principle s of acounting ii

TRANSCRIPT

DEPARTMENT OF ACCOUNTING,SCHOOL OF MANAGEMENT STUDIES,

NUHU BAMALLI POLYTECHNIC,ZARIA.

LECTURE NOTE

ON

PRINCIPLES OF ACCOUNTS II(ACC 111)

FOR

NATIONAL DIPLOMA I STUDENTS

PREPARED BY THE DEPARTMENT

i

© 2013

ii

Course outline:

1. Understand Control Accounts.

2. Know the different methods for the collection of data for Final Accounts from Incomplete Records.

3. Understand Manufacturing Accounts.

4. Understand the accounts of Non-trading organization.

5. Understand Partnership Accounts.

6. Understand the preparation of simple company’s Final Accounts.

3

1. UNDERSTAND CONTROL ACCOUNTS

IntroductionBusinesses are sub-divided in to small scale or large scalebusiness. Error committed where a trial balance failed to agree,suspense account is if the business is relatively small, butcontrol account is used to correct errors if it is large scalebusiness.Control account use only two ledgers to thoroughly check to locateand correct the error(s). Each ledger will have a control account.A ledger that has a control account is referred to as self-balancing ledger or total account. The two ledgers are purchasesledger control account and sales ledger control account.

DefinitionControl account is a summary of individual account in each ledger.It is also a summary of the account to which it relate. Therefore,the balance in the account will be equal to the total of allindividual balances in the ledger. If it fails to balance, then itis an indication that there is error in the ledger. The ruleagainst control account applies to all ledgers but it isrestricted to only sales and purchases ledger. It is thereforeanother form of control mechanism.

ApplicationFigures posted to debtors and creditors control account are notobtained from individual debtors and creditors accountrespectively. Examples of figures posted to debtors controlaccount are total sales, total returns from customers, totaldiscount allowed, among others. These items are obtained fromsales day book, returns inward day book and discount allowedcolumn of the three column cash book respectively. Moreover,examples of items posted to creditors control account are totalcredit purchases, total returns to suppliers, total discountreceived sourced from purchase day book, returns outward day book

4

and discount received column of the three column cash bookrespectively.

Note: Control account is a memoranda record. This means the entries

are not based not principles of double entry, but actualentries are made in personal account.

Other scholars argued that entries in the control account arebased on the principles of double entry while entries in theindividual account are memoranda.

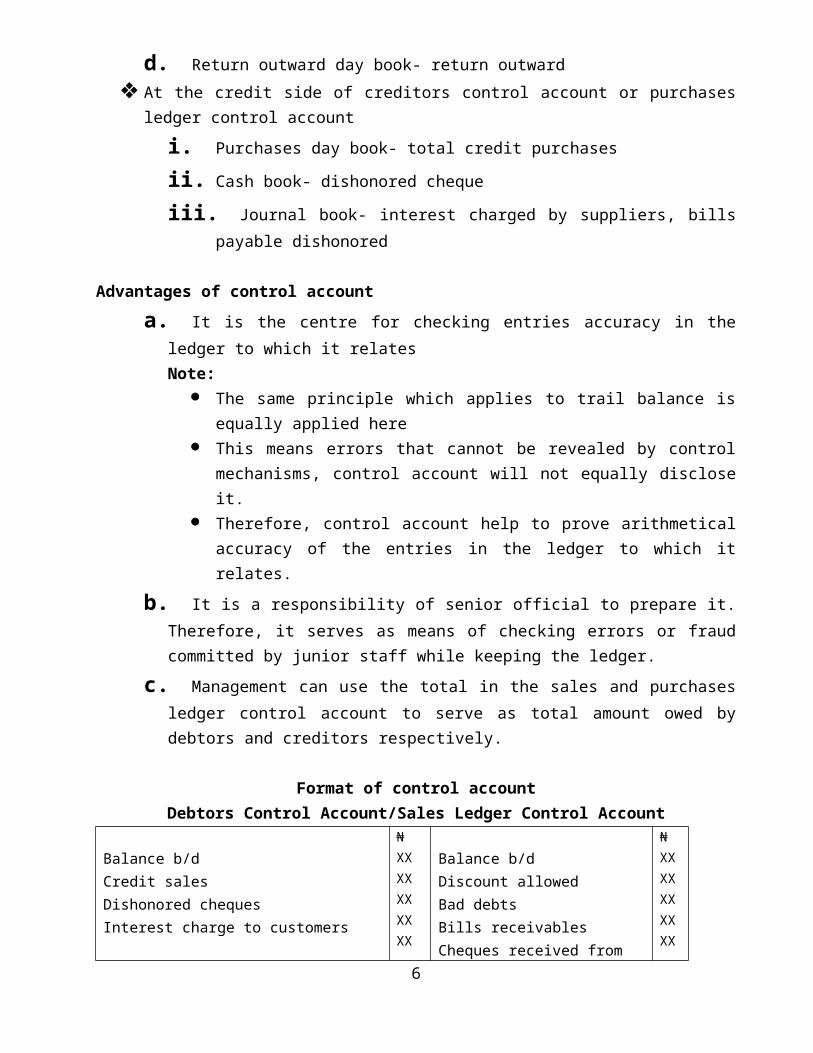

Where to source the entry At the debit side of debtors control account or sales ledger

control account:1. Sales day book- total credit sales

2. Cash book- dishonored check form customers

3. Journal day book- interest charged to customers andbills receivable dishonored

At the credit side of debtors control account or sales ledgercontrol account:1. Cash book- cheque & cash received from customers

2. Discount allowed columns- discount allowed

3. Journal book- bad debt, bills receivables accepted bycustomers & purchase ledger contra (set-off)

4. Return inward day book- returns inward

At the debit side of creditors control account or purchaseledger control accounta. Cash book- cheque and cash paid to suppliers

b. Discount received column- discount received

c. Journal book- bills payable accepted in favor ofsuppliers, self-ledger contra (set-off)

5

d. Return outward day book- return outward At the credit side of creditors control account or purchases

ledger control accounti. Purchases day book- total credit purchases

ii. Cash book- dishonored cheque

iii. Journal book- interest charged by suppliers, billspayable dishonored

Advantages of control accounta. It is the centre for checking entries accuracy in the

ledger to which it relatesNote:

The same principle which applies to trail balance isequally applied here

This means errors that cannot be revealed by controlmechanisms, control account will not equally discloseit.

Therefore, control account help to prove arithmeticalaccuracy of the entries in the ledger to which itrelates.

b. It is a responsibility of senior official to prepare it.Therefore, it serves as means of checking errors or fraudcommitted by junior staff while keeping the ledger.

c. Management can use the total in the sales and purchasesledger control account to serve as total amount owed bydebtors and creditors respectively.

Format of control accountDebtors Control Account/Sales Ledger Control Account

Balance b/dCredit salesDishonored chequesInterest charge to customers

₦XXXXXXXXXX

Balance b/dDiscount allowedBad debtsBills receivablesCheques received from

₦XXXXXXXXXX

6

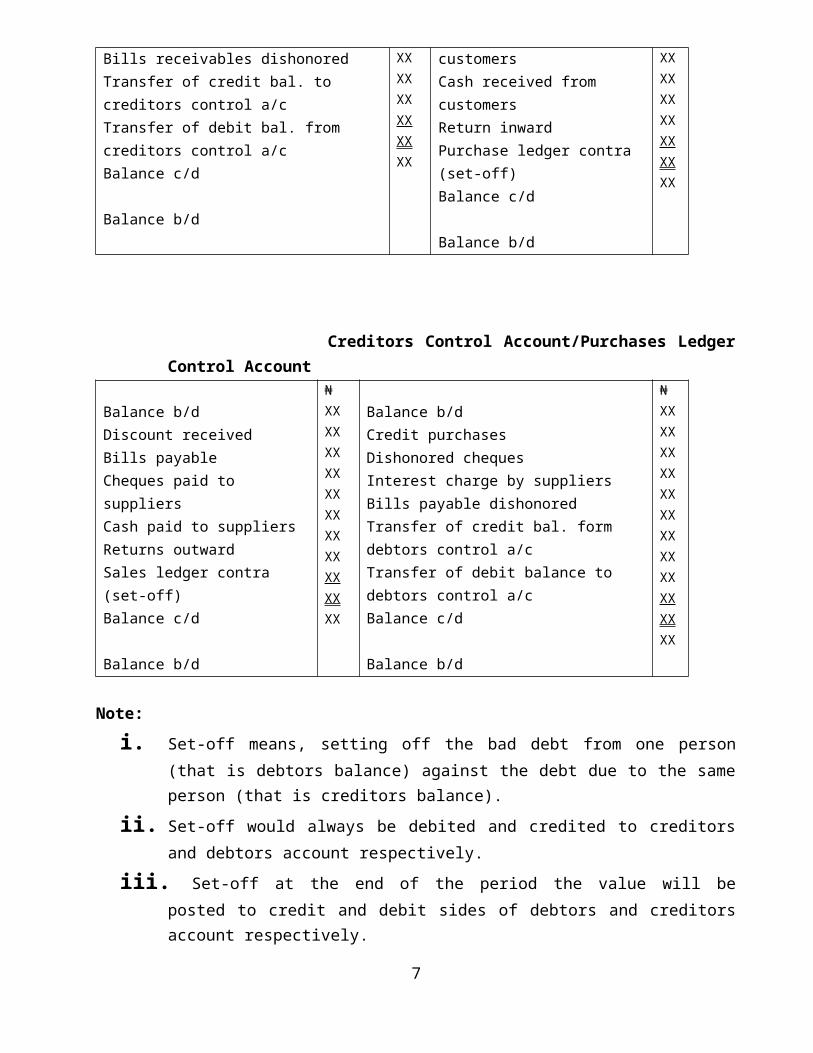

Bills receivables dishonoredTransfer of credit bal. to creditors control a/cTransfer of debit bal. from creditors control a/cBalance c/d

Balance b/d

XXXXXXXXXXXX

customersCash received from customersReturn inwardPurchase ledger contra (set-off)Balance c/d

Balance b/d

XXXXXXXXXXXXXX

Creditors Control Account/Purchases LedgerControl Account

Balance b/dDiscount receivedBills payableCheques paid to suppliersCash paid to suppliersReturns outwardSales ledger contra (set-off)Balance c/d

Balance b/d

₦XXXXXXXXXXXXXXXXXXXXXX

Balance b/dCredit purchasesDishonored chequesInterest charge by suppliersBills payable dishonoredTransfer of credit bal. form debtors control a/cTransfer of debit balance to debtors control a/cBalance c/d

Balance b/d

₦XXXXXXXXXXXXXXXXXXXXXXXX

Note:i. Set-off means, setting off the bad debt from one person

(that is debtors balance) against the debt due to the sameperson (that is creditors balance).

ii. Set-off would always be debited and credited to creditorsand debtors account respectively.

iii. Set-off at the end of the period the value will beposted to credit and debit sides of debtors and creditorsaccount respectively.

