finance and human resources committee - east valley water

TRANSCRIPT

FINANCE AND HUMAN RESOURCES COMMITTEE

May 30, 2017 - 3:30 PM

31111 Greenspot Road, Highland CA 92346

AGENDA

CALL TO ORDER

PLEDGE OF ALLEGIANCE

PUBLIC COMMENTS

NEW BUSINESS

1. Approve the April 25, 2017 Finance and Human Resources Standing CommitteeMeeting Minutes

2. Present Entrance Conference Items for Auditing District Financials

3. Review Surplus Property Policy 7.1.1

ADJOURNPLEASE NOTE: Pursuant to Government Code Section 54954.2(a), any request for a disability-related modification oraccommodation, including auxiliary aids or services, that is sought in order to participate in the above-agendized public meeting should be directed to the District Clerk at (909) 885-4900 at least 72 hours priorto said meeting.

Page 1 of 2 Minutes 4/25/17 cmk

Subject to Approval

EAST VALLEY WATER DISTRICT April 25, 2017 FINANCE AND HUMAN RESOURCES STANDING COMMITTEE MEETING

MINUTES Ms. Koide called the meeting to order at 3:30 p.m. and Mr. Tompkins led the flag salute. PRESENT: Directors: Smith, Morales ABSENT: None STAFF: Brian Tompkins, Chief Financial Officer; Kerrie Bryan, Human

Resources/Risk & Safety Manager; Rudy Guerrero, Accountant; Christi Koide, Administrative Assistant

GUEST(s): Members of the Public PUBLIC COMMENTS The Administrative Assistant declared the public participation section of the meeting open at 3:32 p.m. There being no written or verbal comments, the public participation section was closed. APPROVE THE MARCH 28, 2017 FINANCE AND HUMAN RESOURCES STANDING COMMITTEE MEETING MINUTES M/S/C (Morales-Smith) to approve the March 28, 2017 Finance and Human Resources Standing Committee meeting minutes as submitted. DISCUSS CONTRACT AWARD FOR PROFESSIONAL AUDITING SERVICES The Chief Financial Officer provided an overview of the review process for the six proposals that were submitted, which included: technical qualifications, audit approach, cost comparison of fee proposals, and references. HUMAN RESOURCES UPDATE The Human Resources/Risk & Safety Manager provided recruitment updates for the following: Customer Service Recruitment for one permanent and one temporary Customer Service Representative; Field Service Worker I internal recruitment.

Page 2 of 2 Minutes 4/25/17 cmk

ADJOURN The meeting adjourned at 3:50 p.m. James Morales, Jr., David E. Smith, Governing Board Member Governing Board Member

STAFF REPORT

Agenda Item #2.Meeting Date: May 30, 2017

Discussion ItemTo: FINANCE AND HUMAN RESOURCES COMMITTEE From: Chief Financial Officer

Subject: Present Entrance Conference Items for Auditing District Financials

RECOMMENDATION:

Staff recommends that the Finance and Human Resources Standing Committee (Committee) review theEngagement Letters and planning document from Vicenti, Lloyd & Stutzman, LLP (VLS) for ProfessionalAuditing Services of EVWD and NFWC for the year ended June 30, 2017.

BACKGROUND / ANALYSIS:

Staff has placed this item on the Committee meeting agenda in order to introduce the principals from theDistrict’s new audit firm. In addition, as auditing is a review of managements’ activities, best practices dictatethat a line of communication be established between the District auditors and Governing Board. Therefore, attached for the Board to review are Engagement Letters from VLS to provide auditing services toEVWD for the fiscal year ended June 30, 2017, and an independent review of the North Fork Water Companyfor the year ended January 31, 2018. The Engagement Letters explain what the objectives of these services willbe, and describe the procedures that will be used to perform their work. We have also attached the firm’s‘Overall Plan to Accomplish the Audit’ document. This letter gives insight as to what audit services will beprovided along with the timing of the audit. Auditing Standards require for these documents to be communicated to those charged with Governance andVLS is present to answer any questions.

AGENCY IDEALS AND ENDEAVORS:

Ideals and Endeavor II - Maintain An Environment Committed To Elevated Public Service

(E) - Practice transparent & accountable fiscal management

REVIEW BY OTHERS:

This agenda item has been reviewed by the Administration Department.

FISCAL IMPACT:

There is no fiscal impact associated with this agenda item.

ATTACHMENTS:Description TypeAuditing Plan Backup MaterialEVWD Engagement Letter Backup MaterialNFWC Engagement Letter Backup Material

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT For the Year Ended June 30, 2017

Presented by Vicenti, Lloyd & Stutzman LLP Renee Graves, CPA, CGFM

Leslie Ward, CPA

AUDIT SERVICES/OBJECTIVES Our audit will be made in accordance with auditing standards generally accepted in the United States of America and the Standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. The audit will include such tests of the accounting records and other auditing procedures as we consider necessary to enable us to express our professional opinion whether the financial statements are presented fairly, in all material respects, in accordance with accounting principles generally accepted in the United States of America. The audit of the financial statements does not relieve management or those charged with governance of their responsibilities. An essential feature of our audit is to gain an understanding of your system of internal controls upon which the scope and extent of our audit tests will be determined. Such an audit is not intended to be sufficiently conclusive to assure the discovery of errors, fraudulent financial reporting, misappropriation of assets, or violations of laws or governmental regulations, although their discovery may result. However, we feel that it offers an acceptable balance between conclusive reliability and reasonable audit costs. It provides for inquiries and selective tests of your operating procedures, including those designed to safeguard property and the accuracy and timeliness of cash disbursements. It gives reasonable assurance that the overall financial position and the results of operations are fairly presented on the basis indicated. It should be recognized, however, that it gives less assurance as to the accuracy of the individual items appearing in the financial statements since the tests are directed toward forming an opinion on the financial statements taken as a whole. 2017 AUDIT SERVICES We will audit the Statement of Net Position, Statement of Revenues, Expenses and Changes in Net Position and Statement of Cash Flows as of and for the year ended June 30, 2017. The audit referred to above will include all supplementary schedules required by generally accepted accounting standards, the State Controller’s Office, and Single Audit Uniform Guidance. We will also ensure that the District’s comprehensive annual financial report (CAFR) is prepared in conformity with the current Governmental Accounting, Auditing, and Financial Reporting (GAAFR).

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT

For the Year Ended June 30, 2017

2017 AUDIT REQUIREMENTS (continued) We have not been engaged to report on any other statements, reports or forms that require an auditors’ opinion. We will perform review procedures for the North Fork Water Company and will issue an Independent Accountant’s Review Report. Management will prepare the financial statements, including footnotes and supplementary schedules in compliance with the reporting format required by Governmental Accounting Standards Board (GASB) No. 34; this includes financial reporting and disclosures for GASB No. 45 Other Postemployment Benefits Other Than Pensions (OPEB) and GASB No. 68 Accounting and Financial Reporting for Pensions—an amendment of GASB Statement No. 27. We can assist management in the preparation of the financial statements. The audit referred to above also includes reporting on internal control related to the financial statements and compliance with the provisions of applicable laws, regulations, contracts, agreements, and grants, noncompliance with which could have a material effect on the financial statements in accordance with Government Auditing Standards. COMMUNICATIONS ARISING FROM THE AUDIT We will communicate to the audit sub-committee certain other matters related to the conduct of our audit, in accordance with, generally accepted auditing standards on The Auditor’s Communication with Those Charged with Governance, this communication will include:

The Auditor’s Responsibilities with Regard to the Financial Statement Audit Planned Scope and Timing of the Audit Significant Findings from the Audit:

♦ Qualitative aspects of significant accounting practices of the District such as accounting policies, accounting estimates and financial statement disclosures

♦ Significant difficulties, if any, encountered in performing the audit ♦ Uncorrected misstatements ♦ Disagreements with management ♦ Material, corrected misstatements as a result of audit procedures ♦ Representations the auditor has requested from management ♦ Management’s consultations with other accountants ♦ Significant issues such as business conditions affecting the District or the

application of accounting principles and auditing standards – especially if discussed prior to our retention as the auditor

