macroeconomics (ecs2602) 03 - the financial market (ch 4)

TRANSCRIPT

Slide 1 of 27

ECS 2602Macroeconomics

Errol Goetsch 078 573 5046 [email protected] 082 770 4569 [email protected]

www.facebook.com/groups/ecs2602

Boston | UNISA 2015Unit 03 - Financial Markets

Slide 2 of 27

01 – Overview of the SA macroeconomy

02 – The goods market

03 – Financial Markets

04 – The IS-LM model

05 – Openness in goods and financial markets

06 – The goods market in an open economy

07 – Output, the interest and the exchange rates

08 – The labour market

09 – The AS-AD model

4.0 IntroductionDefinition: Money and InvestmentThe 4 measures of Money: M1A, M1, M2 and M3The 3 functions of MoneyPortfolio Decisions; Money vs. Bonds4.1 The demand for MoneyThe determinants of demandDeriving the demand for moneyFigure 4-1 Deriving the demand for money4.2 The interest rateThe equiibrium condition and LM relationFigure 4-2 The equilibrium interest rateFigure 4-3 The effects of an increase in nominal incomeFigure 4-4 The effects of an increase in the money supplyMonetary policy and open market operationsFigure 4-5 Effect of expansionary OMBond prices and bond yieldsChoosing to change the money suppy or the interest rate4.3 What banks doMoney, bonds, banking, deposits, loans and reservesFigure 4-6 The supply and demand for Central Bank MoneyFigure 4-8 The determination of the interest rate4.4 Adjustment process in the Financial MarketRelationship between price of a bod and interest rate4.5 The Role of the SARB4.6 Monetary Policy in SATermsOutcomesExplain in words, and via chain of events, equations and diagrams,1. How the interest rate is determined2. What causes a change in the interest rate4. The impact of monetary policy on the interest rate4. Monetary policy in SA

MacroeconomicsUnits 01 - 09

Slide 3 of 27

Macroeconomics03 Financial Markets: Terms

Federal Reserve Bank (Fed) income flow saving savings financial wealth, wealth stock investment financial investment money currency chequable deposits bonds money market funds LM relation open market operation

expansionary, and contractionary, open market operations

Treasury bill, (T-bill) financial intermediaries (bank) reserves reserve ratio bank runFears that a bank will not repay their loans will lead people to close their accounts. If enough people do so, the bank will run out of reserves—a bank run. To avoid bank runs, the U.S. government provides federal deposit insurance. An alternative solution is narrow banking, where banks must hold liquid, safe, government bonds, such as T-bills. federal deposit insurance narrow banking central bank money federal funds market federal funds rate money multiplier high-powered money monetary base

Slide 4 of 27

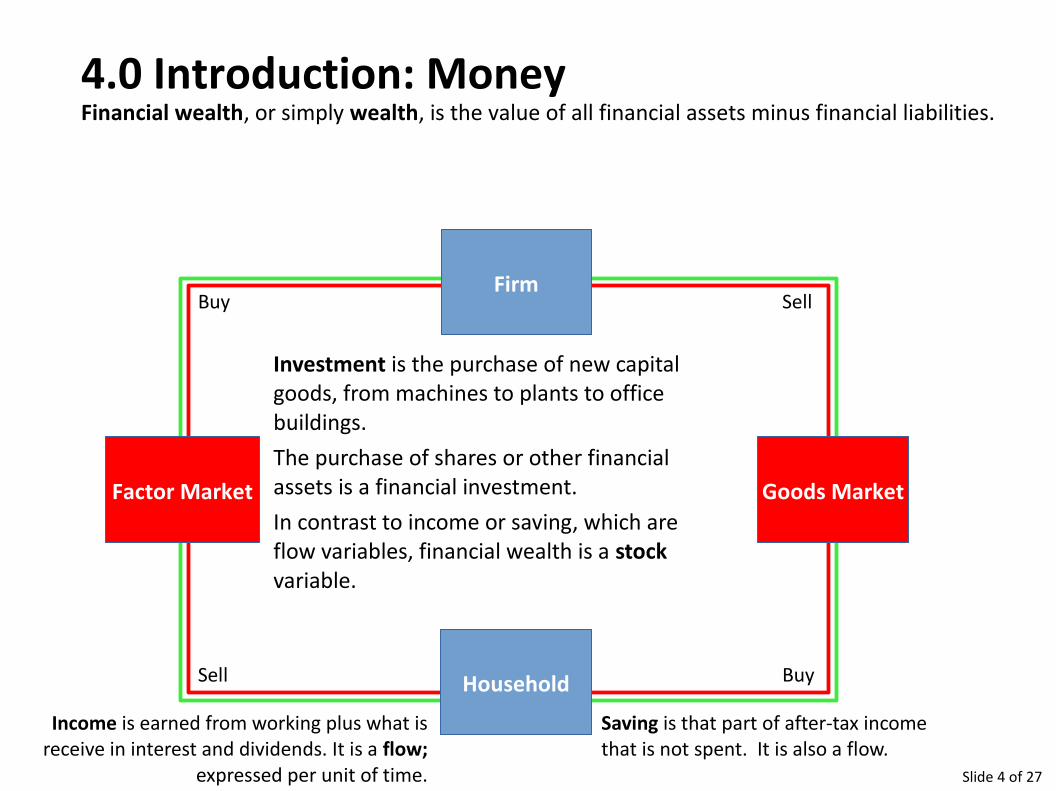

4.0 Introduction: MoneyFinancial wealth, or simply wealth, is the value of all financial assets minus financial liabilities.

