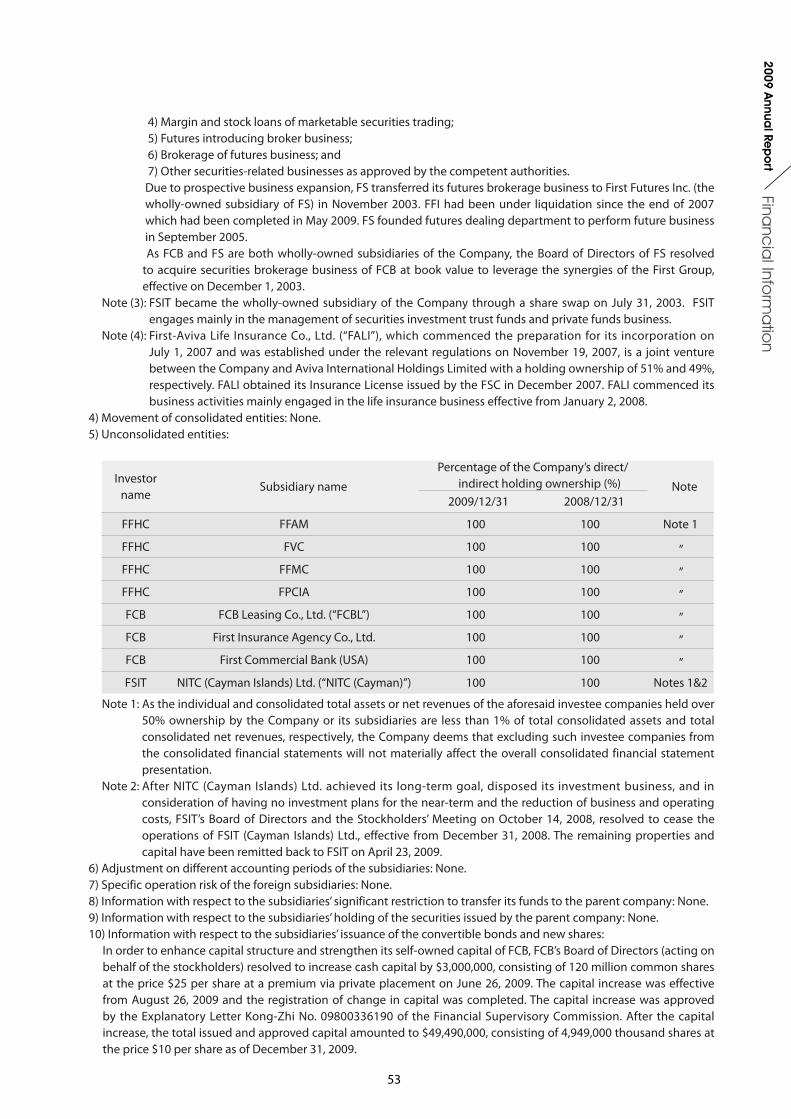

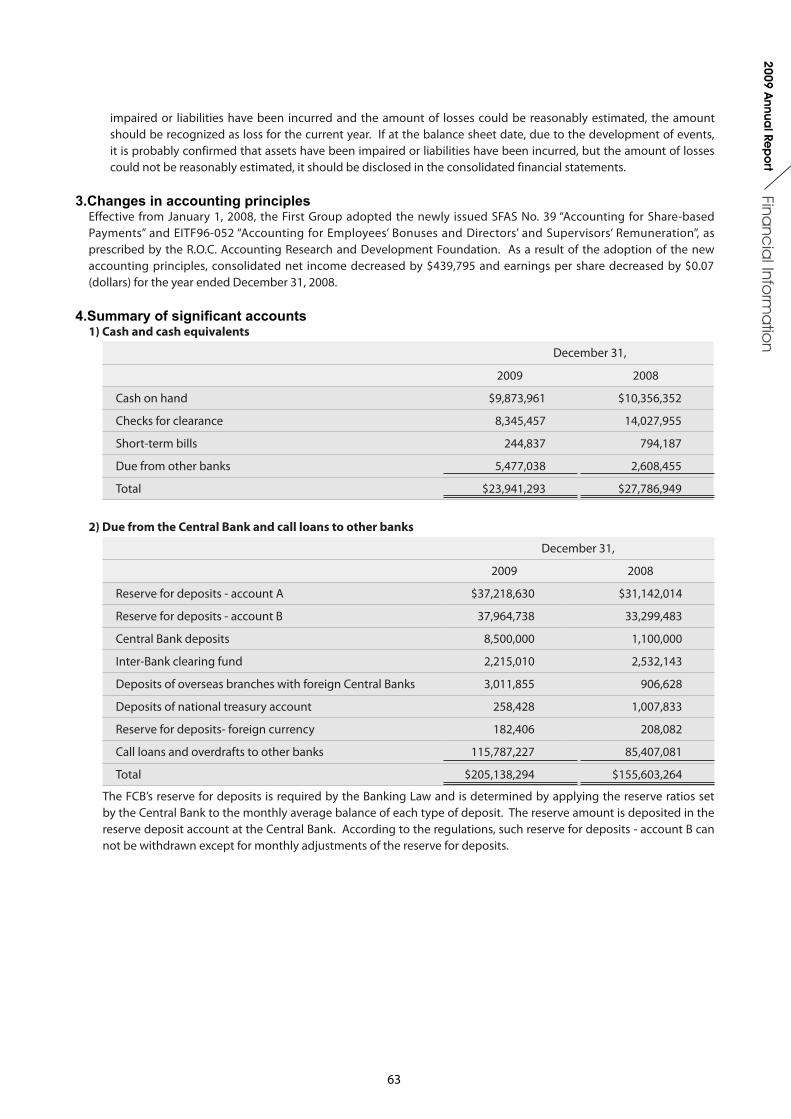

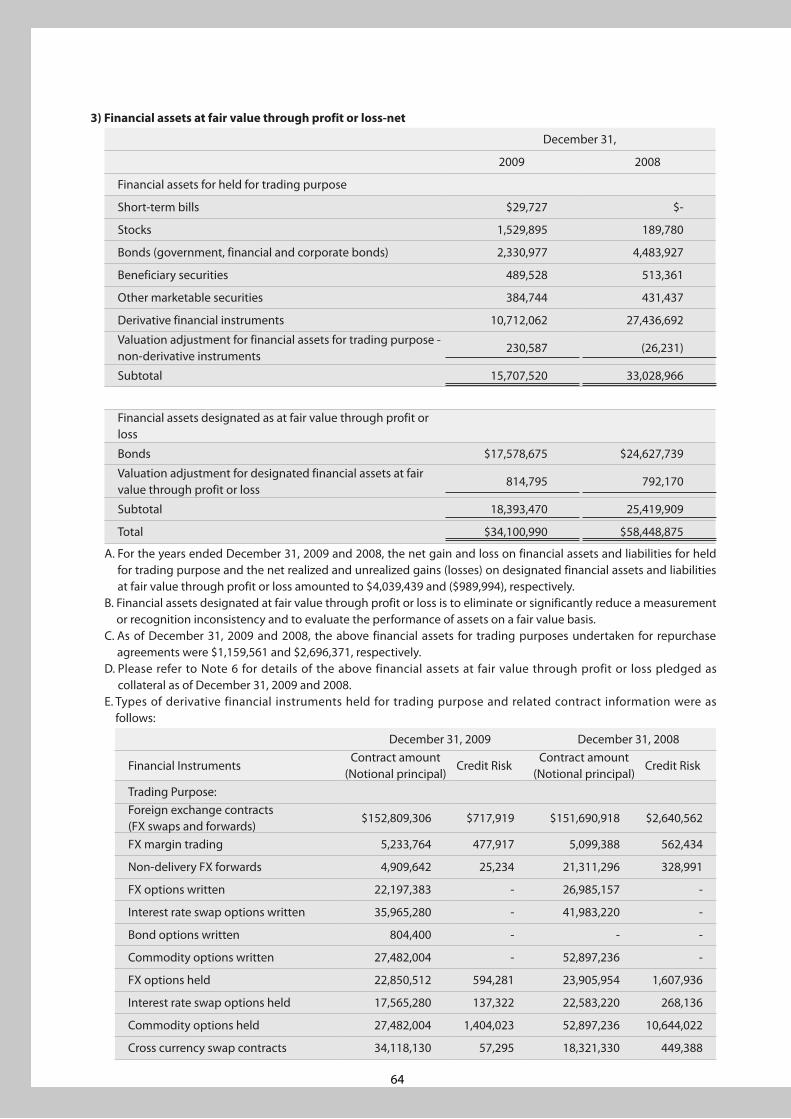

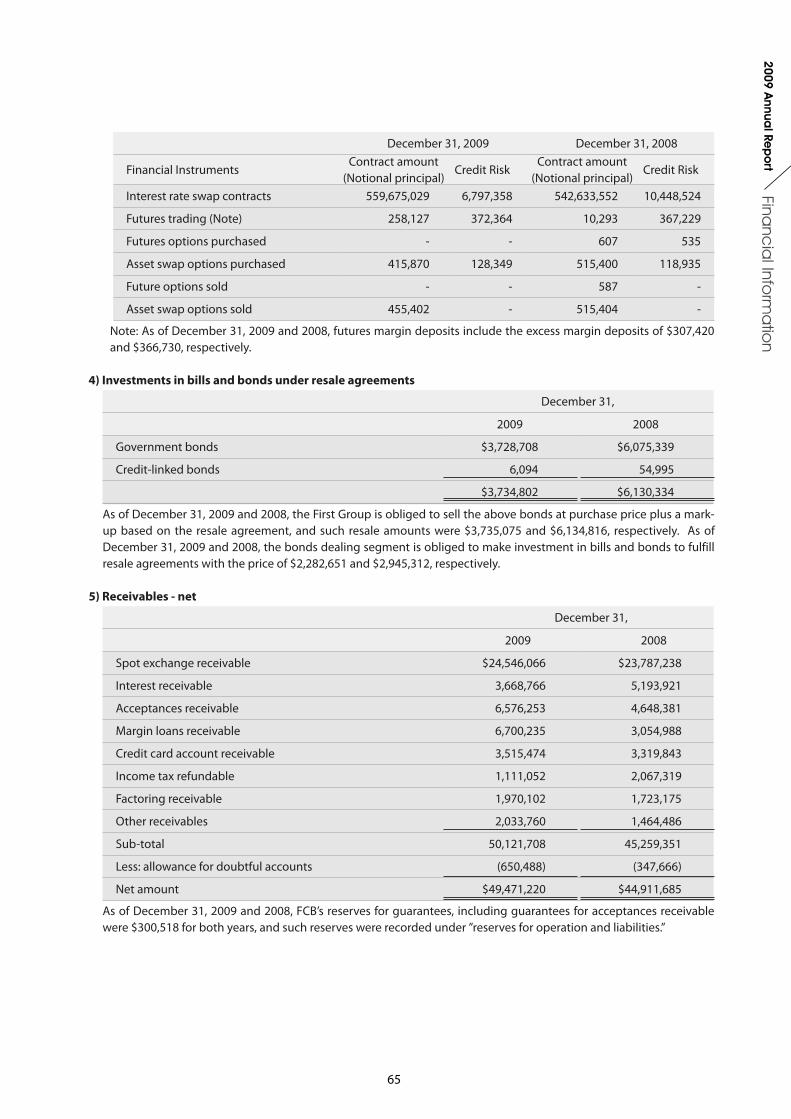

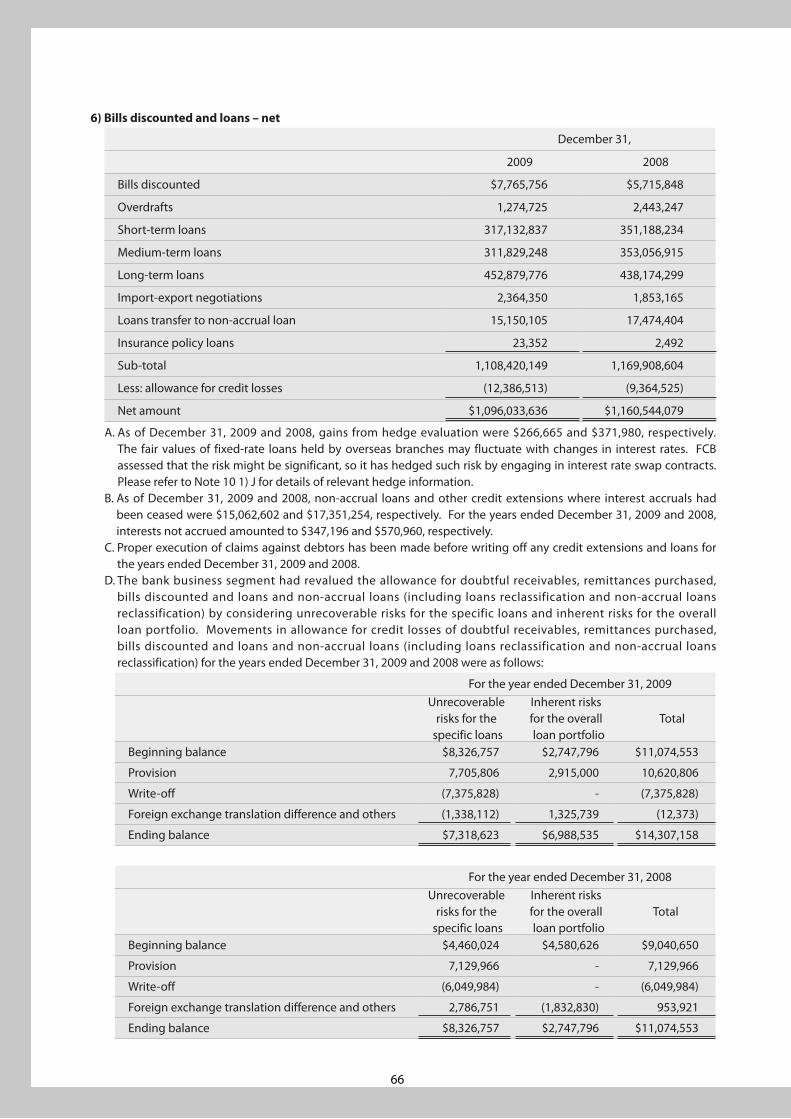

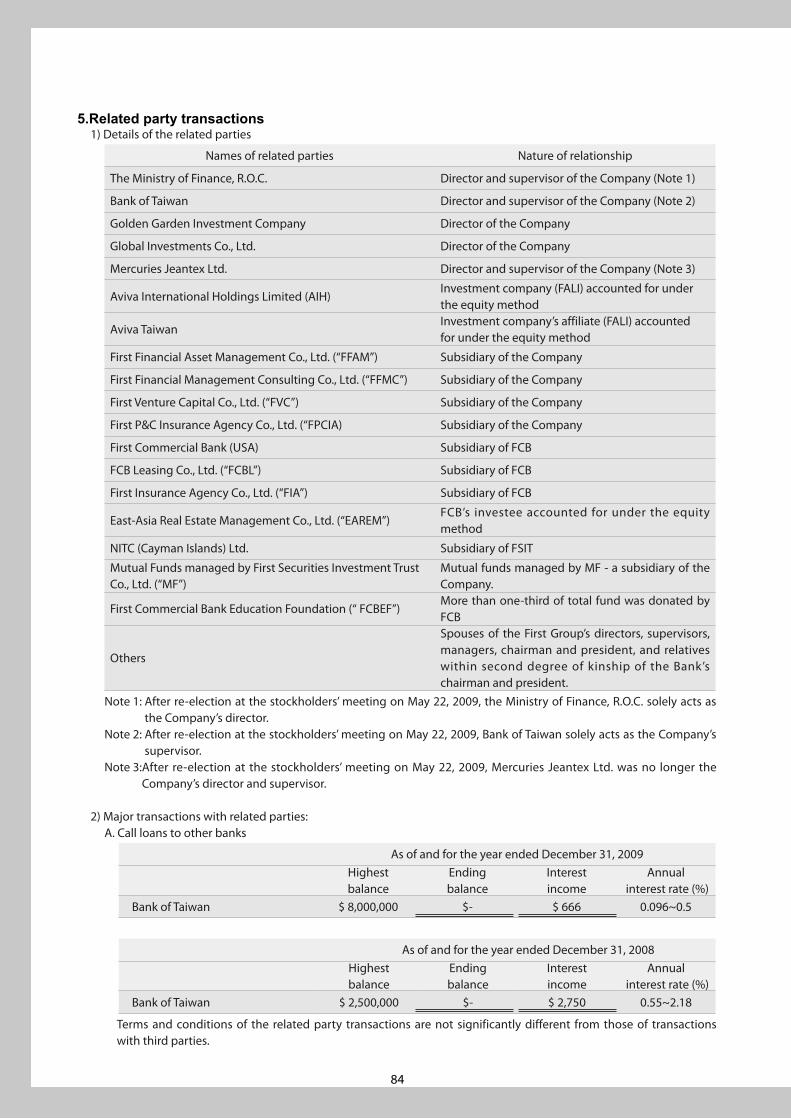

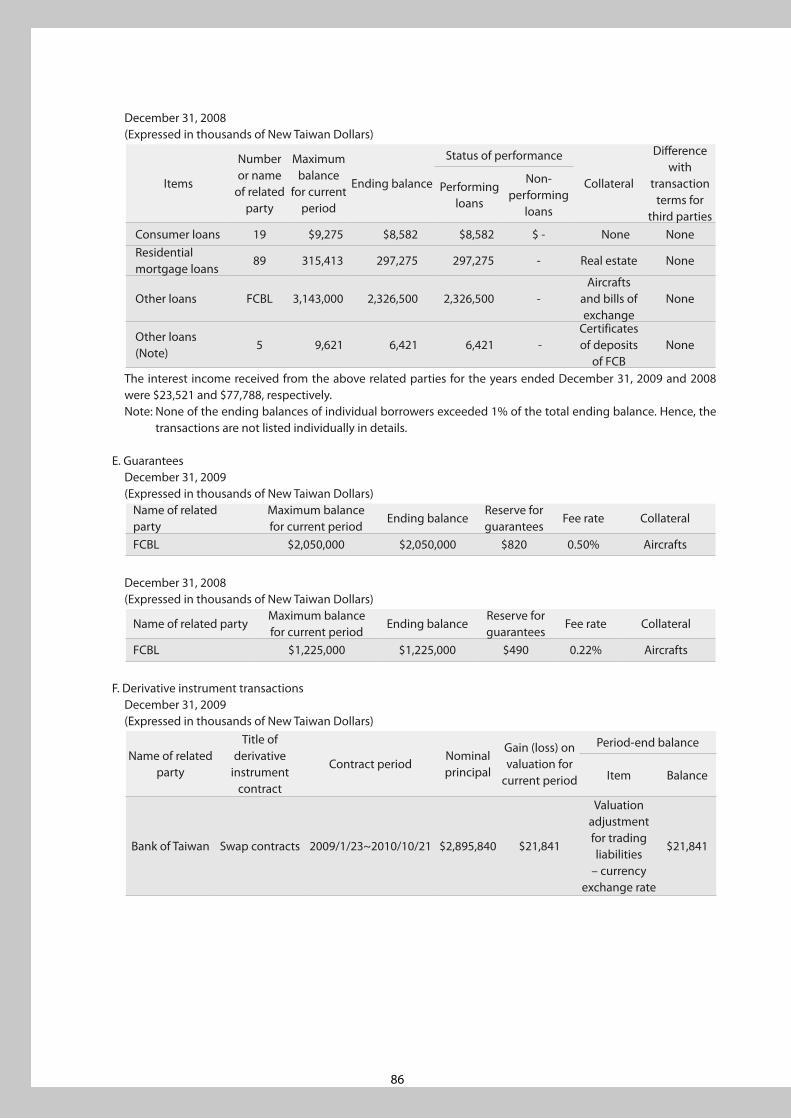

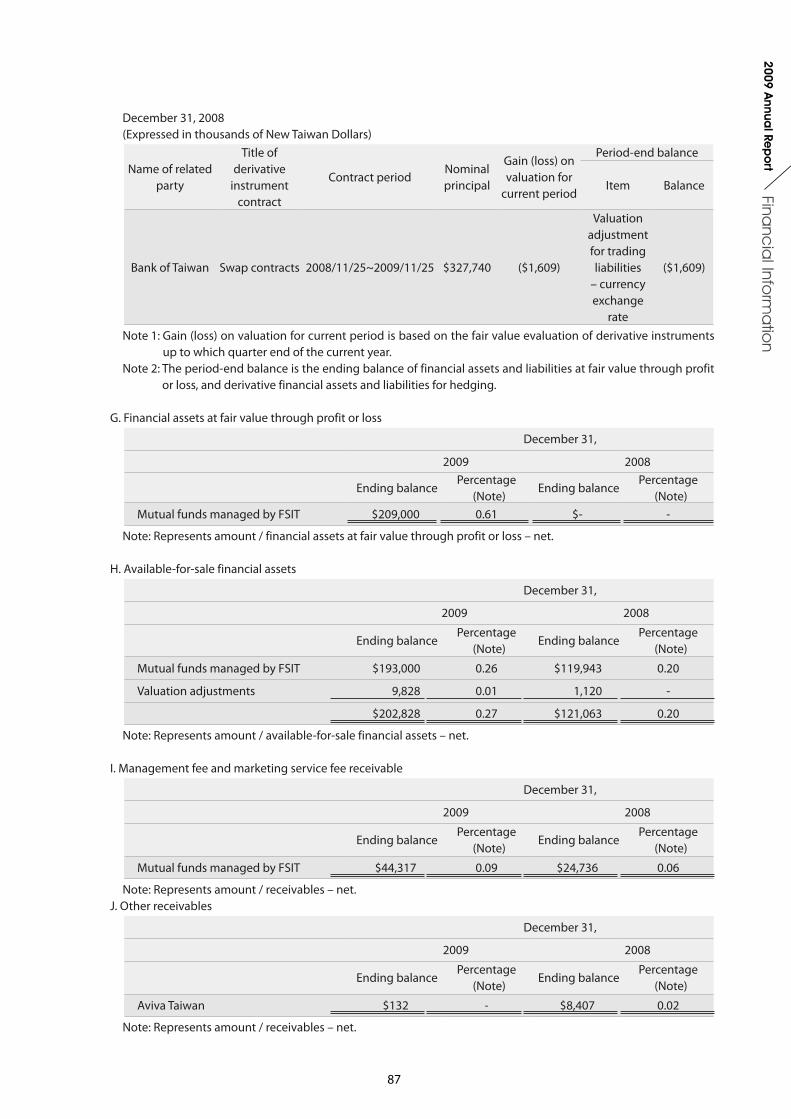

first financial holding - todayir.com

TRANSCRIPT

This English version annual report is a summary translation of the Chinese

version and is not an official document of the shareholders’ meeting. If

there is any discrepancy between the English version and Chinese version,

the Chinese version shall prevail.

Disclaimer: This shareholder report cannot be expected to provide as full understanding of the financial performance, financial position, operating, financing and investment activities of the First Financial Group as the 2009 FFHC annual report in Chinese and the full annual financial statements. This publication contains certain forward-looking statements and future expectations. These expectations are based on management’s current views and assumptions and involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. There can be no assurance that actual outcomes will not differ materially from these statements. FFHC assumes no obligation to update any forward-looking information contained in this report.