♦ Other findings or issues that we believe to be significant and relevant to those responsible for the financial reporting process

Independence – communication of any non-audit services performed or expected to be performed

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT For the Year Ended June 30, 2017

COMMUNICATIONS ARISING FROM THE AUDIT (continued) As part of the required communications, we will communicate, to the extent that they come to our attention, material errors, fraud or other illegal acts that are clearly not inconsequential, and any control deficiencies. Any internal control or compliance related matters that are required to be communicated under professional standards or Federal and State agencies will be included in our audit report. We may also have other comments for management on matters we have observed and possible ways to improve the efficiency of your operations, or other recommendations concerning the internal control structure. With respect to these other communications, it is our normal practice to discuss comments, if appropriate, with the level of management responsible for the matters prior to their communication to senior management and/or the Finance Committee. Before our reports are issued, draft copies are reviewed with management and Finance Committee. These reports are also subjected to firm technical review procedures by an independent partner. ORGANIZATION AND STAFF Our staffing has been planned to obtain the optimum blend of efficiency and quality. Renee Graves is the engagement partner, Leslie Ward is the engagement manager and Daphne Liu is the senior in-charge over the engagement. The partner, manager and in-charge all have significant industry knowledge. The manager and in-charge will have responsibility for coordinating all of the audit areas on the 2017 engagement. TIMING OF THE AUDIT Our audit of the financial statements will be performed in three phases: (1) planning, (2) test of controls and risk assessment, and (3) account balance procedures. We will maintain regular contact with appropriate members of management to ensure all due dates will be met.

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT For the Year Ended June 30, 2017

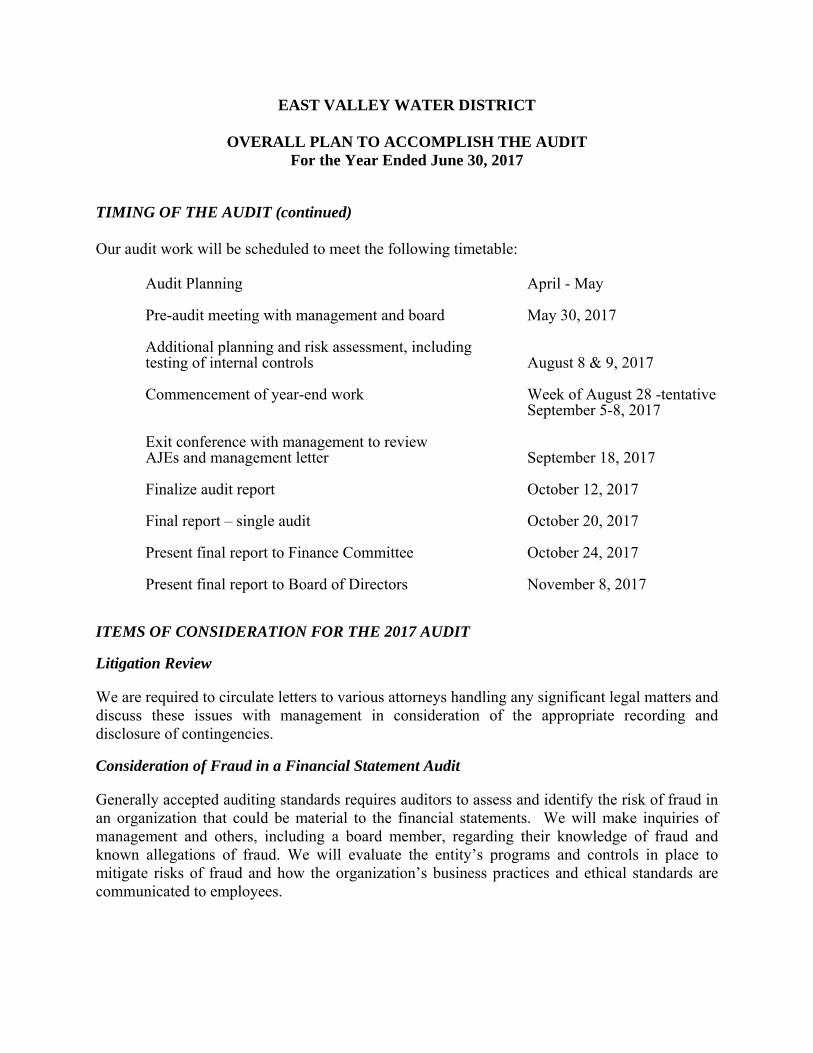

TIMING OF THE AUDIT (continued) Our audit work will be scheduled to meet the following timetable:

Audit Planning April - May

Pre-audit meeting with management and board May 30, 2017 Additional planning and risk assessment, including testing of internal controls August 8 & 9, 2017 Commencement of year-end work Week of August 28 -tentative September 5-8, 2017 Exit conference with management to review AJEs and management letter September 18, 2017

Finalize audit report October 12, 2017

Final report – single audit October 20, 2017 Present final report to Finance Committee October 24, 2017 Present final report to Board of Directors November 8, 2017

ITEMS OF CONSIDERATION FOR THE 2017 AUDIT Litigation Review We are required to circulate letters to various attorneys handling any significant legal matters and discuss these issues with management in consideration of the appropriate recording and disclosure of contingencies. Consideration of Fraud in a Financial Statement Audit Generally accepted auditing standards requires auditors to assess and identify the risk of fraud in an organization that could be material to the financial statements. We will make inquiries of management and others, including a board member, regarding their knowledge of fraud and known allegations of fraud. We will evaluate the entity’s programs and controls in place to mitigate risks of fraud and how the organization’s business practices and ethical standards are communicated to employees.

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT For the Year Ended June 30, 2017

NEW GOVERNMENTAL ACCOUNTING STANDARDS As deemed necessary, the Governmental Accounting Standard Board (GASB) will issue new accounting standards that may impact financial presentations. It is management’s responsibility to implement the appropriate GASB Statement as they pertain to District operations. We can provide assistance to the District with implementation of a new standard under a separate agreement. Statement No. 74 – Financial Reporting for Postemployment Benefit Plans Other than Pension Plans

In June 2015, the GASB issued Statement No. 74 and establishes standards of financial reporting for defined benefit OPEB plans and defined contribution OPEB plans. This statement is closely related in some areas to Statement No. 75. The statement is effective for the fiscal year 2016–17. Governmental Accounting Standards Board Statement No. 80 In January 2016, the GASB issued Statement No. 80 Blending Requirements for Certain Component Units—an amendment of GASB Statement No. 14. This statement establishes an additional blending requirement for the financial statement presentation of component units. A component unit should be included in the reporting entity financial statements if the component unit is organized as a not-for-profit corporation in which the primary government is the sole corporate member, as identified in the component unit’s articles of incorporation or bylaws, and the component unit is included in the financial reporting entity pursuant to the provisions in paragraphs 21−37 of Statement 14, as amended. The statement is effective for the fiscal year 2016-17. Governmental Accounting Standards Board Statement No. 82 In March 2016, the GASB issued Statement No. 82 Pension Issues—an amendment of GASB Statements No. 67, No. 68, and No. 73. This statement addresses issues regarding (1) the presentation of payroll-related measures in required supplementary information, (2) the selection of assumptions and the treatment of deviations from the guidance in an Actuarial Standard of Practice for financial reporting purposes, and (3) the classification of payments made by employers to satisfy employee (plan member) contribution requirements. The statement is effective for the fiscal year 2016-17. NEW GOVERNMENTAL ACCOUNTING STANDARDS ISSUED, NOT YET EFFECTIVE Future GASB Statements In addition, to the GASB Statements noted above, there are several exposure drafts with potential implementation dates ranging from fiscal years 2017-18 and beyond.

