fasb taxonomy advisory group meeting

TRANSCRIPT

1

FASB Taxonomy Advisory

Group Meeting

Date: August 14, 2014

Location: Web Conference

2

Contents

I. Agenda ................................................................................................................................................................. 3

II. Sessions and Highlights ........................................................................................................................................ 4

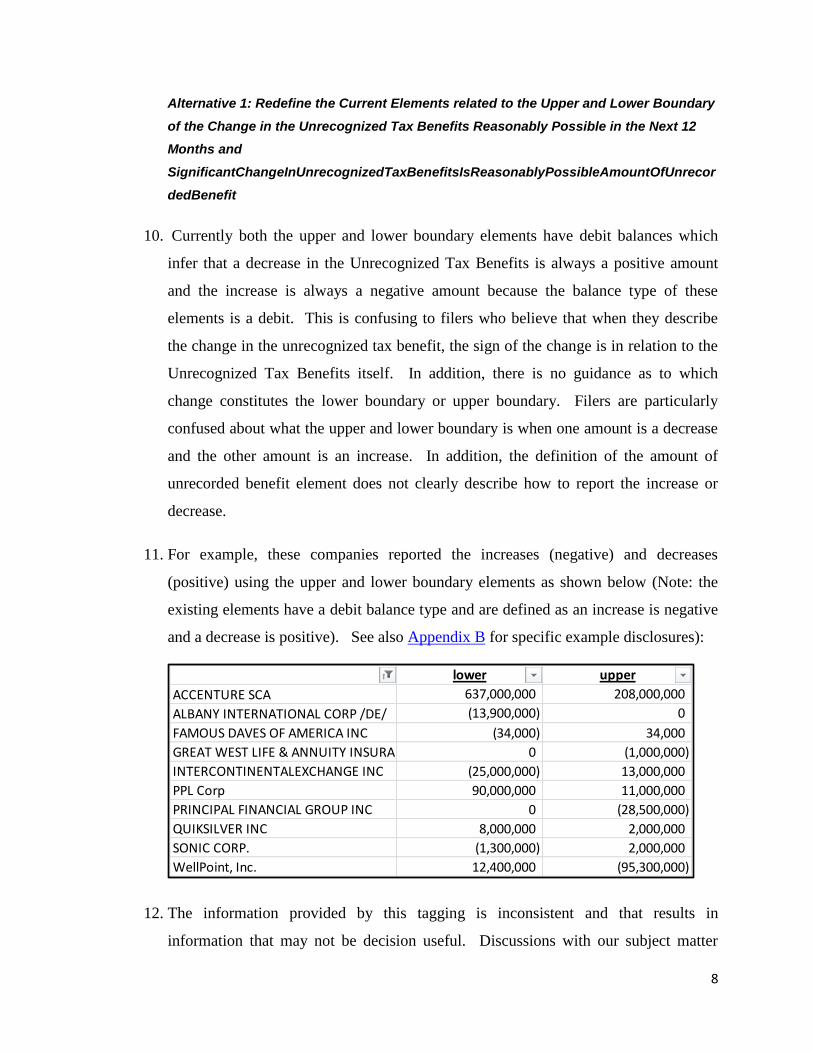

Session 1 – Unrecognized Tax Benefits .................................................................................................................... 4

A. Meeting Highlights ....................................................................................................................................... 4

B. Unrecognized Tax Benefits .......................................................................................................................... 4

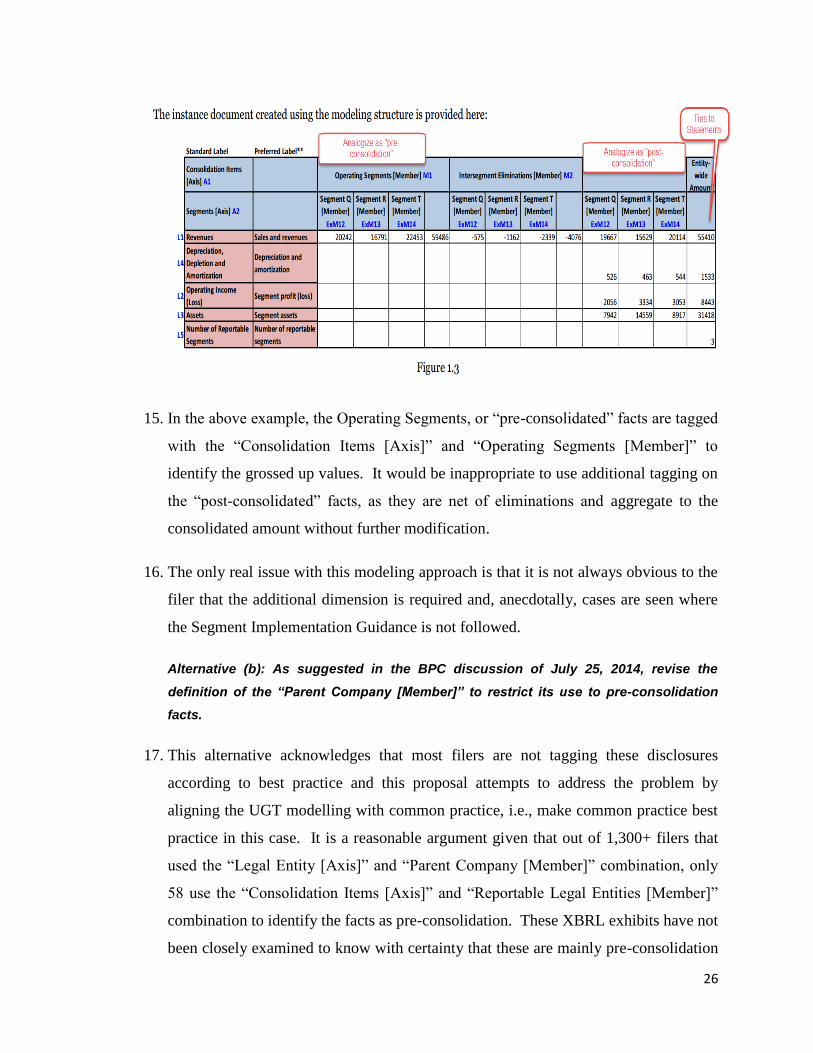

Session 2 – Legal Entity Axis Issues ........................................................................................................................ 19

A. Meeting Highlights ..................................................................................................................................... 19

B. Legal Entity Axis Issues ............................................................................................................................... 19

Session 3 – Special Label Discussion ...................................................................................................................... 28

A. Meeting Highlights ..................................................................................................................................... 28

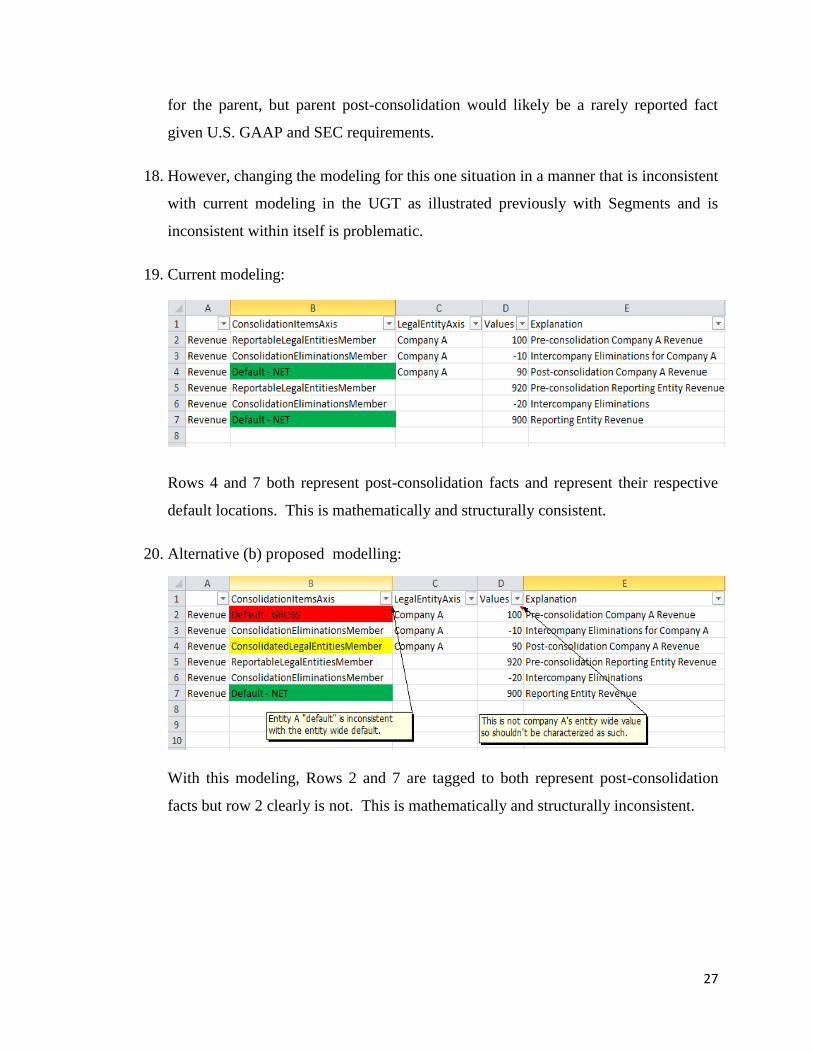

B. Special Label Discussion ............................................................................................................................. 29

3

I. Agenda

Session Presenter

1. Unrecognized Tax Benefits Vickie

2. Legal Entity Axis Issues Louis

3. Special Label Discussion Vickie

4

II. Sessions and Highlights

Session 1 – Unrecognized Tax Benefits

A. Meeting Highlights

B. Unrecognized Tax Benefits

Purpose or Objective of This Memo

1. At the August 14, 2014 TAG Meeting the Taxonomy staff is proposing certain

changes to the taxonomy (UGT) which will better reflect the requirements in ASC

740-10-50-15(d) related to reporting the amount of increase (decrease) reasonably

possible of the unrecognized tax benefits taken or expected to be taken in the next

twelve months.

Two alternatives were presented for inconsistent use of the elements related to upper or lower bound of significant changes in the unrecognized tax benefits reasonably possible to occur in next 12 months. Taxonomy staff and TAG members discussed two alternatives to address inconsistent application of elements for pre- and post-consolidated facts when using the “Legal Entity [Axis]” in combination with the “Consolidation Items [Axis]”. As a result of a prior meeting’s discussion around the deprecation decision tree, three options were provided to identify substantive changes to elements that would normally require deprecation, but based on certain criteria, are changed and not deprecated.