7

iv. Transfer cases are made in order to move credit balance inthe sales ledger (that is debtors account with creditbalance) to the purchases ledger or move debit balance inthe purchase ledger (that is creditors account with debitbalance) to the sales ledger.

v. Transfers:

a. Are debited to the debtors account and credited tothe creditors account

b. Increase the total of debtors and creditors balancerespectively

c. Do not amount to the cancellation or settlement ofany debt

Treatment of some items in control accounta. Creditors control account

i. Bills payable When bills payable and bills payable accepted are

both given. The latter should be used. When only bills payable is given, it should be

assumed that, it is acceptedii. Bills payable honored

Bills payable honored should be disregarded. Thisis due to the fact that, bills payable has no entryin the creditors account and creditors controlaccount.

iii. Provision for discount receivables Provision for discount receivables should be

disregarded Provision for discount receivables does not affect

creditors account and creditors control accountiv. Cash purchases should be disregarded and has no business

whatsoever with creditors and or creditors controlaccount

8

b. Debtors control account

i. Bills receivables Where bills receivable and bills receivables

accepted are both give, the later should be used. When only bills receivable is given, then it should

be assumed as bills receivables accepted.ii. Bills receivable discounted

Bills receivables discounted should be disregarded No entry is to be made in debtors and debtors

control accountiii. Bills receivables honored

Bills receivables honored should be disregarded andno entry is to be made

iv. Bad debt s recovered It should be ignored unless it had been entered to

the credit of debtors control account as such bedebited to debtors control account.

v. Provision for bad and doubtful debt/ provision fordiscount allowable

It should be disregarded and has no correlationwith debtors and debtors control account.

vi. Cash sales should be disregarded and no entry is to bemade in customers account.

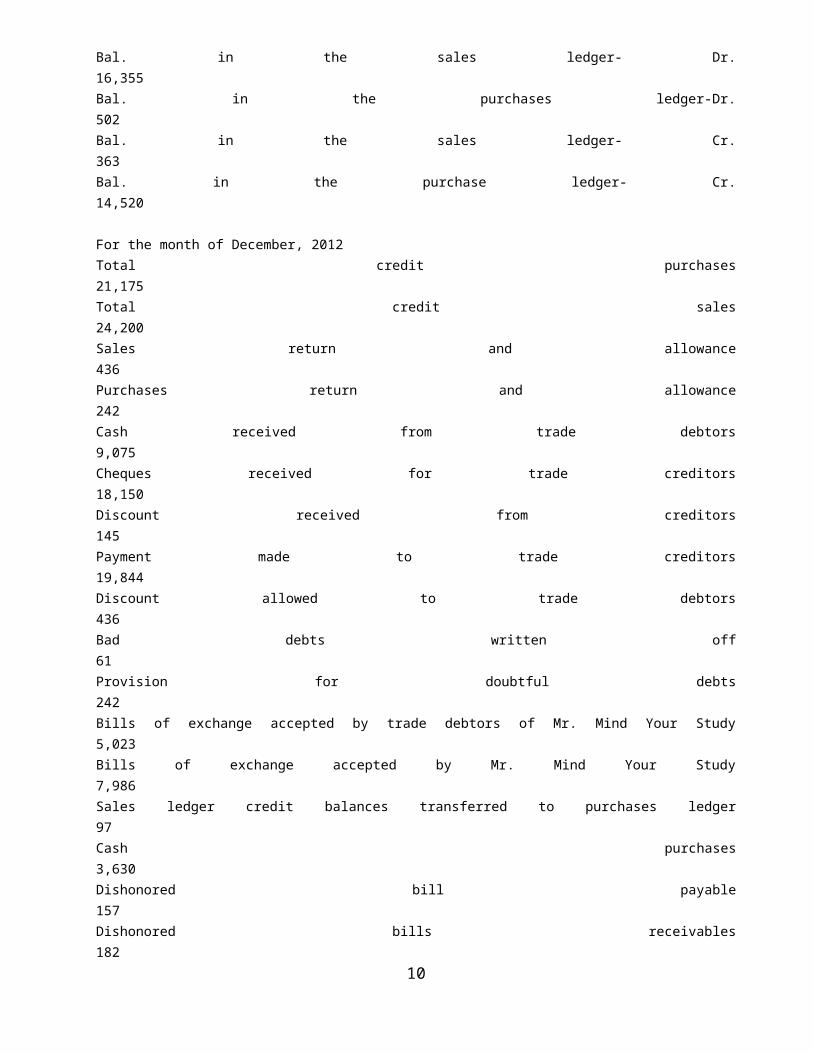

ILLUSTRATION Mr. Mind Your Study, a sole trader, keep his books so that a salesledger control account and a purchase ledger control account areshown in his general ledger and balanced at the end of the month.Form the information below show how these two control account willappear in the general ledger for the month of December, 2012

At December, 2012₦

9

Bal. in the sales ledger- Dr.16,355Bal. in the purchases ledger-Dr.502Bal. in the sales ledger- Cr.363Bal. in the purchase ledger- Cr.14,520

For the month of December, 2012Total credit purchases21,175Total credit sales24,200Sales return and allowance436Purchases return and allowance242Cash received from trade debtors9,075Cheques received for trade creditors18,150Discount received from creditors145Payment made to trade creditors19,844Discount allowed to trade debtors436Bad debts written off61Provision for doubtful debts242Bills of exchange accepted by trade debtors of Mr. Mind Your Study5,023Bills of exchange accepted by Mr. Mind Your Study7,986Sales ledger credit balances transferred to purchases ledger97Cash purchases3,630Dishonored bill payable157Dishonored bills receivables182

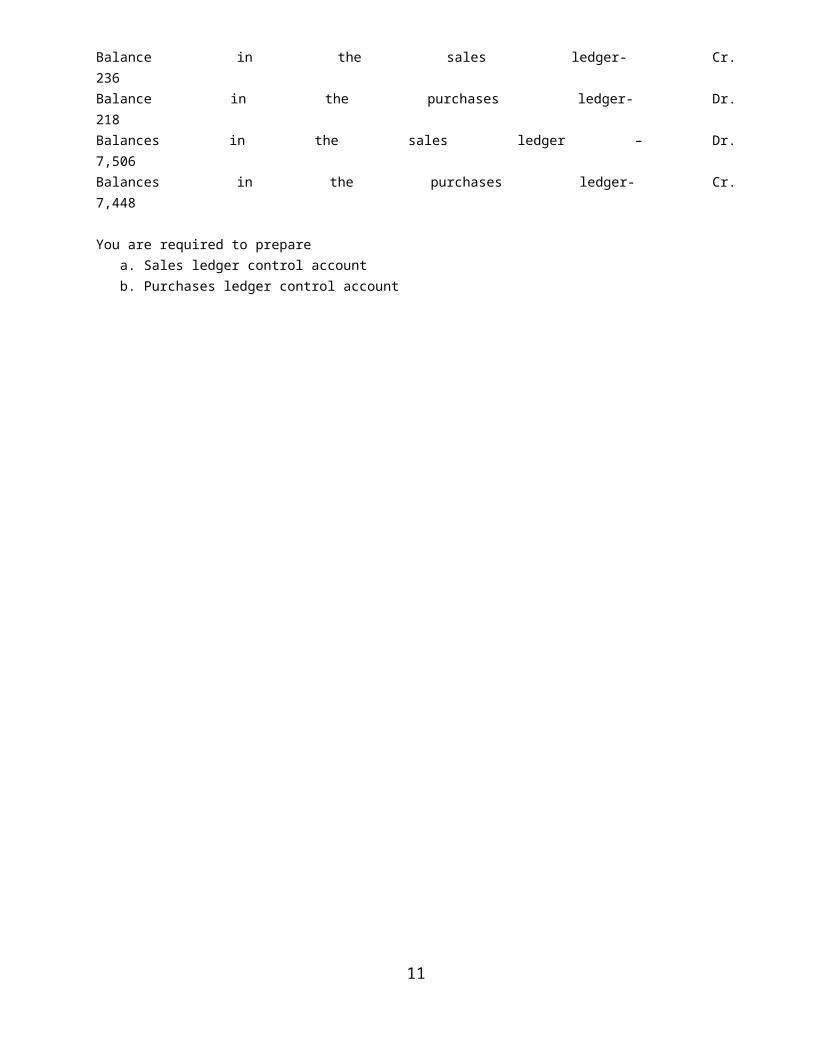

10

Balance in the sales ledger- Cr.236Balance in the purchases ledger- Dr.218Balances in the sales ledger – Dr.7,506Balances in the purchases ledger- Cr.7,448

You are required to preparea. Sales ledger control accountb. Purchases ledger control account

11

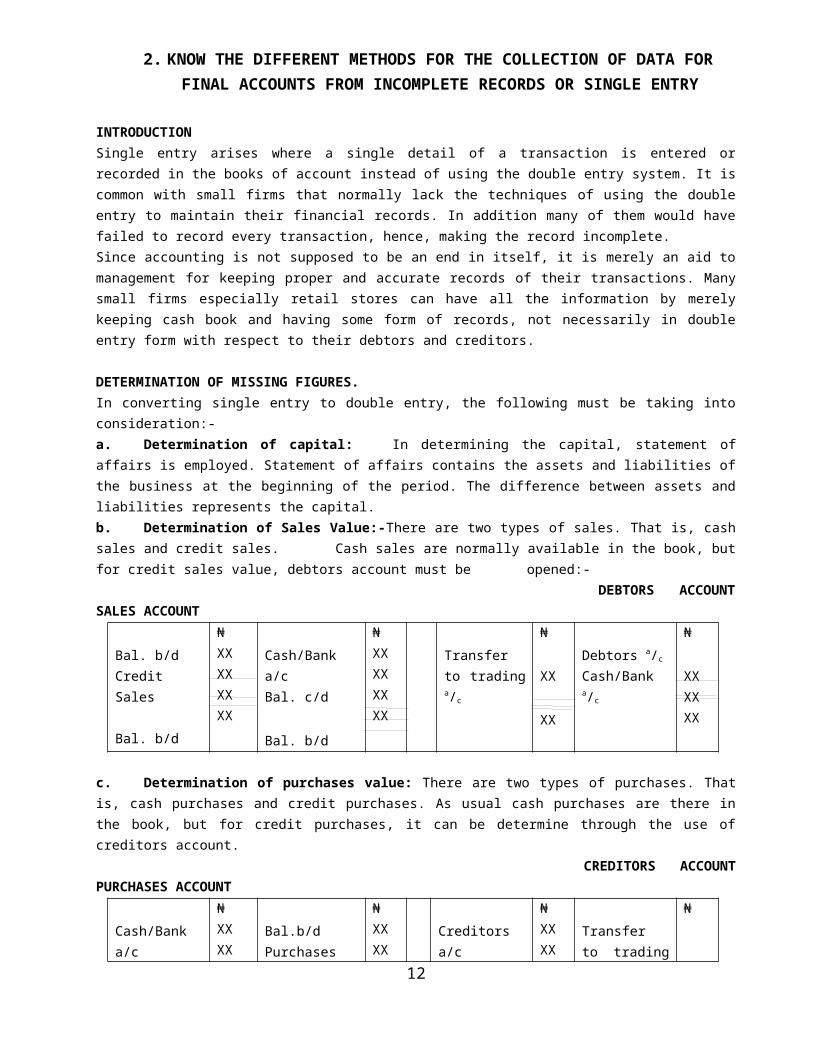

2. KNOW THE DIFFERENT METHODS FOR THE COLLECTION OF DATA FORFINAL ACCOUNTS FROM INCOMPLETE RECORDS OR SINGLE ENTRY

INTRODUCTIONSingle entry arises where a single detail of a transaction is entered orrecorded in the books of account instead of using the double entry system. It iscommon with small firms that normally lack the techniques of using the doubleentry to maintain their financial records. In addition many of them would havefailed to record every transaction, hence, making the record incomplete.Since accounting is not supposed to be an end in itself, it is merely an aid tomanagement for keeping proper and accurate records of their transactions. Manysmall firms especially retail stores can have all the information by merelykeeping cash book and having some form of records, not necessarily in doubleentry form with respect to their debtors and creditors.

