housing finance gses: who gets the subsidy?

TRANSCRIPT

Journal of Financial Services Research 15:3 197±209 (1999)

# 1999 Kluwer Academic Publishers, Boston. Manufactured in The Netherlands.

Housing Finance GSEs: Who Gets the Subsidy?

EDWARD J. KANE

Boston College

Abstract

Taxpayer subsidies that ¯ow toward housing-®nance GSEs are implicit in nature. This makes the size and

distribution of subsidy values hard to measure directly. An array of indirect analyses indicates that incentive-

con¯icted GSE managers can and do extract substantial annual subsidies for GSE stockholders. Currently,

stockholders are allowed to encourage managers to exploit taxpayers by tying incentive compensation implicitly

to increases in the discounted present value of expected future subsidies. To counteract this inappropriate

incentive, managers should be made accountable to taxpayers for returning all compensation that can be fairly

attributed to increases in subsidies captured by GSE stockholders.

Key words: GSE subsidy; Fannie Mae; incentive compensation

Among the legacies of the 1930s program for ending the Great Depression is a layered

federal involvement in promoting and subsidizing the ¯ow of housing ®nance. Until the

Federal Savings and Loan Insurance Corporation (FSLIC) broke down in 1989, the largest

layer of subsidies for housing credit ¯owed through FSLIC-insured thrift institutions

(S&Ls) that concentrated on originating and holding home mortgages. These subsidies

were routed through generously priced deposit insurance and subsidized borrowing

opportunities from the Federal Home Loan Bank System (``Flubbie''). A second, smaller

layer of subsidies ¯owed through federal mortgage insurance offered directly to

mortgagors through the Federal Housing Administration and the Veterans

Administration. In recent years, the ®rst two layers have shrunk and a third layer of

subsidies for housing credit has expanded. This sturdiest layer of subsidies ¯ows through

the activities of government-sponsored credit enterprises (GSEs) in secondary mortgage

markets. The assigned mission of the GSEs is to buy or insure mortgages from ®nancial

institutions that originate mortgages and to issue (or support the issue of ) bonds backed by

pools of mortgages.

In addition to Flubbie, the principal housing GSEs were chartered as the Federal

National Mortgage Association (FNMA) and the Federal Home Loan Mortgage

Corporation (FHLMC). To better market their products to ordinary folks, the managers

of these GSEs have turned their ®rms' acronyms into the user-friendly names Fannie Mae

and Freddie Mac. Both institutions may be described as ``stockholder-owned''

corporations chartered by the federal government speci®cally to increase the ¯ow of

housing ®nance. In corporate governance, Fannie and Freddie are far from ordinary

corporations. They retain many of the characteristics of a federal agency. These

characteristics create some potentially burdensome responsibilities and some valuable

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

special privileges for owners and managers. They also assign taxpayers an implicit stake in

resolving dif®culties that these ®rms might encounter in covering their contractual

obligations.

Subsidies may be de®ned as aid a government provides to a private undertaking. This

aid may be direct or indirect. Direct aid includes explicit funding. But (and more

importantly in the case of Fannie, Freddie, and Flubbie,) implicit bene®ts enhance the

value of the recipient enterprise in subtler ways. Responsible government requires that

authorities measure the costs and bene®ts of every subsidy program and strike a lasting

balance between social costs and social bene®ts over time.

Common law and case law clearly establish that government employees owe duties of

loyalty, competence, and care to taxpayers [Bear and Maldonado-Bear (1994)]. Although

the precise issue may not have been litigated, by logical extension a GSE's federal status

imposes parallel duties to taxpayers on its employees. These duties of public stewardship

con¯ict with and temper the duties GSE employees owe their corporate stockholders. As a

matter of principle, managers' duties to taxpayers should increase with the size of the

subsidies that pass through a GSE's accounts.

In the absence of adequate oversight of this incentive con¯ict, it is unlikely that a subsidy

program can be counted on to serve meritorious public purposes in fair and ef®cient ways.

Agency costs are unlikely to be minimized if a privately owned enterprise is managed to

make long-term and growing use of government support and at the same time its managers

resist efforts to make the enterprise accountable for the distribution made of the support

received. Part of the problem is that receiving the subsidy in implicit ways blurs the con¯ict

of interest and misleads taxpayers about the extent of their stake in managerial decisions.

As off-budget values, the character, size, and distribution of GSE subsidies are hard for

government of®cials, the press, and academics to pin down. Efforts to measure implicit

subsidies and track their ultimate distribution between intended and unintended recipients

are inherently imprecise and controversial. Imprecision in how to measure and track

implicit subsidies adds to their durability by making the extent and violation of managerial

duties hard for outsiders to communicate to a noneconomist audience.

Although this paper focuses on Fannie and Freddie, readers should understand that these

®rms' success in capturing taxpayer subsidies was bound to evoke imitation. Flubbie has

asked Congress to expand its statutory mission so that it can reap subsidized pro®ts in

parallel ways [Federal Home Loan Bank of Chicago (1997)].

Fannie and Freddie understand that the political environment keeps every subsidy

recipient under the threat of closer public review. To de¯ect political pressure for increased

accountability, they characterize themselves as mere ``conduits'' for subsidies rather than

as subsidy recipients per se. They routinely deny that their managers or owners hold onto

any of the subsidies that ¯ow through their pipeline. Echoing the rascally cartoon

character, Bart Simpson, they assure us that they don't receive any subsidies, that nobody

has seen them receive any subsidies, and that nobody can prove they hold onto federal

subsidies anyway.

