inflation targeting in armenia: monetary policy in transition

TRANSCRIPT

Symposium Paper

Inflation Targeting in Armenia: MonetaryPolicy in Transition

KING BANAIAN1,2, DAVID M KEMME3 & GRIGOR SARGSYAN2,4

1Department of Economics, St. Cloud State University, 386 Stewart Hall, 720 4thAve.S., St. Cloud, Minnesota 56301, USA. E-mail: [email protected]

2Armenian International Policy Research Group, 6303 Massachusetts Avenue,Bethesda, MD 20816, USA.

3Department of Economics, University of Memphis, Memphis, TN 38152, USA.E-mail: [email protected]

4Central Bank of Armenia, 6 Vazgen Sargsyan, St. Yerevan 375010, Armenia.E-mail: [email protected]

As the monetary and financial systems in transition economies have evolved so have

monetary policies. Many central banks have followed a course from exchange rate

targeting, to targeting monetary aggregates to targeting inflation. We examine the

development of monetary policy in Armenia, a small, open transition economy that

adopted inflation targeting in January 2006. First, we review monetary policy in

Armenia. Then we evaluate the capacity of the Central Bank of Armenia to

implement inflation targeting. Finally, we estimate and simulate reaction functions

to evaluate the effectiveness of monetary policy. We find that the Central Bank may

have been overly restrictive.

Comparative Economic Studies (2008) 50, 421–437. doi:10.1057/ces.2008.22

Keywords: Armenia, monetary policy, inflation targeting, Taylor Rule

JEL Classifications: E42, E52, E58, P24

INTRODUCTION

As the economic structure and institutions of transition economies of EasternEurope and the former Soviet Union have evolved so have their economicpolicies. Initially all had fiscal and monetary institutions ill-suited for amarket economy. In particular, as transition progressed a new system ofmoney and banking was created to implement market economy monetary

Comparative Economic Studies, 2008, 50, (421–437)r 2008 ACES. All rights reserved. 0888-7233/08

www.palgrave-journals.com/ces

policies and improve financial intermediation. Monetary policy options wereseverely limited in the early transition period however. Transition economiesfound a fixed nominal exchange rate anchor as the monetary policy of choice.

Targeting a monetary aggregate, base or reserves, proved untenable asthese were difficult to measure, money demand was unstable and foreignassistance flows, inter alia, distorted measures of base money. In addition,there were large, often unpredictable, transition shocks that compoundedmeasurement of monetary aggregates. During the early transition period thelong and varying lags between changes in money and changes in inflationintroduced too much uncertainty at a time when building central bankcredibility was essential. A fixed nominal exchange rate anchor served twoimportant purposes. First, it was a highly visible policy target, which thecentral bank could manage and therefore effectively gain credibility. Second,there was a real need to limit exchange rate volatility in order to promoteinternational trade and investment during a period when these economieswere opening to world markets. Within a few years, however, thedisadvantages of a fixed exchange rate policy became apparent: loss ofmonetary autonomy, the potential for currency mismatches within thebanking system and speculative attacks leading to financial and bankingcrises, and equilibrating the real exchange rate only via domestic pricechanges and real output decreases. Relatively quickly many transitioneconomies moved to a heavily managed exchange rate policy as otheroptions were explored. Only with the maturing of institutions and domesticfinancial markets did alternative monetary policies, inflation forecasttargeting in particular, become a viable option.1

There are several critical prerequisites for inflation targeting. The first isthe institutional capacity of the central bank to forecast inflation, theintermediate target, and utilise an array of instruments to meet the target. Thesecond is reasonably well-functioning, sound financial markets that linkcentral bank instruments, a particular interest rate, to the ultimate policyvariable, a measure of inflation. Third, the central bank must be operationallyindependent of the government and free of fiscal obligations, that is, fiscaldominance must be absent. Fourth, a market-oriented economic structurewith predominantly deregulated prices, low level of dollarisation and lowexchange rate pass-through must be in place (or nearly so). Finally, theremust be a political willingness, both within the central bank and thegovernment, to support a commitment to low inflation. The Czech Republic,

1 See IMF, September 2005.‘Does Inflation Targeting Work in Emerging Markets?’Also note that

technically it is inflation forecast targeting that is the best policy descriptor, and the targets may be

explicit or implicit. Below we will simply use the term inflation targeting.

K Banaian et alInflation Targeting in Armenia

422

Comparative Economic Studies

Poland and Hungary were the first three transition economies to adoptinflation targeting and it took from 8 to nearly 12 years into the transition andpressures to move into the Euro area to convince policy makers to adoptinflation targeting in some form.2 But even for these early adopters it isunclear whether or not their policy actions are comparable to similar inflationtargeting central banks in well-developed market economies.

Siklos (2006) notes that central bank behaviour with respect to interestrate setting is often summarised for analytical purposes by its estimatedreaction function.3 If this is the case he suggests that the instrument rule ofthe Hungarian National Bank should then be similar to that of Euro areacentral banks. Gerdesmeier and Roffia (2004) also note estimating reactionfunctions provides a basis for forecasting changes in central bank policyinstruments and evaluation of central bank policies. It may be reasonable alsoto suggest that in general the reaction function of an inflation targetingtransition economy central bank should be similar to that of an inflationtargeting market economy central bank. Thus, for recent transitioneconomy adopters of inflation targeting a comparison of the central bankreaction function with other central banks may reveal both whether or notthe prerequisites for inflation targeting have been met and whether ornot the central bank is committed to and effective in carrying out theannounced policies.