The highlights and resolutions from the July 10, 2014 TAG meeting, the workflow report and the ASU report were provided for review, but were not discussed.

The Taxonomy staff discussed whether the following three elements related to unrecognized tax benefits should be deprecated and replaced with two new elements: (IncreaseInUnrecognizedTaxBenefitsReasonablyPossible and DecreaseInUnrecognizedTaxBenefitsReasonablyPossible).

These three elements are as follows:

(1)SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleAmountOfUnrecordedBenefit

(2)SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossible EstimatedRangeOfChangeUpperBound

(3)SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleEstimatedRangeOfChangeLowerBound

Most TAG member supported the deprecation of the Upper and Lower Bound limits, but a consensus was not clearly reached and the topic will be addressed at a future meeting.

5

2. The Taxonomy staff is proposing revisions to the UGT that we believe will enhance

the information provided by filers and reduce ambiguity about what the expected

change that is reported for the unrecognized tax benefits. The Taxonomy staff is

interested in the view of the TAG members as to whether they believe the suggested

modifications to the taxonomy address the questions raised in practice as described at

the XBRL US Best Practice Committee (BPC) Discussion Document prepared for the

July 25, 2014 BPC Call.

Background Information

3. At the July 25, 2014 BPC Call, the BPC discussed what the appropriate tagging

should be for reporting the positions for which it is reasonably possible that the total

amounts of unrecognized tax benefits will significantly increase or decrease within 12

months of the reporting date. The discussion focused in particular on the requirement

in ASC 740-10-50-15(d)(3) that requires filers to disclose:

For positions for which it is reasonably possible that the total amounts of

unrecognized tax benefits will significantly increase or decrease within 12

months of the reporting date:

(1) The nature of the uncertainty

(2) The nature of the event that could occur in the next 12 months that

would cause the change

(3) An estimate of the range of the reasonably possible change or a

statement that an estimate of the range cannot be made.

4. The basis for conclusions of the original standard provided additional guidance as to

what the Board meant by item (3). The basis for conclusions for FASB Interpretation

No. 48, paragraphs B42 and B43 states (emphasis added)—

The Board initially selected best estimate, as the term is used in FASB

Concepts Statement No. 7, Using Cash Flow Information and Present

Value in Accounting Measurements, to measure tax benefits that are

within the scope of this Interpretation. The best estimate represents the

6

single most likely amount in a range of possible estimated amounts. Some

respondents to the Exposure Draft indicated that a best-estimate

measurement might yield counterintuitive results, especially if there is a

wide dispersion of possible estimated outcomes, each with a low

probability of being ultimately realized. The Board agreed with those

respondents and decided to modify the approach.

This Interpretation specifies that a tax position that meets the threshold for

recognition should be measured at the largest amount that is greater than

50 percent likely of being realized upon ultimate settlement. That

measurement is based on an analysis of the distribution of potential

outcomes (that is, potential realized tax benefits) and their related

probabilities. In the case of tax positions, the distribution is bounded from

below by zero and from above by the amount taken in a tax return. This

Interpretation requires an enterprise to determine the largest amount of

benefit that is greater than 50 percent likely of being realized upon

ultimate settlement.

5. The BPC considered four example disclosures, provided in Appendix A of this

memorandum. The BPC members did not all agree with the Discussion Papers

Recommendations for each example. The Taxonomy staff agreed to do more research

on this matter and discuss our finding and recommendations with the TAG.

Issues with Current Usage of Elements related to Unrecognized Tax Benefits

6. The Taxonomy staff conducted research on how filers were using the elements

associated with the “estimate of the range of the reasonably possible change.”

7. The Taxonomy Staff found that filers were not using

SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleEstimatedR

angeOfChangeLowerBound and

SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleEstimatedR

angeOfChangeUpperBound consistently and appeared to be confused as to what

7

constituted a lower boundary or upper boundary especially when there was an

increase and a decrease being disclosed.

8. Specifically the research found:

(a) Of the 122 who used the Upper Bound Element (28 filers sampled) and

found: 11 used the phrase “up to”, 6 used “as much as” and 11 had no

particular language pattern.

(b) Of the 19 who used the Lower Bound Element: 5 used “up to”; 8 used

“decrease by”; 1 used “amounting to”; 1 used “in excess of”; 1 used

“settled”; 2 used “reduce”; 1 had none.

(c) Of the 181 who used both: 160 used the elements with only positive

numbers, with the smaller number being the Lower Bound and the larger

number being the Upper Bound, 8 used it with negative numbers with the

smaller number being the Lower Bound and the larger number being the

Upper Bound, 9 used the Upper and Lower Bound inconsistently to report

the ends of the range and 4 used the Upper Bound for the larger positive

number and Lower Bound for the smaller positive number.

Taxonomy Staff Analysis

9. The Taxonomy staff considered two alternatives

(a) Redefining the elements related to the upper and lower bound of the change

in the Unrecognized Tax Benefits.

(b) Deprecating the current upper and lower boundary elements and the element

Significant Change in Unrecognized Tax Benefits is Reasonably Possible,

Amount of Unrecorded Benefit and creating two new elements that are more

descriptive of what is required by “An estimate of the range of the

reasonably possible change.”

8

Alternative 1: Redefine the Current Elements related to the Upper and Lower Boundary

of the Change in the Unrecognized Tax Benefits Reasonably Possible in the Next 12

Months and

SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleAmountOfUnrecor

dedBenefit

10. Currently both the upper and lower boundary elements have debit balances which

infer that a decrease in the Unrecognized Tax Benefits is always a positive amount

and the increase is always a negative amount because the balance type of these

elements is a debit. This is confusing to filers who believe that when they describe

the change in the unrecognized tax benefit, the sign of the change is in relation to the

Unrecognized Tax Benefits itself. In addition, there is no guidance as to which

change constitutes the lower boundary or upper boundary. Filers are particularly

confused about what the upper and lower boundary is when one amount is a decrease

and the other amount is an increase. In addition, the definition of the amount of

unrecorded benefit element does not clearly describe how to report the increase or

decrease.

11. For example, these companies reported the increases (negative) and decreases

(positive) using the upper and lower boundary elements as shown below (Note: the

existing elements have a debit balance type and are defined as an increase is negative

and a decrease is positive). See also Appendix B for specific example disclosures):

12. The information provided by this tagging is inconsistent and that results in

information that may not be decision useful. Discussions with our subject matter

lower upper

ACCENTURE SCA 637,000,000 208,000,000

ALBANY INTERNATIONAL CORP /DE/ (13,900,000) 0

FAMOUS DAVES OF AMERICA INC (34,000) 34,000

GREAT WEST LIFE & ANNUITY INSURANCE CO 0 (1,000,000)

INTERCONTINENTALEXCHANGE INC (25,000,000) 13,000,000

PPL Corp 90,000,000 11,000,000

PRINCIPAL FINANCIAL GROUP INC 0 (28,500,000)

QUIKSILVER INC 8,000,000 2,000,000

SONIC CORP. (1,300,000) 2,000,000

WellPoint, Inc. 12,400,000 (95,300,000)

9

experts suggested possibly redefining the lower boundary to be either the largest

increase in the change or the smallest decrease and the upper boundary to be the

smallest increase in the change or the largest decrease. However, that might be

perceived as giving accounting guidance which should be coming from the Board, not

the Taxonomy staff. Also, it may give the impression that the information is

comparable among companies which it is not. It is a number whose comparison is

meaningless out of context. In addition, the Taxonomy staff is concerned that those

boundary elements will continue to be used inconsistently.

13. The Taxonomy staff is concerned that this option will not adequately address the

inconsistent use of the elements as it is may not be clear what the notion of “range”

means when one value is positive and one is negative.

Alternative 2: Deprecate the Current Elements related to the Upper and Lower

Boundary of the Change in the Unrecognized Tax Benefits Reasonably Possible in the

Next 12 Months and the

SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleAmountOfUnrecor

dedBenefit and Create New Elements

14. Under this alternative the Taxonomy staff would make the following changes to the

taxonomy:

(a) Deprecate the following three elements as they do not clearly describe the

facts:

(i) SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyP

ossibleAmountOfUnrecordedBenefit defined as “The amount

of the unrecognized tax benefit of a position taken for which it is

reasonably possible that the total amount thereof will

significantly increase or decrease within twelve months of the

balance sheet date.”1 The Taxonomy staff found that while 534

companies used this element, they used the elements in the same

manner as the elements proposed in paragraph 15. Leaving this

1 The two new elements could be used to describe either the range or the amount of the increase (decrease)

depending on whether the range axis was used.

10

element in place creates two ways of tagging the same data and

results in an incomplete picture (a change is either an increase or

decrease). The Taxonomy staff tested the five largest filers who

used this element. Their disclosures are provided in Appendix C.

(ii) SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyP

ossibleEstimatedRangeOfChangeUpperBound defined as

“Amount of (increase) decrease reasonably possible in the

estimated upper bound of the unrecognized tax benefit for a tax

position taken or expected to be taken.”

(iii) SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyP

ossibleEstimatedRangeOfChangeLowerBound defined as

“Amount of (increase) decrease reasonably possible in the

estimated lower bound of the unrecognized tax benefit for a tax

position taken or expected to be taken.”

15. Create the following two elements

(a) Increase in Unrecognized Tax Benefits Reasonably Possible-- Amount of

increase of the unrecognized tax benefit reasonably possible in the next 12

months. [credit, monetary, instant]

(b) Decrease in Unrecognized Tax Benefits Reasonably Possible--Amount of

decrease of the unrecognized tax benefit reasonably possible in the next 12

months. [debit, monetary, instant]

Taxonomy Staff Recommendations

16. The Taxonomy staff discussed the requirements of ASC 740-10-50-15(d)(3) with

Cullen Walsh, FASB Assistant Director and Nick Cappiello, Project Manager and

Ron Lott, Senior Technical Advisor.

17. Based on those discussions, the Taxonomy staff recommends Alternative 2 as

described above.

11

Question for the TAG Members

1. Do TAG Members agree with the Taxonomy staff’s proposed changes to the

taxonomy?

2. Do TAG Members agree with the Taxonomy staff’s application of those

elements?

Next Steps

18. If TAG members agree with the Taxonomy staff’s proposal the appropriate changes

will be made to the 2015 Draft Taxonomy that will be sent out for comment by

August 31, 2014.

