committee - niyamasabha.org

TRANSCRIPT

I

I

i

;FOURTEENTH KERAIA LEGISLAIIVE AS SEMBLY

COMMITTEEON

PUBLIC TJITDERTAKINGS(2016-2019)

THIRTYFOTJRTH REPORT

On

TRACO CABLE COMPANY LIMITED

(Based on the Report of the comptroller and Auditor General of India for theyear ended 31st l!{arch, 2004)

927t20t7.

CONTENTS

Composition of the Committee

Introduction

Report

Appendix I:Summary of main Conclusions/Recommendations

Appendix II :

Notes furnished by Government on the Audit paragraph

Annexures referred to in the Audit Reports:

Annexure L4

Annexure L5

Annexure L6

Annexure 17

Annexure 18

Page

v

vii

1

21.

22

32

33

34

35

36

COMMITTEE ON PUBLIC UNDERTAKINGS (2016-2019)

COMPOSITION OF THE COMMITTEE

Chairman:

Shri C. Divakaran

Members:

Shri T. A. Ahammed Kabeer

Shri K. B. Ganesh Kumar

Shri C. Krishnan

Shri S. Rajendran

Shri Thiruvanchoor Radhakrishnan

Shri P. T.A. Rahim

Shri Raju Abraham

Shri Sunny JosePh

Shri C. F. Thomas

Shri P. Unni'

Legislature Secretar iat :

Shri V. K. Babu Prakash, SecretarY

Smt. P, K. Giriia Additional Secretary

Shri P. B. Suresh Kumar, Deputy Secretary

Smt. DeePa.V., Under SecretarY.

INTRODUCTION

I, the chairman, committee on public Undertakings (2016-2019) havingbeen authorised by the committee to present the Report on its behalf, present thisThirty Fourth Report on Traco cable company Limited, based on the Report(Commercial) of the Comptroller and Auditor General of India for the year ended31 March, 2004 relating to the public Sector undertakings of the state of Kerala.

The Report of the comptroller and Auditor General of India for the yearended on 31 March 2004, was laid on the Table of the House on s-7-2005.The consideration of the audit paragraphs included in this report andthe examination of the departmental witness in connection thereto was made by thecommittee on Public undertakings constituted for the years 2014-2016 at itsmeeting held on 6-1-2016.

This Report was considered and approved by the committee (2016-2019) atits meeting held on 26-4-201,7.

The Committee place on record its appreciation for the assistance renderedby the Accountant General (Audit), Kerala in the examination of the AuditParagraphs included in this Report.

The Committee wishes to thank the officials of the Industries Department ofthe Government secretariat and Traco cable company Limited for placing thematerials and information solicited in connection with the examination of thesubject. The committee also wishes to thank in particular the secretaries toGovernment, Industries and Finance Departments and the officials of Ttaco Cablecompany Limited who appeared for evidence and assisted the committee byplacing their views before it.

Thiruvananthapuram,

26'hApril,2017.

C. DIVAKARAN,

Chairmon,

Committee on Public Undertakinqs.

REPORT

ONTRACO CABLE COMPANY LIMITED

AUDru PARAGRAPH

Introduction

2'2.r rraco cable company Limited was incorporated in February 1960with the main objective of manufacturing all types and sizes of wires, cables andflexibles for electrical power transmission and distribution, telecommunication,building wiring etc. The company has a power cable manufacturing division atIrimpanam and a telephone cable manufacturing division at Thiruvalla. The power

cables Division was commissioned in 196s with annual capacity to produce 1s00MT of aluminium throughput and 2.5 Lakh conductor Kilometer (LCKM)respectively. It manufactures Poly vinyl chloride(pvc) insulated heavy dutycables, wires, fledbles, bare aluminium conductors and smaller size Jelly FilledTelephone cables(JFTC). The installed capacity (7.30 LCKM per annum) of theJelly Filled Telephone cable (JFTC) Division commissioned in March 199L wasfurther expanded (March 1996) to 15 LCKM per annum.

Organisational set-up

2.2.2 As on 31't March, 2004 the management of the Company was vested ina Board comprising 10 directors including two Government nominees. TheManaging Director is the chief Executive of the company who is assisted byChief of Works(at each of the two divisions), Chief of Finance, a CompanySecretary and heads of Marketing, Personnel and Administration, etc.

Scope of Audit

Extent of Coverage

2.2.3 The performance of the company was last reviewed and results thereofincluded in the Report of the comptroller and Auditor General of India for the year1994-95(commercial). The Report was discussed by the copu in August 2002and their recommendations included in the 3f'report were presented (June 2003)

to the Legislature. Action Taken Notes thereon were awaited (August 2004).

927r2U7.

2

The present review conducted during the period January to May 2004 covers

and activities of the Company for the five years ending 2003-04'

2.2.4 Audit findings as a result of review on the performance and working of

the company were reported to GovernmenvManagement in July 2004 with a

specific request to attend the meeting of Audit Review Committee for State Public

sector Enterprise(ARCPSE) so that the view point of Government/Management

was taken into account before finalising the review. The meeting of ARCPSE was

held on 5,h August, 2004 and attended by the Additional secretary, Industries

Department, Government of Kerala and Managing Director of the company. The

views expressed by the members have been taken into account during finalisation

of the review.

Share Capital

2.2.5 The authorised share capital of Rs.l-S crore comprised 1.475 crore

equity shares of Rs.10 each and 2.50 lakh preference shares of Rs.10 each' The

paid-up share capital as on 3f' March, 2004 amounted to Rs, 13'02 crore'

contributed by Government of Kerala (Rs. 12.82 crore); KSIDC, KFC, other

institutions (Rs. 10lakh) and public (Rs. 9.76 lakh)'

Financial position and Working Results

2.2.6 The Company had finalised its accounts for the period up to 31"'

March, 2003. The financial position and working results of the Company for the

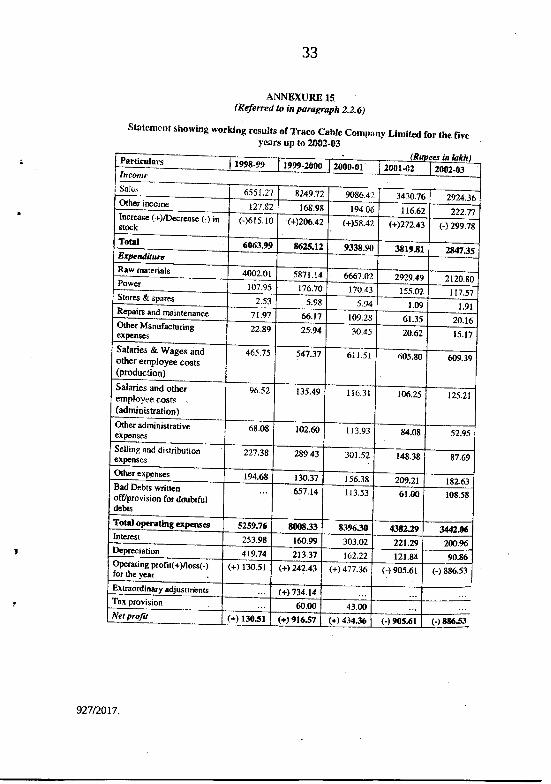

five years up to 31" March, 2003 were as given in Annexure 14 and 15

respectively. Analysis thereof revealed that ;

. The company's paid-up capital of Rs. 13.02 crore as on 31."'March, 2003

was fully eroded by accumulated loss of Rs. 17'65 crore due to dismal performance

since 200L-02. The net worth of the Company was negative.

. The liabilities of the Company included Rs. 6.67 crore being guarantee

commission payable to Government since 1998-99. Interest on Government loans

amounting to Rs. 1.61 crore as well as interest and penal interest on loan from

KIRFB amounting to Rs. 2.L3 crore were also over due as on 31" March, 2003.

3

.ThesalesperformanceoftheCompanyhadsubstantiallydeclinedfrom

90.86 crore in 2000-01 to 29'24 crore in 2002-03' Consequently'

theCompanywhichwasearningprofittill2000.0l,incurredlossestothetune of Rs' 9.06 crore and Rs' B' 87 crore in 2001-02 and 2002-03

resPectivelY.

