monthly insight

TRANSCRIPT

January 2018

Monthly InsighTOutlook for IT appears solidWonjae [email protected]

Chuljoong [email protected]

Young-gun [email protected]

Seungho [email protected]

Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S.PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Mirae Asset Daewoo Research2| Monthly InsighT

Contents

I. Investment strategy

II. Top picks

III. Sector view

IV. Think big

V. Global IT navigation

Spotlight stocks & other notable stocks

.......................................... 3

........................................................... 8

....................................................... 10

......................................................... 15

...................................... 21

…………….… 24

Mirae Asset Daewoo Research3| Monthly InsighT

I. Investment strategyPositive 4Q17 results expected despite won appreciation; IT shares to rise in steps

II. Top picks

III. Sector view

IV. Think big

V. Global IT navigation

Spotlight stocks & other notable stocks

Mirae Asset Daewoo Research4| Monthly InsighT

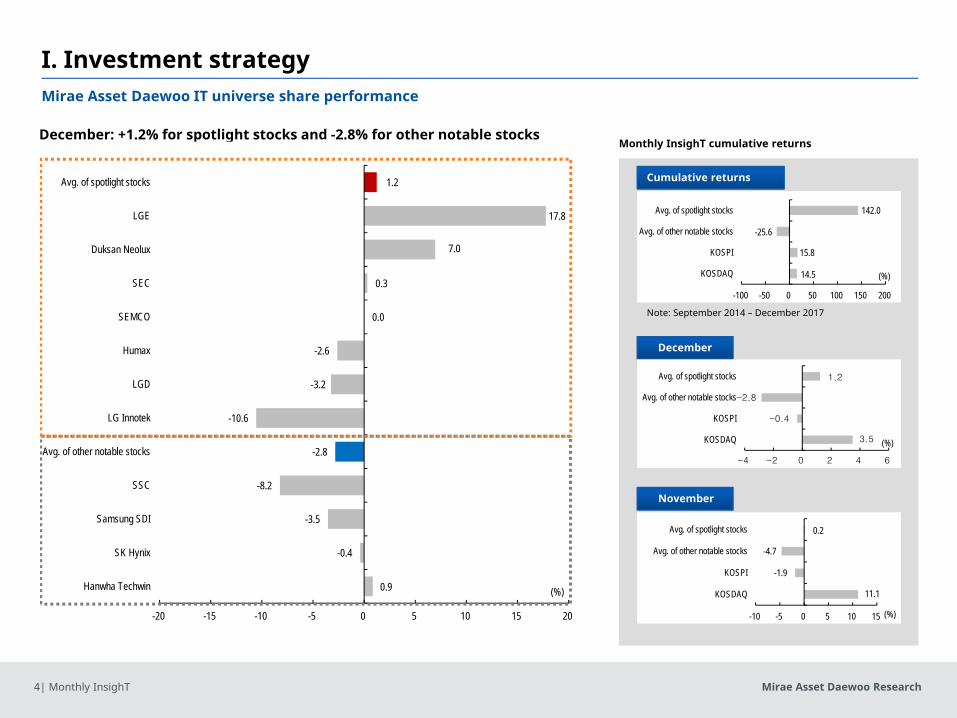

I. Investment strategy Mirae Asset Daewoo IT universe share performance

Monthly InsighT cumulative returns

Note: September 2014 – December 2017

November

December

Cumulative returns

December: +1.2% for spotlight stocks and -2.8% for other notable stocks

3.5

-0.4

-2.8

1.2

-4 -2 0 2 4 6

KOSDAQ

KOSPI

Avg. of other notable stocks

Avg. of spotlight stocks

(%)

14.5

15.8

-25.6

142.0

-100 -50 0 50 100 150 200

KOSDAQ

KOSPI

Avg. of other notable stocks

Avg. of spotlight stocks

(%)

0.9

-0.4

-3.5

-8.2

-2.8

-10.6

-3.2

-2.6

0.0

0.3

7.0

17.8

1.2

-20 -15 -10 -5 0 5 10 15 20

Hanwha Techwin

SK Hynix

Samsung SDI

SSC

Avg. of other notable stocks

LG Innotek

LGD

Humax

SEMCO

SEC

Duksan Neolux

LGE

Avg. of spotlight stocks

(%) 11.1

-1.9

-4.7

0.2

-10 -5 0 5 10 15

KOSDAQ

KOSPI

Avg. of other notable stocks

Avg. of spotlight stocks

(%)

Mirae Asset Daewoo Research5| Monthly InsighT

I. Investment strategy

Source: WISEfn, Mirae Asset Daewoo Research

Share performance & OP consensus revision rates for Korean IT large caps

Mirae Asset Daewoo IT large-cap universe

Source: WISEfn, Mirae Asset Daewoo Research

(W, %, x)

Company Rating TP Currentprice (12/28) Upside

Share performance P/E P/B ROE1W 1M 17F 18F 17F 18F 17F 18F

LGE Buy 129,000 106,000 21.7 6.7 17.8 9.7 8.5 1.4 1.2 15.2 15.0LGD Buy 42,000 29,900 40.5 1.4 -3.2 5.7 11.7 0.8 0.7 14.2 6.4Samsung SDI Buy 270,000 204,500 32.0 1.2 -3.5 19.5 12.6 1.2 1.1 6.7 9.7SEMCO Buy 131,000 100,000 31.0 1.3 0.0 46.4 25.6 1.7 1.6 3.9 6.7LG Innotek Buy 210,000 144,000 45.8 3.6 -10.6 15.5 11.3 1.7 1.5 11.7 14.0SSC Buy 37,800 27,850 35.7 2.4 -8.2 26.4 19.8 2.5 2.2 9.8 12.0Hanwha Techwin Buy 45,400 35,550 27.7 0.9 0.9 39.3 21.3 0.8 0.8 2.1 3.7SEC - - 2,548,000 - 3.7 0.3 9.4 7.5 1.6 1.4 20.2 20.7SK Hynix - - 76,500 - -0.6 -0.4 5.1 4.3 1.6 1.2 37.3 32.0

Positive 4Q17 results expected despite won appreciation; IT shares to rise in steps

■ IT sector update- Semiconductor: Share performance will likely be better than expected despite

concerns over the potential peaking of earnings; SEC is forecast to fare better than peers based on its market leadership.

- Display: Panel prices remained on the decline in December, and are projected to hit bottom in 1Q18; OLED materials and component shipments are projected to continue to grow robustly in 1Q18.

- Handset/component: New smartphone models could provide a boost to component producers’ earnings in the traditional low-demand season of 4Q17; concerns about iPhone X shipments and Apple’s battery issue will likely have only a limited impact on earnings.

- Consumption will become increasingly polarized; the sales mixes of high-priced products, including home appliances and TVs, will likely remain on the rise.

- Companies continue to search for new growth drivers; the recent won appreciation is concerning.

■ Strategy1) Semiconductor supply/demand conditions are expected to be more positive than expected. 2) LGD is worthy of attention in light of expectations for a market recovery in 2Q and a potential re-rating of large-sized OLED panel prices. 3) OLED materials producers merit attention as OLED capacities are projected to increase. 4) New smartphone models, namely the Galaxy S9 and X, could further boost the shares of mobile component players.

■ Spotlight stocks- LGE, LGD, Samsung SDI, SEMCO, LG Innotek, SSC

-12

-6

0

6

12

18

-16

-8

0

8

16

24

LGE HanwhaTechwin

SEC SEMCO SK Hynix LGD SamsungSDI

SSC LG Innotek

(%)(%)Share performance (1M,L) 4Q OP consensus revision rate(R)

Mirae Asset Daewoo Research6| Monthly InsighT

Previous Revised % chg. Notes4Q17F 2017F 2018F 4Q17F 2017F 2018F 4Q17F 2017F 2018FLGE Revenue 16,029 60,462 65,266 16,268 60,701 65,308 1.5 0.4 0.1

OP 523 2,624 3,626 562 2,664 3,618 7.5 1.5 -0.2 LG Innotek’s earnings growth NP 356 1,967 2,250 356 1,967 2,250 -0.1 0.0 0.0

LGD Revenue 6,813 27,477 27,401 6,813 27,477 27,401 0.0 0.0 0.0 OP 326 2,743 1,393 326 2,743 1,393 0.0 0.0 0.0 NP 182 1,949 945 182 1,949 945 0.0 0.0 0.0

Samsung SDI Revenue 2,027 6,493 8,246 2,027 6,493 8,246 0.0 0.0 0.0

OP 109 108 501 109 108 501 0.0 0.0 0.0

NP 319 738 1,142 319 738 1,142 0.0 0.0 0.0

SEMCO Revenue 1,726 6,847 7,825 1,726 6,847 7,825 0.0 0.0 0.0

OP 106 305 535 106 305 535 0.0 0.0 0.0

NP 60 167 303 60 167 303 0.0 0.0 0.0

LG Innotek Revenue 2,570 7,341 8,518 2,809 7,581 8,561 9.3 3.3 0.5

OP 155 310 461 194 350 453 25.5 12.7 -1.7 Optic solutions earnings improvedNP 107 195 312 132 220 301 23.4 12.8 -3.7

SSC Revenue 287 1,115 1,264 287 1,115 1,264 0.0 0.0 0.0

OP 25 103 123 25 103 123 0.0 0.0 0.0

NP 16 61 82 16 61 82 0.0 0.0 0.0

Hanwha Revenue 1,552 4,232 4,322 1,552 4,232 4,322 0.0 0.0 0.0

Techwin OP 56 92 133 56 92 133 0.0 0.0 0.0

NP 38 48 88 38 48 88 0.0 0.0 0.0

SEC Revenue 68,069 241,382 271,372 67,045 240,660 271,163 -1.5 -0.3 -0.1 (Based on the market consensus)OP 16,292 54,691 64,558 15,951 54,449 66,157 -2.1 -0.4 2.5

NP 12,302 41,459 48,625 12,012 41,274 49,858 -2.4 -0.4 2.5

SK Hynix Revenue 8,883 29,932 35,225 8,976 30,064 36,254 1.0 0.4 2.9 (Based on the market consensus)OP 4,229 13,495 15,668 4,310 13,566 16,369 1.9 0.5 4.5

NP 3,393 10,809 12,403 3,414 10,843 12,860 0.6 0.3 3.7

I. Investment strategy

(Wbn, %)

Source: Mirae Asset Daewoo Research

Earnings forecast revisions for large-cap IT plays

Mirae Asset Daewoo Research7| Monthly InsighT

I. Investment strategy

(Wbn, %)

Source: WISEfn, Mirae Asset Daewoo Research

Consensus vs. Mirae Asset Daewoo estimates

Mirae Asset Daewoo Consensus % diff. Notes4Q17F 2017F 2018F 4Q17F 2017F 2018F 4Q17F 2017F 2018FLGE Revenue 16,029 60,462 65,266 16,083 60,591 64,656 -0.3 -0.2 0.9

OP 523 2,624 3,626 457 2,569 3,103 14.3 2.2 16.9 Robust home appliance salesNP 356 1,967 2,250 262 1,818 1,918 35.7 8.2 17.3

LGD Revenue 6,813 27,477 27,401 6,893 27,530 26,641 -1.2 -0.2 2.9

OP 326 2,743 1,393 311 2,725 1,384 4.9 0.7 0.7

NP 182 1,949 945 217 2,014 953 -16.1 -3.2 -0.8

Samsung SDI Revenue 2,027 6,493 8,246 1,976 6,432 7,821 2.6 0.9 5.4

OP 109 108 501 101 93 390 7.9 16.1 28.5 Improvement in mid/large-sized battery earnings

