restricted general agreement l/7466 7 june 1994

TRANSCRIPT

RESTRICTED GENERAL A G R E E M E N T L/7466

7 June 1994 ON TARIFFS AND TRADE Limited Distribution

(94-1166)

Original: English

ACCESSION OF CROATIA

Memorandum on the Foreign Trade Régime

The following Memorandum on the Foreign Trade Régime has been received from the Government of Croatia. In order that the matter may be examined by the Working Party (L/7319/Rev. 1), contracting parties are requested to communicate to the Secretariat by 22 July 1994 any questions they may wish to put concerning the matters dealt with in the Memorandum, for transmission to the authorities of Croatia.

L/7466 Page 2

CONTENTS1

Page

I. Introduction 7

II. Economy and Foreign Trade 8

11.1 Economy 8

11.1.(a) General Description 8

ll.1.(b) Main Directions of Ongoing Economic Policies 11

ll.1.(b).1 Privatisation 13

ll.1.(c) Current Economic Situation 16

ll.1.(d) Division of Authority between Central and Local Governments 17

II.2. Basic Features of Foreign Trade of the Republic of

Croatia 18

ll.2.(a) Foreign Trade 18

ll.2.(b) Balance of Payments 19

II.2.(c) Foreign Debt of the Republic of Croatia 20

III. Instruments and Measures of the Foreign Trade System of the Republic of Croatia 21

111.1 The Law on Foreign Trade Operat ions 21

lll.1.(a) Entities Engaged in Foreign Trade 21

The contents of this Memorandum are based on the outline established by the Council of Representatives on 27 October 1993 and reproduced in document L/7317. However, it should be noted that some modifications had to be made to avoid repetition especially as some laws cover both exports and imports.

Due to the modifications it should also be noted that the numeric sequence of the contents of this Memorandum differs from the outline.

L/7466 Page 3

lll.1.(b) Engaging in Business Activities in Foreign Countries 22

lll.1.(c) Special Forms of Foreign Trade Operations 22

lll.1.(d) Long-term Production Co-operation 23

lll.1.(e) Compensation Agreements with Foreign Countries 23

lll.1.(f) Re-export Agreements 24

lll.1.(g) ^Services in Foreign Trade Operations 24

lll.1.(h) New Legal Requirements in Operations with Foreign Countries 25

lll.1.(i) Measures Against Unfair Trade Practices 27

lll.2.(a) Evolution of Customs Tariff Regulation 28

lll.2.(b) Customs Tariff Nomenclature, Types of Duties, General Description of the Customs Tariff Structure, Weighted Average Level of Duties on Main Customs Tariff Groupings 29

lll.2.(c) Import Charges and Fees 33

lll.2.(d) Taxation Regime 33

lll.2.(e) Tariff Preferences 34

lll.2.(f) Non-tariff Measures Applied to Imports and Exports of Goods 34

lll.2.(f).1 Quotas 34

lll.2.(f).2 Licences 35

lll.2.(g) Customs Valuation 35

lll.2.(h) Rules of Origin 36

lll.2.(i) Customs Formalities 37

lll.2.(j) Standards and Certification 37

lll.2.(k) Organisation of Inspection Services at Border Crossings in the Republic of Croatia 38

L/7466 Page 4 III.3 Expert Regulations

III.3.(a) Customs Tariff Nomenclature. Types of Duties, General Description of the Customs Tariff Structure, Weighted Average Level of Duties on Main Customs Tariff Groupings

l l l .3. (b) Rules of origin for Croatian goods

111.4 Incentives for Exports of Goods and Services

III.4.(a) Protective Measures

111.5 Regulations on Trade in Transit

IV. OTHER POLICIES AFFECTING FOREIGN TRADE

IV.1 Industrial Policy

IV.1.(a) Industrial Property

IV.1.(b) Copyright and Related Rights

IV.2 Agricultural Policy

IV.2.(a) System of Subsidies in Agricultural Production

IV.2.(b) System of Guaranteed Prices

IV.2.(c) Special Fees on Imports of Agricultural and Food (surtax)

IV.3 Financial, Budgetary and Fiscal Policy

IV.3. (a) Taxation Regime

IV.3.(b) Budgetary Policy

IV.4. Foreign Exchange System and Exchange Rate Policy

IV.4. (a) Law on Foundation of Foreign Exchange System, Foreign Exchange Operations and Gold Trading

IV.4.(a).1

IV.4.(a).2

IV.4.(b)

IV.4.(c)

IV.5

IV.6

IV.6.(a)

IV.6.(b)

IV.7

IV.8

IV.9

L/7466 Page 5

Home Currency Internal Convertibility 50

Home Currency Exchange Rate 51

Law on Credit Relations with Foreign Countries 52

Relationship of Croatia with International Monetary Fund 52

System of Foreign Investments in the Republic of Croatia • 54

Government Procurement 56

Government Purchases 56

Government Commodity Reserves 57

State Trading Enterprises 58

Free Zones 58

Subsidy Policy 59

V. INSTITUTIONAL BASE FOR TRADE AND ECONOMIC RELATIONS WITH THIRD COUNTRIES 60

V.1 Brief Description of Bilateral Trade and Economic Agreements and Integration Agreements 60

V.2 Multilateral Economic Co-operation, Membership in Multilateral Economic Organisations 61

ANNEX 1. LIST OF TRADE AGREEMENTS WITH THIRD COUNTRIES 62

A1.1 List of bilateral trade and economic agreements 62

A1.2 List I of international organisations of which the Republic of Croatia is a member 64

L/7466 Page 6

A1.3 List II of international organisations where Republic of Croatia has a different status

A1.4 List of multilateral economic agreements that Republic of Croatia has joined to date

ANNEX 2. Laws and Regulations

A2.1 List of laws and legai acts relating to trade and the market

A2.2 List of laws and legal acts relating to banking and foreign exchange operations

A2.3 List of laws and legal acts relating to the customs system (since 8 Octooer 1991)

ANNEX 3. MAIN ECONOMIC INDICATORS AND FOREIGN TRADE STATISTICS

A3.(a) Foreign trade statistics and agencies

A3.(b) Statistical publications

ANNEX 4.

A4.1 The Definition of small and medium-sized enterprises according to the Accountancy Law

ANNEX 5.

Privatisation Update - Croatia

L/7466 Page 7

I. INTRODUCTION

The process of transition from a socialist to a modern society based on political democracy and an open market economy was initiated in Croatia, when a multi-party system and the first multi-party elections took place in 1990, and the Republic of Croatia adopted a new" Constitution and declared its independence in 1991, . The Croatian Constitution has declared the right of ownership and entrepreneurship and the free market to be the foundations of the economic system in the Republic of Croatia.

The political aspect of the process of transition means not only the development of democracy and the rule of law, but also protection of human rights and freedoms, while the economic aspect includes privatisation and the opening of the economy to market forces and international competition.

These strategic goals cannot be met unless a legal and institutional framework is created that is compatible to frameworks existing in market economies in the international environment. Other conditions for the fulfilment of the strategic goals mentioned are macroeconomic stabilisation and economic restructuring as necessary prerequisites for the process of reconstruction, the dynamic growth of the economy and living standards together with socially, regionally and ecologically balanced development.

Concerning the accession of the Republic of Croatia to the General Agreement on Tariffs and Trade (GATT), the Council of Representatives established a Working Party at its meeting on the 27 October 1993 with the following terms of reference: "to examine the application of the Government of Croatia to accede to the General Agreement under Article XXXIII, and to submit to the Council recommenaations which may include a draft Protocol of Accession'1.

The following comprehensive Mémorandum constitutes the basis for the examination of the foreign trade regime of the Repuoiic of Croatia by the contracting parties of the General Agreement.2

The Memorandum describes measures ana legal provisions valid at the time of its preparation. Although the Republic of Croatia has already made many changes to its legal system in support of a market economy, some laws and regulations are still being revised. The Government of the Republic of Croatia will inform the contracting parties, through the GATT Secretariat, of any changes to tne foreign trade regime covered in this Memorandum

The information and statistics given are generally oasea on data up to the end of 1993, unless otherwise indicated.

L/7466 Page 8

II ECONOMY AND FOREIGN TRADE

i l .1. Economy

11.1.(a) General Description

The Republic of Croatia is a Centrai European and a Mediterranean country, with an area of 56,538 km2 and a population of 4,784,265 people. Croatia's most important natural resources are, first of all. the sea, with a well-indented coast suitable for the development of tourism, maritime activities, ports, and shipbuilding, then agricultural and rich forest areas providing the basis for food production and wood processing, also relatively important oil and gas fields ( annual production of 2 million tons of oil and 3 billion m3 of gas covers 70% of domestic needs) and finally, rich reserves of non-metal raw materials.