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT For the Year Ended June 30, 2017

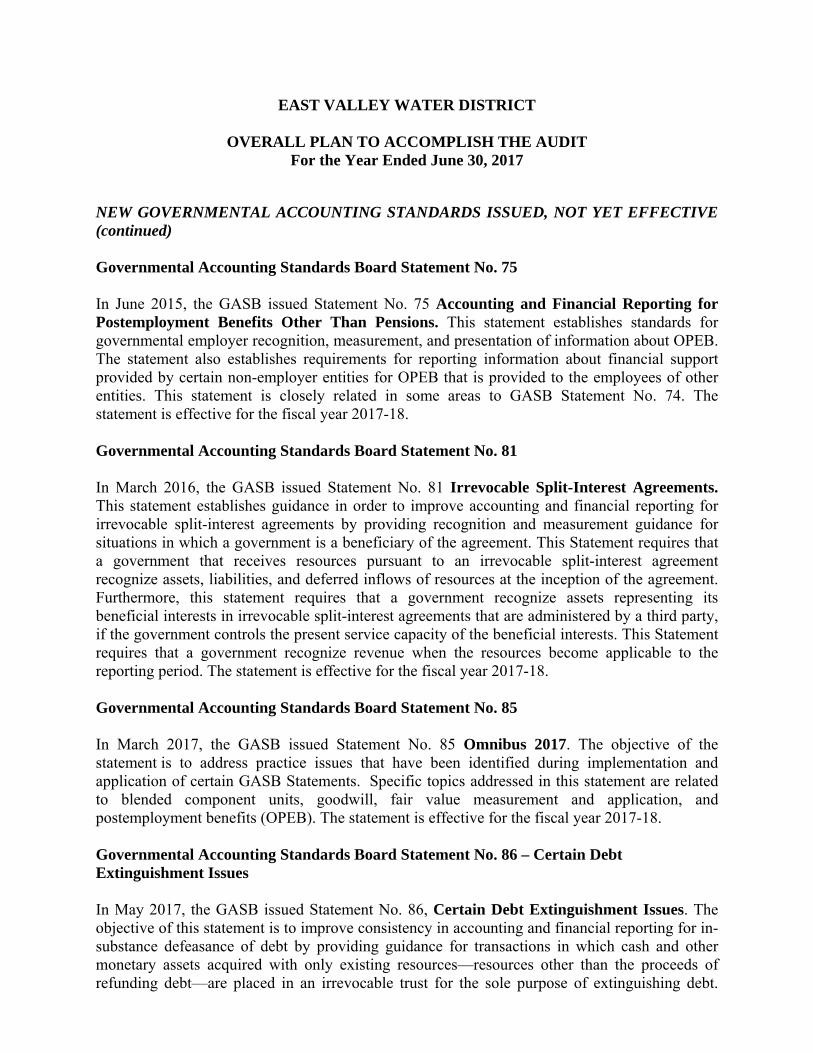

NEW GOVERNMENTAL ACCOUNTING STANDARDS ISSUED, NOT YET EFFECTIVE (continued) Governmental Accounting Standards Board Statement No. 75 In June 2015, the GASB issued Statement No. 75 Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions. This statement establishes standards for governmental employer recognition, measurement, and presentation of information about OPEB. The statement also establishes requirements for reporting information about financial support provided by certain non-employer entities for OPEB that is provided to the employees of other entities. This statement is closely related in some areas to GASB Statement No. 74. The statement is effective for the fiscal year 2017-18. Governmental Accounting Standards Board Statement No. 81 In March 2016, the GASB issued Statement No. 81 Irrevocable Split-Interest Agreements. This statement establishes guidance in order to improve accounting and financial reporting for irrevocable split-interest agreements by providing recognition and measurement guidance for situations in which a government is a beneficiary of the agreement. This Statement requires that a government that receives resources pursuant to an irrevocable split-interest agreement recognize assets, liabilities, and deferred inflows of resources at the inception of the agreement. Furthermore, this statement requires that a government recognize assets representing its beneficial interests in irrevocable split-interest agreements that are administered by a third party, if the government controls the present service capacity of the beneficial interests. This Statement requires that a government recognize revenue when the resources become applicable to the reporting period. The statement is effective for the fiscal year 2017-18. Governmental Accounting Standards Board Statement No. 85 In March 2017, the GASB issued Statement No. 85 Omnibus 2017. The objective of the statement is to address practice issues that have been identified during implementation and application of certain GASB Statements. Specific topics addressed in this statement are related to blended component units, goodwill, fair value measurement and application, and postemployment benefits (OPEB). The statement is effective for the fiscal year 2017-18. Governmental Accounting Standards Board Statement No. 86 – Certain Debt Extinguishment Issues In May 2017, the GASB issued Statement No. 86, Certain Debt Extinguishment Issues. The objective of this statement is to improve consistency in accounting and financial reporting for in-substance defeasance of debt by providing guidance for transactions in which cash and other monetary assets acquired with only existing resources—resources other than the proceeds of refunding debt—are placed in an irrevocable trust for the sole purpose of extinguishing debt.

EAST VALLEY WATER DISTRICT

OVERALL PLAN TO ACCOMPLISH THE AUDIT For the Year Ended June 30, 2017

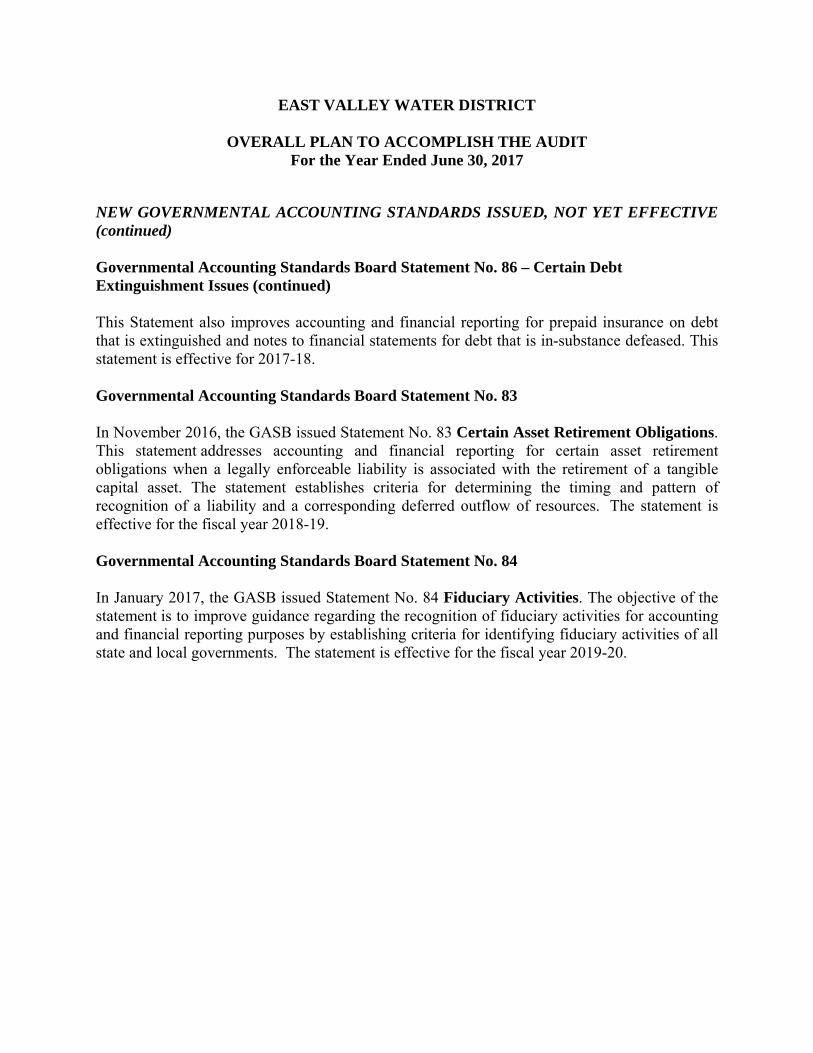

NEW GOVERNMENTAL ACCOUNTING STANDARDS ISSUED, NOT YET EFFECTIVE (continued) Governmental Accounting Standards Board Statement No. 86 – Certain Debt Extinguishment Issues (continued) This Statement also improves accounting and financial reporting for prepaid insurance on debt that is extinguished and notes to financial statements for debt that is in-substance defeased. This statement is effective for 2017-18. Governmental Accounting Standards Board Statement No. 83 In November 2016, the GASB issued Statement No. 83 Certain Asset Retirement Obligations. This statement addresses accounting and financial reporting for certain asset retirement obligations when a legally enforceable liability is associated with the retirement of a tangible capital asset. The statement establishes criteria for determining the timing and pattern of recognition of a liability and a corresponding deferred outflow of resources. The statement is effective for the fiscal year 2018-19. Governmental Accounting Standards Board Statement No. 84 In January 2017, the GASB issued Statement No. 84 Fiduciary Activities. The objective of the statement is to improve guidance regarding the recognition of fiduciary activities for accounting and financial reporting purposes by establishing criteria for identifying fiduciary activities of all state and local governments. The statement is effective for the fiscal year 2019-20.