This paper seeks to rebut these contradictory defenses in turn. The ®rst section focuses

on the character of the subsidized business advantages that federal sponsorship confers on

a GSE. It seeks to explain how the size of a GSE's subsidy is affected by competitive

forces in the market structure for GSE services and that the value of the subsidy is

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

198 EDWARD J. KANE

expandable at the initiative of incentive-con¯icted GSE managers. The second section

reviews estimates of the subsidy that observers in watchdog institutions have offered. The

®nal section outlines reforms in accountability that could help society to better limit the

size of the subsidies that the housing GSEs do manage to retain.

1. How Fannie and Freddie receive subsidies

What value does a GSE's charter name convey? Let us suppose that Fannie had been

chartered under the name Private National Mortgage Corporation and Freddie's charter

name was Private Home Loan Mortgage Corporation. Let us suppose further that both

corporate charters had been issued by the state of Delaware.

The loss of federal sponsorship would have four main effects:

1. It would change the relationships these GSEs have with state and local government,subjecting them to taxes and regulations from which they now have speci®c

exemptions.

2. It would change their relationships with federal agencies, particularly with the

Securities and Exchange Commission (both GSEs now are exempt from SEC ®ling

and disclosure requirements), the Federal Reserve (which serves as ®scal agent), and

the Of®ce of Federal Housing Enterprise Oversight (OFHEO, which was set up to

monitor the safety and soundness of these GSEs).

3. It would change their relationships with competitors, investors, and counterparties in

®nancial markets by removing access to Treasury credit and each corporation's

perceived claim to credit support from federal taxpayers.

4. It would change their relationships with elected of®cials, by eliminating their loosely

de®ned and self-determined corporate obligation to ``assist'' disadvantaged

mortgagors and by making the maintenance of lobbying skills and political clout a

less important part of their enterprise.

The potential economic losses to Fannie and Freddie and potential gains to other parties

from adjusting the ``direct bene®ts'' inherent in the ®rst two relationships are sizeable but

less variable over the business cycle than the ``indirect'' losses and gains from adjusting

its other relationships. Federal sponsorship means that, while positive returns on corporate

equity belong to GSE shareholders, the deep downside of negative returns are transferred

to taxpayers. This asymmetric division of potential revenues and potential costs stands at

the heart of the issues of subsidy measurement and control.

Fannie and Freddie may be likened to government-insured ®nancial intermediaries that

private investors con®dently perceive to be too big to fail (TBTF). Holders of the debt

instruments that TBTF institutions either guarantee or use to fund their asset portfolio

enjoy an informal or conjectural federal guarantee of promised payments. This de facto

federal guarantee extracts a subsidy from general taxpayers in the form of an unpaid credit

enhancement.

This credit enhancement increases GSE pro®ts in several ways. It lowers the GSE's cost

of capital by lowering the explicit and implicit interest cost of GSE debt. It increases

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

HOUSING FINANCE GSEs 199

revenues by raising the fees a GSE can collect for guaranteeing the performance of

mortgage-backed securities (MBS) or writing swaps. It also tends to lower the interest rate

that mortgagors have to pay on the loans that Fannie or Freddie fund or enhance.

How the subsidy divides itself between GSE pro®ts and reduced interest rates for

mortgagors (and therefore higher demand for builder services) depends on how

competitive the market is for the so-called conforming mortgages the GSEs are authorized

to deal in. The issue turns on how vigorously Fannie and Freddie compete against each

other and how much pressure private competitors can bring to bear on the prices and fees

that GSEs charge. Although Fannie and Freddie note that one cannot prove that markets do

not fully shift the subsidy away from their stockholders [e.g., FNMA (1996a)], Flubbie,

private competitors [Capitol Financial Insights (1998)], industrial-organization theory, and

the GSE's extraordinary pro®tability and market dominance [Goodman and Passmore

(1992); Hermalin and Jaffee (1996)] strongly suggest otherwise.

1.1. Managerial control of the subsidies

Direct bene®ts that GSEs get from their hybrid agency-corporate status may be conceived

as targeted reductions in their tax and regulatory burdens. The value of these bene®ts may

be modeled as growing with the volume of business they write. GSE revenues consist of

returns on the assets they hold and returns from the various guarantee and contingent

liability contracts they write.

Indirect bene®ts may be conceived as reductions in the costs a GSE must incur to

ef®ciently convince its counterparties that it can be relied on to ful®ll its contractual

commitments. Merton and Perold (1993) de®ne the capitalized value of these costs of

persuasion to be a ®rm's risk capital. The Merton-Perold de®nition implies that the

capitalized value of the indirect bene®ts of a GSE's status constitute taxpayer-contributed

risk capital. Other things equal, persuasion costsÐand therefore aggregate and taxpayer-

contributed risk capitalÐincrease with a ®rm's leverage, asset risk, interest-rate risk, and

the riskiness of its guarantees and contingent liabilities.

GSE growth and riskiness are constrained in two ways: by limits on the types of

mortgages that Fannie and Freddie may ®nance and by OFHEO oversight. However, the

constraint system remains poorly targeted and riddled with loopholes. Unless, or until,

enforceable duties of adequate and truthful disclosure of subsidy bene®ts can be imposed

on the managers of Fannie and Freddie, government control of GSE subsidies will remain

distressingly cosmetic.

2. Estimates of the value of direct and indirect subsidies to Fannie and Freddie

Spokespersons for Fannie and Freddie sometimes claim that they operate at no cost to

government because they receive no explicit subsidy [e.g., Zoellick (1996)]. This claim is

only half true, and it is circulated for its disinformational effect on the public policy

debate. It confuses taxpayers and provides accounting cover for friendly politicians.

