portfolio maagement

TRANSCRIPT

SUMMARY

Working capital management refers to the administration of all

aspects of current assets, namely cash, marketable securities, debtors

and stock (inventories) and current liabilities. The financial manager

must determine levels and composition of current assets. He must see

that right sources are tapped to finance current assets, and that

current liabilities are paid in time. He must see that right sources

are tapped to finance current assets, and that current liabilities are

paid in time.

There are many aspects of working capital management, which

make it an important function of the financial manager:

Time: working capital management requires much of the

financial manager’s time.

Investment: working capital represents a large portion of

the total investments in assets.

Significance: working capital management has great

significance for all firms but it is very critical for small

firms.

Growth: the need for working capital is directly related to

the firm’s growth.

Investment in current assets represents a very significant portion of

the total investment in assets. Working capital management is critical

for all firms. A small firm may not have much investment in fixed

1

assets, but it has to invest to in current assets. Small firms in

India face a severe problem of collecting their debtors.

Companies have their own policies to assess the working capital

of the firm to finance them with the shortage.

Maddi Lakshmaiah Company adopts certain method for financing

their customer’s working capital requirements. There are certain

recommendations from the committees for the companies to finance the

working capital.

It may, thus, be concluded that all precautions should be taken

for the effective and efficient management of working capital. The

finance manager should pay regular attention to the levels of current

assets and the financing of current assets.

2

CONTENTS

Chapter

No. Name of the concept Page No.

I

Introduction 3

Need of the study 5

Objectives of the study 5

Scope of the study 6

Methodology of the study 7

Limitations of the study 8

II Review of Literature 9

III Industry Profile 18

IV Company Profile 26

VData analysis and

interpretation41

VIFindings, Suggestions and

Conclusion64

VII Bibliography 67

3

CHAPTER I – INTRODUCTION

4

INTRODUCTION

Working capital may be regarded as the life blood of a business. A

study of working capital is a major importance to internal and

external analysis because of its close relationship with the current

day to day operations of a business.

The goal of a working capital management is to manage

the firm’s public undertaking which has been selected for the study.

The topic selected is “A study on working capital management with

reference to M.L & Company Ltd.,

Working capital has become the most important task of

top executive to this increasing troubleshoot in the environment of

the business. This project work provides a conceptual frame work for

the study of various aspects of working capital in M.L. & Company

Ltd.,

The goal of working capital management is to manage

the firm’s current assets and current liabilities in such a way that a

satisfactory level of working capital is maintained.

The most important activities of a business firm are

finance, Production, marketing and human’s resources. Among them

financial management is the very important. Finance management

involves the application of a general management principal is a

particular financial operation. The management of a working capital is

one of the most important aspects of the firm’s overall finance

management.

5

OBJECTIVES OF THE STUDY

To study the existing system of working capital management in

M.L. & Company Ltd.,

To examine the feasibility of present system of Managing cash,

Debtors and Inventory in M.L. Company Ltd.,

Suggesting a better way if any improving management of working

capital.

To analyze the financial performance of the company with

reference to its working capital components.

SOURCES OF DATA

6

The Data is collected from the following sources.

Six years annual reports of M.L. & Company Ltd., from 2009 to

2014.

Interaction with the related finance department.

Ten years financial data of M.L. & Company Ltd., and

consolidation statements.

Past six year’s operating results and Balance sheet of M.L. &

Company Ltd.,

METHODOLOGY AND TECHINIQUES

The working capital management mechanism is studied in detail.

The various factors of working capital management are studied in

detail.

7

The existing scenario of Debt’s management collection period,

cash system, Inventory. Procurement was studied to correlate

with the working capital management components.

Activities regional operating divisions as well as power sector,

industrial sector and international operational division were

studied in depth to analyze the bills receivable system, sales

and debts.

Considering all these factors, we have designed analysis

techniques for determination of ideal working capital management

in M.L. & Company Ltd.,

SCOPE AND PERIOD OF STUDY

The scope and period of study is restricted to the following:

The scope is limited to the operations of M.L. & Company Ltd.,

The information obtained from the Primary and Secondary sources

were limited to M.L. & Company Ltd.,

The key performance indications were taken from 2009-2014.

The operating results, the Balance sheet was of last six years.

Comparison analysis was done in comparison of its sister units.

8

DESIGN OF STUDY

Working capital management is a vital importance in

an organization like M.L. Company Ltd., which deals with its customers

like State tobacco boards, Private industries and public sectors. Even

though it’s internal resources for diversifications and for expansion

projects supported most of its working capital requirements. They

have designed working capital management by keeping the nature of the

industry and its product lifecycle.

The design of the study is as follows:

Streamlining of Cash inputs.

Forecasting of Material requirements.

Keeping the track of system of centralize cash collections.

Computerized bill passing system and customer payment schedule.

Existing Inventory procurements system for both Indigenous nature

and import consignment.

9

NEED FOR THE STUDY

The Study is continued for the following needs:

To know various procedure and patterns followed for computation

of working capital in the organization

To have a personal exposure by visiting the organization for

many times

To study the role of working capital and application in the

organization

To know more information about working capital management both

theoretically and practically

LIMITATION OF THE STUDY

Some aspects of financial information were not available because

of the confidentiality

Information provided is mostly of secondary nature so the

accuracy of the study is limited

Current year’s information is not available

The period of study is limited to only Eight weeks

10

The data and analysis given in the report is applicable to

similar purpose of study

11

CHAPTER II - REVIEW OF LITERATURE

12

WORKING CAPITAL MANAGEMENT

Working capital management involves the relationship between a

firm’s short-term assets and its short-term liabilities. The goal of

working capital management is to ensure that a firm is able to

continue its operations and this it has sufficient ability to satisfy

both maturing short-term debt and upcoming operational expenses. The

management of working capital involves managing inventories, accounts

receivable and payable and cash to pay current liabilities as they

fall due. This implies a clearly designed risk policy to determine

the required liquidity level.

Why Firms Hold Cash

The finance profession recognizes the three

primary reasons offered by economist John Maynard Keynes to explain

why firms hold cash. The three reasons are for the purpose of

speculation, for the purpose of precaution, and for the purpose of

making transactions. All three of these reasons stem from the need

for companies to possess liquidity.

SPECULATION Economist Keynes described this reason for holding

cash as creating the ability for a firm to take advantage of special

opportunities that if acted upon quickly will favour the firm. An

example of this would be purchasing extra inventory at a discount that

is greater than the carrying costs of holding the inventory.

PRECAUTION

13

Holding cash as a precaution serves as an

emergency fund for a firm. If expected cash inflows are not received

as expected cash held on a precautionary basis could be used to

satisfy short-term obligations that the cash inflow may have been

bench marked for.TRANSACTION Firms are in existence to create products or

provide services. The providing of services and creating of products

results in the need for cash inflows and outflows. Firms hold cash in

order to satisfy the cash inflow and cash outflow needs that they

have.

CONCEPTS OF WORKING CAPITALThere are two concepts of working capital

Gross Working Capital

Net working Capital

In the broad sense, the term working capitalrefers to the gross working capital and represents the amount of funds

invested in current assets. Current assets are those assets, which in

the ordinary course of business can be converted into cash within a

short period of normally one accounting year.

14

In a narrow sense, the term working capital refers

to the net working capital. Net working capital is the excess of

current assets over current liabilities.

Net working capital may be positive or negative.

When the current assets exceed the current liabilities, the working

capital is positive and the negative working capital results when the

current liabilities are more than the current assets. Current

liabilities are those liabilities which are intend to be paid in the

ordinary course of business within a short period or normally one

accounting year out of the current assets or the income of the

business.

The gross working capital concept is financial

or going concern concept whereas net working capital is an accounting

concept of working capital. These two concepts of working capital are

not exclusive; rather both have their own merits.

Gross concept is very suitable to the company

form of organization where there is divorce between ownership,

management and control. The net concept of working capital may be

suitable only for proprietary from of organizations such as sole-

trader or partnership firms. However, it may be made clear that as

15

Working Capital = Current Assets –Current Liabilities

per the general practice net working capital is referred to simply as

working capital.

TYPES OF WORKING CAPITALWorking capital may be classified in two ways

1. On the basis of concept

2. On the basis of time

On the basis of concept, working capital Gross working capital

Net working capital

Based on time, working capital can be further classified

into Permanent or fixed working capital.

Temporary or variable working capital.

PERMANENT WORKING CAPITAL: Permanent or fixed working capital isthe minimum amount, which is required to ensure effective utilization

of fixed facilities and for maintaining the circulation of current

assets. There is always a minimum level of current assets, which is

continuously required by the enterprise to carry out its normal

business operations. For example, every firm has to maintain a

16

minimum levels of raw materials, work-in-process, finished goods and

cash balance. This minimum level of current assets is called fixed

working capital.

TEMPORARY WORKING CAPITAL: Any amount over and above the permanent level

of working capital is temporary, fluctuating or variable working

capital. This portion of the required working capital is needed to

meet fluctuations in demand consequent upon changes in production and

sales as a result of seasonal changes

WORKING CAPITAL CYCLE: Cash flows in a cycle into, around and out of

a business. It is the business’s lifeblood and every manager’s

primary task is to help keep it flowing and to use the cash flow to

generate profits. If a business is operating profitably, then it

should, in theory, generate cash surpluses. If it doesn’t generate

surpluses, the business will eventually run out of cash and expire.

The faster a business expands the more cash

it will need for working capital and investment. The cheapest and

best sources of cash exist as working capital right within business.

Good management of working capital will generate cash will help

improve profits and reduce risks. Bear in mind that the cost of

providing credit customers and holding stocks can represent a

substantial proportion of a firm’s total profits.

There are two elements in the business

cycle that absorb cash – inventory (stocks and work-in-progress) and

17

receivables (debtors owing you money). The main sources of cash are

payables (your creditors) and equity and loans.

Each component of working capital (namely

inventory, receivables and payables) has two dimensions … TIME. and

MONEY. When it comes to managing working capital – TIME IS MONEY. If

you can get money to move faster around the cycle (e.g. collect money

due from debtors more quickly) or reduce the amount of money tied up.

(e.g. reduce inventory levels relative to sales), the business will

generate more cash or it will need to borrow less money to fund

working capital. Consequently, you could reduce the cost of bank

interest or you’ll have additional free money available to support

additional sales growth or investment. Similarly, if you can

negotiate, improved terms with suppliers e.g. get longer credit or an

increased credit limit; you effectively create free finance to help

find future sales.

ADVANTAGES OF ADEQUATE WORKING CAPITAL Working capital is the lifeblood and nerve

center of business. Just as circulation of blood is essential in the

human body for maintaining life, working capital is very essential to

maintain the smooth running of a business. No business can run

successfully without an adequate amount of working capital. The main

advantages of maintaining adequate amount of working capital are as

follows:

Solvency of the business: Adequate working capital helps in maintaining

solvency of the business by providing uninterrupted flow of

production.

18

Goodwill: Sufficient working capital enables abusiness concern to make prompt payments and hence helps in creating

and maintaining goodwill.

Easy loans: A concern hacking adequate working capital,high solvency and good credit standing can arrange loans from banks

and others on easy and favorable terms.

Cash Discounts: Adequate working capital also enables aconcern to avail cash discounts on the purchases and hence it reduces

costs. Regular payment of salaries, wages and other day-to-day

commitments company which has ample working capital can make regular

payment of salaries, wages and other day-to-day commitments which

raises the morale of its employees, increases their efficiency,

reduces wastage’s and costs and enhances production and profits.