Factor Market

Household

Goods Market

Firm

Sell Buy

Buy Sell

Investment is the purchase of new capital goods, from machines to plants to office buildings. The purchase of shares or other financial assets is a financial investment.In contrast to income or saving, which are flow variables, financial wealth is a stock variable.

Income is earned from working plus what is receive in interest and dividends. It is a flow;

expressed per unit of time.

Saving is that part of after-tax income that is not spent. It is also a flow.

Slide 5 of 27

4.0 Definition: MoneyAnything that is generally accepted in payment for goods and services

Factor Market

HouseholdLender-SaverBorrower-Spender

Goods Market

FirmLender-Saver

Borrower-Spender

Sell Buy

Buy SellMoney for transactions pays no interest. There are two types of money;

1 Currency (coins and bills)

2 Cheque deposits (the bank deposits on which you can write cheques).

Bonds pay a positive interest rate, i, but they cannot be used for transactions.

Money as stock of demandM = Currency + Deposits+ Notes + Coins+ Cheques (deposits in cheque accounts)+ Savings (deposits in savings accounts)

Not- Income (flow of earnings over time)- Wealth (store of value)

Slide 6 of 27

4.0 The 4 Measures of MoneyM1A, M1, M2, M3

M1A and M1 = “narrow money”

Name Note Form

M1A most liquid measure of the money supply

= coins and notes in circulation + deposits of domestic | private | non-bank sector at commercial banks (are easily convertible into cash).

M1 very sensitive to interest rates

+ “other demand deposts” of the domestic private sector held at banks

M2 + “near money”(short and medium term deposits held at all financial institutions)Short = 1 – 31 days, Medium = 32 – 180 days

M3 + long term deposits of the domestic private sector at financial institutions(> 180 days)

