international economics: “country studies - the republic of ireland”

TRANSCRIPT

International Business

Summer semester 12

International Economics

Topic:

“Country Studies - The Republic of Ireland”

Supervisor: - Prepared by:- Prof. Claus Thomasberger Rajab H. Kaoneka - 0529990

Due: 14 June 2012

1

Table of Contents

1. Introduction 2

2. Country Overview and History 2

2.1. History 2

2.2. Economy - overview 4

3. Balance of Payments 5

4. Public Deficit/Debt 6

4.1. Overview for Ireland's gross national debt 6

4.2. Housing bubble 7

4.3. Unemployment 8

4.4. Migration 8

4.5. Exports strength continues to define economic growth 9

4.6. Investment 9

4.7. Interest rate 9

4.8. The road to recovery 10

5. Fiscal Austerity 10

5.1. European fiscal compact 12

6. Conclusion 13

7. References 14

8. Appendix 15

Figure 1: Irish GDP.................................................................................................15

Figure 2:balance of payment, Source: http://trueeconomics.blogspot.de ..................15

Figure 3: Balance of payment decomposition of invisible sector, ............................15

Figure 4: Balance of Payments: Current and Capital Accounts ................................16

Figure 5: Emigration in Ireland ...............................................................................16

Figure 6: Ireland Unemployment rate ......................................................................16

2

1. Introduction

This paper studies the economy of Republic of Ireland in which explain much on

Balance of payments, Public Deficit/Debt and Financial Austerity, Starting with

History and Country Overview especially before financial Crisis and After Financial

crisis, What happened during the financial crisis and to what extent the country have

been affected and what measure taken to come out of financial crisis.

It seems that the main factors dominating the Irish Economy are Budget deficit,

public debt and Austerity. Iris economy was strongest before thus why we can see

that the country affected much on financial crisis. The days of Ireland enjoying one

of the fastest growing economies in Europe are over, at least for now. The story is all

too familiar, as easy credit fuelled a housing bubble that burst and damaged

consumer confidence.

There are so many different parts of an economy that you have to take in notice when

evaluating why Ireland came to be in that financial crisis. This paper attempted to

describe the elements that have affected the Irish economy the most. Also explain the

emergence of the problem by going through historic economic events around Ireland

and showed how Ireland has been trying to deal with the problem and what they

could have done differently. Throughout this paper give an analysis on the current

economic situation that Ireland is facing as well as looking at Irelands past and

comparing the changes over the years. The paper also takes into account the

economic situations in Europe which may have an effect on Ireland

2. Country Overview and History

2.1. History

The Anglo–Irish Treaty of 1921 formally partitioned Ireland roughly along

Catholic–Protestant lines into the Irish Free State, which in 1948 became the

Republic of Ireland, and Northern Ireland, which remains under British rule.

Sectarian violence declined in the 1990s, and the Irish Republican Army formally

renounced armed struggle in 2005. (http://www.heritage.org, 09.06.2012)

3

In October 2009, Ireland became the final country to ratify the European Union‟s

Lisbon Treaty. Enda Kenny‟s Fine Gael government was elected in February 2011.

Ireland‟s modern, highly industrialized economy performed extraordinarily well

throughout the 1990s, encouraged by free-market policies that made the country one

of the world‟s most attractive destinations for investment capital. However, the burst

of a speculative housing bubble in 2008 and the results of lax bank lending sent the

economy into a tailspin. In 2010, the government nationalized several banks and

accepted a $90 billion European Union–International Monetary Fund rescue

package. (http://www.heritage.org, 09.06.2012)

For many years ago Ireland was among the poorest country among regions of

Europe. Its economy depended much on agricultural and the country couldn‟t

compete well during the industrial revolution. Ireland economy had been virtually

peasant in 1949; approximately 46% of the working population was involved in

agriculture. Because of this, sadly it could be said Ireland‟s chief export was its

people as millions migrated off the island in pursuit of a decent living.