Regular supply of raw materials: Sufficient working capital ensures regular

supply of raw materials and continuous production.Ability to face Crisis: Adequate working capital enables a concern to

face business crisis in emergencies such as Ability to face Crisis:

Adequate working capital enables a concern to face business crisis in

19

emergencies such as depression because during such periods, generally,

there is much pressure on working capital.Quick and regular return on Investments: Every Investor wants a quick and regularreturn on investments. Sufficient of working capital enables a

concern to pay quick and regular dividends to its investors, as there

may not be much pressure to plough back profits. This gains the

confidence of its investors and creates a favorable market to raise

additional funds in the future.

High morale: Adequacy of working capital creates anenvironment of security, confidence, and high morale and creates

overall efficiency in a business.

DISADVANTAGES OF EXCESSIVE WORKING CAPITAL Every business concern should have adequate

working capital to run its business operations. It should have

neither redundant or excessive working capital nor inadequate nor

shortage of working capital. Both excessive as well as short working

capital positions are bad for any business.

Excessive working capital means idle funds which earn no profits

for the business and hence the business cannot earn a proper rate

of return on its investments.

When there is redundant working capital, it may lead to

unnecessary purchasing and accumulation of inventories causing

more chances of theft, waste and losses.

20

Excessive working capital implies excessive debtors and defective

credit policy, which may cause higher incidence of bad debts.

It may result into overall inefficiency in the organization.

When there is an excessive working capital relation with the

banks and other financial institutions may not be maintained.

Due to low rate of return on investments the value of shares may

also fall.

DETERMINANTS OF WORKING CAPITAL

Nature or character of business: The working capital requirements of a firm

basically depend upon the nature of its business. Public utility

undertakings like electricity, water and railway need very limited

working capital because they offer cash sales only and supply

services.

Size of business, Scale of operations: The working capital requirements of a concern are

directly influenced by the size of its business which may be measured

in terms of scale of operations. Greater the size of business units,

generally larger will be the requirements of working capital.

Production policy: In certain industries the wide fluctuations may

be due to seasonal variations. The requirements of working capital in

such a case depend upon the production policy.

21

Seasonal variations: In certain industries the raw material maynot be available throughout the year. They have to buy raw materials

in bulk during the season to ensure an uninterrupted flow of

production.

Working capital cycle: In a manufacturing concern the working capital

starts with the purchase of raw materials and ends with realization of

cash from the sales of finished products. The speed with which the

working capital completes one cycle determines the requirements of

working capital. Longer the period of cycle larger is the requirement

of working capital.

Credit policy: The credit policy of a concern in itsdealings with debtors and creditors considerably influence the

requirements of working capital. A concern that purchases its

requirements on credit and sells its products on cash requires less

amount of working capital.

Business cycles: Business cycle refers to alternativeexpansion and contraction in general business activity. In a period

of boom i.e., when the business is prosperous, there is a need for

22

larger amount of working capital due to increase in sales, rise in

prices, optimistic expansion of business, etc.

On the contrary in the times of depression i.e.,

when there is a down swing of the cycle, the business contracts, sales

decline, difficulties are faced in collections from debtors and firms

may have large amount of working capital lying idle.

Rate of growth of Business: The working capital requirements of a concern

increases with the growth and expansion of its business activities.

Although, it is difficult to determine the relationship between the

growth in the volume of business and working capital of a business,

yet it may be concluded that for normal rate of expansion in the

volume of business, we may have retained profits to provide for more

working capital but in fast growing concern, we shall require large

working capital.

Earning capacity and dividend policy: Some firms have more earning capacity than other

due to quality of their products, monopoly conditions etc. such firms

with high earning capacity may generate cash profits from operations

and contribute to their working capital. The dividend policy of a

concern also influences the requirements of its working capital.

Price level changes: Changes in the price level also affectthe working capital requirements. Generally, the rising prices will

require the firm to maintain large amount of working capital as more

funds will be required to maintain the same current assets. The

23

effect of rising prices may be different for different firms. Some

firms may be affected much while some others may not be affected at

all by the rise in prices.

Other factors: Certain other factors such as operatingefficiency, management ability, irregularities of supply, import

policy, asset structure, importance of labor, banking facilities, etc,

also influence the requirements of working capital.

MANAGEMENT OF CASH Cash management is one of the key areasof working capital management. Cash, the most liquid asset is of

vital importance to the daily operations of business firms need cash

to meet the needs of daily transactions, to take advantage of

unexpected investment opportunities. While cash serves these

functions, it is an idle resource with an opportunity cost. The

liquidity provided by the holding cash is at the expense of profits

that could from alternative investment opportunities. Hence the firm

should plan and control cash carefully.

Cash management details with the following

Cash inflows and out flows

Cash flows within the firm

Cash balances held by a firm at a point of time

24

Cash management need strategies to deal with following various

facts of cash.

INVESTMENT OF SURPLUS FUNDS There are sometimes, surplus funds with thecompanies, which are required after sometime. These funds can be

employed in liquid and risk free securities to earn some income.

There are number of avenues where these funds can be invested

Unit 1964 scheme

Ready forwards

Investment in marketable securities

Bald financing

Negotiable certificate of deposit.

25

CHAPTER III - INDUSTRY PROFILE

26

HISTORY:Tobacco is a plant that grows natively in north and South

America. It is in the same family as the potato, pepper and the

poisonous nightshade, a very dead plant. The seed of a tobacco plant

is very small. A ‘1’ ounce sample contains about 300,000 seeds.

It is believed that tobacco began growing in the America about

6,000 B.C. As early as ‘1’ B.C., American Indians began using tobacco

in many different ways, such as in religious and medicinal practices.

Tobacco was believed to be a cure-all, and was used to dress wounds,

as well as a pain killer. Chewing tobacco was believed to relieve the

pain of a toothache.

Soon after, sailors brought tobacco back to Europe, and the plant

was being grown all over Europe. The major reason for tobacco’s

growing popularity in Europe was its supposed healing properties.

Europeans believed that tobacco could cure almost anything, from bad

breath to cancer.

In 1571, a Spanish doctor named Nicolas Monardes wrote a book

about the history of medicinal plants of the new world. In this he

claimed that tobacco could cure 36 health problems.

In 1588, a Virginian named Thomas Harriet promoted smoking

tobacco as a viable way to get one’s daily dose of tobacco.

Unfortunately, he died of nose cancer (because it was popular then to

breathe the smoke out through the nose).

During the 1600’s, tobacco was so popular that it was frequently

used as money! Tobacco was literally “as good as gold!” This was also

a time when some of the dangerous effects of smoking tobacco were

27

being realised by some individuals. In 1610 sir Francis Bacon noted

that trying to quit the bad habit was really hard.

In 1632, 12 years after the mayflower arrived on Plymoth Rock, it

was illegal to smoke publicly in Massachusetts! This had more to do

with moral beliefs of the day, than health concerns about smoking

tobacco.

In 1760, Pierre Lorilliard establishes a company in New York City

to process tobacco, cigar, and snuff. Today, P. Lorillard is the

oldest tobacco company in the U.S.

GROWTH:In 1776, during the American revolutionary war, tobacco helped

finance the revolution by serving as collateral for loans the

Americans borrowed from France! Over the years, more and more

scientists began to understand the chemical in tobacco, as well as the

dangerous health effects smoking produces.

In 1826, the pure form of nicotine was finally discovered. Soon

after, scientists concluded that nicotine was dangerous poison.

In 1836, New Englander Samuel Green stated that tobacco was an

insecticide, a poison, and can kill a man.

In 1847, the famous Phillip Morris was established, selling hand

rolled Turkish cigarettes. Soon after in 1849, J. E. Liggett and

Brother was established in St. Louis, Mo. (the company that has

settled out of the big lawsuits recently). Cigarettes became popular

around this time when soldiers brought it back to England from the

Russian and Turkish soldiers.

Cigarettes in the U.S. were mainly made from scraps left over

after the production of other tobacco products, especially chewing

28

tobacco. Chewing tobacco became quite popular at this time with the

“cowboys” of the American West.

In 1875, R. J. Reynolds Tobacco Company (better known for its

Reynolds wrap aluminium foil) was established to produce chewing

tobacco. It wasn’t until the 1900’s that the cigarette became the

major tobacco product made and sold. Still, in 1901 3.5 billion

cigarettes were sold, while 6 billion cigars were sold. Along with the

popularity of cigarettes however, was a small but growing anti-tobacco

campaign, with some states proposing a total ban on tobacco?

In 1902, the British Phillip Morris set up a New York

headquarters to market its cigarettes, including a now famous Marlboro

brand. The demand for cigarettes grew however, and in 1913 R.J.

Reynolds began to market a cigarette brand called Camel.

WAR & CIGARETTES: A DEADLY COMBO:The cigarette exploded during world war (1914-1918), where

cigarettes were called the “soldier’s smoke”. By 1923, Camel controls

45% of the U.S. market! In 1924, Phillip Morris began to market

Marlboro as a woman’s cigarette that is a “Mild as May”!

To battle this, American Tobacco Company, maker of the lucky

strike brand, began to market its cigarettes to women and gains 38% of

the market. Smoking rates among female teenagers soon tripled during

the years between 1925-1935. In 1939, American Tobacco Company

introduced a new brand, Pall Mall, which allowed American to become

the largest tobacco company in the U.S.

During World War II (1939-1945), cigarette rates were at an all

time high. Cigarettes were included in a soldier’s C-Rations (like

food). Tobacco companies sent millions of cigarettes to the soldiers

29

for free, and when these soldiers came home, the companies had a

steady stream of loyal customers. During the 1950’s, more and more

evidence was surfacing that smoking was linked to lung cancer.

In 1952 P. Lorillard markets its Kent brand with the ’Micronite’

filter, which contained asbestos! This was fortunately discontinued in

1956. In 1953, Dr. Ernst L. Wynders find that putting cigarette tar on

the backs of mice causes tumors! In 1954, RJ Reynolds introduced the

salem brand, which was the first filter-tipped menthol cigarette.

HEALTH HAZARDS REVEALED:In 1964, the Surgeon General’s Report on “Smoking and Health”

came out. This report assisted in allowing the government to regulate

the advertisement and sales of cigarettes. The 1960’s in general was a

time when much of health hazards of smoking were reported.

In 1965, television cigarette ads were taken off the air in Great

Britain. In 1966, those health warnings on cigarette packs began

propping up. In 1968, Bravo, a non-tobacco cigarette brand was

marketed made primarily of Lettuce, it failed miserably!

Because of the negative press about tobacco, the major tobacco

companies began to diversify their products. Phillip Morris began to

buy into the Miller Brewing company, makers of Miller Beer, Miller

Lite, and Red Dog Beer. RJ Reynolds Tobacco Company drops the “Tobacco

Company” in its name, and becomes RJ Reynolds industries.

It also began to buy into other products, such as aluminium.

American Tobacco Company also drops “Tobacco” from its name, becoming

American Brands, Inc. In 1971, television ads for cigarettes are

finally taken off the air in the U.S. cigarettes, however, were still

30

the most heavily advertised product second to automobiles. In 1977,

the first national great American Smoke out took place.

In 1979, the surgeon general reported on the health consequences

of smoking for women. This is in light to the increasing number of

women who were taking up the bad habit. Some attribute is to slick and

campaign of the Virginia Slims brand, “you’ve come a long way baby”.

THE RECENT PAST:During the 1980’s there were many lawsuits filed against the

tobacco industry because of the harmful effects of its products.

Smoking became politically incorrect, with more public places

forbidding smoking. In 1982, the surgeon general reported that second

hand smoke may cause lung cancer. Smoking in pubic areas was soon

restricted, especially at the work place. In 1985, lung cancer became

the No.1 killer of women, beating out breast cancer! Phillip Morris

continued to diversify into other products, buying into General Foods

Corporation and Kraft Inc in 1985. R. Reynolds also diversified,

buying Nabisco and becoming RJR / Nabisco.

