sustainable procurement practice

TRANSCRIPT

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment

* Correspondence to: Dr Joanne Meehan, Senior Lecturer in Strategic Purchasing, Liverpool Business School. Faculty of Business and Law, Liverpool John Moores University, John Foster Building, 98 Mount Pleasant, Liverpool, L3 5UZ, UK. E-mail: [email protected]

Business Strategy and the EnvironmentBus. Strat. Env. 20, 94–106 (2011)Published online 3 May 2010 in Wiley Online Library(wileyonlinelibrary.com) DOI: 10.1002/bse.678

Sustainable Procurement Practice

Joanne Meehan1* and David Bryde2

1 Liverpool Business School, Faculty of Business and Law, Liverpool John Moores University, Liverpool, UK

2 School of the Built Environment, Liverpool John Moores University, Peter Jost Enterprise Centre, Byrom Street, Liverpool L3 3AF

ABSTRACTProcurement has a key role in sustainability as policies and practices need to extend beyond organisations’ boundaries incorporating their whole supply chains. Guidelines on sustain-ability encourage procurement to make decisions that encompass the environmental, economic and social elements of the Triple Bottom Line (TBL). Taking a supply chain per-spective, procurement also need to analyse how decisions impact on the TBL in respect of suppliers. The results of a survey of sustainable procurement practices in 44 English-based UK Housing Associations (HAs), who are responsible for the provision of social housing, confi rms prior research of other sectors that suggests 1) a failure to overcome inertia in relation to sustainable procurement; and 2) in the few examples where practices have been established, only the environmental element of the TBL is considered. The organisations surveyed have sustainability-related issues in their missions and external and internal pres-sures to embed sustainability, yet this has not translated into widespread establishment of sustainable procurement. Recommendations to neutralise inertia are: fi rstly, take the expe-riences from other areas, e.g. innovation management, which stress the importance of inter-organisational relationships; secondly, develop a small number of sustainable devel-opment indicators for procurement and, to take advantage of the relatively more-advanced environmental practices to show how these elements have socio-economic impacts; and fi nally, rather than focus on just the pressures and drivers of sustainability (as suggested in strategic models of sustainability), emphasise the triggers that overcome inertia and lead to changes in behaviour amongst procurement staff i.e. the establishment of ethical pricing models. Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment.

Received 18 August 2009; revised 22 January 2010; accepted 2 February 2010

Keywords: Sustainability; Procurement; Social Housing; Green Procurement; Triple Bottom Line; Sustainable Procurement;

Organisational Inertia

Sustainable Procurement Practice 95

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

Introduction

THE BUSINESS MODELS USED BY MANY ORGANIZATIONS INCREASINGLY SEEK TO INCLUDE ENVIRONMENTAL ASPECTS of performance in line with the triple bottom line (TBL) concept (Birkin et al., 2009). The TBL has emerged

as a paradigm for sustainable development, whereby meeting the needs of the present and of future gen-

erations are classed under three dimensions: environmental, economic and social (Dyllick and Hockerts,

2002). For true sustainable development to take place, strategy formulation and implementation need to extend

along an organization’s supply chain (Green et al., 1996; Nathan, 2005). For example, fi rms seeking to improve

their environmental performance may work with suppliers to reduce materials’ toxicity or the amount of packag-

ing used in supplies (Sharfman et al., 2009). The need to look outside an organization’s boundaries highlights

the key role of procurement in sustainable development, which is refl ected in the high volume of case research

relating to green supply chain management and sustainable procurement (e.g. Bowen et al., 2001; Zsidisin and

Siferd, 2001; Dyllick and Hockerts, 2002; Rao, 2002; Seitz and Wells, 2006). It was posited in early research on

sustainable procurement that focusing on the environmental aspects of the supply chain may provide a transitional

route toward full sustainability (Green et al., 1998). Empirical research from the pharmaceutical industry provides

some support for this theory, suggesting that the environmental focus frequently presents fi nancial savings, which

has the added bonus of contributing to economic sustainability, thus addressing two of the three dimensions of

the TBL (Veleva et al., 2003). However, research in the fi eld of sustainable procurement is still its infancy and

further empirical study of how sustainability is integrated into the procurement strategies of organizations is called

for (Linton et al., 2007). The remainder of this paper presents the fi ndings of a study of sustainable procurement

practice in the UK social housing industry.

Conceptual Framework

Organizational Inertia

This study is based on the knowledge that the concept of sustainability, and in particular the TBL, is a diffi cult

one to translate into practice. It can involve a high degree of complexity for strategy and decision making (Matos

and Hall, 2007; Preuss, 2007) and necessitates a fundamental shift in operations, causing signifi cant upheaval

for organizations (Shriberg, 2000). The diffi culty of this task arguably becomes greater still when activities extend

beyond organizational boundaries, as in the case of procurement. As a result of this complexity, although many

organizations may have sustainability on their agenda and believe it to be important, the inherent diffi culties of

translating these principles into practice lead to organizational inertia.

Organizational inertia is the inability to enact change in the face of a changing external environment (Miller

and Friesen, 1980) and the phenomenon is highlighted in studies of consumers’ attitudes toward sustainability.

Such studies demonstrate that, on the whole, people verbally endorse environmental sustainability schemes, yet

this endorsement does not correlate with a change in their behaviour (McDonald and Oates, 2006; Vining and

Ebreo, 1990). This may be mirrored by organizations’ procurement practices; certainly, one would expect organi-

zations to say sustainability is an important organizational consideration – it would be a brave organization in the

current climate to state it is not important, but such importance, even if stated as an explicit corporate aim, may

not necessarily be refl ected in procurement strategy and practice. Therefore, in relation to sustainable procurement,

one might expect to fi nd some evidence of this inertia.

The Focus of Sustainability

A further response to the complexity of translating the sustainability concept into procurement strategies and

practice is a focus exclusively on the environmental element of the TBL. Evidence suggests that many organiza-

tions have taken an attenuated view of sustainability, being concerned with environmentally orientated topics such

as eco-effi ciency (Dyllick and Hockerts, 2002; Cozens et al., 1999; Ball et al., 2006). While environmental issues

are key aspects of sustainability, it is acknowledged that the economic and social dimensions need equal attention,

96 J. Meehan and D. Bryde

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

yet they are lacking in many corporate agendas (Sharma and Ruud, 2003; von-Geibler et al., 2006; Yongvanich

and Gutherie, 2006; Diniz and Fabbe-Costes, 2007). An integrated view of sustainability is particularly important

as the three elements are interrelated. For example, the effect of economic growth (economic) may increase an

organization’s carbon footprint (environmental) yet lead to the development of long-term employment opportuni-

ties for local communities (social) (Kirchgeorg and Winn, 2006).

