relationship between working capital management and profitability

TRANSCRIPT

DECLARATION

This Research project is my original work and has not been presented for award of an

MBA degree in any other University or for any other award.

Signed_________________________ Date: _________________NICHOLAS KIMANZI MUMOD53/OL/14685/2009

This research project has been submitted for examination with my approval as the

university supervisor.

Signed: _________________________ Date: _________________Mr. Ngaba (Supervisor)

Department of Accounting & Finance, School of Business

For and on behalf of Kenyatta University,

Mr. Fredrick W. Ndende

Signature ___________________________ Date_______________

Chairman, Department of Accounting & Finance

Kenyatta University.

i

DEDICATION

I dedicate this research project report to my lovely family, parents, my brothers and

sisters and my friends who in one way or another assisted me.

Above all glory to God for the opportunity to be alive and healthy to partake this work.

ii

ACKNOWLEDGMENTS

The following people were key contributors to this project. First and foremost is my fam-

ily, my wife Nitah Rael Kimanzi, Son Shawn Ray Kimanzi, Daughter Iddah Mueni Ki-

manzi, Parents Mr & Mrs Mumo Kituku, Brothers Alex Kituku & Fred Sammy, and Sis-

ters Patricia Syovata & Silvia Nduku. Not forgetting my work mates and fellow class

mates. Supervisor Mr. Ngaba was fundamental in this research for his insightful advice.

I must thank God for his gift of life and peace; he deserves special thanks as well.

iii

ABSTRACT

The importance of working capital management to the profitability of a business has been

extensively studied by scholars and practitioners. The theoretical importance of the

working capital component over the profitability ratio is very clear, that is, the lesser the

time a firm needs to realize cash from its customers relative to the time it requires to pay

off its creditors, the better it is for its liquidity position and thus reduces the risk of

dependency on external and more expensive sources of capital. So firms with lesser

duration of cash conversion cycle are considered more efficient. The purpose of the study

was to establish the relationship between Working Capital Management and Profitability

of retail supermarket chains in Kenya. The research was a causal study design. The

population of this study was consisted of the 6 retail supermarket chains in Kenya these

are Nakumatt, Tuskys, Uchumi, Ukwala, Naivas, and Eastmatt. The research used data of

the selected retail chains, the data covered a five year period starting from 2007 to 2011.

The research used secondary data that was obtained from financial statements of the

companies and Multiple regression analysis was employed. The study found that there

exist a relationship between Working Capital Management and Profitability of retail

supermarket chains in Kenya. It was also established that there was a variation 100% of

the profits of supermarket in Kenya with changes in working capital management at a

confidence level of 95%. This means that 100% of the profits of supermarkets in Kenya is

attributable to working capital management. The study found that holding the working

capital variables under study to a constant zero net operating profit would be equal to

0.399. a unit increase in CCC lead to decrease by 0.002, unit increase in ACP increases

profitability by0.019. The study concludes that there exists relationship between Working

Capital Management and Profitability of retail supermarket chains in Kenya; leverage

was found to positively influence the profitability of supermarkets in Kenya. The study

recommends that future research should be conducted on the same topic with different

firms both listed and non-listed and extending the number of years of the sample. The

scope of further research may be extended to other working capital components including

cash, current ratio and marketable securities.

iv

TABLE OF CONTENTS

DECLARATION..................................................................................................................i

DEDICATION....................................................................................................................ii

ACKNOWLEDGMENTS..................................................................................................iii

ABSTRACT.......................................................................................................................iv

TABLE OF CONTENTS....................................................................................................v

LIST OF FIGURES..........................................................................................................viii

LIST OF TABLES..............................................................................................................ix

DEFINITION FOR RESEARCH TERMS..........................................................................x

LIST OF ABBREVIATIONS...........................................................................................xii

CHAPTER ONE..................................................................................................................1

1.0 Introduction....................................................................................................................1

1.1 Background....................................................................................................................1

1.1.1 Working Capital Management....................................................................................3

1.2 Statement of the Problem...............................................................................................6

1.3 Research Objectives.......................................................................................................8

1.3.1 Specific objectives......................................................................................................8

1.3.2 The research questions................................................................................................8

1.4 Significance of the Study...............................................................................................9

1.4.1To the Management of Supermarkets..........................................................................9

1.4.2To Academia................................................................................................................9

1.5 Limitations of the Study..............................................................................................10

1.6 Scope of the Study.......................................................................................................10

CHAPTER TWO...............................................................................................................11

LITERATURE REVIEW..................................................................................................11

2.1 Introduction..................................................................................................................11

2.2 Theoretical Framework................................................................................................11

2.3 Working Capital Management.....................................................................................142.3.1 Cash Management....................................................................................................14

2.3.2 Inventory Management.............................................................................................16

v

2.3.3 Accounts Receivable Management...........................................................................18

2.3.4 Accounts Payable Management................................................................................20

2.4 Working Capital Management Policies.......................................................................21

2.5 Measures of working capital management..................................................................23

2.6 Strategies for Improving Working Capital Management............................................26

2.7 Empirical Review........................................................................................................27

2.8 Conceptual Framework................................................................................................33

CHAPTER THREE...........................................................................................................35

RESEARCH METHODOLOGY......................................................................................35

3.0 Introduction..................................................................................................................35

3.1 Research Design..........................................................................................................35

3.2 The target population...................................................................................................36

3.3 Sampling......................................................................................................................36

3.4 Data Collection............................................................................................................36

3.5 Data Analysis...............................................................................................................36

3.5.1 Model Specifications................................................................................................37

CHAPTER FOUR.............................................................................................................39

DATA ANALYSIS AND INTERPRETATION OF THE RESULTS..............................39

4.0 Introductions................................................................................................................39

4.1 Descriptive Statistics for Selected Measures of Working Capital Management and Profitability........................................................................................................................39

4.1.1 Comparative means of various WCM ratios and NOP for each of the supermarkets...........................................................................................................................................40

4.2 Comparative Means Of Various WCM Ratios And NOP For The Years Under Re-view....................................................................................................................................41

4.3 Correlation analysis.....................................................................................................42

4.4 Regression Analysis.....................................................................................................43

