introduction to business economics introduction to business economics

TRANSCRIPT

Introduction to Business EconomicsIntroduction to Business Economics

Topics to be Discussed• Aims and objectives of the module• Module structure• The Themes of Microeconomics• What Is a Market?• What Is a Market?• Real Versus Nominal Prices• Why Study Microeconomics?

Aim of the module

• To analyse the principles of microeconomics and their application to business

Introductory ideas

The basic economic problem is that of scarce resources (and unlimited wants).

Given this problem we wish to know:What to produceHow to produce it, and How to produce it, and Who to give it to

Economics is concerned with:The production of goods and servicesThe consumption of goods and servicesin order to address the problem of scarcity

Preliminaries• Microeconomics deals with:

– Behavior of individual units when consuming– Behavior of individual units when producing– Markets: The interaction of consumers and producers

• Macroeconomics deals with:• Macroeconomics deals with:– Analysis of aggregate issues:

• Economic growth• Inflation• Unemployment

• Microeconomics is the foundation of macroeconomic analysis

– How we choose what to buy

Positive and normative economics

Positive statements (description)• What is, was or will be• Alleged facts about the universeNormative statements (prescription)Normative statements (prescription)• What ought to be• Require judgement about good and bad• Depend on philosophical, cultural & religious positions

Positive and normative economics

• Positive analysis is the use of theories and models to predict the impact of a choice:

– What will be the impact of an import quota on foreign cars?– What will be the impact of an increase in the gasoline excise – What will be the impact of an increase in the gasoline excise

tax?• Normative analysis addresses issues from the

perspective of “What ought to be?”:– Consider the equity and efficiency trade-off of an increase in

the gasoline excise tax versus import restriction on foreign oil.

Economic questions

• Technical efficiency (TE)– Minimising costs of production– Maximising output from given inputs

• Allocative efficiency (AE)• Allocative efficiency (AE)– Choice of how much to produce of which goods– Maximising welfare for given resources

• Equity (EQ)– Distribution between individuals & groups

The Themes of Microeconomics

• Allocation of Scarce Resources and Trade-offs– In a planned economy– In a market economy

• Microeconomics and Optimal Trade-offs1. Consumer Theory1. Consumer Theory2. Workers3. Theory of the Firm

• Microeconomics and Prices– The role of prices in a market economy– How prices are determined

Theories and Models• Microeconomic Analysis

– Theories are used to explain observed phenomena in terms of a set of basic rules and assumptions.

– For example• The Theory of the Firm • The Theory of Consumer Behavior• The Theory of Consumer Behavior

– Models:• a mathematical representation of a theory used to make a prediction.

– Validating a Theory• The validity of a theory is determined by the quality of its prediction, given

the assumptions.

– Evolving the Theory• Testing and refining theories is central to the development of the science

of economics.

Module structure

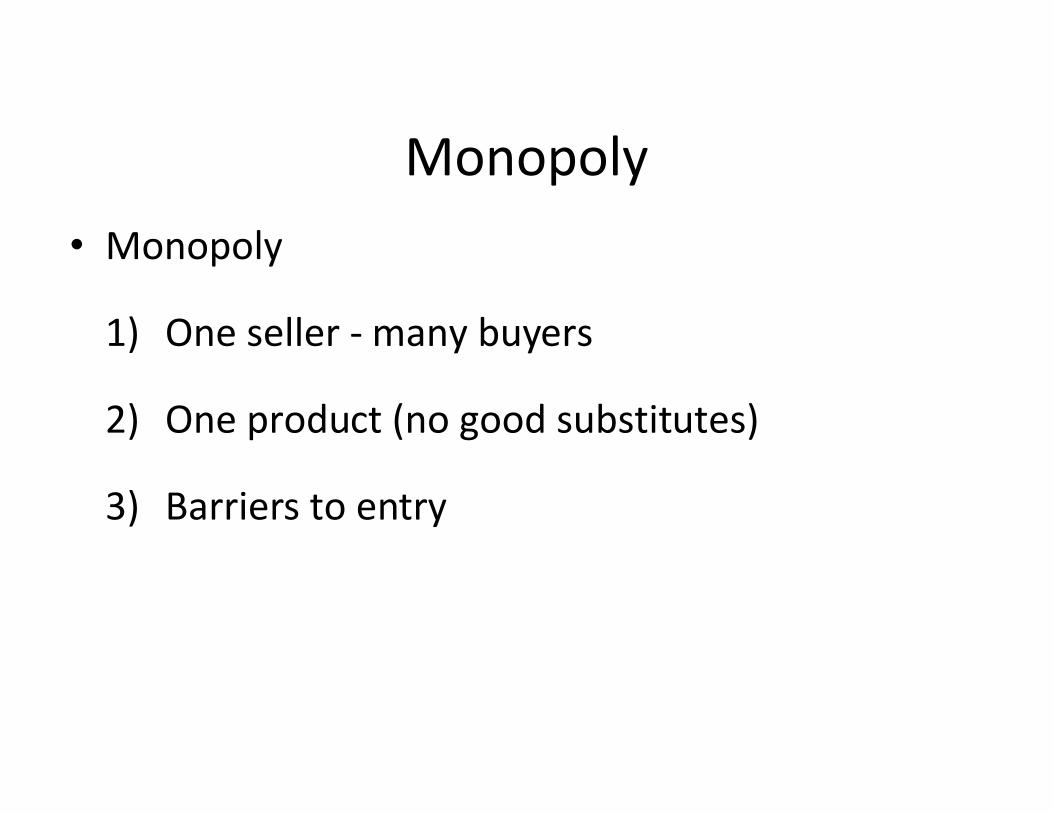

1. Introduction to business economics2. Supply and demand3. Production4. Costs of production4. Costs of production5. Profit maximisation and perfect competition6. Analysis of competitive markets7. Monopoly8. Pricing with market power9. Monopolistic competition and oligopoly10. Game theory

What is a Market?

• Markets– A geographically defined area where buyers and sellers

interact to determine the price of a product or a set of products.

• Markets vs. Industries• Markets vs. Industries– Industries are the supply side of the market.

• Defining the Market– The market parameters must be set before an analysis of the

market can take place.• Arbitrage

– Buying a product at a low price in one location and selling at a high price in another

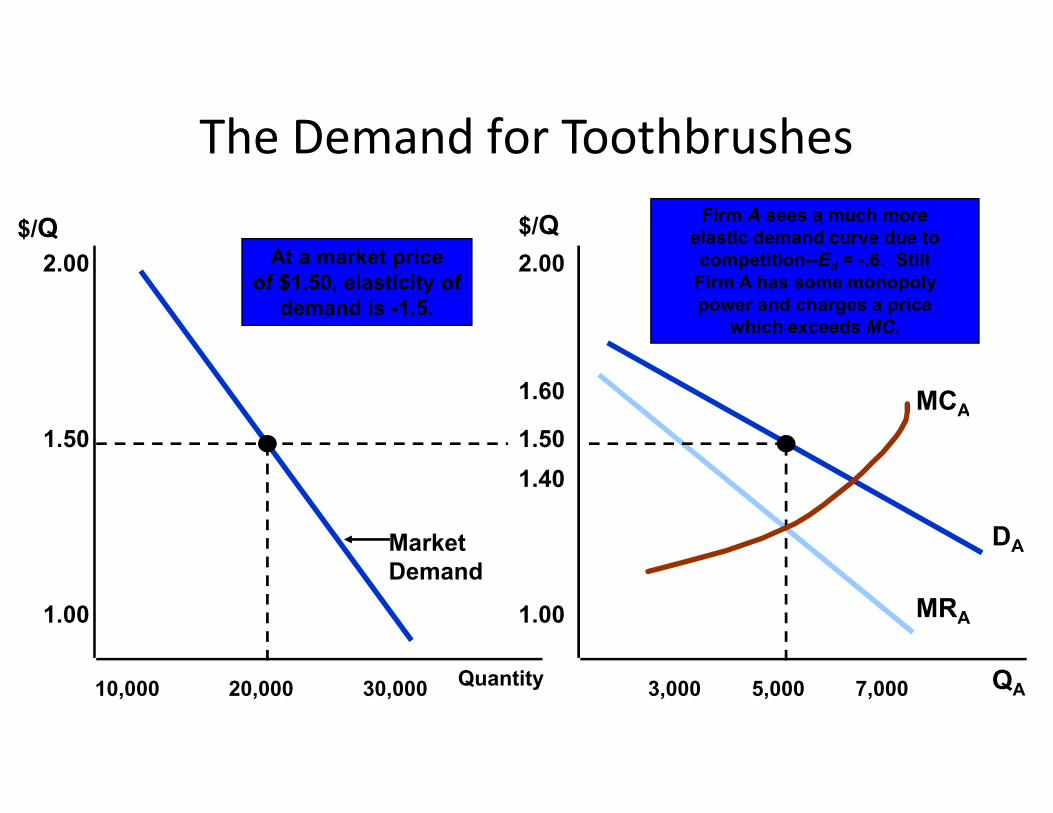

Competitive vs. NoncompetitiveMarkets

• Competitive Markets– Because of the large number of buyers and sellers, no

individual buyer or seller can influence the price.– Example: Most agricultural markets

Noncompetitive Markets• Noncompetitive Markets– Markets where individual producers can influence the price.– Example: OPEC

• Market Price– Competitive markets establish one price.– Noncompetitive markets may set many prices for the same

product.

Real Versus Nominal Prices• Nominal price is the absolute or current price of a

good or service when it is sold.• Real price is the price relative to an aggregate

measure of prices or constant price.measure of prices or constant price.

Real Versus Nominal Prices• The Consumer Price Index (CPI) is an aggregate

measure.– Real prices are emphasized to permit the analysis of

relative prices. relative prices.

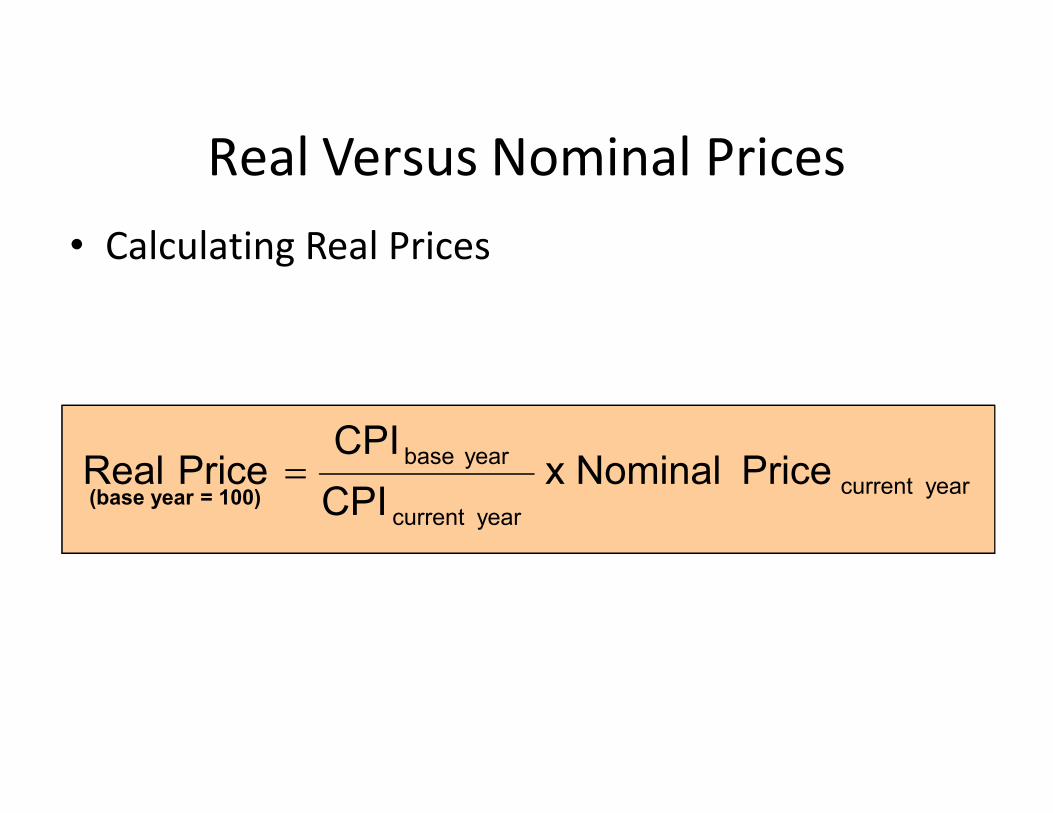

Real Versus Nominal Prices• Calculating Real Prices

yearcurrent yearcurrent

yearbase PriceNominal x CPI

CPIPriceReal

(base year = 100)

Example: the Real Price of Milk

Nominal Price Real Price of MilkYear of Milk CPI in 1970 dollars

1970 .40 38.8 .40 = 38.8/38.8 x .40

1980 .65 82.4 .31 = 38.8/82.4 x .65

1999 1.05 167.0 .24 = 38.8/167.0 x 1.05

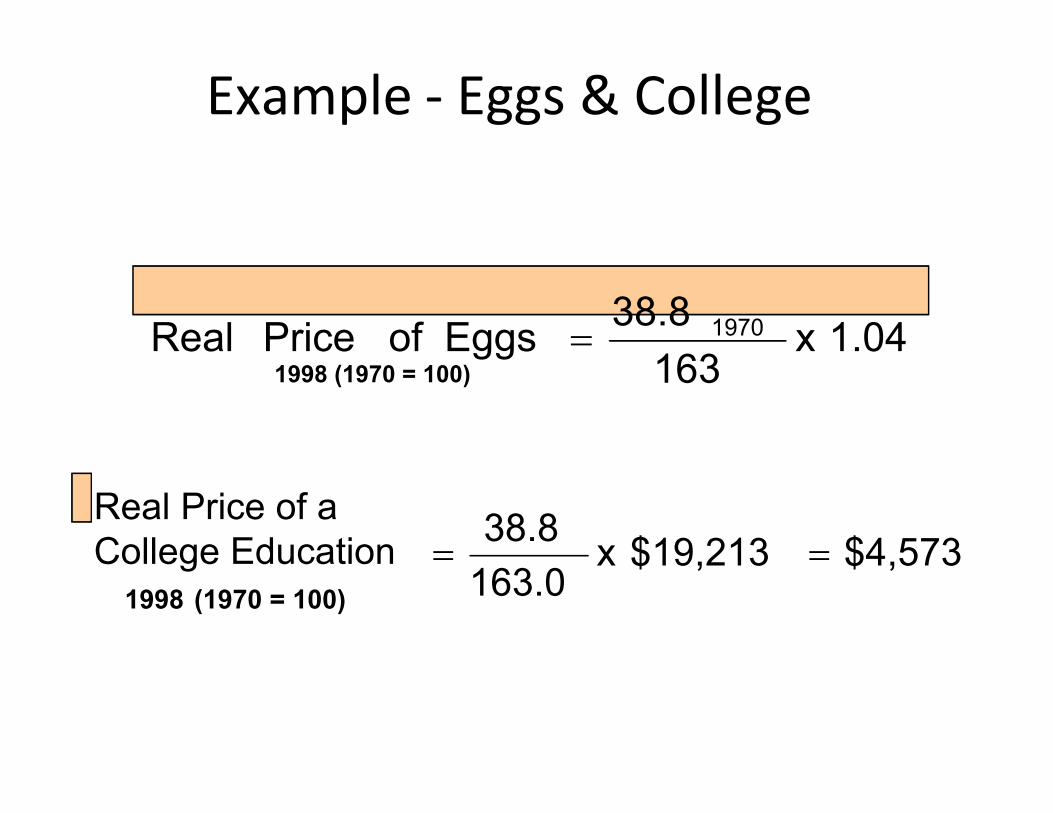

Example - Eggs & College

1.04x163

38.8EggsofPriceReal 1970

1998 (1970 = 100)

$4,573$19,213x 163.0

38.8

Real Price of a College Education

1998 (1970 = 100)

Example - Eggs & College

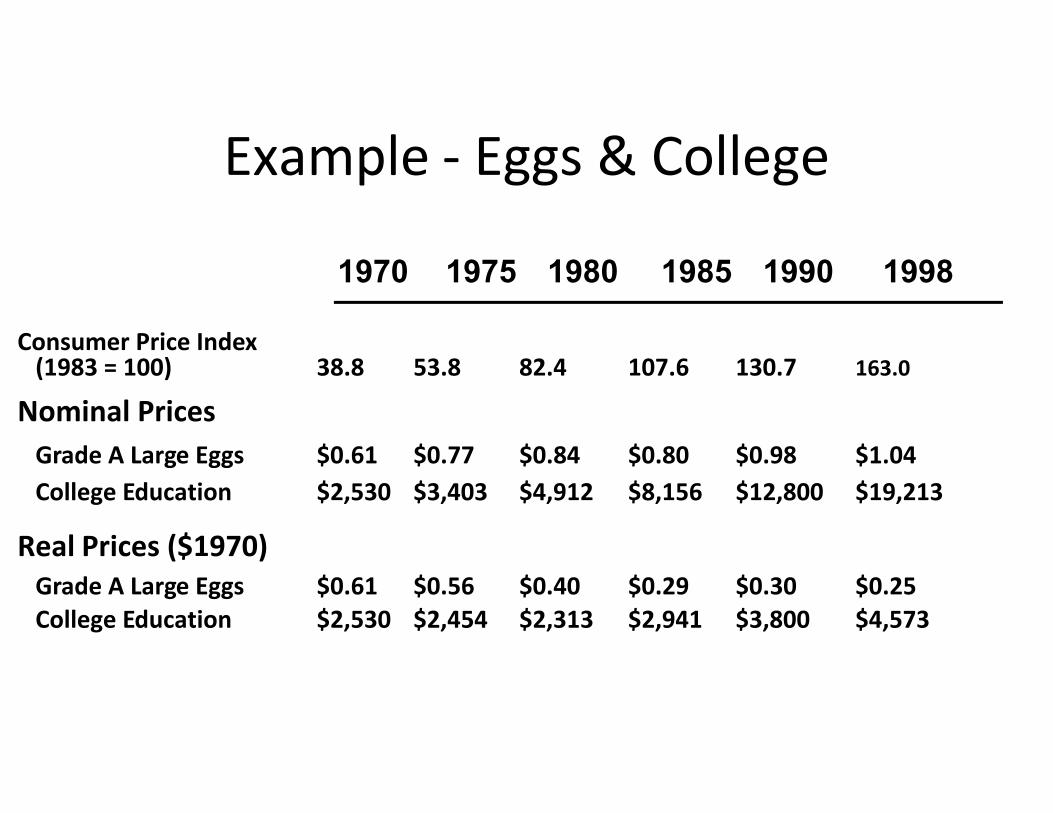

Consumer Price Index(1983 = 100) 38.8 53.8 82.4 107.6 130.7 163.0

Nominal Prices

1970 1975 1980 1985 1990 1998

Nominal PricesGrade A Large Eggs $0.61 $0.77 $0.84 $0.80 $0.98 $1.04College Education $2,530 $3,403 $4,912 $8,156 $12,800 $19,213

Real Prices ($1970)Grade A Large Eggs $0.61 $0.56 $0.40 $0.29 $0.30 $0.25College Education $2,530 $2,454 $2,313 $2,941 $3,800 $4,573

Why Study Microeconomics?• Microeconomic concepts are used by everyone to

assist them in making choices as consumers and producers.

Two Examples

• Ford and the development of its SUV’s• Public Policy Design: Automobile emission

standards for the 21st century

Ford and the development of itsSUV’s

• Issues– Consumer acceptance and demand– Production cost– Pricing strategy– Pricing strategy– Risk analysis– Organizational decisions– Government regulation

Auto emission standards for the 21stcentury

• Issues– Impact on consumers– Impact on producers– How to enforce the standards– How to enforce the standards– What are the benefits and costs?

Summary• Microeconomics is concerned with the decisions

made by small economic units.• Microeconomics relies heavily on the use of

theory and models.theory and models.

Summary• Microeconomics is concerned with positive

questions and normative analysis.• A market refers to a collection of buyers and

sellers who interact and to the possibility for sales sellers who interact and to the possibility for sales and purchases that results from that interaction.

Summary

• The market price is established by the interaction of buyers and sellers.

• A market’s geographic boundaries and range of products must be defined. A market’s geographic boundaries and range of products must be defined.

• To eliminate the effects of inflation we measure real prices, rather than nominal prices.

Supply and demandSupply and demand

Topics to Be Discussed

• Supply and Demand

• The Market Mechanism

• Changes in Market Equilibrium• Changes in Market Equilibrium

• Elasticities of Supply and Demand

• Effects of Government Intervention - Price Controls

Introduction• Applications of Supply and Demand Analysis

– Understanding and predicting how world economic conditions affect market price and production

– Analyzing the impact of government price controls, minimum wages, price supports, and production incentivesminimum wages, price supports, and production incentives

– Analyzing how taxes, subsidies, and import restrictions affect consumers and producers

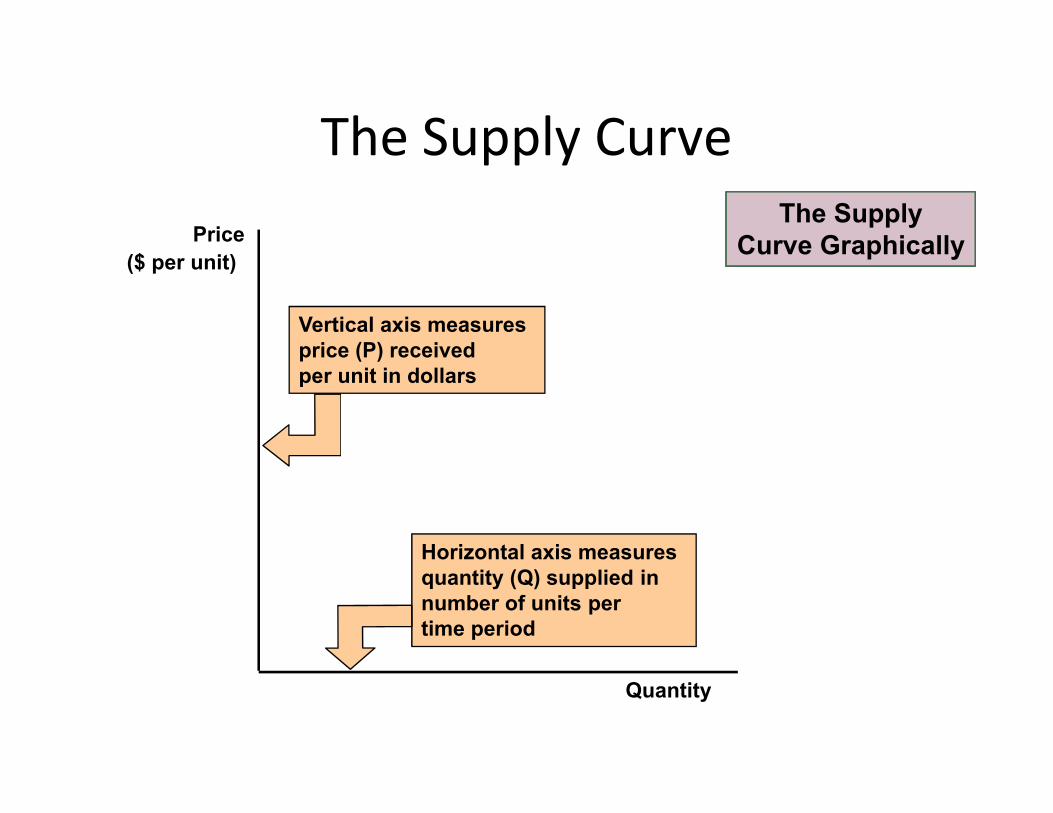

The Supply Curve

• The supply curve shows how much of a good producers are willing to sell at a given price, holding constant other factors that might affect quantity suppliedsupplied

• This price-quantity relationship can be shown by the equation:

)(PQQ ss

Vertical axis measures price (P) receivedper unit in dollars

The Supply CurveThe Supply

Curve GraphicallyPrice($ per unit)

Horizontal axis measures quantity (Q) supplied innumber of units per time period

Quantity

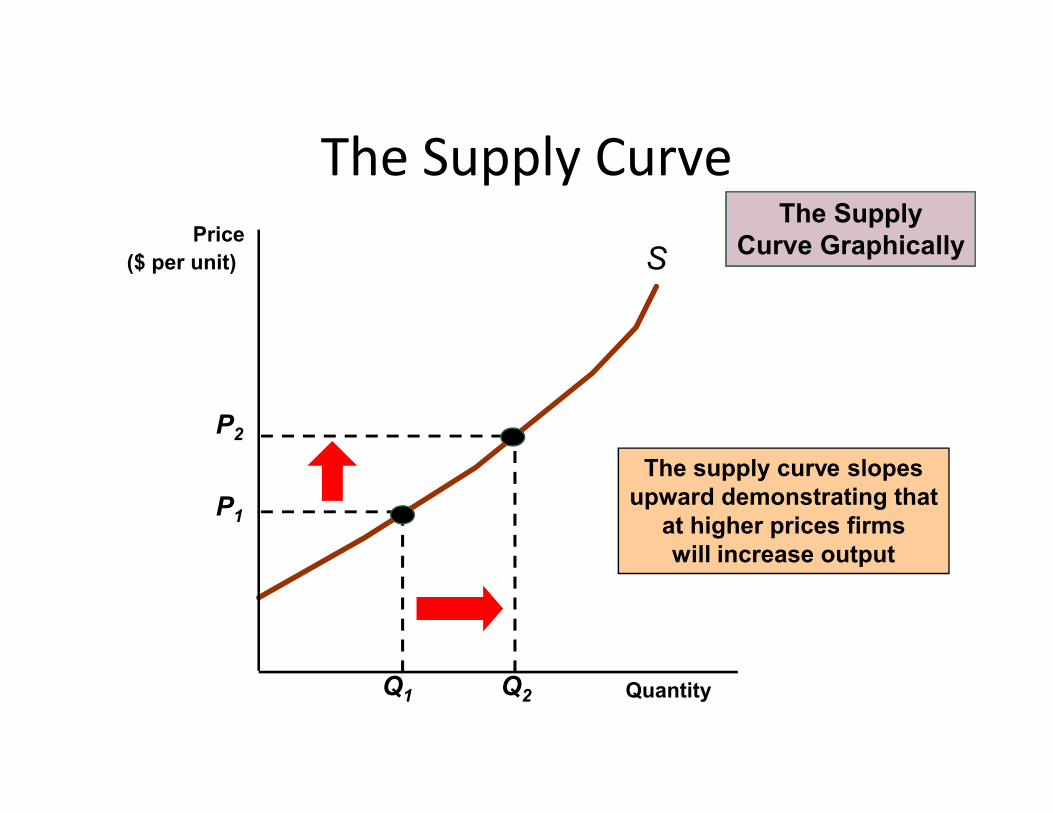

The Supply Curve

S

The SupplyCurve GraphicallyPrice

($ per unit)

The supply curve slopesupward demonstrating that

at higher prices firmswill increase output

Quantity

P1

Q1

P2

Q2

The Supply Curve• Non-price Determining Variables of Supply

– Costs of Production• Labor

• Capital• Capital

• Raw Materials

The Supply Curve• The cost of raw

materials falls– At P1, produce Q2

P S

Change in Supply

S’

– At P2, produce Q1

– Supply curve shifts right to S’

– More produced at any price on S’ than on S

Q

P1

P2

Q1Q0 Q2

The Supply Curve

• Supply - A Review– Supply is determined by non-price supply-

determining variables such as the cost of labor, capital, and raw materials.capital, and raw materials.

– Changes in supply are shown by shifting the entire supply curve.

– Changes in quantity supplied are shown by movements along the supply curve and are caused by a change in the price of the product.

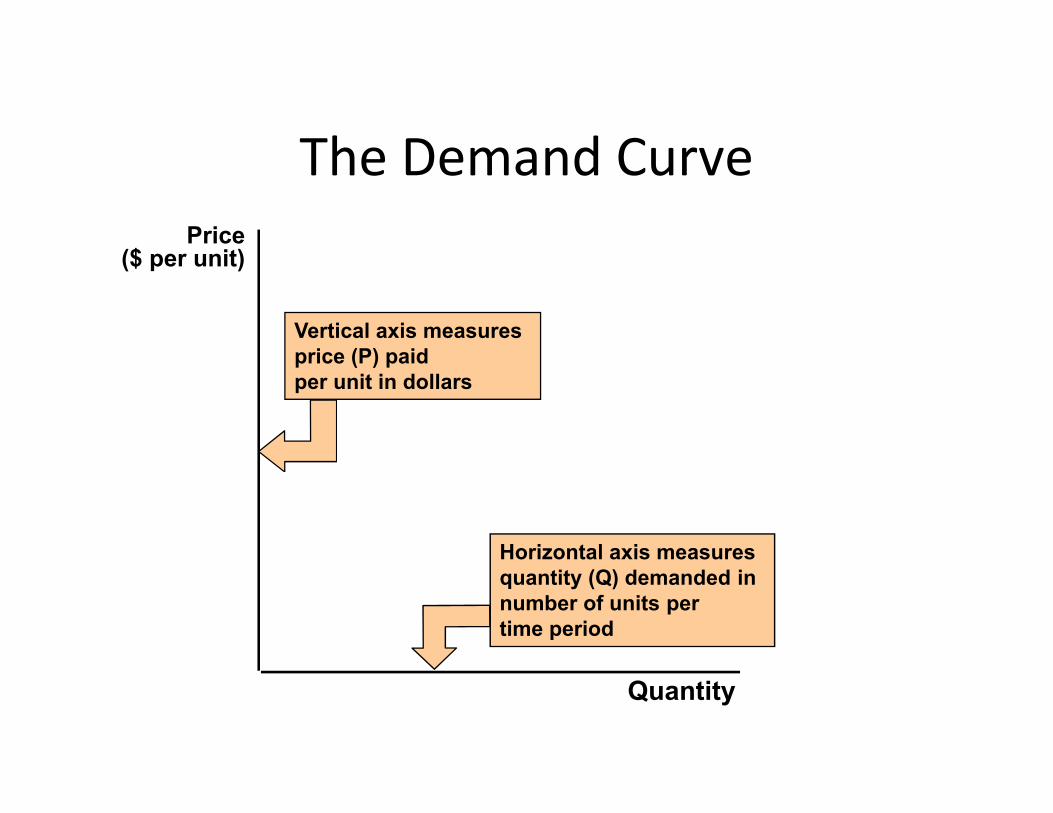

The Demand Curve

• The demand curve shows how much of a good consumers are willing to buy as the price per unit changes holding non-price factors constant.constant.

• This price-quantity relationship can be shown by the equation:

(P)QQ DD

The Demand Curve

Vertical axis measures price (P) paidper unit in dollars

Price($ per unit)

Quantity

Horizontal axis measures quantity (Q) demanded innumber of units per time period

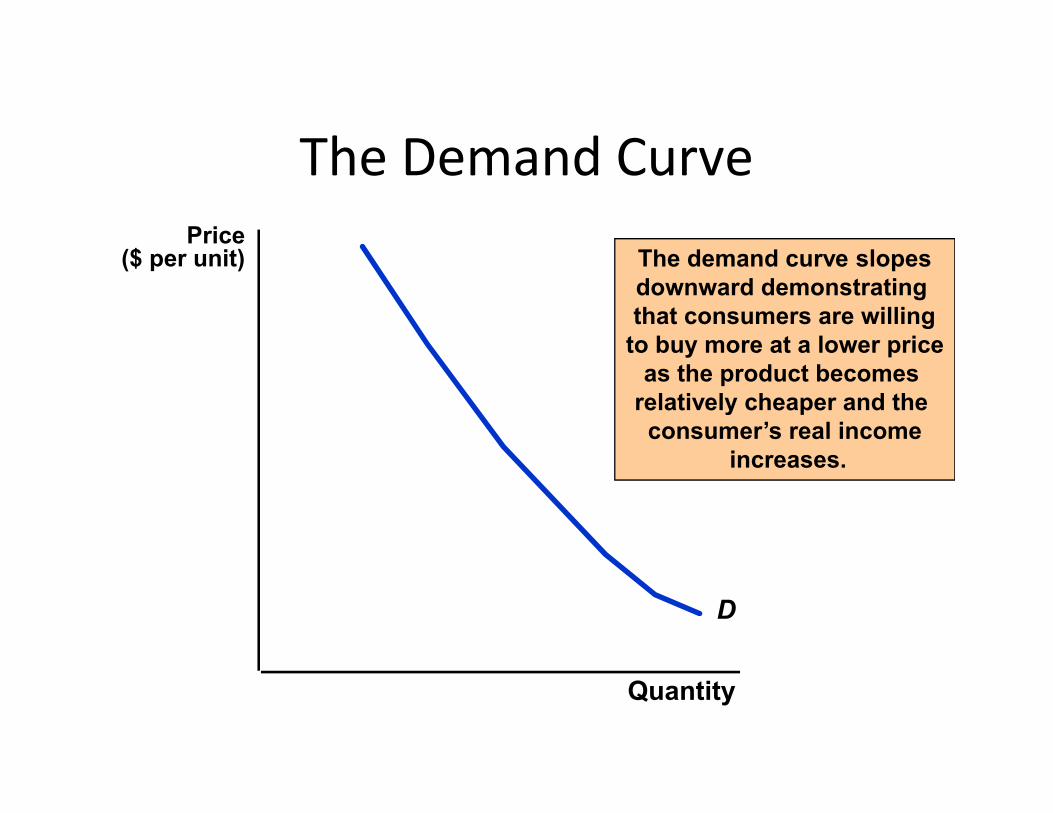

The Demand Curve

The demand curve slopesdownward demonstrating that consumers are willing

to buy more at a lower priceas the product becomes

relatively cheaper and the

Price($ per unit)

D

relatively cheaper and the consumer’s real income

increases.

Quantity

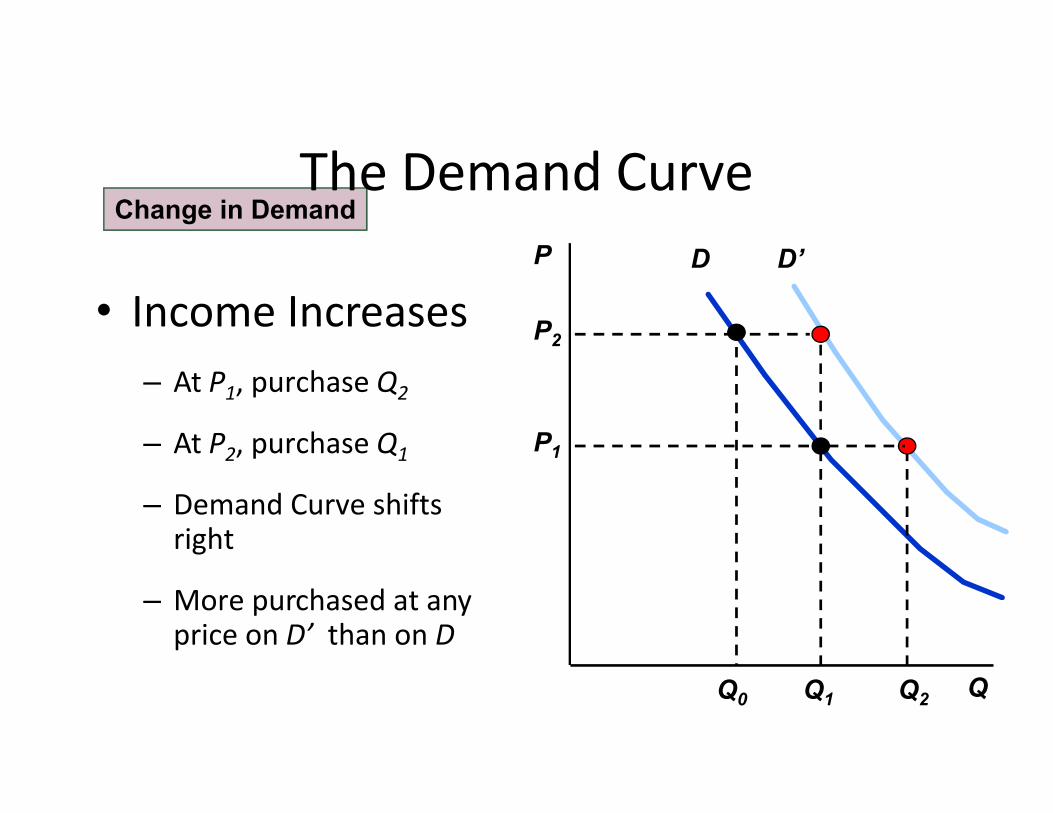

The Demand Curve• Non-price Determining Variables of Demand

– Income– Consumer Tastes– Price of Related Goods– Price of Related Goods

• Substitutes• Complements

DP

P2

D’

Change in DemandThe Demand Curve

• Income Increases– At P1, purchase Q2

QQ1Q0

P1

Q2

– At P2, purchase Q1

– Demand Curve shifts right

– More purchased at any price on D’ than on D

The Demand Curve• Demand - A Review

– Demand is determined by non-price demand-determining variables, such as, income, price of related goods, and tastes.goods, and tastes.

– Changes in demand are shown by shifting the entire demand curve.

– Changes in quantity demanded are shown by movements along the demand curve.

The Market MechanismS

The curves intersect atequilibrium, or market-

clearing, price. At P0 the

Price($ per unit)

Quantity

D

clearing, price. At P0 thequantity supplied is equalto the quantity demanded

at Q0 .

P0

Q0

The Market Mechanism

• Characteristics of the equilibrium or market clearing price:– QD = QS

– No shortage– No shortage– No excess supply– No pressure on the price to change

The Market MechanismS

If price is above equilibrium:

1) Price is above the

P1

Surplus

Price($ per unit)

Quantity

D

P0

Q0

1) Price is above themarket clearing price

2) Qs > Qd

3) Price falls to themarket-clearing price

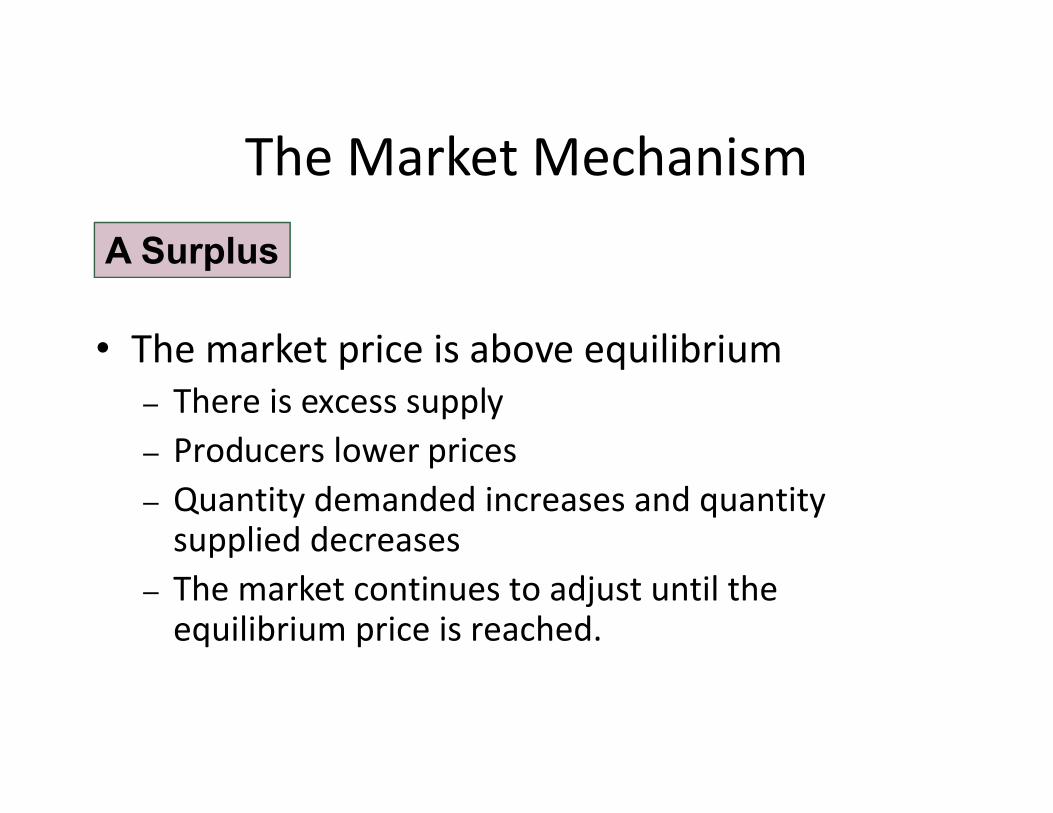

The Market Mechanism

• The market price is above equilibrium– There is excess supply

A Surplus

– There is excess supply– Producers lower prices– Quantity demanded increases and quantity

supplied decreases– The market continues to adjust until the

equilibrium price is reached.

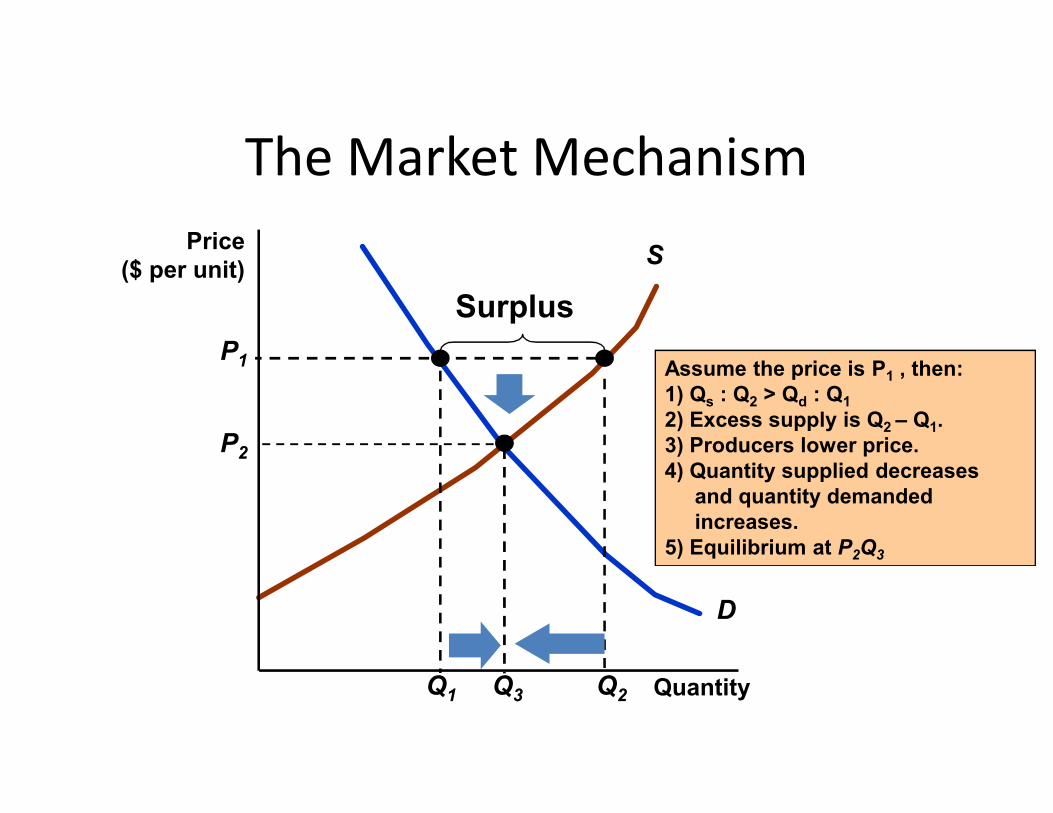

The Market MechanismS

Assume the price is P1 , then:1) Qs : Q2 > Qd : Q1

P1

Surplus

Price($ per unit)

D

Q1

s 2 d 1

2) Excess supply is Q2 – Q1.3) Producers lower price.4) Quantity supplied decreases

and quantity demanded increases.

5) Equilibrium at P2Q3

Q2 Quantity

P2

Q3

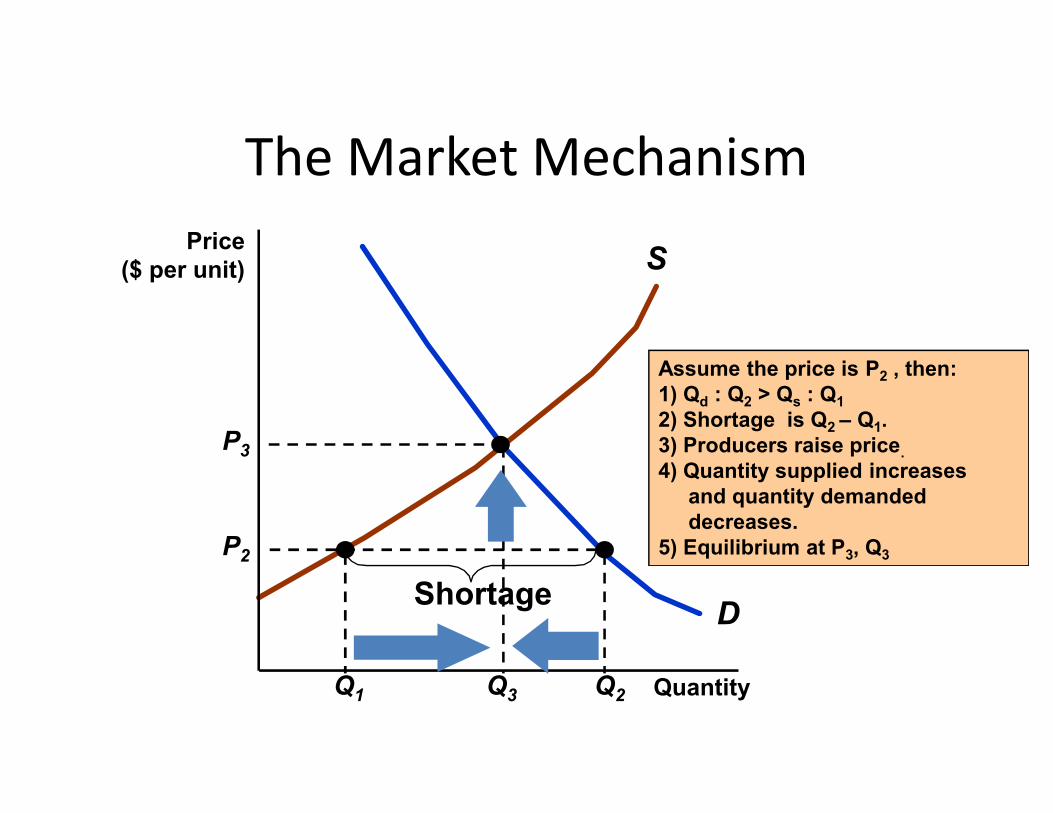

The Market Mechanism

• The market price is below equilibrium:– There is a shortage

Shortage

– There is a shortage– Producers raise prices– Quantity demanded decreases and quantity

supplied increases– The market continues to adjust until the new

equilibrium price is reached.

The Market Mechanism

SPrice

($ per unit)

Assume the price is P2 , then:1) Qd : Q2 > Qs : Q1

D

Q1 Q2

P2

Shortage

Quantity

d 2 s 1

2) Shortage is Q2 – Q1.3) Producers raise price.

4) Quantity supplied increases and quantity demanded decreases.

5) Equilibrium at P3, Q3

Q3

P3

The Market Mechanism

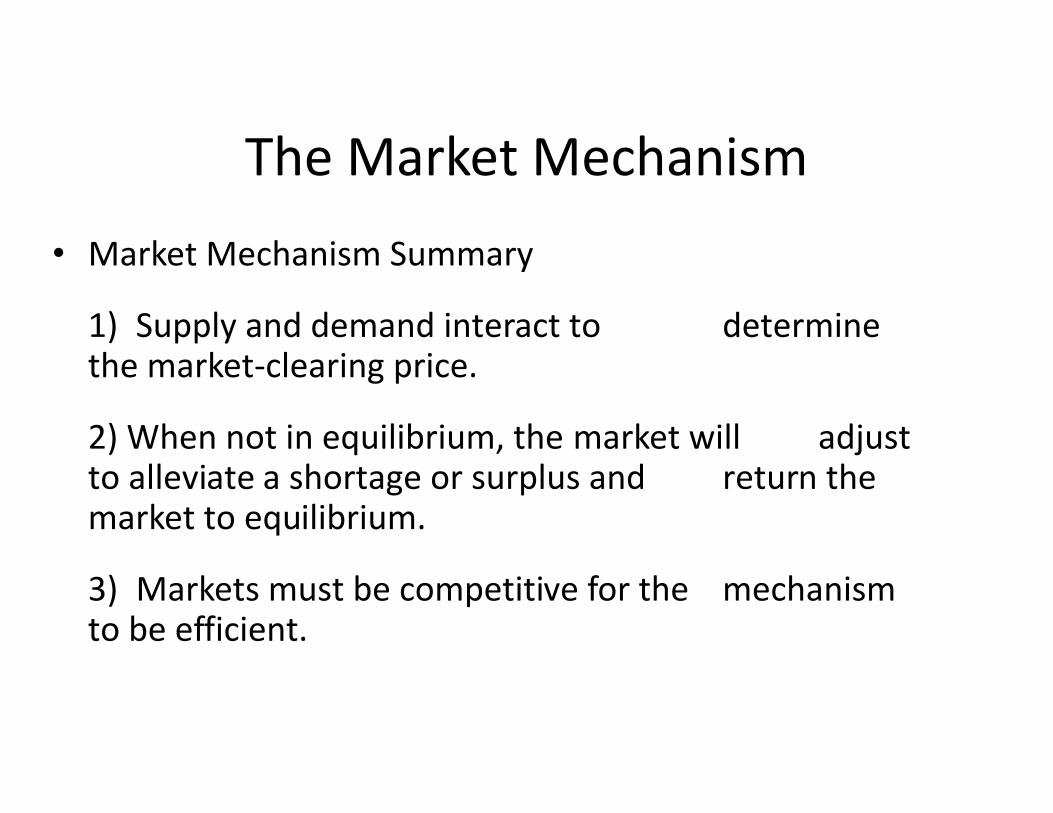

• Market Mechanism Summary

1) Supply and demand interact to determine the market-clearing price.

2) When not in equilibrium, the market will adjust to alleviate a shortage or surplus and return the market to equilibrium.

3) Markets must be competitive for the mechanism to be efficient.

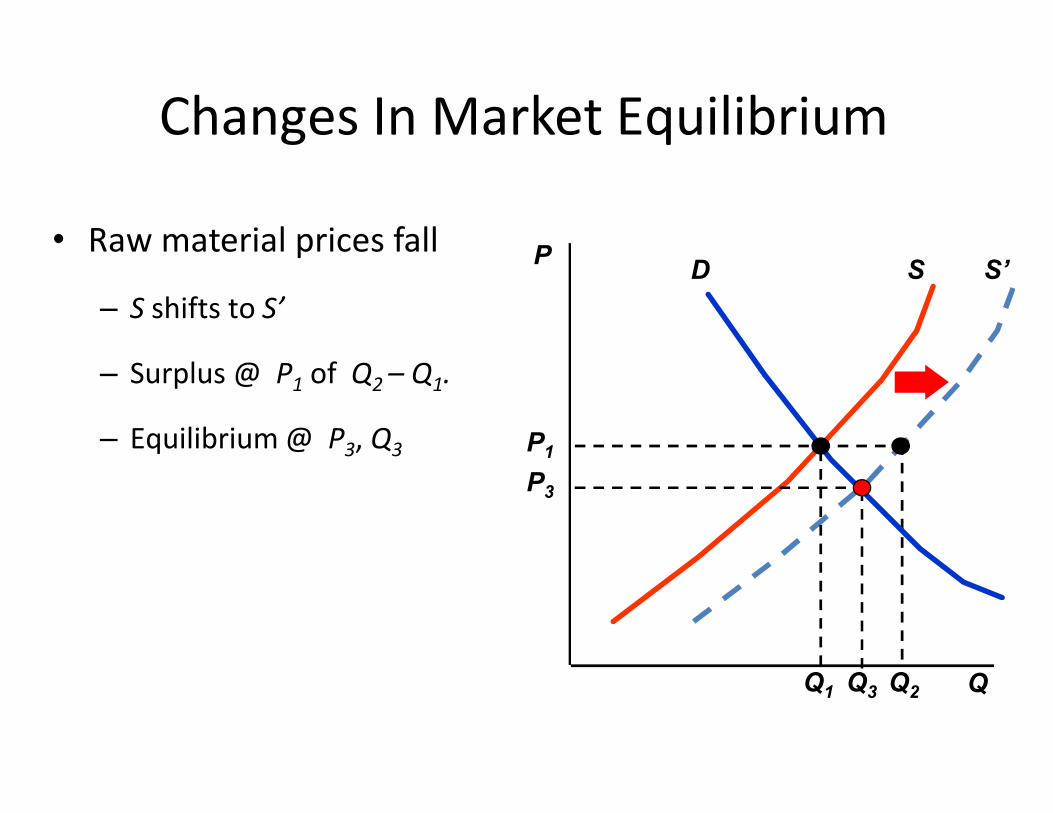

Changes In Market Equilibrium

• Equilibrium prices are determined by the relative level of supply and demand.

