publication.pdf - al mazaya holding company

TRANSCRIPT

His Highness SheikhSabah Al-Ahmad Al-Jaber Al-Sabah

Amir of the State of Kuwait

His Highness SheikhNawaf Al-Ahmad Al-Jaber Al-Sabah

The Crown Prince of the State of Kuwait

His Highness SheikhJaber Mubarak Al-Hamad Al-Sabah

Prime Minister

020406070810121212131416172022252628303335

Message From the ChairmanMessage From the Group CEOVisionMissionBoard of DirectorsExecutive Management Company EstablishmentCapital StructureMajor Shareholders StructureListingOperations / ServicesAl Mazaya HeadquartersSubsidiaries & AssociatesKuwait ProjectsUAE ProjectsRegional ProjectsNew Project - DubaiNew Project - BahrainNew Market - TurkeyFinancial Report 2013Independent Auditors’ Report

CONTENT

01

Mr. Rashid Al NafisiChairman

Dear shareholders,

We are delighted to have this opportunity to meet you here at the beginning of this new year, which carries with it news of optimism and hope, and indicators of the company’s vitality and work, assuring you once again that we have fulfilled the promise we made one year ago: which was that Al Mazaya Holding Company would continue its steady and strong movement throughout 2013, measured by internal external milestones and indicators.

MESSAGEfrom the Chairman

02

03

Today, Al Mazaya has announced its results for the fiscal year up to December 31, 2013, which have been highlighted by a 2000% increase in profits year-on-year, up to KD 6 million.

At the end of the fiscal year just passed, the total assets of the company were KD 228 million, compared to KD 221 million in 2012, while the total shareholders’ equity at was KD 91 million, compared to 83.3 million a year earlier - an increase of 9.2%. Additionally, the total short-term obligations of the company have fallen by 13.55%.

Because of this, we must offer our heartfelt thanks to both the Board of Directors and the excellent executive management, as well as the highly experienced engineering, technical and professional workers, and all the employees of Al Mazaya Company for their strong support of the company, a support without which these results could not have been achieved, and has allowed Al Mazaya Holding to remain among the most influential companies in the Gulf and Arab region.

Shareholders of Al Mazaya: You know very well that our path has not always been easy in recent years, characterized by many political, economic and funding changes, and yet the vision of the Board of Directors, as well as the flexible, dynamic and adaptive strategies that have been put in place, has enabled the company to overcome many of the challenges experienced. The company has succeeded in transforming its focus into income-generating assets, especially those assets formerly under development, which is an achievement to the great credit of the current board of directors and the executive management team.

All of this has come as the positive consequence of a number of corrective actions that we have followed, on top of which has been the restructuring of the company, and reordering it from inside in cooperation with competent institutions, as well as the establishment of a new regulation of internal systems and procedures that best serve the management, staff and workers, and support the company›s activity - internally and externally.

Finally, I would like to assure you that your company today has become more influential and stronger than ever before. I therefore take the liberty here of congratulating you on behalf of your company, and congratulating your company on behalf of you.

Thank you.

Mr. Rashid Al Nafisi Chairman

Eng. Ibrahim Al SoqabiGroup CEO

Esteemed Shareholders,Peace Be Upon You,

I am honored, after having become a member of the Al Mazaya Holding Company family, to welcome you here today, and to offer my heartfelt congratulations on the remarkable success achieved by everyone in this great company at the beginning of a new era of further development and progress.

I am delighted to be able to outline the strong position that Al Mazaya Holding Company is in; a position in the real estate development sector which could never be achieved other than with reliance on strategic planning, trust, well determination, and integrity. This can be seen in Al Mazaya’s progression from conception to implementation to growth, and while we can be allowed a moment of pride to recognize what we’ve done, we must therefore continue to innovate, grow, and expand.

MESSAGEfrom the Group CEO

04

05

Shareholders of Al Mazaya: I wish to take this opportunity to confirm that Al Mazaya has been able to maintain its strong operational performance, and its prestigious position in the market within the framework of an ambitious (but realistic) plan and long term strategic objectives. Short-termism can be a curse, and it is one we have avoided by keeping sight at all times of out long term goals.

2013 witnessed a whole series of achievements and successes of which we can rightly be proud. Despite global financial circumstances since 2008, Al Mazaya has managed to remain strong and solid through the continuous implementation of its projects, which have become more resilient and recognized, with increased revenues through the completion of new projects and income-generating assets.

Shareholders: Your company has succeeded during 2013 by entrenching itself in the market through a number of active steps, including the restructuring of all financial obligations, which has provided the liquidity necessary for operational projects and support for the timely delivery of existing projects, including the Villa Residential Project and «Liwan» Project” in Dubai.

Moreover,The company has also been able to close a large number of successful transactions, which have contributed to the upgrading of the financial situation of the company and increase in its assets, including taking possession of a third tower in the heart of the capital of Kuwait (Al Mazaya Tower 3) through a swap deal that resulted in the sale of office space in Mazaya Business Avenue in Dubai, in exchange for the Kuwait City tower and two pieces of land in the Q-Point Project .

Furthermore, the company has entered the sector of Warehouse and Logistics through the development of an industrial project in Bahrain Investment Warf worth more than KD 6 million. The company has recently finished the design and licensing procedures, as well as the establishment of steel work tender to the specialist contractors. The implementation and leasing work will be completed by the end of this year.

Esteemed shareholders,

Speaking on behalf of Al Mazaya’s management team, I wish to assure you that our ambition has no limits, and that Al Mazaya›s future will be replete with further studies for new income-generating and available-for-sale projects. Al Mazaya has conducted extensive studies of the local, Gulf, and regional markets, as preparations to enter into the right sectors that achieve the returns we expect with the low risk we need, taking advantage of the company’s previous experience and the current market factors. We at this time emphasize that Al Mazaya still has many investment opportunities under study, which are intended to see the light in the near future, in accordance with the strategic plan of the company. These projects will help the company achieve another quantum leap ahead.

The company›s plans for the current year are to focus on getting into investments in new markets, following a strict schedule in the execution and delivery of the current projects, bringing a broad marketing plan to market, selling all the current projects, and completing the Al Mazaya Logistics project, so it can be fully leased.

Thank you for your vision, patience and integrity, and Peace Be Upon You.

Eng. Ibrahim Al Soqabi

Group CEO

To be ONE of the MARKET LEADERS in Real Estate Development Locally, Regionally and Internationally with a STRONG BRAND that provides VALUABLE and QUALITY life style.

06

VISION

• DEVELOP the most DISTINGUISHED projects based on location, sector and value.

• PROVIDE sustainable VALUE for project delivery, customer loyalty and property services.

• DEVELOP the company manpower with a HIGH CALIBER, ambitious and GOAL ORIENTED team members.

• Maintain and grow a STRONG BRAND position.

07

MISSION

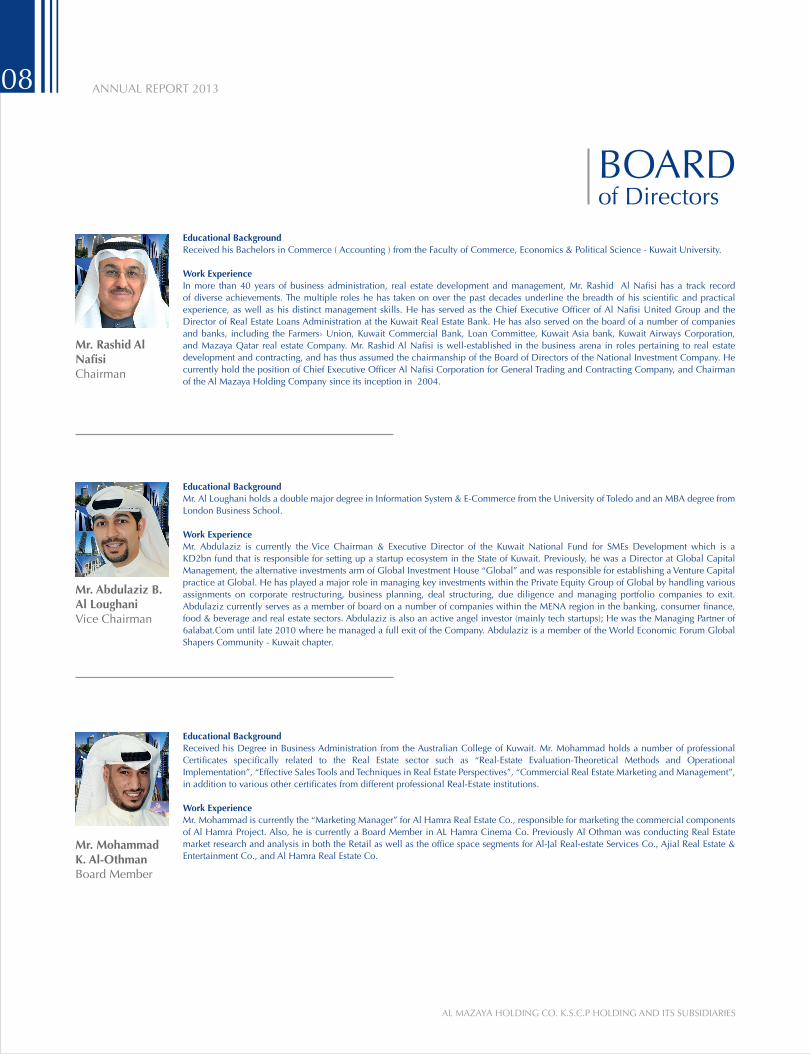

Educational BackgroundMr. Al Loughani holds a double major degree in Information System & E-Commerce from the University of Toledo and an MBA degree from London Business School.

Work ExperienceMr. Abdulaziz is currently the Vice Chairman & Executive Director of the Kuwait National Fund for SMEs Development which is a KD2bn fund that is responsible for setting up a startup ecosystem in the State of Kuwait. Previously, he was a Director at Global Capital Management, the alternative investments arm of Global Investment House “Global” and was responsible for establishing a Venture Capital practice at Global. He has played a major role in managing key investments within the Private Equity Group of Global by handling various assignments on corporate restructuring, business planning, deal structuring, due diligence and managing portfolio companies to exit. Abdulaziz currently serves as a member of board on a number of companies within the MENA region in the banking, consumer finance, food & beverage and real estate sectors. Abdulaziz is also an active angel investor (mainly tech startups); He was the Managing Partner of 6alabat.Com until late 2010 where he managed a full exit of the Company. Abdulaziz is a member of the World Economic Forum Global Shapers Community - Kuwait chapter.

Educational BackgroundReceived his Bachelors in Commerce ( Accounting ) from the Faculty of Commerce, Economics & Political Science - Kuwait University.

Work ExperienceIn more than 40 years of business administration, real estate development and management, Mr. Rashid Al Nafisi has a track record of diverse achievements. The multiple roles he has taken on over the past decades underline the breadth of his scientific and practical experience, as well as his distinct management skills. He has served as the Chief Executive Officer of Al Nafisi United Group and the Director of Real Estate Loans Administration at the Kuwait Real Estate Bank. He has also served on the board of a number of companies and banks, including the Farmers› Union, Kuwait Commercial Bank, Loan Committee, Kuwait Asia bank, Kuwait Airways Corporation, and Mazaya Qatar real estate Company. Mr. Rashid Al Nafisi is well-established in the business arena in roles pertaining to real estate development and contracting, and has thus assumed the chairmanship of the Board of Directors of the National Investment Company. He currently hold the position of Chief Executive Officer Al Nafisi Corporation for General Trading and Contracting Company, and Chairman of the Al Mazaya Holding Company since its inception in 2004.

Educational BackgroundReceived his Degree in Business Administration from the Australian College of Kuwait. Mr. Mohammad holds a number of professional Certificates specifically related to the Real Estate sector such as “Real-Estate Evaluation-Theoretical Methods and Operational Implementation”, “Effective Sales Tools and Techniques in Real Estate Perspectives”, “Commercial Real Estate Marketing and Management”, in addition to various other certificates from different professional Real-Estate institutions.

Work ExperienceMr. Mohammad is currently the “Marketing Manager” for Al Hamra Real Estate Co., responsible for marketing the commercial components of Al Hamra Project. Also, he is currently a Board Member in AL Hamra Cinema Co. Previously Al Othman was conducting Real Estate market research and analysis in both the Retail as well as the office space segments for Al-Jal Real-estate Services Co., Ajial Real Estate & Entertainment Co., and Al Hamra Real Estate Co.