GSE managers have a duty to taxpayers to limit the size of whatever subsidies ¯ow to

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

200 EDWARD J. KANE

stockholders. Managers cannot ful®ll this duty simply by claiming that proofs of the

existence of such a subsidy ¯ow have some loose ends. Many of these loose ends come

from the informational disadvantage under which GSE disclosure policies force outside

investigators to operate [Feldman (1998)]. Of®cials who pride themselves on being in

charge of an ``instrumentality'' of the U.S. government should not dismiss so lightly the

evidence that has been assembled by informationally handicapped critics in watchdog

institutions.

Duties of loyalty, truthfulness, and care to taxpayers could be discharged more

conscientiously by measuring the value of taxpayer credit enhancements in open,

principled, and robust ways. An appropriate policy would be to collect and release

information that GSE staff and outside ®nancial analysts alike could use to account with

reasonable accuracy for the distribution of the subsidy between mortgagors, originators,

and GSE investors.

That Fannie and Freddie dominate the conduit market for conforming loans and act in

important respects the way ``tacitly colluding duopolists'' would be expected to behave

[Hermalin and Jaffee (1996)] is beyond dispute. Of course, this behavior and the GSEs'

extraordinary pro®tability do not prove that Fannie and Freddie in fact tacitly collude. But

these worrisome facts should shift the burden of proof from critics to the GSEs.

Stockholders in Fannie and Freddie stand to lose almost nothing if managerial claims

about subsidy shifting are right, whereas taxpayers stand to lose a great deal if these claims

are mistaken.

In a noncongressional forum last year, a GSE spokesperson ®rmly acknowledged that

Fannie derives value from its federal credit enhancement. In a February 3, 1998, comment

letter written to the Of®ce of the Comptroller of the Currency, Fannie's general counsel

wrote:

Fannie Mae standard domestic obligations, like Treasuries, typically receive no rating

on an issue-by-issue basis, because investors and the rating agencies view the implied

government backing of Fannie Mae as a suf®cient indication of the investment quality

of Fannie Mae obligations [Marra (1998, p. 4)].

To reinforce the point, he goes on to quote the Fitch credit-rating service's explanation of

why it assigns FNMA a AAA rating:

The ``AAA'' ratings are based primarily on the Federal government's compelling

incentives to insure FNMA's continued viability. Although FNMA's obligations are not

explicitly guaranteed by the U.S. government, Fitch believes that in the unlikely event

of ®nancial dif®culties, the Federal government would support the company to the

extent necessary to provide for full and timely payment of FNMA mortgage-backed

securities and unsecured senior debt [Marra (1998, p. 5)].

Thus, the implicit guarantee short-circuits the debt market's discipline of GSE risk-

taking. The market does not require disclosure of projected risks and returns to price GSE

debt or securitization. This makes full and honest disclosure of these projections all the

more important for taxpayers.

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

HOUSING FINANCE GSEs 201

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

Tabl

e1.

Su

mm

ary

of

stud

ies

esti

mat

ing

the

val

ue

of

Fan

nie

Mae

'san

dF

reddie

Mac

'ssu

bsi

dy

Stu

dy

What

Was

Rev

iew

ed?

Met

hod

Fin

din

gs

U.S

.G

ener

alA

cco

un

tin

gO

f®ce

(1996a)

Sav

ings

from

tax

and

SE

C

regis

trat

ion

exem

pti

ons

(``d

irec

tsu

bsi

die

s'')

Apply

aver

age

stat

eta

xra

tean

d

regis

trat

ion

fee

and

assu

me

GS

Es

do

not

chan

ge

beh

avio

r

$400

mil

lion

in1995

on

an

asse

tbas

eof

roughly

$450

bil

lion

Kan

ean

dFo

ster

(19

86

)V

alue

of

impli

edfe

der

al

cred

itsu

pport

for

Fan

nie

Mae

from

1978

to1985

Mar

kFan

nie

'sbal

ance

shee

tto

mar

ket

and

com

par

eto

mar

ket

capit

aliz

atio

n

Fro

m$600

mil

lion

to$11

bil

lion

indif

fere

nt

yea

rs

Sch

war

tzan

dV

anO

rder

(19

88)

``E

xplo

itat

ion''

of

impli

ed

guar

ante

eby

Fan

nie

Mae

from

1978

to1985

Opti

ons

pri

cing

toex

amin

eau

dit

per

iod

and

asse

tvola

tili

ty

Par

tial

explo

itat

ion;

longer

audit

per

iod

and

hig

her

vola

tili

tyco

rres

ponds

toper

iods

when

Fan

nie

is®

nan

cial

lyw

eak

Po

zden

aan

dM

arti

n(1

99

1)

Updat

eS

chw

artz

and

Van

Ord

erfr

om

1986

to1990

Opti

ons

pri

cing

Par

tial

explo

itat

ion

even

when

condit

ions

support

Fan

nie

pro

®ta

bil

ity

Co

ok

and

Sp

ellm

an(1

99

2)

Val

ue

from

impli

edsu

pport

of

ahousi

ng

GS

E

Opti

ons

Pri

cing

Subsi

dy

dep

ends

on

capit

aliz

atio

nan

d

``bai

lout

pre

miu

m''

assu

mpti

ons;

low

er

esti

mat

esar

ound

20

bas

ispoin

tsfo

und

tobe

the

most

likel

y

Gat

tian

dS

pah

r(1

99

7)

Val

ue

of

impli

edguar

ante

eon

Fre

ddie

Mac

MB

Sin

1993

Opti

ons

pri

cing

Ran

ge

wit

hpoin

tes

tim

ate

of

8.3

bas

is

poin

tsor

$410

mil

lion

in1993

Th

yg

erso

n(1

99

0)