4.4.1 Regression Results For 2007....................................................................................43

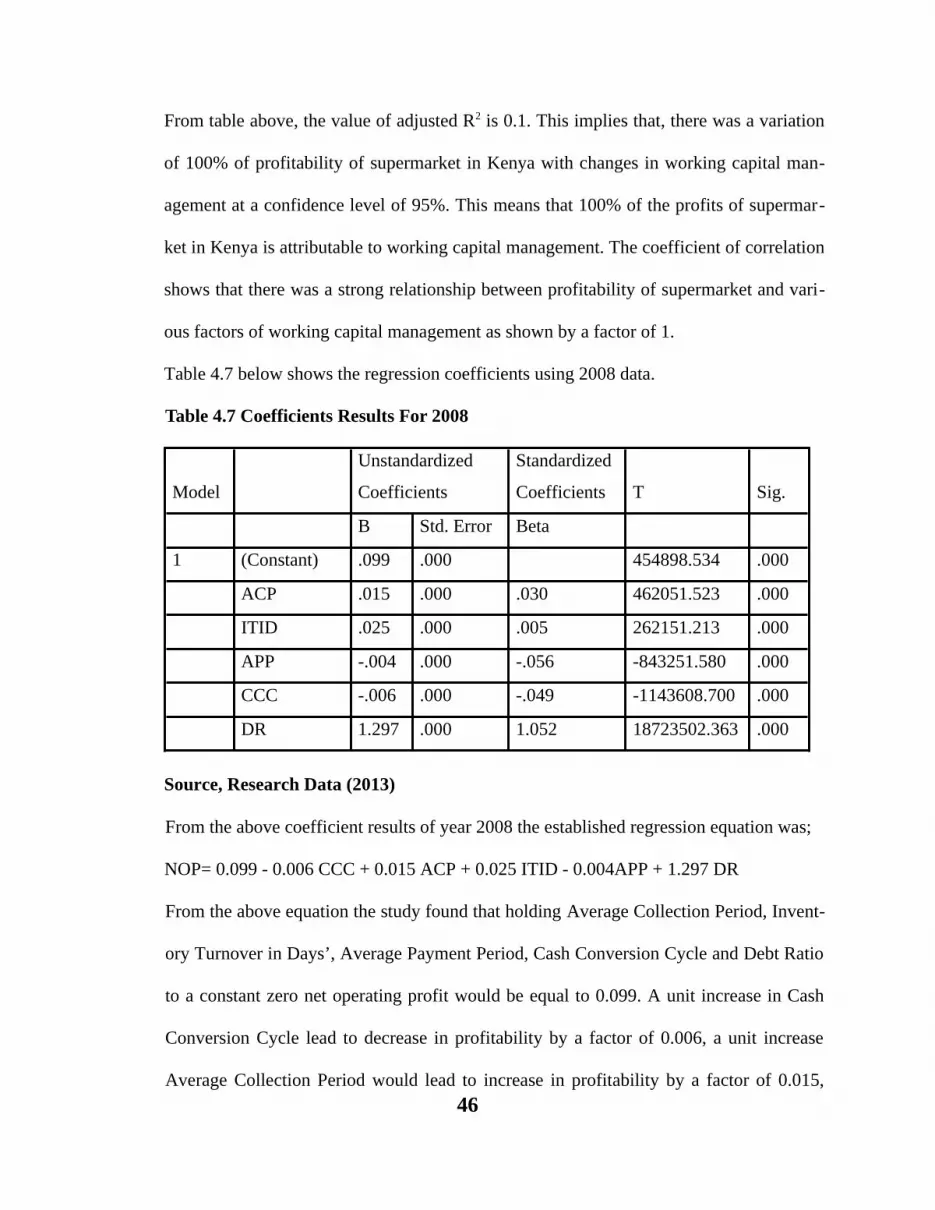

4.4.2 Regression Results For 2008....................................................................................45

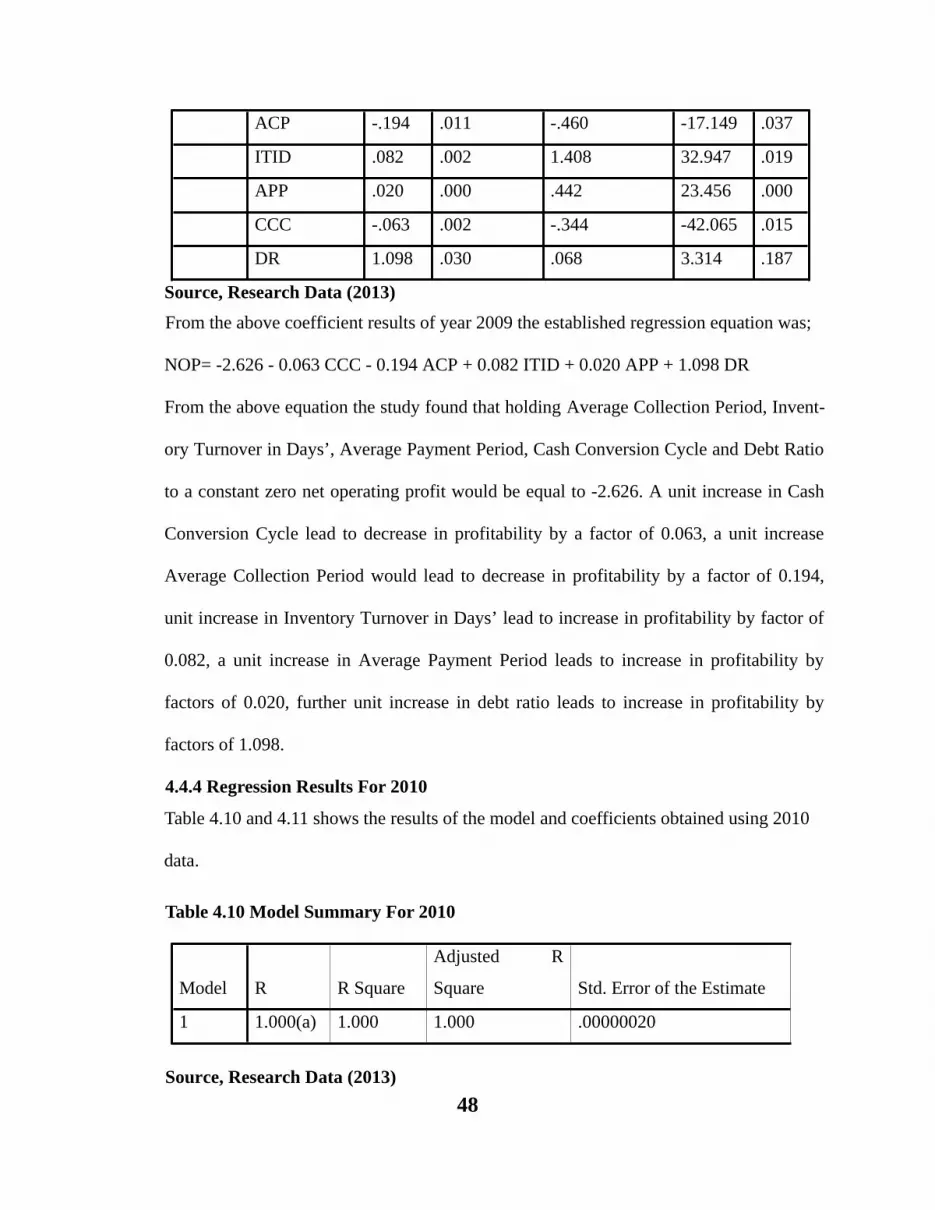

4.4.3 Regression Results For 2009....................................................................................47

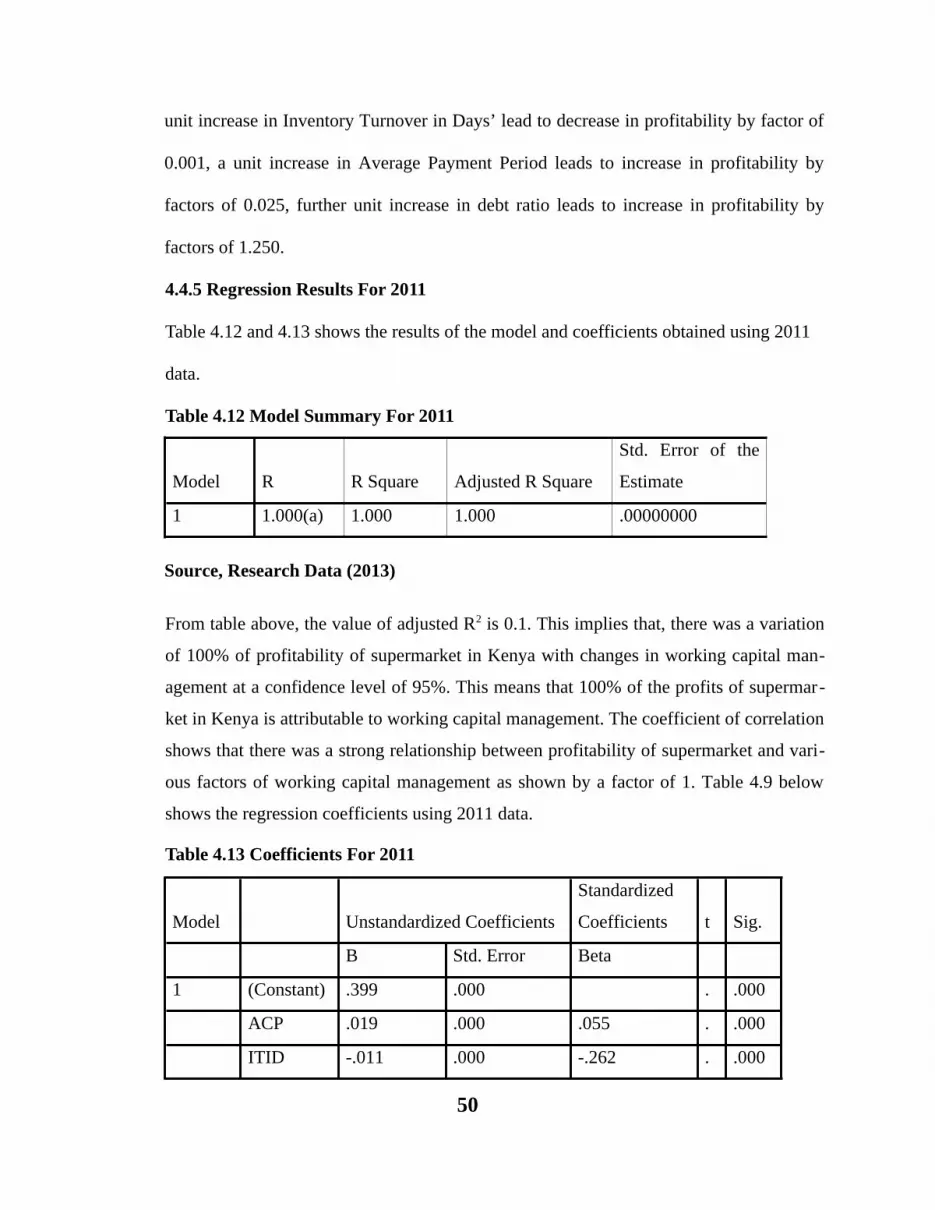

4.4.4 Regression Results For 2010....................................................................................48

4.4.5 Regression Results For 2011....................................................................................50

vi

CHAPTER FIVE:..............................................................................................................52

