family firms and high technology mergers & acquisitions

TRANSCRIPT

Family firms and high technology Mergers &Acquisitions

Paul Andre • Walid Ben-Amar • Samir Saadi

Published online: 11 May 2012

� Springer Science+Business Media, LLC. 2012

Abstract We examine whether family firms undertake value creating high tech-

nology M&A. We also examine whether level of ownership, diversification, agency

issues and CEO type matter. Our sample consists of high-technology M&A

undertaken by Canadian firms over the period 1997–2006. Canada offers a setting

with many family firms and the use of control enhancing mechanisms such as dual

class shares and pyramid structures. We find a positive relationship between family

ownership and announcement period abnormal returns. This relationship, however,

starts to decrease at higher levels of ownership but remains overall positive. We also

show that the agency conflict between shareholders and professional managers has a

detrimental impact on announcement period abnormal returns whereas the conflict

between controlling and minority shareholders via control enhancing mechanisms

does not. Finally, we document that founder CEO undertake better high tech M&A

than descendant or hired CEO.

Keywords Family firms � Family ownership � Mergers & Acquisitions �Corporate governance � Control enhancing mechanisms � High-technology

firms � Event studies

JEL Classification G14 � G34

P. Andre (&)

ESSEC Business School, Av. Bernard Hirsch, B.P. 50105, 95021 Cergy, France

e-mail: [email protected]

W. Ben-Amar

Telfer School of Management, University of Ottawa, 55 Laurier East,

Ottawa, ON K1N 6N5, Canada

e-mail: [email protected]

S. Saadi

Queen’s School of Business, Queen’s University, Kingston, ON K7L 3N6, Canada

e-mail: [email protected]

123

J Manag Gov (2014) 18:129–158

DOI 10.1007/s10997-012-9221-x

1 Introduction

There is a substantial amount of evidence showing that family firms represent a

large fraction of public and private firms around the world (e.g. Claessens et al.

2000; Faccio and Lang 2002; Pedersen and Thomsen 2003; Anderson and Reeb

2003a). However, there exists considerable debate as to whether family firms are

superior or inferior performers (Villalonga and Amit 2006; Miller et al. 2007) and

whether founder CEO matter compared to descendants or hired CEO (Perez-

Gonzalez 2006; He 2008). We examine this issue in a specific yet important context

where family firms pursue risky investments by way of high technology mergers

and acquisitions (M&A). Formally, our paper aims to answer the following research

questions: How does the stock market react to the announcement of high technology

M&A undertaken by family firms? Does the family firms’ governance character-

istics (e.g. use of control enhancing mechanisms, family involvement in manage-

ment) and strategy affect this reaction?

Prior M&A studies have mostly focused on managers’ incentives to undertake

acquisitions (Miller et al. 2010) and few studies (Ben-Amar and Andre 2006; Feito-

Ruiz and Menedez-Requejo 2010) have examined the impact of family ownership

on the value creation from acquisitions. High technology M&A represent a special

class of M&A given their high growth potential but also high risk (Kohers and

Kohers 2000, 2001; Hagedoorn and Duysters 2002; Benou and Madura 2005).

These are often motivated by the acquirer’s need to obtain highly developed

technical expertise and cutting-edge technology (Tsai and Wang 2008). Ranft and

Lord (2000, p. 296) suggest that ‘acquiring firm may not have the ability to develop

these valuable knowledge-based resources internally or, alternatively, internal

development may take too long or be too costly.’ The acquisition of external

technology should enhance acquirer’s innovation level and knowledge base

resulting in better performance.

High-tech takeover targets are also highly risky because the valuations of these

companies are based on uncertain information (Kohers and Kohers 2001). Many

technology firms are young start-ups without any current revenues and whose value

lies heavily on the future development and commercial success of a new technology

(Benou and Madura 2005). Therefore, investors may have difficulties in under-

standing the technological complexity and to adequately evaluate future outcomes.

High-tech M&A provide an interesting setting to examine the ability of family

founders and their heirs in choosing high growth but risky investment projects.

This study contributes to the literature in at least two ways. First, to the best of

our knowledge, this is one of very few papers to examine how shareholders view the

effect of family ownership on firm value when the firm undertakes specific

investments. Second, we investigate the interactions between family firms, the

nature of the agency problems and their impact on the value creation from high tech

M&A. Villalonga and Amit (2006) posit that academic research should distinguish

between ownership, control and management to properly understand their effect on

firm value. Previous studies (Ben-Amar and Andre 2006; Feito-Ruiz and Menedez-

Requejo 2010; Miller et al. 2010) do not consider the specific interactions of the

various agency problems that can be encountered in family firms.

130 P. Andre et al.

123

We investigate the stock market reaction to high technology M&A undertaken by

family firms in Canada as it offers a setting with many family firms and use of

control enhancing mechanisms. Further, Canada offers a corporate governance

regime that is ‘‘principles-based’’ rather than ‘‘rules-based’’ like in the US. These

features are often considered as a ‘weaker’ governance setting. Nevertheless,

Canada offers a strong legal protection regime for minority shareholders.

We find a positive relationship between family ownership and announcement

period abnormal returns. This relationship, however, starts to decrease at higher levels

of ownership but remains overall positive. Diversifying acquisitions undertaken by

family firms are not associated with value destruction to their shareholders. We also

show that the agency conflict between shareholders and professional managers has a

detrimental impact on announcement period abnormal returns whereas the conflict

between family block-holders and minority investors via control enhancing

mechanisms does not. Finally, we document that firms managed by founder CEO

earn higher returns than firms managed by the founder’s descendants or hired CEO.

The remainder of this paper is organised as follows. The next section reviews the

related literature and derives our testable hypotheses. The third section describes the

methodology and Sect. 4 presents and discusses the results. Section 5 offers a

conclusion and suggestions for future research.

2 Related literature and hypotheses

2.1 Family firms and value creation in M&A

The agency literature (Jensen and Meckling 1976) discusses the agency costs arising

from the conflict of interests between shareholders and professional managers

(agency problem 1). In a M&A setting, managers may undertake acquisitions to

increase their compensation and private benefits at the expense of dispersed

shareholders (Shleifer and Vishny 1997). According to the interest alignment

hypothesis (Jensen and Meckling 1976), family ownership concentration should

reduce costs associated with this agency problem and therefore should enhance

value. Large investors such as families have strong incentives and resources to

collect information and monitor professional managers (Shleifer and Vishny 1997;

Claessens et al. 2002). This active family monitoring should increase the quality of

the selection of target firms which should result in better acquisition decisions than

in non-family firms.

Furthermore, family members often hold the CEO and/or chairperson position in

the family firm (Anderson and Reeb 2003a). This active involvement should

improve their knowledge of the firm (firm-specific knowledge) and enhance their

investment decisions particularly in knowledge-based investments like R&D

projects or high-tech acquisitions (Chen and Hsu 2009; Chang et al. 2010).

In addition, family blockholders should have a longer investment horizon. Family

ties within family firms may create a culture of commitment, altruism and loyalty

which favour a focus on long term interests in investment decisions (Chen and Hsu

2009). Moreover, James (1999) argues that founding families often try to transfer

Family firms and high technology Mergers & Acquisitions 131

123

their firm to the next generation and thus should have a long-term orientation and be

more efficient in their investment strategies than non family firms.

However, large family shareholders can also pursue personal objectives that can

differ from profit maximization and be detrimental to minority shareholders (agency

problem 2). Prior research suggests that family blockholders impose significant

costs to the firm because they may undertake sub-optimal investments (Zhang

1998). Given that a large proportion of the family wealth is invested in the firm and

their active involvement in the management, managers of family firms tend to be

more risk-averse managers (Chen and Hsu 2009; Chang et al. 2010; Miller et al.

2010). Therefore, family firms may be reluctant to undertake profitable innovative

strategies through high-tech acquisitions because it may increase the family’s risk

and threatens the survival of the family firm. Chen and Hsu (2009) report that family

control is negatively related to the level of R&D investments which suggests that

family owners may limit risky but profitable R&D investments. Chang et al. (2010)

also document a negative association between family ownership and stock market

reaction to innovation announcements by Taiwanese firms.

The above effect is likely to be more severe as the amount of family wealth

invested in the firm increases. At high-levels of ownership, family blockholders

become entrenched and have sufficient power to undertake investment projects to

increase their private benefits or to reduce the firm’s risk (Zhang 1998; Connelly

et al. 2010). Given the existence of the alignment and entrenchment effects of

family ownership, prior research (Morck et al. 1988; Sanchez-Ballesta and Garcıa-

Meca 2007; Cascino et al. 2010) suggests that family ownership may have a non

linear effect on firm performance.

The above arguments lead to the following hypothesis1:

H1: Family ownership has a positive effect on the stock market reaction to

high-tech M&A at low levels of family ownership (as a result of the

monitoring effect), and has a negative effects on the stock market reaction to

high-tech M&A at high levels of family ownership (as a consequence of the

expropriation effect)

Previous studies obtain mixed evidence on the effect of family ownership on firm

performance (Anderson and Reeb 2003a; Maury 2006; Villalonga and Amit 2006;

Miller et al. 2007; Sciascia and Mazzola 2008). Looking to M&A, Ben-Amar and

Andre (2006) document that family ownership has a positive effect on acquiring

firm performance in Canada while Feito-Ruiz and Menedez-Requejo (2010) report a

non linear relationship between family ownership and announcement period

cumulative abnormal returns in European M&A. Yen and Andre (2007) examine a

set of deals in English origin countries and find that value creating deals are

associated with higher levels of ownership concentration consistent with decreasing

agency costs as the dominant shareholder’s wealth invested in the acquiring firm

increases.