East Valley Water District Page 3 May 10, 2017

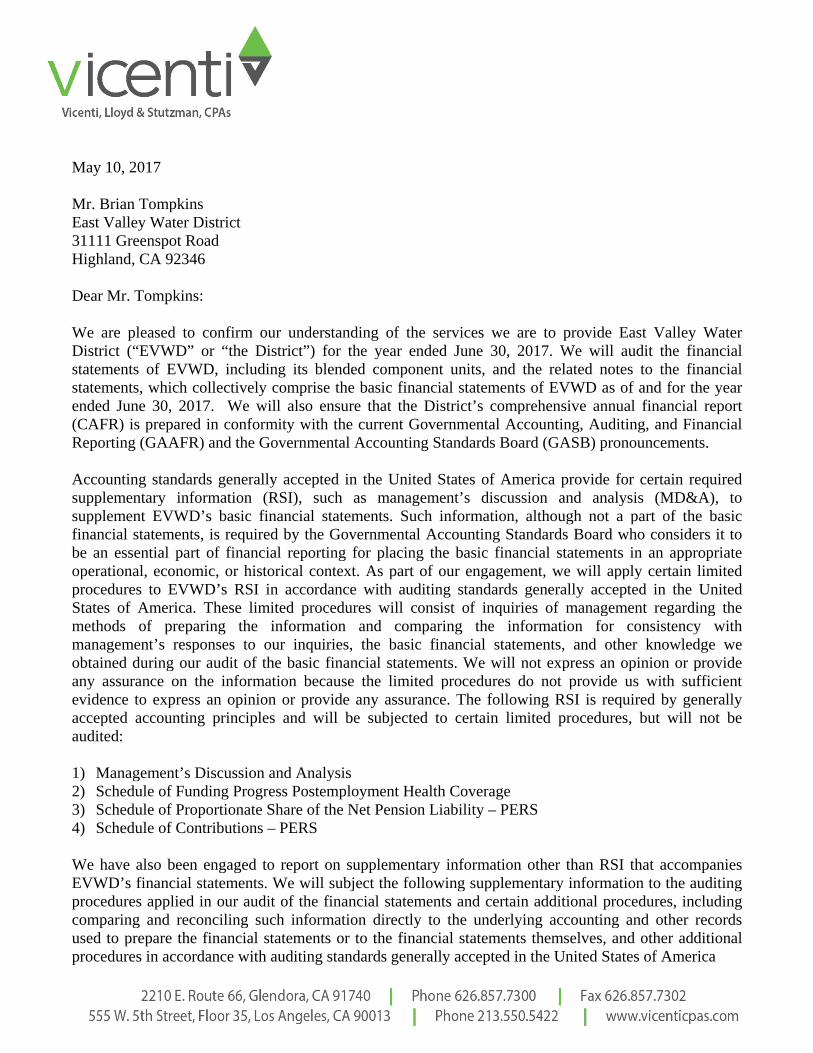

May 10, 2017 Mr. Brian Tompkins East Valley Water District 31111 Greenspot Road Highland, CA 92346 Dear Mr. Tompkins: We are pleased to confirm our understanding of the services we are to provide East Valley Water District (“EVWD” or “the District”) for the year ended June 30, 2017. We will audit the financial statements of EVWD, including its blended component units, and the related notes to the financial statements, which collectively comprise the basic financial statements of EVWD as of and for the year ended June 30, 2017. We will also ensure that the District’s comprehensive annual financial report (CAFR) is prepared in conformity with the current Governmental Accounting, Auditing, and Financial Reporting (GAAFR) and the Governmental Accounting Standards Board (GASB) pronouncements. Accounting standards generally accepted in the United States of America provide for certain required supplementary information (RSI), such as management’s discussion and analysis (MD&A), to supplement EVWD’s basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. As part of our engagement, we will apply certain limited procedures to EVWD’s RSI in accordance with auditing standards generally accepted in the United States of America. These limited procedures will consist of inquiries of management regarding the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We will not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. The following RSI is required by generally accepted accounting principles and will be subjected to certain limited procedures, but will not be audited: 1) Management’s Discussion and Analysis 2) Schedule of Funding Progress Postemployment Health Coverage 3) Schedule of Proportionate Share of the Net Pension Liability – PERS 4) Schedule of Contributions – PERS We have also been engaged to report on supplementary information other than RSI that accompanies EVWD’s financial statements. We will subject the following supplementary information to the auditing procedures applied in our audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America

East Valley Water District Page 2 May 10, 2017

and we will provide an opinion on it in relation to the financial statements as a whole in a report combined with our auditor’s report on the financial statements, except for the schedule of expenditures of federal awards that will be in a separate written report accompanying our auditor’s report: 1) Schedule of Expenditures of Federal Awards 2) Combining Schedule of Net Position 3) Combining Schedule of Revenues, Expenses, and Changes in Net Position 4) Combining Schedule of Cash Flows 5) Refunding Revenue Bonds – Series 2010 6) Refunding Revenue Bonds – Series 2013 7) US Bancorp Installment Purchase Agreement 8) Department of Water Resources Construction Loan – Contract 00C412 9) Department of Water Resources Construction Loan – Contract 10CX110 Audit Objectives The objective of our audit is the expression of an opinion as to whether your financial statements are fairly presented, in all material respects, in conformity with U.S. generally accepted accounting principles and to report on the fairness of the supplementary information referred to in the second paragraph when considered in relation to the financial statements as a whole. The objective also includes reporting on—

• Internal control over financial reporting and compliance with provisions of laws, regulations, contracts, and award agreements, noncompliance with which could have a material effect on the financial statements in accordance with Government Auditing Standards.

• Internal control over compliance related to major programs and an opinion (or disclaimer of opinion) on compliance with federal statutes, regulations, and the terms and conditions of federal awards that could have a direct and material effect on each major program in accordance with the Single Audit Act Amendments of 1996 and Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance).

The Government Auditing Standards report on internal control over financial reporting and on compliance and other matters will include a paragraph that states that (1) the purpose of the report is solely to describe the scope of testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance, and (2) the report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. The Uniform Guidance report on internal control over compliance will include a paragraph that states that the purpose of the report on internal control over compliance is solely to describe the scope of testing of internal control over compliance and the results of that testing based on the requirements of the Uniform Guidance. Both reports will state that the report is not suitable for any other purpose. Our audit will be conducted in accordance with auditing standards generally accepted in the United States of America; the standards for financial audits contained in Government Auditing Standards,

East Valley Water District Page 3 May 10, 2017

issued by the Comptroller General of the United States; the Single Audit Act Amendments of 1996; and the provisions of the Uniform Guidance, and will include tests of accounting records, a determination of major program(s) in accordance with the Uniform Guidance, and other procedures we consider necessary to enable us to express such an opinion. We will issue a written report upon completion of our Single Audit. Our report will be addressed to the Board of Directors of EVWD. We cannot provide assurance that an unmodified opinion will be expressed. Circumstances may arise in which it is necessary for us to modify our opinion or add emphasis-of-matter or other-matter paragraphs. If our opinion is other than unmodified, we will discuss the reasons with you in advance. If, for any reason, we are unable to complete the audit or are unable to form or have not formed an opinion, we may decline to express an opinion or issue our report, or we may withdraw from this engagement.