Mr. Mohammad K. Al-OthmanBoard Member

Mr. Rashid Al NafisiChairman

Mr. Abdulaziz B. Al LoughaniVice Chairman

BOARDof Directors

08

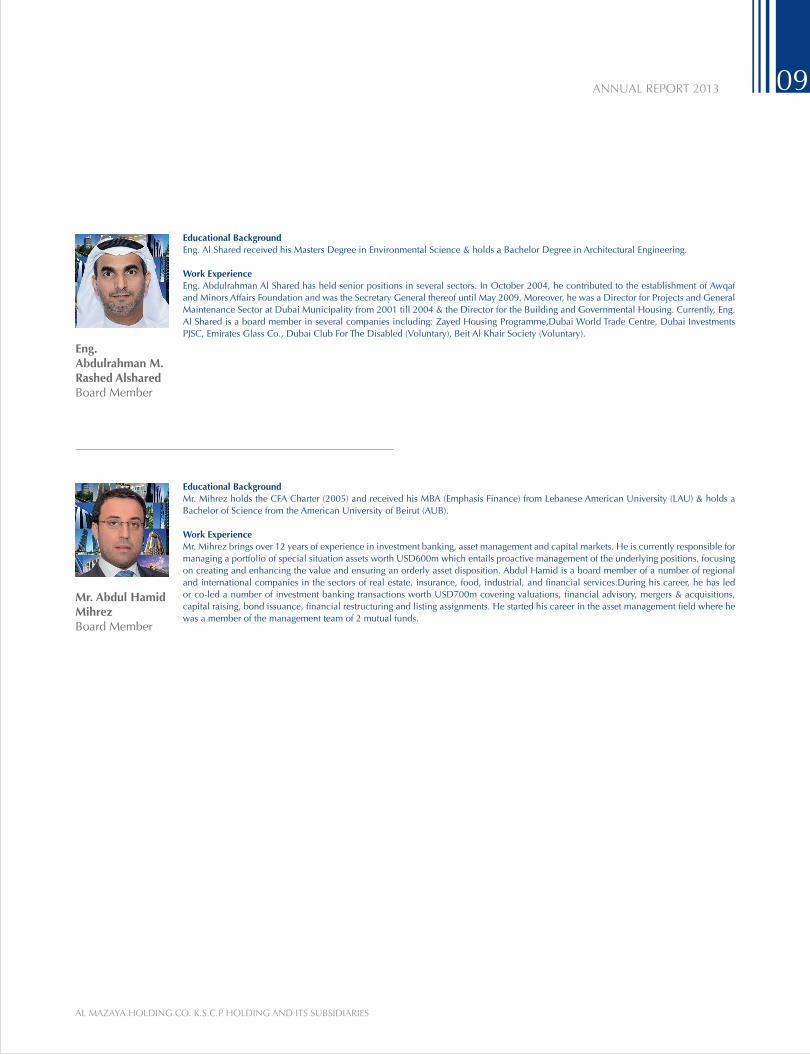

Educational BackgroundMr. Mihrez holds the CFA Charter (2005) and received his MBA (Emphasis Finance) from Lebanese American University (LAU) & holds a Bachelor of Science from the American University of Beirut (AUB).

Work ExperienceMr. Mihrez brings over 12 years of experience in investment banking, asset management and capital markets. He is currently responsible for managing a portfolio of special situation assets worth USD600m which entails proactive management of the underlying positions, focusing on creating and enhancing the value and ensuring an orderly asset disposition. Abdul Hamid is a board member of a number of regional and international companies in the sectors of real estate, insurance, food, industrial, and financial services.During his career, he has led or co-led a number of investment banking transactions worth USD700m covering valuations, financial advisory, mergers & acquisitions, capital raising, bond issuance, financial restructuring and listing assignments. He started his career in the asset management field where he was a member of the management team of 2 mutual funds.

Educational BackgroundEng. Al Shared received his Masters Degree in Environmental Science & holds a Bachelor Degree in Architectural Engineering.

Work ExperienceEng. Abdulrahman Al Shared has held senior positions in several sectors. In October 2004, he contributed to the establishment of Awqaf and Minors Affairs Foundation and was the Secretary General thereof until May 2009. Moreover, he was a Director for Projects and General Maintenance Sector at Dubai Municipality from 2001 till 2004 & the Director for the Building and Governmental Housing. Currently, Eng. Al Shared is a board member in several companies including: Zayed Housing Programme,Dubai World Trade Centre, Dubai Investments PJSC, Emirates Glass Co., Dubai Club For The Disabled (Voluntary), Beit Al Khair Society (Voluntary).

Mr. Abdul Hamid MihrezBoard Member

Eng. Abdulrahman M. Rashed AlsharedBoard Member

09

Educational BackgroundEng. Salwa Malhas - holds a Bachelor and a Master Degree in Civil Engineering from the Jordanian University and has more than 20 years experience in Real Estate Development, Business Models and Feasibility Studies.

Work ExperienceEng. Malhas has held several senior positions & in particular in the Real Estate sector and she has a high profile in managing and developing projects from conducting feasibility studies to development, construction & marketing. Her management skills are highly suited to real estate development, project management, investments, establishing of financial models for new realty opportunities, the business development model for any company including the creation of subsidiaries, and the acquisition and the creating of new companies. Eng. Malhas is also experienced in setting up sales & marketing plans for various projects that now stand at over $500m as well as the running of a research department that issues specialized reports tackling the real estate analysis & investment world. Currently Eng.Salwa is a Board member of Al Nawadi Holding Co. She has held remarkable positions as a General Manager of Al Masaken International Company, a member of ACICO, and as the Head of tendering and marketing in Ghassan Ahmed Al Khalid Co. and tendering Engineer in Al Zaben International Co. while currently at Al Mazaya Holding, where she joined from its inception in 2004 till date; currently a board member in Seven Zones Real Estate Co.

Educational BackgroundReceived his Bachelors Degree in Business Administration (with emphasis on Accounting) from the Lebanese American University - Lebanon. He is also a Certified Public Accountant from the State of New Hampshire, USA.

Work ExperienceServed for more than 4 years for RSM International as an Assistant Manager for Assurance & Business Advisory where he managed a portfolio worth of more than USD 650,000. In addition to working on financial audit assignments, he was responsible for Risk Consulting, Internal Auditing and Financial Consulting including M&A transactions and IPO’s. In 2006 Mr. Sheet joined KGL Investment at it’s inception, as Financial Controller, and was very involved in the establishment of finance and support services departments. By 2008, he was promoted to be the Group Financial Controller where he head up the Groups Financial Accounting & Reporting, Budgeting Control, Compliance & Treasury sections. In addition, Mr. Sheet is currently a Board Member of First Dubai Real Estate Development Co.

Mr. Ayman SheetChief FinancialOfficer

Eng. Ibrahim Al SoqabiGroup CEO

Eng. Salwa MalhasChief Business Development &Marketing Officer

Educational BackgroundEng. Al Soqabi holds an MBA from Kuwait Maastricht Business School, and a B.S. (Civil Eng.) from George Washington University in the USA. In addition to that, he was a member of the boards in several companies in different sections, mostly in real estate inside and outside Kuwait.

Work ExperienceEng. Al Soqabi was the General Manager of the KMC Group of Companies, owned by the Kuwait Finance House which is considered one of the top Sharia’a-compliant companies in the Middle East, at which Eng. Al Soqabi managed the holding company – which consists of seven subsidiaries that provide different, variant and specialized real estate services development, including implementation and management of projects. Eng. Al Soqabi has extensive experience in corporate restructuring and the implementation of governance systems, which include companies’ operational systems, and the development of work plans and strategies to enhance the company’s market share.

EXECUTIVEManagement

10

Educational BackgroundReceived his Bachelor and Master of Science Degrees in Civil Engineering from The University of South Carolina, Columbia, USA, and a Doctor of Philosophy (Ph.D.) Degree in Construction Engineering and Projects Management from the University of Dundee, Scotland, UK. Dr. Jarkas is a Fellow of the UK Society of Professional Engineers, Registered Chartered Engineer (CEng) by the UK Engineering Council (ECUK), recognized and placed on the International Professional Engineers registry of the UK Engineering Council. He is also an active member in several International Professional Associations, Engineering Institutes/Societies, and Arbitration Tribunal Panels. Dr. Jarkas is an authority in Projects and Construction Management with an extensive research record, publications and contribution in the area of Projects and Construction Management, in particular, in the fields of Constructability, Buildability, Construction productivity, Lean Construction, Bidding Practices, Learning Phenomenon in Construction, and Motivation.

Work ExperienceDr. Jarkas’s practical experience spanning over twenty years and encompasses; Planning and Design Management, Structural Design, Structural Damage Assessment, Risk Analysis and Management, Value Engineering, Mediation, Arbitration and ADR, Projects and Construction Management. His Managerial and Technical skills are especially suited to Real Estate Developments, Projects and Construction Management. Currently, he is the Vice Chairman of Al Mazaya Real Estate Development Co., KSCC.

Dr. Abdulaziz M. JarkasChief Projects Officer

Educational BackgroundMr. Khaled holds a Bachelor Degree in Accounting from Faculty of Commerce – English Department, Alexandria University, Egypt. He holds designations for Certified Public Accountant «CPA», Certified Management Accountant «CMA» and Certified Financial Manager «CFM».

Work ExperienceMr. Khaled has over 20 years of operations, corporate finance, consulting, audit, banking, and accounting experience. Mr. Khaled was Chief Operating Officer of F&S Holding Company. From 2005 to 2011, he was Senior Vice President – Finance & Operations of Al-Muthanna Investment Company, a wholly owned subsidiary of Kuwait Finance House. He served as Chief Financial Officer, Vice President and Assistant Secretary of couple of U.S. Property Co. He also was Board Member of Florida Atlantic BOCA Research Park And Deerfield Research Park, State Of Florida, USA. He was Board Member of Muthanna Financial Brokerage Company. He started his career with Barclays Bank, where he worked in the corporate and investment banking department. He has wide and extensive experience in audit and consulting having previously worked with Ernst & Young and Arthur Andersen. During his service with those firms, he was acting manager of a large portfolio of medium to large size clients and was responsible for overall assignment control, client relationship coordination, and quality control assurance.Mr. Khaled is a Board Member of The Kuwaiti Manager Company for Managing Real Estate Projects and internal audit committee member of Mawared United Investment Company. He also is an instructor for full courses of professional designations.

Educational BackgroundMr. Al Hajraf received his Bachelor Degree in Law from Cairo University.

Work ExperienceMr. Al Hajraf has been in the real estate field for over ten years with experience in Kuwait in Commercial, Civil, Real Estate and Criminal law. Having decision-making skills with professional experience in top management works, he brings a rational and analytical approach to problem solving, a high level of integrity and professionalism. He has extensive and professional experience in establishing and managing companies, corporate governance, and has strong skills in the management of Boards, extensive experience in judicial decisions, ten years experience in commercial and civil cases, and strong leadership skills as demonstrated by an ability to recruit manage and motivate a team of in-house employees and high skills in negotiation and settlements.

Mr. Khaled AbdulatifChief Corporate Services Officer

Educational BackgroundEng. Abdullah holds a Bachelor Degree in Civil Engineering from the Kuwait Petroleum and Engineering University and has more than 12 years experience in the real estate sector .

Work ExperienceEng. Abdullah held senior positions in real estate sector as business development manager in first Dubai Real Estate, Deputy Manager of project department in Commercial Real Estate Company (CRC) and as head of development unit in project department in Commercial Real Estate Company (CRC). He has an extensive experience in management, development and operation of the projects from initial study to operate the projects; also he has a high experience in design and construction phase. In addition he has good skills in property management (setting up models to manage the properties of company), preparing study to reduce the expenses cost of properties and establishing of lease plan and strategy for property, currently Al Sultan is a board member in Water Front Real Estate Co.

Eng. AbdullahAl SultanChief Property Management Officer

Mr. Shlash Al HajrafActing CEO –Mazaya FZ

11

MAJORShareholders Structure

Commercial Bank Of Kuwait

Gimbal Holding Company

AL MAZAYA HOLDING CO. IS CONSIDERED ONE OF THE LEADING COMPANIES IN ITS LINE OF BUSINESS. THE COMPANY FOCUSES ON REAL ESTATE DEVELOPMENTS & INVESTMENTS IN THE REGION.

The company was established in 1998 and started operations as AL Mazaya Holding Company in 2004 with a paid up capital of KD 15 million which has increased to reach KD 64.9 million. Al Mazaya Holding Company is listed both in the Kuwait Stock Exchange and in the Dubai Financial Market.

