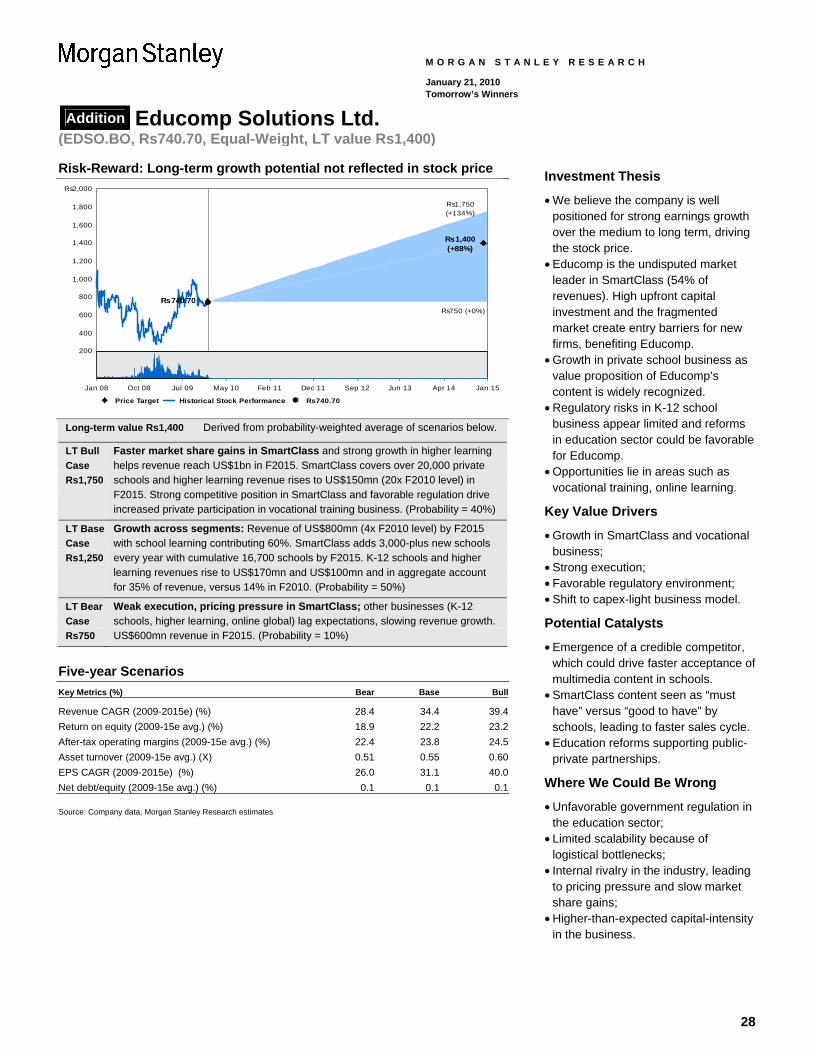

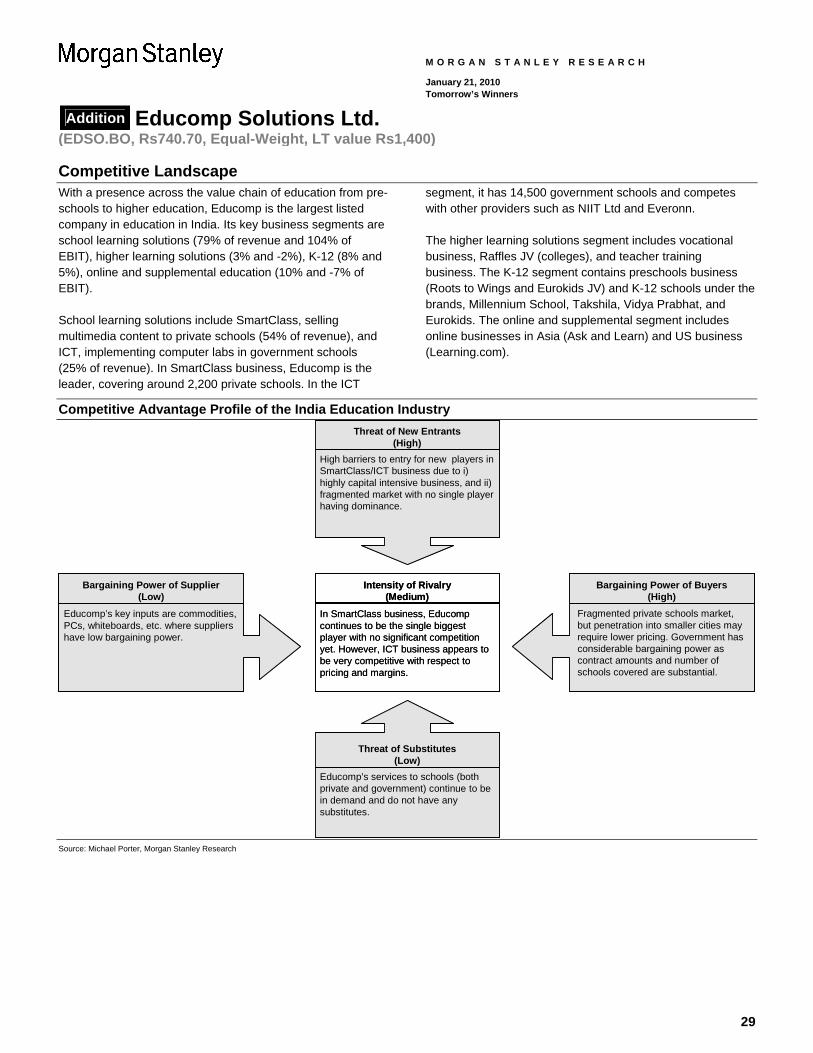

morgan-stanley-jan-2010.pdf - educomp

TRANSCRIPT

X

XX

XX

XX

XX

1

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Signs of a nascent economic recovery in countries around Asia Pacific, after unprecedented financial market turmoil over the past 18 months, have provided an ideal opportunity to revisit the Tomorrow’s Winners, which we started in February 2008. In this update, following on from our last in November 2008, we examine how the companies we identified as having a compelling, long-term competitive advantage weathered the financial storm. Did they stand head-and-shoulders above their peers, or have they yet to show their full promise? Our analysts examine a range of valuation metrics that highlight the strengths of their companies’ various business models. As for previous editions, we asked our analysts to review their industries for companies they felt had a distinct competitive advantage that would drive share price performance over the long term. The companies included lead their domestic competitors and are strong enough to withstand competition from abroad. The majority operate in industries that have high barriers to entry. In addition, the companies’ expected growth rates outpace those of the markets and countries in which they operate. We have not mandated balance across countries; the selections naturally lean towards those countries where GDP growth is stronger than elsewhere in the region. Of the companies included the skew remains towards China and India. Many of these are capitalizing on major long-term trends, such as infrastructure investment and per capita consumption growth. In this issue, we are adding India-based technology solutions provider Educomp and removing Brambles and Bharti Airtel. The competitive advantages identified in early 2008 for these two companies now seem less compelling. As a reminder, Morgan Stanley’s fundamental research is usually predicated on a 12-18 month horizon. However, for the purposes of Tomorrow’s Winners, we extend the time horizon to five years. As always, we welcome feedback from our clients as we progress to future editions of Tomorrow’s Winners.

2

Tomorrow’s Winners: Valuation Metrics

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Perf. vs. Perf. vs. Up/down Up Down Absolute Absolute Perf. vs. Country Perf. vs. Country to LT to LT to LT perf. perf. APxJ MSCI APxJ MSCI Date Close Market Cap value bull bear (12 mths) (24 mths) (12 mths) (12 mths) (24 mths) (24 mths) Industry Name Ticker Rating Curr added price (US$ mn) LT value (%) (%) (%) (%) (%) (%) (%) (%) (%) Country Sub-Industry View Belle International 1880.HK OW HK$ 02/22/08 9.82 10,664 17.80 81 141 6 161.83 -22.75 103.46 99.11 -10.42 -2.28 China Textiles, Apparel and Footwear Attractive

China Mengniu Dairy 2319.HK OW HK$ 02/22/08 27.45 6,140 45.60 66 127 14 171.29 -3.70 112.93 108.58 8.63 16.77 China Food, Bev. & Tobacco Attractive

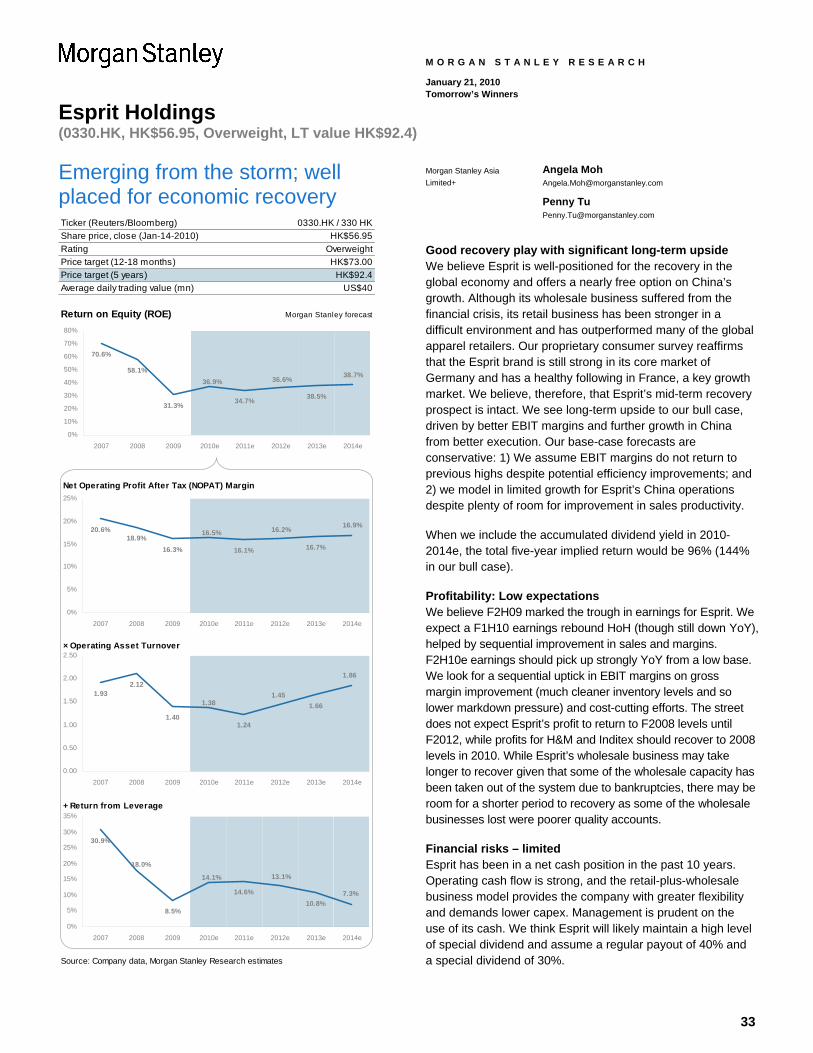

Educomp Solutions Ltd. EDSO.BO EW Rs 01/14/10 726.85 1,502 1,400.00 93 141 3 44.82 -24.36 -13.55 -43.77 -12.03 -8.91 India Education Services Attractive Esprit Holdings 0330.HK OW HK$ 02/22/08 54.50 8,974 92.40 70 114 -24 18.90 -54.52 -39.46 -41.33 -42.19 -32.23 Hong Kong Retail In-Line

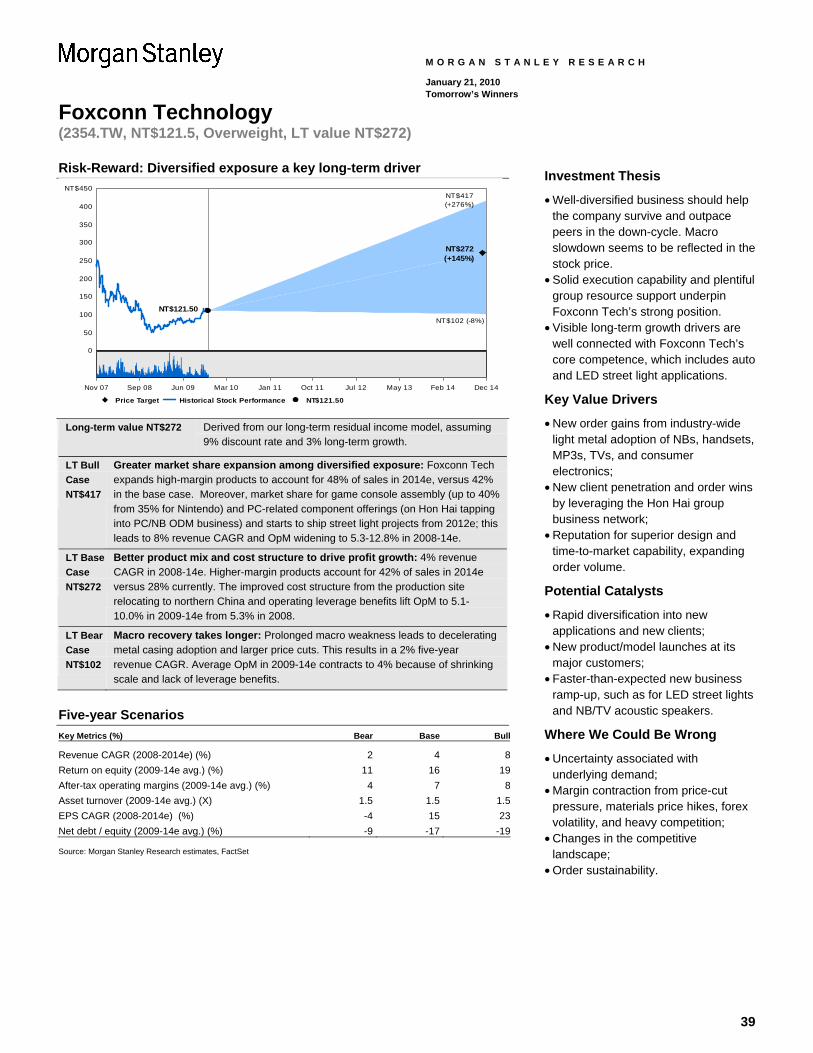

Foxconn Technology 2354.TW OW NT$ 02/22/08 139.00 4,244 272.00 96 200 -27 81.37 -41.56 23.01 5.70 -29.23 -37.77 Taiwan Hardware Technology In-Line

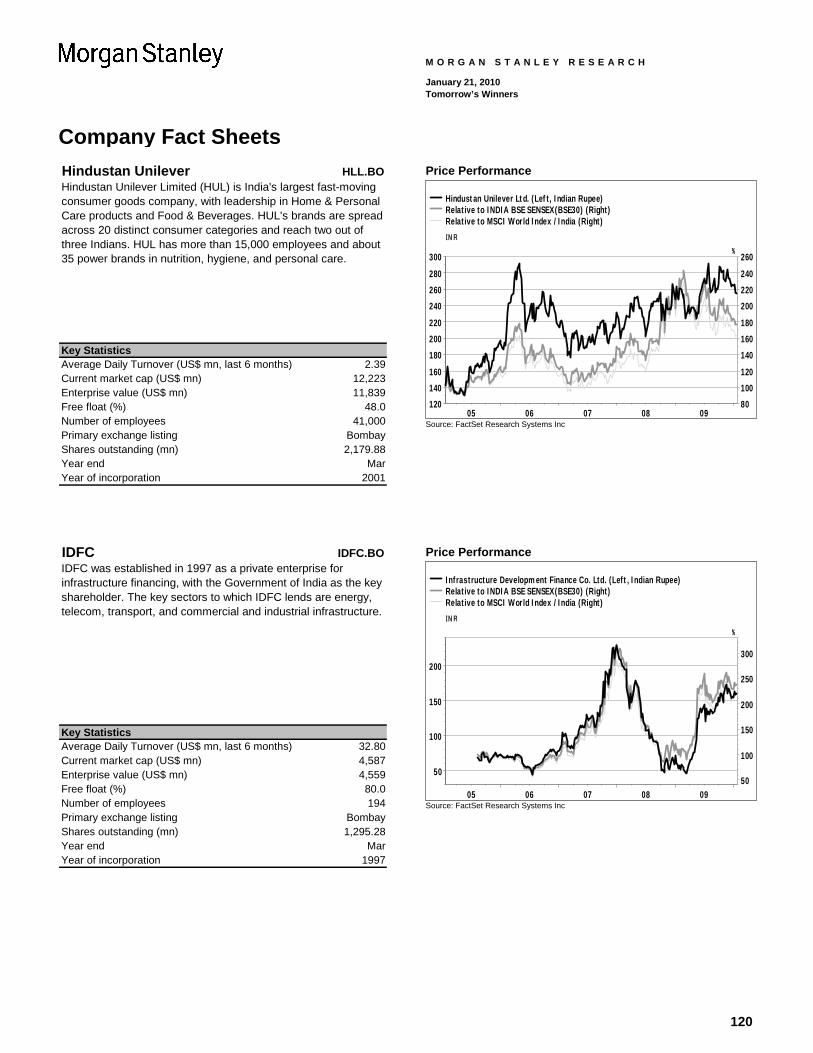

Gemtek Technology 4906.TW EW NT$ 02/22/08 55.60 478 120.00 116 227 4 32.83 11.47 -25.53 -42.84 23.80 15.27 Taiwan Hardware Technology In-Line Hindustan Unilever HLL.BO UW Rs 11/03/08 257.70 12,237 514.00 99 271 -10 6.31 22.00 -52.05 -82.27 34.33 37.45 India Consumer In-Line

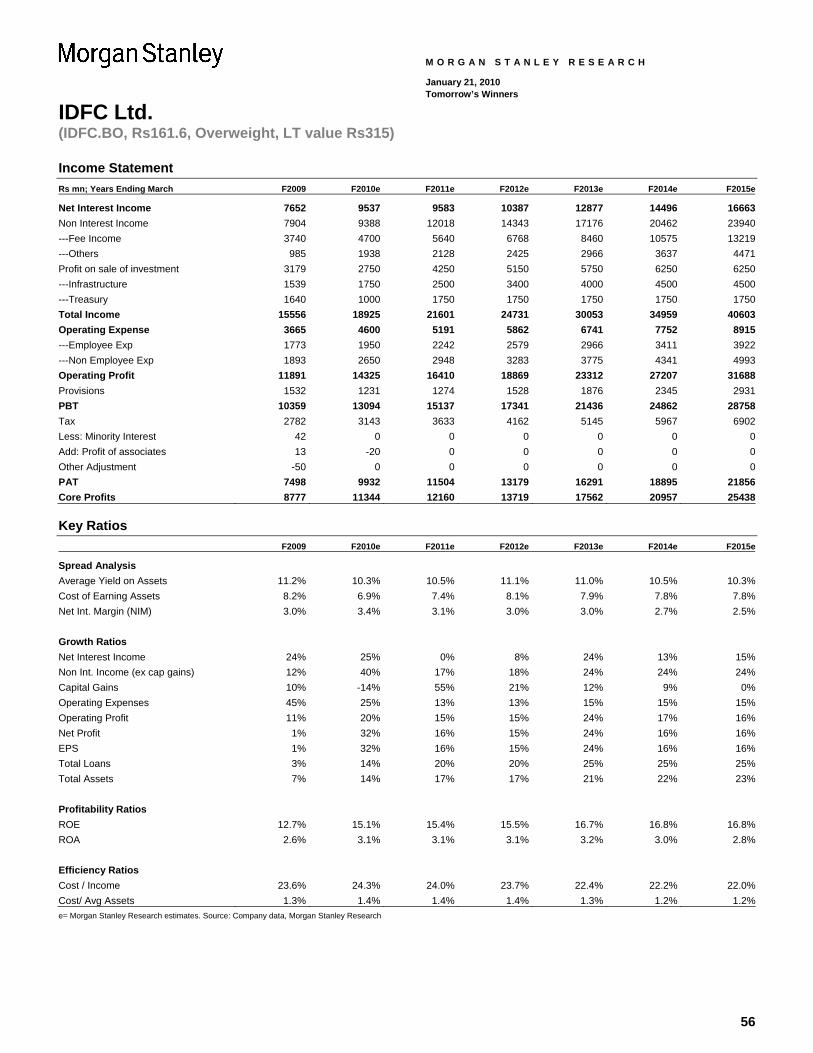

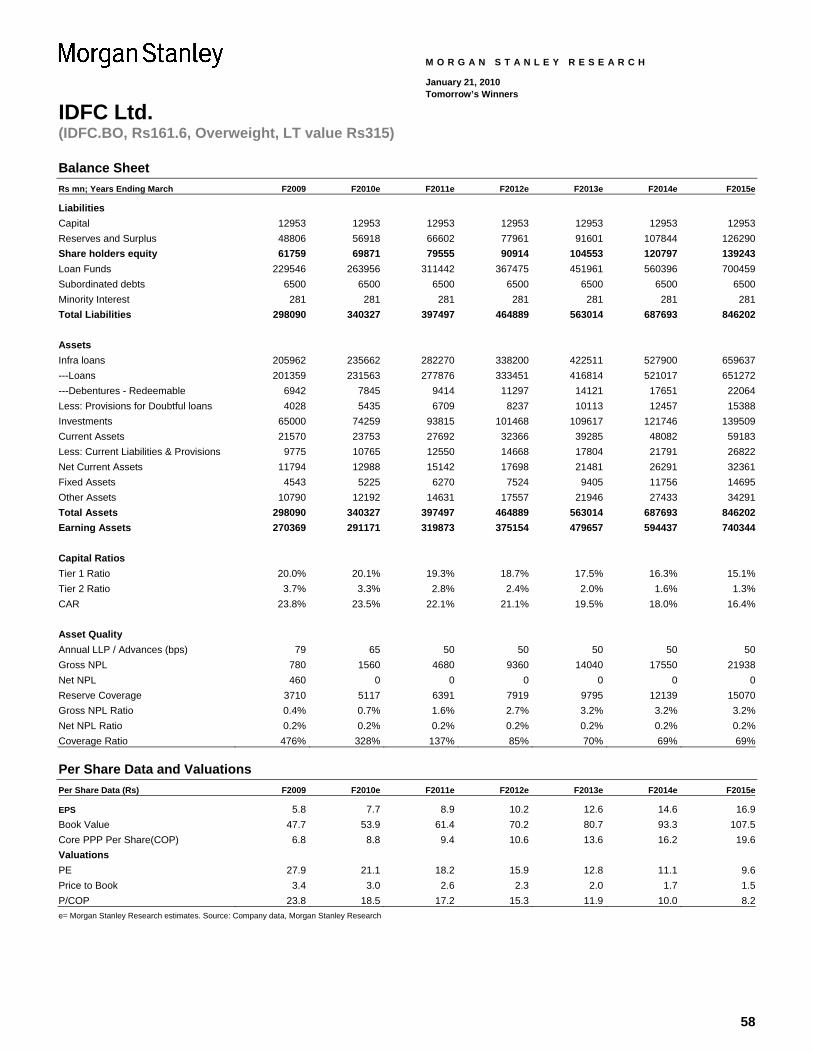

IDFC IDFC.BO OW Rs 02/22/08 160.00 4,514 315.00 97 156 25 126.49 -33.37 68.12 37.90 -21.04 -17.92 India Financial Services Attractive

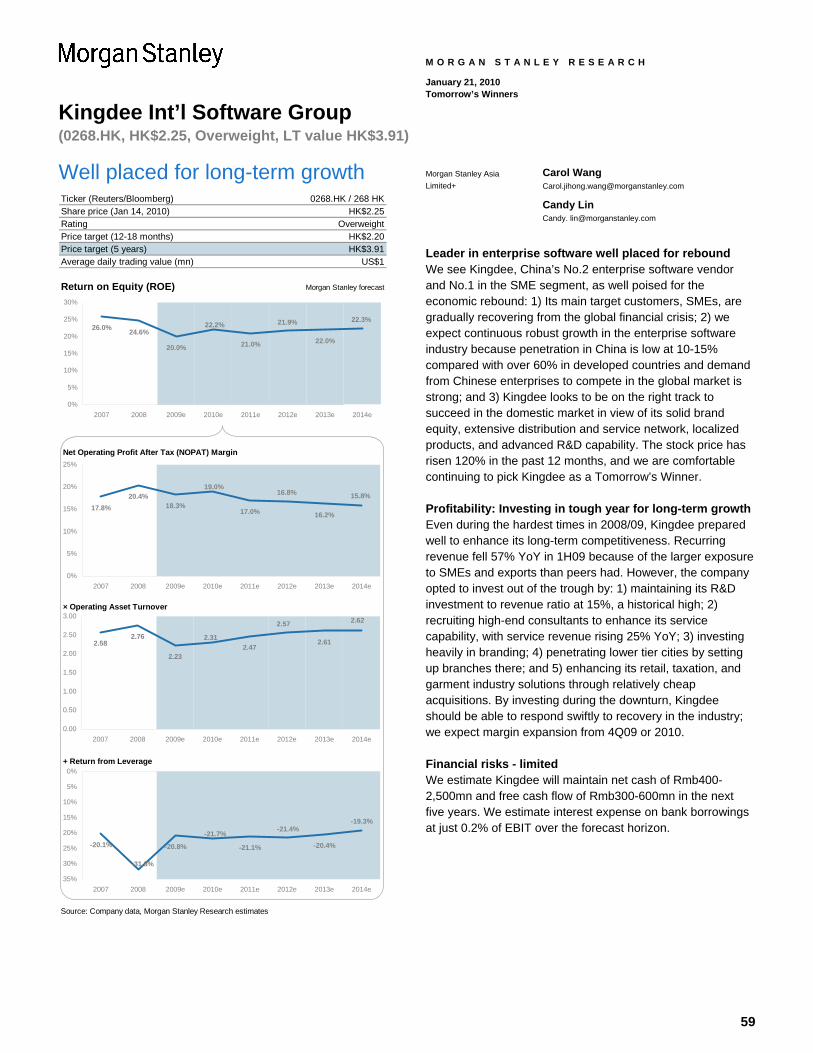

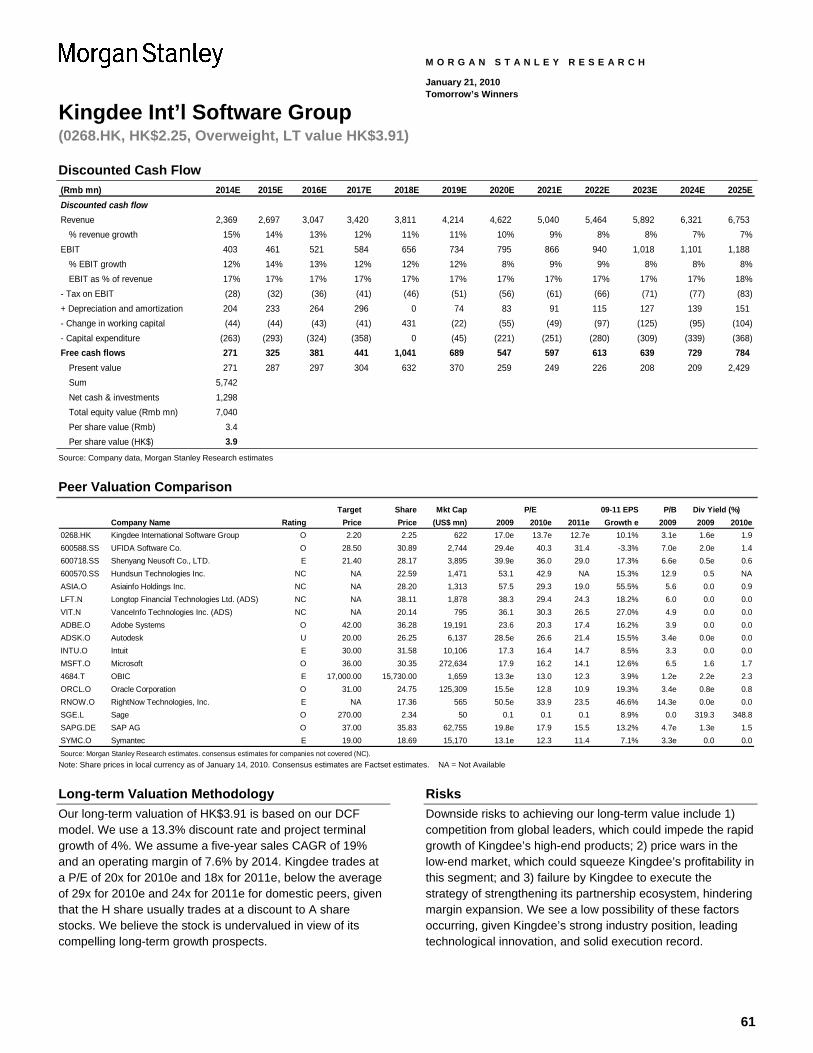

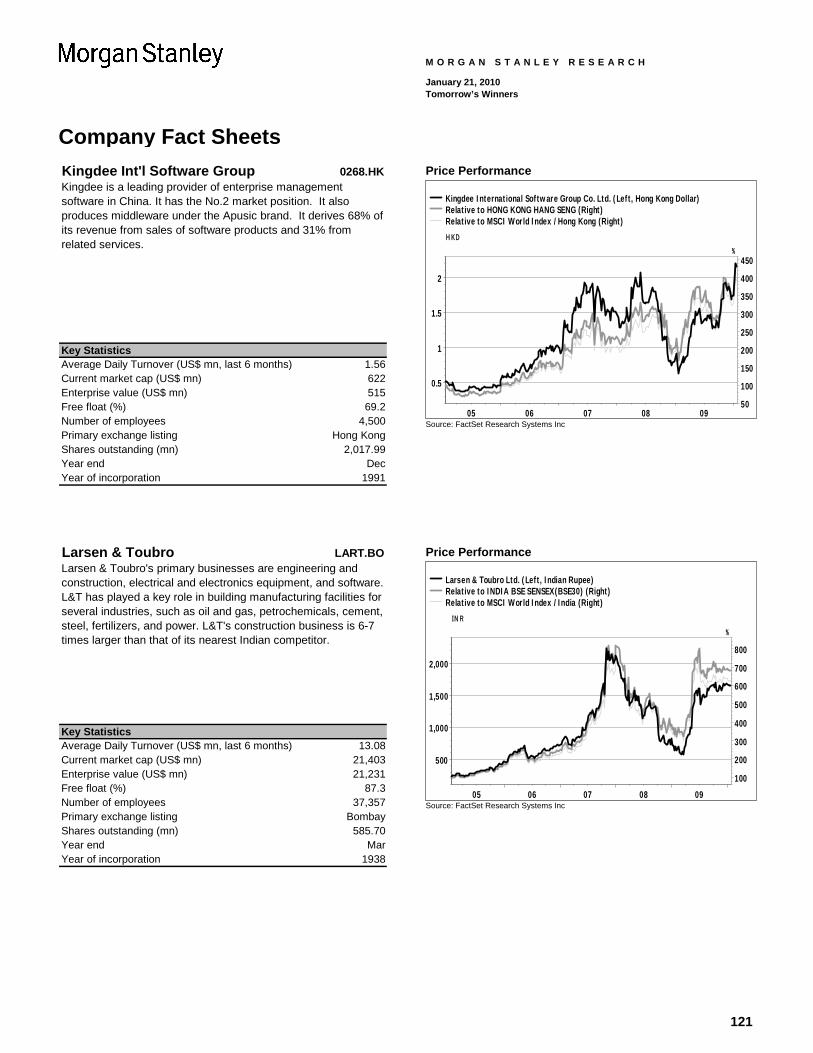

Kingdee Int’l Software Group 0268.HK OW HK$ 11/03/08 2.05 542 3.91 91 135 -9 119.54 15.56 61.17 56.83 27.89 36.03 China Technology In-Line Larsen & Toubro LART.BO OW Rs 02/22/08 1,636.45 21,383 3,095.00 89 172 18 109.25 -19.09 50.88 20.66 -6.76 -3.64 India Construction & Infrastructure Attractive

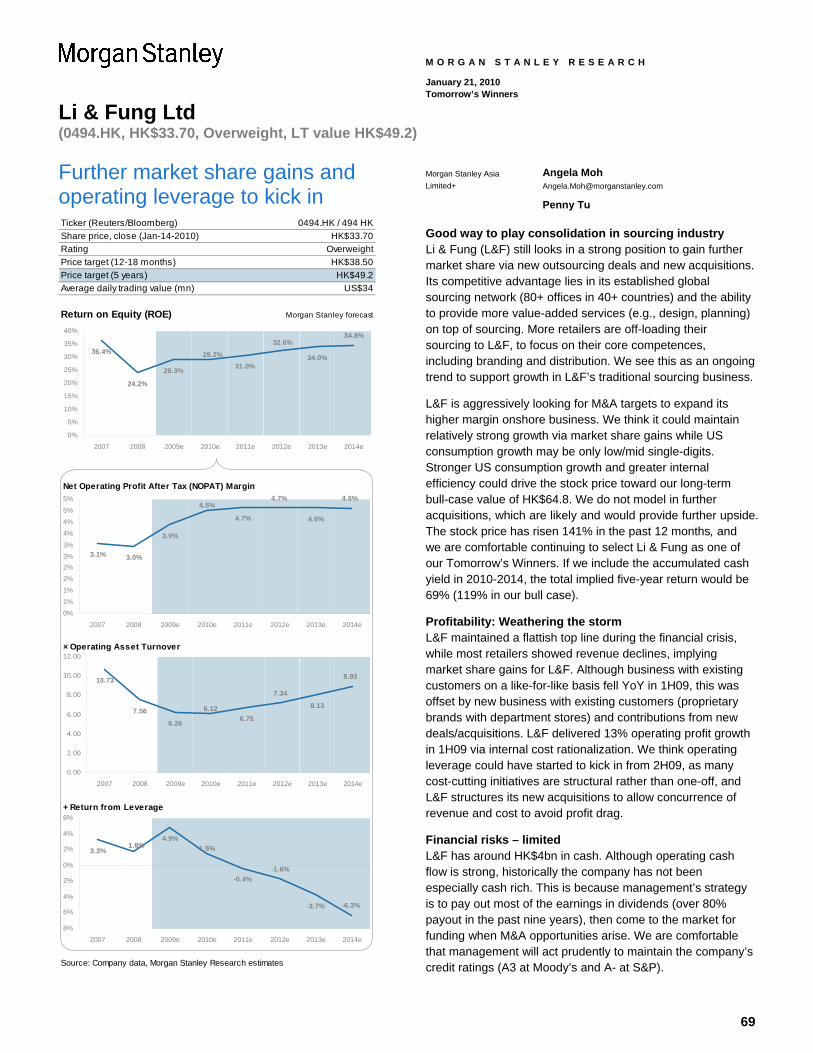

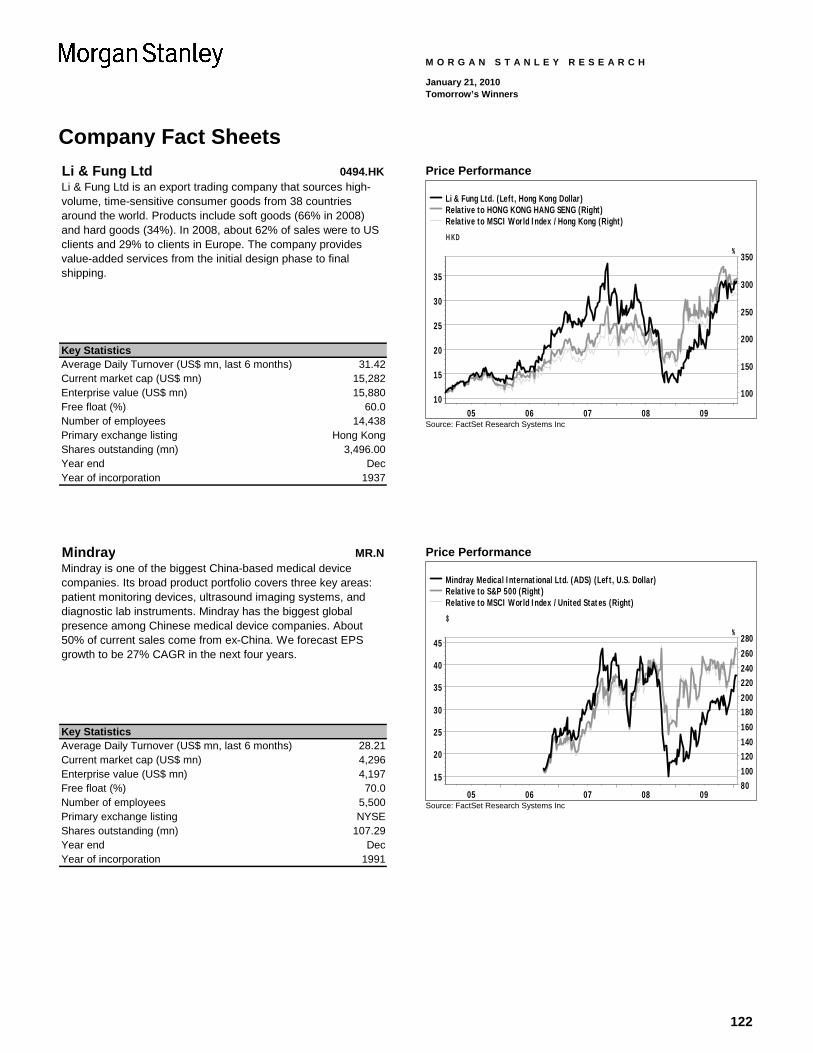

Li & Fung Ltd 0494.HK OW HK$ 02/22/08 33.00 16,045 49.20 49 96 2 141.29 1.74 82.92 81.05 14.07 24.04 Hong Kong Consumer Attractive

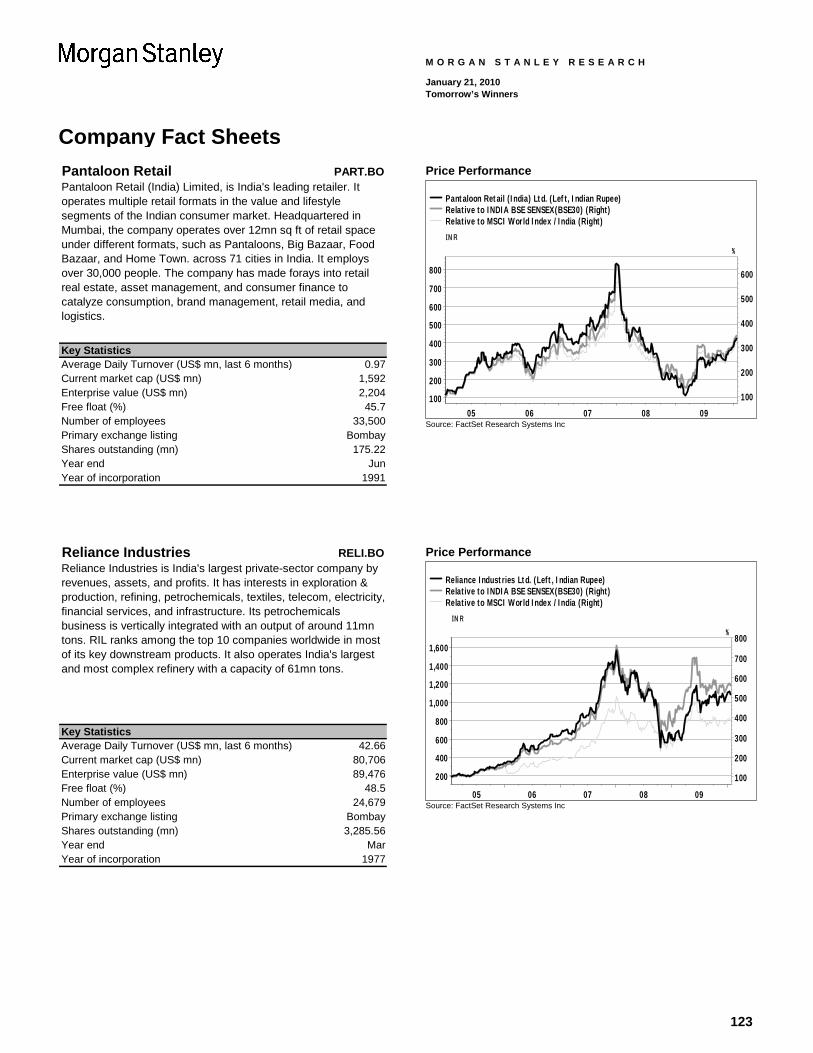

Mindray MR.N OW US$ 11/03/08 37.57 2,838 70.00 86 140 33 90.15 -20.35 31.79 27.44 -8.01 0.12 China Medical Devices Attractive Pantaloon Retail PART.BO OW Rs 02/22/08 445.95 1,700 1,243.00 179 392 -38 73.28 -54.14 14.92 -15.30 -41.81 -38.69 India Retail In-Line

Reliance Industries RELI.BO OW Rs 02/22/08 1,077.75 76,716 2,989.00 177 252 25 74.47 -23.87 16.11 -14.12 -11.53 -8.41 India Oil & Gas In-Line