DISCUSSIONS, CONCLUSIONS AND RECOMMENDATIONS.................................52

5.0 Introduction..................................................................................................................52

5.1 Discussions..................................................................................................................52

5.2 Conclusions..................................................................................................................55

5.3 Recommendations for further Research......................................................................55

REFERENCES..................................................................................................................56

vii

LIST OF FIGURES

Figure 1. 1 Conceptual Framework..................................................................................34

viii

LIST OF TABLES

Table 4. 1 Descriptive Statistics......................................................................................39Table 4. 2 Comparative means of various WCM ratios and NOP for each of the supermarkets....................................................................................................................41Table 4. 3 Correlation Analysis.......................................................................................42Table 4. 4 Regression Model Summary For 2007...........................................................43Table 4. 5 2007 Coefficients results................................................................................44Table 4. 6 Model Summary For 2008..............................................................................45Table 4. 7 Coefficients Results For 2008.........................................................................46Table 4. 8 Model Summary for 2009...............................................................................47Table 4. 9 Coefficients For 2009.....................................................................................47Table 4. 10 Model Summary For 2010............................................................................48Table 4. 11 Coefficients For 2010...................................................................................49Table 4. 12 Model Summary For 2011............................................................................50Table 4. 13 Coefficients For 2011...................................................................................50

ix

DEFINITION FOR RESEARCH TERMS

Working capital management: Padachi, (2008) defines this as a managerial accounting

strategy focusing on maintaining efficient levels of both components of working capital,

current assets and current liabilities, in respect to each other. It ensures a company has

sufficient cash flow in order to meet its short-term debt obligations and operating

expenses.

Profitability: The ability of the firm to earn a profit. Profitability can also be labeled as a

measurement of business success where a company is able to generate profits from its

operations (Keane & Wang, 1995).

Cash conversion cycle: Shin & Soenen, (1998) define the cash conversion cycle as the

continuing cash flow from suppliers to inventory to accounts receivable and back into

cash.

Trade receivables: The term trade receivables refer to the amounts due to a business

following the sale of goods or services to another company (Brealey, 2004).

Trade payables: are also known as accounts payable and refers to money owed to

creditors, lenders, vendors or suppliers for products or services rendered (Brealey, 2004).

Net-trade cycle: it’s similar to cash conversion cycle but only differs in the manner

where Net Trade Cycle shows how long the cash is tied up in the trade cycle before

coming back out as cash again (Deloof, 2003).

x

Return on assets (ROA): measures how profitable a company is relative to its total

assets, In turn, it measures how efficiently a company uses its assets. Normally, ROA is

used to compare companies in the same industry. Everything else being equal, a higher

ROA is better, as it means that a company is more efficient about using its assets (Nazir

& Afza, 2007).

Return on equity: Nazir & Afza, (2007), the ratio of net profit to shareholders' equity

also called book value, net assets or net worth, expressed as a percentage. A measure of

how well a company uses shareholders' funds to generate a profit.

Return on net assets (RONA): is a comparison of net income with fixed assets and net

working income. This is a metric of financial performance of a company that takes into

account earnings of a company with regard to fixed assets and net working income (Nazir

& Afza, 2007).

xi

LIST OF ABBREVIATIONS

CCC Cash conversion cycle

NOP Net operating profitability

NWC Net Working Capital

NSE Nairobi Stock Exchange

WCM Working capital management

CCCM Cash Conversion Cycle Model

OLI Optimum Level of Investment

LTC Long Term Capital

NTC Net-trade cycle

NOA Return on assets

ROE Return on equity

RONA Return on net assets

SPSS Statistical package for social sciences

ACP Average Collection period

ITID Inventory turnover in days

APP Average payment period

DR Debt ratio

xii

CHAPTER ONE

1.0 Introduction

This chapter contains the overall overview of the research project. It basically contains:

the background of the study, statement of the problem, objectives of the study, research

questions, significance of the study, limitations of the study and scope of the study.

1.1 Background

Working capital management, which consists of current assets and current liabilities

management, is the main function of financial managers in all corporations. While the

working capital management takes up a major part of executive manager’s attention and

time, there is a deserved attention to working capital management in finance literature

(Jose, Lancaster, & Stevens, 1996; Deloof, 2003; Ŝen & Oruč, 2009). The utmost

important component of working capital related to inventories, accounts receivables and

accounts payables (Ross, Westerfield, & Jaffe, 2002). Financial executives have to make

different decisions about the level of these components in order to get best results. The

dynamic nature of short-term business emporium, the daily need to substituting current

assets, and liquidation current liabilities help to clarify the importance of working capital

management and financial executive duties. The direct effect of working capital

management on profitability and liquidity position of firms also refers to the importance

of working capital management (Nobanee, Abdullatif, & Al Hajjar, 2011). Firms may

face to bankruptcy if they select and use improper working capital strategies, even though

they experience positive profitability (Śamiloġlo & Demirgũneş, 2008).

1

Management of these current assets and current liabilities is important in creating value

for shareholders (Nazir and Afza, 2009). If a firm can minimize its investment tied up in

current assets, the resulting funds can be invested in value-creating projects, thereby

increasing the firm’s growth opportunities and shareholders’ return (Eramus, 2010).

However, management can also confront liquidity problems due to underinvestment in

working capital (Nazir and Afza, 2009). As pointed out by Filbeck and Krueger (2005),

the ability of financial managers to effectively manage receivables, inventories, and

payables has a significant impact on the success of the business (Nazir and Afza, 2009).

If capital invested in cash, trade receivables, or inventories is not sufficient, the firm may

have difficulty in carrying out its daily business operations (Eramus, 2010). This may

result in declining sales and, in the end, a reduction in profitability (Deloof, 2003). Smith

(1980) emphasized the trade-off between liquidity and profitability when he argued that

working capital management can play an essential role not only in a firm’s profitability

and risk, but also in its value. Decisions regarding an increase in profitability are likely to

involve increased risk, and risk-reducing decisions are likely to result in a reduction in

profitability (Garcia-Teruel and Martínez-Solono, 2007). An accepted measure of

working capital management is the cash conversion cycle (Abuzayed, 2012) which

represents the average number of days between the day the firm begins paying its

suppliers and the day it starts to receive cash for products sold (Deloof, 2003). Longer

cash conversion cycles mean more time between cash expenditure and cash retrieval

(Deloof, 2003). Previous research has used the cash conversion cycle as a measure of

working capital management to analyze whether reducing the time allowed for this cycle

2

has positive or negative effects on corporate profitability (Garcia-Teruel and Martínez-

Solono, 2007; Abuzayed, 2012).

On the whole, empirical evidence related to working capital management and

profitability has substantiated the fact that managers can create value for shareholders by

shortening the cash conversion cycle to the shortest rational amount of time (Raheman,

and Nasr, 2007; Banos-Caballero et al., 2007). The objective of this study is to investigate

the relationship between working capital management, as measured through the cash

conversion cycle, and corporate profitability in Kenya. This study enriches the finance

literature on the relationship between working capital management and profitability.