Val

ue

of

impli

edguar

ante

efo

r

Fre

ddie

and

Fan

nie

inte

rms

of

reduce

dco

stof

funds

Com

par

ison

wit

hban

ks'

cost

of

funds

and

bre

ak-e

ven

inves

tmen

tra

te

Impli

cit

guar

ante

epro

vid

esa

70

to154

bas

ispoin

tsco

stad

van

tage

toth

eG

SE

s

Hem

el(1

99

4)

Cost

advan

tage

for

GS

Es

in

issu

ing

MB

S

Com

par

eyie

lds

of

top-r

ated

pri

vat

e

conduit

MB

Sw

ith

GS

EM

BS

Fan

nie

and

Fre

ddie

save

30

to40

bas

is

poin

tsin

the

MB

Sm

arket

due

toG

SE

stat

us

Am

bro

sean

dW

arga

(19

96

)Fan

nie

and

Fre

ddie

'sco

st-o

f-fu

nds

advan

tage

due

toG

SE

stat

us

Mat

chG

SE

deb

tw

ith

sim

ilar

non-G

SE

corp

ora

tedeb

t;det

erm

ine

wei

gh

ted

cost

of

capit

alfo

rFan

nie

ifit

had

risk

ines

sof

non-G

SE

®nan

cial

®rm

IfFan

nie

/Fre

ddie

deb

tw

asra

ted

`AA

'

wit

hout

GS

Est

atus,

deb

tco

sts

rise

by

100

bas

ispoin

tsin

1993.

IfFan

nie

/Fre

ddie

had

`A'

rate

ddeb

t,co

sts

would

rise

by

200

bas

is

poin

ts;

cost

sof

capit

alw

ould

incr

ease

by

$3.6

bil

lion

in1993

ifF

annie

is`A

'ra

ted

202 EDWARD J. KANE

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

Tabl

e1.

(con

tinu

ed)

Stu

dy

What

Was

Rev

iew

ed?

Met

hod

Fin

din

gs

Co

ng

ress

ional

Bud

get

Of®

ce(1

996)

Fan

nie

and

Fre

ddie

'sco

st-o

f-fu

nds

advan

tage

from

GS

Est

atus;

Val

ue

of

impli

edfe

der

alsu

pport

Com

par

eyie

lds

on

GS

Ese

curi

ties

to

non-G

SE

secu

riti

es;

mar

kG

SE

bal

ance

shee

tsto

mar

ket

and

com

par

eto

mar

ket

capit

aliz

atio

n

Sav

ings

on

deb

tan

dM

BS

wer

eab

out

$6.5

bil

lion

in1995

for

Fan

nie

and

Fre

ddie

;

mar

kto

mar

ket

puts

aver

age

val

ue

of

the

impli

edsu

pport

at$7.8

duri

ng

1993

to1995

U.S

.D

epar

tmen

to

fT

reas

ury

(1996)

Val

ue

of

Fan

nie

and

Fre

ddie

's

expli

cit

and

impli

cit

subsi

die

s

Com

par

eyie

lds

on

GS

Ese

curi

ties

to

non-G

SE

secu

riti

esplu

sG

AO

esti

mat

e

of

dir

ect

subsi

die

s

The

val

ue

of

the

subsi

die

sfo

rFan

nie

and

Fre

ddie

was

$5.8

bil

lion

in1995

wit

h

range

of

$5

bil

lion

to$6.5

bil

lion.

Co

tter

man

and

Pea

rce

(19

96),

Hen

der

shott

and

Sh

illi

ng

(19

89)

and

ICF

Inc.

(19

90

)

Red

uct

ion

inra

tes

on

one

tofo

ur

fam

ily

mort

gag

esdue

toG

SE

acti

vit

y

Use

regre

ssio

ns

todet

erm

ine

the

dif

fere

nce

bet

wee

nra

tes

of

confo

rmin

gan

dnonco

nfo

rmin

g

mort

gag

es

Aco

nfo

rmin

gm

ort

gag

eis

about

30

bas

ispoin

tsch

eaper

than

anonco

nfo

rmin

g

mort

gag

e

Sour

ce:

Fel

dm

an(1

99

8).