NP 319 738 1,142 288 689 1,096 10.8 7.1 4.2

SEMCO Revenue 1,726 6,847 7,825 1,783 6,912 8,211 -3.2 -0.9 -4.7

OP 106 305 535 110 311 603 -3.6 -1.9 -11.3

NP 60 167 303 75 176 394 -20.0 -5.1 -23.1

LG Innotek Revenue 2,809 7,581 8,561 2,604 7,366 8,846 7.9 2.9 -3.2

OP 194 350 453 162 318 504 19.7 9.8 -10.0 The iPhone X impactNP 132 220 301 98 200 346 34.8 9.9 -13.2

SSC Revenue 287 1,115 1,264 287 1,114 1,218 0.0 0.0 3.8

OP 25 103 123 27 105 125 -5.2 -1.3 -1.9

NP 16 61 82 14 65 86 12.4 -6.0 -5.1

Hanwha Revenue 1,552 4,232 4,322 1,494 4,230 4,524 3.9 0.0 -4.5

Techwin OP 56 92 133 55 98 148 1.2 -5.9 -10.1

NP 38 48 88 41 60 96 -5.6 -20.5 -8.3

SEC Revenue - - - 67,045 240,660 271,163 - - -

OP - - - 15,951 54,449 66,157 - - -

NP - - - 12,012 41,274 49,858 - - -

SK Hynix Revenue - - - 8,976 30,064 36,254 - - -

OP - - - 4,310 13,566 16,369 - - -

NP - - - 3,414 10,843 12,860 - - -

Mirae Asset Daewoo Research8| Monthly InsighT

I. Investment strategy

II. Top picksLGE, LGD, Samsung SDI, SEMCO, LG Innotek, SSC

III. Sector view

IV. Think big

V. Global IT navigation

Spotlight stocks & other notable stocks

Mirae Asset Daewoo Research9| Monthly InsighT

II. Top picks(W, Wbn, %) 4Q16 3Q17

4Q17FNotesMirae Asset

Daewoo Consensus YoY QoQ

LGE Revenue 14,777.8 15,224.1 16,268.1 16,083.4 10.1 6.9 - 4Q17 preview: Revenue of W16.27tr (+10.1% YoY) and OP of W562bn (TTB YoY)- Home appliance/TV OP is projected at W3.21tr for 2017 and W3.32tr for 2018. TV earnings are expected to

improve on panel price declines and a greater mix of OLED TVs; sales of vacuums, dryers, and aesthetic products are growing.

- The MC unit’s losses are expected to narrow from W737.6bn in 2017 to W184.7bn in 2018.

CP: 106,000 OP -35.2 516.1 562.0 457.0 TTB 8.9

TP: 129,000 (OPM) -0.2 3.4 3.5 2.8 3.7 0.1

Upside: 21.7% Pretax -83.1 515.7 576.5 413.5 TTB 11.8

NP -322.7 318.1 355.6 262.0 TTB 11.8

LGD Revenue 7,936.0 6,973.0 6,812.8 6,893.1 -14.2 -2.3 - 4Q17 preview: Revenue of W6.8tr (-2.3% QoQ) and OP of W326bn (-44.3% QoQ)- OP downtrend will likely continue in 4Q, due to steady panel price declines.- Depreciation cost burden will likely increase, resulting from the operation of new small/mid-sized OLED lines. - Won appreciation should also be negative. - The LCD market should rebound in 2Q, on the back of: 1) TV demand growth; and 2) yield issues at BOE’s new

facilities. - We advise investors to accumulate LGD shares before CES 2018 (scheduled for January 8th).

CP: 29,900 OP 904.3 586.0 326.1 310.9 -63.9 -44.4

TP: 42,000 (OPM) 11.4 8.4 4.8 4.5 -6.6 -3.6

Upside: 40.5% Pretax 1,064.5 598.6 334.0 309.7 -68.6 -44.2

NP 798.0 443.7 181.8 216.6 -77.2 -59.0

Samsung SDI Revenue 1,302.9 1,707.3 2,026.6 1,976.3 55.5 18.7 - 4Q17 preview: Revenue of W2tr (+18.7% QoQ) and OP of W109bn (+81.5% QoQ) - Small batteries: Galaxy 9-bound component supplies may begin in 4Q, amid continued growth in North

America-bound shipments. - Mid/large-sized batteries: Entered peak-demand season- Earnings for OLED/semiconductor materials business to remain solid- EV battery business is forecast to turn to profit in 2Q18, with its revenue set to climb to W2.2tr in 2018 (from

W1.4tr in 2017).

CP: 204,500 OP -58.0 60.2 109.2 100.8 TTB 81.4

TP: 270,000 (OPM) -4.5 3.5 5.4 5.1 9.8 1.9

Upside: 32.0% Pretax 99.6 174.3 369.2 320.1 270.7 111.8

NP 7.5 145.3 319.0 287.7 4,153.3 119.5

SEMCO Revenue 1,345.1 1,841.1 1,725.7 1,782.7 28.3 -6.3 - 4Q17 preview: Relatively strong earnings, despite weak seasonality

• Camera/telecom modules: Began to supply components for SEC’s Galaxy S9• Substrates: Growth in RF-PCB revenue from a US customer to drive up profitability • Components: Sales mix of value-added MLCC products to expand; ASP to rise for fourth consecutive quarter

- 2018 OP forecast to climb 75.1% on uptrend in MLCC prices

CP: 100,000 OP -46.5 103.2 106.1 110.2 TTB 2.8

TP: 131,000 (OPM) -3.5 5.6 6.1 6.2 9.6 0.5

Upside: 31.0% Pretax -59.0 98.5 81.8 101.2 TTB -17.0

NP -35.3 71.9 59.7 74.7 TTB -17.0

LG Innotek Revenue 2,054.6 1,787.2 2,809.2 2,604.1 36.7 57.2 - 4Q17 preview: Record-breaking earnings likely, with revenue of W2.81tr (+36.7% YoY)- Solid iPhone X sales should drive up the firm’s revenue from dual camera/3D sensing modules.

• The outlook for new businesses is also positive.• The firm has begun supplying other components, like RFPCBs (annual revenue of W200bn) and wireless

charging modules (revenue of W150bn).- Earnings will likely remain solid in 1Q18, although our OP forecast has been lowered to W130.4bn due to won

appreciation.

CP: 144,000 OP 117.8 55.9 194.4 162.5 65.0 247.8

TP: 210,000 (OPM) 5.7 3.1 6.9 6.2 1.2 3.8

Upside: 45.8% Pretax 115.3 42.3 173.2 144.8 50.2 309.5

NP 87.0 34.8 131.6 97.6 51.3 278.2

SSC Revenue 241.5 304.5 286.9 286.8 18.8 -5.8 - 4Q17 preview: OP of W25.3bn (+23.5% YoY)

• For 4Q17, we see revenue of W286.9bn (+18.8% YoY) and operating profit of W25.3bn (+23.5% YoY).• Increased exposure to automotive lighting and tight SG&A expense control should keep OP margin steady.• LED market conditions are gradually improving; ongoing restructuring in the TV BLU industry has led to a

slowdown in the decline in LED chip prices (and even some hikes); the company is exploring new markets, including the automotive market.

CP: 27,850 OP 20.5 30.6 25.3 26.7 23.4 -17.3

TP: 37,800 (OPM) 8.5 10.0 8.8 9.3 0.3 -1.2

Upside: 35.7% Pretax 25.6 30.4 23.4 24.3 -8.6 -23.0

NP 17.6 17.3 16.0 14.3 -9.1 -7.5

Mirae Asset Daewoo Research10| Monthly InsighT

I. Investment strategy

II. Top picks

III. Sector view

• Display: LCD market conditions to bottom out in 1Q18

• Handsets/components: iPhone X and Galaxy S9 serving as dual drivers; Watch out for won appreciation

IV. Think big

V. Global IT navigation

Spotlight stocks & other notable stocks

Mirae Asset Daewoo Research11| Monthly InsighT

Source: WitsView, Mirae Asset Daewoo Research

Decline in 55” panel prices starting to slow down

Source: IHS, Mirae Asset Daewoo Research

LCD panel inventory trends

III. Sector view Display

LG Electronics

Growth rate (R)

Other

-8

-6

-4

-2

0

2

4

1/16 7/16 1/17 7/17

(%)

55인치패널가격변동률55” panel price change

2.5

3.0

3.5

4.0

4.5

5.0

1/14 7/14 1/15 7/15 1/16 7/16 1/17 7/17 1/18

(Weeks)IT용패널재고일수TV용패널재고일수IT panel inventoryTV panel inventory

■ Key issues

- In December, panel prices continued to decline

- 1) TV panel prices: -1.7% for 5.5”; -3.3% for 6.5”; -4% to -6% for 40-50” panels

- 2) IT panel prices: –0.5% for notebook panels; -0.4% for monitor panels

- November LCD TV shipments: 24.43mn units (+2.7% YoY)

- November OLED TV shipments: 271,000 units (+133% YoY)

- The Korean government granted conditional approval for LGD’s plan to build an OLED plant in Guangzhou, China.

- SKC announced investments in CPI lines.

■ Implications

- Declines in prices for 55” and 65” TV panels slowed on solid demand, while prices for 40-50” panels continued falling on shipment growth driven by Chinese and Taiwanese panel makers.

- LCD market conditions should turn around in 2Q18 on a pickup in TV demand amid stabilizing LCD panel inventory. Major sporting events, including the Winter Olympics (early February) and FIFA World Cup (June), the Chinese New Year (mid-February), and new TV product launches (April) are expected to bolster TV demand.

- LGD confirmed significant OLED spending in Guangzhou in December: Large-sized OLED equipment makers include YAS, Jusung Engineering, Avaco, and Invenia.

- SEC is highly likely to launch foldable devices in 2018: Focus on relevant materials and component suppliers.

- Samsung Display will likely make additional investments upon the launch of foldable devices. Shares of OLED equipment suppliers should bottom out in 1Q.

Check point

LCD market conditions to bottom out in 1Q18

TV set makers’ new products (e.g., rollable displays, Mini LED) to be unveiled at CES2018

Apple to report 4Q17 results at end-January

Mirae Asset Daewoo Research12| Monthly InsighT

-15

-10

-5

0

5

10

15

0

7

14

21

28

1/15 7/15 1/16 7/16 1/17 7/17

LCD TV 출하량 (L)YoY 증감률 (R)

(Mn) (%)

-8

-6

-4

-2

0

2

4

6

1/14 7/14 1/15 7/15 1/16 7/16 1/17 7/17

NotebookMonitorTV (Open-cell)TV (4K x 2K)

(%)

Key charts

Monthly LCD TV shipments

LCD panel prices

Monthly LCD panel shipment area (by application)

LCD panel cumulative inventory

Source: IHS, Mirae Asset Daewoo Research

Source: WitsView, Mirae Asset Daewoo Research

Source: IHS, Mirae Asset Daewoo Research

Source: IHS, Mirae Asset Daewoo Research

III. Sector view Display

LCD TV shipments (L)YoY growth (R)

-25

0

25

50

0

6,000

12,000

18,000

1/15 7/15 1/16 7/16 1/17 7/17

(%)(Km2) TV panel (L) Monitor panel (L)Notebook panel (L) Tablet panel (L)Others (L) YoY growth (R)

-15

-10

-5

0

5

10

15

8

10

12

14

16

18

1/15 7/15 1/16 7/16 1/17 7/17 1/18

Production Area (L)Shipment Area (L)MoM 누적재고증감률 (R)

(mn m2) (%)

MoM cumulative inventory growth (R)

Mirae Asset Daewoo Research13| Monthly InsighT

Handsets/components III. Sector view

Source: Company data, Mirae Asset Daewoo Research

SEC smartphone shipments and OP margin of IM division

Source: Counterpoint, FactSet, Company data, Mirae Asset Daewoo Research

Apple smartphone shipments and OP margin

-30

-15

0

15

30

0

25

50

75

100

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17

(%)(mn units) Smartphone shipments (L)Shipments YoY growth (R)ASP YoY growth (R)IM OP margin (R)

GalaxyS8

GalaxyNote 7

GalaxyS7/E

GalaxyNote 8

GalaxyS6E+Note 5Galaxy

S6/E

GalaxyNote 4Galaxy

S5

GalaxyNote 3

-20

0

20

40

60

0

25

50

75

100

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17

(%)(mn units) iPhone shipments (L)Shipments YoY growth (R)Apple M/S (R)OP margin (R)

iPhone8/8+/X

iPhone7/7+

iPhoneSE

iPhone X and Galaxy S9 serving as dual drivers; Watch out for won appreciation

■ Key issues- The global smartphone market is maturing. - SEC: Attention is now turning to the Galaxy S9 and Galaxy X (tentatively named;

expected to feature a foldable display).- LGE: The firm looks set to report wider-than-expected smartphone losses for 2017,

leading to concerns over its brand value.- Apple: Sales of the iPhone X have been faring well; the new model is projected to have

a greater impact on pricing than on volume; Korean parts makers should benefit.- Chinese players’ competitiveness continues to improve; however, there are risks of a

slowdown in growth.- Memory chip/panel price growth in China is pushing up the prices of components,

including MLCC and LED.