In 1987, congress banned smoking on all domestic flights lasting

less than 2 hours. In 1990, smoking is banned, except to Alaska and

Hawaii. In 1990, Ben & Jeery’s (of ice cream fame) boycotts RJR /

Nabisco, and dropped Oreos from its ice cream products.

During the 80’s and 90’s, the tobacco started marketing heavily

in areas outside the U.S., especially developing countries in Asia.

Marlboro is considered the world’s no.1 most valuable brand of any

product with a value over $30 billion! Over this period, there is a

battle between Coca Cola and Marlboro as the No.1 brand in the world.

31

In the recent years there is growing evidence that the tobacco

industry has known all along that cigarettes are harmful, but continue

to market and sell them. There is also evidence that they know that

nicotine was addictive and exploited this hidden knowledge to get

millions of people hooked on this dangerous habit!

Tobacco industry is an agro based industry. Tobacco is cultivated

mainly in the states of Andhra Pradesh and Karnataka most of the

tobacco is used for the manufacture of cigarettes and for exports.

Tobacco is also grown in Tamilnadu, West Bengal, Uttar Pradesh,

Gujarat, Madhya Pradesh, Maharashtra and Orissa also.

However the tobacco grown in these states is of very less quality

and is not used for manufacture of cigarettes and exports. Several

varieties of tobacco such as Virginia flue cured ,Virginia air cured

light soil burley, sun cured Virginia ,nature, chewing. Tobacco,

HDBRG, wrapper tobacco, beedi tobacco and hookah tobacco etc. are

grown in India. Virginia flue cured is a major variety grown in India.

More than 80% of Indian tobacco crop belongs to this variety.

In Virginia flue cured variety the tobacco leaves are separated

from the plant and are cured in tobacco barns. Tobacco barns are

like a furnace where the fumes are used to cure the green leaves of

tobacco plant. tobacco barns appear like small go downs with firing

chambers at the bottom fixed to the walls .the green tobacco leaves

of the plant will be arranged in the form of rows inside the

barns .the temperature inside the barn will be regulated by means of

flow of hot air through the firing chambers .

The tobacco cultivation exports and some other industrial

activities are regulated by central government (ministry of

commerce) through Tobacco board. Tobacco board is headed by I.A.S

32

officer of senior category generally from the central government.

The board consists of several central government officers, state

government officers, political leaders, representatives of farmers

and reputed industrialists. One of the directors of ML group is

always representing the industrialists in the tobacco board.

Tobacco board issues licenses to the farmers who are permitted to

grow tobacco. The licenses regulate the cultivations area the

farmers have to restrict the cultivation to the given area and must

sell the grown tobacco through tobacco board auctions only any

violation is an offence and is punishable.

This is simple technical process by which the green leaf exposed

to hot air at high temperature and cooled slowly over a period of

time. After the curing process, the primary leaf tobacco turns into

lemon yellow color, gold color, brownish yellow color, brown color and

dark brown color. This tobacco is called katcha tobacco leaf and is

ready for sale. The formers pack different colors as a separate grade

which has a separate price in the market.

Tobacco must be sold only through tobacco board auction platforms

under strict rules and regulations. Farmer or buyer is permitted to

transact in tobacco board auction platforms. Central government has

also established several tobacco research institutes for betterment of

quality of tobacco in India. The other varieties of tobacco are not

regulated by tobacco board.

The tobacco purchased from the tobacco board auction platforms

will be graded further wherever required. Grading is a process of

manual separation of one variety of leaf from the other and is done

mainly on the basis if color. Each grade will generally have unique

quality parameters.

33

The graded tobacco is further processed either manually or on

machines; this processing is called DEBUTTING and STRIPPING. Workers

separate the butt of the tobacco leaf from the leaf. This process

can also be done on machines .The machines processing is called

THRESHING.

After stripping/threshing, the tobacco will be further processed

for stabilization of moisture. And this process is called

“REDRYING”. In this process the tobacco first of all will be dried

completely then it will be given steam at the required temperature.

After redrying process the tobacco will be packed in the required

packing say bale packing /case packing etc. The packed tobacco is

ready for export. In India, the first threshing plant which is

working uninterruptedly for the last 25/30 years an imported one by

Maddi Lakshmaiah &co ltd. This was installed at Ganapavaram and the

plant is still running at high efficiency levels in the country with

98% average efficiency level for the last 3 years. There are two

plants owned by ITC which can be compared with this plant in the

country. ITC uses their threshing plants for their own consumption.

Tobacco industry is fetching more than Rs 9000 crores of revenue

to the Central Government. It is providing employment to lakh of

people directly and millions of people indirectly and is also

contributing RS 1000 corers of forex reserves to the country. The

Central Government is announcing several restrictions on

advertisement and consumption of cigarettes in the country.

Encouraging the farmers by providing subsidized fertilizers and by

supporting through tobacco board.

34

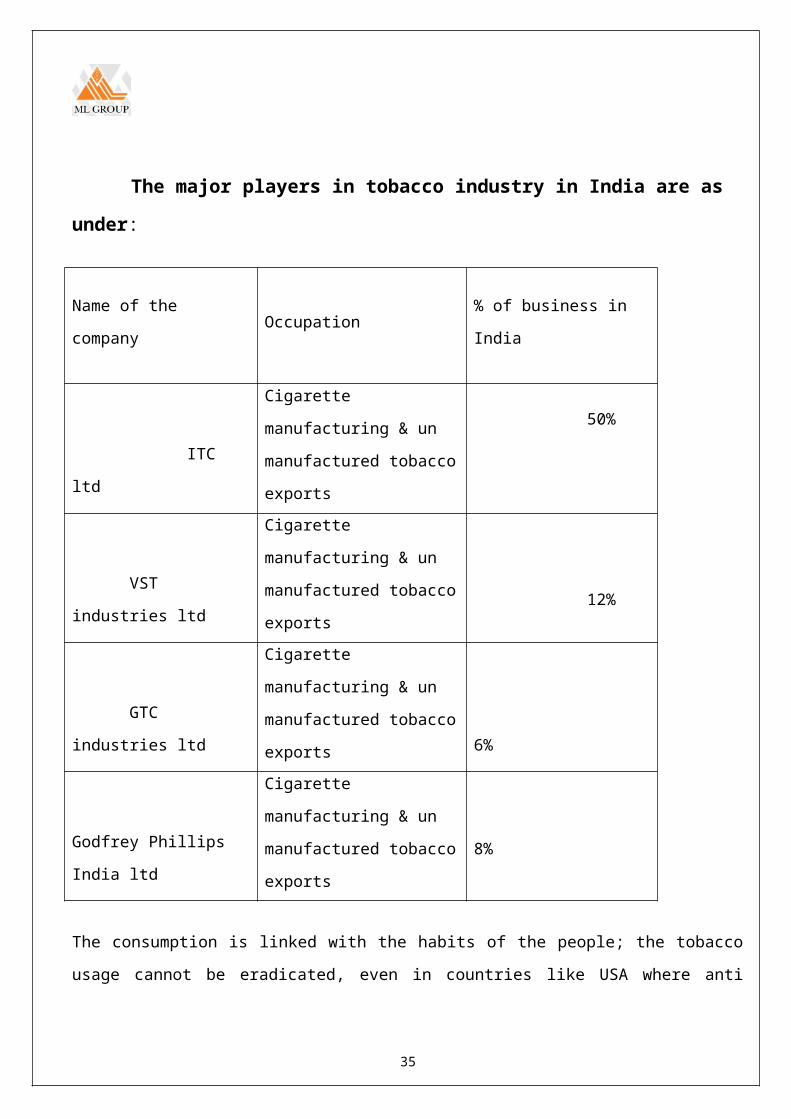

The major players in tobacco industry in India are as

under:

Name of the

companyOccupation

% of business in

India

ITC

ltd

Cigarette

manufacturing & un

manufactured tobacco

exports

50%

VST

industries ltd

Cigarette

manufacturing & un

manufactured tobacco

exports12%

GTC

industries ltd

Cigarette

manufacturing & un

manufactured tobacco

exports

6%

Godfrey Phillips

India ltd

Cigarette

manufacturing & un

manufactured tobacco

exports

8%

The consumption is linked with the habits of the people; the tobacco

usage cannot be eradicated, even in countries like USA where anti

35

tobacco campaign started in 1962, the production of cigarettes and

consumption of cigarettes is still progressing.

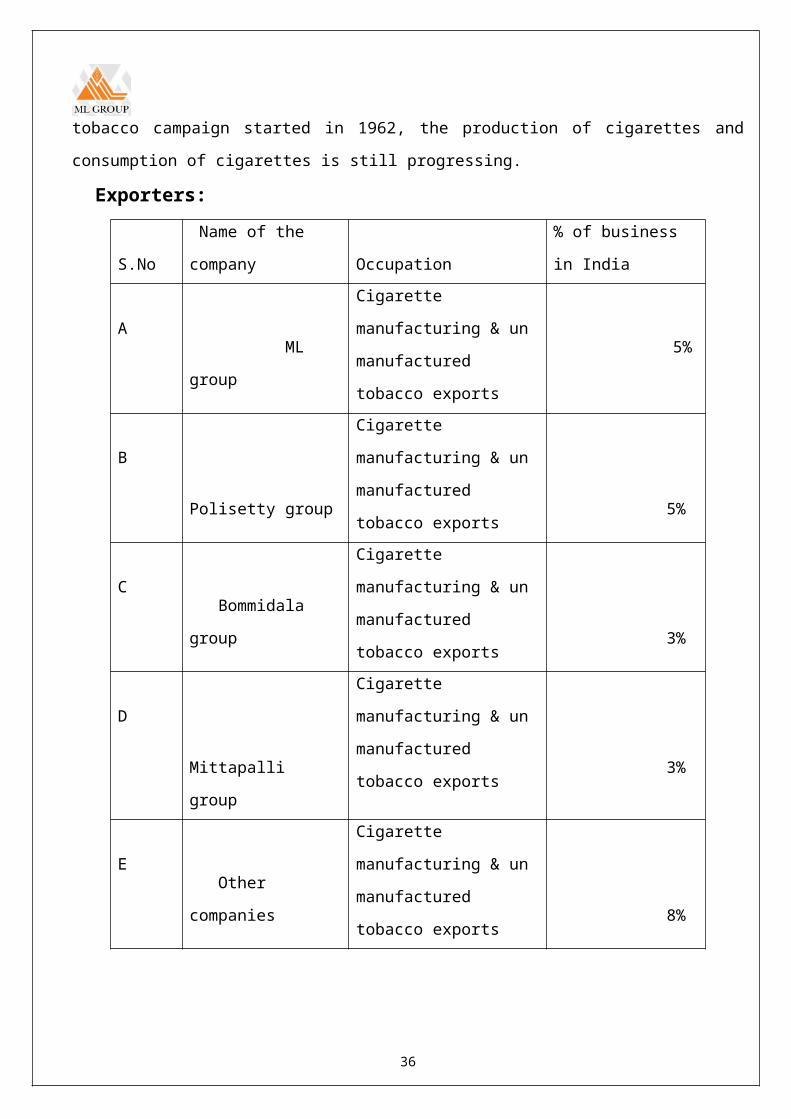

Exporters:

S.No

Name of the

company

Occupation

% of business

in India

A ML

group

Cigarette

manufacturing & un

manufactured

tobacco exports

5%

B

Polisetty group

Cigarette

manufacturing & un

manufactured

tobacco exports5%

C Bommidala

group

Cigarette

manufacturing & un

manufactured

tobacco exports3%

D

Mittapalli

group

Cigarette

manufacturing & un

manufactured

tobacco exports3%

E Other

companies

Cigarette

manufacturing & un

manufactured

tobacco exports8%

36

Our ML company has developed strong relationship with overseas

manufacturing in Europe, Russia and Middle East though there is very

good demand from Russian market. Our company is not exporting much

because of poor economic conditions of the country.

