request for comment: global methodology and assumptions

TRANSCRIPT

Criteria | Structured Finance | Request for Comment:

Request For Comment: GlobalMethodology And Assumptions ForCorporate Securitizations

Analytical Contacts:

Greg M Koniowka, London (44) 20-7176-1209; [email protected]

Alexander Dennis, CFA, Chicago (1) 312-233-7069; [email protected]

Andrew M Bowyer, CFA, London (44) 20-7176-3761; [email protected]

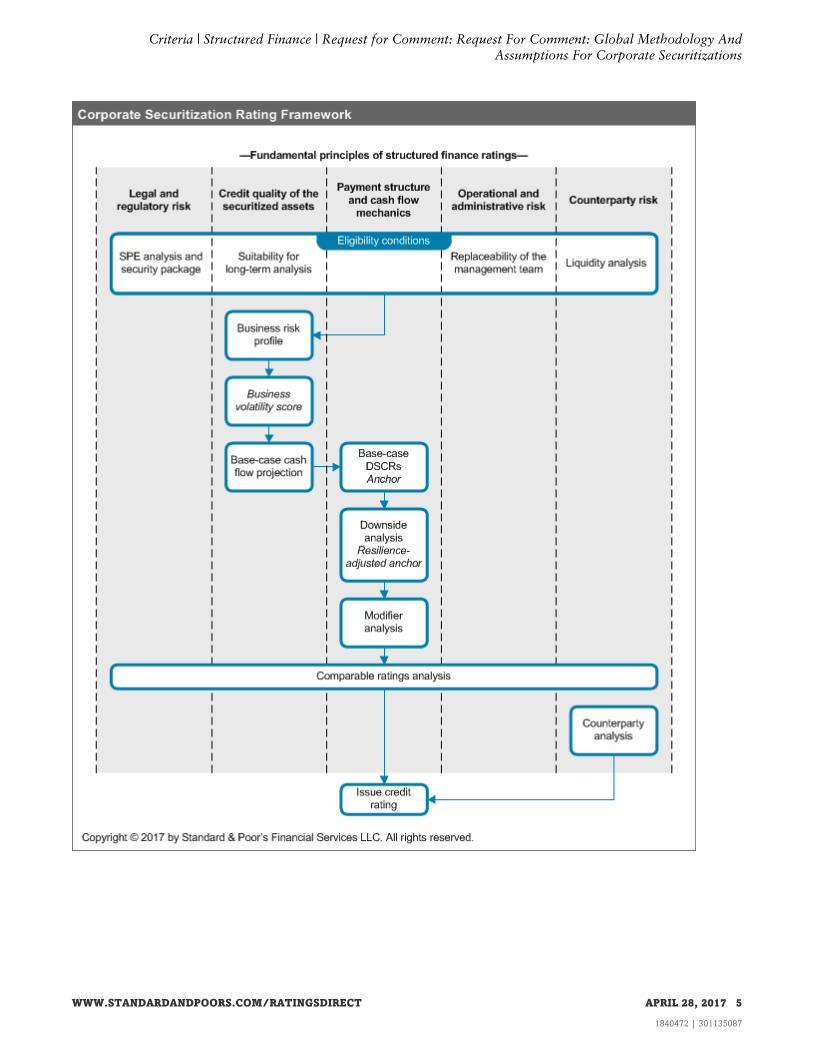

Beata Sperling-Tyler, London (44) 20-7176-3687; [email protected]

Criteria Contacts:

Herve-Pierre P Flammier, Paris (33) 1-4420-7338; [email protected]

Peter Kernan, London (44) 20-7176-3618; [email protected]

Table Of Contents

SCOPE AND OVERVIEW

IMPACT ON OUTSTANDING RATINGS

SUMMARY OF PROPOSED REVISIONS

QUESTIONS

RESPONSE DEADLINE

FRAMEWORK

PROPOSED METHODOLOGY AND ASSUMPTIONS

Step 1: Eligibility Conditions

Step 2: Base Case And Business Risk Profile Analysis

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 1

1840472 | 301135087

Table Of Contents (cont.)

Step 3: Business Volatility Score And DSCR Analysis

Step 4: Modifiers

Step 5: Comparable Rating Analysis

APPENDIX A: DESCRIPTION OF CORPORATE SECURITIZATION

ASSET CLASS

APPENDIX B: DOWNSIDE-SCENARIO ASSUMPTIONS

RELATED CRITERIA

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 2

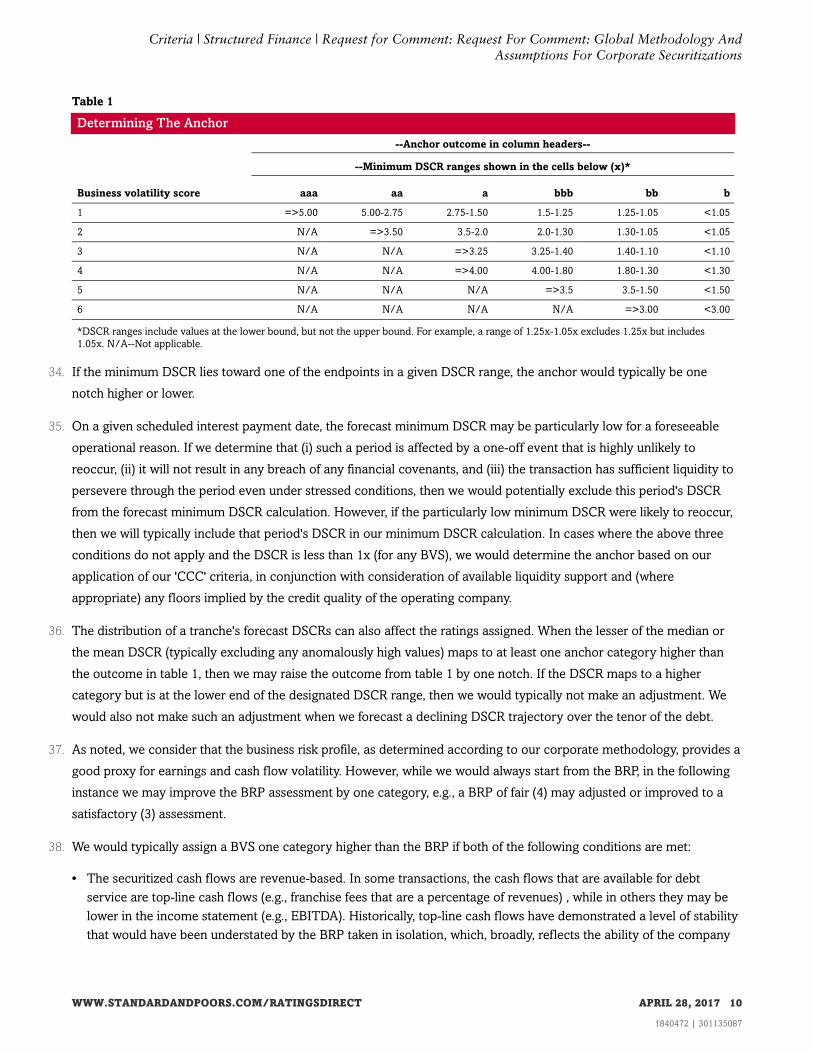

1840472 | 301135087

Criteria | Structured Finance | Request for Comment:

Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

SCOPE AND OVERVIEW

1. This Request for Comment (RFC) sets out proposed methodology and assumptions for rating corporate securitizations

globally. If adopted, these proposed criteria would replace "European Corporate Securitizations," published on Feb. 12,

2016, and "U.S. Corporate Securitization Transactions," published on Oct. 24, 2006. They would apply to all new and

existing ratings on corporate securitizations globally. See Appendix A for a description of the asset class.

