marketing opportunities for fruits in machakos - equator prize

TRANSCRIPT

Market Survey Report

on

Market Opportunities for Fruits and Vegetables Processing in Ukambani,

Eastern Kenya

{PRIVATE } Project Supported by

USAID funds through the FOODNET competitive grants scheme.

By Frederick M. Kiilu (Kamumo Products), Lutta Muhammad (Kenya Agricultural

Research Institute) and Samuel M. Wambugu (Kenya Industrial Research and Development Institute).

2

Acknowledgements{PRIVATE } We wish to record our debt of gratitude to the many individuals and institutions that contributed to successful planning and implementation of this study but are not mentioned here. At the FOODNET Co-ordinating office, we wish to thank Dr Shaun Ferris and John Jagwe for ensuring smooth flow of funds. We specifically mention the FOODNET Co-ordination Office (located in Kampala, Uganda) who provided the funds to meet the operational costs of the study. These funds were drawn from a USAID competitive grant administered by FOODNET. Mr Kyalo Mulinge, Mr Thomas Katua, Mr David Mutinda, Mr Stephen Kituku, Mr Silas M’Ragwa and Mr Mutuku Nthuli conducted Field interviews with farmers and traders of fruits and vegetables as well as intermediate consumers of processed products. Ms Carol Wafula gave valuable assistance with data management. To the lady and the gentlemen, our gratitude. We also wish to thank company officials who assisted us but remain anonymous. Last, but not least we thank all respondents who generously spent their time answering questions they sometimes thought were not important, and for the lessons learnt from them.

November 2001

3

TABLE OF CONTENTS Acknowledgements………………………………………………………………………………3 1 Introduction……………………………………………………………………………………..6 The Agro-ecological, socio-economic, infrastructure and Institutional Environment in Ukambani ……….….4

2.1 Agro-ecological conditions…………………………..……………..6 2.2 Farming Systems and soci-economic conditions……………………..6 2.3 Infrastructure…………………………………………………………7

3. The Company - Kamumo Products…………………………………………………….8 3.1 Status of the firm……………………………………………………..8 3.2 Marketing……………………………………………………………..8 3.3 Constraints…………………………………………………………....8 4. Objectives of the market Survey……………………………………………………..…9 5. Methods……………………………………………………………………………..……9 5.1 The survey of fruits and vegetables farmers…………………………9 5.2 Survey of fruits and vegetables traders………………………………9 5.3 Survey of intermediate consumers of the processed products of fruits and

vegetables………10 5.4 Survey of small, medium and large-scale enterprises processing fruits and

vegetables……..10 6. Availability of Fruits and Vegetables for processing in Kenya and Ukambani……….10 7. The Market for Fruits and Vegetables and Processed Products……………………….12 7.1 Gender……………………………………….…………….…………..13 7.2 Age………………………………………..……………………………13 7.3 Level of formal education……………………………………………..13 8. Processing of Fruits and Vegetables……………………………………………………..17 8.1 Fruits for processing…………………………………………………...17 8.2 Products made from Fruits and vegetables …………………………..17 8.3 Trends in traded volumes and prices of processed fruit and vegetables

products…………...18 8.4 Transportation of Fruits and vegetables products…………………….19 8.5 Sources of fruits and Vegetables……..………………………………..19 9. Intermediate Consumers of Processed Products Made from Fruits and Vegetables in

Ukambani…………20 10. Conclusions and Recommendations …………………………………………………….21 11. References………….…………………………………………………………………….23

4

List of Tables Table 1. Population distribution in the Four Ukambani Districts Table 2a. Hectarage, volume and yields of fruits and vegetables in Kenya Table 2b. Hectarage of fruits and vegetables in four districts of Eastern Province Table 2c. Production and yields of fruits and vegetables in the four districts of Eastern Province Table 3. Characteristics of the main players in the fruit and vegetables sub-sector Table 4. Major fruits and vegetables production seasons in the Ukambani region Table 5. Volumes and prices of processed products made from fruits and vegetables Table 6. Proportion of manufacturers processing various types of fruits and vegetables and annual production and prices Table 7. Trends in traded volumes and prices of processed fruit and vegetable products Table 8. Sources quantities and prices and uses of some processed fruits Table 9. Quantities of processed fruit and vegetable products stocked by intermediate consumers per year Table 10. Characteristics of the businesses dealing with fruit and vegetable processed products

5

List of Figures Figure 1. Kamumo products at a recent trade exhibition Figure 2. The HCDA fruits and vegetables handling facility in Machakos town Figure 3. Fresh fruits used by processing firms Figure 4. Growth trends in intermediate consumers

6

1. Introduction The agriculture sector plays the leading role in the economy of Kenya. Agriculture fulfills this role by providing export earnings, internal self sufficiency in basic foods, employment supply of raw materials for the processing industry. Kenyan agricultural production is dominated by cereals, grain legumes, root crops and several industrial crops. Many of the horticultural crops have a dual subsistence as well as cash function. The importance of the horticulture sub-sector within the Kenyan agriculture sector has been widely acclaimed. Talking to journalists in Nairobi recently, the chairman of the Fresh Produce Exporters Association of Kenya said `Horticulture is the last bastion of growth in an economy which shrunk by 0.4 per cent during the year 2000. It is Kenya's second foreign exchange earner. In the year 2000, foreign exchange earnings from horticulture alone totaled KShs 14 bilion accruing from the sale of 99,000 tons, up from KShs 4 bilion from the sale of 70,000 tons in 1995 (Akumu 2001).' Ukambani area (Machakos, Kitui, Makueni and Mwingi Districts) is a major player in horticulture production for the export as well as the domestic consumers. Although impressive gains in numbers of farmers, hectarage, tonnage and value have been achieved, many factors still constrain exploitation of the development potential offered by the sub-sector. First, transport and communication, storage and processing infrastructure is not well developed in much of the area. Since production and marketing of fruits and vegetables are chacterised by seasonality, there are periods of surplus and scarcity during the year and ensuing wastage and low income. Increased capacity for processing could ease this constraint by utilizing surplus production by transforming these into high value shelf stable products. Following the liberalization of the economy a decade or so ago, some entrepreneurs have set up small to medium scale processing concerns. Such businesses need information about the markets for fresh produce and other raw materials, availability of skills and intermediate inputs as well as the market for final products. There is a need for a market study addressing this need. 2. The Agro-ecological, socio-economic, infrastructure and Institutional Environment in Ukambani 2.1 Agro-ecological Conditions Rainfall patterns in the four Ukambani Districts exhibit distinct bimodal distributions. The first rains fall between mid-March and end of May and are locally known as the long rains (LR). The second rains, the short rains (SR), are received between mid-October and end of December. Average seasonal rainfall is between 250-400 mm. Inter-seasonal rainfall variation is large with a coefficient of variation ranging between 45-58 per cent. Temperature ranges between 17-240c. Evapo-transpiration rates are high and exceed the amount of rainfall, most of the year except the month of November. The main Agro-ecological Zones (AEZ) in the region are: Upper Midland (UM), Lower Highland (LH), Lower Midland (LM) and Lower Lowlands (IL). The LM zone is the most predominant. Based on rainfall criteria, the following main zones can be found: Sub-humid (2) Semi-humid (3), Transitional (4), Semi-arid (5) and Arid (6). The major soils of the dryland areas are developed on basement rocks (gneisses), quartzite and plio-pleistocene bay sediments. The most predominant soils include alfisols, acrisols, ferralsols, vertisols, and andasols (FAO classification).

7

2.2 Farming Systems and socio-economic conditions The main food crops are maize, beans and cowpeas. However, the growing conditions allow a wider range of food crops to be grown. The main on-farm cash generating activities revolve around coffee, horticulture, agro-forestry and cross-bred based dairy farming under the zero and semi-zero grazing systems. Population density within the region (see Table 1) is high and thus the average farm size is within the range 1-7.5 ha. Like in the rest of the country, the majority (about 60%) of the farmers in this region live below the poverty line and they can’t therefore meaningfully contribute to personal or national wealth creation. Poverty and low production risk only permit some of them to use purchased inputs. Farm operations are generally based on hand labour. High value horticultural crops such as tomatoes, onions and Asian vegetables are the main crops and these are raised mainly in Matuu in Yatta division and Kibwezi. Virtually every smallholding has at least some horticultural crop. There may be a combination of tree types on the farm. There are smallholdings where distinct plots are dedicated to the production of one or more types of horticultural crops. This may be under rain-fed or irrigation. There are also medium to large-scale horticulture farms in the area. The main problems are that the quality is low, production constraints such as damage by pests and diseases, and lack of appropriate varieties. These crops exhibit seasonality. They are bulky and highly perishable. They come onto the market at short intervals and then the prices fall, then times of shortage prices increase. 2.3 Infrastructure and Institutional Environment Machakos district is served by 1682 km of roads, out of which 75 per cent are only motorable during the dry season. Makueni district has 1593 km of roads. Kitui and Mwingi districts have a combined 3373 km of roads (3 per cent are all weather). Telecommunication services are more developed in the major town centres such as Machakos and Kitui. Electrical power is supplied to major town centres by the Kenya Power and Lighting Company (KPLC). The government, NGOs and community self help groups have sponsored projects that provide wells, dams and piped water in main areas of human settlement. However, most of the water development ventures are for domestic use and not for agricultural production except in areas where high value crops are raised under irrigation. The area is served by a number of suppliers of seeds, fertilizers, pesticides and fungicides nationwide in the major town centres. A variety of tools and implements can be purchased at these outlets and maintained and serviced through networks of local artisans. The Kenya Industrial Estates (KIE), a public corporation established for the purpose of assisting small-scale industry also participates in the production and marketing of farm implements. Participation by KIE in the farm implements business is however, not extensive. There is considerable local market trade in farm produce, clothing, tools and implements. Loans for agricultural purposes can be obtained from sources such as the Agricultural Finance Corporation (AFC), the co-operative movement and commercial banks. However due to various factors most small-scale subsistence farmers do not have access to the credit facilities.