However, over the past decade the Republic of Ireland has transformed itself from a

struggling agricultural nation to experiencing possibly the greatest level of economic

growth in the world. This accomplishment prompted the naming of Ireland as the

“Celtic Tiger1.” Now, Ireland‟s non-agricultural employment exceeds 40% while

agricultural workers make up less than 8.6%. As can be seen in Appendix: graph 1,

in less than a decade Ireland‟s per capita Gross Domestic Product (GDP) leaped past

the economies of Germany, France, Japan and the average of the 15 European Union

(EU) countries.

Amazingly, Ireland‟s economic output per capita in 2010 exceeds those of these

major industrialized and developed nations by more than 20%2

1 http://www.thomaswhite.com/explore-the-world/ireland.aspx 2 http://www.taxpayersnetwork.org/_Rainbow/Documents/Irelands%20Economic%20Progress.pdf

4

2.2. Economy - overview

Ireland is a small, modern, trade-dependent economy. Ireland was among the first

Countries to join EU, as started to use euro in January 2002. Ireland had growth

average of 6% from 1995 to 2007, since financial crisis the economy dropped

sharply which contributed much to the falling of GDP over 3% in 2008 which also

rose to 8% in 2009 and 1%2010. Ireland was in great depression in 2008 which it

was the first time since more than decades, the financial crisis brought Ireland to the

collapse of its domestic property and construction markets

(www.taxpayersnetwork.org, 12.06.2012).

In 2007 the prices was too high compared to other developed countries, on the same

year the prices of houses fallen by 50%. And that was the downturn in export sector,

consumer spending and business investment along with collapse of construction

sector; all these were dominated by foreign multinationals companies which was the

key factor for Ireland‟s economy. The most important sector was Agriculture where

now is led by Industry and services. In 2008 the government moved to guarantee all

bank deposits, recapitalize the banking system, and establish partly-public venture

capital funds in response to the country's economic downturn

(www.taxpayersnetwork.org, 12.06.2012)

The Irish Government established the National Asset Management Agency (NAMA)

in 2009 to stabilize the banking sector which the roles was to tackle the problem

commercial property and development loans from Irish banks. Whereby there was

huge reduction in revenues and burgeoning budget deficit, in 2009 the government

introduced the first series on draconian budgets. It affected many sectors including