DETERMINATION OF MISSING FIGURES.In converting single entry to double entry, the following must be taking intoconsideration:-a. Determination of capital: In determining the capital, statement ofaffairs is employed. Statement of affairs contains the assets and liabilities ofthe business at the beginning of the period. The difference between assets andliabilities represents the capital.b. Determination of Sales Value:-There are two types of sales. That is, cashsales and credit sales. Cash sales are normally available in the book, butfor credit sales value, debtors account must be opened:- DEBTORS ACCOUNTSALES ACCOUNT

Bal. b/dCreditSales Bal. b/d

₦XXXXXXXX

Cash/Banka/cBal. c/d

Bal. b/d

₦XXXXXXXX

Transferto tradinga/c

₦

XX

XX

Debtors a/c

Cash/Banka/c

₦

XXXXXX

c. Determination of purchases value: There are two types of purchases. Thatis, cash purchases and credit purchases. As usual cash purchases are there inthe book, but for credit purchases, it can be determine through the use ofcreditors account. CREDITORS ACCOUNTPURCHASES ACCOUNT

Cash/Banka/c

₦XXXX

Bal.b/dPurchases

₦XXXX

Creditorsa/c

₦XXXX

Transferto trading

₦

12

Bal. c/d

XX a/c

Bal. b/d

XXXX

Cash/Banka/c XX

a/cXXXX

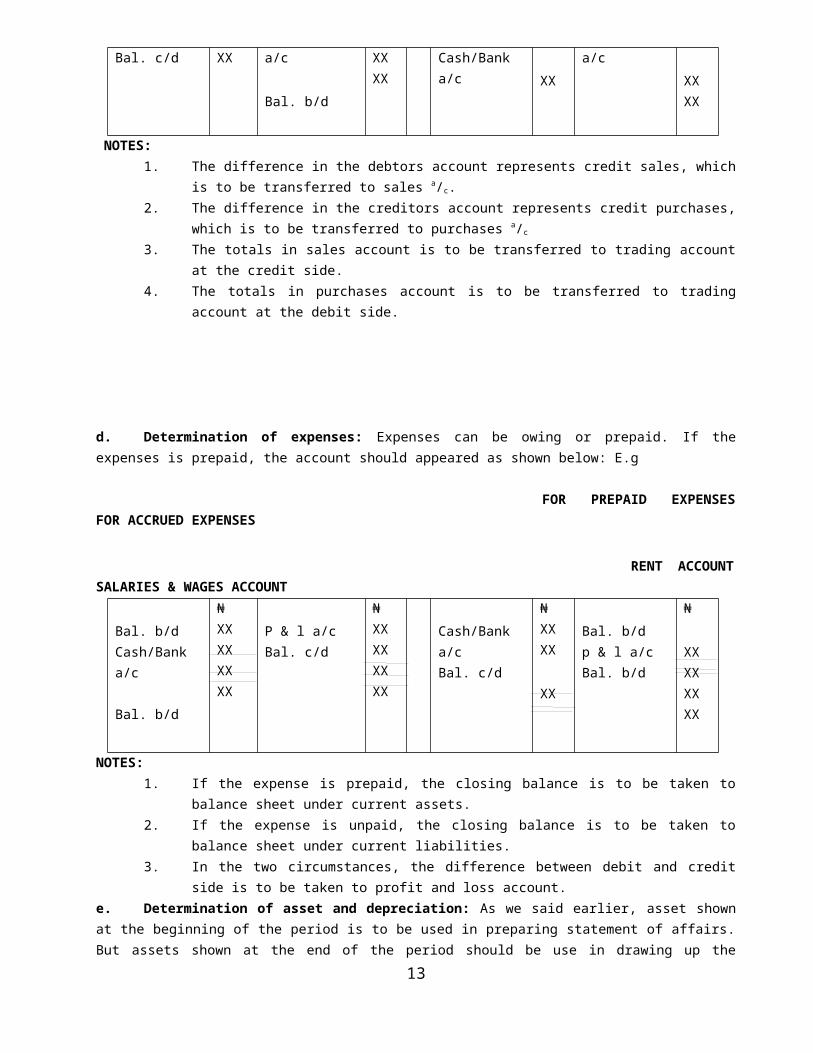

NOTES:1. The difference in the debtors account represents credit sales, which

is to be transferred to sales a/c. 2. The difference in the creditors account represents credit purchases,

which is to be transferred to purchases a/c

3. The totals in sales account is to be transferred to trading accountat the credit side.

4. The totals in purchases account is to be transferred to tradingaccount at the debit side.

d. Determination of expenses: Expenses can be owing or prepaid. If theexpenses is prepaid, the account should appeared as shown below: E.g

FOR PREPAID EXPENSESFOR ACCRUED EXPENSES RENT ACCOUNTSALARIES & WAGES ACCOUNT

Bal. b/dCash/Banka/c Bal. b/d

₦XXXXXXXX

P & l a/cBal. c/d

₦XXXXXXXX

Cash/Banka/cBal. c/d

₦XXXX

XX

Bal. b/d p & l a/cBal. b/d

₦

XXXXXXXX

NOTES:1. If the expense is prepaid, the closing balance is to be taken to

balance sheet under current assets.2. If the expense is unpaid, the closing balance is to be taken to

balance sheet under current liabilities.3. In the two circumstances, the difference between debit and credit

side is to be taken to profit and loss account.e. Determination of asset and depreciation: As we said earlier, asset shownat the beginning of the period is to be used in preparing statement of affairs.But assets shown at the end of the period should be use in drawing up the

13

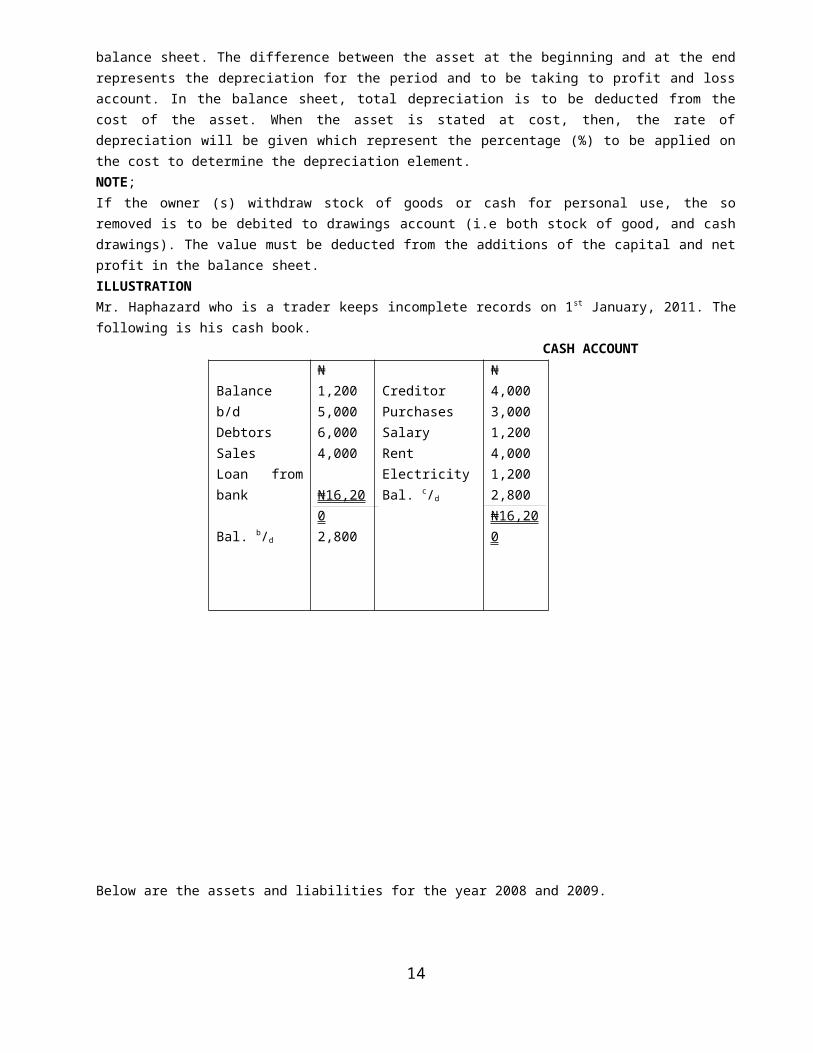

balance sheet. The difference between the asset at the beginning and at the endrepresents the depreciation for the period and to be taking to profit and lossaccount. In the balance sheet, total depreciation is to be deducted from thecost of the asset. When the asset is stated at cost, then, the rate ofdepreciation will be given which represent the percentage (%) to be applied onthe cost to determine the depreciation element.NOTE;If the owner (s) withdraw stock of goods or cash for personal use, the soremoved is to be debited to drawings account (i.e both stock of good, and cashdrawings). The value must be deducted from the additions of the capital and netprofit in the balance sheet.ILLUSTRATION Mr. Haphazard who is a trader keeps incomplete records on 1st January, 2011. Thefollowing is his cash book. CASH ACCOUNT

Balanceb/dDebtorsSalesLoan frombank

Bal. b/d

₦1,2005,0006,0004,000

₦16,2002,800

CreditorPurchasesSalaryRentElectricityBal. c/d

₦4,0003,0001,2004,0001,2002,800₦16,200

Below are the assets and liabilities for the year 2008 and 2009.

14

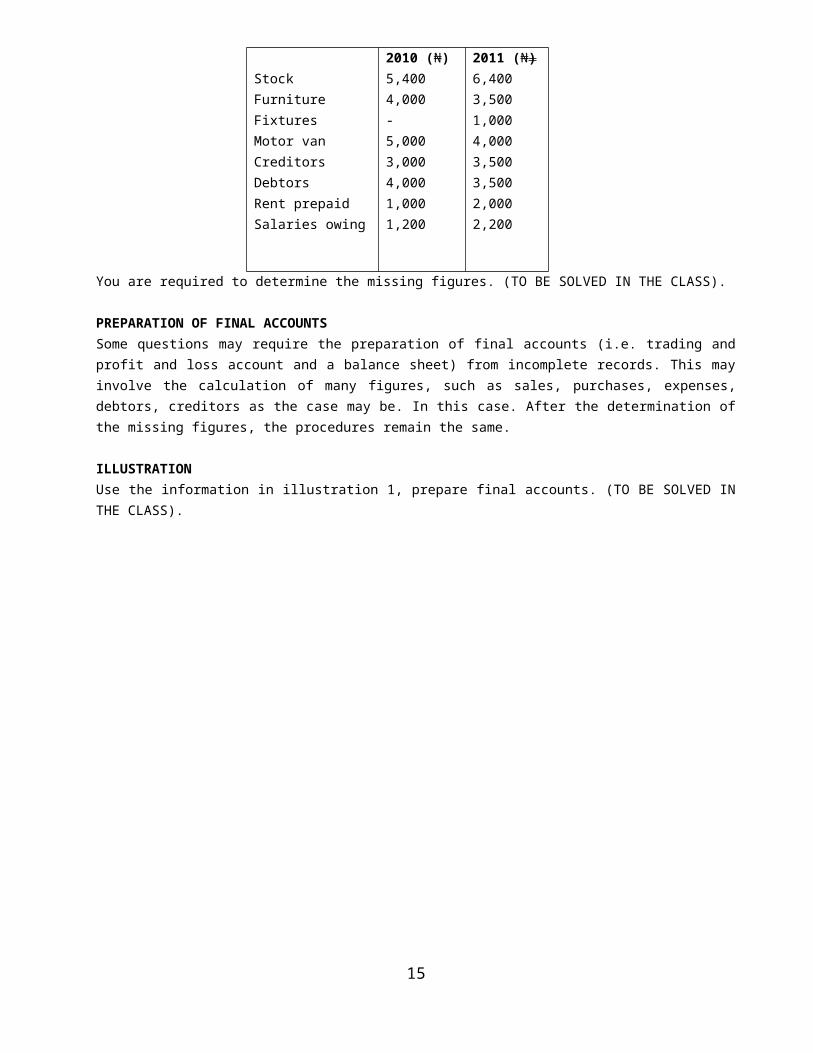

StockFurnitureFixturesMotor vanCreditorsDebtorsRent prepaidSalaries owing

2010 (₦)5,4004,000-5,0003,0004,0001,0001,200

2011 (₦)6,4003,5001,0004,0003,5003,5002,0002,200

You are required to determine the missing figures. (TO BE SOLVED IN THE CLASS).