8

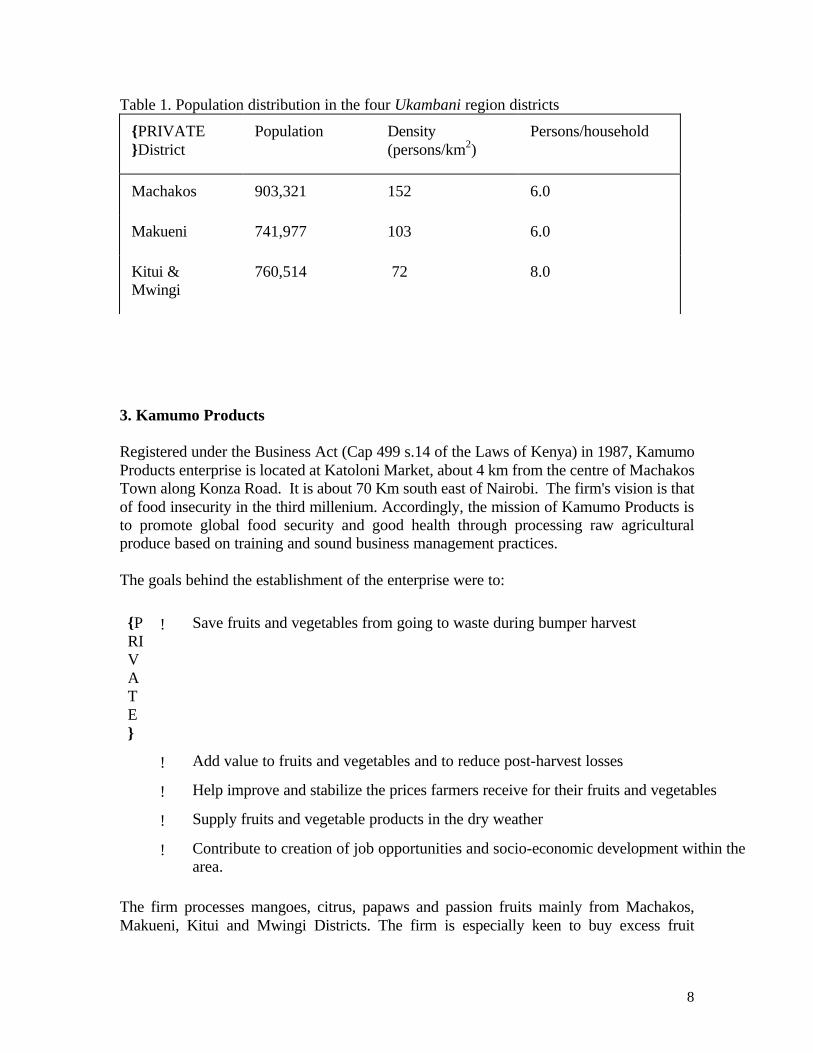

Table 1. Population distribution in the four Ukambani region districts

{PRIVATE }District

Population Density (persons/km2)

Persons/household

Machakos 903,321 152 6.0

Makueni 741,977 103 6.0

Kitui & Mwingi

760,514 72 8.0

3. Kamumo Products Registered under the Business Act (Cap 499 s.14 of the Laws of Kenya) in 1987, Kamumo Products enterprise is located at Katoloni Market, about 4 km from the centre of Machakos Town along Konza Road. It is about 70 Km south east of Nairobi. The firm's vision is that of food insecurity in the third millenium. Accordingly, the mission of Kamumo Products is to promote global food security and good health through processing raw agricultural produce based on training and sound business management practices. The goals behind the establishment of the enterprise were to:

{PRIVATE }

! Save fruits and vegetables from going to waste during bumper harvest

! Add value to fruits and vegetables and to reduce post-harvest losses

! Help improve and stabilize the prices farmers receive for their fruits and vegetables

! Supply fruits and vegetable products in the dry weather

! Contribute to creation of job opportunities and socio-economic development within the area.

The firm processes mangoes, citrus, papaws and passion fruits mainly from Machakos, Makueni, Kitui and Mwingi Districts. The firm is especially keen to buy excess fruit

9

whenever there is surplus production and process these into products that can be used when shortages occur. These are transformed into fruit pulps, juices, jam and sauces. 3.1 Status of the firm At inception, Kamumo Products employed one full time person. The number of employees has since risen to four. All the members of staff receive on-the job training and work under direct supervision of the proprietor. The enterprise has also witnessed significant changes in production technology used. The aluminium utencils which were used in the beginning have been replaced with those made of stainless steel. Small scale semi-automatic tools have largely replaced hand tools based manual procedures. This technical progress has facilitated improvement in product quality, and, at the same time, reduction in unit costs. All these improvements have culminated into increased productivity as well as product diversification. Initially, the firm processed horticultural produce into a single product. The range of products has increased to six. Total production has increased from 50 kg/litres per week to 3,500 kg/litres per week. Annual turn-over rose from U$ 10,000 to 25,000. 3.2 Marketing Kamumo Products sells its finished products to wholesalers, supermarkets, hotels, cafes, hospitals and schools. The firm also reaches its market through participation in trade fairs, symposia, exhibitions, business net-works, etc. In Figure 1., some of the firm's products are on display at a recent International Trade Fair in Nairobi. 3.3 Constraints Like many Jua Kali enterprises, Kamumo Products faces a severe capital constraint. Conditions for accessing credit from either the business community or commercial banks in the Machakos area can not be met by many of the small enterprises. Thus the only realistic source of investible funds is the profits they make and these are, by any standards, meager. This has seriously impaired the firms capacity to undertake investment that should facilitate adoption of efficient technologies. Availability of raw material for processing is constrained by a number of factors, among them, competition from exports, low quality produce from local farmers and the deplorable state of the transport, storage and communications infrastructure. Kamumo Products suffers from adverse effects arising from lack of fruit processing infrastructure, inaccessibility to research findings, lack of training opportunities for staff, inadequate exposure to local as well as international markets and the impact of unpredictable climatic factors on both quality and quantity of fresh horticultural produce for processing. Lack of market research information (international, regional and local) is a serious constraint. There is a general lack of regional and international standards and product specifications. Poor finishing and packaging also pause as serious threats to the marketing of Kamumo Products.

Figure 1. President Daniel Arap Moi being explained about Kamumo products by the Director of Kamumo Products at the KICC in Nairobi.

10

Figure 1. .Mr Frederick Kiilu, Managing Director of Kamumo Products describes to H.E. the President some the products of the firm during a recent trade exhibition in Nairobi. 4. Objectives The goal of the study was to identify market opportunities (and constraints) for the fruit and vegetable processing industry in Machakos district. Objectives of the study were to: 1. Identify the main players in the production, distribution, processing and marketing of

fruits and vegetables in Ukambani. 2. Assess the availability of raw materials (fresh produce), and intermediate inputs (fruit

pulp, and concentrates). 3. Assess the need for local production of semi-processed products (fruit pulps, pastes

and concentrates). 4. Identify volume, prices and revenue trends associated with the production and trade in

intermediate as well as final products. 5. Methods The strategy that was adopted for this study embraced five distinct sets of activities. The first set of activities entailed collection, collation and analysis of information about production, trade and processing of fruits and vegetables in the area from secondary sources and through discussions with the key persons in the area and in Nairobi. These were facilitated by visits to the libraries, the horticulture Division of the Ministry of Agriculture and Rural development, traders, processors, the Departments of Trade and Industry, the HCDA and many others. This yielded information which guided identification of gaps in information and the design of the surveys. Following Rapid Rural Appraisal procedures, four surveys were carried out during the months of May and June 2001. These were, the survey of fruits and vegetable farmers, entities which trade in fruits and vegetables, intermediate consumers of processed fruit and vegetable products, and, small, medium and large scale processors of fruits and vegetables. 5.1 The survey of fruits and vegetables farmers A survey of 35 fruits and vegetables farmers was carried out in Kitui, Machakos Makueni and Districts. Selection of participating farms was effected in two stages. In stage one, areas within the four districts where growing of fruits and vegetables is most intense, taking the variability in production as well as socio-economic conditions in the area and the need to represent this variation into consideration. The second stage involved the actual selection of farmers within the fruit and vegetable farming areas identified in stage one. In each of the areas selected, field interviewers identified rural access tracks branching off the main roads, and selected every third fruits or vegetable farm and interviewed the head of the

11

household. Each field interviewer repeated this procedure until his quota of farmers to be interviewed was completed. A formal questionnaire had been drawn up and pre-tested before being used in the survey. 5.2 Survey of fruits and vegetables traders The survey of fruits and vegetable traders was carried out during the months of May and June 2001. The survey involved the interviewing of 40 small and medium scale traders in Machakos, Nairobi, Kitui and Makueni areas. First, the main markets in which fruits and vegetables are traded in those areas were identified. Within each market, interviewers selected every third fruit or vegetable trader, requested an interview and if granted, applied the questionnaire. 5.3 Survey of intermediate consumers of the processed products of fruits and vegetables Various entities were classified as intermediate consumers of processed products of fruits and vegetables if they acquired these from identifiable sources for passing on to final or other intermediate consumers. These entities included shops, supermarkets and a variety of institutions. Trading centres in Nairobi, Machakos, Kathiani, Kibwezi, Kitui and Matuu areas were selected because they represent existing and potential loci of the market for goods processed by Kamumo Products. A total of 45 entities were selected. Interviewers obtained information about trade in processed fruits and vegetables products using a structured questionnaire. The survey of intermediate consumers of fruits and vegetables processed products took place during the months of May and June 2001. 5.4 Survey of small, medium and large-scale enterprises processing fruits and vegetables In a recent study of the fruit processing sub-sector in Kenya (K-MAP 1994), 29 firms which process or otherwise use intermediate inputs derived from fruits and vegetables were identified. While more than half of the 29 firms are to be found in the city of Nairobi and its environs, the remainder are located far outside the catchment area of Kamumo products, in places such as Mombasa, Nakuru, Kisumu and Eldoret. Largely because of the small numbers of firms that are involved in processing fruits and vegetables, no attempt was made to apply formal sampling procedures for this survey. In lieu of this, it was decided that the firms which are located in the vicinity of Nairobi and Machakos be approached and requested to supply the information that was needed for this study. Nine of the firms obliged and supplied information in varying degrees of completeness. Of the remainder, some declined to participate citing the potentially sensitive nature of information that was being sought, while others were not able to release the relevant officers due to time constraints. Respondents representing the nine firms which

