striped catfish farming in the mekong delta: vulnerability to development & climate change

TRANSCRIPT

Striped catfish farming in the Mekong Delta:

Vulnerability to development & climate change

Ashley S. Halls, Matthew Johns & Anton Immink

Introduction

Introduction

Introduction

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Val

ue

(0

00

's U

S$)

Pro

du

ctio

n (

ton

ne

s)

Year

Production (tonnes)

Value (000's US$)

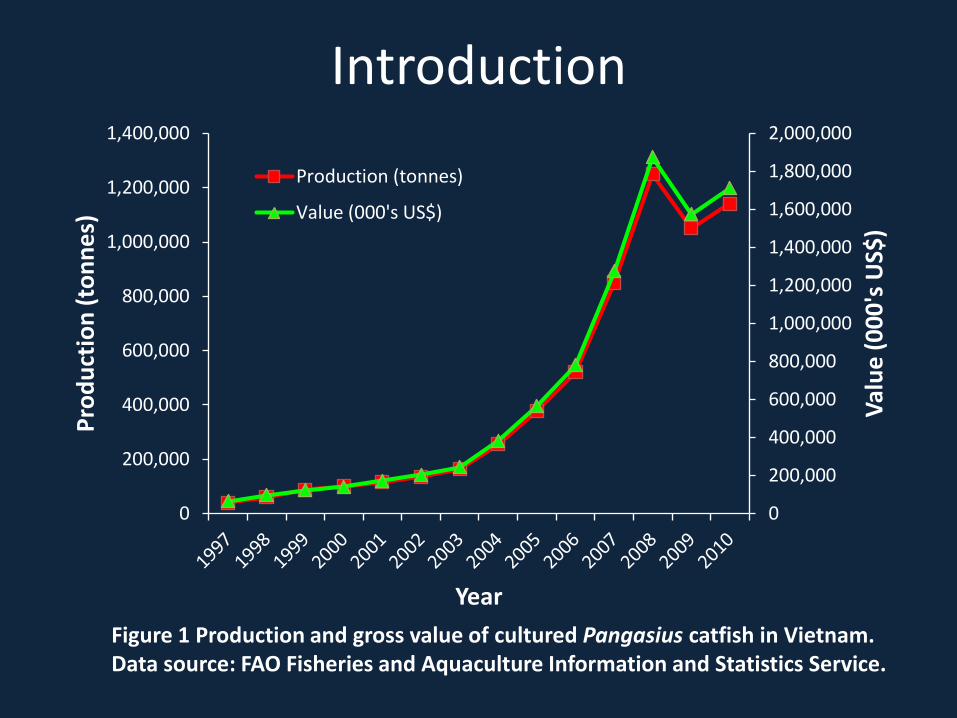

Figure 1 Production and gross value of cultured Pangasius catfish in Vietnam. Data source: FAO Fisheries and Aquaculture Information and Statistics Service.

Introduction

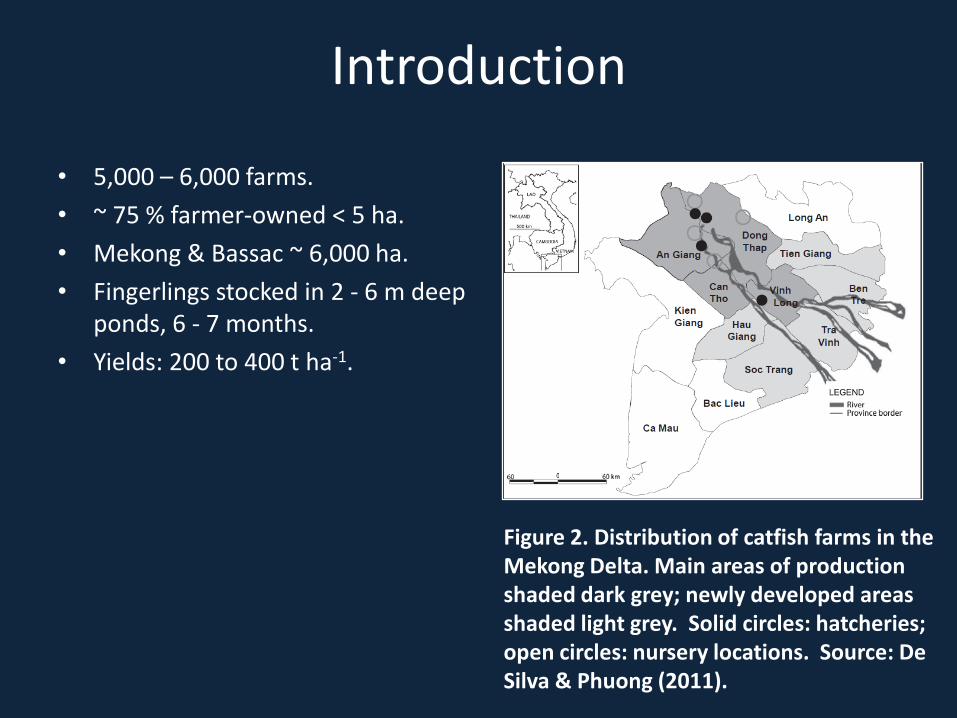

• 5,000 – 6,000 farms.