Al Mazaya has a diversified structure that is divided among high net worth of investors and solid corporate organizations.

Since its inception, Al Mazaya has adopted a balanced expansion strategy that allowed for mitigating risk, while maximizing investment return and witnessing strong growth. By maintaining diversified business allocations within the building industry and geographical distribution of investments in the region, the company has been able to maintain steady growth in its net profits as a result of such a strategy.

Al Mazaya’s investments have also focused on building alliances and strategic partnerships that allow for developing the company’s competitive edge especially in as far as competing for top-tier business opportunities is concerned.

COMPANYEstablishment

CAPITALStructure

12

DUBAI FINANCIAL MARKET

KUWAIT FINANCIAL MARKET

In February 2006, Mazaya Holding Company was listed on the Dubai Financial Market in an effort to become a regional company.

Al Mazaya Holding Company’s great success in the real estate sector was revealed through the company’s listing in the Kuwait Stock Exchange in 2005.

LISTING

13

Marketing & Sales Management AL MAZAYA’s marketing services are grounded by an experienced in-house team with a great vision and strategy for brand development. These extensive real estate marketing services provided by the Marketing department both in Kuwait and Dubai prove AL MAZAYA as one of the leading brands in its field. AL MAZAYA’s marketing team is disciplined in providing contingent studies and solutions for: Corporate Identity & Brand Development, Corporate Theme, Marketing & Sales Strategies, Event Planning, Website design & management, Marketing Tools, Advertising Campaigns & PR, and Social Media.

Property ManagementAL MAZAYA Property Management is reputable to provide a safe, physical working environment through preventive, daily and emergency maintenance, guarding and housekeeping services. Property management, a specialist in total project management, plan, implement and manage the maintenance operations for facilities and renovate enduring facilities. Property management is offering a customized service based on clients’ needs with tactical recommendations and future facility strategic engineering and much about the quality of life aspects in the work environment.

Property ValuationPart of AL MAZAYA Holding’s services is valuation in order to fully evaluate all aspects of the deal through an experienced department resulting in determining the true value of property. With an accurate valuation; then prepare the necessary feasibility studies for projects meant for sale or future expansion, as well as accurately calculating a company’s underlying assets. There is a developed and maintained in house database, as well as our management team’s experience and contacts to ensure an up-to-date and most accurate information to present a comprehensive report and study, which can then be used to help finance the real estate project done through banks or finance companies.

OPERATIONS /Services

Real Estate Market Research AL MAZAYA Holding’s Research Department comprises of an experienced team that assesses the large number of risk factors that are associated with the rapidly growing industry of real estate development. Building on a quantitative approach to understanding the processes of the market that provides information, figures, data, and the reasoning behind each change are all analyzed. The Research Department harnesses and compares all of this to prevent conflicting figures, statistics, and data regarding the growth entailed.

14

Master Developments Purchasing and apportionment of large spaces to develop in selected areas is considered one of the largest assets AL MAZAYA owns in terms of its services. A fully fledged experienced team assesses the different feasible locations in which the company plans to invest in, or develop, to extract the optimum value for the price purchased through searching for new opportunities and developing opportunities at hand, systematically complete due diligence and gathering information to enable a realistic assessment of the highest potential for any given opportunity, with complete feasibility studies in close support with the finance department. Moreover, the team structure the mainstream plans of the key tasks, assign and continually monitor projects throughout all stages of the development process, develop a project management team to ensure the maximum efficiencies of the projects are met and help administer the project up to the tending phase.

Project Management & Consultancy

AL MAZAYA Holding manages a construction project and operates as an extension to your company, and represents the company interests while leveraging the best possible performance out of all the entities employed on the project. AL MAZAYA Holding direct the day-to day work of all entities involved on the project, while you retain all the major decision making authority. Experience, influencing skills, and leadership style are paramount in determining the effectiveness of a Project from assessing the viability of the development, controlling the design and construction phases to providing the required facility and operation management through leadership and exceptional real estate construction experience & assist avoiding both financial obstacles, and development problems.

Portfolio & Fund ManagementAL MAZAYA Holding provides professional management services to clients and other real estate companies that encompass a variety of consultation on various real estate management aspects including: overall management services, strategic planning and budgeting, business operations, including business development, marketing/sales, administration, and financial & project feasibilities, policies & procedures, operational manuals, setup of information technology systems, organizational and functional structure, staffing, and training.

Real Estate BrokerageAL MAZAYA Holding’s Brokerage is based on the desire to personalize and increase the level of service toward its clients. This service will provide AL MAZAYA Holding’s clients the ability to view its projects online using the latest forms of technology, and allow the ability to follow up this with personalized VIP site visits.

Real Estate Development & InvestmentsThere is a variety of different approaches for development in which AL MAZAYA Holding can be involved in. The range from master developments to individual projects in different sectors, including residential, commercial, industrial, educational and health. These endeavors can be directly owned, owned through a partnership with investors, Joint Venture, and BOT’s (Build, Operate and Transfer).

15

Allocation By Geography - 2013 Allocation By Sector - 2013 Sources of Income Allocation - 2013

%72

21%

1%0%

3%2%

1%

Medical

Offices

Retail

Residential

Logistics

Residential - Land

= 5 %

= 23 %

= 2 %

= 62 %

= 1 %

= 8 %

Rent

Sales of Properties

Management Fees

= 36 %

= 56 %

= 8 %

%62

23%

4%

2%

1%8%

%56

8% 36%

Kuwait

UAE

Bahrain

Oman

Saudi Arabia

Lebanon

Turkey

= 21 %

= 72 %

= 1 %

= 2 %

= 3 %

= 1 %

= 0 %

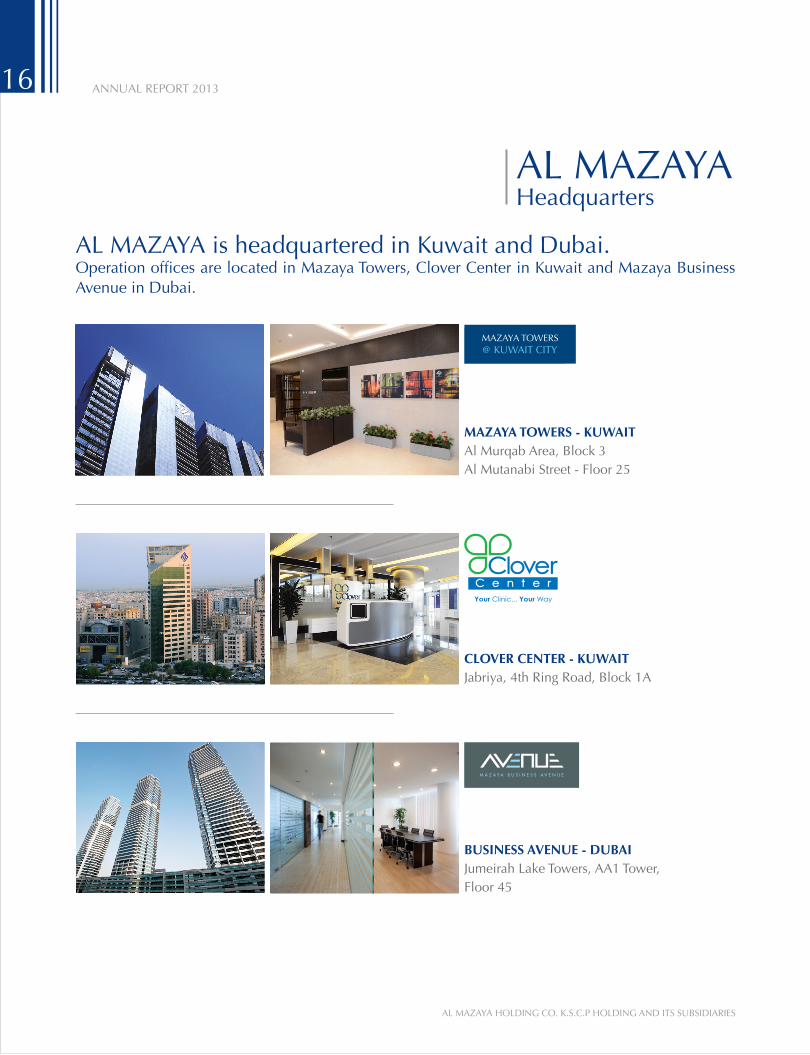

AL MAZAYA is headquartered in Kuwait and Dubai.Operation offices are located in Mazaya Towers, Clover Center in Kuwait and Mazaya Business Avenue in Dubai.

BUSINESS AVENUE - DUBAIJumeirah Lake Towers, AA1 Tower,Floor 45

CLOVER CENTER - KUWAITJabriya, 4th Ring Road, Block 1A

MAZAYA TOWERS - KUWAITAl Murqab Area, Block 3Al Mutanabi Street - Floor 25

DU

BAI

AL MAZAYAHeadquarters

16

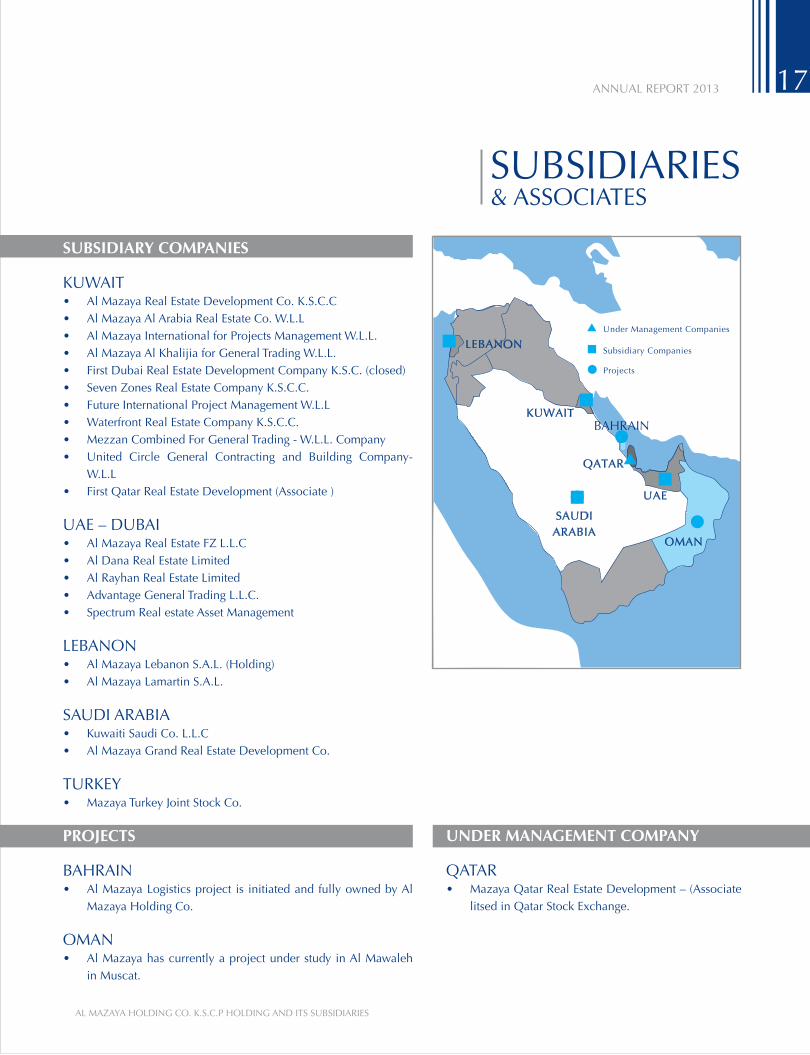

UNDER MANAGEMENT COMPANY

QATAR• Mazaya Qatar Real Estate Development – (Associate

litsed in Qatar Stock Exchange.

SUBSIDIARIES & ASSOCIATES

SUBSIDIARY COMPANIES

KUWAIT• Al Mazaya Real Estate Development Co. K.S.C.C• Al Mazaya Al Arabia Real Estate Co. W.L.L• Al Mazaya International for Projects Management W.L.L.• Al Mazaya Al Khalijia for General Trading W.L.L.• First Dubai Real Estate Development Company K.S.C. (closed)• Seven Zones Real Estate Company K.S.C.C.• Future International Project Management W.L.L• Waterfront Real Estate Company K.S.C.C.• Mezzan Combined For General Trading - W.L.L. Company• United Circle General Contracting and Building Company-

W.L.L• First Qatar Real Estate Development (Associate )

UAE – DUBAI• Al Mazaya Real Estate FZ L.L.C• Al Dana Real Estate Limited• Al Rayhan Real Estate Limited• Advantage General Trading L.L.C.• Spectrum Real estate Asset Management

LEBANON• Al Mazaya Lebanon S.A.L. (Holding)• Al Mazaya Lamartin S.A.L.