• Supply and demand are determined by particular values of supply and demand determining variables.values of supply and demand determining variables.

• Changes in any one or combination of these variables can cause a change in the equilibrium price and/or quantity.

S’

Changes In Market Equilibrium

• Raw material prices fall

– S shifts to S’

– Surplus @ P1 of Q2 – Q1.

P SD

Q2

– Equilibrium @ P3, Q3

Q

P3

Q3Q1

P1

D’ SD

P3

Changes In Market Equilibrium

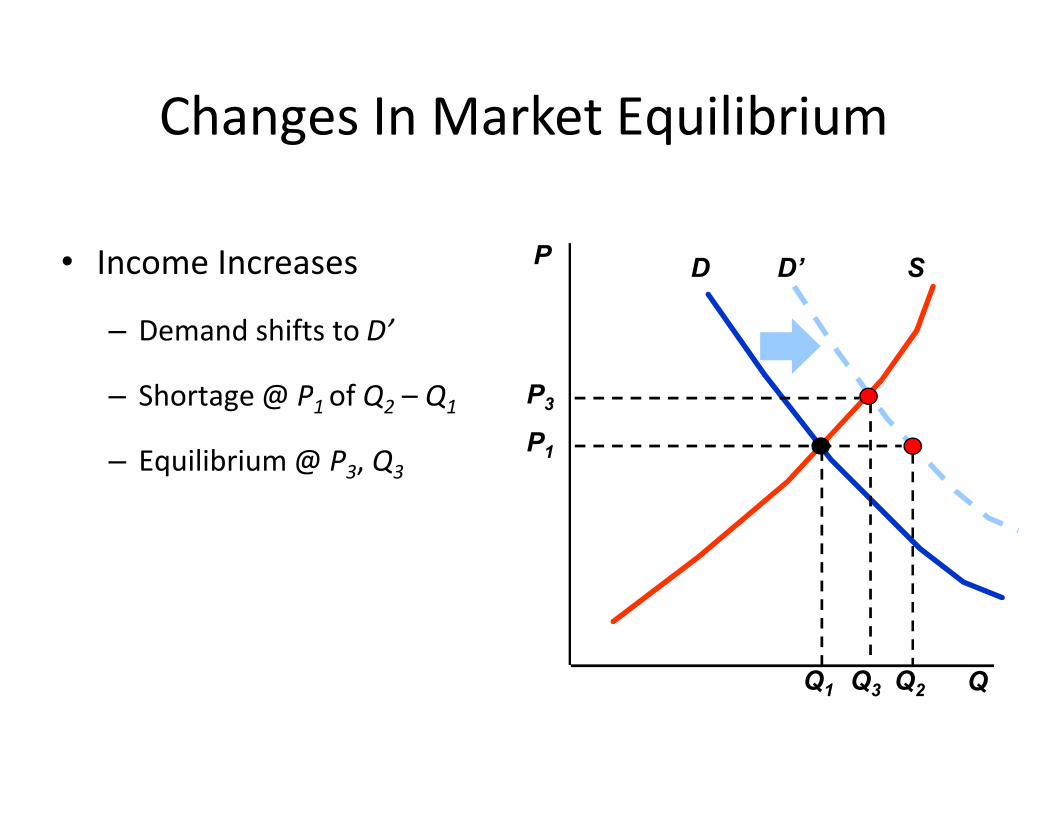

• Income Increases

– Demand shifts to D’

– Shortage @ P1 of Q2 – Q1

P

Q3

P3– Shortage @ P1 of Q2 – Q1

– Equilibrium @ P3, Q3

QQ2Q1

P1

D’ S’

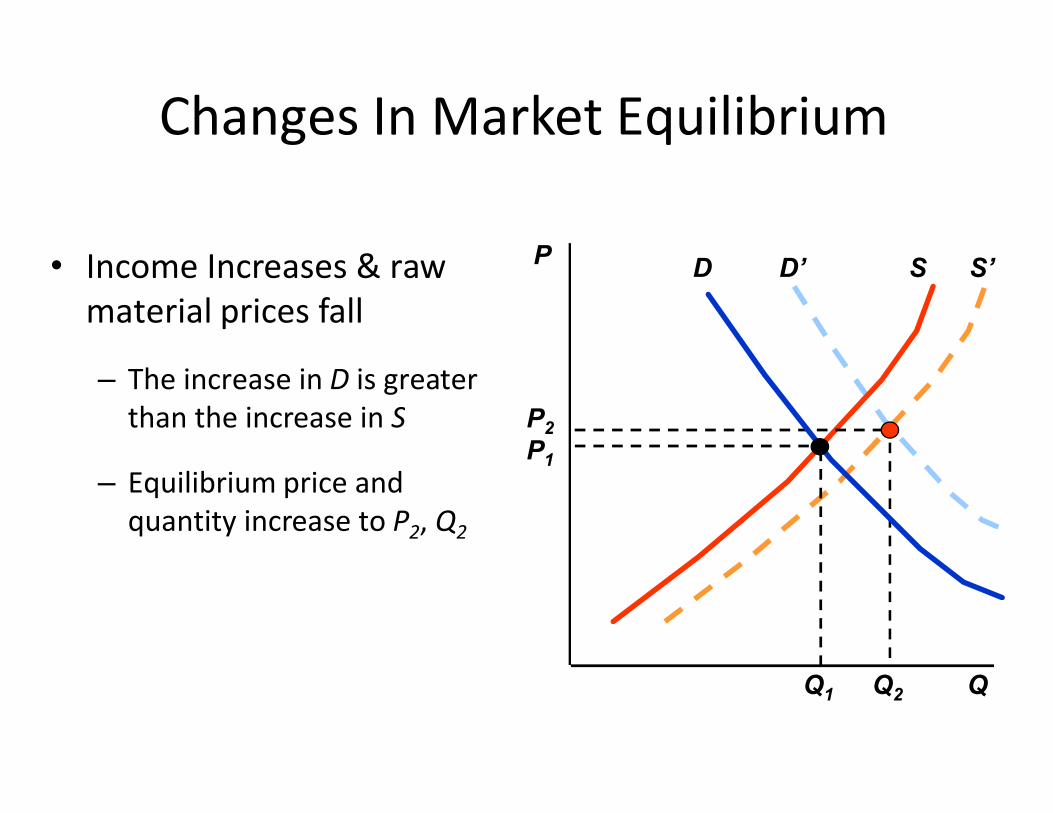

Changes In Market Equilibrium

• Income Increases & raw material prices fall

– The increase in D is greater than the increase in S

P S

P

D

than the increase in S

– Equilibrium price and quantity increase to P2, Q2

Q

P2

Q2

P1

Q1

Shifts in Supply and Demand• When supply and demand change simultaneously,

the impact on the equilibrium price and quantity is determined by:

1) The relative size and direction of the change1) The relative size and direction of the change

2) The shape of the supply and demand curves

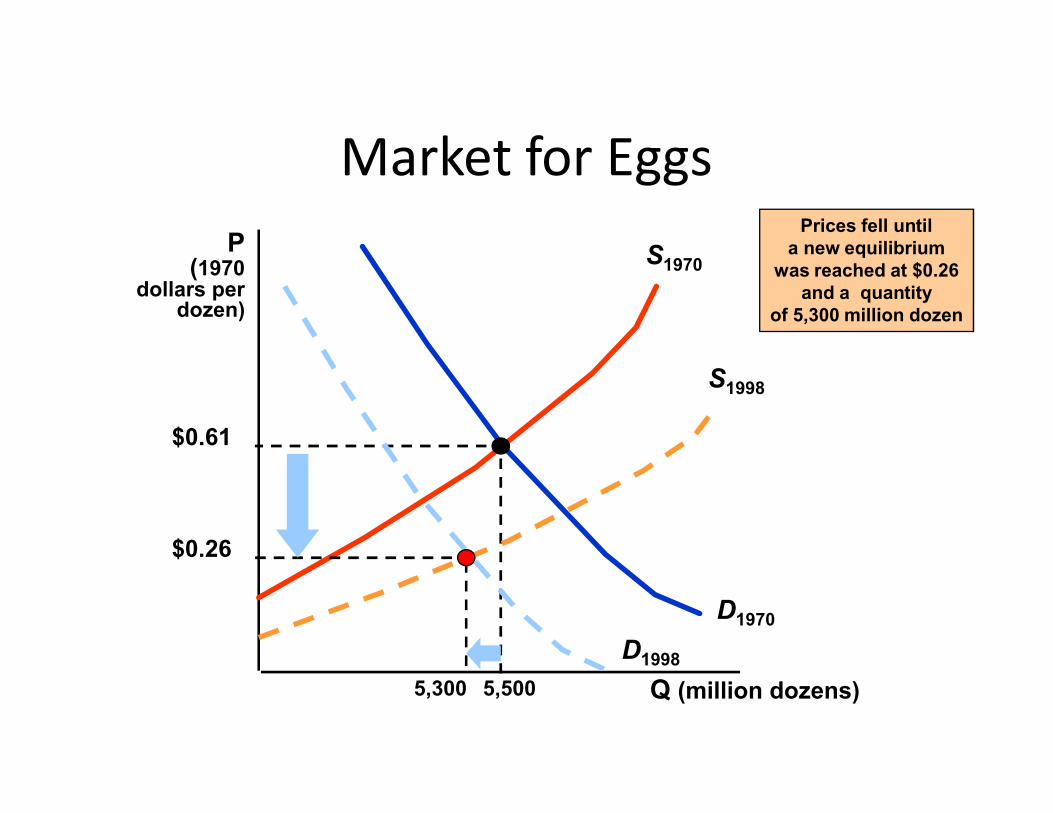

The Price of Eggs and College Education Revisited

• The real price of eggs fell 59% from 1970 to 1998.

• Supply increased due to the increased mechanization of poultry farming and the reduced cost of production.

• Demand decreased due to the increasing consumer concern over the health and cholesterol consequences of eating eggs.

Market for EggsP

(1970dollars per

dozen)

S1970

S1998

Prices fell untila new equilibrium

was reached at $0.26and a quantity

of 5,300 million dozen

Q (million dozens)

D1970

$0.61

5,500

D1998

$0.26

5,300

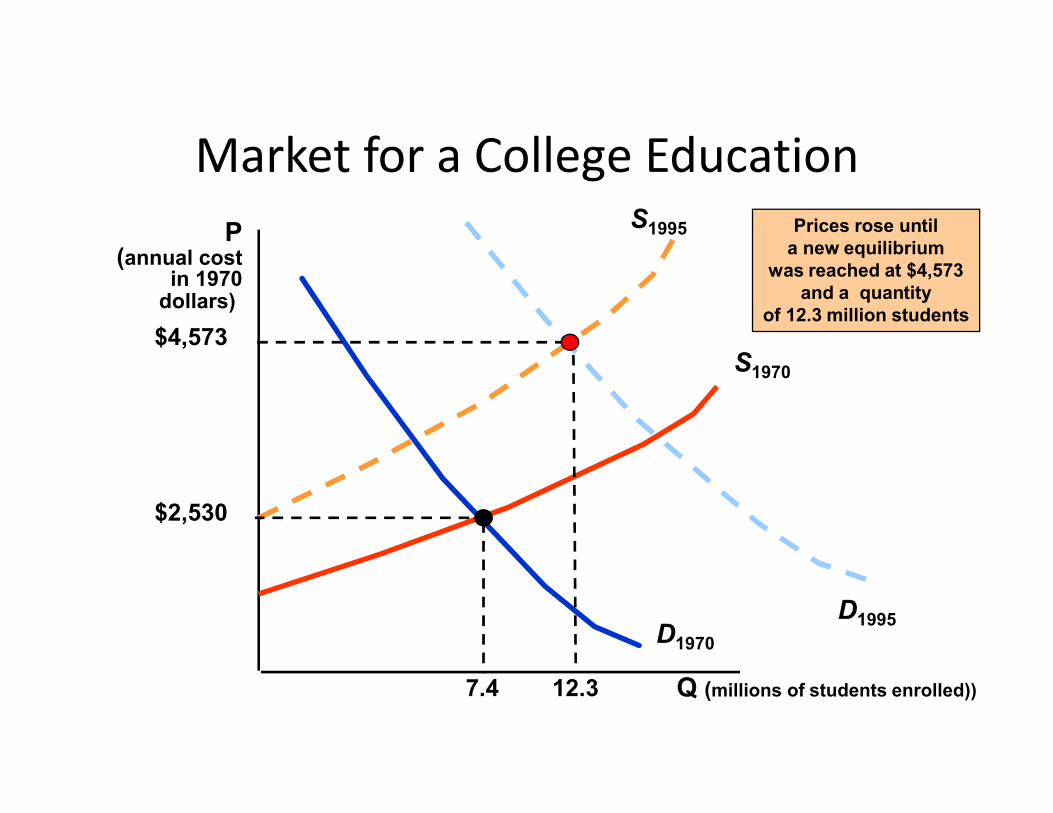

The Price of a College Education

• The real price of a college education rose 68 percent from 1970 to 1995.

• Supply decreased due to higher costs of equipping and maintaining modern classrooms, laboratories and maintaining modern classrooms, laboratories and libraries, and higher faculty salaries.

• Demand increased due to a larger percentage of a growing number of high school graduates attending college.

Market for a College EducationP

(annual costin 1970

dollars)

S1970

S1995

$4,573

Prices rose untila new equilibrium

was reached at $4,573and a quantity

of 12.3 million students

Q (millions of students enrolled))

D1970

D1995

12.3

$2,530

7.4

Elasticities of Supply and Demand

• Generally, elasticity is a measure of the sensitivity of one variable to another.

• It tells us the percentage change in one variable • It tells us the percentage change in one variable in response to a one percent change in another variable.

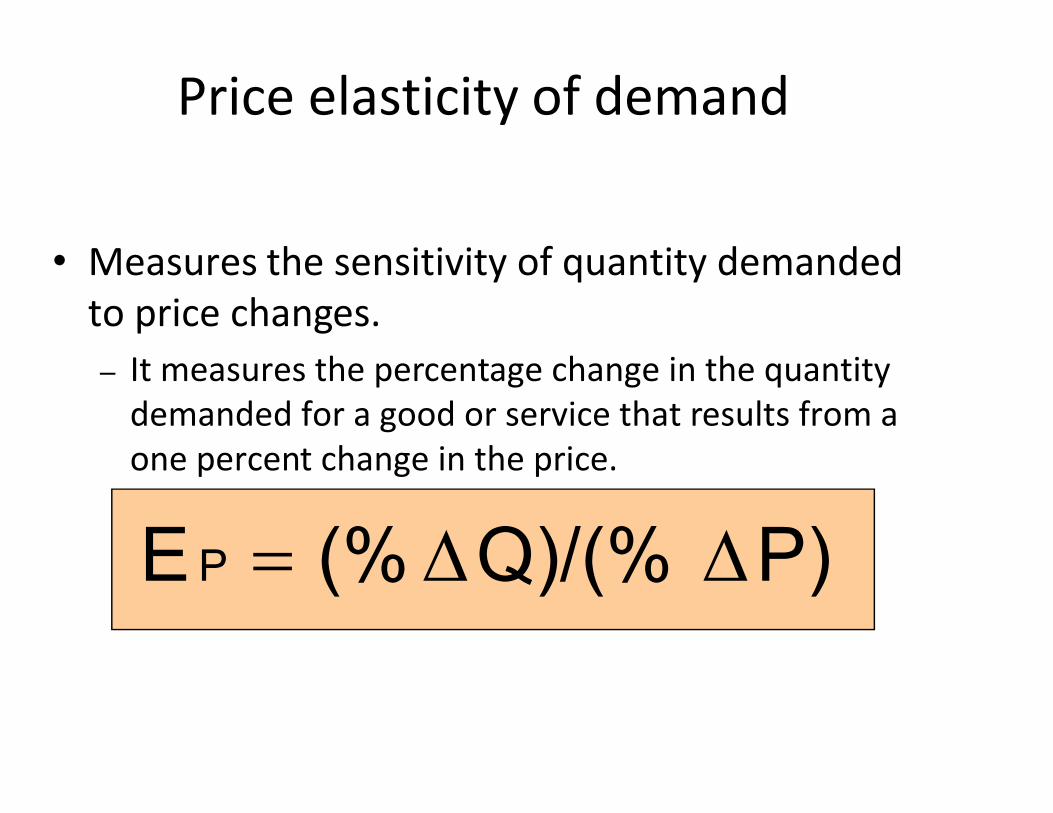

Price elasticity of demand

• Measures the sensitivity of quantity demanded to price changes.– It measures the percentage change in the quantity

demanded for a good or service that results from a demanded for a good or service that results from a one percent change in the price.

P)Q)/(%(%E P

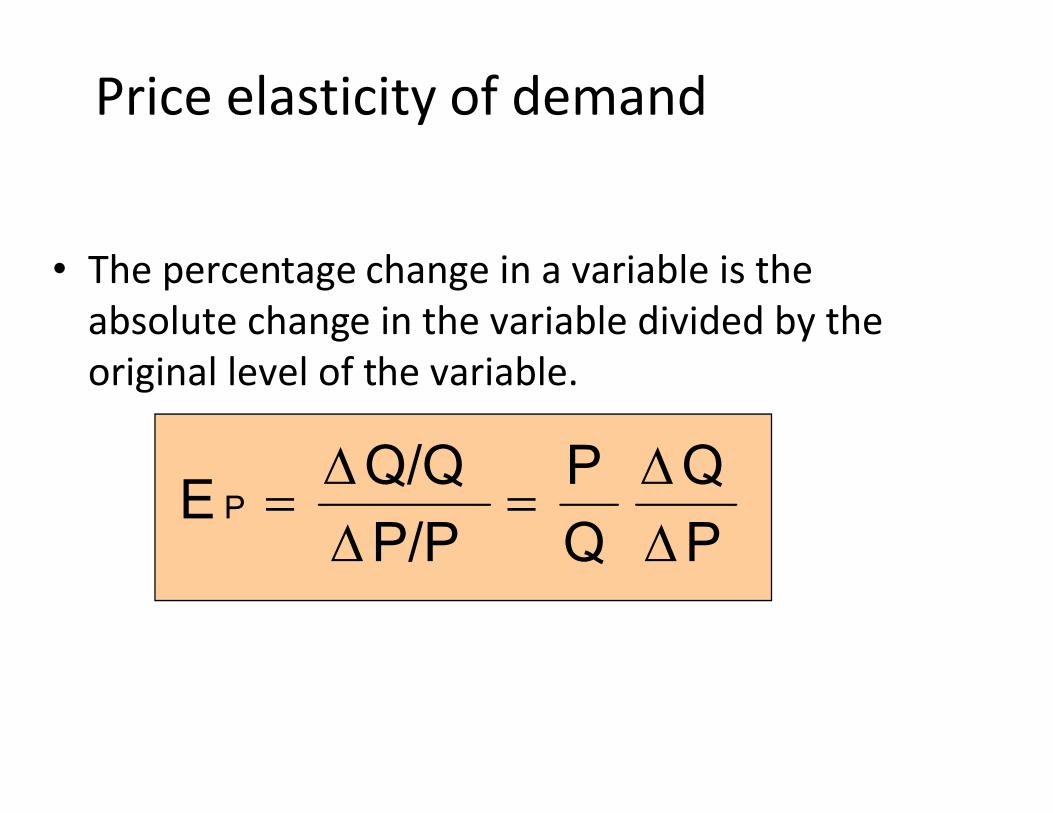

Price elasticity of demand

• The percentage change in a variable is the absolute change in the variable divided by the original level of the variable.

P

Q

Q

P

P/P

Q/QE P

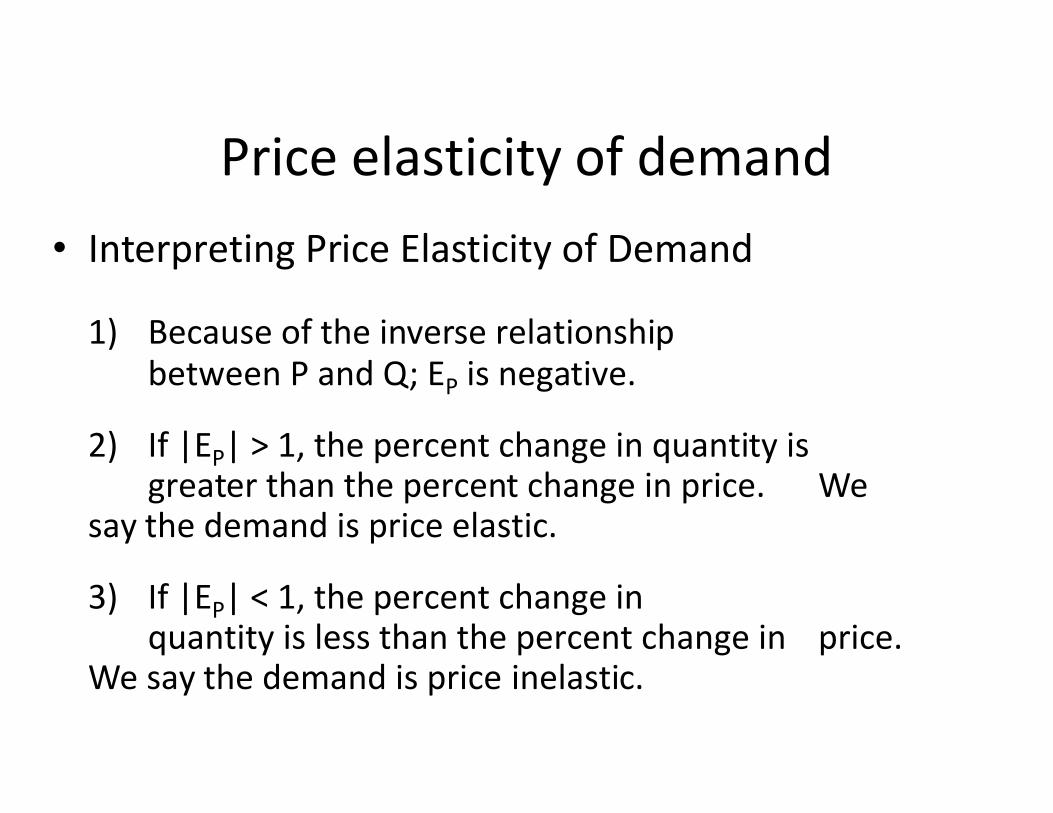

Price elasticity of demand• Interpreting Price Elasticity of Demand

1) Because of the inverse relationship between P and Q; EP is negative.

2) If |EP| > 1, the percent change in quantity is greater than the percent change in price. We

say the demand is price elastic.

3) If |EP| < 1, the percent change in quantity is less than the percent change in price.

We say the demand is price inelastic.

Price elasticity of demand

• The primary determinant of price elasticity of demand is the availability of substitutes.– Many substitutes: demand is price elastic– Few substitutes: demand is price inelastic

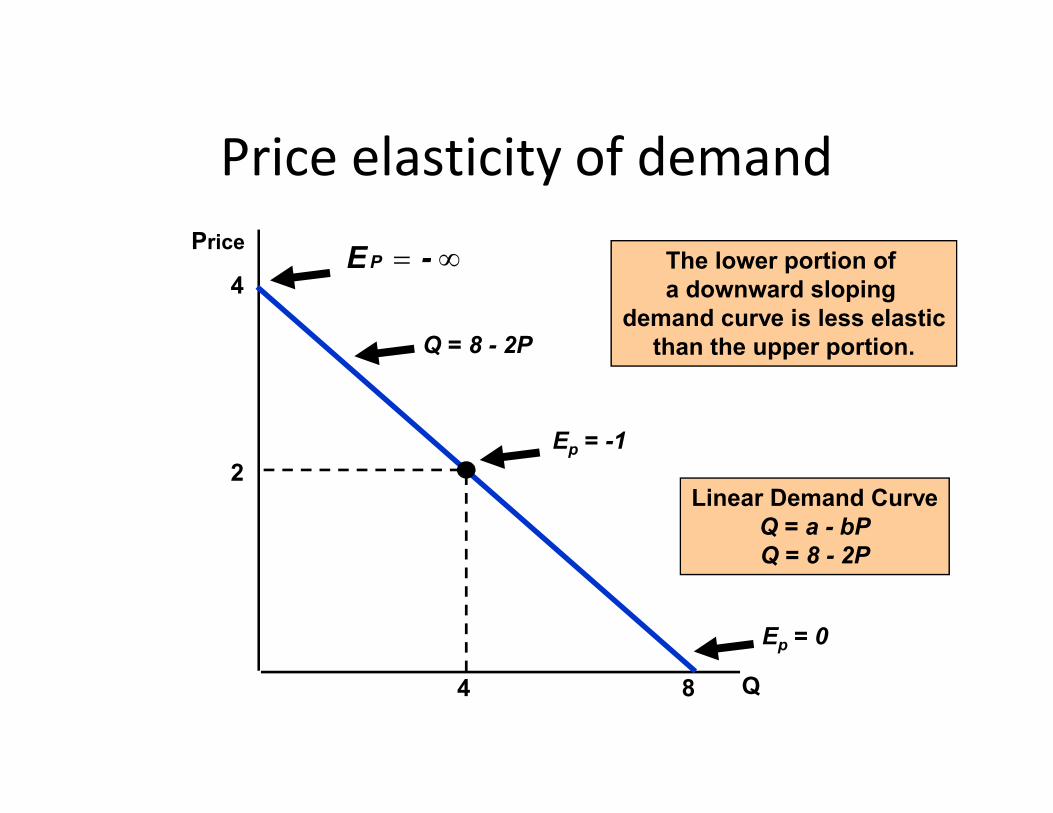

Price elasticity of demandPrice

Q = 8 - 2P

-EP The lower portion of a downward sloping

demand curve is less elasticthan the upper portion.

4

Q

Ep = -1

Ep = 0

8

2

4

Linear Demand CurveQ = a - bPQ = 8 - 2P

Price elasticity of demand

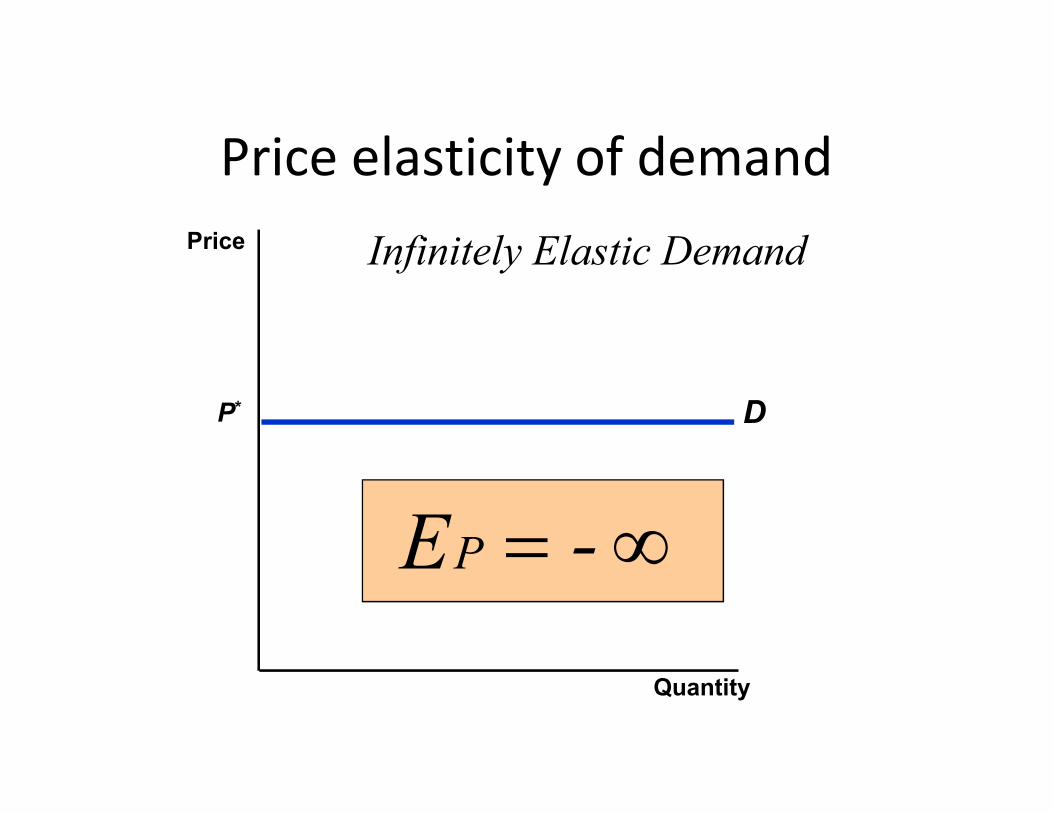

DP*

Price Infinitely Elastic Demand

DP*

-EP

Quantity

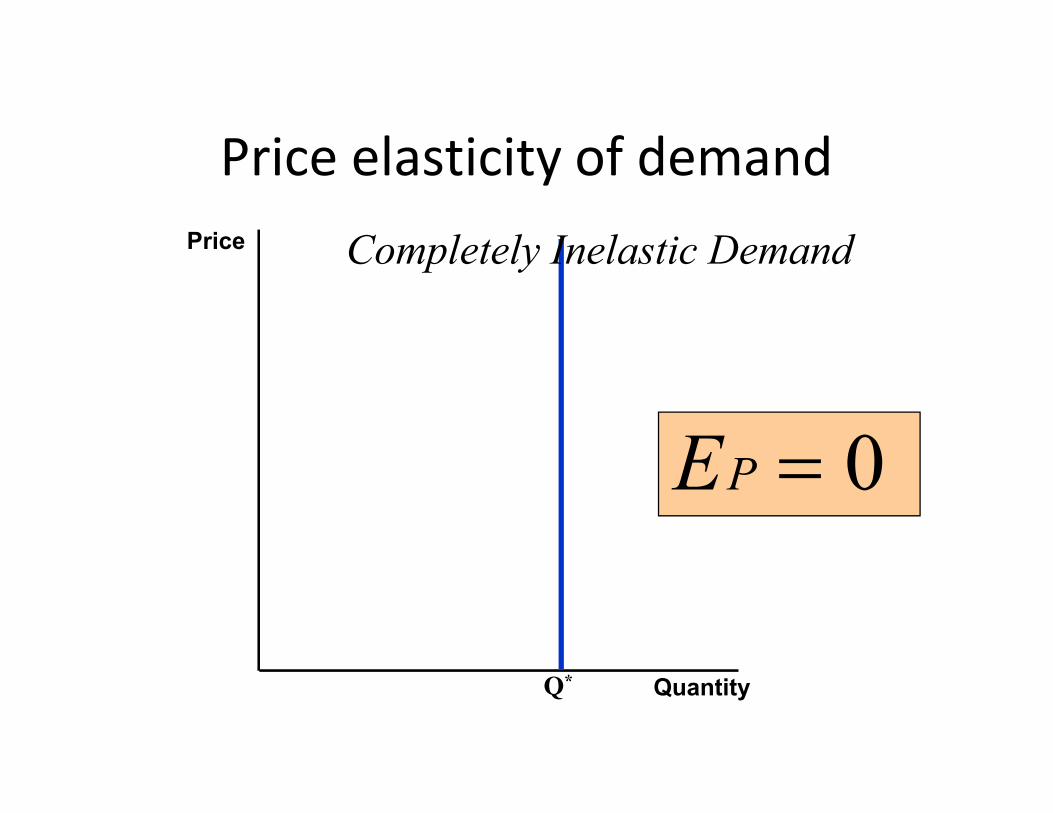

Price elasticity of demandPrice Completely Inelastic Demand

Q*

0EP

Quantity

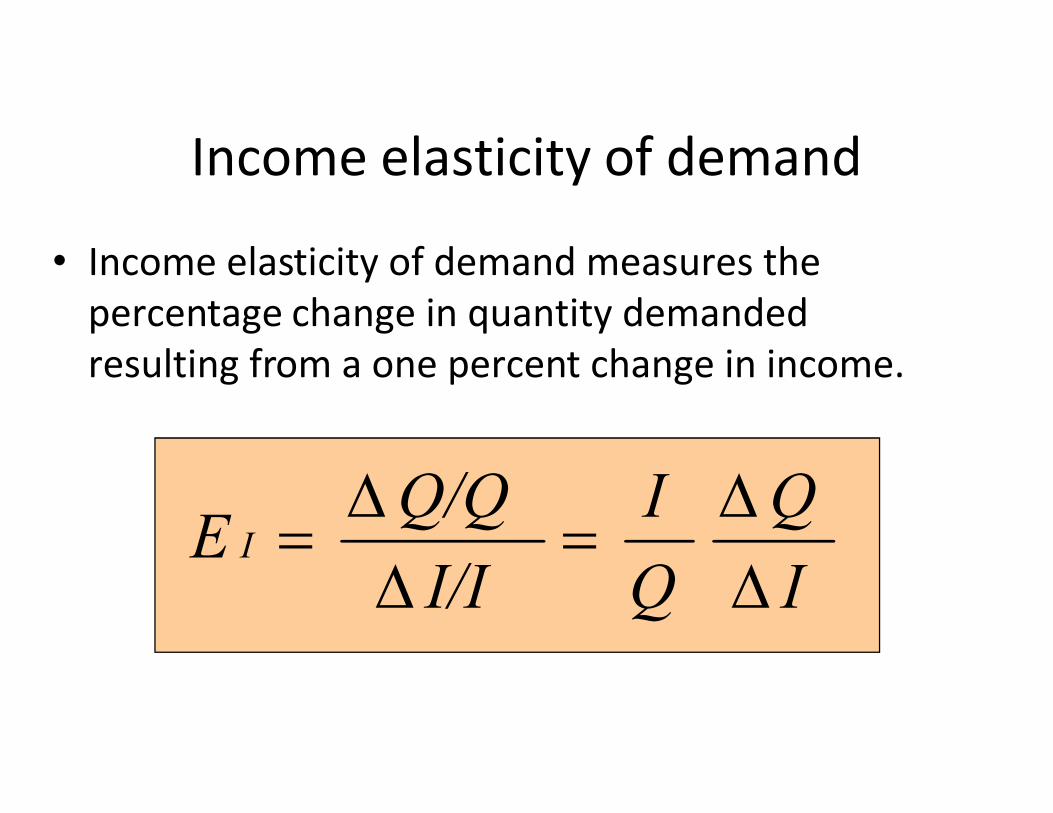

Income elasticity of demand

• Income elasticity of demand measures the percentage change in quantity demanded resulting from a one percent change in income.

I

Q

Q

I

I/I

Q/QE I

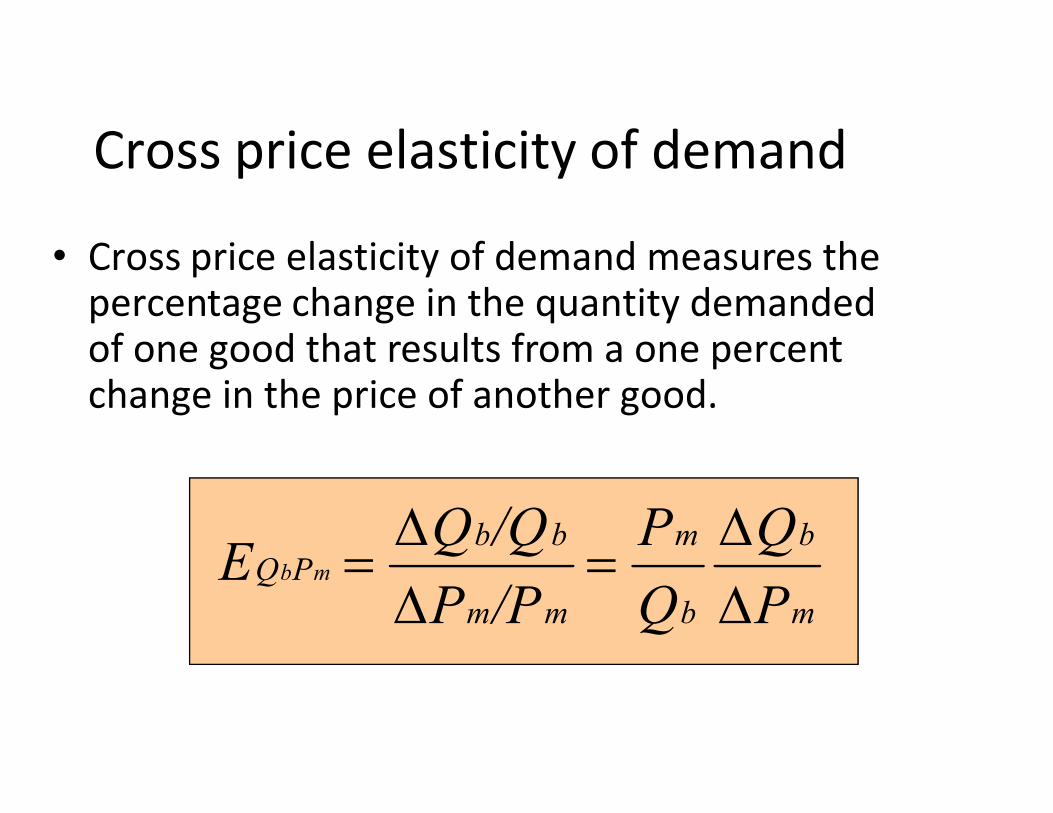

Cross price elasticity of demand

• Cross price elasticity of demand measures the percentage change in the quantity demanded of one good that results from a one percent change in the price of another good.change in the price of another good.

m

b

b

m

mm

bbPQ

P

Q

Q

P

/PP

/QQE mb

Price elasticity of demand• Price elasticity of supply measures the percentage change

in quantity supplied resulting from a 1 percent change in price.

• The elasticity is usually positive because price and quantity • The elasticity is usually positive because price and quantity supplied are positively related.

– Higher price gives producers an incentive to increase output

• We can refer to elasticity of supply with respect to interest rates, wage rates, and the cost of raw materials.

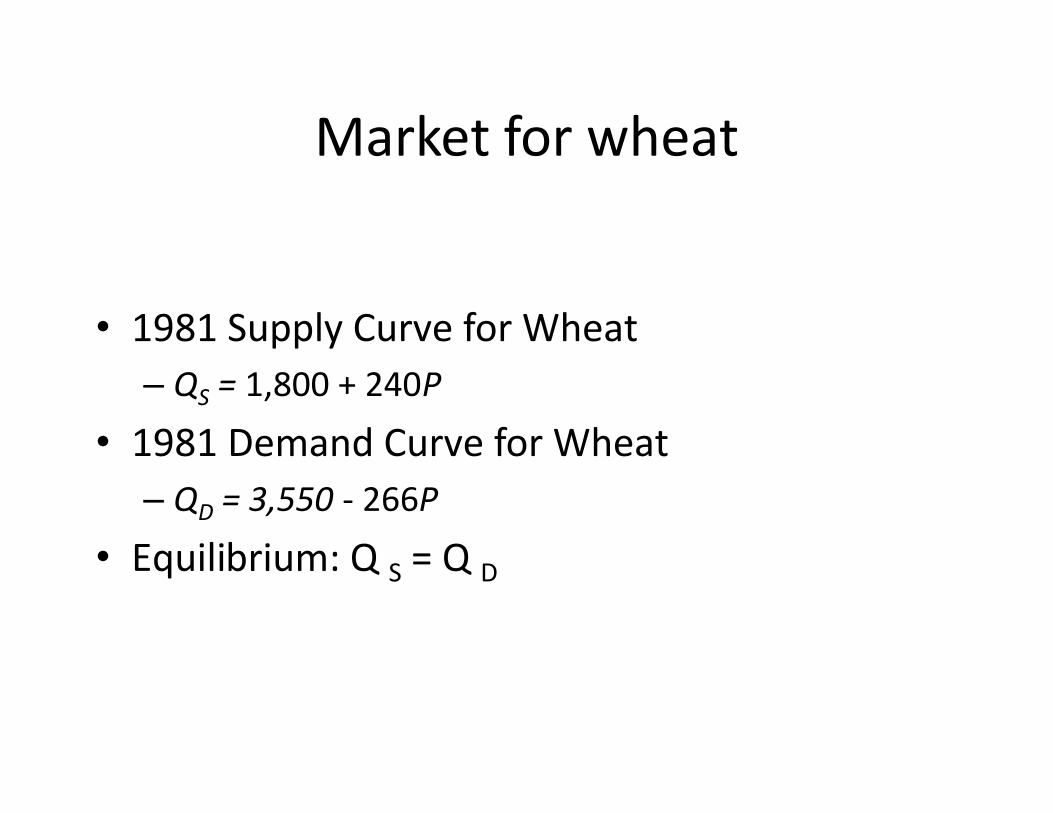

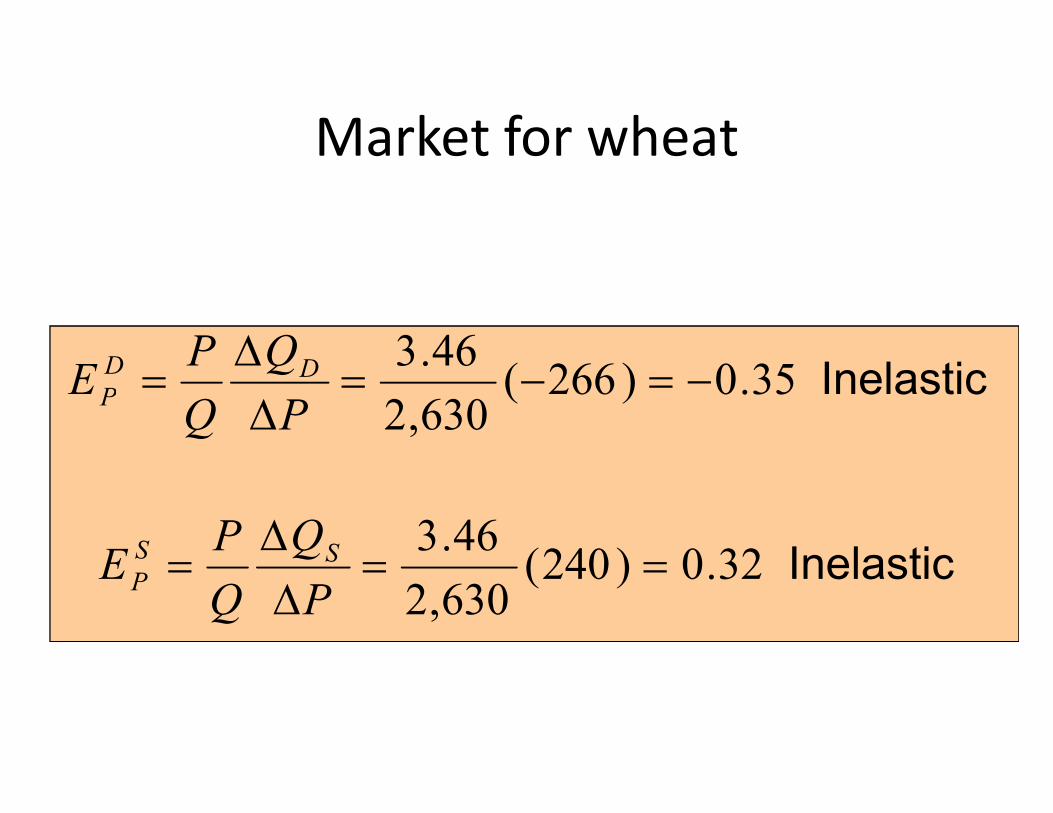

Market for wheat

• 1981 Supply Curve for Wheat– QS = 1,800 + 240PS

• 1981 Demand Curve for Wheat– QD = 3,550 - 266P

• Equilibrium: Q S = Q D

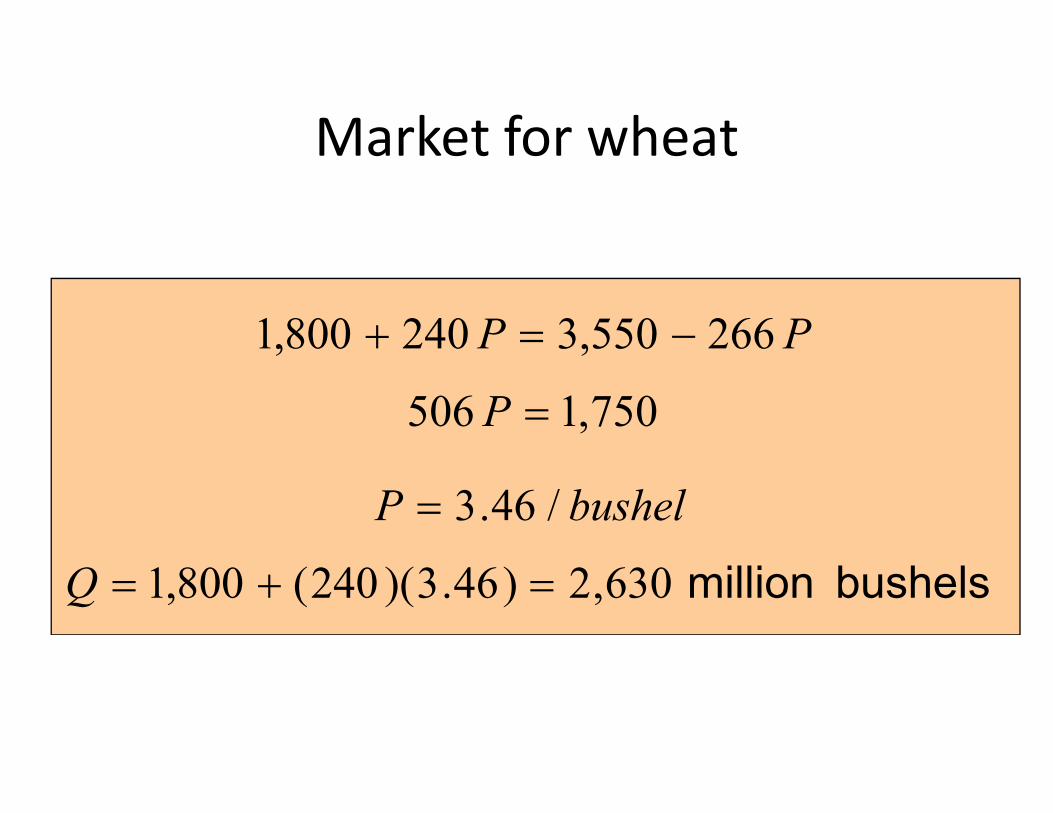

Market for wheat

PP 266550,3240800,1

750,1506 P 750,1506 P

bushelP /46.3

bushelsmillion630,2)46.3)(240(800,1 Q

Market for wheat

Inelastic 35.0)266(630,2

46.3

P

Q

Q

PE DD

P 630,2PQP

Inelastic 32.0)240(630,2

46.3

P

Q

Q

PE SS

P

Market for wheat

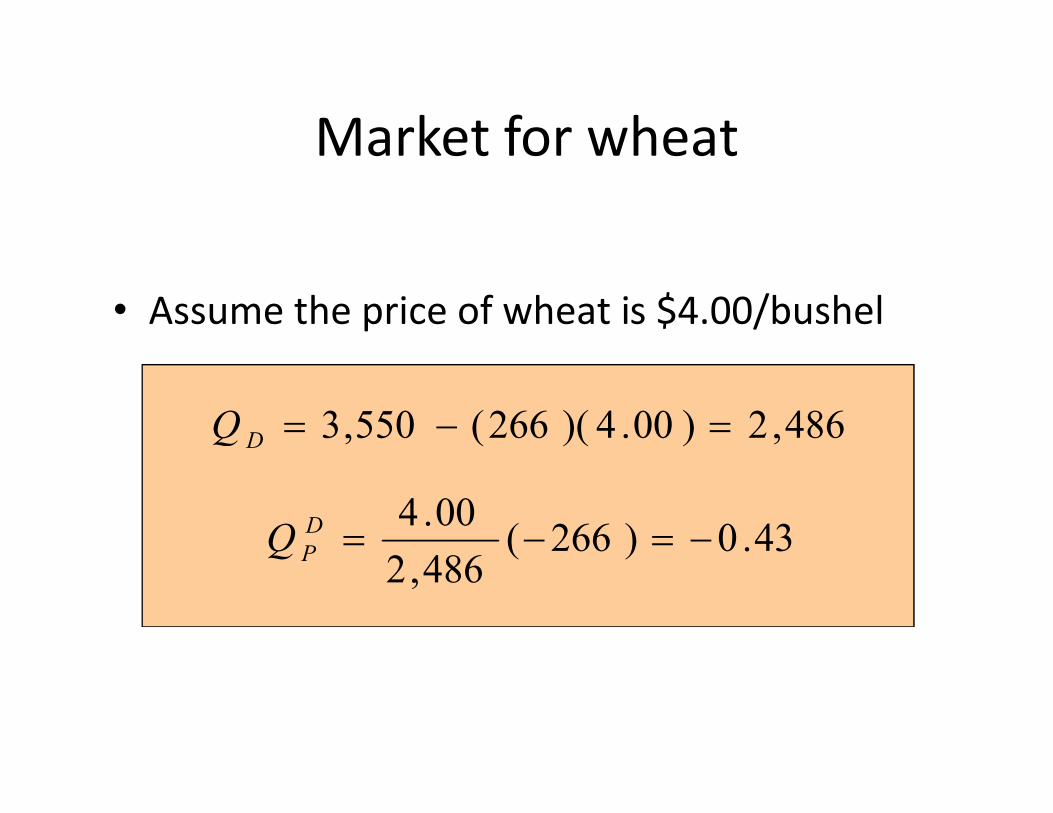

• Assume the price of wheat is $4.00/bushel

486,2)00.4)(266(550,3 Q 486,2)00.4)(266(550,3 DQ

43.0)266(486,2

00.4D

PQ

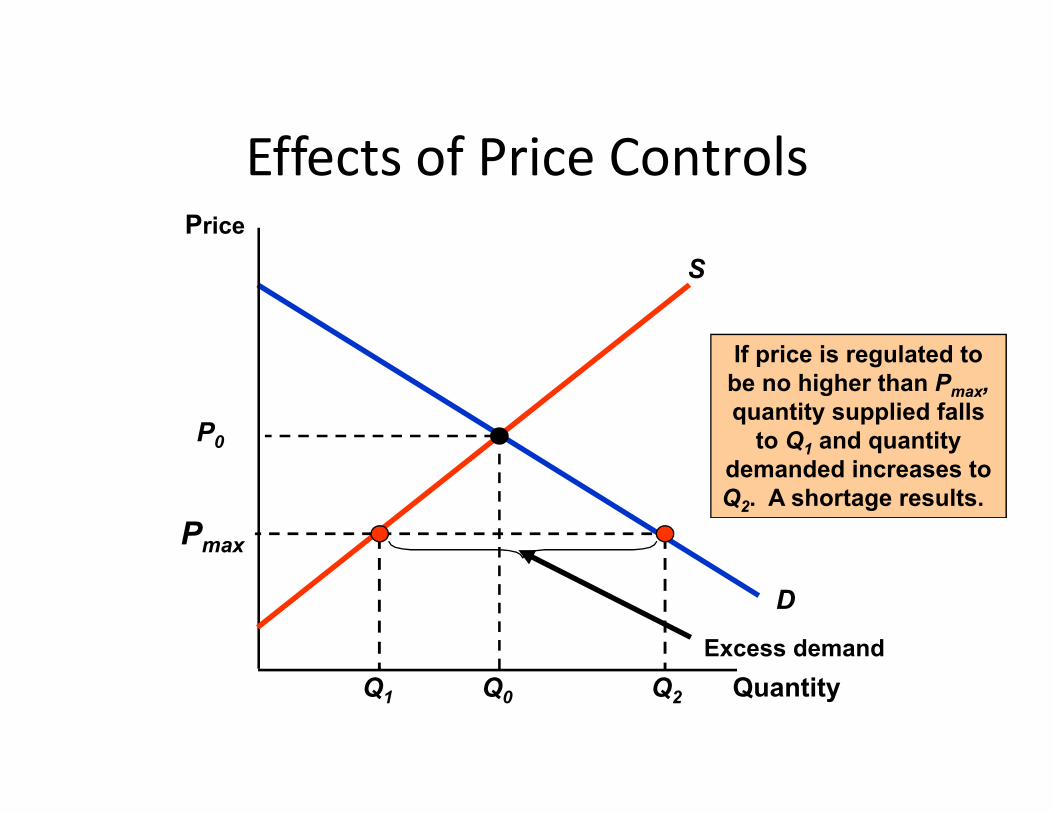

Effects of Price ControlsPrice

S

If price is regulated tobe no higher than Pmax,quantity supplied falls

D

Quantity

P0

Q0

Pmax

Excess demand

quantity supplied fallsto Q1 and quantity

demanded increases toQ2. A shortage results.