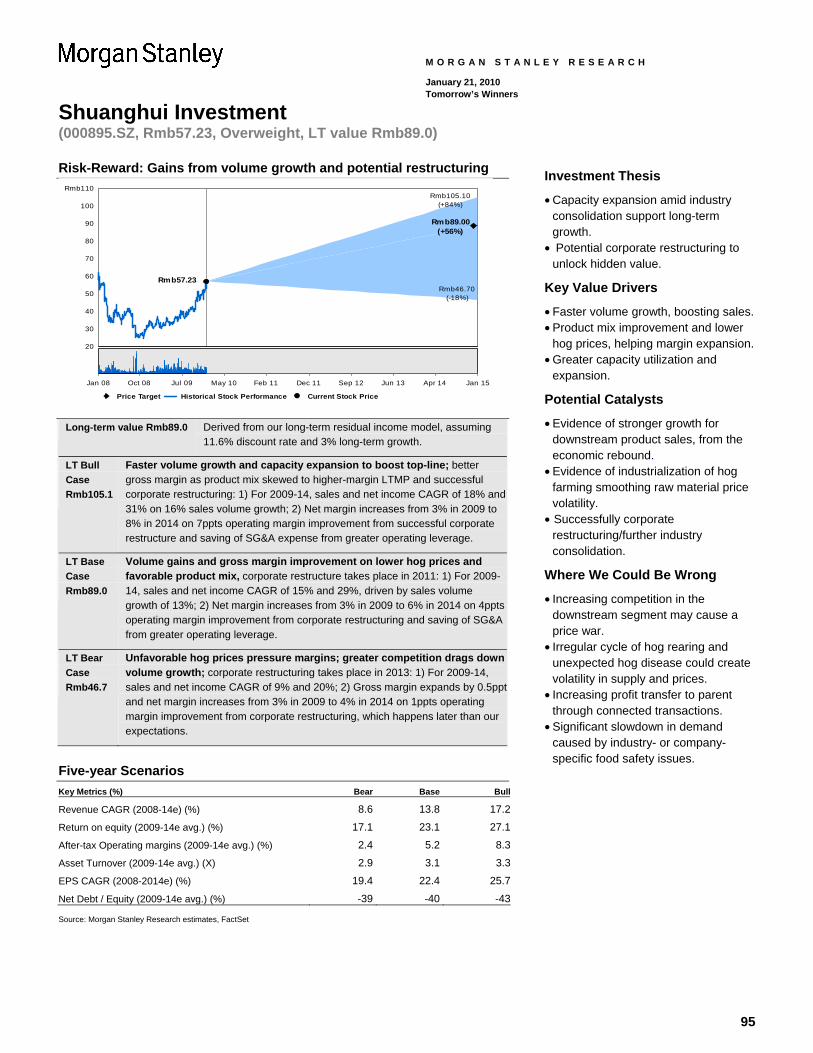

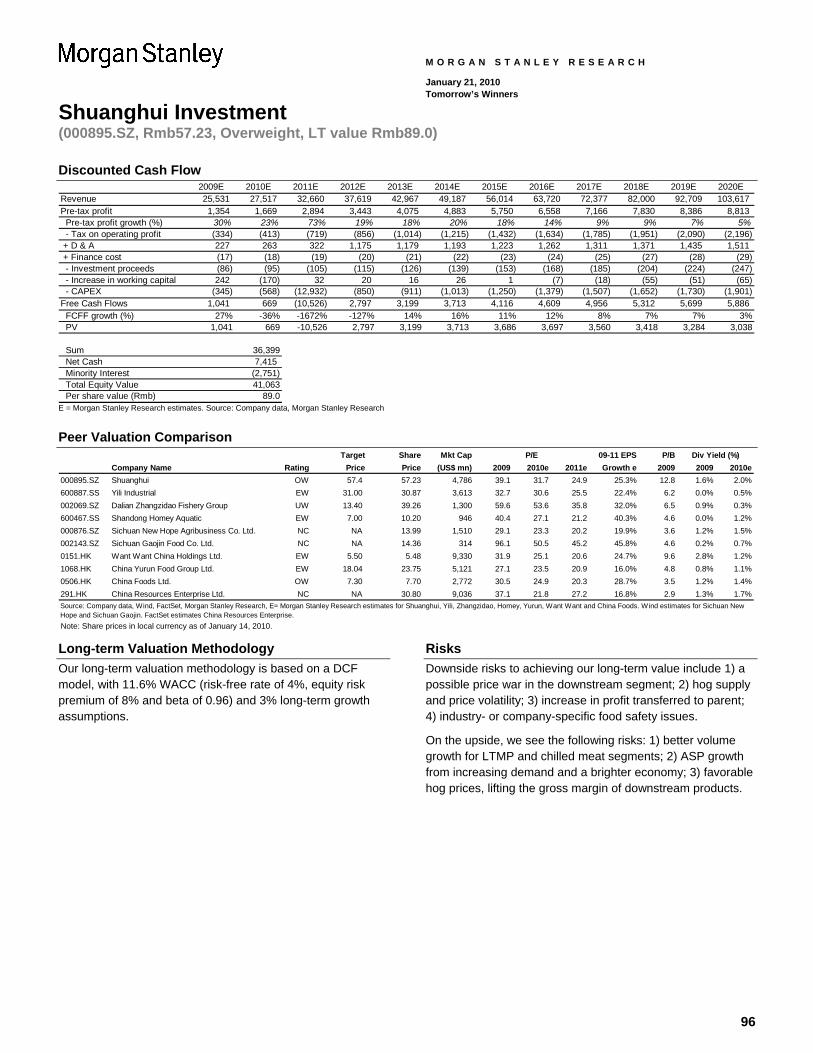

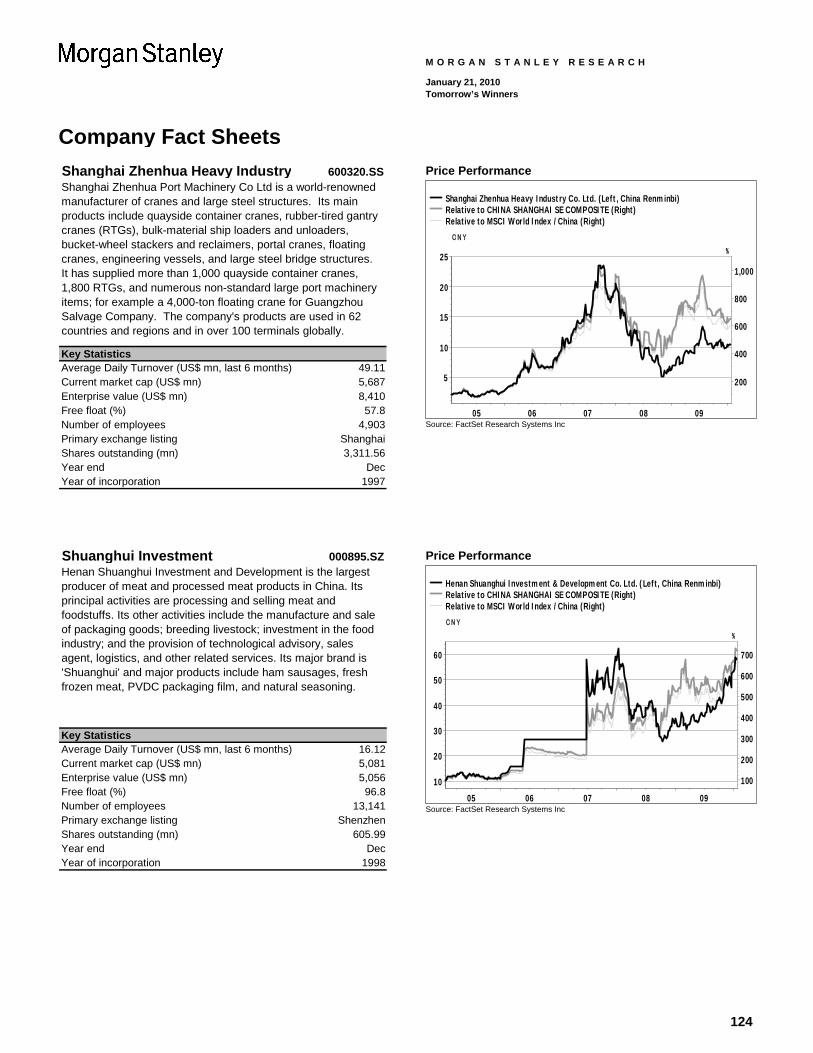

Shanghai Zhenhua 600320.SS EW Rmb 02/22/08 10.20 5,277 22.90 125 266 39 63.72 -47.67 5.36 1.01 -35.34 -27.20 China Capital Goods In-Line Shuanghui Investment 000895.SZ OW Rmb 02/22/08 57.95 5,144 89.20 54 81 -19 50.07 -11.76 -8.30 -12.64 0.58 8.72 China Food, Bev. & Tobacco Attractive

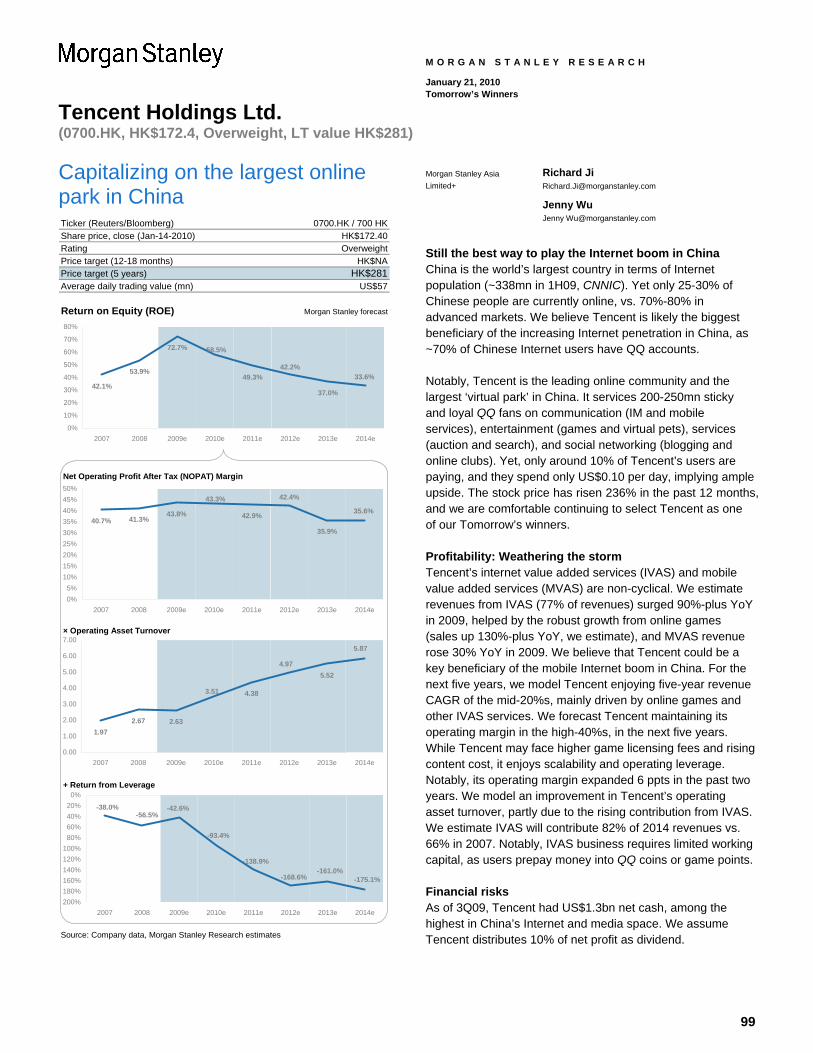

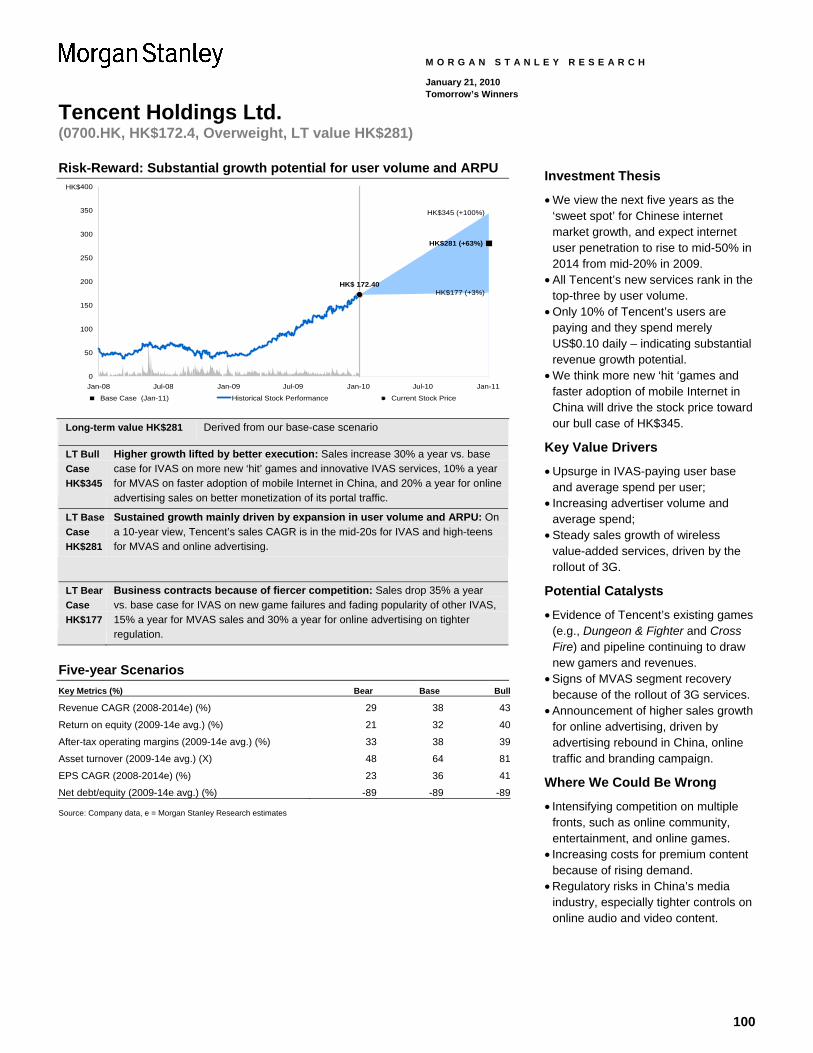

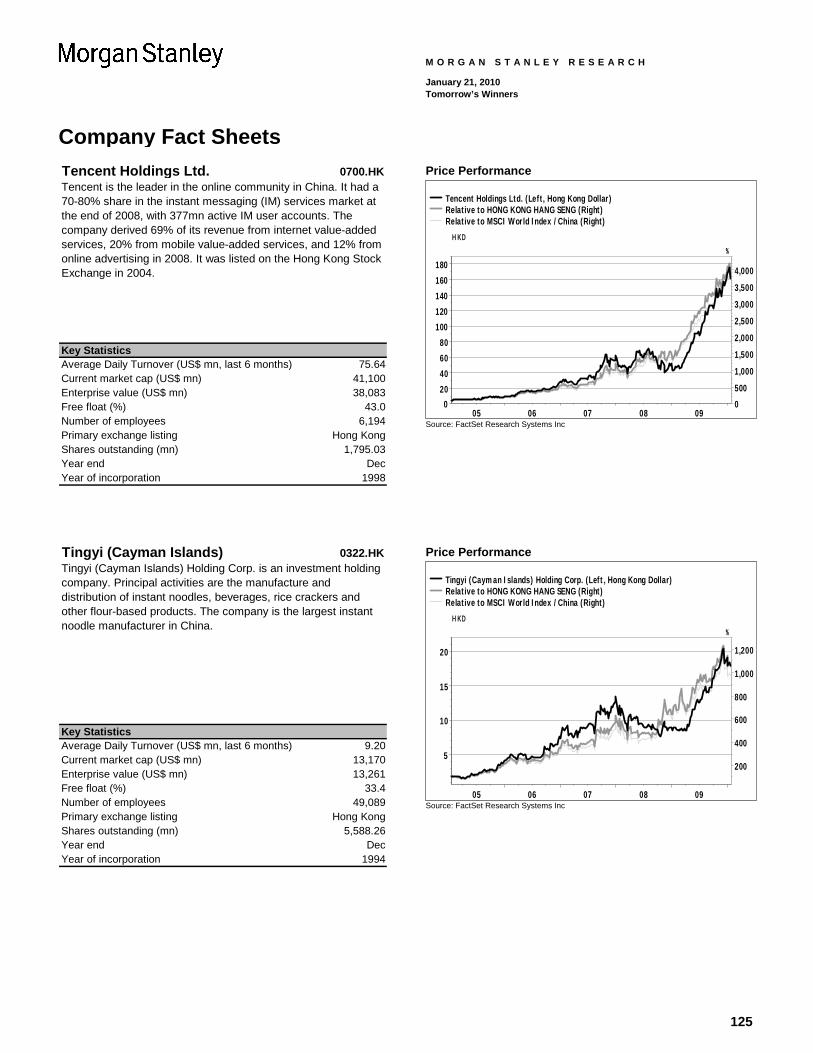

Tencent Holdings Ltd. 0700.HK OW HK$ 02/22/08 155.40 36,466 281.00 81 122 14 236.02 189.82 177.65 173.31 202.15 210.29 China Internet Attractive

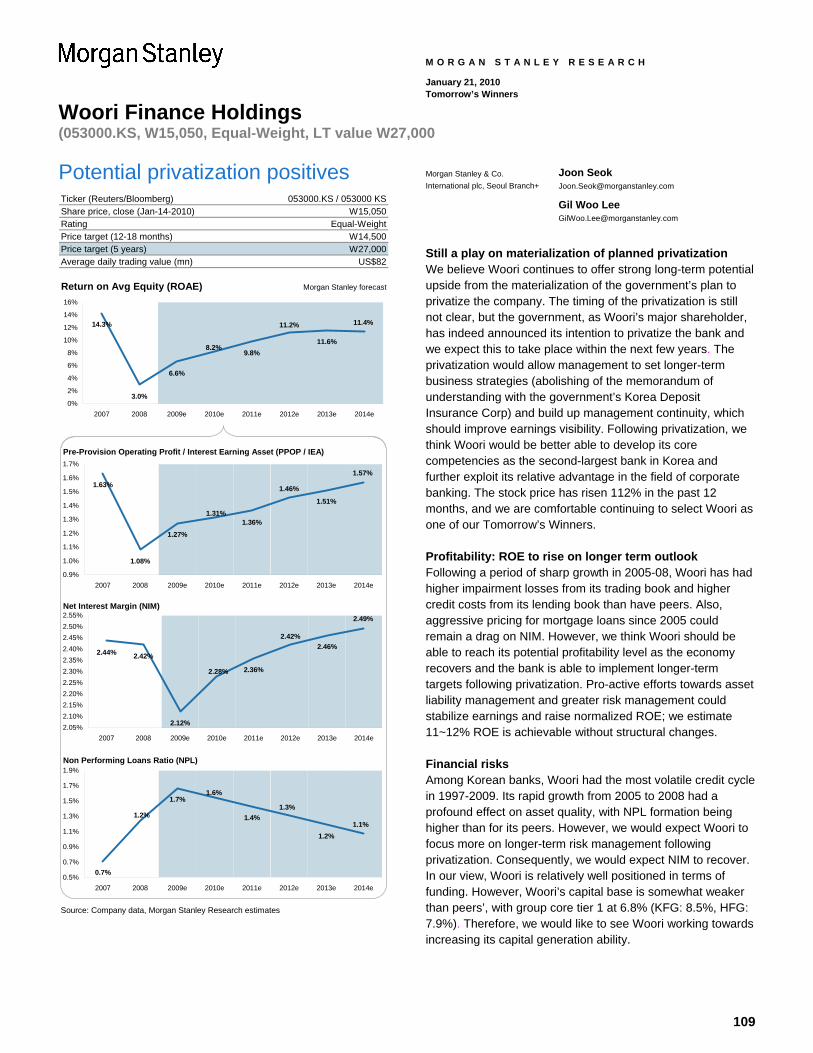

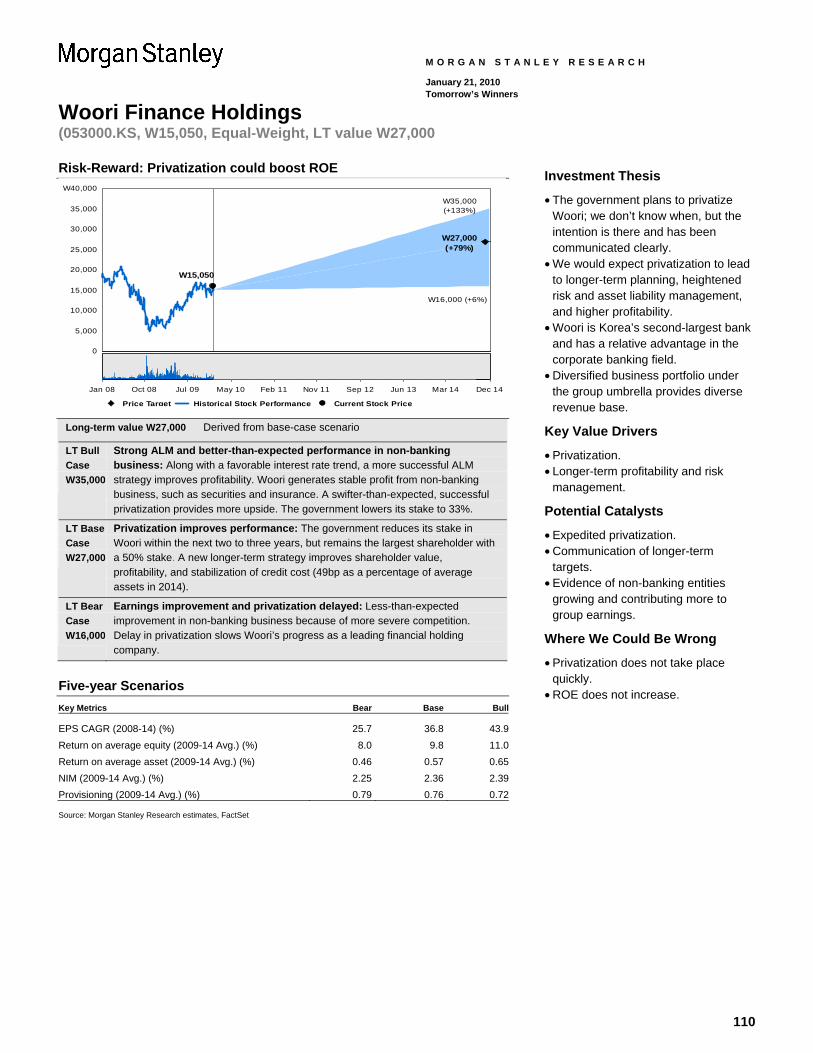

Tingyi (Cayman Islands) 0322.HK EW HK$ 02/22/08 17.58 12,645 25.00 42 96 14 115.49 51.68 57.13 52.78 64.01 72.15 China Food, Bev. & Tobacco Attractive Woori Finance Holdings 053000.KS EW W 02/22/08 15,700 11,121 27,000 72 123 2 112.96 -26.53 54.59 53.88 -14.19 -22.70 S. Korea Financial Services Attractive

MSCI Asia exJapan 58.36 -12.33 MSCI Australia 37.04 -13.64

MSCI China 62.71 -20.47

MSCI Hong Kong 60.23 -22.30 MSCI India 88.59 -15.45

MSCI S. Korea 59.08 -3.82

MSCI Taiwan 75.67 -3.80

Closing prices as of January 20, 2010. Source: Morgan Stanley Research

Removals Perf. vs. Perf. vs. Up/down Up Down Absolute Absolute Perf. vs. Country Perf. vs. Country to LT to LT to LT perf. perf. APxJ MSCI APxJ MSCI Date Date Close value bull bear (12 mths) (24 mths) (12 mths) (12 mths) (24 mths) (24 mths) Industry Name Ticker Rating Curr added removed price LT value (%) (%) (%) (%) (%) (%) (%) (%) (%) Country Sub-Industry View

Bharti Airtel Limited BRTI.BO EW Rs 02/22/08 01/14/10 330.90 470.00 42 81 -46 -8.53 -32.49 -66.89 -97.12 -20.16 -17.04 India Telecommunications Cautious Brambles Ltd. BXB.AX EW A$ 02/22/08 01/14/10 6.77 9.65 43 85 3 -8.79 -41.16 -67.16 -45.83 -28.83 -27.52 Australia Business Services In-Line

Reliance Capital RLCP.BO EW Rs 02/22/08 11/03/08 891.95 2,350.00 163 390 85 54.73 -67.10 -3.63 -33.85 -54.76 -51.64 India Financial Services Attractive

Samsung Techwin 012450.KS OW W 02/22/08 11/03/08 79,500 106,000 33 114 -35 121.35 48.64 62.98 62.27 60.97 52.46 S. Korea Hardware Components In-Line Sobha Developers Ltd. SOBH.BO NAV Rs 02/22/08 11/03/08 306.00 495.00 62 111 -29 128.27 -73.15 69.90 39.68 -60.82 -57.70 India Property In-Line

Closing prices as of January 20, 2010. Source: Morgan Stanley Research

3

Contents

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Tomorrow’s Winners: Valuation Metrics .............................................................................................................................................. 2

Company Analysis

Belle International: Integration of acquisitions boosts long-term earnings growth ............................................................................ 5

Removal Bharti Airtel Ltd.: Facing pressure as incumbent ............................................................................................................ 10

Removal Brambles Ltd: The penalty of past maintenance under-spending.................................................................................... 16

China Mengniu Dairy: Industry leader to capitalize on industry growth........................................................................................... 22

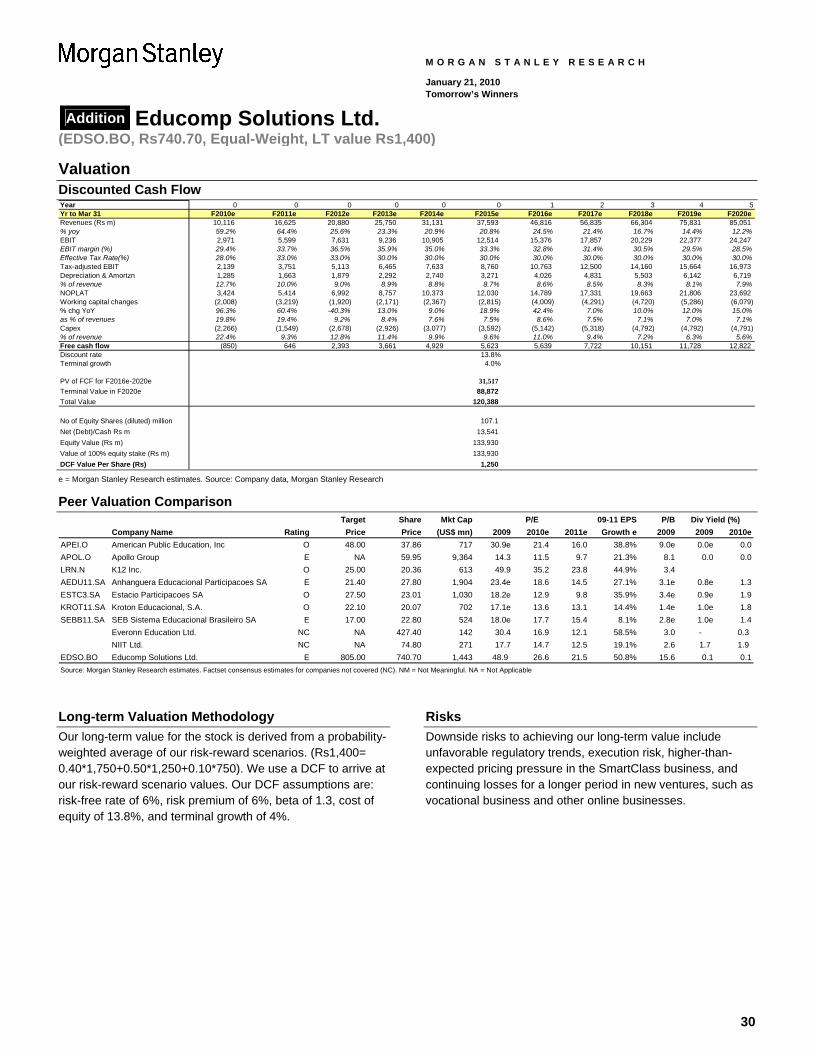

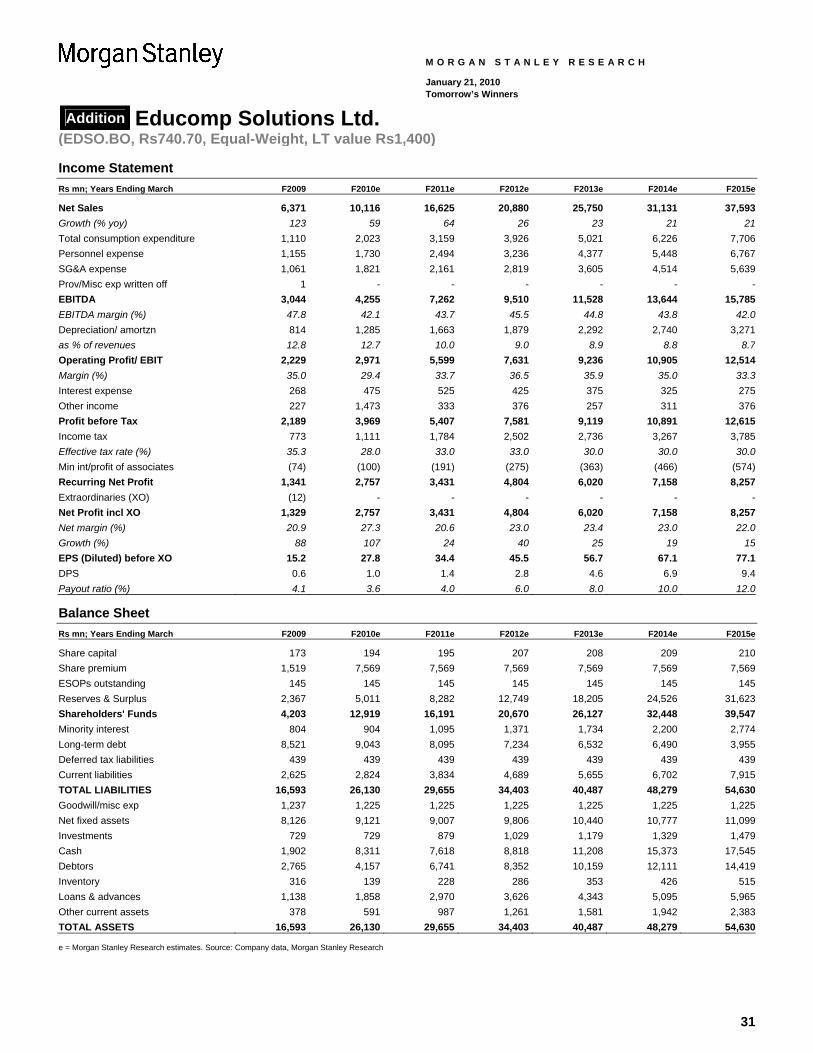

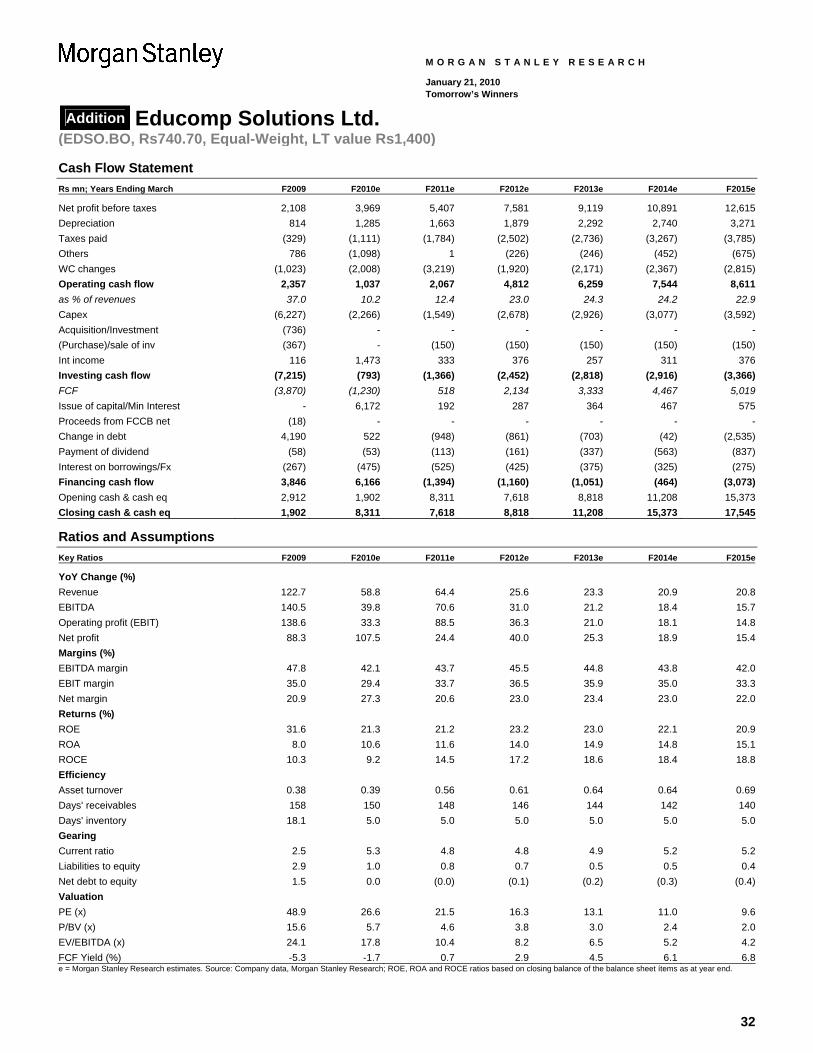

Addition Educomp Solutions Ltd.: Substantial scope long term in an emerging industry ............................................................. 27

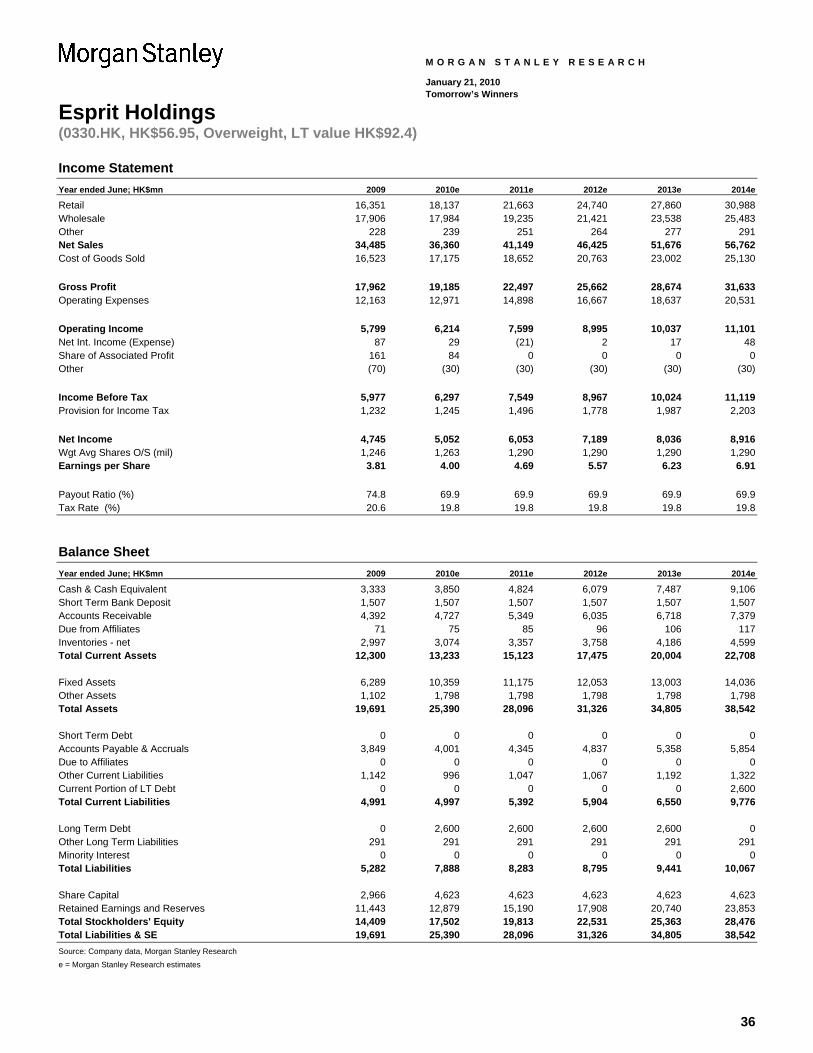

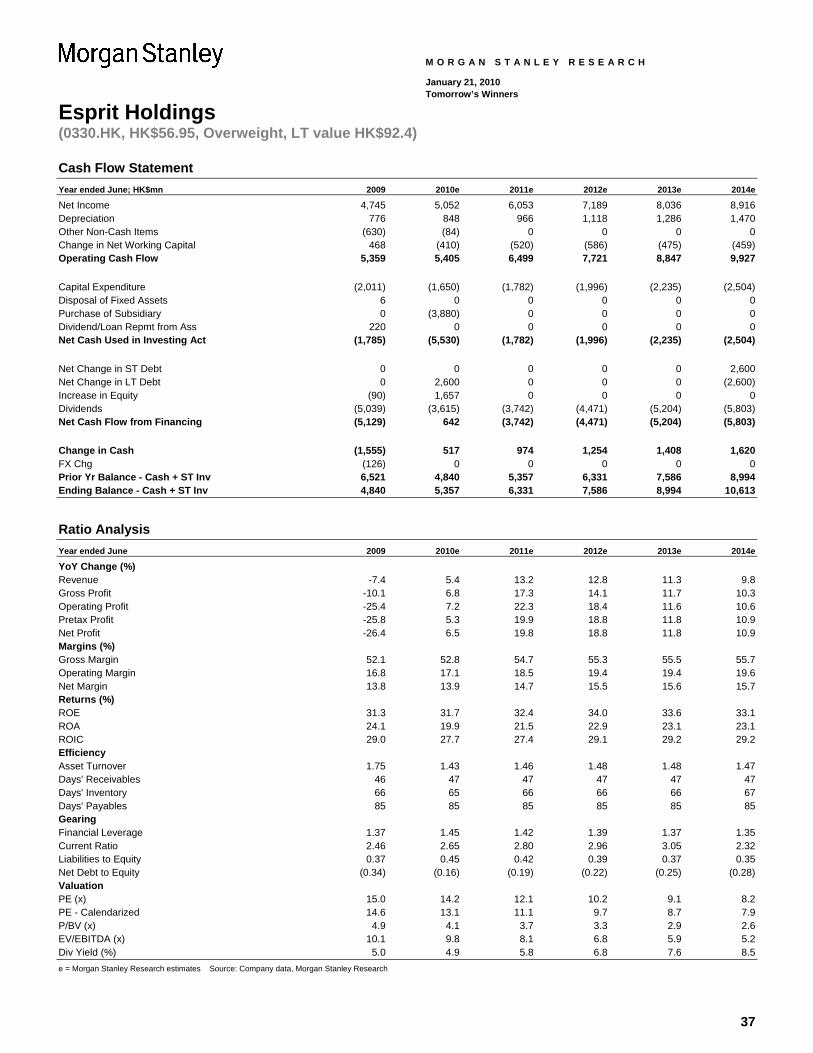

Esprit Holdings: Emerging from the storm; well placed for economic recovery .............................................................................. 33