1 While some of the above issues could relate to other types of ownership concentration, we do not have

large state ownership in Canada and very large institutional ownership is rare in publicly listed companies

because of portfolio and risk considerations (see King and Santor 2008).

132 P. Andre et al.

123

Prior research (Miller et al. 2010; Gomez-Mejia et al. 2010; Anderson and Reeb

2003b) also suggests that family owners’ priorities should have a significant impact on

their firm’s strategic decisions (growth through M&A and diversification decisions).

Given that family blockholders would like to retain control over the firm for a long

period to transfer it to future generations (James 1999), they invest a large proportion

of their wealth in the family firm which increases their financial risk (Anderson and

Reeb 2003a). Unlike other blockholders, e.g., institutional investors who hold

diversified portfolios, family owners cannot diversify their personal portfolios

without diluting their voting rights as well as the socio-emotional wealth derived from

the control over the family firm (Gomez-Mejia et al. 2007). As a consequence, Miller

et al. (2010, p. 204) argue that family owners may try to diversify their personal

investment portfolios through diversifying acquisitions outside the core industry of

the family firm. These diversifying acquisitions allow them to reduce the family’s

portfolio risk without losing control of the firm. Previous studies obtain mixed results

on the relation between family firms, diversification levels and firm value. Anderson

and Reeb (2003b) as well as Gomez-Mejia et al. (2010) find that family firms are less

diversified than non family firms. In contrast, Miller et al. (2010) document a positive

relation between family ownership and the likelihood of diversifying acquisitions.

We therefore examine the impact of diversifying acquisitions undertaken by

family firms. We argue that stock markets may react differently depending on the

acquisition motives. If family firms are expected to select efficiently their targets in

diversifying acquisitions to maximize firm value in the long term in order transfer it

to later generations, we should observe a positive stock market around the

announcement date.

H2: Diversifying acquisitions undertaken by family firms have a positive

effect on the stock market reaction to high-tech M&A

2.2 Family firms, agency problems and value creation in M&A

The conflict opposing family blockholders and minority shareholders is exacerbated

when the controlling family maintains control of the voting rights while holding a

small fraction of cash flow rights through control enhancing mechanisms such as

dual class shares and stock pyramids. These ownership structures involve large

agency costs due to the presence of both entrenchment and incentive problems.

Since the controlling shareholders have the power to make decisions but do not bear

the full cost, (Bebchuk et al. 2000) show how these ownership structures distort

decision making with regard to investment projects choice, firm size and transfer of

control. Prior studies (Cronqvist and Nilsson 2003; Anderson and Reeb 2003a;

Villalonga and Amit 2006) show that family use of control enhancing mechanisms

has a negative impact on firm performance.2

Prior studies testing the expropriation hypothesis through M&A obtain mixed

results. Bae et al. (2002) find evidence that controlling shareholders in large Korean

business groups (chaebols) use M&A to tunnel wealth from minority shareholders to

2 See Adams and Ferreira (2008) for a review of the literature on the impact of the use of control

enhancing mechanisms (dual class shares, stock pyramids and cross-ownership) on firm performance.

Family firms and high technology Mergers & Acquisitions 133

123

themselves. Bigelli and Mengoli (2004) report a negative association between the

separation of ownership and control and the bidder’s announcement returns in Italy.

Holmen and Knopf (2004) as well as Faccio and Stolin (2006) do not find evidence

supporting the hypothesis of minority shareholders expropriation through mergers

and acquisitions in Western Europe. Recently, Wong et al. (2010) and Chang et al.

(2010) document a negative association between family excess control and stock

market reaction to corporate venturing and innovation announcements in Taiwan.

Based on the above discussion, we formulate the following hypothesis:

H3: The use of control enhancing mechanisms by family firms has a negative

effect on the stock market reaction to high-tech M&A

2.3 The effect of family management on value creation in M&A

Prior research documents mixed results on the relation between family management

and firm performance. Smith and Amoako-Adu (1999) and Perez-Gonzalez (2006)

report a negative stock market’s reaction to the appointment of founder-descendants

as CEOs. Villalonga and Amit (2006) and He (2008) report that when the firm’s

founder is active in management (either as CEO or board chairperson), family

ownership has a positive effect on firm performance. In contrast, when founder

descendants serve as CEO, Villalonga and Amit find that family ownership is

negatively related to firm performance. Sciascia and Mazzola (2008) document a

quadratic negative association between the level of family involvement in

management (measured as the percentage of the firm’s managers related to the

controlling family) and firm performance in Italy.

Agency theory predicts that family management should attenuate agency

problem 1 opposing a professional manager to dispersed shareholders (Villalonga

and Amit 2006). A family CEO with a long experience within the firm (a founder or

a descendent) is likely to have a better knowledge about the family firm and should

pursue value creating acquisition strategies. Thus family management is likely to

enhance firm value. We test this prediction in the context of high-tech M&A:

H4: Family management has a positive effect on stock market reaction to

high-tech M&A

3 Data and methodology

3.1 Data

We obtain our data set of Canadian high tech acquisitions from the Thomson

Financial Securities Data’s SDC PlatinumTM Worldwide Mergers & Acquisitions

Database (SDC database). We rely on SDC classification for high tech industries

which include biotechnology & health, communications, computers hardware and

software, electronics, among others industries.3 Our sample meets the following

3 See Kohers and Kohers (2000) for a list of SDC database high tech industries sectors.

134 P. Andre et al.

123

criteria: (1) Observations are for January 1997–2006; (2) Acquiring firms are listed

Canadian companies; (3) Deals are completed and are mergers, exchange offers, or

acquisitions of majority interest; (4) For companies with more than one merger

within a 1-year period, we consider only the first merger in order to circumvent the

contamination effect that results from multiple mergers announcement in the

estimation period; (5) Only transactions greater than US$10 million are included;

(6) Companies have merger announcement dates and others merger-related

information available from the SDC database, ownership and corporate governance

data available from company proxies on the SEDAR web site and stock return and

other financial data available from the CFMRC database and Stock-Guide database,

respectively. After eliminating observations with missing data and outliers, we end

up with a sample of 215 mergers undertaken between January 1997 and 2006.4

3.2 Canadian institutional setting

The Canadian governance setting is interesting since there is a fairly high level of

ownership concentration by dominant family shareholdings (Gadhoum 2006; King

and Santor 2008; Bozec and Laurin 2008). Recent financial research has shown that a

high degree of corporate ownership concentration is the norm around the world (La

Porta et al. 1999; Claessens et al. 2000; Faccio and Lang 2002). Further, in many

countries such as Canada, large publicly listed corporations have family shareholders

who exercise control over the voting rights with a small fraction of cash flow rights.

This separation between ownership and control rights is achieved through the use of

multiple voting shares, stock pyramids and cross-shareholdings (La Porta et al. 1999;

Cronqvist and Nilsson 2003). These findings have changed the focus of researchers

from the traditional conflict of interests between a professional manager and dispersed

shareholders—Agency problem 1—towards another conflict of interests between

controlling and minority shareholders—Agency problem 2. The presence of separation

of control and ownership in Canada allows an examination of the effect of family

control, ownership and management as proposed by Villalonga and Amit (2006).

In addition, the Canadian approach to corporate governance is significantly

different from the one adopted in the US. Following the enactment of the Sarbanes–

Oxley Act, the US adopted a ‘‘rules-based approach’’ that requires full compliance

with prescribed corporate governance rules (see section 303A of the NYSE listed

company manual). In contrast, the Canadian corporate governance regime is still

largely voluntary. This ‘‘principles-based’’ approach requires publicly listed firms to

4 Our sample selection procedure is consistent with prior M&A research using the SDC worldwide M&A

database (see for example, Rau and Vermaelen (1998) and Faccio and Stolin (2006)). The first five

selection criteria resulted in an initial sample of 342 high-tech takeovers. Consistent with the event-study

methodology, 46 observations with less than 100 valid returns over the 200-day estimation period were

dropped from the sample. We further eliminated 58 observations because their proxy circulars were not

available on the SEDAR website to code their ownership structure, governance and executive

compensation data. Finally, following normality diagnostic test on our dependent variable CAR (-1, ?1),

23 outliers were excluded. Our final sample includes 215 high-technology M&A undertaken by 105

unique acquirers. Given that our sample includes multiple acquirers over the period 1997–2006, Huber/

White/Sandwich estimators of variance allowing for observations that are not independent within clusters

(105 unique acquirers) are used to compute t-statistics in all regression models.

Family firms and high technology Mergers & Acquisitions 135

123

disclose the extent of their compliance with the a proposed list of ‘best practices’

guidelines or to explain why they did not adopt these suggested practices (Broshko

and Li 2006).5

3.3 Variables definition

Table 1 provides a description of independent and control variables.

3.3.1 Dependent variable: announcement period abnormal returns

We use the well established event study methodology (Brown and Warner 1985) to

evaluate the change in wealth of acquiring firm’s shareholders around the

announcement of the transactions. The stock’s expected return is computed using

the market model which parameters are estimated during the period of -240 and

-40 days from the announcement date.6 We use daily returns of the TSX/S&P

composite index as a proxy for market returns. Abnormal returns are cumulated

over 3 days (-1, ?1) around the announcement date.

3.3.2 Independent variables

Family ownership, control and management structure

Family ownership

Following prior research (Smith and Amoako-Adu 1999; Faccio and Lang 2002;

Maury 2006), we define family firms as those in which the founder or a member of

his or her family by either blood or marriage is the largest shareholder of the firm

either individually or as a group. The minimum threshold for family blockholding is

10 % of the voting shares and above, the imposed Toronto Stock Exchange

reporting requirement. We code a dummy variable for the presence of a family

blockholder at various levels and a continuous variable capturing the level of

ownership blockholding of the family.7

We use the same methodology as La Porta et al. (1999), Faccio and Lang (2002) and

Claessens et al. (2002) to measure the ultimate voting and ownership rights held by the

acquiring firm’s largest shareholder. Ultimate voting rights (family control) are

measured as the weakest link in the control chain while ultimate ownership (family

ownership) is measured as the fraction of equity capital held by the family blockholder.