HOUSING FINANCE GSEs 203

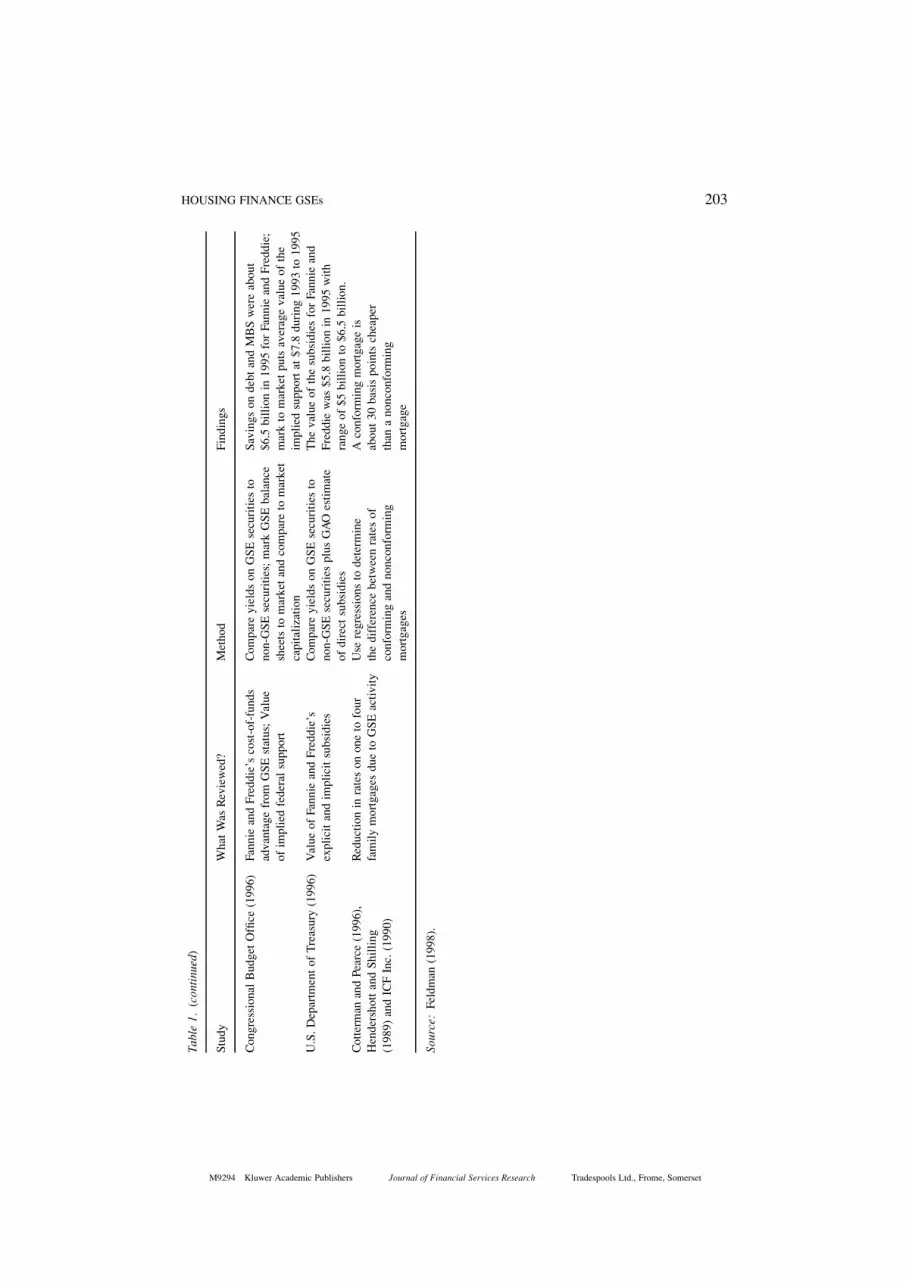

GSE of®cials have criticized public policy economists' efforts to estimate the value of

stockholder subsidies as ``highly theoretical and subjective'' exercises that are unreliable

precisely because of the indirect manner in which the subsidy is provided [Feldman

(1998)]. This criticism is unfounded.

The reliability of empirical research is strengthened rather than weakened by being

clearly rooted in economic theory. Similarly, it is not inappropriate for subjective elements

to be incorporated into individual pieces of research. Conscientious researchers labor to

make sure that the impact of their subjectivity on the reliability of the inferences they draw

is minor. In making inferences about the size of GSE subsidies, the impact that subjectivity

might have can be addressed by assessing, across the universe of individual studies, how

sensitive the order-of-magnitude value of subsidy measurements is to variations in the

particular assumptions employed. It is ironic that ®rms that portray themselves as leaders

in the application of statistical tools to credit scoring and customer outreach criticize the

use of statistical efforts to measure the size and distribution of the federal subsidies that

¯ow through their potentially spongy ``conduit.''

Table 1 is taken from Feldman (1998). This table allows us to undertake a sensitivity

assessment. The ®rst item in the table is the GAO's estimate of the direct subsidies the

GSEs received in 1995. The weakness of this estimate is that the GSEs might have been

able to adapt their behavior to lighten the tax and regulatory burdens if the exemptions did

not exist. However, it is unreasonable to assume that such adaptation could be either

costless or fully effective. A conservative way to generate a ®gure that can be applied to

other years is to halve the dollar estimate and divide the result by total assets. This gives an

order-of-magnitude estimate for direct subsidies of 4.5 basis points.

The last item in the table summarizes three studies of how GSE activity bene®ts

households that issue conforming mortgages by lowering the contract interest rates they

are charged. Passmore and Sparks (1995) raise the possibility that adverse selection by

originators could short-circuit households' interest-rate bene®t. The three studies

nevertheless ®nd a 30 basis-point bene®t.Most other studies in the table indicate that the indirect bene®ts of the taxpayer credit

enhancement to Fannie and Freddie are higher in magnitude than the average bene®t

passed on to mortgage borrowers. This is especially true in years in which either GSE's

®nancial condition is weak.

It is inappropriate for two reasons to dismiss the research efforts summarized in this

table as uninformative simply because the results show substantial variation. First, we

should expect to observe different estimates for the value of the subsidy at different points

in time. Because of the contingent nature of the bene®t, the subsidy's value changes as the

riskiness of GSE activities change. Some portion of the subsidy comes from variation in

interest rates and other macro-economic variables. Because movement in variables such as

expected in¯ation are due to events and policies external to Freddie and Fannie, the size

and distribution of the subsidy can vary even when the GSEs' portfolio composition does

not change at all. The possibility that the subsidy could suddenly become very large makes

it important from the taxpayer's perspective to track the exposure that exists and to put in

place procedures to control it over time.

Second, the focus of statistical inference is to underscore central tendencies. Treating

the results of individual studies as a scatter of data points, the scatter supports the

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

204 EDWARD J. KANE

hypothesis that, on average, Fannie and Freddie stockholders retain a substantial portion of

their credit-enhancement subsidy. A standard way to correct for potentially excessive

variation is to ``trim'' the range of results. Throwing out the two highest and two lowest

estimates of interest savings would generate a low value for the indirect subsidy of 30 to 40

basis points and high value of over 100 basis points. The midpoint of this range is more

than twice the value of the interest-rate bene®t passed on to mortgage borrowers.