Slide 7 of 27

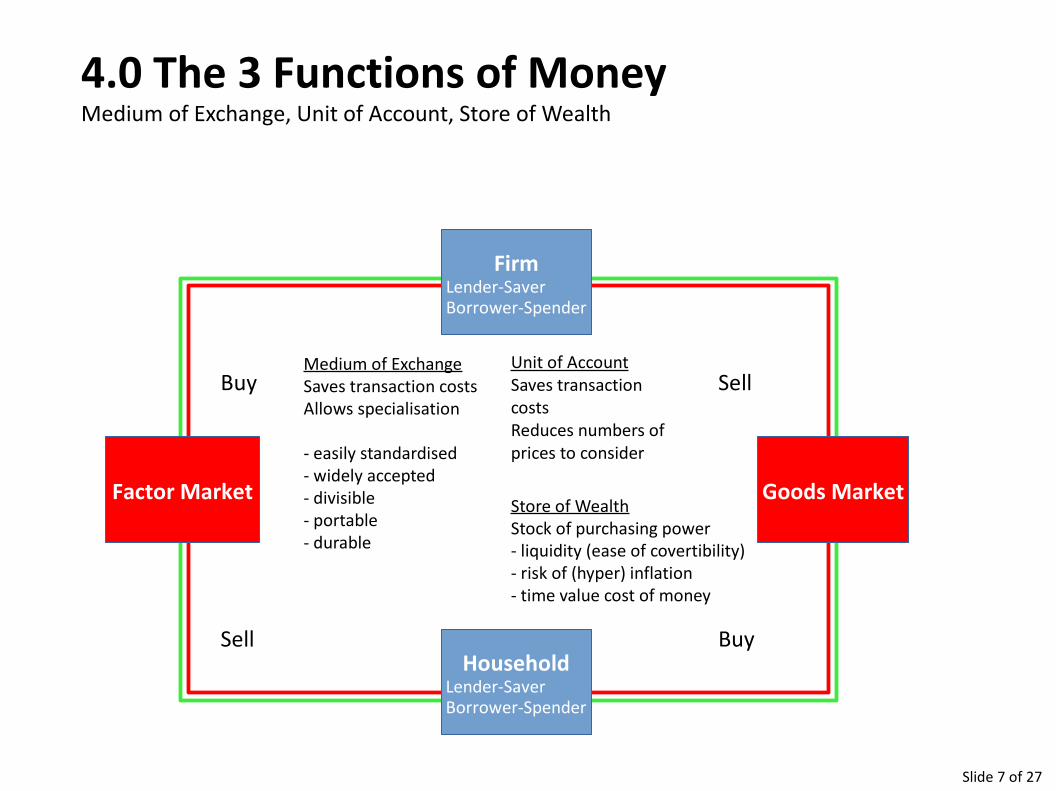

4.0 The 3 Functions of MoneyMedium of Exchange, Unit of Account, Store of Wealth

Medium of ExchangeSaves transaction costsAllows specialisation

- easily standardised- widely accepted- divisible- portable- durable

Factor Market

HouseholdLender-SaverBorrower-Spender

Goods Market

FirmLender-SaverBorrower-Spender

Sell Buy

Buy SellUnit of AccountSaves transaction costsReduces numbers of prices to consider

Store of WealthStock of purchasing power- liquidity (ease of covertibility)- risk of (hyper) inflation- time value cost of money

Slide 8 of 27

4.0 Portfolio Decisions: MoneyMedium of Exchange, Unit of Account, Store of Wealth

Choice between types of assetsStocksBondsReal assetsForeign exchangeMoney

Money vs BondsPortfolio equilibrium = selected composition based on current and expected conditions

Factor Market

HouseholdLender-SaverBorrower-Spender

Goods Market

FirmLender-SaverBorrower-Spender

Sell Buy

Buy Sell

Slide 9 of 27

4.1 The demand for moneyThe mix of money and bonds in your portfolio depends on transactions and interest rates

Factor Market

Household

Goods Market

Firm

Sell Buy

Buy Sell

Price

The proportion of money to bonds depends on

1. Your level of transactions

2. The interest rate on bondsActive balances - The need for money for transactionsY↑ → active transactions↑ → Md↑Y↓ → active transactions↓ → Md↓Passive balances - The need for wealth in form of moneyi↑ → passive demand↓ → Md↓i↓ → passive demand↑ → Md↑

Slide 10 of 27

4.1 The demand for moneyDeriving the demand for money

Factor Market

Household

Goods Market

Firm

Sell Buy

Buy Sell

Price

PricePrice

Read this equation in the following way:

The demand for money, Md , is equal to nominal income, $Y, times a function of the interest rate, i, with the function denoted by L(i ).The demand for money increases in proportion to nominal income ($Y), and depends negatively on the interest rate (L(i)

Md = Y L(i)(+) (-)

Slide 11 of 27

For a given level of nominal income, a lower interest rate increases the demand for money. At a given interest rate, an increase in nominal income shifts the demand for money to the right.

4.1 The demand for moneyFigure 4-1 Deriving the demand for money

Md = Y L(i)(+) (-)

Shift = Change in Money Demand

Move = Change in Demand for Money

Slide 12 of 27

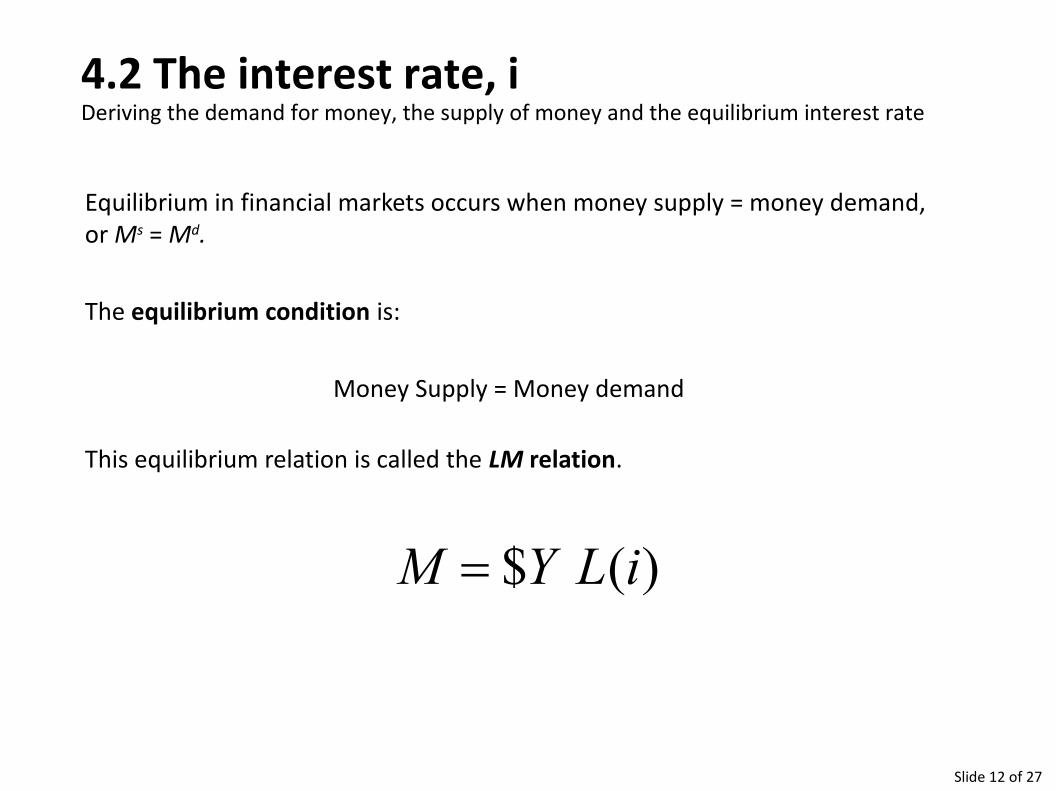

Equilibrium in financial markets occurs when money supply = money demand, or Ms = Md.