12

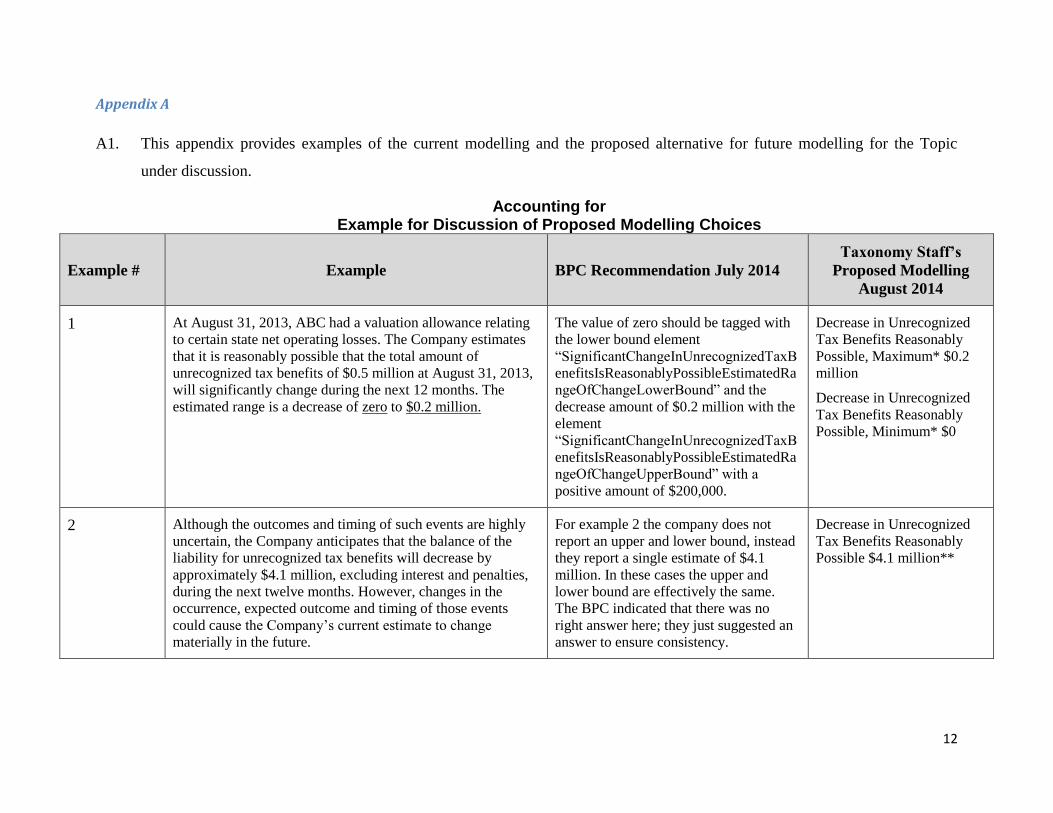

Appendix A

A1. This appendix provides examples of the current modelling and the proposed alternative for future modelling for the Topic

under discussion.

Accounting for Example for Discussion of Proposed Modelling Choices

Example # Example BPC Recommendation July 2014

Taxonomy Staff’s

Proposed Modelling

August 2014

1 At August 31, 2013, ABC had a valuation allowance relating

to certain state net operating losses. The Company estimates

that it is reasonably possible that the total amount of

unrecognized tax benefits of $0.5 million at August 31, 2013,

will significantly change during the next 12 months. The

estimated range is a decrease of zero to $0.2 million.

The value of zero should be tagged with

the lower bound element

“SignificantChangeInUnrecognizedTaxB

enefitsIsReasonablyPossibleEstimatedRa

ngeOfChangeLowerBound” and the

decrease amount of $0.2 million with the

element

“SignificantChangeInUnrecognizedTaxB

enefitsIsReasonablyPossibleEstimatedRa

ngeOfChangeUpperBound” with a

positive amount of $200,000.

Decrease in Unrecognized

Tax Benefits Reasonably

Possible, Maximum* $0.2

million

Decrease in Unrecognized

Tax Benefits Reasonably

Possible, Minimum* $0

2 Although the outcomes and timing of such events are highly

uncertain, the Company anticipates that the balance of the

liability for unrecognized tax benefits will decrease by

approximately $4.1 million, excluding interest and penalties,

during the next twelve months. However, changes in the

occurrence, expected outcome and timing of those events

could cause the Company’s current estimate to change

materially in the future.

For example 2 the company does not

report an upper and lower bound, instead

they report a single estimate of $4.1

million. In these cases the upper and

lower bound are effectively the same.

The BPC indicated that there was no

right answer here; they just suggested an

answer to ensure consistency.

Decrease in Unrecognized

Tax Benefits Reasonably

Possible $4.1 million**

13

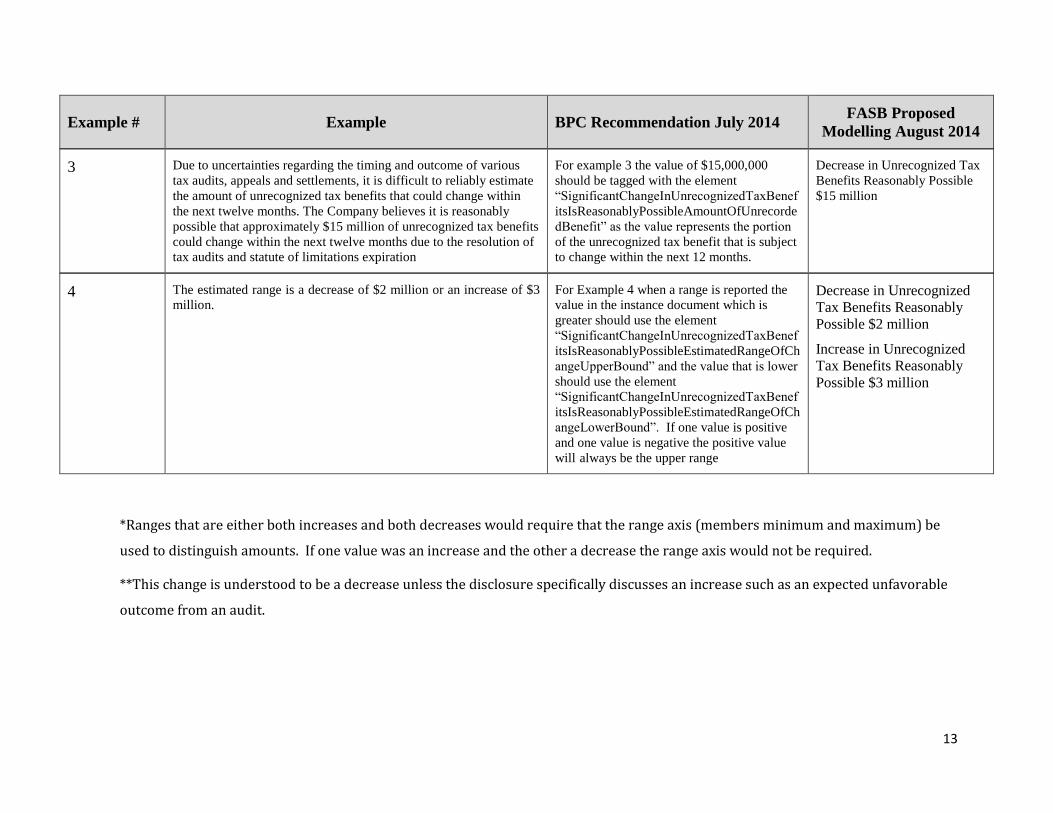

Example # Example BPC Recommendation July 2014 FASB Proposed

Modelling August 2014

3 Due to uncertainties regarding the timing and outcome of various

tax audits, appeals and settlements, it is difficult to reliably estimate

the amount of unrecognized tax benefits that could change within

the next twelve months. The Company believes it is reasonably

possible that approximately $15 million of unrecognized tax benefits

could change within the next twelve months due to the resolution of

tax audits and statute of limitations expiration

For example 3 the value of $15,000,000

should be tagged with the element

“SignificantChangeInUnrecognizedTaxBenef

itsIsReasonablyPossibleAmountOfUnrecorde

dBenefit” as the value represents the portion

of the unrecognized tax benefit that is subject

to change within the next 12 months.

Decrease in Unrecognized Tax

Benefits Reasonably Possible

$15 million

4 The estimated range is a decrease of $2 million or an increase of $3

million. For Example 4 when a range is reported the

value in the instance document which is

greater should use the element

“SignificantChangeInUnrecognizedTaxBenef

itsIsReasonablyPossibleEstimatedRangeOfCh

angeUpperBound” and the value that is lower

should use the element

“SignificantChangeInUnrecognizedTaxBenef

itsIsReasonablyPossibleEstimatedRangeOfCh

angeLowerBound”. If one value is positive

and one value is negative the positive value

will always be the upper range

Decrease in Unrecognized

Tax Benefits Reasonably

Possible $2 million

Increase in Unrecognized

Tax Benefits Reasonably

Possible $3 million

*Ranges that are either both increases and both decreases would require that the range axis (members minimum and maximum) be

used to distinguish amounts. If one value was an increase and the other a decrease the range axis would not be required.

**This change is understood to be a decrease unless the disclosure specifically discusses an increase such as an expected unfavorable

outcome from an audit.

14

Appendix B

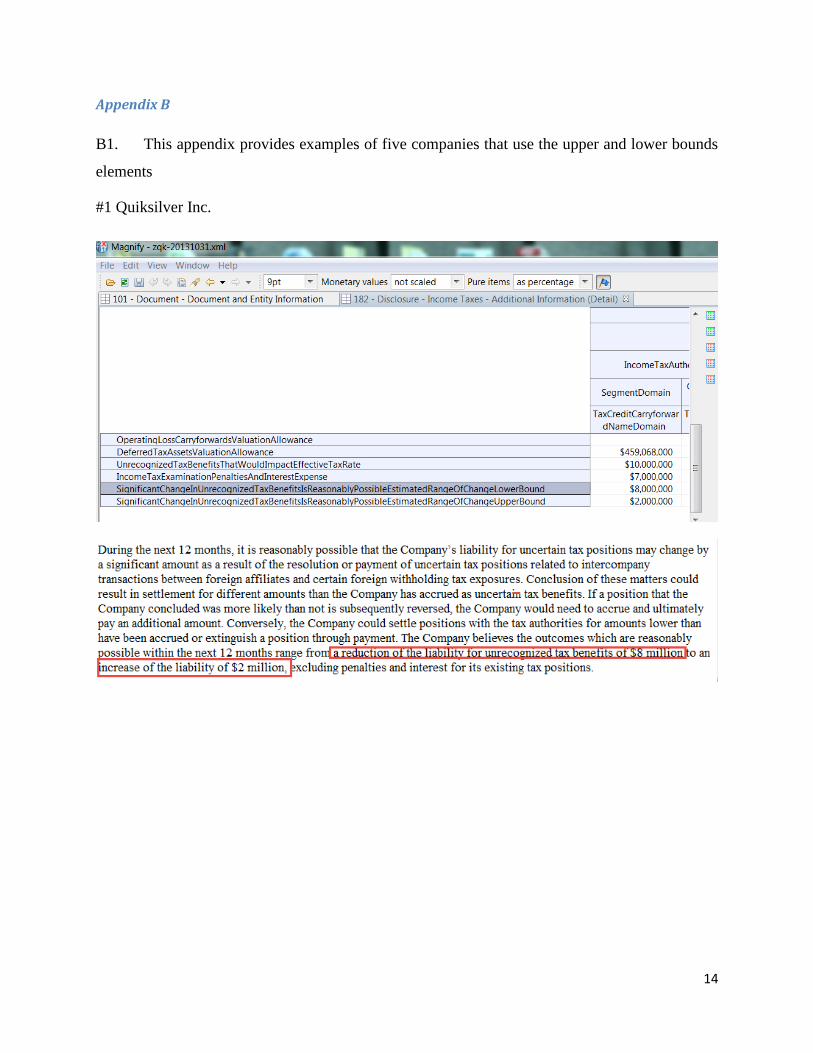

B1. This appendix provides examples of five companies that use the upper and lower bounds

elements

#1 Quiksilver Inc.