12

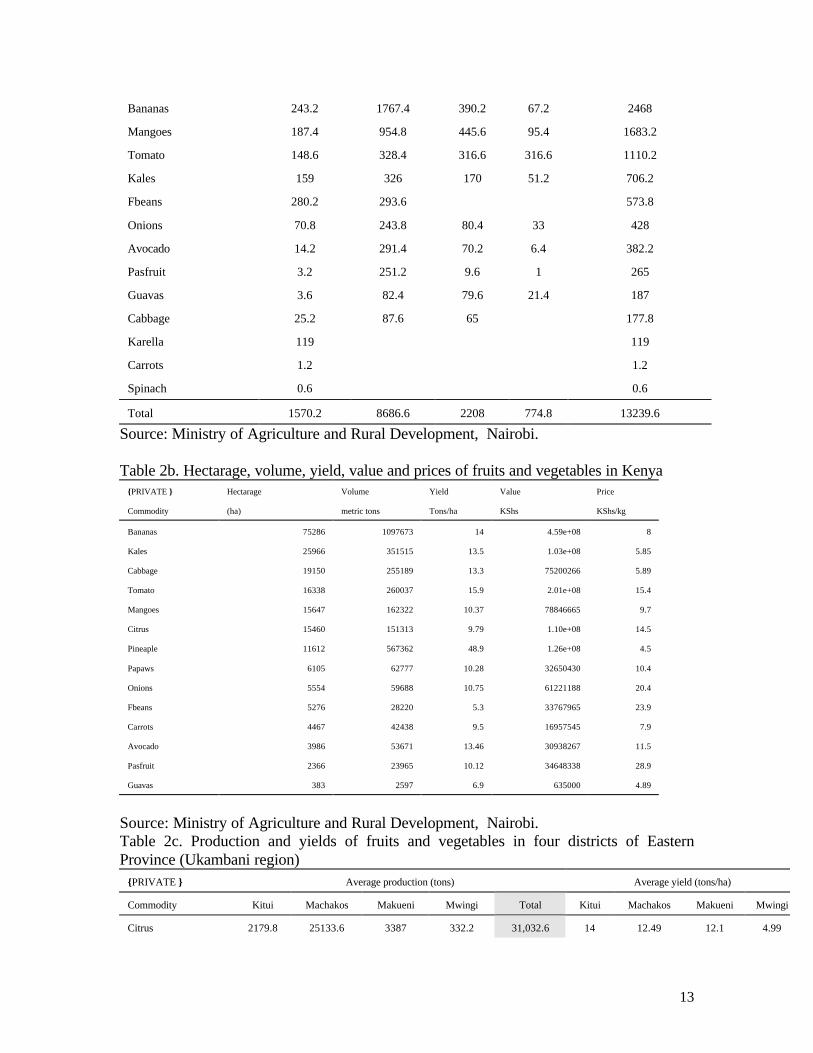

agreed to participate were interviewed during the months of May, June and July 2001. These interviews were guided by a structured questionnaire. 6. Availability of Fruits and Vegetables for processing in Kenya and Ukambani A reliable supply raw materials of acceptable quality is a major determinant of the viability of the processing industry. As noted in the preceding sections, Kenyan farmers have committed a sizeable hectarerage to production of fruits and vegetables. In 1999, for example, 134,000 ha of prime land were planted to fruits and 97,000 ha to vegetables. The leading commodities by hectarage, volume and value were bananas, mangoes, citrus, papaws and avocado (fruits) and kales, cabbage and tomatoes (vegetables). This hectarage yielded 3,276,000 tons of fresh produce. Out of this production, a small proportion (70,000 tons) was exported. The bulk the fruits and vegetables that did not find its way into the export market was used by farm families for subsistence. The remainder was sold to Kenyan consumers through direct purchases from farms, retail outlets or various other arrangements. The range of fruits and vegetables grown in the Ukambani area is wide. Citrus, papaws, bananas, avocado and mangoes (fruits) and tomatoes, cabbage and kales (vegetables) are the most important fruits and vegetables commodities in the Ukambani area. The hectarage of fruits and vegetables grown in four districts of Eastern Province (Ukambani region) is shown in Table 2a below. The contribution of this region to the national fruit and vegetable production is shown in Table 2b. As shown in Table 2c, the average fruit and vegetable yields within the Ukambakani region is comparable and in some cases much higher than the national yields. Thus, it is evident that the Ukambani districts account for a significant proportion of the Kenyan fruit and vegetable production. These districts produce two thirds of guavas, half of papaws, two fifths of citrus and one tenth of mangoes, avocado and passion fruit. Machakos is the leading producer of fruits and vegetables. Neighboring Makueni and Kitui districts are important producers of papaws, bananas and mangoes. Some of the fruits and vegetables were used as raw materials for production of shelf stable products for the local as well as the export market. The need to tap this huge potential through promotion of local industries that add value to the farm produce is hereby strongly indicated. Table 2a. Hectarage of fruits and vegetables in four districts of Eastern Province (Ukambani region)

{PRIVATE } Average area under fruits and vegetable (ha)

Commodity Kitui Machakos Makueni Mwingi Total (ha)

Citrus 259.6 1973.4 336.6 71 2640.6

Papaws 54.4 2086.6 244.2 111.6 2496.8

13

Bananas 243.2 1767.4 390.2 67.2 2468

Mangoes 187.4 954.8 445.6 95.4 1683.2

Tomato 148.6 328.4 316.6 316.6 1110.2

Kales 159 326 170 51.2 706.2

Fbeans 280.2 293.6 573.8

Onions 70.8 243.8 80.4 33 428

Avocado 14.2 291.4 70.2 6.4 382.2

Pasfruit 3.2 251.2 9.6 1 265

Guavas 3.6 82.4 79.6 21.4 187

Cabbage 25.2 87.6 65 177.8

Karella 119 119

Carrots 1.2 1.2

Spinach 0.6 0.6

Total 1570.2 8686.6 2208 774.8 13239.6

Source: Ministry of Agriculture and Rural Development, Nairobi. Table 2b. Hectarage, volume, yield, value and prices of fruits and vegetables in Kenya

{PRIVATE } Hectarage Volume Yield Value Price

Commodity (ha) metric tons Tons/ha KShs KShs/kg

Bananas 75286 1097673 14 4.59e+08 8

Kales 25966 351515 13.5 1.03e+08 5.85

Cabbage 19150 255189 13.3 75200266 5.89

Tomato 16338 260037 15.9 2.01e+08 15.4

Mangoes 15647 162322 10.37 78846665 9.7

Citrus 15460 151313 9.79 1.10e+08 14.5

Pineaple 11612 567362 48.9 1.26e+08 4.5

Papaws 6105 62777 10.28 32650430 10.4

Onions 5554 59688 10.75 61221188 20.4

Fbeans 5276 28220 5.3 33767965 23.9

Carrots 4467 42438 9.5 16957545 7.9

Avocado 3986 53671 13.46 30938267 11.5

Pasfruit 2366 23965 10.12 34648338 28.9

Guavas 383 2597 6.9 635000 4.89

Source: Ministry of Agriculture and Rural Development, Nairobi. Table 2c. Production and yields of fruits and vegetables in four districts of Eastern Province (Ukambani region)

{PRIVATE } Average production (tons) Average yield (tons/ha)