1.1.1 Working Capital Management

The main objective of working capital management is to ensure that companies have

sufficient cash flow to continue normal operations in such a way that minimize risk of

inability to pay short-term commitment. Moreover, managers should try to avoid from

unnecessary investment in working capital. While, more investment in working capital

may reduce the risk of liquidity, insufficient amount of working capital may cause

shortages and problems in daily operations. However, more investment in working capital

means more funds tied up to business operation and would increase the opportunity cost

of investment especially when firms rely on external financing to finance working

capital. Therefore, efficiency of working capital management depends on balances

between liquidity and profitability (Filbeck, Krueger, & Preece, 2007; Faulkender &

Wang, 2006). The profound understanding of the role of working capital and its effect on

firm’s profitability would help managers to look for strategic plans for management of

working capital.

3

One of the standard performance measures to evaluate how well a firm does managing

the working capital is Cash Conversion Cycle (CCC) that was introduced by Richards

and Laughlin (1980). It refers to time-period between buying raw material, convert to

finished goods, sales products, and collect account receivables. Firms with Shorter cash

conversion cycle have less investment in working capital and as a result the cost of

financing is less for these firms. The importance of cash conversion cycle was well

pointed out by a study that was conducted by Shin & Soenen (1998). They compared two

corporations with the same capital structure, Kmart and Wal-Mart. The former had a CCC

of 61 days and the latter had a CCC of 40 days. The differences of 19 days in cash

conversion cycle made Kmart to face 198.3 million US dollars extra to finance their

working capital and faced more financial constraints. Consequently, shorter cash

conversion cycle would increase profitability, and would show the efficiency of

management performance in managing working capital (Deloof, 2003; Nazir et al., 2009;

Zariyawati et al, 2009). Thus, Cash conversion cycle integrates three components of

management efficiency include, production, inventory management, as well as supply

chain management (Moyer, Mcguigan, & Kretlow, 2003).

Operation cycle includes both inventory conversion period and receivables conversion

period. The length of operation cycle should be financed by corporations directly if they

buy the raw materials on cash. But majority of corporations have strong tending to use

trade credits to financing some parts of operation cycle and also suppliers are willing to

provide financial intermediary services to corporations (Niskanen & Niskanen, 2006).

Inventory conversion period refers that how long it takes a firm coverts the raw material

to finished goods. This period is just available in manufacturing firms and it cannot be

4

applied to services or banking sectors. Supply-chain management, economic order

quantity, just in time system and economic production quantity are common techniques to

management inventories and managers can use these tools to shorten the period of

inventory conversion. Receivables conversion period is defined as the time -period

between sales products on credit and collecting the cash from the customers. Financial

managers should select and use appropriate credit policies not only to attract clients in a

manner that enable firms to compete with their competitors but also to minimize the

financing cost of these credits. Last part of cash conversion cycle connected to payables

deferral period that refers to time-period between buying raw material on credit and

paying cash to suppliers. Although, extending the length of payable deferral period may

reduce the length of cash conversion cycle but it should consider that more lengthening of

deferral payable period may damage the firm’s reputations (Nobanee et al., 2011). The

shorter the length of the cash conversion cycle means effective working capital

management and indicates the better management performance with regards to the

inventory conversion period, collecting receivables period and short term financing using

payables.

This study will contribute to the body of knowledge by identifying how working capital

management affects a firm’s profitability and how managers can use working capital

strategies to increase the firm’s profitability. Moreover, This study focus on the effect of

working capital management on firm’s performance and shed more light to how

managers affect firm’s profitability by managing working capital efficiently. The

theoretical contribution of this research is to enrich the existing literature by investigating

5

the effect of working capital management on profitability in Kenya’s firms as a

developing market.

1.2 Statement of the Problem

A firm is required to maintain a balance between profitability while conducting its day to

day operations. While inadequate amount of working capital impairs a firm's liquidity,

holding of excess working capital results in the reduction of the profitability (Ghosh &

Maji, 2003). A firm can be very profitable if it can translate cash from operations within

the same operating cycle, otherwise the firm would need to borrow to support its

continued working capital needs. Thus, the twin objectives of profitability must be

synchronized (Brigham & Houston, 2004). Empirical results show that ineffective

management of working capital is one of the important factors causing industrial

sickness. Modern Financial management aims at reducing the level of current assets

without ignoring the risk of stock outs (Bhattacharya, 1997). Efficient management of

working capital is thus an important indicator of sound health of an organization, which

requires reduction of unnecessary blocking of capital in order to bring down the cost of

financing.

Previous research has documented that working capital management influences a firm’s

profitability (Deloof, 2003; Lazaridis & Tryfonidis, 2006; Eljelly, 2004; Wang, 2002;

Johnson & Soenen, 2003). The studies also reported that efficient working capital

management is one of the crucial characteristics of financially flourishing firms. Most of

the empirical research into the relationship between working capital management and

profitability has confirmed the notion that reducing current assets in comparison to total

assets reduces working capital investment; therefore, it would positively affect the firm’s

6

profitability. Many scholars have measured working capital using the cash conversion

cycle (Lazaridis & Tryfonidis, 2006; Raheman, &Nasr, 2007; Eljelly, 2004)

Deloof (2003) analyzed a sample of Belgian firms and found that firms can raise their

performance by shortening the periods for receivables collection and inventory

conversion. He also reported an unanticipated negative impact associated with the

number of days for accounts payable; poorer firms prolong the time to pay their debts.

Wang (2002) analyzed a sample of Japanese and Taiwanese firms, Lazaridis and

Tryfonidis (2006) examined a sample of firms listed on the Athens Stock Exchange,

Nazir and Afza (2007) investigated a sample of firms listed on the Karachi Stock

Exchange, and Abuzayed (2012) looked at a sample of firms listed on the Amman Stock

Exchange; they all found that shortening the cash conversion cycle enhances firm

performance. Shin and Soenen (1998) used a sample of US firms and Erasmus (2010)

used a sample of South African firms, and both studies employed the net trading cycle

(NTC). NTC is calculated by summing trade receivables and inventories then subtracting

accounts payable and expressing the result as a percentage of sales, as the comprehensive

measure of working capital management. The results were similar to results of studies

that used the cash conversion cycle; the researchers discovered a significant negative

relationship between NTC and profitability.

As noted in the preceding paragraphs, previous studies have studied the correlation

between efficient working capital management and profitability (e.g. Deloof, 2003; Shin

& Soenen 1998). The question arises if we can see that efficient working capital

management in Kenyan firms, with a focus at supermarkets in Kenya, would improve

corporate profitability. In addition, which are the key metrics that are used to define

7

working capital management efficiency? In other words, what drivers should companies

look to when minimizing their investment in working capital?

1.3 Research Objectives

The main objective of the study was to examine the relationship between working capital

management and profitability of supermarkets in Kenya

1.3.1 Specific objectives

The study was guided by the following specific objectives:

(i) To determine the relationship between average collection period and the

profitability of supermarkets in Kenya

(ii) To establish the relationship between inventory turnover in days and the

profitability of supermarkets in Kenya

(iii) To determine the relationship between average payment period and the

profitability of supermarkets in Kenya

(iv)To establish the relationship between cash conversion cycle and the profitability

of supermarkets in Kenya

(v) To determine the relationship between debt ratio and the profitability of

supermarkets in Kenya

1.3.2 The research questions

To fulfill the study’s objectives, the study was guided by the following research

questions:

(i) What is the relationship between average collection period and the profitability of

supermarkets in Kenya?

8

(ii) What is the relationship between inventory turnover in days and the profitability of

supermarkets in Kenya?

(iii) What is the relationship between average payment period and the profitability of

supermarkets in Kenya?

(iv) What is the relationship between cash conversion cycle and the profitability of

supermarkets in Kenya?

(v) What is the relationship between debt ratio and the profitability of supermarkets in

Kenya?

1.4 Significance of the Study

This study will be important to various stakeholders including the management of

supermarkets and companies in Kenya and to academia.

1.4.1To the Management of Supermarkets

The findings and recommendations of this study will be useful to new and existing

managers of supermarkets and other firms on the importance of capital management to

the profitability of their businesses. In addition the management will understand the ideal

capital management ration for their businesses that is ideal for profitability.