.TheprofitofRs'9.17croreachievedin1999-2000wasduetowriteback

ofinterestonlDBlandlFClloan(Rs'7'34crore)onthebasisofwaiverallowed as part of a One Time Settlement Scheme'

Production Performance

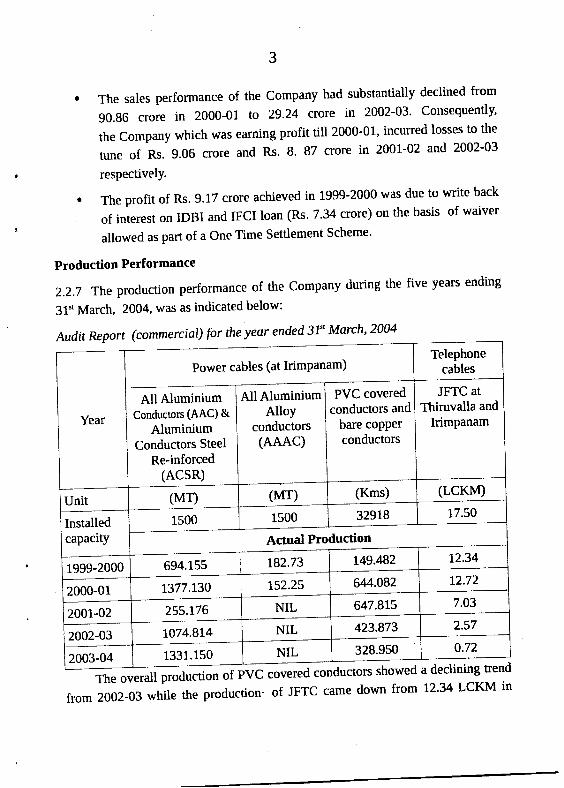

2.2.7 The production performance of the Company during the five years ending

31" March, 2004, was as indicated below:

Audit Report (commercial) for the year ended 37' March' 2004

ered conductors showed a declining trend

from 2002-03 while the production- of JFTC came down from 12'34 LCKM in

Power cables (at lrimPanam)

JFTC At

Thiruvalla and

Irimpanam

PVC coveredconductors and

bare coPPer

conductors

AllAluminiumAlloy

conductors(AAAC)

AllAluminiumConductors (AAC) &

AluminiumConductors Steel

Re-inforced(ACSR)

Actual Production

694.1ss \ 182.73

1377.t30 I 152.2s

647.815

4

1999-2000 to 0.72 LCKM in 2003-04 which was mainry due to non-receipt oforders from Department of Telecommunication (Dor)/Bharat sanchar NigamLimited (BSNL).

The production of AIr Aruminium Ailoy conductors (AAAC) had to bediscontinued since the project was taken up without any firm commitments fromthe State Electricity Board as discussed ln paragraph 2.2.10 infra.Division-wise production is analysed in the succeeding paragraphs.

Power Cables Division

Production of ACSR & AAC

2'2'B Irimpanam Division of the company had been producing Aluminiumconductor steer Reinforced (ACSR) and Alr Aluminium conductors(AAC).The major customer was Kerara state Erecrricity Board (KSEB). whire theDivision had installed capacity to produce 1s00 MT of conductors per annum,based on aluminium throughput, the actuar annual production during the five yearsending 2003-04 ranged between 2ss.1g MT and lz77.r3MT. Th;percentage ofcapacity utilisation during the above period ranged between 17.01 and g1.g1.

The lowest capacity utirisation of 17.07 per centof instailed capacity wasrecorded during 2001-02, which was attributed to non-receipt of adequate ordersfrom the state Electricity Board. The production of conductors at the Divisionwas not cost effective on account of high labour cost and overhead charges. As aresult' the company could not secure enough orders from potential customers anddepended heaviry on KSEB for order. wo cost contror measures were initiated toreduce actuar cost and capture market from other customers at competitive rates.Telephone Cables

2'2'9 In order to supplement the annuar producrion capacity of15 LCKM at JFTC Division, Thiruvata,-the company .ru"i"a (1996-97)additional installed capacity of 2.50 LCKM, at the power cable Division,Irimpanam at a capitar cost of ns- ris crore. The maximum capacityutilisation at Thiruvara, ever since the irrrtutt"tio' of additionar capacity atIrimpanam' was g1.38 per cent of trre insta'ed capacity and capaciryequivalent to 279300 cKM all arong remained unutirised. The maximum

5

annual production of JFTC at Irimpanam was only 61500 CKM'-The production

ofJFTCatthedivisionwasultimatelydiscontinuedinMay2002duetodeclineindemand from DOT/BSNL. The typu

"pp'ou"l by the custom€r for

-the product

which was a pre-requisite ior production-of JFTC was also not obtained since then'

Thus, the decision to create surplus capacity at Irimpanam despite lower

demand and under utilisation of the then existing capacity at Thiruvalla, resulted in

wasteful investment of Rs. 1'45 crore'

Management stated (August 2004) ttrat phasing out of JFTC technology at

such a rapid pace, introduction of cellular telephones on massive scale and excess

capacity creation for optical fibre cables, were developments not anticipated at the

time of caPacitY exPansion'

The reply is not tenable since the pre-expansion capacity at JFTC division'

ThiruvallaitselfwasnotfullyutilisedevenaftergoinginforcapacityexpansionatIrimpanam, and the unutilised capacity (279300 CKM) was more than the

additional capacity created (250000 CKM)' The company should have also taken

noteoftheobsolescenceintheJFTCtechnologyduetoemergingtechnologicalimprovements in the field by other firms in the country'

Creation of idle caPacitY

2.2.1O In antrcipation of demand from KSEB' the company :e:-up

(June 1995) facilities flr manufacture of 1500 MT per annum of All Aluminium

Alloy Condu.tors leneC)' at a cost of Rs' 62'50 lakh' Production with this

facilitycouldnotbestabitisedtillJanuary2000duetooperationalproblemsinthemain equipment' Despite this, the Company accepted (February/March 1998) bulk

orders from XSfe ior supply ol tZiS km and could not deliver 1341.66 km

within the stipulatea derivery period, due to non-Stabilisation of production.

Supplies against repeat orders ior 51-8 km accepted during April 2000 to June

2000werealsodelayed.Thelossduetopenaltyandunfavourablepricevariationon account of the delayed delivery amounted to Rs' 31'11 lakh'

2'2.l.l.Theproductionofthematerialbeforerectifyingtheoperationalproblemsalsocausedhigherlevelofrejection.Thelosssufferedduetoexcessconsumption of elumiiium Alloy during production without stabilisation

amounted to Rs. 3g.18 lakh (net of scrap vilue). Further sales were executed at

prices below tte cost of iroduction' Ieading to short recovery of cost of

Rs.L.81 crore.

6

Audit also observed that KSEB discontinued procurement of AAAC since

2000-01 without assigning any reason though the material was technically and

commercially more advantageous than AAC/ACSR. The company also did notinitiate measures to enter the market in neighbouring states by reducing its cost ofproduction.

Thus, the decision of the company to install production facility at a cost ofRs. 62.50lakh without any firm commitment from KSEB, being the only potentialcustomer, resulted in locked up investment since December 2000.

PVC covered Conductors and Bare Copper Conductors

2'2.12 Details of actual production of pVC covered and bare copperconductors for the five years ending 2003-04 were as follows:-

YearTotal

capacity(in km)

Drop wireAerialcable

Weatherproofcables

Housewire

Totalproduction

Percentage

of actual

to total

production

capacity(Quantity in km)

1999-2000 32918 46.389 64.46 38.183 r49.482 0.45

2000-01 32918 3I4.404 Nil 329.678 644.082 1.96

2001-02 32918 NiI Nil 647.8r5 647.815 1..97

2002-03 329L8 Nil Nil 423.873 423.873 1..29

2003-04 32918 3.050 Nil 32s.900 328.950 1.00

Though the Division was having an annual capacity to produce 32918 km ofconductors, it produced only 0.45 to L.gz per cent during the five years ending31" March, 2004 mainly due to reluctance in entering the competitive market.

Management stated (August 2004) that the market for pvc covered cableswas very competitive due to presence of several small-scale rnanufacturersenjoying tax concessions.

The company had, however, not taken any measure to reduce the excessivecost of production with a view to compete in the market. In the absence of

7

full fledged production, the related activities suchdocumentation of machine/manpower udlisation, etc.,consideradon.

Production Control

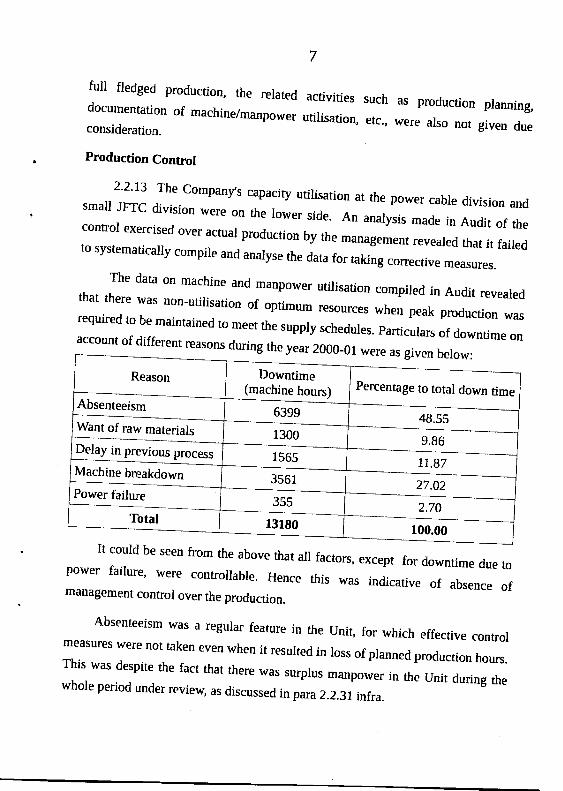

2'2'13 The company's capacity utilisation at the power cable division andsmall JFTC division were on the Iower side. An analysis made in Audit of thecontrol exercised over actuar production by the management reveared that it failedto systematicalry compire and analyse the data for taking corrective measures.The data on machine and manpower utirisation compiled in Audit revealedthat there was non-utilisation of optimum resources when peak production wasrequired to be maintained to meet the supply schedures. particurars of downtime on

as production planning,

were also not given due

account of different reasons during the year 2000-01 were as given below:

It could be seen from the above that alr factors, except for downtime due topower fairure' were controlrable. Hence this was indicative of absence ofmanagement control over the production.

