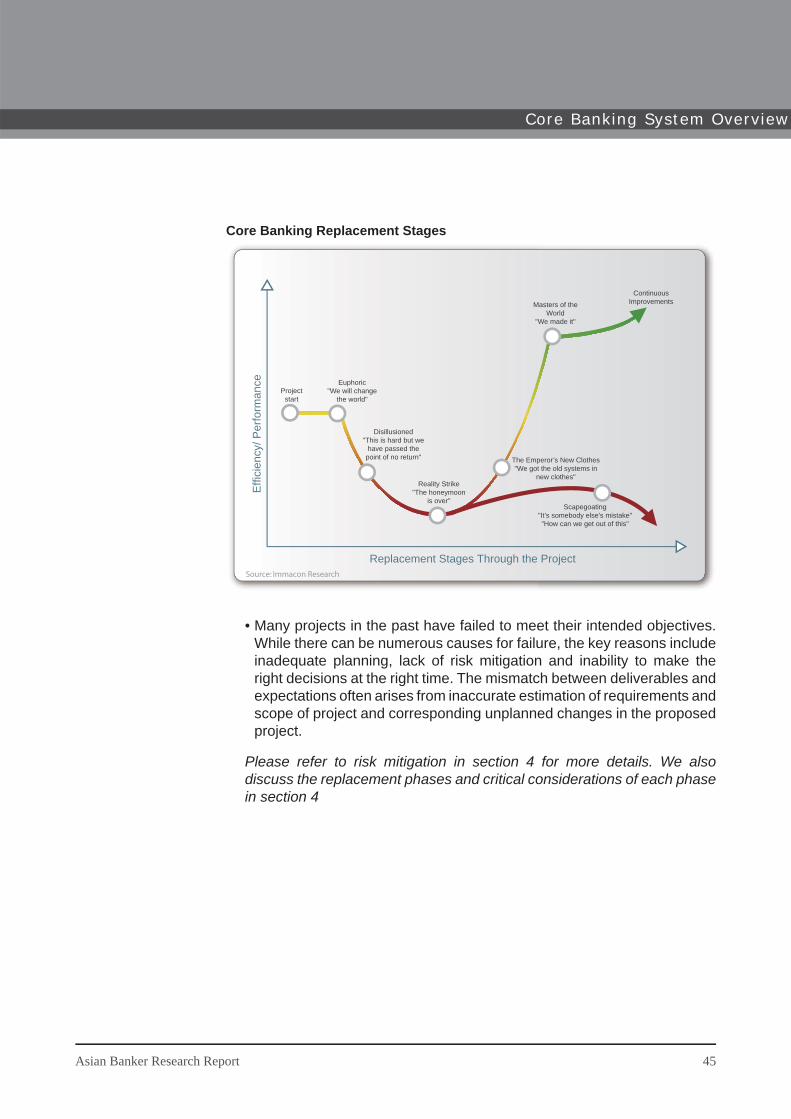

roadmap to successful core banking system replacement

TRANSCRIPT

w w w . t h e a s i a n b a n k e r . c o m

Management Report:Roadmap to Successful Core Banking System Replacement Critical Success Factors and Best Practices

Neeti Aggarwal, CFA

Published September 2006©2006 The Asian Banker

Management Report:

Roadmap to SuccessfulCore Banking System ReplacementCritical Success Factors and Best Practices

IMPORTANT NOTICEAlthough the author and publisher have tried to provide information as accurately as possible, they accept no responsibility for any loss, injury or inconveniences suffered by any person using this document. The author and publisher have taken all reasonable care to ensure the data and information in this report is accurate and presents a fair representation of the subject matter.

First Publication: 15 September 2006

ISBN: 981-05-6643-3

© 2006 The Asian Banker. All rights reserved

The Asian Banker, incorporated in Singapore as T.A.B. International Pte Ltd, claims all rights as owner of intellectual property in this report. No part of this document may be reproduced, stored in a retrieval system or transmitted in any form by any means, electronic, mechanical, photocopying, recording or otherwise, without the written permission of the publisher and the copyright owner.

IMPORTANT NOTICE

ABOUT THE ASIAN BANKERAsia’s fi nancial service landscape is undergoing tremendous change and evolution. Liberalisation, consolidation and rapid technological advances have opened up tremendous opportunities for fi nancial institutions and, it is vital for banks to benchmark themselves against their competitors and to keep abreast of global developments.

Decision-makers need accurate, incisive, timely and continuous information to bring their organisation to the next level, meet competitive challenges successfully and manage their own future. The Asian Banker has long recognised the importance of information as a strategic management and decision-making tool and is positioned to provide banks and partner organisations useful, crucial and timely business intelligence.

The Asian Banker achieves this through three synergistic services:

Asian Banker Research: current, continuous and in-depth research on best practices and market developments and trends

Proprietary & generic research servicesSubscription-based research support services for different programs

Asian Banker Publications: incisive news and information on transformational issues

The Asian Banker JournalAsian Banker E-newsletters on different segments in the fi nancial services industry such as operations & technology, wealth management, CRM, retail distribution and payment systems amongst othersAnnual Publication: The CEO Collection; The Asian Banker 300 Banks RankingSpecial Reports on M&A; Internet Banking; Payments Systems; Retail Banking; CRM; Risk Management; Wealth Management and Operations & Technology

Asian Banker Forums: exclusive gathering of industry leaders and senior decision makers to network and exchange information

Annual Major ConferencesThe Asian Banker SummitThe Future of Banking in ChinaAsia Pacifi c Heads of Retail Banking Annual MeetingChina International Risk Convention (CIRC)

Roundtable Series / Consultative ForumsWealth Management Advisory ForumConsumer Credit Advisory ForumRisk Advisory Forum

Industry Briefi ngs

Contact:THE ASIAN BANKER10 Hoe Chiang Road#14-06 Keppel TowerSingapore 0899315Tel: (65) 6236 6500 Fax: (65) 6236 6530http://www.theasianbanker.com

••

••

••

•

•

•

ABOUT THE ASIAN BANKER

ACKNOWLEDGEMENTWe would like to convey our sincere thanks to Mr Hubert Knapp for sparing his valuable time and providing us with important insights into core banking systems for the preparation of this report.

Mr Knapp is one of our International Resource Directors. He is currently a Managing Partner in Immacon Pte Ltd and holds a dual responsibility as Executive Partner in Motif Technologies Bangkok.

Mr Knapp has 25 years of experience in the fi nancial services industry. He specialises in core banking enabled change, business transformation, credit risk management and strategy development. His career in banking and consulting covers assignments in Germany, United Kingdom, Switzerland, Turkey, Nepal, Sri Lanka, ASEAN and many other parts of the world.

He has managed retail and wholesale banking operations for major global banks in Europe and Asia. After his stint as Deputy General Manager of a joint-venture merchant bank in Indonesia, his interest turned to fi nancial services consulting. His consulting assignments constitute a highly diversifi ed portfolio that includes some of the largest commercial banks in Asia.

ACKNOWLEDGEMENT

Core Banking TransformationCritical Success Factors and Best Practices

Table of Contents

1. Core Banking Trends in Asia Pacifi cMarket Trends1.1 Prominent recent deals in the region1.2 Geographic dispersion of deals in recent years and 2006

estimates1.3 Activity within countries and their vendor preferences1.4 Estimates of system and software spending in Asia

Pacifi cTechnical Trends1.5 Evolution and convergence of core banking systems1.6 Technology integration in Asian countries1.7 Trends in platform usage among Asian countries1.8 Trends in deployment approach

2. Bankers’ Perception Survey on Core Banking System Selection 2.1 Survey results on key reasons for replacement2.2 Survey results on factors considered in system selection2.3 UNIX versus mainframe – survey results on

considerations in system selection

3. Core Banking System – An Overview3.1 Core banking system – an introduction and defi nition

3.1.1 Defi nition of core banking system3.1.2 What to expect in core banking replacement

3.1.3 Rationale for front-end systems replacement3.2 Overview of the core banking system replacement

project3.3 Approaches to replacement

4. Phases of Core Banking Replacement and Critical Considerations 4.1 Phases of core banking replacement – an overview4.2 Timeline of replacement project stages4.3 Phase 1 – Business justifi cation and blueprint

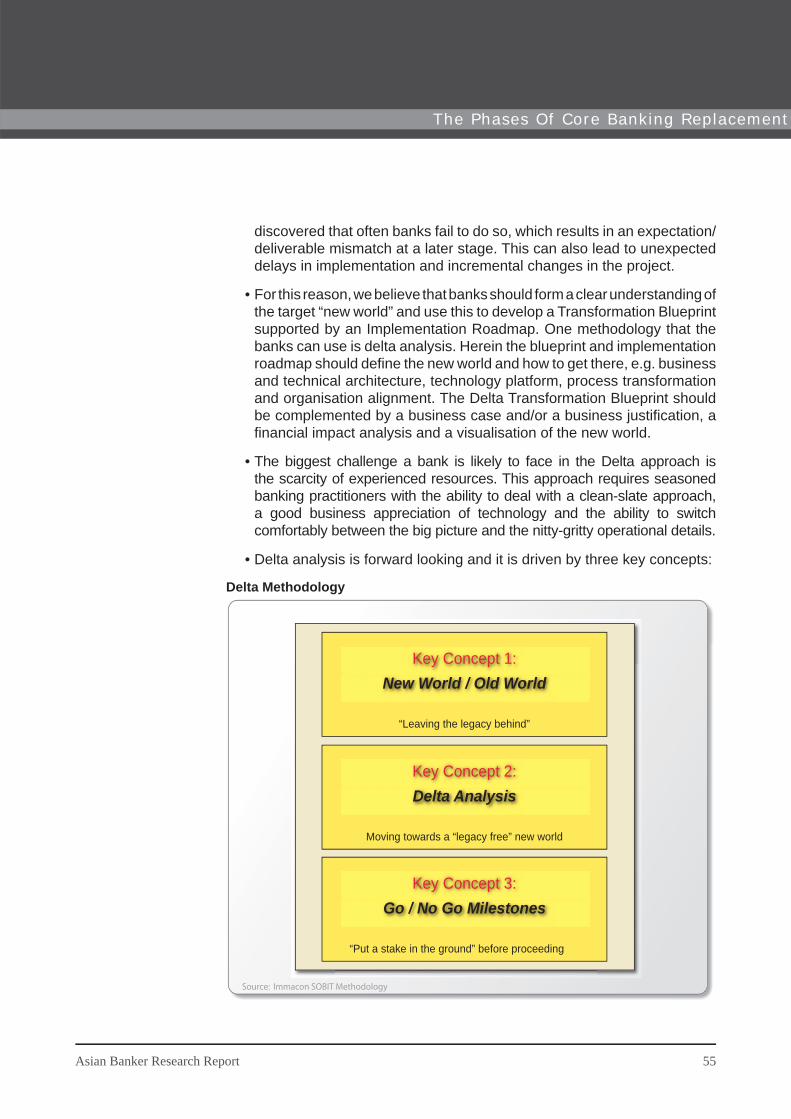

4.3.1 Developing business objectives4.3.2 Delta methodology – assessing future requirements

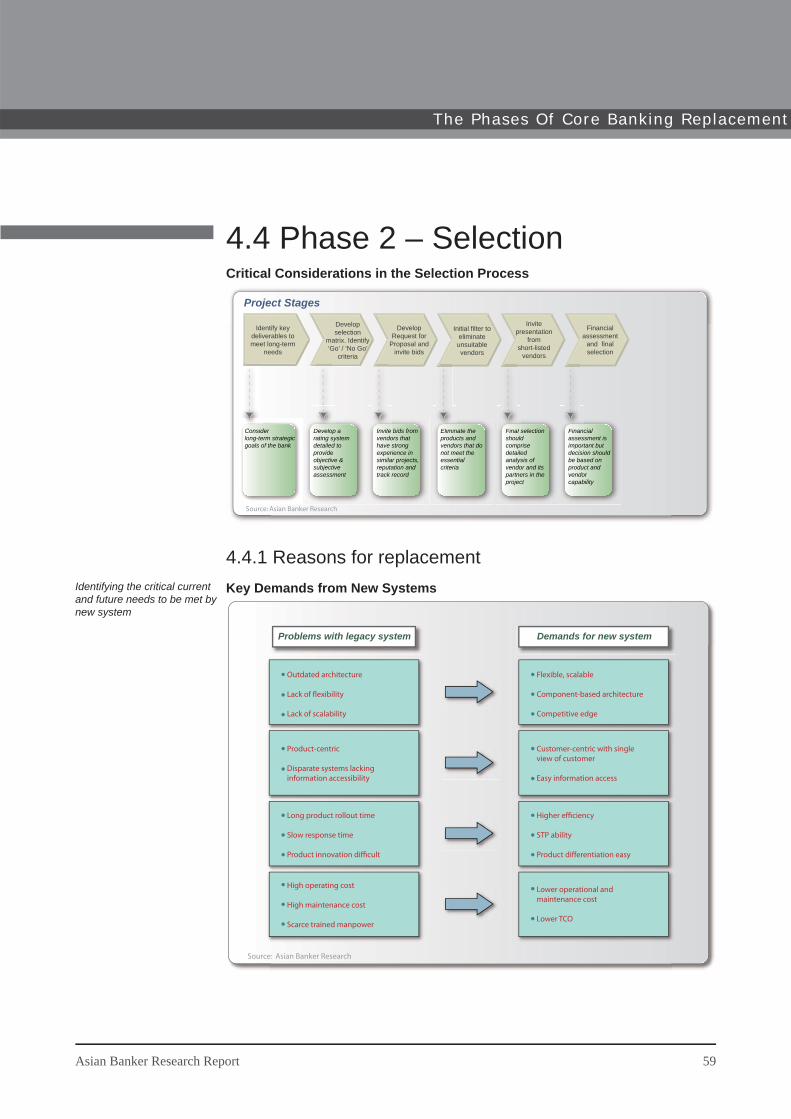

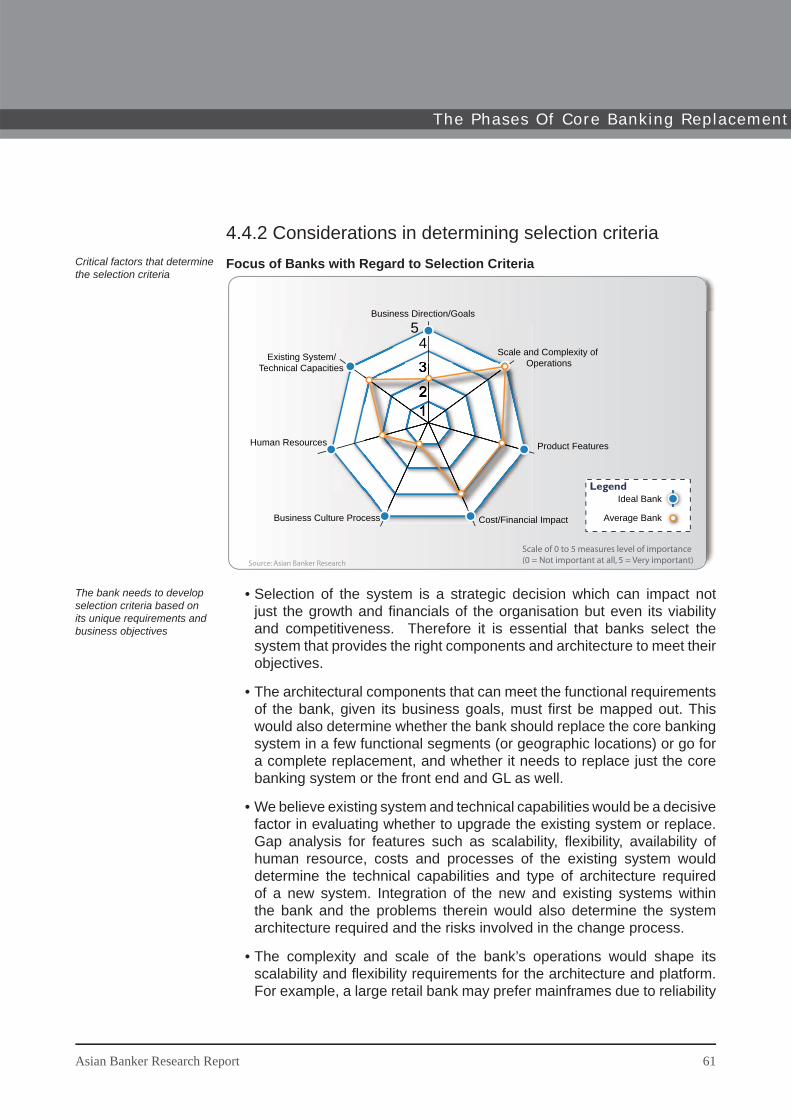

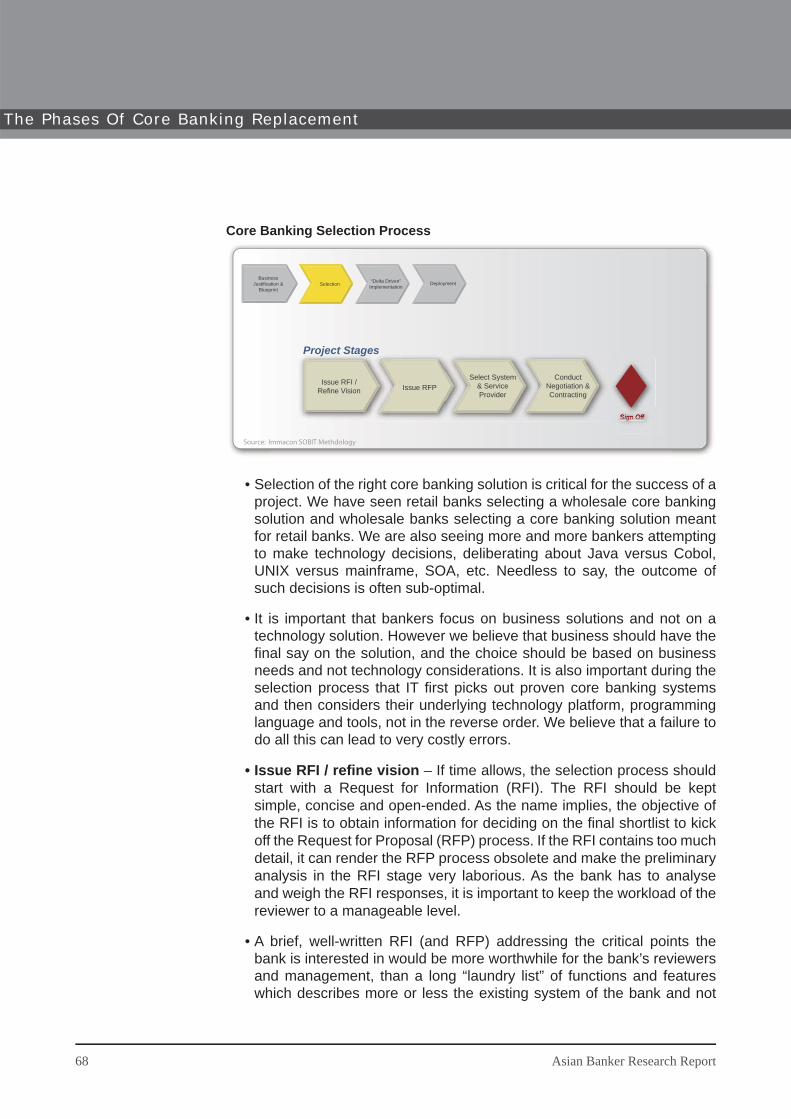

4.4 Phase 2 – Selection 4.4.1 Reasons for replacement 4.4.2 Considerations in determining selection criteria 4.4.3 Key considerations in vendor selection4.4.4 The right architecture and platform4.4.5 Selection process

