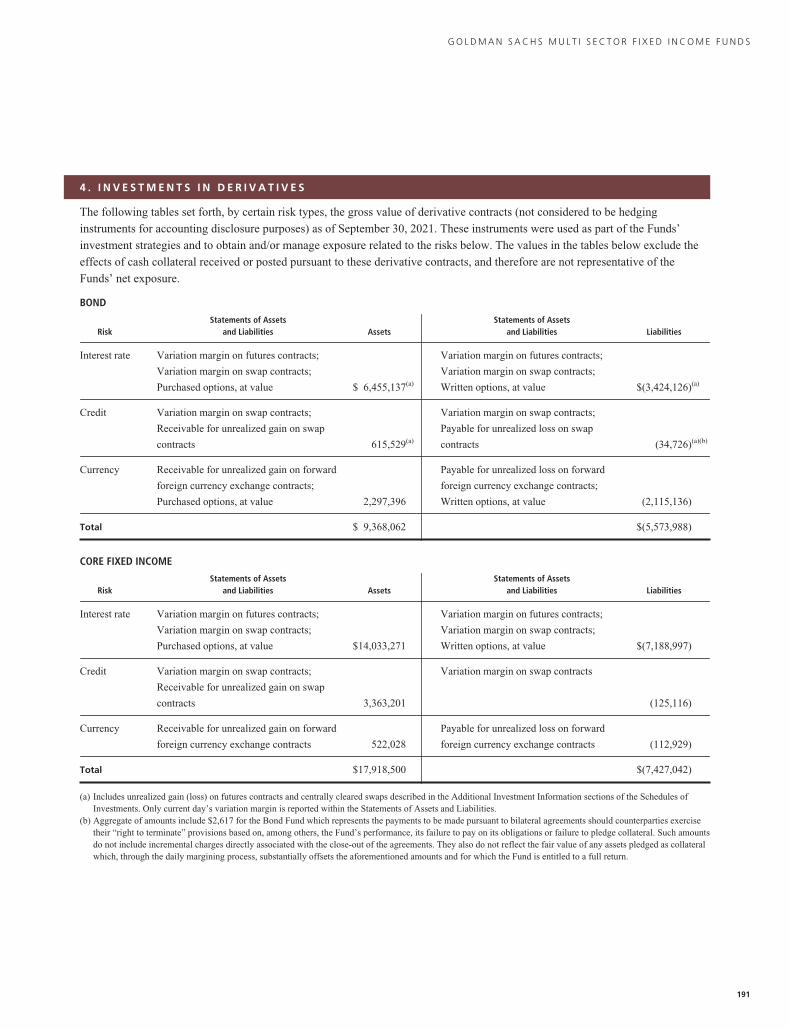

multi sector fixed income funds - goldman sachs asset

TRANSCRIPT

Goldman Sachs Funds

Semi-Annual Report September 30, 2021

Multi Sector Fixed Income FundsBondCore Fixed IncomeGlobal Core Fixed IncomeIncomeLong Short Credit StrategiesStrategic Income