Commodity Kitui Machakos Makueni Mwingi Total Kitui Machakos Makueni Mwingi

Citrus 2179.8 25133.6 3387 332.2 31,032.6 14 12.49 12.1 4.99

14

Pawpaws 524 24013 1639.2 924.8 27,101.0 3.71 11.51 7.94 8.03

Bananas 5384 12827.8 2071.6 270.6 20,554.0 34.8 7.27 3.18 2.81

Mangoes 2474 13291 3403.8 670.8 19,839.6 13.5 13.88 7.62 7.12

Tomato 3296 4687.2 1741.2 1741.2 11,465.6 21 14.24 4.68 4.68

Kales 4509.4 3007.2 824.8 171.4 8,512.8 26.3 9.2 4.89 3.11

Avocado 192.8 5686.6 366.8 24.4 6,270.6 13.7 19.48 4 2.47

Onions 1078 2805 351 153.6 4,387.6 11.7 11.4 4.27 4.8

Passion fruit 16 2863.6 67 2.4 2,949.0 1 11.39 3.25 1.2

French beans 1218 831.2 2,049.2 4.14 3.3

Guavas 21.6 910 476.2 156.4 1,564.2 1.2 11.05 2.55 5.5

Cabbage 96.2 790.6 266.6 1,153.4 1.3 8.71 4.4

Karella 435.2 435.2 3.79

Carrots 3.8 3.8 2.47

Spinach 1 1.0 0.33

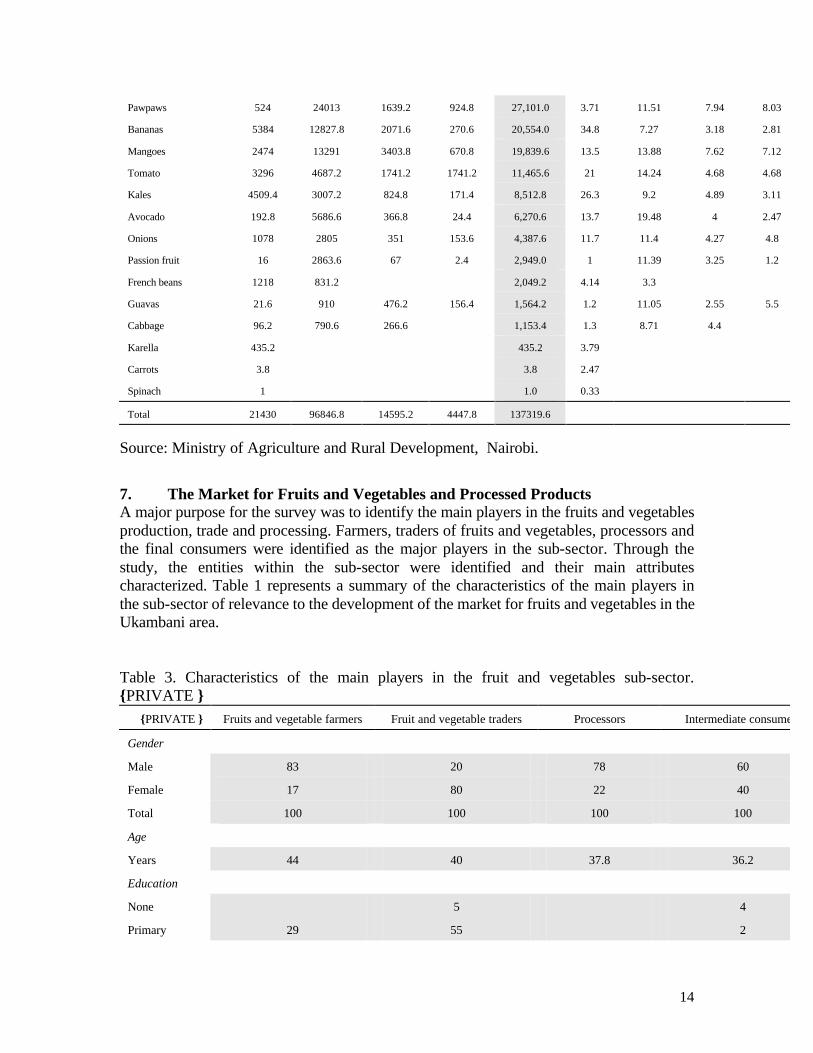

Total 21430 96846.8 14595.2 4447.8 137319.6

Source: Ministry of Agriculture and Rural Development, Nairobi.

7. The Market for Fruits and Vegetables and Processed Products A major purpose for the survey was to identify the main players in the fruits and vegetables production, trade and processing. Farmers, traders of fruits and vegetables, processors and the final consumers were identified as the major players in the sub-sector. Through the study, the entities within the sub-sector were identified and their main attributes characterized. Table 1 represents a summary of the characteristics of the main players in the sub-sector of relevance to the development of the market for fruits and vegetables in the Ukambani area. Table 3. Characteristics of the main players in the fruit and vegetables sub-sector. {PRIVATE }

{PRIVATE } Fruits and vegetable farmers Fruit and vegetable traders Processors Intermediate consumers

Gender

Male 83 20 78 60

Female 17 80 22 40

Total 100 100 100 100

Age

Years 44 40 37.8 36.2

Education

None 5 4

Primary 29 55 2

15

Secondary 46 37.5 11 58

College 9 33 16

University 14 56 7

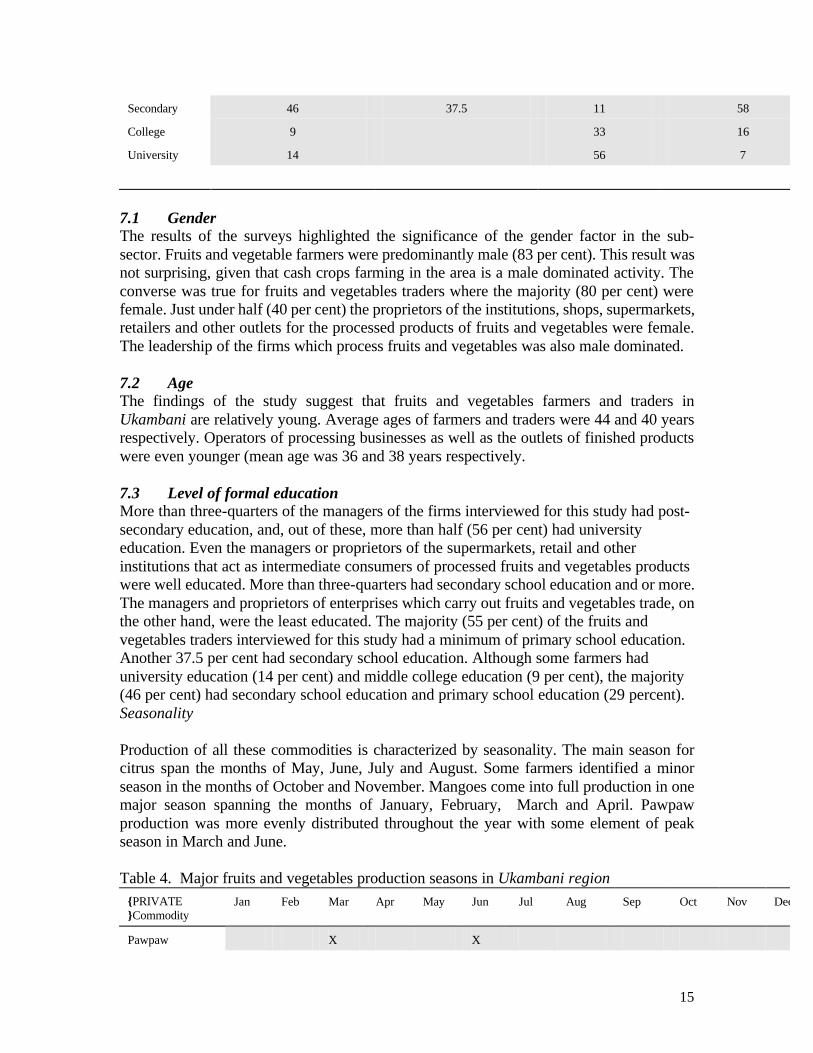

7.1 Gender The results of the surveys highlighted the significance of the gender factor in the sub-sector. Fruits and vegetable farmers were predominantly male (83 per cent). This result was not surprising, given that cash crops farming in the area is a male dominated activity. The converse was true for fruits and vegetables traders where the majority (80 per cent) were female. Just under half (40 per cent) the proprietors of the institutions, shops, supermarkets, retailers and other outlets for the processed products of fruits and vegetables were female. The leadership of the firms which process fruits and vegetables was also male dominated. 7.2 Age The findings of the study suggest that fruits and vegetables farmers and traders in Ukambani are relatively young. Average ages of farmers and traders were 44 and 40 years respectively. Operators of processing businesses as well as the outlets of finished products were even younger (mean age was 36 and 38 years respectively. 7.3 Level of formal education More than three-quarters of the managers of the firms interviewed for this study had post-secondary education, and, out of these, more than half (56 per cent) had university education. Even the managers or proprietors of the supermarkets, retail and other institutions that act as intermediate consumers of processed fruits and vegetables products were well educated. More than three-quarters had secondary school education and or more. The managers and proprietors of enterprises which carry out fruits and vegetables trade, on the other hand, were the least educated. The majority (55 per cent) of the fruits and vegetables traders interviewed for this study had a minimum of primary school education. Another 37.5 per cent had secondary school education. Although some farmers had university education (14 per cent) and middle college education (9 per cent), the majority (46 per cent) had secondary school education and primary school education (29 percent). Seasonality Production of all these commodities is characterized by seasonality. The main season for citrus span the months of May, June, July and August. Some farmers identified a minor season in the months of October and November. Mangoes come into full production in one major season spanning the months of January, February, March and April. Pawpaw production was more evenly distributed throughout the year with some element of peak season in March and June. Table 4. Major fruits and vegetables production seasons in Ukambani region

