 48

3.1 INTRODUCTION ................................................................................................. 48

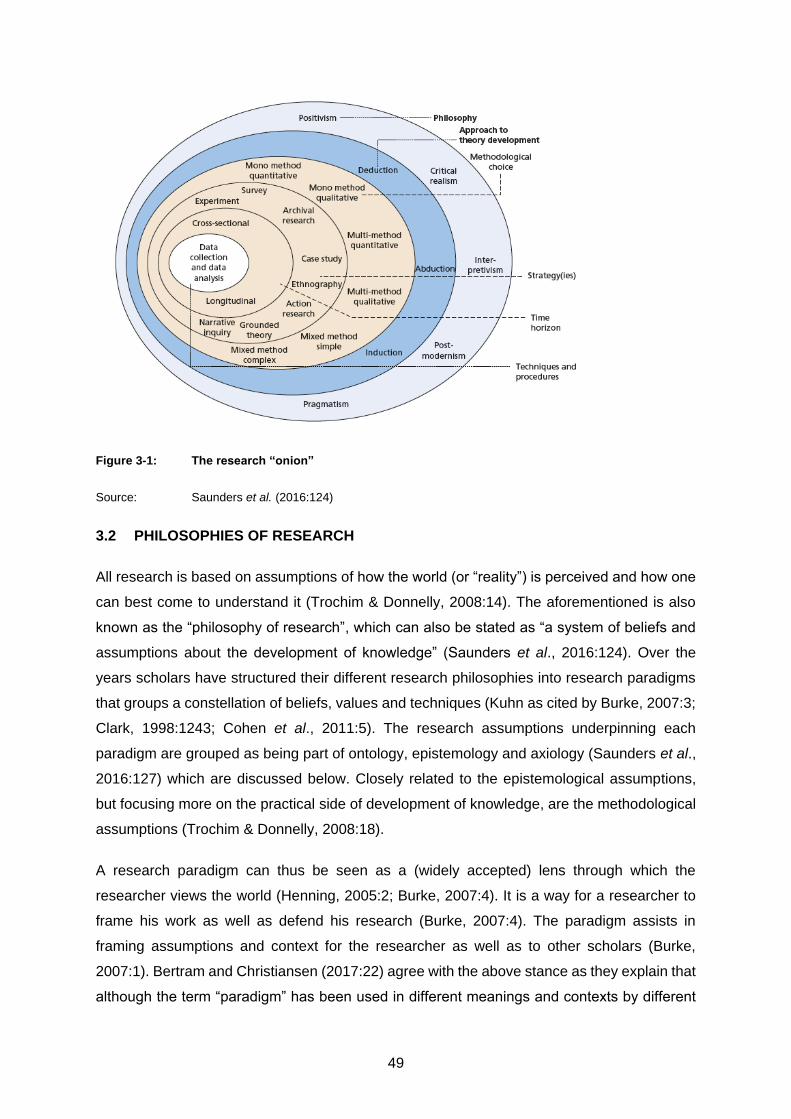

3.2 PHILOSOPHIES OF RESEARCH ...................................................................... 49

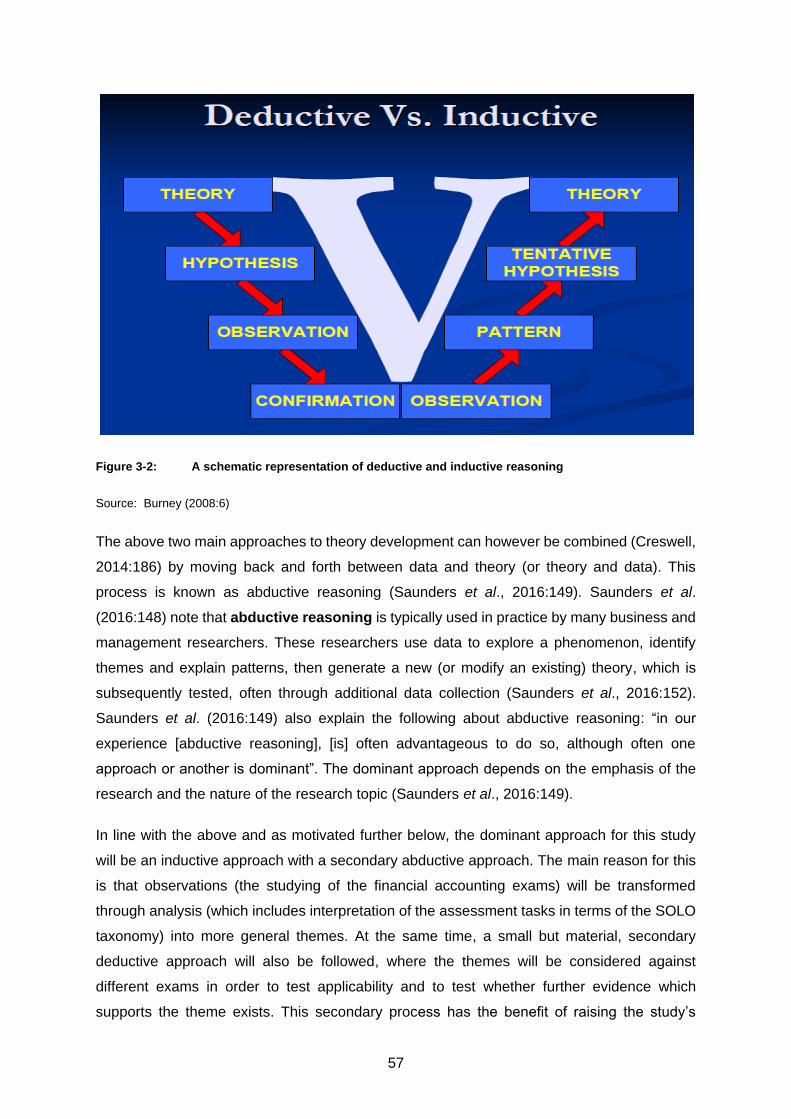

3.3 APPROACH TO THEORY DEVELOPMENT ..................................................... 55

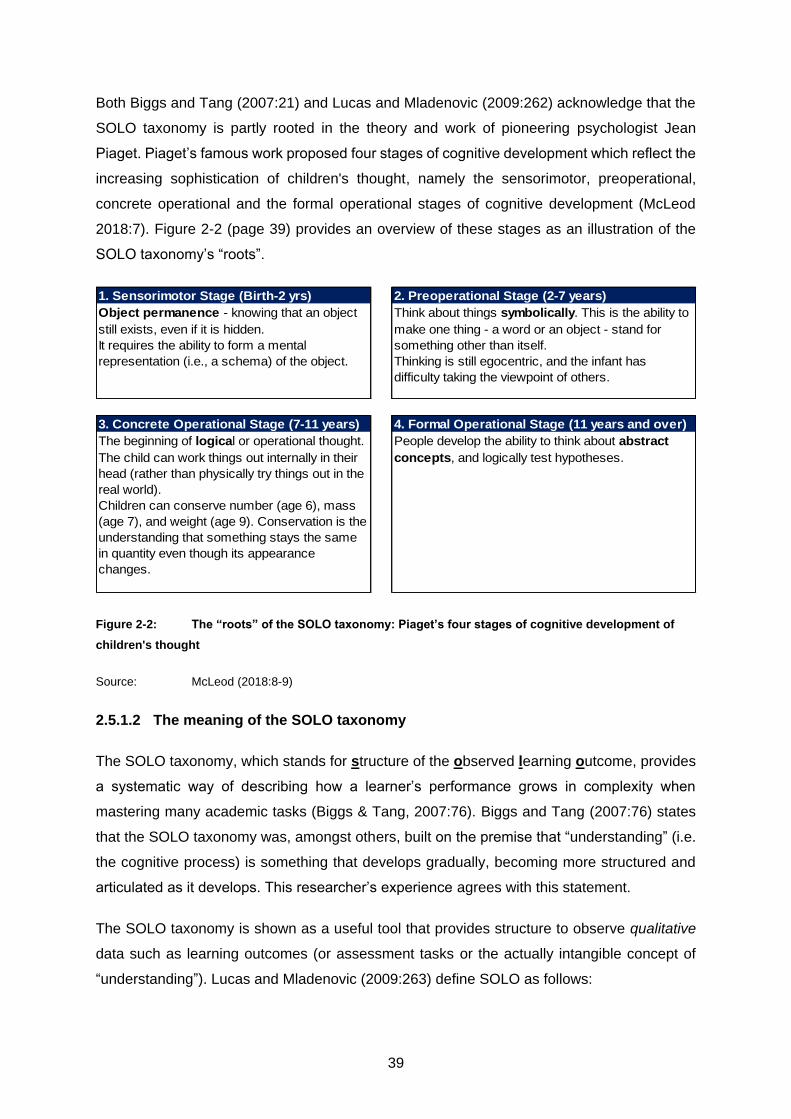

3.4 RESEARCH DESIGN ......................................................................................... 58

3.4.1 Methodological choice ......................................................................................... 59

3.4.2 Research strategy ............................................................................................... 64

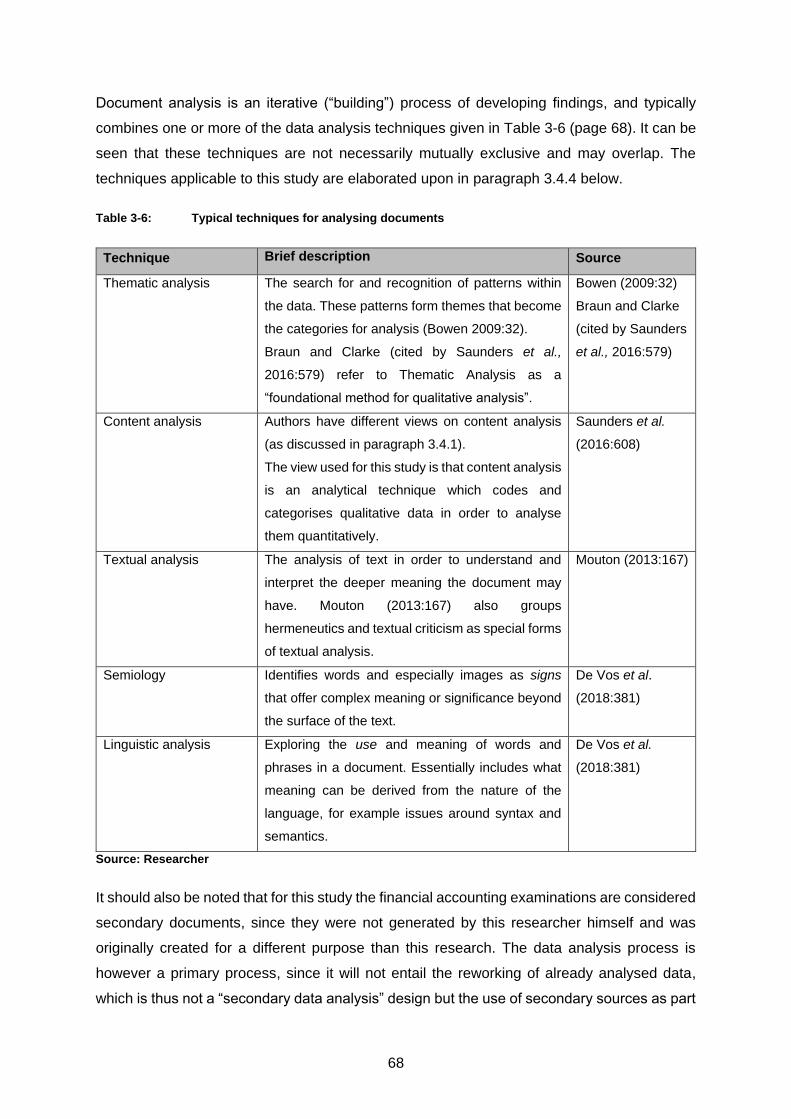

3.4.2.1 Case studies ....................................................................................................... 66

3.4.2.2 Document analysis .............................................................................................. 67

3.4.3 Time horizon ....................................................................................................... 70

3.4.4 Data collection and analysis (research methods) ............................................... 71

3.4.4.1 Target population and sampling frame ................................................................ 72

3.4.4.2 Sample method ................................................................................................... 73

3.4.4.3 Sample size ......................................................................................................... 74

viii

3.4.4.4 The process of coding ......................................................................................... 75

3.4.4.5 Thematic analysis ............................................................................................... 76

3.4.4.6 Content analysis .................................................................................................. 77

3.4.4.7 Textual analysis .................................................................................................. 77

3.4.4.8 Reliability and validity .......................................................................................... 78

3.5 SUMMARY .......................................................................................................... 80

CHAPTER 4 ANALYSIS AND FINDINGS ................................................................................ 81

4.1 INTRODUCTION ................................................................................................. 81

4.2 CONTENT ANALYSIS APPLIED IN SUPPORT OF THE THEMATIC

ANALYSIS .......................................................................................................... 81

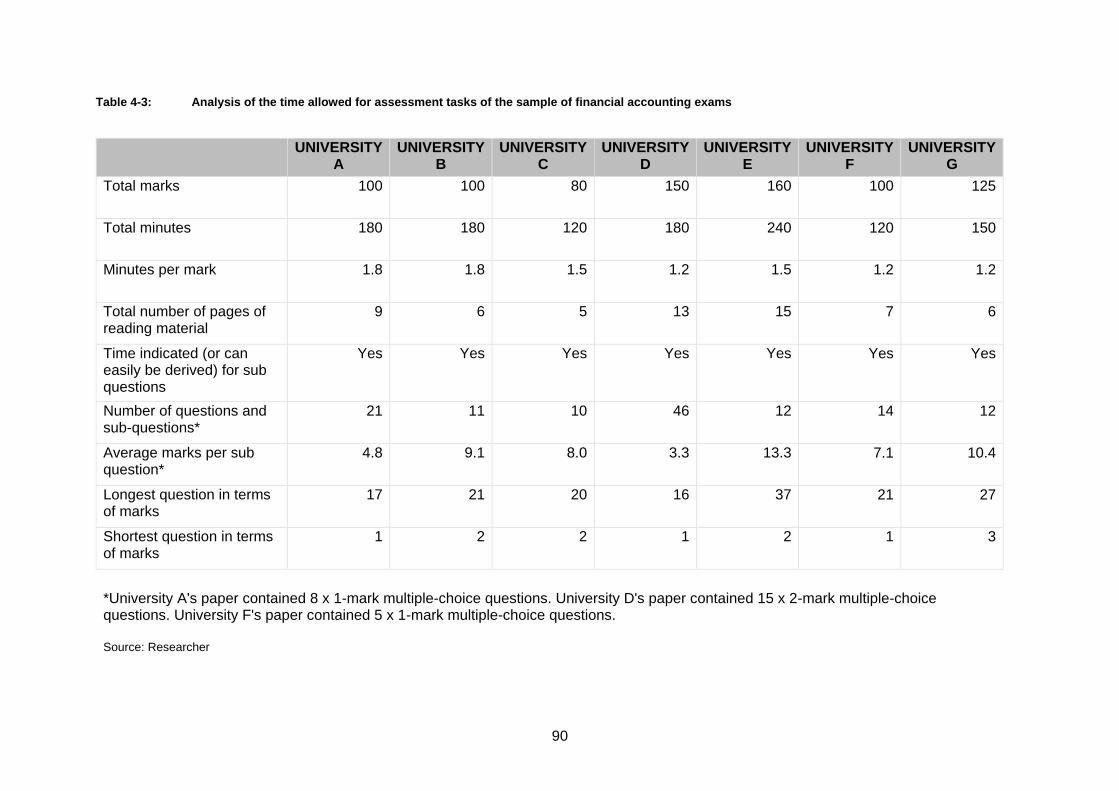

4.3 ANALYSIS OF ASSESSMENT TASKS AND THE EMANATING THEMES ..... 87

4.3.1 Theme 1: Time allowed for the assessment tasks .............................................. 87

4.3.2 Theme 2: The layout of the assessment ............................................................. 91

4.3.3 Theme 3: Conventional wisdom .......................................................................... 94

4.3.4 Reflecting on Themes 1 to 3 ............................................................................... 97

4.3.5 Theme 4: The “dimensional method” of applying SOLO to the Financial

Accounting 1 examinations’ assessment tasks ................................................... 98