2. To date, we have assigned ratings to corporate securitizations subject to either U.K. or U.S. insolvency law. As such,

the proposed criteria mostly discuss jurisdictional application in the context of either the U.S. or the U.K. However, the

proposed criteria could be applied in other developed jurisdictions with similar insolvency laws, or equivalent creditor

protection mechanisms.

3. The businesses that we would assess under these proposed criteria securitize cash flows from a range of industry

sectors where we can establish reasonable confidence in sustainable, long-term cash flow projections.

4. Corporate securitizations are subject to additional criteria that address the fundamentals set out in "Principles Of

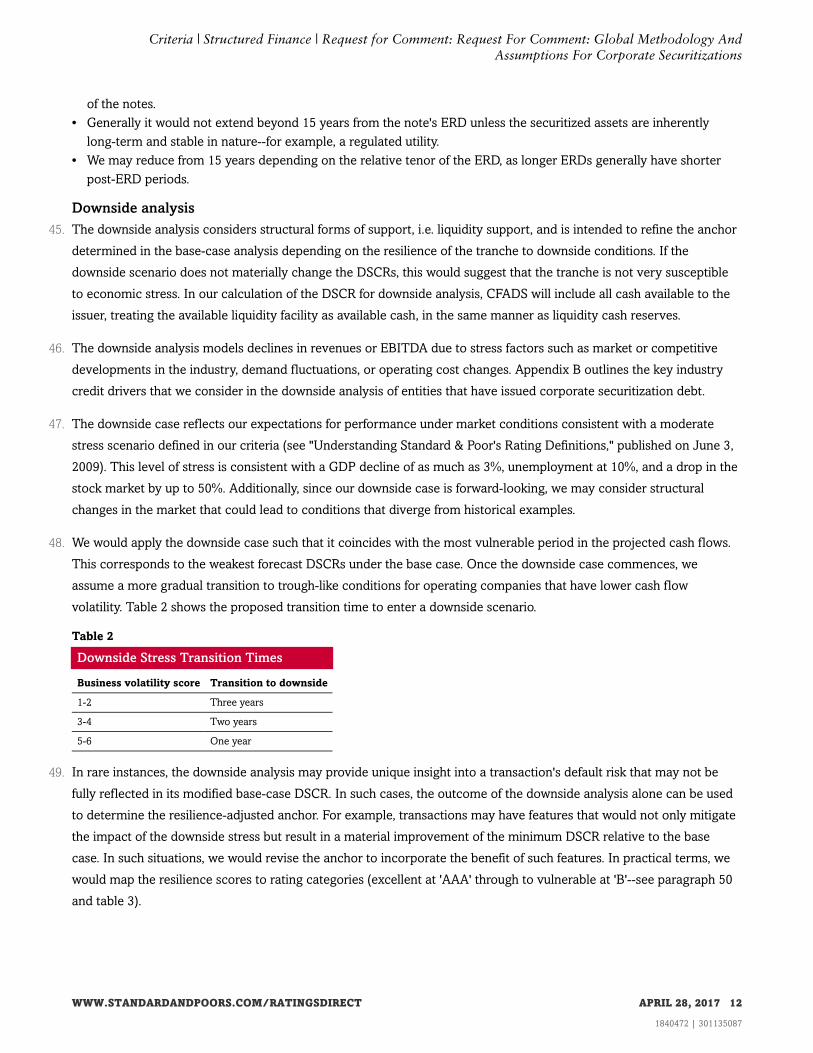

Credit Ratings," published on Feb. 16, 2011. These other criteria address rating above the relevant sovereign rating for

structured finance, counterparty risk, certain legal and regulatory risks, cash flow and payment structure analysis,

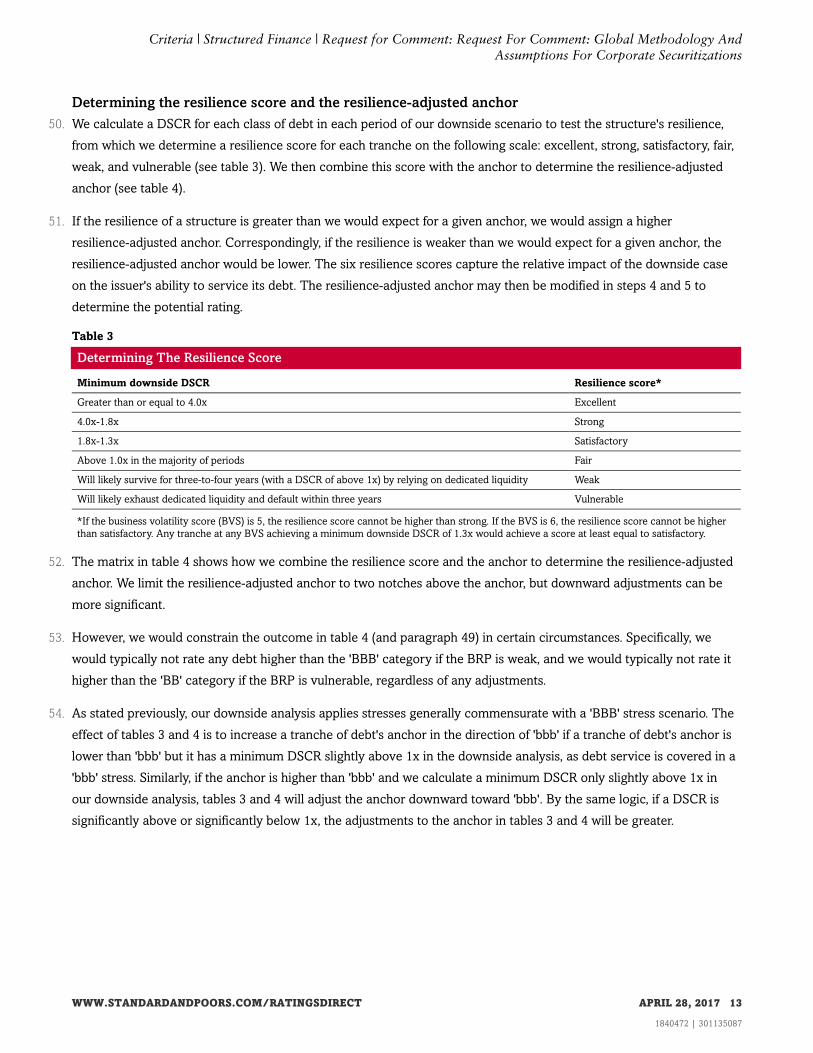

operational administrative risks, and credit stability (see Related Criteria).