{PRIVATE }Commodity

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Pawpaw X X

16

Banana X X

Mango X

Orange X

Tangerine X

Lime X

Guava X

Avocado X

Governor plum X

Passion X

Tomato X X

Carrots X X

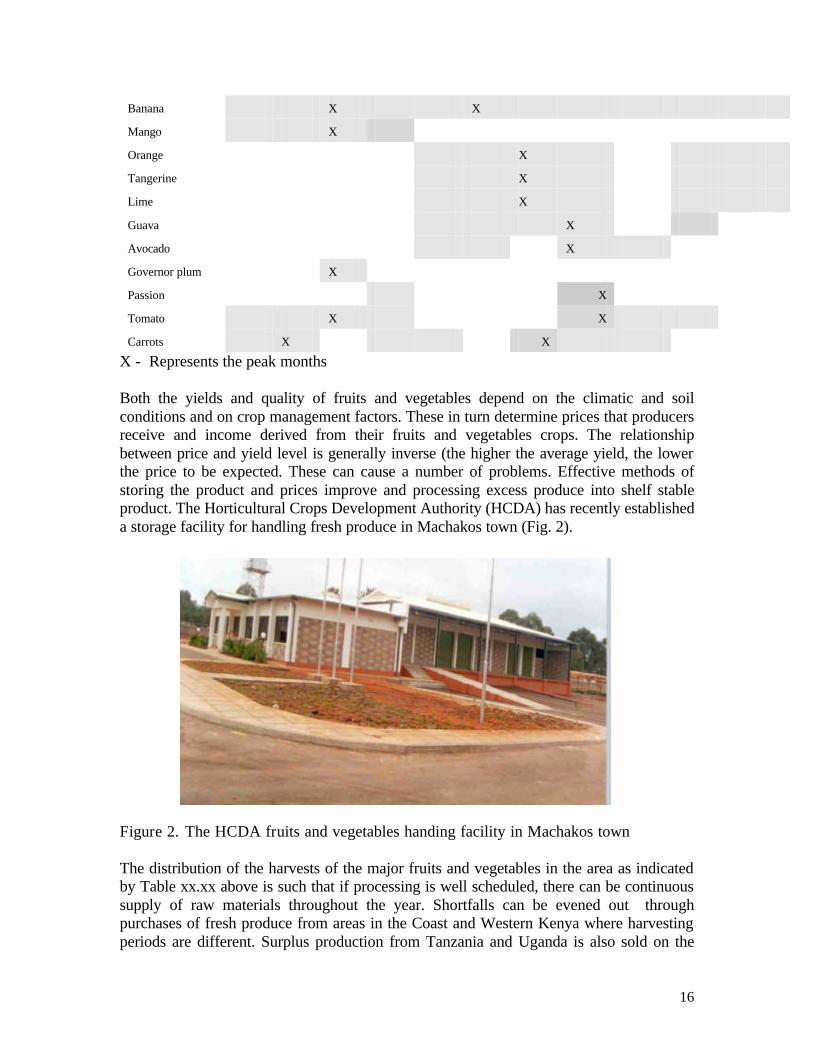

X - Represents the peak months Both the yields and quality of fruits and vegetables depend on the climatic and soil conditions and on crop management factors. These in turn determine prices that producers receive and income derived from their fruits and vegetables crops. The relationship between price and yield level is generally inverse (the higher the average yield, the lower the price to be expected. These can cause a number of problems. Effective methods of storing the product and prices improve and processing excess produce into shelf stable product. The Horticultural Crops Development Authority (HCDA) has recently established a storage facility for handling fresh produce in Machakos town (Fig. 2). Figure 2. The HCDA fruits and vegetables handing facility in Machakos town The distribution of the harvests of the major fruits and vegetables in the area as indicated by Table xx.xx above is such that if processing is well scheduled, there can be continuous supply of raw materials throughout the year. Shortfalls can be evened out through purchases of fresh produce from areas in the Coast and Western Kenya where harvesting periods are different. Surplus production from Tanzania and Uganda is also sold on the

17

Nairobi market and can be accessed by Kamumo Products. Some of the processing firms stated that they import fresh produce from the East African Community member states and beyond. Fresh produce is often supplemented with concentrates and other ingredients purchased from suppliers in Nairobi. The findings of this study provided evidence that even at current levels, Ukambani farmers are producing fruits and vegetables in quantities that are sufficient for small, medium and large scale processors. The main commodities are citrus, papaws, bananas, avocado and mangoes (fruits) and tomatoes, cabbage and kales (vegetables). Kamumo Products' medium term target of raising processing capacity from the present 0.5 tons to 5 tons per day is likely to be met from its immediate vicinity. However, constraints such as competition from exporters, inappropriate varieties (low yields and poor quality), poor infrastructure, lack of investment still remain. Policy interventions to improve in the transport, storage and handling infrastructure, agronomic research to improve yield as well as quality, farmer education, increased support for input supply and marketing opportunities for producers are needed. 8. Processing of Fruits and Vegetables Seasonality of production results into large quantities of fruits and vegetables being brought to the respective markets at the end of the growing season, and the period following this with scarcity. Apart from the traditional functions of increasing job opportunities, enterprises to process fruits and vegetables into shelf stable products, can help farmers achieve stability in prices they receive and make the products available to consumers at reasonable cost. A number of firms now undertake processing of fruits and vegetables into a number of products. While a broad spectrum of products could be processed in Kenya, only a few products are made. KMAP (1994) listed 29 of the processors in various categories who process fruits and vegetables in Kenya. Most of these tended to be located in Nairobi, Nakuru, Kisumu, Mombasa and in other major urban centres country-wide. 8.1 Fruits for processing Fruits processed by these firms are shown in Fig.3. The most frequently mentioned commodities were citrus, bananas, papaws, plums and berries. The sources of these commodities were varied. A significant proportion of the fresh produce that was processed originated from the Ukambani area.. Fig.3. Fresh fruits used by processing firms 8.2 Products made from Fruits and vegetables The main products are canned fruits, sugar preserves beverages and drinks. Some fresh produce is also processed into fruit juices, juice concentrates, fruit nectars, fruit drinks but many process fruit as a line among a diversity of products.

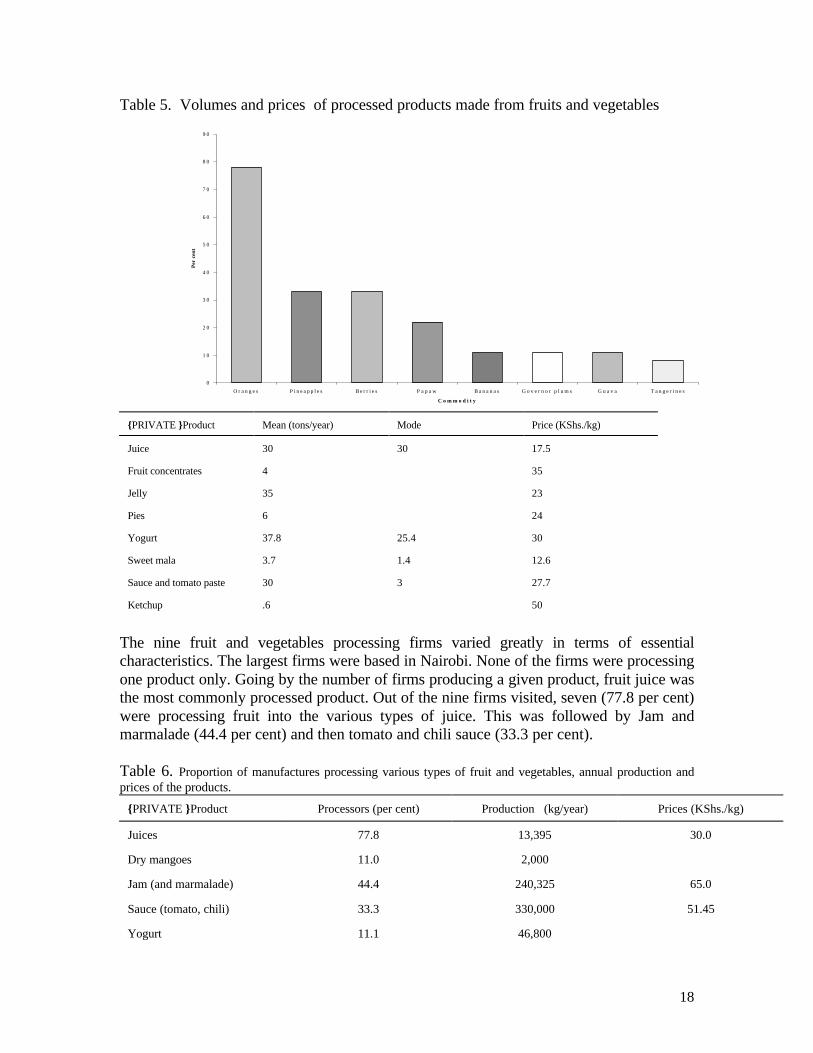

18

Table 5. Volumes and prices of processed products made from fruits and vegetables

{PRIVATE }Product Mean (tons/year) Mode Price (KShs./kg)

Juice 30 30 17.5

Fruit concentrates 4 35

Jelly 35 23

Pies 6 24

Yogurt 37.8 25.4 30

Sweet mala 3.7 1.4 12.6

Sauce and tomato paste 30 3 27.7

Ketchup .6 50

The nine fruit and vegetables processing firms varied greatly in terms of essential characteristics. The largest firms were based in Nairobi. None of the firms were processing one product only. Going by the number of firms producing a given product, fruit juice was the most commonly processed product. Out of the nine firms visited, seven (77.8 per cent) were processing fruit into the various types of juice. This was followed by Jam and marmalade (44.4 per cent) and then tomato and chili sauce (33.3 per cent). Table 6. Proportion of manufactures processing various types of fruit and vegetables, annual production and prices of the products.