• ~ 75 % farmer-owned < 5 ha.

• Mekong & Bassac ~ 6,000 ha.

• Fingerlings stocked in 2 - 6 m deep ponds, 6 - 7 months.

• Yields: 200 to 400 t ha-1.

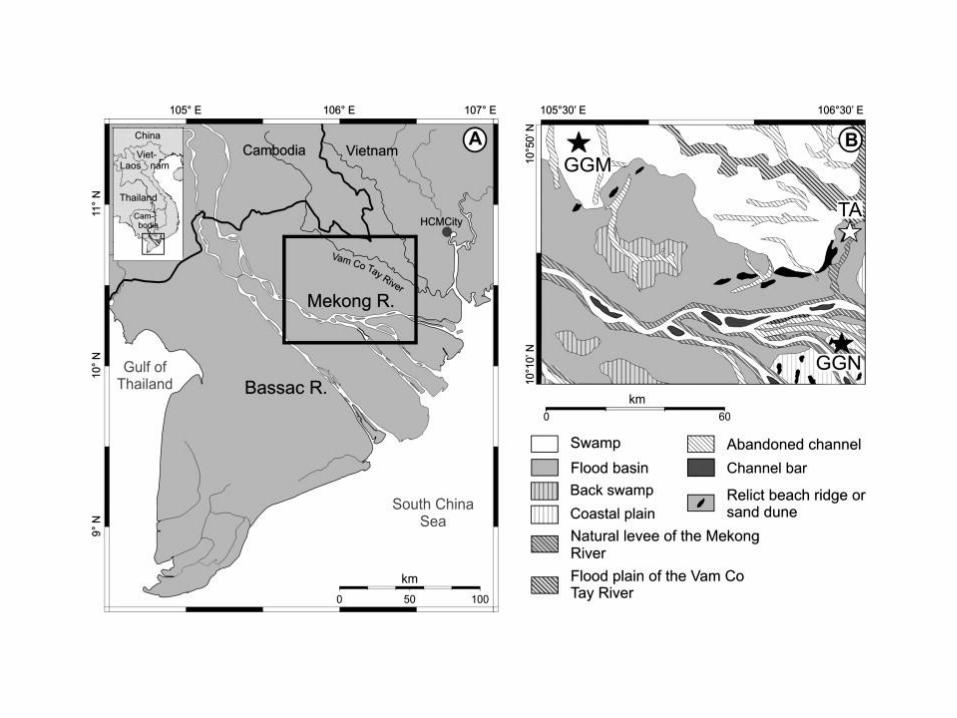

Figure 2. Distribution of catfish farms in the Mekong Delta. Main areas of production shaded dark grey; newly developed areas shaded light grey. Solid circles: hatcheries; open circles: nursery locations. Source: De Silva & Phuong (2011).

Introduction

• Industry will be exposed to changes in biophysical conditions:

• Upstream development;

• Climate change.

• Study purpose:

• Raise awareness of sector’s vulnerability to this exposure

• Mitigate or manage impacts.

Methods

• Intensive (20 day) review of > 75 relevant scientific papers and reports, datasets…etc.

• Impact assessments (MRC) for BDP.

• What do we mean by vulnerability?

• V = Potential Impact – Adaptive Capacity

• PI = Exposure, Sensitivity

• Adaptive capacity – ability to manage or mitigate impacts.