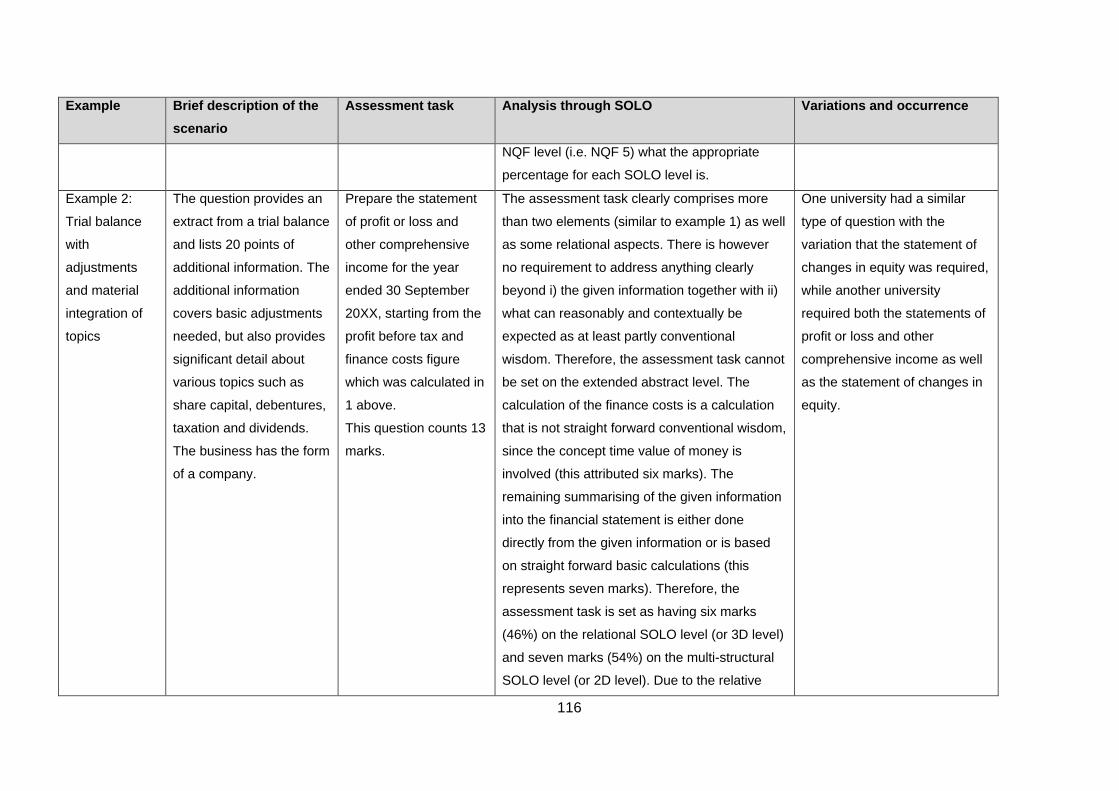

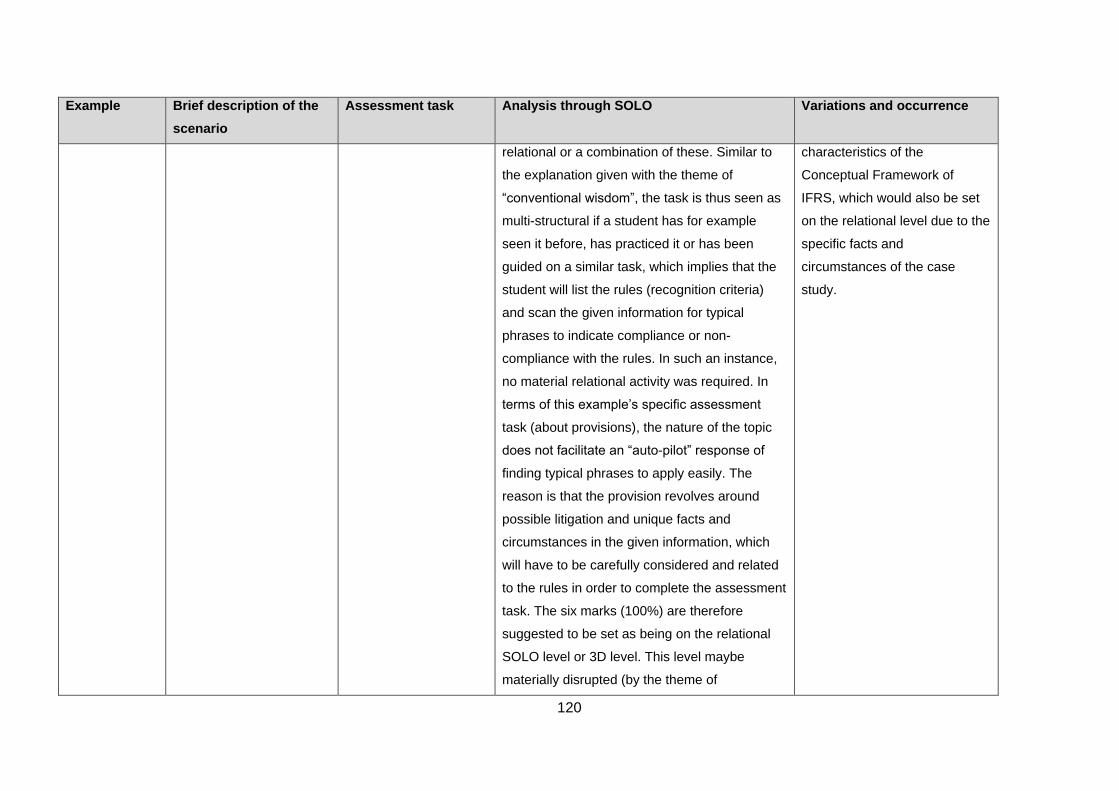

4.3.5.1 Example 1: Trial balance with adjustments ....................................................... 100

4.3.5.2 Example 2: Trial balance with adjustments and material integration of topics .. 101

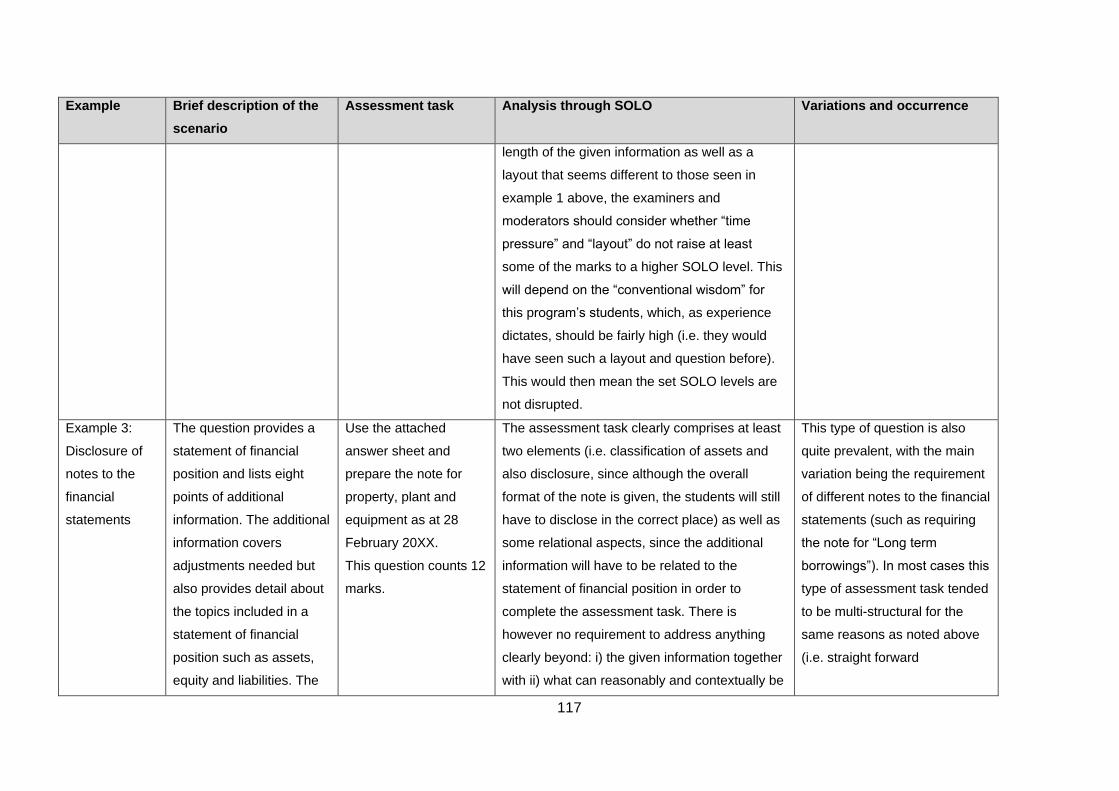

4.3.5.3 Example 3: Disclosure of notes to the financial statements .............................. 102

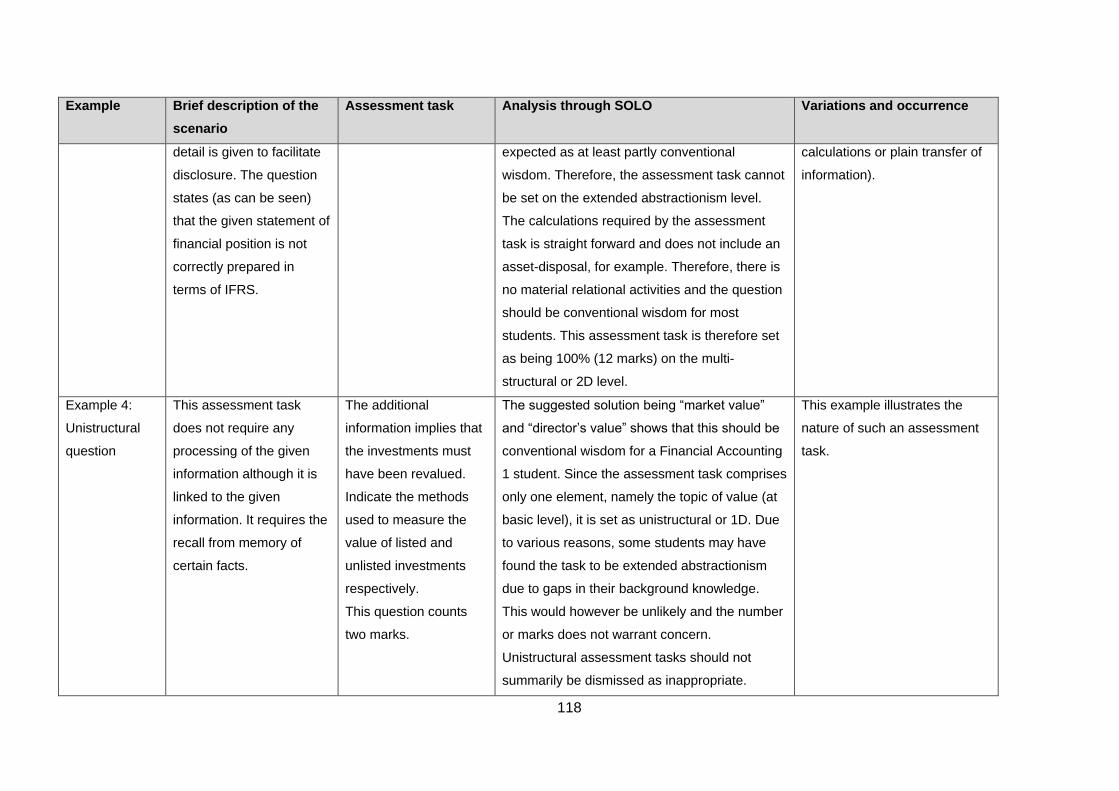

4.3.5.4 Example 4: Unistructural question .................................................................... 103

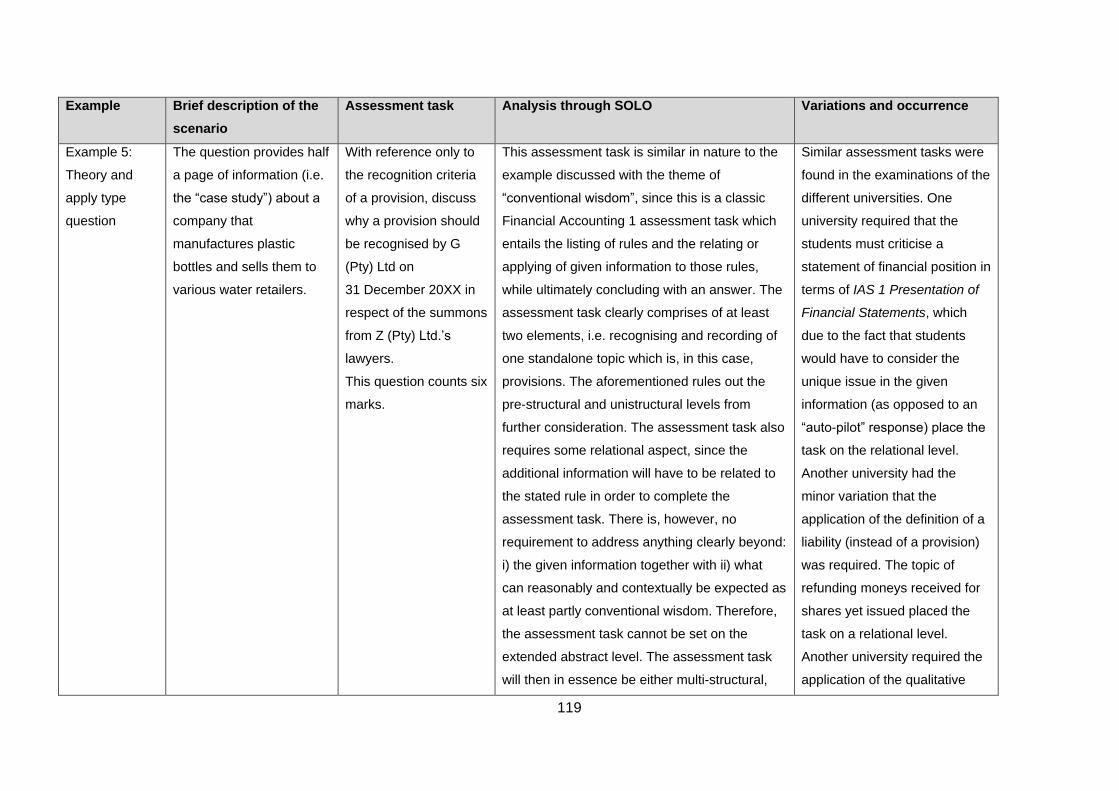

4.3.5.5 Example 5: Theory and apply type question ..................................................... 103

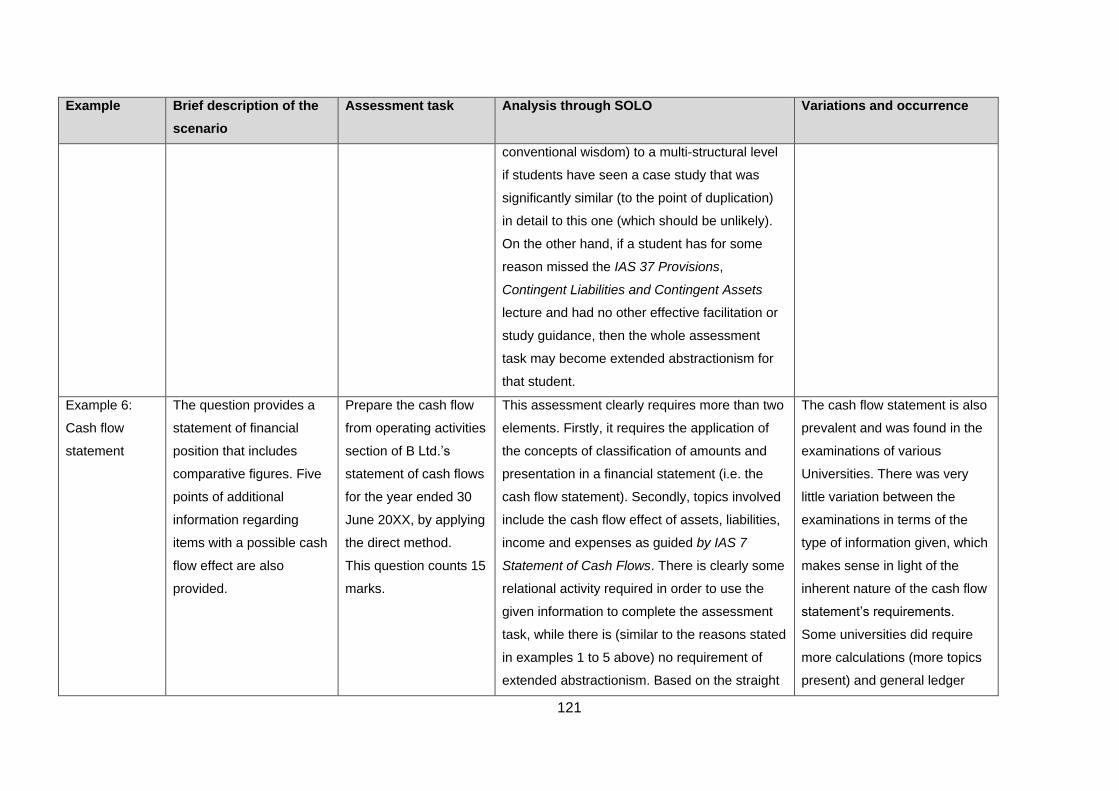

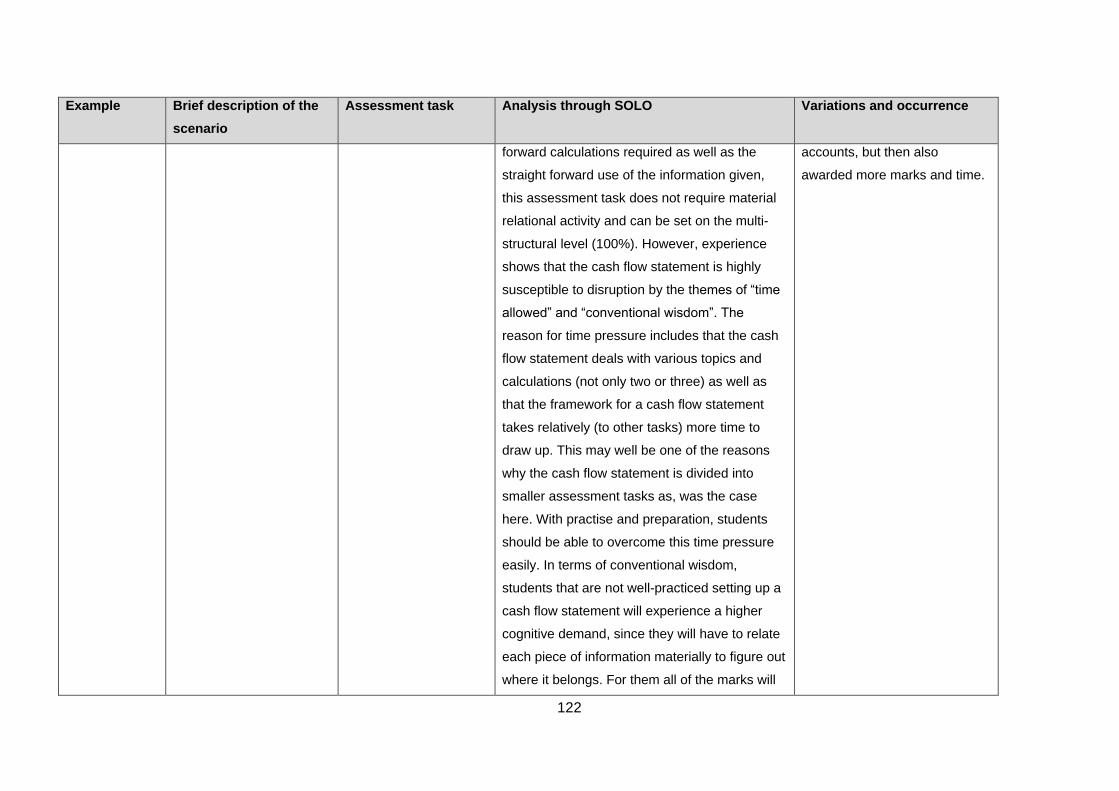

4.3.5.6 Example 6: Cash flow statement ....................................................................... 105

ix

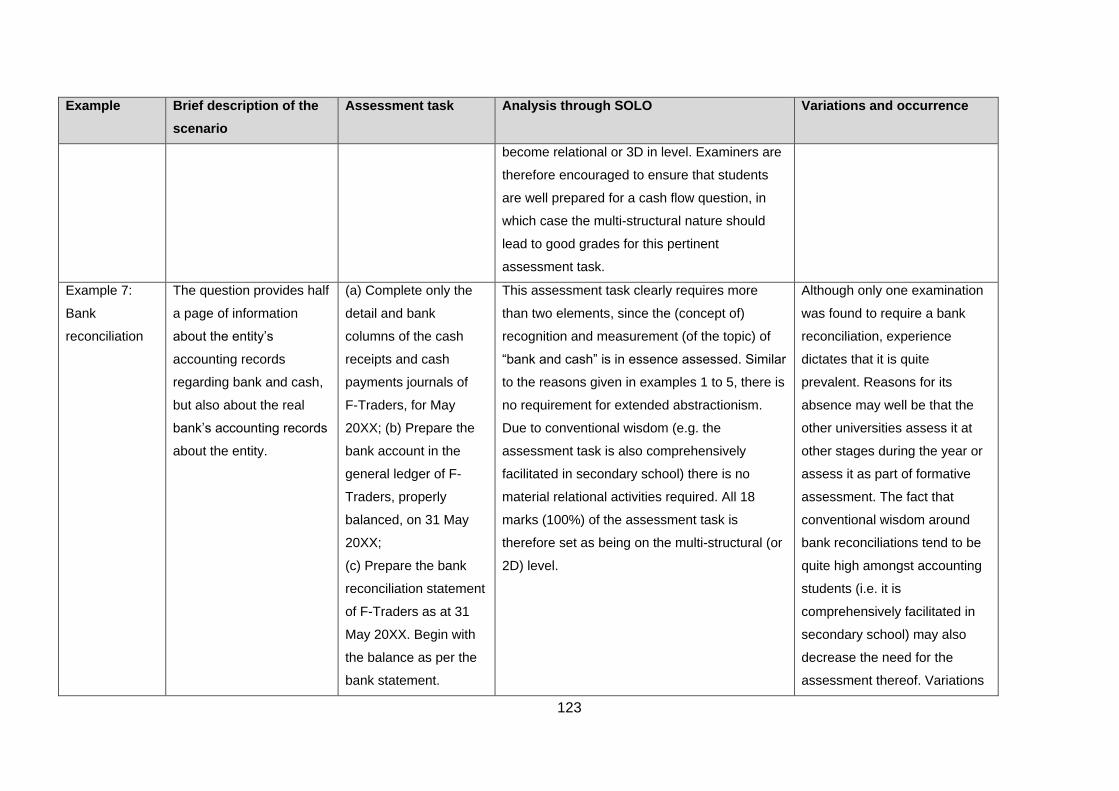

4.3.5.7 Example 7: Bank reconciliation ......................................................................... 106

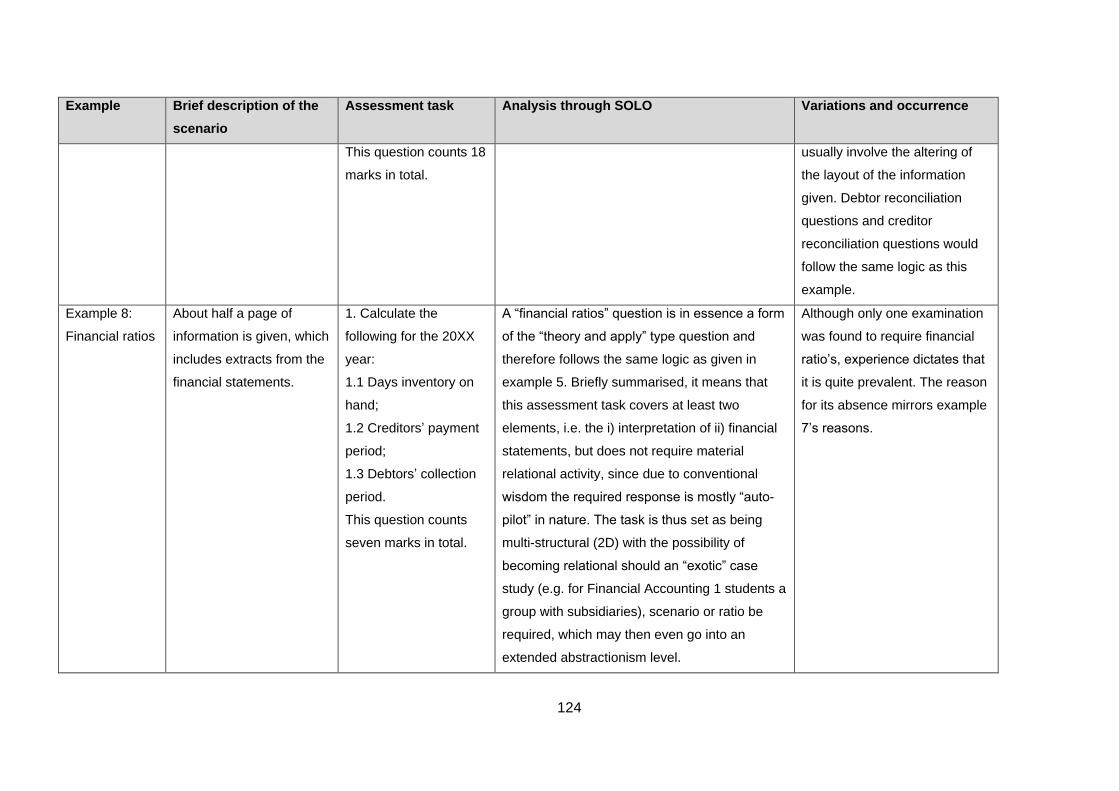

4.3.5.8 Example 8: Financial ratios ............................................................................... 107

4.3.5.9 About journal entries and general ledger accounts ........................................... 107

4.3.6 Reflecting on Theme 4 ...................................................................................... 107

4.4 SUMMARY ........................................................................................................ 108

CHAPTER 5 CONCLUSIONS AND RECOMMENDATIONS ................................................. 109

5.1 INTRODUCTION ............................................................................................... 109

5.2 CONFIRMATION OF THE RESEARCH OBJECTIVES ACHIEVED................ 109