Croatia's geographical location provides a link between Western Europe and South-eastern Europe on the one hand, and Central Europe and the Mediterranean on the other, thus allowing for the development of different forms of transit transport.

Human capital constitutes the most precious potential for development since the people of Croatia are well-educated and trained and have a good industrial culture and tradition. Statistical data support this statement, as fully 69.5% of the 1.5 million working population have at least a secondary school education (53% hold a secondary school diploma and 16.5% hold a university degree).

In 1990, Croatia had a GDP of 15,910 million USD, or 3,350 USD per capita. Sectoral analysis of the economy shows the high and increasing importance of services. Industrial production is still important, although it recorded a fali over recent years, as a result of loss of markets and adjustments in relation to international competition and transition to a market economy. A decrease in building and construction activities, due to lack of investment, has also contributed to the decreasing share of industry in the Croatian economy. (See Table 1.)

TABLE 1. GDP Structure 1990. 1991. 1992.

GDP (factor prices), structure by sector 100.0 1. Agriculture 1* 10.6 2. Industry 2* 30.4 3. Services 59.0 a) Traditional 3* 25.0 b) Other 4* 34.0

100.0 10.2 26.5 63.3 24.0 39.3

100.0 10.6 25.0 64.4 21.8 42.6

Source: Estimates made by the State Institute for Macroeconomic Analysis and Forecasting (SIMAF)

L/7466 Page 9

*1 Includes agriculture, forestry, hunting and fishing and water resources management

*2 Includes mining, oil and gas production, processing industry and building and construction

*3 Includes trade, transport, catering, tourism and crafts M Includes financial and other business services, general government services

and housing and municipal utility services

Traditionally strong sectors of the processing industry, such as clothes, footwear, and food products together with shipbuilding and chemicals have maintained a significant share of Croatia's international trade. Services are another important sector of the Croatian economy, with tourism and maritime transport being especially well developed and earning important amounts of foreign currency ( net foreign currency inflows from tourism amounted to cca 1 billion US$ in 1990). Croatia has a very open economy, a fact illustrated by the total value of exports and imports within the GDP. The ratio was 90.8% in 1990 and 96.8% in 1993.

In recent years, major changes have taken place in the ownership structure of the economy with small and medium-sized enterprises expanding to fill the existing gap in the business sector (for the definition of small and medium sized companies according to the Accountancy Law, see Annex 4). The changes have been encouraged by a speeding up in the process of establishing new companies and privatising existing ones. (See Table 2.)

As a result of these changes, the private sector produced about 37% of the total value added in 1992 , and provided employment for about 40% of the total labour force, including the self-employed and farmers.

TABLE 2 Ownership structure of companies operating in the business sector of the Republic of Croatia

Dec. 1990. Dec.1991. Dec.1992. June 1993.

No. of comp. in the business sector 10.859 16,504 27,138 31,387

A. ownership structure: - private - socially-owned - mixed structure accord, to origin of caoitai - domestic - foreign and mixea - unknown

100.0 62.5 33.5

4.0

100.0 93.3

1.3 5.4

100.0 74.0 21.8

4.2

100.0 98.5

1.3 0.2

100.0 83.4 12.9 3.7

100.0 98.0

1.8 0.2

100.0 88.2

7.0 4.8

100.0 98.1

1.8 0.1

Source: Domestic'Payment Transfers Agency

L/7466 Page 10

The number of companies operating in mid-1993 was two and a half times greater than at the end of 1990, with the largest number of business start-ups in trade, financial and other business services.

The importance of the so-called "socially-owned" companies within the business sector is still considerable, especially with regard to the level of capital invested and that of employment as most of them are large and medium-sized companies. The number of social companies operating in the business sector fell from 33.5% in 1990 to a mere 7% in mid-1993 (See Annex 4, Table A4.2). Two thirds of these companies are in the process of being'privatised. The private sector has been expanding not only in regard to the number of companies but also in terms of capital, employment and overall activity. Therefore, its share of total capital employed amounts to 14.1%, share of employment is 34.2%, share in total business activity measured by revenues is 42.8%,wnile a 51.4% share in profits is a clear indication of its superior efficiency.

Although Croatia has created a very liberal legal framework, foreign investments remain relatively low, with 2,184 foreign investment deals valued at 617 million DEM registered in 1992 while the 1.276 foreign investment deals registered in the first haif of 1993 had a total value of 165 million DEM.

The overall performance of the Croatian economy has deteriorated due to the following factors: structural changes related to the process of transition to a market economy; loss of an important segment of former markets ( Eastern Europe and former Yugoslavia); impact of war ( destruction and blockade of one part of nfrastructurai and industrial installations, disruption of transport and other •nfrastructural links); and as a result of an increased risk factor. The fall of business activities was most evident in 1991, with negative trends slowing down over the following two years.

The cumulative fall in gross domestic product amounted to 24.6% in the period 1991-1993. War risk had a particularly disastrous impact on tourist activities, where results in 1993, although better than in the previous two years, only amounted to a meagre 25% of the prewar level. These developments caused the unemployment rate to double in comparison with the late eighties, as the growing private sector was unable to absorb the excess labour force. (See Table 3.).

L/7466 Page 11

Table 3. Main Macroeconomic Indicators

1991. 1992. 1993.

GDP (% change) ' industrial product. (% change) tourism (% change) rate of unemployment General Government deficit (%GDP). CAB (% GDP)"" CP (annual rate of change)

-14.4 -28.5 -80.7 15.5 -4.5 -4.3

249.5

-9.0 -14.6

5.6 17.8 -2.8 6.6

937.3

-3.2 -5.9 20.3 17.5 -1.2 2.4

1149.3

* GDP estimated by SIMAF ** CAB 1991 does not include newly established Republics on the territory of the

former Yugoslavia

Growing budget expenditure as a result of increasing expenses for defence, care for refugees and displaced persons, growing social benefits, coupled with the fall in tax revenues (due to a reduced taxable base) resulted in a considerable fiscal deficit.

Inflation strongly increased due to an increased disequilibrium both in the real and nominal sphere of the economy.

Croatian international economic relations to some extent reflect the negative trends present in the domestic economy. After a drastic deterioration in international economic relations in 1991, the following two years have seen a gradual improvement, mostly due to increased earnings in tourism and increased transfers from foreign countries. As a result, total foreign currency reserves increased and amounted to 1266 million USS on December 31, 1993.

Il.1.(b) Main Directions of Ongoing Economic Policies

Certain improvements in export demand during 1993 resulted in a slow down in the adverse trends present in the real sector of the economy, which were carried over from 1991 and 1992. In spite of this, inflation continued to accelerate, mostly due to increasing inflationary expectations.

Curbing inflation thus became the most important task of economic policy, as conditions encouraging the continued process of transition to a market economy, restructuring and growth had to be created. As monétisation of the public sector deficit was located as the main direct generator of inflation, a number of measures were taken in the course of 1993 to help implement the stabilisation program adoptea at the end of 1992. The measures were aimed at reducing the public sector deficit and improving the mechanism of monetary regulation.

L/7466 Page 12

The relative prices of basic infrastructurai products and services were increased in order to stop a deficit from being generated in the course of the regular operations of public enterprises. Also, the Government Office responsible for the economy and restructuring of public enterprises was established in order to improve the monitoring of public companies. Its main task will be to coordinate the preparation of new laws for basic public infrastructure activities as well as to work out a strategy for their -estructuring and eventual privatisation.

The process of monitoring expenses incurred in the health sector has also been improved, and accumulated debts have been partly dealt with. New laws on health care and health insurance have been passed, opening the way for privatisation with a view to increasing efficiency in health care sector operations.

Attempts have been made to balance the Government budget by reducing the tax rates, widening the tax base, abolishing the different tax exemptions, and strengthening the activities that reduce tax evasion. A new law on tax administration has been passed together with laws on financing the local tax administration and local self-government, personal income tax and profit tax.

According to new laws, personal income tax will be payable as one single tax. while profit tax will be payable in such a way that equity revaluation and interest on equity are not included in the tax base. Preparations for the introduction of the new value added tax are also drawing to a close, and the old turnover tax system wiil be replaced in the course of next year. The above changes will make the Croatian tax system fully compatible with tax systems in developed European countries.