Absenteeism was a regurar feature in the Unit, for which effective contrormeasures were not taken even when it resurted in loss of pranned production hours.This was despite the fact that there was surprus manpower in the Unit during thewhole period under review, as discussed in para 2.2.31 infra.

Reason

Absenteeism

Downtime(machine hours) Percentage to total down time

48.55

9.86

11.87

27.02 i

-

2.70 I

100.00 I

6399

1300uelay ln previous Drocpss 1565

3561rower larlure

Tbtal355

r3180

Excess (+)/short(-)

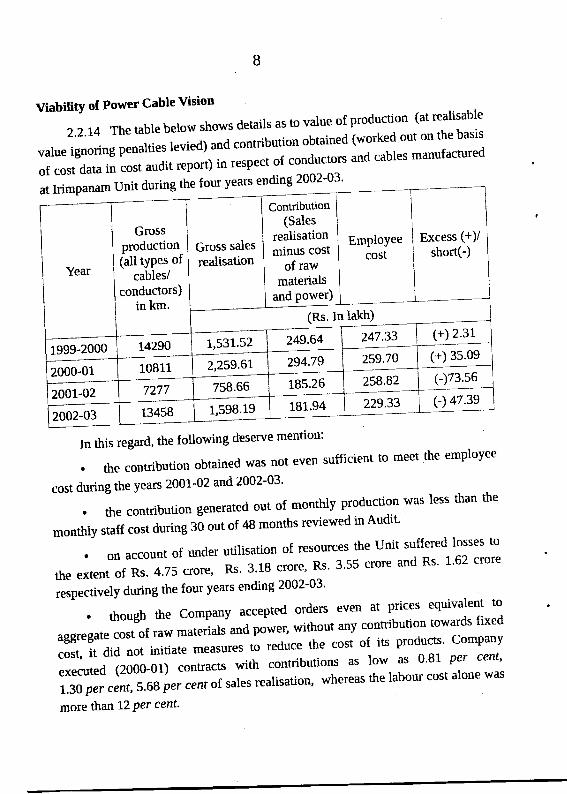

In this regard, the following deserve mention:

' the contribution obtained was not even sufficient to meet the employee

cost during the years 2001-02 and 2002-03'

' the contribution generated out of monthly production was less than the

monthly staff cost during 36 out of 48 months reviewed in Audit'

.onaccountofunderutilisationofresourcestheUnitsufferedlossesto

the extent of Rs' 4'75 crore' Rs' 3'L8 crore' Rs' 3'55 crore and Rs' 1'62 crore

respectively during the four years ending 2002-03'

' thouBh the Company accepted orders even at prices equivalent to

aggregate cost of '"* mutttiul' "nd

po*t" without any contribution towards fixed

cost, it did not initiate measures to reduce the cost of its products' Company

executed (2000-01) "ont""t' with contributions as low as }'Bt per cent'

1.30 per cenf, 5'68 per centof sales realisation' whereas the labour cost alone was

more than !2 Per cent'

EmploYeecost

Contribution(Sales

realisadonminus cost

of rawmaterials

and power)

Gross sales

realisation

Grossproduction(all tyPes of

cables/conductors)

inkm'(Rs. In lakh)

(+) 2.31

(+) 35.09

9

Management attributed (August 2004) the row level of contribution to lackof facilities for manufactu.ing wide range of cabres, highry competitive marketsituation and locationar disadvantages -d1e

to which higher transportation costswere incurred for both raw materials and finished proau"ti

' The reply is not tenable as the Management had not taken any action either toupgrade the technology or to capture market for its products through effective costcontrol measures and marketing techniques.' JFTC Division

Production planning

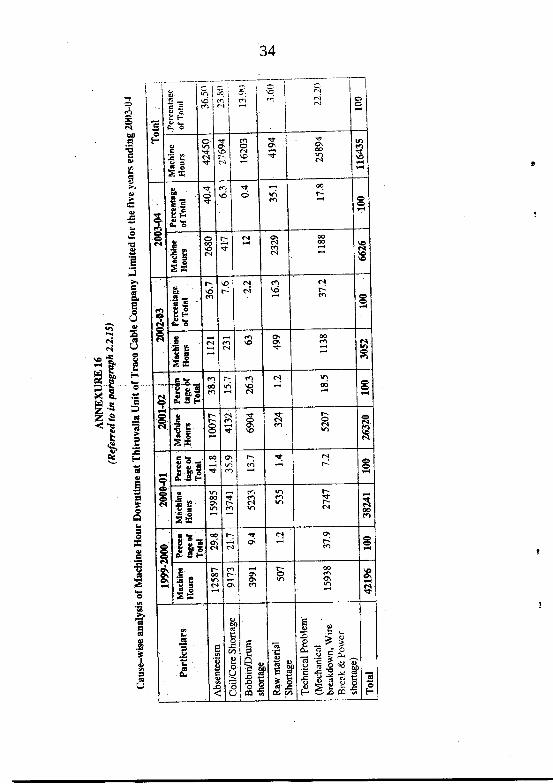

2'2'15 Since the company was not receiving ord.ers for JFTC on a regurarand consistent basis, the producdon pranning activity was confined scheduring ofproduction as per derivery schedules given in the confirmed orders. Auditscrutiny, however, reveared that pranned levels of production were rareryachieved in fuu and deviations from plans were quite common. This was onaccount of reasons such as absence of machine oour"a,'.oivcore shortage,bobbin/drum shortage, etc., as per detairs indicated inAnnexure-r6. The divisionfailed to maintain a steady production and consequentry there was underutilisation of resources to a huge extent especialry since 200L_02.The fact thatmost of the causes were controlable indicated inadequacy of controls on the partof the Management.

The details of variations in production rever on a month_to-month basis, andcapacity utirisation on annual basis for the five years ending 2003_04 areindicated in Annexure L7. As wourd be observed trerefrom the productiondeclined from g'.3Bper centin 2000-01 to 4.7g per centin 2003-04. There wasno production for eight months and four months respectivery during the years2002-03 and 2003_04 due to non_receipt of orders from BSNL.Management stated (August 2004) that the ut'isation of plant was dependentupon the product mix, as ordered for by BSNL from time to time, which differedeach time and courd not be predicted accuratery at the time of ,"*il;;i]nr*a

The fact, howevel remained that the compa.ly did not take any effective action toexplore the market outside BSNL so as to achieve better capacii ut'irrtioo.927n0n.

10

InventorY Control

2.2,1'6 The Management adopted a policy of 'just-in-time' procurement

of raw materials for the Company' A review of stock holding conducted in

Audit revealed that the policy was not being strictly followed by the

Company, as discussed in succeeding paragraph:

Accumulation of stock of raw materials/work in progress

2.2.t7 The Company held an average monthly inventory of raw

marerials worth Rs. 1.03 crore during June 2002 to January 2003 and Rs' 59

lakh from JuIy to october 2003. There was hold-up in production at JFTC

Thiruvalla, from June 2002 to January 2003 and again from JuIy to october

ioo, ,l' want of orders. Based on Company's policy of 'just-in-time'

procurement of raw materials, the unit should not have carried inventory worth

Rs'l.03croreduringtheperiodsofproductionhold-upsincetheprocurement

was to be made against confirmed order only. This led to blocking up of funds

ofRs.l.03crorebesideslossofinterestofRs'12lakhsustainedduetoidleinventory during the periods of production hold up'

Management stated (August 2004) that the procurement' in the instant

case was on the basis of requirements prior to re-engineering and the reduced

requirements resulted out of re-engineering caused excess inventory holding'

Management,sreplyisnotacceptableirrviewofthefactthatthoughtherawmaterialstandardswererevisedinApril2002'theCompanydidnotadopt

the same for procurements made from June 2002 onwards' leading to

accumulationofstockofrawmaterialandconsequentlossofinterest.

Stock of non-saleable telephone cables

2.2.|BAsperthecontractwithBSNLthemanufacturedcablesdelivered

after a period of six months would not be accepted' The JFTC division'

however,manufactured(AprilL999toMarch2003)andheldinstockfinished

cablesofdifferentsizesworthRs.22lakhwithoutobtainingformalorders

11

from BSNL. As a result the cables could not be sold since the stock period

exceeded six months and the finished products became dead stock.

Management stated (August 2004) that the additional quantity was

produced in anticipation of rejection of 10 to L5 per cent by BSNL. The reply

is not tenable since the cables were being cleared after spot inspection by

BSNL and hence there was no need for producing and stocking materials to

make up the rejected quantity. Audit also observed that stock worth Rs. 68;82

lakh was retained in production floor for want of orders'

Marketing

2.2.LgThecompanyhasbeenmarketingitsproductsamongtraditional customers; viz. State Electricity Boards for Power

conductors/cables and DoT/BSNL for Telephone cables. No Marketing

strategy was evolved to enter in to markets outside Electricity

Boards/DoT/BSNL. As far as power cables are concerned, supplies to

other State Electricity Boards were rendered uneconomical, due to the

company's inability to control the cost of production and offer prices

matching with that of competitors. The company, as such, depended solely

on KSEB.