Q1 Q2

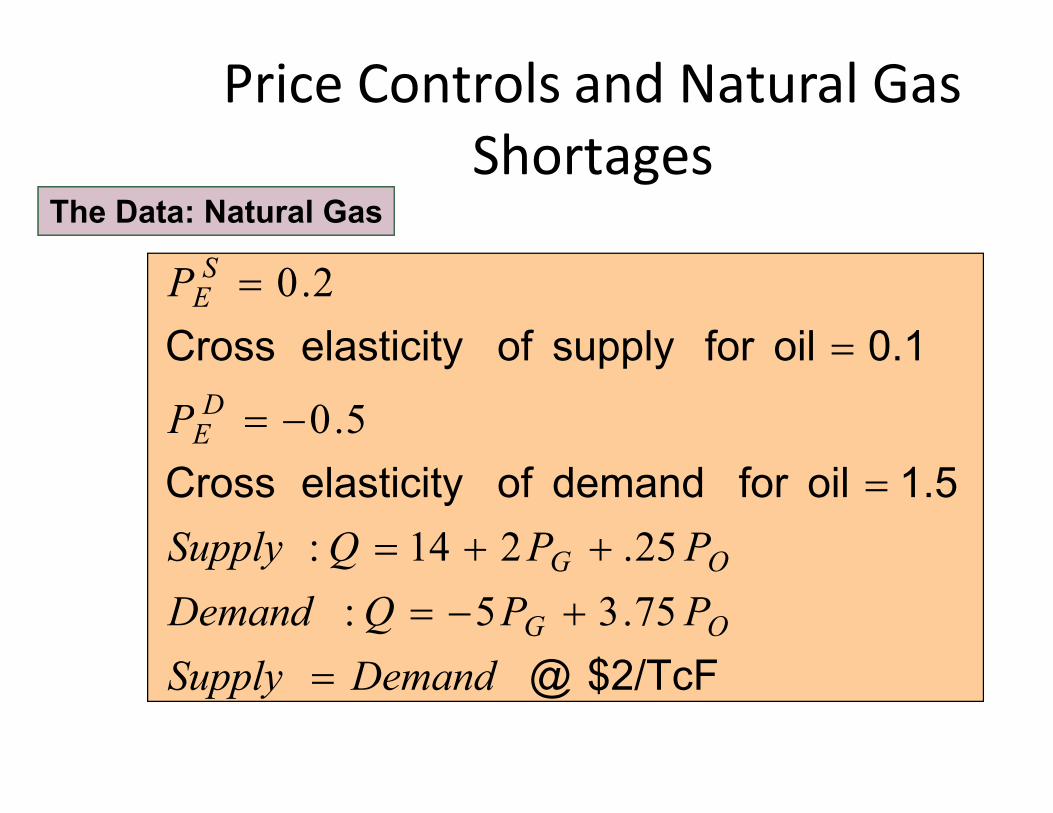

Price Controls and Natural GasShortages

• In 1954, the federal government began regulating the wellhead price of natural gas.

• In 1962, the ceiling prices that were imposed • In 1962, the ceiling prices that were imposed became binding and shortages resulted.

Price Controls and Natural GasShortages

• Price controls created an excess demand of 7 trillion cubic feet.

• Price regulation was a major component of U.S. • Price regulation was a major component of U.S. energy policy in the 1960s and 1970s, and it continued to influence the natural gas markets in the 1980s.

0.1oilforsupply ofelasticityCross

P

P

D

SE

5.0

2.0

Price Controls and Natural GasShortages

The Data: Natural Gas

$2/TcF@

1.5oilfordemandofelasticityCross

DemandSupply

PPQDemand

PPQSupply

P

OG

OG

DE

75.35:

25.214:

5.0

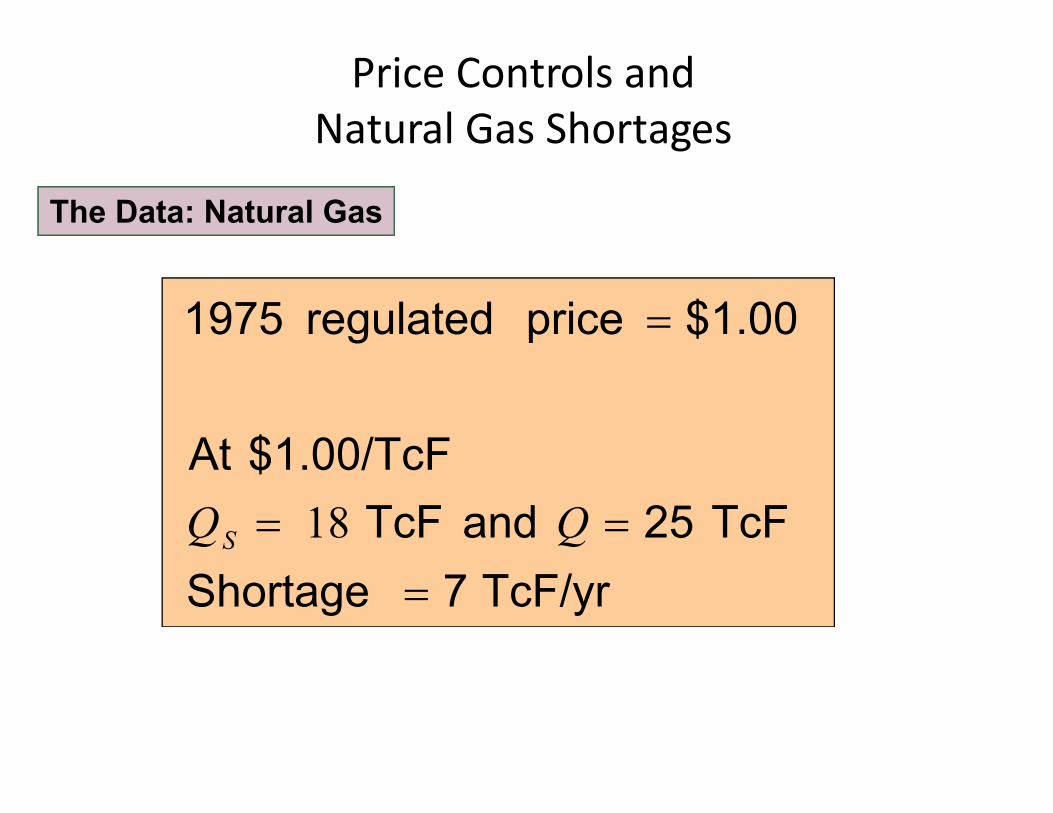

Price Controls andNatural Gas Shortages

The Data: Natural Gas

$1.00priceregulated1975

TcF/yr7Shortage

TcF25andTcF

$1.00/TcFAt

QQS 18

Summary• Supply-demand analysis is a basic tool of

microeconomics.

• The market mechanism is the tendency for supply and demand to equilibrate, so that there is neither excess demand nor excess supplydemand nor excess supply

• Elasticities describe the responsiveness of supply and demand to changes in price, income, and other variables. They pertain to a time frame.

• If we can estimate the supply and demand curves for a particular market, we can calculate the market clearing price.

ProductionProduction

Topics to be Discussed• The Technology of Production

• Isoquants

• Production with One Variable Input (Labor)• Production with One Variable Input (Labor)

• Production with Two Variable Inputs

• Returns to Scale

Introduction

• Our focus is the supply side.

• The theory of the firm addresses:

– How a firm makes cost-minimizing production decisions

– How cost varies with output

– Characteristics of market supply

– Issues of business regulation

The Technology of Production

• The Production Process– Combining inputs or factors of production to achieve an output

• Categories of Inputs (factors of production)– Labor– Materials– Capital

The Technology of Production

• Production Function:

– Indicates the highest output that a firm can produce for every specified combination of inputs given the state of technology.state of technology.

– Shows what is technically feasible when the firm operates efficiently.

The Technology of Production

• The production function for two inputs:

Q = F(K,L)

Q = Output, K = Capital, L = LaborQ = Output, K = Capital, L = Labor

• For a given technology

Isoquants• Curves showing all possible combinations of inputs

that yield the same output

• Assumptions

– Food producer has two inputs, Labor (L) & Capital (K)– Food producer has two inputs, Labor (L) & Capital (K)

• Observations:

– For any level of K, output increases with more L.

– For any level of L, output increases with more K.

– Various combinations of inputs produce the same output.

Production Function for Food

1 20 40 55 65 75

2 40 60 75 85 90

Capital Input 1 2 3 4 5

Labor Input

2 40 60 75 85 90

3 55 75 90 100 105

4 65 85 100 110 115

5 75 90 105 115 120

Production with Two Variable Inputs(L,K)

4

5

The isoquants are derivedfrom the production

function for output of

ECapitalper year The Isoquant Map

Labor per year

1

2

3

1 2 3 4 5

Q1 = 55

function for output ofof 55, 75, and 90.A

D

B

Q2 = 75

Q3 = 90

C

Short-run versus Long-run

• Short-run:– Period of time in which quantities of one or more

production factors cannot be changed.

– These inputs are called fixed inputs.

• Long-run– Amount of time needed to make all production

inputs variable.

Amount Amount Total Average Marginalof Labor (L) of Capital (K) Output (Q) Product Product

Production with One Variable Input(Labour)

0 10 0 --- ---

1 10 10 10 10

2 10 30 15 20

3 10 60 20 303 10 60 20 30

4 10 80 20 20

5 10 95 19 15

6 10 108 18 13

7 10 112 16 4

8 10 112 14 0

9 10 108 12 -4

10 10 100 10 -8

Production with One Variable Input(Labour)

• Observations:

– With additional workers, output (Q) increases, reaches a maximum, and then decreases.

– The average product of labor (AP), or output per worker, increases and then decreases.

L

Q

InputLabor

OutputAP

Production with One Variable Input(Labour)

• Observations (cont.d):

– The marginal product of labor (MP), or output of the additional worker, increases rapidly initially and the additional worker, increases rapidly initially and then decreases and becomes negative.

L

Q

InputLabor

OutputMP L

Outputper

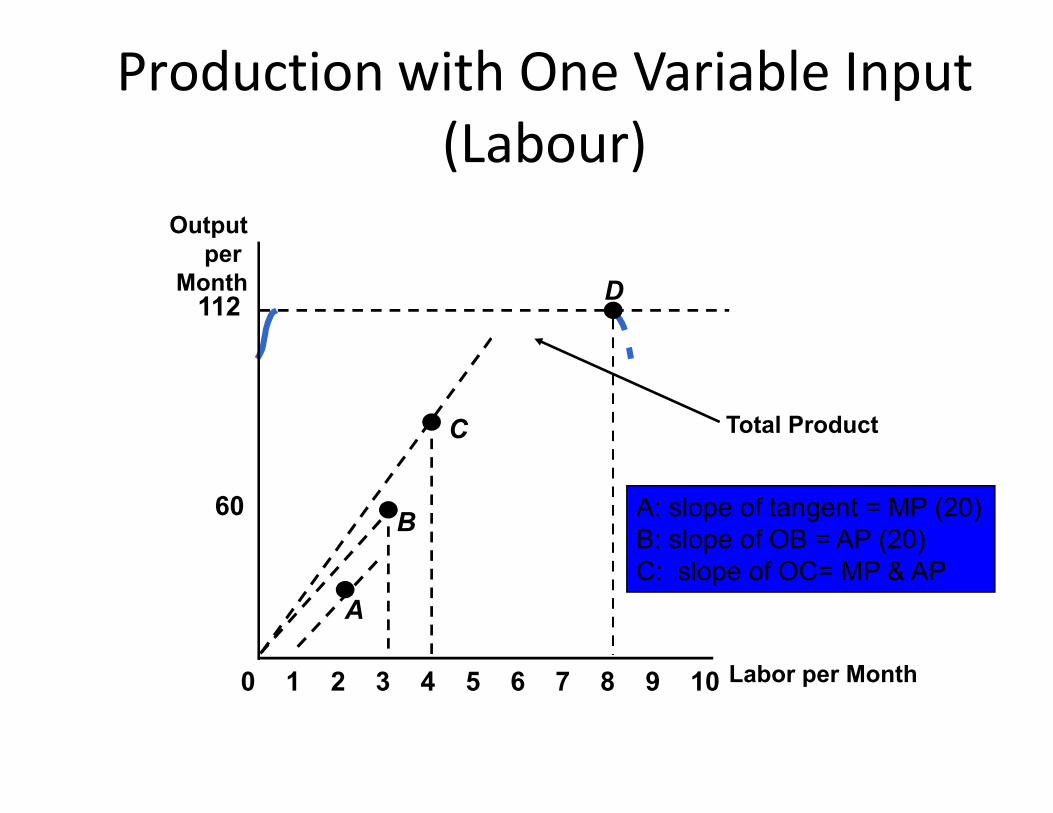

Month112

D

Production with One Variable Input(Labour)

Total Product

A: slope of tangent = MP (20)B: slope of OB = AP (20)C: slope of OC= MP & AP

Labor per Month

60

0 2 3 4 5 6 7 8 9 101

A

B

C

Production with One Variable Input(Labour)

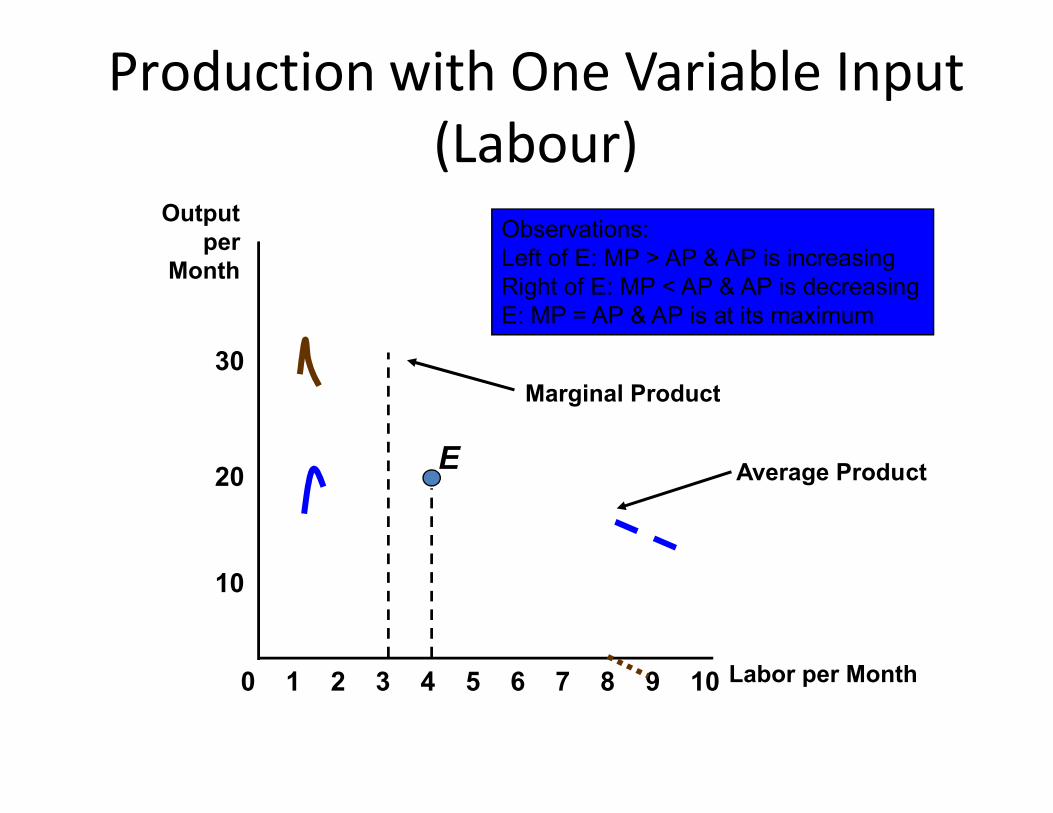

Outputper

Month

30Marginal Product

Observations:Left of E: MP > AP & AP is increasingRight of E: MP < AP & AP is decreasingE: MP = AP & AP is at its maximum

Average Product

8

10

20

0 2 3 4 5 6 7 9 101 Labor per Month

E

Marginal Product

Production with One Variable Input(Labour)

• Observations:– When MP = 0, TP is at its maximum– When MP > AP, AP is increasing– When MP < AP, AP is decreasing– When MP < AP, AP is decreasing– When MP = AP, AP is at its maximum

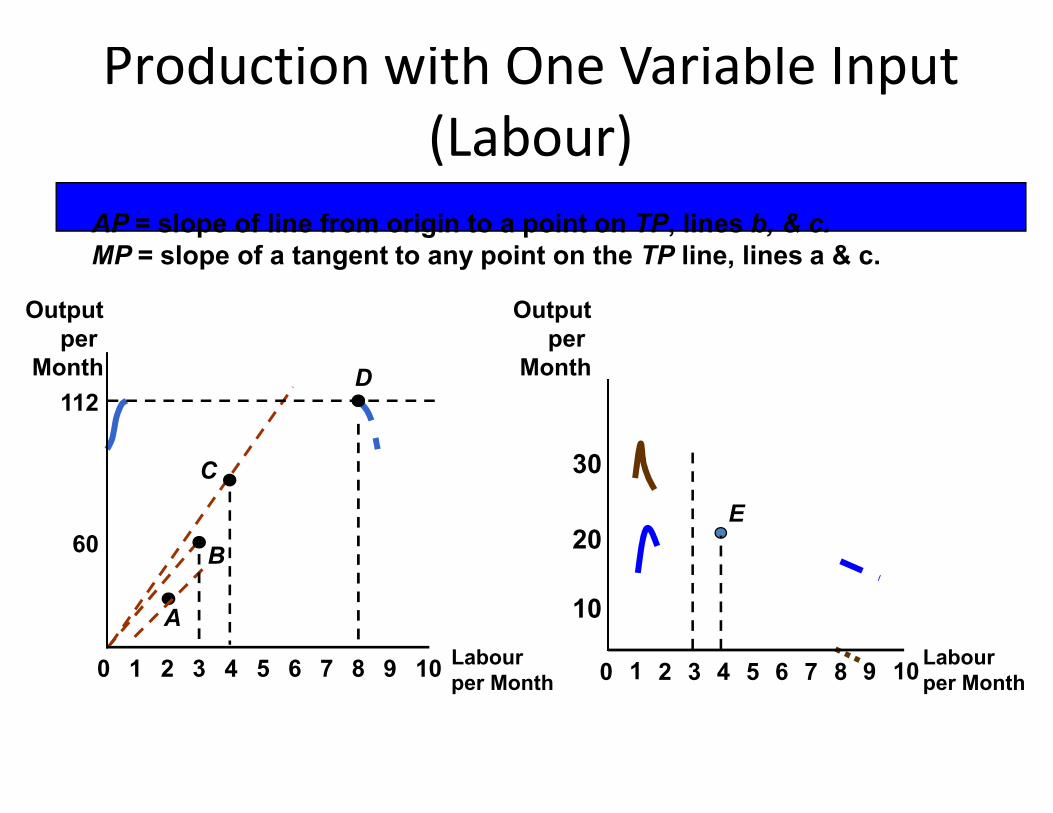

Production with One Variable Input(Labour)

AP = slope of line from origin to a point on TP, lines b, & c.MP = slope of a tangent to any point on the TP line, lines a & c.

112D

Outputper

Month

Outputper

Month

Labourper Month

60

112

0 2 3 4 5 6 7 8 9 101

A

B

C

8

10

20E

0 2 3 4 5 6 7 9 101

30

Labourper Month

Law of diminishing marginal returns

• As the use of an input increases in equal increments, a point will be reached at which the resulting additions to output decreases (i.e. MP declines):

– When the labor input is small, MP increases due to – When the labor input is small, MP increases due to specialization.

– When the labor input is large, MP decreases due to inefficiencies.

• Assumes technology and the quality of the variable input is constant

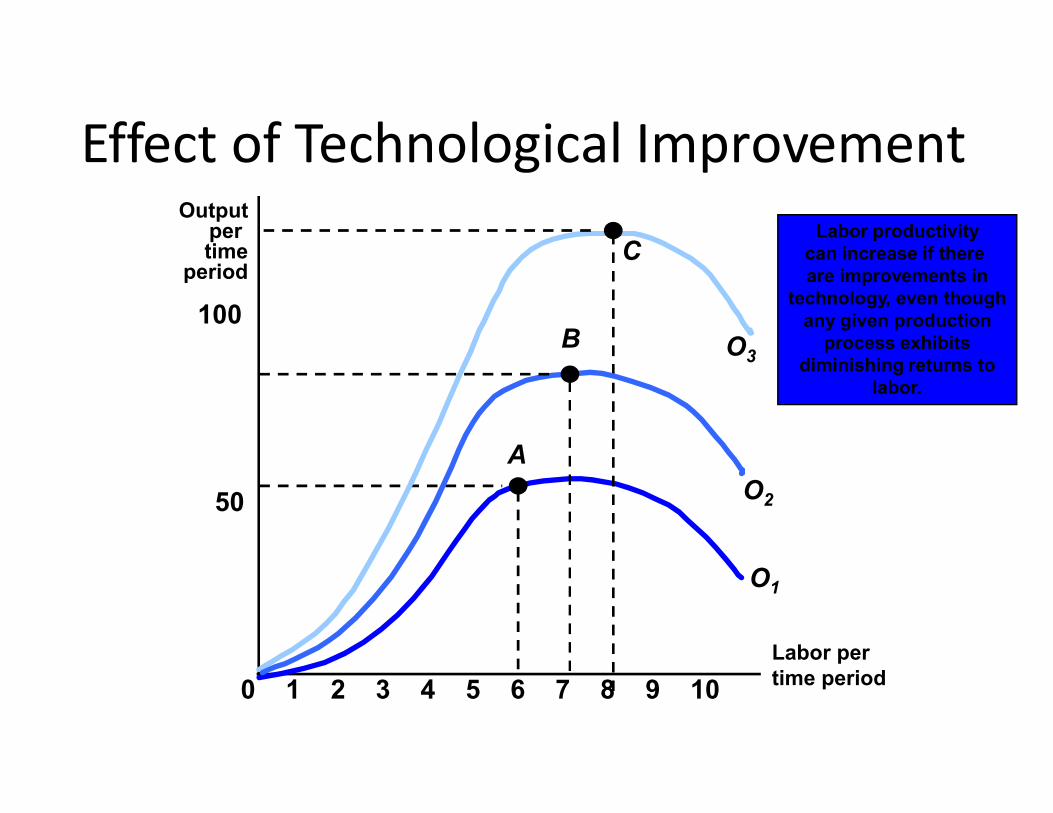

Effect of Technological ImprovementOutput

per time

period

100

C

O3B

Labor productivitycan increase if there are improvements in

technology, even thoughany given production

process exhibitsdiminishing returns to

labor.

Labor pertime period

50

0 2 3 4 5 6 7 8 9 101

A

O1

O2

Malthus and the Food Crisis

• Malthus predicted mass hunger and starvation as diminishing returns limited agricultural output and the population continued to grow.

• Why did Malthus’ prediction fail?

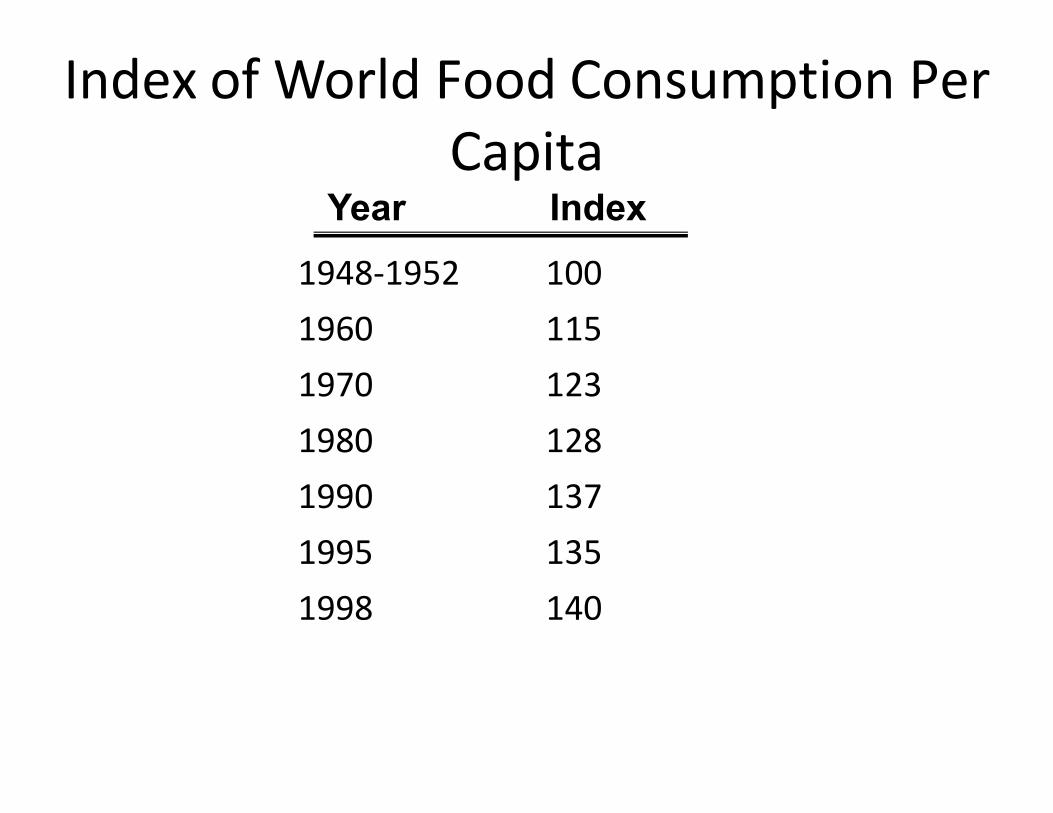

Index of World Food Consumption PerCapita

1948-1952 1001960 1151970 123

Year Index

1970 1231980 1281990 1371995 1351998 140

Malthus and the Food Crisis

• The data show that production increases have exceeded population growth.

• Malthus did not take into consideration the potential impact of technology which has allowed the supply of impact of technology which has allowed the supply of food to grow faster than demand.

• Technology has created surpluses and driven the price down.

Production with Two Variable Inputs• There is a relationship between production and

productivity.

• Long-run production K& L are variable.Long-run production K& L are variable.

• Isoquants analyze and compare the different combinations of K & L and output

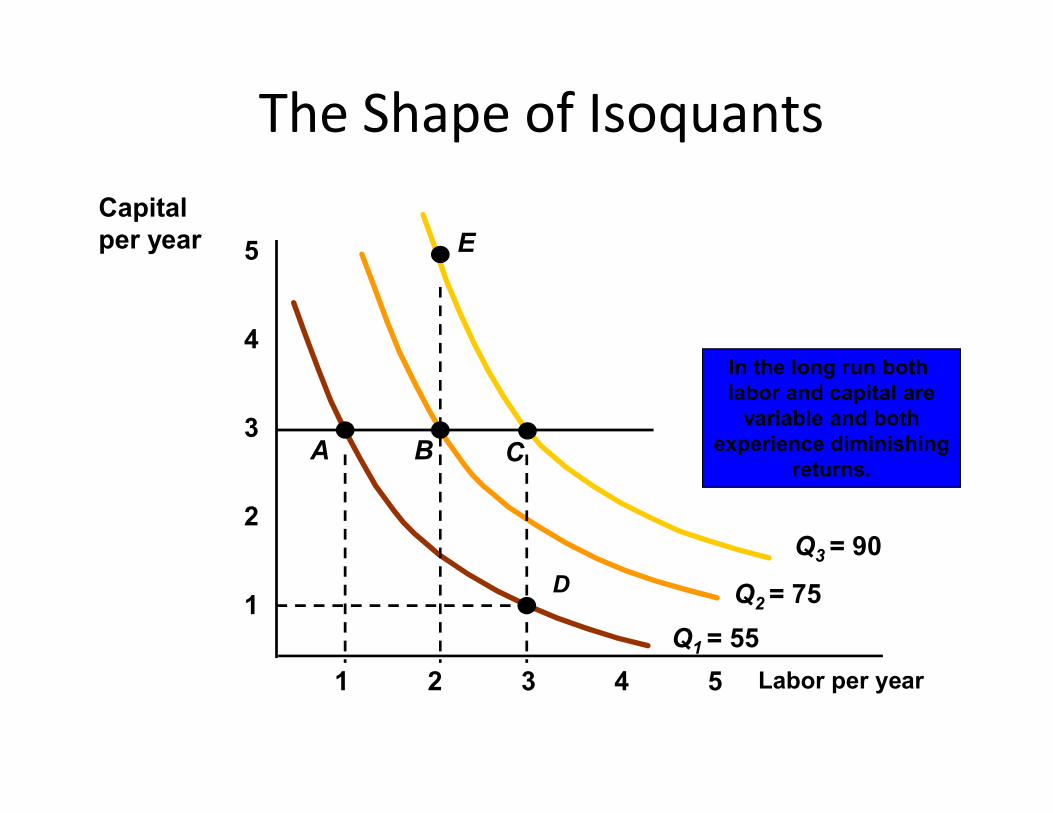

The Shape of Isoquants

4

5

In the long run both labor and capital are

variable and both

Capitalper year E

Labor per year

1

2

3

1 2 3 4 5

variable and bothexperience diminishing

returns.

Q1 = 55

Q2 = 75

Q3 = 90

A

D

B C

Understanding the Isoquant Model

1) Assume capital is 3 and labor increases from 0 to 1 to 2 to 3.• Notice output increases at a decreasing rate (55, 20, 15)

illustrating diminishing returns from labor in the short-run and long-run.long-run.

2) Assume labor is 3 and capital increases from 0 to 1 to 2 to 3.• Output also increases at a decreasing rate (55, 20, 15) due to

diminishing returns from capital.

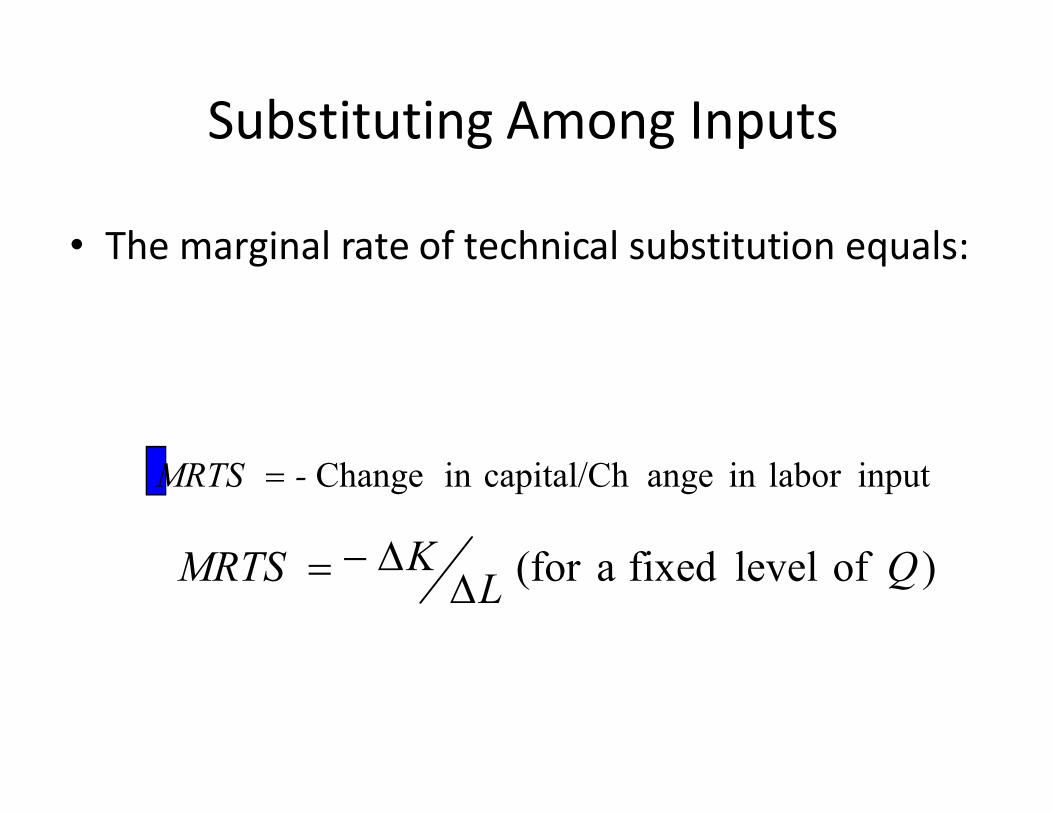

Substituting Among Inputs

• Managers want to determine what combination of inputs to use.

• They must deal with the trade-off between inputs.

• The slope of each isoquant gives the trade-off between two inputs while keeping output constant.

Substituting Among Inputs

• The marginal rate of technical substitution equals:

inputlabor in angecapital/Chin Change-MRTS

)oflevelfixeda(for QLKMRTS

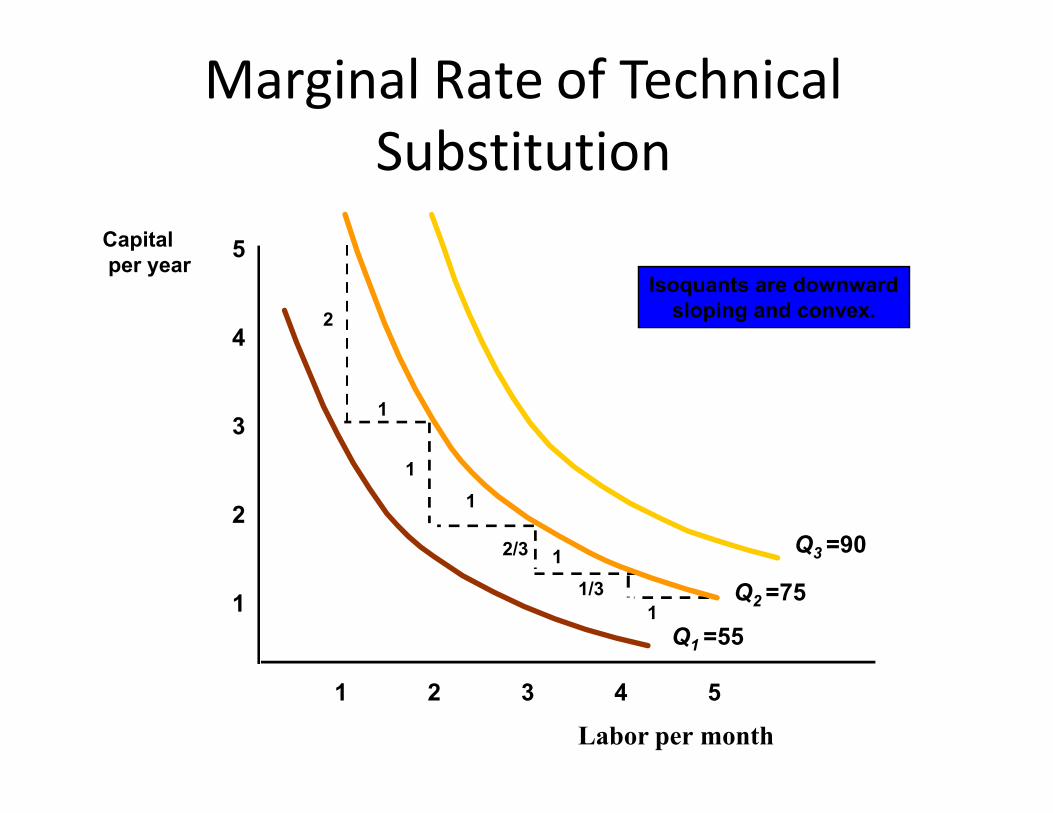

Marginal Rate of TechnicalSubstitution

4

5Capitalper year

Isoquants are downwardsloping and convex.

1

2

Labor per month

1

2

3

1 2 3 4 5

1

1

1

1

1

2/3

1/3

Q1 =55

Q2 =75

Q3 =90

Marginal Rate of TechnicalSubstitution

• Observations:

1) Increasing labour in one unit increments from 1 to 5 results in a decreasing MRTS from 2 to 1/3.1/3.

2) Diminishing MRTS occurs because of diminishing returns and implies isoquants are convex.

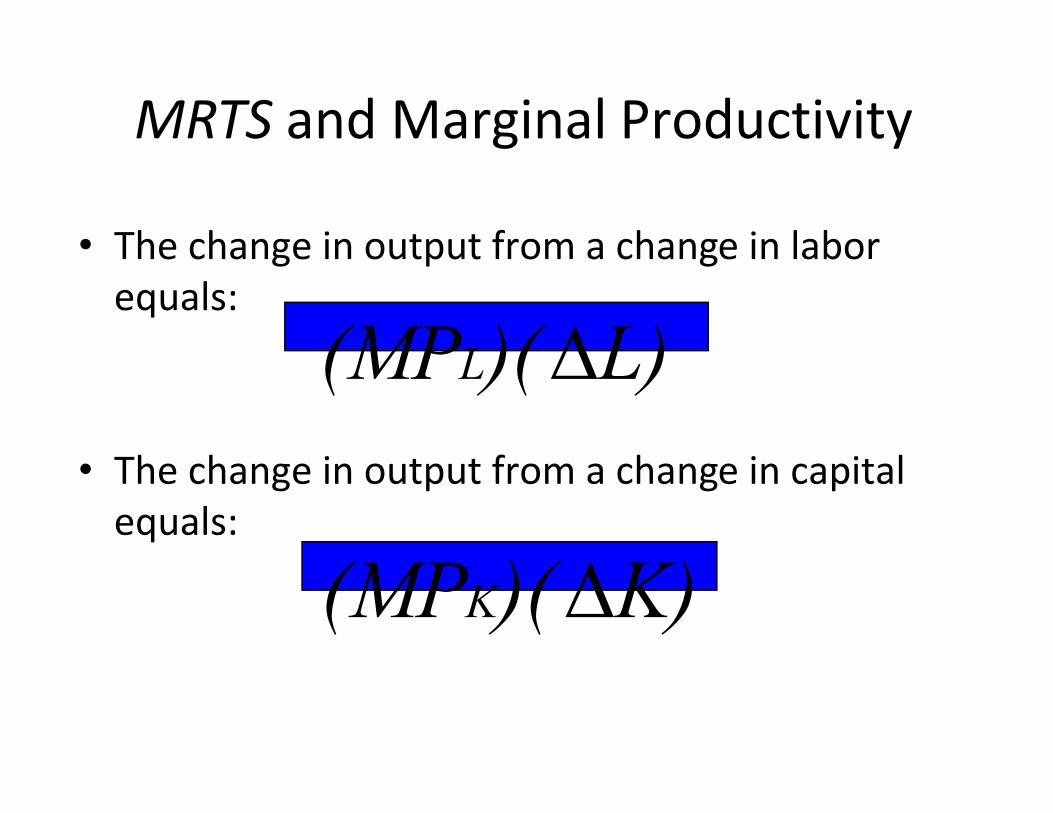

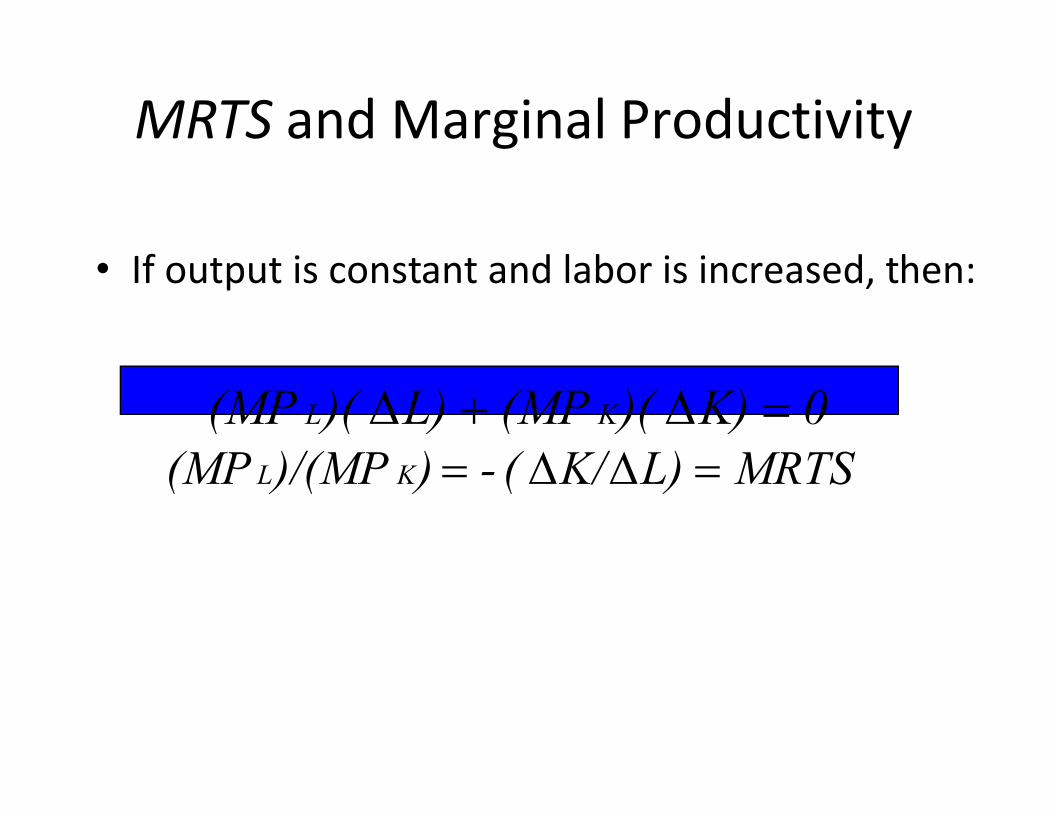

MRTS and Marginal Productivity

• The change in output from a change in labor equals:

L))((MPL • The change in output from a change in capital

equals:

K))((MPK

MRTS and Marginal Productivity

• If output is constant and labor is increased, then:

0K))((MPL))((MP KL 0K))((MPL))((MP KL MRTSL)K/(-))/(MP(MP KL

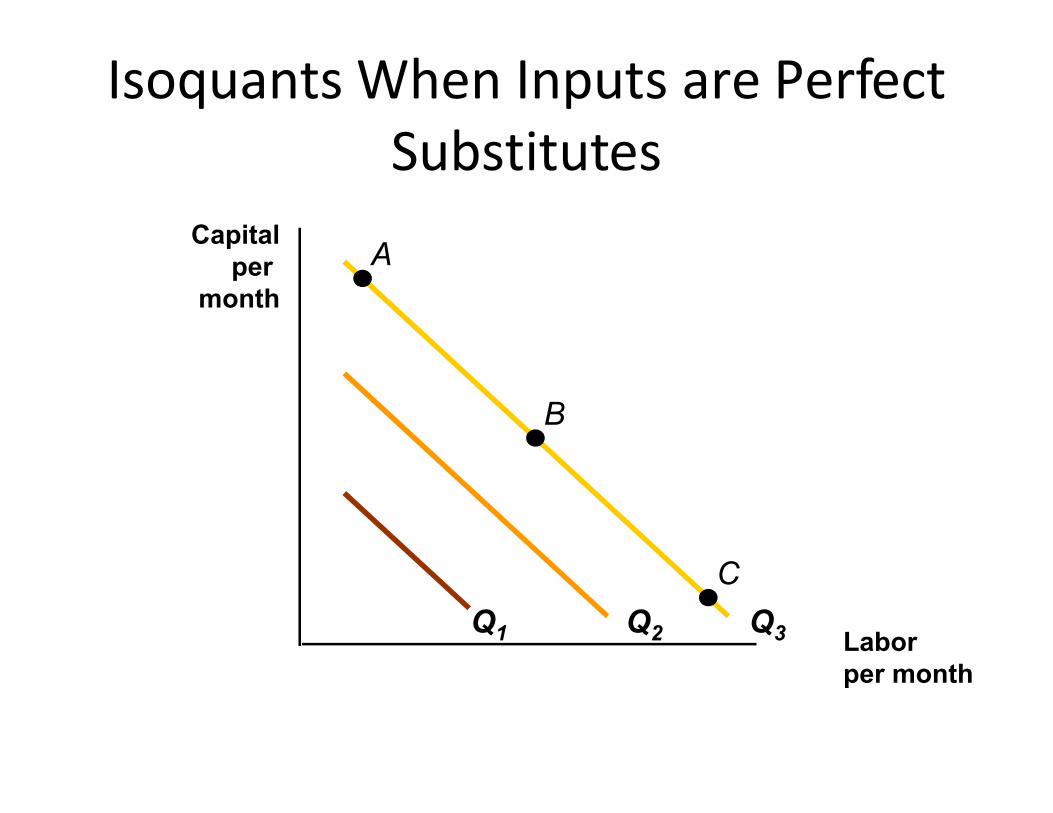

Isoquants When Inputs are PerfectSubstitutes

Capitalper

month

A

B

Laborper month

Q1 Q2 Q3

B

C

Production with Two Variable Inputs

• When inputs are perfectly substitutable:

1) The MRTS is constant at all points on the

Perfect Substitutes

1) The MRTS is constant at all points on the isoquant.

2) For a given output, any combination of inputs can be chosen (A, B, or C) to generate the same level of output (e.g. toll booths & musical instruments)

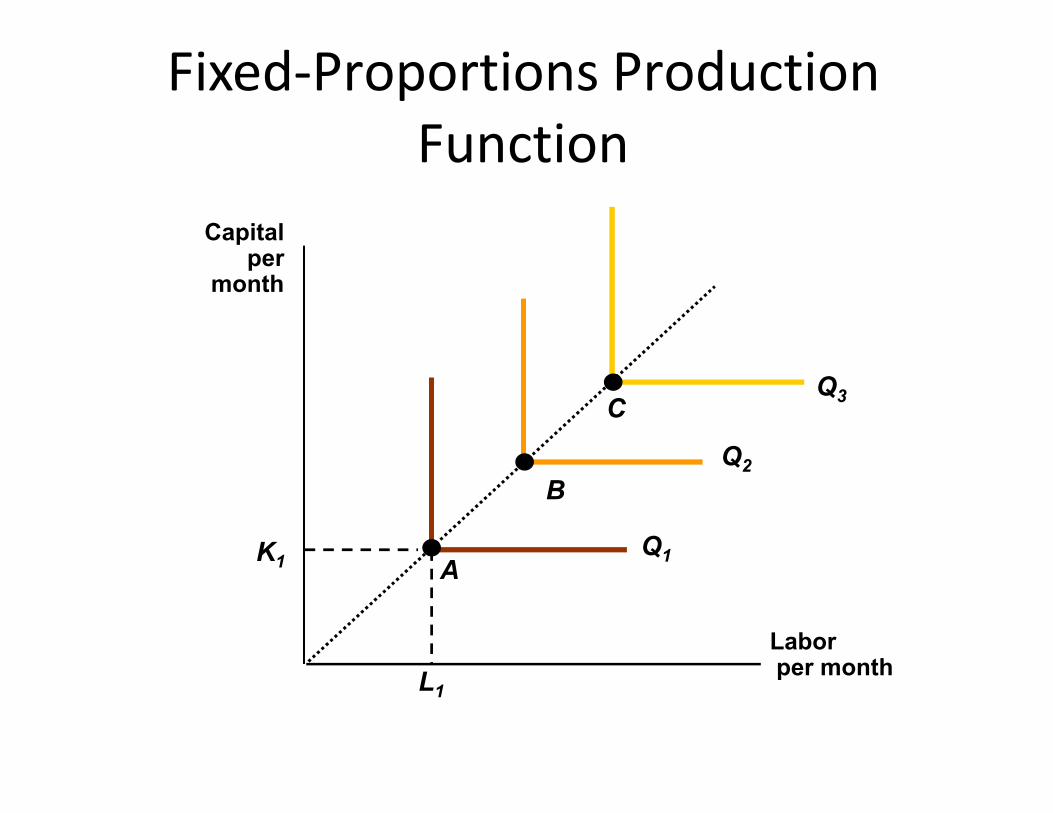

Fixed-Proportions ProductionFunction

Capitalper

month

Q3C

Laborper month

L1

K1Q1

Q2

A

B

C

Production with Two Variable Inputs

• Observations when inputs must be in a fixed-proportion:

1) No substitution is possible. Each output

Fixed-Proportions Production Function

1) No substitution is possible. Each output requires a specific amount of each input (e.g. labour and jackhammers).

2) To increase output requires more labour and capital (i.e. moving from A to B to C which is technically efficient).

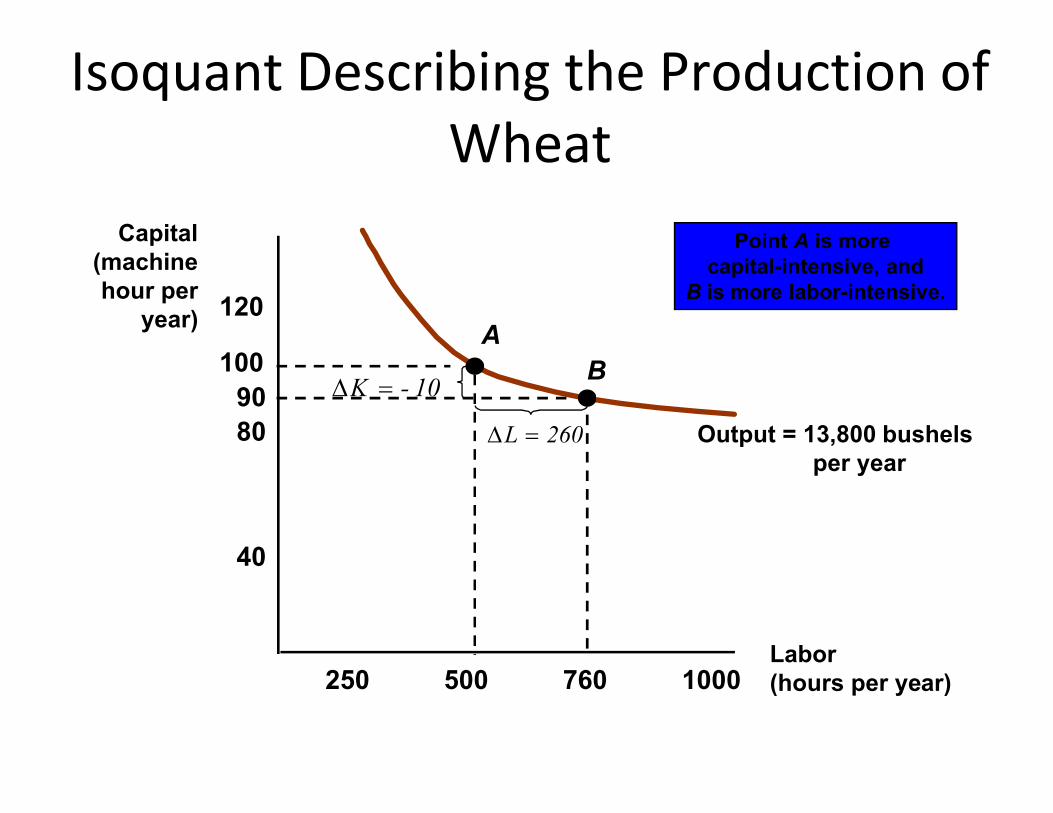

Isoquant Describing the Production ofWheat

Capital(machinehour per

year) 120

10090

AB

10-K

Point A is more capital-intensive, and

B is more labor-intensive.

Labor(hours per year)250 500 760 1000

40

8090

Output = 13,800 bushelsper year

260L

Production of Wheat

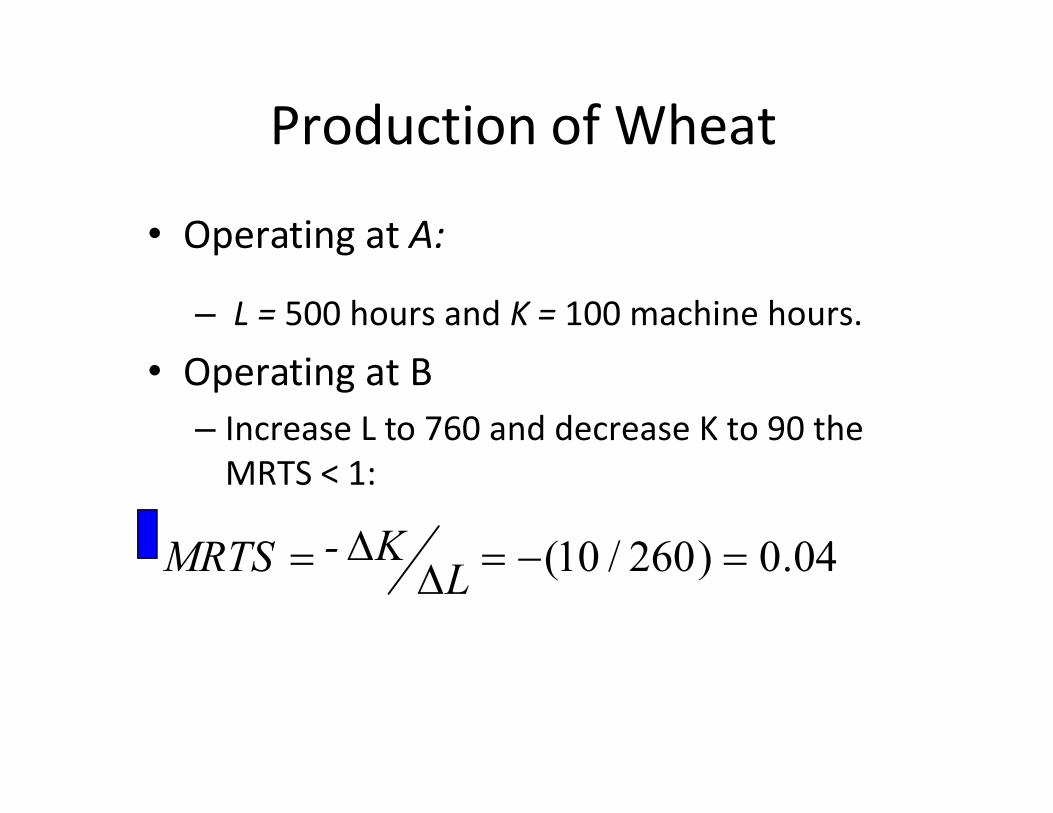

• Operating at A:

– L = 500 hours and K = 100 machine hours.