In this paper we focus on one transition economy recently adoptinginflation targeting, Armenia. For both analysts and policy makers theexistence and understanding of monetary channels that link interest ratesand inflation is critical. To this end we specify and estimate a Taylor rule-typereaction function for the Central Bank of Armenia (CBA). In the next twosections we first briefly describe the evolution of Armenian monetary policyand we ask whether the prerequisites for inflation targeting are met. In thesubsequent section we outline a Taylor rule-type reaction function andestimate it for Armenia. To determine whether the CBA is inflation targetingor exchange rate targeting we estimate the reaction function without theexchange rate and then with three alternative measures: the nominalexchange rate, the real exchange rate and the de-trended real exchangerate. Then we provide interest rate simulations for the empirical ruleand compare the actual interest rate path with that of three alternatives:

2 If we take January 1990 as the beginning of transition, the Czech Republic was the quickest

taking about 8 years, adopting inflation targeting in the first quarter of 1998, then Poland in the first

quarter of 2001 and Hungary in the third quarter of 2001. See Jonas and Mishkin (2005) and

Orlowski (2006).3 See also Poole (2005) and Gerdesmeier and Roffia (2004).

K Banaian et alInflation Targeting in Armenia

423

Comparative Economic Studies

the estimated reaction function, a strict inflation targeting rule and exchangerate pass-through and a strict inflation targeting rule with interest ratesmoothing. The final section presents conclusions and suggestions forfuture research.

ARMENIAN MONETARY POLICY – A BRIEF OVERVIEW

The Central Bank of Armenia (hereinafter CBA) was formed by a charter ‘Lawon the Central Bank of the Republic of Armenia’ in 1996. Article 4 states that the‘primary objective’ of the CBA ‘shall be to ensure stability of prices’ and section2 of that article specifies that this objective is not to be sacrificed to any other.4

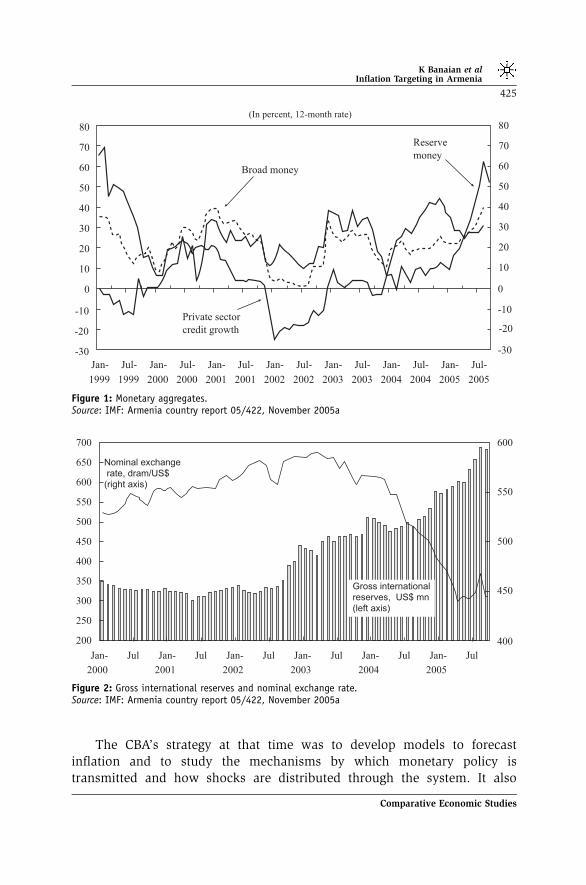

Monetary targeting was announced in 1994 and fully implemented in1996 with Decree 122, July 19 on Foreign Exchange Policy Principles, whichestablished a floating exchange rate. The strategy of employing a nominalanchor, either the exchange rate or quantity of money, was problematic,particularly since 2002 when large inflows of international reserves couldonly be partially sterilised. The exchange rate appreciated sharply, and whilereserve money growth was held to fairly strict quantity targets in 2004private credit and broad money growth continued to increase. The CBAattempted to sell its own bills to banks to absorb some of the excess liquidityin the system, but was not able to restrict reserve money growth in 2005(Figures 1,2).

The Bank had already seen the problem growing as early as 2003:

‘Since mid 1990s, the Central Bank has chosen the regime of volumeadjustment or monetary targeting for its monetary policy, which had enabledthe CB to manage inflation quite effectively by maintaining it within theprogram figures over the last 5 years.Recent years’ experience, however, has shown that the Central Bank hadoften departed from the programmed figures of the monetary aggregates, givingpreference to the provision of stable inflation and financial markets. While theCentral Bank has had many meetings with banks to explicate the cause why theopted nominal anchor-had departed from the program, such deviationshowever, complicate the process of formation of steady expectations amongbusinesses and further effective management of inflation’.5

4 The other objectives in Article 5 do not include any other macroeconomic objective, but make

reference to assuring smooth functioning of the banking and payments systems. The law may be

read online at http://www.cba.am/legal/central.pdf.5 CBA, ‘Development Vision’. http://www.cba.am/publications/vision.pdf, 11 November 2003,

last viewed 16 April 2006.

K Banaian et alInflation Targeting in Armenia

424

Comparative Economic Studies

The CBA’s strategy at that time was to develop models to forecastinflation and to study the mechanisms by which monetary policy istransmitted and how shocks are distributed through the system. It also

Figure 1: Monetary aggregates.Source: IMF: Armenia country report 05/422, November 2005a

Figure 2: Gross international reserves and nominal exchange rate.Source: IMF: Armenia country report 05/422, November 2005a

K Banaian et alInflation Targeting in Armenia

425

Comparative Economic Studies

argued that the switch would lead to better cooperation between the CBA andfiscal authorities. Its vision was to make monetary policy ‘much more open,transparent and closer to public perception’.