SAUDI ARABIA• Kuwaiti Saudi Co. L.L.C• Al Mazaya Grand Real Estate Development Co.

TURKEY• Mazaya Turkey Joint Stock Co.•PROJECTS•BAHRAIN• Al Mazaya Logistics project is initiated and fully owned by Al

Mazaya Holding Co.

OMAN• Al Mazaya has currently a project under study in Al Mawaleh

in Muscat.

17

18

AIM TO LEAD

19

REAL ESTATE DEVELOPMENT & INVESTMENTSPORTFOLIO & FUND MANAGEMENT

PROJECT MANAGEMENT & CONSULTANCYREAL ESTATE BROKERAGE

MARKETING & SALES MANAGEMENT MASTER DEVELOPMENTS

PROPERTY MANAGEMENTPROPERTY VALUATION

REAL ESTATE MARKET RESEARCH

KUWAITProjects

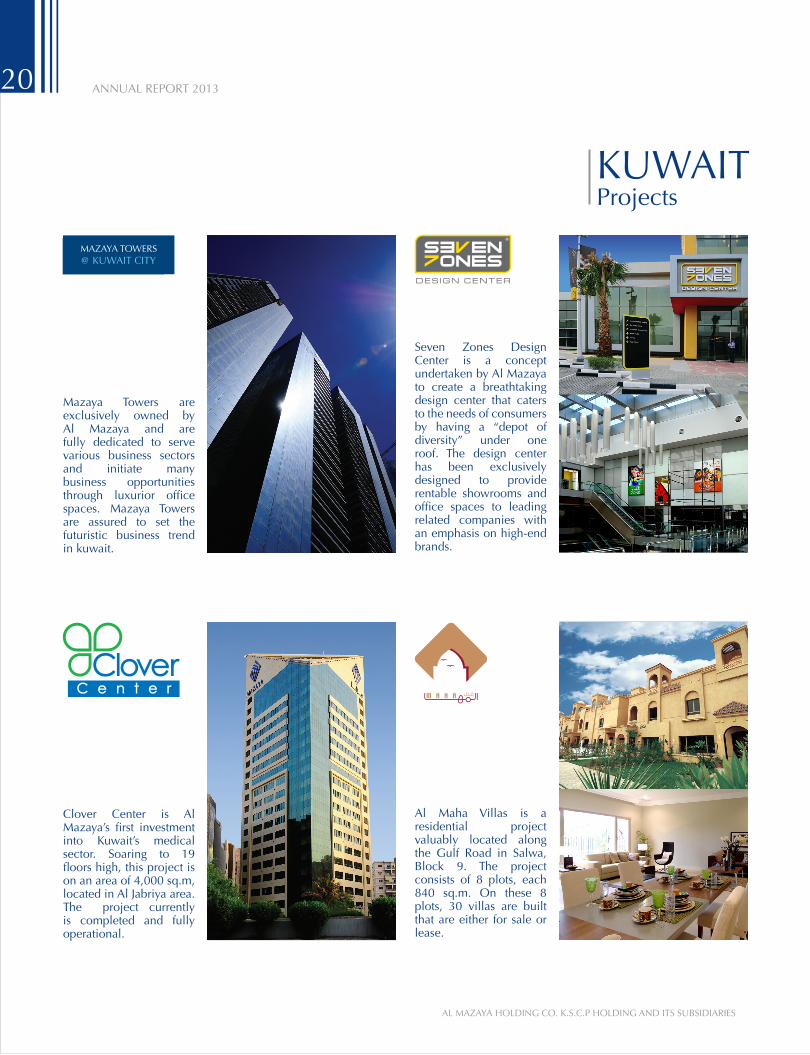

Mazaya Towers are exclusively owned by Al Mazaya and are fully dedicated to serve various business sectors and initiate many business opportunities through luxurior office spaces. Mazaya Towers are assured to set the futuristic business trend in kuwait.

Seven Zones Design Center is a concept undertaken by Al Mazaya to create a breathtaking design center that caters to the needs of consumers by having a “depot of diversity” under one roof. The design center has been exclusively designed to provide rentable showrooms and office spaces to leading related companies with an emphasis on high-end brands.

Al Maha Villas is a residential project valuably located along the Gulf Road in Salwa, Block 9. The project consists of 8 plots, each 840 sq.m. On these 8 plots, 30 villas are built that are either for sale or lease.

Clover Center is Al Mazaya’s first investment into Kuwait’s medical sector. Soaring to 19 floors high, this project is on an area of 4,000 sq.m, located in Al Jabriya area. The project currently is completed and fully operational.

20

Global Tower is a business tower strategically located in Sharq, in close proximity to other business ventures in Kuwait City. The tower consists of 22 levels offering luxurious office spaces. Al Mazaya had developed the project and sell it out.

Al Roya project is a residential complex located in Al Mahboulah area, it consists of 61 residential units that vary in area and interior design to attract clients looking for a particular apartment or villa.

It is an idea initialed by Al Mazaya to develop an ambitious real estate project to turn Kuwait into a new financial center and a cultural city. The project is inspired by and in accordance with the desire of the Amir of Kuwait, in order to turn Kuwait into a hub that will attract many investments, both locally and internationally, in addition to a culture and civilization center.

Surra Villas are individual villas located in different areas in Surra with prime locations. Each villa portrays an authentic style and is built with specific engineering and architectural detail that works in accordance with the highest class specifications including swimming pools and beautiful garden surroundings.

21

UAEProjects

Sky Gardens, a luxurious residential tower, is uniquely located at the entry to the prestigious Dubai International Financial Center (DIFC), south of the Dubai Emirates Towers.Sky Gardens consists of 40 floors of luxurious apartments.

Mazaya Business Avenue comprises of three commercial towers, each one rising to an imposing 45 storey building. The development contains ultra modern offices business centers, state of the art recreational centers, meeting rooms, retail plazas, cafes and more.

The Villa project is situated just off the Emirates Road at the North East Corner of Dubailand. It is considered to be “The Ultimate Spanish Lifestyle”, inspired by generous spaces for outdoor living, including expert landscaping and the coolness and tranquility of Spanish style courtyard housing.

22

Mazaya developed 7 medical buildings in the Dubai Healthcare City - DHCC. The DHCC site comprises of 500 acres and offers all forms of medical facilities, disease prevention centers, as well as wellness amenities. The services provided serve residents from the UAE, GCC, and surrounding regions.

The Icon Towers 1 and 2 in Jumeirah Lakes are residential towers that consist of up to 400 units that vary in area and interior design. The towers have a wonderful lake view from one side and a spectacular view of Jumeirah Islands from the other side.

Morina Residence, owned by First Dubai, a Mazaya subsidiary, is located along the canal near the entrance of Shams Abu Dhabi on Reem Island. Morina is a luxurious 29 storey residential tower offering phenomenal views onto the canal and mangroves. Morina Residence offers exclusive 1, 2, 3 bedroom apartments, duplexes and townhouses.

Located at Al Manara and Al Safa, positioned either side of Interchange 3 on Sheikh Zayed Road, Indigo is an office and retail use building registered with the Dubai Lands Department as Freehold for GCC citizens and companies.

23

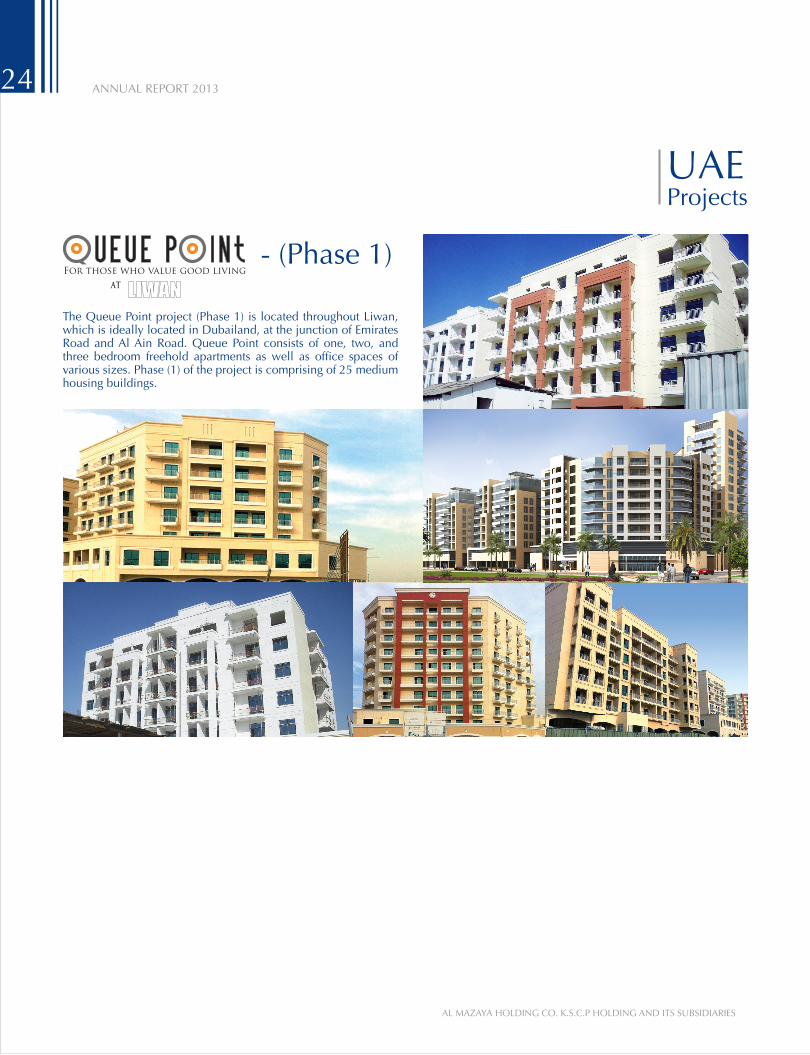

The Queue Point project (Phase 1) is located throughout Liwan, which is ideally located in Dubailand, at the junction of Emirates Road and Al Ain Road. Queue Point consists of one, two, and three bedroom freehold apartments as well as office spaces of various sizes. Phase (1) of the project is comprising of 25 medium housing buildings.

24

- (Phase 1)

UAEProjects

REGIONALProjects

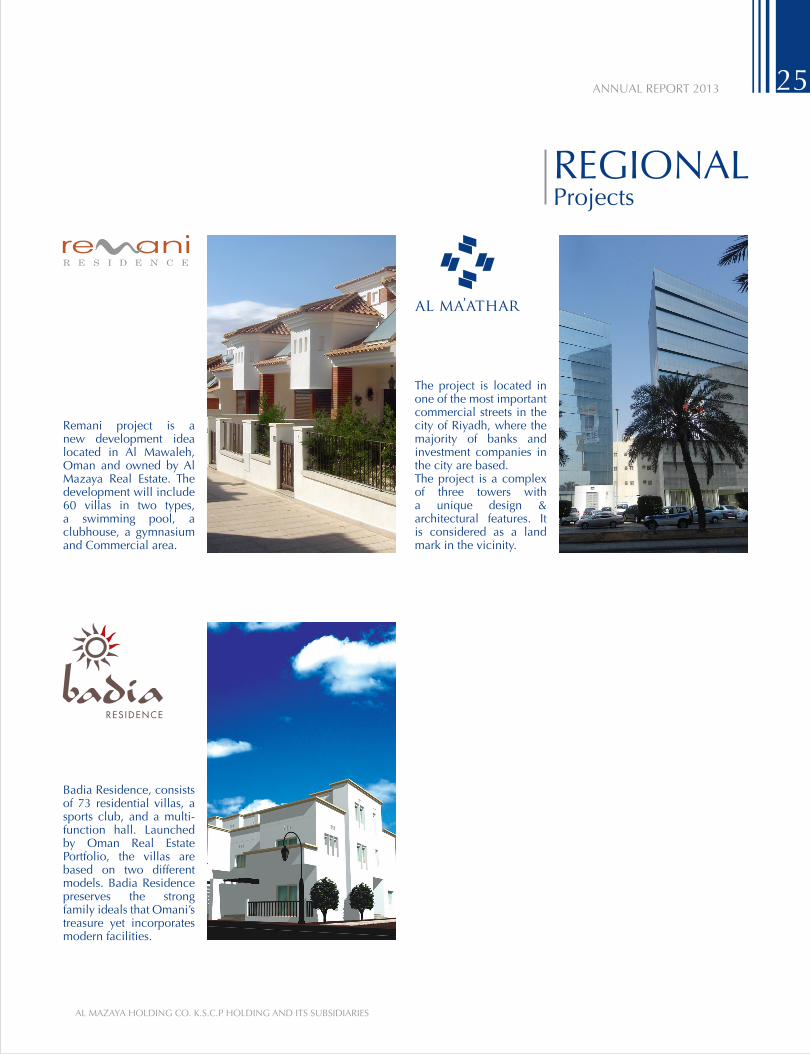

Remani project is a new development idea located in Al Mawaleh, Oman and owned by Al Mazaya Real Estate. The development will include 60 villas in two types, a swimming pool, a clubhouse, a gymnasium and Commercial area.