Goldman Sachs Multi Sector Fixed Income Funds

� BOND

� CORE FIXED INCOME

� GLOBAL CORE FIXED INCOME

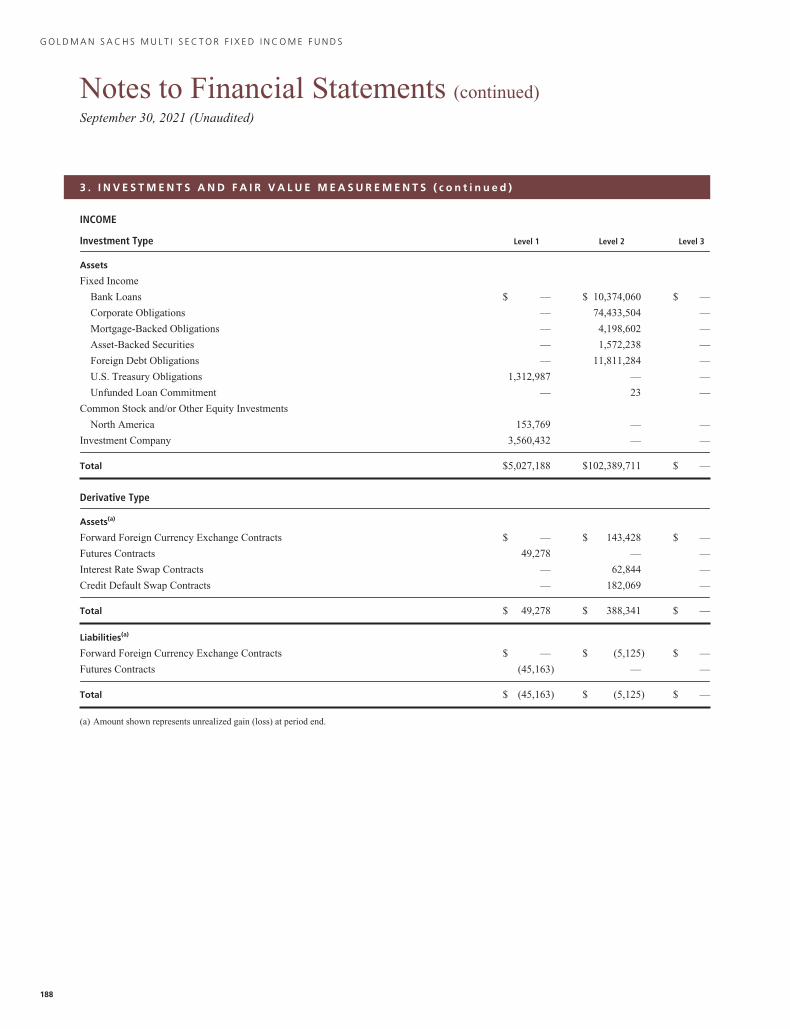

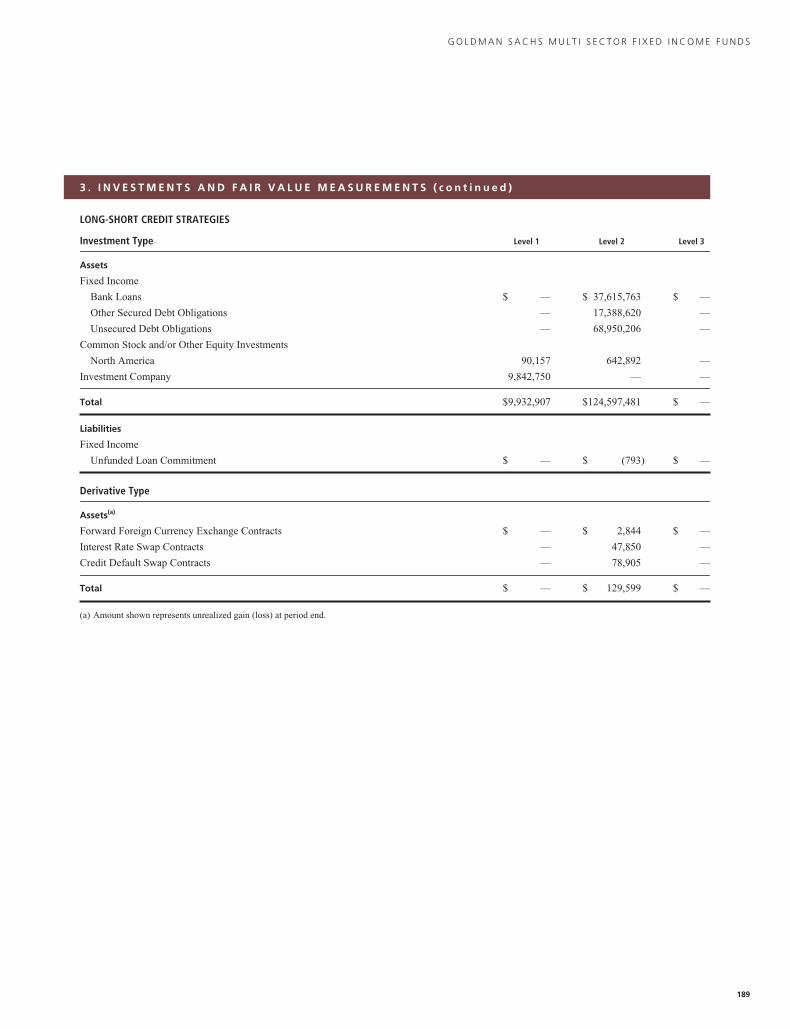

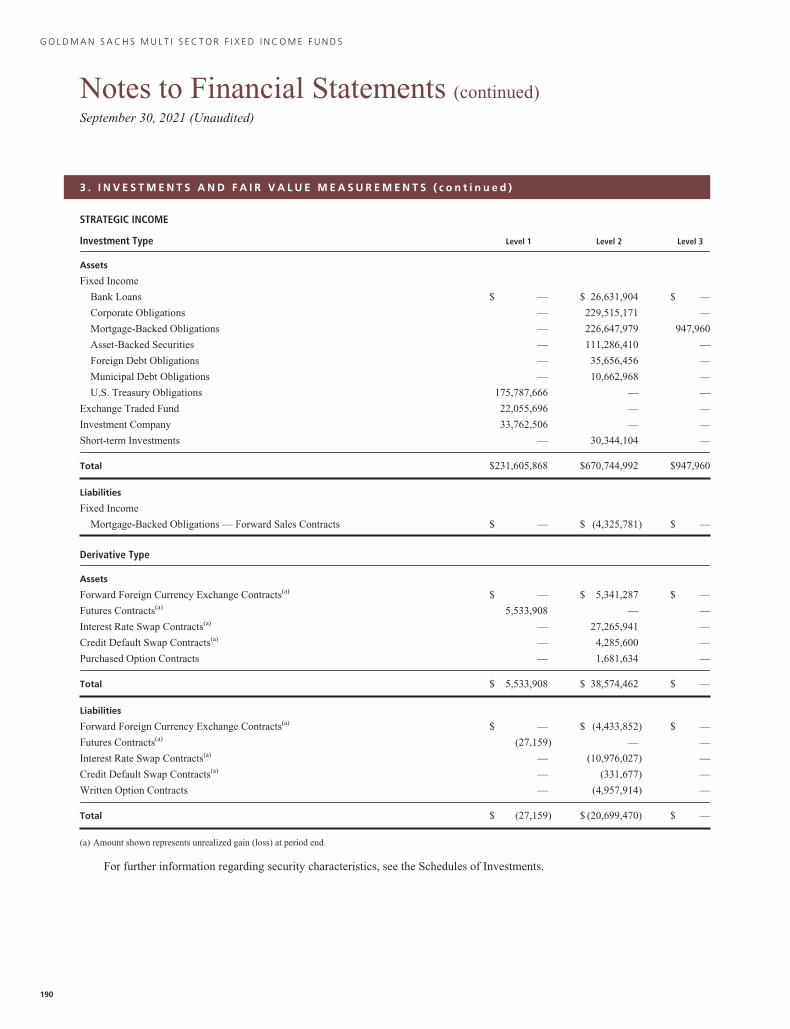

� INCOME

� LONG SHORT CREDIT STRATEGIES

� STRATEGIC INCOME

TABLE OF CONTENTS

Fund Basics 2

Schedules of Investments 15

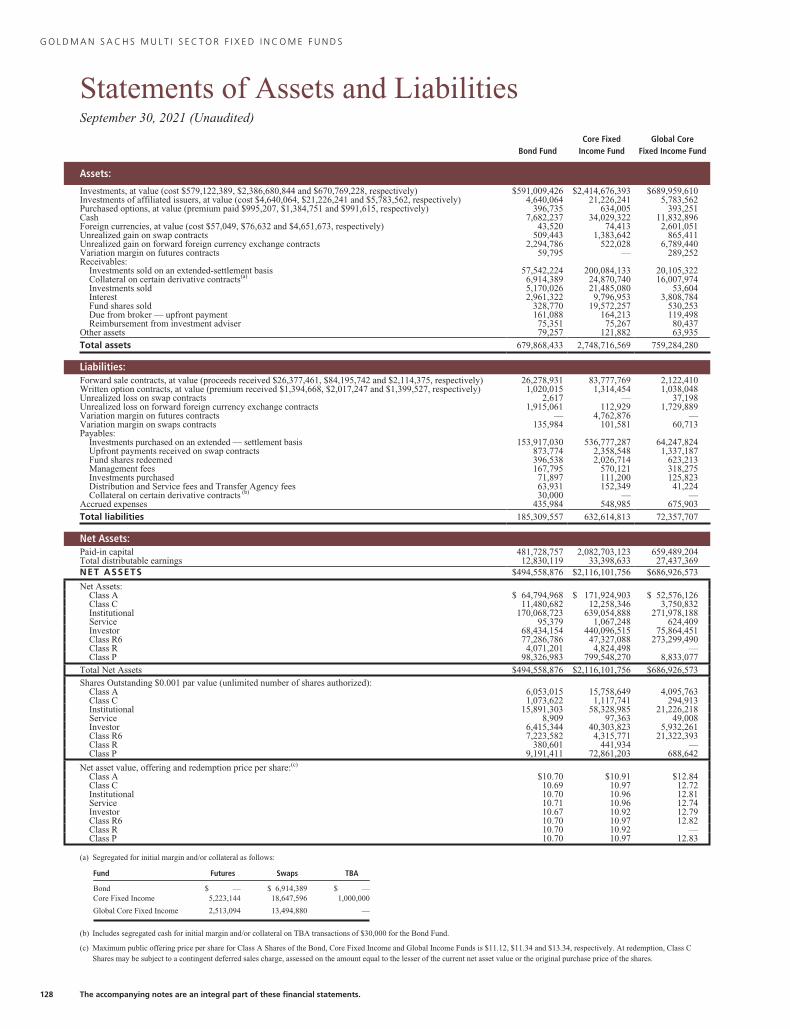

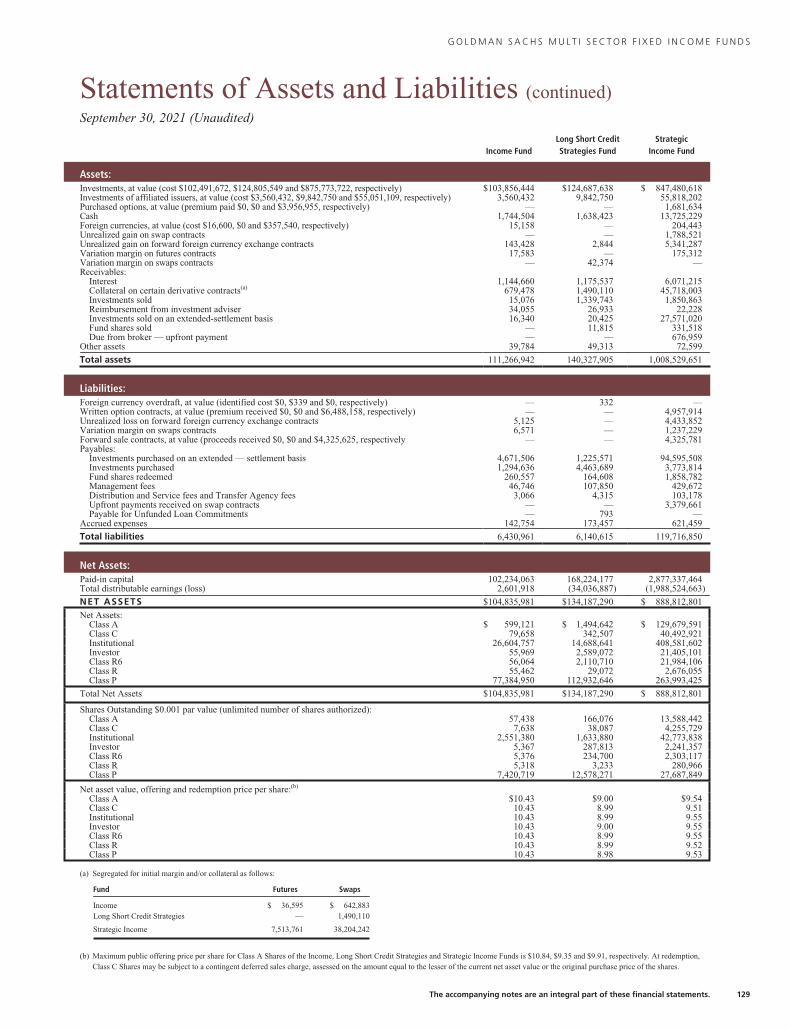

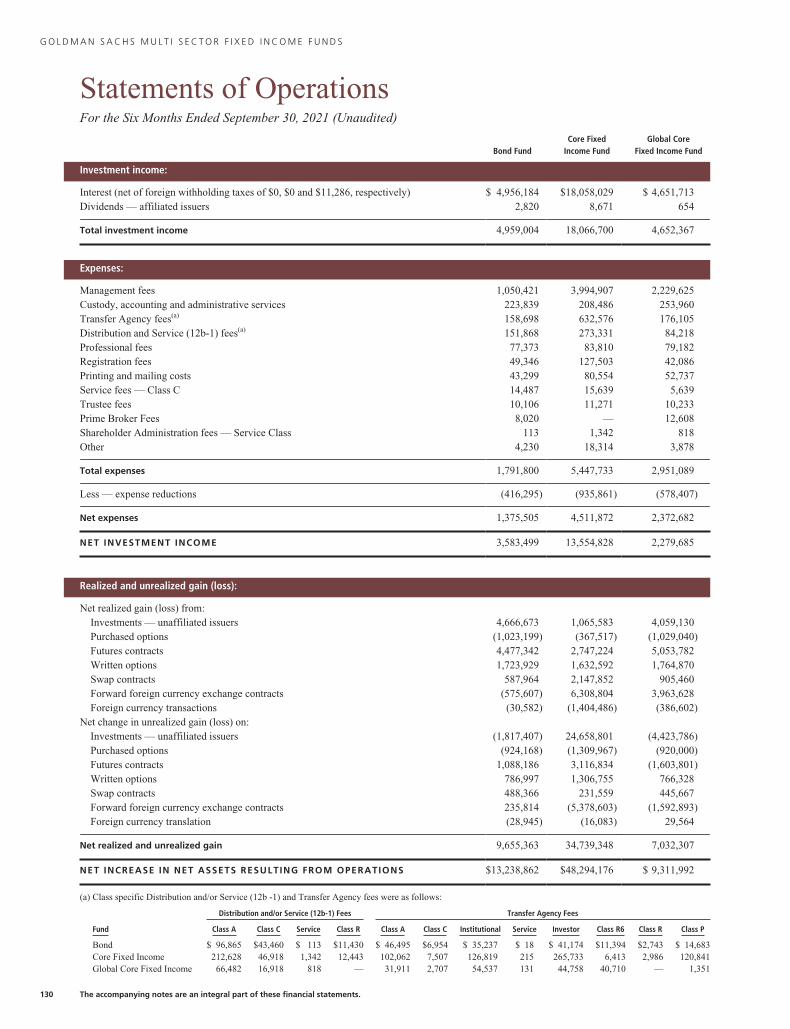

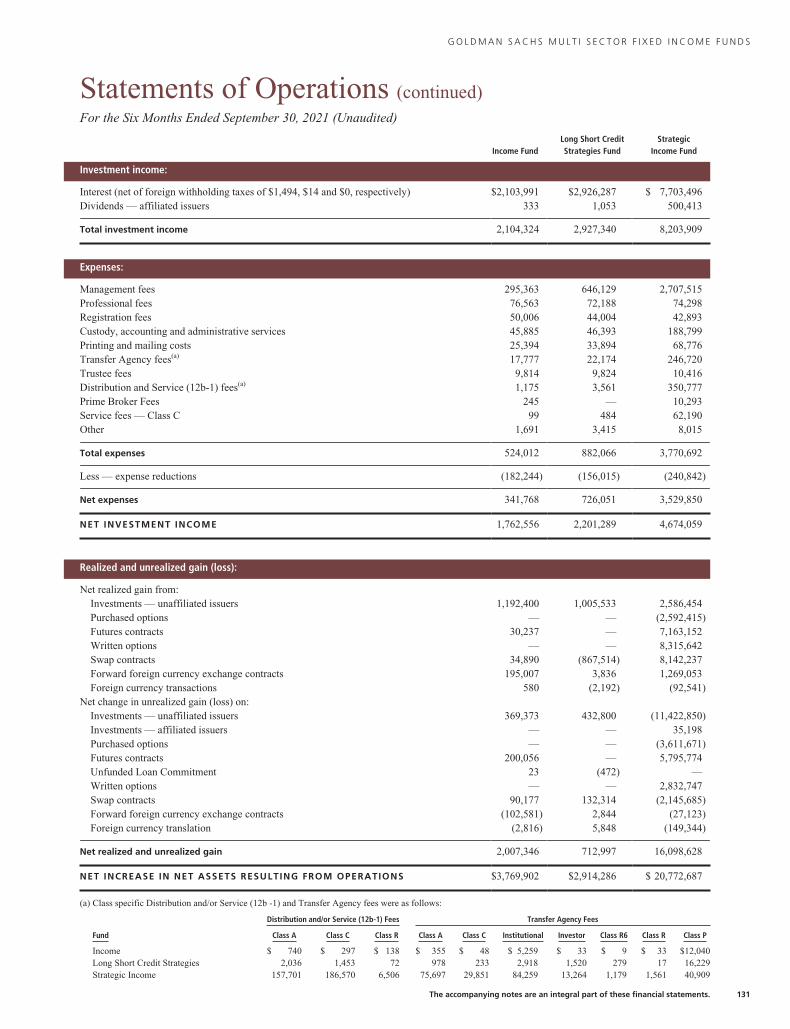

Financial Statements 128

Financial Highlights 135

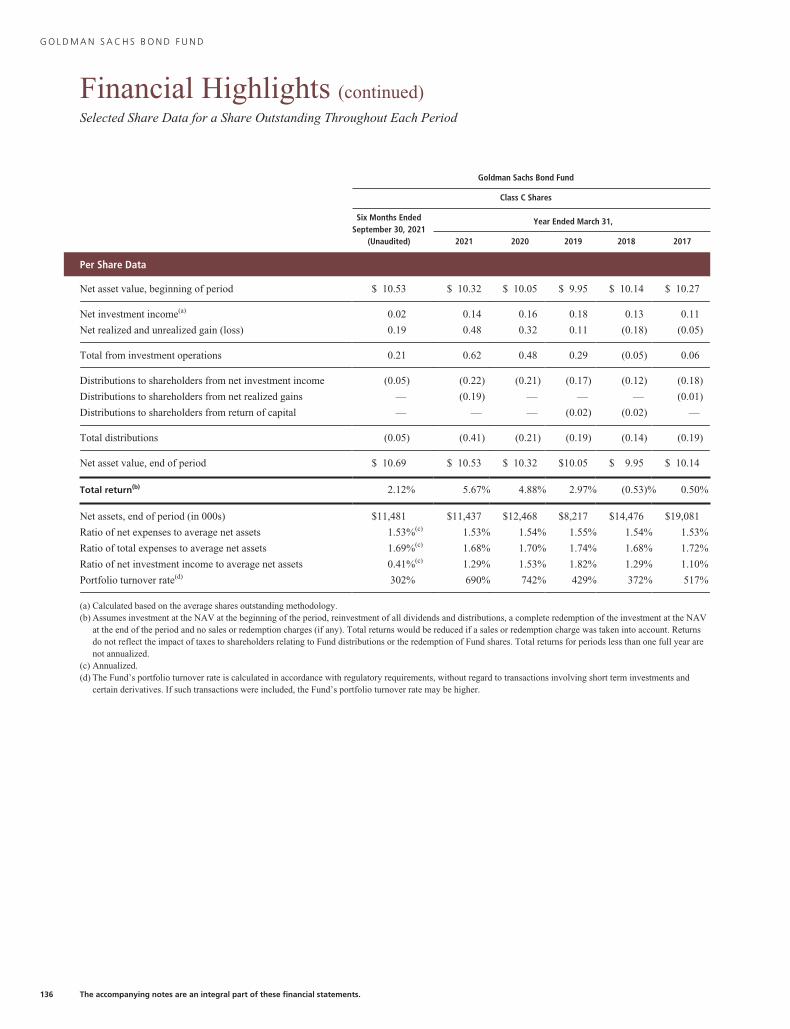

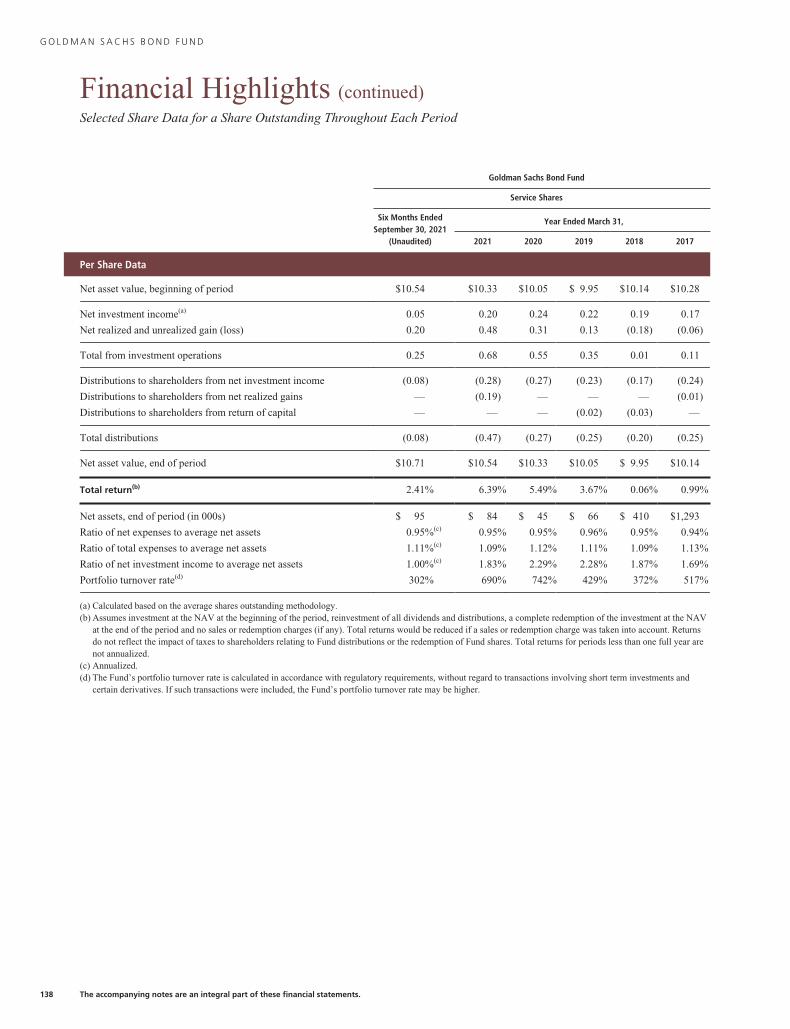

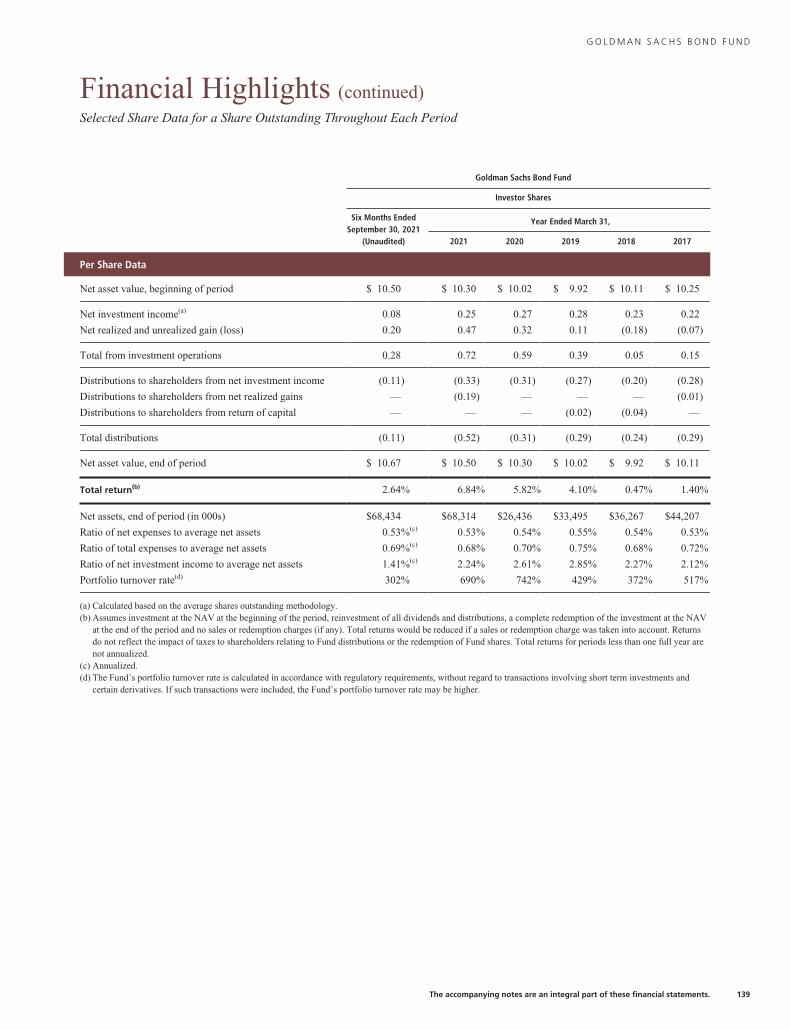

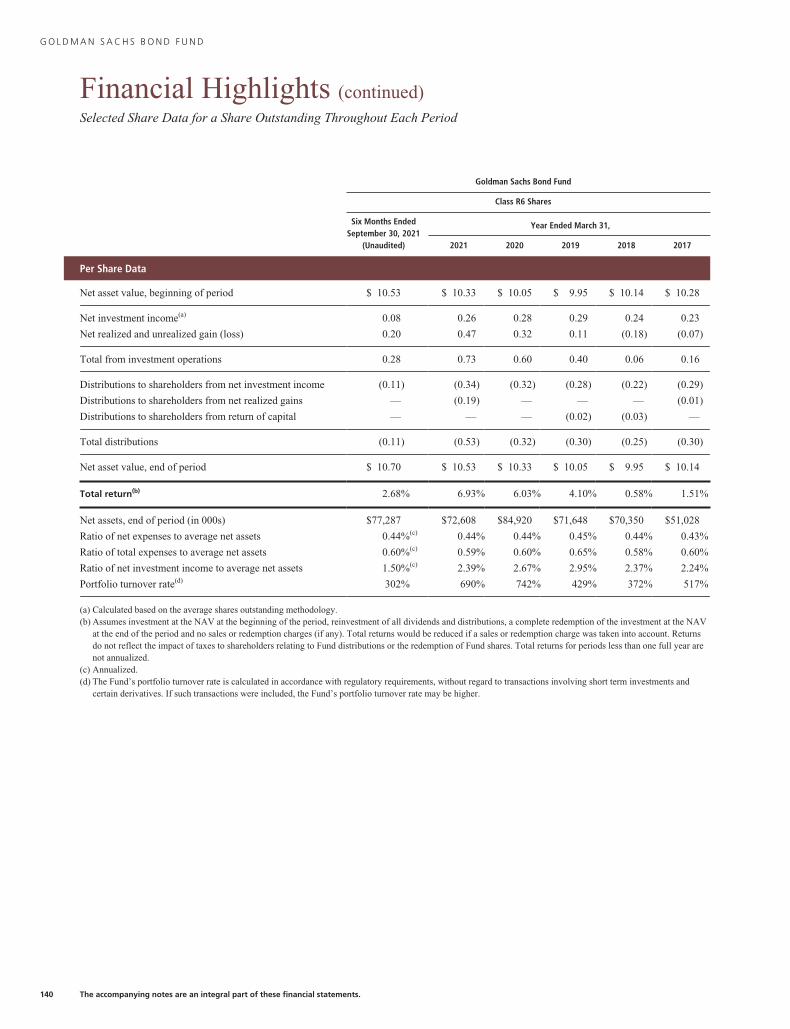

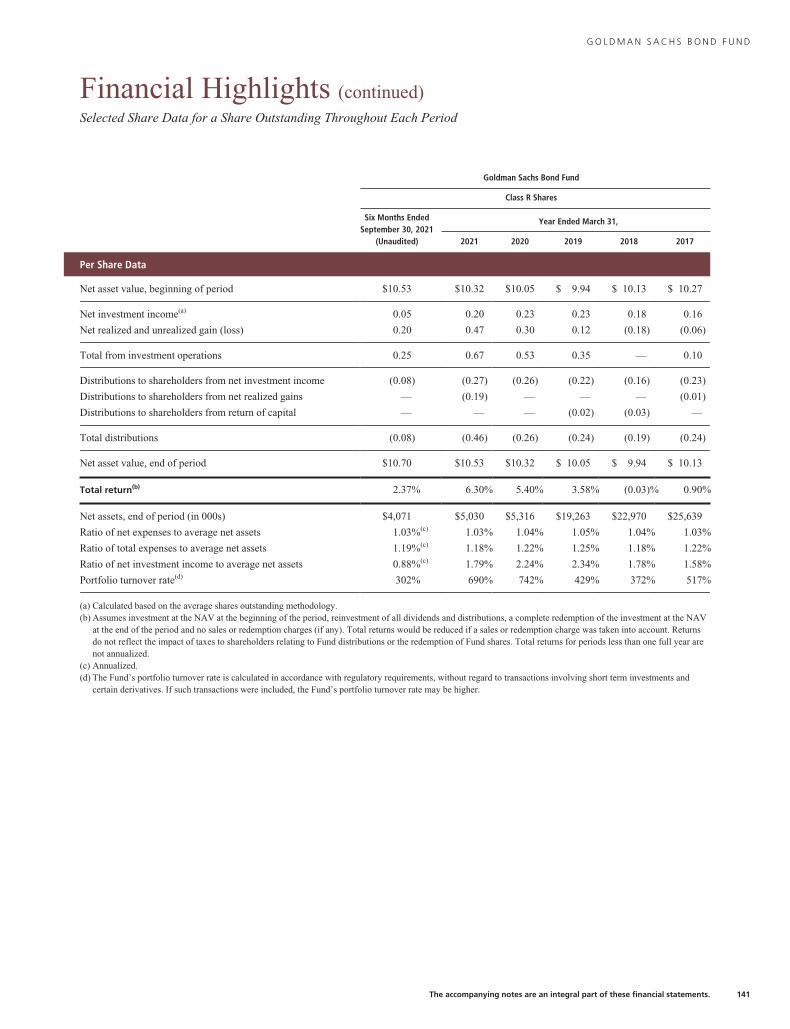

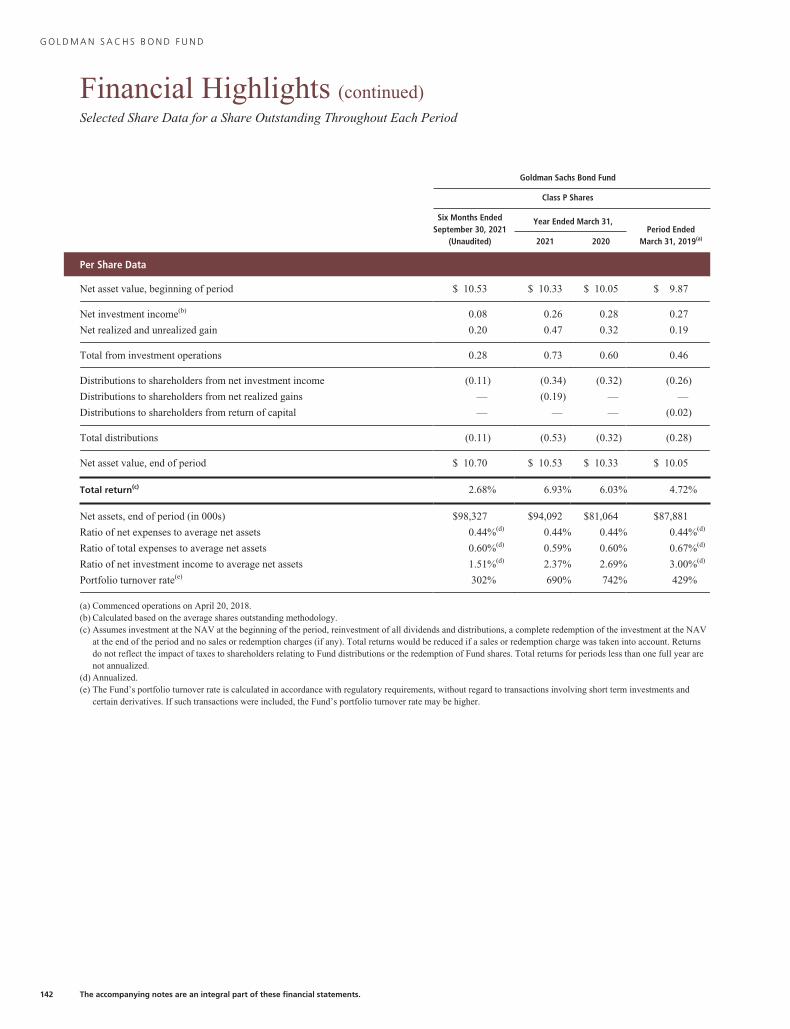

Bond 135

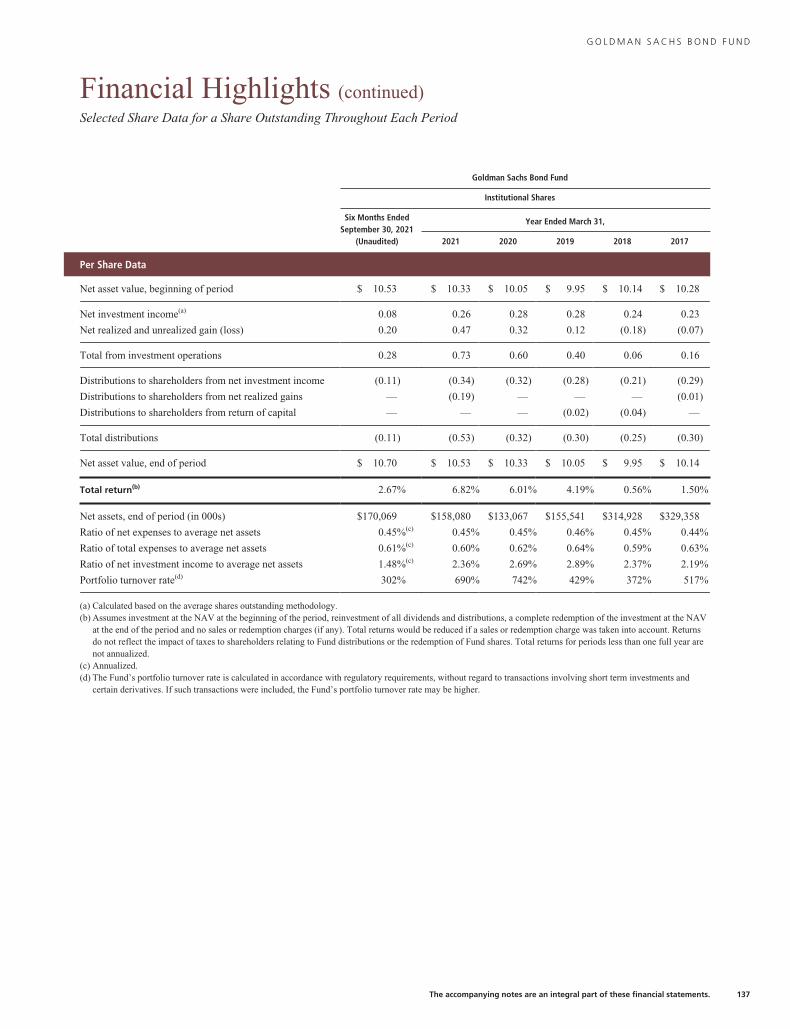

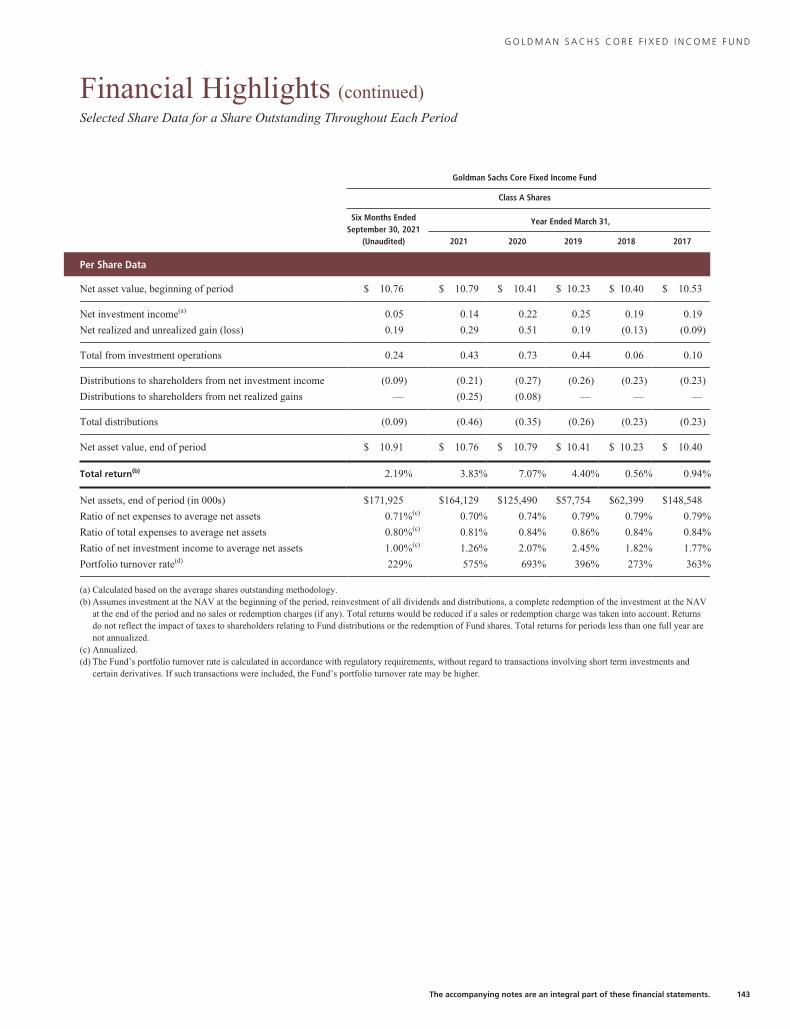

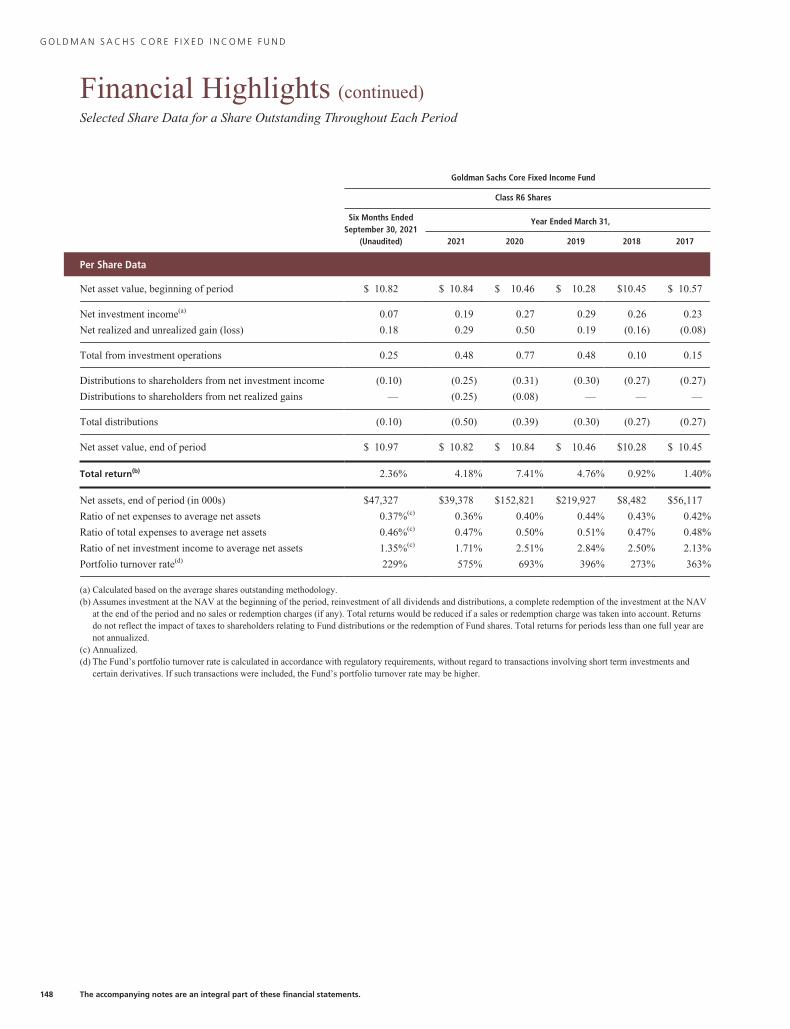

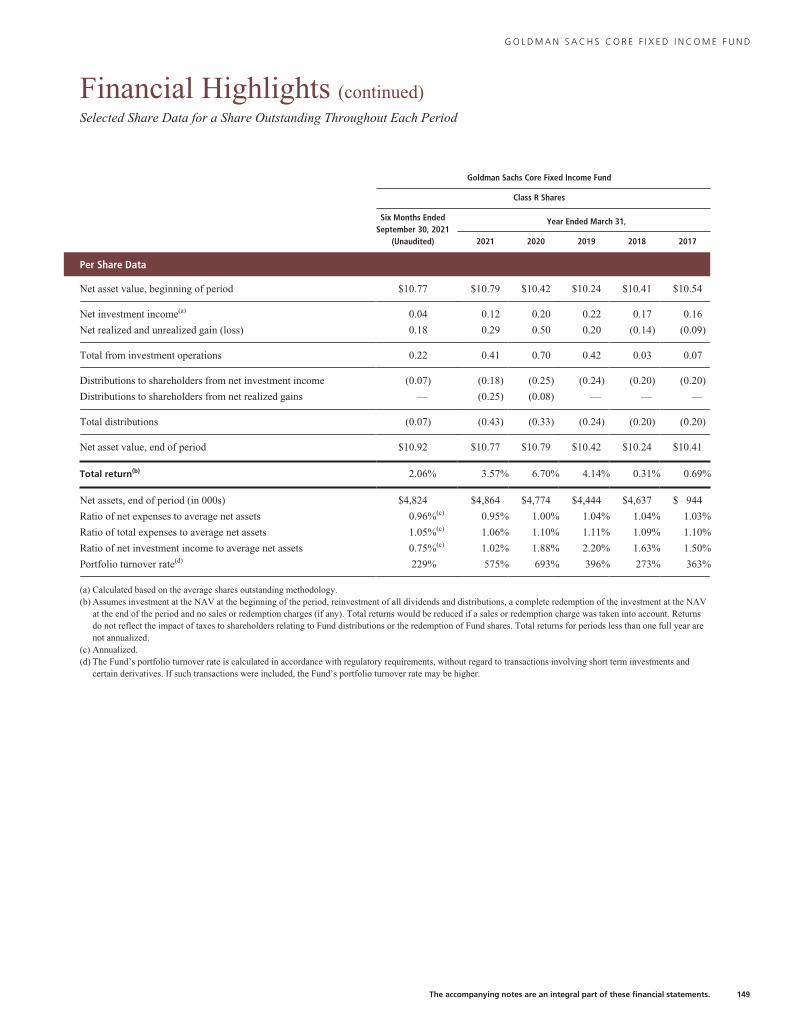

Core Fixed Income 143

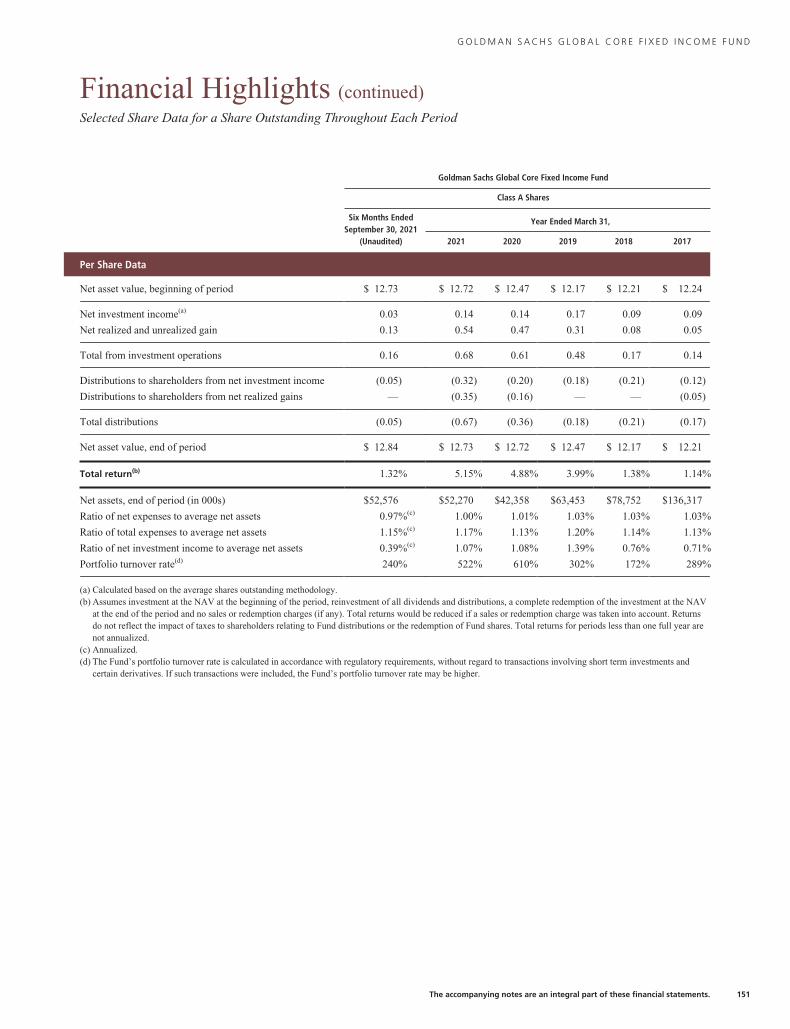

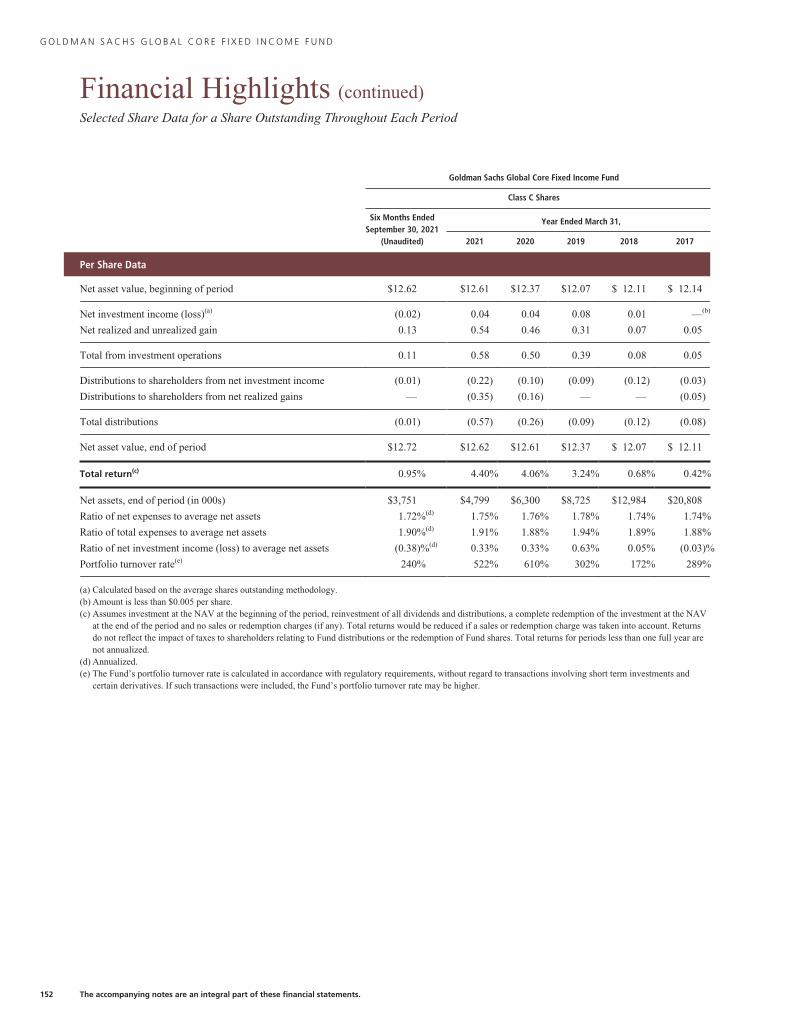

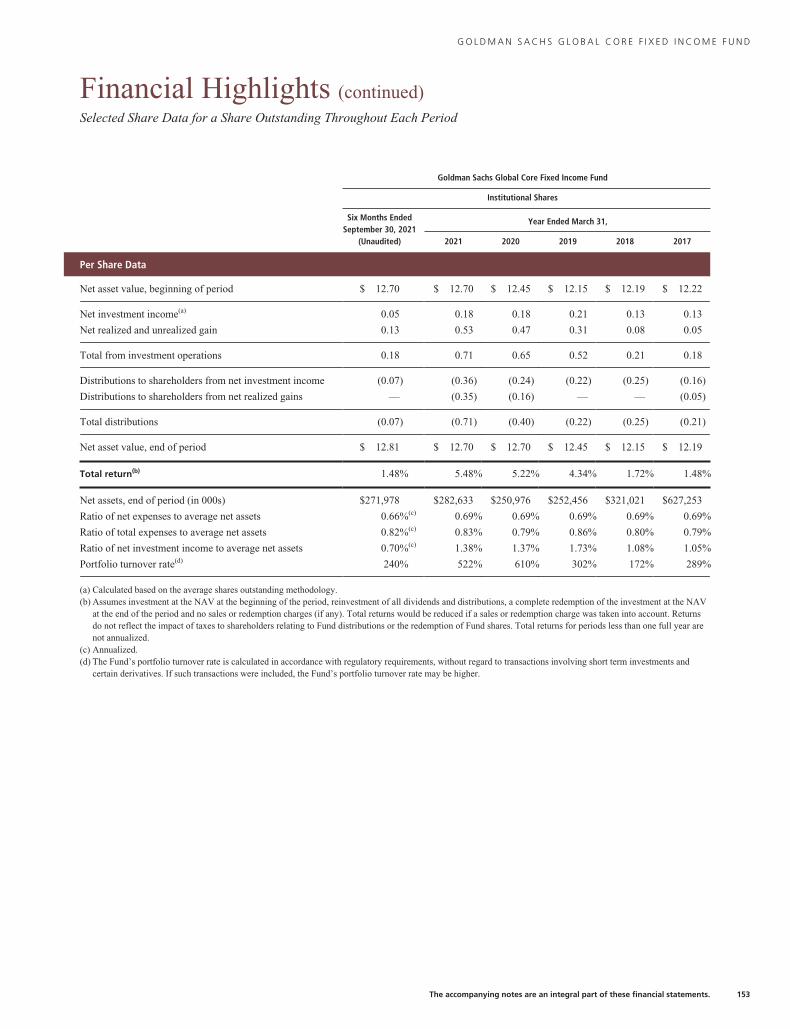

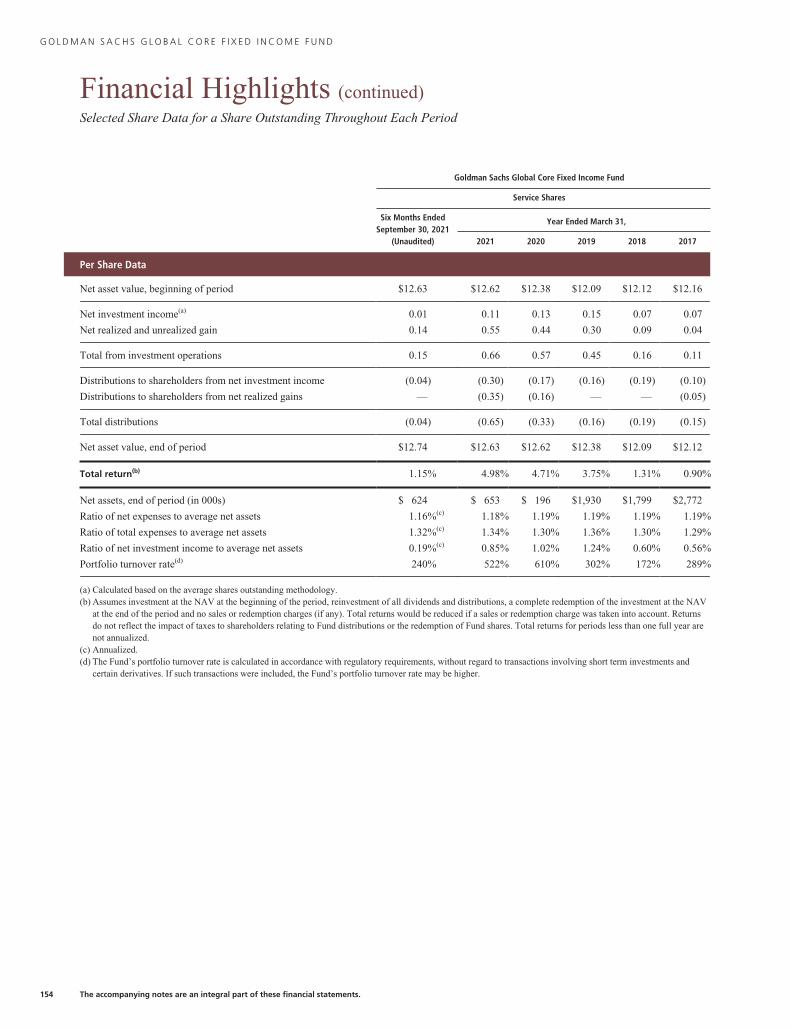

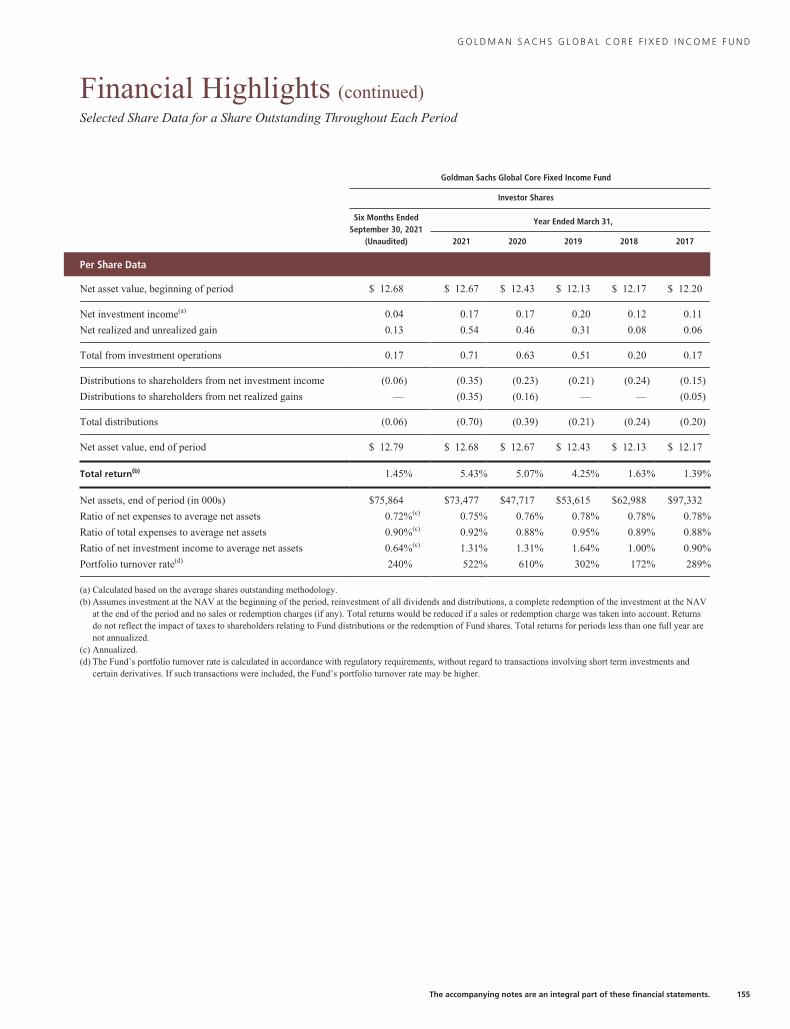

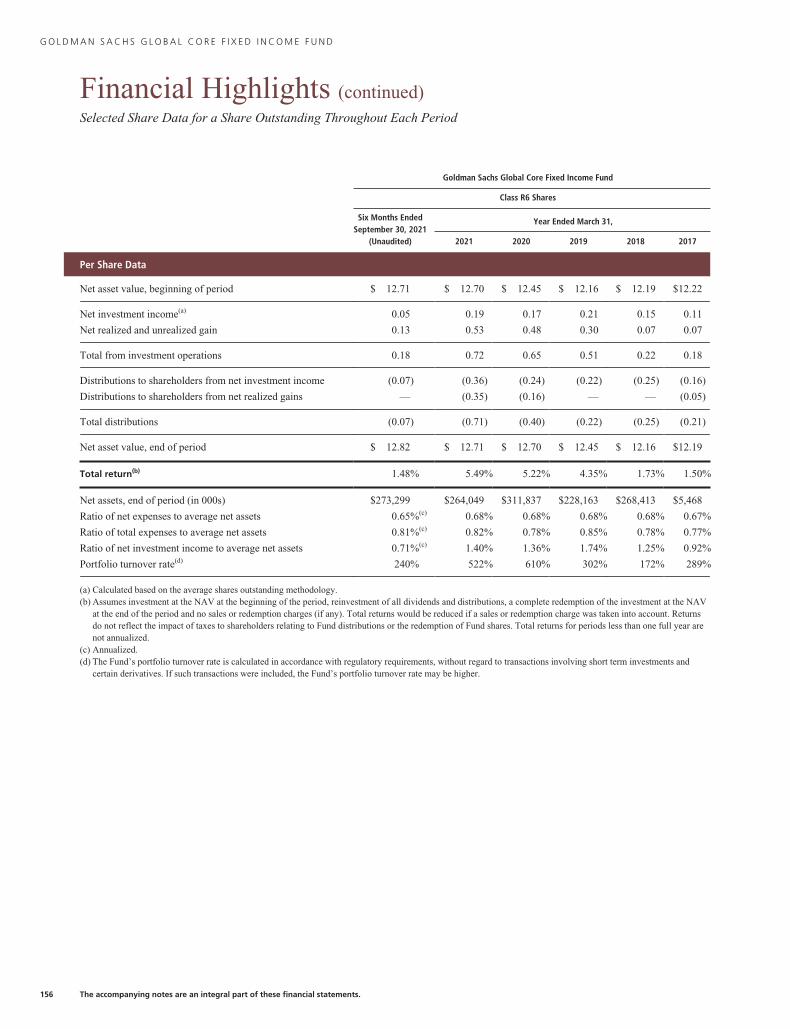

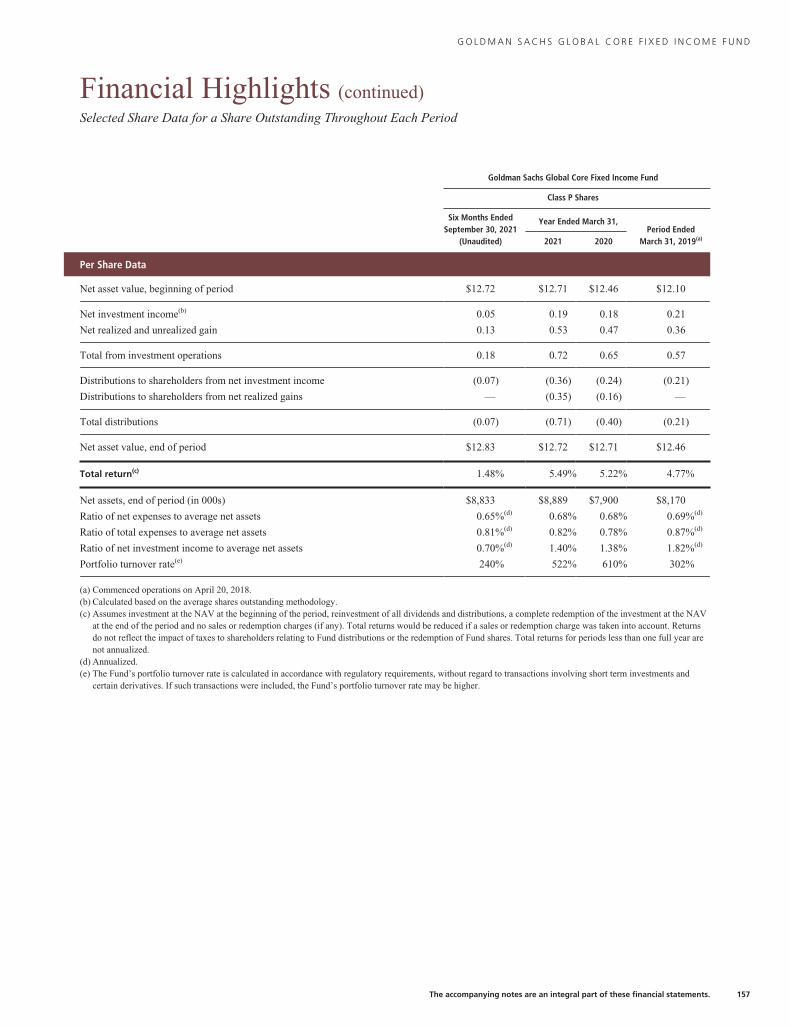

Global Core Fixed Income 151

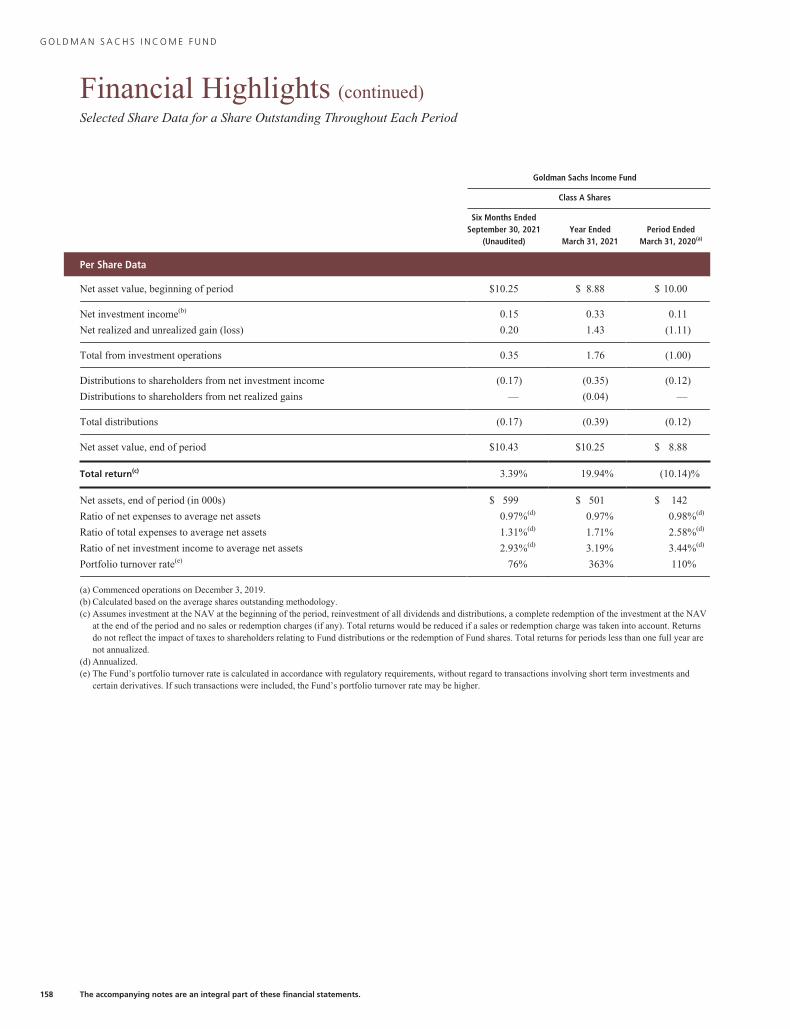

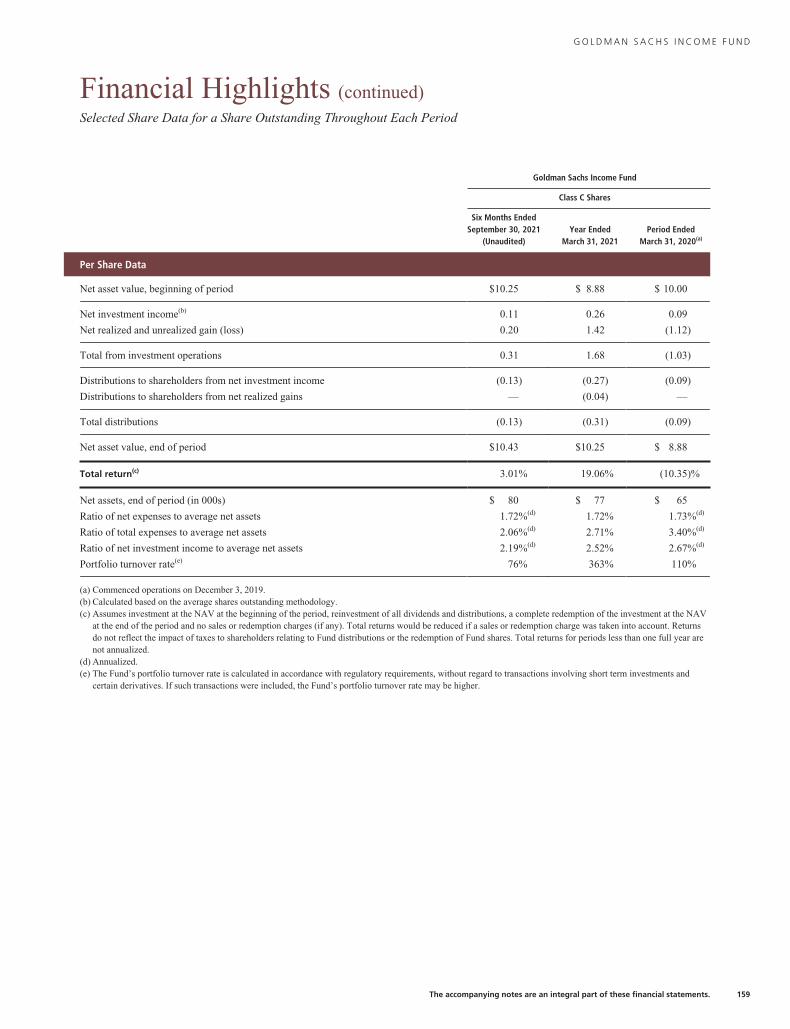

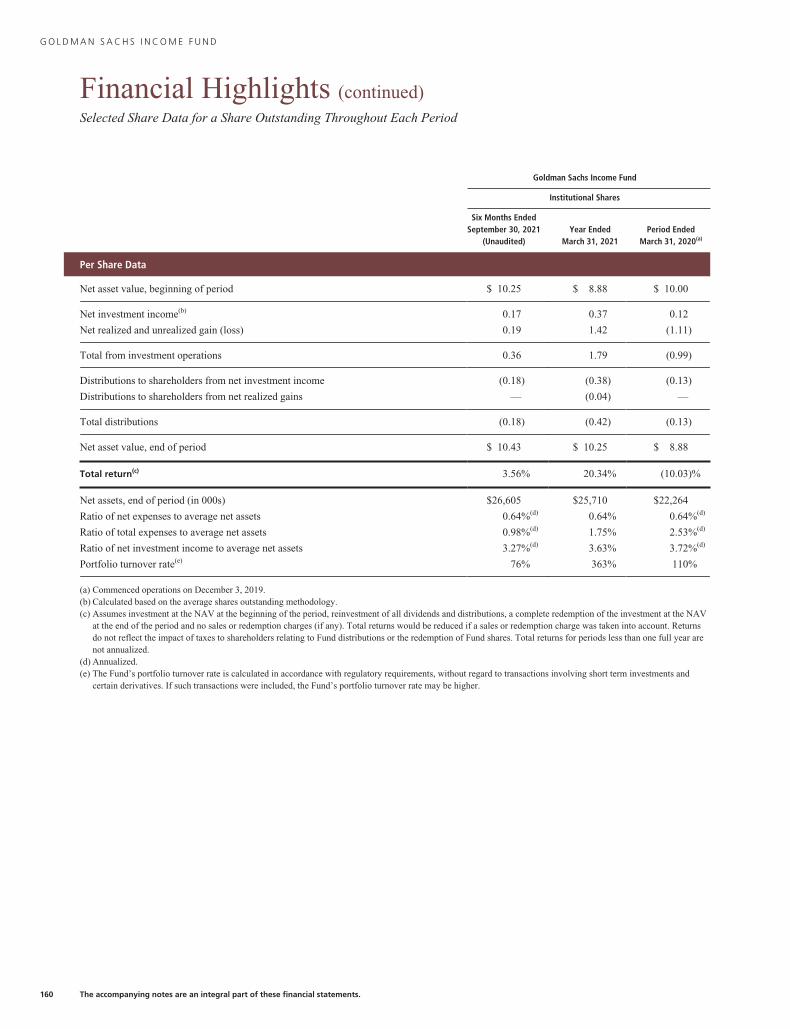

Income 158

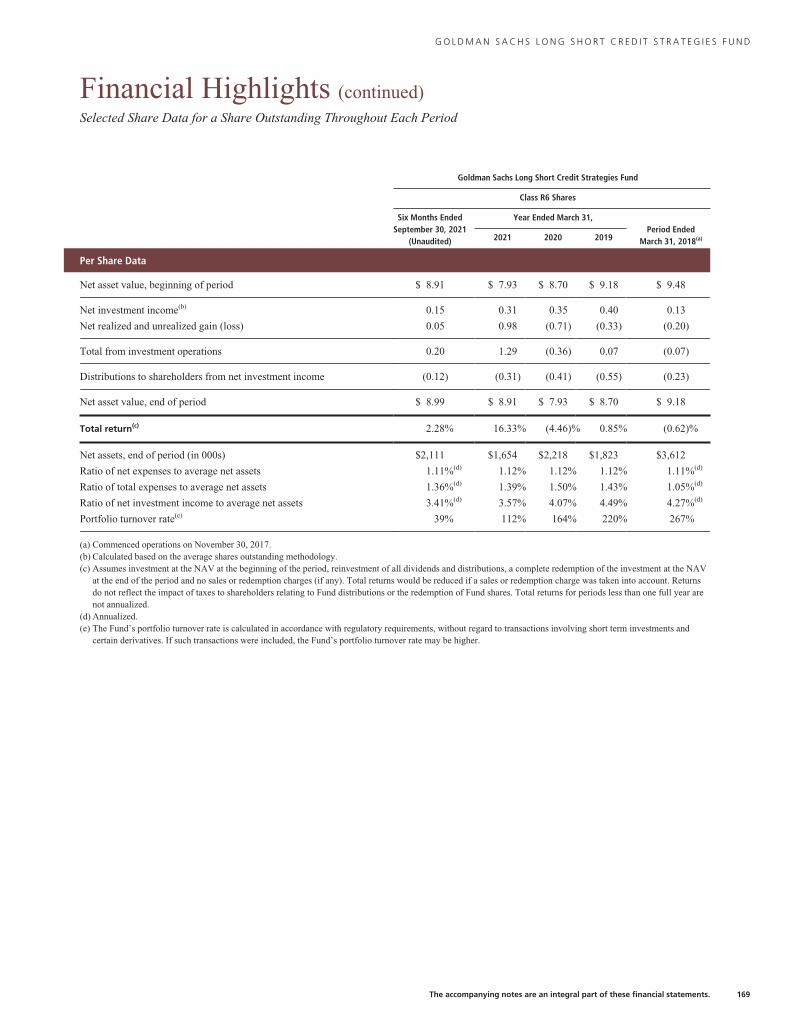

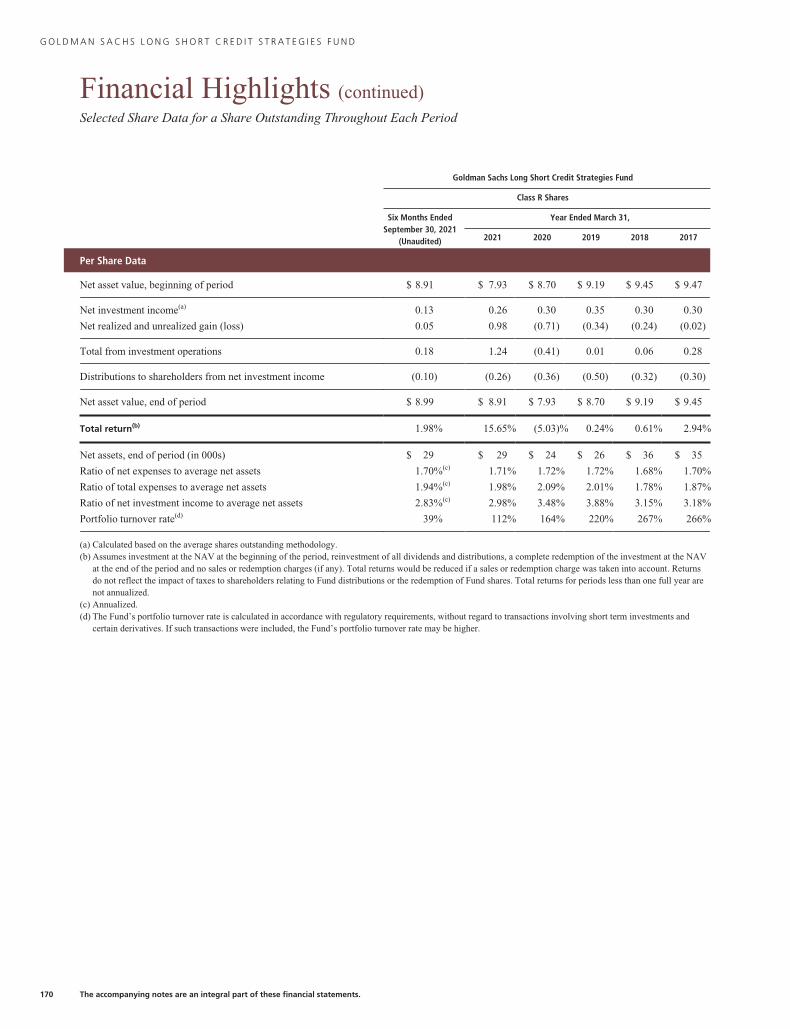

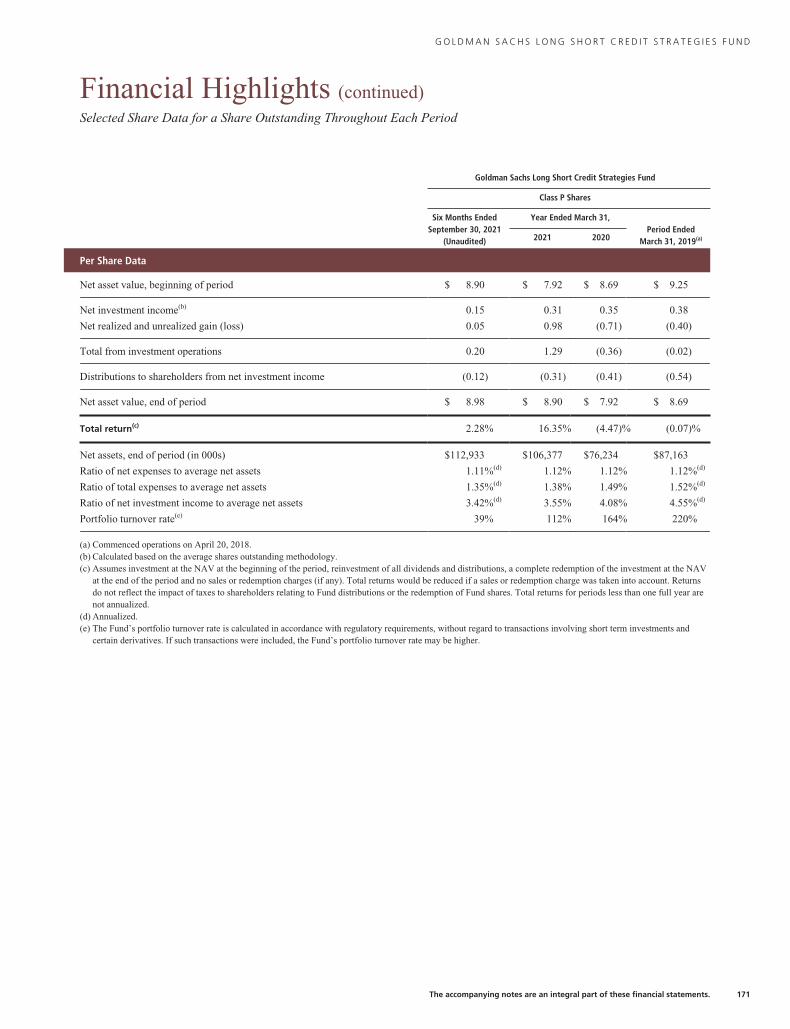

Long Short Credit Strategies 165

Strategic Income 172

Notes to the Financial Statements 179

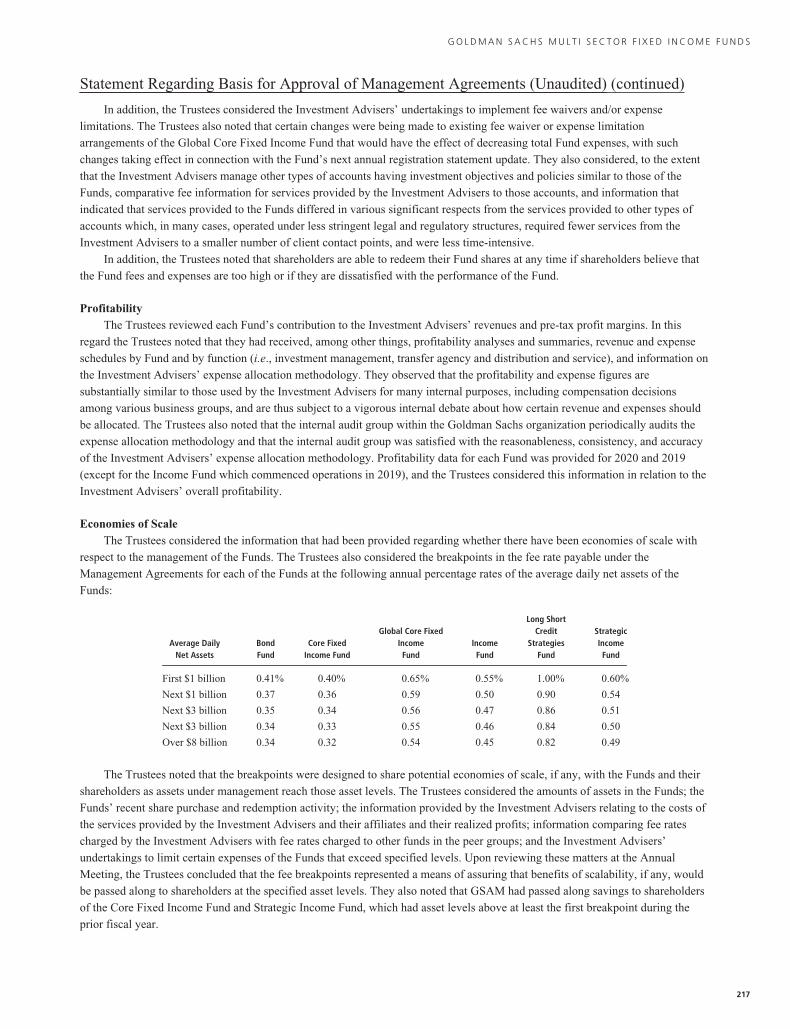

Other Information 212

NOT FDIC-INSURED May Lose Value No Bank Guarantee

Goldman Sachs Multi-Sector Fixed Income Funds

The following are highlights both of key factors affecting the fixed income market and of any changes made to the Goldman Sachs

Multi-Sector Fixed Income Funds (the “Funds”) during the six months ended September 30, 2021 (the “Reporting Period”). A

fuller review of the market and these changes will appear in the Funds’ annual shareholder report covering the 12 months ended

March 31, 2022.