Audit Procedures—General

An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; therefore, our audit will involve judgment about the number of transactions to be examined and the areas to be tested. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We will plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether from (1) errors, (2) fraudulent financial reporting, (3) misappropriation of assets, or (4) violations of laws or governmental regulations that are attributable to the government or to acts by management or employees acting on behalf of the government. Because the determination of abuse is subjective, Government Auditing Standards do not expect auditors to provide reasonable assurance of detecting abuse.

Because of the inherent limitations of an audit, combined with the inherent limitations of internal control, and because we will not perform a detailed examination of all transactions, there is a risk that material misstatements or noncompliance may exist and not be detected by us, even though the audit is properly planned and performed in accordance with U.S. generally accepted auditing standards and Government Auditing Standards. In addition, an audit is not designed to detect immaterial misstatements or violations of laws or governmental regulations that do not have a direct and material effect on the financial statements or on major programs. However, we will inform the appropriate level of management of any material errors, any fraudulent financial reporting, or misappropriation of assets that come to our attention. We will also inform the appropriate level of management of any violations of laws or governmental regulations that come to our attention, unless clearly inconsequential, and of any material abuse that comes to our attention. We will include such matters in the reports required for a Single Audit. Our responsibility as auditors is limited to the period covered by our audit and does not extend to any later periods for which we are not engaged as auditors.

Our procedures will include tests of documentary evidence supporting the transactions recorded in the accounts, and may include tests of the physical existence of inventories, and direct confirmation of receivables and certain other assets and liabilities by correspondence with selected individuals, funding sources, creditors, and financial institutions. We may request written representations from your attorneys as part of the engagement. At the conclusion of our audit, we will require certain written representations from you about your responsibilities for the financial statements; schedule of expenditures of federal awards; federal award programs; compliance with laws, regulations, contracts, and grant agreements; and other responsibilities required by generally accepted auditing standards.

East Valley Water District Page 4 May 10, 2017

Audit Procedures—Internal Control

Our audit will include obtaining an understanding of the government and its environment, including internal control, sufficient to assess the risks of material misstatement of the financial statements and to design the nature, timing, and extent of further audit procedures. Tests of controls may be performed to test the effectiveness of certain controls that we consider relevant to preventing and detecting errors and fraud that are material to the financial statements and to preventing and detecting misstatements resulting from illegal acts and other noncompliance matters that have a direct and material effect on the financial statements. Our tests, if performed, will be less in scope than would be necessary to render an opinion on internal control and, accordingly, no opinion will be expressed in our report on internal control issued pursuant to Government Auditing Standards.

As required by the Uniform Guidance, we will perform tests of controls over compliance to evaluate the effectiveness of the design and operation of controls that we consider relevant to preventing or detecting material noncompliance with compliance requirements applicable to each major federal award program. However, our tests will be less in scope than would be necessary to render an opinion on those controls and, accordingly, no opinion will be expressed in our report on internal control issued pursuant to the Uniform Guidance.

An audit is not designed to provide assurance on internal control or to identify significant deficiencies or material weaknesses. However, during the audit, we will communicate to management and those charged with governance internal control related matters that are required to be communicated under AICPA professional standards, Government Auditing Standards, and the Uniform Guidance.

Audit Procedures—Compliance

As part of obtaining reasonable assurance about whether the financial statements are free of material misstatement, we will perform tests of EVWD’s compliance with provisions of applicable laws, regulations, contracts, and agreements, including grant agreements. However, the objective of those procedures will not be to provide an opinion on overall compliance and we will not express such an opinion in our report on compliance issued pursuant to Government Auditing Standards.

The Uniform Guidance requires that we also plan and perform the audit to obtain reasonable assurance about whether the auditee has complied with federal statutes, regulations, and the terms and conditions of federal awards applicable to major programs. Our procedures will consist of tests of transactions and other applicable procedures described in the OMB Compliance Supplement for the types of compliance requirements that could have a direct and material effect on each of EVWD’s major programs. The purpose of these procedures will be to express an opinion on EVWD’s compliance with requirements applicable to each of its major programs in our report on compliance issued pursuant to the Uniform Guidance.

Other Services

We will assist in preparing the financial statements, schedule of expenditures of federal awards, and related notes of EVWD in conformity with U.S. generally accepted accounting principles and the Uniform Guidance based on information provided by you. We will also assist in the preparation of the State Controller’s Report, and preparation of the Continuing Disclosure Annual Report based on

East Valley Water District Page 5 May 10, 2017

information provided by you. These nonaudit services do not constitute an audit under Government Auditing Standards and such services will not be conducted in accordance with Government Auditing Standards. We will perform the services in accordance with applicable professional standards. The other services are limited to the financial statement services previously defined. We, in our sole professional judgment, reserve the right to refuse to perform any procedure or take any action that could be construed as assuming management responsibilities. We will also conduct our review engagement of the North Fork Water Company as specified in a separate engagement letter.

Management Responsibilities

Management is responsible for (1) designing, implementing, and maintaining effective internal controls, including internal controls over federal awards, and for evaluating and monitoring ongoing activities to help ensure that appropriate goals and objectives are met; (2) following laws and regulations; (3) ensuring that there is reasonable assurance that government programs are administered in compliance with compliance requirements; and (4) ensuring that management and financial information is reliable and properly reported. Management is also responsible for implementing systems designed to achieve compliance with applicable laws, regulations, contracts, and grant agreements. You are also responsible for the selection and application of accounting principles; for the preparation and fair presentation of the financial statements, schedule of expenditures of federal awards, and all accompanying information in conformity with U.S. generally accepted accounting principles; and for compliance with applicable laws and regulations (including federal statutes) and the provisions of contracts and grant agreements (including award agreements). Your responsibilities also include identifying significant contractor relationships in which the contractor has responsibility for program compliance and for the accuracy and completeness of that information.

Management is also responsible for making all financial records and related information available to us and for the accuracy and completeness of that information. You are also responsible for providing us with (1) access to all information of which you are aware that is relevant to the preparation and fair presentation of the financial statements, (2) access to personnel, accounts, books, records, supporting documentation, and other information as needed to perform an audit under the Uniform Guidance, (3) additional information that we may request for the purpose of the audit, and (4) unrestricted access to persons within the government from whom we determine it necessary to obtain audit evidence.

Your responsibilities include adjusting the financial statements to correct material misstatements and confirming to us in the management representation letter that the effects of any uncorrected misstatements aggregated by us during the current engagement and pertaining to the latest period presented are immaterial, both individually and in the aggregate, to the financial statements as a whole.

You are responsible for the design and implementation of programs and controls to prevent and detect fraud, and for informing us about all known or suspected fraud affecting the government involving (1) management, (2) employees who have significant roles in internal control, and (3) others where the fraud could have a material effect on the financial statements. Your responsibilities include informing us of your knowledge of any allegations of fraud or suspected fraud affecting the government received in communications from employees, former employees, grantors, regulators, or others. In addition, you are responsible for identifying and ensuring that the government complies with applicable laws, regulations,

East Valley Water District Page 6 May 10, 2017

contracts, agreements, and grants. Management is also responsible for taking timely and appropriate steps to remedy fraud and noncompliance with provisions of laws, regulations, contracts, and grant agreements, or abuse that we report. Additionally, as required by the Uniform Guidance, it is management’s responsibility to evaluate and monitor noncompliance with federal statutes, regulations, and the terms and conditions of federal awards; take prompt action when instances of noncompliance are identified including noncompliance identified in audit findings; promptly follow up and take corrective action on reported audit findings; and prepare a summary schedule of prior audit findings and a separate corrective action plan. The summary schedule of prior audit findings should be available for our review at the time of our final audit fieldwork.