PREPARATION OF FINAL ACCOUNTSSome questions may require the preparation of final accounts (i.e. trading andprofit and loss account and a balance sheet) from incomplete records. This mayinvolve the calculation of many figures, such as sales, purchases, expenses,debtors, creditors as the case may be. In this case. After the determination ofthe missing figures, the procedures remain the same.

ILLUSTRATIONUse the information in illustration 1, prepare final accounts. (TO BE SOLVED INTHE CLASS).

15

3. MANUFACTURING ACCOUNTINTRODUCTIONFirms engaged in the manufacturing process usually prepare manufacturingaccounts. Manufacturing accounts is an extension of the trading accounts. Amanufacturing account is prepared for two reasons: (1) To find the cost of the goods manufactured; and (2) To ascertain the amount of any profit on the manufacturing process.

APPORTIONMENT AND CLASSIFICATION OF COSTIn general, four (4) elements of manufacturing costs are usually recognized inmanufacturing accounts. These are:

i. Direct materials;ii. Direct Labour;iii. Other direct expenses (e.g. royalties);

Note: The summation of the above ( i.e. i,ii,iii) will give us Prime Cost;and iv. Factory overhead expenses. Note: The summation of prime cost and iv will give us production cost orcost of goods completed.

The word Direct shows the relationship of the cost element to the actual goodsbeen produced. Direct Labour is the cost of personnel actually working on thegoods produced and does not include cost of supervision and other labour costwhich cannot be associated with actual work on the product. Cost of supervision isclassified as an indirect labour and it forms part of the factory over headexpenses.Other direct expenses include royalties (calculated per unit of goods produce),hire of a special plant for a particular job. Factory overhead expenses consistof all expenses that took place in the factory where production is carried on,but which cannot easily be trace to the unit been produce or manufactured.Example of Indirect labour cost is the wages of supervision, cleaners,maintenance. Also examples of indirect material include factory cleaning

16

materials, machinery lubricants, factory rent, and factory electricity, amongothers.

Notes:1. All administrative and selling expenses as well as distribution expensesare charged to the profit and loss account.2. The tradition usually regard the factory as quite distinct from thewarehouse, so, the production cost is transferred to the trading account.3. Since manufacturing account is mainly concern with expenses, then, all theitems would appear on the debit side of the manufacturing account.4. With regard to Stock, there are three (3) levels of stock in amanufacturing firm. These include:

a. Raw materials;b. Work in progress; andc. Finished goods.

Stock related to raw materials and works in progress (W.I.P) are shown in themanufacturing account, while stock of finished goods is shown in the tradingaccount.5. Wages described as factory wages, production wages or manufacturing wagesshould be regarded as direct labour cost unless otherwise stated or indicated.“Factory salaries” (as distinct from administrative or office salaries) shouldbe regarded as factory overhead.

17

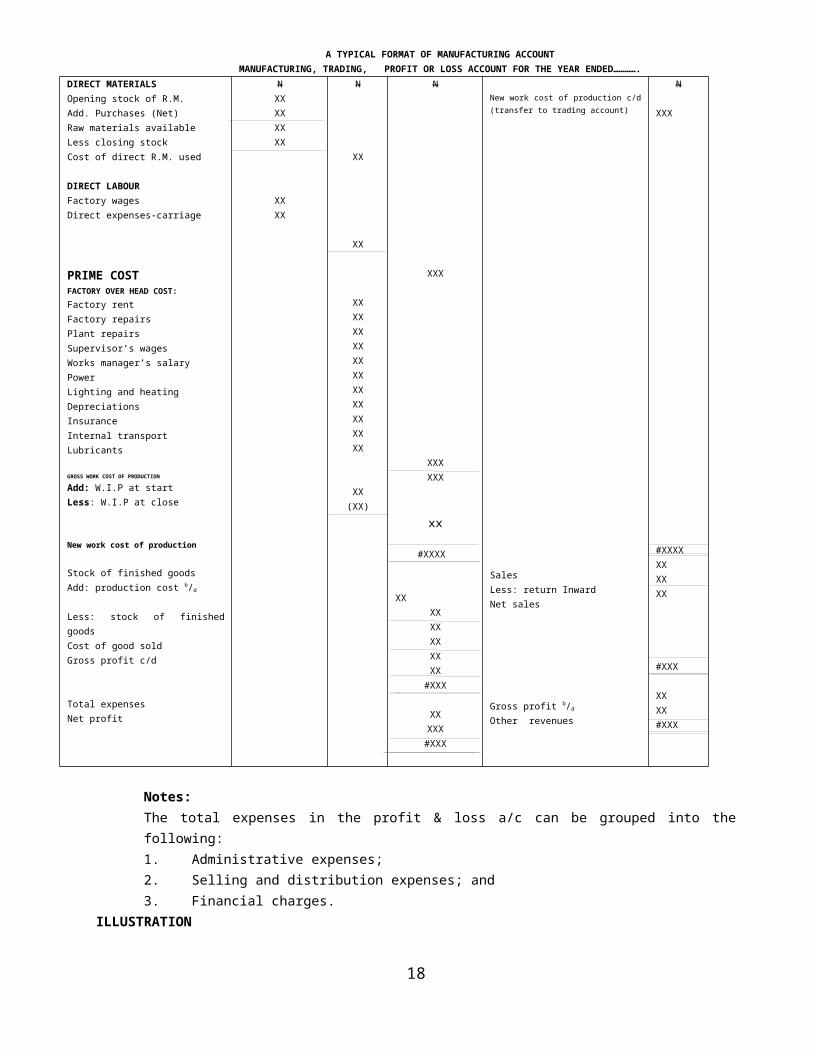

A TYPICAL FORMAT OF MANUFACTURING ACCOUNTMANUFACTURING, TRADING, PROFIT OR LOSS ACCOUNT FOR THE YEAR ENDED………….

DIRECT MATERIALSOpening stock of R.M.Add. Purchases (Net)Raw materials availableLess closing stockCost of direct R.M. used

DIRECT LABOURFactory wagesDirect expenses-carriage

PRIME COSTFACTORY OVER HEAD COST:Factory rentFactory repairsPlant repairsSupervisor’s wagesWorks manager’s salaryPowerLighting and heatingDepreciationsInsuranceInternal transportLubricants

GROSS WORK COST OF PRODUCTION

Add: W.I.P at startLess: W.I.P at close

New work cost of production

Stock of finished goodsAdd: production cost b/d

Less: stock of finishedgoodsCost of good soldGross profit c/d

Total expensesNet profit

NXXXXXXXX

XXXX

N

XX

XX

XXXXXXXXXXXXXXXXXXXXXX

XX(XX)

N

XXX

XXXXXX

xx

#XXXX

XX

XXXXXXXXXX

#XXX

XXXXX#XXX

New work cost of production c/d(transfer to trading account)

SalesLess: return InwardNet sales

Gross profit b/d

Other revenues

N

XXX

#XXXXXXXXXX

#XXX

XXXX#XXX

Notes:The total expenses in the profit & loss a/c can be grouped into thefollowing:1. Administrative expenses;2. Selling and distribution expenses; and3. Financial charges.

ILLUSTRATION

18

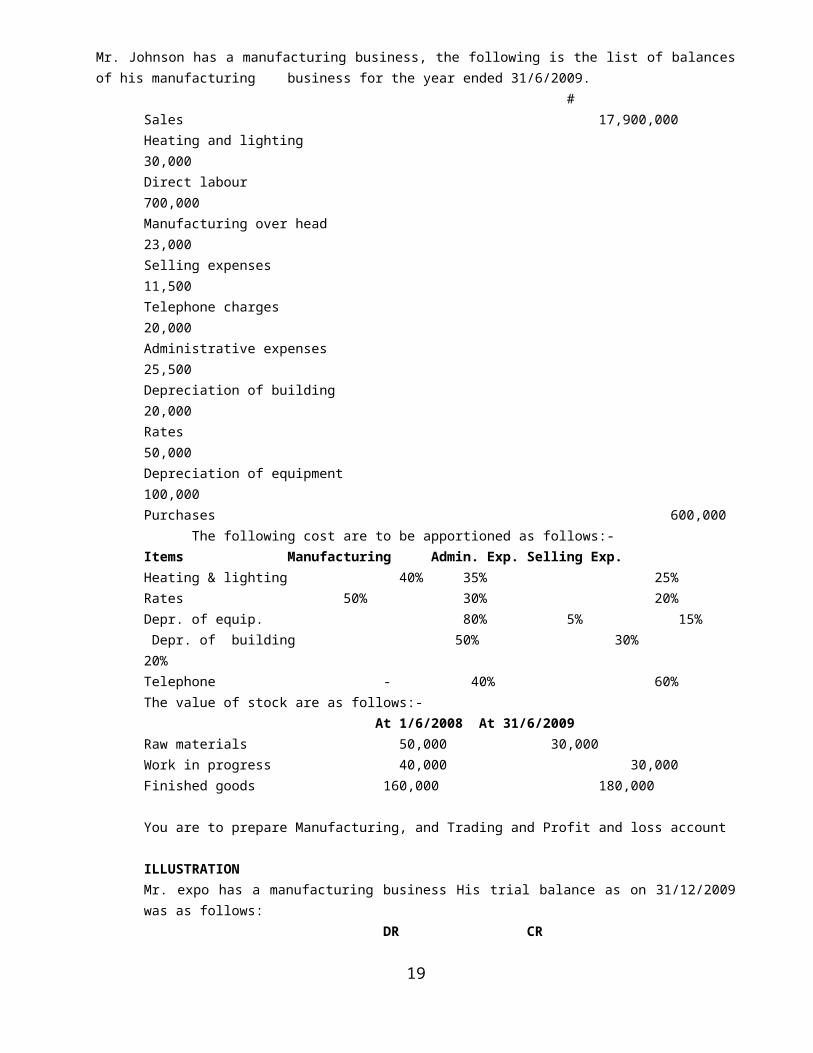

Mr. Johnson has a manufacturing business, the following is the list of balancesof his manufacturing business for the year ended 31/6/2009.

