the aftermath of information technology outsourcing: an empirical study of firm performance...

TRANSCRIPT

125

JOURNAL OF INFORMATION SYSTEMSVol. 22, No. 1Spring 2008pp. 125–159

The Aftermath of Information TechnologyOutsourcing: An Empirical Study of

Firm Performance FollowingOutsourcing Decisions

Li WangThe University of Akron

Kholekile L. GwebuUniversity of New Hampshire

Jing WangUniversity of New Hampshire

David X. ZhuKent State University

ABSTRACT: Increasingly, organizations are jumping onto the information technology(IT) outsourcing bandwagon in an effort to create value. However, evidence indicatingthe positive economic consequences of such initiatives has been limited. This studyattempts to fill this void by synthesizing the process-oriented research in IT businessvalue literature and the resource-based theory to develop an integrative research frame-work for assessing the value proposition of IT outsourcing. With a process-orientedlens, the framework suggests that the effects of IT outsourcing are best documentedat the process level and hence, it is imperative that one takes into consideration theimpact of IT outsourcing on performance at both the process level as well as the firmlevel. Grounded in the resource-based view, the framework also accounts for the com-plementary role of firms’ core IT capability as a critical condition for the value creationof IT outsourcing. Consistent with the process-oriented prediction, the findings suggestthat the positive effects of IT outsourcing appear mostly at the process level, but notat the firm level. Moreover, it is found that the level of business value created by IToutsourcing is contingent on firms’ core IT capability. Firms with superior core IT ca-pability are found to enjoy an advantage in leveraging their outsourcing initiatives toenhance firm value.

Keywords: information technology (IT); outsource; firm performance; IT capability;business value; resource-based view (RBV).

Data Availability: All data are available from public sources.

126 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

I. INTRODUCTION

Information Technology (IT) outsourcing is an increasingly common business practicein which a client transfers property or decision rights over physical and/or human ITresources to a vendor for delivery of IT services such as network management, appli-

cation development, data management, or infrastructure maintenance (Barthelemy andGeyer 2004; Hall and Liedtka 2005; Levina and Ross 2003). For over a decade, it has beena key method used by firms in various industrial sectors to manage IT resources (Choudhuryand Sabherwal 2003; Kishore et al. 2003; Lacity and Willcocks 1998). By the year 2000,it accounted for approximately 30 percent of IT budgets (Mason 2000) and according toone recent estimate (De Souza et al. 2004), worldwide spending on IT outsourcing isexpected to rise from approximately $176 billion in 2003 to well over $230 billion by theend of 2007.

While sizable investments in IT outsourcing are continuously being made, researchersare struggling to determine whether these expenditures deliver any business value to firms.The main reasons often cited by corporate executives for outsourcing their IT infrastructureinclude the belief that it inevitably leads to reduced operating expenses, increased flexibility,improved management focus, improved quality of service, and access to state-of-the-arttechnology (Barthelemy 2001; Kishore et al. 2003). However, there are a number of po-tential adverse financial effects associated with this practice such as vendor selection costs,costs to transition IT infrastructure to the vendor, layoff costs, legal contract costs, the lossof intellectual assets, and possible exploitation from the vendors (Barthelemy 2001;Pfannenstein and Tsai 2004). Due to the high risks involved, it is currently unclear whetherIT outsourcing can deliver economic benefits that outweigh its costs.

Given the scale of IT outsourcing expenditure as well as the possibility for both largesuccesses and failures, one would expect that substantial effort would have been devotedto establishing evidence of the returns on IT outsourcing investments. However, to dateonly a few studies have examined the performance and economic implications of this strat-egy (Dibbern et al. 2004; Jiang and Qureshi 2006). Therefore, this study aims to bridgethe gap in the literature by examining the linkages between IT outsourcing and firms’ short-term and long-term financial performance. To examine how IT outsourcing impacts firmperformance, this study adopts an approach that is consistent with two streams of research:the process perspective of IT business value and the resource-based view of IT. Follow-ing the process perspective in IT business value literature (Barua et al. 1995; Dehning andRichardson 2002; Dehning et al. 2006), the paper postulates that the impact of IT outsourc-ing should be measured through intermediate (i.e., process) level contributions. The under-lying logic is that outsourced IT is intended to support activities and processes, and there-fore, its impact should be assessed at the intermediate process level where its direct effectsare expected to be manifested. Subsequently, these intermediate level contributions mayimpact overall firm performance. Further, consistent with the resource-based view of IT,the paper argues that outsourced IT may not act alone in creating competitive advantage.Rather, the value of IT outsourcing may be contingent upon a firm’s overall IT capabilitythat enables the firm to leverage its IT outsourcing strategy to enhance firm value. In thissense, outsourced IT and firms’ overall IT capability are examples of complementary ITassets as discussed by Barua et al. (1996) and by Bharadwaj (2000). When integrated, theybecome more effective in producing business value.

Moreover, in the current literature, most evidence regarding the business value of IToutsourcing has been drawn from research that uses subjective perceptual measures and isoften based on small samples or case studies (Jiang et al. 2006; Smith et al. 1998). Thispaper adds to the literature by employing objective accounting performance measures, a

The Aftermath of Information Technology Outsourcing 127

Journal of Information Systems, Spring 2008

rigorous methodology and offers empirical insights into whether or not sizable investmentsin IT outsourcing deliver various economic benefits to business entities. Although studiesof this nature are rare, they are very important as IT sourcing decisions represent large anddifficult-to-reverse investments that directly influence firms’ capabilities and property rights.Firms should be well equipped with empirical evidence that illustrates how IT outsourcingcan influence various dimensions of firms’ actual performance. Accounting performancemetrics, as opposed to perceptual performance measures, have the advantage of providingobjective and quantified evidence of the returns on IT outsourcing. Thus, the findings ofthis study can improve the understanding of the value propositions of IT outsourcing andhelp firms make more informed sourcing decisions.

The remainder of the paper is structured as follows. The subsequent section synthesizesrelevant literature. Thereafter, the analytical framework—including hypotheses, variabledefinitions, and sampling procedures—is developed. A discussion of the findings and theireconomic implications follows. Finally, the limitations of the study and suggestions forfuture research are presented.

II. LITERATURE REVIEWIT Outsourcing: Expected Benefits and Inherent Costs and Risks

In 1989, Kodak initiated a landmark ten-year IT outsourcing agreement for $250 millioncontract with three providers (Hall et al. 2005). Since then, the growth of the IT outsourcingphenomenon in practitioner circles has intensified (Barthelemy 2001; DiRomualdo andGurbaxani 1998). Academic work considering IT outsourcing has continued to evolve,reflecting changes in the outsourcing practice and its impact on firms. One research schoolfocuses on the drivers behind outsourcing decisions and attempts to answer questions suchas ‘‘why do organizations outsource?’’ Scholars have suggested that sourcing decisions aregenerally motivated by various expected benefits of IT outsourcing. IT vendors typicallyspecialize in providing cutting-edge information technologies and services. They tend toserve a large client base and have easier access to high-quality and lower-cost labor pools.Therefore, a commonly held belief is that they enjoy the benefits of economies of scaleand can ensure improved IT performance, cost reduction, and deeper source of talent,knowledge, and expertise (Barthelemy 2001; Loh and Venkatraman 1992a; Smith et al.1998). By delegating their IT responsibilities to vendors, outsourcing firms have the poten-tial to enjoy the aforementioned vendor-offered benefits that could not be realized otherwise.From a strategic standpoint, firms that outsource their IT may refocus internal resources ontheir high-value core competencies by transferring the time-consuming and non-core ITfunctions to third-party vendors (Hayes et al. 2000; Lacity et al. 1998). Through extensiveinterviews, a number of studies have sought to identify IT executives and managers’ ex-pectations of IT outsourcing. Table 1 summarizes some of the most common benefits thatcompanies expect IT outsourcing to deliver. Such expectations continue to serve as strongdrivers behind the rapid growth in the IT outsourcing market.

Nevertheless, IT outsourcing also bears inherent costs and risks for the contract-grantingfirms. Both practitioners and researchers have acknowledged concerns over the hidden haz-ards associated with this practice. Some even caution that the benefits of IT outsourcingmay never materialize because they can be consumed by its costs and risks. Numerousunexpected costs and risks could arise during IT outsourcing operations, including unan-ticipated transition and management costs (Aubert and Dussault 1999; Barthelemy 2001;Earl 1996), potential loss associated with lock-ins (Aubert et al. 1999; Hall et al. 2005;Ngwenyama and Bryson 1999), service debasement (Aubert et al. 1999), and loss of or-ganizational competencies (Aubert et al. 1999; Earl 1996). Studies show that managers tend

128 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

TABLE 1Company’s Expectations/Reasons for Outsourcing IT

Expected Benefits /Reasons for Outsourcing IT Author(s) and Studies

1. Cost Reduction Lacity and Hirschheim 1994; Lacityet al. 1998; Seddon et al. 2002

2. Improved Cost Control Lacity et al. 1994; Lacity et al. 19983. Improved Technology or Technical Service Lacity et al. 1994; Lacity et al. 1998;

Seddon et al. 20024. Focus Business on Core Competencies Lacity et al. 1994; Lacity et al. 1998;