15

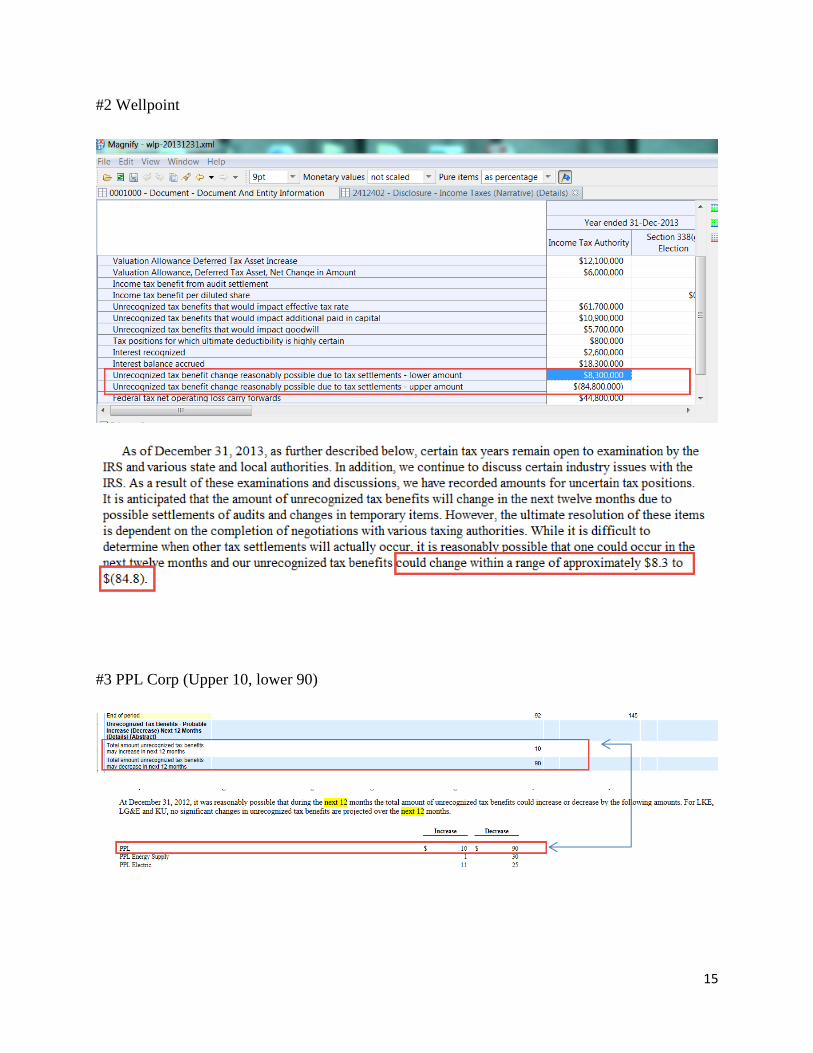

#2 Wellpoint

#3 PPL Corp (Upper 10, lower 90)

16

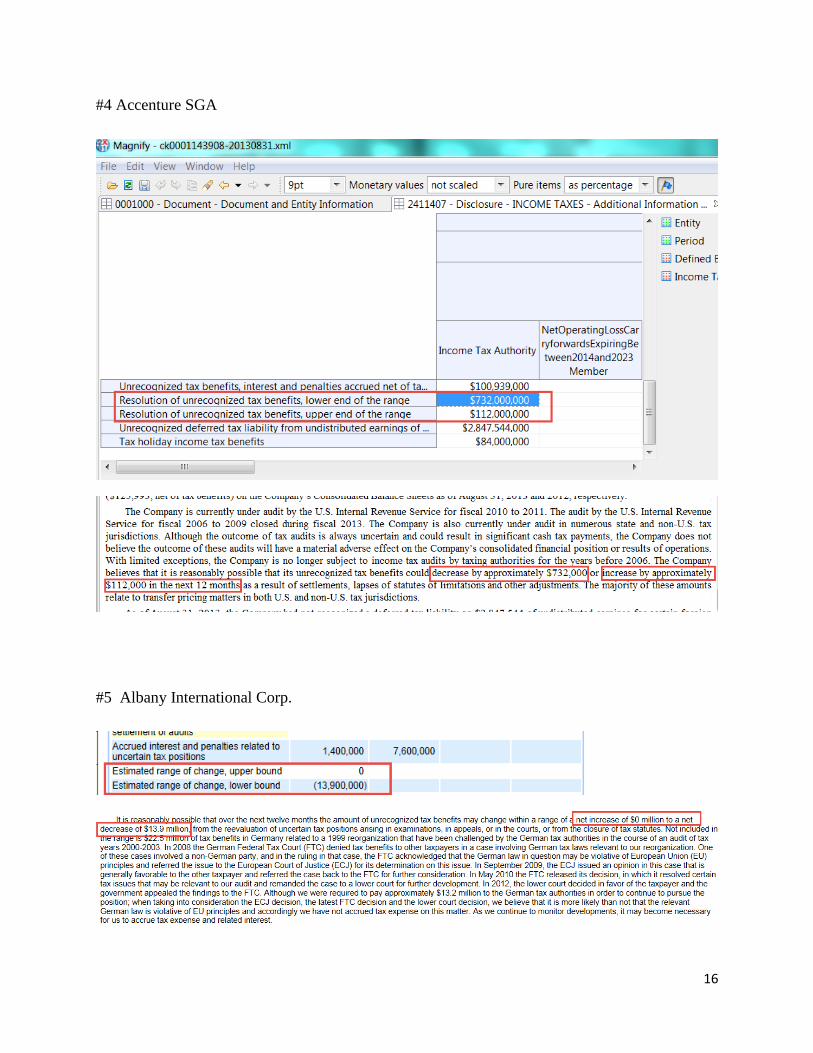

#4 Accenture SGA

#5 Albany International Corp.

17

Appendix C

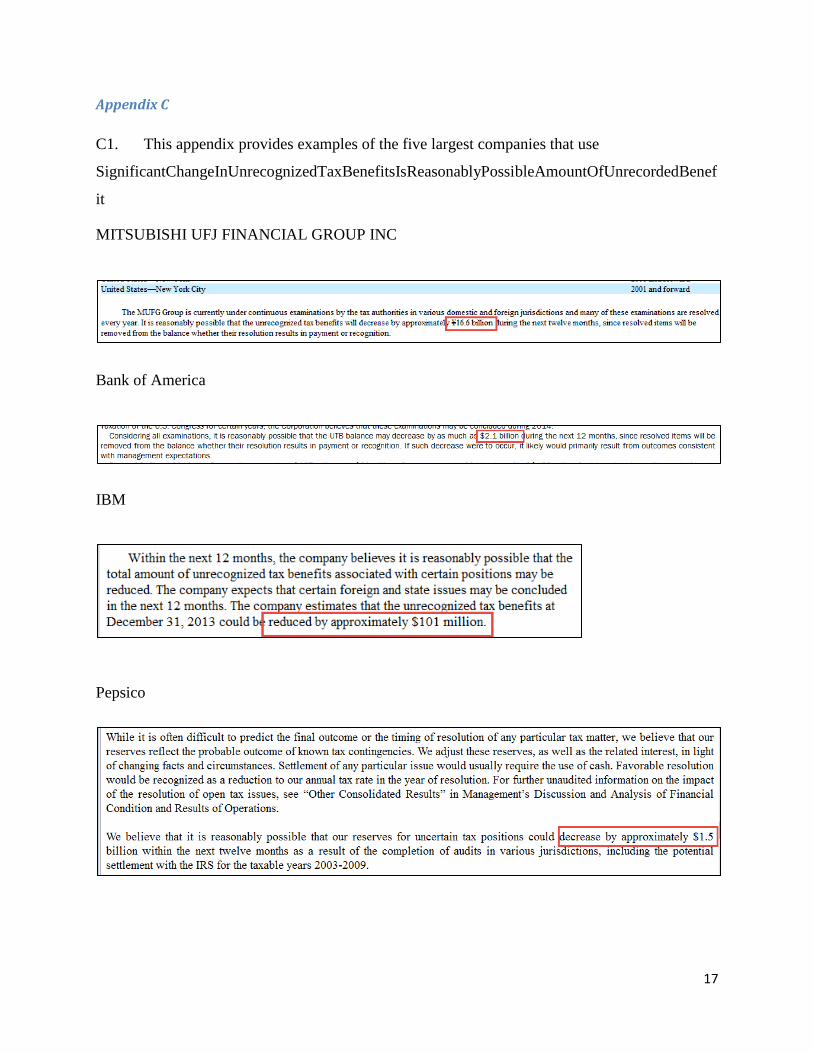

C1. This appendix provides examples of the five largest companies that use

SignificantChangeInUnrecognizedTaxBenefitsIsReasonablyPossibleAmountOfUnrecordedBenef