■ Implications- SEC needs to focus on protecting its brand value and market share to boost sales

volume in 2018.- LGE needs to restore its brand value by leveraging unique and differentiated

products; the company needs to improve profitability via cost controls in 2018.- Apple is likely to post decent sales of the iPhone X: Improvement in earnings needs to

be confirmed during its 4Q17 earnings call (slated for January 30th).- Chinese smartphone makers have begun to show differentiated performances;

attention needs to be paid to the possibility of restructuring (risks to domestic component suppliers).

- Parts suppliers will likely benefit from price growth and the 4th Industrial Revolution.

■ Strategy- We advise investors to lower expectations for smartphone market growth; new model

releases will benefit select parts makers; follow closely those that are able to secure new technologies/new markets.

- SEC’s strategy for 2018 deserves attention; high pricing vs. high volume; new models (foldable).

- Parts makers are becoming more differentiated; focus on those that have secured medium/long-term competitiveness and/or new technologies; further rallies of the tech-heavy KOSDAQ market are likely.

- Parts makers that stand to benefit from the price uptrend and the 4th Industrial Revolution (e.g., the development of autonomous cars and AI technologies) deserve attention.

iPhone X and Galaxy S9 to drive market through 1Q18 Component stocks related to 4th Industrial Revolution

Check point

Mirae Asset Daewoo Research14| Monthly InsighT

Key charts

Source: IDC, Mirae Asset Daewoo Research

Smartphone shipments and market value

Source: IDC, Mirae Asset Daewoo Research

Smartphone shipments by price

Source: IDC, Mirae Asset Daewoo Research

Smartphone quarterly M/S trends

Source: IDC, Mirae Asset Daewoo Research

Smartphone shipments by pixel count

Handsets/components III. Sector view

0

25

50

75

100

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16

(%) High-end(>12MP) Mid-end(8-12MP) Low-end(<8MP)

0

25

50

75

100

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16

(%) Premium (>US$700) High-end (US$400-700) Mid-end (US$150-400) Low-end (<US$150)

0

10

20

30

40

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17

(%)Apple Samsung HuaweiOppo+Vivo Xiaomi LG

1.7 5.0

9.2 6.5

-30

0

30

60

90

0.0

0.5

1.0

1.5

2.0

2006 2009 2012 2015 2018F

(%)(bn units) Shipments (L) Shipments YoY (R) Value YoY (R)

Mirae Asset Daewoo Research15| Monthly InsighT

I. Investment strategy

II. Top picks

III. Sector view

IV. Think big

V. Global IT navigation

Spotlight stocks & other notable stocks

Mirae Asset Daewoo Research16| Monthly InsighT

First CES (1967) vs CES 2017

Source: Press materials

IV. Think big: CES 2018 previewCES 2018: The future of smart cities

Flagship products presented in past CES

Source: Press materials, Mirae Asset Daewoo Research

1970: VCR (Philips)

1967: First CES

1996: DVD

2008: OLED TVs (Panasonic)

1981: CD & camcorders (Sony)

1998: HD TVs

2011: Tablets

2001: Xbox (Microsoft)

2017: AI robots

■ CES: 50 years as the IT trendsetter

- First held in New York in 1967, CES now takes place in in Las Vegas each January.

- New IT products/technologies unveiled at past CES events include the following: VCRs (1970); camcorders (1981); DVD players (1996); HDTVs (1998); and OLED TVs (2008).

- New products/technologies showcased at recent CES events include the following: 3D TVs (2011), smart watches (2012); UHD TVs (2013); curved TVs and wearables (2014); IoT (2015); smart cars and VR devices (2016); and autonomous vehicles 2017).

- While the Mobile World Congress (MWC) held in March each year focuses on mobile devices, CES is a home appliance-oriented show.

- Technologies related to smart cities and cyber security and future growth engines related to AI technologies should garner attention at CES 2018.

- Key words for CES 2018 (January 9th to 12th) include: 1) 5G mobile technology; 2) autonomous driving; 3) cyber security; 4) robotics; and 5) IoT.

Mirae Asset Daewoo Research17| Monthly InsighT

■ 5G to give rise to a super-connected world - In a super-connected world, humans and humans, humans and devices, and

devices and devices will be connected via networks; IoT technologies, namely smart homes and smart cars, are the key to fostering the rise of a super-connected world.

- At CES 2018, the potential of 5G to aid in the establishment of smart cities is expected to be put on the spotlight.

- 5G, which could offer mobile speeds 40 to 100 times faster than 4G LTE, is anticipated to sharply improve connectivity between devices.

- 5G should enable the smooth operation of smart roads (traffic congestion analysis, intelligent traffic management, etc.), autonomous vehicles, automated EV charging stations, and emergency control systems.

- According to the Consumer Technology Association (CTA), the global smart city project market expanded by 38% in 2013-16, and will grow to US$34.4bn by 2020.

- Recently, Intel unveiled a 5G modem chip, announcing its shift of focus from personal computers to servers and communication.

- Once 5G gains traction, inter-device communication costs will likely decrease significantly, and the markets for wearable fitness devices, smartwear, and security devices will likely expand sharply.

IV. Think big: CES 2018 preview

Source: Press materials, Mirae Asset Daewoo Research

4G vs. 5G wireless technology

Source: Press materials, Mirae Asset Daewoo Research

Intel releases 5G modem lineup

4G 5G

Max. data transfer rate 1Gbps 20Gbps

Effective transfer rate 10Mbps 100-1,000Mbps

Relative spectral efficiency - 3x 4G

Mobility 350km/h 500km/h

Relative energy efficiency - 100x 4G

Area traffic capacity 0.1Mbps/m² 10Mbps/m²

Source: CTA, Mirae Asset Daewoo Research

Global smart city project market

1) Smart cities based on 5G mobile technology

34.4

0

5

10

15

20

25

30

35

40

2014 2015 2016 2020F

(US$bn)

Mirae Asset Daewoo Research18| Monthly InsighT

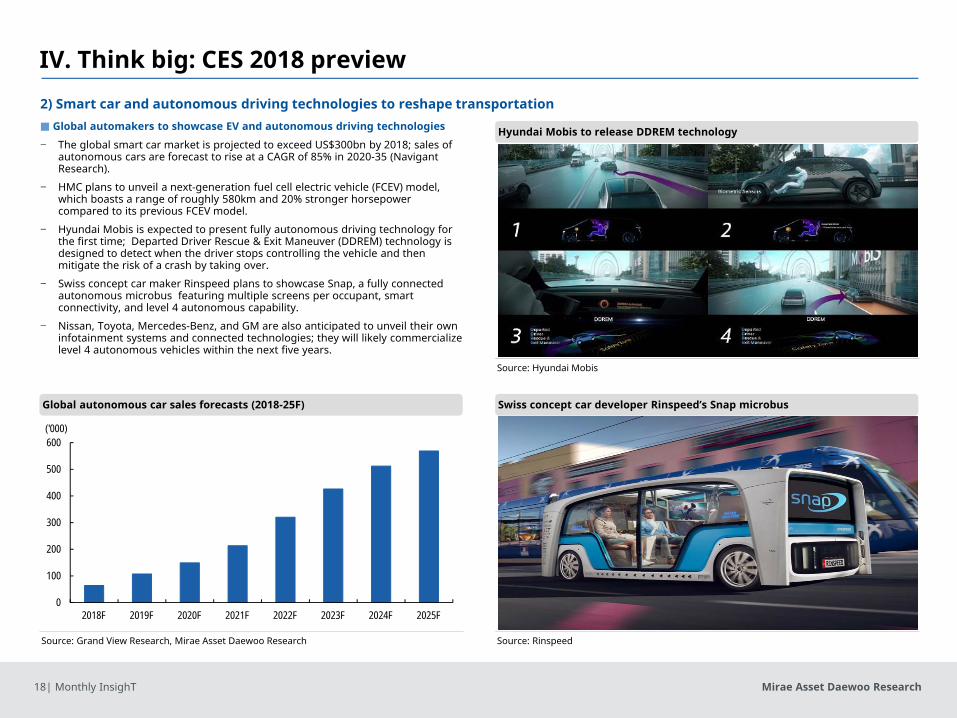

■ Global automakers to showcase EV and autonomous driving technologies

- The global smart car market is projected to exceed US$300bn by 2018; sales of autonomous cars are forecast to rise at a CAGR of 85% in 2020-35 (Navigant Research).

- HMC plans to unveil a next-generation fuel cell electric vehicle (FCEV) model, which boasts a range of roughly 580km and 20% stronger horsepower compared to its previous FCEV model.

- Hyundai Mobis is expected to present fully autonomous driving technology for the first time; Departed Driver Rescue & Exit Maneuver (DDREM) technology is designed to detect when the driver stops controlling the vehicle and then mitigate the risk of a crash by taking over.

- Swiss concept car maker Rinspeed plans to showcase Snap, a fully connected autonomous microbus featuring multiple screens per occupant, smart connectivity, and level 4 autonomous capability.

- Nissan, Toyota, Mercedes-Benz, and GM are also anticipated to unveil their own infotainment systems and connected technologies; they will likely commercialize level 4 autonomous vehicles within the next five years.

Source: Hyundai Mobis

Hyundai Mobis to release DDREM technology

Source: Rinspeed

Swiss concept car developer Rinspeed’s Snap microbus

Source: Grand View Research, Mirae Asset Daewoo Research

Global autonomous car sales forecasts (2018-25F)

IV. Think big: CES 2018 preview2) Smart car and autonomous driving technologies to reshape transportation

0

100

200

300

400

500

600

2018F 2019F 2020F 2021F 2022F 2023F 2024F 2025F

('000)

Mirae Asset Daewoo Research19| Monthly InsighT

■ Robots becoming part of our daily lives

- The International Federation of Robotics (IFR) expects China’s robot sales to triple (to 150,000 units) from 2015 to 2017, and China’s commercial robot market to expand 10-fold by end-2019.

- At CES 2018, Honda is set to unveil its new 3E (empower, experience, empathy) robotics concept.

- At the trade show, the Industrial Technology Research Institute (ITRI), a Taiwan-based high-tech applied research organization, plans to showcase a robot running on its Intelligent Vision System. The robot, designed to recognize the surrounding environment, is expected to be used at companies, hotels, hospitals, and shopping malls.

- LGE has continued launching new commercial robots, deploying cleaning robots at Incheon International Airport and a guide robot at Starfield Hanam in Gyeonggi Province. Sony has recently begun to develop robots for ordinary consumers by reviving its Aibo robot dog 11 years after shelving its original line of robot dogs.

- Hancom Group is also set to showcase a variety of commercial robots (e.g., educational service bots) that are currently being developed via Hancom MDS.