The equilibrium condition is:

Money Supply = Money demand

This equilibrium relation is called the LM relation.

$ ( ) M Y L i=

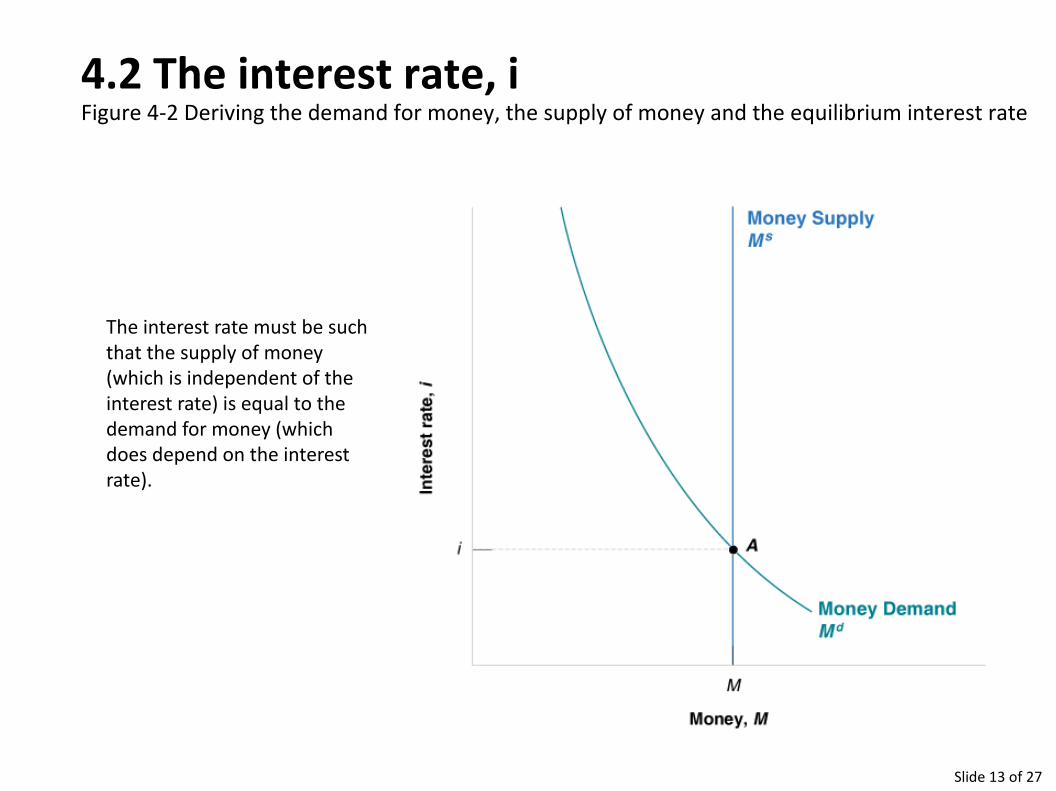

4.2 The interest rate, iDeriving the demand for money, the supply of money and the equilibrium interest rate

Slide 13 of 27

The interest rate must be such that the supply of money (which is independent of the interest rate) is equal to the demand for money (which does depend on the interest rate).

