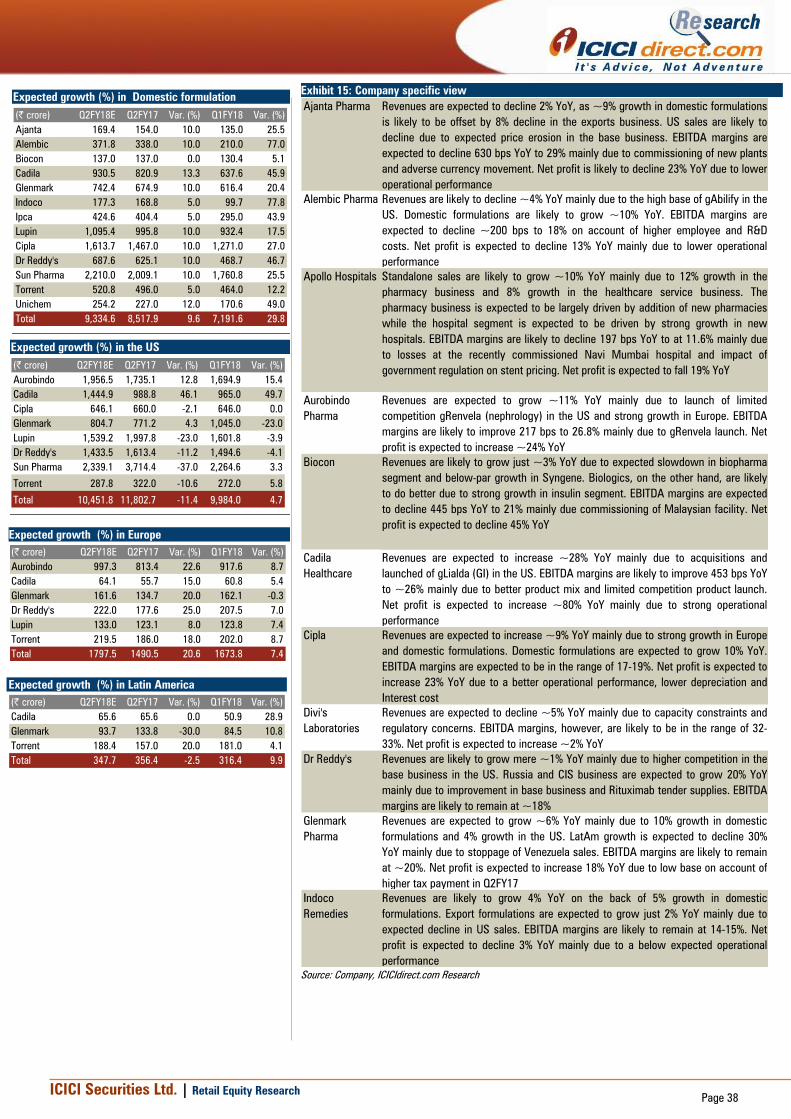

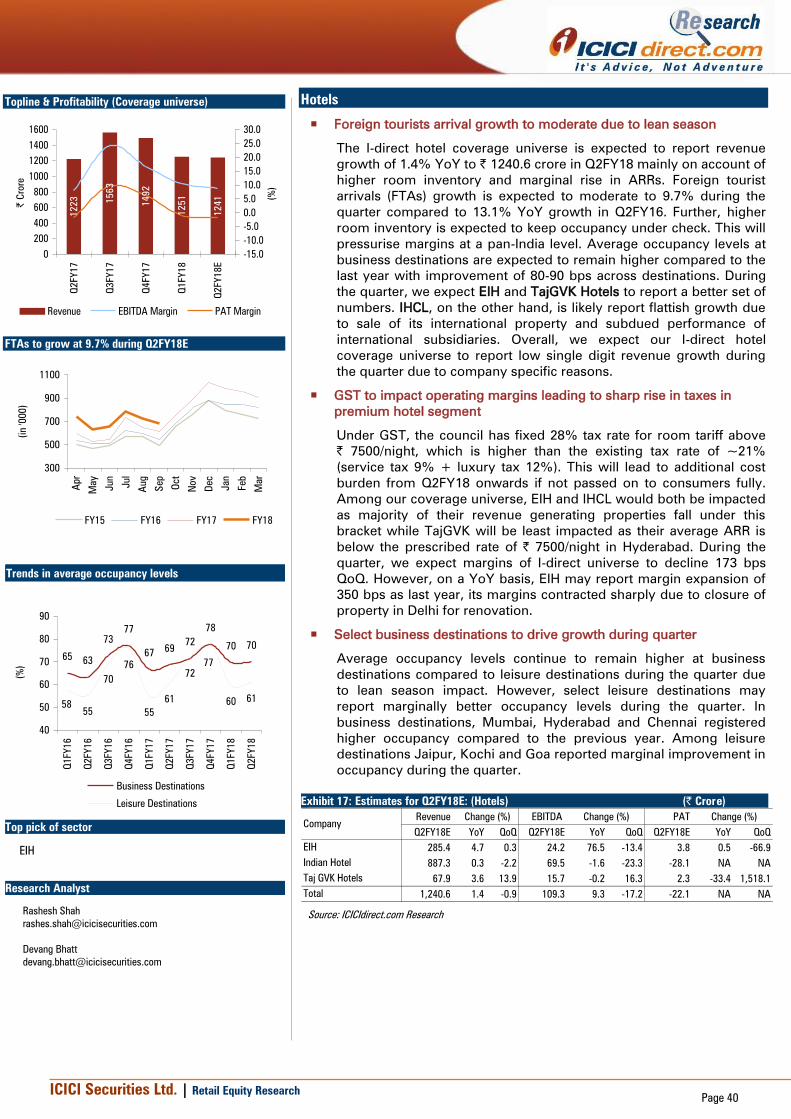

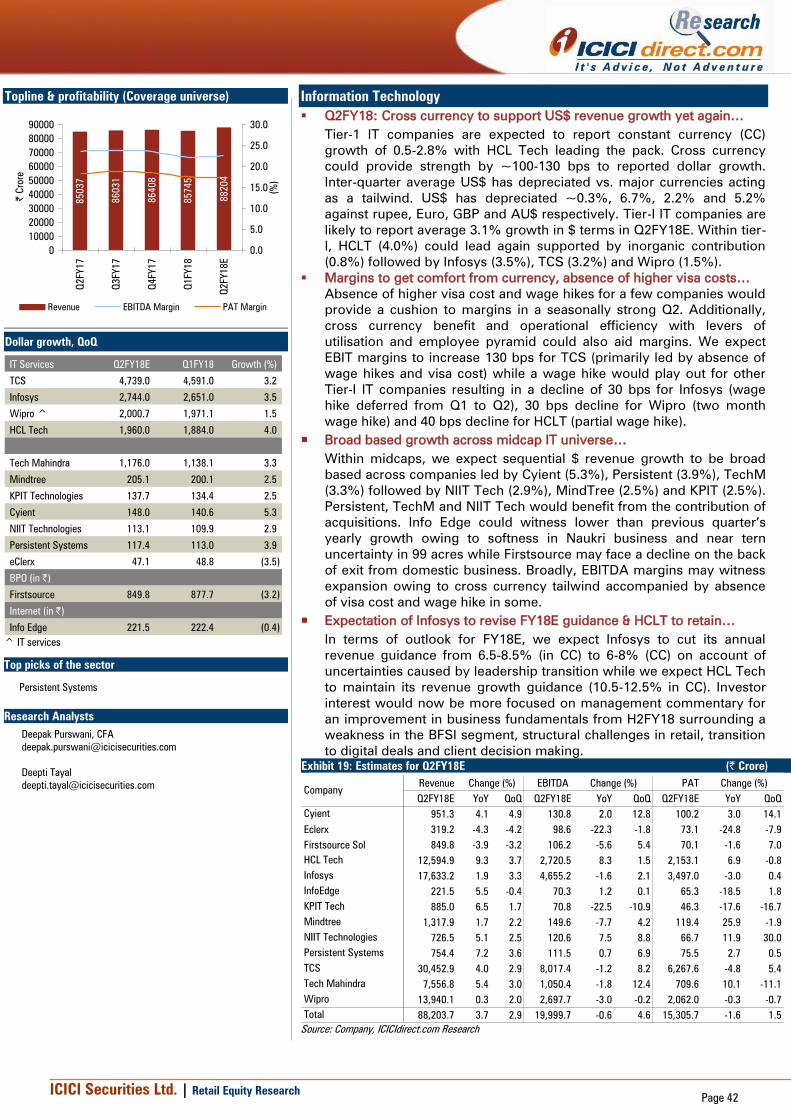

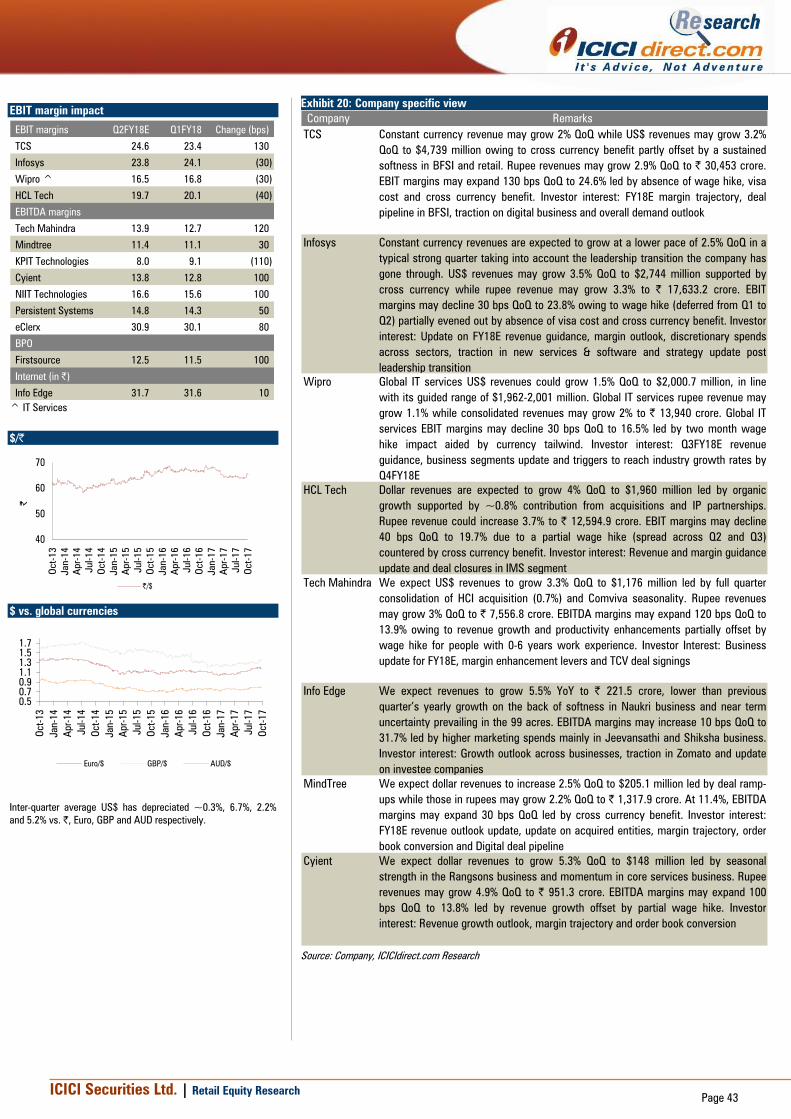

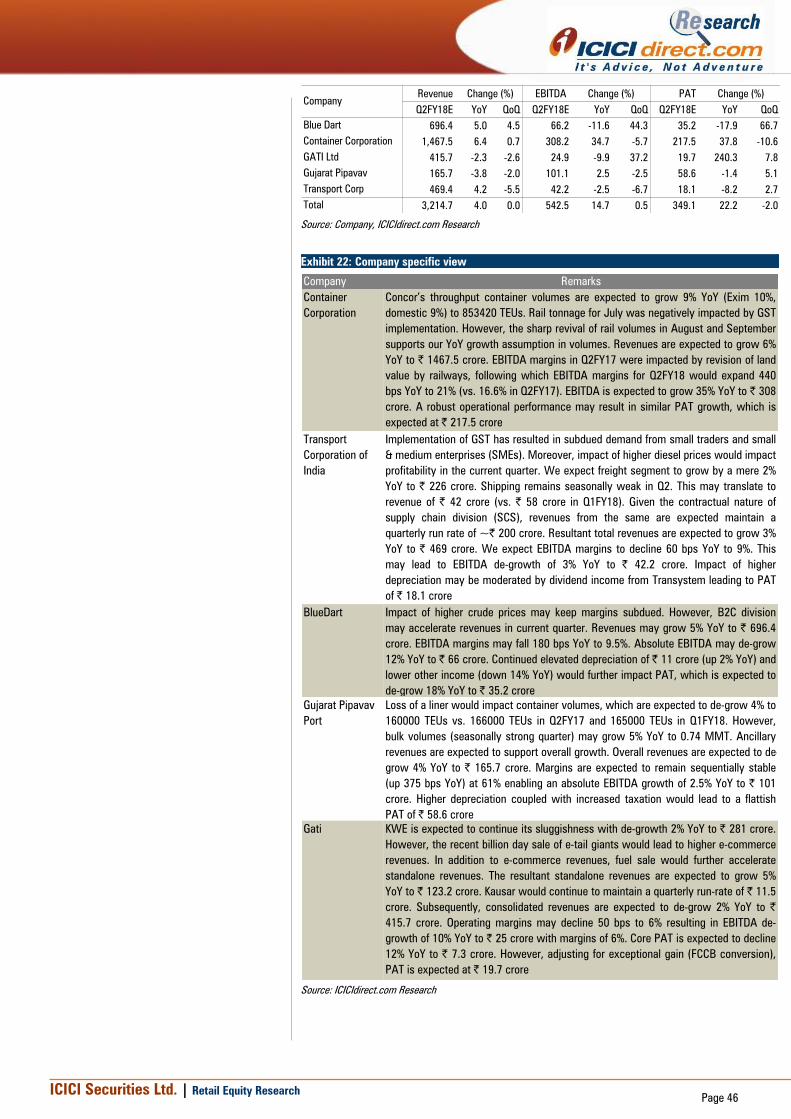

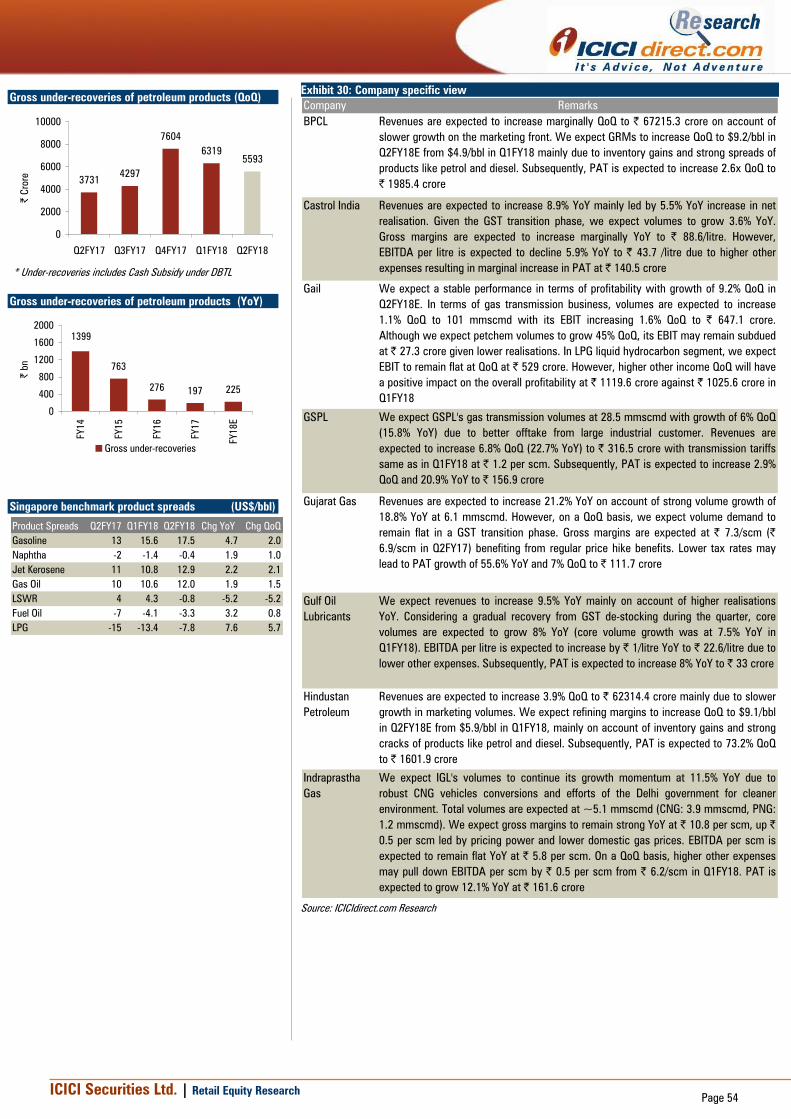

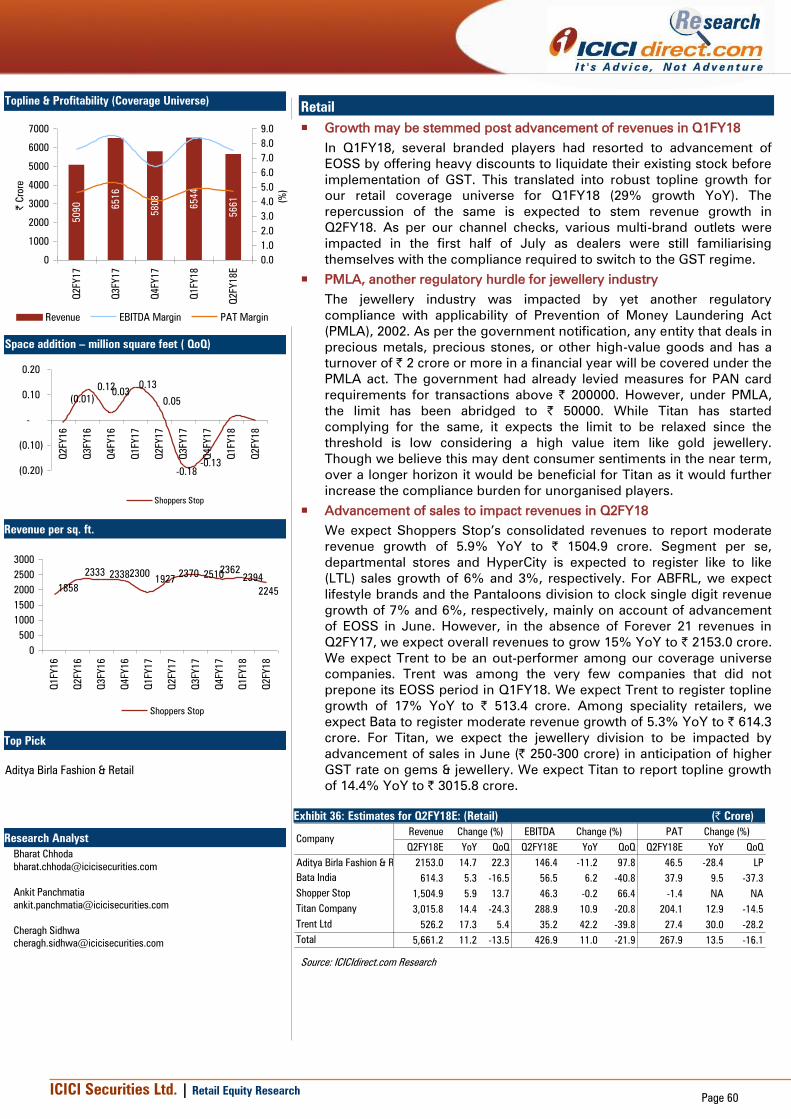

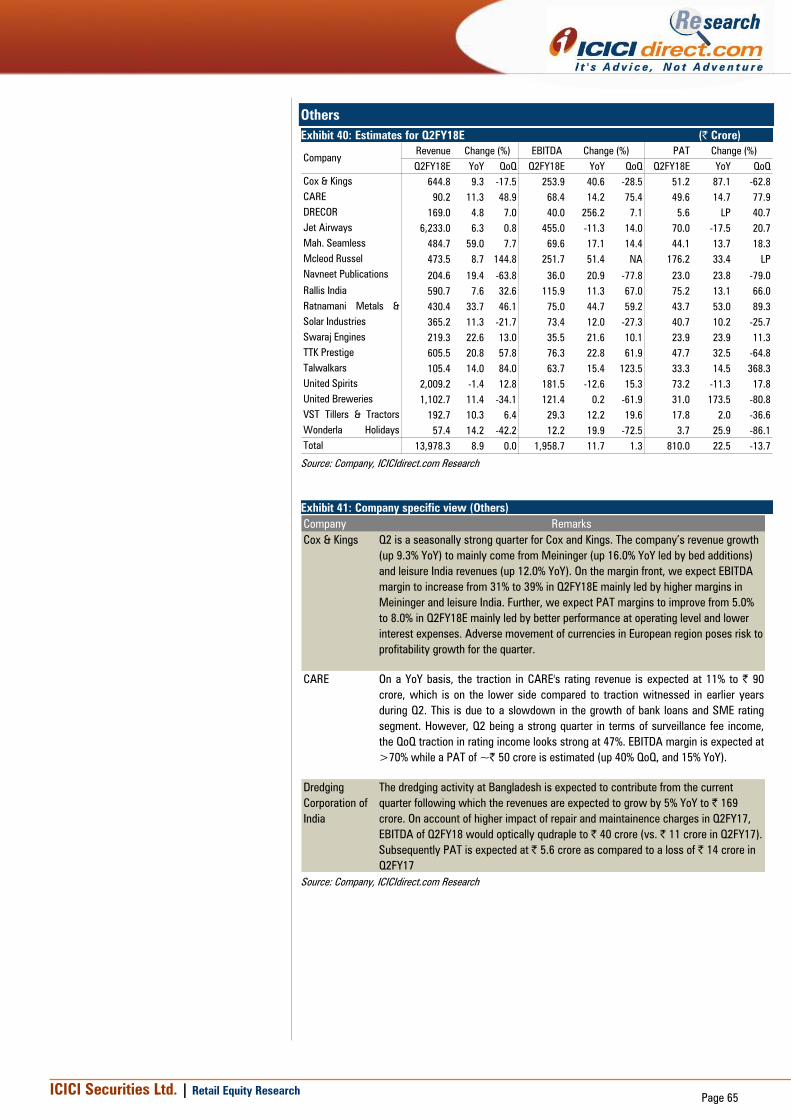

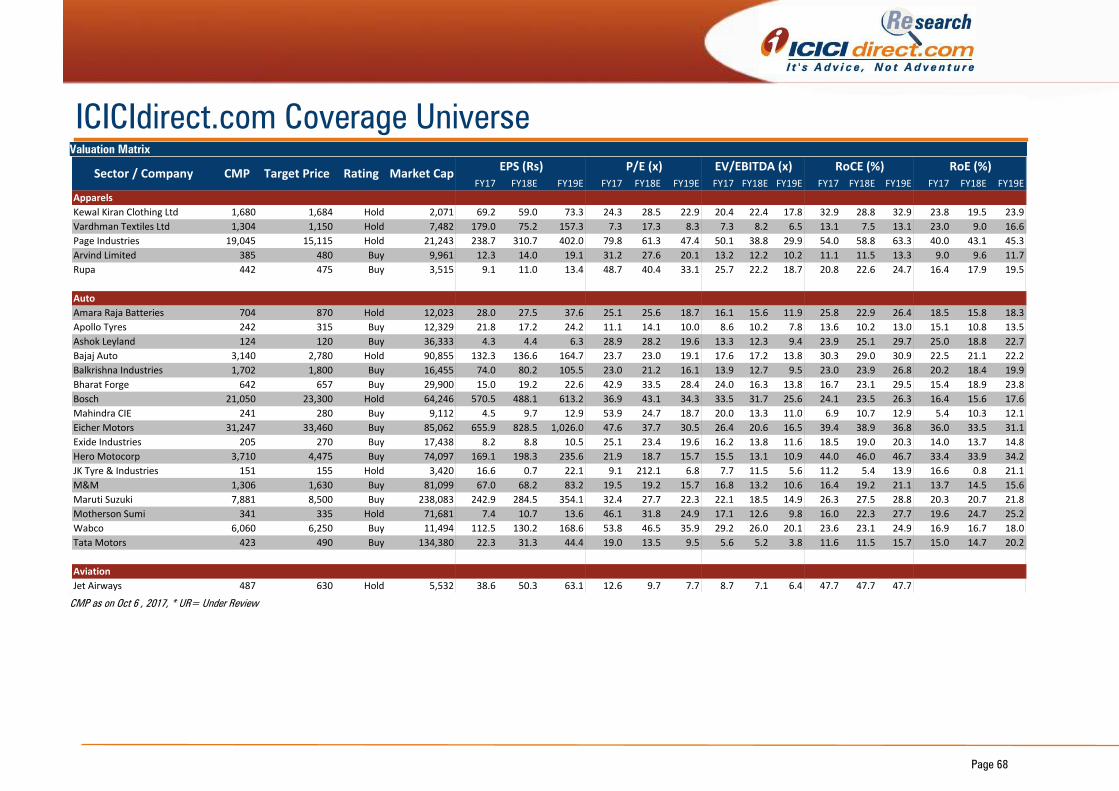

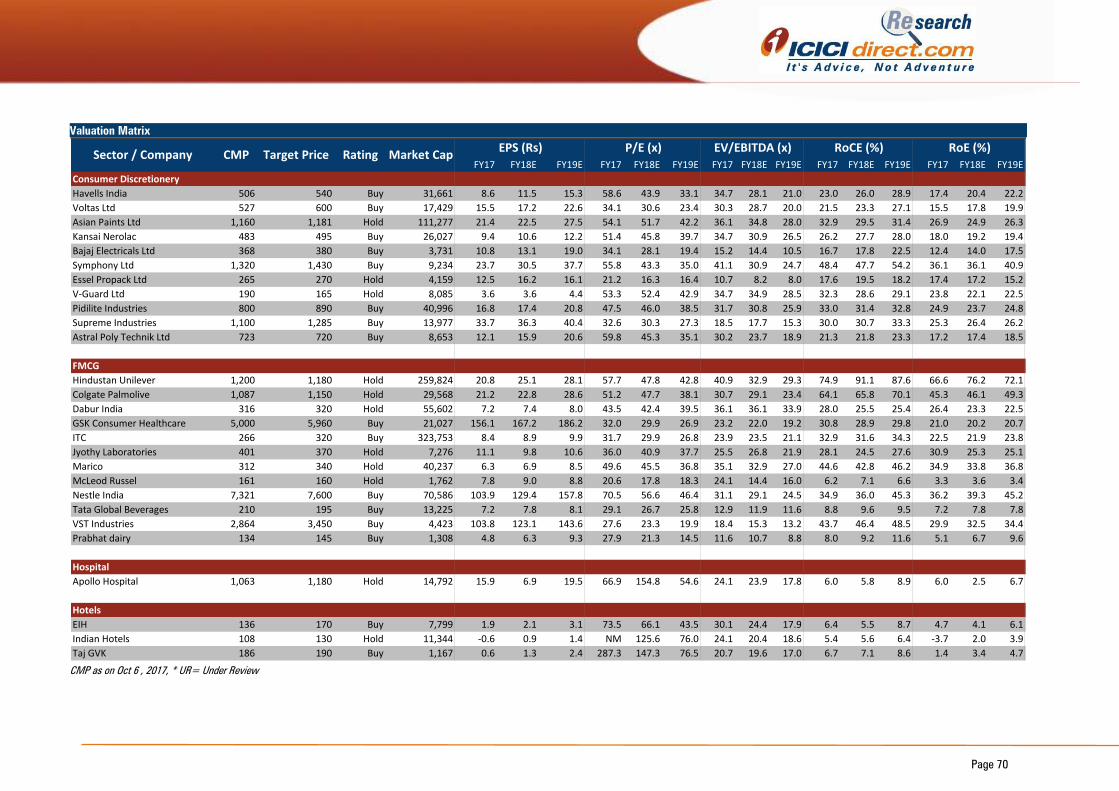

nifty highlights - icici direct

TRANSCRIPT

ICICI Securities Ltd. | Retail Equity Research

October 6, 2017

Q2FY18 Result Preview

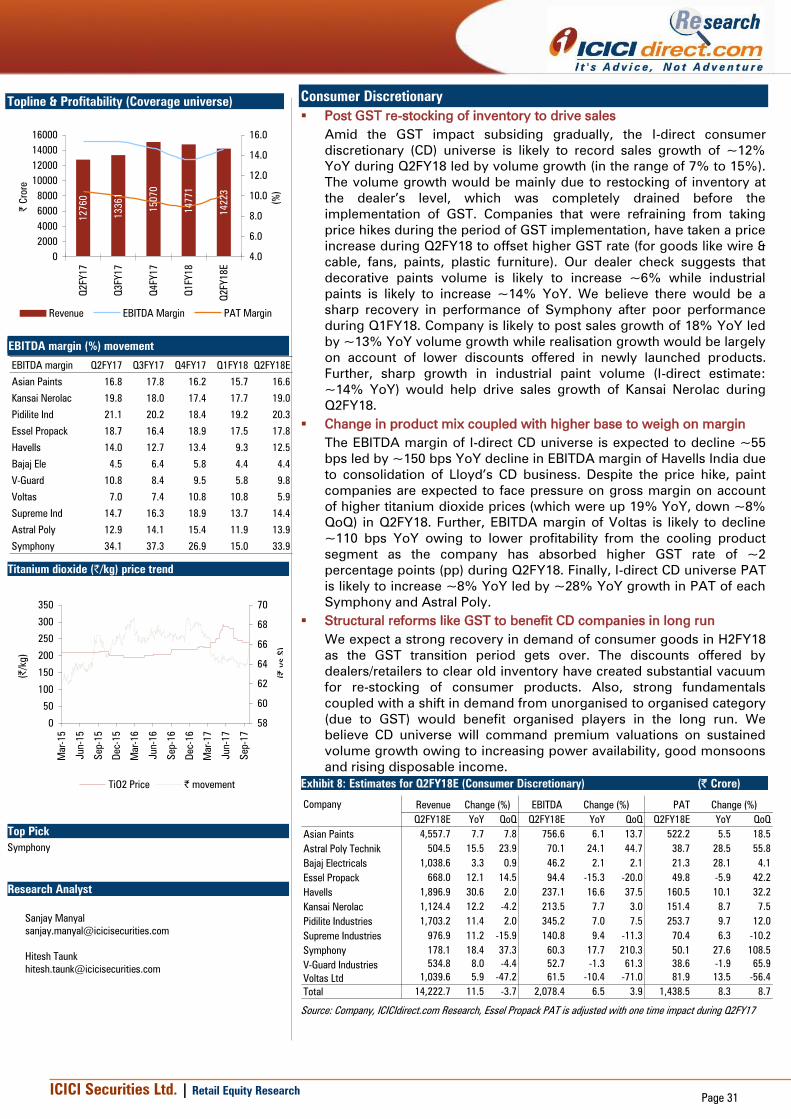

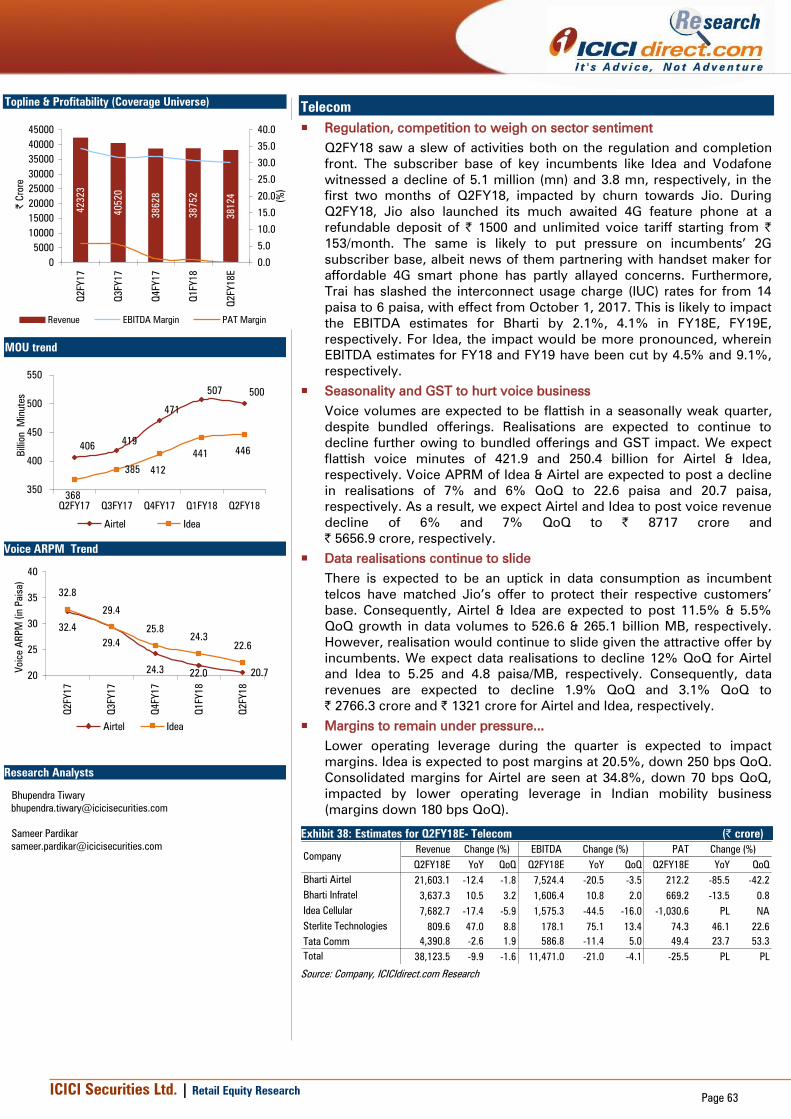

Robust topline growth shaking off GST jitters…

The last three quarters were interspersed with one-time structural

events of demonetisation and GST implementation, which led to

subdued topline growth for sectors characterised by long supply

chains. However, contrary to the expectation of GST putting brakes on

the structural story of strong domestic consumption led growth, post

implementation, Q2FY18E is expected to witness strong topline growth

of 8.8% YoY (ex BFSI and oil & gas) with most sectors warding off the

GST jitters. Re-stocking post GST is expected to accentuate the growth

in this festivity laden quarter

Consumer driven sectors like FMCG & consumer discretionary that

witnessed muted business activity in Q1FY8 amid de-stocking of

channel inventory are expected to exhibit a growth revival in Q2FY18

on account of re-stocking and price revision in items like cigarette, fans,

cables, etc, due to change in tax slab post GST implementation.

Another beneficiary of re-stocking was auto and ancillary that witnessed

strong double digit volume growth of ~12% (vs. 7% in Q1FY18) across

sub-segments (except 3-W). Major sectors like oil & gas and metal &

mining will benefit from higher commodity prices. They may prove to

be key contributors in the topline growth of our coverage universe

However, certain export driven sectors, viz. pharma & IT have been

witnessing a slowdown in business in recent quarters. The same trend

is expected in Q2FY18E. While the IT sector is facing an uncertain

demand environment due to emerging technologies & protectionist

measures across regions, the pharma space is experiencing acute

pricing pressure in US, albeit domestic pharma has experienced

recovery post GST. The telecom sector also continues to witness steep

pricing led competition, leading to sharp decline in financials

The I-direct coverage (ex-BFSI and oil & gas) is likely to witness revenue

growth of 8.8% YoY, primarily driven by sectors like metals & mining

(+20.9% YoY), auto & ancillary (+13.2% YoY) and FMCG (+7.8% YoY).

