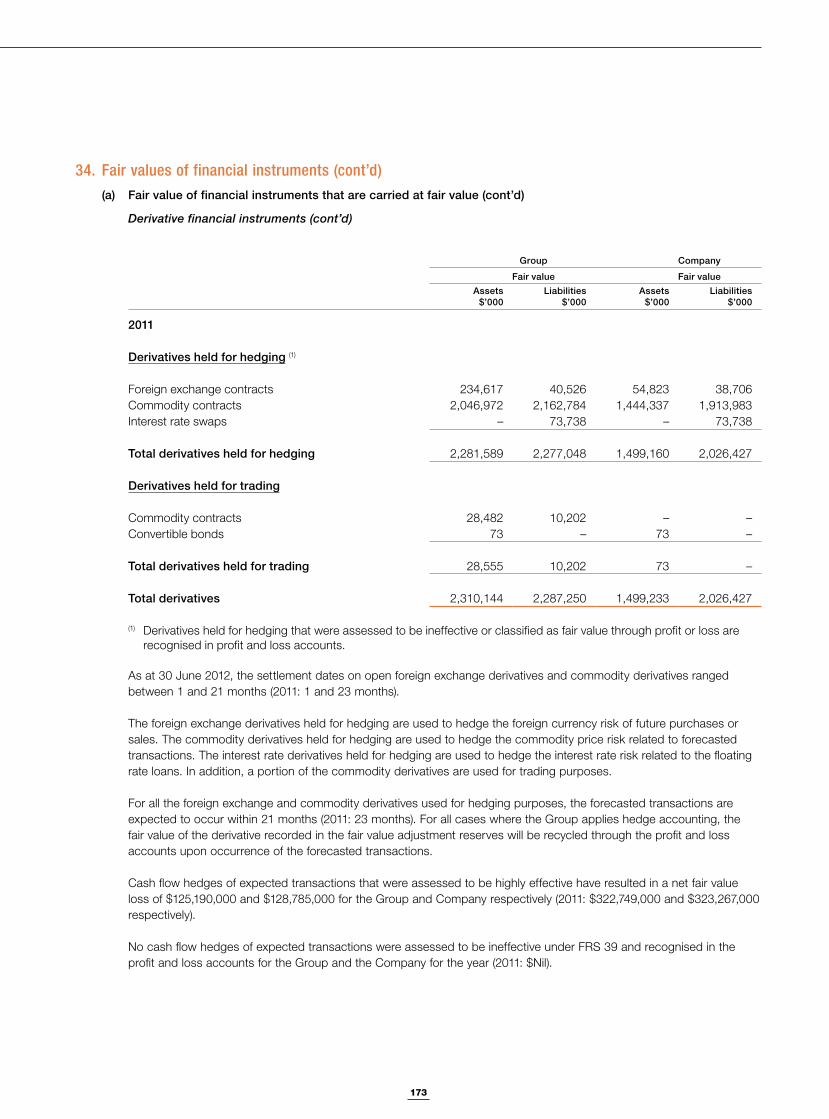

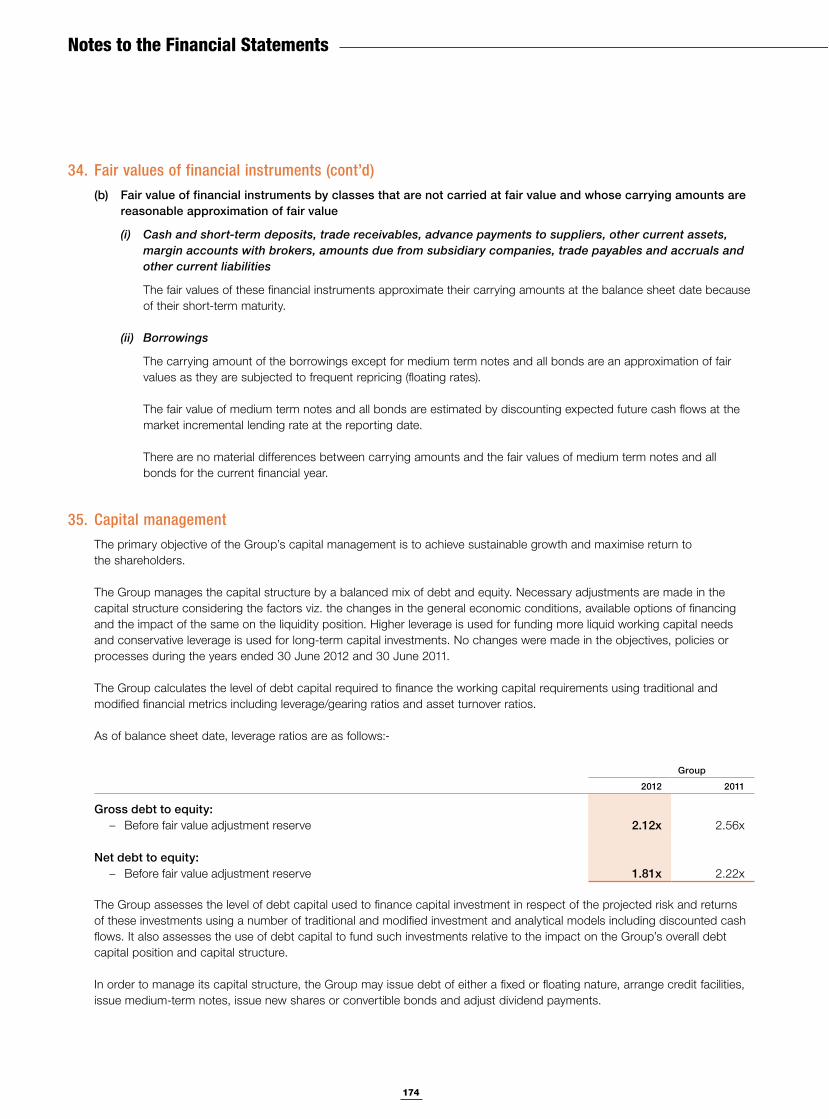

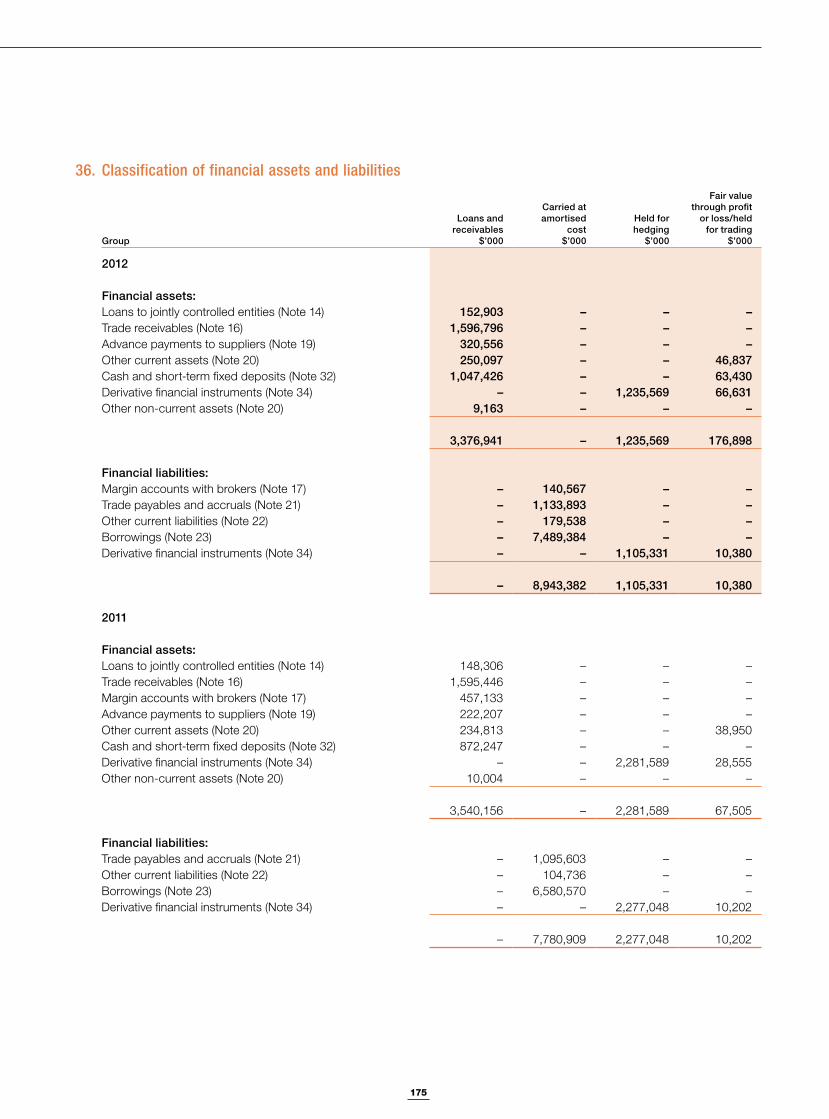

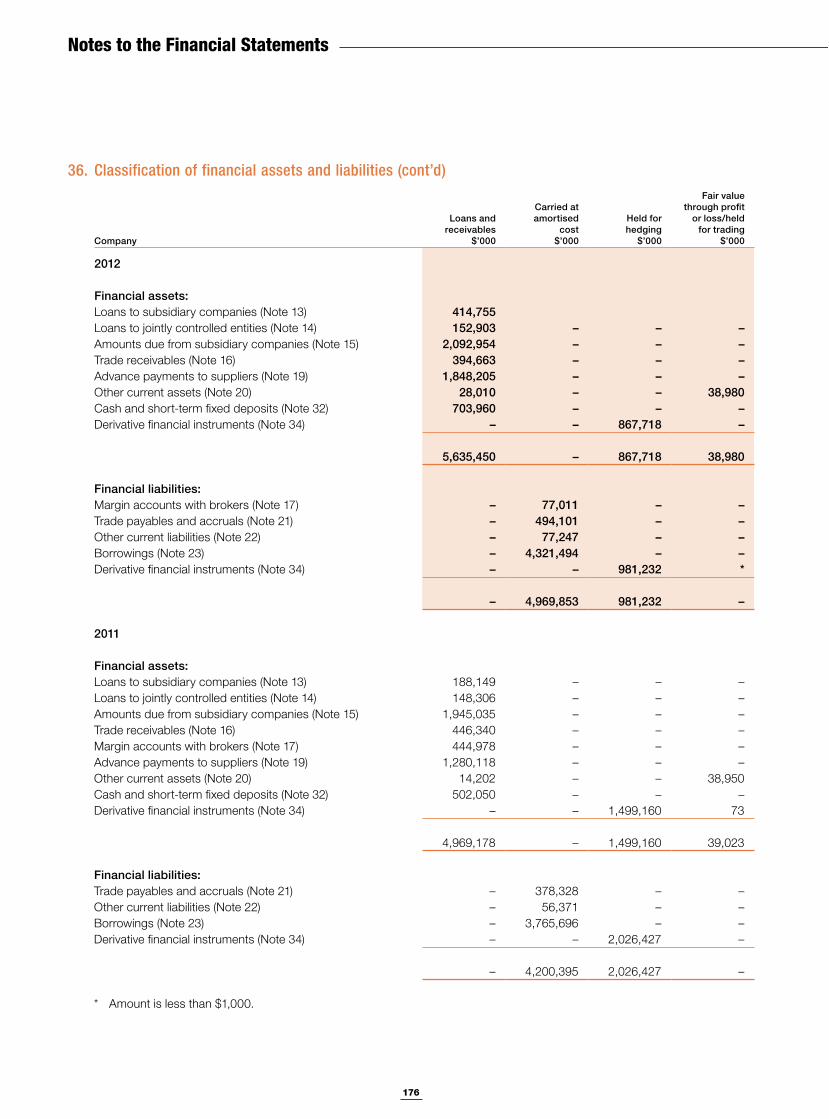

shaping the future - olam international

TRANSCRIPT

Olam

International Limited

Annual R

eport 2012

Shaping the FutureHow Olam is driving sustainable growth while solving for risk

Seeing the Big Picture Addressing the global supply demand imbalance in the agri-complex

Empowering Our People Leveraging our strengths by developing global leaders

Growing Responsibly Improving small-scale farmer incomes & livelihoods

Olam International Limited9 Temasek Boulevard11-02 Suntec Tower TwoSingapore 038989

Telephone (65) 6339 4100Facsimile (65) 6339 9755www.olamonline.com

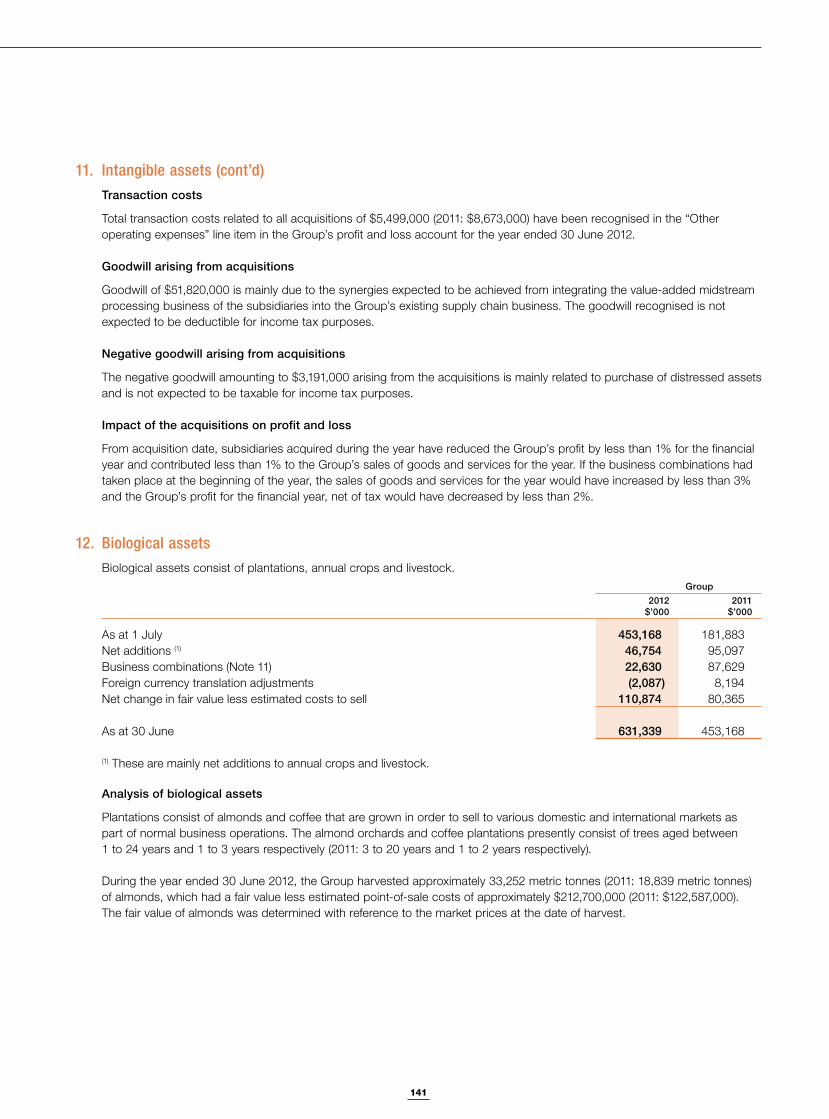

Shaping The Future - CEO and Executive Directors’ Dialogue Pg 14

Midstream - Addressing Global Needs Pg 42

Olam is helping shape the future of agri-commodities by partnering with farmers worldwide to bring new resources into play.

Olam is a custodian of our investors’ resources so we need to show how we are growing these resources responsibly, for profit and for the benefit of all our stakeholders

CR&S - Supporting Rural Livelihoods Pg 50

Our People - Growing Global Leaders Pg 54

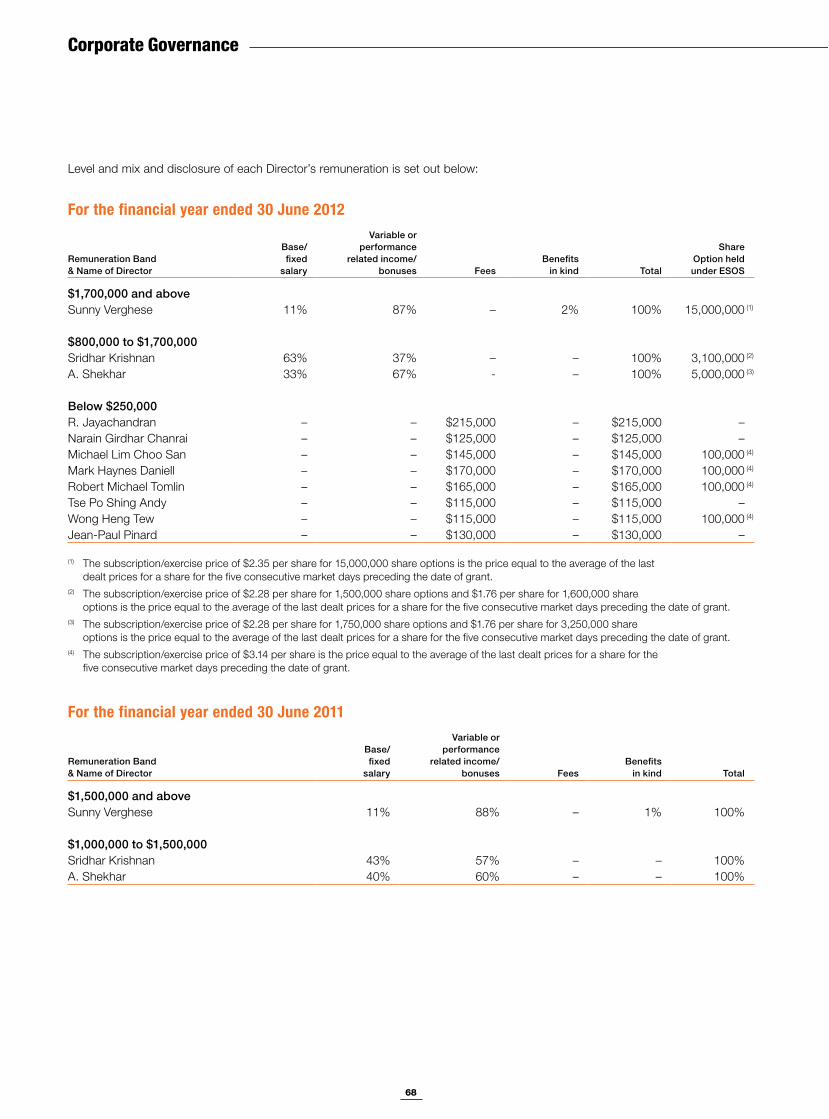

1

02 Performance Overview

04 Performance Analysis

06 Financial Summary

07 Financial Highlights

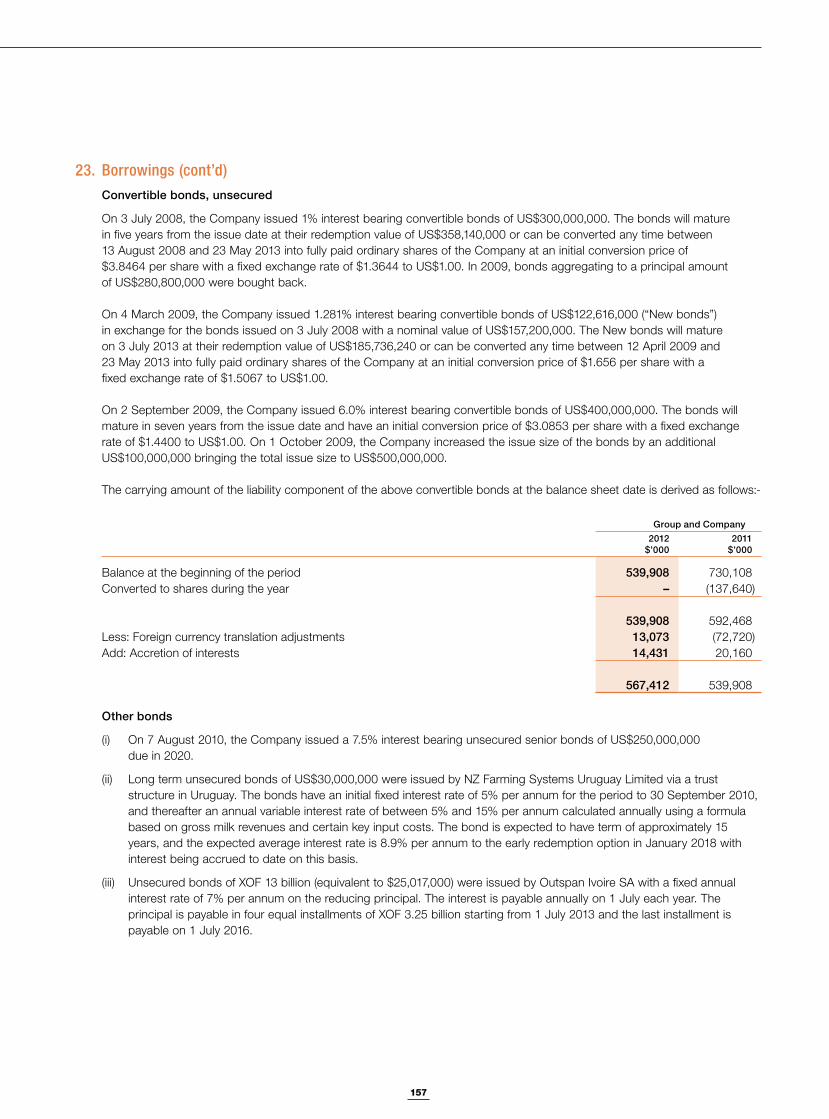

08 Chairman’s Statement

10 Board of Directors

14 CEO and Executive Directors’ Dialogue CEO Sunny Verghese and Executive Directors Sridhar Krishnan and A. Shekhar discuss Olam’s approach to sustainable long-term growth