ML Company is now exporting cigarettes to Middle East and U.S.A

by manufacturing the cigarettes on job work basis. The company

foresees a very bright future for this company in tobacco in the

coming years.

ML group is the first tobacco company who exported tobacco to

China and is the first company who imported tobacco also from China.

There was imported tobacco in Indian tobacco history before this and

after till now. The group maintains good relationship with the Chinese

tobacco monopoly.

One of the trade delegates that accompanied our honorable Prime

Minister during his recent visit to China is from ML Company. Three

ambassadors of China have visited our company in the past as our

guests and expressed their satisfaction on our infrastructure

facilities.

Production of different varieties of tobacco in India: VFC Tobacco Traditional/NCOs/My

sore

200 million

VFC Tobacco HDBRG 12 millionISB Tobacco ISB

(Releswaram/Warangal)

10 million

IAS Tobacco 25 million

37

CHAPTER IV - COMPANY PROFILE

38

HISTORY:The highly competitive tobacco market represented tremendous

growth potential to Mr. Maddi Lakshmaiah. Foreseeing the and for

quality Indian tobacco a long term strategy was formulated. Right from

its inception, the company adhered to international standards and made

rapid in roads to global tobacco markets.

A sophisticated threshing plant of international standards was

commissioned in 1976 first in Andhra Pradesh. It created a revolution

in tobacco processing and led to a huge upsurge in demand. This led to

the commissioning of two modern plants with threshers, redryers and

other sophisticated equipment for the processing of quality tobacco.

ML Group has taken its credo of total quality to the furthest,

whether in the quality of process, products or working conditions for

the vast workforce. The foresighted innovation of Sri Maddi Lakshmaiah

has given the group strong edge. The personal involvement of the

directors in all aspects of the business has resulted in high quality

operational parameters.

The company can proudly claim some of the most skilled work force

and a highly efficient management people who have contributed

significantly to the prominent position the company. The company has

earned recognition from apex institutions and is a recognized leader

in tobacco markets the world over.

The quantum growth in ML Co: Spread of investment in infra

structure and diversification into other business.

“ML GROUP” under its umbrella, various companies have an annul

turnover of Rs 1550 million and an asset base of Rs 2000 million. A

real estate development wing was setup to develop and lease commercial

39

properties with working environment that rival the best

internationally.

The information about the establishment of the group which

consists of five concerns as displayed on the preceding pages, let us

have a look on the various concerns of ML Group individually:

ML group of companies (ML group) was founded by Mr.Maddi

Lakshmaiah in 1970. He joined in his family business in 1952 after

completing his engineering degree. The joint family business started

payback in 1943 dealing with tobacco exports, well before India.

ML group of companies (ML group), a pioneer in Indian un

manufactured tobacco industry has been exporting tobacco to all over

the world for the past three decades. It has solidified its

relationship with overseas tobacco merchants& manufactures.

Maddi Lakshmaiah & Co Ltd, was set up at Chilakaluripet, a

village in Andhra Pradesh that produces some of the best tobacco in

the country. Today it has evolved into a diversified, multi products

conglomerate known as ML Group that is recognised world over for its

excellence. The company processes tobacco and another agro based

products that are used both in the country and exported to the most

quality conscious world markets.

An emphasis on total quality and dedication to the interests of

its client’s world wide is a hallmark of ML group. The group is

performing excellently well from the date of its incorporation and

has been exporting large volume of tobacco to Russia, CIS countries,

U.K, Europe, African countries, China, Latin American countries,

Middle East countries, Bangladesh & Nepal etc. The group established

its branches in Russia & European countries and has strong tie up

40

with African and Latin American countries and especially with the

neighbour giant China.

The group is founded by Sri Maddi Lakshmaiah, a mechanical

engineer after 15 years of versatile experience in tobacco industry

in 1970 at Chilakaluripet , Günter dist, A.P .the group has 5 major

concern namely;

Maddi Lakshmaiah & Co Ltd (MLCO)

ML Agro Products (MLAP)

K.S Subbaiah Pillai & co ltd (KSSP)

ML Exports (MLE)

Coromandal Agro Products & Oils Ltd (CAPOL)

Expecting CAPOL which is engaged in edible oils all are engaged

in tobacco industry. MLCO & MLAP have concentrated on processing

activities where as KSSP&MLE are leading exporters and are

recognised by government of India as export house.

Vision: Descriptions of some thing can organization corporate culture,

business technology an activity in the future.

The company is trying to develop world class information

technology building in Bangalore, china and Hyderabad in the

coming 5 years time.

The company is going for sheet tobacco plant in joint venture

with on of the Indian best tobacco cigarette manufacturer.

The company is also contemplating for 100% tobacco joint venture

association with one of the best cigarette manufacturer.

The company exports with second strongest country china, Russia

and Germany.

41

The ambassadors are coming to Maddi Lakshmaiah Company limited in

August.

The ambassadors of South Africa are hold up and the company is

having top joint venture with U.K.

Mission:A mission statement is an enduring statement of purpose that

distinguishes one business from others similar firms. This statement

identifies the scope of firms operations in product and market terms.

M.L & company limited mission is to produce good quality of

tobacco and get number one position in India in producing and

exporting tobacco.

Policies:Policies can be considered a guide to action it is desirable that

persons responsible for implementation of policies use discretion and

judgment in appraising and deciding among alternative courses of

action.

The company has well defined policies for exports the quality

tobacco.

To conduct its operation with honesty integrity and

transpoarency.

Employment policy is formulation and adoption.

This company shall maintain quality leadership by providing

products and services that completely and consistently meet the

agreed.

Requirements of all customs and unsure fitness for use of all

products there by ensuring total confidence to every customer.

42

Employment policy formulation and adoption.

Canteen, cleaning, security maintenance of good industrial

relation.

Future plans:- The company (Maddi Lakshmaiah) for an ECB for 50 million

dollars and development of regular trade and also

infrastructure projects in India.

Maddi Lakshmaiah Company is also working on joint venture basis

with UK based Commodities Company for supply of agri products

to South Asian countries.

The company already entered into joint venture with an US based

company by name CARGIL for the south Indian needs.

They have worked for joint venture arrangements with

Yugoslavian government for their requirement for India.

This for above five million dollars of investment in supply of

5000 tonnes every year.

Achievements / awards:- Maddi Lakshmaiah Company has no particular achievements/ awards.

Maddi Lakshmaiah group (CAPOL Chirala, Prakasam Dist ) got

several achievement awards .

All India Cotton Feed Crushers Association, Mumbai awarded CAPOL

as III highest exporter and II highest domestic seller of cotton

seed extraction for the year 1992-93.

43

CAPOL is the highest exporter and III highest domestic set of

cotton seed extraction for the year 1993-94.

CAPOL is the III highest domestic seller of cotton seed

extraction in the year 1994-95.

CAPOL is the II highest domestic seller of cotton seed extraction

in the year 1995-96.

CAPOL is the II highest domestic seller of cotton seed extraction

in the year 1997-98

CAPOL is the III highest domestic seller of cotton seed

extraction for the year 1999-2000.

CAPOL is the II highest extraction of cotton linter for the year

2000-01.

CAPOL is the III highest exporter of cotton linter and III

highest domestic seller of cotton seed extraction for the year

2001-02.

The company (CAPOL) has been awarded may commendation led by

government of AP for its continuous harmonious relations with its

employees in the years 1994,95,96,97.

Track record:- The company has 30 years of performance.

It never failed in meeting the scheduled repayments of loans with

the bank. Rather it postponed most of the loans with the lenders.

LAND MARKS:- Maddi Lakshmaiah Company was the first Indian company to join

with China to do business.

It was the first company to import tobacco and export tobacco.

44

Ambassadors have already come here and 4th one is coming in this

august.

NEGOTIATIONS:- The company is trying to develop world class information

technology building in Bangalore, Chennai and Hyderabad in the

coming five years time

The company is going for sheet tobacco plant in joint venture

with one of the Indian best tobacco cigarette manufacture.

The company is also contemplating for 100% tobacco joint venture

in association with one of the best cigarette manufacture.

The company exports with the second strongest country china,

Russia and India.

The finance manager is assisted by a team of experienced

management and non management staff who takes care of finance &

accounts activities of the organisation.

The export manager (ML Company) deals all the matters regarding

the exports department and directly reports to the managing

director.

ML group was a multifaceted corporate leader of which the

group consists of five concerns namely.

Maddi Lakshmaiah and Co Ltd - Tobacco threshers, packers &

exporters, real estate &leasing.

ML Agro Products - Tobacco threshers, packers &exporters.

KS Subbaiah Pillai & Co (India) ltd - Tobacco export.

ML Exports. - Exports house.

45

Coromandal Agro Products & Oils ltd. - Bulk producers of oils.

Maddi Lakshmaiah & Co Ltd:-ML & company Limited, the fore runner of all the companies of ML

group, the company enjoys a pre eminent standing in the world of

tobacco, exporting to China, Russia, Western Europe, Africa and

Bangladesh among others.

Supported by a team of experts, technicians, engineering and a

skilled world –force, the company has forged a head setting standards

that have become benchmarks in the industry. Today Chilakaluripet is a

well known name in the global tobacco business in no little measure

due to the pioneering efforts of the intrepid founder, Sri Maddi

Lakshmaiah.

ML AGRO PRODUCTS LTD:-ML agro products ltd was born of a increase in demand for quality

tobacco in both the domestic and foreign markets. Building on the rich

experience of running a profitable operation, a new plant was set up

in 1976 at Martur, Prakasam district.

It is fully self sufficient with modern threshers, lamina

redryers, automatic double ram press, sophisticated quality control

laboratory and mammoth ware houses. It ranks among the largest

threshing units in the country apart from its export commitments.

KS Subbiah Pillai & Co (India) ltd:

46

K.S.S.P & Co Ltd was acquired in 1982 with all its

assets K.S Subbaiah Pillai & Co (India) Ltd is the group with leading

tobacco exporting unit. In a field that is extremely competitive, the

excellent performance of the company is an indicator of the trust that

it enjoys across the globe.

COROMANDAL AGRO PRODUCTS & OILS LTD (CAPOL):CAPOL started in 1976, extracts and refines cotton seed oil.

Today it is a multi products company with equipment to process all

kinds of oil seeds. The plant has a storage capacity of 2100 tones for

different types of oil.

Extreme care is taken to ensure that at every stage in the

process of production right from selection of the raw material to

packing the products, only the best is passed.

Minimum human intervention and rigorous application of quality

control process ensures the final product conform to all appropriate

standards. The by-products, hulls and de-oil cakes are in high demand

in many parts of the world.

ML EXPORTS: ML exports is a totally export oriented unit, with clients in a

variety of markets around the world. The company enjoys a reputation

for excellent delivery schedules and transparent business practice in

global markets.

SHARE HOLDING PATTERN & MANAGEMENT OF GROUP:The group has been successfully improving its business in all of

its activities such as domestic sales, export sales, tobacco

processing & other tobacco development activities, warehousing

47

facilities etc. The group has two tobacco processing plants and one

solvent extraction plant in South India. The group owns around 1,

00,000 sq. mts of warehousing complexes in south India.