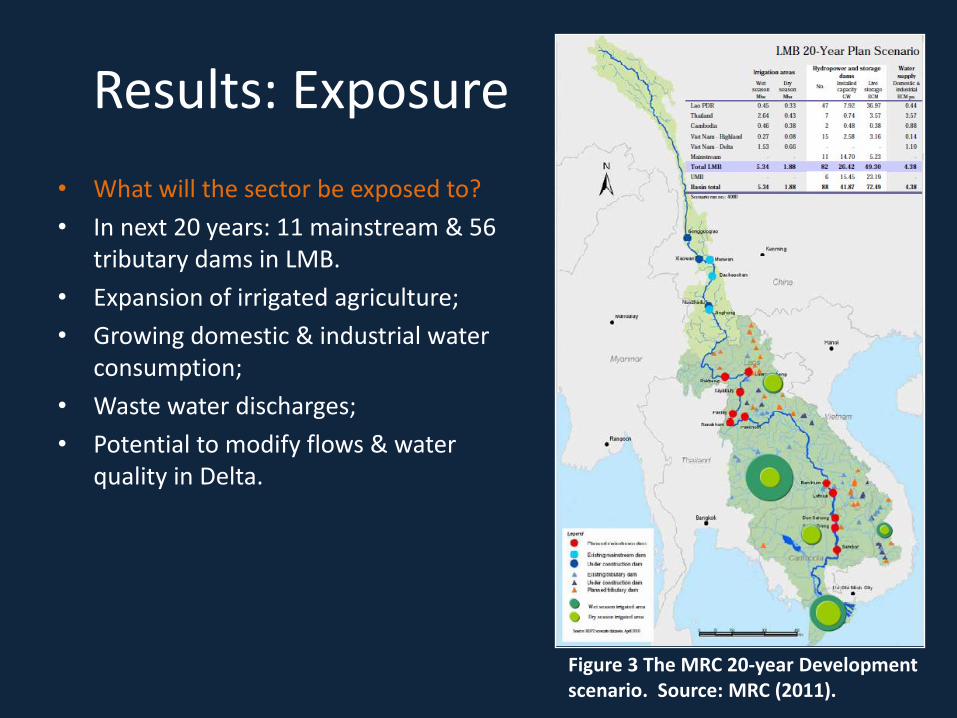

Results: Exposure

• What will the sector be exposed to?

• In next 20 years: 11 mainstream & 56 tributary dams in LMB.

• Expansion of irrigated agriculture;

• Growing domestic & industrial water consumption;

• Waste water discharges;

• Potential to modify flows & water quality in Delta.

Figure 3 The MRC 20-year Development scenario. Source: MRC (2011).

Exposure

• Climate in Delta already changing.

• 0.7 – 0.8 o C (1.9 o C ?) rise expected by 2050.

• Sea levels up 17 cm by 2030.

• More frequent & intense typhoons.

• Changes in precipitation in the LMB expected:

• + 1 % - 10 % in most areas, but up to – 8 % in Delta.

• How will flows and water quality in the Delta respond?

Exposure

• Dry season flows: + 17 to + 20 %.

• Wet season flows: - 3 to + 1 %.

• Average annual flows: + 2 to + 6 %.

• Water temperature: + 0.7 – 0.8 o C

• Marginal decline in O2 solubility in ponds.

• More saline water intrusion into Mekong (affecting Ben Tre, Tra Vinh and Vinh Long).

• Intrusion into Bassac will decrease (improving conditions in parts of Tra Vinh, Can Tho, Hau Giang & Soc Tranh).

• Overall area affected unchanged.

Exposure

• Nutrient (N&P) loading (agri.): +12% ; +28 %.

• Nutrient loading (urban sources): + 50 %.

• Herbicide / pesticide concs: + 15 % / + 5%

• Downstream supply of sediment: - 75 %.

• Delivery of nutrients to Delta / offshore coastal zones.

• Structural stability of river channels / coastline.

Exposure

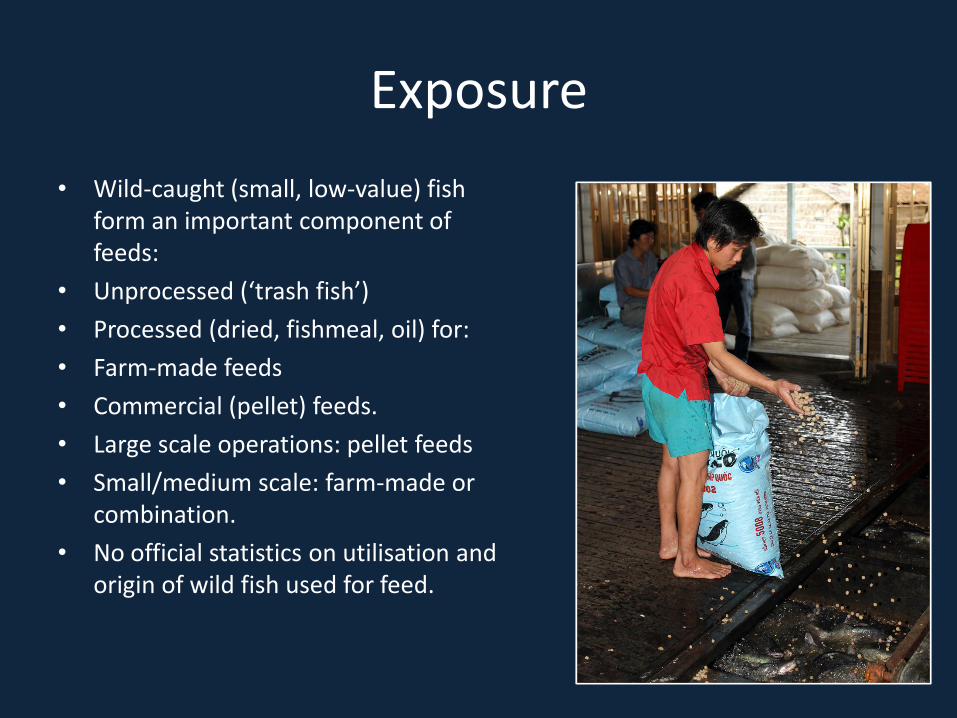

• Wild-caught (small, low-value) fish form an important component of feeds:

• Unprocessed (‘trash fish’)

• Processed (dried, fishmeal, oil) for:

• Farm-made feeds

• Commercial (pellet) feeds.