5 National Policy NP 58-201 ‘Corporate Governance Guidelines’ and National Instrument NI-58-101

‘Disclosure of Corporate Governance Practices’ provide a comprehensive description of the Canadian

corporate governance regime. Broshko and Li (2006) discuss also the main differences between corporate

governance regimes in Canada and the US.6 Firms with \100 valid returns over the estimation period were excluded from the sample.7 We reran the regressions with a dummy using 20 % threshold, spline dummies at the 10–25 % level

and more than 25 % (in Canada the disclosure threshold is 10 %, contrary to the US disclosure threshold

of 5 %) and one with a 10–50 % and more than 50 % dummy (consistent with the Cascino et al. (2010)

discussion of majority ownership and control). Results are consistent across various specifications so for

brevity we only present those at the 10 % level.

136 P. Andre et al.

123

Control enhancing mechanisms and family excess vote-holding

We code a dummy variable for voting structures that enable the family’s voting

rights (family control) to exceed its cash flow rights (family ownership) via multiple

share classes with differential voting rights and pyramids where the family holds

shares in the firm through one or more intermediate entities of which the family

owns less than 100 %. The family excess vote-holding is the difference between the

voting rights and the cash flow rights.

Family firm management

We create a dummy variable to take into account the implication of founding-

family or professional CEO in the management of the family firm. Professional

CEO is a dummy variable equals 1 if the acquiring firm prior to the transaction is

managed by a professional CEO. We further code whether the family CEO is the

founder or descendant.

3.3.3 Control variables

Acquiring firm characteristics

Institutional ownership in the acquiring firm

According to the efficiency-augmentation hypothesis, institutional investors have

strong incentives to effectively monitor managers. This enhances managerial

efficiency and the quality of corporate decision making including M&A (Duggal

and Millar 1999; Wright et al. 2002). On the other hand, according to the efficiency-

abatement hypothesis, they do not act as effective monitors due to their short term

vision and passivity. It is argued that they have myopic investment objectives,

which causes them to sell the stock of an underperforming company rather than to

have a long term perspective and to pressure managers to favour value-enhancing

changes. Prior empirical studies (Duggal and Millar 1999; Kohers and Kohers 2000;

Wright et al. 2002) provide mixed evidence on the relationship between institutional

ownership and acquiring firm performance. Institutional ownership is measured as

the level of voting rights held by all institutional investors in the acquiring firm.

Board composition

Empirical studies examining the role of independent boards on value creation in

the case of M&A provide mixed evidence. Faleye and Huson (2002)8 find a positive

relationship while Byrd and Hickman (1992) present evidence that this relation is

non linear. Subrahmanyam et al. (1997) find a negative relationship in the case of

announcement date CAR of bank M&A. In a Canadian setting, Ben-Amar and

Andre (2006) find a significant positive association between the proportion of

unrelated directors and acquiring firm announcement period excess returns.

In this study, we rely on the TSX guidelines definition (TSX 1994) of unrelated

board members which considers a director as unrelated if he-she is not a manager of

the firm or of its subsidiaries; is not related to the controlling shareholder and does

not have business dealings with the firm which could create a conflict of interests.

8 Faleye and Huson (2002) find a positive relation between a measure of board effectiveness and bidder

returns. Firms receive high scores on the board effectiveness factor when they have small, independent

board that meet frequently.

Family firms and high technology Mergers & Acquisitions 137

123

Board independence is measured as the ratio of the number of unrelated directors to

board size.

Board size

The governance literature (Jensen 1993; Yermack 1996; Eisenberg et al. 1998)

has also explored the effect of board size on firm value. The increase of board size

should enhance its expertise, counterbalance the CEO’s dominance of the board and

enhance board effectiveness. On the other hand, larger boards may encounter

communication and coordination problems that reduce their effectiveness. Yermack

(1996) and Eisenberg et al. (1998) confirm this negative relationship between board

size and firm performance. Looking at M&A, Faleye and Huson (2002) and Ben-

Amar and Andre (2006) document a negative relationship between board size and

acquiring firm CAR.

Leadership structure

Several studies have examined the effect of CEO duality (i.e., the CEO is also the

board chairman) on firm performance. Duality reduces firm performance because it

promotes CEO entrenchment, exacerbates CEO power and reduces board

effectiveness. Scholars from the organization theory argue, however, that duality

improves firm performance since it provides clear leadership to the firm (Kang and

Zardkoohi 2005). The empirical evidence does not generally support the idea that

duality is harmful to firm performance.9 Boyd (1995) finds that duality has a

positive effect while Baliga et al. (1996) find that it has no impact. In the context of

M&A, Faleye and Huson (2002) find that duality has no effect on acquiring firm

announcement period CARs.

Managerial incentives (equity based compensation)

While the issue of managerial incentive pay has been the topic of much

controversy over the past few years, the agency literature generally considers that

incentive pay is a useful mechanism to align managers’ interests with those of the

shareholders (Core et al. 1999). Shleifer and Vishny (1989) predict that equity based

compensation should reduce agency costs and limit the non-value-maximising

behaviour of managers of acquiring companies. Prior finance research (Datta et al.

2001) documents a positive association between equity based compensation and

acquirer’s announcement period CARs. Consistent with Bushman et al. (1996), the

relative importance of the CEO’s performance-contingent compensation is

measured by the ratio of cash bonus plus stock options granted to the total

compensation earned by the CEO in the same period. The CEO’s total

compensation includes salary, cash bonuses, other compensations and stock options.

Stock options are valued at 25 % of their exercise price at the time of the grant.10

US cross-listing

Charitou et al. (2007, 1282) points out that ‘Canadian firms make up the single

largest group of foreign firms listed on a US stock exchange’. Furthermore, and

9 See Dalton et al. (1998), Kang and Zardkoohi (2005) for a review of the board leadership structure

literature.10 Similar to, among others, Brick et al. (2006), Archambeault et al. (2008), we implement the stock

option valuation method of Core et al. (1999) where we value stock options at 25 % of their exercise

price. Besides its simplicity, Core et al.’s approach produces results that are in the range of those

generated by complex valuation models (see, for instance, Lambert et al. 1991; Core et al. 1999).

138 P. Andre et al.

123

unlike firms from other countries, Canadian companies are required to cross-list

ordinary shares (not ADRs) and submit to all filing and disclosure requirements.

Prior research (Doidge, Karolyi and Stulz 2004) suggests that cross-listing in the US

is a signal used by these firms to indicate their willingness to accept tougher

governance rules and further regulatory oversight. Charitou et al. (2007) document

an improvement in the governance practices of Canadian firms in the years

following their cross-listing in the US. Cross-listing in the US is measured through a

dichotomous variable that is equal to one if the acquiring firm is listed on a US stock

exchange and zero otherwise.

Free cash flows (FCF)

Jensen (1986) argues that managers of firms with large free cash flows are more

likely to undertake non-value creating acquisition strategies. In the tradition of Lang

et al. (1991) and more recent papers such as Gregory (2005), we control for the level

the acquirer’s free cash flows. Free cash flows are measured as cash flows from

operations divided by book value of assets.

Market-to-book ratio (MarkettoBook)

Jensen (2005) suggests that firms with high valuations have greater managerial

discretion which allows their managers to make poor deals once they have run out of

good ones. Dong et al. (2006) and Moeller et al. (2004) document that high

valuation firms make poor M&A deals. We measure firm valuation as the ratio of

market value of equity plus the book value of debt to the book value of assets.

Acquiring firm industry

We also control for the acquiring firm’s industry using the SDC database macro

industry identifier.

Target firm and deal characteristics

Public target

Kohers and Kohers (2000, 42) argue ‘the market may perceive that the growth

opportunities of privately held high-tech companies are more valuable than those of

publicly traded high-tech companies’. Benou and Madura (2005) and Kohers and

Kohers (2000) find the acquirers of privately held high-tech targets obtain higher

returns than the acquirers of public high-tech targets. Looking at Canadian

acquirers, Yuce and Ng (2005) as well as Ben-Amar and Andre (2006) document

that the acquisition of private targets is associated with higher announcement period

abnormal returns.

Payment method (Cash only)

Prior research finds that the mode of payment is one of the consistent factors that

influence the level of value creation in M&A (Andrade et al. 2001). In the context of

high tech acquisitions, Benou and Madura (2005) find that acquirer returns are

higher in cash offers than in stock or mixed offers. In contrast, Kohers and Kohers

(2000) find that both stock and cash financing are associated with significant

positive excess returns.

Related industries

Datta et al. (1992) note that the relatedness of the activities of the acquiring and

target firms is a key determinant of the level of value creation in M&A since

Family firms and high technology Mergers & Acquisitions 139

123

synergies are easier to achieve when firms have related business than when creating

conglomerates. Looking at acquisitions of high tech targets in the US, Kohers and

Kohers (2000) find that high tech acquirers obtain significantly higher returns than

non high-tech acquiring firms. Related industries is a dummy variable equal to 1 if

the acquirer and the target share the same 4-digit SIC code and zero otherwise.

Cross-border transactions (cross-border)

Cross-border transactions should benefit shareholders of both firms when the

merged firm can exploit market imperfections in outside markets (Eun et al. 1996).

However, integration costs and cultural problems often undermine these gains.