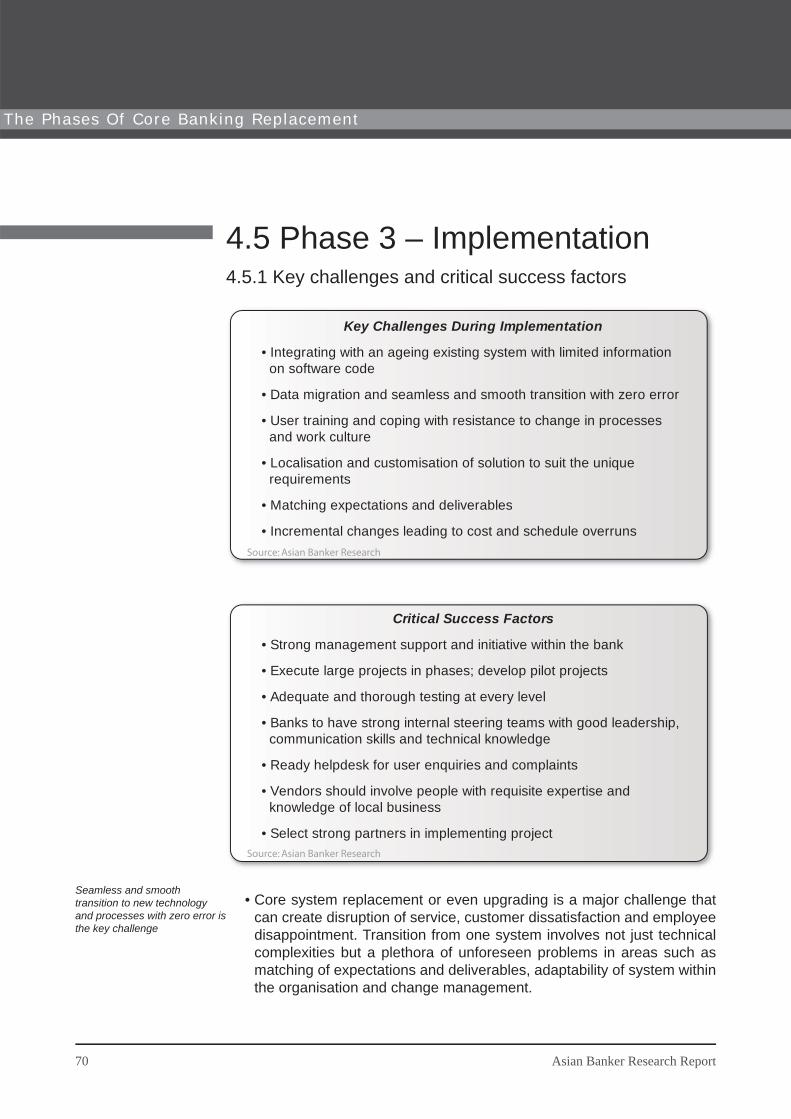

4.5 Phase 3 – Implementation 4.5.1 Key challenges and critical success factors4.5.2 Implementation process

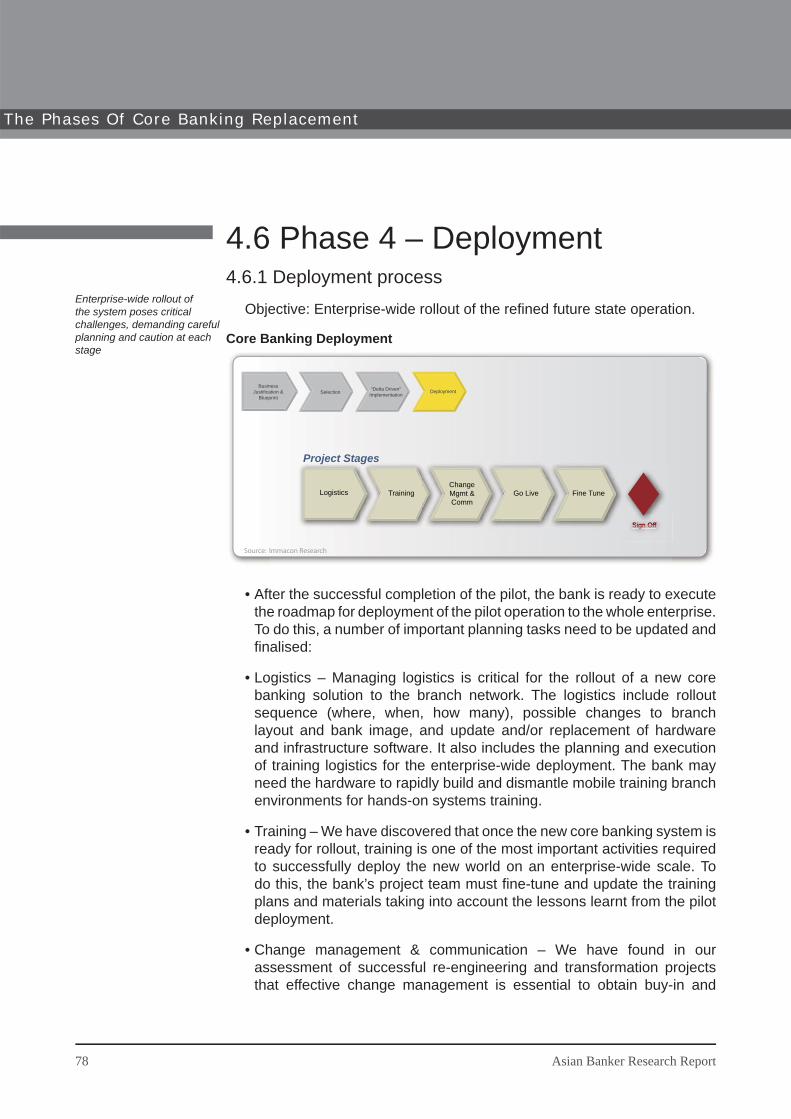

4.6 Phase 4 – Deployment4.6.1 Deployment process4.6.2 Deployment approaches

4.7 Risk mitigation4.8 Financial implications

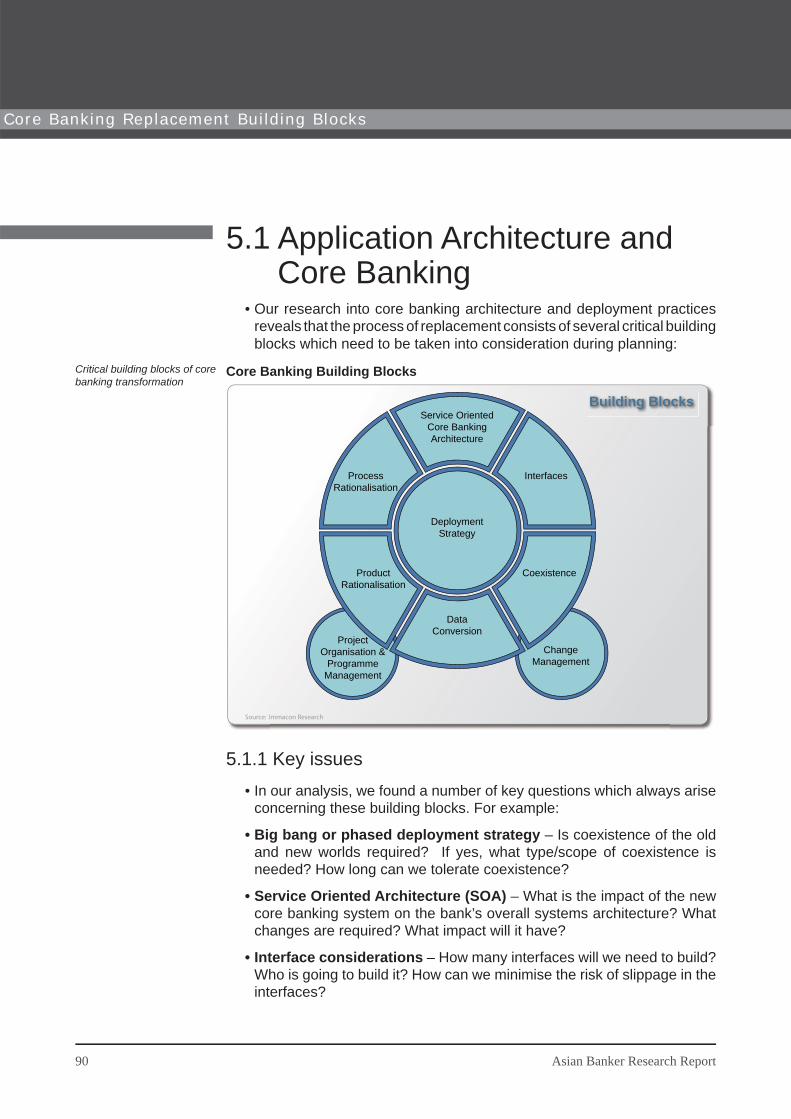

5. Core Banking Replacement Building Blocks5.1 Application architecture and core banking

5.1.1 Key issues5.1.2 Deployment strategy

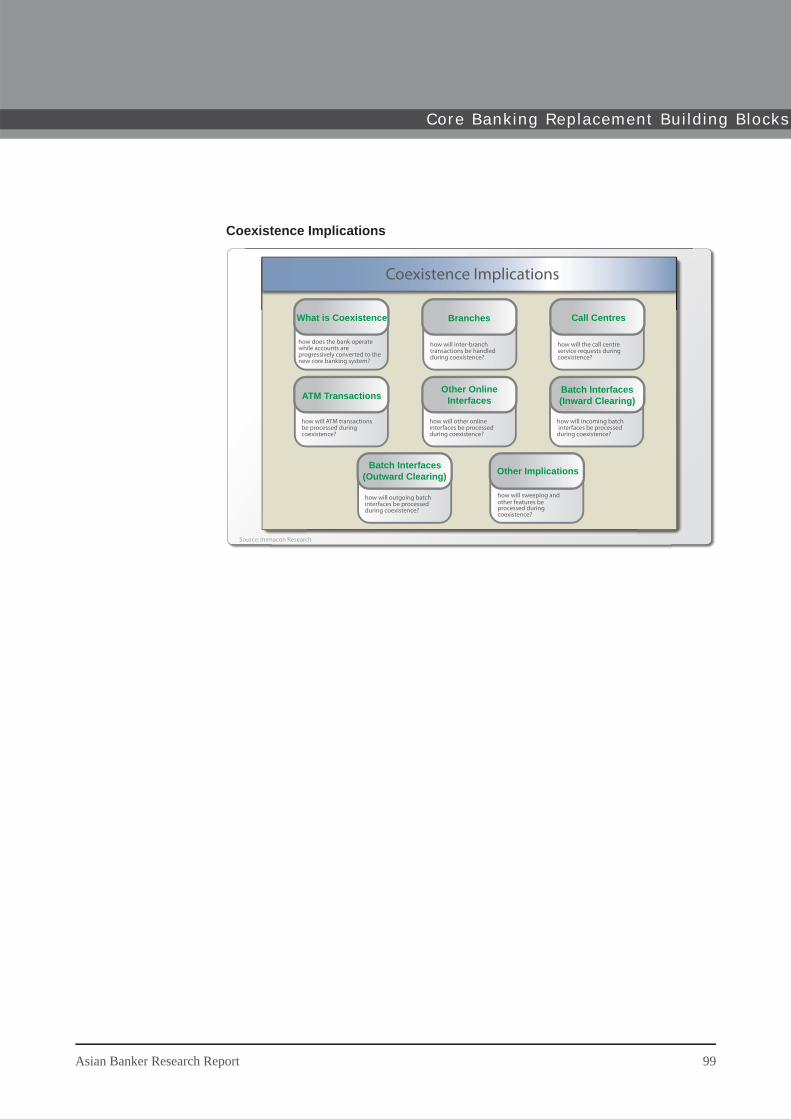

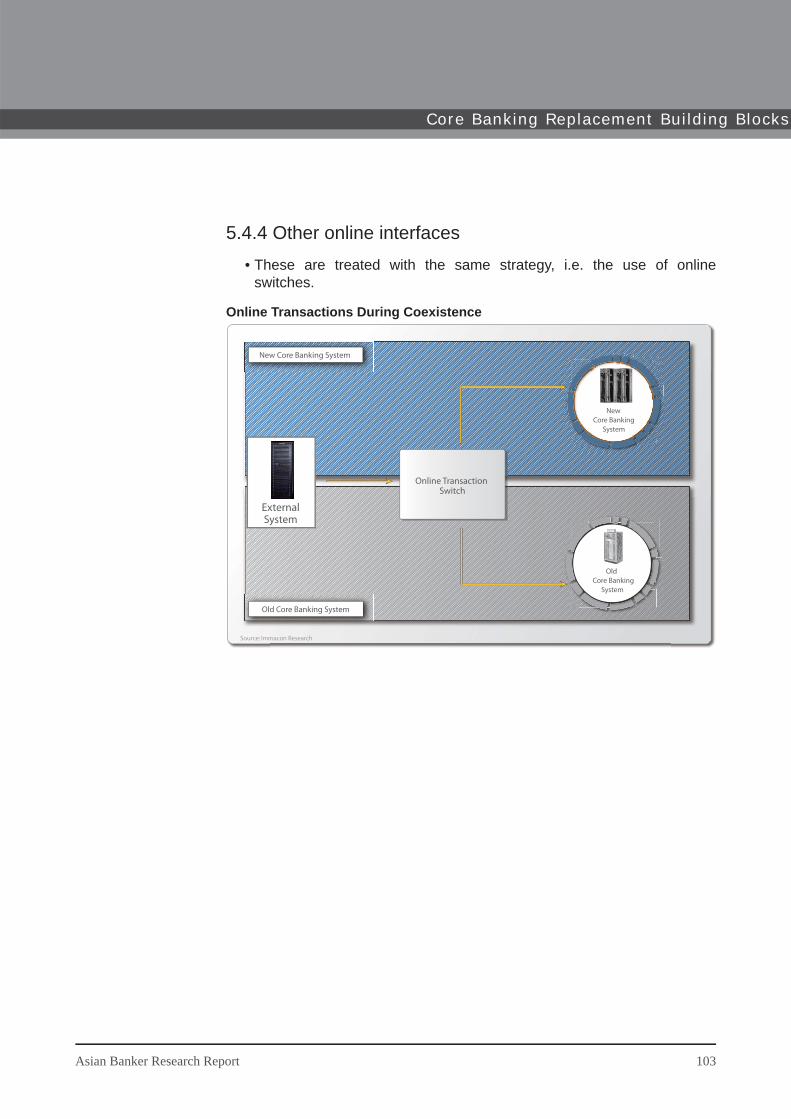

5.2 Service oriented architecture5.3 Interface considerations 5.4 Coexistence

Table of Contents

2 Asian Banker Research Report

Table of Contents

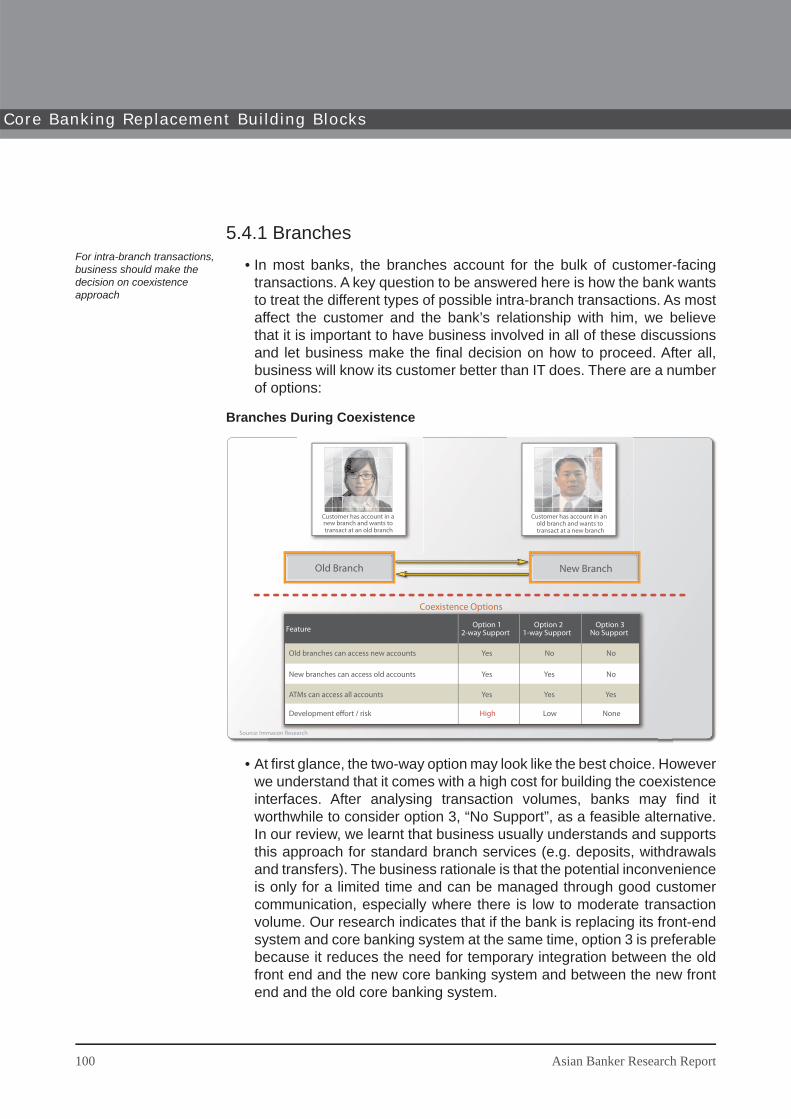

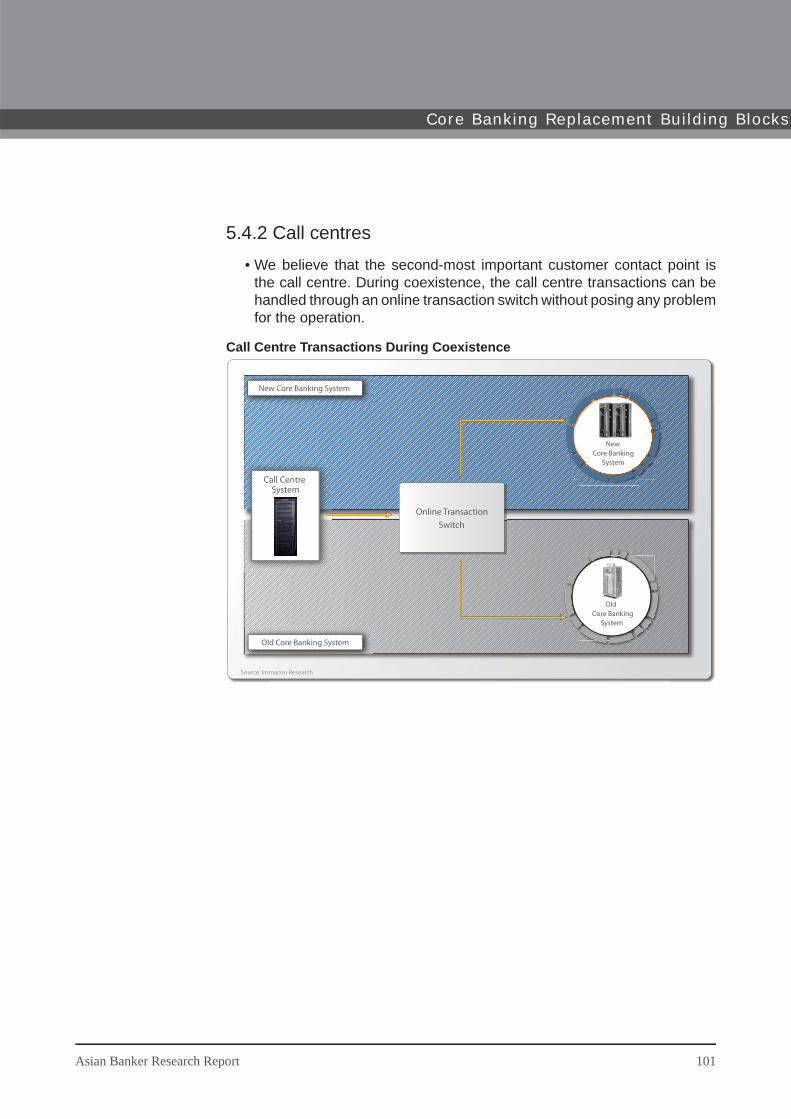

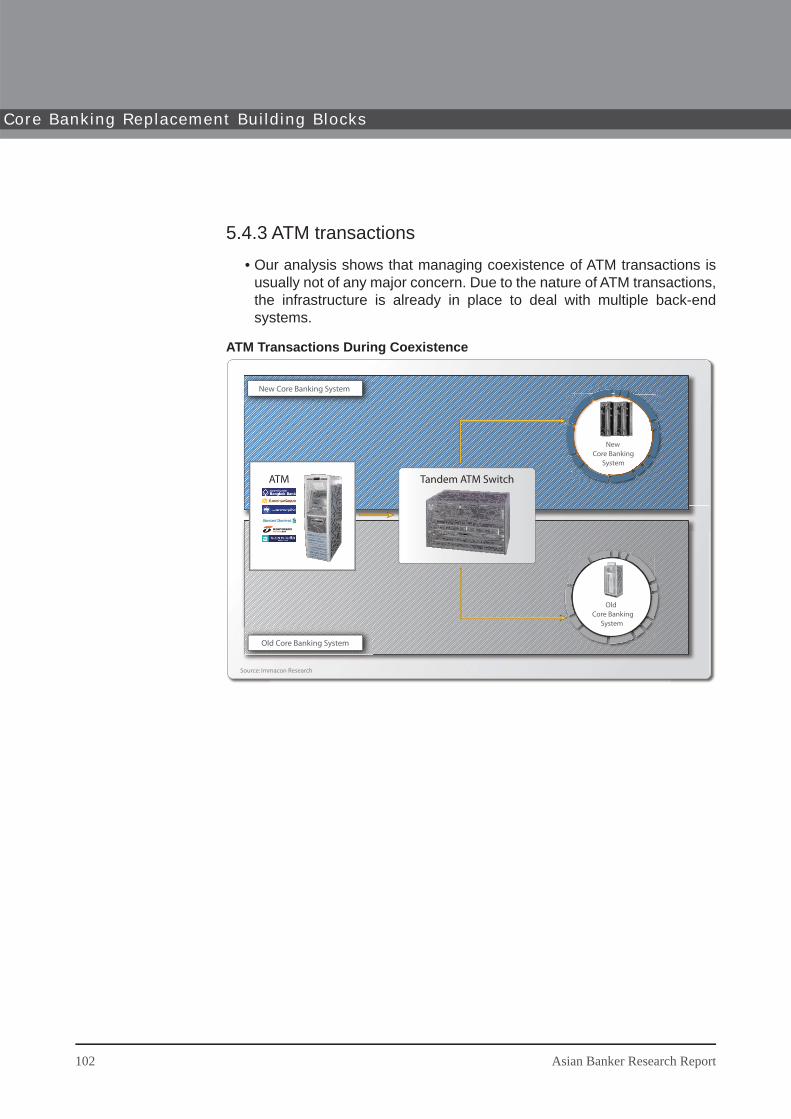

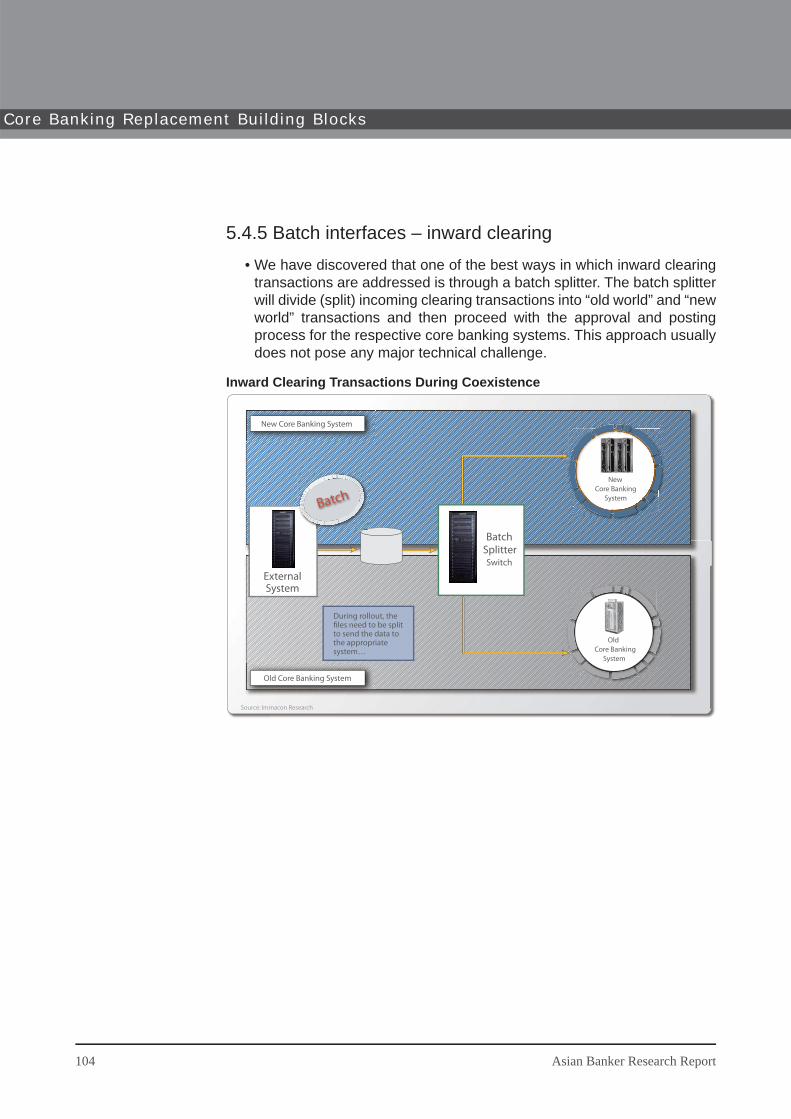

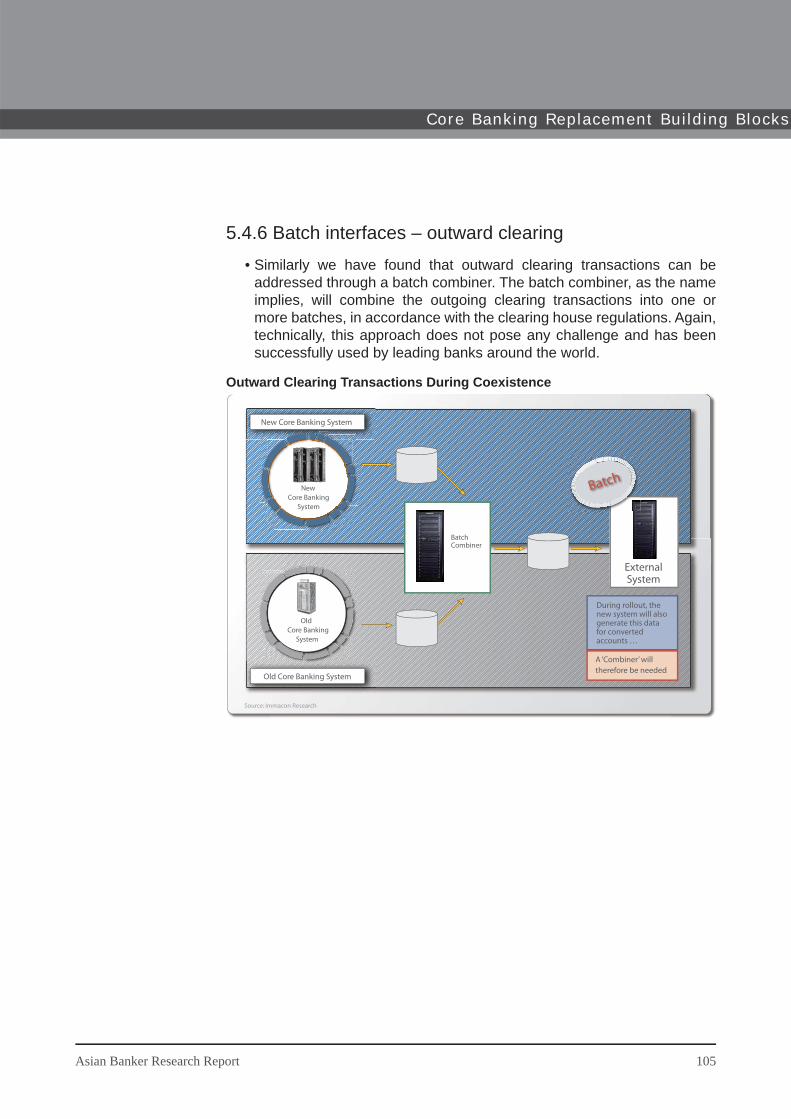

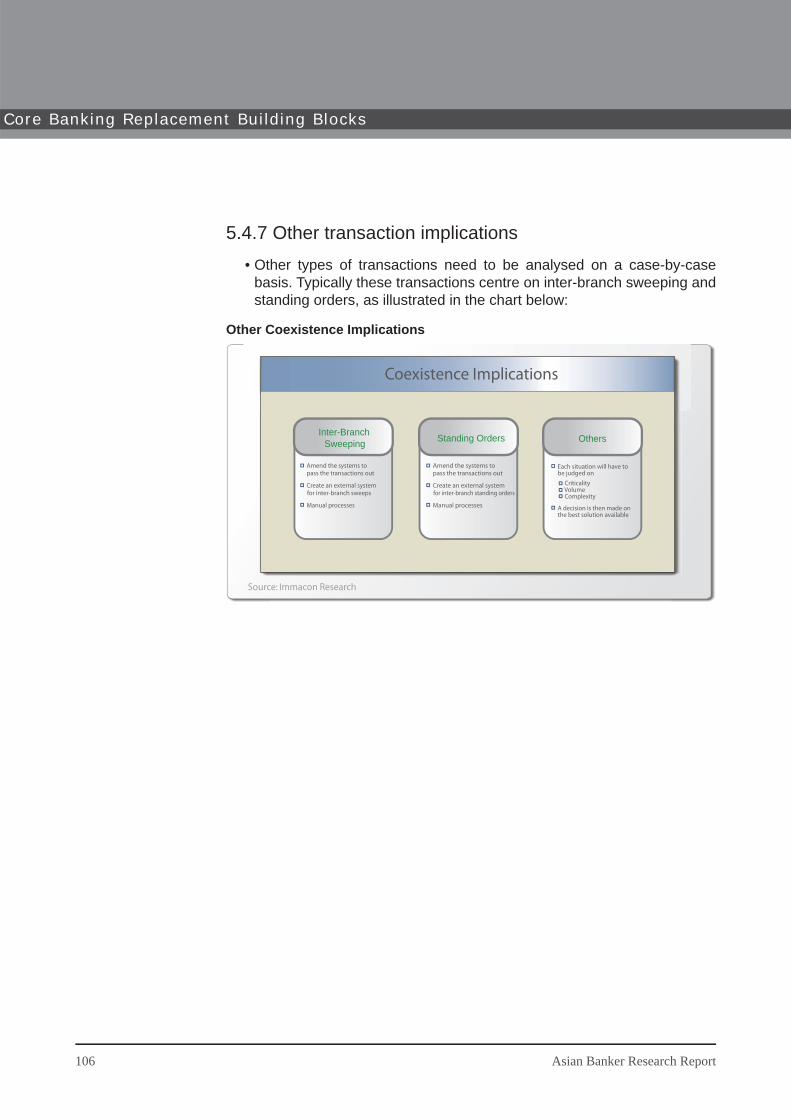

5.4.1 Branches5.4.2 Call centres5.4.3 ATM transactions5.4.4 Other online interfaces5.4.5 Batch interfaces – inward clearing5.4.6 Batch interfaces – outward clearing5.4.7 Other transaction implications