First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding Co., Ltd. First Financial Holding

Letter to Shareholders 02

Company Profile 07

Financial Highlights 08

Corporate Governance 12

Capital Overview 28

Subsidiaries Overview 32

Corporate Social Responsibilities 42

Financial Information 44

General Information 155

Contents

2

Letter to Shareholders

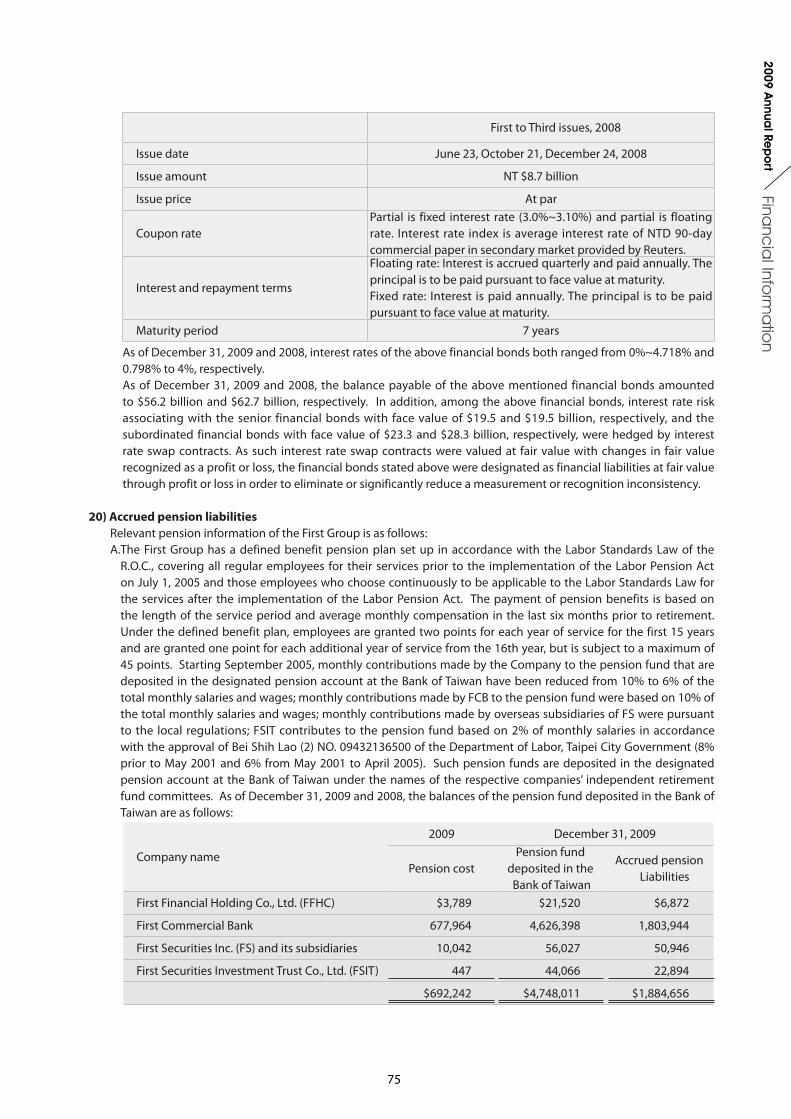

Dear Shareholders,

Looking back in 2009, thanks to stimulus actions taken by governments around the world, the economy progressively stabilized. Nevertheless, the recent Dubai standstill and sovereign debt crisis of the Southern Europe countries showed that the risks of a relapse were high. Excess liquidity triggered fears over inflation and asset bubble, while capital injections into the financial systems widened budget deficit and threatened to undermine the still fragile economy. Unemployment rates remained high, leaving central banks around the world in a dilemma over when to unwind their stimulus measures, fiscal- and monetary-wise.

In Taiwan, starting from the third quarter 2009, the capital market regained momentum and the GDP growth turned positive in the fourth quarter at an estimated 9.22%, as Government’s economic stimulus actions fueled trade activities and capital inflows from overseas. Increased export demand drove up capacity utilization rates at major technology and electronics manufacture facilities, triggering a new wave of capital raising plans in the private sector. On the domestic front, consumer confidence firmed up and brought forth the growth of private consumption back to positive territory at an estimated 1.48%. Benefiting from export volumes arising from strong bounce-back in Emerging-Asia economies, Taiwan’s GDP was expected to shrink by 1.87% for 2009, better than the previous forecast of -2.53%, according to Directorate-General of Budget, Accounting and Statistic. Statistics also indicated positive signs of recovery in financial and insurance sector, with a 2.8% growth projected for the fourth quarter of 2009, versus double-digit contraction seen in the first and second quarter of 2009.

Uncertainty Lays Still AheadWhile signs of a global recovery were observed in 2009, we remain cautious about the high level of uncertainty in a number of respects. The financial crisis has not only helped materialize the rise of world’s new economic power, the change in global business structure, but further addressed the power of emerging economic entities, such as China and India, will impact the global economy. In the wake of the financial crisis, the “jobless” recovery in developed economies appears inevitable. Capital injections into the global financial system have accelerated the expansion of debt at an alarming rate. Increasing liquidity that resulted from “loose” monetary and fiscal policy now risks new wave of asset bubbles. Growing needs for raw materials such as petros and minerals from developing economies are heightening inflationary pressure. While the “imbalances” described above might worsen or even cause further fluctuations in the global economic cycles, the key to stabilize and sustain the economy can not be short-lived fiscal or monetary initiatives alone, but continued innovation and governmental incentives that encourage investments and consumption.

Operating Strategy: from Stable to StrongIn the backdrop of an economic upturn and thawing relations between Taiwan and China, First Financial Holdings gradually climbed out of the trough in 2008. Thanks to a combination of sound risk oversight, improving margin expansion, earnings recovery for the banking business and subsidiaries profit growth aided by market rebounds and revived investor optimism, the group reported consolidated net revenue of NT$29,573 million. Net Income was NT$2,689 million, of which NT$2,779 million was attributable to equity holders of parent company and a loss of NT$90 million to minority shareholders. Post-tax EPS was NT$0.44. In light of the adoption of SFAS Article 34 (which requires a general provision to be made against all outstanding loans), First Financial Holdings moved to further set aside provisions for its bank subsidiary to lower NPL ratio and improve Bad-Debt Coverage. Although undertaking such precaution delivered an adverse impact on bottom-line, it was understood by institutional investors at home and abroad that such action was taken for a necessary cause in order to strengthen the group’s financial soundness as well as China deployment plan.

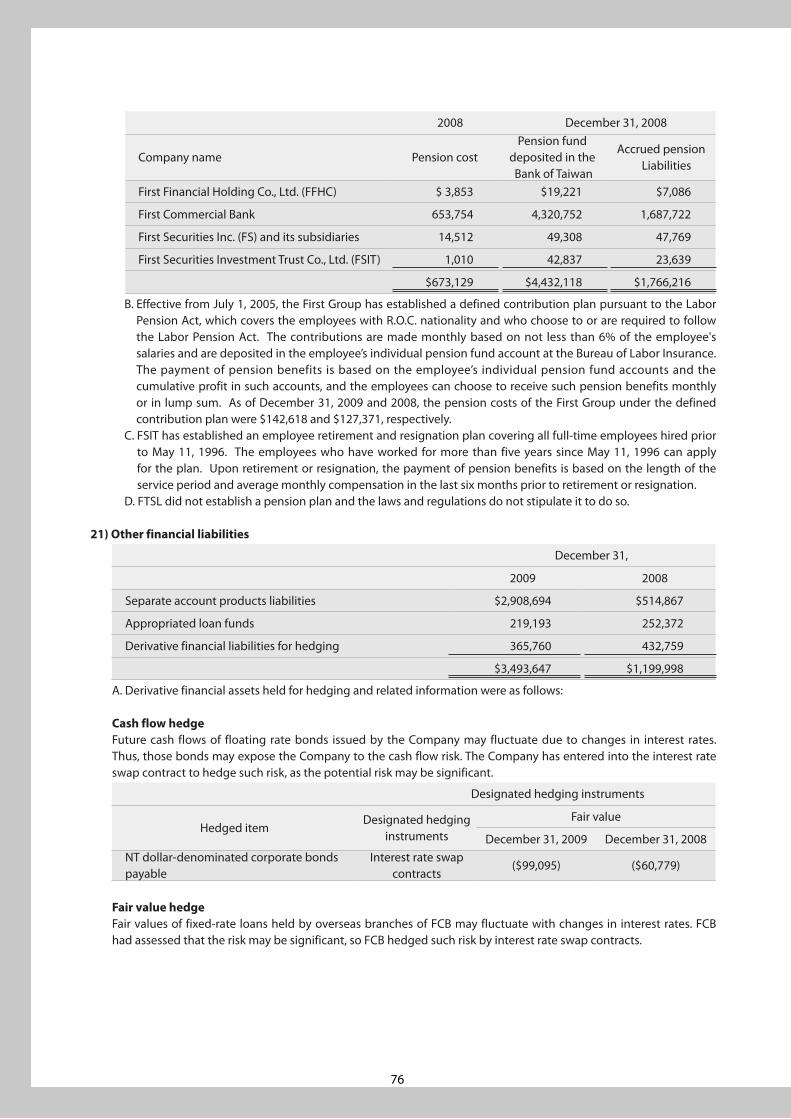

The 2009 operating performance of group subsidiaries is described separately below:

In 2009, First Bank benefited from a rebound in Net Interest Margin and steady recovery of Net Interest Income, started from the third quarter. Though Fee Income contracted due to financial crisis and structured note compensation during the first half of 2009, fee momentum resumed in the second half of the year and still accounted for as much as 15% of net

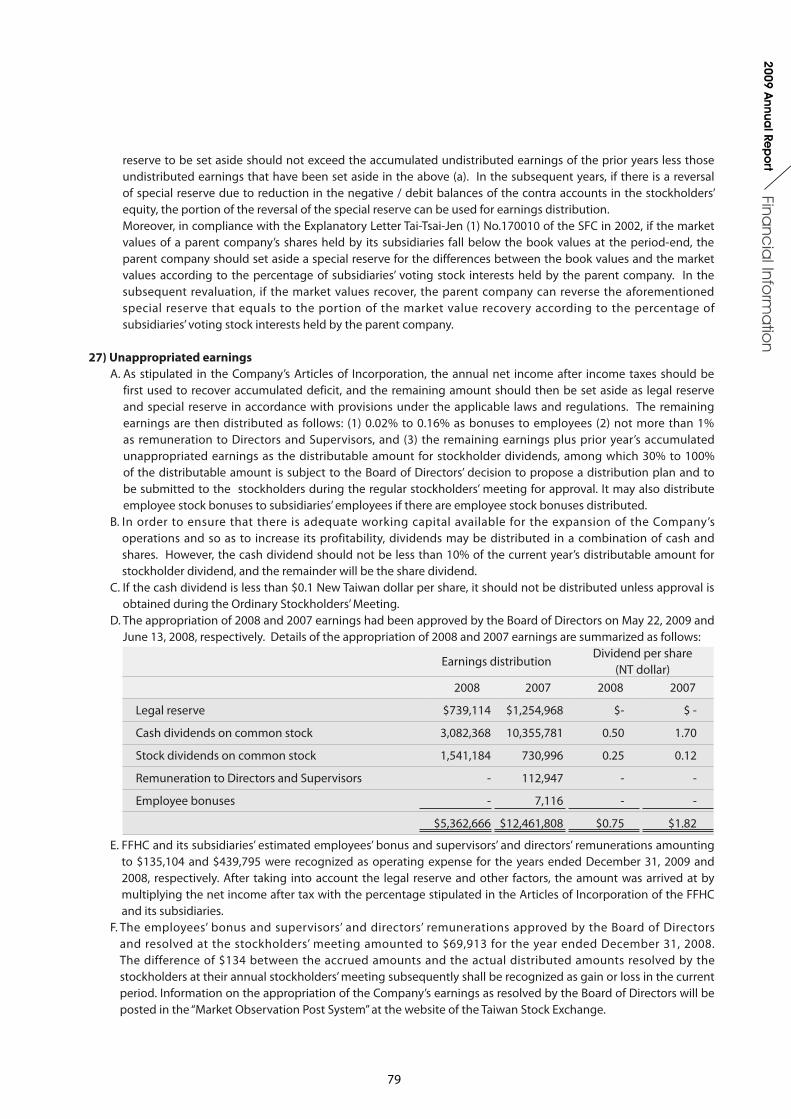

3

Lette

r to Sha

reho

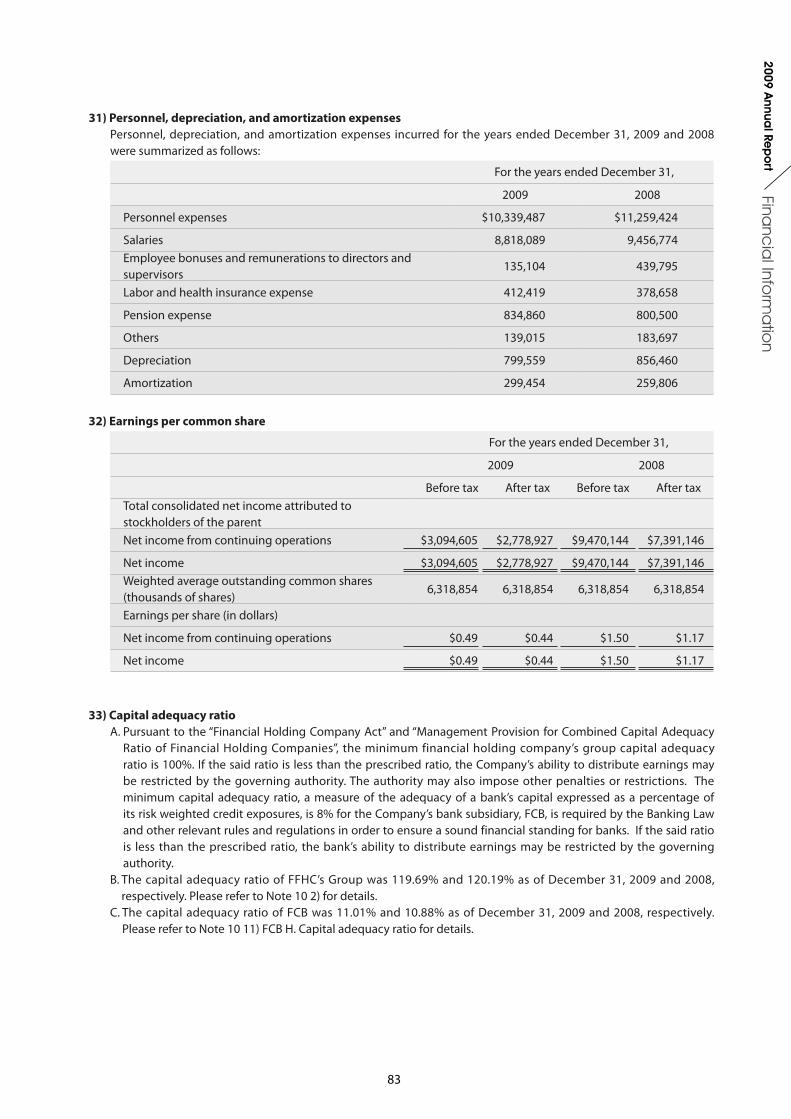

lde

rs2009 A

nnual Re

po

rt

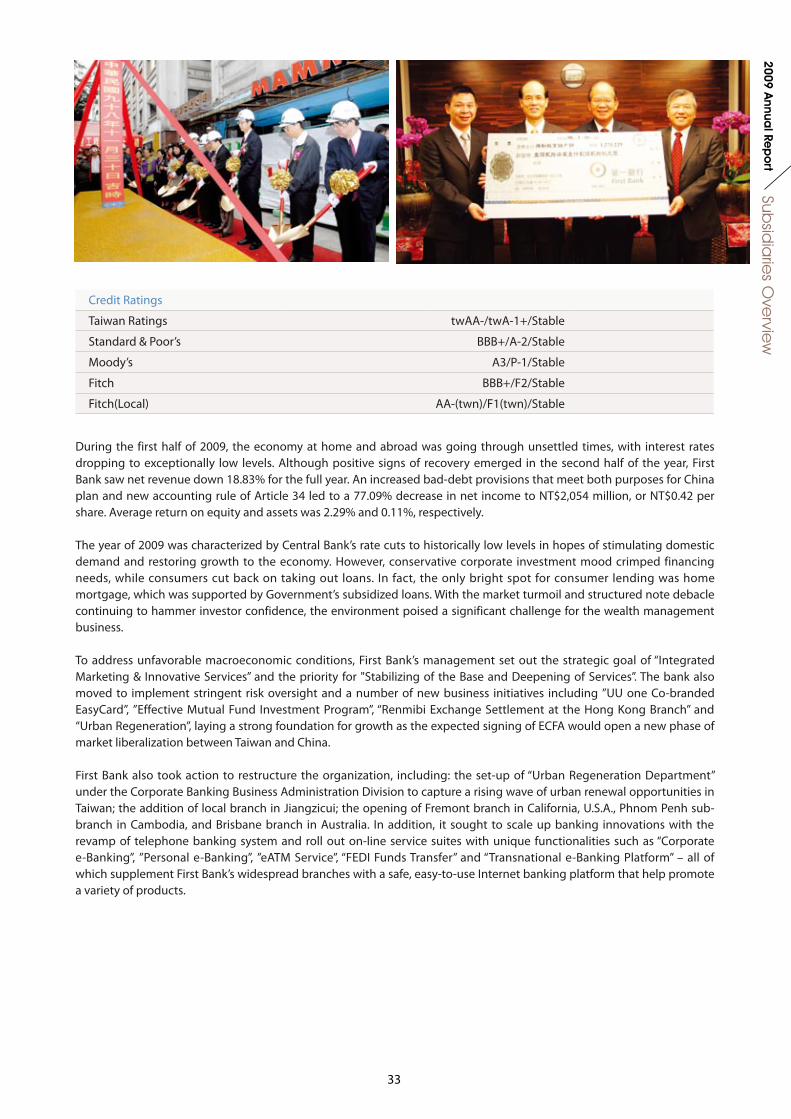

revenue for the full year. Increased Bad-Debt Provision in response to new regulations governing banks’ financial viability led to a 77.09% decrease in net income to NT$2,054 million, or NT$0.42 per share, meeting just 26.84% of First Bank’s budget goal. However, with delinquency rate cut down to 1.32% and coverage ratio raised to 84.75%, First Bank’s restored financial strength has laid the ground work for its China expansion and profit growth plans.

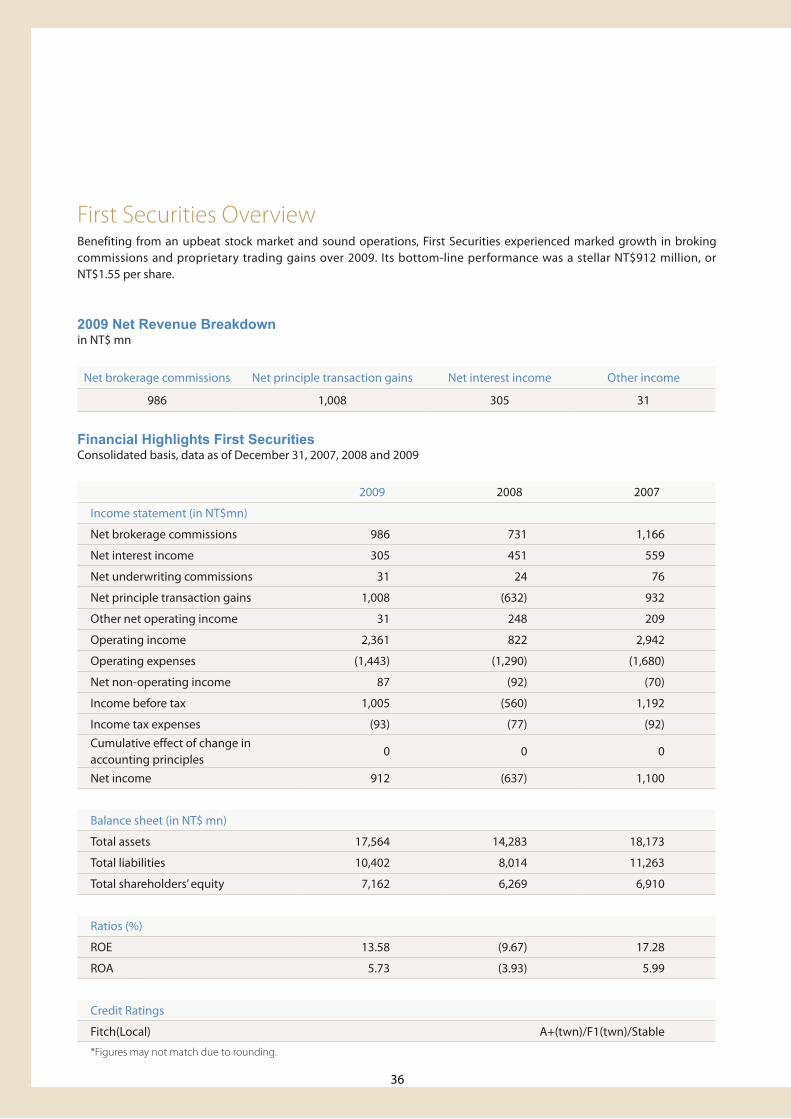

Riding on a wave of liquidity momentum and stock market rallies, Taiwan stock market saw brokerage volumes grow by 38.47% to NT$1,226,107 million in 2009. The brokerage market share of First Securities jumped to 1.723% from 1.465% a year earlier. In addition, it was ranked No.1 in broking volumes on the Emerging Board. During 2009, First Securities actively explored the new business of advising Taiwanese corporations that operate overseas for local listings, and advanced strongly in the competition for IPO and SPO underwriting – with 7 cases acting as a lead underwriter and 27 cases as a co-manager, doubling its record of the prior year. Its bottom-line performance underscored the result of its optimization of risk management and modular portfolios to maximize proprietary trading profit: 2009 net income was NT$912 million or NT$1.55 per share, exceeding its budget goal by 51.05%.

Yuh-Chang ChenChairman, First Financial

4

Letter to Shareholders

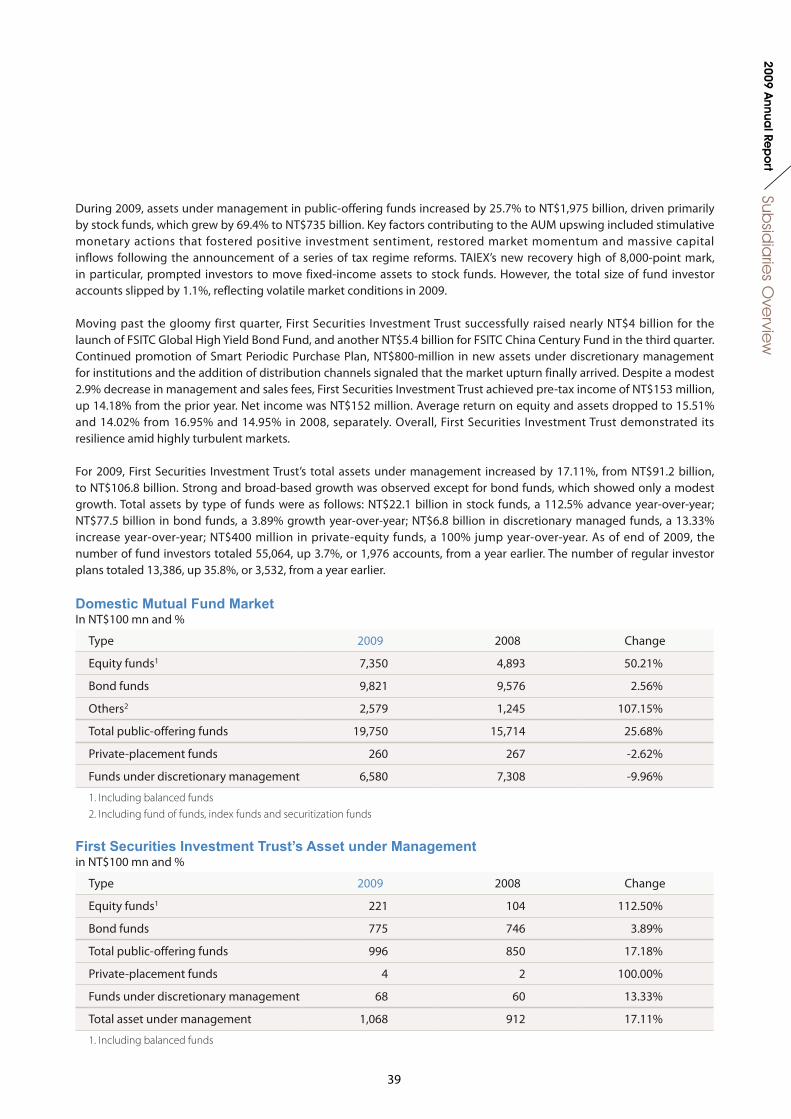

With investor optimism surging back in the second quarter, combined with Government’s stimulus actions, First Securities Investment Trust’s Asset Under Management increased to NT$106.8 billion for 2009. Public-offering fund assets increased by NT$14.6 billion to NT$99.6 billion, with stock funds registering the strongest growth rate of 112.5% to NT$22.1 billion. As of end of 2009, the account of First Securities Investment Trust’s investors grew by 3.7% to 55,064, while the size of regular investor plans grew by 35.8% to 13,386 from the prior year. The company’s profit returned to the historical baseline, with net income of NT$152 million, or NT$2.53 per share, beating its budget goal by 26.25%.