The role of procurement in driving forward the corporate sustainability agenda is critical, given its position and

its ability to infl uence external organizations in the supply chain (Green et al., 1996; Seuring, 2004). However,

the available procurement frameworks for assessing supplier sustainability, such as ISO 14001, take an attenuated

view of sustainability, focusing only on environmental standards (Corbett and Kirsch, 2001). The complexity,

formal procedures and structures can also be prohibitive, particularly for SMEs (Perrini and Tencati, 2006). There

is empirical evidence that suggests that the collection of suppliers’ environmental information does not necessary

translate to an evaluation of this data (Preuss, 2007); thus it serves as proxy control mechanisms for evaluation

and selection of suppliers (Koplin et al., 2007), moving procurement’s involvement to policing, rather than devel-

opment. Similarly, suppliers’ adherence to standards does not necessarily lead procurement staff to become fully

engaged in the sustainability agenda (Preuss, 2007). Such engagement may be crucial, as the requirement to focus

on medium- and long-term change requires commitment from staff (Wilkinson et al., 2001). This commitment

is particularly signifi cant in environments where sustainability is critical to the organizational values, as in the

case of the social housing industry. Empirical research cites the importance of external collaboration, which pro-

motes the sharing of values (along with data availability), as a key enabler in developing supply chain sustainabil-

ity (Veleva et al., 2003).

The Drivers of Sustainability

As much of the sustainability debate has been at the global level, the drive towards corporate sustainability has

been particularly felt by multinational organizations in the public eye (de Man and Burns, 2006). For example,

the car manufacturing industry is publicly visible and operates in competitive global markets: both factors that

create powerful drivers for change (Koplin et al., 2007; Seitz and Wells, 2006). Similar external pressures are

evident in other publicly visible industries, for example the global pharmaceuticals industry (Veleva et al., 2003).

In these situations, increasing customer pressure and expectation are making corporate reputation increasingly

critical (Koplin et al., 2007; Preuss, 2001). Consumers, fuelled by the mounting press attention on carbon foot-

prints and the environment, assume that in these highly visible industries it is the focal organization’s responsibil-

ity to take the lead in the sustainability agenda (Thogersen, 2006).

However, despite the external pressures, many of these organizations are not fully embracing sustainability

throughout their supply chains and are only just beginning to place prerequisites on their suppliers (Koplin et al., 2007). Much of the activity on sustainability has arguably been driven (certainly in some industries) through the

statutory necessity of environmental management; the imposition of which is approached as risk reduction and

thus creates negative connotations, rather than being viewed as an area for value creation (Tregidga and Milne,

2006). Furthermore, consumers’ knowledge of sustainable development is relatively narrow, focusing largely on

the environmental issues of recycling, remanufacturing, re-use and reverse logistics (Angell, 2000).

If these external drivers have a narrow focus they can create barriers to consideration of a broad approach

encompassing the full spectrum of sustainable development. In response, organizations may tend to focus on

these issues, as they have a high public relations value compared with other equally important issues that are

more diffi cult to promote (de Man and Burns, 2006; Cerrin, 2002; von-Geibler et al., 2006). Yet if these external

drivers have a narrow focus they can create barriers to a more holistic approach encompassing the full spectrum

of sustainable development. In addition, external drivers may not be as powerful in less visible, non-regulated

and non-consumer markets. In such organizations it is argued that managers, through sharing the values of the

organization, will be motivated to progress organizational goals related to sustainability (Mason et al., 2007).

Empirical research on six European organizations provides support for the power of internal drivers for sustain-

ability. Here, it was observed that organizations will initiate and implement sustainability-orientated learning when

these requirements are anchored in the cultural attributes of the organization and supported by corresponding

learning mechanisms (Siebenhuner and Arnold, 2007). Other research identifi ed further internal drivers of

Sustainable Procurement Practice 97

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

sustainability, such as the need for internal change management and the adoption of organizational structures

(Griffi ths and Petrick, 2001), and the pivotal role of individuals in facilitating and embedding sustainability, par-

ticularly in smaller organizations (Siebenhuner and Arnold, 2007). Therefore, one may expect to fi nd the drivers

of sustainable procurement to be contingent upon the organization context.

Empirical Study

Empirical study was undertaken in the UK social housing industry. This industry was chosen as sustainability in

social housing is a high government priority. Social housing describes residential properties made available for

rental at affordable rates. The UK’s aging population coupled with the current economic climate creates an unprec-

edented and growing need for social housing (Feinstein et al., 2008). Many local authorities have transferred their

existing social housing stock to registered social landlords (RSLs), who also provide new social housing. Most RSLs

are housing associations (HAs), though a small number operate as trusts and cooperatives. Demand for social

housing is anticipated to grow by 50% by 2011 (Chevin et al., 2008), and in 2009 the UK government provided

£1.2b support for affordable housing to buy or rent, with a plan to provide £1.5 billion to deliver 20 000 additional

energy-effi cient affordable homes in 2009/2010 (Her Majesty’s Government (HMG), 2009). Furthermore, most

of the government’s sustainable development indicators underpin the impact of social housing on national eco-

nomic, social and environmental development (Housing Corporation, 2005). Regulatory and funding bodies within

the social housing sector are therefore pushing for HAs to demonstrate sustainability policies throughout their

supply chains.

The study undertaken was an exploratory survey of staff working in HAs. The survey was sent to HAs belonging

to Procurement for Housing (PfH), a national procurement consortium of more than 650 RSLs, which is sup-

ported by the National Housing Federation, the Chartered Institute of Housing and HouseMark. PfH has limited

reach in Scotland and Northern Ireland – and these countries have different regulatory frameworks, so to ensure

consistency the HAs surveyed were all based in England. PfH manages the purchase and supply of over £1 m of

goods and services every week and is committed to sustainable procurement (PfH, 2009). PfH members include

some of the largest HAs in England, with annual turnovers in excess of £20 m and over 10 000 managed proper-

ties including new builds, and some of the smallest, with less than £5 m annual turnover and fewer than 1000

managed properties (and no new builds). This targeted sampling allows investigation and provides insights of an

emerging fi eld, and has been adopted in prior study of supply-chain environmental management (Sharfman et al., 2009). The objective was to understand sustainable procurement by exploring the attitudes of a key stakeholder

group, namely staff responsible for formulating and implementing procurement strategy. The research questions

are how and why sustainable procurement takes place.