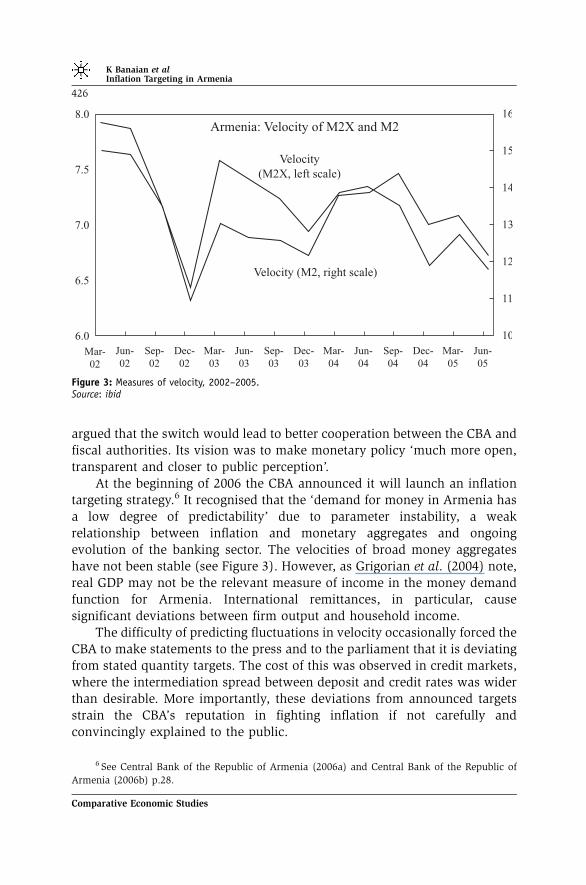

At the beginning of 2006 the CBA announced it will launch an inflationtargeting strategy.6 It recognised that the ‘demand for money in Armenia hasa low degree of predictability’ due to parameter instability, a weakrelationship between inflation and monetary aggregates and ongoingevolution of the banking sector. The velocities of broad money aggregateshave not been stable (see Figure 3). However, as Grigorian et al. (2004) note,real GDP may not be the relevant measure of income in the money demandfunction for Armenia. International remittances, in particular, causesignificant deviations between firm output and household income.

The difficulty of predicting fluctuations in velocity occasionally forced theCBA to make statements to the press and to the parliament that it is deviatingfrom stated quantity targets. The cost of this was observed in credit markets,where the intermediation spread between deposit and credit rates was widerthan desirable. More importantly, these deviations from announced targetsstrain the CBA’s reputation in fighting inflation if not carefully andconvincingly explained to the public.

Figure 3: Measures of velocity, 2002–2005.Source: ibid

6 See Central Bank of the Republic of Armenia (2006a) and Central Bank of the Republic of

Armenia (2006b) p.28.

K Banaian et alInflation Targeting in Armenia

426

Comparative Economic Studies

To improve credibility the CBA decided to use headline, or total inflation,as its target. It will make announcements for a variety of events thatmight cause deviation from the target, including shocks to world prices,sharp external shocks to the exchange rate, agricultural shocks, such asdroughts, and other natural disasters. In short, if it finds an external adversesupply shock, it will explain why a short-term deviation from the inflationtarget might be warranted. As long as these supply shocks are infrequent andpolicy remedies carefully explained, this may not cause much harm to theCBA’s reputation.

The CBA has moved slowly towards inflation targeting, planning to makea full transition to inflation targets by 2008. It will maintain limits on netforeign assets (ie, a floor) and on net domestic assets (ceiling) during thetransition period. However, in Article 6 of the central bank law the process offiling a monetary policy programme to the government calls for monetaryaggregates to be included; this will need to be changed in order to move toinflation targeting, no longer stating quantity forecasts.7

ARE THE PREREQUISITES FOR INFLATION TARGETING MET IN ARMENIA?

The prerequisites for inflation targeting have been discussed extensively inthe literature. Siklos and Abel (2003) provide a clear discussion for the case ofHungary, emphasising the institutional and economic pre-conditions neces-sary. These are discussed in a broader context in IMF (2005b). However,Stone (2003) argues that many developing economies announce an inflationtarget to define their policy objective, but are unable to achieve full-fledgedinflation targeting because various preconditions, lack of a strong fiscalposition and a fully developed financial system in particular, are not met.As a result they opt for a set of policies he labels ‘inflation targeting lite’.8 Thismay not be a monetary policy regime per se, but simply a transitionalregime that attempts to maintain monetary stability while structural reformsnecessary to support a nominal anchor take place. Once fiscal and financialsystems improve and transparency and bank credibility increases, movingto a more full-fledged inflation targeting regime may be possible.9 Armeniais clearly in transition, as the CBA just announced the adoption ofinflation targeting, believing that the fundamental preconditions are met.

7 Ibid, p. 30. One can see that while CBA states its goal of 3% inflation for 2006, it nevertheless

must file forecasts for monetary aggregates, including reserve money. See pp. 31–32.8 Note that this is quite different than the case of fully developed economies like the G3, the US,

Japan and Germany, which pursue what Clarida et al. (1998) call ‘soft-hearted inflation targeting’.9 See also Batini and Laxton (2005), Carare et al. (2002) and Dabla-Norris et al. (2007).

K Banaian et alInflation Targeting in Armenia

427

Comparative Economic Studies

The Central Bank of Armenia (2006c) casts the conditions in a slightlydifferent framework emphasising institutional, operational and macroeco-nomic pre-conditions. The Bank emphasises that these conditions aremet or sufficiently met to proceed with full-fledged inflation targeting. Letus review them.