Source: Press materials, Mirae Asset Daewoo Research

LGE and Hancom Group begin production of commercial robots

Source: Honda, Mirae Asset Daewoo Research

Honda to release four types of 3E commercial robots

Source: IFR, Mirae Asset Daewoo Research

Global commercial robot sales

IV. Think big: CES 2018 preview3) Robots enter the mainstream

13.2

9.1

1.2 1.01.2 1.0

0

2

4

6

8

10

12

14

Household robot Entertainment robot

2016-19F 2015 2014(US$mn)

Mirae Asset Daewoo Research20| Monthly InsighT

Source: SEC, Mirae Asset Daewoo Research

One Samsung: Connecting smartphones, TVs, and home appliances

Source: LGE

LGE’s ThinQ AI network

Source: Press materials, Mirae Asset Daewoo Research

Smart home network centering on the consumer

IV. Think big: CES 2018 preview

■ IOT-connected devices - CES 2018 will showcase a variety of smart home devices, with existing AI

speakers, such as the Amazon Echo and Google Home, providing upgraded features and more seamless connectivity to TVs and other entertainment systems.

- Smart home-related devices expected to garner the most attention at the upcoming tech fair include 4K UHD TVs, voice recognition devices, wearable devices, and wireless speakers.

- SEC and LGE are set to unveil consumer electronics integrated with AI and big data technologies to enhance user convenience.

- SEC is expected to reveal a new IoT-connected AI device, as well as a proprietary AI platform that offers connectivity to smartphones, TVs, and other home appliances.

- LGE announced plans to promote its deep learning-driven AI brand, ThinQ (which is set to be employed by all AI-enabled devices of LGE), operating a dedicated booth at the upcoming show.

4) Smart home devices (IoT)

AI platformBixby

Homeappliances

AutoAI speaker

TV

Smartphone

Smart TV

Smartphone Smart work

Smart education

Smart city

Smart appliancesSmart Car

Smart care

Smart grid

Health/wellness

Safety

Economic benefits

Smart home

Mirae Asset Daewoo Research21| Monthly InsighT

I. Investment strategy

II. Top picks

III. Sector view

IV. Think big

V. Global IT navigation

Spotlight stocks & other notable stocks

Mirae Asset Daewoo Research22| Monthly InsighT

Source: Bloomberg, Mirae Asset Daewoo Research

Global IT index performance table (12/28)

Source: Bloomberg, Mirae Asset Daewoo Research

December share performance (MoM)

IndexPerformance (%)

1W 1M 3M 6M 12MDow Jones 24,719 -0.3 2.0 10.3 15.8 25.1 NASDAQ 6,903 -0.9 0.8 6.3 12.4 28.2 KOSPI 2,467 -0.2 -1.8 3.0 3.0 21.8 KOSDAQ 798 5.7 2.1 22.3 19.5 26.4

MSCI IT

World 221 -1.0 0.6 8.1 16.9 36.9 US 253 -1.1 0.6 8.7 17.5 36.8 Korea 1,282 -0.1 -3.0 -0.2 6.9 43.5 Japan 167 -1.7 -1.3 7.5 16.2 35.3

Taiwan 202 0.8 -1.9 0.3 -0.8 18.3

China 690 0.9 2.0 9.4 33.6 93.2

Source: Bloomberg, Mirae Asset Daewoo Research

December sector performance (MoM)

V. Global IT navigation Concerns over slowing iPhone sales

■ Global industry performance- While the MSCI World IT index rose 0.6%, the MSCI Korea IT index slipped 3.0%.- IT companies in Korean, Japan, and Taiwan largely underwent corrections.

■ Sector performance- Some stocks experienced strong rallies driven by non-operating events: Sharp

by 9.5% after returning to the Tokyo Stock Exchange first section; Toshiba by 14.9% thanks to its successful issuance of new shares worth JPY600bn.

- Apple supply chain stocks broadly dropped amid concerns over the iPhone sales slowdown and the recent battery issue: Sunny Optical (-23.2%), Largan (-21.8%), AAC (-10.8%), and LG Innotek (-10.6%).

- The display panel and semiconductor foundry segments advanced, driven by BOE and Sharp, respectively.

■ Company performance- Sunny Optical (-23.2%): Weaker investment sentiment on iPhone supply chain

stocks and camera module shipment decline in November (-3.9% MoM)

-10

-5

0

5

10

Dis

play

pan

el

Foun

dry

Auto

mat

ion

PC

Dis

play

com

pone

nts

Non

-mem

ory

Mem

ory

Dis

play

gla

ss

Dis

tribu

tion

Han

dset LIB

Sem

icon

. equ

ip.

Appl

ianc

es

Dis

play

equ

ip.

Mat

eria

ls

EMS/

OD

M

LED

Touc

hscr

een

Com

pone

nts

(%)

-30

0

30

60

SMIC

KC T

ech

Acer

LGE

Best

Buy

Tosh

iba

Lite

-On

Shar

p

Anap

ass

Rad

iant

Skyw

orks

Med

iaTe

k

Alps

Ele

ctric

LG In

note

k

AAC

Iljin

Dis

play

APS

Hol

ding

s

Epis

tar

Larg

an

Sunn

y O

ptic

al

(%)

Mirae Asset Daewoo Research23| Monthly InsighT

Source: Bloomberg, Mirae Asset Daewoo Research

MSCI World and MSCI World IT

Source: Bloomberg, Mirae Asset Daewoo Research

P/E comparison by country (2017F)

Source: Bloomberg, Mirae Asset Daewoo Research

MSCI IT performance by country

Source: Bloomberg, Mirae Asset Daewoo Research

IT sector P/B-ROE comparison (2017F)

V. Global IT navigation Key charts

80

120

160

200

240

280

1/12 1/13 1/14 1/15 1/16 1/17 1/18

MSCI World MSCI World IT(1/1/12=100)

80

130

180

230

280

1/12 1/13 1/14 1/15 1/16 1/17 1/18

MSCI US ITMSCI Korea ITMSCI Japan ITMSCI Taiwan IT

(1/1/12=100)

35.3

21.3 19.9 19.5 15.2

8.9

0

10

20

30

40

China Japan World US Taiwan Korea

(x)

0

2

4

6

8

0 5 10 15 20 25 30

ROE (%)

P/B (x)

WorldUS

China

TaiwanJapan

Korea

Mirae Asset Daewoo Research24| Monthly InsighT

I. Investment strategy

II. Top picks

III. Sector view

IV. Think big

V. Global IT navigation

Spotlight stocks

• LGE, LGD, Samsung SDI, SEMCO, LG Innotek, SSC

Other notable stocks

• Hanwha Techwin

Mirae Asset Daewoo Research25| Monthly InsighT

LG Electronics (066570 KS)

Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimates

FY (Dec.) 12/14 12/15 12/16 12/17F 12/18F 12/19F

Revenue (Wbn) 59,041 56,509 55,367 60,701 65,308 69,466

OP (Wbn) 1,829 1,192 1,338 2,664 3,618 3,991

OP margin (%) 3.1 2.1 2.4 4.4 5.5 5.7

NP (Wbn) 399 124 77 1,967 2,250 2,446

EPS (W) 2,208 688 425 10,875 12,440 13,527

ROE (%) 3.4 1.1 0.7 15.2 15.0 14.2

P/E (x) 26.8 78.2 121.4 9.7 8.5 7.8

P/B (x) 0.9 0.8 0.8 1.4 1.2 1.0

(Maintain) Buy

Target Price (12M, W) ▲129,000

Share price (12/28/17, W) 106,000

Expected Return 22%

OP (17F, Wbn) 2,664

Consensus OP (17F, Wbn) 2,569

EPS Growth (17F, %) 2,458.0

Market EPS Growth (17F, %) 46.7

P/E (17F, x) 9.7

Market P/E (17F, x) 10.0

KOSPI 2,467.49

Market Cap (Wbn) 17,347

Shares Outstanding (mn) 181

Free Float (%) 65.6

Foreign Ownership (%) 33.6

Beta (12M) 0.93

52-Week Low 51,500

52-Week High 107,000

(%) 1M 6M 12M

Absolute 15.5 33.7 105.8

Relative 17.7 29.1 68.9

Wonjae [email protected]

Smartphone losses expected to narrow in 2018

■ 4Q17 preview: OP of W562.0bn (TTB YoY) - For 4Q17, we project revenue of W16.27tr (+10.1% YoY) and operating profit of W562.0bn (TTB YoY). Excluding LG Innotek, revenue is projected at W13.46tr (+3.4% YoY) and operating profit at W367.6bn (TTB YoY).

- The home entertainment (HE) division is expected to post operating profit of W426.2bn and an OP margin of 8% (+4.6%p YoY); margins will likely be supported by an increasing mix of premium products (including OLED TVs), panel price declines, and wonappreciation.

- The home appliance & air solution (H&A) division is expected to post operating profit of W19.3bn and OP margin of W4.5% (+0.9%p YoY).

- The mobile communications (MC) division is expected to suffer an operating loss of W233.6bn (narrowing QoQ and YoY).

■ Home appliance/TV units to generate annual OP of W3tr; Smartphone business to stabilize - For 2017, we forecast revenue of W3.21tr and operating profit of W3.32tr. TV earnings are expected to improve on panel price declines and a higher sales mix of OLED TVs. Sales of vacuum cleaners, dryers, and aesthetic products are growing.

- The MC division’s losses are anticipated to narrow from W737.6bn in 2017 to W184.7bn in 2018.

■ Maintain Buy and raise TP to W129,000 from W113,000 - Margins are improving in line with top-line growth; we are positive about the automotive electronics business; the smartphone

business is expected to recover in 2018. - In deriving our target price, we applied a P/B of 1.45x (20% premium to the upper end of the five-year average) to our 2018F

BPS of W89,004.

Spotlightstocks

70

100

130

160

190

220

250

12/16 4/17 8/17 12/17

LGE KOSPI

Mirae Asset Daewoo Research26| Monthly InsighT

LG Electronics (066570 KS)

Source: Company data, Mirae Asset Daewoo Research

(Wbn, %,, ‘000 units)2017F 2018F

2016 2017F 2018F4Q17F

1Q 2Q 3QP 4QF 1QF 2QF 3QF 4QF YoY QoQ Previous Diff.