Methodology

A survey-based approach was adopted, as prior work highlights its usefulness in undertaking an initial exploration

of organizational buyers’ attitudes and decision-making (Heide and Weiss, 1995; Love et al., 1998). Respondents

were asked to use the following defi nitions of sustainability and sustainable procurement when completing the

questionnaire:

‘Sustainability’ encompasses environmental, social and economic factors (e.g. reducing carbon emissions and

waste, increasing water effi ciency, diversity, promotion of well-being, equal opportunities, creating a strong,

stable, effi cient and fair economy). ‘Sustainable procurement’ can be defi ned as the process used to secure

the acquisition of goods and services (‘products’) in a way that ensures that there is the least impact on society

and the environment throughout the full life cycle of the product.

This encompasses the TBL concept and refl ects the widely adopted defi nitions of the Bruntland Report, which

states that sustainable development ‘seeks to meet the needs and aspirations of the present without compromising

the ability to meet those of the future’ (Bruntland, 1987).

98 J. Meehan and D. Bryde

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

To explore inertia in developing and implementing sustainable purchasing strategies the questionnaire con-

tained statements relating to the importance of sustainability, both currently and in the future, the expectation

being that sustainability would be perceived to be more important in the future and hence not necessarily a current

priority. Respondents rated their attitudes towards these statements using fi ve-point Likert scales. Then data were

elicited on the specifi c sustainable procurement activities. Previous research highlights the role of the development

of policies, target setting, contract management, training, supply chain management including policing and use

of standards (see Koplin et al., 2007; Preuss, 2007; Maxwell et al., 2006; Veleva et al., 2003; Wilkinson et al., 2001).

Implicit in three of these ten activities is development and collaboration (staff training, supplier awareness raising

and helping suppliers’ improve their performance), while the remaining seven activities are policy and compliance

activities. Ten statements were derived encompassing these activities and three options were offered to respon-

dents: ‘yes’, ‘no’ and ‘working towards’, the expectation being that there would be a larger proportion of ‘no’ and

‘working towards’ than ‘yes’ responses, providing further evidence of inertia.

The next section identifi ed if sustainable procurement was attenuated towards environmental elements. Respon-

dents rated the importance of sustainability when purchasing specifi c products and services using a fi ve-point

Likert scale (1 = not important to 5 = very important). A list of 22 products and services was presented, refl ecting

the full range of purchasing activity undertaken by PfH on behalf of its members. If an attenuated view of sustain-

ability existed, one would expect the focus to be on products and services with an environmental focus.

The questionnaire also considered the drivers of sustainable procurement. Nine drivers were presented, refl ect-

ing external and internal factors. Each driver’s strength was rated on a fi ve-point scale of 1 = very weak through to

5 = very strong. Given that HAs are not multi-national organizations or highly visible to consumers, there is an

expectation that internal drivers will be important. The fi nal section gathered classifi cation data on respondents’

organization and role, which would be used in the second stage of the research. After piloting the questionnaire

with PfH and a member organization, the questionnaire was sent via email to all 550 PfH member organizations.

In total 44 usable questionnaires were returned, giving a response rate of 8%. Although this is low, it is a typical

fi gure for email questionnaires (Michaelidou and Dibb, 2006) and, given the exploratory nature of the research,

the dataset was regarded as acceptable.

Results

Of the 44 respondents, 27% had procurement-related role titles, 66% had other role titles and 7% did not specify

their role. Other role titles refl ected a variety of functions including strategy, operations, fi nance, human resources,

facilities management and asset management. Only one respondent (head of sustainability) had sustainability as

an explicit role title. All except two respondents had the words manager, head or director as part of their role title.

21% of respondents had roles specifi cally related to housing, with 70% in roles not directly related to the develop-

ment or maintenance of the housing stock. 9% of respondents did not specify this.

A post-survey analysis of responses in terms of the scale of the HA (turnover and number of properties) showed

no discernible patterns. Some respondents in large HAs reported relatively advanced procurement policies and

practices in relation to sustainability compared with smaller HAs, though the converse was also true.

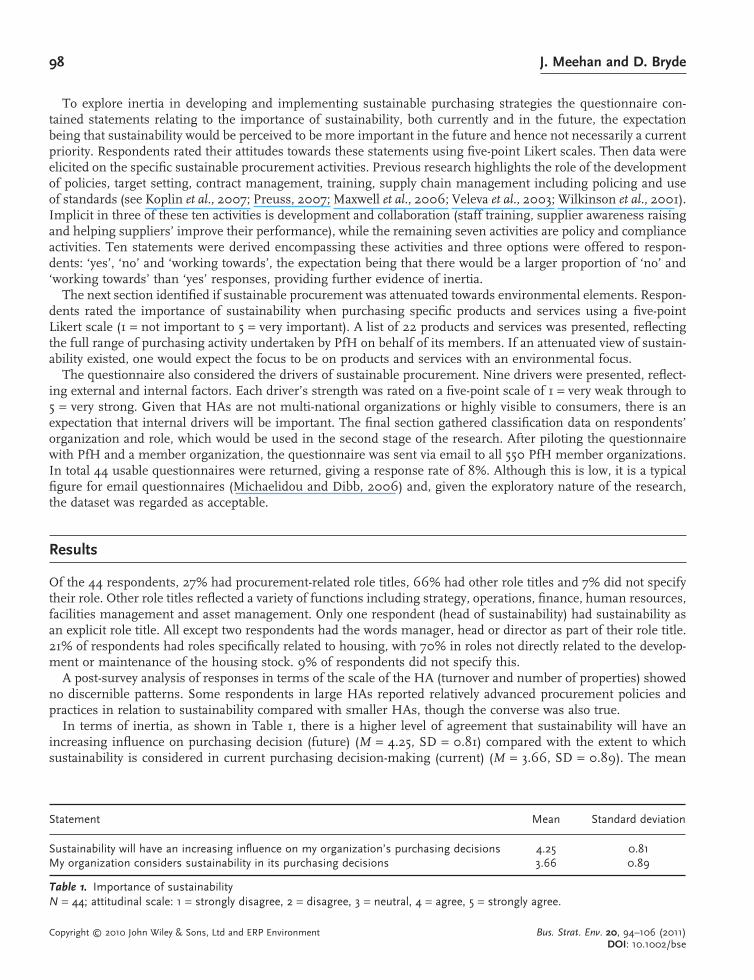

In terms of inertia, as shown in Table 1, there is a higher level of agreement that sustainability will have an

increasing infl uence on purchasing decision (future) (M = 4.25, SD = 0.81) compared with the extent to which

sustainability is considered in current purchasing decision-making (current) (M = 3.66, SD = 0.89). The mean

Statement Mean Standard deviation

Sustainability will have an increasing infl uence on my organization’s purchasing decisions 4.25 0.81My organization considers sustainability in its purchasing decisions 3.66 0.89

Table 1. Importance of sustainabilityN = 44; attitudinal scale: 1 = strongly disagree, 2 = disagree, 3 = neutral, 4 = agree, 5 = strongly agree.

