mergers and acquisitions by multinational firms

TRANSCRIPT

Masa ryk Unive r s i ty Faculty of Economics and Administration Field of study: Business Management

MERGERS AND ACQUISITIONS BY MULTINATIONAL FIRMS

Master Thesis

Thesis Supervisor: Author: Ing. Bc. Sylva Žáková Talpová, Ph.D. Bc. Luis E. Marquez Balderas, B.A.

Brno, 2019

MUNI ECON

MASARYKOVA UNIVERZITA

Faculty of Economics and Administration Lipová 41a, 602 00 Brno

IČ: 00216224 DIČ: CZ00216224

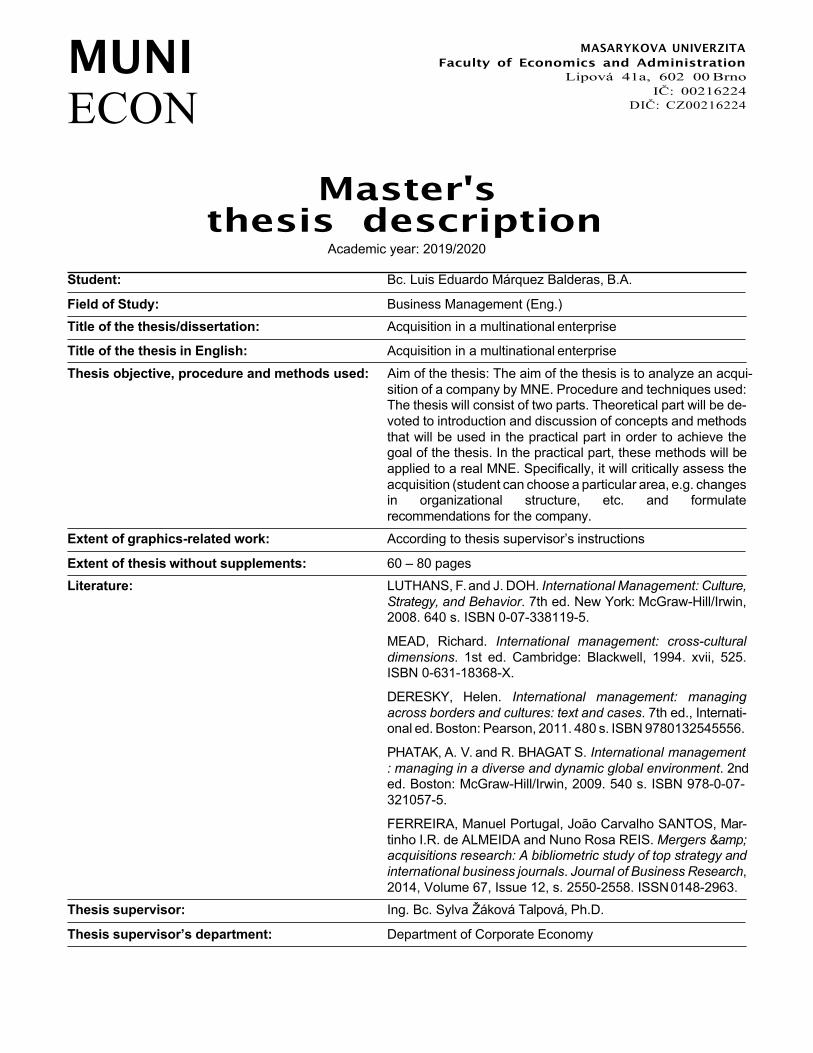

Master's thesis description

Academic year: 2019/2020 Student: Bc. Luis Eduardo Márquez Balderas, B.A.

Field of Study: Business Management (Eng.) Title of the thesis/dissertation: Acquisition in a multinational enterprise

Title of the thesis in English: Acquisition in a multinational enterprise Thesis objective, procedure and methods used: Aim of the thesis: The aim of the thesis is to analyze an acqui-

sition of a company by MNE. Procedure and techniques used: The thesis will consist of two parts. Theoretical part will be de- voted to introduction and discussion of concepts and methods that will be used in the practical part in order to achieve the goal of the thesis. In the practical part, these methods will be applied to a real MNE. Specifically, it will critically assess the acquisition (student can choose a particular area, e.g. changes in organizational structure, etc. and formulate recommendations for the company.

Extent of graphics-related work: According to thesis supervisor’s instructions

Extent of thesis without supplements: 60 – 80 pages Literature: LUTHANS, F. and J. DOH. International Management: Culture,

Strategy, and Behavior. 7th ed. New York: McGraw-Hill/Irwin, 2008. 640 s. ISBN 0-07-338119-5.

MEAD, Richard. International management: cross-cultural dimensions. 1st ed. Cambridge: Blackwell, 1994. xvii, 525. ISBN 0-631-18368-X.

DERESKY, Helen. International management: managing across borders and cultures: text and cases. 7th ed., Internati- onal ed. Boston: Pearson, 2011. 480 s. ISBN 9780132545556.

PHATAK, A. V. and R. BHAGAT S. International management : managing in a diverse and dynamic global environment. 2nd ed. Boston: McGraw-Hill/Irwin, 2009. 540 s. ISBN 978-0-07- 321057-5.

FERREIRA, Manuel Portugal, João Carvalho SANTOS, Mar- tinho I.R. de ALMEIDA and Nuno Rosa REIS. Mergers & acquisitions research: A bibliometric study of top strategy and international business journals. Journal of Business Research, 2014, Volume 67, Issue 12, s. 2550-2558. ISSN 0148-2963.

Thesis supervisor: Ing. Bc. Sylva Žáková Talpová, Ph.D.

Thesis supervisor’s department: Department of Corporate Economy

Thesis assignment date: 2018/11/01 The deadline for the submission of master’s thesis and uploading it into IS can be found in the academic year calendar.

In Brno, date: 2020/01/07

Name and Surname of the author: Bc. Luis Eduardo Marquez Balderas, B.A. Master’s thesis title: Mergers and Acquisitions by Multinational Firms

Department: Department of Corporate Economy

Master’s thesis supervisor: Ing. Bc. Sylva Žáková Talpová, Ph.D.

Master’s thesis date: 2020

Abstract

Research over the last few decades shows clearly that the rate of failures of mergers and acquisitions is at least fifty percent. In a global survey of mergers and acquisitions that had taken place over the last decade, Deloitte established that 83% of the transactions failed to achieve the management’s desired goals. These findings suggest that senior managers and the board of directors would avoid merger and acquisition transactions as much as possible. However, the research shows that the trend in mergers and acquisitions has been increasing. Further, the value of the money invested in the deals has been increasing. The aim of this thesis was to understand the reasons why firms undertake mergers and acquisitions, the reasons for failure, and the remedial actions taken to deal with the failure. The objectives of the thesis were achieved through a case study of Cemex Cement Company which has an extensive history of mergers and acquisitions, some of which ended in failure. Data for the study was collected through interviews with the senior managers of Cemex. The reasons for mergers and acquisitions were found to include technological considerations, entry into foreign markets, market power and efficiency gains, diversification, investor demands, the emergence of multinationals, national economic trends, and economies of scale and scope. The reasons for failure included stiff competition, financial crises, organisational culture, overestimation of synergies, high energy costs, and complexities of operating in foreign markets. The remedial actions undertaken to correct the failures include rebalancing of the portfolio, enhanced sales, operational improvements, alternative energy sources, refinance agreements, and improving organisational culture. The thesis established that for managers, the probability of failure of the merger and acquisition is taken into consideration, however, the potential benefits outweigh the fear of failure.

Keywords

Mergers, Acquisitions, Performance, Failures, Hubris, Pre-merger, Post-merger, Integration.

Declaration I certify that I have written the master’s Thesis Mergers and Acquisitions by Multinational Firms by myself under the supervision of Ing. Bc. Sylva Žáková Talpová, Ph.D., and I have listed all the literary and other specialist sources in accordance with legal regulations, Masaryk University internal regulations, and the internal procedural deeds of Masaryk University and the Faculty of Economics and Administration.

Brno, …………………………... Luis E. Marquez Balderas

Acknowledgement I would like to express my sincerest thanks and appreciation to all the people who supported me during the time of writing this thesis. I would especially like to thank my thesis supervisor Sylva Žáková Talpová, for all her insight, guidelines, advice, and corrections. I would also like to express gratitude to CEMEX S.A.B. de C.V for agreeing to participate in this thesis, and finally, but not least, I would like to express my sincere gratitude to my family for supporting and encouraging me throughout my whole studies in order to become better.

Table of Contents INTRODUCTION ......................................................................................................................... 1

1 MULTINATIONAL CORPORATIONS .................................................................................. 4

1.1 Multinational Corporation ..................................................................................................... 4

1.2 Theories of Multinational Firms ....................................................................................... 4

1.2.1 Macro-economic Theories .................................................................................................. 4

1.2.2 Micro-Theories ............................................................................................................... 6

2 MERGERS AND ACQUISITIONS .......................................................................................... 8

2.1 Definition of Mergers and Acquisitions ............................................................................ 8

2.2 Reasons for Mergers and Acquisitions ................................................................................ 10

2.2.1 Synergy .................................................................................................................... 10

2.2.2 Agency Theory ........................................................................................................ 11

2.2.3 Value Creation ......................................................................................................... 12

2.2.4 Market Power ........................................................................................................... 13

2.2.5 Efficiency Gains ...................................................................................................... 13

2.2.6 Economies of Scale and Scope ................................................................................ 14

2.2.7 Strategic Realignment .............................................................................................. 14

2.2.8 Diversification ......................................................................................................... 15

2.2.9 Reduction of Tax Liabilities .................................................................................... 16

2.3 Motives from the Sellers Perspectives ................................................................................. 17

2.4 Cross Border Mergers and Acquisitions from firms in Emerging Markets ......................... 17

2.5 Summary .............................................................................................................................. 18

3 PHASES AND PROCESS OF MERGERS AND ACQUISITIONS .................................... 19

3.1 Merger and Acquisition Process ..................................................................................... 19

3.2 Effect of the Merger and Acquisition Process on Outcome of the Deal ......................... 21

4 CHALLENGES AND REASONS FOR FAILURE OF MERGERS AND

ACQUISITIONS ....................................................................................................................... 22