Market and Economic Review� The broad U.S. fixed income market, as measured by the Bloomberg U.S. Aggregate Bond Index, posted a return of 1.88%

during the Reporting Period, significantly underperforming the broad U.S. equity market.

� Early in the Reporting Period, global central banks generally remained accommodative, with the U.S. Federal Reserve (“Fed”)

indicating it needed to see “substantial progress” on its employment and inflation goals before altering U.S. monetary policy.

� Remarkably strong U.S. inflation data, deemed “transitory” by the Fed, a disappointing U.S. jobs report released in April 2021

and the spread of the COVID-19 Delta variant suggested pandemic-related dynamics could continue distorting economic data as

the Reporting Period progressed.

� In September 2021, as inflationary trends continued, driven by a sharp rise in energy prices and persistent supply-chain bottlenecks,

developed markets central banks delivered or hinted at sooner than previously consensus expected policy normalization, with the

Fed stating it might start raising interest rates during 2022 and the tapering of its asset purchases “may soon be warranted.”

� Shorter-term U.S. Treasury yields rose modestly during the Reporting Period overall, while intermediate- and longer-term U.S.

Treasury yields fell moderately.

� Corporate bonds, both investment grade and high yield, outperformed U.S. Treasuries during the Reporting Period. So, too, did

Treasury inflation protected securities and emerging markets debt. Securitized assets, including mortgage-backed securities and

asset-backed securities, underperformed U.S. Treasuries during the Reporting Period.

Fund Changes and Highlights

Goldman Sachs Bond Fund

� Effective October 1, 2021, just after the close of the Reporting Period, Michael Swell no longer served as a portfolio manager

for the Fund. Ashish Shah continues to serve as a portfolio manager for the Fund.

Goldman Sachs Core Fixed Income Fund

� Effective October 1, 2021, just after the close of the Reporting Period, Michael Swell no longer served as a portfolio manager

for the Fund. Ashish Shah continues to serve as a portfolio manager for the Fund.

Goldman Sachs Long Short Credit Strategies Fund

� Effective July 29, 2021, the Fund’s benchmark index changed from the ICE Bank of America Merrill Lynch U.S. Dollar Three-

Month LIBOR Constant Maturity Index to the ICE Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index.

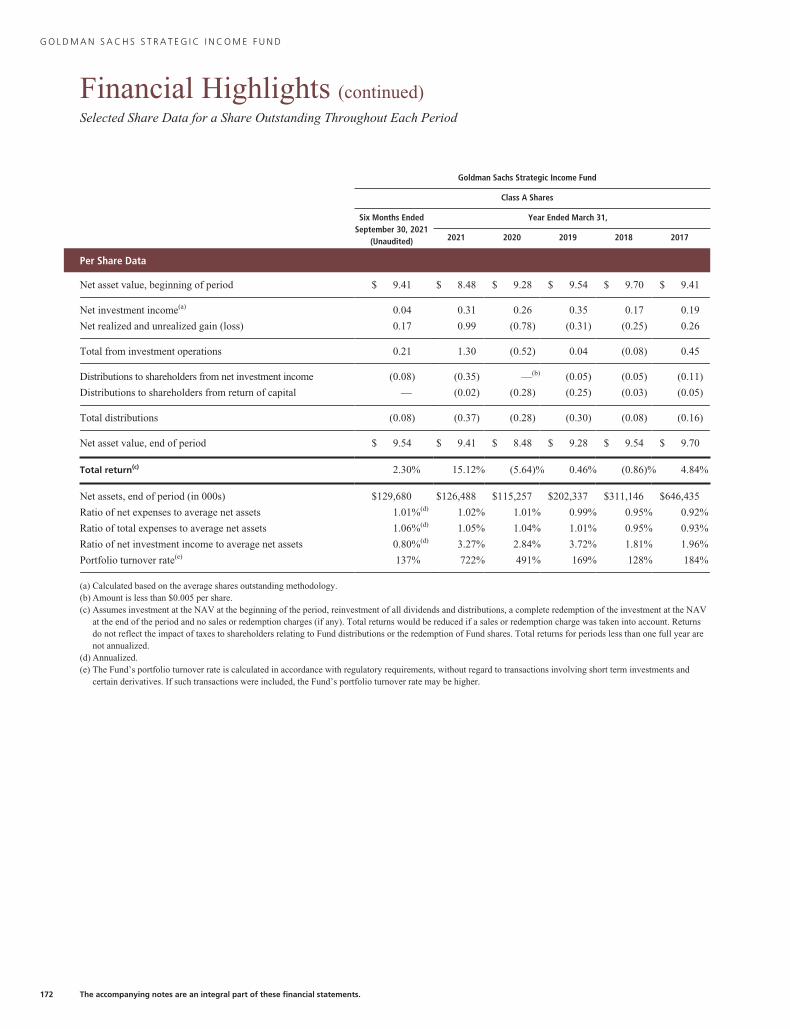

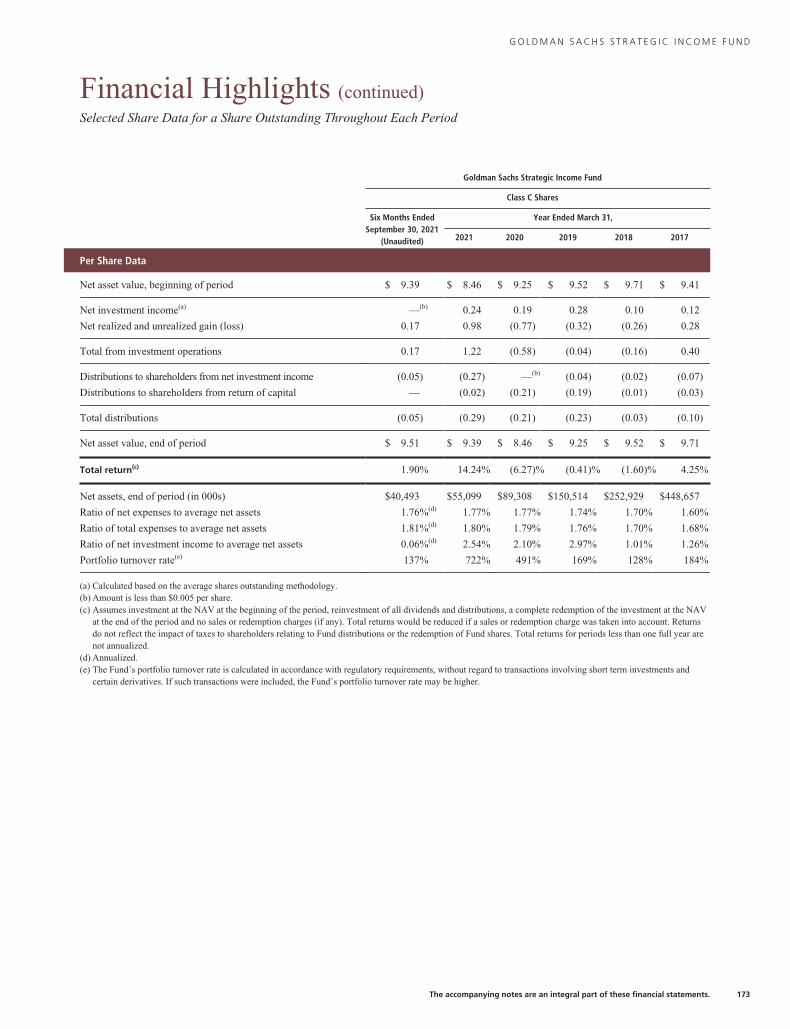

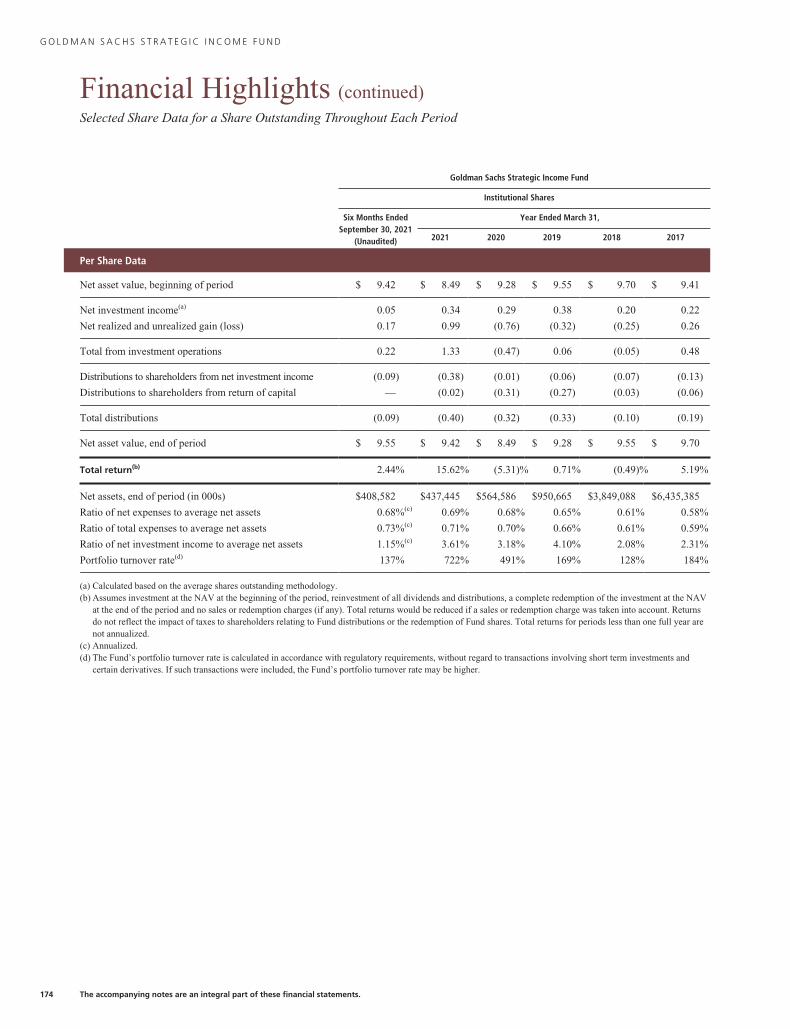

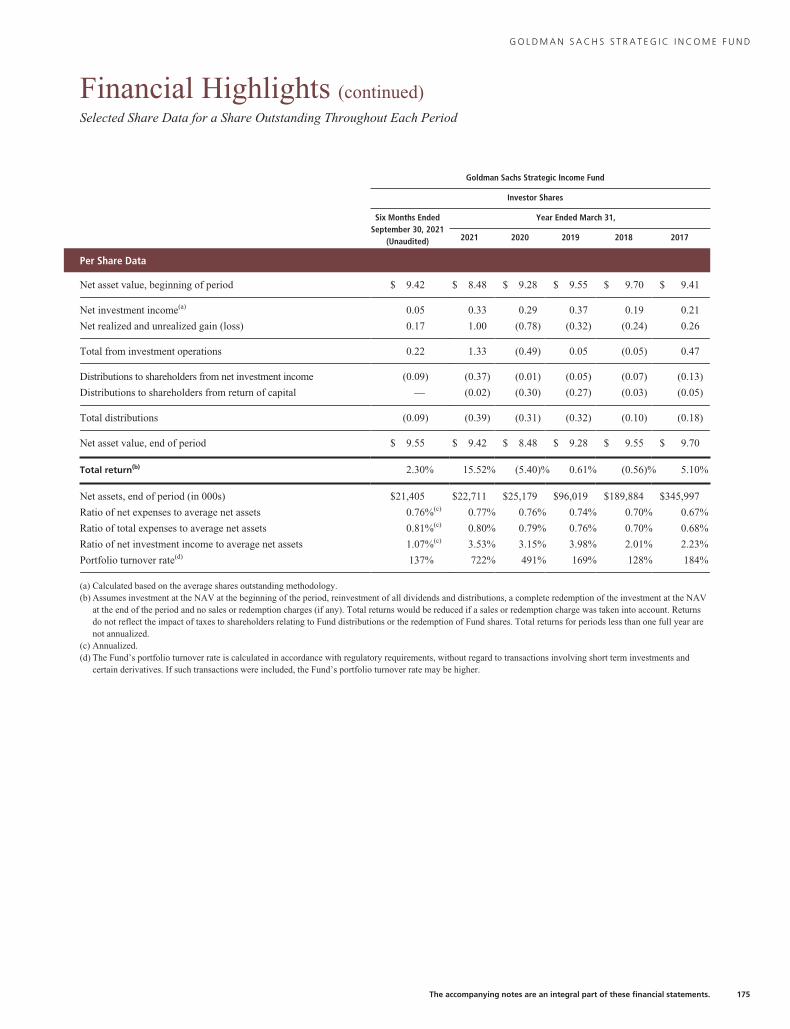

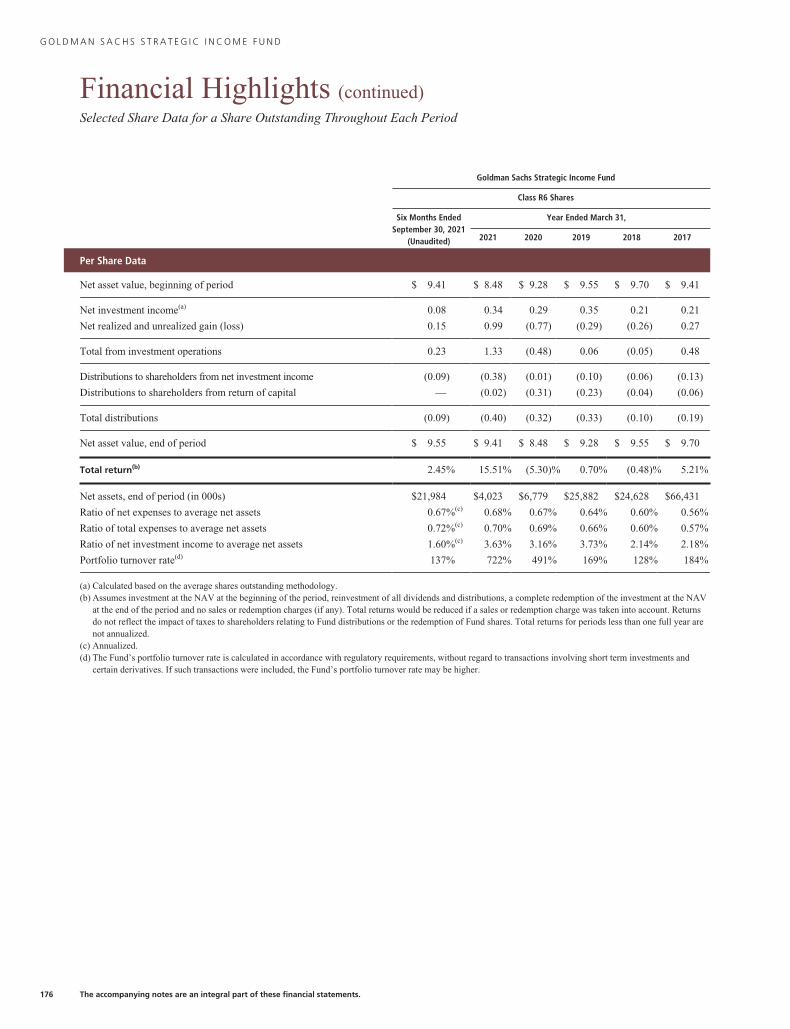

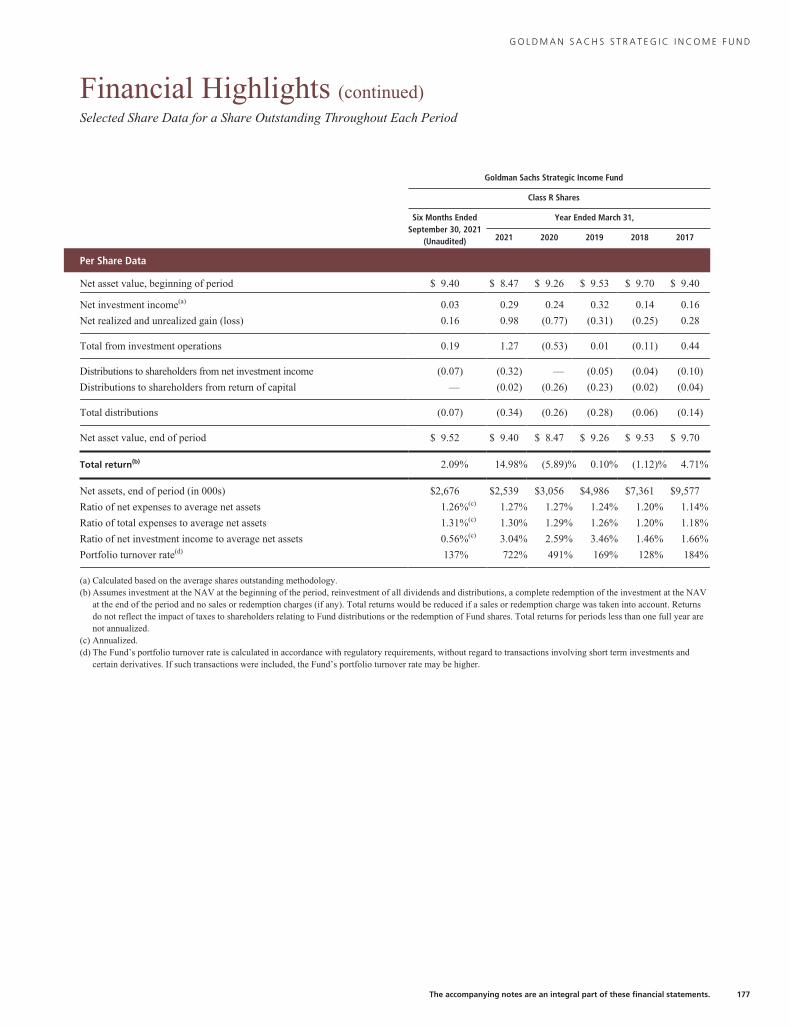

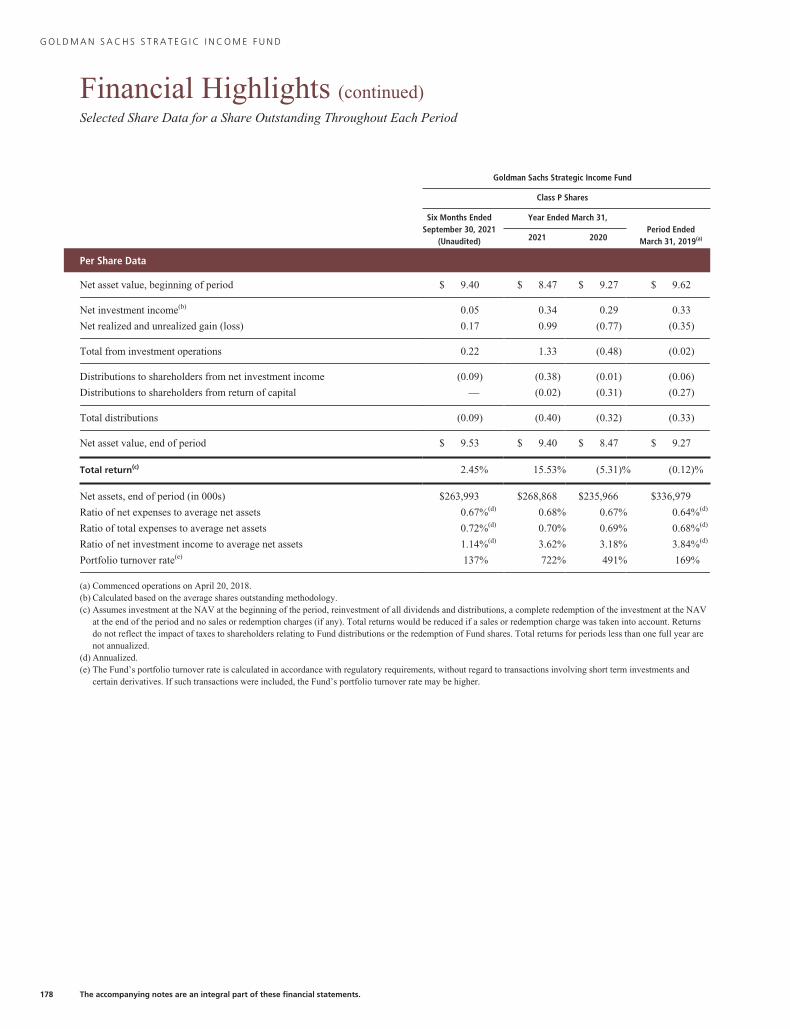

Goldman Sachs Strategic Income Fund

� Effective July 29, 2021, the Fund’s benchmark index changed from the ICE Bank of America Merrill Lynch U.S. Dollar Three-

Month LIBOR Constant Maturity Index to the ICE Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index.

� Effective October 1, 2021, just after the close of the Reporting Period, Michael Swell no longer served as a portfolio manager

for the Fund. Ashish Shah continues to serve as a portfolio manager for the Fund.

� The Strategic Income Fund is a dynamic fund which may have large fluctuations in sector allocations within a time period.

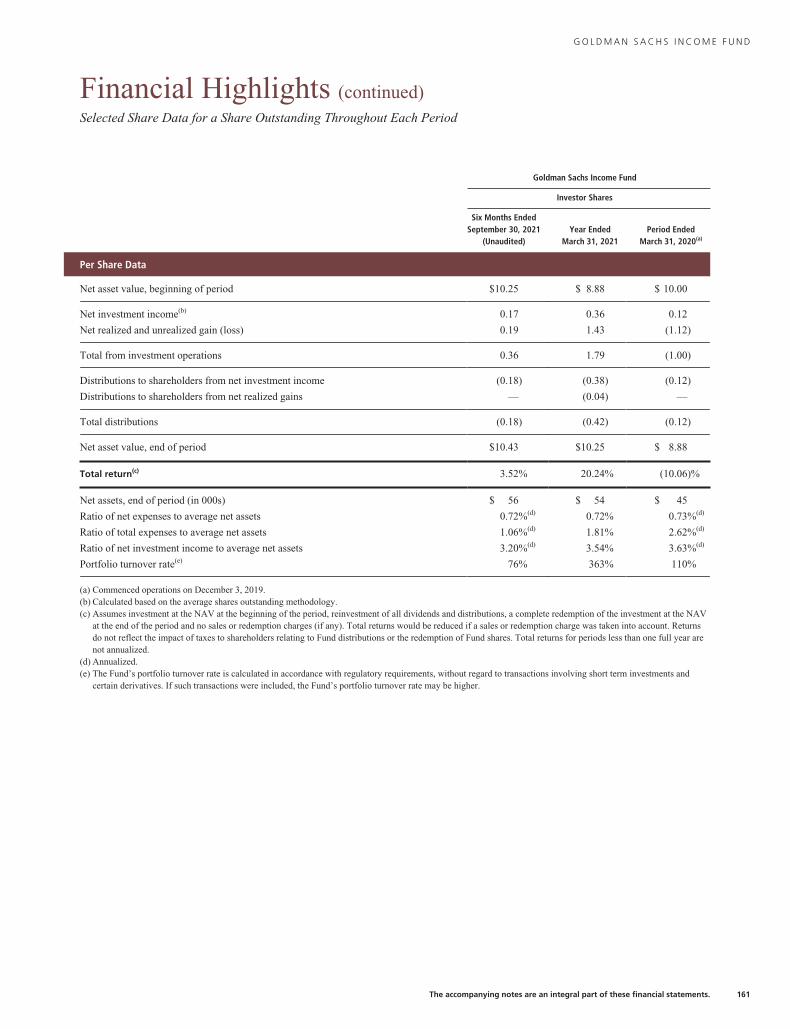

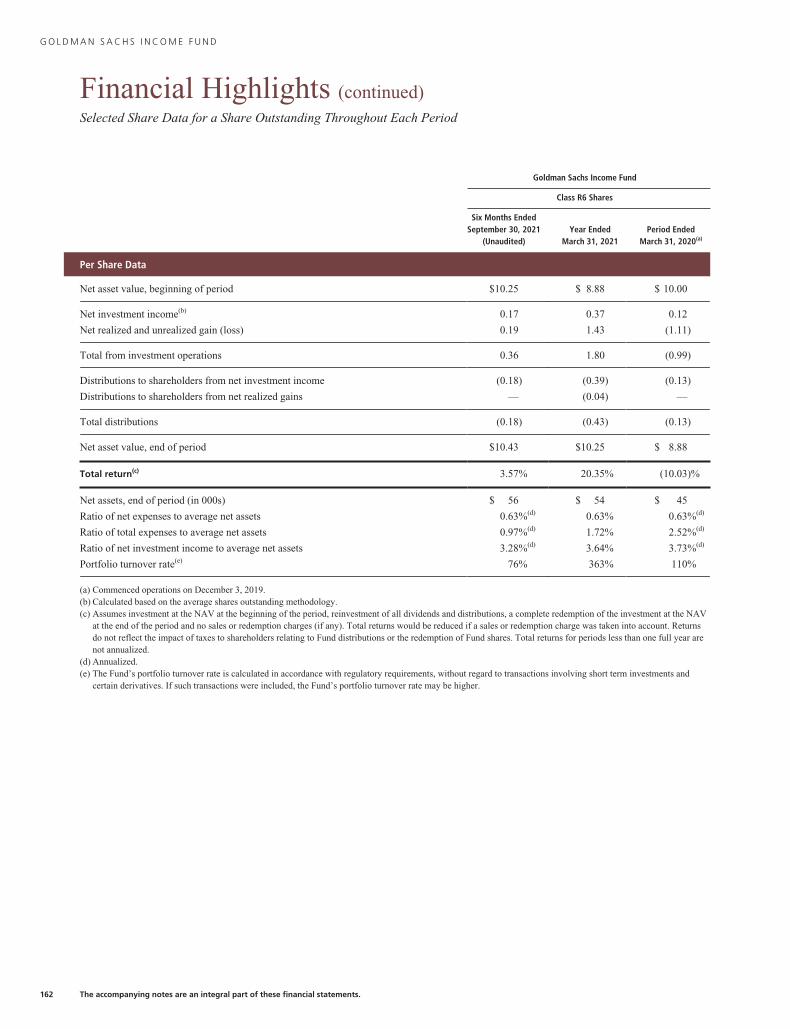

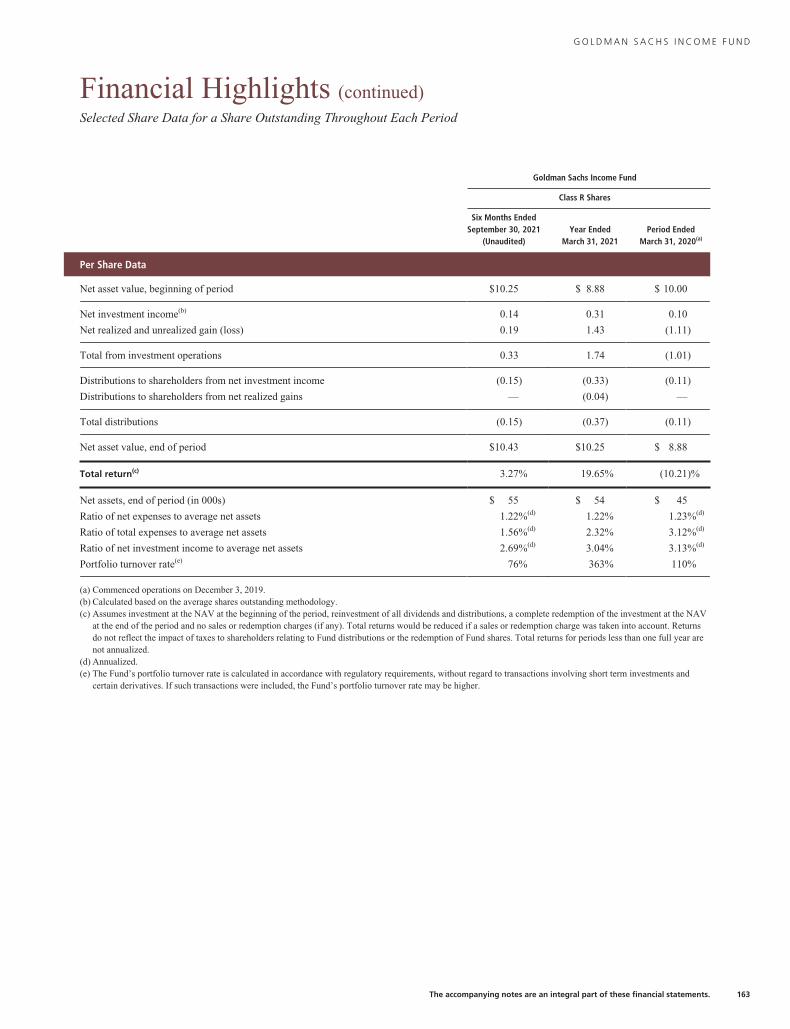

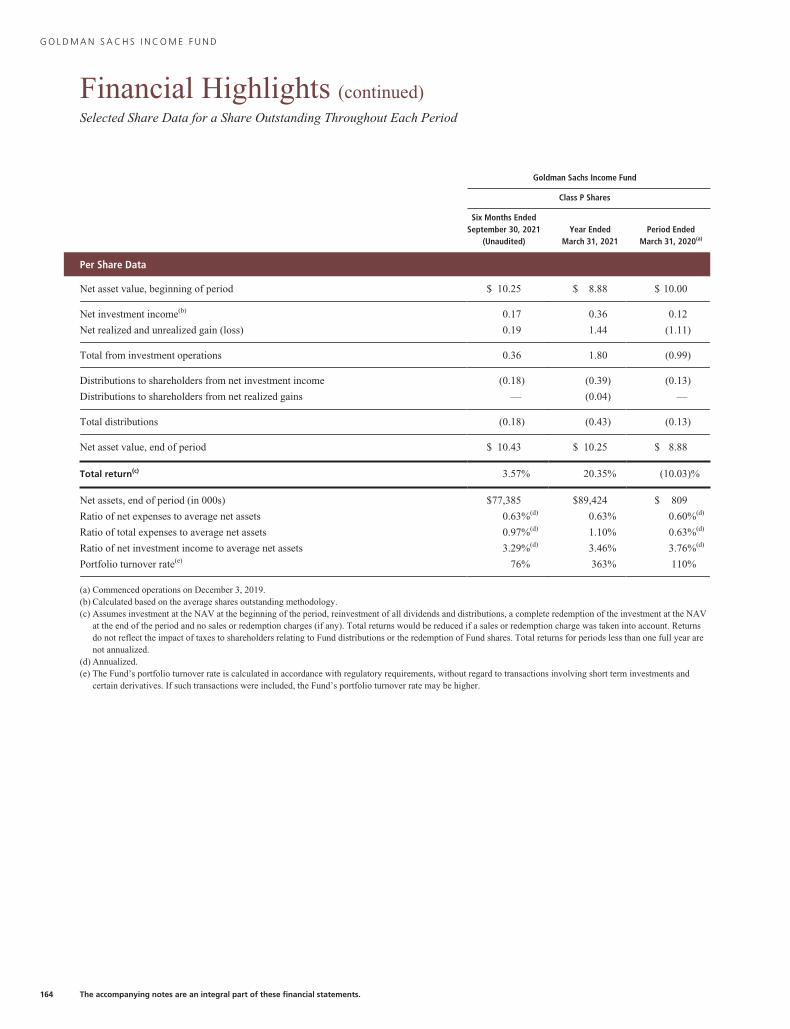

Goldman Sachs Income Fund

� The Fund outperformed its relative benchmark due to the Fund’s overweight allocations to high yield and investment grade

corporate bonds. Spread Sectors (High yield and investment grade corporate bond) remain generally resilient against rate market

volatility and supply chain pressures.

1

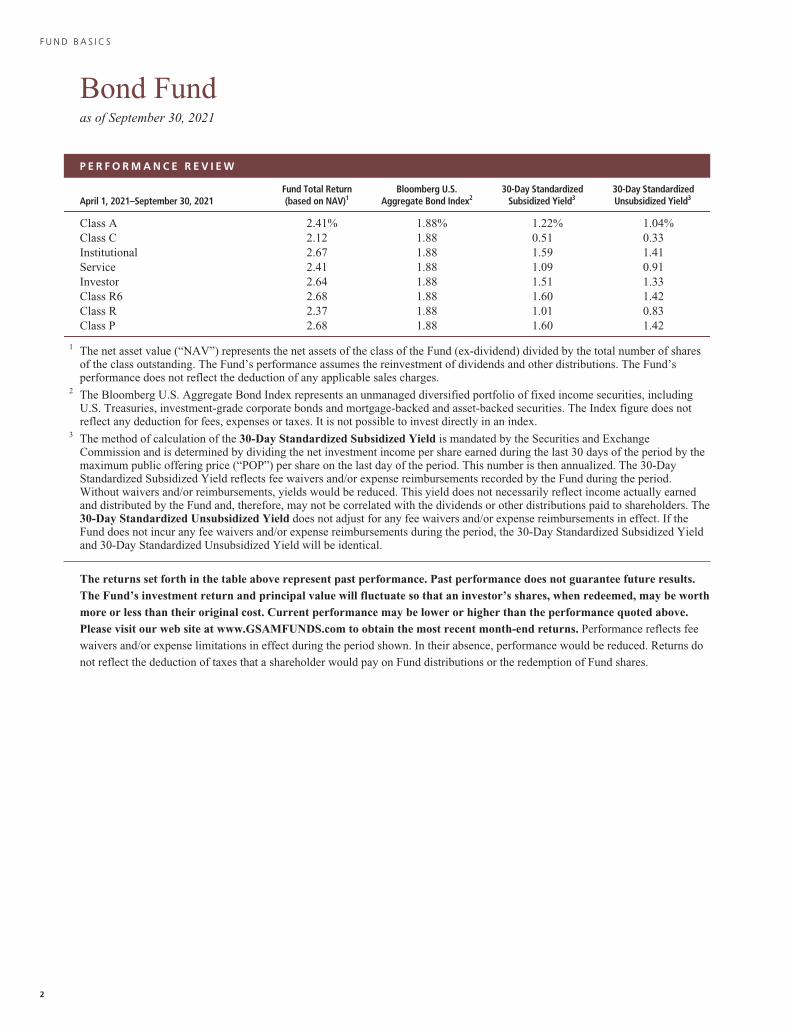

F U N D B A S I C S

Bond Fundas of September 30, 2021

P E R F O R M A N C E R E V I E W

April 1, 2021–September 30, 2021Fund Total Return(based on NAV)1

Bloomberg U.S.Aggregate Bond Index2

30-Day StandardizedSubsidized Yield3

30-Day StandardizedUnsubsidized Yield3

Class A 2.41% 1.88% 1.22% 1.04%Class C 2.12 1.88 0.51 0.33Institutional 2.67 1.88 1.59 1.41Service 2.41 1.88 1.09 0.91Investor 2.64 1.88 1.51 1.33Class R6 2.68 1.88 1.60 1.42Class R 2.37 1.88 1.01 0.83Class P 2.68 1.88 1.60 1.42

1 The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of sharesof the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’sperformance does not reflect the deduction of any applicable sales charges.

