technical innovation and competitive advantage in retail financial services: a case study of change...

TRANSCRIPT

British Journal of Management, Vol. 7, 45-61 (1996)

Technical Innovation and Competitive Services: and

Advantage in Retail Financial A Case Study of Change

Industry Response

Timothy Morris and Roy Westbrook London Business School, Sussex Place, Regent’s Park, London NW14SA, UK

This article presents a case study of a major technical innovation in the core activity of payment processing in a UK bank. In describing the strategic rationale for the change and the process of implementation, the degree of consistency between the operational and organizational dimensions of the new system are examined. As this system is widely regarded as the benchmark for future paper processing in the industry, the factors contributing to successful innovation are discussed and the management rather than the technological aspects of this are emphasized. Competitor responses to the innovation are explained by the influence of traditional assumptions about the basis of competitive advantage in banking.

Introduction

In 1989 Midland Bank’s branch back office oper- ation was much the same as that of any other UK bank. By November 1991, Midland had effect- ively abolished the traditional back office and revolutionized the operation’s largest single task - cheque processing. The new system, based on eight large district service centres (DSCs), was not only put in place 1 month ahead of its tight schedule but also within its &50 million budget. The technological innovations of the project made the DSCs the first nationally integrated system of its type in the UK, and according to US experts, the world’s largest banking application of such pr0cesses.l Through the dramatic quality and cost improvements which resulted, the bank gained a

I The project can perhaps be seen as an early and sub- stantial example of business process re-engineering (BPR), although it was conceived before re-engineering became a popular term, and it is not our intention here to interpret the scheme in terms of the BPR literature.

new competitive edge and opened up further strategic opportunities, but its competitors chose not to imitate Midland’s example.

The paper briefly reviews the organizational literature on information technology (IT) innova- tion. It then describes the Midland DSC project in terms of its strategic rationale, the process of change management and the operational conse- quences of the new system. The final part ana- lyses the reasons for success and reflects on the responses of the rest of the industry before re- viewing what this case reveals about models of IT change in financial services.

IT innovation and organizational change

Models of IT innovation usually suggest that change occurs through strategic decision making in response to environmental demands and the opportunities presented by a menu of technical innovations (Earl, 1988; Scott Morton, 1991). There tends to be a built in assumption that man- agers know enough about the environment of the

0 1996 British Academy of Management

46 7: Morris and R. Westbrook

organization to respond appropriately and have the resources, time and incentive so to do and this may be reinforced by research methods which ex post ask actors involved in the process to recon- struct decisions about intention, process and outcomes.

In practice, many innovations fail to live up to end user expectations. Hidden set up and oper- ating costs diminish the expected benefits (Pavitt, 1991) and, because much technical change is relatively easily imitated, it does not lead to last- ing comparative advantage (Kay and Willman, 1993). Competitors catch up by acquiring techno- logies off the shelf from suppliers and may even benefit from not having to bear the costs of dev- elopment. In mature industries such as auto- mobile manufacture and banking the adoption of a new generation of technologies usually leads to new industry-wide standards of product quality and cost which become the minimum expected by customers and levels of process automation vary quite marginally between firms (Hayes and Aber- nathy, 1980; Womack et al., 1990). With their large and widely distributed customer base, retail banks have adopted broadly similar product and process innovations to manage core activities like money transmission and account information services. This enables them to provide generic products like cash distribution or debit card transactions through automated tellers.

Competitive pressures and technological oppor- tunities may explain the broad dimensions of technical innovation but a number of important organizational issues remain. First, technical in- novation does not on its own lead to competitive success. The work of the Massachusetts Institute of Technology group has concluded that IT is the platform on which success can be built but organ- izational factors are crucial to realizing the benefits of automating and ‘informating’ processes (Scott Morton, 1992; Zuboff, 1988). Hence, the reason why the benefits offered by IT have not been more frequently realized in banking as well as other industries relates to organizational issues and management failures rather than technical short- comings - although practising managers contest this claim. Second, the relationship between the properties of IT and organization design is not fixed. There is, of course, a long literature on the extent to which technology determines organiza- tional features and, as Willman (1986; 1993) has pointed out, part of the problem of the debate is

’

simply a definitional one regarding what is en- compassed by the term technology. However, very large IT applications create what Clark calls ‘strong imperatives’ for aspects of work and organ- ization (Clark, 1993, p. 13; McLoughlin and Clark, 1988). The effect is to impose a series of constraints and opportunities on management decisions about task design and the use of technology.

This raises the question of managerial object- ives and specifically the role of the chief executive (CEO). Schein (1992) observed that little is known about this role in the innovation process even though much of the literature on IT decision making emphasizes the importance of senior management commitment for success. Either management is treated in a relatively undiffer- entiated way, or the perspectives of specialists, such as IT experts, are contrasted with those of line managers. Schein’s work suggested distin- guishing features existed between CEOs’ basic assumptions about IT; some saw IT as having the potential to transform the organization including the way tasks were performed, work was organ- ized and indeed the basis of industry competition. Others were more pragmatic, limiting their sights to incremental cost saving and quality improve- ment. As the latter view was more prevalent among his (smallish) sample, Schein concluded that the heroic change agents of various case studies are unrepresentative: CEOs tend to re- spond to the myriad of forces acting on them and to see the limits and risks of technical inno- vation as much as the grand opportunities, balan- cing long and much shorter term considerations of cost and actual benefits of automation. Rarely do they lead innovation with a grand design of total transformation. This paper aims to contri- bute to this debate by exploring the role of the CEO in initiating and leading change, but we also emphasize the importance of taking into account the bank’s competitive situation and the norms of the industry regarding technical innovation, because of the way they framed managers’ assumptions about the timing, scope and object- ives of change.

The role of top managers links to the dynamics of the decision-making process. One dimension of this concerns the choice of technology and how this was ‘sold’ within the organization; another concerns the involvement of particular functional groups in the decisions about the innovation. Major IT changes tend to disrupt existing ways of

Technical Innovation and Competitive Advantage in Retail Financial Services 47

working, involve substantial resources and job loss and/or redesign. New power bases are often created thereby impinging on the distribution of power and influence within the organization. Understanding decisions about the design and process of change therefore involves exploring the extent to which rational actor models and straightforward costlbenefit analyses provide an explanation of change. Rational actor models would suggest there was a strong link between the strategic goals of the organization and the selec- tion and evaluation of the technological solution using analytical tools to guide decision making. Implementation plans would flow directly from the basic objectives involving different functions developing proposals which were consistent with the overall plan. By contrast, political approaches would see decision making as more of a negoti- ated process between different interest groups and a looser coupling between strategic goals and technology solutions (Pettigrew, 1973; Pfeffer and Salancik, 1974).

In the empirical analysis we explore these issues. We emphasize the context in which change oc- curred in the bank after a long period of decline as being critical to understanding the sort of decision making that took place and the nature of the technical solution that was chosen. We look at the formal business case which articulated the rationale for change and then consider what the priorities of the managers charged with carrying out the DSC project actually were. We suggest that a broadly consistent set of priorities gov- erned the actions of all of the managers involved, and that micropolitical differences, while not absent, were dwarfed by the overwhelming rec- ognition of the need to innovate successfully because of the deteriorating financial position of the bank. The new CEO was able to seize the opportunity this situation presented to galvanize his managers into action by a combination of a persuasive financial case and a promise that the technical solution was tried and tested. The project therefore combined (i) risk minimization in technical innovation with (ii) great potential reward in the short term and (iii) maintenance of continuity with existing organizational arrange- ments which we suggest underpinned the success of the change in the bank’s terms. Midland became the clear industry leader in processing costs but, intriguingly, its competitors did not seek to imitate it. We argue that this response reflects

widely held assumptions about how the industry competes and accepted ways of working. It also reflects a competitor perception that Midland was not a good role model given its previous failures. These factors acted as a brake on further tech- nical innovation in processing in the industry.

Research method

This research was carried out over a period of 2 years. A new DSC was visited and videotape used to record the process and interviews with a manager and a supervisor. This formed the basis of a teaching case in 1991. We were also given access to all the key documentation of Midland Bank, including the business case authorized by the board of directors, internal reports and com- munication videos and detailed quality and pro- ductivity data. Between November 1992 and June 1993 we visited another DSC where observation of work activities took place, performance meas- ures were examined and interviews with person- nel at various levels were conducted. We also gathered performance data from other sites, by which time they were well established. Between mid-1991 and July 1993 we interviewed the senior managers involved in the DSC project, who also commented in detail on an earlier draft of the paper. However, they sought only to correct facts, and not to influence our interpretation of events.