Operational preconditions include inflation forecasting capabilities and aclear understanding on the part of policymakers of the monetary transmissionmechanism. While the CBA has developed methods for forecasting inflationand these are typically explained in the Monetary Policy Program documents,most have only recently been implemented.10 Formal forecasting models arenow employed, but their usefulness is sometimes limited due to the extremeseasonality of inflation, exogenous shocks, unstable money demand duringtransition and ongoing structural reforms which make stochastic modelsdifficult to estimate. All of these factors, along with relatively short time seriesfor critical data make modeling efforts challenging. While reaching a betterunderstanding of the monetary channels does require careful analysis andmodelling efforts, these limitations are not unique to inflation targeting as apolicy choice. Other monetary policies, monetary aggregate targeting andexchange rate targeting, require similar efforts as well, and these difficultieswill likely be overcome in due course.

Macroeconomic preconditions include a developed financial market,absence of fiscal dominance and both internal and external stability.Developed financial markets are essential as a deep and liquid interbankmarket relieves the central bank of the need to conduct intermediatingtransactions and contributes to broad distribution of central bank paper thusfacilitating open market operations. The benefits of a more fully developedfinancial system, lower median interest rates due to greater competition, alsotend to make the central bank an advocate for financial system reforms.11 TheCBA acknowledges that the relatively underdeveloped domestic financialmarket is the ‘most serious obstacle to the effective implementation of aninflation targeting strategy’.12 The small banking industry and few financialinstruments limit the typical interest rate channel of monetary policy criticalfor the influence of monetary policy on macroeconomic performance.Insufficient competition, the size of the second economy and opaqueownership structures remain problematic.13

10 See Table 11a, p. 28 of Dabla-Norris et al. (2007).11 Stone (2003), p. 8 notes that median interest rates in 1998–1999 were 12.4% for countries

engaged in inflation targeting lite versus 9.9% for full-fledged inflation targeters.12 Central Bank of the Republic of Armenia (2006c), p. 10.13 See Dabla-Norris et al. (2007) section IV.D and Table 10 for additional details.

K Banaian et alInflation Targeting in Armenia

428

Comparative Economic Studies

Fiscal dominance is a constraint on the implementation of any monetarypolicy. In Armenia several traditional measures, like central bank lending tothe government or the share of seniorage in GDP indicate that fiscaldominance is not an issue. However, other indicators, such as confidence thatthe government can manage an external shock without central bankassistance, contribute to uncertainty in this area. Large seasonal governmentexpenditures and the large remittances from abroad pose special challenges.Nonetheless, relatively stable fiscal policies and priorities now indicate fiscaldominance, per se, does not appear to be a major obstacle. Further, overallinternal balance also appears to be satisfactory as average inflation during1998–2004 was 2.4% and growth has been strong.14 External balance is moreproblematic, however, due to the unusual role of foreign private remittances.Because foreign remittances are critical in reducing the current accountdeficit, economic conditions abroad must be carefully monitored. Stronggrowth in exports and foreign direct investment in the longer term mayeventually limit the dependency on remittances.

Institutional preconditions include designating price stability as theprinciple goal of the central bank, selecting a particular inflation target,empowering the central bank with policy discretion, providing mechanismsfor transparency and accountability and operational independence. Pricestability was declared the primary goal of the CBA early on.15 However,as in most transition economies, attaining that goal was initially sub-ordinated to finding an equilibrium exchange rate and ensuring internationalcompetitiveness. Even with the declaration of inflation targeting as themonetary policy, important caveats include concerns for exchange ratestability. The extent to which exchange rate intervention is legitimatelyimplemented to reduce volatility versus maintaining competitiveness remainsto be seen.

For an inflation forecast targeting regime the policy target must be clear.Headline inflation has the advantage that the public understands andobserves it with ease. The link between the intermediate target, the inflationforecast and the headline consumer price index should be clear and the lagshort. A serious limitation, however, is the extent to which inflation may beinfluenced by non-monetary shocks. In Armenia the monetary policychannels may be overwhelmed by real shocks, domestic (in agriculture, eg)or foreign (energy, eg), that may confuse public perceptions of the Bank’spolicy signals. Selection of the appropriate target, core inflation or a trimmedCPI, rather than headline CPI may ameliorate this problem. Further, coping

14 See Table 5 of Dabla-Norris et al. (2007), p. 14.151996 Republic of Armenia Law on the Central Bank.

K Banaian et alInflation Targeting in Armenia

429

Comparative Economic Studies

with exogenous shocks requires adjustments to policy, and the bank musthave the discretion to make these changes quickly and to providesimultaneously clear explanations to the public. Monetary policy discretionincludes the ability to make policy changes without extensive negotiationswith the legislature or Ministry of Finance. In addition, policy discretiontypically requires the use of an inflation forecast as the primary guide forpolicy, but also consideration of other indictors ranging from changes tomonetary aggregates, international capital flows and exchange rate pressures– all at the Bank’s discretion.16 The CBA appears to have the necessarydiscretion to implement inflation targeting. Further, operational indepen-dence appears to be sufficient. In fact, when compared to other transitioneconomy central banks quantitative measures of central bank independenceindicate the CBA is among the most independent – ranked first or secondmost independent by some measures.17

Effectively communicating central bank policies is essential for full-fledged inflation targeting. Policy must be transparent and the Bank must beaccountable. In Armenia this appears to be the case. The CBA has adopted theIMF’s Code of Good Practices in Transparency of Monetary and FinancialPolicies and has made it part of its operating philosophy.18 The CBA publishesregular, monthly, quarterly and annual reports and the Monetary PolicyProgram. The Inflation Report is expected to be published quarterly alongwith minutes of the meetings of the Bank Board. Transparency andaccountability are not expected to be an issue in the transition to full-fledgedinflation targeting. It appears the CBA authorities have adopted and are firmlycommitted to inflation targeting.