Audit noticed that the percentage of company's supply with reference to

total procurement of power cables by KSEB ranged between 27 '67 and76.07

during the five years ended 31 March 2004. In respect of telephone cables,

theCompany'ssupplyincomparisontototalprocurementbyDoT/BSNLwasin the range of 0.38 per cent to 2.88 per cent during the four years ending 31

March 2003.

The gradual fall in market share of power cables was attributable to

emergence of new suppliers and company's incapacity to offer competitive

prices. with the entry of more manufactures in the market, the capacity far

exceeded the demand, and company could not match its prices to ttrat of the

new entrants due to excessive cost'

2.2.20 The sole dependence oB KSEB for power cables and DOT/BSNL

for telephone cables acted as a constraint in all the spheres of activity of the

L2

Company right from capacity utilisation to sales realisation. The suppliesmade by the Company were subjected to levy of penalties, belated salesrealisation, lowering of prices, etc. There were no earnest efforts on the partof the company to avoid losses by streamlining its systems, reducing costsand improving efficiency of performance, as highlighted in the succeedingparagraphs.

Power Cables

Payment of Liquidated damages

2'2,2L As per the general terms and conditions of supply of conductors toKSEB, delay in supply by the company attracted payment of liquidateddamages @ one per cent of value of materials per month of delay or partthereof subject to a maximum of 10 per cent of such value. Audit observedthat out of the 15 supply orders executed during the period April l-999 toMarch 200d supplies against eight supply order's attracted levy of liquidateddamages amounting to Rs. 35.92 lakh for belated (one to four months) suppty.

The delays in delivery were mainly attributable to avoidable reasons suchas want of raw materials (9.87 per cent of. downtime recorded), absenteeism(4gper cent) and machine breakdown(27 per cent).

Management stated(August 2004) that the optimum product mix andmonthly requirement of consignees as per delivery schedule in purchase orderswere different and hence backlogs in supply occurred.

The reply is not tenable in view of the fact that the production required tomeet the delivery schedule was always achievable, had the company exercisedproper control over the loss of production hours on account of avoidablereasons, such as shortage of raw materials, absenteeism, downtime of machinesdue to inadequate maintenance and repairs, etc.

Delay in preferring claims

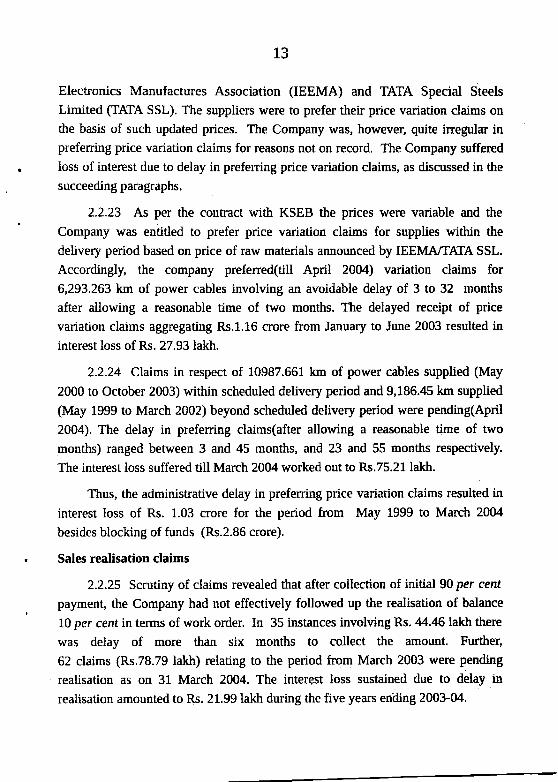

Price variation claims

2-2.22 KSEB publishes the updated prices for power cabres every monrhbased on the raw material prices announced by the Indian Electrical and

L3

Electonics Manufactures Association (IEEMA) and TATA Special Steels

Limited (TAIA SSL). The suppliers were to prefer their price variation daims on

the basis of such updated prices. The Company was, however, quite inegular inprefening price variation claims for reasons not on record, The Company suffered

loss of interest due to delay in prefening price variation claims, as discussed in the

succeeding paragraphs,

2.2.23 As per the contact witb KSEB the prices were variable and the

Company was entitled to prefer price variation claims for supplies within the

delivery period based on price of raw materials announced by IEEMA/IAIA SSL.

Accordingly, the company prefened(till April 2004) variation claims for

6,293.263 km of power cables involving an avoidable delay of 3 to 32 months

after allowing a reasonable time of two months. The delayed receipt of price

variation claims aggregating Rs.1.16 crore from January to June 2003 resulted in

interest loss of Rs. 27.93 lakh.

2.2.24 Clums in respect of 10987.661 km of power cables supplied (May

2000 to October 2003) within scheduled delivery period and 9,1.86.45 km supplied

(May 1999 to March 2002) beyond scheduled delivery period were pending(April

2004). The delay in preferring claims(after allowing a reasonable time of two

months) ranged between 3 and 45 months, and 23 and 55 months respectively.

The interest loss suffered till March 2004 worked out to Rs.75.2L lakh.

Thus, the administrative delay in preferring price variation claims resulted in

interest loss of Rs. 1.03 crore for the period from May 1999 to March 20M

besides blocking of fqnds (Rs.2.86 crore).

Sales realisation claims

2.2.25 Scrutiny of claims revealed that after collection of initial 9O per cent

payment, the Company had not effectively followed up the realisation of balance

1A per cent in terms of work order. In 35 instances involving Rs. 214.46 lakh there

was delay of more than six months to collect the amount. Further,

62 claims (Rs.78.79 lakh) relating to the period from March 2003 were pending

realisation as on 31 March 2004. The interest loss sustained due to delay in

realisation amounted to Rs. 2L.99 lakh during the five years ending 2003-04.

L4

Managementsmted(August2004)thatl0percentofthevalueofbillswasusually paid only after the power conductors supplied were consumed by

consignees.Thereplyisnotcorrectsincetheagreementspecificallyprovidedforrelease of. I0 per cent payments on acceptance of material'

Telephone Cables

Lower Vendor - rating

2,2.26TheDepartmentofTelecommunication(DoT)effected(1997-98)a

majorchangeintenderevaluation,introducinga'vendorrating'System,whichwasbased on quality (ISO certification), promptness in delivery and contpetitiveness

of prices quoted. Company's vendor rating ever since the introduction of the

system, was below the industrial average, mainly because of the delays in delivery

of cables. To compensate for the drop in delivery rating and maintain competitive

vendor rating the company had to quote prices lesser than potential market price'

2.2.27 Audit observed that the delivery rating of the company' came down

from 0.86 to 0.72during 2000-01 when the industrial average stood at 0'82' As per

the Management'S own assessment, the sales revenue that the Company had to

forgobyquotinglowerratestoensurecompetitivevendorratingfortheyearwasRs.1.50 crore.

Payment of liquidated damages

2.2.2EAsperthetermsofthepurchaseorder'delayedsuppliestoDOT/BSNL atrracred levy of liquidated damages @ ll2 per cent of value of such

supplies for each week or part thereof up to 10 weeks, and thereafter @ 7 per cent

of the value of delayed supplies for each week of delay for another L0 weeks.

Further, delayed supplies were not eligible for price variation claims for the

delayed period but the advantage of any reduction in price for basic raw material

would be passed on to BSNL.

The Company could not adhere to the schedule for a sizeable portion of the

supplies every year. The amount of liquidated damages, price cuts and related

recoveries, suffered on delayed supplies amounted to Rs.4'35 crore during the

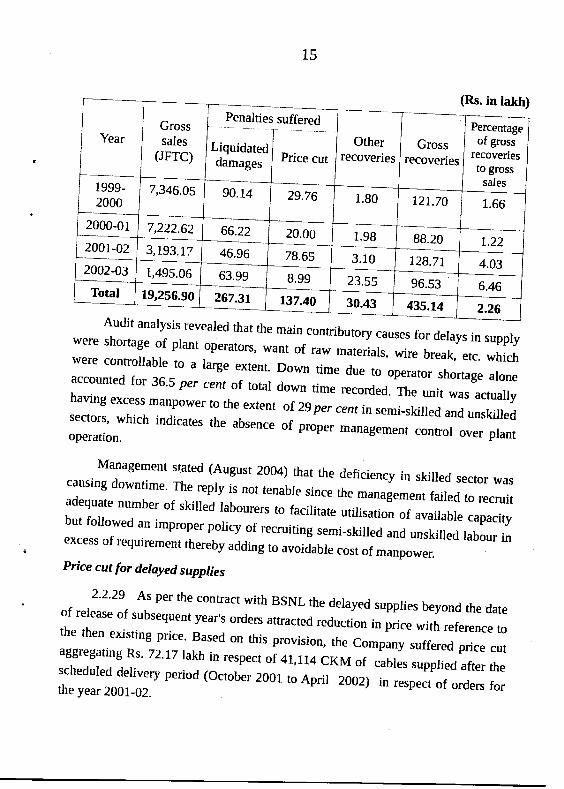

period 1999-2000 to 2002-03 as shown in the table below:

15

(Rs. in takh)

Audit analysis reveared that the main contributory causes ,o, our"rlffi;:: :::::i:ji::l

operators, want of ..* ,"*",r-;,;il; etc. whichwere controtable to a large extent. Down time due to operator shortage aroneaccounted for 36.5 per cent of totar down time recorded. The unit was actuailyhaving excess manpower to the extent of 2g per cent insemiskilled and unskilled

;::"":lJn,"h indicates the absence of proper management contror over pranr

Management stated (August 2004) that the deficiency in skilled sector wascausing downtime. The reply is not tenabre since the management failed to recruitadequate number of skilled labourers to fac'itate utilisation of avairabre capacitybut followed an improper policy of recruiting semi-skilred and unskilled labour inexcess of requirement thereby adding to avoidlble cost of manpower.Price cut for delayed supplies

2'2'29 As per rhe conrracr with BSNL the delayed supplies beyond the dateof release of subsequent year's orders attracted redrrction in price with reference tothe then existing price. Based on this provision, the company suffered price cutaggregating R' 72.17lakh in respect of 41,,174cKM of cables suppried after thescheduled delivery period (ocrober 2001 to Aprir 2002) in respecr of orders forthe year 200t-02.