MC(MobileCommunications)

Revenue 3,091.7 2,701.4 2,807.7 2,956.8 2,974.2 3,155.9 3,238.0 3,065.9 12,023.9 11,557.6 12,434.0 -0.8 5.3 2,956.8 0.0 OP 3.7 -132.4 -375.3 -233.6 -89.2 -31.6 -48.6 -15.3 -1,218.1 -737.6 -184.7 -49.1 -37.8 -233.6 0.0 OPM 0.1 -4.9 -13.4 -7.9 -3.0 -1.0 -1.5 -0.5 -10.1 -6.4 -1.5 7.5 5.5 -7.9 0.0

HE(HomeEntertainment)

Revenue 4,326.1 4,234.9 4,637.6 5,327.1 4,456.6 4,668.6 5,367.0 5,283.8 17,425.4 18,525.7 19,776.1 11.1 14.9 5,327.1 0.0 OP 382.2 343.0 458.0 426.2 371.5 368.8 476.4 428.0 1,237.4 1,609.4 1,644.6 159.9 -6.9 426.2 0.0 OPM 8.8 8.1 9.9 8.0 8.3 7.9 8.9 8.1 7.1 8.7 8.3 4.6 -1.9 8.0 0.0

H&A(HomeAppliance & Air Solution)

Revenue 4,647.7 5,264.6 4,984.4 4,293.1 4,877.2 5,573.4 5,393.5 4,419.4 17,278.1 19,189.8 20,263.5 5.9 -13.9 4,293.1 0.0 OP 519.1 464.3 424.9 193.2 471.6 551.8 449.0 207.7 1,317.6 1,601.5 1,680.0 31.6 -54.5 193.2 0.0 OPM 11.2 8.8 8.5 4.5 9.7 9.9 8.3 4.7 7.6 8.3 8.3 0.9 -4.0 4.5 0.0

VC(VehicleComponents)

Revenue 876.4 882.6 873.4 873.4 917.1 962.9 1,011.1 1,061.6 2,773.1 3,505.8 3,952.7 0.9 0.0 873.4 0.0 OP -14.5 -16.4 -29.0 -26.2 -27.5 5.8 15.2 18.0 -63.3 -86.1 11.5 80.7 -9.6 -26.2 0.0 OPM -1.7 -1.9 -3.3 -3.0 -3.0 0.6 1.5 1.7 -2.3 -2.5 0.3 -1.3 0.3 -3.0 0.0

Internal&other

Revenue 609.4 679.1 1,088.6 709.2 737.0 790.9 1,137.3 783.4 2,578.5 3,086.3 3,448.6 13.7 -34.9 709.2 0.0 OP -32.4 -4.4 31.6 6.3 8.6 15.0 30.6 8.2 -16.1 1.1 62.4 -51.0 -80.0 6.3 0.0 OPM -5.3 -0.6 2.9 0.9 1.2 1.9 2.7 1.0 -0.6 0.0 1.8 -1.2 -2.0 0.9 0.0

LGInnotek Revenue 1,644.7 1,339.6 1,787.2 2,809.2 2,122.1 1,606.4 1,941.3 2,890.8 5,754.6 7,580.7 8,560.6 36.7 57.2 2,569.9 9.3 OP 66.8 32.5 55.9 194.4 130.4 58.7 93.2 171.0 104.8 349.7 453.3 65.0 247.6 154.9 25.5

Total Revenue 14,657.2 14,551.4 15,224.1 16,268.1 15,358.2 16,064.5 17,158.1 16,727.6 55,367.0 60,700.9 65,308.4 10.1 6.9 16,028.9 1.5 OP 921.5 664.0 516.1 562.0 863.1 956.2 981.4 817.0 1,337.7 2,663.7 3,617.7 -1,693.0 8.9 522.5 7.6 OPM 6.3 4.6 3.4 3.5 5.6 6.0 5.7 4.9 2.4 4.4 5.5 3.7 0.1 3.3 0.2

LGE Revenue 13,012.5 13,211.8 13,436.9 13,459.0 13,236.1 14,458.1 15,216.8 13,836.8 50,845.7 53,120.2 56,747.8 3.4 0.2 13,459.0 0.0 (excludingLG Innotek) OP 854.7 631.5 460.2 367.6 732.7 897.6 888.2 646.0 1,245.2 2,314.0 3,164.4 -342.5 -20.1 367.6 0.0

OPM 6.6 4.8 3.4 2.7 5.5 6.2 5.8 4.7 2.4 4.4 5.6 3.9 -0.7 2.7 0.0 Pretaxprofit 1,091.9 742.3 515.7 576.5 918.7 1,011.4 940.9 776.0 721.7 2,926.3 3,647.0 -793.7 11.8 538.1 7.1 Pretaxmargin 7.4 5.1 3.4 3.5 6.0 6.3 5.5 4.6 1.3 4.8 5.6 4.1 0.2 3.4 0.2 Netprofit 795.3 497.5 318.1 355.6 566.7 623.9 580.4 478.7 76.9 1,966.5 2,249.7 -210.2 11.8 331.9 7.1 Netmargin 5.4 3.4 2.1 2.2 3.7 3.9 3.4 2.9 0.1 3.2 3.4 4.4 0.1 2.1 0.1 Handsetsalesvolume 16,200 14,700 15,600 16,107 15,813 16,425 17,246 17,189 68,900 62,607 66,673 -1.8 3.2 16,107 0.0

-Smartphones 14,800 13,300 13,700 14,844 14,588 15,236 16,116 16,116 55,000 56,644 62,056 5.3 8.3 14,844 0.0 TVsalesvolume 6,100 6,100 6,800 7,024 5,709 6,026 6,792 6,556 27,500 26,024 25,083 -8.8 3.3 7,024 0.0

-OLEDTVsalesvolume 188 200 255 357 321 386 463 555 666 1,000 1,725 22.3 40.0 357 0.0

Spotlightstocks

Earnings table

Mirae Asset Daewoo Research27| Monthly InsighT

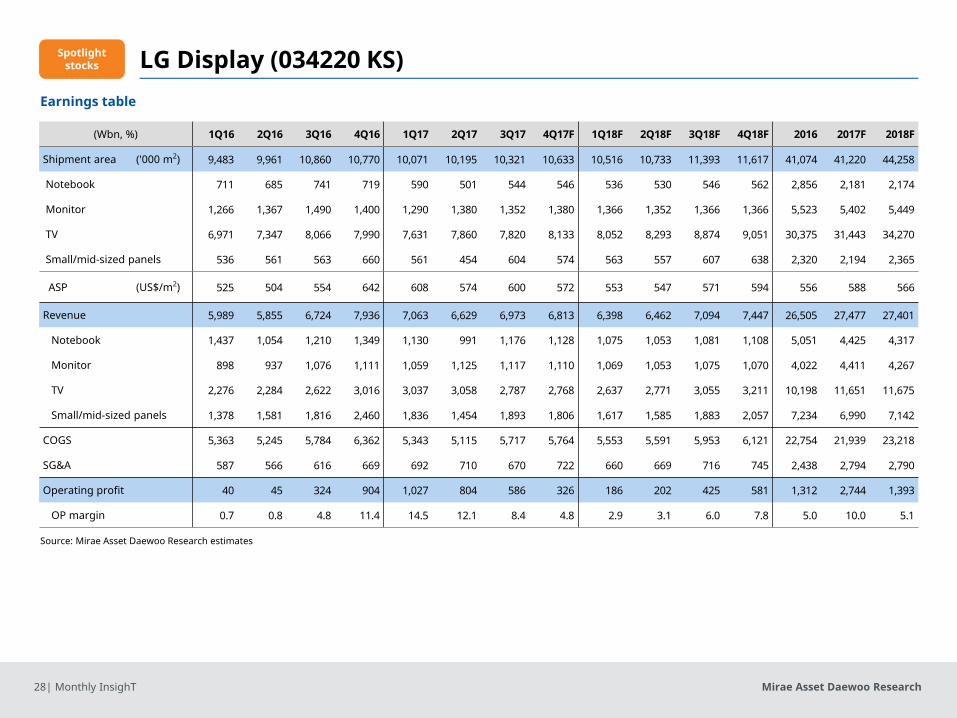

LG Display (034220 KS)

FY (Dec.) 12/14 12/15 12/16 12/17F 12/18F 12/19F

Revenue (Wbn) 26,456 28,384 26,504 27,477 27,401 31,827

OP (Wbn) 1,357 1,626 1,311 2,743 1,393 2,722

OP margin (%) 5.1 5.7 4.9 10.0 5.1 8.6

NP (Wbn) 904 967 907 1,949 945 1,876

EPS (W) 2,527 2,701 2,534 5,448 2,641 5,243

ROE (%) 8.2 8.2 7.2 14.2 6.4 11.7

P/E (x) 13.3 9.1 12.4 5.7 11.7 5.9

P/B (x) 1.1 0.7 0.9 0.8 0.7 0.7

(Maintain) Buy

Target price (12M, W) 42,000

Share price (12/28/17, W) 29,900

Expected Return 40%

OP (17F, Wbn) 2,743

Consensus OP (17F, Wbn) 2,725

EPS growth (17F, %) 115.0

Market EPS growth (17F, %) 46.7

P/E (17F, x) 5.5

Market P/E (17F, x) 10.0

KOSPI 2,467.49

Market cap (Wbn) 10,699

Shares outstanding (mn) 358

Free float (%) 62.1

Foreign ownership (%) 24.8

Beta (12M) 0.45

52-week low 27,300

52-week high 38,900

(%) 1M 6M 12M

Absolute -2.9 -19.7 -6.0

Relative -1.1 -22.5 -22.9Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimatesChuljoong Kim

Panel price downtrend is slowing

■ 4Q17 preview: Revenue of W6.8tr (-2.3% QoQ) and OP of W326bn (-44.3% QoQ)

- Operating profit is expected to remain on the decline QoQ in 4Q amid the steady downtrend in TV panel prices. - Depreciation cost burden will likely increase, as a result of the operation of new small/mid-sized OLED lines. - Won appreciation should also be negative.

■ Catalysts: To transform into an OLED maker in 2018

- The LCD market is expected to rebound in 2Q18, on the back of: 1) improvement in TV demand, driven by the FIFA World Cup; and 2) yield issues at BOE’s new facilities.

- Large-sized OLED: Losses are expected to narrow on solid OLED TV sales and customer base expansion.- Investments in OLED lines in Guangzhou are expected to be confirmed in December; the OLED TV market will likely enter a

virtuous cycle in 2018.

■ Valuation: Maintain Buy and TP of W42,000

- The stock has fallen to a P/B of 0.7-0.8x amid falling panel prices. We recommend buying at the lower end of the P/B band.

- Earnings are expected to pick up starting in 2Q18, in line with market recovery. To be re-rated as an OLED maker - Historically, LGD’s share price hit bottom whenever the panel price downtrend began to slow. - We advise investors to accumulate LGD shares before CES 2018.

Spotlightstocks

70

80

90

100

110

120

130

12/16 4/17 8/17 12/17

LGD KOSPI

Mirae Asset Daewoo Research28| Monthly InsighT

LG Display (034220 KS)

(Wbn, %) 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17F 1Q18F 2Q18F 3Q18F 4Q18F 2016 2017F 2018F

Shipment area ('000 m2) 9,483 9,961 10,860 10,770 10,071 10,195 10,321 10,633 10,516 10,733 11,393 11,617 41,074 41,220 44,258

Notebook 711 685 741 719 590 501 544 546 536 530 546 562 2,856 2,181 2,174

Monitor 1,266 1,367 1,490 1,400 1,290 1,380 1,352 1,380 1,366 1,352 1,366 1,366 5,523 5,402 5,449

TV 6,971 7,347 8,066 7,990 7,631 7,860 7,820 8,133 8,052 8,293 8,874 9,051 30,375 31,443 34,270

Small/mid-sized panels 536 561 563 660 561 454 604 574 563 557 607 638 2,320 2,194 2,365

ASP (US$/m2) 525 504 554 642 608 574 600 572 553 547 571 594 556 588 566

Revenue 5,989 5,855 6,724 7,936 7,063 6,629 6,973 6,813 6,398 6,462 7,094 7,447 26,505 27,477 27,401

Notebook 1,437 1,054 1,210 1,349 1,130 991 1,176 1,128 1,075 1,053 1,081 1,108 5,051 4,425 4,317

Monitor 898 937 1,076 1,111 1,059 1,125 1,117 1,110 1,069 1,053 1,075 1,070 4,022 4,411 4,267

TV 2,276 2,284 2,622 3,016 3,037 3,058 2,787 2,768 2,637 2,771 3,055 3,211 10,198 11,651 11,675

Small/mid-sized panels 1,378 1,581 1,816 2,460 1,836 1,454 1,893 1,806 1,617 1,585 1,883 2,057 7,234 6,990 7,142

COGS 5,363 5,245 5,784 6,362 5,343 5,115 5,717 5,764 5,553 5,591 5,953 6,121 22,754 21,939 23,218

SG&A 587 566 616 669 692 710 670 722 660 669 716 745 2,438 2,794 2,790

Operating profit 40 45 324 904 1,027 804 586 326 186 202 425 581 1,312 2,744 1,393

OP margin 0.7 0.8 4.8 11.4 14.5 12.1 8.4 4.8 2.9 3.1 6.0 7.8 5.0 10.0 5.1

Earnings table

Source: Mirae Asset Daewoo Research estimates

Spotlightstocks

Mirae Asset Daewoo Research29| Monthly InsighT

Samsung SDI (006400 KS)

FY (Dec.) 12/14 12/15 12/16 12/17F 12/18F 12/19F

Revenue (Wbn) 5,474 4,955 5,201 6,493 8,246 9,818

OP (Wbn) 71 -267 -926 108 501 730

OP margin (%) 1.3 -5.4 -17.8 1.7 6.1 7.4

NP (Wbn) -84 54 219 738 1,142 1,274

EPS (W) -1,426 765 3,117 10,490 16,227 18,104

ROE (%) -0.9 0.5 2.0 6.7 9.7 9.9

P/E (x) - 149.0 35.0 19.5 12.6 11.3

P/B (x) 0.7 0.7 0.7 1.2 1.1 1.0

(Maintain) Buy

Target price (12M, W) 270,000

Share price (11/30/17, W) 204,500

Expected Return 32%

OP (17F, Wbn) 108

Consensus OP (17F, Wbn) 93

EPS growth (17F, %) 236.5

Market EPS growth (17F, %) 46.7

P/E (17F, x) 19.5

Market P/E (17F, x) 10.0

KOSPI 2,467.49

Market cap (Wbn) 14,062

Shares outstanding (mn) 70

Free float (%) 74.6

Foreign ownership (%) 41.7

Beta (12M) 2.45

52-week low 105,500

52-week high 232,500

(%) 1M 6M 12M

Absolute -7.0 19.9 90.2

Relative -5.3 15.8 56.1

Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimates

Chuljoong [email protected]

EV market’s growth potential is indisputable

■ 4Q17 preview: Revenue of W2tr (+18.7% QoQ), OP of W109bn (+81.5% QoQ)

- Small batteries: Galaxy 9-bound component supplies may begin in 4Q, amid continued growth in North America-bound shipments.