We have also co-directed a series of general management courses for Midland bank managers for several years. Hence we have had frequent formal and informal contact with many members of the bank during the whole period of the DSC initiative, in a situation where they felt able to express freely their hopes and anxieties. We have attended various in-house presentations when top management, including the chairman of the Mid- land Group and chief executive of the UK bank, outlined the strategy of the bank and the role of the DSC project within it. Lastly, we conducted interviews with senior managers within four other UK retail banks during 1992 and 1993, to obtain their reaction to Midland’s initiative and an in- dication of their own plans.

Part 1: Description of the DSC project Context: recent development of UK banks UK retail banks effectively operated as a cartel until 20 years ago. They monopolized money

48 Z Morris and R. Westbrook

transmission and were closely regulated by the Bank of England. Full disclosure of profits was not required until 1970. Thereafter, the emer- gence of new currency markets attracted foreign banks and competition for wholesale funds intensified (Nevin and Davis, 1970; Shaw and Coulbeck, 1983). On the retail side, building societies gradually encroached into the banks’ markets and competed particularly effectively for deposits. The banks responded by international diversification either through acquisition and direct representation or by establishing consort- ium arrangements with other banks. However, lending in both developed and less developed countries subsequently proved problematic and bad debt problems were evident by the end of the 1970s. During the early 1980s UK bank profit- ability was further depressed by the severe reces- sion. Progressive deregulation of the financial services industry permitted new competitors to become established.

Traditionally, a bank had grown by adding more branches to its network; ‘strategy’ was seen essentially in a number and location of branches. New technologies revolutionized several import- ant areas of banking, notably payment methods, currency trading, cash distribution and money transmission (Child and Tarbuck, 1985; Willman and Cowan, 1984) and new products, such as cash and debit cards, were developed on the back of the process innovation. These product and pro- cess innovations began to alter the role of branch networks. Customers rarely required a full range of services and could, and in some cases did, con- duct all their business without visiting a branch. Automatic teller machines could be located not only outside a bank branch but outside any other building. As early as 1977, the banks themselves prophetically observed: ‘The traditional bank branch, which virtually attempted to be a clearing bank in microcosm, is thus in some ways inap- propriate for contemporary needs.’ (CLCB, 1977) but only in 1992 with the Midland Bank’s DSC project was the logical consequence of this obser- vation realized. In the range of services to cus- tomers and in accounting and operational terms each branch stood as a self-contained unit. UK banks computerized their networks by the early 1970s and each branch processed its work and reconciled its ledgers daily. The cheques and cred- its were then cleared or exchanged at the clearing house. Up to two-thirds of each branch was given

over to back office operations and approximately 66 per cent of all staff were involved in this process (Morris, 1986).

The Midland Bank

Fifty years ago, Midland Bank was the largest in the world; by 1992 it was not even listed in the top 100 largest banks by net asset value. Its decline began in the immediate post-war years when its senior management proved over-cautious. Later, when mergers and acquisitions created fewer, larger competitors it failed to take the oppor- tunity to protect its competitive position in the domestic market by pursuing a merger. The Midland also chose not to establish a wholly owned international structure as it already had the largest correspondent banking network. It became more reliant on the weak UK economy than the other clearing banks and from the late 1970s had been consistently out of line in terms of the costhcome ratio which measured operating efficiency.

More urgent problems occurred with the pur- chase of Crocker Bank in California in 1980. This looked like a sound strategic move to provide the Midland with an entree to the richest regional market in the world, but Crocker was over- exposed to the volatile local Californian property market wherein it incurred considerable bad debts which Midland had to take on to its own books. It subsequently sold Crocker for a nominal sum but under the terms of the sale was obliged to retain a substantial proportion of the outstanding debt. The episode badly affected the morale of the organization and weakened Midland’s ability to compete by eating into its asset base.

Despite (or perhaps because of) this setback, Midland was an innovative organization, adding many new product lines in the marketing-led 1 9 8 0 ~ ~ experimenting with branding and new branch design, and setting up the UK’s first telephone-based, full-banking service. At that stage, however, the bank’s systems could not always deliver all these products satisfactorily. This division between marketing and operations was compounded by the difficulty of communic- ating the developing strategic rationale to all 50000 staff. This led to more frustration in the branch network.

To revive the bank’s fortunes, a new team under chairman Sir Kit McMahon was appointed

Technical Innovation and Competitive Advantage in Retail Financial Services 49

in the mid-1980s and a new corporate strategy was developed. One aspect of this was a proposed partnership with the Hong Kong and Shanghai Bank to establish an international network and bring in new assets on which the new group’s lending could expand. Another was a dramatic cost reduction in the UK banking arm, principally by developing a new system of centralized pay- ment clearing through DSCs. The bank’s inten- tion was to become by 1992 the lowest cost processor in Europe of cheques and credits and ultimately of other types of payment.

Pressure for cost reduction

In all of the retail banks, much of their operating cost was traditionally bound up with the proces- sing of cheques and credits through the clearing system. In 1989, some 72 per cent of Midland’s total operating cost was estimated to be incurred by the back office area of the branches which undertook this processing. Although the UK retail bank made profits throughout the 1980s, senior executives believed that centralization would reduce the cost of clearing an item sub- stantially and, given an annual volume of over 300 million items of clearing, a reduction of the scale forecast would improve the bank’s perform- ance considerably.

It is worth emphasizing that Midland’s need to exploit its assets more productively was greater than its competitors following the Crocker losses. These left the balance sheet so weakened that there were severe limits on its ability to lend to generate profits and meant that it had to pursue cost reduction more aggressively instead. This prompted it to replace managers associated with the old regime with senior executives from out- side the bank, an unprecedented move in the banking industry. Among the new managers was Gene Lockhart, an American with wide consult- ing experience in IT in financial services. Lock- hart had taken responsibility for IT, then run the whole of the operations side before becoming the CEO of the bank. He brought new ideas and models of organizing based on best practice in the US and a very good knowledge of industry technology. He strongly advocated the strategy of separating operations and sales functions by centralizing the main payment operations on the grounds that this would realize cost reductions in under 4 years. Evidence from the US, where some

of the new managers had worked showed savings from centralizing processing of the order of 20-30 per cent in retail banks. As part of the 1988 Group Cost Reduction Programme, the strategy of func- tional separation was endorsed and, as one part of this, the proposal to centralize payment process- ing was agreed in principle.

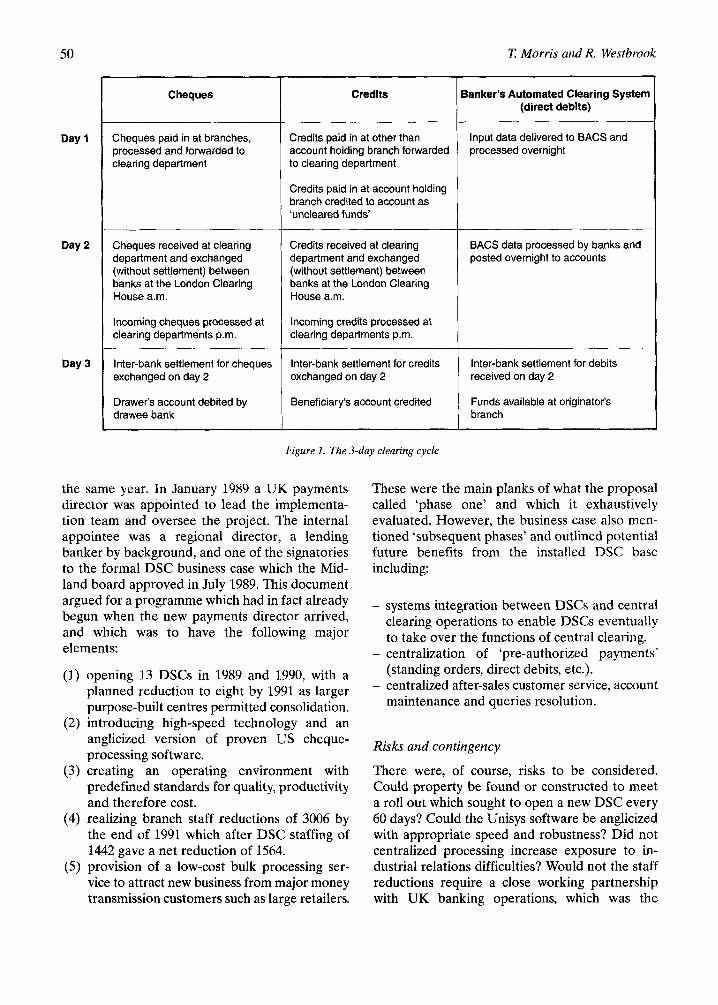

Payment processing - an early centralization initiative

The 3-day clearing system for UK banks is described in Figure 1. An early initiative to cen- tralize day 1 of this process had been tried by Midland in the late 1970s when operational centres were established to service geographical areas of the network. These centres handled not only money transmission but other functions such as account opening and standing orders with the longer term objective of minimizing paper processing in branches. By the early 1980s the initiative was in difficulty because:

the removal of data from the branches made it more difficult to resolve customer problems as the branches had to refer to the centres for the appropriate information and corrective action. operational efficiency suffered because the centres were multipurpose and staffed and managed by branch employees with little experience of mass processing. centres operated on the bank’s standard opening hours (0900-1700 hours) but most of the work arrived in the evening, when staff had to be retained on overtime. many of the centres were located in urban areas and difficult to access, which created distribution delays and increased costs.

The outcome was a decision not to extend the coverage of the operations centres but to keep some of them operating in order to realize the re- turn on the capital investment. However, the basic strategy of cost reduction through centralized processing remained. It was to be embodied in a new project to provide the network with DSCs as a major part of the attack on the cost base.

DSC: the proposal

Feasibility analysis began in March 1988, and a pilot operation was conducted in September of

T Morris and R. Westbrook 50

Day 1

Day 2

Day 3

Cheques

Cheques paid in at branches, processed and forwarded to clearing department

Cheques received at clearing department and exchanged (without settlement) between banks at the London Clearing House a.m.

Incoming cheques processed at clearing departments p.m.

Inter-bank settlement for cheques exchangedonday2

Drawer’s account debited by drawee bank

~ ~~

Credits

Credits paid in at other than account holding branch forwarded to clearing department

Credits paid in at account holding branch credited to account as ‘uncleared funds’

Credits received at clearing department and exchanged (without settlement) between banks at the London Clearing House a.m.

Incoming credits processed at clearing departments p.m.

Inter-bank settlement for credits exchangedonday2

Beneficiary’s account credited

~

Sanker’s Automated Clearing System (direct debits)

Input data delivered to BACS and processed overnight

BACS data processed by banks and posted overnight to accounts

Inter-bank settlement for debits received on day 2

Funds available at originator’s branch

Figure 1. The 3-day clearing cycle

the same year. In January 1989 a UK payments director was appointed to lead the implementa- tion team and oversee the project. The internal appointee was a regional director, a lending banker by background, and one of the signatories to the formal DSC business case which the Mid- land board approved in July 1989. This document argued for a programme which had in fact already begun when the new payments director arrived, and which was to have the following major elements:

(1) opening 13 DSCs in 1989 and 1990, with a planned reduction to eight by 1991 as larger purpose-built centres permitted consolidation.

(2) introducing high-speed technology and an anglicized version of proven US cheque- processing software.

(3) creating an operating environment with predefined standards for quality, productivity and therefore cost.

(4) realizing branch staff reductions of 3006 by the end of 1991 which after DSC staffing of 1442 gave a net reduction of 1564.

( 5 ) provision of a low-cost bulk processing ser- vice to attract new business from major money transmission customers such as large retailers.

These were the main planks of what the proposal called ‘phase one’ and which it exhaustively evaluated. However, the business case also men- tioned ‘subsequent phases’ and outlined potential future benefits from the installed DSC base including:

- systems integration between DSCs and central clearing operations to enable DSCs eventually to take over the functions of central clearing.

- centralization of ‘pre-authorized payments’ (standing orders, direct debits, etc.).

- centralized after-sales customer service, account maintenance and queries resolution.

Risks and contingency

There were, of course, risks to be considered. Could property be found or constructed to meet a roll out which sought to open a new DSC every 60 days? Could the Unisys software be anglicized with appropriate speed and robustness? Did not centralized processing increase exposure to in- dustrial relations difficulties? Would not the staff reductions require a close working partnership with UK banking operations, which was the

Technical Innovation and Competitive Advantage in Retail Financial Services 51

central operations function of Midland, embraced all central processing, and which had its own separate organization? The proposers were here rightly prudent, for most of these points became issues which hindered implementation. Their approach was to plan an implementation process which would contain these risks. Thus, in the case of potential industrial relations difficulties, the following steps were taken:

- a formal negotiating structure was agreed with the banking union.

- detailed contingency plans for each DSC to cover labour or other disruption.

- capacity planning which embraced the whole national system, including formal ‘twinning’ of DSCs, for mutual coverage.

- systems and telecommunications configura- tions in which no single failure point could have wider impact.

Similar caution prevailed in selecting a supplier. Although only two companies, IBM and Unisys, were feasible choices, a thorough selection pro- cess decided on the latter because they had:

- undertaken to relocate experienced support resources to the UK.

- resolved to meet Midland’s rapid roll out schedule.

- offered a total solution not involving third- party suppliers.

- shown the capability to provide a system which would ultimately integrate into central clearing.

- the ability to be upgraded for ‘image’ processing.

- already anglicized their software for a building society.

None the less, on this last point major modifica- tions were still needed for Midland’s application which were developed with the supplier through structured project reviews to, in the words of the proposal,

‘contain the risks to an acceptable level.’

Implementation

Formal board approval (July 1989) was followed within 2 months by the opening of the first

purpose built DSC at Bristol. The need for rapid implementation thereafter was increased by Midland’s worsening trade position. The DSC programme was a major commitment at a time of severe cash constraint yet the UK payments director received handwritten notes from the chairman specifically exempting the project from the general group-wide policy to contain costs and emphasizing the importance of speedy pro- gress. Despite the haste, there was no cutting of corners on project management; the programme consisted at one stage of 136 individual projects, each with specific tasks and targets.

Responsibility for the project development and implementation lay in the central operations division which was separate from the sales divi- sion of the bank which ran the branches. There- fore the DSC project team consisted of operations managers whose concerns were to make the centralized processing work and thereby achieve the unit cost improvements set out in the business plan. It is worth noting, however, that the actual payback for the project investment was to come through head-count reductions in the branches, and although feasibility exercises calculated the numbers involved, this had been a central exer- cise. Little concern with the application of the resulting formula at branch level existed at this stage, and there was no representative from the branch hierarchy in the project team. This was to have ramifications subsequently.