Empirical results have been somewhat mixed. Moeller and Schlingemann (2005)

show that US firms that acquire cross-border targets experience lower abnormal

performance and that the results are negatively associated with global and industrial

diversification but positively associated to legal systems offering better shareholder

protection. Faccio et al. (2006) report a positive association between the acquisition

of foreign targets and acquirer returns for a sample of European M&A. Ben-Amar

and Andre (2006) document that Canadian bidders involved in cross-border

transactions obtain higher returns than domestic acquisitions.

Deal size (log deal value)

Asquith et al. (1983) argue that bidder returns increase with relative size of the

target to the acquirer. Kohers and Kohers (2000), as well as Benou and Madura

(2005), report a positive relation between the relative transaction size and acquirer

abnormal returns in high-tech acquisitions. We control for transaction size and

measure deal size as the log of the deal value.

Time period

To control for the high technology wave that occurred in the period 1997–2000

we introduce a dummy variable equals to one if the deal occurs in that period.

4 Results

4.1 Descriptive statistics

Our sample consists of 215 transactions between January 1997 and 2006 with an

annual average value of US $ 352.2 million and total value of over US $ 75.7

billion. These figures are smaller than those reported in US studies. For example, the

average transaction value in Benou and Madura (2005) is US $ 433.2 million. The

largest numbers of deals occurs in the year 2000, the peak of the new economy

bubble, with 53 deals worth some 27.6 billion dollars, an average deal size of 520

million. Most acquirers are high-tech firms, followed by telecoms and health

industry firms. The largest deals were initiated by telecom companies.

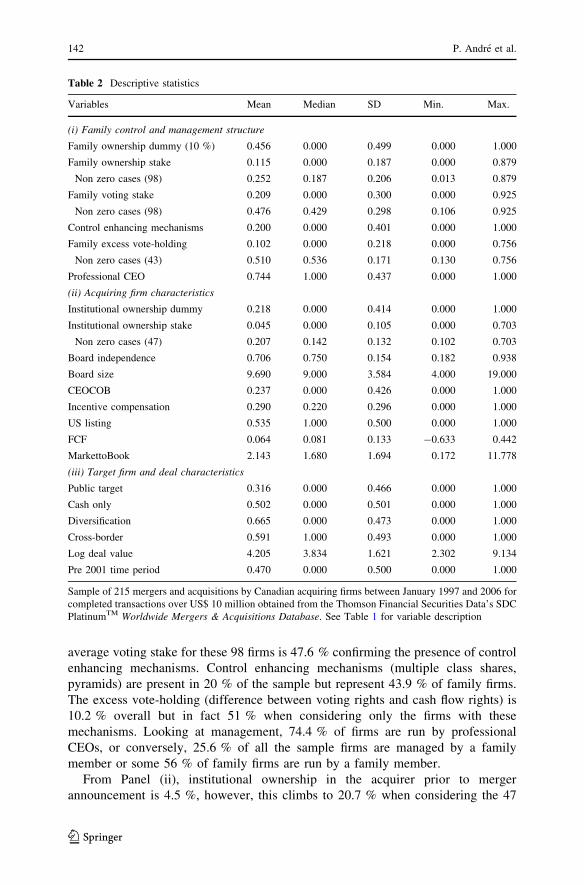

Table 2 provides descriptive statistics of variables examined in this study. As

shown in Panel (i), the average family ownership stake in the acquirer prior to

merger announcement is 11.5 %, however, this level increases to 25.2 % when

considering the 98 family firms only (45.6 % of total sample). These figures confirm

significant corporate ownership concentration in Canada as reported in previous

studies (Gadhoum 2006; Ben-Amar and Andre 2006; Bozec and Laurin 2008). The

140 P. Andre et al.

123

Table 1 Variable description

Variable Description

(i) Family control and family structure

Family ownership dummy Dummy variable that equals one if the acquirer’s largest shareholder is a family

(the founder or a member of his or her family by either blood or mariage) and

zero otherwise. A large shareholder is an individual or an entity with a voting

stake of 10 % or more

Family ownership stake Percentage of ownership (cash-flow) rights of all classes of the acquiring firm’s

shares held by the family as a group prior to the transaction

Family voting stake Percentage of voting rights of all classes of the acquiring firm’s shares held by

the family as a group prior to the transaction

Control-enhancing

mechanisms dummy

Dummy variable equals 1 if there are multiple voting share classes, pyramids or

cross-holdings in the acquiring firm

Family excess vote-holding Difference between the percentage of voting rights of the family and cash flow

rights held by the family in the acquiring firm prior to the transaction

Professional CEO dummy Dummy variable equals 1 if the acquiring firm prior to the transaction is

managed by a professional CEO, i.e., someone who is not a family member

(ii) Acquiring firm characteristics

Institutional ownership

dummy

Dummy variable equal 1 if one or more institutional investors own 10 % or

more of the acquiring firm’s cash flow rights prior to the transaction

Institutional ownership stake Percentage of cash flow rights held by institutional investors in the acquiring

firm prior to the transaction

Board independence Ratio of unrelated directors to number of board members in the acquiring firm

prior to the transaction

Board size Number of board members in the acquiring firm prior to the transaction

CEOCOB Dummy variable equals 1 if the acquiring firm CEO is also board chairman prior

to the transaction

Incentive compensation The ratio of the market value of options granted to the acquiring firm CEO

divided by his/her total compensation in the year prior to the deal

US listing Dummy variable equals 1 if the acquiring firm is listed on a US exchange

(NYSE, NASDAQ, AMEX) prior to the transaction, and 0 otherwise

FCF Acquiring firm cash-flow from operations divided by the book value of assets at

end of year prior to the transaction

MarkettoBook The ratio of the market value of equity plus the book value of debt to the book

value of assets at end of year prior to the transaction

(iii) Target firm and deal characteristics

Public target Dummy variable equals 1 if target firm is listed on a stock exchange

Cash only Dummy variable equals 1 if transaction is entirely financed with cash

Diversification Dummy variable equals 1 if acquirer and target do not share the same 4-digit

SIC code

Cross-border Dummy variable equals 1 if target nation is not Canada

Log deal value Logarithm of the deal total value

Pre 2001 time Period Dummy variable equals 1 if the transaction is announced between January 1997

and December 2000

Governance information is collected from Information Circulars available on SEDAR (sedar.com). Transaction

characteristics are obtained from the Thomson Financial Securities Data’s SDC PlatinumTM Worldwide Mergers

& Acquisitions Database. Financial information is from Compustat or StockGuide

Family firms and high technology Mergers & Acquisitions 141

123

average voting stake for these 98 firms is 47.6 % confirming the presence of control

enhancing mechanisms. Control enhancing mechanisms (multiple class shares,

pyramids) are present in 20 % of the sample but represent 43.9 % of family firms.

The excess vote-holding (difference between voting rights and cash flow rights) is

10.2 % overall but in fact 51 % when considering only the firms with these

mechanisms. Looking at management, 74.4 % of firms are run by professional

CEOs, or conversely, 25.6 % of all the sample firms are managed by a family

member or some 56 % of family firms are run by a family member.

From Panel (ii), institutional ownership in the acquirer prior to merger

announcement is 4.5 %, however, this climbs to 20.7 % when considering the 47

Table 2 Descriptive statistics

Variables Mean Median SD Min. Max.

(i) Family control and management structure

Family ownership dummy (10 %) 0.456 0.000 0.499 0.000 1.000

Family ownership stake 0.115 0.000 0.187 0.000 0.879

Non zero cases (98) 0.252 0.187 0.206 0.013 0.879

Family voting stake 0.209 0.000 0.300 0.000 0.925

Non zero cases (98) 0.476 0.429 0.298 0.106 0.925

Control enhancing mechanisms 0.200 0.000 0.401 0.000 1.000

Family excess vote-holding 0.102 0.000 0.218 0.000 0.756

Non zero cases (43) 0.510 0.536 0.171 0.130 0.756

Professional CEO 0.744 1.000 0.437 0.000 1.000

(ii) Acquiring firm characteristics

Institutional ownership dummy 0.218 0.000 0.414 0.000 1.000

Institutional ownership stake 0.045 0.000 0.105 0.000 0.703

Non zero cases (47) 0.207 0.142 0.132 0.102 0.703

Board independence 0.706 0.750 0.154 0.182 0.938

Board size 9.690 9.000 3.584 4.000 19.000

CEOCOB 0.237 0.000 0.426 0.000 1.000

Incentive compensation 0.290 0.220 0.296 0.000 1.000

US listing 0.535 1.000 0.500 0.000 1.000

FCF 0.064 0.081 0.133 -0.633 0.442

MarkettoBook 2.143 1.680 1.694 0.172 11.778

(iii) Target firm and deal characteristics

Public target 0.316 0.000 0.466 0.000 1.000

Cash only 0.502 0.000 0.501 0.000 1.000

Diversification 0.665 0.000 0.473 0.000 1.000

Cross-border 0.591 1.000 0.493 0.000 1.000

Log deal value 4.205 3.834 1.621 2.302 9.134

Pre 2001 time period 0.470 0.000 0.500 0.000 1.000

Sample of 215 mergers and acquisitions by Canadian acquiring firms between January 1997 and 2006 for

completed transactions over US$ 10 million obtained from the Thomson Financial Securities Data’s SDC

PlatinumTM Worldwide Mergers & Acquisitions Database. See Table 1 for variable description

142 P. Andre et al.

123

non zero cases. Moreover, the average board size is 9.69 members where a majority

are unrelated directors (70 %). The roles of CEO and chairman of the board are

cumulated in 23.7 % of the firms of our sample. CEO incentive compensation is on

average 29.0 % of total compensation. Canadian acquirers are listed in the US in

53.5 % percent of cases. Panel (ii) also indicates that the average level of free cash

flows is 0.06 and the average market to book is 2.143.