You are responsible for identifying all federal awards received and understanding and complying with the compliance requirements and for the preparation of the schedule of expenditures of federal awards (including notes and noncash assistance received) in conformity with the Uniform Guidance. You agree to include our report on the schedule of expenditures of federal awards in any document that contains and indicates that we have reported on the schedule of expenditures of federal awards. You also agree to make the audited financial statements readily available to intended users of the schedule of expenditures of federal awards no later than the date the schedule of expenditures of federal awards is issued with our report thereon. Your responsibilities include acknowledging to us in the written representation letter that (1) you are responsible for presentation of the schedule of expenditures of federal awards in accordance with the Uniform Guidance; (2) you believe the schedule of expenditures of federal awards, including its form and content, is stated fairly in accordance with the Uniform Guidance; (3) the methods of measurement or presentation have not changed from those used in the prior period (or, if they have changed, the reasons for such changes); and (4) you have disclosed to us any significant assumptions or interpretations underlying the measurement or presentation of the schedule of expenditures of federal awards.

You are also responsible for the preparation of the other supplementary information, which we have been engaged to report on, in conformity with U.S. generally accepted accounting principles. You agree to include our report on the supplementary information in any document that contains, and indicates that we have reported on, the supplementary information. You also agree to make the audited financial statements readily available to users of the supplementary information no later than the date the supplementary information is issued with our report thereon. Your responsibilities include acknowledging to us in the written representation letter that (1) you are responsible for presentation of the supplementary information in accordance with GAAP; (2) you believe the supplementary information, including its form and content, is fairly presented in accordance with GAAP; (3) the methods of measurement or presentation have not changed from those used in the prior period (or, if they have changed, the reasons for such changes); and (4) you have disclosed to us any significant assumptions or interpretations underlying the measurement or presentation of the supplementary information.

Management is responsible for establishing and maintaining a process for tracking the status of audit findings and recommendations. Management is also responsible for identifying and providing report copies of previous financial audits, attestation engagements, performance audits, or other studies related to the objectives discussed in the Audit Objectives section of this letter. This responsibility includes relaying to us corrective actions taken to address significant findings and recommendations resulting from those audits, attestation engagements, performance audits, or studies. You are also responsible for

East Valley Water District Page 7 May 10, 2017

providing management’s views on our current findings, conclusions, and recommendations, as well as your planned corrective actions, for the report, and for the timing and format for providing that information.

You agree to assume all management responsibilities relating to the financial statements, schedule of expenditures of federal awards, and related notes, and any other nonaudit services we provide. You will be required to acknowledge in the management representation letter our assistance with preparation of the financial statements, schedule of expenditures of federal awards, and related notes and that you have reviewed and approved the financial statements, schedule of expenditures of federal awards, and related notes prior to their issuance and have accepted responsibility for them. Further, you agree to oversee the nonaudit services by designating an individual, preferably from senior management, with suitable skill, knowledge, or experience; evaluate the adequacy and results of those services; and accept responsibility for them.

Engagement Administration, Fees, and Other The audit documentation for this engagement is the property of Vicenti, Lloyd & Stutzman LLP (VLS) and constitutes confidential information. However, pursuant to authority given by law or regulation, we may be requested to make certain audit documentation available to a cognizant or oversight agency or its designee, or the U.S. Government Accountability Office for purposes of a quality review of the audit, to resolve audit findings, or to carry out oversight responsibilities. We will notify you of any such request. If requested, access to such audit documentation will be provided under the supervision of VLS personnel. Furthermore, upon request, we may provide copies of selected audit documentation to the aforementioned parties. These parties may intend, or decide, to distribute the copies or information contained therein to others, including other governmental agencies. The audit documentation for this engagement will be retained for a minimum of seven years after the report release date or for any additional period requested by the cognizant or oversight agency, or pass-through Entity. If we are aware that a federal awarding agency, pass-through entity, or auditee is contesting an audit finding, we will contact the party(ies) contesting the audit finding for guidance prior to destroying the audit documentation. We utilize a third-party service provider in serving your account. It is possible for the service provider to access confidential information about your organization, but we remain committed to maintaining the confidentiality and security of your information. Accordingly, we maintain internal policies, procedures, and safeguards to protect the confidentiality of your information. In addition, we have an agreement with the service provider that includes confidentiality and non-disclosure clauses and we will take reasonable precautions to determine that they have appropriate procedures in place to prevent the unauthorized release of your confidential information to others. You will be asked to provide your consent prior to the sharing of your confidential information with the third-party service provider. Furthermore, we will remain responsible for the service provided by the third-party service provider. Government Auditing Standards require that we provide you with a copy of our most recent external peer review report and any letter of comment. We will also provide you any subsequent peer review reports and letters of comment received during the period of the contract. Our 2016 peer review report can be found on our website at http://vicenticpas.com/about/peer-review/.

East Valley Water District Page 8 May 10, 2017

We expect to begin our audit in early August 2017 for interim procedures and early September 2017 for year-end procedures; the final report will be issued in October 2017. Renee Graves is the engagement partner and is responsible for supervising the engagement and signing the reports or authorizing another individual to sign them. We understand that your employees will prepare the schedules and obtain the documents requested in the “Prepared by Client” (PBC) list provided to you. The final trial balance and key audit schedules will be uploaded to the EVWD client portal hosted by VLS five days prior to the start of fieldwork. In addition, your employees will locate any documents selected by us for testing and prepare any confirmations we may request. Our fee for these services (excluding the separate financial review and report for the North Fork Water Company) is $22,500. The fee is based on anticipated cooperation from your personnel and the assumption that unexpected circumstances will not be encountered during the audit. If significant additional time is necessary, we will discuss it with you and arrive at a new fee estimate before we incur the additional costs. Closing We appreciate the opportunity to be of service to the East Valley Water District and believe this letter accurately summarizes the significant terms of our engagement. If you have any questions, please let us know. If you agree with the terms of our engagement as described in this letter, please sign a copy and return it to us. Very truly yours,

Renee S. Graves, CPA, CGFM Vicenti, Lloyd & Stutzman LLP RESPONSE: This letter correctly sets forth the understanding of East Valley Water District. Management signature:

Title:

Date:

May 10, 2017 Mr. Brian Tompkins East Valley Water District 31111 Greenspot Road Highland, CA 92346 RE: North Fork Water District Dear Mr. Tompkins:

We are pleased to confirm our acceptance and understanding of the services we are to provide for the year ended January 31, 2018.

We will perform a review engagement with respect to the financial statements of North Fork Water District ( the Company), which comprise the statement of financial position as of January 31, 2018, and the related statements of activities, changes in shareholders’ equity and cash flows for the year then ended, and the related notes to the financial statements.

Our Responsibilities

The objective of our engagement is to obtain limited assurance as a basis for reporting whether we are aware of any material modifications that should be made to the financial statements in order for them to be in accordance with accounting principles generally accepted in the United States of America.

We will conduct our review engagement in accordance with Statements on Standards for Accounting and Review Services promulgated by the Accounting and Review Services Committee of the AICPA and comply with the AICPA’s Code of Professional Conduct, including the ethical principles of integrity, objectivity, professional competence, and due care.

A review engagement includes primarily applying analytical procedures to your financial data and making inquiries of management. A review engagement is substantially less in scope than an audit engagement, the objective of which is the expression of an opinion regarding the financial statements as a whole. A review engagement does not contemplate obtaining an understanding of the Company’s internal control; assessing fraud risk; testing accounting records by obtaining sufficient appropriate audit evidence through inspection, observation, confirmation, or other examination of source documents; or other procedures ordinarily performed in an audit engagement. Accordingly, we will not express an opinion regarding the financial statements.

Our engagement cannot be relied upon to identify or disclose any financial statement misstatements, including those caused by fraud or error, or to identify or disclose any wrongdoing within the Company or noncompliance with laws and regulations. However, we will inform the appropriate level of management of any material errors and any evidence or information that comes to our attention during the performance of our review procedures that fraud may have occurred. In addition, we will inform you of any evidence or information that comes to our attention during the performance of our review procedures regarding noncompliance with laws and regulations that may have occurred, unless they are clearly inconsequential. We have no responsibility to identify and communicate deficiencies or material weaknesses in your internal control as part of this engagement.