The DSC: operations

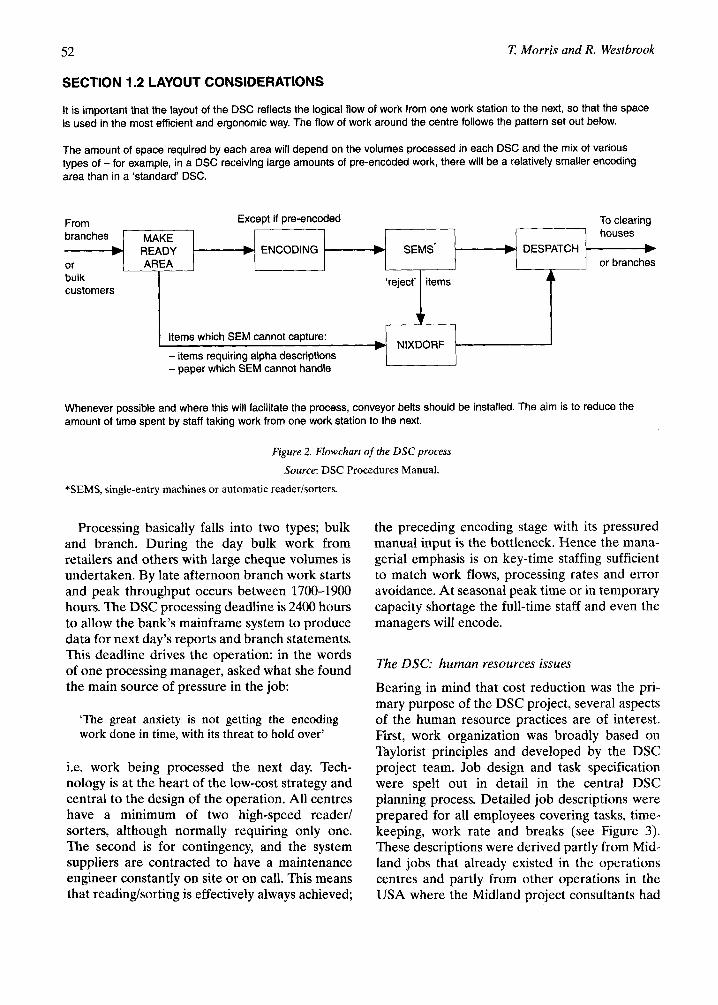

The DSC contrasts with a branch back office in two main ways: scale and dedication. Unlike the range of tasks undertaken in a back office, a DSC (in 1992) existed only to process cheques and credits. It is a prime example in a service industry of what in manufacturing is called a ‘focused factory’ (Skinner, 1974). Processing over 300 mil- lion items from branches each year in only eight centres is possible because a dedicated process can be engineered for continuous work flow at peak periods. Also the scale permits investment in very high speed technology with over 60000 items read and sorted per hour. Automatic reading and sorting are, however, not the only stages of the process; cheques must first be manually encoded to enable them to be machine read. The whole DSC process is shown in Figure 2.

52 T Morris and R. Westbrook

branches MAKE

or AREA b READY b ENCODING + SEMS’ b DESPATCH

SECTION 1.2 LAYOUT CONSIDERATIONS

houses * or branches

It is important that the layout of the DSC reflects the logical flow of work from one work station to the next, so that the space is used in the most efficient and ergonomic way. The flow of work around the centre follows the pattern set out below.

The amount of space required by each area will depend on the volumes processed in each DSC and the mix of various types of - for example, in a DSC receiving large amounts of pre-encoded work, there will be a relatively smaller encoding area than in a ‘standard‘ DSC.

bulk ‘reject’ customers

items 4

Whenever possible and where this will facilitate the process, conveyor belts should be installed. The aim is to reduce the amount of time spent by staff taking work from one work station to the next.

Items which SEM cannot capture:

- items requiring alpha descriptions 7

Figure 2. Flowchart of the DSC process

Source: DSC Procedures Manual.

NIXDORF

*SEMS, single-entry machines or automatic readerkorters.

Processing basically falls into two types; bulk and branch. During the day bulk work from retailers and others with large cheque volumes is undertaken. By late afternoon branch work starts and peak throughput occurs between 1700-1900 hours. The DSC processing deadline is 2400 hours to allow the bank’s mainframe system to produce data for next day’s reports and branch statements. This deadline drives the operation: in the words of one processing manager, asked what she found the main source of pressure in the job:

‘The great anxiety is not getting the encoding work done in time, with its threat to hold over’

i.e. work being processed the next day. Tech- nology is at the heart of the low-cost strategy and central to the design of the operation. All centres have a minimum of two high-speed reader/ sorters, although normally requiring only one. The second is for contingency, and the system suppliers are contracted to have a maintenance engineer constantly on site or on call. This means that readinghorting is effectively always achieved;

the preceding encoding stage with its pressured manual input is the bottleneck. Hence the mana- gerial emphasis is on key-time staffing sufficient to match work flows, processing rates and error avoidance. At seasonal peak time or in temporary capacity shortage the full-time staff and even the managers will encode.

The DSC: human resources issues

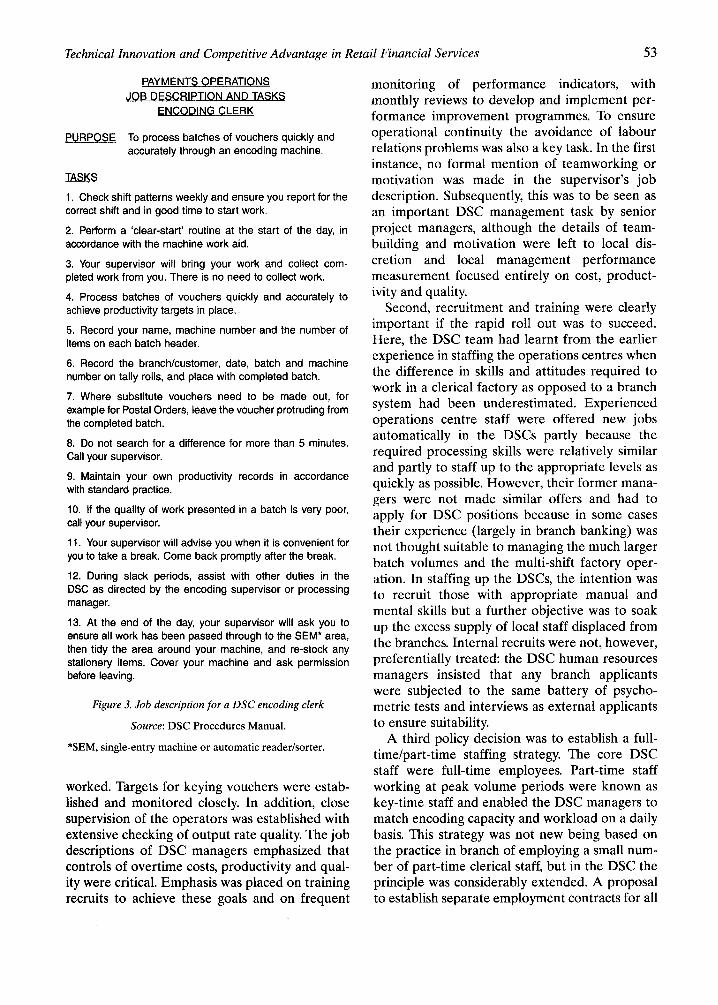

Bearing in mind that cost reduction was the pri- mary purpose of the DSC project, several aspects of the human resource practices are of interest. First, work organization was broadly based on Taylorist principles and developed by the DSC project team. Job design and task specification were spelt out in detail in the central DSC planning process. Detailed job descriptions were prepared for all employees covering tasks, time- keeping, work rate and breaks (see Figure 3) . These descriptions were derived partly from Mid- land jobs that already existed in the operations centres and partly from other operations in the USA where the Midland project consultants had

Technical Innovation and Competitive Advantage in Retail Financial Services 53

PAYMENTS OPERATIONS JOB DESCRIPTION AND TASKS

ENCODING CLERK

PURPOSE To process batches of vouchers quickly and accurately through an encoding machine.

TASKS

1. Check shift patterns weekly and ensure you report for the correct shift and in good time to start work.

2. Perform a ‘clear-start‘ routine at the start of the day, in accordance with the machine work aid.

3. Your supervisor will bring your work and collect com- pleted work from you. There is no need to collect work.

4. Process batches of vouchers quickly and accurately to achieve productivity targets in place.

5. Record your name, machine number and the number of items on each batch header.

6. Record the branch/customer, date, batch and machine number on tally rolls, and place with completed batch.

7. Where substitute vouchers need to be made out, for example for Postal Orders, leave the voucher protruding from the completed batch.

8. Do not search for a difference for more than 5 minutes. Call your supervisor.

9. Maintain your own productivity records in accordance with standard practice.

10. If the quality of work presented in a batch is very poor, call your supervisor.

11. Your supervisor will advise you when it is convenient for you to take a break. Come back promptly after the break.

12. During slack periods, assist with other duties in the DSC as directed by the encoding supervisor or processing manager.

13. At the end of the day, your supervisor will ask you to ensure all work has been passed through to the SEM* area, then tidy the area around your machine, and re-stock any stationery items. Cover your machine and ask permission before leaving.

Figure 3. Job description for a DSC encoding clerk

Source: DSC Procedures Manual.