28 Executive Committee

30 Global Presence

32 Business Review Senior managers discuss what is driving global growth in the agri-businesses sector

34 Upstream

38 Origination

42 Midstream

46 New Growth

50 Corporate Responsibility & Sustainability Implementing processes to deliver sustainable products across all our geographies

54 Our People

56 Risk Management

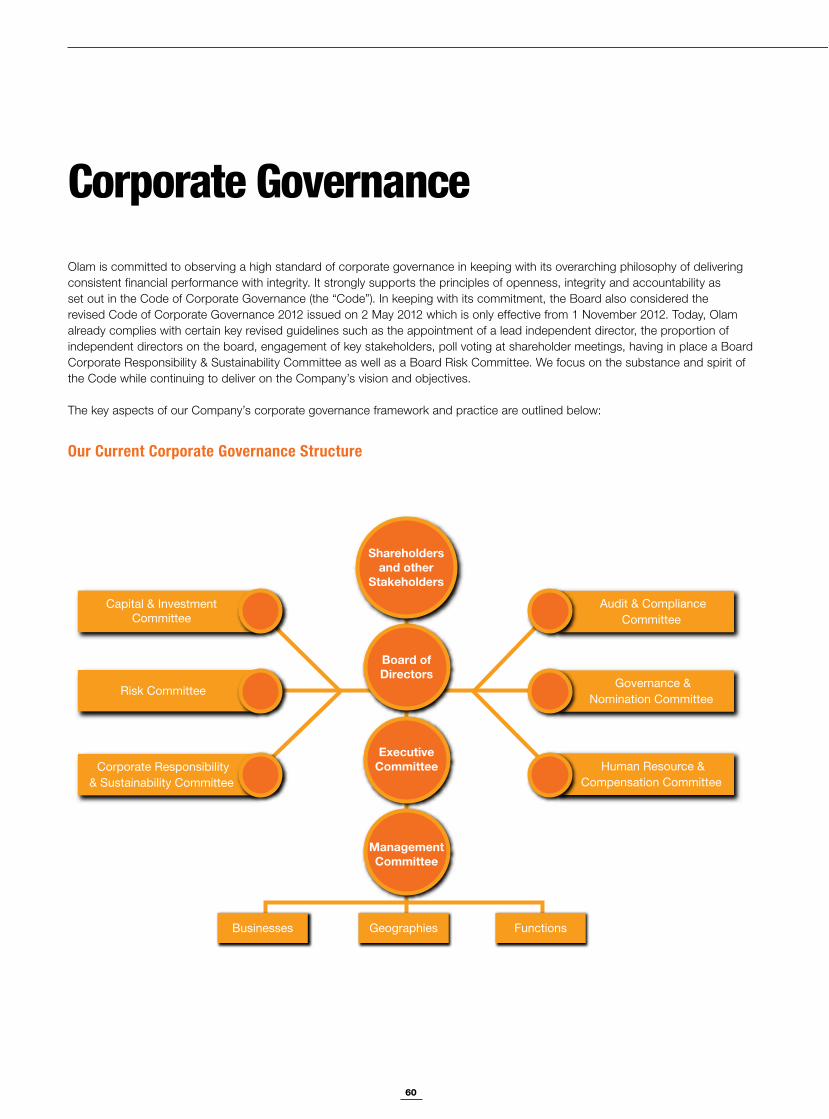

58 Corporate Governance Why good Corporate Governance is vital for success

77 Key Information Regarding Directors

81 Corporate Information

82 6-Year Financial Analysis

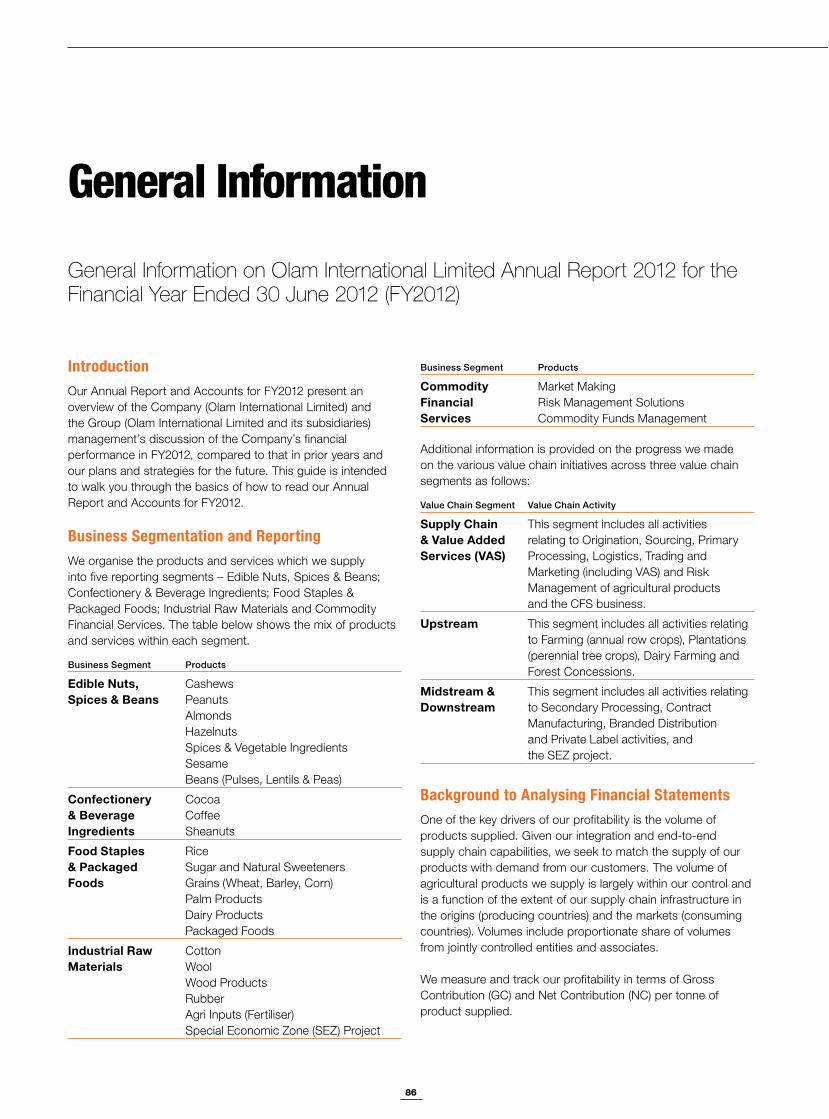

86 General Information

89 Directors’ Report and Audited Financial Statements

Contents

Embracing ChangeChange is an inherent and accelerating factor in today’s business. It is a threat if we don’t anticipate it, but also a source of great opportunity if we do. Many of the world’s most successful businesses have gained in strength during turbulent times.

Commodity markets have seen volatile swings in recent years and this has led to stress and pressure on many participants. Some have withdrawn and others have reduced their commitment under these market conditions.

Olam’s business model has proven its strength and resilience to volatility. As a result, we are capitalising on emerging opportunities as we implement our strategy to build a unique and globally capable company.

The foundation of our strategy was laid two decades ago as we developed our business in the emerging markets, based on a repeatable model of adjacency growth. Today we remain true to our core, but see new potential as agri-resources grow scarce, global markets re-balance and consumption patterns and demand change. In this annual report, we explore the wider story of how Olam is positioning itself to be at the forefront of the agri-complex which has attractive growth prospects.

Our organisational advantage – our people, culture and values, make us what we are today.

Coffee in Brazil

2

VOLUME

SALES REVENUE

NET CONTRIBUTION

NET CONTRIBUTION / TONNE

EBITDA

NPAT

FY2011

FY2012

8.5mtonnes

10.7mtonnes

+26.3%

FY2011

FY2012

S$1.4bS$1.2b

+13.0%

FY2011

FY2012

S$957.8mS$863.0m

+11.0%

FY2011

FY2012

S$129

S$145

(11.0%)

FY2011

FY2012

S$403.8m

S$444.6m

(9.2%)

FY2011

FY2012

S$17.1bS$15.8b

+8.2%

Performance Overview

3

EPS

FY2011

FY2012

(26.2%)

S$0.203

S$0.150

ROIC

FY2011

FY2012

10.7%14.3%

(3.6%)

ROE

FY2011

FY2012

14.2%21.3%

(7.1%)

EQUITY SPREAD

FY2011

FY2012

4.2%11.3%

(7.1%)

CAPITAL SPREAD

FY2011

FY2012

3.5%7.1%

(3.6%)

NET ASSET VALUE PER SHARE*

* Before Fair Value Adujstment Reserve

FY2011

FY2012

S$1.45

S$1.15 +25.8%

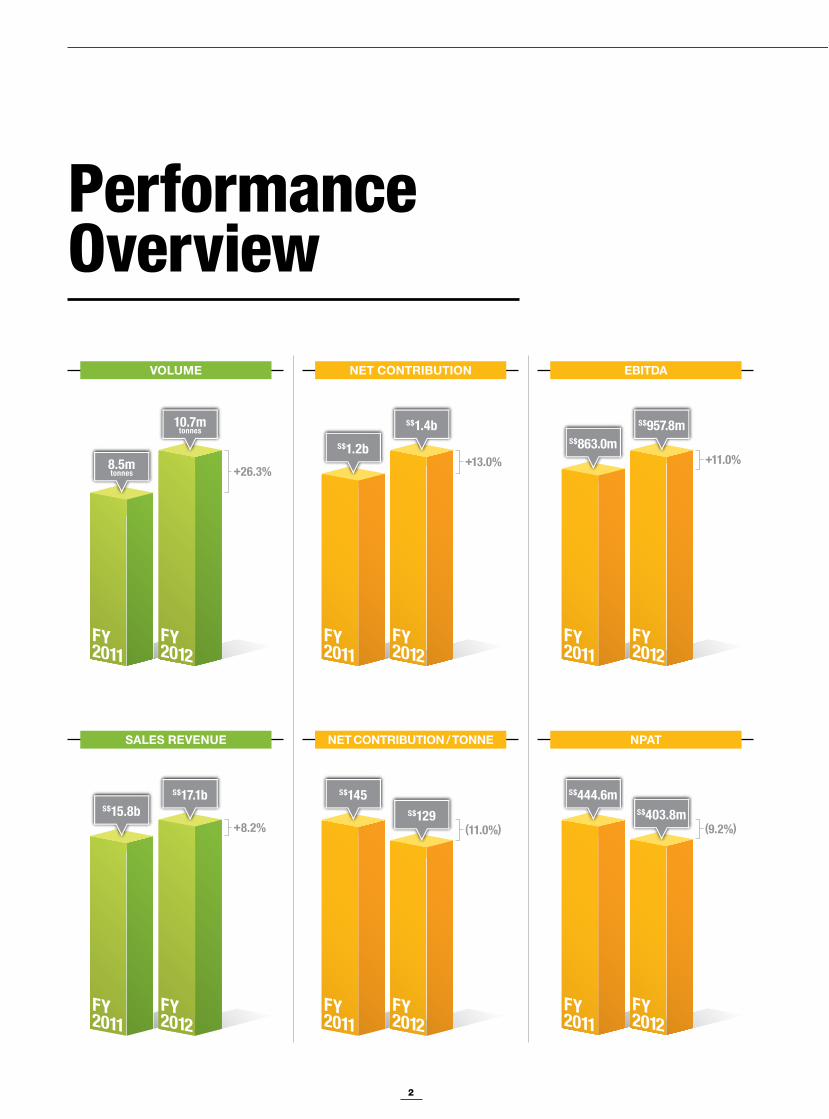

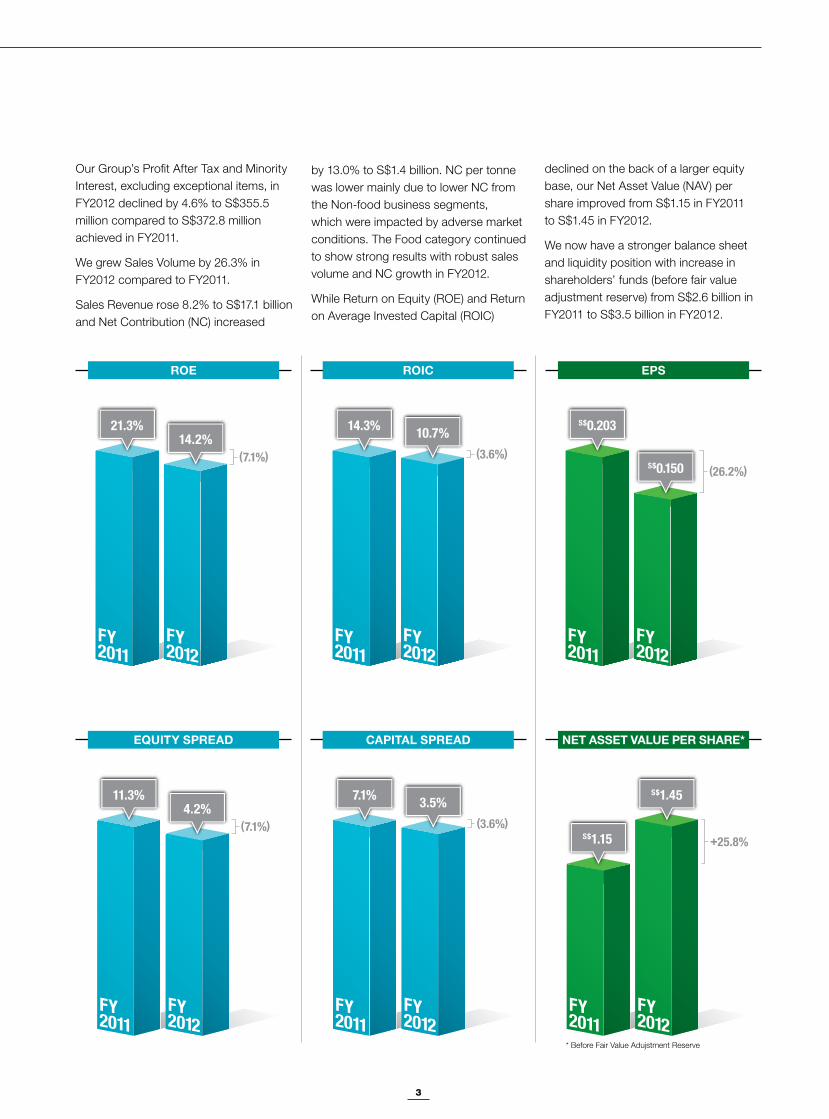

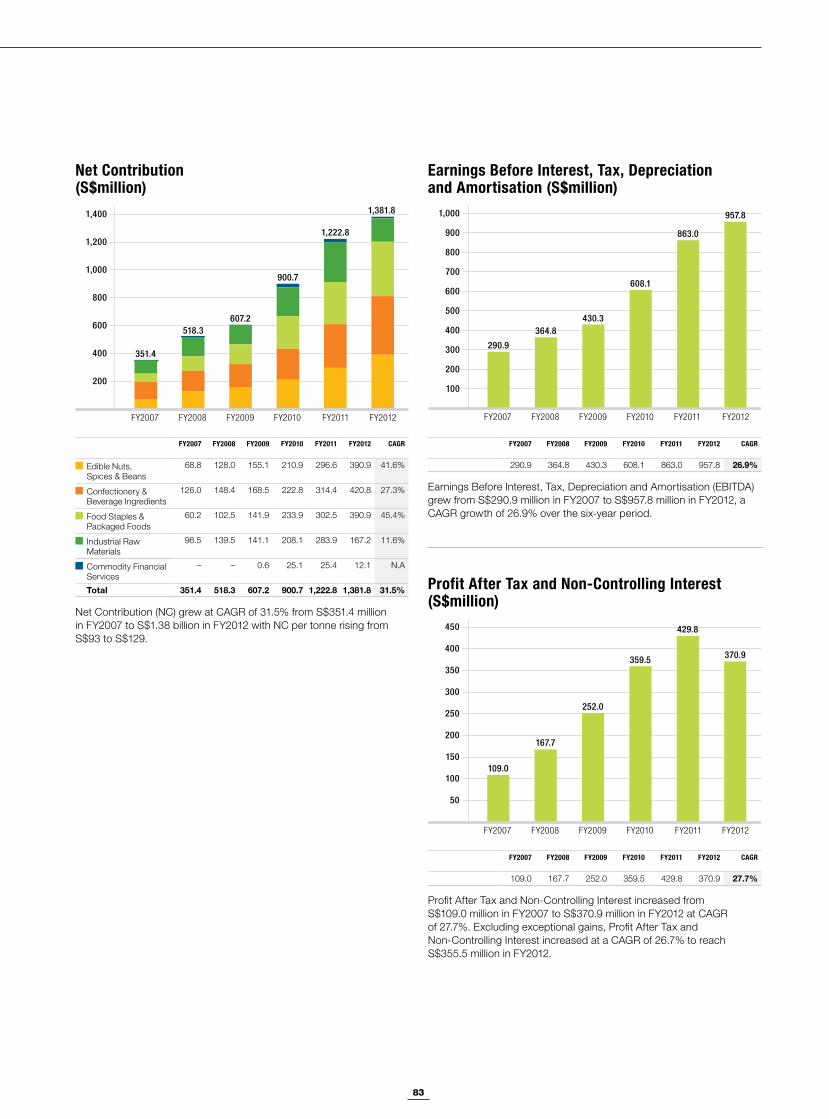

by 13.0% to S$1.4 billion. NC per tonne was lower mainly due to lower NC from the Non-food business segments, which were impacted by adverse market conditions. The Food category continued to show strong results with robust sales volume and NC growth in FY2012.