Operating margins (ex-BFSI and oil & gas) may contract 18 bps YoY to

19.9% while earnings are expected to grow 6.7% YoY. We expect

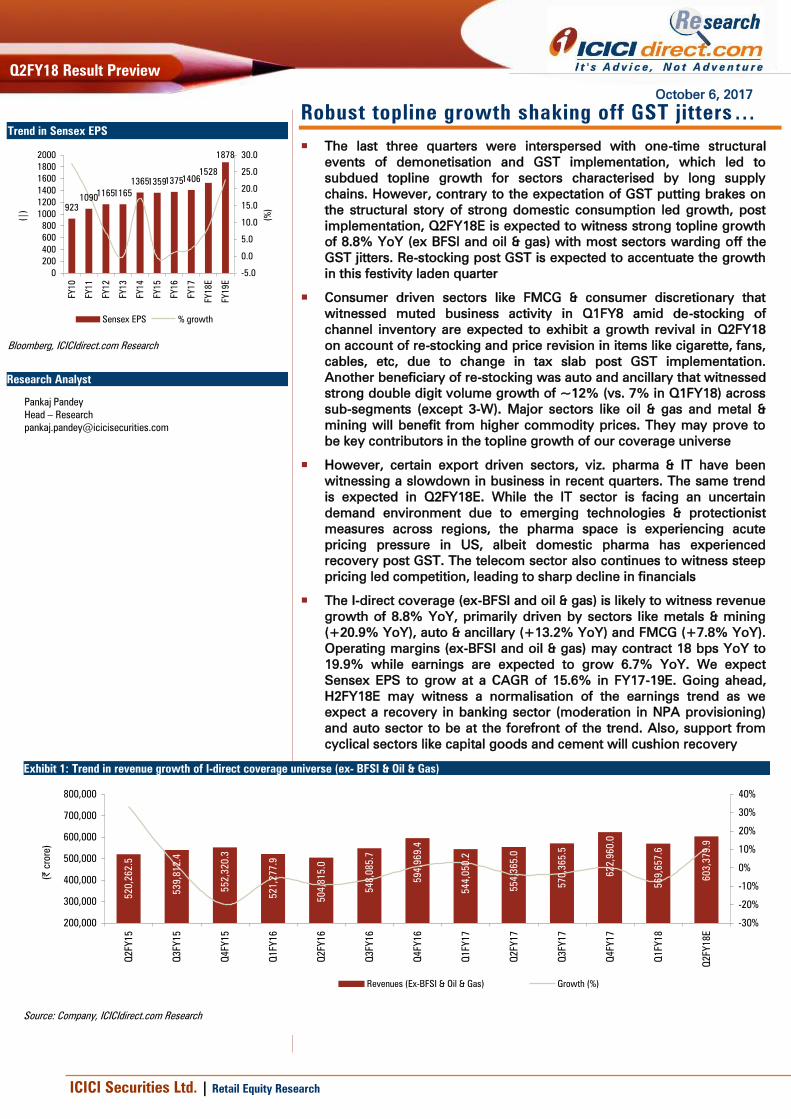

Sensex EPS to grow at a CAGR of 15.6% in FY17-19E. Going ahead,

H2FY18E may witness a normalisation of the earnings trend as we

expect a recovery in banking sector (moderation in NPA provisioning)

and auto sector to be at the forefront of the trend. Also, support from

cyclical sectors like capital goods and cement will cushion recovery

Exhibit 1: Trend in revenue growth of I-direct coverage universe (ex- BFSI & Oil & Gas)

520,2

62.5

539,8

12.4

552,3

20.3

521,2

77.9

504,8

15.0

548,0

85.7

594,9

69.4

544,0

50.2

554,3

65.0

570,3

65.5

622,9

60.0

569,6

57.6

603,3

79.9

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Q2FY15

Q3FY15

Q4FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(|

crore)

-30%

-20%

-10%

0%

10%

20%

30%

40%

Revenues (Ex-BFSI & Oil & Gas) Growth (%)

Source: Company, ICICIdirect.com Research

Trend in Sensex EPS

923

109011651165

1365135913751406

1528

1878

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18E

FY19E

(|

)

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

(%

)

Sensex EPS % growth

Source:

Bloomberg, ICICIdirect.com Research

Research Analyst

Pankaj Pandey

Head – Research

ICICI Securities Ltd. | Retail Equity Research

Page 2

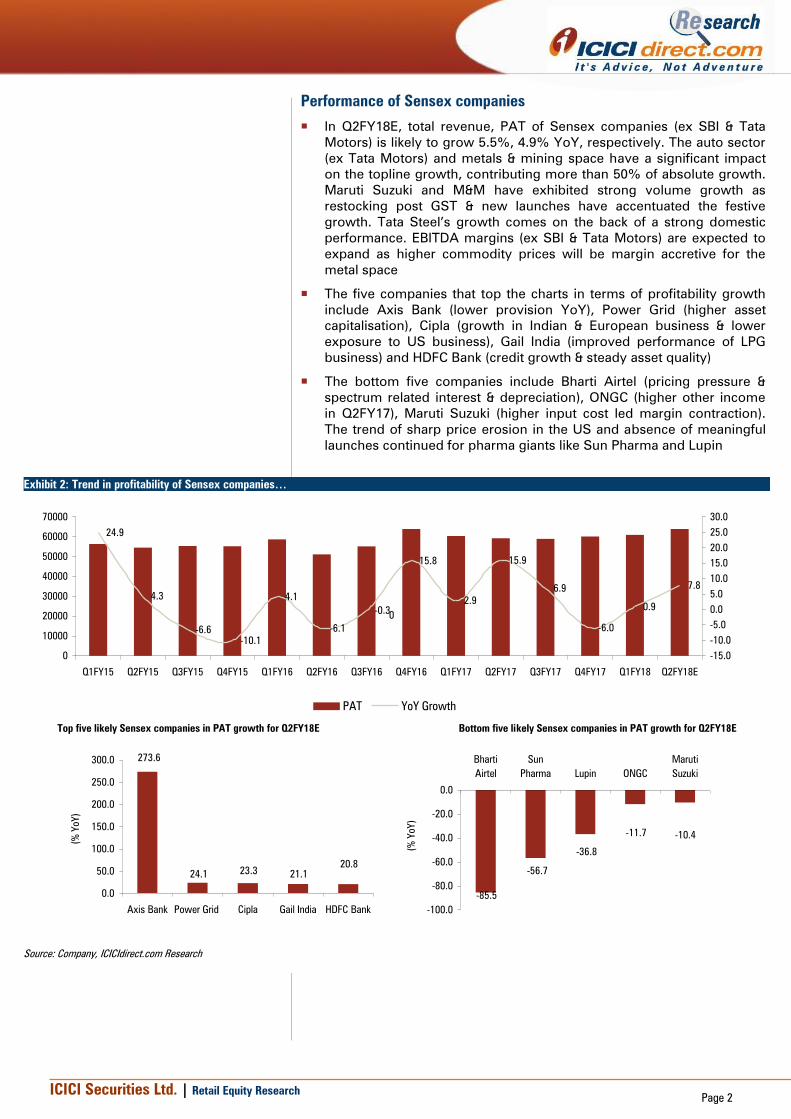

Performance of Sensex companies

In Q2FY18E, total revenue, PAT of Sensex companies (ex SBI & Tata

Motors) is likely to grow 5.5%, 4.9% YoY, respectively. The auto sector

(ex Tata Motors) and metals & mining space have a significant impact

on the topline growth, contributing more than 50% of absolute growth.

Maruti Suzuki and M&M have exhibited strong volume growth as

restocking post GST & new launches have accentuated the festive

growth. Tata Steel’s growth comes on the back of a strong domestic

performance. EBITDA margins (ex SBI & Tata Motors) are expected to

expand as higher commodity prices will be margin accretive for the

metal space

The five companies that top the charts in terms of profitability growth

include Axis Bank (lower provision YoY), Power Grid (higher asset

capitalisation), Cipla (growth in Indian & European business & lower

exposure to US business), Gail India (improved performance of LPG

business) and HDFC Bank (credit growth & steady asset quality)

The bottom five companies include Bharti Airtel (pricing pressure &

spectrum related interest & depreciation), ONGC (higher other income

in Q2FY17), Maruti Suzuki (higher input cost led margin contraction).

The trend of sharp price erosion in the US and absence of meaningful

launches continued for pharma giants like Sun Pharma and Lupin

Exhibit 2: Trend in profitability of Sensex companies…

24.9

4.3

-6.6

-10.1

4.1

-6.1

-0.3

15.8

2.9

15.9

6.9

-6.0

0.9

7.8

0

10000

20000

30000

40000

50000

60000

70000

Q1FY15 Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18E

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

PAT YoY Growth

0

Top five likely Sensex companies in PAT growth for Q2FY18E Bottom five likely Sensex companies in PAT growth for Q2FY18E

273.6

24.123.3

21.1

20.8

0.0

50.0

100.0

150.0

200.0

250.0

300.0

Axis Bank Power Grid Cipla Gail India HDFC Bank

(%

YoY)

-85.5

-56.7

-36.8

-11.7 -10.4

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

Bharti

Airtel

Sun

Pharma Lupin ONGC

Maruti

Suzuki

(%

YoY)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 3

What we expect our coverage universe to report; emerging trends

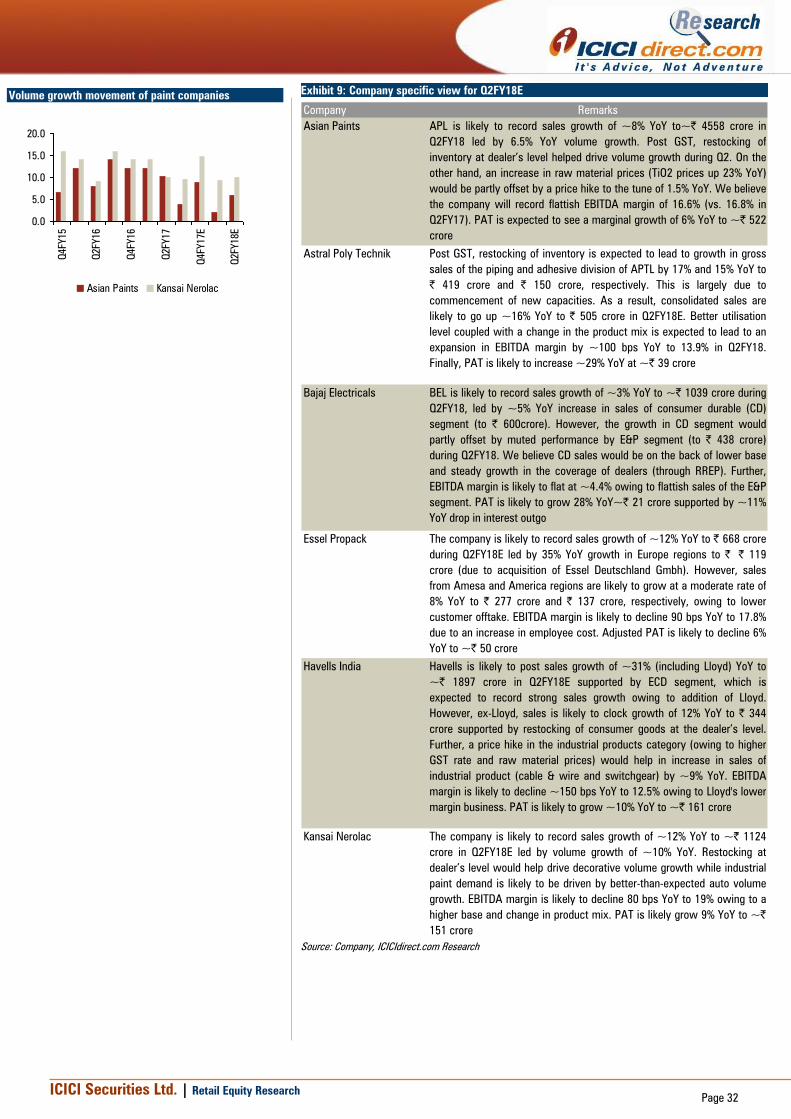

From a sectoral perspective, sectors like auto (ex-Tata Motors 22%

YoY), metals & mining (20.9% YoY), oil & gas (17.1% YoY) and cement

(11.7% YoY) are expected to report strong revenue growth backed by

both volume & realisation growth and also led by inorganic growth in

certain auto ancillary & cement companies . However, the telecom

sector is expected to witness a sales decline of 9.9% YoY as post GST

jitters added to the competitive pressure

In the banking space, credit growth remains muted at 6.8% YoY. PSU

banks are expected to continue to see single digit growth of ~5.5% YoY

while private banks continue to clock strong 17.9% YoY growth.

Positive developments in the steel sector and large players evincing

buying interest in companies referred to NCLT under IBC (viz. Essar

Steel, Bhushan Steel & Monnet Ispat) may lead to provisions write-back

in coming quarters. Savings interest rate cut of 50 bps by the largest

bank remained the highlight of the quarter, with other banks following

suit. Accordingly, a decline in interest expense would support NII. A

higher cut in deposit rates, compared to a decline in MCLR, is expected

to result in NII growth of 13.1% YoY and 3.1% QoQ for our coverage

universe. We expect our banking coverage universe PPP to grow 14.9%

YoY and 2.9% QoQ while PAT is seen growing 39% YoY and 8.7% QoQ

For Q2FY18E, overall auto volumes registered strong ~12% YoY

growth mainly due to 1) re-stocking of vehicles by dealers post

implementation of GST and 2) higher inventory build-up across the

dealer network ahead of the festive season. The quarter was among the

best, as all segments reported healthy volume growth. The standout

from the space was the 2-W & tractor segment, which reported robust

growth of ~12% YoY & ~30% YoY, respectively. The PV space

maintained its growth momentum with volumes up ~10% YoY. Further,

a demand revival was seen in 3-W (volumes up ~8% YoY backed by

both domestic & export demand) and CV (volumes up ~15% YoY,

mainly due to a recovery in the M&HCV segment). The quarter was

among the best for most OEMs, which reported healthy YoY and QoQ

volume growth. Thus, we estimate our universe [ex-Tata Motors (TML)]

to report topline growth of ~22% YoY. Further, higher raw material cost

(prices of key commodities viz. steel & aluminium were up 19% YoY

each) is likely to impact EBITDA margins of our universe (ex-TML),

which is expected to decline 170 bps YoY to 14.1%

In the capital goods space in Q2FY18E, EPC companies are expected to

face interim headwinds in execution and elongation of working capital

cycle due to transition of the sub contractor/vendor value chain in the

GST process. This may lead EPC companies to lend support to their

vendor base and, hence, will impact working capital in Q2FY18E. In

turn, the move may lead to some rise in interest cost. However, the

same may be contained till Q2FY18E. We expect EPC companies to

post muted revenue growth of 3.9%YoY (lower execution from sub

contractor will slow execution in Q2FY18E). However, PAT is expected

to grow 9.6% YoY on the back of a margins expansion. For Q2FY18E,

product based companies are expected to report 9.1% YoY revenue

growth. However, pressure on EBITDA margins is likely to continue.

The same is expected to contract 50 bps to 16.1% for the quarter.

Consequently, absolute EBITDA is expected to grow by only 0.8% in

Q2FY18E.

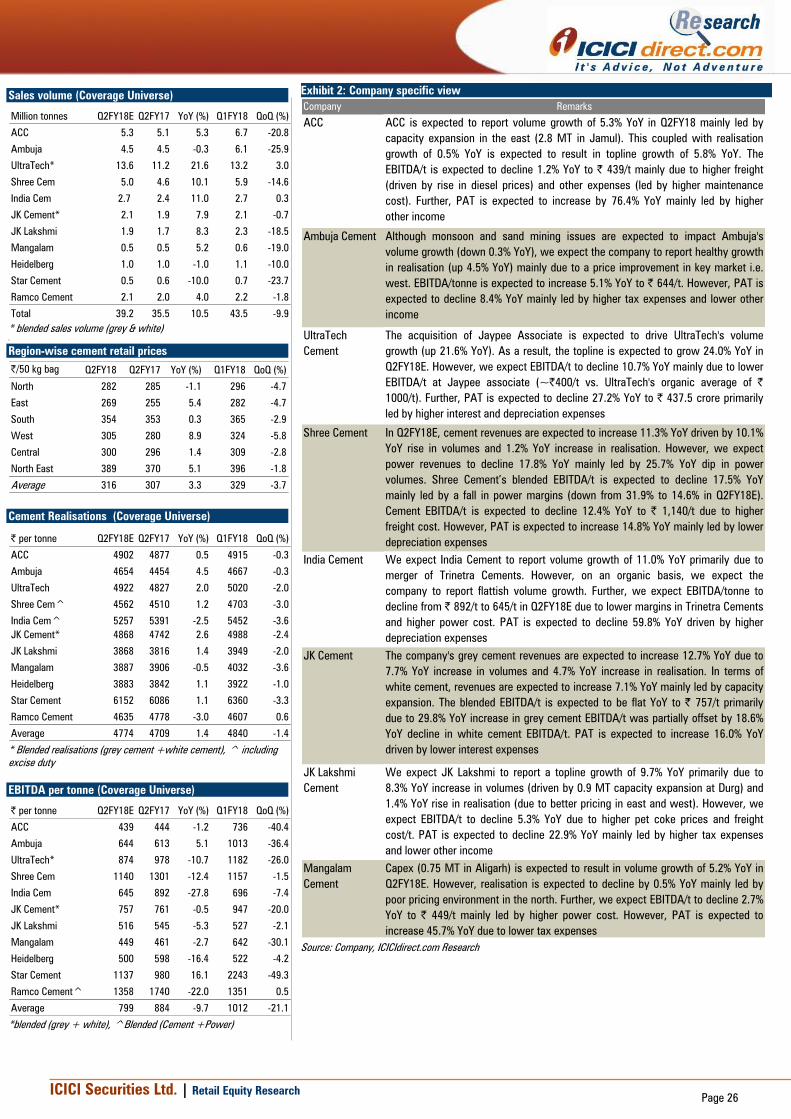

Cement demand is expected to remain muted mainly due to the impact

of monsoon and sand mining issue in many parts of India. Hence, on an

organic basis, we expect companies under our coverage to report flat

to negative volume growth. However, considering the acquisition of

ICICI Securities Ltd. | Retail Equity Research

Page 4

Jaypee by UltraTech, merger of Trinetra Cement by India Cement and

capacity expansion by various companies under our coverage universe,

we expect companies to report optically higher volume growth.