*SEM, single-entry machine or automatic readerlsorter.

worked. Targets for keying vouchers were estab- lished and monitored closely. In addition, close supervision of the operators was established with extensive checking of output rate quality. The job descriptions of DSC managers emphasized that controls of overtime costs, productivity and qual- ity were critical. Emphasis was placed on training recruits to achieve these goals and on frequent

monitoring of performance indicators, with monthly reviews to develop and implement per- formance improvement programmes. To ensure operational continuity the avoidance of labour relations problems was also a key task. In the first instance, no formal mention of teamworking or motivation was made in the supervisor’s job description. Subsequently, this was to be seen as an important DSC management task by senior project managers, although the details of team- building and motivation were left to local dis- cretion and local management performance measurement focused entirely on cost, product- ivity and quality.

Second, recruitment and training were clearly important if the rapid roll out was to succeed. Here, the DSC team had learnt from the earlier experience in staffing the operations centres when the difference in skills and attitudes required to work in a clerical factory as opposed to a branch system had been underestimated. Experienced operations centre staff were offered new jobs automatically in the DSCs partly because the required processing skills were relatively similar and partly to staff up to the appropriate levels as quickly as possible. However, their former mana- gers were not made similar offers and had to apply for DSC positions because in some cases their experience (largely in branch banking) was not thought suitable to managing the much larger batch volumes and the multi-shift factory oper- ation. In staffing up the DSCs, the intention was to recruit those with appropriate manual and mental skills but a further objective was to soak up the excess supply of local staff displaced from the branches. Internal recruits were not, however, preferentially treated: the DSC human resources managers insisted that any branch applicants were subjected to the same battery of psycho- metric tests and interviews as external applicants to ensure suitability.

A third policy decision was to establish a full- time/part-time staffing strategy. The core DSC staff were full-time employees. Part-time staff working at peak volume periods were known as key-time staff and enabled the DSC managers to match encoding capacity and workload on a daily basis. This strategy was not new being based on the practice in branch of employing a small num- ber of part-time clerical staff, but in the DSC the principle was considerably extended. A proposal to establish separate employment contracts for all

54 i7 Morris and R. Westbrook

DSC staff was put forward but rejected as too sensitive in industrial relations terms, thereby raising the risk of delay in the roll out. It was also thought likely to give the wrong impression to other operations staff about the importance attached to the DSC and potentially to restrict mobility in and out of the DSCs.

This had important consequences for jobs, careers and rewards. For the job structure it meant that specific jobs were not allocated to full- or key-time staff as the DSC team had first planned as part of their employment model. Additionally, a career development path was established through the DSC jobs from encoder to supervisor which was open to full- and key- time staff. This career path was designed to aid recruitment from within and without the bank and for that reason it mirrored the practices of the branch banking system. Also, employees who transferred from full-time clearing to key-time DSC work retained their right to shift premia, although former key-time clearing staff did not, which caused some friction.

Similarly, the conventional hourly based pay structure was transferred from the bank to the DSC. This was despite efforts to develop an indi- vidual based performance-pay system initiated by the DSC team and investigated by a consulting firm on their behalf. The performance pay model was rejected for a number of reasons. These included the difficulty of establishing reliable per- formance measures in a greenfield operation, the lack of reliable management information in the early phase of the project and because a number of tasks were not susceptible to meaningful per- formance measures. Information difficulties also made group-based bonuses difficult to apply and although subsequently the quality of performance data improved to the extent that a DSC-wide bonus would have been feasible, by then it was deemed unnecessary as productivity and cost targets had been achieved.

The progress of the DSC programme was not without problems. The first DSC was reviewed 5 months into the programme, and an internal report made the following points.

(1) The volumes of work processed by all DSCs were broadly in line but the mix differed from plan: bulk (i.e. retailers and other big corpor- ate cheque processors) levels were 50 per cent above plan; branch volumes were 50 per

cent lower. Midland appeared to have gained market share in the bulk processing market, which produced over 51 million new revenue, but it then faced stiff competition on pricing and processing times from other banks using their branches to provide similar levels of service (i.e. next day crediting of funds).

(2) The roll out of the DSC in Bristol had not gone smoothly and was suspended as recti- fication of problems with the anglicization of American software for the new high product- ivity readerkorters took place. This delayed the transfer of bulk processing by 4 weeks and branch processing by 6 weeks with conse- quent delays in the branch linkage to the DSC and thus delays in head-count reductions.

(3) The slippage in the roll out could partly be made up by staff savings in future as actual productivity standards in the DSC were higher than planned. The achievement of the low-voucher processing cost was realistic, representing a significant gain on the branch processing system.

(4) Branch reductions in staff were much lower than planned. Investigation by the imple- mentation review team put expected head- count savings at 77-80 per cent of original plan. The impact on the financing of the DSCs was an extension in the payback period.

A further review of the same DSC in April 1990 focused on staff performance. Several prob- lems between the branches and the DSC were un- covered including:

(1) standards of presentation of work from the branches, affecting DSC throughput and productivity.

(2) encoding and voucher problems at the DSC which caused customer account problems at the branch and customer complaints over quality.

These difficulties arose out of the forementioned software problems and the speed of the roll out which made it difficult to communicate the rationale for the changes adequately. They were compounded by the reliance in the DSCs on key- time staff who had little experience of bank work. By February 1990, some full-time DSC staff were calling for a ballot on industrial action to resolve their grievances. These revolved around changes

Technical Innovation and Competitive Advantage in Retail Financial Services 55

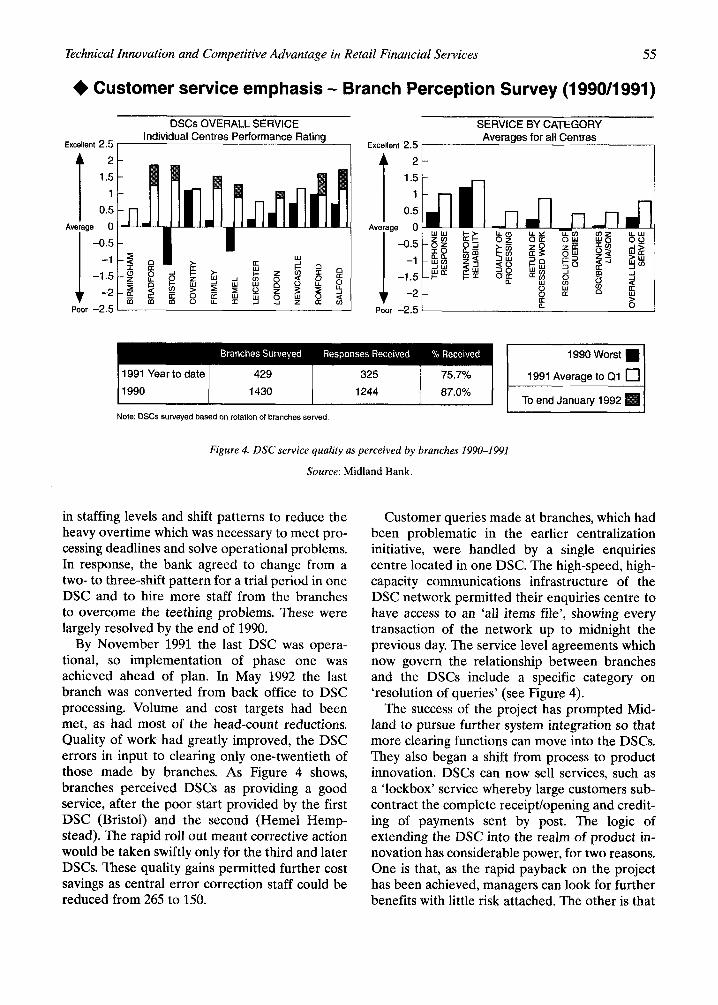

+ Customer service emphasis - Branch Perception Survey (1 990/1991)

DSCs OVERALL SERVICE SERVICE BY CATEGORY Individual Centres Performance Rating Averages for all Centres

Excellent 2.5 I I Excellent 2.5 I

a

1991 Year to date 429 325 75.7% 1990 1430 1244 87.0%

I Note: DSCs surveyed based on rotation of branches Served.

Figure 4. DSC service quality as perceived by branches 1990-1991

Source: Midland Bank.

in staffing levels and shift patterns to reduce the heavy overtime which was necessary to meet pro- cessing deadlines and solve operational problems. In response, the bank agreed to change from a two- to three-shift pattern for a trial period in one DSC and to hire more staff from the branches to overcome the teething problems. These were largely resolved by the end of 1990.