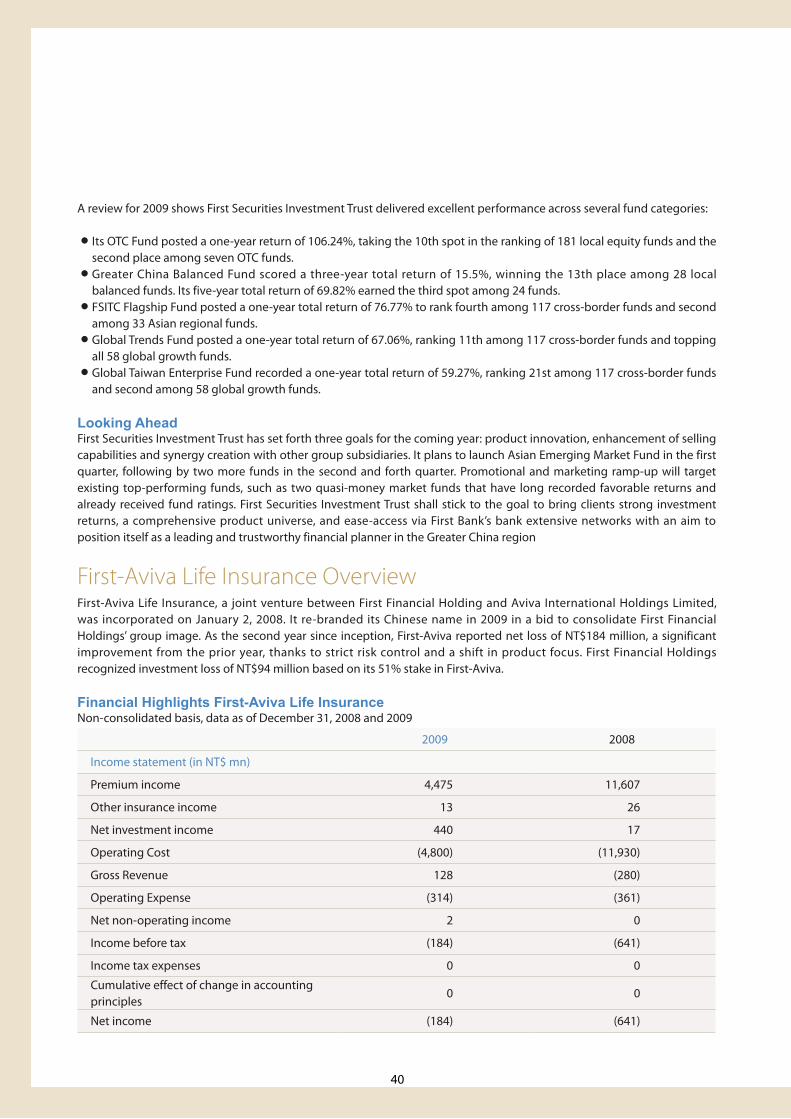

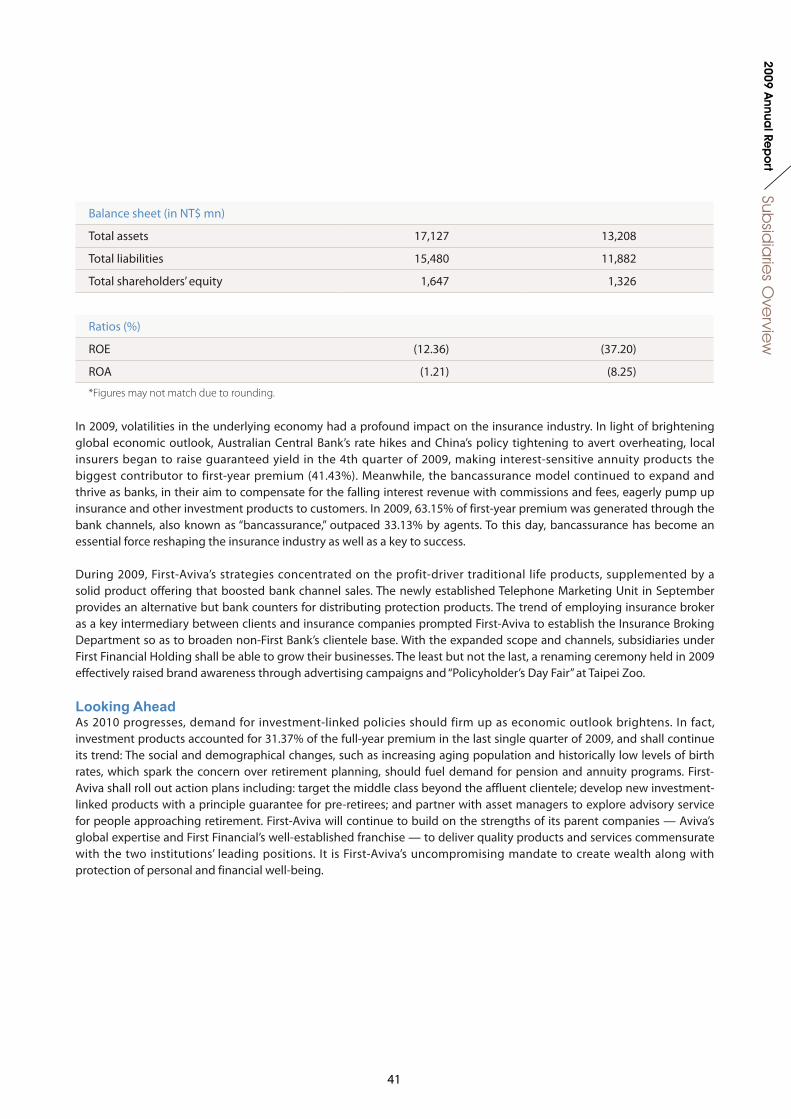

In 2009, First-Aviva shifted its product focus to traditional life policies and retirement-plan programs, steering away from investment-linked and interest-sensitive annuity insurance products against an unfavorable interest rate environment. By leveraging cross-sell efforts on mortgage insurance and accident insurance through First Bank’s branch networks, First-Aviva achieved first-year premium of NT$3.34 billion. The company was ranked the 16th insurer in terms of bancassurance with a 0.56% market share. Improved investment returns and stringent cost control helped narrow 2009 net loss to NT$184 million, or -NT$0.82 per share, easing the pressure for re-capitalization.

As for other subsidiaries with smaller-scale operations, First AMC, First Consulting and First P & C Insurance Agency met earnings targets on the back of cost-cutting measures and upward volume and price movement in markets– except for First Venture Capital, which dragged by impairment losses on its equity portfolio under volatile market conditions. For 2009, First AMC reported net income of NT$43.58 million, exceeding its budget goal by 1.29%; First Venture Capital reported NT$25.98 million, short of its budget goal by 35.74%; First Consulting reported net income of NT$8.97 million, exceeding its budget goal by 24.22%; First P & C Insurance Agency reported net income of NT$6.51 million, exceeding its budget goal by 29.07%.

China Reach, Taiwan Experience We see 2010 as a year of new opportunities given a turnaround in the economy at home and abroad, and gradually tie-up between Taiwan and China. A number of focal points are identified to guide our business strategy and forward-looking initiatives in the coming year; implement joint-marketing and resources integration across group subsidiaries; pioneer overseas expansion; establish a group-wide financial products and services platform to enhance one-stop shopping for customers; reinforce the compliance regime and strengthen risk management practices; optimize processes and procedures to manage the group’s asset and liability profile; target to act as a benchmark for best corporate citizen. To conclude, our vision is firmly rooted in our bank franchise, through which we will continue to promote joint marketing, integrate resources, innovate on customer services, sustain profitability and maximize value for the group and shareholders.

To ensure compliance with changing legal and financial regulations, we will continue to educate employees, management and directors about the latest reforms via periodical training to enhance corporate governance. We have put into place an IFRS (International Financial Reporting Standards) task force responsible for the implementation and personnel training relating to IFRS. Yet another dedicated team was established to be responsible for the origination, review and monitoring of China business plans for the group’s subsidiaries, while devising strategies through our in-house policy research into the financial Memorandum of Understanding (MOU) and Economic Cooperation Framework Agreement(ECFA) between Taiwan and China.

To lead the race of human capital, we will accelerate the development of talent for core businesses important to sustain our competitive advantages for the future. In addition, we will proactively recruit, train and deploy management associates, equipping them with certificates applicable to financial professions in China, Hong Kong and Macau to support China expansion strategy.

For risk management, we will incorporate risk monitoring from subsidiaries’ ALM (Asset and Liability Management)

5

Lette

r to Sha

reho

lde

rs2009 A

nnual Re

po

rt

commissions into the group’s risk management regime. A regular review and update of our internal control processes and procedures will be in place to ensure the validity and effectiveness of such controls. We will also continue to strengthen internal control at subsidiary levels and on-going employee training to raise awareness of ethical behavior as part of the group-wide efforts to reinforce risk management.

In light of the signing of the financial MOU and negotiations over the “early harvest list” of industries under the ECFA framework between Taiwan and China, we have set forth the priority of establishing a bank branch in Shanghai, followed by a securities brokerage representative office, as early preparatory steps to build a financial service platform for Taiwanese businesses that operate overseas. As we are positive on the potentials of emerging markets in the Asia-Pacific region, our goal for the next stage of China business development will be incorporating a subsidiary company in China after the Shanghai branch’s operation gets on track.

With regard to marketing, core banking business shall continue to act as the foundation from which to tap into stock broking, asset management and insurance, so as to solidify primary profit sources such as corporate banking, retail banking, foreign exchange and wealth management. To help our customers meet their financial goals as well as to

Ming-Ren ChienPresident, First Financial

6

discover cross-sell opportunities for the group, we will continue promoting our unique “Financial Services Integration System”, which integrates a wide range of financial products alongside a sales referral platform in a bid to boost business volume.

Meanwhile, to fortify corporate image and fulfill social responsibilities, we will adhere to our centennial corporate tradition and virtue by gaining clients trust through persistent quality financial services and products, which better safeguard the First Financial brand. Based on existing ample resources and business franchise, we manage to integrate group sales and upgrade brand awareness by consolidating subsidiaries business and CSR campaign as a whole. We believe our brand re-engineering efforts will pay off and bring to the attention of our customers, shareholders and employees the compelling advantages that keep First Financial ahead in the financial industry.

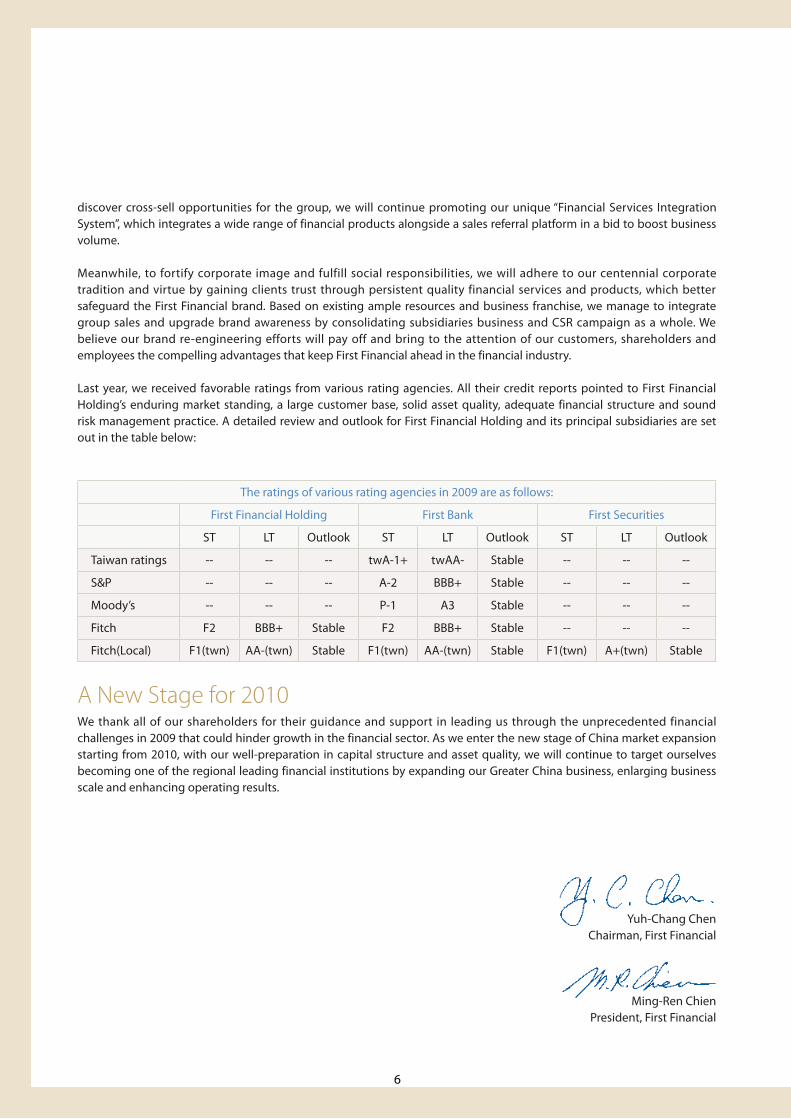

Last year, we received favorable ratings from various rating agencies. All their credit reports pointed to First Financial Holding’s enduring market standing, a large customer base, solid asset quality, adequate financial structure and sound risk management practice. A detailed review and outlook for First Financial Holding and its principal subsidiaries are set out in the table below:

The ratings of various rating agencies in 2009 are as follows:

First Financial Holding First Bank First Securities

ST LT Outlook ST LT Outlook ST LT Outlook

Taiwan ratings -- -- -- twA-1+ twAA- Stable -- -- --

S&P -- -- -- A-2 BBB+ Stable -- -- --

Moody’s -- -- -- P-1 A3 Stable -- -- --

Fitch F2 BBB+ Stable F2 BBB+ Stable -- -- --

Fitch(Local) F1(twn) AA-(twn) Stable F1(twn) AA-(twn) Stable F1(twn) A+(twn) Stable

A New Stage for 2010We thank all of our shareholders for their guidance and support in leading us through the unprecedented financial challenges in 2009 that could hinder growth in the financial sector. As we enter the new stage of China market expansion starting from 2010, with our well-preparation in capital structure and asset quality, we will continue to target ourselves becoming one of the regional leading financial institutions by expanding our Greater China business, enlarging business scale and enhancing operating results.

Yuh-Chang ChenChairman, First Financial

Ming-Ren ChienPresident, First Financial

7

Co

mp

any Pro

file2009 A

nnual Re

po

rt

First Financial Holding Co., Ltd. was incorporated on January 2, 2003 with First Commercial Bank as its flagship entity. It is

listed on Taiwan Stock Exchange under the stock code 2892.

Founded in 1899, First Bank was one of the three government-affiliated banks with the mission to allocate credit to

underserved industrial and commercial businesses, finance national infrastructure, and serve as an underlying force of

Taiwan’s great economic advancement. In 1998, First Bank became the largest private-owned bank on the island after

privatization. Since then it has been able to secure leadership positions in such selected areas as the corporate banking,

SME business, home mortgages, mutual-fund distribution, trade finance, deposit and lending. It currently owns 190

branches at home along with 26 overseas branches and representative offices including the U.S. subsidiary of First

Commercial Bank (USA).

With the historical groundwork well laid by First Bank, First Financial Holding Co. further diversified its business portfolio

into securities trading, property and casualty insurance and asset management on July 31, 2003, by acquiring First Taisec

Securities Co., Ltd., Mingtai Fire & Marine Insurance Co., Ltd. and National Investment Trust Co., Ltd. On July 28, 2003, it

successfully raised the equivalent of NT$17.3 billion via a global depository receipt program, the first ever issued by a

Taiwanese financial institution, which significantly shored up capital bases of the group and its subsidiaries. From May

through September of 2004, in its second round of penetrating into new markets to deliver full product range and high

quality services, First Financial Holding Co. established First Financial Asset Management Co., Ltd., First Venture Capital Co.,

Ltd., First Financial Management Consulting Co., Ltd., and First P&C Insurance Agency Co., Ltd.

First Financial Holding, in an aim to capture growth in wealth management, expand product offerings, retain clients and

address personal retirement planning needs, sought to form a joint venture with U.K’s largest insurer Aviva in 2007. First-

Aviva Life, a 51:49 joint-venture between the two companies, was incorporated on December 11, 2007.

In order to solidify group image, raise popular awareness of its subsidiaries and promote employee loyalty, First Financial

Holding rebranded subsidiaries First Taisec Securities, National Securities Investment Trust and First Taisec Capital

Management under the names “First Securities”, “First Securities Investment Trust” and “First Capital Management” on

December 31, 2008. And in September of 2009, First-Aviva’s Chinese brand was successfully renamed.

With NT$1.96 trillion in assets, over five million customer accounts and strong client relationships, First Financial Holding

operates across multiple financial sectors. The holding company enhances efficiency via economies of scale and allows

for effective joint marketing, resource sharing and personnel assignment within the group. First Financial Holding will

continue to leverage its diversified scope to create greater value for clients, shareholders and employees, with the goal of

becoming the most competitive financial institution in Taiwan and across the Asian-Pacific region.

Company Profile

8

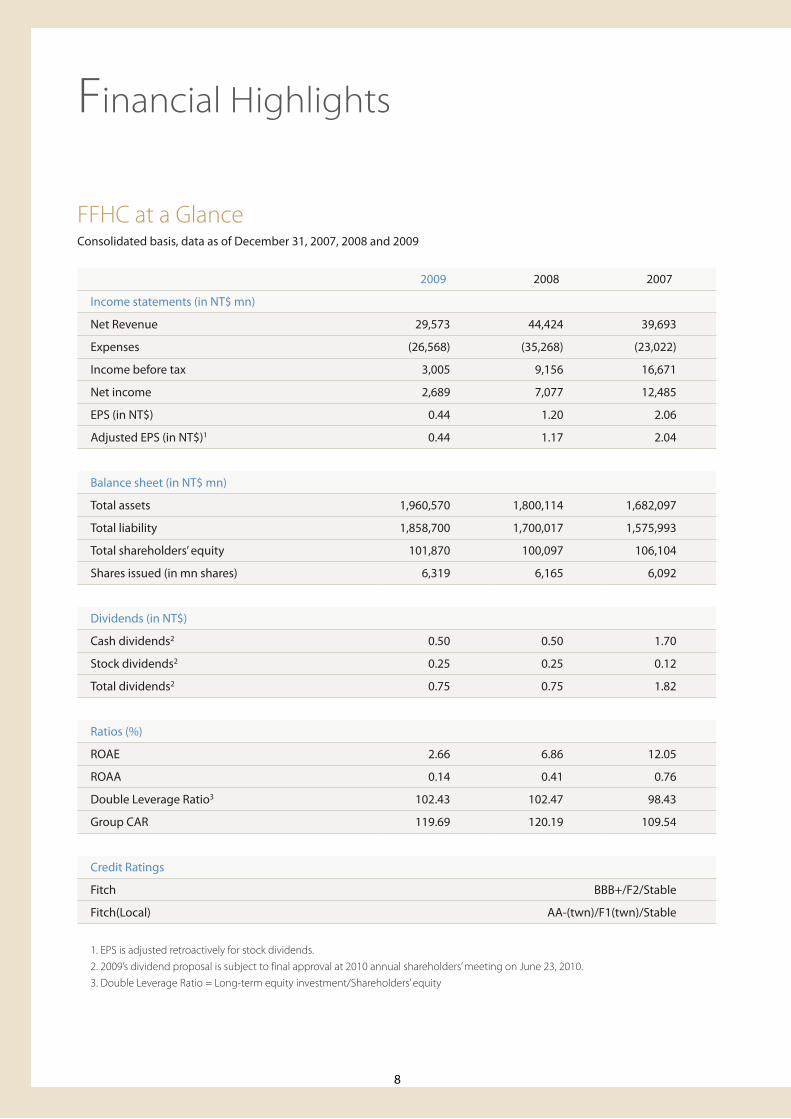

FFHC at a GlanceConsolidated basis, data as of December 31, 2007, 2008 and 2009

2009 2008 2007

Income statements (in NT$ mn)

Net Revenue 29,573 44,424 39,693

Expenses (26,568) (35,268) (23,022)

Income before tax 3,005 9,156 16,671

Net income 2,689 7,077 12,485

EPS (in NT$) 0.44 1.20 2.06

Adjusted EPS (in NT$)1 0.44 1.17 2.04

Balance sheet (in NT$ mn)

Total assets 1,960,570 1,800,114 1,682,097

Total liability 1,858,700 1,700,017 1,575,993

Total shareholders’ equity 101,870 100,097 106,104

Shares issued (in mn shares) 6,319 6,165 6,092

Dividends (in NT$)

Cash dividends2 0.50 0.50 1.70

Stock dividends2 0.25 0.25 0.12

Total dividends2 0.75 0.75 1.82

Ratios (%)

ROAE 2.66 6.86 12.05

ROAA 0.14 0.41 0.76

Double Leverage Ratio3 102.43 102.47 98.43

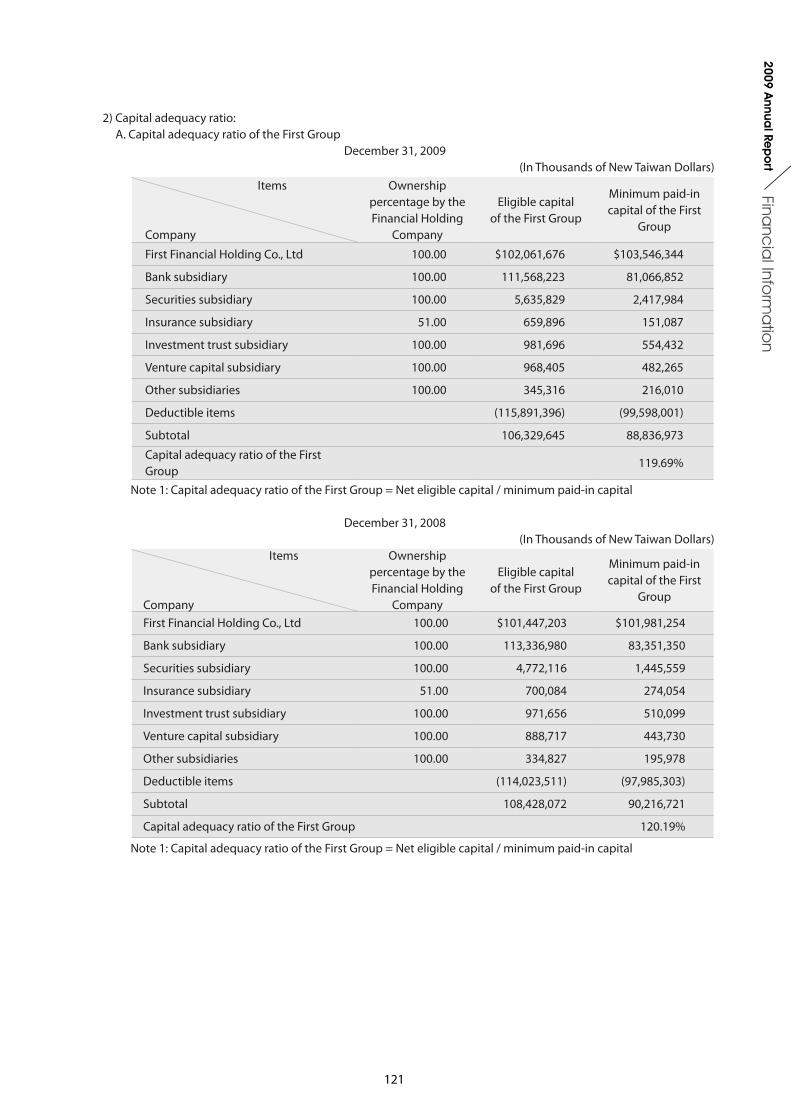

Group CAR 119.69 120.19 109.54

Credit Ratings

Fitch BBB+/F2/Stable

Fitch(Local) AA-(twn)/F1(twn)/Stable

1. EPS is adjusted retroactively for stock dividends. 2. 2009’s dividend proposal is subject to final approval at 2010 annual shareholders’ meeting on June 23, 2010.3. Double Leverage Ratio = Long-term equity investment/Shareholders’ equity

Financial Highlights

9

Financ

ial H

ighlig

hts2009 A

nnual Re

po

rt

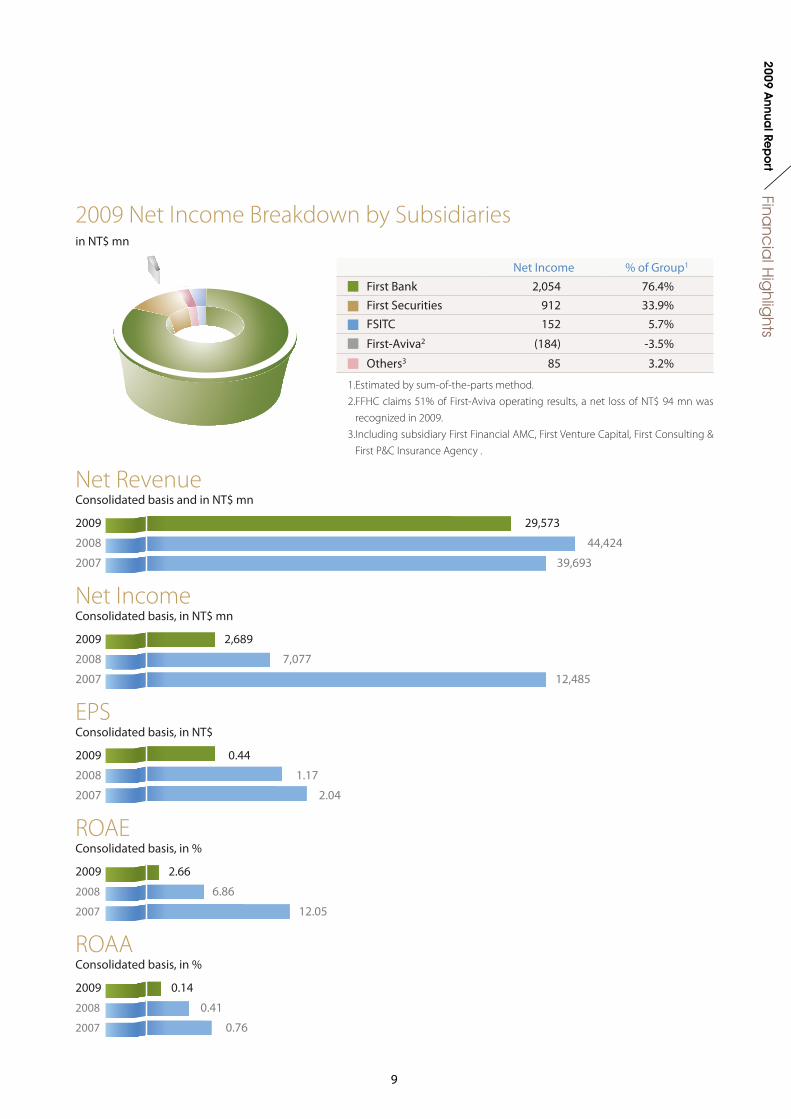

2009 Net Income Breakdown by Subsidiariesin NT$ mn

1.Estimated by sum-of-the-parts method.2. FFHC claims 51% of First-Aviva operating results, a net loss of NT$ 94 mn was

recognized in 2009.3. Including subsidiary First Financial AMC, First Venture Capital, First Consulting &

First P&C Insurance Agency .