Consequently, we expect companies in our coverage universe to

register volume growth of 10.5% YoY in Q2FY18E. In addition, we

expect realisation to increase 1.4% YoY leading to revenue growth of

11.7% YoY in Q2FY18E. However, higher other expenses (due to

increase in maintenance cost), rise in power (led by higher pet coke

prices) and freight cost may dent EBITDA/t (down 9.7% YoY to | 799/t)

in Q2FY18E

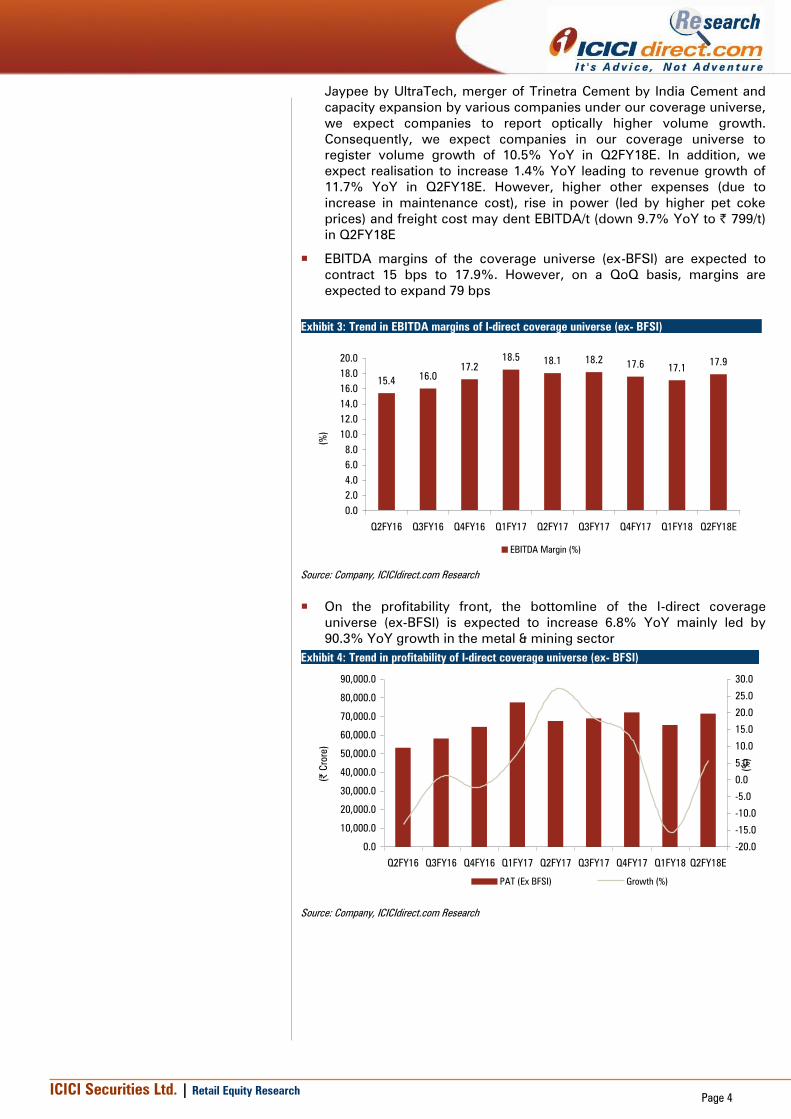

EBITDA margins of the coverage universe (ex-BFSI) are expected to

contract 15 bps to 17.9%. However, on a QoQ basis, margins are

expected to expand 79 bps

On the profitability front, the bottomline of the I-direct coverage

universe (ex-BFSI) is expected to increase 6.8% YoY mainly led by

90.3% YoY growth in the metal & mining sector

Exhibit 4: Trend in profitability of I-direct coverage universe (ex- BFSI)

0.0

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

90,000.0

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18E

(|

Crore)

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

(%

)

PAT (Ex BFSI) Growth (%)

Source: Company, ICICIdirect.com Research

Exhibit 3: Trend in EBITDA margins of I-direct coverage universe (ex- BFSI)

15.416.0

17.2

18.518.1 18.2

17.617.1

17.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18E

(%

)

EBITDA Margin (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 5

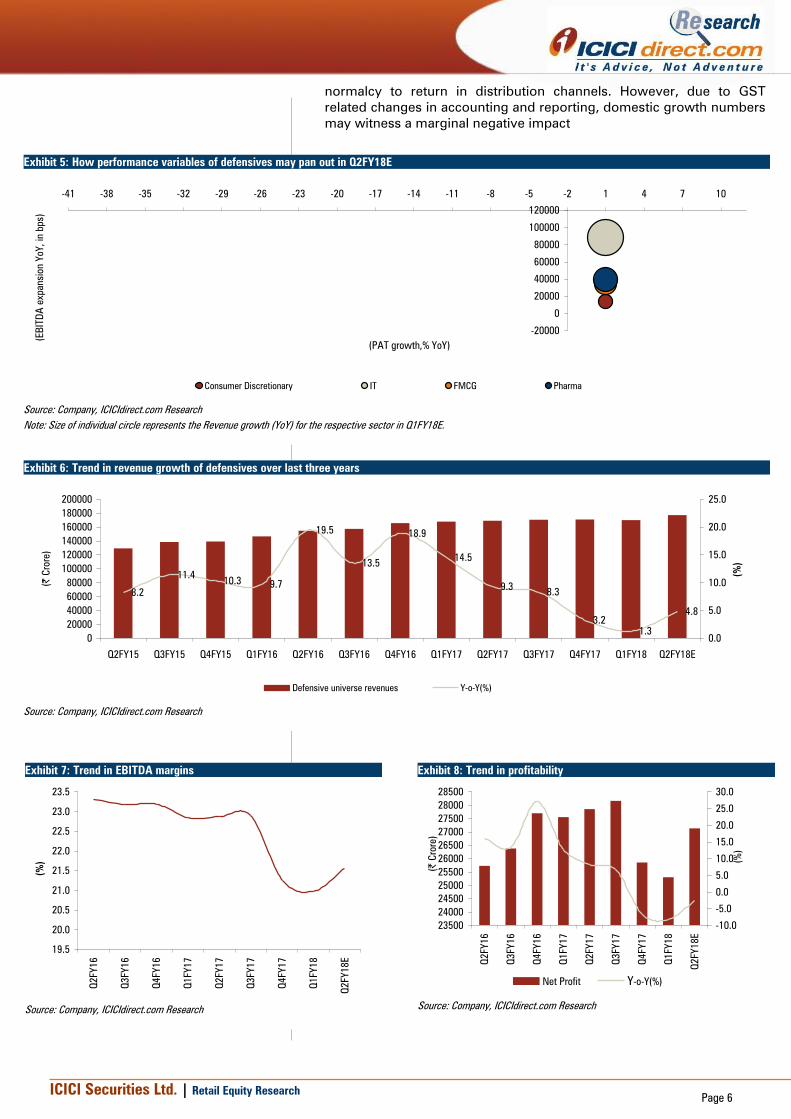

Defensives: Consumption sectors impacted by GST…

(Sector composition: consumer discretionary, IT, FMCG, healthcare)

Key highlights:

In the past seven years, the defensive sector has never reported

revenue de-growth in any quarter. However, events like demonetisation

& GST rollout have slowed down the topline growth from Q3FY17

onwards. Defensives are expected to post revenue growth of 4.8% YoY

compared to average revenue growth of 10.7% in the previous 12

quarters. Although the FMCG sector continues to witness some

pressure on account of GST in the form of disruption in wholesale

channel & slower rural recovery, the topline growth can be attributed to

price hikes like in cigarette post GST rate revision. In the healthcare

space, a slowdown in the US is likely to overshadow domestic growth,

which is expected to see revival post-GST implementation. The EBITDA

margin of the defensive universe is expected to contract 131 bps YoY

mainly due to margin contraction of 388 bps in the pharma space on

account of sharp price erosion in the US. The ensuing EBITDA, PAT of

the defensive universe is expected to decline 1.2% YoY & 2.6% YoY,

respectively

Tier-1 IT companies are expected to report constant currency (CC)

growth of 0.5-2.8% with HCL Tech leading the pack. Cross currency

could provide strength by ~100-130 bps to reported dollar growth.

Inter-quarter average US$ has depreciated vs. major currencies acting

as a tailwind. US$ has depreciated ~0.3%, 6.7%, 2.2% and 5.2%

against rupee, Euro, GBP and AU$, respectively. Tier-I IT companies are

likely to report average 3.1% growth in $ terms in Q2FY18E. Within tier-

I, HCLT (4.0%) may lead again supported by inorganic contribution

(0.8%) followed by Infosys (3.5%), TCS (3.2%) and Wipro (1.5%). Within

midcaps, we expect sequential dollar revenue growth to be broad

based across companies led by Cyient (5.3%), Persistent (3.9%), TechM

(2.5%) followed by NIIT Tech (2.9%), MindTree (2.5%) and KPIT (2.5%).

Persistent, TechM and NIIT Tech would benefit from the contribution of

acquisitions. On the operating margins front, absence of higher visa

cost and wage hikes for a few companies would provide a cushion to

margins in a seasonally strong Q2

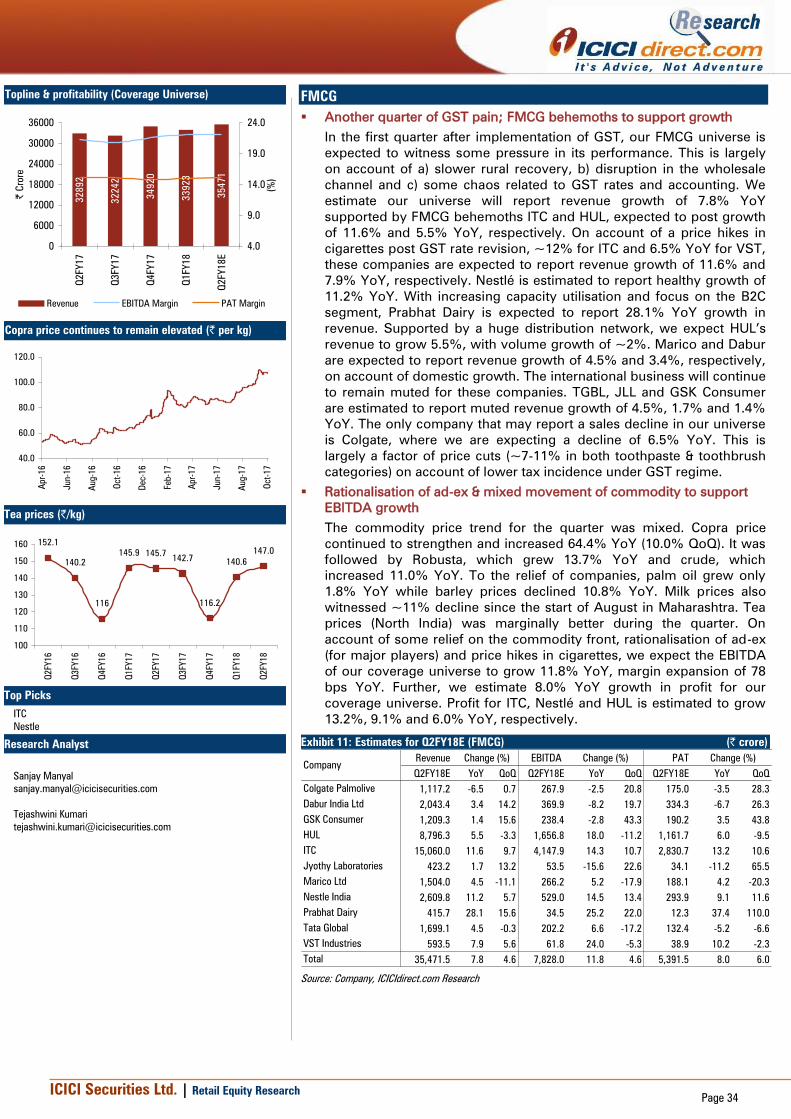

In the first quarter, after implementation of GST, our FMCG universe is

expected to witness some pressure in its performance. This is largely

on account of a) slower rural recovery, b) disruption in the wholesale

channel and c) some chaos related to GST rates and accounting. We

estimate our universe will report revenue growth of 7.8% YoY

supported by FMCG behemoths ITC and HUL, expected to post growth

of 11.6% and 5.5% YoY, respectively. The only company that may

report a sales decline in our universe is Colgate, where we are

expecting a decline of 6.5% YoY, on account of price cuts on account of

lower tax incidence under GST regime. On account of some relief on

the commodity front, rationalisation of ad-ex (for major players) and

price hikes in cigarettes, we expect the EBITDA of our coverage

universe to grow 11.8% YoY. Further, we estimate 8.0% YoY growth in

profit for our coverage

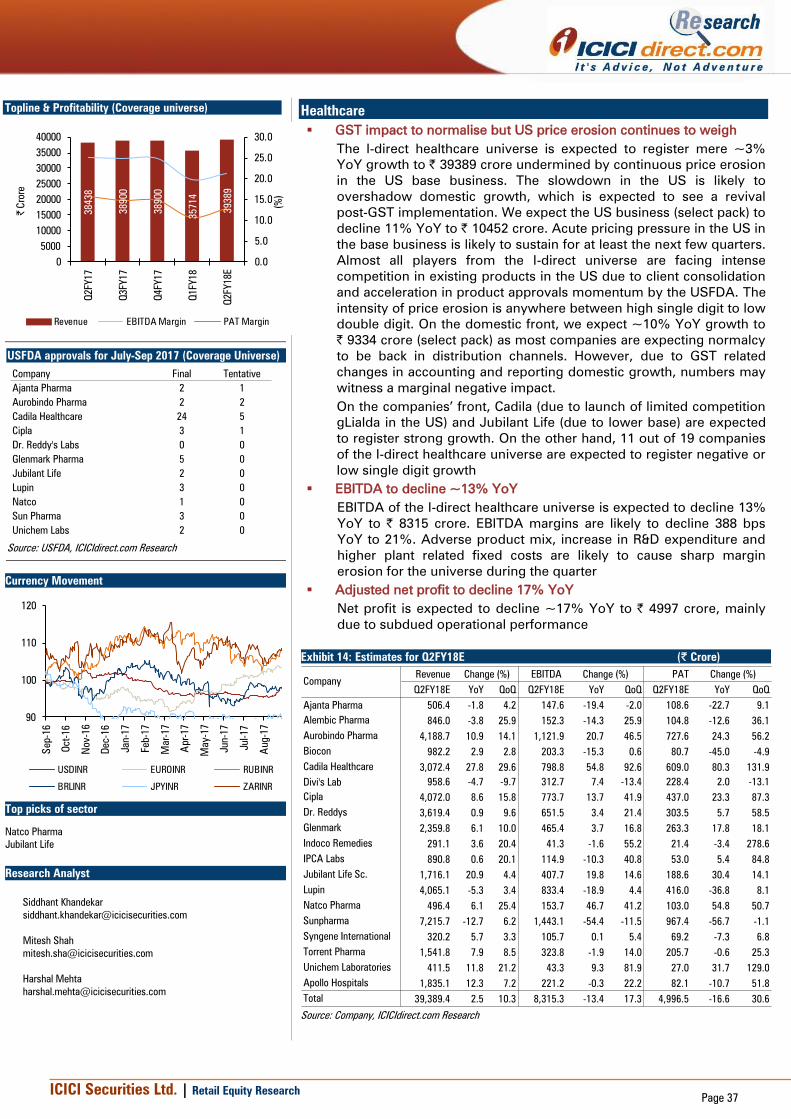

I-direct healthcare universe is expected to register mere ~3% YoY

growth to | 39389 crore undermined by continuous price erosion in the

US base business. We expect US business (selected pack) to decline

11% YoY to | 10452 crore. Almost all players from the universe are

facing intense competition in existing products in the US due to client

consolidation and acceleration in product approvals momentum by the

USFDA. The intensity of price erosion is anywhere between high single

digit to low double digit. On the domestic front, we expect ~10% YoY

growth to | 9334 crore (select pack) as most companies are expecting

ICICI Securities Ltd. | Retail Equity Research

Page 6

normalcy to return in distribution channels. However, due to GST

related changes in accounting and reporting, domestic growth numbers

may witness a marginal negative impact

Exhibit 5: How performance variables of defensives may pan out in Q2FY18E

-20000

0

20000

40000

60000

80000

100000

120000

-41 -38 -35 -32 -29 -26 -23 -20 -17 -14 -11 -8 -5 -2 1 4 7 10

(PAT growth,% YoY)

(EB

ITD

A e

xpansio

n Y

oY,

in b

ps)

Consumer Discretionary IT FMCG Pharma

Source: Company, ICICIdirect.com Research

Note: Size of individual circle represents the Revenue growth (YoY) for the respective sector in Q1FY18E.

Exhibit 6: Trend in revenue growth of defensives over last three years

8.2

11.410.3

9.7

19.5

13.5

18.9

14.5

9.38.3

3.2

1.3

4.8

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18E

(|

Crore)

0.0

5.0

10.0

15.0

20.0

25.0

(%

)

Defensive universe revenues Y-o-Y(%)

Source: Company, ICICIdirect.com Research

Exhibit 7: Trend in EBITDA margins

19.5

20.0

20.5

21.0

21.5

22.0

22.5

23.0

23.5

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(%

)

Source: Company, ICICIdirect.com Research

Exhibit 8: Trend in profitability

23500

24000

24500

25000

25500

26000

26500

27000

27500

28000

28500

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(|

Crore)

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

(%

)

Net Profit Y-o-Y(%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 7

Cyclicals: Visible signs of pick-up in capex cycle

(Sector composition: auto, cement, capital goods, power, infrastructure,

real estate, oil & gas and telecom)

Key Highlights

Cyclicals are expected to witness strong growth of 13% YoY after 11

quarters of de-growth. This high growth is expected to be mainly driven

by 17% YoY growth in the oil & gas sector led by higher gross refining

margins reported by oil marketing companies. The power sector is

likely to continue its growth momentum (~7.2% YoY growth) on the

back of generation & capacity addition

We expect the oil & gas sector to report a decent set of numbers in

Q2FY18E. Realisations of upstream oil & gas companies are expected to

grow QoQ on account of 3.3% QoQ growth in average Brent crude oil

prices to US$ 51.7/bbl. Also, increase in oil & gas production is

expected to augur well for upstream companies. On the OMCs front, we

expect strong GRMs supported by high product spreads and inventory

gains with benchmark Singapore GRMs rising from US$6.4/bbl in

Q1FY18 to US$8.3/bbl in Q2FY18. However, marketing volumes are

expected to remain muted. On the gas utility front, we expect stable

growth in volumes due to increase in domestic gas production and

imported LNG. Continued demand from city gas distribution, lower

domestic gas prices and relatively stable spot LNG prices are expected

to bode well for gas utility companies

In the metal space, on a sequential basis, we expect the EBITDA/tonne

of steel players to increase while non-ferrous players are also likely to

report healthy revenues and profitability. On account of an increase in

domestic steel prices and moderation in the prices of coking coal (key

raw material), we expect steel players to report healthy EBITDA/tonne

sequentially. During Q2FY18, majority of base metal prices witnessed

an increase on a YoY and QoQ basis. Average zinc prices during the

quarter were at US$2962/tonne (up 32% YoY, 14% QoQ). Average lead

prices were at US$2331/tonne (up 24% YoY, 8% QoQ). The average

price of aluminium was at US$2010/tonne (up 24% YoY, 6% QoQ) while

average copper prices were at US$6351/tonne (up 33% YoY, 12%

QoQ). We expect higher prices to augment the topline and profitability

of non-ferrous players

Overall, the power generation during April-August 2017 is up 4.6% YoY

while in August 2017 the same was up 7.9% YoY. In terms of segmental

(YTD) basis, thermal generation is up 5% YoY while hydro has seen

moderate growth of 5.8% YoY albeit peak season. On the other hand,

renewable segment witnessed 30.2% YoY growth in generation during

April-July 2017, mainly on the back of strong capacity addition in FY17.