The project is located in one of the most important commercial streets in the city of Riyadh, where the majority of banks and investment companies in the city are based.The project is a complex of three towers with a unique design & architectural features. It is considered as a land mark in the vicinity.

Badia Residence, consists of 73 residential villas, a sports club, and a multi-function hall. Launched by Oman Real Estate Portfolio, the villas are based on two different models. Badia Residence preserves the strong family ideals that Omani’s treasure yet incorporates modern facilities.

25

26

(Phase 2)

The Queue Point project (Phase 2) is located throughout Liwan, which is ideally located in Dubailand, at the junction of Emirates Road and Al Ain Road. Queue Point consists of one, two, and three bedroom freehold apartments as well as office spaces of various sizes.

27

NEW PROJECTDubai

MAZAYA LOGISTICS is a concept initiated and wholly owned by Al Mazaya in the world of Industry to construct, develop, and operate ideal key storage solutions. Mazaya Logistics is a reliable, flexible and experienced warehousing solution with a state of the art warehousing management system. Its prime location in Bahrain Investment Wharf (BIW) makes it the key choice for many local, international and national companies.

28

NEW PROJECTBahrain

29

Al Mazaya is planning to Develop a Residential complex in Turkey-Istanbul after the completion of Mazaya Turkey Incorporation. The plan is to engage the company into a partnership throughout a joint venture with a good reputable Real Estate Turkish Developer.

30

NEW MARKETTurkey

31

32

AL MAZAYA HOLDING COMPANY K.S.C.AND ITS SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENT 31 DECEMBER 2013

FINANCIAL REPORT2013

33

Independent auditors’ reportConsolidated statement of financial positionConsolidated statement of incomeConsolidated statement of comprehensive incomeConsolidated statement of changes in equityConsolidated statement of cash flowsNotes to the consolidated financial statements

3536373839

40-4142-78

Index Page

34

INDEPENDENT AUDITORS' REPORT TO THE SHAREHOLDERS OF AL MAZAYA HOLDING COMPANY K.S.C.P.

Report on the Consolidated Financial StatementsWe have audited the accompanying consolidated financial statement of Al Mazaya Holding Company K.S.C.P. (the “Parent Company”) and its subsidiaries (collectively the “Group”), which comprise the consolidated statement of financial position as at 31 December 2013, and the consolidated statement of income, consolidated statement of comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial StatementsThe management of the Parent Company is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ ResponsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Group as at 31 December 2013, and its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards. Report on Other Legal and Regulatory RequirementsFurthermore, in our opinion proper books of account have been kept by the Parent Company and the consolidated financial statements, together with the contents of the report of the Parent Company’s Board of Directors relating to these consolidated financial statements, are in accordance therewith. We further report that we obtained all the information and explanations that we required for the purpose of our audit and that the consolidated financial statements incorporate all information that is required by the Companies Law No. 25 of 2012, as amended, and by the Parent Company's Memorandum of Incorporation and Articles of Association, that an inventory was duly carried out and that, to the best of our knowledge and belief, no violations of the Companies Law No. 25 of 2012, as amended, or of the Parent Company’s Memorandum of Incorporation and Articles of Association have occurred during the year ended 31 December 2013 that might have had a material effect on the business of the Parent Company or on its financial position.

WALEED A. AL OSAIMI LICENCE NO. 68-A OF ERNST & YOUNGAL AIBAN, AL OSAIMI & PARTNERS

26 January 2014Kuwait

DR. SAUD HAMAD AL-HUMAIDILICENSE NO. 51 AOF DR. SAUD HAMAD AL-HUMAIDI & PARTNERSMEMBER OF BAKER TILLY INTERNATIONAL

15

01 35

2,266,732358,706

89,094,87114,250,13512,750,873

118,721,317

86,385,9375,563,047

17,445,840109,394,824228,116,141

64,931,97721,655,39310,289,8987,354,9781,408,173

)21,788,181(673,551636,546

5,797,886

90,960,2216,207,117

97,167,338

337,21120,497,70522,000,00042,874,916

1,500,0002,399,595

--

68,662,79812,523,8672,987,627

88,073,887

130,948,803228,116,141

2,266,732160,913

74,474,14618,630,80312,894,223

108,426,817

93,788,2465,446,486

13,391,425112,626,157221,052,974

64,931,97721,655,3939,675,7806,740,860

927,863(21,788,181)

(369,033)487,818

1,025,071

83,287,5484,552,280

87,839,828

336,911-

31,000,00031,336,911

7,000,000-

8,500,0003,947,108

62,069,97917,443,3522,915,796

101,876,235

133,213,146221,052,974

7

89.1011

121314

15151616

17

1918

18191920

2114

2013KD

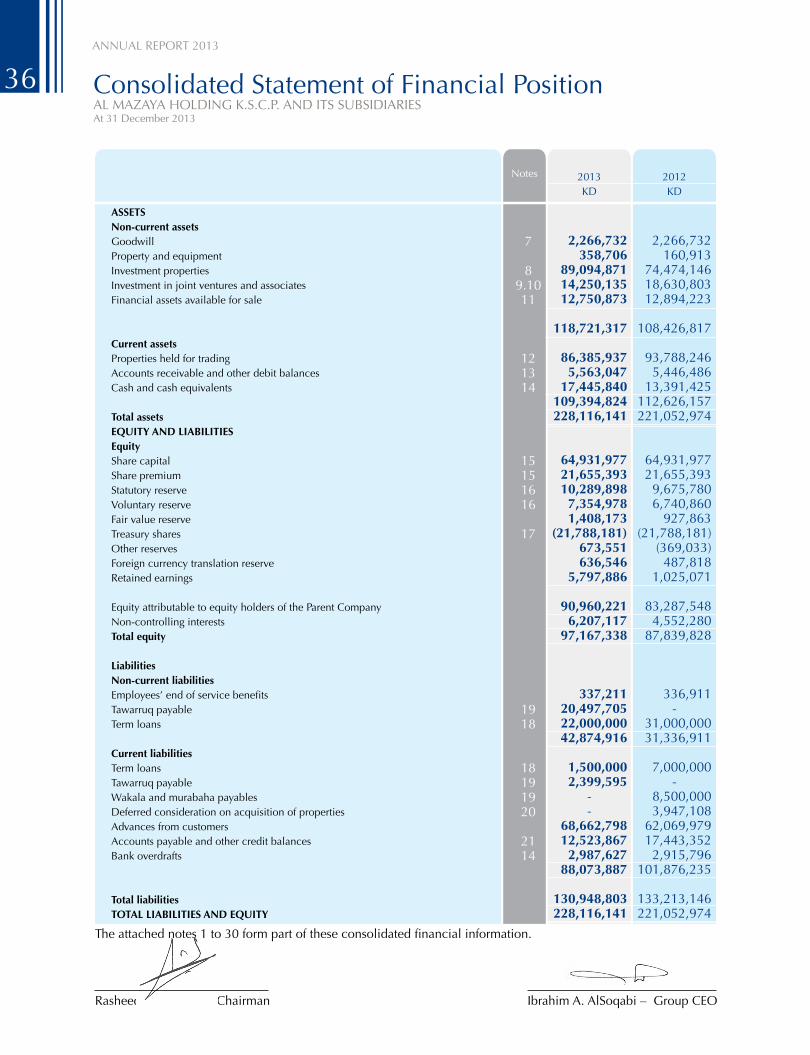

ASSETSNon-current assetsGoodwillProperty and equipmentInvestment propertiesInvestment in joint ventures and associatesFinancial assets available for sale

Current assetsProperties held for tradingAccounts receivable and other debit balances Cash and cash equivalents

Total assetsEQUITY AND LIABILITIESEquityShare capitalShare premiumStatutory reserveVoluntary reserveFair value reserveTreasury sharesOther reservesForeign currency translation reserveRetained earnings

Equity attributable to equity holders of the Parent CompanyNon-controlling interestsTotal equity

LiabilitiesNon-current liabilitiesEmployees’ end of service benefitsTawarruq payableTerm loans

Current liabilitiesTerm loansTawarruq payableWakala and murabaha payablesDeferred consideration on acquisition of propertiesAdvances from customersAccounts payable and other credit balancesBank overdrafts

Total liabilitiesTOTAL LIABILITIES AND EQUITY

2012KD

Notes

Rasheed Y. Al-Nafisi – Chairman

Ibrahim A. AlSoqabi – Group CEO

Consolidated Statement of Financial PositionAL MAZAYA HOLDING K.S.C.P. AND ITS SUBSIDIARIESAt 31 December 201316

The attached notes 1 to 30 form part of these consolidated financial information.

36

22

78

9,10

12232430

15

6

2013KD

2012KD

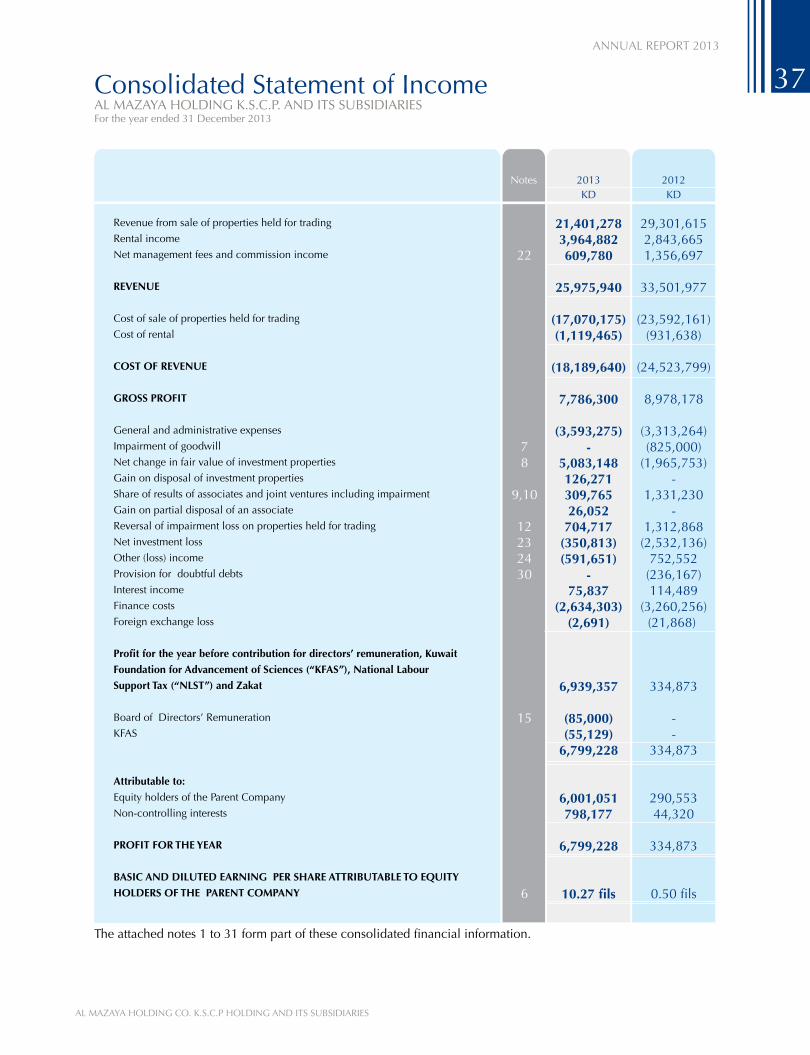

Revenue from sale of properties held for trading

Rental income

Net management fees and commission income

REVENUE

Cost of sale of properties held for trading

Cost of rental

COST OF REVENUE

GROSS PROFIT

General and administrative expenses

Impairment of goodwill

Net change in fair value of investment properties

Gain on disposal of investment properties

Share of results of associates and joint ventures including impairment

Gain on partial disposal of an associate

Reversal of impairment loss on properties held for trading

Net investment loss

Other (loss) income

Provision for doubtful debts

Interest income

Finance costs

Foreign exchange loss

Profit for the year before contribution for directors’ remuneration, Kuwait

Foundation for Advancement of Sciences )“KFAS”(, National Labour

Support Tax )“NLST”( and Zakat

Board of Directors’ Remuneration

KFAS

Attributable to:

Equity holders of the Parent Company

Non-controlling interests

PROFIT FOR THE YEAR

BASIC AND DILUTED EARNING PER SHARE ATTRIBUTABLE TO EQUITY

HOLDERS OF THE PARENT COMPANY

The attached notes 1 to 31 form part of these consolidated financial information.