Sustainable Procurement Practice 99

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

perception of the future importance of sustainability in procurement being increased on the rating scale is between

agree and strongly agree, whilst the perception that it is currently considered is between neutral and agree.

A comparison using a paired sample t-test indicates that there is a statistically signifi cant difference at the 5%

level (t(43) = −4.98, p < 0.001) between the mean scores for respondents’ answers to the two statements shown

in Table 1.

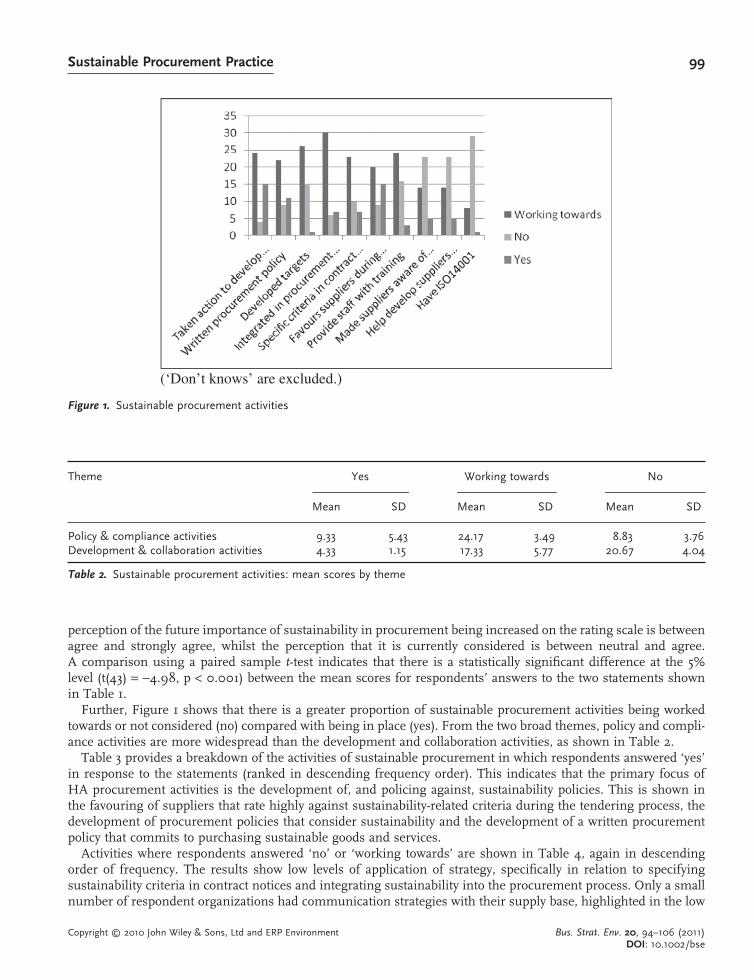

Further, Figure 1 shows that there is a greater proportion of sustainable procurement activities being worked

towards or not considered (no) compared with being in place (yes). From the two broad themes, policy and compli-

ance activities are more widespread than the development and collaboration activities, as shown in Table 2.

Table 3 provides a breakdown of the activities of sustainable procurement in which respondents answered ‘yes’

in response to the statements (ranked in descending frequency order). This indicates that the primary focus of

HA procurement activities is the development of, and policing against, sustainability policies. This is shown in

the favouring of suppliers that rate highly against sustainability-related criteria during the tendering process, the

development of procurement policies that consider sustainability and the development of a written procurement

policy that commits to purchasing sustainable goods and services.

Activities where respondents answered ‘no’ or ‘working towards’ are shown in Table 4, again in descending

order of frequency. The results show low levels of application of strategy, specifi cally in relation to specifying

sustainability criteria in contract notices and integrating sustainability into the procurement process. Only a small

number of respondent organizations had communication strategies with their supply base, highlighted in the low

Figure 1. Sustainable procurement activities

(‘Don’t knows’ are excluded.)

Theme Yes Working towards No

Mean SD Mean SD Mean SD

Policy & compliance activities 9.33 5.43 24.17 3.49 8.83 3.76Development & collaboration activities 4.33 1.15 17.33 5.77 20.67 4.04

Table 2. Sustainable procurement activities: mean scores by theme

100 J. Meehan and D. Bryde

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

number of responses related to improving supplier awareness and developing suppliers’ sustainability perfor-

mance. ISO 14001 was not on the agenda for most of the HAs.

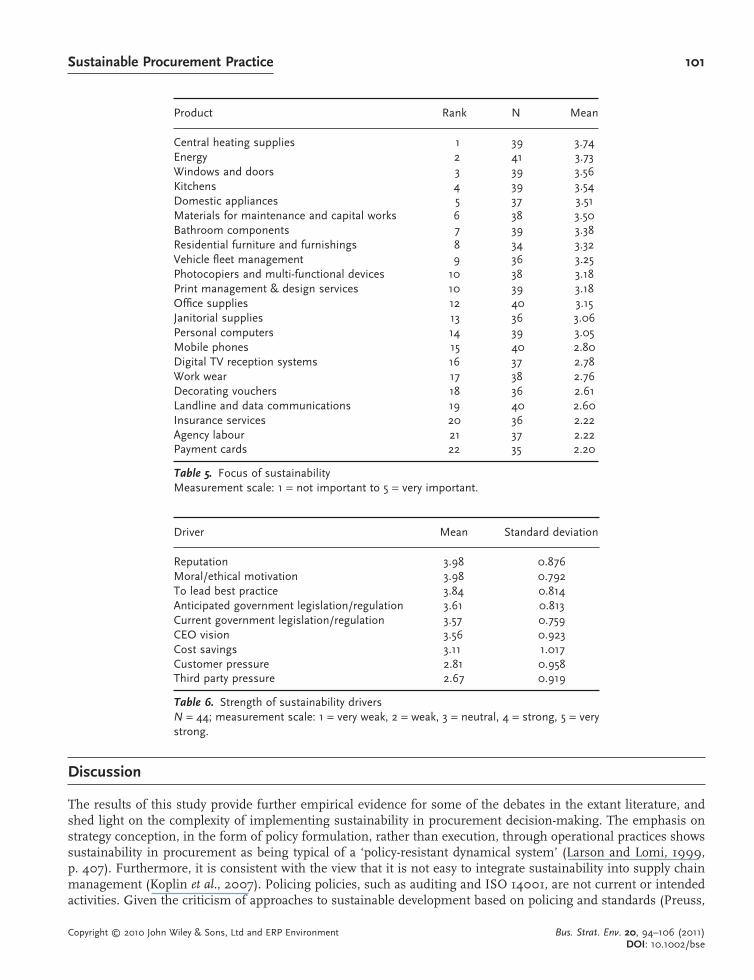

The results indicate attenuation of the TBL. In terms of relative importance, as shown in Table 5, the mean

scores for all areas are relatively low, with all scores under 4 (4 = important). The top two areas (central heating

and energy) were related to environmental and energy, suggesting that an eco-effi ciency view is prominent. The

next top six areas of focus for sustainable procurement decisions centred predominantly on products and services

directly associated with building and furnishing the housing stock. The next tier of products (ranked 9–13) related

to the organization’s own internal requirements, and here less importance was given to sustainability issues in

procurement. The fi nal tier of products (ranked 14–22 with a mean less than 3) comprised a mix of telecoms/data

communication products, general consumables and services and those relating to the social element of the TBL

(e.g. agency labour).