On a segmental basis, central level utilities saw higher than average

PLFs at 70% while that of state and private IPPs meaningfully improved

to 64% and 55%, respectively. On the conventional side, no capacity

addition was reported in Q2FY18E

ICICI Securities Ltd. | Retail Equity Research

Page 8

Exhibit 9: How performance variables of cyclicals may pan out in Q2FY18E

-4

-2

0

2

4

6

-40 -20 0 20 40 60 80 100 120

(PAT growth, % YoY)

(EB

ITD

A M

argin

expansio

n, in

bps)

Capital Goods Power Auto Cement Metals

Source: Company, ICICIdirect.com Research

Exhibit 10: Trend in revenue growth of cyclicals

35.4

19.4

-1.7

-14.2

-7.8

-12.9-11.2

-3.6 -2.8

-10.6

-6.4

-1.0

-10.6

12.1

0

100000

200000

300000

400000

500000

600000

700000

800000

Q1FY15 Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18E

(|

Crore)

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

(%

)

Total Cylical revenues Y-o-Y(%)

Source: Company, ICICIdirect.com Research

Exhibit 11: Trend in EBITDA margins

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(%

)

Source: Company, ICICIdirect.com Research

Exhibit 12: Interest costs …

12000

12500

13000

13500

14000

14500

15000

15500

16000

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(|

Crore)

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

(%

)

Interest costs (| cr) Y-o-Y(%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 9

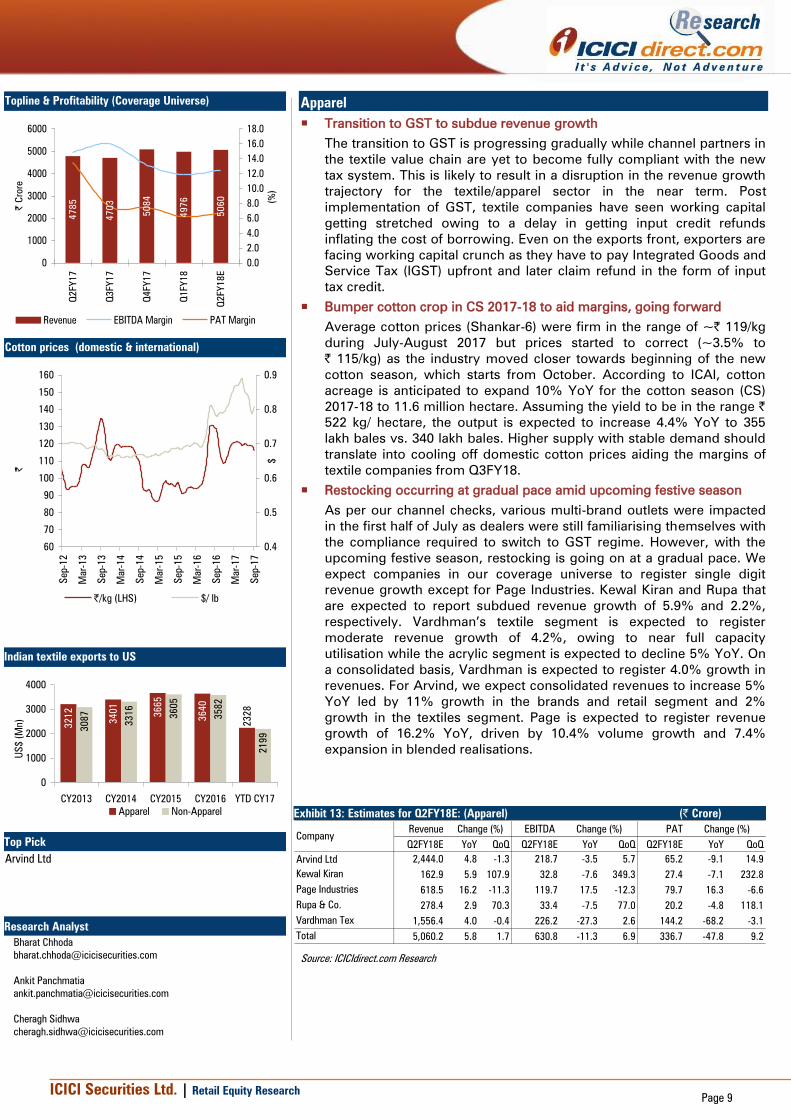

Apparel

Transition to GST to subdue revenue growth

The transition to GST is progressing gradually while channel partners in

the textile value chain are yet to become fully compliant with the new

tax system. This is likely to result in a disruption in the revenue growth

trajectory for the textile/apparel sector in the near term. Post

implementation of GST, textile companies have seen working capital

getting stretched owing to a delay in getting input credit refunds

inflating the cost of borrowing. Even on the exports front, exporters are

facing working capital crunch as they have to pay Integrated Goods and

Service Tax (IGST) upfront and later claim refund in the form of input

tax credit.

Bumper cotton crop in CS 2017-18 to aid margins, going forward

Average cotton prices (Shankar-6) were firm in the range of ~| 119/kg

during July-August 2017 but prices started to correct (~3.5% to

| 115/kg) as the industry moved closer towards beginning of the new

cotton season, which starts from October. According to ICAI, cotton

acreage is anticipated to expand 10% YoY for the cotton season (CS)

2017-18 to 11.6 million hectare. Assuming the yield to be in the range |

522 kg/ hectare, the output is expected to increase 4.4% YoY to 355

lakh bales vs. 340 lakh bales. Higher supply with stable demand should

translate into cooling off domestic cotton prices aiding the margins of

textile companies from Q3FY18.

Restocking occurring at gradual pace amid upcoming festive season

As per our channel checks, various multi-brand outlets were impacted

in the first half of July as dealers were still familiarising themselves with

the compliance required to switch to GST regime. However, with the

upcoming festive season, restocking is going on at a gradual pace. We

expect companies in our coverage universe to register single digit

revenue growth except for Page Industries. Kewal Kiran and Rupa that

are expected to report subdued revenue growth of 5.9% and 2.2%,

respectively. Vardhman’s textile segment is expected to register

moderate revenue growth of 4.2%, owing to near full capacity

utilisation while the acrylic segment is expected to decline 5% YoY. On

a consolidated basis, Vardhman is expected to register 4.0% growth in

revenues. For Arvind, we expect consolidated revenues to increase 5%

YoY led by 11% growth in the brands and retail segment and 2%

growth in the textiles segment. Page is expected to register revenue

growth of 16.2% YoY, driven by 10.4% volume growth and 7.4%

expansion in blended realisations.

Exhibit 13: Estimates for Q2FY18E: (Apparel) (| Crore)

Revenue EBITDA PAT

Q2FY18E YoY QoQ Q2FY18E YoY QoQ Q2FY18E YoY QoQ

Arvind Ltd 2,444.0 4.8 -1.3 218.7 -3.5 5.7 65.2 -9.1 14.9

Kewal Kiran 162.9 5.9 107.9 32.8 -7.6 349.3 27.4 -7.1 232.8

Page Industries 618.5 16.2 -11.3 119.7 17.5 -12.3 79.7 16.3 -6.6

Rupa & Co. 278.4 2.9 70.3 33.4 -7.5 77.0 20.2 -4.8 118.1

Vardhman Tex 1,556.4 4.0 -0.4 226.2 -27.3 2.6 144.2 -68.2 -3.1

Total 5,060.2 5.8 1.7 630.8 -11.3 6.9 336.7 -47.8 9.2

Change (%) Change (%) Change (%)

Company

Source: ICICIdirect.com Research

Topline & Profitability (Coverage Universe)

4785

4703

5084

4976

5060

0

1000

2000

3000

4000

5000

6000

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

| C

rore

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

(%

)

Revenue EBITDA Margin PAT Margin

Cotton prices (domestic & international)

60

70

80

90

100

110

120

130

140

150

160

Sep-12

Mar-13

Sep-13

Mar-14

Sep-14

Mar-15

Sep-15

Mar-16

Sep-16

Mar-17

Sep-17

|

0.4

0.5

0.6

0.7

0.8

0.9

$

|/kg (LHS) $/ lb

Indian textile exports to US

3212

3401

3665

2199

3640

2328

3087

3316

3605

3582

0

1000

2000

3000

4000

CY2013 CY2014 CY2015 CY2016 YTD CY17

US

$ (

Mn)

Apparel Non-Apparel

Top Pick

Arvind Ltd

Research Analyst

Bharat Chhoda

Ankit Panchmatia

Cheragh Sidhwa

ICICI Securities Ltd. | Retail Equity Research

Page 10

Decline in duty drawback to impact garment exports

According to the data provided by Office of Textile and Apparel

(OTEXA), India’s apparel exports to the US for YTD CY17 declined 0.2%

to US$2328 million while non-apparel exports continued to register

growth of 6.1% to US$2199 million. Recently, The Government of India

has announced new duty drawback rates for garments effective from

October 1, 2017. The duty drawback rate for cotton garments has been

fixed at 2% vs. existing 7.7%. Duty drawback rates on garments of

blended and manmade fibres have been fixed at 2.5% vs. existing 9.5%

and 9.8%, respectively. The new lower rates are expected to negatively

impact the global competitiveness of Indian garment exporters as the

industry is already facing pressure due to rupee appreciation.

Exhibit 14: Company specific view (Apparel)

Company Remarks

Kewal Kiran Traditionally, Q2 is a strong quarter for KKCL as various dealers replenish their

inventory a month prior to the start of the new festive season. However, we expect

revenues to be impacted due to GST compliance related issues at the dealer’s level.

We expect revenues to increase 5.9% YoY to | 162.9 crore led by 2.8% increase in

volumes to 15.2 lakh pieces and 3% increase in realisation to | 1072/piece. Operating

margins are likely to dip 290 bps YoY to 20.1. Subsequently, we expect PAT to decline

7.1% YoY to | 27.4 crore

Page

Industries

We expect Page to continue on its strong revenue growth trajectory and register a

healthy topline growth of 16.2% YoY to | 618.5 crore led by 10.4% volume growth to

42 million pieces and 7.4% realisation growth to | 147/piece. We expect leisure

segment to be the key growth driver by registering YoY volume growth of 24%.

Operating margins are likely to expand 30 bps YoY to 19.4% owing to improved

realisations and positive operating leverage. We expect PAT to increase 16.3% YoY to

| 79.7 crore

Rupa &

Company

We expect Rupa to register subdued revenue growth of 2.9% YoY to | 278.4 crore.

EBITDA margins are likely to contract 130 bps YoY to 12.0% on account of negative

operating leverage while absolute EBITDA is expected to decline 7.5% YoY to | 33.4

crore. On account of a decline in interest expense, we expect PAT de-growth to be

curtailed at 4.8% YoY to | 20.2 crore

Vardhman

Textiles

Consolidated revenues are likely to report moderate growth of 4.0% YoY to | 1556.4

crore. On the segmental front, we expect textiles segment to register subdued growth

rate of 4.2% while the acrylic business is expected to decline 5% YoY. In Q2FY17,

operating margins were abnormally high owing to low cost cotton inventory gains.

However we expect operating margins to be severely impacted in the quarter on

account of high cost cotton inventory. EBITDA margins are expected to contract 630

bps YoY to 14.5%. On account of a 40% stake sale in Vardhman yarn and threads in

Q2FY17 (exceptional income: | 251 crore), PAT was significantly higher at | 454

crore. In the absence of extraordinary income, PAT for Q2FY18 is expected to decline

68% to | 144.2 crore

Arvind Ltd The negative impact of GST, which dented revenues for July, was to an extent

moderated by the revival in August and September. In addition to the same, optimum

utilisation of capacity at the garment facility and lower demand for textiles could result

in a flattish performance for the textile business. We expect textile revenues to grow

2% YoY (vs. an average of 12% over past four quarter). Likewise, on the back of large

base impact of Q2FY17 (growth of 33%), retail revenues are expected to grow 11%

YoY to | 834 crore. The resultant consolidated revenues are expected to grow 5% YoY

to | 2444 crore. The impact of GST on operating expenses is expected to dent EBITDA

margins by 70 bps to 9% with an absolute EBITDA de-growth of 4% YoY to | 219

crore. Increase in interest expenses due to increased working capital requirement may

lead PAT de-growth of 11% YoY to | 65.2 crore

Source: Company, ICICIdirect.com Research

China’s cotton yarn import

80

110

140

170

200

230

260

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

Mar-16

Jun-16

Sep-16

Dec-16

Mar-17

Jun-17

Million k

gs

China’s cotton yarn imports have declined 2.7% YoY in

YTDFY18, which would impact revenue growth and

margins of Indian cotton yarn exporters

ICICI Securities Ltd. | Retail Equity Research

Page 11

Auto and auto ancillary

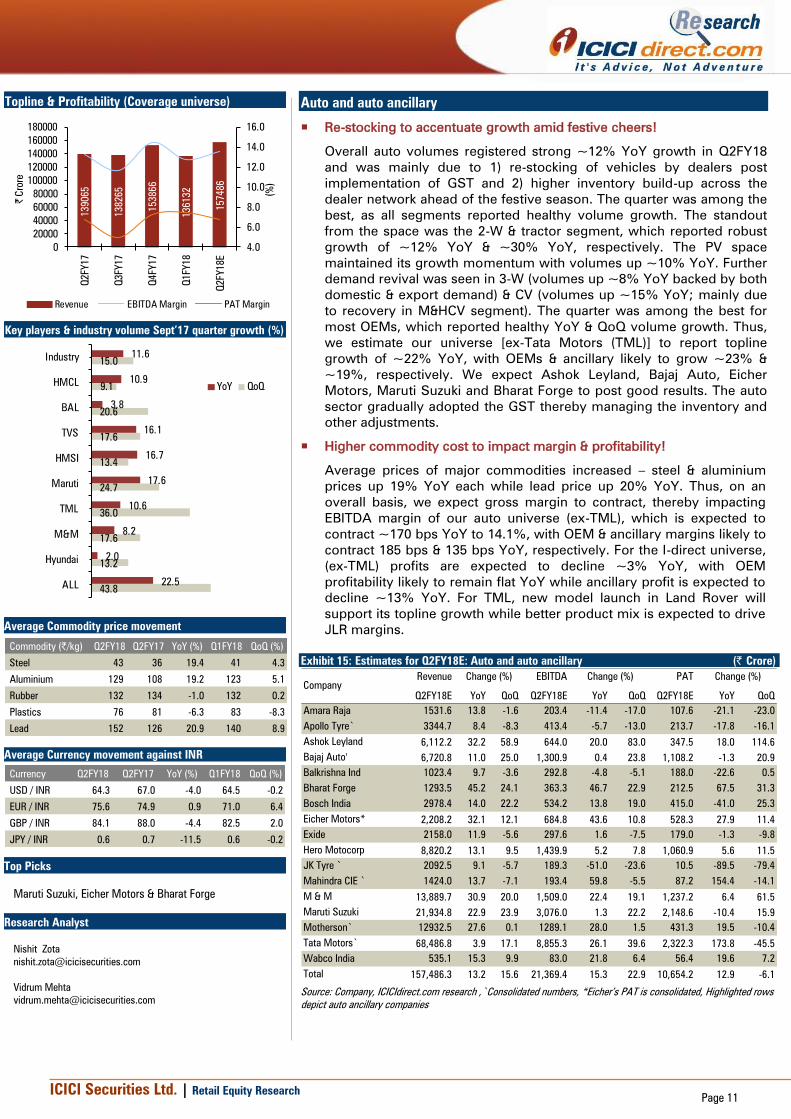

Re-stocking to accentuate growth amid festive cheers!

Overall auto volumes registered strong ~12% YoY growth in Q2FY18

and was mainly due to 1) re-stocking of vehicles by dealers post

implementation of GST and 2) higher inventory build-up across the

dealer network ahead of the festive season. The quarter was among the

best, as all segments reported healthy volume growth. The standout

from the space was the 2-W & tractor segment, which reported robust

growth of ~12% YoY & ~30% YoY, respectively. The PV space

maintained its growth momentum with volumes up ~10% YoY. Further

demand revival was seen in 3-W (volumes up ~8% YoY backed by both

domestic & export demand) & CV (volumes up ~15% YoY; mainly due

to recovery in M&HCV segment). The quarter was among the best for

most OEMs, which reported healthy YoY & QoQ volume growth. Thus,

we estimate our universe [ex-Tata Motors (TML)] to report topline

growth of ~22% YoY, with OEMs & ancillary likely to grow ~23% &

~19%, respectively. We expect Ashok Leyland, Bajaj Auto, Eicher

Motors, Maruti Suzuki and Bharat Forge to post good results. The auto

sector gradually adopted the GST thereby managing the inventory and

other adjustments.

Higher commodity cost to impact margin & profitability!

Average prices of major commodities increased – steel & aluminium

prices up 19% YoY each while lead price up 20% YoY. Thus, on an

overall basis, we expect gross margin to contract, thereby impacting

EBITDA margin of our auto universe (ex-TML), which is expected to

contract ~170 bps YoY to 14.1%, with OEM & ancillary margins likely to

contract 185 bps & 135 bps YoY, respectively. For the I-direct universe,

(ex-TML) profits are expected to decline ~3% YoY, with OEM

profitability likely to remain flat YoY while ancillary profit is expected to

decline ~13% YoY. For TML, new model launch in Land Rover will

support its topline growth while better product mix is expected to drive

JLR margins.