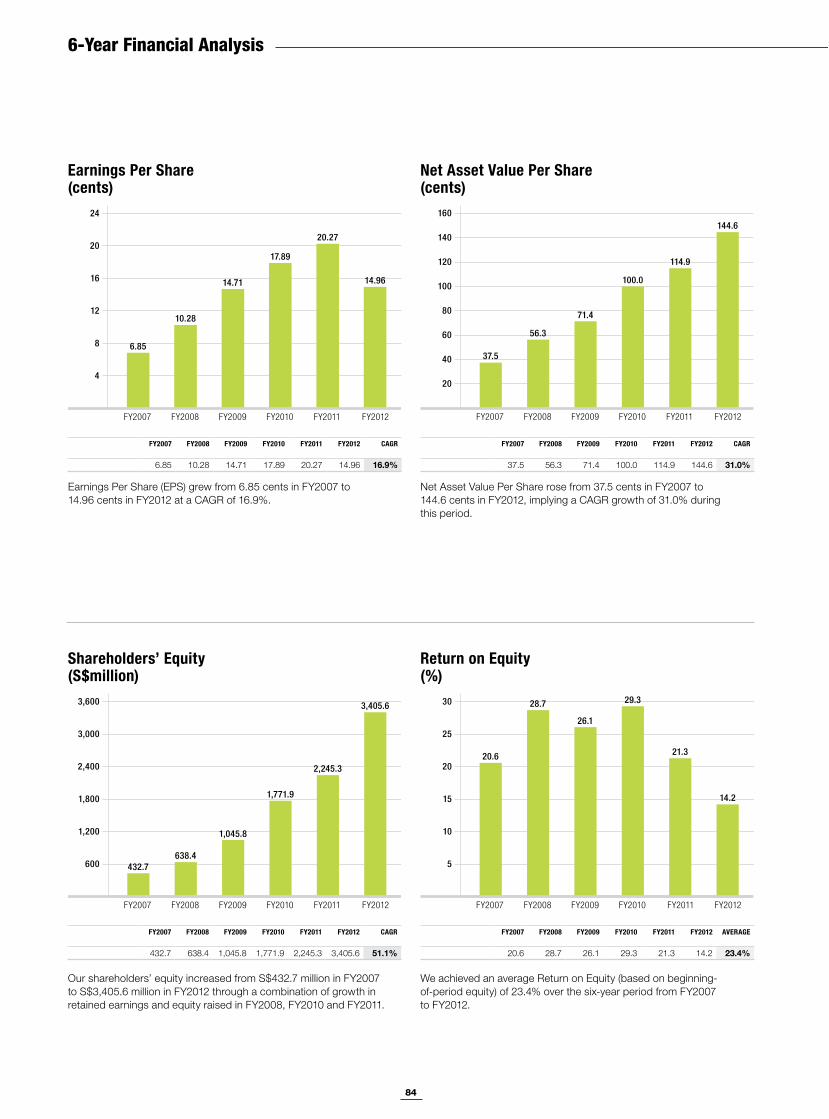

While Return on Equity (ROE) and Return on Average Invested Capital (ROIC)

declined on the back of a larger equity base, our Net Asset Value (NAV) per share improved from S$1.15 in FY2011 to S$1.45 in FY2012.

We now have a stronger balance sheet and liquidity position with increase in shareholders’ funds (before fair value adjustment reserve) from S$2.6 billion in FY2011 to S$3.5 billion in FY2012.

Our Group’s Profit After Tax and Minority Interest, excluding exceptional items, in FY2012 declined by 4.6% to S$355.5 million compared to S$372.8 million achieved in FY2011.

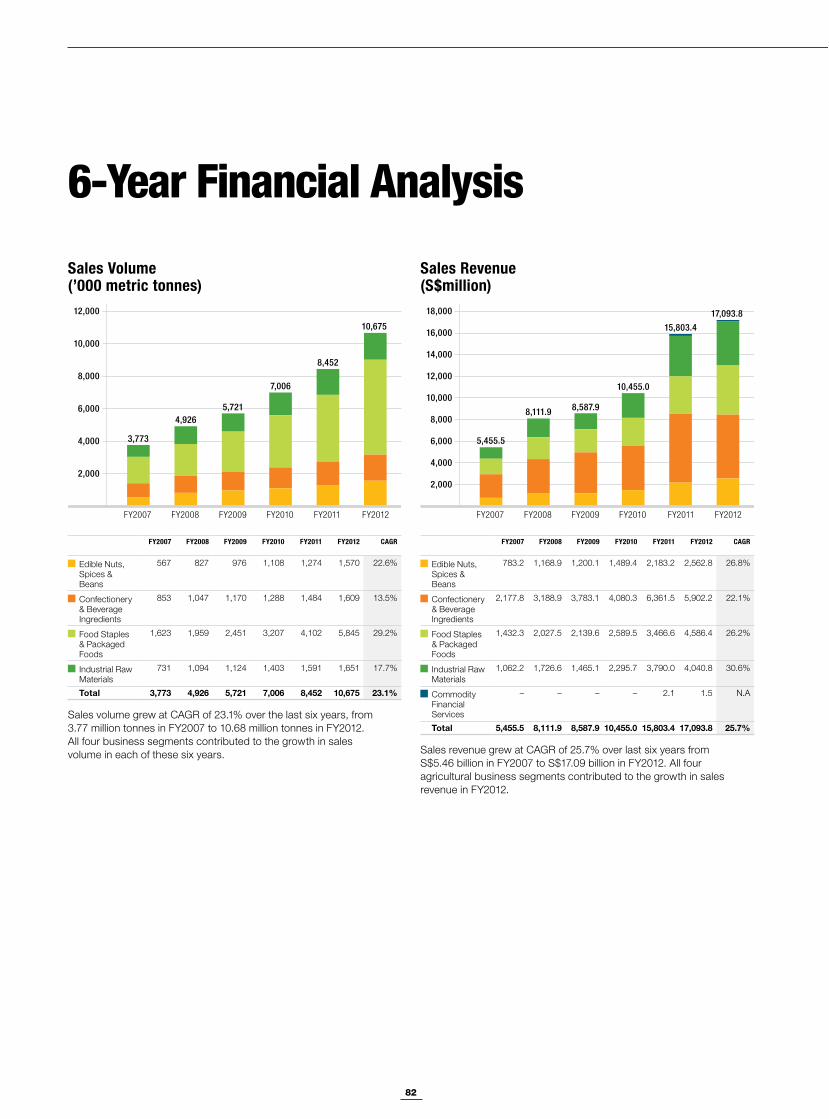

We grew Sales Volume by 26.3% in FY2012 compared to FY2011.

Sales Revenue rose 8.2% to S$17.1 billion and Net Contribution (NC) increased

4

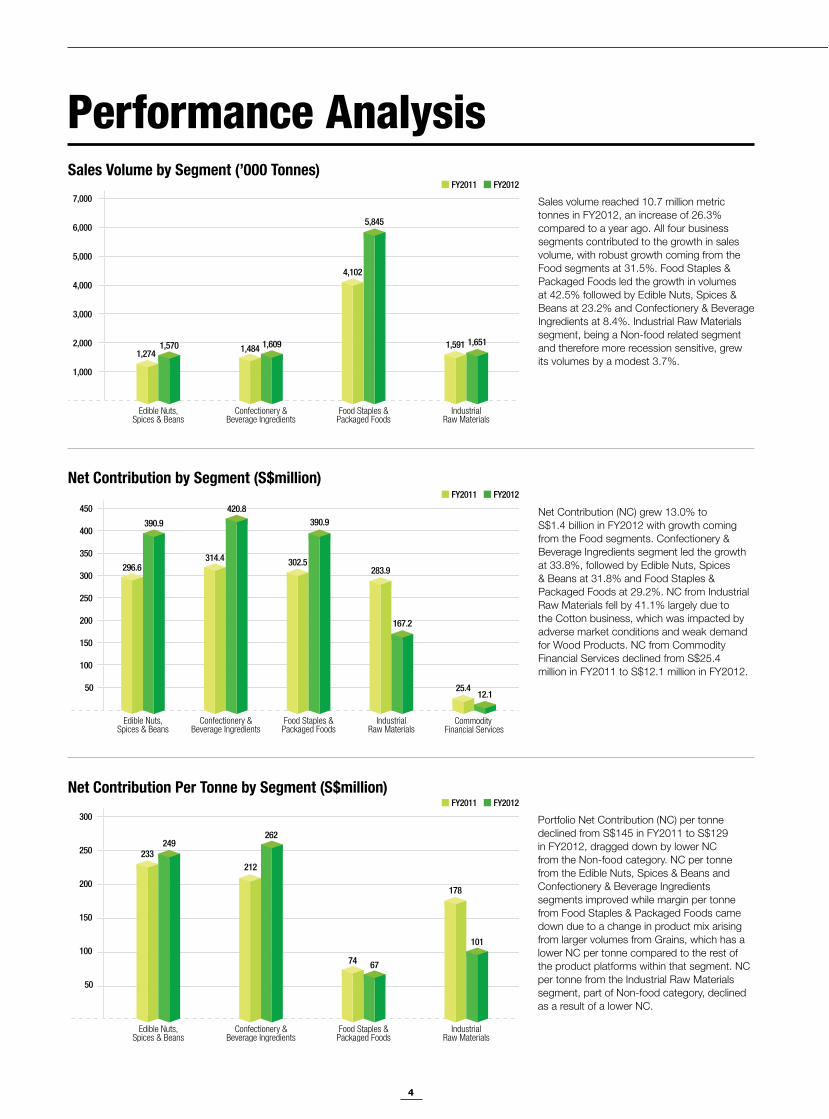

Sales volume reached 10.7 million metric tonnes in FY2012, an increase of 26.3% compared to a year ago. All four business segments contributed to the growth in sales volume, with robust growth coming from the Food segments at 31.5%. Food Staples & Packaged Foods led the growth in volumes at 42.5% followed by Edible Nuts, Spices & Beans at 23.2% and Confectionery & Beverage Ingredients at 8.4%. Industrial Raw Materials segment, being a Non-food related segment and therefore more recession sensitive, grew its volumes by a modest 3.7%.

Edible Nuts,Spices & Beans

Confectionery &Beverage Ingredients

Food Staples &Packaged Foods

IndustrialRaw Materials

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1,2741,570

4,102

5,845

1,591 1,651

FY2011 FY2012

1,484 1,609

Sales Volume by Segment (’000 Tonnes)

Net Contribution (NC) grew 13.0% to S$1.4 billion in FY2012 with growth coming from the Food segments. Confectionery & Beverage Ingredients segment led the growth at 33.8%, followed by Edible Nuts, Spices & Beans at 31.8% and Food Staples & Packaged Foods at 29.2%. NC from Industrial Raw Materials fell by 41.1% largely due to the Cotton business, which was impacted by adverse market conditions and weak demand for Wood Products. NC from Commodity Financial Services declined from S$25.4 million in FY2011 to S$12.1 million in FY2012.

Edible Nuts,Spices & Beans

Confectionery &Beverage Ingredients

Food Staples &Packaged Foods

Commodity Financial Services

IndustrialRaw Materials

50

100

150

200

250

300

350

400

450

314.4

420.8

302.5

390.9

283.9

167.2

25.412.1

296.6

390.9

FY2011 FY2012

Net Contribution by Segment (S$million)

Portfolio Net Contribution (NC) per tonne declined from S$145 in FY2011 to S$129 in FY2012, dragged down by lower NC from the Non-food category. NC per tonne from the Edible Nuts, Spices & Beans and Confectionery & Beverage Ingredients segments improved while margin per tonne from Food Staples & Packaged Foods came down due to a change in product mix arising from larger volumes from Grains, which has a lower NC per tonne compared to the rest of the product platforms within that segment. NC per tonne from the Industrial Raw Materials segment, part of Non-food category, declined as a result of a lower NC.

50

100

150

200

250

300

233249

212

262

74 67

178

101

FY2011 FY2012

Edible Nuts,Spices & Beans

Confectionery &Beverage Ingredients

Food Staples &Packaged Foods

IndustrialRaw Materials

Net Contribution Per Tonne by Segment (S$million)

Performance Analysis

5

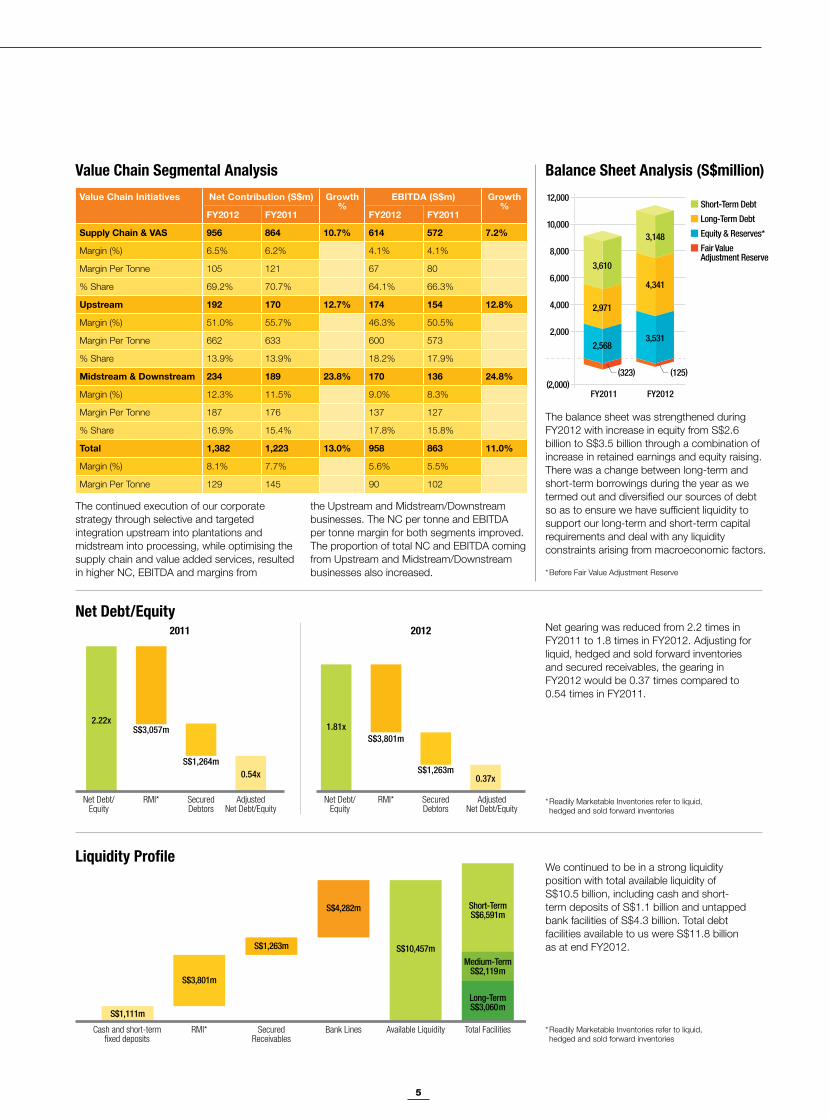

Value Chain Initiatives Net Contribution (S$m) Growth %

EBITDA (S$m) Growth %

FY2012 FY2011 FY2012 FY2011

Supply Chain & VAS 956 864 10.7% 614 572 7.2%

Margin (%) 6.5% 6.2% 4.1% 4.1%

Margin Per Tonne 105 121 67 80

% Share 69.2% 70.7% 64.1% 66.3%

Upstream 192 170 12.7% 174 154 12.8%

Margin (%) 51.0% 55.7% 46.3% 50.5%

Margin Per Tonne 662 633 600 573

% Share 13.9% 13.9% 18.2% 17.9%

Midstream & Downstream 234 189 23.8% 170 136 24.8%

Margin (%) 12.3% 11.5% 9.0% 8.3%

Margin Per Tonne 187 176 137 127

% Share 16.9% 15.4% 17.8% 15.8%

Total 1,382 1,223 13.0% 958 863 11.0%

Margin (%) 8.1% 7.7% 5.6% 5.5%

Margin Per Tonne 129 145 90 102

The balance sheet was strengthened during FY2012 with increase in equity from S$2.6 billion to S$3.5 billion through a combination of increase in retained earnings and equity raising. There was a change between long-term and short-term borrowings during the year as we termed out and diversified our sources of debt so as to ensure we have sufficient liquidity to support our long-term and short-term capital requirements and deal with any liquidity constraints arising from macroeconomic factors.

The continued execution of our corporate strategy through selective and targeted integration upstream into plantations and midstream into processing, while optimising the supply chain and value added services, resulted in higher NC, EBITDA and margins from

Net Debt/Equity

* Readily Marketable Inventories refer to liquid, hedged and sold forward inventories

* Readily Marketable Inventories refer to liquid, hedged and sold forward inventories

* Before Fair Value Adjustment Reserve

FY2012

2,000

(2,000)

4,000

6,000

8,000

10,000

12,000

FY2011

3,610

2,971

2,568

(323)

3,148

4,341

3,531

(125)

Balance Sheet Analysis (S$million)

Net Debt/Equity

RMI* SecuredDebtors

AdjustedNet Debt/Equity

2.22x

0.54x

S$3,057mS$3,801m

S$1,264m

Net Debt/Equity

RMI* SecuredDebtors

AdjustedNet Debt/Equity

1.81x

0.37xS$1,263m

2011 2012

Cash and short-termfixed deposits

RMI* SecuredReceivables

Bank Lines Available Liquidity Total Facilities

S$1,111m

S$3,801m

S$1,263m

S$4,282m

S$10,457m

Short-TermS$6,591m

Medium-TermS$2,119m

Long-TermS$3,060m

Net gearing was reduced from 2.2 times in FY2011 to 1.8 times in FY2012. Adjusting for liquid, hedged and sold forward inventories and secured receivables, the gearing in FY2012 would be 0.37 times compared to 0.54 times in FY2011.

We continued to be in a strong liquidity position with total available liquidity of S$10.5 billion, including cash and short-term deposits of S$1.1 billion and untapped bank facilities of S$4.3 billion. Total debt facilities available to us were S$11.8 billion as at end FY2012.

Liquidity Profile

Value Chain Segmental Analysis

the Upstream and Midstream/Downstream businesses. The NC per tonne and EBITDA per tonne margin for both segments improved. The proportion of total NC and EBITDA coming from Upstream and Midstream/Downstream businesses also increased.