Table 6 shows the extent to which various external and internal factors are perceived to be driving sustainability.

The three strongest drivers identifi ed by the respondents are to enhance reputation, a moral/ethical motivation

and a desire to lead best practice. Although these emerge as the strongest mean values, these are all still under

the value of 4 (strong), highlighting the lack of force behind them. Anticipated legislative pressures are seen as

stronger drivers than current ones, suggesting that respondents believe that these external forces will strengthen.

These forces are followed closely by the vision of the chief executive offi cer. The three weakest drivers are cost

savings, customer pressure and third party pressure.

Statement No/WT %

My organization has developed targets for sustainable procurement 41 93.2All our procurement staff receive training on the impact of sustainability on purchasing decision-making 40 90.1We have made our suppliers aware of our sustainable procurement policy and practices 37 84.1My organization helps to develop its suppliers’ sustainability performance (e.g. through auditing) 37 84.1We currently have ISO14001 certifi cation 37 84.1My organization has integrated sustainability into its procurement process 36 81.8My organization specifi es sustainability criteria in its contract notices 33 75.0We have a written procurement policy stating our commitment to purchasing sustainable goods & services 31 70.1My organization favours suppliers that rate highly on sustainability during the tender process 29 66.0We have taken action to develop procurement policies that consider sustainability 28 63.6

Table 4. Sustainable procurement activities – respondents answering ‘no’/’working towards (WT)’N = 44.

Statement Yes %

We have taken action to develop procurement policies that consider sustainability 15 34.1My organization favours suppliers that rate highly on sustainability during the tender process 15 34.1We have a written procurement policy stating our commitment to purchasing sustainable goods & services 11 25.0My organization has integrated sustainability into its procurement process 7 15.9My organization specifi es sustainability criteria in its contract notices 7 15.9We have made our suppliers aware of our sustainable procurement policy and practices 5 11.4My organization helps to develop its suppliers’ sustainability performance (e.g. through auditing) 5 11.4All our procurement staff receive training on the impact of sustainability on purchasing decision-making 3 6.8My organization has developed targets for sustainable procurement 1 2.3We currently have ISO14001 certifi cation 1 2.3

Table 3. Sustainable procurement activities – respondents answering ‘yes’

Sustainable Procurement Practice 101

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

Discussion

The results of this study provide further empirical evidence for some of the debates in the extant literature, and

shed light on the complexity of implementing sustainability in procurement decision-making. The emphasis on

strategy conception, in the form of policy formulation, rather than execution, through operational practices shows

sustainability in procurement as being typical of a ‘policy-resistant dynamical system’ (Larson and Lomi, 1999,

p. 407). Furthermore, it is consistent with the view that it is not easy to integrate sustainability into supply chain

management (Koplin et al., 2007). Policing policies, such as auditing and ISO 14001, are not current or intended

activities. Given the criticism of approaches to sustainable development based on policing and standards (Preuss,

Driver Mean Standard deviation

Reputation 3.98 0.876Moral/ethical motivation 3.98 0.792To lead best practice 3.84 0.814Anticipated government legislation/regulation 3.61 0.813Current government legislation/regulation 3.57 0.759CEO vision 3.56 0.923Cost savings 3.11 1.017Customer pressure 2.81 0.958Third party pressure 2.67 0.919

Table 6. Strength of sustainability driversN = 44; measurement scale: 1 = very weak, 2 = weak, 3 = neutral, 4 = strong, 5 = very strong.

Product Rank N Mean

Central heating supplies 1 39 3.74Energy 2 41 3.73Windows and doors 3 39 3.56Kitchens 4 39 3.54Domestic appliances 5 37 3.51Materials for maintenance and capital works 6 38 3.50Bathroom components 7 39 3.38Residential furniture and furnishings 8 34 3.32Vehicle fl eet management 9 36 3.25Photocopiers and multi-functional devices 10 38 3.18Print management & design services 10 39 3.18Offi ce supplies 12 40 3.15Janitorial supplies 13 36 3.06Personal computers 14 39 3.05Mobile phones 15 40 2.80Digital TV reception systems 16 37 2.78Work wear 17 38 2.76Decorating vouchers 18 36 2.61Landline and data communications 19 40 2.60Insurance services 20 36 2.22Agency labour 21 37 2.22Payment cards 22 35 2.20

Table 5. Focus of sustainabilityMeasurement scale: 1 = not important to 5 = very important.

102 J. Meehan and D. Bryde

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

2007; Corbett and Kirsch, 2001) this might not be a major limitation, though on the other hand it may be further

evidence of the failure to translate policy into procurement practice. Despite the lack of use of ISO 14001, the

specifi c areas of focus for procurement activity relate predominantly to policy and compliance rather than develop-

ment and collaboration. This supports previous concerns as to procurement’s role (Preuss, 2007). The lack of

development suggests that suppliers’ compliance is being mandated through tendering and contract criteria, as

opposed to the promotion of the sharing of sustainability values. This lack of engagement with suppliers is a

potential barrier to driving forward the sustainability agenda (Veleva et al., 2003).

Viewed through the lens of organizational inertia, the fi ndings suggest this is widespread, owing to structural

issues. Institutional theory contends that over time organizations foster stability and permanence, which contrib-

utes to long-term success, yet this process of ‘institutionalization’ also generates inertia and resistance to change.

To survive, organizations institutionalize their goals and routinize their activities, becoming highly ‘reliable’ and

‘accountable’ for their actions (Larsen and Lomi, 1999, p. 407). Procurement functions are as prone to such insti-

tutionalization as other functions. The ‘reliability’ of procurement has increasingly focused on acquiring the right

products at the right price, quality and time and its ‘accountability’ is predicated on demonstrating value for money.

Introducing sustainability to procurement decision-making potentially re-defi nes reliable and accountable, adding

an additional dimension to the price, quality and time triumvirate. Owing to structural inertia as organizations

increase with age and in size they may become more resistant to adopting these new procurement practices.

Experience of other industries suggests that structural inertia can be overcome. Fleck (2007) studied General

Electric (GE), a long-lived US electrical manufacturing company, and concluded that to neutralize structural inertia

it institutionalized those practices that allowed renewal of routines and redefi nition of its relationship with its

environment.

