saints and sinners; how to make it big on wall street

TRANSCRIPT

Istanbul, Turkey ©Ceyhun K. Yildiz

Econ 281: Wall Street Program Ceyhun K. Yıldız Summer 2014 Drew University

How could one hit the sky high on the most famous financial district, Wall Street? Is it worth to work way longer hours than human body should naturally elevate?

How to master all of the many skills in conjunction with scarce time limitation? I intend to analyze what drives man to renounce his best era of youthfulness,

dedicating to hard-work and diving into a harshly intense environment in which excessive information intake, dedication and success may precede family, at times creativity, or even health. Growing competition, parental oppression, increasing

inflation have exponentially forced students enter into an arguably obnoxious environment of struggle even before high school graduation.

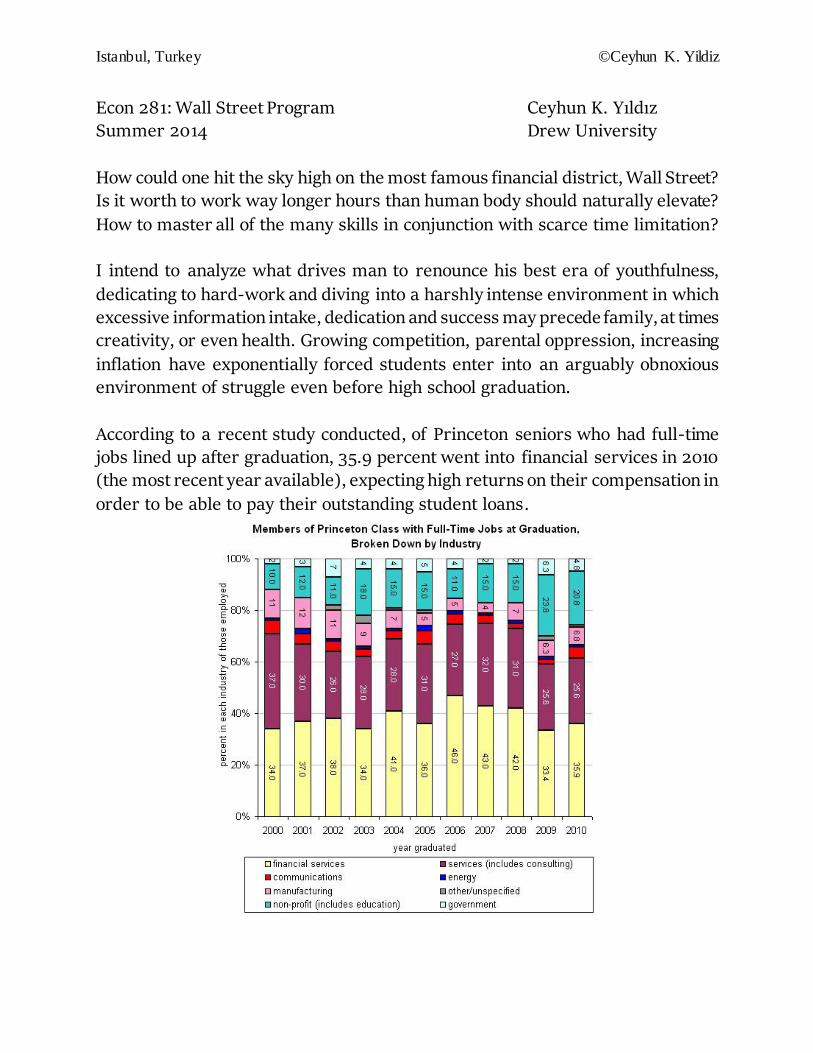

According to a recent study conducted, of Princeton seniors who had full-time jobs lined up after graduation, 35.9 percent went into financial services in 2010 (the most recent year available), expecting high returns on their compensation in

order to be able to pay their outstanding student loans.