4.2 The interest rate, iFigure 4-2 Deriving the demand for money, the supply of money and the equilibrium interest rate

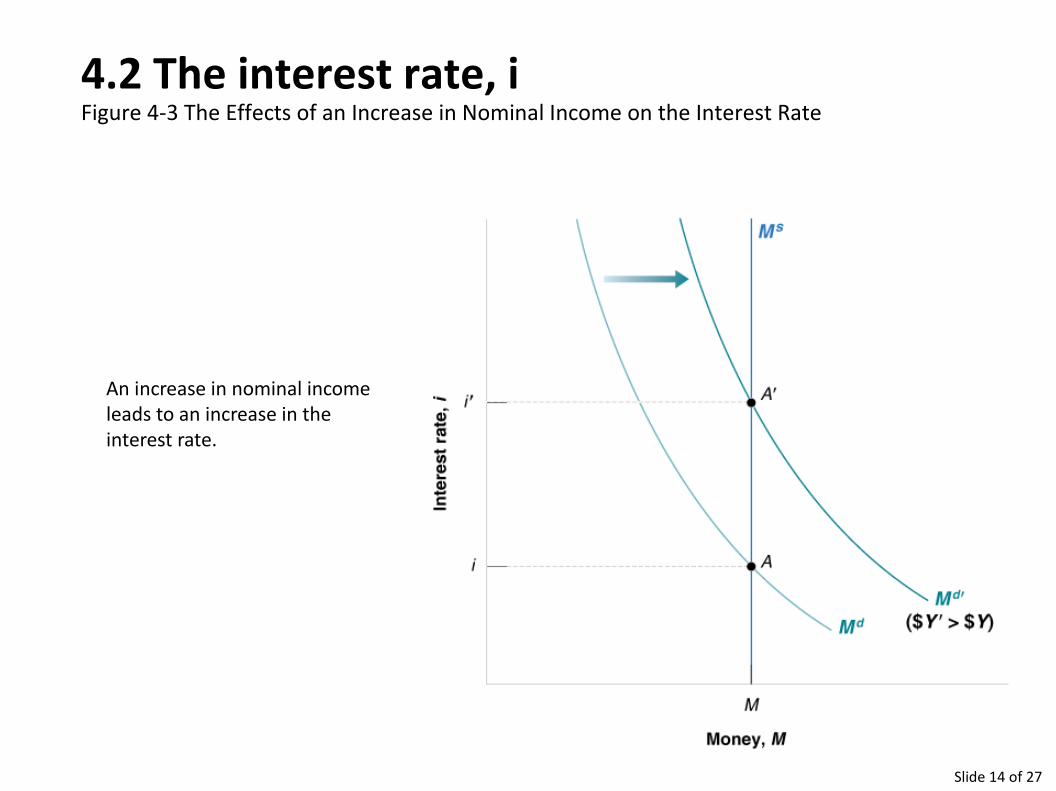

Slide 14 of 27

An increase in nominal income leads to an increase in the interest rate.

4.2 The interest rate, iFigure 4-3 The Effects of an Increase in Nominal Income on the Interest Rate

Slide 15 of 27

An increase in the supply of money leads to a decrease in the interest rate.

4.2 The interest rate, iFigure 4-4 The Effects of an Increase in the Money Supply on the Interest Rate

Taxes and imports reduce money stockGrants and exports increase money stockBank deposits increase D and reduce C

Slide 16 of 27

Open-market operations, which take place in the “open market” for bonds, are the standard method central banks use to change the money stock in modern economies.

If the central bank buys bonds, this operation is called an expansionary open market operation because the central bank increases (expands) the supply of money.

If the central bank sells bonds, this operation is called a contractionary open market operation because the central bank decreases (contracts) the supply of money.

4.2 The interest rate, iMonetary Policy and Open Market Operations

Slide 17 of 27

The assets of the central bank are the bonds it holds. The liabilities are the stock of money in the economy. An open market operation in which the central bank buys bonds and issues money increases both assets and liabilities by the same amount.

4.2 Monetary Policy | Open Market OperationsFigure 4-5 Effects of an Expansionary Open Market Operation

Slide 18 of 27

iP

PB

B

$100 $

$ $

$100P

iB 1

Treasury bills, or T-bills are issued by the U.S. government promising payment in a year or less. If you buy the bond today and hold it for a year, the rate of return (or interest) on holding a $100 bond for a year is ($100 - $PB)/$PB.The relation between the interest rate and bond pricesGiven the interest rate, we calculate the price of the bond with the same formula.

4.2 The interest rate, iBond Prices and Bond Yields

Summary1.The interest rate is determined by the equality of the supply of money and the demand for money.2.By changing the supply of money, the central bank can affect the interest rate.3.The central bank changes the supply of money through open market operations, which are purchases or sales of bonds for money.4.Open market operations in which the central bank increases the money supply by buying bonds lead to an increase in the price of bonds and a decrease in the interest rate.5.Open market operations in which the central bank decreases the money supply by selling bonds lead to a decrease in the price of bonds and an increase in the interest rate.