5.3 FRAMEWORK FOR THE APPLICATION OF THE SOLO TAXONOMY IN

EVALUATING THE LEVEL OF INTRODUCTORY FINANCIAL

ACCOUNTING ASSESSMENTS ...................................................................... 110

5.3.1 Introduction ....................................................................................................... 110

5.3.2 Time allowed to complete assessment tasks .................................................... 110

5.3.3 The layout of the assessment ........................................................................... 111

5.3.4 The effect of “conventional wisdom” ................................................................. 111

5.3.5 The link to a more structured and formalised way of applying SOLO to the

Financial Accounting 1 examinations’ assessment tasks ................................. 112

5.3.6 The “dimensional method” of applying SOLO to the Financial Accounting 1

examinations’ assessment tasks ....................................................................... 112

5.3.7 Conclusion ........................................................................................................ 126

5.4 LIMITATIONS OF THE STUDY ........................................................................ 126

5.5 AREAS FOR FURTHER RESEARCH .............................................................. 127

5.5.1 Topics noted as extending beyond the defined research objectives ................. 127

5.5.2 Further topics that may logically build on this study .......................................... 127

x

5.6 REFLECTIVE LEARNING ................................................................................ 128

5.7 SUMMARY ........................................................................................................ 128

BIBLIOGRAPHY ...................................................................................................................... 129