- Mid/large-sized batteries: Entered peak-demand season

- Earnings for the OLED/semiconductor materials business should remain solid.

■ Catalyst: Robust mid/large-sized battery earnings; Rising value of stake in Samsung Display

- The EV battery business is forecast to turn to profit in 2Q18, and its revenue is set to climb to W2.2tr in 2018 (from W1.4tr in2017).

- Safety issues have emerged in the small and mid/large-sized battery markets: top-tier firms with advanced technology will likely continue to benefit.

- Solid sales of the iPhone X and China-bound OLED panel shipments should boost earnings at subsidiary Samsung Display in 2018.

■ Valuation: Maintain Buy and TP of W270,000

- Our target price was derived by summing the value of investment assets (W9.6tr; including Samsung Display stake) and operations (W9.1tr; including the mid/large-sized battery business).

- The firm should see its cost structure improvement accelerate, driven by EV market expansion and market share gains.

- Conditions are ripe for a re-rating of the mid/large-sized battery division.

80

110

140

170

200

230

260

290

11/16 3/17 7/17 11/17

Samsung SDI KOSPI

Other notable stocks

Spotlightstocks

Mirae Asset Daewoo Research30| Monthly InsighT

Samsung SDI (006400 KS) Earnings table

Source: Mirae Asset Daewoo Research estimates

(Wbn, %) 1Q17 2Q17 3Q17 4Q17F 1Q18F 2Q18F 3Q18F 4Q18F 2016 2017F 2018F

Revenue 1,305 1,454 1,707 2,027 1,992 1,948 2,090 2,215 5,203 6,493 8,246

LIB 823 987 1,169 1,467 1,425 1,345 1,457 1,562 3,425 4,447 5,790

Small-sized (IT) 551 690 814 945 962 845 907 901 2,488 3,000 3,615

Mid/large-sized (EV, ESS) 272 298 355 523 463 501 551 660 937 1,447 2,175

Electronic materials 482 467 538 559 567 603 633 653 1,773 2,046 2,456

Operating profit -67 6 60 109 110 94 133 165 -926 108 501

LIB -114 -48 3 49 47 29 66 96 -349 -110 239

Small-sized (IT) -23 15 49 73 73 43 60 60 -28 114 236

Mid-large-sized (EV, ESS) -90 -63 -45 -25 -26 -13 6 37 -321 -223 3

Electronic materials 46 54 57 60 63 65 67 69 167 218 263

Other -744 0 0

OP margin -5.2 0.4 3.5 5.4 5.5 4.8 6.3 7.5 -17.8 1.7 6.1

LIB -13.8 -4.9 0.3 3.3 3.3 2.2 4.5 6.2 -10.2 -2.5 4.1

Electronic materials 9.6 11.5 10.5 10.8 11.0 10.8 10.5 10.5 9.4 10.6 10.7

Other notable stocks

Spotlightstocks

Mirae Asset Daewoo Research31| Monthly InsighT

FY (Dec.) 12/14 12/15 12/16 12/17F 12/18F 12/19F

Revenue (Wbn) 6,100 6,176 6,033 6,847 7,825 8,637

OP (Wbn) 65 301 24 305 535 609

OP margin (%) 1.1 4.9 0.4 4.5 6.8 7.1

NP (Wbn) 503 11 15 167 303 355

EPS (W) 6,478 144 190 2,154 3,902 4,580

ROE (%) 11.5 0.3 0.3 3.9 6.7 7.4

P/E (x) 8.4 436.3 268.0 46.4 25.6 21.8

P/B (x) 0.9 1.1 0.9 1.7 1.6 1.5

(Maintain) Buy

Target Price (12M, W) 131,000

Share price (11/30/17, W) 100,000

Expected Return 31%

(%) 1M 6M 12M

Absolute -2.4 -2.4 98.4

Relative -0.6 -5.8 62.8

Samsung Electro-Mechanics (009150 KS)

Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimatesWonjae Park

Higher MLCC prices to drive up 2018 earnings

■ 4Q17 preview: OP of W106.1bn (TTB YoY); Strong seasonality expected for 1Q18

- For 4Q17, we project solid revenue (W1.73tr) and operating profit (W106.1bn; TTB YoY) despite weak seasonality.• Camera/telecom modules: Supply of components for SEC’s Galaxy S9 has begun. • Substrates (HDI, RF-PCB, etc.): Growth in RF-PCB revenue from a US customer to drive up profitability• Components (MLCC, inductors, etc.): Sales mix of value-added MLCC products to expand; ASP to rise for the fourth consecutive quarter

- For 1Q18, we forecast revenue of W1.84tr (+17.1% YoY) and operating profit of W136.6bn (+435.1% YoY).• The anticipated launch of the Galaxy S9 will likely boost dual-camera module and SLP (substrate-like PCB) sales. Despite 4Q being a weak season, the company will likely move straight into a high season, thanks to the

launches of new smartphone models; however, the won’s recent appreciation is negative.

■ 2018 OP forecast to climb 75.1% on uptrend in MLCC prices

- SEMCO’s full-year operating profit is projected to come in at W305.5bn for 2017, and climb 75.1% to W535bn in 2018 (supported by full-fledged sales of dual camera modules and a continued uptrend in MLCC prices).

■ Maintain Buy and TP of W131,000

- The won’s recent appreciation and changes in FO-PLP technology trend deserve attention.

OP (17F, Wbn) 305

Consensus OP (17F, Wbn) 311

EPS Growth (17F, %) 1,036.5

Market EPS Growth (17F, %) 46.7

P/E (17F, x) 46.4

Market P/E (17F, x) 10.0

KOSPI 2,467.49

Market Cap (Wbn) 7,469

Shares Outstanding (mn) 78

Free Float (%) 73.3

Foreign Ownership (%) 20.3

Beta (12M) 1.62

52-Week Low 50,400

52-Week High 112,000

70

110

150

190

230

270

12/16 3/17 6/17 9/17 12/17

SEMCO KOSPI

Spotlightstocks

Mirae Asset Daewoo Research32| Monthly InsighT

Earnings table

Source: Company data, Mirae Asset Daewoo Research estimates

Samsung Electro-Mechanics (009150 KS) Spotlightstocks

(Wbn, %)2017F 2018F

2016 2017F 2018F1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue Module solutions 773.0 835.5 822.0 639.2 792.3 908.4 912.3 781.3 2,658.2 3,069.7 3,394.2

Component solutions 490.4 542.4 608.0 630.6 623.8 678.0 754.2 707.0 1,929.2 2,271.4 2,763.0

Substrate solutions 292.5 319.5 399.6 438.4 403.6 320.7 381.5 482.2 1,316.0 1,450.0 1,587.9

Other 14.6 12.5 11.5 17.4 18.9 22.7 20.0 18.4 129.7 56.0 80.0

Total 1,570.5 1,709.9 1,841.1 1,725.7 1,838.6 1,929.8 2,068.0 1,988.8 6,033.1 6,847.1 7,825.2

Operating profit Module solutions 18.9 39.7 32.7 17.1 38.1 47.8 42.7 26.5 28.8 108.4 155.2