Seddon et al. 20025. Access to New Technologies and Technical Talents Lacity et al. 1994; Seddon et al. 20026. Improved Flexibility Seddon et al. 2002

to underestimate the risks associated with IT outsourcing as well as the underlying expenseson vendor search, vendor contracting, transitioning to the vendor, and the ongoing effortof outsourcing management (Barthelemy 2001). According to a survey conducted byBarthelemy (2001), companies on the average spend 3 percent of their total IT outsourcingcost on vendor search and contracting and may take as long as 12 months to completelyswitch their in-house IT functions to the vendor. Once the transition is completed and thesourcing client is locked in, unanticipated costs can skyrocket (Ngwenyama et al. 1999).For instance, in many cases, contractual amendments are necessary either due to the chang-ing needs of the clients or the incompleteness of the original contracts. As a result, sourcingfirms are susceptible to vendor exploitation and have seen their outsourcers charge excessivepremiums for new services or changes for the services rendered (Aubert et al. 1998). Servicedegradation has also been documented as a major issue in IT outsourcing: poor responsetime, poor turnaround time, late updates of software, applications that do not meet therequirements, and so on (Aubert et al. 1998; Barthelemy 2003b). According to a surveyconducted by Software Development Magazine in October 2003, of the 414 surveyed U.S.IT developers and managers, 56 percent claimed that outsourcing IT work was worse thanwhat could be achieved in-house and, in the worst cases, unusable (Morales 2004). Often,parallel to unsatisfactory services, costs could rise. For instance, two years into an out-sourcing contract, companies could be spending as much as 35 percent of their annualcontract amount on relational and performance management with their vendors (Barthelemy2001). One of the firms studied by Lacity and Hirschheim (1993) reported that its out-sourcing costs were almost three times the cost of in-house services.

Assessing the Outcome of IT OutsourcingDespite the ongoing debate on its benefits and risks, firms worldwide continue to invest

extensively in IT outsourcing (Barthelemy 2001; Mason 2000; Oh et al. 2006). The rapidgrowth in the outsourcing market signals that firms of all sizes believe that this practicewill ultimately deliver value (Levina et al. 2003). Clearly, as more firms move towards IToutsourcing to enhance profitability and performance, there is a need for rigorous empiricalassessment on the effects of IT outsourcing on firm performance. Investigation of this natureis crucial as it provides managers and policy makers with concrete evidence on whether IToutsourcing should be considered as a strategy for the creation of firm competitive advan-tage. Nevertheless, the literature has not yet adequately addressed the question of whetherthe claimed advantages of IT outsourcing have really materialized and been realized by

The Aftermath of Information Technology Outsourcing 129

Journal of Information Systems, Spring 2008

TABLE 2IT Outsourcing Outcome Measures

Outcome Constructs Outcome DimensionsMethodologies

UsedAuthors and

Studies

Technological Benefits (i.e.,access to IT talents andavoidance of technologicalobsolescence)

Surveys Grover and Cheon1996; Lee andKim 1999; Leeet al. 2004

Strategic Benefits (i.e.,improved focus on corecompetency and improvedIS competency)

Surveys Grover et al. 1996;Lee et al. 1999;Lee et al. 2004

Satisfaction (with) Economic Benefits (i.e.,improved cost control andeconomies of scale in bothhuman and technologicalresources)

Surveys Grover et al. 1996;Lee et al. 1999;Lee et al. 2004

Interviews/CaseStudies

Marcolin andMcLellan 1998

Overall Satisfaction Survey Lee et al. 2004;Poppo et al.2002

Expectations/ObjectivesRealized

Costs (i.e., reduced cost andimproved cost control)

Interviews/CaseStudies

Lacity et al. 1994;Lacity et al.1998

Market Value of theClient Firms

Stock Price Event Study Hayes et al. 2000;Oh et al. 2006;Farag et al.2003

Firm Valuation, PerceivedRisk, and Stock Price

Event Study/Case Study

Peak et al. 2002

client firms. Both conceptual and empirical research that assesses the effect of IT outsourc-ing on firm performance remains underdeveloped. Even with the few exceptions that in-vestigate the outcome of IT outsourcing, they tend to be descriptive and anecdotal in natureand rely on self-reported and perceptual data for their analyses (Jiang et al. 2006; Smith etal. 1998). Table 2 summarizes some of the measures and methodologies used by priorresearch in studying the outcome of IT outsourcing.

As shown in Table 2, much of the inquisition on both the success and failure of IToutsourcing has been in the form of individual case studies or industrial surveys(Hirschheim 2000; Smith et al. 1998). In the extant research, success or performance of IToutsourcing has been measured using participants’ self-reported perception of whether theoutcome of their IT sourcing decisions met their expectations or objectives and their sat-isfaction with the achieved strategic, economic, and technological benefits. For instance, inan effort to identify the best practice of IT outsourcing, Lacity et al. (1998) interviewed145 U.S. and U.K. IT managers (61 sourcing decisions). Using expected cost savingsachieved as an indicator of IT outsourcing success, they found that 56 percent of the totalsourcing decisions achieved expected cost savings, 23 percent did not, and 16 percent werenot able to determine. There are also a few studies that employ an event study methodologyand use publicly available financial data rather than self-reported data to examine the impact

130 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

of IT outsourcing announcement on the market value of the contract-granting firms (Hayeset al. 2000; Oh et al. 2006). These studies provide evidence that outsourcing is a value-added business exchange for outsourcing firms contingent on the level of transaction riskand the size and industry of the firm. The findings indicate that investors tend to react morefavorably to the outsourcing announcement when the transactional risk is low and whenfirms are small and are in the service industry. Although stock price data is not self-reporteddata, to a large extent, it still constitutes a perceptual measure as it represents investors’perception of the benefits and risks of IT outsourcing. Further, this body of research in-vestigates the impact of IT outsourcing announcement on the contract-granting firms’ value.It is not clear how well the firms’ actual performance after IT outsourcing implementationsupports evidence found using capital market measures.

Recent progress notwithstanding, important gaps remain. From an empirical perspec-tive, although perceptual measures have the advantage of capturing intangible impacts(Chan 2000), they also exhibit several inherent limitations. Perceptions and feelings maybe susceptible to bias due to the difficulty for human beings to provide accurate estimates(Chan 2000). In survey studies, this problem could be confounded by respondents’ recallerrors and the potential tendency among respondents to provide answers that they think thequestioner wants to hear. IT sourcing decisions represent large and difficult-to-reverse in-vestments, thereby putting pressure on researchers and professionals to ensure that firmsmake informed decisions. Paradoxically, the dominance of subjective and perceptual evi-dence in the literature forces firms to make their IT sourcing decisions based on commit-ment of faith. It is inconceivable that large expenditures such as those incurred for out-sourcing IT could be made without an accompanying economic evaluation of more objectiveevidence. Audited accounting measures, rather than perception-based metrics, are used inthis study to provide business entities with quantifiable and objective evidence on the effectof IT outsourcing on firms’ performance. There is no doubt that firms’ decision makingwill be strengthened by the systematic appraisal and analysis of objective accounting mea-sures. Without such validation and confirmation, there will likely remain some lingeringdoubt as to whether IT outsourcing is truly delivering on its promise.

Theoretically, current studies have primarily sought to establish a direct link betweenIT outsourcing and broad high-level firm performance indicators such as overall cost ob-jective achieved (Lacity and Hirschheim 1994; Lacity et al. 1998), stock price changesaround the announcement of IT outsourcing (Hayes et al. 2000; Oh et al. 2006), or satis-faction with the overall economic benefits of IT outsourcing (Grover and Cheon 1996; Leeand Kim 1999; Lee et al. 2004). This approach does not consider the possibilities thatthe effects of IT outsourcing on overall firm performance can be detected only throughintermediate level contributions to business processes (Barua et al. 1995; Dehning andRichardson 2002). They also do not consider the possibility that the outcome of IT out-sourcing may be contingent on firms’ overall IT capability that enables them to leveragetheir IT outsourcing strategy to enhance firm value. If these intermediate-level contributionsand contingency effects are not taken into account, the business value of IT outsourcingmay be obscured.

III. CONCEPTUAL FRAMEWORK AND HYPOTHESES DEVELOPMENTBased on the review of the literature, this study develops a conceptual framework to

guide the examination of the business value of IT outsourcing (see Figure 1). As shown inFigure 1, while certain firms choose to make and manage their IT in-house, others maychoose to outsource part or their entire IT to external vendors. Regardless of which choice

The Aftermath of Information Technology Outsourcing 131

Journal of Information Systems, Spring 2008

FIGURE 1Proposed Conceptual Model

IT Capability

Non-Outsourcer

Outsourcer

IT STRATEGY OUTCOME

Firm Level

Process Level

Managerial

Operational

the firms make, IT is intended to support business activities and processes and deliverbusiness value. Hence, consistent with the process-oriented tradition in the IT business valueliterature (Barua, et al 1995; Dehning and Richardson 2002; Dehning et al. 2006), thisframework proposes that the contribution of outsourced IT to business value should beassessed not only at the firm level, but also at the intermediate process level where thedirect effects of outsourced IT take place.

Further, researchers adopting the resource-based view have long suggested that IT re-sources rarely act alone in creating or sustaining competitive advantage. For instance,researchers have found that sizable investment in IT per se may not create sustained ad-vantage because technologies can be easily duplicated by others. Nevertheless, a firm withsuperior IT capability can leverage this complex and hard-to-duplicate capability to realizethe full competitive potential of invested IT (Bharadwaj 2000). In other words, researchershave acknowledged that IT capability complements information technologies and moderatesthe effects of IT on firm performance in such a way that firms with superior IT capabilitywill be at an advantage in using IT to enhance firm value.