Exhibit 15: Estimates for Q2FY18E: Auto and auto ancillary (| Crore)

Revenue EBITDA PAT

Q2FY18E YoY QoQ Q2FY18E YoY QoQ Q2FY18E YoY QoQ

Amara Raja 1531.6 13.8 -1.6 203.4 -11.4 -17.0 107.6 -21.1 -23.0

Apollo Tyre` 3344.7 8.4 -8.3 413.4 -5.7 -13.0 213.7 -17.8 -16.1

Ashok Leyland 6,112.2 32.2 58.9 644.0 20.0 83.0 347.5 18.0 114.6

Bajaj Auto' 6,720.8 11.0 25.0 1,300.9 0.4 23.8 1,108.2 -1.3 20.9

Balkrishna Ind 1023.4 9.7 -3.6 292.8 -4.8 -5.1 188.0 -22.6 0.5

Bharat Forge 1293.5 45.2 24.1 363.3 46.7 22.9 212.5 67.5 31.3

Bosch India 2978.4 14.0 22.2 534.2 13.8 19.0 415.0 -41.0 25.3

Eicher Motors* 2,208.2 32.1 12.1 684.8 43.6 10.8 528.3 27.9 11.4

Exide 2158.0 11.9 -5.6 297.6 1.6 -7.5 179.0 -1.3 -9.8

Hero Motocorp 8,820.2 13.1 9.5 1,439.9 5.2 7.8 1,060.9 5.6 11.5

JK Tyre ` 2092.5 9.1 -5.7 189.3 -51.0 -23.6 10.5 -89.5 -79.4

Mahindra CIE ` 1424.0 13.7 -7.1 193.4 59.8 -5.5 87.2 154.4 -14.1

M & M 13,889.7 30.9 20.0 1,509.0 22.4 19.1 1,237.2 6.4 61.5

Maruti Suzuki 21,934.8 22.9 23.9 3,076.0 1.3 22.2 2,148.6 -10.4 15.9

Motherson` 12932.5 27.6 0.1 1289.1 28.0 1.5 431.3 19.5 -10.4

Tata Motors` 68,486.8 3.9 17.1 8,855.3 26.1 39.6 2,322.3 173.8 -45.5

Wabco India 535.1 15.3 9.9 83.0 21.8 6.4 56.4 19.6 7.2

Total 157,486.3 13.2 15.6 21,369.4 15.3 22.9 10,654.2 12.9 -6.1

Change (%)

Company

Change (%) Change (%)

Source: Company, ICICIdirect.com research ,`Consolidated numbers, *Eicher’s PAT is consolidated, Highlighted rows

depict auto ancillary companies

Topline & Profitability (Coverage universe)

139065

138265

153866

136132

157486

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(%

)

| C

rore

Revenue EBITDA Margin PAT Margin

Key players & industry volume Sept’17 quarter growth (%)

11.6

10.9

3.8

16.1

16.7

17.6

10.6

8.2

2.0

22.5

15.0

9.1

20.6

17.6

13.4

24.7

36.0

17.6

13.2

43.8

Industry

HMCL

BAL

TVS

HMSI

Maruti

TML

M&M

Hyundai

ALL

YoY QoQ

Average Commodity price movement

Commodity (|/kg) Q2FY18 Q2FY17 YoY (%) Q1FY18 QoQ (%)

Steel 43 36 19.4 41 4.3

Aluminium 129 108 19.2 123 5.1

Rubber 132 134 -1.0 132 0.2

Plastics 76 81 -6.3 83 -8.3

Lead 152 126 20.9 140 8.9

Average Currency movement against INR

Currency Q2FY18 Q2FY17 YoY (%) Q1FY18 QoQ (%)

USD / INR 64.3 67.0 -4.0 64.5 -0.2

EUR / INR 75.6 74.9 0.9 71.0 6.4

GBP / INR 84.1 88.0 -4.4 82.5 2.0

JPY / INR 0.6 0.7 -11.5 0.6 -0.2

Top Picks

Maruti Suzuki, Eicher Motors & Bharat Forge

Research Analyst

Nishit Zota

Vidrum Mehta

ICICI Securities Ltd. | Retail Equity Research

Page 12

Company Remarks

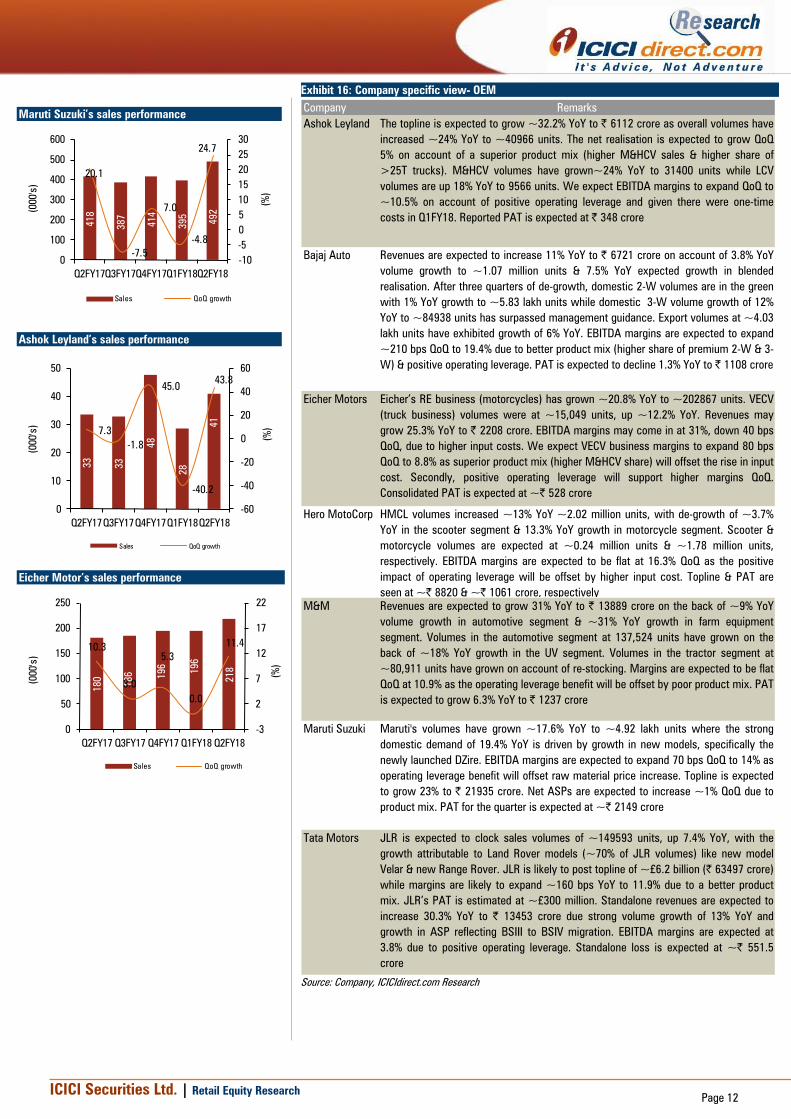

Ashok Leyland The topline is expected to grow ~32.2% YoY to | 6112 crore as overall volumes have

increased ~24% YoY to ~40966 units. The net realisation is expected to grow QoQ

5% on account of a superior product mix (higher M&HCV sales & higher share of

>25T trucks). M&HCV volumes have grown~24% YoY to 31400 units while LCV

volumes are up 18% YoY to 9566 units. We expect EBITDA margins to expand QoQ to

~10.5% on account of positive operating leverage and given there were one-time

costs in Q1FY18. Reported PAT is expected at | 348 crore

Bajaj Auto Revenues are expected to increase 11% YoY to | 6721 crore on account of 3.8% YoY

volume growth to ~1.07 million units & 7.5% YoY expected growth in blended

realisation. After three quarters of de-growth, domestic 2-W volumes are in the green

with 1% YoY growth to ~5.83 lakh units while domestic 3-W volume growth of 12%

YoY to ~84938 units has surpassed management guidance. Export volumes at ~4.03

lakh units have exhibited growth of 6% YoY. EBITDA margins are expected to expand

~210 bps QoQ to 19.4% due to better product mix (higher share of premium 2-W & 3-

W) & positive operating leverage. PAT is expected to decline 1.3% YoY to | 1108 crore

Eicher Motors Eicher’s RE business (motorcycles) has grown ~20.8% YoY to ~202867 units. VECV

(truck business) volumes were at ~15,049 units, up ~12.2% YoY. Revenues may

grow 25.3% YoY to | 2208 crore. EBITDA margins may come in at 31%, down 40 bps

QoQ, due to higher input costs. We expect VECV business margins to expand 80 bps

QoQ to 8.8% as superior product mix (higher M&HCV share) will offset the rise in input

cost. Secondly, positive operating leverage will support higher margins QoQ.

Consolidated PAT is expected at ~| 528 crore

Hero MotoCorp HMCL volumes increased ~13% YoY ~2.02 million units, with de-growth of ~3.7%

YoY in the scooter segment & 13.3% YoY growth in motorcycle segment. Scooter &

motorcycle volumes are expected at ~0.24 million units & ~1.78 million units,

respectively. EBITDA margins are expected to be flat at 16.3% QoQ as the positive

impact of operating leverage will be offset by higher input cost. Topline & PAT are

seen at ~| 8820 & ~| 1061 crore, respectively

M&M Revenues are expected to grow 31% YoY to | 13889 crore on the back of ~9% YoY

volume growth in automotive segment & ~31% YoY growth in farm equipment

segment. Volumes in the automotive segment at 137,524 units have grown on the

back of ~18% YoY growth in the UV segment. Volumes in the tractor segment at

~80,911 units have grown on account of re-stocking. Margins are expected to be flat

QoQ at 10.9% as the operating leverage benefit will be offset by poor product mix. PAT

is expected to grow 6.3% YoY to | 1237 crore

Maruti Suzuki Maruti's volumes have grown ~17.6% YoY to ~4.92 lakh units where the strong

domestic demand of 19.4% YoY is driven by growth in new models, specifically the

newly launched DZire. EBITDA margins are expected to expand 70 bps QoQ to 14% as

operating leverage benefit will offset raw material price increase. Topline is expected

to grow 23% to | 21935 crore. Net ASPs are expected to increase ~1% QoQ due to

product mix. PAT for the quarter is expected at ~| 2149 crore

Tata Motors JLR is expected to clock sales volumes of ~149593 units, up 7.4% YoY, with the

growth attributable to Land Rover models (~70% of JLR volumes) like new model

Velar & new Range Rover. JLR is likely to post topline of ~£6.2 billion (| 63497 crore)

while margins are likely to expand ~160 bps YoY to 11.9% due to a better product

mix. JLR’s PAT is estimated at ~£300 million. Standalone revenues are expected to

increase 30.3% YoY to | 13453 crore due strong volume growth of 13% YoY and

growth in ASP reflecting BSIII to BSIV migration. EBITDA margins are expected at

3.8% due to positive operating leverage. Standalone loss is expected at ~| 551.5

crore

Source: Company, ICICIdirect.com Research

Exhibit 16: Company specific view- OEM

Maruti Suzuki’s sales performance

418

387

414

395

492

20.1

-7.5

7.0

-4.8

24.7

-10

-5

0

5

10

15

20

25

30

0

100

200

300

400

500

600

Q2FY17Q3FY17Q4FY17Q1FY18Q2FY18

(%

)

(000's

)

Sales QoQ growth

Ashok Leyland’s sales performance

33

33

48

28

41

7.3

-1.8

45.0

-40.2

43.8

-60

-40

-20

0

20

40

60

0

10

20

30

40

50

Q2FY17Q3FY17Q4FY17Q1FY18Q2FY18

(%

)

(000's

)

Sales QoQ growth

Eicher Motor’s sales performance

180

186 196

196

218

10.3

3.0

5.3

0.0

11.4

-3

2

7

12

17

22

0

50

100

150

200

250

Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18

(%

)

(000's

)

Sales QoQ growth

ICICI Securities Ltd. | Retail Equity Research

Page 13

Exhibit 17: Company specific view- Ancillaries

Company Remarks

Amara Raja

Batteries

(ARBL)

Good growth in the automotive segment (OEM + replacement) is likely to drive

ARBL's revenue, which is expected to grow 14% YoY to | 1,532 crore. EBITDA

margins are expected to decline 379 bps YoY to 13.3% as average lead prices (key

raw material) increased 20% YoY & 8% QoQ to |151/kg. PAT is expected to decline

21% YoY to | 108 crore

Apollo Tyres

(APL)

Consolidated revenue is likely to grow 8.4% YoY to | 3,345 crore mainly supported by

its Indian operations. The re-stocking of tyres (post GST) is expected to drive its

replacement segment. Average natural rubber price remained flat (down 1% YoY & up

0.2% QoQ to |132/kg). However, we believe APL will enjoy the benefit of low cost raw

material inventory in Q2FY18. EBITDA margins are likely to expand 403 bps QoQ to

12.4%. PAT is expected to decline 18.4% YoY to | 212 crore

Balkrishna

Industries (BIL)

BIL's revenues are expected to grow 9.7% YoY to | 1,023 crore, with volume likely to

increase 11% YoY to 47,231 MT. The management expects the margin to sharply

recover from Q2FY18 onwards (to its traditional level of 28-30%). Thus, we expect

EBITDA margins to expand 726 bps QoQ (down 436 bps YoY) to 28.6%. PAT is

expected to decline 6.1% YoY to | 188 crore

Bharat Forge Revenues are likely to increase 45% YoY to | 1292 crore. Net domestic revenues are

expected to grow 9.9% QoQ to | 554 crore, mainly driven by M&HCV volume growth.

Export revenues are expected to increase 58% YoY to | 712 crore as class 8 truck

volumes have grown YoY while oil & gas revenues are expected to grow significantly.

EBITDA margins are expected to be almost unchanged QoQ at 28.1%. PAT is likely to

increase 67% YoY to | 163 crore

Bosch Its revenue is expected to increase 14% YoY to | 2,978 crore mainly due to strong

recovery in domestic CV & tractor volumes. Its EBITDA margins are expected at 17.9%

flat YoY and up 140 bps QoQ due to a better product mix (lower share of traded of

goods) & cost efficiencies. Bosch had an exceptional gain from sale of its starter

motor & generator division worth | 281 crore in Q2FY17. Thus, a decline of 41% YoY

to |415 crore in PAT is not comparable YoY

Exide Industries

(EIL)

EIL is expected to post highest ever quarterly revenue (up 12% YoY to | 2,158 crore)

supported by good growth in its automotive segment. Further, despite a price hike in

the past (yet to be fully passed on), higher raw material cost will impact its margin,

which is expected to decline 139 bps YoY & 163 bps QoQ to 13.8%. PAT is expected

to decline marginally by 1% YoY to | 179 crore

JK Tyre (JKTIL) Consolidated revenues are expected to grow 9% YoY to | 2,093 crore primarily driven

by Indian operation. The acquired Cavendish Industries (CIL) has witnessed a

turnaround thereby driving its overall performance. EBITDA margins are expected to

improve 910 bps QoQ to 9% as JKTIL will benefit from lower cost inventory in Q2FY18

(unlike in Q1FY18). Higher interest & depreciation (>8% of sales) is likely to impact

PAT that is expected at | 11 crore

MCIE

Automotive

Its standalone business will largely be driven by production volumes of its top two

clients M&M & TML, which account for ~45% of its revenue. Standalone revenue,

EBITDA & PAT are estimated at ~| 479 crore, ~| 47 crore and ~| 21 crore,

respectively. On a consolidated basis, we expect revenue, EBITDA & PAT of | 1424

crore, | 193 crore and | 87 crore, respectively

Motherson

Sumi

MSSL's consolidated revenues are expected to grow 27.6% YoY to | 12,933 crore. The

result would not be comparable on like-to-like basis, as it would include the

performance of newly acquired PKC group (revenue of ~|1900 crore). Its European

operations (SMR & SMP) are expected to continue with its decent performance.

Consolidated EBITDA margin is likely to expand 100 bps QoQ & 10 bps YoY to 10%.

PAT is expected at | 431 crore

Wabco India

(WIL)

WIL’s revenue is expected to grow 15.3% YoY to | 535 crore mainly due to 1)

recovery in domestic M&HCV production volume up >13% YoY, 2) continued growth

momentum in exports and 3) partly driven by new product launches. EBITDA margins

are likely to improve 83 bps YoY & 50 bps QoQ to 15.5%. Subsequently, PAT is

expected to increase 19.6% YoY to | 56 crore

Source: Company, ICICIdirect.com Research

Hero MotoCorp’s sales performance

1823

1474

1622

1854

2023

4.5

-19.2

10.0

14.3

9.1

-25

-15

-5

5

15

1000

1200

1400

1600

1800

2000

2200

Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18

(%

)

(000's

)

Sales QoQ growth

ICICI Securities Ltd. | Retail Equity Research

Page 14

Banking and Financial Institutions

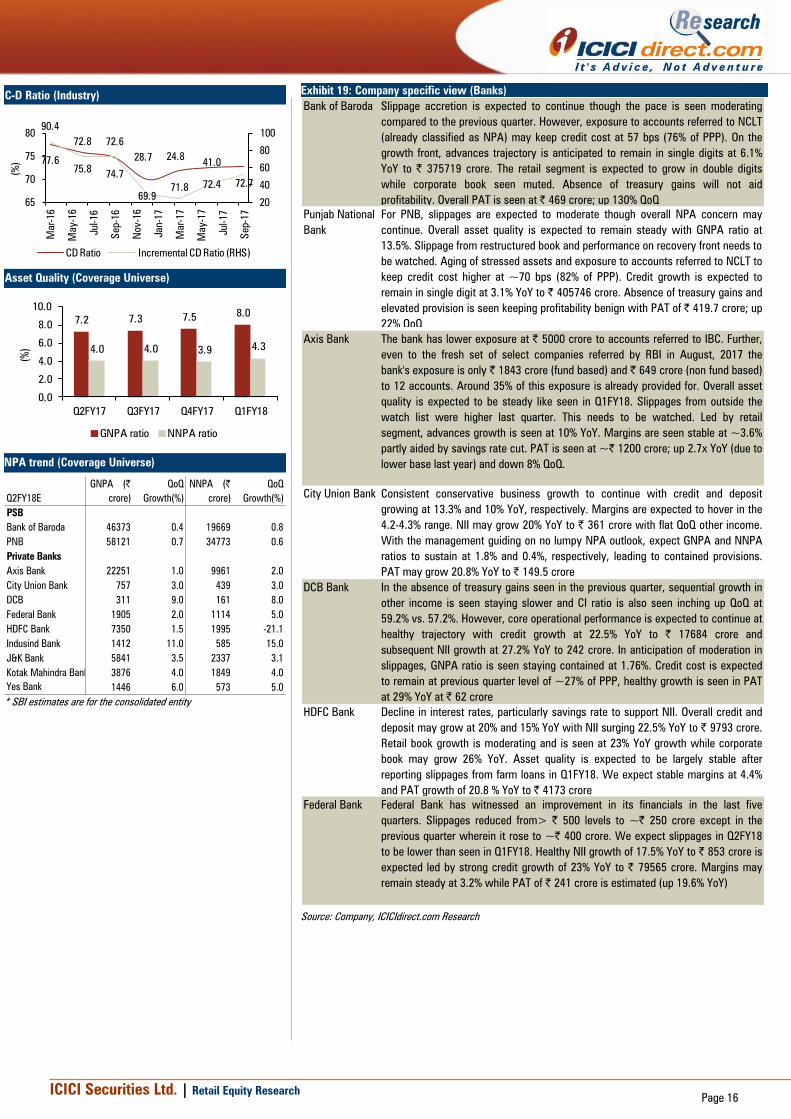

Improvement in credit not yet visible, marginally better CD ratio

Credit growth remained flat at 6.8% YoY as on September 15, 2017.