Net Income % of Group1

First Bank 2,054 76.4%First Securities 912 33.9%FSITC 152 5.7%

First-Aviva2 (184) -3.5%

Others3 85 3.2%

Net RevenueConsolidated basis and in NT$ mn

2009 29,573

2008 44,424

2007 39,693

Net Income Consolidated basis, in NT$ mn

2009 2,689

2008 7,077

2007 12,485

EPSConsolidated basis, in NT$

2009 0.44

2008 1.17

2007 2.04

ROAEConsolidated basis, in %

2009 2.66

2008 6.86

2007 12.05

ROAAConsolidated basis, in %

2009 0.14

2008 0.41

2007 0.76

10

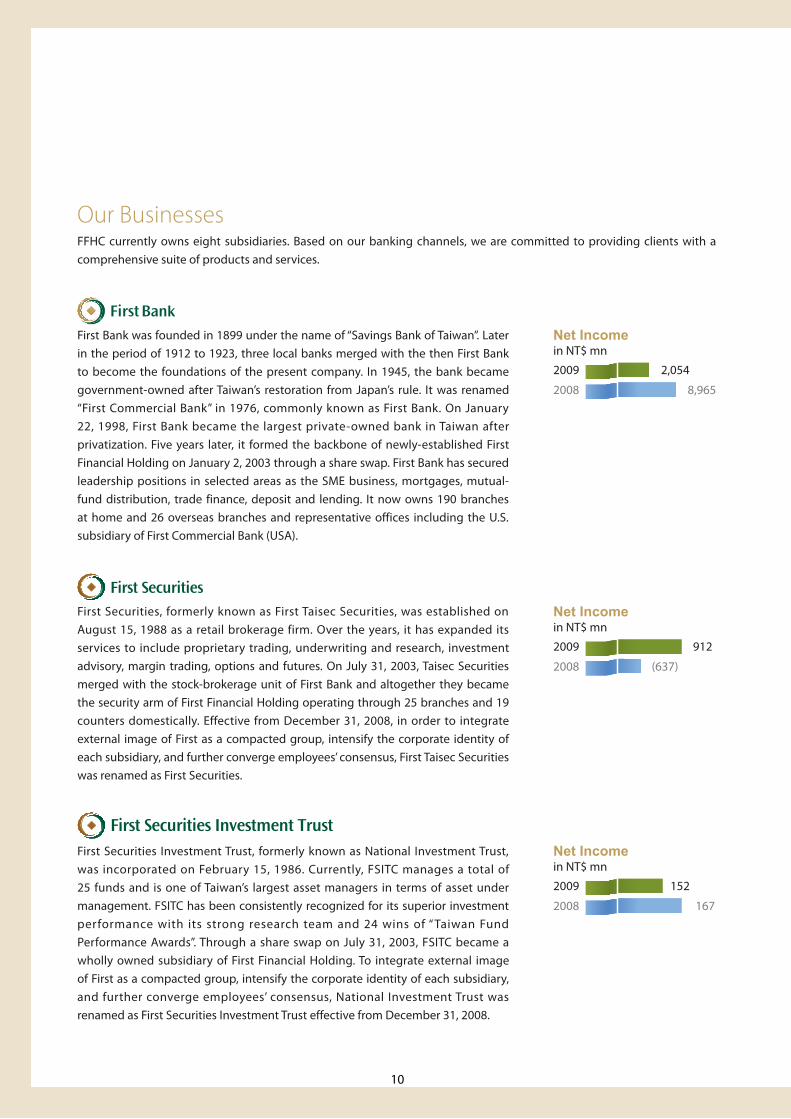

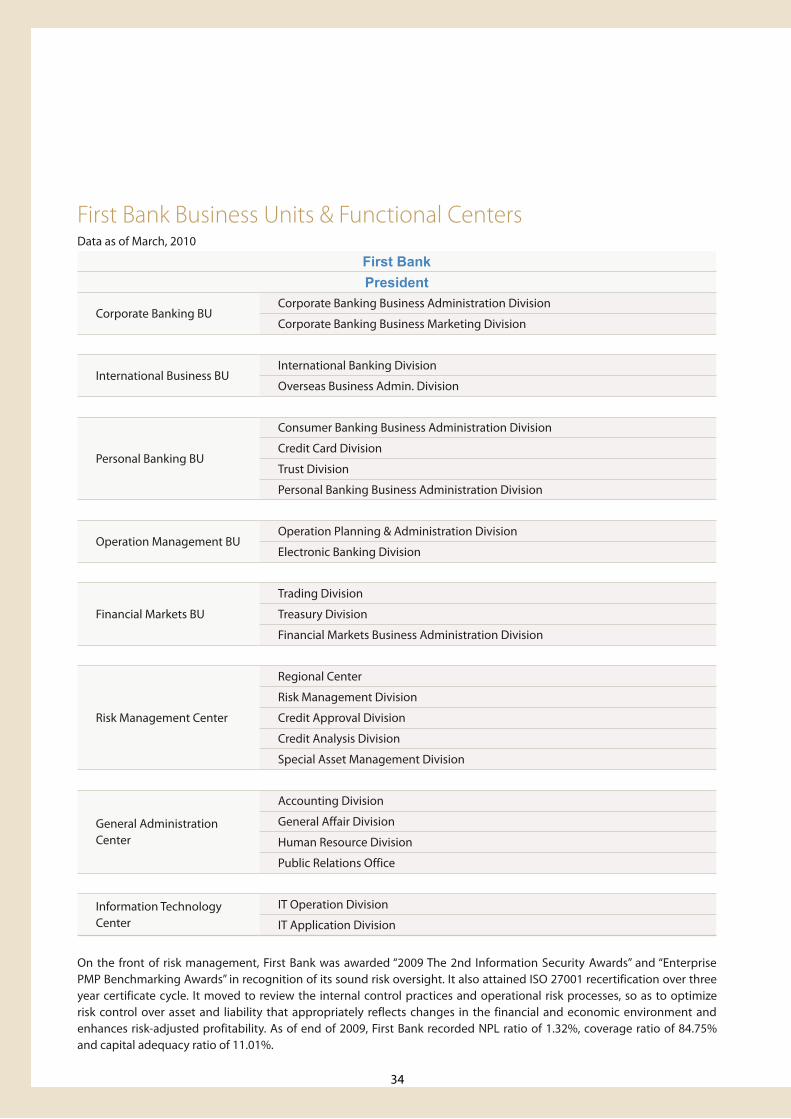

Our BusinessesFFHC currently owns eight subsidiaries. Based on our banking channels, we are committed to providing clients with a comprehensive suite of products and services.

First Bank was founded in 1899 under the name of “Savings Bank of Taiwan”. Later in the period of 1912 to 1923, three local banks merged with the then First Bank to become the foundations of the present company. In 1945, the bank became government-owned after Taiwan’s restoration from Japan’s rule. It was renamed “First Commercial Bank” in 1976, commonly known as First Bank. On January 22, 1998, First Bank became the largest private-owned bank in Taiwan after privatization. Five years later, it formed the backbone of newly-established First Financial Holding on January 2, 2003 through a share swap. First Bank has secured leadership positions in selected areas as the SME business, mortgages, mutual-fund distribution, trade finance, deposit and lending. It now owns 190 branches at home and 26 overseas branches and representative offices including the U.S. subsidiary of First Commercial Bank (USA).

First Securities, formerly known as First Taisec Securities, was established on August 15, 1988 as a retail brokerage firm. Over the years, it has expanded its services to include proprietary trading, underwriting and research, investment advisory, margin trading, options and futures. On July 31, 2003, Taisec Securities merged with the stock-brokerage unit of First Bank and altogether they became the security arm of First Financial Holding operating through 25 branches and 19 counters domestically. Effective from December 31, 2008, in order to integrate external image of First as a compacted group, intensify the corporate identity of each subsidiary, and further converge employees’ consensus, First Taisec Securities was renamed as First Securities.

First Securities Investment Trust, formerly known as National Investment Trust, was incorporated on February 15, 1986. Currently, FSITC manages a total of 25 funds and is one of Taiwan’s largest asset managers in terms of asset under management. FSITC has been consistently recognized for its superior investment performance with its strong research team and 24 wins of “Taiwan Fund Performance Awards”. Through a share swap on July 31, 2003, FSITC became a wholly owned subsidiary of First Financial Holding. To integrate external image of First as a compacted group, intensify the corporate identity of each subsidiary, and further converge employees’ consensus, National Investment Trust was renamed as First Securities Investment Trust effective from December 31, 2008.

2009 2,054

2008 8,965

2009 912

2008 (637)

2009 152

2008 167

Net Incomein NT$ mn

Net Incomein NT$ mn

Net Incomein NT$ mn

11

Financ

ial H

ighlig

hts2009 A

nnual Re

po

rt

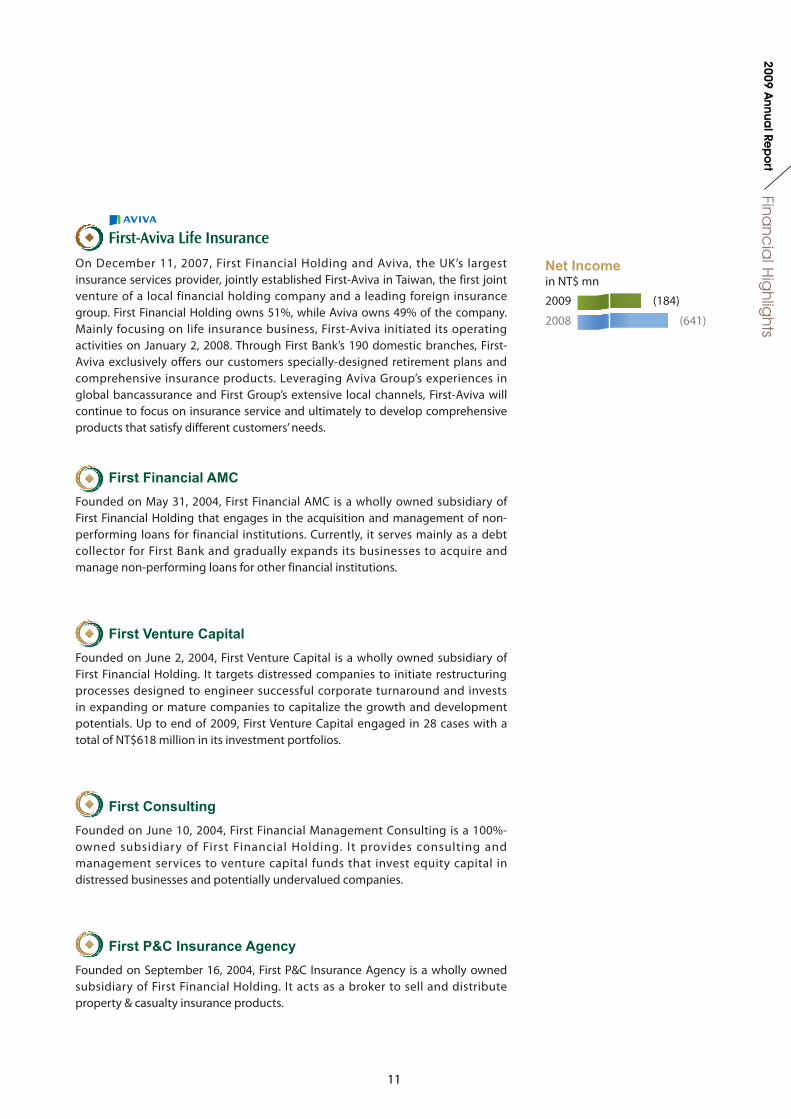

On December 11, 2007, First Financial Holding and Aviva, the UK’s largest insurance services provider, jointly established First-Aviva in Taiwan, the first joint venture of a local financial holding company and a leading foreign insurance group. First Financial Holding owns 51%, while Aviva owns 49% of the company. Mainly focusing on life insurance business, First-Aviva initiated its operating activities on January 2, 2008. Through First Bank’s 190 domestic branches, First-Aviva exclusively offers our customers specially-designed retirement plans and comprehensive insurance products. Leveraging Aviva Group’s experiences in global bancassurance and First Group’s extensive local channels, First-Aviva will continue to focus on insurance service and ultimately to develop comprehensive products that satisfy different customers’ needs.

First Financial AMC

Founded on May 31, 2004, First Financial AMC is a wholly owned subsidiary of First Financial Holding that engages in the acquisition and management of non-performing loans for financial institutions. Currently, it serves mainly as a debt collector for First Bank and gradually expands its businesses to acquire and manage non-performing loans for other financial institutions.

First Venture Capital

Founded on June 2, 2004, First Venture Capital is a wholly owned subsidiary of First Financial Holding. It targets distressed companies to initiate restructuring processes designed to engineer successful corporate turnaround and invests in expanding or mature companies to capitalize the growth and development potentials. Up to end of 2009, First Venture Capital engaged in 28 cases with a total of NT$618 million in its investment portfolios.

First Consulting

Founded on June 10, 2004, First Financial Management Consulting is a 100%-owned subsidiary of First Financial Holding. It provides consulting and management services to venture capital funds that invest equity capital in distressed businesses and potentially undervalued companies.

First P&C Insurance Agency Founded on September 16, 2004, First P&C Insurance Agency is a wholly owned subsidiary of First Financial Holding. It acts as a broker to sell and distribute property & casualty insurance products.

2009 (184)

2008 (641)

Net Incomein NT$ mn

12

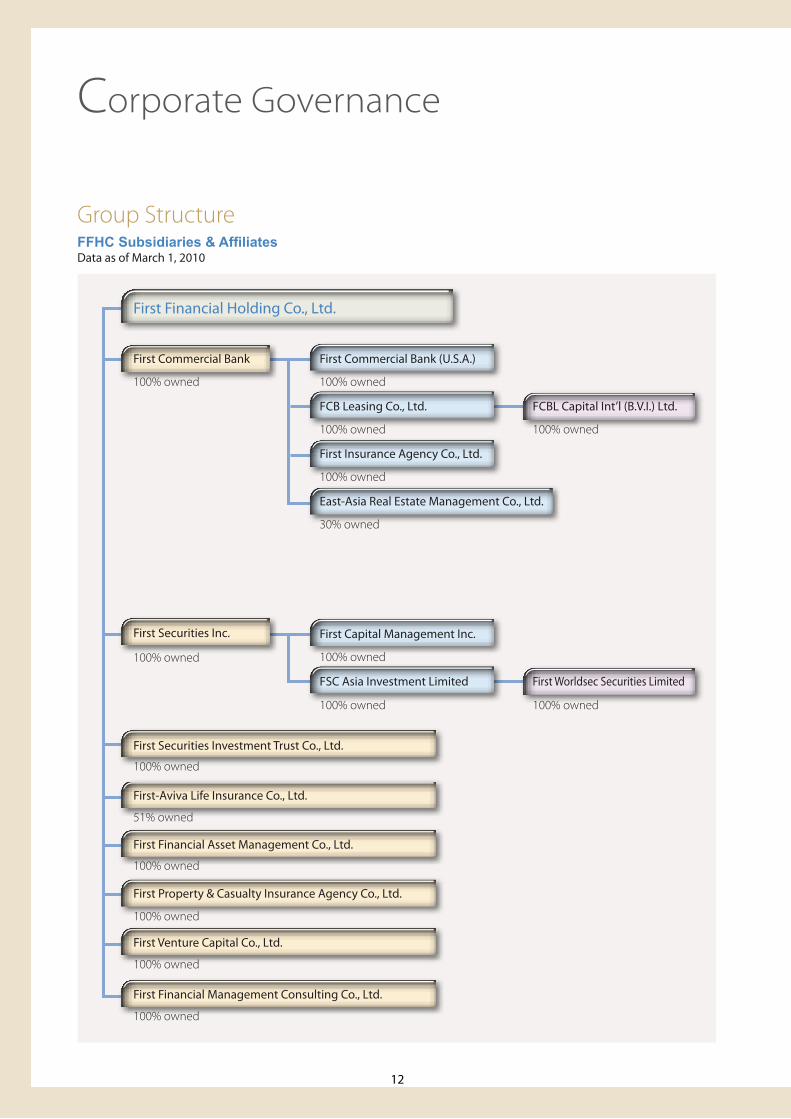

Group StructureFFHC Subsidiaries & AffiliatesData as of March 1, 2010

Corporate Governance

First Financial Holding Co., Ltd.

100% owned

100% owned

51% owned

100% owned

100% owned

100% owned

100% owned

First Securities Investment Trust Co., Ltd.

First-Aviva Life Insurance Co., Ltd.

First Financial Asset Management Co., Ltd.

First Property & Casualty Insurance Agency Co., Ltd.

First Financial Management Consulting Co., Ltd.

First Venture Capital Co., Ltd.

First Commercial Bank First Commercial Bank (U.S.A.)

First Capital Management Inc.

FCB Leasing Co., Ltd.

FSC Asia Investment Limited

FCBL Capital Int’l (B.V.I.) Ltd.

First Worldsec Securities Limited

First Insurance Agency Co., Ltd.

East-Asia Real Estate Management Co., Ltd.

100% owned 100% owned

100% owned

100% owned 100% owned

100% owned 100% owned

100% owned

30% owned

First Securities Inc.

13

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

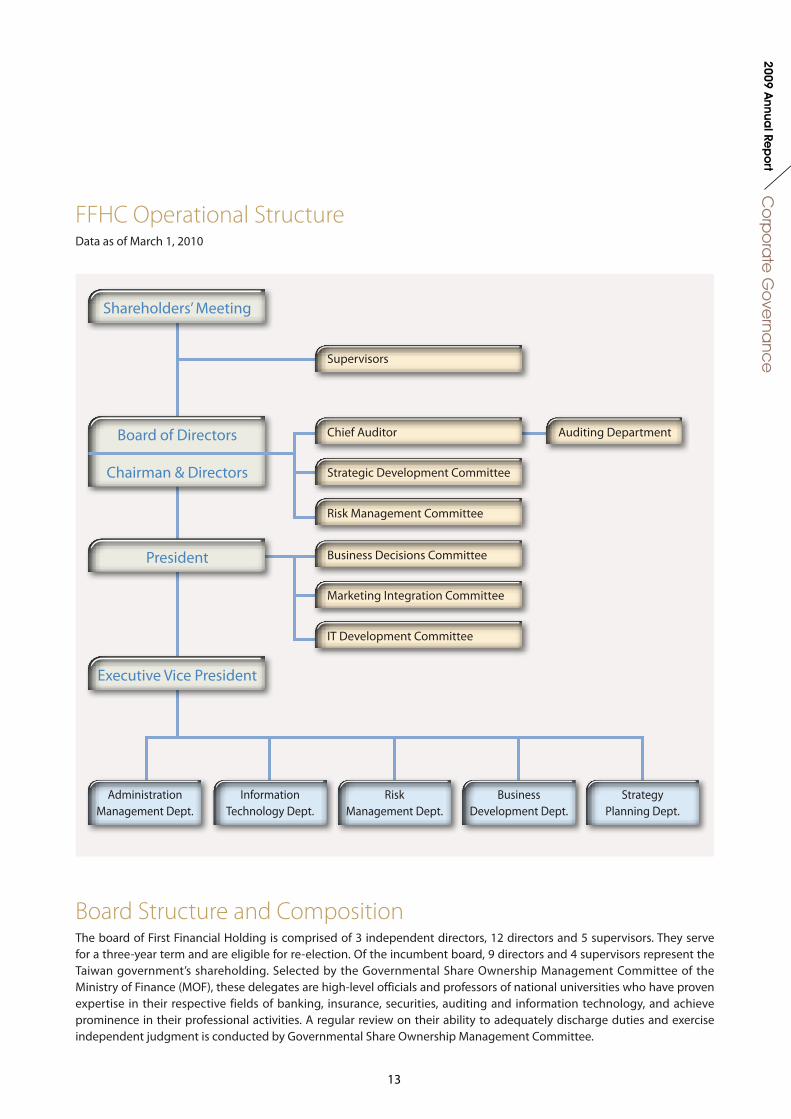

FFHC Operational StructureData as of March 1, 2010

Shareholders’ Meeting

Board of Directors

Chairman & Directors

President

Executive Vice President

Supervisors

Chief Auditor

Business Decisions Committee

Auditing Department

Strategic Development Committee

Marketing Integration Committee

Risk Management Committee

IT Development Committee

Administration Management Dept.

Information Technology Dept.

Risk Management Dept.

Business Development Dept.

Strategy Planning Dept.

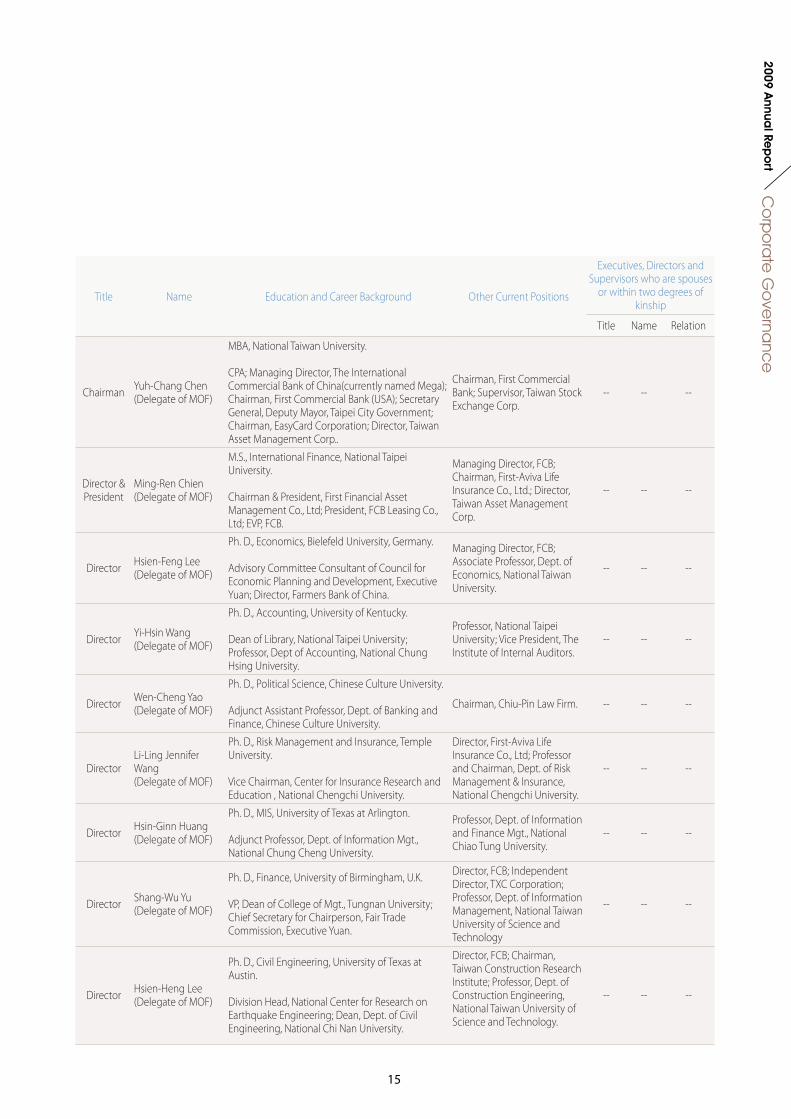

Board Structure and CompositionThe board of First Financial Holding is comprised of 3 independent directors, 12 directors and 5 supervisors. They serve for a three-year term and are eligible for re-election. Of the incumbent board, 9 directors and 4 supervisors represent the Taiwan government’s shareholding. Selected by the Governmental Share Ownership Management Committee of the Ministry of Finance (MOF), these delegates are high-level officials and professors of national universities who have proven expertise in their respective fields of banking, insurance, securities, auditing and information technology, and achieve prominence in their professional activities. A regular review on their ability to adequately discharge duties and exercise independent judgment is conducted by Governmental Share Ownership Management Committee.