• Large scale operations: pellet feeds

• Small/medium scale: farm-made or combination.

• No official statistics on utilisation and origin of wild fish used for feed.

Exposure

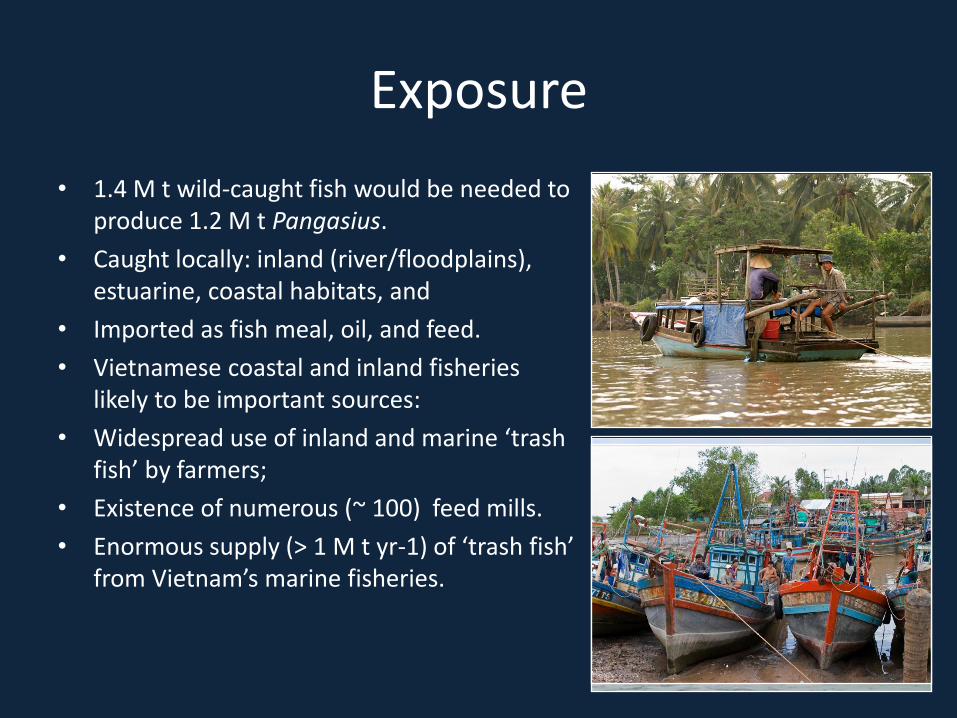

• 1.4 M t wild-caught fish would be needed to produce 1.2 M t Pangasius.

• Caught locally: inland (river/floodplains), estuarine, coastal habitats, and

• Imported as fish meal, oil, and feed.

• Vietnamese coastal and inland fisheries likely to be important sources:

• Widespread use of inland and marine ‘trash fish’ by farmers;

• Existence of numerous (~ 100) feed mills.

• Enormous supply (> 1 M t yr-1) of ‘trash fish’ from Vietnam’s marine fisheries.