Short-Term Debt

Long-Term Debt

Fair Value Adjustment Reserve

Equity & Reserves*

6

Financial Summary

SALES REVENUE BY REGION

EBITDA SHARE BY VALUE CHAIN SEGMENT

SOURCING VOLUME BY REGION

NET CONTRIBUTION SHARE BY SEGMENT

38.7%

18.9%

23.0%

19.4%

64.0%

18.2%

17.8%

44.0%

16.3%

18.3%

21.4%

Supply Chain & Value-added Services

Upstream Midstream & Downstream

Edible Nuts, Spices & Beans

Confectionery & Beverage Ingredients

Food Staples & Packaged Foods

Industrial Raw Materials

Commodity Financial Services

Asia & Middle East AfricaEurope Americas

28.3%

30.4%

28.3%

12.1%

0.9%

7

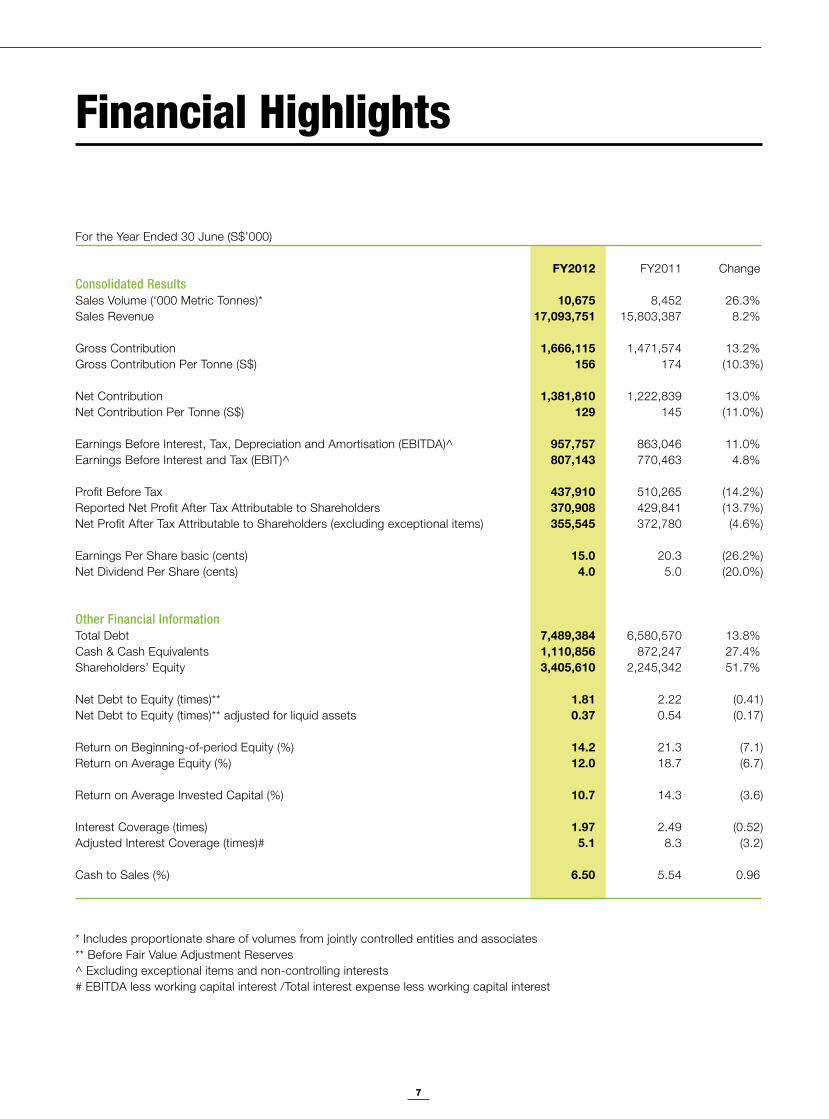

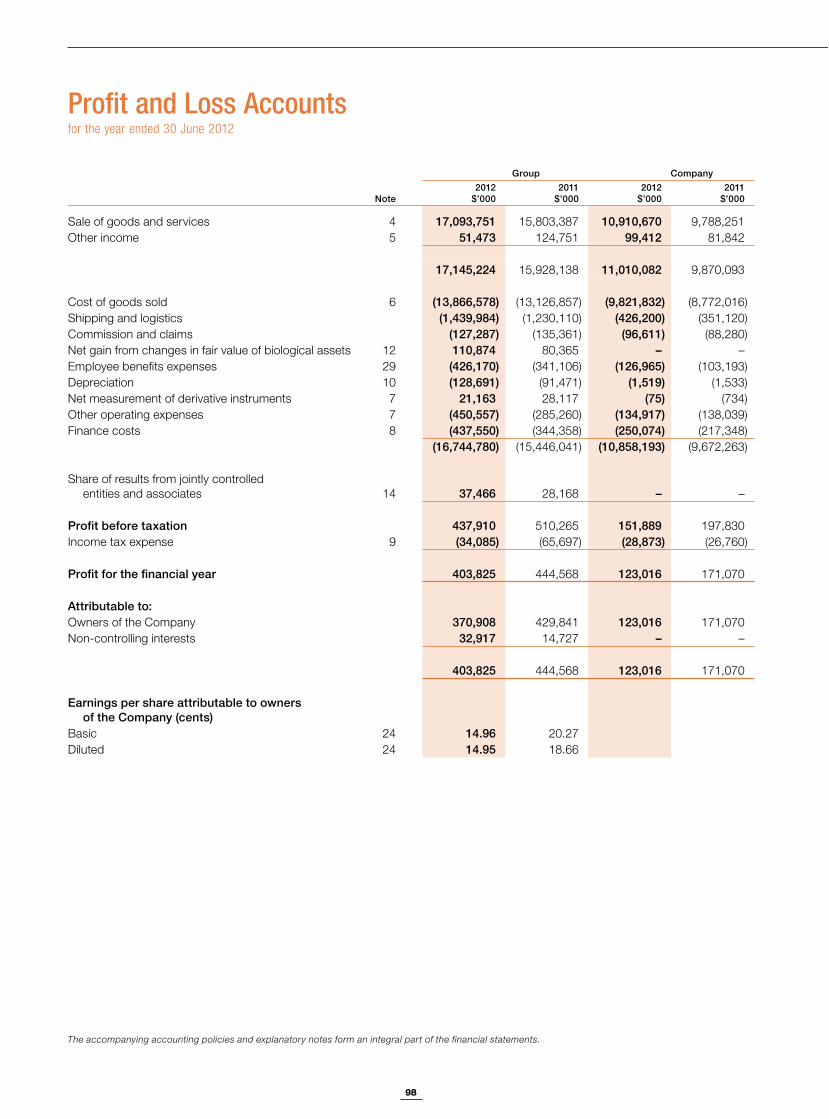

For the Year Ended 30 June (S$’000) FY2012 FY2011 Change Consolidated Results Sales Volume (‘000 Metric Tonnes)* 10,675 8,452 26.3% Sales Revenue 17,093,751 15,803,387 8.2% Gross Contribution 1,666,115 1,471,574 13.2% Gross Contribution Per Tonne (S$) 156 174 (10.3%) Net Contribution 1,381,810 1,222,839 13.0% Net Contribution Per Tonne (S$) 129 145 (11.0%) Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA)^ 957,757 863,046 11.0% Earnings Before Interest and Tax (EBIT)^ 807,143 770,463 4.8% Profit Before Tax 437,910 510,265 (14.2%) Reported Net Profit After Tax Attributable to Shareholders 370,908 429,841 (13.7%) Net Profit After Tax Attributable to Shareholders (excluding exceptional items) 355,545 372,780 (4.6%) Earnings Per Share basic (cents) 15.0 20.3 (26.2%) Net Dividend Per Share (cents) 4.0 5.0 (20.0%) Other Financial Information Total Debt 7,489,384 6,580,570 13.8% Cash & Cash Equivalents 1,110,856 872,247 27.4% Shareholders’ Equity 3,405,610 2,245,342 51.7% Net Debt to Equity (times)** 1.81 2.22 (0.41) Net Debt to Equity (times)** adjusted for liquid assets 0.37 0.54 (0.17) Return on Beginning-of-period Equity (%) 14.2 21.3 (7.1) Return on Average Equity (%) 12.0 18.7 (6.7) Return on Average Invested Capital (%) 10.7 14.3 (3.6) Interest Coverage (times) 1.97 2.49 (0.52) Adjusted Interest Coverage (times)# 5.1 8.3 (3.2) Cash to Sales (%) 6.50 5.54 0.96

* Includes proportionate share of volumes from jointly controlled entities and associates ** Before Fair Value Adjustment Reserves^ Excluding exceptional items and non-controlling interests # EBITDA less working capital interest /Total interest expense less working capital interest

Financial Highlights

8

Chairman’s Statement

Executing Our Strategy

Olam has weathered the uncertainties and fluctuations of a challenging year, delivering

creditable results while continuing to build on a strong platform for growth.

9

FY2012 has been a challenging year for Olam characterised by macroeconomic uncertainties emanating broadly from Europe and the Middle East. The European sovereign debt crisis has cast a long shadow over global economic performance and the recovery is expected to be slow. Olam has weathered the resultant uncertainties and fluctuations, delivering creditable results and continuing to build on a strong platform for growth.

Our results were achieved under these difficult market conditions. However, our investments continue to lay the foundations that will shape the future of our company. We remain focused on our strategy and I am optimistic about the long-term prospects for continuing growth in the agri-commodity complex, as well as the opportunities this presents for delivering our strategy going forward.

We recorded a sales revenue growth of 8.2% in FY2012 to S$17.1 billion and a Profit after Tax and Minority Interest of S$355.5 million, excluding exceptional items, which was 4.6% below our excellent FY2011 performance. Our FY2012 results, while marginally lower than last year, demonstrate by and large, the resilience of the Olam model and our ability to deliver across highly volatile commodity and economic cycles.

I am optimistic about the long-term prospects for continuing growth in our sector and the opportunities this presents for delivering our strategy going forward. ”

The optimism, energy and determination of our talented multi-cultural team has enabled us to navigate this difficult period skilfully. Our Food-related business segments continued on their strong upward trajectory, delivering good volume and margin growth in FY2012. However our Non-food related segments registered a decline in Net Contribution this year, due to unfavourable market conditions that were driven by exceptional events.

I would like to take this opportunity to thank all our shareholders for their unstinting support and confidence in Olam. The Board of Directors is pleased to recommend a first and final dividend of 4.00 cents per share, subject to the approval of our shareholders. This amounts to a dividend pay-out of S$95.61 million and a pay-out ratio of 26% for FY2012.

A more detailed review of our results for the year and the operating performance of the Group is contained in the Financial Report on pages 90 to 183 of this report.

Good governance is the foundation on which we have built our business and this is deeply embedded in our business culture. We remain firmly committed to maintaining high standards in governance processes as a part of our accountability to all our shareholders.

The Board works closely with our management team on areas of strategy, risk, compliance and sustainability, all of which are critical to investors. We continue the process of evaluating the Board and individual members in their roles on our Board and Board Committees. We have a talented and committed team. We continue to invest in our people and develop leaders.

On behalf of the Board, I would like to congratulate and thank our global team of 18,000 Olamites for continuing to display an extraordinary commitment and putting in the discretionary effort which resulted in a strong performance under difficult economic and market conditions.

I would also like to thank my fellow Directors on the Board, our shareholders, investors, business partners and other stakeholders for their ongoing support of Olam. We will continue to build on our distinctive strengths and valuable experience gained through tough times to deliver value to our shareholders.

R. Jayachandran Chairman

“

10

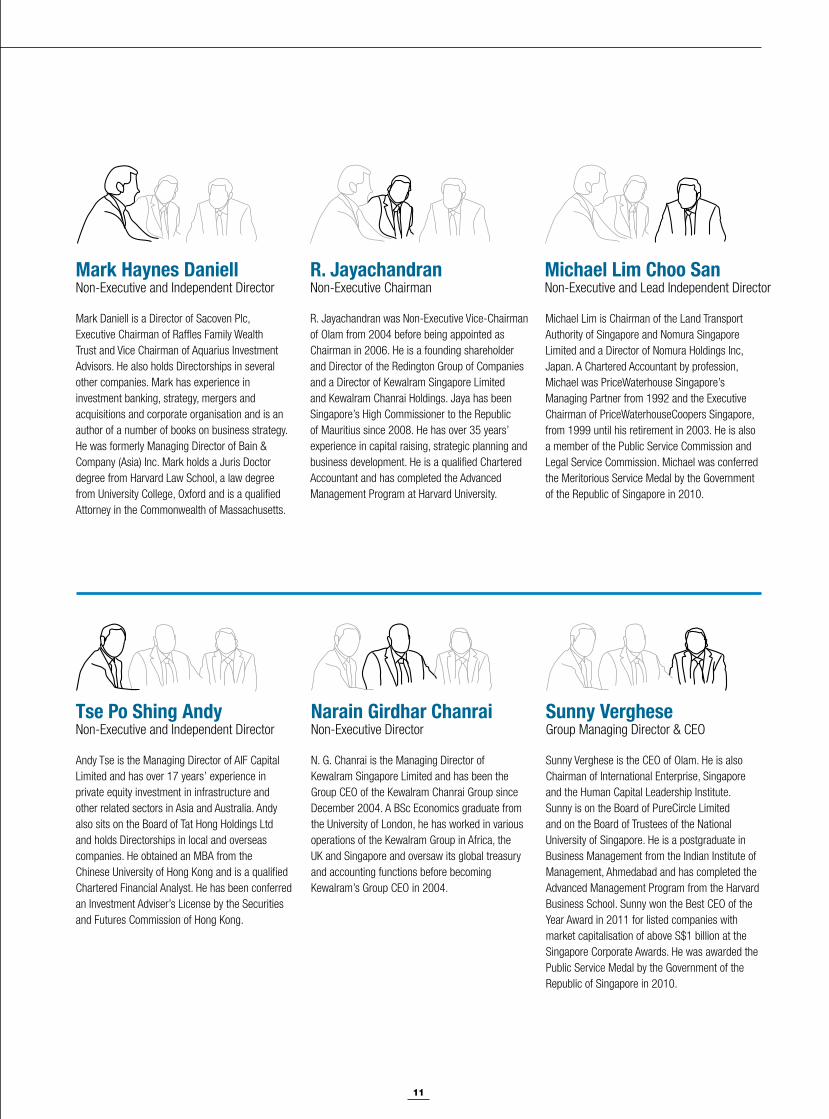

Board of DirectorsBoard of Directors

11

Narain Girdhar ChanraiNon-Executive Director

N. G. Chanrai is the Managing Director of Kewalram Singapore Limited and has been the Group CEO of the Kewalram Chanrai Group since December 2004. A BSc Economics graduate from the University of London, he has worked in various operations of the Kewalram Group in Africa, the UK and Singapore and oversaw its global treasury and accounting functions before becoming Kewalram’s Group CEO in 2004.

Sunny VergheseGroup Managing Director & CEO

Sunny Verghese is the CEO of Olam. He is also Chairman of International Enterprise, Singapore and the Human Capital Leadership Institute. Sunny is on the Board of PureCircle Limited and on the Board of Trustees of the National University of Singapore. He is a postgraduate in Business Management from the Indian Institute of Management, Ahmedabad and has completed the Advanced Management Program from the Harvard Business School. Sunny won the Best CEO of the Year Award in 2011 for listed companies with market capitalisation of above S$1 billion at the Singapore Corporate Awards. He was awarded the Public Service Medal by the Government of the Republic of Singapore in 2010.

Tse Po Shing AndyNon-Executive and Independent Director

Andy Tse is the Managing Director of AIF Capital Limited and has over 17 years’ experience in private equity investment in infrastructure and other related sectors in Asia and Australia. Andy also sits on the Board of Tat Hong Holdings Ltd and holds Directorships in local and overseas companies. He obtained an MBA from the Chinese University of Hong Kong and is a qualified Chartered Financial Analyst. He has been conferred an Investment Adviser’s License by the Securities and Futures Commission of Hong Kong.

R. JayachandranNon-Executive Chairman

R. Jayachandran was Non-Executive Vice-Chairman of Olam from 2004 before being appointed as Chairman in 2006. He is a founding shareholder and Director of the Redington Group of Companies and a Director of Kewalram Singapore Limited and Kewalram Chanrai Holdings. Jaya has been Singapore’s High Commissioner to the Republic of Mauritius since 2008. He has over 35 years’ experience in capital raising, strategic planning and business development. He is a qualified Chartered Accountant and has completed the Advanced Management Program at Harvard University.

Michael Lim Choo SanNon-Executive and Lead Independent Director

Mark Haynes DaniellNon-Executive and Independent Director

Mark Daniell is a Director of Sacoven Plc, Executive Chairman of Raffles Family Wealth Trust and Vice Chairman of Aquarius Investment Advisors. He also holds Directorships in several other companies. Mark has experience in investment banking, strategy, mergers and acquisitions and corporate organisation and is an author of a number of books on business strategy. He was formerly Managing Director of Bain & Company (Asia) Inc. Mark holds a Juris Doctor degree from Harvard Law School, a law degree from University College, Oxford and is a qualified Attorney in the Commonwealth of Massachusetts.

Michael Lim is Chairman of the Land Transport Authority of Singapore and Nomura Singapore Limited and a Director of Nomura Holdings Inc, Japan. A Chartered Accountant by profession, Michael was PriceWaterhouse Singapore’s Managing Partner from 1992 and the Executive Chairman of PriceWaterhouseCoopers Singapore, from 1999 until his retirement in 2003. He is also a member of the Public Service Commission and Legal Service Commission. Michael was conferred the Meritorious Service Medal by the Government of the Republic of Singapore in 2010.

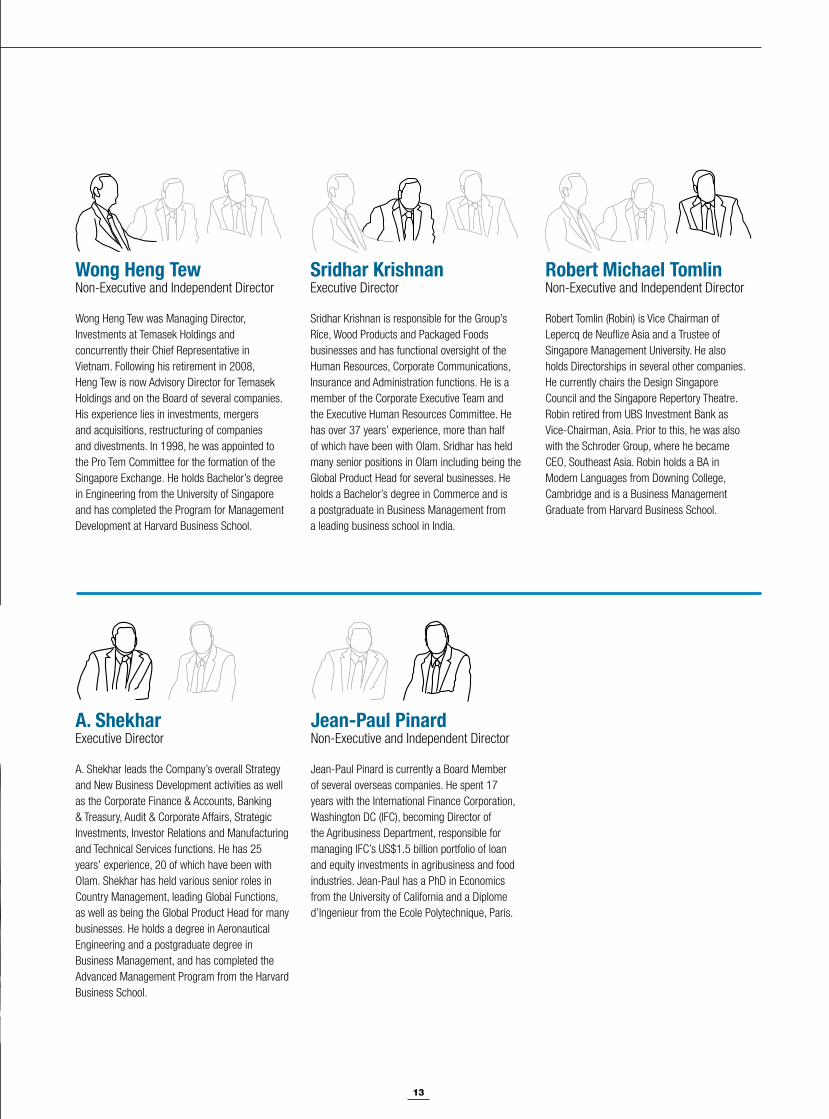

12

Board of Directors

13

Sridhar KrishnanExecutive Director

Sridhar Krishnan is responsible for the Group’s Rice, Wood Products and Packaged Foods businesses and has functional oversight of the Human Resources, Corporate Communications, Insurance and Administration functions. He is a member of the Corporate Executive Team and the Executive Human Resources Committee. He has over 37 years’ experience, more than half of which have been with Olam. Sridhar has held many senior positions in Olam including being the Global Product Head for several businesses. He holds a Bachelor’s degree in Commerce and is a postgraduate in Business Management from a leading business school in India.

Wong Heng TewNon-Executive and Independent Director

Wong Heng Tew was Managing Director, Investments at Temasek Holdings and concurrently their Chief Representative in Vietnam. Following his retirement in 2008, Heng Tew is now Advisory Director for Temasek Holdings and on the Board of several companies. His experience lies in investments, mergers and acquisitions, restructuring of companies and divestments. In 1998, he was appointed to the Pro Tem Committee for the formation of the Singapore Exchange.!He holds Bachelor’s degree in Engineering from the University of Singapore and has completed the Program for Management Development at Harvard Business School.