14

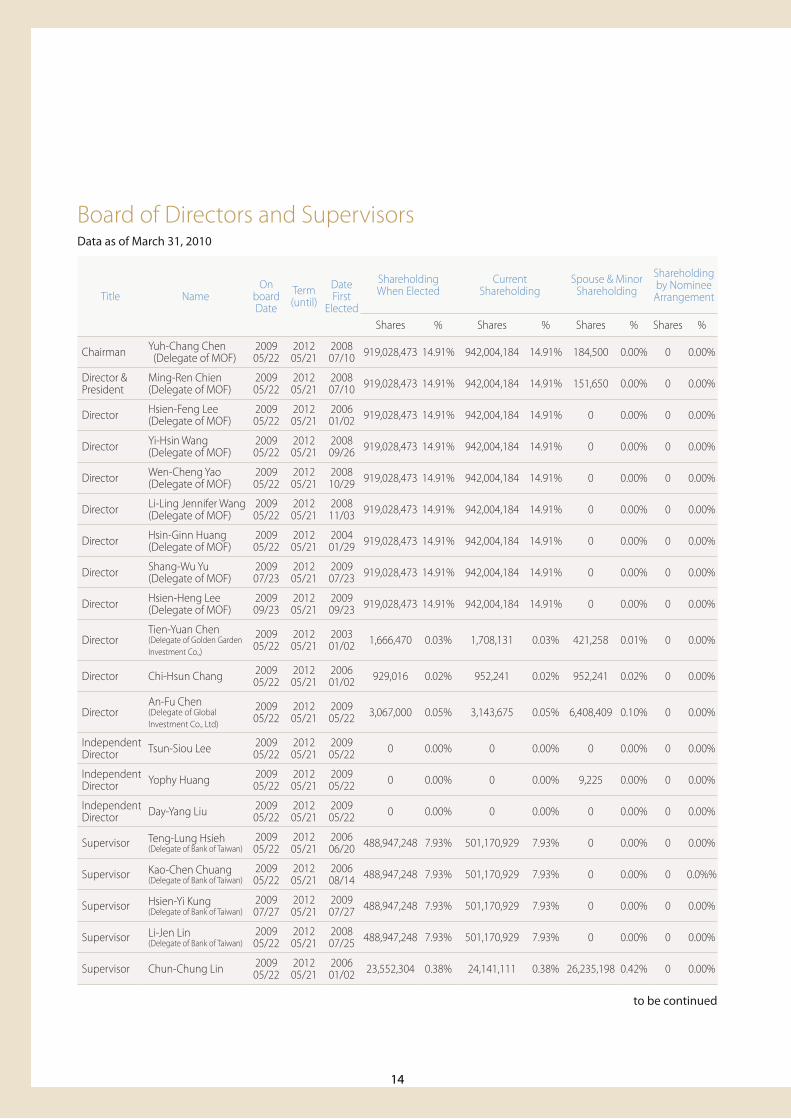

Board of Directors and SupervisorsData as of March 31, 2010

to be continued

Title NameOn

boardDate

Term(until)

Date First

Elected

ShareholdingWhen Elected

CurrentShareholding

Spouse & Minor Shareholding

Shareholding by Nominee

Arrangement

Shares % Shares % Shares % Shares %

Chairman Yuh-Chang Chen (Delegate of MOF)

200905/22

201205/21

200807/10 919,028,473 14.91% 942,004,184 14.91% 184,500 0.00% 0 0.00%

Director & President

Ming-Ren Chien(Delegate of MOF)

200905/22

201205/21

200807/10 919,028,473 14.91% 942,004,184 14.91% 151,650 0.00% 0 0.00%

Director Hsien-Feng Lee(Delegate of MOF)

200905/22

201205/21

200601/02 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

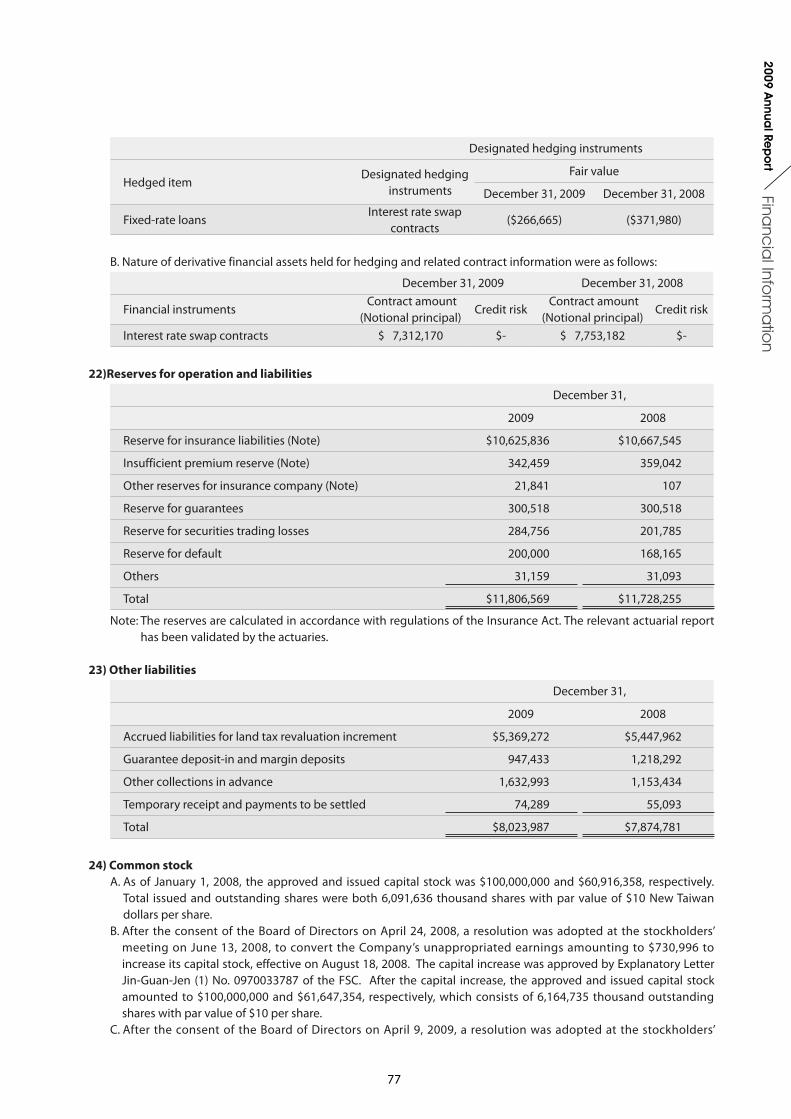

Director Yi-Hsin Wang(Delegate of MOF)

200905/22

201205/21

200809/26 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

Director Wen-Cheng Yao(Delegate of MOF)

200905/22

201205/21

200810/29 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

Director Li-Ling Jennifer Wang(Delegate of MOF)

200905/22

201205/21

200811/03 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

Director Hsin-Ginn Huang(Delegate of MOF)

200905/22

201205/21

200401/29 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

Director Shang-Wu Yu(Delegate of MOF)

200907/23

201205/21

200907/23 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

Director Hsien-Heng Lee(Delegate of MOF)

200909/23

201205/21

200909/23 919,028,473 14.91% 942,004,184 14.91% 0 0.00% 0 0.00%

DirectorTien-Yuan Chen(Delegate of Golden Garden Investment Co.,)

200905/22

201205/21

200301/02 1,666,470 0.03% 1,708,131 0.03% 421,258 0.01% 0 0.00%

Director Chi-Hsun Chang 200905/22

201205/21

200601/02 929,016 0.02% 952,241 0.02% 952,241 0.02% 0 0.00%

DirectorAn-Fu Chen(Delegate of Global Investment Co., Ltd)

200905/22

201205/21

200905/22 3,067,000 0.05% 3,143,675 0.05% 6,408,409 0.10% 0 0.00%

Independent Director Tsun-Siou Lee 2009

05/22201205/21

200905/22 0 0.00% 0 0.00% 0 0.00% 0 0.00%

Independent Director Yophy Huang 2009

05/22201205/21

200905/22 0 0.00% 0 0.00% 9,225 0.00% 0 0.00%

Independent Director Day-Yang Liu 2009

05/22201205/21

200905/22 0 0.00% 0 0.00% 0 0.00% 0 0.00%

Supervisor Teng-Lung Hsieh(Delegate of Bank of Taiwan)

200905/22

201205/21

200606/20 488,947,248 7.93% 501,170,929 7.93% 0 0.00% 0 0.00%

Supervisor Kao-Chen Chuang(Delegate of Bank of Taiwan)

200905/22

201205/21

200608/14 488,947,248 7.93% 501,170,929 7.93% 0 0.00% 0 0.0%%

Supervisor Hsien-Yi Kung(Delegate of Bank of Taiwan)

200907/27

201205/21

200907/27 488,947,248 7.93% 501,170,929 7.93% 0 0.00% 0 0.00%

Supervisor Li-Jen Lin(Delegate of Bank of Taiwan)

200905/22

201205/21

200807/25 488,947,248 7.93% 501,170,929 7.93% 0 0.00% 0 0.00%

Supervisor Chun-Chung Lin 200905/22

201205/21

200601/02 23,552,304 0.38% 24,141,111 0.38% 26,235,198 0.42% 0 0.00%

15

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

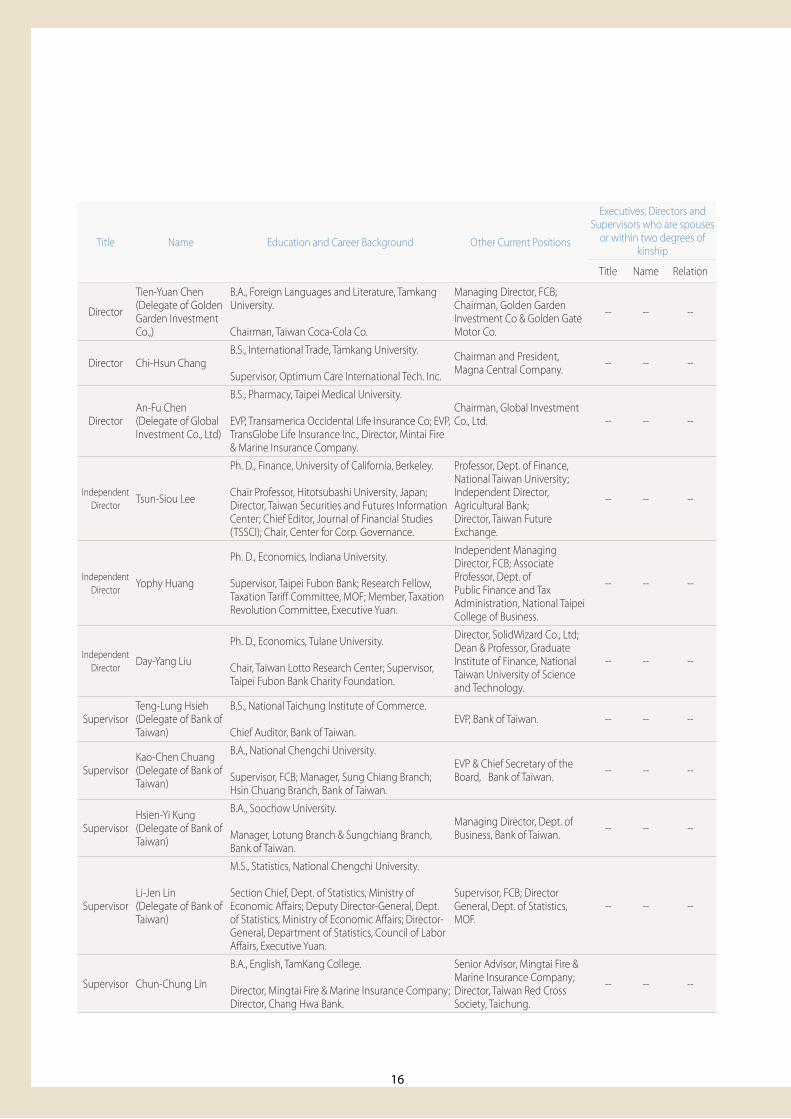

Title Name Education and Career Background Other Current Positions

Executives, Directors and Supervisors who are spouses

or within two degrees of kinship

Title Name Relation

Chairman Yuh-Chang Chen(Delegate of MOF)

MBA, National Taiwan University.

CPA; Managing Director, The International Commercial Bank of China(currently named Mega); Chairman, First Commercial Bank (USA); Secretary General, Deputy Mayor, Taipei City Government; Chairman, EasyCard Corporation; Director, Taiwan Asset Management Corp..

Chairman, First Commercial Bank; Supervisor, Taiwan Stock Exchange Corp.

-- -- --

Director & President

Ming-Ren Chien(Delegate of MOF)

M.S., International Finance, National Taipei University.

Chairman & President, First Financial Asset Management Co., Ltd; President, FCB Leasing Co., Ltd; EVP, FCB.

Managing Director, FCB; Chairman, First-Aviva Life Insurance Co., Ltd.; Director, Taiwan Asset Management Corp.

-- -- --

Director Hsien-Feng Lee(Delegate of MOF)

Ph. D., Economics, Bielefeld University, Germany.

Advisory Committee Consultant of Council for Economic Planning and Development, Executive Yuan; Director, Farmers Bank of China.

Managing Director, FCB; Associate Professor, Dept. of Economics, National Taiwan University.

-- -- --

Director Yi-Hsin Wang(Delegate of MOF)

Ph. D., Accounting, University of Kentucky.

Dean of Library, National Taipei University; Professor, Dept of Accounting, National Chung Hsing University.

Professor, National Taipei University; Vice President, The Institute of Internal Auditors.

-- -- --

Director Wen-Cheng Yao(Delegate of MOF)

Ph. D., Political Science, Chinese Culture University.

Adjunct Assistant Professor, Dept. of Banking and Finance, Chinese Culture University.

Chairman, Chiu-Pin Law Firm. -- -- --

DirectorLi-Ling Jennifer Wang(Delegate of MOF)

Ph. D., Risk Management and Insurance, Temple University.

Vice Chairman, Center for Insurance Research and Education , National Chengchi University.

Director, First-Aviva Life Insurance Co., Ltd; Professor and Chairman, Dept. of Risk Management & Insurance, National Chengchi University.

-- -- --

Director Hsin-Ginn Huang(Delegate of MOF)

Ph. D., MIS, University of Texas at Arlington.

Adjunct Professor, Dept. of Information Mgt., National Chung Cheng University.

Professor, Dept. of Information and Finance Mgt., National Chiao Tung University.

-- -- --

Director Shang-Wu Yu(Delegate of MOF)

Ph. D., Finance, University of Birmingham, U.K.

VP, Dean of College of Mgt., Tungnan University; Chief Secretary for Chairperson, Fair Trade Commission, Executive Yuan.

Director, FCB; Independent Director, TXC Corporation; Professor, Dept. of Information Management, National Taiwan University of Science and Technology

-- -- --

Director Hsien-Heng Lee(Delegate of MOF)

Ph. D., Civil Engineering, University of Texas at Austin.

Division Head, National Center for Research on Earthquake Engineering; Dean, Dept. of Civil Engineering, National Chi Nan University.

Director, FCB; Chairman, Taiwan Construction Research Institute; Professor, Dept. of Construction Engineering, National Taiwan University of Science and Technology.

-- -- --

16

Director

Tien-Yuan Chen(Delegate of Golden Garden Investment Co.,)

B.A., Foreign Languages and Literature, Tamkang University.

Chairman, Taiwan Coca-Cola Co.

Managing Director, FCB; Chairman, Golden Garden Investment Co & Golden Gate Motor Co.

-- -- --

Director Chi-Hsun ChangB.S., International Trade, Tamkang University.

Supervisor, Optimum Care International Tech. Inc.

Chairman and President, Magna Central Company. -- -- --

DirectorAn-Fu Chen(Delegate of Global Investment Co., Ltd)

B.S., Pharmacy, Taipei Medical University.

EVP, Transamerica Occidental Life Insurance Co; EVP, TransGlobe Life Insurance Inc., Director, Mintai Fire & Marine Insurance Company.

Chairman, Global Investment Co., Ltd. -- -- --

Independent Director Tsun-Siou Lee

Ph. D., Finance, University of California, Berkeley.

Chair Professor, Hitotsubashi University, Japan; Director, Taiwan Securities and Futures Information Center; Chief Editor, Journal of Financial Studies (TSSCI); Chair, Center for Corp. Governance.

Professor, Dept. of Finance, National Taiwan University; Independent Director, Agricultural Bank; Director, Taiwan Future Exchange.

-- -- --

Independent Director Yophy Huang

Ph. D., Economics, Indiana University.

Supervisor, Taipei Fubon Bank; Research Fellow, Taxation Tariff Committee, MOF; Member, Taxation Revolution Committee, Executive Yuan.

Independent Managing Director, FCB; Associate Professor, Dept. of Public Finance and Tax Administration, National Taipei College of Business.

-- -- --

Independent Director Day-Yang Liu

Ph. D., Economics, Tulane University.

Chair, Taiwan Lotto Research Center; Supervisor, Taipei Fubon Bank Charity Foundation.

Director, SolidWizard Co., Ltd; Dean & Professor, Graduate Institute of Finance, National Taiwan University of Science and Technology.

-- -- --

SupervisorTeng-Lung Hsieh(Delegate of Bank of Taiwan)

B.S., National Taichung Institute of Commerce.

Chief Auditor, Bank of Taiwan. EVP, Bank of Taiwan. -- -- --

SupervisorKao-Chen Chuang(Delegate of Bank of Taiwan)

B.A., National Chengchi University.

Supervisor, FCB; Manager, Sung Chiang Branch; Hsin Chuang Branch, Bank of Taiwan.

EVP & Chief Secretary of the Board, Bank of Taiwan. -- -- --

SupervisorHsien-Yi Kung(Delegate of Bank of Taiwan)

B.A., Soochow University.

Manager, Lotung Branch & Sungchiang Branch, Bank of Taiwan.

Managing Director, Dept. of Business, Bank of Taiwan. -- -- --

SupervisorLi-Jen Lin(Delegate of Bank of Taiwan)

M.S., Statistics, National Chengchi University.

Section Chief, Dept. of Statistics, Ministry of Economic Affairs; Deputy Director-General, Dept. of Statistics, Ministry of Economic Affairs; Director-General, Department of Statistics, Council of Labor Affairs, Executive Yuan.

Supervisor, FCB; Director General, Dept. of Statistics, MOF.

-- -- --

Supervisor Chun-Chung Lin

B.A., English, TamKang College.

Director, Mingtai Fire & Marine Insurance Company; Director, Chang Hwa Bank.

Senior Advisor, Mingtai Fire & Marine Insurance Company; Director, Taiwan Red Cross Society, Taichung.

-- -- --

Title Name Education and Career Background Other Current Positions

Executives, Directors and Supervisors who are spouses

or within two degrees of kinship

Title Name Relation

17

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

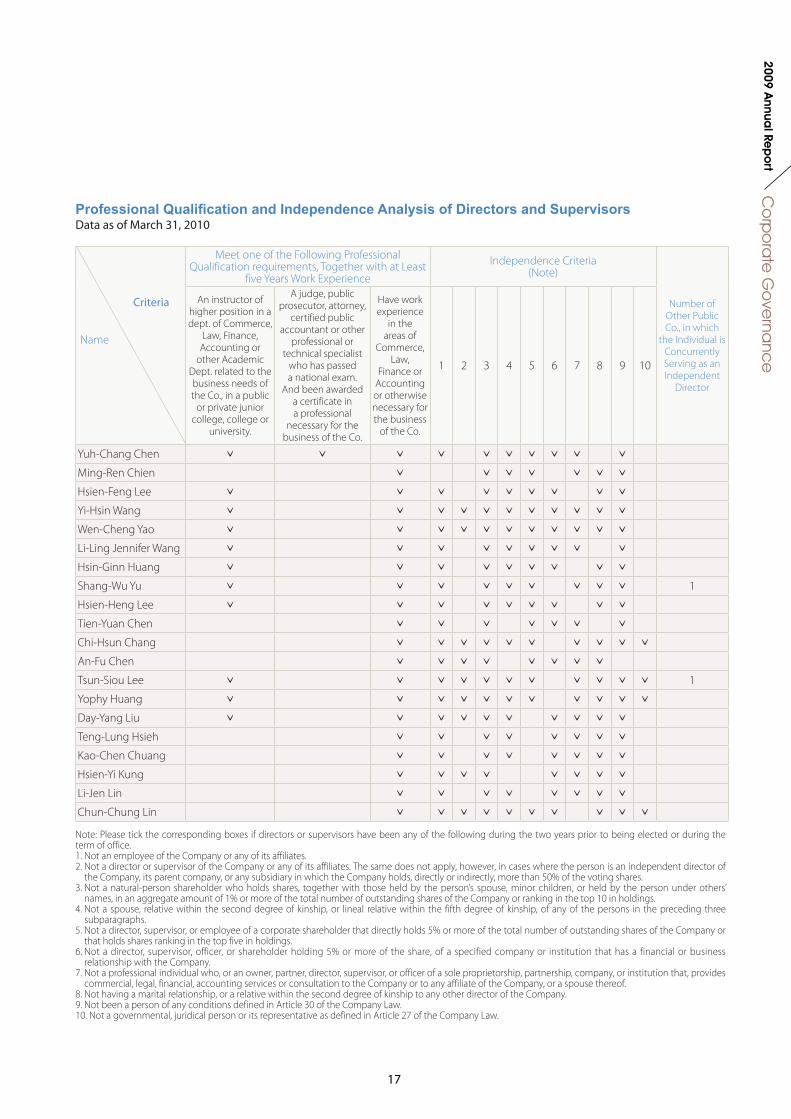

Professional Qualification and Independence Analysis of Directors and SupervisorsData as of March 31, 2010

Name

Meet one of the Following Professional Qualification requirements, Together with at Least

five Years Work Experience

Independence Criteria(Note)

Number of Other Public Co., in which

the Individual is Concurrently Serving as an Independent

Director

An instructor of higher position in a dept. of Commerce,

Law, Finance, Accounting or

other Academic Dept. related to the business needs of the Co., in a public

or private junior college, college or

university.

A judge, public prosecutor, attorney,

certified public accountant or other

professional or technical specialist

who has passed a national exam.

And been awarded a certificate in a professional

necessary for the business of the Co.

Have work experience

in the areas of

Commerce, Law,

Finance or Accounting or otherwise necessary for the business

of the Co.

1 2 3 4 5 6 7 8 9 10

Yuh-Chang Chen ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Ming-Ren Chien ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Hsien-Feng Lee ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Yi-Hsin Wang ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Wen-Cheng Yao ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Li-Ling Jennifer Wang ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Hsin-Ginn Huang ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Shang-Wu Yu ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ 1

Hsien-Heng Lee ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Tien-Yuan Chen ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Chi-Hsun Chang ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

An-Fu Chen ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Tsun-Siou Lee ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ 1

Yophy Huang ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Day-Yang Liu ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Teng-Lung Hsieh ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Kao-Chen Chuang ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Hsien-Yi Kung ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Li-Jen Lin ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Chun-Chung Lin ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ ˇ

Criteria

Note: Please tick the corresponding boxes if directors or supervisors have been any of the following during the two years prior to being elected or during the term of office.1. Not an employee of the Company or any of its affiliates.2. Not a director or supervisor of the Company or any of its affiliates. The same does not apply, however, in cases where the person is an independent director of

the Company, its parent company, or any subsidiary in which the Company holds, directly or indirectly, more than 50% of the voting shares.3. Not a natural-person shareholder who holds shares, together with those held by the person’s spouse, minor children, or held by the person under others’

names, in an aggregate amount of 1% or more of the total number of outstanding shares of the Company or ranking in the top 10 in holdings.4. Not a spouse, relative within the second degree of kinship, or lineal relative within the fifth degree of kinship, of any of the persons in the preceding three

subparagraphs.5. Not a director, supervisor, or employee of a corporate shareholder that directly holds 5% or more of the total number of outstanding shares of the Company or

that holds shares ranking in the top five in holdings.6. Not a director, supervisor, officer, or shareholder holding 5% or more of the share, of a specified company or institution that has a financial or business

relationship with the Company.7. Not a professional individual who, or an owner, partner, director, supervisor, or officer of a sole proprietorship, partnership, company, or institution that, provides

commercial, legal, financial, accounting services or consultation to the Company or to any affiliate of the Company, or a spouse thereof.8. Not having a marital relationship, or a relative within the second degree of kinship to any other director of the Company.9. Not been a person of any conditions defined in Article 30 of the Company Law.10. Not a governmental, juridical person or its representative as defined in Article 27 of the Company Law.