Exposure

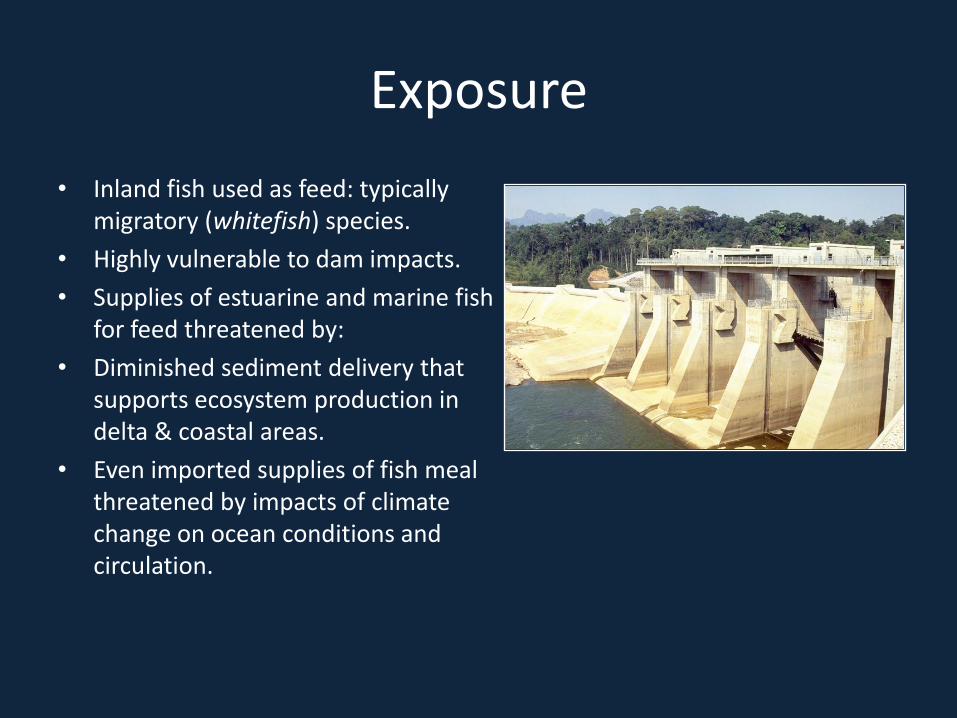

• Inland fish used as feed: typically migratory (whitefish) species.

• Highly vulnerable to dam impacts.

• Supplies of estuarine and marine fish for feed threatened by:

• Diminished sediment delivery that supports ecosystem production in delta & coastal areas.

• Even imported supplies of fish meal threatened by impacts of climate change on ocean conditions and circulation.

Sensitivity & Potential Impacts

• Nutrient concentrations in Delta expected to remain acceptable: – Diluting effects of increasing dry season

flows; – Diminished transport of sediments; – Improvements to waste water

treatment

• Local eutrophication? • Uncertain whether herbicides and

pesticides concs. will rise to levels that threaten food safety of Pangasius products.

• Maintaining market confidence in food safety paramount importance to sector.

Johanna Da Cruz

Sensitivity & Potential Impacts

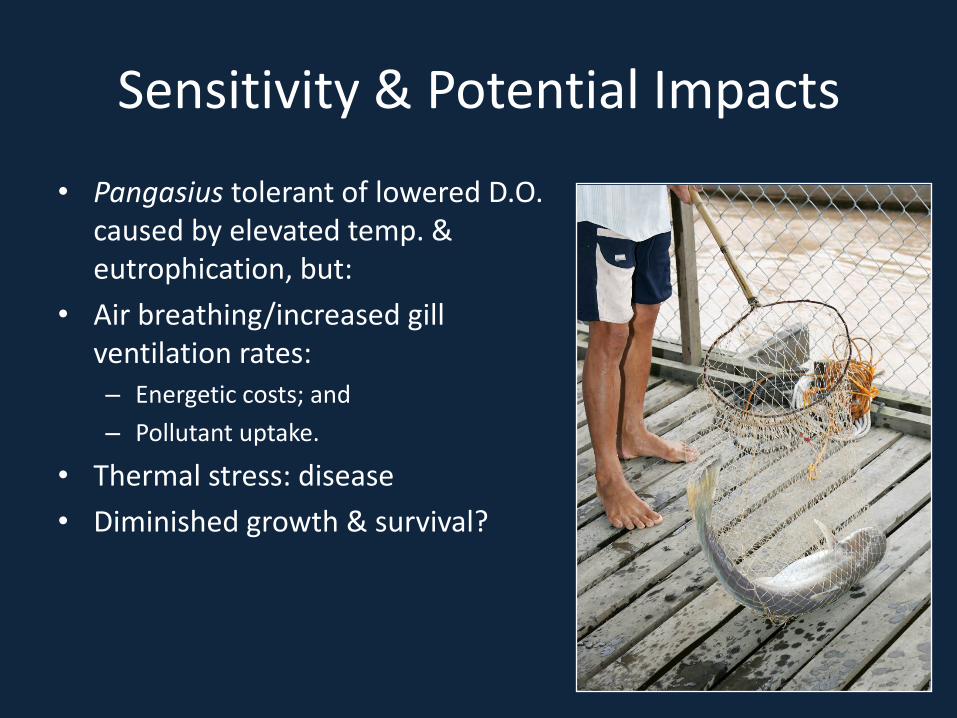

• Pangasius tolerant of lowered D.O. caused by elevated temp. & eutrophication, but:

• Air breathing/increased gill ventilation rates: – Energetic costs; and

– Pollutant uptake.

• Thermal stress: disease

• Diminished growth & survival?