ANNEXURES ........................................................................................................................... 135

xi

LIST OF TABLES

Table 1-1: Examples of research involving Bloom's and the revised Bloom's

taxonomy ........................................................................................................ 15

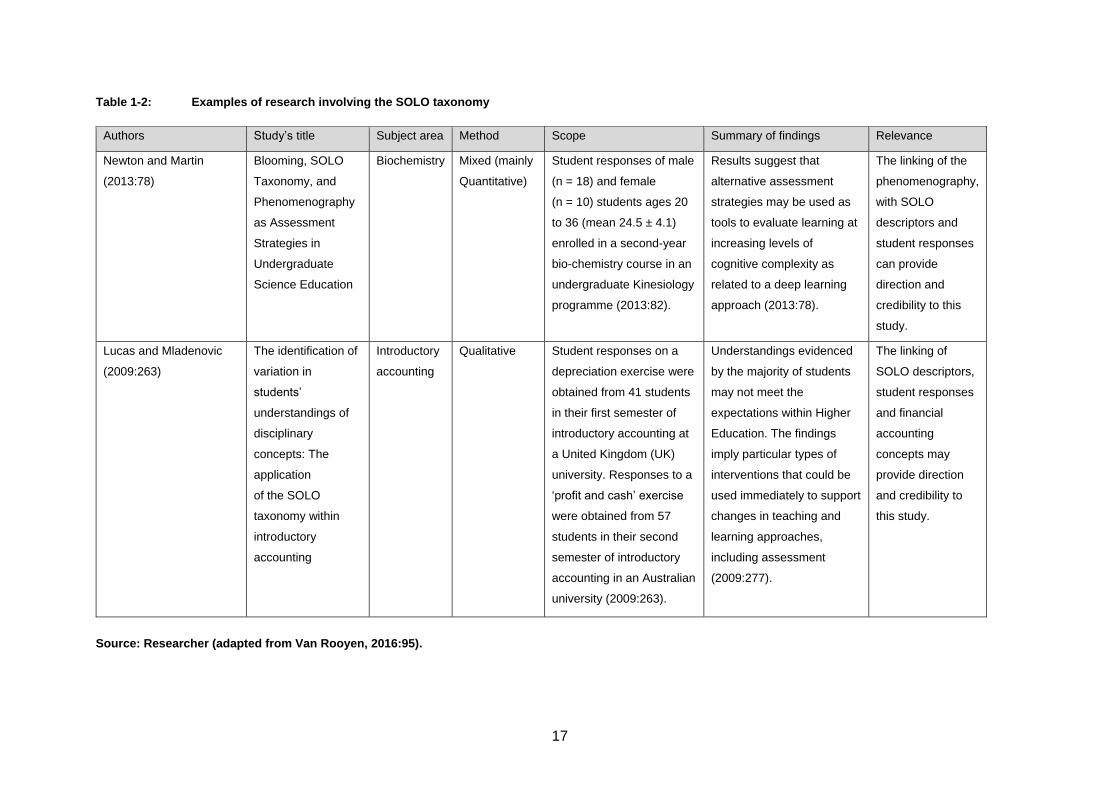

Table 1-2: Examples of research involving the SOLO taxonomy .................................... 17

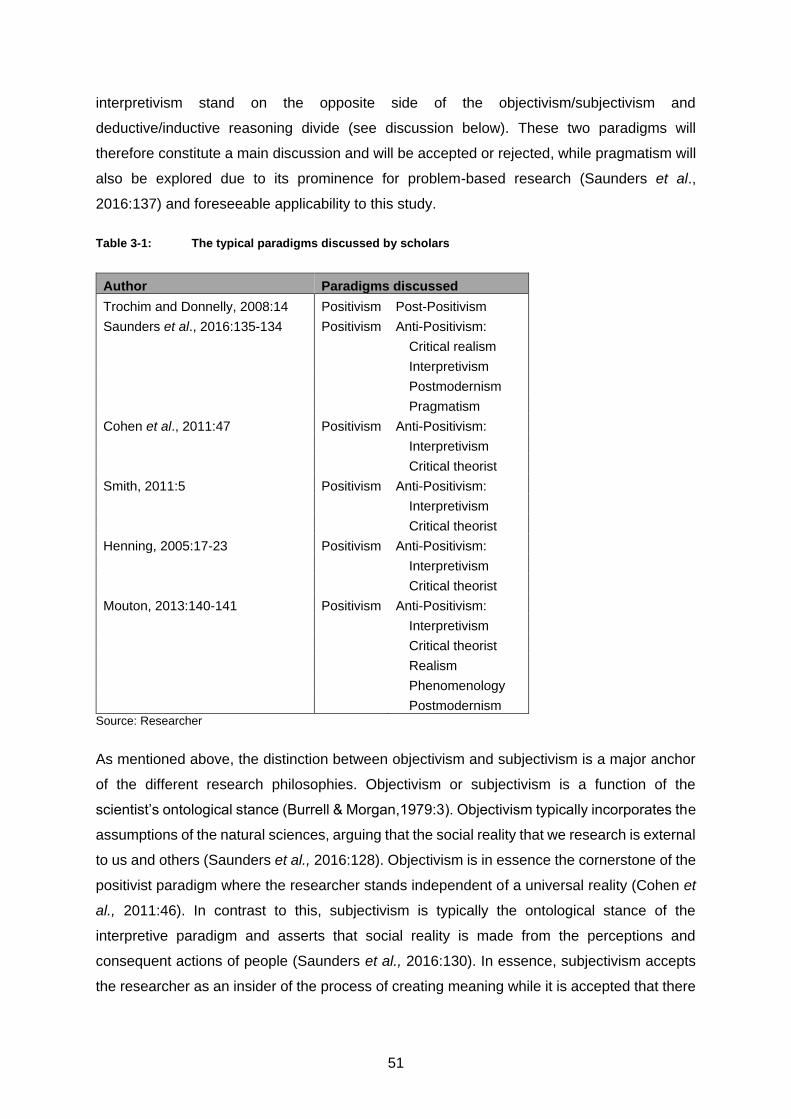

Table 3-1: The typical paradigms discussed by scholars ................................................ 51

Table 3-2: Further justification of the applicability of the interpretive paradigm ............... 52

Table 3-3: Assumptions under pragmatism ..................................................................... 55

Table 3-4: Typical characteristics of qualitative research as applied in this study ........... 61

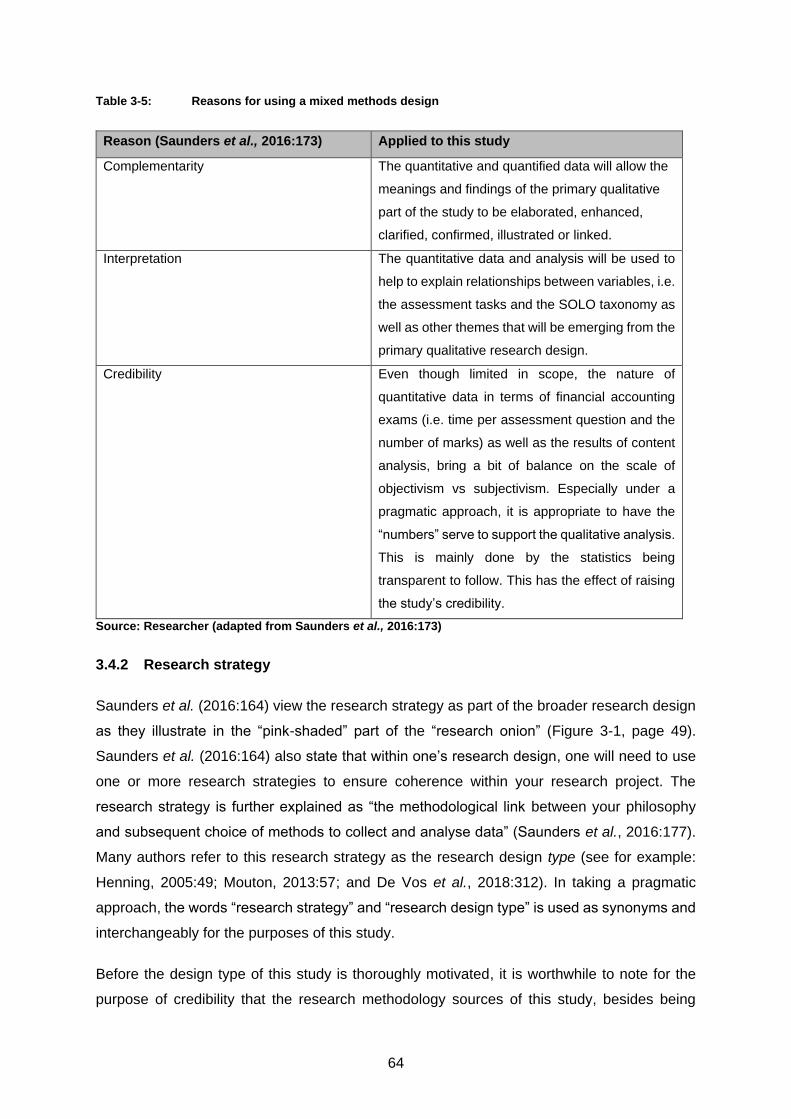

Table 3-5: Reasons for using a mixed methods design ................................................... 64

Table 3-6: Typical techniques for analysing documents .................................................. 68

Table 3-7: Reflecting on the advantages and disadvantages of document analysis ....... 69

Table 3-8: Practical steps of document analysis ............................................................. 71

Table 4-1: An illustration of the word frequency in the examinations .............................. 85

Table 4-2: An illustration of the word frequency of the examinations’ assessment

tasks ............................................................................................................... 86

Table 4-3: Analysis of the time allowed for assessment tasks of the sample of

financial accounting exams ............................................................................ 90

Table 5-1: Research objectives achieved ...................................................................... 109

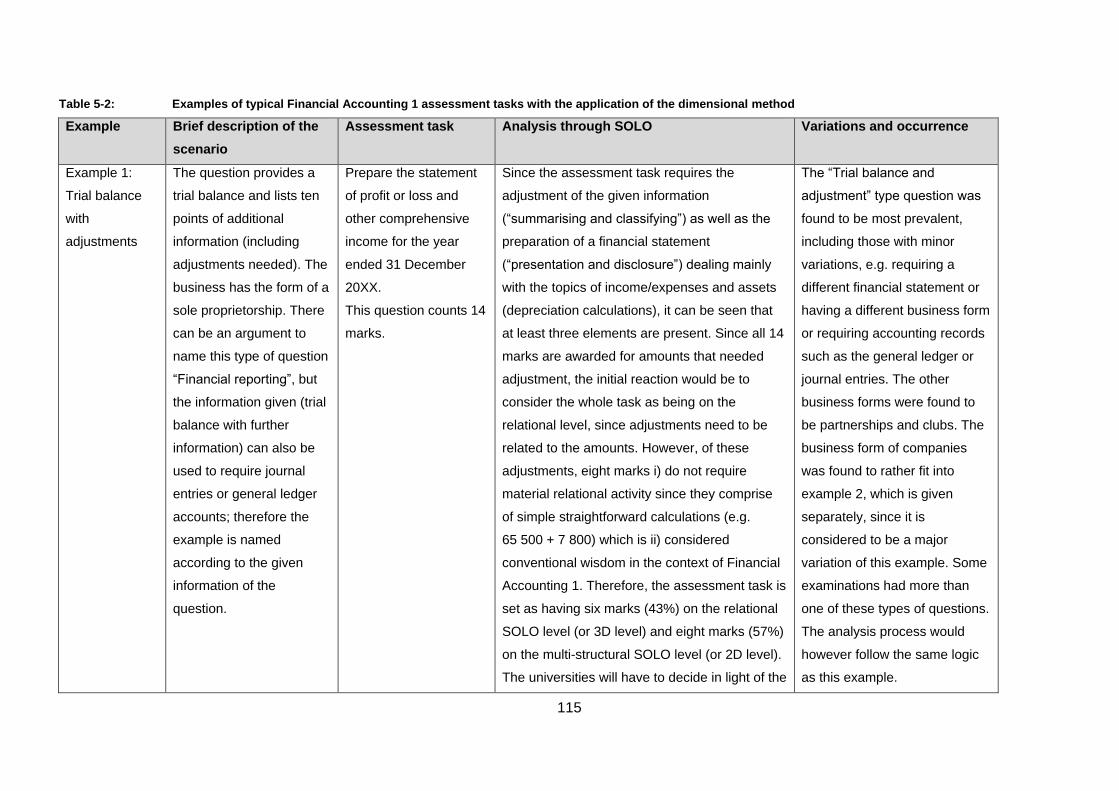

Table 5-2: Examples of typical Financial Accounting 1 assessment tasks with the

application of the dimensional method ......................................................... 115

xii

LIST OF FIGURES

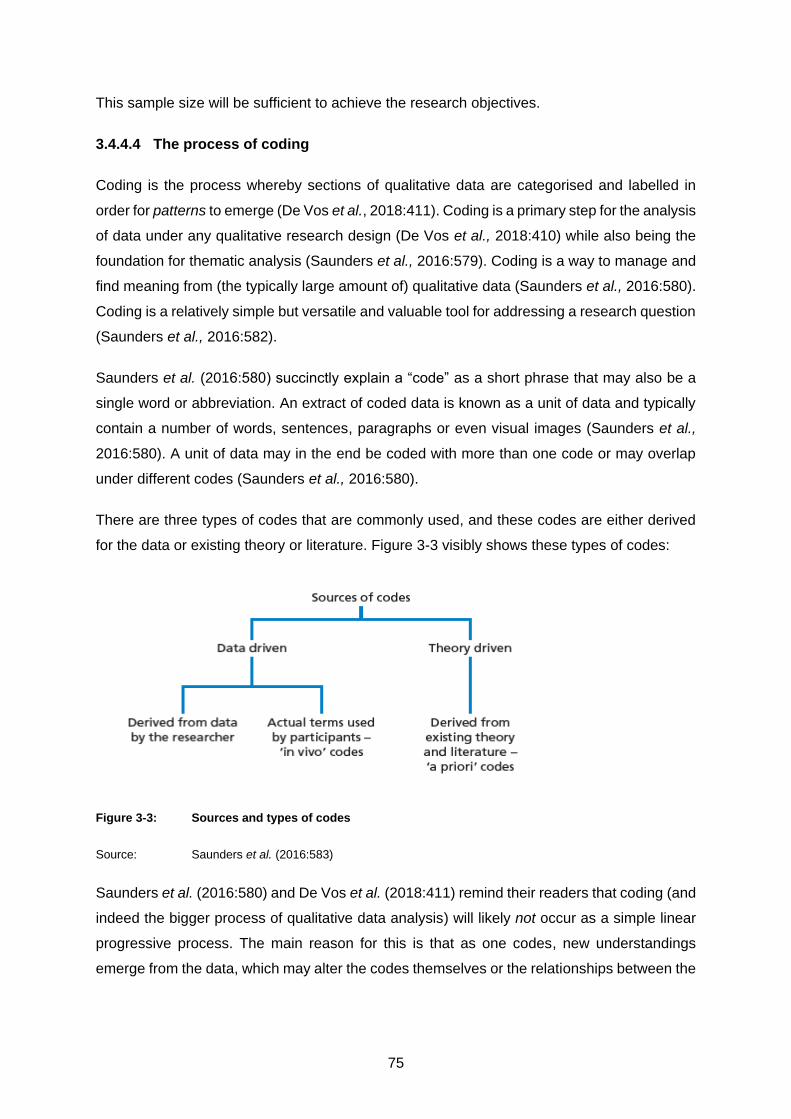

Figure 2-1: External influences on, and alignment of, assessment .................................. 32