Istanbul, Turkey ©Ceyhun K. Yildiz

But how are the students, who want to work in financial services industry, going to make it big on Wall Street? Can semi-target and non-target school graduates

break into Wall Street ever? What kind of different skills are students expected to eventually possess? We will examine with care each of these questions on this paper. But first, let’s take a look at the roots of investment banking.

Philadelphia financier Jay Cooke established the first modern American

investment bank during the Civil War era. However, private banks had been providing investment banking functions since the beginning of the 19th century and many of those evolved into investment banks in the post-bellum era (Moulton

212). During the Civil War, banking houses were syndicated to meet the federal government’s need for money to fund its war efforts. Jay Cooke launched the first mass securities selling operation in U.S. history employing thousands of salesmen

to float what ultimately amounted to $830 million worth of government bonds to a wide group of investors. (Oberholtzer 299)

The market for financial services evolved dramatically in the post-Civil War era. One of the most significant changes was the emergence of “active investment banking”, also known as “Private Equity”, in which investment bankers

Istanbul, Turkey ©Ceyhun K. Yildiz

influenced the management of client companies through sitting on the finance committees and even directly on the board of directors of those companies

(Williamson 15). Jewish banking houses were instrumental to the process of capital formation in

the United States in the late 19th and early 20th century (Baron 224). Modern banking in Europe and the Unites States was influenced by Jewish financiers, such as Rottschild family and Warburg family, and Jews were major contributors to

the establishment of important investment banks on Wall Street. In the middle of the 19th century, a number of German Jews founded investment

banking firms which later became mainstays of the industry. Most prominent Jewish banks in the United States were investment banks, rather than commercial banks (Krefetz 54-55). Jonathan Knee postulates that Jews were forced to focus

on the development of investment banks because they were excluded from the commercial banking sector (Knee 31).

Several major banks were started following the mid-19th century by Jews, including Goldman Sachs, Kuhn Loeb, Lehman Brothers, Salomon Brothers, and Bache & Co. (Krefetz 46)

(Wechsberg 235) Lehman Brothers entered investment banking in the 1880s, becoming a member of the Coffee Exchange as early as 1883 and finally the New

York Stock Exchange in 1887. In 1889, it underwrote its first public offering, the common stock of the International Steam Pump Company. In 1906, under Philip Lehman, the firm partnered with Goldman Sachs & Co. (Geisst 51, 285), to bring

the General Cigar Co. to the market, followed closely by Sears, Roebuck and Company. (Wechsberg 238) During the following two decades, almost one hundred new issues were underwritten by Lehman, many times in conjunction

with Goldman, Sachs. During the period from 1890 – 1925, in the early 20th century, the investment

banking industry was highly concentrated and dominated by an oligopoly that consisted of JP Morgan & Co.; Kuhn, Loeb & Co.; Brown Brothers; and Kidder, Peabody & Co. There was no legal requirement to separate the operations of

commercial and investment banks; as a result deposits from the commercial banking side of the business constituted an in-house supply of capital that could

Istanbul, Turkey ©Ceyhun K. Yildiz

be used to fund the underwriting business of the investment banking side (Stowell 22).

Before moving on, I would like to point out some of the most important historical events and acts took place during the 20th century.

By the beginning of 1933, the banking system in the United States had effectively ceased to function. The incoming Roosevelt administration and the incoming

Congress took immediate steps to pass legislation to respond to the Great Depression. A major component of Roosevelt’s New Deal was reform of the nation’s banking system.