Component solutions 45.6 60.5 86.0 97.7 90.5 89.2 110.5 77.8 132.9 289.8 367.9

Substrate solutions -39.0 -29.5 -15.5 -8.8 8.1 -3.2 9.5 -2.4 -137.3 -92.8 12.0

Total 25.5 70.7 103.2 106.1 136.6 133.8 162.7 101.9 24.4 305.5 535.0

OP margin Module solutions 2.4 4.7 4.0 2.7 4.8 5.3 4.7 3.4 1.1 3.5 4.6

Component solutions 9.3 11.2 14.1 15.5 14.5 13.2 14.6 11.0 6.9 12.8 13.3

Substrate solutions -13.3 -9.2 -3.9 -2.0 2.0 -1.0 2.5 -0.5 -10.4 -6.4 0.8

Total 1.6 4.1 5.6 6.1 7.4 6.9 7.9 5.1 0.4 4.5 6.8

Pretax profit 11.5 64.0 98.5 81.8 118.1 117.3 147.2 77.7 32.1 255.8 460.3

Net profit 2.2 33.3 71.9 59.7 75.9 77.8 97.6 51.5 14.7 167.2 302.8

Pretax margin 0.7 3.7 5.4 4.7 6.4 6.1 7.1 3.9 0.5 3.7 5.9

Net margin 0.1 2.0 3.9 3.5 4.1 4.0 4.7 2.6 0.2 2.4 3.9

Mirae Asset Daewoo Research33| Monthly InsighT

FY (Dec.) 12/14 12/15 12/16 12/17F 12/18F 12/19F

Revenue (Wbn) 6,466 6,138 5,755 7,581 8,561 8,754

OP (Wbn) 314 224 105 350 453 456

OP margin (%) 4.9 3.6 1.8 4.6 5.3 5.2

NP (Wbn) 113 95 5 220 300 303

EPS (W) 5,020 4,018 209 9,296 12,697 12,786

ROE (%) 7.5 5.5 0.3 11.7 14.0 12.4

P/E (x) 22.4 24.5 422.4 15.5 11.3 11.3

P/B (x) 1.6 1.3 1.2 1.7 1.5 1.3

(Maintain) Buy

Target Price (12M, W) ▼210,000

Share price (11/30/17, W) 144,000

Expected Return 46%

OP (17F, Wbn) 350

Consensus OP (17F, Wbn) 318

EPS Growth (17F, %) 4,342.0

Market EPS Growth (17F, %) 46.7

P/E (17F, x) 15.5

Market P/E (17F, x) 10.0

KOSPI 2,467.49

Market Cap (Wbn) 3,408

Shares Outstanding (mn) 24

Free Float (%) 59.2

Foreign Ownership (%) 22.9

Beta (12M) 1.10

52-Week Low 85,600

52-Week High 184,500

(%) 1M 6M 12M

Absolute -14.8 -10.8 63.6

Relative -13.2 -13.9 34.3

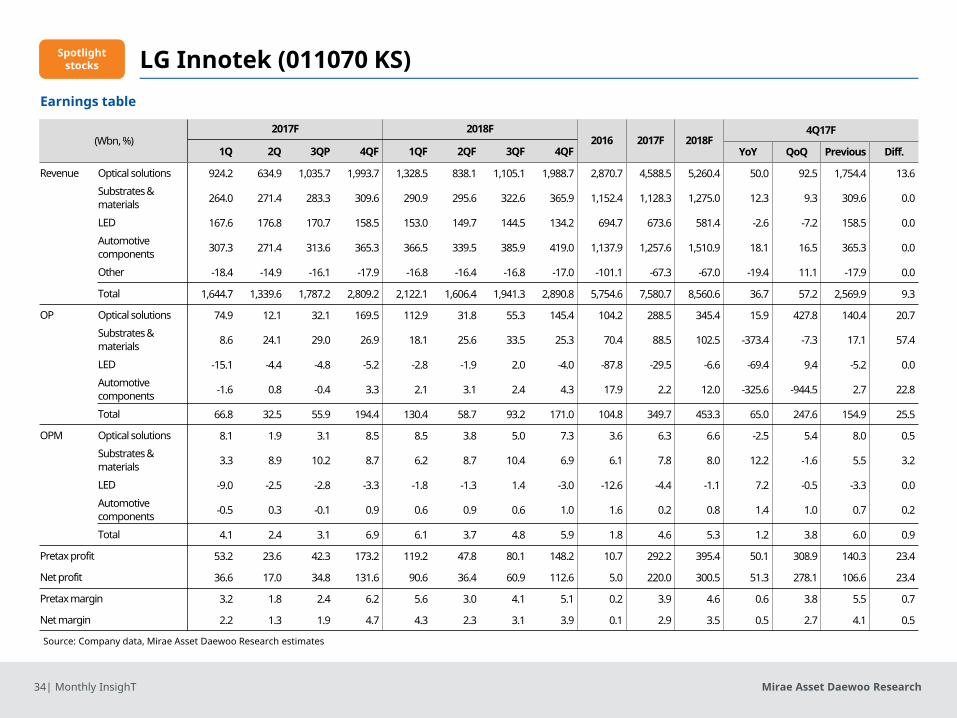

LG Innotek (011070 KS)

Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimatesWonjae Park

Spotlightstocks

Strong competitiveness remains intact

■ 4Q17 preview: OP estimate raised to W194.4bn (from W154.9bn)

- For 4Q17, we expect LG Innotek to deliver record-breaking earnings, with revenue of W2.81tr (+36.7% YoY).

- We believe that solid iPhone X sales are driving up the firm’s revenue from dual camera/3D sensing modules. • The outlook for new businesses is also positive.• The firm has begun supplying other components, like RFPCBs (annual revenue of W200bn) and wireless

charging modules (revenue of W150bn).

■ Earnings to remain robust in 1Q18; Automotive electronics business is also positive; Won appreciation is negative

- Earnings will likely remain solid in 1Q18, although our operating profit forecast has been lowered to W130.4bn (from W147bn) due to the won’s recent appreciation.

- LG Group’s potential acquisition of an automotive components supplier would also benefit LG Innotek by boosting sales of the firm’s automotive LEDs.

■ Maintain Buy and lower TP to W210,000 (from W232,000)

- Our new target price is based on our 2018F BPS of 97,775 and a target P/B of 2.16x (20% discount to the five-year peak), lowered from 2.5x due to the won’s recent appreciation and deteriorating investor sentiment.

80

120

160

200

240

12/16 4/17 8/17 12/17

LG Innotek KOSPI

Mirae Asset Daewoo Research34| Monthly InsighT

Earnings table

Source: Company data, Mirae Asset Daewoo Research estimates

LG Innotek (011070 KS) Spotlightstocks

(Wbn, %)2017F 2018F

2016 2017F 2018F4Q17F

1Q 2Q 3QP 4QF 1QF 2QF 3QF 4QF YoY QoQ Previous Diff.

Revenue Optical solutions 924.2 634.9 1,035.7 1,993.7 1,328.5 838.1 1,105.1 1,988.7 2,870.7 4,588.5 5,260.4 50.0 92.5 1,754.4 13.6

Substrates & materials 264.0 271.4 283.3 309.6 290.9 295.6 322.6 365.9 1,152.4 1,128.3 1,275.0 12.3 9.3 309.6 0.0

LED 167.6 176.8 170.7 158.5 153.0 149.7 144.5 134.2 694.7 673.6 581.4 -2.6 -7.2 158.5 0.0

Automotive components 307.3 271.4 313.6 365.3 366.5 339.5 385.9 419.0 1,137.9 1,257.6 1,510.9 18.1 16.5 365.3 0.0

Other -18.4 -14.9 -16.1 -17.9 -16.8 -16.4 -16.8 -17.0 -101.1 -67.3 -67.0 -19.4 11.1 -17.9 0.0

Total 1,644.7 1,339.6 1,787.2 2,809.2 2,122.1 1,606.4 1,941.3 2,890.8 5,754.6 7,580.7 8,560.6 36.7 57.2 2,569.9 9.3

OP Optical solutions 74.9 12.1 32.1 169.5 112.9 31.8 55.3 145.4 104.2 288.5 345.4 15.9 427.8 140.4 20.7

Substrates & materials 8.6 24.1 29.0 26.9 18.1 25.6 33.5 25.3 70.4 88.5 102.5 -373.4 -7.3 17.1 57.4

LED -15.1 -4.4 -4.8 -5.2 -2.8 -1.9 2.0 -4.0 -87.8 -29.5 -6.6 -69.4 9.4 -5.2 0.0

Automotive components -1.6 0.8 -0.4 3.3 2.1 3.1 2.4 4.3 17.9 2.2 12.0 -325.6 -944.5 2.7 22.8

Total 66.8 32.5 55.9 194.4 130.4 58.7 93.2 171.0 104.8 349.7 453.3 65.0 247.6 154.9 25.5

OPM Optical solutions 8.1 1.9 3.1 8.5 8.5 3.8 5.0 7.3 3.6 6.3 6.6 -2.5 5.4 8.0 0.5

Substrates & materials 3.3 8.9 10.2 8.7 6.2 8.7 10.4 6.9 6.1 7.8 8.0 12.2 -1.6 5.5 3.2

LED -9.0 -2.5 -2.8 -3.3 -1.8 -1.3 1.4 -3.0 -12.6 -4.4 -1.1 7.2 -0.5 -3.3 0.0

Automotive components -0.5 0.3 -0.1 0.9 0.6 0.9 0.6 1.0 1.6 0.2 0.8 1.4 1.0 0.7 0.2

Total 4.1 2.4 3.1 6.9 6.1 3.7 4.8 5.9 1.8 4.6 5.3 1.2 3.8 6.0 0.9

Pretax profit 53.2 23.6 42.3 173.2 119.2 47.8 80.1 148.2 10.7 292.2 395.4 50.1 308.9 140.3 23.4

Net profit 36.6 17.0 34.8 131.6 90.6 36.4 60.9 112.6 5.0 220.0 300.5 51.3 278.1 106.6 23.4

Pretax margin 3.2 1.8 2.4 6.2 5.6 3.0 4.1 5.1 0.2 3.9 4.6 0.6 3.8 5.5 0.7

Net margin 2.2 1.3 1.9 4.7 4.3 2.3 3.1 3.9 0.1 2.9 3.5 0.5 2.7 4.1 0.5

Mirae Asset Daewoo Research35| Monthly InsighT

Seoul Semiconductor (046890 KQ)

Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimates

FY (Dec.) 12/13 12/14 12/15 12/16 12/17F 12/18F

Revenue (Wbn) 939 1,011 954 1,115 1,264 1,445

OP (Wbn) 3 46 58 103 123 142

OP margin (%) 0.3 4.5 6.1 9.2 9.7 9.8

NP (Wbn) -7 17 36 61 82 95

EPS (W) -118 291 621 1,054 1,407 1,635

ROE (%) -1.2 3.0 6.1 9.8 12.0 12.5

P/E (x) - 54.0 25.1 26.4 19.8 17.0

P/B (x) 2.1 1.6 1.5 2.5 2.2 2.0

(Maintain) Buy

Target Price (12M, W) 37,800

Share price (12/28/17, W) 27,850

Expected Return 36%

OP (17F, Wbn) 103

Consensus OP (17F, Wbn) 105

EPS Growth (17F, %) 69.8

Market EPS Growth (17F, %) 46.7

P/E (17F, x) 26.4

Market P/E (17F, x) 10.0

KOSDAQ 798.42

Market Cap (Wbn) 1,624

Shares Outstanding (mn) 58

Free Float (%) 64.2

Foreign Ownership (%) 18.5

Beta (12M) 0.68

52-Week Low 14,750

52-Week High 33,150

(%) 1M 6M 12M

Absolute -12.7 29.5 78.5

Relative -15.5 8.0 40.3

Wonjae [email protected]

Other notable stocks

Spotlightstocks

80

120

160

200

240

12/16 4/17 8/17 12/17

Seoul Semiconductor

KOSDAQ

Improving market conditions

■ 4Q17 preview: OP of W25.3bn (+23.5% YoY)

- For 4Q17, we see revenue of W286.9bn (+18.8% YoY) and operating profit of W25.3bn (+23.5% YoY).

- Increased exposure to automotive lighting and tight SG&A expense control should keep OP margin steady.

- LED market conditions are gradually improving: The ongoing restructuring in the TV BLU industry has led to a slowdown in the decline in LED chip prices (and even some price hikes); the company is exploring new markets, including the automotive market.

■ 2018F revenue of W1.26tr; Patents, top-line growth, and potential industry restructuring are positives

- We expect 2017 revenue to exceed the W1tr mark again, reaching W1.11tr (+16.8% YoY).

- Top-line growth will likely continue in 2018, with record-high revenue of W1.26tr (+13.4% YoY) supported by expansion of automotive LED sales and operation of a new Vietnam plant (due to be completed in March 2018).

- Growth of the OLED market is a risk, but at the same time could accelerate LED industry restructuring.

■ Maintain Buy and TP of W37,800

- Although the stock is not undervalued, expectations for the LED industry could provide a boost.

Mirae Asset Daewoo Research36| Monthly InsighT

Seoul Semiconductor (046890 KQ)Earnings table

Source: Company data, Mirae Asset Daewoo Research estimates

(Wbn, W, %)2017F 2018F

2016 2017F 2018F1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue 256.2 267.0 304.5 286.9 284.5 307.8 346.9 324.4 953.8 1,114.5 1,263.6

Operating profit 23.4 24.1 30.6 25.3 26.6 29.6 37.7 28.9 57.5 103.4 122.8

Pretax profit 10.5 29.7 30.4 23.4 25.9 29.0 37.0 28.2 49.6 94.0 119.9

Net profit 6.8 21.4 17.3 16.0 17.7 19.8 25.3 19.3 36.2 61.4 82.0

EPS 116 366 296 275 303 340 434 330 621 1,054 1,407

OP margin 9.1 9.0 10.1 8.8 9.4 9.6 10.9 8.9 6.0 9.3 9.7

Pretax margin 4.1 11.1 10.0 8.2 9.1 9.4 10.7 8.7 5.2 8.4 9.5

Net margin 2.6 8.0 5.7 5.6 6.2 6.4 7.3 5.9 3.8 5.5 6.5

Other notable stocks

Spotlightstocks

Mirae Asset Daewoo Research37| Monthly InsighT

Hanwha Techwin (012450 KS)

Notes: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interestsSource: Mirae Asset Daewoo Research estimates

FY (Dec.) 12/14 12/15 12/16 12/17F 12/18F 12/19F

Revenue (Wbn) 2,616 2,613 3,519 4,232 4,322 4,918

OP (Wbn) 8 -60 151 92 133 173

OP margin (%) 0.3 -2.3 4.3 2.2 3.1 3.5

NP (Wbn) -119 6 345 48 88 119

EPS (W) -2,236 108 6,498 905 1,669 2,257

ROE (%) -7.1 0.3 15.1 2.1 3.7 4.9

P/E (x) - 329.2 6.7 39.3 21.3 15.8

P/B (x) 0.8 0.8 1.0 0.8 0.8 0.7

(Maintain) Buy

Target Price (12M, W) ▼45,400

Share price (12/28/17, W) 35,550

Expected Return 52%

OP (17F, Wbn) 92

Consensus OP (17F, Wbn) 98

EPS Growth (17F, %) -86.1

Market EPS Growth (17F, %) 46.7

P/E (17F, x) 39.3

Market P/E (17F, x) 10.0

KOSPI 2,467.49

Market Cap (Wbn) 1,870

Shares Outstanding (mn) 53

Free Float (%) 67.3

Foreign Ownership (%) 18.0

Beta (12M) 0.89

52-Week Low 32,750

52-Week High 53,100

(%) 1M 6M 12M

Absolute 0.7 -21.7 -17.3

Relative 2.6 -24.4 -32.2

Wonjae [email protected]

Earnings to normalize in 2018

■ 4Q17 preview: OP to rise 83.3% YoY to W55.9bn on self-propelled howitzer exports

- After remaining sluggish through 3Q, earnings will likely see a pickup in 4Q (revenue of W1.55tr and operating profit of W55.9bn), driven by increased exports of the K9 self-propelled howitzer (estimated at W170bn).