From Panel (iii), we can see that 50.2 % of deals are paid exclusively with cash

or cash equivalent. Furthermore, most transactions in our sample involve private

targets; only 31.6 % of the acquired firms in our sample are publicly held firms. In

addition, close to 60 % of our observations involve cross-border transactions. We

denote 66.5 % of deals are diversifying acquisitions involving two firms in

unrelated industries (i.e., high tech acquirers with a different 4-digit SIC code as the

target). Panel (iii) also reports that the average log of deal value is 4.205 and 47 %

of deals occur prior to 2001 during what some have called the new economy bubble.

4.2 Announcement period abnormal returns

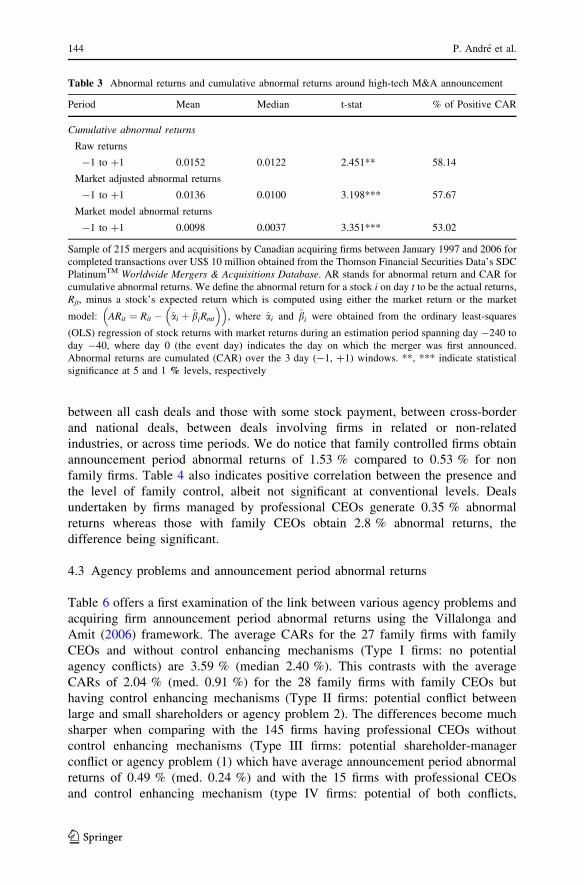

We begin by analysing the average impact of mergers and acquisitions on the

change in wealth of acquiring shareholders around the announcement for our sample

of Canadian high tech M&A over the January 1997–2006 period. As shown in

Table 3, there are positive and statistically significant abnormal returns around the

transaction announcement.

Cumulative abnormal returns (CAR) obtained by acquiring firms’ shareholders

around the announcement day are positive and significant at 0.98 % within days -1

and ?1 (1.52 % for raw returns and 1.36 % for market adjusted returns). Also,

53.02 % of deals have positive CARs (58.14 % of raw returns and 57.67 % of

market adjusted returns). The positive short term CARs around announcement day

are consistent with prior Canadian studies (Eckbo and Thorburn 2000; Yuce and Ng

2005; Ben-Amar and Andre 2006). These results are also consistent with the prior

US short window studies (Kohers and Kohers 2000; Benou and Madura 2005)

investigating investors’ initial reaction to the announcement of high-tech M&A. Our

results suggest that stock market participants had a positive perception of the

potential value creation of high tech M&A undertaken by Canadian acquirers over

the period January 1997–2006.

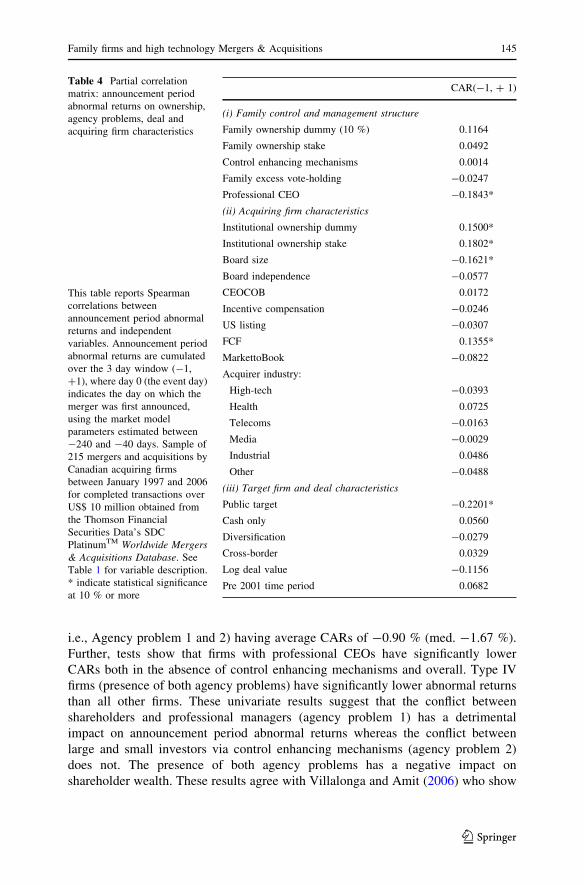

Table 4 presents the partial correlation matrix between CAR and the independent

variables. The announcement abnormal returns are positively and significantly

correlated with the presence and level of institutional ownership but negatively and

significantly correlated with the presence of professional (non-family) CEO and

with the size of the board. The CARs are also negatively correlated with the deals

involving publicly listed targets and with the size of the deal. These results are

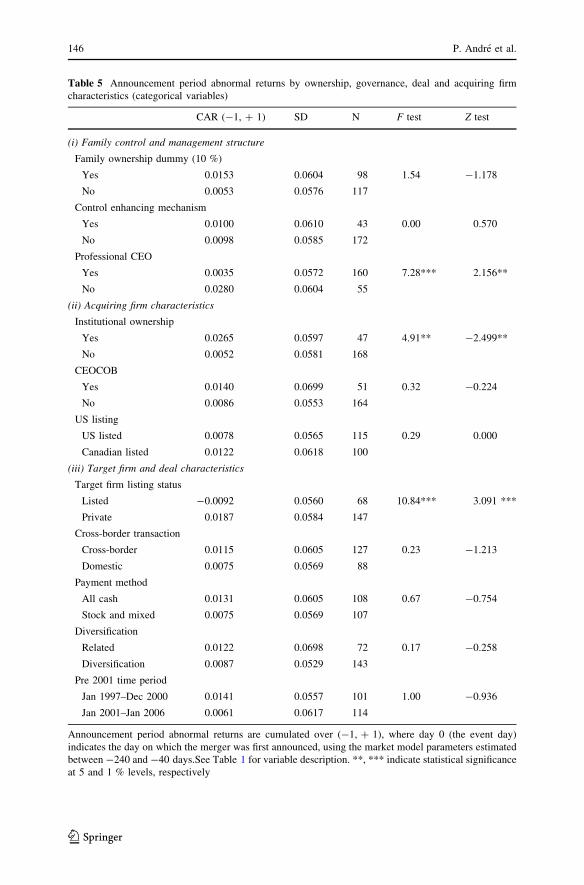

consistent with Moeller et al. (2004). Table 5 presents the announcement period

abnormal returns, cumulated over the 3-day window (-1, ?1), by dichotomous

variables. Our results confirm those in Table 3, that is, acquirer shareholders enjoy

significant positive excess returns in the presence of institutional ownership and

when purchasing private firms rather than public ones. On a univariate dimension,

there is no significant difference in the CARs of US and non-US listed acquirers,

Family firms and high technology Mergers & Acquisitions 143

123

between all cash deals and those with some stock payment, between cross-border

and national deals, between deals involving firms in related or non-related

industries, or across time periods. We do notice that family controlled firms obtain

announcement period abnormal returns of 1.53 % compared to 0.53 % for non

family firms. Table 4 also indicates positive correlation between the presence and

the level of family control, albeit not significant at conventional levels. Deals

undertaken by firms managed by professional CEOs generate 0.35 % abnormal

returns whereas those with family CEOs obtain 2.8 % abnormal returns, the

difference being significant.

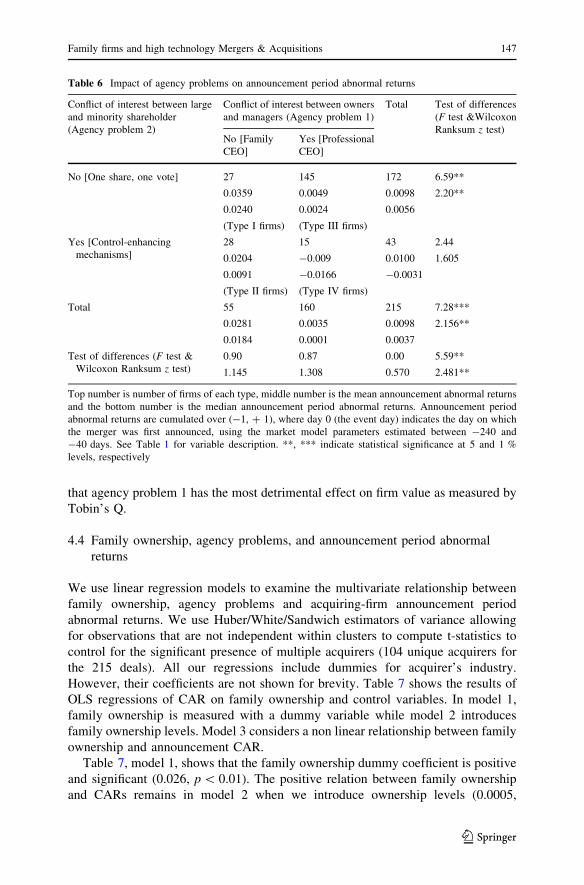

4.3 Agency problems and announcement period abnormal returns

Table 6 offers a first examination of the link between various agency problems and

acquiring firm announcement period abnormal returns using the Villalonga and

Amit (2006) framework. The average CARs for the 27 family firms with family

CEOs and without control enhancing mechanisms (Type I firms: no potential

agency conflicts) are 3.59 % (median 2.40 %). This contrasts with the average

CARs of 2.04 % (med. 0.91 %) for the 28 family firms with family CEOs but

having control enhancing mechanisms (Type II firms: potential conflict between

large and small shareholders or agency problem 2). The differences become much

sharper when comparing with the 145 firms having professional CEOs without

control enhancing mechanisms (Type III firms: potential shareholder-manager

conflict or agency problem (1) which have average announcement period abnormal

returns of 0.49 % (med. 0.24 %) and with the 15 firms with professional CEOs

and control enhancing mechanism (type IV firms: potential of both conflicts,

Table 3 Abnormal returns and cumulative abnormal returns around high-tech M&A announcement