The Glass–Steagall Act of 1933 was passed in reaction to the collapse of a large portion of the American commercial banking system in early 1933. One of its

provisions introduced the separation of bank types according to their business (commercial and investment banking). In order to comply with the regulation, most large banks split into separate entities. For instance, JP Morgan split into

three entities: JP Morgan continued to operate as a commercial bank, Morgan Stanley was formed to operate as an investment bank, and Morgan Grenfell operated as a British merchant bank. (Essvale 4)

Congress enacted The Securities Exchange Act of 1934, a law governing the secondary trading of securities (stocks, bonds, and debentures) in the United

States of America. It was a sweeping piece of legislation. The Act and related statutes form the basis of regulation of the financial markets and their participants in the Unites States. The 1934 Act also established the Securities and

Exchange Commission (SEC), the agency primarily responsible for enforcement of United States federal securities law. (Cox 11)

After the reforms of the mid-20th century, the major Wall Street investment banks focused on dealmaking, serving as advisors to corporations on mergers and acquisitions as well as public offerings of securities. These ‘bulge-bracket’ firms

included Goldman Sachs, Morgan Stanley, Lehman Brothers, First Boston and others. (Essvale 5)

In the 1980’s, the emphasis on dealmaking shifted to a new focus on trading. Firms such as Salomon Brothers, Merrill Lynch and Drexel Burnham Lambert

Istanbul, Turkey ©Ceyhun K. Yildiz

became prominent as investment banks earned an increasing amount of their profits from trading for their own account. Advances in computing technology

enabled banks to use sophisticated mathematical models to develop and execute trading strategies. The high frequency and large volume of trades allowed them to generate a profit by taking advantages of small changes in market conditions

within milliseconds. (Morrison 15-16) During the 80s decade, Michael Milken, head of the high-yield bond department

at Drexel Burnham Lambert, popularized the use of high yield debt (also known as junk bonds) in corporate finance, especially in mergers and acquisitions. This new source of capital sparked an explosion in leveraged buyouts and hostile

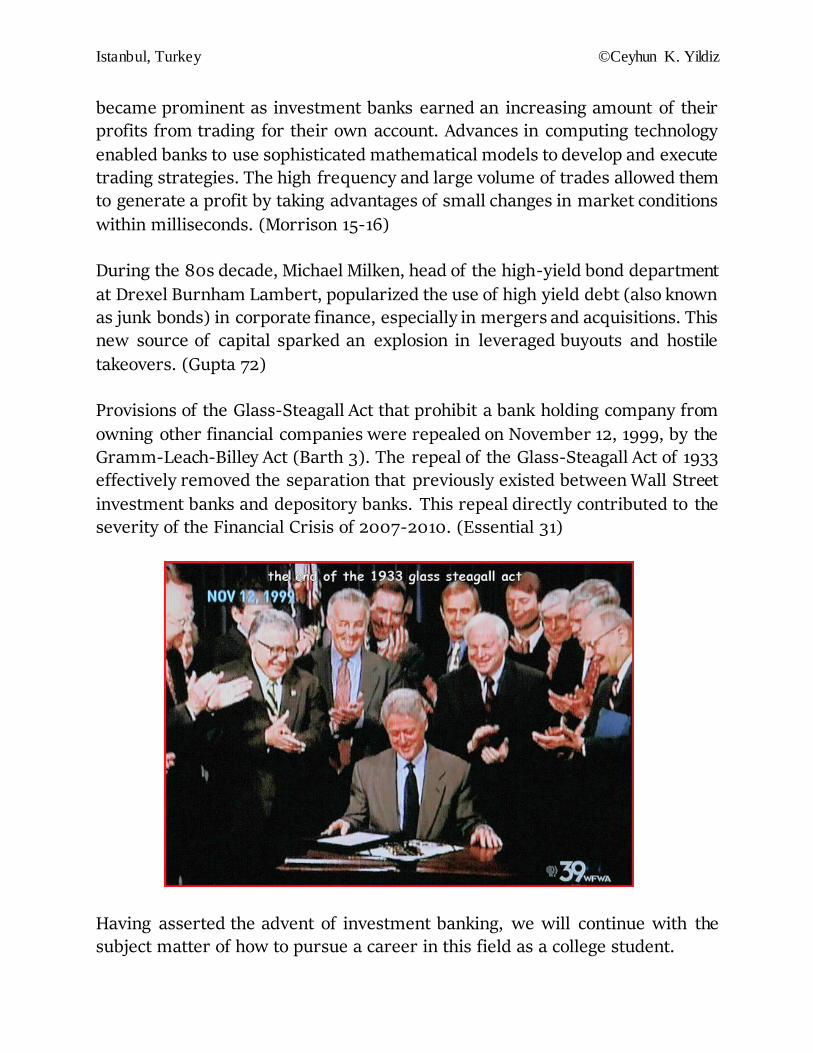

takeovers. (Gupta 72) Provisions of the Glass-Steagall Act that prohibit a bank holding company from