4.1 Indicators of the Performance of the Merger and Acquisition ............................................ 22

4.2 Reasons for Failures of Mergers and Acquisitions .............................................................. 23

4.2.1 Hubris Hypothesis ........................................................................................................ 23

4.2.2 Managerial Discretion Hypothesis ................................................................................ 24

4.2.3 Price Bubbles ................................................................................................................ 25

4.2.4 Administrative Costs .................................................................................................... 26

4.2.5 Contagion and Capacity Effects ................................................................................... 26

4.2.6 Information Asymmetry ............................................................................................... 26

4.2.7 Lack of Common Vision .............................................................................................. 26

4.2.8 Rapid growth of Substitutes .......................................................................................... 27

4.2.9 Culture .......................................................................................................................... 27

4.2.10 Poorly Managed Integration ....................................................................................... 27

4.2.11 Managerial Challenges ............................................................................................... 28

4.2.12 Target Valuation Challenges ...................................................................................... 28

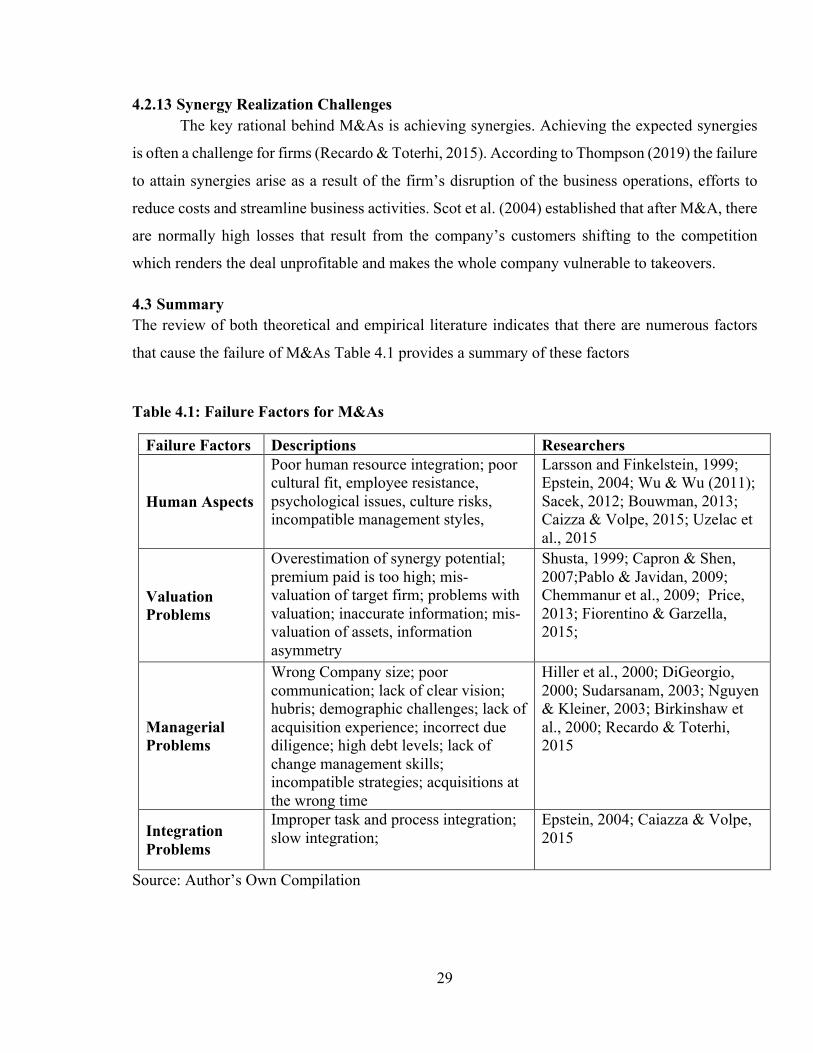

4.2.13 Synergy Realization Challenges ................................................................................. 29

4.3 Summary .............................................................................................................................. 29

5 RESEARCH APPROACH ...................................................................................................... 30

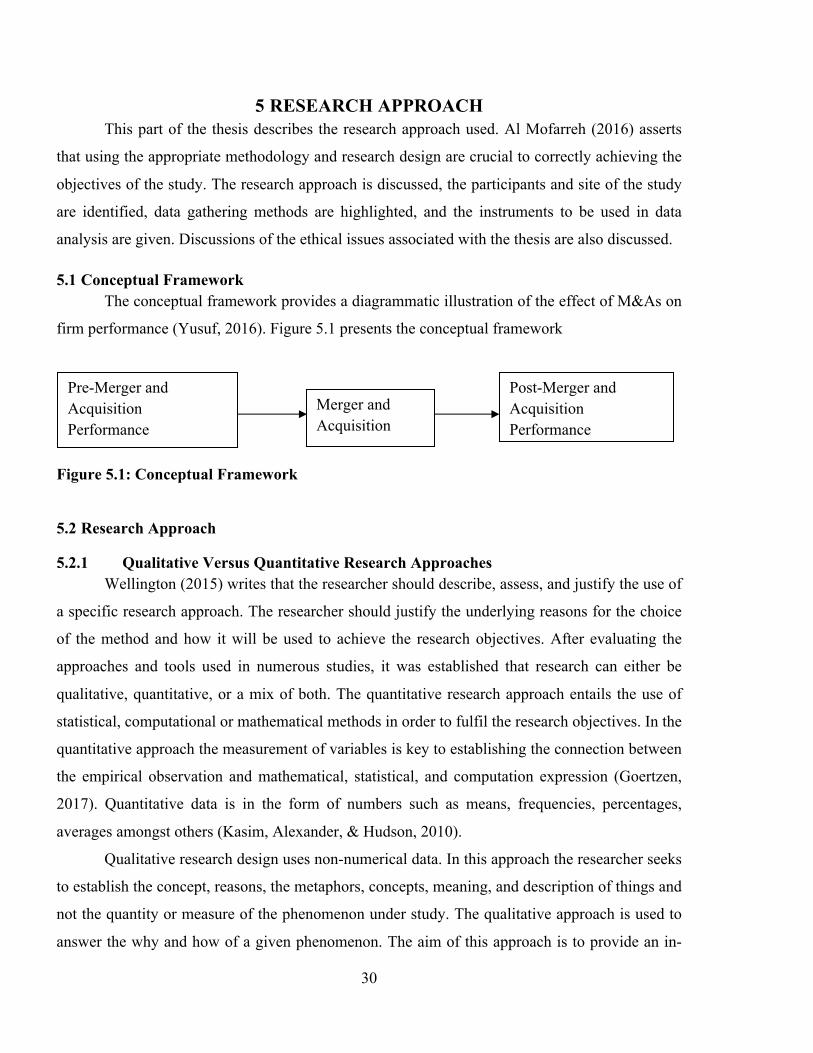

5.1 Conceptual Framework ........................................................................................................ 30

5.2 Research Approach .............................................................................................................. 30

5.2.1 Qualitative Versus Quantitative Research Approaches ........................................... 30

5.2.2 Case Study Qualitative Research Design ................................................................ 31

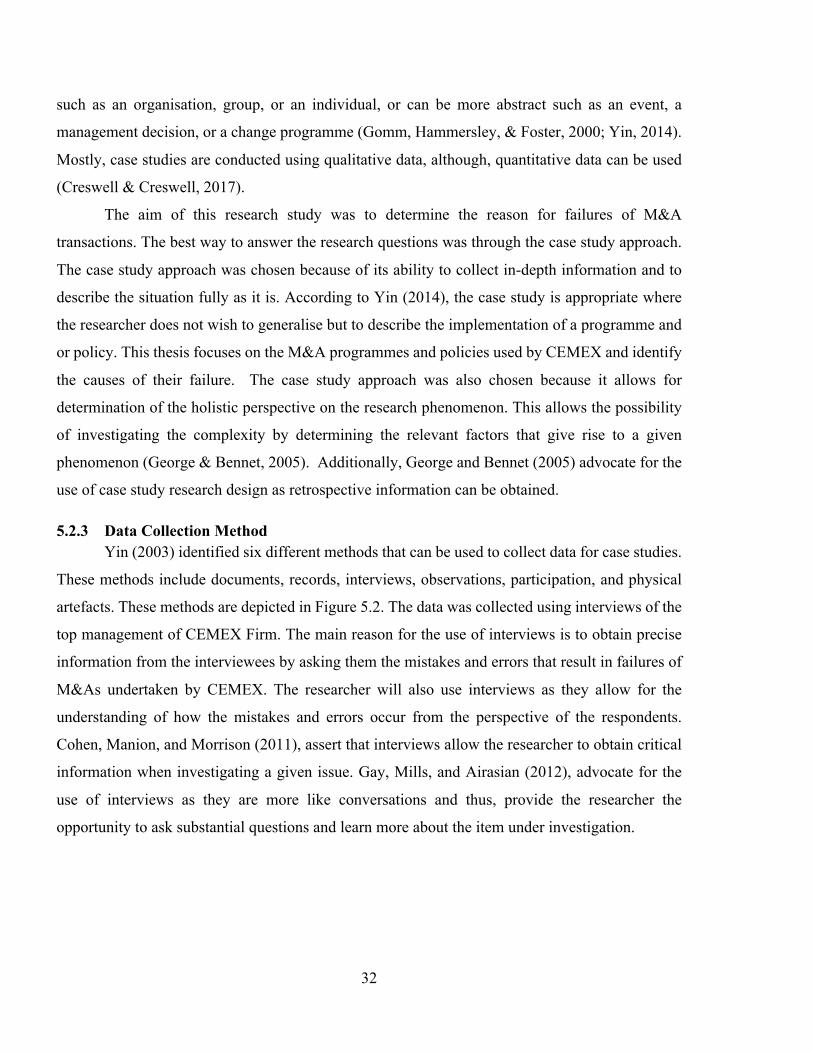

5.2.3 Data Collection Method ........................................................................................... 32

5.2.4 Interview Guide ....................................................................................................... 33

5.3 Location of the Study ........................................................................................................... 34