YearGrosssales

(JFTC)

I Penalties suffered

trtr*/ ,;"";. Other

recoveriesGross

recoveries

Percentageof gross

recoveriesto gross

sales1999-2000

7,346.05 vu.14 29.76 1.80 121.70 1.66

2000-01 7,222.62 66.22 20.00 1.98 88.20 1.222001,-02 3,793.17 46.96 78.65 3.10 128.71 4.032002-03 1,495.06 63.99 8.99 23.55 96.53 6.46TotaI 19,256.90 267.3r 137.40 30.43 435.14 2.26

16

Delay in sales realisation from DOT/BSNL

2.2.30 The contract for supply of telephone cables to DOT/BSNL stipulated

payment of 95 per cent of the value against proof of receipt of goods by the

consignee and the balance 5 per cent within a period of six months or at an early

date against bank guarantee'

Audit,however,observedthatevenafterallowing15daysfordocumentsto

reachDoT/BsNLthePaymentagainstl,4l0invoiceswasde}ayedforperiodsranging from 3 to :aziays f'o* d"t" oI delivery during the five years ending

2003-04. The interest loss sustained by the Company due to delay in realisation

worked out to Rs'2'95 crore'

ManPower AnalYsis

Surplus ManPower

2.2.31 The Company had manpower in excess -of

re{uirement',::^rt1:

recruitments were made without conducting Prcper work-study 1d the level of

tl a tima n{

:ffiTffiff#;" much resser than those initia'v projected at the time of- r! r -^+ +^1.^ orlonrrlfP

il,#;;ffi;;;.rhe.flanae'T:*Y:"u'l;-iu*n1":':"";1;t":::ti:ftr'T;;;;;; the labour/staff strength. After ir was pointed out

-r-- +L^+ rLora rglc

(August 2001) bv the consurtants enqaqf 9-"-1Y.it3;|;t;l-ll'"Tllffig#r,u;ffi; the exrent of 40 to 45 per cent at Head office and

o\ l-" Etnrrrl

Jt1ffi-::'ffi'tr,e"unis, a committee constituted (December 2002) by Boaid

identified (March 2003) the surplus manpower as follows:

Theoverallreductioninstaffcostafterdownsizingonthelinesproposedwas

estimated at Rs.L.44 crore per annum. Based on this, the extra cost bome by the

Company due to retention of surplus manpower for the five years ending 2003-04

amountedtoRs'T.20crore.TheCompanylaterrequested(June2003)Government

Particulars Men in Position ActuallY required Excess manpower

35Head office 55 20

Thiruvalla Unit 376 198

150IrimPanamUnit 2t5 65

283 363Tbtal tr6

L7

to refer the company to Enter?rises Reforms committee for resuucturing/diversification' Further developments were awaited (september 2004).Avoidable payment of overtime wages/production incentive

2.2.32 Despite holding surprus manpower in both the Divisions and the orderposition much below the capacity revels, the Management resorted to engagementof workers on overtime basis, as a matter of routine, without conducting any cost_benefit analysis.

Tlte overtime wag€s paid during the four years ended 31 March 2003amounted to Rs'86.65 lakh. In addition , the company also disbursed productionincentive amounting to Rs.s3.43 rakh at JFTC unit during the three years up to2001,-02. Payment of incentive was not justifiable as;

' The company could neither avoid levy of riquidated damages byBSNL/DOT for derayed derivery nor the drop in derivery rating whichwere considered as a basis for approval (october lggg) of tie scheme.

. There was large scale absenteeism,

. There was no extra/additional production.

Management stated (August 2004) that the incidence of riquidated damageswould have been much more, had it not introduced the production incentivescheme' The repry was not acceptabre as the payment of overtime wages andproduction incentive was not justifiabre when the company had huge surplusmanpower, high level of absenteeism coupled with poor production performance.Incidence of idle wages

2'2'33 The production activities at JFTC Division Thiruvala came to astand stilr with effect from 31 May 2002, for want of orders. The Irimpanam unitalso had to stop production with effect from 23 July 2002 awaiting further ordersfrom KSEB against tenders in process. The company, therefore, informed (october2002) the Government that there would be considerable savings in establishmentexpenses, in case a ray off was declared. Though the Government anowed(February 2003) the company to lay'off, the Board defened the decision anddecided to canvass further orders. Thereafter Thiruvalla Division had not been in927t2017.

18

operation during the period JuIy to October 2003' for want of further orders from

BSNL.Theoptiontolayoffwas'however'notevenconsideredandtheidlewagespaid during the period of production hold up worked out to Rs' 4'07 crore'

Management Information System (MIS)

2'2.34TheCompanydidnothaveasystematicandefficientMlsforbetterCorporate Gouernance' In the absence of proper MIS the Management could not

add,ress problem areas as discussed below:

' Delay in execution of work orders and high cost of production were the

main problem areas for the Company' which adversely affected its order

position, sales realisation and profitability' No regular and systematic

analysis of the causes of delays were conducted by the top

Management/Board'

' There was absence of proper reporting system and remedial measures

were not initiated in time'

.ThedirectionsfromBoardofDirectorsinvitalareaswerenotalways

PromPtlY comPlied with'

Internal Audit and Internal Control

Internal Audit

2.2.35TheCompanywasnothavingitsownlnternalAuditwing'TheInternalAuditwasbeingconductedbyengagingafirmofCharteredAccountants'Audit observed that the findings and related recommendations by Internal Audit

werenotproperlyacteduponbytheManagement.Mostofthesystemdeficienciespointed out in Internal Audit were persisting as indicated below:

.InspiteofobjectionsinlnternalAudit,InternalControlSysteminareasof

debtors control and cash management left scope for substantial

imProvement.

.Productionstandardsfixedattheti'meofcommissioningremainedunchangedandimprovementsbroughtinsincethenwerenotproperlyincorporated in the system for better Internal Control'

L9

' stock levels remained to be fixed and there was absence of a foorproofsystem of coding and crassification of inventory and proper storage andup-keep of finished goods.

' Though the company was generating high value scrap materiars likeAluminium and copper, weighments recorded at the time of removal ofscrap were often erroneous.

' There was no system in the company for regurar identification anddisposal of scrap. The total value of scrap as on 31 March 2003 wasRs.56.19 lakh and it consisted of items dating back to 1963-64.

Audit observed that the observations and recommendations by the internalauditors were not acted upon and were still pending (September ZOOAj.

Internal control

2'2.36 The Internal control systems in the company were found to beinadequate in many respects. The deficiencies observed in Internal control systemsare indicated in Annexure 18. The nature of inegularities were as foilows:

' The company did not exercise adequate contror over consumption ofmaterials resulting in excessive scrap generation.

' The company failed to reconcile the input and output in respect of copperconsumed. The excess consumption and unaccounted shortage noticed inAudit amounted to Rs.31.g9lakh (Sl.No .l of.Annexure 7g).

' The corporate governance lacked in many respects (sr.Nos.3 & g ofAnnexure L8).

' The procurement was often made on the basis of limited tenders whichdeprived the benefis of open tenders (Sl. No.S ofAnnexure L8)

' Different rates were paid for same materiars procured during the sameperiod at the two divisions involving additional avoidable expenditure ofRs. 16.08lakh (Sl. No.6 of Annexure 1B).

' Absence of internal check system led to fraudulent claims to the extent ofRs.13.58lakh (Sl. No.7 of Annexure 7B).

20

TheabovematterswerereportedtoGoverntnentinJuly2004;theirreplyhadnot been received (September 2004)'

[Audit Paragraph 2.2 (2'2't to 2'2'36) contained in the Report of the

Comptroller and Auditor General of India for the year ended 31st March 20041'

The Notes furnished by the Government on Audit paragraph is given in

Appendix II.

1'TheCommitteeobservedthatthefailureoftheCompanytocapturemarketforitsproductsthrougheffectivecostcontrolmeasuresandmarketingtechniquesresultedindelayedsalesrealizationandblockingupoffundsininventory'TheCommitteealsonoticedthattheCompanyhadtopayheavypenaltiesfordelayedsuppliesandsufferedsubstantiallossesduetononupgradation of technology and excess consumption of raw materials'

2. As of now the Company is going on progress and sufficiently good

.o*Ju"k has been reported and hence the committee decided to drop the above

said para' conclusion/Recommendations

3. The committee observes that the company is cu$ently making good

progress and good comeback has been reported by the Company'

Inthelightoftheaboveobservation,theCommitteedecidestodroptheaudit para.

ThiruvananthaPuram,26th April,2017.