owning other financial companies were repealed on November 12, 1999, by the Gramm-Leach-Billey Act (Barth 3). The repeal of the Glass-Steagall Act of 1933 effectively removed the separation that previously existed between Wall Street

investment banks and depository banks. This repeal directly contributed to the severity of the Financial Crisis of 2007-2010. (Essential 31)

Having asserted the advent of investment banking, we will continue with the subject matter of how to pursue a career in this field as a college student.

Istanbul, Turkey ©Ceyhun K. Yildiz

If you decided to pursue an investment banking career on Wall Street, there are prominent decisions you must make. Investment banking is a fast-moving, high-

stress, ferociously competitive business that requires specialized knowledge and experience – not to mention commitment, focus, and the physical, mental, and psychological stamina required to work long hours. Obtaining a job in this

potentially lucrative profession usually requires a solid skill-set and qualities – although a strong recommendation from someone of influence may surpass all of them. (Davis 1)

Potential employers in the investment banking field will look for candidates with the following qualifications in education and work experience. A college degree

in any or both of the following: Accounting, Banking, Business Administration, Business Law, Computer Science, Economics, Finance, Human Resources, International Trade, Tax Law. Davis continues, this is not set in stone, as potential

employers will consider other business, law, and technology related disciplines that are not listed here. Basically, employers want to see what the nominees will bring to the table.

As Marc Davis suggests, if you are short on specific skills, you may also cite personal skills. For example, you might say that you are highly motivated,

energetic, enthusiastic, detail-oriented and so on. Many of these things will be implied in your investment banking skill set – that is, accounting skills generally suggests a detail-oriented personality – so you can omit overlap for the sake of

brevity. According to O-Connell; banks, brokerages, and other financial services firms will

favor job candidates who bring the following attributes to the negotiation table: Deep insight into changing financial consumer demographics, including

millennial investors who will inherit $40 trillion from their Baby Boomer

parents and overseas investors climbing out of the middle class and into affluent investors status.

A pitch-perfect grasp of investment bank risk and securities analysis.

A clear, concise and compelling handle on the new banking business model, which emphasizes caution over aggressive risk taking.

Deep experience in statistics, quantitative analysis and information

modeling.

Istanbul, Turkey ©Ceyhun K. Yildiz

While investment firms continue to hone their wish lists for analysts, the good news is that the need for candidates who possess the above skill sets are already

in great demand, confirms Brian O-Connell. Viable candidates will have finance or business degrees, and preferably advanced

Masters of Business Administration (MBA) degrees for plum investment banking analyst posts, although financial services firms do recruit finance and business undergraduates from high-end schools for entry-level analyst positions. New

analysts can expect long work weeks – 60-80 hours isn’t out of the norm – and will work closely with firm managing directors to “fill in the blanks” on the investment strategies favored by those directors. (O’Connell)

For junior-level positions, trainee positions or internships in investment banking, qualifications may not be confined to the areas cited above. Education and

experience that is less focused on finance may be acceptable to potential employers with a view toward training new hires in investment banking specialties. In fact, last week in a meeting with JP Morgan marketing head, I was

informed that they are willing to recruit from any educational background due to a high demand for different masterminds to conduct different parts of their business and make a skill-set pool that will feed the business in all aspects.

Communication is key. Investment bankers need to be effective team players with excellent communication skills in order to avoid disconnects and wasted effort.