21,401,2783,964,882609,780

25,975,940

)17,070,175()1,119,465(

)18,189,640(

7,786,300

)3,593,275(-

5,083,148126,271309,76526,052704,717

)350,813()591,651(

-75,837

)2,634,303( )2,691(

6,939,357

)85,000()55,129(

6,799,228

6,001,051798,177

6,799,228

10.27 fils

29,301,6152,843,6651,356,697

33,501,977

(23,592,161)(931,638)

(24,523,799)

8,978,178

(3,313,264)(825,000)

(1,965,753)-

1,331,230-

1,312,868(2,532,136)

752,552(236,167)114,489

(3,260,256)(21,868)

334,873

--

334,873

290,55344,320

334,873

0.50 fils

Notes

Consolidated Statement of IncomeAL MAZAYA HOLDING K.S.C.P. AND ITS SUBSIDIARIESFor the year ended 31 December 2013 17

37

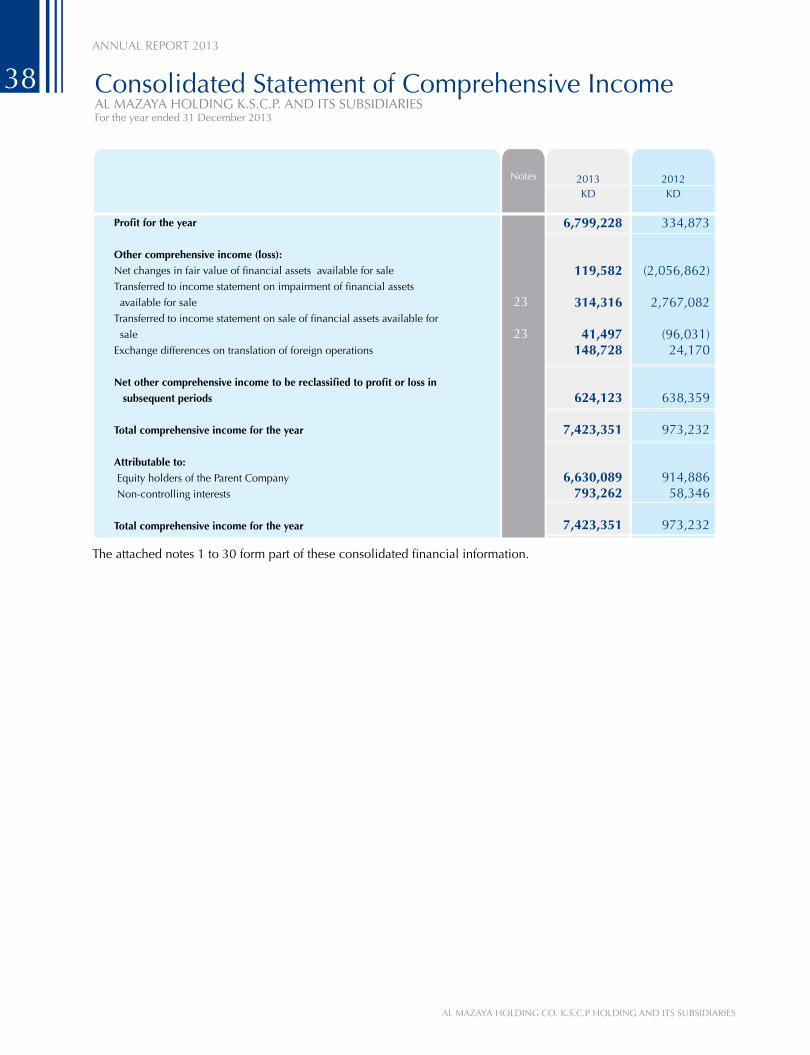

6,799,228

119,582

314,316

41,497148,728

624,123

7,423,351

6,630,089793,262

7,423,351

334,873

(2,056,862)

2,767,082

(96,031)24,170

638,359

973,232

914,88658,346

973,232

Profit for the year

Other comprehensive income )loss(:

Net changes in fair value of financial assets available for sale

Transferred to income statement on impairment of financial assets

available for sale

Transferred to income statement on sale of financial assets available for

sale

Exchange differences on translation of foreign operations

Net other comprehensive income to be reclassified to profit or loss in

subsequent periods

Total comprehensive income for the year

Attributable to:

Equity holders of the Parent Company

Non-controlling interests

Total comprehensive income for the year

2013KD

2012KD

The attached notes 1 to 30 form part of these consolidated financial information.

Consolidated Statement of Comprehensive IncomeAL MAZAYA HOLDING K.S.C.P. AND ITS SUBSIDIARIESFor the year ended 31 December 2013

23

23

Notes

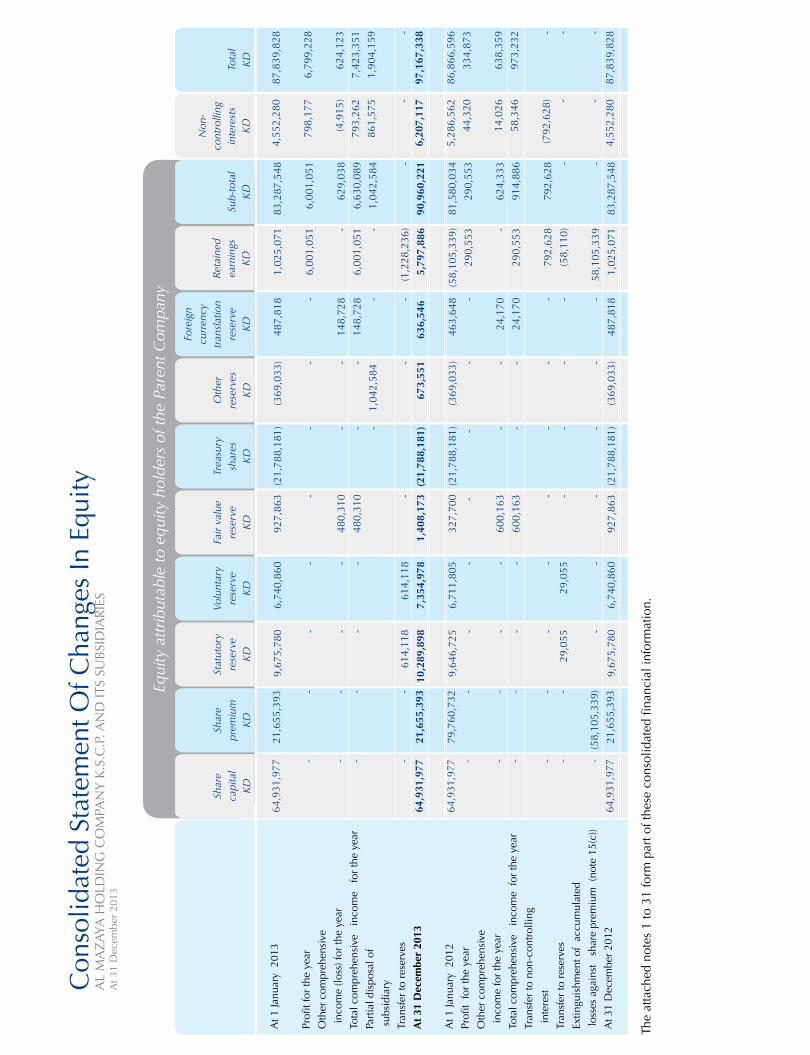

18

38

Con

solid

ated

Sta

tem

ent O

f Cha

nges

In E

quity

AL

MA

ZAY

A H

OLD

ING

CO

MPA

NY

K.S

.C.P

. AN

D IT

S SU

BSI

DIA

RIE

SA

t 31

Dec

embe

r 20

13

64,9

31,9

77 -

- -

-

64,9

31,9

77

64,9

31,9

77

-

- -

-

- -

64,9

31,9

77

21,6

55,3

93 -

- -

-

21,6

55,3

93

79,7

60,7

32 -

-

-

- -

(58,

105,

339)

21,6

55,3

93

9,67

5,78

0

-

- -

614,

118

10,2

89,8

98

9,64

6,72

5 -

- -

-

2

9,05

5 -

9,67

5,78

0

6,74

0,86

0

-

- -

614,

118

7,35

4,97

8

6,71

1,80

5 -

- -

-

2

9,05

5 -

6,74

0,86

0

927,

863

-

48

0,31

0

48

0,31

0

-

1,40

8,17

3

327

,700 -

6

00,1

63

6

00,1

63

- - -

927,

863

(21,

788,

181)

- - -

-

)21,

788,

181(

(21

,788

,181

) -

-

- - - -

(21,

788,

181)

(369

,033

)

-

- -

1,0

42,5

84

-

673

,551

(369

,033

) - - - - - -

(369

,033

)

487,

818

-

148,

728

148,

728 -

-

636

,546

463,

648 -

24,1

70

24,1

70

- - -

487,

818

1,02

5,07

1

6,00

1,05

1 -

6,00

1,05

1 -

(1,2

28,2

36)

5,79

7,88

6

(58,

105,

339)

290,

553 -

2

90,5

53

79

2,62

8

(58,

110)

58,1

05,3

39

1,02

5,07

1

At 1

Janu

ary

201

3

Profi

t for

the

year

Oth

er c

ompr

ehen

sive

inc

ome

(loss

) for

the

year

Tota

l com

preh

ensi

ve

inco

me

for

the

year

Part

ial d

ispo

sal o

f

sub

sidi

ary

Tran

sfer

to r

eser

ves

At

31 D

ecem

ber

2013

At 1

Janu

ary

201

2

Profi

t fo

r th

e ye

ar

Oth

er c

ompr

ehen

sive

inc

ome

for

the

year

Tota

l com

preh

ensi

ve

inco

me

for

the

year

Tran

sfer

to n

on-c

ontr

ollin

g

int

eres

t

Tran

sfer

to r

eser

ves

Extin

guis

hmen

t of

accu

mul

ated

loss

es a

gain

st

shar

e pr

emiu

m (

note

15(

c))

At 3

1 D

ecem

ber

2012

Shar

e ca

pita

lK

D

Stat

utor

yre

serv

eK

D

Shar

e pr

emiu

mK

D

Volu

ntar

yre

serv

eK

D

Fair

valu

ere

serv

eK

D

Trea

sury

shar

esK

D

Oth

er

rese

rves

KD

Fore

ign

curr

ency

tr

ansl

atio

n re

serv

eK

D

Ret

aine

d ea

rnin

gs

KD

83,2

87,5

48

6,00

1,05

1

629,

038

6,63

0,08

9

1,04

2,58

4

-

90,9

60,2

21

81,5

80,0

34

290,

553

624,

333

914,

886

792,

628 - -

83,2

87,5

48

Sub-

tota

lK

D

4,55

2,28

0

798,

177

(4,9

15)

793,

262

861,

575 -

6,2

07,1

17

5,

286,

562

44,3

20

14,0

26

5

8,34

6

(792

,628

) - -

4,55

2,28

0

87,8

39,8

28

6,79

9,22

8

624,

123

7,42

3,35

1

1,90

4,15

9

-

97

,167

,338

86

,866

,596

334,

873

638,

359

973,

232 - - -

87,8

39,8

28

Non

-co

ntro

lling

inte

rest

sK

DTo

tal

KD

The

atta

ched

not

es 1

to 3

1 fo

rm p

art o

f the

se c

onso

lidat

ed fi

nanc

ial i

nfor

mat

ion.