it

MITSUBISHI UFJ FINANCIAL GROUP INC

Bank of America

IBM

Pepsico

18

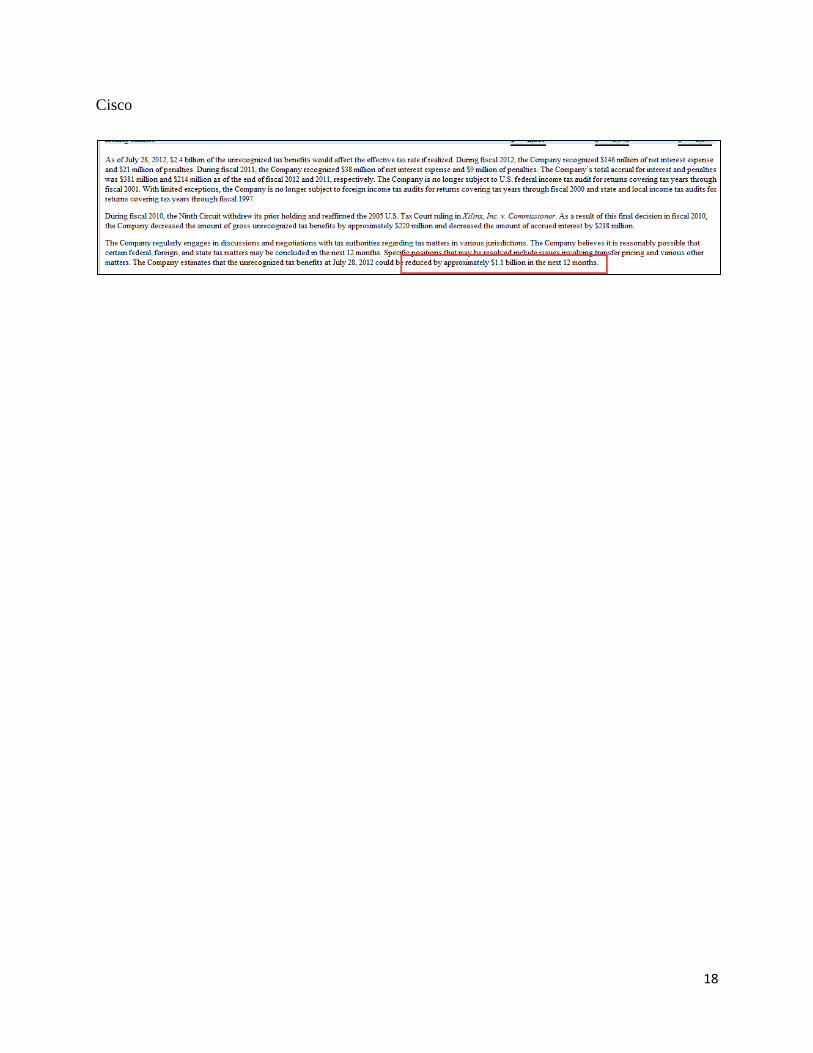

Cisco

19

Session 2 – Legal Entity Axis Issues

A. Meeting Highlights

B. Legal Entity Axis Issues

Purpose or Objective of This Memo

1. At the August 14, 2014 TAG Meeting the Taxonomy staff is proposing guidance and

certain changes to the US GAAP Financial Reporting Taxonomy (UGT) that will

better reflect the requirements for identifying pre- and post-consolidated facts when

using the “Legal Entity [Axis]” jointly with the “Consolidation Items [Axis]”.

Background Information

2. Use of the “Legal Entity [Axis]” has been an unresolved topic of discussion with the

Taxonomy Advisory Group (TAG) (September 17, 2013), the Dimension Working

Group (DWG) (November 7, 2013), and most recently with the XBRL US Best

Practice Committee (BPC) (July 25, 2014).

3. The core issues have revolved around the appropriate use and meaning of the

Document and Entity Information (DEI) Dimension, “Legal Entity [Axis]”:

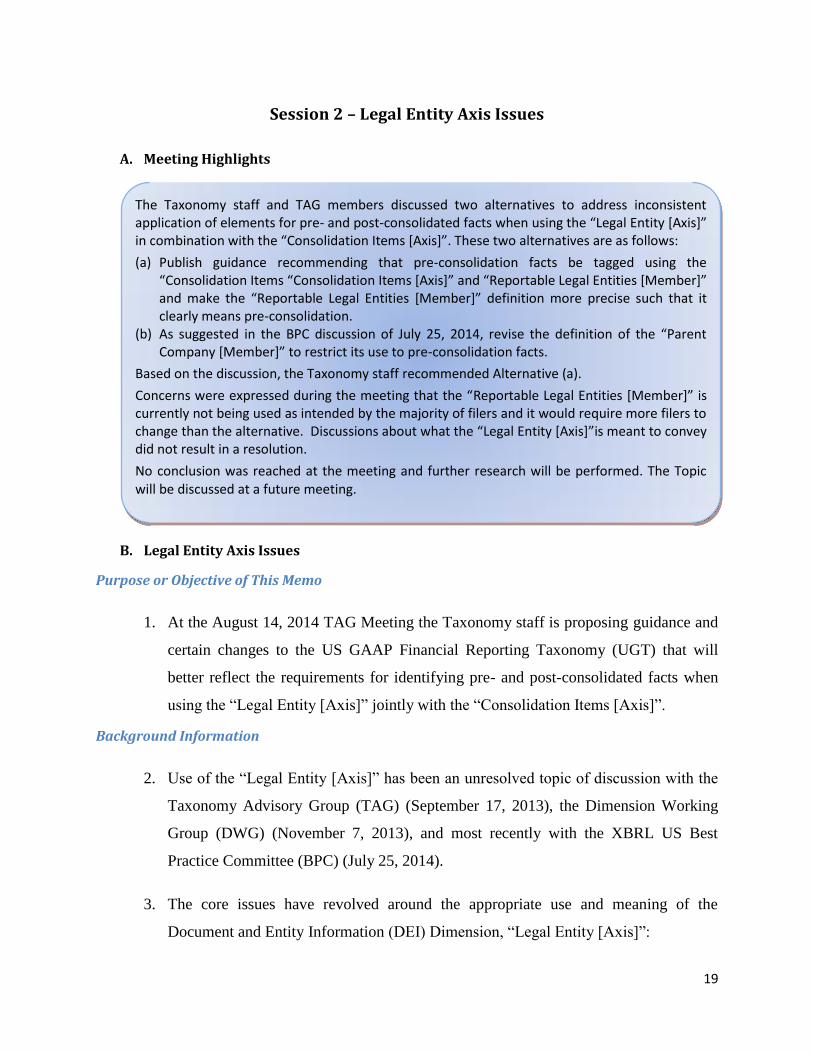

The Taxonomy staff and TAG members discussed two alternatives to address inconsistent application of elements for pre- and post-consolidated facts when using the “Legal Entity [Axis]” in combination with the “Consolidation Items [Axis]”. These two alternatives are as follows:

(a) Publish guidance recommending that pre-consolidation facts be tagged using the “Consolidation Items “Consolidation Items [Axis]” and “Reportable Legal Entities [Member]” and make the “Reportable Legal Entities [Member]” definition more precise such that it clearly means pre-consolidation.

(b) As suggested in the BPC discussion of July 25, 2014, revise the definition of the “Parent Company [Member]” to restrict its use to pre-consolidation facts.

Based on the discussion, the Taxonomy staff recommended Alternative (a).

Concerns were expressed during the meeting that the “Reportable Legal Entities [Member]” is currently not being used as intended by the majority of filers and it would require more filers to change than the alternative. Discussions about what the “Legal Entity [Axis]”is meant to convey did not result in a resolution.

No conclusion was reached at the meeting and further research will be performed. The Topic will be discussed at a future meeting.

20

Attributes identified: entity names / identifiers, type of entity, pre- and post-

consolidation values, nature of entities (relationship to reporting entity) – parent,

subsidiary, VIE, etc.

Orthogonal attributes that should be broken out as separate dimensions from the

“Legal Entity [Axis]” to better identify key entity attributes and remove

ambiguity in the “Legal Entity [Axis]”.

Members (domainItemTypes) that should be used with these dimensions.

4. In this memo the Taxonomy staff will not directly address these issues but it is

important to understand the context they provide for the specific issue this memo

addresses. These topics will be addressed at a later TAG meeting.

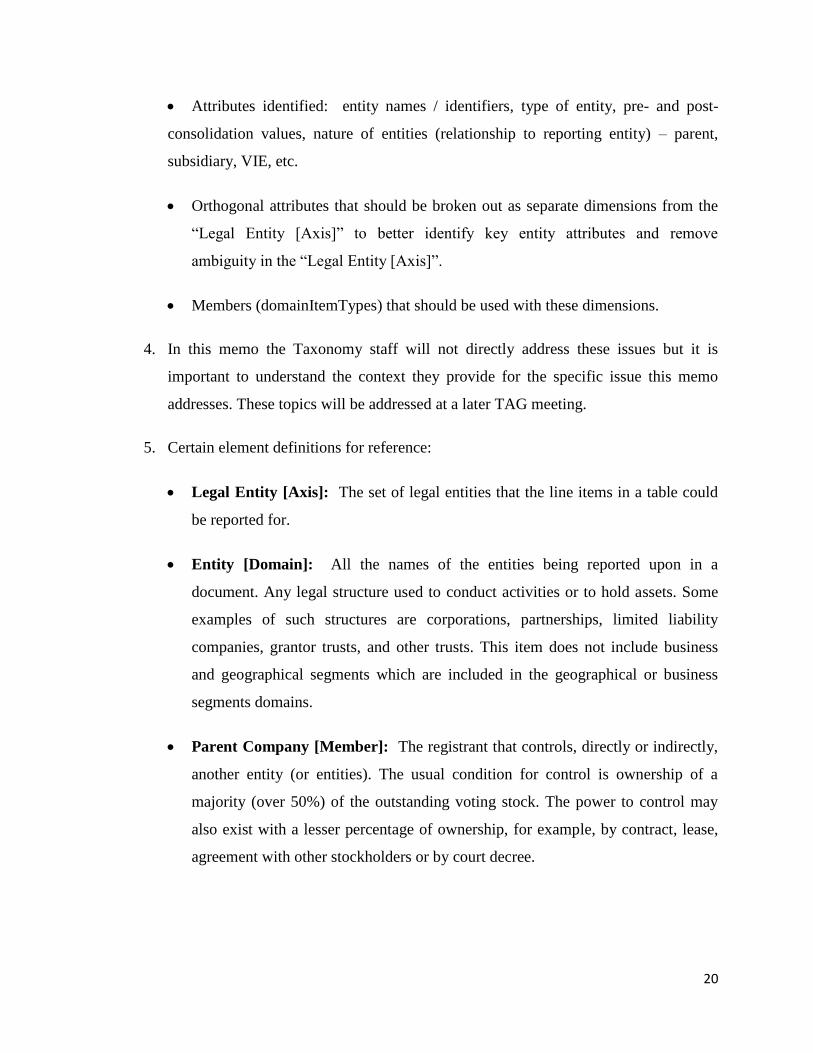

5. Certain element definitions for reference:

Legal Entity [Axis]: The set of legal entities that the line items in a table could

be reported for.