INCORPORTATION:ML Company is a limited company (m/s Maddi Lakshmaiah and Company

Limited) which was originally incorporated on 8th day of October 1970

under the name, Maddi Lakshmaiah and Company Private Limited having

passed the necessary special resolution on the 23rd day of March 2002,

in terms of Sec 31(1)/44 of the Companies Act 1956 the name of the

company changed to Maddi Lakshmaiah and Company Limited.

NATURE OF ACTIVITY:o This factory produces good quality tobacco.

o The production capacity per each day is 1 lakh 20 tones

FINANCIAL STRUCTURE;The initial investment of ML Company is 10, 00,000.

TURN OVER OF THE GROUP:The turn over of the group for the financial year 1989-99

standards is at around Rs 800 million. The net earnings after taxes of

the group have been maintained at Rs 150/200 million per annum.

The group has sound assets base having assets spread in most of

the prime centres & ports of South India.

The group has developed excellent infrastructure during the

past 30 years which has been yielding a promising regular income of

more than Rs 225 million every year.

The products of the M.L Company &their main uses:

48

The various products of the MLCompany and their economic uses are

as follows.

Karnataka light soil-Mysore:This tobacco is preferred for low nicotine content, high filling

capacity and suitability to blend well with any tobacco.

Monsoon burley:Used in U.S. blended cigarettes

Traditional burley:Used for pipe mixture, chewing plugs and hookah tobacco paste.

Kurnool and Telangana (natu):Primarily used for cigarette blending and for hookah tobacco

paste making.

Eluru (natu tobacco):Mainly used for cheroots, snuff pipe tobacco, cigarette blending

and for hookah paste making.

Oriental: Used for cigarette blending.

Century fire cured tobacco:Used in pipe mixtures and hookah tobacco paste

Bidi tobacco:Used in the manufacture of bidis, a hand rolled smoking products

made by wrapping tobacco with natured bony leaves.

Cigar wrapper tobacco:

Mainly used for wrapping the cigars.

49

Cigar filler tobacco:Mainly used in the manufacture of cigars &exported to some

countries for use in hookah tobacco paste.

Cheroot tobacco:Used for the manufacture of cheroots and hookah tobacco paste.

Lanka tobacco: Used for the manufacture of cigars & cheroots

Tamilnadu:

Used for chewing & cheroot.

Red Chopadia:Mostly used for chewing also called lat Chopadia and safna. The

export packing ranges from 250gms-1000gms and is available in bales of

up to 100kg.

Rustic tobacco: Used as chewing tobacco, hookah tobacco for tobacco sheet

making, for kreteks in Indonesia, pipe mixers& cigarette blending to

some extent

Motihari: Used in manufacture of various tobacco products such aschewing tobacco, hookah paste, bidis etc.

Northern light soil (nls):This tobacco is flavoured to semi flavoured with excellent ageing

properties.

50

Objectives of the company: To serve the nation’s vital interest in the tobacco related

sectors.

To earn a reasonable return on investment.

To work towards achievement of self reliance in the field of

tobacco, threshing formulation& distribution system.

To create strong research& development in the field of tobacco

and stimulate R&D of exports.

To maximise utilisation of the existing facilities in order to

improve efficient and increased productivity.

To import training, conduct seminars, workshops and

educational courses on computers, computer maintenance

software development and software exports and to develop and

design software in India.

Abroad and to start software technology part in India or

abroad and to offer relationship management solutions for

individuals and organisations both individually and through

strategic alliances with others companies.

To employ experts to investigate and examine into the

conditions, prospects, value character and circumstance of any

business concern and undertaking and generally of any assets

property or right.

51

To carry on all kinds of agency business.

To carry on business as merchants in all kinds of goods.

BOARD OF DIRECTORS:Managing Director : Sri Maddi Lakshmaiah

Director : Sri Maddi Seetha Devi

Director : Sri Maddi Venkateswara Rao (M.B.A in USA)

Director : Sri Maddi Ramesh

Excutive Director : Sri Mallavarapu Rama Mohana Rao

Excutive Director : Sri Meaden Sekhar

MANAGEMENT TEAM:Managing Director : M. Venkateswara Rao

Director : M. Lakshmaiah

General Director : M. Rama Mohana Rao

Personnel Manager : B. Babu Rao

Leaf Manager : M. Rama Mohana Rao

Finance Manager : M. Shekhar

Export Manager : M. Shekhar

Production Manager : K.S. Rami Reddy

Circle Manager : Anji Babu

Factory coordinator : P. Subba Rao

52

ORGANIZATION STRUCTURE: The company (ML Company) is under the complete administrative control

of the managing director and he is reported by the director and he is

reported by general manager.

The General Manager (ML Company) is assisted by five

General Managers.

o Manager personnel.

o Manager leaf department.

o Manger finance.

o Manager exports.

o Manager production.

53

54

Managing DirectorDeputy Managing DirectorGeneral Managing DirectorPersonnel ManagerPersonnel officerWelfare officerSafty officerStaffLeaf ManagerFinancial ManagerAccouns OfficerStaffExport ManagerExport OfficerProduction ManagerPlant EngineerAssist. EngineerStaff workers

Responsibilities:The M.L Company managing director M.Venkateswara Rao is under the

complete administrative control of the managing direction and he is

reported by the director and he is reported by general manager

The general manager of ML Company is M. Ram Mohan Rao assisted by

fine general manager i.e., personal manager, leaf manager or

department manager, finance manager, exports manager and production

manager.

The personal department manager B. Babu Rao is headed by who

reports directly to G.M. he looks after the areas of personnel &

administration under there may be a personal offices welfare officer

and a safely officer.

The finance manager M.Shekhar is assisted by a team of

experienced management and non management staff who tekes care of the

finance is accounts activities of the organization.

The export manager M.Shakhar deals all the matters regarding the

export departments and directly reports to managing director.

The production manager K.S.Rami Reddy is headed by the G.M. is

assisted by a plant engineer and staff of the production department.

FUNCTIONS OF THE COMPANY: The group has the following different departments.

PERSONNEL DEPARTMENT:This department deals with the matters of industrial relations,

HRD, welfare activities, labour legislations, recruitment and issues

of wages etc. which is the main department in the organisation.

LEAF DEPARTMENT:

55

This department deals with the matters of tobacco leaf. It looks

after buying tobacco from the farmers for the processing of tobacco.

EXPORT DEPARTMENT:It looks after the export matters of the organisation. This

organisation exports tobacco leaf to China, Bangladesh & UK.

PRODUCTION DEPARTMENT: This department takes care to produce quality tobacco to

customers.

MARKETING DEPARTMENT:This department takes care of marketing the company tobacco to

other countries such as Russia, Europe, Middle East, Bangladesh,

African countries etc. They sell varieties of tobacco in market and maintain goodrelationship with the customers. This is one of the main/important

departments in this organization.

M.L group was concentrating on domestic market.

It ties up with Indian strongest cigarette manufacturing company,

ITC.

Methods:-In ML Company the methods of purchasing tobacco is of various types

i.e.

With tenders raised in market, documents will be filled up by

various companies or merchants can purchase them.

They have good contacts with various merchants (mediators between

manufacture & exporters) in reputed companies at Guntur.

56

Every year they are procuring 1000 tonnes of various varieties

/grades of tobacco.

They usually do their business with the international reputed

companies like.

o Universal

o Dimon

o Standard commercial

The company have some direct contacts with other

countries and they directly ask them at the time of requirement.

Marketing channels:- Normally they send samples/verities.

At the time of requirement, they send samples through couriers.

Participating in exhibitions- every year ML Company was taking

participation in 5-6 exhibitions.

The people who have connection in tobacco visit tobacco stalls

usually, even from Europe, Russia & china.

People like manufactures, dealers, bankers, merchants of tobacco

may visit the tobacco exhibitions.

They display the samples of the company and sell the samples.

Another mode:-The other mode of marketing (channel) is through business

delegations of Tobacco Board of Central government, Ministry of

Commerce. Government. of India, Guntur. The tobacco board usually:

Regularize crop.

Register of foreigners. Fixing the crop size.

57

The board explore marketing possibilities with the help of

exporters.

Another type of business mode is tobacco trade delegations from

different countries (usually every year 5-6 delegations may takes

place).

The tobacco delegations meet exporters and inspect all the

tobacco.

They get the business through reputation.

Customers usually approach them because of the good will of

the company.

Mode of payment:- Exporters normally receive payment from their buyers through

L.C’S (letters of credit).

Some time through advance payment ion terms of D.A&D.P.

o Document against payment

o Document against acceptance.

After customers checkers in the Madras port it may send to

abroad.

Shipment of tobacco is through Chennai port only.

At the same time shipment of tobacco the pay/buyers send payment

to bank in the company’s account.

Credit:- Some parties ask/need some time for payment with in certain

period from the date of bill of payment (up to 180 days).

In India there is a rule that on credit basis, the payment must

be done with in 180 days from the date.

Market range:-

58

ML Company was marketing 7-10 million kilos of tobacco every year.

But the market range is not fixed. The market range depends on supply

&demand forces.

When there is demand, the company produces more.

In the tobacco field, the marketing/market range may be flexible

based on international supply -demand.

FINANCE DEPARTMENT: In this department

Cash payments will be checked by cashiers.

Cash bills and credit bills may be received from trashing factory

and engineering department.

Concerned accounts may be generalized by the accountants and may

be sent to concerned heads.

Credit bills payment will be given in the form of cheque’s or DD’s

CHAPTER V

DATA ANALYSIS & INTERPRETATIONS

59

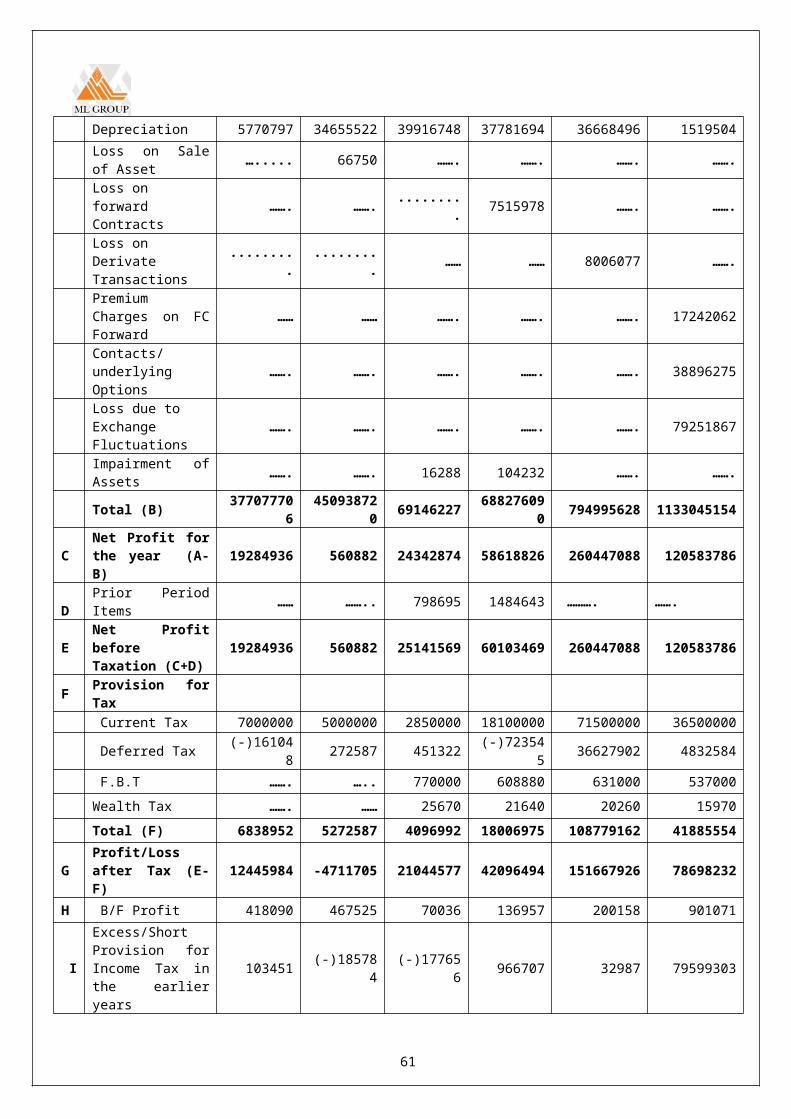

TABLE No. :1 PROFIT & LOSS ACCOUNTS

SL.No

DESCRIPTIONACTUALS

2008-09 2009-10 20010-11 2011-12 2012-13 2013-14

A Income Sales 13177274

5 96695127 255762587

257993866 280678564 588655944

Threshing & Re-drying Charges

64895977 122756852

121348304

102639420 147816539 126595125

Exchange Fluctuation Gain

……. ……. ……. 14388067 30583174 …….