Period Mean Median t-stat % of Positive CAR

Cumulative abnormal returns

Raw returns

-1 to ?1 0.0152 0.0122 2.451** 58.14

Market adjusted abnormal returns

-1 to ?1 0.0136 0.0100 3.198*** 57.67

Market model abnormal returns

-1 to ?1 0.0098 0.0037 3.351*** 53.02

Sample of 215 mergers and acquisitions by Canadian acquiring firms between January 1997 and 2006 for

completed transactions over US$ 10 million obtained from the Thomson Financial Securities Data’s SDC

PlatinumTM Worldwide Mergers & Acquisitions Database. AR stands for abnormal return and CAR for

cumulative abnormal returns. We define the abnormal return for a stock i on day t to be the actual returns,

Rjt, minus a stock’s expected return which is computed using either the market return or the market

model: ARit ¼ Rit � ai þ biRmt

� �� �, where ai and bi were obtained from the ordinary least-squares

(OLS) regression of stock returns with market returns during an estimation period spanning day -240 to

day -40, where day 0 (the event day) indicates the day on which the merger was first announced.

Abnormal returns are cumulated (CAR) over the 3 day (-1, ?1) windows. **, *** indicate statistical

significance at 5 and 1 % levels, respectively

144 P. Andre et al.

123

i.e., Agency problem 1 and 2) having average CARs of -0.90 % (med. -1.67 %).

Further, tests show that firms with professional CEOs have significantly lower

CARs both in the absence of control enhancing mechanisms and overall. Type IV

firms (presence of both agency problems) have significantly lower abnormal returns

than all other firms. These univariate results suggest that the conflict between

shareholders and professional managers (agency problem 1) has a detrimental

impact on announcement period abnormal returns whereas the conflict between

large and small investors via control enhancing mechanisms (agency problem 2)

does not. The presence of both agency problems has a negative impact on

shareholder wealth. These results agree with Villalonga and Amit (2006) who show

Table 4 Partial correlation

matrix: announcement period

abnormal returns on ownership,

agency problems, deal and

acquiring firm characteristics

This table reports Spearman

correlations between

announcement period abnormal

returns and independent

variables. Announcement period

abnormal returns are cumulated

over the 3 day window (-1,

?1), where day 0 (the event day)

indicates the day on which the

merger was first announced,

using the market model

parameters estimated between

-240 and -40 days. Sample of

215 mergers and acquisitions by

Canadian acquiring firms

between January 1997 and 2006

for completed transactions over

US$ 10 million obtained from

the Thomson Financial

Securities Data’s SDC

PlatinumTM Worldwide Mergers

& Acquisitions Database. See

Table 1 for variable description.

* indicate statistical significance

at 10 % or more

CAR(-1, ? 1)

(i) Family control and management structure

Family ownership dummy (10 %) 0.1164

Family ownership stake 0.0492

Control enhancing mechanisms 0.0014

Family excess vote-holding -0.0247

Professional CEO -0.1843*

(ii) Acquiring firm characteristics

Institutional ownership dummy 0.1500*

Institutional ownership stake 0.1802*

Board size -0.1621*

Board independence -0.0577

CEOCOB 0.0172

Incentive compensation -0.0246

US listing -0.0307

FCF 0.1355*

MarkettoBook -0.0822

Acquirer industry:

High-tech -0.0393

Health 0.0725

Telecoms -0.0163

Media -0.0029

Industrial 0.0486

Other -0.0488

(iii) Target firm and deal characteristics

Public target -0.2201*

Cash only 0.0560

Diversification -0.0279

Cross-border 0.0329

Log deal value -0.1156

Pre 2001 time period 0.0682

Family firms and high technology Mergers & Acquisitions 145

123

Table 5 Announcement period abnormal returns by ownership, governance, deal and acquiring firm

characteristics (categorical variables)

CAR (-1, ? 1) SD N F test Z test

(i) Family control and management structure

Family ownership dummy (10 %)

Yes 0.0153 0.0604 98 1.54 -1.178

No 0.0053 0.0576 117

Control enhancing mechanism

Yes 0.0100 0.0610 43 0.00 0.570

No 0.0098 0.0585 172

Professional CEO

Yes 0.0035 0.0572 160 7.28*** 2.156**

No 0.0280 0.0604 55

(ii) Acquiring firm characteristics

Institutional ownership

Yes 0.0265 0.0597 47 4.91** -2.499**

No 0.0052 0.0581 168

CEOCOB

Yes 0.0140 0.0699 51 0.32 -0.224

No 0.0086 0.0553 164

US listing

US listed 0.0078 0.0565 115 0.29 0.000

Canadian listed 0.0122 0.0618 100

(iii) Target firm and deal characteristics

Target firm listing status

Listed -0.0092 0.0560 68 10.84*** 3.091 ***

Private 0.0187 0.0584 147

Cross-border transaction

Cross-border 0.0115 0.0605 127 0.23 -1.213

Domestic 0.0075 0.0569 88

Payment method

All cash 0.0131 0.0605 108 0.67 -0.754

Stock and mixed 0.0075 0.0569 107

Diversification

Related 0.0122 0.0698 72 0.17 -0.258

Diversification 0.0087 0.0529 143

Pre 2001 time period

Jan 1997–Dec 2000 0.0141 0.0557 101 1.00 -0.936

Jan 2001–Jan 2006 0.0061 0.0617 114

Announcement period abnormal returns are cumulated over (-1, ? 1), where day 0 (the event day)

indicates the day on which the merger was first announced, using the market model parameters estimated

between -240 and -40 days.See Table 1 for variable description. **, *** indicate statistical significance

at 5 and 1 % levels, respectively

146 P. Andre et al.

123

that agency problem 1 has the most detrimental effect on firm value as measured by

Tobin’s Q.

4.4 Family ownership, agency problems, and announcement period abnormal

returns

We use linear regression models to examine the multivariate relationship between

family ownership, agency problems and acquiring-firm announcement period

abnormal returns. We use Huber/White/Sandwich estimators of variance allowing

for observations that are not independent within clusters to compute t-statistics to

control for the significant presence of multiple acquirers (104 unique acquirers for

the 215 deals). All our regressions include dummies for acquirer’s industry.

However, their coefficients are not shown for brevity. Table 7 shows the results of

OLS regressions of CAR on family ownership and control variables. In model 1,

family ownership is measured with a dummy variable while model 2 introduces

family ownership levels. Model 3 considers a non linear relationship between family

ownership and announcement CAR.

Table 7, model 1, shows that the family ownership dummy coefficient is positive

and significant (0.026, p \ 0.01). The positive relation between family ownership

and CARs remains in model 2 when we introduce ownership levels (0.0005,

Table 6 Impact of agency problems on announcement period abnormal returns

Conflict of interest between large

and minority shareholder

(Agency problem 2)

Conflict of interest between owners

and managers (Agency problem 1)

Total Test of differences

(F test &Wilcoxon

Ranksum z test)No [Family

CEO]

Yes [Professional

CEO]

No [One share, one vote] 27

0.0359

0.0240

(Type I firms)

145

0.0049

0.0024

(Type III firms)

172

0.0098

0.0056

6.59**

2.20**

Yes [Control-enhancing

mechanisms]

28

0.0204

0.0091

(Type II firms)

15

-0.009

-0.0166

(Type IV firms)

43

0.0100

-0.0031

2.44

1.605

Total 55

0.0281

0.0184

160

0.0035

0.0001

215

0.0098

0.0037

7.28***

2.156**

Test of differences (F test &

Wilcoxon Ranksum z test)

0.90

1.145

0.87

1.308

0.00

0.570

5.59**

2.481**

Top number is number of firms of each type, middle number is the mean announcement abnormal returns

and the bottom number is the median announcement period abnormal returns. Announcement period

abnormal returns are cumulated over (-1, ? 1), where day 0 (the event day) indicates the day on which

the merger was first announced, using the market model parameters estimated between -240 and