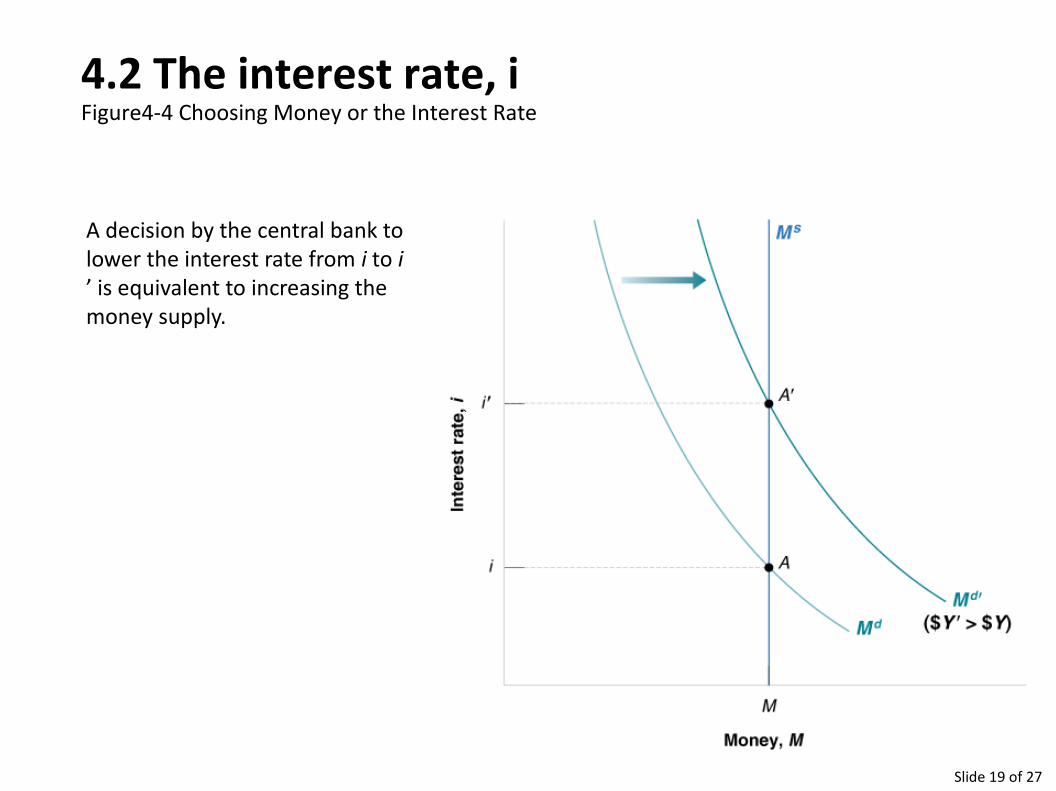

Slide 19 of 27

A decision by the central bank to lower the interest rate from i to i ’ is equivalent to increasing the money supply.

4.2 The interest rate, iFigure4-4 Choosing Money or the Interest Rate

Slide 20 of 27

Economies have more financial assets than money and bonds. Money = currency + chequable deposits.Financial intermediaries are institutions that receive funds from people and firms, and use these funds to buy bonds or stocks, or to make loans to other people and firms. Loans are roughly 70% of banks’ non-reserve assets. Bonds count for the rest, 30%.What Banks do1) Banks receive funds from people and firms who either deposit funds directly or have funds sent to

their checking accounts. The liabilities of the banks are therefore equal to the value of these checkable deposits.

2) Banks keep as reserves some of the funds they receive.

Banks hold reserves for three reasons3) On any given day, some depositors withdraw cash and others deposit cash4) On any given day, people with accounts at the bank write cheques to people with accounts at other

banks, and people with accounts at other banks write cheques to people with accounts at the bank.

5) Banks are subject to reserve requirements. The required reserve ratio – the ratio of bank reserves to bank checkable deposits – is 10% in the US and 2.5% in SA

Assets of the SARBThe SARB's assets are the bonds it holds. It's liabilities are the money it has issued, central bank money. Not all of central bank money is held as currency by the public. Some of it is held as reserves by banks.