• Operating at BIncrease L to 760 and decrease K to 90 the – Increase L to 760 and decrease K to 90 the MRTS < 1:

04.0)260/10( L

K-MRTS

Production of Wheat

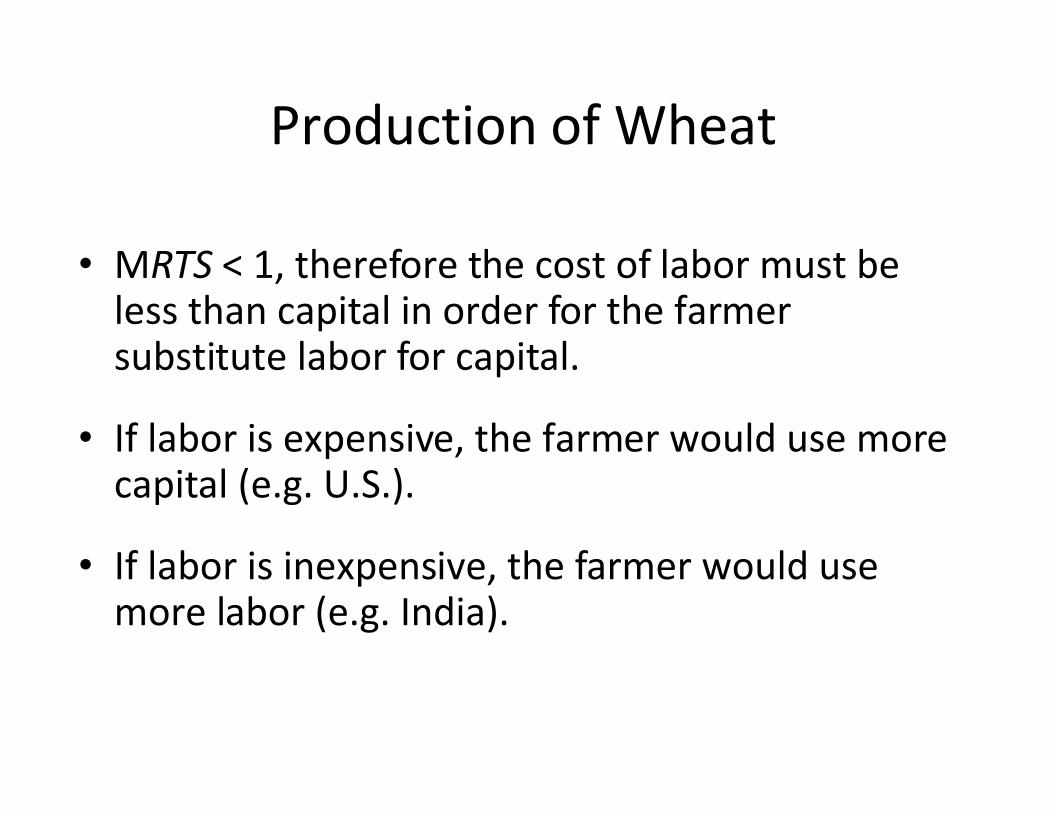

• MRTS < 1, therefore the cost of labor must be less than capital in order for the farmer substitute labor for capital.

• If labor is expensive, the farmer would use more capital (e.g. U.S.).

• If labor is inexpensive, the farmer would use more labor (e.g. India).

Returns to Scale• Measuring the relationship between the scale

(size) of a firm and output

• Increasing returns to scale: output more than doubles when all inputs are doubleddoubles when all inputs are doubled– Larger output associated with lower cost (autos)

– One firm is more efficient than many (utilities)

– The isoquants get closer together

Increasing returns to Scale

Capital(machine

hours)

Increasing Returns:The isoquants move closer together

A

Labor (hours)

10

20

30

5 10

2

4

0

Returns to Scale

• Measuring the relationship between the scale (size) of a firm and output

• Constant returns to scale: output doubles when all inputs are doubledwhen all inputs are doubled– Size does not affect productivity– May have a large number of producers– Isoquants are equidistant apart

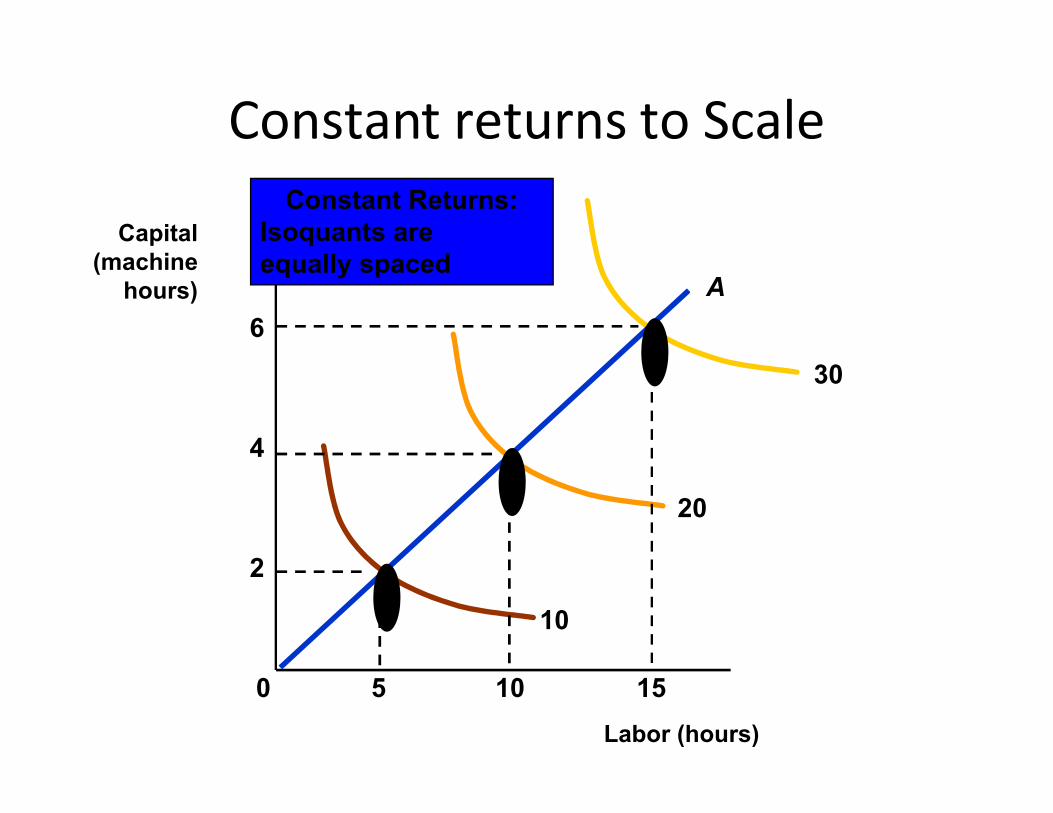

Constant returns to Scale

Capital(machine

hours)

Constant Returns:Isoquants are equally spaced

30

A

6

Labor (hours)

10

20

155 10

2

4

0

Returns to Scale

• Measuring the relationship between the scale (size) of a firm and output

• Decreasing returns to scale: output less than doubles when all inputs are doubled

• Decreasing returns to scale: output less than doubles when all inputs are doubled– Decreasing efficiency with large size– Reduction of entrepreneurial abilities– Isoquants become farther apart

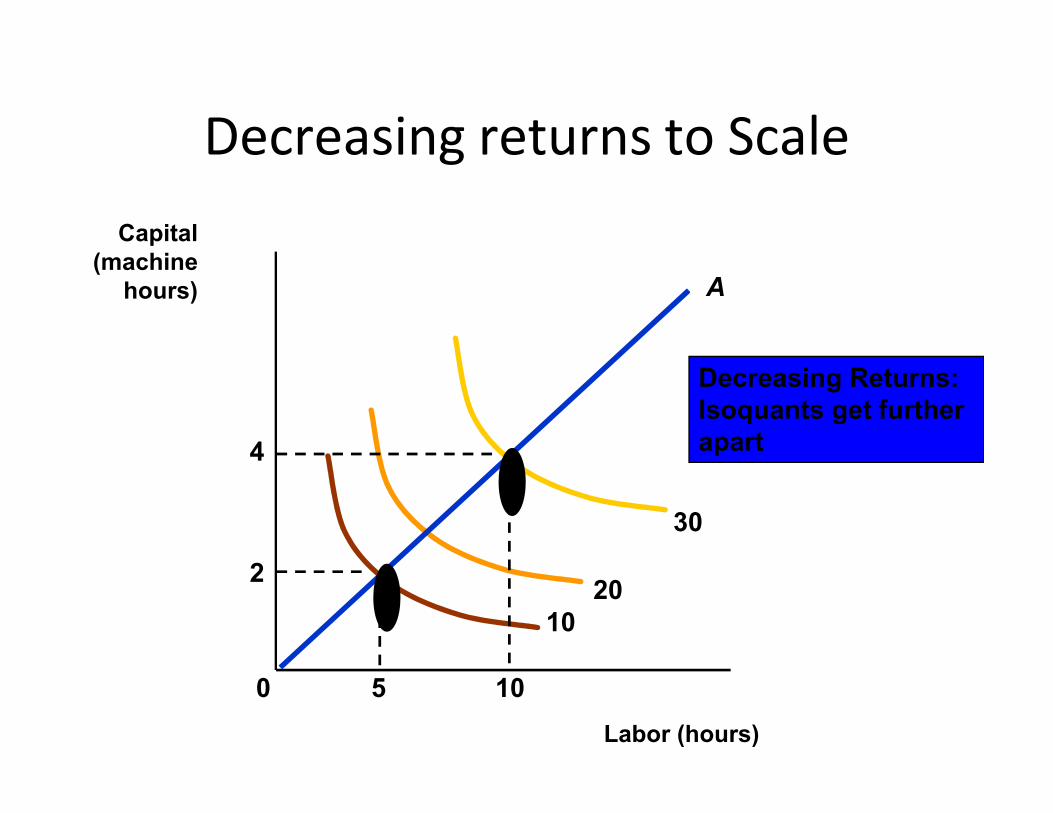

Decreasing returns to ScaleCapital

(machinehours)

Decreasing Returns:Isoquants get further

A

Labor (hours)

Isoquants get further apart

1020

30

5 10

2

4

0

Returns to Scale in the U.S. CarpetIndustry

• The carpet industry has grown from a small industry to a large industry with some very large firms.

• Can the growth be explained by the presence of economies to scale?

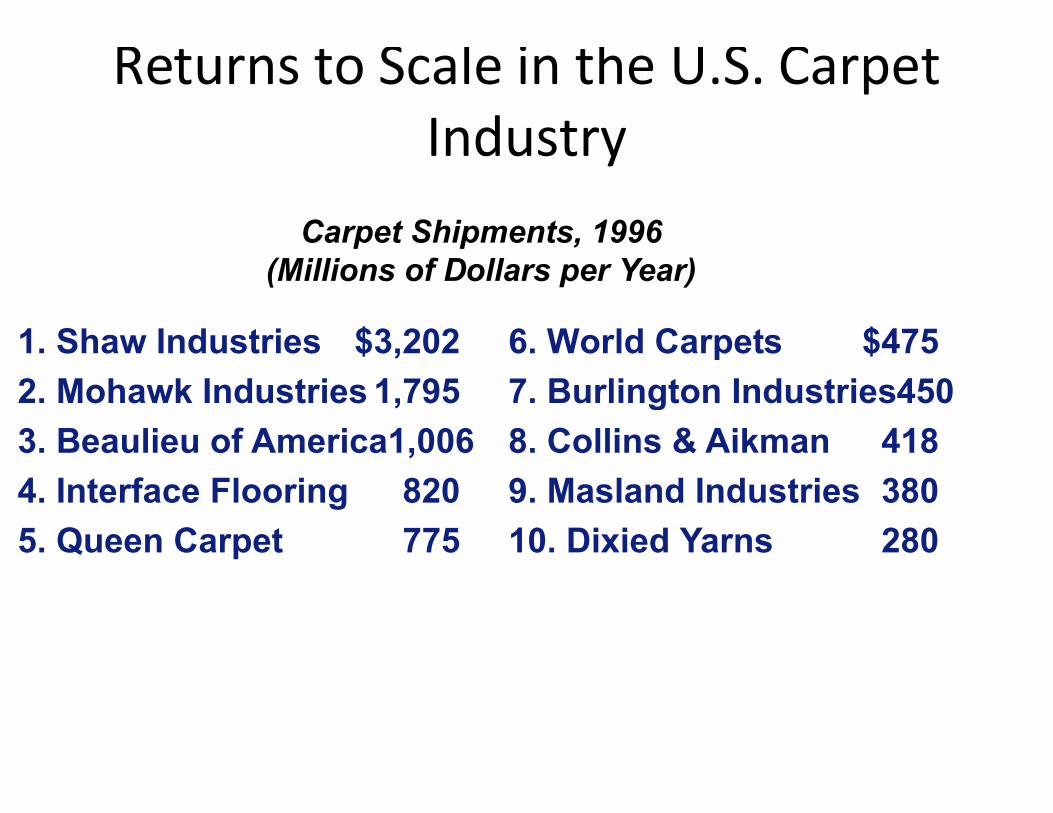

Returns to Scale in the U.S. CarpetIndustry

Carpet Shipments, 1996(Millions of Dollars per Year)

1. Shaw Industries $3,202 6. World Carpets $475

2. Mohawk Industries 1,795 7. Burlington Industries4502. Mohawk Industries 1,795 7. Burlington Industries450

3. Beaulieu of America1,006 8. Collins & Aikman 418

4. Interface Flooring 820 9. Masland Industries 380

5. Queen Carpet 775 10. Dixied Yarns 280

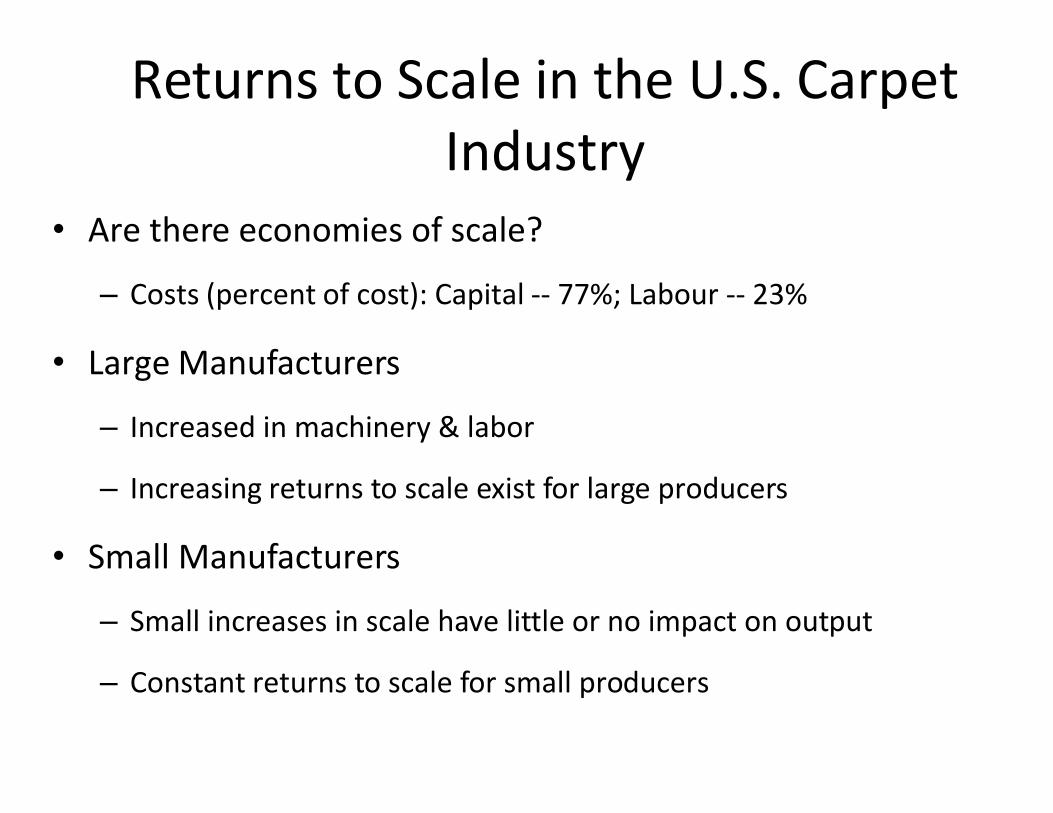

Returns to Scale in the U.S. CarpetIndustry

• Are there economies of scale?

– Costs (percent of cost): Capital -- 77%; Labour -- 23%

• Large Manufacturers

– Increased in machinery & labor

– Increasing returns to scale exist for large producers

• Small Manufacturers

– Small increases in scale have little or no impact on output

– Constant returns to scale for small producers

Summary• A production function describes the maximum output

a firm can produce for each specified combination of inputs.

• An isoquant is a curve that shows all combinations of • An isoquant is a curve that shows all combinations of inputs that yield a given level of output.

• Average product of labor measures the productivity of the average worker, whereas marginal product of labor measures the productivity of the last worker added.

Summary

• The law of diminishing returns explains that the marginal product of an input eventually diminishes as its quantity is increased.

• Isoquants always slope downward because the • Isoquants always slope downward because the marginal product of all inputs is positive.

• In long-run analysis, we tend to focus on the firm’s choice of its scale or size of operation.

Costs of productionCosts of production

Topics to be Discussed

• Measuring Cost: Which Costs Matter?

• Cost in the Short Run

• Cost in the Long Run• Cost in the Long Run

• Long-Run Versus Short-Run Cost Curves

Introduction• The production technology measures the relationship

between input and output.

• Given the production technology, managers must choose how to produce.choose how to produce.

• To determine the optimal level of output and the input combinations, we must convert from the unit measurements of the production technology to dollar measurements or costs.

Economic cost versus Accountingcost

• Accounting Cost– Actual expenses plus depreciation charges for

capital equipmentcapital equipment

• Economic Cost– Cost to a firm of utilizing economic resources in

production, including opportunity cost

Opportunity cost

• Cost associated with opportunities that are foregone when a firm’s resources are not put to their highest-value use.

• E.g.:

– A firm owns its own building and pays no rent for office space

– Does this mean the cost of office space is zero?

Sunk Cost

• Expenditure that has been made and cannot be recovered

• Should not influence a firm’s decisions.

• E.g.:• E.g.:

– A firm pays $500,000 for an option to buy a building.

– The cost of the building is $5 million or a total of $5.5 million.

– The firm finds another building for $5.25 million.

– Which building should the firm buy?

Fixed and variable costs

• Total output is a function of variable inputs and fixed inputs.

• Therefore, the total cost of production equals • Therefore, the total cost of production equals the fixed cost (the cost of the fixed inputs) plus the variable cost (the cost of the variable inputs), or…

VCFCTC

Fixed and variable costs

• Fixed Cost

– Does not vary with the level of output

• Variable Cost

– Cost that varies as output varies

Fixed versus sunk costs

• Fixed Cost

– Cost paid by a firm that is in business regardless of the level of output

• Sunk Cost

– Cost that has been incurred and cannot be recovered

Some examples

• Personal Computers: most costs are variable

– Components, labour

• Software: most costs are sunk• Software: most costs are sunk

– Cost of developing the software

• Pizza: most costs are fixed

– Largest cost component is fixed

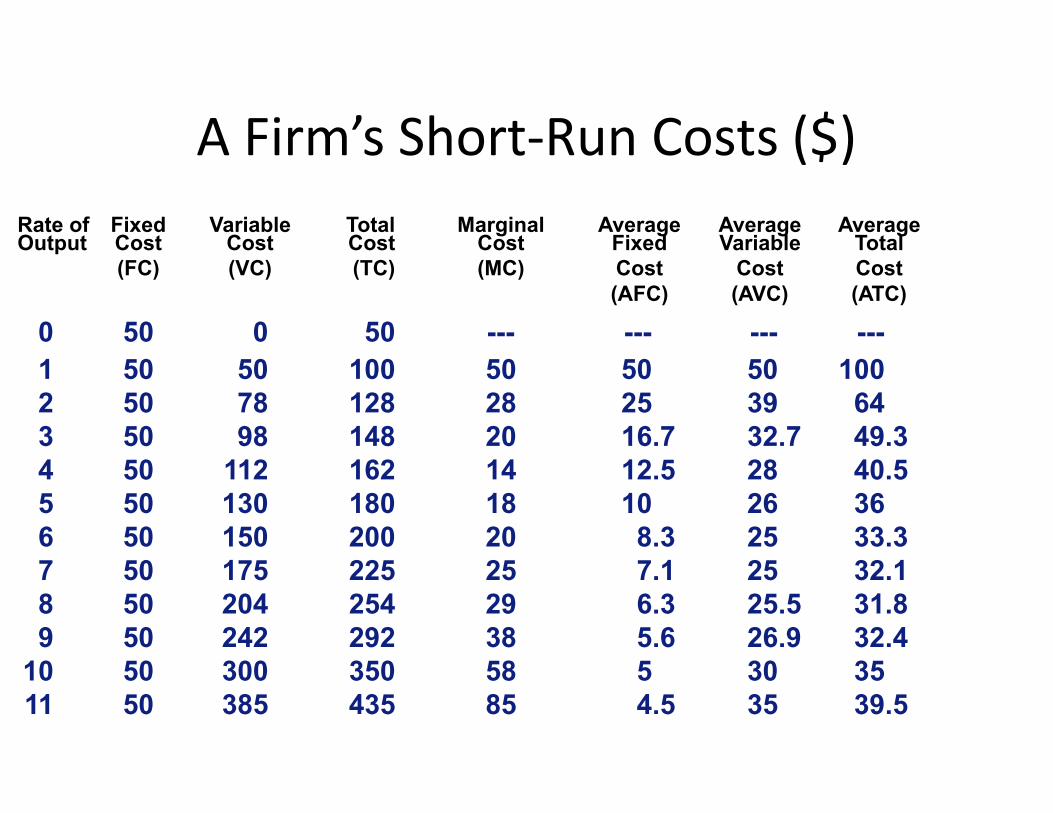

A Firm’s Short-Run Costs ($)

0 50 0 50 --- --- --- ---1 50 50 100 50 50 50 1002 50 78 128 28 25 39 64

Rate of Fixed Variable Total Marginal Average Average AverageOutput Cost Cost Cost Cost Fixed Variable Total

(FC) (VC) (TC) (MC) Cost Cost Cost(AFC) (AVC) (ATC)

2 50 78 128 28 25 39 643 50 98 148 20 16.7 32.7 49.34 50 112 162 14 12.5 28 40.55 50 130 180 18 10 26 366 50 150 200 20 8.3 25 33.37 50 175 225 25 7.1 25 32.18 50 204 254 29 6.3 25.5 31.89 50 242 292 38 5.6 26.9 32.4

10 50 300 350 58 5 30 3511 50 385 435 85 4.5 35 39.5

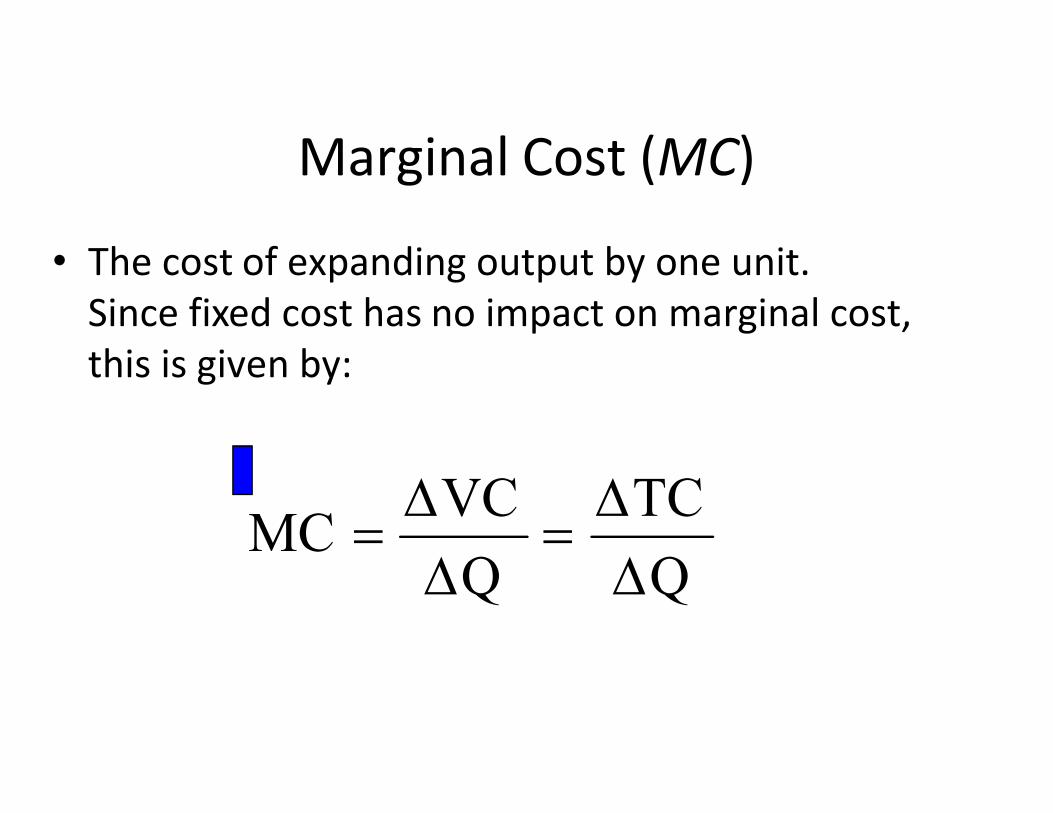

Marginal Cost (MC)

• The cost of expanding output by one unit. Since fixed cost has no impact on marginal cost, this is given by:

Q

TC

Q

VCMC

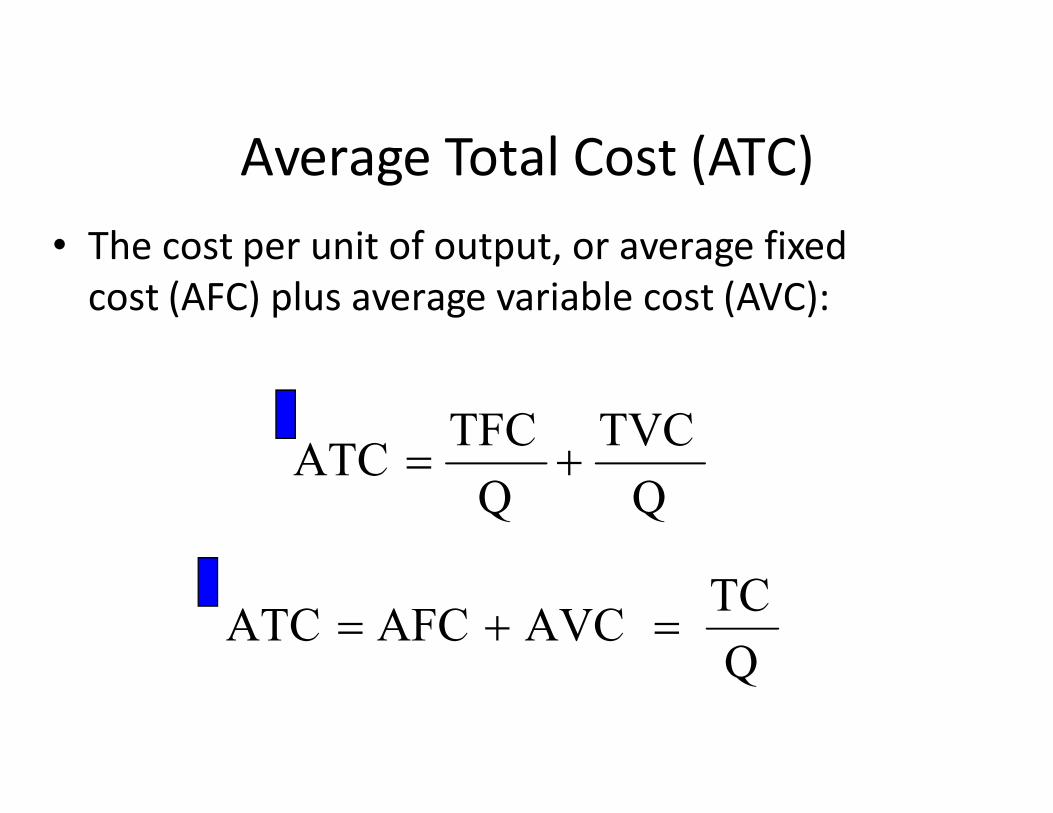

Average Total Cost (ATC)• The cost per unit of output, or average fixed

cost (AFC) plus average variable cost (AVC):

TVCTFC

Q

TVC

Q

TFCATC

Q

TC AVCAFCATC

The Determinants of Short-RunCost

• The relationship between the production function and cost is determined be whether there are increasing or decreasing returns to inputs.

• Increasing returns and cost– With increasing returns, output is increasing relative to input and

variable cost and total cost will fall relative to output.• Decreasing returns and cost

– With decreasing returns, output is decreasing relative to input and variable cost and total cost will rise relative to output.

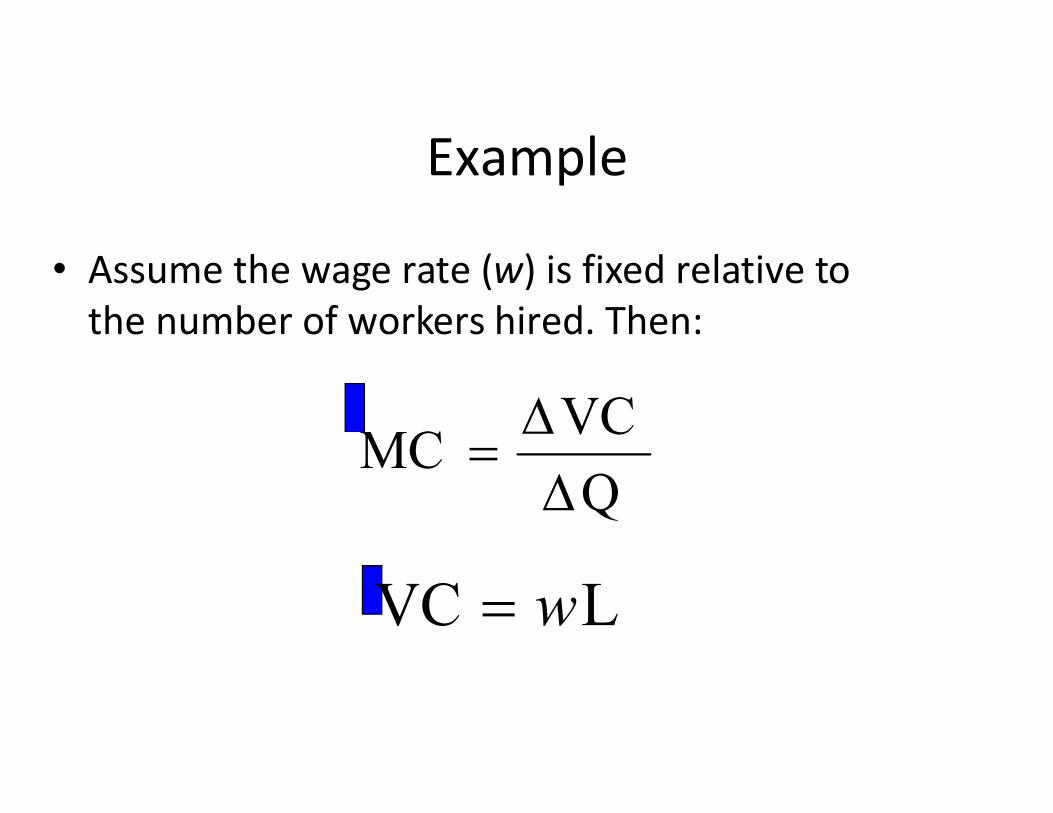

Example

• Assume the wage rate (w) is fixed relative to the number of workers hired. Then:

VCQ

VCMC

LVC w

Example

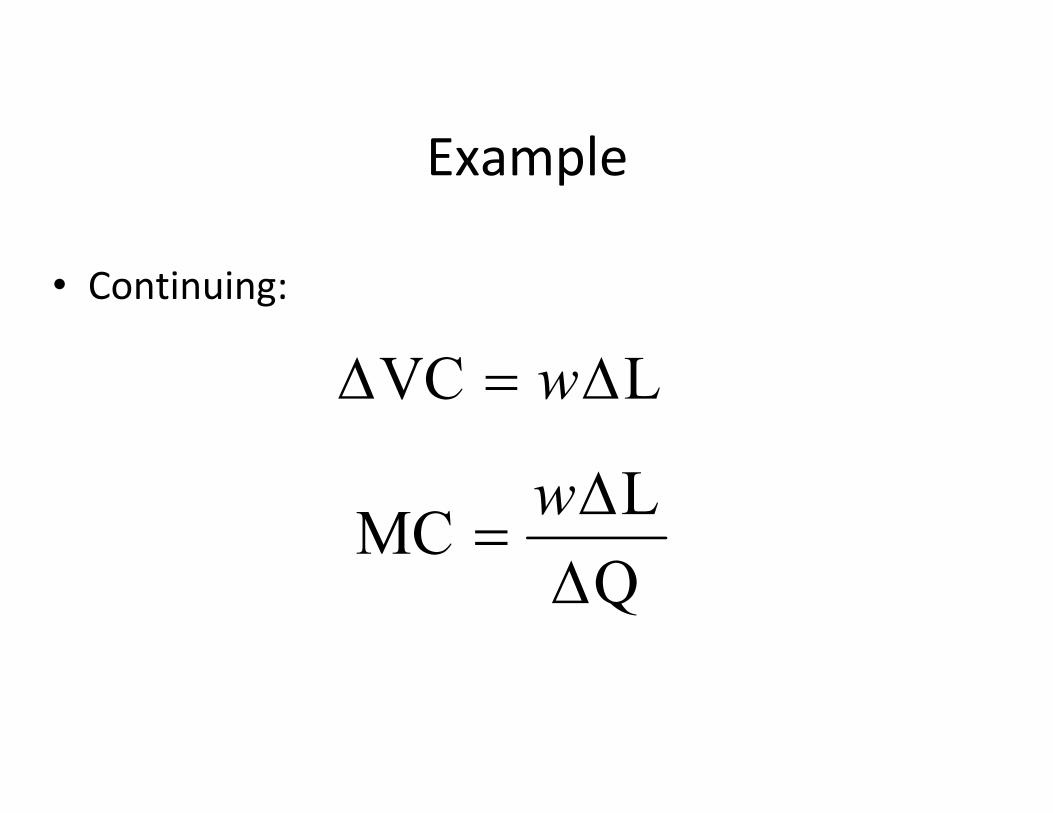

• Continuing:

LVC w LVC w

Q

LMC

w

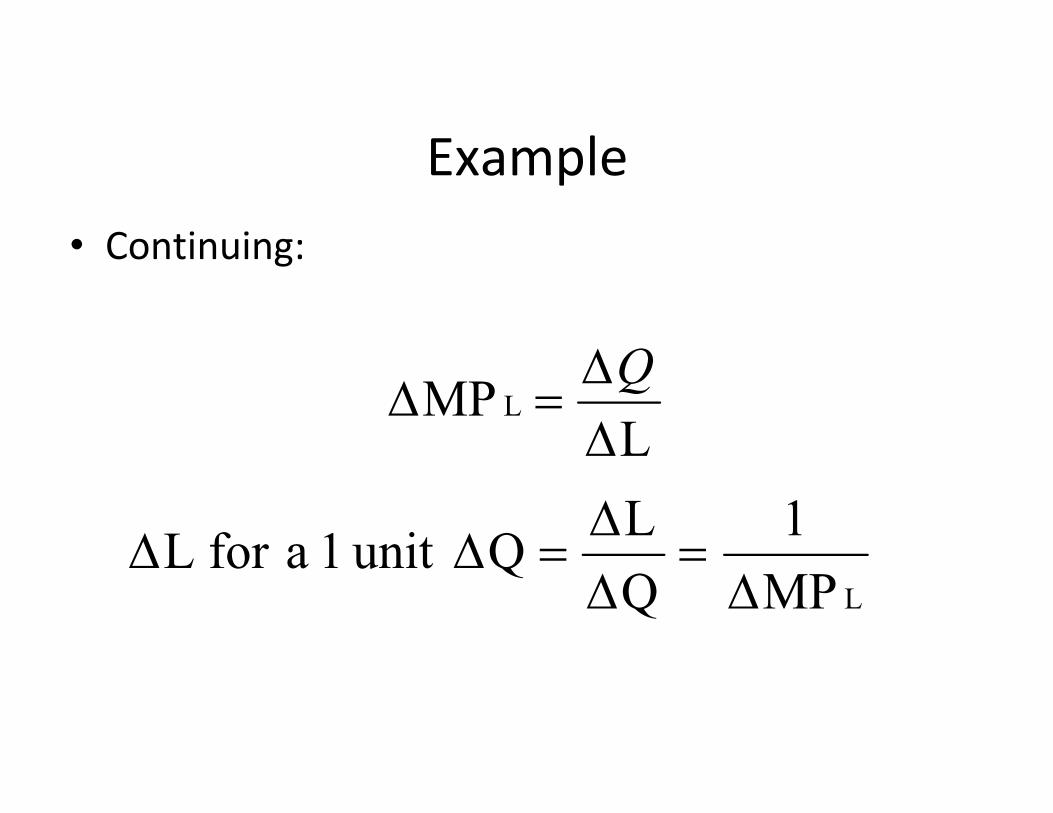

Example• Continuing:

MP L

Q

LMP L

LMP

1

Q

LQunit1aforL

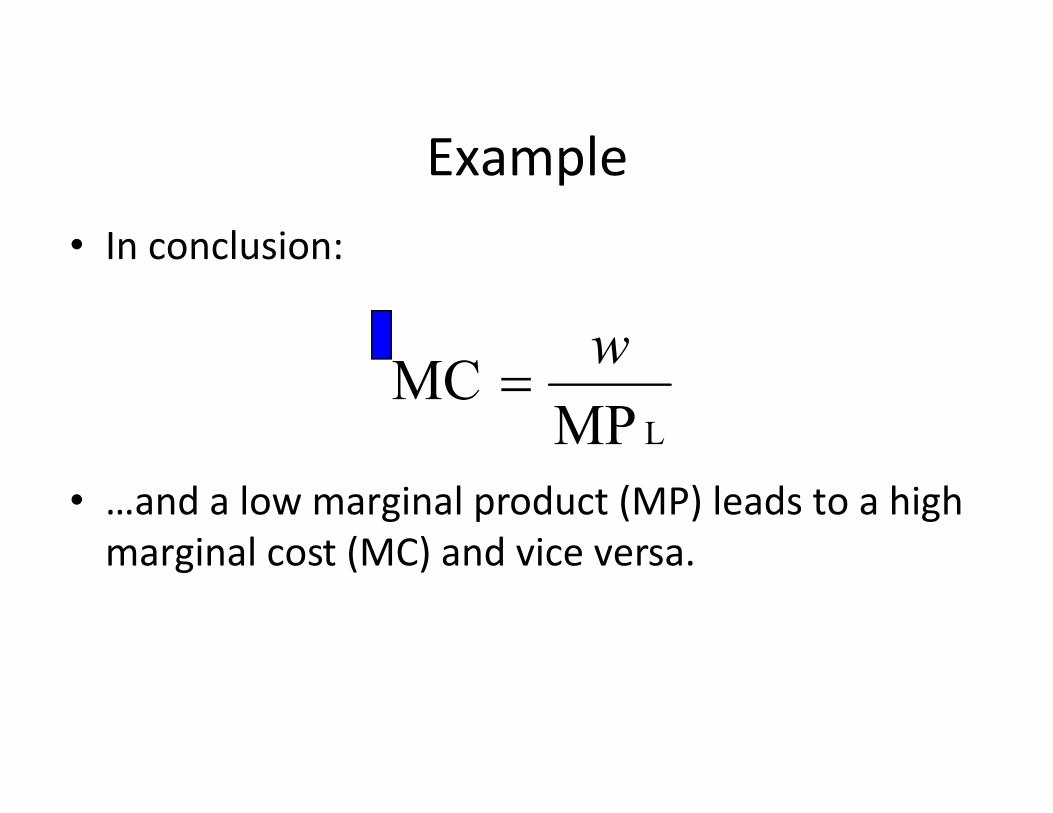

Example• In conclusion:

MPMC

w

• …and a low marginal product (MP) leads to a high marginal cost (MC) and vice versa.

LMPMC

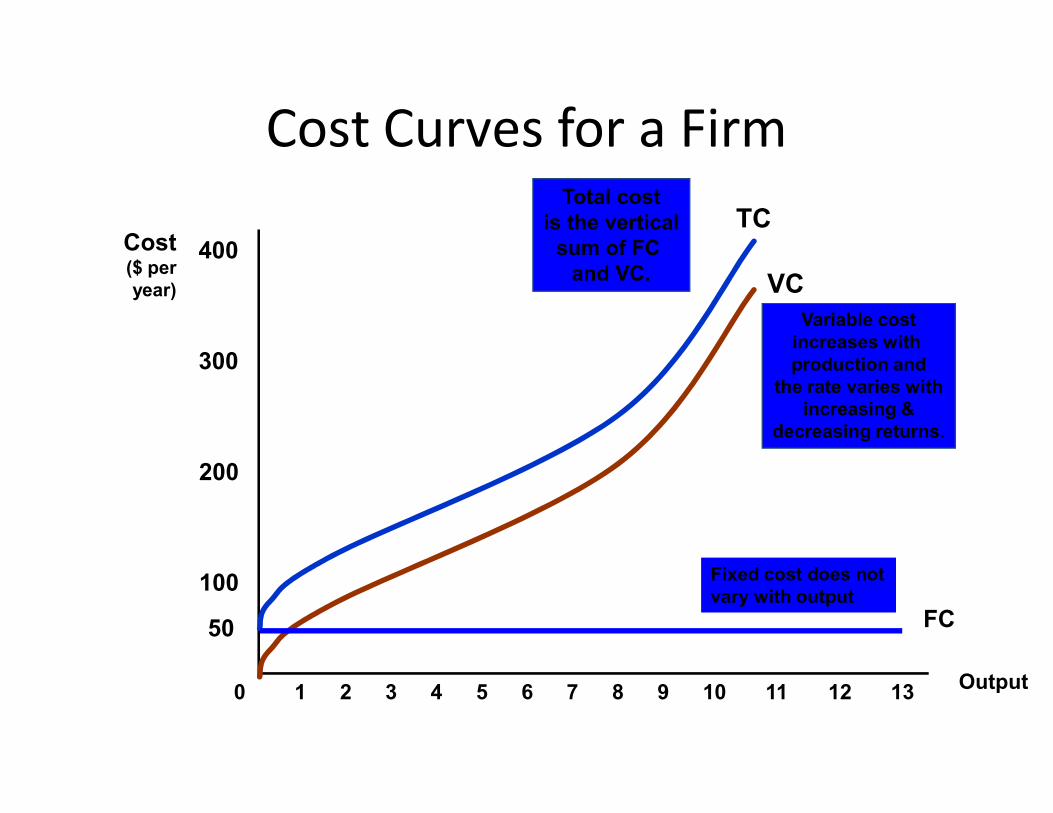

Cost Curves for a Firm

Cost($ peryear)

300

400

VCVariable cost

increases with production and

the rate varies withincreasing &

TCTotal cost

is the verticalsum of FC

and VC.

Output

100

200

0 1 2 3 4 5 6 7 8 9 10 11 12 13

increasing &decreasing returns.

FC50

Fixed cost does notvary with output

Cost Curves for a FirmCost($ perunit)

75

100

MC

Output (units/yr.)

25

50

0 1 2 3 4 5 6 7 8 9 10 11

ATC

AVC

AFC

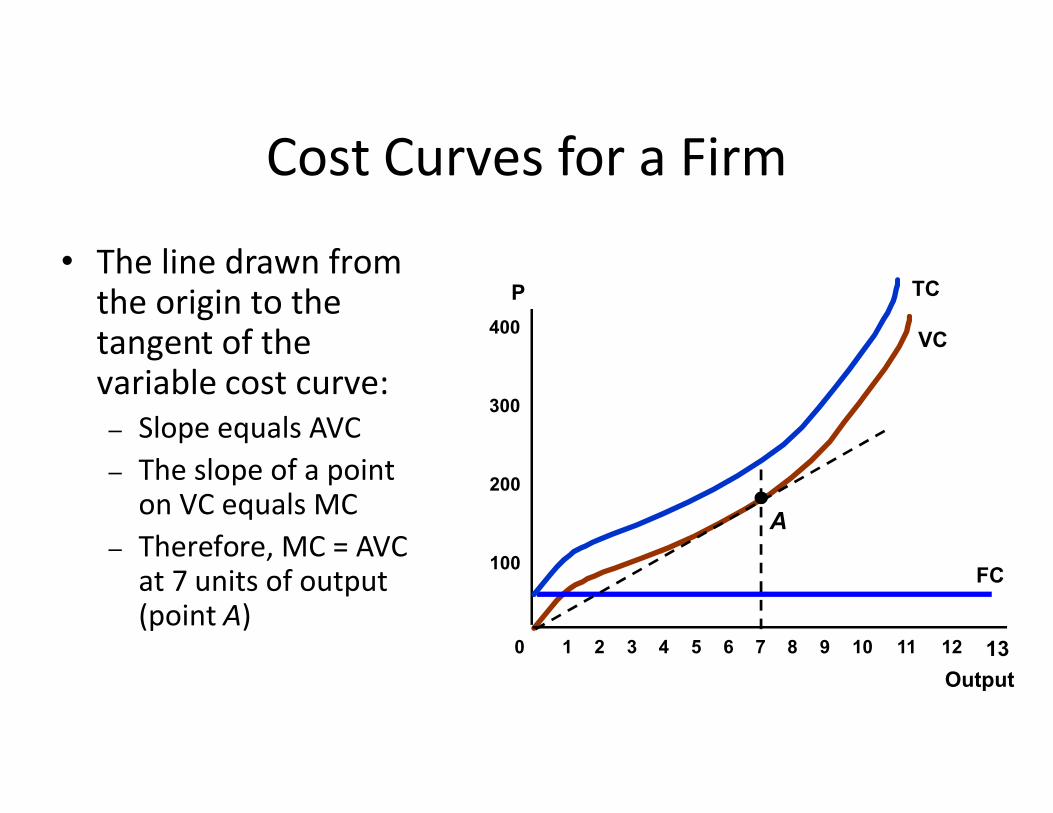

Cost Curves for a Firm

• The line drawn from the origin to the tangent of the variable cost curve:

P

300

400VC

TC

– Slope equals AVC– The slope of a point

on VC equals MC– Therefore, MC = AVC

at 7 units of output (point A)

Output

100

200

300

0 1 2 3 4 5 6 7 8 9 10 11 12 13

FC

A

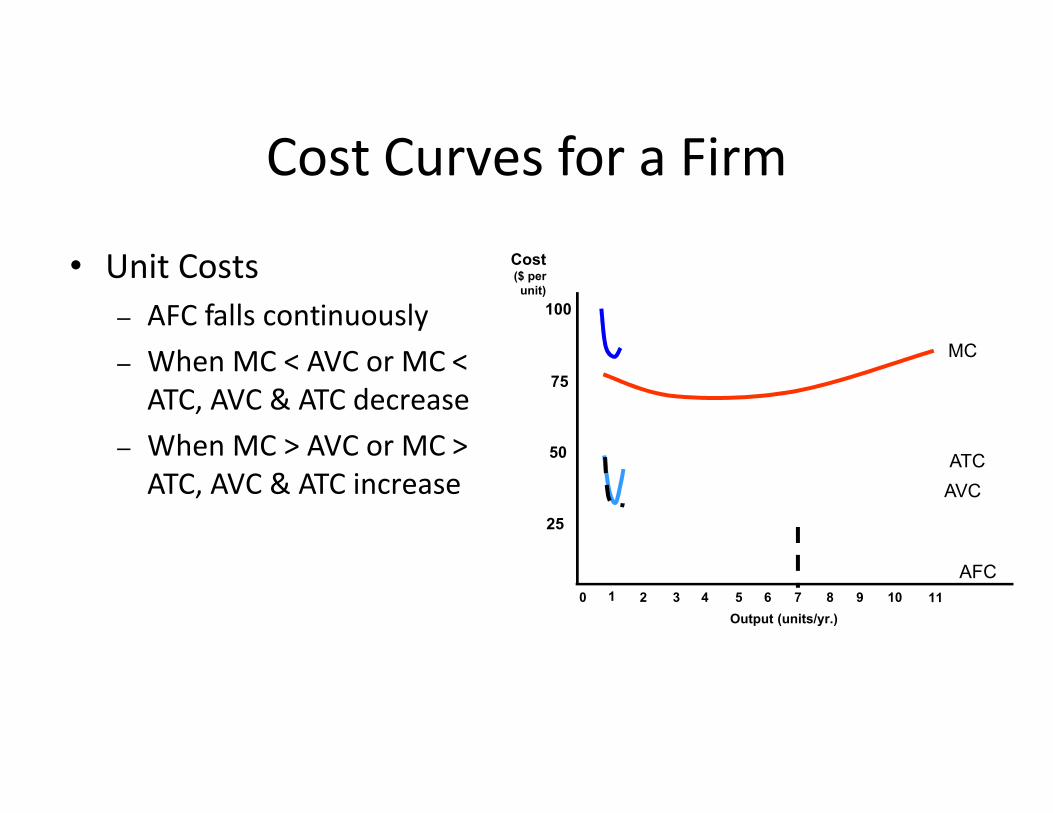

Cost Curves for a Firm

• Unit Costs– AFC falls continuously– When MC < AVC or MC <

ATC, AVC & ATC decrease

Cost($ perunit)

75

100

MC

ATC, AVC & ATC decrease– When MC > AVC or MC >

ATC, AVC & ATC increase

Output (units/yr.)

25

50

0 1 2 3 4 5 6 7 8 9 10 11

ATC

AVC

AFC

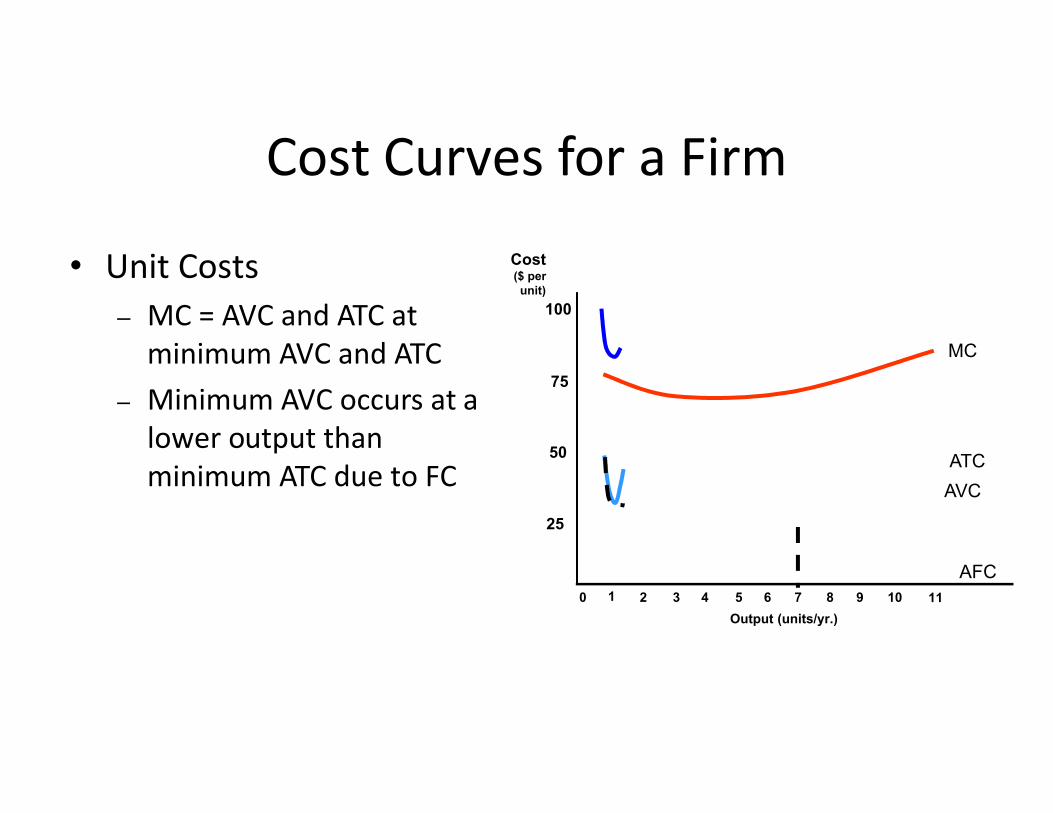

Cost Curves for a Firm

• Unit Costs– MC = AVC and ATC at

minimum AVC and ATC– Minimum AVC occurs at a

Cost($ perunit)

75

100

MC

– Minimum AVC occurs at a lower output than minimum ATC due to FC

Output (units/yr.)