Profit on Forward Contacts

……. ……. ……. ……. ……. 12986303

Other Income 41145403 54219836 45775357 60206090 143913688 52984780Licence fee &Amenities fromIT Park

……. ……. 65001628 90007058 136987132 145331345

Closing Stock 158548517

177827787

227917226

221660415 315463618 327075443

Total (A) 396362642

451499602

715805102

746894916 1055442716 1253628940

B Expenditure

Opening Stock 124793176

158548517

177827787

227917226 221660415 315463618

Purchases 155880478

111121750

280314175

211640666 336888367 441026464

Manufacturing& TradingExpenses

47914280 74069521 92767953 100518972 85887573 97948079

AdministrativeExp. 20353905 25796364 32312207 34106300 42886670 46204417

SellingExpenses 1073226 1676574 2533525 1045901 2069214 3941191

Rent onBuilding &Machinery

4608518 3762398 8217482 5450732 6928277 6692952

Repairs toBuilding 2449847 6772217 8774221 13061646 17310485 38314867

Interest &Bank Charges 14233479 34469107 40357291 49132743 36690054 46543858

60

Depreciation 5770797 34655522 39916748 37781694 36668496 1519504Loss on Saleof Asset …..... 66750 ……. ……. ……. …….

Loss on forward Contracts

……. ……. ......... 7515978 ……. …….

Loss on Derivate Transactions

.........

......... …… …… 8006077 …….

PremiumCharges on FCForward

…… …… ……. ……. ……. 17242062

Contacts/underlyingOptions

……. ……. ……. ……. ……. 38896275

Loss due to ExchangeFluctuations

……. ……. ……. ……. ……. 79251867

Impairment ofAssets ……. ……. 16288 104232 ……. …….

Total (B) 377077706

450938720 69146227 68827609

0 794995628 1133045154

CNet Profit forthe year (A-B)

19284936 560882 24342874 58618826 260447088 120583786

DPrior PeriodItems …… …….. 798695 1484643 ………. …….

ENet ProfitbeforeTaxation (C+D)

19284936 560882 25141569 60103469 260447088 120583786

F Provision forTax Current Tax 7000000 5000000 2850000 18100000 71500000 36500000

Deferred Tax (-)161048 272587 451322 (-)72354

5 36627902 4832584

F.B.T ……. ….. 770000 608880 631000 537000Wealth Tax ……. …… 25670 21640 20260 15970Total (F) 6838952 5272587 4096992 18006975 108779162 41885554

GProfit/Lossafter Tax (E-F)

12445984 -4711705 21044577 42096494 151667926 78698232

H B/F Profit 418090 467525 70036 136957 200158 901071

I

Excess/ShortProvision forIncome Tax inthe earlieryears

103451 (-)185784

(-)177656 966707 32987 79599303

61

JTransferred toGeneralReserve

12500000 ……. 20800000 43000000 151000000 79000000

KTransferred from General Reserve

…… 4500000 ……. …… ….. ……

L

Balance ProfitCarried toBalance Sheet(G+H+I-J+K)

467525 70036 136957 200158 901071 599303

62

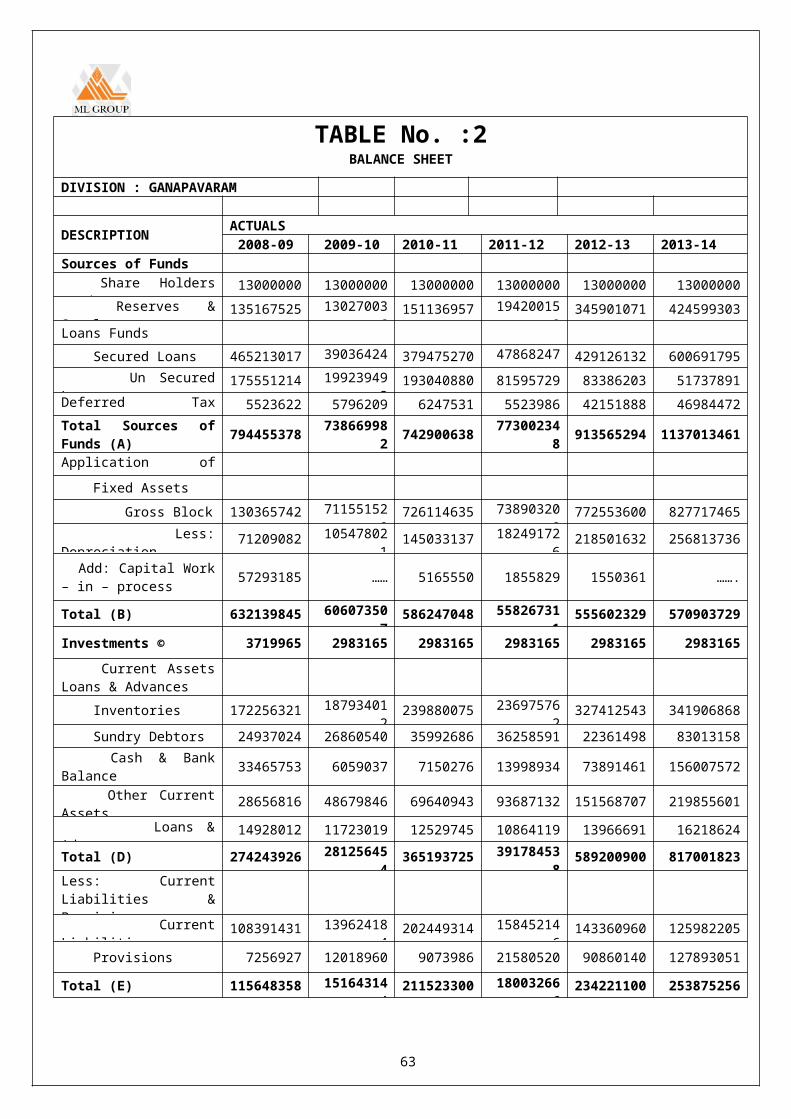

TABLE No. :2BALANCE SHEET

DIVISION : GANAPAVARAM

DESCRIPTION ACTUALS2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Sources of Funds Share HoldersFunds

13000000 13000000 13000000 13000000 13000000 13000000 Reserves &Surplus

135167525 130270036

151136957 194200158

345901071 424599303Loans Funds Secured Loans 465213017 39036424

4379475270 47868247

5429126132 600691795

Un SecuredLoans

175551214 199239493

193040880 81595729 83386203 51737891Deferred TaxLiability

5523622 5796209 6247531 5523986 42151888 46984472Total Sources ofFunds (A) 794455378 73866998

2 742900638 773002348 913565294 1137013461

Application ofFunds Fixed Assets Gross Block 130365742 71155152

8726114635 73890320

8772553600 827717465

Less:Depreciation

71209082 105478021

145033137 182491726

218501632 256813736

Add: Capital Work– in – process 57293185 …… 5165550 1855829 1550361 …….

Total (B) 632139845 606073507

586247048 558267311

555602329 570903729

Investments © 3719965 2983165 2983165 2983165 2983165 2983165 Current AssetsLoans & Advances Inventories 172256321 18793401

2239880075 23697576

2327412543 341906868

Sundry Debtors 24937024 26860540 35992686 36258591 22361498 83013158 Cash & BankBalance 33465753 6059037 7150276 13998934 73891461 156007572

Other CurrentAssets

28656816 48679846 69640943 93687132 151568707 219855601 Loans &Advances

14928012 11723019 12529745 10864119 13966691 16218624

Total (D) 274243926 281256454

365193725 391784538

589200900 817001823Less: CurrentLiabilities &Provisions CurrentLiabilities

108391431 139624184

202449314 158452146

143360960 125982205

Provisions 7256927 12018960 9073986 21580520 90860140 127893051

Total (E) 115648358 151643144

211523300 180032666

234221100 253875256

63

Total Applicationof Funds (B+C+D-E) 794455378 73866998

2 742900638 773002348 913565294 1137013461

64

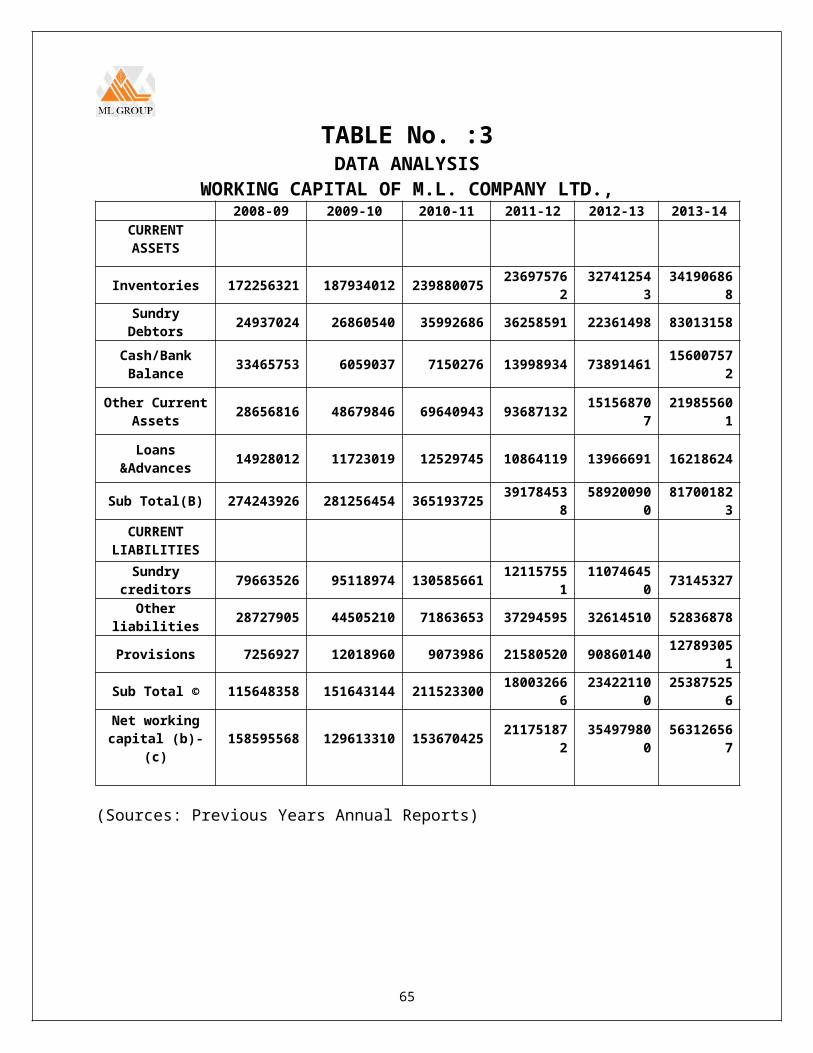

TABLE No. :3DATA ANALYSIS

WORKING CAPITAL OF M.L. COMPANY LTD.,2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