C. DIVAKARAN'

Chairman'Committee on Public Undertakings'

2L

APPENDIX.I

SUMMARY OF MAIN CONCLUSION/RECOMMENDATIONS

sl.No.

Para.

No.DepartmentConcerned

Conclusions/Recommendations

'L 2 3 41 3 Industries The Committee observes that the Company is

currently making good progress and goodcomeback has been reported by the Company.In the light of the above observation,the Committee decides to drop the audit para.

22

g$Eg

s i;flE$iEiEEE#i

gEE$

$ T,E *l

$gf,ElFE E;IE;E.EIclsEl&r€gE,s e gi

€!i;1gF€*I

HTEEI

{+ EEI

flE BEJ8bE rl

LG'8".e

?*.ee-EE;ll >

!!EFUFovxoEFE.xEEiEoE

E;?s€s(J >.pE.I 6g{8o=drE.g

i'g's';.EE.E.YFv:9FE'E{rE8;

E.

E

$EgEEgE

ffigE

faEigEsg

g€EE

Es$g

EEFg

9a

!

Fx

EIt:l.€cH

$TzEoo7T6tI-8

E

Eg'

I

f

Tg

V)

F

l{F

z

xz7=afr

II1

azH

aFz

rmB

EEigHo ,€ ^ElgErEgI

'EE igEl

Eg€ifl

gls€fl

EE€EEIeE;#€lEE E;EI

r $E:+iEE* E El

flE!: eI

E:'g:lE:Er"{e:ig{j

I

I

_l

--l

23

;Hi;;fi;i;Pu*u

iiggg[$gggggil

iEEE€EBEfg€EEE-

9ts9beitE€ r; F5 €" 9.3

!sif{ P o!

; tEg

3€Eg€"E $-e E.Q

g5;ii

?q$; E

EaiEE3E EE€e gE';&

EE$si

gq:eg

*$Fqg

Ib$i€H

.E

9sitF"Fg6aEsEEE.Hb:tbu'tE99d,EsEEH.ld E

EAgE8Eb'aF$6BSE3Et'EF6

iE=: Uri'i..E e.l gloE" g=I 6..i

IE

EEE

-85

EE.tl

5

8EP

vIT

5E!.aEIaa

fr

$o€6

I

e

24

s€EtS.EEg

E gE€bE dgit9:fETE! Ei*:

Egaa€

E 6E€E,E

e3 EE

iEEEE€

IgEiBE-

ie ne € fr€E

o€u{g€ea8soda4-gtErgHS9sEEgH*oc66-J>

?CE'g.FrE:

$:>ts:d

.z!6104

6

o

r,€ils

.EE:ao€

,6-

€dri 3€q!!

o€

o!

1.jEaa-

:iTirll:rr aii'; ':t

i3il€i-o3t.trO3!_F g:

= 6laa

;o=L

5E*3EnB.e

Ea!lq=

t'2

ii:-=E.6>>L<

!0i.'i ;e-9l

oae,i€i

iEt;.or9'i;si:o!€i r't:':-9.'Eroi q.a1D-=,=:3FEt:E.E

8.3aE8:-6€-E€Ec6"8iaF!

.2iF6o.=

EgOtr€'.ELg€

.=q

&'=F95E3i9i

te l:?i I,66

isit6,:tja?iiEitE.DE:; i'lif.B ",3bb.E'2=YGe€EXgEEBEA,EaodIr=>6EeE-cFc.:

vi&F

.d.=AF.ooEnoEo

Fi.;EeE6;grOC

.oCFtFa

.giiEJ

i E'r:-o.r&l€'rPt,=acao

3 Eb.

3 2.D.Yd6

:_ggEU39.E:od=9!

<;Ut

BS€t21

9tE,}rie!9=F:

oltlat

o.6

oEti

€ie

.{

to€o6

dgdoe

=

25

-;.;l3Elca €l3Fiv;lcfl

ELItrtlF6l

4: -rl

€EiE€I,. oJohl

rEl'a al

Hoi:FIo ol.E

=li'xlid bls-lo9l

^: dl;elsslaiV ":l

EEI:?lE'01tr

'lth:IeEla.=loolxelq clEslc 6!.r 9l

b3laclI|E E]

'ogo,0o

qo.

.li

da

qd

oo

a'9oa

=

c

=,)I

ctoO

xl?c-.tl -otl cisl EfrlgNt*.il 9

1ll$le6il PNIA

E€ E gE

€gg?E6E E 6F

3*- i g'E

I€E sEi* s fsE.E 9 :.8€t e E.s

igig€s

iaitggis

i?EEsE-ggi

€3':SX"t f€;13€l

cfiEiE.* ai$s?i

EEiEiiESEiEj.E FSE-Us EYE= a;-s{H:EE EEs=:E9g.E:F TH.;:E.ET iE: * ;3Es Ii€ sEE'. ts-€ii:Eflei3i: Es5.ag.rE;.8 8E -^ e.r€ HE'E0_ E o,, E ? € _ O.- -cEo6E.o,E -SgEI:.E EE EE E FsE*€iE!eEI'g eeE{.pEFaEE;E n;A$E;s 5E::i lt5

"=-leEEUfiir 9-tcE.9'= 0 E'= H b € e.9=.9-€elEgE= .iEE!t'EBEeEEET {=EF.€Fgrtr:e.EE lP':.H't"1, ae€= - ;.= !

H3€ g:,;a HEtf Eg:FIF':g e€g€i9Pi5 !r*; tt otr q= - E e.E

E H€ F b€€ qEi!t;8":?f,gE EEEEPE;gPc*a t.!:Ee-gg#?fiF=rE;cE;te9BeH*l;€*i€

q

€

o

q,(l

6

q€o

q.:

$l

cl

d5cl

I

I

-__tI

J

92720L7.

26

ggigF€s{ggFsii

alg€i$ggEffifigEFgF$-EB€gFgEi

ffigii;ffffg;*ig

qal€<Er3Befra'-E.F,sFEosEH:PQto60stEE!jjE->Eq8-.3e.e 8.EIIs.q

E€.9c;TEEe3oor35e,:E€EPT>rxEoootr i'ri

x!

Ei! E-H.g E.E"ss;E

;€$!

$$gE

e€gE

$fgst *T 9e

$FFs€$E FE B

eie€ *

F [!isE{ sgtll

6I

t)€

EL

5

oc

ooca0

oog

U&d

od

3

oI

.hlg.il5dledlexlodl

Edl

Itl€ta

l3.l8Idlo.

l6T

27

>,a!3

ETb-rEA

.9tEgr.g>6

TFH€sE-gEp€e U

86eE.E Ea?EFstH,€.8oi a

s€;>sE8E;€ EE6.s a3^=EEggs $H 5'E..UE€f € s

H3FI€9

4.2*Ea.i x.=; # EeirisEsEF;E oE 9-9

E:f E l€ Feisg€Esi

g€i $s

gFsgi

sEE; E*

$Egggs

FiE€g€

fsg€ g$

'\t6rcIEi8rei .11rO

l9

oErEd

EdEEO

o5c6oo

=

co6Q

o'g}E8o.inl#5tidgE

=6

E.'8.Et <)00a

:,8gEi!6Y3o.EI7o

isi

iEi,€ )lslisrie,t.*::isil= t|r&ar9FEt.qPFt5+26gt42o.:l90uo.:i!5*c.=6€s9=

wg c

"bxsE E=;el:.E: aJA C

=qo

is$lq 3rOL--o

5 3..=i 3sa de:39ieE!- tr

igg:€ e.

igg.;Egi

!'- rAJ

H F.iI OsKltr

aE!oci tF g'E3 E

5e€'5()cg.F$.EEE6;EE T.E9ge

96ELs*9e6n:,a33x.<i(,

$l:6H.

8;rE€

|

e €.1\Eia'- J! brrr€o- 6rig !tF!i s.:

iBilPrlaiE6tHgiEa&"1eft6XEE3c'F*

.b€E$OEo.-a6iExo

ilo.E€3pOE

E;;'EO^

Ig2q

Yg

E,EegeeFE.ritg.oEIE:r:9.g'6g g..rtE I

6'El i60pE I

f,8reEi'!,1e€ ID:JO

: I'E3g:)otigrrEE,9 d,

15 ciE€

ilE'6ooE

o

B

i,o

5orE,xlgi

EII

T':g'i6l'5 1

rtt6'ictagfit(

!