Figure 2-2: The “roots” of the SOLO taxonomy: Piaget’s four stages of cognitive

development of children's thought .................................................................. 39

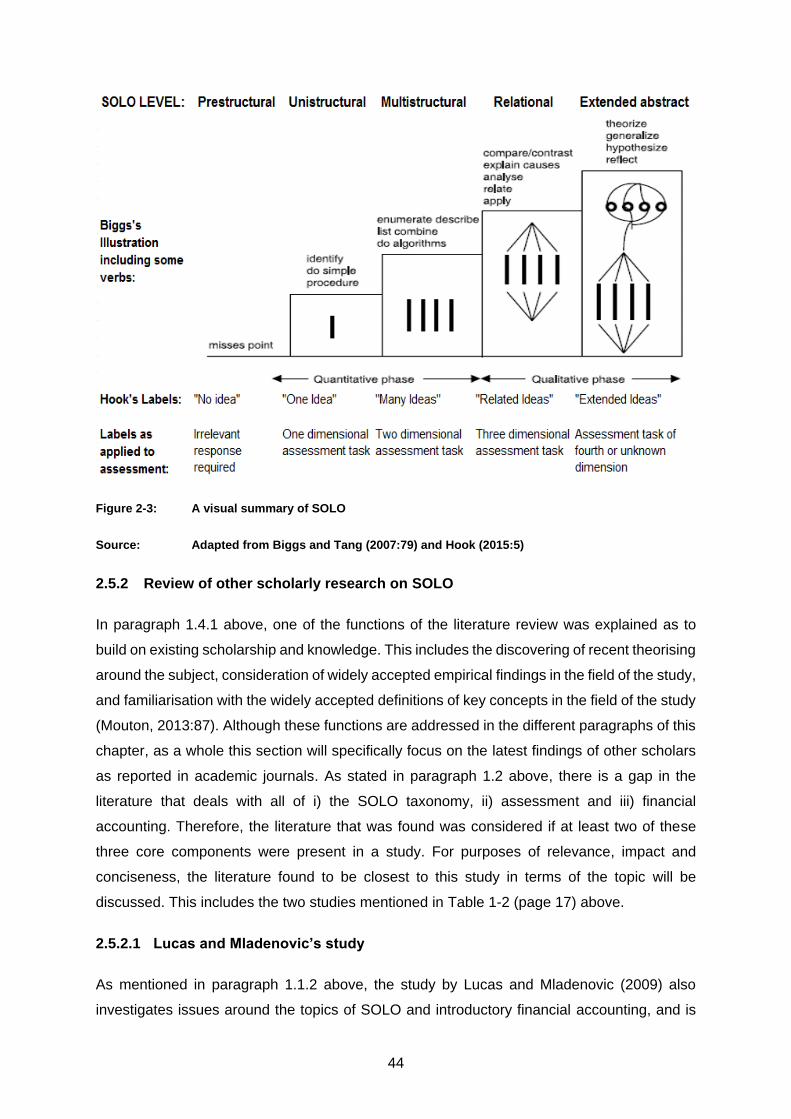

Figure 2-3: A visual summary of SOLO ............................................................................ 44

Figure 3-1: The research “onion” ...................................................................................... 49

Figure 3-2: A schematic representation of deductive and inductive reasoning ................. 57

Figure 3-3: Sources and types of codes ........................................................................... 75

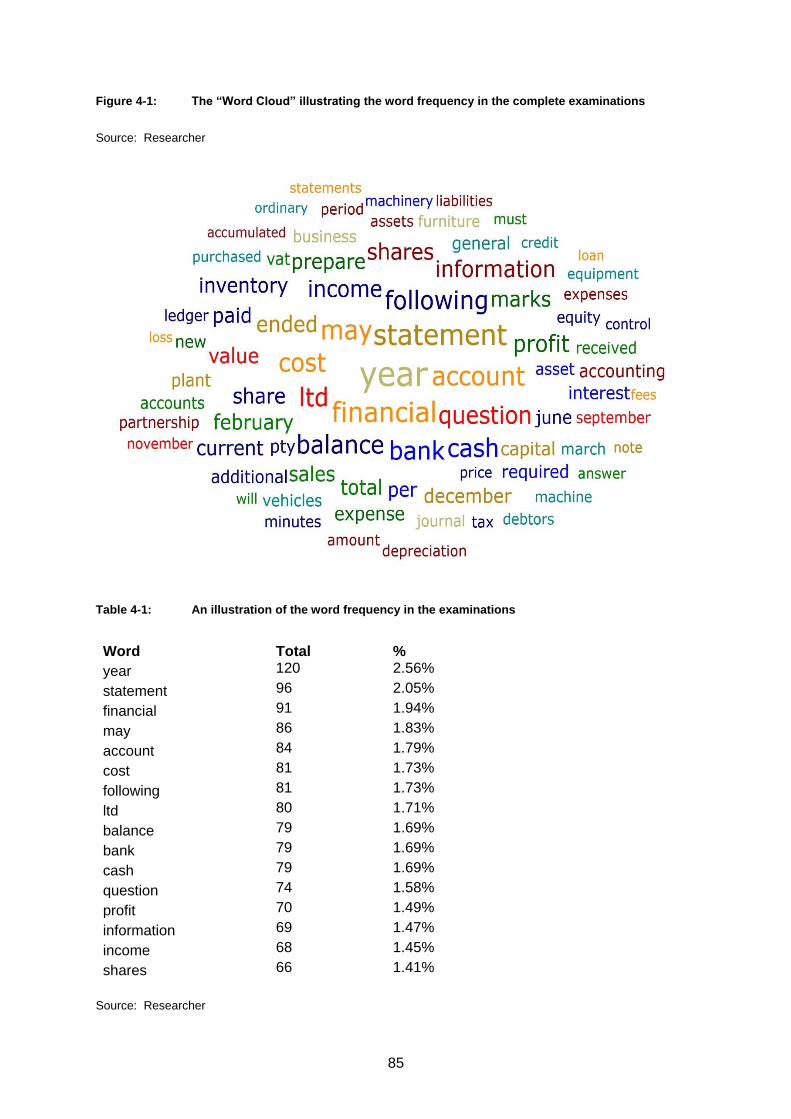

Figure 4-1: The “Word Cloud” illustrating the word frequency in the complete

examinations .................................................................................................. 85

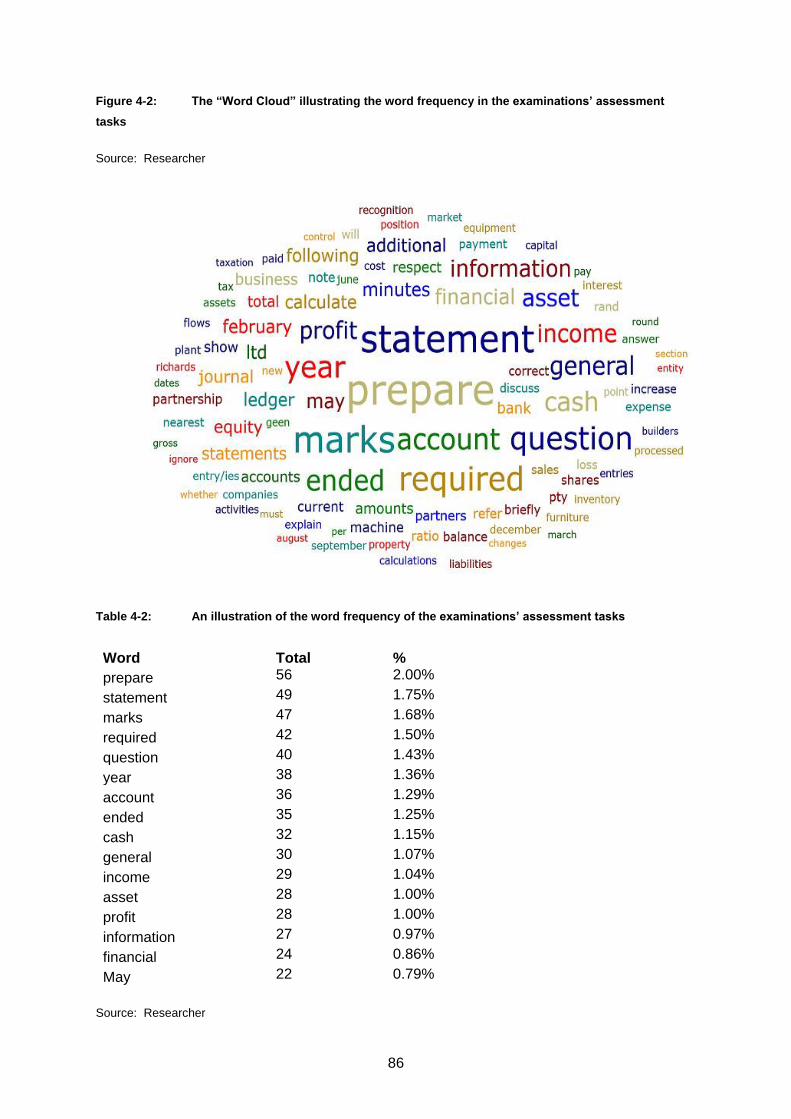

Figure 4-2: The “Word Cloud” illustrating the word frequency in the examinations’

assessment tasks ........................................................................................... 86

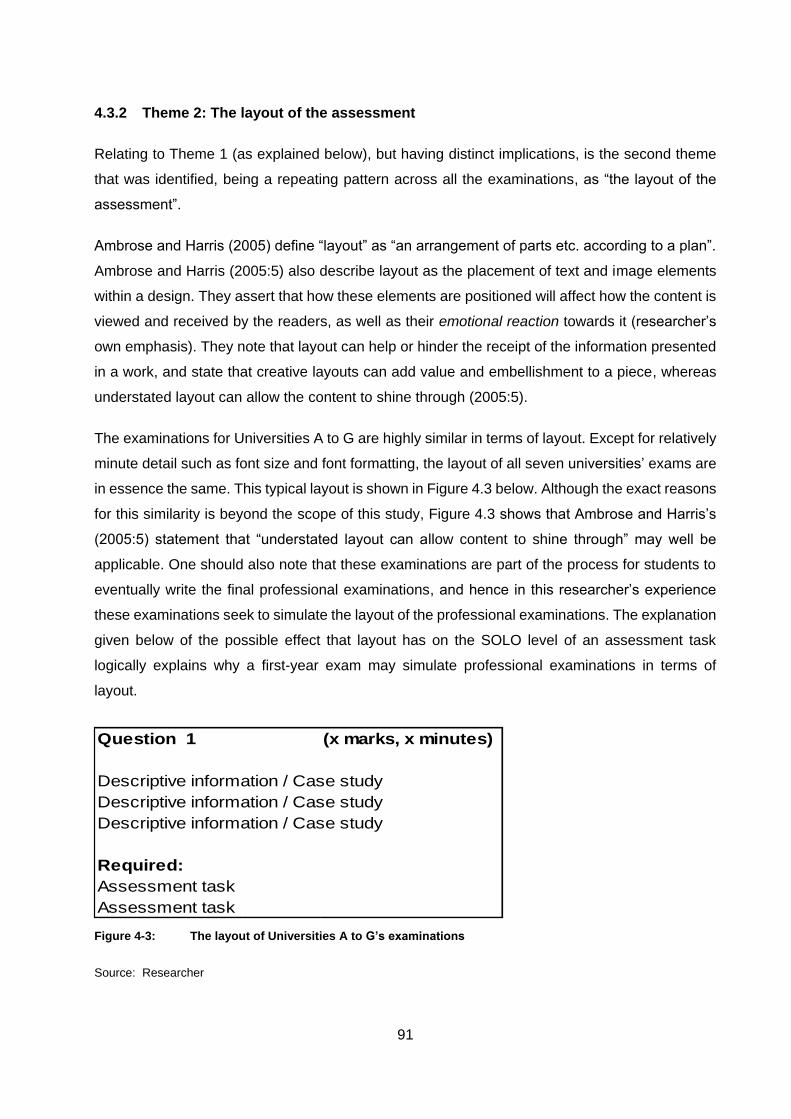

Figure 4-3: The layout of Universities A to G’s examinations ........................................... 91

Figure 5-1: A visual summary of the SOLO taxonomy and assessment ........................ 114

13

CHAPTER 1 INTRODUCTION

1.1 INTRODUCTION

1.1.1 Background

There is wide consensus that assessment is a centre pillar of the learning process (Brown

2001:4). A major reason for assessment’s prominence is that it fundamentally affects students’

behaviour during the teaching and learning process (Rowntree 1987:1; Biggs & Tang,

2007:169). This also applies to financial accounting students in a South African context, since

assessment as a concept is key to measure whether these students demonstrate, as is

expected from them, a wide base of knowledge, skills, abilities and attributes by the time they

enter the accountancy profession (Van Rooyen, 2016:1). This agrees with the view of the

South African Qualifications Authority (SAQA), which states “… (a)s assessment is central to

the recognition of achievement, the quality of the assessment is therefore important to provide

credible certification.” (SAQA, 2001:16).

It is therefore important to recognise that amongst all the variables of the teaching and learning

process, assessment (and by analogy the standard thereof): i) facilitates student behaviour

such as deep learning (Biggs & Tang, 2007:25), and ii) has to incorporate the requirements

from various stakeholders such as the university, professional bodies and government policy.

An example of a stakeholder’s requirements is found in the government policy of the South

African Qualifications Authority’s (SAQA) level descriptors for the South African National

Qualifications Framework (NQF). The SAQA level descriptors are statements describing

learning achievement at a particular level of the NQF, and provides a broad indication of the

types of learning outcomes and assessment criteria that are appropriate for a qualification at

that level (SAQA, 2012:4).