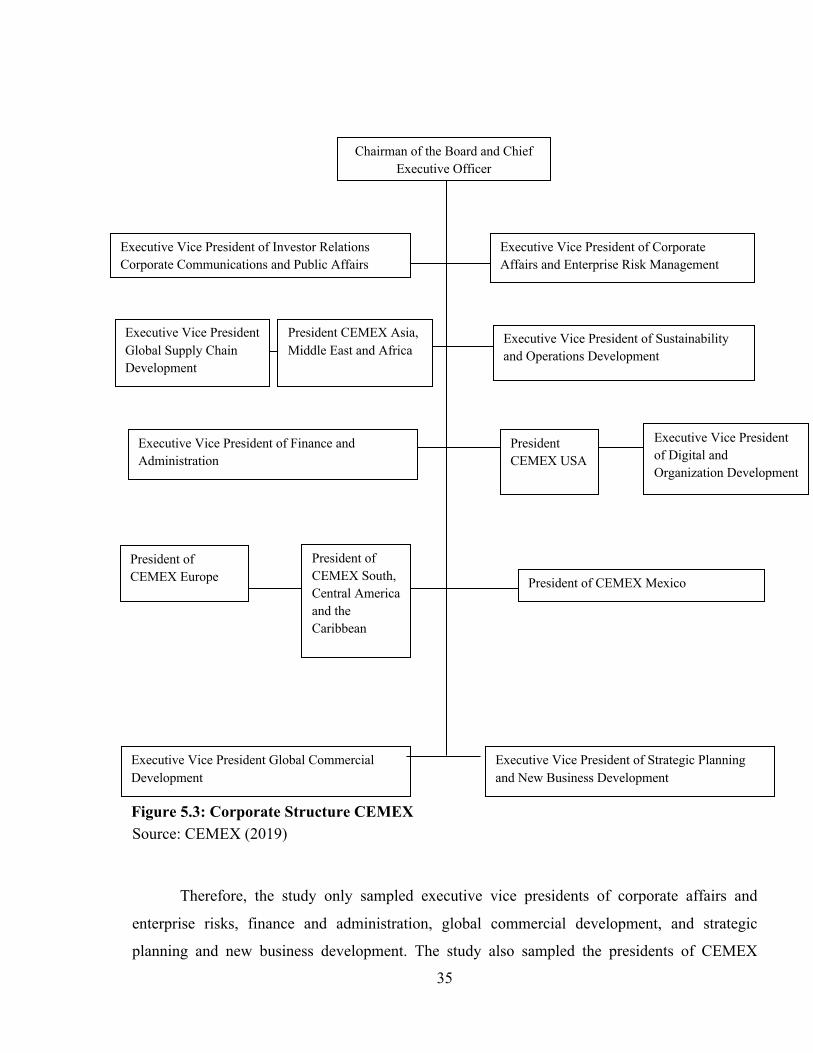

5.4 Study Participants ................................................................................................................ 34

5.5 Ethical Considerations ......................................................................................................... 36

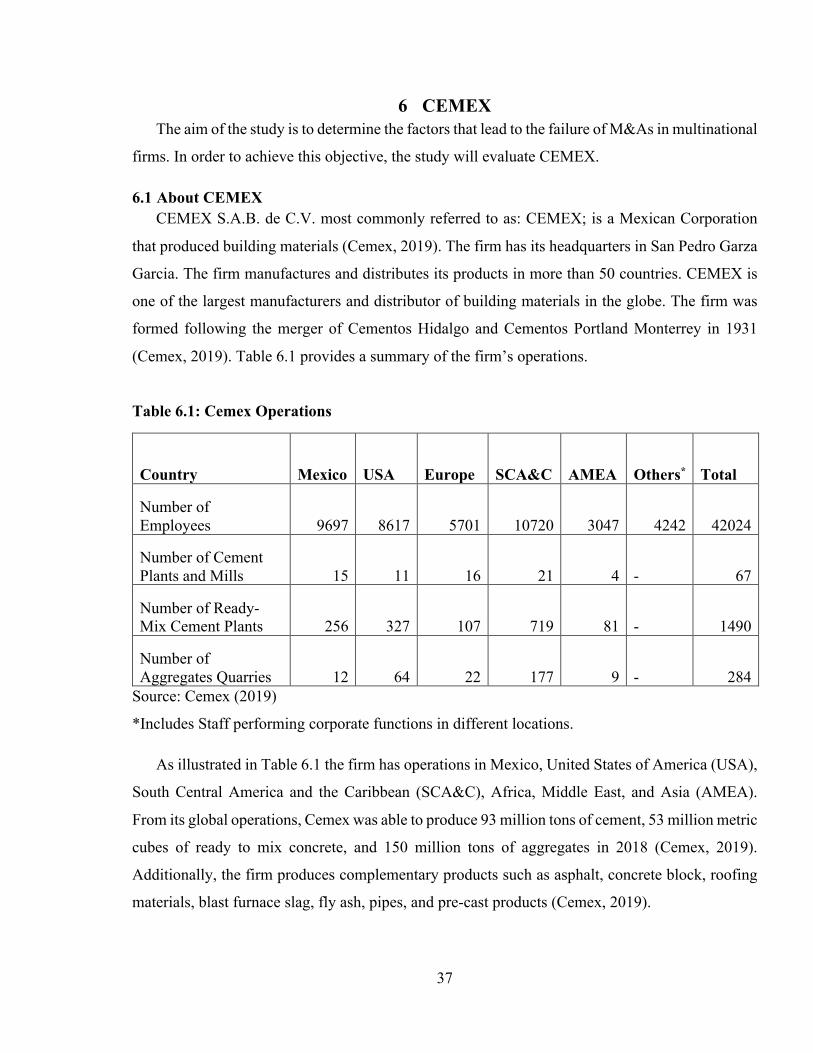

6 CEMEX ..................................................................................................................................... 37

6.1 About CEMEX .................................................................................................................... 37

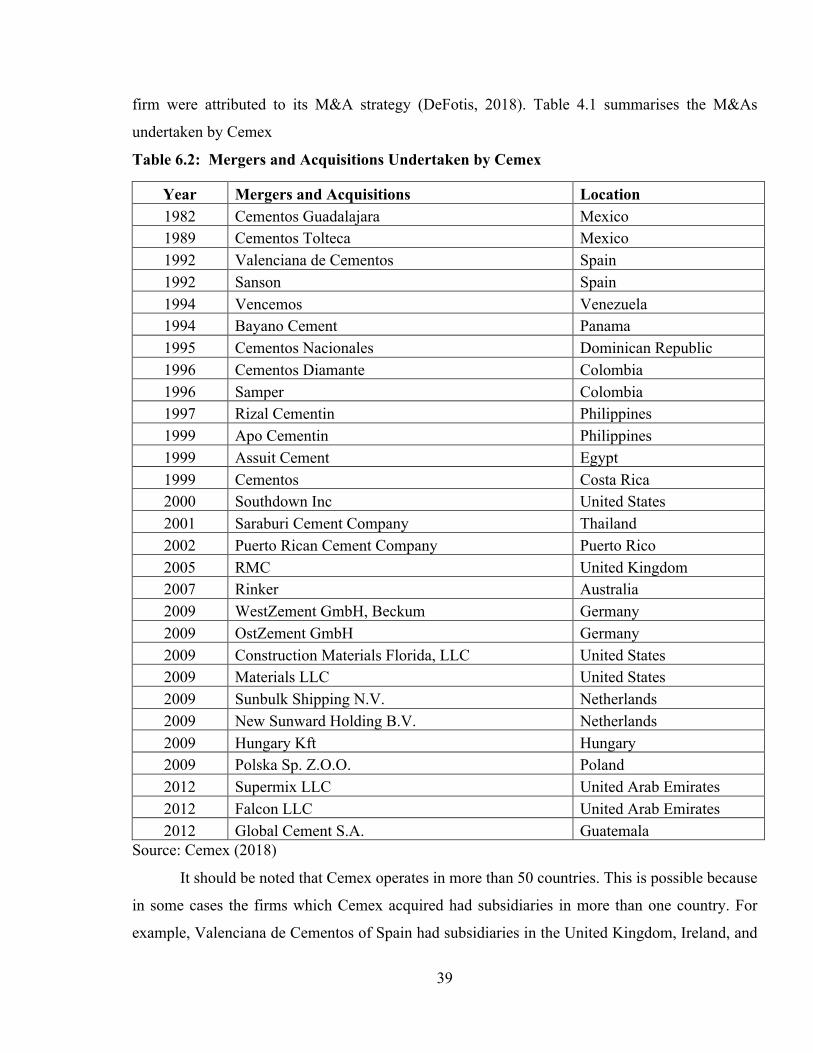

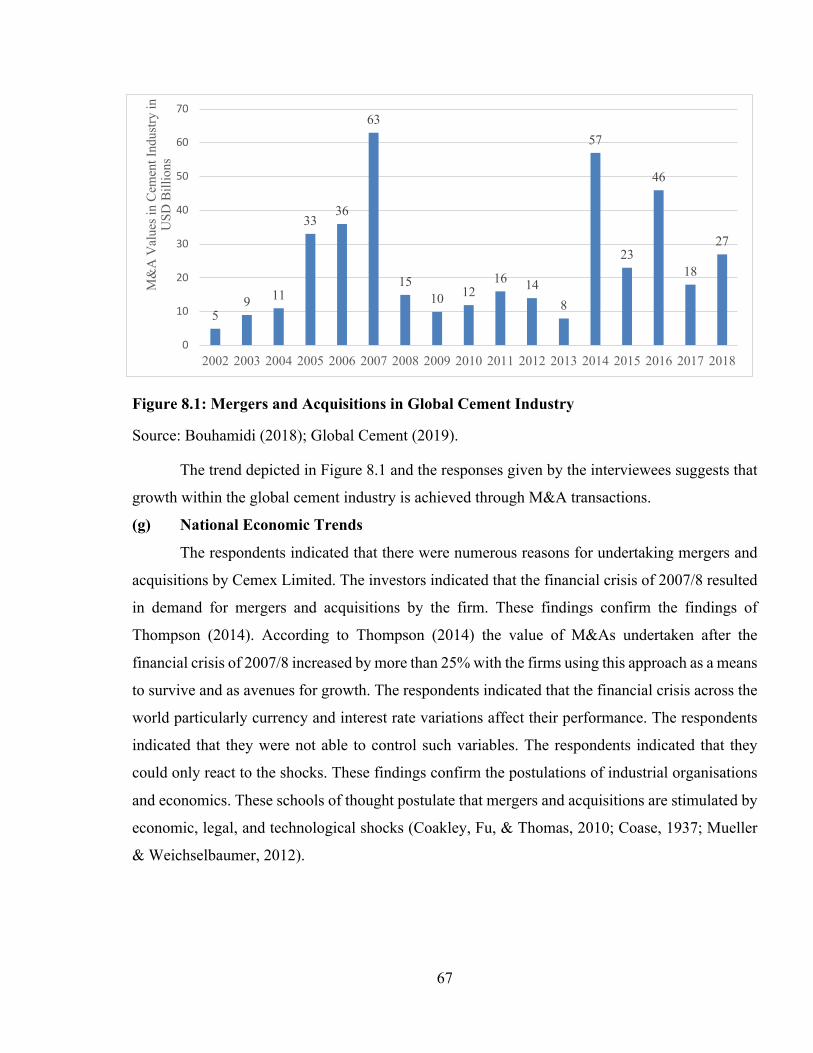

6.2 Mergers and Acquisitions by Cemex ................................................................................... 38