18

Board MeetingThe board of directors convenes every month to approve financial and other reporting, discuss the management’s performance, monitor the internal compliance and control system, and review the development of corporate strategies and performance objectives, which reflect changes in the competitive environment. All board members receive written material on the proposals in advance and meetings of the board of directors shall be convened by the chairman of the board of directors. Unless otherwise provided for in the Company Charter, resolutions of the board of directors shall be passed by one-half of the directors at a meeting attended by one-half of the directors.

Attendance at Board Meetings

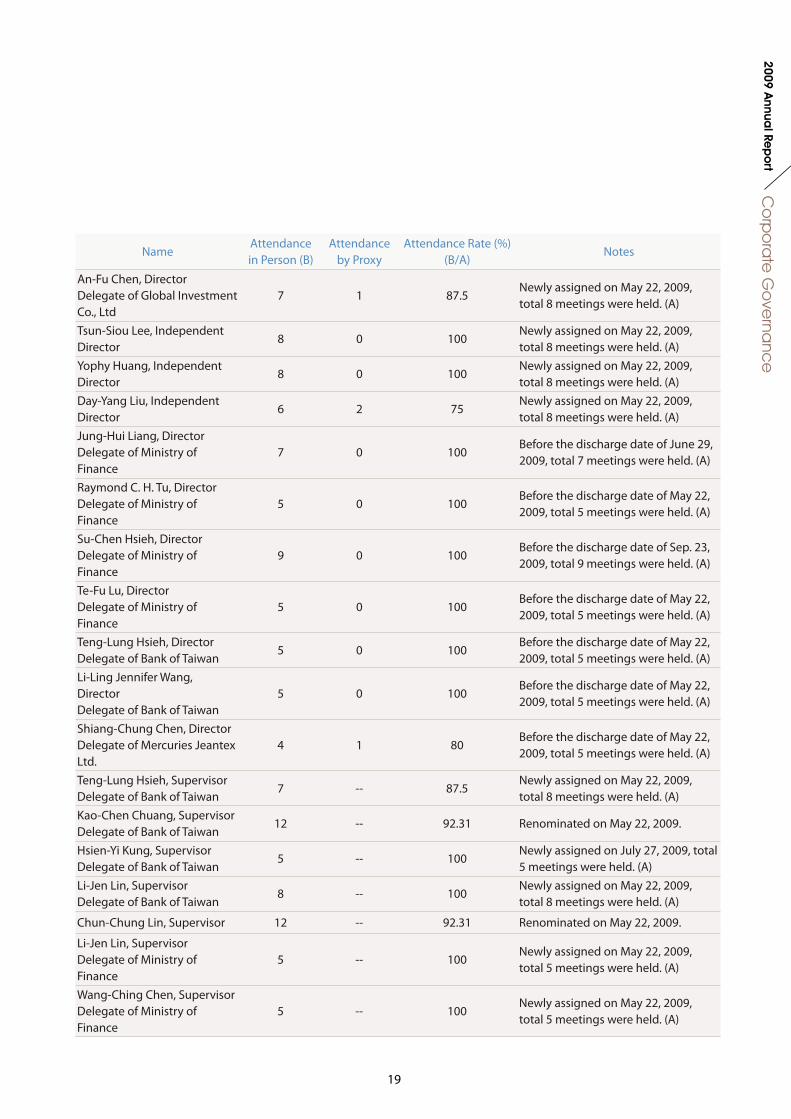

During 2009, there were 13 board of director meetings held. The number of meetings attended by each Director and Supervisor was as follows:

NameAttendancein Person (B)

Attendance by Proxy

Attendance Rate (%)(B/A)

Notes

Yuh-Chang Chen, ChairmanDelegate of Ministry of Finance

13 0 100 Renominated on May 22, 2009.

Ming-Ren Chien, DirectorDelegate of Ministry of Finance

12 1 92.31 Renominated on May 22, 2009.

Hsien-Feng Lee, DirectorDelegate of Ministry of Finance

12 1 92.31 Renominated on May 22, 2009.

Yi-Hsin Wang, DirectorDelegate of Ministry of Finance

11 2 84.62 Renominated on May 22, 2009.

Wen-Cheng Yao, DirectorDelegate of Ministry of Finance

13 0 100 Renominated on May 22, 2009.

Li-Ling Jennifer Wang, DirectorDelegate of Ministry of Finance

7 1 87.5Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Hsin-Ginn Huang, DirectorDelegate of Ministry of Finance

10 3 76.92 Renominated on May 22, 2009.

Shang-Wu Yu, DirectorDelegate of Ministry of Finance

5 0 100Newly assigned on July 23, 2009, total 5 meetings were held. (A)

Hsien-Heng Lee, DirectorDelegate of Ministry of Finance

4 0 100Newly assigned on Sep. 23, 2009, total 4 meetings were held. (A)

Tien-Yuan Chen, DirectorDelegate of Golden Garden Investment Co.

12 1 92.31 Renominated on May 22, 2009.

Chi-Hsun Chang, Director 13 0 100 Renominated on May 22, 2009.

19

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

An-Fu Chen, DirectorDelegate of Global Investment Co., Ltd

7 1 87.5Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Tsun-Siou Lee, Independent Director

8 0 100Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Yophy Huang, Independent Director

8 0 100Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Day-Yang Liu, Independent Director

6 2 75Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Jung-Hui Liang, DirectorDelegate of Ministry of Finance

7 0 100Before the discharge date of June 29, 2009, total 7 meetings were held. (A)

Raymond C. H. Tu, DirectorDelegate of Ministry of Finance

5 0 100Before the discharge date of May 22, 2009, total 5 meetings were held. (A)

Su-Chen Hsieh, DirectorDelegate of Ministry of Finance

9 0 100Before the discharge date of Sep. 23, 2009, total 9 meetings were held. (A)

Te-Fu Lu, DirectorDelegate of Ministry of Finance

5 0 100Before the discharge date of May 22, 2009, total 5 meetings were held. (A)

Teng-Lung Hsieh, DirectorDelegate of Bank of Taiwan

5 0 100Before the discharge date of May 22, 2009, total 5 meetings were held. (A)

Li-Ling Jennifer Wang, DirectorDelegate of Bank of Taiwan

5 0 100Before the discharge date of May 22, 2009, total 5 meetings were held. (A)

Shiang-Chung Chen, DirectorDelegate of Mercuries Jeantex Ltd.

4 1 80Before the discharge date of May 22, 2009, total 5 meetings were held. (A)

Teng-Lung Hsieh, SupervisorDelegate of Bank of Taiwan

7 -- 87.5Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Kao-Chen Chuang, SupervisorDelegate of Bank of Taiwan

12 -- 92.31 Renominated on May 22, 2009.

Hsien-Yi Kung, SupervisorDelegate of Bank of Taiwan

5 -- 100Newly assigned on July 27, 2009, total 5 meetings were held. (A)

Li-Jen Lin, SupervisorDelegate of Bank of Taiwan

8 -- 100Newly assigned on May 22, 2009, total 8 meetings were held. (A)

Chun-Chung Lin, Supervisor 12 -- 92.31 Renominated on May 22, 2009.

Li-Jen Lin, SupervisorDelegate of Ministry of Finance

5 -- 100Newly assigned on May 22, 2009, total 5 meetings were held. (A)

Wang-Ching Chen, SupervisorDelegate of Ministry of Finance

5 -- 100Newly assigned on May 22, 2009, total 5 meetings were held. (A)

NameAttendancein Person (B)

Attendance by Proxy

Attendance Rate (%)(B/A)

Notes

20

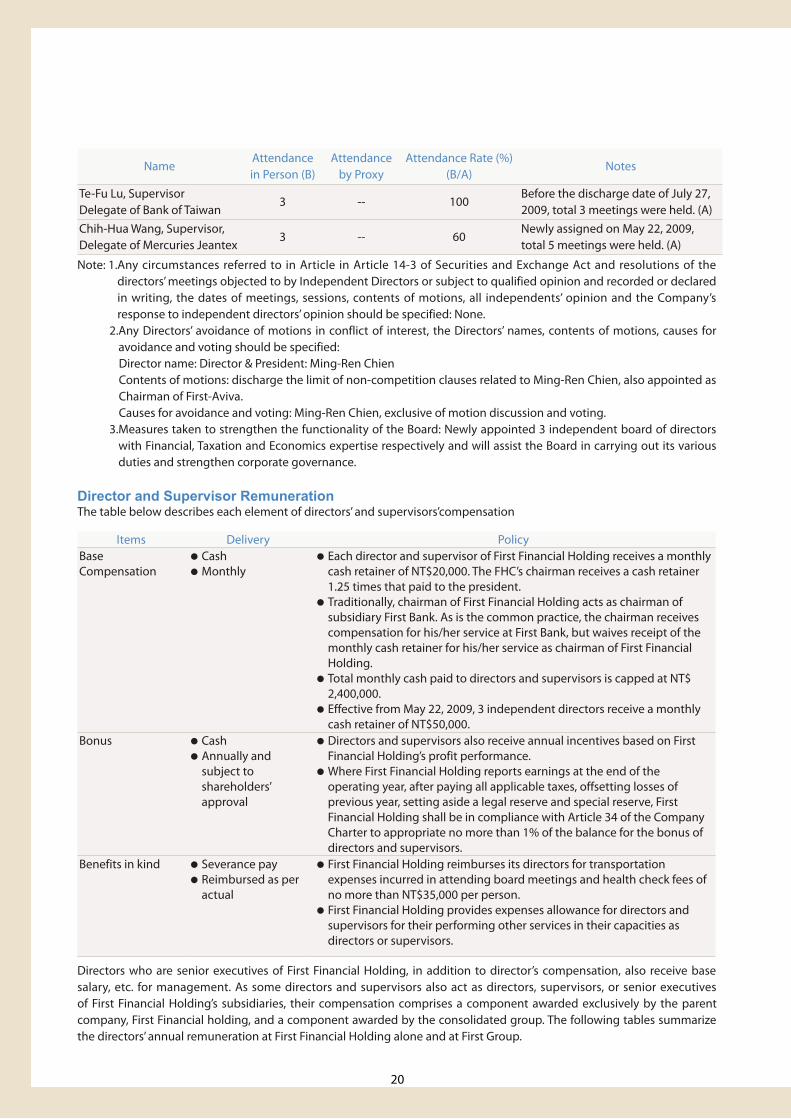

Director and Supervisor RemunerationThe table below describes each element of directors’ and supervisors’compensation

Items Delivery PolicyBase Compensation

● Cash ● Monthly

● Each director and supervisor of First Financial Holding receives a monthly cash retainer of NT$20,000. The FHC’s chairman receives a cash retainer 1.25 times that paid to the president.

● Traditionally, chairman of First Financial Holding acts as chairman of subsidiary First Bank. As is the common practice, the chairman receives compensation for his/her service at First Bank, but waives receipt of the monthly cash retainer for his/her service as chairman of First Financial Holding.

● Total monthly cash paid to directors and supervisors is capped at NT$ 2,400,000.

● Effective from May 22, 2009, 3 independent directors receive a monthly cash retainer of NT$50,000.

Bonus ● Cash ● Annually and

subject to shareholders’ approval

● Directors and supervisors also receive annual incentives based on First Financial Holding’s profit performance.

● Where First Financial Holding reports earnings at the end of the operating year, after paying all applicable taxes, offsetting losses of previous year, setting aside a legal reserve and special reserve, First Financial Holding shall be in compliance with Article 34 of the Company Charter to appropriate no more than 1% of the balance for the bonus of directors and supervisors.

Benefits in kind ● Severance pay ● Reimbursed as per

actual

● First Financial Holding reimburses its directors for transportation expenses incurred in attending board meetings and health check fees of no more than NT$35,000 per person.

● First Financial Holding provides expenses allowance for directors and supervisors for their performing other services in their capacities as directors or supervisors.

Directors who are senior executives of First Financial Holding, in addition to director’s compensation, also receive base salary, etc. for management. As some directors and supervisors also act as directors, supervisors, or senior executives of First Financial Holding’s subsidiaries, their compensation comprises a component awarded exclusively by the parent company, First Financial holding, and a component awarded by the consolidated group. The following tables summarize the directors’ annual remuneration at First Financial Holding alone and at First Group.

Te-Fu Lu, SupervisorDelegate of Bank of Taiwan

3 -- 100Before the discharge date of July 27, 2009, total 3 meetings were held. (A)

Chih-Hua Wang, Supervisor, Delegate of Mercuries Jeantex

3 -- 60Newly assigned on May 22, 2009, total 5 meetings were held. (A)

Note: 1. Any circumstances referred to in Article in Article 14-3 of Securities and Exchange Act and resolutions of the directors’ meetings objected to by Independent Directors or subject to qualified opinion and recorded or declared in writing, the dates of meetings, sessions, contents of motions, all independents’ opinion and the Company’s response to independent directors’ opinion should be specified: None.

2. Any Directors’ avoidance of motions in conflict of interest, the Directors’ names, contents of motions, causes for avoidance and voting should be specified: Director name: Director & President: Ming-Ren ChienContents of motions: discharge the limit of non-competition clauses related to Ming-Ren Chien, also appointed as Chairman of First-Aviva.Causes for avoidance and voting: Ming-Ren Chien, exclusive of motion discussion and voting.

3. Measures taken to strengthen the functionality of the Board: Newly appointed 3 independent board of directors with Financial, Taxation and Economics expertise respectively and will assist the Board in carrying out its various duties and strengthen corporate governance.

NameAttendancein Person (B)

Attendance by Proxy

Attendance Rate (%)(B/A)

Notes

21

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

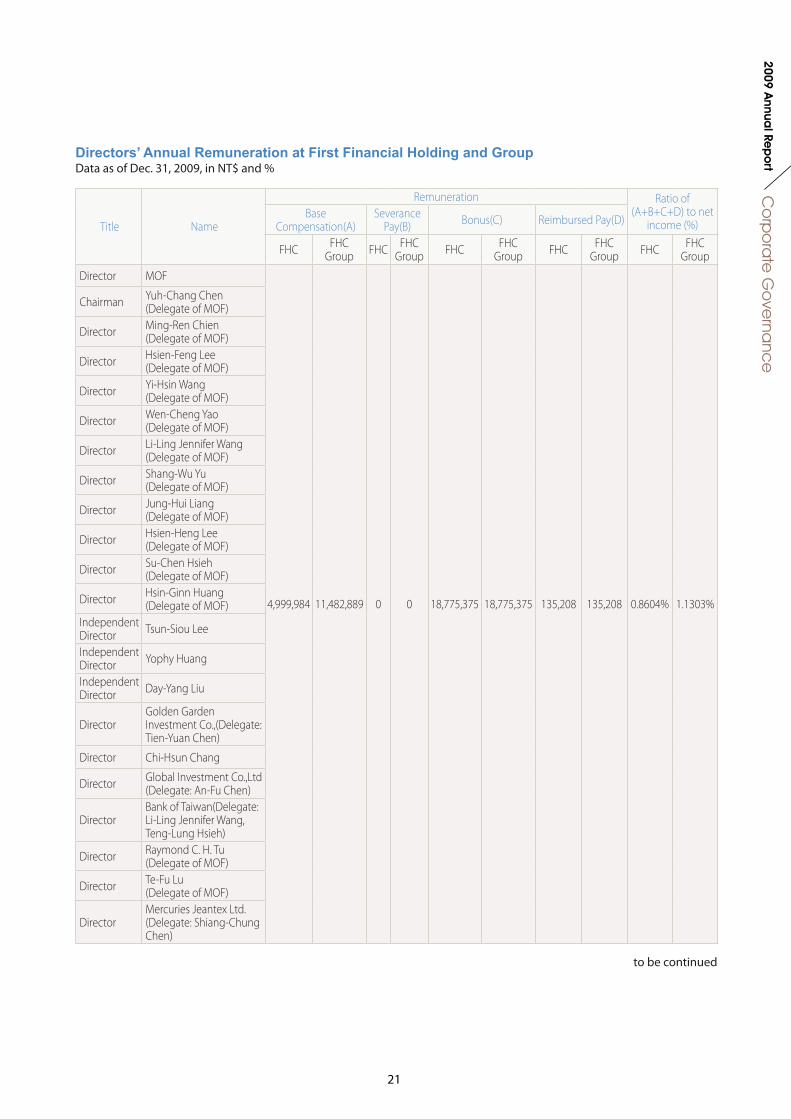

Title Name

Remuneration Ratio of (A+B+C+D) to net

income (%)Base

Compensation(A)Severance

Pay(B) Bonus(C) Reimbursed Pay(D)

FHC FHC Group FHC FHC

Group FHC FHC Group FHC FHC

Group FHC FHC Group

Director MOF

4,999,984 11,482,889 0 0 18,775,375 18,775,375 135,208 135,208 0.8604% 1.1303%

Chairman Yuh-Chang Chen(Delegate of MOF)

Director Ming-Ren Chien(Delegate of MOF)

Director Hsien-Feng Lee(Delegate of MOF)

Director Yi-Hsin Wang(Delegate of MOF)

Director Wen-Cheng Yao(Delegate of MOF)

Director Li-Ling Jennifer Wang(Delegate of MOF)

Director Shang-Wu Yu(Delegate of MOF)

Director Jung-Hui Liang (Delegate of MOF)

Director Hsien-Heng Lee(Delegate of MOF)

Director Su-Chen Hsieh(Delegate of MOF)

Director Hsin-Ginn Huang(Delegate of MOF)

IndependentDirector Tsun-Siou Lee

IndependentDirector Yophy Huang

IndependentDirector Day-Yang Liu

DirectorGolden Garden Investment Co.,(Delegate: Tien-Yuan Chen)

Director Chi-Hsun Chang

Director Global Investment Co.,Ltd (Delegate: An-Fu Chen)

DirectorBank of Taiwan(Delegate: Li-Ling Jennifer Wang, Teng-Lung Hsieh)

Director Raymond C. H. Tu(Delegate of MOF)

Director Te-Fu Lu(Delegate of MOF)

DirectorMercuries Jeantex Ltd. (Delegate: Shiang-Chung Chen)

Directors’ Annual Remuneration at First Financial Holding and GroupData as of Dec. 31, 2009, in NT$ and %

to be continued

22

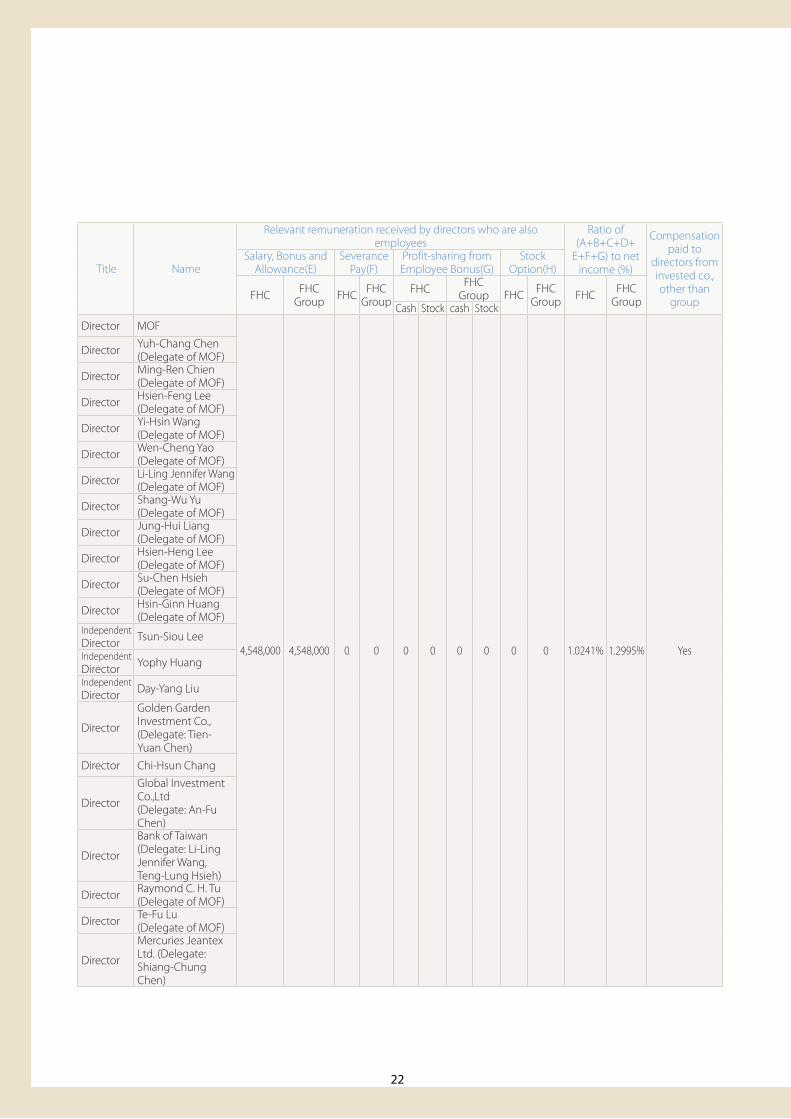

Title Name

Relevant remuneration received by directors who are also employees

Ratio of (A+B+C+D+

E+F+G) to net income (%)

Compensation paid to

directors from invested co., other than

group

Salary, Bonus and Allowance(E)

Severance Pay(F)

Profit-sharing from Employee Bonus(G)

Stock Option(H)

FHC FHC Group FHC FHC

GroupFHC FHC

Group FHC FHC Group FHC FHC

GroupCash Stock cash StockDirector MOF

4,548,000 4,548,000 0 0 0 0 0 0 0 0 1.0241% 1.2995% Yes

Director Yuh-Chang Chen(Delegate of MOF)

Director Ming-Ren Chien(Delegate of MOF)

Director Hsien-Feng Lee(Delegate of MOF)

Director Yi-Hsin Wang(Delegate of MOF)

Director Wen-Cheng Yao(Delegate of MOF)

Director Li-Ling Jennifer Wang(Delegate of MOF)

Director Shang-Wu Yu(Delegate of MOF)

Director Jung-Hui Liang (Delegate of MOF)

Director Hsien-Heng Lee(Delegate of MOF)

Director Su-Chen Hsieh(Delegate of MOF)

Director Hsin-Ginn Huang(Delegate of MOF)

IndependentDirector Tsun-Siou Lee

IndependentDirector Yophy Huang

IndependentDirector Day-Yang Liu

Director

Golden Garden Investment Co.,(Delegate: Tien-Yuan Chen)

Director Chi-Hsun Chang

Director

Global Investment Co.,Ltd (Delegate: An-Fu Chen)

Director

Bank of Taiwan(Delegate: Li-Ling Jennifer Wang, Teng-Lung Hsieh)

Director Raymond C. H. Tu(Delegate of MOF)

Director Te-Fu Lu(Delegate of MOF)

Director

Mercuries Jeantex Ltd. (Delegate: Shiang-Chung Chen)

23

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

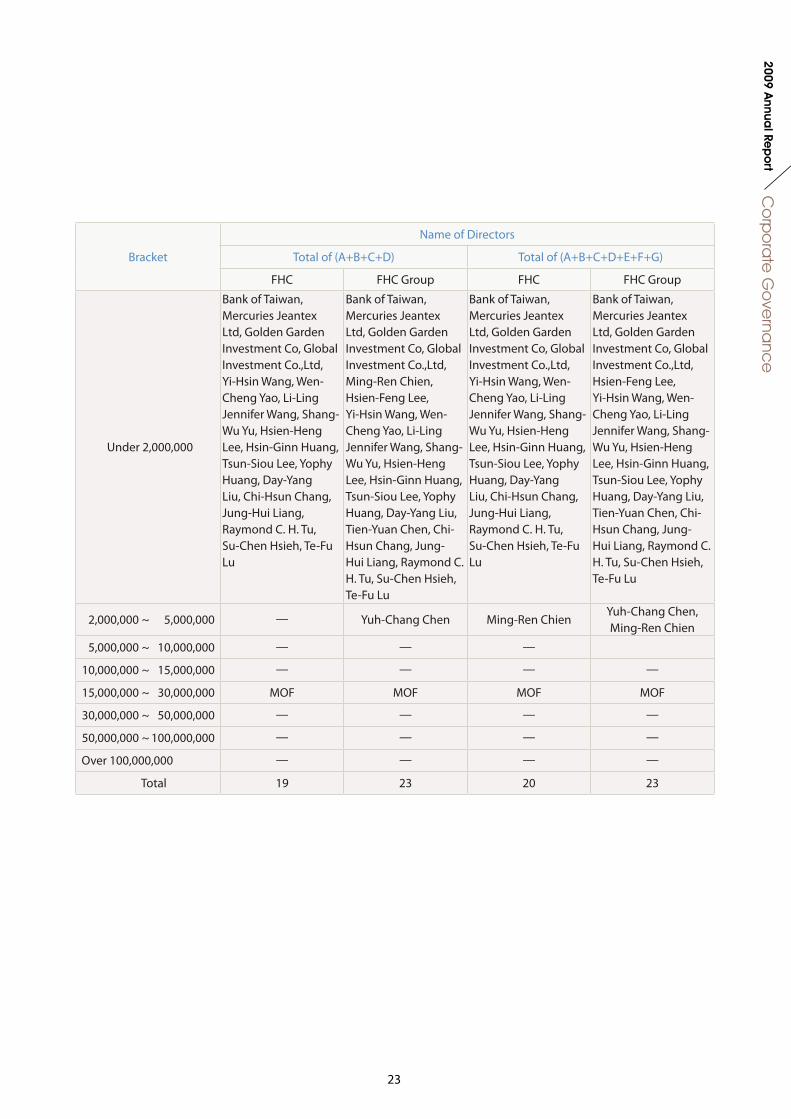

Bracket

Name of Directors

Total of (A+B+C+D) Total of (A+B+C+D+E+F+G)