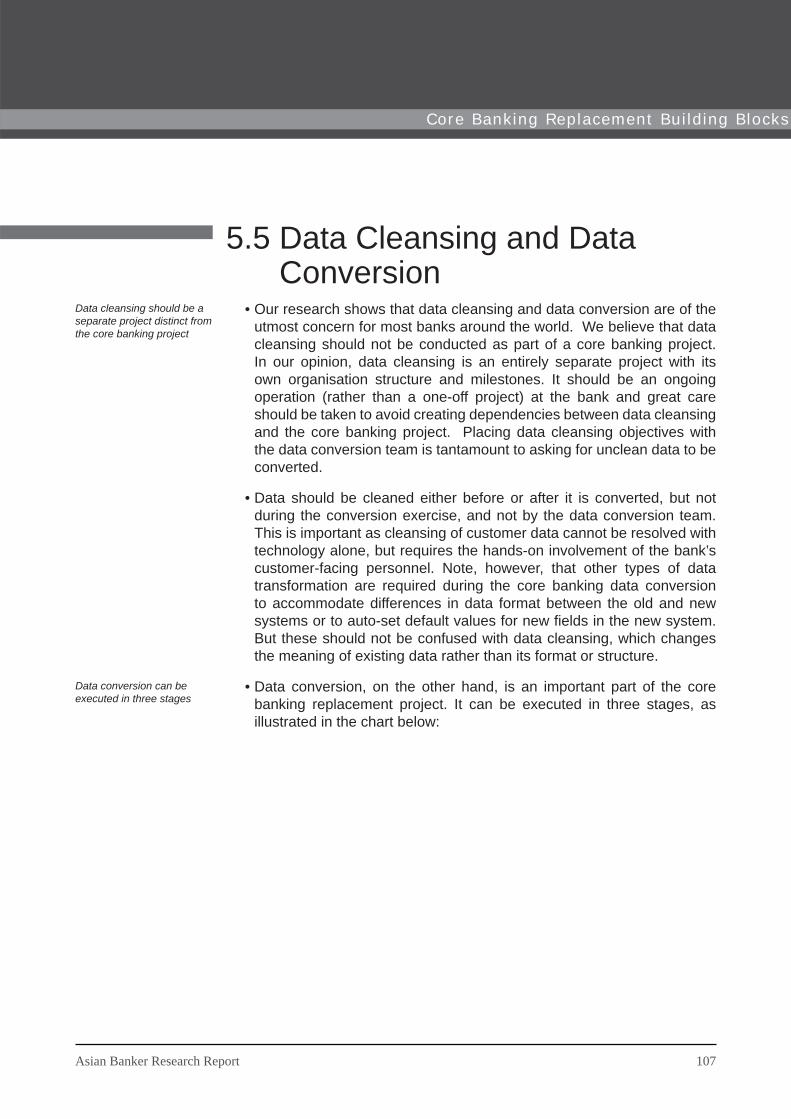

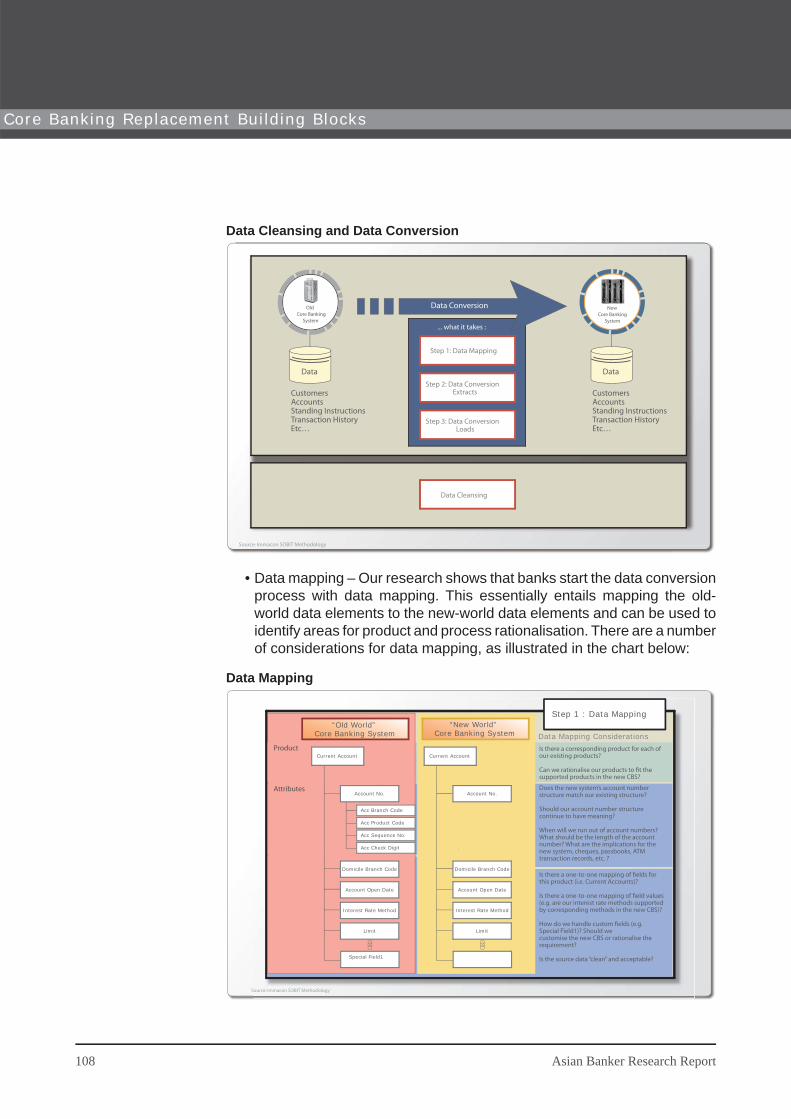

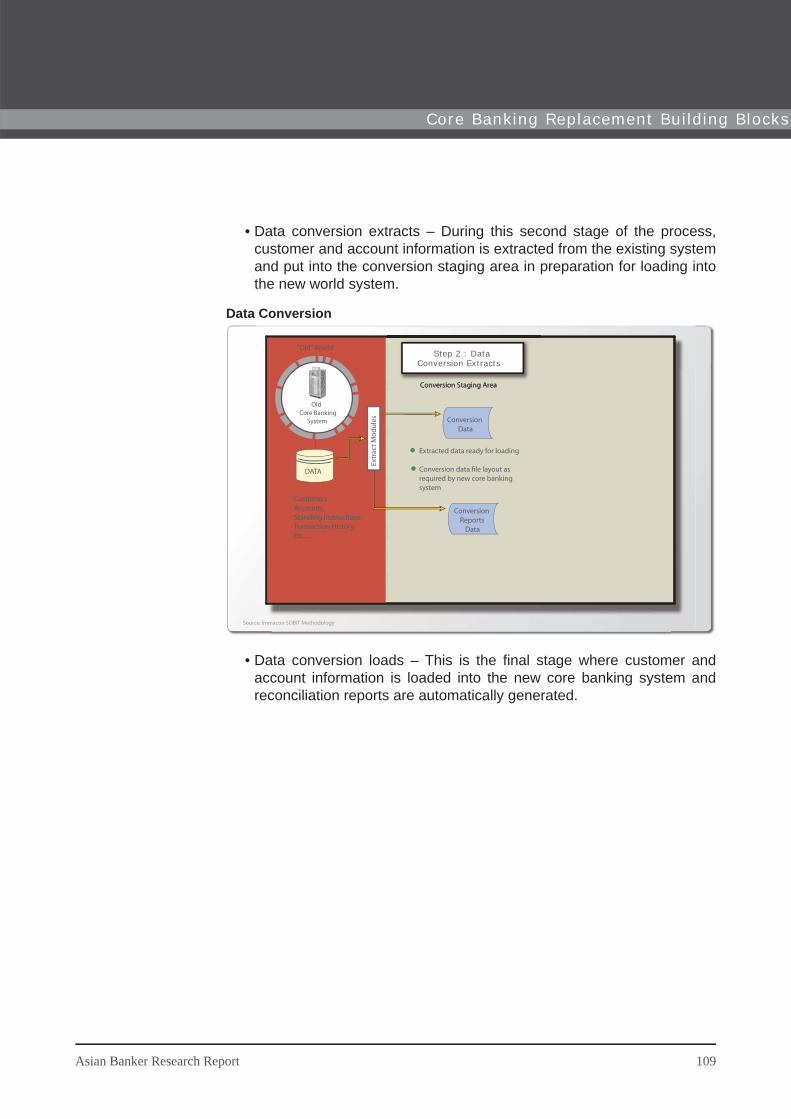

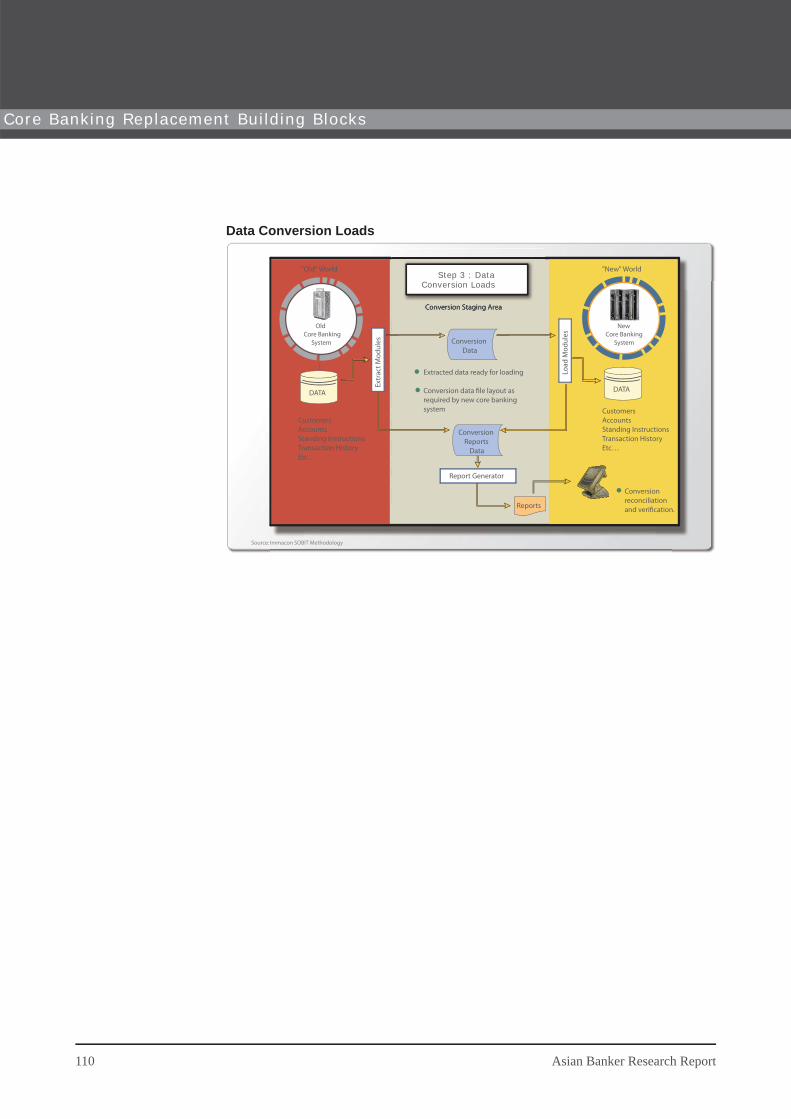

5.5 Data conversion and data cleansing5.6 Product rationalisation 5.7 Process rationalisation

6. Critical Success Factors and Best Practices6.1 Project organisation and programme management

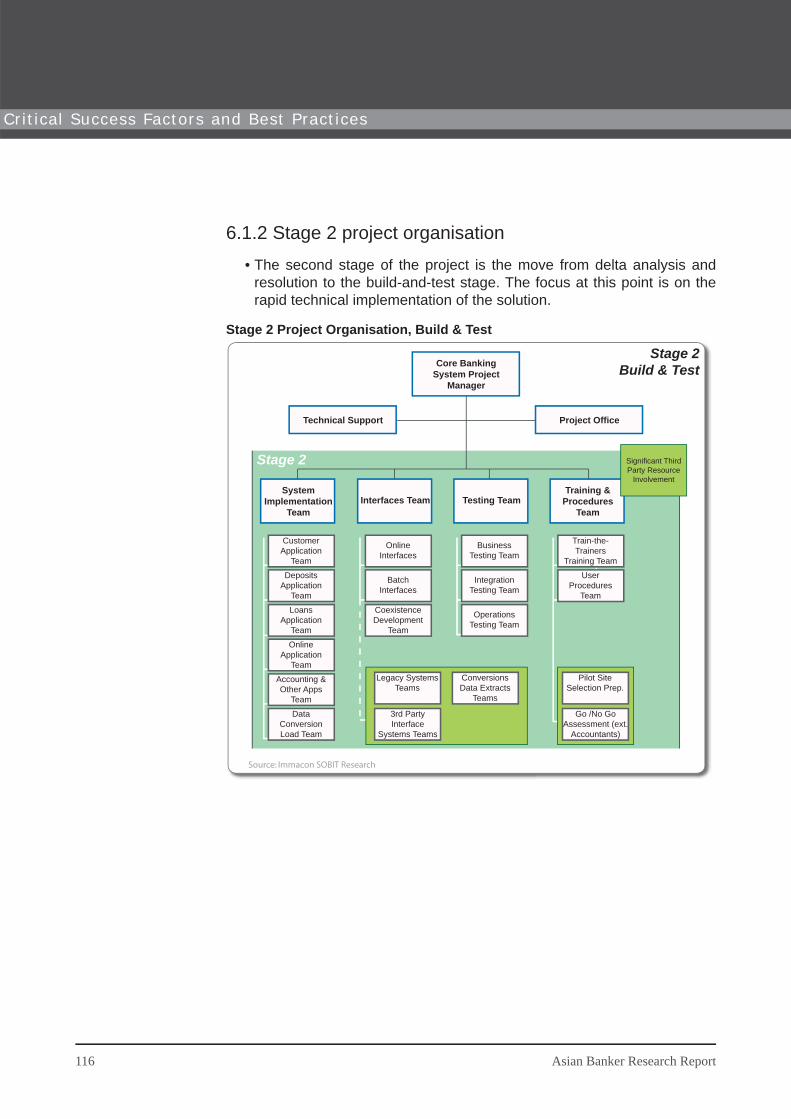

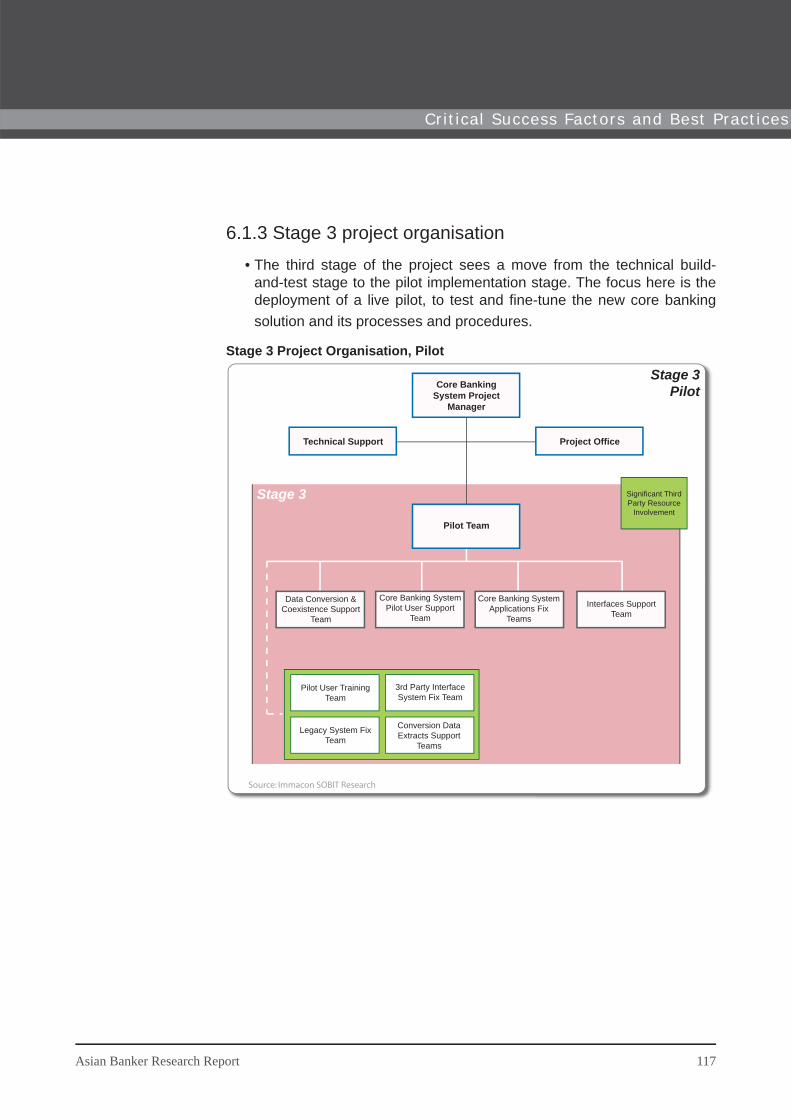

6.1.1 Stage 1 project organisation6.1.2 Stage 2 project organisation6.1.3 Stage 3 project organisation

6.2 Critical success factors and best practices in system selection

6.3 Critical success factors and best practices in vendor selection

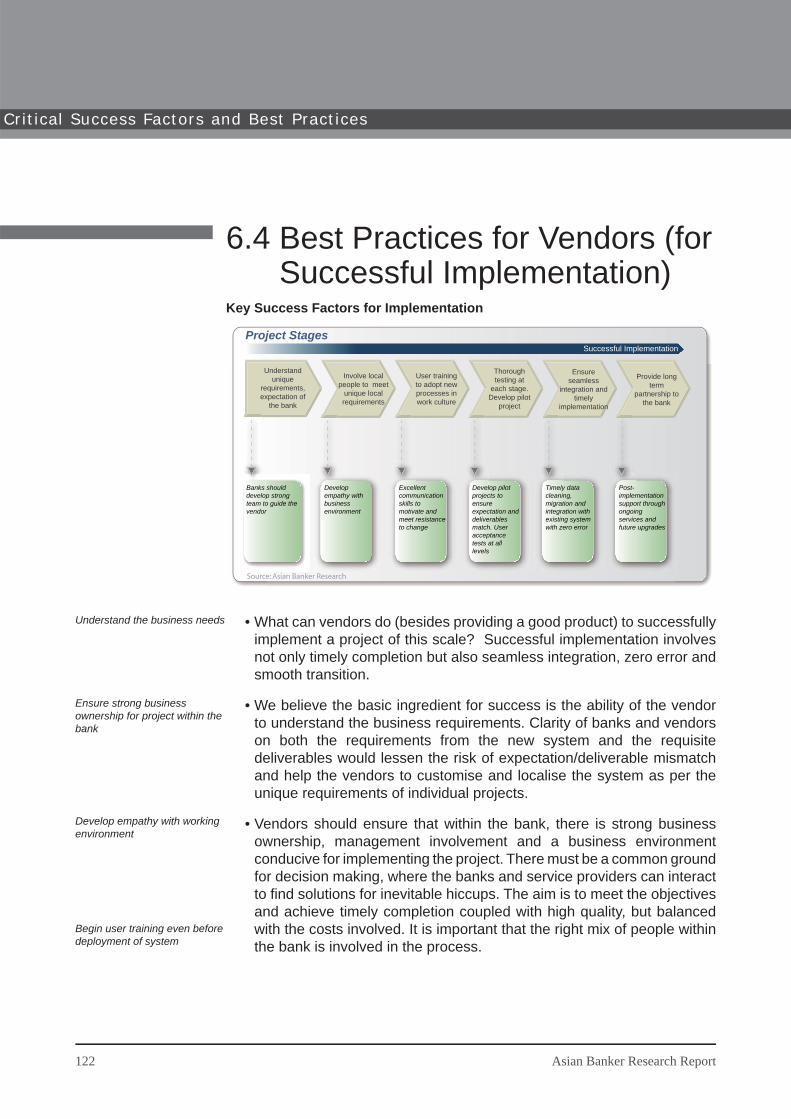

6.4 Best practices for vendors (for successful implementation)

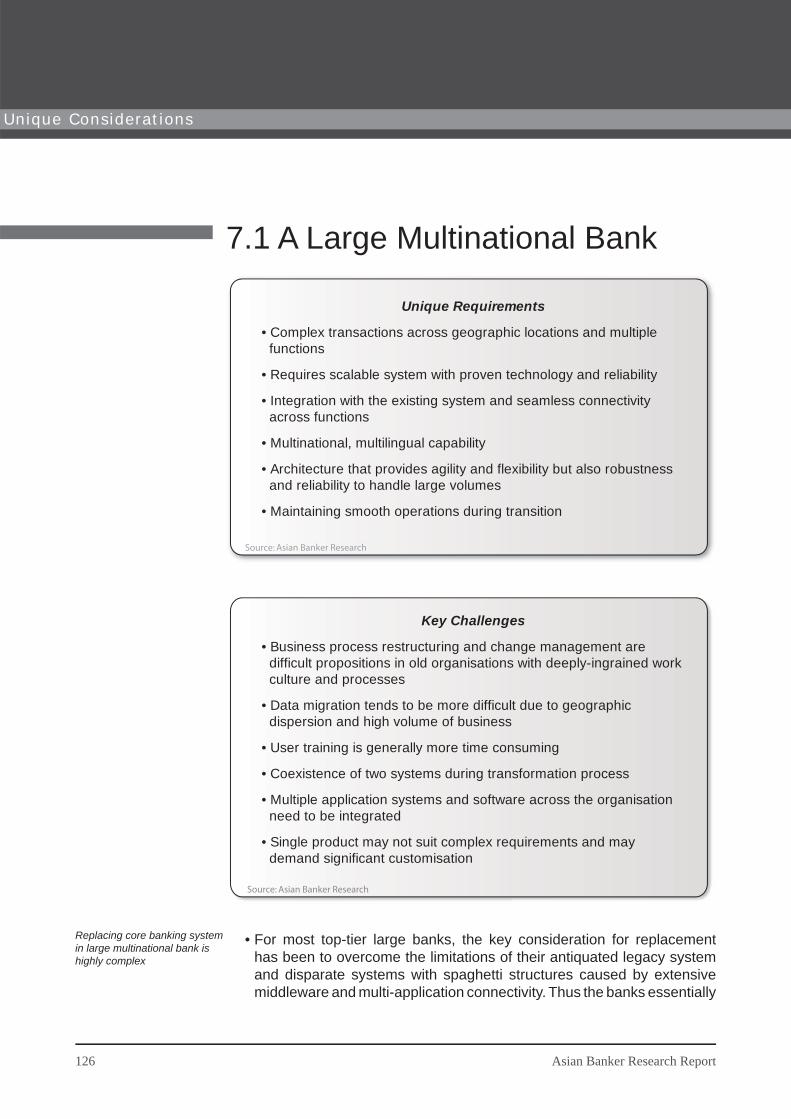

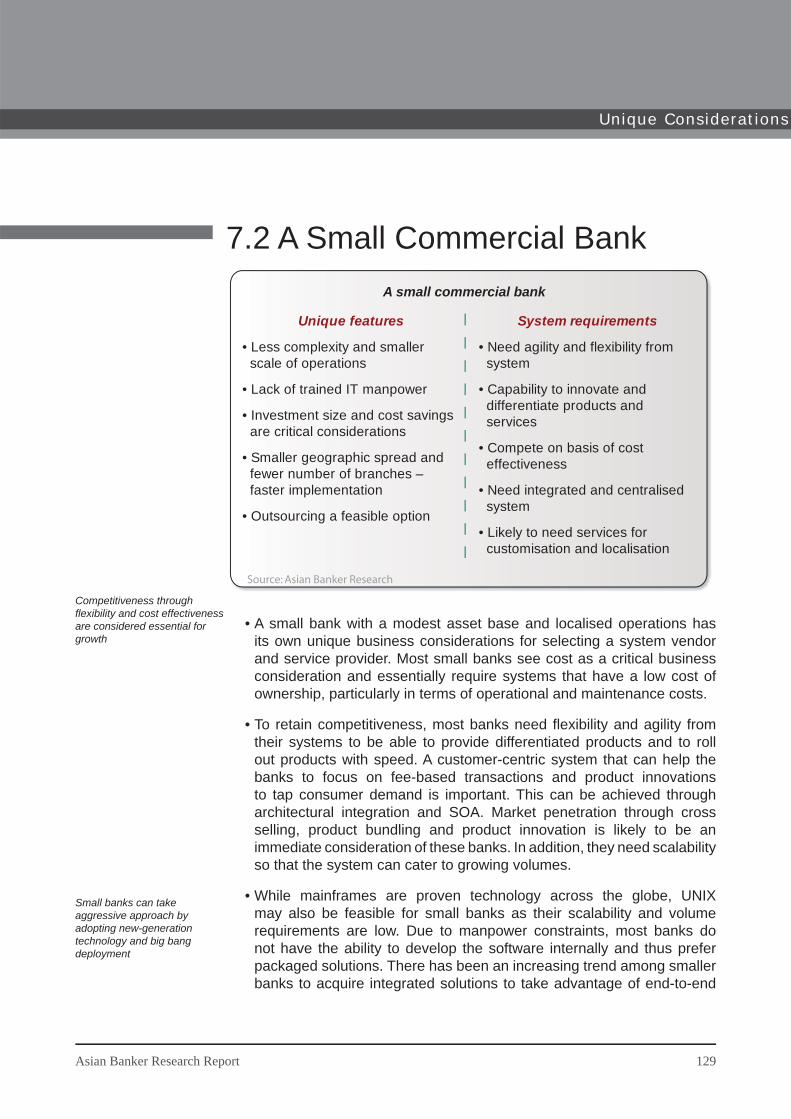

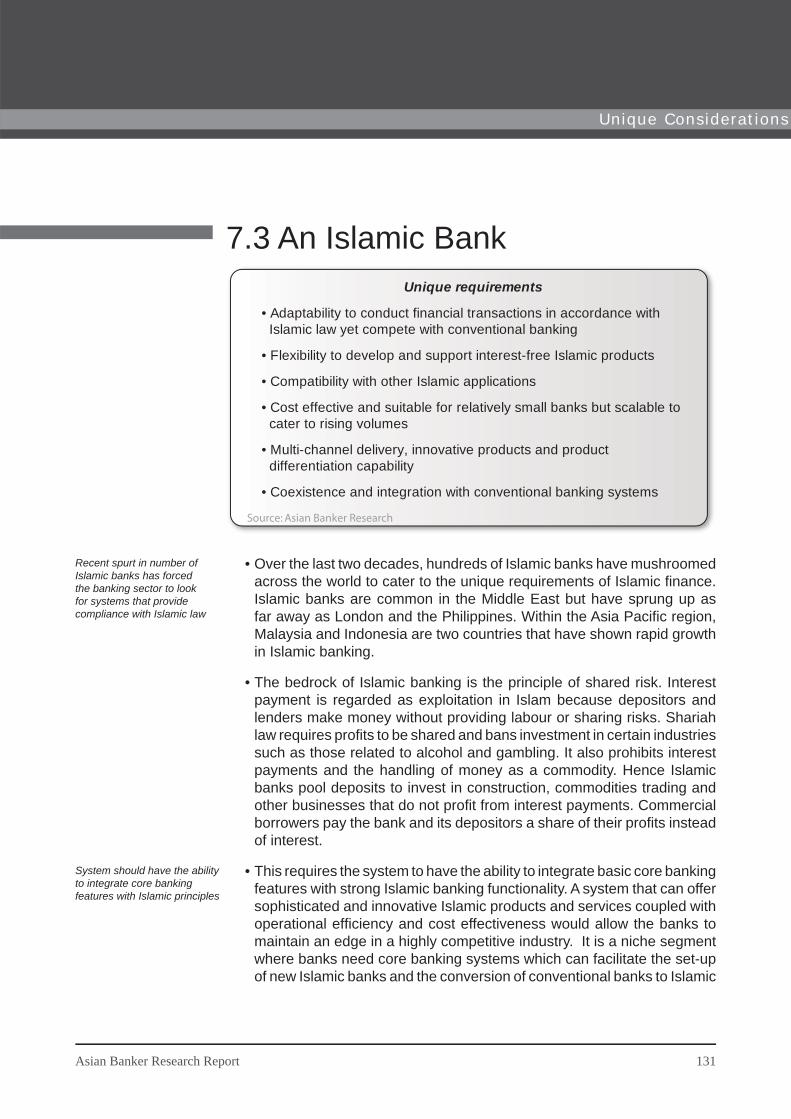

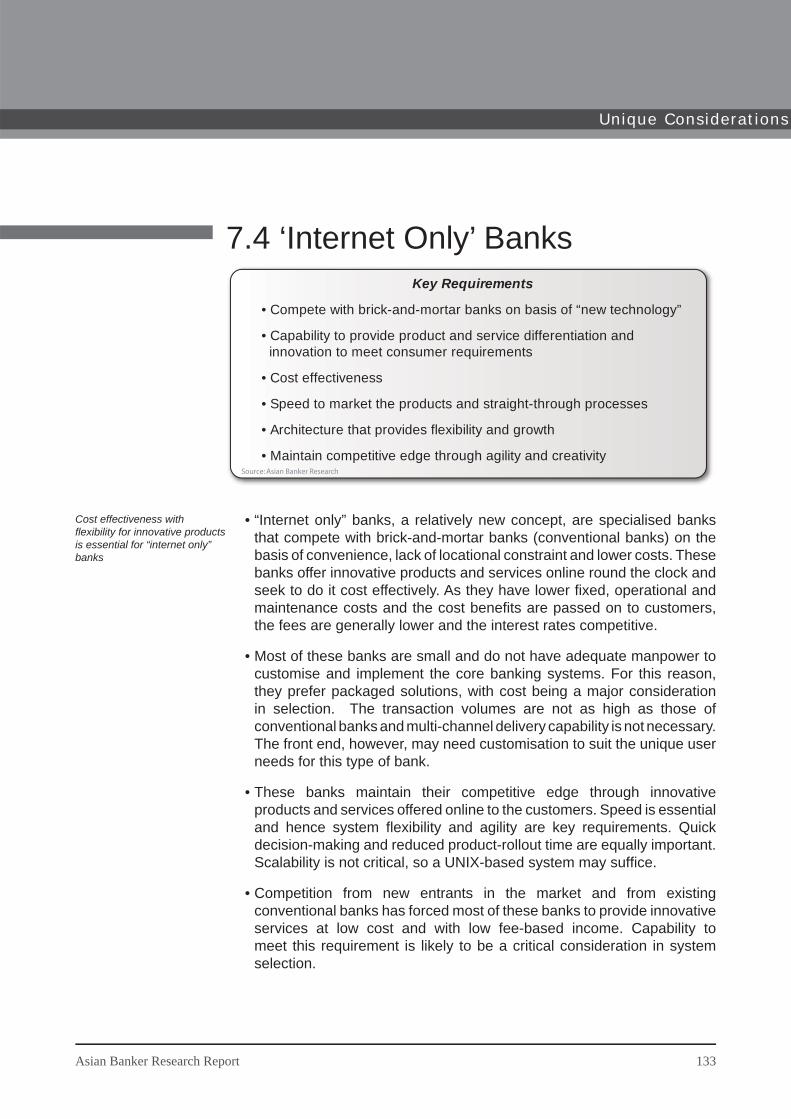

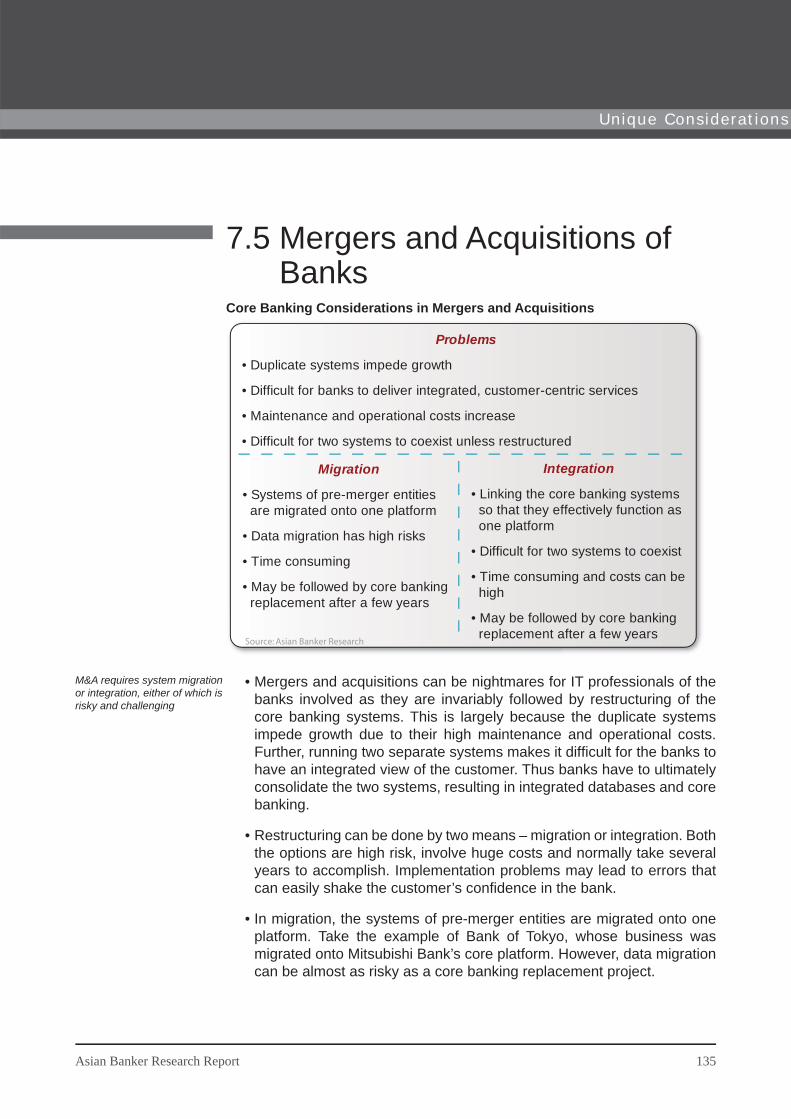

7. Unique Core Banking Replacement Considerations7.1 A large multinational bank7.2 A small commercial bank7.3 An Islamic bank7.4 “Internet only” banks7.5 Mergers and acquisitions of banks

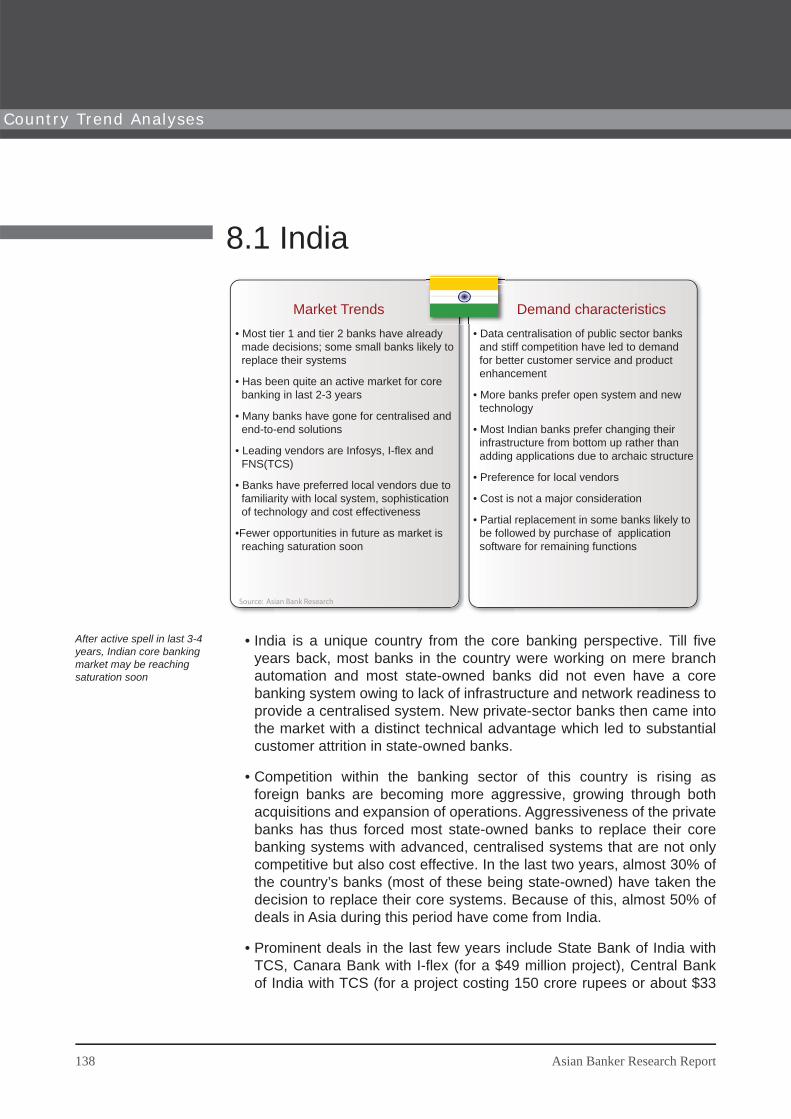

8. Country Trend Analyses 8.1 India8.2 China8.3 Japan, Korea and Taiwan

Asian Banker Research Report 3

8.4 South East Asia – Indonesia, Malaysia, Thailand and Singapore

9. Vendor Assessment9.1 Vendor and product assessment 9.2 Market positioning

10. Conclusions10.1 Conclusion 1 – for bankers10.2 Conclusion 2 – for vendors

A1. Appendix I – Case StudiesA1.1. State bank of IndiaA1.2 Union bank of Philippines

A1. Appendix II – An Average Request for Proposal

4 Asian Banker Research Report

Table of Contents

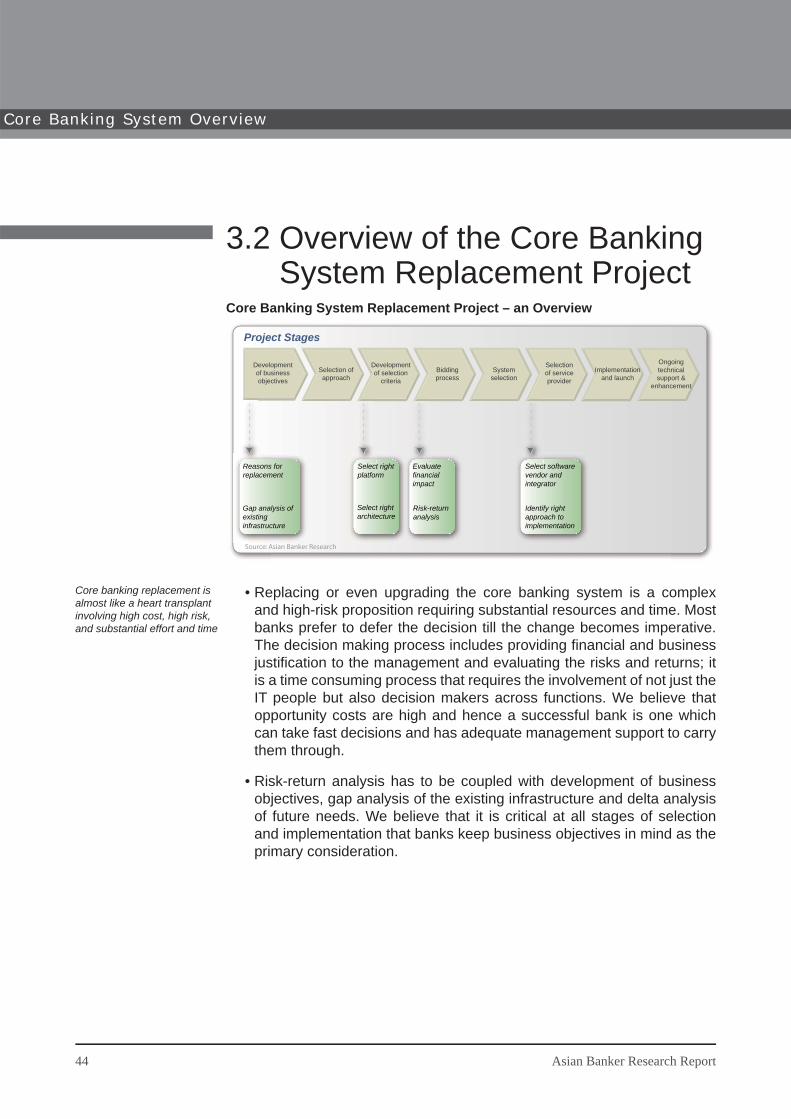

Executive SummaryIncreasing consumer demands, high costs and widespread dissatisfaction with ageing systems are making it increasingly diffi cult for Asian bankers to put off decisions to replace their core banking systems. We feel that the banking industry worldwide is nearing a time when replacing core banking systems would be a necessity rather than an option. However the complexity of the task is such that it is often compared to a heart transplant, involving huge risks, high costs and substantial time and human resources.

The critical need for replacement stems from rising customer expectations and existing technical limitations. Banks are fi nding it imperative to expand their channels and services while managing operational and technical costs even as margins are shrinking due to stiff competition. But this is hampered by technical limitations as many traditional fi nancial institutions are shackled by a series of heavily siloed non-integrated back-offi ce legacy systems in which customer information resides in multiple and unconnected locations. Attempts to integrate these through layers of middleware have just made the structure more complicated in many cases. On the other hand, abandoning the antiquated structure itself presents a major challenge from the organisation and fi nancial perspectives. But competitive pressures are forcing banks to take speedy actions, as can be seen in our analysis of trends in Asian markets.