4.3 What banks doMoney, Bonds and Banking

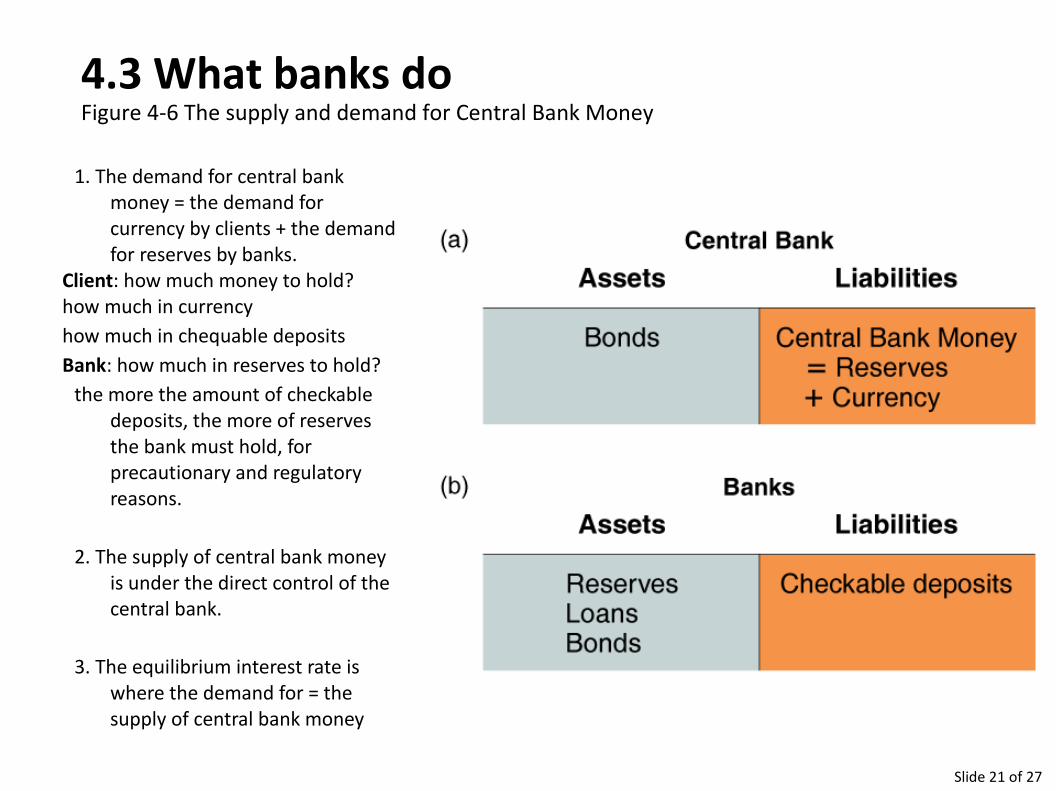

Slide 21 of 27

4.3 What banks doFigure 4-6 The supply and demand for Central Bank Money

1. The demand for central bank money = the demand for currency by clients + the demand for reserves by banks.

Client: how much money to hold?how much in currencyhow much in chequable depositsBank: how much in reserves to hold?

the more the amount of checkable deposits, the more of reserves the bank must hold, for precautionary and regulatory reasons.

2. The supply of central bank money is under the direct control of the central bank.

3. The equilibrium interest rate is where the demand for = the supply of central bank money

Slide 22 of 27

The equilibrium interest rate is such that the supply of central bank money is equal to the demand for central bank money.

4.3 What banks doFigure 4-8 Equilibrium for Central Bank Money and the Determination of the Interest Rate

The federal funds market is a market for bank reserves. In equilibrium, demand (Rd) must equal supply (H - CUd). The interest rate determined in the market is called the federal funds rate in the US and the repo rate in SA

The overall supply of money = central bank money x the money multiplier:

High-powered money is the term used to reflect the fact that the overall supply of money depends in the end on the amount of central bank money (H), or monetary base.

The Money Multiplier The ultimate increase in the money supply is the result of successive rounds of purchases of bonds—the first started by the SARB in its open market operation, the following rounds by banks.

Slide 23 of 27

Factor Market

Household

Goods Market

Firm

Sell Buy

Buy Sell

Price

Md = Y L(i)(+) (-)

Y↑ → Md↑→ P

B↓ → i↑

Y↓ → Md↓→ P

B↑ → i↓

4.4 Adjustment process in the Fin MarketRelationship between Price of Bond and i: P

B↓ → i↑ or P

B↓ → i↑

Slide 24 of 27

4.5 The Role of the SARBManagement of the South African money and banking system

Formulates and implements monetary policy (the measures to influence the quantity of money and the rate of interest in a country, with a view to achieving stable prices and facilitating full employment and sustainable economic growth). South Africa's monetary policy targets inflation and uses the refinancing system for its implementation. Provides liquidity to banks (fill gaps during periods of temporary shortages of cash) as “lender-of-last-resort” to protect depositors.

Make banknotes and coin through the SA Mint Company (the subsidiary that mints all the coins) and the SA Bank Note Company (the subsidiary that prints all banknotes). The SARB does not care whether the public holds cash, demand deposits at banks or has pre-arranged but unutilised credit lines. The potential supply of banknotes and coin is limited by banks to the extent that the public can only withdraw cash held as deposits or draw cash against pre-arranged credit facilities.

Distribute banknotes and coin as a wholesaler through seven branch offices (Bloemfontein, Cape Town, Durban, East London, Johannesburg, Port Elizabeth and Pretoria North) and settle claims for mutilated banknotes. Banker of other Banks and change the minimum cash reserves that banks are required to hold and can use such adjustments to influence bank liquidity and the amount of money in circulation. Settlement of interbank claims via the South African Multiple Option Settlement (SAMOS) system.