IMPACT ON OUTSTANDING RATINGS

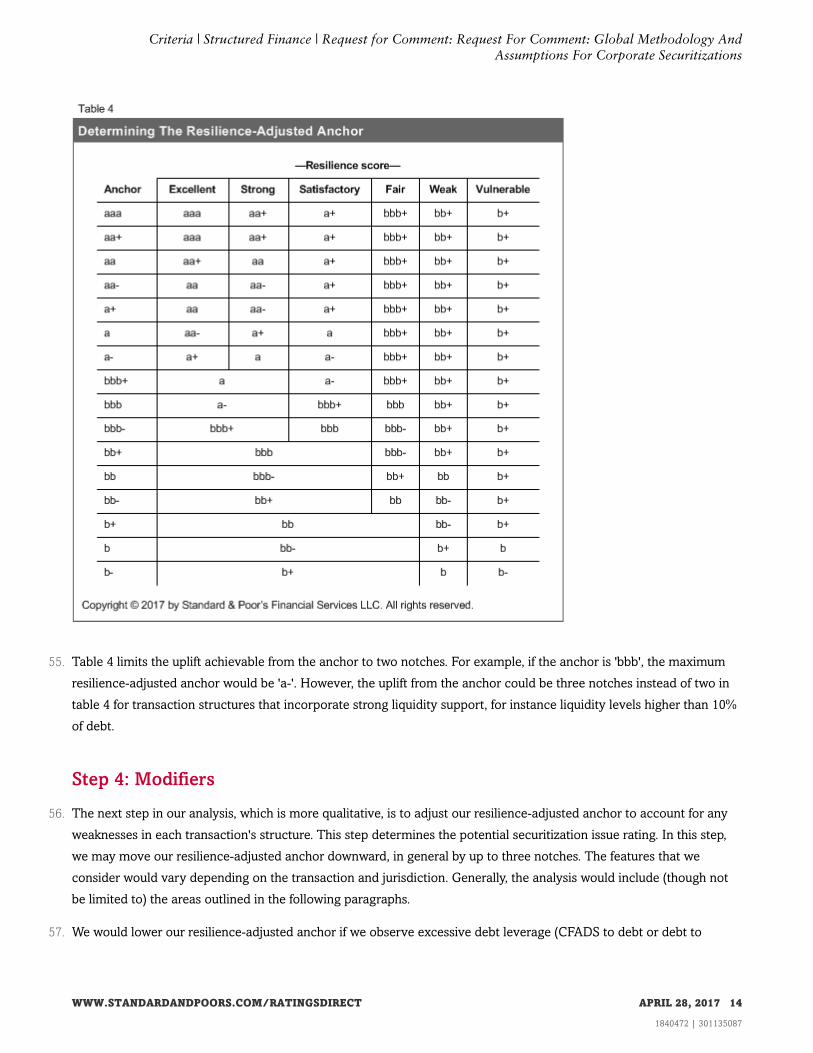

5. We expect the proposed criteria to have limited impact on outstanding ratings. About 85% of outstanding ratings are

currently not expected to be subject to rating change as a result of the adoption of the proposed criteria. We anticipate

that the remaining rated debt may be subject to rating actions ranging from a one-to-three notch downgrade (about

10%) to a one-to-three notch upgrade (about 5%).

SUMMARY OF PROPOSED REVISIONS

6. The proposed methodology adopts a cash flow analysis framework based around debt service coverage ratio (DSCR)

analysis. Apart from this change, most of the proposed framework builds on our current approach, and we are not

proposing to change our current legal and structural analysis or the basis of our analysis of the underlying corporate

assets.

7. The proposed revision to our cash flow analysis is intended to provide greater transparency with regard to how we

assess the ability of the securitized business to service ongoing debt payments.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 3

1840472 | 301135087

8. There are five key steps in the proposed approach.

9. Step 1: Eligibility conditions. This is a list of attributes a transaction must possess for S&P Global Ratings to consider

rating it using a corporate securitization approach. The fundamental premise of corporate securitization is that we can

rate through the insolvency of the operating company and differentiate the rating on the corporate securitization debt

from the creditworthiness of the operating company. The use of bankruptcy-remote special-purpose entities (SPEs),

the granting of security over the securitization assets, and sufficient liquidity are some of the features that allow us to

differentiate the credit risk of the securitization and the operating company. We also do not expect to see refinancing

risk in corporate securitization structures.

10. Step 2: Base-case cash flow projection and business risk profile analysis. We formulate our base-case operating cash

flow projection for the securitized assets and derive the company's business risk profile (BRP) using our corporate

methodology. This is unchanged from our current approach.

11. Step 3: DSCR analysis. This represents the main change that we are proposing. We would adopt a cash flow analysis

framework that uses projected minimum debt service coverage ratios (DSCRs) to assess whether cash flows will be

sufficient to service debt through the life of the rated transaction. The proposed framework outlines minimum DSCR

levels to achieve a given anchor outcome, calculated separately for each tranche of securitized debt. These minimum

DSCR levels vary depending on our assessment of the earnings and cash flow volatility for each business. We use the

BRP as a proxy for earnings and cash flow volatility. This means that we would look for higher DSCRs for a weak BRP

than for a strong BRP to achieve the same anchor, all else being equal, because we assume that a weak BRP signifies a

more volatile business.

12. Our DSCR analysis has two main stages. First, the base-case analysis considers operating-level cash flows and does

not consider issuer-level structural features (such as liquidity). The output of the base-case DSCR analysis would be an

anchor for each tranche. We then run a downside DSCR analysis to derive the "resilience-adjusted anchor," whereby

we test whether the issuer-level structural enhancements improve the resilience of the transaction under a stress

scenario. The downside analysis could lead us to revise the anchor upward or downward depending on how the

structure responds to the stress. We base this downside analysis on a moderate stress, equivalent to the industry 'BBB'

scenario (see "Appendix B: Downside-Scenario Assumptions"), plus any company-specific adjustments. This analysis

considers all issuer-level credit supports. We would apply the downside stress to the base-case cash flow forecast (see

step 2) at the point where we believe the stress would be greatest.

13. Step 4: Modifiers. We could then adjust the resilience-adjusted anchor depending on our assessment of the structural

package. For example, we could make adjustments for differing debt repayment structures, leverage, or weak financial

covenant packages. The output of this step would be the potential tranche rating.

14. Step 5: Comparable ratings analysis. Finally, we may adjust the potential tranche rating up or down by one notch

based on our holistic comparable analysis and our assessment of the transaction's credit characteristics relative to its

peers. The output would be the issue rating for each class of debt, although it would be subject to additional limitations

resulting from considerations of other factors such as counterparty exposure or sovereign rating constraints.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 4

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 5

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

QUESTIONS

15. S&P Global Ratings is seeking responses to the following questions, in addition to any other general comments on the

proposed criteria.

• What are your views on the methodology we have discussed in this article?

• Are there any other factors you believe should be considered in the proposed criteria for cash flow stress

assumptions that are not already noted in this proposal?

• Is the DSCR framework appropriate for corporate securitization structures?

• Does the way in which we have set out the link to the BRP and business volatility score (BVS) seem appropriate?

• Does the downside analysis seem appropriate?

• Are there major factors that we have not noted in our modifier analysis or comparable rating analysis?

• Is the 15-year benchmark amortization profile an appropriate method of normalizing turbo structure DSCR results?

RESPONSE DEADLINE

16. We encourage interested market participants to submit their written comments on the proposed criteria by May 29,

2017, to http://www.standardandpoors.com/en_US/web/guest/ratings/rfc where participants must choose from the

list of available Requests for Comment links to launch the upload process (you may need to log in or register first). We

will review and take such comments into consideration before publishing our definitive criteria once the comment

period is over. S&P Global Ratings, in concurrence with regulatory standards, will receive and post comments made

during the comment period to

www.standardandpoors.com/en_US/web/guest/ratings/ratings-criteria/-/articles/criteria/requests-for-comment/filter/all#rfc.

Comments may also be sent to [email protected] should participants encounter technical difficulties.

All comments must be published but those providing comments may choose to have their remarks published

anonymously or they may identify themselves. Generally, we publish comments in their entirety, except when the full

text, in our view, would be unsuitable for reasons of tone or substance.

FRAMEWORK

17. Corporate securitization transactions have credit risks and features associated with both traditional corporate debt and

traditional securitizations. Similar to traditional corporate debt, the servicing of ongoing debt payments depends on the

company's competitive advantage and ability to generate cash flow. The difference in corporate securitizations is the

use of securitization techniques to differentiate the credit risk of the business' operating company and that of the debt.

Corporate securitization features include asset isolation, bankruptcy-remote issuers, management replacement

features, and the absence of refinancing risk.

PROPOSED METHODOLOGY AND ASSUMPTIONS

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 6

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

Step 1: Eligibility Conditions

18. In order to be able to differentiate the issue rating on the corporate securitization debt from the creditworthiness of the

operating company, we must conclude that the debt would continue to be serviced notwithstanding the insolvency of

the operating company. This assumption is the fundamental building block of corporate securitization analysis. The

following subsections describe the features we would typically expect to see, in order to gain comfort that it is possible

to rate through the insolvency of the operating company.