FHC FHC Group FHC FHC Group

Under 2,000,000

Bank of Taiwan, Mercuries Jeantex Ltd, Golden Garden Investment Co, Global Investment Co.,Ltd, Yi-Hsin Wang, Wen-Cheng Yao, Li-Ling Jennifer Wang, Shang-Wu Yu, Hsien-Heng Lee, Hsin-Ginn Huang, Tsun-Siou Lee, Yophy Huang, Day-Yang Liu, Chi-Hsun Chang, Jung-Hui Liang, Raymond C. H. Tu, Su-Chen Hsieh, Te-Fu Lu

Bank of Taiwan, Mercuries Jeantex Ltd, Golden Garden Investment Co, Global Investment Co.,Ltd, Ming-Ren Chien, Hsien-Feng Lee, Yi-Hsin Wang, Wen-Cheng Yao, Li-Ling Jennifer Wang, Shang-Wu Yu, Hsien-Heng Lee, Hsin-Ginn Huang, Tsun-Siou Lee, Yophy Huang, Day-Yang Liu, Tien-Yuan Chen, Chi-Hsun Chang, Jung-Hui Liang, Raymond C. H. Tu, Su-Chen Hsieh, Te-Fu Lu

Bank of Taiwan, Mercuries Jeantex Ltd, Golden Garden Investment Co, Global Investment Co.,Ltd, Yi-Hsin Wang, Wen-Cheng Yao, Li-Ling Jennifer Wang, Shang-Wu Yu, Hsien-Heng Lee, Hsin-Ginn Huang, Tsun-Siou Lee, Yophy Huang, Day-Yang Liu, Chi-Hsun Chang, Jung-Hui Liang, Raymond C. H. Tu, Su-Chen Hsieh, Te-Fu Lu

Bank of Taiwan, Mercuries Jeantex Ltd, Golden Garden Investment Co, Global Investment Co.,Ltd, Hsien-Feng Lee, Yi-Hsin Wang, Wen-Cheng Yao, Li-Ling Jennifer Wang, Shang-Wu Yu, Hsien-Heng Lee, Hsin-Ginn Huang, Tsun-Siou Lee, Yophy Huang, Day-Yang Liu, Tien-Yuan Chen, Chi-Hsun Chang, Jung-Hui Liang, Raymond C. H. Tu, Su-Chen Hsieh, Te-Fu Lu

2,000,000 ~ 5,000,000 — Yuh-Chang Chen Ming-Ren ChienYuh-Chang Chen, Ming-Ren Chien

5,000,000 ~ 10,000,000 — — —

10,000,000 ~ 15,000,000 — — — —

15,000,000 ~ 30,000,000 MOF MOF MOF MOF

30,000,000 ~ 50,000,000 — — — —

50,000,000 ~ 100,000,000 — — — —

Over 100,000,000 — — — —

Total 19 23 20 23

24

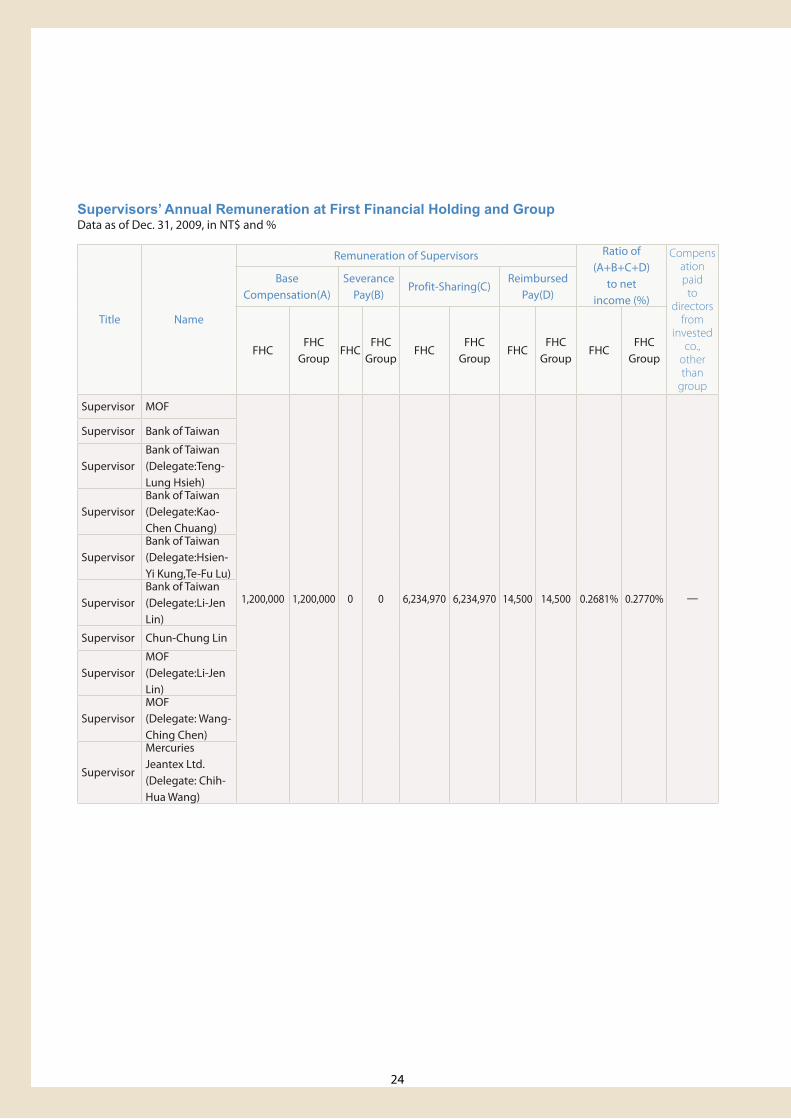

Supervisors’ Annual Remuneration at First Financial Holding and GroupData as of Dec. 31, 2009, in NT$ and %

Title Name

Remuneration of Supervisors Ratio of (A+B+C+D)

to net income (%)

Compensation paid

to directors

from invested

co., other than

group

Base Compensation(A)

Severance Pay(B)

Profit-Sharing(C)Reimbursed

Pay(D)

FHCFHC

GroupFHC

FHC Group

FHCFHC

GroupFHC

FHC Group

FHCFHC

Group

Supervisor MOF

1,200,000 1,200,000 0 0 6,234,970 6,234,970 14,500 14,500 0.2681% 0.2770% —

Supervisor Bank of Taiwan

SupervisorBank of Taiwan(Delegate:Teng-Lung Hsieh)

SupervisorBank of Taiwan(Delegate:Kao-Chen Chuang)

SupervisorBank of Taiwan(Delegate:Hsien-Yi Kung,Te-Fu Lu)

SupervisorBank of Taiwan(Delegate:Li-Jen Lin)

Supervisor Chun-Chung Lin

SupervisorMOF(Delegate:Li-Jen Lin)

SupervisorMOF(Delegate: Wang-Ching Chen)

Supervisor

Mercuries Jeantex Ltd.(Delegate: Chih-Hua Wang)

25

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

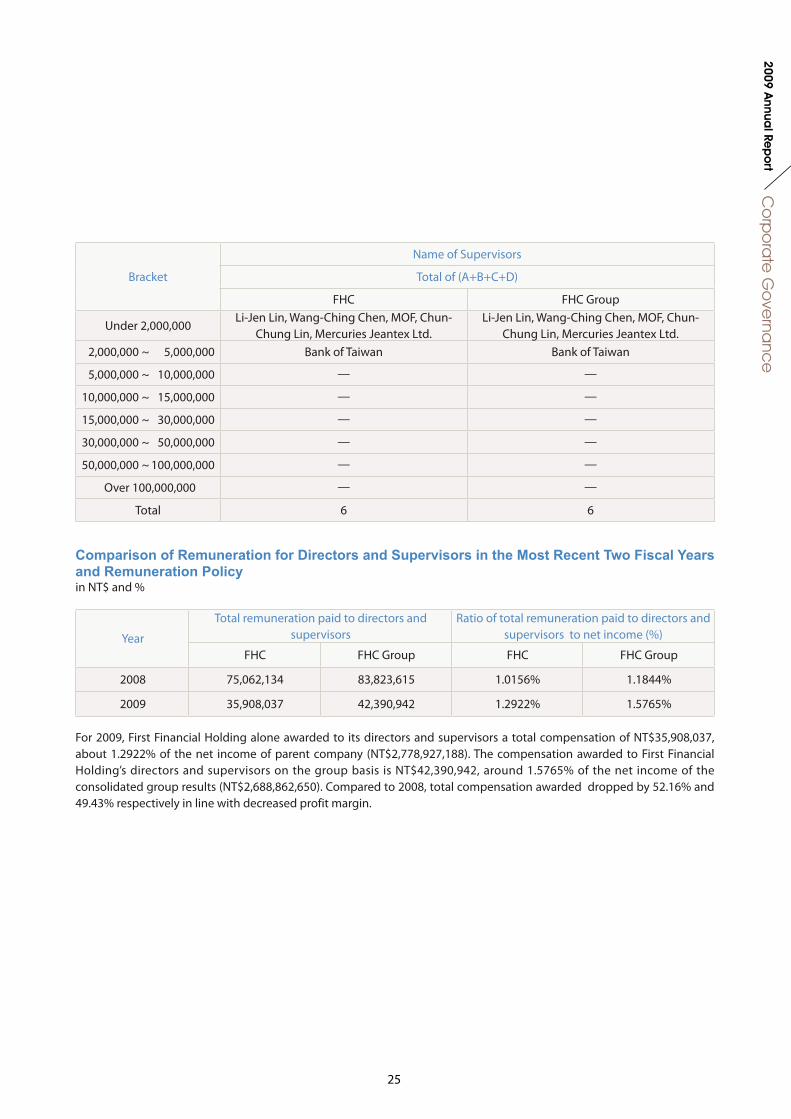

Bracket

Name of Supervisors

Total of (A+B+C+D)

FHC FHC Group

Under 2,000,000Li-Jen Lin, Wang-Ching Chen, MOF, Chun-

Chung Lin, Mercuries Jeantex Ltd.Li-Jen Lin, Wang-Ching Chen, MOF, Chun-

Chung Lin, Mercuries Jeantex Ltd. 2,000,000 ~ 5,000,000 Bank of Taiwan Bank of Taiwan

5,000,000 ~ 10,000,000 — —

10,000,000 ~ 15,000,000 — —

15,000,000 ~ 30,000,000 — —

30,000,000 ~ 50,000,000 — —

50,000,000 ~ 100,000,000 — —

Over 100,000,000 — —

Total 6 6

Year

Total remuneration paid to directors and supervisors

Ratio of total remuneration paid to directors and supervisors to net income (%)

FHC FHC Group FHC FHC Group

2008 75,062,134 83,823,615 1.0156% 1.1844%

2009 35,908,037 42,390,942 1.2922% 1.5765%

Comparison of Remuneration for Directors and Supervisors in the Most Recent Two Fiscal Years and Remuneration Policyin NT$ and %

For 2009, First Financial Holding alone awarded to its directors and supervisors a total compensation of NT$35,908,037, about 1.2922% of the net income of parent company (NT$2,778,927,188). The compensation awarded to First Financial Holding’s directors and supervisors on the group basis is NT$42,390,942, around 1.5765% of the net income of the consolidated group results (NT$2,688,862,650). Compared to 2008, total compensation awarded dropped by 52.16% and 49.43% respectively in line with decreased profit margin.

26

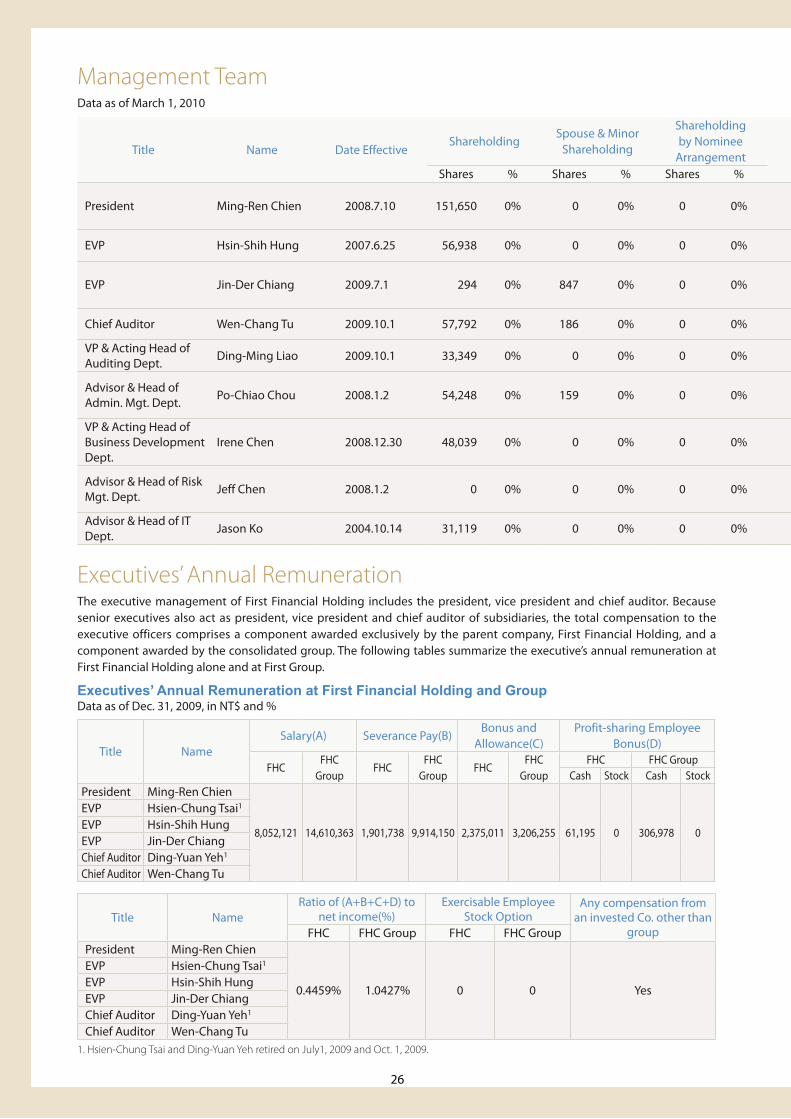

Title Name Date EffectiveShareholding

Spouse & Minor Shareholding

Shareholding by Nominee

Arrangement Education & Experience Other Position

Managers who are spouses or within 2 degrees of kinship

Shares % Shares % Shares % Title Name Relation

President Ming-Ren Chien 2008.7.10 151,650 0% 0 0% 0 0%M.S. International finance, National Taipei University; President, FCB Leasing Co.; EVP, FCB; Chairman & President, First Financial Asset Mgt. Co., Ltd.

Managing Director, FCB; Chairman, First Aviva Life Insurance Co., Ltd; Director, TWN Asset Mgt. Corp.

- - -

EVP Hsin-Shih Hung 2007.6.25 56,938 0% 0 0% 0 0%B.S., International Trade, National Taiwan University; EVP, Financial Markets BU of FCB; Director, FS Inc.

Chairman, FSITC Co., Ltd. - - -

EVP Jin-Der Chiang 2009.7.1 294 0% 847 0% 0 0%M.S., Banking and Finance, Tam Kang University; Head of IT Center of FCB; Director of FSITC.

EVP, FCB; Chairman, First Venture Capital and First Financial Mgt. Consulting Co.; Supervisor, FS Inc; Director, TWN Financial Asset Service Corp.

- - -

Chief Auditor Wen-Chang Tu 2009.10.1 57,792 0% 186 0% 0 0%LL.B., Soochow University; Chief Auditor of FCB; AVP & Manager, Credit Approval Division of FCB.

Supervisor, FS Inc., First Venture Capital and First Financial Mgt. Consulting Co.

- - -

VP & Acting Head of Auditing Dept.

Ding-Ming Liao 2009.10.1 33,349 0% 0 0% 0 0%B.S., Economics, Soochow University; Head of Taichung Regional Center of FCB.

Head of Auditing Dept, FCB. - - -

Advisor & Head of Admin. Mgt. Dept.

Po-Chiao Chou 2008.1.2 54,248 0% 159 0% 0 0%B.S., Accounting, National Cheng Kung University; SAVP & Manager, General Affair Division of FCB.

EVP, General Admin. Center of FCB; Supervisor, FSITC Co. and Tang Eng Iron Works; Director, TWN Asset Mgt. Corp.

- - -

VP & Acting Head of Business Development Dept.

Irene Chen 2008.12.30 48,039 0% 0 0% 0 0%B.A., National Taiwan University; Senior Manager, Marketing Integration Unit, Business Development Dept. and Admin. & Planning Dept.

Director of FSITC Co. - - -

Advisor & Head of Risk Mgt. Dept.

Jeff Chen 2008.1.2 0 0% 0 0% 0 0%B.S., International trade, Feng Chia College of Engineering and Business; SVP, Credit Approval Division and Credit Analysis Division of FCB

EVP, Risk Mgt. Center of FCB. - - -

Advisor & Head of IT Dept.

Jason Ko 2004.10.14 31,119 0% 0 0% 0 0%M.S., Computer Science, George Washington University; SVP, IT Division of FCB

EVP, IT Center of FCB. - - -

Management TeamData as of March 1, 2010

Title NameRatio of (A+B+C+D) to

net income(%)Exercisable Employee

Stock OptionAny compensation from

an invested Co. other than groupFHC FHC Group FHC FHC Group

President Ming-Ren Chien

0.4459% 1.0427% 0 0 Yes

EVP Hsien-Chung Tsai1

EVP Hsin-Shih HungEVP Jin-Der ChiangChief Auditor Ding-Yuan Yeh1

Chief Auditor Wen-Chang Tu1. Hsien-Chung Tsai and Ding-Yuan Yeh retired on July1, 2009 and Oct. 1, 2009.

Executives’ Annual RemunerationThe executive management of First Financial Holding includes the president, vice president and chief auditor. Because senior executives also act as president, vice president and chief auditor of subsidiaries, the total compensation to the executive officers comprises a component awarded exclusively by the parent company, First Financial Holding, and a component awarded by the consolidated group. The following tables summarize the executive’s annual remuneration at First Financial Holding alone and at First Group.

Executives’ Annual Remuneration at First Financial Holding and GroupData as of Dec. 31, 2009, in NT$ and %

Title NameSalary(A) Severance Pay(B)

Bonus and Allowance(C)

Profit-sharing Employee Bonus(D)

FHCFHC

GroupFHC

FHC Group

FHCFHC

GroupFHC FHC Group

Cash Stock Cash StockPresident Ming-Ren Chien

8,052,121 14,610,363 1,901,738 9,914,150 2,375,011 3,206,255 61,195 0 306,978 0

EVP Hsien-Chung Tsai1

EVP Hsin-Shih HungEVP Jin-Der ChiangChief Auditor Ding-Yuan Yeh1

Chief Auditor Wen-Chang Tu

27

Co

rpo

rate

Go

verna

nce

2009 Annua

l Rep

ort

Title Name Date EffectiveShareholding

Spouse & Minor Shareholding

Shareholding by Nominee

Arrangement Education & Experience Other Position

Managers who are spouses or within 2 degrees of kinship

Shares % Shares % Shares % Title Name Relation

President Ming-Ren Chien 2008.7.10 151,650 0% 0 0% 0 0%M.S. International finance, National Taipei University; President, FCB Leasing Co.; EVP, FCB; Chairman & President, First Financial Asset Mgt. Co., Ltd.

Managing Director, FCB; Chairman, First Aviva Life Insurance Co., Ltd; Director, TWN Asset Mgt. Corp.

- - -

EVP Hsin-Shih Hung 2007.6.25 56,938 0% 0 0% 0 0%B.S., International Trade, National Taiwan University; EVP, Financial Markets BU of FCB; Director, FS Inc.

Chairman, FSITC Co., Ltd. - - -

EVP Jin-Der Chiang 2009.7.1 294 0% 847 0% 0 0%M.S., Banking and Finance, Tam Kang University; Head of IT Center of FCB; Director of FSITC.

EVP, FCB; Chairman, First Venture Capital and First Financial Mgt. Consulting Co.; Supervisor, FS Inc; Director, TWN Financial Asset Service Corp.

- - -

Chief Auditor Wen-Chang Tu 2009.10.1 57,792 0% 186 0% 0 0%LL.B., Soochow University; Chief Auditor of FCB; AVP & Manager, Credit Approval Division of FCB.

Supervisor, FS Inc., First Venture Capital and First Financial Mgt. Consulting Co.

- - -

VP & Acting Head of Auditing Dept.

Ding-Ming Liao 2009.10.1 33,349 0% 0 0% 0 0%B.S., Economics, Soochow University; Head of Taichung Regional Center of FCB.

Head of Auditing Dept, FCB. - - -

Advisor & Head of Admin. Mgt. Dept.

Po-Chiao Chou 2008.1.2 54,248 0% 159 0% 0 0%B.S., Accounting, National Cheng Kung University; SAVP & Manager, General Affair Division of FCB.

EVP, General Admin. Center of FCB; Supervisor, FSITC Co. and Tang Eng Iron Works; Director, TWN Asset Mgt. Corp.

- - -

VP & Acting Head of Business Development Dept.

Irene Chen 2008.12.30 48,039 0% 0 0% 0 0%B.A., National Taiwan University; Senior Manager, Marketing Integration Unit, Business Development Dept. and Admin. & Planning Dept.

Director of FSITC Co. - - -

Advisor & Head of Risk Mgt. Dept.

Jeff Chen 2008.1.2 0 0% 0 0% 0 0%B.S., International trade, Feng Chia College of Engineering and Business; SVP, Credit Approval Division and Credit Analysis Division of FCB

EVP, Risk Mgt. Center of FCB. - - -

Advisor & Head of IT Dept.