Deposit growth is seen moderating around 10% YoY as interest rates

decline and demonetisation money flushes out from banks.

Accordingly, the incremental CD ratio has gone up to 51.5% in

September 2017 from lows of 30-40% in the past. For our coverage

universe, credit growth is estimated at 10% YoY. PSU banks are

expected to continue to see single digit growth of ~5.5% YoY while

private banks continue to clock strong 17.9% YoY growth to | 1569368

crore. Retail focused private banks like IndusInd Bank, HDFC Bank, DCB

Bank and even Federal Bank are expected to maintain their strong

growth trajectory of >20% YoY.

Positive trends in steel sector to prevent liquidation risk provisions

Banks have been making additional provisions required to reach 50% in

case of initial 12 accounts referred to NCLT from Q1FY18. In addition,

new list of stressed borrowers would also entail further provisions.

Large banks like PNB & BoB (| 7200 crore exposure in 10 accounts) and

Axis Bank (| 5283 crore in eight accounts) had indicated their exposure

to the 12 accounts is provided for by ~40-50% of the portfolio.

Provisions on a QoQ basis may be largely stable as provision impact

from agri loan slippages in Q1 seems over.

Positive developments in steel sector resulted in large domestic and

international players evincing buying interest in companies referred to

NCLT under IBC (namely Essar Steel, Bhushan Steel & Monnet Ispat).

Any buyout can result in upgradation of status to standard and lower

haircuts may lead to provisions write-back in coming quarters.

Rise in yields, slower quarter to dent other income

Volatility in rupee led by sharp depreciation may impact forex fee

income positively. However, treasury gains were seen muted due to 15

bps rise in 10 year G-Sec to 6.66%. Accordingly, we factor in lower non-

interest income growth for banks in our coverage.

Improving NII to support ageing led higher provisions

Savings interest rate cut of 50 bps by the largest bank remained the

highlight of the quarter, with other banks following suit. Accordingly, a

decline in interest expense would support NII. A higher cut in deposit

rates compared to a decline in MCLR is expected to result in NII growth

of 13.1% YoY and 3.1% QoQ for our coverage universe. We expect our

banking coverage universe PPP to grow at 14.9% YoY and 2.9% QoQ

while PAT is seen growing 39% YoY and 8.7% on a QoQ basis.

We expect fresh NPA accretion to moderate in Q2FY18E. Slippages

from watchlist would be key monitorable. Restructured assets and SDR

is gradually flowing to NPA category. For our coverage universe, we

expect net addition in GNPA at | 7830 crore (| 15154 crore was added

in Q1FY18). Despite moderation in slippages, GNPA ratio is apparently

expected to inch up owing to muted growth in advances.

Within our coverage, mid size banks like Federal Bank, DCB Bank and

City Union Bank are expected to deliver a healthy set of numbers.

Earnings of large private banks like HDFC Bank, IndusInd Bank, Yes

Bank and Kotak Mahindra Bank are expected to continue to remain

strong both on business and earnings growth. Axis Bank’s earnings are

expected to remain stable QoQ but surge 275% YoY, mainly due to

lower provisions (| 2369 crore) in Q2FY18E vs. steep provisions in Q2

last year (| 3622 crore). Large PSBs including PNB and BoB are

expected to report strong PAT growth QoQ with largely stable GNPA.

NBFCs like Bajaj Finance are expected to report stellar PAT growth of

33.3% and expect consistent earnings for HDFC Ltd.

Net interest income (Coverage Universe)

7306

6865

7265

7260

7467

19268

19670

21280

21904

22594

15103

15260

17407

16722

18233

0

10000

20000

30000

40000

50000

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(| C

rore)

PSB Private NBFC

PPP (Coverage Universe)

6002

5750

9252

5865

6233

15421

16745

17808

18059

18383

5869

6209 6

605

6308

6804

0

10000

20000

30000

40000

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(|

Crore)

NBFC Private PSB

Net Profit (Coverage Universe)

417

547

888

5865

6843

7741

8360

8797

3558

3579

3975

3523

3885

0

2000

4000

6000

8000

10000

12000

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(| C

rore)

NBFC Private PSB

Top Picks

Axis Bank

Bank of Baroda

Research Analyst

Kajal Gandhi

Vishal Narnolia

Vasant Lohiya

ICICI Securities Ltd. | Retail Equity Research

Page 15

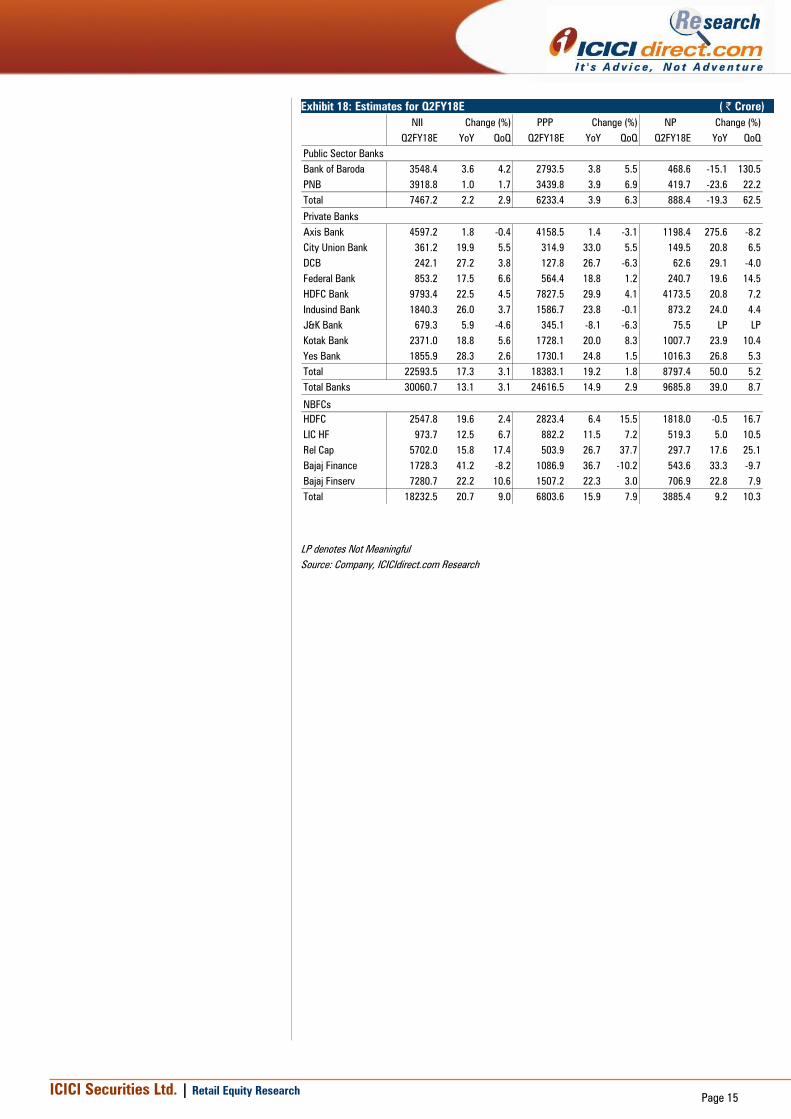

Exhibit 18: Estimates for Q2FY18E ( | Crore)

NII PPP NP

Q2FY18E YoY QoQ Q2FY18E YoY QoQ Q2FY18E YoY QoQ

Bank of Baroda 3548.4 3.6 4.2 2793.5 3.8 5.5 468.6 -15.1 130.5

PNB 3918.8 1.0 1.7 3439.8 3.9 6.9 419.7 -23.6 22.2

Total 7467.2 2.2 2.9 6233.4 3.9 6.3 888.4 -19.3 62.5

Axis Bank 4597.2 1.8 -0.4 4158.5 1.4 -3.1 1198.4 275.6 -8.2

City Union Bank 361.2 19.9 5.5 314.9 33.0 5.5 149.5 20.8 6.5

DCB 242.1 27.2 3.8 127.8 26.7 -6.3 62.6 29.1 -4.0

Federal Bank 853.2 17.5 6.6 564.4 18.8 1.2 240.7 19.6 14.5

HDFC Bank 9793.4 22.5 4.5 7827.5 29.9 4.1 4173.5 20.8 7.2

Indusind Bank 1840.3 26.0 3.7 1586.7 23.8 -0.1 873.2 24.0 4.4

J&K Bank 679.3 5.9 -4.6 345.1 -8.1 -6.3 75.5 LP LP

Kotak Bank 2371.0 18.8 5.6 1728.1 20.0 8.3 1007.7 23.9 10.4

Yes Bank 1855.9 28.3 2.6 1730.1 24.8 1.5 1016.3 26.8 5.3

Total 22593.5 17.3 3.1 18383.1 19.2 1.8 8797.4 50.0 5.2

Total Banks 30060.7 13.1 3.1 24616.5 14.9 2.9 9685.8 39.0 8.7

HDFC 2547.8 19.6 2.4 2823.4 6.4 15.5 1818.0 -0.5 16.7

LIC HF 973.7 12.5 6.7 882.2 11.5 7.2 519.3 5.0 10.5

Rel Cap 5702.0 15.8 17.4 503.9 26.7 37.7 297.7 17.6 25.1

Bajaj Finance 1728.3 41.2 -8.2 1086.9 36.7 -10.2 543.6 33.3 -9.7

Bajaj Finserv 7280.7 22.2 10.6 1507.2 22.3 3.0 706.9 22.8 7.9

Total 18232.5 20.7 9.0 6803.6 15.9 7.9 3885.4 9.2 10.3

Change (%) Change (%) Change (%)

Public Sector Banks

Private Banks

NBFCs

LP denotes Not Meaningful

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 16

Exhibit 19: Company specific view (Banks)

Bank of Baroda Slippage accretion is expected to continue though the pace is seen moderating

compared to the previous quarter. However, exposure to accounts referred to NCLT

(already classified as NPA) may keep credit cost at 57 bps (76% of PPP). On the

growth front, advances trajectory is anticipated to remain in single digits at 6.1%

YoY to | 375719 crore. The retail segment is expected to grow in double digits

while corporate book seen muted. Absence of treasury gains will not aid

profitability. Overall PAT is seen at | 469 crore; up 130% QoQ

Punjab National

Bank

For PNB, slippages are expected to moderate though overall NPA concern may

continue. Overall asset quality is expected to remain steady with GNPA ratio at

13.5%. Slippage from restructured book and performance on recovery front needs to

be watched. Aging of stressed assets and exposure to accounts referred to NCLT to

keep credit cost higher at ~70 bps (82% of PPP). Credit growth is expected to

remain in single digit at 3.1% YoY to | 405746 crore. Absence of treasury gains and

elevated provision is seen keeping profitability benign with PAT of | 419.7 crore; up

22% QoQ

State Bank of Axis Bank The bank has lower exposure at | 5000 crore to accounts referred to IBC. Further,

even to the fresh set of select companies referred by RBI in August, 2017 the

bank's exposure is only | 1843 crore (fund based) and | 649 crore (non fund based)

to 12 accounts. Around 35% of this exposure is already provided for. Overall asset

quality is expected to be steady like seen in Q1FY18. Slippages from outside the

watch list were higher last quarter. This needs to be watched. Led by retail

segment, advances growth is seen at 10% YoY. Margins are seen stable at ~3.6%

partly aided by savings rate cut. PAT is seen at ~| 1200 crore; up 2.7x YoY (due to

lower base last year) and down 8% QoQ.

City Union Bank Consistent conservative business growth to continue with credit and deposit

growing at 13.3% and 10% YoY, respectively. Margins are expected to hover in the

4.2-4.3% range. NII may grow 20% YoY to | 361 crore with flat QoQ other income.

With the management guiding on no lumpy NPA outlook, expect GNPA and NNPA

ratios to sustain at 1.8% and 0.4%, respectively, leading to contained provisions.

PAT may grow 20.8% YoY to | 149.5 crore

DCB Bank In the absence of treasury gains seen in the previous quarter, sequential growth in

other income is seen staying slower and CI ratio is also seen inching up QoQ at

59.2% vs. 57.2%. However, core operational performance is expected to continue at

healthy trajectory with credit growth at 22.5% YoY to | 17684 crore and

subsequent NII growth at 27.2% YoY to 242 crore. In anticipation of moderation in

slippages, GNPA ratio is seen staying contained at 1.76%. Credit cost is expected

to remain at previous quarter level of ~27% of PPP, healthy growth is seen in PAT

at 29% YoY at | 62 crore

HDFC Bank Decline in interest rates, particularly savings rate to support NII. Overall credit and

deposit may grow at 20% and 15% YoY with NII surging 22.5% YoY to | 9793 crore.

Retail book growth is moderating and is seen at 23% YoY growth while corporate

book may grow 26% YoY. Asset quality is expected to be largely stable after

reporting slippages from farm loans in Q1FY18. We expect stable margins at 4.4%

and PAT growth of 20.8 % YoY to | 4173 crore

Federal Bank Federal Bank has witnessed an improvement in its financials in the last five

quarters. Slippages reduced from> | 500 levels to ~| 250 crore except in the

previous quarter wherein it rose to ~| 400 crore. We expect slippages in Q2FY18

to be lower than seen in Q1FY18. Healthy NII growth of 17.5% YoY to | 853 crore is

expected led by strong credit growth of 23% YoY to | 79565 crore. Margins may

remain steady at 3.2% while PAT of | 241 crore is estimated (up 19.6% YoY)

Source: Company, ICICIdirect.com Research

C-D Ratio (Industry)

77.6

75.874.7

69.9

71.872.4 72.7

90.4

72.8 72.6

28.7 24.841.0

20

40

60

80

100

65

70

75

80

Mar-16

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

(%

)

CD Ratio Incremental CD Ratio (RHS)

Asset Quality (Coverage Universe)

7.2 7.3 7.58.0

4.0 4.0 3.94.3

0.0

2.0

4.0

6.0

8.0

10.0

Q2FY17 Q3FY17 Q4FY17 Q1FY18

(%)

GNPA ratio NNPA ratio

NPA trend (Coverage Universe)

PSB

Bank of Baroda 46373 0.4 19669 0.8

PNB 58121 0.7 34773 0.6

Private Banks

Axis Bank 22251 1.0 9961 2.0

City Union Bank 757 3.0 439 3.0

DCB 311 9.0 161 8.0

Federal Bank 1905 2.0 1114 5.0

HDFC Bank 7350 1.5 1995 -21.1

Indusind Bank 1412 11.0 585 15.0

J&K Bank 5841 3.5 2337 3.1

Kotak Mahindra Bank 3876 4.0 1849 4.0

Yes Bank 1446 6.0 573 5.0

Q2FY18E

GNPA (|

crore)

QoQ

Growth(%)

NNPA (|

crore)

QoQ

Growth(%)

* SBI estimates are for the consolidated entity

ICICI Securities Ltd. | Retail Equity Research

Page 17

Exhibit 20: Company specific view contd. (Banks)

Jammu &

Kashmir Bank

For J&K Bank, moderation is expected in slippages. However, a robust recovery in

Q1FY18 remains unlikely. Therefore, GNPA ratio is expected to inch up to 11.5%.

High proportion of stressed assets and provision on NCLT exposure to keep credit

cost higher at 53 bps (72% of PPP), though lower compared to previous quarters.

Floating provision of | 349 crore and increased PCR at 70.3% provides comfort.

Credit growth is expected to remain flattish at | 47759 crore. With credit cost,

lower than previous quarter and steady operational performance, PAT is seen at |

75 crore

Kotak Mahindra

Bank

Expect continuance of steady performance on both asset quality as well as

earnings. Advances trajectory is expected to remain healthy at 18.5% YoY to |

149328 crore, led by retail segment. With margins seen stable at ~4.5%, NII

growth is expected at 18.8% YoY to | 2371 crore. Stable credit cost at ~15 bps,

with no major impact from exposure to NCLT referred accounts, is seen aiding

profitability. Asset quality is expected to remain steady with GNPA ratio at 2.6%.

The management's commentary on strategy on insurance business needs to

watched

Yes Bank Earnings growth is expected to continue at healthy pace at 26.8% YoY to | 1016

crore, led by 28.3% and 27.2% YoY growth in NII and other income respectively. On

the growth front, the advances trajectory is seen remaining robust at 30.2% YoY to

| 143471 crore. A recent cut in saving interest rates would aid stability in margins

at ~3.6-3.7%, though the impact will be fully visible from Q3FY18 onwards. Asset

quality is seen remaining steady with GNPA ratio at 1.01%, with bias towards

improvement on reversal of ~| 365.9 crore exposure to JP Associate out of total

exposure of | 911 crore

IndusInd Bank We expect IndusInd Bank's overall consistent performance to continue in Q2FY18E.

We expect growth of 25% YoY to | 123836 crore led by corporate finance segment.