Investment banks communicate with external parties such as investors, accountants, consultants, and lawyers. Moreover, many client representatives tend to be extremely scrutinizing, well-respected and often short-tempered, and

you’ll need to know how to deal with them. (Dumon 2) In addition to these facts about how to make it big on Wall Street, we also need

to discuss how to join the elite rafting boat without a pre-purchased ticket given by a target school degree.

Mike Moran, CFA, set out to answer this question by studying the backgrounds of the 25 highest paid hedge fund managers. These men (he feels sorry for ladies, they are all men) are the true BSDs of Wall Street. They are the masters of the

universe that take home more pay than the GDP of some small countries. They are outliers. We can learn from outliers.

Istanbul, Turkey ©Ceyhun K. Yildiz

As mentioned earlier, it is common knowledge going to a target school is the guaranteed path to breaking into Wall Street. But yet, there is empirical evidence

that an elite degree is not what determines your success rather the elite degree just gets your foot in the door. The rest is up to you, rather than your degree. As a matter of fact, in a recent meeting I took part with a JP Morgan Chase associate,

who has been working in the company for over 10 years; she stated the fact that most of the high-end school alumni do not sit on their chairs after a decade. This statement is consistent with the idea that we mentioned earlier.

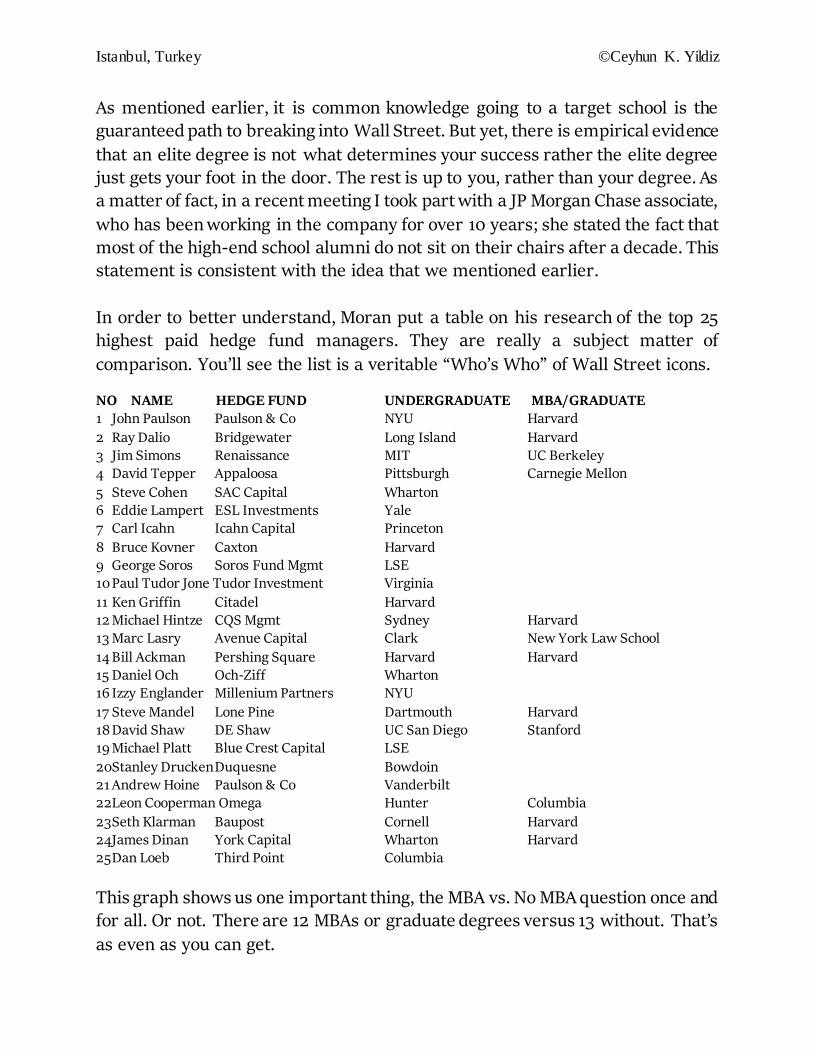

In order to better understand, Moran put a table on his research of the top 25 highest paid hedge fund managers. They are really a subject matter of

comparison. You’ll see the list is a veritable “Who’s Who” of Wall Street icons.