1.4.2To Academia

Knowledge seekers in the fields of economics, research methods, management, and

finance will find this research study useful. In particular, this research study will be

beneficial to the researchers with research interests in capital management and firm

profitability, by serving as a point of reference. In addition, future researchers will be able

to formulate further studies based on the recommendations of this study.

9

1.5 Limitations of the Study

Limitation for the purpose of this research was regarded as a factor that was present and

contributed to the researcher getting either inadequate information or responses or if

otherwise the response given would have been totally different from what the researcher

expected.

The main limitations of this study were; some data was not readily available. This

reduced the probability of reaching a more conclusive study. However, conclusions were

made with the available data. The small size of the sample could have limited confidence

in the results and this might limit generalizations to other situations. Time due to official

duties was a major concern.

1.6 Scope of the Study

The study focused on the relationship between working capital management and

profitability of supermarkets in Kenya and used audited and published financial

statements from supermarkets as data for analysis.

10

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter summarises the information from other researchers who had carried out their

research in the same study on the relationship between capital management and

profitability of firms. The study specifically covers the theoretical discussions, research

gap and conceptual framework.

2.2 Theoretical Framework

The theoretical relationship between working capital and profitability has been discussed

extensively in the literature. From the perspective of working capital, firms have two

main objectives, namely maximization of profit and minimization of liquidity risk. As

pointed by Walker (1980) risk means, risk of not maintaining adequate liquidity; risk of

having too much or too little inventory to maintain production and sales; and the risk of

not granting adequate credit to support the proper level of sales.

Profitability is concerned with the overall objective of owner wealth maximization. The

problem with the dual objectives of profitability and liquidity is that they tend to conflict.

Decisions that tend to maximize profitability tend to create the problem of inadequate

liquidity and vice versa. In addition, the way in which working capital is managed can

have a significant impact on profitability and liquidity goals of the firm.Corporations can

have a best possible amount of working capital that leads to their value maximization

(Deloof, 2003). On the other hand, maintaining a huge inventory, readily granting credit

to customers, and being willing to wait a longer time to receive payment may result in

11

higher sales (Deloof, 2003). The downside of granting generous trade credit and

maintaining high levels of inventory is that money is stashed in working capital (Deloof,

2003). On the liabilities side, postponing payment to suppliers lets a firm to get the goods

prior to paying, therefore increases spontaneous financing and thus reduces the need for

costly external funding (Lasher, 2008).Efficient working capital management involves

managing short-term assets and short-term liabilities in a way that provides balance

between eliminating potential inability to cope with short-term debts and avoiding

unnecessary holdings in these assets (Eljelly, 2004). Previous research has documented

that working capital management influences a firm’s profitability (Lazaridis and

Tryfonidis, 2006), (Eljelly, 2004), (Wang, 2002)). Johnson and Soenen (2003) also

reported that efficient working capital management is one of the crucial characteristics of

financially flourishing firms.

Most of the empirical research into the relationship between working capital management

and profitability has confirmed the notion that reducing current assets in comparison to

total assets reduces working capital investment; therefore, it would positively affect the

firm’s profitability. Many scholars have measured working capital using the cash

conversion cycle (Eljelly, 2004).Deloof (2003) analyzed a sample of Belgian firms and

found that firms can raise their performance by shortening the periods for receivables

collection and inventory conversion. He also reported an unanticipated negative impact

associated with the number of days for accounts payable; poorer firms prolong the time to

pay their debts. Wang (2002) analyzed a sample of Japanese and Taiwanese firms,

Lazaridis and Tryfonidis (2006) examined a sample of firms listed on the Athens Stock

12

Exchange, Nazir and Afza (2007) investigated a sample of firms listed on the Karachi

Stock Exchange, and Abuzayed (2012) looked at a sample of firms listed on the Amman

Stock Exchange; they all found that shortening the cash conversion cycle enhances firm

performance. Shin and Soenen (1998) used a sample of US firms and Erasmus (2010)

used a sample of South African firms, and both studies employed the net trading cycle

(NTC). NTC is calculated by summing trade receivables and inventories then subtracting

accounts payable and expressing the result as a percentage of sales, as the comprehensive

measure of working capital management. The results were similar to results of studies

that used the cash conversion cycle; the researchers discovered a significant negative

relationship between NTC and profitability.To make sure the optimal level of working

capital management can be reached, there are four dimensions of working capital

management should be considered: cash management, inventory management, account

receivable management (debtor management) and account payable management (creditor

management). Each element has its own characteristics. However, managers should take

each component into consideration as a whole, since a trade-off exists in the relationship

of each component. For instance, a large inventory and a generous trade credit policy

may lead to higher sales, large inventory and a generous trade credit allows customers to

assess product quality before paying (Long, Malitz and Ravid, 1993; Deloof and Jegers,

1996). However, the flip side of granting trade credit and keeping inventory is that,

money is locked in working capital (Deloof, 2003). Therefore, having a good knowledge

on each element of working capital management can be very helpful in financial decision

making.

13

2.3 Working Capital Management

2.3.1 Cash Management

In a business, having sufficient cash is very important. Cash is like the oxygen for a com-

pany to survive, company needs cash to deal with their daily operations. Padachi (2006)

points out that just as circulation of blood is very necessary in the human body to main-

tain life, cash flow is necessary to maintain business. Akinwande (2009) also mentions in

his study that Cash is lifeblood of a business, and a manager’s key mission is to assist in

keeping it to flow and to take the advantage of the cash flow in making profit. Therefore,

maintaining sufficient cash can decide the destiny of a business. Cash management is

mainly about the decision of cash distribution, which is also the most important compo-

nent of working capital management.

Although cash does not earn profit, there are three motives for a company to hold cash:

Transaction motive: company needs certain level of cash to meeting their daily transac-

tions, such as payment for supplier, salaries and so on. Cash holding ensures company to

meet their regular cash outflow; Precautionary motives: Sometimes, cash flow is hard for

a company to predict because of the difference between the firms and industries. Cash

holding can help to relieve the problem of unexpected cash needs, for instance, raised

cost of raw material and default of third party and Speculative motives: during the busi-

ness operation, unexpected investment opportunities can raise, sufficient cash holding al-

lows the company to take advantage of these opportunities and grow in the future.

As one can see, companies can enjoy several benefits under holding sufficient cash.

However, holding excessive cash does not make good business sense, since excessive

14

cash can earn interest if they are used in the proper investment (Banjerjee, 2005). Mar-

tinez-Sola, Garcia-Teruel and Martinez-Solano (2011) tested two questions in their inves-

tigation: first, whether there is an optimal cash level that can maximize firm value, and

second whether firm value would be reduced if the cash deviates from the optimal level.

Results denote that there is a concave relationship between cash holding and firm value,

which means that optimal cash level that maximized firm value, does exist. Firm value

will be decreased if the cash holding is different from this optimal level. Trade-off theory

can also explain that there is an optimal level of cash holding which can balance the mar-

ginal benefit and cost (Saddour, 2006). These results suggest that having optimal cash

holding is the central task of cash management.

Banjerjee (2005) mentions that two constraints which decide how much cash a firm

should maintain. The First is the compensating balances, which is the cash balance re-

quired compensating for the services that are rendered by banks to the firms (p. 213). The

second is self-imposed balance, which is determined by considering factors like the need

for cash, the predictability of this need, the interest rate on marketable securities or the

borrowing rate, and the fixed cost of effecting a transfer between marketable securities

and cash or effecting a loan transaction (p.213). Saddour (2006) studies the determinants

of cash holding by using a sample of French firms. Results confirm that cash holding en-

able firms to take profitable investment opportunities, which leads to the fact that cash

holding level of growth firm is higher than the matured firms. They also find that the de-

terminants of cash holding are different between growth firms and matured firms. Cash

holdings in growth companies decrease with the raise of firms’ characteristics: size, level

15

of liquid assets and short-term debt. However, in matured firms, cash level shows a posi-

tive relationship with firm size and dividend payout and negative relationship with firms’

research and development expenses. Within a similar study, cash-holding level in firms

from Canada is strongly affected by their market to book ratio, cash flow, net working

capital leverage, and firm size (Gill and Shah, 2012). Bensoussan, Chutani and Sethi

(2009) explain the optimization problem of meeting demands for cash over time with

cash deposit in bank or invested in stock. Study shows the solutions of optimal level of

cash holding a company should have under different uncertainty by using different

model.