Equi

ty a

ttrib

utab

le to

equ

ity h

olde

rs o

f the

Par

ent C

ompa

ny

334,873

93,706

236,167

1,965,753

-

(1,312,868)

825,000

2,532,136

(1,331,230)

-

(114,489)

3,260,256

21,868

99,706

6,610,878

17,100,323

(5,249,109)

(18,887,860)

80,938

(8,657,323)

1,496,065

(49,685)

1,446,380

2,405,076

(124,916)

(2,198,232)

-

(174,054)

(2,055,815)

-

(344,234)

1,720,810

-

-

-

138,915

114,489

(517,961)

30

8

12

7

23

8

9

9

9

2013KD

2012KD

Notes

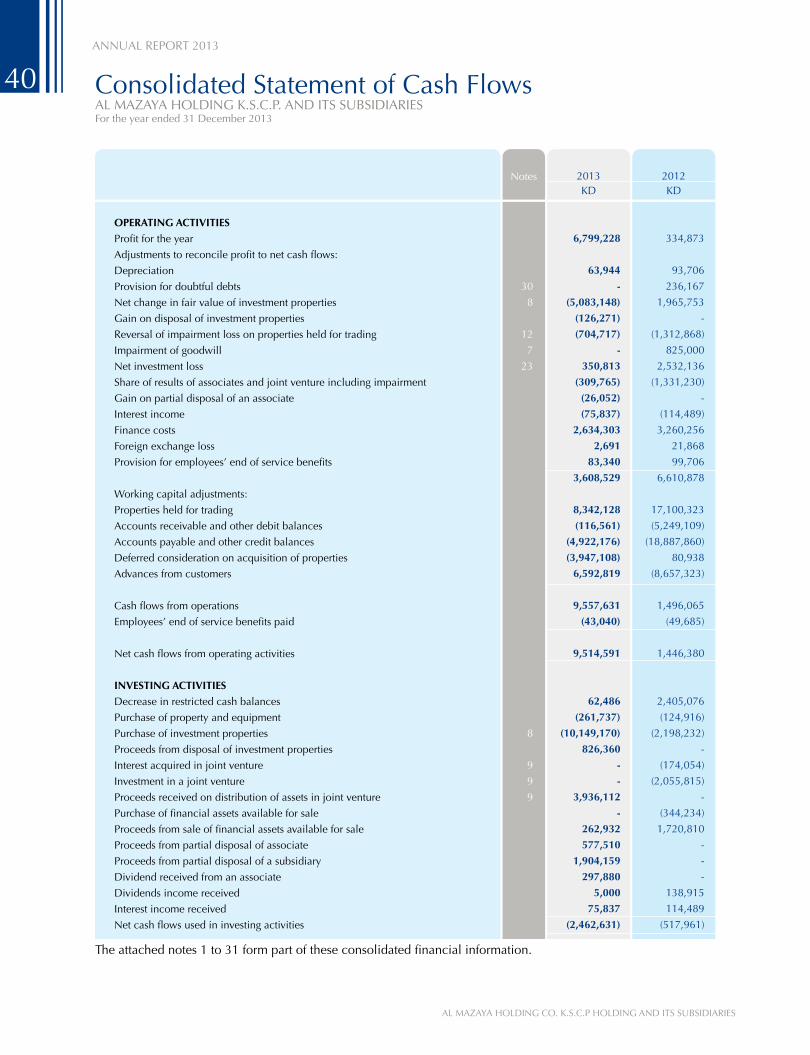

OPERATING ACTIVITIES

Profit for the year

Adjustments to reconcile profit to net cash flows:

Depreciation

Provision for doubtful debts

Net change in fair value of investment properties

Gain on disposal of investment properties

Reversal of impairment loss on properties held for trading

Impairment of goodwill

Net investment loss

Share of results of associates and joint venture including impairment

Gain on partial disposal of an associate

Interest income

Finance costs

Foreign exchange loss

Provision for employees’ end of service benefits

Working capital adjustments:

Properties held for trading

Accounts receivable and other debit balances

Accounts payable and other credit balances

Deferred consideration on acquisition of properties

Advances from customers

Cash flows from operations

Employees’ end of service benefits paid

Net cash flows from operating activities

INVESTING ACTIVITIES

Decrease in restricted cash balances

Purchase of property and equipment

Purchase of investment properties

Proceeds from disposal of investment properties

Interest acquired in joint venture

Investment in a joint venture

Proceeds received on distribution of assets in joint venture

Purchase of financial assets available for sale

Proceeds from sale of financial assets available for sale

Proceeds from partial disposal of associate

Proceeds from partial disposal of a subsidiary

Dividend received from an associate

Dividends income received

Interest income received

Net cash flows used in investing activities

6,799,228

63,944

-

)5,083,148(

)126,271(

)704,717(

-

350,813

)309,765(

)26,052(

)75,837(

2,634,303

2,691

83,340

3,608,529

8,342,128

)116,561(

)4,922,176(

)3,947,108(

6,592,819

9,557,631

)43,040(

9,514,591

62,486

)261,737(

)10,149,170(

826,360

-

-

3,936,112

-

262,932

577,510

1,904,159

297,880

5,000

75,837

)2,462,631(

Consolidated Statement of Cash FlowsAL MAZAYA HOLDING K.S.C.P. AND ITS SUBSIDIARIESFor the year ended 31 December 201320

The attached notes 1 to 31 form part of these consolidated financial information.

40

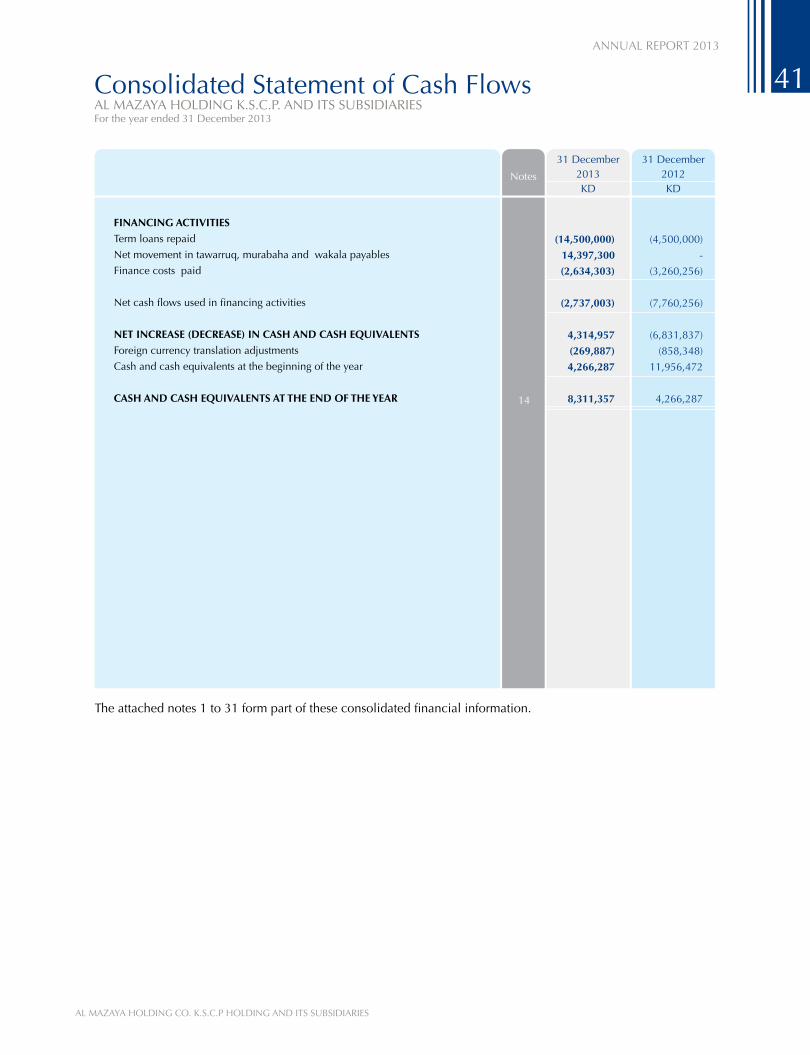

14

)14,500,000(

14,397,300

)2,634,303(

)2,737,003(

4,314,957

)269,887(

4,266,287

8,311,357

(4,500,000)

-

(3,260,256)

(7,760,256)

(6,831,837)

(858,348)

11,956,472

4,266,287

FINANCING ACTIVITIES

Term loans repaid

Net movement in tawarruq, murabaha and wakala payables

Finance costs paid

Net cash flows used in financing activities

NET INCREASE )DECREASE( IN CASH AND CASH EQUIVALENTS

Foreign currency translation adjustments

Cash and cash equivalents at the beginning of the year

CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR

31 December2013KD

31 December2012KD

Notes

The attached notes 1 to 31 form part of these consolidated financial information.

Consolidated Statement of Cash FlowsAL MAZAYA HOLDING K.S.C.P. AND ITS SUBSIDIARIESFor the year ended 31 December 2013 21

07 41

Notes to The Consolidated Financial StatementAL MAZAYA HOLDING COMPANY K.S.C.P. AND ITS SUBSIDIARIES31 December 2013

1. CORPORATE INFORMATION

Al Mazaya Holding Company - K.S.C.P. (the “Parent Company”) was incorporated on 7 November 1998 under the

Companies Law No. 25 of 2012 and amended thereto. The Parent Company is engaged in investment in local and foreign

companies, real estate properties and consultancy services. This consolidated financial statement presents the results of the

Parent Company and its subsidiaries (collectively referred to as the “Group”).

The registered head office of the Parent Company is at Mazaya Tower 01, Al Murqab, P.O. Box 3546, Safat 13036, State

of Kuwait.

The principal activities of the Parent Company as per the article of association are as follows:

Ownership of Kuwaiti and foreign shareholding companies, ownership of shares and portions of limited liability Kuwaiti

and foreign companies or participating in the formation of those companies, as well as managing and guaranteeing those

companies, granting loans to the companies in which it owns shares in and guaranteeing them towards others, provided

that the percentage of participation of the holding company in the capital of the borrowing company is not less than 20%,

ownership of industrial property rights including intellectual rights, trade marks, industrial marks, industrial fees or any

other rights relating to such assets and leasing them to other companies to utilize them whether inside or outside the state

of Kuwait, ownership of the movable assets and real properties needed to operate within the applicable laws, utilization

of its available financial surpluses by investing them in financial real estate portfolios managed by specialized companies.

The Parent Company has the right to practice its aforementioned objectives inside the State of Kuwait and abroad for itself

or as agent or representative to other, the Company has the right as well to have interest or to participate with entities that

practice similar operations or assist the Company in achieving its objectives inside and outside Kuwait, and such it has the

right to establish, form partnership, purchase or merge with those entities.

The consolidated financial statements of the Group for the year ended 31 December 2013 were authorised for issue by

the Board of Directors on 26 January 2014, and are issued subject to the approval of the Ordinary General Assembly of

the shareholders of the Parent Company. The shareholders’ General Assembly has the power to amend the consolidated

financial statements after issuance.

The New Companies Law issued on 26 November 2012 by Decree Law no. 25 of 2012 (the “Companies Law”), cancelled

the Commercial Companies Law No. 15 of 1960. The Companies Law was subsequently amended on 27 March 2013 by

Decree Law no. 97 of 2013 (the Decree). The Executive Regulations of the new amended law issued on 29 September 2013

and was published in the official Gazette on 6 October 2013.

As per article three of the executive regulations, the companies have one year from the date of publishing the executive

regulations to comply with the new amended law.

2. BASIS OF PREPERATION

The consolidated financial statements of the Group have been prepared on the historical cost basis, except for financial

assets available for sale, and investment properties that have been measured at fair value.

The consolidated financial statements are presented in Kuwaiti Dinars (“KD”), which is the functional currency of the Parent

Company. The consolidated financial statements have been prepared in accordance with International Financial Reporting

Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and applicable requirements of

Ministerial Order No. 18 of 1990.

42

Notes to The Consolidated Financial StatementAL MAZAYA HOLDING COMPANY K.S.C.P. AND ITS SUBSIDIARIES31 December 2013

3. CHANGES IN ACCOUNTING POLICIES

New and amended standards and interpretationsThe accounting policies adopted are consistent with those of the previous financial year, except for the following new and amended IFRS effective as of 1 January 2013:

The adoption of the standards or interpretations is described below:

IAS 1 Presentation of Items of Other Comprehensive Income – Amendments to IAS 1

The amendments to IAS 1 change the grouping of items presented in OCI. Items that could be reclassified (or ‘recycled’)

to profit or loss at a future point in time would be presented separately from items that will never be reclassified. The

amendment affects presentation only and therefore has no impact on the Group’s financial position or performance.

IFRS 7 Disclosures — Offsetting Financial Assets and Financial Liabilities - Amendments to IFRS 7

These amendments require an entity to disclose information about rights to set-off and related arrangements (e.g., collateral

agreements). The disclosures would provide users with information that is useful in evaluating the effect of netting

arrangements on an entity’s financial position. The new disclosures are required for all recognised financial instruments

that are set off in accordance with IAS 32 financial instruments: presentation. The disclosures also apply to recognised

financial instruments that are subject to an enforceable master netting arrangement or similar agreement, irrespective of

whether they are set off in accordance with IAS 32. The Group does not have any assets with these characteristics so there

has been no effect on the presentation of its consolidated financial statements.