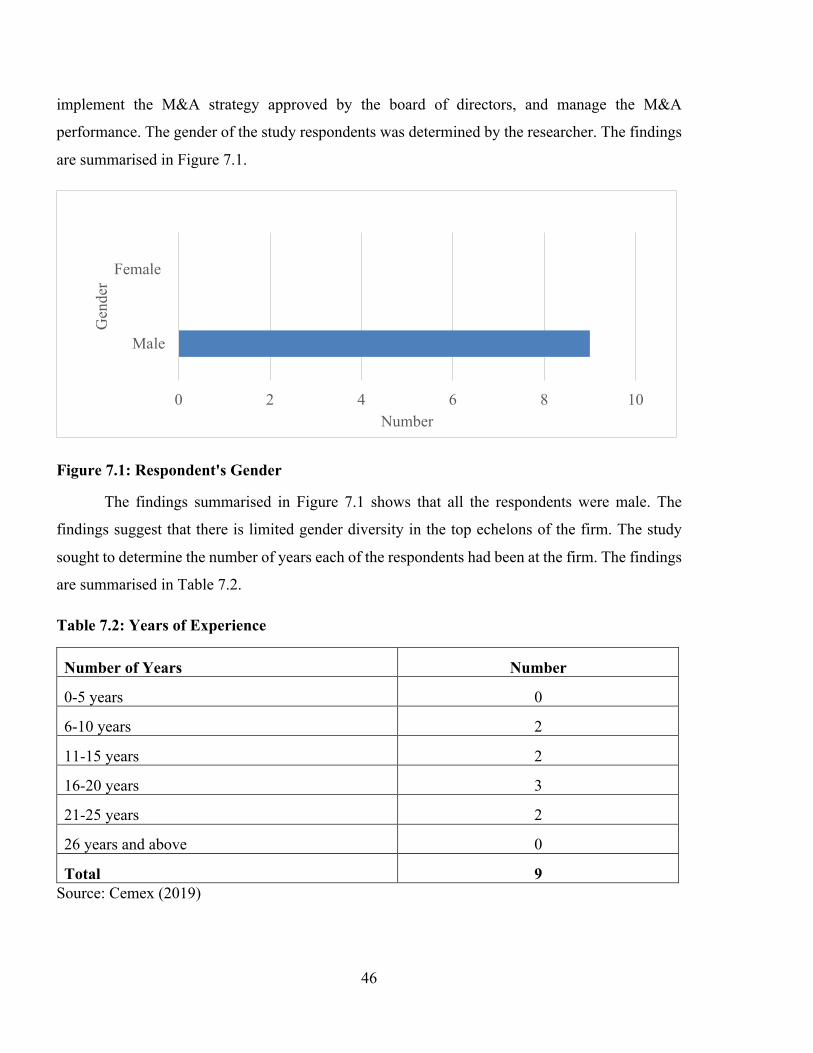

7 FINDINGS ................................................................................................................................. 45

7.1 General Information ............................................................................................................. 45