Entity [Domain]: All the names of the entities being reported upon in a

document. Any legal structure used to conduct activities or to hold assets. Some

examples of such structures are corporations, partnerships, limited liability

companies, grantor trusts, and other trusts. This item does not include business

and geographical segments which are included in the geographical or business

segments domains.

Parent Company [Member]: The registrant that controls, directly or indirectly,

another entity (or entities). The usual condition for control is ownership of a

majority (over 50%) of the outstanding voting stock. The power to control may

also exist with a lesser percentage of ownership, for example, by contract, lease,

agreement with other stockholders or by court decree.

21

Consolidation Items [Axis]: Information by components, eliminations, non-

segment corporate-level activity and reconciling items used in consolidating a

parent entity and its subsidiaries or its operating segments.

Reportable Legal Entities [Member]: Legal entities of the consolidated entity

reporting separate financial information in the entity's financial statements.

Current Issue

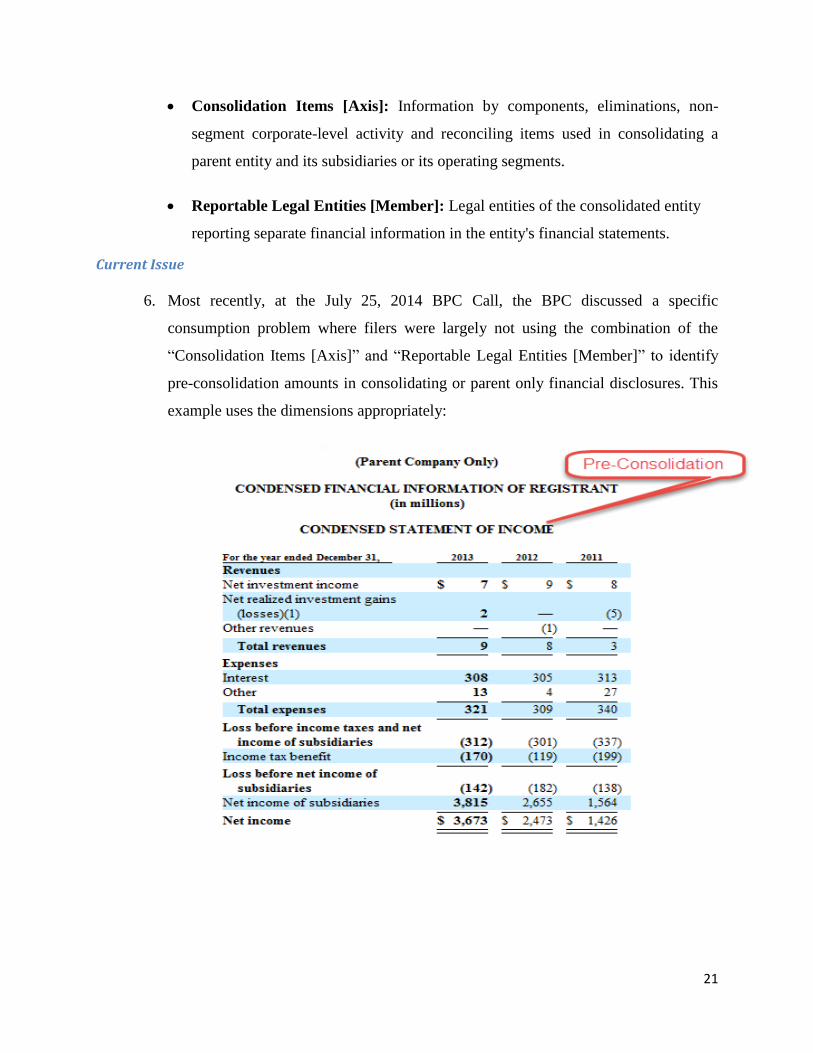

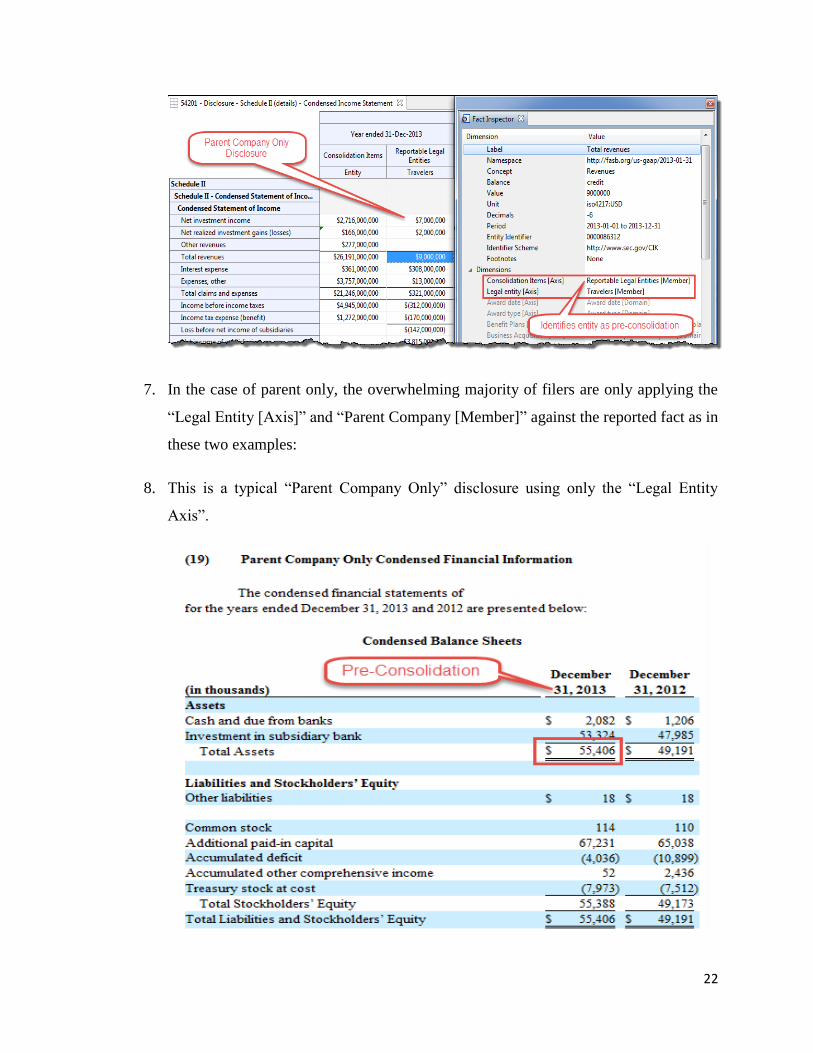

6. Most recently, at the July 25, 2014 BPC Call, the BPC discussed a specific

consumption problem where filers were largely not using the combination of the

“Consolidation Items [Axis]” and “Reportable Legal Entities [Member]” to identify

pre-consolidation amounts in consolidating or parent only financial disclosures. This

example uses the dimensions appropriately:

22

7. In the case of parent only, the overwhelming majority of filers are only applying the

“Legal Entity [Axis]” and “Parent Company [Member]” against the reported fact as in

these two examples:

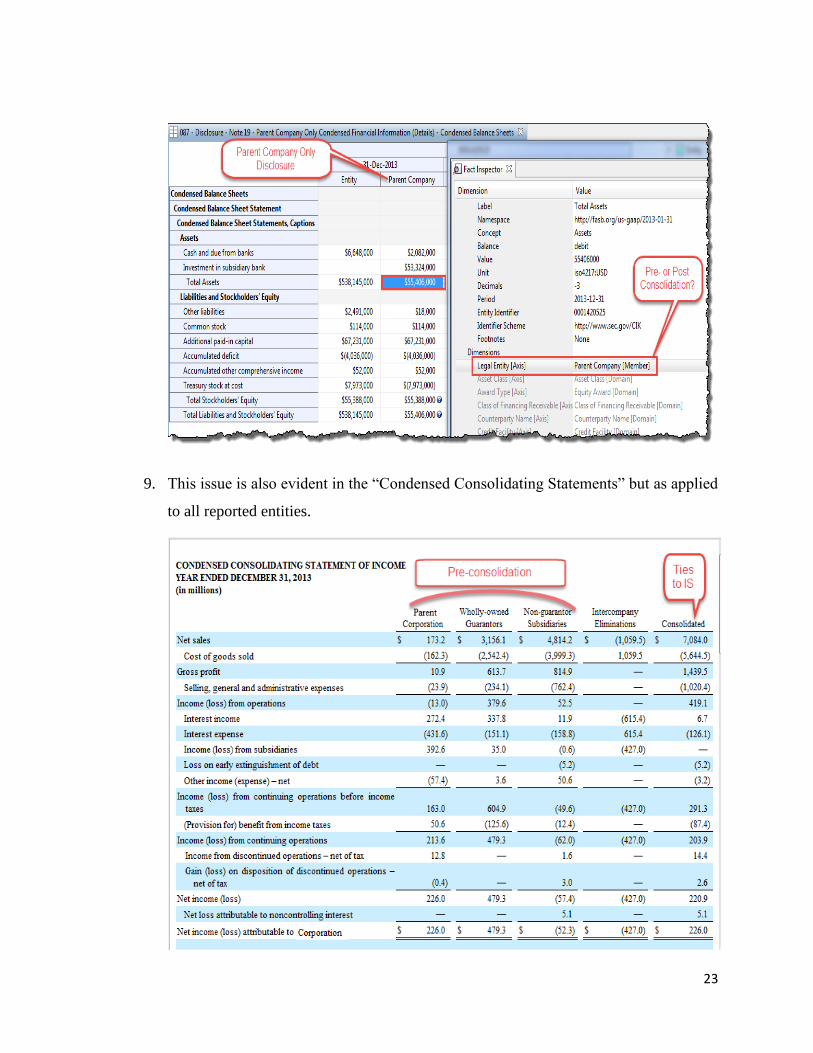

8. This is a typical “Parent Company Only” disclosure using only the “Legal Entity

Axis”.

23

9. This issue is also evident in the “Condensed Consolidating Statements” but as applied

to all reported entities.