■ Operating profit to normalize in 2018

- We forecast 2017 operating profit at a mere W92.5bn (-38.6% YoY), in light of the persistent sluggishness of the security camera business.

- For 2018, operating profit is projected to recover to W133.2bn (+44% YoY), on a turnaround of the security camera business and continuous exports of defense products.

- The engine division will likely continue to incur revenue & risk-sharing program expenses, but such expenses need to be viewed as investments for the future.

■ Maintain Buy but lower TP to W45,400 (from W54,000)

- Our new target price is based on 2018F BPS of W45,437 and a P/B of 1.0x (20% discount to the five-year average).

- We continue to recommend expanding positions in the event of correction.

- We caution that the results of the ongoing tax investigation could be reflected in 4Q17.

Other notable stocks

50

70

90

110

130

12/16 4/17 8/17 12/17

Hanwha Techwin KOSPI

Mirae Asset Daewoo Research38| Monthly InsighT

Hanwha Techwin (012450 KS)Earnings table

Source: Company data, Mirae Asset Daewoo Research estimates

(Wbn, %, %p)2017F 2018F

2016 2017F 2018F1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue CCTV 136.7 168.1 143.5 165.0 143.5 184.9 200.9 178.2 637.8 613.3 707.5 Engine/energy equip. 221.2 234.6 213.3 354.5 238.9 254.3 266.6 283.6 1,050.7 1,023.6 1,043.4 Hanwha Power Systems 23.5 67.7 36.6 75.0 47.0 47.4 54.9 71.3 197.1 202.8 220.5 Hanwha Precision Machinery 55.9 73.1 56.3 59.5 56.5 62.2 71.5 67.9 169.3 244.8 258.1 Hanwha Systems 134.6 153.0 150.3 345.0 155.3 176.5 194.2 242.7 217.3 782.9 768.7

Hanwha Land Systems 110.5 187.7 149.8 301.0 150.5 165.6 173.8 208.6 714.4 749.0 698.5

Hanwha Defense 92.0 152.1 129.5 263.0 105.2 167.1 183.8 211.4 532.0 636.6 667.6

Total 774.3 1,036.3 868.6 1,552.3 886.2 1,047.3 1,135.1 1,253.0 3,518.8 4,231.5 4,321.7

Operatingprofit

CCTV -0.1 -3.7 -10.3 -21.5 -4.3 0.0 5.0 3.4 33.7 -35.6 4.1

Engine/energy equip. 12.6 5.2 -1.3 4.6 6.0 5.6 7.5 3.7 58.0 21.1 22.7

Hanwha Power Systems -7.1 -2.2 -0.7 -3.0 -1.4 -1.4 -0.9 -1.4 -12.8 -13.0 -5.1 Hanwha Precision Machinery 3.7 10.0 4.1 3.3 2.9 4.0 5.1 3.8 -15.4 21.2 15.9

Hanwha Systems -1.5 -1.8 2.2 20.4 2.3 2.6 6.8 8.5 13.5 19.2 20.3

Hanwha Land Systems 1.3 9.9 2.6 42.1 15.1 14.1 14.8 11.5 38.6 56.0 55.4

Hanwha Defense 2.3 5.8 9.4 13.7 3.4 8.3 12.0 11.5 35.1 31.2 35.2

Total 11.2 23.2 2.2 55.9 20.1 29.4 46.4 37.2 150.7 92.5 133.2

OP margin 1.4 2.2 0.3 3.6 2.3 2.8 4.1 3.0 4.3 2.2 3.1

Pretax profit 5.9 19.1 -10.1 48.0 14.9 24.0 40.4 30.4 418.5 62.9 109.8

Net profit 9.9 17.1 -17.6 38.4 11.9 19.2 32.3 24.4 345.2 47.8 87.8

Pretax margin 0.8 1.8 -1.2 3.1 1.7 2.3 3.6 2.4 11.9 1.5 2.5

Net margin 1.3 1.7 -2.0 2.5 1.3 1.8 2.8 1.9 9.8 1.1 2.0

Other notable stocks

Mirae Asset Daewoo Research39| Monthly InsighT

APPENDIX 1

Important Disclosures & Disclaimers 2-Year Rating and Target Price History

Company (Code) Date Rating Target Price Company (Code) Date Rating Target Price LG Electronics(066570) 01/01/2018 Buy 129,000 01/01/2017 Buy 38,000 10/26/2017 Buy 113,000 12/31/2016 No Coverage 08/30/2017 Buy 100,000 07/27/2016 Buy 37,000 07/10/2017 Buy 95,000 04/01/2016 Buy 32,000 04/09/2017 Buy 96,000 01/27/2016 Buy 29,000 03/13/2017 Buy 87,700 11/29/2015 Buy 31,000 03/01/2017 Buy 79,000 Samsung SDI(006400) 10/31/2017 Buy 270,000 01/26/2017 Buy 65,600 09/01/2017 Buy 240,000 10/28/2016 Buy 64,000 07/27/2017 Buy 210,000 10/03/2016 Buy 67,000 07/03/2017 Trading Buy 180,000 07/28/2016 Buy 75,000 01/01/2017 Hold 03/01/2016 Buy 78,000 12/31/2016 No Coverage 01/26/2016 Buy 67,000 10/28/2016 Trading Buy 107,000 11/27/2015 Buy 70,000 09/11/2016 Trading Buy 120,000 LG Display(034220) 10/25/2017 Buy 42,000 04/29/2016 Trading Buy 129,000 07/03/2017 Buy 50,000 01/25/2016 Buy 138,000 04/26/2017 Buy 40,000 11/29/2015 Buy 148,000

0

50,000

100,000

150,000

Jan 16 Jan 17 Jan 18

(W) LG Electronics

0

10,000

20,000

30,000

40,000

50,000

60,000

Jan 16 Jan 17 Jan 18

(W) LG Display

0

50,000

100,000

150,000

200,000

250,000

300,000

Jan 16 Jan 17 Jan 18

(W) Samsung SDI

Mirae Asset Daewoo Research40| Monthly InsighT

2-Year Rating and Target Price History

Company (Code) Date Rating Target Price Company (Code) Date Rating Target Price Samsung Electro-Mechanics(009150) 07/23/2017 Buy 131,000 01/25/2016 Buy 115,000 07/03/2017 Buy 123,000 07/26/2015 Buy 123,000 05/31/2017 Buy 100,000 Seoul Semiconductor(046890) 11/30/2017 Buy 37,800 05/01/2017 Buy 93,000 10/25/2017 Buy 34,300 04/02/2017 Buy 85,000 10/10/2017 Buy 31,000 02/20/2017 Buy 76,000 09/01/2017 Buy 28,000 01/26/2017 Buy 68,000 07/03/2017 Buy 26,900 10/03/2016 Buy 65,300 04/02/2017 Buy 23,400 08/31/2016 Buy 72,200 02/02/2017 Buy 20,300 04/26/2016 Buy 73,700 10/03/2016 Buy 19,900 01/31/2016 Buy 74,600 07/31/2016 Buy 21,500 10/30/2015 Buy 93,000 02/01/2016 Buy 19,500 LG Innotek(011070) 01/01/2018 Buy 210,000 10/27/2015 Buy 24,000 10/25/2017 Buy 232,000 Hanwha Techwin(012450) 01/02/2018 Buy 45,400 09/01/2017 Buy 230,000 11/05/2017 Buy 54,000 07/03/2017 Buy 199,000 10/10/2017 Buy 47,000 04/02/2017 Buy 171,000 07/18/2017 Buy 57,000 03/01/2017 Buy 156,000 05/01/2017 Buy 69,000 01/25/2017 Buy 130,000 04/23/2017 Buy 61,000 01/01/2017 Buy 119,000 01/31/2017 Buy 62,000 11/29/2016 Buy 115,000 11/02/2016 Buy 71,000 10/03/2016 Buy 105,000 10/03/2016 Buy 80,000 07/27/2016 Buy 117,000 07/31/2016 Buy 77,000 06/01/2016 Buy 107,000 06/08/2016 Buy 61,000 04/27/2016 Buy 96,000 05/01/2016 Buy 59,000 04/01/2016 Buy 102,000 10/28/2015 Buy 49,000

0

50,000

100,000

150,000

Jan 16 Jan 17 Jan 18

(W) Samsung Electro-Mechanics

0

50,000

100,000

150,000

200,000

250,000

Jan 16 Jan 17 Jan 18

(W) LG Innotek

0

10,000

20,000

30,000

40,000

Jan 16 Jan 17 Jan 18

(W) Seoul Semiconductor

0

20,000

40,000

60,000

80,000

100,000

Jan 16 Jan 17 Jan 18

(W) Hanwha Techwin

Mirae Asset Daewoo Research41| Monthly InsighT

Equity Ratings Distribution & Investment Banking Services Buy Trading Buy Hold Sell

Equity Ratings Distribution 74.52% 12.50% 12.98% 0.00% Investment Banking Services 70.73% 19.51% 9.76% 0.00% * Based on recommendations in the last 12-months (as of September 30, 2017)

Disclosures As of the publication date, Mirae Asset Daewoo Co., Ltd. and/or its affiliates do not have any special interest with the subject company and do not own 1% or more of the subject company's shares outstanding.

Analyst Certification The research analysts who prepared this report (the “Analysts”) are registered with the Korea Financial Investment Association and are subject to Korean securities regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws or regulations thereof. Each Analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the personal views of the Analyst about any and all of the issuers and securities named in this report and (ii) no part of the compensation of the Analyst was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report. Mirae Asset Daewoo Co., Ltd. (“Mirae Asset Daewoo”) policy prohibits its Analysts and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer, director or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this report. Like all employees of Mirae Asset Daewoo, the Analysts receive compensation that is determined by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment banking, proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or Mirae Asset Daewoo except as otherwise stated herein.

Stock Ratings Industry Ratings Buy : Relative performance of 20% or greater Overweight : Fundamentals are favorable or improving Trading Buy : Relative performance of 10% or greater, but with volatility Neutral : Fundamentals are steady without any material changes Hold : Relative performance of -10% and 10% Underweight : Fundamentals are unfavorable or worsening Sell : Relative performance of -10%

Ratings and Target Price History (Share price (─), Target price (▬), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆)) * Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months. * Although it is not part of the official ratings at Mirae Asset Daewoo Co., Ltd., we may call a trading opportunity in case there is a technical or short-term material development. * The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of future earnings. * The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic conditions.

Mirae Asset Daewoo Research42| Monthly InsighT