Sensitivity & Potential Impacts

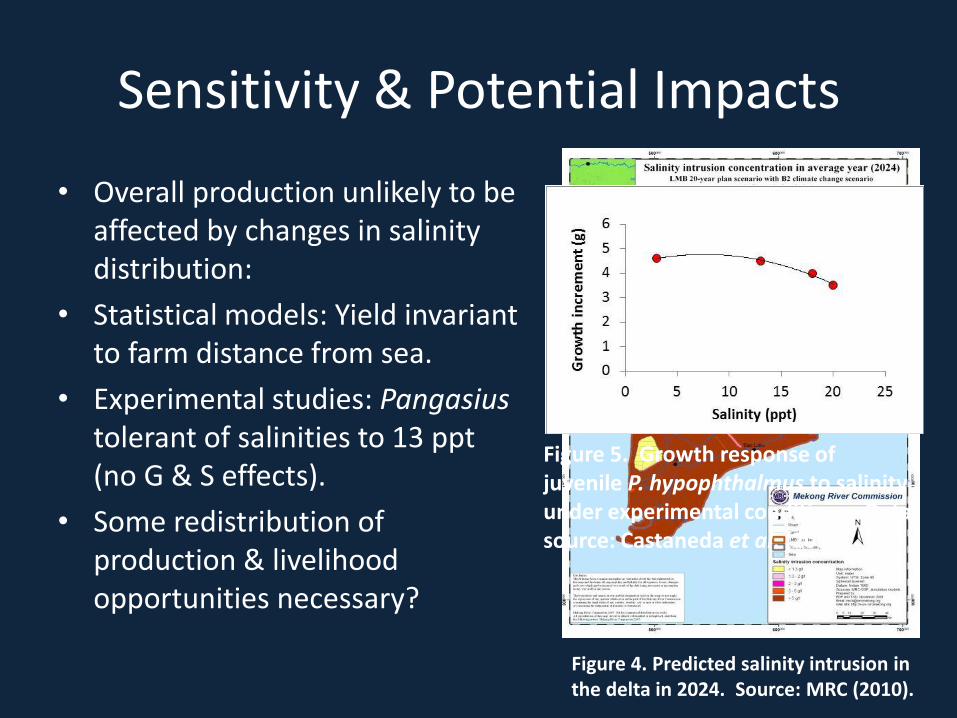

• Overall production unlikely to be affected by changes in salinity distribution:

• Statistical models: Yield invariant to farm distance from sea.

• Experimental studies: Pangasius tolerant of salinities to 13 ppt (no G & S effects).

• Some redistribution of production & livelihood opportunities necessary?

Figure 4. Predicted salinity intrusion in the delta in 2024. Source: MRC (2010).

Figure 5. Growth response of juvenile P. hypophthalmus to salinity under experimental conditions. Data source: Castaneda et al. (2010).

Sensitivity & Potential Impacts

• Marginal profits for most small-scale farmers.

• Sensitive: – Market prices (downward

trend)

– Feed costs (75 – 85 % of var. costs)

• Farmers suspend production until prices rise.

1,50

2,00

2,50

3,00

2003 2004 2005 2006 2007 2008 2009 2010 2011

Exp

ort

val

ue

(US$

/kg)

Year

Figure 6 Unit value of exports, 2003-2010. Data source: Dzung (2012)

Sensitivity & Potential Impacts

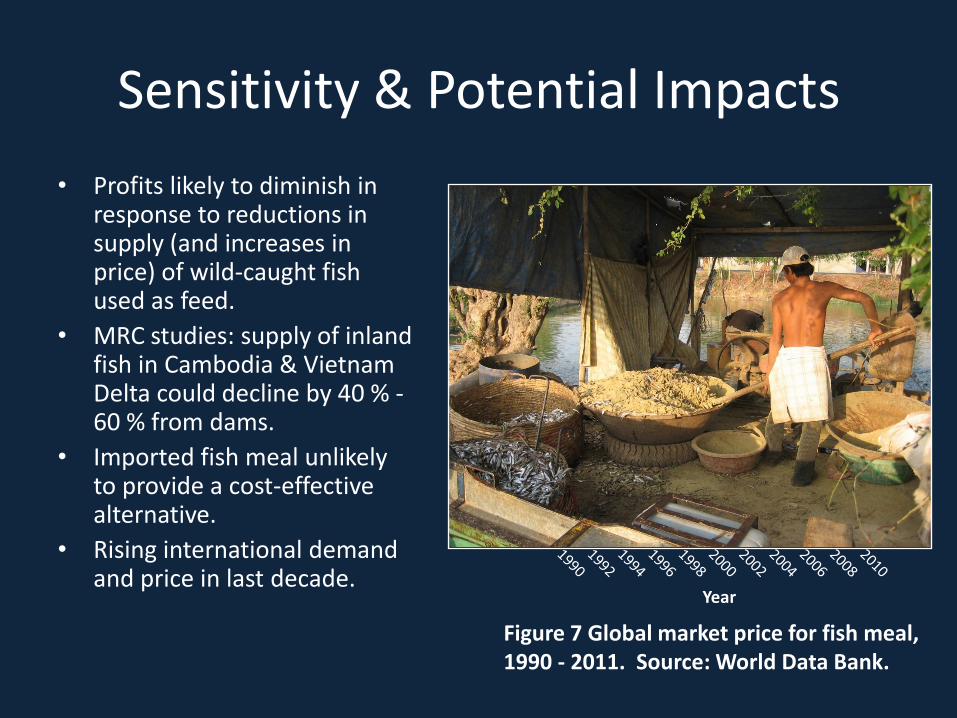

• Profits likely to diminish in response to reductions in supply (and increases in price) of wild-caught fish used as feed.