cut in spending, wage reductions for all public servants. Budget deficit reached

32.4% of GDP in 2010 which it was the world‟s largest deficit

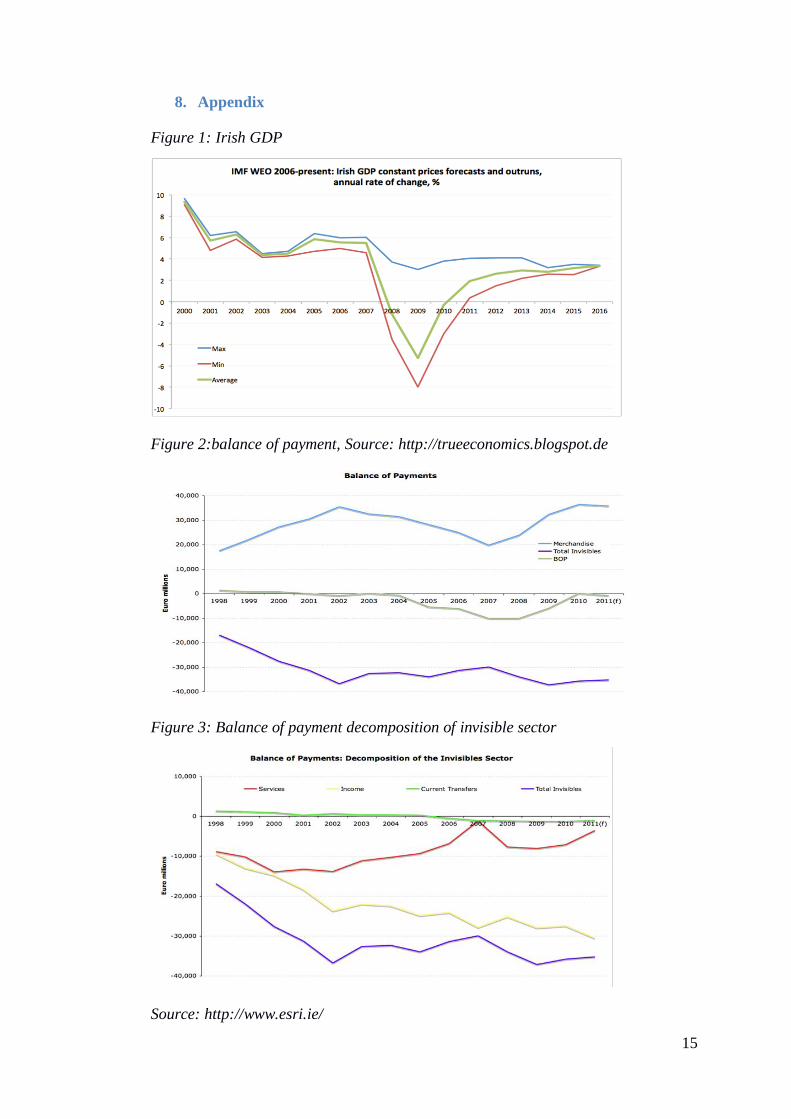

(www.taxpayersnetwork.org, 12.06.2012). See Appendix: figure 1.

EU and IMF issued the package of $112 billion to rescue the Irish government‟s

banking sector and avoiding defaulting on its sovereign debt. Since entering office in

March 2011, the KENNY government has intensified austerity measures to try to

meet the deficit targets under Ireland's EU-IMF program.

5

Ireland achieved moderate growth in 2011 and cut the budget deficit to 10.1% of

GDP, although the recovery is expected to slow in 2012 as a result of the euro-zone

debt crisis.3

3. Balance of Payments

The Central Statistics Office published, the surplus is at €761 million, which revised

from a deficit of €1.113 billion when the first estimate was published in March.

(http://www.theodora.com, 10.06.2012)

In 2011, a deficit of €1 billion was recorded in the 1st quarter. This doesn‟t mean that

this is good forecast toward the surplus; evidence can be taken in two year.

It has been published in the Central Statistics Office that: - “In each of the past five

years the first quarter of the year was the period in which the largest deficit was

registered (the figures are not seasonally adjusted).

The balance of payments nets export earnings against spending on imports; incomes

on foreign investments of Irish residents against incomes of foreign residents‟ Irish

investments; and cash transfers to Ireland (mostly from the EU) against Irish cash

transfers to the rest of the world. ”

Irish services export has been seen as most changing fast sector on the economy for

past ten years, so you can see that the balance of payment give all information about

the services exports (www.theodora.com, 10.06.2012)

Services exports did worse in the first quarter of the year which when you compare

to other previous years. But as the figure are not adjusted for the seasonal factors, as

compared to the previous which can give the wide indicator of trends4

3 http://www.theodora.com/wfbcurrent/ireland/ireland_economy.html 4 As is usually the case, services exports declined in the first quarter of the year compared to the previous quarter. However, as the figures are not adjusted for seasonal factors, comparison with the year earlier period usually provides the best indicator of trends.

6

See appendix: figure 2. Illustrate the trends on the annual basis, providing forecast

for 2011 based on data through September.

ICT services are seems to be the sources which have largest services export earnings

see Appendix figure. 3& 4 where it put overall increase since statistics were to put in

accordance in the year of 1990s

This service of ICT has increased the exports at least 15 per cent on the previous

years which it was €7.2 billion in the first quarter of the year. Business services are

second largest source or export, which contribute €5.4billion in the first three months

which it was 8 per cent increase (http://www.esri.ie, 11.06.2012) 5

Financial services and insurance are the third and fourth largest services exports.

Both increased modestly in the first three months of the year compared to the year

earlier period. (http://www.esri.ie, 11.06.2012)

The travails of the tourism sector are to be seen in the chart. Revenue from foreign

visitors, which is classified as a services export, remained just short of €500 million

in the first quarter, barely changed on the same period in 20106

.