24

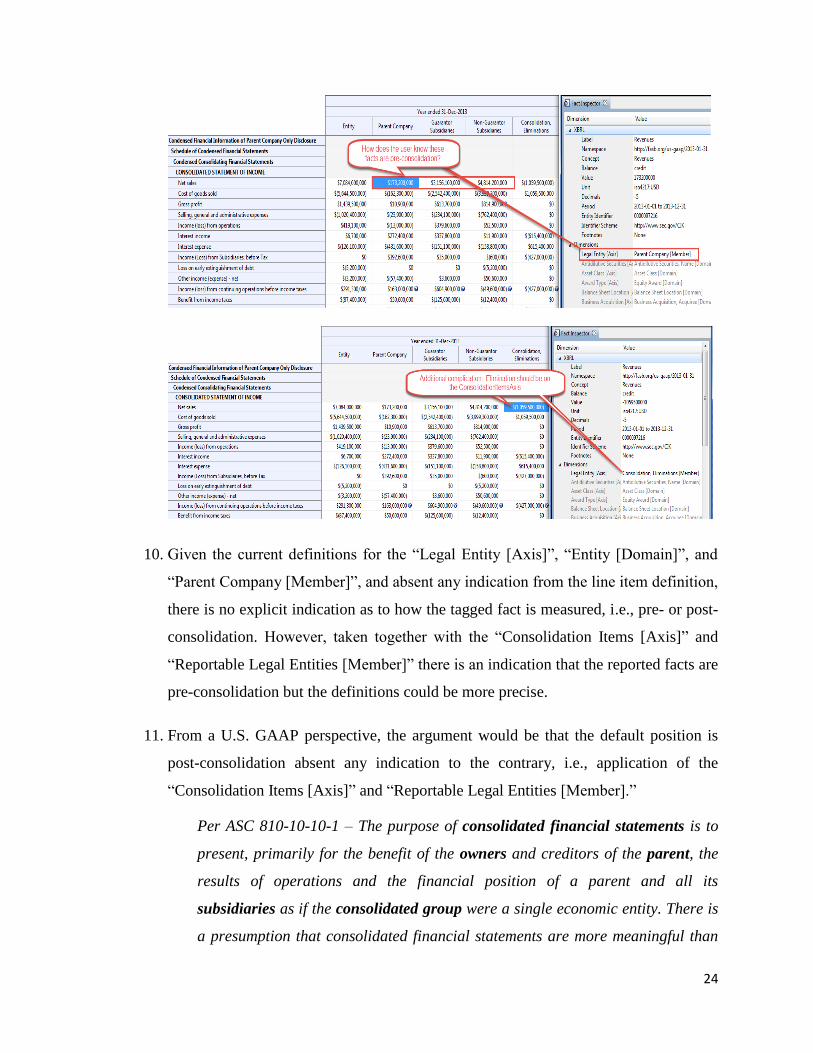

10. Given the current definitions for the “Legal Entity [Axis]”, “Entity [Domain]”, and

“Parent Company [Member]”, and absent any indication from the line item definition,

there is no explicit indication as to how the tagged fact is measured, i.e., pre- or post-

consolidation. However, taken together with the “Consolidation Items [Axis]” and

“Reportable Legal Entities [Member]” there is an indication that the reported facts are

pre-consolidation but the definitions could be more precise.

11. From a U.S. GAAP perspective, the argument would be that the default position is

post-consolidation absent any indication to the contrary, i.e., application of the

“Consolidation Items [Axis]” and “Reportable Legal Entities [Member].”

Per ASC 810-10-10-1 – The purpose of consolidated financial statements is to

present, primarily for the benefit of the owners and creditors of the parent, the

results of operations and the financial position of a parent and all its

subsidiaries as if the consolidated group were a single economic entity. There is

a presumption that consolidated financial statements are more meaningful than

25

separate financial statements and that they are usually necessary for a fair

presentation when one of the entities in the consolidated group directly or

indirectly has a controlling financial interest in the other entities.

Taxonomy Staff Analysis

12. The Taxonomy staff considered two alternatives to address this issue:

(a) Publish guidance recommending that pre-consolidation facts be tagged using

the “Consolidation Items [Axis]” and “Reportable Legal Entities [Member]”

and make the “Reportable Legal Entities [Member]” definition more precise

such that it clearly means pre-consolidation.

(b) As suggested in the BPC discussion of July 25, 2014, revise the definition of

the “Parent Company [Member]” to restrict its use to pre-consolidation facts.

Alternative (a): Publish guidance recommending that pre-consolidation facts be tagged

using the “Consolidation Items [Axis]” and “Reportable Legal Entities [Member]” and

make the “Reportable Legal Entities [Member]” definition more precise such that it

clearly means pre-consolidation.

13. This approach would include the following definition modification for “Reportable

Legal Entities [Member]” to clarify intent for using this member:

“Legal entities of the consolidated entity reporting pre-consolidated separate

financial information in the entity's financial statements.”

14. This approach is consistent with U.S. GAAP (ASC 810-10-10-1) and how

consolidated financial statements are considered. Additionally, it is consistent with

the UGT modelling as developed for Segments over the last couple of years and as

published in the Segments Implementation Guide. For example:

26

15. In the above example, the Operating Segments, or “pre-consolidated” facts are tagged

with the “Consolidation Items [Axis]” and “Operating Segments [Member]” to

identify the grossed up values. It would be inappropriate to use additional tagging on

the “post-consolidated” facts, as they are net of eliminations and aggregate to the

consolidated amount without further modification.

16. The only real issue with this modeling approach is that it is not always obvious to the

filer that the additional dimension is required and, anecdotally, cases are seen where

the Segment Implementation Guidance is not followed.

Alternative (b): As suggested in the BPC discussion of July 25, 2014, revise the

definition of the “Parent Company [Member]” to restrict its use to pre-consolidation

facts.

17. This alternative acknowledges that most filers are not tagging these disclosures

according to best practice and this proposal attempts to address the problem by

aligning the UGT modelling with common practice, i.e., make common practice best

practice in this case. It is a reasonable argument given that out of 1,300+ filers that

used the “Legal Entity [Axis]” and “Parent Company [Member]” combination, only

58 use the “Consolidation Items [Axis]” and “Reportable Legal Entities [Member]”

combination to identify the facts as pre-consolidation. These XBRL exhibits have not

been closely examined to know with certainty that these are mainly pre-consolidation

27

for the parent, but parent post-consolidation would likely be a rarely reported fact

given U.S. GAAP and SEC requirements.

18. However, changing the modeling for this one situation in a manner that is inconsistent

with current modeling in the UGT as illustrated previously with Segments and is

inconsistent within itself is problematic.

19. Current modeling:

Rows 4 and 7 both represent post-consolidation facts and represent their respective

default locations. This is mathematically and structurally consistent.

20. Alternative (b) proposed modelling:

With this modeling, Rows 2 and 7 are tagged to both represent post-consolidation

facts but row 2 clearly is not. This is mathematically and structurally inconsistent.

28

Taxonomy Staff Recommendations

21. Based on the above, the Taxonomy staff recommends Alternative (a).

Question for the TAG Members

1. Do TAG Members agree with the Taxonomy staff’s proposal?

Next Steps

22. If TAG members agree with the Taxonomy staff’s proposal, the appropriate changes

will be made to the 2015 Draft Taxonomy that will be sent out for comment by

August 31, 2014. Additionally, an Implementation Guide will be issued illustrating

this structure and the elements would be candidates for implementation guidance

labels as the label is developed.

Session 3 – Special Label Discussion

A. Meeting Highlights

The Taxonomy staff presented three alternatives to identify substantive changes to elements that would normally require deprecation, but based on certain criteria, are changed and not deprecated.

These three alternatives are as follows:

(1) Including in the definition, a statement about how the element has changed (for example, measurement) and whether the use of the element should be restricted to a particular location in the financial statements.

(2) Modifying the existing change label classifications to notify the filer with a new “sub-label” (Similar to “Modified: Documentation Label”).

(3) Creating a new “special” label to describe changes made in lieu of deprecating the element.

After considering the advantages and disadvantages of all of the options, the Taxonomy staff recommended Option (3).

Concerns regarding an excess of labels and managing those were expressed during the meeting.

Conclusion reached during the meeting was to provide option 2 in the proposed 2015 Taxonomy for comment for four elements related to deferred taxes as an example for feedback.

29

B. Special Label Discussion

Purpose or Objective of This Memo

1. The purpose of this memorandum is to discuss what alternatives should be considered

to identify taxonomy changes that would normally require deprecation, but based on

certain criteria, are changed and not deprecated.

2. The Taxonomy staff is presenting three alternatives to deprecating the elements when

certain criteria are met. The Taxonomy staff is interested in getting feedback from

TAG members about the options.

Background Information

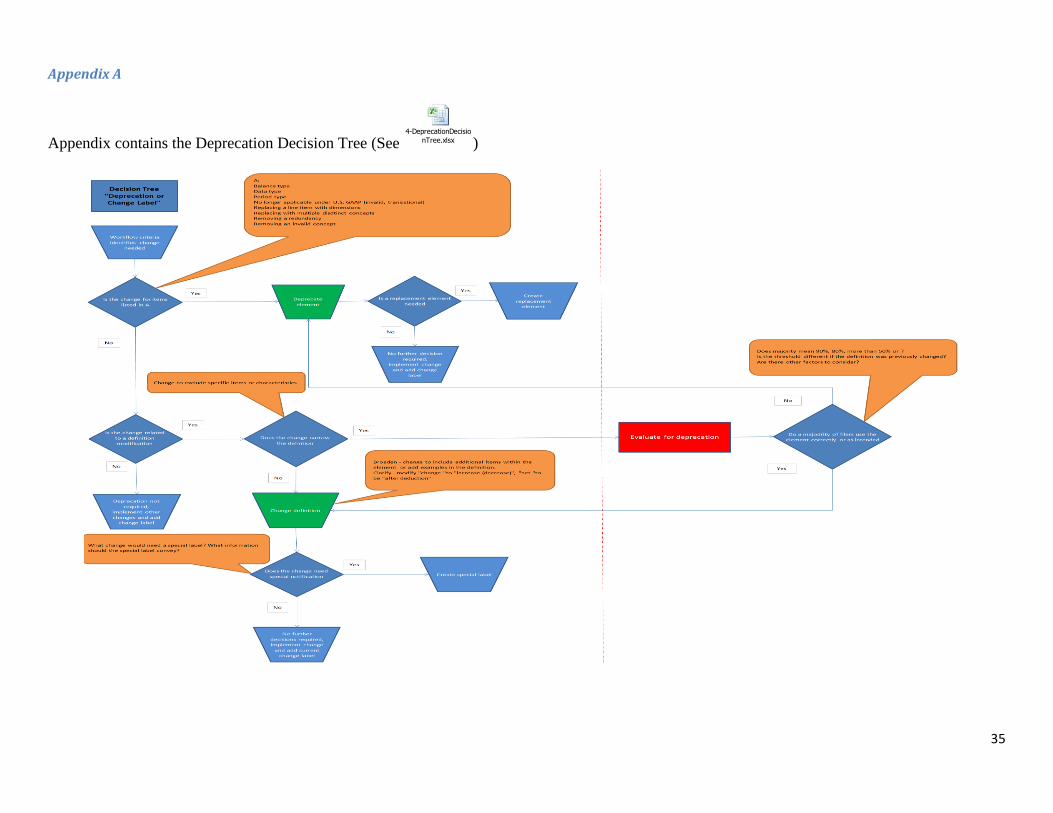

3. At the July 10, 2014 Taxonomy Advisory Group (TAG) Meeting, the Taxonomy staff

asked TAG members whether they agreed with the criteria for deprecation as

illustrated to the left side of the dotted red line of the deprecation decision tree (See

Appendix A), namely:

(a) Balance type

(b) Data type

(c) Period type

(d) Item no longer applicable under U.S. GAAP (invalid, transitional)

(e) Replacing a line item with dimensions

(f) Replacing with multiple distinct concepts

(g) Removing a redundancy

(h) Removing an invalid concept

(i) Narrowing the definition of an element to exclude specific items or

characteristics*

*With the understanding that deprecation was subject to further discussion and consideration of the

effect that deprecation.