Overall we believe that the preconditions for inflation targeting inArmenia have essentially been met and at this point the CBA is well on itsway to full-fledged inflation targeting. The next question is what does theCBA reaction function look like? Can it be estimated and is it similar to that ofan established market economy central bank? Further, how does the patternof interest rates set by the bank compare to that from the estimated reaction

16 It is worth noting that, while the CBA is adopting an inflation targeting strategy, it specifically

notes that it is also not abandoning ‘all of the principles of the monetary aggregate targeting

strategy’. Central Bank of the Republic of Armenia (2006c), p. 11. Such explicit pronouncements may

confound public perceptions of monetary policy.17 Cukierman et al. (2002) attribute this in part to being a latecomer to central bank reforms

and also for countries which had two central bank reform laws, the second tends to make the central

bank even more independent. This was indeed the case for the Central Bank of Armenia.

See pp. 241–244, and in particular Tables 1, p. 242 and 2, p. 244. Also see Table 6, p.16 of Dabla-

Norris et al. (2007).18 Central Bank of the Republic of Armenia (2006b).

K Banaian et alInflation Targeting in Armenia

430

Comparative Economic Studies

function and how does it compare with that which would have resulted ifinflation targeting had been the prevailing policy?

THE MODEL AND ESTIMATION

Given the state of the monetary and fiscal system described above, inflationtargeting – lite or otherwise – may be a feasible monetary policy option. Itthen seems likely that a Taylor rule may be useful in describing the centralbank reaction function and useful for comparative policy analysis as well.There are numerous formulations of Taylor rules. We begin by assuming thatthe central bank faces a quadratic loss function for both inflation and output.If there is a connection between nominal interest rates and aggregate demand,we can find that the central bank will minimise losses by targeting the interestrate according to the following rule:

r�t ¼ r� þ f½EðptþkjOtÞ � p�� þ j½EðytþkjOtÞ� ð1Þ

where r* is the nominal interest rate when inflation and the output gap areat their target levels of p* and zero and E(pt+k|Ot) is the expectation ofinflation at time t+k given the information set O at time t (and likewise for y.)This is the forward-looking Taylor Rule described by Svensson (1997). It isforward looking because it sets the target interest rate based on a forecast forinflation and the output gap. Svensson refers to such a rule as inflationforecast targeting. A country engaged in strict inflation targeting will set thevalue of j¼ 0.

Sgherri (2005) varies the model in two ways. First, she argues for interestrate smoothing either as a response to uncertainty about the inflation andoutput forecasts or as a means of dealing with fragility in the banking system(banks may not be able to withstand the balance sheet effects of large adversechanges in deposit and lending rates.) Second, central banks may viewmovements in the exchange rate as useful indicators of inflationary pressurein the economy. Gerdesmeier and Roffia (2004) also consider a ‘baseline’Taylor rule similar to (1) adding lagged interest rates as a measure of inertiaor interest rate smoothing, and then additional specifications includingvarious exchange rate measures. We use an augmented form of equation (1)to test whether deviations from exchange rates, inflation and output affect theconduct of monetary policy:

r�t ¼art�1 þ ð1� aÞfb½EðptþkjOtÞ � p��þ g½EðytþkjOtÞ� þ d½EðetþkjOtÞ�g þ et

ð2Þ

K Banaian et alInflation Targeting in Armenia

431

Comparative Economic Studies

where e is the deviation of the exchange rate from its long-run trend.Following Sgherri (2005) we assume purchasing power parity to hold in thelong run so that e is a stationary process.

A question arises whether the nominal or real effective exchange ratecontains additional information about the future of inflation. Sgherri uses thereal rate for this purpose. Devereux and Engel (2006) use the nominalexchange rate. In a country with sticky nominal prices, the exchange rate canreflect changes in relative prices of non-durable goods as well as changingasset prices. The nominal exchange rate thus contains news that themonetary authority can use in inflation forecast targeting.19

We define the information set O as containing all relevant informationavailable to the policymaker, which includes observations on inflation, theGDP gap, nominal exchange rate versus the US dollar or the real effec-tive exchange rates, and broad M2 including foreign currency deposits, forthe current and two most recent quarters. This information set provides theorthogonality conditions required to estimate equation (2) by the generalisedmethod of moments (GMM). We estimate the equation using quarterlyobservations for 1998:I through 2005:I.