-40 days. See Table 1 for variable description. **, *** indicate statistical significance at 5 and 1 %

levels, respectively

Family firms and high technology Mergers & Acquisitions 147

123

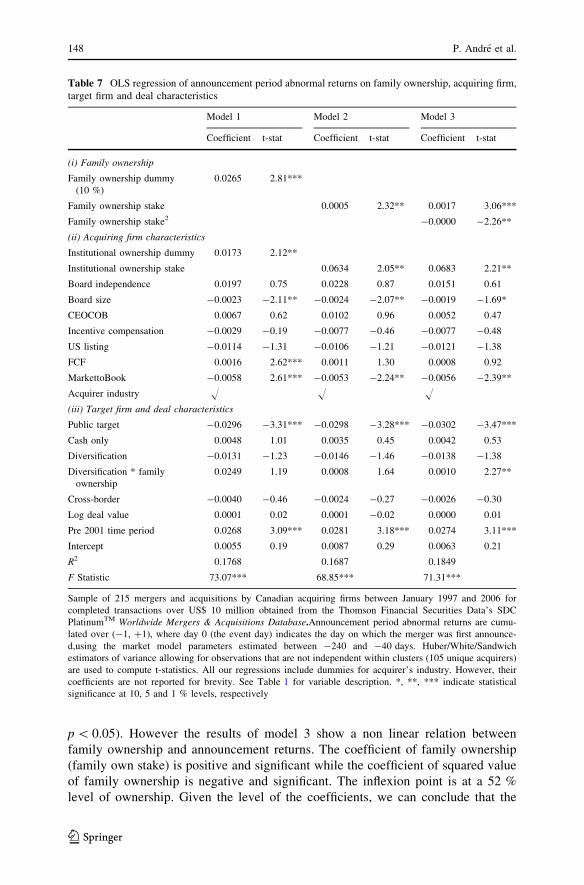

p \ 0.05). However the results of model 3 show a non linear relation between

family ownership and announcement returns. The coefficient of family ownership

(family own stake) is positive and significant while the coefficient of squared value

of family ownership is negative and significant. The inflexion point is at a 52 %

level of ownership. Given the level of the coefficients, we can conclude that the

Table 7 OLS regression of announcement period abnormal returns on family ownership, acquiring firm,

target firm and deal characteristics

Model 1 Model 2 Model 3

Coefficient t-stat Coefficient t-stat Coefficient t-stat

(i) Family ownership

Family ownership dummy

(10 %)

0.0265 2.81***

Family ownership stake 0.0005 2.32** 0.0017 3.06***

Family ownership stake2 -0.0000 -2.26**

(ii) Acquiring firm characteristics

Institutional ownership dummy 0.0173 2.12**

Institutional ownership stake 0.0634 2.05** 0.0683 2.21**

Board independence 0.0197 0.75 0.0228 0.87 0.0151 0.61

Board size -0.0023 -2.11** -0.0024 -2.07** -0.0019 -1.69*

CEOCOB 0.0067 0.62 0.0102 0.96 0.0052 0.47

Incentive compensation -0.0029 -0.19 -0.0077 -0.46 -0.0077 -0.48

US listing -0.0114 -1.31 -0.0106 -1.21 -0.0121 -1.38

FCF 0.0016 2.62*** 0.0011 1.30 0.0008 0.92

MarkettoBook -0.0058 2.61*** -0.0053 -2.24** -0.0056 -2.39**

Acquirer industry H H H

(iii) Target firm and deal characteristics

Public target -0.0296 -3.31*** -0.0298 -3.28*** -0.0302 -3.47***

Cash only 0.0048 1.01 0.0035 0.45 0.0042 0.53

Diversification -0.0131 -1.23 -0.0146 -1.46 -0.0138 -1.38

Diversification * family

ownership

0.0249 1.19 0.0008 1.64 0.0010 2.27**

Cross-border -0.0040 -0.46 -0.0024 -0.27 -0.0026 -0.30

Log deal value 0.0001 0.02 0.0001 -0.02 0.0000 0.01

Pre 2001 time period 0.0268 3.09*** 0.0281 3.18*** 0.0274 3.11***

Intercept 0.0055 0.19 0.0087 0.29 0.0063 0.21

R2 0.1768 0.1687 0.1849

F Statistic 73.07*** 68.85*** 71.31***

Sample of 215 mergers and acquisitions by Canadian acquiring firms between January 1997 and 2006 for

completed transactions over US$ 10 million obtained from the Thomson Financial Securities Data’s SDC

PlatinumTM Worldwide Mergers & Acquisitions Database.Announcement period abnormal returns are cumu-

lated over (-1, ?1), where day 0 (the event day) indicates the day on which the merger was first announce-

d,using the market model parameters estimated between -240 and -40 days. Huber/White/Sandwich

estimators of variance allowing for observations that are not independent within clusters (105 unique acquirers)

are used to compute t-statistics. All our regressions include dummies for acquirer’s industry. However, their

coefficients are not reported for brevity. See Table 1 for variable description. *, **, *** indicate statistical

significance at 10, 5 and 1 % levels, respectively

148 P. Andre et al.

123

positive relationship starts to decrease at higher levels of ownership but remains

overall positive. Our results confirm hypothesis 1.

These results are similar to those of Feito-Ruiz and Menedez-Requejo (2010)

who find that family ownership has a positive and significant effect on acquirer

shareholders’ wealth up to an ownership level of 34 %. Beyond this ownership

level, family ownership has a negative effect. Our results suggest that at higher

levels of ownership, i.e., the family has a higher amount of wealth invested in the

firm, the market perceives that the family are making deals with less value creation

potential. One explanation presented in the literature is that family owners may limit

their risk taking strategies as the level of investment in the firm increases (Miller

et al. 2010).

Table 7 also presents the results of the effect of diversifying acquisitions

undertaken by family firms on the announcement period abnormal returns (H2).

This effect is measured through the interaction term between family ownership and

relatedness dummy (Diversification * Family ownership). The coefficient of the

interaction variable is positive in the three models and is statistically significant in

model 3 only although not necessarily economically significant. These results

suggest that the stock market does not perceive diversifying acquisitions undertaken

by family owners as value-decreasing. In contrast, our results seem to imply that

family owners select carefully their target firms in diversifying acquisitions as much

as in related type deals.

Table 7 also shows that the presence and level of institutional ownership

positively affects announcement period abnormal returns. Consistent with the

efficiency augmentation hypothesis of institutional ownership benefits, our results

are consistent with Wright et al. (2002) but contrasts with Kohers and Kohers (2000)

who report a negative relation between institutional shareholdings and high-tech

acquirers’ excess returns. These results confirm the effective monitoring role of

institutional investors. Given their ownership stake and their large resources,

institutional investors can impact corporate strategy and enhance corporate decision

making including M&A. We further find a negative relationship between

announcement date CAR and board size consistent with results by Yermack

(1996) and Eisenberg et al. (1998). We also document a negative association

between market-to-book and excess returns earned by acquirer shareholders. This is

consistent with Jensen’s (2005) conjecture that firms with high valuations make

poorer acquirers and confirmed by Moeller et al. (2004) and Dong et al. (2006).

When we control for variables related to the target firms and deal characteristics,

we find that acquisitions of public targets are negatively associated to announcement

period abnormal returns, consistent with prior literature. Deals prior to 2001, i.e.,

during the high-tech bubble, generate higher abnormal returns to acquiring firm

shareholders than subsequent deals. The payment method, relatedness, location and

deal size have no significant effect on acquiring firm performance.11

11 As additional sensitivity tests (un-tabulated results), we run regressions using market adjusted returns

and find similar results. We also use alternative definitions for related industry (same SDC macro industry

code, same 1 digit SIC codes) and replace the all cash dummy by the level of cash paid and results remain

the same.

Family firms and high technology Mergers & Acquisitions 149

123

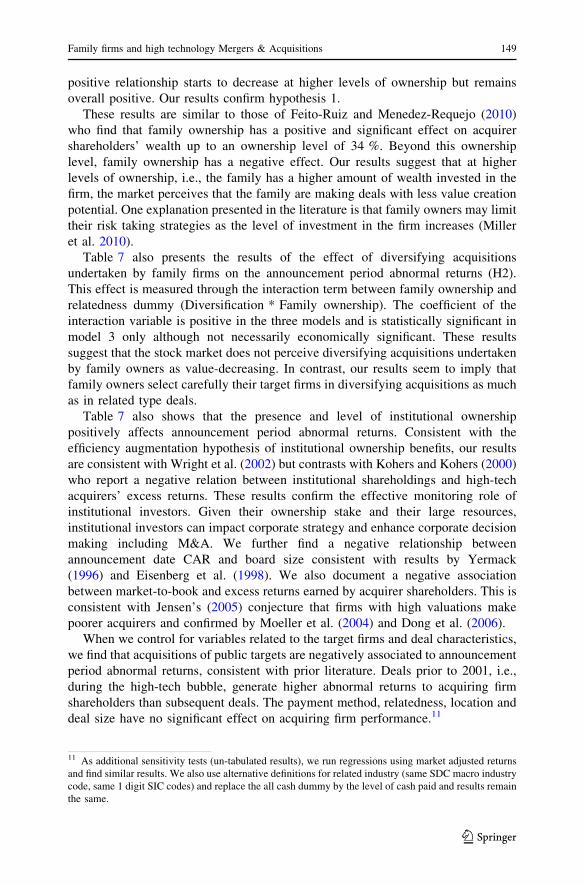

Turning more specifically to the potential agency problems, multivariate results

in Table 8 support those found in Table 6. The coefficient on professional CEO

(non-family CEO, i.e., agency problem 1) is negative and significant in both models