4. TAG members agreed with many of these reasons for change, however they did not

agree that deprecation was always the most appropriate action to take for substantive

changes in definition, especially when more filers than not were using the element

appropriately. There was no determination at that time about how many filers needed

30

to use the element correctly to avoid deprecation, instead the discussion focused on

whether deprecation was the appropriate vehicle to change filer behavior. TAG

members suggested that there needs to be another way to alert filers about substantive

definition changes without deprecation, as deprecation punishes those who use the

element appropriately. The Taxonomy staff believes that deprecation is appropriate

when the meaning of the element has changed substantively, however the Taxonomy

staff agreed to an alternative by not deprecating and creating a way of alerting users

of the Taxonomy when substantive definition modifications were made by using a

label to report these situations.

Multiple Methods to Identify Substantive Changes to Elements

5. Identification of changes can be made in a number of ways and selection of the most

effective method needs to be determined. Options for identification:

(a) Including in the definition, a statement about how the element has changed

(for example, measurement) and whether the use of the element should be

restricted to a particular location in the financial statements.*

(b) Modifying the existing change label classifications to notify the filer with a

new “sub-label” (Similar to “Modified: Documentation Label”)

(c) Creating a new “special” label to describe changes made in lieu of

deprecating the element.

*Option 1 is similar to what was found in previous UGTs and some tagging guidance. That

information was deemed too restrictive and ultimately removed.

6. For purposes of this discussion the element DeferredTaxAssetsLiabilitiesNet will be

used to demonstrate the three options. DeferredTaxAssetsLiabilitiesNet is currently

defined as “Amount after allocation of valuation allowances of deferred tax asset

attributable to deductible temporary differences and carryforwards, net of deferred tax

liability attributable to taxable temporary differences.”

7. Not every filer using the element is aware that (1) this element was revised in 2012 so

that it can only be used when the amount of deferred tax assets (DTAs) net of

deferred tax liabilities (DTLs) results in a net deferred tax asset (that is, it is no longer

31

a two-way element) and (2) the intended use is within the notes to the financial

statements. There is a difference between the net amounts presented on the Statement

of Financial Position and the net amounts presented in the notes because of the way

DTAs and DTLs are netted. The amounts on the Statement of Financial Position are

jurisdictionally netted, whereas the amounts in the notes is the net of the gross

deferred tax liabilities and the deferred tax assets after valuation allowance (not

jurisdictionally netted).

Option 1: Include Distinguishing Information in the Definition

8. Currently, certain legacy documentation labels in the Taxonomy contain a location.

For example, Defined Benefit Plan, Current Assets is defined as “For a classified

balance sheet, the amount recognized in balance sheet as a current asset associated

with the plan.”

9. In the case of elements that have been historically inappropriately used such as

DeferredTaxAssetsLiabilitiesNet, the definition could be modified to incorporate

both of the characteristics that distinguish it from the net deferred tax asset reported in

the Statement of Financial Position:

Amount reported in the notes to the financial statement after

allocation of valuation allowances of deferred tax asset attributable to

deductible temporary differences and carryforwards, net of deferred

tax liability attributable to taxable temporary differences not netted by

jurisdiction. {italics added for emphasis}

10. The principle advantage of this option is that the filer is put on notice as to any

restrictions on its use. The principle disadvantage of this option is that an element

should not be bounded by location. The period type (instant/duration), data type,

balance type (credit/debit), definition (documentation label) and reference should be

enough for appropriate element selection. Understanding of the underlying

accounting concepts is outside of the purpose of the elements. Also, many elements

can appear in either the notes or the statements.

32

Option 2: Modify the Existing Change Label

11. Under this alternative the Taxonomy staff would modify the existing Change Labels

to include another label to highlight any special characteristics or accounting

differences.

12. Currently there are generally 6 types of changes described in the 201X Change Label.

Those changes relate to:

(i) The creation of new elements (including but not limited to those

created by new ASUs)

(ii) The deprecation of an element (including modifications to the

deprecation label or deprecation date).

(iii) The change in the definition of an element

(iv) The change in type (data type, balance type, and period type)

(v) A new reference or change in a current reference (either to amend

or remove the reference entirely).

(vi) A change in one of the element labels (standard, period start, period

end and total labels)

13. Under this option, another label “Clarification Label” (using this name for discussion

purposes) would be added which would be a type of Change Label used to highlight

any special characteristics or accounting differences that result in a substantive

change in the definition of the element. The Clarification Label would only appear

on elements that would normally be deprecated but because the element is used

correctly by a significant number of filers (or some other agreed-upon criteria)

deprecation would not be cost beneficial.

14. Possible proposed language that could be included in the label:

DeferredTaxAssetsLiabilitiesNet

2015 Change Label {Modified Documentation Label. Originally read as

follows: Amount after allocation of valuation allowances of deferred tax asset

attributable to deductible temporary differences and carryforwards, net of

deferred tax liability attributable to taxable temporary differences.}

33

{Clarification Label: The definition of this element has been significantly

changed to restrict its use; this change may require reconsideration of its use.

Possible replacement element may be DeferredIncomeTaxAssetsNet.}

15. The language could be made more specific. For example, instead of “to restrict its

use”

(a) to limit its use to the primary financial statements

(b) to limit its use to the notes to the financial statements

(c) to clarify the underlying measurement

(d) to exclude certain transactions

16. The advantage of this option is that the 201X Change label already exists for the

UGT, so users of the UGT will not need to adjust their systems for a new label. The

principle disadvantage of this option is that it may be lost among the other change

labels and as noted in Option 1, appropriateness of element is determined by its

attributes, not defined by location as more specific language may imply.

Option 3: Create a New “Special” Label to Describe Change that are more Significant than Usual

17. The only difference between choosing Option 3 and Option 2 is that Option 3 creates

a new field/location outside of the Change label location.

18. The principle advantage of this option is that it will stand out from the other changes

currently in the Change Label; however its principle disadvantage is that, users of the

UGT and service providers may need to rework processes and systems to

accommodate the new label. This adds cost and there is the risk that it will not

communicate the change effectively.

Taxonomy Staff Recommendations

19. After considering the advantages and disadvantages of all of the options, the

Taxonomy staff recommends Option 3 as described above.

34

Next Steps

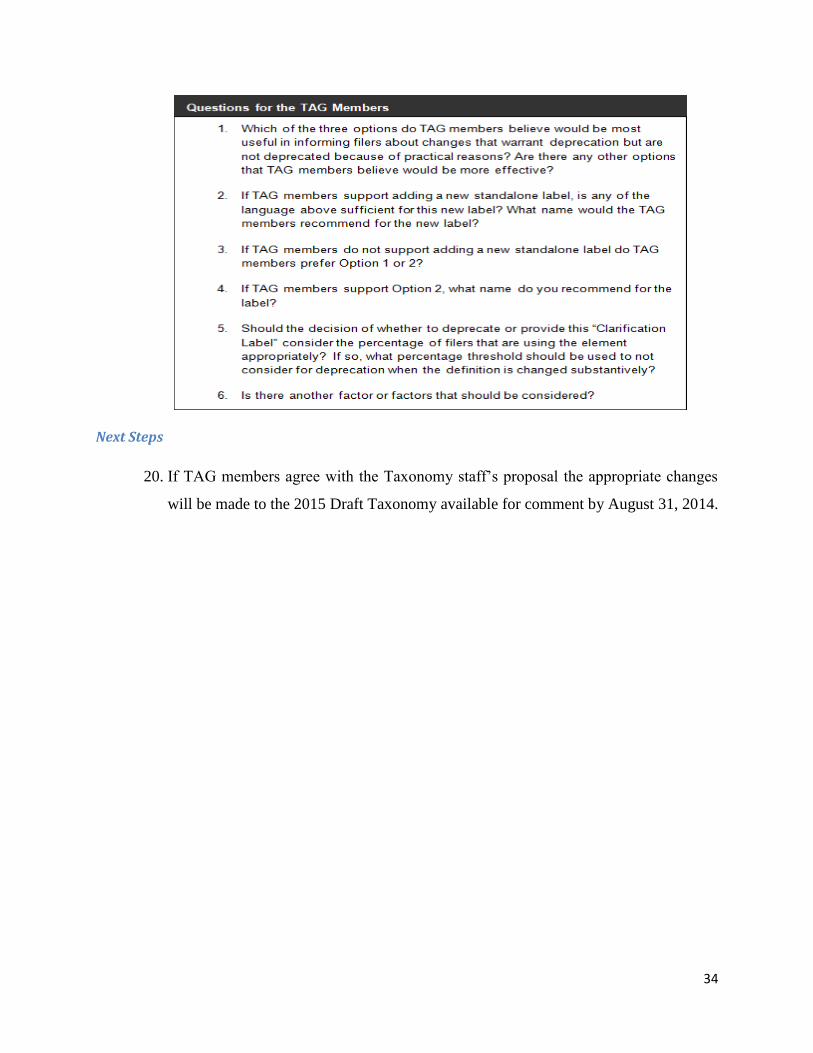

20. If TAG members agree with the Taxonomy staff’s proposal the appropriate changes

will be made to the 2015 Draft Taxonomy available for comment by August 31, 2014.

35

Appendix A

Appendix contains the Deprecation Decision Tree (See 4-DeprecationDecisio

nTree.xlsx )