Furthermore, important standard setting bodies such as SAQA (2016:1) and the International

Accounting Education Standards Board (IAESB, 2019:79) are in agreement as to the

importance of assessment as well as the principles underlying good assessment. These

principles are summarised as: fairness, validity, reliability, practicability, validity, equity,

transparency, and sufficiency within professional accounting education programmes. All these

principles can be collectively noted as “credible assessment” (SAQA, 2001:16).

Credibility of assessment is also recognised by Higher Education Institutions (HEIs) in South

Africa through their various assessment policies (NWU, 2011:1; CUT, 2016:3). An initial review

of some of these policies shows that in order to aid the implementation of principles of credible

14

assessment, documents are provided to evaluate the assessment tasks itself (NWU, 2011:1,

CUT, 2016:57). These documents are typically identified by descriptions such as

“Questionnaire on the Quality of Assessment Papers” (CUT, 2016:57), “Moderator's Report”

(NWU, 2012) or “Report by external examiner” (UNIZULU, 2015), etc. It is noted that these

reports almost universally utilise the revised Bloom’s taxonomy (refer below) to evaluate the

appropriateness of the cognitive demands (i.e. the level) of the assessment. This is no surprise

since a common conceptual framework is needed to assist in the alignment of the learning

outcomes with the assessment thereof (Lucas et al., 2014:578) and the best-known example

of such a framework, according to Herbert et al. (2009:23), is Bloom’s Taxonomy.

In 1956 Bloom’s Taxonomy was created as a classification system for educational goals

(Bloom et al., 1956; Bush et al., 2014:3). The major idea of the taxonomy is that what

educators want students to know, as encompassed in the statements of educational

objectives, can be arranged in a hierarchy from less to more complex (Huitt, 2011:1). The

taxonomy distinguishes six levels of cognitive processes (Clark, 2015), from knowledge (the

lowest level) to evaluation (the highest level) and it has been widely used to write objectives,

activities, and assessments (Bush et al., 2014:3). Bloom’s Taxonomy was later updated by

Anderson and Krathwohl (2001), who revised it to fit the more outcome-focused modern

education objectives (Huit, 2011:2). The revision included switching the names of the levels

from nouns to active verbs, reversing the order of the highest two levels and the addition of a

conceptualization of knowledge dimensions as factual, conceptual, procedural, and meta-

cognitive (Bush et al., 2014:2; Clark, 2015; Huit, 2011:2). This revision, which is known as the

revised Bloom’s taxonomy (Biggs & Tang, 2007:80), ranks the thinking skills in ascending

order as "remembering, understanding, applying, analysing, evaluating and creating" (Biggs

& Tang, 2007:81; Bush et al., 2014:2).

Biggs and Tang (2007:80) acknowledge that the revision of Bloom's Taxonomy is an

improvement, but that it still has some shortcomings such as that under the verbs of

“‘understanding’ you can find ‘identify’, ‘discuss’ and ‘explain’, which [can] represent three

different [cognitive] levels”. They therefore advocate their Structure of the Observed Learning

Outcome (SOLO) taxonomy as an alternative to the revised Bloom's taxonomy (Biggs & Tang,

2007:80). The SOLO taxonomy provides a systematic way of describing how a learner’s

performance grows in complexity when mastering many academic tasks (Biggs & Tang,

2007:76). It suggests five levels of understanding (in order of depth): pre-structural, uni-

structural, multistructural, relational and extended abstract (Biggs & Tang, 2007:79).

15

1.1.2 Motivation of the study and previous research

An initial review of the literature showed that some researchers typically used Bloom’s

Taxonomy and the revised Bloom’s Taxonomy to evaluate the cognitive level (demand) of

learning outcomes, student responses and/or assessment. Table 1-1 (Van Rooyen, 2016:95)

lists some examples:

Table 1-1: Examples of research involving Bloom's and the revised Bloom's taxonomy

Source: Van Rooyen (2016:95).

It is, however, due to the nature of a Financial Accounting 1 examination (especially in the

context of high stakes summative assessment), no easy task to evaluate this assessment to

determine a level of cognitive demand required, as explained in the following paragraphs.

Even with the aid of the revised Bloom’s taxonomy, this evaluation will remain a challenge.

Biggs and Tang (2007:80) support this observation by stating: “Anderson and Krathwohl’s

revision is an improvement, but even then under ‘understanding’ you can find ‘identify’,

‘discuss’ and ‘explain’, which represent three different SOLO levels”.

Authors Subject area Summary of findings

Example of studies using the original Bloom’s taxonomy

Momsen et al. (2010) Biology It was found that learning outcomes were written to

address the higher-order cognitive skills, but that

assessment tended to focus on the lower-order skills.

Yap et al. (2014) Accounting Results indicated that 80% of learning outcomes were

in the three lower cognitive levels (knowledge,

comprehension and application).

Ahmed et al. (2014) Engineering It was found that the cognitive domains were not

balanced within the degree programme.

Example of studies using the revised Bloom’s taxonomy

Williams (2013) Information

technology

The authors concluded that there was a shift towards

higher cognitive levels with progression through the

year levels of study. The revised Bloom’s Taxonomy

was found to be feasible in analysing the learning

outcomes for a course.

Lakshmi (2013) Finance The learning outcomes of finance modules were

categorised according to the revised taxonomy’s

cognitive levels. The lower-level skills along with the

application of knowledge dominated the learning

outcomes analysed. The results across the different

universities did, however, differ.

16

The major reason for this difficulty in evaluating a Financial Accounting 1 examination’s level

is that (in line with Biggs and Tang’s (2007:80) observation noted above), for an assessment

of Financial Accounting 1, verbs that indicate assessment tasks, such as “remember”, “apply”

or “evaluate”, which are usually associated with the revised Bloom’s taxonomy (Biggs & Tang,

2007:80-81) may imply different cognitive demands within a context which can differ

significantly for each assessment task, even if the same verb occurs.

Furthermore, Ramsden (cited by Biggs, 2007:xvi) states that

Biggs’s most outstanding single contribution to education has been the creation of the

Structure of the Observed Learning Outcome (SOLO) taxonomy. Rather than read about

the extraordinary practical utility of this device in secondary sources, get it from the

original here. From assessing clinical decision making by medical students to classifying

the outcomes of essays in history, SOLO remains the assessment apparatus of choice.

Literature (Table 1-2, page 17) on the SOLO taxonomy (defined in Biggs & Tang, 2007:76 and

discussed in paragraph 2.5.1.2 below) suggests it may well (amongst its various other uses)

provide a more objective and defensible way to evaluate a summative assessment task. A

relevant example (noted in Table 1-2, page 17) is found in Lucas and Mladenovic (2009:263),

where the application of SOLO in an introductory accounting course, regarding the evaluation

of the level of students’ understanding of subject specific concepts, is explored. None of these

scholars focused on the exact topic of this study, but their work can be incorporated and built

upon in order to meet the research objectives.

It is the application of the SOLO taxonomy to the summative assessment of a Financial

Accounting 1 module that is of interest to this study.

17

Table 1-2: Examples of research involving the SOLO taxonomy

Source: Researcher (adapted from Van Rooyen, 2016:95).

Authors Study’s title Subject area Method Scope Summary of findings Relevance

Newton and Martin

(2013:78)

Blooming, SOLO

Taxonomy, and

Phenomenography

as Assessment

Strategies in

Undergraduate

Science Education

Biochemistry Mixed (mainly

Quantitative)

Student responses of male

(n = 18) and female

(n = 10) students ages 20

to 36 (mean 24.5 ± 4.1)

enrolled in a second-year

bio-chemistry course in an

undergraduate Kinesiology

programme (2013:82).

Results suggest that

alternative assessment

strategies may be used as

tools to evaluate learning at

increasing levels of

cognitive complexity as

related to a deep learning

approach (2013:78).

The linking of the

phenomenography,

with SOLO

descriptors and

student responses

can provide

direction and

credibility to this

study.

Lucas and Mladenovic

(2009:263)

The identification of

variation in

students’

understandings of

disciplinary

concepts: The

application

of the SOLO

taxonomy within

introductory

accounting

Introductory

accounting

Qualitative Student responses on a

depreciation exercise were

obtained from 41 students

in their first semester of

introductory accounting at

a United Kingdom (UK)

university. Responses to a

‘profit and cash’ exercise

were obtained from 57

students in their second

semester of introductory

accounting in an Australian

university (2009:263).

Understandings evidenced

by the majority of students

may not meet the

expectations within Higher

Education. The findings

imply particular types of

interventions that could be

used immediately to support

changes in teaching and

learning approaches,

including assessment

(2009:277).

The linking of

SOLO descriptors,

student responses

and financial

accounting

concepts may

provide direction

and credibility to

this study.

18

1.1.3 The context of the study

Since this study contains a good measure of being cross-discipline (i.e. accounting and

education), it is useful to provide some context for the readers of the study.

It is therefore clarified that this study is concerned with the measuring and aiding of fair and

appropriate assessment for a student that is starting an accounting qualification (i.e. for

Financial Accounting 1) and that this qualification is primarily influenced by international

accounting standards (currently known as IFRS), professional bodies and government

regulations (e.g. SAQA). Although this study encompasses theory of education as a discipline,

the main aim and focus is on financial accounting as a professional discipline in a higher

education context.

It should also be mentioned that the term “introductory” in the study’s title refers to a financial

accounting module pitched at i) NQF level 5 in terms of ii) a financial accounting programme

(see paragraphs 1.4.2.1 and 2.3.3) that may typically lead to a professional designation. There

are other introductory accounting modules being part of, for example, a business course, of

which the goal is to give students an overview of different organisational functions. Such

introductory modules are not included in the scope of this study. A further comprehensive

discussion of stakeholders including SAQA and the NQF is given in paragraph 2.3 below.

1.2 PROBLEM STATEMENT

The above described background and motivation shows: i) the need for credible assessment,

as well as ii) the practical utility of the SOLO taxonomy in evaluating assessment tasks.

Although literature strongly supports these notions, there is a clear gap in the literature in that

the application of the SOLO taxonomy to evaluate the level of assessment of Financial

Accounting 1 written examinations (as a form of summative assessment) has not been

explored. As other studies (see Table 1-2, page 17) do show SOLO as a valuable tool of

analysis, it confirms that there is value in investigating the application of the SOLO taxonomy

in evaluating the standard of financial accounting assessments.

As part of the aforementioned, there is also the pertinent issue that, due to the nature of a

Financial Accounting 1 examination, it is no easy task to evaluate the assessment to determine

a level of cognitive demand required, even with the aid of the revised Bloom’s taxonomy. The

major reason for this is that for an assessment of Financial Accounting 1, verbs that indicate

assessment tasks, such as “remember”, “apply” or “evaluate” which are usually associated

with the revised Bloom’s taxonomy, may imply different cognitive demands within a context

that can differ significantly for each assessment task even if the same verb occurs.

19

The research problem can thus be summarised by the following questions:

How can the SOLO taxonomy be applied in order to evaluate the level of assessment

of a Financial Accounting 1 written summative assessment?

What are some typical themes and their influence on the standard or level of a

Financial Accounting 1 summative assessment that can be identified if the SOLO

taxonomy is applied as a tool for analysis?

1.3 OBJECTIVES OF THE STUDY

The following objectives have been formulated for the study:

1.3.1 Primary objective/s

The primary objective of this study is to provide a framework for the application of the SOLO

taxonomy in evaluating the standard of summative assessment of a Financial Accounting 1

module.

1.3.2 Secondary objectives

In order to achieve the primary objective, the following secondary objectives are formulated

for the study:

1. To contextualise from the literature the significant matters surrounding summative

assessment, including the matters of stakeholders’ interest and principles that should

be adhered to when setting and delivering assessments (Chapter 2).

2. To conceptualise the application of the SOLO taxonomy in evaluating the standard or

level of summative assessments (Chapter 2).

3. To document as part of the proposed framework, typical Financial Accounting 1

summative assessment tasks with the analysis through the SOLO taxonomy (Chapter

4).

4. To determine by analysis through the SOLO taxonomy, typical themes that have an

influence on the standard or level of a Financial Accounting 1 summative assessment

(Chapter 4).

5. To synthesise the insight gained through the study into a framework which can guide

the application of the SOLO taxonomy in evaluating the standard of summative

assessment of a Financial Accounting 1 module (Chapters 4 and 5).

20

1.4 RESEARCH DESIGN AND METHODOLOGY

In order to meet the research objectives, the study comprised a literature review and an

empirical study.

1.4.1 Literature review

There is little doubt that the literature review is of critical importance to every research project

(Mouton, 2013:86; Hart, 1998:13). It is in essence the review of the existing body of

scholarship and knowledge (Mouton, 2013:87) that can be built on with the main aim being to

add value and make a contribution to one’s field of research. It is evident from the research

objectives of this specific study that the literature review was compulsory.

The literature review has other important functions as well. The aims of the literature review,

as applied to this study, are as follows:

1.) “To ensure that one does not merely duplicate a previous study” (Mouton, 2013:87):

A review of the Nexus database that provides information on approximately 170 000

South African current and completed research projects including theses and

dissertations (NRF, 2015) was done. The North-West University’s electronic database

was searched (including, amongst others, EBSCOhost, WorldCat, Scopus, Lexis, Web

of Science, etc.) This review of Nexus and database searches showed that this study

is not a duplicate.

2.) Some of the aims can be grouped together as building on existing scholarship and

knowledge. Mouton (2013:87), for example, lists these aims as:

To discover the most recent and authoritative theorising about the subject;

To find what the most widely accepted empirical findings in the field of study are;

and

To ascertain what the most widely accepted definition of key concepts in the field

of study are.

The literature search provided references of scholarly work on assessment and the

SOLO taxonomy.

3.) The literature review sets the motivation for context and value of the research (Hart,

1998:14).

21

In order to achieve the above, the data sources for this study included relevant textbooks,

journal articles, unpublished studies, the NQF, the IES’s and SAQA’s guidance, and the

universities’ assessment forms.

The background section (paragraph 1.1 above) incorporates the result of the preliminary

literature review, which is expanded on in Chapter 2 below.

1.4.2 Empirical study

From the research objectives it can be seen that the Financial Accounting 1 summative

examinations, as a form of document that comprise mainly qualitative (textual) data, is

analysed by applying the SOLO taxonomy. Thus, qualitative research, using the document

analysis design as listed by Tesch (1990:58) and further outlined by Bowen (2009:27) and De

Vos et al. (2018:380), was mainly used for the empirical portion of the study (discussed in

paragraph 3.4.2.2). The main technique for analysing the documents was set as thematic

analysis including coding (paragraph 3.4.4).