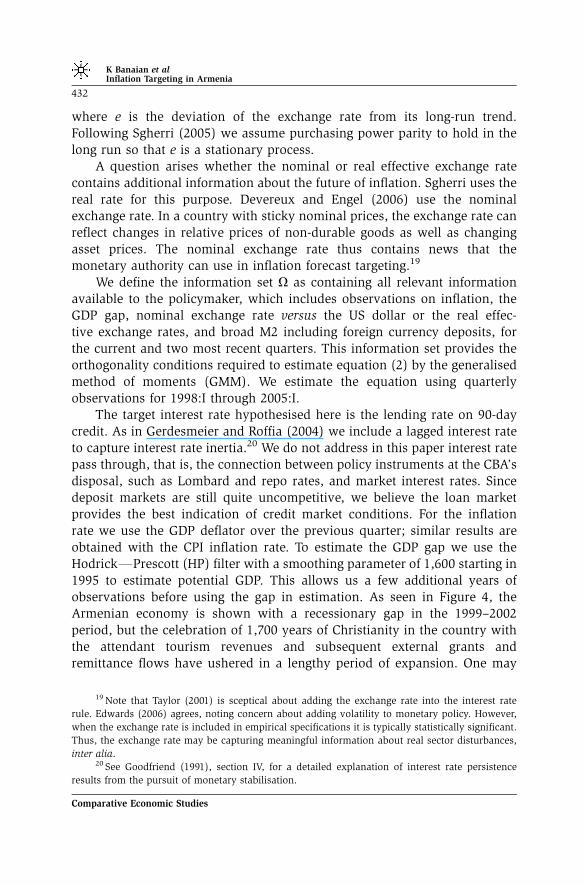

The target interest rate hypothesised here is the lending rate on 90-daycredit. As in Gerdesmeier and Roffia (2004) we include a lagged interest rateto capture interest rate inertia.20 We do not address in this paper interest ratepass through, that is, the connection between policy instruments at the CBA’sdisposal, such as Lombard and repo rates, and market interest rates. Sincedeposit markets are still quite uncompetitive, we believe the loan marketprovides the best indication of credit market conditions. For the inflationrate we use the GDP deflator over the previous quarter; similar results areobtained with the CPI inflation rate. To estimate the GDP gap we use theHodrickFPrescott (HP) filter with a smoothing parameter of 1,600 starting in1995 to estimate potential GDP. This allows us a few additional years ofobservations before using the gap in estimation. As seen in Figure 4, theArmenian economy is shown with a recessionary gap in the 1999–2002period, but the celebration of 1,700 years of Christianity in the country withthe attendant tourism revenues and subsequent external grants andremittance flows have ushered in a lengthy period of expansion. One may

19 Note that Taylor (2001) is sceptical about adding the exchange rate into the interest rate

rule. Edwards (2006) agrees, noting concern about adding volatility to monetary policy. However,

when the exchange rate is included in empirical specifications it is typically statistically significant.

Thus, the exchange rate may be capturing meaningful information about real sector disturbances,

inter alia.20 See Goodfriend (1991), section IV, for a detailed explanation of interest rate persistence

results from the pursuit of monetary stabilisation.

K Banaian et alInflation Targeting in Armenia

432

Comparative Economic Studies

argue that the potential GDP is too small by ignoring earlier years – theArmenian economy was quite depressed in the period after transition – butthis likely only affects the intercept of the trend line for potential GDP. Sinceall we are interested in is the deviation from the trend, the HP filter serves as areasonable approximation.

Grigorian et al. (2004) show that many of the macroeconomic time seriesin Armenia contain unit roots, so before we estimate the above equation wetest for stationarity. The results of unit root tests are presented in Table 1. Theinflation and GDP gap measures are stationary in levels, but the interest rate,real exchange rate and broad money are difference stationary. Grigorian,Khachatryan and Sargsyan found cointegration between money, wages andexchange rates; only the terms of trade was found to be level-stationary intheir monthly model. Also exchange rate changes passed through quickly to

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

1998 1999 2000 2001 2002 2003 2004 2005

GDPGAP

Figure 4: GDPGAP

Table 1: Unit root tests

ADF test, levels Lags ADF test,first difference

Lags

90-day lending rate �1.632 1 �8.706* 0Inflation (GDP deflator) �11.864* 0 FGDP gap �5.891* 0 FNominal exchange rate �1.513 1 �2.993* 0Real effective exchange rate �0.601 0 �5.235* 1Broad M2, incl. foreign currency deposits 2.140 4 �5.579* 2

* indicates 0.01 level of significance. Lag length determined by Schwarz Information Criterion.

K Banaian et alInflation Targeting in Armenia

433

Comparative Economic Studies

price changes in their model. For us the question is whether the lending rateis connected to exchange rates as hypothesised in equation (2).

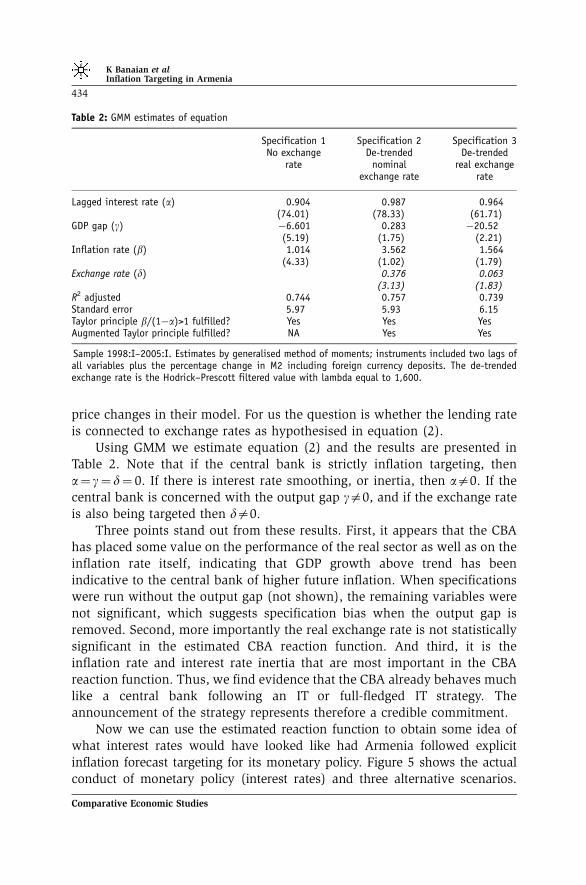

Using GMM we estimate equation (2) and the results are presented inTable 2. Note that if the central bank is strictly inflation targeting, thena¼ g¼ d¼ 0. If there is interest rate smoothing, or inertia, then aa0. If thecentral bank is concerned with the output gap ga0, and if the exchange rateis also being targeted then da0.