The value of cash holding and use of cash holding vary between good and bad-governed

firms. This can be illustrated by looking at influence on firm value by using of cash hold-

ing in different business environment: In a poorly-governed firm, 1 dollar cash is only

valued at 0.88 dollar. To be a contrast to that, in a well-governed firm, 1 dollar cash can

double its price.

Firm’s future performance in poorly corporate governance will be reduced since cash can

be dissipated very fast. On the opposite, in well-governed firms, firms’ future operating

performance will get a big improvement due to the negative impact of cash holding can

be cancelled out (Dittmar, Mahrt-Smith, 2006).

2.3.2 Inventory Management

Usually, inventory can be decomposed by three parts: raw materials, work-in-process in-

ventory and finished inventory. Just like cash management, inventory management also

has trade-off in its management system. According to Damodaran (1997), there are three

motives for a company to hold inventories. First, raw materials are held to make sure that

16

the production process goes well and not interrupted by a shortage of raw materials. Sec-

ondly, inventories of intermediate goods appear in the middle of process, it will be used

to continue process. Thirdly, holding enough finished goods is to avoid the risk of losing

sales, and to avoid the large ordering and administration cost which caused by replenish-

ing inventory. However, the down side of holding too many inventories can cause large

carrying cost, for instance, storage cost, security cost, and goods obsolescence and goods

perishing. Therefore, with an efficient inventory management, a lot of the risks and costs

can be avoided. Singh (2008) studies the relationship between inventory management and

working capital management, and he supports the importance of inventory management.

He thinks that firms with a poor inventory management can cause serious problems

which destroy the long-term profitability and firms’ survival chances. A contrary result,

with a well-thought inventory management, firm can reduce the inventory to an optimal

level which has no negative effect on production and sales. The paper also denotes that

the size of inventory directly affects the working capital and its management. Thus, in-

ventory management does attract manager’s attentions.

Considerable level of inventories is the main goal of inventory management. In order to

find the solution for optimal inventory, Swaminathan (2001) studies the how structural

reforms affects inventory management in public and private sectors in India. Findings of

this paper verify that adjusting raw material and finished goods as a component of inven-

tory is faster than the inventory as a whole to reach the reasonable level. There are some

other methods that can easily affect inventory management, such as, order quantity

method, just-in-time inventories, etc. (AutuKaite and Molay, 2011).

17

2.3.3 Accounts Receivable Management

Accounts receivable management, which is also known as debtor management, is a com-

pany giving their customers a specific credit term to pay for products or services. These

credit terms, which are called trade credit, can help ease customer’s financial frictions

(Meltzer, 1960). Customers who buy products or service on trade credit are called sundry

debtor for the company. Account receivable is a major component in business finance. In

European countries, such as Germany and Italy, account receivable is more than one

quarter of their total asset (Bougheas, Mateut and Mizen, 2009). Rajan and Zingales

(1995) study capital structure of firms. They show that in a sample of American firms,

17.8 percent of total assets are the accounts receivable. We can see that an efficient ac-

count receivable management is indispensable. Smith (1987) points out that providing

trade credit to customers is very important to suppliers whose sales or investment depend

on consumer’s financing ability. Emery (1984) uses operational and financial method to

explain the reasons that behind extending trade credit: firstly, extending trade credit is

due to pure operating flexibility. He explains that the demand of customers is irregular

since the market is imperfect. There is always a deviation from expected demand, which

may cause the excess production.

Temporary relaxations of credit terms allows account receivable account fluctuate corre-

spond to the deviation in demand, which illustrates the formation of a sale queen instead

of customer or products queen. Secondly, pure financial intermediary motive explicates

extension of trade credit. Due to the imperfect market, firms are required to maintain liq-

uid reserve for the unexpected needs of cash. Offering trade credit to customers can be

18

seen as offering loan to customers, which is also a part of liquid reserve. Ferris (1981) de-

fines trade credit as a particular type of short term loan: a loan that is tied in both timing

and value to the exchange of goods (p. 243). Therefore, firms can receive lending rate of

return from this loaned liquid reserve. Extending trade credit gives suppliers an opportu-

nity to earn a higher rate of return than the marginal return. Hill, Kelly and Lockhart

(2012) reveal that trade receivable significantly and positively affect shareholders wealth

by studying all non-financial, non- utility, and SIC classifiable firms in the period 1971-

2006. This result confirms the importance of a reasonable trade credit policy. However,

the risks behind offering trade credit to customers are: firstly, customers may default,

which causes the company to run the risk of bad debts. Secondly, company will lose the

interest between time of sale and time of payment by the customer (Damodaran, 1997).

Based on the trade-off of credit sale, controlling and managing account receivables be-

come very important. Kumar (2010) explains the meaning of debtor management as a

process of making decision which relates to the investment in the business debtors. And

the aim of debtor management is to stimulate the sales and meanwhile minimize the risk

of not receiving money from the debtors. If debtor management is in a poor condition,

working capital ratio could be stressful which causes the needs of more capital input or

increased debt (Turner Hopkins, 2009). Gillbert and Reichert (1995) find out that 59 per-

cent firms of Fortune 500 are using account receivable management model to improve

their working capital management.

In order to achieve effective account receivables management, there are two elements

should be focused. On the one hand, company needs to know which credit policy is suit

19

for their business. Credit policy gives firms a guideline about how to deal with the debtor

and how much credit they should liberalize to their customers. With a liberated credit

policy, the sale and profitability of a firm may increase largely, but the risk of bad debts

or interest foregone may also increase. With a strict credit policy, the security and liquid-

ity of a firm may rise, but profitability of the firm may go down. Obtaining the optimal

level of security and profitability is the one task of financial manager (graph 1). On the

other hand, company should know their customers well, that is what we called credit

analysis. Damodaran (1997) defines credit analysis is an analysis designed to evaluate the

creditworthiness of customer (p.378). Based on customers’ capacity analysis, company

can make their credit decision, which is whether to sell the products or service on credit.

2.3.4 Accounts Payable Management

Suppliers offer trade credit will create account receivable, opposite to that, customers ac-

cept the trade credit will generate account payable. Account payable, which occurs when

firms purchase goods or services on credit, is the payment for vendors for products, ser-

vices inventories and supplies. One merit of having trade credit from sellers is that com-

pany can reduce some investment in working capital management and save some re-

source (Damodaran, 1997). Maximizing the account payable and stretching the payment

term could be a competitive advantage for firms. In the United Kingdom, on average

there are 70 percentage of the total short-term debt. 55 percentage of these short-term

debt are recorded under account payable (Kohler et al, 2000, Guariglia and Mateut,

2006). However, the risk of maximizing account payables by having a longer credit pe-

riod from the supplier is that firms may not get a discount from their vendors or bad qual-

ity products or service may get from suppliers, which can ruin the business relationship

20

between suppliers and demanders. Finally, it will affect firm’s profitability (Ganesan,

2007). Some elements of account payable management, such as account payable policy,

implementation of the policy and monitoring result, can help manager ensure that effi-

ciency of account payable management reached (Sagner, 2011).

2.4 Working Capital Management Policies

Characteristics of each component of working capital management alert that the manage-

ment should not underestimate the importance of working capital management. Decision

of working capital management can be affected by a company’s working capital manage-

ment policy as well. Working capital management policy is a method of making invest-

ment by using current assets and financing firms’ assets by using short-term liabilities

(Bandara, and Weerakoon-Banda, 2011). Basically, there are three types of working capi-

tal policies: matching working capital policy, aggressive working capital policy and con-

servative working capital policy.

First, matching working capital policy is by using current asset to match current liability

perfectly. It implies that company will simply keep enough cash on hand to pay for their

due liabilities. Second, aggressive working capital policy is that companies usually has

low account receivable and try to pay their payable as late as possible. They invest most

of their asset into the investment and keep less cash on hand. Though this policy has high

return, the risk is high. Third, conservative working capital policy is preferred by risk

aversion. Companies under this policy usually make sure they can pay their liability on

time, and they keep extra cash on hand just for the uncertainty (Kulkarni, 2011).