The financial accounting examinations, however, also contain a limited amount of numeric

data (such as the number of marks), which is quantitative in nature. A limited analysis utilising

basic descriptive statistics (Saunders et al., 2016:527) as well as content analysis were used

with this data in order to support the qualitative approach. The study therefore ultimately drew

on mixed methods research as discussed by Creswell (2015:6) (see paragraph 3.4.1).

It can thus be seen that in the main, an inductive approach (Burney 2008:5) was followed by

transforming observations (the studying of the financial accounting exams) through analysis

(which included interpretation of the assessment task in terms of the SOLO taxonomy) into

more general themes. In line with Creswell (2014:186), a secondary deductive approach was

also followed, where the themes were considered against different exams in order to test their

value through applicability, but also to test whether there was further evidence that supported

the theme.

The empirical portion of this study also comprised the following methodology dimensions:

1.4.2.1 Target population and sampling frame

The target population, which is also the sampling frame for the study, is discussed and motived

in paragraph 3.4.4.1, and was set as final summative financial accounting examinations

pitched at NQF level 5 at the 26 public South African universities. In paragraph 3.4.4.1 it is

also motivated why 2016’s examinations are used but not detracting from the study’s validity.

22

1.4.2.2 Sample method

The sample method was motivated and set as non-probability purposive sampling (paragraph

3.4.4.2).

1.4.2.3 Sample size

The sample size consists of examinations from seven universities that were purposively

selected (paragraph 3.4.4.3).

1.4.3 Paradigmatic assumptions and perspectives

1.4.3.1 Ontological assumptions

Grey (2014:19) who builds on the work of amongst others Tesch (1994), Crotty (1998) and

Easterby-Smith (2002), describes ontology as the study of being, that is, the nature of

existence and what constitutes reality. Grey (2014:19) and Cohen et al. (2011:5) are in

agreement that in essence the researcher’s ontological stance is one of either i) reality being

external to the individual thus objective, positivist and nominalist in nature, or ii) there are

multiple realities and ways of accessing them and this is seen subjectively, a result of

individual cognition, relativist or nominalist.

In light of the research problem (paragraph 1.2) and objectives (paragraph 1.3), it can be seen

that this study is in essence one of describing “a way” of “how to”. This study is thus set in an

ontological stance of multiple and subjective realities since a solution will be proposed

(founded in research), but it is acknowledged that there can be other solutions and

interpretations. It is submitted that as long as the study is credible, this stance does not detract

from the value of the research.

1.4.3.2 Epistemological assumptions

While ontology embodies understanding what is, epistemology tries to understand what it

means to know. Epistemology provides a philosophical background for deciding what kinds of

knowledge are legitimate and adequate (Grey, 2014:19).

In line with the ontological stance motivated above, this study involves the researcher as the

main research participant as opposed to being an objective observer. In terms of Crotty (cited

by Grey, 2014:19) this can be stated as subjectivism. This epistemological stance is also

known as anti-positivism as is described by Cohen et al. (2011:6). In terms of this study, this

anti-positivist epistemology can be further refined as one of “interpretivism”. Grey (2014:23)

describes interpretivism as “the world is interpreted through the classification schemas of the

23

mind”. This description is apt since in terms of this study, documents will be analysed and

interpreted through the lens of the SOLO taxonomy.

Cohen et al.’s (2011:46) list of typical indications of applicability of the interpretative paradigm

is also applicable to this study. These include research that is qualitative, subjective, small

scale, interpretative, concerned with understanding and explanation, it concerns the individual,

is of practical interest, has personal involvement of the researcher, is non-statistical, and

accepts multiple directions of causality.

1.4.3.3 Rhetorical assumptions

According to O’Neil (cited by Young, 2013) rhetoric is the art of persuasion. Young (2013)

continues by explaining that the rhetorical structure of your paper is how you go about

persuading your reader that what you are saying is worth something, and that this structure

includes issues around the use of language and formatting. Mouton (2013:129-134) also

emphasises the importance of the style, content and form of scientific writing and provides 12

rules (that he compiled from various sources) to assist with effective scientific writing.

Young (2013) furthermore emphasises that the overall rhetorical assumption for qualitative

research is that it is not “truth seeking” or omniscient, but instead reporting what reality is

through the eyes of the research participants.

In the light of the above and in order to persuade the reader that this study is worthy of being

seriously considered, the study’s credibility will be enhanced through i) thick description of

logical and transparent reasoning where the reader will be able to follow the thought process

through transparent writing, as well as ii) the documenting of the systematic and referenced

process of this research in the research methodology chapter (Chapter 3).

1.4.3.4 Methodological assumptions

Methodological assumptions consist of the assumptions made by the researcher regarding

the methods used in the process of research (Dave, 2013).

As derived from Dave (2013), in terms of this study, the procedures used by the researcher

are mainly inductive and are based on the researcher’s own experience in collecting and

analysing data. The research here is the product of the values of the researcher. Through an

inductive approach, raw textual data is condensed into themes. Clear links are established

between research objectives and summary findings derived from raw data. A framework of

24

the underlying structure of experiences or processes that are evident from the raw data is then

developed. In Chapter 3 this study’s methodology (including assumptions) is comprehensively

described and motivated.

1.4.3.5 Theoretical framework

It can be seen throughout Biggs and Tang’s (2007) work that the SOLO taxonomy is

inextricably tied to, and flows from, their theory of constructive alignment (Biggs & Tang,

2007:50-62). The theory of "constructive alignment" entails the systematic alignment of the

intended learning outcomes, teaching and learning activities, and the assessment tasks while

knowledge is constructed throughout the process (Biggs & Tang, 2007:7). This specific theory

underpins this study and is further discussed in paragraph 2.2.

1.5 ETHICAL CONSIDERATIONS

As stated by Cohen et al. (2011:542), the overriding principle of ethical considerations is one

of “do no harm to participants”.

In light of this overriding principle the risk of any harm to participants was carefully considered.

This author, in light of his auditing and chartered accounting background, considers himself

capable of meticulously assessing risk.

The risk to participants of this study is subsequently considered minimal since:

1.) Data gathered (the financial accounting exams) is already in the public domain due to

the fact that students already wrote the exams and hence the exams can be obtained

from former or current students or from exam resources on different websites. An

example of easy access can be found on the website of Course Hero (2018).

2.) Initial discussions with possible participants (applicable representatives) indicated that

they are comfortable with especially the use of examinations that are at least one-year-

old (i.e. 2016 for this study) since the risk of being accused of “leaking” exams are then

completely avoided. The nature of Financial Accounting 1 topics, being about the

fundamental and introductory principles, leads to these exams still being sufficient for

this study’s purposes and hence this suggestion will be implemented.

3.) Although point 1 and 2 already show a low risk, the following principles of ethics, as

outlined by Smith (2011:99), will also be adhered to, so as to indicate how serious the

author considers ethics: Voluntary participation will be emphasised. Confidentially of

25

the research data will be strictly applied by electronic and physical protection of the

data. The researcher alone will have access to the primary data. The universities

whose exams will be analysed will be de-linked as specific identifiable participants from

the final research findings through the use of neutral labels.

Therefore, the nature of the study does not indicate any further risk of participation. In addition

ethical clearance was obtained for the study from the Faculty of Economic and Management

Sciences Research Ethics Committee (EMS-REC) (approval number NWU-00646-20-A4).

1.6 CHAPTER CLASSIFICATION

This study will comprise the following chapters:

Chapter 1 Introduction, background and planning

This chapter serves as an introduction to the study and provides an overview of the

background, motivation, research objectives and an outline description of the planned

research methodology of the study.

Chapter 2 Contextualising summative assessment

This chapter will be based on a systematic literature review which includes i) addressing the

research objectives of:

contextualising from literature the significant matters surrounding summative

assessment including the matters of stakeholders’ interest and principles that should

be adhered to when setting and delivering assessments (research objective 1);

conceptualising the application of the SOLO taxonomy in evaluating the standard or

level of summative assessments (research objective 2);

and ii) summarising and building on the work of selected other scholars.

Chapter 3 Research design and methodology

In this chapter the chosen design and methodology will be motivated and defended. This

includes paradigmatic assumptions.

Chapter 4 Analysis and findings

In this chapter the empirical evidence generated in order to further complete the following

research objectives will be documented:

26

As part of the proposed framework, typical Financial Accounting 1 summative assessment

tasks will be documented with an analysis through the SOLO taxonomy thereof (research

objective 3).

Typical themes that have an influence on the standard or level of a Financial Accounting

1 exam will be determined by analysis through the SOLO taxonomy (research objective

4).

The insight gained through the study will be synthesised to flow into the framework that

will be given in Chapter 5 and which can guide the application of the SOLO taxonomy in

evaluating the standard of summative assessment of a Financial Accounting 1 module

(research objective 5).

Chapter 5 Conclusions and recommendations

This chapter will include the study’s conclusions and recommendations. It will also clearly link

the findings to the problem statement and ensure that every objective has been achieved. The

final suggested coherent framework will be given. Areas for further research and reflective

learning will also be briefly discussed.

1.7 SUMMARY

This chapter served as an introduction to the study and provided an overview of the

background, motivation, research objectives and an outline description of the planned

research methodology of the study.

27

CHAPTER 2 CONTEXTUALISING SUMMATIVE ASSESSMENT

2.1 INTRODUCTION

This chapter will be based on a systematic literature review which includes i) addressing the

research objectives of:

contextualising from literature the significant matters surrounding summative

assessment including the matters of stakeholders’ interest and principles that should

be adhered to when setting and delivering assessments (research objective 1);

conceptualising the application of the SOLO taxonomy in evaluating the standard or

level of summative assessments (research objective 2);

and ii) summarising and building on the work of selected other scholars.

In paragraph 1.4.1 the purpose and function of the literature review was explained, while

paragraph 1.1.1 provided background to summative assessment and the importance of the

credibility thereof. In this chapter these matters will also be expanded on.

2.2 CONSTRUCTIVE ALIGNMENT

It is mentioned in paragraph 1.4.3.5 that the SOLO taxonomy is tied to the theory of

constructive alignment and that this theory also underpins the study. In the following

paragraphs the theory of constructive alignment is further discussed.

Biggs and Tang (2007:52) explain that the “constructive” part is based on the constructivist

theory, i.e. that learners use their own activity to construct their knowledge. Biggs and Tang

(2007:52) suggest that the best way to achieve this “construction of knowledge” is that the

learning outcomes (they refer to these as “intended learning outcomes” or “ILOs”) should

specify activities and content that students should engage in, while the teacher’s task is to:

i) set up a learning environment that encourages the student to perform these learning

activities, and ii) then to assess what the learning outcomes required in order to determine

whether the intended learning took place. Biggs and Tang (2007:13) refer to this process as

their version of the “often confused concept” of outcomes-based education, which they refer

to as outcomes-based teaching and learning (OBTL) which is “solely concerned with

enhancing teaching and learning” and which is to be implemented using constructive

alignment. Biggs and Tang (2007:21) acknowledge that this form of constructivist theory (and

28

their use thereof) has its roots in cognitive psychology as pioneered by Jean Piaget in 1950

(see Figure 2-2, page 39).

As is the case with any theory, this constructivist theory can of course be challenged, but what

is certainly applicable in this researcher’s experience is that deep authentic learning goes

hand-in-hand with true understanding. Understanding is seen as a personal process for each

individual. One cannot “understand” on someone’s behalf, that person must do it themself if

their desire is to learn the skill or content so as to be able to use it themself. A person wishing

to understand something must therefore construct a connection in his own mind. It therefore

seems logical and desirable that teaching and learning activities (TLAs) and assessment

should be geared towards assisting a learner in constructing connections in his mind (i.e.

“learning”).

Biggs and Tang (2007:52) furthermore explain that the “alignment” part of constructive

alignment means that learning activities, teaching activities and assessment tasks all stem

from well-written (in terms of using verbs) learning outcomes and therefore all having the same

aim.

Constructive alignment can thus be stated as the process where the intended learning

outcomes, the teaching and learning activities, as well as the assessment tasks are

systematically aligned, to be done in accordance with the learning activities required in the

outcomes (Biggs & Tang, 2007:7) so as to facilitate the construction of “understanding” and

ultimately true knowledge. One can also view this form of alignment as inherently constructive

(or “building-up”) in the same way as feedback or criticism is often said to be constructive.

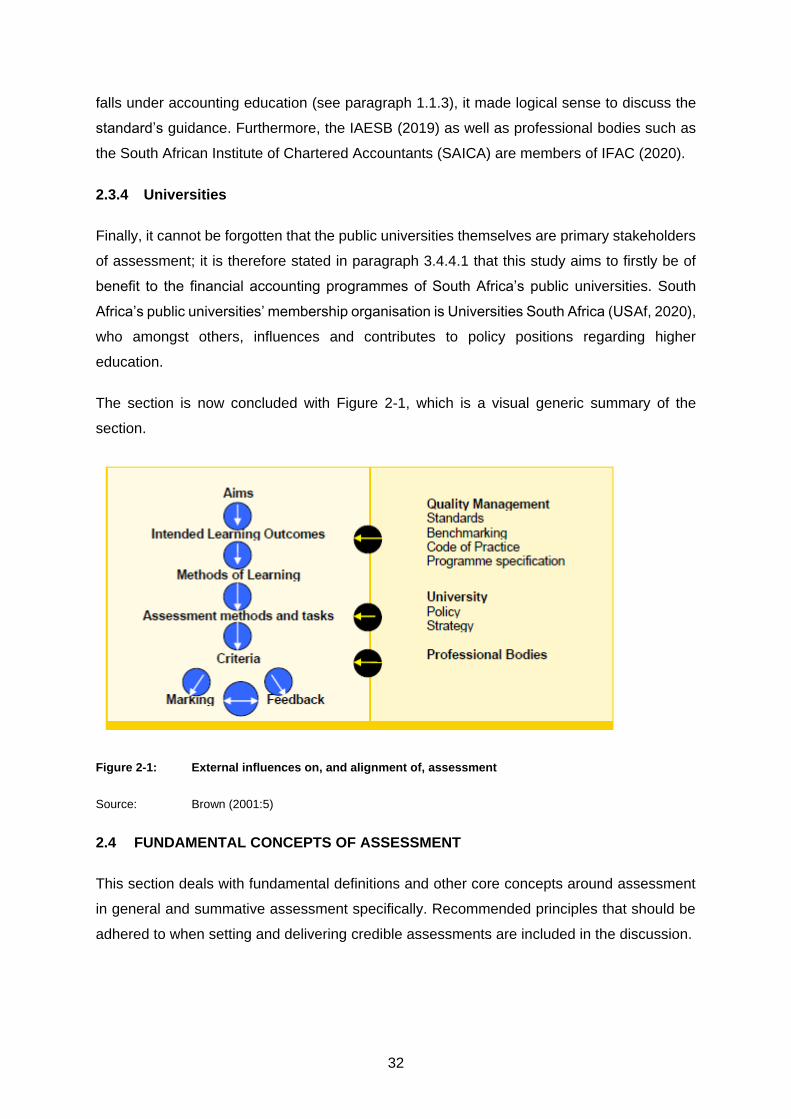

Figure 2-1 (page 32) visually represents the process of constructive alignment. It can also be

seen that the assessment criteria have a pertinent place in this process.