Three points stand out from these results. First, it appears that the CBAhas placed some value on the performance of the real sector as well as on theinflation rate itself, indicating that GDP growth above trend has beenindicative to the central bank of higher future inflation. When specificationswere run without the output gap (not shown), the remaining variables werenot significant, which suggests specification bias when the output gap isremoved. Second, more importantly the real exchange rate is not statisticallysignificant in the estimated CBA reaction function. And third, it is theinflation rate and interest rate inertia that are most important in the CBAreaction function. Thus, we find evidence that the CBA already behaves muchlike a central bank following an IT or full-fledged IT strategy. Theannouncement of the strategy represents therefore a credible commitment.

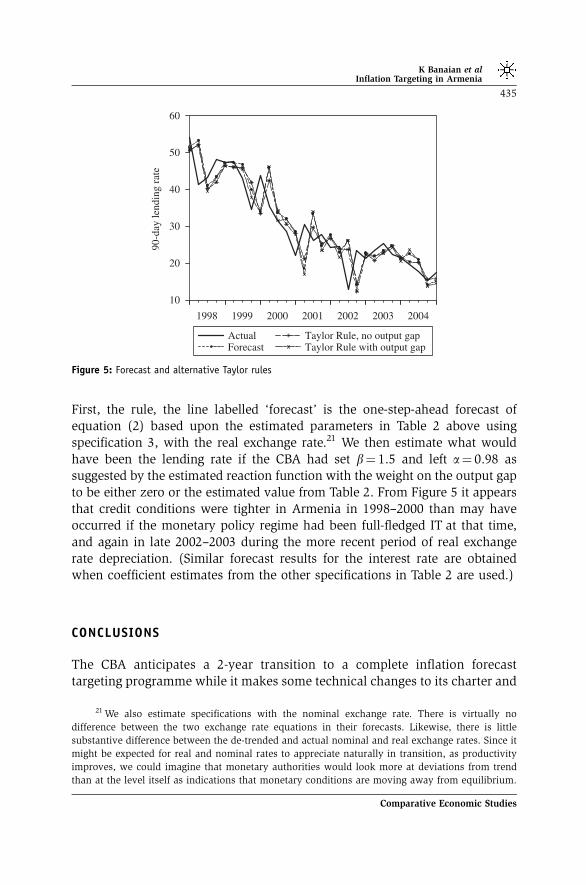

Now we can use the estimated reaction function to obtain some idea ofwhat interest rates would have looked like had Armenia followed explicitinflation forecast targeting for its monetary policy. Figure 5 shows the actualconduct of monetary policy (interest rates) and three alternative scenarios.

Table 2: GMM estimates of equation

Specification 1No exchange

rate

Specification 2De-trended

nominalexchange rate

Specification 3De-trended

real exchangerate

Lagged interest rate (a) 0.904 0.987 0.964(74.01) (78.33) (61.71)

GDP gap (g) �6.601 0.283 �20.52(5.19) (1.75) (2.21)

Inflation rate (b) 1.014 3.562 1.564(4.33) (1.02) (1.79)

Exchange rate (d) 0.376 0.063(3.13) (1.83)

R2 adjusted 0.744 0.757 0.739Standard error 5.97 5.93 6.15Taylor principle b/(1�a)>1 fulfilled? Yes Yes YesAugmented Taylor principle fulfilled? NA Yes Yes

Sample 1998:I–2005:I. Estimates by generalised method of moments; instruments included two lags ofall variables plus the percentage change in M2 including foreign currency deposits. The de-trendedexchange rate is the Hodrick–Prescott filtered value with lambda equal to 1,600.

K Banaian et alInflation Targeting in Armenia

434

Comparative Economic Studies

First, the rule, the line labelled ‘forecast’ is the one-step-ahead forecast ofequation (2) based upon the estimated parameters in Table 2 above usingspecification 3, with the real exchange rate.21 We then estimate what wouldhave been the lending rate if the CBA had set b¼ 1.5 and left a¼ 0.98 assuggested by the estimated reaction function with the weight on the output gapto be either zero or the estimated value from Table 2. From Figure 5 it appearsthat credit conditions were tighter in Armenia in 1998–2000 than may haveoccurred if the monetary policy regime had been full-fledged IT at that time,and again in late 2002–2003 during the more recent period of real exchangerate depreciation. (Similar forecast results for the interest rate are obtainedwhen coefficient estimates from the other specifications in Table 2 are used.)

CONCLUSIONS

The CBA anticipates a 2-year transition to a complete inflation forecasttargeting programme while it makes some technical changes to its charter and

10

20

30

40

50

60

1998 1999 2000 2001 2002 2003 2004

ActualForecast

Taylor Rule, no output gapTaylor Rule with output gap

90-d

ay le

ndin

g ra

te

Figure 5: Forecast and alternative Taylor rules

21 We also estimate specifications with the nominal exchange rate. There is virtually no

difference between the two exchange rate equations in their forecasts. Likewise, there is little

substantive difference between the de-trended and actual nominal and real exchange rates. Since it

might be expected for real and nominal rates to appreciate naturally in transition, as productivity

improves, we could imagine that monetary authorities would look more at deviations from trend

than at the level itself as indications that monetary conditions are moving away from equilibrium.