{PRIVATE }Product Processors (per cent) Production (kg/year) Prices (KShs./kg)

Juices 77.8 13,395 30.0

Dry mangoes 11.0 2,000

Jam (and marmalade) 44.4 240,325 65.0

Sauce (tomato, chili) 33.3 330,000 51.45

Yogurt 11.1 46,800

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

O r a n g e s P i n e a p p l e s B e r r i e s P a p a w B a n a n a s G o v e r n o r p l u m s G u a v a T a n g e r i n e s

C o m m o d i t y

Per

cen

t

19

Fruit pulp 11.1

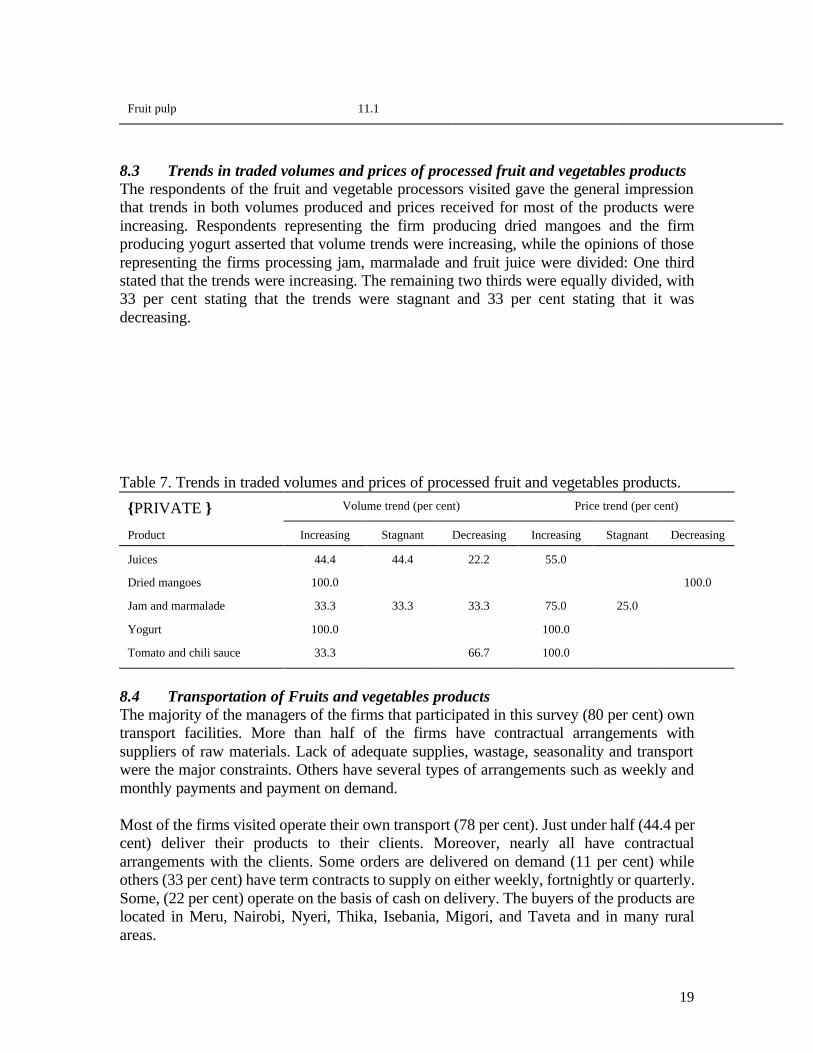

8.3 Trends in traded volumes and prices of processed fruit and vegetables products The respondents of the fruit and vegetable processors visited gave the general impression that trends in both volumes produced and prices received for most of the products were increasing. Respondents representing the firm producing dried mangoes and the firm producing yogurt asserted that volume trends were increasing, while the opinions of those representing the firms processing jam, marmalade and fruit juice were divided: One third stated that the trends were increasing. The remaining two thirds were equally divided, with 33 per cent stating that the trends were stagnant and 33 per cent stating that it was decreasing. Table 7. Trends in traded volumes and prices of processed fruit and vegetables products.

{PRIVATE } Volume trend (per cent) Price trend (per cent)

Product Increasing Stagnant Decreasing Increasing Stagnant Decreasing

Juices 44.4 44.4 22.2 55.0

Dried mangoes 100.0 100.0

Jam and marmalade 33.3 33.3 33.3 75.0 25.0

Yogurt 100.0 100.0

Tomato and chili sauce 33.3 66.7 100.0

8.4 Transportation of Fruits and vegetables products The majority of the managers of the firms that participated in this survey (80 per cent) own transport facilities. More than half of the firms have contractual arrangements with suppliers of raw materials. Lack of adequate supplies, wastage, seasonality and transport were the major constraints. Others have several types of arrangements such as weekly and monthly payments and payment on demand. Most of the firms visited operate their own transport (78 per cent). Just under half (44.4 per cent) deliver their products to their clients. Moreover, nearly all have contractual arrangements with the clients. Some orders are delivered on demand (11 per cent) while others (33 per cent) have term contracts to supply on either weekly, fortnightly or quarterly. Some, (22 per cent) operate on the basis of cash on delivery. The buyers of the products are located in Meru, Nairobi, Nyeri, Thika, Isebania, Migori, and Taveta and in many rural areas.

20

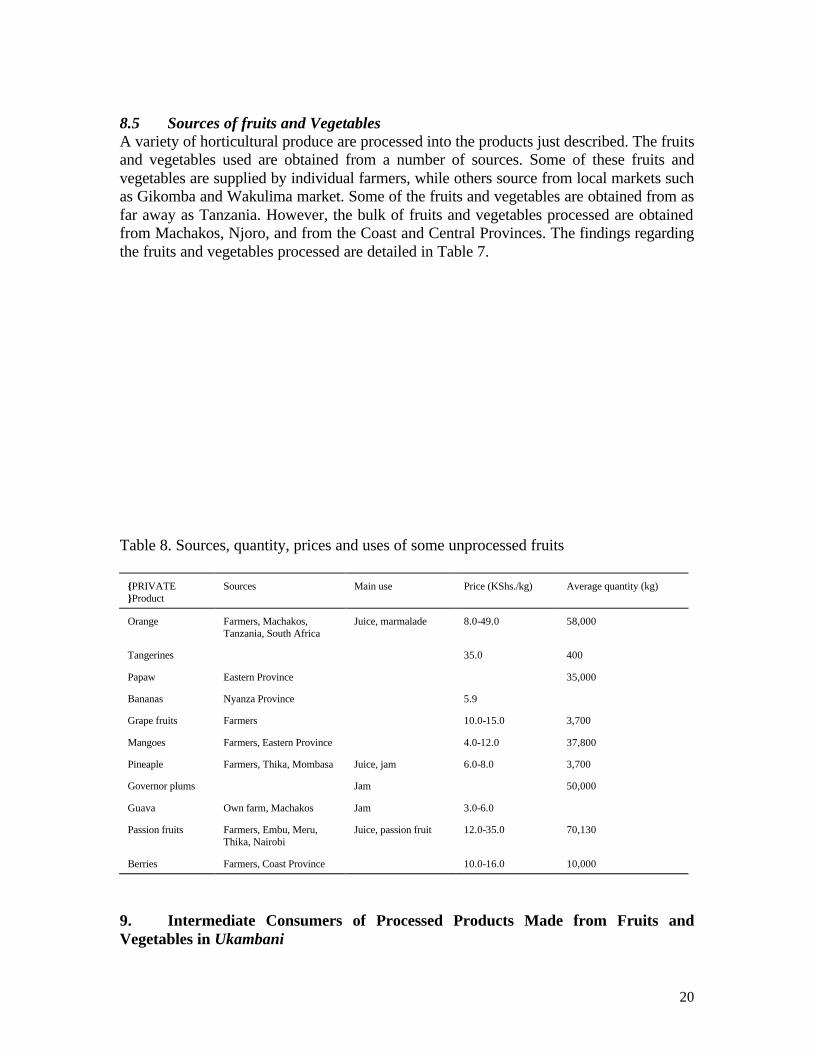

8.5 Sources of fruits and Vegetables A variety of horticultural produce are processed into the products just described. The fruits and vegetables used are obtained from a number of sources. Some of these fruits and vegetables are supplied by individual farmers, while others source from local markets such as Gikomba and Wakulima market. Some of the fruits and vegetables are obtained from as far away as Tanzania. However, the bulk of fruits and vegetables processed are obtained from Machakos, Njoro, and from the Coast and Central Provinces. The findings regarding the fruits and vegetables processed are detailed in Table 7. Table 8. Sources, quantity, prices and uses of some unprocessed fruits

{PRIVATE }Product

Sources Main use Price (KShs./kg) Average quantity (kg)