However, the importance of the complementary synergy between IT and IT capabilityis yet to be fully explored in the IT outsourcing context. Outsourcing IT to high-qualityvendors has the potential to enhance firms’ competitive advantage because vendors maypossess valuable IT assets that are costly to imitate by in-house IT functions. Nevertheless,whether or not firms can fully realize the potential of IT outsourcing may also depend ontheir overall IT capability. After all, it is the firms’ overall IT capability that determineswhether or not firms can select the right vendors, choose the right component of IT tooutsource, successfully manage the ongoing relationship with the vendors, and effectivelyuse the IT provided by the vendors to achieve their business goals. In almost all respects,outsourced IT can produce greater returns in conjunction with a high level of overall ITcapability. Overall IT capability is vital to firms that outsource their IT. Hence, the frame-work proposes that IT capability moderates the relationship between outsourced IT and

132 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

firm performance. The essence here is that outsourced IT and firms’ overall IT capabilityare mutually reinforcing and performance enhancing and when combined, they will be moreeffective in helping firms create business value.

The following provides an in-depth discussion on the selection of performance mea-sures, explaining how IT outsourcing creates value through its impact on these measuresand the moderating effect of IT capability on the link between IT outsourcing and firmperformance.

Performance MeasuresPrior to assessing the impact of IT outsourcing on firm performance, it is necessary to

first identify appropriate performance metrics for evaluation. When doing so, it is importantto note that this study involves evaluating the business value of heterogeneous informationsystems (network, telecommunication, database, and data processing technologies and ser-vices) outsourced in diverse industry environments (see the Appendix). Since systems differin the domain or processes on which they exert impact and activities are also highly idio-syncratic across industry sectors, an attempt must be made to capture impacts that havesome sense of commonality across outsourced systems and industry sectors when identi-fying the performance metrics. To do so in this study a framework proposed by Mooneyet al. (1995) is employed.

Mooney et al.’s (1995) framework classifies business processes into operational andmanagerial processes. Operational processes constitute activities associated with ‘‘primarybusiness operations’’ while managerial processes include activities associated with the ad-ministration, allocation, monitoring, and control of resources within organizations. Mooneyet al. (1995) suggest that, with its automational, informational, and transformational bene-fits, IT impacts both operational and managerial processes and subsequently overall firmperformance. Automational benefits stem from the ability of IT to automate tasks. Forexample, in an organizational task as pervasive as order entry and processing, technologiessuch as data processing, database, network, and telecommunication all contribute to taskautomation (Porter 1985). Mooney et al. (1995) argue that automation benefits operationalprocesses because labor costs and inventory can be reduced while productivity, efficiency,and reliability can be improved. Automation may also enhance managerial processesthrough cost reduction and efficiency improvement in reporting, control, monitoring, andadministration.

The informational benefits of IT stem from the fact that IT aids organizations to bettermanage information, i.e., collect, store, process, and discriminate information. From anoperational perspective, the ability to manage information should improve resource utili-zation, responsiveness, and operational flexibility. From a managerial perspective, it shouldimprove decision quality, resource usage, and managerial effectiveness. Finally, the trans-formational effect of IT refers to its ability to facilitate process transformation. From anoperational perspective, the transformational benefits of IT could lead to improved productsand/or services, enhanced customer relationship management, downsizing, and reducedcycle times to develop and bring products/services to market. From a managerial perspec-tive, such transformational effects may improve managerial responsiveness and coordination(Mooney et al. 1995).

To encapsulate, IT offers three categories of benefits: automational, informational, andtransformational. These benefits impact organizations’ operational and managerial processesthrough two dimensions: reduction in cost and improvement in efficiency. IT-enabled costreductions in operational and managerial processes range from cost in monitoring, search-ing, and reporting, to recording, communication, and documentation. Decreases in these

The Aftermath of Information Technology Outsourcing 133

Journal of Information Systems, Spring 2008

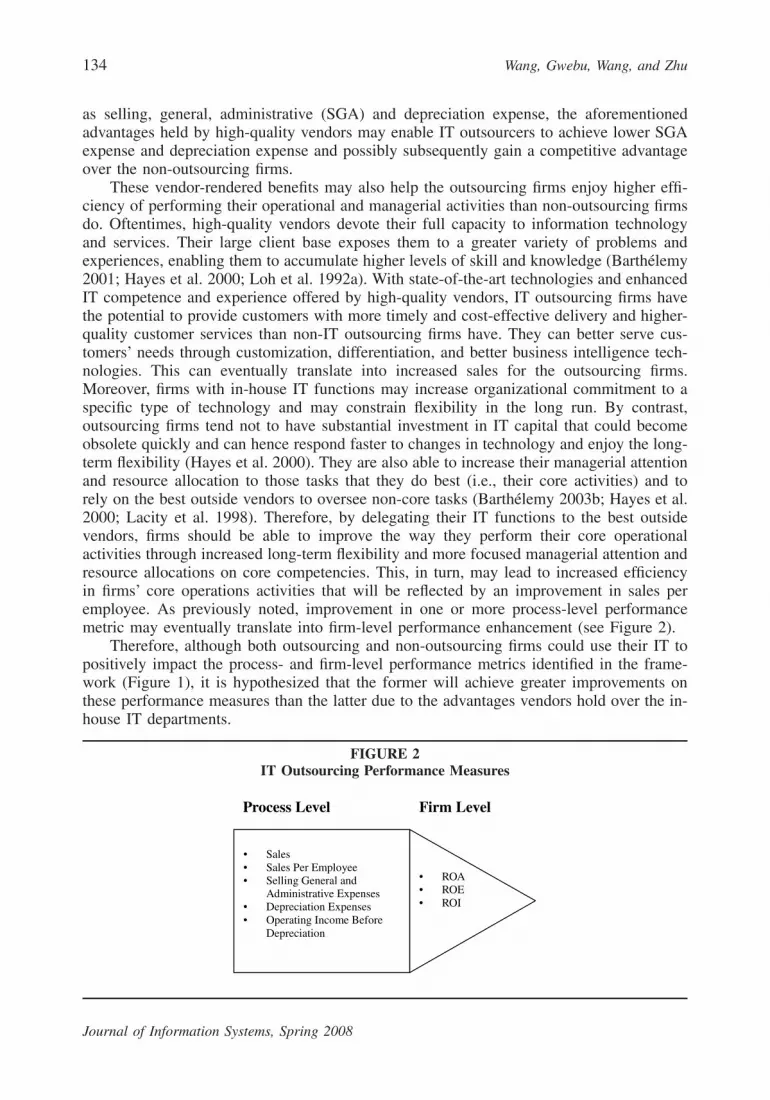

costs should manifest in improvement in the selling, general, and administrative expenses(SGAS). Improvements in operational and managerial efficiency should lead to higherquality in decision making, products or services, customer reach and relationship. Theseenhancements should be reflected in increased sales and increased sales per employee.Increased sales and reduced SGAS in turn should lead to improved operating income beforedepreciation (OBIBD) since OBIBD is calculated as net sales less cost of goods sold andSGAS before deducting depreciation, depletion, and amortization. In the IT business valueliterature, sales, sales per employee, OBIBD, and SGAS have been employed as performancemeasures in the assessment of IT payoff (Rai et al. 1997; Bharadwaj 2000; Poston andGrabski 2000, Hitt et al. 2002).

Collectively, improvements in one or more of these process-level measures may even-tually be translated into firm-level performance improvements reflected in Return on Asset(ROA), Return on Investment (ROI), and Return on Equity (ROE). These three measureshave been extensively used in prior studies to assess the effect of IT on firm-level perform-ance (Hitt and Brynjolfsson 1996; Barua et. al 1995; Alpar and Kim 1990; Brown et al.1995; Rai et al. 1997; Bharadwaj 2000; Dehning and Stratopoulos 2002).

By applying Mooney et al.’s (1995) framework, this study is able to identify the genericeffects of IT on both operational and managerial processes. As depicted in the proposedframework (Figure 1), IT in general impacts the aforementioned process and firm-levelperformance measures due to the IT-enabled automational, informational, and transforma-tional effects. However, the degree of the impact may differ significantly between outsourc-ing and non-outsourcing firms. With the outsourcing firms, they allow ‘‘experts’’ with su-perior IT resources, skills, and knowledge to manage their IT. Hence, their outsourced IThas the potential to exert greater impact on these process- and firm-level measures comparedto firms that make and manage IT in-house. Outsourcing firms could also achieve loweroperational expenditure on IT because they do not have to invest significant amounts in ITcapital. This consequently may lead to lower depreciation expense (DEP).

The following section discusses how IT outsourcing can impact these performancemetrics. A series of hypotheses will be developed based on the discussion.