(www.irishtimes.com, 11.06.2012)

4. Public Deficit/Debt

4.1. Overview for Ireland's gross national debt

The Irelands debt is more than 100% of the GDP in 2011 followed by Italy and

Greece which are only countries having larger debt burden in the Eurozone. The

European Stability and Growth Pact criteria states that “national debt should not

exceed 60% of GDP”. Ireland as one of indebted countries, this is enough sign to

show that Ireland is in pre-recession in terms of Gross national debt in the Eurozone

(www.accountancyireland.ie, 11.06.2012)

5 Overall we expect imports of goods and services to rise by 1.1 per cent this year and 1.6 per cent in 2013. Net factor payments are estimated at €30 billion in 2011. The net figure is the difference between very large gross flows. The net income figure from the balance of payments in 2010 is €27.4 billion, almost identical to the net factor payments figure for that year. 6 http://www.irishtimes.com/newspaper/finance/2011/0624/1224299524666.html

7

The interest rate will be above 5% for the bailout packages where by the economic

advisers say that there will be many years before the nominal GDP growth in Ireland.

The nominal GDP will be high as the interest rate on borrowing. Also they the

economist they expect that the EU will cut 1% present average rate of borrowing to

Ireland. The economist says that this will reduce the time taken to bring down the

gross debt ratio to a more sustainable level and reduce the share of tax revenue being

spent annually on servicing the national debt. Secondly, there is likely to be a re-

profiling of the debt burden with an extension of maturity dates for repayment and

possibly „haircuts‟ imposed on part of the debt burden. (www.accountancyireland.ie,

11.06.2012)

Gibson explains, “However, any terms of the deal would still require ROI to push

ahead or even accelerate fiscal consolidation and reforms, taking more money out of

the economy and leading to a very subdued domestic economy. It is this outcome

that the Economic Eye has factored into its forecasts.” 7

4.2. Housing bubble

According to Ernst--Young-Economic-Eye says that housing demand won‟t reach

1980‟s level until 2015

"Average annual new ROI private housing completions are projected to be fewer

than 20,000 through this period, and fall as low as 5,000-7,000 in 2011 and 2012.

Demand for new-housing is unlikely to get back up to 1980‟s levels until 2015. Once

current excess supply is added to the equation, the true net demand for new private

housing is even lower."

The said there is also great fall of housing demands in the North Ireland compared to

other boom years; there is prediction that the demand may be higher if there is

increase in migration

7 http://www.accountancyireland.ie/Archives/Extra/Articles/Ireland-to-emerge-from-recession-in-2012--says-latest-Ernst--Young-Economic-Eye/

8

4.3. Unemployment

Economic Eye said the jobs level in Ireland will not reach the previous year boom for

almost two decades. Unemployment has been big issue in Ireland and it will take

more than two decades to back the peak level of employment which occurred during

the boom years (http://www.ey.com, 12.06.2012)

The primary source of job creation in the future (2012–2020) in Ireland will be

business services sectors, where Ernst & Young Economic Eye Summer forecast

2011 forecasted more than 43,000 jobs will be created and they said more than 4,000

will be created on manufacturing will is small number of jobs and construction sector

will contribute nothing to the number of jobs

The employment growth will be modest with predicted loss in public services; public

administration is predicted to lose 2,000 jobs and education more than 3,000 jobs,

although they said that employment may be high depending on the government

decisions and negotiations with public services union (Ernst & Young Economic Eye

Summer forecast 2011)