Robert Michael TomlinNon-Executive and Independent Director

Robert Tomlin (Robin) is Vice Chairman of Lepercq de Neuflize Asia and a Trustee of Singapore Management University. He also holds Directorships in several other companies. He currently chairs the Design Singapore Council and the Singapore Repertory Theatre. Robin retired from UBS Investment Bank as Vice-Chairman, Asia. Prior to this, he was also with the Schroder Group, where he became CEO, Southeast Asia. Robin holds a BA in Modern Languages from Downing College, Cambridge and is a Business Management Graduate from Harvard Business School.

A. ShekharExecutive Director

A. Shekhar leads the Company’s overall Strategy and New Business Development activities as well as the Corporate Finance & Accounts, Banking & Treasury, Audit & Corporate Affairs, Strategic Investments, Investor Relations and Manufacturing and Technical Services functions. He has 25 years’ experience, 20 of which have been with Olam. Shekhar has held various senior roles in Country Management, leading Global Functions, as well as being the Global Product Head for many businesses. He holds a degree in Aeronautical Engineering and a postgraduate degree in Business Management, and has completed the Advanced Management Program from the Harvard Business School.

Jean-Paul PinardNon-Executive and Independent Director

Jean-Paul Pinard is currently a Board Member of several overseas companies. He spent 17 years with the International Finance Corporation, Washington DC (IFC), becoming Director of the Agribusiness Department, responsible for managing IFC’s US$1.5 billion portfolio of loan and equity investments in agribusiness and food industries. Jean-Paul has a PhD in Economics from the University of California and a Diplome d’Ingenieur from the Ecole Polytechnique, Paris.

14

CEO and Executive Directors’ Dialogue

Shaping the Future

Olam’s CEO Sunny Verghese and Executive Directors A. Shekhar and Sridhar Krishnan talk about the company’s approach to sustainable long-term growth across its businesses.

BUSINESS STRATEGY

We talked to Sunny Verghese about Olam’s medium and long-term business strategy and how this is focused to enable the company to take advantage of the opportunities open to it over the coming decade.

Olam has a unique business model that has enabled you to build a distinct competitive advantage in the market. What are the most important components of this and how scalable is your strategy?

Sunny: At Olam, our Governing Objective is to maximise long-term intrinsic value for

our continuing shareholders in an ethical, socially responsible and an environmentally sustainable manner. In order to maximise long-term intrinsic value we need to impact three key drivers:

1 Open up the capital spread (ROE-KE & ROIC-WACC) 2 Increase the rate of profitable growth 3 Increase the duration of growth

Our long-term strategic choices are guided by developing pathways that will impact these three key drivers. In order to impact these three drivers, we need to build differentiation and develop a distinct competitive advantage that will allow us to grow above market rates and generate excess returns.

Our Governing Objective is to maximise long-term intrinsic value for our continuing shareholders in an ethical, socially responsible

& environmentally sustainable manner.

Sustain duration of

growthPAT growth Horizon 2

Increase the rate of profitable

growthPAT growth

FY11-16: 26%

Open up capital spreads

ROE-KE ROIC-WACC

15

From left to right:Executive Directors, Sridhar Krishnan, A. Shekhar, and CEO, Sunny Verghese

16

Superior origination,

trading & risk

managementskills

Emerging market expertise

Repeatableand

scalable adjacency

based growth formula

Organisationaladvantage

DeliveryModel

Well diversi!edacross scale platforms

- global footprint

Leadershipand relevantglobal scale

Focusedon single

asset class

Defensible position

Unique PortfolioSelective

integration across value

chain

Olam’sCompetitiveAdvantage

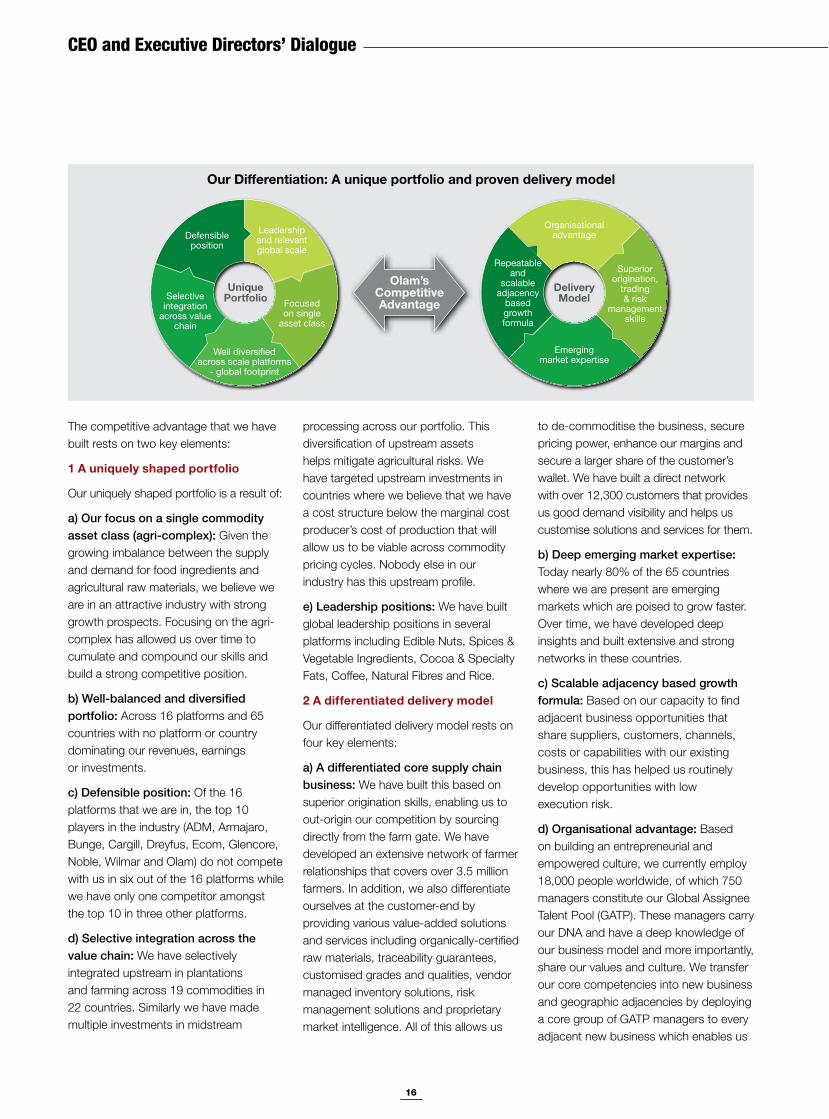

Our Differentiation: A unique portfolio and proven delivery model

CEO and Executive Directors’ Dialogue

The competitive advantage that we have built rests on two key elements:

1 A uniquely shaped portfolio

Our uniquely shaped portfolio is a result of:

a) Our focus on a single commodity asset class (agri-complex): Given the growing imbalance between the supply and demand for food ingredients and agricultural raw materials, we believe we are in an attractive industry with strong growth prospects. Focusing on the agri-complex has allowed us over time to cumulate and compound our skills and build a strong competitive position.

b) Well-balanced and diversified portfolio: Across 16 platforms and 65 countries with no platform or country dominating our revenues, earnings or investments.

c) Defensible position: Of the 16 platforms that we are in, the top 10 players in the industry (ADM, Armajaro, Bunge, Cargill, Dreyfus, Ecom, Glencore, Noble, Wilmar and Olam) do not compete with us in six out of the 16 platforms while we have only one competitor amongst the top 10 in three other platforms.

d) Selective integration across the value chain: We have selectively integrated upstream in plantations and farming across 19 commodities in 22 countries. Similarly we have made multiple investments in midstream

processing across our portfolio. This diversification of upstream assets helps mitigate agricultural risks. We have targeted upstream investments in countries where we believe that we have a cost structure below the marginal cost producer’s cost of production that will allow us to be viable across commodity pricing cycles. Nobody else in our industry has this upstream profile.

e) Leadership positions: We have built global leadership positions in several platforms including Edible Nuts, Spices & Vegetable Ingredients, Cocoa & Specialty Fats, Coffee, Natural Fibres and Rice.

2 A differentiated delivery model

Our differentiated delivery model rests on four key elements:

a) A differentiated core supply chain business: We have built this based on superior origination skills, enabling us to out-origin our competition by sourcing directly from the farm gate. We have developed an extensive network of farmer relationships that covers over 3.5 million farmers. In addition, we also differentiate ourselves at the customer-end by providing various value-added solutions and services including organically-certified raw materials, traceability guarantees, customised grades and qualities, vendor managed inventory solutions, risk management solutions and proprietary market intelligence. All of this allows us

to de-commoditise the business, secure pricing power, enhance our margins and secure a larger share of the customer’s wallet. We have built a direct network with over 12,300 customers that provides us good demand visibility and helps us customise solutions and services for them.

b) Deep emerging market expertise: Today nearly 80% of the 65 countries where we are present are emerging markets which are poised to grow faster. Over time, we have developed deep insights and built extensive and strong networks in these countries.

c) Scalable adjacency based growth formula: Based on our capacity to find adjacent business opportunities that share suppliers, customers, channels, costs or capabilities with our existing business, this has helped us routinely develop opportunities with low execution risk.

d) Organisational advantage: Based on building an entrepreneurial and empowered culture, we currently employ 18,000 people worldwide, of which 750 managers constitute our Global Assignee Talent Pool (GATP). These managers carry our DNA and have a deep knowledge of our business model and more importantly, share our values and culture. We transfer our core competencies into new business and geographic adjacencies by deploying a core group of GATP managers to every adjacent new business which enables us

17

grains, sugar and cotton complexes. Our results were particularly impacted by the fat tail events in the cotton business and to a lesser extent, demand erosion in the Wood Products business. We believe that these developments are mostly cyclical in nature and not structural. While this will post near-term headwinds in some of our platforms, the

Sustaining our competitive advantage is driven by a strategy that rests on proprietary insights built over the last 23 years of our operating history. ”

“

Sunny Verghese

to transfer our DNA into the new operation and also reduce execution risk.

Having secured this differentiation, growth has become more routine and reflexive allowing us to replicate and build a scalable business.

How has Olam been impacted by the ongoing difficulties in the global economy? Has this influenced your long-term strategy for growth and how are you addressing the heightened level of risk in uncertain times?

Sunny: FY2012 has been a challenging year for the industry as a whole, with nearly every participant posting a significant decline in earnings from the corresponding period before. While on a relative basis we performed better than our peers, we had our first ever decline in earnings since our listing seven years ago. Industry under-performance was a function of both the deteriorating global macroeconomic conditions and specific product market developments in the

medium and long-term prospects for our industry remain very attractive given the growing imbalance between supply and demand for agricultural raw material and food ingredients.

Our long-term strategy of:

i) Building a well-balanced and diversified portfolio biased towards the food raw materials category which is relatively more recession resistant

ii) Selectively integrating upstream into excess return plantation and farming initiatives

iii) Selective integration into midstream manufacturing and processing assets

iv) Building choke points in our supply chain business

v) Leveraging our latent assets and capabilities to enter into three new businesses, namely Packaged Foods business in Africa, the Agri-Input business (fertiliser manufacturing) in Gabon and the Commodity Financial Services business

remains relevant.

CEO, Sunny Verghese

18

CEO and Executive Directors’ Dialogue

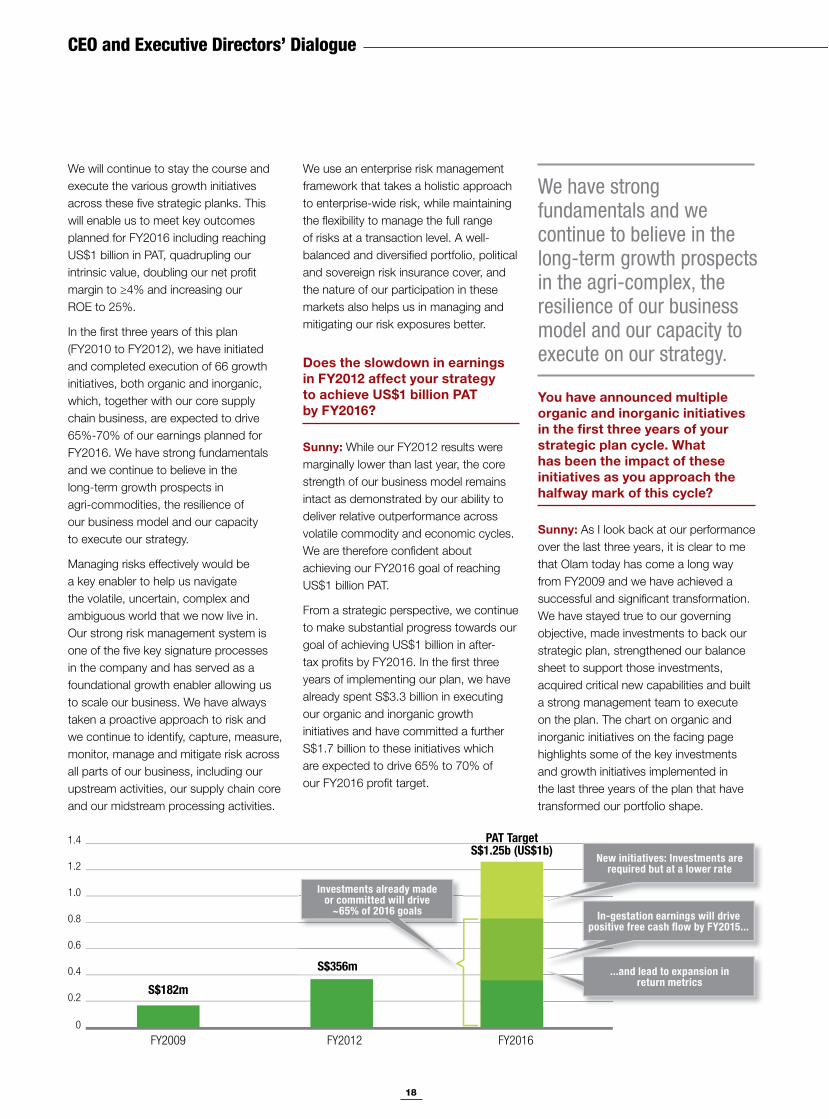

We will continue to stay the course and execute the various growth initiatives across these five strategic planks. This will enable us to meet key outcomes planned for FY2016 including reaching US$1 billion in PAT, quadrupling our intrinsic value, doubling our net profit margin to !4% and increasing our ROE to 25%.

In the first three years of this plan (FY2010 to FY2012), we have initiated and completed execution of 66 growth initiatives, both organic and inorganic, which, together with our core supply chain business, are expected to drive 65%-70% of our earnings planned for FY2016. We have strong fundamentals and we continue to believe in the long-term growth prospects in agri-commodities, the resilience of our business model and our capacity to execute our strategy.

Managing risks effectively would be a key enabler to help us navigate the volatile, uncertain, complex and ambiguous world that we now live in. Our strong risk management system is one of the five key signature processes in the company and has served as a foundational growth enabler allowing us to scale our business. We have always taken a proactive approach to risk and we continue to identify, capture, measure, monitor, manage and mitigate risk across all parts of our business, including our upstream activities, our supply chain core and our midstream processing activities.

We use an enterprise risk management framework that takes a holistic approach to enterprise-wide risk, while maintaining the flexibility to manage the full range of risks at a transaction level. A well-balanced and diversified portfolio, political and sovereign risk insurance cover, and the nature of our participation in these markets also helps us in managing and mitigating our risk exposures better.

Does the slowdown in earnings in FY2012 affect your strategy to achieve US$1 billion PAT by FY2016?

Sunny: While our FY2012 results were marginally lower than last year, the core strength of our business model remains intact as demonstrated by our ability to deliver relative outperformance across volatile commodity and economic cycles. We are therefore confident about achieving our FY2016 goal of reaching US$1 billion PAT.

From a strategic perspective, we continue to make substantial progress towards our goal of achieving US$1 billion in after-tax profits by FY2016. In the first three years of implementing our plan, we have already spent S$3.3 billion in executing our organic and inorganic growth initiatives and have committed a further S$1.7 billion to these initiatives which are expected to drive 65% to 70% of our FY2016 profit target.

You have announced multiple organic and inorganic initiatives in the first three years of your strategic plan cycle. What has been the impact of these initiatives as you approach the halfway mark of this cycle?

Sunny: As I look back at our performance over the last three years, it is clear to me that Olam today has come a long way from FY2009 and we have achieved a successful and significant transformation. We have stayed true to our governing objective, made investments to back our strategic plan, strengthened our balance sheet to support those investments, acquired critical new capabilities and built a strong management team to execute on the plan. The chart on organic and inorganic initiatives on the facing page highlights some of the key investments and growth initiatives implemented in the last three years of the plan that have transformed our portfolio shape.

FY2009

S$182m

S$356m

PAT TargetS$1.25b (US$1b)

FY2012 FY2016

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0

b)New initiatives: Investments are

required but at a lower rate

S$356m

Investments already made or committed will drive

~65% of 2016 goals In-gestation earnings will drive positive free cash flow by FY2015...

...and lead to expansion in return metrics

We have strong fundamentals and we continue to believe in the long-term growth prospects in the agri-complex, the resilience of our business model and our capacity to execute on our strategy.

19

Edible Nuts, Spices & Beans

Almond orchards (Australia, USA) Peanut farming (Argentina) Tomato, Garlic, Onion and

other Vegetables (California)

Argentina shelling and blanching expansion

Spices (SK Foods/Gilroy); Sesame hulling in Nigeria Cashew mechanisation Pepper and Garlic processing Vietnam/China

Hazelnuts procurement (Turkey/Progida) Spices (India/VKL) Cashew processing (Expansion) Cashew ingredients

Confectionery & Beverage Ingredients

Coffee plantations (Laos/Tanzania/Ethiopia)

Coffee sourcing origins (Mexico/Guatemala)

Specialty fats (UK/Britannia) Cocoa grinding (IVC) Soluble Coffee manufacturing (VN)

Cocoa ingredients (Spain/Macao)

Food Staples and Packaged Foods

Dairy farm (Uruguay/NZFSU) Palm plantations (WAF/SIFCA)

Grains sourcing and elevation (Australia, Russia)

Sugar refinery (Indonesia/PT DUS, Nigeria) Sugar milling in India Wheat milling (Nigeria/CFM, Ghana)

Dairy & Grains (Russia/Rusmolco) Rice farming (East Africa)

Grains trading (Canada/Lansing) Grains terminal (Australia/NAT)

Sugar milling (India/Hemarus) Dairy/Juice (WAF/Kayass) Biscuits (WAF/Titan.) Sugar milling (Brazil/UAP) Wheat milling (WAF/CFM) Dairy processing (IVC)

Industrial Raw Materials

Timber forestry concession (Gabon/ROC/Mozambique) Rubber plantations (WAF) Fertiliser manufacturing (Gabon)

Cotton (Australia/US/Africa) Wood sourcing

(Panama/Costa Rica)

Rubber (Gabon)

Commodity Financial Services

Upstream Supply Chain Midstream and Downstream

Initiatives up to 2011 2012 initiatives

Organic and Inorganic Initiatives

Cashew processing in Côte d’Ivoire

20

CEO and Executive Directors’ Dialogue

The mix of business units and selective value chain participation has enhanced our market position and extended our competitive advantage. These are also favourably impacting our financial results as shown in the sustained Net Contribution (NC) growth across all our business units and value chain segments.

This strong early momentum, together with the investments already committed for future growth, gives us the confidence that we are well on track towards achieving our FY2016 goals.

that 21st century companies must serve two roles equally. We must deliver long-term and lasting value for our continuing shareholders, while being a positive force for sustainable change in the communities and contexts in which we operate.