• MRC studies: supply of inland fish in Cambodia & Vietnam Delta could decline by 40 % - 60 % from dams.

• Imported fish meal unlikely to provide a cost-effective alternative.

• Rising international demand and price in last decade.

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

$ /

to

nn

e

Year

Fishmeal, $/mt, nominal$

Fishmeal, $/mt, real 2005$

Figure 7 Global market price for fish meal, 1990 - 2011. Source: World Data Bank.

Sensitivity & Potential Impacts

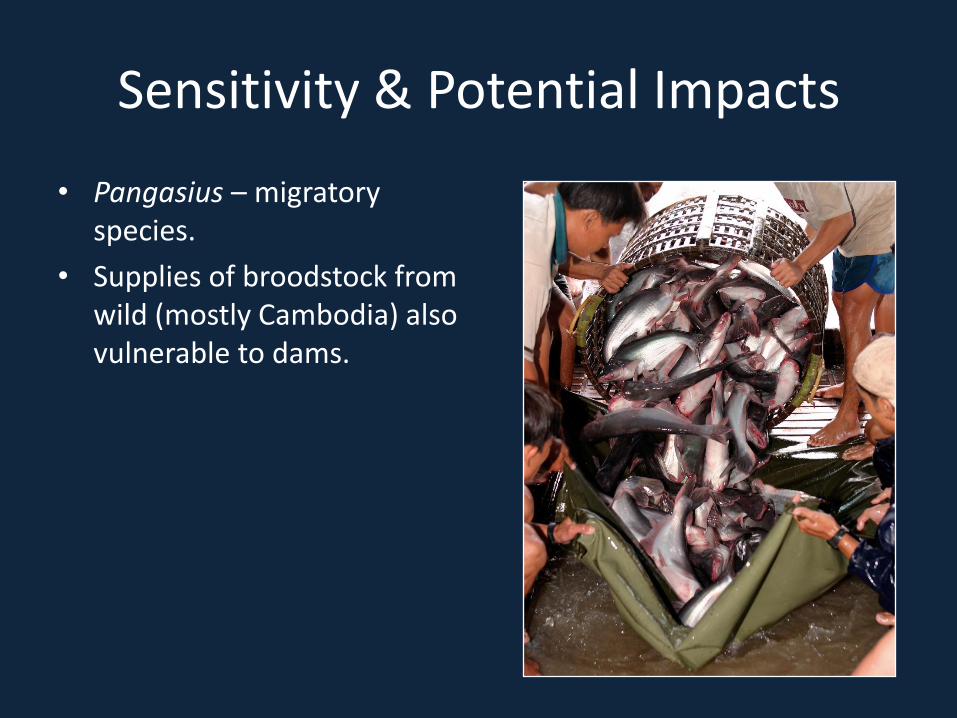

• Pangasius – migratory species.

• Supplies of broodstock from wild (mostly Cambodia) also vulnerable to dams.

Adaptive Capacity

• Where water quality is affected (by pollution, eutrophication and temperature):

• Autonomous adaptation: – feed inputs,

– drug applications,

– stocking densities

• Diminish profit & product safety

• Planned adaptation (more effective but also costly): – Treatment facilities at water intakes and (waste water) off-takes.

– Pond aeration

– Greater regulation over drug use

Adaptive Capacity

• Improved broodstock management practices to reduce reliance wild-caught individuals.

• Flood protection works in longer term.