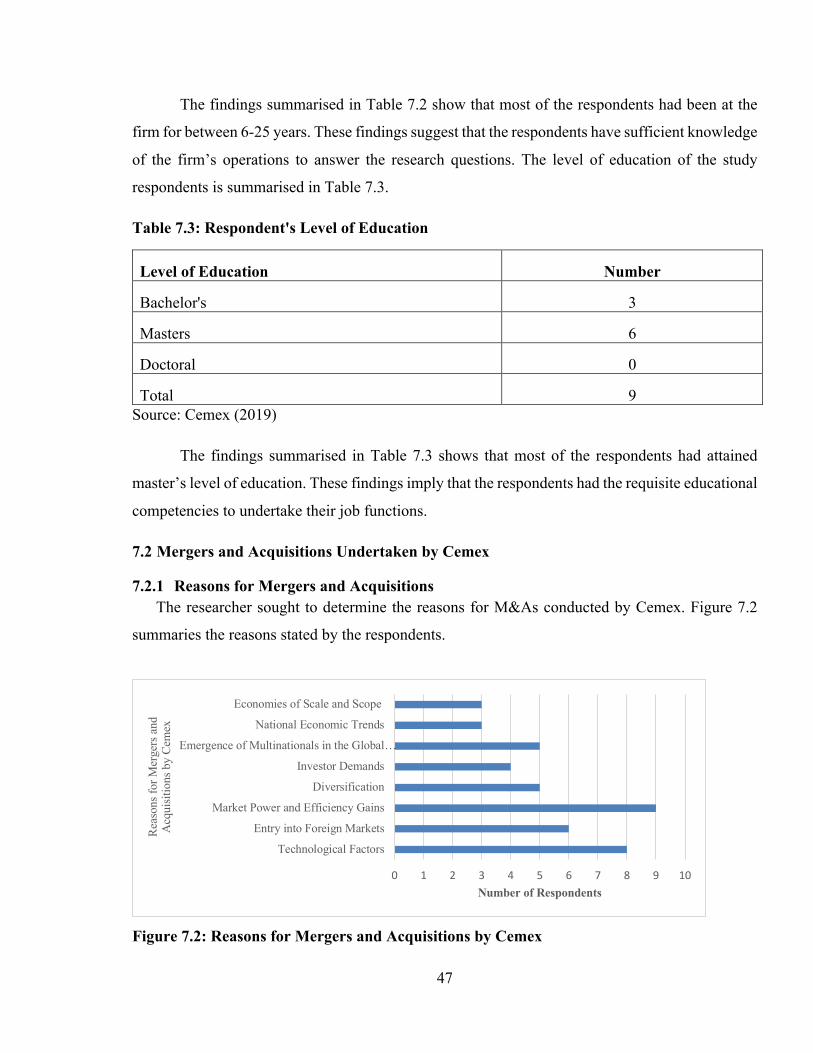

7.2 Mergers and Acquisitions Undertaken by Cemex ............................................................... 47

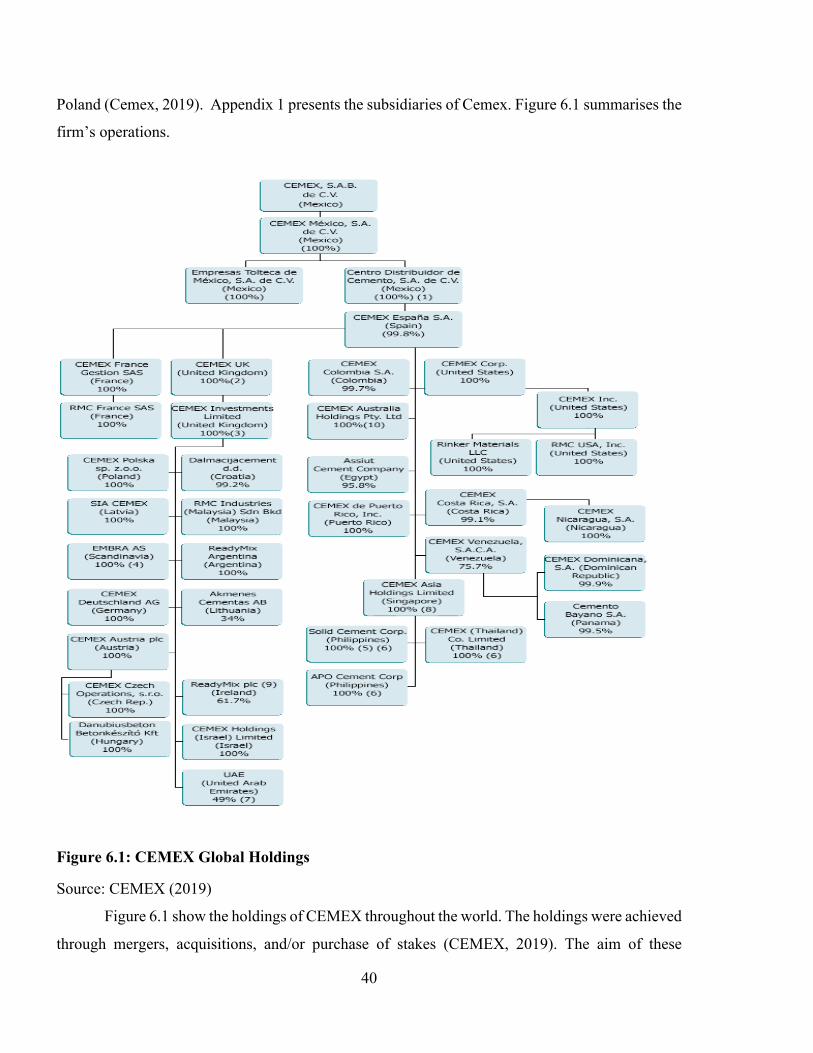

7.2.1 Reasons for Mergers and Acquisitions .................................................................... 47

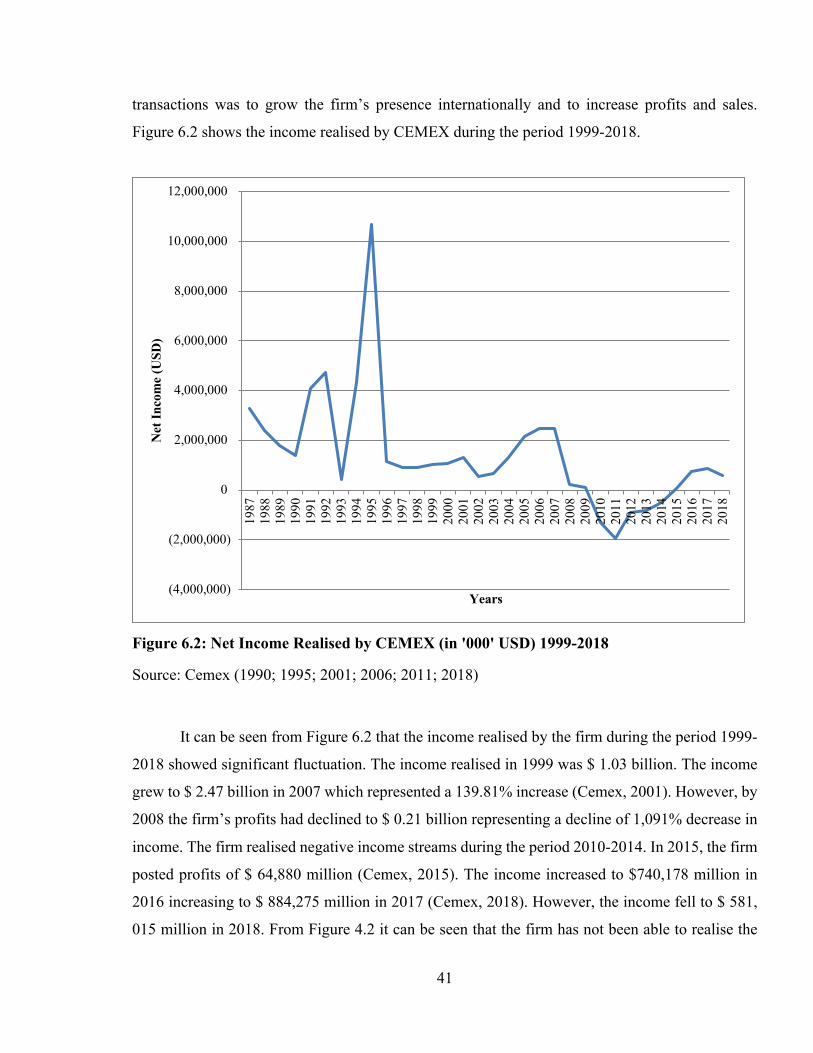

7.2.2 Process for the Mergers and Acquisitions ............................................................... 51

7.2.3 Challenges Experienced During the Merger and Acquisition Process .................... 53

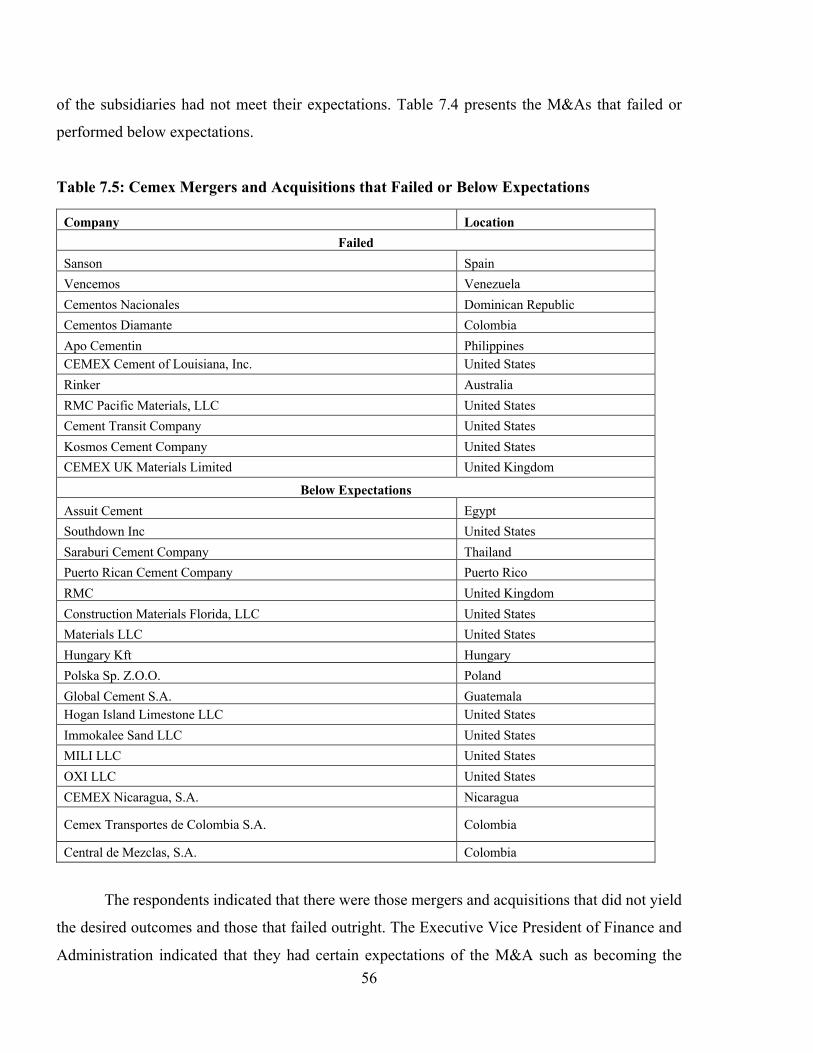

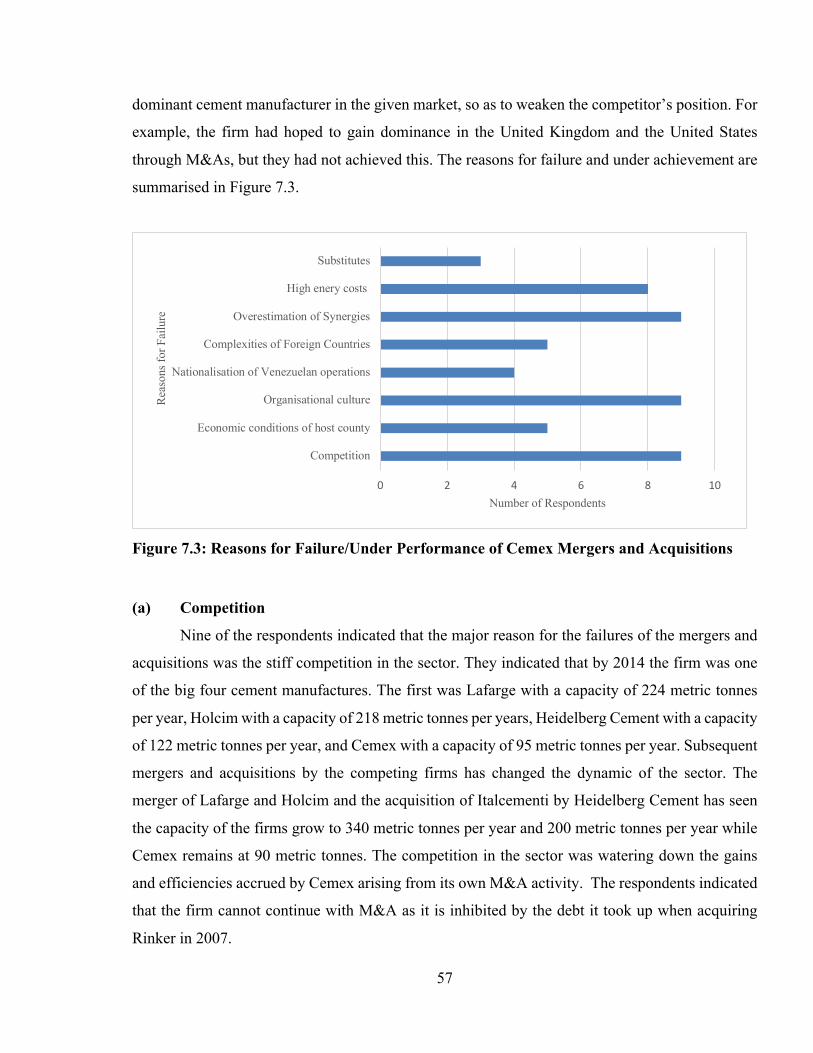

7.2.4 Reasons for Failure .................................................................................................. 55

7.2.5 Remedies for the Failures ........................................................................................ 61

8 DISCUSSIONS .......................................................................................................................... 65

8.1 Reasons for Mergers and Acquisitions ................................................................................ 65

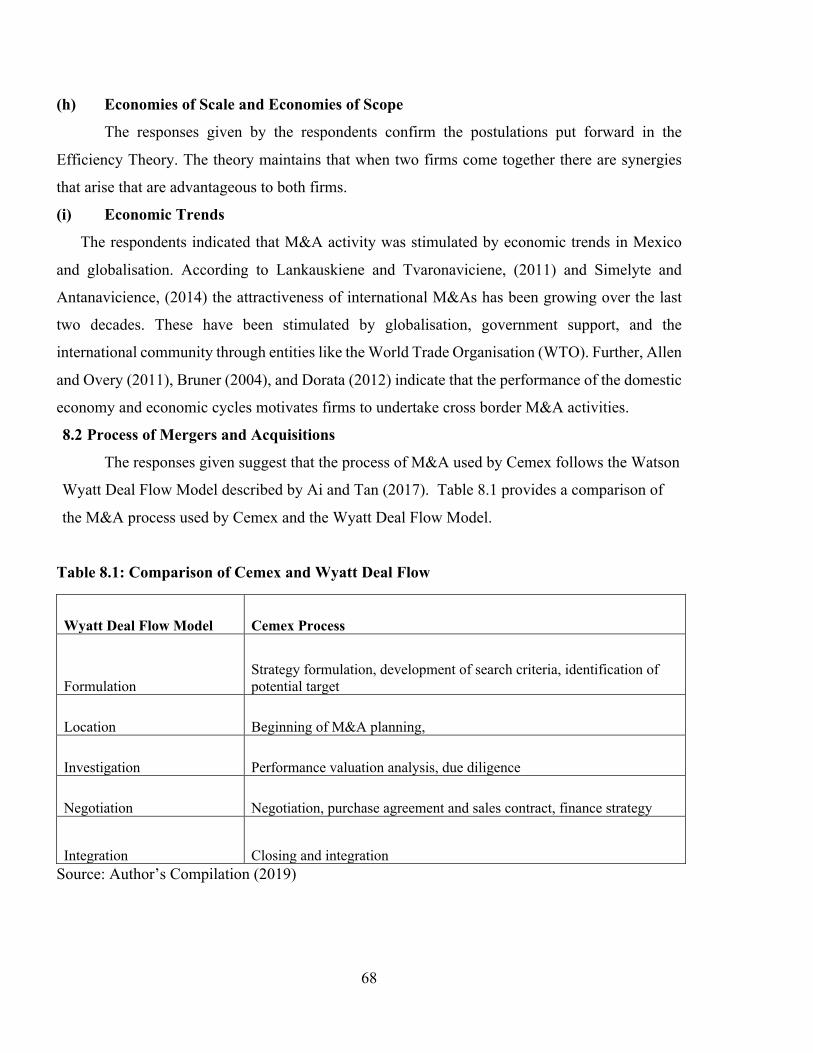

8.2 Process of Mergers and Acquisitions ................................................................................... 68