25

50

0 1 2 3 4 5 6 7 8 9 10 11

ATC

AVC

AFC

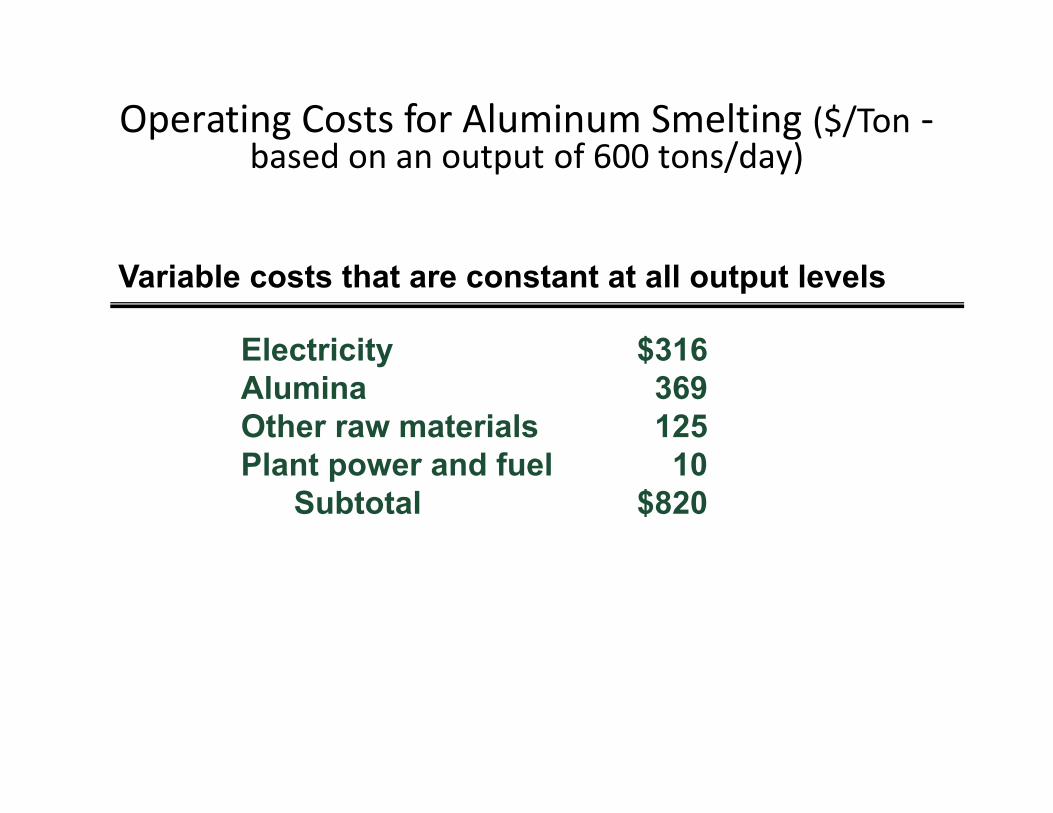

Operating Costs for Aluminum Smelting ($/Ton -based on an output of 600 tons/day)

Variable costs that are constant at all output levels

Electricity $316Alumina 369Other raw materials 125Plant power and fuel 10

Subtotal $820

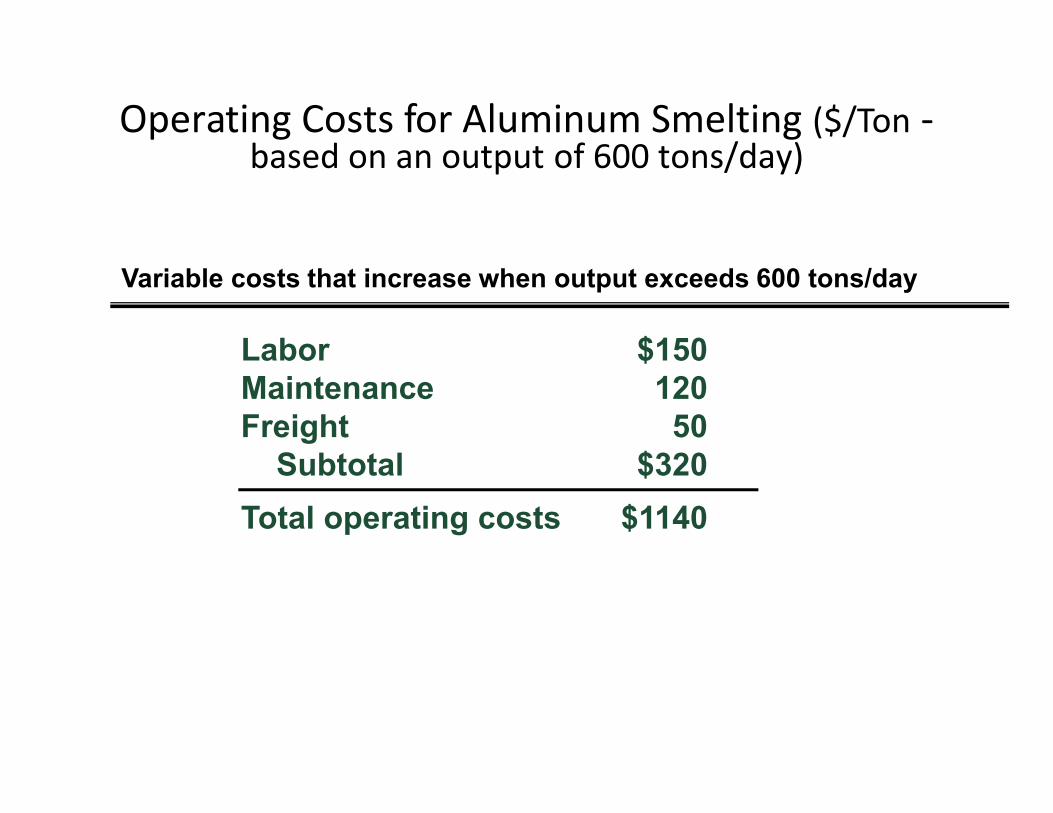

Operating Costs for Aluminum Smelting ($/Ton -based on an output of 600 tons/day)

Variable costs that increase when output exceeds 600 tons/day

Labor $150Maintenance 120Freight 50

Subtotal $320

Total operating costs $1140

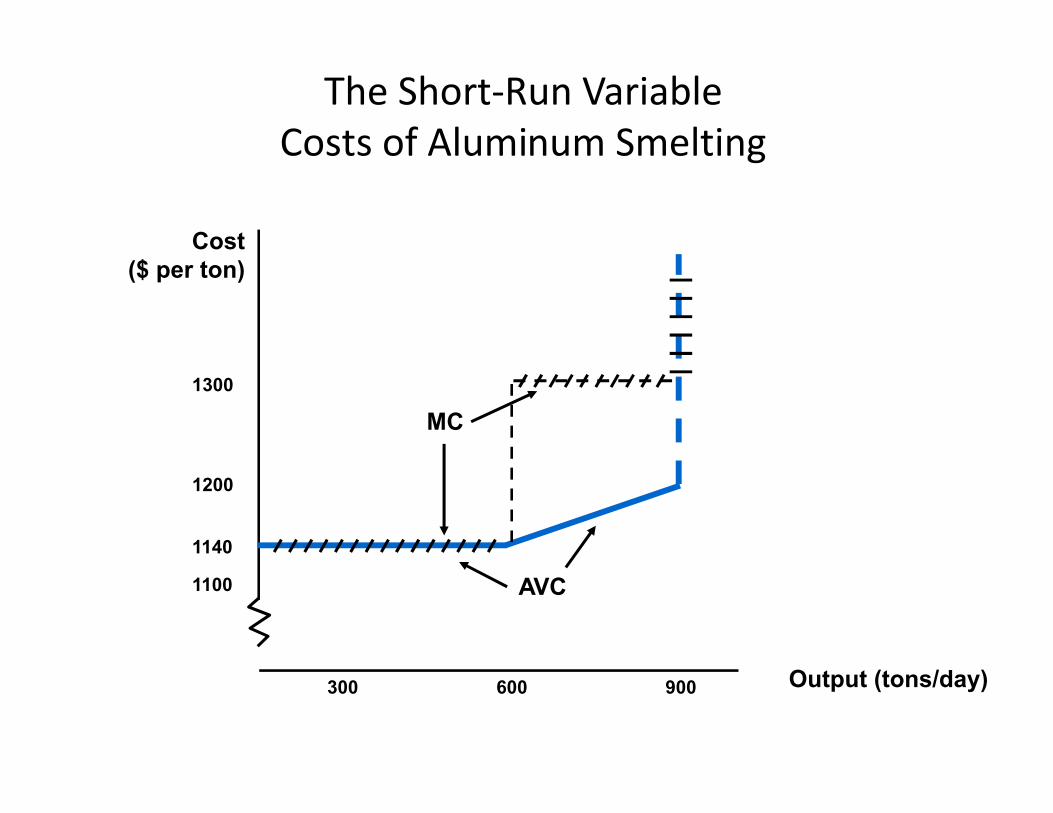

The Short-Run VariableCosts of Aluminum Smelting

Cost($ per ton)

1300

Output (tons/day)

1100

1200

300 600 900

1140

MC

AVC

Cost in the Long Run

• Assumptions

– Two Inputs: Labor (L) & capital (K)

– Price of labor: wage rate (w)

The Cost Minimizing Input Choice

– The price of capital: R = depreciation rate + interest rate

Cost in the Long Run

• The Isocost Line– C = wL + rK

The User Cost of CapitalThe Cost Minimizing Input Choice

– C = wL + rK

– Isocost: A line showing all combinations of L & Kthat can be purchased for the same cost

Cost in the Long Run

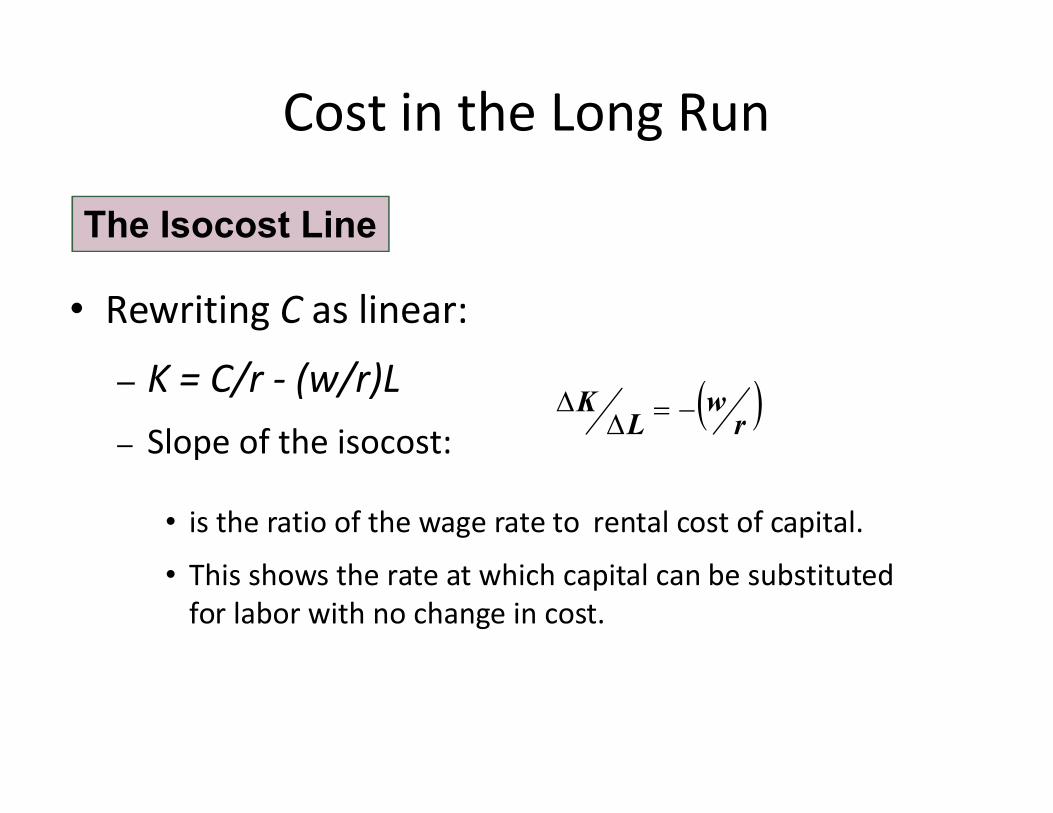

• Rewriting C as linear:

– K = C/r - (w/r)L wK

The Isocost Line

– Slope of the isocost:

• is the ratio of the wage rate to rental cost of capital.

• This shows the rate at which capital can be substituted for labor with no change in cost.

rw

LK

Choosing Inputs• We will examine how to minimize cost for a given

level of output (by combining isocosts with isoquants)

Producing a Given Output atMinimum Cost

Capitalper

year

Isocost C2 shows quantity Q can be produced with

Q1 is an isoquantfor output Q1.

Isocost curve C0 showsall combinations of K and L

that cost C0.

CO C1 C2 are

K2

Labour per year

Q1 can be produced withcombination K2L2 or K3L3.

However, both of theseare higher cost combinations

than K1L1.

Q1

C0 C1 C2

CO C1 C2 arethree

isocost lines

AK1

L1

K3

L3L2

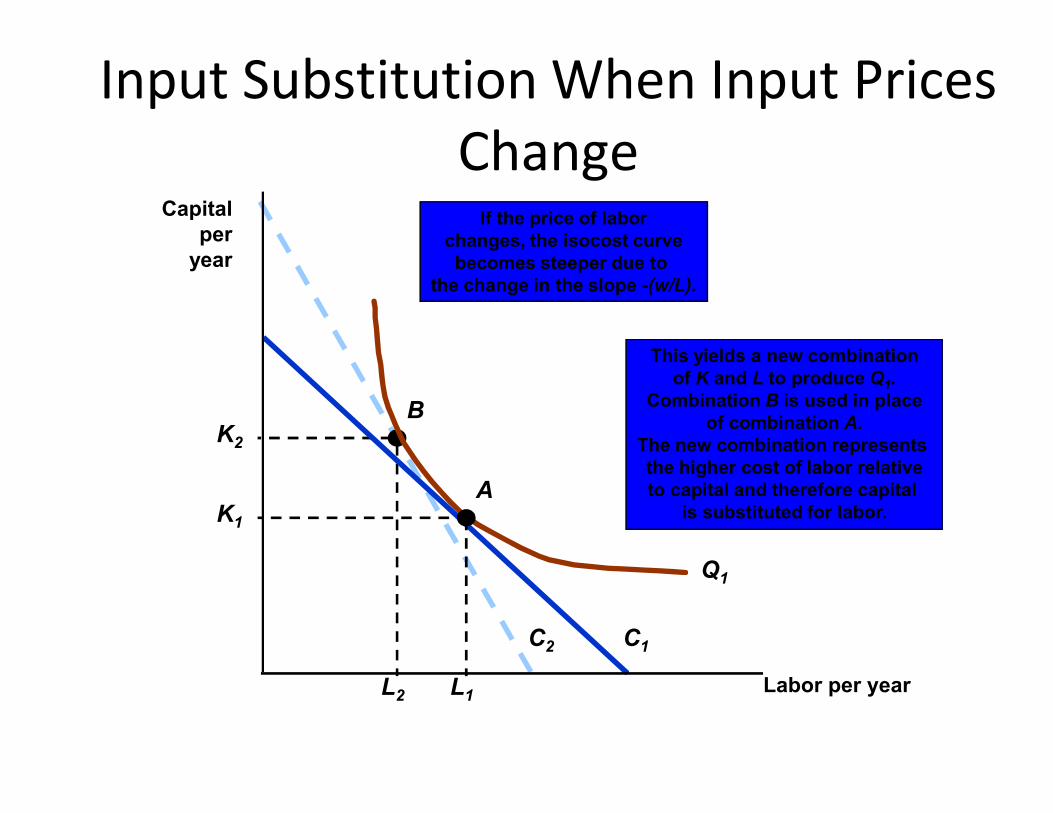

Input Substitution When Input PricesChange

This yields a new combinationof K and L to produce Q1.

Combination B is used in placeB

If the price of laborchanges, the isocost curvebecomes steeper due to

the change in the slope -(w/L).

Capitalper

year

C2

Combination B is used in placeof combination A.

The new combination represents the higher cost of labor relativeto capital and therefore capital

is substituted for labor.

K2

L2

B

C1

K1

L1

A

Q1

Labor per year

Cost in the Long Run

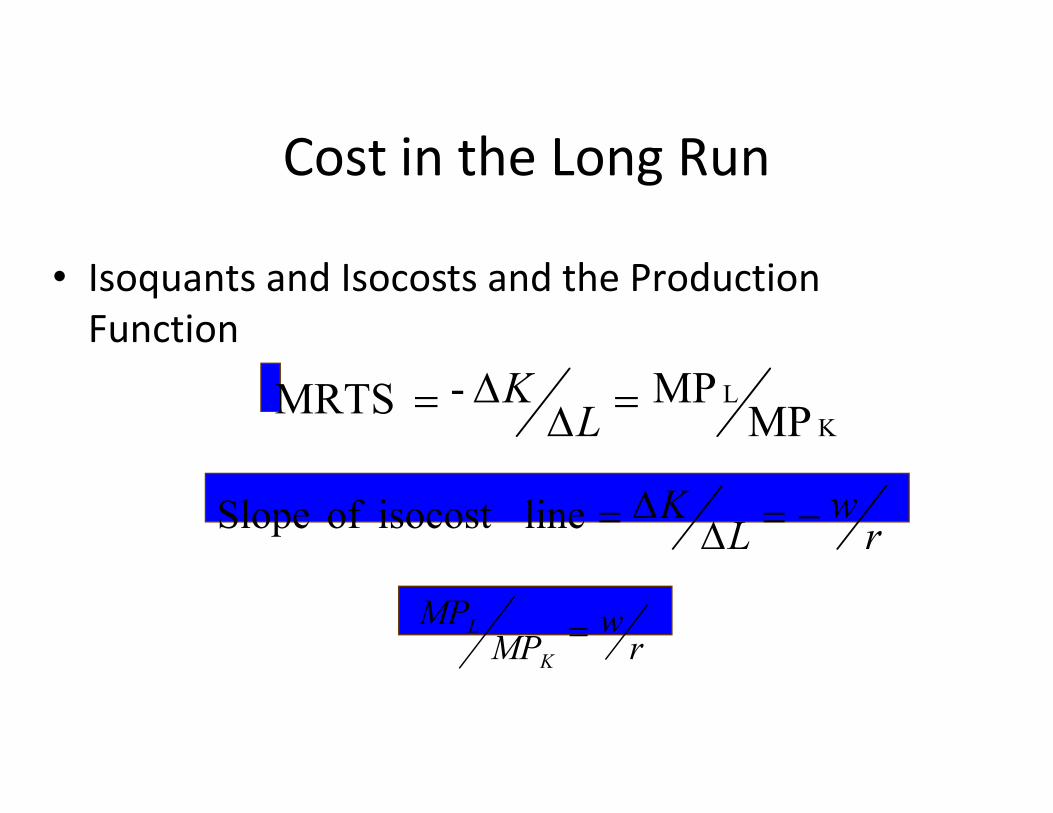

• Isoquants and Isocosts and the Production Function

LMP

MP-MRTS L

KK

LMP

MP-MRTS L

K

rw

LK

lineisocost ofSlope

rw

MPMP

K

L

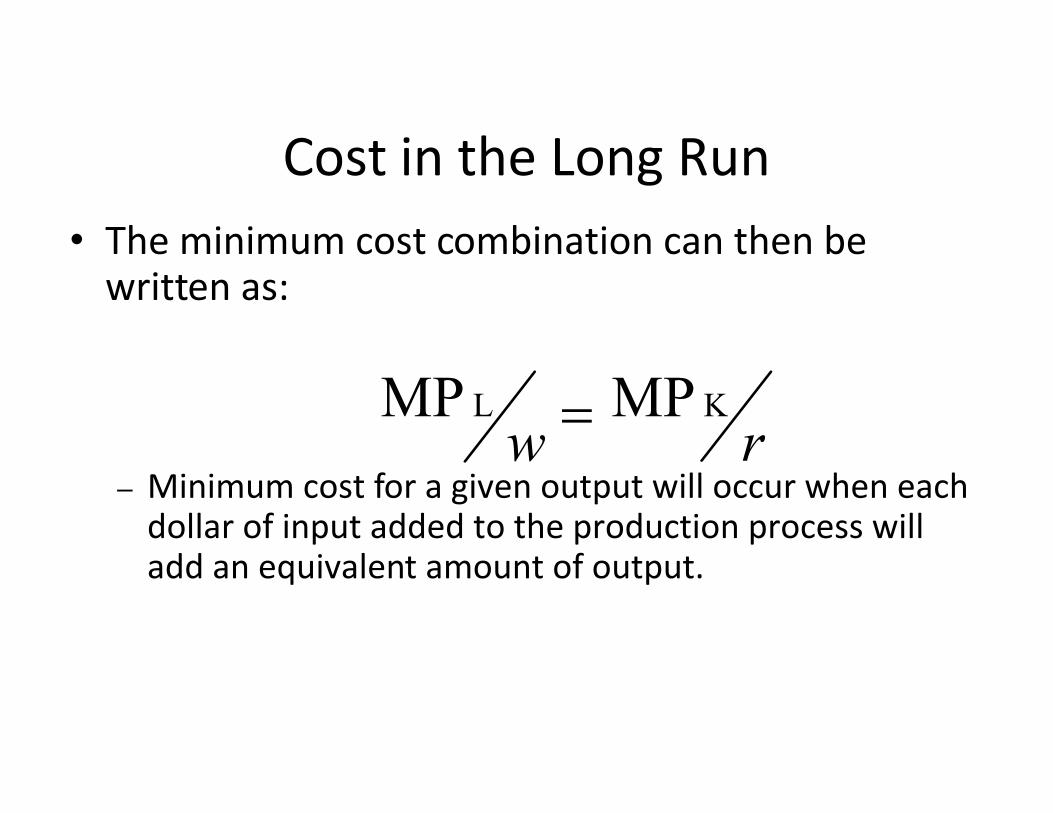

Cost in the Long Run• The minimum cost combination can then be

written as:

KL MPMP – Minimum cost for a given output will occur when each

dollar of input added to the production process will add an equivalent amount of output.

rwKL MPMP

Effect of Effluent Fees on Input Choices

• Firms that have a by-product to production produce an effluent.

• An effluent fee is a per-unit fee that firms must • An effluent fee is a per-unit fee that firms must pay for the effluent that they emit.

• How would a producer respond to an effluent fee on production?

Effect of Effluent Fees on InputChoices

• The Scenario: Steel Producer

1) Located on a river: Low cost transportation and emission disposal (effluent).and emission disposal (effluent).

2) EPA imposes a per unit effluent fee to reduce the environmentally harmful effluent.

3) How should the firm respond?

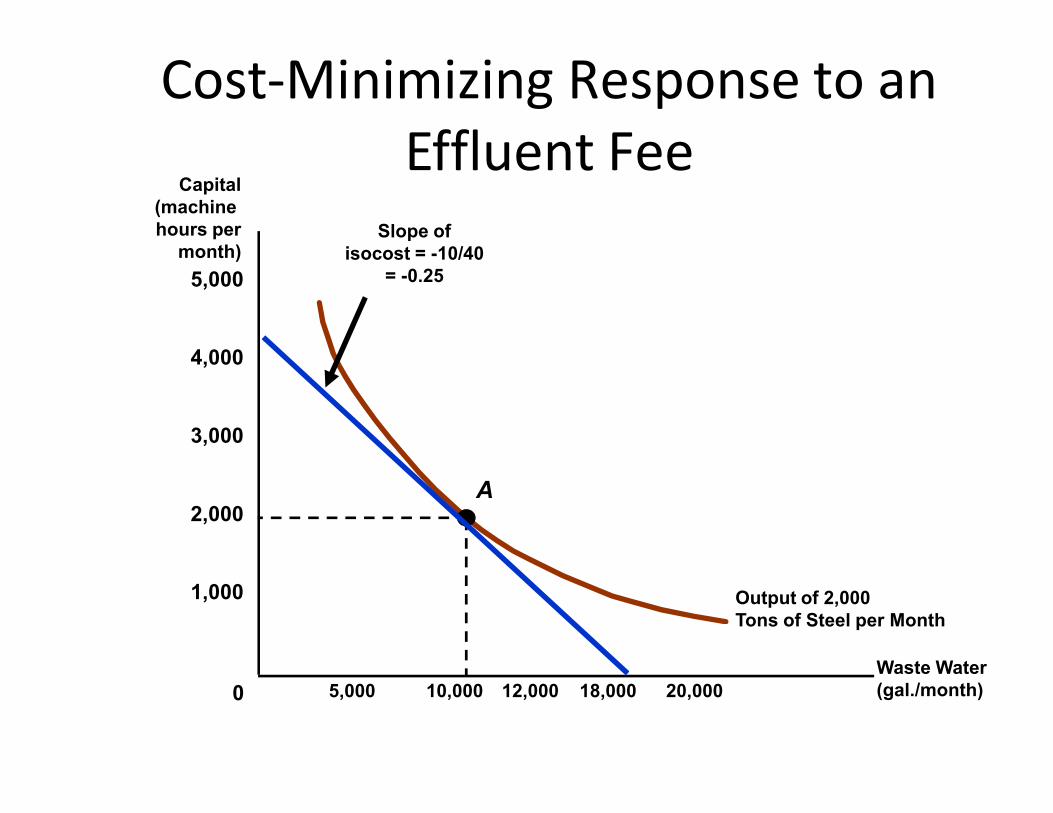

Cost-Minimizing Response to anEffluent Fee

Capital(machine hours per

month)Slope of

isocost = -10/40 = -0.25

4,000

5,000

Waste Water(gal./month)

Output of 2,000Tons of Steel per Month

A

10,000 18,000 20,0000 12,000

2,000

1,000

3,000

5,000

Cost-Minimizing Response to anEffluent Fee

4,000

5,000

Capital(machine hours per

month)

3,500

Slope ofisocost = -20/40

= -0.50

B Following the impositionof the effluent fee of $10/gallon

Prior to regulation the firm chooses to produce an output using 10,000

gallons of water and 2,000machine-hours of capital at A.

F

Output of 2,000Tons of Steel per Month

2,000

1,000

3,000

10,000 18,000 20,0000 12,000

E

5,000

3,500 of the effluent fee of $10/gallonthe slope of the isocost changeswhich the higher cost of water to

capital so now combination Bis selected.A

CWaste Water(gal./month)

Effect of Effluent Fees on InputChoices

• The more easily factors can be substituted, the more effective the fee is in reducing the effluent.

• The greater the degree of substitutes, the less the firm will have to pay (for example: $50,000 with firm will have to pay (for example: $50,000 with combination B instead of $100,000 with combination A)

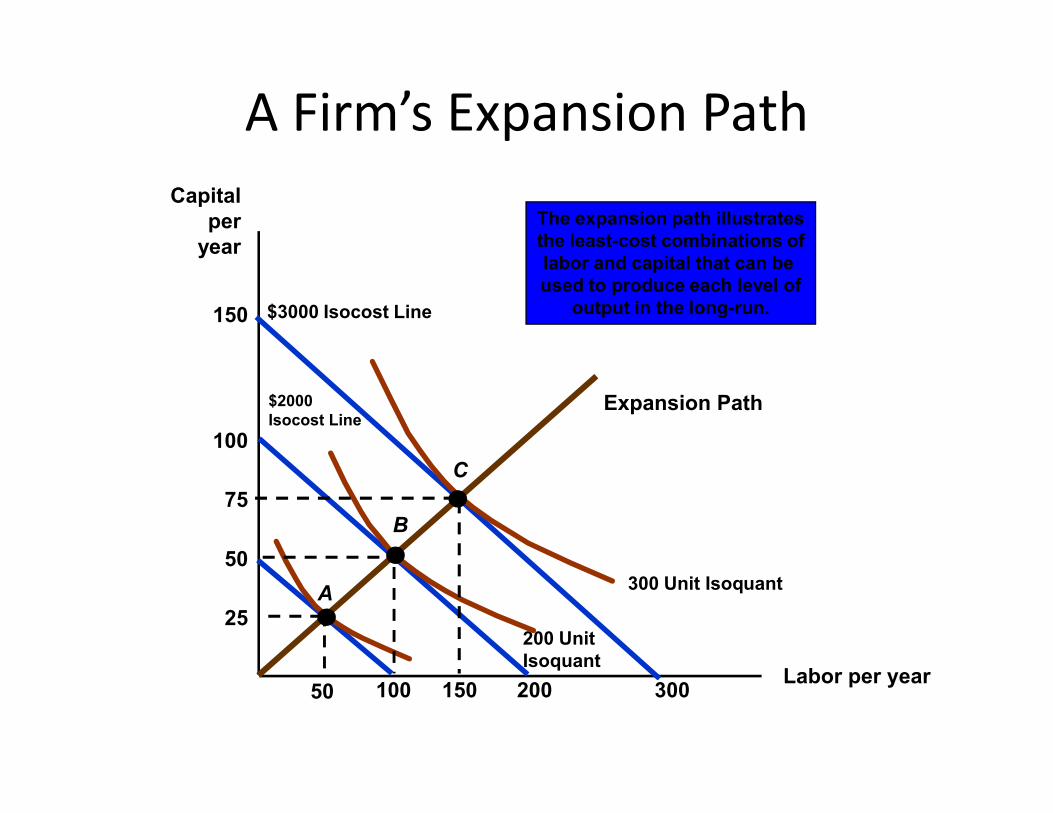

Costs in the Long Run

• Cost minimization with Varying Output Levels– A firm’s expansion path shows the minimum cost

combinations of labor and capital at each level of output.output.

A Firm’s Expansion PathCapital

peryear

Expansion Path

The expansion path illustratesthe least-cost combinations oflabor and capital that can be used to produce each level of

output in the long-run.150

$2000

$3000 Isocost Line

Labor per year

Expansion Path

25

50

75

100

10050 150 300200

A

$2000Isocost Line

200 UnitIsoquant

B

300 Unit Isoquant

C

A Firm’s Long-Run Total Cost CurveCost

perYear

Expansion Path

3000F

Output, Units/yr

1000

100 300200

2000

D

E

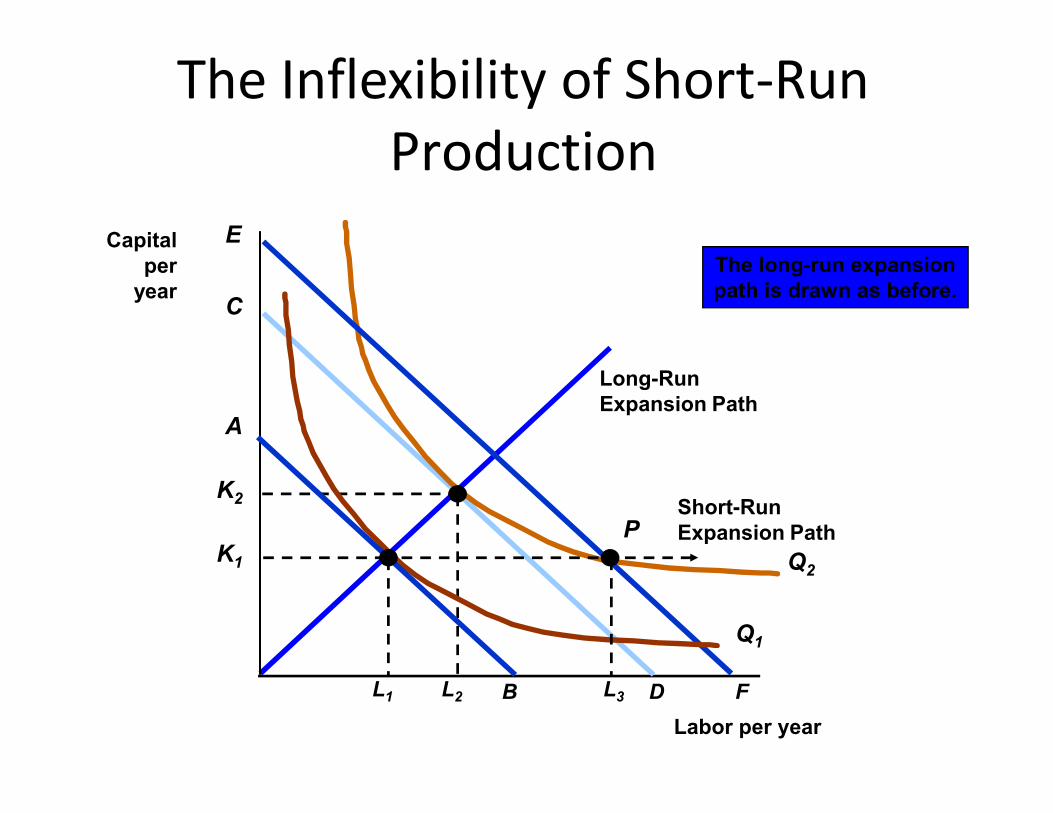

Long-Run Versus Short-Run CostCurves

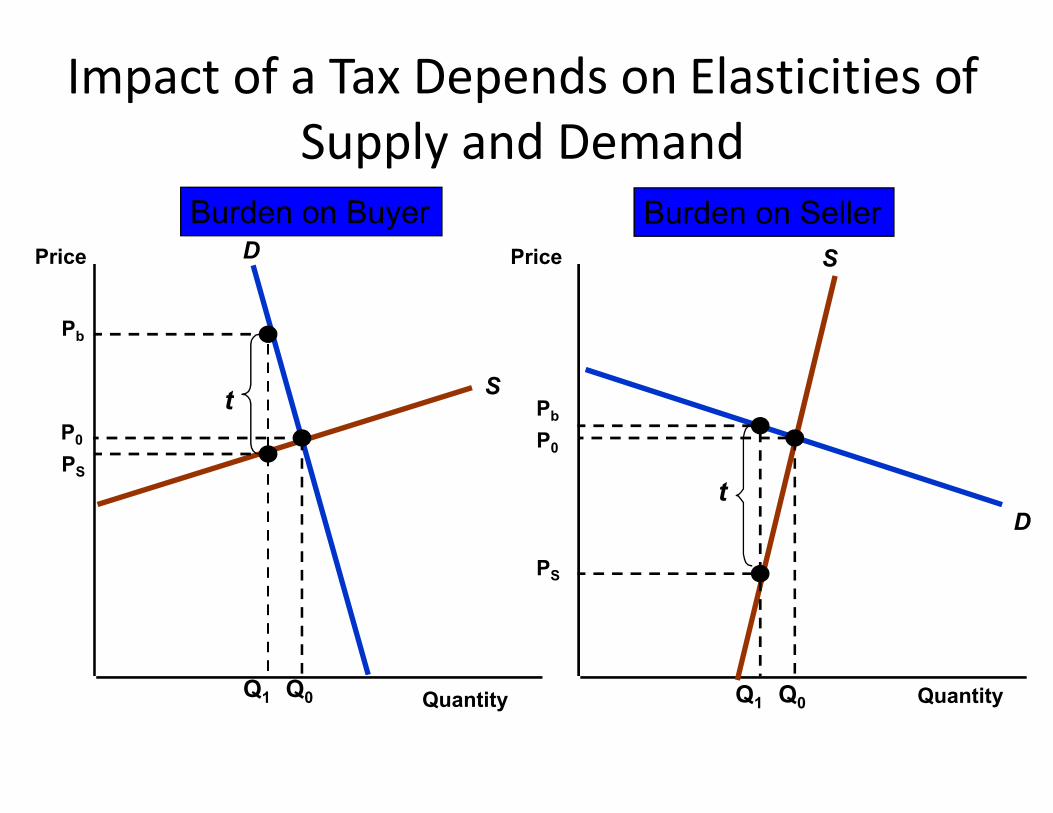

• What happens to average costs when both inputs are variable (long run) versus only having one input that is variable (short run)?

Long-RunExpansion Path

The long-run expansionpath is drawn as before.

The Inflexibility of Short-RunProduction

Capitalper

yearC

E

Expansion Path

Labor per year

L2

Q2

K2

D F

Q1

A

BL1

K1

L3

PShort-RunExpansion Path

Long-Run Average Cost (LAC)

• Constant Returns to Scale– If input is doubled, output will double and average cost is

constant at all levels of output.• Increasing Returns to ScaleIncreasing Returns to Scale

– If input is doubled, output will more than double and average cost decreases at all levels of output.

• Decreasing Returns to Scale– If input is doubled, the increase in output is less than twice

as large and average cost increases with output.• In the long-run:

– Firms experience increasing and decreasing returns to scale and therefore long-run average cost is “U” shaped.

Long-run marginal cost

• Long-run marginal cost leads long-run average cost:– If LMC < LAC, LAC will fall

– If LMC > LAC, LAC will rise

– Therefore, LMC = LAC at the minimum of LAC

Long-run average and marginal cost

Cost($ per unitof output

LAC

LMC

Output

A

Economies and Diseconomies ofScale

• Economies of Scale– Increase in output is greater than the increase in

inputs.

• Diseconomies of Scale• Diseconomies of Scale– Increase in output is less than the increase in

inputs.

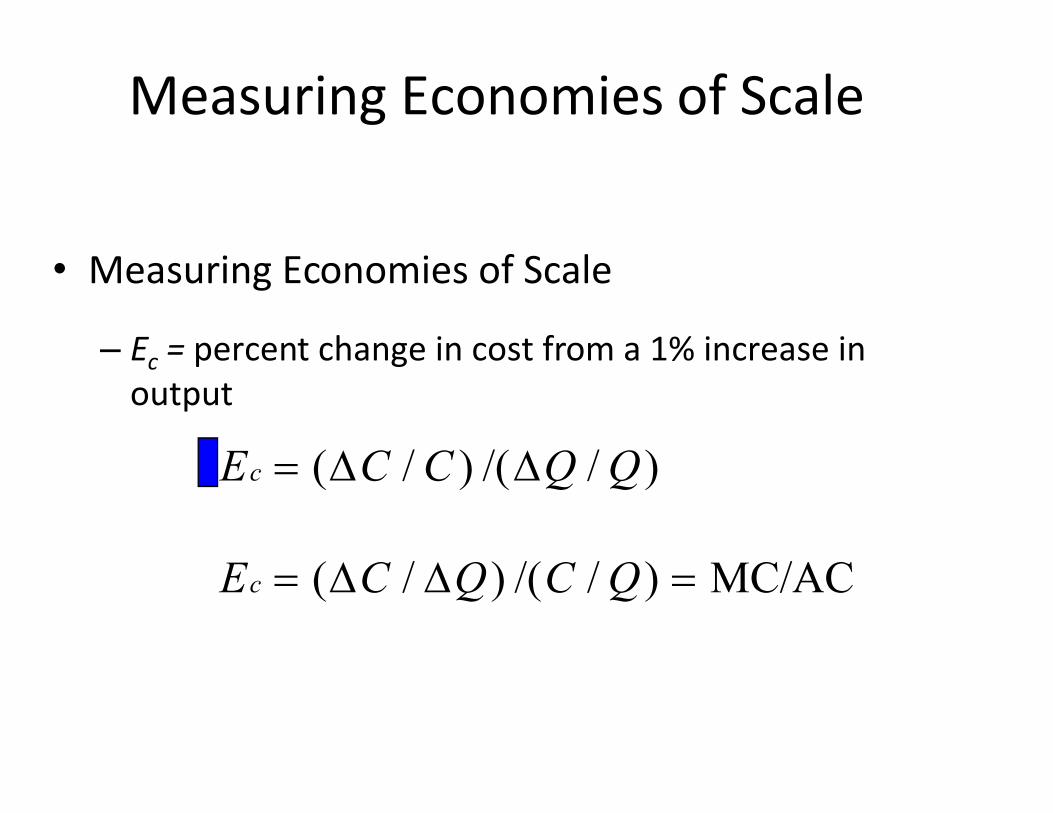

Measuring Economies of Scale

• Measuring Economies of Scale

– Ec = percent change in cost from a 1% increase in outputoutput

)//()/( QQCCEc

MC/AC)//()/( QCQCEc

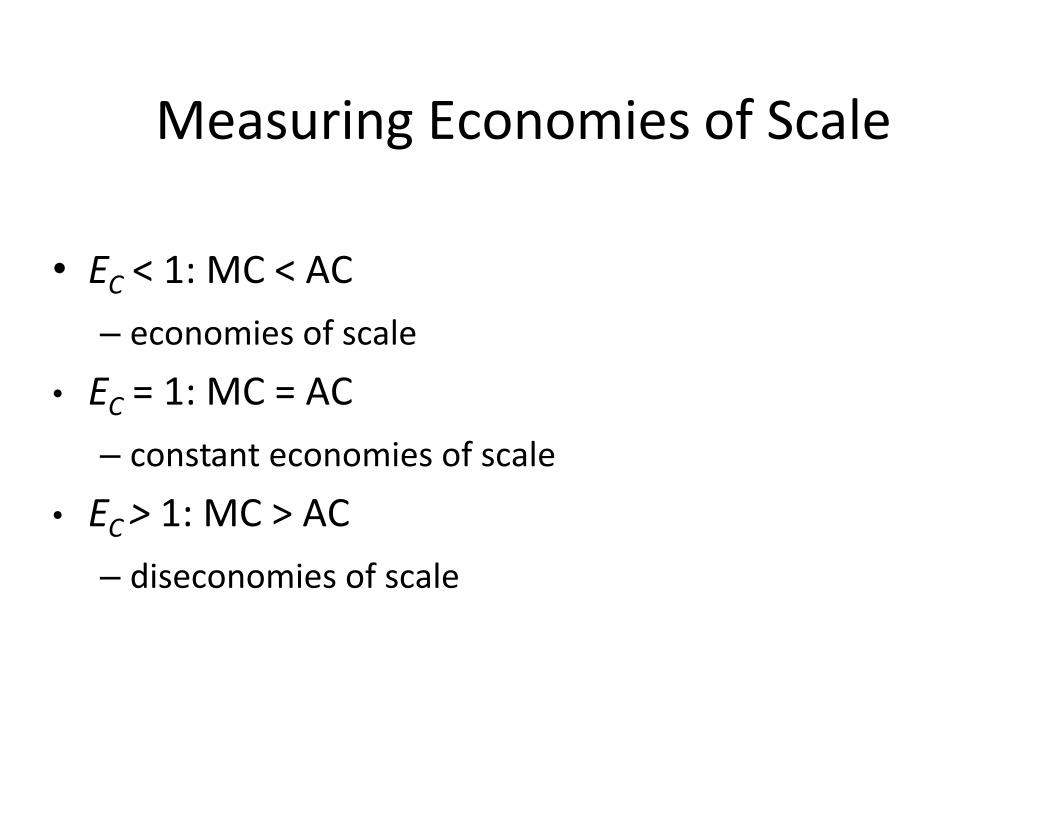

Measuring Economies of Scale

• EC < 1: MC < AC– economies of scale

• EC = 1: MC = AC• EC = 1: MC = AC– constant economies of scale

• EC > 1: MC > AC– diseconomies of scale

Long-Run Versus Short-Run CostCurves

• The Relationship Between Short-Run and Long-Run Cost– We will use short and long-run cost to determine the

optimal plant sizeoptimal plant size

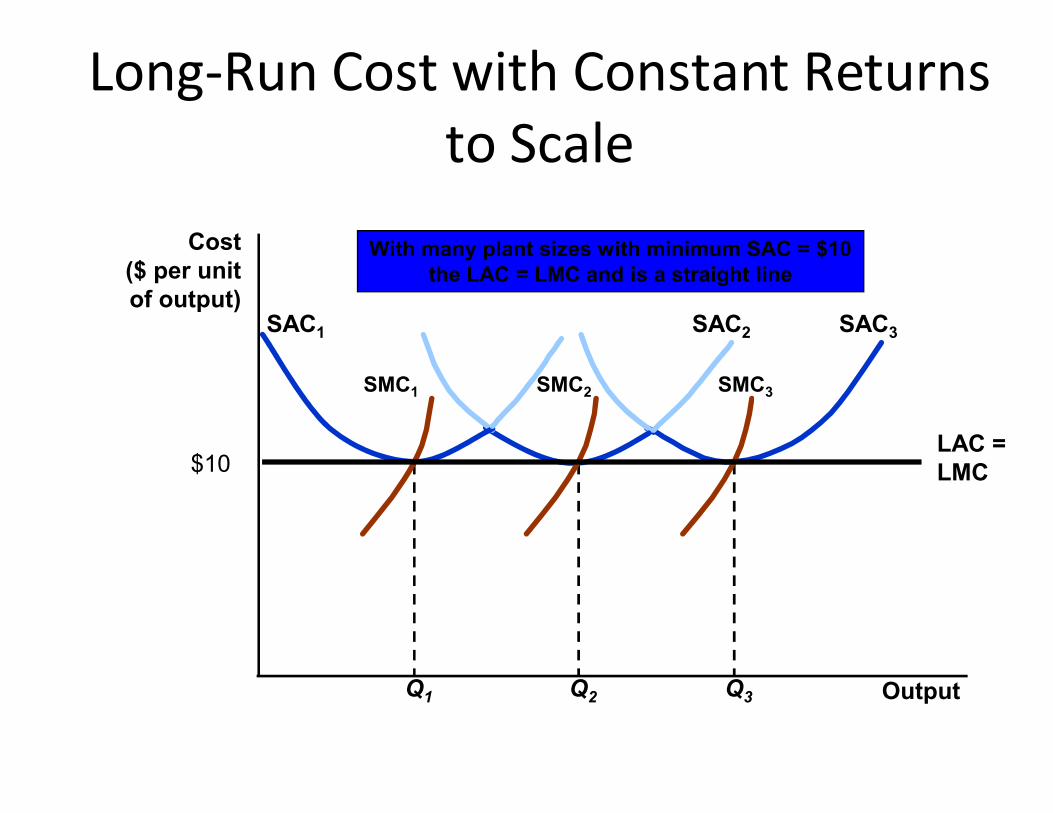

Long-Run Cost with Constant Returnsto Scale

Cost($ per unitof output)

SAC3

SMC3

SAC2

SMC2

SAC1

SMC1

With many plant sizes with minimum SAC = $10the LAC = LMC and is a straight line

OutputQ3Q2Q1

LAC =LMC$10

Long-Run Cost with Constant Returns toScale

• The optimal plant size will depend on the anticipated output (e.g. Q1 choose SAC1,etc).

• The long-run average cost curve is the envelope of The long-run average cost curve is the envelope of the firm’s short-run average cost curves.

Long-Run Cost with Economies and Diseconomies of Scale

Cost($ per unitof output

SAC1

SAC2

$10

$8B

A

LAC SAC3

Output

SMC1

SMC2LMC

If the output is Q1 a managerwould chose the small plant

SAC1 and SAC $8.Point B is on the LAC because

it is a least cost plant for a given output.

Q1

B

SMC3

Long-Run Cost with Economies and Diseconomies of Scale

• What is the firms’ long-run cost curve?– Firms can change scale to change output in the long-

run.– The long-run cost curve is the dark blue portion of the – The long-run cost curve is the dark blue portion of the

SAC curve which represents the minimum cost for any level of output.

Summary

• Managers, investors, and economists must take into account the opportunity cost associated with the use of the firm’s resources.

• Firms are faced with both fixed and variable costs • Firms are faced with both fixed and variable costs in the short-run.

• When there is a single variable input, as in the short run, the presence of diminishing returns determines the shape of the cost curves.

Summary• In the long run, all inputs to the production process

are variable.

• The firm’s expansion path describes how its cost-minimizing input choices vary as the scale or output of minimizing input choices vary as the scale or output of its operation increases.

• The long-run average cost curve is the envelope of the short-run average cost curves.

• A firm enjoys economies of scale when it can double its output at less than twice the cost.

Profit maximisation and perfectProfit maximisation and perfectcompetition

Objectives

• Perfectly competitive markets• Profit maximisation• Marginal revenue, marginal cost and profit

maximisationmaximisation• Choosing output in the short-run and in the long-

run

Topics to be Discussed• Perfectly Competitive Markets

• Profit Maximization

• Marginal Revenue, Marginal Cost, and Profit Maximization

• Choosing Output in the Short-Run• Choosing Output in the Short-Run

• The Competitive Firm’s Short-Run Supply Curve

• Short-Run Market Supply

• Choosing Output in the Long-Run

• The Industry’s Long-Run Supply Curve

Perfectly Competitive Markets

• Characteristics of Perfectly Competitive Markets

1) Price taking1) Price taking

2) Product homogeneity

3) Free entry and exit

Perfectly Competitive Markets

• Price Taking

– The individual firm sells a very small share of the total market output and, therefore, cannot influence market price.influence market price.

– The individual consumer buys too small a share of industry output to have any impact on market price.

Perfectly Competitive Markets

• Product Homogeneity

– The products of all firms are perfect substitutes.

– Examples: Agricultural products, oil, copper, iron, – Examples: Agricultural products, oil, copper, iron, lumber

Perfectly Competitive Markets

• Free Entry and Exit

– Buyers can easily switch from one supplier to another.another.

– Suppliers can easily enter or exit a market.

Profit Maximization• Do firms maximize profits?

• Possibility of other objectives?– Revenue maximization?– Revenue maximization?

– Dividend maximization?

– Short-run profit maximization?