Analysing the Asian markets and the recent core banking replacement decisions, we found that there has been a gradual rise in the number of core banking deals in the last two years. Interestingly, almost half of the deals during this period have come from state-owned Indian banks. These banks had faltered due to competitive pressure from private banks and have found it imperative to purchase (in most cases for the fi rst time) new core banking systems and upgrade themselves technically to improve product innovation, agility in decision making and cost effectiveness. We expect the Asia-wide trend to continue in the year 2006; but as the Indian market nears saturation, there are likely to be fewer deals from this country in the following years.

Looking at the trend in countries that have fi rst-generation technical sophistication, we have discovered that core banking replacement is considered a cyclical industry as banks come to the market about every 15 years to replace an ageing system and improve their effi ciencies. In the last two years, many banks in countries like China, Taiwan and Malaysia have shown initial signs of awakening to the need for technical advancement. We expect to see increasing activity in China with foreign banks getting full access to the sector in 2007 under WTO stipulations and with China’s hosting of the

Execut ive Summary

Asian Banker Research Report 5

Olympics in 2008. On the other hand, we have found that banks in countries like Japan and Indonesia are still mulling over the wisdom of replacing.

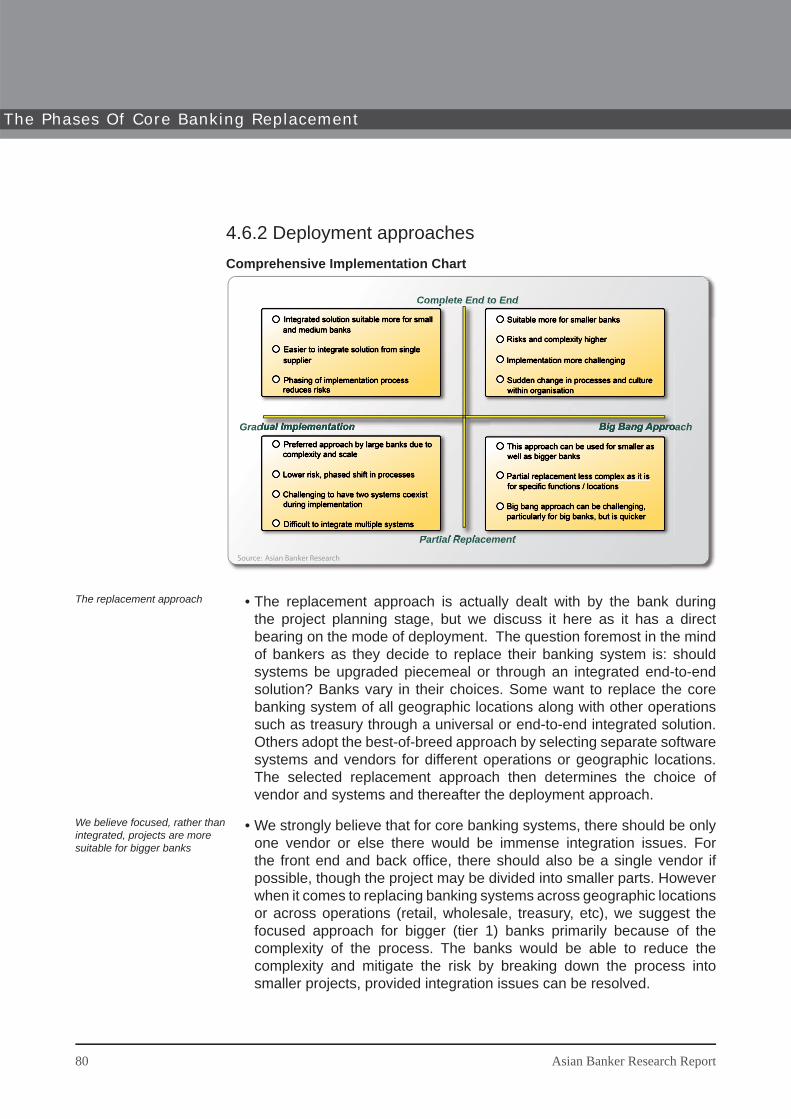

Once a bank has decided to replace its system, it embarks on a complex process involving a series of critical choices. To start with, the bank has to decide on the most appropriate approach to system replacement. The choices vary with the availability of technical skills, complexity of the project, availability of products and costs involved. As banks weigh their options, they often have to consider the pros and cons of “buying” versus “building” and “purchasing” versus “outsourcing”. We have discovered that most Asian banks increasingly prefer to focus on their core business rather than lock their resources in building a system and there is a distinct trend towards the purchase of packaged solutions. However for large multinational banks, a ready packaged solution often does not meet the complex requirements and hence may require further development (as in the case of HSBC) or substantial customisation at the minimum.