Orange Farmers, Machakos, Tanzania, South Africa

Juice, marmalade 8.0-49.0 58,000

Tangerines 35.0 400

Papaw Eastern Province 35,000

Bananas Nyanza Province 5.9

Grape fruits Farmers 10.0-15.0 3,700

Mangoes Farmers, Eastern Province 4.0-12.0 37,800

Pineaple Farmers, Thika, Mombasa Juice, jam 6.0-8.0 3,700

Governor plums Jam 50,000

Guava Own farm, Machakos Jam 3.0-6.0

Passion fruits Farmers, Embu, Meru, Thika, Nairobi

Juice, passion fruit 12.0-35.0 70,130

Berries Farmers, Coast Province 10.0-16.0 10,000

9. Intermediate Consumers of Processed Products Made from Fruits and Vegetables in Ukambani

21

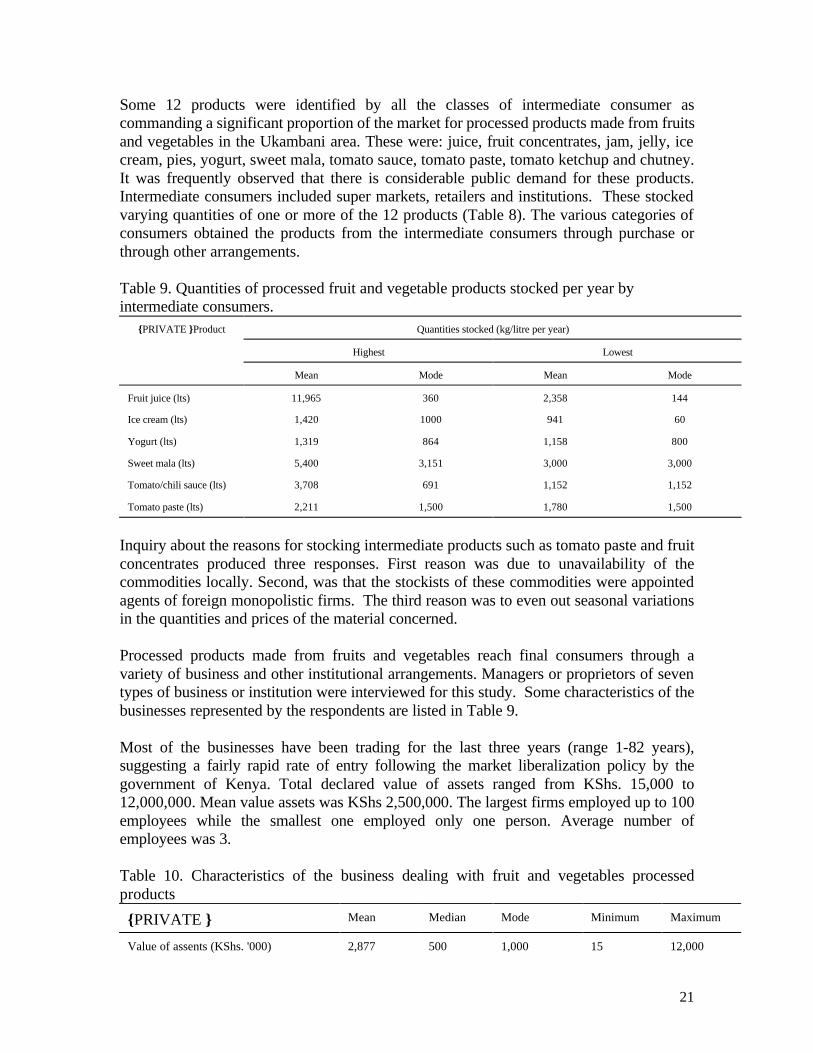

Some 12 products were identified by all the classes of intermediate consumer as commanding a significant proportion of the market for processed products made from fruits and vegetables in the Ukambani area. These were: juice, fruit concentrates, jam, jelly, ice cream, pies, yogurt, sweet mala, tomato sauce, tomato paste, tomato ketchup and chutney. It was frequently observed that there is considerable public demand for these products. Intermediate consumers included super markets, retailers and institutions. These stocked varying quantities of one or more of the 12 products (Table 8). The various categories of consumers obtained the products from the intermediate consumers through purchase or through other arrangements. Table 9. Quantities of processed fruit and vegetable products stocked per year by intermediate consumers.

{PRIVATE }Product Quantities stocked (kg/litre per year)

Highest Lowest

Mean Mode Mean Mode

Fruit juice (lts) 11,965 360 2,358 144

Ice cream (lts) 1,420 1000 941 60

Yogurt (lts) 1,319 864 1,158 800

Sweet mala (lts) 5,400 3,151 3,000 3,000

Tomato/chili sauce (lts) 3,708 691 1,152 1,152

Tomato paste (lts) 2,211 1,500 1,780 1,500

Inquiry about the reasons for stocking intermediate products such as tomato paste and fruit concentrates produced three responses. First reason was due to unavailability of the commodities locally. Second, was that the stockists of these commodities were appointed agents of foreign monopolistic firms. The third reason was to even out seasonal variations in the quantities and prices of the material concerned. Processed products made from fruits and vegetables reach final consumers through a variety of business and other institutional arrangements. Managers or proprietors of seven types of business or institution were interviewed for this study. Some characteristics of the businesses represented by the respondents are listed in Table 9. Most of the businesses have been trading for the last three years (range 1-82 years), suggesting a fairly rapid rate of entry following the market liberalization policy by the government of Kenya. Total declared value of assets ranged from KShs. 15,000 to 12,000,000. Mean value assets was KShs 2,500,000. The largest firms employed up to 100 employees while the smallest one employed only one person. Average number of employees was 3. Table 10. Characteristics of the business dealing with fruit and vegetables processed products

{PRIVATE } Mean Median Mode Minimum Maximum

Value of assents (KShs. '000) 2,877 500 1,000 15 12,000

22

Total work force (persons) 13.3 4.0 4.0 1.0 100.00

Duration in business (years) 8.9 5.0 3.0 1.0 82.0 The inquiry covered 12 products: juice, fruit concentrates, jam, jelly, ice cream, pies, yogurt, sweet mala, tomato sauce, tomato paste, tomato ketchup and chutney. These are the products for which there is an increasing demand (see Fig. 4) and this prompts importation and stocking of the same by intermediate consumers such as super markets, retailers, e.t.c.

Going by the observations and responses offered by respondents from these businesses, fruit concentrates and tomato paste were not stocked by many businesses because most of these are monopolized imported by a few businesses whom either directly import in bulk (which many SME businesses cannot afford) or process just enough to sustain their processing needs Fig. 4. Growth trends in intermediate consumers 10. Conclusions and Recommendations The results of the study confirmed that farmers in the area in the immediate vicinity of where Kamumo Products produce high volumes of fruits and vegetables, notably, citrus, bananas, mangoes, avocado and guavas, (fruits) and tomatoes, brasicas and onions (vegetables). Most farmers interviewed indicated that production, price and revenue trends

for these commodities were increasing. However, harvesting time for these commodities is confined to within short periods in the year. There is also increasing competition from producers in neighboring (e.g., Tanzania and Uganda) and distant countries (e.g., South Africa, and Egypt) whose produce now reaches the Kenyan market sometimes at unreasonably subsidized prices. Apart from the 10-20 per cent wastage that takes place (cf. Food security), seasonal price fractuations results in farmers' lowered incomes leading to rural poverty and in some cases rural-urban migration, which further undermines agricultural productivity in the region with dire consequences on the national economy! Several firms (e.g., Kamumo Products) have set up enterprises, which acquire fresh fruits and vegetables for processing into shelf stable products. Many of these are located in Nairobi and its environs and beyond. Kamumo Products and Matinyani Multi-purpose Women Group in Kitui (about 130 Km from Machakos town) are the only two micro-enterprises located in the Ukambani area that do processing of fruits and vegetables. However, the Women Group only deals with dried mango processing. There is thus a real and pressing need to address the issue of processing the bountiful fruits and vegetables into shelf-stable intermediate and/or final household consumer goods. The major intermediate products from fruits and vegetables of immediate concern include fruit juice concentrates and tomato paste- this last product is only made by one company in Kenya which is situated about 250 Km from Nairobi. The study showed that there is substantial demand for finished products of fruits and vegetables, notably, fruit juices, jam and marmalade and tomato and chili sauce. This

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Juices Jam and marmalade Ice cream Yogurt Sweet mala Tomato and chilisauce

IncreasingStagnantFluctuating

23

demand is currently satisfied by processors of fruits and vegetables who are located outside the Ukambani Districts. Such processors used significant amounts of imported raw materials for processing (fruit juice concentrates and tomato paste - mainly). The Ukambani Districts are major producers of tomatoes, citrus, avocado, guavas and bananas in Kenya. Production of these commodities however, comes under adverse influence of seasonality. Harvesting takes place over short periods which are followed by periods of scarcity and high prices. The findings of the study suggest that at harvest time about 10 -20% of the fresh produce harvested goes to waste because of lack of marketing opportunities. There is need to establish a mechanism for processing this `surplus production' which otherwise goes to waste into shelf stable products including fruit concentrates, pastes, etc. These could be further processed into final products, demand for which the survey results have shown, is increasing. The demand emanates from the general public (domestic/households and micro to medium-scale food processors in Kenya and some neighboring countries), and from institutions such as hospitals, and schools (including school-feeding programs). This survey indicated that production of preserved fruits and vegetables (particularly the very perishable tomato) was insignificant within the region. In particular, Kamumo Products sources its raw materials for processing from local farmers through various arrangements and sometimes uses some imported intermediate products (mainly tomato paste and fruit juice concentrate) imported from as far away as South Africa and Egypt. This is a very sorry state of affairs taking into account the huge potential of the Ukambani region to produce and supply the needed raw materials! In view of the above, it is recommended that local production, processing and marketing of fruits anf vegetables within the Ukambani region be given adequate technical and financial support. This will reduce wastage and guarantee higher returns to the farmer, reduce rural poverty through employment creation, curb rural-urban migration which undermines agricultural productivity socio-economical development. 11. References

24

Ministry of Agriculture. 2000. `An overview of market price trends of fruits and vegetables in Kenya 1994-1999.' Marketing Information Branch. Ministry of Agriculture and Rural Development. Nairobi, Kenya. K-MAP. 1994. Preliminary analysis of the fruit processing sub-sector in Kenya. A study by Kenya Management Assistance Program (K_MAP) funded by ILO/FIT Project, Geneva, Switzerland. Mungai, J.K. 2000. `Processing of fruits and vegetables in Kenya. Miscellaneous monograph, Market Information Branch, Ministry of Agriculture. Republic of Kenya. Sessional Paper No.2 of 1994 on National Food Policy. April 1994. Akumu, W. 2001. Industry says no to new law: horticulture players argue proposed bill will strangle private enterprise. Daily Nation, September 7, 2001.

Lutta Muhammad and Frederick M. Kiilu

The agricultural sector plays the leading role in the economy of Kenya, providing export earnings, self-sufficiency in food,employment and raw materials for the processing industry.Agricultural production is dominated by cereals, grain legumes,root crops and several industrial crops but horticulture is gainingimportance as a result of the general decline in performance ofthe agricultural sector. However, fresh fruit and vegetable cropsare harvested over short periods and this leads to surpluses andlow prices during the harvesting season, followed by shortagesduring the rest of the year. Moreover, fresh produce isperishable, bulky and susceptible to attacks by pests anddiseases and as a result farmers incur losses through spoilage,wastage and low prices.

Processing of fresh produce into shelf-stable products couldmitigate the effects of fluctuation in demand and supply, addvalue to farm production, help stabilize smallholder income andat the same time increase the range of products available toconsumers. This article highlights the experiences of a localmicro-enterprise in the processing of fruits and vegetables inUkambani area, Kenya.