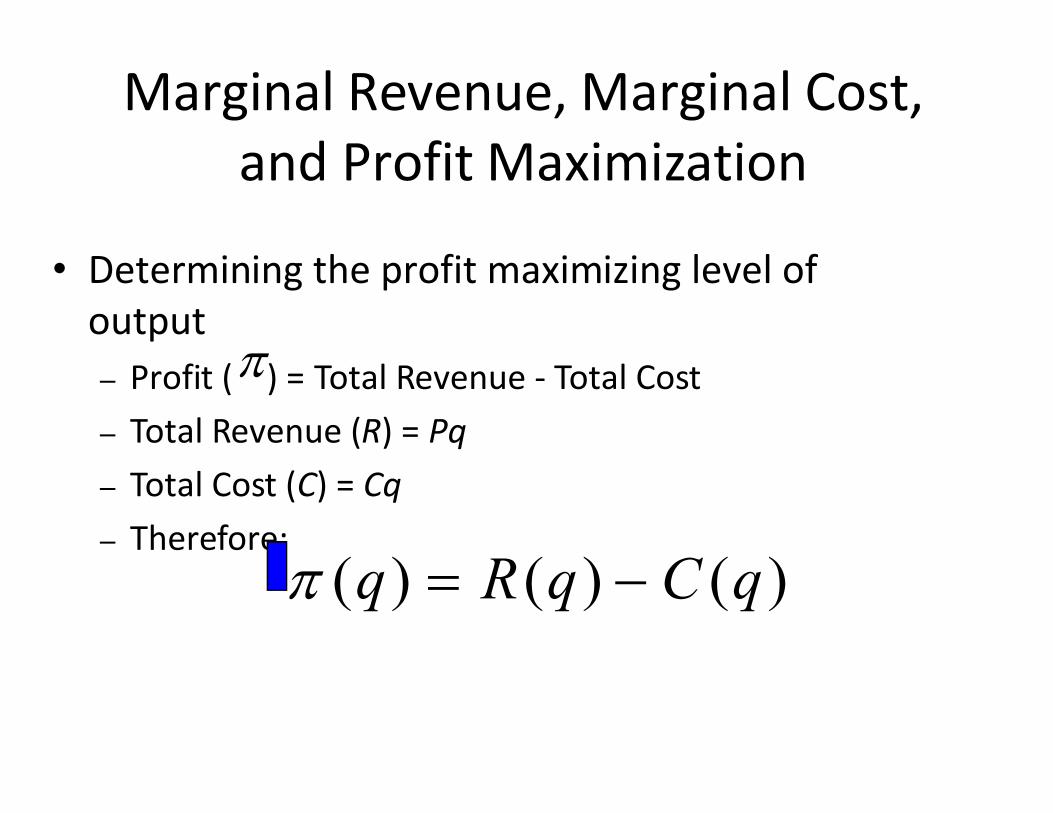

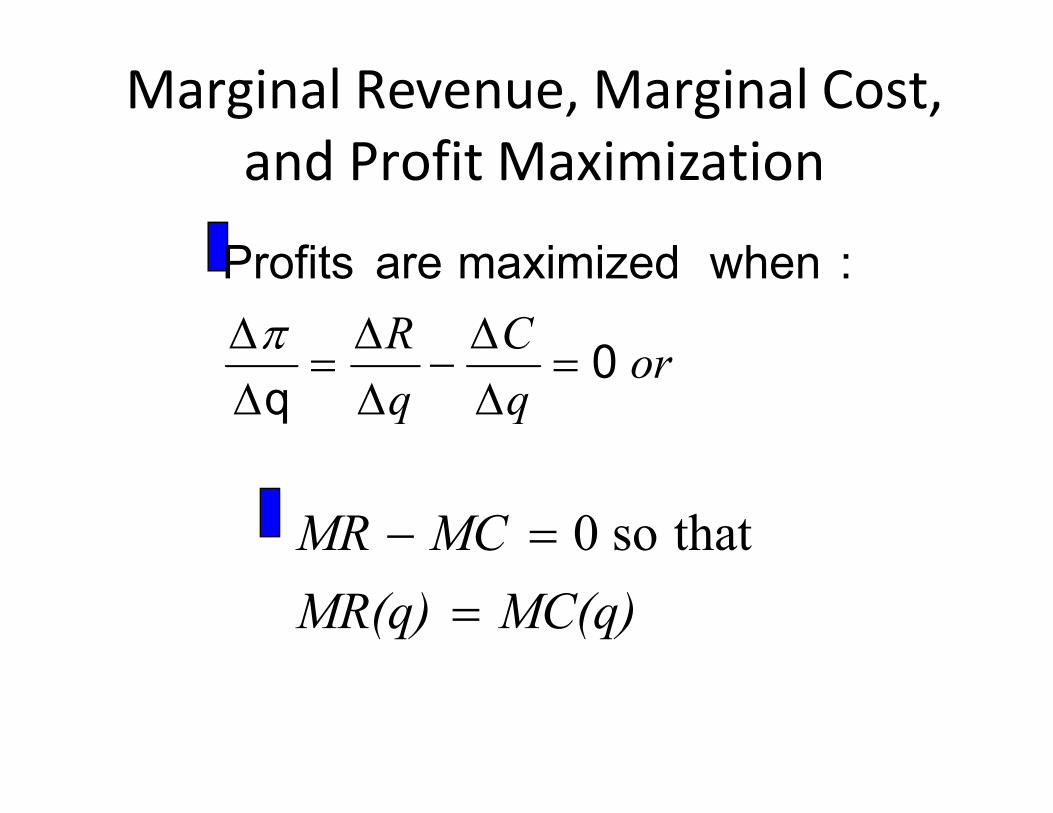

Marginal Revenue, Marginal Cost,and Profit Maximization

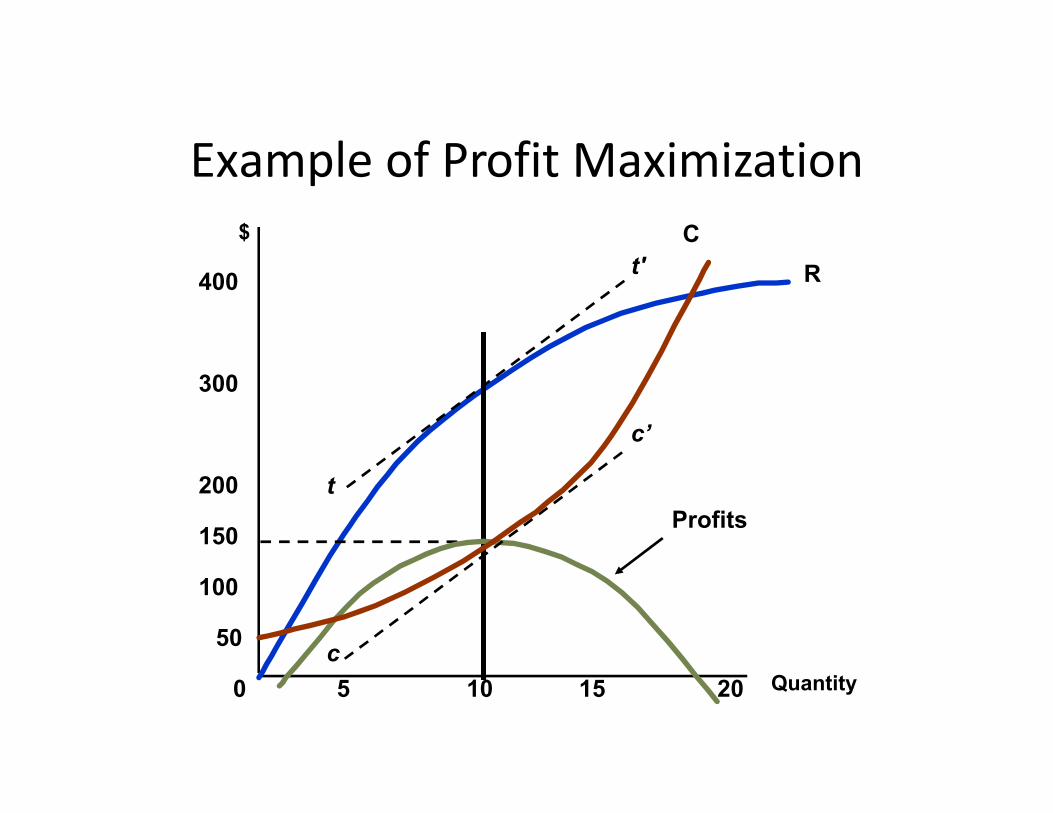

• Determining the profit maximizing level of output– Profit ( ) = Total Revenue - Total Cost– Total Revenue (R) = Pq– Total Cost (C) = Cq– Therefore:

)()()( qCqRq

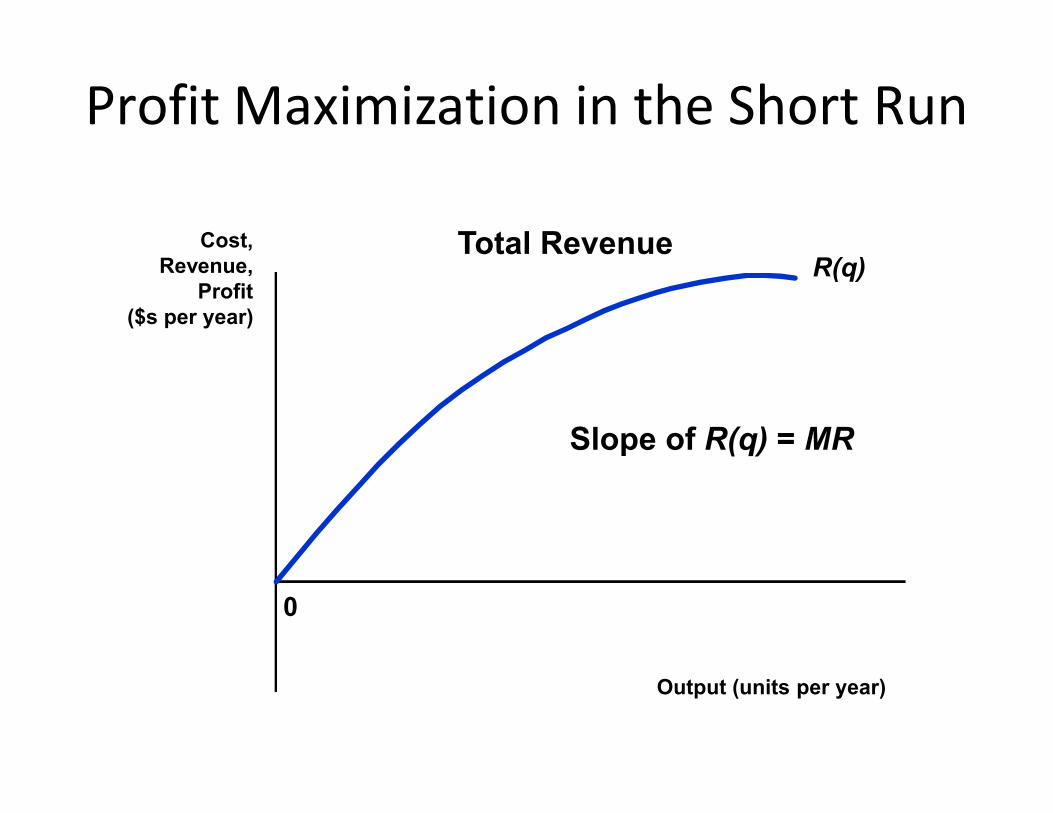

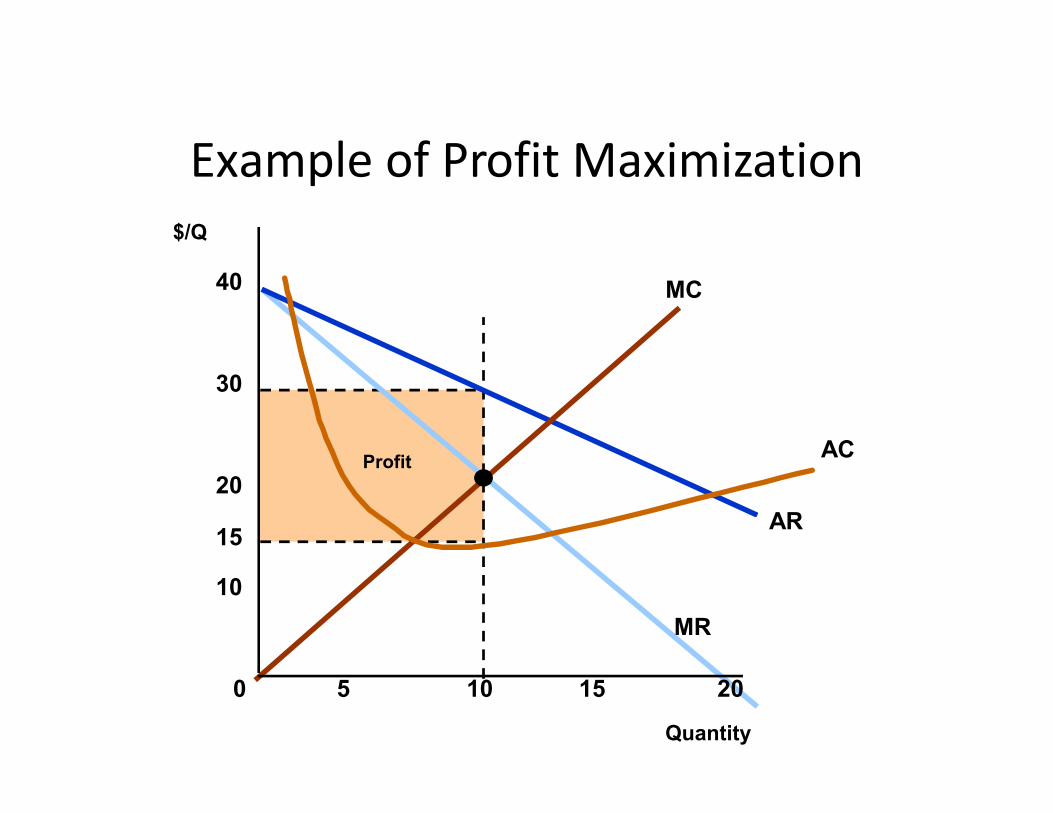

Profit Maximization in the Short Run

Cost,Revenue,

Profit($s per year)

R(q)Total Revenue

0

Output (units per year)

Slope of R(q) = MR

Cost,Revenue,

Profit$ (per year)

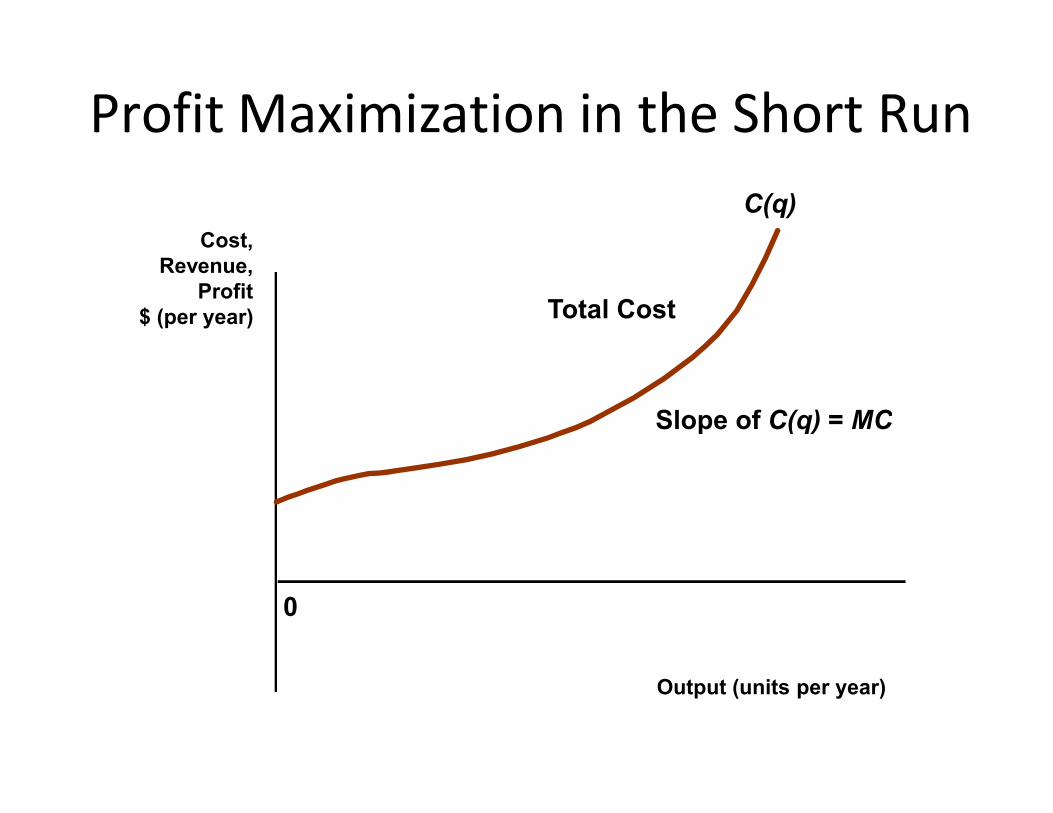

Profit Maximization in the Short RunC(q)

Total Cost

Slope of C(q) = MC

0

Output (units per year)

Slope of C(q) = MC

Marginal Revenue and Marginal Cost

• Marginal revenue is the additional revenue from producing one more unit of output.

• Marginal cost is the additional cost from Marginal cost is the additional cost from producing one more unit of output.

Marginal Revenue, Marginal Cost,and Profit Maximization

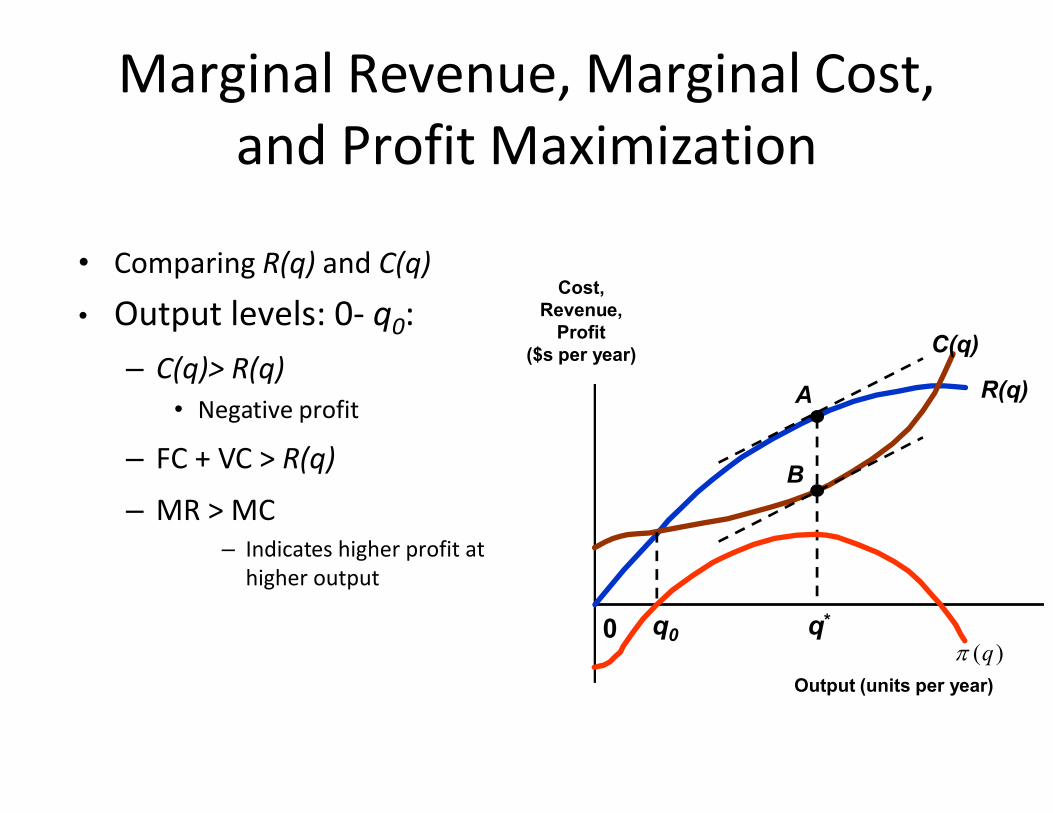

• Comparing R(q) and C(q)

• Output levels: 0- q0: – C(q)> R(q)

• Negative profit

Cost,Revenue,

Profit($s per year)

R(q)

C(q)

A• Negative profit

– FC + VC > R(q)

– MR > MC– Indicates higher profit at

higher output

0

Output (units per year)

A

B

q0 q*

)(q

Marginal Revenue, Marginal Cost,and Profit Maximization

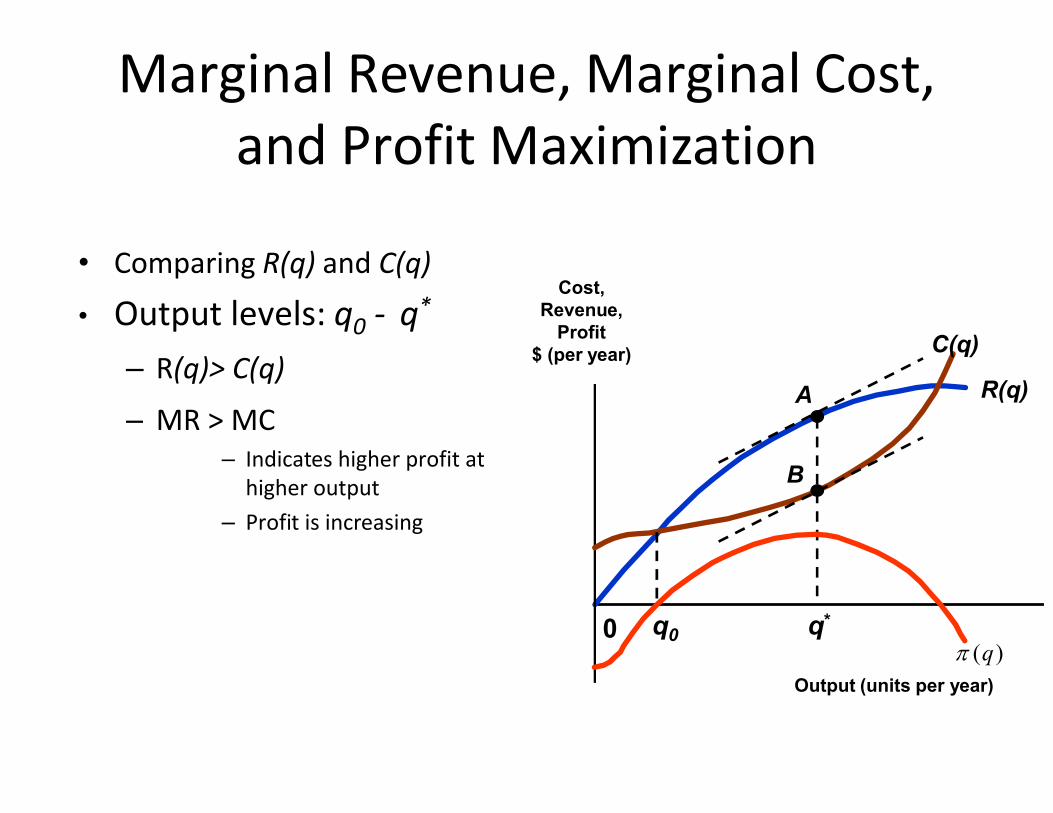

• Comparing R(q) and C(q)

• Output levels: q0 - q*

– R(q)> C(q)

– MR > MCR(q)

Cost,Revenue,

Profit$ (per year) C(q)

A– MR > MC

– Indicates higher profit at higher output

– Profit is increasing

0

Output (units per year)

A

B

q0 q*

)(q

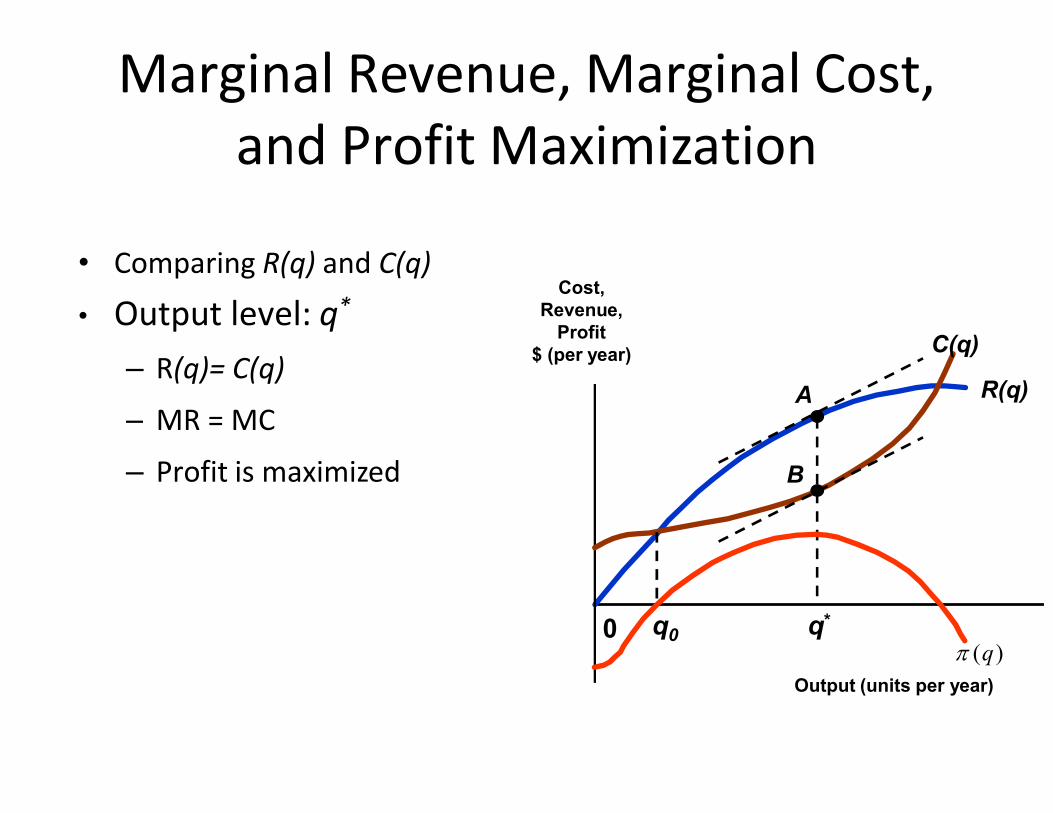

Marginal Revenue, Marginal Cost,and Profit Maximization

• Comparing R(q) and C(q)

• Output level: q*

– R(q)= C(q)

– MR = MCR(q)

Cost,Revenue,

Profit$ (per year) C(q)

A– MR = MC

– Profit is maximized

0

Output (units per year)

A

B

q0 q*

)(q

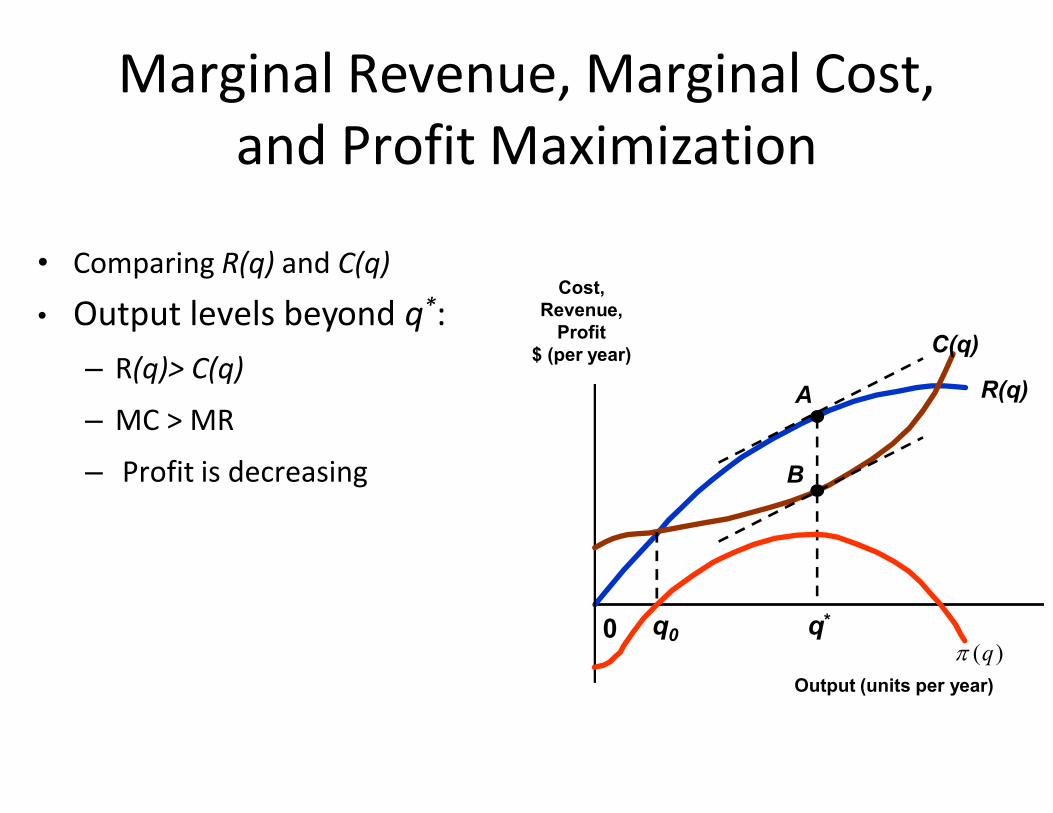

Marginal Revenue, Marginal Cost,and Profit Maximization

• Comparing R(q) and C(q)

• Output levels beyond q*: – R(q)> C(q)

– MC > MRR(q)

Cost,Revenue,

Profit$ (per year) C(q)

A– MC > MR

– Profit is decreasing

0

Output (units per year)

A

B

q0 q*

)(q

C-Rq

RMR

Marginal Revenue, Marginal Cost,and Profit Maximization

C-Rq

q

CMC

orq

C

q

R0

q

: whenmaximizedareProfits

Marginal Revenue, Marginal Cost,and Profit Maximization

qqq

MC(q)MR(q)

MCMR

thatso0

Demand and MR

• The Competitive Firm

– Price taker

– Market output (Q) and firm output (q)– Market output (Q) and firm output (q)

– Market demand (D) and firm demand (d)

– R(q) is a straight line

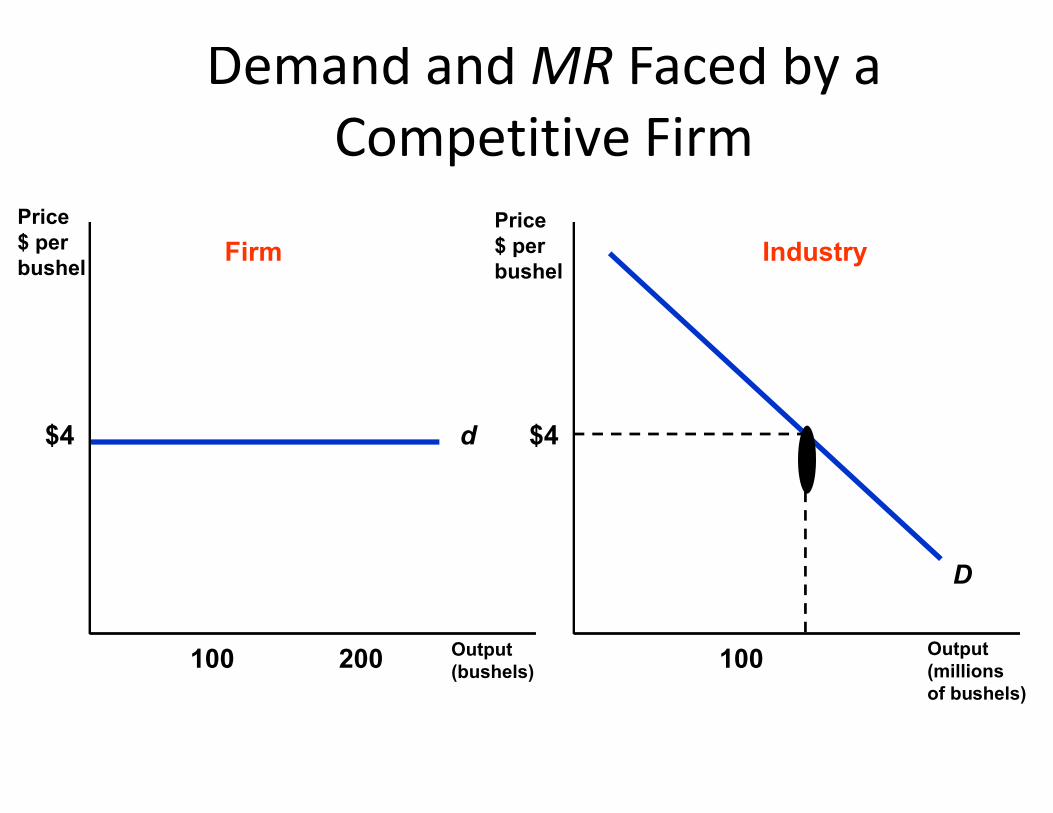

Demand and MR Faced by aCompetitive Firm

Price$ per bushel

Firm IndustryPrice$ per bushel

Output (bushels)

Output (millions of bushels)

d$4

100 200 100

D

$4

Demand and MR Faced by aCompetitive Firm

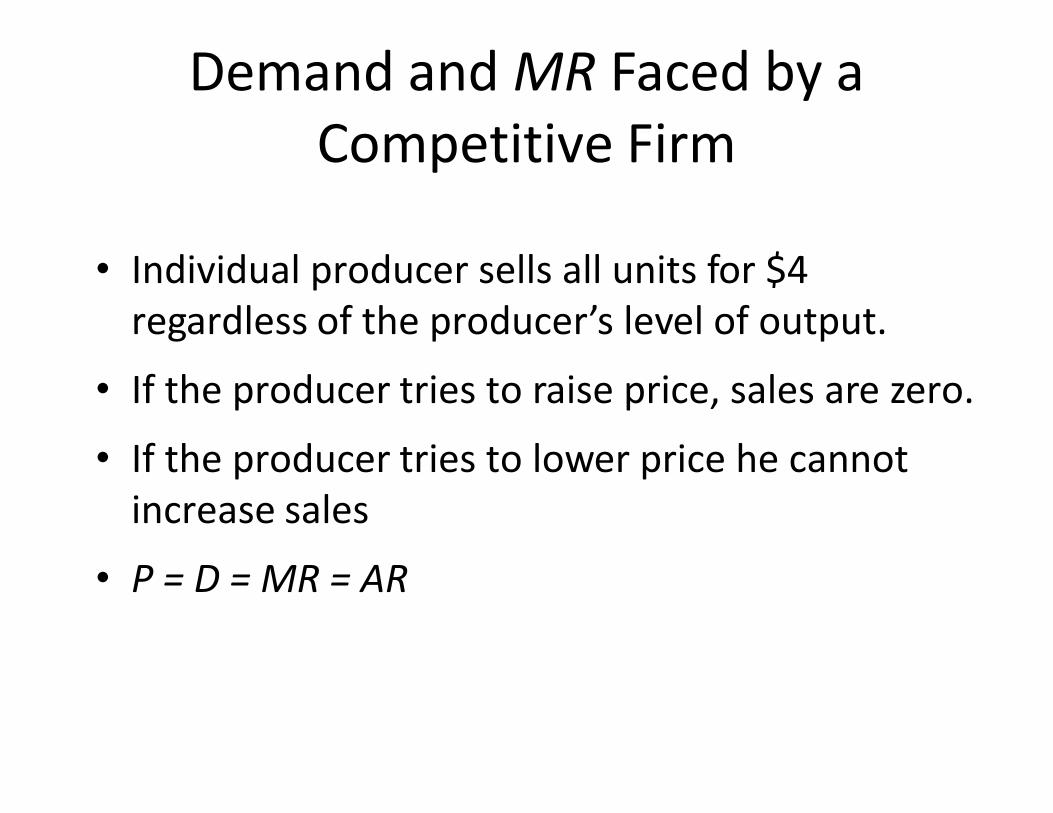

• Individual producer sells all units for $4 regardless of the producer’s level of output.

• If the producer tries to raise price, sales are zero.• If the producer tries to raise price, sales are zero.

• If the producer tries to lower price he cannot increase sales

• P = D = MR = AR

Choosing Output in the Short Run

• We will combine production and cost analysis with demand to determine output and profitability.

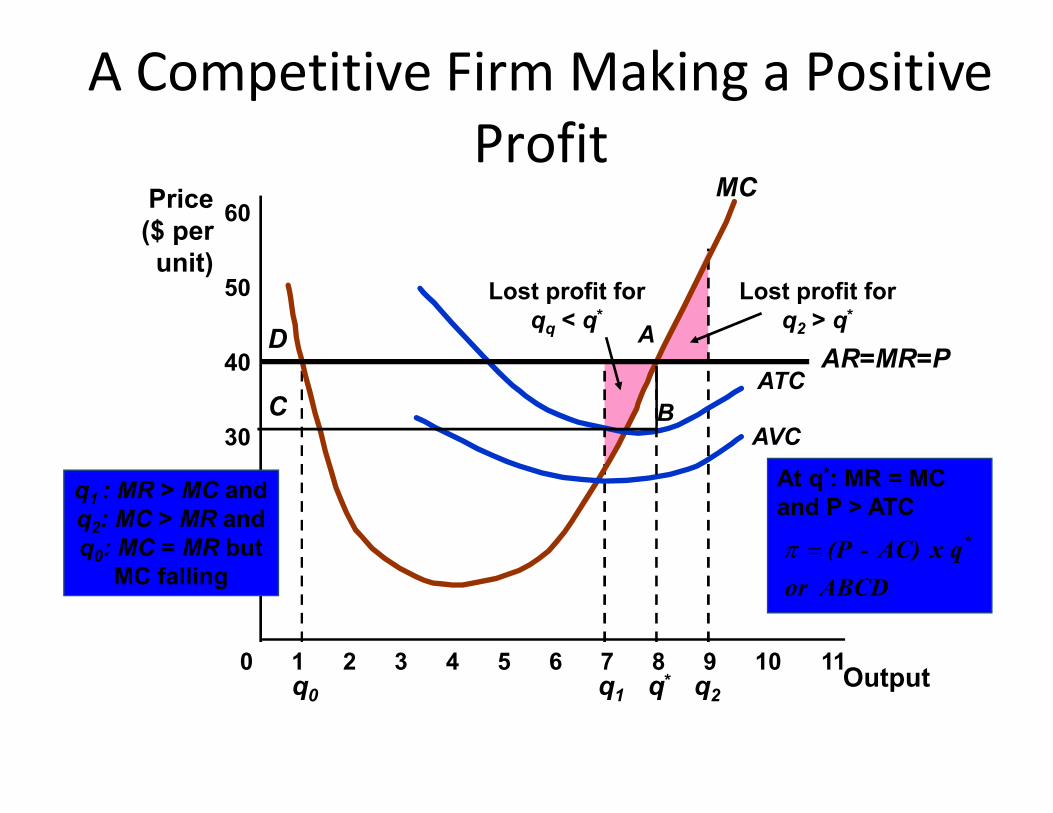

Lost profit forqq < q*

Lost profit forq2 > q*

A Competitive Firm Making a PositiveProfit

40

Price($ perunit)

50

60MC

ATCAR=MR=P

D A

BC

q0 q1 q2

10

20

30

0 1 2 3 4 5 6 7 8 9 10 11

AVC

Outputq*

At q*: MR = MCand P > ATC

ABCDor

qx AC) -(P *

BC

q1 : MR > MC andq2: MC > MR andq0: MC = MR but

MC falling

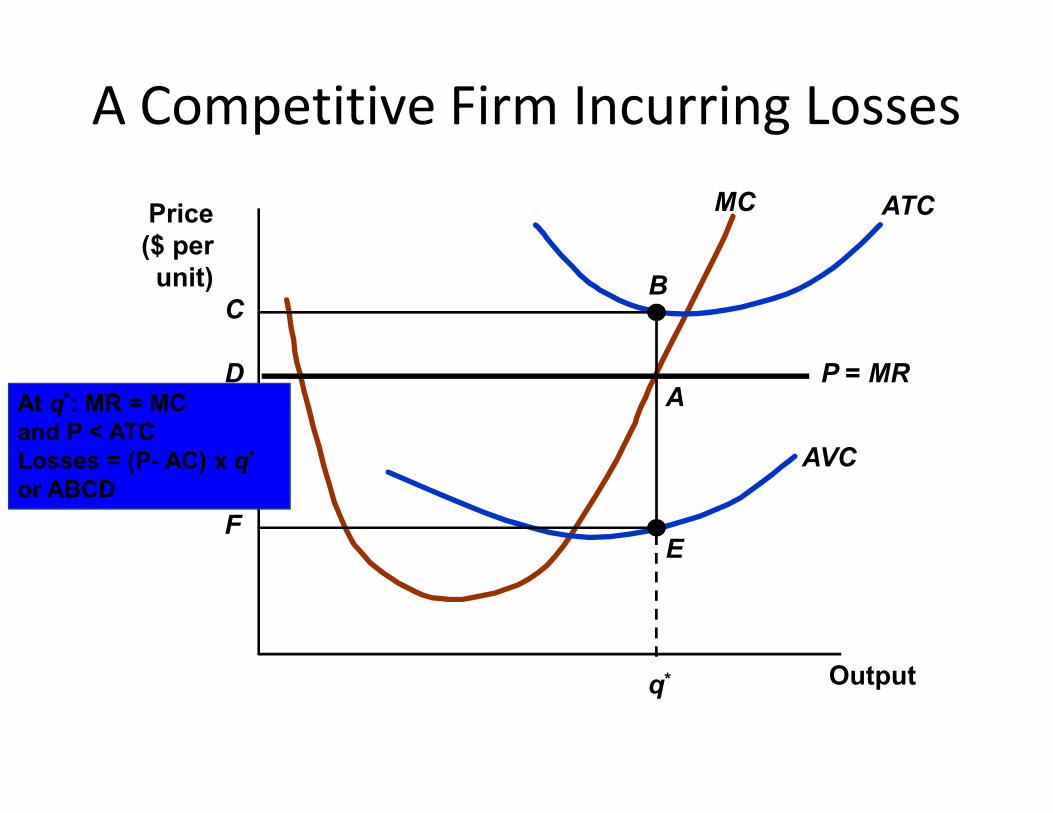

A Competitive Firm Incurring Losses

Price($ perunit)

ATCMC

P = MR

BC

AD

At q*: MR = MC

Output

AVC

q*

F

A

E

At q*: MR = MCand P < ATCLosses = (P- AC) x q*

or ABCD

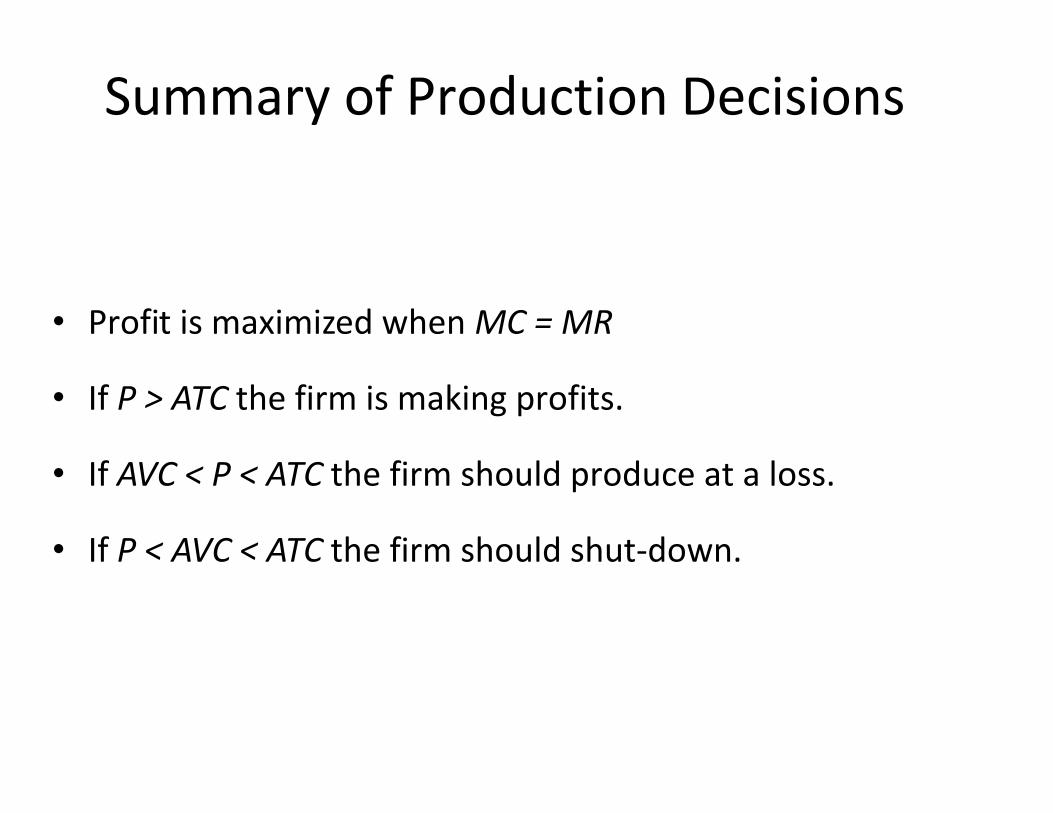

Summary of Production Decisions

• Profit is maximized when MC = MR

• If P > ATC the firm is making profits.• If P > ATC the firm is making profits.

• If AVC < P < ATC the firm should produce at a loss.

• If P < AVC < ATC the firm should shut-down.

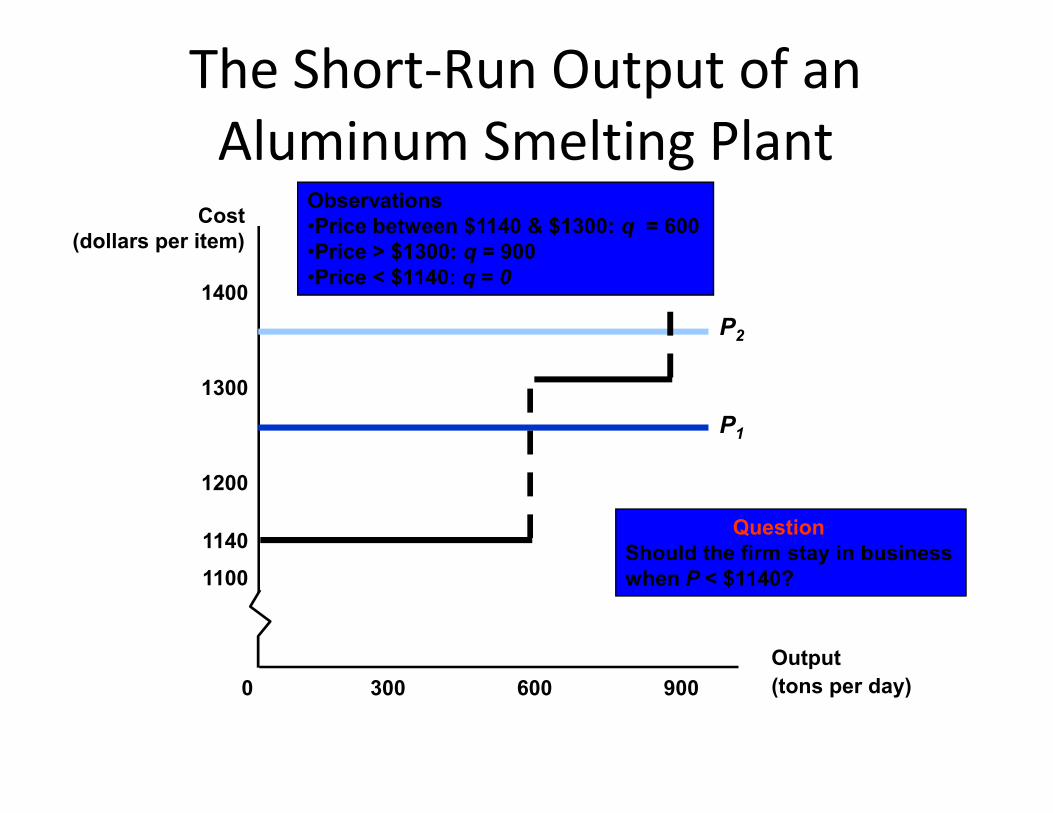

The Short-Run Output of anAluminum Smelting Plant

Cost(dollars per item)

1300

1400

P2

Observations•Price between $1140 & $1300: q = 600•Price > $1300: q = 900•Price < $1140: q = 0

Output (tons per day)300 600 9000

1100

1200

1140

P1

QuestionShould the firm stay in businesswhen P < $1140?

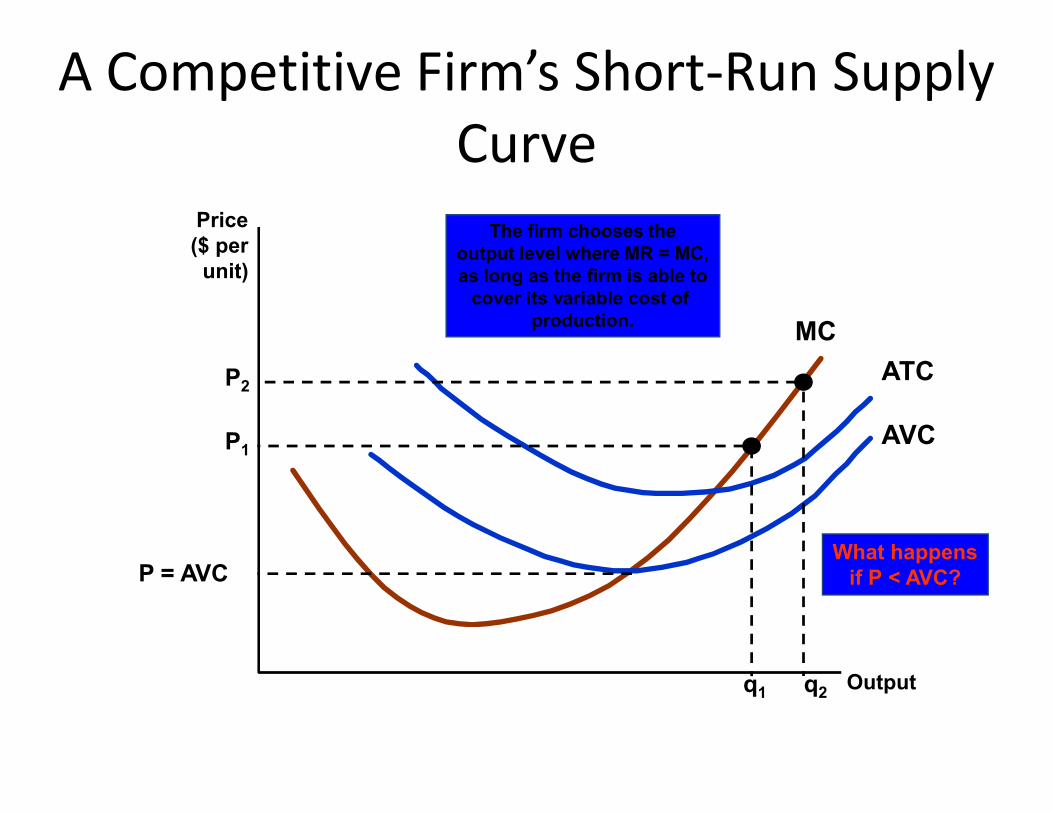

A Competitive Firm’s Short-Run SupplyCurve

Price($ per

unit)

MC

ATCP2

The firm chooses theoutput level where MR = MC,as long as the firm is able to

cover its variable cost of production.

Output

AVC

P = AVCWhat happens

if P < AVC?

q2

P1

q1

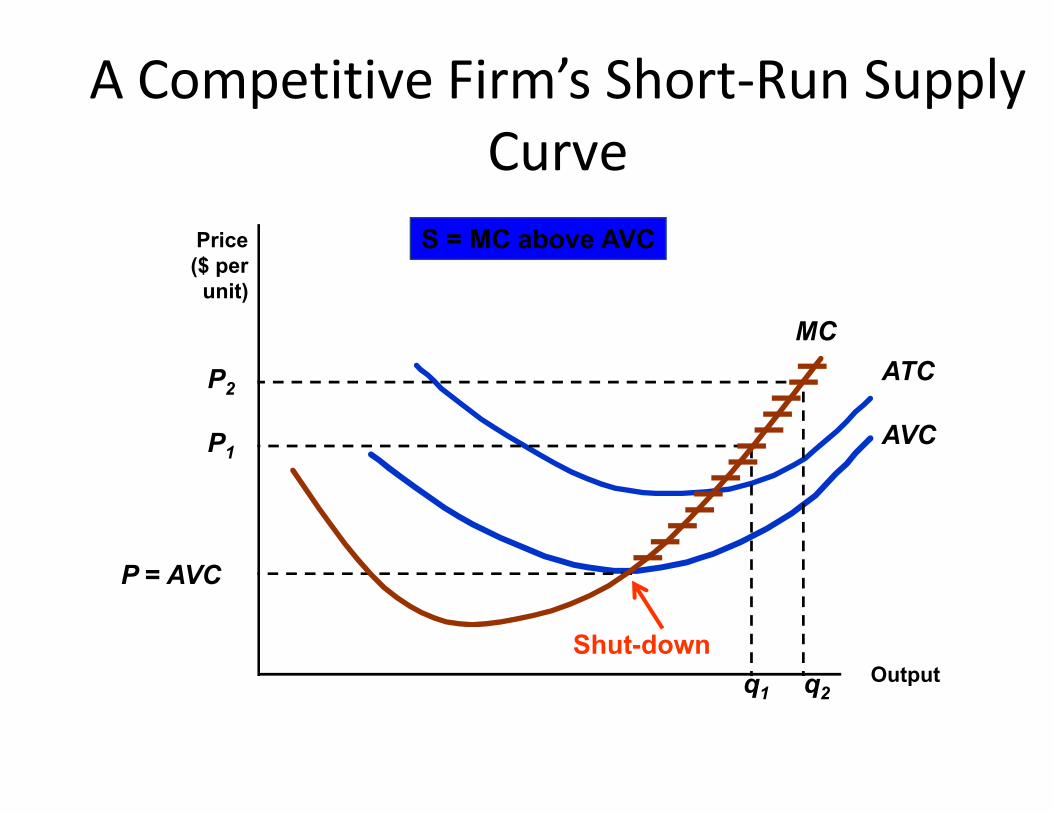

Price($ per

unit)

MC

ATCP2

S = MC above AVC

A Competitive Firm’s Short-Run SupplyCurve

Output

AVC

P = AVC

P1

q1 q2

Shut-down

A Competitive Firm’s Short-Run SupplyCurve

• Supply is upward sloping due to diminishing returns.• Higher price compensates the firm for higher cost of

additional output and increases total profit because it applies to all units.applies to all units.

• When the price of a firm’s input changes, the firm changes its output level, so that the marginal cost of production remains equal to the price.