To better comprehend the complicated process of core banking replacement, we begin with a defi nition of the core banking system. We defi ne it as a highly effi cient “customer accounting” and transaction processing engine, for high volumes of back-offi ce transactions and customer-level accounting and reporting of the deposit and loan products processed in the bank. However it does not include the front offi ce. Thus we believe that the bank has to fi rst determine whether it really needs to replace its core system or it can manage with just front-offi ce replacement. In many cases, it is likely that the bank needs to replace both along with the general ledger – which would be a project of even bigger magnitude. If the bank has to change both front end and core banking, we recommend it be done through the same vendor to avoid integration issues.

Our research shows that banks which go ahead with replacement should make a clear transition from their legacy system to the new system. Partially bringing old elements such as codes, process automation and loss-making legacy products into the new environment will lead to sub-optimal returns.

We have divided the process of core banking replacement into four phases. The fi rst phase is business justifi cation and identifi cation of business requirements through delta analysis. We believe that the bank should, fi rst and foremost, determine its long-term strategic goals as these would guide the bank towards the critical requirements for its system. With the business objectives in mind, banks need to analyse the capabilities and defi ciencies of their existing core banking system to determine the new system’s requirements – yet during our research, we discovered that only 70% of the banks in our sample do so. In addition to setting the objectives, the bank should establish the business and fi nancial justifi cation for the project at this

6 Asian Banker Research Report

Execut ive Summary

early stage of the process.

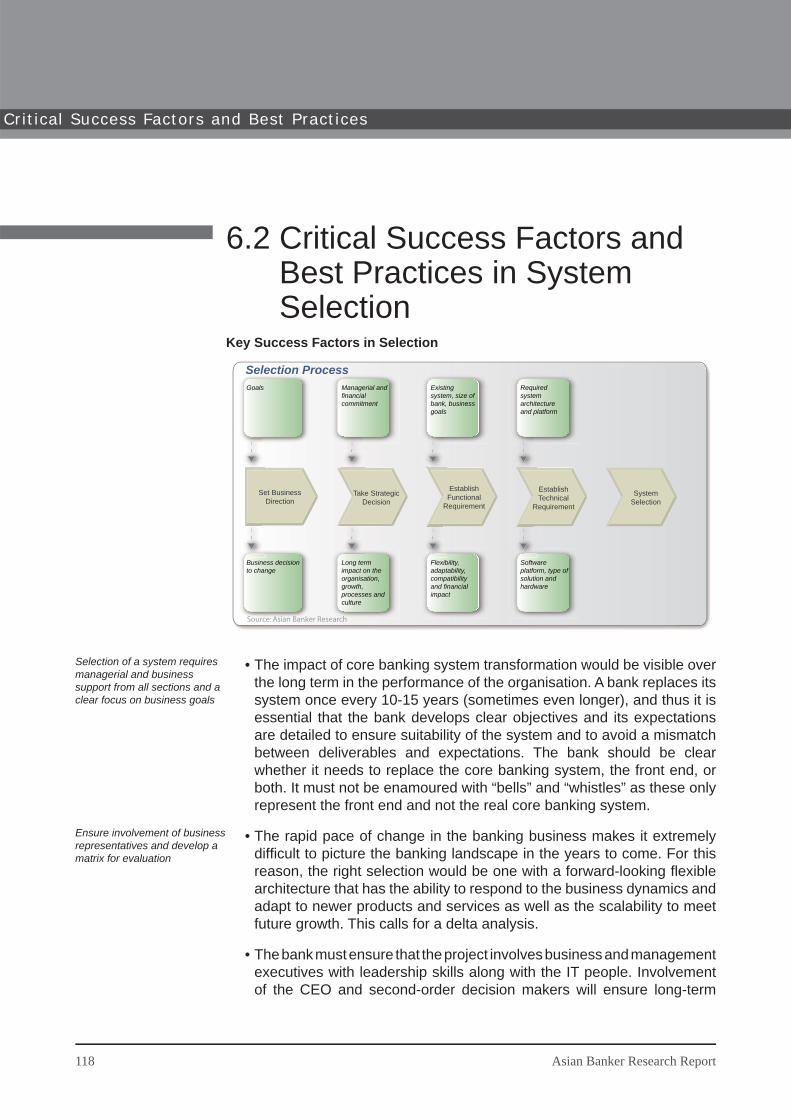

The second phase of the project is selection of the system and the vendor. Selection of a core banking system will affect not only the growth and fi nancials of the organisation but also its viability and competitiveness. Hence banks need to critically evaluate all available options and select the system that provides the right DNA (the architecture) to meet its business and strategic requirements. We believe that the selection process should involve business representatives from all functional divisions owing to the pervasive nature of these systems within the organisation. Viewing the project as just an IT project would be a recipe for failure.

The selection process begins with the issuance of a Request for Proposal to various vendors. Each of the bids is assessed on both qualitative and quantitative terms across a matrix of selection criteria. The critical requirements from a new system are fl exibility and scalability to cater to future growth. We advise banks to ensure that with the new system, they are not simply shifting to a bigger box which may become a constraint again in a few years’ time, as this would defeat the whole purpose of replacing the system. Equally important is that banks should not be enamoured with “bells” and “whistles” (which are more often than not the front-end features) and should look for a system that has the requisite processing power rather than just a user friendly front-end screen.

We have discovered that one of the challenges is picturing the banking landscape in years to come due to the rapid pace of change in the banking business. Thus the right selection would be one with a forward-looking fl exible architecture that has the ability to support the business ambitions of the bank and allows for future modifi cations with ease. This can come from Service Oriented Architecture (SOA). SOA is a relatively recent development which, in its purest sense, is centred on loosely coupled components which support generic services and are based on web technology. In a core banking context, it essentially means reducing barriers in antiquated infrastructure and creating real-time integration of disparate systems and sharing of databases on a fl exible and easily upgradeable infrastructure. We advise banks to look for a system that has the fl exibility of SOA and to integrate their systems and components in an SOA-based framework within the bank.

Banks need to select not the “best” system available but the one that is most appropriate for their particular requirements. Different banks and their unique requirements are discussed in section 8.

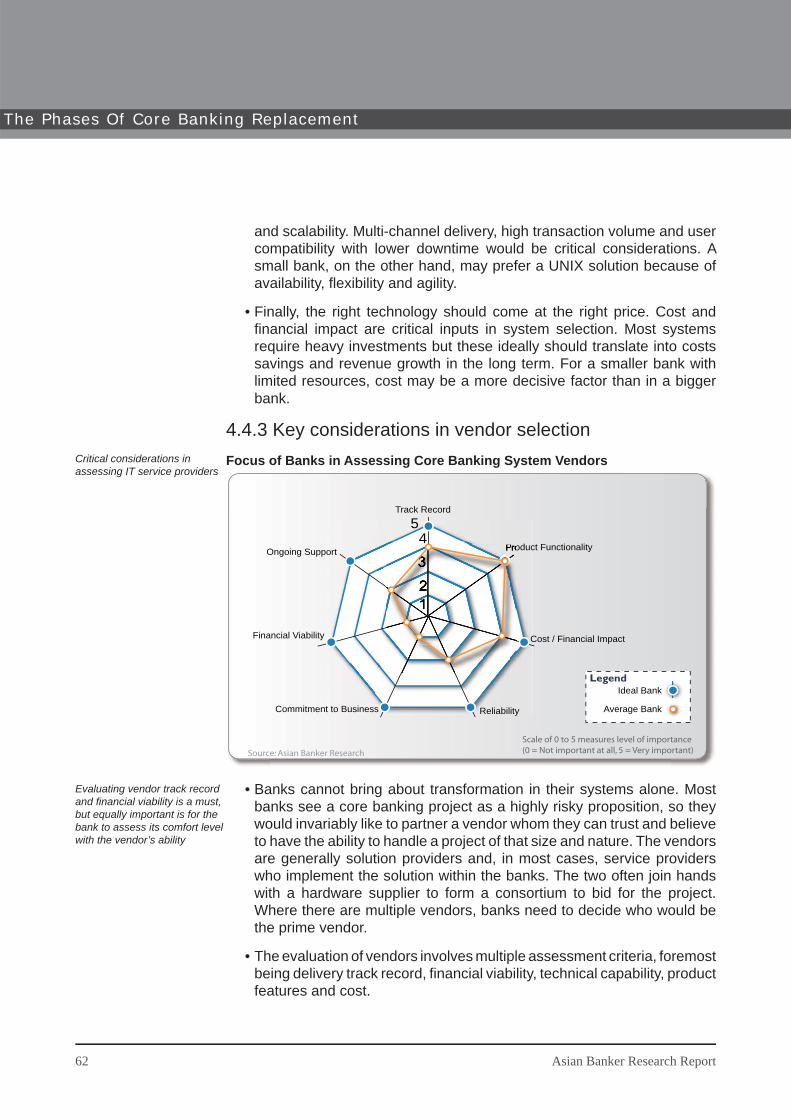

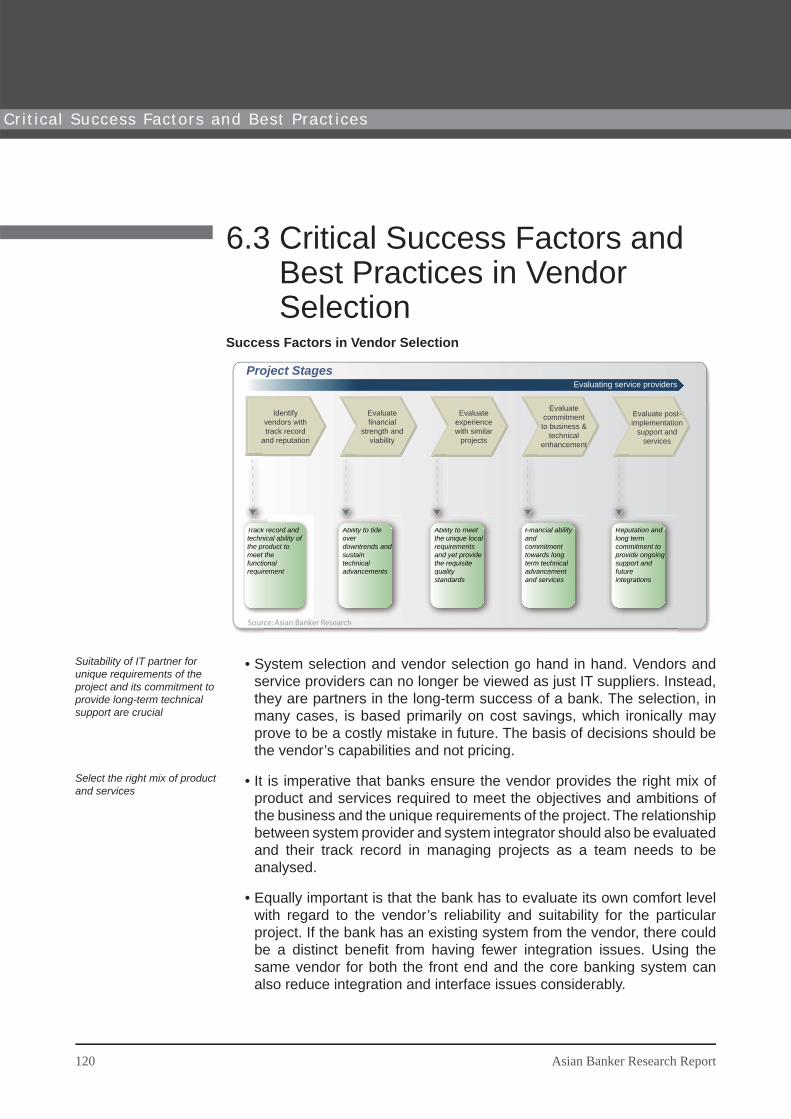

Equally critical is selecting the right vendor. We believe that it is imperative for banks to consider vendors as long-term partners in growth in today’s fast-paced environment. The critical vendor assessment criteria include trust

Asian Banker Research Report 7

Execut ive Summary

in the vendor’s ability to meet the business objectives (through optimum customisation and localisation of the product) as well as the vendor’s reliability, implementation capabilities and fi nancial strength. Vendors that have a track record of providing international-quality products while meeting the local needs of banks are more likely to achieve long-term success. The mix of product and services coupled with pricing are critical considerations. We have rated leading vendors in Asian markets based on our assessment and a survey done among bankers – this is discussed in our section on vendor assessment.

Platform choice is one other critical factor in selection. While mainframe remains unbeaten in its robustness and stability, UNIX-based systems are becoming more popular. We have discovered that banks in Asian countries are increasingly shifting towards the more agile and fl exible UNIX systems, which are perceived to have lower operational and maintenance costs. While this is true for banks that have lower transaction volumes, it may not be so for large retail banks. We believe that mainframes continue to have a distinct advantage in terms of stability and scalability. Hence for mission critical projects, mainframes would still be preferred for their reliability. However for small banks (and those banks that are acquiring a core banking system for the fi rst time and whose transaction volumes are not very high), a UNIX-based system could meet their requirements. As more than 50% of the deals in Asia have come from small banks, UNIX-based systems have become more common.

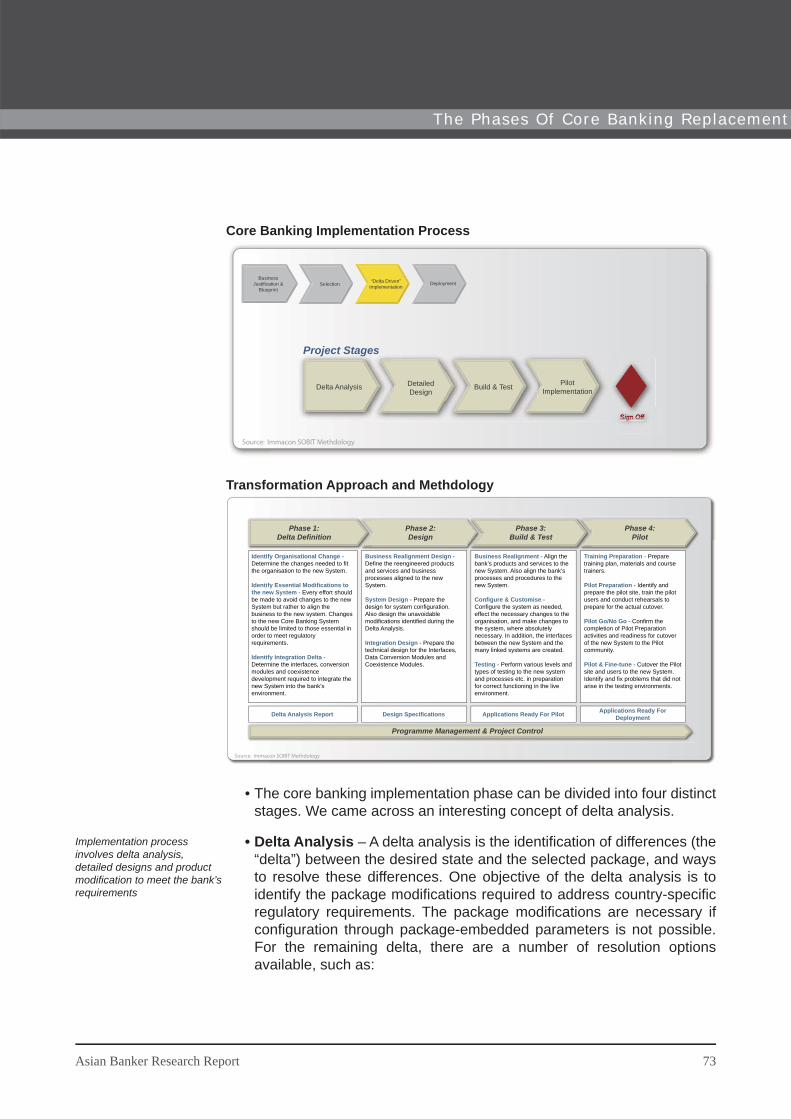

The third phase of the project is implementation. The key objective is to operationalise and pilot the transformed future state, including technology, process and organisational change. This involves developing detailed designs, including system designs for confi guration and customisation and designs for interfaces and data conversion. The other critical elements of this phase are building and testing the system, implementing pilot projects and conducting business acceptance tests at each stage. We recommend that banks limit customisation of the core banking system to what is essential as it may affect the core processing ability of the system. Rather, the banks should customise the front end which interacts with the users.

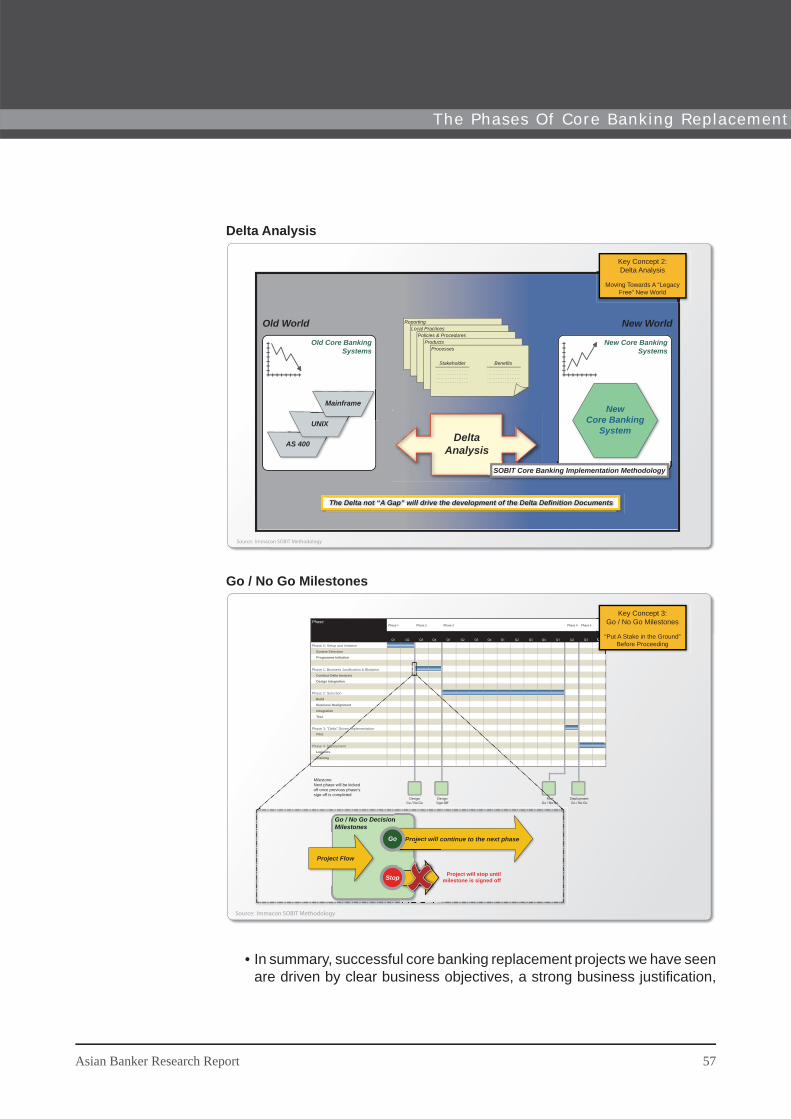

At each stage, the bank should undertake delta analysis to determine the effi cacy and success of the project; this would determine whether it progresses to the next stage. Delta analysis and sign-off at each stage are essential to ensure that deliverables and expectations match, or else the project can easily digress from its initial plan and increase in scope through incremental changes which will lead to schedule and cost overruns.

The next and fi nal phase of the project is deployment. This is probably the most critical and challenging stage, where the bank undertakes the actual

8 Asian Banker Research Report

Execut ive Summary

deployment of the new system. The process involves numerous logistical issues such as data conversion, interfacing and coexistence.

Banks can approach this transition in two ways – big bang implementation and gradual deployment. Big bang essentially means all systems go live at the same time. While this is quicker, it is also riskier. Instead we recommend phased implementation, where deployment is done in small clusters, though the bank has to tackle the tricky issue of coexistence. We believe that the gradual step-by-step approach is appropriate in most cases as it entails lower risks, facilitates change management and allows changes to be incorporated in the technical framework as it is being installed (to provide a better fi t with the business).

Data conversion and data mapping are two crucial elements that the bank has to deal with during deployment. The data migration and conversion process is often hampered by lack of available information on the old system. Mass migration requires a large capital investment, takes a few years to implement and poses a signifi cant risk of service interruptions that can reduce customer satisfaction. The other critical challenge is to maintain smooth operations and develop interfaces across delivery channels during transition through coexistence of two systems.

We believe that banks should predefi ne the milestones at each stage of the replacement process and ensure they are adhered to. At any stage, if the bank fi nds that it cannot achieve these milestones, it may review its project and decide whether and how it wants to continue the project.

Our research into change management during replacement shows that the majority of banks upgrade their system or implement a new one to meet existing users’ process and work culture requirements. Instead, however, we recommend that banks align their products, processes and work culture with the new system. In other words, the replacement should be undertaken together with product and process rationalisation coupled with work culture transformation in order to optimise the returns from the new system.

This embracing of new technology requires tremendous effort in change management, which demands extensive user training and re-engineering of processes across the organisation. There is often resistance to change and employee dissatisfaction during the transition. We believe this can be countered only through effective communication and developing the right business environment.

We have discovered that just 30% of recent replacement projects had active CEO involvement. However our research shows that successful projects require the backing of a strong leader from top management with a strategic

Asian Banker Research Report 9

Execut ive Summary

mindset and the duty to see the project through. Strong leadership support and a capable steering team (which can harness the bank’s resources, take quick decisions and motivate staff to see the project through) are critical for success. Banks need to develop strong internal teams that have effective communication and technical skills, to share decision-making with the service provider to overcome problems. The complexity of the process and inevitable hiccups will demand that banks engage in the process with thorough planning and programme organisation.

10 Asian Banker Research Report

Execut ive Summary

1Core Banking Trends in Asia Pacifi c

This section examines the trends in core banking transformation among Asian countries and covers a wide spectrum of issues ranging from pattern in deals, replacement approach, platform selection, implementation and key architectural trends. The aim is to learn from recent decisions and understand the market dynamics of this region.

Core Banking Trends in Asia Pacifi c

Market Trends1.1 Prominent recent deals in the region1.2 Geographic dispersion of deals in recent years and 2006

estimates1.3 Activity within countries and their vendor preferences1.4 Estimates of system and software spending in Asia Pacifi c

Technical Trends 1.5 Evolution and convergence of core banking systems1.6 Technology integration in Asian countries1.7 Trends in platform usage among Asian countries1.8 Trends in deployment approach

1.1 Prominent Recent Deals in the Region

Major Asian Core Banking Deals in Last two Years

In keeping with the worldwide trend, Asian banks have been active in replacing and upgrading their core banking systems in the last few years. We believe high demand and competitive pressures are forcing many banks in the region to improve their technical base.

Analysing the recent decisions, we noticed three signifi cant trends. Firstly, more than 50% of banks that decided to replace their core banking systems were small banks with an asset base of less than $1 billion. Medium to large Asian banks are taking considerably long to mull over the wisdom of replacing. Secondly, banks are increasingly favouring the UNIX platform. Part of the reason for this observation is that most of the recent deals came from small banks, for which the UNIX platform is more feasible. Thirdly, no vendor dominates the region, but Asian service providers have been given preference by banks while vendors with strongholds in Europe and the United States fi nd it diffi cult to develop a solid position here.

Looking at the geographic dispersion of recent decisions, we discovered that the concentration of replacements has varied in the last two years. However the Indian banking industry has taken a clear lead in core banking transformation. Most of the deals came from state-owned banks like Bank of Baroda, Allahabad Bank and Central Bank of India.