Managing monetary flow has also been improved, with the so-called selective lending and budget deficit financing by the National Bank of Croatia being discontinued. Changes in the monetary base are now mostly related to the monétisation of foreign exchange transactions and to changes in the level of statutory reserves held by commercial banks. The National Bank of Croatia is also developing open money market activities in order to improve the regulation of overall liquidity. The new law on the National Bank of Croatia stipulates that it is an independent institution whose operations are controlled by Parliament and whose main task is to protect the value of the national currency.

Financial discipline will also be strengthened when commercial banks bring their operations in line with the new law on banks and savings institutions that introduces banking standards and criteria set by BIS and the European Union. Another factor contributing to financial discipline has been the introduction of international accounting standards and auditing procedures into the business sector with the new Accountancy and Audit laws. Still another important element has been the protection offered to creditors in the course of bankruptcy proceedings handled by the courts.

This was the macroeconomic, legal and institutional environment in October 1993 when the Government introduced strict measures aimed at radical disinflation. The measures included a tight monetary and fiscal policy, restrictions in nominal wage growth, and stabilisation of the foreign exchange rate through central bank

L/7466 Page 13

interventions in the foreign exchange market.

The new role of the central bank was made possible by the new Foreign Exchange Law, which stipulates that the foreign exchange rate is set by the foreign exchange market, while foreign exchange reserves accumulated in the course of 1992 and 1993 are considered to be adequate to ensure a satisfactory overall foreign exchange liquidity. In addition to the existing convertibility of current transactions, internal domestic currency convertibility for the household sector has also been introduced, and domestic legal entities are now allowed to hold foreign exchange accounts with domestic banks.

Although domestic prices of tradeable goods are expected to become stable due to a stable exchange rate, the present highly liberal trade system with very few goods on import quotas, relatively low average rate of customs duties levied and all barriers to entry abolished, will also play an important role.

The period to come will see further trade liberalisation coupled with application of international multilateral agreements, establishment of free trade areas with European countries and gradual integration into the European Community (Union).

The further liberalisation of the foreign trade system has been set up in tandem with liberalisation of the pricing system. The majority of prices are set by the market, the only exception being the prices of some utility services that are set by local authorities. Price ranges in the group of products and services that include wheaten flour, brown bread, and domestic postal and telephone services must be reported to the authorities. In 1993, the Government abandoned direct price control of infrastructural products and services, i.e. natural monopolies such as electricity, the most important energy products, rail transport, radio, television and telephone subscription and opted for indirect control through membership on the boards of directors of the enterprises providing these services.

The Government is determined to prevent monopolistic behaviour in the market especially for agricultural and food products where some limitations to trade still exist in the form of interventions from the State commodity reserves.

11.1.(b).1 PRIVATISATION

Privatisation of the economy is a priority among the goals of economic policy. Not only is a market economy with a dominant private sector one of the main strategic goals, but it is also essential to privatise existing socially-owned companies and banks if long-term stabilisation and integration into the international economic system are to be achieved.

Although Croatia has already committed itself to privatising its economy, there are some distinct differences that should be noted before any comparison is made with other Central and Eastern European countries undergoing a transition into a market economy. •

L/7466 Page 14

Firstly, Croatia had a strong private sector in the form of small handicrafts, shops, hair salons etc.. Although this sector was in contradiction to the former centrally planned economy it was somehow allowed to exist due to its strong tradition in Croatia

Secondly, State ownership officially did not exist due to the "self-management" system that introduced a so-called "socially-owned" status under the former economic system. Therefore, the new democratic Croatian Government could not conduct a privatisation process as an official "owner" but rather as a regulatory "care-taker" body that monitored the transition of ownership and partial privatisation of so called "socially-owned" enterprises.

Thirdly, in recognising that some former socially-owned enterprises fell into the category of public enterprises/utilities, the new democratic Croatian Government separated these from the list of "socially-owned" enterprises undergoing transformation and has allowed individual privatisation/restructuring programmes to be made for each of these entities.

The fourth and last issue that needs to be taken into account is that over 80% of Croatian land is privately owned.

As can be seen from the above facts Croatia has some clear advantages when compared to other Central and Eastern European countries in privatising its economy due to the presence of existing private ownership. Also, it should be noted that Croatian citizens were very much exposed to "Western" cultures through the tourist industry which has always been a traditionally strong sector. This exposure was not only evident through tourism but also through the far less restrictive international movements/travel of its citizens compared with other former "communist" countries.

Privatisation of socially-owned companies is being carried out according to the Law on the Transformation of Socially-Owned Enterprises, which was adopted in the first half of 1991, with the Croatian Privatisation Fund being the central institution responsible for the transformation and privatisation process. An autonomous privatisation process in Croatian companies can take one or a combination of any of the four forms included in the Law: sale of entire companies or parts thereof, additional capital investments in companies, debt equity swaps, and free transfer of all remaining company shares to the Croatian Privatisation Fund and to the two Pension funds.

The present law on privatisation does not deal with privatisation of public enterprises, banks, insurance companies, cooperatives, ports, marinas, hospitals and schools. Special regulations will be passed to deal with these.

The process of privatisation is open to all domestic and foreign natural persons and legal entities. Domestic natural persons enjoy a discount on purchase of a stake not exceeding 20,000 DEM, i.e. a total stake not exceeding 50% of company value.

The process of privatisation, i.e. owner identification, saw a slow down in 1991

L/7466 Page 15

due to the war, but continued in 1992 and 1993, so that the first stage of the process is now almost complete. Most small and medium-sized companies (48% of the total number of companies and 10% of their total value) have been fully privatised, 37% of medium-sized companies representing 48% of total company value have seen the CPF and Pension funds become their minority owners with a 30% stake in ownership. The remaining 15% are large companies. They represent 42% of the total capital invested. State funds are their majority owners, with a 52% stake in their capital.

The second stage of the privatisation process, which started in the course of 1993, was initiated by the Croatian Privatisation Fund selling shares held in its portfolio by organising auctions and inviting public tenders. Trading also started in the off-the-counter secondary stock market both with fully owned shares and with those not yet fully owned (purchased to be paid for in instalments).

A number of shares held by the Croatian Privatisation Fund will be used to compensate former company owners in the process of restitution, and a number of them will be distributed freely to certain groups of citizens.

The process of company privatisation is planned to be completed in the course of 1994 using a combination of flexible sales, other trading methods and free distribution of shares held in the Croatian Privatisation Fund portfolio. 1994 is the year in which the privatisation process in banks and public enterprises is scheduled to start.

Before the process of privatisation started, housing and other forms of accommodation were largely (75%) under private ownership. The process of privatisation has been extended to the remaining 25% of housing and accommodation which was classified as "socially-owned". To date over 40% of this category has also been transferred into private ownership.

Macroeconomic stabilisation and the privatisation of most companies are expected to create the conditions necessary for successful restructuring of banks and companies, which in turn should result not only in their increased competitiveness but also in the increased competitive strength of the whole economy in the global market.

The process of structural adjustments will encompass modernisation of traditionally strong industrial sectors, continued market entry of new small and medium-sized companies and liquidation of companies without orospects. At the same time, expenses created by reduced employment levels will be transferred from companies to the state, as it is the responsibility of the state to ensure a well-developed network of social benefits so that social tensions cannot impede the restructuring process.

New legislation of companies, labour and related fields will come into force during 1994 and 1995 and will provide a legal framework compatible with international standards, thus creating prerequisites for the development of all the labour and capital market institutions needed in a fully operational market economy, and also ensuring

L/7466 Page 16

the flexibility necessary for the smooth running of the structural adjustments process.

Foreign investments are considered to be a very important element of economic restructuring and reconstruction. That is why the entire legal and macroeconomic framework will be geared towards ensuring liberal, stable, and encouraging conditions for all kinds of foreign investments.