8.3 Factors that lead to the Failure of the Mergers and Acquisitions ........................................ 69

9 CONCLUSIONS AND RECOMMENDATIONS ................................................................. 72

9.1 Conclusions Based on Study Findings ................................................................................ 72

9.2 Recommendations ................................................................................................................ 73

9.3 Contributions and Implications ............................................................................................ 74

9.4 Limitations of the Study ...................................................................................................... 75

REFERENCES ............................................................................................................................ 76

LIST OF TABLES ....................................................................................................................... 89

LIST OF FIGURES ..................................................................................................................... 90

ABBREVEIATION AND ACRONMYS ................................................................................... 91

INTERVIEW GUIDE ................................................................................................................. 92

APPENDICES .............................................................................................................................. 93

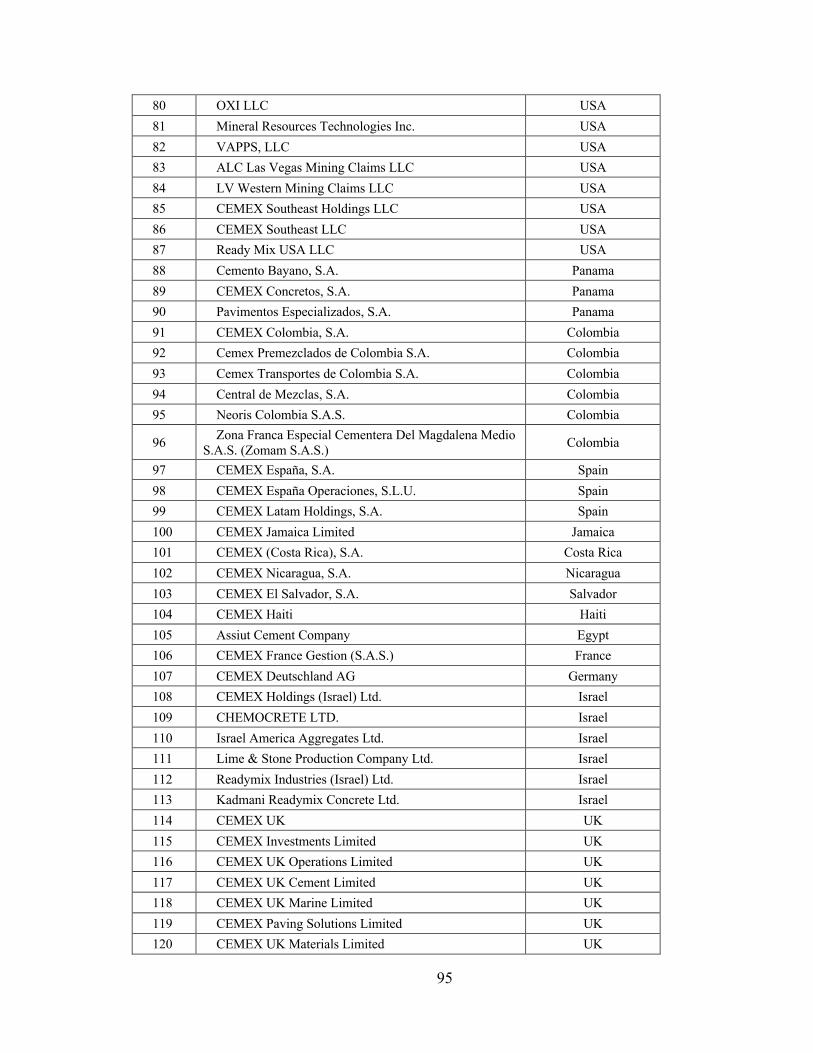

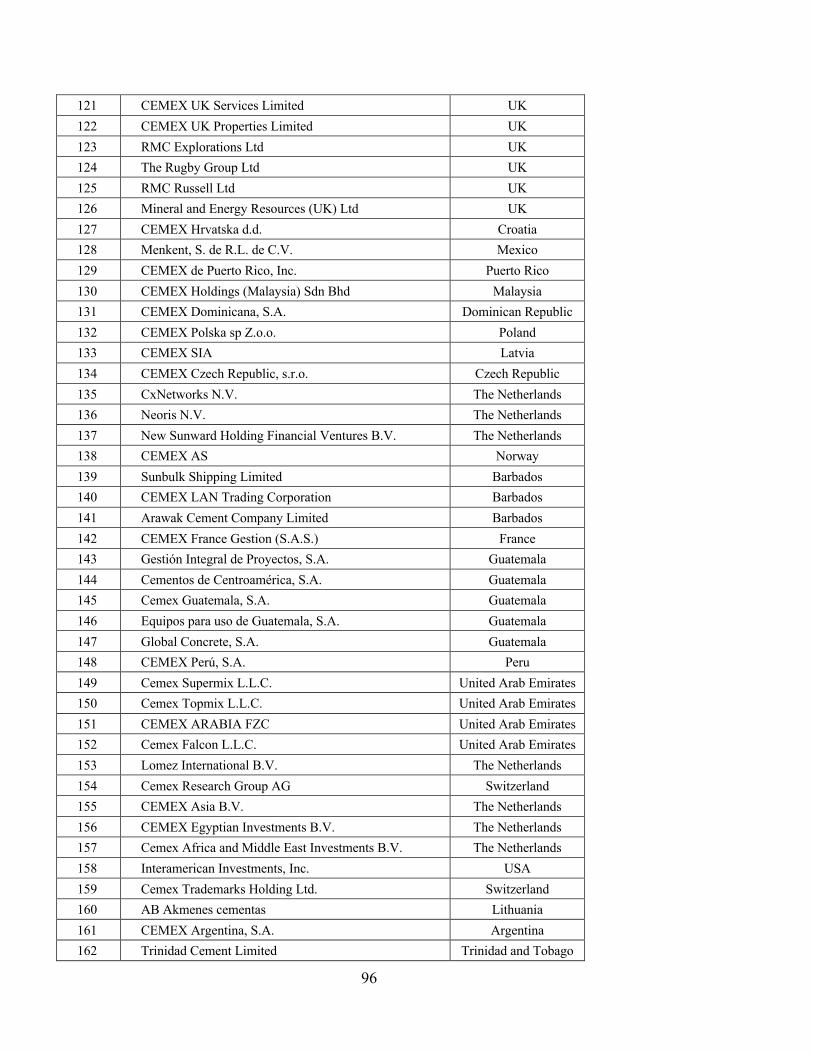

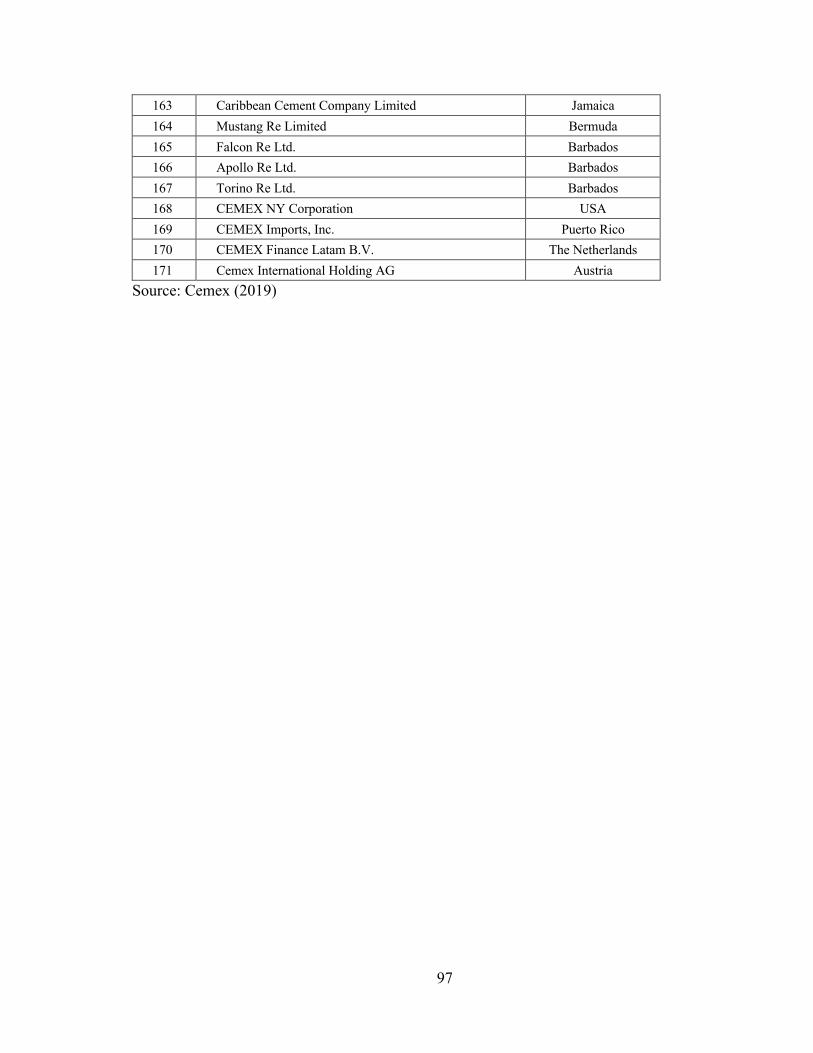

Appendix1: List of Cemex Subsidiaries as at December 31st 2018 ........................................... 93

1

INTRODUCTION Globalisation has stimulated major changes in the business world over the past decade.