Bankruptcy remoteness

19. The rated debt should be issued by a bankruptcy-remote special-purpose entity (SPE). We assess the bankruptcy

remoteness of the issuer SPE by applying our criteria for SPEs. Relevant factors typically include restrictions on

objects and powers, separation provisions between the issuer and the operating company, the presence of an

independent director (with veto rights in cases of an insolvency vote), and sufficiently robust security over the assets.

For example, where assets remain on the balance sheet of the operating company (balance sheet transactions), the

noteholders should be able to enforce their interest on the assets of the business ahead of the insolvency and/or

restructuring of the operating company. For true sale transactions (true sale is defined in various published legal

criteria regarding SPEs--see Appendix A for further details), where the assets of the business are typically sold to the

SPE, true sale and nonconsolidation opinions are often provided to give comfort that the asset transfer will not be

characterized as debt, and the assets of the issuer will not become part of the operating company's bankruptcy estate.

Replaceability of the management team

20. Corporate securitizations rely on the company's management to transform the assets of the business into cash to pay

interest and principal on the debt. However, in order to differentiate the corporate securitization issue ratings from the

credit risk of the operating company, the management of the business must be replaceable. This is a critical step in

corporate securitizations, and we have observed that not all industries and businesses meet this condition. For

example, businesses where winning contracts or customer retention is heavily influenced by relationships with

management or other specific individuals at the operating company may experience significant contract loss, customer

churn, and cash flow disruption following a bankruptcy proceeding. Alternatively, businesses like a franchised system

of restaurants in the U.S. are likelier to maintain cash flow continuity following the bankruptcy of the operating

company. This is because each franchise owner invests significant capital into the success of their stores, and as a

result we have seen franchisees continue to operate their stores following the system franchisor (the operating

company) filing for bankruptcy protection.

21. Once we establish whether management is likely to be replaceable without materially weakening the underlying

strength of the securitized assets and their cash flows, we then look for mechanisms to ensure the replacement takes

place in a time frame that is unlikely to disrupt the ability to make debt payments. For example, this could be achieved

in a true sale transaction with a backup manager or a restructuring agent in place at the transaction's closing.

Alternatively, for balance-sheet transactions, it could be achieved where court-led administration can be blocked and

security over the assets enforced ahead of the bankruptcy of the operating company, including if necessary the

appointment of a new management team to facilitate the continued operation of the business in the best interest of the

secured noteholders.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 7

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

Compatibility with long-term cash flow projections

22. The business risk profile (BRP) assessment is typically based on a short-term or medium-term horizon, but corporate

securitization transactions have debt maturities stretching out to 15 years and longer. We may form the view that

certain industries or product offerings are not compatible with longer-term ratings due to risks of structural changes in

the industry or obsolescence. Further, the risk of a fundamental change in the business' operating model can also

challenge the visibility of long-term performance.

23. For example, in balance-sheet transactions there can be a risk that an operating company will restructure, make

certain sales and acquisitions, or take on new debt. Not only can this make cash flow projections less certain, but it can

also affect our post-insolvency assumptions. In determining the eligibility of the corporate securitization, we look for

features that mitigate such risks, for example restrictive operating covenants and financial restrictions. For true-sale

transactions, we typically take comfort from the terms of the management agreement and sometimes from the nature

of the business, in the case of franchisees.

Sufficient liquidity

24. The rated notes should benefit from liquidity provisions at the level of the securitization issuer, to cover for disruption

of cash flows arising from an insolvency of the operating company. The factors that we consider to determine the

sufficiency of available liquidity include, but are not limited to:

• The nature of the securitized assets, and specifically the likely impact of the operating company insolvency on cash

flows;

• For balance-sheet transactions, our assessment of the likely time frame for security enforcement in the given

jurisdiction for the specific type of assets, also accounting for different security structures, regulatory constraints,

and possible government interference;

• The level of specialization required and the depth of the market for replacement servicers or management team; and

• A review of the backup servicer (if in place).

25. Our assessments of liquidity sufficiency could also differ depending on the economic scenarios that we expect a given

tranche to survive. This means that for higher rating categories we may look for greater liquidity.

Isolation from refinancing risk

26. Corporate securitizations retain a more direct linkage to the operating company than typical structured finance

transactions. Nonetheless, in common with most of our structured finance criteria, we do not expect to see refinancing

risk in corporate securitizations. For example, we do not expect to see hard bullet notes, which are to be repaid by

further issuance at a specified date, and where nonrepayment would constitute a note event of default.

Step 2: Base Case And Business Risk Profile Analysis

27. When we conduct cash flow analysis for corporate securitizations, we project the operating cash flows of the business

and test its ability to service the transaction's liability structure in a timely way. The starting point for our proposed

cash flow analysis is the base-case operating cash flow projection. The assumptions for the base case are based on our

outlook for the industry and the operating company, and would take into account our near-term financial projections

to the extent we deem appropriate. The assessment is based only on forecast cash flow and does not account for

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 8

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

external credit supports such as liquidity or liquidity reserve accounts.

28. We develop a base-case forecast for each transaction, with a horizon equal to the term of the rated debt. We would

typically not give credit to growth after the first two years, unless we see reliable long-term sources of revenue growth,

such as contract structures or a regulatory framework. For transactions based on EBIT or EBITDA where we do not

give credit to growth, we would typically assume only the minimum maintenance capital expenditure (capex) to keep

the business going. The minimum maintenance capex is generally the covenanted level of capex, but we may assume

a higher level based on the business' track record or our assessment of the minimum maintenance capex. In certain

instances, for example in industries that are highly competitive or have weak growth prospects, we may consider it

appropriate to assume zero growth from the outset of the transaction.

29. We then determine the BRP for the operating company according to our corporate methodology, which provides a

good proxy for the volatility of the business (see "Corporate Methodology," published on Nov. 19, 2013).

Step 3: Business Volatility Score And DSCR Analysis

Base-case DSCR

30. The proposed methodology adopts a debt service coverage ratio (DSCR) analysis framework assessing whether the

cash flow generated by the business is sufficient for the issuer to service its obligations. The analysis considers the

minimum DSCR produced by the base-case projection. We consider that, in order to achieve a given anchor outcome,

a stronger business with more stable cash flows will require a lower DSCR than a weaker business with more volatile

cash flows.

31. The DSCR for any class of debt is calculated as cash flow available for debt service (CFADS) divided by debt service

payments that are pari passu and senior to that class. CFADS for a given period is calculated as revenues from

operations less operating expenses and (where relevant) taxes, capex (which is defined as general maintenance to

support ongoing operations), working capital, and pension liabilities. As an operating cash flow figure, CFADS

excludes any cash balances that a transaction could draw on to service debt, such as the debt service reserve fund or

maintenance fund, or cash balances that are not required to be kept in the structure.

Determining the business volatility score

32. To calibrate the strength and stability of a given business, we derive the business volatility score (BVS). To determine a

BVS for a given business, we start by mapping to a 1 through 6 scale from the BRP (excellent = 1 to vulnerable = 6),

which may then be subject to additional adjustments as per paragraphs 37-40.