4.4. Migration

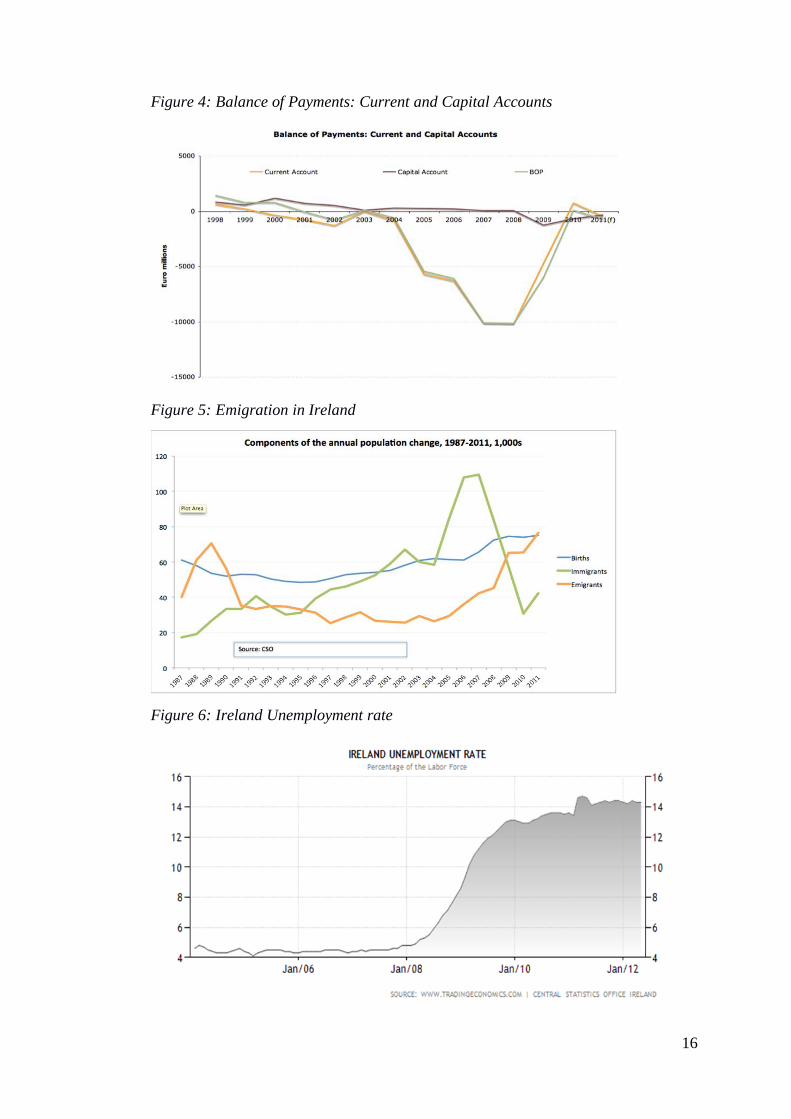

The labour forces in Ireland have decreased by 5% which is equal to 100, 000 people

in which indicated huge increase in emigration and fall in force participation, see

Appendix figure 5

Neil Gibson Economic Advisor to Ernst & Young comments8

: - “These

unemployment rate forecasts are based on an assumption that there will be

significant migration outflows for much of the next decade.

If these outflows do not materialize for reasons such as people struggling to selling

their houses, for example, the unemployment rate for Ireland could be even higher”.

8 Gibson says that “this has helped to keep unemployment from rising further, which benefits the Exchequer; but that the loss of population has reduced domestic demand in terms of consumer spending and housing, in addition to the loss of key skills. The summer forecast is for unemployment rates across the Island to peak in 2011/2012 before slowly falling.”

9

4.5. Exports strength continues to define economic growth

In Ireland there were worse falling in export during the recession in 2009 where by it

was better for pharmaceuticals products. Ireland is one of the few Eurozone countries

exporting more today than pre-recession. Between 2008 and 2010 Irish exports grew

by almost 5% in comparison to US (1.1%), UK (-5.3%), German (-2.5%), Portugal (-

3.8%), Greece (-20.7%). (Ernst & Young Economic Eye Summer forecast 2011)

Ireland currently has $3.3bn worth of sells on merchandise goods export to china,

where by 0.24% of total Chines goods imports which is huge. Economic Eye

forecasts that If ROI‟s share of Chinese goods imports doubled by 2020, and

assuming strong Chinese import growth, this would mean US$21bn worth of

additional goods exports compared to the current level, equivalent to 6.5% of

additional GDP. (Ernst & Young Economic Eye Summer forecast 2011)

4.6. Investment

In Ireland the Investment suffered as any other many countries during the economy

downturn, the economy of Ireland failed almost two-third between 2007 to 2010

which is twice the rate of decline on Greece by -32.3%, three times that of Portugal

(-16%), and four times the rate of decline in the US where the sub-prime mortgage

crisis started, from which the global credit crunch emerged

4.7. Interest rate

As the ECB responds to the economies of France and Germany, the Irelands interest

rate has been risen up at the wrong time. As ECB seeking to reduce Inflation, The