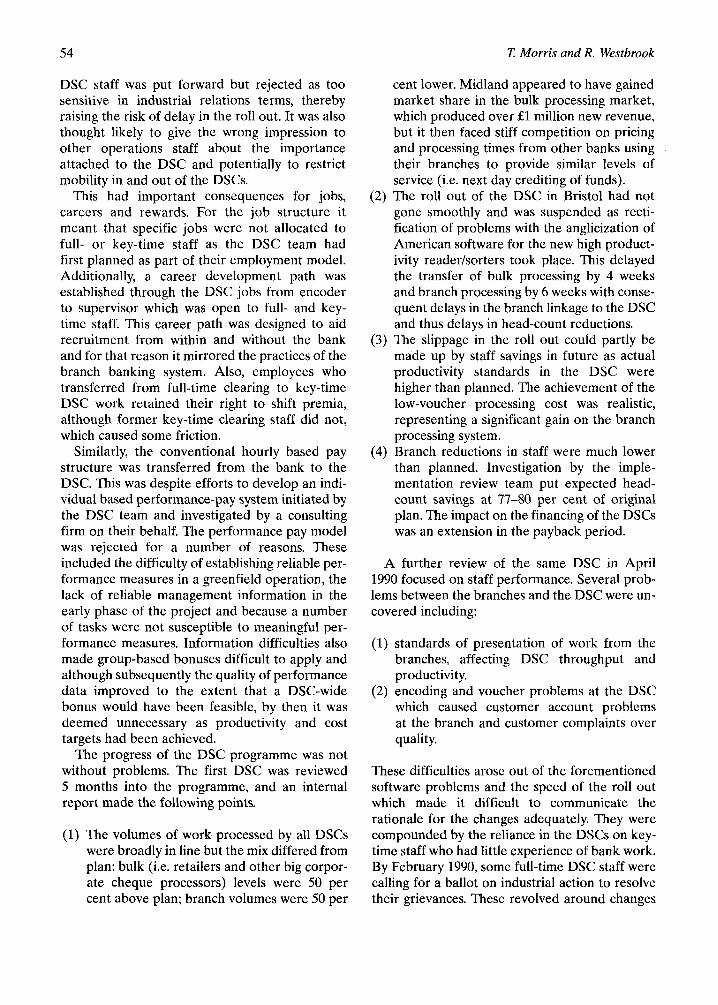

By November 1991 the last DSC was opera- tional, so implementation of phase one was achieved ahead of plan. In May 1992 the last branch was converted from back office to DSC processing. Volume and cost targets had been met, as had most of the head-count reductions. Quality of work had greatly improved, the DSC errors in input to clearing only one-twentieth of those made by branches. As Figure 4 shows, branches perceived DSCs as providing a good service, after the poor start provided by the first DSC (Bristol) and the second (Hemel Hemp- stead). The rapid roll out meant corrective action would be taken swiftly only for the third and later DSCs. These quality gains permitted further cost savings as central error correction staff could be reduced from 265 to 150.

Customer queries made at branches, which had been problematic in the earlier centralization initiative, were handled by a single enquiries centre located in one DSC. The high-speed, high- capacity communications infrastructure of the DSC network permitted their enquiries centre to have access to an ‘all items file’, showing every transaction of the network up to midnight the previous day. The service level agreements which now govern the relationship between branches and the DSCs include a specific category on ‘resolution of queries’ (see Figure 4).

The success of the project has prompted Mid- land to pursue further system integration so that more clearing functions can move into the DSCs. They also began a shift from process to product innovation. DSCs can now sell services, such as a ‘lockbox’ service whereby large customers sub- contract the complete receipt/opening and credit- ing of payments sent by post. The logic of extending the DSC into the realm of product in- novation has considerable power, for two reasons. One is that, as the rapid payback on the project has been achieved, managers can look for further benefits with little risk attached. The other is that

56 T Morris and R. Westbrook

they have a first-mover strategic advantage in central processing which may be exploited, for example to become the processing specialist for the industry as a whole, an attractive strategy given the number of competitiors seeking to provide lending facilities and hence the poor margins to be earned there. But other retail banks have been prepared to lower their processing prices to bulk customers to match Midland’s offer, thereby limiting its gains. Meanwhile, discussion of the rationalization of processing in the industry has continued at the industry level but without radical change being achieved.

Competitor reaction

What was the reaction of other UK banks to Midland’s DSC initiative? We asked senior mana- gers in four other retail banks to describe their own approach to cheque processing, and their view of the Midland approach.

Decentralized processing. Each of the other banks currently does cheque processing either in most branch back offices as before (one example) or uses some version of ‘clustering’, i.e. smaller branches send work to the nearest large branch which has dedicated staff and equipment to pro- cess it. One of the four was planning to become much more centralized than Midland using just two service centres by the end of the decade. No one intended following Midland’s regionalized set up, although all had considered it with varying degrees of thoroughness.

Redundancies. All the banks had announced substantial branch closure and redundancy pro- grammes, which were later and, pro-rata, larger than the Midlands. All had come under the same costhncome ratio pressure in an environment commonly described as ‘overbanked’.

Reaction to Midland. Admiration for the effect- iveness with which Midland had carried out its change was tempered with views that the result- ant configuration was not the right longer term solution. There was a clear sense that Midland had acted speedily because it had to, and suc- ceeded because the change had a high profile in the organization and top management support. One change manager, envious of the resources given to Midland’s project, remarked

‘I am Gene Lockhart and Chris Thorn (the DSC project director) rolled into one, and when I started I was a low grade middle manager. They started with a pull from the top.’

(Also worthy of note was that the banks were very familiar with what the others were doing and who the key individuals were.)

Although the Midland system was agreed to be an impressive achievement, this was mainly due to the dramatic improvement in error reduction.

‘There are internal targets for reject rates ... and league tables between the individual banks are published to humiliate. Years ago we used to laugh at Midland because they were always bottom of the heap, we had a great time pointing this out to the Midland guy . . . But they’ve had a good sort out and now they’re doing very well.’

One reason for not changing was the falling cheque volumes which started to occur after 1992 as substitute card-based systems devel- oped. All the banks took the view that Midland had excess processing capacity of 2 years after the DSC programme was completed and would need to close a number of centres. Also, as the quote here suggests, there was an implicit re- luctance to accept Midland, the UK banking world’s underperformer in the ’eighties, as a model for change.

Subsequent developments 1992-1 994

In a sense this scepticism on the part of Midland’s competitors was justified, for the improvement in Midland’s fortunes was insufficient to keep it independent. After the announcement of disap- pointing results in 1991, Sir Kit McMahon was replaced as CEO by Brian Pearse. Pearse came from Barclays Bank and his arrival signalled a reassertion of traditional branch banking values and a strong emphasis on improving customer service. In 1992 there followed a takeover struggle for Midland, with Lloyds Bank, reportedly keen to gain access to Midland’s DSC network, eventually losing out to the Hong Kong and Shanghai Banking Corporation Group (HSBC). In seeking a return for its g3.7 billion purchase, HSBC has switched Midland’s strategy from cost reduction to growth in market share. In 1994, Keith Whitson, whose whole career has been in HSBC, became Midland CEO on Pearse’s

Technical Innovation and Competitive Advantage in Retail Financial Services 57

retirement. (Lockhart had departed once the HSBC takeover had gone through.)

In 1993, partly due to the rapid success of debit cards in the UK - another innovation in which Midland played a leading role - cheque volumes fell for the first time. Midland therefore closed one DSC (Heme1 Hempstead) in late summer 1994, and pressed ahead with plans to move more back office functions from branches into the DSC network.

Part 2: Discussion Why did it succeed?

Midland’s DSC programme is in the bank’s own terms a success story of IT-based innovation which has attracted international interest. We have seen that the research literature emphasizes such factors as the role of top management and the importance of organizational innova- tion and commitment to change. This case shows the need to look at the internal and external contexts and supports the role of multidisciplinary case research in understanding complex change processes.

In many ways the DSC programme was a high- risk project. To introduce new technology on such a scale and in a very short time was unpreced- ented in the industry. There are many reasons why the organization achieved it, and we organize these into five categories: top management com- mitment, project management, past experience of centralization, human resource management, and internal marketing.

Top management commitment. Traditional strat- egy in the industry had, in the words of one senior manager,

‘always been “me-too”.’