NO NAME HEDGE FUND UNDERGRADUATE MBA/GRADUATE 1 John Paulson Paulson & Co NYU Harvard

2 Ray Dalio Bridgewater Long Island Harvard 3 Jim Simons Renaissance MIT UC Berkeley 4 David Tepper Appaloosa Pittsburgh Carnegie Mellon

5 Steve Cohen SAC Capital Wharton 6 Eddie Lampert ESL Investments Yale 7 Carl Icahn Icahn Capital Princeton

8 Bruce Kovner Caxton Harvard 9 George Soros Soros Fund Mgmt LSE 10 Paul Tudor Jone Tudor Investment Virginia

11 Ken Griffin Citadel Harvard 12 Michael Hintze CQS Mgmt Sydney Harvard 13 Marc Lasry Avenue Capital Clark New York Law School

14 Bill Ackman Pershing Square Harvard Harvard 15 Daniel Och Och-Ziff Wharton 16 Izzy Englander Millenium Partners NYU

17 Steve Mandel Lone Pine Dartmouth Harvard 18 David Shaw DE Shaw UC San Diego Stanford 19 Michael Platt Blue Crest Capital LSE

20Stanley Drucken Duquesne Bowdoin 21 Andrew Hoine Paulson & Co Vanderbilt 22Leon Cooperman Omega Hunter Columbia

23Seth Klarman Baupost Cornell Harvard 24James Dinan York Capital Wharton Harvard 25 Dan Loeb Third Point Columbia

This graph shows us one important thing, the MBA vs. No MBA question once and for all. Or not. There are 12 MBAs or graduate degrees versus 13 without. That’s

as even as you can get.

Istanbul, Turkey ©Ceyhun K. Yildiz

Do you need an MBA? No. But can it help? Yes. Moving on.

By now you have probably read or heard about the role of deliberate practice in determining expert performance. Many books and studies (K. Anders Ericsson is the leading researcher in this field) have shown that a minimum of ten years of

deliberate practice is necessary to reach a world-class level of performance. Let’s look at how many years after college three of our outliers had before getting

their break: PTJ – 11 years

Druckenmiller – 11 years Hoine – 11 years

See a pattern here? The fact that they are all exactly 11 years is probably a coincidence, but Mike does not believe it is a coincidence that all three are above 10 years.

Learning any profession and becoming proficient takes time. These three worked hard over a decade before they made it big. If you break into Wall Street right out

of the college, chances are you will be living a much better life than your friends who aren’t in finance.

For some people, this is all they want in life. And that’s OK. But if you really want to make it big, you need to take advantage of your opportunity and work very hard at getting better.

At the end of the day, the people who say you need a target school degree are partially right. However, the people who say you don’t need a fancy degree to

succeed are also right. The two are not mutually exclusive. Anyone can become an outlier success on Wall Street and make enough money to

buy small countries. The key rule is to always work hard play hard. Don’t just work hard for work’s sake. Work hard to improve.

And use those networking skills to find a proper mentor or the right boss. Find someone who will teach you and push you to improve. (Moran 4)

Istanbul, Turkey ©Ceyhun K. Yildiz

From this point on until the end of the page I will highlight very few facts about female professionals on Wall Street.