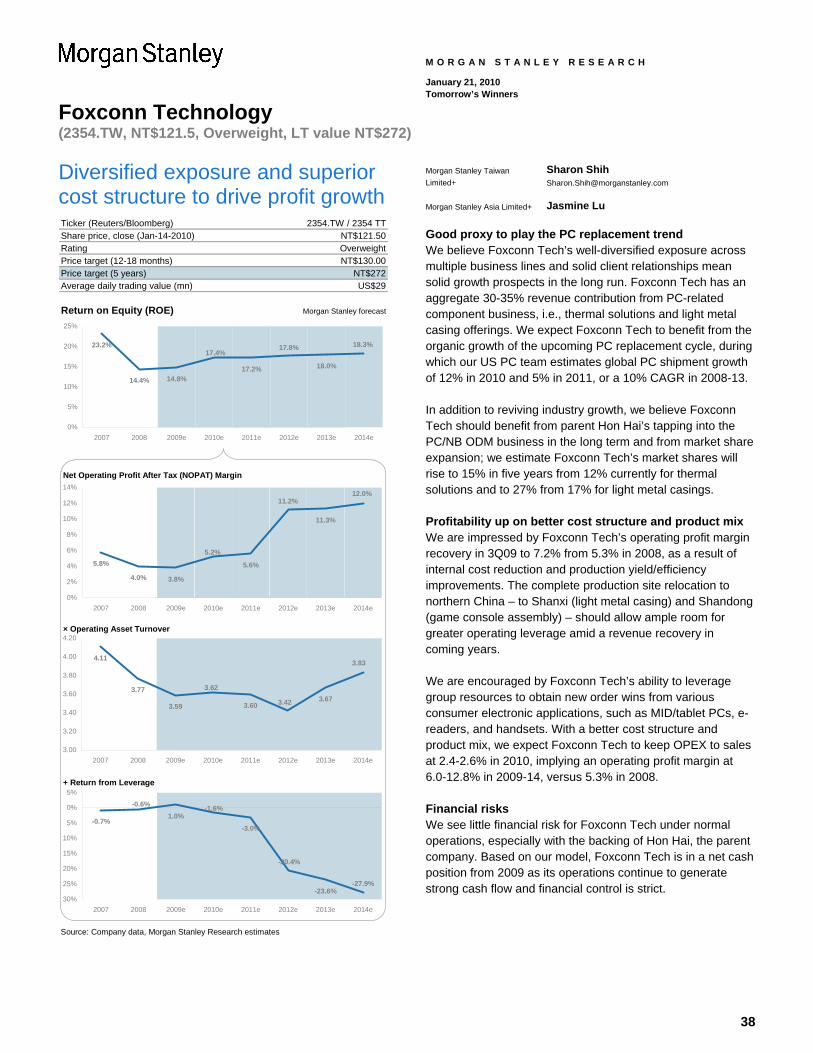

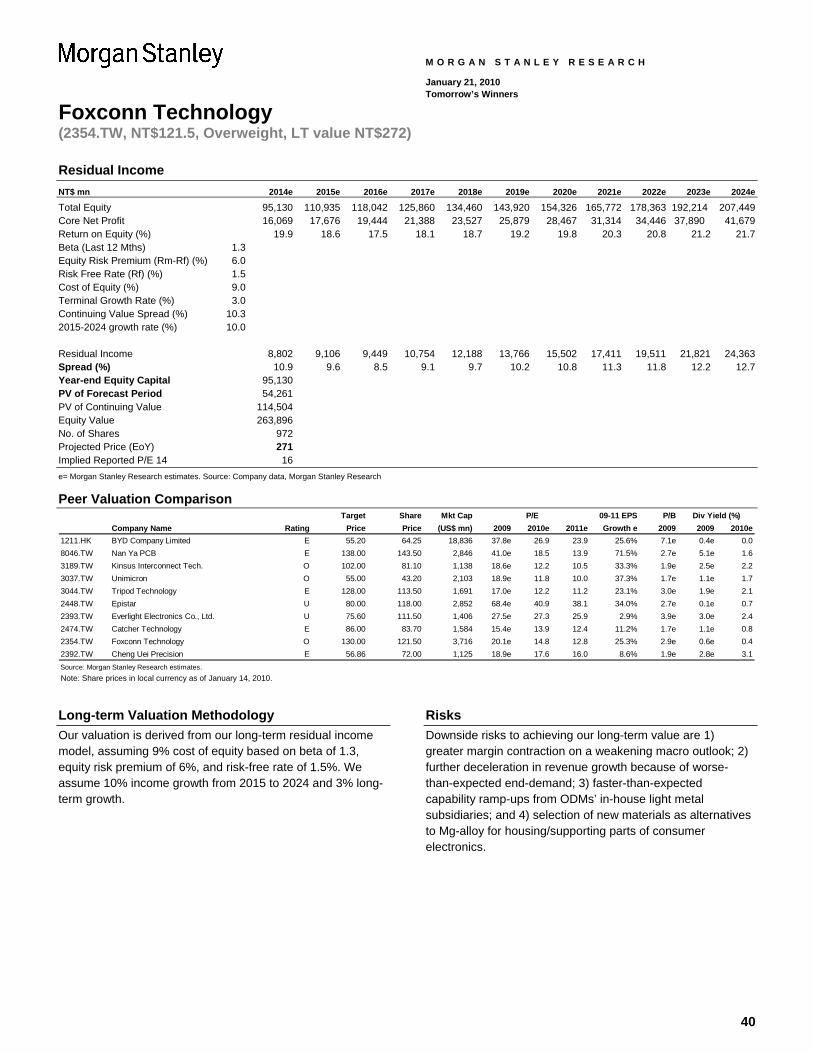

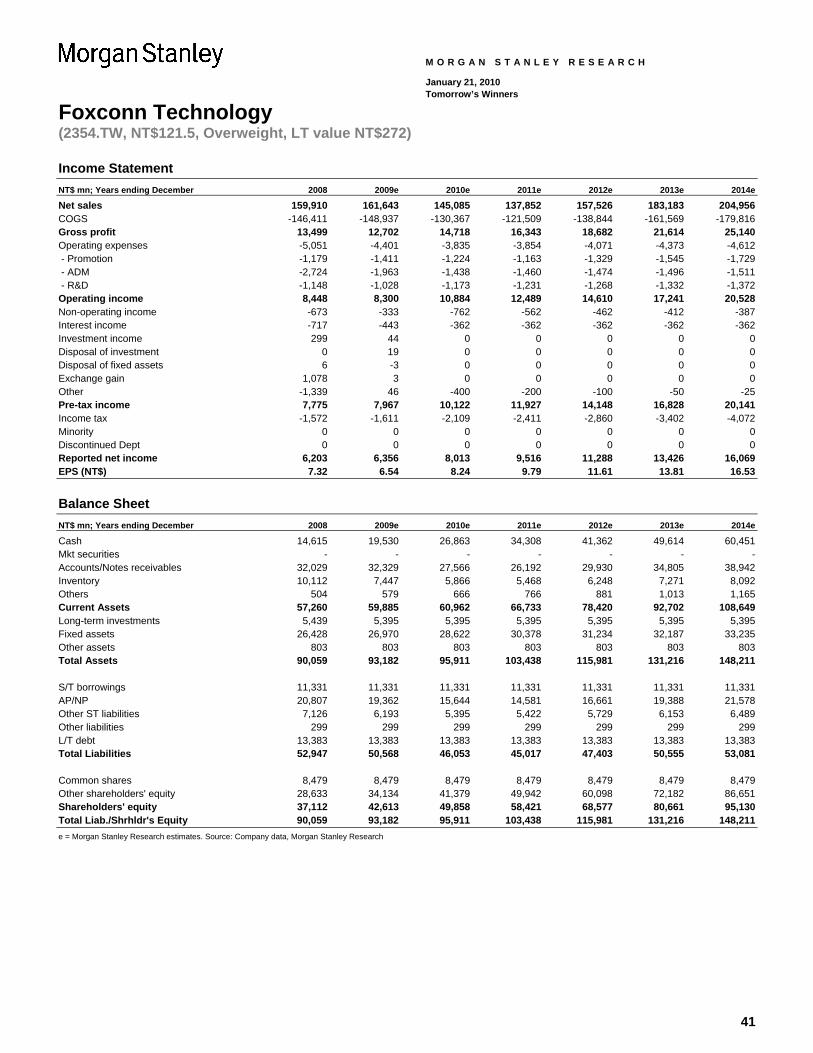

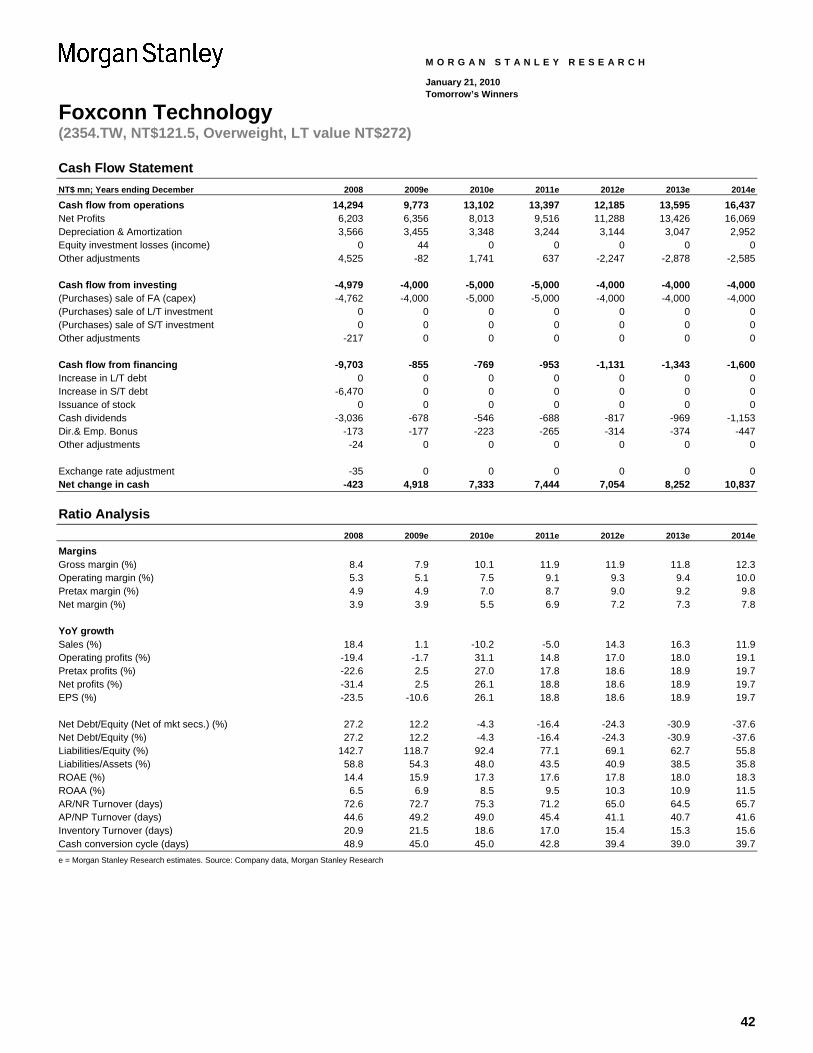

Foxconn Technology: Diversified exposure and superior cost structure to drive profit growth ....................................................... 38

Gemtek Technology: Play on upcoming fixed-mobile convergence................................................................................................ 43

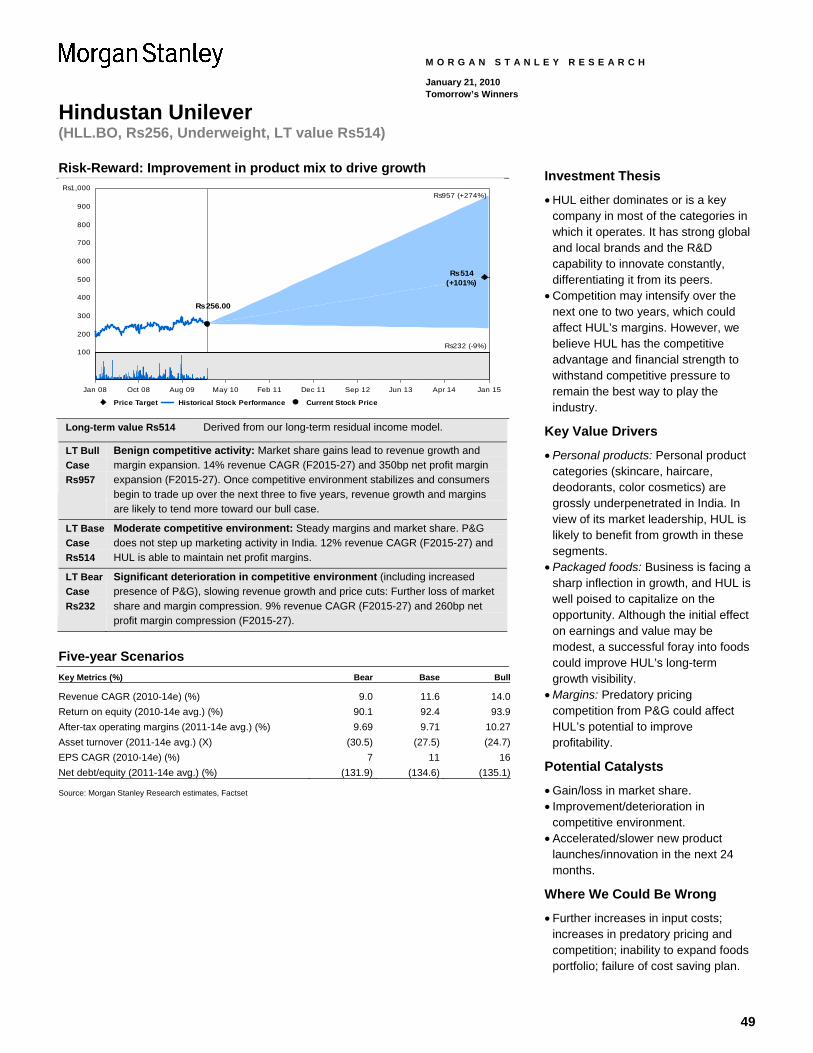

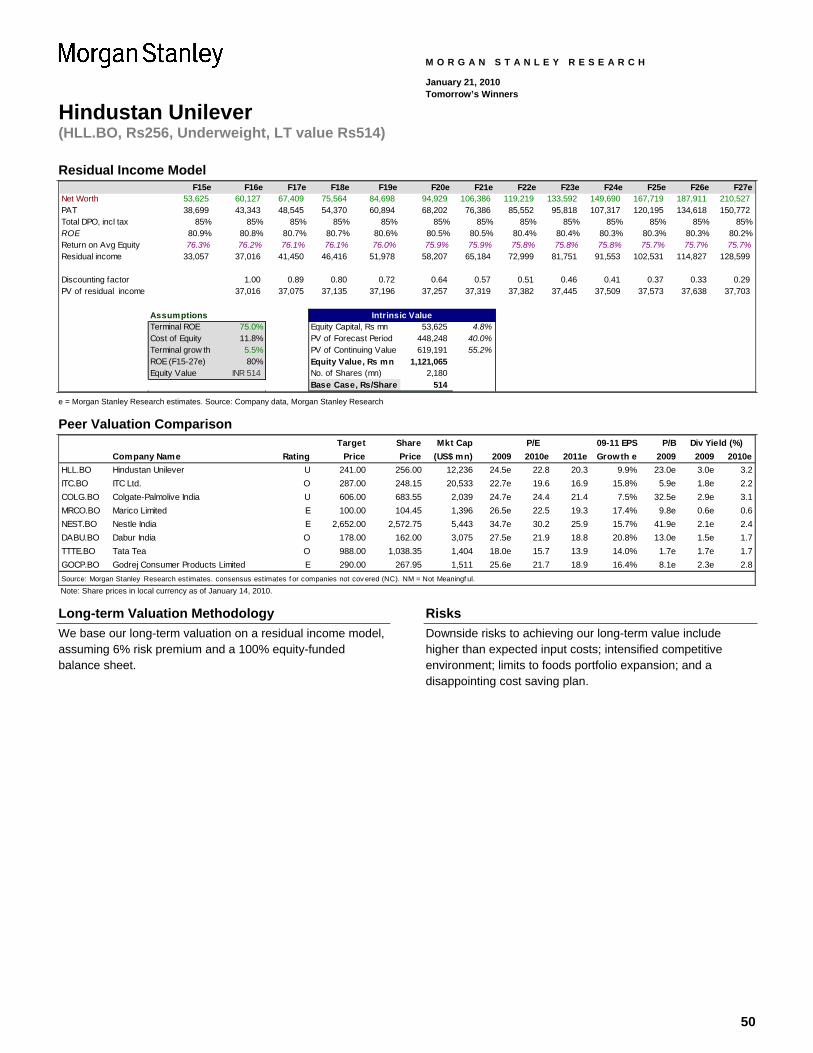

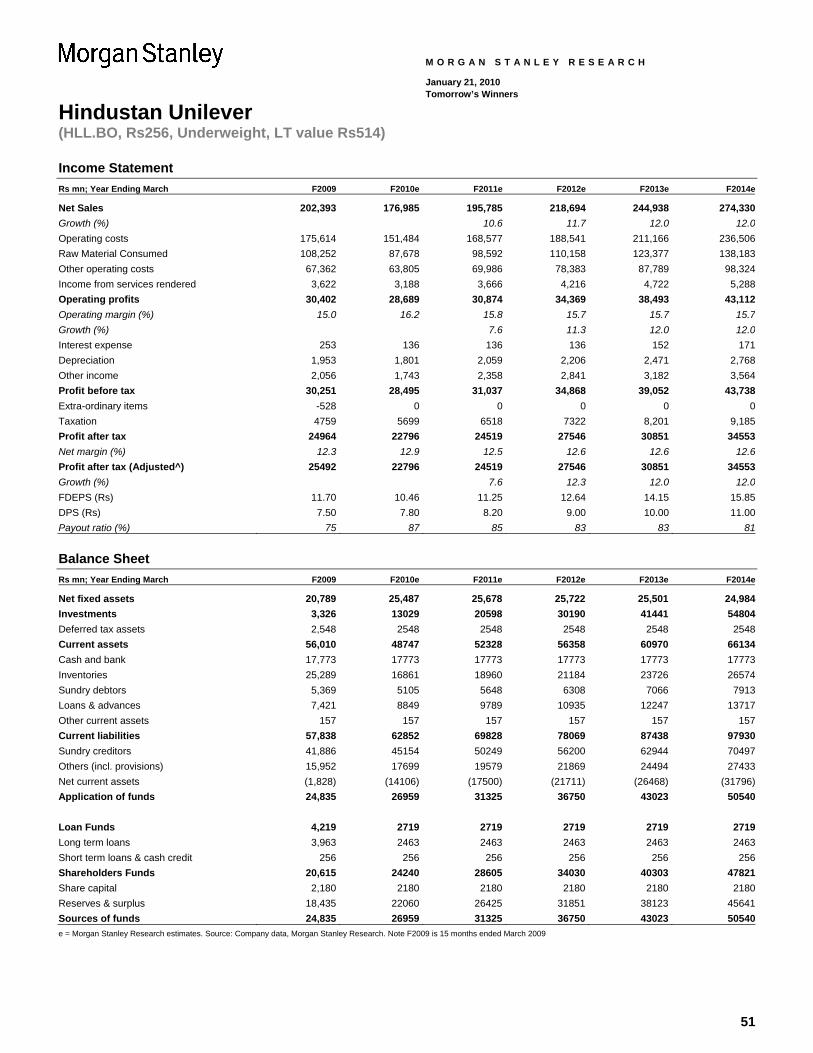

Hindustan Unilever: Long-term story intact, but some hurdles ahead ............................................................................................ 48

IDFC: Financing the infrastructure boom .......................................................................................................................................... 53

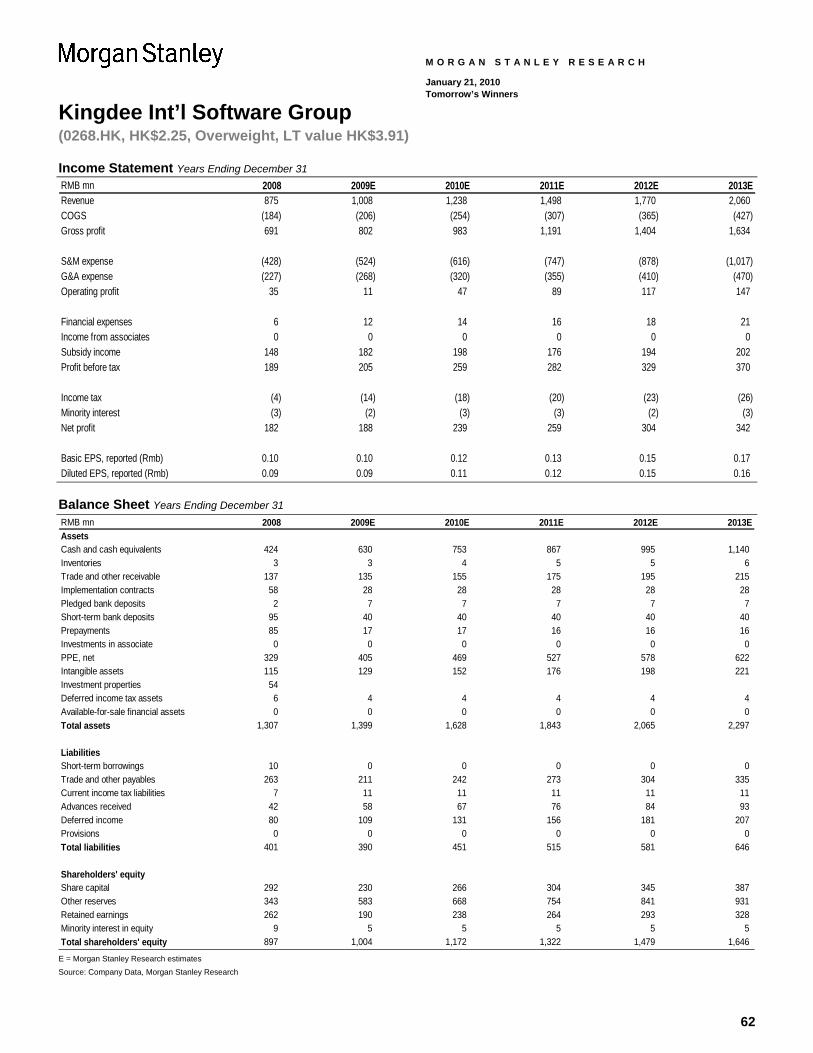

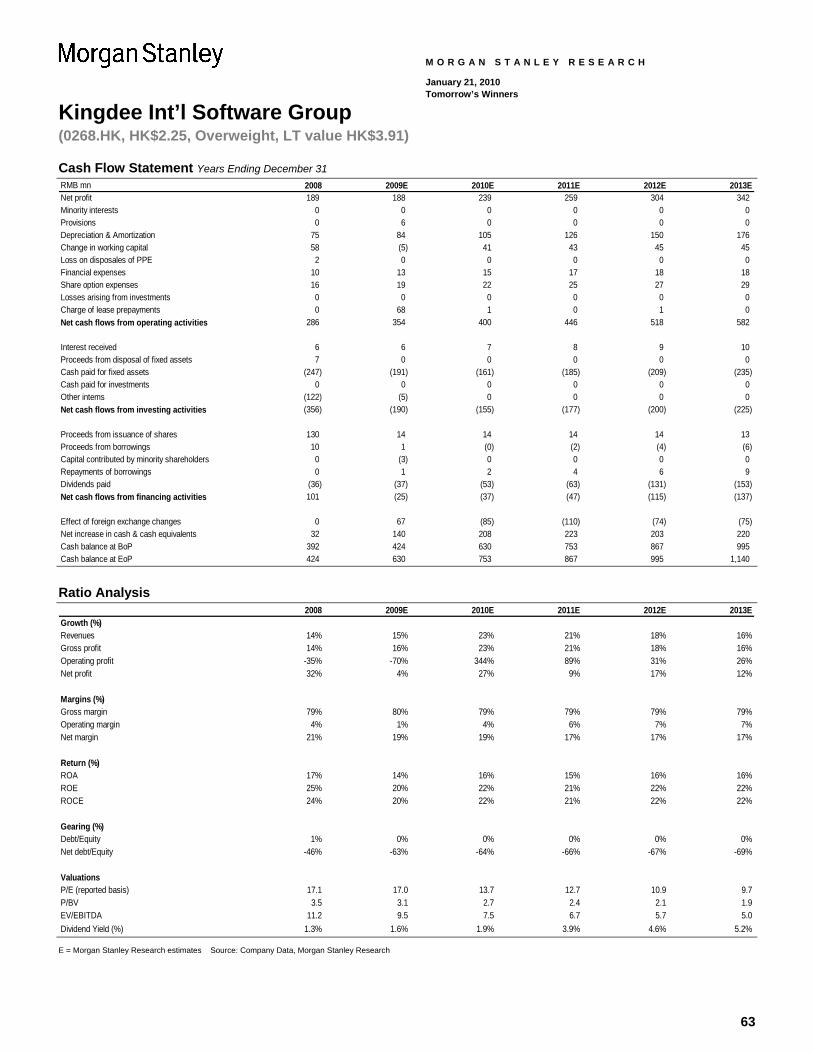

Kingdee International Software Group: Well placed for long-term growth .................................................................................... 59

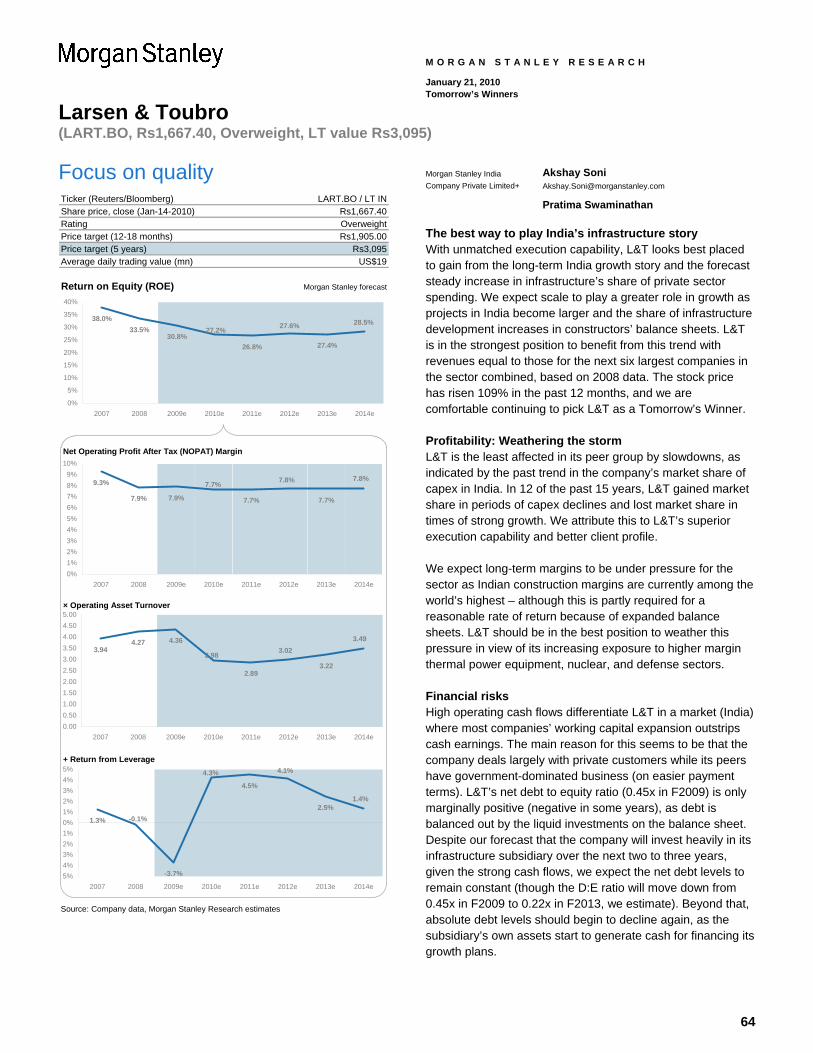

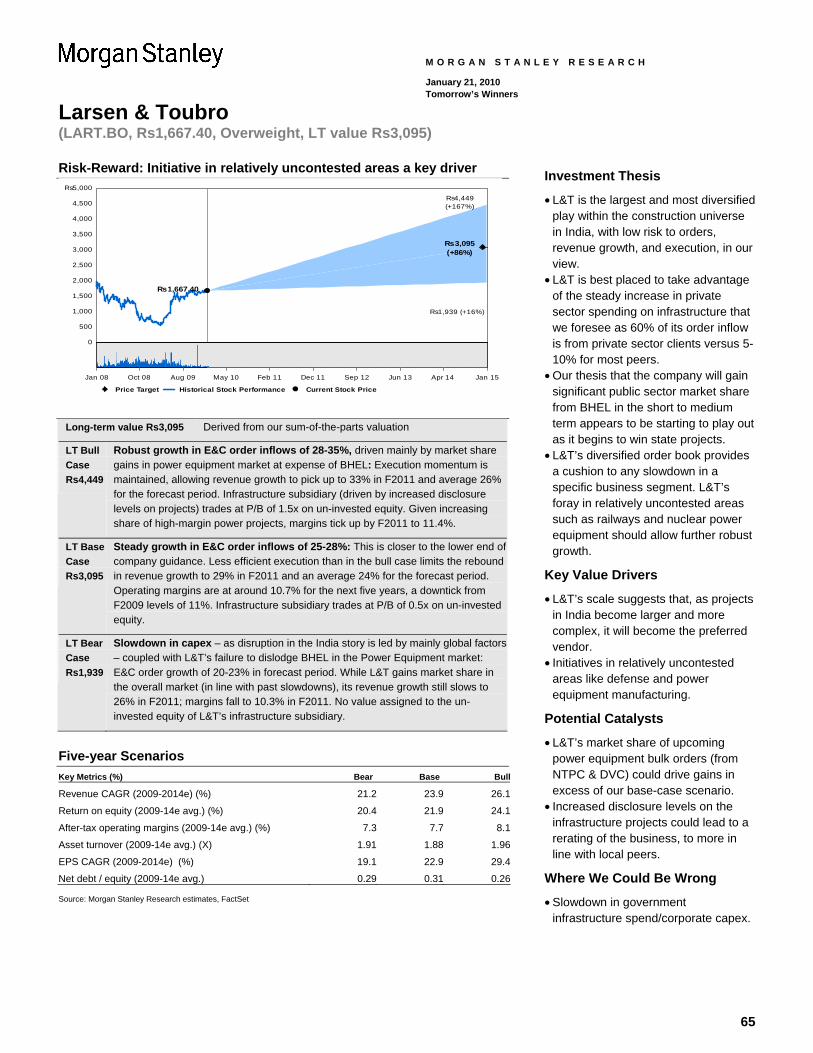

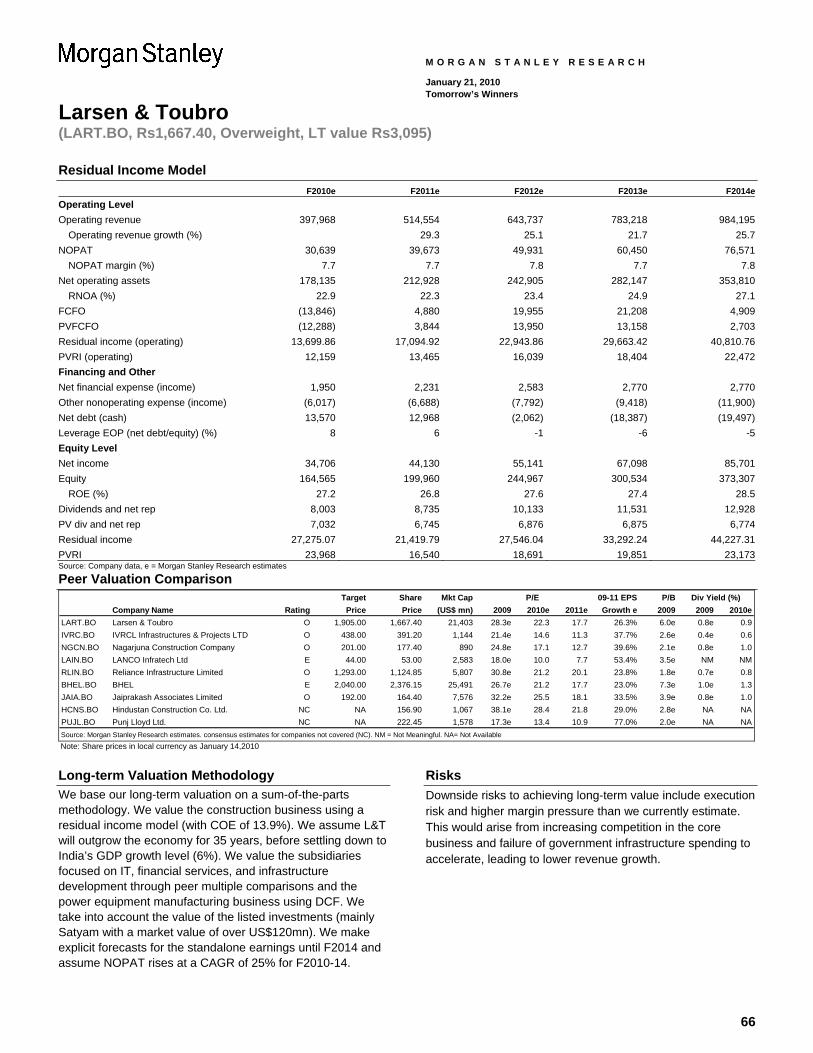

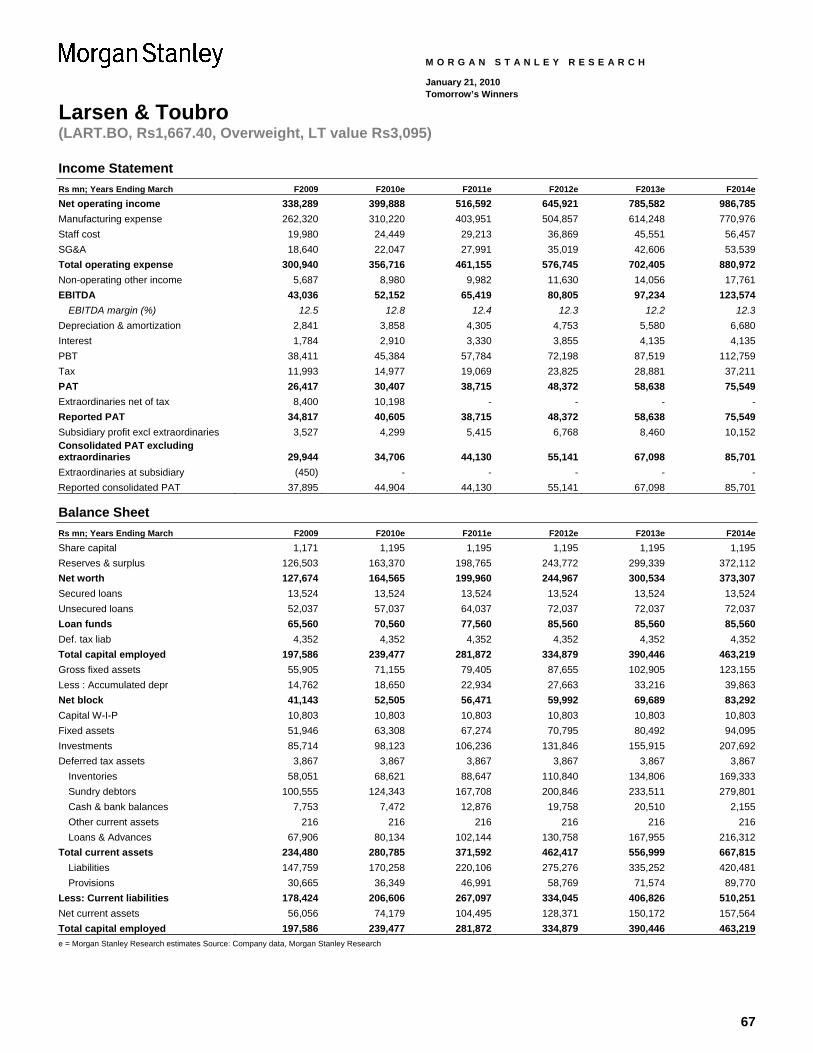

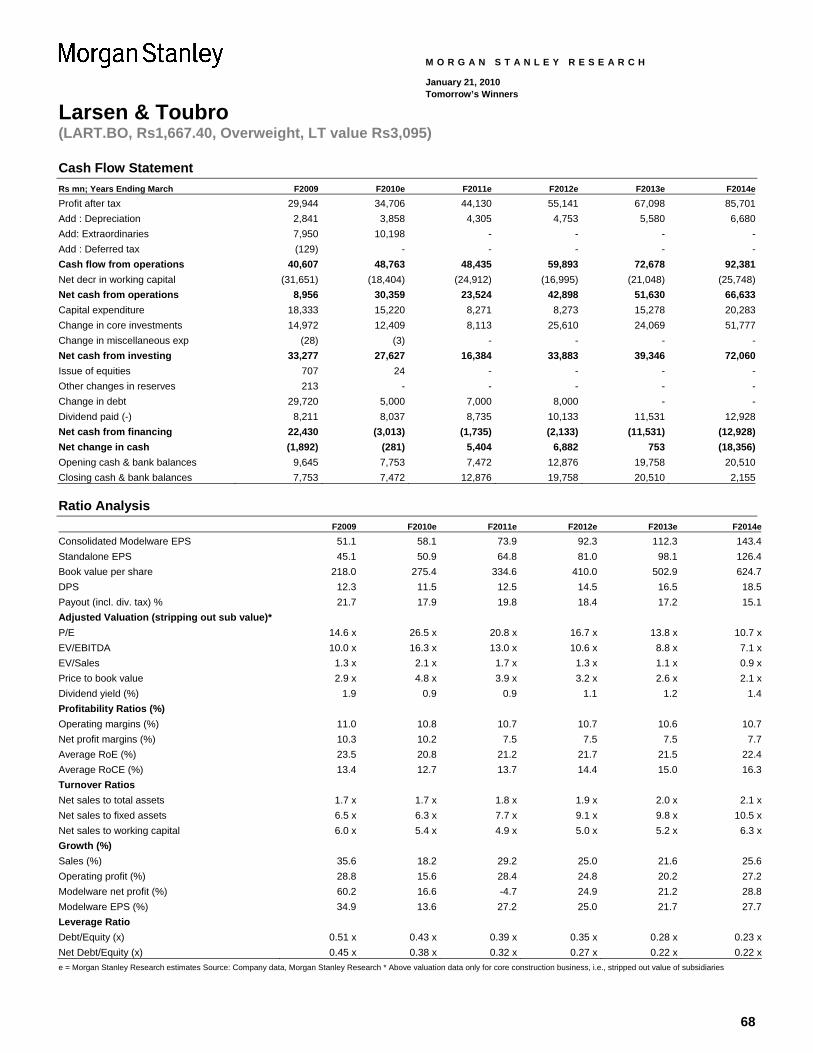

Larsen & Toubro: Focus on quality ................................................................................................................................................. 64

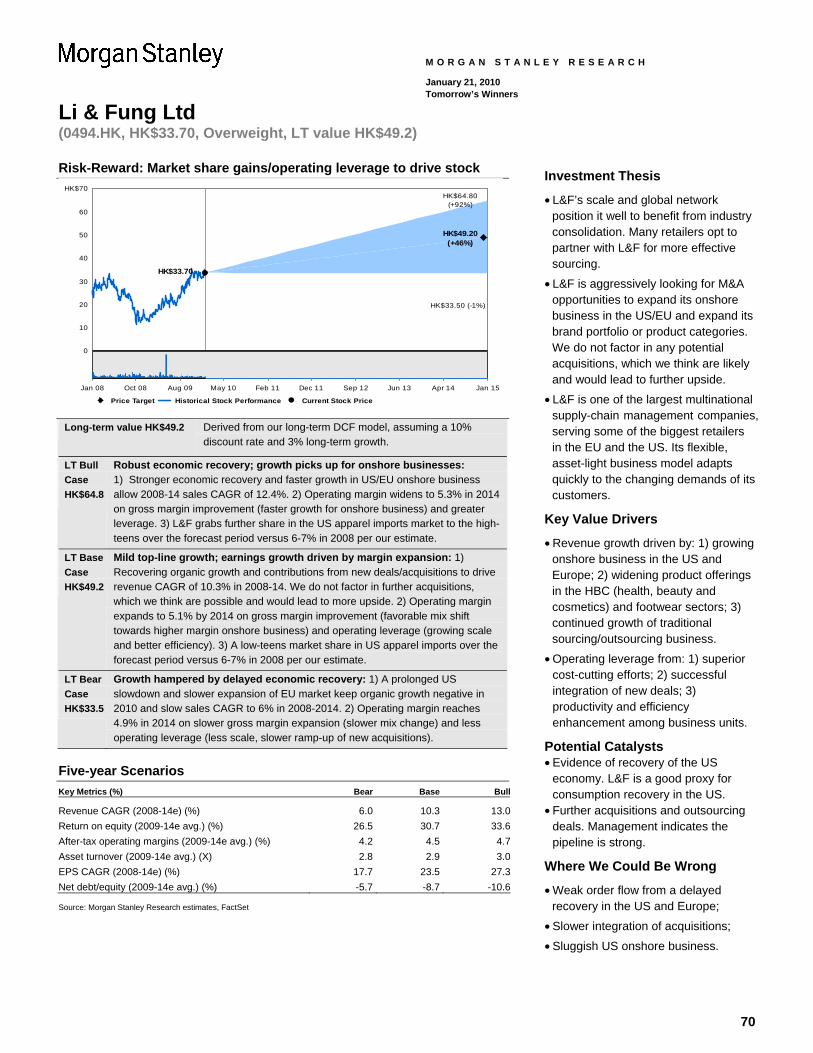

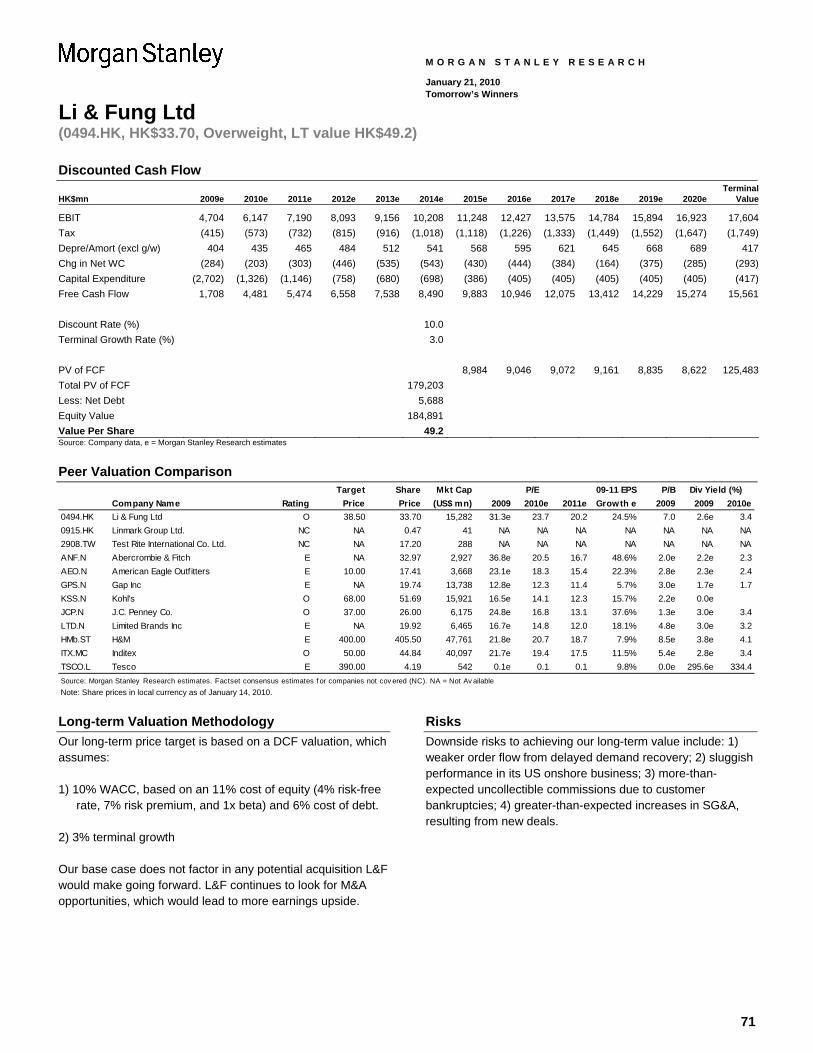

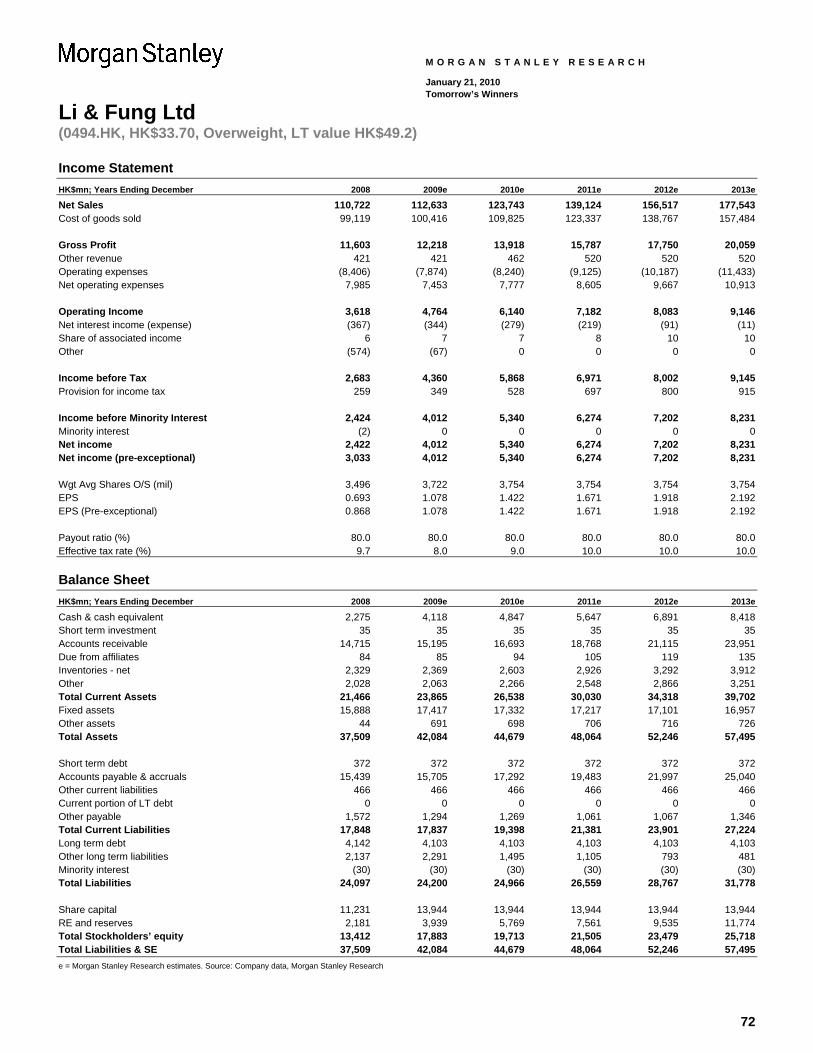

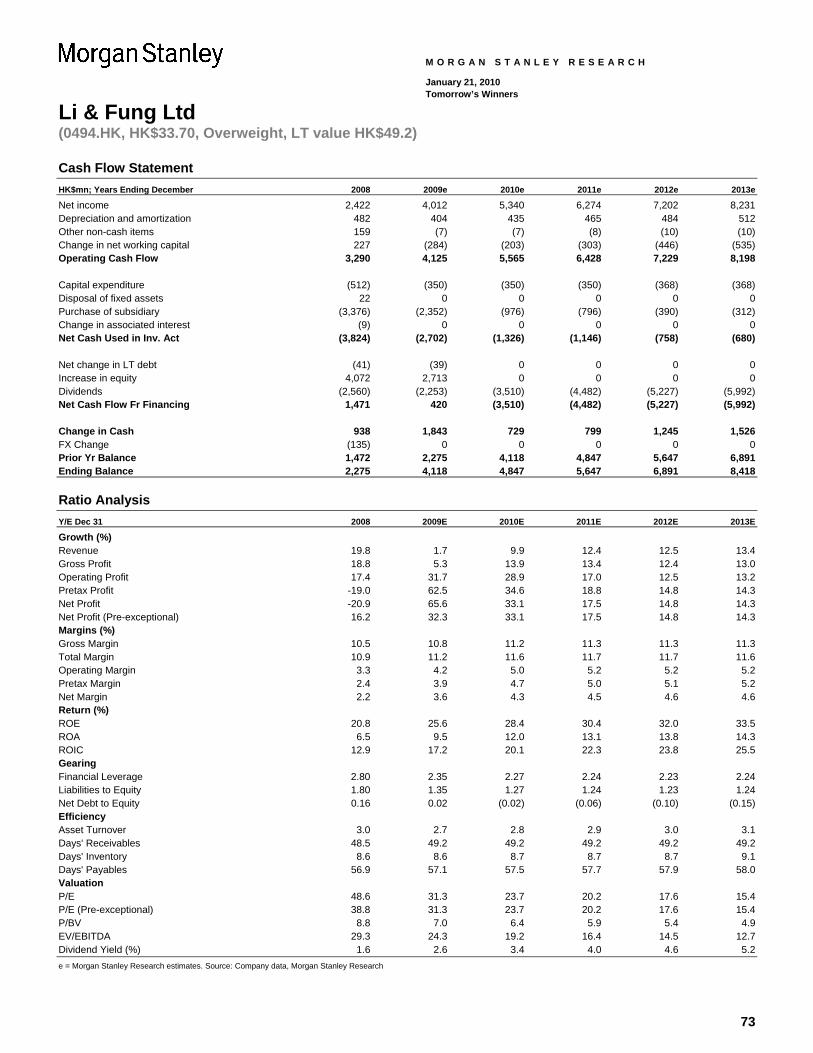

Li & Fung Ltd: Further market share gains and operating leverage to kick in.................................................................................. 69