The Impact of IT Outsourcing on Firm PerformanceCompared with the non-outsourcers, the outsourcing firms have the potential to perform

both their operational and managerial activities at lower costs for the following reasons.Large vendors can provide the sourcing firms with access to economies of scale due tovendors’ large client base. Their size enables them to negotiate lower prices with hardwareand software providers (Barthelemy 2001). Moreover, vendors are often located in coun-tries and regions where high-quality and lower-cost labor pools are easily accessible (Smithet al. 1998). Due to rapid technological advances, firms’ technical expertise and equipmentcould face the threat of becoming obsolete (Hayes et al. 2000; Smith et al. 1998). Never-theless, as specialists of information technology and service providers, vendors can oftenafford to invest in state-of-the-art technologies, high-quality IT personnel, and innovativepractices at a scale that cannot be realized by many firms’ in-house IT departments(Antonucci et al. 1998; DiRomualdo et al. 1998). With the aforementioned advantages,high-quality vendors can hence provide the same if not higher levels of service at a lowerunit cost than in-house IT departments (Ang and Straub 1998; Barthelemy 2001; Smith etal. 1998). Through delegating their IT responsibilities to vendors, an outsourcer may reduceexpenses because it does not have to invest significant amounts in both capital and IThuman resources (Hayes et al. 2000; Smith et al. 1998). Therefore, although IT in generalhelps both outsourcing and non-outsourcing firms decrease the process-level expenses such

134 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

FIGURE 2IT Outsourcing Performance Measures

• Sales • Sales Per Employee • Selling General and

Administrative Expenses • Depreciation Expenses • Operating Income Before

Depreciation

• ROA • ROE • ROI

Process Level Firm Level

as selling, general, administrative (SGA) and depreciation expense, the aforementionedadvantages held by high-quality vendors may enable IT outsourcers to achieve lower SGAexpense and depreciation expense and possibly subsequently gain a competitive advantageover the non-outsourcing firms.

These vendor-rendered benefits may also help the outsourcing firms enjoy higher effi-ciency of performing their operational and managerial activities than non-outsourcing firmsdo. Oftentimes, high-quality vendors devote their full capacity to information technologyand services. Their large client base exposes them to a greater variety of problems andexperiences, enabling them to accumulate higher levels of skill and knowledge (Barthelemy2001; Hayes et al. 2000; Loh et al. 1992a). With state-of-the-art technologies and enhancedIT competence and experience offered by high-quality vendors, IT outsourcing firms havethe potential to provide customers with more timely and cost-effective delivery and higher-quality customer services than non-IT outsourcing firms have. They can better serve cus-tomers’ needs through customization, differentiation, and better business intelligence tech-nologies. This can eventually translate into increased sales for the outsourcing firms.Moreover, firms with in-house IT functions may increase organizational commitment to aspecific type of technology and may constrain flexibility in the long run. By contrast,outsourcing firms tend not to have substantial investment in IT capital that could becomeobsolete quickly and can hence respond faster to changes in technology and enjoy the long-term flexibility (Hayes et al. 2000). They are also able to increase their managerial attentionand resource allocation to those tasks that they do best (i.e., their core activities) and torely on the best outside vendors to oversee non-core tasks (Barthelemy 2003b; Hayes et al.2000; Lacity et al. 1998). Therefore, by delegating their IT functions to the best outsidevendors, firms should be able to improve the way they perform their core operationalactivities through increased long-term flexibility and more focused managerial attention andresource allocations on core competencies. This, in turn, may lead to increased efficiencyin firms’ core operations activities that will be reflected by an improvement in sales peremployee. As previously noted, improvement in one or more process-level performancemetric may eventually translate into firm-level performance enhancement (see Figure 2).

Therefore, although both outsourcing and non-outsourcing firms could use their IT topositively impact the process- and firm-level performance metrics identified in the frame-work (Figure 1), it is hypothesized that the former will achieve greater improvements onthese performance measures than the latter due to the advantages vendors hold over the in-house IT departments.

The Aftermath of Information Technology Outsourcing 135

Journal of Information Systems, Spring 2008

H1a: IT Outsourcing firms will have higher sales than their non-outsourcing counter-parts will.

H1b: IT Outsourcing firms will have a higher ratio of sales per employee than theirnon-outsourcing counterparts will.

H1c: IT Outsourcing firms will exhibit lower selling, general, and administrative ex-penses than their non-outsourcing counterparts will.

H1d: IT Outsourcing firms will exhibit lower depreciation expenses than their non-outsourcing counterparts will.

H1e: IT Outsourcing firms will have higher operating income before depreciation thantheir non-outsourcing counterparts will.

H1f: IT Outsourcing firms will have higher ROA, ROI, and ROE than their non-outsourcing counterparts will.

Complementarity between IT Outsourcing and IT CapabilityAlthough the paper has argued that IT outsourcing firms could achieve greater improve-

ments on the identified process- and firm-level performance metrics than the non-outsourcers, it is unwise to assume that IT outsourcing will be equally effective in enhancingfirm value under all situations. The positive effects of IT outsourcing on performance couldbe contingent upon factors such as the level of a firm’s core IT capability.

Following Bharadwaj (2000, 171), a firm’s core IT capability is defined in this studyas ‘‘its ability to mobilize and deploy IT-based resources in combination or copresent withother resources and capabilities.’’ The argument that a firm’s core capability is an importantcontingency factor for the effects of IT outsourcing on performance is supported by theresource-based view (RBV) of IT. With the RBV of IT, researchers realize that a firm’s ITresources or resource combinations have to be valuable, relatively scarce, and difficult toimitate and substitute in order to generate sustained competitive advantage for the firm(Bharadwaj 2000; Mata et al. 1995; Ross et al. 1996; Ray et al. 2005). They also realizethat valuable IT resources and capabilities rarely act alone. IT resources and capabilitiesproduce greater returns in conjunction with each other than they do alone (Ravichandranand Lertwongsatien 2002). Complementary IT resources are more valuable and more dif-ficult to imitate when employed together than when used separately and, therefore, theyare important sources of sustainable competitive advantage.

Similarly, outsourced IT may not act alone in creating value for firms. As previouslydiscussed, high-quality IT outsourcing vendors may enjoy resource endowments and ITcapabilities that could be difficult for firms with in-house IT to duplicate, including econ-omies of scale, state-of-the-art-technology, specialized knowledge and expertise, and rela-tively easier access to high-quality and lower-cost labor pools. Nevertheless, the advantagesbestowed by high-quality vendors may only be fully realized by firms with superior coreIT capability. A firm’s overall IT capability drives how the valuable vendor-rendered ITresources and capabilities can be mobilized, deployed, and leveraged in order to achievethe business objectives of the firm.

Important organizational IT capabilities include IT leadership, business systems think-ing, architectural planning, making technology work, informed buying, contract facilitation,contract monitoring, and vendor development (Feeny and Willcocks 1998). Such capabili-ties are crucial for the success of IT outsourcing because the business value of IT out-sourcing can only be enhanced and realized to the fullest with the complementarity of these

136 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

capabilities. Specifically, in the initiation and implementation of IT outsourcing strategy,firms face a series of challenging but important decisions. In the process of making andimplementing these decisions, firms that have developed high core IT capabilities in thepast will be at an advantage compared to those that lack core IT capabilities.

For example, even before the outsourcing decision, firms have to decide what consti-tutes their competitive core IT so that it remains in house, and which of the firm’s ITactivities can be outsourced? While outsourcing of non-core IT functions may benefit firmsthrough increased managerial attention and improved resource allocation to the firms’ corecompetencies, the distinction between core and non-core IT may not always be clear(Insinga and Werle 2000). When companies are unable to distinguish their core- from non-core IT, they might engage in the outsourcing of mission-critical IT competencies and firm-specific IT assets and may incur extremely high levels of unexpected risks and costs (Hallet al. 2005; Ngwenyama et al. 1999). Theoretically, IT assets can be classified into eithercommodity or specific assets depending on whether they are designed for standardizedprocesses or the unique strategic needs of a particular firm. Outsourcing highly firm-specificIT assets can be a fairly difficult, costly, and risky endeavor (Miranda and Kim 2006). IT-specific assets tend to be unique to the outsourcing firm. Thus, the vendor cannot achieveeconomies of scale by spreading the costs across many clients and hence will recover allassociated costs from the outsourcing firm by charging a premium fee (Hall et al. 2005).Further, firm-specific IT assets are difficult to obtain from the market. Outsourcing firmsneed to determine whether they should completely rely on a single vendor, in which casethey could be subject to vendor opportunism and vendor failure vulnerability (Hall et al.2005; Ngwenyama et al. 1999). Once a vendor seizes control of the IT assets, it can exploitthe client’s dependence through client lock-in, opportunistic new term negotiation, or charg-ing the service rate at a premium (Hall et al. 2005; Ngwenyama et al. 1999). Further, theoutsourcing firm would have to incur substantial switching costs should the vendor under-perform on the contracted activities or viciously exploit this client dependence (Ngwenyamaet al. 1999). Strategically, the transfer of firm-specific, mission-critical IT assets to thecontrol of external agents could also increase the client firm’s vulnerability and threaten itslong-term flexibility and competitiveness. Its success may be entirely dependent on theexternal vendor—it may lose its ability to use IT efficiently and effectively, and it may losecontrol over important IT decisions, such as using IT in an innovative fashion and aligningIT with its business strategies (Aubert et al. 1999; Aubert et al. 1998; Hall et al. 2005). Inlight of the high risks and costs involved in the outsourcing of core and firm-specific ITassets, firms with superior IT capabilities will be at an advantage in distinguishing corefrom non-core and commodity from specific IT assets. A firm’s IT leadership skills andbusiness systems thinking capability enhance its ability to envision how IT can be integratedwith business processes and objectives (Feeny et al. 1998). Such capabilities improve thefirm’s understanding of which of its IT activities serve firm-specific and mission-criticalbusiness objectives and hence should be kept and nurtured in-house.