The final argument to persuade anyone was usually

‘and anyway, it’s what the other banks are doing,’

Deregulation and the freeing of competition meant more radical sources of advantage had to be found. Midland was the bank under most cost pressure and had already shown an ability to innovate in products and marketing.

This partly explains why the DSC programme and the timing of the initiative came from Mid- land. But it still required top management to push it through and give some of the group’s increas- ingly scarce resources to it. Factors behind this include, first, the high-public prowe of a major bank faced with falling profits, and the conse- quent need to be seen by the market to be taking action; second, the influence of Gene Lockhart, who had recently joined the bank but knew this solution could be made to work. Several inter- views emphasized the importance of Lockhart’s persuasive ability to communicate his vision to the other senior management and get them to support the change. Third, the project was protected by the Midland chairman from cost- cutting pressures which could have changed its scale and delayed implementation. Additionally, the collective experience in the bank of former centralizing initiatives, which were seen as flawed in execution rather than conception, was impor- tant. Once committed, top management gave the fullest possible support to the implementation team because they believed in the principle of centralization. Thus the key role of top man- agement, so much emphasized in innovation literature, is reinforced by this case.

Project management. The scheme was ambitious in scale, but appropriately limited in scope. The project goals were very clearly, even narrowly, defined (see section on the proposal described earlier). Not only was there no ambiguity but there was no internal conflict between the operational parameters by which success would be measured - volume, cost and quality. Once the volumes were achieved the costs would fall, and the automation which made volume and cost targets feasible also would ensure fewer errors than the less integrated and more manual processes it replaced. This congruence of goals is not always characteristic of service environments, where higher quality can mean higher cost; it was the advanced technology, production engineering and work-flow tracking which showed the way to gain simultaneous improvement in cost and quality. (At least in a control-oriented, ‘errors/ million’ definition of quality.)

As this was a large-scale initiative in which much was new, the first two DSCs were also effectively pilot operations in which experiments with the hardware and software and with the

58 T. Morris and R. Westbrook

allocation of tasks were conducted. Considerable teething problems were experienced but the solu- tions were documented and fed into a central model for operations and human resources for application in subsequent DSCs as they came on line. This allowed the bank to achieve a rapid implementation programme despite the novelty of the scale of the DSCs.

We have also shown how the project team assessed risk, made contingencies and managed suppliers. The team contained (or could draw on) all the relevant disciplines and the key role of project leader was given to the UK payments director, a lending banker who well understood the needs of the customers in the branch network. The high internal profile of the project meant that help could be obtained on any issue as it arose.

Past experience of centralization. Midland learned from the earlier centralization initiative that if the strategic gains were to be made certain then the operational detail had to be completely rethought. Each error made in the late 1970s - locationltransport, staff hours, scale, focus, etc. - was specifically reversed in the model of the late 1980s. Indeed, an earlier version of Midland’s internal communications video begins with the UK payments director enumerating the past errors and explaining specifically how the DSCs will overcome them, not least to persuade those staff with longer memories to see the move in a positive light. New technology and greenfield sites facilitated a thorough review of the process engineering, and the implementation team frankly referred (at least among themselves) to DSCs as ‘factories’, but saw this as having no negative con- notation, rather it conveyed an image associated with high productivity and low cost.

A further aspect of learning concerned the value of greater centralization as a means to cut costs. Hence, the bank began to think about the benefits of further centralizing including other forms of payment processing such as automated payments and account management. With the latter initiative customers would have their ac- counts handled from an area office rather than a local branch. Associated with centralization was the perceived benefit of management specializa- tion. DSCs were staffed and run by operation specialists who ran large batch, high-volume pro- cessing factories with shift working. Traditionally, the bank had based its management development

on the virtues of generalism so that branch bankers had to have some experience of opera- tions. This had provided flexibility in manage- ment deployment but also led to unnecessary duplication of skills. In the new system, staffing policy was based on a much clearer differentia- tion between the management skills required for processing work and that required for selling in the branches.

Human resource management. The bank sought limited change in its management of human resources and in many respects emphasized continuity to gain acceptance of change. As processing factories, the DSCs were organized in classic Taylorist terms. Taylorism in organization theory and human resource management terms is problematical (Walton, 1985; Wood, 1989), but from an operations viewpoint it remains a viable path to high productivity in a process requiring varying staff capacity. A Taylorist solution fitted with the existing model of centrally organizing staff in a large number of branches to do a range of tasks in similar ways, thereby ensuring consist- ency of output and staff transferability. It was thus a familiar strategy to implement and one that managers felt confident they could apply. This was important given the need for a rapid imple- mentation programme and the capacity to trans- fer staff in from the existing branch network. Longer term questions of staff retention and motivation were deliberately postponed until it was evident that the financial payback was occur- ring. DSC managers were then encouraged more to think about developing teamwork and morale.

However, it is worth noting that the bank did not rely solely on tight managerial control to achieve productivity. Midland followed the strong advice of their US consultants that staff product- ivity would require a high-grade environment, and the DSCs are appropriately clean, well lit and have well appointed facilities. One of the subtler messages that this was intended to reinforce was that the management of banking operations, pre- viously seen in the organization’s culture as a less valued activity than lending, was now a key to the group’s future.

In industrial relations terms the central concern was to minimize the risk of disruption while implementing the DSC programme and gain the benefits of centralization as soon as possible. For a start the bank openly offered the union full

Technical Innovation and Competitive Advantage in Retail Financial Services 59

recognition, to avoid the possibility of a union campaign. Managers determined what could be conceded (in the interests of rapid implement- ation) and what could not. The full-time/key-time ratio is an example where management saw a growing proportion of key-time workers as essen- tial for rising productivity, and could not concede to union demands for fixed ratios. Yet DSC shift premia which the union wished to be the same as in branches were seen by management as an issue which would take months to resolve if resisted and not essential to productivity in an operation based mainly on key-time staff. It was therefore conceded, The clear focus on productivity en- abled the DSC team to separate the essential, the desirable and the dispensable features of their goal at each stage.

While the human resource function was not an architect of the change it became involved in all of the implementation stages. Human resource managers saw their goal as being to ensure that the DSCs were staffed as quickly as possible and that efficiency levels were reached within planned times. The function was strongly conformist with business principles and with the traditions of personnel management in the bank so that issues of job redesign or innovation in work organiza- tion did not arise. It was also of importance to the function that to retain the respect of line mana- gers no very radical changes were proposed. In Legge’s terms, this was a classic case of conformist personnel management rather than innovation (Legge, 1993). The explanation for the policy line adopted by the human resource function was based on the need for a pragmatic and quick solution to a one-off event and one that offered predictability of outcome.

Internal marketing. The Bristol episode re- vealed that communications problems, always an issue in such a large and dispersed organization, had been exacerbated by the speed of the roll out and the association of the DSC initiative with branch cost cuts. A video was produced to explain the rationale for the changes and what they meant for the branch network. The message was very much one of reorienting the branches to a role focused on selling and on customer service. The DSC would remove back office functions so that staff would not be distracted from their key role. Those staff who preferred processing tasks would be able to concentrate on that work in a DSC.

DSCs enter into formal service level agree- ments with the branches that they serve, in which performance standards are set for both parties. At the same time regular branch perception surveys have been instituted to monitor the service given by DSCs. These surveys show a steady increase in the satisfaction expressed by branches with DSC service (compare January 1992 with earlier per- formance in Figure 4). But they also showed that management was determined to measure and monitor progress, not just to assume it would happen.

Conclusion

We have, then, a case of successful IT change which was not imitated by competitors and in our conclusions we want to consider why this was the case. One argument might be that technical change is progressively rendering the DSCs redundant: cheques volumes are falling and card payments rising. The number of DSCs has already been reduced. However, the Midland DSC pro- ject has already paid for itself because the cost and quality benefits of centralization have been so high and similar benefits could also have been exploited by any other bank if it had chosen to centralize. The technology is not new; indeed, it was developed nearly 20 years ago. Furthermore, the benefits of centralized processing may also be applied to card vouchers as well as cheques. The reluctance to centralize therefore still has to be explained.

To do this we need to focus on the assumptions of managers in the industry both about the process of technical change and about sources of comparative advantage. Banking has been seen as an extremely institutionalized field (DiMaggio and Powell, 1983). Institutional theories of organ- ization provide a contrasting approach to the rational actor emphasis of much management literature based around the assumption of strat- egic choice. Starting from the question of why organizations are so similar, institutional theories contend that much of organizational life is based on the need to maintain stability and survival by adopting prevailing norms. Extraorganizational norms and taken for granted assumptions about the best ways of working create a tendency to homogeneity between organizations facing similar environments.