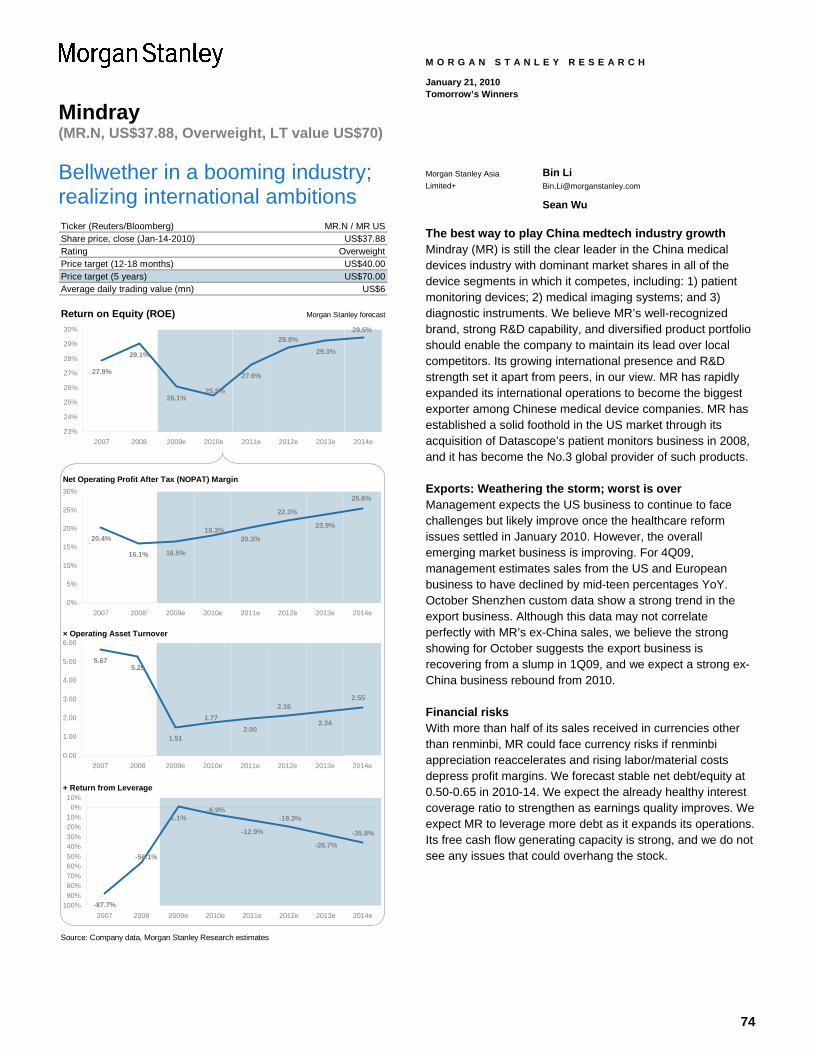

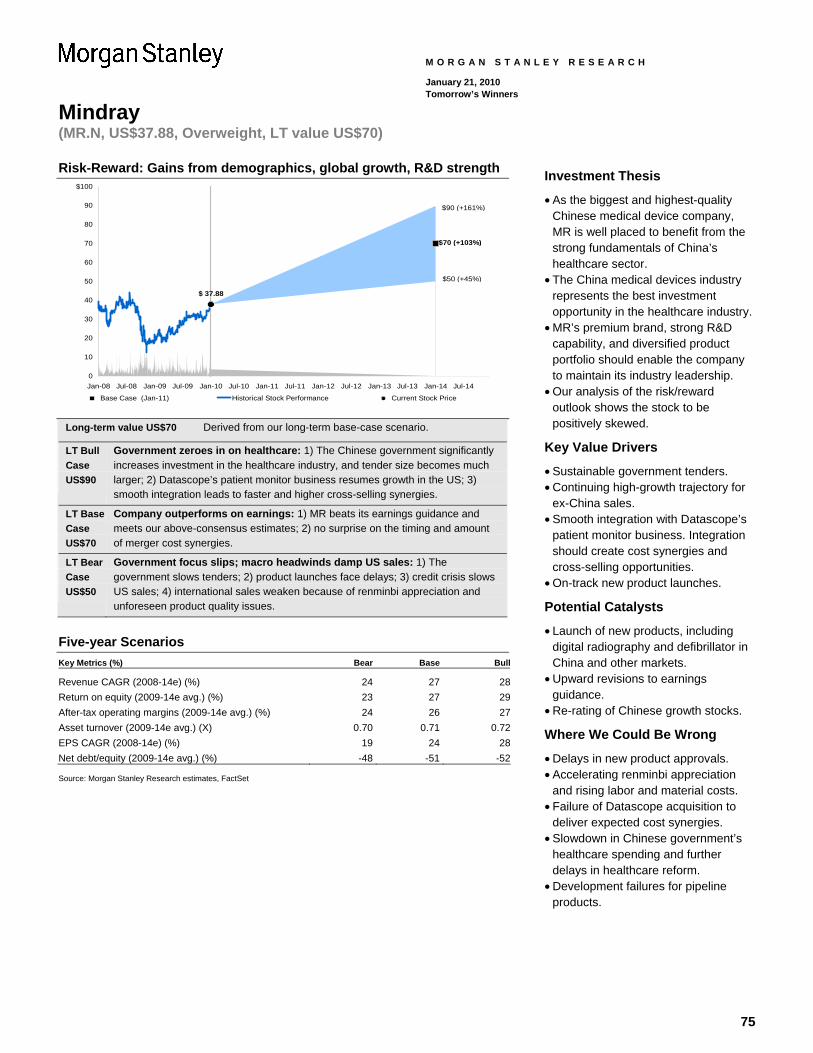

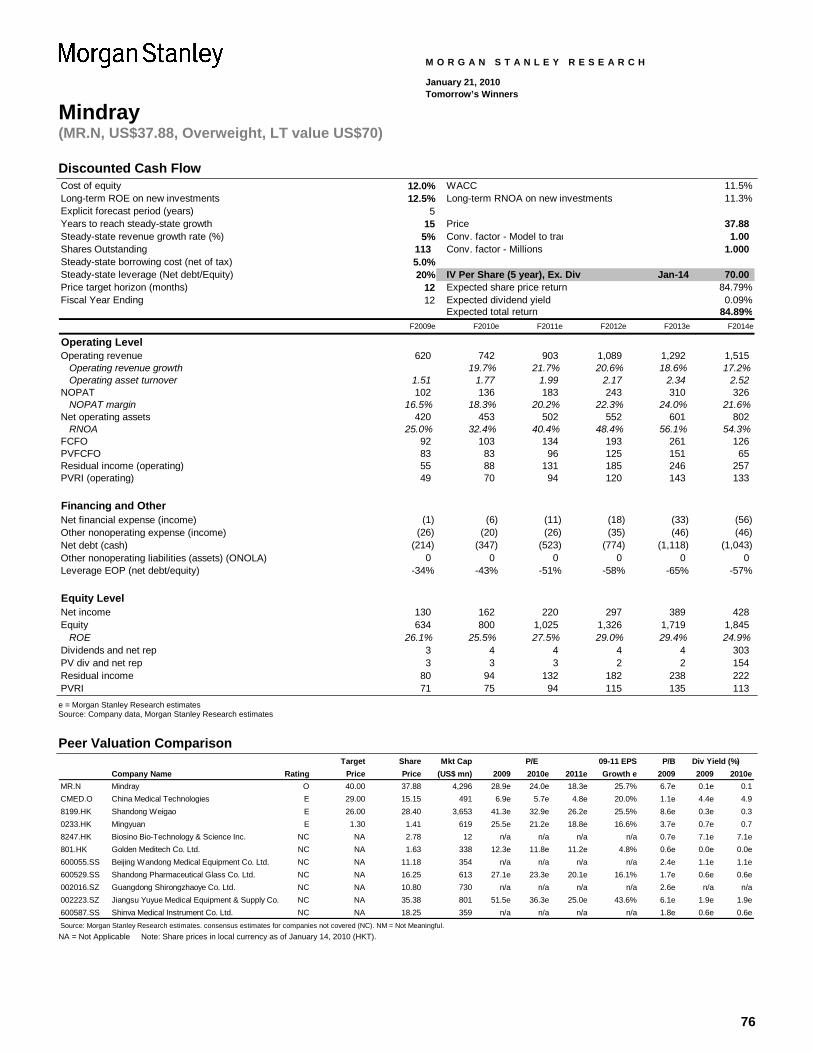

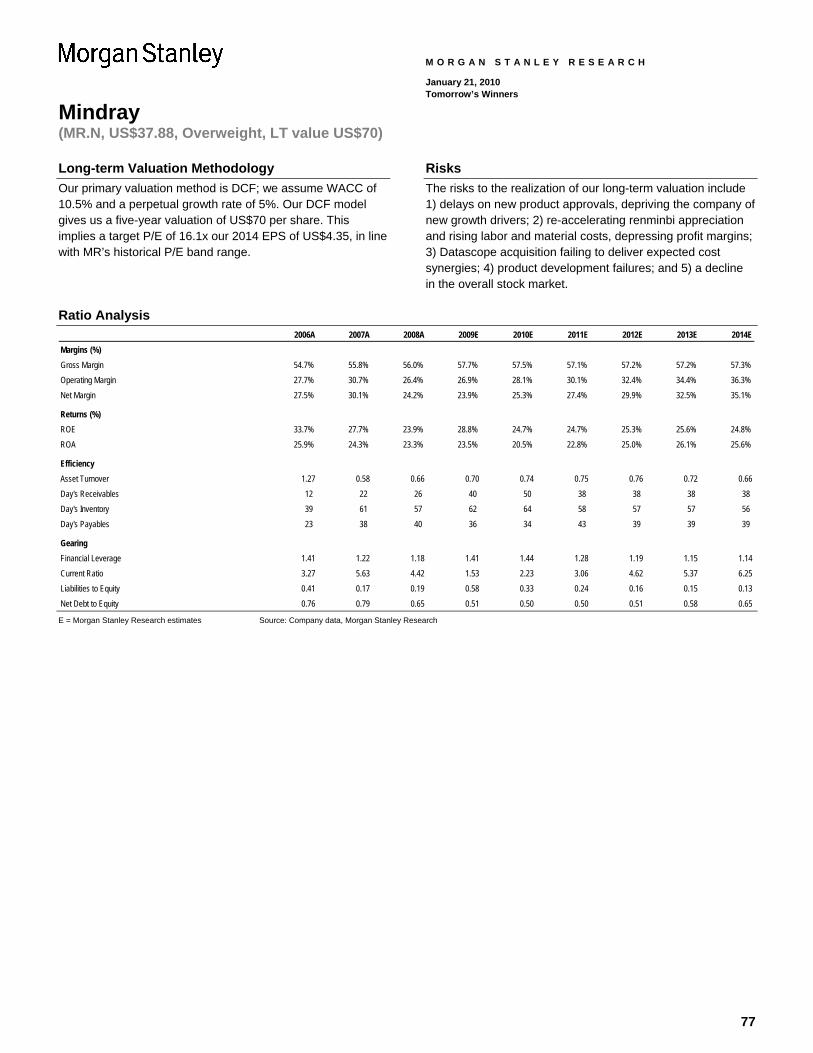

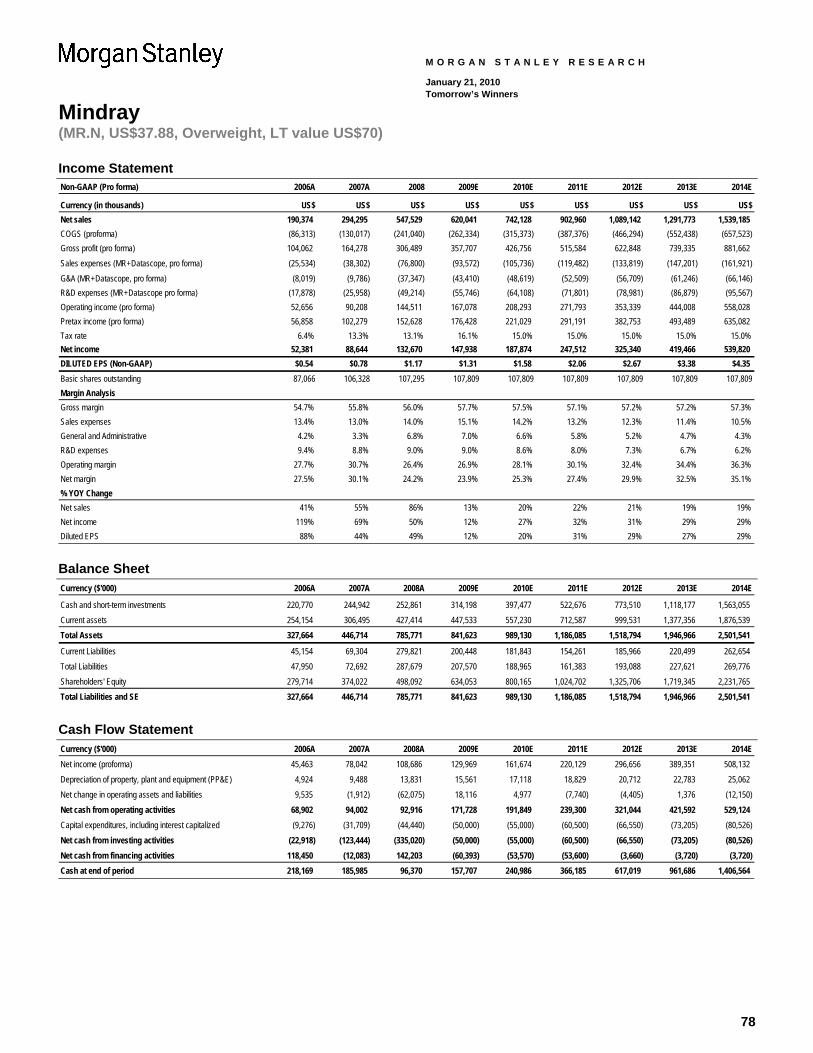

Mindray: Bellwether in a booming industry; realizing international ambitions................................................................................... 74

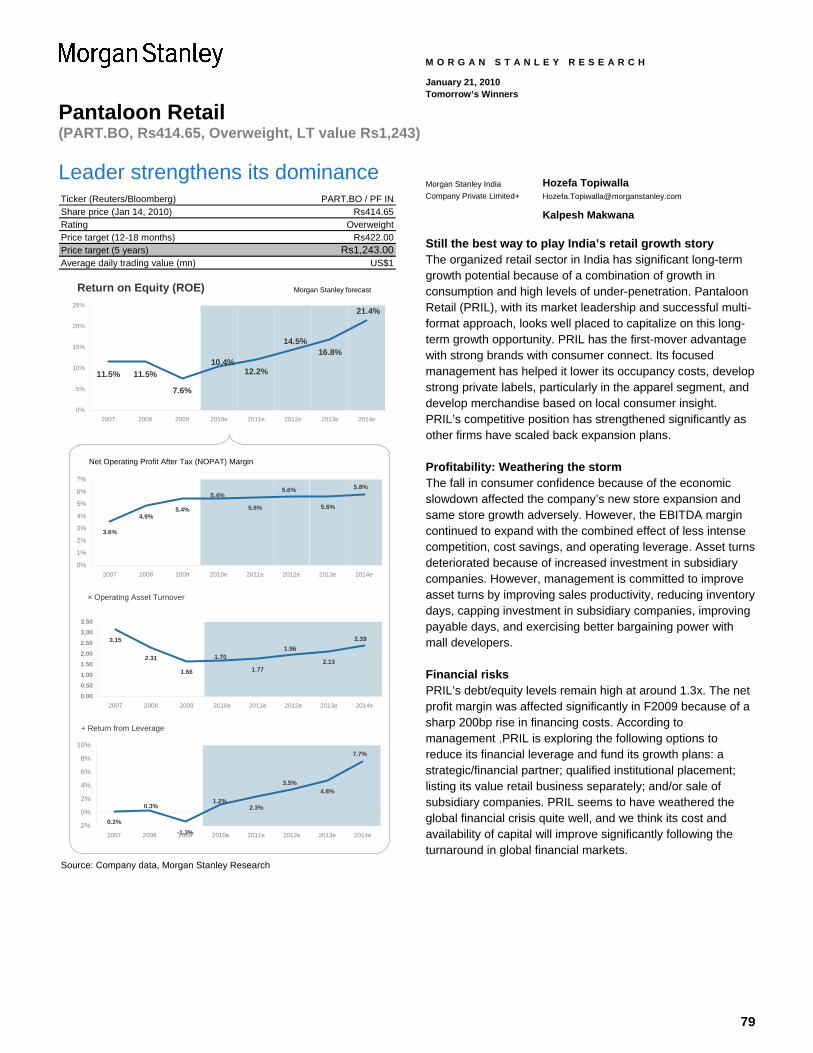

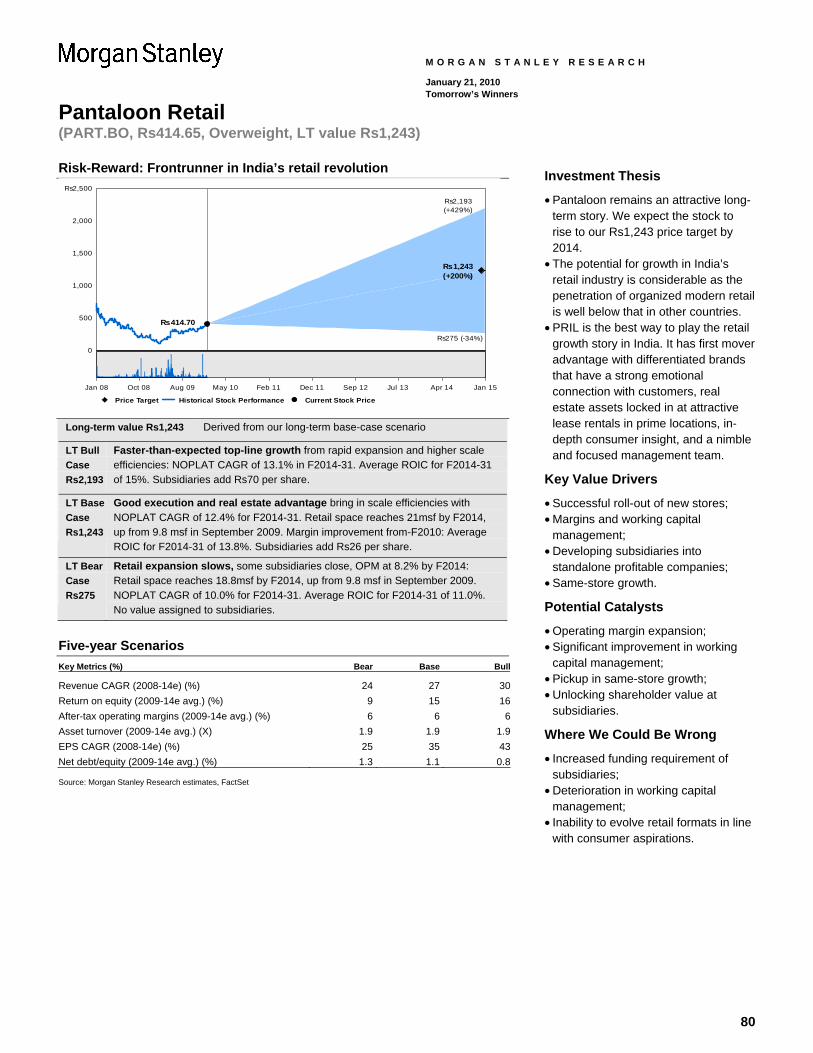

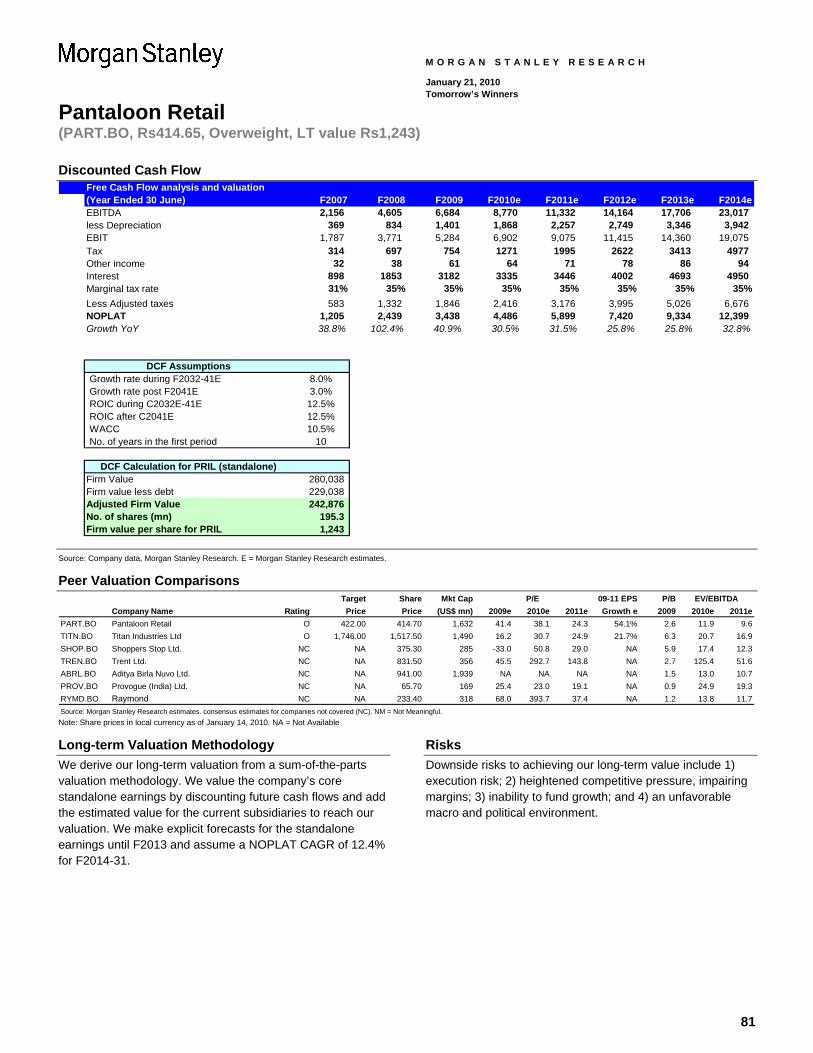

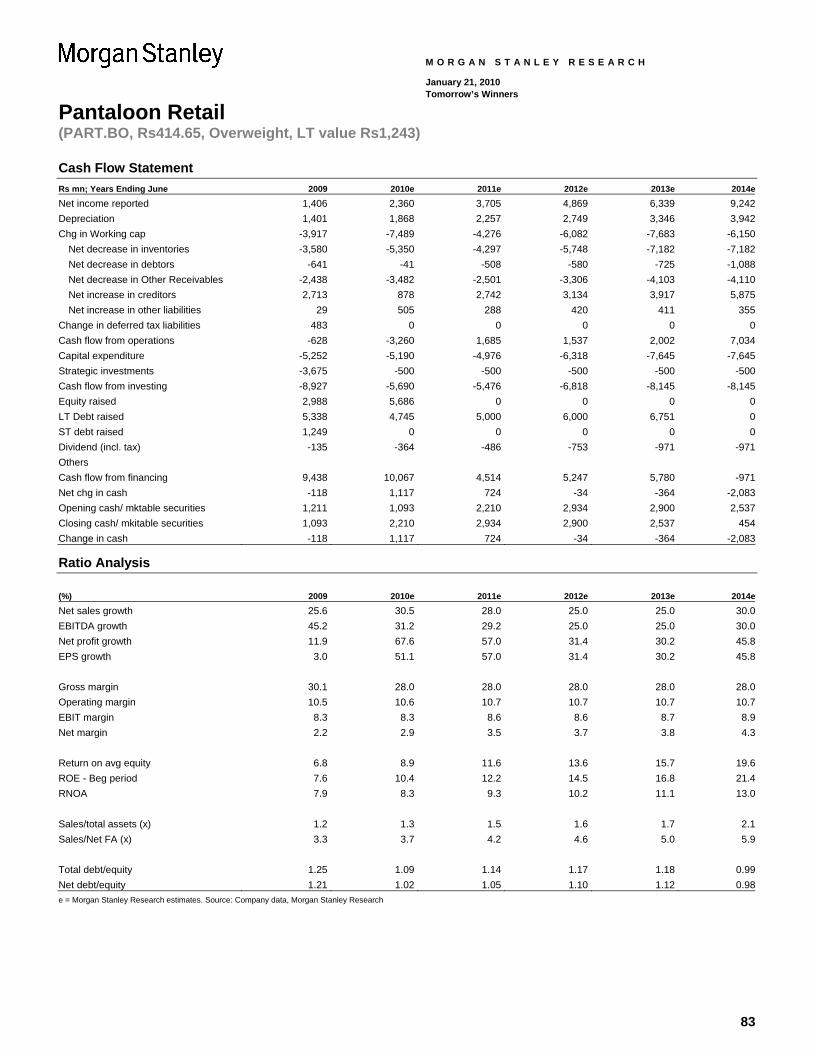

Pantaloon Retail: Leader strengthens its dominance ...................................................................................................................... 79

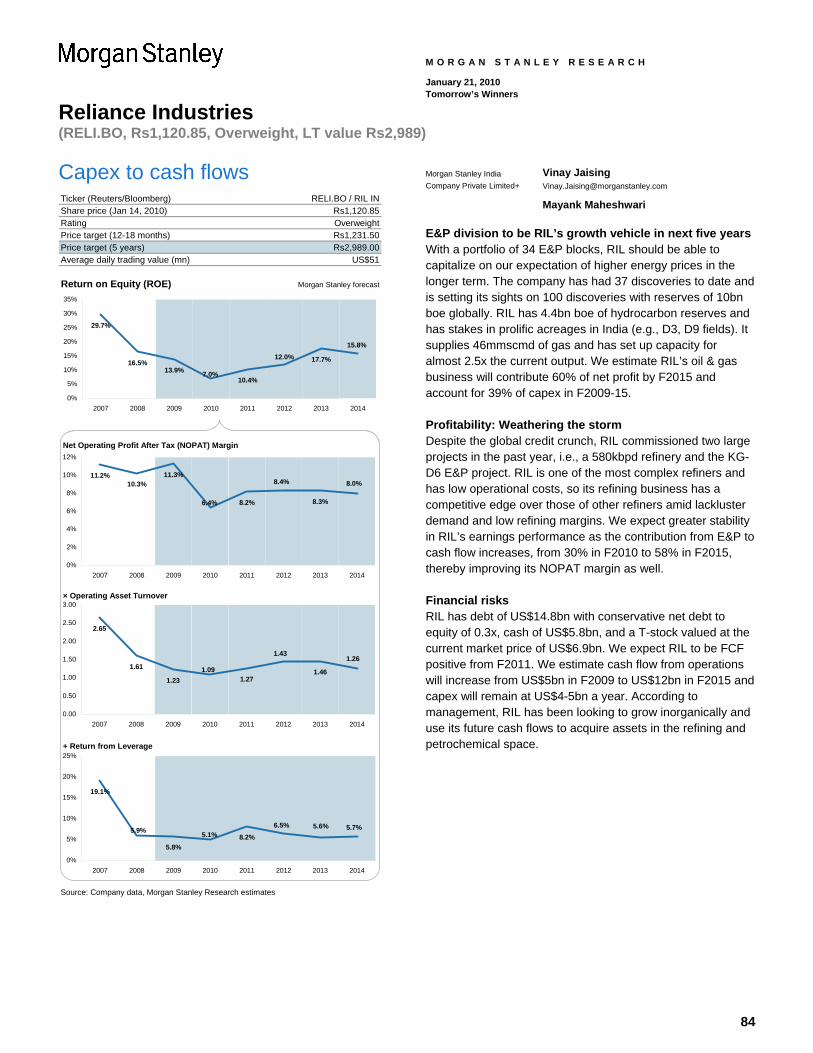

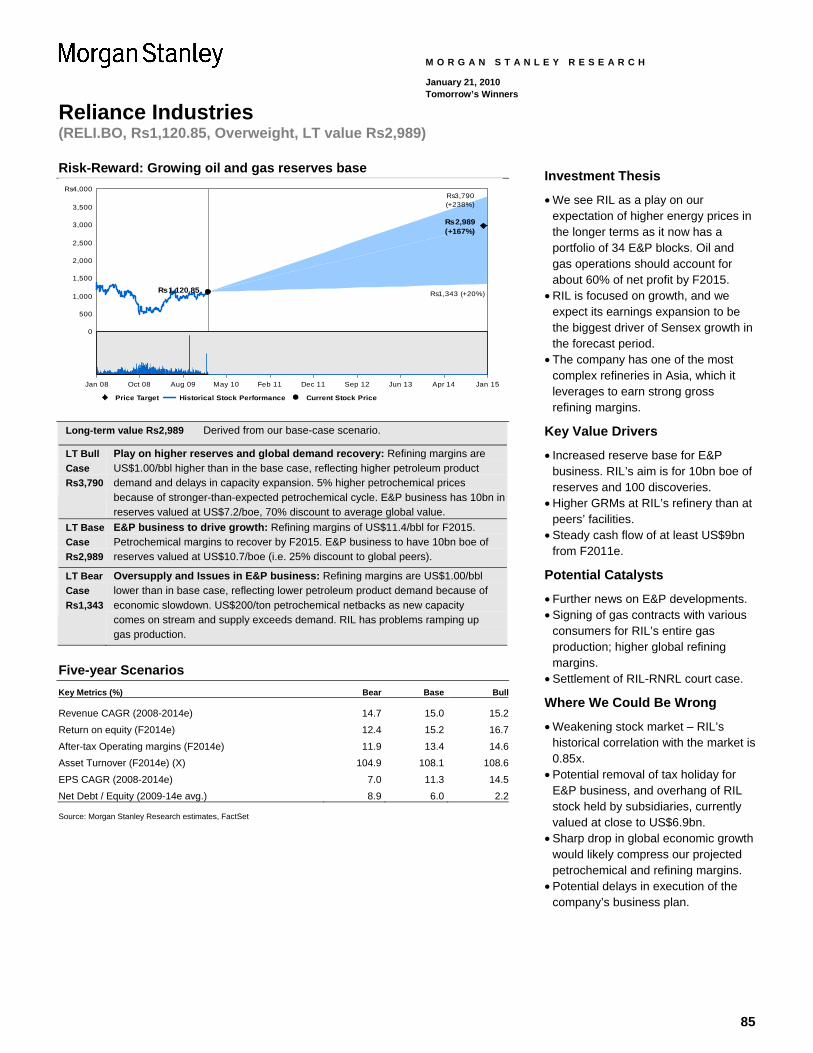

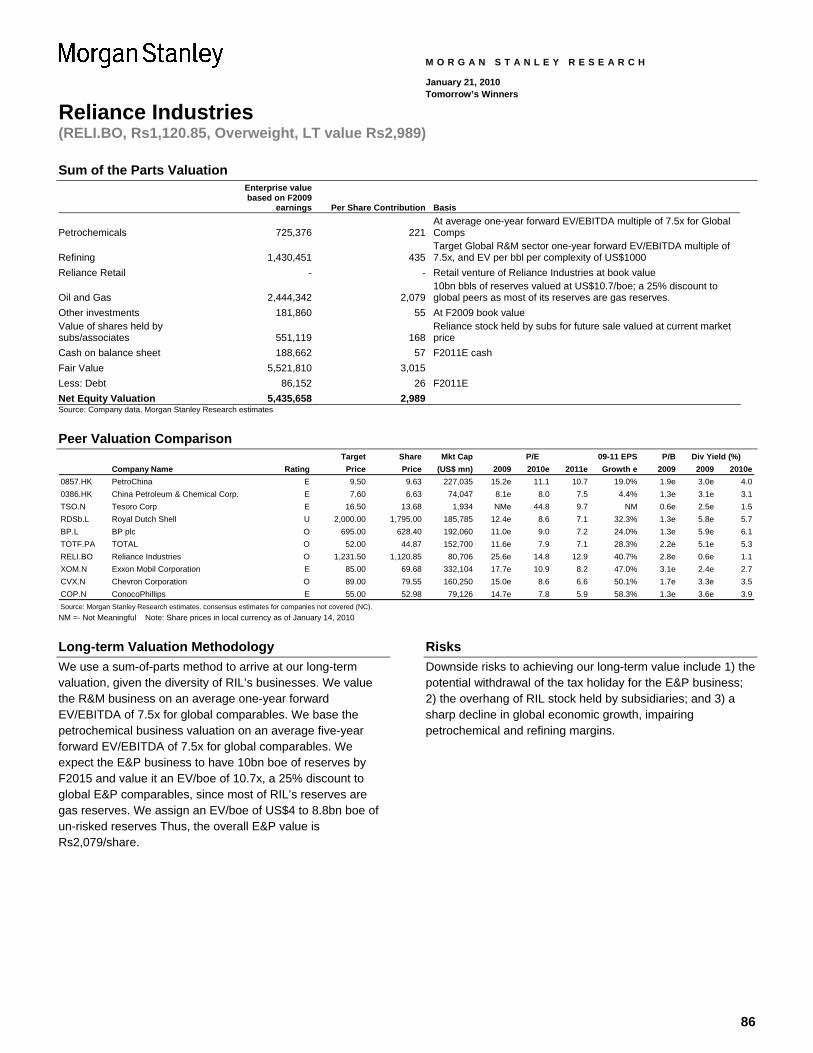

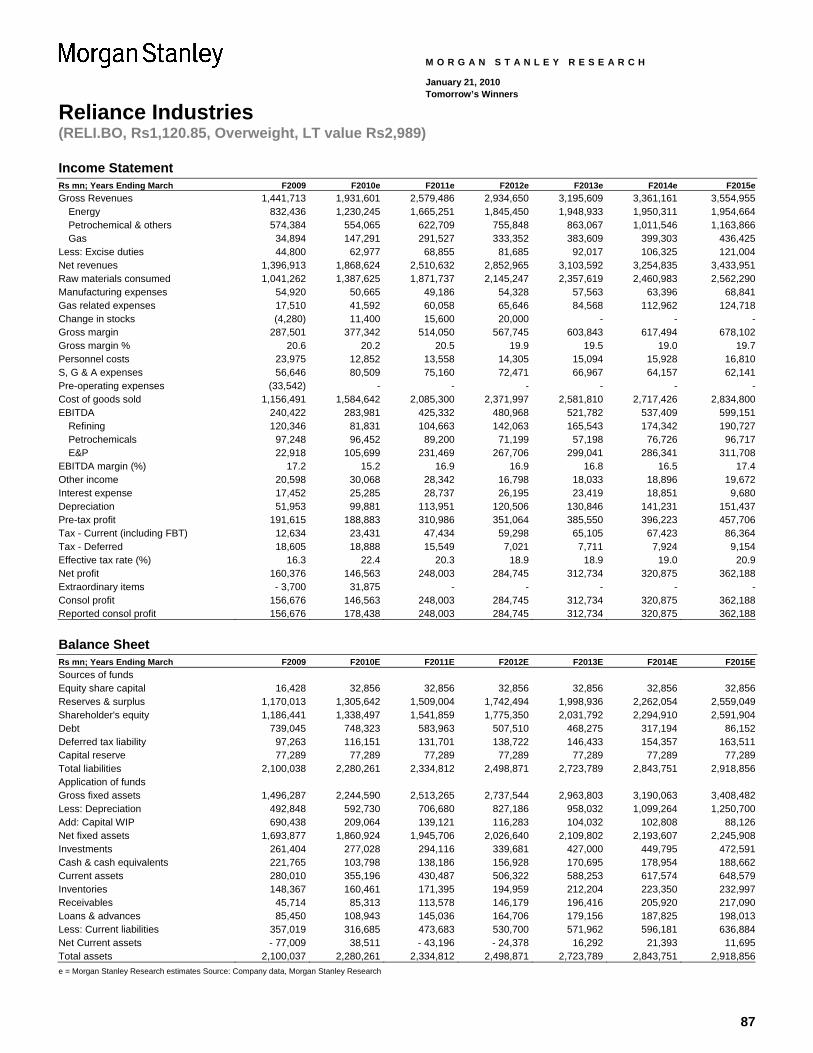

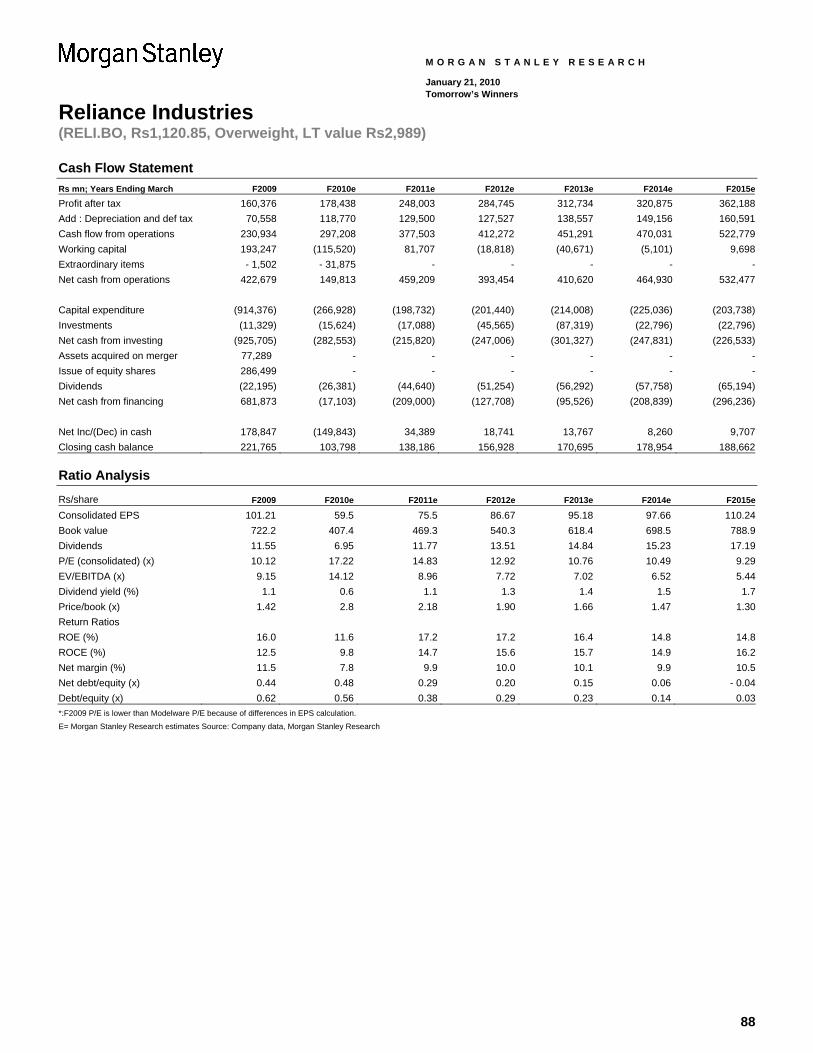

Reliance Industries: Capex to cash flows ....................................................................................................................................... 84