Just look at the statistics for the “C-suite” – top corporate jobs such as Chief Executive Officer (CEO), chief operating officer (COO), and chief financial officer

(CFO). In 2011, only 8 percent of CFOs and 1.5 percent of CEOs of large U.S. corporations were women, compared with 3 percent and 0.5 percent, respectively, in 1994. Very well, this is a huge increase over that period. But the

percentages have not increased much over the past five years, and the low absolute figures contrast sharply with women’s advancement in education and labor force participation. Why is Wall Street still unfriendly to females, even after

decades of promoting gender – and other forms of – diversity? (Fang 20) In a recent study, academicians found interesting patterns in their subjects of

thousands of analysts spanning 17 years (1993-2009). Female analysts are, on average, better educated than their male co-workers, at least as measured by the number with Ivy League degrees. Approximately 35 percent of the female workers

are Ivy Leaguers, compared with 25 percent of men. This figure is consistent with the idea that most of the competitive female graduates sign up for the Wall Street labor market. (Fang 21)

It is also worth mentioning in spite of the fact that 14 percent of Wall Street all-star analysts are women, virtually none of the top bosses in any of those big firms

are. Where did all the highly educated, highly connected, high-potential women go? They largely remain in analytical roles rather than being promoted into general management division, which entails subjective evaluations.

There is slow progress, in the C-suite. A recent Bloomberg article reported that in 2012, the number of women CFOs at Standard and Poor’s 500 companies

increased 35 percent, from 40 to 54, to a record high of 14 percent. But climbing to the top remains difficult. The ratio for women in CEO roles

remained at 4 percent in 2012, also a record but one that has not changed for five years. They asymmetry in women’s success at breaking these two C-suite glass ceilings is telling: it is far easier for women to demonstrate technical and

measurable skills than to overcome potential bias in subjective qualitative evaluations such as connectedness. (Fang 21)

Istanbul, Turkey ©Ceyhun K. Yildiz

I would like to underline some information about intelligence and leadership.

What lies in the spine of huge success is reacting different situations with different types of leadership, says Daniel Goleman, psychologist and noted author. Superb and effective leaders have a high degree of what has come to be

known as emotional intelligence. In fact, Goleman’s research at approximately 200 large, global companies

revealed that without emotional intelligence, a person can have first-class training, an incisive mind, and an endless supply of good ideas, but he still won’t make a great leader. (Goleman 94)

The components of EQ are self-awareness, self-regulation, motivation, empathy and social skills. But exhibiting emotional intelligence at the workplace does not

mean simply controlling your anger or getting along with people. Rather, it means understanding your own and other people’s emotional makeup well enough to move people in the direction of accomplishing your company’s goals.

Can emotional intelligence be learned? IT takes time and, most of all, commitment. But the benefits that come from having a well-developed emotional

intelligence, both for the individual and the organization, make it worth the effort. When he analyzed the data he gathered from 188 companies, Goleman was

convinced by the link between a company’s success and the emotional intelligence of its leaders. And of the same importance, research has also demonstrated that people can, if they take the right approach, develop their emotional intelligence.

“People who are in control of their feelings can tame their emotional impulses and redirect them in useful ways”, says noted author Daniel Goleman. For ages,

people have debated if leaders are born or made. Though the the answer is both, the research clearly demonstrate that emotional intelligence can be learned. There is a certain thing which is emotional intelligence increases with age. It’s

important to emphasize that building emotional intelligence will not happen without sincere desire and commitment. But it can be done. “Nothing great was ever achieved without enthusiasm” wrote Emerson. If your goal is to become a

great leader, these words can serve as a guidepost in your efforts to develop high EQ. (Goleman 97)

Istanbul, Turkey ©Ceyhun K. Yildiz

And I will gladly wrap up the course work.

To be an investment banker, you should focus on your undergraduate studies, along with extra-curricular activities, and some work experience.

There is an increasing demand curve for potential employees in the field of investment banking. Understanding the needs of employers and climbing those stairs in time will vastly increase your chances for landing onto your dream job

on Wall Street. Past data has shown that investment firms will give an edge to candidates who

can speak multiple languages and to candidates who have a firm grasp on technology and social media.

As Davis suggested, in a competitive job market, a persuasive resume will give the applicant a definite edge among the many who may apply for the position. Relevance should always be your guide in deciding what to include and expand

upon in your investment banking resume. Following the suggestions above may not guarantee that you'll be hired, but if you're qualified, you'll be in the running.