60 ‘7: Morris and R. Westbrook

The perspective is therefore quite different from much of the strategic choice and leadership literature which tends to emphasize diversity and focus on the mechanisms for achieving this, through product differentiation, brand develop- ment and market segmentation. Institutional theories do not generally deny the possibility of decision making being based on competitive pres- sure, nor wholly dismiss the influence of purpo- sive managerial strategies shaping organizational ends (DiMaggio, 1988; Oliver, 1991) but conven- tions and embedded ways of organizing create high psychological switching costs. To be carried through, change has to challenge conventional ways of understanding success in relation to exist- ing arrangements. A major implication of the in- stitutional approach is that IT innovation depends on perceptions of how well it fits with prevailing norms as well as the expected competitive benefits.

We believe that isomorphism is an important characteristic of banking and it explains much about the process and dynamics of technical inno- vation. Isomorphic pressures are partly the result of the banks’ intermediate role in the distribution of money, allocation of credit and deposit taking. Because these functions can affect the implemen- tation of government policy and because of the importance of public confidence for the operation of the banking system, the banks have tradition- ally cultivated a public image of respectability and prudence and worked closely with the monetary authorities. For instance, the chairmen of the re- tail banks meet regularly with representatives of the Bank of England. There are also sound eco- nomic and strategic reasons for some of the colla- borative decision making. Notably, their common ownership of the cheque and credit clearing sys- tems favours collaboration in technical innovation to maintain common standards and spread costs.

Other areas of similarity are not so easily explained by reference to costs. For example, they chose to compete for many years by extending their retail networks rather than service differ- entiation; they aimed to cover broadly the same market segments until quite recently with similar product offerings and charging structures. For many years they operated as an oligopsony in the labour market, coordinating not just pay but a range of other conditions, entry requirements and trade union recognition policies, reinforced by ‘no poaching’ agreements (Morris, 1986). Indeed, the cartel-like behaviour of retail banking over

pricing and service quality has been repeatedly criticized by consumer groups. Accepted wisdom in Midland and the other retail banks was that centralization was either too difficult or too time- consuming to pursue and that it was not worth- while. Furthermore, the industry norm with respect to technical innovation of processing was that it should broadly be managed collectively: the banks had always moved roughly together in terms of the timing and the content of innovations even if they differed in terms of supplier and architectural specifics. Each had adopted back office processing at about the same time; each had upgraded at more or less the same pace (and not at a pace dictated by technological availability). Each had experimented at the same time with centralizing initiatives which fell far short of the DSC programme.

Change could therefore only occur because the decline and then crisis within Midland following the Crocker Bank disaster prompted the removal of the old guard at the top of the bank and the hiring of newcomers from without the banking industry. Even so, it can be said that the DSC pro- ject was a bold initiative characterized by caution. Where it has gone for more radical innovation, as in its First Direct telephone banking, the bank has sealed it off from the mainstream of its activ- ities and created a separate entity.

The disinclination to copy Midland was not because the other banks did not know of the benefits. Rather, it reflected the perspectives of other bank leaders about the nature of competi- tion: banks did not see processing as an important source of long-term comparative advantage and as they struggled to deal with debt crises mana- gerial priorities were elsewhere, even though cost savings from centralization would have been highly valued. Furthermore, Midland was not an exemplar of success in the industry. Much of what it had done seemed to smack of desperation and went against the norms of the industry; it was not an obvious benchmark for good practice.

Generally, then, technical change can be resisted even if it is feasible and financially worthwhile. In UK financial services, firms tend to move cau- tiously, isolating technical from organizational dimensions. They prefer to avoid using untried technologies and to innovate broadly in similar ways even though they operate independ- ently. They distrust or discount the experience of innovators who have not been financially

Technical Innovation and Competitive Advantage in Retail Financial Services 61

successful. Moreover, outside their core activity (lending) they have deferred change initiatives. Overcoming such restrictions has required a financial crisis, a top management team from out- side retail banking, awareness of best standards elsewhere and ability to ‘sell’ innovation in terms which not only appealed rationally but also resonated with the general desire to end the demoralization of long-term decline.

References Child, J. and M. Tarbuck (1985). ‘The Introduction of New

Technology in Banking: Managerial Initiative and Union Response’, Industrial Relations Journal, 16, pp. 3-20.

Clark, J. (ed.) (1993). Human Resource Management and Technical Change. Sage, London.

CLCB (1977). The London Clearing Banks: Evidence by the Committee of London Clearing Banks to the Committee to Review the Functioning and Financial Institutions. CLCB, London.

DiMaggio, P. (1988). ‘Interest and Agency in Institutional Theory’. In: L. Zucker (ed.), Institutional Patterns in Organizations, pp. 3-22. Ballinger, Cambridge, MA.

DiMaggio, P. and W. Powell (1983). ‘The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organization Fields’, American Sociological Review, 48 (April), pp. 147-160.

Earl, M. (ed.) (1988). Information Management: The Strategic Dimension. Clarendon Press, Oxford.

Hayes, R. and W. Abernathy (1980). ‘Managing Our Way to Economic Decline’, Harvard Business Review, July-August.

Kay, J. and I? Willman (1993). ‘Managing Technology Innova- tion: Architecture, Trust and Organisational Relationships in the Firm’. In: P. Swam (ed.), New Technologies and the Firm: Innovation and Competition. Routledge, London.

Legge, K. (1993). ‘The Role of Personnel Specialists: Centrality or Marginalisation?’. In: J. Clark (ed.), Human Resource Management and Technical Change, pp. 20-42. Sage. London.

McLoughlin, I. and J. Clark (1988). Technological Change at Work. Open University Press, Milton Keynes.

Morris, T. (1986). Innovations in Banking: Business Strategies and Employees Relations. Croom Helm, London.

Nevin, E. and E. Davis (1970). The London Clearing Banks. Elek Books, London.

Oliver, C. (1991). ‘Strategic Responses to Institutional Pro- cesses’, Academy of Management Review, 16( l), pp. 145-179.

Pavitt, K. (1991). ‘Key Characteristics of the Large Innovating Firm’, British Journal of Management, 2, pp. 41-50.

Pettigrew, A. (1973). The Politics of Organizational Decision- Making. Tavistock, London.

Pfeffer, J. and G. Salancik (1974). ‘Organizational Decision Making as a Political Process: The case of a university budget’, Administrative Science Quarterly, 19, pp. 135-151.

Schein, E. (1992). ‘The Role of the CEO in the Management of Change: The Case of Information Technology’. In: T. Kochan and M. Useem (eds), Transforming Organiza- tions, pp. 97-117. Oxford University Press, New York.

Scott Morton, M. (ed.) (1991). The Corporation ofthe 2990s. Oxford University Press, New York.

Scott Morton, M. (1992). ‘The Effects of Information Tech- nology on Management and Organizations’. In: T. Kochan and M. Useem (eds), Transforming Organizations, pp. 261- 278. Oxford University Press, New York.

Shaw, E. and N. Coulbeck (1983). UK Retail Banking Prospects in the Competitive 1980s. Staniland Hall, London.

Skinner, W. (1974). ‘The Focused Factory’, Harvard Business Review, 52(3), pp. 112-113.

Walton, R. I. (1985). ‘From Control to Commitment in the Workplace’, Harvard Business Review, 63, pp. 76-84.

Willman, I? (1986). Technological Change, Collective Bargaining and Industrial Efficiency. Oxford University Press, Oxford.

Willman, P. (1993). Appropriability of Technology and Internal Organisation. Centre for Organisational Research Working Paper No. 31, London Business School.

Willman, P. and R. Cowan (1984). ‘New Technology in Bank- ing: The Impact of Autotellers on Staff Numbers’. In: M. Warner (ed.), Microprocessors, Manpower & Society, Gower, Aldershot, Hants.

Womack, J., D. Jones and D. Ross (1990). The Machine that Changed the World. Rawson-Macmillan, New York.

Wood, S. (ed.) (1989). The Transformation of Work? Unwin Hyman, London.

Zuboff, S. (1988). In the Age of the Smart Machine. Basic Books, New York.