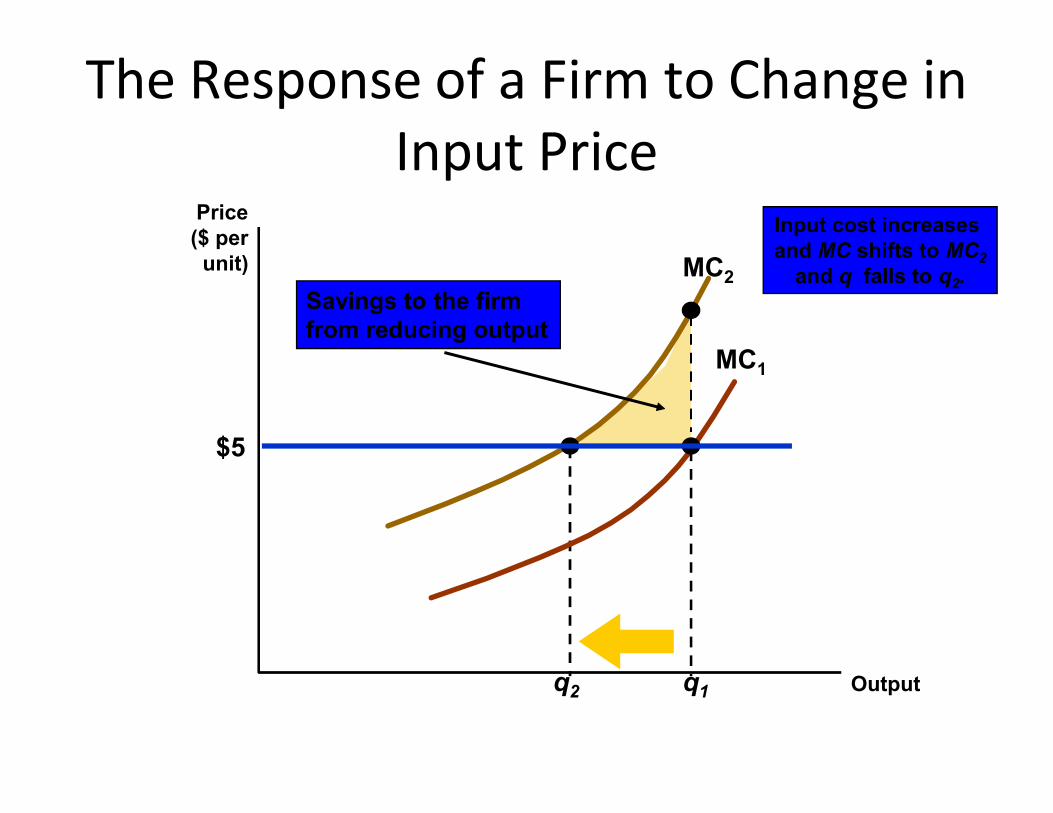

MC2

Input cost increases and MC shifts to MC2

and q falls to q2.

MC1

The Response of a Firm to Change inInput Price

Price($ per

unit)

Savings to the firmfrom reducing output

q2 q1 Output

$5

The Short-Run Production ofPetroleum Products

Cost($ per

barrel)

26

27 SMC

The MC of producinga mix of petroleum products

from crude oil increasessharply at several levelsof output as the refinery

shifts from one processingunit to another.

Output(barrels/day)

8,000 9,000 10,000 11,000

23

24

25How much wouldbe produced if

P = $23? P = $24-$25?

MC3

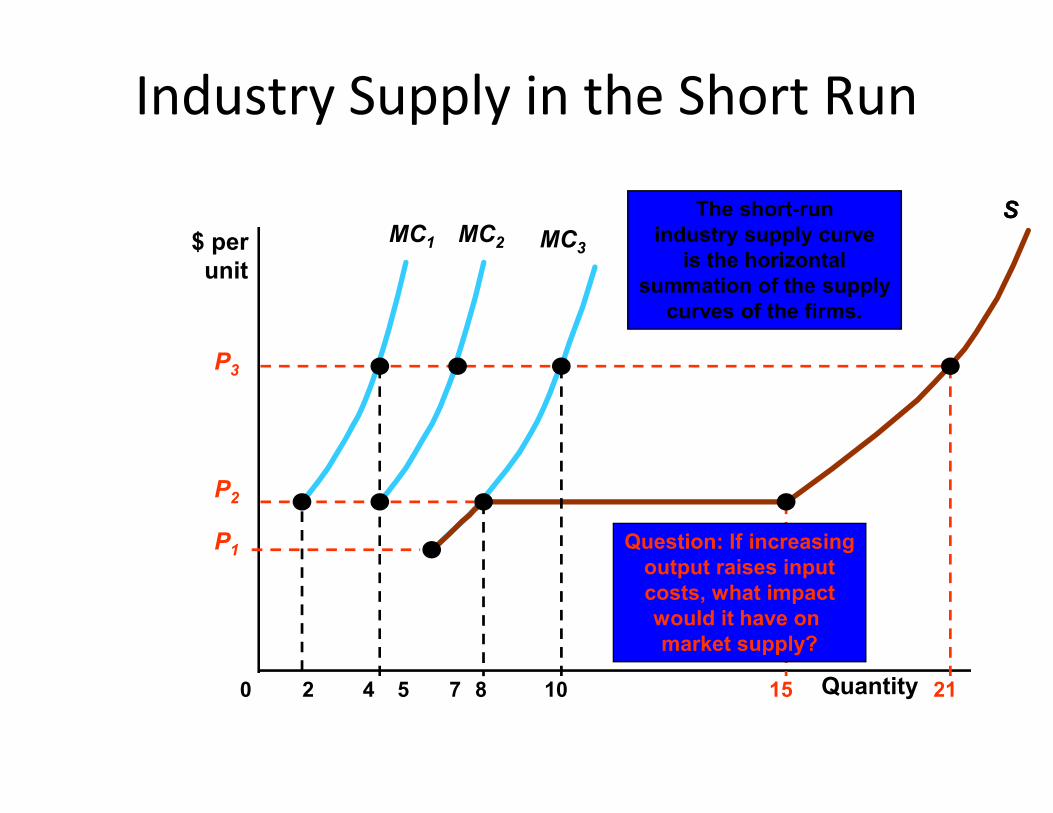

Industry Supply in the Short Run

$ perunit

MC1

SSThe short-runindustry supply curve

is the horizontalsummation of the supply

curves of the firms.

MC2

P3

0 2 4 8 105 7 15 21Quantity

P1

P2

Question: If increasingoutput raises inputcosts, what impactwould it have on market supply?

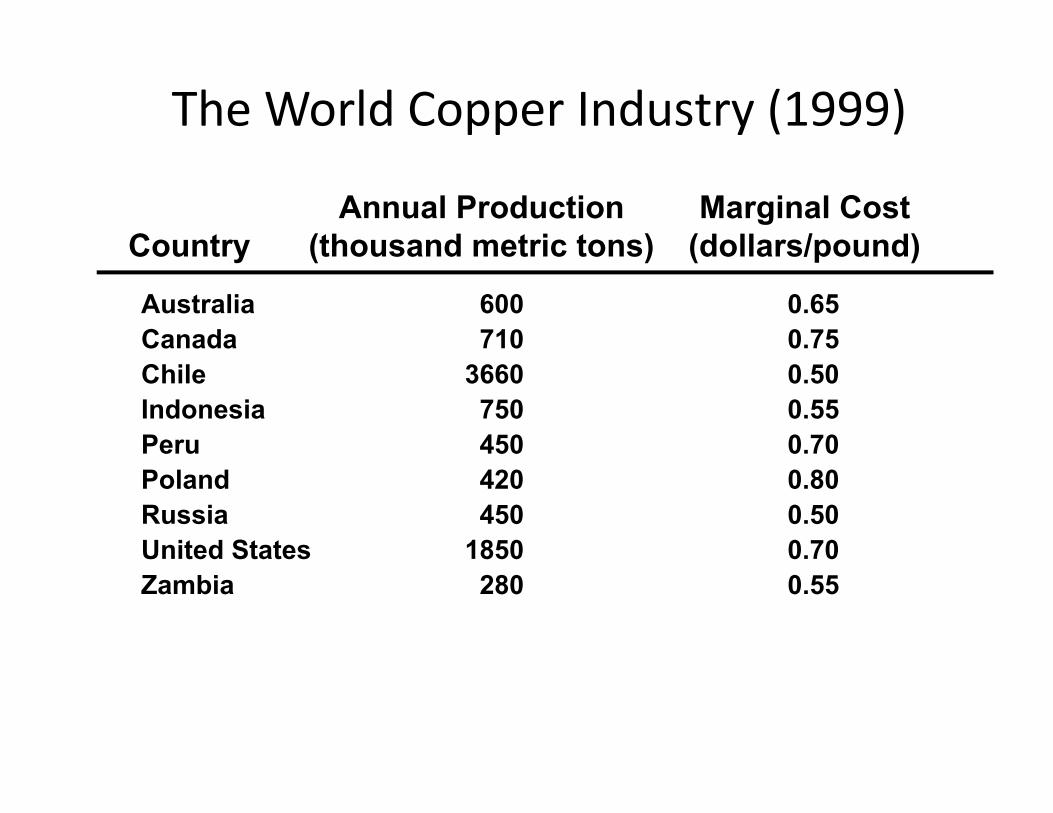

The World Copper Industry (1999)

Annual Production Marginal CostCountry (thousand metric tons) (dollars/pound)

Australia 600 0.65Canada 710 0.75Chile 3660 0.50Indonesia 750 0.55Indonesia 750 0.55Peru 450 0.70Poland 420 0.80Russia 450 0.50United States 1850 0.70Zambia 280 0.55

The Short-Run World Supply ofCopper

Price($ per pound)

0.80

0.90

MC ,MC

MCCa

MCPo

Production (thousand metric tons)0 2000 4000 6000 8000 10000

0.40

0.50

0.60

0.70

MCC,MCR

MCJ,MCZ

MCA

MCP,MCUS

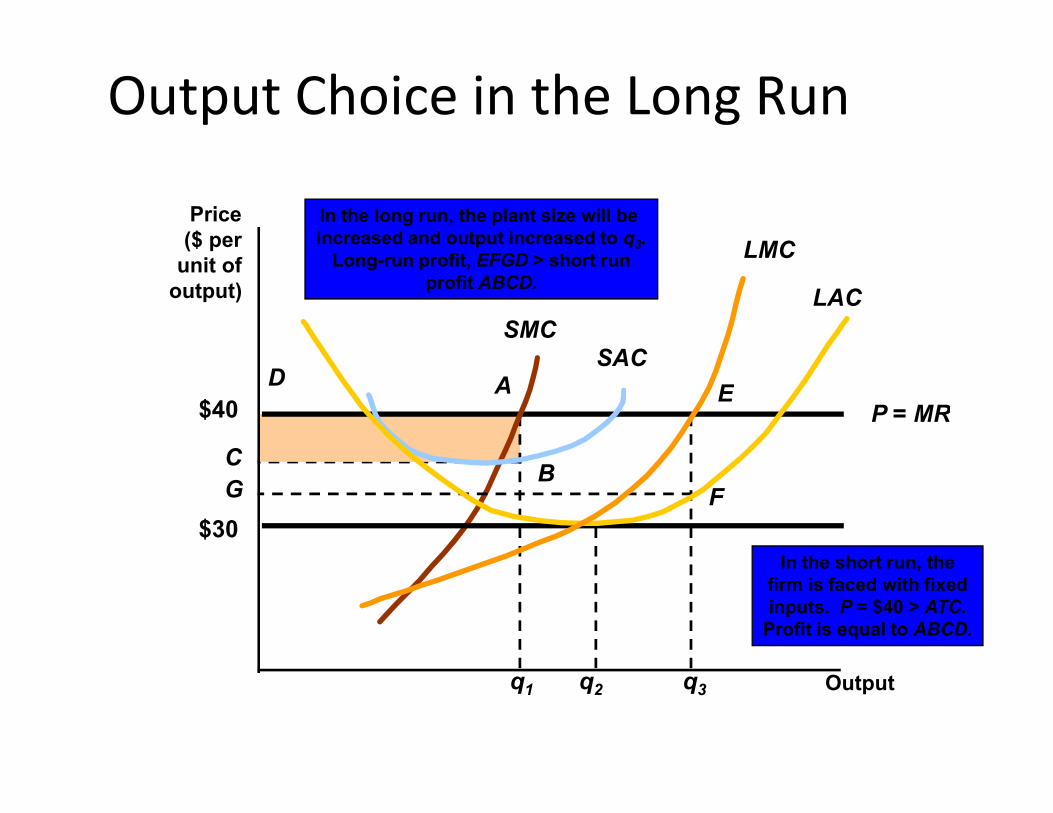

Choosing Output in the Long Run

• In the long run, a firm can alter all its inputs, including the size of the plant.

• We assume free entry and free exit.We assume free entry and free exit.

AD

Output Choice in the Long Run

Price($ per

unit ofoutput)

P = MR$40

SACSMC

In the long run, the plant size will be increased and output increased to q3.

Long-run profit, EFGD > short runprofit ABCD.

LAC

E

LMC

q1

BC

In the short run, thefirm is faced with fixedinputs. P = $40 > ATC.

Profit is equal to ABCD.

Output

P = MR$40

q3q2

G F$30

E

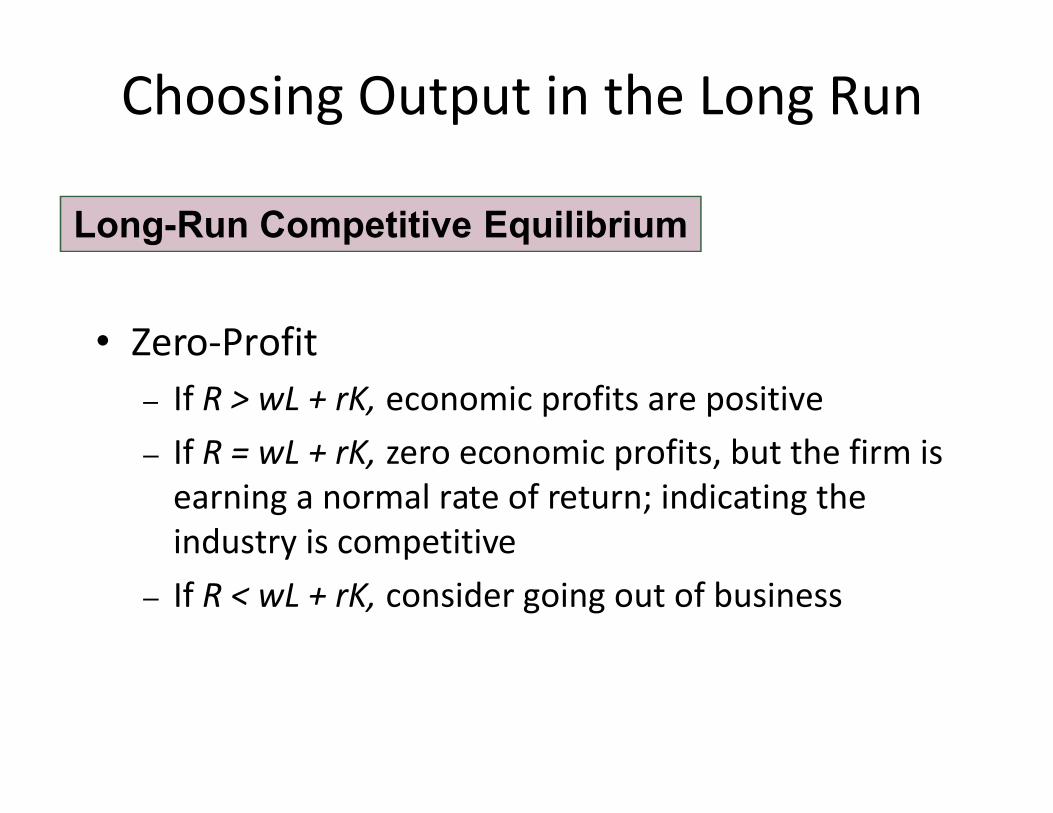

Choosing Output in the Long Run

• Zero-Profit– If R > wL + rK, economic profits are positive

Long-Run Competitive Equilibrium

– If R > wL + rK, economic profits are positive– If R = wL + rK, zero economic profits, but the firm is

earning a normal rate of return; indicating the industry is competitive

– If R < wL + rK, consider going out of business

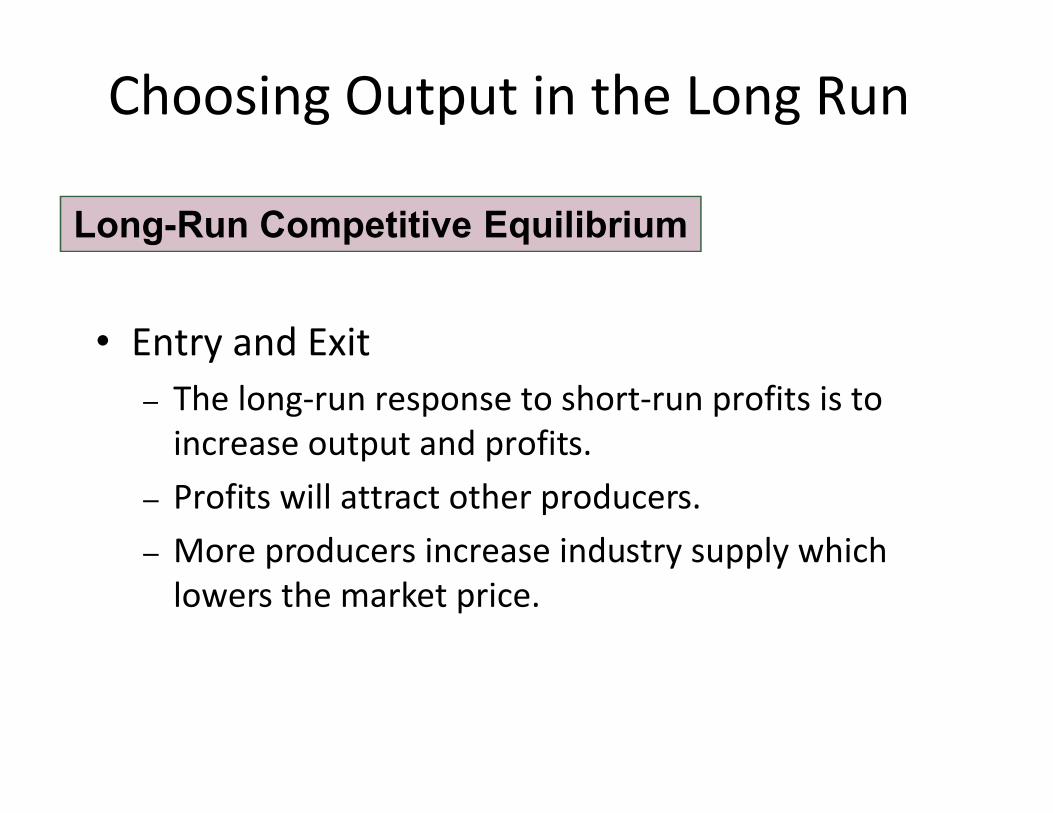

Choosing Output in the Long Run

• Entry and Exit– The long-run response to short-run profits is to

Long-Run Competitive Equilibrium

– The long-run response to short-run profits is to increase output and profits.

– Profits will attract other producers.– More producers increase industry supply which

lowers the market price.

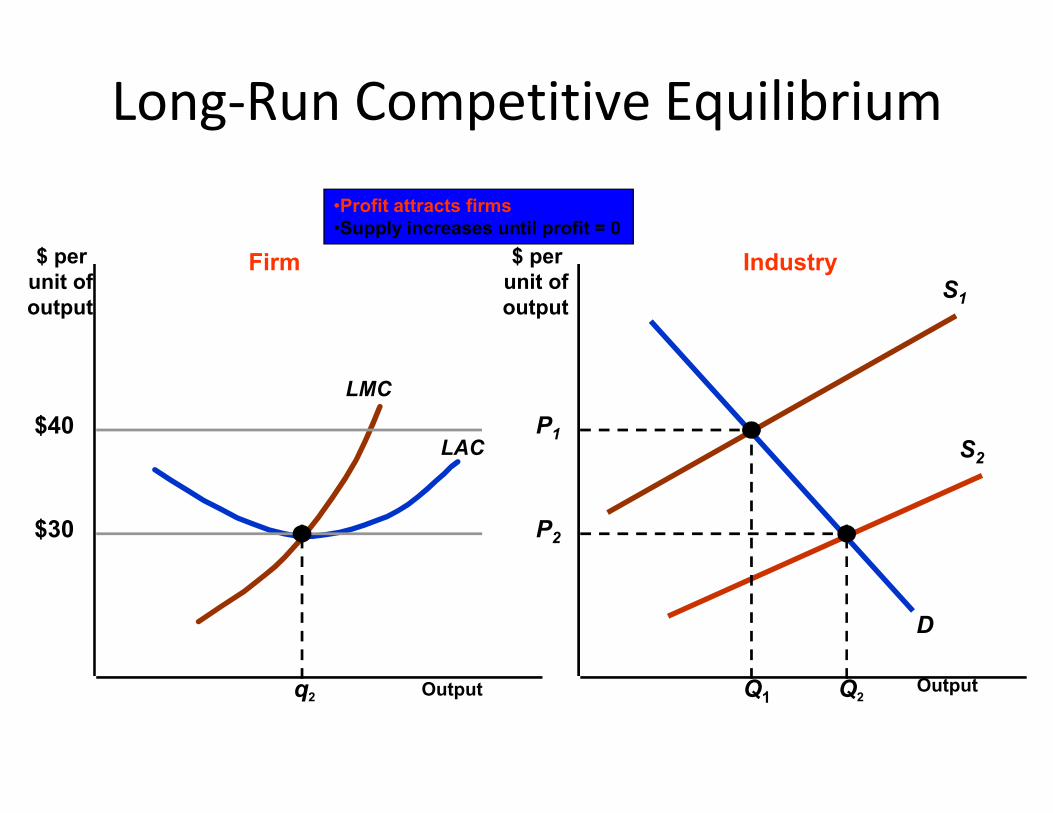

Long-Run Competitive Equilibrium

S1

$ per unit ofoutput

$ per unit ofoutput

LMC

Firm Industry

•Profit attracts firms•Supply increases until profit = 0

Output Output

$40LAC

D

S2

P1

Q1q2

$30

Q2

P2

Long-Run Competitive Equilibrium

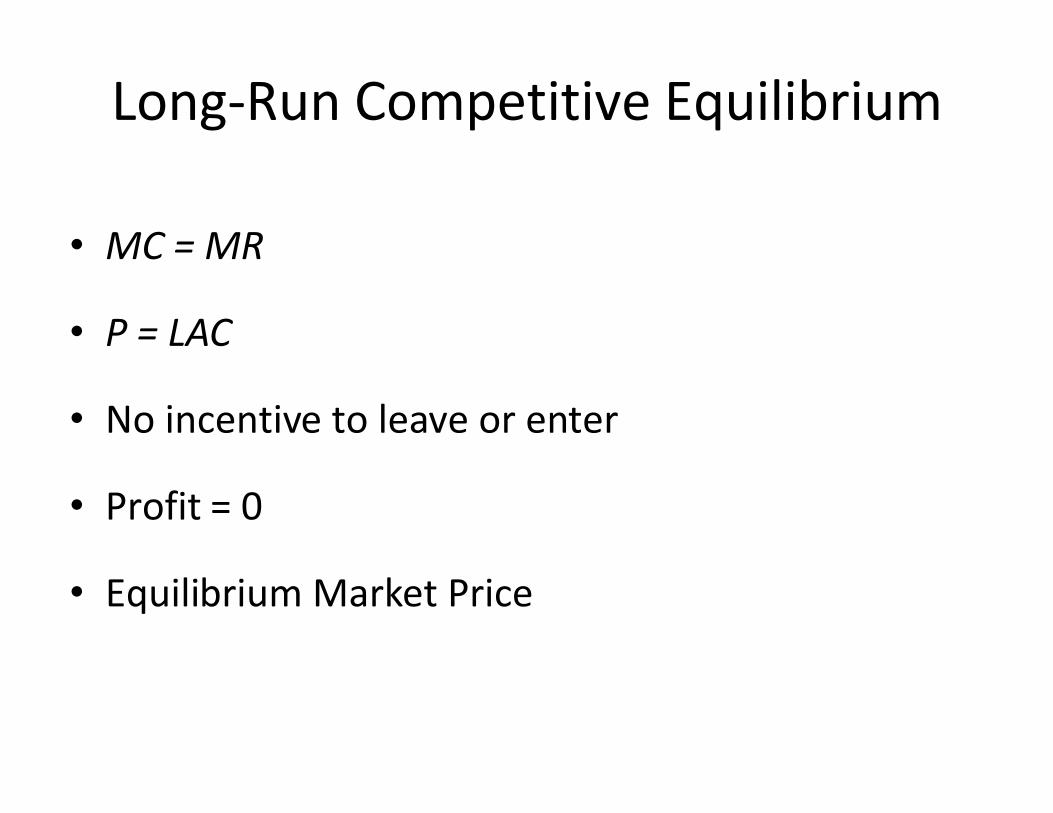

• MC = MR

• P = LAC

• No incentive to leave or enter• No incentive to leave or enter

• Profit = 0

• Equilibrium Market Price

The Industry’s Long-Run Supply Curve

• The shape of the long-run supply curve depends on the extent to which changes in industry output affect the prices the firms must pay for inputs.

• To determine long-run supply, we assume:• To determine long-run supply, we assume:

– All firms have access to the available production technology.

– Output is increased by using more inputs, not by invention.

– The market for inputs does not change with expansions and contractions of the industry.

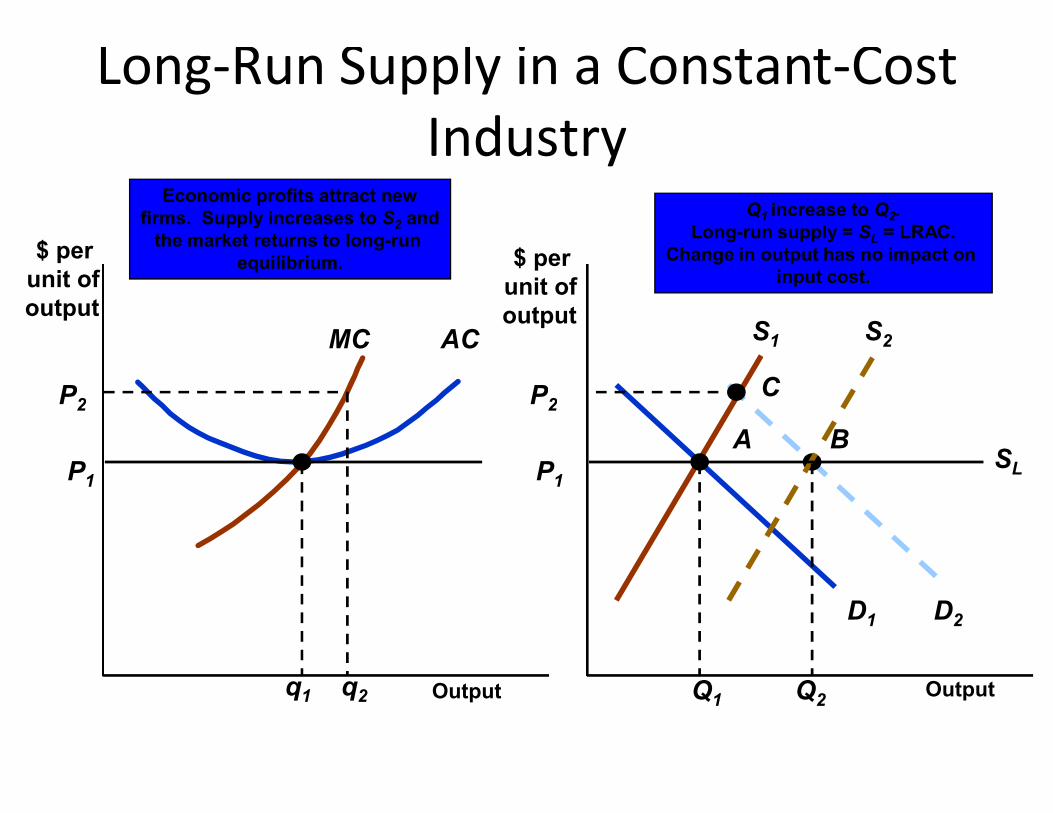

Long-Run Supply in a Constant-CostIndustry

ACMC S1

CP2P2

S2

Economic profits attract newfirms. Supply increases to S2 and

the market returns to long-run equilibrium. $ per

unit ofoutput

Q1 increase to Q2.Long-run supply = SL = LRAC.

Change in output has no impact on input cost.

$ per unit ofoutput

AP1 P1

q1

D1

Q1

D2

P2P2

q2

B

Q2Output Output

SL

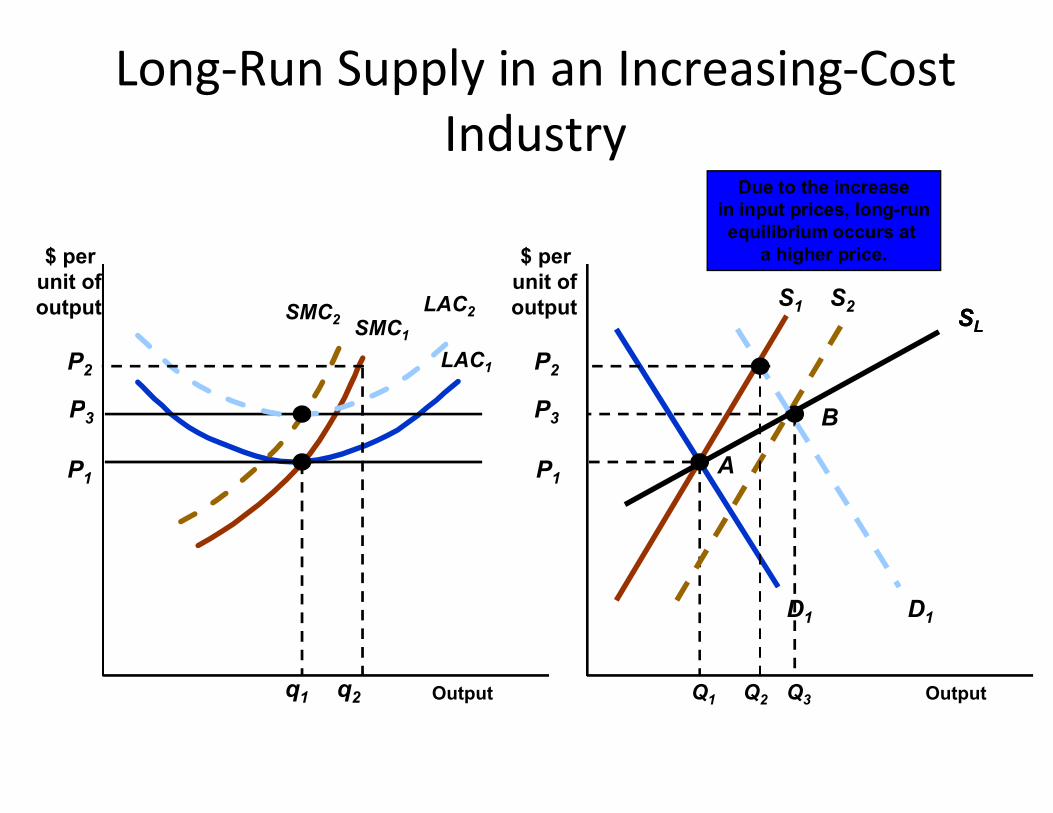

Long-Run Supply in an Increasing-Cost Industry

$ per unit ofoutput

$ per unit ofoutput S1

LAC1

SMC1SSLL

P

SMC2

Due to the increasein input prices, long-runequilibrium occurs at

a higher price.

LAC2

B

S2

P

P2 P2

Output Output

D1

P1 P1

q1 Q1

A

P3 BP3

Q3q2

D1

Q2

Long-Run Supply in an Decreasing-Cost Industry

S2

SMC2

Due to the decreasein input prices, long-runequilibrium occurs at

a lower price.$ per unit ofoutput

$ per unit ofoutput

SMC1

S1

LAC1

P2 P2

B

SL

P3

Q3

P3

LAC2

Output Output

P1P1

A

D1

Q1q1 Q2q2

P2 P2

D2

Long-Run Supply

• In a constant-cost industry, long-run supply is a horizontal line at a price that is equal to the minimum average cost of production.

• In an increasing-cost industry, the long-run supply • In an increasing-cost industry, the long-run supply curve is upward sloping.

• In a decreasing-cost industry, long-run supply curve is downward sloping.

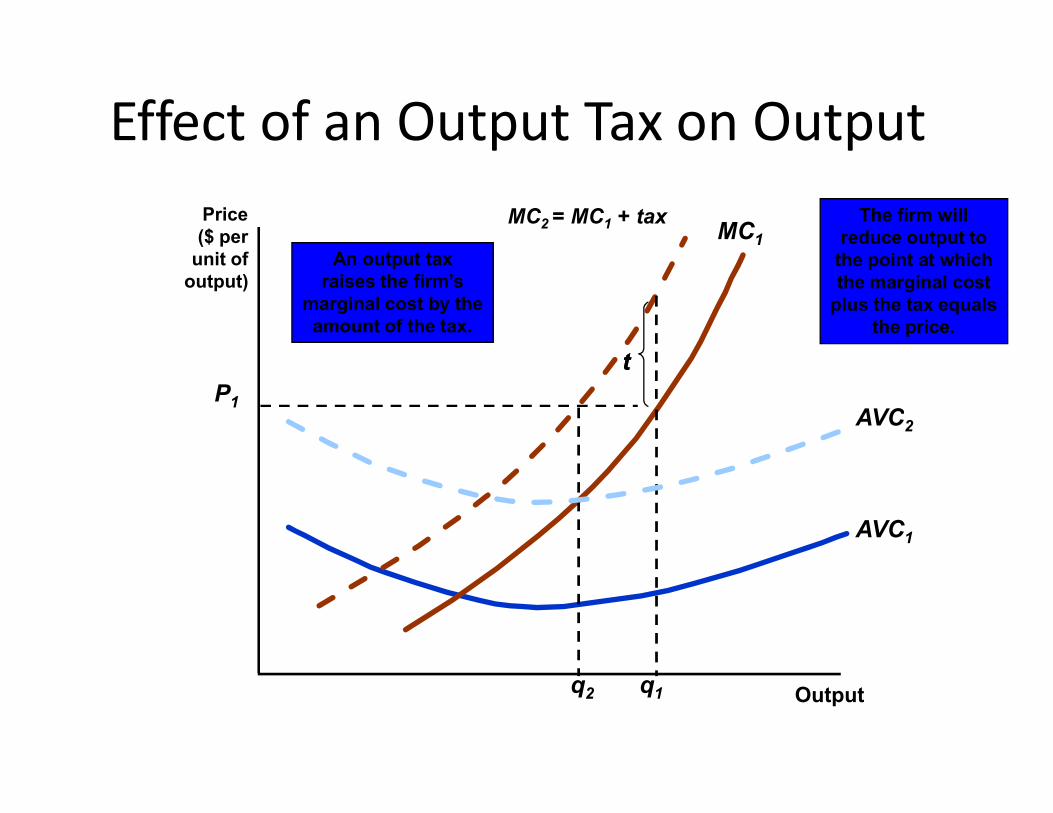

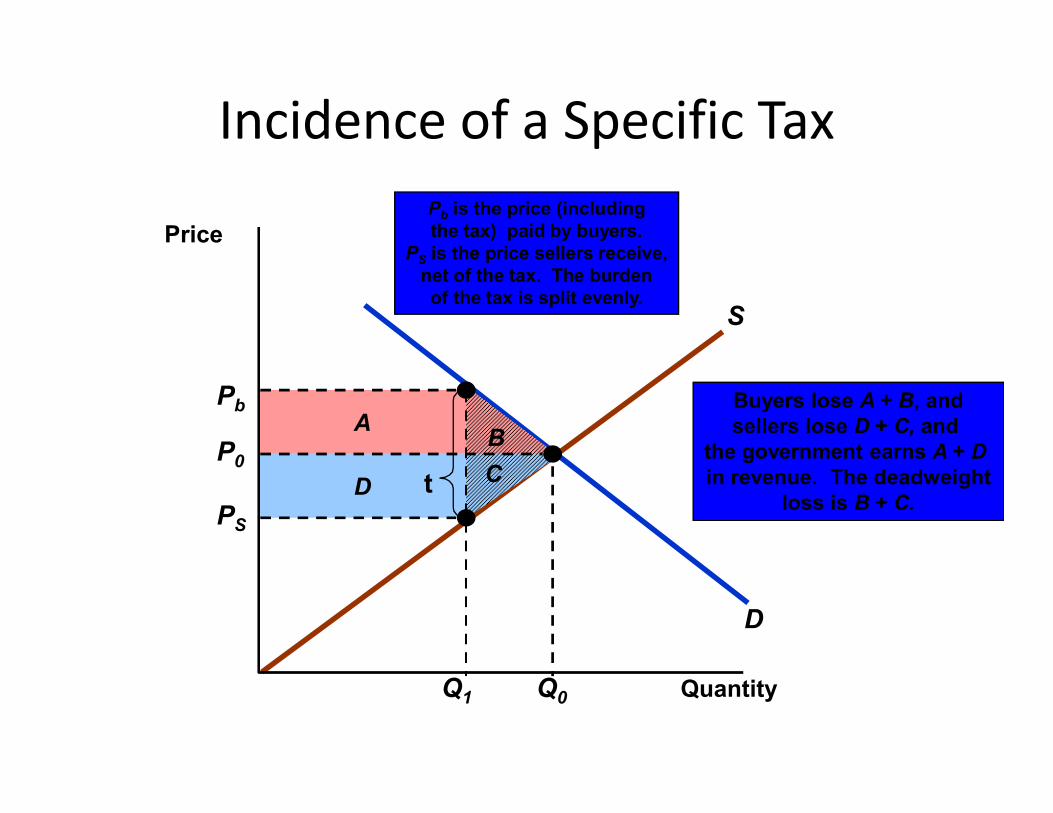

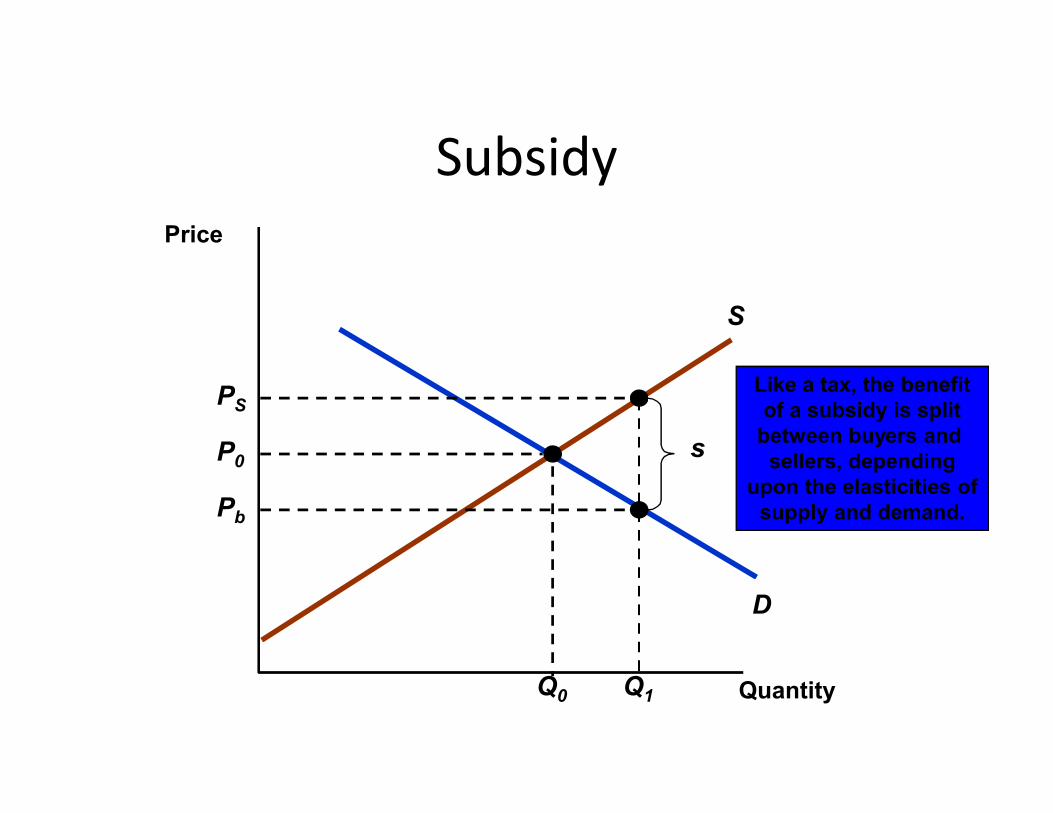

Effect of an Output Tax on OutputPrice($ per

unit ofoutput)

MC1

P1

The firm willreduce output to

the point at whichthe marginal cost

plus the tax equalsthe price.

tt

MC2 = MC1 + tax

AVC

An output taxraises the firm’s

marginal cost by theamount of the tax.

Output

AVC1

P1

q1q2

AVC2

Effect of an Output Tax on OutputPrice($ per

unit ofoutput) SS1

P

SS2 = S1 + t

t

Output

DD

P1

Q1

P2

Q2

t

Tax shifts S1 to S2 andoutput falls to Q2. Price

increases to P2.

Summary• The managers of firms can operate in accordance with a

complex set of objectives and under various constraints.

• A competitive market makes its output choice under the assumption that the demand for its own output is horizontal.

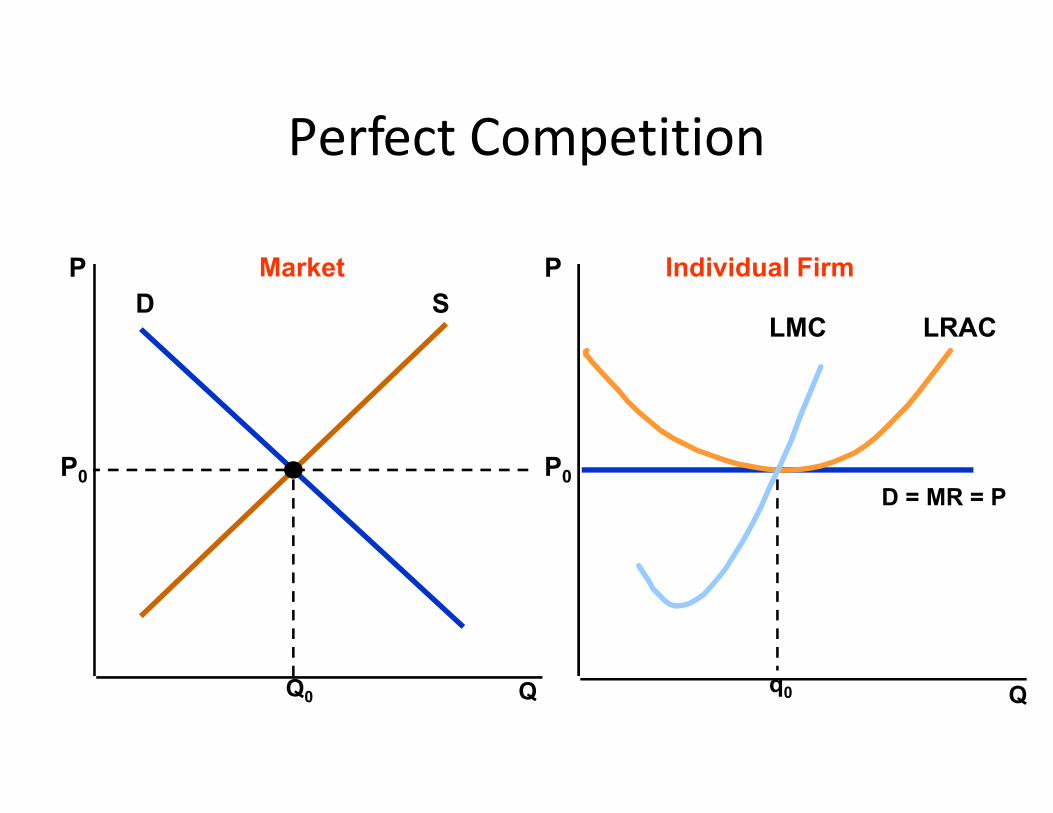

• In the short run, a competitive firm maximizes its profit by choosing an output at which price is equal to (short-run) marginal cost.

• The short-run market supply curve is the horizontal summation of the supply curves of the firms in an industry.

Summary

• In the long-run, profit-maximizing competitive firms choose the output at which price is equal to long-run marginal cost.

• The long-run supply curve for a firm can be horizontal, upward sloping, or downward sloping.

Analysis of competitive marketsAnalysis of competitive markets

Topics to be Discussed• Evaluating the Gains and Losses from Government Policies-

-Consumer and Producer Surplus

• The Efficiency of a Competitive Market

• Minimum Prices• Minimum Prices

• Price Supports and Production Quotas

• Import Quotas and Tariffs

• The Impact of a Tax or Subsidy

Consumer and Producer Surplus

• Consumer surplus is the total benefit or value that consumers receive beyond what they pay for the good.

• Producer surplus is the total benefit or revenue • Producer surplus is the total benefit or revenue that producers receive beyond what it cost to produce a good.

Consumer and Producer Surplus

ConsumerSurplus

Price

S

10

7 Between 0 and Q0

consumers A and B

ProducerSurplus

Between 0 and Q0

producers receive a net gain from

selling each product--producer surplus.

Quantity0

D

5

Q0

Consumer CConsumer BConsumer A

consumers A and Breceive a net gain from

buying the product--consumer surplus

Consumer and Producer Surplus

• To determine the welfare effect of a government policy we can measure the gain or loss in consumer and producer surplus.

• Welfare Effects

– Gains and losses caused by government intervention in the market.

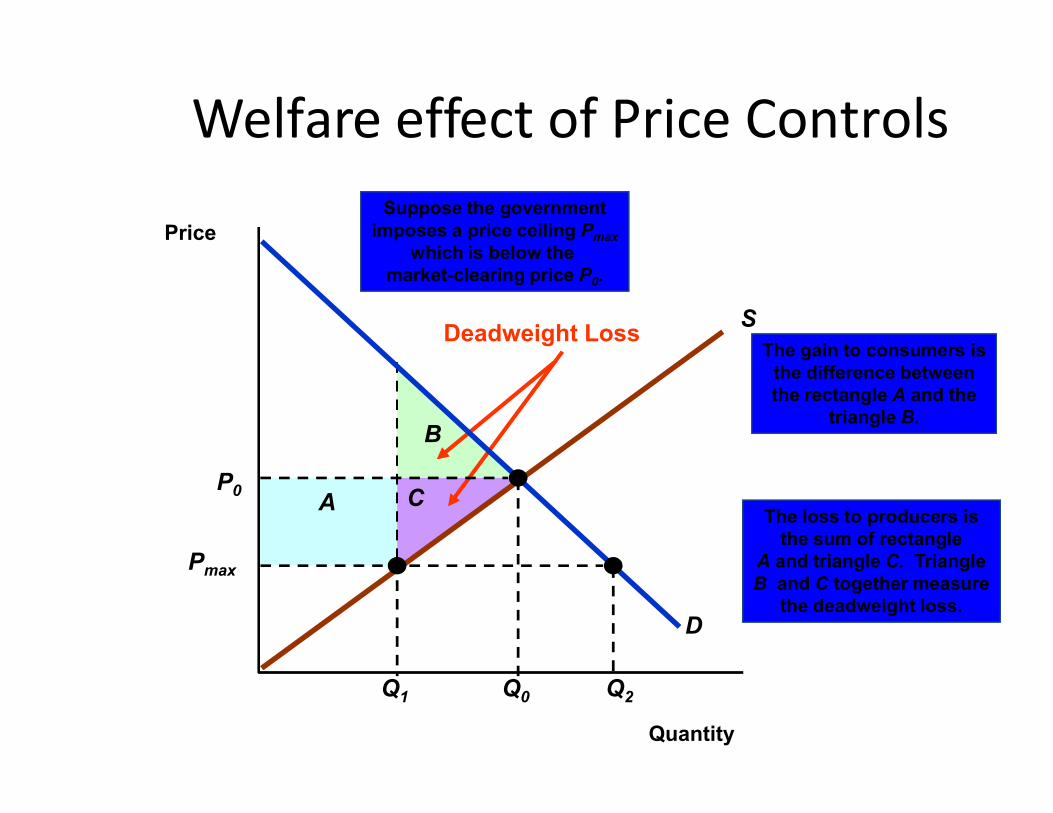

The gain to consumers isthe difference betweenthe rectangle A and the

Deadweight Loss

Welfare effect of Price Controls

Price

S

Suppose the governmentimposes a price ceiling Pmax

which is below the market-clearing price P0.

The loss to producers isthe sum of rectangle

A and triangle C. TriangleB and C together measure

the deadweight loss.

B

A C

triangle B.

Quantity

D

P0

Q0

Pmax

Q1 Q2

Welfare effect of Price Controls

• The total loss is equal to area B + C.• The total change in surplus =

(A - B) + (-A - C) = -B - C

The deadweight loss is the inefficiency of the price • The deadweight loss is the inefficiency of the price controls.– The loss of producer surplus exceeds the gain from

consumer surplus.

Welfare effect of Price Controls

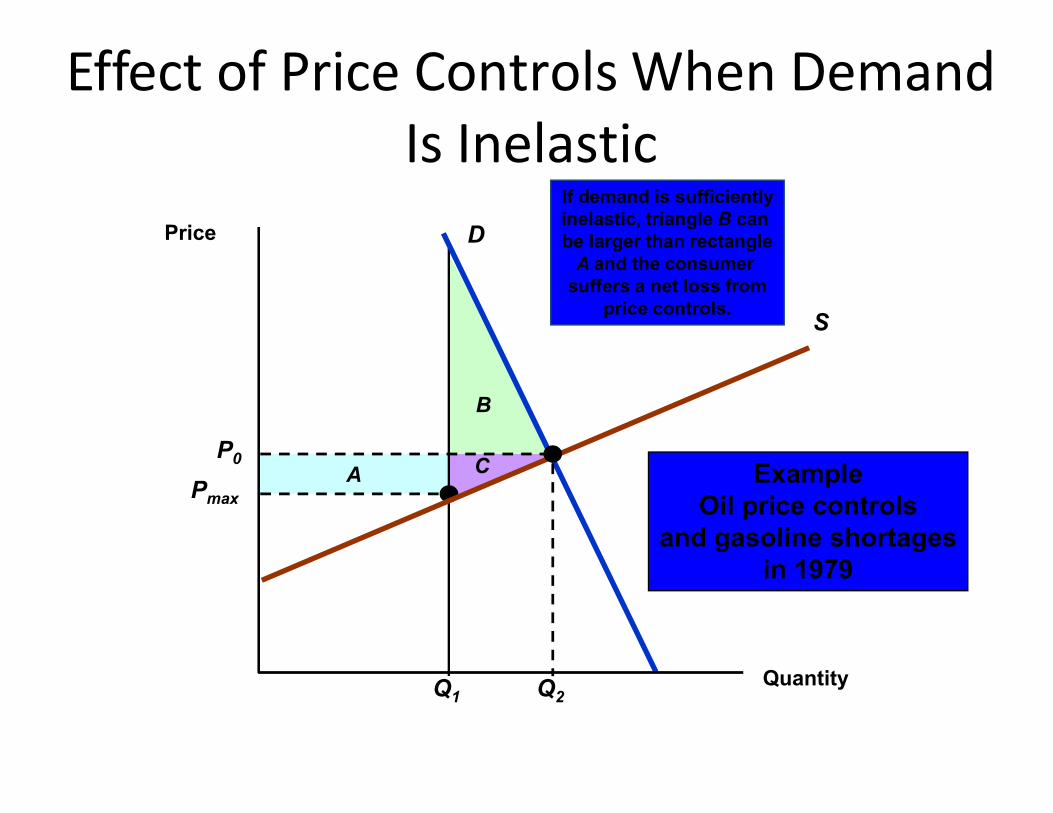

• Consumers can experience a net loss in consumer surplus when the demand is sufficiently inelastic

B

If demand is sufficientlyinelastic, triangle B can be larger than rectangle

A and the consumer suffers a net loss from

price controls.S

D

Effect of Price Controls When DemandIs Inelastic

Price

B

APmax

C

Q1

ExampleOil price controls

and gasoline shortagesin 1979

Quantity

P0

Q2

Price Controls and Natural Gas Shortages

• 1975 U.S.price controls created a shortage of natural gas.

• What was the deadweight loss?What was the deadweight loss?