•

•

•

Market Trends

12 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

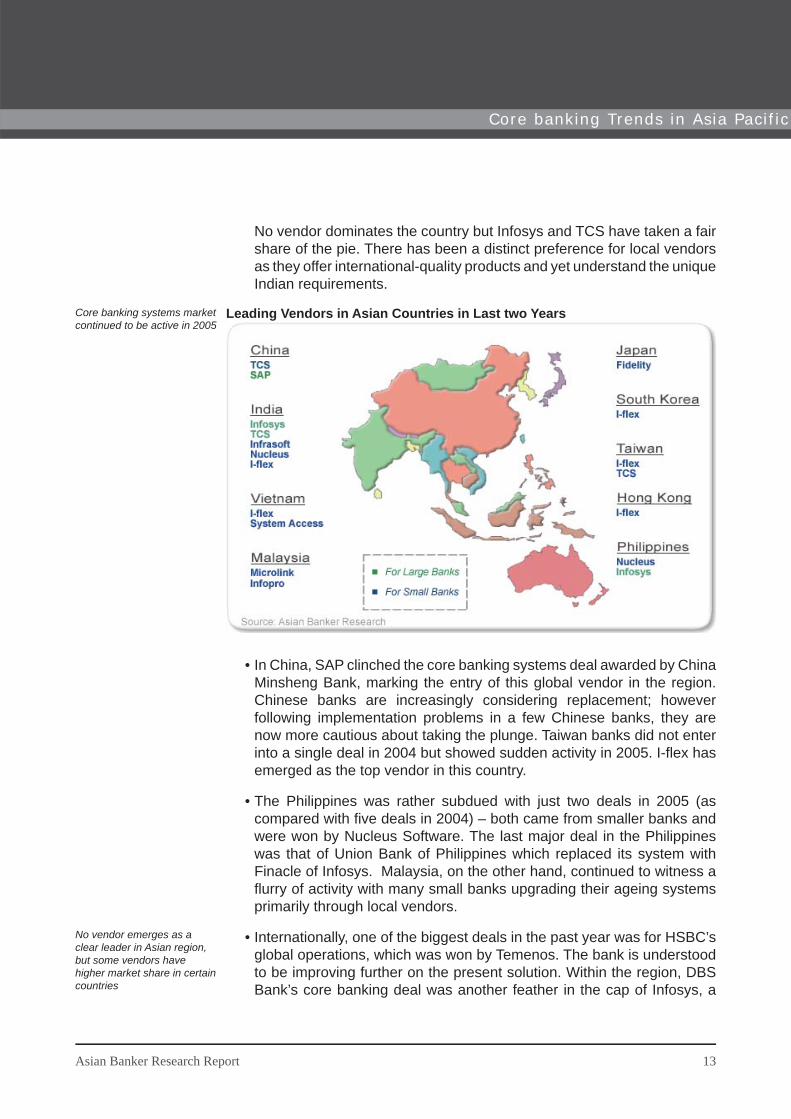

No vendor dominates the country but Infosys and TCS have taken a fair share of the pie. There has been a distinct preference for local vendors as they offer international-quality products and yet understand the unique Indian requirements.

Leading Vendors in Asian Countries in Last two Years

In China, SAP clinched the core banking systems deal awarded by China Minsheng Bank, marking the entry of this global vendor in the region. Chinese banks are increasingly considering replacement; however following implementation problems in a few Chinese banks, they are now more cautious about taking the plunge. Taiwan banks did not enter into a single deal in 2004 but showed sudden activity in 2005. I-fl ex has emerged as the top vendor in this country.

The Philippines was rather subdued with just two deals in 2005 (as compared with fi ve deals in 2004) – both came from smaller banks and were won by Nucleus Software. The last major deal in the Philippines was that of Union Bank of Philippines which replaced its system with Finacle of Infosys. Malaysia, on the other hand, continued to witness a fl urry of activity with many small banks upgrading their ageing systems primarily through local vendors.

Internationally, one of the biggest deals in the past year was for HSBC’s global operations, which was won by Temenos. The bank is understood to be improving further on the present solution. Within the region, DBS Bank’s core banking deal was another feather in the cap of Infosys, a

•

•

•

Core banking systems market continued to be active in 2005

No vendor emerges as a clear leader in Asian region, but some vendors have higher market share in certain countries

Asian Banker Research Report 13

Core banking Trends in Asia Pacif ic

leading player in the region, particularly in India.

Analysing vendor dominance in the region, we discovered that I-fl ex, Infosys, TCS-FNS, Nucleus Software and System Access have been popular among second-tier banks in Asia. For large banks, the preferred vendors include Temenos, TCS, SAP and Infosys. Leading international vendors such as Fiserv and Fidelity have shown little activity in the region in the last two years.

TCS-FNS and Infosys are strong in this region, particularly in India. Temenos, however, has had no signifi cant deal in Asia in the recent two years though it continues to be a fi erce contender for deals from top-tier banks across the world. Its last big project in the region was for Industrial Bank of Korea.

Globally, Islamic banking is a fast growing sector with banks demanding a system specifi cally catering to this segment. Within Asia, Islamic banking has been popular largely in Malaysia and Indonesia. The leading vendors for Islamic banking in the region are Silverlake, Infopro and Microlink who have done a fair number of deals in Malaysia.

In summary, we believe that international vendors have found it diffi cult to establish a stronghold in Asian markets as there is distinct preference for vendors who are perceived to have knowledge of the unique local market conditions in addition to a solid track record. Please see our section on vendor analysis for more details.

•

•

•

•

14 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

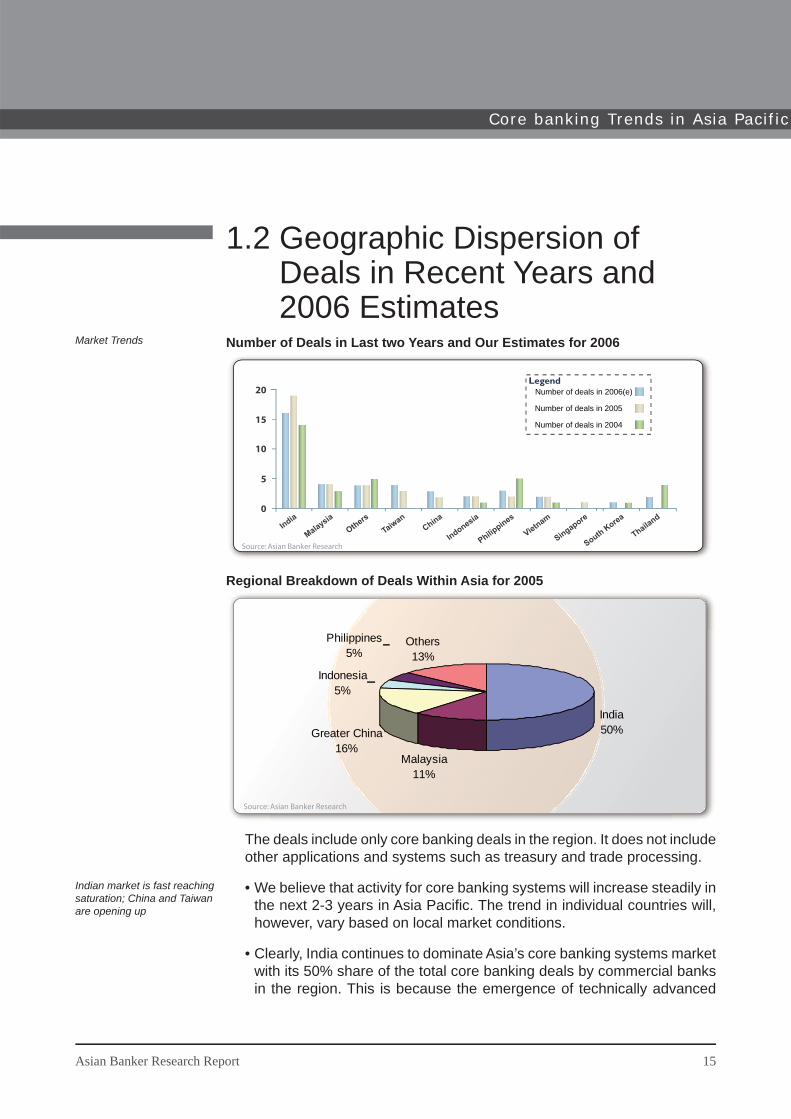

1.2 Geographic Dispersion of Deals in Recent Years and 2006 Estimates

Number of Deals in Last two Years and Our Estimates for 2006

20

15

10

5

0

India

MalaysiaOthers

TaiwanChina

Indonesia

Philippines

Vietnam

Singapore

South Korea

Thailand

Number of deals in 2006(e)

Number of deals in 2005

Number of deals in 2004

Legend

Source: Asian Banker Research

Regional Breakdown of Deals Within Asia for 2005

India50%

Malaysia11%

Greater China16%

Indonesia5%

Philippines5%

Others13%

Source: Asian Banker Research

The deals include only core banking deals in the region. It does not include other applications and systems such as treasury and trade processing.

We believe that activity for core banking systems will increase steadily in the next 2-3 years in Asia Pacifi c. The trend in individual countries will, however, vary based on local market conditions.

Clearly, India continues to dominate Asia’s core banking systems market with its 50% share of the total core banking deals by commercial banks in the region. This is because the emergence of technically advanced

•

•

Market Trends

Indian market is fast reaching saturation; China and Taiwan are opening up

Asian Banker Research Report 15

Core banking Trends in Asia Pacif ic

private banks in the country has forced most state-owned banks to substitute (and in most cases acquire for the fi rst time) a centralised core banking system to improve their competitiveness and retain their market share. However we expect the trend to slow down in the next couple of years as most leading banks have already entered into core banking deals. A few banks that have not yet upgraded their systems are fi nding it increasingly diffi cult to compete and are currently evaluating available products and vendors.

Taiwan witnessed a recent surge in core banking deals, though mostly from smaller banks. In China, the number of deals has been rising slowly but steadily as more and more banks evaluate the need for replacement; however most of these deals have been from smaller banks. We expect the current trend in both Taiwan and China to continue this year.

Malaysia has also been active with four deals in 2005, though most of these were again from smaller banks. However we believe some big banks like Maybank are actively considering core banking replacement. We expect to see more core banking deals in Malaysia with Islamic banks favouring local vendors who can meet Islamic banking requirements.

Most other countries saw just a few small deals with the exception of Singapore, where DBS has entered into a core banking deal for its retail business. Thailand and Korea were noticeably absent from the scene in 2005, but we expect activity in both countries to pick up over the next couple of years.

•

•

•

16 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

1.3 Activity Within Countries and Their Vendor Preferences

Activity in Banking Sectors for Core Banking Replacement in Last two Years

05 10 15 20 25 30

VendorPreference

InternationalVendors

LocalVendors

Less active, international demand High activity, international demand

Less active, unique local needs Highly active, unique local needs

Trends indicate likely shift in future

% of banking sector replacing CBS in last 2 years

Singapore

SouthKorea

Taiwan

Vietnam

Philippines

Thailand

India

MalaysiaIndonesia

China Legend

Source: Asian Banker Research

The level of activity is represented by the percentage of commercial banks in each country that have awarded core banking system deals in the last two years. It is based on number of deals and gives the same rating to big and small banks.

We believe that almost 25% of the Indian banking sector has entered into core banking replacement deals in the last two years. In absolute terms, the number is far higher than that of any other country – though as a percentage of the whole sector, it may not be as signifi cant. Most banks in this country have preferred local vendors owing to not just the international level of expertise and reputation of the vendors but also their higher level of trust in them. Contributing to this is also the fact that many Indian vendors have advanced in these last few years to become some of the leading vendors in the world.

Interestingly, the banking sectors of Thailand and Korea saw no new deals in 2005 despite being active in 2004. However there was increased activity in Taiwan and China. Increasing competition from foreign banks in these countries is forcing banks to evaluate their core banking replacement needs. We believe the core banking transformation in these countries is set to accelerate over the next few years.

•

•

Market Trends

Indian banks have favoured technical advancement through local vendors

Other Asian countries expected to continue to show demand for core banking transformation

Asian Banker Research Report 17

Core banking Trends in Asia Pacif ic

Most Chinese banks have shown a strong preference for systems that are designed to suit their specifi c and unique requirements. For this reason, smaller Chinese banks have preferred domestic vendors while larger banks have preferred international vendors that can meet their local needs. Similarly, many Malaysian banks have preferred local vendors that can meet their Islamic banking requirements.

Banks from developed markets like Singapore and Hong Kong have fi rst-generation technical sophistication and are undertaking a cyclical replacement of their ageing systems. In contrast, banks in countries like India, Pakistan and Vietnam are purchasing core banking systems for the fi rst time now. For obvious reasons, activity among the banks that lack technical sophistication will increase.

We believe that most Asian banks prefer to select vendors that either involve local people through a setup in their country or partner local vendors. This is because there is a perception among the bankers that a local is more likely to understand and adapt to the unique local needs of a particular country. However in many countries, the availability of international-quality products from local vendors is a limiting factor which has forced banks to look for alternatives.

•

•

•

China banks have preference for systems that cater to their unique needs

18 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

1.4 Estimates of System and Software Spending in Asia Pacifi c

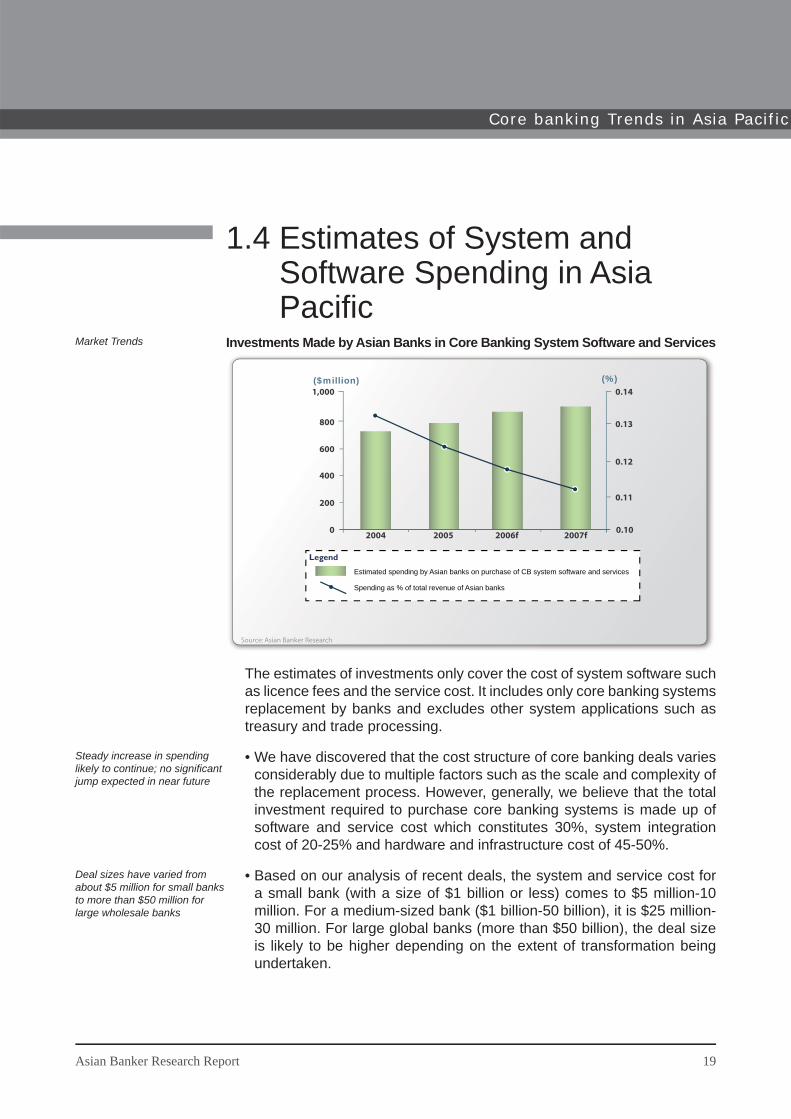

Investments Made by Asian Banks in Core Banking System Software and Services

800

600

1,000

400

200

0.14

2004 2005 2006f 2007f0

(%)($million)

0.10

0.13

0.12

0.11

Estimated spending by Asian banks on purchase of CB system software and services

Legend

Spending as % of total revenue of Asian banks

Source: Asian Banker Research

The estimates of investments only cover the cost of system software such as licence fees and the service cost. It includes only core banking systems replacement by banks and excludes other system applications such as treasury and trade processing.

We have discovered that the cost structure of core banking deals varies considerably due to multiple factors such as the scale and complexity of the replacement process. However, generally, we believe that the total investment required to purchase core banking systems is made up of software and service cost which constitutes 30%, system integration cost of 20-25% and hardware and infrastructure cost of 45-50%.

Based on our analysis of recent deals, the system and service cost for a small bank (with a size of $1 billion or less) comes to $5 million-10 million. For a medium-sized bank ($1 billion-50 billion), it is $25 million-30 million. For large global banks (more than $50 billion), the deal size is likely to be higher depending on the extent of transformation being undertaken.

•

•

Market Trends

Steady increase in spending likely to continue; no signifi cant jump expected in near future

Deal sizes have varied from about $5 million for small banks to more than $50 million for large wholesale banks

Asian Banker Research Report 19

Core banking Trends in Asia Pacif ic

A critical cost item is system software cost; this includes the cost of software licences, which varies depending on project. For example, for FNS customers, software licence cost has varied from $1 million to over $7 million, with an average of $1.8 million in 2005.

Overall, we have seen a steady rise in investment made by banks in Asia over recent years. We expect the trend to continue. However, as a percentage of total revenue, we believe the investments are likely to show a declining trend as the banks have witnessed even higher growth in revenue. We also believe that there is stiff price competition among vendors and that this will keep the costs in core banking replacement under control.

•

•

20 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

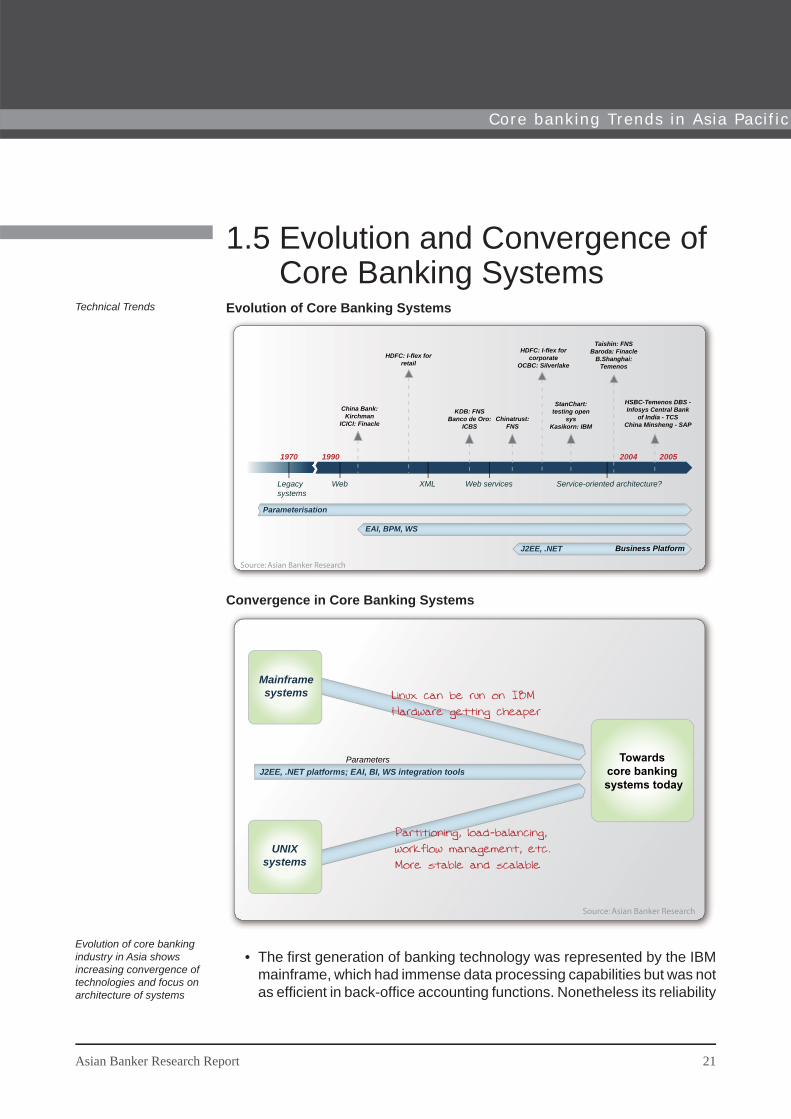

1.5 Evolution and Convergence of Core Banking Systems

Evolution of Core Banking Systems

Business Platform J2EE, .NET

EAI, BPM, WS

Parameterisation

Legacysystems

1970 1990 2004 2005

Web XML Web services Service-oriented architecture?

China Bank: Kirchman

ICICI: Finacle

HDFC: I-flex for retail

KDB: FNSBanco de Oro:

ICBSChinatrust:

FNS

HDFC: I-flex for corporate

OCBC: Silverlake

StanChart:testing open

sysKasikorn: IBM

Taishin: FNS Baroda: Finacle

B.Shanghai:Temenos

HSBC-Temenos DBS - Infosys Central Bank

of India - TCS China Minsheng - SAP

Source: Asian Banker Research

Convergence in Core Banking Systems

Parameters

Mainframesystems

UNIXsystems

J2EE, .NET platforms; EAI, BI, WS integration toolsTowards

core banking systems today

Source: Asian Banker Research

The fi rst generation of banking technology was represented by the IBM mainframe, which had immense data processing capabilities but was not as effi cient in back-offi ce accounting functions. Nonetheless its reliability

•

Technical Trends

Evolution of core banking industry in Asia shows increasing convergence of technologies and focus on architecture of systems

Asian Banker Research Report 21

Core banking Trends in Asia Pacif ic

and scalability remain unbeaten today. In the next stage of evolution came parameterisation of processing rules and enhancement in automation from back- to front-offi ces. Here, the UNIX platform solutions have shown high functionality, with some of them using relational database technology to maintain accounting and administrative data.

UNIX systems have borrowed ideas freely from mainframes such as logical partitioning, the ability for isolation, the ability to share across partitions, and common interfaces. Integration tools and other technological advancements have brought about a certain level of standardisation and convergence of technologies today at the platform, application and architectural layers.

Banks are increasingly looking for solutions that have the technical capability to meet their unique functional requirements while improving their competitiveness. There is also increasing demand for component-based modular systems that do not have integration issues.

Trends in Requirements

• Architecture that supports flexibility, growth and services such as Service Oriented Architecture (SOA)

• Systems capable of global deployment – multi-channel, multilingual with high connectivity

• Customer centric focus with increased connectivity across processes and functions. Integrated solution increasingly available

• Convergence of old and new technology with increased scalability and flexibility

Source: Asian Banker Research

Service Oriented Architecture (SOA) is a relatively new concept that has gained popularity quickly. Herein, business applications are constructed from independent reusable interoperable services that can be reconfi gured without a vast amount of technical labour. The concept is based on web services and components that are brought together to perform specifi c business tasks. It essentially means reducing barriers in antiquated infrastructure and creating a real-time integration of disparate systems and a sharing of databases on a fl exible and easily upgradeable infrastructure. We discuss this in more detail in section 5.

On the architectural front, J2EE and .NET are two architectural frameworks that have evolved in the last few years. These are new-generation fl exible

•

•

•

•

Banks need to adopt Service Oriented Architecture

22 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

and interoperable architectures that facilitate the complete meshing of core banking solutions with the complex technology fabric of the bank.

The key attributes that banks require from their architecture are fl exibility, scalability and agility. With customer expectations increasing, banks have moved towards centralised systems with customer-centric architecture, where they drive the business through a single view of the customer and the paramount consideration in all decisions is the consumer.

IT Service Providers in the Region

• Vendor consolidation through mergers and acquisitions.

• Partnership among vendors to mix and match solutions.

• Standard protocols and fierce competition among IT service providers leading to increased product offerings and price competition.

Source: Asian Banker Research

The growth in demand for core banking systems in Asia Pacifi c has prompted many international vendors such as SAP, Temenos, Fidelity and Misys to focus increasingly on the region. At the same time, vendors that began their operations in Asian countries have grown to become recognised names across the world; these include companies like Infosys, I-fl ex and TCS.

Desire to become the leading player in the market has led to mergers and acquisitions among IT service providers. At the global level, Fidelity’s acquisition of Sanchez broadened its reach to a larger collection of banks. Among leading vendors in Asia, TCS acquired FNS in a leap from their previous alliance. Another example of consolidation in the industry is Oracle’s acquisition of a stake in I-fl ex. These players are developing an increasingly strong foothold in the core banking systems market.

Greater convergence makes it diffi cult for bankers to differentiate between vendors’ value propositions. However standard protocols and fi erce competition have led to more product offerings and price wars – a boon for the industry as a whole.