Other evidence that the subsidy holdback is substantial can be found in the stiffening of

GSE yields and the softening of GSE stock prices that occurs at times when Congress

seems to contemplate weakening the federal ties that Fannie and Freddie enjoy (such as in

August±September 1996).

3. Exerting better taxpayer control over the GSE subsidy

Skillful lobbying by Fannie and Freddie (and their friends in the housing industry) has

established considerable autonomy for incentive-con¯icted GSE managers. It has

prevented the Treasury from collecting appropriate fees for taxpayers' credit

enhancements. It has even blocked budget of®cers and Congress from of®cially certifying

and controlling the annual value of GSE credit enhancements as part of the federal budget.

Although the GSEs have accepted OFHEO oversight, they used lobbying pressure to deny

OFHEO of®cials the authority and information they would need to measure and control in

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

Source: Philadelphia Inquirer, Universal Press Syndicate. With permission, this rendition substitutes ``GSE

Stockholder'' for the word Corporate, which appeared in the cartoonist's original drawing.

HOUSING FINANCE GSEs 205

timely fashion the activities by which the federal credit enhancement can be made more

valuable to GSE shareholders. For example, late in 1998, Fannie was reported to be

drumming up support from housing trade groups to ``derail'' an OFHEO effort to link

GSE capital requirements to credit and interest-rate risk [Barancik (1998)]. Ironically,

Congress added con¯ict to OFHEO's interest in controlling stockholder subsidies by

making OFHEO dependent on Fannie and Freddie for its funding [Feldman (1998)].

The root problem in controlling the subsidy is GSE managers' lack of adequate

accountability for the size and distribution of the taxpayer subsidies their ®rms receive.

Incentive-con¯icted GSE managers get to frame their obligations to taxpayers as

affordable housing goals and decide more or less on their own what other behaviors

discharge the ethical obligations their federal status creates for them. The accounting

standards under which the GSEs report to OFHEO and society at large aggravate rather

than mitigate managers' incentive con¯ict. GSE managers should be required, under

penalties for fraud or negligent misrepresentation, to document how much their activity

bene®ts mortgagors and to measure (and return to the Treasury) the value of all direct or

indirect bene®ts from GSE status that are not successfully passed through to targeted

mortgage borrowers.

Procedures for limiting GSE activities leave GSE managers wide latitude to expand

their subsidies by undertaking new activities. They also allow GSE managers to hold back

information on the marginal impact these activities have had on the overall riskiness of

their ®rms. The dif®culty of constraining interest-arbitrage pro®ts that GSEs can earn from

expanding activities that are unrelated to the GSE's social mission is analyzed by Seiler

(1998) and the GAO (1998).

The cartoon on p. 197 stresses that these defects in accountability to taxpayers are not

accidents. The GSEs have insulated themselves from criticism by making careful

investments of stockholder funds. Stockholder funds have been used to maintain a

balanced portfolio of lobbying resources and to support the careers of friendly politicians

and researchers [McKinley (1997)]. Harry Truman once advised us that if we want a friend

in Washington, we should buy a dog. As long as the U.S. electorate remains willing to

tolerate the lightly masked shell game of trading laundered political investments for

subsidized implicit returns to GSE investors, incentives for accountability enhancement

will be minuscule.

3.1. The policy impasse

Ironically, strong incentives do exist for Congress to entertain proposals to increase GSE

accountability. Holding hearings on these proposals helps members of Congress populate

their campaign fund-raisers and milk GSE managers and construction-industry PACs in

other ways. Preparing reform proposals is a task that occupies many public policy

economists and many conscientious government of®cials. Most proposals fall into three

categories: (1) severing the corporate umbilical cords that link GSE obligations to

taxpayers, (2) fully pricing at least some of the privileges and credit enhancements that

GSE corporate obligations enjoy, and (3) plugging particular loopholes in the inherited

fabric of subsidy generation and control.

To this longstanding mix of useful reforms, this paper adds the idea of directly

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

206 EDWARD J. KANE

disciplining the incentive con¯ict under which top GSE managers labor. This can be done

by outlawing or rede®ning allowable stock-based and pro®t-related bonuses that can be

passed to GSE managers or by permitting managers to receive supplementary pay for

demonstrably lowering the interest rates at which low-income mortgagors can borrow and

demonstrably reducing the value of taxpayer-contributed risk capital.

It is dangerous to allow only stockholders to offer incentive compensation and tie that

compensation to the performance of GSE stock. The public-policy defect in this

compensation scheme is that GSE stock price performance increases with increases in the

size of the federal subsidy that their ®rms retain. To balance managers' natural incentives

to seek stock-based incentive rewards, incentive-based bonuses should be reduced by a

substantial multiple of estimated increases in the value of the taxpayer credit enhancement

imbedded in GSE stock. In addition, managers' ability to orchestrate political donations

and other bene®ts for elected of®cials should be subjected to special reporting restrictions

and other ethical controls that recognize GSE managers' quasi-civil-servant status.

The range of proposed reforms makes it clear that the problem of measuring and

controlling GSE subsidies is not due to a shortage of promising ideas. It is rooted in

informational asymmetries that mask congressional incentives to keep Fannie, Freddie,

and their friends happy.

Acknowledgments

This paper was prepared for the May 14, 1998, Appraising Fannie Mae and Freddie Mac

Conference, sponsored by Essential Information. I am grateful to Ron Feldman, Stephen

Kane, and two editors of this journal for helpful comments on previous drafts of this paper.