Prior argument that the concept of sustainability is complex and diffi cult to operationalize (Matos and Hall,

2007) suggests a second lens through which to view inertia: namely, the interaction between organizations and

individual procurement staff responsible for implementing operational policies. Van der Steen (2009, p. 738)

describes how inertia occurs due to ‘routine rigidity’ of staff adopting new rules for management accounting. New

rules challenge routine behaviours and inertia manifests in limited behavioural changes or unintended conse-

quences. Individuals become insecure if new rules are perceived as ambiguous, leading to two forms of inertia:

new rules interpreted using existing knowledge inappropriate to the situation and ontological anxiety arising from

multiple, inconsistent and confl icting rules. For sustainable procurement, routine inertia extends to encompass

various sustainability policy documents and guidelines that proliferate. These become the ‘rules’ that infl uence

behaviour. For many these rules are certainly new and therefore challenge existing behaviour amongst procure-

ment decision-makers.

Arguably, in relation to procurement, they are also ambiguous. First, a great deal of knowledge focuses on defi n-

ing and measuring sustainability. The UK Government established 15 headline indicators of sustainable develop-

ment in the UK, with a framework of 132 other indicators (DETR, 1999) and 29 local indicators (DETR, 2000).

An update in 2009 comprised 68 indicators and, additionally, complemented 32 of the national indicators with a

set of 46 international indicators (DEFRA, 2009). At the local level the indictors encompass environmental indi-

cators, in terms of ‘prudent use of resources’ and ‘protection of the environment’, social indicators of ‘better health

and education for all’, ‘access to local services and travel’, ‘shaping our surroundings’ and ‘empowerment and

participation’, and economic indicators relating to a ‘sustainable local economy’, yet it is not clear which of these

indicators, and how, procurement can help to meet. It is easier to understand how procurement can contribute to

the local economic indicator of ‘social and community enterprises’ by sourcing products and services from such

organizations, yet its ability to infl uence a social indicator, such as ‘fear of crime’, is less clear. The sheer volume

of indicators may lead to ontological anxiety. Second, the existing knowledge focuses on national and local sustain-

ability goals. Many supply chains transcend local and national boundaries, raising the possibility of inconsistency

and confl ict when making sourcing decisions. For example, buying environmentally friendly products from over-

seas might help achieve the environmental goal of ‘protection of the environment’ but be in confl ict and incon-

sistent with the economic goal of ‘employment’ in the local community. The ontological anxiety may be further

exacerbated when sustainability procurement is seen to involve a trade-off against cost, time or quality.

Those responsible for embedding sustainability into organizations are encouraged to develop a strategy. A typical

example of such encouragement is the guidelines from Sustainability of Work, a UK-based group, a product of

Sustainable Procurement Practice 103

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

The Prince of Wales’ Accounting for Sustainability project. They recommend a six-step strategic approach involv-

ing (1) indentifying key issues and drivers, (2) developing strategy, (3) establishing governance and accountability,

(4) setting targets and an action plan, (5) monitoring, (6) reporting and evaluating (Sustainability at Work, 2010).

In terms of step (1), identify key issues and drivers, organizations are advised to ask the question ‘what are the

internal and external drivers?’. The survey fi ndings showed a number of internal and external drivers. Some were

relatively strong, i.e. reputation and moral/ethical motivation (internal) and anticipated government legislation

(external), whilst others were weaker, i.e. cost savings (internal) and customer pressure (external). Despite this

multitude of drivers there was still a widespread failure to translate the drivers into sustainable procurement

practices. Theory relating to neutralizing organizational inertia suggests the need for a catalytic event or trigger to

change behaviour (van der Steen, 2009). An absence of triggers could explain the lack of sustainable procurement

found in the survey. If one looks to other industry sectors a possible trigger is found in the establishment of ethical

economics or ethical pricing models. Halliday (2009) interviewed the head of Oxfam’s Sustainable Livelihood

Strategy, who claimed that food and beverages are at the forefront driving sustainability in the supply chain. Here

the trigger is not the external pressure of customer demand (although this is present), but the development of

internal structures involving conscious decisions to integrate sustainability into economic models (Partos, 2009).

Without this pressure ideals may not translate into action. Words of caution are sounded relating to strategies

where triggers involve managing reputational loss caused by regulatory infringements with the associated censures

and bad publicity (Sustainability at Work, 2010).

The survey shows that the focus of sustainability in procurement is predominantly on the environmental element

of the TBL, particularly energy and eco-effi ciencies. This attenuation refl ects the extent literature (Dyllick and

Hockerts, 2002; Bowen et al., 2001; Zsidisin and Siferd, 2001; Rao, 2002; Seitz and Wells, 2006; Ball et al., 2006).

The fi ndings add weight to prior arguments that corporate sustainability agendas prioritize the environmental

element as this is the most visible to customers, and where customers are more informed (de Man and Burns,

2006; Cerrin, 2002; von-Geibler et al., 2006). It is evident from government policy, discussed in the previous

section, that there are national and local sustainability-related indicators relating to the economic and social dimen-

sions that organizations are being encouraged to consider in their procurement activities, for example sourcing

products to add to the economic well-being of local communities and ethical purchasing of materials from devel-

oping countries where employees have safe and humane working conditions (which can be related to a social

indicator of ‘better health’). This survey showed no strong evidence that this potential is being used. An example

of a missed opportunity is illustrated through procuring agency labour (Table 5), where sustainability consider-

ations were perceived to be relatively unimportant. Procurement of agency labour could consider the economic

element of the TBL by targeting the unemployed, and could contribute to the social element by providing training

and educational opportunities to those employed.

The environmental focus of the TBL also suggests a failure to integrate economic, social and environmental

concerns, an integration that is stressed in guidelines as being a policy priority and crucial to sustainable develop-

ment (Ekins, 2000). The organizations in the survey would all be expected to contribute to delivering against the

economic and social sustainability indicators described in the previous section. Paradoxically, an unintended con-

sequence of the holistic TBL concept is fragmentation and a lack of integration in sustainability-related decision-

making. Policy and strategic guidelines favour separate, distinct lists of indicators for each of the TBL elements.

The UK Government through its Offi ce of Government Commerce and Department for the Environment, Food

and Rural Affairs provided lengthy guidelines on how to incorporate social issues into the different stages of the

procurement process (OGC, 2003). This was followed three years later by a similar guide, which focused exclusively

on social issues in purchasing (OGC, 2006). Yet these guidelines provided little detail of how environmental and

social considerations can be integrated into decision-making in general and procurement decisions in particular.