Jason Ko 2004.10.14 31,119 0% 0 0% 0 0%M.S., Computer Science, George Washington University; SVP, IT Division of FCB

EVP, IT Center of FCB. - - -

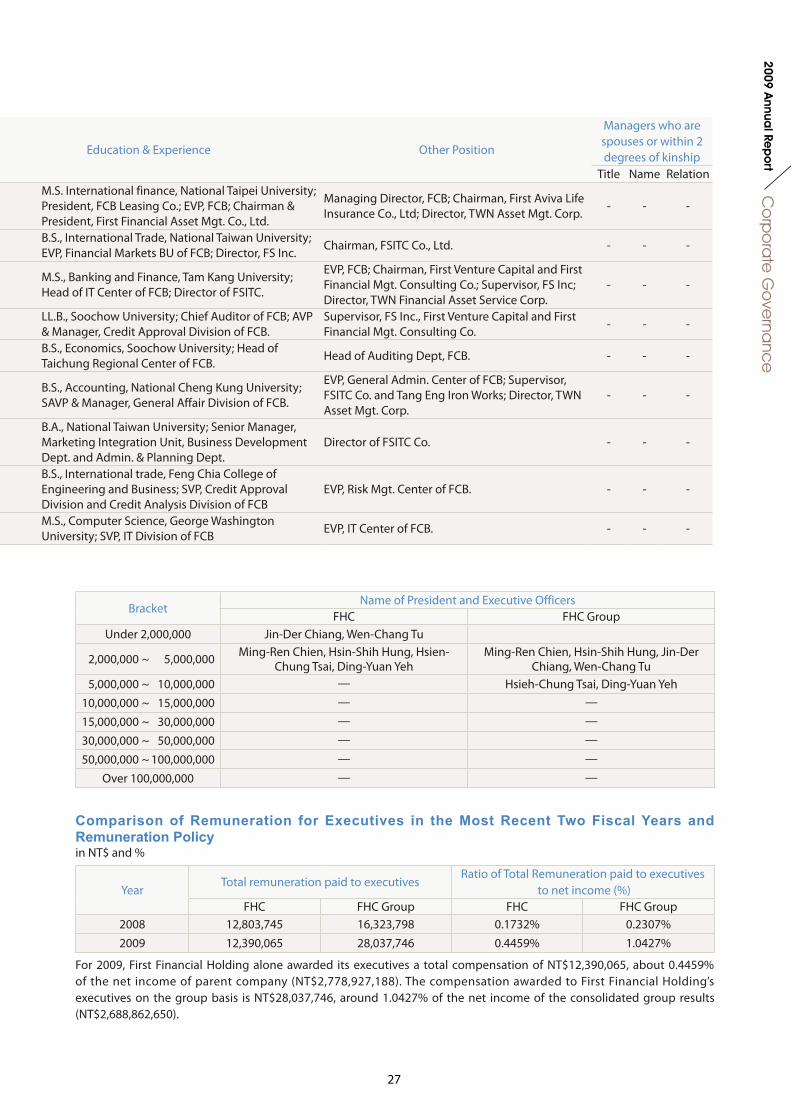

BracketName of President and Executive Officers

FHC FHC GroupUnder 2,000,000 Jin-Der Chiang, Wen-Chang Tu

2,000,000 ~ 5,000,000 Ming-Ren Chien, Hsin-Shih Hung, Hsien-Chung Tsai, Ding-Yuan Yeh

Ming-Ren Chien, Hsin-Shih Hung, Jin-Der Chiang, Wen-Chang Tu

5,000,000 ~ 10,000,000 — Hsieh-Chung Tsai, Ding-Yuan Yeh 10,000,000 ~ 15,000,000 — — 15,000,000 ~ 30,000,000 — — 30,000,000 ~ 50,000,000 — — 50,000,000 ~ 100,000,000 — —

Over 100,000,000 — —

Comparison of Remuneration for Executives in the Most Recent Two Fiscal Years and Remuneration Policyin NT$ and %

YearTotal remuneration paid to executives

Ratio of Total Remuneration paid to executives to net income (%)

FHC FHC Group FHC FHC Group2008 12,803,745 16,323,798 0.1732% 0.2307%2009 12,390,065 28,037,746 0.4459% 1.0427%

For 2009, First Financial Holding alone awarded its executives a total compensation of NT$12,390,065, about 0.4459% of the net income of parent company (NT$2,778,927,188). The compensation awarded to First Financial Holding’s executives on the group basis is NT$28,037,746, around 1.0427% of the net income of the consolidated group results (NT$2,688,862,650).

28

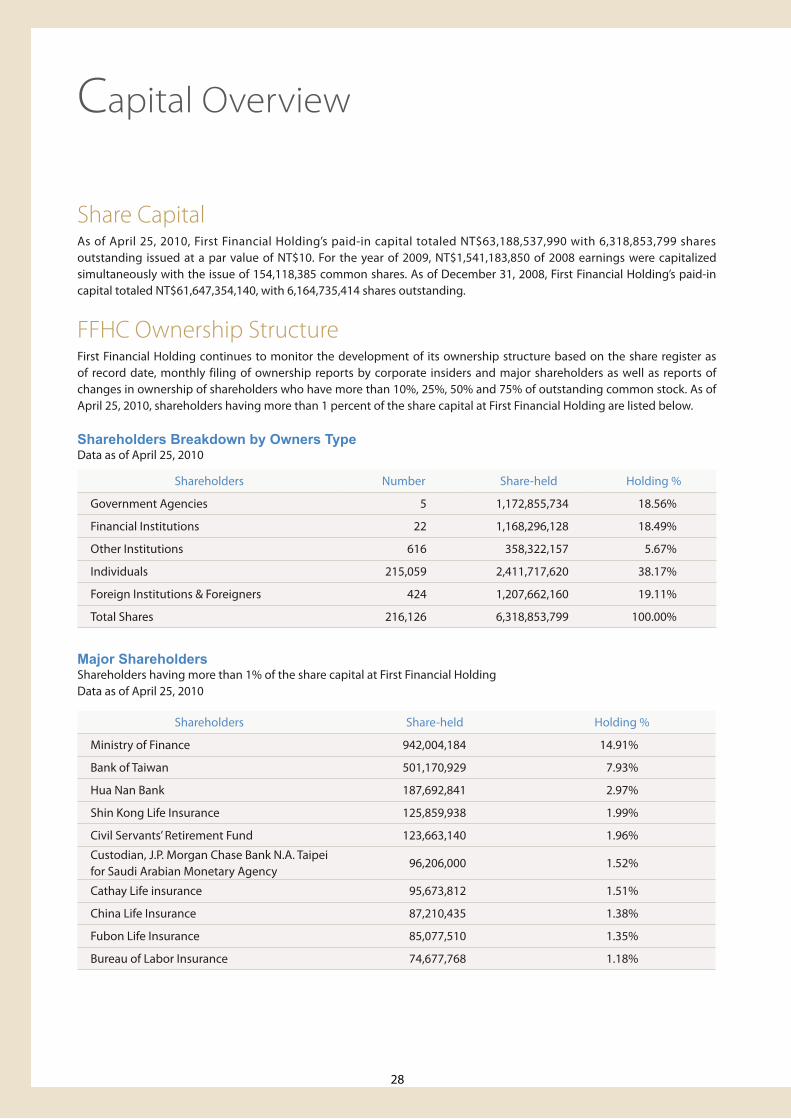

Shareholders Share-held Holding %

Ministry of Finance 942,004,184 14.91%

Bank of Taiwan 501,170,929 7.93%

Hua Nan Bank 187,692,841 2.97%

Shin Kong Life Insurance 125,859,938 1.99%

Civil Servants’ Retirement Fund 123,663,140 1.96%

Custodian, J.P. Morgan Chase Bank N.A. Taipei for Saudi Arabian Monetary Agency

96,206,000 1.52%

Cathay Life insurance 95,673,812 1.51%

China Life Insurance 87,210,435 1.38%

Fubon Life Insurance 85,077,510 1.35%

Bureau of Labor Insurance 74,677,768 1.18%

Share CapitalAs of April 25, 2010, First Financial Holding’s paid-in capital totaled NT$63,188,537,990 with 6,318,853,799 shares outstanding issued at a par value of NT$10. For the year of 2009, NT$1,541,183,850 of 2008 earnings were capitalized simultaneously with the issue of 154,118,385 common shares. As of December 31, 2008, First Financial Holding’s paid-in capital totaled NT$61,647,354,140, with 6,164,735,414 shares outstanding.

FFHC Ownership StructureFirst Financial Holding continues to monitor the development of its ownership structure based on the share register as of record date, monthly filing of ownership reports by corporate insiders and major shareholders as well as reports of changes in ownership of shareholders who have more than 10%, 25%, 50% and 75% of outstanding common stock. As of April 25, 2010, shareholders having more than 1 percent of the share capital at First Financial Holding are listed below.

Shareholders Breakdown by Owners TypeData as of April 25, 2010

Capital Overview

Shareholders Number Share-held Holding %

Government Agencies 5 1,172,855,734 18.56%

Financial Institutions 22 1,168,296,128 18.49%

Other Institutions 616 358,322,157 5.67%

Individuals 215,059 2,411,717,620 38.17%

Foreign Institutions & Foreigners 424 1,207,662,160 19.11%

Total Shares 216,126 6,318,853,799 100.00%

Major ShareholdersShareholders having more than 1% of the share capital at First Financial HoldingData as of April 25, 2010

29

Ca

pita

l Ove

rview

2009 Annua

l Rep

ort

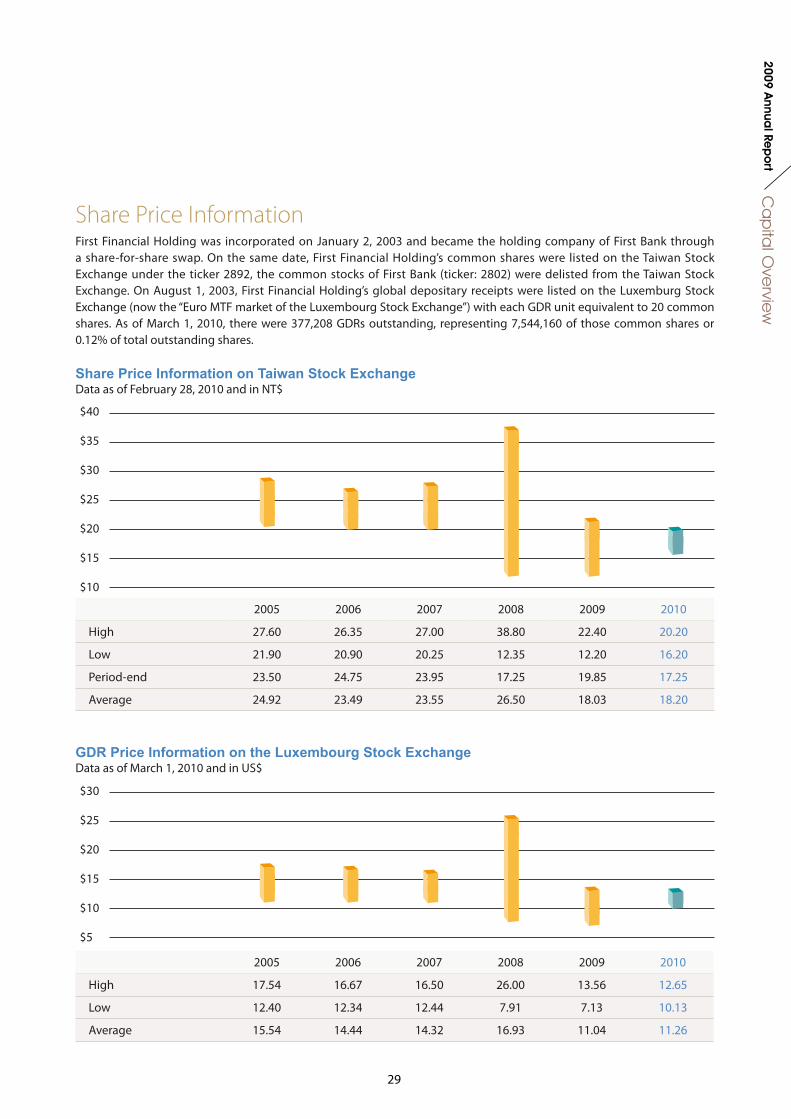

2005 2006 2007 2008 2009 2010

High 27.60 26.35 27.00 38.80 22.40 20.20

Low 21.90 20.90 20.25 12.35 12.20 16.20

Period-end 23.50 24.75 23.95 17.25 19.85 17.25

Average 24.92 23.49 23.55 26.50 18.03 18.20

2005 2006 2007 2008 2009 2010

High 17.54 16.67 16.50 26.00 13.56 12.65

Low 12.40 12.34 12.44 7.91 7.13 10.13

Average 15.54 14.44 14.32 16.93 11.04 11.26

Share Price InformationFirst Financial Holding was incorporated on January 2, 2003 and became the holding company of First Bank through a share-for-share swap. On the same date, First Financial Holding’s common shares were listed on the Taiwan Stock Exchange under the ticker 2892, the common stocks of First Bank (ticker: 2802) were delisted from the Taiwan Stock Exchange. On August 1, 2003, First Financial Holding’s global depositary receipts were listed on the Luxemburg Stock Exchange (now the “Euro MTF market of the Luxembourg Stock Exchange”) with each GDR unit equivalent to 20 common shares. As of March 1, 2010, there were 377,208 GDRs outstanding, representing 7,544,160 of those common shares or 0.12% of total outstanding shares.

Share Price Information on Taiwan Stock ExchangeData as of February 28, 2010 and in NT$

GDR Price Information on the Luxembourg Stock ExchangeData as of March 1, 2010 and in US$

$40

$35

$30

$25

$20

$15

$10

$30

$25

$20

$15

$10

$5

30

Dividend First Financial Holding’s board of directors has the right to propose an annual dividend, which becomes effective after

being approved by the shareholders’ meeting. The dividend scheme takes into account the operating and investment

requirements of the company, the profit performance of the current year, cost of capital, taxation, the overall financial

industry development and the movement of the money market, and shareholders’ interests.

To finance new capital investments, enhance earnings capacity and comply with local regulations, First Financial Holding

uses the residual dividend policy. If First Financial Holding reports a net income at the end of the operating year, the

net income shall be used to pay relevant taxes, offset cumulative losses of previous years (if any), and set aside a legal

reserve and special capital reserve as required by local regulations. After the distribution of the aforementioned items, the

balance shall be appropriated as follows:

(1) 0.02%~0.16% for bonuses to employees;

(2) no more than 1% for compensation for directors and supervisors;

The remainder after deducting employee bonuses and directors’ compensation, plus cumulative undistributed earnings

of the previous year, make up the total amount available for the distribution of shareholder dividends. The board has the

discretion to propose shareholder dividends equivalent to 30%-100% of that available amount, pending the approval of

shareholders’ meeting. Subjects eligible to participate in the employee stock bonus plan may include employees of First

Financial Holding’s affiliated companies, with the stock bonus plan set forth by the board.

According to First Financial Holding’s operating scheme, the amount of cash dividend must exceed 10% of the total

amount available for the distribution of shareholder dividends. A cash dividend of less than NT$0.1 per share need not be

distributed unless otherwise provided for in the resolution of the shareholder’s meeting.

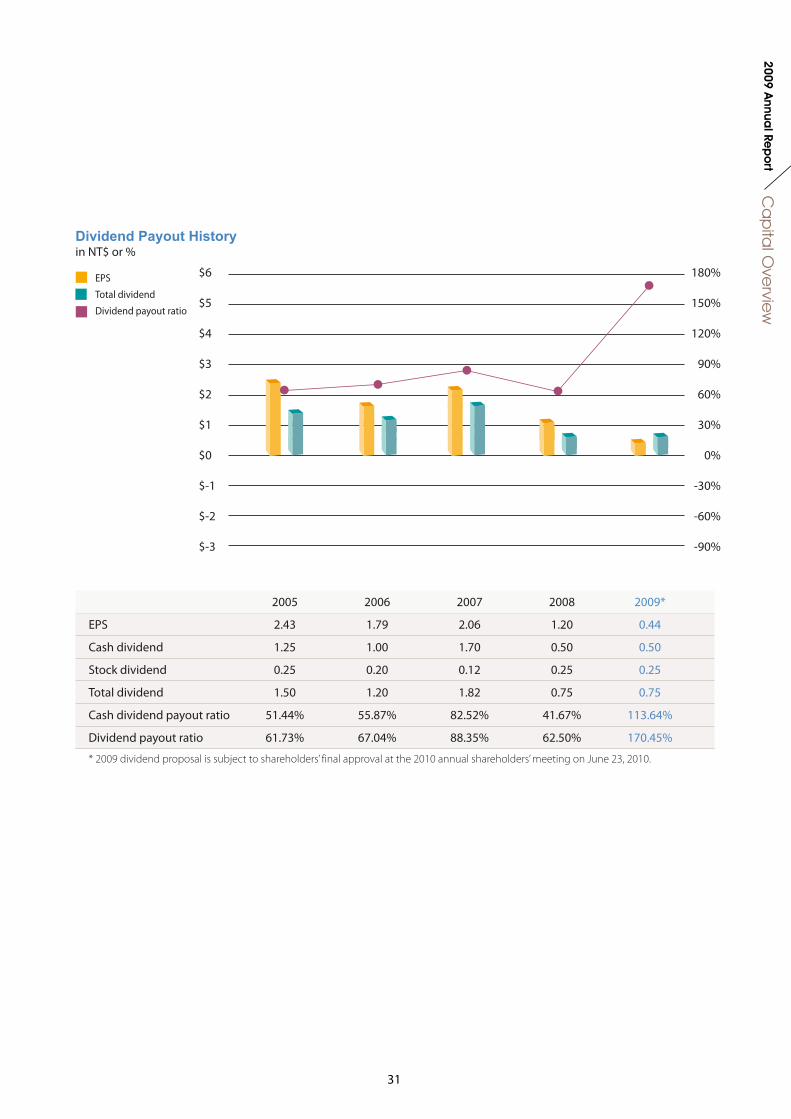

For the fiscal year 2007 and 2008, First Financial Holding’s dividend payout ratio was 88.35% and 62.50%, respectively.

Retroactively adjusted for cash dividend payout ratio would be 82.52% and 41.67%.

31

Ca

pita

l Ove

rview

2009 Annua

l Rep

ort

Dividend Payout Historyin NT$ or %

2005 2006 2007 2008 2009*

EPS 2.43 1.79 2.06 1.20 0.44

Cash dividend 1.25 1.00 1.70 0.50 0.50

Stock dividend 0.25 0.20 0.12 0.25 0.25

Total dividend 1.50 1.20 1.82 0.75 0.75

Cash dividend payout ratio 51.44% 55.87% 82.52% 41.67% 113.64%

Dividend payout ratio 61.73% 67.04% 88.35% 62.50% 170.45%

* 2009 dividend proposal is subject to shareholders’ final approval at the 2010 annual shareholders’ meeting on June 23, 2010.

$6

$5

$4

$3

$2

$1

$0

$-1

$-2

$-3

180%

150%

120%

90%

60%

30%

0%

-30%

-60%

-90%

EPS

Total dividend

Dividend payout ratio

32

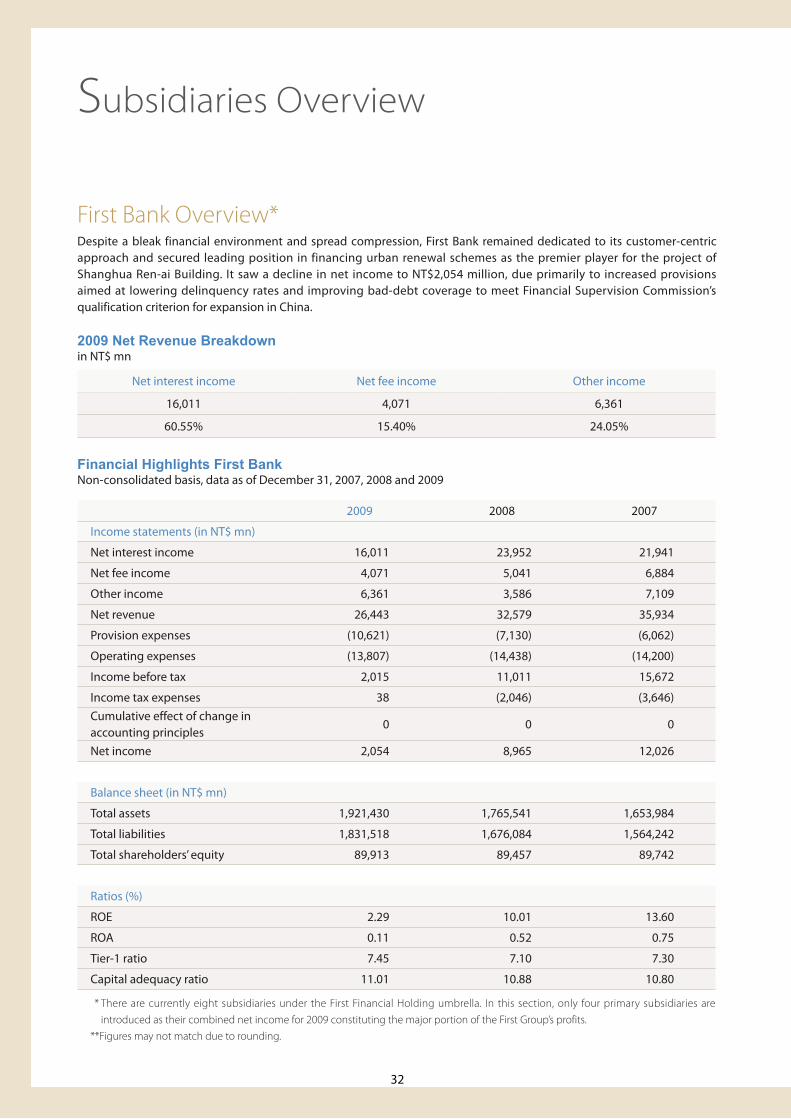

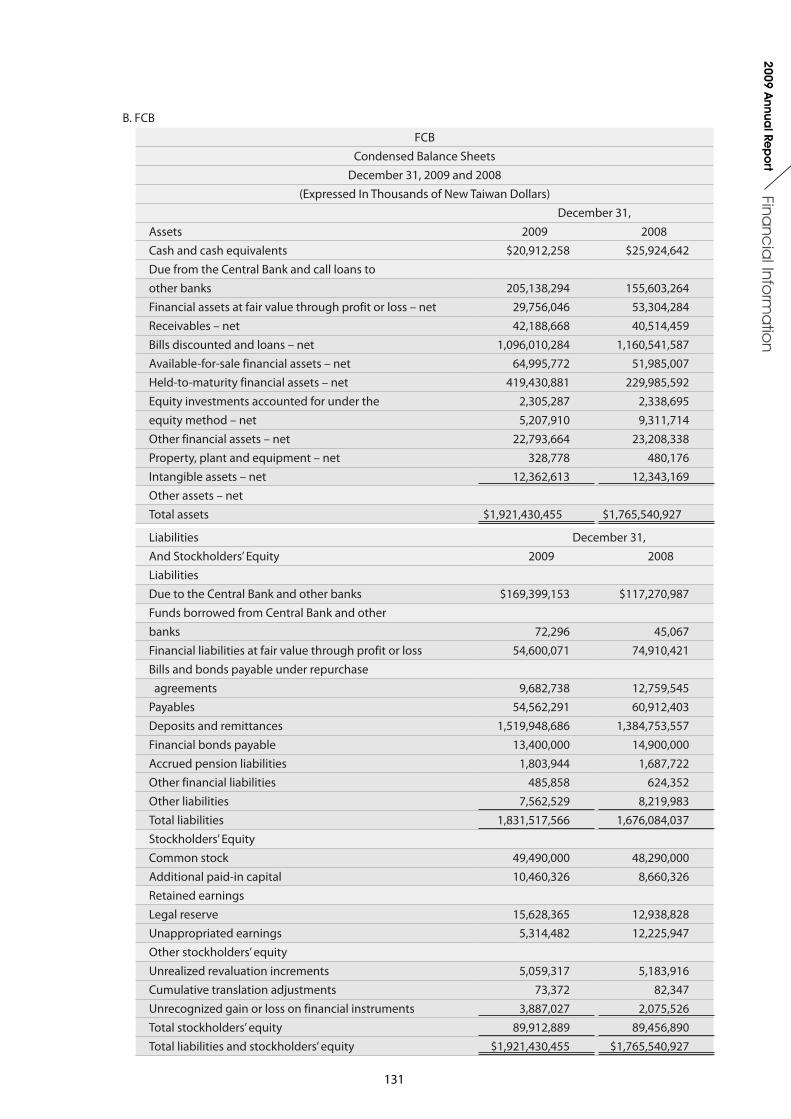

First Bank Overview*Despite a bleak financial environment and spread compression, First Bank remained dedicated to its customer-centric approach and secured leading position in financing urban renewal schemes as the premier player for the project of Shanghua Ren-ai Building. It saw a decline in net income to NT$2,054 million, due primarily to increased provisions aimed at lowering delinquency rates and improving bad-debt coverage to meet Financial Supervision Commission’s qualification criterion for expansion in China.

2009 Net Revenue Breakdownin NT$ mn

Subsidiaries Overview

Net interest income Net fee income Other income

16,011 4,071 6,361

60.55% 15.40% 24.05%

Financial Highlights First BankNon-consolidated basis, data as of December 31, 2007, 2008 and 2009

2009 2008 2007

Income statements (in NT$ mn)

Net interest income 16,011 23,952 21,941

Net fee income 4,071 5,041 6,884

Other income 6,361 3,586 7,109

Net revenue 26,443 32,579 35,934

Provision expenses (10,621) (7,130) (6,062)

Operating expenses (13,807) (14,438) (14,200)

Income before tax 2,015 11,011 15,672

Income tax expenses 38 (2,046) (3,646)Cumulative effect of change in accounting principles

0 0 0

Net income 2,054 8,965 12,026

Balance sheet (in NT$ mn)

Total assets 1,921,430 1,765,541 1,653,984

Total liabilities 1,831,518 1,676,084 1,564,242

Total shareholders’ equity 89,913 89,457 89,742

Ratios (%)

ROE 2.29 10.01 13.60

ROA 0.11 0.52 0.75

Tier-1 ratio 7.45 7.10 7.30

Capital adequacy ratio 11.01 10.88 10.80

* There are currently eight subsidiaries under the First Financial Holding umbrella. In this section, only four primary subsidiaries are introduced as their combined net income for 2009 constituting the major portion of the First Group’s profits.