In consumer finance, non vehicle segment like LAP and credit cards would continue

to drive growth. Margins are expected to be strong at ~3.8-3.9% range with partial

positive impact of savings rate cut. This would lead to NII growth of 26% YoY to |

1840 crore. PAT of | 873 crore is expected, up 24% YoY while asset quality should

remain largely steady

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 18

Exhibit 21: Company specific view (NBFCs)

LIC Housing

Finance

We expect advances growth of ~15.0% YoY (| 150760 crore) to be maintained.

Individual home loans (~96% of the portfolio) are also expected to increase 13.7%

YoY while developer loans traction is expected to be at higher rate YoY. Margins,

which had risen to ~3%, have fallen back to 2.5% levels in Q1FY18 owing to a rise

in NPAs. We expect NPAs to be lower than in Q1FY18. This, in turn, would support

NIMs at ~2.55%. PAT growth of 5% YoY to | 519 crore is estimated

Reliance Capital Demerger and listing of housing finance is over. It still continues to stay in

consolidated financials. NII may grow 26% YoY with strong loan book growth of

>50% in home and ~12% growth in commercial finance. Life insurance and

general insurance are expected to report an improvement in premium growth. AMC

is expected to report PBT of | 150 crore, AUMs are seen flat QoQ led by equity

market corrections and debt yields rising in September. Revenues are seen rising

16% YoY to | 5702 crore led by premium growth. PAT growth is estimated to be |

298 crore rising 18% YoY

HDFC Ltd In case of HDFC Ltd, credit growth is estimated to be steady at 15% YoY to |

316717 crore led by higher traction in corporate loans and ~13% YoY growth in

individual segment (~70% of portfolio). GNPA ratio is expected to be lower than

1.12% in Q1FY18. This would support reported margins at ~3.9-4%. NII growth of

19.6% YoY to | 2548 crore is estimated. Gains on sale of investments would be

muted in Q2FY18 while dividend income of >| 300 crore is expected. PAT is seen

at | 1818 crore, flat YoY and up 17% QoQ

Bajaj Finance For Bajaj Finance Q2 is seasonally a weak quarter compared to Q1 and Q3.

However, led by consumer finance segment, we estimate AUM will increase 34%

YoY to | 70000 crore. Healthy sales by e-commerce companies would support

AUM traction, which along with healthy calculated margins of ~9.5% could lead to

NII growth of 41% YoY | 1728 crore. Asset quality may stay healthy while

provisions are seen lower QoQ. PAT of | 544 crore is expected, up 33% YoY (down

10% QoQ)

Bajaj Finserv Bajaj Finserv’s consolidated revenue is expected to grow at a healthy pace of

22.2% YoY to | 7281 crore, while PBT is seen at | 1507 crore, up 22.3% YoY.

Among segments, AUM of lending business is expected to continue to grow at a

healthy pace of more than 30% YoY. Subsequently, topline and PBT of finance

segment is expected to grow 31.1% and 31.6% YoY, respectively. Seasonality and

higher retention in crop insurance is seen keeping healthy traction in general

insurance premium at 22% YoY. Pick up in rated individual new business premium

seen in Q1FY18, is expected to continue ahead. Total premium (new as well as

renewal) growth in life insurance is expected at 7% YoY. On profitability, PBT is

expected at | 232 crore. Overall PAT is expected at | 707 crore; up 22.8% YoY

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 19

Building materials

Re-stocking begins at dealer’s level…

The GST impact continued to weigh on the building materials

segment as significant de-stocking took place at the dealer’s level

during June-July 2017. However, recent media interaction of

various company managements indicates that things have

improved August 2017 onwards & a recovery has been seen.

Further, companies are expected to witness strong growth in

H2FY18E led by improvement in demand, re-stocking at dealer’s

level and implementation of e-way bill from October 1, 2017.

Overall, in Q2FY18E, our building material universe is expected to

post topline growth of 4.0% YoY to | 2674.3 crore.

We believe that in the long term, GST would be positive for

organised players as it would establish a level playing field & help

them gain market share from unorganised players who would now

come under the tax ambit. Currently, the organised segment

accounts for only ~50% in tiles industry and ~25% in plywood

industry, which could significantly rise over the next few years

given the GST implementation.

Tiles universe revenues expected to grow 3.5% YoY...

Our tiles universe is expected to post subdued sales volume

growth of 3.0% YoY to 29.4 MSM as sales would be impacted by

dealer de-stocking in the first half of Q2FY18. Hence, we expect

topline to grow moderately by 3.5% YoY to | 1114.0 crore.

However, we expect EBITDA margins to contract 120 bps YoY to

14.1% due to 200 bps YoY contraction in Kajaria’s EBITDA margins

to 18.0%. Hence, we expect the bottomline to de-grow 1.2% YoY to

| 86.6 crore.

Plywood universe revenues expected to grow 3.0% YoY...

With Century’s revenues expected to grow 5.1% YoY, we expect

the plywood universe’s topline to grow 3.0% YoY to | 921.7 crore.

EBITDA margins are expected to contract 70 bps YoY to 15.0% due

to higher input costs. Consequently, we expect the bottomline of

our plywood universe to de-grow 4.3% YoY to | 80.7 crore.

Exhibit 22: Estimates for Q2FY18E (Tiles) (| crore)

Revenue EBITDA PAT

Q2FY18E YoY QoQ Q2FY18E YoY QoQ Q2FY18E YoY QoQ

Kajaria Ceramics 652.8 3.8 4.0 117.5 -6.4 13.3 61.9 -2.7 21.5

Somany Ceramics 461.2 3.1 38.4 39.2 0.3 198.3 24.6 2.7 309.9

Total 1,114.0 3.5 15.9 156.7 -4.8 34.1 86.6 -1.2 51.9

Company

Change (%) Change (%) Change (%)

Source: Company, ICICIdirect.com Research

Exhibit 23: Estimates for Q2FY18E (Plywood) (| crore)

Revenue EBITDA PAT

Q2FY18E YoY QoQ Q2FY18E YoY QoQ Q2FY18E YoY QoQ

Century Plyboards 482.8 5.1 10.1 72.8 -3.9 19.1 43.6 -11.5 27.8

Greenply Industries 438.9 0.9 12.4 65.8 2.3 35.1 37.1 5.8 21.2

Total 921.7 3.0 11.2 138.5 -1.0 26.2 80.7 -4.3 24.7

Change (%)

Company

Change (%) Change (%)

Source: Company, ICICIdirect.com Research

Exhibit 24: Estimates for Q2FY18E (Home Improvement) (| crore)

Revenue EBITDA PAT

Q2FY18E YoY QoQ Q2FY18E YoY QoQ Q2FY18E YoY QoQ

Shankara Building 638.6 6.1 7.9 41.9 8.3 7.1 19.0 33.9 10.4

Total 638.6 6.1 7.9 41.9 8.3 7.1 19.0 33.9 10.4

Company

Change (%) Change (%) Change (%)

Source: Company, ICICIdirect.com Research

Topline & Profitability (Tiles universe)

1076

1025

1279

961

1114

0

300

600

900

1200

1500

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

| C

rore

3.0

6.0

9.0

12.0

15.0

18.0

(%

)

Revenue EBITDA Margin PAT Margin

Topline & Profitability (Plywood universe)

894

783 934

829

922

0

250

500

750

1000

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

| C

rore

0.0

4.0

8.0

12.0

16.0

20.0

(%

)

Revenue EBITDA Margin PAT Margin

Sales Volume Trend (Tiles Universe)

16.6

15.9

19.3

16.4

17.2

11.9

11.2

15.6

9.3

12.3

4

8

12

16

20

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18E

(M

SM

)

Kajaria Ceramics Somany Ceramics

Top pick of the sector

Shankara Building Products

Century Plyboards

Research Analyst

Deepak Purswani, CFA

Vaibhav Shah

ICICI Securities Ltd. | Retail Equity Research

Page 20

Exhibit 25: Company specific view (Tiles coverage universe)

Company Remarks

Kajaria Ceramics Though sales in July 2017 were impacted by dealer de-stocking amid GST roll-out,

a recovery at the dealer’s level has started from August onwards. Consequently, we

expect sales volumes to grow moderately at 3.1% YoY to 17.2 million square metre

(MSM). Hence, the topline is expected to grow 3.8% YoY to | 652.8 crore. Further,

we expect EBITDA margins to decline 200 bps YoY to 18.0% due to the high base

effect (the company recorded EBITDA margins of 20% due to lower gas prices in

the base quarter). Consequently, we expect the bottomline to de-grow 2.7% YoY to

| 61.9 crore mainly due to EBITDA margin contraction

Somany

Ceramics

With sales impacted in July 2017 post GST implementation, the management has

mentioned that re-stocking has begun from mid-August onwards. Hence, we expect

Somany to post subdued volume growth of 2.9% YoY to 12.3 MSM. Consequently,

we expect the topline to grow 3.1% YoY to | 461.2 crore. Further, we expect

EBITDA margins to contract 30 bps YoY to 8.5% led by higher raw material costs

(60.9% in Q2FY18E vs. 60.7% in Q2FY17). Consequently, we expect the bottomline

to grow moderately at 2.7% YoY to | 24.6 crore

Source: Company, ICICIdirect.com Research

Exhibit 26: Company specific view (Plywood coverage universe)

Company Remarks

Century Plyboard With a steady improvement in the demand environment, we expect Century to post

a moderate topline growth of 5.1% YoY to | 482.8 crore. Its plywood and allied

division revenues are expected to grow 3.6% YoY to | 336.8 crore while laminates

and allied division segment is expected to post a topline growth of 5.7% YoY to |

103.5 crore. Further, we expect EBITDA margins to contract 140 bps YoY to 15.1%

mainly on account of a 310 bps YoY contraction in plywood & allied division EBIT

margin to 12% due to a hike in raw material costs. Hence, the bottomline is

expected to decline 11.5% YoY to | 43.6 crore led by EBITDA margin contraction

and higher effective tax rate (19% in Q2FY18E vs. 15.6% in Q2FY17)

Greenply

Industries

Greenply is expected to post flattish topline growth of 0.9% YoY at | 438.9 crore as

its plywood division revenues are expected to post 2.3% YoY de-growth to | 303.8

crore due to the impact of de-stocking in July, 2017. However, MDF revenues are

expected to grow strongly at 10.1% YoY to | 136.1 crore as it is not much impacted

due to destocking. Furthermore, we expect EBITDA margins to expand 20 bps YoY

to 15.0% led by 60 bps YoY improvement in plywood division margins to 11%.

Consequently, we expect the bottomline to grow 5.8% YoY to | 37.1 crore

Source: Company, ICICIdirect.com Research

Exhibit 27: Company specific view (Home Improvement coverage universe)

Company Remarks

Shankara Building

Products

We expect Shankara's topline to grow 6.1% YoY to | 638.6 crore led by robust

growth of 20% YoY to | 319.6 crore in its retail division. On the other hand, we

expect channel and enterprise division revenues to decline 5% YoY to | 319.0 crore

in line with the management's plan to reduce channel division revenues. With a

higher share of high margin retail division (50% share in Q2FY18E revenues vs.

44.2% in Q2FY17), we expect EBITDA margins to expand 20 bps YoY to 6.6%.

Overall, we expect its bottomline to grow robustly at 33.9% YoY to | 19.0 crore led

by the strong performance of retail division and lower interest expenses

Source: Company, ICICIdirect.com Research

Major News during Q2FY18 (Building materials)

The company has opened its 117th retail store at

Mysore admeasuring 22100 sq ft

The company has opened its 118th retail store at

Bangalore admeasuring 3000 sq ft

Shankara

Building

Products

ICICI Securities Ltd. | Retail Equity Research

Page 21

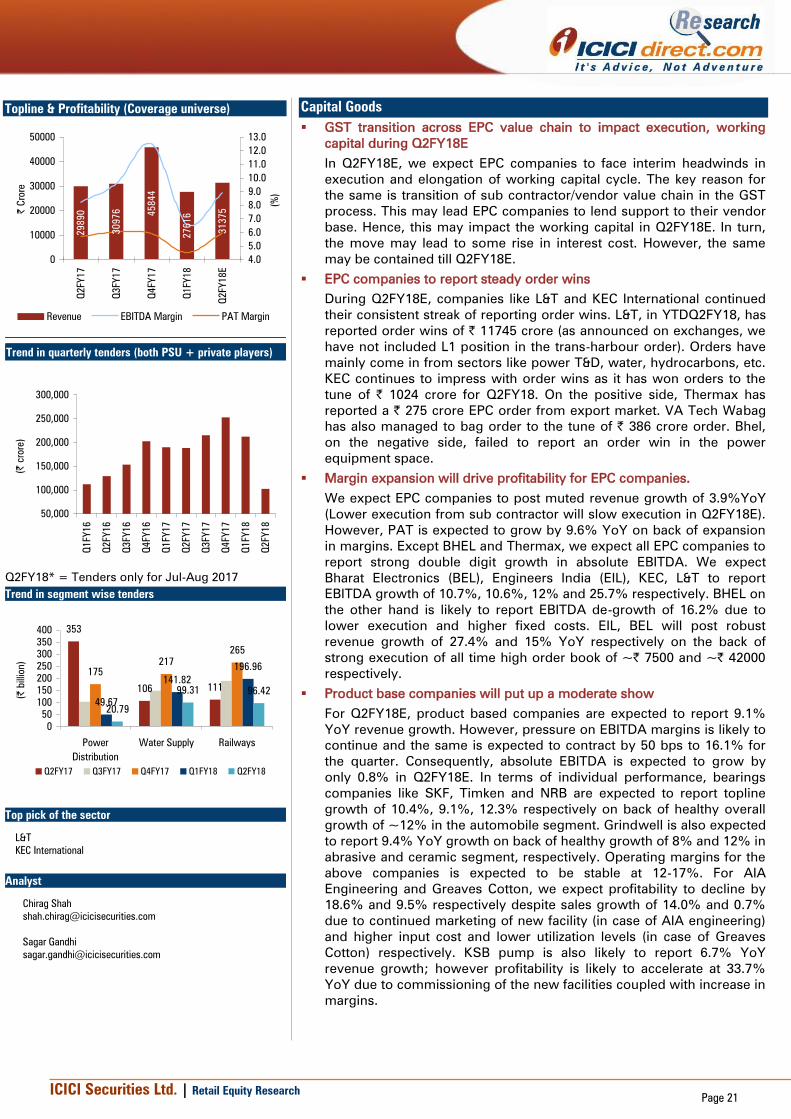

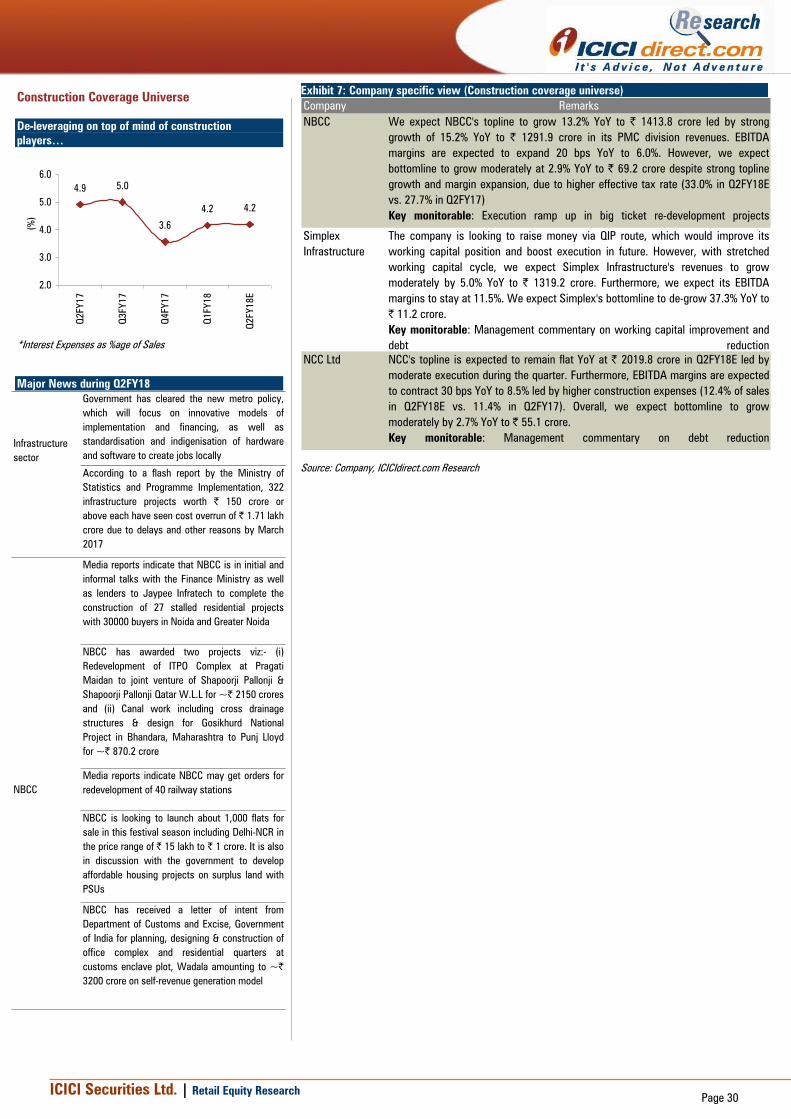

Capital Goods

GST transition across EPC value chain to impact execution, working

capital during Q2FY18E

In Q2FY18E, we expect EPC companies to face interim headwinds in

execution and elongation of working capital cycle. The key reason for

the same is transition of sub contractor/vendor value chain in the GST

process. This may lead EPC companies to lend support to their vendor

base. Hence, this may impact the working capital in Q2FY18E. In turn,

the move may lead to some rise in interest cost. However, the same

may be contained till Q2FY18E.

EPC companies to report steady order wins

During Q2FY18E, companies like L&T and KEC International continued

their consistent streak of reporting order wins. L&T, in YTDQ2FY18, has

reported order wins of | 11745 crore (as announced on exchanges, we

have not included L1 position in the trans-harbour order). Orders have

mainly come in from sectors like power T&D, water, hydrocarbons, etc.

KEC continues to impress with order wins as it has won orders to the

tune of | 1024 crore for Q2FY18. On the positive side, Thermax has

reported a | 275 crore EPC order from export market. VA Tech Wabag

has also managed to bag order to the tune of | 386 crore order. Bhel,

on the negative side, failed to report an order win in the power

equipment space.