East Valley Water District/ North Fork Water District Page 2 May 10, 2017 Your Responsibilities

The engagement to be performed is conducted on the basis that you acknowledge and understand that our responsibility is to obtain limited assurance as a basis for reporting whether we are aware of any material modifications that should be made to the financial statements in order for the statements to be in accordance with accounting principles generally accepted in the United States of America. You have the following overall responsibilities that are fundamental to our undertaking the engagement in accordance with SSARS:

1) The selection of accounting principles generally accepted in the United States of America as the financial reporting framework to be applied in the preparation of the financial statements.

2) The preparation and fair presentation of financial statements in accordance with accounting principles generally accepted in the United States of America and the inclusion of all informative disclosures that are appropriate for accounting principles generally accepted in the United States of America.

3) The design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of the financial statements.

4) The prevention and detection of fraud.

5) To ensure that the Company complies with the laws and regulations applicable to its activities.

6) The accuracy and completeness of the records, documents, explanations, and other information, including significant judgments, you provide to us for the engagement.

7) To provide us with—

• access to all information of which you are aware is relevant to the preparation and fair presentation of the financial statements, such as records, documentation, and other matters.

• additional information that we may request from you for the purpose of the review engagement.

• unrestricted access to persons within the Company of whom we determine it necessary to make inquiries.

8) To provide us, at the conclusion of the engagement, with a letter that confirms certain representations made during the review.

Our Report

We will issue a written report upon completion of our review of the Company’s financial statements. Our report will be addressed to the board of directors of North Fork Water Company. We cannot provide assurance that an unmodified accountant’s review report will be issued. Circumstances may arise in which it is necessary for us to report known departures from accounting principles generally accepted in the United States of America, add an emphasis-of-matter or other-matter paragraph(s), or withdraw from the engagement. If, for any reason, we are unable to complete the review of your financial statements, we will not issue a report on such statements as a result of this engagement.

You agree to include our accountant’s review report in any document containing financial statements that indicates that such financial statements have been reviewed by us and, prior to inclusion of the report, to ask our permission to do so.

East Valley Water District/ North Fork Water District Page 3 May 10, 2017

Other Relevant Information

Renee Graves is the engagement partner and is responsible for supervising the engagement and signing the report or authorizing another individual to sign it.

We estimate that our fees for these services will not exceed $2,000 including out-of-pocket costs such as report production, word processing, postage, travel, etc. The fee estimate is based on anticipated cooperation from your personnel and the assumption that unexpected circumstances will not be encountered during the work performed. If significant additional time is necessary, we will discuss it with you and arrive at a new fee estimate before we incur the additional costs. Our invoices for these fees are payable on presentation.

You agree to hold us harmless and to release, indemnify, and defend us from any liability or costs, including attorney's fees, resulting from management's knowing misrepresentations to us.

We appreciate the opportunity to be of service to you and believe this letter accurately summarizes the significant terms of our engagement. If you have any questions, please let us know. If you acknowledge and agree with the terms of our engagement as described in this letter, please sign a copy and return it to us.

Sincerely,

Renee S. Graves, CPA, CGFM

Acknowledged: East Valley Water District/ North Fork Water District Date

STAFF REPORT

Agenda Item #3.Meeting Date: May 30, 2017

Discussion ItemTo: FINANCE AND HUMAN RESOURCES COMMITTEE From: Chief Financial Officer

Subject: Review Surplus Property Policy 7.1.1

RECOMMENDATION:

Staff recommends that the Finance and Human Resources Committee review the attached Surplus PropertyPolicy.

BACKGROUND / ANALYSIS:

One of East Valley Water District’s Organizational Endeavors is to “Dedicate Effort Toward SystemMaintenance and Modernization”, which occasionally leads to the need to dispose of retired or surplus assets. The attached policy defines the criteria for declaring surplus property, as well as, the authorizations requiredfor proper disposal. After the disposal of the property, proceeds, if received, may be credited to theappropriate equipment replacement fund or the EVWD Employee Events Association.

AGENCY IDEALS AND ENDEAVORS:

Ideals and Endeavor I - Encourage Innovative Investments To Promote Sustainable Benefits (D) – Dedicate effort toward system maintenance & modernization

Ideals and Endeavor II - Maintain An Environment Committed To Elevated Public Service

(E) - Practice transparent & accountable fiscal management

REVIEW BY OTHERS:

This agenda item has been reviewed by Executive Management.

FISCAL IMPACT:

There is no fiscal impact associated with this agenda item.

ATTACHMENTS:Description Type7.1.1 Surplus Property Policy Backup MaterialSurplus Property / Capital Asset Disposition Form Backup Material

EAST VALLEY WATER DISTRICT Administrative Policies & Programs

Policy Title: Surplus Property Policy

Original Approval Date: June 14, 2017

Last Revised:

Policy No: 7.1.1

Page 1 of 5

Purpose

The purpose of this policy is to establish uniform procedures for disposing of property that

has been declared surplus by the District. Generally, property is declared surplus if it is no

longer needed by the using department because of decreased use, poor condition, damage

not worth the cost of repairing, and/or obsolescence.

Scope

For the purposes of this policy, surplus property may include supplies, equipment, and

components of plant facilities. Examples include, but are not limited, office equipment,

furniture and fixtures, pool vehicles and other fleet equipment, pumps, valves, and other

facility components. This policy does not pertain to real property, disposal of which is

subject to additional legal requirements.

Responsibility and Authorization

A Department Head will determine if supplies, a piece of equipment or a capital asset has

become surplus based on the description above. If so, the Department Head, or a designee

will determine the value of the surplus item, either from an existing source document or

a reasonable estimate of replacement value if a source document is unavailable in the

District’s document management system.

Before an asset is sold or otherwise disposed of, it must first be determined if the asset

had originally been purchased with grant monies. If this is the case, the District must refer

to the grant agreement and follow prescribed procedures for disposition.

If the current value of the surplus property is determined to be less than $1,000,

the Department Head should notify the Finance Department, determine the

appropriate method of disposition, and coordinate its disposal. The General

Manager/CEO’s approval is required for items valued between $1,000 - $3,000.

If the property item deemed surplus has an estimated current value of over $3,000,