CURRENTASSETS

Inventories 172256321 187934012 239880075 236975762

327412543

341906868

SundryDebtors 24937024 26860540 35992686 36258591 22361498 83013158

Cash/BankBalance 33465753 6059037 7150276 13998934 73891461 15600757

2

Other CurrentAssets 28656816 48679846 69640943 93687132 15156870

721985560

1

Loans&Advances 14928012 11723019 12529745 10864119 13966691 16218624

Sub Total(B) 274243926 281256454 365193725 391784538

589200900

817001823

CURRENTLIABILITIES

Sundrycreditors 79663526 95118974 130585661 12115755

111074645

0 73145327

Otherliabilities 28727905 44505210 71863653 37294595 32614510 52836878

Provisions 7256927 12018960 9073986 21580520 90860140 127893051

Sub Total © 115648358 151643144 211523300 180032666

234221100

253875256

Net workingcapital (b)-

(c)158595568 129613310 153670425 21175187

235497980

056312656

7

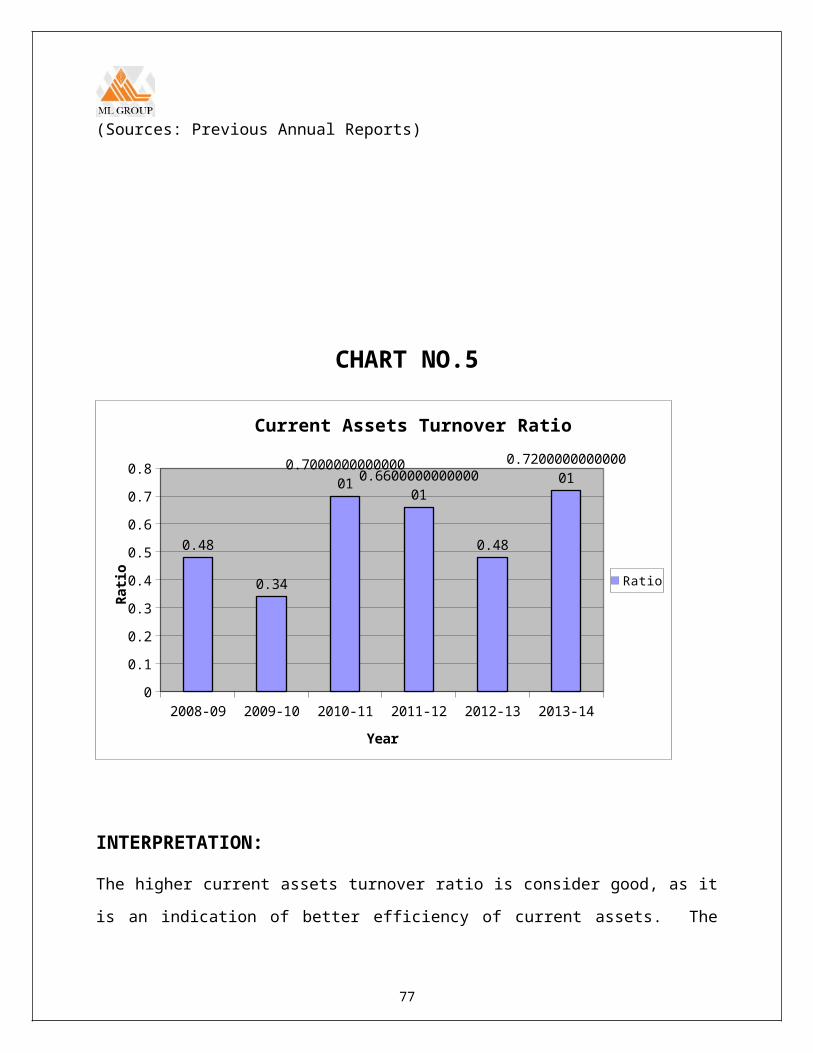

(Sources: Previous Years Annual Reports)

65

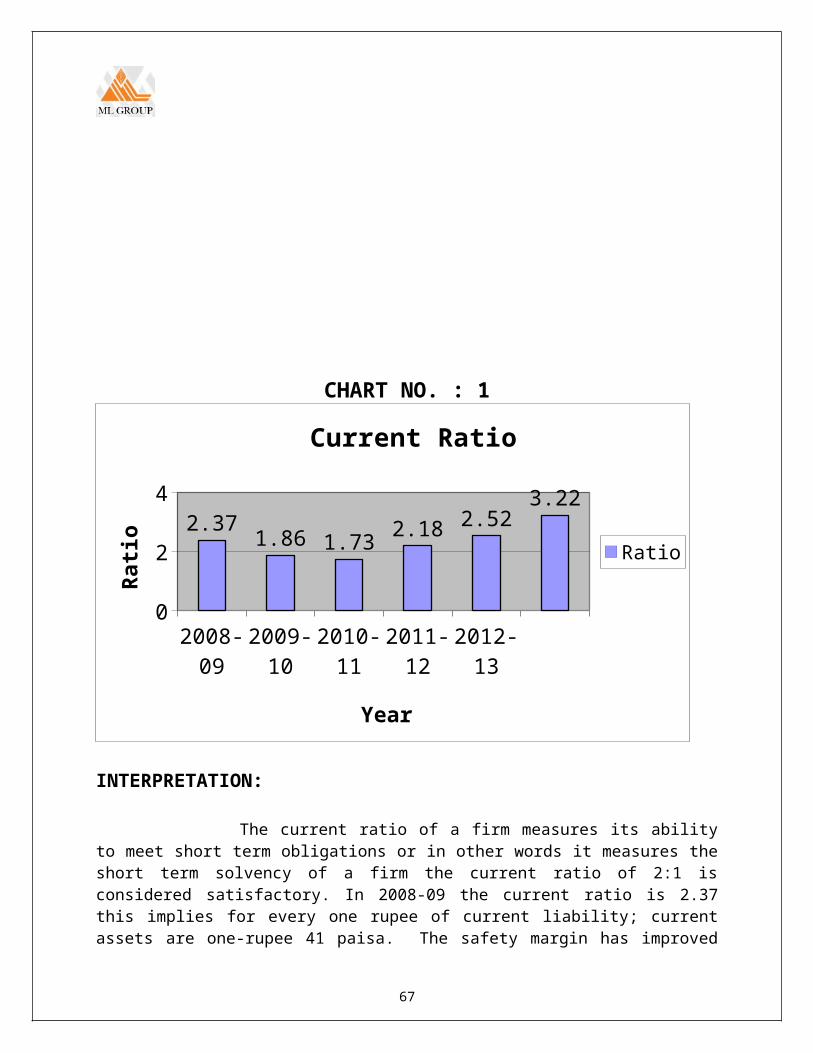

RATIO ANALYSISTABLE No. : 4CURRENT RATIO

Year Currentassets

Currentliabilities Ratio

2008-09 274243926 115648358 2.37

2009-10 281256454 151643144 1.86

2010-11 365193725 211523300 1.73

2011-12 391784538 180032666 2.18

2012-13 589200900 234221100 2.52

2013-14 817001823 253875256 3.22

(Sources: Previous years Annual Reports)

66

CHART NO. : 1

2008-09

2009-10

2010-11

2011-12

2012-13

0

2

42.37 1.86 1.73 2.18 2.52

3.22

Current Ratio

Ratio

Year

Rati

o

INTERPRETATION:

The current ratio of a firm measures its abilityto meet short term obligations or in other words it measures theshort term solvency of a firm the current ratio of 2:1 isconsidered satisfactory. In 2008-09 the current ratio is 2.37this implies for every one rupee of current liability; currentassets are one-rupee 41 paisa. The safety margin has improved

67

over the previous years. In 2009-10 the current ratio decreedover 2008; the current ratio is less than the standard i.e 1.86this implies that for every one rupee of current liability and isless than the previous year

In 2010-11 the current ratio is less than thestandard i.e 1.73; this implies that for every one rupee ofcurrent liability and is less than the previous year. In 2011-12the current ratio is more than the standard i.e 2.18; thisimplies that for every one rupee of current liability and is morethan the previous year. It is a good sing of the company that itis more then the safe margin of solvency.

It is a good sign of the company in 2012-13 thecurrent ratio is more than the standard i.e 2.52; this impliesthat for every one rupee of current liability and is more thanthe previous year. It is a good sign of the company in 2013-14the current ratio is more than the standard i.e 3.22; thisimplies that for every one rupee of current liability and is morethan the previous year it is a good sing of the company that itis more then the safe margin of solvency.

TABLE No. : 5QUICK RATIO

Year Quick assets CurrentLiabilities Ratio

2008-09 101987605 115648358 0.88

68

2009-10 93322442 151643144 0.62

2010-11 125313650 211523300 0.59

2011-12 154808776 180032666 0.86

2012-13 261788357 234221100 1.12

2013-14 475094955 253875256 1.87

(Sources : Previous Years Annual Reports)

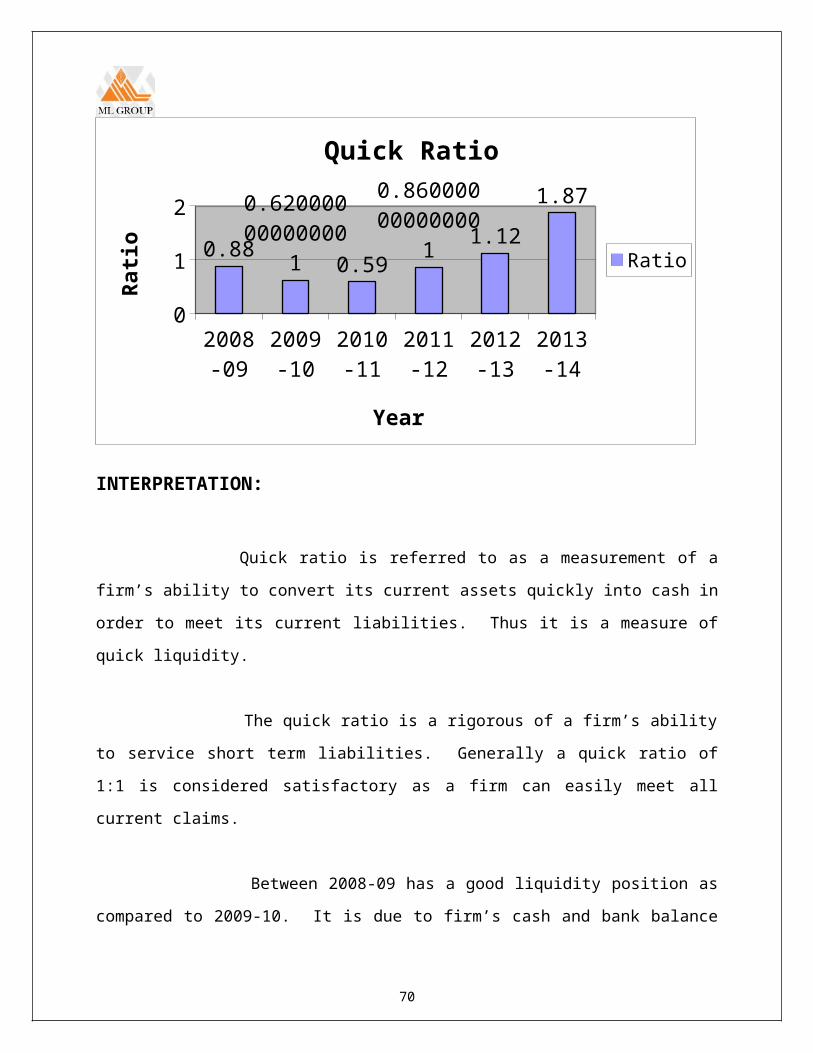

CHART NO. : 2

69

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

0

1

20.88

0.62000000000000

1 0.59

0.86000000000000

1 1.121.87

Quick Ratio

Ratio

Year

Rati

o

INTERPRETATION:

Quick ratio is referred to as a measurement of a

firm’s ability to convert its current assets quickly into cash in

order to meet its current liabilities. Thus it is a measure of

quick liquidity.