Determining the anchor

33. Table 1 sets out the anchor that we would typically expect to assign for any given minimum DSCR ranges and

volatility score.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 9

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

Table 1

Determining The Anchor

--Anchor outcome in column headers--

--Minimum DSCR ranges shown in the cells below (x)*

Business volatility score aaa aa a bbb bb b

1 =>5.00 5.00-2.75 2.75-1.50 1.5-1.25 1.25-1.05 <1.05

2 N/A =>3.50 3.5-2.0 2.0-1.30 1.30-1.05 <1.05

3 N/A N/A =>3.25 3.25-1.40 1.40-1.10 <1.10

4 N/A N/A =>4.00 4.00-1.80 1.80-1.30 <1.30

5 N/A N/A N/A =>3.5 3.5-1.50 <1.50

6 N/A N/A N/A N/A =>3.00 <3.00

*DSCR ranges include values at the lower bound, but not the upper bound. For example, a range of 1.25x-1.05x excludes 1.25x but includes

1.05x. N/A--Not applicable.

34. If the minimum DSCR lies toward one of the endpoints in a given DSCR range, the anchor would typically be one

notch higher or lower.

35. On a given scheduled interest payment date, the forecast minimum DSCR may be particularly low for a foreseeable

operational reason. If we determine that (i) such a period is affected by a one-off event that is highly unlikely to

reoccur, (ii) it will not result in any breach of any financial covenants, and (iii) the transaction has sufficient liquidity to

persevere through the period even under stressed conditions, then we would potentially exclude this period's DSCR

from the forecast minimum DSCR calculation. However, if the particularly low minimum DSCR were likely to reoccur,

then we will typically include that period's DSCR in our minimum DSCR calculation. In cases where the above three

conditions do not apply and the DSCR is less than 1x (for any BVS), we would determine the anchor based on our

application of our 'CCC' criteria, in conjunction with consideration of available liquidity support and (where

appropriate) any floors implied by the credit quality of the operating company.

36. The distribution of a tranche's forecast DSCRs can also affect the ratings assigned. When the lesser of the median or

the mean DSCR (typically excluding any anomalously high values) maps to at least one anchor category higher than

the outcome in table 1, then we may raise the outcome from table 1 by one notch. If the DSCR maps to a higher

category but is at the lower end of the designated DSCR range, then we would typically not make an adjustment. We

would also not make such an adjustment when we forecast a declining DSCR trajectory over the tenor of the debt.

37. As noted, we consider that the business risk profile, as determined according to our corporate methodology, provides a

good proxy for earnings and cash flow volatility. However, while we would always start from the BRP, in the following

instance we may improve the BRP assessment by one category, e.g., a BRP of fair (4) may adjusted or improved to a

satisfactory (3) assessment.

38. We would typically assign a BVS one category higher than the BRP if both of the following conditions are met:

• The securitized cash flows are revenue-based. In some transactions, the cash flows that are available for debt

service are top-line cash flows (e.g., franchise fees that are a percentage of revenues) , while in others they may be

lower in the income statement (e.g., EBITDA). Historically, top-line cash flows have demonstrated a level of stability

that would have been understated by the BRP taken in isolation, which, broadly, reflects the ability of the company

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 10

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

to generate earnings and operating cash flows; and

• The operating company has demonstrated stable revenue generation through multiple economic downturns

(typically assessed based on at least 20 years of performance data).

39. We would typically assign a BVS one or more categories below the BRP for any of the following reasons:

• There is material ongoing exposure to the financial performance of the operating company. For example, in

situations where not all of the operating company's business is being sold to the structured finance issuer, the

performance of certain non-contributed segments of the operating company may still affect the performance of cash

flows servicing the issuer's debt.

• There are a very limited number of companies in the market that could viably replace the operating company if it

were to default. For example, in certain technology companies, it may be difficult to find long-term replacements for

the operating company due to the specialized systems, networks, and knowledge relating to the unique services

being offered.

• If the cash flows are contract-based, and the transaction is exposed to significant contract renewal risk. While

contractual cash flows could appear potentially more stable relative to sales, or to EBITDA-based cash flows when

the contracts cover a long period of time, we may still view cash flow volatility as relatively high to the extent that

the contracts have shorter maturities than the rated notes and may need to be renewed multiple times to meet

interest and principal obligations.

• If we assess that the business is subject to structural decline.

40. If the business has other material, incremental weaknesses related to cash flow volatility that are not captured above,

we may consider further downward adjustments to the BVS.

41. Throughout the life of a given transaction, as amortization occurs, the DSCR levels may evolve. As we rerun our

analysis under these proposed criteria, we would consider DSCR levels in the context of the business risk profile and

taking into account possible adverse macroeconomic conditions within the expected remaining life of the transaction.

Where the DSCR levels have evolved, in order to consider adjusting the ratings we would need to conclude that there

has been a material, persisting change in the fundamentals of the transaction.

Benchmark amortization profiles for turbo structures

42. For transactions that have scheduled principal amortization payments, we calculate all DSCRs (including downside

analysis--see below) for each rated tranche of debt based on the documented payment schedule. For cash sweep

structures (often referred to as turbo structures), a DSCR analysis based on scheduled debt payments is not always

going to be informative. Turbo structures typically require limited principal repayment prior to an expected (principal)

repayment date (ERD--or in U.S. transactions, the "anticipated repayment date"). On the ERD, the bond can be repaid,

but a failure to repay at ERD is not a note event of default. Following the ERD, upon a failure to repay, the cash flows

are allocated according to an accelerated repayment structure.

43. In order to assess the ability of the borrower to service debt in a turbo structure on a comparable DSCR basis, we are

proposing to assume a benchmark principal amortization schedule that will model that the debt is repaid within an

appropriate period over a fixed number of years following its ERD and ahead of its final maturity.

44. The benchmark amortization profile would be based on the following guidelines:

• For all transactions, the amortization profile would not extend beyond the two years prior to the legal final maturity

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 11

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

of the notes.

• Generally it would not extend beyond 15 years from the note's ERD unless the securitized assets are inherently

long-term and stable in nature--for example, a regulated utility.

• We may reduce from 15 years depending on the relative tenor of the ERD, as longer ERDs generally have shorter

post-ERD periods.

Downside analysis

45. The downside analysis considers structural forms of support, i.e. liquidity support, and is intended to refine the anchor

determined in the base-case analysis depending on the resilience of the tranche to downside conditions. If the

downside scenario does not materially change the DSCRs, this would suggest that the tranche is not very susceptible

to economic stress. In our calculation of the DSCR for downside analysis, CFADS will include all cash available to the

issuer, treating the available liquidity facility as available cash, in the same manner as liquidity cash reserves.

46. The downside analysis models declines in revenues or EBITDA due to stress factors such as market or competitive

developments in the industry, demand fluctuations, or operating cost changes. Appendix B outlines the key industry

credit drivers that we consider in the downside analysis of entities that have issued corporate securitization debt.

47. The downside case reflects our expectations for performance under market conditions consistent with a moderate

stress scenario defined in our criteria (see "Understanding Standard & Poor's Rating Definitions," published on June 3,

2009). This level of stress is consistent with a GDP decline of as much as 3%, unemployment at 10%, and a drop in the

stock market by up to 50%. Additionally, since our downside case is forward-looking, we may consider structural

changes in the market that could lead to conditions that diverge from historical examples.

48. We would apply the downside case such that it coincides with the most vulnerable period in the projected cash flows.

This corresponds to the weakest forecast DSCRs under the base case. Once the downside case commences, we

assume a more gradual transition to trough-like conditions for operating companies that have lower cash flow

volatility. Table 2 shows the proposed transition time to enter a downside scenario.

Table 2

Downside Stress Transition Times

Business volatility score Transition to downside

1-2 Three years

3-4 Two years

5-6 One year

49. In rare instances, the downside analysis may provide unique insight into a transaction's default risk that may not be

fully reflected in its modified base-case DSCR. In such cases, the outcome of the downside analysis alone can be used

to determine the resilience-adjusted anchor. For example, transactions may have features that would not only mitigate

the impact of the downside stress but result in a material improvement of the minimum DSCR relative to the base

case. In such situations, we would revise the anchor to incorporate the benefit of such features. In practical terms, we

would map the resilience scores to rating categories (excellent at 'AAA' through to vulnerable at 'B'--see paragraph 50

and table 3).