Livelihood in a risky environmentIn the Ukambani area, the first rains fall between mid-Marchand end of May. The second rains come between mid-Octoberand end of December. Average seasonal rainfall is between 250 - 400 mm. As a result, the major subsistence crops fail intwo out of five seasons, while most fruit trees are able to takeadvantage of the total amount of rain received in both seasonsand produce a good crop.

Ukambani has a high population density and the average farmsize is between 1 - 7.5 ha. About 60 percent of the smallholderhouseholds are thought to live below the poverty line, on lessthan one dollar a day. Virtually every smallholding has at leastone horticultural crop, which is either rain-fed or irrigated. The majority of smallholders grow traditional fruit varieties oflow quality. Some farmers have been replacing these traditionalvarieties with improved varieties, promoted by the KenyaAgricultural Research Institute (KARI), but the low pricesobtained for fresh produce during the harvesting period havetended to discourage the adoption of improved varieties and farming practices. A consequence is that farmers harvestonly 20 - 30 percent of the potential yield.

Production and utilization Recent statistics indicate that Kenyan farmers have committed a sizeable acreage to fruits and vegetables. In 1999 almost 3.3 million tons were produced, out of which 70,000 tons wereexported. The rest were used by farm families for subsistence orsold on the domestic market. In Ukambani the most importanthorticultural crops are papaya, citrus, passion fruit, mangoes,avocado, bananas and tomatoes. Yields are comparable with thenational average and Ukambani contributes a substantial part ofthe total Kenyan production.

The major harvesting season for citrus spans the period Maythrough August, with a minor season in the months of Octoberand November. Mangoes come into full production in one majorseason spanning the months of January, February and March.Papaya and banana production is more evenly distributed

throughout the year, with peak seasons in March and June.This means that there is continuous supply of raw materials forprocessing throughout the year.

A survey to identify market opportunities and constraints for thefruit and vegetable processing industry in the Ukambani areawas carried out in 2001. The aim was to quantify the availabilityof fresh produce and intermediate inputs (fruit pulp, andconcentrates), to assess the market for semi-processed products(fruit pulps, pastes and concentrates) and to quantify the demandfor final products. Seven processed fruit and vegetable productswere identified by traders and consumers as commanding asignificant proportion of the market in Ukambani. Fruit juicewas the leading product, followed by ice cream. Then followedjam (marmalade and jelly) and tomato sauce (paste, ketchup andchutney). According to estimates, the demand for fruit producein Ukambani would correspond to a volume of productionequivalent to 7100 tons of fresh produce per year.

Processing in Ukambani Local retail and wholesale outlets for processed fruit andvegetables products are at present supplied by large-scale foodprocessing concerns located in Nairobi and its environs. Drivenby business objectives, these large concerns have littleinteraction with local farmers. They get their fresh produce fromas far away as Uganda, Tanzania, South Africa and even Egypt.

One consequence of the liberalization of the Kenyan economy inthe eighties was that it became possible to start up local micro-enterprises to take advantage of market opportunities within thearea. Established as a private company in 1987, KamumoProducts Enterprise is located in Machakos town, 70 km southeast of Nairobi. The enterprise was founded with the vision thatfood security in the third millennium will be intricately linkedwith the market. The firm’s mission is to promote betternutrition and health for the population through processing ofagricultural produce, sound business management and skillstransfer. The aims of the enterprise are to:

• Save fruits and vegetables from going to waste duringbumper harvests

• Add value to fruits and vegetables• Help stabilize the prices farmers receive for their fruits and

vegetables• Supply affordable fruit and vegetable products in the dry

season• Contribute to the creation of jobs and socio-economic

development within the area.

The firm buys excess mangoes, citrus, papaya, tomatoes andpassion fruits from farmers in Ukambani (Machakos, Makueni,Kitui and Mwingi districts) for processing into intermediateproducts (fruit pulps, fruit concentrates) and final products(juices, jam and sauces). Over the years productivity hasincreased, as has product diversification. Initially, the firmprocessed horticultural produce only into fruit juice. The rangeof products now includes jam and marmalade, tomato and chilli sauce and chutney. Total production has increased from 50 kg/litres per week to 3500 kg/litres per week. KamumoProducts sells finished products through wholesalers,supermarkets, hotels, cafés, hospitals and schools. The firm alsoreaches its market through participation in trade fairs, symposia,exhibitions and other business networks.

LE

ISA

MA

GA

ZIN

E .

SE

PT

EM

BE

R 2

004

30

Reducing risk by fruit processing

31

LE

ISA

MA

GA

ZIN

E .S

EP

TE

MB

ER

2004

Kennedy A. Mulela

Bunyore lies in the basin of Lake Victoria in Western Kenya andis an area of granite outcrops and small streams. Our village getsenough rain but population is dense and our natural forests andwild life have become degraded. Some farmers try to earn a littlecash by growing tea, others keep a few cows under zero grazingconditions for their milk.I have lived in this community since I left school in 1988. I wastrained for a white-collar future, but once I had my certificates Irealized there weren’t many jobs. I did not see why I should suf-fer when God had given me good health so I decided to go intofarming because it seemed to offer economic independence.Rural life in a traditional setting in a country like Kenya can behard, but gradually I came in contact with individuals and organi-zations that helped me develop my ideas. This is my story and thestory of the organizations that helped me build my farm.

The first organization to influence my farming practices was theInternational Centre for Insect Physiology (ICIPE). Togetherwith other farmers we were shown how to grow neem trees thatcan be used, for example, to treat minor health problems. TheNew Forest Project provided me with trees such as Gliricidiasepia, Sesbania and Leucaena and enabled me to create woodlotsthat now provide me with fodder and firewood and help improvethe quality of my soil. Training by the Forest Action Network, an organization that lobbies for the preservation of forests, has increased my under-standing of the role forestry plays in integrated farming systemsand encouraged me to plant Grivelia trees which, if coppiced,grow very fast and provide good timber and firewood. Networking has really empowered me in terms of contacts andknowledge-based ideas. Magazines like LEISA Magazine andSpore have provided me with references and information onfarming experiences worldwide. CTA, who publishes Spore, hasalso supplied me with books and learning material through theirspecial scheme and I am using them to set up a local resourcecentre. Two other magazines I read are Agroforestry published byICRAF and EcoForum produced by the Environmental LiasonCentre International. Earth Action is another organization that has helped keep me up-to-date and aware of technologies that can help farmers developand manage more sustainable systems. The techniques I havelearned have not only helped me to produce good crops of cassa-va, bananas, sugar cane and sweet potato on my small farm, butsharing my experiences with other farmers has enabled us towork together to restore and preserve our environment.

■

Kennedy Amatsili Mulela. Box 48, Emuhaya 50314, Kenya. Tel: + 254 0733270831

At inception, Kamumo Products employed one full time person.The number of employees has since risen to six. All themembers of staff receive on-the-job training and work underdirect supervision of Mr Frederick Kiilu, the proprietor andManaging Director. Over the years, significant changes inproduction technology have taken place. The aluminium utensilsthat were used in the beginning have been replaced with thosemade of stainless steel. Semi-automatic equipment has largelyreplaced hand tools. This technical progress has facilitated animprovement in product quality and at the same time, areduction in unit costs. The firm finances its capitaldevelopment and recurrent operations solely from profits andsavings.

Several skills-transfer initiatives have also been undertaken byKamumo Products Enterprise. Kakumuti Syondo Women’s SelfHelp Group in Kitui town now processes juice and driedmangoes for sale to the local community, to supermarkets inNairobi and even for export. Training for Kakumuti Women’sGroup was provided by Mr. Kiilu of Kamumo Products.Individual entrepreneurs in Nunguni, Kibwezi and Emali tradingcentres have also benefited from training. These enterprisesprocess tomato sauce and fruit juice, producing about 180 tonsof finished products per year.

Constraints to the development of micro-enterprisesKamumo Products faces severe constraints. Examples are:• Accessing credit from either the business community or

commercial banks in the area is difficult for most smallenterprises. This has seriously impaired the firm’s capacity toundertake investment that should facilitate innovation.

• Variability in the quality of produce from local farmers andthe deplorable state of the transport, storage andcommunications infrastructure represent a major challenge.

• The impact of climatic factors on both quality and quantity offresh produce is difficult to predict.

• Lack of access to research and training opportunities for staffand appropriate specification of standards and productspecifications represent a threat to the firm’s viability.

There is substantial demand for finished products of fruits andvegetables, notably fruit juices, jam and marmalade and tomatoand chilli sauce, but this demand is currently satisfied byprocessors of fruits and vegetables who are located outside theUkambani district and who often resort to imported fruit juiceconcentrates and tomato paste. As a result, at least 10 - 20percent of the fresh produce harvested in the area goes to wastefor lack of marketing opportunities; and the increases in yieldsthat would be possible through better varieties and bettermanagement remain unrealized.

■

Lutta Muhammad. Senior Research Officer. Kenya Agricultural Research Institute,P.O. Box 1764, Machakos, Kenya. Email: [email protected] M. Kiilu. Managing Director. Kamumo Products, P.O. Box 1146,Machakos, Kenya.

References- Hendrix, C.M and J.B. Redd, 1999. Chemistry and technology of citrus juices and by-products. In: P.R, Ashurst (ed.). Production and packaging of non-carbonatedfruit juices and fruit beverages. Aspen Publishers Inc., Gathersburg, Maryland. pp. 53-86.- Ministry of Agriculture, 2000. An overview of market price trends of fruits and vegetables in Kenya 1994-1999. Marketing Information Branch, Ministry ofAgriculture and Rural Development, Nairobi, Kenya.

Building my farm

Universal Youth Group members. From left to right:

Washington Sikinvi, Elly Okemo and

Kennedy Mulela.