K Banaian et alInflation Targeting in Armenia

435

Comparative Economic Studies

develops public confidence in the new monetary policy regime. Our analysisindicates that the path of interest rates in Armenia since 1998 may have beenoccasionally overly restrictive (Figure 5). The inflation targeting regime isseen by some to be too inflation-conscious and insufficiently restrictive indealing with positive supply shocks that might result during the transition toa market economy.

We note that the IMF has recently stated that inflation targeting may be anappropriate policy for developing and transition economies. Indeed, thenecessary ‘technical’ requirements for success of an IT policy regime ‘areessential for the success of virtually any systematic monetary policy framework,and some may be even more important for non-inflation targeting regimes’(IMF, 2006, p. 18). Inflation targeting is an information-intensive strategy formonetary policy, they argue, and we agree that the amount of information usedin forming the current forecasts of inflation, the output gap and real exchangerates (if the augmented form is used) may be large. Although the estimationresults are quite reasonable, we believe at this early stage caution is stillwarranted. The estimates may be fragile due to the short time period involved,but they are highly plausible and the Taylor rule simulations do provideimportant insights into the conduct of monetary policy.

Acknowledgements

The authors would like to thank the anonymous referees for helpful commentson an earlier draft. All errors remain the responsibility of the authors.

REFERENCES

Batini, N and Laxton, D. 2005: Under what conditions can inflation targeting be adopted? The

experience of emerging markets. In: Schmidt-Hebel, K and Mishkin, FS (eds). Monetary Policy

Under Inflation Targeting. Banco Central de Chile: Santiago, 2007.

Carare, A, Schaechter, A and Stone, M. 2002: Establishing initial conditions in support of inflation

targeting. IMF Working Paper No. 02/102, International Monetary Fund: Washington, DC.

Central Bank of the Republic of Armenia. 2006a: Banking System of Armenia: Development,

Supervision, Regulation. CBRA: Yerevan.

Central Bank of the Republic of Armenia. 2006b: Monetary Policy Programme of the Republic of

Armenia. CBRA: Yerevan.

Central Bank of the Republic of Armenia. 2006c: The Rationale for the Adoption of Inflation Targeting

Strategy. CBRA: Yerevan.

Clarida, R, Gali, J and Gertler, M. 1998: Monetary policy rules in practice: Some international

evidence. European Economic Review 42: 1033–1067.

Cukierman, A, Miller, GP and Neyapti, B. 2002: Central Bank reform, liberalization and inflation in

transition economies – An international perspective. Journal of Monetary Economics 49: 237–264.

Dabla-Norris, E, Kim, D, Zermeno, M, Billmeier, A and Kramarenko, V. 2007: Modalities of moving to

inflation targeting in Armenia and Georgia. IMF Working Paper WP/07/133, International

Monetary Fund: Washington, DC.

K Banaian et alInflation Targeting in Armenia

436

Comparative Economic Studies

Devereux, MB and Engel, C. 2006: Expectations and exchange rate policy. NBER Working Paper

#12213, National Bureau of Economic Research: Cambridge, MA.

Edwards, S. 2006: The relationship between exchange rates and inflation targeting revisited. NBER

Working Paper No. 12163, April 2006.

Gerdesmeier, D and Roffia, B. 2004: Empirical estimates of reaction functions for the Euro area.

Swiss Journal of Economics and Statistics 140: 37–66.

Goodfriend, M. 1991: Interest rates and the conduct of monetary policy. Carnegie-Rochester

Conference Series on Public Policy 34: 7, 30.

Grigorian, D, Khachatryan, A and Sargsyan, G. 2004: Exchange rate, money, and wages: What is

driving prices in Armenia? IMF Working Paper, WP/04/229, International Monetary Fund:

Washington, DC.

International Monetary Fund. 2005a: Armenia: Country Report 05/422 (International Monetary

Fund: Washington, DC.

International Monetary Fund. 2005b: Does inflation targeting work in emerging markets? World

Economic Outlook: Building Institutions, September 2005. pp. 161–186, International Monetary

Fund: Washington, DC.

International Monetary Fund. 2006: Inflation targeting and the IMF. Mimeo, Monetary and Financial

Systems Department, 16 March 2006, International Monetary Fund: Washington, DC.

Jonas, J and Mishkin, FS. 2005: Inflation targeting in transition economies: Experiences and

prospects. In: Bernanke, BS and Woodford, M (eds). The Inflation Targeting Debate. University of

Chicago Press: Chicago pp. 353–413.

Orlowski, L. 2006: Advancing inflation targeting in Central Europe: Strategies, policy rules and

empirical evidence. Paper presented at the 9th Bi-Annual Meeting of the European Association of

Comparative Economic Studies, Brighton England, 7–9 September 2006.

Poole, W. 2005: How predictable is fed policy. Review of the Federal Reserve Bank of St. Louis 87:

659–668.

Sgherri, S. 2005: Explicit and implicit targets in open economies. IMF Working Paper, WP/05/176,

International Monetary Fund: Washington, DC.

Siklos, PL. 2006: Hungary’s entry into the euro area: Lessons for prospective members from a

monetary policy perspective, Economic Systems, 30: 366–384.

Siklos, PL and Abel, I. 2003: Is Hungary ready for inflation targeting? Economic Systems 66: 1–25.

Stone, M. 2003: Inflation targeting lite. IMF Working Paper WP/03/12, International Monetary Fund:

Washington, DC.

Svensson, L. 1997: Inflation forecast targeting: Implementing and monitoring inflation targets.

European Economic Review 41: 1111–1146.

Taylor, JB. 2001: The role of the exchange rate in monetary policy rules. American Economic Review

91(2): 263–267.

K Banaian et alInflation Targeting in Armenia

437

Comparative Economic Studies