3EZtvt9l, I

EioPbe'

3Bvt>8(29

qo "E{tg E

\I F E

t--I

I

I

II

II

I

i

II

II

I

II

I

II

txta0

lEilulcl0

l.q

lB

lr

l3lgIF

#s

28

3rEgBE

r El= o=

i Fe g

;Es-E

Ei: E

EE $SB g 8.5

H 3:EE

2 €;€EE is iiEAs:Ei1 A:E$i* sa Bt

iB*E?iE

E'dEitx0o

tsGI

oaeo

lcieist'ti5

ia;8i:rgijE.r3)gD O.! L'u3.EEErEE7t9Etr9.rats'8s

6Zo'EE&,x.9ET

bEaEErs€trg8!r65EtE9e.E! E;ej

letietlsqrll t

=4JItrpElXoo3EHEb.tAEg El

s.g€.Eo,€oggEi3gEgoo.E.E

goo7.E8E-

BEEO2=30_99egEtgr

'E g

EiA:ot't a

rr It€ rts{tE jrElrt*ir EtI t.3c0:93e:E

:sI b,[t 3'Eq

E663E89Eaeo9€c)e=

EEcdq

gE

.bsPEE=EE€E

E

EX6'oe-EE-6b I'5:zl:i3qlE{3,rE'6l

F.v{l

c

€.6oEFIe€tr6

7o

-l!t$$^il cO

.11

sl

ffiilI E$:€

liEtii EF!EI q'ttQ o

I sEEE;

1 EEE;EI EE"f=R

IE€F?E

Iii3gERAESE E

I

I

--! I

29

l0i=,9tot>IEa.=o

IE

'o,

9:g(

6

e

';l

o

=toI

gd

o

oa

.Eo

,9i!i-o

o05l-=Q

9i

c';AJR'g!€jEr€{,tx6at'It.C

oc

::E+

?ut:s35DQ\E

6=r9td

1E

)0rg

-E'6e€

.$aE6

zca

0

3qooEqdqto

6aFoo

d.{OF6G

9l.'11clldl

g9EgB5

$€DO

u=;Ble)xl.{rA

iEi3''Xl:9,p€

Eto,Itu=!E]A;O!o0l

9t

'n;c!=rItFtGC

5i

29X=(E

=!a0

3E:q,. .2ae

o:tferrd?g29;a;Ei8l.t'=)I'ots

9p.o.Ei .

P

SrF]*itttElgi5lolotc,l

:?nd,9o

3ieEbi

€F5ii.:

6.Ed3c&ooEEi3isi.sDE:t

\'d-d

3e;8l0

i8(':) o:t5.rci!>rxto'€ie''oo6!

ilt5'c\i€tol:io,

,8,3ip;EiEE9cgrgE.c3iFc

r o.i34t)u)95 i;EiiF ji# r

t o\-t q

,-iiF!iE ti6t'st; 6..!r-l

i3 E

€54!

EiF6

,6.3.E;

'EEO

=R.E t;FA-Nd€

E33-x=a'o.e3s.g'ii6gg.=o

3

'

,a=J.E. U

?EEl€stld

i a'Ei;€rloiFe:ETrog

E!tr8.B.S

,tEri d

htvaoX

'O =.:a.-cX'tr r

ooo.E-;gE,g e-, orE;t:5trtrg$x'Eg;!3,

+ 8.1aq l

HajEltE9:33iEd:aii9ioEl

UU6.E.;h1.9tl

l.si>rs18't9!0

totfila.0<'Ii9

r.9 i

:t'lc:rooi

tiI,€aE:tto!€:bOr

.=tdqGdkl>'!!5q

Hr,=aFO.=>32E6t9o=

,qt3,friEt5txrE'o

g

I

c

nE

.2 1

5lo(Eo0

Eixl:t .i

f;ib45lf.it(

i 9:Jq>,qa2)c

ici:0-!)=;'rlr.o I

1Ertt(

l9!,E:LFi'[,1s!R'E'ikoztilogsa.!ots

€!

Ef;>ba'FPooAE

€x!!r ai€8o!osoo{"oOL

E€Egg86g-aF€=atro

l€tit>

E

ooo

&UItt

A6

EI

E,

6cc5ao

ihI it.lr=rlt i

i3(HI'e i

:g{g.3J?rxriq';

,l Cj5cqo>

gEAd

.E .E

;€Ed

SFd6u€a6

iiq

8E0=ua5HHtt?bgo=3{v6hoIiFOr5d83sgH

0

q

o

ooB

o

so

EBE60

Fog

oa

(,

I'oE

6'o

b'q6

il"E'ioI€si{ltl

otboq

PilLl-.1

FIEi€!9i

6a

ooq

E

oxa

th-

€;cEfgg

EifF;$E

sEEg EEfl

ggiFggg

{;iE{*E

FigfEFgI

iEEg;ggg,E*EE A $g

o>shiF!'6*or€jc]Eid

i9:3:6i-El.-lo'El!:x

i.En

ii,

i.6

oIoxoO

a\

N

g,a

bE€i<!gi5Aac

ge

aPP

B.Exo,D&i3f}4i*tEEE

;E; 8..:gl8tteigt

3,:i .i

dl5i^l .!

\i\o;trixr,6;oiE9ro .,OV€)tl!tatETg9

lFtotoIOIXl0thtoto

lolotol3Il!lo

t':I&I

IE

Itt'$.lcDtvI

IEto

l€[l=alJ.It\tc rl(t l

lqqIt (

lq .!

te:Itr (

l,! :lo Ila,IE:i8o.!ig t

if

30

dlOI

'l I

.ol-lgl

3ldl:ldleldtol

>lclEIEIot,l,l)lolclat!

€l0l

t-libu!.'tI qlr8li9llbd

pEl

t -lt3i:al\Ol) dl

I

I

II

I---lI

III

I

.s Et

'5.91:r5a'E.EBeEEao-.5E.EsEl.gFEo.!>r6

?"uF

iE;rO.)r< it5 2

,V, ll0c

:*ii ;'ir.Fl46,rdl

r coi2€:iel:0e€t9.ts4

E E.'F5 !F3i-ai iegi-

6_O-:

ESi€61

.g.glEE:gDt

.H OJ

E E,9,'E.E

;

EE:aEt

3Eog5suE0

Ea5Eov€B€'EF8

r isF;9H\O !ge uHei*,99

o

gEI:€ €?EE

E E€E i i!IgE i;: E E€a€9Beei *5fl;Az7 ^s 0E-?

ll€is iE q€

EEE g€ E :E::; E E E : -fiE E

Eig{; si€gE= - F.E ; E b b-Eg:95 *3;aE€*re A€€g:E;€e s=€Ei:s5B* EEi:9?Eali EEXi;

gEEi?:l3giE

F€3 €T3'F 9

E€g E.E:6 o

iHE fEfB ;Ei; E

EiEE€I:;€ E

AAFg 'e

E;EI ;s.ge.E s

E{EE r

iEs€ F,

a??is€= a Ei'.i .- & EE

oa\ol'Il '

E

{

.;€rE

Entg .ilC 6il

31

Ff $iffiF

32

| .l:lllUF.E 1';

iii' f';;i'': it PatugraVh 2)"61

Slalrn,,:ili 5li;tr'.ltr:' li;i;.rr'i;.! iii;:;r: lil;i of TrT co Cal;lc Co;;ipany Limitcti ;:l; ll;'

-',i \ixlth {'i ll'i'livtf lcats uP [o 20i]2-rl3

iliuwes in lul,it)----r----.-'l

l9iItr-9Y

i A. LirL,titic*

o. naio u1, "opit"l 1 trot st I i19l8l

a. Gross Bloct | :rtf'tt :ja i -'t1g

e. lnvesllnint5

427ti.32

370.12 i

l30l.8l

424.54

r30r.8r i;;lt592.42

i)Ll.Jv

45-15.44

,:. (..i:!.:r .;npr,))cd o,.r.,!s r..',1'r'..1: , ,,' r,i,tir..ifilil.s1"l ':lt::i:':; :]:'*orr;lr" cnorrnl

* i.l o,',r, -""n. r!,!-$1.'g!itli\'''J':r9!gss-!q!9:-1999!Util-!5!:-

g. Accumulated I nZo.ll

(.:apital. en plotcdi 3770.98 | 24r3.t4

L'12635 t' 820"74

b. Rescrves and i :Sf.oa

d. Trade dues and

current liabilities(imludingprovisrons)

33

r n "*,,kY!]iX? fi 0,.,. o tStatemeltt shorving xorking rcsults of !}sco Cable Company Limited for the gve

years up to 2002-03

Porticul&m 1998-99 t999-2000 am0.0l 2001.02 2002-03

6551.27 E249.72 9086.42 3430.76 2924.36t27.82 r68.98 t94.A6 tt6.62 J)) 1a

Incrcase (+)/Decrasc (:) instock

G)615. l0 (+)206-42 G)s8.42 (+)272.43 (-)299.78

Totat 6063.99 u25.r2 9338.90 38r9Jl ?84735Etpcnditure

4{,02.ol 587 t.L4 66,67.02 2929.49 2t20.80107.95 t76."t0 t70.4 155.02 t17.57

sPilG 2.53 s.98 5.94 1.09 1.91Repaim and maintenun""- 71.9'l 6.t7 r09.28 6t.35 20.t6Othcr Manufacturingexpcnses

22,89 75.94 30.45 20.62 15.t7

Salaries & Wages andother employee costs(production)

465.75 547.37 611.5t 605.80 609.39

Salaries and otheremploye€ costs(adminisaation)

96.52 135.49 r r6.3t t46.25 125.21

Other administmtiveexPenses

68.08 toz.fi l I 3.93 84.08 52.95

Sclling and distriburioncxPenses

227.38 289.43 301.52 148.38 87.69

exPcn$s 194.68 t30.37 | 56.38 209.21 187.63Bad Debts writteno{Tprovision for dorbfuldebts

657.14 u3.53 6r.00 10E.58

Totrl openting experues s2s9.75 E00833 83963t1 $4229 34/.2,06253.98 160.99 303.O2 221.29 2m'96

Deprcciation 419.74 213.37 162.22 rzt.u 90.86Operaring profi (+)nossc)for the yar

(+) 130.5r (+) U2.43 (+) 4'17.36 G) 905.6r G) 886.s3

!xtmordinsry Edjustm;nts G)734.14Tax provision @.m 43-00Net protir (+) 13051 (+) 915.57 (+) {3{36 (-) 905.51 G) 8t553

927/2017.