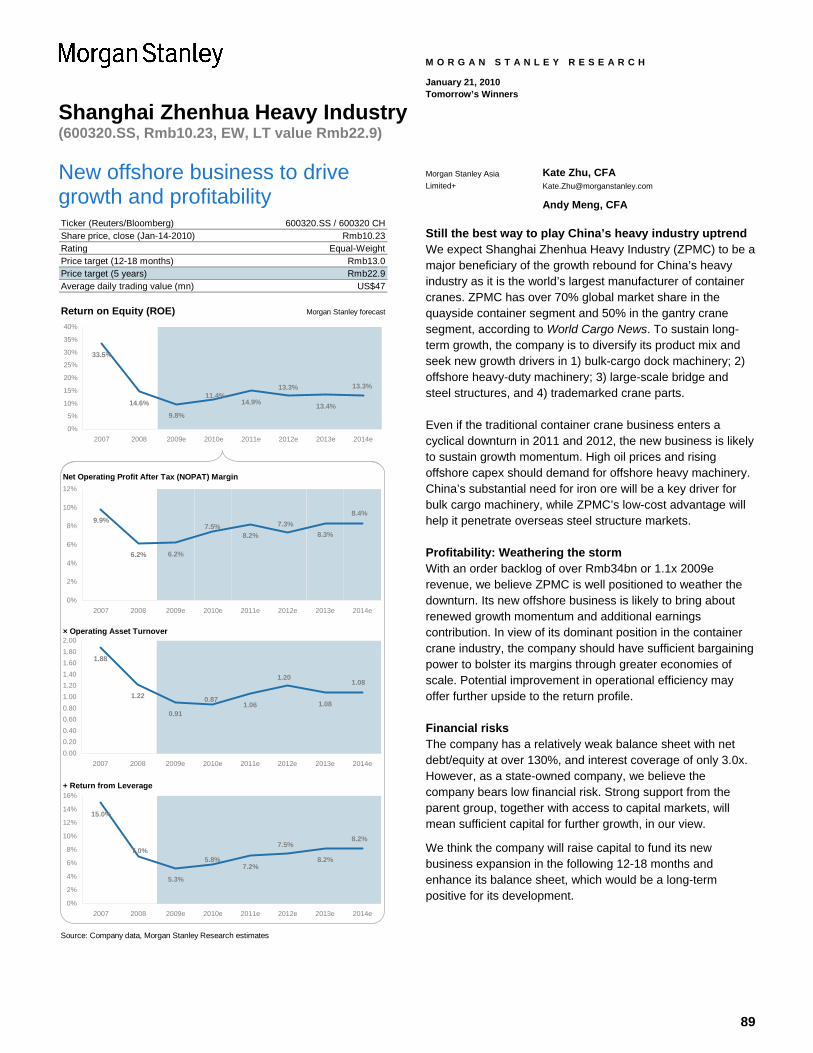

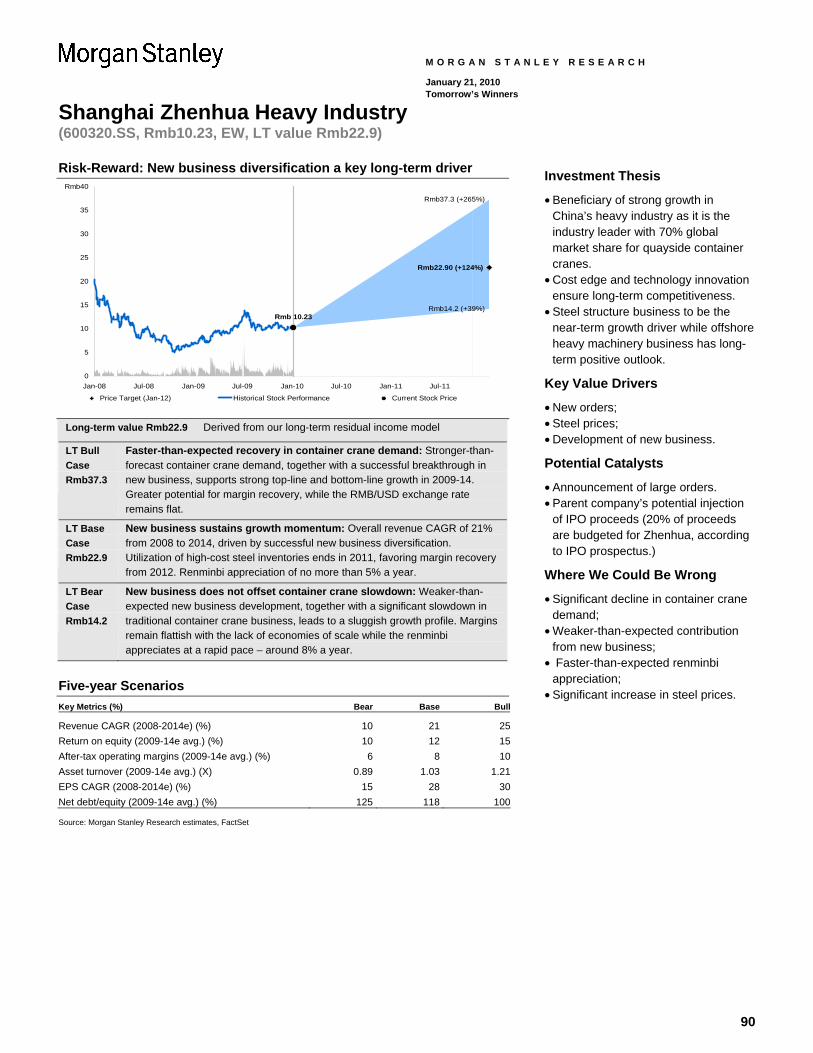

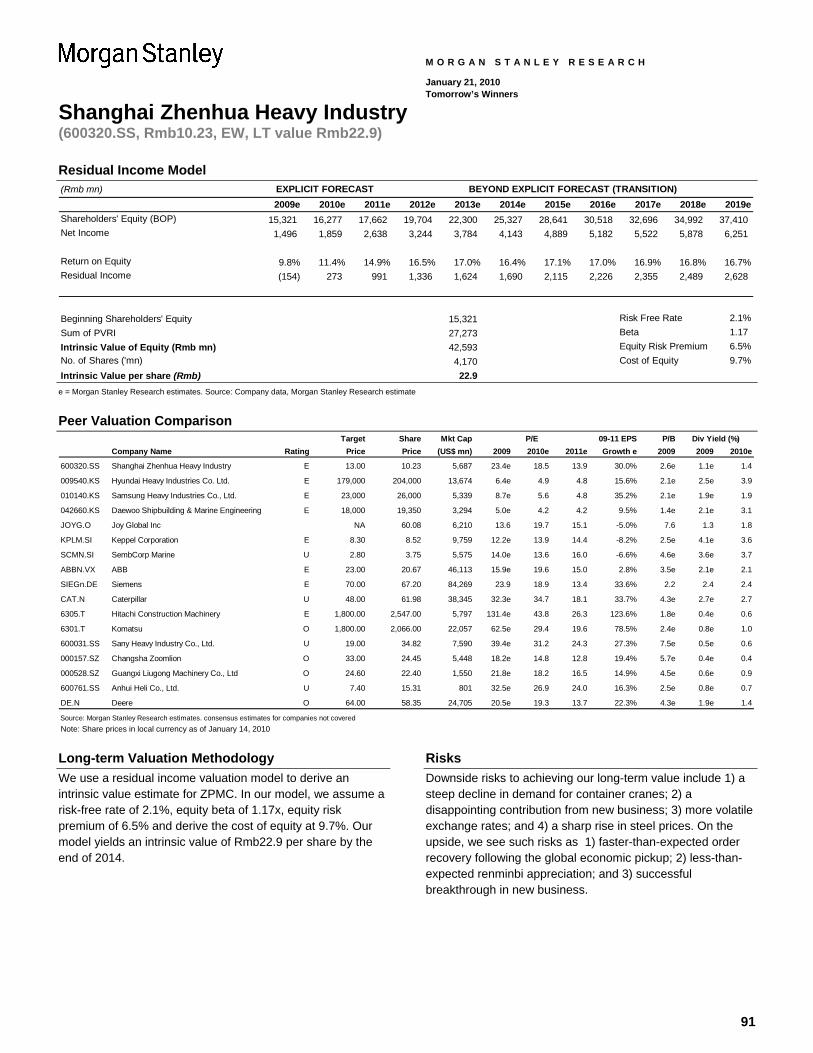

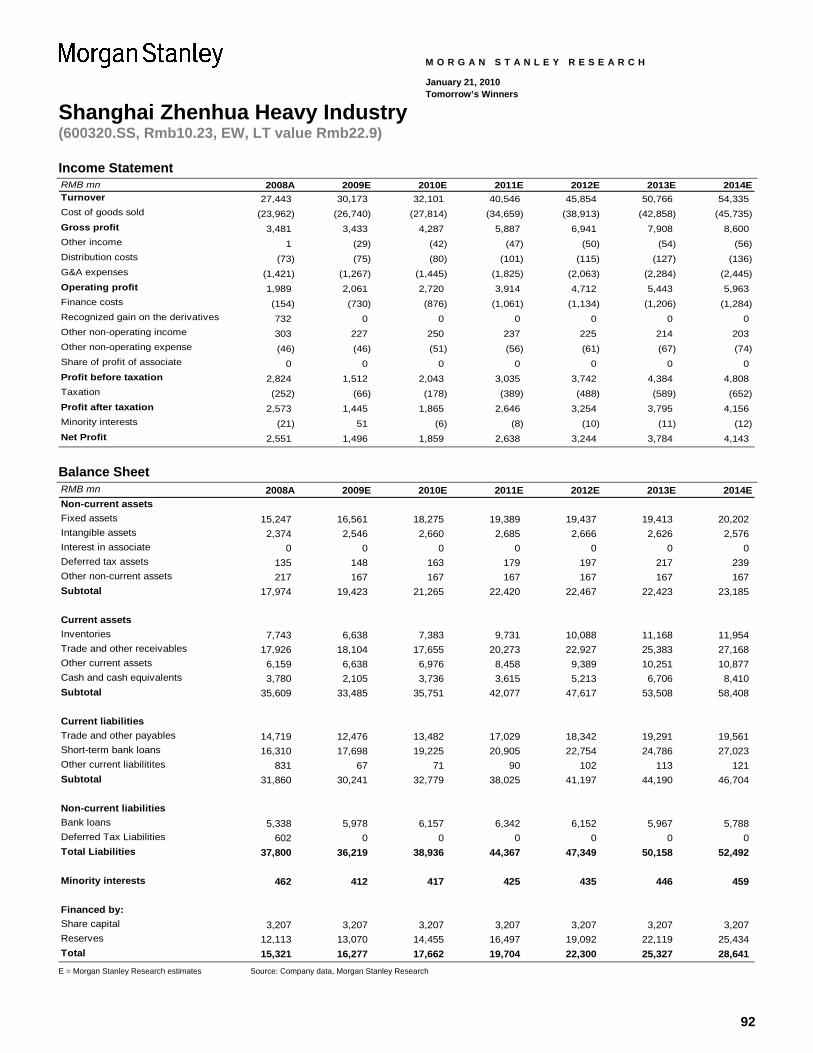

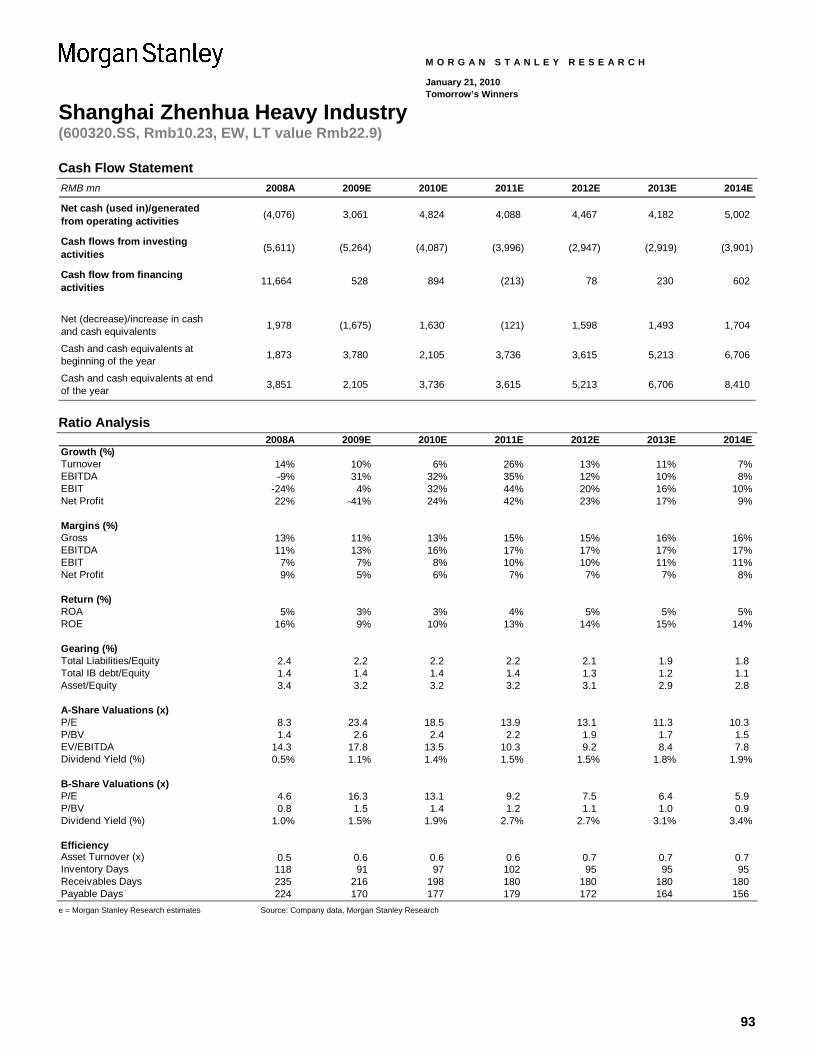

Shanghai Zhenhua Heavy Industry: New offshore business to drive growth and profitability........................................................ 89

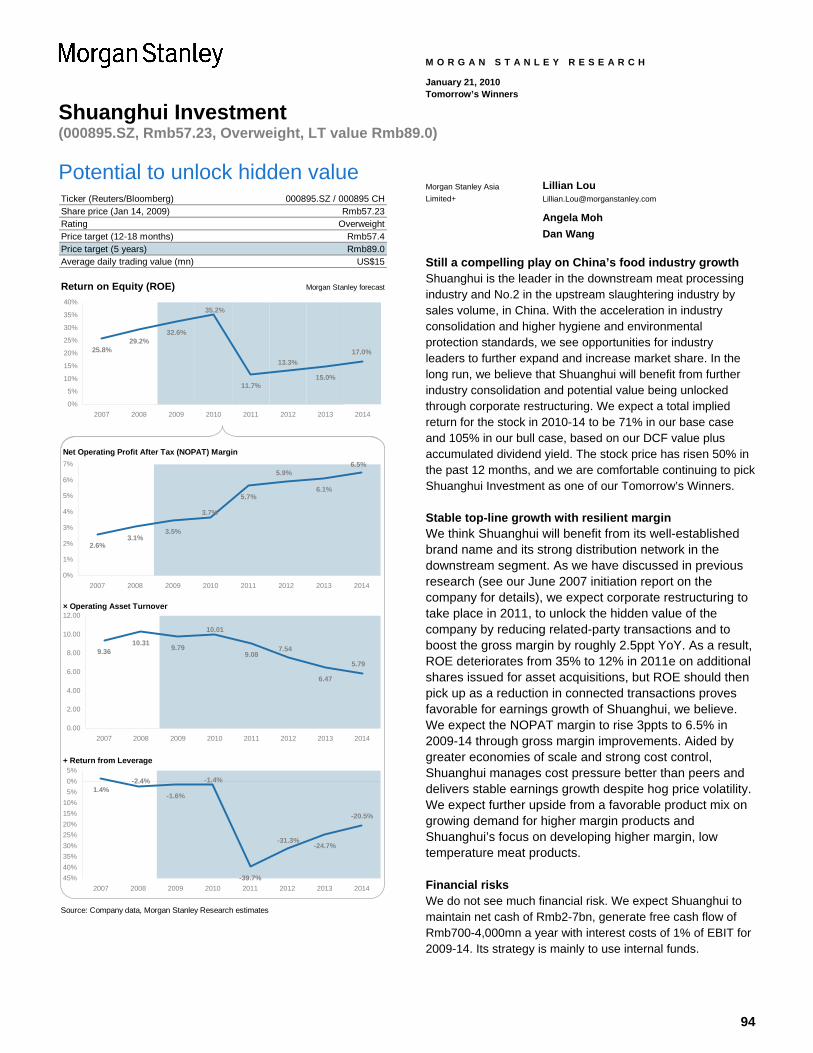

Shuanghui Investment: Potential to unlock hidden value ............................................................................................................... 94

Tencent Holdings Ltd.: Capitalizing on the largest online park in China......................................................................................... 99

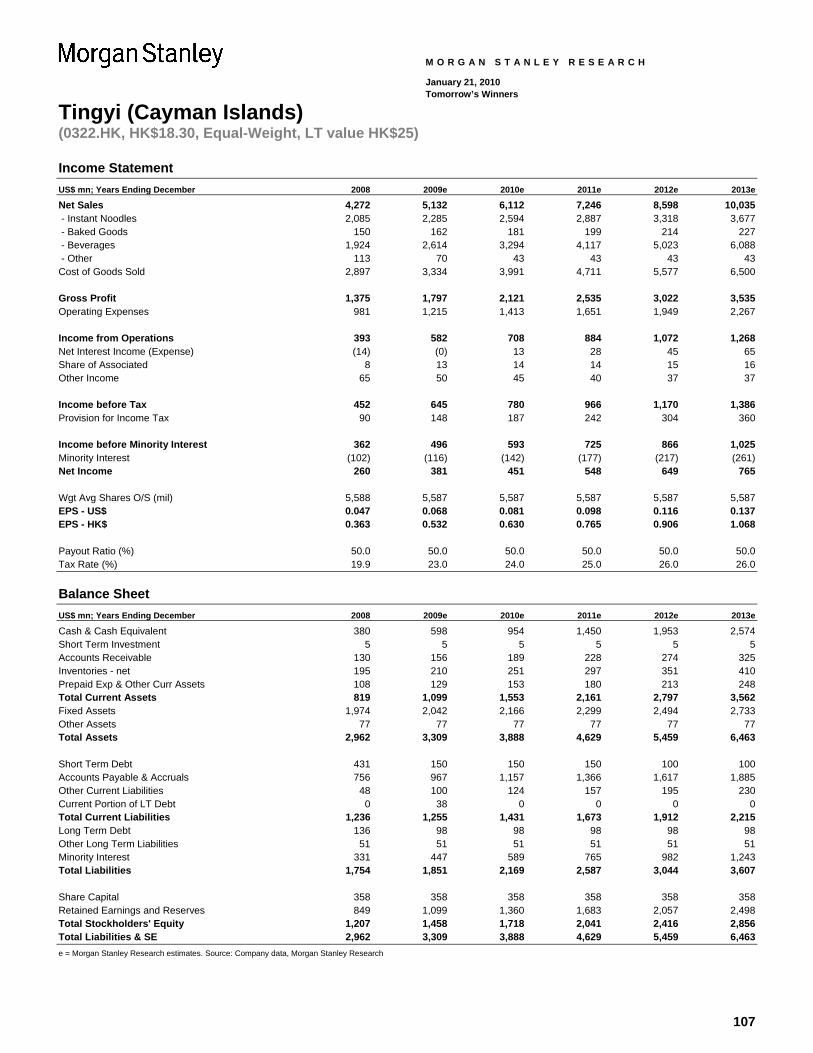

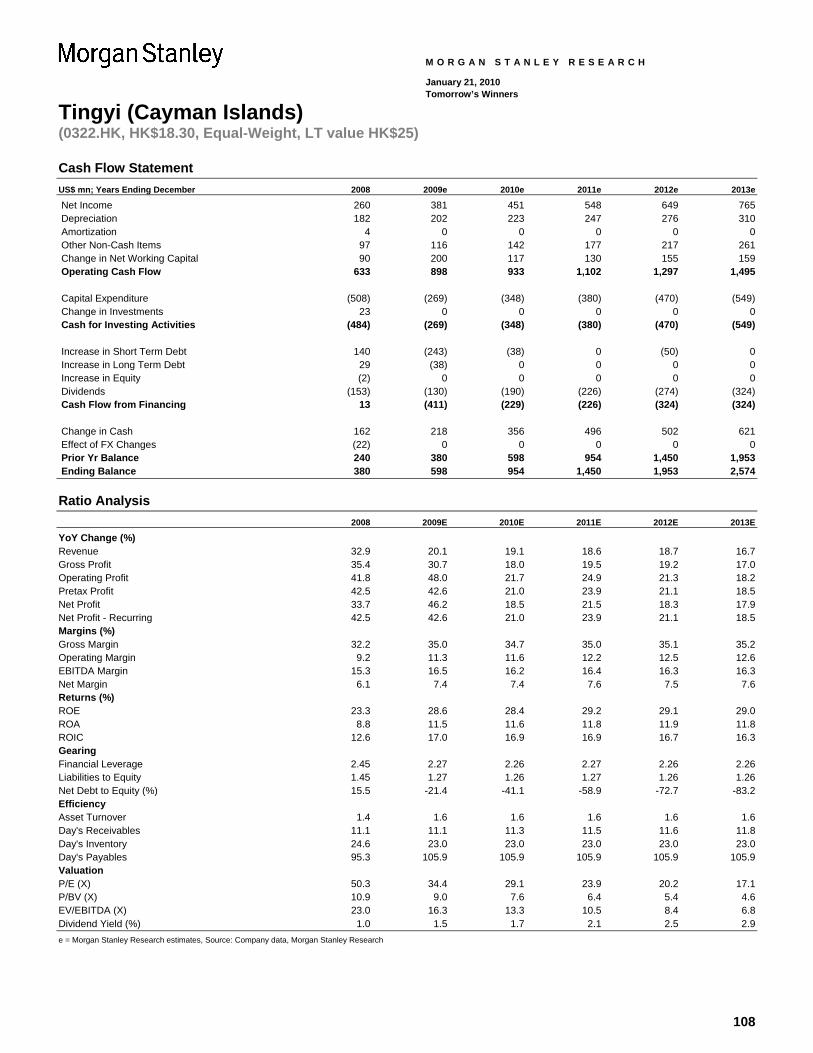

Tingyi (Cayman Islands): Sector leader with compelling growth story.......................................................................................... 104

Woori Finance Holdings: Potential privatization positives ............................................................................................................ 109

Appendix

Company Fact Sheets..................................................................................................................................................................... 116

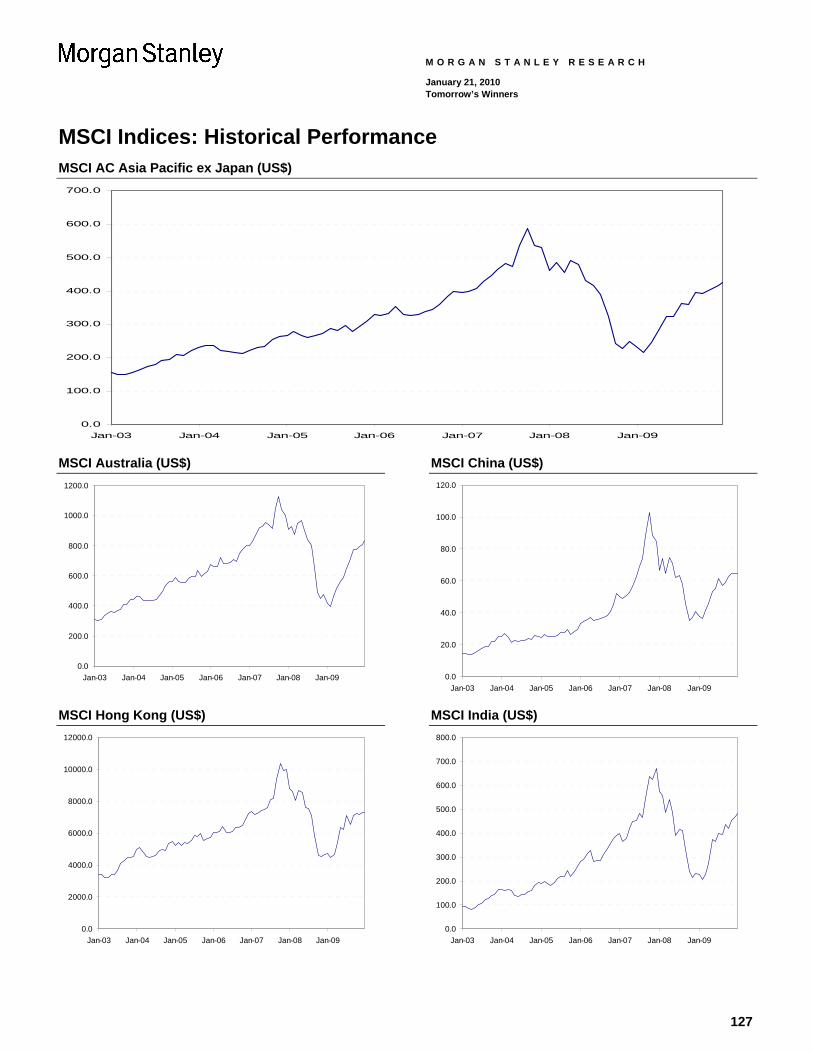

MSCI Indices: Historical Performance............................................................................................................................................. 127

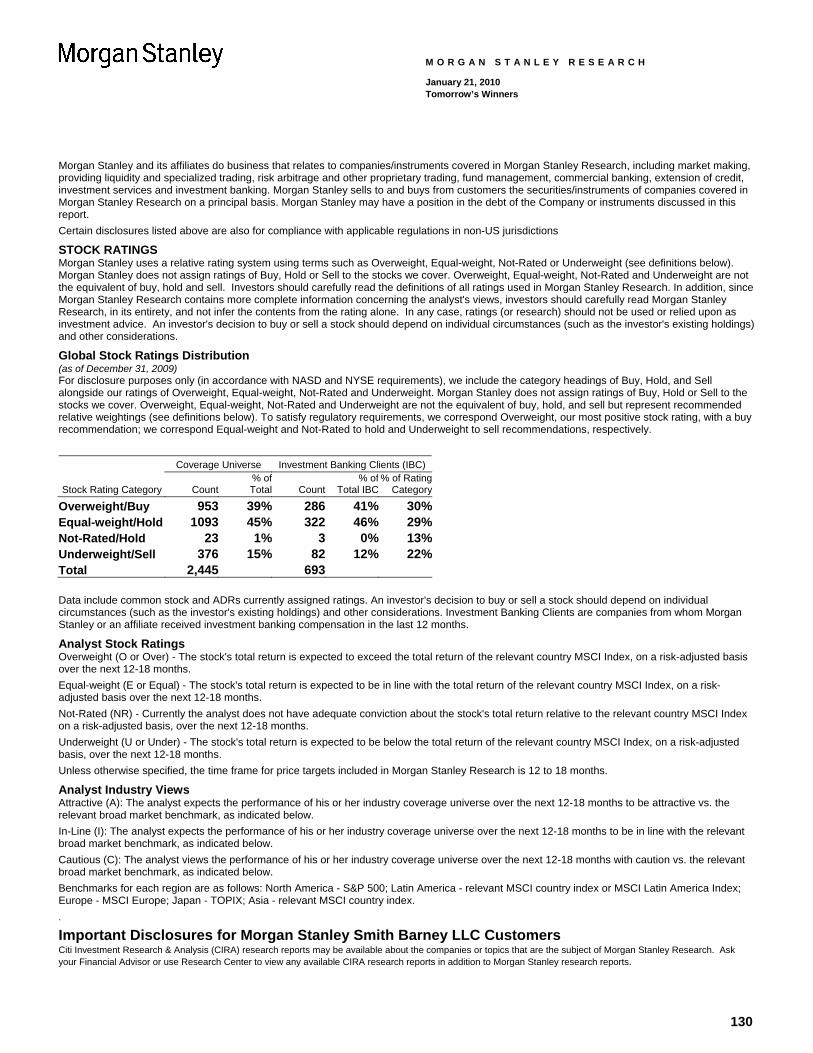

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. += Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

4

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

5

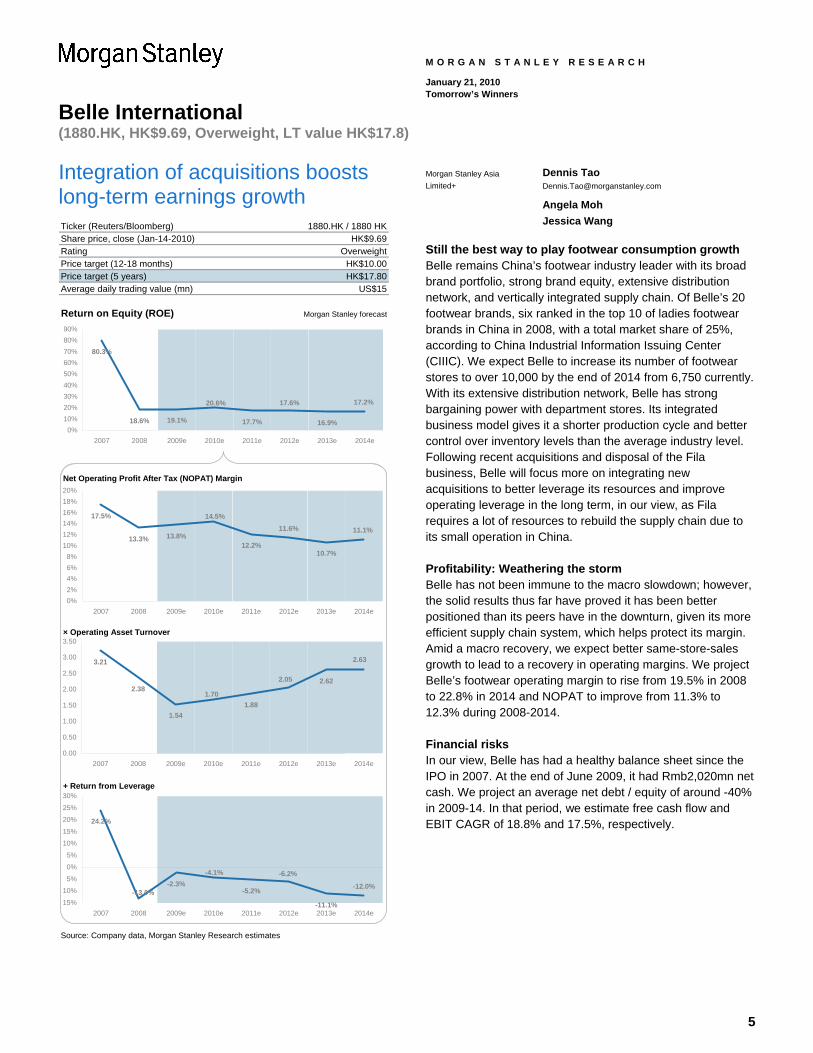

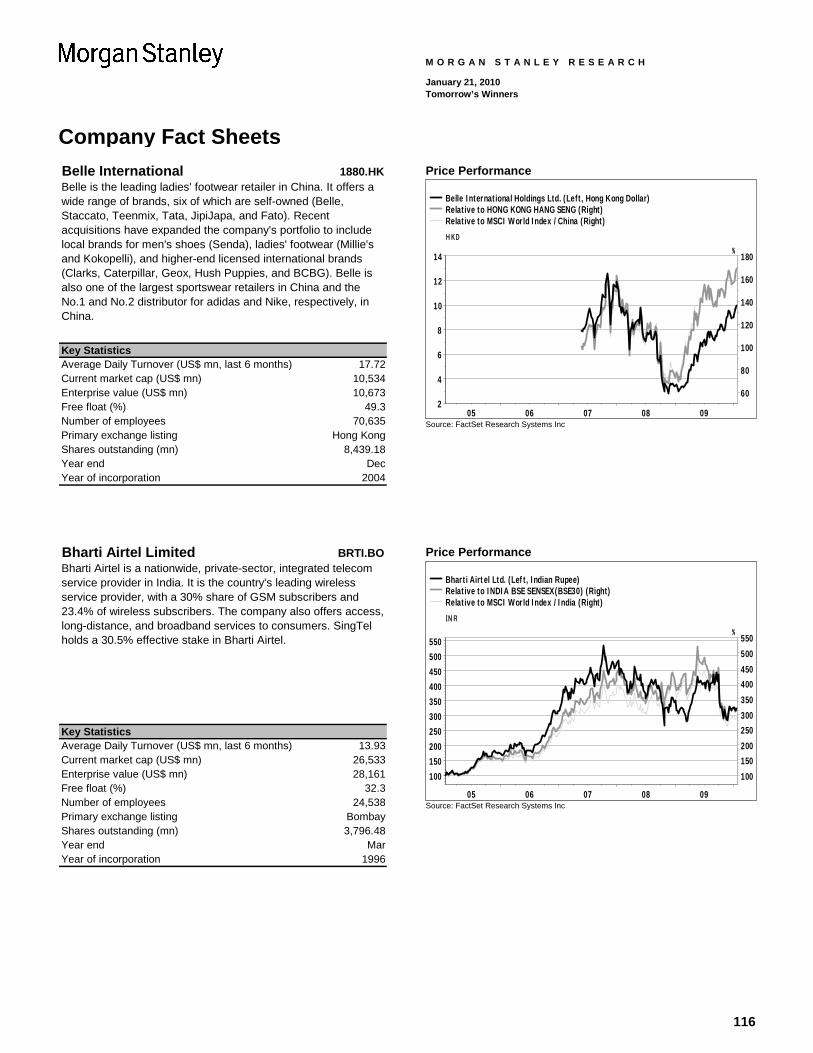

Belle International (1880.HK, HK$9.69, Overweight, LT value HK$17.8)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Integration of acquisitions boosts long-term earnings growth Ticker (Reuters/Bloomberg)Share price, close (Jan-14-2010)RatingPrice target (12-18 months)Price target (5 years) HK$17.80Average daily trading value (mn)

Return on Equity (ROE) Morgan Stanley forecast

Net Operating Profit After Tax (NOPAT) Margin

× Operating Asset Turnover

+ Return from Leverage

Source: Company data, Morgan Stanley Research estimates

US$15

1880.HK / 1880 HKHK$9.69

OverweightHK$10.00

80.3%

18.6% 19.1% 17.7% 16.9%

17.2%17.6%20.6%

0%10%20%30%40%50%60%70%80%90%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

17.5%

13.3% 13.8%12.2%

10.7%

14.5%11.6% 11.1%

0%2%4%6%8%

10%12%14%16%18%20%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

3.21

2.38

1.541.88

2.62

1.70

2.05

2.63

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

24.2%

-2.3%-5.2%

-11.1%

-12.0%

-6.2%-4.1%

-13.0%15%

10%

5%

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

Morgan Stanley Asia Limited+

Dennis Tao [email protected]

Angela Moh Jessica Wang

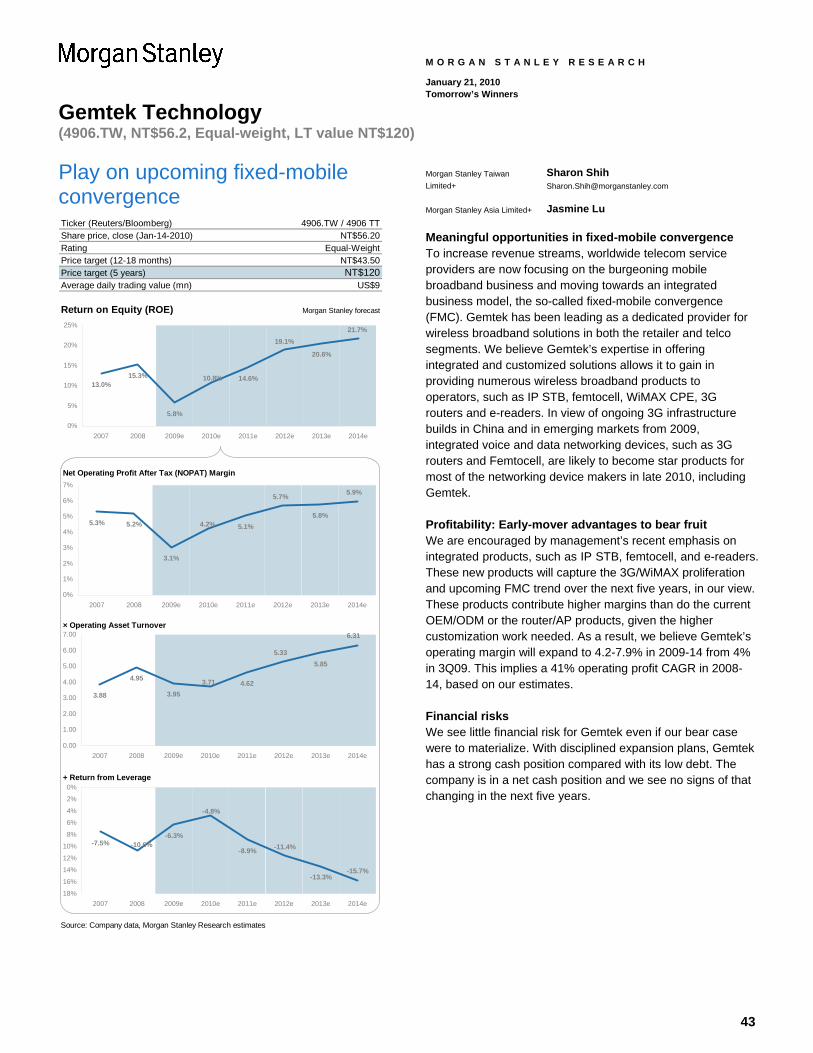

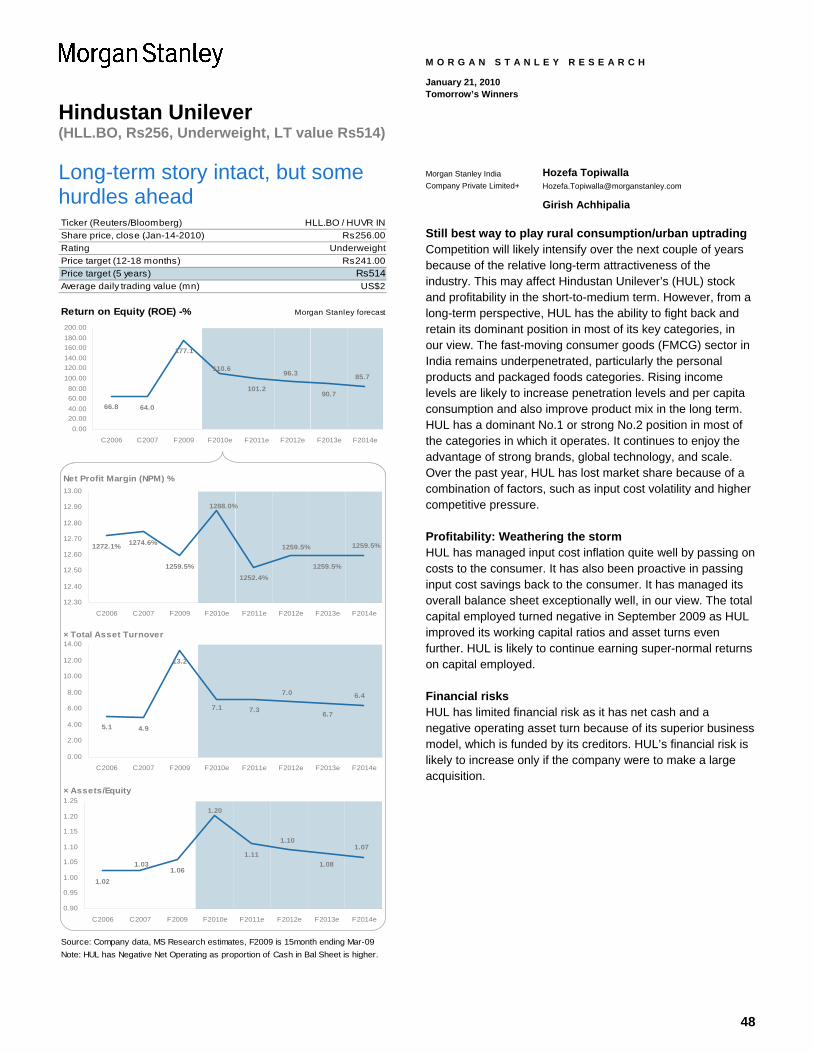

Still the best way to play footwear consumption growth Belle remains China’s footwear industry leader with its broad brand portfolio, strong brand equity, extensive distribution network, and vertically integrated supply chain. Of Belle’s 20 footwear brands, six ranked in the top 10 of ladies footwear brands in China in 2008, with a total market share of 25%, according to China Industrial Information Issuing Center (CIIIC). We expect Belle to increase its number of footwear stores to over 10,000 by the end of 2014 from 6,750 currently. With its extensive distribution network, Belle has strong bargaining power with department stores. Its integrated business model gives it a shorter production cycle and better control over inventory levels than the average industry level. Following recent acquisitions and disposal of the Fila business, Belle will focus more on integrating new acquisitions to better leverage its resources and improve operating leverage in the long term, in our view, as Fila requires a lot of resources to rebuild the supply chain due to its small operation in China.