Slide 25 of 27

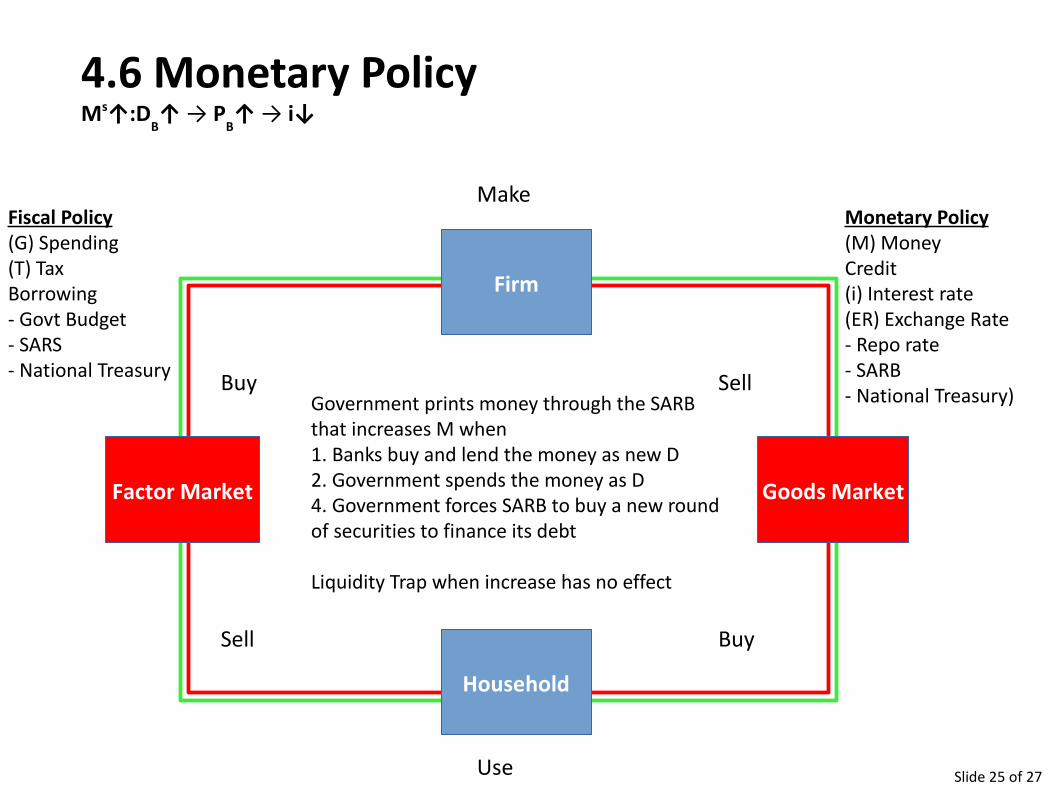

Make

Use

Government prints money through the SARB that increases M when1. Banks buy and lend the money as new D2. Government spends the money as D4. Government forces SARB to buy a new round of securities to finance its debt

Liquidity Trap when increase has no effect

Factor Market

Household

Goods Market

Firm

Sell Buy

Buy Sell

Fiscal Policy(G) Spending(T) TaxBorrowing- Govt Budget- SARS- National Treasury

Monetary Policy (M) MoneyCredit(i) Interest rate(ER) Exchange Rate- Repo rate- SARB- National Treasury)

4.6 Monetary PolicyMs↑:D

B↑ → P

B↑ → i↓

Slide 26 of 27

Macroeconomics03 Financial Markets: Terms

Federal Reserve Bank (Fed) income flow saving savings financial wealth, wealth stock investment financial investment money currency chequable deposits bonds money market funds LM relation open market operation

expansionary, and contractionary, open market operations

Treasury bill, (T-bill) financial intermediaries (bank) reserves reserve ratio bank runFears that a bank will not repay their loans will lead people to close their accounts. If enough people do so, the bank will run out of reserves—a bank run. To avoid bank runs, the U.S. government provides federal deposit insurance. An alternative solution is narrow banking, where banks must hold liquid, safe, government bonds, such as T-bills. federal deposit insurance narrow banking central bank money federal funds market federal funds rate money multiplier high-powered money monetary base

Slide 27 of 27

01 – Overview of the SA macroeconomy

02 – The goods market

03 – Financial Markets

04 – The IS-LM model

05 – Openness in goods and financial markets

06 – The goods market in an open economy

07 – Output, the interest and the exchange rates

08 – The labour market

09 – The AS-AD model

4.0 IntroductionDefinition: Money and InvestmentThe 4 measures of Money: M1A, M1, M2 and M3The 3 functions of MoneyPortfolio Decisions; Money vs. Bonds4.1 The demand for MoneyThe determinants of demandDeriving the demand for moneyFigure 4-1 Deriving the demand for money4.2 The interest rateThe equiibrium condition and LM relationFigure 4-2 The equilibrium interest rateFigure 4-3 The effects of an increase in nominal incomeFigure 4-4 The effects of an increase in the money supplyMonetary policy and open market operationsFigure 4-5 Effect of expansionary OMBond prices and bond yieldsChoosing to change the money suppy or the interest rate4.3 What banks doMoney, bonds, banking, deposits, loans and reservesFigure 4-6 The supply and demand for Central Bank MoneyFigure 4-8 The determination of the interest rate4.4 Adjustment process in the Financial MarketRelationship between price of a bod and interest rate4.5 The Role of the SARB4.6 Monetary Policy in SATermsOutcomesExplain in words, and via chain of events, equations and diagrams,1. How the interest rate is determined2. What causes a change in the interest rate4. The impact of monetary policy on the interest rate4. Monetary policy in SA

MacroeconomicsUnits 01 - 09