Conclusions

The research reported in this paper found no strong presence of sustainable procurement practices in the social

housing sector. Prior research suggests that this is a widespread problem across many industries and is not con-

fi ned to the UK. Organizations responsible for the provision of social housing have a mission to deliver against

104 J. Meehan and D. Bryde

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

social, environmental and economic sustainability targets and the fact that these missions have not been translated

into practice is noteworthy. All organizations, as they grow over time, are susceptible to structural inertia. In the

case of sustainable procurement such inertia may explain a lack of development. Building sustainability consider-

ations into procurement decision-making requires a step change, which increases in diffi culty as traditional pro-

curement approaches embed over time. One area where those responsible for developing strategies in relation to

sustainable procurement can learn lessons relates to the management of innovation. Structural inertia in this area

is overcome by systematic problem-solving in areas including technology, administrative issues, inter-organiza-

tional relationships, renewal of resources, sustained risk management and planned responses to the external

environment (Fleck, 2007). For sustainable procurement, a key factor is the management of inter-organizational

relationships. This requires supplier engagement strategies, moving from policing and compliance activities to

developmental and collaborative activities with suppliers.

Sustainability strategies are being informed by the numerous policy guidelines that set out sustainable develop-

ment indicators at international, national and local levels. These guidelines illustrate the breadth and complexity

of the subject. In respect of sustainable procurement, such breadth and complexity is likely to contribute to anxiety

and confusion at the operational level, leading to inertia amongst those responsible for procurement decision-

making. Strategists will need to establish processes that address this anxiety. Part of the strategic development

process could include (1) the establishment of a small number of indicators that are specifi c and applicable to the

procurement function and (2) a focus on how these indicators integrate each element of the TBL: i.e., rather than

developing distinct and separate environmental, economic and social indicators they would show how procurement

decisions impact on all three elements. The emphasis in procurement on the environmental element of the TBL

reported in this paper – which confi rms earlier research (i.e. Cozens et al., 1999; Dyllick and Hockerts, 2002) –

suggests that a useful starting point in terms of achieving such integration is to focus on the socio-economic

consequences of procurement decisions informed by environmental concerns.

Strategic approaches to embed sustainability are informed by well-established strategic management frame-

works. A strategic approach recommends using the PESTEL (political, economic, social, technological, environ-

mental and legal) method to analyse the sustainability drivers and pressures at the start of the process

(Sustainability at Work, 2010). The research reported in this paper revealed an industry sector in which there were

a multitude of external and internal drivers, yet such drivers had not resulted in widespread sustainable procure-

ment practice. Strategic approaches need to consider the triggers of sustainable development, which provide the

catalyst in converting pressures into practices. Lessons can be learnt from industry sectors that have made relatively

good progress in embedding sustainability in their organization. For example, the use of ethical economics and

ethical pricing models is seen as a trigger to sustainability success stories in the food and beverage sector. The

social housing sector, as with many other industries, will need to question the underlying assumptions of their

procurement business models, which in many cases are predicated on the lowest possible price for bought-in

products and services.

References

Angell LC. 2000. Editorial. International Journal of Operations and Production Management 20(2): 124–126.

Ball A, Broadbent J, Jarvis T. 2006. Waste management, the challenges of the PFI and ‘sustainability reporting’. Business Strategy and the Environment 15(4): 258–274.

Birkin F, Polesie T, Lewis L. 2009. A new business model for sustainable development: an exploratory study using the theory of constraints

in Nordic organizations. Business Strategy and the Environment 18(5): 277–290.

Bowen F, Cousins P, Lamming R, Faruk A. 2001. The role of supply management capabilities in green supply. Production and Operations Management 10(2): 174–189.

Bruntland G (ed.). 1987. Our Common Future: the World Commission on Environment and Development. Oxford University Press: Oxford.

Cerrin P. 2002. Communication in corporate environmental reports. Corporate Social Responsibility and Environmental Management 9(1): 46–66.

Chevin D, Love A, Marsh P, Orr D, Cowans D, Clark R, Shoults T, Titherington T, Cave M, Parker R, Trusler S, Simmons R, Church D. 2008.

Moving Up a Gear: New Challenges for Housing Associations. Smith Institute: London.

Corbett CJ, Kirsch DA. 2001. International Diffusion of ISO 14000 Certifi cation. Production and Operations Management 10(3): 327–342.

Cozens P, Hillier D, Prescott G. 1999. The sustainable and the criminogenic: the case of new-build housing projects in Britain. Property Man-agement 17(3): 252–261.

Sustainable Procurement Practice 105

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

de Man R, Burns TR. 2006. Sustainability: supply chains, partner linkages, and new forms of self-regulation. Human Systems Management 25(1): 1–12.

Department for Environment, Food and Rural Affairs (DEFRA). 2009. Sustainable Development Indicators in Your Pocket 2009: an Update of the UK Government Strategy Indicators. DEFRA: London.

Department for Environment, Transport and the Regions (DETR). 1999. Quality of Life Counts. DETR: London.

Department for Environment, Transport and the Regions (DETR). 2000. Local Quality of Life Counts: a Handbook for a Menu of Local Indicators for Sustainable Development. DETR: London.

Diniz JDAS, Fabbe-Costes N. 2007. Supply Chain Management and Supply Chain Orientation: key factors for sustainable development proj-

ects in developing countries? International Journal of Logistics: Research and Applications 10(3): 235–250.

Dyllick T, Hockerts K. 2002. Beyond the business case for corporate sustainability. Business Strategy and the Environment 11(2): 130–141.

Ekins P. 2000. The Big Picture: Social Housing and Sustainability. Housing Corporation: London.

Feinstein L, Lupton R, Hammond C, Mujtaba T, Salter E, Sorhaindo A. 2008. The Public Value of Social Housing: a Longitudinal Analysis of the Relationship Between Housing and Life Chances. Smith Institute: London.

Fleck D. 2007. Institutionalization and organizational long-term success. Brazilian Administration Review 4(2): 64–80.

Green K, Morton B, New S. 1996. Purchasing and environmental management: interactions, policies and opportunities, Business Strategy and the Environment 5(3): 188–197.

Green K, Morton B, New S. 1998. Green purchasing and supply policies: do they improve companies’ environmental performance? Supply Chain Management: an International Journal 3(2): 89–95.

Griffi ths A, Petrick JA. 2001. Corporate architectures for sustainability. International Journal of Operations and Production Management 21(12):

1572–1585.

Halliday J. 2009. Food Sector at the Forefront of Sustainability, Says Oxfam. http://www.foodnavigator.com/On-your-radar/Sustainability/Food-

sector-at-the-forefront-of-sustainability-says-Oxfam [19 January 2010].

Heide JB, Weiss AM. 1995. Vendor consideration and switching behavior for buyers in high-technology markets. Journal of Marketing 59(3):

30–43.