Companies have been searching for a competitive advantage on a worldwide scale. Companies are

forced to follow their customers- who are going global- as they respond to the competition that is

worldwide in scale. Globalisation in combination with other trends such as deregulation,

privatisation and corporate restructuring has spurred an unprecedented surge in cross-border

merger and acquisition activity. The recent figures in business clearly indicate that cross border

mergers and acquisitions have become a fundamental characteristic of the global business

landscape. Additionally, growing through M&A is one of the main ways in which multinational

firms seek to expand globally. Often, however, expectations outrun reality and the difficulties of

merging two companies are underestimated.

The motivation for mergers and acquisitions (M&As) has been the subject of numerous

research studies across the globe. The interest arises from the fact that empirical findings have

established that more than sixty-six percent of all M&A deals undertaken result in failure (Angwin,

2007; Groen & McCarthy, 2011; Hiltrop, 2019). Further, studies have shown that mergers and

acquisitions are motivated by various factors besides finances. Similarly, researchers have found

that more than sixty percent of mergers and acquisition motivated by factors besides profits, often

do not achieve their objectives (Denison, 2016). Despite the established failures, businesses across

the globe continue to undertake merger and acquisition transactions. The empirical evidence raises

the following questions:

(i) What are the reasons for mergers and acquisitions undertaken by Cemex?

(ii) What is the M&A process used by Cemex?

(iii) What are the challenges faced during the M&A process?

(iv) Which are the failures and the reasons for failure of the mergers and acquisitions

undertaken by Cemex?

(v) What are the remedies put in place by Cemex to deal with the failures?

A review of theoretical and empirical literature showed that there are various reasons why

firms undertake mergers and acquisitions and the reasons for failure. The identified reasons for

mergers and acquisitions include synergy, agency theory, value creation, market power, efficiency

gains, economies of scale and scope, strategic realignment, diversification, and reduction of tax

liabilities. The reasons for failure include hubris hypothesis, managerial discretion, price bubbles,

2

administrative costs, contagion and capacity effects, lack of a common vision, the rapid growth of

substitutes, cultural differences, poorly managed integration process, managerial challenges, target

valuation challenges, and synergy realisation challenges. The literature review also established that

the pre-merger and acquisition process, the actual transaction, and the post-merger and acquisition

process also impact the performance of the transaction. The thesis also investigated a neglected

area of mergers and acquisitions undertaken by firms from emerging markets. Over the last few

decades, the amount of foreign direct investment from emerging markets through mergers and

acquisitions have been increasing. Although the number of M&A undertaken by firms from

emerging markets has been growing, little research has been conducted to understand the reasons

for these transactions, the process, the challenges, and the success and failures.

In order to answer the research questions, a case study of CEMEX S.A.B. de C.V., also known

as Cemex which is a Mexican firm that produces building materials, was undertaken. The firm

operates in more than fifty-two countries across the globe. Over the last three decades, the firm had

undertaken more than a dozen mergers and acquisitions across the globe. Some of the mergers and

acquisitions have been successful while some have resulted in large failures. The data for the thesis

was collected using interviews. The participants of the study were the top management of Cemex.

The significance of this study rests on several grounds. In Mexico, a large number of

mergers and acquisition occur in the financial sector, for example, during the period 2009-2018

seventy-six of the ninety-four merger and acquisitions involved firms operating in the financial

sector (Deloitte, 2017; Rio & Colunga, 2018). Consequently, most of the studies on mergers and

acquisitions in Mexico have been conducted in firms operating in the banking sector (Bohada &

Hector, 2019; Hernàndez, Domìnguez, & Toledo, 2013; Romero & Fajardo, 2017). Thus, there is

limited empirical evidence on the mergers and acquisitions in Mexico that occur outside the

financial sector. In this respect, this thesis evaluated mergers and acquisitions outside the financial

sector. Further, the study explores the merger and acquisition process of a firm from an emerging

market. Over the last few decades, most of the mergers and acquisitions have involved firms in

developed nations (Ai & Tan, 2019).

The thesis is presented in nine chapters. Chapter one provides an analysis of multinational

corporations and the reasons why they exist. Chapter two provides a description of mergers and

acquisitions and the reasons why firms chose to undertake such transactions. Chapter three

summarises the process of mergers and acquisitions. Chapter four presents a theoretical and

empirical review of the challenges and reasons for the failure of mergers and acquisitions. Chapter

3

five identifies the research approach used to answer the research questions. Chapter six provides

an introduction to Cemex which was the company the thesis focused on. Chapter seven provides a

description of the study participants and a summary of their responses to the questions developed

to answer the research questions. Chapter eight provides a discussion of the findings. Chapter nine

contains conclusions drawn from the findings, makes recommendations based on the findings,

indicates the contributions of the study, and highlights the limitations of the study.

4

1 MULTINATIONAL CORPORATIONS This chapter provides a review of the concept and theories that support the emergence of

multinational firms.

1.1 Multinational Corporation There are different definitions of the term multinational corporation which have numerously

termed as denationalized corporations, transnational firms, international corporations, or cosmo-

corparations (Kusluvan, 1998). Pitelis and Sugden (2000) define multinational corporation (MNC)

as an entity that owns and/or control the production of goods and service in one or more than one

country other than its home county. The ownership is usually meant by a majority of more than

50%. Hoskisson, Wright, Filatotchev and Peng (2013) define MNCs as firms that earns 25% or

more of its income from outside its home county. The defining feature of MNCs include they are

often large; their global activities are centrally managed by the parent company; involved in the

importing and exporting of goods and services; make significant investments in foreign countries;

buy and sell licences to its products in foreign markets; participate in contract manufacturing

(Allon, Anderson, Munim, & Ho, 2018).

1.2 Theories of Multinational Firms There are various theories that try to explain the reason for MNCs. The theories attempt to

answer three fundamental questions: what are the factors that stimulate firms to produce goods and

services abroad? What conditions enable them to carry out their activities abroad? Why do the

MNCs have different types of investments? Kojima (1984) classified the theories of MNCs into

macroeconomic theories and microeconomic theories.

1.2.1 Macro-economic Theories (a) Location Theory

The idea that firms expand beyond their national borders due to the location advantages

was first discussed by Richard Cantillon, Etienne Bonnot de Condillac, David Hume, James

Steuard, and David Ricard (Glatte, 2015). It was the work of Johann Heinrich Von Thünen that the

location theory was explicitly stipulated. According to Von Thünen (1826) the cost associated with

the transportation of the goods produced by industry reduces some of the economic rent identified

by Ricardo. Further, Von Thünen noted that the transportation costs and the economic rents, vary

across regions and goods. The transportation costs increase as the distance from the factory to the

marketplace increases. The theory addressed the question of why economic activities are located

5

where they are. Von Thünen argued that firms decide the location that will maximise their profits

while individuals chose those that will maximise utility. In his seminal works ‘Über den

Süddeutschland’, in 1909 Alfred Weber used the freight charges for inputs and outputs, and the

finished production function to develop a framework that could be used to establish the optimal

location for factories. Both works of Von Thünen (1829) and Weber (1909) focused on the national

point of view.

The international perspective was introduced by Hoover (1948) and promulgated by Ohlin

(1952), Sabathil (1969), Moore (1978), Tesch (1980), and Goette (1994). The academics postulated

the firms choose to operate beyond their national boundaries due to economic factors (potential

markets, competitive conditions, infrastructure, communication, transportation costs, labour costs,

monetary (conditions), political factors (tax regulations, environmental requirements, market entry

barriers, government support, political risks), cultural factors (language, attitudes, religion) and

geographical factors (climate, geography, natural resources, and topography). Glatte (2015) found

that it was no longer large corporations that expand abroad. According to Glatte (2015) smaller

firms and foreign direct investment are also determined by location selection.

(b) Absolute Advantage Theory

The main ideas of this theory are attributed to Adam Smith 1776. Smith (1776) argued that

countries attain absolute advantage by allowing for free trade and specialising in what they have

an advantage in. Smith (1776) reasoned that commerce between nations should not be restricted or

regulated by government but should be determined by free market forces. Smith argued that market

forces would increase efficiencies that would benefit the nation. Kojiam (1978) integrated the

absolute theory with MNCs by suggesting that foreign direct investment (FDI) is needed to make

nations / factor markets efficient and competitive internationally. Kojiam (1978) indicated that

MNCs enhanced production and exports through the transfer of capital, managerial competencies,

and technological know-how to the host nation. Kojiam (1978) identified three major factors for

MNCs to move abroad these include resources, labour, and market. The MNCs invest in foreign

nations so as to obtain and secure imports of goods which their home country does not have or

produces at higher costs. Labour-oriented MNCs look for areas were wages in given locations are

cheaper than in their home nation. The MNCs make use of idle or inefficient factor markets. The

market oriented MNCs aim to overcome trade barriers by providing import substitution of the

recipient nations. Additionally, MNCs seek oligopolistic advantages by investing in other markets.

6

1.2.2 Micro-Theories (a) Hymer-Kindleberg Theory This theory can also be referred to as the monopolistic or oligopolistic power, or structural

market imperfection theory. Hymer (1960) sought to answer why do firms go to other countries;

how are they able to survive in foreign markets where they have to incur adjustment costs; and why

do they want to acquire, retain control and ownership. Hymer (1976), found that the firms were

motivated by two incentives which were monopolistic or oligopolistic advantages that arose from

operating in the foreign nation. The second factor was the elimination of competition that the firms

experienced in foreign nations. Hymer (1979) observed that MNCs do not work in conditions of

perfect competition. Hymer (1979) introduced a third motivation for firms to go beyond their

national borders. The economies of scale and the efficient operation of the corporation’s business

and ability to coordinate activities with its subsidiaries.

Kindleberg (1969) introduced the concept of rigidities in the input’s markets. Kindleberg

(1969) argued that where there are factors that inhibit the flow of inputs to competitors, the

multinational enterprises take advantage of these rigidities. These include technology and designs

protected by patents, wages might be significantly different, interest rate paid on credits are

example of rigidities that give MNCs the advantages if they locate their production processes in

different countries and regions. The suppositions of Kindleberger (1969) allow for the cross-border

vertical and horizontal integrations that were put forward by Hymer.