•

•

•

•

Asian vendors are increasing their global reach

Desire to become leading player has led to consolidation in the industry

Asian Banker Research Report 23

Core banking Trends in Asia Pacif ic

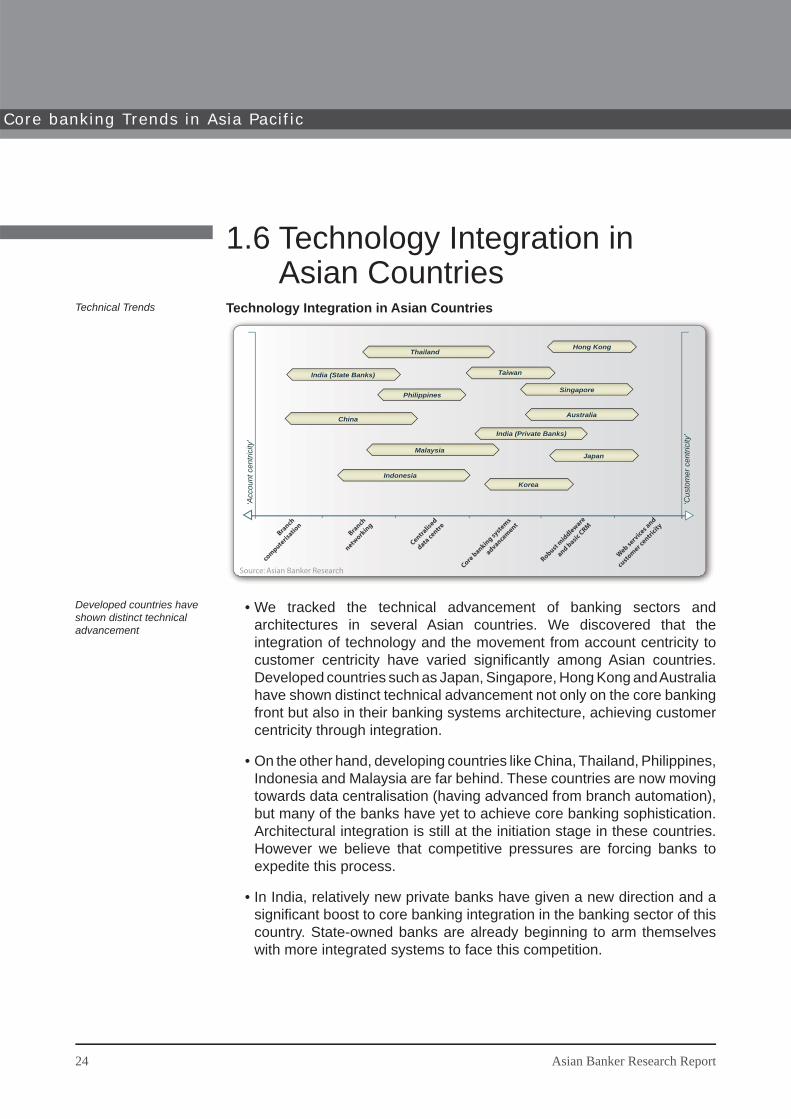

1.6 Technology Integration in Asian Countries

Technology Integration in Asian Countries

‘Acc

ount

cen

trici

ty’

‘Cus

tom

er c

entri

city

’

Thailand

India (State Banks)

Philippines

China

Malaysia

Indonesia

Hong Kong

Taiwan

Singapore

Australia

India (Private Banks)

Japan

Korea

Branch

compute

risatio

nBra

nch

network

ing

Centralis

ed

data centre

Core b

anking syste

ms

advancement

Robust mid

dleware

and basic C

RM

Web serv

ices and

custom

er centri

city

Source: Asian Banker Research

We tracked the technical advancement of banking sectors and architectures in several Asian countries. We discovered that the integration of technology and the movement from account centricity to customer centricity have varied signifi cantly among Asian countries. Developed countries such as Japan, Singapore, Hong Kong and Australia have shown distinct technical advancement not only on the core banking front but also in their banking systems architecture, achieving customer centricity through integration.

On the other hand, developing countries like China, Thailand, Philippines, Indonesia and Malaysia are far behind. These countries are now moving towards data centralisation (having advanced from branch automation), but many of the banks have yet to achieve core banking sophistication. Architectural integration is still at the initiation stage in these countries. However we believe that competitive pressures are forcing banks to expedite this process.

In India, relatively new private banks have given a new direction and a signifi cant boost to core banking integration in the banking sector of this country. State-owned banks are already beginning to arm themselves with more integrated systems to face this competition.

•

•

•

Technical Trends

Developed countries have shown distinct technical advancement

24 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

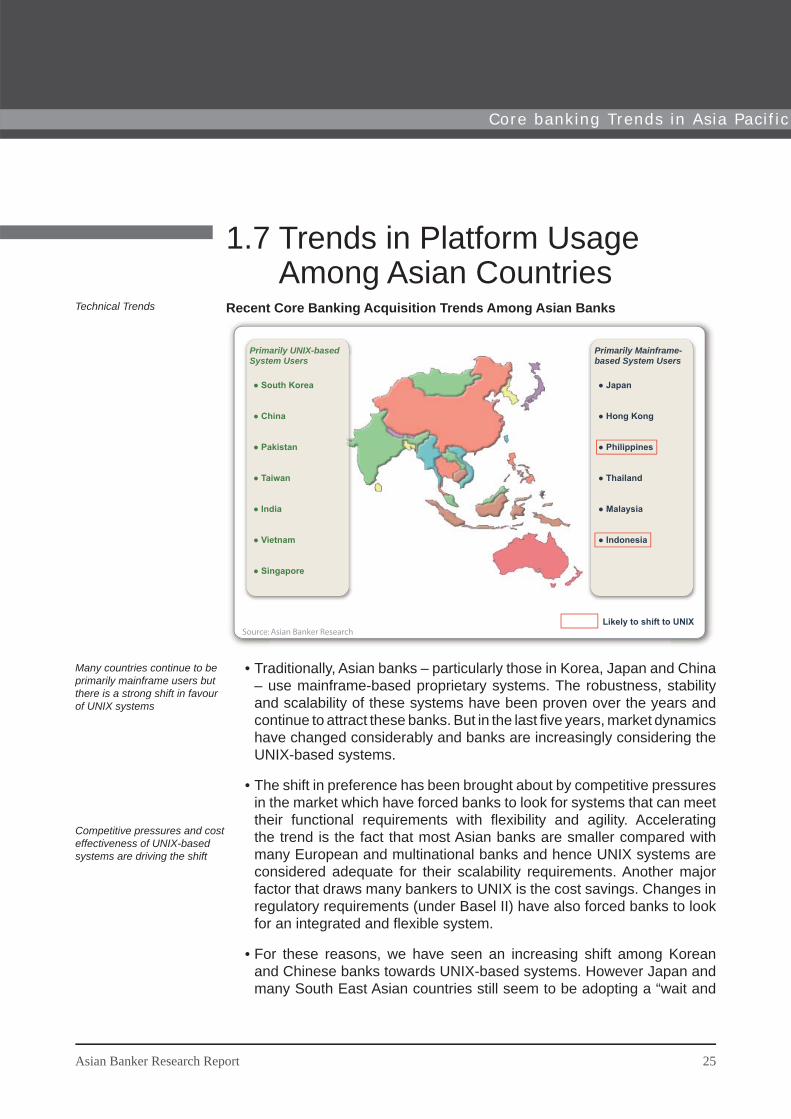

1.7 Trends in Platform Usage Among Asian Countries

Recent Core Banking Acquisition Trends Among Asian Banks

● South Korea

● China

● Pakistan

● Taiwan

● India

● Vietnam

● Singapore

Primarily UNIX-basedSystem Users

● Japan

● Hong Kong

● Philippines

● Thailand

● Malaysia

● Indonesia

Primarily Mainframe-based System Users

Likely to shift to UNIXSource: Asian Banker Research

Traditionally, Asian banks – particularly those in Korea, Japan and China – use mainframe-based proprietary systems. The robustness, stability and scalability of these systems have been proven over the years and continue to attract these banks. But in the last fi ve years, market dynamics have changed considerably and banks are increasingly considering the UNIX-based systems.

The shift in preference has been brought about by competitive pressures in the market which have forced banks to look for systems that can meet their functional requirements with fl exibility and agility. Accelerating the trend is the fact that most Asian banks are smaller compared with many European and multinational banks and hence UNIX systems are considered adequate for their scalability requirements. Another major factor that draws many bankers to UNIX is the cost savings. Changes in regulatory requirements (under Basel II) have also forced banks to look for an integrated and fl exible system.

For these reasons, we have seen an increasing shift among Korean and Chinese banks towards UNIX-based systems. However Japan and many South East Asian countries still seem to be adopting a “wait and

•

•

•

Technical Trends

Many countries continue to be primarily mainframe users but there is a strong shift in favour of UNIX systems

Competitive pressures and cost effectiveness of UNIX-based systems are driving the shift

Asian Banker Research Report 25

Core banking Trends in Asia Pacif ic

see” approach. In mature countries like Singapore, there are very few deals as well; but in the country’s most recent deal, DBS opted in favour of a UNIX platform.

In the Indian subcontinent, most commercial banks are adopting core banking systems for the fi rst time. Thus most banks have taken advantage of this new-generation technology. As there is no problem of integrating with the existing system, implementation is cheaper and less complex. Moreover, the traditional preference of Indian banks (and Indian vendors) is for a UNIX environment.

While smaller Asian banks have favoured UNIX-based systems owing to their cost effectiveness, we believe that mainframe has proved to be more reliable and scalable for a larger size of operations. As transaction volumes increase, the total cost per user in mainframe decreases, making it more competitive.

•

•

26 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

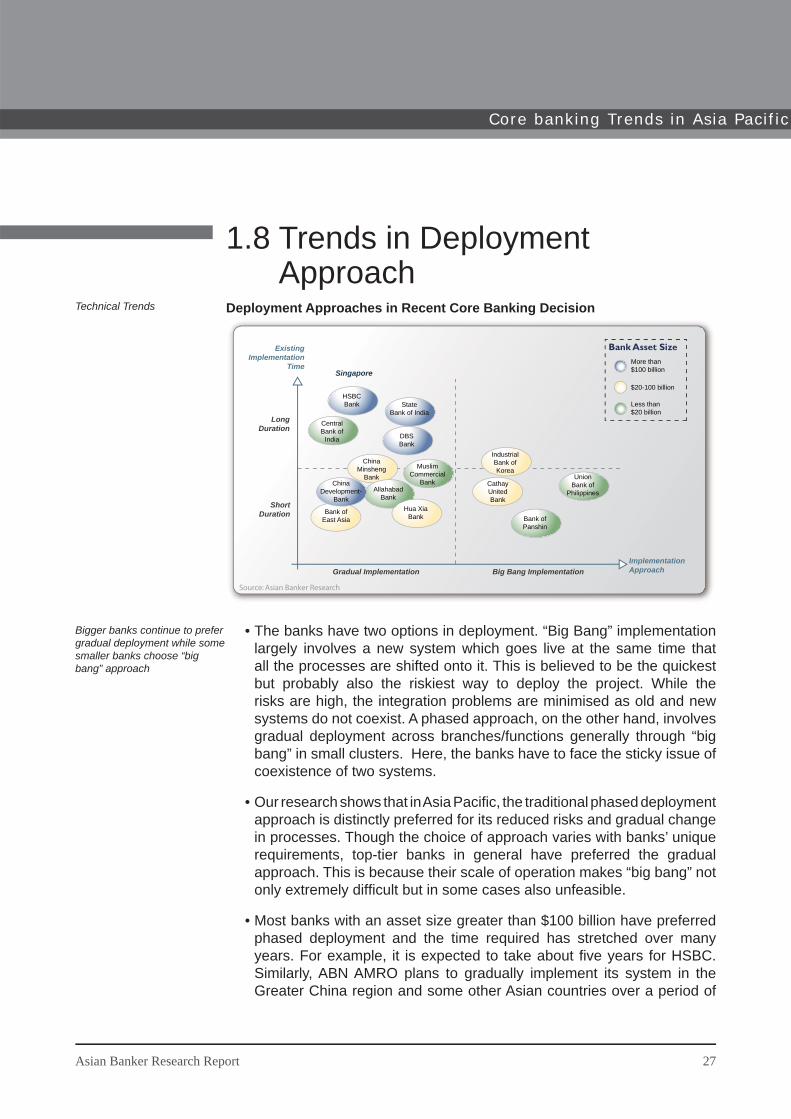

1.8 Trends in Deployment Approach

Deployment Approaches in Recent Core Banking Decision

LongDuration

ExistingImplementation

Time

ShortDuration

Gradual Implementation Big Bang ImplementationImplementationApproach

Singapore

HSBCBank

ChinaMinsheng

Bank

CentralBank of

India

AllahabadBank

MuslimCommercial

Bank

Bank of Panshin

UnionBank of

Philippines

Bank ofEast Asia

Hua Xia Bank

IndustrialBank of Korea

CathayUnitedBank

StateBank of India

DBSBank

ChinaDevelopment-

Bank

Bank Asset SizeMore than $100 billion

$20-100 billion

Less than $20 billion

Source: Asian Banker Research

The banks have two options in deployment. “Big Bang” implementation largely involves a new system which goes live at the same time that all the processes are shifted onto it. This is believed to be the quickest but probably also the riskiest way to deploy the project. While the risks are high, the integration problems are minimised as old and new systems do not coexist. A phased approach, on the other hand, involves gradual deployment across branches/functions generally through “big bang” in small clusters. Here, the banks have to face the sticky issue of coexistence of two systems.

Our research shows that in Asia Pacifi c, the traditional phased deployment approach is distinctly preferred for its reduced risks and gradual change in processes. Though the choice of approach varies with banks’ unique requirements, top-tier banks in general have preferred the gradual approach. This is because their scale of operation makes “big bang” not only extremely diffi cult but in some cases also unfeasible.

Most banks with an asset size greater than $100 billion have preferred phased deployment and the time required has stretched over many years. For example, it is expected to take about fi ve years for HSBC. Similarly, ABN AMRO plans to gradually implement its system in the Greater China region and some other Asian countries over a period of

•

•

•

Technical Trends

Bigger banks continue to prefer gradual deployment while some smaller banks choose “big bang” approach

Asian Banker Research Report 27

Core banking Trends in Asia Pacif ic

fi ve years. For State Bank of India and Central Bank of India, it is likely to be around four years. We believe that it is critical to keep the rollout time and the period that two systems coexist as short as possible.

On the other hand, a few smaller banks have taken the quicker approach of “big bang”. These include: Union Bank of Philippines whose system by Infosys was implemented in just one year; Industrial Bank of Korea by Temenos; and Cathay United Bank, Taiwan by TCS-FNS.

•

28 Asian Banker Research Report

Core banking Trends in Asia Pacif ic

2Bankers’ Perception Survey on Core Banking System SelectionWe have conducted a series of surveys in the Asian banking sector to strengthen our research on various aspects of core banking transformation. Our surveys have given us an insight into how bankers assess various vendors in the region, key considerations in the selection of a new system, and platform preference among Asian banks. We have discovered that some of the common perceptions lack sound foundation.

Bankers’ Perception Survey on Core Banking System Selection

2.1 Survey results on key reasons for replacement 2.2 Survey results on factors considered in system selection2.3 UNIX versus mainframe – survey results on considerations in

system selection

2.1 Survey Results on Key Reasons for Replacement

Perception Survey on Key Reasons for Replacement

% of executives citing area as a problem10 20 30 40 50 60 70 80

Other

Errors in operation

Errors in data

Availability

Errors in processing

Scalability

Timing problems

Technology

Simplification

Integration

Cost

Flexibility

Source: Asian Banker Research

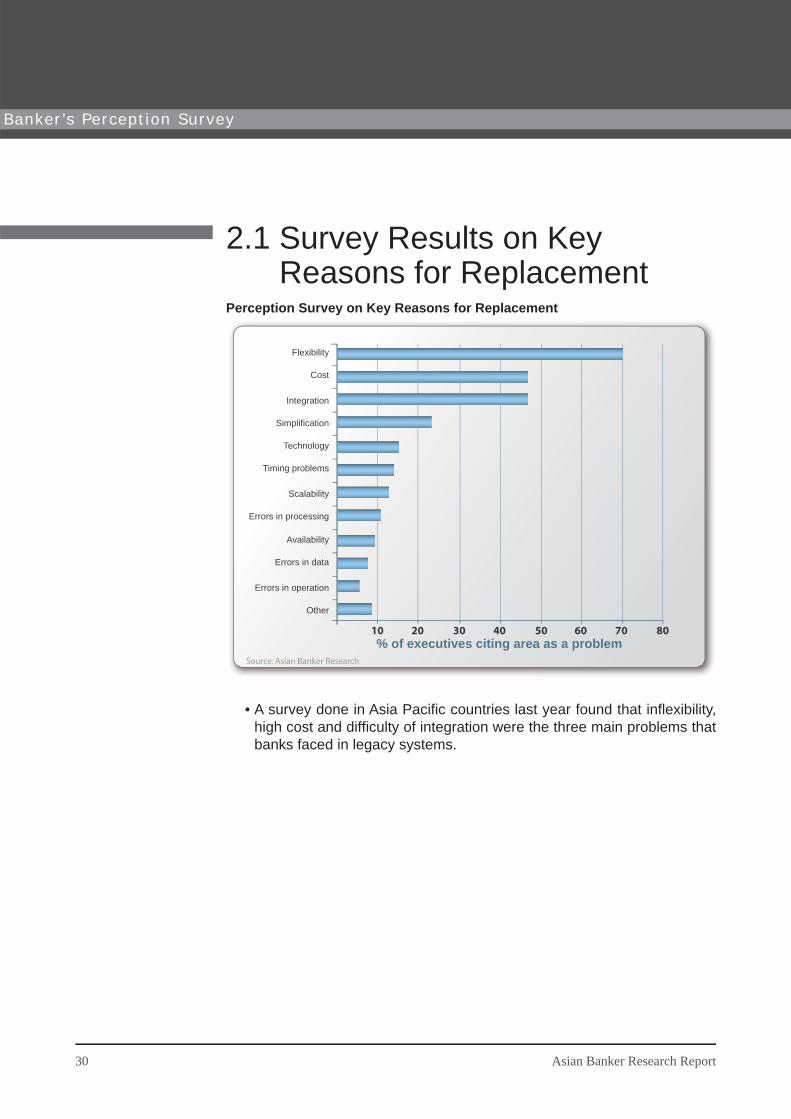

A survey done in Asia Pacifi c countries last year found that infl exibility, high cost and diffi culty of integration were the three main problems that banks faced in legacy systems.

•

30 Asian Banker Research Report

Banker ’s Percept ion Survey

Banker ’s Percept ion Survey

2.2 Survey Results on Factors Considered in System Selection

Perception Survey on Factors Considered

Ran

king

Importance

Cost

Short product time-to-market

Availability of third party applications

Ease of integration

Vendor reputation and track record

Straight through processing/ real-time capability

Truly modular and integrated, single sign-on

Functionality

Scalability

Reliability/ stability

Source: Asian Banker Research

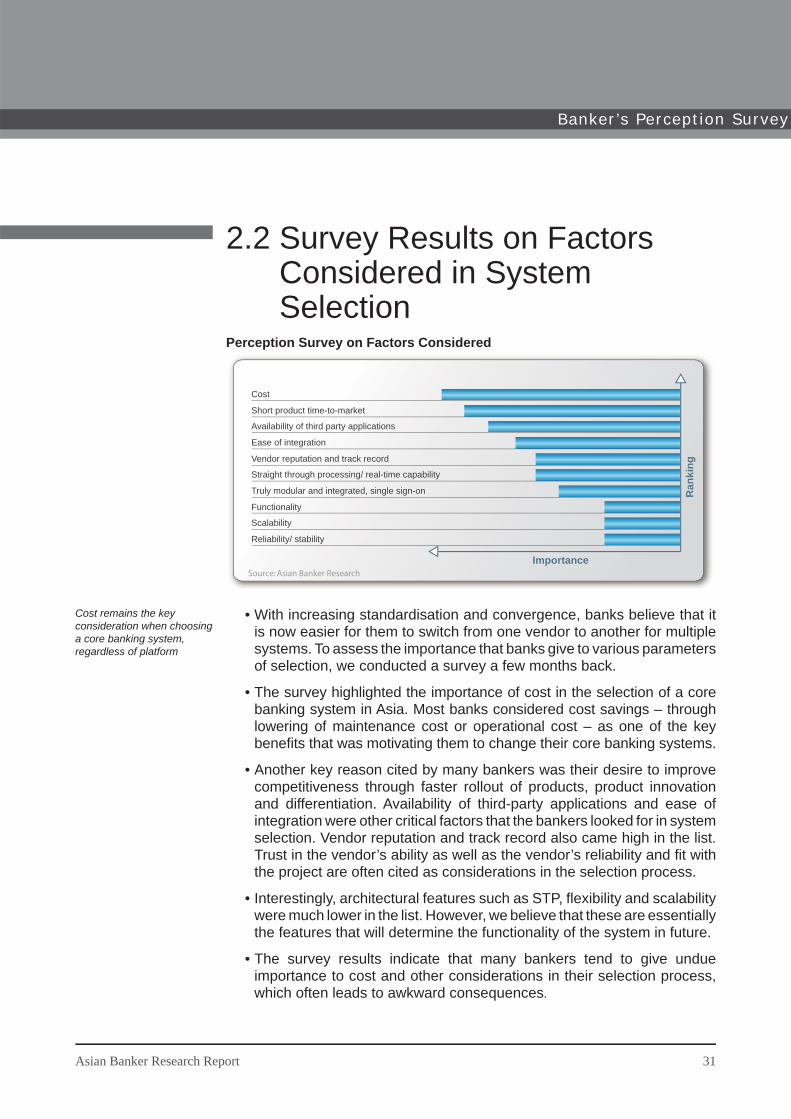

With increasing standardisation and convergence, banks believe that it is now easier for them to switch from one vendor to another for multiple systems. To assess the importance that banks give to various parameters of selection, we conducted a survey a few months back.

The survey highlighted the importance of cost in the selection of a core banking system in Asia. Most banks considered cost savings – through lowering of maintenance cost or operational cost – as one of the key benefi ts that was motivating them to change their core banking systems.

Another key reason cited by many bankers was their desire to improve competitiveness through faster rollout of products, product innovation and differentiation. Availability of third-party applications and ease of integration were other critical factors that the bankers looked for in system selection. Vendor reputation and track record also came high in the list. Trust in the vendor’s ability as well as the vendor’s reliability and fi t with the project are often cited as considerations in the selection process.

Interestingly, architectural features such as STP, fl exibility and scalability were much lower in the list. However, we believe that these are essentially the features that will determine the functionality of the system in future.

The survey results indicate that many bankers tend to give undue importance to cost and other considerations in their selection process, which often leads to awkward consequences.

•

•

•

•

•

Cost remains the key consideration when choosing a core banking system, regardless of platform

Asian Banker Research Report 31

2.3 UNIX Versus Mainframe – Survey Results on Considerations in System Selection

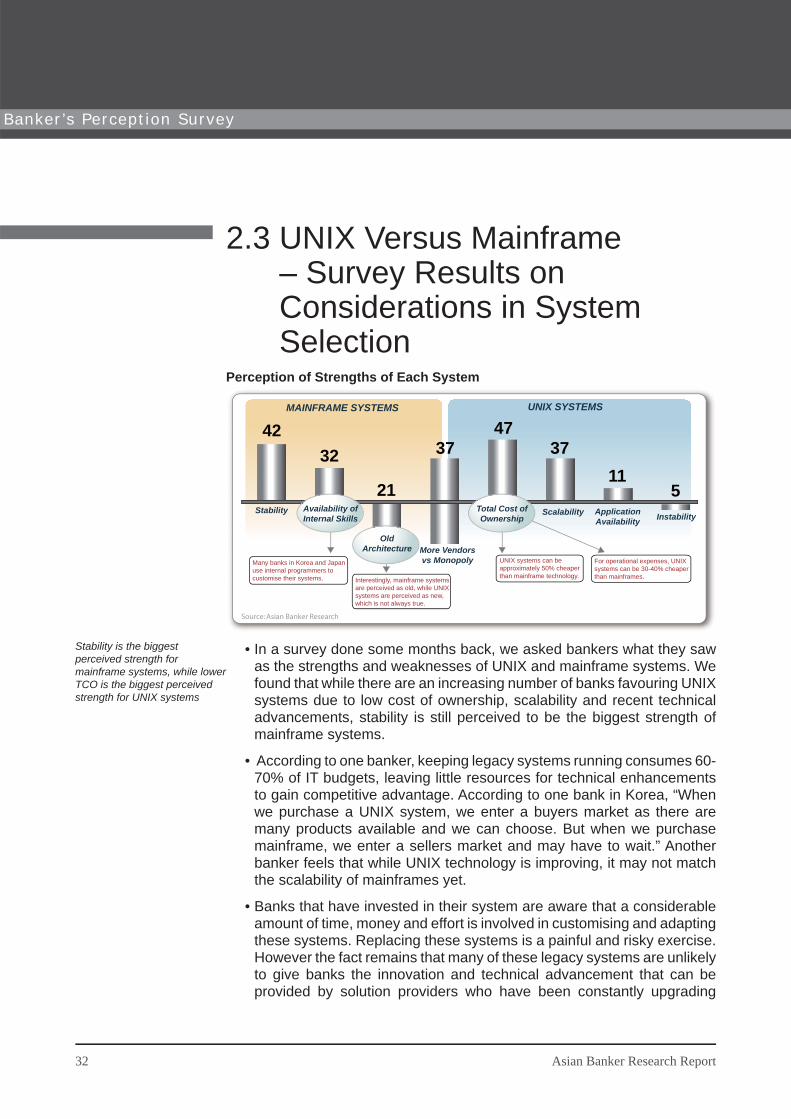

Perception of Strengths of Each System

Interestingly, mainframe systems are perceived as old, while UNIX systems are perceived as new, which is not always true.