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 12

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

Determining the resilience score and the resilience-adjusted anchor

50. We calculate a DSCR for each class of debt in each period of our downside scenario to test the structure's resilience,

from which we determine a resilience score for each tranche on the following scale: excellent, strong, satisfactory, fair,

weak, and vulnerable (see table 3). We then combine this score with the anchor to determine the resilience-adjusted

anchor (see table 4).

51. If the resilience of a structure is greater than we would expect for a given anchor, we would assign a higher

resilience-adjusted anchor. Correspondingly, if the resilience is weaker than we would expect for a given anchor, the

resilience-adjusted anchor would be lower. The six resilience scores capture the relative impact of the downside case

on the issuer's ability to service its debt. The resilience-adjusted anchor may then be modified in steps 4 and 5 to

determine the potential rating.

Table 3

Determining The Resilience Score

Minimum downside DSCR Resilience score*

Greater than or equal to 4.0x Excellent

4.0x-1.8x Strong

1.8x-1.3x Satisfactory

Above 1.0x in the majority of periods Fair

Will likely survive for three-to-four years (with a DSCR of above 1x) by relying on dedicated liquidity Weak

Will likely exhaust dedicated liquidity and default within three years Vulnerable

*If the business volatility score (BVS) is 5, the resilience score cannot be higher than strong. If the BVS is 6, the resilience score cannot be higher

than satisfactory. Any tranche at any BVS achieving a minimum downside DSCR of 1.3x would achieve a score at least equal to satisfactory.

52. The matrix in table 4 shows how we combine the resilience score and the anchor to determine the resilience-adjusted

anchor. We limit the resilience-adjusted anchor to two notches above the anchor, but downward adjustments can be

more significant.

53. However, we would constrain the outcome in table 4 (and paragraph 49) in certain circumstances. Specifically, we

would typically not rate any debt higher than the 'BBB' category if the BRP is weak, and we would typically not rate it

higher than the 'BB' category if the BRP is vulnerable, regardless of any adjustments.

54. As stated previously, our downside analysis applies stresses generally commensurate with a 'BBB' stress scenario. The

effect of tables 3 and 4 is to increase a tranche of debt's anchor in the direction of 'bbb' if a tranche of debt's anchor is

lower than 'bbb' but it has a minimum DSCR slightly above 1x in the downside analysis, as debt service is covered in a

'bbb' stress. Similarly, if the anchor is higher than 'bbb' and we calculate a minimum DSCR only slightly above 1x in

our downside analysis, tables 3 and 4 will adjust the anchor downward toward 'bbb'. By the same logic, if a DSCR is

significantly above or significantly below 1x, the adjustments to the anchor in tables 3 and 4 will be greater.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 13

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

55. Table 4 limits the uplift achievable from the anchor to two notches. For example, if the anchor is 'bbb', the maximum

resilience-adjusted anchor would be 'a-'. However, the uplift from the anchor could be three notches instead of two in

table 4 for transaction structures that incorporate strong liquidity support, for instance liquidity levels higher than 10%

of debt.

Step 4: Modifiers

56. The next step in our analysis, which is more qualitative, is to adjust our resilience-adjusted anchor to account for any

weaknesses in each transaction's structure. This step determines the potential securitization issue rating. In this step,

we may move our resilience-adjusted anchor downward, in general by up to three notches. The features that we

consider would vary depending on the transaction and jurisdiction. Generally, the analysis would include (though not

be limited to) the areas outlined in the following paragraphs.

57. We would lower our resilience-adjusted anchor if we observe excessive debt leverage (CFADS to debt or debt to

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 14

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

EBITDA) relative to peers.

58. We would assess the length of the amortization profile. One consequence of having high leverage is the protracted

time required to deleverage, which would most likely result in a transaction's expected amortization profile being

materially longer than peers with comparable business volatility scores. As a general rule, excessively long principal

payment periods introduce additional risks that we need to reflect in our ratings. We would typically revise down our

resilience-adjusted anchor by up to three notches if an amortization profile results in full repayment beyond 20 years,

lowering by the full three notches where repayment extends beyond 28 years. Beyond this, we may take the view that,

because of the nature of the business, very long-term amortization profiles cannot be supported by long-term cash flow

projections. In these instances, we may therefore not be able to rate the securitization above the credit quality of the

operating company.

59. We would assess the length of the ERD. In our cash flow analysis for transactions with turbo amortization structures,

we will assume a benchmark principal payment period of 15 years that begins immediately following the ERD. The

benchmark is established to improve comparability of our credit ratings. In conjunction, we will consider the tenor to

the ERD. We would typically view an early ERD, for example three years or less after issuance, as a positive mitigating

factor that offsets, fully or partially, any lowering of our resilience-adjusted anchor stemming from structural

weaknesses. Conversely, we would typically revise down our resilience-adjusted anchor by up to three notches when

the ERD window exceeds seven years. A very long ERD window significantly beyond 10 years would introduce

additional operating cash flow forecasting risk--depending on the volatility of the business--and we would typically

apply more than a three-notch adjustment to our resilience adjusted anchor. Typically, if a class of debt is

time-tranched, with each tranche ranking pari passu, we will view the credit quality of all tranches as the same.

60. For balance sheet transactions, if the financial covenants would not, in our view, be effective in identifying a

deterioration in the company's performance and/or allowing the trustee to enforce security and appoint an

administrative receiver, we may take one of two views:

• We can't rate through insolvency (meaning these criteria would not be applicable), which would be the case if we

think that an insolvency could occur ahead of the financial covenant due to it being ineffective (e.g., the definition of

the DSCR may be subject to manipulation or not being tied to operating performance); or

• The financial covenants are weak (a low trigger for restricted payments or default covenant) and the likelihood of

default would be higher as a result.

Step 5: Comparable Rating Analysis

61. The final adjustments to arrive at the corporate securitization rating result from our comparable rating analysis. This

involves taking a holistic review of an issuer's credit characteristics and performance in aggregate, both in absolute

terms and relative to peers. We may assign a final securitization rating one notch higher or lower than the potential

rating based on this analysis. If a transaction does not have direct peers, we may select a broader set of peers.

62. Our analysis of a transaction's credit characteristics recognizes that a transaction can have material differences in key

operating and structural elements relative to its peers. For example, we will consider differences in the scale and

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 15

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

history of the business being securitized. In U.K. transactions that involve operating companies, the structure may

contain a particularly strong set of operating covenants, where the trigger levels are set higher than its peers.

Alternatively, security could be granted over a particularly robust portfolio of property assets with low loan-to-value

ratios, indicating relatively high levels of (shareholder) capital at risk and a strong dynamic alignment of interests

between rated noteholders and other transaction stakeholders.

63. We generally choose peers that are in the same sector or asset class and, where possible, are subject to similar levels

of country risk and have debt with similar tenors.

64. Beyond the impact of the comparable ratings analysis, if any, there may be other constraints on the final rating on the

corporate securitization, for example as a result of counterparty or other overarching criteria (see Related Criteria

below).

65. Note that, for balance-sheet transactions, we would typically assume that the credit quality of a corporate

securitization tranche is at least equal to that of the operating company, regardless of subordination. This does not

apply for true sale transactions. If we identify risks in the structure of the transaction that are not present in the

operating company, we may not apply this floor.