2 The Bloomberg U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, includingU.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities. The Index figure does notreflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index.

3 The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and ExchangeCommission and is determined by dividing the net investment income per share earned during the last 30 days of the period by themaximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-DayStandardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period.Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earnedand distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If theFund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yieldand 30-Day Standardized Unsubsidized Yield will be identical.

The returns set forth in the table above represent past performance. Past performance does not guarantee future results.The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worthmore or less than their original cost. Current performance may be lower or higher than the performance quoted above.Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee

waivers and/or expense limitations in effect during the period shown. In their absence, performance would be reduced. Returns do

not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

2

F U N D B A S I C S

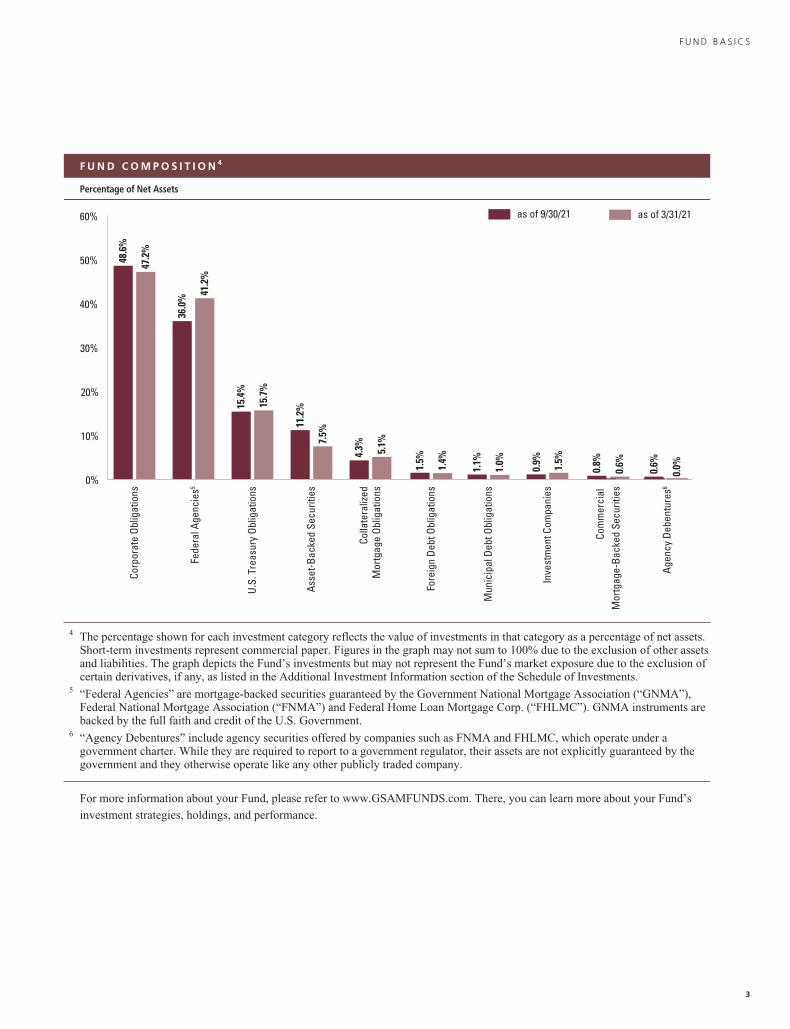

F U N D C O M P O S I T I O N 4

Percentage of Net Assets

as of 9/30/21 as of 3/31/21

Corp

orat

e Ob

ligat

ions

47.2

%

48.6

%

Fede

ral A

genc

ies5

36.0

%

41.2

%

Fore

ign

Debt

Obl

igat

ions

1.4%

1.5%

15.7

%

15.4

%U.

S. T

reas

ury

Oblig

atio

ns

Mun

icip

al D

ebt O

blig

atio

ns1.

1%

1.0%

0.9% 1.5%

Inve

stm

ent C

ompa

nies

Com

mer

cial

M

ortg

age-

Back

ed S

ecur

ities

0.8%

0.6%

0%

10%

20%

60%

50%

40%

30%

0.0%0.6%

Agen

cy D

eben

ture

s6

Asse

t-Bac

ked

Secu

ritie

s7.

5%

11.2

%

4.3% 5.1%

Colla

tera

lized

Mor

tgag

e Ob

ligat

ions

4 The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.Short-term investments represent commercial paper. Figures in the graph may not sum to 100% due to the exclusion of other assetsand liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion ofcertain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments.

5 “Federal Agencies” are mortgage-backed securities guaranteed by the Government National Mortgage Association (“GNMA”),Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corp. (“FHLMC”). GNMA instruments arebacked by the full faith and credit of the U.S. Government.

6 “Agency Debentures” include agency securities offered by companies such as FNMA and FHLMC, which operate under agovernment charter. While they are required to report to a government regulator, their assets are not explicitly guaranteed by thegovernment and they otherwise operate like any other publicly traded company.

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s

investment strategies, holdings, and performance.

3

F U N D B A S I C S

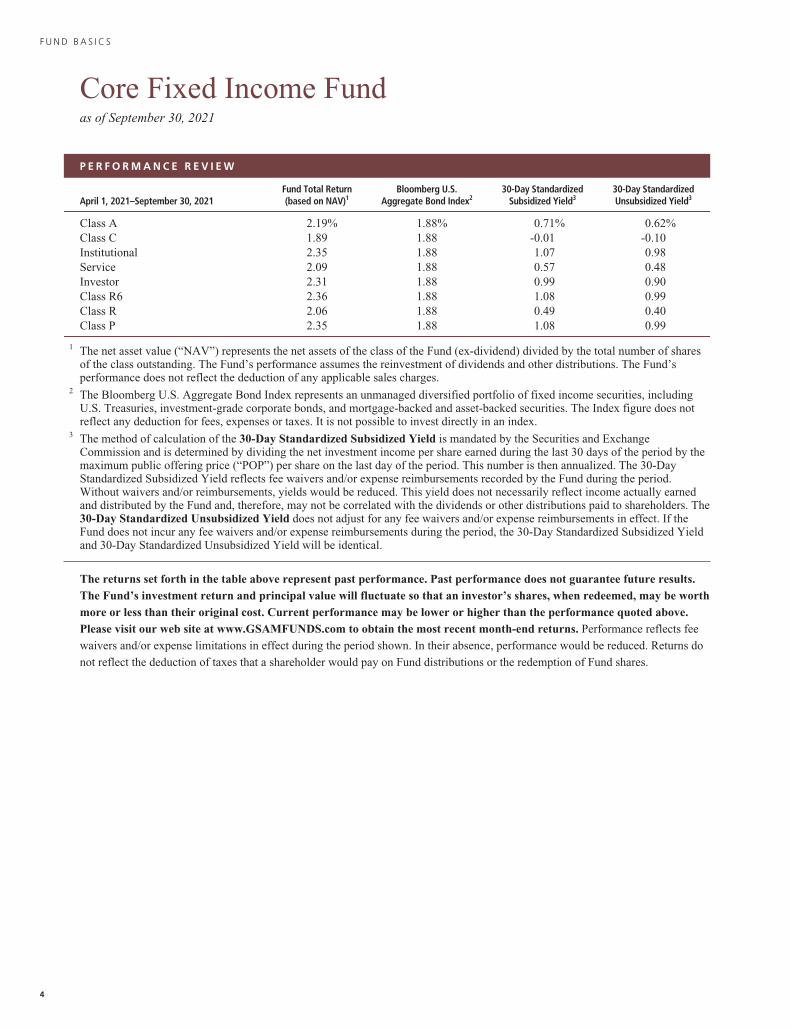

Core Fixed Income Fundas of September 30, 2021

P E R F O R M A N C E R E V I E W

April 1, 2021–September 30, 2021Fund Total Return(based on NAV)1

Bloomberg U.S.Aggregate Bond Index2

30-Day StandardizedSubsidized Yield3

30-Day StandardizedUnsubsidized Yield3

Class A 2.19% 1.88% 0.71% 0.62%Class C 1.89 1.88 -0.01 -0.10Institutional 2.35 1.88 1.07 0.98Service 2.09 1.88 0.57 0.48Investor 2.31 1.88 0.99 0.90Class R6 2.36 1.88 1.08 0.99Class R 2.06 1.88 0.49 0.40Class P 2.35 1.88 1.08 0.99

1 The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of sharesof the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’sperformance does not reflect the deduction of any applicable sales charges.

2 The Bloomberg U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, includingU.S. Treasuries, investment-grade corporate bonds, and mortgage-backed and asset-backed securities. The Index figure does notreflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index.

3 The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and ExchangeCommission and is determined by dividing the net investment income per share earned during the last 30 days of the period by themaximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-DayStandardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period.Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earnedand distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If theFund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yieldand 30-Day Standardized Unsubsidized Yield will be identical.

The returns set forth in the table above represent past performance. Past performance does not guarantee future results.The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worthmore or less than their original cost. Current performance may be lower or higher than the performance quoted above.Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee

waivers and/or expense limitations in effect during the period shown. In their absence, performance would be reduced. Returns do

not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

4

F U N D B A S I C S

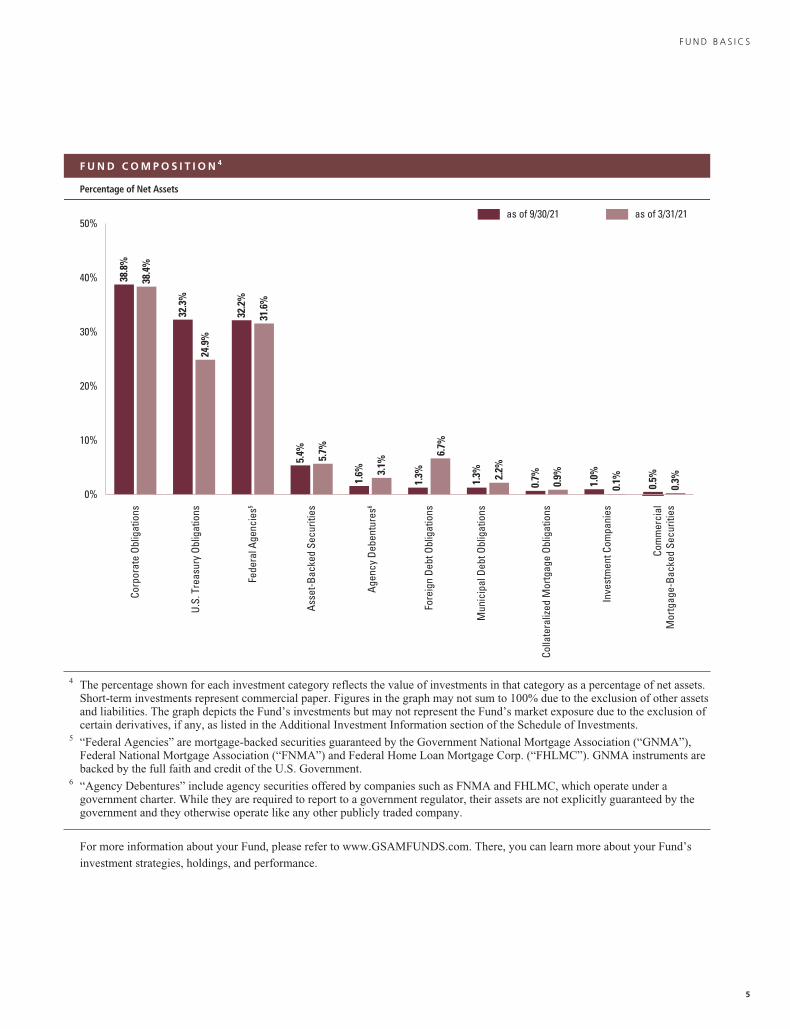

F U N D C O M P O S I T I O N 4

Percentage of Net Assets

as of 3/31/21as of 9/30/21

0%

10%

20%

30%

40%

50%

6.7%

1.3%

Fore

ign

Debt

Obl

igat

ions

0.9%

0.7%

Colla

tera

lized

Mor

tgag

e Ob

ligat

ions

2.2%

1.3%

Mun

icip

al D

ebt O

blig

atio

ns

1.6% 3.

1%Ag

ency

Deb

entu

res6

1.0%

0.1%

Inve

stm

ent C

ompa

nies

5.7%

5.4%

Asse

t-Bac

ked

Secu

ritie

s

32.2

%

31.6

%Fe

dera

l Age

ncie

s5

32.3

%

24.9

%U.

S. T

reas

ury

Oblig

atio

ns

38.4

%

38.8

%Co

rpor

ate

Oblig

atio

ns

Com

mer

cial

Mor

tgag

e-Ba

cked

Sec

uriti

es

0.5%

0.3%

4 The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.Short-term investments represent commercial paper. Figures in the graph may not sum to 100% due to the exclusion of other assetsand liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion ofcertain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments.

5 “Federal Agencies” are mortgage-backed securities guaranteed by the Government National Mortgage Association (“GNMA”),Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corp. (“FHLMC”). GNMA instruments arebacked by the full faith and credit of the U.S. Government.

6 “Agency Debentures” include agency securities offered by companies such as FNMA and FHLMC, which operate under agovernment charter. While they are required to report to a government regulator, their assets are not explicitly guaranteed by thegovernment and they otherwise operate like any other publicly traded company.

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s

investment strategies, holdings, and performance.

5

F U N D B A S I C S

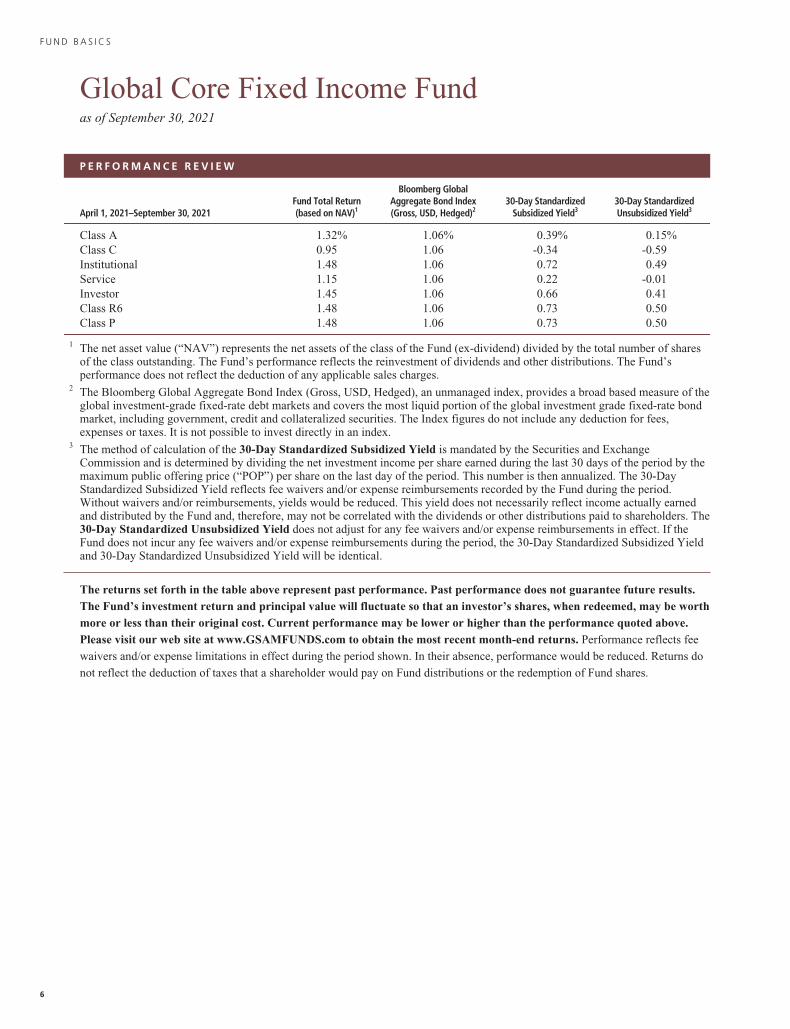

Global Core Fixed Income Fundas of September 30, 2021

P E R F O R M A N C E R E V I E W

April 1, 2021–September 30, 2021Fund Total Return(based on NAV)1

Bloomberg GlobalAggregate Bond Index(Gross, USD, Hedged)2

30-Day StandardizedSubsidized Yield3

30-Day StandardizedUnsubsidized Yield3

Class A 1.32% 1.06% 0.39% 0.15%Class C 0.95 1.06 -0.34 -0.59Institutional 1.48 1.06 0.72 0.49Service 1.15 1.06 0.22 -0.01Investor 1.45 1.06 0.66 0.41Class R6 1.48 1.06 0.73 0.50Class P 1.48 1.06 0.73 0.50

1 The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of sharesof the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’sperformance does not reflect the deduction of any applicable sales charges.

2 The Bloomberg Global Aggregate Bond Index (Gross, USD, Hedged), an unmanaged index, provides a broad based measure of theglobal investment-grade fixed-rate debt markets and covers the most liquid portion of the global investment grade fixed-rate bondmarket, including government, credit and collateralized securities. The Index figures do not include any deduction for fees,expenses or taxes. It is not possible to invest directly in an index.

3 The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and ExchangeCommission and is determined by dividing the net investment income per share earned during the last 30 days of the period by themaximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-DayStandardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period.Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earnedand distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If theFund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yieldand 30-Day Standardized Unsubsidized Yield will be identical.

The returns set forth in the table above represent past performance. Past performance does not guarantee future results.The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worthmore or less than their original cost. Current performance may be lower or higher than the performance quoted above.Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee

waivers and/or expense limitations in effect during the period shown. In their absence, performance would be reduced. Returns do

not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

6

F U N D B A S I C S

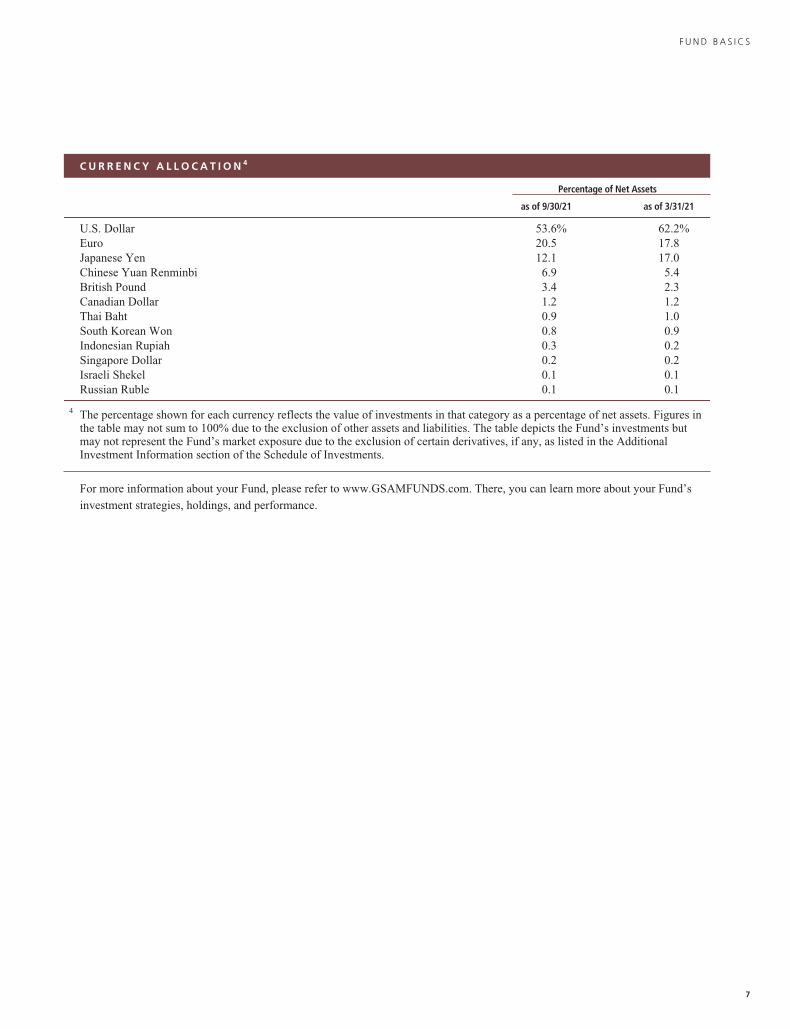

C U R R E N C Y A L L O C A T I O N 4

Percentage of Net Assets

as of 9/30/21 as of 3/31/21

U.S. Dollar 53.6% 62.2%Euro 20.5 17.8Japanese Yen 12.1 17.0Chinese Yuan Renminbi 6.9 5.4British Pound 3.4 2.3Canadian Dollar 1.2 1.2Thai Baht 0.9 1.0South Korean Won 0.8 0.9Indonesian Rupiah 0.3 0.2Singapore Dollar 0.2 0.2Israeli Shekel 0.1 0.1Russian Ruble 0.1 0.1

4 The percentage shown for each currency reflects the value of investments in that category as a percentage of net assets. Figures inthe table may not sum to 100% due to the exclusion of other assets and liabilities. The table depicts the Fund’s investments butmay not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the AdditionalInvestment Information section of the Schedule of Investments.

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s

investment strategies, holdings, and performance.

7

F U N D B A S I C S

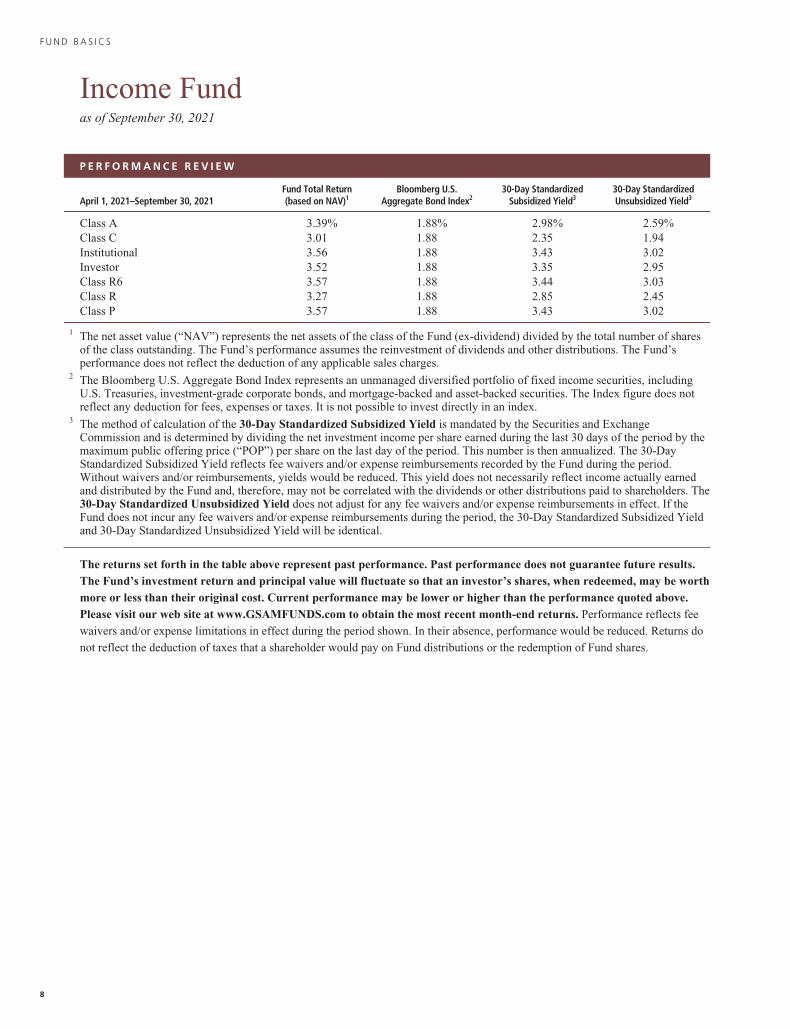

Income Fundas of September 30, 2021

P E R F O R M A N C E R E V I E W

April 1, 2021–September 30, 2021Fund Total Return(based on NAV)1

Bloomberg U.S.Aggregate Bond Index2

30-Day StandardizedSubsidized Yield3

30-Day StandardizedUnsubsidized Yield3

Class A 3.39% 1.88% 2.98% 2.59%Class C 3.01 1.88 2.35 1.94Institutional 3.56 1.88 3.43 3.02Investor 3.52 1.88 3.35 2.95Class R6 3.57 1.88 3.44 3.03Class R 3.27 1.88 2.85 2.45Class P 3.57 1.88 3.43 3.02

1 The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of sharesof the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’sperformance does not reflect the deduction of any applicable sales charges.

2 The Bloomberg U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, includingU.S. Treasuries, investment-grade corporate bonds, and mortgage-backed and asset-backed securities. The Index figure does notreflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index.

3 The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and ExchangeCommission and is determined by dividing the net investment income per share earned during the last 30 days of the period by themaximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-DayStandardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period.Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earnedand distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If theFund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yieldand 30-Day Standardized Unsubsidized Yield will be identical.

The returns set forth in the table above represent past performance. Past performance does not guarantee future results.The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worthmore or less than their original cost. Current performance may be lower or higher than the performance quoted above.Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee

waivers and/or expense limitations in effect during the period shown. In their absence, performance would be reduced. Returns do

not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

8

F U N D B A S I C S

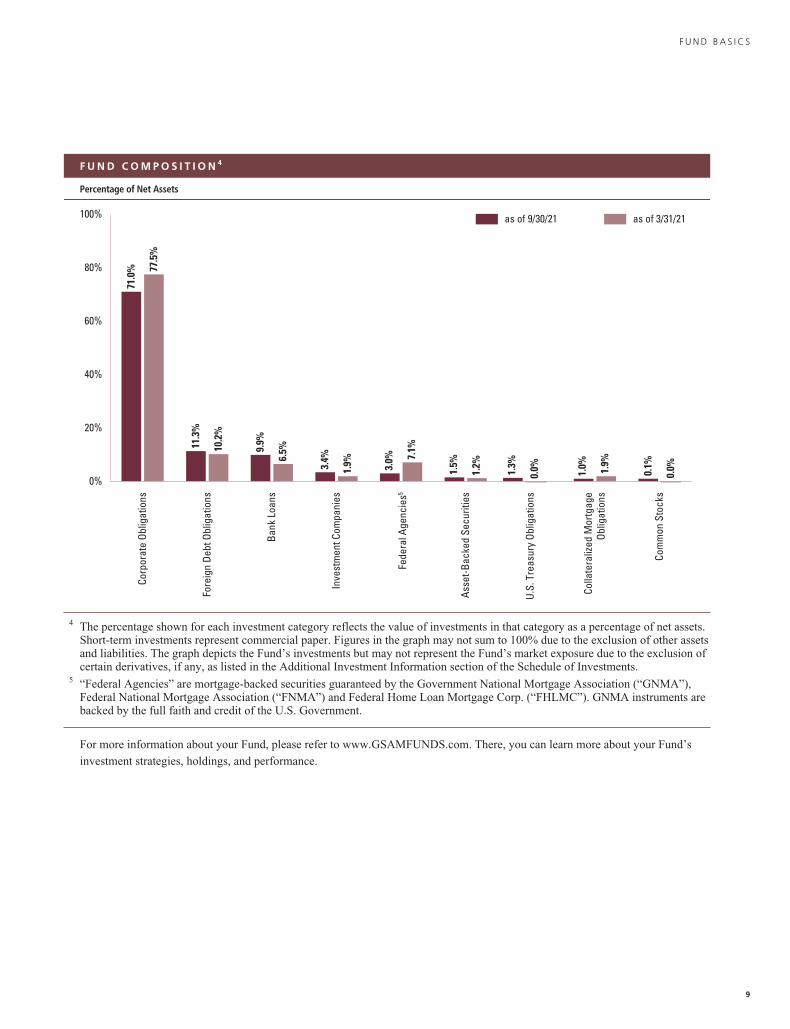

F U N D C O M P O S I T I O N 4

Percentage of Net Assets

Inve

stm

ent C

ompa

nies

Bank

Loa

ns

Fore

ign

Debt

Obl

igat

ions

as of 3/31/21as of 9/30/21

0%

20%

40%

60%

100%

80%

U.S.

Tre

asur

y Ob

ligat

ions

Colla

tera

lized

Mor

tgag

eOb

ligat

ions

Asse

t-Bac

ked

Secu

ritie

s

Fede

ral A

genc

ies5

9.9%

6.5%

3.4%

1.9% 3.0%

7.1%

1.5%

1.2%

Corp

orat

e Ob

ligat

ions

71.0

%

77.5

%

11.3

%

10.2

%

1.3%

0.0%

1.0%

1.9%

Com

mon

Sto

cks

0.1%

0.0%

4 The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.Short-term investments represent commercial paper. Figures in the graph may not sum to 100% due to the exclusion of other assetsand liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion ofcertain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments.

5 “Federal Agencies” are mortgage-backed securities guaranteed by the Government National Mortgage Association (“GNMA”),Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corp. (“FHLMC”). GNMA instruments arebacked by the full faith and credit of the U.S. Government.

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s

investment strategies, holdings, and performance.