In concluding this paragraph, it is submitted that it is hardly possible to overemphasise the

importance of constructive alignment in the current university environment (Brown, 2001:4).

In this environment, which includes increased student numbers, student-centeredness,

serious financial implications, diversity of students (Biggs & Tang, 2007:2), and various but

sometimes conflicting stakeholder interests (paragraph 2.2), it is vital to be able to

demonstrate fairness of assessment (paragraph 1.1.1) and authenticity of assessment

(paragraph 2.4.1) so as to be able to be accountable to all these different stakeholders whilst

coping with this ever-changing and demanding environment.

29

2.3 PRIMARY STAKEHOLDERS

The following paragraphs summarise, from the literature, context around the primary

stakeholders’ interest in summative assessment of introductory financial accounting modules

at public South African universities. The context is given per group of stakeholders.

2.3.1 Students

Brown (2001:6) lists three overall reasons for assessment at HEIs which are still applicable

today (the merits of these reasons are however beyond the scope of this study). These are: i)

to give a licence to proceed to the next stage or to graduation; ii) to classify the performance

of students in rank order; and iii) to improve students’ learning. These reasons also overlap,

but may unfortunately sometimes be in conflict (Brown, 2001:6). What is clear from these

reasons is that students are firstly and foremost the main stakeholders of assessment. Even

by reviewing just these three overall reasons for assessment, one can already see how

assessment may have a life-changing impact on students. Assessment can, amongst others

and especially in the South African context, literally mean the difference between a life of

poverty or a successful career. It is therefore no surprise that there is so much writing,

research, reflection and regulation of assessment worldwide.

Since students are the first primary stakeholders of assessment, it is apt to further discuss

their relationship with assessment. In this aspect it can be seen that scholars on assessment

are strongly in agreement that assessment heavily influences a student’s approach to the

learning process. This influence may in fact be so high that it can be seen that some authors,

such as Brown (2001:4), state that assessment actually drives student behaviour. Brown’s

(2001:6) first principle of effective assessment is that assessment shapes learning, so if you

want to change learning then change the assessment method. Biggs and Tang (2007:169)

agree by noting how teachers usually see the intended learning outcomes as the central pillar

in an aligned teaching system, but that students rather see assessment as the central pillar.

Ramsden (cited by Biggs & Tang, 2007:169) states that “From our students’ point of view,

assessment always defines the actual curriculum”.

Biggs and Tang (2007:169) explain that this effect that assessment has on student behaviour,

whereby assessment determines what and how students learn more than what the curriculum

does, is widely known as “backwash”. Biggs and Tang (2007:169) note that the term was

coined by Lewis Elton (1987). Biggs and Tang (2007:169) furthermore note that “backwash”

is usually seen in a negative light, especially in an exam dominated system, since students for

example spent their time in rote learning of prior year exam papers and focus on exam strategy

30

instead of substance of learning. All of this will lead to surface learning, a concept which

Biggs and Tang (2007:29) describe as learning activities that are too low a level as to achieve

the intended learning outcomes. An example of surface learning would be if rote memorisation

is used to falsely give the impression of real understanding (Biggs & Tang, 2007:29). In

contrast to surface learning, deep learning means activities where a student wants to, and

indeed does, develop real understanding and makes sense of what he or she is learning

(Biggs & Tang, 2007:24).

Biggs and Tang (2007:169) however, do explain that “backwash” can be utilised in a positive

way, mainly by two things being in place: i) constructive alignment (see paragraph 2.2) as well

as ii) criterion-referenced assessment (see paragraph 2.4.3). Doing this will harness students’

high concern for assessment and fit backwash into an overall process that facilitates the

desired effect of deep learning.

The above paragraphs focused on students as the main stakeholders when it comes to

assessment. It follows that students’ family, funders and prospective employers share this

stakeholder interest.

2.3.2 The Government of South Africa

In terms of Financial Accounting 1 as a module at a public South African university, the

government of South Africa is also a major stakeholder of university qualifications and their

eventual assessment processes (not least because it is a major funder of higher education).

It is therefore no surprise that these qualifications are regulated. The process of how such a

qualification is regulated will now be explained in the following paragraphs.

The South African Government is represented by the Department of Higher Education and

Training (SAQA, 2014:2) with its “mother” act being the Higher Education Act 101 of 1997, of

which the main goal was to establish a single co-ordinated higher education system.

Flowing from the mother act is one of the main “daughter” acts, which is the National

Qualifications Framework Act 67 of 2008 (the “NQF Act”), of which a main aim is to provide

for the National Qualifications Framework (NQF). Section 6 of this act mandates the NQF to

consist of ten levels including level descriptors (see SAQA, 2012).

In terms of section 10 of the NQF Act, a juristic person namely the South African Qualifications

Authority (SAQA), is enacted with its objective set as, amongst others, to oversee the further

development and implementation of the NQF. Sections 13-23 regulate SAQA’s further

functions.

31

The NQF Act, in terms of section 25, also enacts a Quality Council i.e. the Council on Higher

Education (CHE). Some of the primary functions of the CHE as prescribed by section 27 of

the NQF Act are i) the development, registration and publication of qualifications as well as ii)

to develop and implement a policy for quality assurance within its sub-framework.

The sub-framework referred to here (as enacted by section 7 of the NQF Act) is the Higher

Education Qualifications Sub-Framework (HEQSF) (Department of Higher Education and

Training, 2014:10) which build on the NQF’s levels to provide detail such as qualification

names, their purpose, characteristics and amount of learning credits.

The HEQSF (Department of Higher Education and Training, 2014:14) summarises the

interrelation of SAQA and the CHE’s roles as follows:

SAQA is responsible for the development of policy and criteria for registering standards

and qualifications on the NQF on the recommendation of the CHE.

The CHE is responsible for the development and management of the HEQSF and for

advising the Minister of Higher Education and Training on matters relating to the

HEQSF. This includes issues such as the development of naming conventions for

qualifications.

Sections 13 and 27 of the NQF Act require that both SAQA and the CHE should develop a

system of collaboration in terms of various issues, which include assessment.

The NQF Act in section 29, as well as the HEQSF (Department of Higher Education and

Training, 2014:14), also recognise the role of professional bodies. Section 29 of the NQF Act

broadly defines professional bodies as “statutory or non-statutory body of expert practitioners

in an occupational field” and provides for professional bodies to register with SAQA so as to

be recognised by the act. The HEQSF (Department of Higher Education and Training,

2014:14) provides for consultation with professional bodies.

2.3.3 Professional bodies

In terms of this study it is acknowledged that professional bodies have material influence on

the assessment in qualifications that eventually forms part of their requirements for

membership. The detailed requirements of the professional bodies are however beyond the

scope of this study. The target population of this study (paragraph 1.4.2.1) was set as

summative financial accounting examinations that are i) pitched at NQF level 5 and ii) forms

part of a financial accounting qualification. Such a qualification may (or may not) eventually

lead to a professional accounting designation. However, since the IAESB issued an

accounting education standard on assessment (see paragraph 2.3) and since this study’s topic

32

falls under accounting education (see paragraph 1.1.3), it made logical sense to discuss the

standard’s guidance. Furthermore, the IAESB (2019) as well as professional bodies such as

the South African Institute of Chartered Accountants (SAICA) are members of IFAC (2020).

2.3.4 Universities

Finally, it cannot be forgotten that the public universities themselves are primary stakeholders

of assessment; it is therefore stated in paragraph 3.4.4.1 that this study aims to firstly be of

benefit to the financial accounting programmes of South Africa’s public universities. South

Africa’s public universities’ membership organisation is Universities South Africa (USAf, 2020),

who amongst others, influences and contributes to policy positions regarding higher

education.

The section is now concluded with Figure 2-1, which is a visual generic summary of the

section.

Figure 2-1: External influences on, and alignment of, assessment

Source: Brown (2001:5)

2.4 FUNDAMENTAL CONCEPTS OF ASSESSMENT

This section deals with fundamental definitions and other core concepts around assessment

in general and summative assessment specifically. Recommended principles that should be

adhered to when setting and delivering credible assessments are included in the discussion.

33

2.4.1 Definitions of assessment

It is apt to begin the discussion with the concept of “assessment” itself. It is possible to provide

many definitions of assessment and it is also submitted that most readers intuitively

understand what “assessment” means, but as an anchor point the following definition is

provided. SAQA (2001:16) defines assessment as “A structured process for gathering

evidence and making judgments about an individual’s performance in relation to registered

national standards and qualifications”. The central idea here is one of having evidence

enabling measurement against a standard. Linking on to this notion of evidence is the concept

of assessment criteria. SAQA (2001:22) states that assessment criteria are “statements

whereby an assessor can judge whether the evidence provided by a learner is sufficient to

demonstrate competent performance”. Assessment criteria are clear, precise and transparent

statements against which performance is assessed (Geyser, 2004:95). Biggs and Tang

(2007:215) mention the use of rubrics as a way to set assessment criteria for some

assessment tasks. The use of assessment criteria fit into the overall process of constructive

alignment (and ultimately fairness of assessment), as discussed in paragraph 2.4.1 below.

Since the title of the study makes it clear that summative assessment is of interest, it is apt

to discuss what is meant by “summative assessment”. The concept of summative assessment

relates to the purpose of the assessment and is often contrasted to assessment with a

formative purpose (formative assessment) (Van Tonder, 2010:19). Hence, if the purpose of

the assessment is to support and improve the learning process, then the assessment is

formative in nature and known as formative assessment, whereas if the purpose of an

assessment is to assess the knowledge, skills, attitudes and/or values of a student at the end

of a particular period of learning, it is known as summative assessment (Van Tonder, 2010:19).

Biggs and Tang (2007:97) agree with these definitions and make it clear that “(f)ormative

assessment is provided during learning, telling students how well they are doing and what

might need improving; summative after learning, informing how well students have learned

what they were supposed to have learned”.

Biggs and Tang (2007:163) also refer to formative assessment as “formative feedback” and

summative assessment as “summative grading” to emphasise that the purpose of these two

forms of assessment is very different. One may wonder why this study then focusses on

summative assessment. The answer is that summative assessment is traditionally used at

public South African universities to grade students at the end of a module or year of study and

to eventually award a qualification or not (SAQA, 2014:8). This is also the case in Biggs and

Tang’s (2007:164) experience where they state that “(i)n summative assessment, the results

are used to grade students at the end of a course or to accredit at the end of a programme”.

34

It can thus be seen that summative assessment is “high stakes” and has serious financial and

other implications for a student (this however does not mean formative assessment is not

important). It is therefore due to this inherent serious implication of summative assessment

crucial that it is as fair as possible. One way of enhancing or demonstrating fairness is by

using a taxonomy such as Bloom’s or SOLO, to more objectively measure the level (or

standard) of a summative assessment.

It was further noted that the financial accounting examinations that make up the data set of

this study is a form of traditional or conventional assessment, since these written

examinations have been used over a long period (Van Tonder, 2010:19). Alternative

assessment utilises instruments that have not been used in particular discipline (e.g. financial

accountancy) for a long time and can be seen as relatively new or innovative, but they are

admittedly not necessarily authentic in nature (Van Tonder, 2010:19). Authentic assessment

is described by Van Tonder (2010:20) as assessment performed in contexts very closely

related to real life situations. Examples of alternative assessment instruments (which is the

case in terms of financial accountancy) include presentations by students, reflective journals,

as well as portfolios of learning evidence (Van Tonder, 2010:19). The principles of credible

assessment will at some point differ between conventional and alternative assessment, and it

is therefore necessary to note that the data for this study is considered to be a form of

conventional assessment.

2.4.2 Kinds of knowledge

Biggs and Tang (2007:72) emphasise that knowledge is the object of understanding (which

can be structured into levels) and that there are two main kinds of knowledge in the context of

assessment. These two main kinds of knowledge are stated as declarative knowledge or

functioning knowledge (Biggs & Tang, 2007:72). In linking to the above discussion it is

therefore also important to consider whether an assessment aims to cover declarative

knowledge or functioning knowledge.

Biggs and Tang (2007:81) describe declarative knowledge as knowing about phenomena,

disciplines and theories (e.g. “what Freud said”). It is content knowledge that accrues from

others’ research, not from personal experience, and is typically found in libraries, textbooks,

and what teachers declare in lectures (Biggs & Tang, 2007:72). On the other hand, Biggs and

Tang (2007:72) explain that functioning knowledge is based on the idea of performance

underpinned by fundamental understanding (e.g. how to physically fly an aeroplane). This

knowledge is within the experience of the learner, who can now put declarative knowledge to

work by solving problems such as performing surgery. Functioning knowledge requires a solid

35

foundation of declarative knowledge (Biggs & Tang, 2007:72). Whether an assessment will

cover declarative knowledge or functioning knowledge will depend on its context. For financial

accounting as a professional discipline, the assessment process is likely to lean more towards

functioning knowledge. Fortunately, due to the inherent nature of financial accounting (e.g.

supporting documentation, standards-based reporting and working with numbers) a traditional

assessment such as an exam can simulate real-life scenarios in order to assess functioning

knowledge to a large extent. This may not be the case for other professionals such as pilots

or surgeons. The SOLO taxonomy can assist in the assessment process of both declarative

as well as functioning knowledge (see paragraph 2.5.1.3 below).

2.4.3 Forms of assessment

According to Biggs and Tang (2007:170) another set of concepts that influences current

practice (and therefore needs discussion) is the distinction between assessment in the form

of norm-referenced assessment and assessment in the form of criterion-referenced

assessment.

Norm-referenced assessment (NRA) is described as assessment with the aim of

differentiating between students based on their results (Biggs & Tang, 2007:179), hence the

focus on a “normal” distribution of results. Criterion-referenced assessment (CRA) in

contrast entails assessment with the aim of judging how well a student’s performance matches

a criterion that has been set in advance (Biggs & Tang, 2007:179). NRA therefore makes

judgments about people whereas CRA makes judgments about performance (Biggs & Tang,

2007:179). For CRA whether a group of students all score full marks or very low marks are

inconsequential, since the issue is whether the outcomes were evidently met or not. Biggs and

Tang (2007:170) admit that there may be instances where a normative approach is applicable,