APPENDIX A: DESCRIPTION OF CORPORATE SECURITIZATION ASSETCLASS

66. The term "securitization" normally implies that the securitized assets are able to support the debt on the basis of the

credit merits, thanks to their successful isolation from the servicer's or seller's bankruptcy risk. Therefore, true

securitizations are rated "through the bankruptcy" of the seller/servicer or originator, the implication being that a

seller/servicer bankruptcy is not expected to affect the debt service of the securitized debt and, therefore, that a

seller/servicer bankruptcy will have no effect on the rating. In a corporate securitization, the continued operation of a

business is necessary to generate the cash flows that service the debt; therefore, rating through an operator bankruptcy

may be difficult unless the operator is, from a practical standpoint, replaceable and the transaction structure allows for

its replacement at critical points during the term of the transaction, or the operator is continuing to operate the assets

through its reorganization.

67. A corporate securitization is more similar to, and incorporates more risks associated with, traditional corporate debt

than debt in a traditional securitization. A securitization risk spectrum ranges from pure corporate risk at one extreme

to "true securitizations" of commoditized assets--such as credit card receivables, mortgages, and auto loans, which

carry virtually no corporate risk--at the other. Corporate securitizations can include many operating components, such

as supply chain management, manufacturing, marketing, and distribution, which are necessary to the ongoing

successful operation of a business. Therefore the general approach in these proposed criteria is to blend the

seller/servicer's corporate business risk with a structured finance analysis, while focusing on maximizing noteholders'

control over the securitized, cash-generating assets. For example, some corporate securitizations are structured as

"true sale" transactions; in others, the securitized assets stay on the consolidated balance sheet of the operating

company, and would only move off balance sheet to the SPE once the security had been enforced.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 16

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

APPENDIX B: DOWNSIDE-SCENARIO ASSUMPTIONS

68. This section relates to the operating cash flow analysis part of our corporate securitization transactions rating process.

Specifically, it sets out our starting assumptions that we use to model the downside case cash flow available for debt

service (CFADS). The DSCR buffer in the downside case is one element we use to assess the strength of the structural

features of a transaction, and to determine potential adjustments to the anchor.

69. Below, we outline the assumptions for the downside case for the industries of the currently rated transactions'

operating companies: leisure and sports, pubs, restaurants and retail, transport infrastructure, business and customer

services, and telecommunications and cable. A downside case for transactions in other sectors not listed in this article

would be informed by our knowledge of the sector, the company in question, and its peers.

70. The downside case reflects our expectations for performance under moderately stressed market conditions. The track

record of a sector over the past 20 years guide our expectation of the performance of rated transactions under a

downside case.

71. Our assumptions for the drop in EBITDA in the downside case are informed by the empirically observed decline

companies experienced during the harshest period in the past 20 years, which is 2007-2010. The next two paragraphs

outline the peak-to-trough declines we would use to test the rated transaction's performance.

72. The declines vary per industry and are informed by the one tailed upper 95% bound of the mean EBITDA declines

experienced in 2007-2010 by a global population of companies analyzed.

• 45% for businesses in the leisure and sports sector, including football stadiums, entertainment venues, hotels, and

others.

• 30% for pubs, restaurants, and retail.

• 25% for transport infrastructure, that is companies that derive most of their earnings from the commercial operation

of airports, marine ports, toll road networks, railways, and other transportation infrastructure assets and services,

such as navigable waterways and air and marine traffic controllers.

• 30% for business and consumer services (for example, the provision of car insurance, driving lessons, breakdown

cover, consumer loans, motoring advice, road maps, and funeral services).

• 30% for telecommunications and cable companies, including traditional fixed-line and wireless telecom network

operators, cable operators, satellite operators, tower companies, and data center operators.

73. In case of transactions where revenues rather than earnings are subject to securitization, we test the rated transaction's

performance under the following peak-to-trough revenue declines, based on performance experienced in 2007-2010.

They are informed by the one tailed upper 95% bound of the population we analyzed.

• 25% for businesses in the leisure and sports sector.

• 15% for pubs, restaurants, and retail businesses.

• 10% for businesses in transport infrastructure.

• 20% for business and consumer services companies.

• 15% for telecommunications and cable companies.

74. The downside stress we apply may depart from the above numbers if we consider that the observed peak-to-trough

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 17

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

decline of the past 20 years are unrepresentative for the individual business. For example, given that our analysis is

forward-looking, we may also consider structural, regulatory, operating, or competitive position changes in the market.

75. We model one downside scenario during the tenor of the transaction's notes. The timing of the downside coincides

with the most vulnerable period in our projected cash flows, i.e., the weakest DSCR under the base case.

76. The transition time to the downside scenario is provided in table 2. We assume a company remains in the downside

scenario until the legal final maturity of the notes.

77. Our downside-case assumptions consist of a combination of market and operating stresses. A market downside

reflects market or competitive developments in the industry that cause a potential drop in EBITDA or revenue

compared with our base case. Possible market stresses include the introduction or obsolescence of products or

services, demand fluctuations, and industrywide operating cost changes. The operating downside takes into account a

business-specific operational stress; for example, key client risk, reputational risk, or event risk. In some situations,

there may be a correlation between market and operating stresses.

78. We describe below the possible industry-specific stresses in a market downside-case.

79. For the leisure and sports sector:

• Economic downturns can have an outsize effect on revenue generation (where trends tend to follow GDP) because

of the generally discretionary nature of leisure products. During economic downturns, revenue will generally

contract more than GDP. A fall in revenue can also result from cyclicality or seasonality affecting demand and price

competition.

• Margins can be under pressure due to increased costs of lease rentals, labor, or input materials.

80. For pubs, restaurants, and retail:

• Industry sales trends are closely correlated with macroeconomic trends. However, in mature, developed markets,

GDP growth is not always a good proxy for retail sales and revenue can be more sensitive to consumer confidence

and expectations about unemployment and discretionary income.

• Revenue may fall as a result of changing demand trends or substitution by other products or services. An example

of this has been a decline in the revenues of U.K. "wet-led" pubs (i.e., those that rely more on alcoholic drinks) due

to the increasing availability of low-price alcohol from retail outlets, and changing customer preferences in favor of

eating out rather than drinking.

• Increase in the nature and number of competitors, as more restaurants compete with pubs for both food and drink

sales.

• Industry developments, for example rapid growth of the discount segment, may pressure gross margins of

traditional operators and force them to lower prices to remain competitive. An influx of new entrants, alternative

business models, and rising cost pressure could squeeze EBITDA margins even for large-scale operations.

• Profit margins could be under pressure due to cost inflation or commodity cost increases, which the pubs may be

unable to pass on to customers. The extent of margin erosion would generally depend on the operator's ability to

generate cost savings or raise prices.

81. For transportation infrastructure companies:

• A decline in demand can occur and fluctuate along with economic cycles, employment levels, trade flows, or

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 18

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

population growth, in particular if a company is operating in a relatively small or weak economy. Some

transportation infrastructure companies have exposure to groups whose usage is more volatile. For instance, toll

road usage by heavy goods vehicles tends to be more volatile than usage by cars; and the number of passengers

transiting at an airport tends to fluctuate more than the number of origin-and-destination passengers. Some

companies may also have part or all of their revenues contracted or guaranteed, which may moderate demand risk.

• While tariffs tend to increase with inflation, tariff restrictions may be imposed through regulation in response to

economic conditions.

• Nonregulated companies that operate in small economies or with a limited number or diversity of customers can

exhibit more volatile revenues.

82. For business and customer services:

• Demand for services generally follows GDP and inflation trends, whereas revenues tend to grow at slightly less than,

or in line with, GDP growth. Demand is generally stable during periods of modest economic weakness because

customers tend to continue outsourcing noncore services even during recessions. However, customers may seek

pricing concessions or fewer services during recessions.

• A fall in margins may exceed a decline in revenue, as companies tend to delay staff reduction, while labor costs

constitute a significant element of the cost structure. The nature of the service performed affects the flexibility of the

expense structure. Companies performing less complex services have more flexible expense structures because they

can more quickly adjust their staff levels to align with demand. This does not necessarily apply for companies with a

highly unionized work force. Companies performing more complex services have less flexible expense structures

because they must maintain consistent staff levels given the time and expense required to train new staff should

demand suddenly increase.