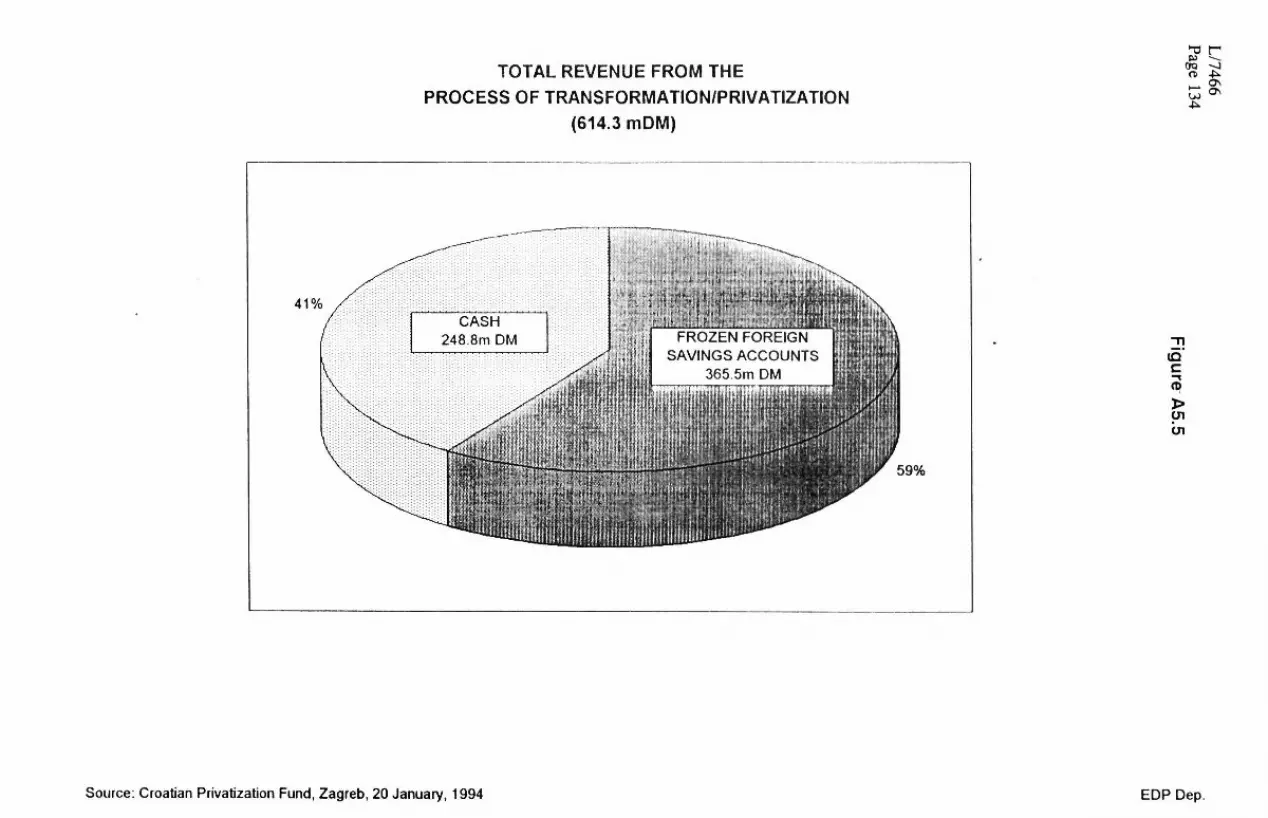

Please refer to Annex 5 for a privatisation update of former "socially-owned" enterprises.

11.1. (c) Current Economic Situation

The economic situation in Croatia at the end of 1993 and at the beginning of 1994 had developed under the decisive influence of Government anti-inflationary measures introduced in October 1993. Factors relating to ownership restructuring and to structural anomalies still present in Croatian production and consumption were also influential. Another influence contributing to difficulties was the recession in the most important Croatian export markets.

Due to the introduction of a tight monetary and fiscal policy supported by income policies, i.e. the abandonment of the backward looking indexation of wages, exchange and interest rates, inflation was drastically reduced from a monthly increase of 40% in October to 1 % in November and -0.5% in December 1993.

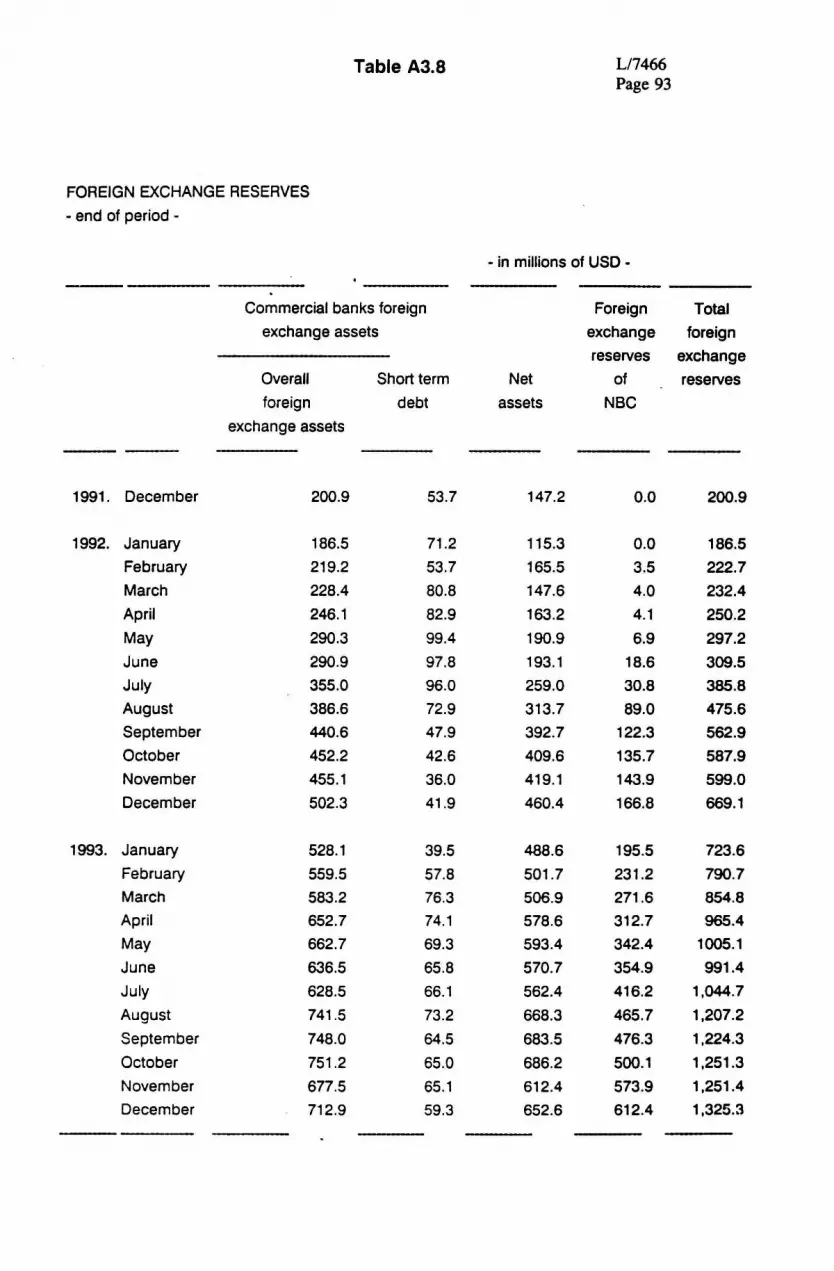

Another important factor in curbing inflation was the stabilisation of the foreign exchange rate in the foreign exchange market due to an increased supply of foreign currency from the domestic sector, as a result of a heavily reduced overall dinar liquidity. Inflows of short-term foreign capital resulted in increased foreign exchange reserves held by the monetary sector in spite of the current account balance deficit.

The increased high demand for money induced by disinflation and coupled with a restricted money supply resulted in high real-term interest rates. A high disinflation has had no substantial adverse effects on production and employment levels as they are predominantly determined by structural factors.

Overall production levels have been levelling off due to low exports and weak home demand. Employment has been falling in the non-privatised business sector and has levelled off in the government services sector. Employment has been increasing slowly in the private sector.

There have been no major changes in the official unemployment figures, mostly due to the considerable level of employment in the informal sector of the economy. However, the process of company restructuring, coupled with bank rehabilitation in the second stage of the stabilisation program implementation, is bound to spur the gradual transformation of presently hidden unemployment into officially declared unemployment levels.

L/7466 Page 17

11.1. (ci) Division of Authority between Central and Local Governments

The Republic of Croatia has set up a system of local self-government and administration based on the European Charter on Local Self-government and following the referendum in local communities held at the end of 1992. The new system introduced decentralisation in the field of public services, and vertical integration in administrative services, thus separating state administration operations on the local level from local self-government.

Within the system of local self-government and local administration twenty-one regions, called "Counties"(including the City of Zagreb) have been introduced. The boundaries of these administrative units are based on historical, communication and economic characteristics.

Counties are not only the local centres of state administration with responsibility for carrying out decentralised administrative tasks, but are also the centres of local self-government. Here the interests of municipalities, towns and districts are being harmonised with a view to encouraging economic and social development and satisfying common public needs at the level of lower self-governing units and of entire regions.