Applicants with a true passion for finance, and market analysis should apply for investment banking, perform self-study on finance, business, and economics. If you’re a rigorous and vigorous professional with strong valuation skills and the

ability to interact with others, this challenging and rewarding job may be just what you are looking for. Latching onto a financial analyst job can be a gateway into a lucrative career on Wall Street. Expect to work hard and be ready to listen.

Do all of the above, and you'll vastly increase your chances of landing that Wall Street analyst dream-job.

My suggestion to you is that never stop asking questions, for you won’t get anything more than a “no”, but if you hesitate to ask and not step forward, you won’t even get that chance. It’s just as simple as that.

People who have self-control, self-discipline, and self-awareness will always surpass the others without. If you can’t control yourself, you can’t control the

business. And like Henry David Thoreau said, “Go confidently in the direction of your dreams. Live the life you have always imagined.”

Istanbul, Turkey ©Ceyhun K. Yildiz

Bibliography

Baron, Salo Wittmayer; Kahan, Arcadius; Gross, Nachum (1975). Economic history of the Jews.

p. 224. "The contribution of such Jewish banking houses to the process of capital formation in the United States in the late 19th and early 20th century was considerable by any standard."

Business knowledge for IT in global investment banking: The complete handbook for IT professionals (2010). London: Essvale Corp. pp. 4-5.

Davis, Mark. How to Write and Effective Investment Banking Resume (2013). Web.

www.investopedia.com

Dumon, Marv. Wanna Be A Bigwig? (2012). Web. www.investopedia.com

Ellis Paxson Oberholtzer, Jay Cooke: financier of the Civil War (1907) - Volume 1. Online edition,

page 299.

Essential Information, Consumer Education Foundation. Sold Out: How Wall Street and Washington Betrayed America, March 2009, page 31. www.wallstreetwatch.org

Fang, L. 2013, "Connections on WALL STREET", Finance & Development, vol. 50, no. 2, pp. 20-21.

Geisst, Charles R. The Last Partnerships. McGraw-Hill, 1997, page 51, 285.

Goleman, Daniel. "What Makes A Leader?." Harvard Business Review 76.6 (1998): 93-102. Business Source Elite. Web. 21 July 2014.

Gupta, Aparna. Risk Management and Simulation. Florida: CRC Press, 2013. Print. pp. 72

Harold Glenn Moulton. The financial organization of society (1921) pp 212f online edition.

James D. Cox, Robert W. Hillman, and Donald C. Langevoort. Securities Regulation: Cases and Materials (6th ed.). Aspen Publishers. 2009. pp. 11.

James R. Barth, R. Dan Brumbaugh Jr., James A. Wilcox: The Repeal of Glass-Steagall and the

Advent of Broad Banking. Economic and Policy Analysis Working Paper, 2000, pp. 3.

Knee, Jonathan A. (2007). The Accidental Investment Banker: Inside the Decade That

Transformed Wall Street. Random House Digital, Inc. p. 31.

Krefetz, Gerald (1982). Jews and money: the myths and the reality. Ticknor & Fields. pp. 54–55 - pp. 46.

Istanbul, Turkey ©Ceyhun K. Yildiz

Morrison, Alan D., Wilhelm, Bill. Investment Banking: Past, Present, and Future: Journal of

Applied Corporate Finance (2007) Volume 19, Number 1. Morgan Stanley Publication. pp. 15-16.

O’Connell, Brian. How to Become an Investment Bank Analyst (2013). www.investopedia.com

Stowell, David (2010). An Introduction to Investment Banks, Hedge Funds, and Private Equity: The New Paradigm. Academic Press. pp. 22.

Wechsberg, Joseph. The Merchant Bankers. Pocket Books, 1966, page 235, 238.

Williamson, John Peter (1988). The Investment banking handbook. John Wiley and Sons. p. 15.