Profitability: Weathering the storm Belle has not been immune to the macro slowdown; however, the solid results thus far have proved it has been better positioned than its peers have in the downturn, given its more efficient supply chain system, which helps protect its margin. Amid a macro recovery, we expect better same-store-sales growth to lead to a recovery in operating margins. We project Belle’s footwear operating margin to rise from 19.5% in 2008 to 22.8% in 2014 and NOPAT to improve from 11.3% to 12.3% during 2008-2014.

Financial risks In our view, Belle has had a healthy balance sheet since the IPO in 2007. At the end of June 2009, it had Rmb2,020mn net cash. We project an average net debt / equity of around -40% in 2009-14. In that period, we estimate free cash flow and EBIT CAGR of 18.8% and 17.5%, respectively.

6

Belle International (1880.HK, HK$9.69, Overweight, LT value HK$17.8)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

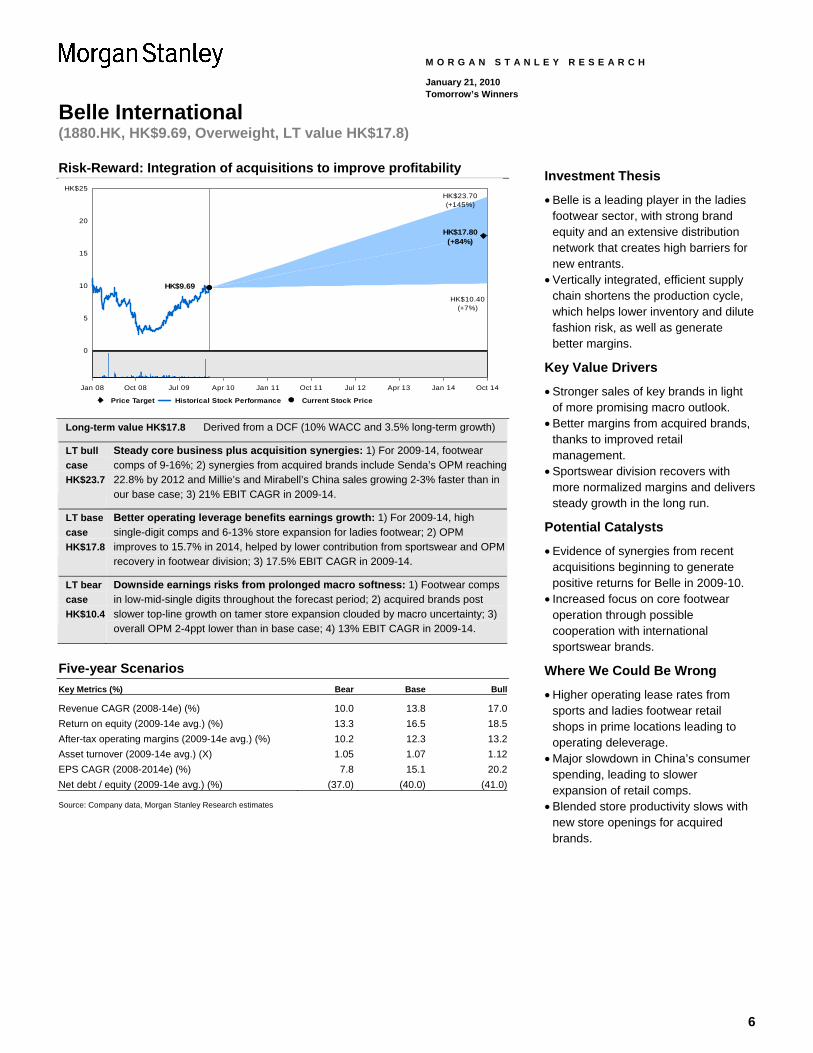

Risk-Reward: Integration of acquisitions to improve profitability

0

5

10

15

20

HK$25HK$23.70(+145%)

HK$17.80(+84%)

HK$10.40(+7%)

HK$9.69

Price Target Historical Stock Performance Current Stock Price

Jan 08 Oct 08 Jul 09 Apr 10 Jan 11 Oct 11 Jul 12 Apr 13 Jan 14 Oct 14

Long-term value HK$17.8 Derived from a DCF (10% WACC and 3.5% long-term growth)

LT bull case HK$23.7

Steady core business plus acquisition synergies: 1) For 2009-14, footwear comps of 9-16%; 2) synergies from acquired brands include Senda’s OPM reaching 22.8% by 2012 and Millie’s and Mirabell’s China sales growing 2-3% faster than in our base case; 3) 21% EBIT CAGR in 2009-14.

LT base case HK$17.8

Better operating leverage benefits earnings growth: 1) For 2009-14, high single-digit comps and 6-13% store expansion for ladies footwear; 2) OPM improves to 15.7% in 2014, helped by lower contribution from sportswear and OPM recovery in footwear division; 3) 17.5% EBIT CAGR in 2009-14.

LT bear case HK$10.4

Downside earnings risks from prolonged macro softness: 1) Footwear comps in low-mid-single digits throughout the forecast period; 2) acquired brands post slower top-line growth on tamer store expansion clouded by macro uncertainty; 3) overall OPM 2-4ppt lower than in base case; 4) 13% EBIT CAGR in 2009-14.

Five-year Scenarios Key Metrics (%) Bear Base Bull

Revenue CAGR (2008-14e) (%) 10.0 13.8 17.0Return on equity (2009-14e avg.) (%) 13.3 16.5 18.5After-tax operating margins (2009-14e avg.) (%) 10.2 12.3 13.2Asset turnover (2009-14e avg.) (X) 1.05 1.07 1.12EPS CAGR (2008-2014e) (%) 7.8 15.1 20.2Net debt / equity (2009-14e avg.) (%) (37.0) (40.0) (41.0) Source: Company data, Morgan Stanley Research estimates

Investment Thesis

• Belle is a leading player in the ladies footwear sector, with strong brand equity and an extensive distribution network that creates high barriers for new entrants.

• Vertically integrated, efficient supply chain shortens the production cycle, which helps lower inventory and dilute fashion risk, as well as generate better margins.

Key Value Drivers

• Stronger sales of key brands in light of more promising macro outlook.

• Better margins from acquired brands, thanks to improved retail management.

• Sportswear division recovers with more normalized margins and delivers steady growth in the long run.

Potential Catalysts

• Evidence of synergies from recent acquisitions beginning to generate positive returns for Belle in 2009-10.

• Increased focus on core footwear operation through possible cooperation with international sportswear brands.

Where We Could Be Wrong

• Higher operating lease rates from sports and ladies footwear retail shops in prime locations leading to operating deleverage.

• Major slowdown in China’s consumer spending, leading to slower expansion of retail comps.

• Blended store productivity slows with new store openings for acquired brands.

7

Belle International (1880.HK, HK$9.69, Overweight, LT value HK$17.8)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

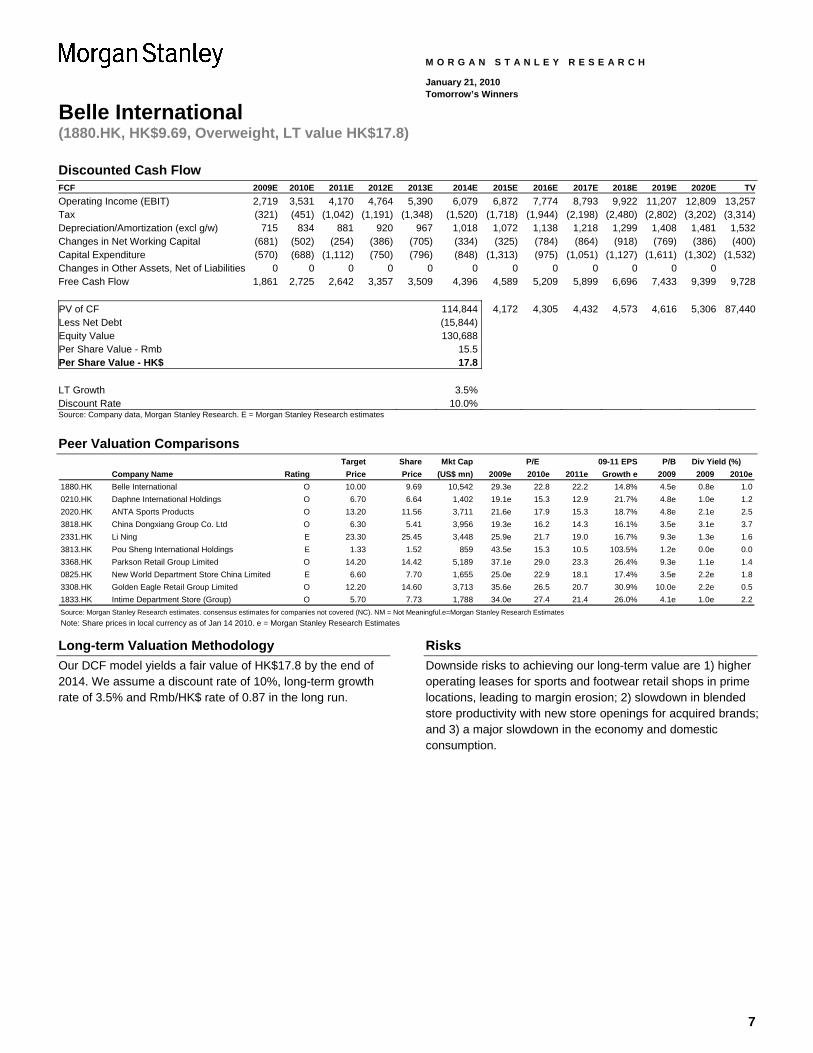

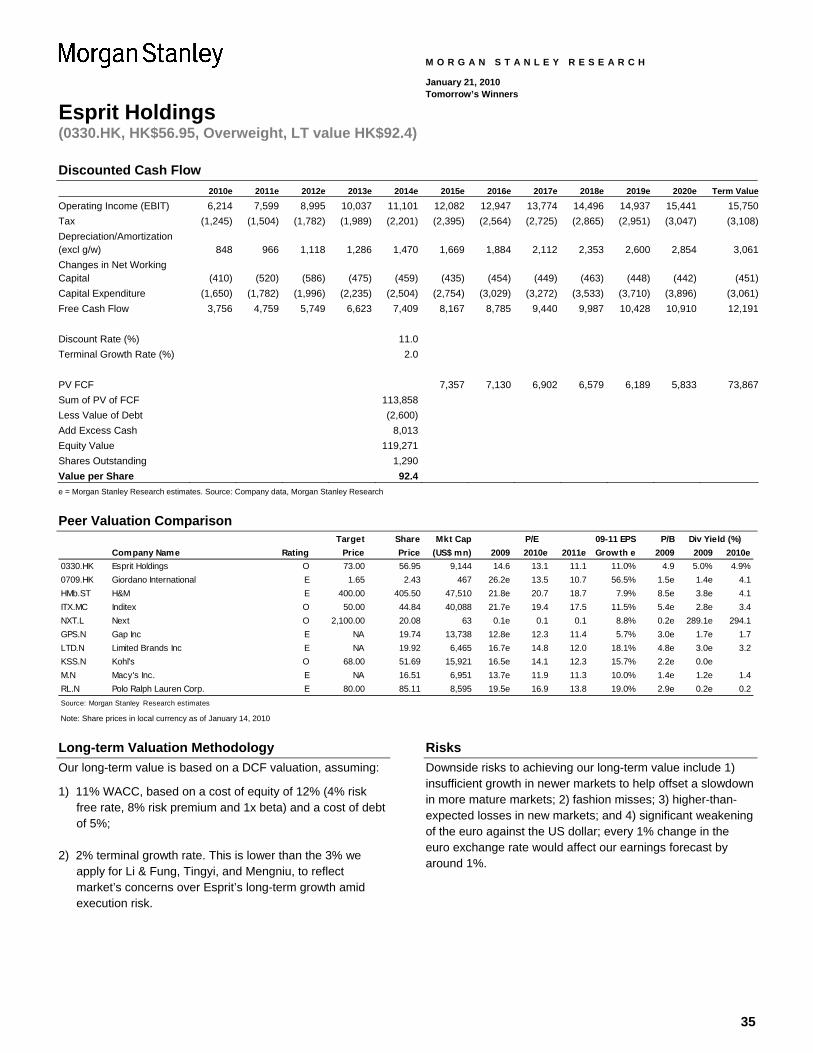

Discounted Cash Flow FCF 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E TVOperating Income (EBIT) 2,719 3,531 4,170 4,764 5,390 6,079 6,872 7,774 8,793 9,922 11,207 12,809 13,257Tax (321) (451) (1,042) (1,191) (1,348) (1,520) (1,718) (1,944) (2,198) (2,480) (2,802) (3,202) (3,314)Depreciation/Amortization (excl g/w) 715 834 881 920 967 1,018 1,072 1,138 1,218 1,299 1,408 1,481 1,532Changes in Net Working Capital (681) (502) (254) (386) (705) (334) (325) (784) (864) (918) (769) (386) (400)Capital Expenditure (570) (688) (1,112) (750) (796) (848) (1,313) (975) (1,051) (1,127) (1,611) (1,302) (1,532)Changes in Other Assets, Net of Liabilities 0 0 0 0 0 0 0 0 0 0 0 0Free Cash Flow 1,861 2,725 2,642 3,357 3,509 4,396 4,589 5,209 5,899 6,696 7,433 9,399 9,728 PV of CF 114,844 4,172 4,305 4,432 4,573 4,616 5,306 87,440Less Net Debt (15,844) Equity Value 130,688 Per Share Value - Rmb 15.5 Per Share Value - HK$ 17.8 LT Growth 3.5% Discount Rate 10.0% Source: Company data, Morgan Stanley Research. E = Morgan Stanley Research estimates

Peer Valuation Comparisons

Target Share Mkt Cap 09-11 EPS P/BCompany Name Rating Price Price (US$ mn) 2009e 2010e 2011e Growth e 2009 2009 2010e

1880.HK Belle International O 10.00 9.69 10,542 29.3e 22.8 22.2 14.8% 4.5e 0.8e 1.00210.HK Daphne International Holdings O 6.70 6.64 1,402 19.1e 15.3 12.9 21.7% 4.8e 1.0e 1.22020.HK ANTA Sports Products O 13.20 11.56 3,711 21.6e 17.9 15.3 18.7% 4.8e 2.1e 2.53818.HK China Dongxiang Group Co. Ltd O 6.30 5.41 3,956 19.3e 16.2 14.3 16.1% 3.5e 3.1e 3.72331.HK Li Ning E 23.30 25.45 3,448 25.9e 21.7 19.0 16.7% 9.3e 1.3e 1.63813.HK Pou Sheng International Holdings E 1.33 1.52 859 43.5e 15.3 10.5 103.5% 1.2e 0.0e 0.03368.HK Parkson Retail Group Limited O 14.20 14.42 5,189 37.1e 29.0 23.3 26.4% 9.3e 1.1e 1.40825.HK New World Department Store China Limited E 6.60 7.70 1,655 25.0e 22.9 18.1 17.4% 3.5e 2.2e 1.83308.HK Golden Eagle Retail Group Limited O 12.20 14.60 3,713 35.6e 26.5 20.7 30.9% 10.0e 2.2e 0.51833.HK Intime Department Store (Group) O 5.70 7.73 1,788 34.0e 27.4 21.4 26.0% 4.1e 1.0e 2.2Source: Morgan Stanley Research estimates. consensus estimates for companies not covered (NC). NM = Not Meaningful.e=Morgan Stanley Research Estimates

P/E Div Yield (%)

Note: Share prices in local currency as of Jan 14 2010. e = Morgan Stanley Research Estimates

Long-term Valuation Methodology Our DCF model yields a fair value of HK$17.8 by the end of 2014. We assume a discount rate of 10%, long-term growth rate of 3.5% and Rmb/HK$ rate of 0.87 in the long run.

Risks Downside risks to achieving our long-term value are 1) higher operating leases for sports and footwear retail shops in prime locations, leading to margin erosion; 2) slowdown in blended store productivity with new store openings for acquired brands; and 3) a major slowdown in the economy and domestic consumption.

8

Belle International (1880.HK, HK$9.69, Overweight, LT value HK$17.8)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

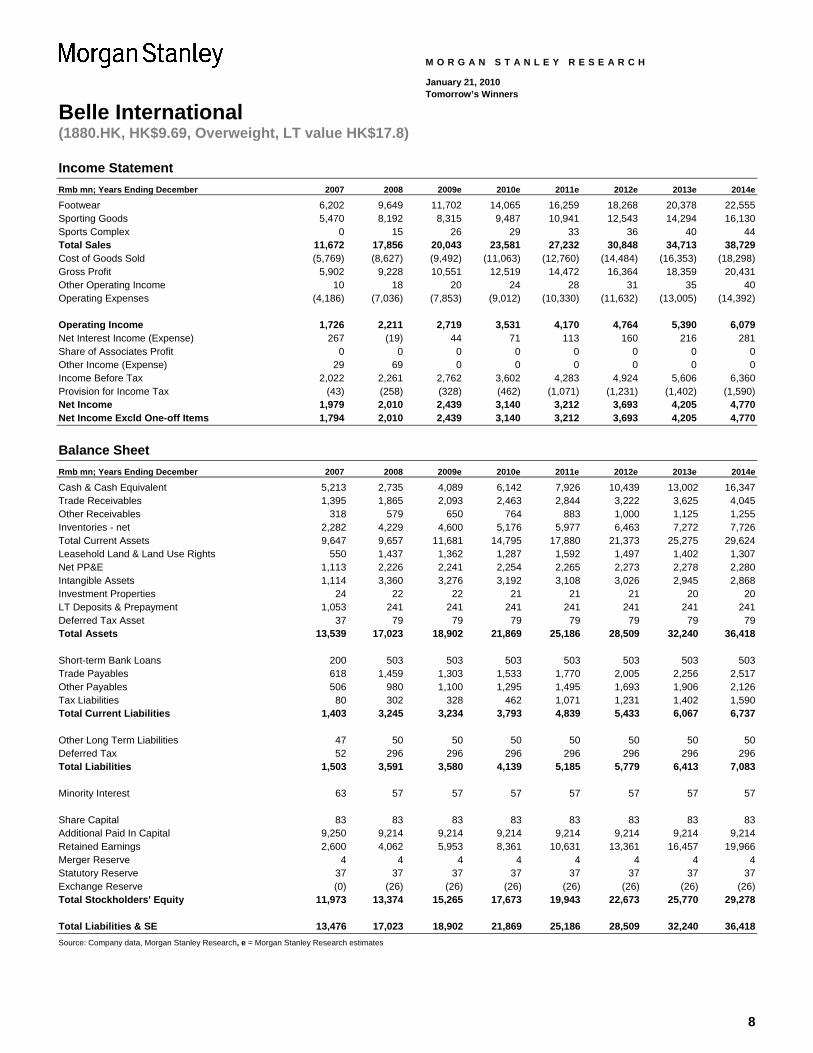

Income Statement Rmb mn; Years Ending December 2007 2008 2009e 2010e 2011e 2012e 2013e 2014e Footwear 6,202 9,649 11,702 14,065 16,259 18,268 20,378 22,555 Sporting Goods 5,470 8,192 8,315 9,487 10,941 12,543 14,294 16,130 Sports Complex 0 15 26 29 33 36 40 44 Total Sales 11,672 17,856 20,043 23,581 27,232 30,848 34,713 38,729 Cost of Goods Sold (5,769) (8,627) (9,492) (11,063) (12,760) (14,484) (16,353) (18,298) Gross Profit 5,902 9,228 10,551 12,519 14,472 16,364 18,359 20,431 Other Operating Income 10 18 20 24 28 31 35 40 Operating Expenses (4,186) (7,036) (7,853) (9,012) (10,330) (11,632) (13,005) (14,392) Operating Income 1,726 2,211 2,719 3,531 4,170 4,764 5,390 6,079 Net Interest Income (Expense) 267 (19) 44 71 113 160 216 281 Share of Associates Profit 0 0 0 0 0 0 0 0 Other Income (Expense) 29 69 0 0 0 0 0 0 Income Before Tax 2,022 2,261 2,762 3,602 4,283 4,924 5,606 6,360 Provision for Income Tax (43) (258) (328) (462) (1,071) (1,231) (1,402) (1,590) Net Income 1,979 2,010 2,439 3,140 3,212 3,693 4,205 4,770 Net Income Excld One-off Items 1,794 2,010 2,439 3,140 3,212 3,693 4,205 4,770

Balance Sheet Rmb mn; Years Ending December 2007 2008 2009e 2010e 2011e 2012e 2013e 2014e Cash & Cash Equivalent 5,213 2,735 4,089 6,142 7,926 10,439 13,002 16,347 Trade Receivables 1,395 1,865 2,093 2,463 2,844 3,222 3,625 4,045 Other Receivables 318 579 650 764 883 1,000 1,125 1,255 Inventories - net 2,282 4,229 4,600 5,176 5,977 6,463 7,272 7,726 Total Current Assets 9,647 9,657 11,681 14,795 17,880 21,373 25,275 29,624 Leasehold Land & Land Use Rights 550 1,437 1,362 1,287 1,592 1,497 1,402 1,307 Net PP&E 1,113 2,226 2,241 2,254 2,265 2,273 2,278 2,280 Intangible Assets 1,114 3,360 3,276 3,192 3,108 3,026 2,945 2,868 Investment Properties 24 22 22 21 21 21 20 20 LT Deposits & Prepayment 1,053 241 241 241 241 241 241 241 Deferred Tax Asset 37 79 79 79 79 79 79 79 Total Assets 13,539 17,023 18,902 21,869 25,186 28,509 32,240 36,418 Short-term Bank Loans 200 503 503 503 503 503 503 503 Trade Payables 618 1,459 1,303 1,533 1,770 2,005 2,256 2,517 Other Payables 506 980 1,100 1,295 1,495 1,693 1,906 2,126 Tax Liabilities 80 302 328 462 1,071 1,231 1,402 1,590 Total Current Liabilities 1,403 3,245 3,234 3,793 4,839 5,433 6,067 6,737 Other Long Term Liabilities 47 50 50 50 50 50 50 50 Deferred Tax 52 296 296 296 296 296 296 296 Total Liabilities 1,503 3,591 3,580 4,139 5,185 5,779 6,413 7,083 Minority Interest 63 57 57 57 57 57 57 57 Share Capital 83 83 83 83 83 83 83 83 Additional Paid In Capital 9,250 9,214 9,214 9,214 9,214 9,214 9,214 9,214 Retained Earnings 2,600 4,062 5,953 8,361 10,631 13,361 16,457 19,966 Merger Reserve 4 4 4 4 4 4 4 4 Statutory Reserve 37 37 37 37 37 37 37 37 Exchange Reserve (0) (26) (26) (26) (26) (26) (26) (26) Total Stockholders' Equity 11,973 13,374 15,265 17,673 19,943 22,673 25,770 29,278 Total Liabilities & SE 13,476 17,023 18,902 21,869 25,186 28,509 32,240 36,418 Source: Company data, Morgan Stanley Research, e = Morgan Stanley Research estimates

9

Belle International (1880.HK, HK$9.69, Overweight, LT value HK$17.8)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

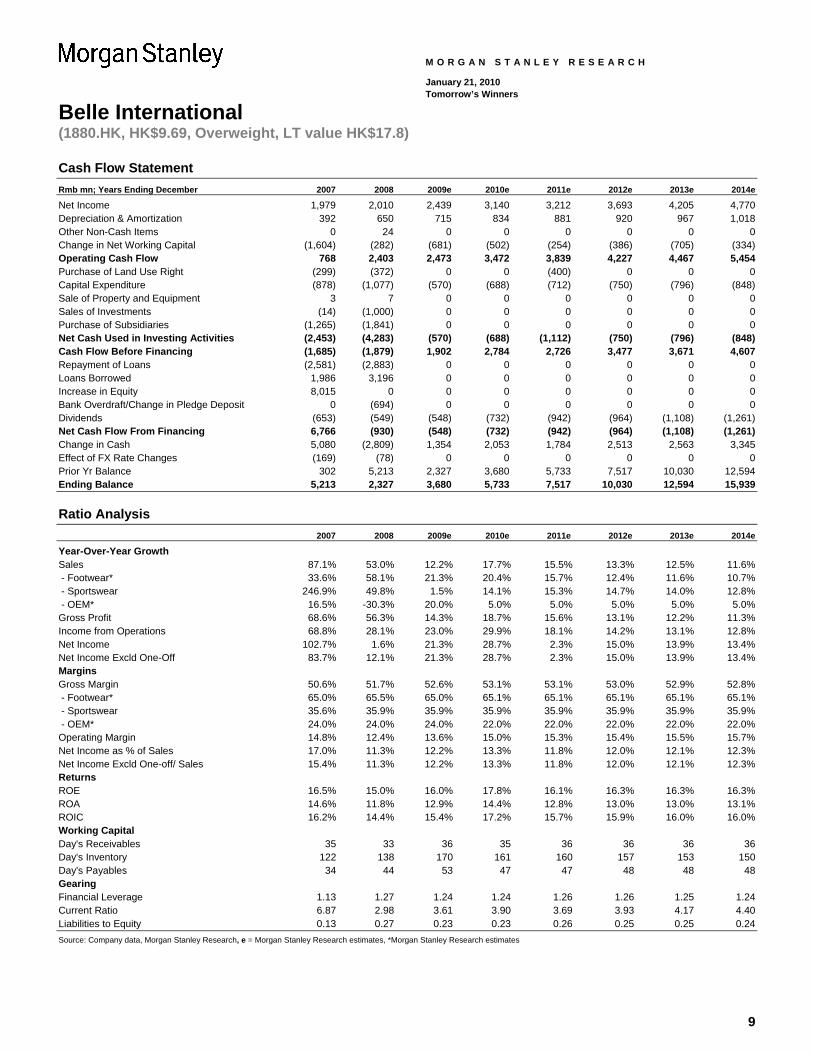

Cash Flow Statement Rmb mn; Years Ending December 2007 2008 2009e 2010e 2011e 2012e 2013e 2014e Net Income 1,979 2,010 2,439 3,140 3,212 3,693 4,205 4,770 Depreciation & Amortization 392 650 715 834 881 920 967 1,018 Other Non-Cash Items 0 24 0 0 0 0 0 0 Change in Net Working Capital (1,604) (282) (681) (502) (254) (386) (705) (334) Operating Cash Flow 768 2,403 2,473 3,472 3,839 4,227 4,467 5,454 Purchase of Land Use Right (299) (372) 0 0 (400) 0 0 0 Capital Expenditure (878) (1,077) (570) (688) (712) (750) (796) (848) Sale of Property and Equipment 3 7 0 0 0 0 0 0 Sales of Investments (14) (1,000) 0 0 0 0 0 0 Purchase of Subsidiaries (1,265) (1,841) 0 0 0 0 0 0 Net Cash Used in Investing Activities (2,453) (4,283) (570) (688) (1,112) (750) (796) (848) Cash Flow Before Financing (1,685) (1,879) 1,902 2,784 2,726 3,477 3,671 4,607 Repayment of Loans (2,581) (2,883) 0 0 0 0 0 0 Loans Borrowed 1,986 3,196 0 0 0 0 0 0 Increase in Equity 8,015 0 0 0 0 0 0 0 Bank Overdraft/Change in Pledge Deposit 0 (694) 0 0 0 0 0 0 Dividends (653) (549) (548) (732) (942) (964) (1,108) (1,261) Net Cash Flow From Financing 6,766 (930) (548) (732) (942) (964) (1,108) (1,261) Change in Cash 5,080 (2,809) 1,354 2,053 1,784 2,513 2,563 3,345 Effect of FX Rate Changes (169) (78) 0 0 0 0 0 0 Prior Yr Balance 302 5,213 2,327 3,680 5,733 7,517 10,030 12,594 Ending Balance 5,213 2,327 3,680 5,733 7,517 10,030 12,594 15,939

Ratio Analysis 2007 2008 2009e 2010e 2011e 2012e 2013e 2014e Year-Over-Year Growth Sales 87.1% 53.0% 12.2% 17.7% 15.5% 13.3% 12.5% 11.6% - Footwear* 33.6% 58.1% 21.3% 20.4% 15.7% 12.4% 11.6% 10.7% - Sportswear 246.9% 49.8% 1.5% 14.1% 15.3% 14.7% 14.0% 12.8% - OEM* 16.5% -30.3% 20.0% 5.0% 5.0% 5.0% 5.0% 5.0% Gross Profit 68.6% 56.3% 14.3% 18.7% 15.6% 13.1% 12.2% 11.3% Income from Operations 68.8% 28.1% 23.0% 29.9% 18.1% 14.2% 13.1% 12.8% Net Income 102.7% 1.6% 21.3% 28.7% 2.3% 15.0% 13.9% 13.4% Net Income Excld One-Off 83.7% 12.1% 21.3% 28.7% 2.3% 15.0% 13.9% 13.4% Margins Gross Margin 50.6% 51.7% 52.6% 53.1% 53.1% 53.0% 52.9% 52.8% - Footwear* 65.0% 65.5% 65.0% 65.1% 65.1% 65.1% 65.1% 65.1% - Sportswear 35.6% 35.9% 35.9% 35.9% 35.9% 35.9% 35.9% 35.9% - OEM* 24.0% 24.0% 24.0% 22.0% 22.0% 22.0% 22.0% 22.0% Operating Margin 14.8% 12.4% 13.6% 15.0% 15.3% 15.4% 15.5% 15.7% Net Income as % of Sales 17.0% 11.3% 12.2% 13.3% 11.8% 12.0% 12.1% 12.3% Net Income Excld One-off/ Sales 15.4% 11.3% 12.2% 13.3% 11.8% 12.0% 12.1% 12.3% Returns ROE 16.5% 15.0% 16.0% 17.8% 16.1% 16.3% 16.3% 16.3% ROA 14.6% 11.8% 12.9% 14.4% 12.8% 13.0% 13.0% 13.1% ROIC 16.2% 14.4% 15.4% 17.2% 15.7% 15.9% 16.0% 16.0% Working Capital Day's Receivables 35 33 36 35 36 36 36 36 Day's Inventory 122 138 170 161 160 157 153 150 Day's Payables 34 44 53 47 47 48 48 48 Gearing Financial Leverage 1.13 1.27 1.24 1.24 1.26 1.26 1.25 1.24 Current Ratio 6.87 2.98 3.61 3.90 3.69 3.93 4.17 4.40 Liabilities to Equity 0.13 0.27 0.23 0.23 0.26 0.25 0.25 0.24 Source: Company data, Morgan Stanley Research, e = Morgan Stanley Research estimates, *Morgan Stanley Research estimates

10

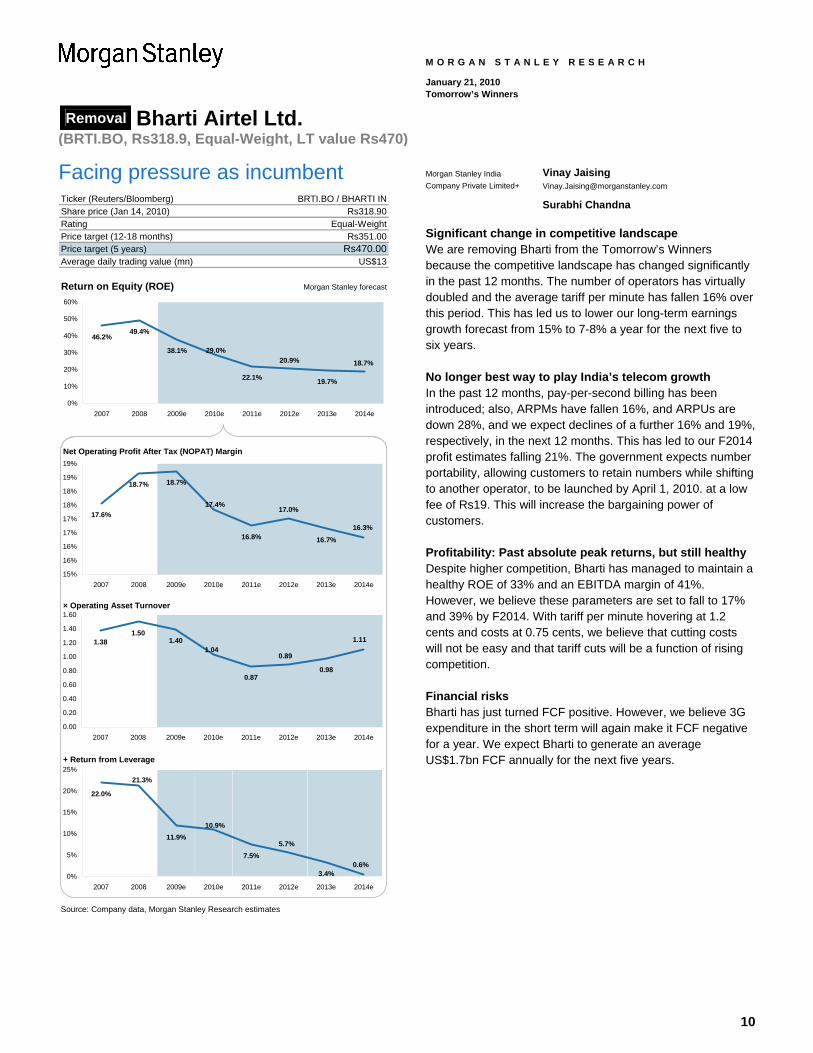

Removal Bharti Airtel Ltd. (BRTI.BO, Rs318.9, Equal-Weight, LT value Rs470)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Facing pressure as incumbent Ticker (Reuters/Bloomberg)Share price (Jan 14, 2010)RatingPrice target (12-18 months)Price target (5 years) Rs470.00Average daily trading value (mn)

Return on Equity (ROE) Morgan Stanley forecast

Net Operating Profit After Tax (NOPAT) Margin

× Operating Asset Turnover

+ Return from Leverage

Source: Company data, Morgan Stanley Research estimates

US$13

BRTI.BO / BHARTI INRs318.90

Equal-WeightRs351.00

46.2%49.4%

38.1%

22.1% 19.7%

18.7%20.9%29.0%

0%

10%

20%

30%

40%

50%

60%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

17.6%

18.7% 18.7%

16.8% 16.7%

17.4%17.0%

16.3%

15%

16%

16%

17%

17%

18%

18%

19%

19%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

1.381.50

1.40

0.870.98

1.040.89

1.11

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

22.0%

11.9%

7.5%

3.4%0.6%

5.7%

10.9%

21.3%

0%

5%

10%

15%

20%

25%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

Morgan Stanley India Company Private Limited+

Vinay Jaising [email protected]

Surabhi Chandna

Significant change in competitive landscape We are removing Bharti from the Tomorrow’s Winners because the competitive landscape has changed significantly in the past 12 months. The number of operators has virtually doubled and the average tariff per minute has fallen 16% over this period. This has led us to lower our long-term earnings growth forecast from 15% to 7-8% a year for the next five to six years.

No longer best way to play India’s telecom growth In the past 12 months, pay-per-second billing has been introduced; also, ARPMs have fallen 16%, and ARPUs are down 28%, and we expect declines of a further 16% and 19%, respectively, in the next 12 months. This has led to our F2014 profit estimates falling 21%. The government expects number portability, allowing customers to retain numbers while shifting to another operator, to be launched by April 1, 2010. at a low fee of Rs19. This will increase the bargaining power of customers.

Profitability: Past absolute peak returns, but still healthy Despite higher competition, Bharti has managed to maintain a healthy ROE of 33% and an EBITDA margin of 41%. However, we believe these parameters are set to fall to 17% and 39% by F2014. With tariff per minute hovering at 1.2 cents and costs at 0.75 cents, we believe that cutting costs will not be easy and that tariff cuts will be a function of rising competition.

Financial risks Bharti has just turned FCF positive. However, we believe 3G expenditure in the short term will again make it FCF negative for a year. We expect Bharti to generate an average US$1.7bn FCF annually for the next five years.

11

Removal Bharti Airtel Ltd. (BRTI.BO, Rs318.9, Equal-Weight, LT value Rs470)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

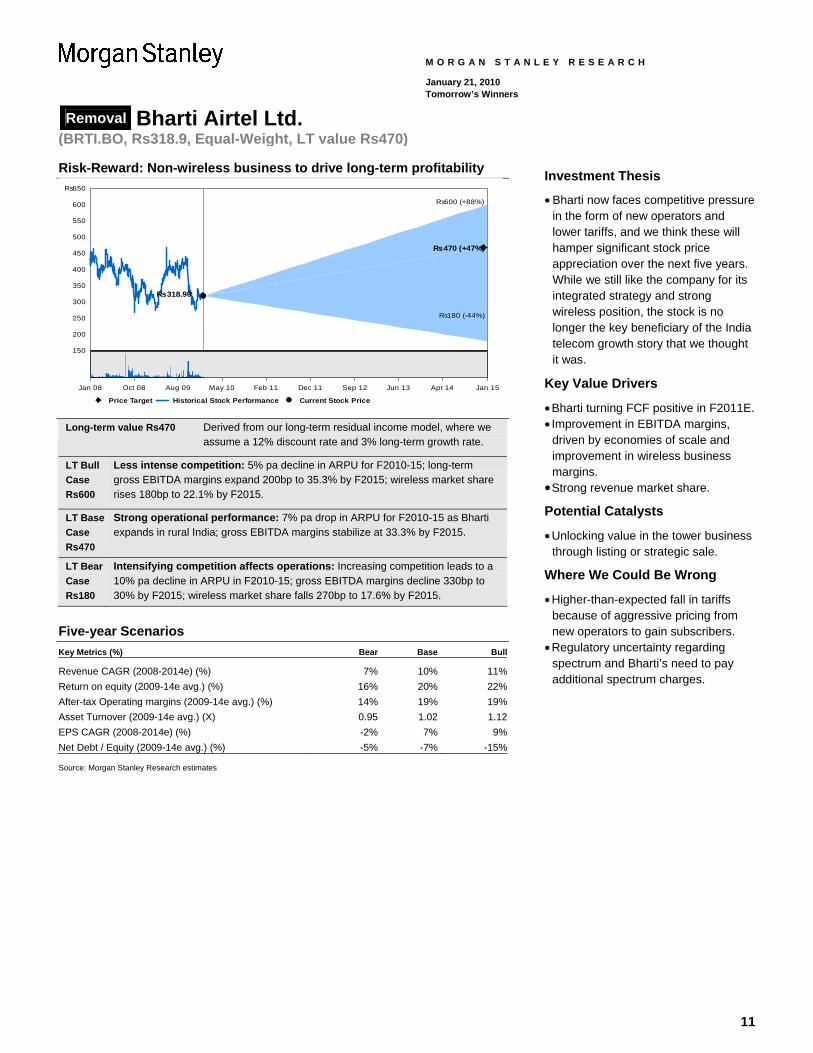

Risk-Reward: Non-wireless business to drive long-term profitability

150

200

250

300

350

400

450

500

550

600

Rs650

Rs600 (+88%)

Rs470 (+47%)

Rs180 (-44%)

Rs318.90

Price Target Historical Stock Performance Current Stock Price

Jan 08 Oct 08 Aug 09 May 10 Feb 11 Dec 11 Sep 12 Jun 13 Apr 14 Jan 15

Long-term value Rs470 Derived from our long-term residual income model, where we assume a 12% discount rate and 3% long-term growth rate.

LT Bull Case Rs600

Less intense competition: 5% pa decline in ARPU for F2010-15; long-term gross EBITDA margins expand 200bp to 35.3% by F2015; wireless market share rises 180bp to 22.1% by F2015.

LT Base Case Rs470

Strong operational performance: 7% pa drop in ARPU for F2010-15 as Bharti expands in rural India; gross EBITDA margins stabilize at 33.3% by F2015.

LT Bear Case Rs180

Intensifying competition affects operations: Increasing competition leads to a 10% pa decline in ARPU in F2010-15; gross EBITDA margins decline 330bp to 30% by F2015; wireless market share falls 270bp to 17.6% by F2015.

Five-year Scenarios Key Metrics (%) Bear Base Bull

Revenue CAGR (2008-2014e) (%) 7% 10% 11%Return on equity (2009-14e avg.) (%) 16% 20% 22%After-tax Operating margins (2009-14e avg.) (%) 14% 19% 19%Asset Turnover (2009-14e avg.) (X) 0.95 1.02 1.12EPS CAGR (2008-2014e) (%) -2% 7% 9%Net Debt / Equity (2009-14e avg.) (%) -5% -7% -15% Source: Morgan Stanley Research estimates

Investment Thesis

• Bharti now faces competitive pressure in the form of new operators and lower tariffs, and we think these will hamper significant stock price appreciation over the next five years. While we still like the company for its integrated strategy and strong wireless position, the stock is no longer the key beneficiary of the India telecom growth story that we thought it was.

Key Value Drivers

• Bharti turning FCF positive in F2011E. • Improvement in EBITDA margins,

driven by economies of scale and improvement in wireless business margins.

• Strong revenue market share.

Potential Catalysts

• Unlocking value in the tower business through listing or strategic sale.

Where We Could Be Wrong

• Higher-than-expected fall in tariffs because of aggressive pricing from new operators to gain subscribers.

• Regulatory uncertainty regarding spectrum and Bharti’s need to pay additional spectrum charges.