Economic Eye forecast is for ECB interest rates to remain above Bank of England

and US Federal Reserve rates until at least 2013. Interest rates are forecast to rise in

both Europe and the UK before the end of 2011, but the gap will widen further as

ECB rate rises are likely to continue to move first. (Ernst & Young Economic Eye

Summer forecast 2011)

10

4.8. The road to recovery

The economy contracted in output by -1.8% in 2011 but there good recovery in 2012,

but it seems that the employment will fall in two consecutive years from 2011 to

2012 whereby there will be total of 400,000 net job lost since the recession started,

while unemployment will rise by 15% in which the rate has never experienced since

1990‟s (www.accountancyireland.ie, 12.06.2012)

Neil Gibson Economic Advisor to Ernst & Young comments “The positive outlook

for global demand means that exports are forecast to continue to grow but this will

not create enough jobs to substantively reduce unemployment and recover the losses

of the recession. Nonetheless, the Economic Eye retains its long-run optimism for

growth of the ROI economy, which remains rooted in its internationally focused

businesses, strong skills base and competitive Corporation Tax regime.”

This outlook is, however, subject to the proviso that the banking problems get

resolved and a sustainable deal is reached on debt. The more insulated NI economy

has a much smaller export base and whilst it‟s short-term growth forecasts are

stronger than for ROI, in the medium to long-term it is projected to return to a rate of

growth below that of its neighbour9.

5. Fiscal Austerity

From the 4th quarter to 3

rd quarter, Ireland has determined the cumulative GPD

decreased by 21 percent, this means Ireland experience the deficit of 11-12 percent

from the fiscal balance. The Ireland over the 2007 to 2010 period the industrialized

economy has seem to decline in National output which is the largest compound.(

www.accountancyireland.ie, 11.06.2012)

As it has been written in the www.accountancyireland.ie:-“Ireland‟s general

government debt has increased by 320% over the same period. The level of national

debt has increased rapidly as a result of successive bank bailouts, allied to the budget

deficits associated with running a pro-cyclical taxation and expenditure mix.”

9 http://www.accountancyireland.ie/Archives/Extra/Articles/Ireland-to-emerge-from-recession-in-2012--says-latest-Ernst--Young-Economic-Eye/

11

Bank as 2nd

largest contribution to the economy has accounted the bailout of 14.5%

of its nominal GDP in 2009 where by 32% in 2010. The general Government of

Ireland planned to stabilize the debt at 108% of GDP by 2014 (www.ul.ie,

11.06.2012)10

. Unemployment rose from 4.6% in 2007 to 14.2% in June 2011 as

shown in the Appendix: figure 6

A report from independent watchdog, the Irish Fiscal Advisory Council (IFAC), has

claimed that current government fiscal policy is working and that if anything, the

Irish government may need to make further cuts to keep Ireland‟s economic

projections on track. On the report says that IFAC has made plan for calculation

which was not valid that the government cuts, austerity measures and taxation

increases are all those which have been included in the last budget11

In June 2011 Ireland established the IFAC (The Irish Fiscal Advisory Council) for

the functions to reforms in the economy. Its functions is asses, suggest if the

government meeting the targets and objectives which may lead to appropriate

government‟s macroeconomic forecasts, budgetary projections and fiscal policy

On the report the IFAC said that: “The government‟s plan to reduce the General

Government deficit from approximately 10 per cent of GDP in 2011 on an

underlying basis to 8.6 per cent of GDP in 2012 was based on a real growth rate of

1.3 per cent in 2012. However, some deterioration in growth prospects since the

Budget announcement raises a question mark as to whether this deficit target can be

attained with currently planned consolidation measures. According to The Irish

Times, additional measures of 400 million euro may be needed this year to achieve

the deficit target, and the government is not doing enough to cut deficit and debt

levels in the period up to 201512

. (www.theepochtimes.com, 11.06.2012)

10 http://www.ul.ie/business/sites/default/files/research_bulletins/April%202012%20-%20KBS%20Research%20Bulletin.pdf 11 As such, the current report recognizes that the pretexts on which the IFAC made their last calculations in late 2011 are no longer valid, and that government cuts, austerity measures and taxation increases outlined in the last budget may be inadequate in meeting Ireland’s planned fiscal targets for 2012 and beyond 12 http://www.theepochtimes.com/n2/ireland/more-austerity-needed-for-ireland-say-fiscal-advisors-219781.html