Her Majesty’s Government (HMG). 2009. Key Government Deliverables for 2009/10. HMG website. http://www.hmg.gov.uk/media/29759/

key_deliverables.pdf [27 July 2009].

Housing Corporation. 2005. Government’s National Strategy for Sustainable Development. Housing Corporation website. http://www.housing-

corp.gov.uk/server/show/conWebDoc.1074 [27 July 2009].

Kirchgeorg M, Winn MI. 2006. Sustainability marketing for the poorest of the poor. Business Strategy and the Environment 15(3): 171–184.

Koplin J, Seuring S, Mesterharm M. 2007. Incorporating sustainability into supply management in the automotive industry – the case of the

Volkswagen AG. Journal of Cleaner Production 15(11/12): 1053–1062.

Larson ER, Lomi A. 1999. Resetting the clock: a feedback approach to the dynamics of organisational inertia, survival and change. Journal of the Operational Research Society 50(4): 406–421.

Linton JD, Klassen R, Jayaraman V. 2007. Sustainable supply chains: an introduction. Journal of Operations Management 25(6): 1075–1082.

Love PED, Skitmore M, Earl G. 1998. Selecting a suitable procurement method for a building project. Construction Management and Economics 16(2): 221–233.

Mason C, Kirkbride J, Bryde DJ. 2007. From stakeholders to institutions: the changing face of social enterprise governance theory. Management Decision 45(2): 284–301.

Matos S, Hall J. 2007. Integrating sustainable development in the supply chain: the case of life cycle assessment in oil and gas and agricultural

biotechnology. Journal of Operations Management 25(6): 1083–1102.

Maxwell D, Sheate W, van der Vorst R. 2006. Functional and systems aspects of the sustainable product and service development approach

for industry. Journal of Cleaner Production 14(17): 1466–1479.

McDonald S, Oates CJ. 2006. Sustainability: consumer perceptions and marketing strategies. Business Strategy and the Environment 15(3):

157–170.

Michaelidou N, Dibb S. 2006. Using email questionnaires for research: good practice in tackling non-response. Journal of Targeting, Measure-ment and Analysis for Marketing 14(4): 289–296.

Miller D, Friesen PH. 1980. Momentum and revolution in organizational adaptation. Academy of Management Journal 23(4): 591–614.

Nathan S. 2005. Supply-side sustainability. Process Engineering February. http://www.theengineer.co.uk/channels/process-engineering/

supply-side-sustainability/289999.article [accessed 25 March 2010].

Offi ce of Government Commerce (OGC). 2003. Offi ce of Government Commerce and Department for the Environment, Food and Rural Affairs Joint Note on Environmental Issues in Purchasing. OGC website. http://www.org.gov.uk/documents/environmental-issues-defra.pdf [19

January 2010].

Offi ce of Government Commerce (OGC). 2006. Social Issues in Purchasing. OGC website. http://www.ogc.gov.uk/documents/Social_Issues_

in_Purchasing/pdf [19 January 2010].

Partos L. 2009. Ethical Economic Model Spells Opportunity for Food Firms. http://www.foodnavigator.com/Financial-Industry/Ethical-economic-

model-spells-opportunity-for-food-fi rms [19 January 2010].

Perrini F, Tencati A. 2006. Sustainability and Stakeholder Management: the Need for New Corporate Performance Evaluation and Reporting

Systems. Business Strategy and the Environment 15(5): 296–308.

Preuss L. 2001. In dirty chains? Purchasing and greener manufacturing. Journal of Business Ethics 7(1): 345–359.

Preuss L. 2007. Buying into our future: sustainability initiatives in local government procurement. Business Strategy and the Environment 16(5):

354–365.

106 J. Meehan and D. Bryde

Copyright © 2010 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 20, 94–106 (2011) DOI: 10.1002/bse

Procurement for Housing (PfH). 2009. Delivering Procurement Effi ciency. PfH website. http://www.procurementforhousing.co.uk/about_us/

sustainable_procurement [25 July 2009].

Rao P. 2002. Greening the supply chain: a new initiative in South East Asia. International Journal of Operations and Production Management 22(6): 632–655.

Seitz MA, Wells PE. 2006. Challenging the implementation of corporate sustainability: the case of automotive engine remanufacturing. Busi-ness Process Management Journal 12(6): 822–836.

Sharfman MP, Shaft TM, Anex RP Jr. 2009. The road to cooperative supply-chain environmental management: trust and uncertainty among

pro-active fi rms. Business Strategy and the Environment 18(1): 1–13.

Seuring S. 2004. Industrial ecology, life cycles, supply chains; differences and interrelations. Business Strategy and the Environment 13(5):

306–319.

Sharma S, Ruud A. 2003. On the path to sustainability; integrating social dimensions into the research and practice of environmental manage-

ment. Business Strategy and the Environment 12(4): 205–214.

Shriberg M. 2000. Sustainability management in campus housing: a case study at the University of Michigan. International Journal of Sustain-ability in Higher Education 1(2): 137–154.

Siebenhuner B, Arnold M. 2007. Organizational learning to manage sustainable development. Business Strategy and the Environment 16(5):

339–353.

Sustainability at Work. 2010. Strategic Approach. http://www.sustainabilityatwork.org.uk/strategy [19 January 2010].

Thogersen J. 2006. Media attention and the market for ‘green’ consumer products. Business Strategy and the Environment 15(3): 145–156.

Tregidga H, Milne MJ. 2006. From sustainable management to sustainable development: a longitudinal analysis of a leading New Zealand

environmental reporter. Business Strategy and the Environment 15(4): 219–241.

Van der Steen M. 2009. Inertia and management accounting change. Accounting, Auditing and Accountability 22(5): 736–761.

Veleva V, Hart M, Greiner T, Crumbley C. 2003. Indicators for measuring environmental sustainability: a case study of the pharmaceutical

industry. Benchmarking: an International Journal 10(2): 107–119.

Vining J, Ebreo A. 1990. What makes a recycler? A comparison of recyclers and non-recyclers. Environment and Behavior 22(1): 55–73.

von-Geibler J, Liedtke C, Wallbaum H, Schaller S. 2006. Accounting for the social dimension of sustainability: experiences from the biotech-

nology industry. Business Strategy and the Environment 15(5): 334–346.

Wilkinson A, Hill M, Gollan P. 2001. The sustainability debate. International Journal of Operations and Production Management 21(12): 1492–

1502.

Yongvanich K, Gutherie J. 2006. An extended performance reporting framework for social and environmental accounting. Business Strategy and the Environment 15(5): 309–321.

Zsidisin GA, Siferd SP. 2001. Environmental purchasing – a framework for theory development. International Journal of Purchasing and Supply Management 7(1): 61–73.