Firms can minimize financial risk and improve its overall performance if firms have a

well- though working capital management policy by understanding the role and drivers of

21

working capital management (Nazir, and Afza, 2009). Weinraub and Visscher (1998) in-

vestigate the relationship between aggressive and conservative working capital practice in

ten diverse industry groups. They find out that industries do have significantly different

policies on their working capital management, and the policy in each industry keeps sta-

ble over time. Besides this, the study also denotes that industry asset and liabilities po-

lices have a significantly negative relationship. Nazir and Afza (2009) reiterate the im-

portance of working capital management policies. They discussed how working capital

management policy affects firms’ profitability. A negative relationship between prof-

itability and degree of aggressiveness of working capital policies is concluded in their re-

search. They suggest that managers can create firm value by adopting a conservative ap-

proach in working capital management.

In recent years, working capital management policy still attracts economists’ attentions.

In 2011, Bandara, and Weerakoon published their research the impact of working capital

management practices on firm value. The study indicates that working capital manage-

ment has impact on firms’ value by studying a sample of 74 companies listed in the

Colombo stock exchange. The result is similar to the result of Nazir and Afza (2009), re-

veals a significant positive relationship between conservative working capital manage-

ment policy and firm value. A significant negative relationship between aggressive work-

ing capital management and firm value proves that aggressive working capital manage-

ment policy may destroy firm value. Moreover, the study explains that firms following

match working capital management policy can generate higher value than the firms with

conversion working capital management. Al-Mwalla (2012) further validates the positive

22

relationship between conservative working capital management policy, which uses more

long-term debt to finance firms’ activities, and firms’ profitability and its value; and the

negative relationship between aggressive working capital management policy, which use

more short-term liabilities to finance firms’ activities, and firms’ profitability and value.

Thus, a well-designed working capital management policy can be a competitive advan-

tage for firms to create value for their shareholders. Furthermore, in the study of Al-Shu-

biri (2011), he confirms that there is no significant relationship between working capital

management policy and operating and financial risk.

2.5 Measures of working capital management

Since working capital management is such important for businesses, how do managers

know whether their management is efficient or not? There are several ways to assess the

efficiency of working capital management. The traditional way is by using liquidity ra-

tios, for instance, current ratio, and quick ratio. The drawback of these ratios is that they

are too general, there is not too much detailed information of working capital manage-

ment can be reached. However, the cash conversion cycle (CCC), which is defined as the

total time that a company takes from the days they bought their raw materials to the mo-

ment when they sell their finished goods, is deemed as the best measure for working capi-

tal management. A short cash conversion cycle implies that company has a good liquid-

ity. Firms have sufficient cash or capital to run their daily operation. If the duration of

cash conversion cycle is too long, it implies that company needs more cash to finance its

cycle (Mathur, 2010). Cash conversion cycle is calculated by Days Sales Outstanding

(DSO) + Days Inventory Outstanding (DIO) -Days Payable Outstanding (DPO). From

this equation, the performance of each dimension of working capital management can be

23

evaluated as well. That is one of the reasons it has been used so often as the measure of

working capital management. Following shows the calculation of each components of

cash conversion cycle.

Days Sales Outstanding (DSO) is used to measure how many days it takes a firm to col-

lect their account receivable. It is calculated by account receivable (trade) / total

revenue*365

Days Inventory Outstanding (DIO) evaluates how many days does a firm take to convert

their inventory to sales. It is calculated by Inventory/ cost of goods sold*365

Days payable Outstanding (DPO) is measuring how many days a firm needs to pay for

their vendors or supplier for the goods or service they use. It is calculated by account

payables (trade) / cost of goods sold*365

From the perspective of Days Sales Outstanding and Days Inventory Outstanding, the re-

sult are expected to be the shorter the better, since shorter Days sales outstanding and

shorter Days inventory outstanding implies that company can get cash in a short time.

Opposite to the Days Sales outstanding and Days inventory outstanding, Days Payable

Outstanding is expected to be longer. Basically, if firms can have a longer payment terms

it can help company to reduce working capital investment. However, the disadvantages of

doing this are: first, companies may lose the opportunity of discount. Second, it may

cause a bad relationship with vendors. In the research of Deloof (2003), the relationship

between three components of cash conversion cycle and firm’s profitability are also stud-

ied. The results exhibit that a negative relationship between the numbers of days account

receivable and cross-operating income. Same applied to the numbers of inventory days

24

and cross operating income in his research. The results confirm that a decrease in Days

Sales Outstanding and Days Inventory Outstanding is an improvement for companies. A

significant and negative relationship between Days Payable Outstanding and cross oper-

ating income (net operating income) is found in the research of Deloof (2003). The po-

tential reason for negative relationship between Days Payable Outstanding and profitabil-

ity is the downside of paying vendors late, such as, no discount and bad quality of ser-

vice, has more effects on the industry which Deloof (2003) used in his study. Garcia-

Teruel and Martinez-Solano (2006) focus on the impact of working capital management

on small and median firms’ profitability. Outcomes are in line with the conclusions from

Deloof (2003) that firm’s profitability is negatively related to days account receivables

and Days Inventory Outstanding. These findings mean that firms’ performance or prof-

itability can be generated by reducing the Days Sales Outstanding and Days Inventory

Outstanding. Equally, Lower cash conversion cycle implies that cash move fast around

the cycle and this can become a competitive advantage for firms (Autukaite, and Molay,

2011).

Net trade cycle (NTC), which is used in the study of Shin and Soenen (1998), is another

measure for working capital management. Basically, NTC is similar to cash conversion

cycle. Three components (account receivable, inventory and account payable) are pre-

sented as a percentage of sales (Shin and Soenen, 1998). Shin and Soenen indicate the ad-

vantage of NTC is that it provides an easy estimate for addition financing needs with re-

gard to working capital expressed as a function of the projected sales growth, and NTC is

25

also closely related to the issue of firm valuation and creation of shareholder value (p.

38).

Research in different industries would like to use different measures of working capital

management, which is proved by Filbeck and Kureger (2005). They examine the working

capital performance across industries by investigating the annul rating of working capital

performance of firms of CFO Magazine. The study illustrates the different measure of

working capital management that is used in companies cross industries, and list how of-

ten each company within an industry change their measure of working capital measure-

ment over time. They concluded that among industries, there is a significant difference

exist regarding to the proxy of working capital management and within an industry,

working capital management measures are different over time.

2.6 Strategies for Improving Working Capital Management

It is vital for leaders in treasury to know how they can improve the working capital man-

agement. Unfortunately, there is no standard solution for all firms. Features of firm de-

cide what kind of working capital management they should apply. However, the follow-

ing dimensions may give managers some insights.

Six Sigma methodologies have been recognized as a helpful method to improve working

capital management. Generally speaking, Six sigma is a disciplined, data-driven approach

and methodology for eliminating defects (driving toward six standard deviations between

the mean and the nearest specification limit) in any process-from manufacturing to trans-

actional and from product to service (six sigma, 2012). It helps companies to measure liq-

uidity and make sure the liquidity goes well in the all areas of institution. Six sigma

methodologies can decrease the Days Sales Outstanding, accelerates the payment cycle,

26

improves customer satisfaction and reduces necessary amount and costs of working capi-

tal needs (Filbeck, and Krueger, 2005). Waxer (2003) tests four companies that applied

six sigma methodologies. The result shows that costs saving are significant in these four

companies. These savings are ranged from 1.2 to 4.5 percentage of revenue. Waxer

(2003) indicates that six sigma methodologies is not a short cut that allows firms to be

profitable immediately. Six Sigma is a saving method which takes some times before

companies be profitable if companies plan properly.

Rule (2004), the director and global head of liquidity and investments in Citigroup, gives

her suggestions to improving working capital management: first, liquidity management is

an effective tool in managing working capital. Liquidity management has been concen-

trated by managers for many years, but there are two parts that are emphasized: 1. the real

time information integration is very important since it help the manager to know where

their position is in the cash cycle, and how to make their budget for next step. 2. Invest

extra money in vehicles to earn higher return instead of putting in the deposition and gen-

erate minimal interest. Second, there are some new tools, for instance, electronic invoice

presentment and payment and continuous linked settlement, which can help improving

working capital management.