After the outsourcing decision, among other things, firms need to decide (1) who theyshould rely on as vendors, (2) what form of vendor relationship is most appropriate for theoutsourced IT, (3) how to manage the on-going vendor relationship, and (4) how to leveragevendors’ resources and capabilities to create value for the firm. As previously noted, despiteits potential benefits, IT outsourcing is associated with numerous unexpected costs andrisks, including vendor selection, unanticipated transition and management costs (Aubert etal. 1999; Barthelemy 2001; Earl 1996), potential loss associated with lock-ins (Aubertet al. 1999; Hall et al. 2005; Ngwenyama et al. 1999), service debasement (Aubert et al.1999), vendor exploitation, and loss of organizational competencies (Aubert et al. 1999;

The Aftermath of Information Technology Outsourcing 137

Journal of Information Systems, Spring 2008

Earl 1996). In light of such high risks and costs, firms may need to do much more thanmerely outsource their IT in order to create business value. Several factors have beendocumented as being important for the success of IT outsourcing initiatives, includingvendor selection (Levina et al. 2003), the client-vendor relationship (Barthelemy 2003a;Poppo and Zenger 2002; Sabherwal 1999), and outsourcing strategies (Currie 1998; Lacityet al. 1998). With strong core IT capabilities, firms will have a better understanding ofinformation technology and can hence better assess a vendors’ competence and its readinessto perform the task, avoiding low-quality subcontractors in a market that could be full oflemons (Mayer and Salomon 2006). Strong technology capabilities can also help firmsbetter craft contracts and monitor the relationship because they have a better understandingof what problems to look for, how to clearly define the roles, responsibilities, and gains ofeach party, how to stipulate monitoring, incentive, and pecuniary mechanisms, and how toidentify appropriate milestone and evaluate the outcomes (Mayer et al. 2006). To a largedegree, superior IT capability translates into superior capability in governing the outsourc-ing transaction (Mayer et al. 2006). With a higher level of core IT capability, firms canleverage leadership skills, business thinking capabilities, their contract facilitation and mon-itoring capabilities, and vendor development skills to ensure that they select the right ven-dor, formulate conducive contractual strategies, facilitate smooth outsourcing transitions,effectively manage the client-vendor relationship, and strategically align vendors’ core com-petencies with the firm’s business objectives.

Therefore, although vendors’ valuable and hard-to-imitate resource endowments and ITcapabilities may confer the outsourcing firms with valuable opportunities and competitivepotential, a firm’s existing core IT capabilities enable it to make the right sourcing decisionand to effectively mobilize, deploy, and leverage the competitive potential offered by thevendors. It thus stands to reason that the complementary synergy between IT outsourcingand firms’ existing core IT capabilities is another critical source of business value for thefirms. Firms that incur the cost of IT outsourcing without developing IT capabilities maybe at a relative disadvantage compared to firms that do because outsourced IT can combinewith the firm’s IT capability to produce complementary synergy that is embedded, valuable,and difficult to imitate. Hence, the actual outcome of an IT outsourcing initiative alsodepends on sourcing firms’ overall IT capability that helps firms leverage their outsourcingstrategy to realize the full competitive potential offered by the high-quality vendors.

H2: IT capability moderates the relationship between IT outsourcing and firm perform-ance in such a way that IT outsourcing in conjunction with superior IT capabilitywill produce better firm performance than IT outsourcing alone will.

IV. RESEARCH METHODOLOGYSample Collection

IT outsourcing initiatives were identified by examining news announcements from theLexisNexis academic database over the period January 1, 1993 to December 31, 2003. Akeyword search method using a combination of search terms ‘‘information technology’’ and‘‘outsource,’’ or ‘‘IT’’ and ‘‘outsource’’ was employed.1 These search terms yielded an initialsample of 4,528 announcements. Subsequent review indicated that a large number of theannouncements were unrelated to IT outsourcing initiatives (e.g., product announcementsfrom IT outsourcing vendors, repeated announcements regarding the same IT outsourcing

1 The sample includes only firms that voluntarily disclosed IT outsourcing announcements. Future studies canbenefit from further expansion of this sampling procedure.

138 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

initiative event, or continued contracts from previous IT outsourcing initiatives). After elim-inating these items, 552 announcements remained in the sample. Next, a search in theCompustat database was conducted to check whether the IT outsourcing companies wereincluded in the database, using either the ticker symbol or company name provided in theannouncements. This procedure filtered out another 426 companies (possibly because theyare nonpublic companies or they ceased operating under that particular name or tickersymbol due to mergers or acquisitions). Additional inspection revealed that six of the re-maining 126 companies had missing data for total assets that were required for a subsequentmatching procedure. After excluding these six companies, the final data sample consistedof 120 companies. The Appendix provides some examples of the announcements retainedand used in the analysis. Table 3 summarizes the sample selection procedure and presentsthe distribution of the 120 companies in the final sample by industry and by year. As shownin Table 3, a large portion of the IT outsourcing firms are from the manufacturing industry(41 or 34 percent) and the service industries (SIC code 6000, 7000, and 8000—49 or 40.8percent).

MetricsIn this study, the impact of IT outsourcing on both process-level and firm-level per-

formance measures were assessed. The process-level metrics identified and discussed insection III include sales, sales per employees, selling, general and administrative expenses,depreciation expenses, and operating income before depreciation. Overall, firm performancemetrics included return on assets (ROA), return on equity (ROE), and return on investment(ROI). Table 4 provides a detailed description of these performance measures as defined inCompustat. Because the goal of the study was to understand both the short-term and long-term effects of IT outsourcing, performance measures from one year before the IT out-sourcing initiative (year t � 1) to three years after the IT outsourcing initiative (year t� 1, t � 2, and t � 3) were used in the tests. Table 5 presents the calculation of theperformance variables from year t � 1 to year t � 3.

Matching ProcedureA matched-pair analysis was employed to examine whether the firm performance of

the IT-outsourcing firms were better than matched non-IT-outsourcing firms subsequentto the IT outsourcing initiatives. According to Barber and Lyon (1996), the best matchingprocedure in event studies should match the sample and control firms by industry, firm size,and pre-event performance. This procedure would yield better-specified tests than matchingon industry alone, or on industry and size. Following this guideline, the IT outsourcingfirms were first matched with a group of control firms on size and industry one year beforethe IT outsourcing announcements (year t � 1). In this procedure, a group of firmswith the same four-digit Standard Industrial Classification (SIC) code were first identifiedfor each outsourcing firm. Then among each group, the firm with the assets size that isclosest to the outsourcing firm was chosen. This chosen firm and the outsourcing firm thusformed a pair that was matched on both the four-digit industry code and firm size. Next, asearch in the Lexis-Nexis academic database was conducted to check whether the matchedcontrol firms had IT outsourcing announcements in years t � 1 to t � 3, using either thecompany name or the ticker symbol of the control firms as the keyword. The search revealedthat none of the control firms had IT outsourcing announcements in years t � 1 to t � 3.Lastly, a series of t-tests were run to check whether the sample and control firms werematched on pre-event performance. As shown in the first section of Table 6, there are nosignificant differences in pre-event performance measures between the outsourcing group

The Aftermath of Information Technology Outsourcing 139

Journal of Information Systems, Spring 2008

TABLE 3Sample Selection

Panel A: Sample Selection Procedure

Initial Sample 4,528Less: announcements unrelated to IT outsourcing

initiatives, repeated announcements, andcontinued contracts from previous IToutsourcing initiatives (3,976)

Less: observations not in the Compustat database (426)Less: observations with missing total assets data (6)Final Sample 120

Panel B: Distribution of the IT Outsourcing Firms by Industry

Industry by SIC Codes Number of Firms

1000-Mining, Construction 22000-Manufacturing 63000-Manufacturing 354000-Transportation, Communications, Utilities 125000-Wholesales and Retail Trade 166000-Finance, Insurance, Real Estate 237000-Services 238000-Health Services 39000-Public Institutions 0Total 120

Panel C: Distribution of the IT Outsourcing Firms by Year

Year Number of Firms

1993 21994 61995 41996 21997 71998 61999 252000 192001 212002 182003 10Total 120

and the matched control group one year before the announcements except on one variable( marginally significant). Also shown here, there is no significant difference in totalSGAS ,t�1

assets ( t � 0.06) between the outsourcing group and the matched control group.TA ,t�1

Therefore, the results presented in the first section of Table 6 validate the soundness of thematching procedure: the outsourcing firms and the control firms are matched on year, four-digit industry code, firm size, and pre-event performance.

140 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

TABLE 4The Definition of the Variables in Compustat

Variables Compustat Definition

Return on Assets (ROA) Income before extraordinary Items, divided by totalassets, multiplied by 100.

Return on Investment (ROI) Income before extraordinary items, divided by totalinvested capital, which is the sum of the followingitems: total long-term debt, preferred stock,minority interest, total common equity. This isthen multiplied by 100.

Return on Equity (ROE) Income before extraordinary items, divided bycommon equity, multiplied by 100.

Net Sales (SALE) Gross sales (the amount of actual billings tocustomers for regular sales completed during theperiod) reduced by cash discounts, trade discounts,and returned sales and allowances for which creditis given to customers.

Selling, General and AdministrativeExpenses (SGA)

All operational selling, general, and administrativeexpenses not allocated to cost of goods sold.

Depreciation Expenses (DEP) Depreciation and amortization expenses.Operating Income Before Depreciation

(OPIBD)Net sales less cost of goods sold and selling, general

and administrative expenses before deductingdepreciation, depletion, and amortization.

TABLE 5The Definition of Performance Variables

Firm-Level Variables

ROAt�j � return-on-assets ratio of year t � j, where j � �1 to 3;ROEt�j � return-on-equity ratio of year t � j, where j � �1 to 3; andROIt�j � return-on-investment ratio of year t � j, where j � �1 to 3.