Municipalities (419), towns (68) and special self-governing districts (2) are defined as local self-governing units, where the needs and interests of the local population are being considered. Residents of an inhabited area or parts thereof, may start a local council as a form of local self-government, where they participate directly in the decision-making process on common local issues.

State administration activities performed in local units of self-government and administration are financed from the State budget. Activities within the field of local self-government (i.e. local level public needs) are financed from the budget of the local self-governing and administrative unit. In cases where the fiscal revenues available are not adequate, or local needs are of importance for a wider community, co-financing from the central government budget will be provided either via transfers to the local government budget or via direct financial support to public institutions.

While a certain number of public services are the responsibility of the centrai government ( national defence, international relations, the system of customs, retirement and disability insurance, the judiciary system, economic policy and infrastructure on the state level), a large number of services are provided at the local level, with the authority for and financing of a certain number of public services being divided between the central and local governments (police, education, health care, housing, social welfare, urban planning, and granting concession rights). Finally, some public services are the sole responsibility of local administration (local urban development planning, environmental protection, building permits and land rates, fire protection, local transport and other local utilities, preschool education, sports and recreation, and cultural activities).

L/7466 Page 18

Financing of local public services within the scope of their authority is derived from the following sources: income from their own assets (companies owned by them, concession rights granted), local taxes (regions collect tax on inheritances and gifts, tax on motor vehicles and vessels, and tax on entertainment and sports events, municipalities and towns collect turnover tax, property tax and advertising tax, districts collect special district taxes and fees in accordance with separate legal provisions). Certain taxes are divided between the central government and local government units in the following way: counties are entitled to 5% of income tax, and 10% of profit tax. municipalities and towns to 25% of ipcome tax, 20% of the profit tax, 50% of the tax on gains from games on chance, and 60% of the tax on real estate transactions, and cities with more than 40,000 inhabitants may introduce an additional rate on income tax up to a certain limit. Local administration revenues will also include cash penalties and confiscated profit on illegal dealings defined by them, administrative dues, communal and other fees for use of municipal or city installations, institutions or land, transfers from the State budget and other revenue following special legal provisions.

II.2. Basic Features of Foreign Trade of the Republic of Croatia

II.2.(a) Foreign Trade

The trade balance of the Republic of Croatia showed a deficit from 1990 to 1993. As a result of 1991 and 1992 imports decreasing faster than exports in the same period, the coverage of imports by exports increased from 77.5% in 1990 to 103.1% in 1992. Exports were again reduced in 1993, while imports went up, so that coverage of imports by exports was down again to 83.7%. The balance of services has traditionally been favourable (due to considerable inflows from tourism and maritime transport), and the surplus has been used to cover the commodity balance deficit. However, the income from exported services was halved in 1991 due to the war, and the surplus in the balance of services fell accordingly, so that the goods and non-factor services balance recorded a deficit of 499 million US$. As the political and economic situation gradually improved in the course of 1992, exports of services were on the increase again while imports went down, with the resulting surplus in the balance of services ensuring a 560 million US$ surplus on the goods and non-factor services account. In the course of 1993 the goods and non-factor services account again showed a deficit due to a considerable deficit in the commodity trade amounting to 762 million US$. The measures taken to intensify exports of services, although successful especially in tourism, were not sufficient to cover the deficit on the commodity trade side.

An analysis of trade in goods shows that two thirds is realised with developed countries, with the European Community currently being the most important partner and absorbing cca 50% of total trade. Croatia's current most important foreign trading partners are Germany and Italy. The beginning of this decade saw a reduced volume of trade with Eastern European and developing countries. The same was true of trade with the republics of former Yugoslavia, although Slovenia still remains one of the

L/7466 Page 19

Croatia's most important foreign trade partners.

The commodity structure of trade shows that finished textile products, footwear, wood processing, chemical and food products are the most important. An important volume of trade is also recorded in machine products and transport equipment, with shipbuilding dominating exports, and machines and vehicles dominating imports. Imports of oil and gas are also important. The most important changes recorded in the structure of trade in 1992 and 1993 are the fall in exports from shipbuilding due to increased risks, and the fall in imports of energy products due to a drastic decline in domestic economic activity.

II.2.(b) Balance of Payments

The most prominent features of current transactions in the balance of payments of the Republic of Croatia are: an adverse balance in commodity trade with foreign countries, net outflows due to interest payments, revenues exceeding expenditure in services, and a favourable balance on transfers. In the sector of lending activities and financial transactions, a considerable net outflow of capital was recorded in the course of 1990 and in the first half of 1991.

Developments in the Croatian balance of payments in 1992 reflected the overall developments in the economy of the country.

Favourable results were recorded in foreign trade, especially in imports and exports of goods, although the total volume of goods traded was much lower than in previous years.

A net inflow of foreign currency from private transfers was recorded, mostly due to increased purchases of cash by banks as the purchasing power of the population went down, but also due to the sale of socially-owned flats for cash, then to aid, gifts, and finally foreign remittances paid into foreign currency accounts held by citizens. The National Bank of Croatia started building its foreign currency reserves in 1992, while current foreign currency assets of business banks also increased. As all the foreign currency reserves that existed in former Yugoslavia remained deposited with the National Bank of Yugoslavia at the time of the demise of the federation, the Republic of Croatia started its monetary independence without any foreign currency reserves held by its centrai bank.

In the first nine month of 1993 there was a current account deficit of 75.7 million US$ on the balance of payments, while the same period of the previous year recorded a surplus of 331.1 million US$. The deficit was caused by an important adverse balance in the commodity trade, (see Annex 3)

The period under scrutiny saw revenues from services amount to 1,323 million US$, which was a 26% increase over the same period in the previous year. Expenses increased by 21% in the same period.

L/7466 Page 20

Medium and long-term foreign loans used in the first nine months of 1993 amounted to 84.5 million US$, i.e. the increase over the same period in the previous year was cca 112%. Of the total amount lent, 88.2% was used to import equipment, only 3.8% to import materials and 7.8% was received in cash.

In regard to the medium and long-term foreign loans, 248.6 million US$ of principal came due for repayment in 1993. 151.8 million US$ was repaid, which is 51.5% more than the amount repaid in 1992. As 96.8 million US$ remained unpaid in 1993 and 384.2 million US$ remained unpaid in the previous years, the total overdue and unsettled amount equals 484.2 million US$.

The balance of capital transactions at the end of September 1993 indicated a net outflow of capital totalling 101.6 million USS as a result of large instalment payments rather than the use of medium and long-term loans.

II.2.(c) Foreign Debt of the Republic of Croatia

The foreign debt of the Republic of Croatia amounted to 2,548 million US$ on 30 September 1993. The debt maturity structure is relatively favourable, as 2,483.3 million US$ or 97.5% of the debt are medium and long-term loans, and 64.7 million US$ or 2.5% is a short-term loan due within a year.

Of the amount mentioned. 347.8 million US$ is owed to international financial institutions, 1,016 million to governments and government agencies and 1,184.2 million US$ to private creditors.

Of the amount owed to governments and government agencies, 690 million US$ in loans has been rescheduled and refinanced.

Of the amount owed to private creditors, 967.6 million US$ are refinanced loans to commercial banks.

The above should not be considered a final account of Croatian indebtedness as negotiations on the succession regarding assets and liabilities of former Yugoslavia have not yet been concluded.

L/7466 Page 21

III. INSTRUMENTS AND MEASURES OF THE FOREIGN TRADE SYSTEM OF THE REPUBLIC OF CROATIA

111.1 The Law on Foreign Trade Operations

The foreign trade system of the Republic of Croatia and its legal regulations stipulate the conditions, limitations and benefits of trading in goods and services with foreign countries, as well as stipulations regulating payments with foreign countries. As in any foreign trade system, the essence is in the measures - instruments to be applied in dealings with foreign countries. These measures have been elaborated in the Law on Foreign Trade Operations and in the appropriate by-laws.

Following the requirements of constitutional law, the Republic of Croatia took over the Law on Foreign Trade Operations from the legal system of former Yugoslavia, and the same law became effective as part of the legislation of Croatia on 7 October 1991.

The Law was not altered until November 1993, when the Parliament of the Republic of Croatia passed alterations and amendments to the Law, with the aim of introducing further liberalisation of imports into the Republic of Croatia.

The Company Law, passed by the Parliament of the Republic of Croatia in November 1993, derogated the stipulations of the Law on Foreign Trade Operations concerning the status of legal entities engaged in foreign trade as well as stipulations setting special requirements for those entities engaged in the same operations.