IFRS 10 Consolidated Financial Statements

IFRS 10 establishes a single control model that applies to all entities including special purpose entities. IFRS 10 replaces the

parts of previously existing IAS 27 Consolidated and Separate Financial Statements that dealt with consolidated financial

statements and SIC-12 Consolidation – Special Purpose Entities. IFRS 10 changes the definition of control such that an

investor controls an investee when it is exposed, or has rights, to variable returns from its involvement with the investee

and has the ability to affect those returns through its power over the investee. To meet the definition of control in IFRS

10, all three criteria must be met, including: (a) an investor has power over an investee; (b) the investor has exposure, or

rights, to variable returns from its involvement with the investee; and (c) the investor has the ability to use its power over

the investee to affect the amount of the investor’s returns. The adoption of this standard did not have any material impact

on the consolidated financial position or performance of the Group.

IFRS 11 Joint Arrangements and IAS 28 Investment in Associates and Joint Ventures

IFRS 11 replaces IAS 31 Interests in Joint Ventures and SIC-13 Jointly-controlled Entities — Non-monetary Contributions by

Venturers. IFRS 11 removes the option to account for jointly controlled entities (JCEs) using proportionate consolidation.

Instead, JCEs that meet the definition of a joint venture under IFRS 11 must be accounted for using the equity method. This

amendment does not have any impact on the consolidated financial statement.

24

09 43

Notes to The Consolidated Financial StatementAL MAZAYA HOLDING COMPANY K.S.C.P. AND ITS SUBSIDIARIES31 December 2013

IFRS 12 Disclosure of Involvement with Other Entities IFRS 12 sets out the requirements for disclosures relating to an entity’s interests in subsidiaries, joint arrangements, associates and structured entities. It does not apply to certain employee benefit plans, separate financial statements to which IAS 27 Separate Financial Statements applies (except in relation to unconsolidated structured entities and investment entities in some cases), certain interests in joint ventures held by an entity that does not share in joint control, and the majority of interests in another entity accounted for in accordance with IFRS 9 Financial Instruments. IFRS 12 adds to the disclosure requirements of IAS 1 by specifically requiring an entity to disclose all significant judgements and estimates made in determining the nature of its interest in another entity or arrangement, and in determining the type of joint arrangement in which it has an interest. Adoption of this standard did not have any impact on the consolidated financial statement of the Group and the new disclosure are made in consolidated financial statement.

IFRS 13 Fair Value Measurement IFRS 13 establishes a single source of guidance under IFRS for all fair value measurements. The standard does not change when an entity is required to use fair value, but rather provides guidance on how to measure fair value under IFRS when fair value is required or permitted. IFRS 13 requires an entity to disclose information that helps users of its financial statements to assess both of the following: (a) For assets and liabilities that are measured at fair value on a recurring or non-recurring basis in the statement of financial position after initial recognition, the valuation techniques and inputs used to develop those measurements. (b) For fair value measurements using significant unobservable inputs, the effect of the measurements on profit or loss or other comprehensive income for the period.

The application of IFRS 13 has not materially impacted the fair value measurements carried out by the Group. IFRS 13 also requires specific disclosures on fair values, some of which replace existing disclosure requirements in other standards, including IFRS 7 Financial Instruments: Disclosures. Some of these disclosures are specifically required for non-financial instruments, thereby affecting the disclosures of consolidated financial statements. The Group provides these disclosures in Note 29.

Standard issue but not yet effectiveStandards issued but not yet effective up to the date of issuance of the Group’s financial statements are listed below. This listing of standards issued is those that the Group reasonably expects to have an impact on disclosures, financial position or performance when applied at a future date. The Group intends to adopt these standards when they become effective.

IFRS 9 ‘Financial Instruments’:The standard was issued in November 2009, however at the IASB meeting in July 2013, the IASB tentatively decided to defer the mandatory effective date of IFRS 9 to be left open. However, IFRS 9 would still be available for early application. The standard improves the ability of the users of the financial statement to assess the amount, timing and uncertainty of future cash flows of the entity by replacing many financial instrument classification categories, measurement and associated impairment methods. The application of IFRS 9 will result in amendments and additional disclosures relating to financial instruments and associated risks.

IAS 32 Offsetting Financial Assets and Financial Liabilities — Amendments to IAS 32These amendments clarify the meaning of “currently has a legally enforceable right to set-off”. The amendments also clarify the application of the IAS 32 offsetting criteria to settlement systems (such as central clearing house systems) which apply gross settlement mechanisms that are not simultaneous. This amendment is not expected to impact the Group’s financial position or performance and becomes effective for annual periods beginning on or after 1 January 2014.

Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27)These amendments are effective for annual periods beginning on or after 1 January 2014 provide an exception to the consolidation requirement for entities that meet the definition of an investment entity under IFRS 10. The exception to consolidation requires investment entities to account for subsidiaries at fair value through profit or loss. This amendment would not be relevant to the Group, since the Group would not qualify to be an investment entity under IFRS 10.

25

44

Notes to The Consolidated Financial StatementAL MAZAYA HOLDING COMPANY K.S.C.P. AND ITS SUBSIDIARIES31 December 2013

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIESBasis of consolidation The consolidated financial statements comprise the financial statements of the Parent Company and its subsidiary as at 31 December 2013. Control is achieved when the Group is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. Specifically, the Group controls an investee if and only if the Group has:• Power over the investee (i.e. existing rights that give it the current ability to direct the relevant activities of the investee)• Exposure, or rights, to variable returns from its involvement with the investee, and• The ability to use its power over the investee to affect its returns

When the Group has less than a majority of the voting or similar rights of an investee, the Group considers all relevant facts and circumstances in assessing whether it has power over an investee, including:• The contractual arrangement with the other vote holders of the investee• Rights arising from other contractual arrangements• The Parent Company’s voting rights and potential voting rights

The financial statements of the Subsidiary are prepared at the same reporting year as the Parent Company using consistent accounting policies. Subsidiaries are consolidated from the date on which the Group obtains control and continues to be consolidated until the date that such control ceases.

All material intra-group balances and transactions, including material unrealised gains and losses arising on intra-group transactions are eliminated on consolidation.

Non-controlling interest represents the portion of profit and loss and net assets not held by the Group and are presented separately in the consolidated statement of income and within equity in the consolidated statement of financial position separately from equity attributable to the equity holders of the Parent Company.

A change in the ownership interest of a subsidiary, without a change of control, is accounted for as an equity transaction. Losses are attributed to the non controlling interest even if that results in a deficit balance. If the Group loses control over a subsidiary, it:• Derecognises the assets (including goodwill) and liabilities of the subsidiary;• Derecognises the carrying amount of any non controlling interest;• Derecognises the cumulative translation differences, recorded in equity;• Recognises the fair value of the consideration received;• Recognises the fair value of any investment retained;• Recognises any surplus or deficit in consolidated statement of income; and• Reclassifies the Parent Company’s share of components previously recognised in other comprehensive income to

consolidated statement of income or retained earnings as appropriate.

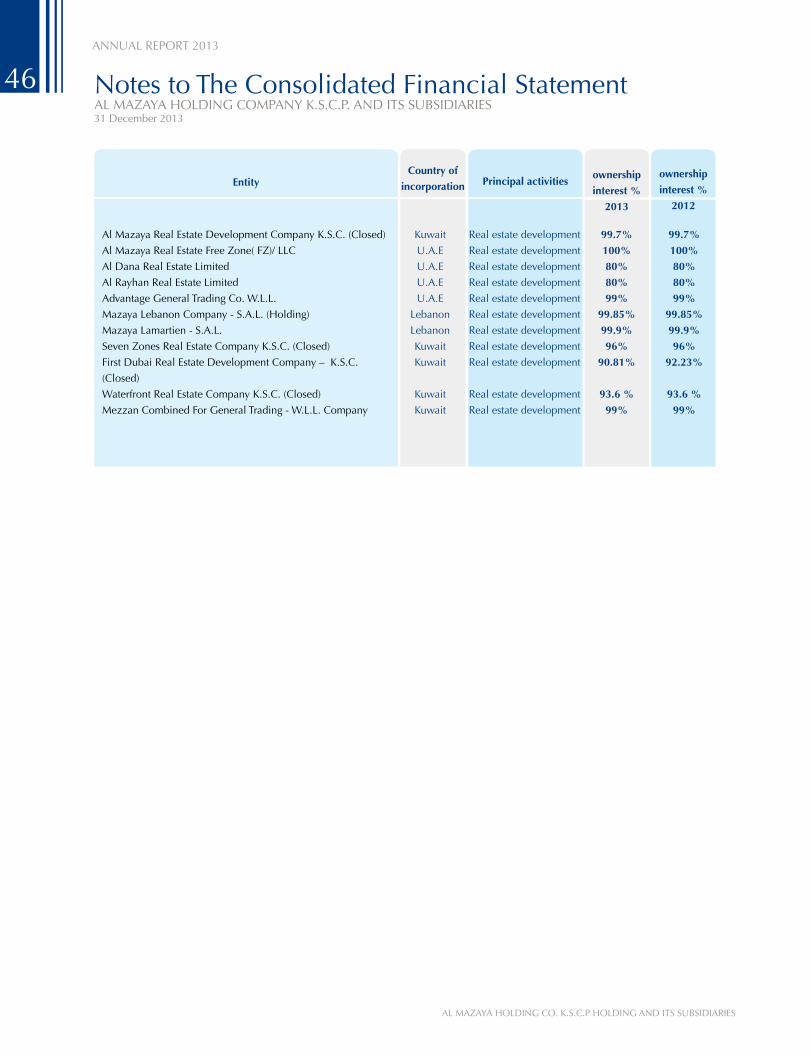

The consolidated financial statements include the financial statements of the Parent Company and the following subsidiaries, where the Parent Company has direct investment :

26

11 45

Notes to The Consolidated Financial StatementAL MAZAYA HOLDING COMPANY K.S.C.P. AND ITS SUBSIDIARIES31 December 2013

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

Real estate development

99.7%

100%

80%

80%

99%

99.85%

99.9%

96%

90.81%

93.6 %

99%

99.7%

100%

80%

80%

99%

99.85%

99.9%

96%

92.23%

93.6 %

99%

Principal activities

Al Mazaya Real Estate Development Company K.S.C. (Closed)

Al Mazaya Real Estate Free Zone( FZ)/ LLC

Al Dana Real Estate Limited

Al Rayhan Real Estate Limited

Advantage General Trading Co. W.L.L.

Mazaya Lebanon Company - S.A.L. (Holding)

Mazaya Lamartien - S.A.L.

Seven Zones Real Estate Company K.S.C. (Closed)

First Dubai Real Estate Development Company – K.S.C.

(Closed)

Waterfront Real Estate Company K.S.C. (Closed)

Mezzan Combined For General Trading - W.L.L. Company

ownership

interest %

2013

ownership

interest %

2012

Country of

incorporationEntity

Kuwait

U.A.E

U.A.E

U.A.E

U.A.E

Lebanon

Lebanon

Kuwait

Kuwait

Kuwait

Kuwait

27

46

Notes to The Consolidated Financial StatementAL MAZAYA HOLDING COMPANY K.S.C.P. AND ITS SUBSIDIARIES31 December 2013

Business combinations and goodwillA business combination is the bringing together of separate entities or businesses into one reporting entity as a result one entity, the acquirer, obtaining control of one or more other businesses. The acquisition method of accounting is used to account for business combinations. The cost of an acquisition is measured as the aggregate of the consideration transferred, measured at acquisition date fair value and the amount of any non-controlling interests in the acquiree. Under this method, the Group recognises, separately from goodwill, identifiable assets acquired, liabilities assumed and any non-controlling interests in the acquiree at the acquisition date. For each business combination, the Group elects to measure the non-controlling interests in the acquiree either at fair value or at the proportionate share of the acquiree’s identifiable net assets. Acquisition costs incurred are expensed and included in other expenses.

When the Group acquires a business, it assesses the financial assets and liabilities assumed for appropriate classification and designation in accordance with the contractual terms, economic circumstances and pertinent conditions as at the acquisition date. This includes the separation of embedded derivatives in host contracts by the acquiree.

If the business combination is achieved in stages, the acquisition date fair value of the acquirer’s previously held equity interest in the acquiree is remeasured to fair value at the acquisition date through profit or loss.