Stability

OldArchitecture More Vendors

vs Monopoly

Scalability ApplicationAvailability Instability

4232

21

3747

3711

5

MAINFRAME SYSTEMS UNIX SYSTEMS

Availability of Internal Skills

Many banks in Korea and Japan use internal programmers to customise their systems.

Total Cost ofOwnership

UNIX systems can be approximately 50% cheaper than mainframe technology.

For operational expenses, UNIX systems can be 30-40% cheaper than mainframes.

Source: Asian Banker Research

In a survey done some months back, we asked bankers what they saw as the strengths and weaknesses of UNIX and mainframe systems. We found that while there are an increasing number of banks favouring UNIX systems due to low cost of ownership, scalability and recent technical advancements, stability is still perceived to be the biggest strength of mainframe systems.

According to one banker, keeping legacy systems running consumes 60-70% of IT budgets, leaving little resources for technical enhancements to gain competitive advantage. According to one bank in Korea, “When we purchase a UNIX system, we enter a buyers market as there are many products available and we can choose. But when we purchase mainframe, we enter a sellers market and may have to wait.” Another banker feels that while UNIX technology is improving, it may not match the scalability of mainframes yet.

Banks that have invested in their system are aware that a considerable amount of time, money and effort is involved in customising and adapting these systems. Replacing these systems is a painful and risky exercise. However the fact remains that many of these legacy systems are unlikely to give banks the innovation and technical advancement that can be provided by solution providers who have been constantly upgrading

•

•

•

Stability is the biggest perceived strength for mainframe systems, while lower TCO is the biggest perceived strength for UNIX systems

32 Asian Banker Research Report

Banker ’s Percept ion Survey

their technology. Banks are increasingly realising that their expertise is in banking and not IT development.

According to a leading global vendor, Asian banks have always been very interested in UNIX solutions and so, proportionately speaking, we have more UNIX centres in Asia than in the United States. We believe this is because the core banking market today is dominated by Indian banks, which have traditionally preferred UNIX-based systems.

While the debate over preferred technology continues, it goes without saying that what may be considered suitable by one bank may not be appropriate for another bank. For example, big banks with an extensive scale of operation may fi nd it risky to switch from mainframe systems to UNIX technology primarily because of complexities, high risks and huge costs involved in the process. However a small bank which is building its core banking system from scratch (or replacing it) may prefer lower-cost open systems.

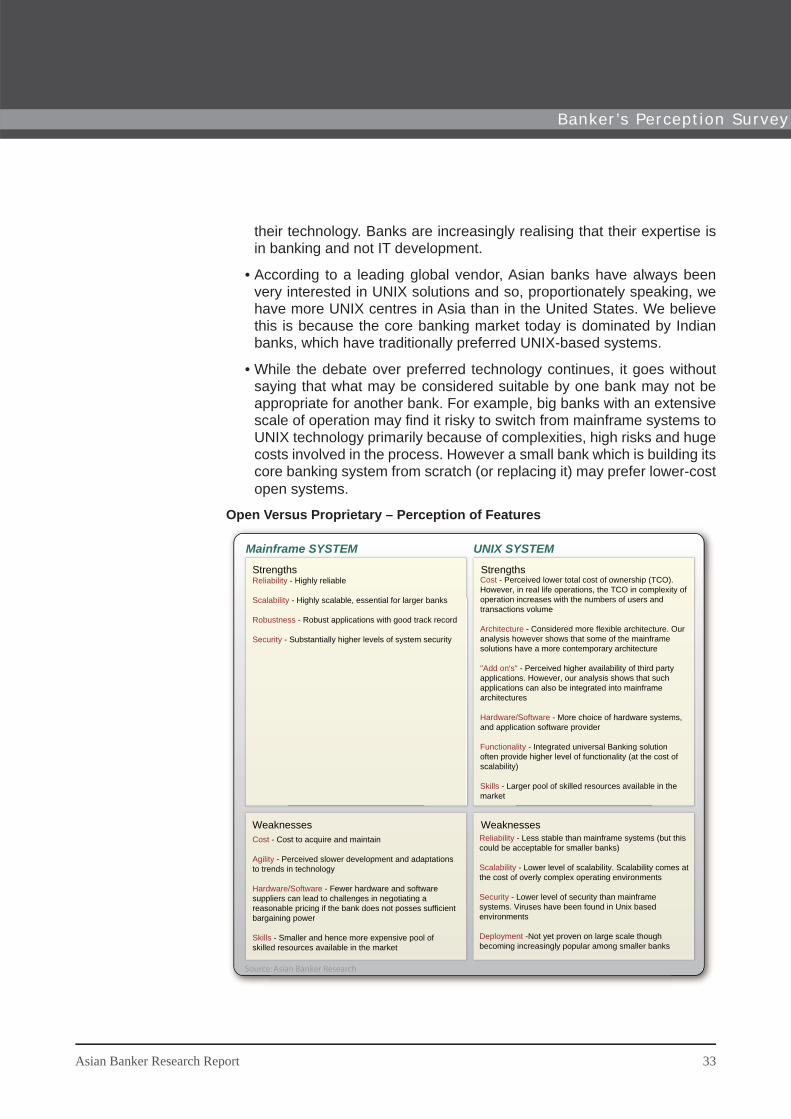

Open Versus Proprietary – Perception of Features

Strengths

Weaknesses

Strengths

Weaknesses

Reliability - Highly reliable

Scalability - Highly scalable, essential for larger banks

Robustness - Robust applications with good track record

Security - Substantially higher levels of system security

Cost - Cost to acquire and maintain

Agility - Perceived slower development and adaptations to trends in technology

Hardware/Software - Fewer hardware and software suppliers can lead to challenges in negotiating a reasonable pricing if the bank does not posses sufficient bargaining power

Skills - Smaller and hence more expensive pool of skilled resources available in the market

Cost - Perceived lower total cost of ownership (TCO). However, in real life operations, the TCO in complexity of operation increases with the numbers of users and transactions volume

Architecture - Considered more flexible architecture. Our analysis however shows that some of the mainframe solutions have a more contemporary architecture

"Add on's" - Perceived higher availability of third party applications. However, our analysis shows that such applications can also be integrated into mainframe architectures

Hardware/Software - More choice of hardware systems, and application software provider

Functionality - Integrated universal Banking solution often provide higher level of functionality (at the cost of scalability)

Skills - Larger pool of skilled resources available in the market

Reliability - Less stable than mainframe systems (but this could be acceptable for smaller banks)

Scalability - Lower level of scalability. Scalability comes at the cost of overly complex operating environments

Security - Lower level of security than mainframe systems. Viruses have been found in Unix based environments

Deployment -Not yet proven on large scale though becoming increasingly popular among smaller banks

UNIX SYSTEMMainframe SYSTEM

Source: Asian Banker Research

•

•

Asian Banker Research Report 33

Banker ’s Percept ion Survey

Open systems have proved their ability to perform from the security and technology points of view. According to one banker, “5-10 years ago a large bank would go for mainframe, no questions asked. But in the last 5-10 years things have changed. Any bank today, no matter how big, may consider switching to open system.”

On the other hand, most big banks still favour the reliability and stability of mainframes. Some bankers are inclined towards proprietary systems as they are used to working on them. Switching to a new technology would not only involve a huge amount of cost and high risks but also require effort to get used to the new processes.

According to one vendor, “Open systems are most appropriate for Asian banks due to their smaller size compared to many international banks. They don’t need the scalability of mainframes and the scalability of open systems has really increased in recent years.” One leading bank in Korea states that the trend in Korea today is to shift towards UNIX systems from IBM “due to the availability of small packages that can be easily integrated in our system [whereas] when we use mainframe we need to code them which would be a time consuming proposition”.

The right choice varies with banks’ requirements

As can be seen from the survey, platform choice is a dilemma that all bankers face when they consider replacement. Our in-depth analysis shows that for smaller Asian banks, a UNIX platform could be more feasible as they may not need the scalability of the mainframe and UNIX can be cost effective for a small number of transactions. However our research shows that for large retail banks, mainframe is likely to still be the preferred choice because:

It is more reliable and keeps the system running through most upgrades. Hence the downtime is low.

It has the capability to support a large number of users, supports multiple applications and allows better resource management. This is especially important where transaction volumes are high.

It requires less server capacity than UNIX for the same amount of work and has higher continuous availability (due to less downtime).

On the cost issue, UNIX-based systems are generally believed to have a lower total cost of ownership (TCO). However the benchmark, we believe, should not be total cost of ownership but total cost per user. Our research indicates that when the bank has large volumes of transactions and users, the operational cost of mainframe could be lower on a per-user

•

•

•

•

-

-

-

•

Strengths and weaknesses of proprietary and open systems, as perceived by respondent banks

Our research and analysis of the platform features reveal a different picture

34 Asian Banker Research Report

Banker ’s Percept ion Survey

basis. Also, while making the cost comparison, banks must consider the switching costs (shifting from existing mainframe to UNIX) and the cost of the coexistence of two systems during the replacement process.

Please see our section on platform choices in section 4 for more details

Asian Banker Research Report 35

Banker ’s Percept ion Survey

This page has been left intentionallly blank

3Core Banking System – An Overview

There are various defi nitions of “core banking system” circulating in the market. We have defi ned the core banking system (as we see it) and researched on aspects that are (and also those that are falsely believed to be) included in the replacement. This section provides an overview of the replacement and transformation process. We believe there should be clarity on the components of core banking system replacement even before the process is initiated.

Core Banking System – An Overview

3.1 Core banking system – an introduction and defi nition3.1.1 Defi nition of core banking system3.1.2 What to expect in core banking replacement3.1.3 Rationale for front-end systems replacement

3.2 Overview of the core banking system replacement project3.3 Approaches to replacement

3.1 Core Banking System – An Introduction and Defi nition

Core banking replacement is becoming a hot topic in banking. We have discovered that many banks are considering core banking system replacement because of the following perceived needs:

Ageing Technology Infrastructure – Ageing technology that is increasingly diffi cult and expensive to maintain and support

No Common Customer View – Multiple customer views and complex processes are not easily integrated with the existing technology infrastructure

No Product Factory – Innovative, highly interdependent product bundles are not supported by the existing core banking system; it is laborious to launch new products and services

Long Deployment Cycle – Technological infl exibility demands lengthy development cycles

No/Limited Basel II Support – New and more complex Basel II-driven risk frameworks are not supported

Due to such perceptions, the business users demand an immediate replacement of the core banking systems. Here are some examples of the justifi cation given for this investment to address all of these issues:

“We are losing market share. We need to replace our core banking system now to increase our competitiveness and regain lost markets.”

“We need to replace our core banking system to have a better understanding of our customer.”

“We need to replace our core banking system to be able to bring new products to the market faster.”

“We need a core banking-enabled product factory.”

These and similar statements are what we hear when talking to leading bankers throughout the region.

The software vendors of course are responding to these needs, by claiming:

•

-

-

-

-

-

•

-

-

-

-

•

Perceived needs justifying replacement of core banking system

38 Asian Banker Research Report

Core Banking System Overview

Core Banking System Overview

“Our system will transform your organisation and make your bank more competitive.”

“With our system, you will be able to signifi cantly enhance your CRM capabilities and gain market share.”

“Our solution will automate your lending process, improve your collateral management capabilities and make you Basel II compliant.”

The key questions which now arise are:

Are the bankers’ perceptions about the outcome of a core banking replacement correct?

Does a “traditional” core banking replacement project address all of these issues?

Do the statements made by software vendors truly refl ect what their clients can expect from a core banking replacement project?

To answer these questions, it is necessary to clearly defi ne what a core banking replacement really is

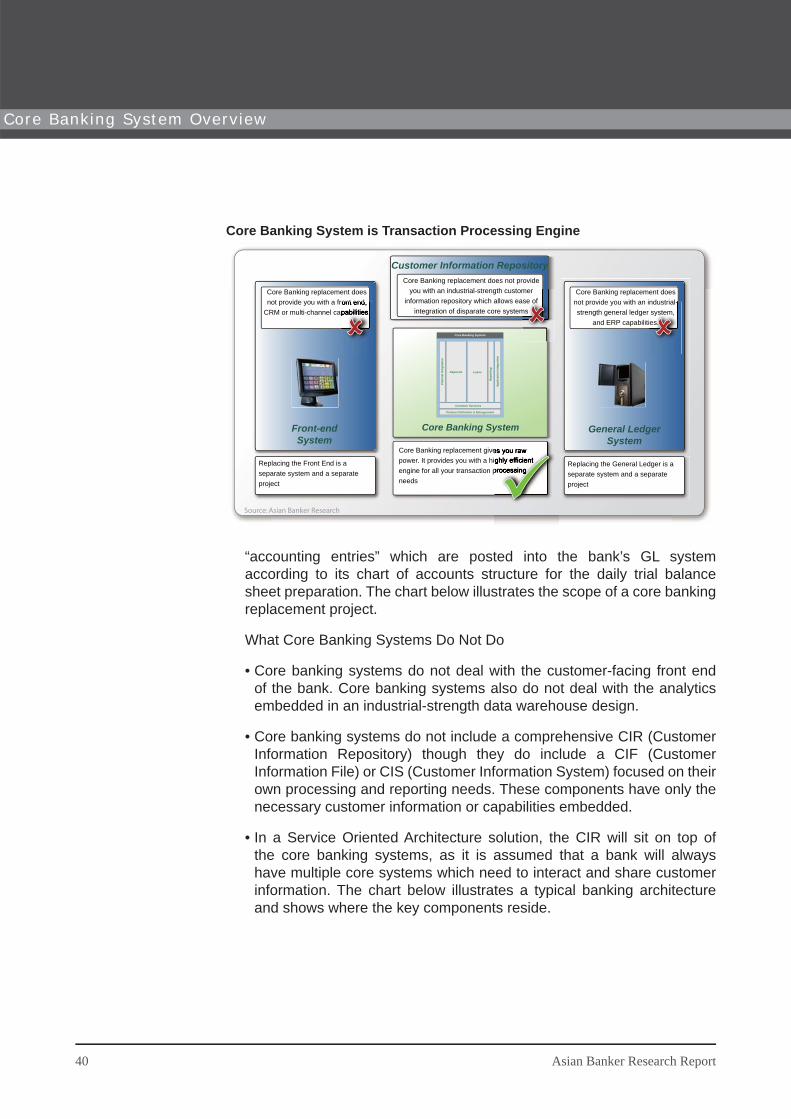

3.1.1 Defi nition of a core banking systemWe have discovered that there are multiple defi nitions of core banking systems today. However based on our discussions with industry experts, we can defi ne core banking, in simple terms, as a highly effi cient “customer accounting” and transaction processing engine for high volumes of back-offi ce transactions. The purpose of a core banking system is thus to give banks the ability to process large transaction volumes in a fast and effi cient way; clearing, transfers and interest/fee calculation are all the fortes of core banking. But let us explore this in more detail and look at some of the myths regarding core banking replacement projects.

What Core Banking Systems Do

A core banking system is a transaction processing engine with customer-level accounting and reporting of the deposit and loan products processed in the bank.

Core banking also deals with transactions such as interest and fee calculation, pre-processing for statement printing, end-of-day processing, and consolidation of daily individual transactions as

-

-

-

•

-

-

-

•

•

•

Core banking system is simply the core processing power of the bank

Asian Banker Research Report 39

Core Banking System is Transaction Processing Engine

Deposits Loans

Common Services

Product Definition & Management

Core Banking System

Cha

nnel

Inte

grat

ion

App

licat

ion

Inte

grat

ion

Rep

ortin

g

Core Banking replacement does not provide you with a front end,

CRM or multi-channel capabilities.

Core Banking replacement does not provide you with an industrial- strength general ledger system,

and ERP capabilities.

Replacing the Front End is a separate system and a separate project

Replacing the General Ledger is a separate system and a separate project

Core Banking replacement does not provide you with an industrial-strength customer

information repository which allows ease of integration of disparate core systems

Core Banking replacement gives you raw power. It provides you with a highly efficient engine for all your transaction processing needs

General Ledger System

Front-endSystem

Core Banking System

Customer Information Repository

Source: Asian Banker Research

“accounting entries” which are posted into the bank’s GL system according to its chart of accounts structure for the daily trial balance sheet preparation. The chart below illustrates the scope of a core banking replacement project.

What Core Banking Systems Do Not Do

Core banking systems do not deal with the customer-facing front end of the bank. Core banking systems also do not deal with the analytics embedded in an industrial-strength data warehouse design.

Core banking systems do not include a comprehensive CIR (Customer Information Repository) though they do include a CIF (Customer Information File) or CIS (Customer Information System) focused on their own processing and reporting needs. These components have only the necessary customer information or capabilities embedded.

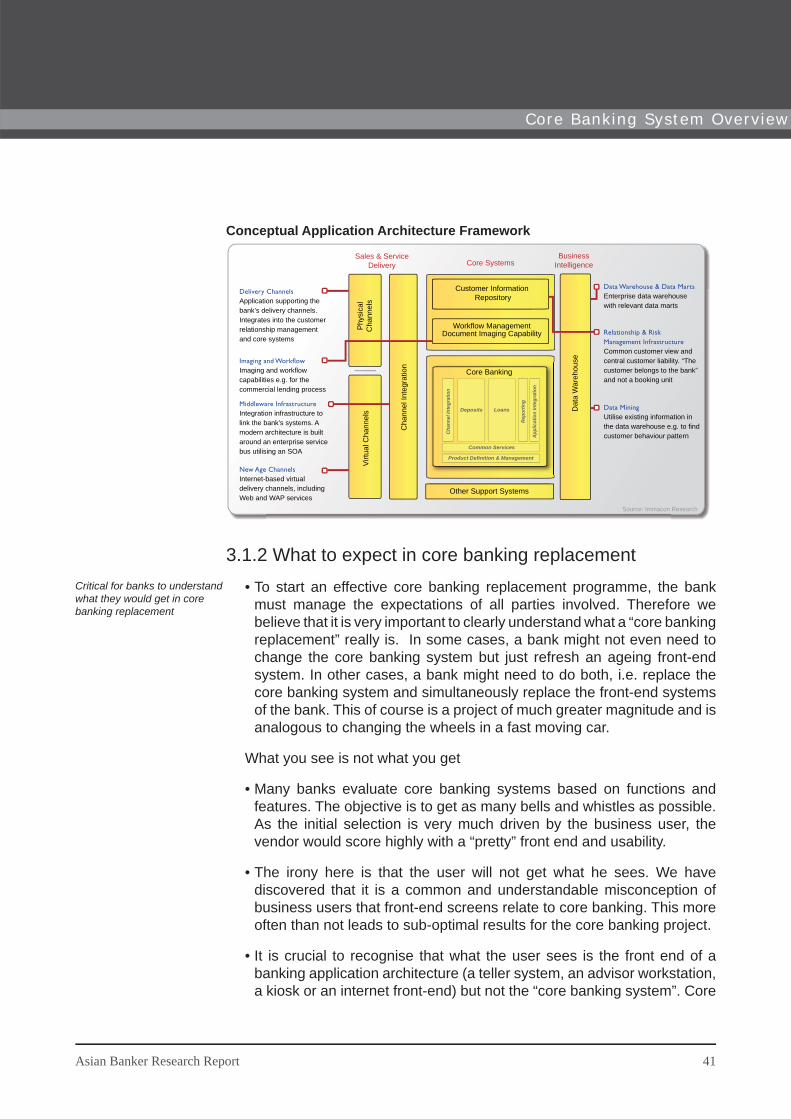

In a Service Oriented Architecture solution, the CIR will sit on top of the core banking systems, as it is assumed that a bank will always have multiple core systems which need to interact and share customer information. The chart below illustrates a typical banking architecture and shows where the key components reside.

•

•

•

40 Asian Banker Research Report

Core Banking System Overview

Conceptual Application Architecture Framework

Sales & ServiceDelivery

BusinessIntelligenceCore Systems

Delivery ChannelsApplication supporting the bank’s delivery channels. Integrates into the customer relationship management and core systems

Data Warehouse & Data MartsEnterprise data warehouse with relevant data marts

Relationship & Risk Management InfrastructureCommon customer view and central customer liability. “The customer belongs to the bank” and not a booking unit

Data MiningUtilise existing information in the data warehouse e.g. to find customer behaviour pattern

Imaging and WorkflowImaging and workflow capabilities e.g. for the commercial lending process

Middleware InfrastructureIntegration infrastructure to link the bank’s systems. A modern architecture is built around an enterprise service bus utilising an SOA

New Age ChannelsInternet-based virtual delivery channels, including Web and WAP services

Customer Information Repository

Dat

a W

areh

ouse

Cha

nnel

Inte

grat

ion

Phy

sica

lC

hann

els

Virtu

al C

hann

els

Other Support Systems

Workflow ManagementDocument Imaging Capability

Core Banking

Deposits Loans

App

licat

ion

Inte

grat

ion

Cha

nnel

Inte

grat

ion

Rep

ortin

g

Common Services

Product Definition & Management

Source: Immacon Research

3.1.2 What to expect in core banking replacementTo start an effective core banking replacement programme, the bank must manage the expectations of all parties involved. Therefore we believe that it is very important to clearly understand what a “core banking replacement” really is. In some cases, a bank might not even need to change the core banking system but just refresh an ageing front-end system. In other cases, a bank might need to do both, i.e. replace the core banking system and simultaneously replace the front-end systems of the bank. This of course is a project of much greater magnitude and is analogous to changing the wheels in a fast moving car.

What you see is not what you get

Many banks evaluate core banking systems based on functions and features. The objective is to get as many bells and whistles as possible. As the initial selection is very much driven by the business user, the vendor would score highly with a “pretty” front end and usability.

The irony here is that the user will not get what he sees. We have discovered that it is a common and understandable misconception of business users that front-end screens relate to core banking. This more often than not leads to sub-optimal results for the core banking project.

It is crucial to recognise that what the user sees is the front end of a banking application architecture (a teller system, an advisor workstation, a kiosk or an internet front-end) but not the “core banking system”. Core

•

•

•

•

Critical for banks to understand what they would get in core banking replacement

Asian Banker Research Report 41

Core Banking System Overview

banking is about raw processing power: transaction throughput, interest and fee calculation, parameterised product setup, clearing, interfacing with existing systems and transaction sources, etc. The good-looking screens have little to do with critical aspects of core banking and are no indicator for the quality of the core banking system.

3.1.3 Rationale for front-end systems replacementTo make matters more complicated, it is often important to also change the front-end applications, to better reap the benefi ts of the core banking replacement. For the front-end replacement, it is critical to make sure that the front-end applications can be integrated with the back-end systems with minimal effort. For a contemporary core banking and front-end replacement project, it is advisable to deploy SOA and an enterprise service bus.

To deploy a front-end solution for a new core banking project, there are three options:

Package solution with minimal customisation: This is typically the going-in position of banks that are accustomed to “best of breed” package implementations. The potential advantages are faster implementation and lower customisation costs. However, the bank that takes this approach must be determined to follow through and use the package capabilities as provided. Many banks fi nd it diffi cult to sustain this approach as the project progresses and the limitations of the package become clearer.

Package solution customised to the bank’s desired processes: This approach requires the bank to defi ne its multi-channel front-end operating model, processes and performance metrics prior to selecting the front-end package. The advantage of this approach is that the upfront design can help establish a realistic business case and give clear requirements for vendor selection and contracting. However, this approach requires experienced business process designers capable of defi ning the future operating model of the bank.

Custom built solution: This approach requires technical and business process designers capable of defi ning the future business and technical architecture to build and implement the solution. Few banks in the world are suitably equipped for such an undertaking at this time.

During package selection, the bank will typically need to choose from the following scenarios:

•

•

-

-

-

•

Banks may also need to replace front end to reap benefi ts from core banking replacement

42 Asian Banker Research Report

Core Banking System Overview