Adaptive Capacity

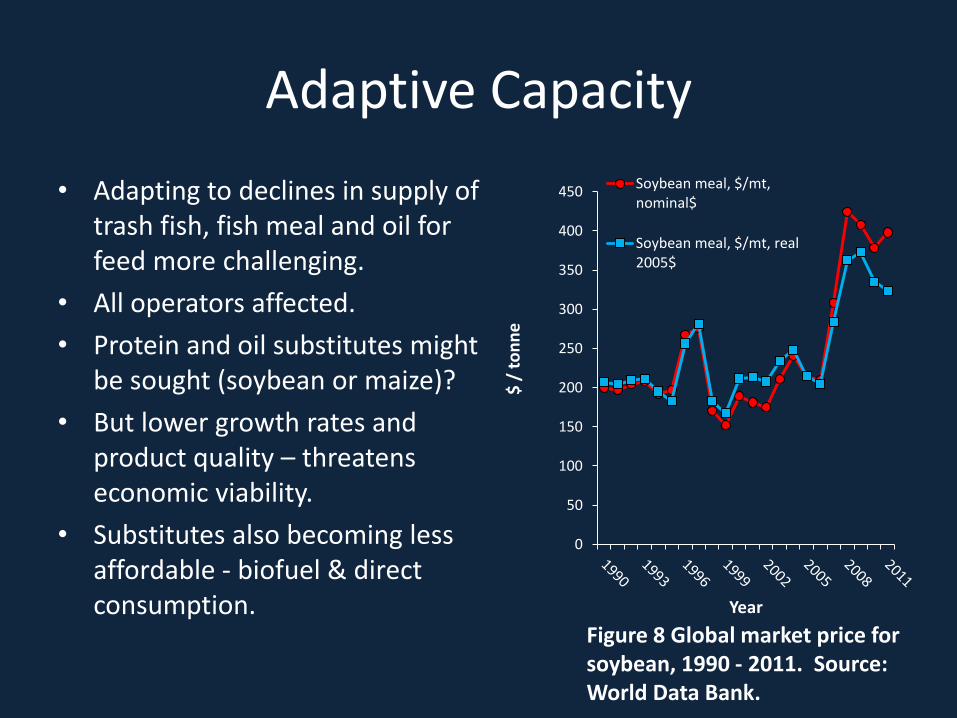

• Adapting to declines in supply of trash fish, fish meal and oil for feed more challenging.

• All operators affected.

• Protein and oil substitutes might be sought (soybean or maize)?

• But lower growth rates and product quality – threatens economic viability.

• Substitutes also becoming less affordable - biofuel & direct consumption.

0

50

100

150

200

250

300

350

400

450

$ /

to

nn

e

Year

Soybean meal, $/mt,nominal$

Soybean meal, $/mt, real2005$

Figure 8 Global market price for soybean, 1990 - 2011. Source: World Data Bank.

Conclusions: Vulnerability

• Sector vulnerable via several pathways of impact.

• Most important impact pathway?

• Particularly whether water quality deteriorate to cause: – Physiological impacts?

– Contaminant-related product safety impacts?

• Very likely that supplies of wild-caught fish used for feed will decline, locally, regionally and globally exacerbating their upward cost trends.

• Doubt surrounds the cost-effectiveness of substitutes.

• Other cost burdens likely: – Farm re-location; flood control; improved broodstock management,

water treatment facilities…etc.

Vulnerability

• To maintain output, demand will need to be inelastic to necessary price rises.

• Unlikely given historic price trends and growing output from other countries e.g. China, Bangladesh, Indonesia…etc.

• Without price rises, declines in profit and output expected, impacting upon dependent livelihoods and wider economy.

• Far reaching implications for food security beyond the Delta.

• Challenges the assertion that aquaculture production will compensate the expected declines in yield from capture fisheries.

Priority Research

• Described in our report : www.sustainablefish.org/

• Reliably determine reliance on wild fish for feed from inland and coastal fisheries most vulnerable to development & CC impacts.

Thank you

Photos: Joe Garrison, MRCS Cuyers & Binh (2008) Johanna Da Cruz Ashley Halls, ASL

Further Information: www.sustainablefish.org/

Priority Research

• Described in our report : www.sustainablefish.org/

• Reliably determine reliance on wild fish for feed from inland and coastal fisheries most vulnerable to development impacts;

• Improve knowledge of physiological responses / tolerances (temp, D.O. salinity);

• Better predict water quality under future basin development scenarios;

• Assess likely food safety of Pangasius products in response to water quality conditions (particularly pollutant and contaminant concentrations);

• Formulate cost-effective feeds using alternative sources of protein/oil to maintain or expand production.

• Improve understanding of international markets for Pangasius products, their driving forces and price elasticity of demand.

Adaptive Capacity

• Relocating farms further upstream – impracticable strategy to salinity changes.

• Development of more saline-tolerant strains advocated:

• Feasibility and necessity?

• Improved broodstock management practices to reduce reliance wild-caught individuals.

• Flood protection works in longer term.

Economics of Production

• Production costs for household-scale intensive pond-reared P. hypophthalmus are relatively stable but margins are extremely tight. Production costs in early 2009 for commercial-scale striped catfish grow-out producers were approximately VND 15 000/kg (USD 0.83/kg) excluding capital investment costs; this was offset by sale prices of VND 16 000/kg (USD 0.89/kg). At that time household-scale grow-out producers were only being paid VND 14 000-15 000 (USD 0.78 – 0.83/kg) for market sized fish by processing plants but their production costs at approximately VND 13 000 – 14 000 (USD 0.72 – 0.78 kg) excluding capital investment costs were lower . Most grow-out farmers view capital investment costs as a ‘sunk cost’. Profit margins in early 2009 were so tight that striped catfish grow-out farmers in Vietnam were unlikely to recover their capital investment costs fully (FAO 2010).