9

F U N D B A S I C S

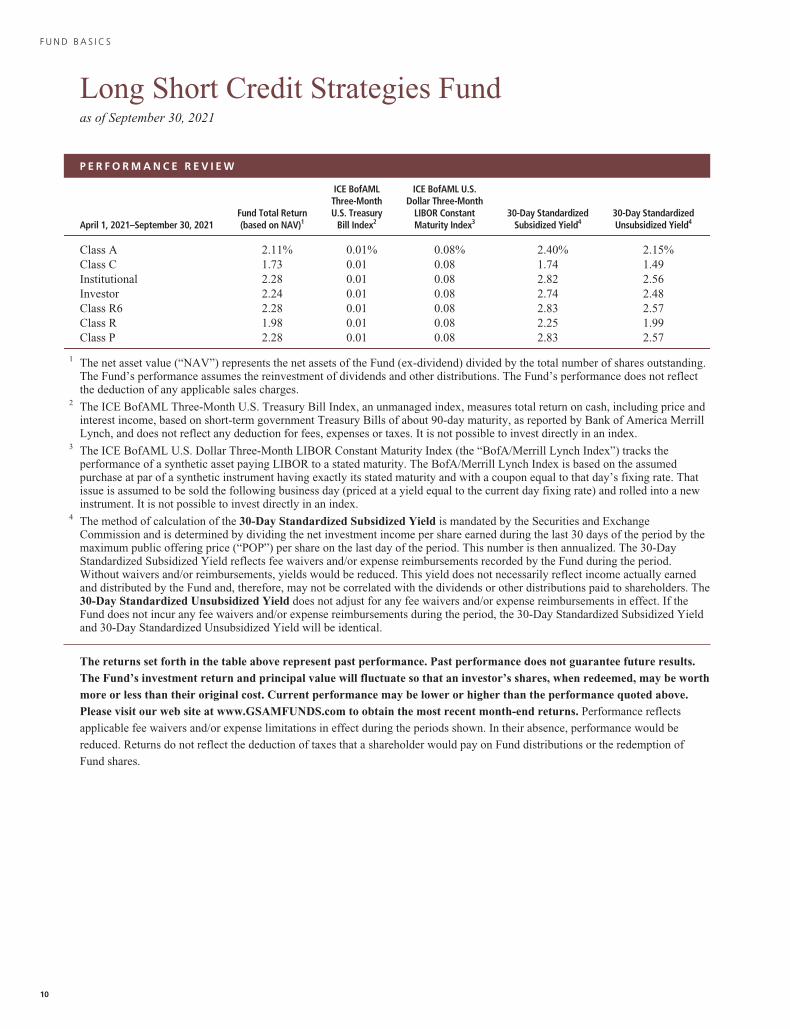

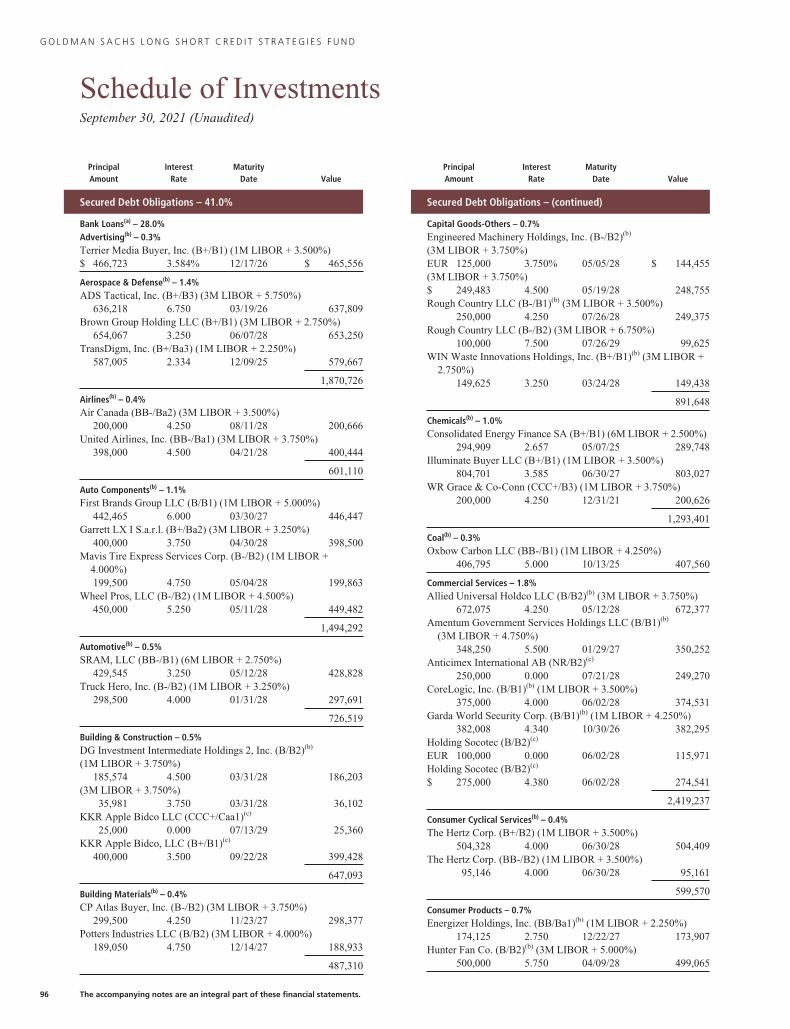

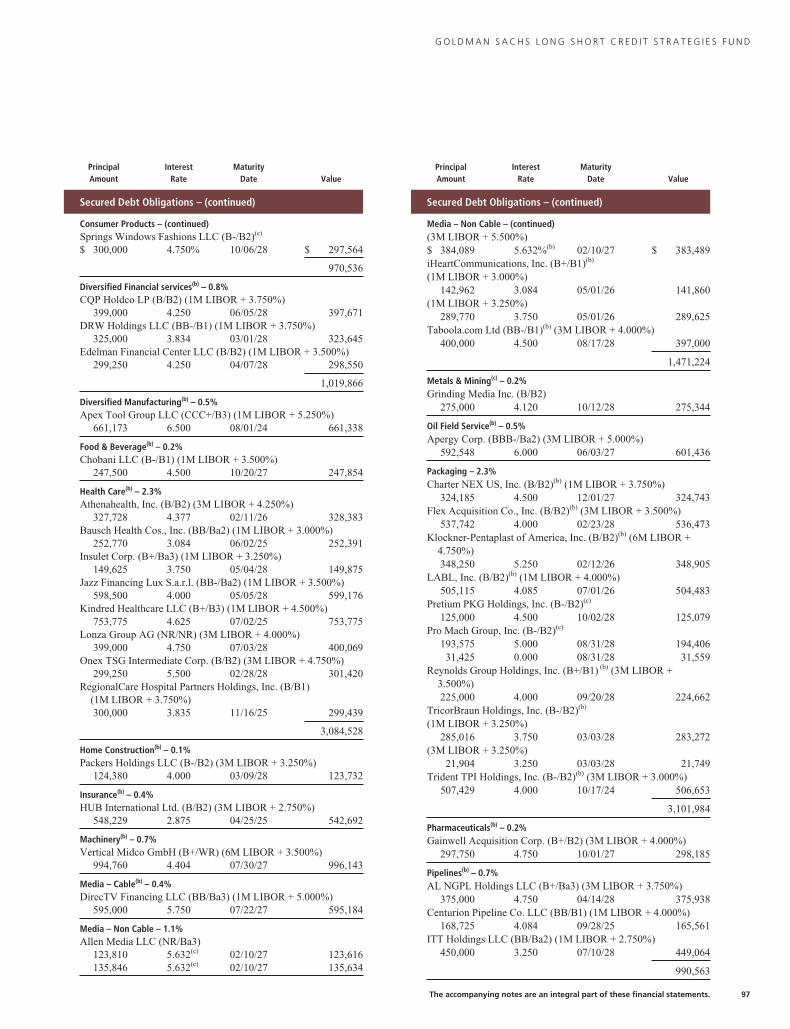

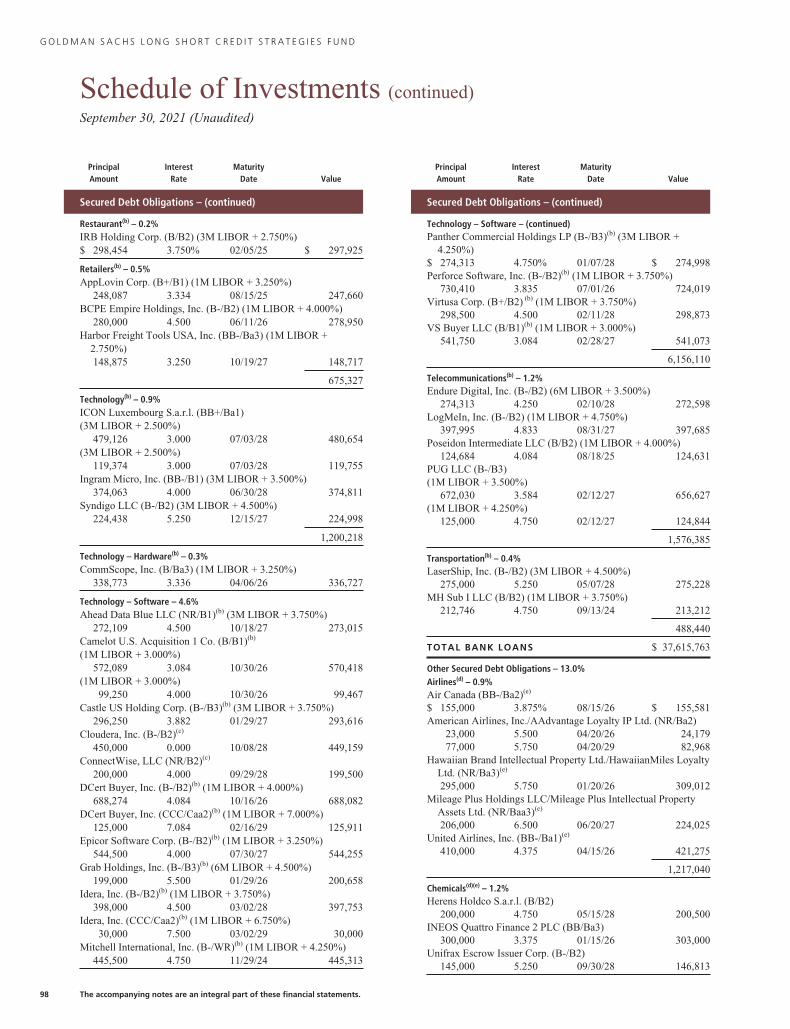

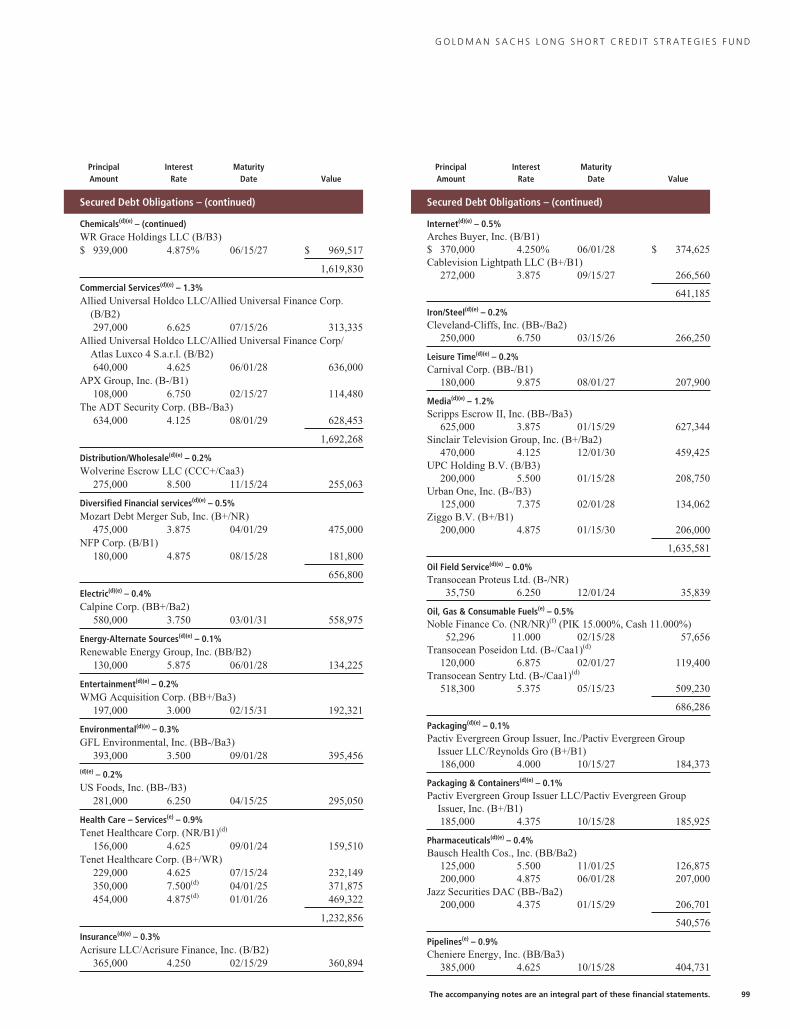

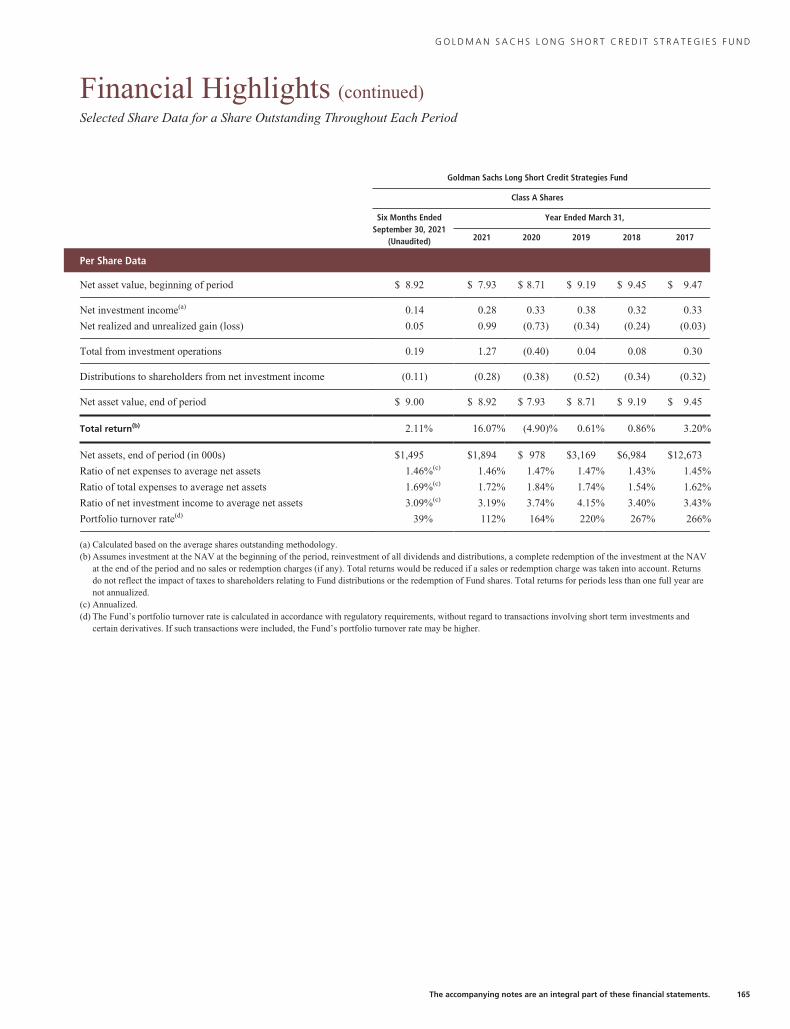

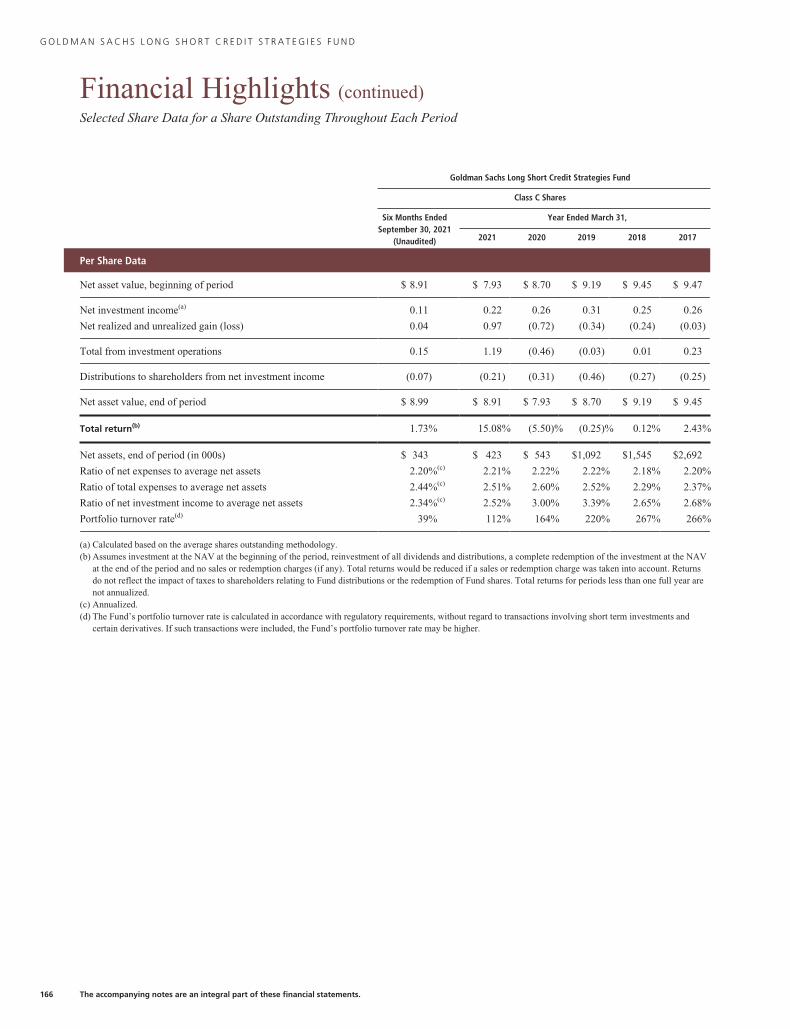

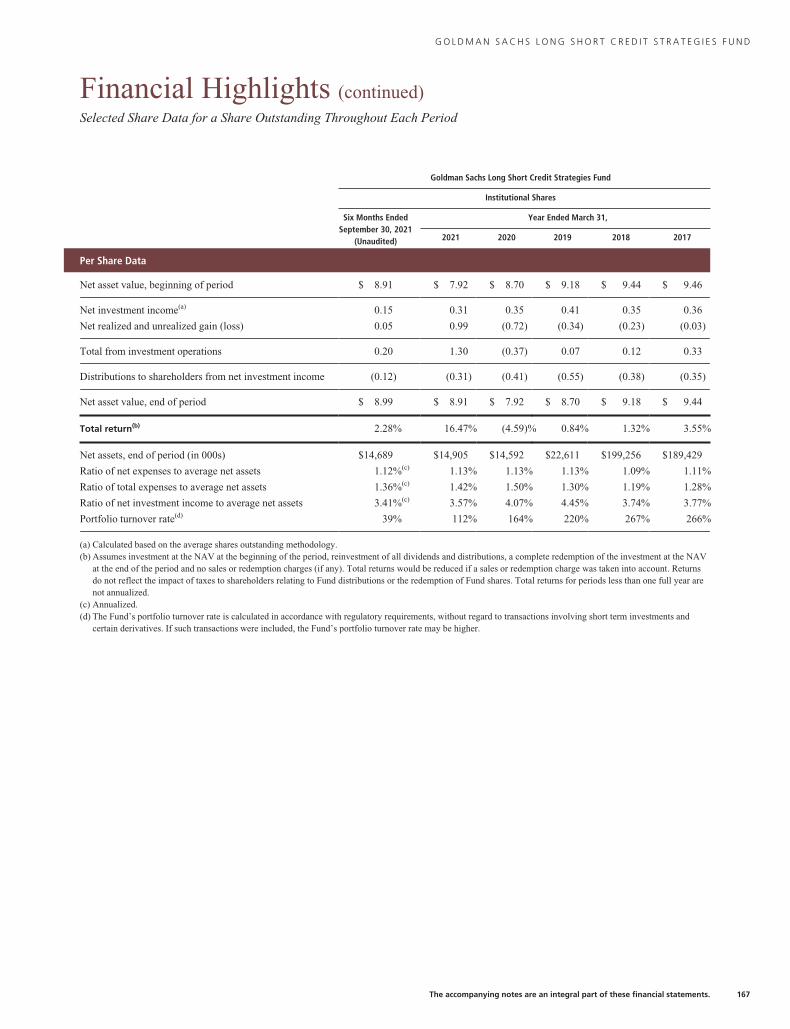

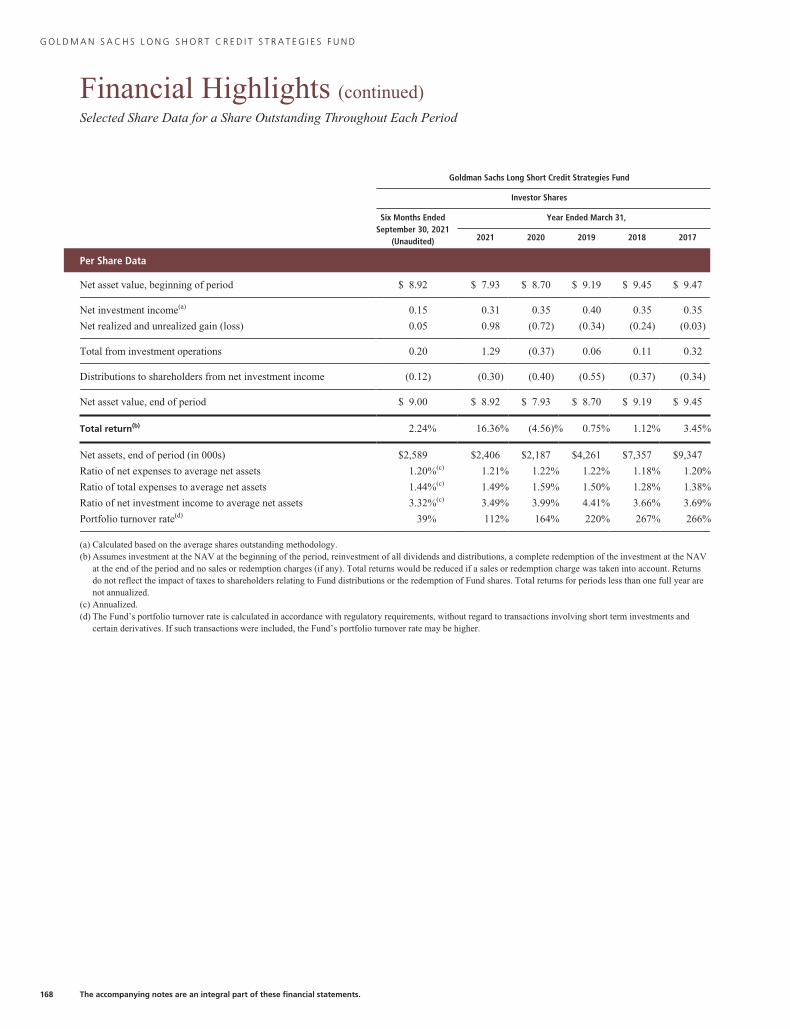

Long Short Credit Strategies Fundas of September 30, 2021

P E R F O R M A N C E R E V I E W

April 1, 2021–September 30, 2021Fund Total Return(based on NAV)1

ICE BofAMLThree-MonthU.S. Treasury

Bill Index2

ICE BofAML U.S.Dollar Three-Month

LIBOR ConstantMaturity Index3

30-Day StandardizedSubsidized Yield4

30-Day StandardizedUnsubsidized Yield4

Class A 2.11% 0.01% 0.08% 2.40% 2.15%Class C 1.73 0.01 0.08 1.74 1.49Institutional 2.28 0.01 0.08 2.82 2.56Investor 2.24 0.01 0.08 2.74 2.48Class R6 2.28 0.01 0.08 2.83 2.57Class R 1.98 0.01 0.08 2.25 1.99Class P 2.28 0.01 0.08 2.83 2.57

1 The net asset value (“NAV”) represents the net assets of the Fund (ex-dividend) divided by the total number of shares outstanding.The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflectthe deduction of any applicable sales charges.

2 The ICE BofAML Three-Month U.S. Treasury Bill Index, an unmanaged index, measures total return on cash, including price andinterest income, based on short-term government Treasury Bills of about 90-day maturity, as reported by Bank of America MerrillLynch, and does not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index.

3 The ICE BofAML U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “BofA/Merrill Lynch Index”) tracks theperformance of a synthetic asset paying LIBOR to a stated maturity. The BofA/Merrill Lynch Index is based on the assumedpurchase at par of a synthetic instrument having exactly its stated maturity and with a coupon equal to that day’s fixing rate. Thatissue is assumed to be sold the following business day (priced at a yield equal to the current day fixing rate) and rolled into a newinstrument. It is not possible to invest directly in an index.

4 The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and ExchangeCommission and is determined by dividing the net investment income per share earned during the last 30 days of the period by themaximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-DayStandardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period.Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earnedand distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If theFund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yieldand 30-Day Standardized Unsubsidized Yield will be identical.

The returns set forth in the table above represent past performance. Past performance does not guarantee future results.The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worthmore or less than their original cost. Current performance may be lower or higher than the performance quoted above.Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects

applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be

reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of

Fund shares.

10

F U N D B A S I C S

F U N D C O M P O S I T I O N 4

Percentage of Net Assets

as of 3/31/21as of 9/30/21

0%

60%

50%

40%

Othe

r Sec

ured

Debt

Obl

igat

ions

13.1

%

13.0

%

Bank

Loa

ns28

.0%

23.7

%

Inve

stm

ent

Com

pani

es4.

0%

7.3%

U.S.

Tre

asur

yOb

ligat

ions

3.9%

0.0%

Com

mon

Sto

cks

0.4%0.6%

Unse

cure

d De

btOb

ligat

ions

51.4

% 54.4

%

10%

20%

30%

4 The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.Figures in the graph may not sum to 100% due to the exclusion of other assets and liabilities. The graph depicts the Fund’sinvestments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in theAdditional Investment Information section of the Schedule of Investments.

11

F U N D B A S I C S

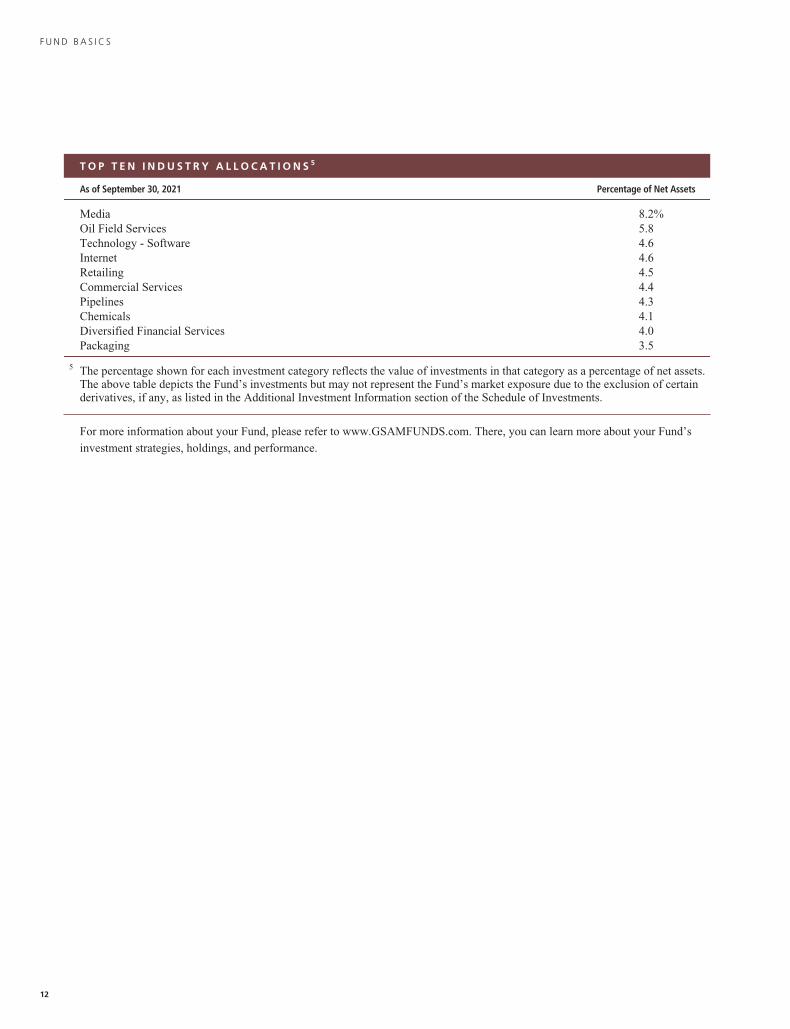

T O P T E N I N D U S T R Y A L L O C A T I O N S 5

As of September 30, 2021 Percentage of Net Assets

Media 8.2%Oil Field Services 5.8Technology - Software 4.6Internet 4.6Retailing 4.5Commercial Services 4.4Pipelines 4.3Chemicals 4.1Diversified Financial Services 4.0Packaging 3.5

5 The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.The above table depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certainderivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments.

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s

investment strategies, holdings, and performance.

12

F U N D B A S I C S

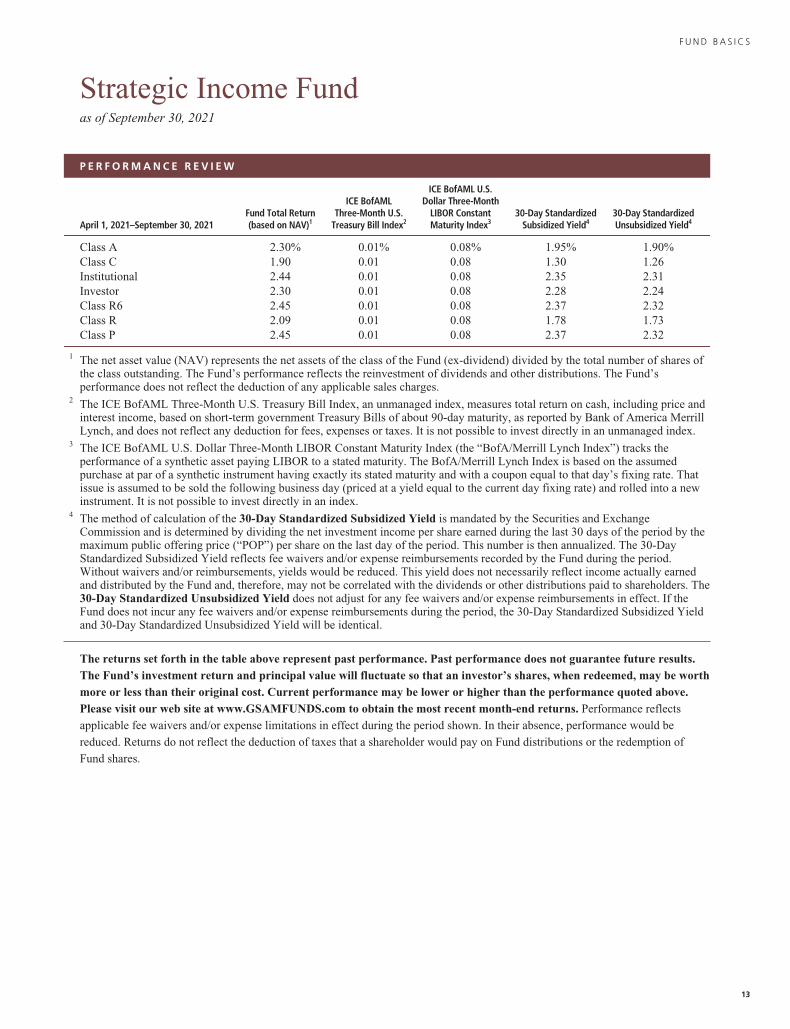

Strategic Income Fundas of September 30, 2021

P E R F O R M A N C E R E V I E W

April 1, 2021–September 30, 2021Fund Total Return(based on NAV)1

ICE BofAMLThree-Month U.S.

Treasury Bill Index2

ICE BofAML U.S.Dollar Three-Month

LIBOR ConstantMaturity Index3

30-Day StandardizedSubsidized Yield4

30-Day StandardizedUnsubsidized Yield4

Class A 2.30% 0.01% 0.08% 1.95% 1.90%Class C 1.90 0.01 0.08 1.30 1.26Institutional 2.44 0.01 0.08 2.35 2.31Investor 2.30 0.01 0.08 2.28 2.24Class R6 2.45 0.01 0.08 2.37 2.32Class R 2.09 0.01 0.08 1.78 1.73Class P 2.45 0.01 0.08 2.37 2.32

1 The net asset value (NAV) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares ofthe class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’sperformance does not reflect the deduction of any applicable sales charges.

2 The ICE BofAML Three-Month U.S. Treasury Bill Index, an unmanaged index, measures total return on cash, including price andinterest income, based on short-term government Treasury Bills of about 90-day maturity, as reported by Bank of America MerrillLynch, and does not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

3 The ICE BofAML U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “BofA/Merrill Lynch Index”) tracks theperformance of a synthetic asset paying LIBOR to a stated maturity. The BofA/Merrill Lynch Index is based on the assumedpurchase at par of a synthetic instrument having exactly its stated maturity and with a coupon equal to that day’s fixing rate. Thatissue is assumed to be sold the following business day (priced at a yield equal to the current day fixing rate) and rolled into a newinstrument. It is not possible to invest directly in an index.

4 The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and ExchangeCommission and is determined by dividing the net investment income per share earned during the last 30 days of the period by themaximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-DayStandardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period.Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earnedand distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/or expense reimbursements in effect. If theFund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yieldand 30-Day Standardized Unsubsidized Yield will be identical.

The returns set forth in the table above represent past performance. Past performance does not guarantee future results.The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worthmore or less than their original cost. Current performance may be lower or higher than the performance quoted above.Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects

applicable fee waivers and/or expense limitations in effect during the period shown. In their absence, performance would be

reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of

Fund shares.

13

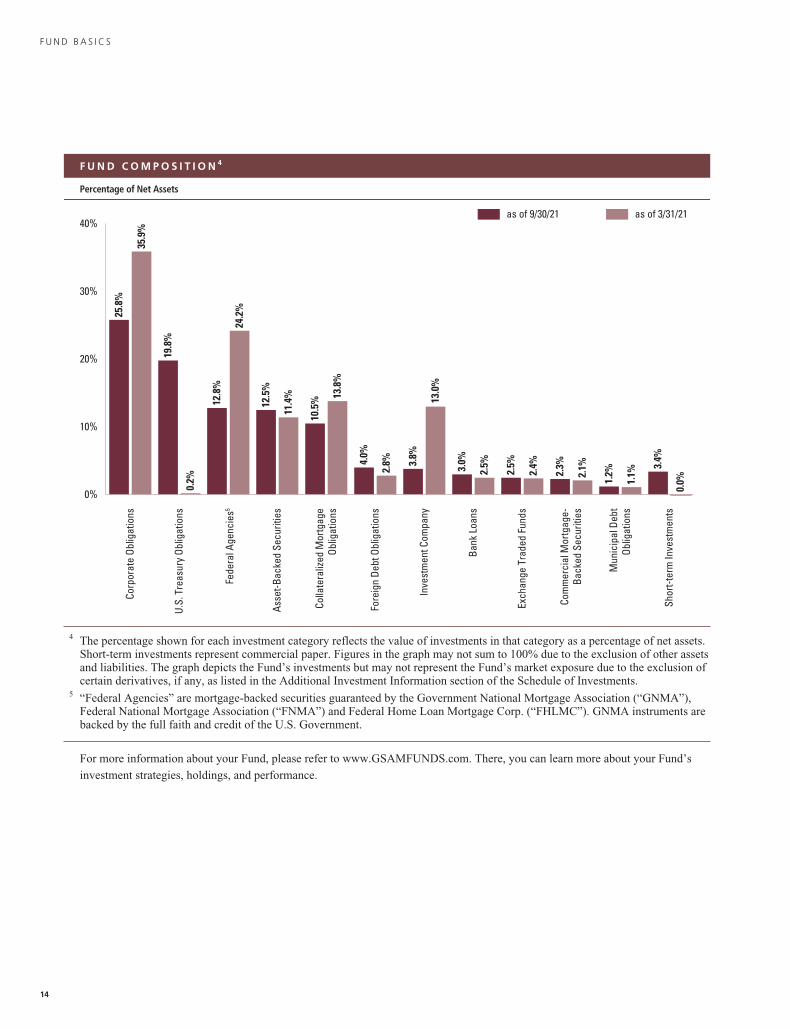

F U N D B A S I C S

F U N D C O M P O S I T I O N 4

Percentage of Net Assets

as of 3/31/21as of 9/30/21

Corp

orat

e Ob

ligat

ions

35.9

%

25.8

%

Mun

icip

al D

ebt

Obl

igat

ions

1.2%

1.1%

Shor

t-ter

m In

vest

men

ts3.

4%

0.0%

U.S.

Tre

asur

y Ob

ligat

ions

19.8

%

0.2%

Colla

tera

lized

Mor

tgag

e O

blig

atio

ns13

.8%

10.5

%

Asse

t-Bac

ked

Secu

ritie

s11

.4%

12.5

%

Inve

stm

ent C

ompa

ny

2.5%3.0%

Com

mer

cial

Mor

tgag

e-Ba

cked

Sec

uriti

es

3.8%

13.0

%

Fede

ral A

genc

ies5

12.8

%

24.2

%

Fore

ign

Debt

Obl

igat

ions

4.0%

2.8%

Exch

ange

Tra

ded

Fund

s

2.1%2.3%

Bank

Loa

ns

2.4%2.5%

0%

10%

20%

30%

40%

4 The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.Short-term investments represent commercial paper. Figures in the graph may not sum to 100% due to the exclusion of other assetsand liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion ofcertain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments.

5 “Federal Agencies” are mortgage-backed securities guaranteed by the Government National Mortgage Association (“GNMA”),Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corp. (“FHLMC”). GNMA instruments arebacked by the full faith and credit of the U.S. Government.

For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s

investment strategies, holdings, and performance.