Foreign trade operations are defined as operations between legal entities with a registered office in the Republic of Croatia and legal entities with a registered office in a foreign country. These operations may be performed by legal and natural persons (traders, sole traders and companies) engaged in economic activity in accordance with the Company Law, i.e. provided they have been entered in the court register.

Ill.1.(a) Entities Engaged in Foreign Trade

All companies and traders prope.ly founded and registered in accordance with the Company Law may engage in foreign trade operations.

Earlier restrictions regarding special requirements when dealing in foreign trade and when registering for foreign trade operations have been abolished by the Company Law (Article 648 of the Comoany Law).

Foreign companies and traders (foreign persons') are subject to the same legal rreatment as domestic companies and persons in their operations in the territory of the Republic of Croatia.

L/7466 Page 22

Foreign persons may operate through companies founded abroad or through subsidiaries founded in Croatia in accordance with the Company Law.

Subsidiaries are founded in accordance with the general and specific provisions of the Company Law, and on condition of reciprocity.

The earlier obligation to found a foreign representative office in order to engage in operations in the Croatian market has been abolished (Article 648 of the Company Law).

ill.1.(b) Engaging in Business Activities in Foreign Countries

Croatian business people and their associations, banks, insurance ana reinsurance companies are free to engage in business activities in foreign countries either by founding companies, subsidiaries, business units and representative offices or by investing in foreign companies in accordance with the legal requirements of the country where the business activity is to take place.

The Law requires that a company wishing to engage in business operations in a foreign country must be entered in the register held by the Ministry of Economy. The Ministry will require data on the company founder, amount and sources of founders' equity, and data on the person responsible for operations in a foreign country. The founder is also required to submit a registration document, and articles of association or a charter, i.e. a legal document testifying to the legality of the company's operations abroad.

A company operating abroad is required to inform the founder of the results of its operations abroad, to send its annual report to the Domestic Payment Transfers Agency, and to transfer the profit earned abroad into the Republic of Croatia, unless it is being used for business purposes abroad.

The Law requires that a company operating abroad be deleted from the register if foreign regulations permanently prevent transfer of profits, if the company has to discontinue operations following the legal requirements of the country where it was founded, or if no transfer of profit to the Republic of Croatia has taken place in the course of the two years following the company foundation.

IIM.(c) Special Forms of Foreign Trade Operations

Foreign trade operations encompass not only import and export of goods and services, but also some special forms of foreign trade operations. According to the Law, special trade operations are especially long-term production co-operations, compensation deals with foreign countries and re-exporting arrangements with foreign countries.

L/7466 Page 23

lll.1.(d) Long-term Production Co-operation

The Law allows domestic entrepreneurs to enter into contracts for long-term production co-operation with foreign persons. The contracts must be in writing and for a term not shorter than three years. The value of export transactions covered by the contract must be at least equal to the value of import transactions covered by the same contract.

At the same time, legal provisions on foreign exchange operations allow payments and collections on imports and exports of goods and services covered by a long-term co-operation contract to be made via a current account.

During any given year, debit or credit balances on the current account may not exceed 40% of the amount of goods and services delivered as imports and exports in the previous year.

All contracts on long-term production co-operation, as well as all alterations and amendments to these contracts, must be entered into the register kept at the Ministry of Economy, and the application for registration must be submitted not later than 30 days after the contract was signed.

It is the obligation of the Ministry to enter the contract into the register in the course of 30 days after the application was submitted. In cases where the contract has not been entered in the course of 30 days, it will nevertheless become valid 30 days after the registration term has expired.

Goods that are the object of a contract for long-term production co-operation, and fall under the regime of import-export quotas or licences, are not automatically exempt from quotas, but an approval for import or export will be issued by the Ministry and it will be valid as long as the contract has not expired. It must be pointed out that the principles of non-discrimination and national treatment were respected in this case, fallowing Articles I and III of GATT.

Ill.1.(e) Compensation Agreements with Foreign Countries

Compensation agreements with foreign countries are aeals involving exports of goods and services which are paid for by imports of goods and services of equal value. The deals are contracted with foreign entities in cases of exports to countries experiencing balance of trade difficulties, when no other form of collection for goods and services exported can be applied, and in cases of import of equipment to be used in production of goods to be later exported, when payment will be made by exports of goods produced on the equipment or Dy sen/ices rendered with the equipment being imported.

Compensation Oeais with foreign countries have to be accrovea by tne Ministry of Economy.

L/7466 Page 24

Detailed stipulations regarding conditions of entering a compensation deal have oeen necessary in order to ensure collection for all exports of goods and services in foreign currency, which is of the utmost importance for the balance of payments of the country.

In practice, compensation deals are being given approval depending on the structure of goods imported and exported and their price and purpose, and are being carried out in accordance with general and specific foreign trade, foreign exchange and customs regulations. In other.words, the deals are not exempt from volume restrictions, customs duties, obligations to the central bank etc..

In the process of approving and carrying out compensation deals with foreign countries, the fundamental GATT principles of non-discrimination and national treatment of imported goods are being observeo.

Ill.1.(f) Re-export Agreements

Legal entities in the Republic of Croatia are allowed to purchase goods abroad with the intention of selling the same goods abroad, either directly or through temporary import of goods into Croatia and consecutive export. Such goods may be re-exported unchanged, or essentially changed or reworked. Re-export deals require the approval of the Ministry of Economy.

The Ministry will not approve a re-export deal only if it is suspected that the deal might violate international trade rules and principles of fair trading.

Ill.1.(g) Services in Foreign Trade Operations

The Law recognises the following services in foreign trade operations: completion of construction projects abroad, cession of construction projects in the Republic of Croatia to foreign entities, international cargo transport, international forwarding, catering and tourist services, agency and representation services, factoring services, attestation, etc.

Domestic entrepreneurs entering into contracts for construction projects abroad may purchase equipment needed for completion of the projects in the same foreign country, and import the same equipment freely into Croatia when the project has been completed or the equipment is no longer needed. Import duty will then be paid only on the non-depreciated asset value in accordance with the customs regulations of the Republic of Croatia.

Foreign entities may engage in construction projects in the Republic of Croatia, provided the engagement is a result of a public invitation for tenders in accordance with the regulations stipulating public auctions and invitations for public tenders in the Republic of Croatia.

L/7466 Page 25

All contracts for construction projects to be completed abroad or by foreign entities in Croatia will be entered into a special register kept by the Ministry of Economy. Other services in foreign trade are performed freely, without obligation to report to authorities and in accordance with the contract entered into by the parties concerned.

Ill.1.(h) New Legal Requirements in Operations with Foreign Countries

New laws that are being gradually introduced in the Republic of Croatia, with the most important changes being laid down in the Company Law, will introduce changes in the field of trade, and especially in the field of transactions with foreign countries.

The new Law on Trade is being prepared and will set common criteria for trade transactions, either at home or abroad, thus abolishing the artificial division of trade into foreign and domestic, since all trade is a single economic activity.

Liberalisation and simplification of procedures in foreign trade transactions are the most important characteristics of the Draft Law concerning import-export deals. Unnecessary licences, approvals and register entries are being abolished for certain types of foreign trade contracts (construction contracts for projects completed abroad, cession of domestic construction contracts for projects to foreign entities, sales contracts from consignment stock, agency contracts etc.)

A foreign trade regime cannot but mirror the current development stage of the national economy and accompanying foreign trade policy. That is why the new legal framework being introduced in Croatia necessarily combines principles of free trade with drastically reduced levels of central administration intervention policies, i.e. new legislation is being adapted to the current development level of the Croatian economy. Another achievement of the new legal framework is the reduction of central administration bodies involved in the necessary regulation and monitoring of foreign trade transactions. The streamlining of operations should increase not only the effectiveness and transparency of necessary operations but also the legal protection offered to all those participating in transactions.

It is envisaged that the legal framework set for international trade in Croatia wiil change in the future in order to reflect the progress achieved in the process of transition and the development of the Croatian economy with its further integration into international trade. The role of the central administration will gradually be reduced, and the Trade Law stipulations concerning international dealings should be regarded as temporary solutions. This is particularly true of stipulations that were, of necessity, taken over from the old legislation.

L/7466 Page 26

The following are the basic features of the new foreign trade legislation:

1) No special registration is required when engaging- either in import-export deals or in other business transactions with foreign countries. Trade is considered to be a single activity and is not divided into foreign and domestic trade, thus making special foreign trade regulation superfluous.