#Sales 17,900,000Heating and lighting30,000Direct labour700,000Manufacturing over head23,000Selling expenses11,500Telephone charges 20,000Administrative expenses25,500Depreciation of building20,000Rates50,000Depreciation of equipment100,000Purchases 600,000

The following cost are to be apportioned as follows:-Items Manufacturing Admin. Exp. Selling Exp.Heating & lighting 40% 35% 25%Rates 50% 30% 20%Depr. of equip. 80% 5% 15% Depr. of building 50% 30% 20%Telephone - 40% 60%The value of stock are as follows:-

At 1/6/2008 At 31/6/2009Raw materials 50,000 30,000Work in progress 40,000 30,000Finished goods 160,000 180,000

You are to prepare Manufacturing, and Trading and Profit and loss account

ILLUSTRATION Mr. expo has a manufacturing business His trial balance as on 31/12/2009was as follows:

DR CR

19

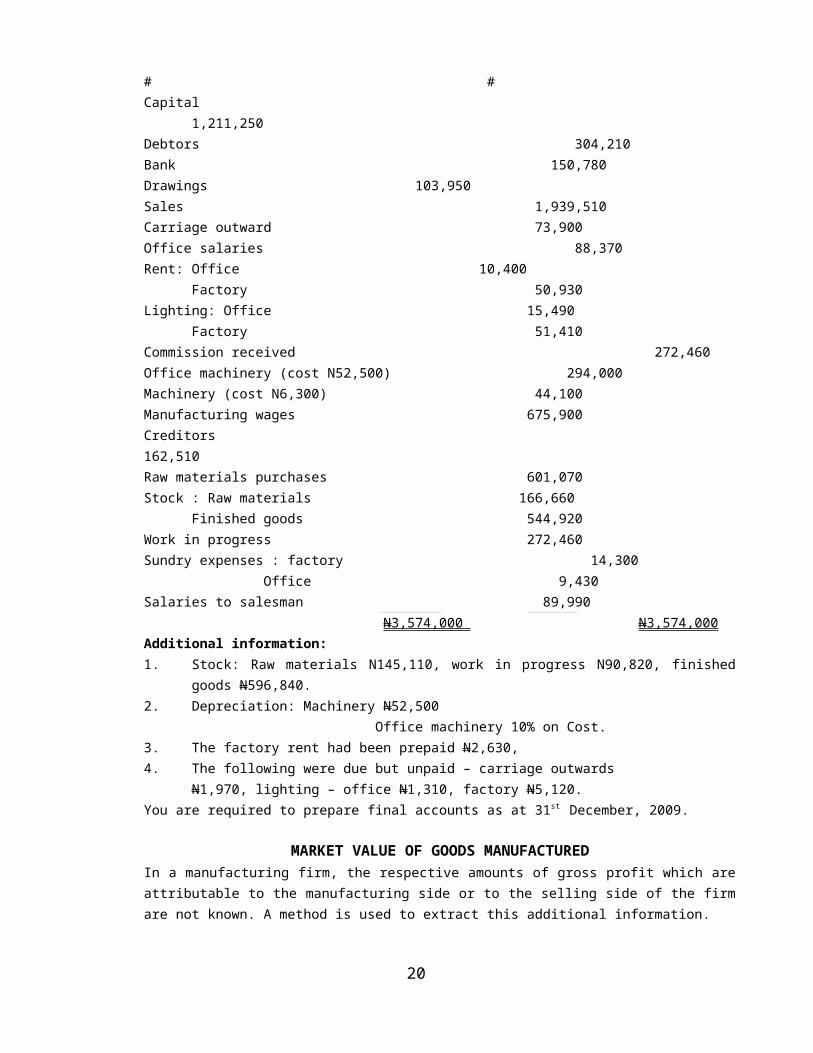

# #Capital

1,211,250Debtors 304,210Bank 150,780Drawings 103,950Sales 1,939,510Carriage outward 73,900Office salaries 88,370Rent: Office 10,400

Factory 50,930Lighting: Office 15,490

Factory 51,410Commission received 272,460Office machinery (cost N52,500) 294,000Machinery (cost N6,300) 44,100Manufacturing wages 675,900Creditors162,510Raw materials purchases 601,070Stock : Raw materials 166,660

Finished goods 544,920Work in progress 272,460Sundry expenses : factory 14,300

Office 9,430Salaries to salesman 89,990

N 3,574,000 N 3,574,000 Additional information:1. Stock: Raw materials N145,110, work in progress N90,820, finished

goods N596,840.2. Depreciation: Machinery N52,500

Office machinery 10% on Cost.3. The factory rent had been prepaid N2,630,4. The following were due but unpaid – carriage outwards

N1,970, lighting – office N1,310, factory N5,120.You are required to prepare final accounts as at 31st December, 2009.

MARKET VALUE OF GOODS MANUFACTUREDIn a manufacturing firm, the respective amounts of gross profit which areattributable to the manufacturing side or to the selling side of the firmare not known. A method is used to extract this additional information.

20

In this method, the cost which would have been involved if the goods hadbeen bought in the finished state instead of been manufacture by the firmis brought into account.The amount (that is, the market value of goods manufactured) is creditedin the manufacturing account and debited in the trading account. In thisway, a two figures of gross profit are reflected (Instead of Just onefigure). The two figures of gross profit are:i. Gross profit on trading; andii. Gross profit on manufacturing.Note:The net profit figure remains unchanged in the Profit & Loss account.ILLUSTRATIONWith reference to Illustration above, if the market value is N2, 000,250,prepare a manufacturing and trading account.

21

4. UNDERSTAND THE ACCOUNTS OF NON-TRADING ORGANIZATION

INTRODUCTIONThe accounts are prepared for organizations set up to render services to theirregistered members. Therefore, not-for-profit making organizations like clubs,societies, charitable organizations, professional bodies, associations, amongothers do not have trading and profit and loss accounts drawn up for them. Astheir principal function is not trading or profit making. Essentially, they aimat promoting activity or group of activities such as sports and culturalactivities, among others. The kind of final accounts prepared by theseorganizations are either receipts and payments or Income and Expenditureaccounts or both.

RECEIPTS AND PAYMENTS ACCOUNTThe receipts and payments accounts are merely a summary of the cash book for theperiod. Because, it shows all cash transaction of the organization regardless ofwhether the cash is paid for the period or not. It generally includes receiptsand payments of a capital nature and receipts and payments of certain item notstrictly applicable to the period under review. The difference between debit andcredit side of receipts and payments accounts represent cash surplus, whichotherwise can be called cash balance.NOTES:1. The accounts show only the receipts and payments of Money;2. It does not show surplus of Income over expenditure or excess ofexpenditure over Income;3. Subscription in arrears and subscription in advance are all included underreceipts;4. Expenses which relate to more than one period are not appointment;5. Information about outstanding liability or subscription due but not paidare not given;6. Capital expenditure is recorded under payment even though the servicesdrive from these asset are used up completely during the accounting period; and7. Being merely as the cash book, the receipts, and payment does not formpart of the double entry system.INCOME AND EXPENDITUREFor most non-profit organization, the preparation of a receipts and paymentsaccount alone is inadequate. This is because, the members would like to know bywhat amount for their Income for the year has exceeded their expenditure or thereverse, and Income and expenditure account is prepared for this purpose. AnIncome and expenditure account differs little in principles and concept fromprofit and loss account, but is almost the same.

22

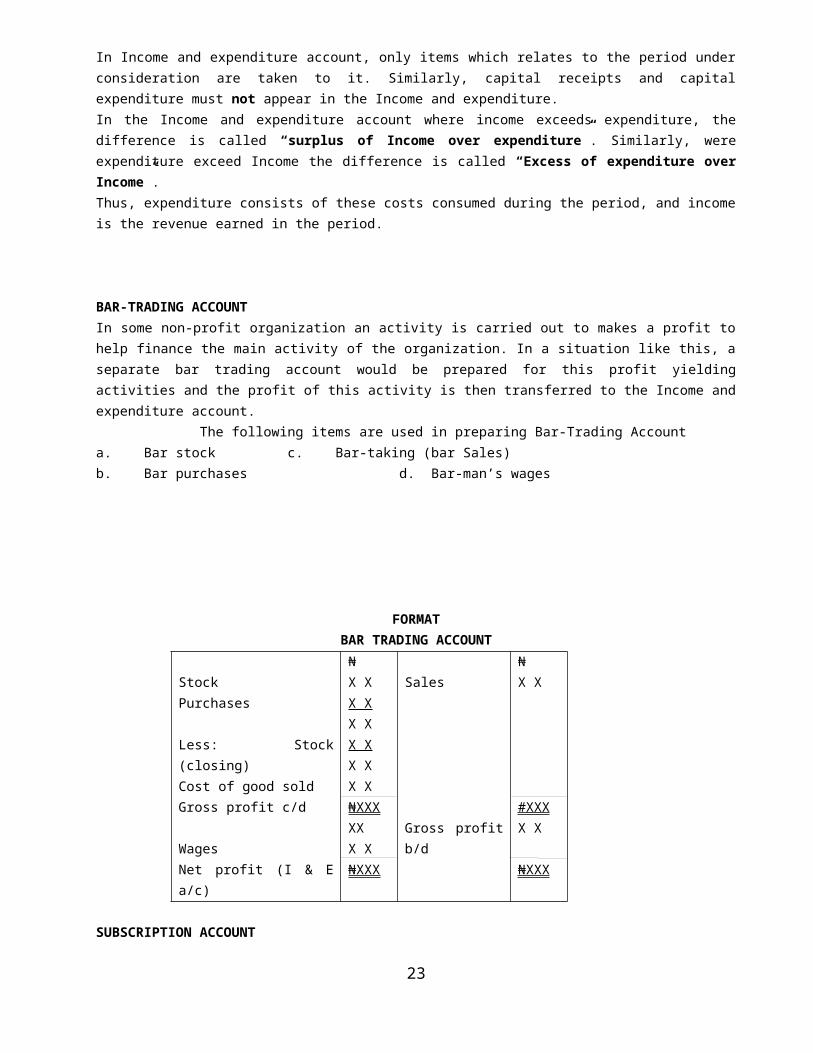

In Income and expenditure account, only items which relates to the period underconsideration are taken to it. Similarly, capital receipts and capitalexpenditure must not appear in the Income and expenditure.In the Income and expenditure account where income exceeds expenditure, thedifference is called “surplus of Income over expenditure”. Similarly, wereexpenditure exceed Income the difference is called “Excess of expenditure overIncome”.Thus, expenditure consists of these costs consumed during the period, and incomeis the revenue earned in the period.

BAR-TRADING ACCOUNTIn some non-profit organization an activity is carried out to makes a profit tohelp finance the main activity of the organization. In a situation like this, aseparate bar trading account would be prepared for this profit yieldingactivities and the profit of this activity is then transferred to the Income andexpenditure account. The following items are used in preparing Bar-Trading Accounta. Bar stock c. Bar-taking (bar Sales)b. Bar purchases d. Bar-man’s wages

FORMATBAR TRADING ACCOUNT

StockPurchases

Less: Stock(closing)Cost of good soldGross profit c/d

WagesNet profit (I & Ea/c)