14

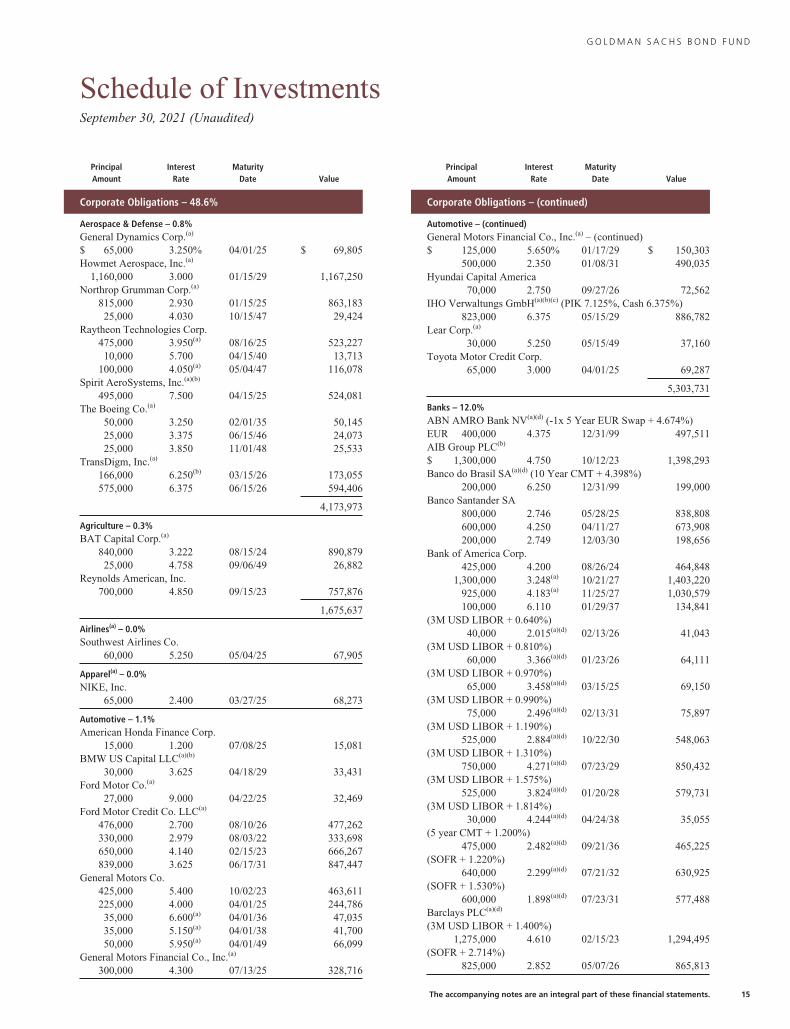

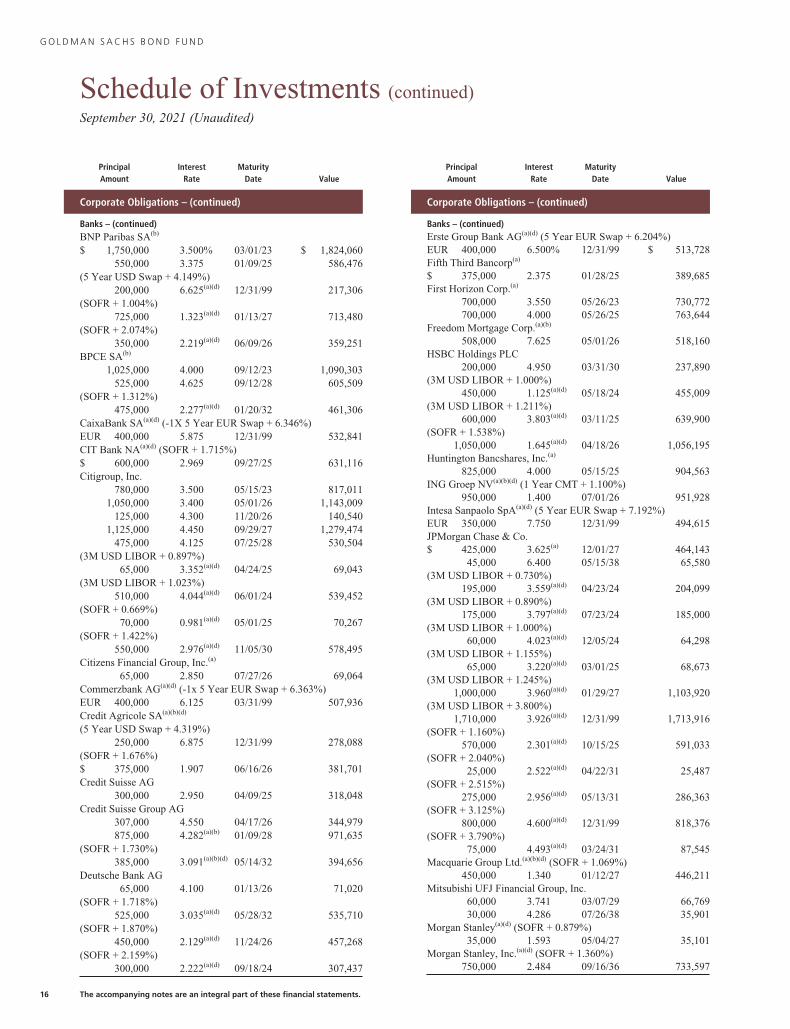

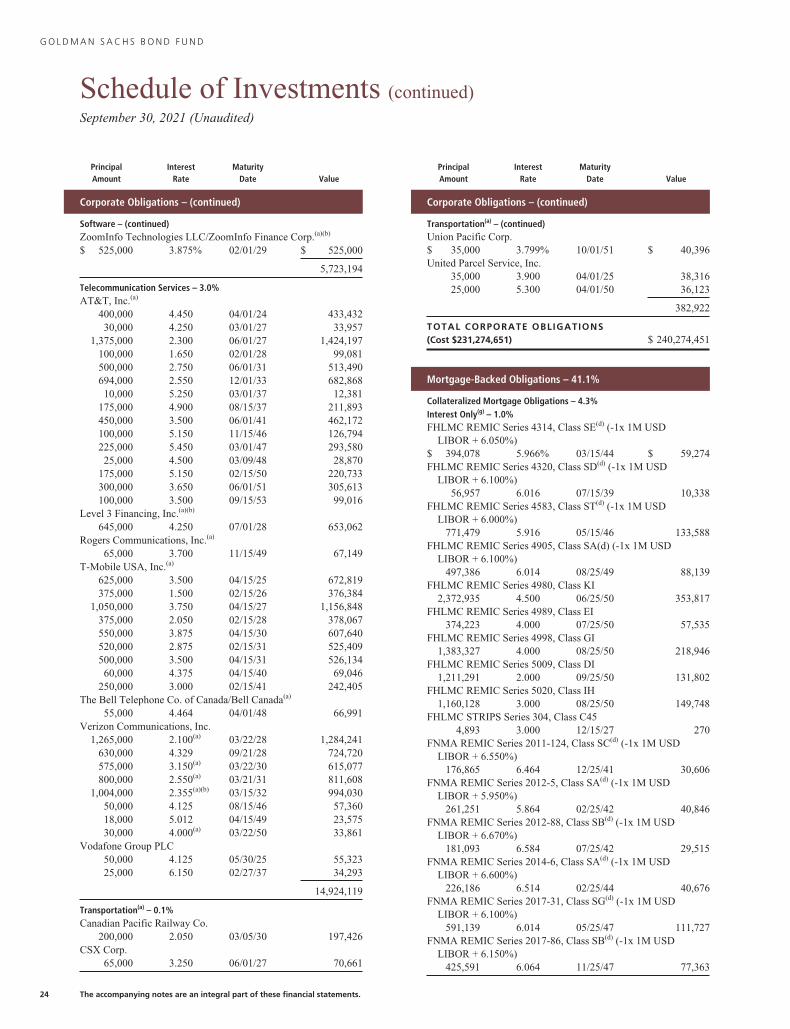

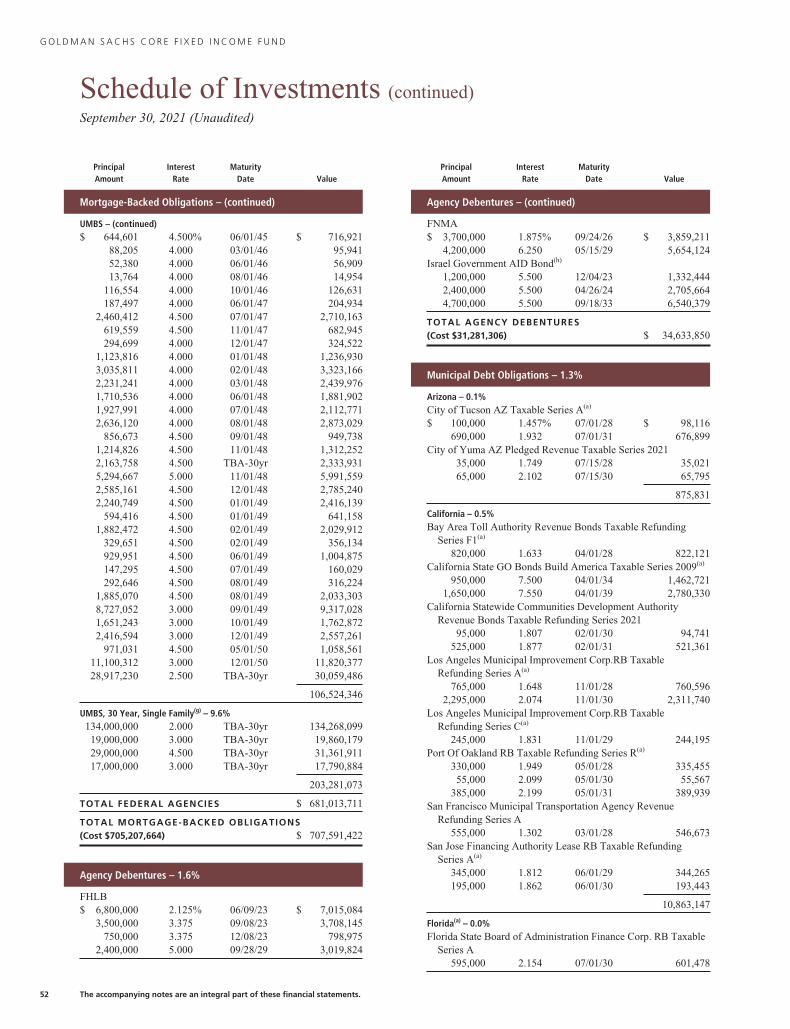

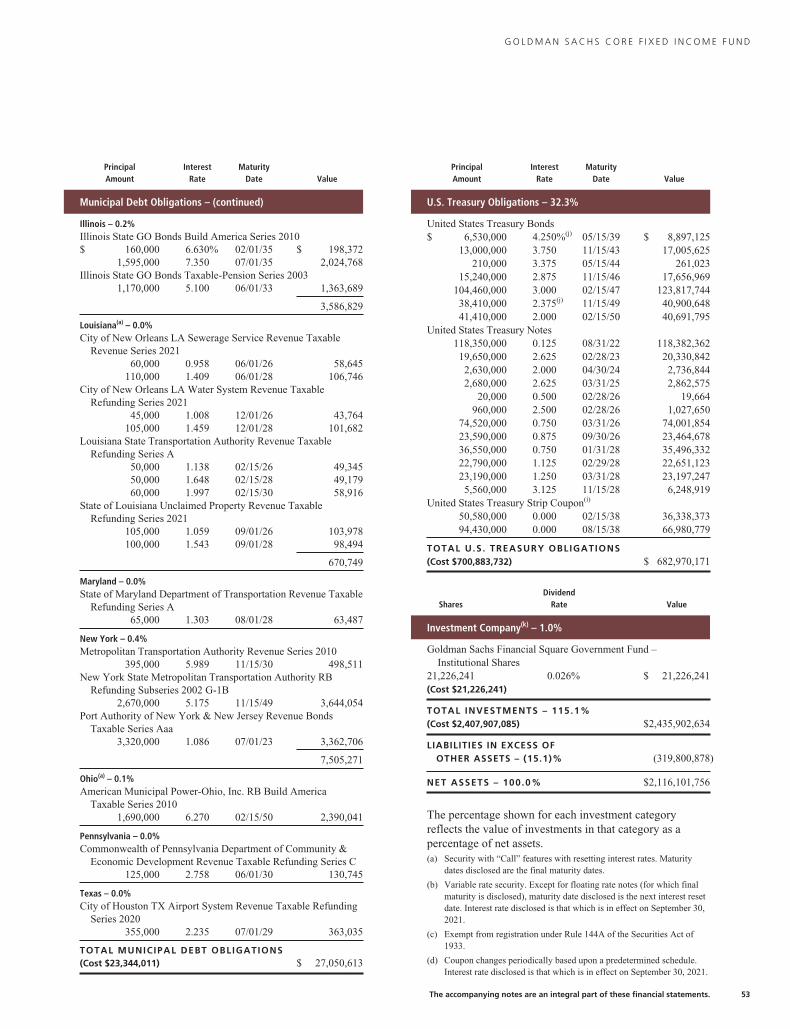

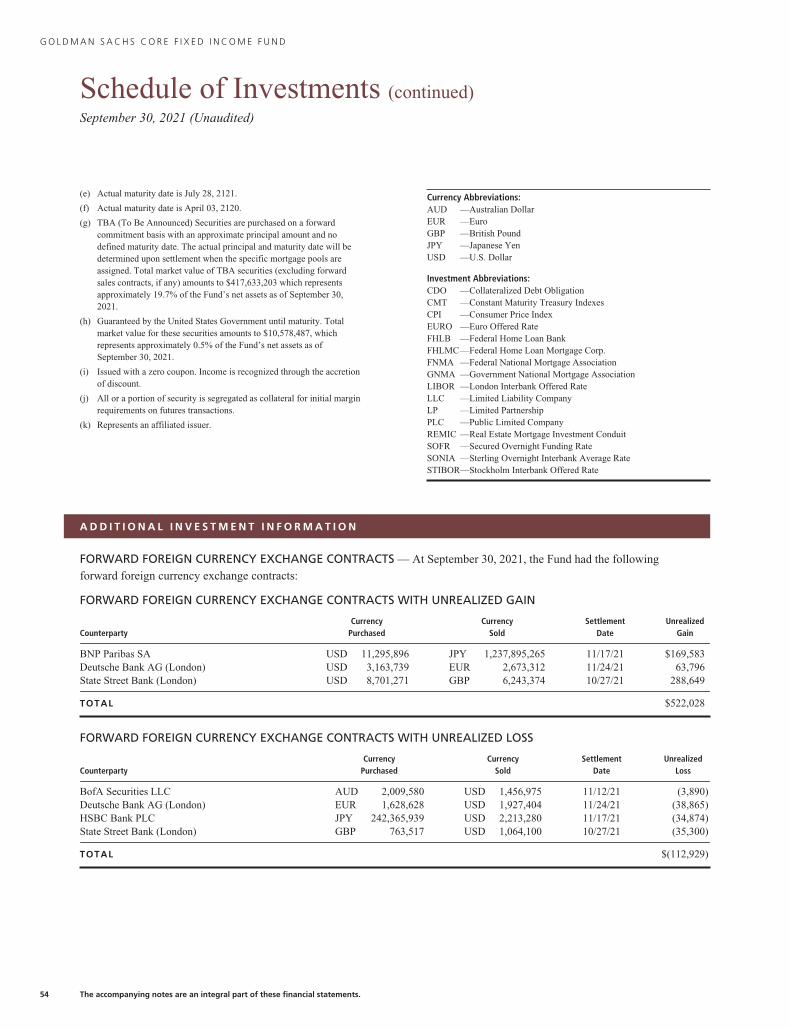

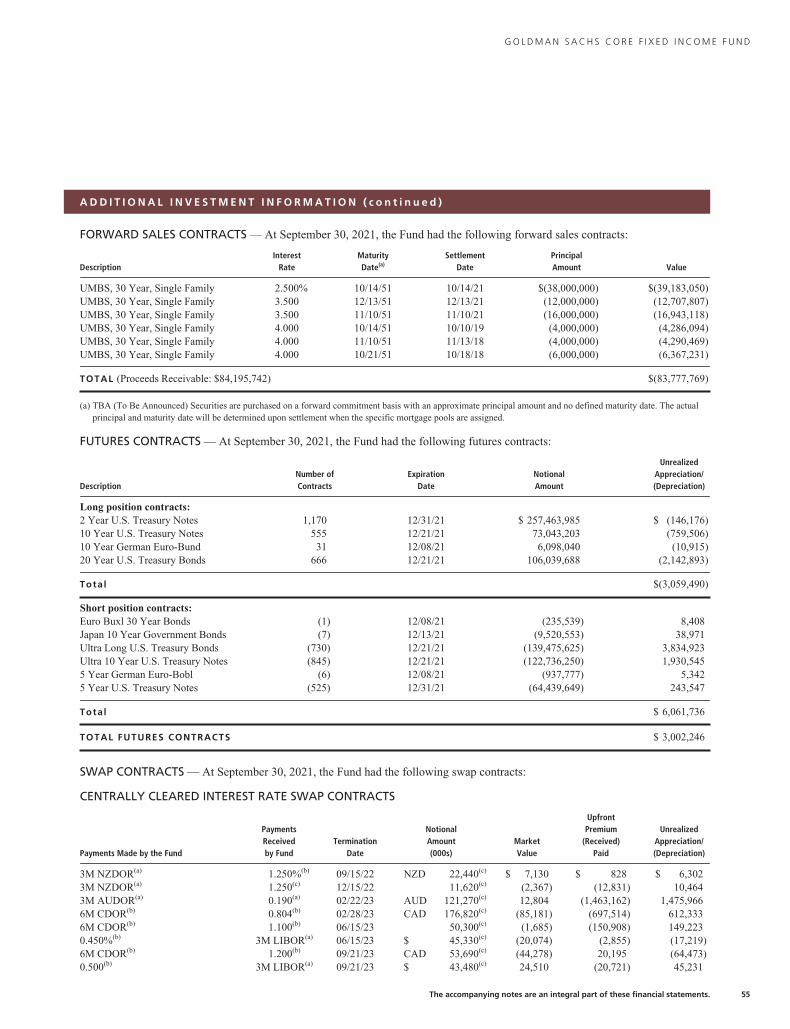

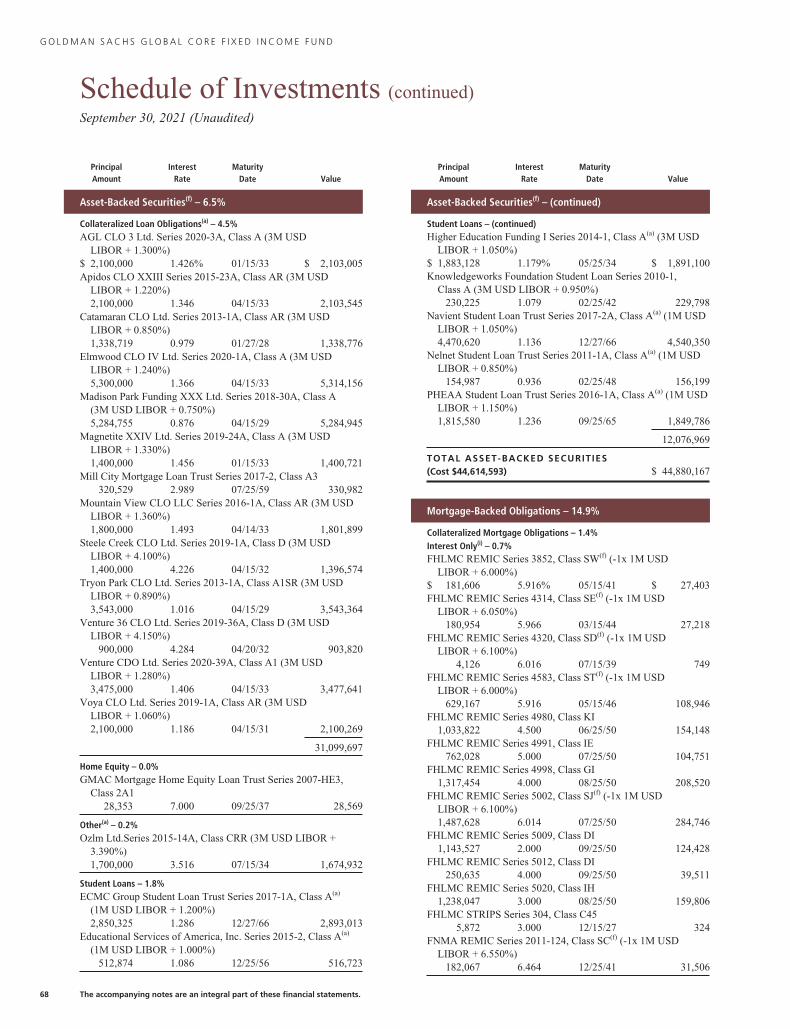

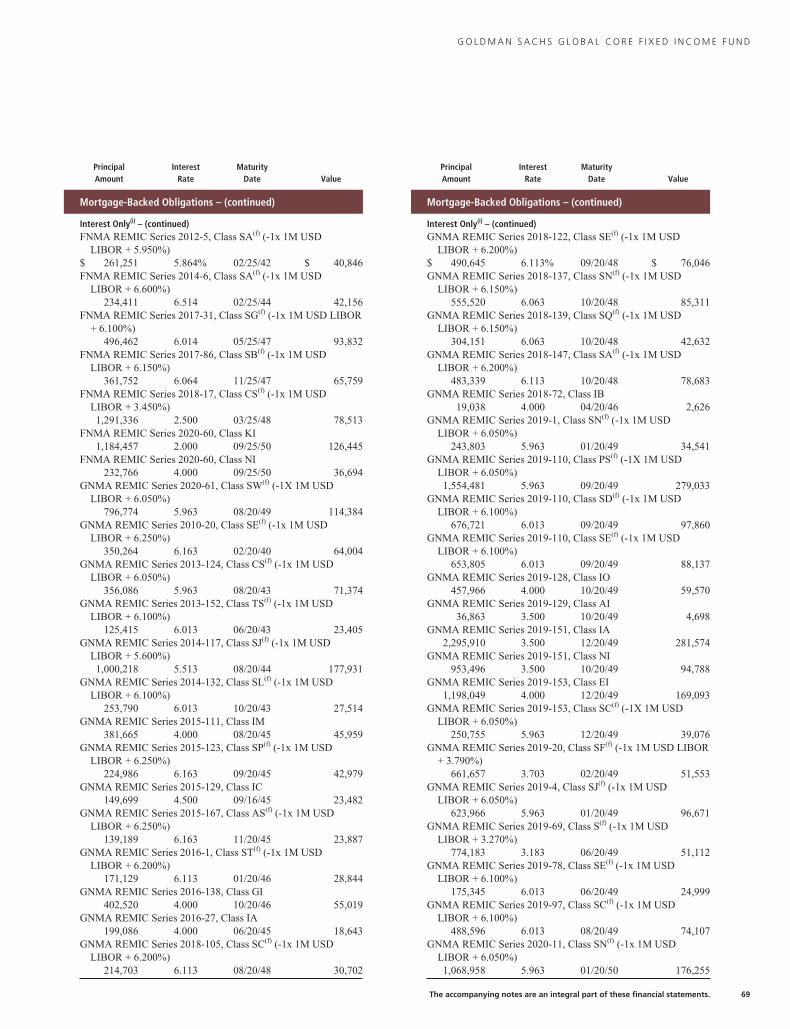

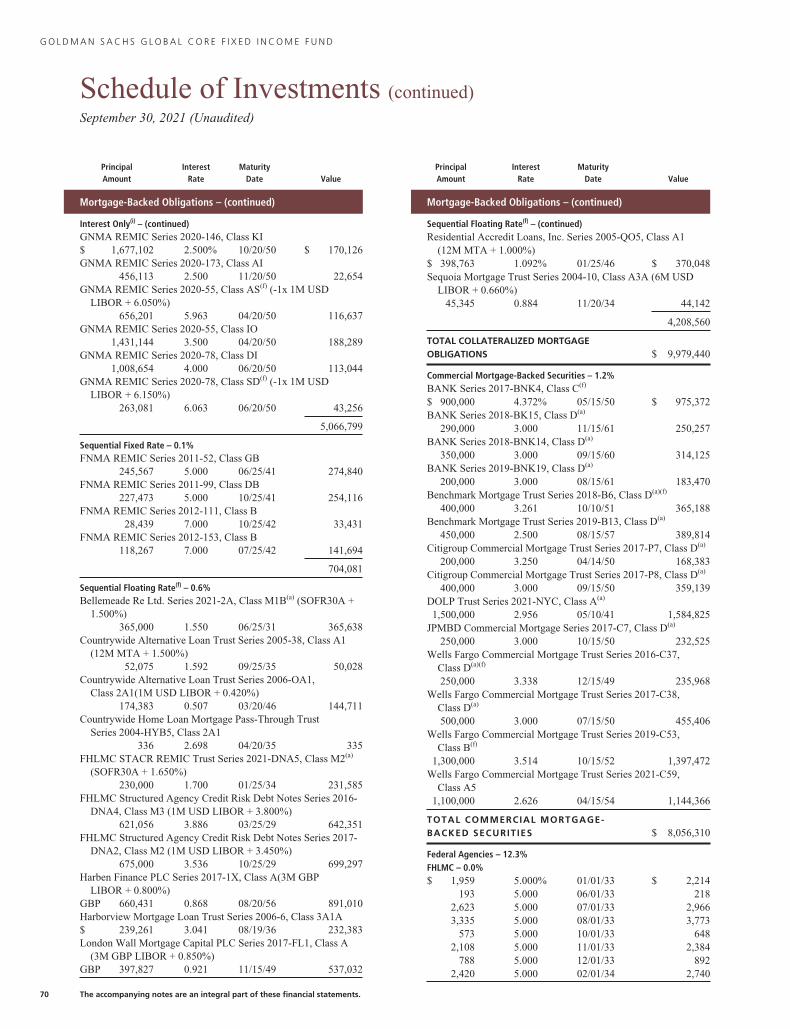

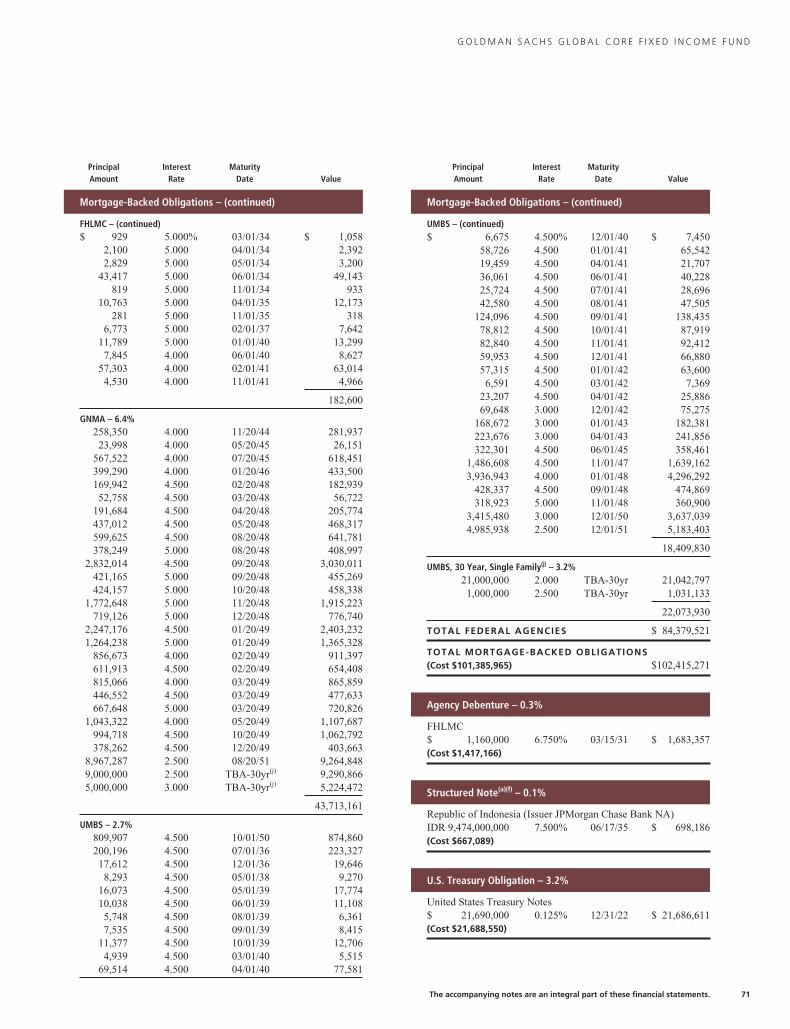

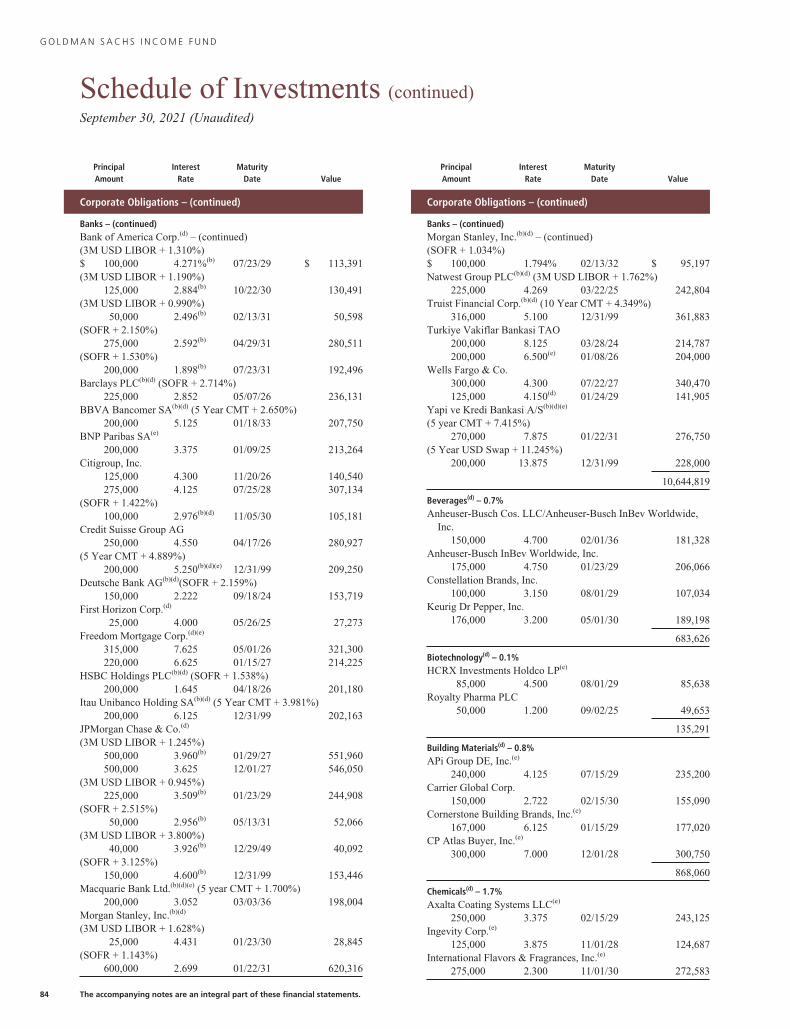

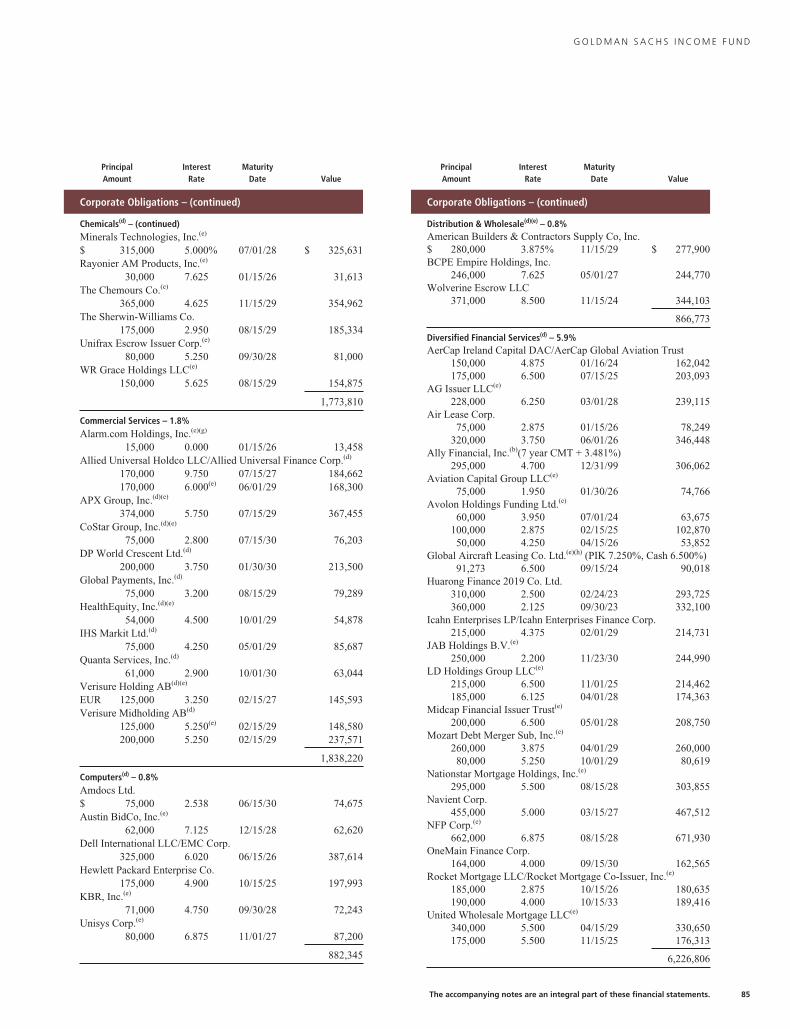

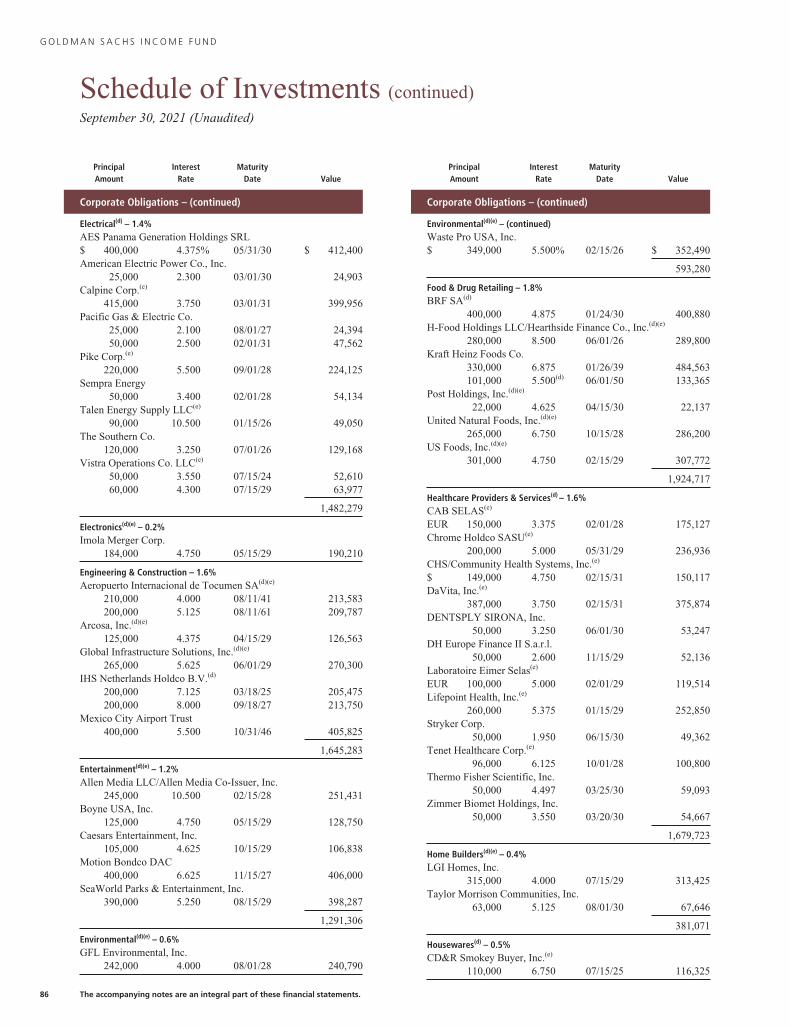

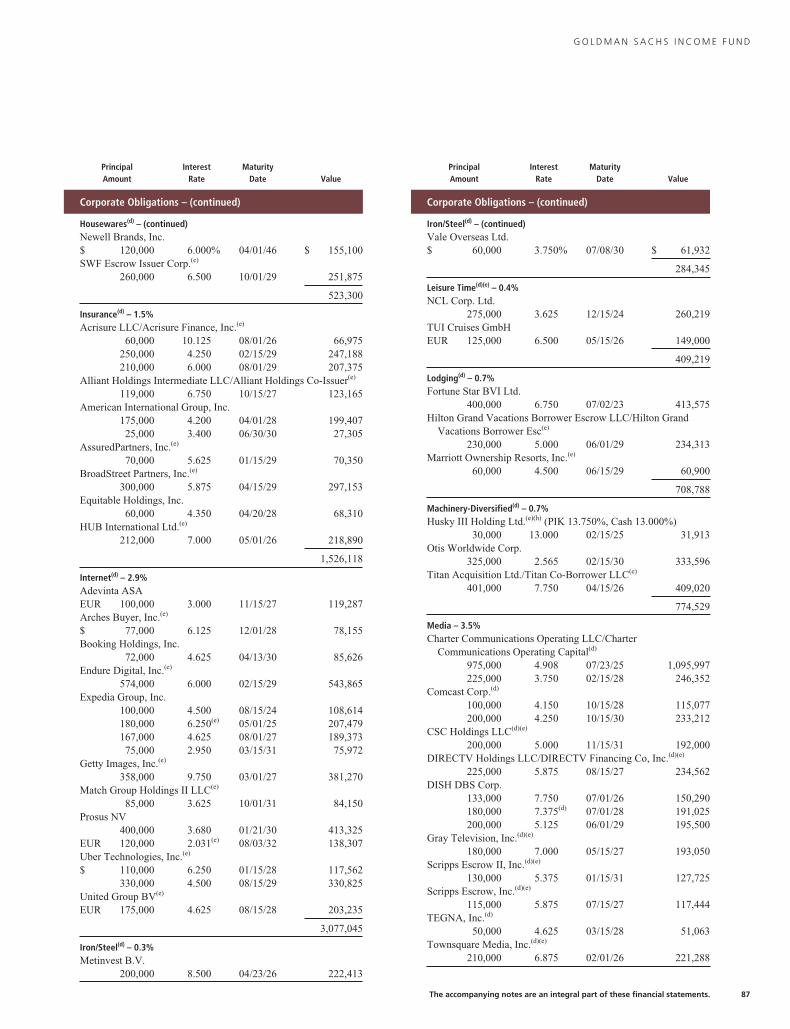

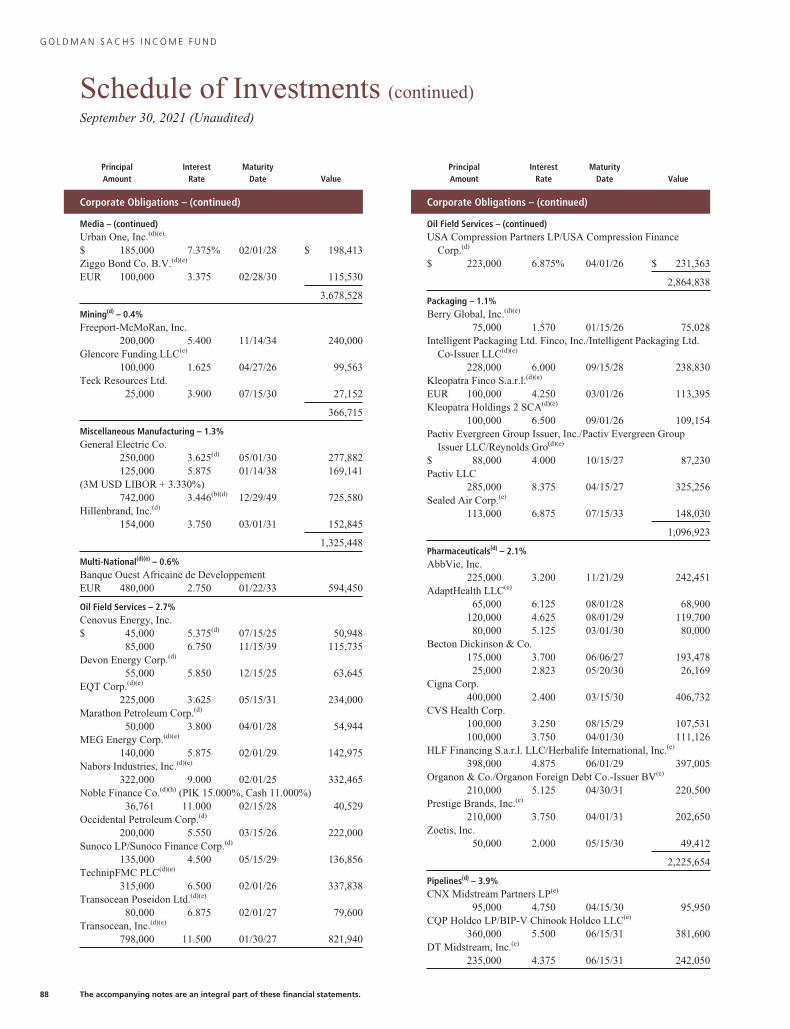

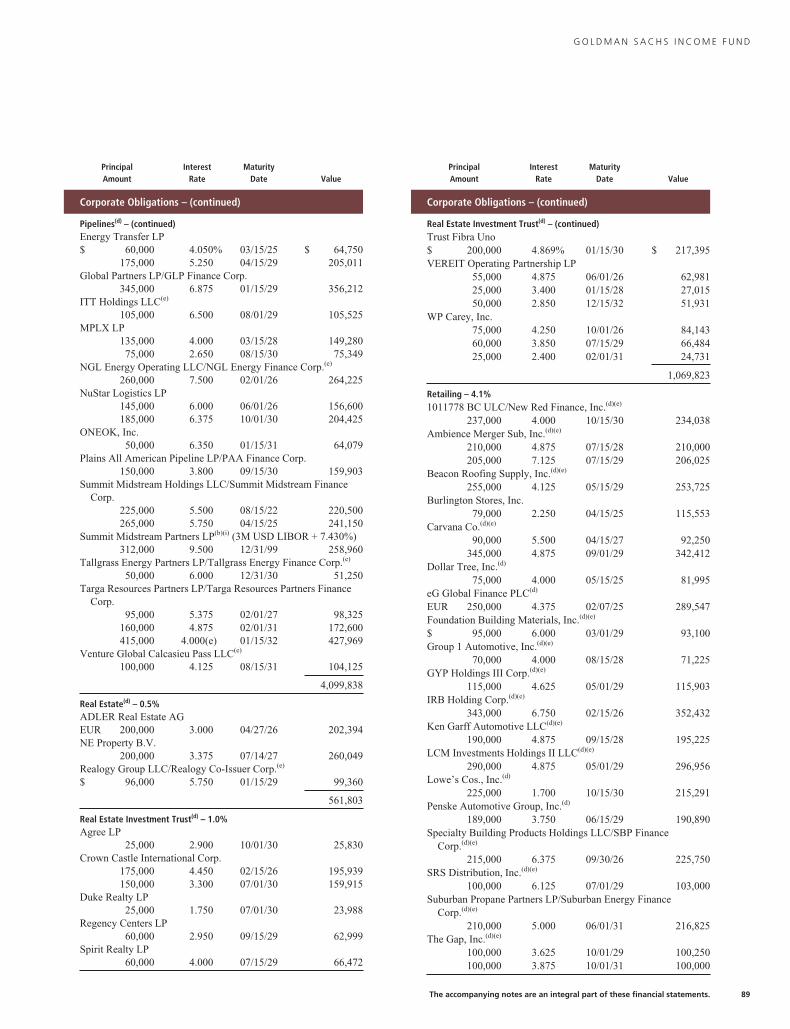

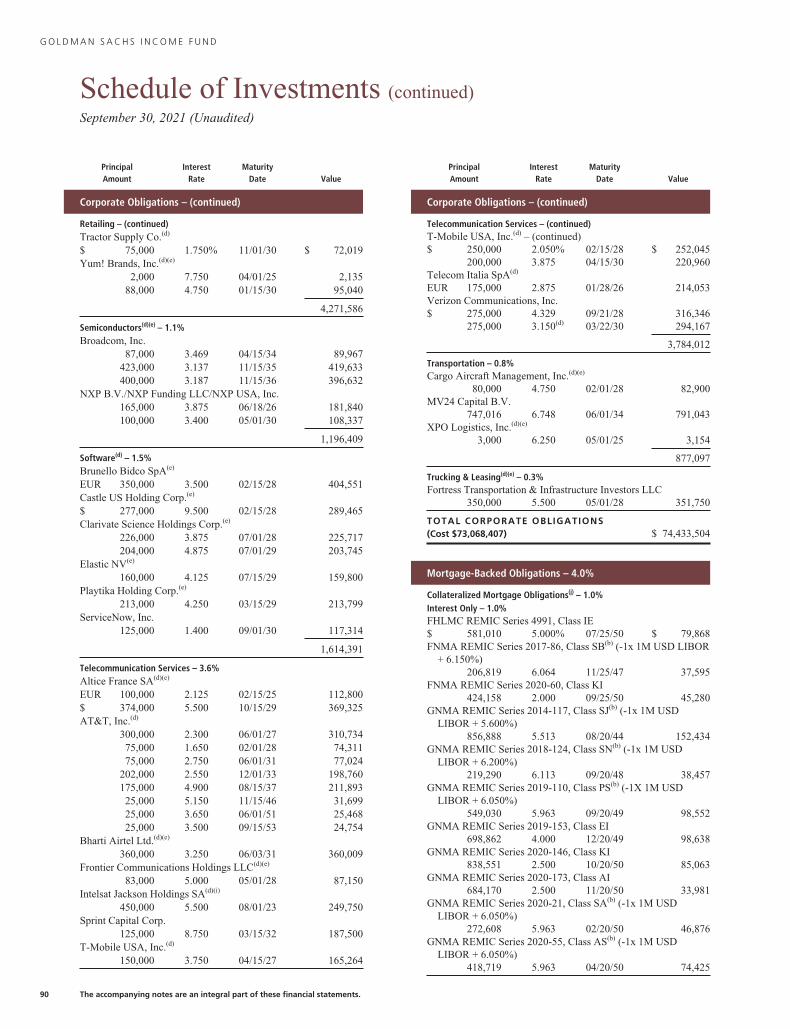

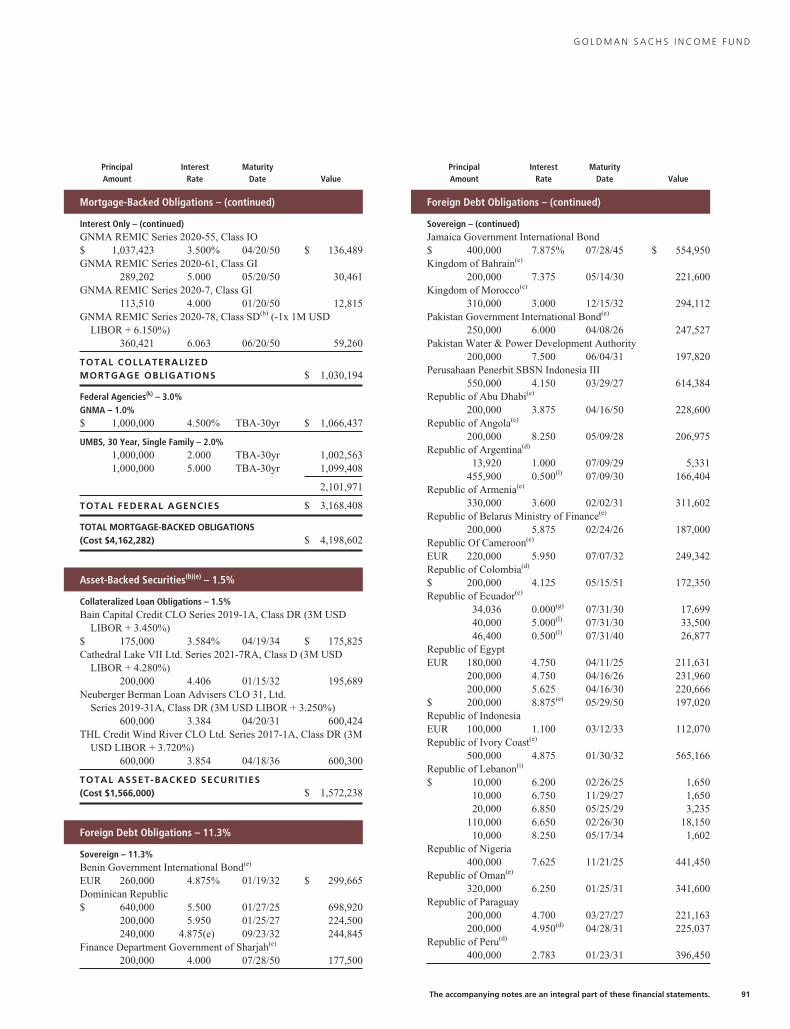

G O L D M A N S A C H S B O N D F U N D

Schedule of InvestmentsSeptember 30, 2021 (Unaudited)

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – 48.6%

Aerospace & Defense – 0.8%General Dynamics Corp.(a)

$ 65,000 3.250% 04/01/25 $ 69,805Howmet Aerospace, Inc.(a)

1,160,000 3.000 01/15/29 1,167,250Northrop Grumman Corp.(a)

815,000 2.930 01/15/25 863,18325,000 4.030 10/15/47 29,424

Raytheon Technologies Corp.475,000 3.950(a) 08/16/25 523,22710,000 5.700 04/15/40 13,713

100,000 4.050(a) 05/04/47 116,078Spirit AeroSystems, Inc.(a)(b)

495,000 7.500 04/15/25 524,081The Boeing Co.(a)

50,000 3.250 02/01/35 50,14525,000 3.375 06/15/46 24,07325,000 3.850 11/01/48 25,533

TransDigm, Inc.(a)

166,000 6.250(b) 03/15/26 173,055575,000 6.375 06/15/26 594,406

4,173,973

Agriculture – 0.3%BAT Capital Corp.(a)

840,000 3.222 08/15/24 890,87925,000 4.758 09/06/49 26,882

Reynolds American, Inc.700,000 4.850 09/15/23 757,876

1,675,637

Airlines(a) – 0.0%Southwest Airlines Co.