Process-Level Variables

SALESt�j � net sales scaled by total assets in year t � j, where j � �1 to 3;SALEEMPt�j � net sales divided by number of employees in year t � j, where j � �1 to 3;

SGASt�j � selling, general and advertising expenses scaled by net sales in year t � j, wherej � �1 to 3;

DEPSt�j � depreciation expenses scaled by net sales in year t � j, where j � �1 to 3; andOPIBDSt�j � operating income before depreciation scaled by net sales in year t � j, where

j � �1 to 3.

Mean Comparison of the Matched PairsAfter finalizing the matched pairs, a series of t-tests were run to compare the means

of the performance variables (as defined in Table 5) between the IT outsourcing groupand the control group in each period after the IT outsourcing initiatives (e.g.,

versus versus etc.).ROA ROA ; ROA ROA ,t�1, IT outsourcing t�1, control t�2, IT outsourcing t�2, control

These tests examined whether outsourcing firms outperformed the control group after theIT outsourcing initiatives. If the means of SGAS and DEPS are lower or the means ofSALES, SALEEMP, and OPIBDS are higher for the outsourcing group than the matchedcontrol group, the results would suggest that outsourcing IT might have helped companies

The Aftermath of Information Technology Outsourcing 141

Journal of Information Systems, Spring 2008

TABLE 6Mean Comparison between the IT Outsourcing Group and the Matched Control Group

IT Outsourcing GroupMean

Matched Control GroupMean Difference t-value

Panel A: Pre-Event Variables

TAt�1 32550.04 31832.23 717.82 0.06ROAt�1 (2.29) (1.11) (1.18) (0.33)ROEt�1 (349.87) (11.47) (338.40) (0.98)ROIt�1 (7.39) (66.80) 59.41 0.92SALESt�1 1.00 0.94 0.06 0.54SALEEMPt�1 0.01 0.01 (0.00) (0.93)SGASt�1 0.45 0.29 0.15 1.95*DEPSt�1 0.16 0.08 0.07 1.03OPIBDSt�1 0.02 0.08 (0.06) (0.59)

Panel B: Firm-Level Variables

ROAt (11.34) (0.26) (11.08) (1.76)*a

ROAt�1 (12.13) (1.67) (10.46) (1.83)*ROAt�2 (2.83) (8.66) 5.82 1.07ROAt�3 (2.92) (7.34) 4.42 1.00ROEt (162.66) 0.62 (163.28) (1.30)ROEt�1 (14.13) (1.03) (13.11) (1.04)ROEt�2 (2.93) (21.20) 18.27 1.07ROEt�3 (3.09) 8.27 (11.36) (1.41)ROIt (13.66) 0.46 (14.12) (1.64)*ROIt�1 (14.01) (7.23) (6.77) (0.55)ROIt� 2 (4.22) (20.37) 16.15 1.04ROIt�3 (12.11) (16.83) 4.73 0.28

Panel C: Process-Level Variables

SALESt 0.06 0.11 (0.05) (0.76)SALESt�1 0.06 0.11 (0.05) (0.82)SALESt�2 (0.01) (0.34) 0.33 0.72SALESt�3 (0.40) (0.02) (0.38) (0.90)SALEEMPt 0.01 0.01 (0.00) (0.52)SALEEMPt�1 0.00 0.01 (0.00) (1.13)SALEEMPt�2 0.01 0.01 (0.00) (0.90)SALEEMPt�3 0.01 0.01 0.00 0.36SGASt 0.40 0.31 0.09 1.98**SGASt�1 0.40 0.31 0.09 1.72*SGASt�2 0.36 0.31 0.06 0.97SGASt�3 0.79 0.54 0.25 0.49DEPSt 0.12 0.09 0.03 0.72DEPSt�1 0.09 0.12 (0.04) (0.93)DEPSt�2 0.08 0.14 (0.05) (1.41)DEPSt�3 0.13 0.09 0.04 0.65OPIBDSt 0.06 0.11 (0.05) (0.76)OPIBDSt�1 0.06 0.11 (0.05) (0.82)OPIBDSt�2 (0.01) (0.34) 0.33 0.72OPIBDSt�3 (0.40) (0.02) (0.38) (0.90)

*, **, *** significant at the 10, 5, and 1 percent levels, respectively, two-tailed.

142 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

improve business processes. If the means of the firm-level metrics (ROA, ROE, and ROI)are higher for the outsourcing group than the matched control group, the results wouldsuggest that outsourcing IT may have contributed to better overall firm performance for theoutsourcing companies.

Statistical ModelMany factors other than IT outsourcing can affect firm performance. Thus, it is nec-

essary to design a test to control possible confounding factors while examining post-eventfirm performance. A multiple regression model was employed to control for other possibleconfounding factors. Brown and Perry (1994) report that performance in a given time periodcan be affected by performance in a prior period. Barber and Lyon (1996) also point outthat controlling pre-event performance can help mitigate test misspecification for post-eventperformance evaluation. Besides controlling for pre-event performance in the matchingprocedure discussed previously, firm performance one year before the IT outsourcing event(year t � 1) was used in the regression to control for this ‘‘halo’’ effect. Growth can affecta company’s future performance by increasing investments that may affect both efficiencyand profitability. In the accounting literature, market-to-book ratio (MB) is often used as aproxy for growth. The reciprocal of MB, i.e., BM, was used as a control factor for growthto avoid the discontinuity in the MB ratio when book value is negative. In addition, IToutsourcing may have different effects on large companies compared with small companies.Total assets (TA) were used to control for the size effect in the regression model. Otherfirm initiatives, such as merger and acquisition or firm restructure, can also affect the growthpotential or the size of a firm, which in turn can affect firm performance. Therefore, BMand TA in the regression model can function as the ‘‘catch-all’’ factors to control for thesefactors. In summary, the regression model used is:

DIFFPERF � � � � DIFFPERF � � DIFFBMi,t�j i,t�j 1 i,t�1 2 i,t�j

� � DIFFTA � � EVENT � e (1)3 i,t�j 4 i,t�j i,t�j

where:

�DIFFPERFi,t�j the difference in performance between the IT outsourcing company jand the matched control company, in year t � j, where j � 0, 1, 2, or3. The performance measures are as defined in Table 5;

�DIFFPERFi,t�1 the difference in performance between the IT outsourcing company jand the matched control company, in year t � 1;

�DIFFBMi,t�j the difference in book-to-market ratio between the IT outsourcingcompany j and the matched control company in year t � j. The bookvalue of equity was obtained from Compustat and the market value ofequity was calculated as stock price at the end of year t � j times thenumber of common stock shares outstanding at the end of year t � j;

�DIFFTAi,t�j the difference in total assets between the IT outsourcing company j andthe matched control company at the end of year t � j; and

�EVENTi,t�j a dummy variable, which takes the value of 1 if the differentialperformance is calculated as IT outsourcing company’s performanceminus the matched control firm’s performance, and takes the value of 0when the differential performance is calculated as the matched controlfirm’s performance minus the IT outsourcing firm’s performance.

The Aftermath of Information Technology Outsourcing 143

Journal of Information Systems, Spring 2008

Data related to the performance variables, BM, and TA were all obtained from Com-pustat. This model is similar to the one employed by Nicolaou (2004) and was estimatedfor each period from year t to year t � 3 for each performance variable, using the OrdinaryLeast Squares (OLS) estimation procedure. is the differential performanceDIFFPERFi,t�1

one year prior to the IT outsourcing initiative. This variable was employed to control forthe ‘‘halo’’ effect. and are control variables for other confoundingDIFFBM DIFFTAi,t�j i,t�j

factors. The EVENT dummy variable captures the directional difference in the dependentvariable in Model (1). According to Nicolaou (2004), the EVENT dummy variable in thisregression helps mitigate concerns of endogeneity. If estimated �4 is positive when ROA,ROE, or ROI is used in Model (1), the results would indicate that IT outsourcing companiesexperienced better firm-level returns subsequent to the outsourcing initiatives when com-pared to the matched non-outsourcing companies. If estimated �4 is negative when SGASor DEPS is used in Model (1), or if estimated �4 is positive when SALES, SALEEMP, orOPIBDS is used in Model (1), the results would indicate that IT outsourcing companiesexperienced improved process performance subsequent to the outsourcing initiative whencompared to the matched non-outsourcing companies.

V. RESULTSThe Effects of IT Outsourcing on Process- and Firm-level Performance Measures

The second section of Table 6 reports the mean differences in performance measuresbetween the IT outsourcing group and the matched control group from year t to year t� 3. The t-tests are two-tailed. The results show that ROAt, and ROIt, are marginallyROA ,t�1

significantly lower for the IT outsourcing group than for the control group; and SGASt andare significantly and marginally significantly higher for the IT outsourcing groupSGASt�1

than for the control group, respectively. Since IT outsourcing initiatives may only havepartial effects on firm performance in the announcement year t, the analysis will focus onperformance measures from years t � 1 to year t � 3 hereafter. Compared to non-outsourcing firms, IT outsourcing firms experienced lower return-on-asset (ROA) in year t� 1, and higher selling, general, and administrative expenses per sales dollar (SGAS) inyear t � 1. However, neither process-level nor firm-level performance measures seem todiffer between the outsourcing and non-outsourcing firms in years t � 2 and t � 3.