References

Ambrose, Brent W., and Arthur D. Warga. ``Implications of Privatization: The Costs to Fannie Mae and Freddie

Mac.'' In: U.S. Department of Housing and Urban Development, ed., Studies on Privatizing Fannie Mae andFreddie Mac. U.S. Department of Housing and Urban Development. Washington, DC: U.S. Department of

Housing and Urban Development, (1996), pp. 169±204.

Barancik, Scott. ``Fannie Mae Bashes Agency on Risk-Based Capital Plan.'' American Banker (1998).

Bear, Larry A., and Rita Maldonado-Bear. Free Markets, Finance, Ethics, and Law. Englewood Cliffs, NJ:

Prentice-Hall, 1994.

Capitol Financial Insights, Inc. The Competitive Threat of Government Sponsored Enterprises. Study prepared

for the Association of Financial Guaranty Insurors, Chevy Chase, MD, 1998.

Congressional Budget Of®ce. Controlling the Risks of Government Sponsored Enterprises. Washington, DC:

Government Printing Of®ce, 1991.

Congressional Budget Of®ce. Assessing the Public Costs and Bene®ts of Fannie Mae and Freddie Mac.

Washington, DC: Government Printing Of®ce, 1996.

Cook, Douglas O. ``Review of the Ambrose-Warga and Cotterman-Pearce Papers.'' In: U.S. Department of

Housing and Urban Development, ed., Studies on Privatizing Fannie Mae and Freddie Mac. U.S.Department of Housing and Urban Development. Washington, DC: U.S. Department of Housing and Urban

Development, (1996), pp. 205±210.

Cook, Douglas O., and Lewis J. Spellman. ``Taxpayer Resistance, Guarantee Uncertainty and Housing Finance

Subsidies.'' Journal of Real Estate Finance and Economics 5 (1992), 181±195.

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

HOUSING FINANCE GSEs 207

Cotterman, Robert F. and James E. Pearce. ``The Effects of the Federal National Mortgage Association and the

Federal Home Loan Mortgage Corporation on Conventional Fixed-Rate Mortgage Yields.'' In: U.S.

Department of Housing and Urban Development, ed., Studies on Privatizing Fannie Mae and Freddie Mac.U.S. Department of Housing and Urban Development. Washington, DC: U.S. Department of Housing and

Urban Development, (1996), pp. 97±168.

Federal Home Loan Bank of Chicago. ``Mortgage Partnership Finance: Rebalancing American Mortgage

Finance.'' Chicago: Author, 1997.

Federal Home Loan Mortgage Corporation. 1996 Annual Report. McLean, VA: FHLMC, 1996b.

Federal National Mortgage Association. ``Fannie Mae Review of the Hermalin-Jaffee Paper.'' In: U.S.

Department of Housing and Urban Development, ed., Studies on Privatizing Fannie Mae and Freddie Mac.U.S. Department of Housing and Urban Development. Washington, DC: U.S. Department of Housing and

Urban Development, (1996a), pp. 314±332.

Federal National Mortgage Association. 1996 Annual Report. Washington, DC: FNMA, 1996b.

Feldman, Ron. ``Estimating and Managing the Federal Subsidy of Fannie Mae and Freddie Mac: Is Either Task

Possible.'' Journal of Public Budgeting, Accounting, and Financial Management (1998), pp. 81-116.

Federal Home Loan Mortgage Corporation. Financing America's Housing. McLean, VA: FHLMC, (1996a), pp.

32±33.

Gatti, James F., and Ronald W. Spahr. ``The Value of Federal Sponsorship: The Case of Freddie Mac.'' RealEstate Economics (1997), pp. 453-485.

Goodman, John L., Jr., and S. Wayne Passmore. ``Market Power and the Pricing of Mortgage Securitization.''

Washington, D.C.: Federal Reserve Board, Finance and Economics Discussion Series, 187 (1992), 1±31.

Hemel, Eric I. ``GSEs and Mortgage Finance.'' Morgan Stanley U.S. Investment Research (1994), 1±5.

Hendershott, Patric H., and James D. Shilling. ``The Impact of Agencies on Conventional Fixed-Rate Mortgage

Yields.'' Journal of Real Estate Finance and Economics 2 (1989), 101±115.

Hermalin, Benjamin E., and Dwight M. Jaffee. ``The Privatization of Fannie Mae and Freddie Mac: Implications

for Mortgage Industry Structure.'' In: U.S. Department of Housing and Urban Development, ed., Studies onPrivatizing Fannie Mae and Freddie Mac. U.S. Department of Housing and Urban Development.Washington, DC: U.S. Department of Housing and Urban Development, (1996), pp. 225±302.

ICF Inc. Effects of the Conforming Loan Limit on Mortgage Markets. Final Report Prepared for the U.S.Department of Housing and Urban Development. Of®ce of Policy Development and Research. Fairfax, VA:

ICF, Incorporated, 1990.

Kane, Edward J., and Chester Foster. ``Valuing the Conjectural Government Guarantees of FNMA Liabilities.''

In: Proceedings of Conference on Bank Structure and Competition. Chicago: Federal Reserve Bank of

Chicago, (1986), pp. 347±368.

Kaufman, Herbert M. ``FNMA's Role in Deregulated Markets: Implications from Past Behavior.'' Journal ofMoney, Credit and Banking 20 (1988), pp. 673±683.

Marra, Anthony F. (deputy general counsel of FNMA). ``Comment Letter on OCC Docket No. 97-22, Risk-

Based Capital Standards: Recourse and Direct Credit Substitutes.'' (1998).