60,000 5.250 05/04/25 67,905

Apparel(a) – 0.0%NIKE, Inc.

65,000 2.400 03/27/25 68,273

Automotive – 1.1%American Honda Finance Corp.

15,000 1.200 07/08/25 15,081BMW US Capital LLC(a)(b)

30,000 3.625 04/18/29 33,431Ford Motor Co.(a)

27,000 9.000 04/22/25 32,469Ford Motor Credit Co. LLC(a)

476,000 2.700 08/10/26 477,262330,000 2.979 08/03/22 333,698650,000 4.140 02/15/23 666,267839,000 3.625 06/17/31 847,447

General Motors Co.425,000 5.400 10/02/23 463,611225,000 4.000 04/01/25 244,78635,000 6.600(a) 04/01/36 47,03535,000 5.150(a) 04/01/38 41,70050,000 5.950(a) 04/01/49 66,099

General Motors Financial Co., Inc.(a)

300,000 4.300 07/13/25 328,716

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Automotive – (continued)General Motors Financial Co., Inc.(a) – (continued)$ 125,000 5.650% 01/17/29 $ 150,303

500,000 2.350 01/08/31 490,035Hyundai Capital America

70,000 2.750 09/27/26 72,562IHO Verwaltungs GmbH(a)(b)(c) (PIK 7.125%, Cash 6.375%)

823,000 6.375 05/15/29 886,782Lear Corp.(a)

30,000 5.250 05/15/49 37,160Toyota Motor Credit Corp.

65,000 3.000 04/01/25 69,287

5,303,731

Banks – 12.0%ABN AMRO Bank NV(a)(d) (-1x 5 Year EUR Swap + 4.674%)EUR 400,000 4.375 12/31/99 497,511AIB Group PLC(b)

$ 1,300,000 4.750 10/12/23 1,398,293Banco do Brasil SA(a)(d) (10 Year CMT + 4.398%)

200,000 6.250 12/31/99 199,000Banco Santander SA

800,000 2.746 05/28/25 838,808600,000 4.250 04/11/27 673,908200,000 2.749 12/03/30 198,656

Bank of America Corp.425,000 4.200 08/26/24 464,848

1,300,000 3.248(a) 10/21/27 1,403,220925,000 4.183(a) 11/25/27 1,030,579100,000 6.110 01/29/37 134,841

(3M USD LIBOR + 0.640%)40,000 2.015(a)(d) 02/13/26 41,043

(3M USD LIBOR + 0.810%)60,000 3.366(a)(d) 01/23/26 64,111

(3M USD LIBOR + 0.970%)65,000 3.458(a)(d) 03/15/25 69,150

(3M USD LIBOR + 0.990%)75,000 2.496(a)(d) 02/13/31 75,897

(3M USD LIBOR + 1.190%)525,000 2.884(a)(d) 10/22/30 548,063

(3M USD LIBOR + 1.310%)750,000 4.271(a)(d) 07/23/29 850,432

(3M USD LIBOR + 1.575%)525,000 3.824(a)(d) 01/20/28 579,731

(3M USD LIBOR + 1.814%)30,000 4.244(a)(d) 04/24/38 35,055

(5 year CMT + 1.200%)475,000 2.482(a)(d) 09/21/36 465,225

(SOFR + 1.220%)640,000 2.299(a)(d) 07/21/32 630,925

(SOFR + 1.530%)600,000 1.898(a)(d) 07/23/31 577,488

Barclays PLC(a)(d)

(3M USD LIBOR + 1.400%)1,275,000 4.610 02/15/23 1,294,495

(SOFR + 2.714%)825,000 2.852 05/07/26 865,813

The accompanying notes are an integral part of these financial statements. 15

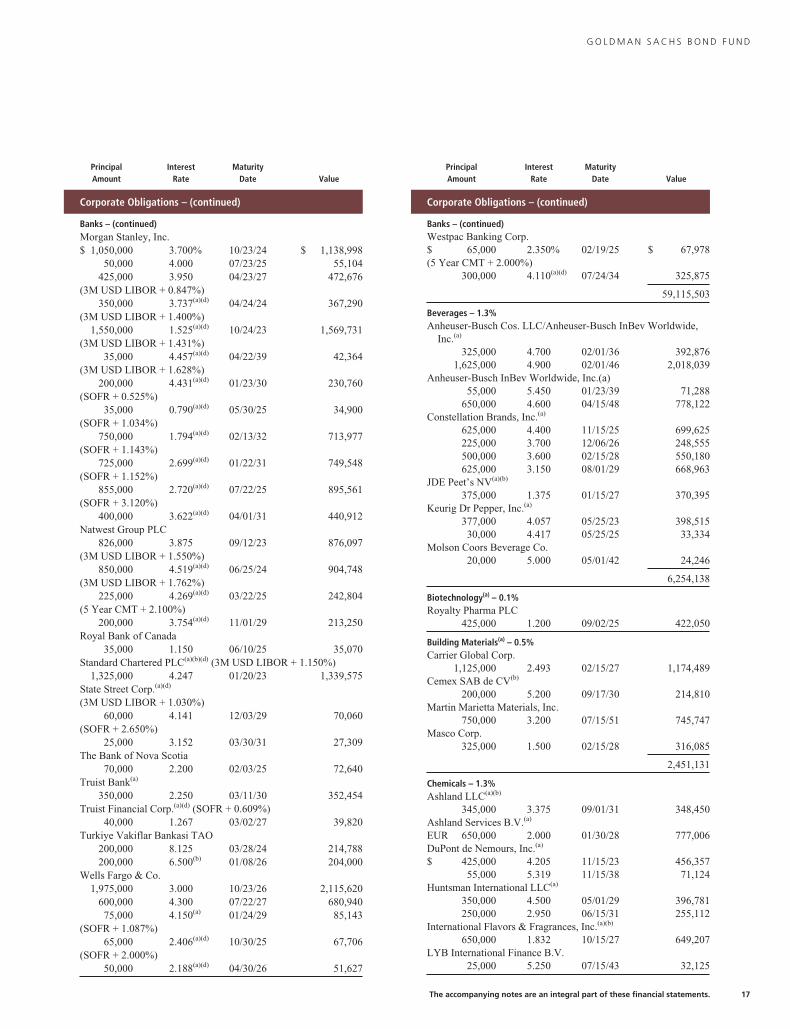

G O L D M A N S A C H S B O N D F U N D

Schedule of Investments (continued)September 30, 2021 (Unaudited)

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Banks – (continued)BNP Paribas SA(b)

$ 1,750,000 3.500% 03/01/23 $ 1,824,060550,000 3.375 01/09/25 586,476

(5 Year USD Swap + 4.149%)200,000 6.625(a)(d) 12/31/99 217,306

(SOFR + 1.004%)725,000 1.323(a)(d) 01/13/27 713,480

(SOFR + 2.074%)350,000 2.219(a)(d) 06/09/26 359,251

BPCE SA(b)

1,025,000 4.000 09/12/23 1,090,303525,000 4.625 09/12/28 605,509

(SOFR + 1.312%)475,000 2.277(a)(d) 01/20/32 461,306

CaixaBank SA(a)(d) (-1X 5 Year EUR Swap + 6.346%)EUR 400,000 5.875 12/31/99 532,841CIT Bank NA(a)(d) (SOFR + 1.715%)$ 600,000 2.969 09/27/25 631,116Citigroup, Inc.

780,000 3.500 05/15/23 817,0111,050,000 3.400 05/01/26 1,143,009

125,000 4.300 11/20/26 140,5401,125,000 4.450 09/29/27 1,279,474

475,000 4.125 07/25/28 530,504(3M USD LIBOR + 0.897%)

65,000 3.352(a)(d) 04/24/25 69,043(3M USD LIBOR + 1.023%)

510,000 4.044(a)(d) 06/01/24 539,452(SOFR + 0.669%)

70,000 0.981(a)(d) 05/01/25 70,267(SOFR + 1.422%)

550,000 2.976(a)(d) 11/05/30 578,495Citizens Financial Group, Inc.(a)

65,000 2.850 07/27/26 69,064Commerzbank AG(a)(d) (-1x 5 Year EUR Swap + 6.363%)EUR 400,000 6.125 03/31/99 507,936Credit Agricole SA(a)(b)(d)

(5 Year USD Swap + 4.319%)250,000 6.875 12/31/99 278,088

(SOFR + 1.676%)$ 375,000 1.907 06/16/26 381,701Credit Suisse AG

300,000 2.950 04/09/25 318,048Credit Suisse Group AG

307,000 4.550 04/17/26 344,979875,000 4.282(a)(b) 01/09/28 971,635

(SOFR + 1.730%)385,000 3.091(a)(b)(d) 05/14/32 394,656

Deutsche Bank AG65,000 4.100 01/13/26 71,020

(SOFR + 1.718%)525,000 3.035(a)(d) 05/28/32 535,710

(SOFR + 1.870%)450,000 2.129(a)(d) 11/24/26 457,268

(SOFR + 2.159%)300,000 2.222(a)(d) 09/18/24 307,437

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Banks – (continued)Erste Group Bank AG(a)(d) (5 Year EUR Swap + 6.204%)EUR 400,000 6.500% 12/31/99 $ 513,728Fifth Third Bancorp(a)

$ 375,000 2.375 01/28/25 389,685First Horizon Corp.(a)

700,000 3.550 05/26/23 730,772700,000 4.000 05/26/25 763,644

Freedom Mortgage Corp.(a)(b)

508,000 7.625 05/01/26 518,160HSBC Holdings PLC

200,000 4.950 03/31/30 237,890(3M USD LIBOR + 1.000%)

450,000 1.125(a)(d) 05/18/24 455,009(3M USD LIBOR + 1.211%)

600,000 3.803(a)(d) 03/11/25 639,900(SOFR + 1.538%)

1,050,000 1.645(a)(d) 04/18/26 1,056,195Huntington Bancshares, Inc.(a)

825,000 4.000 05/15/25 904,563ING Groep NV(a)(b)(d) (1 Year CMT + 1.100%)

950,000 1.400 07/01/26 951,928Intesa Sanpaolo SpA(a)(d) (5 Year EUR Swap + 7.192%)EUR 350,000 7.750 12/31/99 494,615JPMorgan Chase & Co.$ 425,000 3.625(a) 12/01/27 464,143

45,000 6.400 05/15/38 65,580(3M USD LIBOR + 0.730%)

195,000 3.559(a)(d) 04/23/24 204,099(3M USD LIBOR + 0.890%)

175,000 3.797(a)(d) 07/23/24 185,000(3M USD LIBOR + 1.000%)

60,000 4.023(a)(d) 12/05/24 64,298(3M USD LIBOR + 1.155%)

65,000 3.220(a)(d) 03/01/25 68,673(3M USD LIBOR + 1.245%)

1,000,000 3.960(a)(d) 01/29/27 1,103,920(3M USD LIBOR + 3.800%)

1,710,000 3.926(a)(d) 12/31/99 1,713,916(SOFR + 1.160%)

570,000 2.301(a)(d) 10/15/25 591,033(SOFR + 2.040%)

25,000 2.522(a)(d) 04/22/31 25,487(SOFR + 2.515%)

275,000 2.956(a)(d) 05/13/31 286,363(SOFR + 3.125%)

800,000 4.600(a)(d) 12/31/99 818,376(SOFR + 3.790%)

75,000 4.493(a)(d) 03/24/31 87,545Macquarie Group Ltd.(a)(b)(d) (SOFR + 1.069%)

450,000 1.340 01/12/27 446,211Mitsubishi UFJ Financial Group, Inc.

60,000 3.741 03/07/29 66,76930,000 4.286 07/26/38 35,901

Morgan Stanley(a)(d) (SOFR + 0.879%)35,000 1.593 05/04/27 35,101

Morgan Stanley, Inc.(a)(d) (SOFR + 1.360%)750,000 2.484 09/16/36 733,597

16 The accompanying notes are an integral part of these financial statements.

G O L D M A N S A C H S B O N D F U N D

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Banks – (continued)Morgan Stanley, Inc.$ 1,050,000 3.700% 10/23/24 $ 1,138,998

50,000 4.000 07/23/25 55,104425,000 3.950 04/23/27 472,676

(3M USD LIBOR + 0.847%)350,000 3.737(a)(d) 04/24/24 367,290

(3M USD LIBOR + 1.400%)1,550,000 1.525(a)(d) 10/24/23 1,569,731

(3M USD LIBOR + 1.431%)35,000 4.457(a)(d) 04/22/39 42,364

(3M USD LIBOR + 1.628%)200,000 4.431(a)(d) 01/23/30 230,760

(SOFR + 0.525%)35,000 0.790(a)(d) 05/30/25 34,900

(SOFR + 1.034%)750,000 1.794(a)(d) 02/13/32 713,977

(SOFR + 1.143%)725,000 2.699(a)(d) 01/22/31 749,548

(SOFR + 1.152%)855,000 2.720(a)(d) 07/22/25 895,561

(SOFR + 3.120%)400,000 3.622(a)(d) 04/01/31 440,912

Natwest Group PLC826,000 3.875 09/12/23 876,097

(3M USD LIBOR + 1.550%)850,000 4.519(a)(d) 06/25/24 904,748

(3M USD LIBOR + 1.762%)225,000 4.269(a)(d) 03/22/25 242,804

(5 Year CMT + 2.100%)200,000 3.754(a)(d) 11/01/29 213,250

Royal Bank of Canada35,000 1.150 06/10/25 35,070

Standard Chartered PLC(a)(b)(d) (3M USD LIBOR + 1.150%)1,325,000 4.247 01/20/23 1,339,575

State Street Corp.(a)(d)

(3M USD LIBOR + 1.030%)60,000 4.141 12/03/29 70,060

(SOFR + 2.650%)25,000 3.152 03/30/31 27,309

The Bank of Nova Scotia70,000 2.200 02/03/25 72,640

Truist Bank(a)

350,000 2.250 03/11/30 352,454Truist Financial Corp.(a)(d) (SOFR + 0.609%)

40,000 1.267 03/02/27 39,820Turkiye Vakiflar Bankasi TAO

200,000 8.125 03/28/24 214,788200,000 6.500(b) 01/08/26 204,000

Wells Fargo & Co.1,975,000 3.000 10/23/26 2,115,620

600,000 4.300 07/22/27 680,94075,000 4.150(a) 01/24/29 85,143

(SOFR + 1.087%)65,000 2.406(a)(d) 10/30/25 67,706

(SOFR + 2.000%)50,000 2.188(a)(d) 04/30/26 51,627

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Banks – (continued)Westpac Banking Corp.$ 65,000 2.350% 02/19/25 $ 67,978(5 Year CMT + 2.000%)

300,000 4.110(a)(d) 07/24/34 325,875

59,115,503

Beverages – 1.3%Anheuser-Busch Cos. LLC/Anheuser-Busch InBev Worldwide,

Inc.(a)

325,000 4.700 02/01/36 392,8761,625,000 4.900 02/01/46 2,018,039

Anheuser-Busch InBev Worldwide, Inc.(a)55,000 5.450 01/23/39 71,288

650,000 4.600 04/15/48 778,122Constellation Brands, Inc.(a)

625,000 4.400 11/15/25 699,625225,000 3.700 12/06/26 248,555500,000 3.600 02/15/28 550,180625,000 3.150 08/01/29 668,963

JDE Peet’s NV(a)(b)

375,000 1.375 01/15/27 370,395Keurig Dr Pepper, Inc.(a)

377,000 4.057 05/25/23 398,51530,000 4.417 05/25/25 33,334

Molson Coors Beverage Co.20,000 5.000 05/01/42 24,246

6,254,138

Biotechnology(a) – 0.1%Royalty Pharma PLC

425,000 1.200 09/02/25 422,050

Building Materials(a) – 0.5%Carrier Global Corp.

1,125,000 2.493 02/15/27 1,174,489Cemex SAB de CV(b)

200,000 5.200 09/17/30 214,810Martin Marietta Materials, Inc.

750,000 3.200 07/15/51 745,747Masco Corp.

325,000 1.500 02/15/28 316,085

2,451,131

Chemicals – 1.3%Ashland LLC(a)(b)

345,000 3.375 09/01/31 348,450Ashland Services B.V.(a)

EUR 650,000 2.000 01/30/28 777,006DuPont de Nemours, Inc.(a)

$ 425,000 4.205 11/15/23 456,35755,000 5.319 11/15/38 71,124

Huntsman International LLC(a)

350,000 4.500 05/01/29 396,781250,000 2.950 06/15/31 255,112

International Flavors & Fragrances, Inc.(a)(b)

650,000 1.832 10/15/27 649,207LYB International Finance B.V.

25,000 5.250 07/15/43 32,125

The accompanying notes are an integral part of these financial statements. 17

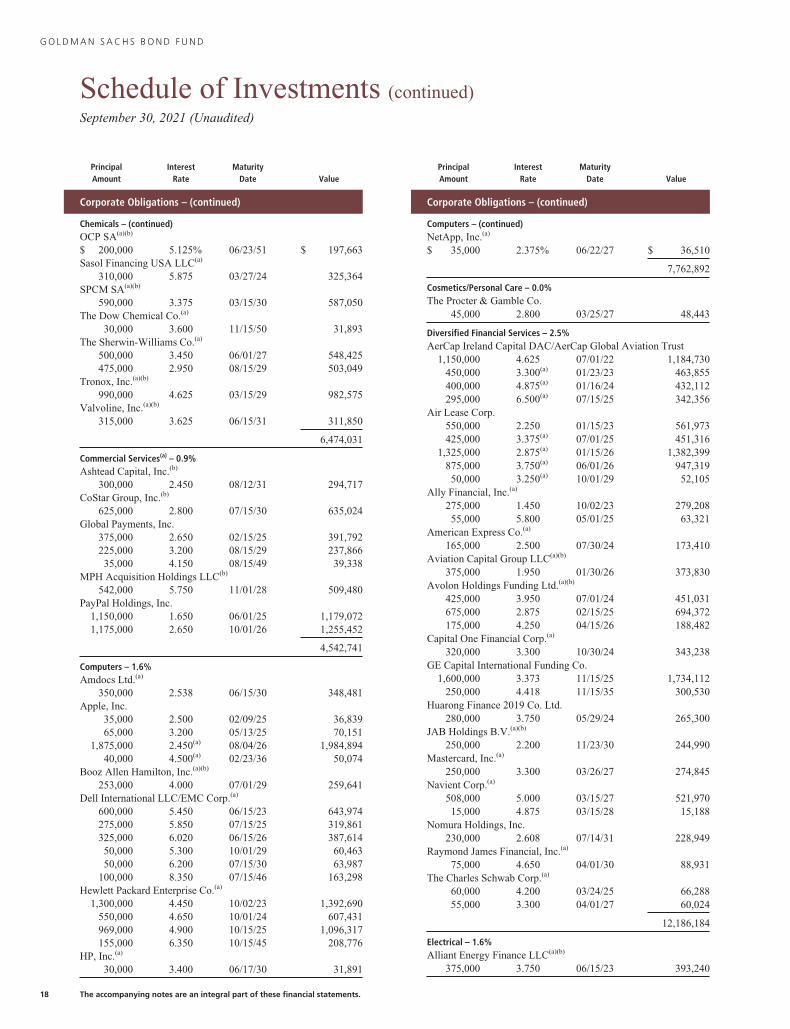

G O L D M A N S A C H S B O N D F U N D

Schedule of Investments (continued)September 30, 2021 (Unaudited)

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Chemicals – (continued)OCP SA(a)(b)

$ 200,000 5.125% 06/23/51 $ 197,663Sasol Financing USA LLC(a)

310,000 5.875 03/27/24 325,364SPCM SA(a)(b)

590,000 3.375 03/15/30 587,050The Dow Chemical Co.(a)

30,000 3.600 11/15/50 31,893The Sherwin-Williams Co.(a)

500,000 3.450 06/01/27 548,425475,000 2.950 08/15/29 503,049

Tronox, Inc.(a)(b)

990,000 4.625 03/15/29 982,575Valvoline, Inc.(a)(b)

315,000 3.625 06/15/31 311,850

6,474,031

Commercial Services(a) – 0.9%Ashtead Capital, Inc.(b)

300,000 2.450 08/12/31 294,717CoStar Group, Inc.(b)

625,000 2.800 07/15/30 635,024Global Payments, Inc.

375,000 2.650 02/15/25 391,792225,000 3.200 08/15/29 237,86635,000 4.150 08/15/49 39,338

MPH Acquisition Holdings LLC(b)

542,000 5.750 11/01/28 509,480PayPal Holdings, Inc.

1,150,000 1.650 06/01/25 1,179,0721,175,000 2.650 10/01/26 1,255,452

4,542,741

Computers – 1.6%Amdocs Ltd.(a)

350,000 2.538 06/15/30 348,481Apple, Inc.

35,000 2.500 02/09/25 36,83965,000 3.200 05/13/25 70,151

1,875,000 2.450(a) 08/04/26 1,984,89440,000 4.500(a) 02/23/36 50,074

Booz Allen Hamilton, Inc.(a)(b)

253,000 4.000 07/01/29 259,641Dell International LLC/EMC Corp.(a)

600,000 5.450 06/15/23 643,974275,000 5.850 07/15/25 319,861325,000 6.020 06/15/26 387,61450,000 5.300 10/01/29 60,46350,000 6.200 07/15/30 63,987

100,000 8.350 07/15/46 163,298Hewlett Packard Enterprise Co.(a)

1,300,000 4.450 10/02/23 1,392,690550,000 4.650 10/01/24 607,431969,000 4.900 10/15/25 1,096,317155,000 6.350 10/15/45 208,776

HP, Inc.(a)

30,000 3.400 06/17/30 31,891

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Computers – (continued)NetApp, Inc.(a)

$ 35,000 2.375% 06/22/27 $ 36,510

7,762,892

Cosmetics/Personal Care – 0.0%The Procter & Gamble Co.

45,000 2.800 03/25/27 48,443

Diversified Financial Services – 2.5%AerCap Ireland Capital DAC/AerCap Global Aviation Trust

1,150,000 4.625 07/01/22 1,184,730450,000 3.300(a) 01/23/23 463,855400,000 4.875(a) 01/16/24 432,112295,000 6.500(a) 07/15/25 342,356

Air Lease Corp.550,000 2.250 01/15/23 561,973425,000 3.375(a) 07/01/25 451,316

1,325,000 2.875(a) 01/15/26 1,382,399875,000 3.750(a) 06/01/26 947,31950,000 3.250(a) 10/01/29 52,105

Ally Financial, Inc.(a)

275,000 1.450 10/02/23 279,20855,000 5.800 05/01/25 63,321

American Express Co.(a)

165,000 2.500 07/30/24 173,410Aviation Capital Group LLC(a)(b)

375,000 1.950 01/30/26 373,830Avolon Holdings Funding Ltd.(a)(b)

425,000 3.950 07/01/24 451,031675,000 2.875 02/15/25 694,372175,000 4.250 04/15/26 188,482

Capital One Financial Corp.(a)

320,000 3.300 10/30/24 343,238GE Capital International Funding Co.

1,600,000 3.373 11/15/25 1,734,112250,000 4.418 11/15/35 300,530

Huarong Finance 2019 Co. Ltd.280,000 3.750 05/29/24 265,300

JAB Holdings B.V.(a)(b)

250,000 2.200 11/23/30 244,990Mastercard, Inc.(a)

250,000 3.300 03/26/27 274,845Navient Corp.(a)

508,000 5.000 03/15/27 521,97015,000 4.875 03/15/28 15,188

Nomura Holdings, Inc.230,000 2.608 07/14/31 228,949

Raymond James Financial, Inc.(a)

75,000 4.650 04/01/30 88,931The Charles Schwab Corp.(a)

60,000 4.200 03/24/25 66,28855,000 3.300 04/01/27 60,024

12,186,184

Electrical – 1.6%Alliant Energy Finance LLC(a)(b)

375,000 3.750 06/15/23 393,240

18 The accompanying notes are an integral part of these financial statements.

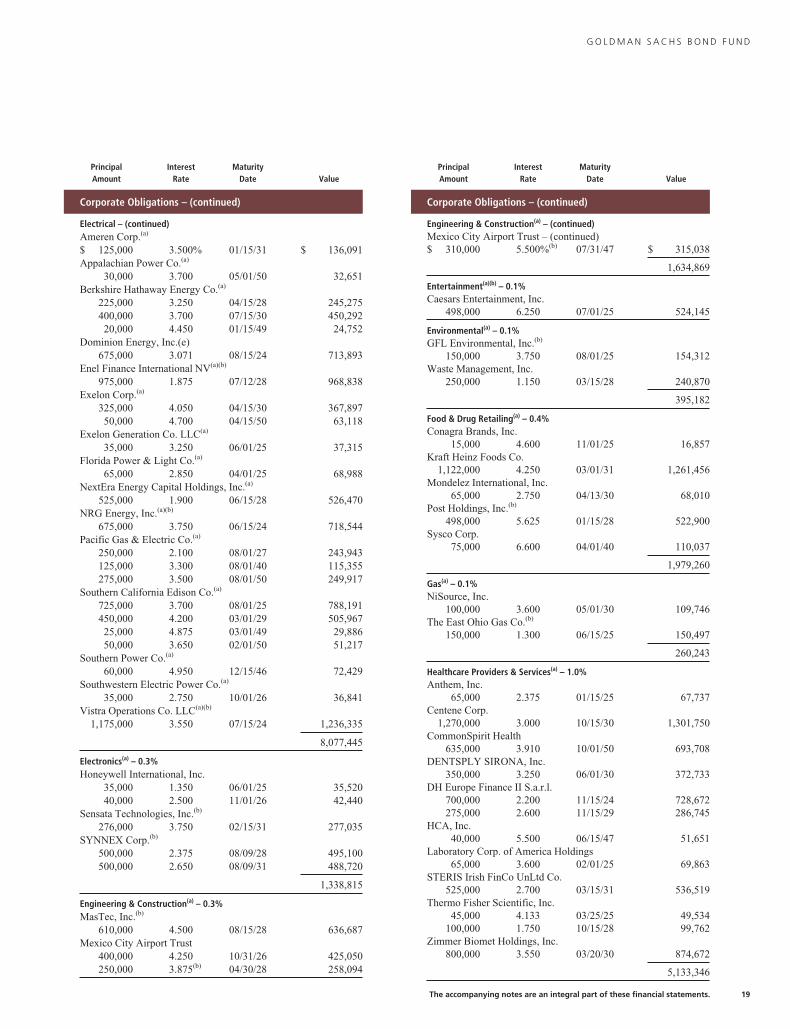

G O L D M A N S A C H S B O N D F U N D

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Electrical – (continued)Ameren Corp.(a)

$ 125,000 3.500% 01/15/31 $ 136,091Appalachian Power Co.(a)

30,000 3.700 05/01/50 32,651Berkshire Hathaway Energy Co.(a)

225,000 3.250 04/15/28 245,275400,000 3.700 07/15/30 450,29220,000 4.450 01/15/49 24,752

Dominion Energy, Inc.(e)675,000 3.071 08/15/24 713,893

Enel Finance International NV(a)(b)

975,000 1.875 07/12/28 968,838Exelon Corp.(a)

325,000 4.050 04/15/30 367,89750,000 4.700 04/15/50 63,118

Exelon Generation Co. LLC(a)

35,000 3.250 06/01/25 37,315Florida Power & Light Co.(a)

65,000 2.850 04/01/25 68,988NextEra Energy Capital Holdings, Inc.(a)

525,000 1.900 06/15/28 526,470NRG Energy, Inc.(a)(b)

675,000 3.750 06/15/24 718,544Pacific Gas & Electric Co.(a)

250,000 2.100 08/01/27 243,943125,000 3.300 08/01/40 115,355275,000 3.500 08/01/50 249,917

Southern California Edison Co.(a)

725,000 3.700 08/01/25 788,191450,000 4.200 03/01/29 505,96725,000 4.875 03/01/49 29,88650,000 3.650 02/01/50 51,217

Southern Power Co.(a)

60,000 4.950 12/15/46 72,429Southwestern Electric Power Co.(a)

35,000 2.750 10/01/26 36,841Vistra Operations Co. LLC(a)(b)

1,175,000 3.550 07/15/24 1,236,335

8,077,445

Electronics(a) – 0.3%Honeywell International, Inc.

35,000 1.350 06/01/25 35,52040,000 2.500 11/01/26 42,440

Sensata Technologies, Inc.(b)

276,000 3.750 02/15/31 277,035SYNNEX Corp.(b)

500,000 2.375 08/09/28 495,100500,000 2.650 08/09/31 488,720

1,338,815

Engineering & Construction(a) – 0.3%MasTec, Inc.(b)

610,000 4.500 08/15/28 636,687Mexico City Airport Trust

400,000 4.250 10/31/26 425,050250,000 3.875(b) 04/30/28 258,094

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Engineering & Construction(a) – (continued)Mexico City Airport Trust – (continued)$ 310,000 5.500%(b) 07/31/47 $ 315,038

1,634,869

Entertainment(a)(b) – 0.1%Caesars Entertainment, Inc.

498,000 6.250 07/01/25 524,145

Environmental(a) – 0.1%GFL Environmental, Inc.(b)

150,000 3.750 08/01/25 154,312Waste Management, Inc.

250,000 1.150 03/15/28 240,870

395,182

Food & Drug Retailing(a) – 0.4%Conagra Brands, Inc.

15,000 4.600 11/01/25 16,857Kraft Heinz Foods Co.

1,122,000 4.250 03/01/31 1,261,456Mondelez International, Inc.

65,000 2.750 04/13/30 68,010Post Holdings, Inc.(b)

498,000 5.625 01/15/28 522,900Sysco Corp.

75,000 6.600 04/01/40 110,037

1,979,260

Gas(a) – 0.1%NiSource, Inc.

100,000 3.600 05/01/30 109,746The East Ohio Gas Co.(b)

150,000 1.300 06/15/25 150,497

260,243

Healthcare Providers & Services(a) – 1.0%Anthem, Inc.

65,000 2.375 01/15/25 67,737Centene Corp.

1,270,000 3.000 10/15/30 1,301,750CommonSpirit Health

635,000 3.910 10/01/50 693,708DENTSPLY SIRONA, Inc.

350,000 3.250 06/01/30 372,733DH Europe Finance II S.a.r.l.

700,000 2.200 11/15/24 728,672275,000 2.600 11/15/29 286,745

HCA, Inc.40,000 5.500 06/15/47 51,651

Laboratory Corp. of America Holdings65,000 3.600 02/01/25 69,863

STERIS Irish FinCo UnLtd Co.525,000 2.700 03/15/31 536,519

Thermo Fisher Scientific, Inc.45,000 4.133 03/25/25 49,534

100,000 1.750 10/15/28 99,762Zimmer Biomet Holdings, Inc.

800,000 3.550 03/20/30 874,672

5,133,346

The accompanying notes are an integral part of these financial statements. 19

G O L D M A N S A C H S B O N D F U N D

Schedule of Investments (continued)September 30, 2021 (Unaudited)

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Household Products(a) – 0.0%Kimberly-Clark Corp.$ 10,000 2.875% 02/07/50 $ 10,152

Housewares(a)(b) – 0.1%The Scotts Miracle-Gro Co.

524,000 4.000 04/01/31 522,690

Insurance – 1.2%Acrisure LLC/Acrisure Finance, Inc.(a)(b)

536,000 4.250 02/15/29 529,970American International Group, Inc.

100,000 4.125 02/15/24 107,9661,075,000 3.900(a) 04/01/26 1,191,078

375,000 4.200(a) 04/01/28 427,301250,000 3.400(a) 06/30/30 273,053

Arch Capital Finance LLC(a)

1,000,000 4.011 12/15/26 1,124,760Arch Capital Group US, Inc.

250,000 5.144 11/01/43 329,375Great-West Lifeco Finance 2018 LP(a)(b)

225,000 4.047 05/17/28 254,426Marsh & McLennan Cos., Inc.(a)

575,000 4.375 03/15/29 667,730Reinsurance Group of America, Inc.(a)

65,000 3.900 05/15/29 72,467Willis North America, Inc.(a)

205,000 2.950 09/15/29 214,217XLIT Ltd.

775,000 4.450 03/31/25 859,808

6,052,151

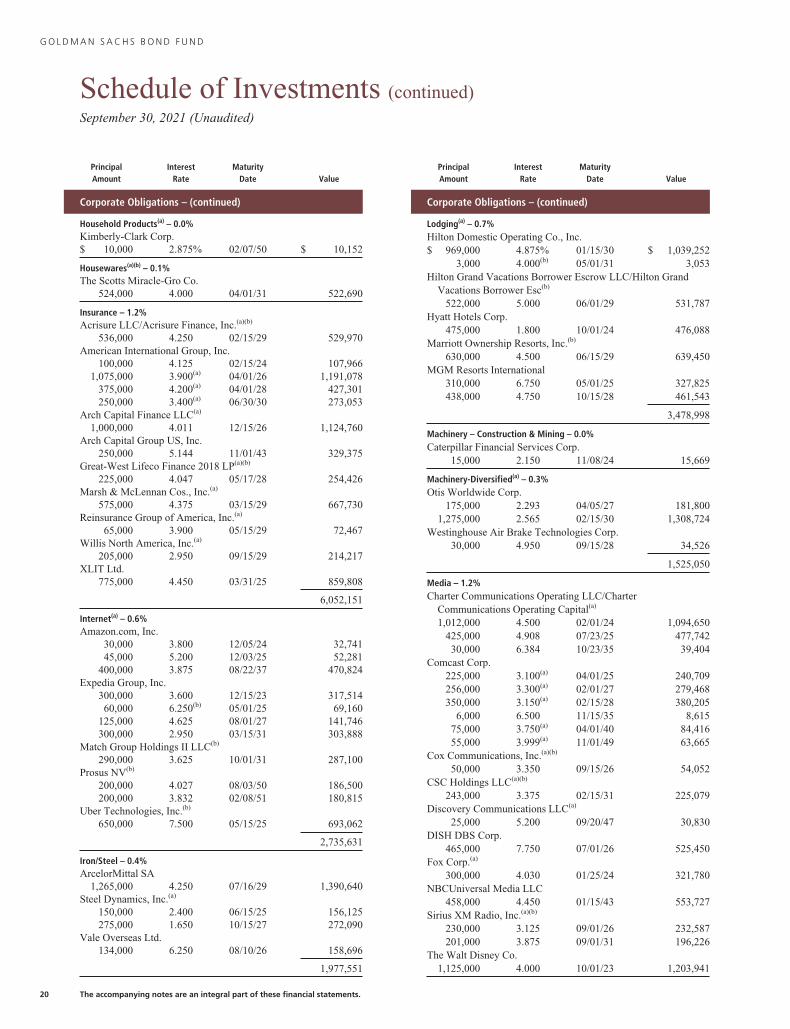

Internet(a) – 0.6%Amazon.com, Inc.

30,000 3.800 12/05/24 32,74145,000 5.200 12/03/25 52,281

400,000 3.875 08/22/37 470,824Expedia Group, Inc.

300,000 3.600 12/15/23 317,51460,000 6.250(b) 05/01/25 69,160

125,000 4.625 08/01/27 141,746300,000 2.950 03/15/31 303,888

Match Group Holdings II LLC(b)

290,000 3.625 10/01/31 287,100Prosus NV(b)

200,000 4.027 08/03/50 186,500200,000 3.832 02/08/51 180,815

Uber Technologies, Inc.(b)

650,000 7.500 05/15/25 693,062

2,735,631

Iron/Steel – 0.4%ArcelorMittal SA

1,265,000 4.250 07/16/29 1,390,640Steel Dynamics, Inc.(a)

150,000 2.400 06/15/25 156,125275,000 1.650 10/15/27 272,090

Vale Overseas Ltd.134,000 6.250 08/10/26 158,696

1,977,551

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Lodging(a) – 0.7%Hilton Domestic Operating Co., Inc.$ 969,000 4.875% 01/15/30 $ 1,039,252

3,000 4.000(b) 05/01/31 3,053Hilton Grand Vacations Borrower Escrow LLC/Hilton Grand

Vacations Borrower Esc(b)

522,000 5.000 06/01/29 531,787Hyatt Hotels Corp.

475,000 1.800 10/01/24 476,088Marriott Ownership Resorts, Inc.(b)

630,000 4.500 06/15/29 639,450MGM Resorts International

310,000 6.750 05/01/25 327,825438,000 4.750 10/15/28 461,543

3,478,998

Machinery – Construction & Mining – 0.0%Caterpillar Financial Services Corp.

15,000 2.150 11/08/24 15,669

Machinery-Diversified(a) – 0.3%Otis Worldwide Corp.

175,000 2.293 04/05/27 181,8001,275,000 2.565 02/15/30 1,308,724

Westinghouse Air Brake Technologies Corp.30,000 4.950 09/15/28 34,526

1,525,050

Media – 1.2%Charter Communications Operating LLC/Charter

Communications Operating Capital(a)

1,012,000 4.500 02/01/24 1,094,650425,000 4.908 07/23/25 477,74230,000 6.384 10/23/35 39,404

Comcast Corp.225,000 3.100(a) 04/01/25 240,709256,000 3.300(a) 02/01/27 279,468350,000 3.150(a) 02/15/28 380,205

6,000 6.500 11/15/35 8,61575,000 3.750(a) 04/01/40 84,41655,000 3.999(a) 11/01/49 63,665

Cox Communications, Inc.(a)(b)

50,000 3.350 09/15/26 54,052CSC Holdings LLC(a)(b)

243,000 3.375 02/15/31 225,079Discovery Communications LLC(a)

25,000 5.200 09/20/47 30,830DISH DBS Corp.