The quick ratio is a rigorous of a firm’s ability

to service short term liabilities. Generally a quick ratio of

1:1 is considered satisfactory as a firm can easily meet all

current claims.

Between 2008-09 has a good liquidity position as

compared to 2009-10. It is due to firm’s cash and bank balance

70

and good receivables management. In 2009-10, company allowed

credit sales in order to expand its sales volume and also the

purchase of the inventory is more as compared to previous year.

It is effect fell on successive year. In 2010-11 the liquidity

position is decreased when compared to 2008-00. In 2011-12 the

liquidity position is increased when compared to 2010-11. In

2012-13, and 2013-14 the quick ratio of the company is

satisfactory i.e. 1.1 which is nearer to the standard.

TURNOVER RATIOTABLE No. : 6

INVENTORY TURNOVER RATIO

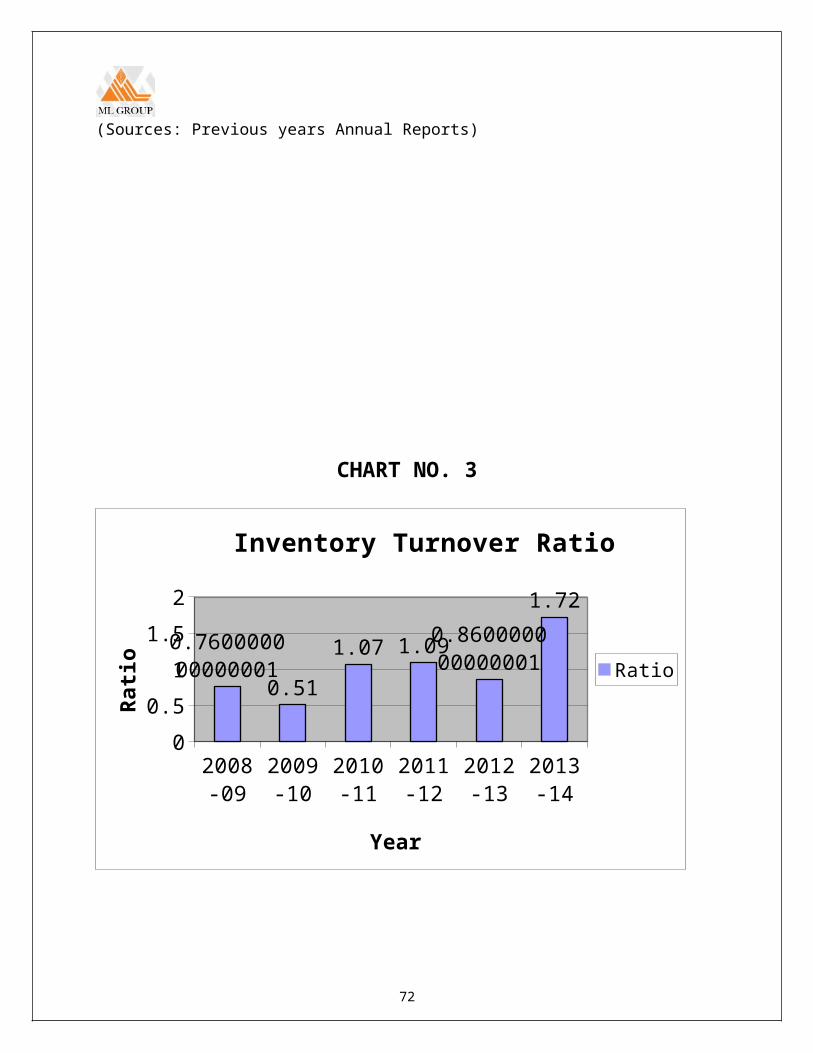

Year Turnover Inventory Ratio

2008-09 131772745 172256321 0.76

2009-10 96695127 187934012 0.51

2010-11 255762587 239880075 1.07

2011-12 257993866 236975762 1.09

2012-13 280678564 327412543 0.86

2013-14 588655944 341906868 1.72

71

(Sources: Previous years Annual Reports)

CHART NO. 3

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

00.5

11.5

2

0.760000000000001

0.511.07 1.090.860000000000001

1.72

Inventory Turnover Ratio

Ratio

Year

Rati

o

72

INTERPRETATION:

The inventory turnover ratio measures how quickly the

inventory is sold. It is a test of efficient inventory

management. In general, a high inventory is better than a low

ratio. A high ratio implies good inventory management.

In 2014 stock are converted into liquid more fatly when

compared to the successive years 2008, 2009, 2010, 2011, 2012,

2013. It shows effective inventory management. In the year

2008-09 there has been decreased in the inventory turnover ratio.

In these year inventory has not been told sold fast. In 2012 the

inventory turnover ratio is high when compared to 2010-11. Here

the inventory value is reduced in 2008-09 inventory turnover

ratio decreased when compared of 2009-10. In 2013-14 the company

maintain high inventory turnover ratio.

TABLE No. : 7

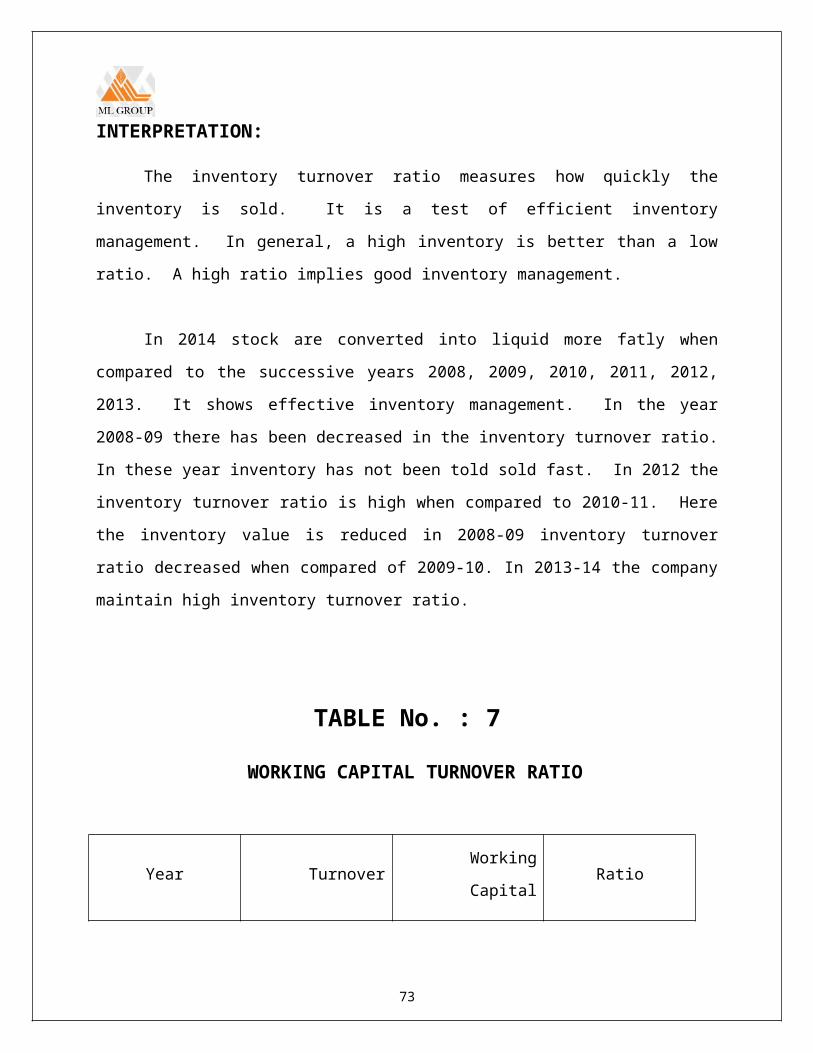

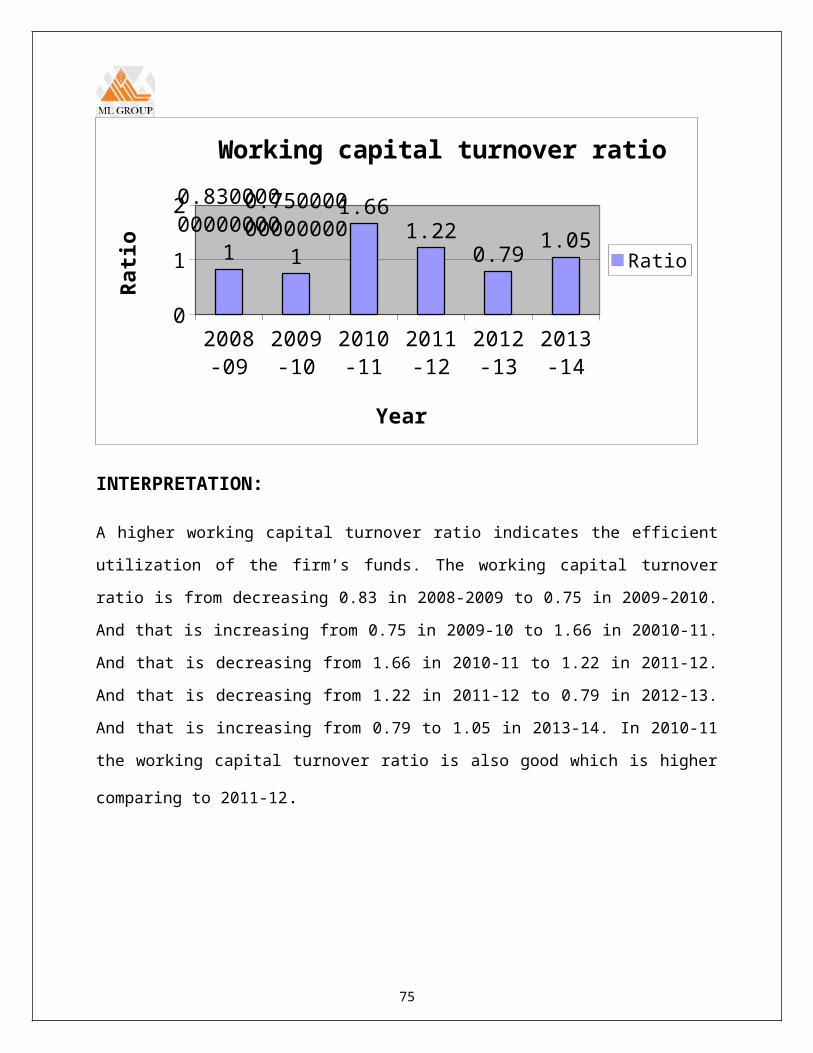

WORKING CAPITAL TURNOVER RATIO

Year TurnoverWorking

CapitalRatio

73

2008-09 131772745 158595568 0.83

2009-10 96695127 129613310 0.75

2010-11 255762587 153670425 1.66

2011-12 257993866 211751872 1.22

2012-13 280678564 354979800 0.79