₦X XX XX XX XX XX X₦XXXXXX X₦XXX

Sales

Gross profitb/d

₦X X

#XXXX X

₦XXX

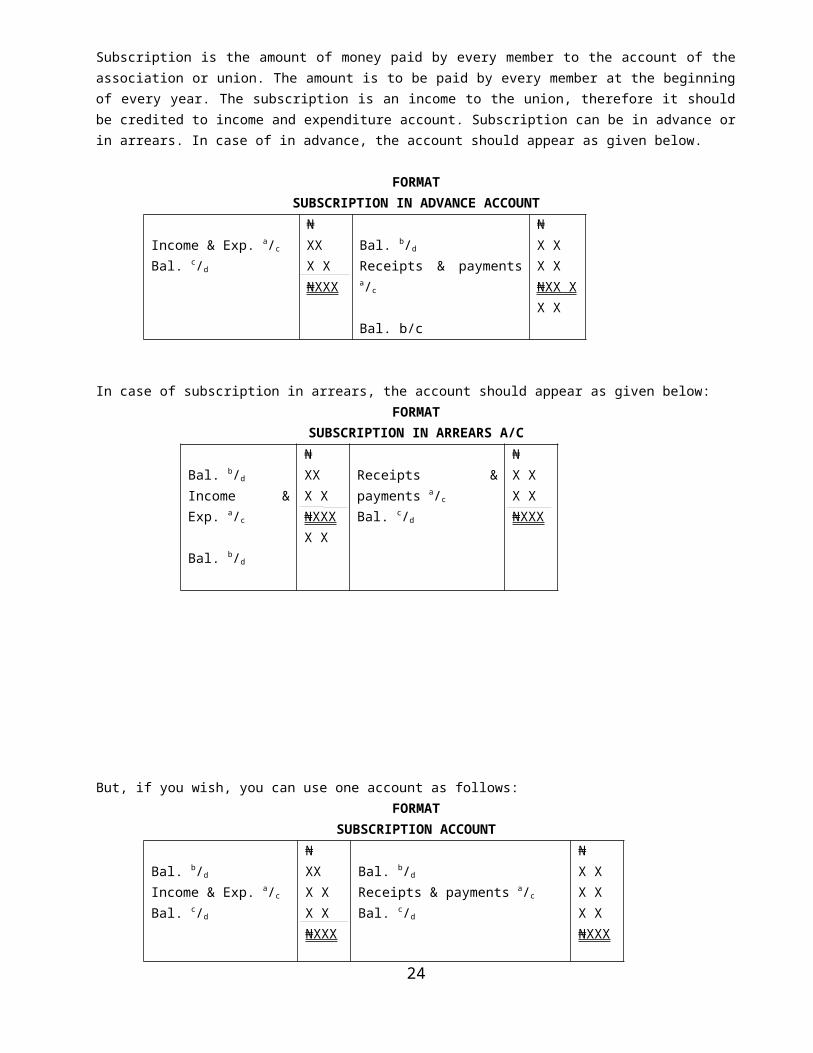

SUBSCRIPTION ACCOUNT

23

Subscription is the amount of money paid by every member to the account of theassociation or union. The amount is to be paid by every member at the beginningof every year. The subscription is an income to the union, therefore it shouldbe credited to income and expenditure account. Subscription can be in advance orin arrears. In case of in advance, the account should appear as given below.

FORMATSUBSCRIPTION IN ADVANCE ACCOUNT

Income & Exp. a/c

Bal. c/d

₦XXX X₦XXX

Bal. b/d

Receipts & paymentsa/c

Bal. b/c

₦X XX X₦XX XX X

In case of subscription in arrears, the account should appear as given below:FORMAT

SUBSCRIPTION IN ARREARS A/C

Bal. b/d

Income &Exp. a/c

Bal. b/d

₦XXX X₦XXXX X

Receipts &payments a/c

Bal. c/d

₦X XX X₦XXX

But, if you wish, you can use one account as follows:FORMAT

SUBSCRIPTION ACCOUNT

Bal. b/d

Income & Exp. a/c

Bal. c/d

₦XXX XX X₦XXX

Bal. b/d

Receipts & payments a/c

Bal. c/d

₦X XX XX X₦XXX

24

Bal. b/d X X Bal. b/d X X

NOTES: Where a club or society received payment from members for benefit which

members are yet to enjoy this payment made in advance (i.e. subscription

received in advance) would be shown under current liability in the balance

sheet. It is a liability because the payments has been made by the members, but

the club has not yet rendered the services to the When members have not yet paid

their subscription in the year (i.e subscription in arrears). Then, they are

owing money to the club/union. The items for the subscription would appear in

the balance sheet as part of current asset.

ACCUMULATED FUND

Most of the union or associations normally keep their records using a single

entry or incomplete records. Therefore, the starting point is that, a statement

of affairs is to be drafted so that an accumulated fund is to be determine.

Accumulated fund represent the capital which should be transfer to the balance

sheet. Assets and liabilities at the beginning of the year are all use in

determining accumulated fund for the association.

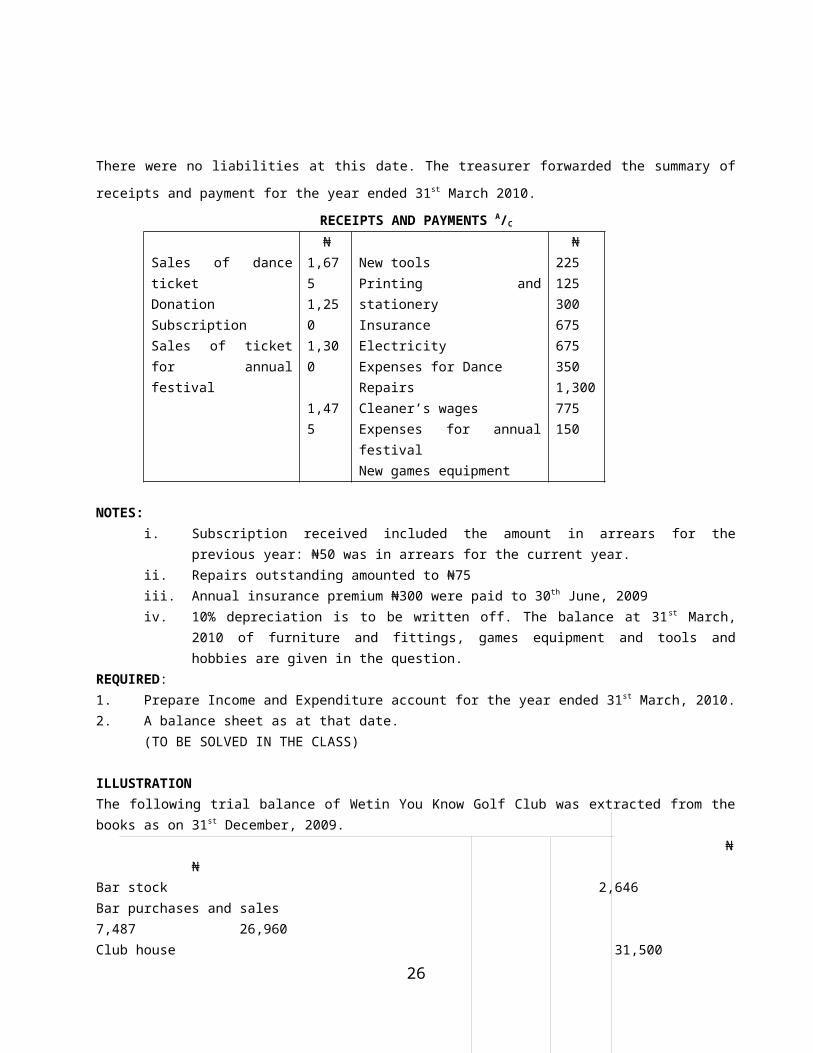

ILLUSTRATION 28Zaria polo club has the following information as on 1st April, 2010.

₦Cash balance 1,150

Subscription in arrears 75

Games equipment 1,600

Insurance prepaid 75

Tools and hobbies equipment 1,025

Furniture and fittings 3,750

25

There were no liabilities at this date. The treasurer forwarded the summary of

receipts and payment for the year ended 31st March 2010.

RECEIPTS AND PAYMENTS A/C

Sales of danceticketDonationSubscriptionSales of ticketfor annualfestival

₦1,6751,2501,300

1,475

New toolsPrinting andstationeryInsuranceElectricityExpenses for DanceRepairsCleaner’s wagesExpenses for annualfestivalNew games equipment

₦2251253006756753501,300775150

NOTES:i. Subscription received included the amount in arrears for the

previous year: ₦50 was in arrears for the current year.ii. Repairs outstanding amounted to ₦75iii. Annual insurance premium ₦300 were paid to 30th June, 2009iv. 10% depreciation is to be written off. The balance at 31st March,

2010 of furniture and fittings, games equipment and tools andhobbies are given in the question.

REQUIRED:1. Prepare Income and Expenditure account for the year ended 31st March, 2010.2. A balance sheet as at that date.

(TO BE SOLVED IN THE CLASS)

ILLUSTRATIONThe following trial balance of Wetin You Know Golf Club was extracted from thebooks as on 31st December, 2009.

₦₦

Bar stock 2,646Bar purchases and sales7,487 26,960Club house 31,500

26

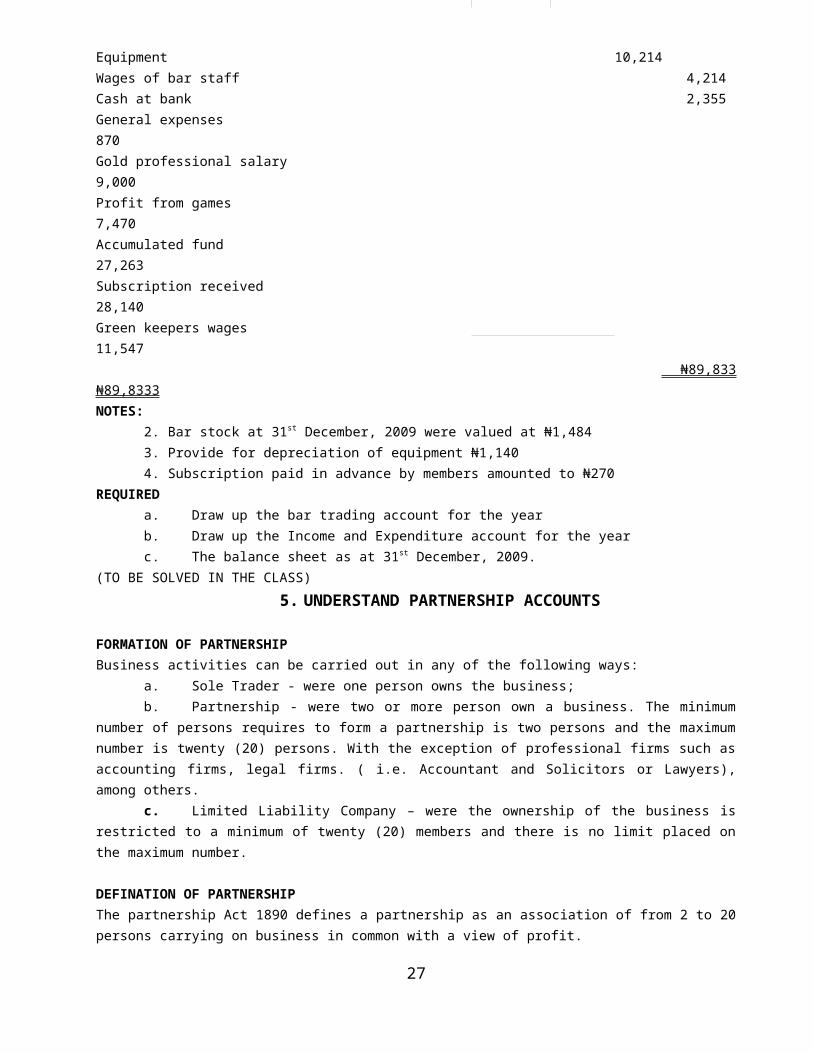

Equipment 10,214Wages of bar staff 4,214Cash at bank 2,355General expenses870Gold professional salary9,000Profit from games7,470Accumulated fund27,263Subscription received28,140Green keepers wages11,547

₦89,833₦89,8333NOTES:

2. Bar stock at 31st December, 2009 were valued at ₦1,4843. Provide for depreciation of equipment ₦1,1404. Subscription paid in advance by members amounted to ₦270

REQUIREDa. Draw up the bar trading account for the yearb. Draw up the Income and Expenditure account for the yearc. The balance sheet as at 31st December, 2009.

(TO BE SOLVED IN THE CLASS)5. UNDERSTAND PARTNERSHIP ACCOUNTS

FORMATION OF PARTNERSHIPBusiness activities can be carried out in any of the following ways: a. Sole Trader - were one person owns the business; b. Partnership - were two or more person own a business. The minimumnumber of persons requires to form a partnership is two persons and the maximumnumber is twenty (20) persons. With the exception of professional firms such asaccounting firms, legal firms. ( i.e. Accountant and Solicitors or Lawyers),among others. c. Limited Liability Company – were the ownership of the business isrestricted to a minimum of twenty (20) members and there is no limit placed onthe maximum number.