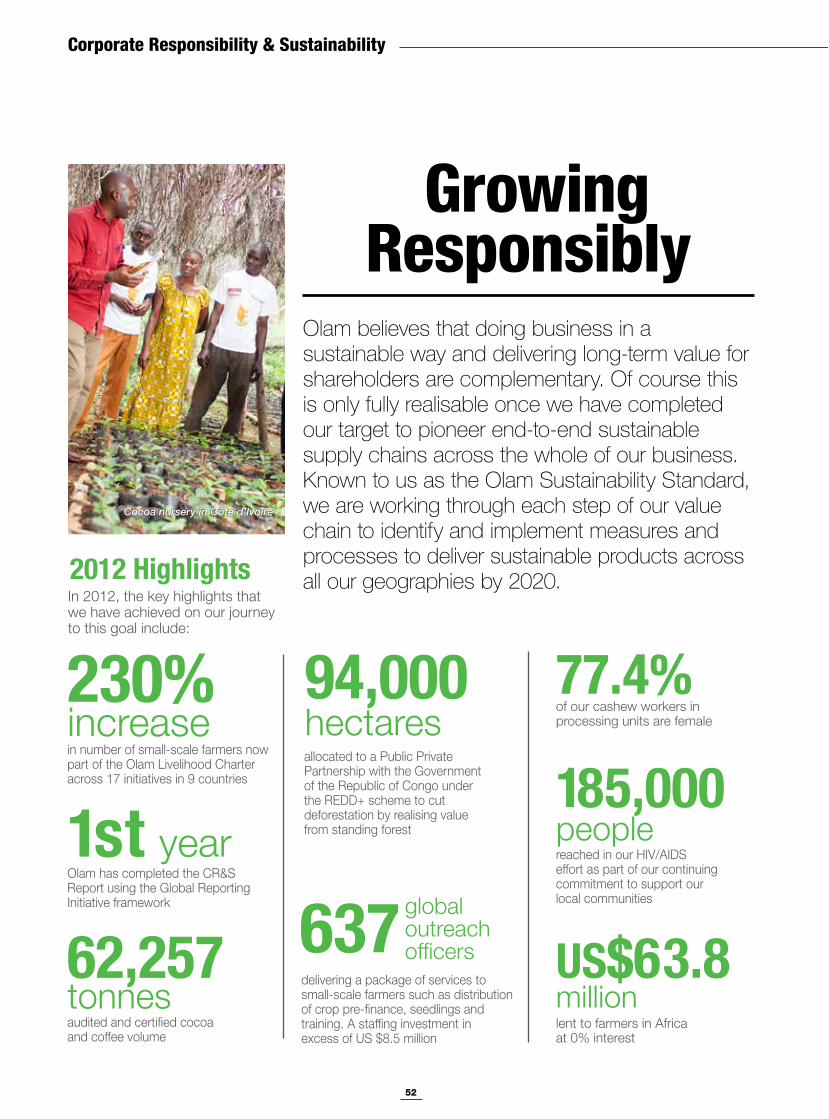

Our aspiration is to pioneer end-to-end sustainable supply chains in the agricultural complex across the whole of our business. Internally, we refer to this as the Olam Sustainability Standard (OSS) and this is at the heart of our vision of Growing Responsibly. We are working through each step of our value chain to identify and implement processes and measures to deliver sustainable agricultural products across all our geographies by 2020. This is a challenging and ‘stretch’ target but it informs the many choices that we make as a company.

The Olam Livelihood Charter (OLC) and our work with more than 200,000 small scale farmers (a 230% increase over last year) demonstrate the power of this model to improve the livelihood of small-scale farmers. We delivered over 62,000 tonnes of certified and audited Cocoa and Coffee to our customers, provided US$63.8 million as pre-finance to farmers in Africa at zero percent interest and employed 637 extension officers to deliver training and services to small-scale farmers including distribution of crop pre-finance, seedlings and agronomic advice. In FY2012 we have also completed our Corporate Responsibility and Sustainability Report (CRSR) using the Global Reporting Initiative (GRI) framework. We hope to move as many of our 3.5 million farmers as possible to the Livelihood Charter Principles by 2020.

You have said that Olam’s business model is built on unlocking mutual value and making sustainability an integral part of corporate strategy. How do you ensure this balance between growth and sustainable development?

Sunny: Olam’s Governing Objective is to maximise long-term intrinsic value for its continuing shareholders. We can only achieve this by building a sustainable business in the fullest sense. We believe

CAGR %NC (S$M)32%

27%

135%

24%

Supply Chain & VAS

Upstream

Midstream/Downstream

FY2009 FY2010 FY2011 FY2012

200

400

600607

901

1,223

1,382

800

10000

14000

12000

12315

469

156

110

635

189

170

864

234

192

956

CAGR %NC (S$M)32%

36%

36%

40%

6%

Confectionery &Beverage Ingredients

Food Staples &Packaged Foods

Industrial RawMaterials

CommodityFinancial Services

FY2009 FY2010 FY2011 FY2012

200

400

600607

901

1,223

1,382

800

10000

14000

12000Edible Nuts,Spices & Beans

234

142

169

155

208

234

223

211

284

303

314

297

167

391

421

391

21

FINANCIAL & OPERATIONAL REVIEW

A. Shekhar, Olam’s Executive Director responsible for Finance and Strategy answers questions on Olam’s performance in 2012 and the ongoing funding needs of the company as it executes on the 2016 growth objectives.

Olam has shown consistent growth and returns over the past seven years since listing. What were the main factors influencing the company’s financial performance in FY2012?

Shekhar: Our FY2012 Net Profit after Tax and Minority Interest (excluding exceptional items) declined 4.6% to S$355.5 million. Our Food-related business segments continued strong trajectory growth from the last two years by delivering an increase in sales volumes of 31.5% and Net Contribution (NC) of 31.6% compared to FY2011. Our Non-food segments consisting

of the Industrial Raw Materials and Commodity Financial Services segments were mainly responsible for lowering our overall earnings as they registered a decline in NC due to unfavourable market conditions and outlier events experienced during the year, especially in the Cotton markets.

This is the first time in our operating history that we recorded a year-on-year decline in our overall earnings. But it has to be seen in the context of the extreme volatility and very tough operating conditions experienced globally in the agricultural space. We believe that considering the overall market conditions, as well as relative to other peers, we navigated through these conditions well.

The Industrial Raw Materials segment, which is relatively more recession sensitive, had a weak performance in FY2012. What is your outlook for this segment going forward and are you re-examining the company’s overall exposure to this segment?

Shekhar: Our Industrial Raw Materials segment which comprises Cotton, Wool, Rubber, Wood Products, Fertiliser and the Special Economic Zone (SEZ) project, accounted for 23.6% of revenues and 15.5% of volumes in FY2012. Sales volume from this segment increased 3.7% but contribution fell mainly because of our Cotton and Wood Products businesses. Our Wool, Rubber and SEZ businesses performed well during the year.

The market events that impacted the Cotton business were exceptional and, we believe, were a fat tail event and one-off in nature. We think the prospects for Cotton should be more positive from the second half of FY2013. Structurally, our competitive position has only improved relative to other industry participants. We are well positioned to consolidate our market position within this industry, since some of the other players have been significantly impacted by the recent market events. While FY2013 is likely to be a recovery year, we remain confident of our growth prospects in the Cotton business over the medium to long-term.

Executive Director, A. Shekhar

22

CEO and Executive Directors’ Dialogue

The Wood Products business saw a decline in overall demand and margin pressures in most markets, including China and India, which were the main drivers of growth over the last few years. We do not foresee any near-term recovery in China, and India continues to struggle with the impact of devaluation of the Indian Rupee making it more expensive for importers. Our move into FSCTM certified Timber is beginning to yield some dividends in Europe and USA and we expect prospects to improve as further regulatory pressures increase for promoting the use of certified and traceable timber in these markets. Overall, we remain well positioned to take advantage of these markets, when recovery occurs.

What are some of the significant acquisitions you have made this year? How are they tracking post-acquisition?

Shekhar: The key acquisitions we announced in FY2012 were Hemarus Industries (Sugar milling in India), Progida (Hazelnut processing in Turkey), OK Foods (Biscuits and Candies in Nigeria) and Rusmolco (Dairy and Grains farming in Russia). Hemarus Industries has had a good start and is tracking above plan

while OK Foods and Rusmolco were concluded only towards the end of the year and are still in their early stages of post-merger integration.

What was the rationale for getting into Fertilisers and why do you think your Gabon Fertiliser project is so attractive?

Shekhar: In 2009 we identified fertiliser and other agri-inputs distribution in Africa as a new business opportunity because it could help leverage the grower and supplier relationships that we have built over the last 23 years. We already supply these farmers with various agri-inputs,

including fertilisers, in order to secure their crop output. The Gabon Fertiliser project, gives us a unique opportunity to enter into the back-end manufacturing of Urea and participate in a financially attractive excess return opportunity. The attractiveness stems from access to low cost natural gas at a fixed price for a 25-year period, economies of scale in manufacturing, a favourable port based plant location from a freight and market access viewpoint; all of which are critical success factors for profitability in Urea manufacturing. Gabon offers us the ability to easily access and viably distribute Urea to our supplier network in Africa, as well as South and North American customers.

Packaged Foods in Nigeria

Hazelnuts in Turkey

23

36%

41%

8%

4%

8%3%

Banks - BilateralBanks - SyndicationConvertible Bonds

Unrated BondsMTNPerpetuals

You have stated that you will not raise any further equity till FY2016. How will you address your funding requirements in the event of another liquidity squeeze like we saw during the global financial crisis?

Shekhar: We have taken various proactive steps to strengthen our balance sheet and align it towards supporting our strategic plan targets.

We have pre-emptively raised additional equity to build an enhanced equity base of S$3.5 billion at the end of FY2012 vs $2.6 billion in FY2011. This has resulted in reducing our net debt to equity ratio to 1.81x in FY2012, and created sufficient additional debt capacity to fund our planned investments. Based on our targeted net debt to equity target of 2.5x, and likely retained earnings over the next few years, we feel quite comfortable at this stage, that we can fund our planned investments without raising further equity. We have also successfully tapped the debt capital markets as well as the bond markets, to build a debt profile and tenor to match our more asset intensive investment profile. We have already front-loaded a lot of investments in the last three years and have raised the required equity and debt for all our committed investments, which should enable us to get to 65-70% of our FY2016 earnings target. As long as the business delivers the forecasted earnings and cash flows, we believe that we can meet our planned cash flow requirements, without raising further equity, while operating within our targeted gearing structure. However, if our earnings trajectory over the next two to three years is below plan, we will drop or phase out some of the planned investments.

What was the rationale for the recent share buy-back and how will it benefit investors in the long-term?

Shekhar: There are a few rules we set for ourselves before considering any share buy-back:

i) The shares should be trading at a discount to our intrinsic value ii) Returns to continuing shareholders through the buy-back of shares should be comparable or better than the universe of alternative growth opportunities available to the company iii) We should not compromise our ability to fund investments that are required to meet our strategic plan targets.

We bought back approximately 52 million shares in June 2012 when our shares were trading at a significant discount to our intrinsic value and almost approaching our net asset value. Therefore, we felt that allocating some part of our capital towards buying back our shares at those price levels would increase long-term value for our continuing shareholders without compromising our ability to fund our investment plans or adversely affect our targeted gearing levels. We have also decided to not cancel these shares and retain them as Treasury Shares, which provides us with flexibility to maximise the impact of this buy-back.

Cotton in USA

Debt Mix 2012

24

CEO and Executive Directors’ Dialogue

PEOPLE & PROCESSES

Sridhar Krishnan is Olam’s Executive Director responsible for the Rice, Packaged Foods and Wood Products businesses in addition to the Human Resources function. We asked him to elaborate on how the company has been able to develop its people and ensure effective management of the business across such a wide portfolio.

Olam has been a highly successful ‘people’ business. How would you characterise the contribution that your people have made to Olam’s development and growth?

Sridhar: We have always believed that our people are the true source of our competitive advantage. Today we employ 18,000 people worldwide and 750 of those are a part of our Global Assignee Talent Pool (GATP), the management team that has an intimate knowledge of our business model, understands

our systems and processes, shares our values and culture and carries our DNA.

Our long-term commitment to the development of our GATP has been one of the main reasons for our continuous growth and consistent performance. We are constantly developing this group by investing management time at the highest level and by putting them through a common rite of passage, which includes posting them to challenging conditions in emerging market countries and providing them with critical experiences that allow them to absorb our DNA and distinctive company culture.

Our greatest strength as a company is our highly engaged, entrepreneurial and empowered managers who have developed an ownership mentality. This has enabled us to produce leaders who are capable of executing our ambitious growth objectives.

We believe our success stems from our ability to concurrently execute multiple growth initiatives across products,

markets and value chain segments. We have managed this by ensuring that each time we start a new business or open a new geography, we are able to deploy a core team of senior leaders who have the capabilities required and a proven track record within Olam to spearhead the new opportunity.

Our culture at Olam is entrepreneurial, team-oriented and non-hierarchical. This encourages managers to take greater responsibility for their careers, both personally and professionally, and to contribute to the success of the company over the longer term.

What fresh challenges has your strategy to move into the upstream and midstream parts of the value chain thrown up for your talent management practices? How have you addressed the capability gaps given these were new areas for Olam?

Executive Director, Sridhar Krishnan

25

Sridhar: Our continued focus over the years on a single asset class (the agri-complex) and an asset-light supply chain model enabled us to build deep insights and capabilities in our core business and consolidate our competitive position. Our immediate goal after the launch of our new strategy in FY2009 was to embed similar levels of capability and expertise in the areas of upstream plantation, midstream manufacturing, farming and primary processing which are new to Olam within a short time frame.

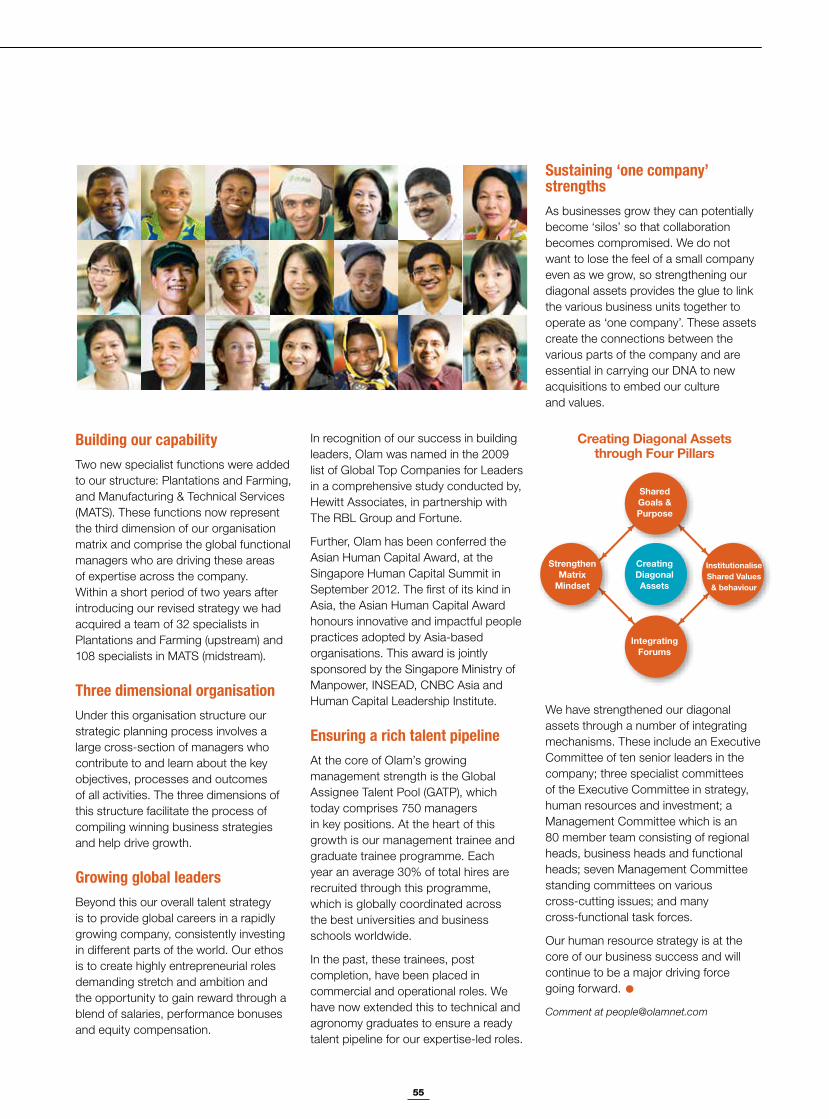

This meant putting in place an accelerated process of building global leaders internally with the right mindset to manage capital intensive assets to minimise execution risks. We established two new centralised functions, namely Plantations and Manufacturing and Technical Services (MATS) to acquire and drive expertise in these new areas across the organisation. We established through a competency mapping process,

the key skills and capabilities required for these new roles. Leveraging on our compelling employee value proposition, we have acquired a team of 32 specialists in plantation and farming, as well as 108 specialists in MATS within a short two year period after embarking on this revised strategy. We also focused on aligning the cultures of the acquired companies with the Olam culture and building a ‘One Company’ mindset across the organisation. We have also rolled out a comprehensive process of culture building across the organisation to strengthen our organisational advantage.

We further initiated a coaching culture to embed coaching skills in the Olam leadership team to ensure expertise is transferred by our senior leaders to their team members. At the same time we have designed and rolled out formal and experiential learning programmes to address the developmental needs of managers.

Olam’s business model is known to be very ‘management-intensive’. With an ever increasing scale of operations and some recent senior management changes, what steps are you taking to ensure the continuity and scalability of your talent pool?

Sridhar: Over the last 23 years, we have competed and won on the basis of our organisational advantage that rests on the strengths and capabilities of our people. Our people management processes and distinctive culture has enabled us to build a high engagement and a strong ownership mentality within the company. This has also enabled us to achieve low attrition rates relative to our industry. We have consistently had high engagement scores in the mid 80s which compares to the top decile companies globally. We have also regularly attracted high calibre managers and over time transformed them into successful leaders who have helped to grow our businesses to the prominent global positions that they have achieved today.

The imports team in Ghana

26

CEO and Executive Directors’ Dialogue

Our practice in creating entrepreneurial roles, our capacity to embed stretch and ambition, the opportunities that we provide as a high-growth company to our people to assume larger roles relatively quickly, our ability to motivate them by providing independence in their roles, and our compensation and reward systems that supports long-term orientation are key elements of this successful model. This has made Olam attractive to some of the best talent in the industry.

In recognition of our success in building leaders, Olam was named in the 2009 list of Global Top Companies for Leaders in a study conducted by Hewitt Associates in partnership with The RBL Group and Fortune Magazine. We also received the 2012 Asian Human Capital Award jointly sponsored by the Singapore Ministry of Manpower, INSEAD, CNBC Asia and Human Capital Leadership Institute, which honours innovative and impactful people practices adopted by Asia-based organisations.

Our Management Trainee and Graduate Trainee Programmes, which comprise 30% of our annual hire, form a key part of our talent management pipeline. Our

manpower plans and succession planning programmes have ensured that there are two to three successors for every critical role in the company that allows us to plan for managerial transition in a smooth and seamless way. This was demonstrated again this year in terms of filling the roles created by some of the management departures that you referred to in your question.