2) Detailed legal regulations are provided only for the foreign trade operations that are exempt from the general principle of free trade (compensation deals with foreign countries) as well as for transactions that have been given preferential treatment, such as long-term production cooperation, imports of equipment treated as foreign investment, imports of equipment purchased abroad in order to complete a construction project abroad, etc.

3) Licence requirements for re-export transactions are being abolished. Record keeping of agency and representation contracts entered into with foreign partners has also been abolished, and the Ministry of Economy does not require registration of services performed in foreign trade.

4) Procedures for starting up a company abroad are being simplified. Croatia must, like any other country, monitor the outflow of capital from the country, and that is why the Ministry of Finance has been given the authority to issue approvals for company start-ups abroad as well as for investments in foreign companies.

5) The Government of Croatia may, in cases it considers necessary, set quotas on imports and exports, but this measure has ceased to be its obligation, while the existing regulations view quotas as a measure aimed at protecting home industry.

6) Passing protective and other regulations that are in full compliance with the principles declared by GATT.

7) Acquisition and cession of the right of industrial property and know-how has ceased to be part of foreign trade legislation.

8) Regulation of temporary imports and exports of goods and regulation of import-export rights granted to citizens have been taken over from existing legislation.

9) Exports of goods and services will be enhanced by means of indirect instruments and measures incorporated in the economic and development policy, and only exceptionally will direct incentives, such as tax and customs refunds, be applied.

L/7466 Page 27

lll.1.(i) Measures Against Unfair Trade Practices

Work on the Law on Competition and Monopolies is in progress.

The draft law deals with conditions prohibiting restraints on trade, exemptions, monopolistic practices, and abuses from dominant position and mergers.

The legal stipulations will apply to all private and public persons and legal entities engaged in business activities in the domestic market and to foreign persons, in case their actions have an impact on the territory of the Republic of Croatia.

Prohibitions incorporated in the law do not apply to export cartels.

Basic prohibitions incorporated in the law are the following:

General prohibition on prevention and restrictions of freedom of competition by means of contracts, agreements, and through actions agreed upon by companies or associations of companies;

Special cases include:

- direct or indirect price agreements, - division of market or supply sources. - tying arrangements, - limitations on production, sales or purchases, - limitations on or hindrance of research and innovation activities,

restrictions regarding access to the market or exclusion from trade imposed on companies that are not parties to agreements, co-ordinated actions or associations.

Exemptions from general ana specific Drohibitions are provided by:

A general clause (rule of reason) stipulating the means and terms of application in cases of non substantial restrictions and

Block exemptions selected following the example of the EEC regulations (contracts for exclusive and selective distribution, franchising, joint ventures, research and development)

Horizontal agreements and group boycotts aimed affixing prices and dividing the market by area or by buyer are Drohibited per se.

Monopolistic intentions and abuse of a dominant market position are prohibited

L/7466 Page 28

The notion of market power is defined together with criteria for establishing its existence

A dominant market position is defined as existing in cases of market share exceeding 30%.

Special cases of aouse are defined within the proposed Law.

Mergers subject to prohibitioa are aiso defined within the proposed Law.

The Competition Protection Agency will be the body responsible for the implementation of the law, with the structure and operations of the Agency being defined by the Law on Competition and Monopolies.

III.2.(a) Evolution of Customs Tariff Regulation

The Parliament of the Republic of Croatia passed, by its decision effective from 8 October 1991, the Customs Law, the Law on Customs Tariff, the Law on Customs Administration and the Law on Free Zones, which, together with corresponding by-laws, constitute the legal framework of the system of customs protection in the Republic of Croatia.

Basic definitions incorporated in the Customs Law express elements of the independence of the Republic of Croatia, i.e. the regaining of responsibilities that were, in the previous period, transferred to the federal bodies of the former Socialist Federal Republic of Yugoslavia.

The Customs Tariff of the former SFRY was used until 15 January 1992, when the Customs Tariff of the Republic of Croatia became effective, following the Decision of the Government of the Republic of Croatia.

The Republic of Croatia has amended and altered the legal framework of the customs protection system inherited from the former SFRY, with a view to making the system compatible both with the contemporary customs regulations of developed countries and with its own specific needs. The new system should enhance the economic development of the Republic of Croatia and minimise the adverse effects of the current difficult economic and political circumstances.

The basic principles underlying the system of customs protection are the following:

a) free and unobstructed exchange of goods with restrictions strictly confined to protection of domestic production and market;

b) acceptance of all international contracts, agreements and other documents that are part of the system of customs and

L/7466 Page 29

non-customs protection signed and ratified by the former SFRY, provided they are not in collision with the Constitution of the Republic of Croatia and are not harmful to the economy or the market of the Republic of Croatia.

c) application of non-discriminatory solutions regarding regulation and monitoring of international transport of goods, objects and people, provided such solutions are common to global foreign trade practices and are related to establishing the customs base, customs obligation, customs clearance procedure, documents to be supplied in cases of imports, exports, or transit, and the definition of customs institutions incorporated in the customs system;

d) the entire territory of the Republic of Croatia constitutes a single customs area, and the system of customs protection is an integral part of the overall integrated system of protection of the economy and the market of the Republic of Croatia;

lll.2.(b) Customs Tariff Nomenclature, Types of Duties. General Description of the Customs Tariff Structure, Weighted Average Level of Duties on Main Customs Tariff Groupings

Imported goods are grouped in the Customs Tariff into 21 sections, 97 chapters, 1241 heading numbers, about 4700 sub-heading numbers and about 6600 H.S. codes, which are used to simplify the process of grouping and are oased on the International Convention on the Harmonised Commodity Description and Coding System and Explanatory Notes issued by the Council for Customs Cooperation in Brussels.

All goods and objects imported, entered or received in the customs area of the Republic of Croatia are liable for customs duty , unless the same Law or the Law on Customs Tariff stipulates otherwise. Customs payment liability and customs duty rate levels are set for protective purposes oniy.

The new tariff is intended for use in trade with the contracting parties of GATT ana with the signatories of the most favoured nation clause, i.e. the countries that apply the same clause to imports of goods of Croatian origin.

Nominal customs duty rates listed in the customs tariff range from 0 to 18%, which is a reduction on the customs duty rates applied in former SFRY, where the range was 0 to 25%. The distribution of the items in the 1992 Customs Tariff is given in Table 4.

L/7466 Page 30

Table 4. Distribution of Customs Items

RANGE NUMBER OF ITEMS RELATIVELY

free to 5% 5551 83.17% 5% to 10% • 1097 16.44% 10% to 18% 26 0.39%

TOTAL 6674 100%

According to the customs tariff applied in 1991, the nominal domestic economy protection rate was cca 10%, with rates applied to raw materials and production materials being 8%, equipment rates being 13%, and consumer goods rates being over 17%. The 1992 Customs Tariff considerably decreased customs duty rates, especially in the raw materials sector where imports of 3599 items are free from duty. Mostly due to the structure of goods imported, the overall level of customs protection is relatively low as total imports consist of 62% raw materials and production materials, 2% equipment and 26% consumer goods.

The Customs Law offers a relatively large number of exemptions from customs duty payment, which also means that import dues are being lowered. The exemptions proposed are non-discriminatory. New amendments to the Customs Law have ^educed the number of exemptions from customs duty payments.

In addition to the import burden set by the customs tariff, protective measures also include import quotas, additional,supplementary, and compensation customs duties, preferential duties, seasonal duties, customs refunds, and special measures of customs protection.

TABLE 5.

SECTION

1 II III IV V VI VII VIII IX X XI XII XIII XIV XV XVI XVII XVIII XIX XX XXI

L/7466 Page 31

CUSTOMS DUTY BURDEN ON IMPORTED GOODS IN %

UNWEIGHTED DUES

3.09 1.51 0.91 4.63 0.19 1.28 3.14 3.70 1.23 1.80 6.39 8.28 2.97 1.66 1.80 1.20 1.09 0.29 12.77 4.08 0

1991

3.94 1.68 0.91 3.78 0.20 1.59 3.66 3.48 1.24 1.74 6.17 9.43 3.04 1.66 1.83 1.21 1.38 0.13

12.77 4.01 0

WEIGHTED DUES 1992

4.05 1.52 0.91 4.56 0.20 1.65 3.31 3.49 1.24 1.90 5.95 9.44 2.97 1.66 1.91 1.21 1.37 0.21

12.77 4.12 0

1993 (1-11)

4.65 1.75 0.91 4.41 0.21 1.63 3.28 3.49 1.25 1.97 5.92 9.44 2.97 1.66 1.81 1.20 1.25 0.23

12.77 3.98 0

TOTAL 2.45 2.49 3.01 2.90

Criteria regarding import quotas are set by the Government of the Republic of Croatia in accordance with the goals of economic and developmental policy and are published in the Official Gazette. It is on the basis of these criteria that the Minister of Finance will permit imports of goods without any customs duty payment, or imports of goods with customs duty below the Customs Tariff Rate (quotas). Goods imported under the regime of quotas are not considered to be free imports.