Price Controls and Natural Gas Shortages

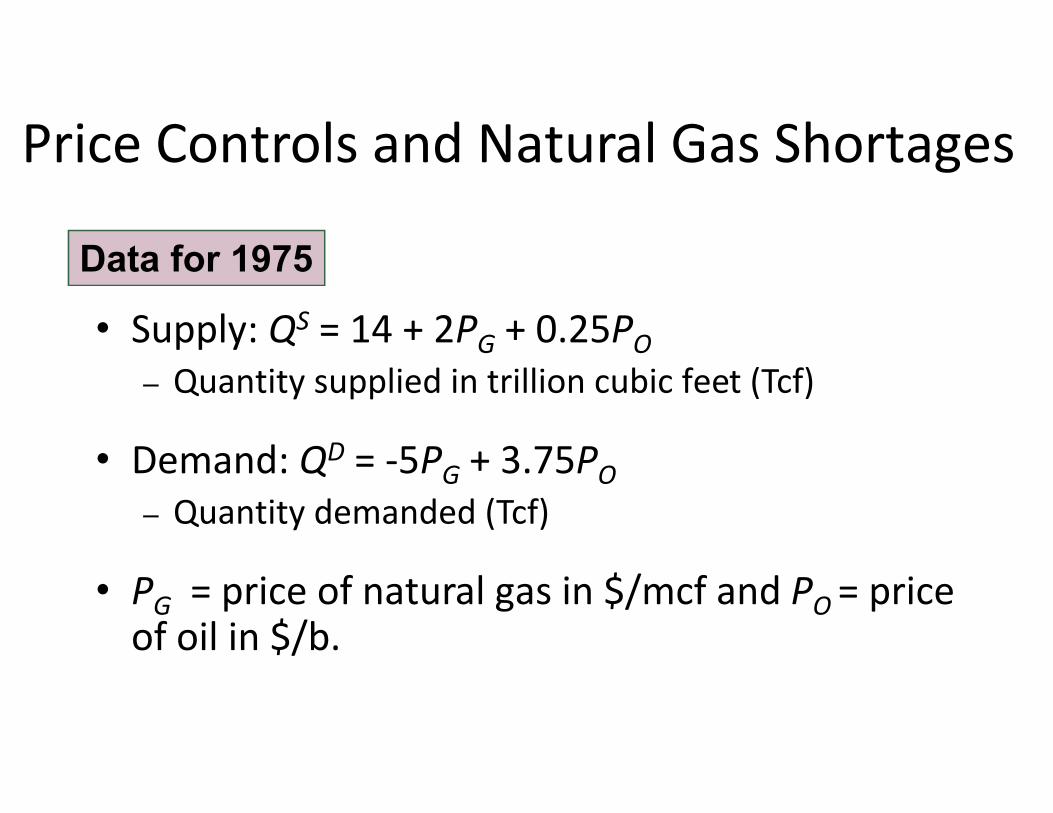

• Supply: QS = 14 + 2PG + 0.25PO– Quantity supplied in trillion cubic feet (Tcf)

Data for 1975

• Demand: QD = -5PG + 3.75PO– Quantity demanded (Tcf)

• PG = price of natural gas in $/mcf and PO = price of oil in $/b.

Price Controls and Natural Gas Shortages

• PO = $8/b

• Equilibrium P = $2/mcf and Q = 20 Tcf

Data for 1975

• Equilibrium PG = $2/mcf and Q = 20 Tcf

• Price ceiling set at $1

• This information can be seen graphically:

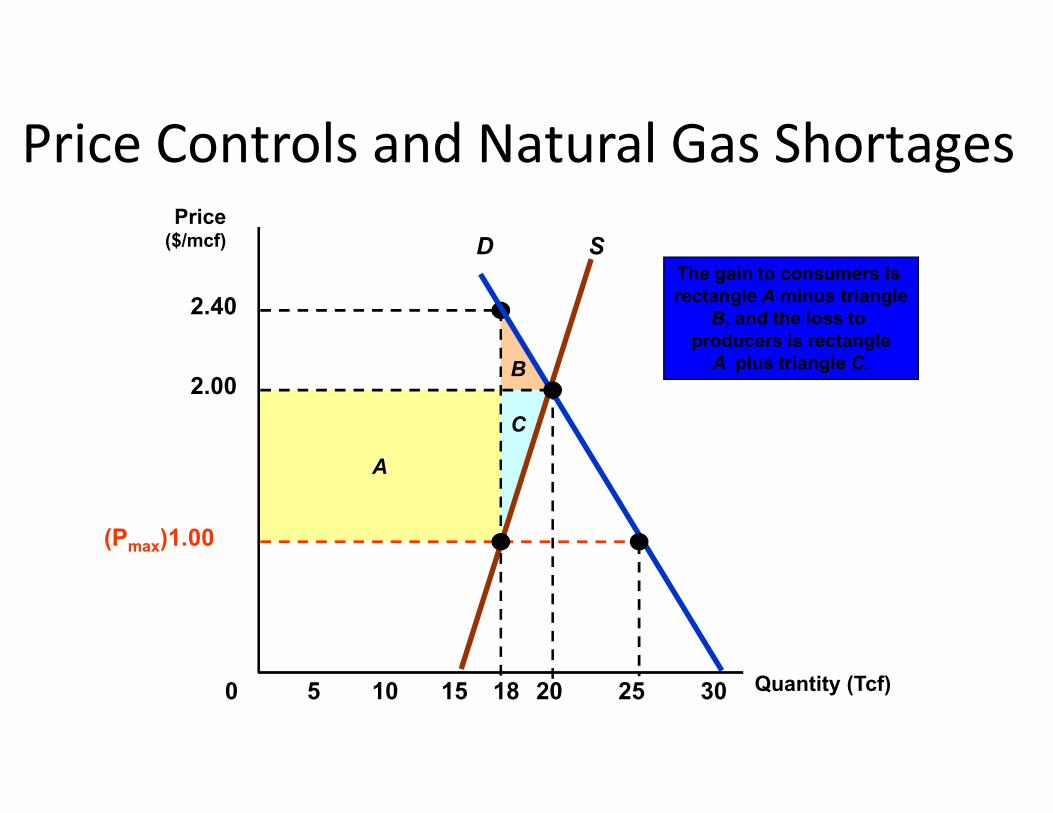

B

2.40

The gain to consumers is rectangle A minus triangle

B, and the loss to producers is rectangle

A plus triangle C.

SD

2.00

Price($/mcf)

Price Controls and Natural Gas Shortages

A

C

Quantity (Tcf)0 5 10 15 20 25 3018

(Pmax)1.00

Price Controls and Natural Gas Shortages

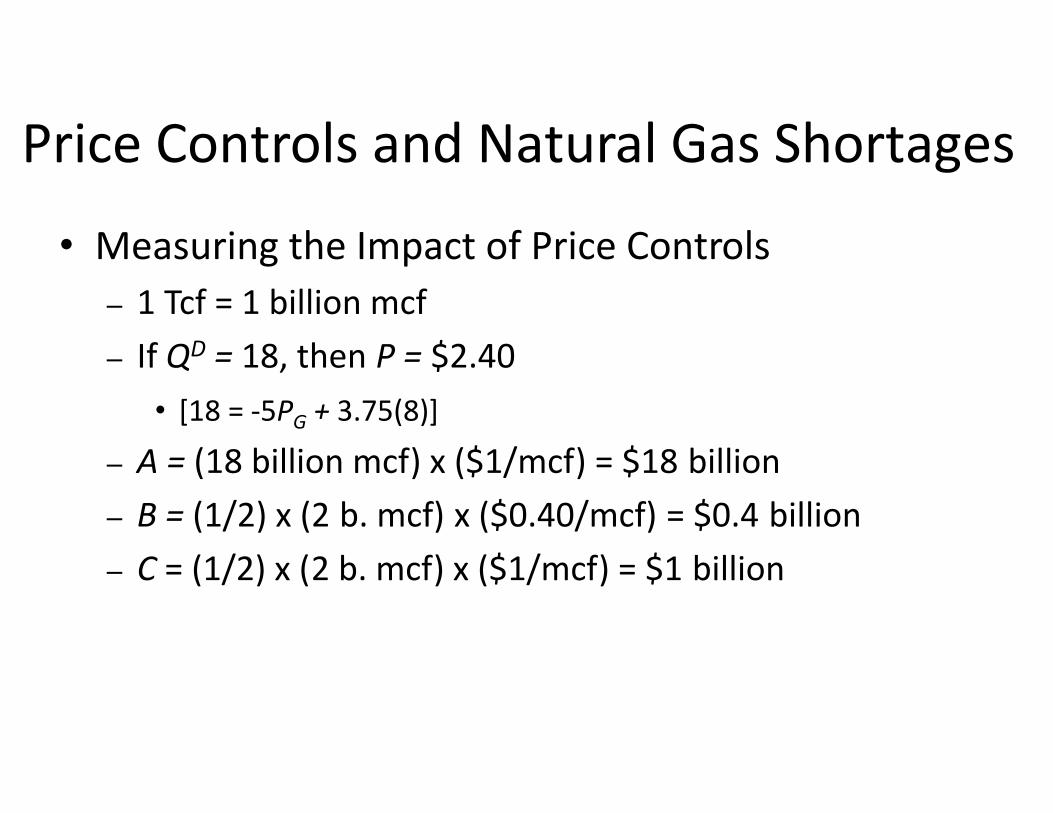

• Measuring the Impact of Price Controls– 1 Tcf = 1 billion mcf– If QD = 18, then P = $2.40

• [18 = -5P + 3.75(8)]• [18 = -5PG + 3.75(8)]

– A = (18 billion mcf) x ($1/mcf) = $18 billion– B = (1/2) x (2 b. mcf) x ($0.40/mcf) = $0.4 billion– C = (1/2) x (2 b. mcf) x ($1/mcf) = $1 billion

Price Controls and Natural Gas Shortages

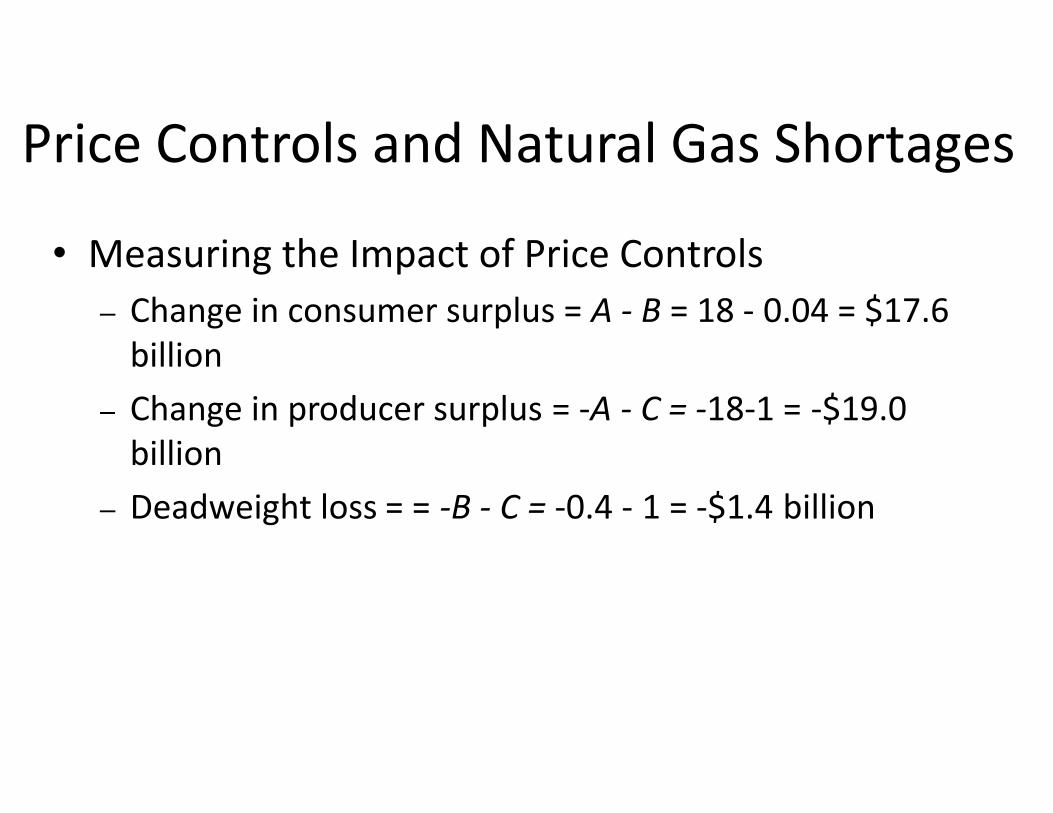

• Measuring the Impact of Price Controls– Change in consumer surplus = A - B = 18 - 0.04 = $17.6

billion– Change in producer surplus = -A - C = -18-1 = -$19.0 – Change in producer surplus = -A - C = -18-1 = -$19.0

billion– Deadweight loss = = -B - C = -0.4 - 1 = -$1.4 billion

Market failure and governmentintervention

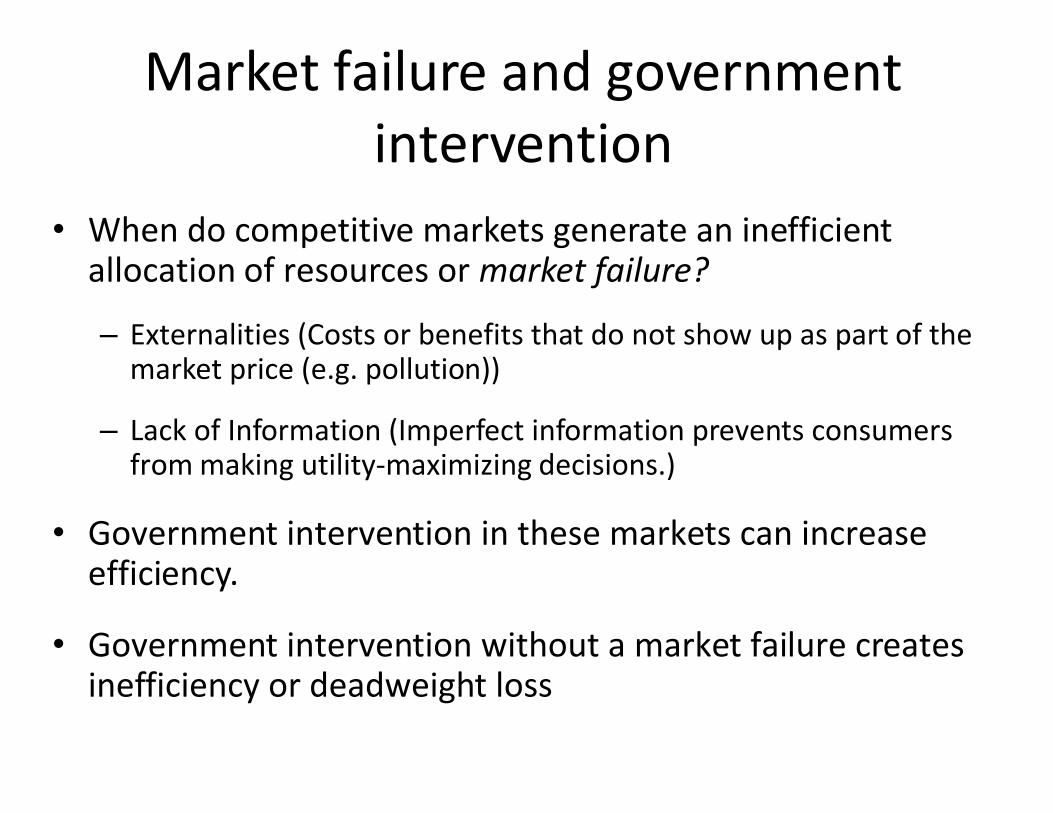

• When do competitive markets generate an inefficient allocation of resources or market failure?

– Externalities (Costs or benefits that do not show up as part of the market price (e.g. pollution))

– Lack of Information (Imperfect information prevents consumers from making utility-maximizing decisions.)

• Government intervention in these markets can increase efficiency.

• Government intervention without a market failure creates inefficiency or deadweight loss

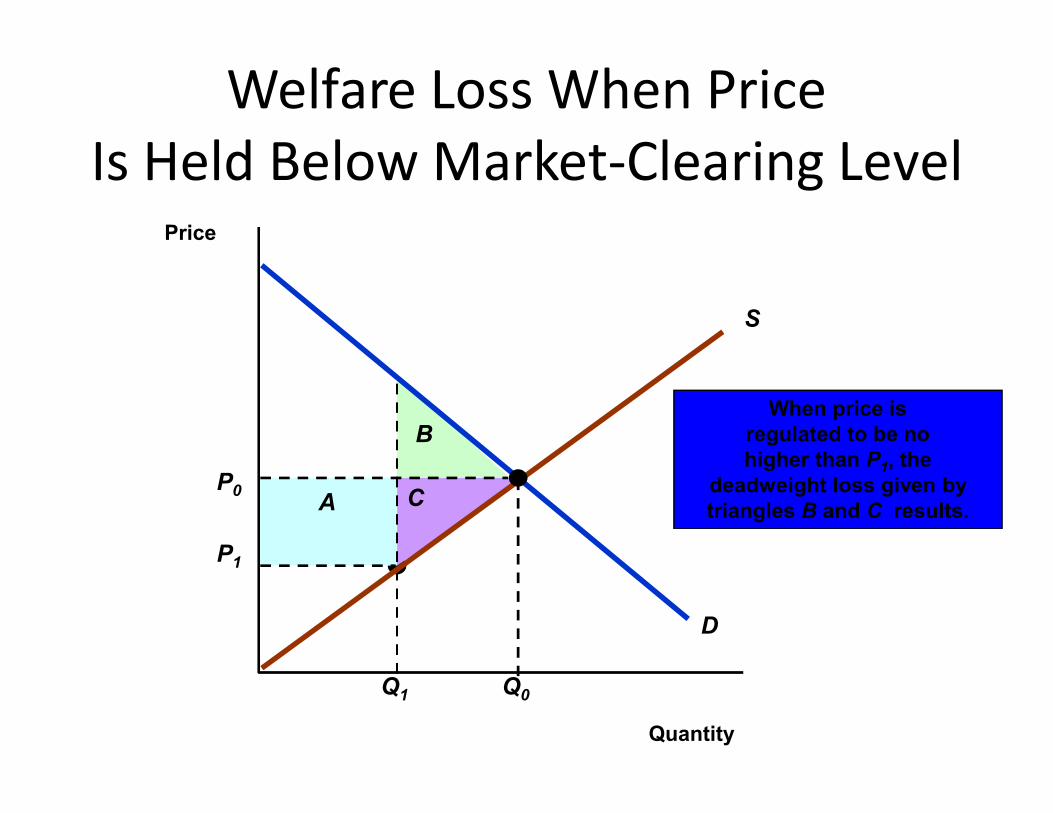

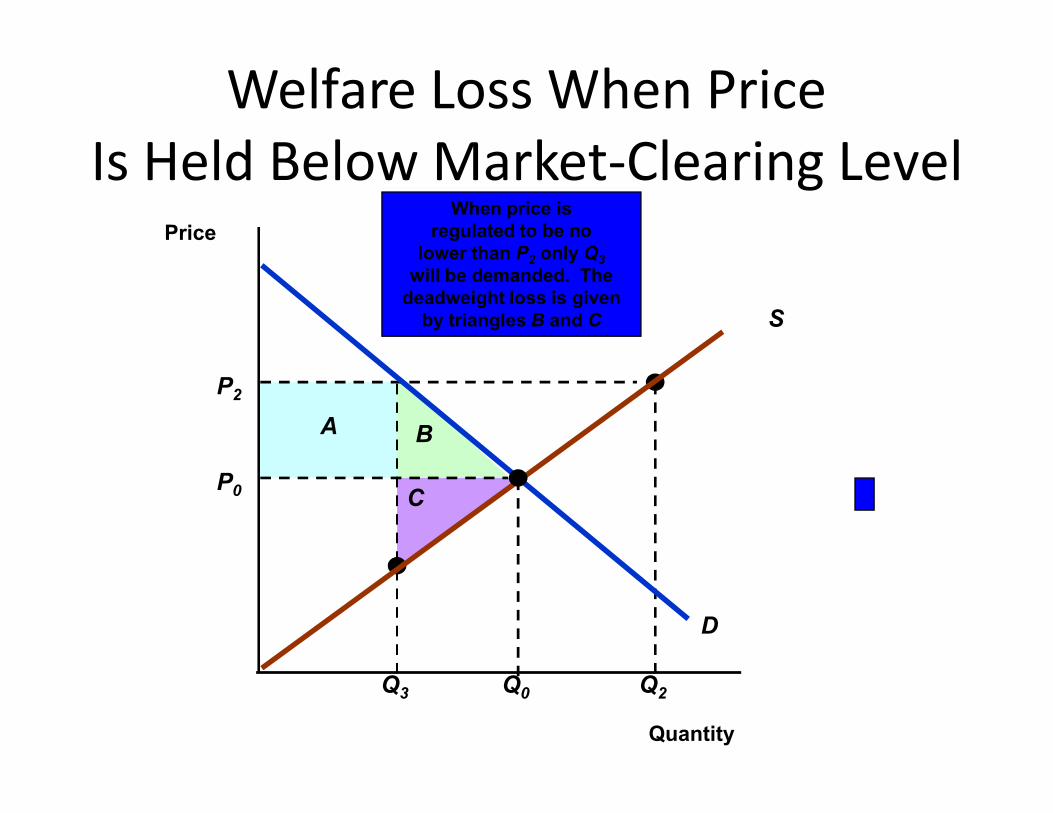

When price is

Welfare Loss When PriceIs Held Below Market-Clearing Level

Price

S

P1

Q1

A

B

C

When price is regulated to be no higher than P1, the

deadweight loss given by triangles B and C results.

Quantity

D

P0

Q0

P2

When price is regulated to be no

lower than P2 only Q3

will be demanded. Thedeadweight loss is given

by triangles B and C

Price

S

Welfare Loss When PriceIs Held Below Market-Clearing Level

Q3

A B

C

Q2

Quantity

D

P0

Q0

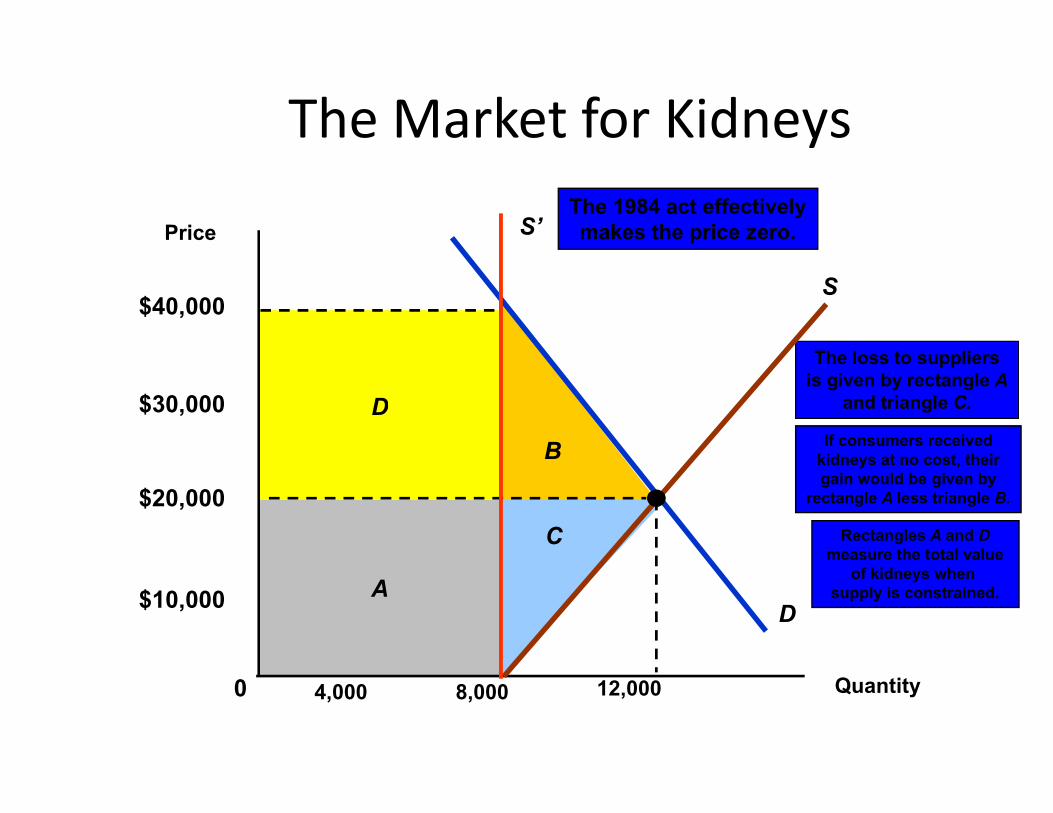

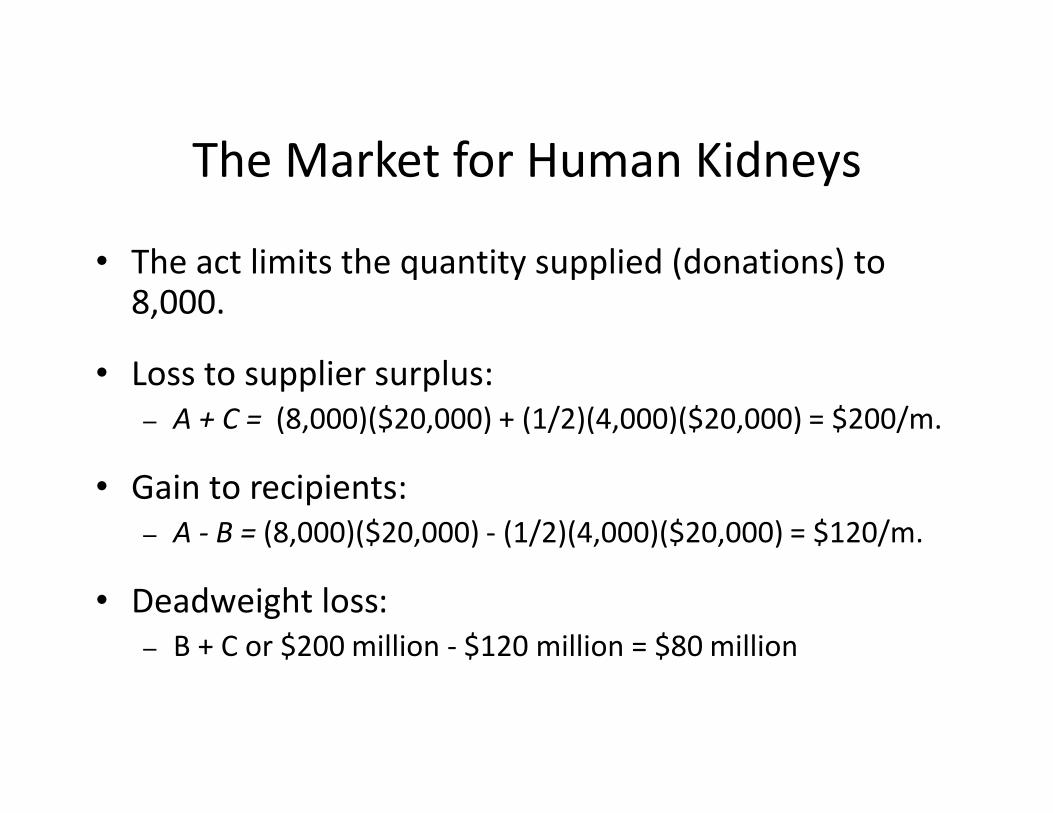

The Market for Human Kidneys

• The 1984 U.S. National Organ Transplantation Act prohibits the sale of organs for transplantation.

• Analyzing the Impact of the Act– Supply: QS = 8,000 + 0.2P

• If P = $20,000, Q = 12,000

– Demand: QD = 16,000 - 0.2P

D

The loss to suppliersis given by rectangle A

and triangle C.

The Market for Kidneys

Price

$30,000

$40,000S

S’The 1984 act effectivelymakes the price zero.

D

Rectangles A and Dmeasure the total value

of kidneys when supply is constrained.A

C

and triangle C.

Quantity8,0004,0000

$10,000

$30,000

B If consumers receivedkidneys at no cost, theirgain would be given by

rectangle A less triangle B.

D

12,000

$20,000

The Market for Human Kidneys

• The act limits the quantity supplied (donations) to 8,000.

• Loss to supplier surplus:A + C = (8,000)($20,000) + (1/2)(4,000)($20,000) = $200/m.– A + C = (8,000)($20,000) + (1/2)(4,000)($20,000) = $200/m.

• Gain to recipients:– A - B = (8,000)($20,000) - (1/2)(4,000)($20,000) = $120/m.

• Deadweight loss:– B + C or $200 million - $120 million = $80 million

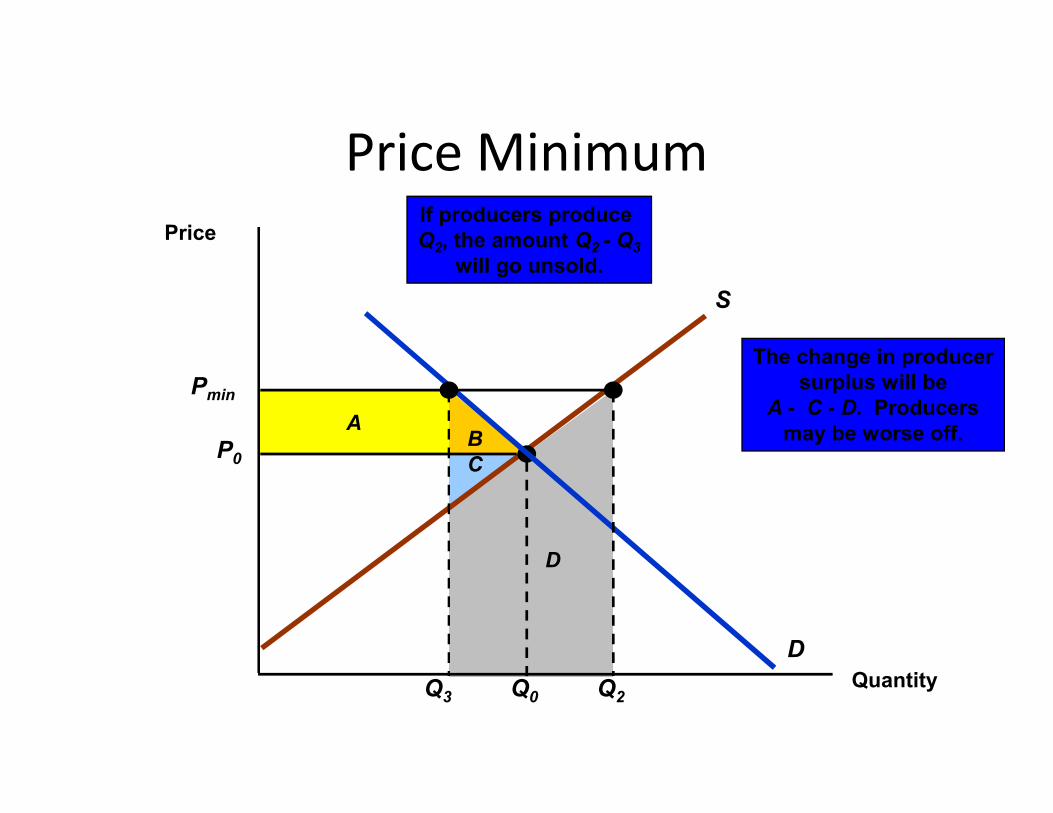

Minimum Prices• Periodically government policy seeks to raise

prices above market-clearing levels.

• We will investigate this by looking at a price We will investigate this by looking at a price minimum (floor) and the minimum wage.

The change in producersurplus will be

A - C - D. Producers

Price MinimumPrice

S

Pmin

If producers produce Q2, the amount Q2 - Q3

will go unsold.

BA

A - C - D. Producersmay be worse off.

C

D

Quantity

D

P0

Q0Q3 Q2

wmin

Firms are not allowed topay less than wmin. This

results in unemployment.

S

The Minimum Wagew

B The deadweight lossis given by

triangles B and C.C

A

L1 L2

UnemploymentD

w0

L0L

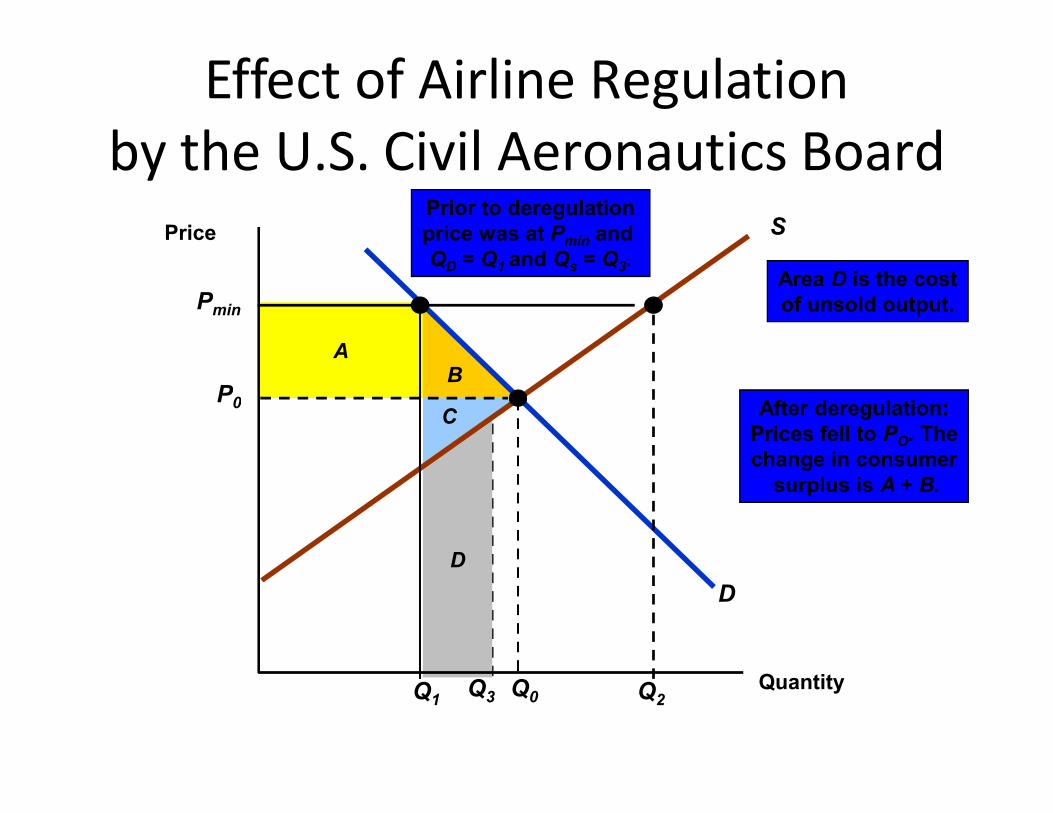

Airline Regulation• During 1976-1981 the airline industry in the U.S.

changed dramatically.

• Deregulation lead to major changes in the industry.industry.

• Some airlines merged or went out of business as new airlines entered the industry.

BA

C After deregulation:

Area D is the costof unsold output.

Effect of Airline Regulationby the U.S. Civil Aeronautics Board

Price S

P0

Pmin

Prior to deregulationprice was at Pmin and QD = Q1 and Qs = Q3.

C After deregulation:Prices fell to PO. Thechange in consumer

surplus is A + B.

Q3

D

Quantity

D

P0

Q0Q1 Q2

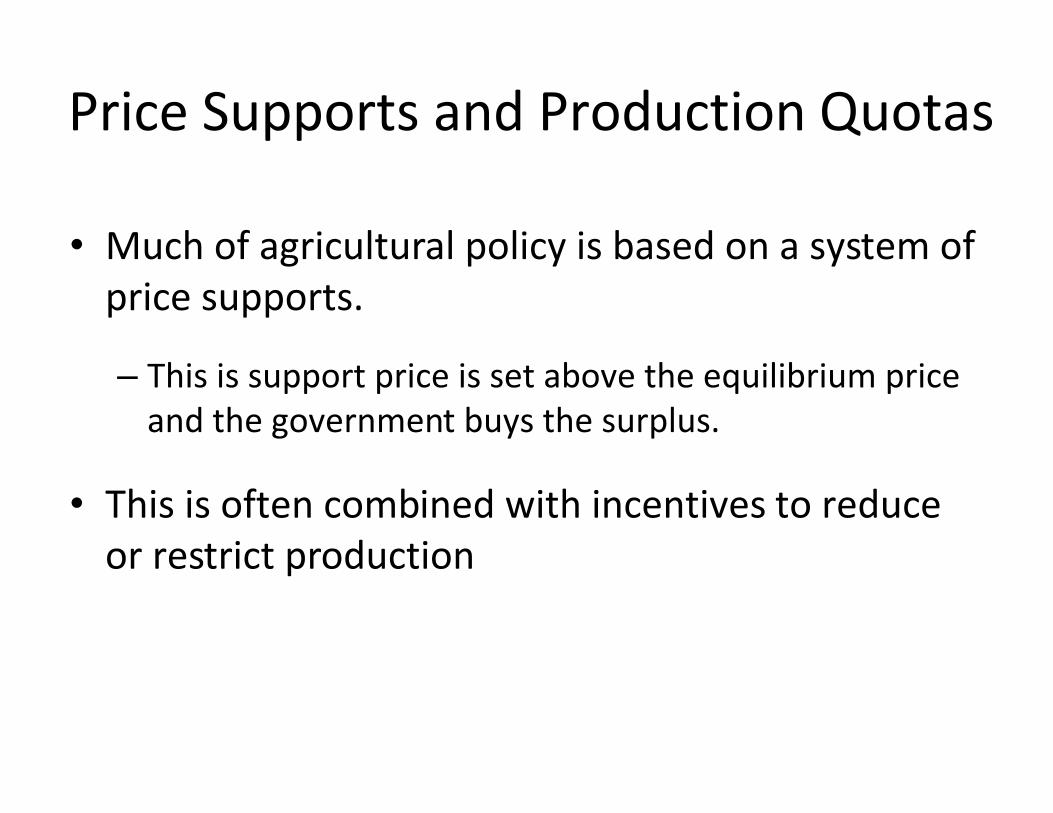

Price Supports and Production Quotas

• Much of agricultural policy is based on a system of price supports.

– This is support price is set above the equilibrium price and the government buys the surplus.and the government buys the surplus.

• This is often combined with incentives to reduce or restrict production

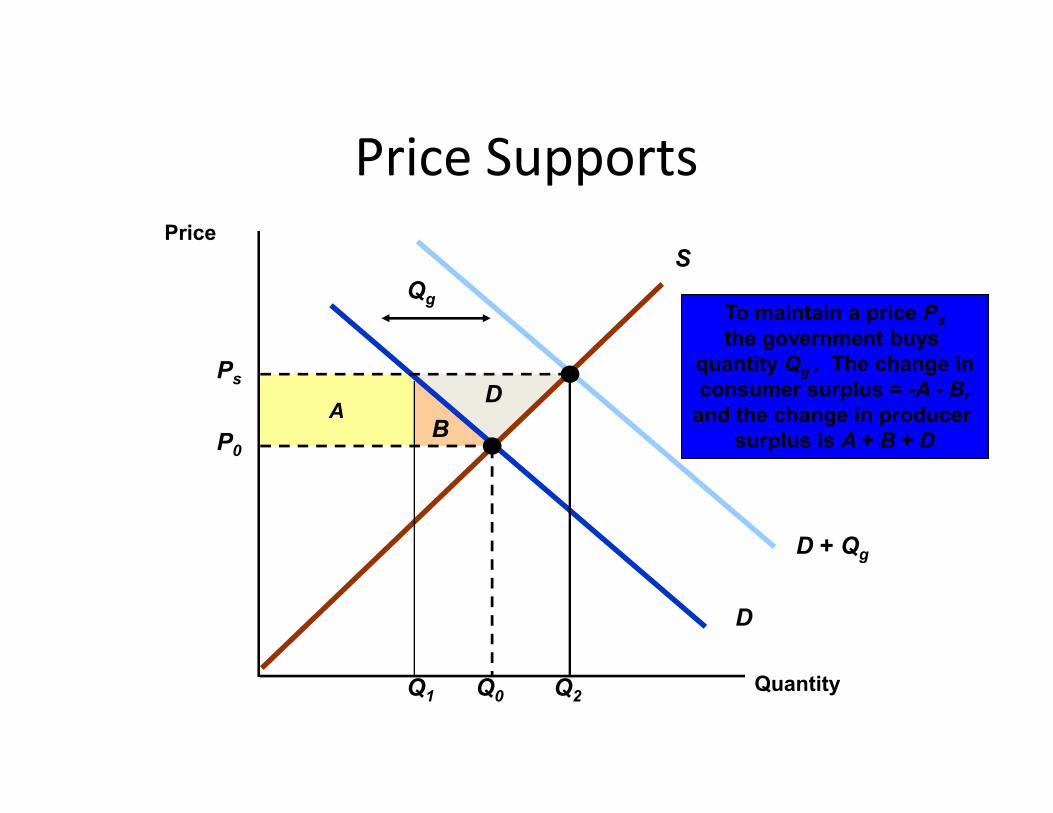

DA

To maintain a price Ps

the government buys quantity Qg . The change inconsumer surplus = -A - B,

and the change in producer

Qg

Price SupportsPrice

S

Ps

B

DA and the change in producer

surplus is A + B + D

D + Qg

Quantity

D

P0

Q0 Q2Q1

Qg

A

Price Supports

PriceS

Ps

The cost to the government is the speckled rectangle

Ps(Q2-Q1)

DTotal welfare loss

D-(Q2-Q1)ps

D + Qg

BA

Quantity

D

P0

Q0 Q2Q1

TotalWelfare

Loss

2 1 s

Production Quotas

• The government can also cause the price of a good to rise by reducing supply.

• E.g.: E.g.: – controlling entry into the taxicab market– controlling the number of liquor licenses

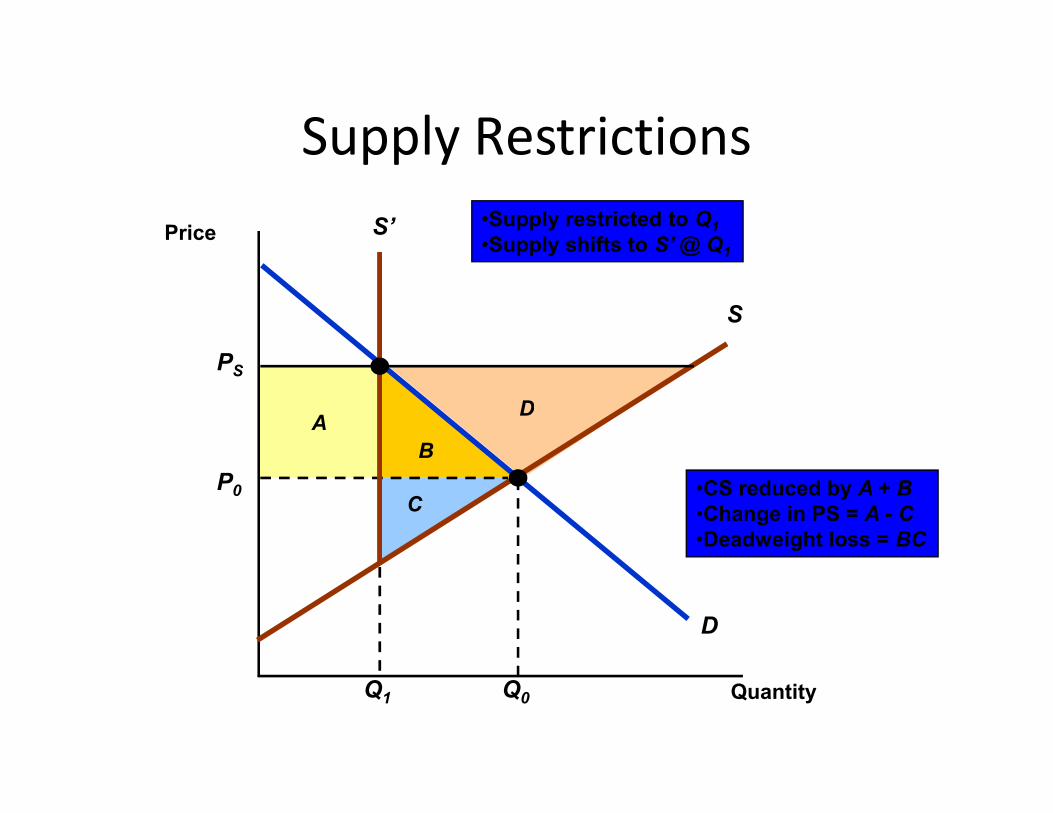

D

Supply RestrictionsPrice

S

PS

S’ •Supply restricted to Q1

•Supply shifts to S’ @ Q1

BA

•CS reduced by A + B•Change in PS = A - C•Deadweight loss = BC

C

D

Quantity

D

P0

Q0Q1

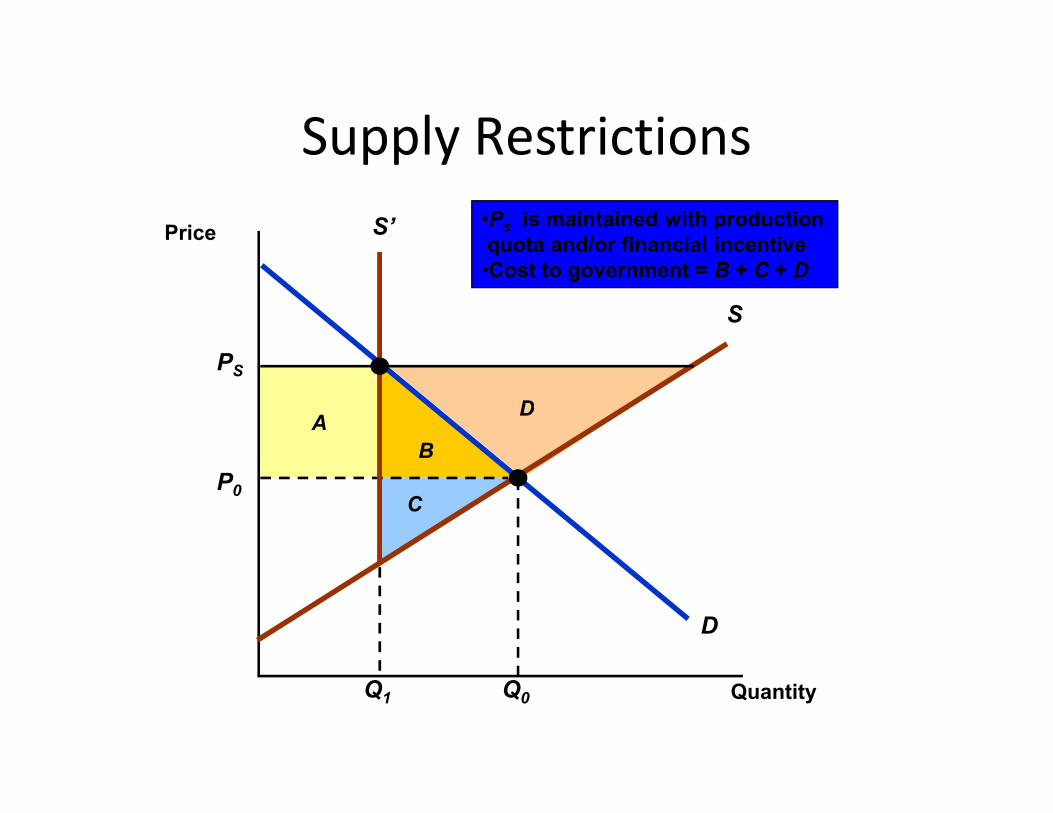

D

Price

S

PS

S’ •Ps is maintained with productionquota and/or financial incentive•Cost to government = B + C + D

Supply Restrictions

BA

C

D

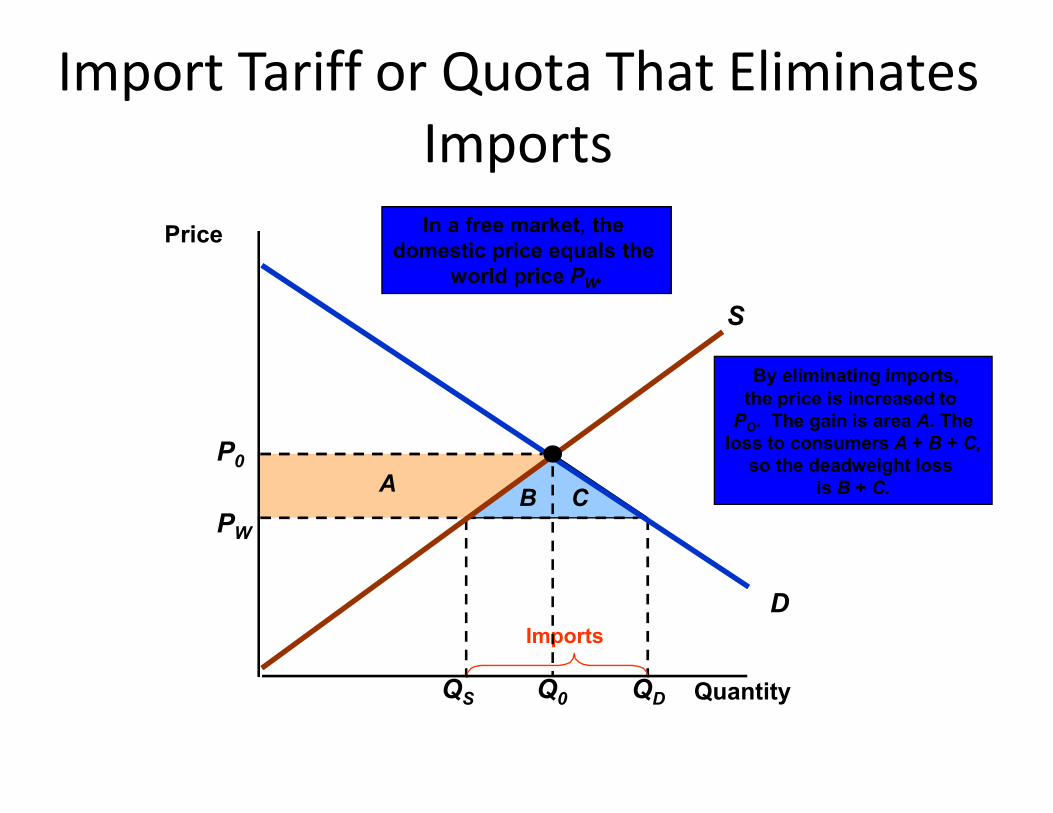

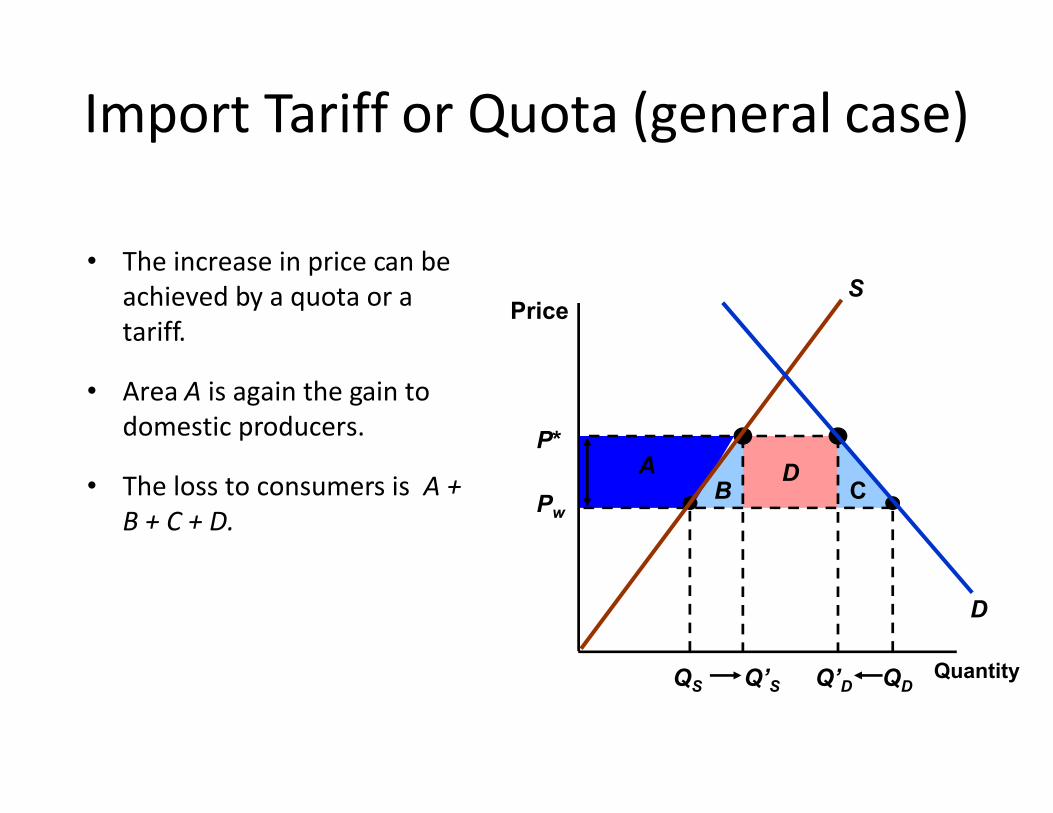

Quantity