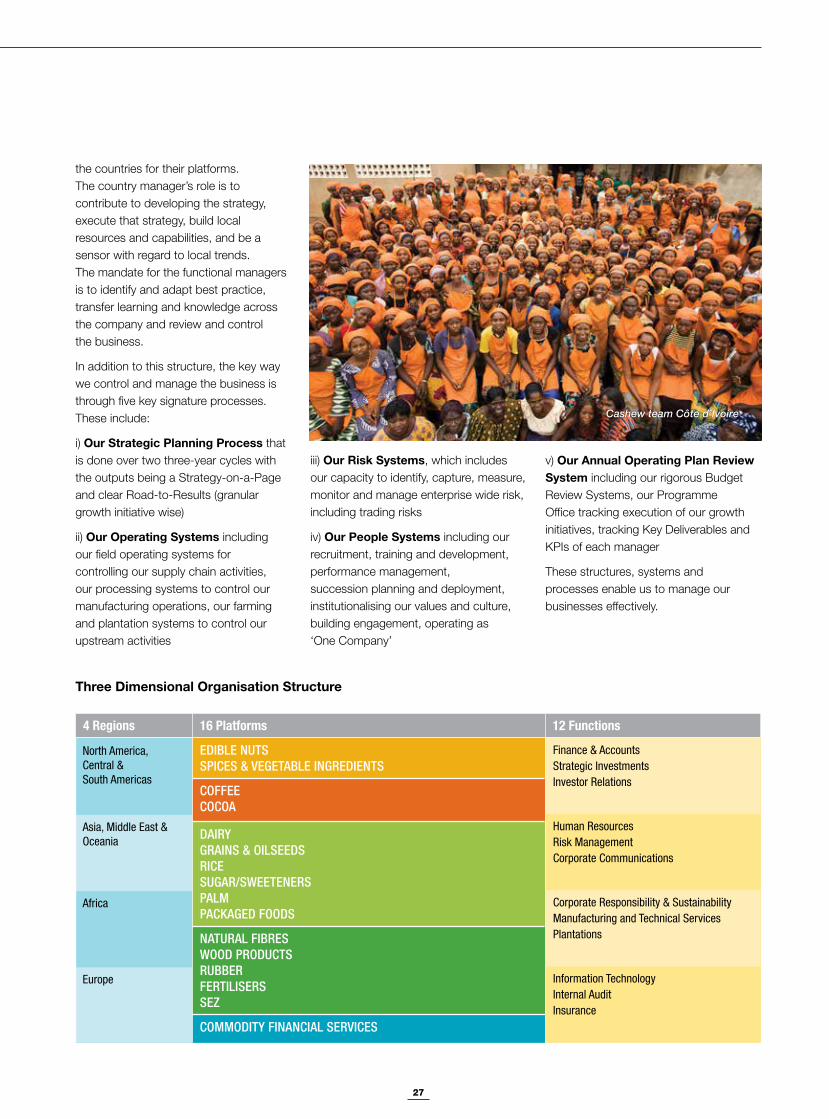

Olam now operates across 65 countries, employs over 18,000 people and is involved in upstream, supply chain, midstream and downstream businesses. How does the management team review, control and direct such diverse operations?

Sridhar: Our company has grown and diversified significantly over the years across businesses, geographies and functions. To ensure that we enhance our capacity to execute our strategy, effectively manage and control our business despite the diversity and be predictable in our performance, we have designed an organisational structure and

Wood products team in Central America

developed key signature processes that will enable us to effectively do this.

Our structure is organised across three dimensions. These are our business platforms, geographies and functions. Today we have 16 business platforms, are present in 65 countries and have 12 functions. This structure allows us to build three complementary capabilities concurrently namely:

i) Secure global scale efficiency and synergies (through the business platforms)

ii) Local country level responsiveness and flexibility (through the country dimension)

iii) The capacity to leverage our knowledge and learning across the company (through the functions)

The global business platform heads capture the full benefit of our integrated worldwide operations by extracting synergies across different countries and furthering global scale efficiency and competitiveness. They help in developing global strategy for the product, co-ordinate transactions across countries and allocate assets and resources across

27

the countries for their platforms. The country manager’s role is to contribute to developing the strategy, execute that strategy, build local resources and capabilities, and be a sensor with regard to local trends. The mandate for the functional managers is to identify and adapt best practice, transfer learning and knowledge across the company and review and control the business.

In addition to this structure, the key way we control and manage the business is through five key signature processes. These include:

i) Our Strategic Planning Process that is done over two three-year cycles with the outputs being a Strategy-on-a-Page and clear Road-to-Results (granular growth initiative wise)

ii) Our Operating Systems including our field operating systems for controlling our supply chain activities, our processing systems to control our manufacturing operations, our farming and plantation systems to control our upstream activities

iii) Our Risk Systems, which includes our capacity to identify, capture, measure, monitor and manage enterprise wide risk, including trading risks

iv) Our People Systems including our recruitment, training and development, performance management, succession planning and deployment, institutionalising our values and culture, building engagement, operating as ‘One Company’

4 Regions 16 Platforms 12 Functions

EDIBLE NUTSSPICES & VEGETABLE INGREDIENTS

Finance & AccountsStrategic Investments Investor Relations

Human ResourcesRisk ManagementCorporate Communications

Corporate Responsibility & SustainabilityManufacturing and Technical ServicesPlantations

Information TechnologyInternal AuditInsurance

COFFEECOCOA

DAIRYGRAINS & OILSEEDSRICESUGAR/SWEETENERSPALMPACKAGED FOODS

NATURAL FIBRESWOOD PRODUCTSRUBBERFERTILISERSSEZ

COMMODITY FINANCIAL SERVICES

North America,Central & South Americas

Asia, Middle East &Oceania

Africa

Europe

Cashew team Côte d’Ivoire

Three Dimensional Organisation Structure

v) Our Annual Operating Plan Review System including our rigorous Budget Review Systems, our Programme Office tracking execution of our growth initiatives, tracking Key Deliverables and KPIs of each manager

These structures, systems and processes enable us to manage our businesses effectively.

28

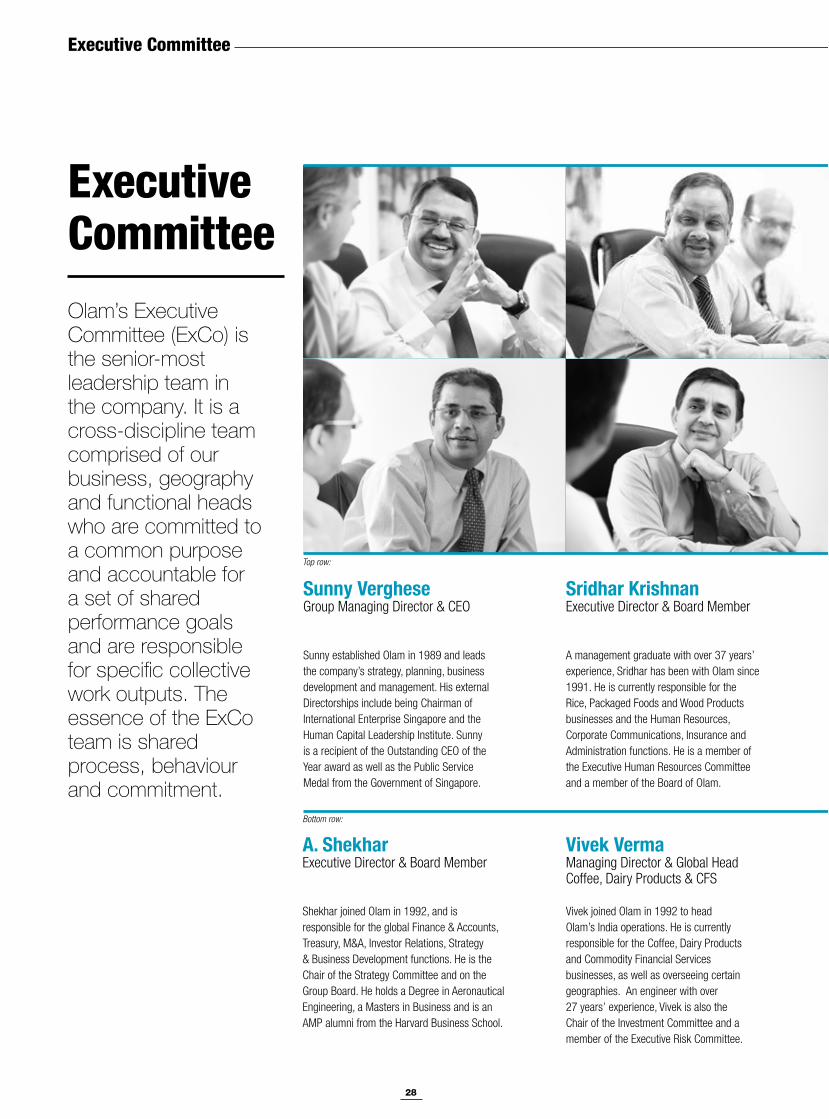

Sunny VergheseGroup Managing Director & CEO

Sunny established Olam in 1989 and leads the company’s strategy, planning, business development and management. His external Directorships include being Chairman of International Enterprise Singapore and the Human Capital Leadership Institute. Sunny is a recipient of the Outstanding CEO of the Year award as well as the Public Service Medal from the Government of Singapore.

Vivek VermaManaging Director & Global Head Coffee, Dairy Products & CFS

Vivek joined Olam in 1992 to head Olam’s India operations. He is currently responsible for the Coffee, Dairy Products and Commodity Financial Services businesses, as well as overseeing certain geographies.! An engineer with over 27 years’ experience, Vivek is also the Chair of the Investment Committee and a member of the Executive Risk Committee.

Sridhar KrishnanExecutive Director & Board Member

A management graduate with over 37 years’ experience, Sridhar has been with Olam since 1991. He is currently responsible for the Rice, Packaged Foods and Wood Products businesses and the Human Resources, Corporate Communications, Insurance and Administration functions. He is a member of the Executive Human Resources Committee and a member of the Board of Olam.

Executive Committee

A. ShekharExecutive Director & Board Member

Shekhar joined Olam in 1992, and is responsible for the global Finance & Accounts, Treasury, M&A, Investor Relations, Strategy & Business Development functions. He is the Chair of the Strategy Committee and on the Group Board. He holds a Degree in Aeronautical Engineering, a Masters in Business and is an AMP alumni from the Harvard Business School.

Top row:

Bottom row:

Executive CommitteeOlam’s Executive Committee (ExCo) is the senior-most leadership team in the company. It is a cross-discipline team comprised of our business, geography and functional heads who are committed to a common purpose and accountable for a set of shared performance goals and are responsible for specific collective work outputs. The essence of the ExCo team is shared process, behaviour and commitment.

29

Venkatramani SrivathsanManaging Director, Regional Head & Global Head Fertiliser

Srivathsan is a Chartered Accountant and joined Olam in 1994. After handling country and regional finance roles, Sri moved into operations and is currently the Global Head of the Fertiliser business in addition to overseeing Olam’s operations in Nigeria, Cameroon and Gabon. He is a member of the Investment Committee and the Executive Internal Audit Committee.

Ashok KrishenManaging Director & Global Head Edible Nuts

Ashok is a management graduate with 26 years’ experience. He has been with Olam since 1992 and is today the Global Head of the Edible Nuts platform which includes Cashew, Peanuts, Almonds and Hazelnuts. He is a member of the Strategy Committee and the Executive Risk Committee.

Gerard ManleyManaging Director & Global Head Cocoa, Specialty Fats, Sugar & Sweeteners

Gerry has 30 years’ experience in the Cocoa and Chocolate industry and is currently Chairman of the Federation of Cocoa Commerce. He has been with Olam since 1998 and is currently Chair of the Executive Corporate Responsibility and Sustainability Executive Committee and a member of the Strategy Committee and the Executive Risk Committee.

Ranveer ChauhanManaging Director, Regional Head & Global Head Palm

Ranveer joined Olam in 1993 and is the Global Head of the Palm business in addition to overseeing Olam’s operations in West, East and South Africa. A management graduate with over 25 years’ experience in agri-commodities, he is an alumni of IIM-A (India). Ranveer is a member of the Executive Human Resources Committee.

Ashok HegdeManaging Director & Global Head Rubber, Risk & IT

Ashok joined Olam in 1994 in Africa and spearheaded Olam’s foray into SE Asia. He has handled Country Head, Regional Controller and Business Head roles over the past 18 years and is currently responsible for the Rubber business and the Risk and IT functions.!He is a member of the Investment Committee and Chair of the Executive Risk Committee.

Jagdish PariharManaging Director & Global Head Natural Fibres

Jagdish has been with Olam since 1990 and over the past 23 years has been involved in the creation of many businesses in Olam’s portfolio. He is now responsible for the Natural Fibres division covering the Cotton and Wool businesses. Jagdish is a member of the Strategy Committee, the Executive Risk Committee and the Chair of the Executive Internal Audit Committee.

30

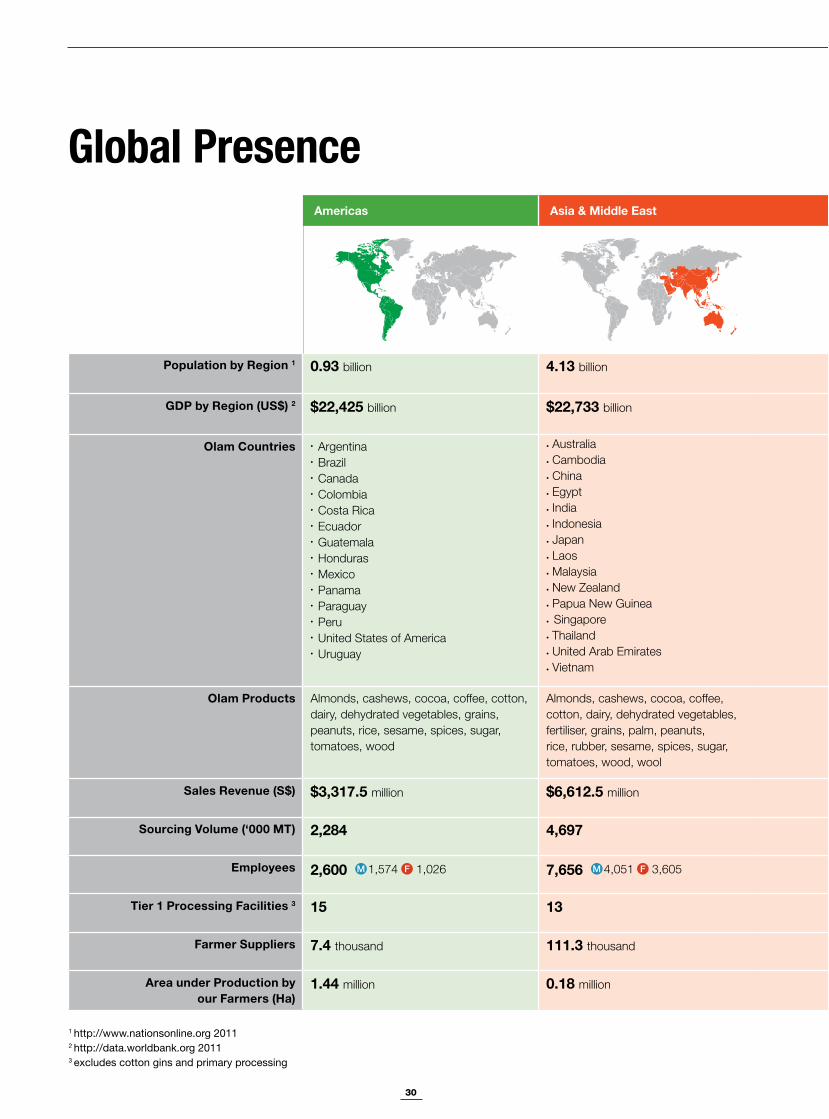

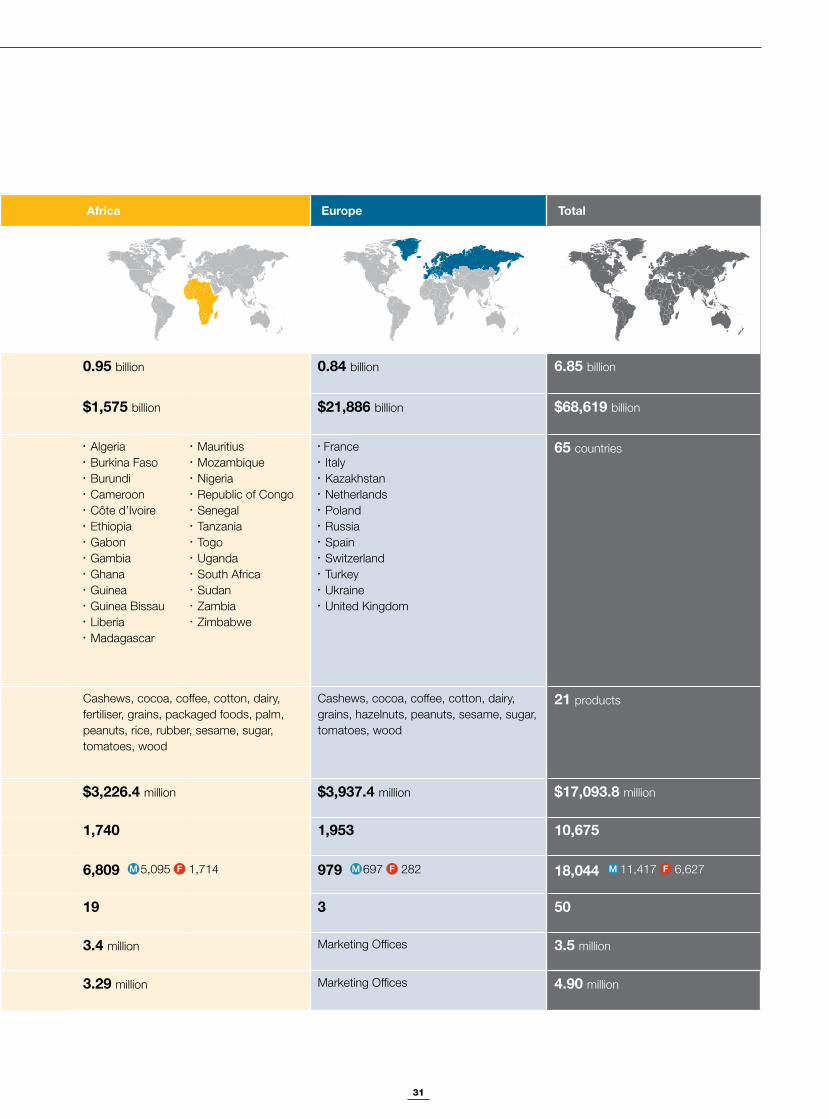

Global Presence Americas Asia & Middle East Africa Europe Total

Population by Region 1 0.93 billion 4.13 billion 0.95 billion 0.84 billion 6.85 billion

GDP by Region (US$) 2 $22,425 billion $22,733 billion $1,575 billion $21,886 billion $68,619 billion

Olam Countries ArgentinaBrazilCanadaColombia

Panama

CambodiaChina

IndiaIndonesia

Laos

Thailand

Vietnam

NetherlandsPoland

65

Olam Products 21

Sales Revenue (S$) $3,317.5 million $6,612.5 million $3,226.4 million $3,937.4 million $17,093.8 million

Sourcing Volume (‘000 MT) 2,284 4,697 1,740 1,953 10,675

Employees 2,600 M 1,574 F 1,026 7,656 M 4,051 F 3,605 6,809 M 5,095 F 1,714 979 M 697 F 282 18,044 M 11,417 F 6,627

Tier 1 Processing Facilities 3 15 13 19 3 50

Farmer Suppliers 7.4 111.3 3.4 million 3.5 million

Area under Production by our Farmers (Ha)

1.44 million 0.18 million 3.29 million 4.90 million

1 http://www.nationsonline.org 2011 2 http://data.worldbank.org 2011 3 excludes cotton gins and primary processing

31

Americas Asia & Middle East Africa Europe Total

Population by Region 1 0.93 billion 4.13 billion 0.95 billion 0.84 billion 6.85 billion

GDP by Region (US$) 2 $22,425 billion $22,733 billion $1,575 billion $21,886 billion $68,619 billion

Olam Countries ArgentinaBrazilCanadaColombia

Panama

CambodiaChina

IndiaIndonesia

Laos

Thailand

Vietnam

NetherlandsPoland

65

Olam Products 21

Sales Revenue (S$) $3,317.5 million $6,612.5 million $3,226.4 million $3,937.4 million $17,093.8 million

Sourcing Volume (‘000 MT) 2,284 4,697 1,740 1,953 10,675

Employees 2,600 M 1,574 F 1,026 7,656 M 4,051 F 3,605 6,809 M 5,095 F 1,714 979 M 697 F 282 18,044 M 11,417 F 6,627

Tier 1 Processing Facilities 3 15 13 19 3 50

Farmer Suppliers 7.4 111.3 3.4 million 3.5 million

Area under Production by our Farmers (Ha)

1.44 million 0.18 million 3.29 million 4.90 million

32

Business Review

32

Seeing the Big Picture

Olam has successfully developed a unique business model that has enabled us to participate globally across the agriculture value chain and achieve leading positions in many of our businesses. This has enhanced our ability to deliver unmatched quality, consistency, innovation and value for our customers, ensuring we continue on our path to growth despite the recent volatility in world markets.