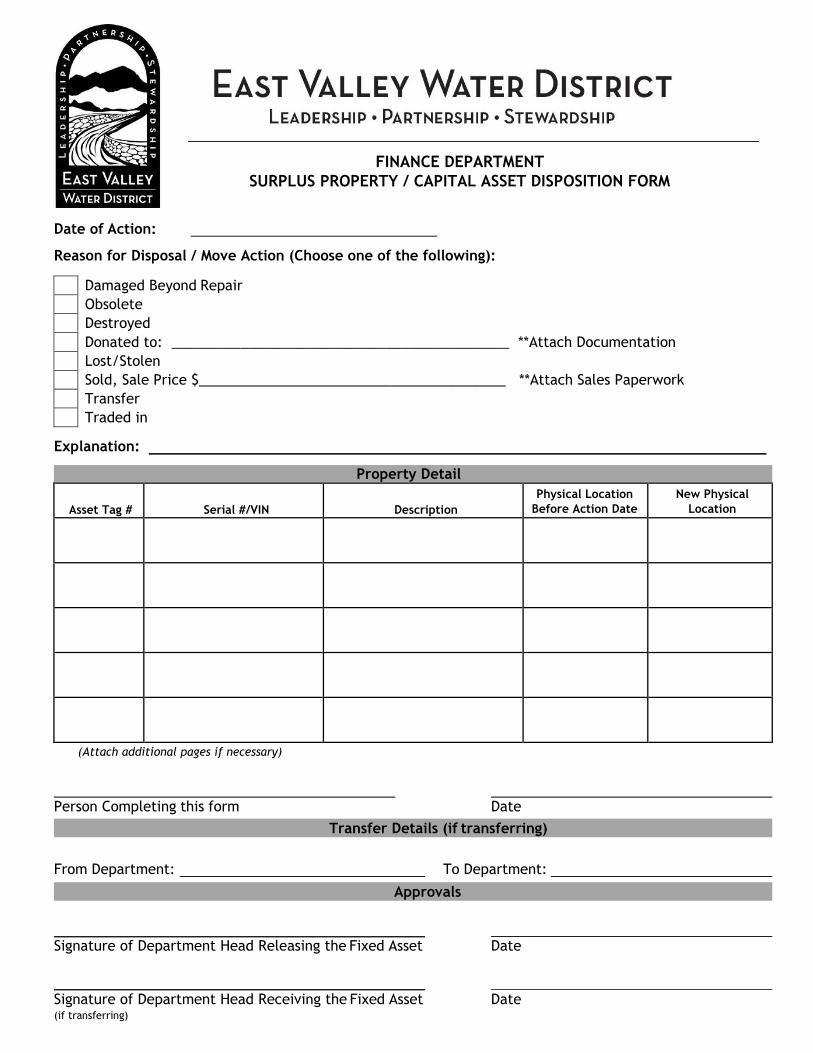

then the Department Head must complete a Surplus Property / Capital Asset

Disposition form. This form is available on the District’s intranet. One copy of the

form should be completed and circulated for signatures. After signatures are

obtained, the property must be declared surplus by the Board of Directors.

EAST VALLEY WATER DISTRICT Administrative Policies & Programs

Policy Title: Surplus Property Policy

Original Approval Date: June 14, 2017

Last Revised:

Policy No: 7.1.1

Page 2 of 5

Methods of Disposal

There are four approved methods for disposal of surplus property including:

Trade in for credit on new material or equipment

Public Sale

Public Donation

Scrap

1. Trade In - Surplus property can be offered as trade-in for new equipment or material

or for credit towards the acquisition of new property. If the current value of a

surplus property item slated for trade-in is $1,000 or over, then a Surplus

Property/Capital Asset Disposition form should be completed. The estimated trade

in value of the surplus property or capital asset should be noted on the Surplus

Property/Capital Asset Disposition form and on the purchase order issued for any

new property resulting from the trade in.

2. Public Sale - Surplus property may be offered for sale. All surplus property is for

sale “as is” and “where is,” with no warranty, guarantee, or representation of any

kind, expressed or implied, as to the condition, utility or usability of the property

offered for sale. For any sale of surplus property with a current value of $1,000 or

above, the Department Head should indicate on the Surplus Property / Capital Asset

Disposition form the recommended selling method and any other notations in the

Department Head approval. Appropriate methods of sale are as follows:

A. Public Auction – District staff may conduct public auctions or the District may

contract with a professional auctioneer and/or an Internet auctioneer for this

service.

B. Sealed Bids – Sealed bids may be solicited for the sale of surplus property.

Surplus property disposed of in this manner shall be sold to the highest

responsible bidder.

C. Negotiated Sale – Surplus property may be sold outright if the Department

Head, with concurrence of the General Manager/CEO, determines that only

one known buyer is available or interested in acquiring the property.

D. Selling as Salvage – Equipment, materials, supplies, fixtures, or facility

components that are no longer capable of performing their intended function

EAST VALLEY WATER DISTRICT Administrative Policies & Programs

Policy Title: Surplus Property Policy

Original Approval Date: June 14, 2017

Last Revised:

Policy No: 7.1.1

Page 3 of 5

without extensive repair, or that are of no value except for reclamation

purposes, may be considered salvage. Surplus property may be sold as salvage

if the Department Head deems that the value of the raw material exceeds

the value of the property.

3. Donation - The Department Head may recommend and the General Manager/CEO

may authorize, the donation of surplus property to a 501(c)(3) nonprofit

organization or school district located or operating within the District’s service area

or, secondarily, to any other non-profit organization or private organization that

aids nonprofit organizations.

A. Noticing - If surplus property has been approved for donation, the

Department Head will notice the availability of such property for donation,

indicating the quantity, description, and location of the surplus property, by

advertisement in a local newspaper and on the District’s web site. This notice

will also indicate a closing date for the receipt of all requests for donation

and indicate the way in which interested parties can receive additional

information.

B. Terms & Conditions - Requests for donation will be accepted on a first-come,

first-serve basis. The Department Head will send a letter to the non-profit

organization(s) or school district(s) that respond to the notice to advise them

of the District’s terms and conditions of the donation. Generally, the terms

and conditions are:

Accepting the property “as is,” with no implied warranties;

Exhibit an immediate need for the property;

Agreeing that the property will never be sold or transferred for

profit; and

Assume all costs and liability associated with the removal and

transportation of the surplus property from the District.

A return letter, signed by an authorized agent from the non-profit

organization or school district, accepting the District’s terms and

conditions is required before the surplus property can be released.

EAST VALLEY WATER DISTRICT Administrative Policies & Programs

Policy Title: Surplus Property Policy

Original Approval Date: June 14, 2017

Last Revised:

Policy No: 7.1.1

Page 4 of 5

C. Release - If, in the opinion of the Department Head, the donated property

has a current value of less than $3,000, then the General Manager/CEO can

approve the release of the property to the recipient(s) that meet the above

criteria and agree to the District’s terms and conditions. If, in the opinion of

the Department Head, the donated property has a current value of $3,000 or

more, the initiating Department Head will prepare a report to identify the

specific property to be donated, the estimated current value of the property,

and the proposed recipient(s) of the property for approval by the Board of

Directors. After Board approval, the surplus property may then be released.

The department from which the donated property is being taken

should remove any District tags or emblems before the property is

officially transferred to the recipient organization(s).

4. Scrap – This method of disposal is recommended only after determining that none

of the other methods – trade-in, sale (including salvage), or donation - is feasible.

It applies when surplus property has no value and there is no expectation of proceeds

from the disposal.

Inoperable or irreparable property with an original cost of $1,000 or less may

be scrapped at the discretion of the Department Head.

Inoperable or irreparable property with an original cost between $1,000 and

$3,000s may be scrapped with the approval of the General Manager/CEO.

Inoperable or irreparable property with an original cost of more than $3,000

requires the completion of a Surplus Property / Capital Asset Disposition Form

and approval of the District Board.

Proceeds

1. Any proceeds received from the trade-in or sale of surplus property will be credited

to the appropriate equipment replacement fund.

2. Proceeds from salvage or scrap will be donated to the EVWD Employee Events

Association in support of its efforts to provide school supplies and necessities to

disadvantaged students at schools within the District’s service area.

EAST VALLEY WATER DISTRICT Administrative Policies & Programs

Policy Title: Surplus Property Policy

Original Approval Date: June 14, 2017

Last Revised:

Policy No: 7.1.1

Page 5 of 5

Prohibited Disposition

1. District surplus property may not be sold or given to a District employee except

through public auction or solicitation of sealed bids open to the public.

2. District employees shall not be permitted to bid on, or knowingly come into

ownership of, any surplus property if the employee participated in any way in the

disposal process.

Revised: June 14, 2017

FINANCE DEPARTMENT

SURPLUS PROPERTY / CAPITAL ASSET DISPOSITION FORM

Date of Action:

Reason for Disposal / Move Action (Choose one of the following):

Damaged Beyond Repair

Obsolete

Destroyed

Donated to: ____________________________________________ **Attach Documentation

Lost/Stolen

Sold, Sale Price $________________________________________ **Attach Sales Paperwork

Transfer

Traded in

Explanation:

Property Detail

Asset Tag # Serial #/VIN Description

Physical Location

Before Action Date

New Physical

Location

(Attach additional pages if necessary)

Person Completing this form Date

Transfer Details (if transferring)

From Department: To Department:

Approvals

Signature of Department Head Releasing the Fixed Asset Date

Signature of Department Head Receiving the Fixed Asset Date (if transferring)