F

TE;t-!o

a{

'=?o,)>E

rtc.ls

'{' I6t9If-irolI

mN 'f

$@(.1

a\o

q?eR

u.zzflEdE

tg

V;m

@r

cz, ?,.5

@N

c- N otdd

@@ \o

at\6E

?d

F

taFEEFtr

r:€ r.le{

(")\o

Nr e

E.zt_gt

Nd

€ Oro\€ ct

IS3€ c: a\o

olol v')

6 oel?tN

t=?

!E

rrt5

N s vd rd cl(.r

\aGI

'YtFi

3Ep

oq

*r .q c..l

r

=v,a6@

tr- cla:trd x

6(.1

tF

e

sEsoid

t:N

s Nr

Ee-83

r€c.l

r 6r €

o\Eo\N$

,6

oo

tt,gotl

()

Ego'= 6

466€

6 -o"trE3-6qt& (tt

6 e.€ _; e

=.9is:E€:t H= c

E Eg; F

34

=tgi a il-alU

O?

o

o

Fl

Oa9EAoi J(

s* I:E. FCE Ll'i oxd. .:trlr Ezs .e<! ?F:i/

J'F

eE

3

o

6

I6

FI

35

.4,nrrr:lrrr'r: l';(ll.r:ft::.ei le in prtn.gr:t;ii i.:,. .,1:

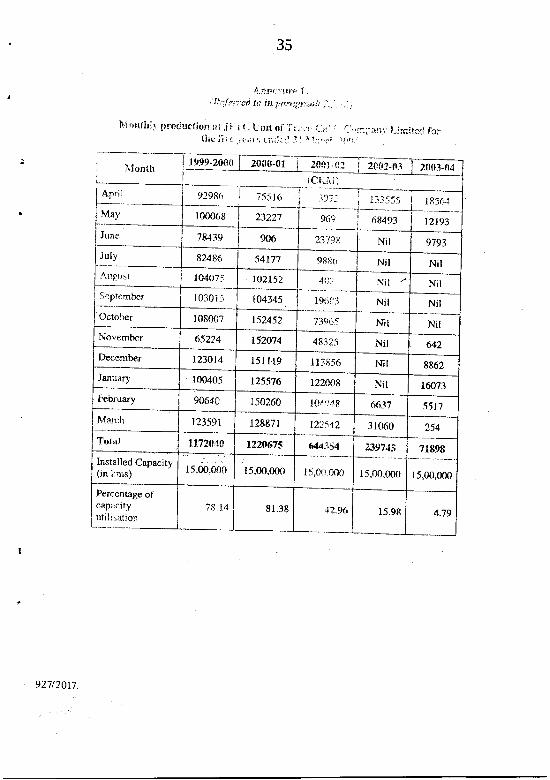

R,lnnlhl.rprodueti<urnl ,ff i{ll,iiltoi"i';:,:.r.a-.r.,:! ,.-,.,,...:3}1..t_irnifcllfc:(liu iji.. .ir::.,r:; ii..;.::1,1: I tl:t.:; lllo i'

--.. i lrg9-2oi'irr \IonlllII

April 91986 75_516 .]i l-1-1i55 2a(

l\{ay r00068 23227 96(,| i 6s493l__*

t2193Junc i813t) 906 217)! Nil 9793July 82,486 54t"77 9886 Nil Nit

.llgr.rcl 10,4.07 r02152 NiI / NitS4ptrmber r030i5 1o1345 I96[1:] Nit NilOctober | 08007 t52452 73.qii5 NiI Nill.lo"embcr 65224 1520?4 483?.5 Nil &2December 123014 l5 I t.l9 I 13856 Nil 8862January 100405 t25576 122A08 Nit t6073February 9064C r 50260 l{!r.r4 8 663'1 55t7l\1[an:h 123591 128871 t?,?"i42 3t060 1<i

Tof.al lI72A4t 1220675 e44.i54 239715 7r898Installed Capacity(in I:rns) 15,00.000 r5.00.000 15,00.to0 15,00,000 t5,00,0fi)

Percentage ofcapr!cltyutiliretion

7&.14 81.38 42..96 l-s.98 4.79

927t2017.

36

ANNEXURE 18

(Referre.l to it, Paragntph 2'2 '16)

Dcficiencics in Internal contiol syete'ms in Traco Cable Company Limited

@ Report for rhe )r'ar 199_.1-95 about the exccss

I usage of Aluminium ro, *anui"ctu'" "{.Ali llTlTX,:T1'::::*(::?",1i:ltlffi#H":ili"" i*'ii"r'iJ'J ilcsnl' coPU hdd recoiwirended in

;;;f ilp* lparagraptr 52) to taks remcdial action to reduce excess

;;"rnd;. ThJ coitpinv' howevor, took 19 99ritr9l measures' There was

;;;;'"i a system of input - output reeonciliation of costly raw mateill:p"tt of inr"ntow control. Audit observed that out of im aggregale consumpnon

Lr ii.gS,ZT X;". of Aiumnium and Steel, there was excess usage of l!:V2.\8".;il;;il anJstot vatucrl at Rs. 18.96 lakh as per the weight of .finishcdrxoducts recorded in thc packing list. The overall scrap gerrcration was

ffi;'""fiil r[. id]f r"r.r,";hich accou_nted for 0.83 per cerr of input

"eii,,t?"..^9t,!.sre1"."*'u:^'*:,*:.Y:-T::3^.:'^:1fr ltl"i:ffiH;"T;#6'K;;'";ffi R"' 12'e3 lakh dwing the period April reee to

March 2003.

Thus. the absence of lnput-ouPut reconiiliation resulted in unaccounted

Th."rh th" C"-fiy followJ 'tust itr Tirre' policy o{ procurenpnt the

#;ilil;;;ir,i-nau ooit was quitc higir'.thi "*:" *Y-f;-Tliiilil"'d;i.Ot

"rore toa R5' 9'83 crore' The iash credit with banks could

have becn reduced substantially with better inventory nanagement'

Thusthedeviation,fromthedeclaredprocufementpolicyresultedin

@ form.an Audit cotnmittee frorn December

2000 onwards, the Comparry constinred the Cornmitt€€ ontV I tvtaln ]!l;ilJ#fi;': ;i,h"'i;,';t,* since then confined to review of annr;d

fi;;;fi;;t*"ts alone and did not irlclud€ othcr prcscribd

i;mrted in interest loss on potential

sales realization to the extent.oi *. 28.58 latJr in respect of Thiruvalla unit and

Rs. ?.?4 lakh in respect of kimpanam unit

R."lt t"qrtt"d as packing ."ttti"l of lower sizc JFTC was being procured

;;;i;A;Jdr""n'ar,i.p"o"1g1o;},9-1'.1fl v-:""ilg.-:-*:#il;;;; ii.i,J ona".t up to 1999-:2000 and when open tenders were

fiil;ilg 20oo-ol, the lowe;t tates obtaincd were substantially lesser-than

il;;;;;i#"g rate of procurement' While lhe rate of 800 mm canre down

to* n . 3?9 t6 ns. 325, the rate of l'000 mm got reduccd from Rs' 529 !o

ir. +ss. Th" rates could be furtber lowered furing 2001-o2-when open tenders

with adequate publicity were invited'

ft u. pr*or*nt made on tlre basis of limited cnders deprived the benefit of

open tenders-

37

i ;,,,,,;i..,,i,.,,i'iJt;;;;;;;;;,il"a ,"iii,t*.l, ',"",i, ,:';rii*-i-";i**'.ali .; l.; ,,t r; . :1i,,, .,,;.." ;i:.:;:11:; rlr.l; : lr,:,:' 'il: 'r; .,'".irt -: af:- 'IlifirtJrlli !l'1i? |

I iinl.il.." ."*,. mnt.ti*t-lrr,ip."t:',r t:i 1h'r !lr::1 lh;il lrilrir::'::lr unit u'rs iocatcrl I

I I me (lompany had been follorving a system of sending r)nc copy each of I

I stores received notes (SRVs) to their linance. wing and materials wi

respectively;'t'lre paynrents wcre made bv tlie financc r':ing rfter recei'ing

checl:s necesstry beforc effecting final payment l)uc ::t this intemal che.ck

systern lacunae, payment! were made by the finance wrrig against SRVs from

Thiruvalla supported by 19 fbrged irlvoices for supplv of battens and drums

during ttre period ftom July 200t to June 200?.'llhc i:ve'r payrnent on this

account amounted to Rs.13.58 lakh. The Company irrtitnlted the mattet to the

GoveInme.nt, which dirmted (October 2002) Vigilance Departnent to conduct

ar] enquiry into the matt€r.

Thus the intetnal check system lapses resulted in Payment against fraudulent

claims.

i i ;n ii;t aciual solkingresults wiih rcfercncc to budgeu.

'ere appro ve<j belatedly

I ! (dut,nl Juie to September). no budget estinrates rvere 2reparcd thereafter' In

| | ,esg,,..I of periods fir which budgets were avaihble, wi,ie variation werc noticed