DEFINATION OF PARTNERSHIPThe partnership Act 1890 defines a partnership as an association of from 2 to 20persons carrying on business in common with a view of profit.

27

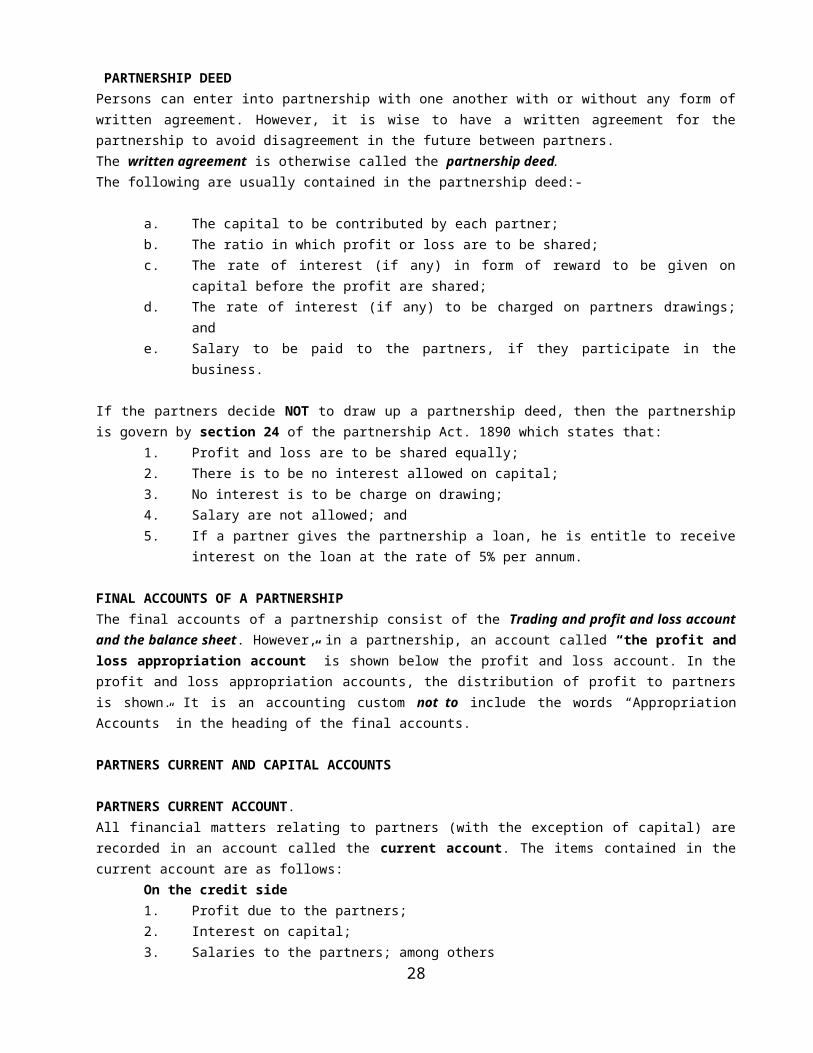

PARTNERSHIP DEEDPersons can enter into partnership with one another with or without any form ofwritten agreement. However, it is wise to have a written agreement for thepartnership to avoid disagreement in the future between partners.The written agreement is otherwise called the partnership deed. The following are usually contained in the partnership deed:-

a. The capital to be contributed by each partner;b. The ratio in which profit or loss are to be shared;c. The rate of interest (if any) in form of reward to be given on

capital before the profit are shared;d. The rate of interest (if any) to be charged on partners drawings;

ande. Salary to be paid to the partners, if they participate in the

business.

If the partners decide NOT to draw up a partnership deed, then the partnershipis govern by section 24 of the partnership Act. 1890 which states that:

1. Profit and loss are to be shared equally;2. There is to be no interest allowed on capital;3. No interest is to be charge on drawing;4. Salary are not allowed; and5. If a partner gives the partnership a loan, he is entitle to receive

interest on the loan at the rate of 5% per annum.

FINAL ACCOUNTS OF A PARTNERSHIPThe final accounts of a partnership consist of the Trading and profit and loss accountand the balance sheet. However, in a partnership, an account called “the profit andloss appropriation account” is shown below the profit and loss account. In theprofit and loss appropriation accounts, the distribution of profit to partnersis shown. It is an accounting custom not to include the words “AppropriationAccounts” in the heading of the final accounts.

PARTNERS CURRENT AND CAPITAL ACCOUNTS

PARTNERS CURRENT ACCOUNT.All financial matters relating to partners (with the exception of capital) arerecorded in an account called the current account. The items contained in thecurrent account are as follows: On the credit side

1. Profit due to the partners;2. Interest on capital;3. Salaries to the partners; among others

28

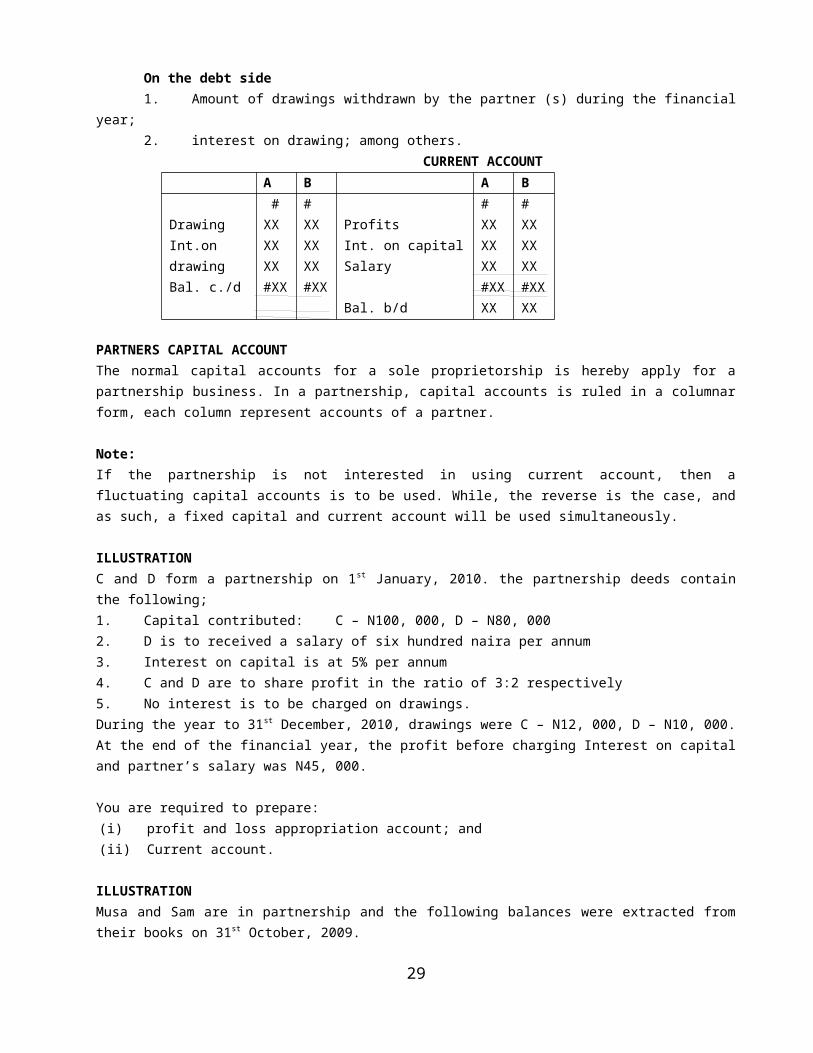

On the debt side1. Amount of drawings withdrawn by the partner (s) during the financial

year;2. interest on drawing; among others.

CURRENT ACCOUNTA B A B

DrawingInt.ondrawingBal. c./d

#XXXXXX#XX

#XXXXXX#XX

ProfitsInt. on capitalSalary

Bal. b/d

#XXXXXX#XXXX

#XXXXXX#XXXX

PARTNERS CAPITAL ACCOUNTThe normal capital accounts for a sole proprietorship is hereby apply for apartnership business. In a partnership, capital accounts is ruled in a columnarform, each column represent accounts of a partner.

Note:If the partnership is not interested in using current account, then afluctuating capital accounts is to be used. While, the reverse is the case, andas such, a fixed capital and current account will be used simultaneously.

ILLUSTRATIONC and D form a partnership on 1st January, 2010. the partnership deeds containthe following;1. Capital contributed: C – N100, 000, D – N80, 0002. D is to received a salary of six hundred naira per annum3. Interest on capital is at 5% per annum4. C and D are to share profit in the ratio of 3:2 respectively5. No interest is to be charged on drawings.During the year to 31st December, 2010, drawings were C – N12, 000, D – N10, 000.At the end of the financial year, the profit before charging Interest on capitaland partner’s salary was N45, 000.

You are required to prepare:(i) profit and loss appropriation account; and (ii) Current account.

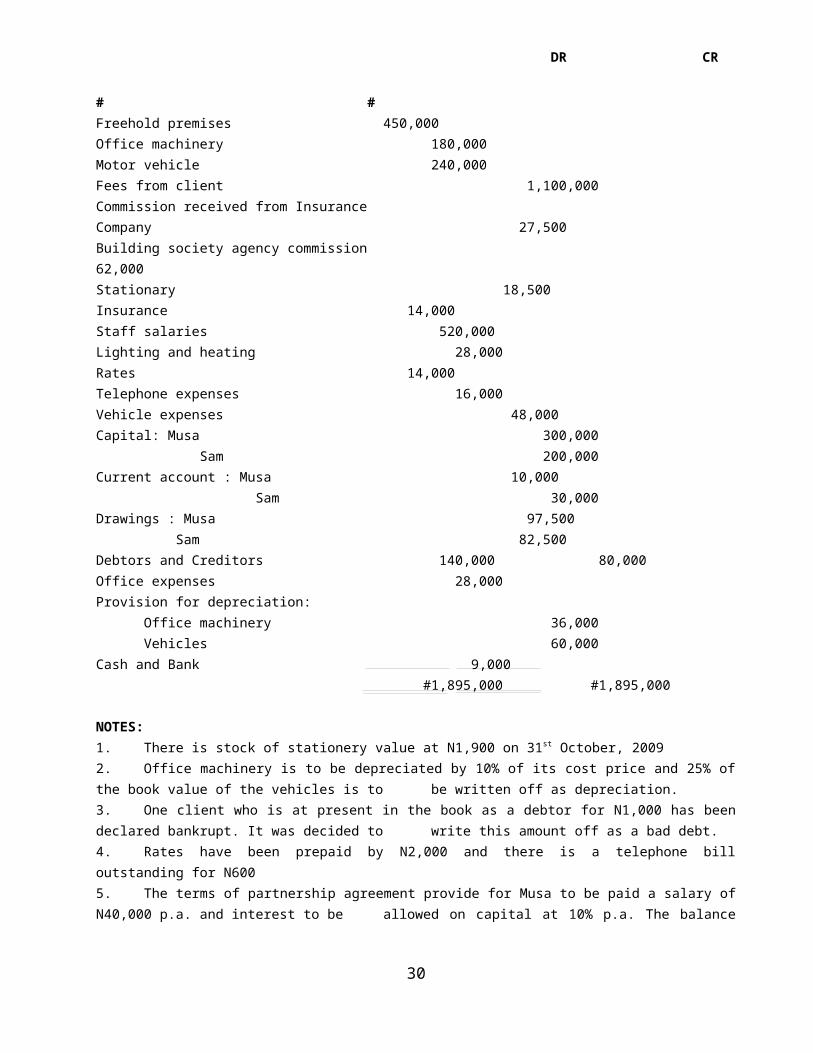

ILLUSTRATIONMusa and Sam are in partnership and the following balances were extracted fromtheir books on 31st October, 2009.