Table 7 presents the OLS estimation results of Model (1). To mitigate the effects ofextreme values, the dependent and independent variables were Winsorized at the 1 percentand 99 percent levels.2 For the firm-level measures, the estimated coefficients of variableEVENT (�4) are negative and significant when the dependent variables are DIFFROAt,

DIFFROEt, DIFFROIt, and TheDIFFROA , DIFFROE , DIFFROE , DIFFROI .t�1 t�1 t�3 t�1

negative and significant estimated coefficients for ROA, ROE, and ROI in year t � 1 con-sistently suggest that IT outsourcing companies experienced worse firm-level profitabilitythan their matched peers one year after the outsourcing initiatives. However, such neg-ative results are not evident two or three years after the initiatives. For process-level mea-sures, the estimated coefficients are positive and significant for andDIFFSGASt�2

This suggests that SGA expenses per sales dollar are higher for the ITDIFFSGAS .t�3

outsourcing companies two and three years after the IT outsourcing initiatives, compared

2 Additional analysis to exclude influential observations were conducted using recommended cutoffs for studentizedresiduals and the DFFITS measure. The main results remained robust after these additional tests. In addition,diagnostic analyses were performed to ensure that the estimated results did not suffer from autocorrelation andmulticollinearity issues and that the assumption of normality was not violated.

144W

ang,G

webu,

Wang,

andZ

hu

Journalof

Information

Systems,

Spring2008

TABLE 7OLS Estimation of Regression Models Differential Performance after IT Outsourcing

Model 1: DIFFPERF � � � � DIFFPERF � � BM � � TA � � EVENT � ei,t�j i,t�j 1 i,t�1 2 i,t�j 3 i,t�j 4 i,t�j i,t�j

DIFFPERFt�ja Intercept DIFFPERFt�1 BM TA EVENT Adj. R2

Firm-Level Variables

DIFFROAt�1b 1.425 0.745*** 0.00000001 0.0000564 (2.850) 0.42

DIFFROAt 4.681* 0.206** (0.00000017) 0.0001441 (9.362)** 0.04DIFFROAt�1 6.631** 0.414*** 0.00000044 0.0004169 (13.263)*** 0.14DIFFROAt�2 1.372 (0.129) 0.00000086 0.0001523 (2.744) 0.01DIFFROAt�3 (2.564) 0.040 0.00000052 0.0000852 5.127 0.01DIFFROEt�1 5.992 3.013*** (0.00000138) 0.0011720 (11.984) 0.25DIFFROEt 61.500 (0.026) (0.00000944) 0.0025904 (123.001)** 0.00DIFFROEt�1 9.938* (0.007) 0.00000076 0.0007253 (19.876)** 0.02DIFFROEt�2 (0.945) 0.057*** (0.00000263) 0.0007367 1.890 0.03DIFFROEt�3 15.817** 0.019 (0.00000165) 0.0011707 (31.634)*** 0.05DIFFROIt�1 5.274 0.684*** (0.00000011) 0.0001208 (10.548) 0.23DIFFROIt 11.802* (0.332)*** 0.00000083 0.0002478 (23.604)** 0.06DIFFROIt�1 6.987 0.334*** 0.00000040 0.0006749 (13.973)** 0.13DIFFROIt�2 3.103 (0.168)** 0.00000053 0.0003135 (6.206) 0.01DIFFROIt�3 8.526 (1.016)*** (0.00000922) 0.0027620* (17.052) 0.14

(continued on next page)

The

Afterm

athof

Information

TechnologyO

utsourcing145

Journalof

Information

Systems,

Spring2008

TABLE 7 (continued)

Process-Level Variables

DIFFSALESt�1 0.003 0.830*** (0.00000001) (0.0000004) (0.005) 0.73DIFFSALESt 0.055 0.675*** 0.00000001 0.0000007 (0.111)* 0.59DIFFSALESt�1 0.006 0.629*** 0.00000001 (0.0000003) (0.011) 0.50DIFFSALESt�2 0.060 0.768*** 0.00000002 (0.0000008) (0.120) 0.55DIFFSALESt�3 (0.022) 0.770*** 0.00000012 (0.0000075) 0.043 0.27DIFFSALEEMPt�1 (7.246) 0.728*** 0.00000953 (0.0001660) 14.491 0.67DIFFSALEEMPt (8.421) 0.745*** 0.00002933*** (0.0018676) 16.842 0.73DIFFSALEEMPt�1 (25.243)* 0.603*** 0.00004113*** (0.0037835)** 50.487** 0.61DIFFSALEEMPt�2 (10.717) 0.812*** 0.00006663*** (0.0075423)*** 21.433 0.63DIFFSALEEMPt�3 (12.239) 0.626*** 0.00004172** (0.0043640) 34.478** 0.38DIFFSGASt�1 (0.087)*** 0.204*** (0.00000002) (0.0000028) 0.173 0.74DIFFSGASt (0.056)** 0.281*** (0.00000002) (0.0000024) 0.113*** 0.46DIFFSGASt�1 (0.042) 0.210*** (0.00000003) (0.0000016) 0.085 0.19DIFFSGASt�2 (0.031) 0.162*** (0.00000001) (0.0000003) 0.062* 0.22DIFFSGASt�3 (0.047)** 0.094*** (0.00000003) (0.0000007) 0.095*** 0.16DIFFDEPSt�1 (0.000) 0.501*** 0.00000001 0.0000001 0.000 0.71DIFFDEPSt (0.010) 2.447*** (0.00000002)** 0.0000001 0.021 0.71DIFFDEPSt�1 0.005 0.582*** (0.00000000) (0.0000001) (0.009) 0.18DIFFDEPSt�2 0.016 0.428*** (0.00000001) (0.0000001) (0.032)** 0.09DIFFDEPSt�3 0.025** 0.019 0.00000000 0.0000009 (0.050)*** 0.05DIFFOPIBDSt�1 0.057** 0.181*** 0.00000002 0.0000017 (0.114) 0.63DIFFOPIBDSt 0.023 0.254*** 0.00000001 0.0000002 (0.046) 0.29DIFFOPIBDSt�1 0.014 0.151*** 0.00000004** 0.0000022 (0.027) 0.09DIFFOPIBDSt�2 (0.026) 0.020 0.00000006*** 0.0000027 0.052 0.09DIFFOPIBDSt�3 0.018 (0.029) 0.00000002 0.0000047* (0.036) 0.04

*, **, *** significant at the 10, 5, and 1 percent levels, respectively, two-tailed. Data are Winsorized at the 1 percent and 99 percent levels.a DIFFPERFt�j is calculated as the differential performance between an IT-outsourcing company and its matched control company in year t � j (j � 0 to 3) for each

performance variable. See Table 5 for the definition of performance variables.b When dependent variable is DIFFPERFt�1, the control variable is DIFFPERFt�2, not DIFFPERFt�1. BMi,t�j is book-to-market ratio for company i in year t � j. The

book value of equity was obtained from Compustat and the market value of equity was calculated as stock price at the end of year t times the number of commonstock shares outstanding at the end of year t � j. TAi,t�j is total assets of firm i at the end of year t � j. Event � 1 if the differential performance is calculated as IToutsourcing company’s performance minus the matched control firm’s performance; � 0 when the differential performance is calculated as the matched control firm’sperformance minus the IT outsourcing firm’s performance.

146 Wang, Gwebu, Wang, and Zhu

Journal of Information Systems, Spring 2008

to the matched non-outsourcing companies. The results also show that the estimated co-efficients are positive and significant for the dependent variables andDIFFSALEEMPt�1

which indicates that IT outsourcing companies improved their efficiencyDIFFSALEEMP ,t�3

in sales per employee one year and three years after the initiatives compared to theirmatched peers. In addition, estimated coefficients are negative and significant for the de-pendent variables and which implies that IT outsourcing com-DIFFDEPS DIFFDEPS ,t�2 t�3

panies improved their efficiency in depreciation expenses per sales dollar two and threeyears after the initiatives, compared to their matched peers. Overall, the results presentedin Table 7 suggest that the IT outsourcing companies were not able to immediately benefitfrom the outsourcing initiatives in the short-run (year t and year t � 1); however, they wereable to improve their process-level efficiency in sales per employee and depreciation ex-pense per sales dollar in the long-run (in years t � 2 and t � 3).

An alternative way to examine the changes in firm performance after IT outsourcingis to employ a double-differencing method as follows:

(PERF � PERF ) � (PERF � PERF ) (2)firm,t�j firm,t�1 match,t�j match,t�1

where:

�PERFfirm,t�j performance variables for IT outsourcing firms in year t � j ( j � 0, 1, 2,or 3).

�PERFfirm,t�1 performance variables for IT outsourcing firms in year t � 1.�PERFmatch,t�j performance variables for matched control firms in year t � j ( j � 0, 1,

2, or 3).�PERFmatch,t�1 performance variables for matched control firms in year t � 1.