83. For the telecommunications and cable industry.

• Revenues and margins in the industry are primarily affected by competition, regulation, technological displacement,

and substitution, as well as the maturity of the market in which a telecom company operates.

• In our view, the telecom and cable industry has low cyclicality given that telecommunications and television

services are near necessities in developed markets. In addition, telecoms infrastructure providers benefit from

long-term contracted revenues. Still, changes in unemployment rates and consumer spending do affect the demand

for telecom services.

• Volatility of revenues and margins differs materially among companies in the industry. Companies could have

more-volatile revenues and margins if they feature: no long-term contracted revenues, concentrated customer base,

operation in fragmented markets with high price competition, exposure to potential material changes in regulation,

service offering can't be differentiated, the cost base is rigid or operating leverage high, or they face very high

country risks in geographies with relatively low disposable incomes.

• Services characterized by a significant portion of customer customization, multiyear customer contracts, or material

customer switching costs such as wireless tower leasing or managed data center services, are subject to lower price

competition and cyclicality than the industry average. However, wholesale services, including long haul transport

and voice, which are often purchased on a spot market basis where customers are seeking least-cost routing and are

relatively indifferent to the particular supplier, may be subject to significant pricing pressures and above-average

volatility.

• The sector has a high level of mergers and acquisitions (M&A) resulting from privatization and subsequent

consolidation. In our downside case, we adjust for this--since elevated M&A distorts historical peak-to-trough

measurements--by overstating volatility (both upside and downside) compared with organic movements.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 19

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

84. In case of noncyclical businesses that are unlikely to experience a decline in EBITDA or revenue as a result of

market-related factors, we model such a drop by applying an operating stress. Such businesses include agriculture

companies, where any drop in revenue or earnings is more likely due to weather conditions; funeral providers, where

services tend to be relatively stable, predictable, and independent from economic cycles, with a relatively high price

inelasticity of demand; and sport and leisure assets or facilities with a large and loyal fan base over an extended period.

Below we outline examples of industry-specific operating stresses.

85. The leisure and sports sector:

• Falling sales as a result of an event risk, such as weather, a political event, disease, stadium damage, terrorism, or

structural changes--for example due to disruptive technologies, particularly in travel-related businesses, or due to

the introduction of new business models.

• A weakening of a brand or competitive standing in the market segment. For example, poor performance by a sports

team that may lead to relegation to a lower league or the loss of a fan base. The consequences are likely to include

reduction of attendance and ticket revenues and in contractual performance-related revenue. We may assume a

more modest decline if we believe the business is highly competitive, can retain greater pricing power, or can secure

additional sources of revenue.

86. Pubs, restaurants, and retail:

• Drop in demand due to changes related to a specific subsector or product, changes in consumer preferences and

spending behavior, the threat of e-commerce, adverse weather trends, intensified competition, or tightened

regulations.

• Food safety scare or lack of attractive or healthier alternative offerings in response to the growing popularity of

healthy eating and drinking choices.

• Business failures of companies that are unable to adequately reduce their cost base or international disposals of

assets to prevent instant liquidation.

• A need to invest in maintenance or renovation of facilities in order to increase sales and maintain the relevance of a

concept. Investment beyond normal maintenance spending is often required to periodically reinvigorate properties,

brands, and offerings, especially in more competitive markets. Companies also need to invest in technology to

support online operations and an efficient supply chain.

87. Transport infrastructure:

• Demand and profitability could be affected significantly by exceptional events for example, weather conditions,

health scares, natural disasters, political unrest, and security concerns, although historically this has been for short

periods of time. For example, a port's earnings would likely be affected by the closure of a large company that is its

main customer.

• Competition from a new infrastructure asset or mode of transport where an operator of the incumbent asset is less

able to adjust their route network.

• Inability to manage the cost base, although the impact is likely to be limited as transportation infrastructure

companies with operational assets, in particular those which are regulated, tend to exhibit stable profit margins.

Although demand can fluctuate with economic cycles, profitability tends to be relatively stable owing to the limited

competitive forces the industry faces. Higher volatility of profitability could occur in case of nonregulated

companies, or companies with high proportion of fixed costs or limited flexibility in adjusting variable costs, for

example due to a highly unionized labor force.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 20

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

• Cash flow available for debt service may be affected by an obligation of a third party (government, regulator, or

concession grantor) to make significant capex commitments.

• An adverse government or regulatory intervention.

88. Business and customer services:

• Reputational damage resulting in a loss of revenue or market share. The extent of the loss would depend on the

specifics of the business. For example, reputational damage could cause a funeral provider to close a number of

funeral locations, but we would not expect any closing of crematoria due to their utility-like characteristics.

• Companies that have a significant proportion of customer contracts with governmental agencies may face the risk of

shifts in political influence, which could give preference to competitors or even decrease the use of service

contractors in favor of internal government departments.

• Regulatory changes can lead to significant increases in companies operating costs.

89. Telecommunications and cable companies:

• Telecom and cable companies may be subject to technological displacement and substitution.

• Companies in particularly mature markets may be subject to customer erosion due to changing customer

preferences or pricing pressure from a substitution product or service.

• For fixed-line or wireless carriers, the key risks are linked to competition dynamics (driving prices and/or market

shares) and include potential new entrants, competition from alternative technologies (e.g., over-the-top

content--delivery of film over the internet without traditional subscriptions), and the need to buy spectrum licences

and invest in new technologies. Companies could be at risk of emergence of a larger and better capitalized

competitor or increased supply in the market.

• Unfavorable reputation that may result in elevated marketing costs, below market pricing, and customer loss.

RELATED CRITERIA

• Structured Finance: Asset Isolation And Special-Purpose Entity Methodology, March 29, 2017

• Ratings Above The Sovereign - Structured Finance: Methodology And Assumptions, Aug. 8, 2016

• European Corporate Securitizations, Feb. 12, 2016

• Global Framework For Assessing Operational Risk In Structured Finance Transactions, Oct. 9, 2014

• Global Framework For Cash Flow Analysis Of Structured Finance Securities, Oct. 9, 2014

• Counterparty Risk Framework Methodology And Assumptions, June 25, 2013

• Corporate Methodology, Nov. 19, 2013

• Criteria For Assigning 'CCC+', 'CCC', 'CCC-', And 'CC' Ratings, Oct. 1, 2012

• Principles Of Credit Ratings, Feb. 16, 2011

• Methodology: Credit Stability Criteria, May 3, 2010

• Understanding Standard & Poor's Rating Definitions, June 3, 2009

• U.S. Corporate Securitization Transactions, Oct. 24, 2006

• Legal Criteria For U.S. Structured Finance Transactions: Criteria Related To Hybrid Asset-Backed Securities, Oct. 1,

2006

• Legal Criteria For U.S. Structured Finance Transactions: Special-Purpose Entities, Oct. 1, 2006

• Global Timber Property Securitizations, May 1, 2003

These criteria represent the specific application of fundamental principles that define credit risk and ratings opinions.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 21

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

Their use is determined by issuer- or issue-specific attributes as well as S&P Global Ratings assessment of the credit

and, if applicable, structural risks for a given issuer or issue rating. Methodology and assumptions may change from

time to time as a result of market and economic conditions, issuer- or issue-specific factors, or new empirical evidence

that would affect our credit judgment.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 22

1840472 | 301135087

Criteria | Structured Finance | Request for Comment: Request For Comment: Global Methodology AndAssumptions For Corporate Securitizations

STANDARD & POOR'S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor's Financial Services LLC.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2017 by Standard & Poor’s Financial Services LLC. All rights reserved.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT APRIL 28, 2017 23

1840472 | 301135087