29

DR CR # #Freehold premises 450,000Office machinery 180,000Motor vehicle 240,000Fees from client 1,100,000Commission received from InsuranceCompany 27,500Building society agency commission 62,000Stationary 18,500Insurance 14,000Staff salaries 520,000Lighting and heating 28,000Rates 14,000Telephone expenses 16,000Vehicle expenses 48,000Capital: Musa 300,000 Sam 200,000Current account : Musa 10,000

Sam 30,000Drawings : Musa 97,500

Sam 82,500Debtors and Creditors 140,000 80,000Office expenses 28,000Provision for depreciation:

Office machinery 36,000Vehicles 60,000

Cash and Bank 9,000 #1,895,000 #1,895,000

NOTES:1. There is stock of stationery value at N1,900 on 31st October, 20092. Office machinery is to be depreciated by 10% of its cost price and 25% ofthe book value of the vehicles is to be written off as depreciation.3. One client who is at present in the book as a debtor for N1,000 has beendeclared bankrupt. It was decided to write this amount off as a bad debt.4. Rates have been prepaid by N2,000 and there is a telephone billoutstanding for N6005. The terms of partnership agreement provide for Musa to be paid a salary ofN40,000 p.a. and interest to be allowed on capital at 10% p.a. The balance

30

of the profit is to be divided in the ratio in which partners have providedcapital.6. The partner maintain fixed capital account, all adjustments been madethrough the current account.

Required:Prepare the profit and loss account and appropriation account together with thepartners current account for the year ended 31st October, 2009 and the balancesheet as at that date.

31

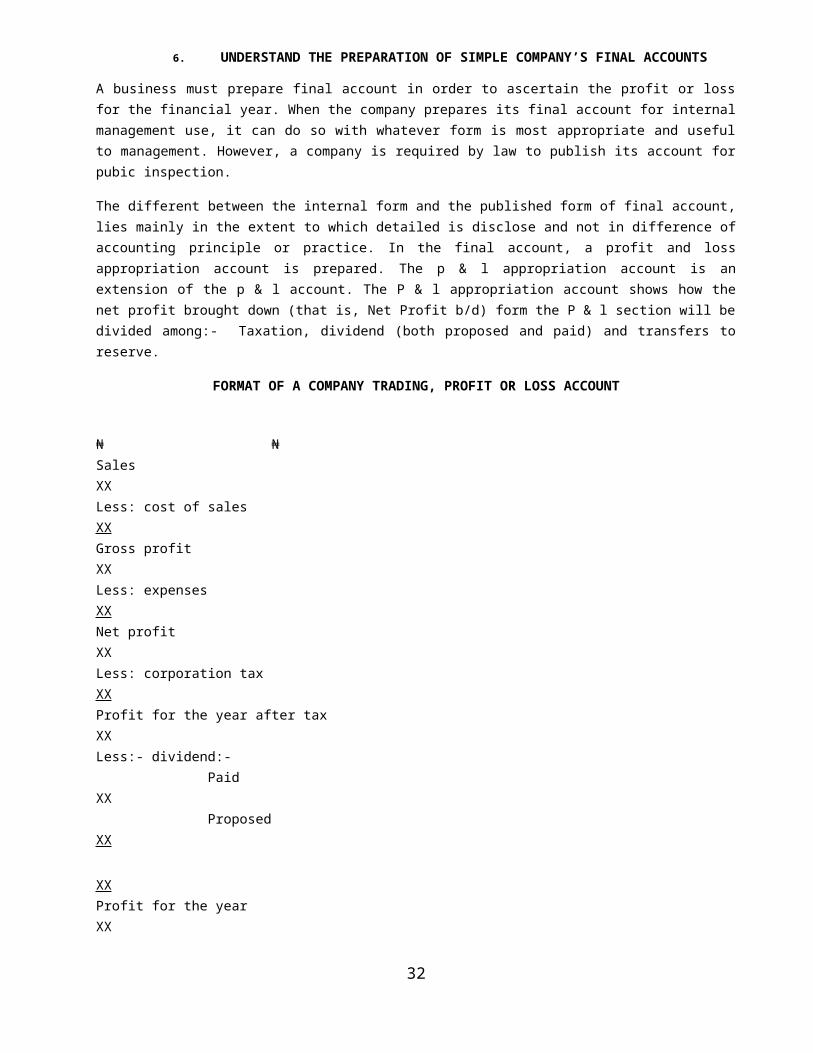

6. UNDERSTAND THE PREPARATION OF SIMPLE COMPANY’S FINAL ACCOUNTS

A business must prepare final account in order to ascertain the profit or lossfor the financial year. When the company prepares its final account for internalmanagement use, it can do so with whatever form is most appropriate and usefulto management. However, a company is required by law to publish its account forpubic inspection.

The different between the internal form and the published form of final account,lies mainly in the extent to which detailed is disclose and not in difference ofaccounting principle or practice. In the final account, a profit and lossappropriation account is prepared. The p & l appropriation account is anextension of the p & l account. The P & l appropriation account shows how thenet profit brought down (that is, Net Profit b/d) form the P & l section will bedivided among:- Taxation, dividend (both proposed and paid) and transfers toreserve.

FORMAT OF A COMPANY TRADING, PROFIT OR LOSS ACCOUNT

₦ ₦Sales XXLess: cost of sales XXGross profit XXLess: expenses XXNet profit XXLess: corporation tax XXProfit for the year after tax XXLess:- dividend:- Paid XX Proposed XX XXProfit for the year XX

32

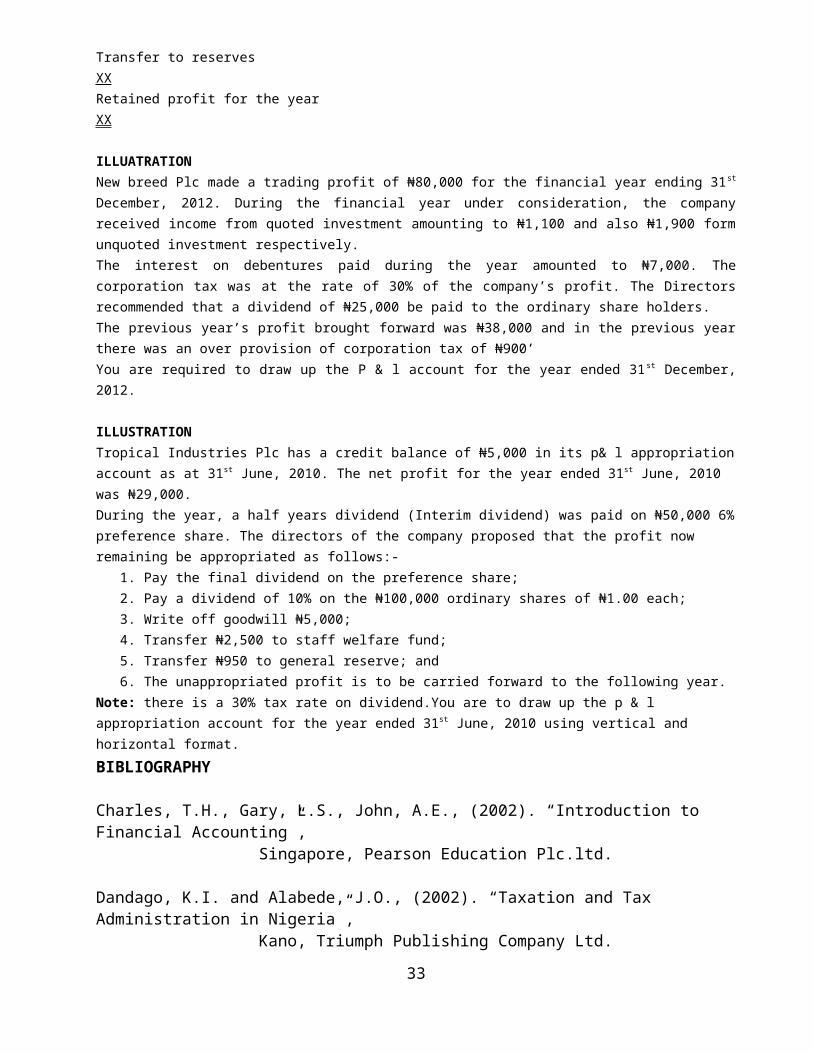

Transfer to reserves XXRetained profit for the year XX

ILLUATRATIONNew breed Plc made a trading profit of ₦80,000 for the financial year ending 31st

December, 2012. During the financial year under consideration, the companyreceived income from quoted investment amounting to ₦1,100 and also ₦1,900 formunquoted investment respectively.The interest on debentures paid during the year amounted to ₦7,000. Thecorporation tax was at the rate of 30% of the company’s profit. The Directorsrecommended that a dividend of ₦25,000 be paid to the ordinary share holders.The previous year’s profit brought forward was ₦38,000 and in the previous yearthere was an over provision of corporation tax of ₦900’You are required to draw up the P & l account for the year ended 31st December,2012.

ILLUSTRATIONTropical Industries Plc has a credit balance of ₦5,000 in its p& l appropriationaccount as at 31st June, 2010. The net profit for the year ended 31st June, 2010 was ₦29,000.During the year, a half years dividend (Interim dividend) was paid on ₦50,000 6%preference share. The directors of the company proposed that the profit now remaining be appropriated as follows:-

1. Pay the final dividend on the preference share;2. Pay a dividend of 10% on the ₦100,000 ordinary shares of ₦1.00 each;3. Write off goodwill ₦5,000;4. Transfer ₦2,500 to staff welfare fund;5. Transfer ₦950 to general reserve; and6. The unappropriated profit is to be carried forward to the following year.

Note: there is a 30% tax rate on dividend.You are to draw up the p & l appropriation account for the year ended 31st June, 2010 using vertical and horizontal format.BIBLIOGRAPHY

Charles, T.H., Gary, L.S., John, A.E., (2002). “Introduction to Financial Accounting”, Singapore, Pearson Education Plc.ltd.

Dandago, K.I. and Alabede, J.O., (2002). “Taxation and Tax Administration in Nigeria”, Kano, Triumph Publishing Company Ltd.

33

Etuk-Udo, J.S., (1999). “Principle of Account for West Africa I”, Ibadan, University Press.

Frank, W. and Slan, S.,(2002). ”Business Accounting I”, 9th Ed., Great Britain, Financial Times, Pretice Hall Publishing.

Frank, W. and Omuya, T.O., (1992). “Business Accounting I”, 5th Ed., Singapore, Longman Publishers Plc.

Jennis, A.R., (2001). “Financial Accounting I”, 2nd Ed., Great Britain, GuernseyCo. Ltd.

Kermit, D.L., (1995). “Essential of Financial Accounting”, 7th Ed.,Irwin/McGraw Hill.

Mill Cham, A.H., (1992). “Foundation of Accounting”, 3rd Ed., London, DP Publication ltd.

Robert, O.I., (2004). “Financial Accounting Made Simple”, 1st Ed., vol. 1.

Vickery, B.G., (1979). “Principle and practice of Book Keeping”, 21st Ed, Cassell Ltd.

Williams, P., (1982). “Accounting”, revised by James, L.L., 4th Ed., Great Britain, Pitman Books Ltd.

34

35