2.7 Empirical Review

Various studies have analyzed the relationship of working capital management and firm

profitability in various markets. The results are quite mixed, but a majority of studies

conclude a negative relationship between WCM and firm profitability. The studies

reviewed have used various variables to analyze the relationship, with different

27

methodology such as linear regression and panel data regression. In this section, we have

presented the chronology of major studies related to our study in order to assess and

identify the research gap.

Soenen (1993) investigated the relationship between the net trade cycle as a measure of

working capital and return on investment in US firms. The results of the study indicated a

negative relationship between the duration of net trade cycle and return on assets (ROA).

Furthermore, this relationship between net trade cycle and return on assets was found to

differ across industries, depending on the type of industry. A significance relationship for

about half of the industries studied indicated that results might vary from industry to

industry. To support the results of Soenen (1993) on a large sample and with a long time

period, Jose et al. (1996) examined the relationship between profitability measures and

management of ongoing liquidity needs for a large cross section of firms over a 20-year

period. They tested the long run equilibrium relationship between the cash conversion

cycle and alternative measures of profitability, using both non-parametric and regression

analysis. The study concluded with strong evidence that aggressive working capital

policies enhance profitability. The authors found no evidence of a positive cross sectional

relationship for the CCC-profitability in any of the industries studied.

In order to examine the relationship between efficient working capital management and a

firm’s profitability Shin and Soenen (1998) used net-trade cycle (NTC) as a measure of

working capital management. The relationship was examined using correlation and

regression analysis, by industry and working capital intensity. Using a sample of 58,985

firm years covering the period 1975–94, in all cases, authors found a strong negative

28

relation between the length of the firm’s net-trade cycle and its profitability. Also, shorter

NTC were associated with higher risk-adjusted stock returns. Shin and Soenen

highlighted the importance of reducing NTC to create shareholder value.

Lyroudi and Lazaridis (2000) used the Greek food industry to examine the cash

conversion cycle as a liquidity indicator of the firms and tried to determine its

relationship with the current and the quick ratios, with its component variables. They

investigated the implications of the CCC in terms of profit- ability, indebtness and firm

size. The results of their study indicated that there is a significant positive relationship

between the cash conversion cycle and the traditional liquidity measures of current and

quick ratios.

Wang (2002) examined the relationship between liquidity management and operating

performance, and that between liquidity management and corporate value for firms in

Japan and Taiwan. The empirical findings for both Japan and Taiwan show negative

CCC–ROA and CCC–ROE relationships which are sensitive to industry factors. The

study supported the results of Jose et al., (1996) and Shin and Soenen (1998) that a lower

CCC corresponds with better operating performance. The study further revealed that

aggressive liquidity management is associated with higher corporate value for both

countries in spite of differences in structural characteristics or in the financial system of a

firm.

Deloof (2003) investigated the relationship between working capital management and

corporate profitability for a sample of 1,009 large Belgian non-financial firms for the

period 1992–96. He used trade credit policy and inventory policy as measured by number

of day’s accounts receivable, accounts payable and inventories, and the cash conversion

29

cycle as a comprehensive measure of working capital management. The results of the

study were as consistent as of Shin and Soenen (1998). Deloof found a significant

negative relation between gross operating income and the number of days accounts

receivable, inventories and accounts payable. Thus, he suggests that managers can create

value for their shareholders by reducing the number of day’s accounts receivable and

inventories to a reasonable minimum.

Eljelly (2004) empirically examined the relation between profitability and liquidity, as

measured by current ratio and cash gap (cash conversion cycle) on a sample of companies

in Saudi Arabia. Using correlation and regression analysis the study found significant

negative relation between the firm’s profit- ability and its liquidity level, as measured by

current ratio. The negative relationship was more evident in firms with high current ratios

and longer cash conversion cycles. At the industry level, however, the study found that

the cash conversion cycle or the cash gap is of more importance as a measure of liquidity

than the current ratio that affects profitability. The size variable was also found to have a

significant effect on profitability at the industry level.

Lazaridis and Tryfonidis (2006) investigated the relationship of corporate profitability

and working capital management of 131 companies listed in the Athens Stock Exchange

(ASE) for the period 2001–04. The purpose of this study was to establish a relationship

that was statistically significant, between profitability, the cash conversion cycle and its

components for listed firms in the ASE. The results of the research showed that there is a

statistical significance between profitability, measured through gross operating profit and

the cash conversion cycle. They observed that lower gross operating profit is associated

with an increase in the number of day’s accounts payables. Moreover, managers can

30

create profits for their companies by correctly handling the cash conversion cycle and

keeping each of the different components (accounts receivables, accounts payables and

inventory) to an optimum level.

Padachi (2006) analyzed the working capital management practices through a sample of

58 small manufacturing companies in Mauritius. The basic purpose of this study was to

examine the trends in working capital management and its impact on firms’ performance.

The regression results show that high investment in inventories and receivables is

associated with lower profitability. This study has also shown that the paper and printing

industry has been able to achieve high scores on the various components of working

capital and this has had a positive impact on its profitability. The findings also reveal an

increasing trend in the short-term component of working capital financing.

Raheman and Nasr (2007) provide further evidence about the relationship of working

capital management and profitability. Using variable and methodology as used by Deloof

(2003) on a sample of 94 companies listed on the Karachi Stock Exchange (KSE) for the

period 1999–2004, the results show that there is strong negative relationship between

variables of WCM and profitability of the firms. It means that as the cash conversion

cycle increases, it leads to decreasing profitability of the firm. Thus, managers can make

the shareholders’ value positive by reducing CCC to the minimum possible level. The

authors also found a positive relationship between the size of the firm and its profitability,

and a significant negative relationship between debt and profitability.

In a related study Afza and Nazir (2007) investigated the relationship between the

aggressive/conservative working capital policies of various industrial groups and a large

sample of 263 companies listed at Karachi Stock Exchange for a period of 1998–2003.

31

Using ANOVA and LSD test, the study found significant differences among the working

capital investment and financing policies across different industries. Using ordinary least

regression analysis, the authors concluded a negative relationship between the

profitability measures of firms and degree of aggressiveness of working capital

investment and financing policies.

Garcia-Teruel and Martinez-Solano (2007) for the first time examined the effect of

working capital management on profitability of small and medium sized Spanish firms.

Using panel data regression methodology, the authors revealed that managers can create

value by reducing their inventories and the number of days for which their accounts are

outstanding. The results of the study are similar to those found in previous studies that

focused on large firms (Deloof, 2003; Jose et al., 1996; Shin and Soenen, 1998; Wang,

2002). The authors further concluded that SMEs have to be concerned with working

capital management because they can also create value by reducing their cash conversion

cycle to a minimum, as far as that is reasonable.

Samiloglu and Demirgunes (2008) in their study examined the effect of working capital

management on firm profitability about companies listed at the Istanbul Stock exchange

(ISE). Using the multiple regression model, the study examined the effect of working

capital on firm profitability for the period of 1998–2007. The findings of the study show

that accounts receivables period, inventory period and lever- age affect firm profitability

negatively; while growth (in sales) affects firm profitability positively.

Zariyawati et al. (2009) used panel data of 1,628 firm years for the period between 1996–

2006 that consisted of six different economic sectors, in order to examine the relationship

between working capital management and firm profitability of the firms listed in

32

Malaysia. Results of this study found that the CCC is significantly negatively associated

with the firm profitability. They further emphasized that managers should focus on

reduction of the cash conversion period in order to create shareholder wealth. The results

of the study are consistent with that of other studies conducted in different markets. Luo

et al., (2009) find that the efficiency of a firm’s working capital management has a lasting

impact on the firm’s performance. Improvement in working capital efficiency leads to

increase in future earnings, as the market responds positively to the improvement of

working capital efficiency. Firm value increases when cash conversion cycle decreases.

Closer examination of literature on the relationship of working capital management and

profitability in general supports the fact that aggressive working capital policies enhance

firm profitability (Jose et al., 1996; Shin and Soenen, 1998 for US companies; Deloof,

2003 for Belgian firms; Wang, 2002 for Japanese and Taiwanese firms; Raheman and