1 and 2. This result suggests that family-managed firms earn higher abnormal

returns than firms managed by a professional CEO. Family managers have generally

Table 8 OLS regression of announcement period abnormal returns on agency problems, acquiring firm,

target firm and deal characteristics

Model 1 Model 2

Coefficient t-stat Coefficient t-stat

(i) Agency problems

Control-enhancing mechanisms ($) 0.0095 0.75

Family excess vote-holding 0.0004 1.63

Professional CEO dummy(&) -0.0252 -2.44** -0.0205 -2.06**

Interaction $ and & -0.0179 -1.05 -0.0007 -2.61**

(ii) Acquiring firm characteristics

Institutional ownership dummy 0.0197 2.53**

Institutional ownership stake 0.0690 2.04**

Board independence 0.0207 0.84 0.0172 0.67

Board size -0.0021 -1.82* -0.0025 -2.21**

CEOCOB 0.0082 0.75 0.0098 0.86

Incentive compensation -0.0023 -0.15 -0.0025 -0.16

US listing -0.0072 -0.85 -0.0067 -0.77

FCF -0.0199 -0.68 -0.0238 -0.82

MarkettoBook -0.0057 2.37** -0.0056 -2.30**

Acquirer industry H H

(iii) Target firm and deal characteristics

Public target -0.0268 -2.92*** -0.0279 -3.06***

Cash only 0.0080 1.00 0.0086 1.09

Diversification 0.0004 0.05 -0.0001 -0.08

Cross–border 0.0009 0.11 0.0010 0.12

Log deal value 0.0001 0.03 0.0004 0.11

Pre 2001 time period 0.0234 2.68*** 0.0235 2.71**

Intercept 0.0221 0.76 0.0255 0.88

R2 0.1802 0.1909

F Statistic 3.71*** 5.85***

Sample of 215 mergers and acquisitions by Canadian acquiring firms between January 1997 and 2006 for

completed transactions over US$ 10 million obtained from the Thomson Financial Securities Data’s SDC

PlatinumTM Worldwide Mergers & Acquisitions Database.Announcement period abnormal returns are

cumulated over (-1, ?1), where day 0 (the event day) indicates the day on which the merger was first

announced, using the market model parameters estimated between -240 and -40 days. Huber/White/

Sandwich estimators of variance allowing for observations that are not independent within clusters (105

unique acquirers) are used to compute t-statistics. All our regressions include dummies for acquirer’s

industry. However, their coefficients are not reported for brevity. See Table 1 for variable description. *,

**, *** indicate statistical significance at 10, 5 and 1 % levels, respectively

150 P. Andre et al.

123

a longer experience within the firm and are likely to have a better knowledge of its

business than a hired CEO. Hence, they may have superior managerial expertise to

pursue value creating acquisition strategies particularly in high-technology

industries.

As shown in Table 8, the coefficients on either the presence of control-enhancing

mechanisms or the level of family excess vote holding (agency problem 2) are both

non significant. H3 is therefore not supported. Family use of controlling enhancing

mechanisms does not seem to affect the success of major investment projects such

as high-tech M&A.

The presence of both agency issues, the interaction term, is negative and

significant in model 2. Overall, the results of Table 8 suggest that the potential

agency conflict between shareholders and professional managers (agency problem

1) has a detrimental impact on announcement period abnormal returns whereas the

potential agency conflict between large and small investors via control enhancing

mechanisms (agency problem 2) does not. The presence of both agency problems

has a further negative impact on shareholder wealth. It is possible that the market

expects the presence of family excess control to amplify the agency costs associated

with the conflict between shareholders and professional managers. When family

block-holders use control enhancing mechanisms, they hold control over the firm

with a small fraction of cash flow rights and internalize only a small portion of the

wealth implications of a non-optimal investment decision. Therefore, stock market

participants may perceive them as less effective in monitoring professional

managers’ acquisition decisions which exacerbate agency costs resulting from

agency problem 1.

These findings are consistent with arguments made by James (1999) and

Anderson and Reeb (2003a) who suggest that the sheer amount of wealth families

have invested in the firm is a sufficient incentive to maximise firm value and restrain

from extracting private benefits which would make it difficult to establish a long

term relationship with the investment community, raise additional capital to grow

the firm and would increase the cost of capital. We can suggest that countries with

well-developed markets and offering good minority shareholder protection can

reduce the agency problems between family owners and minority shareholders, to a

certain extent, as long as the family shareholder continues to play an active role in

the management of the firm.

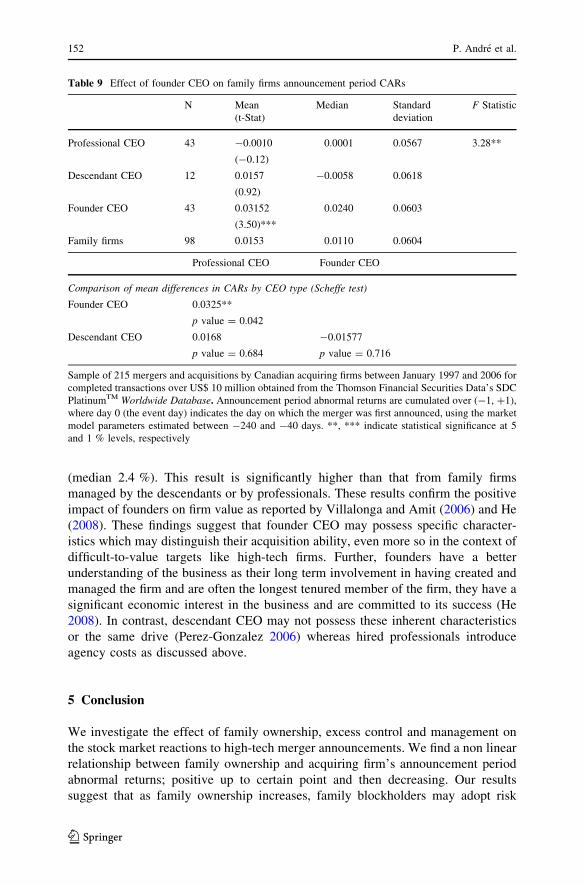

4.5 Do founders matter?

The results of Tables 6 and 8 suggest that family management has a positive effect

on the market reaction to high-technology M&A. We further examine the impact of

family management to see whether the positive effect is limited to the firm’s

founders or remain with descendant CEO. Similar to Villalonga and Amit (2006)

and He (2008), we examine the impact of CEO type (founder, descendant or

professional manager) on the value creation from our risky high tech acquisitions.

The results in Table 9 are consistent with the valuable role played by the founders

of the firm. High tech acquisitions initiated by a founder CEO create significant

value to shareholders. The abnormal announcement returns are 3.2 % on average

Family firms and high technology Mergers & Acquisitions 151

123

(median 2.4 %). This result is significantly higher than that from family firms

managed by the descendants or by professionals. These results confirm the positive

impact of founders on firm value as reported by Villalonga and Amit (2006) and He

(2008). These findings suggest that founder CEO may possess specific character-

istics which may distinguish their acquisition ability, even more so in the context of

difficult-to-value targets like high-tech firms. Further, founders have a better

understanding of the business as their long term involvement in having created and

managed the firm and are often the longest tenured member of the firm, they have a

significant economic interest in the business and are committed to its success (He

2008). In contrast, descendant CEO may not possess these inherent characteristics

or the same drive (Perez-Gonzalez 2006) whereas hired professionals introduce

agency costs as discussed above.

5 Conclusion

We investigate the effect of family ownership, excess control and management on

the stock market reactions to high-tech merger announcements. We find a non linear

relationship between family ownership and acquiring firm’s announcement period

abnormal returns; positive up to certain point and then decreasing. Our results

suggest that as family ownership increases, family blockholders may adopt risk

Table 9 Effect of founder CEO on family firms announcement period CARs

N Mean

(t-Stat)

Median Standard

deviation

F Statistic

Professional CEO 43 -0.0010

(-0.12)

0.0001 0.0567 3.28**

Descendant CEO 12 0.0157

(0.92)

-0.0058 0.0618

Founder CEO 43 0.03152

(3.50)***

0.0240 0.0603

Family firms 98 0.0153 0.0110 0.0604

Professional CEO Founder CEO

Comparison of mean differences in CARs by CEO type (Scheffe test)

Founder CEO 0.0325**

p value = 0.042

Descendant CEO 0.0168

p value = 0.684

-0.01577

p value = 0.716

Sample of 215 mergers and acquisitions by Canadian acquiring firms between January 1997 and 2006 for

completed transactions over US$ 10 million obtained from the Thomson Financial Securities Data’s SDC

PlatinumTM Worldwide Database. Announcement period abnormal returns are cumulated over (-1, ?1),

where day 0 (the event day) indicates the day on which the merger was first announced, using the market

model parameters estimated between -240 and -40 days. **, *** indicate statistical significance at 5

and 1 % levels, respectively

152 P. Andre et al.

123

reducing strategies leading them to forgo profitable but risky investment projects.

These findings contribute to a better understanding of how family owners’

preferences and risk attitude affect firm performance. Moreover, the non linear

association between family ownership and stock market reaction to high-tech M&A

qualifies the question as to whether family firms are superior or inferior performers.

We also show that the conflict of interests between shareholders and professional

managers (agency problem 1) has the most harmful effect on shareholders’ wealth

whereas the conflict between large family owners and minority shareholders via

control enhancing mechanisms (agency problem 2) does not. To the best of our

knowledge, our paper is the first to consider the interactions between the two agency

problems and to test which of the two has the most detrimental effect on the quality

of an important business decision: high technology M&A. Furthermore, following

Villalonga and Amit (2006), this paper distinguishes between ownership, control

and management to better understand the family effect.

Adding to the family business literature, we find that family involvement in

management has a positive effect on the wealth creation of high-tech M&A and that

founders CEO are associated with better performance than hired CEOs. These

results confirm the valuable role played by founders in the success of family firms.

Given their long-term involvement in the firm and their better understanding of the

business, founders have more expertise in the selection of difficult to value targets

(such as high-tech firms) which results in value-creating acquisition strategies. Our

findings do not support the altruism argument (Lubatkin et al. 2005) that family

firms protect and favour incompetent family CEO who likely lack the expertise to

undertake value-creating acquisitions.