Martin, Deborah L., and Pozdena, Randall J. ``Taxpayer Risk in Mortgage Policy.'' Federal Reserve Bank of SanFrancisco Weekly Letter (1991), pp. 91±94.

McKinley, Vern. The Mounting Case for Privatizing Fannie Mae and Freddie Mac. Policy Analysis No. 293.

Washington, DC: Cato Institute, 1997.

Merton, Robert C., and Andre F. Perold. ``Theory of Risk Capital in Financial Firms.'' Journal of AppliedCorporate Finance 6 (1993), pp. 16±32.

Miles, Barbara L. ``Proposed Offset Fees for Fannie Mae and Freddie Mac.'' Congressional Research ServiceMemorandum to House Banking and Financial Services Committee (1995).

Of®ce of Federal Housing Enterprise Oversight. 1997 Report to Congress. Washington, DC: Of®ce of Federal

Housing Enterprise Oversight, 1997.

Passmore, S. Wayne, and Sparks, Roger. ``Putting the Squeeze on a Market for Lemons: Government-Sponsored

Mortgage Securitization.'' Washington D.C.: Federal Reserve Board, Finance and Economics Discussion

Series. 95-13 (1995), pp. 1±31.

Pozdena, Randall, and Deborah Martin. ``Taxpayer Risk in Mortgage Policy.'' FRBSF Weekly Letter (1991),

91±44.

Retinas, Nicolas (assistant secretary for Housing, federal housing commissioner, U.S. Department of Housing

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

208 EDWARD J. KANE

and Urban Development). ``Testimony Before the Subcommittee on Capital Markets, Securities and

Government Sponsored Enterprises of the Committee on Banking and Financial Services.'' (1996), 5±7.

Schwartz, Eduardo, and Robert Van Order. ``Valuing the Implicit Guarantee of the Federal National Mortgage

Association.'' Journal of Real Estate Finance and Economics 1 (1988), pp. 23±34.

Seiler, Robert S. ``Fannie Mae and Freddie Mac as Investor-Owned Public Utilities.'' Journal of PublicBudgeting, Accounting, and Financial Management (1998) pp. 117-154.

Shadow Financial Regulatory Committee. ``Extending the Credit Reform Act to GSEs.'' Statement No. 131.

Chicago: Loyola University, February 12, 1996.

Shilling, James D. ``Comments on the Ambrose-Warga and Cotterman-Pearce Paper.'' In: U.S. Department of

Housing and Urban Development, ed., Studies on Privatizing Fannie Mae and Freddie Mac. U.S.Department of Housing and Urban Development. Washington, DC: U.S. Department of Housing and Urban

Development, (1996), pp. 211±217.

Stanton, Thomas H. ``Restructuring Fannie Mae and Freddie Mac: Framework and Policy Options.'' In: U.S.

Department of Housing and Urban Development, ed., Studies on Privatizing Fannie Mae and Freddie Mac.U.S. Department of Housing and Urban Development. Washington, DC: U.S. Department of Housing and

Urban Development, (1996), pp. 1±47.

Thygerson, Kenneth J. ``Federal Mortgage Credit Agencies and the Decline in Thrift Charter Value.'' Paper

presented at the Annual Meeting of the American Real Estate and Urban Economics Association, 1990.

U.S. Department of Treasury. Report of the Treasury on Government Sponsored Enterprises. Washington, DC:

Government Printing Of®ce, 1990.

U.S. Department of Treasury. Report of the Treasury on Government Sponsored Enterprises. Washington, DC:

Government Printing Of®ce, 1991.

U.S. Department of Treasury. Government Sponsorship of the Federal National Mortgage Association and theFederal Home Loan Mortgage Corporation. Washington, DC: Government Printing Of®ce, 1996.

U.S. General Accounting Of®ce. The Federal National Mortgage Association in a Changing EconomicEnvironment. Washington, DC. Government Printing Of®ce, 1985.

U.S. General Accounting Of®ce. Government Sponsored Enterprises: A Framework for Limiting theGovernment's Exposure to Risk. Washington, DC: Government Printing Of®ce, 1991a.

U.S. General Accounting Of®ce. Government Sponsored Enterprises: A Government's Exposure to Risk.

Washington, DC: Government Printing Of®ce, 1991b.

U.S. General Accounting Of®ce. FNMA and FHLMC: Bene®ts Derived from Federal Ties. Washington, DC:

Government Printing Of®ce, 1996a.

U.S. General Accounting Of®ce. Housing Enterprises: Potential Impacts of Severing Government Sponsorship.

Washington, DC: Government Printing Of®ce, 1996b.

U.S. General Accounting Of®ce. Government-Sponsored Enterprises: Federal Oversight Needed forNonmortgage Investments. Washington, DC: Government Printing Of®ce, 1998.

Weicher, John C. ``The New Structure of the Housing Finance System.'' Federal Reserve Bank of St. LouisReview 76 (1994), pp. 47±65.

Woodward, Thomas. ``Testimony Before the Subcommittee on Capital Markets. Securities and Government

Sponsored Enterprises of the Committee on Banking and Financial Services.'' (1997).

Zimmerman, Dennis. ``Unfunded Mandates and State Taxation of the Income of Fannie Mae, Freddie Mac and

Sallie Mae: Implications for D.C. Finances.'' CRS Report for Congress (1995), pp. 95±952.

Zoellick, Robert (executive vice president of Fannie Mae). ``Testimony Before the Subcommittee on Capital

Markets, Securities and Government Sponsored Enterprises of the Committee on Banking and Financial

Services.'' (1996), pp. 5±6.

M9294 Kluwer Academic Publishers Journal of Financial Services Research Tradespools Ltd., Frome, Somerset

HOUSING FINANCE GSEs 209