12

Removal Bharti Airtel Ltd. (BRTI.BO, Rs318.9, Equal-Weight, LT value Rs470)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Competitive Landscape

Key Changes

• Greater intensity in tariff competition among operators;

• Increased competition with new launches;

• More new operators to increase competition further.

Bharti is one of India’s private integrated telecom operators providing wireless, enterprise, and long-distance services. Bharti has historically enjoyed a first mover advantage and its

pan-India presence had helped secure higher net adds than its competitors. Although it still has the top position in terms of subscribers, Bharti’s market share in net adds is declining because of new launches by operators such as Reliance Communications, Tata Teleservices, and Aircel, which have been giving special offers to attract customers. This has also led to steep falls in ARPMs and ARPUs in the industry.

The number of operators virtually doubled in 2009 and we expect a further four to five operators to launch services in the next 12 months – the operators could include Loop Telecom, Datacom, Stel, Swan and Sistema.

Competitive Advantage Profile of the Telecom Industry

Spectrum is no longer a constraint and new licensees can share passive and partly active infrastructure to launch services faster.

Threat of New Entrants(High)

High growth market; lowest average revenues per minute (ARPMs) in the world; lowest capex per sub.

Intensity of Rivalry(High)

Key buyers: Telecom subscribersIntroduction of number portability will lead to churn among subscribers.

Bargaining Power of Buyers(High)

Key suppliers: Equipment manufacturers Capex is on a decline around the world, increasing the attractiveness of the Indian market. Large size of contracts makes suppliers dependent on telecom operators.

Bargaining Power of Supplier(Low)

Both Data and Voice face little or no risk of substitutes since they are basic ingredients for communications today.

Threat of Substitutes(Low)

Spectrum is no longer a constraint and new licensees can share passive and partly active infrastructure to launch services faster.

Threat of New Entrants(High)

High growth market; lowest average revenues per minute (ARPMs) in the world; lowest capex per sub.

Intensity of Rivalry(High)

Key buyers: Telecom subscribersIntroduction of number portability will lead to churn among subscribers.

Bargaining Power of Buyers(High)

Key suppliers: Equipment manufacturers Capex is on a decline around the world, increasing the attractiveness of the Indian market. Large size of contracts makes suppliers dependent on telecom operators.

Bargaining Power of Supplier(Low)

Both Data and Voice face little or no risk of substitutes since they are basic ingredients for communications today.

Threat of Substitutes(Low)

Source: Michael Porter, Morgan Stanley Research

13

Removal Bharti Airtel Ltd. (BRTI.BO, Rs318.9, Equal-Weight, LT value Rs470)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

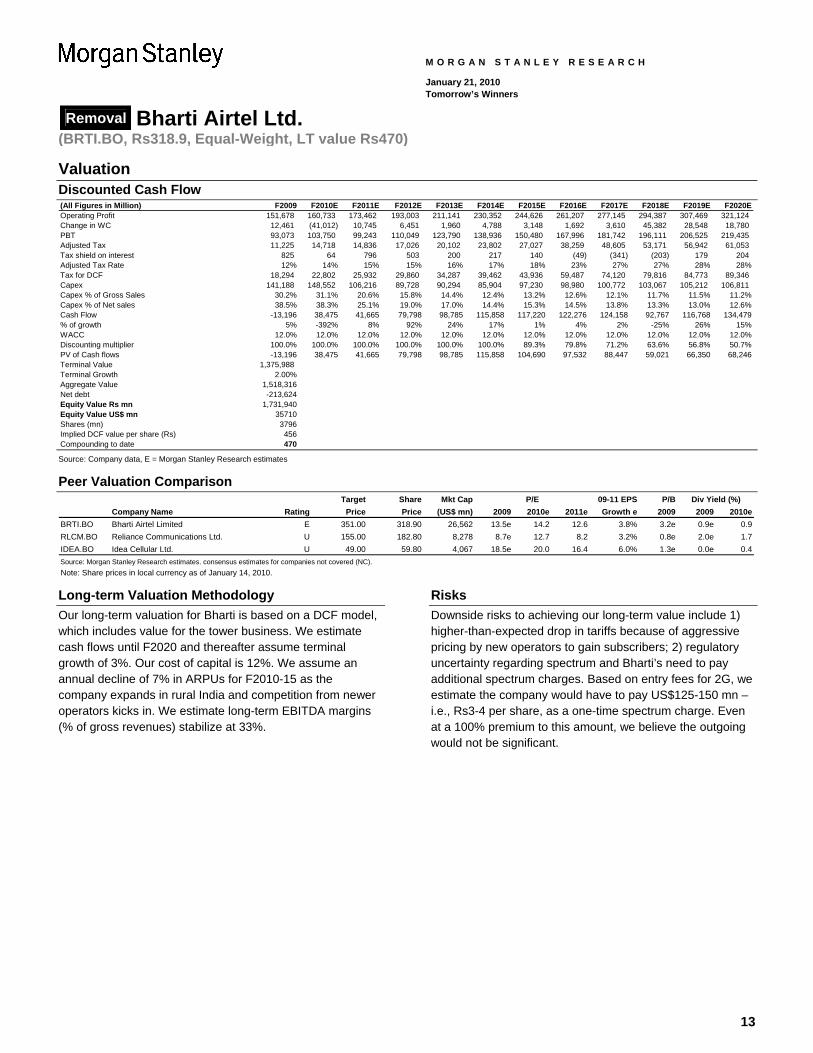

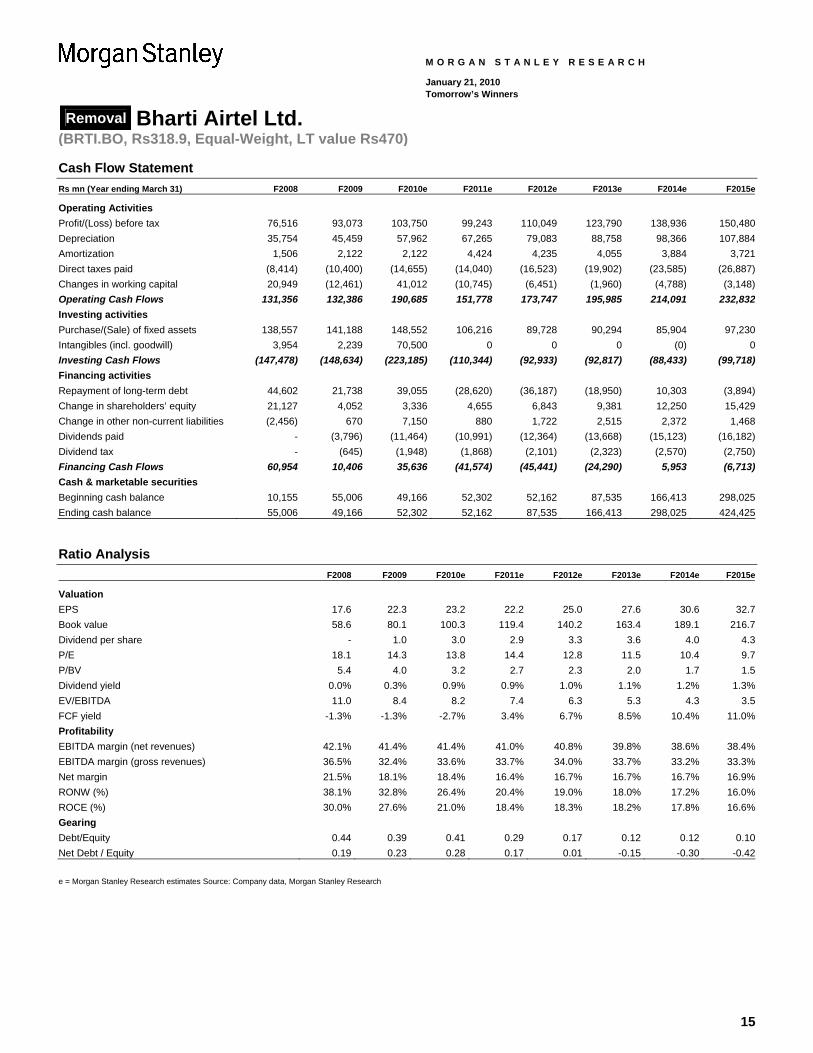

Valuation Discounted Cash Flow (All Figures in Million) F2009 F2010E F2011E F2012E F2013E F2014E F2015E F2016E F2017E F2018E F2019E F2020EOperating Profit 151,678 160,733 173,462 193,003 211,141 230,352 244,626 261,207 277,145 294,387 307,469 321,124 Change in WC 12,461 (41,012) 10,745 6,451 1,960 4,788 3,148 1,692 3,610 45,382 28,548 18,780 PBT 93,073 103,750 99,243 110,049 123,790 138,936 150,480 167,996 181,742 196,111 206,525 219,435 Adjusted Tax 11,225 14,718 14,836 17,026 20,102 23,802 27,027 38,259 48,605 53,171 56,942 61,053 Tax shield on interest 825 64 796 503 200 217 140 (49) (341) (203) 179 204 Adjusted Tax Rate 12% 14% 15% 15% 16% 17% 18% 23% 27% 27% 28% 28%Tax for DCF 18,294 22,802 25,932 29,860 34,287 39,462 43,936 59,487 74,120 79,816 84,773 89,346 Capex 141,188 148,552 106,216 89,728 90,294 85,904 97,230 98,980 100,772 103,067 105,212 106,811 Capex % of Gross Sales 30.2% 31.1% 20.6% 15.8% 14.4% 12.4% 13.2% 12.6% 12.1% 11.7% 11.5% 11.2%Capex % of Net sales 38.5% 38.3% 25.1% 19.0% 17.0% 14.4% 15.3% 14.5% 13.8% 13.3% 13.0% 12.6%Cash Flow -13,196 38,475 41,665 79,798 98,785 115,858 117,220 122,276 124,158 92,767 116,768 134,479% of growth 5% -392% 8% 92% 24% 17% 1% 4% 2% -25% 26% 15%WACC 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0%Discounting multiplier 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 89.3% 79.8% 71.2% 63.6% 56.8% 50.7%PV of Cash flows -13,196 38,475 41,665 79,798 98,785 115,858 104,690 97,532 88,447 59,021 66,350 68,246Terminal Value 1,375,988 Terminal Growth 2.00%Aggregate Value 1,518,316 1,397,215Net debt -213,624 5,513Equity Value Rs mn 1,731,940 1,391,702Equity Value US$ mn 35710 33,433 Shares (mn) 3796 3,796 Implied DCF value per share (Rs) 456 367 367 Compounding to date 470 411 2.43% 13% Source: Company data, E = Morgan Stanley Research estimates

Peer Valuation Comparison Target Share Mkt Cap 09-11 EPS P/B

Company Name Rating Price Price (US$ mn) 2009 2010e 2011e Growth e 2009 2009 2010eBRTI.BO Bharti Airtel Limited E 351.00 318.90 26,562 13.5e 14.2 12.6 3.8% 3.2e 0.9e 0.9RLCM.BO Reliance Communications Ltd. U 155.00 182.80 8,278 8.7e 12.7 8.2 3.2% 0.8e 2.0e 1.7IDEA.BO Idea Cellular Ltd. U 49.00 59.80 4,067 18.5e 20.0 16.4 6.0% 1.3e 0.0e 0.4Source: Morgan Stanley Research estimates. consensus estimates for companies not covered (NC).

P/E Div Yield (%)

Note: Share prices in local currency as of January 14, 2010.

Long-term Valuation Methodology Our long-term valuation for Bharti is based on a DCF model, which includes value for the tower business. We estimate cash flows until F2020 and thereafter assume terminal growth of 3%. Our cost of capital is 12%. We assume an annual decline of 7% in ARPUs for F2010-15 as the company expands in rural India and competition from newer operators kicks in. We estimate long-term EBITDA margins (% of gross revenues) stabilize at 33%.

Risks Downside risks to achieving our long-term value include 1) higher-than-expected drop in tariffs because of aggressive pricing by new operators to gain subscribers; 2) regulatory uncertainty regarding spectrum and Bharti’s need to pay additional spectrum charges. Based on entry fees for 2G, we estimate the company would have to pay US$125-150 mn – i.e., Rs3-4 per share, as a one-time spectrum charge. Even at a 100% premium to this amount, we believe the outgoing would not be significant.

14

Removal Bharti Airtel Ltd. (BRTI.BO, Rs318.9, Equal-Weight, LT value Rs470)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

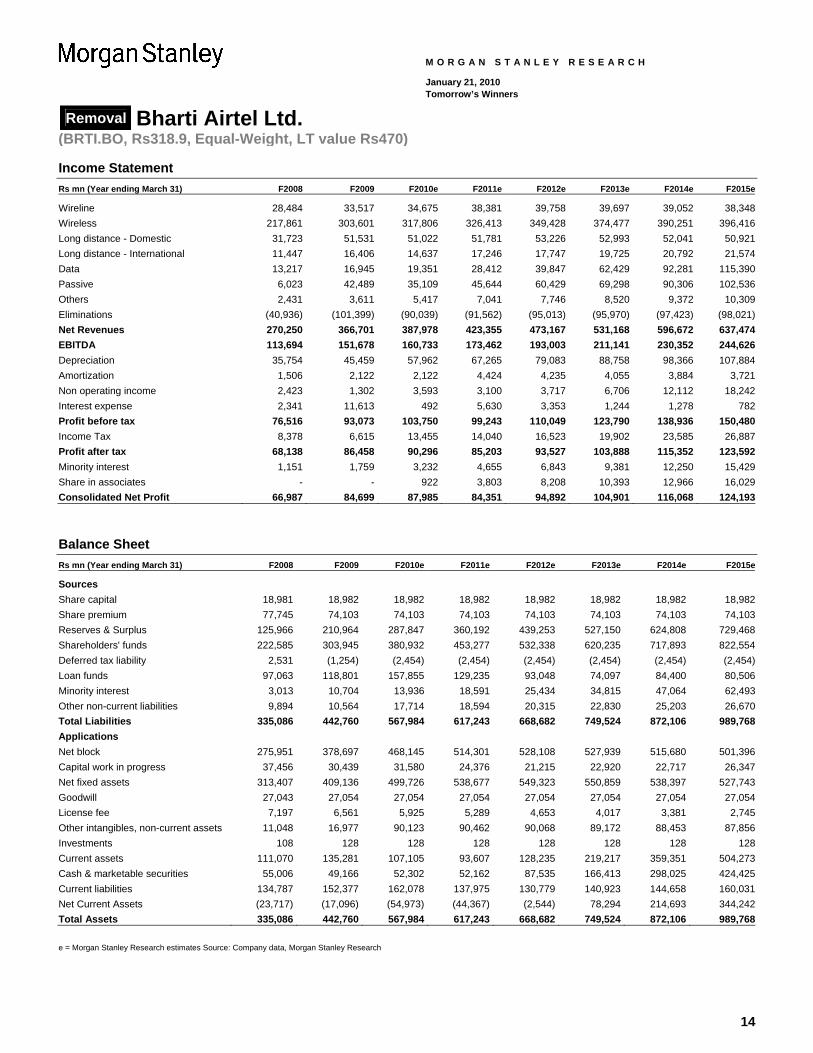

Income Statement Rs mn (Year ending March 31) F2008 F2009 F2010e F2011e F2012e F2013e F2014e F2015e

Wireline 28,484 33,517 34,675 38,381 39,758 39,697 39,052 38,348Wireless 217,861 303,601 317,806 326,413 349,428 374,477 390,251 396,416Long distance - Domestic 31,723 51,531 51,022 51,781 53,226 52,993 52,041 50,921Long distance - International 11,447 16,406 14,637 17,246 17,747 19,725 20,792 21,574Data 13,217 16,945 19,351 28,412 39,847 62,429 92,281 115,390Passive 6,023 42,489 35,109 45,644 60,429 69,298 90,306 102,536Others 2,431 3,611 5,417 7,041 7,746 8,520 9,372 10,309Eliminations (40,936) (101,399) (90,039) (91,562) (95,013) (95,970) (97,423) (98,021)Net Revenues 270,250 366,701 387,978 423,355 473,167 531,168 596,672 637,474EBITDA 113,694 151,678 160,733 173,462 193,003 211,141 230,352 244,626Depreciation 35,754 45,459 57,962 67,265 79,083 88,758 98,366 107,884Amortization 1,506 2,122 2,122 4,424 4,235 4,055 3,884 3,721Non operating income 2,423 1,302 3,593 3,100 3,717 6,706 12,112 18,242Interest expense 2,341 11,613 492 5,630 3,353 1,244 1,278 782Profit before tax 76,516 93,073 103,750 99,243 110,049 123,790 138,936 150,480Income Tax 8,378 6,615 13,455 14,040 16,523 19,902 23,585 26,887Profit after tax 68,138 86,458 90,296 85,203 93,527 103,888 115,352 123,592Minority interest 1,151 1,759 3,232 4,655 6,843 9,381 12,250 15,429Share in associates - - 922 3,803 8,208 10,393 12,966 16,029Consolidated Net Profit 66,987 84,699 87,985 84,351 94,892 104,901 116,068 124,193

Balance Sheet Rs mn (Year ending March 31) F2008 F2009 F2010e F2011e F2012e F2013e F2014e F2015e

Sources Share capital 18,981 18,982 18,982 18,982 18,982 18,982 18,982 18,982Share premium 77,745 74,103 74,103 74,103 74,103 74,103 74,103 74,103Reserves & Surplus 125,966 210,964 287,847 360,192 439,253 527,150 624,808 729,468Shareholders' funds 222,585 303,945 380,932 453,277 532,338 620,235 717,893 822,554Deferred tax liability 2,531 (1,254) (2,454) (2,454) (2,454) (2,454) (2,454) (2,454)Loan funds 97,063 118,801 157,855 129,235 93,048 74,097 84,400 80,506Minority interest 3,013 10,704 13,936 18,591 25,434 34,815 47,064 62,493Other non-current liabilities 9,894 10,564 17,714 18,594 20,315 22,830 25,203 26,670Total Liabilities 335,086 442,760 567,984 617,243 668,682 749,524 872,106 989,768Applications Net block 275,951 378,697 468,145 514,301 528,108 527,939 515,680 501,396Capital work in progress 37,456 30,439 31,580 24,376 21,215 22,920 22,717 26,347Net fixed assets 313,407 409,136 499,726 538,677 549,323 550,859 538,397 527,743Goodwill 27,043 27,054 27,054 27,054 27,054 27,054 27,054 27,054License fee 7,197 6,561 5,925 5,289 4,653 4,017 3,381 2,745Other intangibles, non-current assets 11,048 16,977 90,123 90,462 90,068 89,172 88,453 87,856Investments 108 128 128 128 128 128 128 128Current assets 111,070 135,281 107,105 93,607 128,235 219,217 359,351 504,273Cash & marketable securities 55,006 49,166 52,302 52,162 87,535 166,413 298,025 424,425Current liabilities 134,787 152,377 162,078 137,975 130,779 140,923 144,658 160,031Net Current Assets (23,717) (17,096) (54,973) (44,367) (2,544) 78,294 214,693 344,242Total Assets 335,086 442,760 567,984 617,243 668,682 749,524 872,106 989,768

e = Morgan Stanley Research estimates Source: Company data, Morgan Stanley Research

15

Removal Bharti Airtel Ltd. (BRTI.BO, Rs318.9, Equal-Weight, LT value Rs470)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Cash Flow Statement Rs mn (Year ending March 31) F2008 F2009 F2010e F2011e F2012e F2013e F2014e F2015e

Operating Activities Profit/(Loss) before tax 76,516 93,073 103,750 99,243 110,049 123,790 138,936 150,480Depreciation 35,754 45,459 57,962 67,265 79,083 88,758 98,366 107,884Amortization 1,506 2,122 2,122 4,424 4,235 4,055 3,884 3,721Direct taxes paid (8,414) (10,400) (14,655) (14,040) (16,523) (19,902) (23,585) (26,887)Changes in working capital 20,949 (12,461) 41,012 (10,745) (6,451) (1,960) (4,788) (3,148)Operating Cash Flows 131,356 132,386 190,685 151,778 173,747 195,985 214,091 232,832Investing activities Purchase/(Sale) of fixed assets 138,557 141,188 148,552 106,216 89,728 90,294 85,904 97,230Intangibles (incl. goodwill) 3,954 2,239 70,500 0 0 0 (0) 0Investing Cash Flows (147,478) (148,634) (223,185) (110,344) (92,933) (92,817) (88,433) (99,718)Financing activities Repayment of long-term debt 44,602 21,738 39,055 (28,620) (36,187) (18,950) 10,303 (3,894)Change in shareholders’ equity 21,127 4,052 3,336 4,655 6,843 9,381 12,250 15,429Change in other non-current liabilities (2,456) 670 7,150 880 1,722 2,515 2,372 1,468Dividends paid - (3,796) (11,464) (10,991) (12,364) (13,668) (15,123) (16,182)Dividend tax - (645) (1,948) (1,868) (2,101) (2,323) (2,570) (2,750)Financing Cash Flows 60,954 10,406 35,636 (41,574) (45,441) (24,290) 5,953 (6,713)Cash & marketable securities Beginning cash balance 10,155 55,006 49,166 52,302 52,162 87,535 166,413 298,025Ending cash balance 55,006 49,166 52,302 52,162 87,535 166,413 298,025 424,425

Ratio Analysis F2008 F2009 F2010e F2011e F2012e F2013e F2014e F2015e

Valuation EPS 17.6 22.3 23.2 22.2 25.0 27.6 30.6 32.7Book value 58.6 80.1 100.3 119.4 140.2 163.4 189.1 216.7Dividend per share - 1.0 3.0 2.9 3.3 3.6 4.0 4.3P/E 18.1 14.3 13.8 14.4 12.8 11.5 10.4 9.7P/BV 5.4 4.0 3.2 2.7 2.3 2.0 1.7 1.5Dividend yield 0.0% 0.3% 0.9% 0.9% 1.0% 1.1% 1.2% 1.3%EV/EBITDA 11.0 8.4 8.2 7.4 6.3 5.3 4.3 3.5FCF yield -1.3% -1.3% -2.7% 3.4% 6.7% 8.5% 10.4% 11.0%Profitability EBITDA margin (net revenues) 42.1% 41.4% 41.4% 41.0% 40.8% 39.8% 38.6% 38.4%EBITDA margin (gross revenues) 36.5% 32.4% 33.6% 33.7% 34.0% 33.7% 33.2% 33.3%Net margin 21.5% 18.1% 18.4% 16.4% 16.7% 16.7% 16.7% 16.9%RONW (%) 38.1% 32.8% 26.4% 20.4% 19.0% 18.0% 17.2% 16.0%ROCE (%) 30.0% 27.6% 21.0% 18.4% 18.3% 18.2% 17.8% 16.6%Gearing Debt/Equity 0.44 0.39 0.41 0.29 0.17 0.12 0.12 0.10Net Debt / Equity 0.19 0.23 0.28 0.17 0.01 -0.15 -0.30 -0.42

e = Morgan Stanley Research estimates Source: Company data, Morgan Stanley Research

16

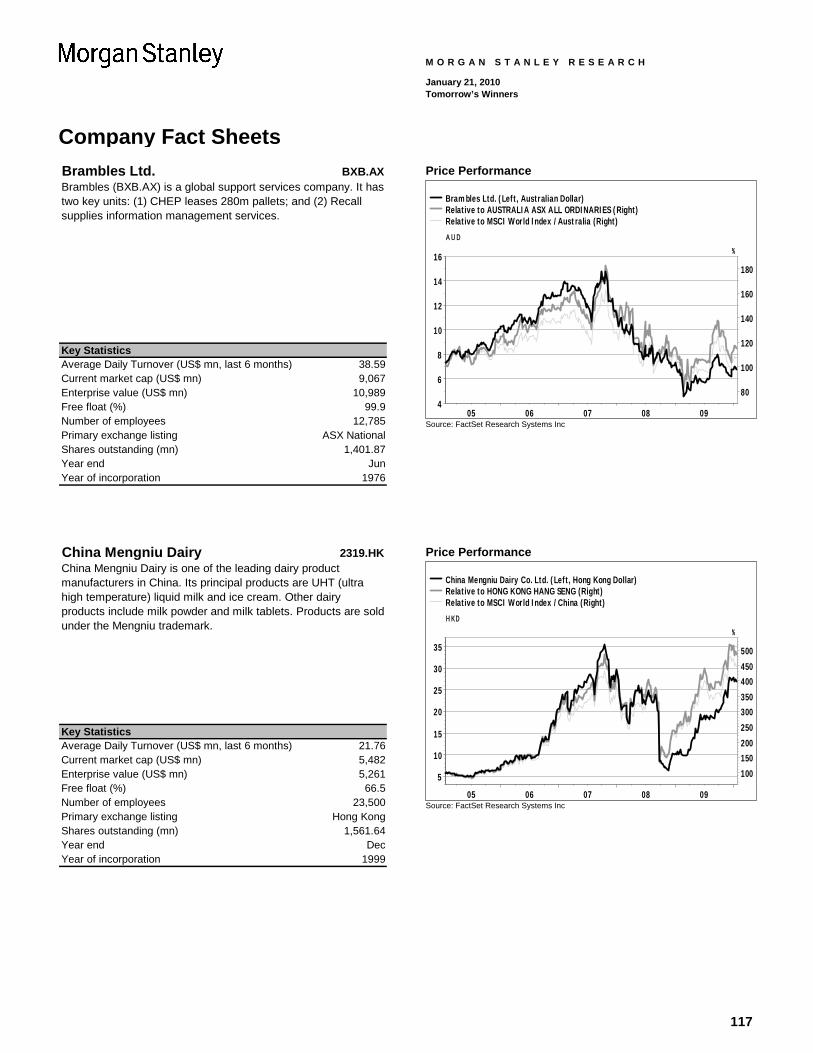

Removal Brambles Ltd (BXB.AX, A$6.96, Equal-Weight, LT value A$9.65)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

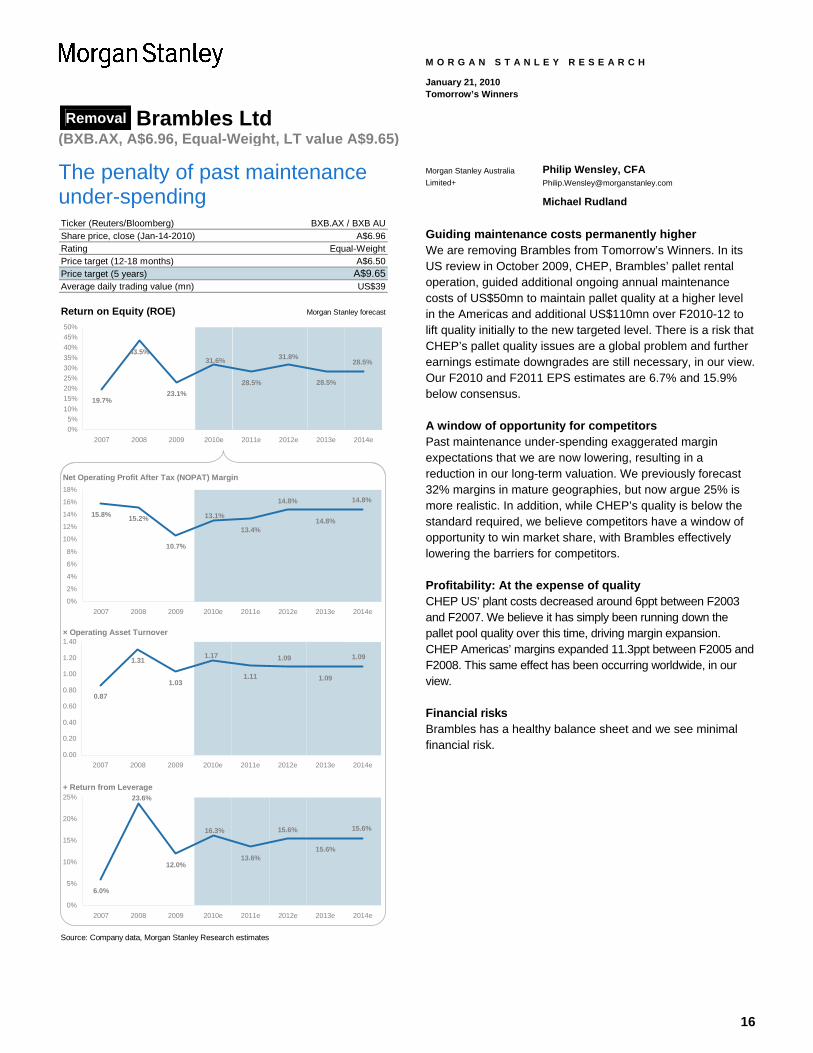

The penalty of past maintenance under-spending Ticker (Reuters/Bloomberg)Share price, close (Jan-14-2010)RatingPrice target (12-18 months)Price target (5 years) A$9.65Average daily trading value (mn)

Return on Equity (ROE) Morgan Stanley forecast

Net Operating Profit After Tax (NOPAT) Margin

× Operating Asset Turnover

+ Return from Leverage

Source: Company data, Morgan Stanley Research estimates

BXB.AX / BXB AUA$6.96

Equal-WeightA$6.50

US$39

19.7%

43.5%

23.1%28.5% 28.5%

28.5%31.8%31.6%

0%5%

10%15%20%25%30%35%40%45%50%

2007 2008 2009 2010e 2011e 2012e 2013e 2014e

15.8% 15.2%

10.7%

13.4%14.8%

13.1%

14.8% 14.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2007 2008 2009 2010e 2011e 2012e 2013e 2014e

0.87

1.31

1.031.11 1.09

1.17 1.09 1.09

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2007 2008 2009 2010e 2011e 2012e 2013e 2014e

6.0%

12.0%13.6%

15.6%

15.6%15.6%16.3%

23.6%

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010e 2011e 2012e 2013e 2014e

Morgan Stanley Australia Limited+

Philip Wensley, CFA [email protected]

Michael Rudland

Guiding maintenance costs permanently higher We are removing Brambles from Tomorrow’s Winners. In its US review in October 2009, CHEP, Brambles’ pallet rental operation, guided additional ongoing annual maintenance costs of US$50mn to maintain pallet quality at a higher level in the Americas and additional US$110mn over F2010-12 to lift quality initially to the new targeted level. There is a risk that CHEP’s pallet quality issues are a global problem and further earnings estimate downgrades are still necessary, in our view. Our F2010 and F2011 EPS estimates are 6.7% and 15.9% below consensus.

A window of opportunity for competitors Past maintenance under-spending exaggerated margin expectations that we are now lowering, resulting in a reduction in our long-term valuation. We previously forecast 32% margins in mature geographies, but now argue 25% is more realistic. In addition, while CHEP’s quality is below the standard required, we believe competitors have a window of opportunity to win market share, with Brambles effectively lowering the barriers for competitors.

Profitability: At the expense of quality CHEP US’ plant costs decreased around 6ppt between F2003 and F2007. We believe it has simply been running down the pallet pool quality over this time, driving margin expansion. CHEP Americas’ margins expanded 11.3ppt between F2005 and F2008. This same effect has been occurring worldwide, in our view.

Financial risks Brambles has a healthy balance sheet and we see minimal financial risk.

17

Removal Brambles Ltd (BXB.AX, A$6.96, Equal-Weight, LT value A$9.65)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

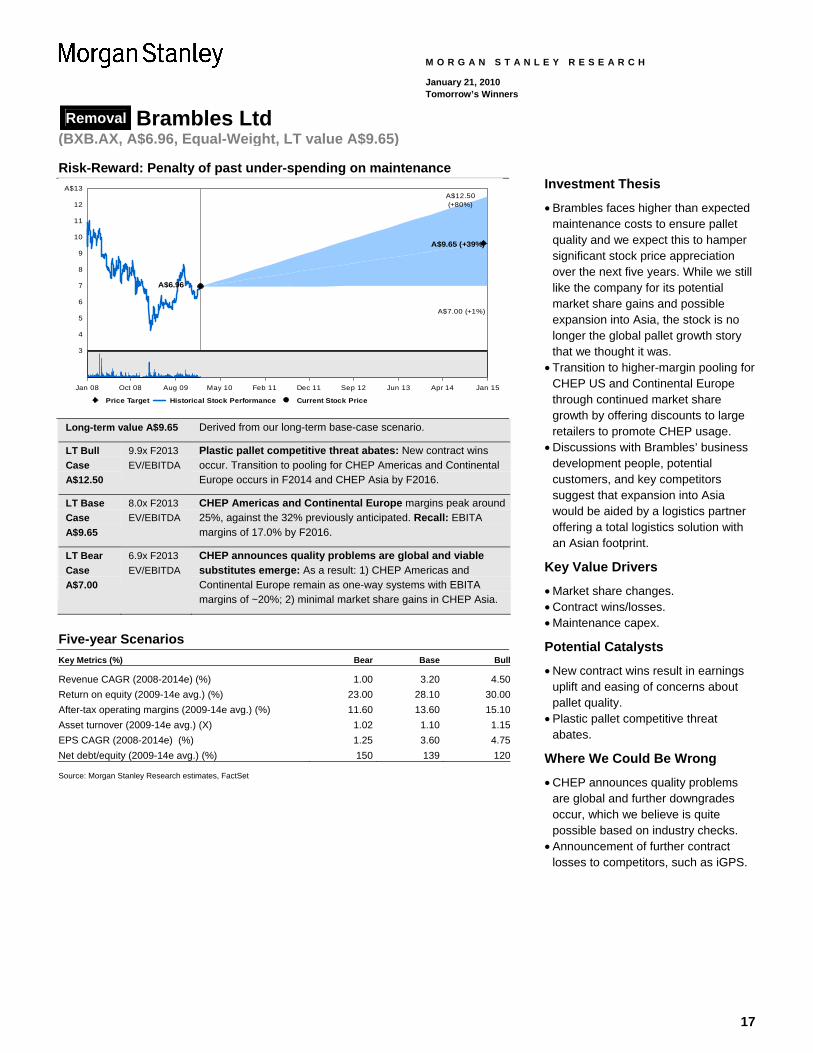

Risk-Reward: Penalty of past under-spending on maintenance

3

4

5

6

7

8

9

10

11

12

A$13A$12.50(+80%)

A$9.65 (+39%)

A$7.00 (+1%)

A$6.96

Price Target Historical Stock Performance Current Stock Price

Jan 08 Oct 08 Aug 09 May 10 Feb 11 Dec 11 Sep 12 Jun 13 Apr 14 Jan 15

Long-term value A$9.65 Derived from our long-term base-case scenario.

LT Bull Case A$12.50

9.9x F2013 EV/EBITDA

Plastic pallet competitive threat abates: New contract wins occur. Transition to pooling for CHEP Americas and Continental Europe occurs in F2014 and CHEP Asia by F2016.

LT Base Case A$9.65

8.0x F2013 EV/EBITDA

CHEP Americas and Continental Europe margins peak around 25%, against the 32% previously anticipated. Recall: EBITA margins of 17.0% by F2016.

LT Bear Case A$7.00

6.9x F2013 EV/EBITDA

CHEP announces quality problems are global and viable substitutes emerge: As a result: 1) CHEP Americas and Continental Europe remain as one-way systems with EBITA margins of ~20%; 2) minimal market share gains in CHEP Asia.

Five-year Scenarios Key Metrics (%) Bear Base Bull

Revenue CAGR (2008-2014e) (%) 1.00 3.20 4.50Return on equity (2009-14e avg.) (%) 23.00 28.10 30.00After-tax operating margins (2009-14e avg.) (%) 11.60 13.60 15.10Asset turnover (2009-14e avg.) (X) 1.02 1.10 1.15EPS CAGR (2008-2014e) (%) 1.25 3.60 4.75Net debt/equity (2009-14e avg.) (%) 150 139 120 Source: Morgan Stanley Research estimates, FactSet

Investment Thesis

• Brambles faces higher than expected maintenance costs to ensure pallet quality and we expect this to hamper significant stock price appreciation over the next five years. While we still like the company for its potential market share gains and possible expansion into Asia, the stock is no longer the global pallet growth story that we thought it was.

• Transition to higher-margin pooling for CHEP US and Continental Europe through continued market share growth by offering discounts to large retailers to promote CHEP usage.

• Discussions with Brambles’ business development people, potential customers, and key competitors suggest that expansion into Asia would be aided by a logistics partner offering a total logistics solution with an Asian footprint.

Key Value Drivers

• Market share changes. • Contract wins/losses. • Maintenance capex.

Potential Catalysts

• New contract wins result in earnings uplift and easing of concerns about pallet quality.

• Plastic pallet competitive threat abates.

Where We Could Be Wrong

• CHEP announces quality problems are global and further downgrades occur, which we believe is quite possible based on industry checks.

• Announcement of further contract losses to competitors, such as iGPS.

18

Removal Brambles Ltd (BXB.AX, A$6.96, Equal-Weight, LT value A$9.65)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

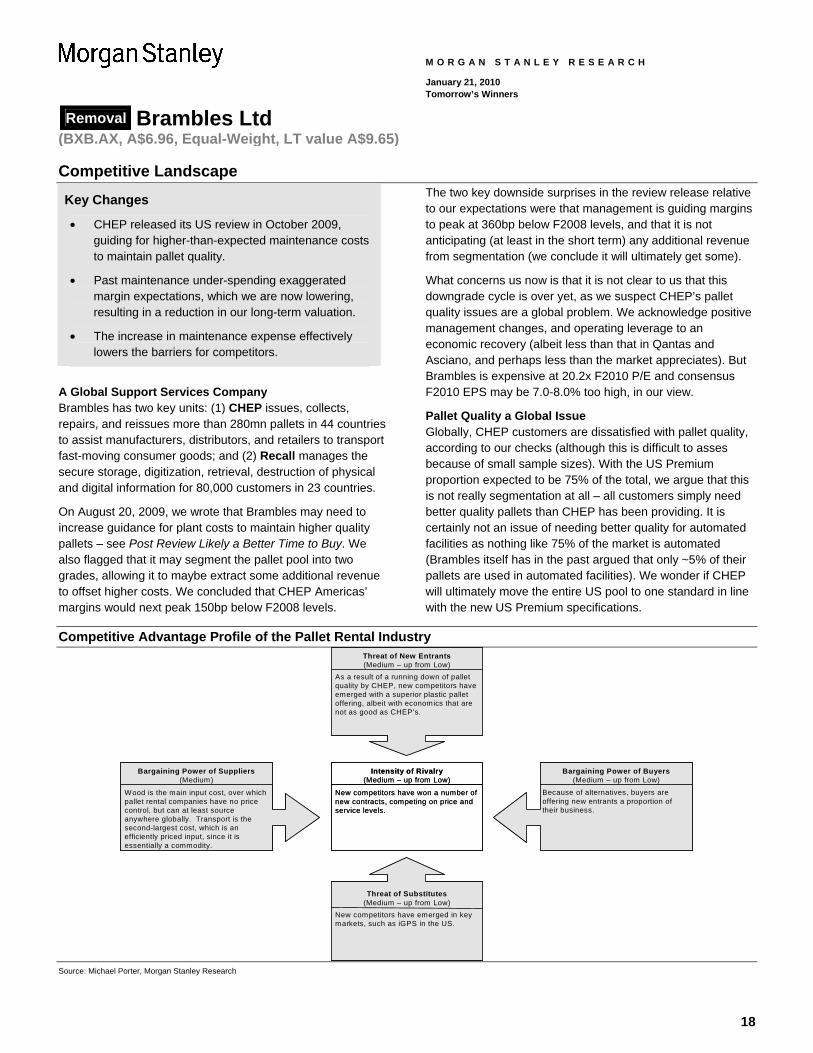

Competitive Landscape

Key Changes

• CHEP released its US review in October 2009, guiding for higher-than-expected maintenance costs to maintain pallet quality.

• Past maintenance under-spending exaggerated margin expectations, which we are now lowering, resulting in a reduction in our long-term valuation.

• The increase in maintenance expense effectively lowers the barriers for competitors.

A Global Support Services Company Brambles has two key units: (1) CHEP issues, collects, repairs, and reissues more than 280mn pallets in 44 countries to assist manufacturers, distributors, and retailers to transport fast-moving consumer goods; and (2) Recall manages the secure storage, digitization, retrieval, destruction of physical and digital information for 80,000 customers in 23 countries.

On August 20, 2009, we wrote that Brambles may need to increase guidance for plant costs to maintain higher quality pallets – see Post Review Likely a Better Time to Buy. We also flagged that it may segment the pallet pool into two grades, allowing it to maybe extract some additional revenue to offset higher costs. We concluded that CHEP Americas’ margins would next peak 150bp below F2008 levels.

The two key downside surprises in the review release relative to our expectations were that management is guiding margins to peak at 360bp below F2008 levels, and that it is not anticipating (at least in the short term) any additional revenue from segmentation (we conclude it will ultimately get some).

What concerns us now is that it is not clear to us that this downgrade cycle is over yet, as we suspect CHEP’s pallet quality issues are a global problem. We acknowledge positive management changes, and operating leverage to an economic recovery (albeit less than that in Qantas and Asciano, and perhaps less than the market appreciates). But Brambles is expensive at 20.2x F2010 P/E and consensus F2010 EPS may be 7.0-8.0% too high, in our view.

Pallet Quality a Global Issue Globally, CHEP customers are dissatisfied with pallet quality, according to our checks (although this is difficult to asses because of small sample sizes). With the US Premium proportion expected to be 75% of the total, we argue that this is not really segmentation at all – all customers simply need better quality pallets than CHEP has been providing. It is certainly not an issue of needing better quality for automated facilities as nothing like 75% of the market is automated (Brambles itself has in the past argued that only ~5% of their pallets are used in automated facilities). We wonder if CHEP will ultimately move the entire US pool to one standard in line with the new US Premium specifications.

Competitive Advantage Profile of the Pallet Rental Industry

As a result of a running down of pallet quality by CHEP, new competitors have emerged with a superior plastic pallet offering, albeit with economics that are not as good as CHEP’s.

Threat of New Entrants(Medium – up from Low)

New competitors have won a number of new contracts, competing on price and service levels.

Intensity of Rivalry(Medium – up from Low)

Because of alternatives, buyers are offering new entrants a proportion of their business.