In this procedure, the post-event performance of an IT outsourcing firm is first com-pared to the performance in year t � 1 of the same firm, then that change in performanceis adjusted by the corresponding change in performance of the matched non-outsourcingfirm during the same period. This method is similar to the one employed in Dehning et al.(2006). One key advantage of employing this method is that the double-adjusted post-eventperformance can reveal whether there is improvement in performance attributable to theevent regardless of whether there is difference in performance in year t � 1 betweenthe outsourcing firm and the control firm. This method is useful in this study especiallyfor the performance measure SGAS. Recall that in the pre-event performance matchingprocedure discussed previously the SGAS measure is marginally significantly different be-tween the outsourcing group and the control group in year t � 1. Therefore, this double-differencing procedure can help provide more valid analysis particularly for this variable.As shown in Table 8, the double-adjusted and are negative and marginallySGAS SGASt�1 t�2

significant (�0.11, t � �1.66; � 0.13, t � �1.92, respectively), indicating that SGA ex-penses of the outsourcing firms decreased more in years t � 1 and t � 2 than that of thematched non-outsourcing firms. In summary, even though (see Table 6),SGAS SGASt�1 t�2

and (see Table 7) are higher for the IT outsourcing firms than the matched controlSGASt�3

firms, IT outsourcing companies achieved greater improvements in andSGAS SGASt�1 t�2

over than the matched control companies (see Table 8). This pattern can be directlySGASt�1

observed in Table 6, where the means of SGASt, andSGAS , SGAS , SGAS ,t�1 t�1 t�2

are 0.45, 0.40, 0.40, 0.36 and 0.79, respectively, for the IT outsourcing companies;SGASt�3

while the means of SGASt, and are 0.29, 0.31, 0.31,SGAS , SGAS , SGAS , SGASt�1 t�1 t�2 t�3

0.31 and 0.54, respectively, for the matched control companies. Thus, even though SGAS

The

Afterm

athof

Information

TechnologyO

utsourcing147

Journalof

Information

Systems,

Spring2008

TABLE 8Double Differencing T-Tests

Mean STD t-valuea

Firm-Level Variables

(ROAfirm,t � ROAfirm,t�1) � (ROAmatch,t � ROAmatch,t�1) �9.50 69.43 �1.46(ROAfirm,t�1 � ROAfirm,t�1) � (ROAmatch,t�1 � ROAmatch,t�1) �8.53 46.35 �1.95**(ROAfirm,t�2 � ROAfirm,t�1) � (ROAmatch,t�2 � ROAmatch,t�1) 0.89 46.68 0.19(ROAfirm,t�3 � ROAfirm,t�1) � (ROAmatch,t�3 � ROAmatch,t�1) 2.69 44.71 0.59(ROEfirm,t � ROEfirm,t�1) � (ROEmatch,t � ROEmatch,t�1) 214.83 4263.54 0.50(ROEfirm,t�1 � ROEfirm,t�1) � (ROEmatch,t�1 � ROEmatch,t�1) 400.87 4055.49 0.97(ROEfirm,t�2 � ROEfirm,t�1) � (ROEmatch,t�2 � ROEmatch,t�1) 482.72 4387.01 1.00(ROEfirm,t�3 � ROEfirm,t�1) � (ROEmatch,t�3 � ROEmatch,t�1) �24.06 268.54 �0.78(ROIfirm,t � ROIfirm,t�1) � (ROImatch,t � ROImatch,t�1) �8.55 105.23 �0.84(ROIfirm,t�1 � ROIfirm,t�1) � (ROImatch,t�1 � ROImatch,t�1) 6.06 77.56 0.79(ROIfirm,t�2 � ROIfirm,t�1) � (ROImatch,t�2 � ROImatch,t�1) �70.10 773.76 �0.86(ROIfirm,t�3 � ROIfirm,t�1) � (ROImatch,t�3 � ROImatch,t�1) �73.09 805.47 �0.84

(continued on next page)

148W

ang,G

webu,

Wang,

andZ

hu

Journalof

Information

Systems,

Spring2008

TABLE 8 (continued)

Mean STD t-valuea

Process-Level Variables

(SALESfirm,t � SALESfirm,t�1) � (SALESmatch,t � SALESmatch,t�1) �0.06 0.57 �1.13(SALESfirm,t�1 � SALESfirm,t�1) � (SALESmatch,t�1 � SALESmatch,t�1) �0.02 0.65 �0.35(SALESfirm,t�2 � SALESfirm,t�1) � (SALESmatch,t�2 � SALESmatch,t�1) �0.06 0.67 �0.89(SALESfirm,t�3 � SALESfirm,t�1) � (SALESmatch,t�3 � SALESmatch,t�1) 0.02 1.06 0.17(SALEEMPfirm,t � SALEEMPfirm,t�1) � (SALEEMPmatch,t � SALEEMPmatch,t�1) 5.93 133.55 0.41(SALEEMPfirm,t�1 � SALEEMPfirm,t�1) � (SALEEMPmatch,t�1 � SALEEMPmatch,t�1) 11.49 162.57 0.67(SALEEMPfirm,t�2 � SALEEMPfirm,t�1) � (SALEEMPmatch,t�2 � SALEEMPmatch,t�1) �3.53 186.80 �0.17(SALEEMPfirm,t�3 � SALEEMPfirm,t�1) � (SALEEMPmatch,t�3 � SALEEMPmatch,t�1) 1.34 240.47 0.05(SGASfirm,t � SGASfirm,t�1) � (SGASmatch,t � SGASmatch,t�1) �0.08 0.51 �1.43(SGASfirm,t�1 � SGASfirm,t�1) � (SGASmatch,t�1 � SGASmatch,t�1) �0.11 0.56 �1.66*(SGASfirm,t�2 � SGASfirm,t�1) � (SGASmatch,t�2 � SGASmatch,t�1) �0.13 0.56 �1.92*(SGASfirm,t�3 � SGASfirm,t�1) � (SGASmatch,t�3 � SGASmatch,t�1) �0.12 0.60 �1.60(DEPSfirm,t � DEPSfirm,t�1) � (DEPSmatch,t � DEPSmatch,t�1) �0.01 0.22 �0.57(DEPSfirm,t�1 � DEPSfirm,t�1) � (DEPSmatch,t�1 � DEPSmatch,t�1) �0.08 0.53 �1.65*(DEPSfirm,t�2 � DEPSfirm,t�1) � (DEPSmatch,t�2 � DEPSmatch,t�1) �0.10 0.86 �1.15(DEPSfirm,t�3 � DEPSfirm,t�1) � (DEPSmatch,t�3 � DEPSmatch,t�1) �0.12 0.89 �1.30(OPIBDSfirm,t � OPIBDSfirm,t�1) � (OPIBDSmatch,t � OPIBDSmatch,t�1) 0.03 0.40 0.82(OPIBDSfirm,t�1 � OPIBDSfirm,t�1) � (OPIBDSmatch,t�1 � OPIBDSmatch,t�1) 0.06 0.55 1.20(OPIBDSfirm,t�2 � OPIBDSfirm,t�1) � (OPIBDSmatch,t�2 � OPIBDSmatch,t�1) 0.07 0.99 0.70(OPIBDSfirm,t�3 � OPIBDSfirm,t�1) � (OPIBDSmatch,t�3 � OPIBDSmatch,t�1) 0.03 1.01 0.25

*, **, *** significant at the 10, 5, and 1 percent levels, respectively.a Based on two-tailed tests.See Table 2 for the definition of performance variables.

The Aftermath of Information Technology Outsourcing 149

Journal of Information Systems, Spring 2008

is higher for the outsourcing firms from year t � 1 to year t � 3, the improvements inand over are better for the outsourcing firms than for the controlSGAS SGAS SGASt�1 t�2 t�1

firms (changes in SGAS over year t � 1 are �0.05, �0.05, �0.09, and 0.34, respectively,for the outsourcing companies in year t , t � 1, t � 2 and t � 3; and �0.02, �0.02, �0.02and 0.25, respectively, for the matched control companies). Through this analysis, one cansee that the double-differencing procedure yields a more valid and insightful understandingof the post-event performance when there is significant difference in pre-event performance( in this case).SGASt�1

The results in Table 8 also reveal that the double-adjusted firm-level measure ROAt�1

is significantly negative, which suggests that return-on-assets for the IT outsourcing com-panies declined one-year after the IT outsourcing initiatives. On the other hand, the double-adjusted process-level measure is marginally negative, indicating that the out-DEPSt�1

sourcing companies improved their efficiency in depreciation expenses in year t � 1 betterthan their counterparts did. These results are consistent with previous findings in Tables 6and 7.

The Moderating Effects of IT CapabilityInformationWeek tracks the IT agendas of the most innovative companies in employing

IT resources in the United States and publishes an InformationWeek500 (IW500 hereafter)ranking list annually. In the IT business value literature, the IW500 annual ranking and asub-list of the annual ranking (IT leaders) have been used as proxies for IT capability(Bharadwaj 2000; Santhanam and Hartono 2003; Wang and Alam 2007). Studies find thatIT capability is positively associated with firm performance because firms with high ITcapability can more effectively integrate IT resources with other organizational resourcesto create business value (Bharadwaj 2000; Santhanam et al. 2003; Wang et al. 2007). Recallthat the proposed conceptual framework posits that firms’ overall IT capability could playa similar complementary role even when IT is outsourced. Outsourcing firms with superiorIT capability will be at an advantage because they can leverage this capability to fullyrealize the benefits of IT outsourcing. To examine this moderating effect of IT capability,one more variable (IW500) was incorporated into the regression to examine whether IW500companies are able to obtain better firm performance results after the IT outsourcing ini-tiatives, when compared to other outsourcing companies. The regression model used istherefore:

DIFFPERF � � � � DIFFPERF � � DIFFBM � � DIFFTAi,t�j i,t�j 1 i,t�1 2 i,t�j 3 i,t�j

� � EVENT � � EVENT IW500 � e*4 i,t�j 5 i,t�j i,t�j (3)

where:

IW500 � 1 if company i is listed in IW500 in year t � j, 0 otherwise.

Among the 120 IT outsourcing companies, 22 companies are listed in IW500,3 whilenone of the matched control companies are listed in IW500 during the examination period.Assuming that IW500 companies can manage their IT outsourcing activities better than thenon-IW500 companies, it is expected that �5, which captures the incremental firm perform-ance difference between the IW500 and non-IW500 outsourcing companies, will be positive