12

5.1. European fiscal compact

On May 31st Ireland voted the European fiscal compact where by only half of the

voted but according to The Irish Times the results has a favor on the ratifying the

treaty that sets the rules to control the debt and deficit of euro-zone members

(60.29% for, 39.71% against) was greeted with relief by Enda Kenny, the prime

minister, who had staked both his government‟s and his own reputation on a win for

the “Yes” camp. The outcome closely mirrored the opinion polls, which had

indicated solid public support for the treaty throughout a dull campaign.

(www.theepochtimes.com, 11.06.2012)

According to the Irish Times: “The referendum debate was dominated by a single

question: how can Ireland, which leaves an EU/IMF bailout programme next year,

fund itself if it cannot then borrow on sovereign debt markets, and needs a second

bailout in 2014? For the Yes campaign, led by the government parties and supported

by Fianna Fail, the leading opposition party, that was the central argument. Only

countries that ratify the fiscal treaty can access the European Stability Mechanism,

the euro zone‟s permanent €500 billion ($618 billion) bailout fund. So, if voters

rejected the treaty and access to EU finance was thereby denied, who would lend

Ireland money? On that, Sinn Fein and some smaller left-wing parties that led the No

campaign struggled to produce an answer to convince a skeptical electorate in

somber mood.”

There is now hope for the bailout-box to turn into success which will lead to the

greater advantage in Europe. Ireland was only euro-zone to use referendum which

leads them to ratify the fiscal compact, as written on the Irish Times that this was

ninth plebiscite on EU matters since it voted to join the union in 1972. The middle-

class and rural voters supported much the treaty which turned to great opposition

from the urban class13

.

13 Mr. Kenny’s government will use the referendum win in Europe as a mandate for change. Certainly, it buys some time to restructure Ireland’s bank debt, and to help advance a growth strategy to complement the fiscal compact. But Mr Kenny also knows that without major progress to report on either of these issues, winning a future referendum on further European integration becomes far harder to achieve.

13

6. Conclusion

Ireland returned to growth last year and the economic recovery is projected to gain

further momentum, despite on-going budgetary consolidation. A recovery in Europe

and North America should boost exports in 2013. With activity improving gradually,

the labor market situation will slowly turn around and unemployment will stabilize.

Inflation is projected to remain low, apart from a temporary energy and VAT-related

spike in prices.

Progress in narrowing macroeconomic and financial imbalances is being made and

needs to continue. It is the only way to gain further confidence of financial markets.

Adjustment would be aided by a rapid resolution of growing mortgage arrears. Given

the risk that high unemployment might become structural, reforms to public

employment services and job training should be fully implemented to help job

seekers return to work.

14

7. References

History (http://www.heritage.org/index/pdf/2012/countries/ireland.pdf,

09.06.2112)

Imports and the Balance of Payments

(http://www.esri.ie/UserFiles/publications/QEC2011Win.pdf, 11.06.2012)

Balance of payments

(http://www.irishtimes.com/newspaper/finance/2011/0624/1224299524666.ht

ml, 11.06.2012)

Ireland: Celtic Tiger Licking its Wounds

(http://www.thomaswhite.com/explore-the-world/ireland.aspx, 11.06.2012)

Irish Fiscal Advisory Council, Fiscal Assessment Report

(http://www.fiscalcouncil.ie, 11.06.2012)

Ernst & Young Economic Eye Summer forecast 2011 (http://www.ey.com,

12.06.2012)

OECD (http://www.oecd.org, 13.06.2012)

15

8. Appendix

Figure 1: Irish GDP

Figure 2:balance of payment, Source: http://trueeconomics.blogspot.de

Figure 3: Balance of payment decomposition of invisible sector

Source: http://www.esri.ie/

16

Figure 4: Balance of Payments: Current and Capital Accounts

Figure 5: Emigration in Ireland

Figure 6: Ireland Unemployment rate