465,000 7.750 07/01/26 525,450Fox Corp.(a)

300,000 4.030 01/25/24 321,780NBCUniversal Media LLC

458,000 4.450 01/15/43 553,727Sirius XM Radio, Inc.(a)(b)

230,000 3.125 09/01/26 232,587201,000 3.875 09/01/31 196,226

The Walt Disney Co.1,125,000 4.000 10/01/23 1,203,941

20 The accompanying notes are an integral part of these financial statements.

G O L D M A N S A C H S B O N D F U N D

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

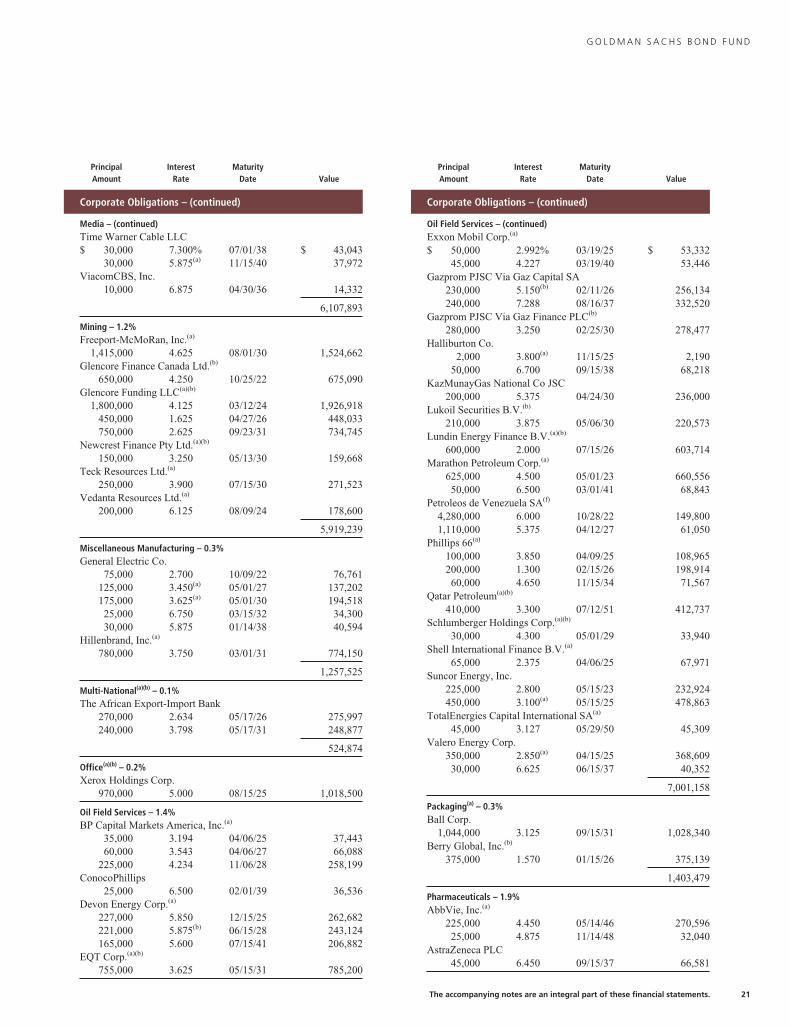

Media – (continued)Time Warner Cable LLC$ 30,000 7.300% 07/01/38 $ 43,043

30,000 5.875(a) 11/15/40 37,972ViacomCBS, Inc.

10,000 6.875 04/30/36 14,332

6,107,893

Mining – 1.2%Freeport-McMoRan, Inc.(a)

1,415,000 4.625 08/01/30 1,524,662Glencore Finance Canada Ltd.(b)

650,000 4.250 10/25/22 675,090Glencore Funding LLC(a)(b)

1,800,000 4.125 03/12/24 1,926,918450,000 1.625 04/27/26 448,033750,000 2.625 09/23/31 734,745

Newcrest Finance Pty Ltd.(a)(b)

150,000 3.250 05/13/30 159,668Teck Resources Ltd.(a)

250,000 3.900 07/15/30 271,523Vedanta Resources Ltd.(a)

200,000 6.125 08/09/24 178,600

5,919,239

Miscellaneous Manufacturing – 0.3%General Electric Co.

75,000 2.700 10/09/22 76,761125,000 3.450(a) 05/01/27 137,202175,000 3.625(a) 05/01/30 194,51825,000 6.750 03/15/32 34,30030,000 5.875 01/14/38 40,594

Hillenbrand, Inc.(a)

780,000 3.750 03/01/31 774,150

1,257,525

Multi-National(a)(b) – 0.1%The African Export-Import Bank

270,000 2.634 05/17/26 275,997240,000 3.798 05/17/31 248,877

524,874

Office(a)(b) – 0.2%Xerox Holdings Corp.

970,000 5.000 08/15/25 1,018,500

Oil Field Services – 1.4%BP Capital Markets America, Inc.(a)

35,000 3.194 04/06/25 37,44360,000 3.543 04/06/27 66,088

225,000 4.234 11/06/28 258,199ConocoPhillips

25,000 6.500 02/01/39 36,536Devon Energy Corp.(a)

227,000 5.850 12/15/25 262,682221,000 5.875(b) 06/15/28 243,124165,000 5.600 07/15/41 206,882

EQT Corp.(a)(b)

755,000 3.625 05/15/31 785,200

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Oil Field Services – (continued)Exxon Mobil Corp.(a)

$ 50,000 2.992% 03/19/25 $ 53,33245,000 4.227 03/19/40 53,446

Gazprom PJSC Via Gaz Capital SA230,000 5.150(b) 02/11/26 256,134240,000 7.288 08/16/37 332,520

Gazprom PJSC Via Gaz Finance PLC(b)

280,000 3.250 02/25/30 278,477Halliburton Co.

2,000 3.800(a) 11/15/25 2,19050,000 6.700 09/15/38 68,218

KazMunayGas National Co JSC200,000 5.375 04/24/30 236,000

Lukoil Securities B.V.(b)

210,000 3.875 05/06/30 220,573Lundin Energy Finance B.V.(a)(b)

600,000 2.000 07/15/26 603,714Marathon Petroleum Corp.(a)

625,000 4.500 05/01/23 660,55650,000 6.500 03/01/41 68,843

Petroleos de Venezuela SA(f)

4,280,000 6.000 10/28/22 149,8001,110,000 5.375 04/12/27 61,050

Phillips 66(a)

100,000 3.850 04/09/25 108,965200,000 1.300 02/15/26 198,91460,000 4.650 11/15/34 71,567

Qatar Petroleum(a)(b)

410,000 3.300 07/12/51 412,737Schlumberger Holdings Corp.(a)(b)

30,000 4.300 05/01/29 33,940Shell International Finance B.V.(a)

65,000 2.375 04/06/25 67,971Suncor Energy, Inc.

225,000 2.800 05/15/23 232,924450,000 3.100(a) 05/15/25 478,863

TotalEnergies Capital International SA(a)

45,000 3.127 05/29/50 45,309Valero Energy Corp.

350,000 2.850(a) 04/15/25 368,60930,000 6.625 06/15/37 40,352

7,001,158

Packaging(a) – 0.3%Ball Corp.

1,044,000 3.125 09/15/31 1,028,340Berry Global, Inc.(b)

375,000 1.570 01/15/26 375,139

1,403,479

Pharmaceuticals – 1.9%AbbVie, Inc.(a)

225,000 4.450 05/14/46 270,59625,000 4.875 11/14/48 32,040

AstraZeneca PLC45,000 6.450 09/15/37 66,581

The accompanying notes are an integral part of these financial statements. 21

G O L D M A N S A C H S B O N D F U N D

Schedule of Investments (continued)September 30, 2021 (Unaudited)

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

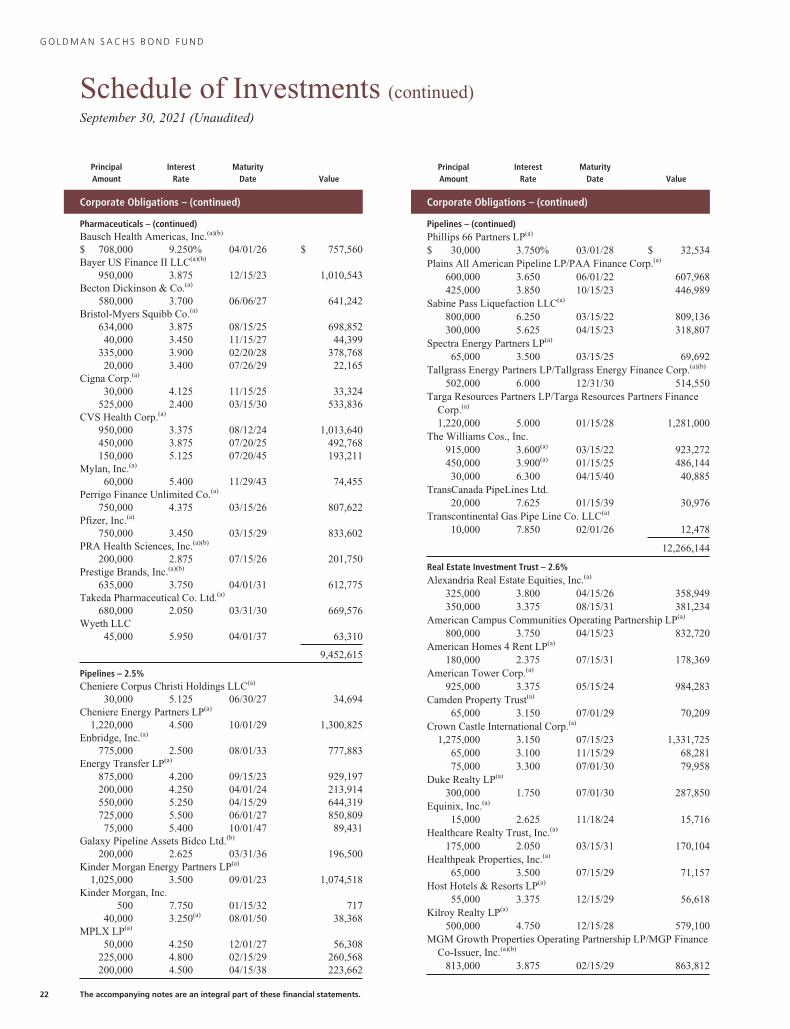

Pharmaceuticals – (continued)Bausch Health Americas, Inc.(a)(b)

$ 708,000 9.250% 04/01/26 $ 757,560Bayer US Finance II LLC(a)(b)

950,000 3.875 12/15/23 1,010,543Becton Dickinson & Co.(a)

580,000 3.700 06/06/27 641,242Bristol-Myers Squibb Co.(a)

634,000 3.875 08/15/25 698,85240,000 3.450 11/15/27 44,399

335,000 3.900 02/20/28 378,76820,000 3.400 07/26/29 22,165

Cigna Corp.(a)

30,000 4.125 11/15/25 33,324525,000 2.400 03/15/30 533,836

CVS Health Corp.(a)

950,000 3.375 08/12/24 1,013,640450,000 3.875 07/20/25 492,768150,000 5.125 07/20/45 193,211

Mylan, Inc.(a)

60,000 5.400 11/29/43 74,455Perrigo Finance Unlimited Co.(a)

750,000 4.375 03/15/26 807,622Pfizer, Inc.(a)

750,000 3.450 03/15/29 833,602PRA Health Sciences, Inc.(a)(b)

200,000 2.875 07/15/26 201,750Prestige Brands, Inc.(a)(b)

635,000 3.750 04/01/31 612,775Takeda Pharmaceutical Co. Ltd.(a)

680,000 2.050 03/31/30 669,576Wyeth LLC

45,000 5.950 04/01/37 63,310

9,452,615

Pipelines – 2.5%Cheniere Corpus Christi Holdings LLC(a)

30,000 5.125 06/30/27 34,694Cheniere Energy Partners LP(a)

1,220,000 4.500 10/01/29 1,300,825Enbridge, Inc.(a)

775,000 2.500 08/01/33 777,883Energy Transfer LP(a)

875,000 4.200 09/15/23 929,197200,000 4.250 04/01/24 213,914550,000 5.250 04/15/29 644,319725,000 5.500 06/01/27 850,80975,000 5.400 10/01/47 89,431

Galaxy Pipeline Assets Bidco Ltd.(b)

200,000 2.625 03/31/36 196,500Kinder Morgan Energy Partners LP(a)

1,025,000 3.500 09/01/23 1,074,518Kinder Morgan, Inc.

500 7.750 01/15/32 71740,000 3.250(a) 08/01/50 38,368

MPLX LP(a)

50,000 4.250 12/01/27 56,308225,000 4.800 02/15/29 260,568200,000 4.500 04/15/38 223,662

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Pipelines – (continued)Phillips 66 Partners LP(a)

$ 30,000 3.750% 03/01/28 $ 32,534Plains All American Pipeline LP/PAA Finance Corp.(a)

600,000 3.650 06/01/22 607,968425,000 3.850 10/15/23 446,989

Sabine Pass Liquefaction LLC(a)

800,000 6.250 03/15/22 809,136300,000 5.625 04/15/23 318,807

Spectra Energy Partners LP(a)

65,000 3.500 03/15/25 69,692Tallgrass Energy Partners LP/Tallgrass Energy Finance Corp.(a)(b)

502,000 6.000 12/31/30 514,550Targa Resources Partners LP/Targa Resources Partners Finance

Corp.(a)

1,220,000 5.000 01/15/28 1,281,000The Williams Cos., Inc.

915,000 3.600(a) 03/15/22 923,272450,000 3.900(a) 01/15/25 486,14430,000 6.300 04/15/40 40,885

TransCanada PipeLines Ltd.20,000 7.625 01/15/39 30,976

Transcontinental Gas Pipe Line Co. LLC(a)

10,000 7.850 02/01/26 12,478

12,266,144

Real Estate Investment Trust – 2.6%Alexandria Real Estate Equities, Inc.(a)

325,000 3.800 04/15/26 358,949350,000 3.375 08/15/31 381,234

American Campus Communities Operating Partnership LP(a)

800,000 3.750 04/15/23 832,720American Homes 4 Rent LP(a)

180,000 2.375 07/15/31 178,369American Tower Corp.(a)

925,000 3.375 05/15/24 984,283Camden Property Trust(a)

65,000 3.150 07/01/29 70,209Crown Castle International Corp.(a)

1,275,000 3.150 07/15/23 1,331,72565,000 3.100 11/15/29 68,28175,000 3.300 07/01/30 79,958

Duke Realty LP(a)

300,000 1.750 07/01/30 287,850Equinix, Inc.(a)

15,000 2.625 11/18/24 15,716Healthcare Realty Trust, Inc.(a)

175,000 2.050 03/15/31 170,104Healthpeak Properties, Inc.(a)

65,000 3.500 07/15/29 71,157Host Hotels & Resorts LP(a)

55,000 3.375 12/15/29 56,618Kilroy Realty LP(a)

500,000 4.750 12/15/28 579,100MGM Growth Properties Operating Partnership LP/MGP Finance

Co-Issuer, Inc.(a)(b)

813,000 3.875 02/15/29 863,812

22 The accompanying notes are an integral part of these financial statements.

G O L D M A N S A C H S B O N D F U N D

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

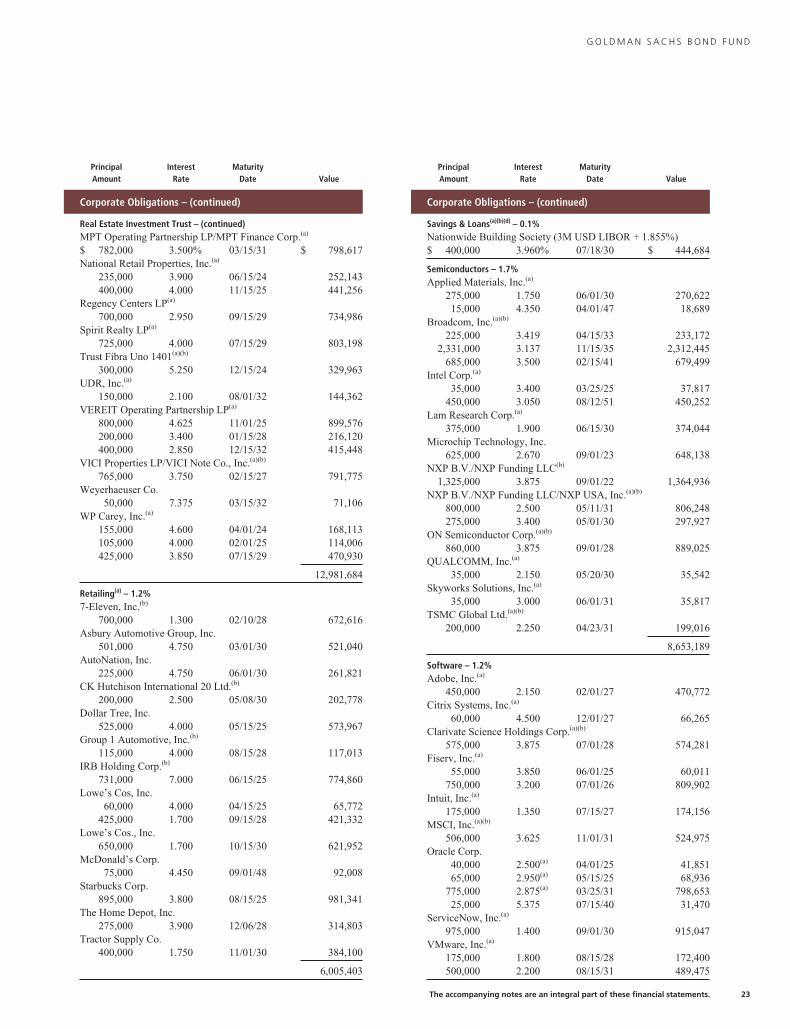

Real Estate Investment Trust – (continued)MPT Operating Partnership LP/MPT Finance Corp.(a)

$ 782,000 3.500% 03/15/31 $ 798,617National Retail Properties, Inc.(a)

235,000 3.900 06/15/24 252,143400,000 4.000 11/15/25 441,256

Regency Centers LP(a)

700,000 2.950 09/15/29 734,986Spirit Realty LP(a)

725,000 4.000 07/15/29 803,198Trust Fibra Uno 1401(a)(b)

300,000 5.250 12/15/24 329,963UDR, Inc.(a)

150,000 2.100 08/01/32 144,362VEREIT Operating Partnership LP(a)

800,000 4.625 11/01/25 899,576200,000 3.400 01/15/28 216,120400,000 2.850 12/15/32 415,448

VICI Properties LP/VICI Note Co., Inc.(a)(b)

765,000 3.750 02/15/27 791,775Weyerhaeuser Co.

50,000 7.375 03/15/32 71,106WP Carey, Inc.(a)

155,000 4.600 04/01/24 168,113105,000 4.000 02/01/25 114,006425,000 3.850 07/15/29 470,930

12,981,684

Retailing(a) – 1.2%7-Eleven, Inc.(b)

700,000 1.300 02/10/28 672,616Asbury Automotive Group, Inc.

501,000 4.750 03/01/30 521,040AutoNation, Inc.

225,000 4.750 06/01/30 261,821CK Hutchison International 20 Ltd.(b)

200,000 2.500 05/08/30 202,778Dollar Tree, Inc.

525,000 4.000 05/15/25 573,967Group 1 Automotive, Inc.(b)

115,000 4.000 08/15/28 117,013IRB Holding Corp.(b)

731,000 7.000 06/15/25 774,860Lowe’s Cos, Inc.

60,000 4.000 04/15/25 65,772425,000 1.700 09/15/28 421,332

Lowe’s Cos., Inc.650,000 1.700 10/15/30 621,952

McDonald’s Corp.75,000 4.450 09/01/48 92,008

Starbucks Corp.895,000 3.800 08/15/25 981,341

The Home Depot, Inc.275,000 3.900 12/06/28 314,803

Tractor Supply Co.400,000 1.750 11/01/30 384,100

6,005,403

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Savings & Loans(a)(b)(d) – 0.1%Nationwide Building Society (3M USD LIBOR + 1.855%)$ 400,000 3.960% 07/18/30 $ 444,684

Semiconductors – 1.7%Applied Materials, Inc.(a)

275,000 1.750 06/01/30 270,62215,000 4.350 04/01/47 18,689

Broadcom, Inc.(a)(b)

225,000 3.419 04/15/33 233,1722,331,000 3.137 11/15/35 2,312,445

685,000 3.500 02/15/41 679,499Intel Corp.(a)

35,000 3.400 03/25/25 37,817450,000 3.050 08/12/51 450,252

Lam Research Corp.(a)

375,000 1.900 06/15/30 374,044Microchip Technology, Inc.

625,000 2.670 09/01/23 648,138NXP B.V./NXP Funding LLC(b)

1,325,000 3.875 09/01/22 1,364,936NXP B.V./NXP Funding LLC/NXP USA, Inc.(a)(b)

800,000 2.500 05/11/31 806,248275,000 3.400 05/01/30 297,927

ON Semiconductor Corp.(a)(b)

860,000 3.875 09/01/28 889,025QUALCOMM, Inc.(a)

35,000 2.150 05/20/30 35,542Skyworks Solutions, Inc.(a)

35,000 3.000 06/01/31 35,817TSMC Global Ltd.(a)(b)

200,000 2.250 04/23/31 199,016

8,653,189

Software – 1.2%Adobe, Inc.(a)

450,000 2.150 02/01/27 470,772Citrix Systems, Inc.(a)

60,000 4.500 12/01/27 66,265Clarivate Science Holdings Corp.(a)(b)

575,000 3.875 07/01/28 574,281Fiserv, Inc.(a)

55,000 3.850 06/01/25 60,011750,000 3.200 07/01/26 809,902

Intuit, Inc.(a)

175,000 1.350 07/15/27 174,156MSCI, Inc.(a)(b)

506,000 3.625 11/01/31 524,975Oracle Corp.

40,000 2.500(a) 04/01/25 41,85165,000 2.950(a) 05/15/25 68,936

775,000 2.875(a) 03/25/31 798,65325,000 5.375 07/15/40 31,470

ServiceNow, Inc.(a)

975,000 1.400 09/01/30 915,047VMware, Inc.(a)

175,000 1.800 08/15/28 172,400500,000 2.200 08/15/31 489,475

The accompanying notes are an integral part of these financial statements. 23

G O L D M A N S A C H S B O N D F U N D

Schedule of Investments (continued)September 30, 2021 (Unaudited)

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Software – (continued)ZoomInfo Technologies LLC/ZoomInfo Finance Corp.(a)(b)

$ 525,000 3.875% 02/01/29 $ 525,000

5,723,194

Telecommunication Services – 3.0%AT&T, Inc.(a)

400,000 4.450 04/01/24 433,43230,000 4.250 03/01/27 33,957

1,375,000 2.300 06/01/27 1,424,197100,000 1.650 02/01/28 99,081500,000 2.750 06/01/31 513,490694,000 2.550 12/01/33 682,86810,000 5.250 03/01/37 12,381

175,000 4.900 08/15/37 211,893450,000 3.500 06/01/41 462,172100,000 5.150 11/15/46 126,794225,000 5.450 03/01/47 293,58025,000 4.500 03/09/48 28,870

175,000 5.150 02/15/50 220,733300,000 3.650 06/01/51 305,613100,000 3.500 09/15/53 99,016

Level 3 Financing, Inc.(a)(b)

645,000 4.250 07/01/28 653,062Rogers Communications, Inc.(a)

65,000 3.700 11/15/49 67,149T-Mobile USA, Inc.(a)

625,000 3.500 04/15/25 672,819375,000 1.500 02/15/26 376,384

1,050,000 3.750 04/15/27 1,156,848375,000 2.050 02/15/28 378,067550,000 3.875 04/15/30 607,640520,000 2.875 02/15/31 525,409500,000 3.500 04/15/31 526,13460,000 4.375 04/15/40 69,046

250,000 3.000 02/15/41 242,405The Bell Telephone Co. of Canada/Bell Canada(a)

55,000 4.464 04/01/48 66,991Verizon Communications, Inc.

1,265,000 2.100(a) 03/22/28 1,284,241630,000 4.329 09/21/28 724,720575,000 3.150(a) 03/22/30 615,077800,000 2.550(a) 03/21/31 811,608

1,004,000 2.355(a)(b) 03/15/32 994,03050,000 4.125 08/15/46 57,36018,000 5.012 04/15/49 23,57530,000 4.000(a) 03/22/50 33,861

Vodafone Group PLC50,000 4.125 05/30/25 55,32325,000 6.150 02/27/37 34,293

14,924,119

Transportation(a) – 0.1%Canadian Pacific Railway Co.

200,000 2.050 03/05/30 197,426CSX Corp.

65,000 3.250 06/01/27 70,661

PrincipalAmount

InterestRate

MaturityDate Value

Corporate Obligations – (continued)

Transportation(a) – (continued)Union Pacific Corp.$ 35,000 3.799% 10/01/51 $ 40,396United Parcel Service, Inc.

35,000 3.900 04/01/25 38,31625,000 5.300 04/01/50 36,123

382,922

TOTAL CORPORATE OBLIGATIONS(Cost $231,274,651) $ 240,274,451

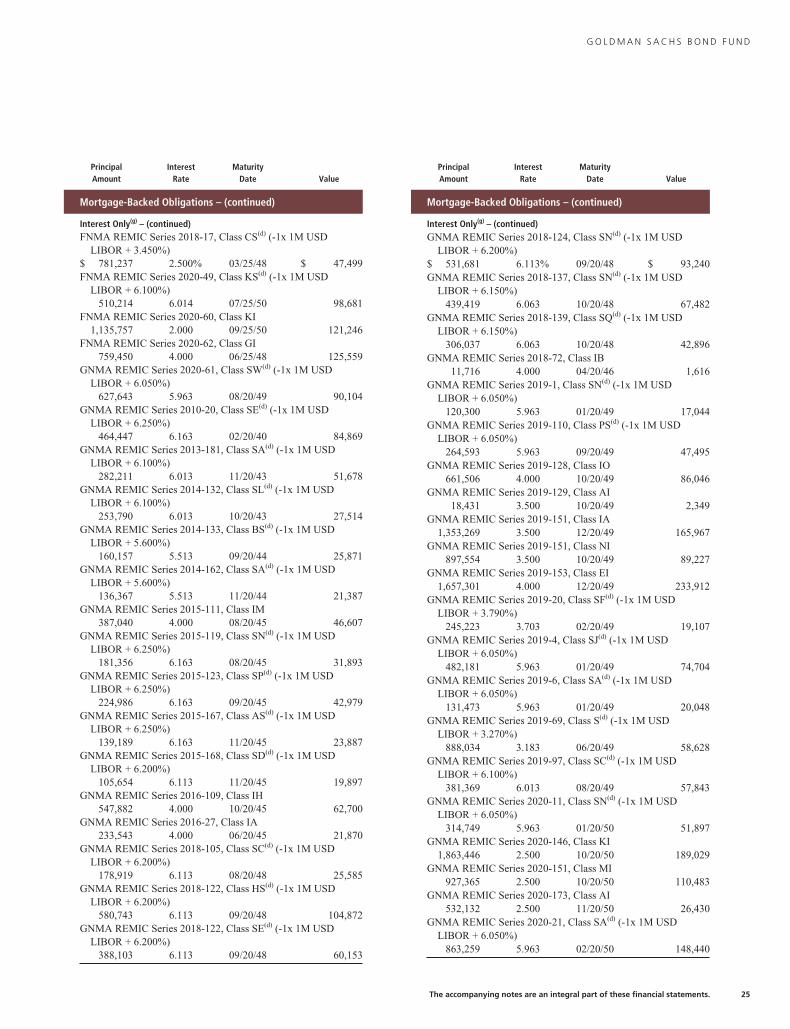

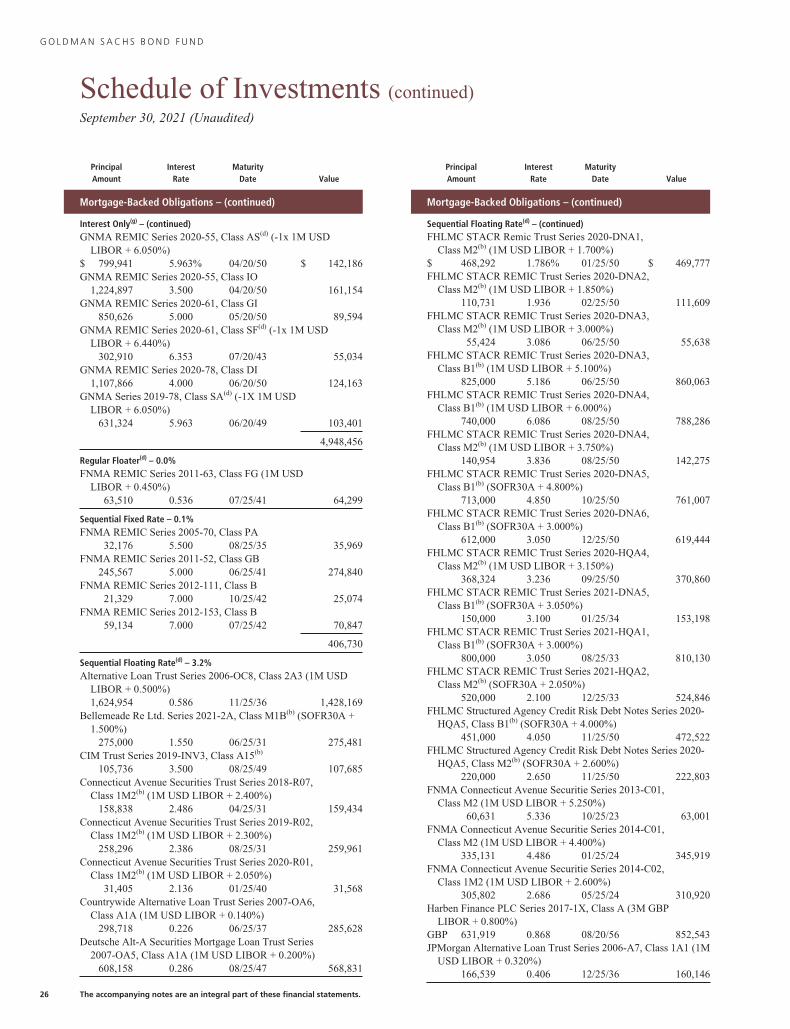

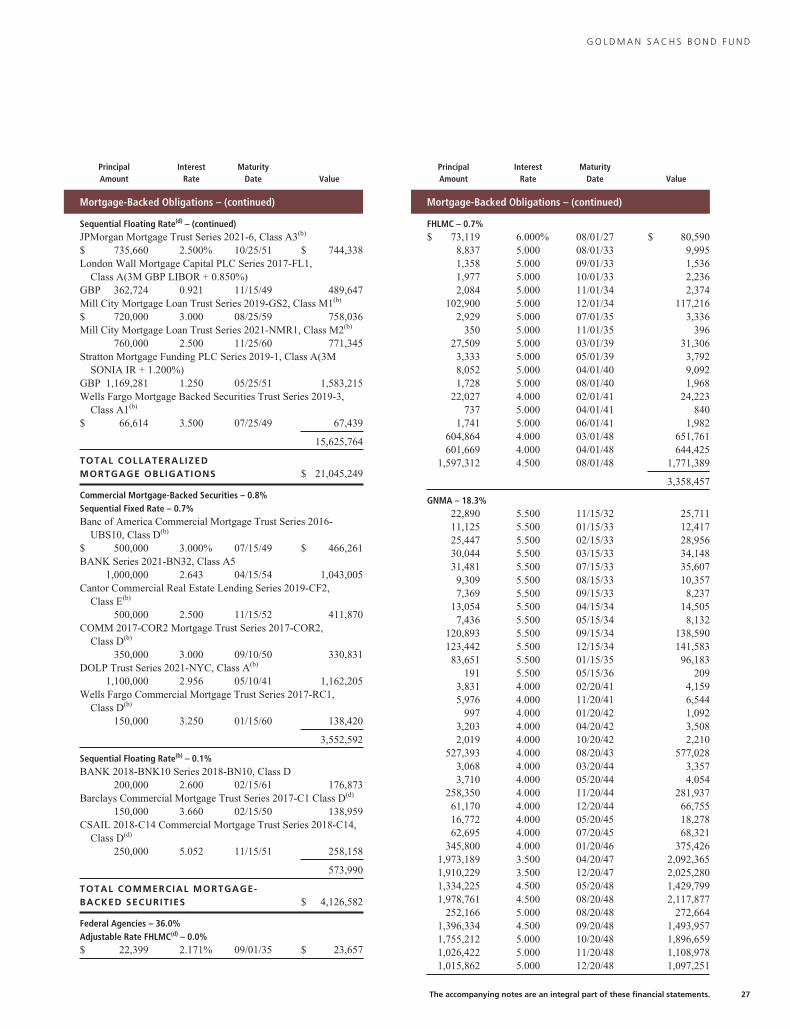

Mortgage-Backed Obligations – 41.1%

Collateralized Mortgage Obligations – 4.3%Interest Only(g) – 1.0%FHLMC REMIC Series 4314, Class SE(d) (-1x 1M USD

LIBOR + 6.050%)$ 394,078 5.966% 03/15/44 $ 59,274FHLMC REMIC Series 4320, Class SD(d) (-1x 1M USD

LIBOR + 6.100%)56,957 6.016 07/15/39 10,338

FHLMC REMIC Series 4583, Class ST(d) (-1x 1M USDLIBOR + 6.000%)

771,479 5.916 05/15/46 133,588FHLMC REMIC Series 4905, Class SA(d) (-1x 1M USD

LIBOR + 6.100%)497,386 6.014 08/25/49 88,139

FHLMC REMIC Series 4980, Class KI2,372,935 4.500 06/25/50 353,817

FHLMC REMIC Series 4989, Class EI374,223 4.000 07/25/50 57,535

FHLMC REMIC Series 4998, Class GI1,383,327 4.000 08/25/50 218,946

FHLMC REMIC Series 5009, Class DI1,211,291 2.000 09/25/50 131,802

FHLMC REMIC Series 5020, Class IH1,160,128 3.000 08/25/50 149,748

FHLMC STRIPS Series 304, Class C454,893 3.000 12/15/27 270

FNMA REMIC Series 2011-124, Class SC(d) (-1x 1M USDLIBOR + 6.550%)

176,865 6.464 12/25/41 30,606FNMA REMIC Series 2012-5, Class SA(d) (-1x 1M USD

LIBOR + 5.950%)261,251 5.864 02/25/42 40,846

FNMA REMIC Series 2012-88, Class SB(d) (-1x 1M USDLIBOR + 6.670%)

181,093 6.584 07/25/42 29,515FNMA REMIC Series 2014-6, Class SA(d) (-1x 1M USD

LIBOR + 6.600%)226,186 6.514 02/25/44 40,676

FNMA REMIC Series 2017-31, Class SG(d) (-1x 1M USDLIBOR + 6.100%)

591,139 6.014 05/25/47 111,727FNMA REMIC Series 2017-86, Class SB(d) (-1x 1M USD

LIBOR + 6.150%)425,591 6.064 11/25/47 77,363

24 The accompanying notes are an integral part of these financial statements.

G O L D M A N S A C H S B O N D F U N D

PrincipalAmount

InterestRate

MaturityDate Value

Mortgage-Backed Obligations – (continued)

Interest Only(g) – (continued)FNMA REMIC Series 2018-17, Class CS(d) (-1x 1M USD

LIBOR + 3.450%)$ 781,237 2.500% 03/25/48 $ 47,499FNMA REMIC Series 2020-49, Class KS(d) (-1x 1M USD

LIBOR + 6.100%)510,214 6.014 07/25/50 98,681

FNMA REMIC Series 2020-60, Class KI1,135,757 2.000 09/25/50 121,246

FNMA REMIC Series 2020-62, Class GI759,450 4.000 06/25/48 125,559

GNMA REMIC Series 2020-61, Class SW(d) (-1x 1M USDLIBOR + 6.050%)

627,643 5.963 08/20/49 90,104GNMA REMIC Series 2010-20, Class SE(d) (-1x 1M USD

LIBOR + 6.250%)464,447 6.163 02/20/40 84,869

GNMA REMIC Series 2013-181, Class SA(d) (-1x 1M USDLIBOR + 6.100%)

282,211 6.013 11/20/43 51,678GNMA REMIC Series 2014-132, Class SL(d) (-1x 1M USD

LIBOR + 6.100%)253,790 6.013 10/20/43 27,514

GNMA REMIC Series 2014-133, Class BS(d) (-1x 1M USDLIBOR + 5.600%)

160,157 5.513 09/20/44 25,871GNMA REMIC Series 2014-162, Class SA(d) (-1x 1M USD

LIBOR + 5.600%)136,367 5.513 11/20/44 21,387

GNMA REMIC Series 2015-111, Class IM387,040 4.000 08/20/45 46,607

GNMA REMIC Series 2015-119, Class SN(d) (-1x 1M USDLIBOR + 6.250%)

181,356 6.163 08/20/45 31,893GNMA REMIC Series 2015-123, Class SP(d) (-1x 1M USD

LIBOR + 6.250%)224,986 6.163 09/20/45 42,979

GNMA REMIC Series 2015-167, Class AS(d) (-1x 1M USDLIBOR + 6.250%)

139,189 6.163 11/20/45 23,887GNMA REMIC Series 2015-168, Class SD(d) (-1x 1M USD

LIBOR + 6.200%)105,654 6.113 11/20/45 19,897

GNMA REMIC Series 2016-109, Class IH547,882 4.000 10/20/45 62,700

GNMA REMIC Series 2016-27, Class IA233,543 4.000 06/20/45 21,870

GNMA REMIC Series 2018-105, Class SC(d) (-1x 1M USDLIBOR + 6.200%)

178,919 6.113 08/20/48 25,585GNMA REMIC Series 2018-122, Class HS(d) (-1x 1M USD

LIBOR + 6.200%)580,743 6.113 09/20/48 104,872

GNMA REMIC Series 2018-122, Class SE(d) (-1x 1M USDLIBOR + 6.200%)

388,103 6.113 09/20/48 60,153

PrincipalAmount

InterestRate

MaturityDate Value

Mortgage-Backed Obligations – (continued)

Interest Only(g) – (continued)GNMA REMIC Series 2018-124, Class SN(d) (-1x 1M USD

LIBOR + 6.200%)$ 531,681 6.113% 09/20/48 $ 93,240GNMA REMIC Series 2018-137, Class SN(d) (-1x 1M USD

LIBOR + 6.150%)439,419 6.063 10/20/48 67,482

GNMA REMIC Series 2018-139, Class SQ(d) (-1x 1M USDLIBOR + 6.150%)

306,037 6.063 10/20/48 42,896GNMA REMIC Series 2018-72, Class IB

11,716 4.000 04/20/46 1,616GNMA REMIC Series 2019-1, Class SN(d) (-1x 1M USD

LIBOR + 6.050%)120,300 5.963 01/20/49 17,044

GNMA REMIC Series 2019-110, Class PS(d) (-1x 1M USDLIBOR + 6.050%)

264,593 5.963 09/20/49 47,495GNMA REMIC Series 2019-128, Class IO

661,506 4.000 10/20/49 86,046GNMA REMIC Series 2019-129, Class AI

18,431 3.500 10/20/49 2,349GNMA REMIC Series 2019-151, Class IA

1,353,269 3.500 12/20/49 165,967GNMA REMIC Series 2019-151, Class NI

897,554 3.500 10/20/49 89,227GNMA REMIC Series 2019-153, Class EI

1,657,301 4.000 12/20/49 233,912GNMA REMIC Series 2019-20, Class SF(d) (-1x 1M USD

LIBOR + 3.790%)245,223 3.703 02/20/49 19,107

GNMA REMIC Series 2019-4, Class SJ(d) (-1x 1M USDLIBOR + 6.050%)

482,181 5.963 01/20/49 74,704GNMA REMIC Series 2019-6, Class SA(d) (-1x 1M USD

LIBOR + 6.050%)131,473 5.963 01/20/49 20,048

GNMA REMIC Series 2019-69, Class S(d) (-1x 1M USDLIBOR + 3.270%)

888,034 3.183 06/20/49 58,628GNMA REMIC Series 2019-97, Class SC(d) (-1x 1M USD

LIBOR + 6.100%)381,369 6.013 08/20/49 57,843

GNMA REMIC Series 2020-11, Class SN(d) (-1x 1M USDLIBOR + 6.050%)

314,749 5.963 01/20/50 51,897GNMA REMIC Series 2020-146, Class KI