Bargaining Power of Buyers(Medium – up from Low)

Wood is the main input cost, over which pallet rental companies have no price control, but can at least source anywhere globally. Transport is the second-largest cost, which is an efficiently priced input, since it is essentially a commodity.

Bargaining Power of Suppliers(Medium)

New competitors have emerged in key markets, such as iGPS in the US.

Threat of Substitutes(Medium – up from Low)

As a result of a running down of pallet quality by CHEP, new competitors have emerged with a superior plastic pallet offering, albeit with economics that are not as good as CHEP’s.

Threat of New Entrants(Medium – up from Low)

New competitors have won a number of new contracts, competing on price and service levels.

Intensity of Rivalry(Medium – up from Low)

Because of alternatives, buyers are offering new entrants a proportion of their business.

Bargaining Power of Buyers(Medium – up from Low)

Wood is the main input cost, over which pallet rental companies have no price control, but can at least source anywhere globally. Transport is the second-largest cost, which is an efficiently priced input, since it is essentially a commodity.

Bargaining Power of Suppliers(Medium)

New competitors have emerged in key markets, such as iGPS in the US.

Threat of Substitutes(Medium – up from Low)

Source: Michael Porter, Morgan Stanley Research

19

Removal Brambles Ltd (BXB.AX, A$6.96, Equal-Weight, LT value A$9.65)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

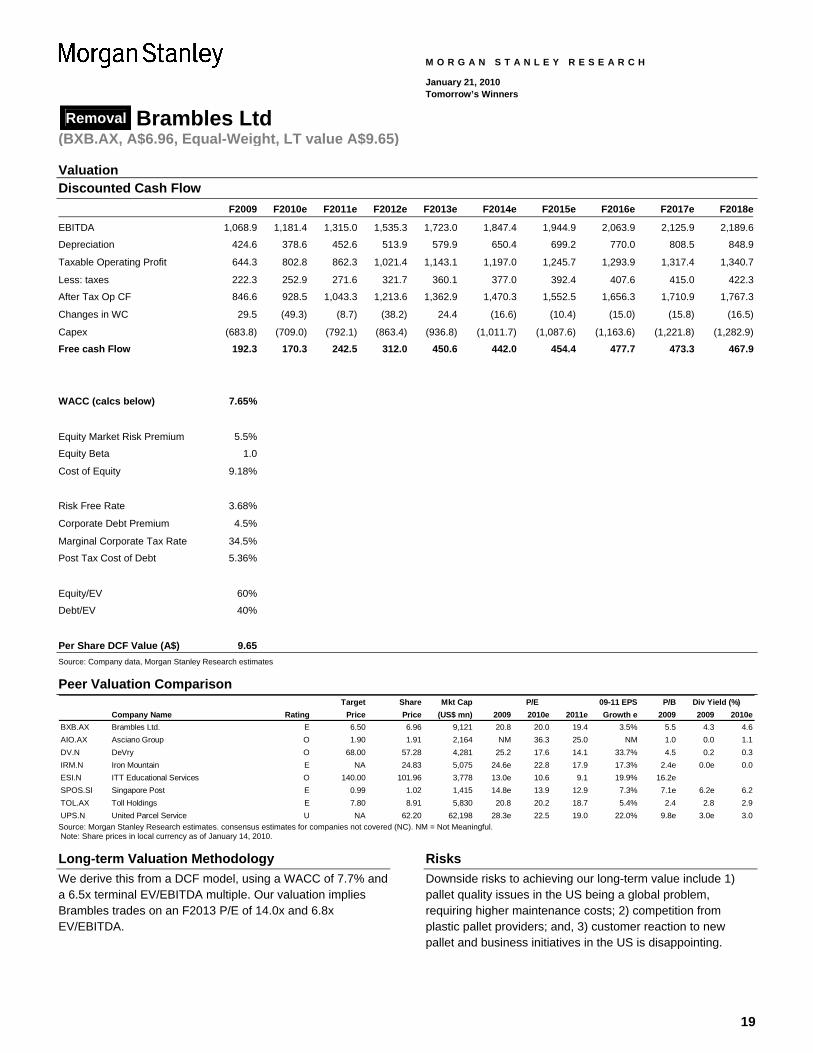

Valuation Discounted Cash Flow F2009 F2010e F2011e F2012e F2013e F2014e F2015e F2016e F2017e F2018e

EBITDA 1,068.9 1,181.4 1,315.0 1,535.3 1,723.0 1,847.4 1,944.9 2,063.9 2,125.9 2,189.6

Depreciation 424.6 378.6 452.6 513.9 579.9 650.4 699.2 770.0 808.5 848.9

Taxable Operating Profit 644.3 802.8 862.3 1,021.4 1,143.1 1,197.0 1,245.7 1,293.9 1,317.4 1,340.7

Less: taxes 222.3 252.9 271.6 321.7 360.1 377.0 392.4 407.6 415.0 422.3

After Tax Op CF 846.6 928.5 1,043.3 1,213.6 1,362.9 1,470.3 1,552.5 1,656.3 1,710.9 1,767.3

Changes in WC 29.5 (49.3) (8.7) (38.2) 24.4 (16.6) (10.4) (15.0) (15.8) (16.5)

Capex (683.8) (709.0) (792.1) (863.4) (936.8) (1,011.7) (1,087.6) (1,163.6) (1,221.8) (1,282.9)

Free cash Flow 192.3 170.3 242.5 312.0 450.6 442.0 454.4 477.7 473.3 467.9

WACC (calcs below) 7.65%

Equity Market Risk Premium 5.5%

Equity Beta 1.0

Cost of Equity 9.18%

Risk Free Rate 3.68%

Corporate Debt Premium 4.5%

Marginal Corporate Tax Rate 34.5%

Post Tax Cost of Debt 5.36%

Equity/EV 60%

Debt/EV 40%

Per Share DCF Value (A$) 9.65 Source: Company data, Morgan Stanley Research estimates

Peer Valuation Comparison Target Share Mkt Cap 09-11 EPS P/B

Company Name Rating Price Price (US$ mn) 2009 2010e 2011e Growth e 2009 2009 2010eBXB.AX Brambles Ltd. E 6.50 6.96 9,121 20.8 20.0 19.4 3.5% 5.5 4.3 4.6AIO.AX Asciano Group O 1.90 1.91 2,164 NM 36.3 25.0 NM 1.0 0.0 1.1DV.N DeVry O 68.00 57.28 4,281 25.2 17.6 14.1 33.7% 4.5 0.2 0.3IRM.N Iron Mountain E NA 24.83 5,075 24.6e 22.8 17.9 17.3% 2.4e 0.0e 0.0ESI.N ITT Educational Services O 140.00 101.96 3,778 13.0e 10.6 9.1 19.9% 16.2eSPOS.SI Singapore Post E 0.99 1.02 1,415 14.8e 13.9 12.9 7.3% 7.1e 6.2e 6.2TOL.AX Toll Holdings E 7.80 8.91 5,830 20.8 20.2 18.7 5.4% 2.4 2.8 2.9UPS.N United Parcel Service U NA 62.20 62,198 28.3e 22.5 19.0 22.0% 9.8e 3.0e 3.0

P/E Div Yield (%)

Source: Morgan Stanley Research estimates. consensus estimates for companies not covered (NC). NM = Not Meaningful. Note: Share prices in local currency as of January 14, 2010.

Long-term Valuation Methodology We derive this from a DCF model, using a WACC of 7.7% and a 6.5x terminal EV/EBITDA multiple. Our valuation implies Brambles trades on an F2013 P/E of 14.0x and 6.8x EV/EBITDA.

Risks Downside risks to achieving our long-term value include 1) pallet quality issues in the US being a global problem, requiring higher maintenance costs; 2) competition from plastic pallet providers; and, 3) customer reaction to new pallet and business initiatives in the US is disappointing.

20

Removal Brambles Ltd (BXB.AX, A$6.96, Equal-Weight, LT value A$9.65)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

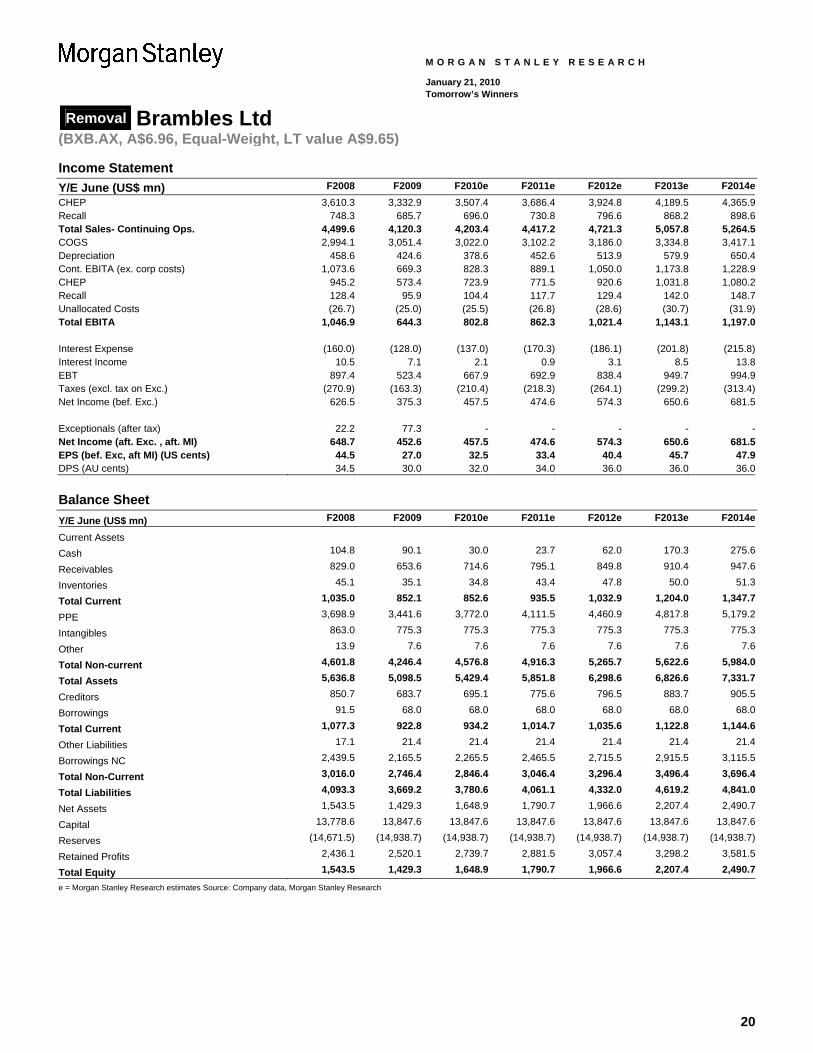

Income Statement Y/E June (US$ mn) F2008 F2009 F2010e F2011e F2012e F2013e F2014eCHEP 3,610.3 3,332.9 3,507.4 3,686.4 3,924.8 4,189.5 4,365.9Recall 748.3 685.7 696.0 730.8 796.6 868.2 898.6Total Sales- Continuing Ops. 4,499.6 4,120.3 4,203.4 4,417.2 4,721.3 5,057.8 5,264.5COGS 2,994.1 3,051.4 3,022.0 3,102.2 3,186.0 3,334.8 3,417.1Depreciation 458.6 424.6 378.6 452.6 513.9 579.9 650.4Cont. EBITA (ex. corp costs) 1,073.6 669.3 828.3 889.1 1,050.0 1,173.8 1,228.9CHEP 945.2 573.4 723.9 771.5 920.6 1,031.8 1,080.2Recall 128.4 95.9 104.4 117.7 129.4 142.0 148.7Unallocated Costs (26.7) (25.0) (25.5) (26.8) (28.6) (30.7) (31.9)Total EBITA 1,046.9 644.3 802.8 862.3 1,021.4 1,143.1 1,197.0 Interest Expense (160.0) (128.0) (137.0) (170.3) (186.1) (201.8) (215.8)Interest Income 10.5 7.1 2.1 0.9 3.1 8.5 13.8EBT 897.4 523.4 667.9 692.9 838.4 949.7 994.9Taxes (excl. tax on Exc.) (270.9) (163.3) (210.4) (218.3) (264.1) (299.2) (313.4)Net Income (bef. Exc.) 626.5 375.3 457.5 474.6 574.3 650.6 681.5 Exceptionals (after tax) 22.2 77.3 - - - - -Net Income (aft. Exc. , aft. MI) 648.7 452.6 457.5 474.6 574.3 650.6 681.5EPS (bef. Exc, aft MI) (US cents) 44.5 27.0 32.5 33.4 40.4 45.7 47.9DPS (AU cents) 34.5 30.0 32.0 34.0 36.0 36.0 36.0

Balance Sheet Y/E June (US$ mn) F2008 F2009 F2010e F2011e F2012e F2013e F2014e

Current Assets Cash 104.8 90.1 30.0 23.7 62.0 170.3 275.6

Receivables 829.0 653.6 714.6 795.1 849.8 910.4 947.6

Inventories 45.1 35.1 34.8 43.4 47.8 50.0 51.3

Total Current 1,035.0 852.1 852.6 935.5 1,032.9 1,204.0 1,347.7

PPE 3,698.9 3,441.6 3,772.0 4,111.5 4,460.9 4,817.8 5,179.2

Intangibles 863.0 775.3 775.3 775.3 775.3 775.3 775.3

Other 13.9 7.6 7.6 7.6 7.6 7.6 7.6

Total Non-current 4,601.8 4,246.4 4,576.8 4,916.3 5,265.7 5,622.6 5,984.0

Total Assets 5,636.8 5,098.5 5,429.4 5,851.8 6,298.6 6,826.6 7,331.7

Creditors 850.7 683.7 695.1 775.6 796.5 883.7 905.5

Borrowings 91.5 68.0 68.0 68.0 68.0 68.0 68.0

Total Current 1,077.3 922.8 934.2 1,014.7 1,035.6 1,122.8 1,144.6

Other Liabilities 17.1 21.4 21.4 21.4 21.4 21.4 21.4

Borrowings NC 2,439.5 2,165.5 2,265.5 2,465.5 2,715.5 2,915.5 3,115.5

Total Non-Current 3,016.0 2,746.4 2,846.4 3,046.4 3,296.4 3,496.4 3,696.4

Total Liabilities 4,093.3 3,669.2 3,780.6 4,061.1 4,332.0 4,619.2 4,841.0

Net Assets 1,543.5 1,429.3 1,648.9 1,790.7 1,966.6 2,207.4 2,490.7

Capital 13,778.6 13,847.6 13,847.6 13,847.6 13,847.6 13,847.6 13,847.6

Reserves (14,671.5) (14,938.7) (14,938.7) (14,938.7) (14,938.7) (14,938.7) (14,938.7)

Retained Profits 2,436.1 2,520.1 2,739.7 2,881.5 3,057.4 3,298.2 3,581.5

Total Equity 1,543.5 1,429.3 1,648.9 1,790.7 1,966.6 2,207.4 2,490.7

e = Morgan Stanley Research estimates Source: Company data, Morgan Stanley Research

21

Removal Brambles Ltd (BXB.AX, A$6.96, Equal-Weight, LT value A$9.65)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Cash Flow Statement Y/E June (US$ mn) F2008 F2009 F2010e F2011e F2012e F2013e F2014eEBITA 1,046.9 644.3 802.8 862.3 1,021.4 1,143.1 1,197.0 Depreciation 458.6 424.6 378.6 452.6 513.9 579.9 650.4 WC Changes 66.6 29.5 (49.3) (8.7) (38.2) 24.4 (16.6)Tax (232.9) (129.2) (210.4) (218.3) (264.1) (299.2) (313.4)Interest Expense (146.4) (131.8) (137.0) (170.3) (186.1) (201.8) (215.8)Interest Earnings 9.6 8.0 2.1 0.9 3.1 8.5 13.8 Operating Cash flow 1,166.3 1,023.0 786.8 918.6 1,050.1 1,254.9 1,315.3 Capex- Maintenance (458.6) (424.6) (378.6) (452.6) (513.9) (579.9) (650.4)Capex Growth (410.8) (259.2) (330.4) (339.5) (349.5) (356.9) (361.3)Non PP&E Investments (82.7) (24.4) - - - - -Disposals 140.7 101.6 - - - - -Investing Cash flow (811.4) (606.6) (709.0) (792.1) (863.4) (936.8) (1,011.7) Ordinary and Special Dividend (444.8) (277.6) (237.9) (332.8) (398.4) (409.8) (398.3)Share Issue 38.5 0.8 - - - - -Buyback (392.0) - - - - - -Other financing Cash Flow 128.3 (8.6) - - - - -Changes in borrowings 269.7 (109.3) 100.0 200.0 250.0 200.0 200.0 Financing Cash flow (400.3) (394.7) (137.9) (132.8) (148.4) (209.8) (198.3)Effect of foreign Exchange 19.8 (36.4) - - - - -Closing Cash 104.8 90.1 30.0 23.7 62.0 170.3 275.6

Ratio Analysis Y/E June (US$ mn) F2008 F2009 F2010e F2011e F2012e F2013e F2014eCHEP AMERICAS Revenues 1,581.3 1,556.9 1,611.4 1,692.0 1,751.2 1,824.7 1,916.0 Growth % 9.9% -1.5% 3.5% 5.0% 3.5% 4.2% 5.0%EBIT 452.8 229.0 319.1 329.9 395.8 456.2 479.0 EBIT Margin % 28.6% 14.7% 19.8% 19.5% 22.6% 25.0% 25.0% EMEA Revenues 1,642.1 1,452.6 1,531.5 1,608.0 1,744.7 1,893.0 1,959.3 Growth % 12.7% -11.5% 5.4% 5.0% 8.5% 8.5% 3.5%EBIT 396.5 286.5 340.0 365.0 429.2 469.5 489.8 EBIT Margin % 24.1% 19.7% 22.2% 22.7% 24.6% 24.8% 25.0% ASIA-PACIFIC Revenues 386.9 323.4 364.5 386.4 428.9 471.8 490.6 Growth % 19.9% -16.4% 12.7% 6.0% 11.0% 10.0% 4.0%EBIT 95.9 57.9 64.9 76.5 95.6 106.1 111.4 EBIT Margin % 24.8% 17.9% 17.8% 19.8% 22.3% 22.5% 22.7% CHEP Revenues 3,610.3 3,332.9 3,507.4 3,686.4 3,924.8 4,189.5 4,365.9 Growth % 12.2% -7.7% 5.2% 5.1% 6.5% 6.7% 4.2%CHEP EBIT 945.2 573.4 723.9 771.5 920.6 1,031.8 1,080.2 EBIT Margin % 26.2% 17.2% 20.6% 20.9% 23.5% 24.6% 24.7%e = Morgan Stanley Research estimates Source: Company data, Morgan Stanley Research

22

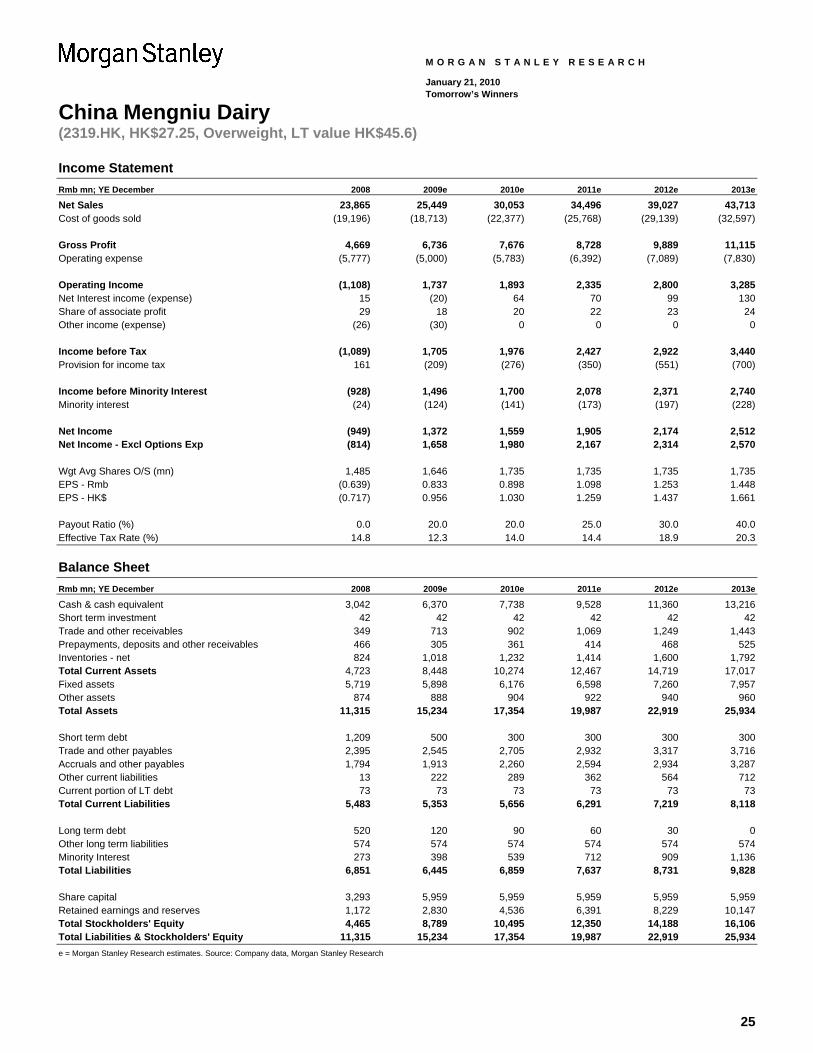

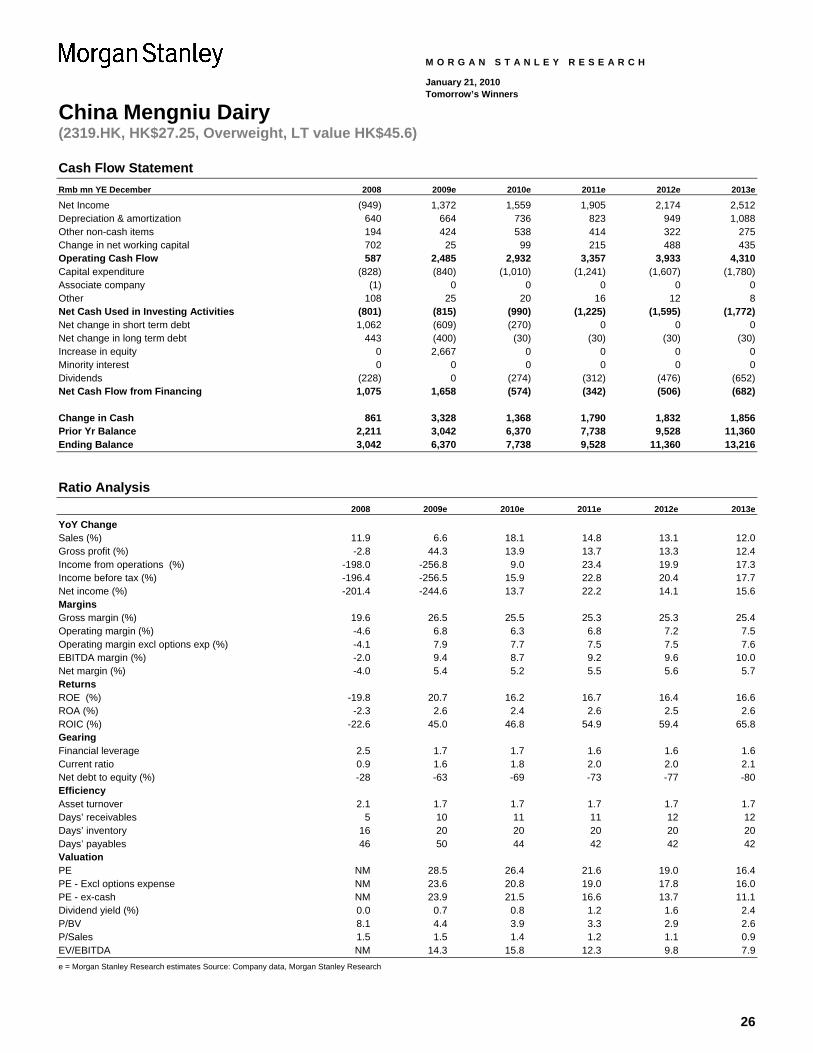

China Mengniu Dairy (2319.HK, HK$27.25, Overweight, LT value HK$45.6)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Industry leader to capitalize on industry growth Ticker (Reuters/Bloomberg)Share price, close (Jan-14-2010)RatingPrice target (12-18 months)Price target (5 years) HK$45.60Average daily trading value (mn)

Return on Equity (ROE) Morgan Stanley forecast

Net Operating Profit After Tax (NOPAT) Margin

× Operating Asset Turnover

+ Return from Leverage

Source: Company data, Morgan Stanley Research estimates

2319.HK / 2319 HKHK$27.25

OverweightHK$32.00

US$20

31.2%

-18.6%

30.7%

18.1% 17.8%

18.2%17.6%17.7%

30%

20%

10%

0%

10%

20%

30%

40%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

5.2%

-4.0%

6.0% 5.8% 6.0%5.4%

5.8% 6.2%

6%

4%

2%

0%

2%

4%

6%

8%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

6.06 5.70

7.12

9.01

10.508.19

9.72

11.04

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

-0.3%

-11.9%

-34.1%

-45.0%

-50.6%

-39.0%

-26.7%

3.9%

60%

50%

40%

30%

20%

10%

0%

10%

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

Morgan Stanley Asia Limited+

Angela Moh [email protected]

Penny Tu

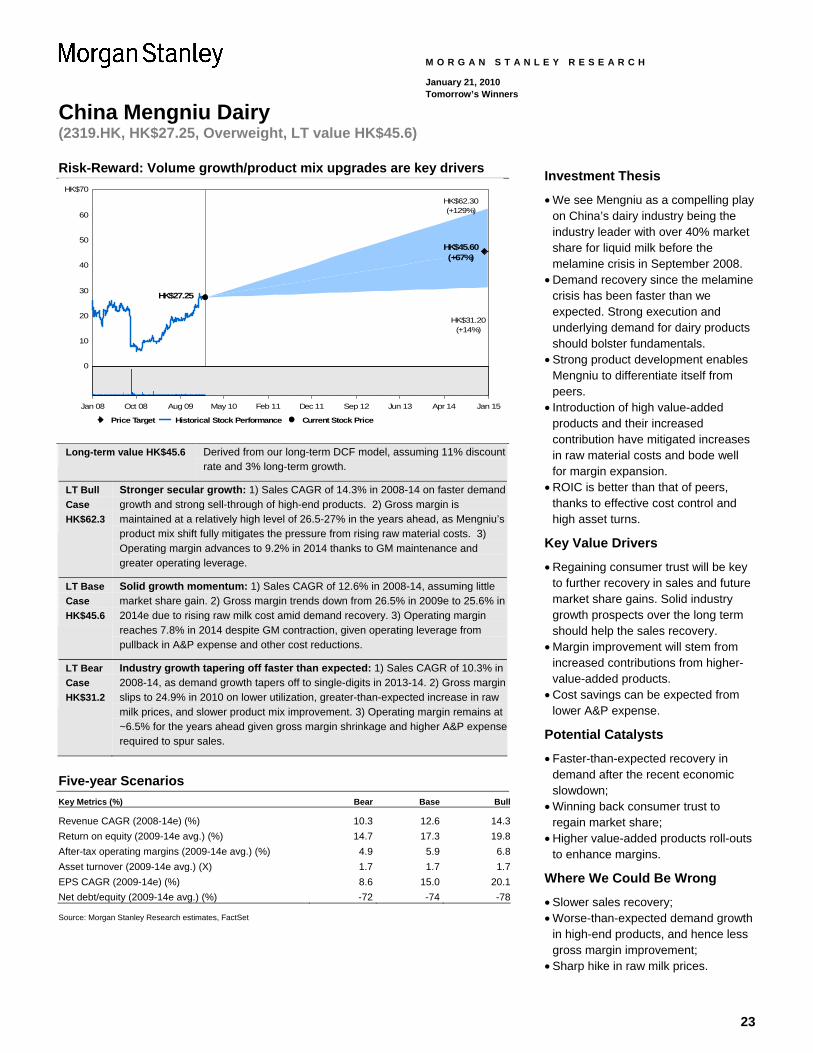

Best proxy to China’s dairy industry growth We believe that Mengniu will stand out as a long-term winner in China’s dairy industry by gaining market share. Mengniu’s key competitive advantages include strong product development capabilities, a robust distribution platform, effective management execution, and a more proactive and flexible strategy compared with those of other dairy companies. We expect its long-term growth to come from: First, secular growth of China’s dairy industry: China’s per capita consumption of liquid milk was around 10 liters in 2008, versus 20-70 liters in developed markets. We believe that sustained growth in liquid milk consumption will be driven by improving affordability, with disposable income expected to rise much faster than average product prices. Second, product mix upgrades to support top-line growth and margin expansion: Higher-margin value-added products now account for around 15% of sales, and management aims to increase this proportion to ~20% in the next three years.

When we include the accumulated dividend yield for 2010-2014e, the total implied five-year return would be 76.8% (or 140.6% in our bull case).

Profitability: Upside likely to come from better margins Our base case conservatively assumes the gross margin will trend down from 26.5% in 2009e to ~25.5% in the next few years on potential raw milk price increases. In our bull case, we assume Mengniu will be able to maintain its gross margins in coming years because 1) its sourcing of higher quality milk from larger scale farms will enhance the stability of raw milk costs; and 2) product mix upgrading brought by a greater revenue contribution from high-end products could mitigate fluctuations in raw material costs. In the longer term, there is also room for greater operating leverage from growing scale and a lower advertising and promotion (A&P) expense ratio.

Financial risks – limited Mengniu has nearly Rmb7bn in cash after the investment by COFCO Group in July 2009; we expect it to remain in a net cash position in our forecast years. Strong operating cash flow is more than sufficient to cover capex. Mengniu plans to continue consolidating its upstream operations in the following ways: 1) building milking infrastructure for individual farmers; 2) providing financing for milk farms upgrades or expansion; and 3) offering technical training to farmers. Its strategy remains to invest in minor stakes in farms instead of in raising cows itself, so funding needs should not be excessive.

23

China Mengniu Dairy (2319.HK, HK$27.25, Overweight, LT value HK$45.6)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Risk-Reward: Volume growth/product mix upgrades are key drivers

0

10

20

30

40

50

60

HK$70HK$62.30(+129%)

HK$45.60(+67%)

HK$31.20(+14%)

HK$27.25

Price Target Historical Stock Performance Current Stock Price

Jan 08 Oct 08 Aug 09 May 10 Feb 11 Dec 11 Sep 12 Jun 13 Apr 14 Jan 15

Long-term value HK$45.6 Derived from our long-term DCF model, assuming 11% discount rate and 3% long-term growth.

LT Bull Case HK$62.3

Stronger secular growth: 1) Sales CAGR of 14.3% in 2008-14 on faster demand growth and strong sell-through of high-end products. 2) Gross margin is maintained at a relatively high level of 26.5-27% in the years ahead, as Mengniu’s product mix shift fully mitigates the pressure from rising raw material costs. 3) Operating margin advances to 9.2% in 2014 thanks to GM maintenance and greater operating leverage.

LT Base Case HK$45.6

Solid growth momentum: 1) Sales CAGR of 12.6% in 2008-14, assuming little market share gain. 2) Gross margin trends down from 26.5% in 2009e to 25.6% in 2014e due to rising raw milk cost amid demand recovery. 3) Operating margin reaches 7.8% in 2014 despite GM contraction, given operating leverage from pullback in A&P expense and other cost reductions.

LT Bear Case HK$31.2

Industry growth tapering off faster than expected: 1) Sales CAGR of 10.3% in 2008-14, as demand growth tapers off to single-digits in 2013-14. 2) Gross margin slips to 24.9% in 2010 on lower utilization, greater-than-expected increase in raw milk prices, and slower product mix improvement. 3) Operating margin remains at ~6.5% for the years ahead given gross margin shrinkage and higher A&P expense required to spur sales.

Five-year Scenarios Key Metrics (%) Bear Base Bull

Revenue CAGR (2008-14e) (%) 10.3 12.6 14.3Return on equity (2009-14e avg.) (%) 14.7 17.3 19.8After-tax operating margins (2009-14e avg.) (%) 4.9 5.9 6.8Asset turnover (2009-14e avg.) (X) 1.7 1.7 1.7EPS CAGR (2009-14e) (%) 8.6 15.0 20.1Net debt/equity (2009-14e avg.) (%) -72 -74 -78 Source: Morgan Stanley Research estimates, FactSet

Investment Thesis

• We see Mengniu as a compelling play on China’s dairy industry being the industry leader with over 40% market share for liquid milk before the melamine crisis in September 2008.

• Demand recovery since the melamine crisis has been faster than we expected. Strong execution and underlying demand for dairy products should bolster fundamentals.

• Strong product development enables Mengniu to differentiate itself from peers.

• Introduction of high value-added products and their increased contribution have mitigated increases in raw material costs and bode well for margin expansion.

• ROIC is better than that of peers, thanks to effective cost control and high asset turns.

Key Value Drivers

• Regaining consumer trust will be key to further recovery in sales and future market share gains. Solid industry growth prospects over the long term should help the sales recovery.

• Margin improvement will stem from increased contributions from higher-value-added products.

• Cost savings can be expected from lower A&P expense.

Potential Catalysts

• Faster-than-expected recovery in demand after the recent economic slowdown;

• Winning back consumer trust to regain market share;

• Higher value-added products roll-outs to enhance margins.

Where We Could Be Wrong

• Slower sales recovery; • Worse-than-expected demand growth

in high-end products, and hence less gross margin improvement;

• Sharp hike in raw milk prices.

24

China Mengniu Dairy (2319.HK, HK$27.25, Overweight, LT value HK$45.6)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

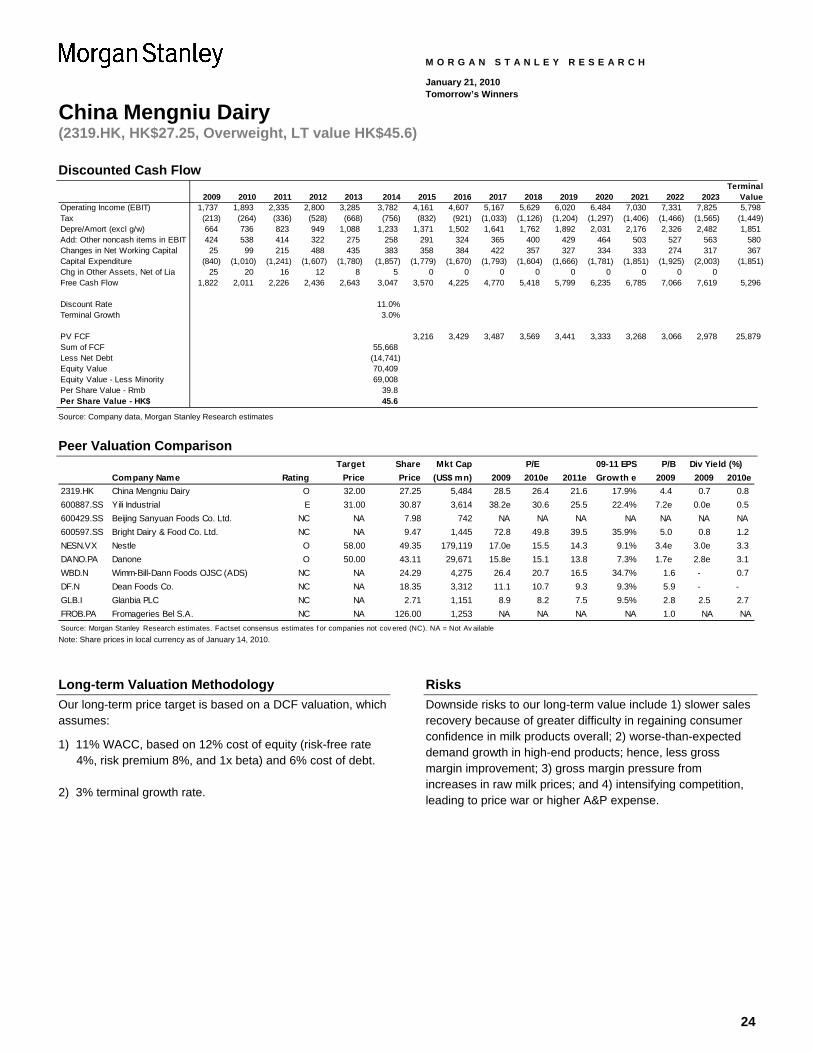

Discounted Cash Flow

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023Terminal

ValueOperating Income (EBIT) 1,737 1,893 2,335 2,800 3,285 3,782 4,161 4,607 5,167 5,629 6,020 6,484 7,030 7,331 7,825 5,798Tax (213) (264) (336) (528) (668) (756) (832) (921) (1,033) (1,126) (1,204) (1,297) (1,406) (1,466) (1,565) (1,449)Depre/Amort (excl g/w) 664 736 823 949 1,088 1,233 1,371 1,502 1,641 1,762 1,892 2,031 2,176 2,326 2,482 1,851Add: Other noncash items in EBIT 424 538 414 322 275 258 291 324 365 400 429 464 503 527 563 580Changes in Net Working Capital 25 99 215 488 435 383 358 384 422 357 327 334 333 274 317 367Capital Expenditure (840) (1,010) (1,241) (1,607) (1,780) (1,857) (1,779) (1,670) (1,793) (1,604) (1,666) (1,781) (1,851) (1,925) (2,003) (1,851)Chg in Other Assets, Net of Lia 25 20 16 12 8 5 0 0 0 0 0 0 0 0 0Free Cash Flow 1,822 2,011 2,226 2,436 2,643 3,047 3,570 4,225 4,770 5,418 5,799 6,235 6,785 7,066 7,619 5,296

Discount Rate 11.0%Terminal Growth 3.0%

PV FCF 3,216 3,429 3,487 3,569 3,441 3,333 3,268 3,066 2,978 25,879Sum of FCF 55,668Less Net Debt (14,741)Equity Value 70,409Equity Value - Less Minority 69,008Per Share Value - Rmb 39.8Per Share Value - HK$ 45.6 Source: Company data, Morgan Stanley Research estimates

Peer Valuation Comparison

Target Share Mkt Cap 09-11 EPS P/BCompany Name Rating Price Price (US$ mn) 2009 2010e 2011e Growth e 2009 2009 2010e

2319.HK China Mengniu Dairy O 32.00 27.25 5,484 28.5 26.4 21.6 17.9% 4.4 0.7 0.8 600887.SS Yili Industrial E 31.00 30.87 3,614 38.2e 30.6 25.5 22.4% 7.2e 0.0e 0.5600429.SS Beijing Sanyuan Foods Co. Ltd. NC NA 7.98 742 NA NA NA NA NA NA NA600597.SS Bright Dairy & Food Co. Ltd. NC NA 9.47 1,445 72.8 49.8 39.5 35.9% 5.0 0.8 1.2 NESN.VX Nestle O 58.00 49.35 179,119 17.0e 15.5 14.3 9.1% 3.4e 3.0e 3.3DANO.PA Danone O 50.00 43.11 29,671 15.8e 15.1 13.8 7.3% 1.7e 2.8e 3.1WBD.N Wimm-Bill-Dann Foods OJSC (ADS) NC NA 24.29 4,275 26.4 20.7 16.5 34.7% 1.6 - 0.7 DF.N Dean Foods Co. NC NA 18.35 3,312 11.1 10.7 9.3 9.3% 5.9 - - GLB.I Glanbia PLC NC NA 2.71 1,151 8.9 8.2 7.5 9.5% 2.8 2.5 2.7 FROB.PA Fromageries Bel S.A. NC NA 126.00 1,253 NA NA NA NA 1.0 NA NASource: Morgan Stanley Research estimates. Factset consensus estimates f or companies not cov ered (NC). NA = Not Av ailable

P/E Div Yield (%)

Note: Share prices in local currency as of January 14, 2010.

Long-term Valuation Methodology Our long-term price target is based on a DCF valuation, which assumes:

1) 11% WACC, based on 12% cost of equity (risk-free rate 4%, risk premium 8%, and 1x beta) and 6% cost of debt.

2) 3% terminal growth rate.

Risks Downside risks to our long-term value include 1) slower sales recovery because of greater difficulty in regaining consumer confidence in milk products overall; 2) worse-than-expected demand growth in high-end products; hence, less gross margin improvement; 3) gross margin pressure from increases in raw milk prices; and 4) intensifying competition, leading to price war or higher A&P expense.

25

China Mengniu Dairy (2319.HK, HK$27.25, Overweight, LT value HK$45.6)

M O R G A N S T A N L E Y R E S E A R C H

January 21, 2010 Tomorrow’s Winners

Income Statement Rmb mn; YE December 2008 2009e 2010e 2011e 2012e 2013e Net Sales 23,865 25,449 30,053 34,496 39,027 43,713 Cost of goods sold (19,196) (18,713) (22,377) (25,768) (29,139) (32,597) Gross Profit 4,669 6,736 7,676 8,728 9,889 11,115 Operating expense (5,777) (5,000) (5,783) (6,392) (7,089) (7,830) Operating Income (1,108) 1,737 1,893 2,335 2,800 3,285 Net Interest income (expense) 15 (20) 64 70 99 130 Share of associate profit 29 18 20 22 23 24 Other income (expense) (26) (30) 0 0 0 0 Income before Tax (1,089) 1,705 1,976 2,427 2,922 3,440 Provision for income tax 161 (209) (276) (350) (551) (700) Income before Minority Interest (928) 1,496 1,700 2,078 2,371 2,740 Minority interest (24) (124) (141) (173) (197) (228) Net Income (949) 1,372 1,559 1,905 2,174 2,512 Net Income - Excl Options Exp (814) 1,658 1,980 2,167 2,314 2,570 Wgt Avg Shares O/S (mn) 1,485 1,646 1,735 1,735 1,735 1,735 EPS - Rmb (0.639) 0.833 0.898 1.098 1.253 1.448 EPS - HK$ (0.717) 0.956 1.030 1.259 1.437 1.661 Payout Ratio (%) 0.0 20.0 20.0 25.0 30.0 40.0 Effective Tax Rate (%) 14.8 12.3 14.0 14.4 18.9 20.3