There is an increasing desire for product traceability, as well as a growing emphasis on food safety and responsible sourcing. This has an impact across all our supply chains in products as diverse as cocoa, coffee, dairy, dehydrated vegetables, rice, timber, cotton and palm. At Olam we are pioneering new ways to meet this demand across our portfolio of products.

Several Olam businesses are expanding their reach by investing in selective upstream assets and developing manufacturing capabilities that will enhance our ability to meet increased demand, improve our margins and returns, and help achieve Olam’s goal to be a !4% NPAT and 25% ROE company by 2016.

In this review Olam’s senior managers discuss what’s driving global growth in agri-business, how we are responding to the opportunities this presents and some of the initiatives that are coming to fruition through the innovation and commitment of our people.

3333

Upstream Pg 34-37

Changing Global Consumption

Origination Pg 38-41

Meeting Future Demand

Midstream Pg 42-45

Addressing Global Needs

New Growth Pg 46-49

Establishing New Growth

Palm processing facility in Côte d’Ivoire

3434

Upstream

Where global growth meets local demand

Changing Global Consumption

Vivek Verma talks about the need to balance the fast growing demand for cereals being driven by the rise in population and increasing prosperity, resulting in a rapid migration to meat consumption by an emerging middle class. He considers why these factors are constrained by the location and availability of arable land to meet global needs and how the resulting pressure on markets is leading to increased volatility, as well as greater exposure to extreme weather events.

Developing our diminishing land supply

Rapid changes in consumption patterns and continuing constraints on global supply require significant investment in arable land, and improved agricultural productivity to maintain parity with demand for agri-commodities in both developing and developed economies. Available land is primarily in areas constrained by lack of infrastructure and productivity challenges, where knowledge and experience will be important factors in developing new sources of production and supply.

Vivek Verma

Managing Director and Global Head, Coffee, Dairy Products & Commodity Financial Services

Upstream

3535

More limited supplies of fresh water

Impact on global stock ratios

Growing opportunities

Comment at [email protected]

Onion farming in USA

Cotton plantation in Côte d’Ivoire Almond orchard in Australia

Dairy farm in Uruguay

36

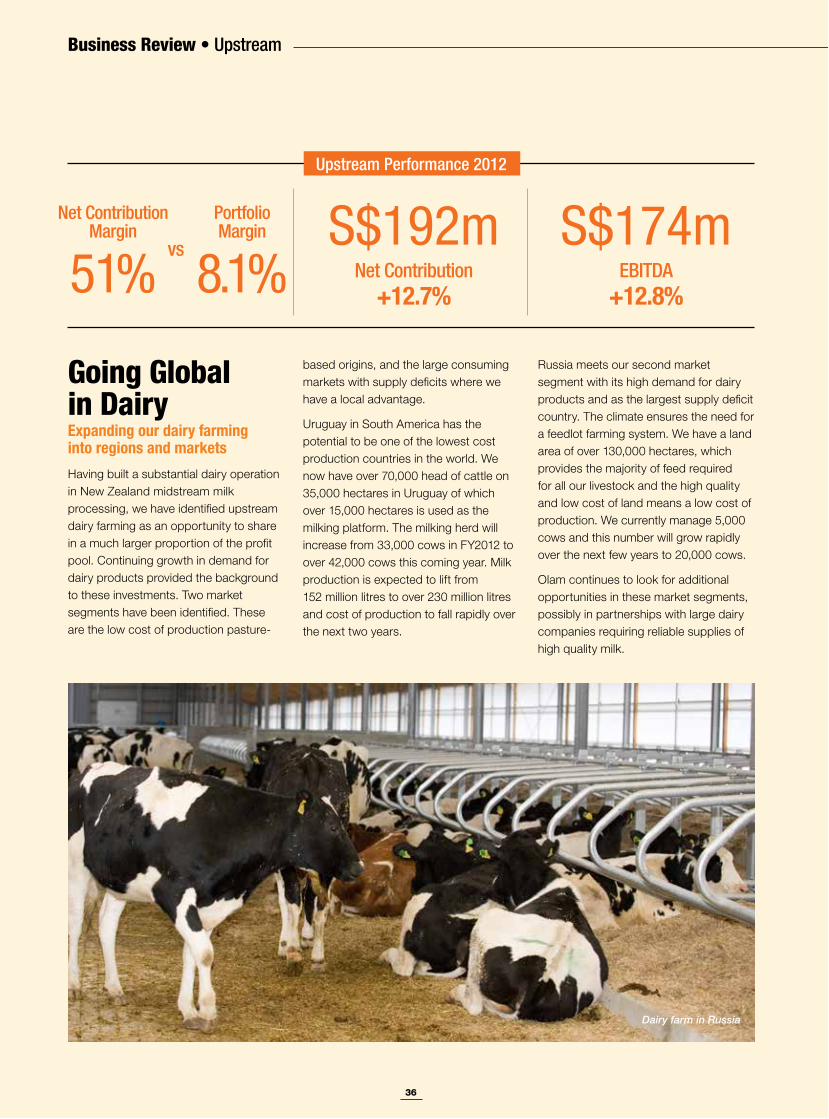

Upstream

Going Global in DairyExpanding our dairy farming into regions and markets

Dairy farm in Russia

Upstream Performance 2012

Portfolio Margin

8.1%Net Contribution

Margin

51%S$192m

Net Contribution +12.7%

S$174mEBITDA

+12.8%

vs

37

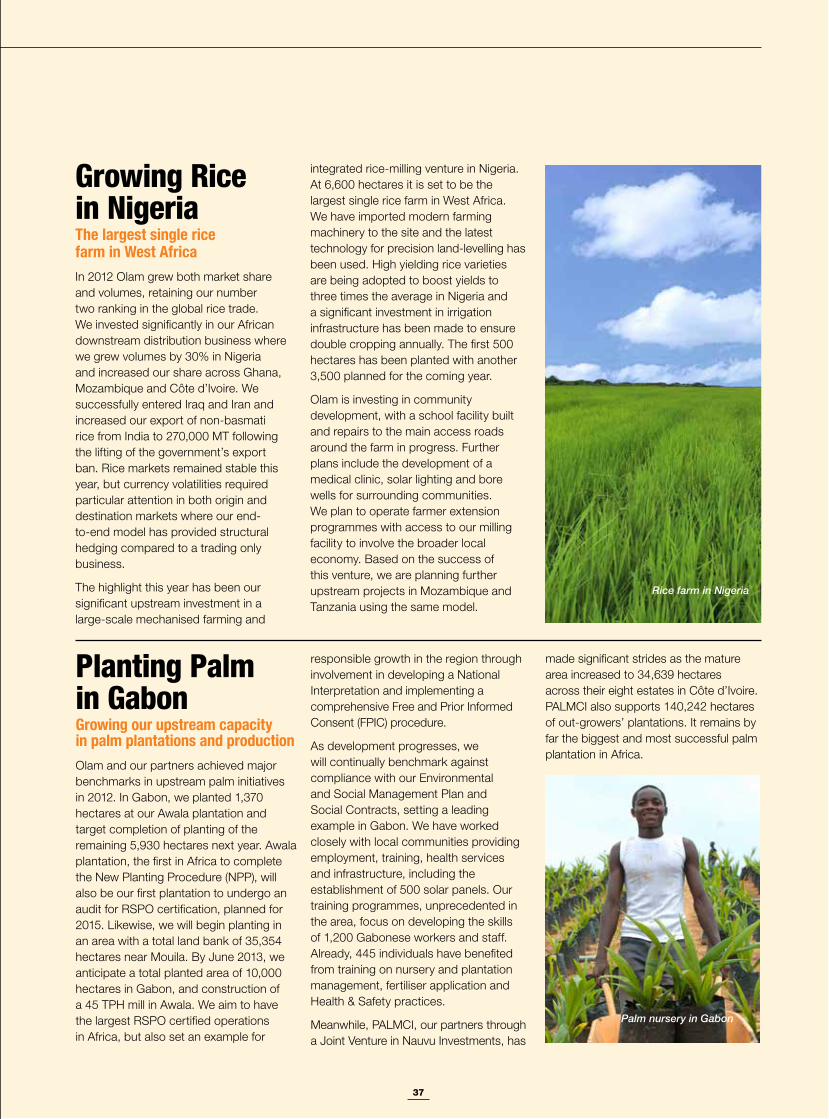

Rice farm in Nigeria

Planting Palm in GabonGrowing our upstream capacity in palm plantations and production

Palm nursery in Gabon

Growing Rice in NigeriaThe largest single rice farm in West Africa

38

Origination

Meeting Future Demand

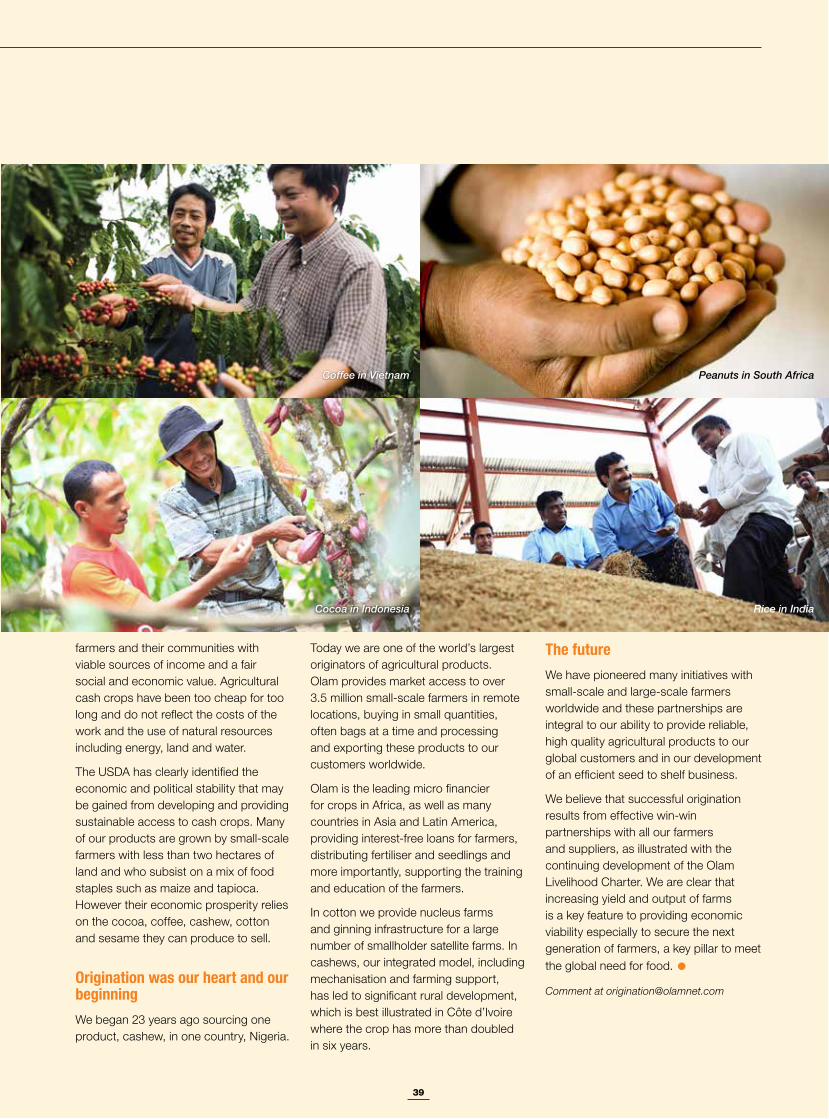

Gerry Manley looks at the long-term trends in food commodities, what is driving such consistent demand across the markets and the likely scenario for commodity prices going forward. He also examines the drivers of this growth and how Olam’s origination position enables it to help support and influence the necessary changes.

Food prices have been on a steady rise over the past two decades with almost all food commodities showing at least double-digit growth. This has evidently become a structural rather than cyclical trend and is driven by both supply and demand factors. Origination of agricultural products is complex and requires commitment, resources and long-term relationships to deliver the needed supply growth.

Gerry Manley

Managing Director and Global Head of Cocoa, Specialty Fats, Sugar & Sweeteners

Origination

A growing momentum

Factors affecting demand

Impact on rural communities

39

Origination was our heart and our beginning

The future

Comment at [email protected]

Cocoa in Indonesia

Coffee in Vietnam Peanuts in South Africa

Rice in India

40

Origination

Integrated Strategy in CoffeeGrowing our origin presence

Origination Performance 2012

S$14,825mSales Revenue

+7.0%

S$956mNet Contribution

+10.7%

S$614mEBITDA +7.2%

Coffee in Colombia

41

Producing Better CottonIntegrating better cotton practices across our supply chain

Global presence with a local spiritExpanding our cocoa footprint in Latin America

Cocoa in Ecuador

Cotton in Mozambique

42

Midstream

Delivering cost-effective manufacturing solutions

Greg Estep

President and Global Head, Spices & Vegetable Ingredients

Addressing Global Needs

Greg Estep talks about the increasing shift by brand owners in the developed economies towards contract manufacturing to minimise manufacturing costs. He looks at how the move towards processed foods is helping consumers in the developing world as incomes rise and economic growth increases the demand for convenience and choice.

Partnering for consistency and traceability

Food manufacturing is experiencing a period of rapid change as branded food companies aim to become asset light and focus on value addition through marketing and innovation, while contract manufacturers are scaling up to fill the gap. The developing world is also seeing rapid expansion to meet the changing habits of consumers in fast-growing markets, where processed foods are providing the answers to meet demand for nutritious, convenient meals.

Midstream

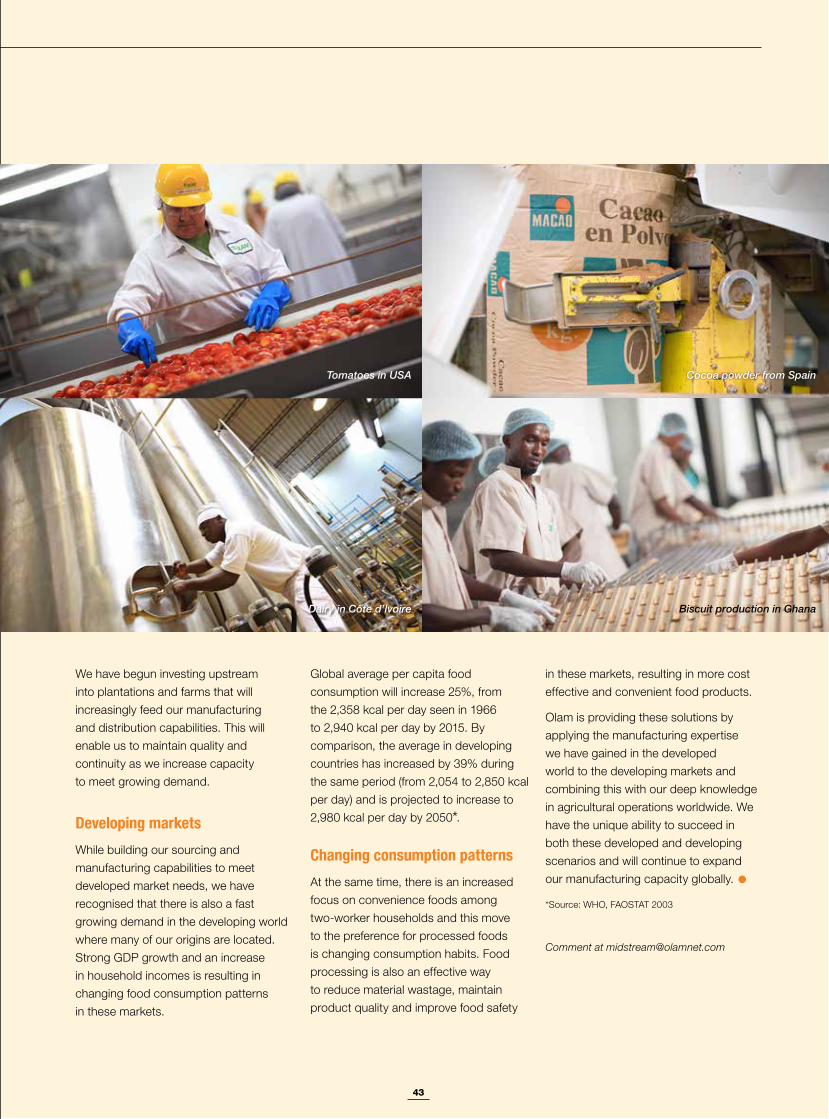

43

Dairy in Côte d’Ivoire

Cocoa powder from Spain

Biscuit production in Ghana

Tomatoes in USA

Developing markets *

Changing consumption patterns

Comment at [email protected]

44

Midstream

Hazelnuts in TurkeyExpanding our edible nut portfolio through adjacency growth

Midstream Performance 2012

Hazelnut processing in Turkey

S$1,892mSales Revenue

+15.0%

S$234mNet Contribution

+23.8%

S$170mEBITDA

+24.8%

45

Sugar Milling in BrazilEntering the world’s largest sugar origin

Spicing Up Our PortfolioLeveraging our diverse product range in Spices & Vegetable Ingredients

Onion processing in USA

Sugar milling in Brazil

46

New Growth

A. Shekhar Executive Director and Board Member

Establishing New Growth

A. Shekhar discusses some of the unique qualities that have enabled us to expand over the years and create opportunities in new growth areas that bring extended capabilities and enhanced returns for our business. These opportunities have themselves become significant businesses that are growing fast and contributing to our success today.

Olam’s involvement over the past 23 years in diverse geographies and markets has enabled us to build a wealth of proprietary knowledge. Our deep participation across the entire value chain has helped us to develop relationships and leverage opportunities that have been open to us as we have grown our business.

Utilising valuable latent assetsAs we have grown as a company, we have built deep knowledge and insight into the products and various steps of our supply chain. We have developed significant local knowledge, context and contacts in our various geographies and created strong, well differentiated grower and customer franchises that are quite unique within our Industry.

Each aspect of our business model has helped in the accumulation and understanding of this knowledge. Our participation in sourcing at the farm gate has enabled us to reach and build a strong mutual interdependence with more than 3.5 million farmers and suppliers worldwide. We have been able to gain access to key assets and resources such as critical warehousing, logistics and port-based infrastructure, and feedstock such as natural gas.

Cross-sourcing of multiple agri-commodities has helped us identify commonalities, linkages and similar trends between them. We have also derived proprietary insights into the fundamentals driving supply and demand, and the cost of production across regions for a wide range of these commodities.

Growing unique capabilitiesThis deep emerging market execution and project management expertise has been aided by the extensive feet-on-the-ground quality that defines our business. Olam managers in our markets help assess key trends and define the unique characteristics of the operations, brands and consumption behaviour in those markets. This proprietary information is invaluable to our large base of more than 12,300 loyal customers worldwide.

In addition, our strong inbound and outbound supply chain distribution network in key emerging markets, as well as our deeply embedded global relationships with all the food majors, has resulted in the proven ability to offer solutions which will integrate into the back-end of their supply chain.