If a foreign country importing goods of Croatian origin, aoes not apply to Croatian vessels or other means of transport and the same customs clearance procedure that it normally applies to goods, vessels and vehicles from other countries, the Croatian Minister of Finance is entitled to levy additional customs duty on goods imported from that country and to appiy a special customs clearance procedure.

L/7466 Page 32

provided the measures do not run contrary to the international contract obligations. In case imports of the same goods are free, the Minister of Finance is entitled to order that a percentage of the value of goods be paid as customs duty.

If goods are imported at a price below the price quoted in the contract (as defined in Article 36 of the Customs Law), and if imports of the same goods may seriously harm the economy of the Republic of Croatia, additional customs duty will be levied, equal to the difference between the contracted price and the price actually paid for the goods imported.

In case of imports of goods from countries that have not entered into the contract containing the most favoured nation clause with the Republic of Croatia, or that do not observe the clause when importing goods from Croatia, the customs duty rate applied will be 75%.

The Government of the Republic of Croatia may, on the basis of reciprocity, either lower or increase the customs duties levied in case of such imports, or restrict imports and apply a certain customs duty rate in accordance with the stipulations of the Customs Law.

In case of imports of goods from developing countries, preferential customs rates may be set. Preferential customs duties will be levied on goods imported from certain countries, provided the value of the goods has been increased through industrial processing by at least 51%. These customs duty rates are set by the Government of the Republic of Croatia.

In cases where customs duties levied on certain agricultural produce do not ensure stable home production and a home market in accordance with the current price policy over a certain period of time, the Government of the Republic of Croatia may, following the proposal made by the Minister of Finance and after it has received the opinions of the Ministries of Agriculture and Economy, levy seasonal customs duties in addition to existing ones, although for a limited period of time. Seasonal customs duties thus levied may not exceed 30%.

In cases where imported goods are used in the production of domestic goods and services which are later exported, customs duties paid maybe refunded in part or fully. The Government of the Republic of Croatia will define the terms and modes of customs duty refunds.

The Government of the Republic of Croatia may, following a proposal by the Minister of Finance, and after it has obtained opinions from the Croatian Chamber of Commerce and from the Ministry of Economy, increase, decrease or abolish the currently applied customs duties. It may also levy a 15% customs duty on goods classified as "free" imports in the Customs Tariff, if it can be expected that the price of such goods will cause major disruptions in the home market, or that the goods will enable a company or another person to enjoy a monopolistic position or a monopolistic price in the market. Regulation thus passed can only be effective for a limited period of time, (special customs protection measures).

L/7466 Page 33

A unified customs duty of 8% will be applied to goods imported by companies and other legal entities, if the goods are classified under more than two tariff numbers and their import is free. The same unified customs rate of 8% is levied on goods valued up to 500 US$, if the goods are brought or received from abroad by Croatian or foreign citizens, and will be used by them in their households, except if customs preferentials apply to the same goods or the customs tariff classifies the goods as "free" imports.

Ill.2.(c) Import Charges and Fees

All imported goods are charged at 1 % of the customs base for customs record keeping. The Government of the Republic of Croatia may stipulate which goods will be exempt from paying the charge. The aim of the customs record keeping fee is to provide funds for financing the modernisation of the Customs service.

The Government of the Republic of Croatia may, in order to ensure that the balance of payments reflects the Governments development and economic policy proclaimed for the period, levy a special provisional tax on imports of certain goods. The Government of the Republic of Croatia will decide which goods and groups of goods will be taxed, what the tax level will be, and how long the tax will be levied.

An equalising charge as part of import taxation, that was levied within the protective measures introduced in the Republic of Croatia in the course of 1991 ana 1992, was abandoned in 1993.

A special fee is levied on imports of agricultural and food products in order to protect home agricultural production. The fee is levied on goods listed in the Decision taken every year.

The impact of the above-mentioned fees and charges may be measured by the range of the total burden on goods imoorted, including both customs duties ana non-custom fees in each section of the Customs Tariff (with the exception of agricultural products).

Ill.2.(d) Taxation Regime

Sales tax rates levied on gooas and services traded in the market within the Republic of Croatia ao not create a price aifference between goods of foreign origin as opposed to domestic goods.

L/7466 Page 34

lll.2.(e) Tariff Preferences

Preferential customs duties were levied in the course of 1991, 1992, and 1993 following Article 51 of the Customs Law of the Republic of Croatia and the Decision on preferential customs duties and non-payment of other import dues on goods imported from certain developing countries, from republics of former Yugoslavia ( 'free" customs rate in case of reciprocity in preferential treatment of all goods), Bosnia and Hercegovina, Macedonia and Slovenia, as well as on goods from the Republic of Tunisia, the Republic of Turkey, the Republic of Uruguay and from Spain ( for certain goods included in the preferential list attached to the Decision).

Ill.2.(f) Non-tariff Measures Applied to Imports and Exports of Goods

lll.2.(f).1 Quotas

Imports and exports of goods are free. In case of exceptional circumstances, the Law provides for the possibility of introducing or imposing quantity limitations, i.e. quotas on imports and exports of goods applied for a limited period of time. The purpose of quotas is to protect domestic production and to support the development policy of certain key economic sectors.

Quotas as a means of regulating imports and exports had to be used because of limitations present in the national economy and with a view to enabling domestic business organisations to enter international trade with the support of specific Government measures. The Government of Croatia will, therefore, decide on the list of goods to be included in the quota regime, on the level of quotas, on the dynamics of import and export and on the terms of quota allocation at the end of each year.

The Chamber of Commerce is responsible for the allocation of quotas and is obliged to inform all interested parties of the venue and date of the quota allocation. Information should reach the interested parties not later than eight days before the allocation procedure takes place.

The Law considers quotas to be measures that are non-discriminatory against third countries. Quotas are autonomous and global, i.e. they apply to all goods irrespective of the origin of those goods or the exporting country. The whole system of quotas is set up and applied in accordance with the GATT regulations, Articles XIII and XVIII in particular.

Import quotas are set for a limited number of agricultural products, some food products, iron, steel and machine industry products, cement, as well as artificial textile fibres and fabrics. (See Annex 3, Table A3.22)

In the Republic of Croatia only 203 items (or 3%) on a list of 6674 tariff items are affected by import quotas, so that 97% of goods are imported freely.

L/7466 Page 35

Any existing quantitative restrictions will gradually be removed depending on the following factors: the restoration of war damaged areas; the advancement of the process of reconstruction; and the further implementation of a market economy including the process of restructuring the Croatian economy.

Ill.2.(f).2 Licences

Import and export licences are applied for the purpose of fulfilling international contracts and agreements, monitoring import and export of historical and artistic artifacts, certain precious metals, and arms and military equipment.

Licences are issued by the Government body responsible for foreign trade, and they are used for import and export of goods up to a certain value or quantity, with transactions under licences completed in a given period of time.

The current licences regime in the Republic of Croatia is applied to foreign trade transactions involving substances damaging the ozone layer according to the Montreal Convention, unprocessed gold and silver, coins and securities, arms and ammunition, narcotics, historical works and art works.

Ill.2.(g) Customs Valuation

The customs base of goods wnl be valued according to Articles 36-48 of the Customs Law of the Republic of Croatia. These Articles are fully in accordance with the Agreement on the Implementation of Article VII of the GATT.

Principles of customs valuation are explained in Article 36 (imports of goods) and Article 37 ( exports of goods).

Article 36 (1) stipulates that the customs base, on wnich rates set by the customs tariff are applied, is the value of goods. The value of goods representing the customs base is the contract price (transactional value). The contract price is the actual price paid, or the price to be paid, for goods purchased in order to be imported nto Croatia (Article 36 (2). The same Article (36 (3)) defines the contract price usea as the customs base on which the customs tariff rates are applied, as follows:

(1) it includes all costs and other expenses connected with the sale and delivery of goods to any port or place of entry into the customs area of the Republic of Croatia (Article 2);

(2) it excludes all costs, fees and cnarges collected in tne customs area of the ReDublic of Croatia;

L/7466 Page 36