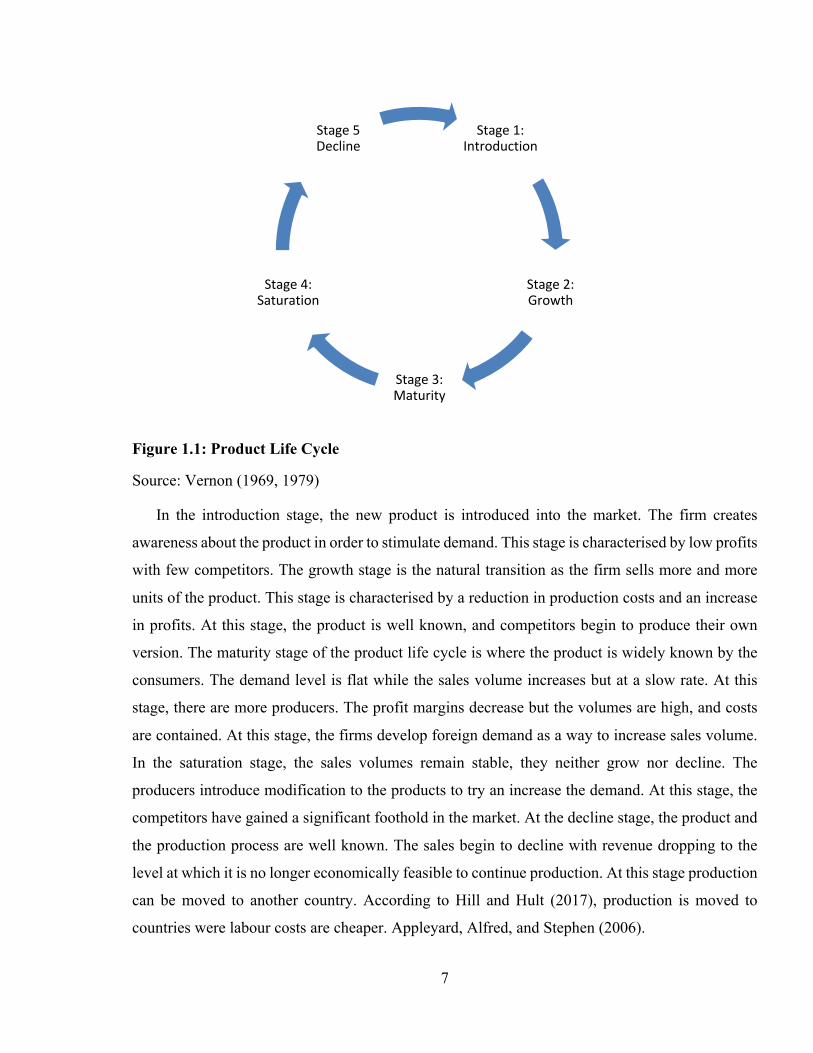

(b) Product Life Cycle Theory

This hypothesis was put forward by Vernon (1969; 1979) as a means of explaining patterns

that emerged from international traded. Vernon suggested that in the initial stages, the product’s

life cycle all the factors associated with the product are sourced from the area where the product

was invented (Hill, 2007). Thereafter, the product is used in world markets. As the consumption in

world markets increases the production process progressively moves away from the area it was

invented. The life cycle of the product is depicted in Figure 1.1

7

Figure 1.1: Product Life Cycle

Source: Vernon (1969, 1979)

In the introduction stage, the new product is introduced into the market. The firm creates

awareness about the product in order to stimulate demand. This stage is characterised by low profits

with few competitors. The growth stage is the natural transition as the firm sells more and more

units of the product. This stage is characterised by a reduction in production costs and an increase

in profits. At this stage, the product is well known, and competitors begin to produce their own

version. The maturity stage of the product life cycle is where the product is widely known by the

consumers. The demand level is flat while the sales volume increases but at a slow rate. At this

stage, there are more producers. The profit margins decrease but the volumes are high, and costs

are contained. At this stage, the firms develop foreign demand as a way to increase sales volume.

In the saturation stage, the sales volumes remain stable, they neither grow nor decline. The

producers introduce modification to the products to try an increase the demand. At this stage, the

competitors have gained a significant foothold in the market. At the decline stage, the product and

the production process are well known. The sales begin to decline with revenue dropping to the

level at which it is no longer economically feasible to continue production. At this stage production

can be moved to another country. According to Hill and Hult (2017), production is moved to

countries were labour costs are cheaper. Appleyard, Alfred, and Stephen (2006).

Stage 1: Introduction

Stage 2: Growth

Stage 3: Maturity

Stage 4: Saturation

Stage 5 Decline

8

2 MERGERS AND ACQUISITIONS This chapter provides a review of the concept and theories that support the need and purpose

of mergers and acquisitions. The aim of this chapter is to provide the main concepts and terms that

cover the topic area of the thesis.

2.1 Definition of Mergers and Acquisitions The main objectives of any business entity are to achieve the highest level of profits. However,

most business entities have limited capabilities and resources necessary to attain the highest levels

of profits (Rashid & Naeem, 2017). Therefore, in order to attain their goals, firms employ various

options; these options can either be organic or inorganic. Organic growth strategic involve the

expansion of business through new products, productivity enhancements, increased production,

streamlining of business operations and cost reduction, entry into new markets, and increasing

customer base (Dash, 2010). In organic growth is the process of growth of assets and sales

expansion through mergers and acquisitions (Dash,2010). Koi-Akrofi (2016) uses the term mergers

and acquisitions interchangeable to describe the fusion, joining, union, or coming together of two

or more entities through the process of acquisition or a pooling of interests (Koi-Akrofi, 2016).

The result of a merger is the formation of a new entity. According to Unoki (2013), an acquisition

occurs when a target company is purchased by another firm. The firm that purchases the target firm

treats the acquired entity as an asset. The firm is included as an asset in the balance sheet; the

amount paid above the target firm’s book value and/or market value is recognised as goodwill that

will be charged against future income (Unoki, 2013).

According to Wang, Pauleen, & Chan, 2013, a merger is the combination of two entities

whereby one entity transfers all its assets to the other entity which continues to exist. Put simply,

one entity is consumed by the other. The shareholders of the consumed firm obtain shares in the

surviving firm (Huh, 2015). On the other hand, an acquisition involves the buying of assets and

stocks of the target firm. The distinction between mergers and acquisitions is often blurred.

According to Popp (2013), the main difference between mergers and acquisitions is the position of

the shareholders. In merged firms, the shareholders of the target firm receive shares in the new

firm. In acquired firms, the shares of the target firm are transferred to the purchasing firm in the

form of cash or debt. Netter, Stegemoller, and Wintoki (2011) indicate that mergers and

acquisitions involve a wide variety of transactions, with different frameworks, and different effects

on the various stakeholders. Netter et al. (2011) argued that the difference between M&As is seen

9

in the governing structure that arises from the deal whereby mergers result in the equitable

combination of the firms while acquisitions entails less equitable combination of the firms with

more emphasis being place on streamlining and replacing the target-firms structures.

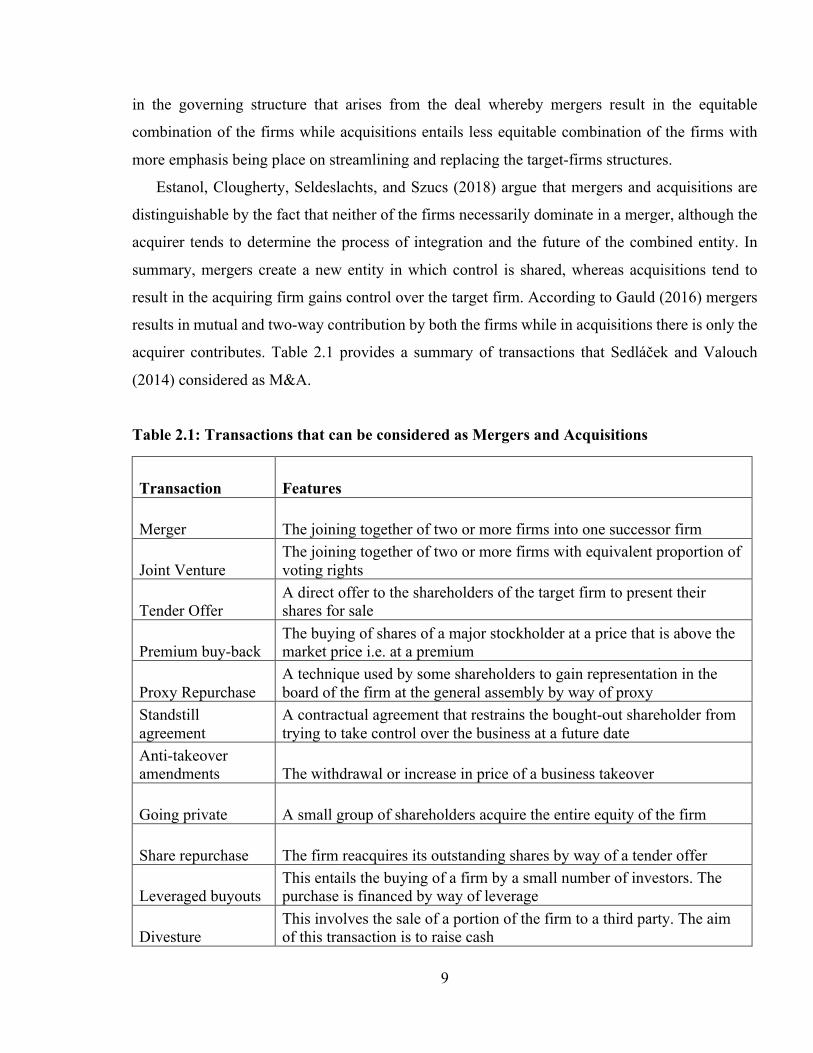

Estanol, Clougherty, Seldeslachts, and Szucs (2018) argue that mergers and acquisitions are

distinguishable by the fact that neither of the firms necessarily dominate in a merger, although the

acquirer tends to determine the process of integration and the future of the combined entity. In

summary, mergers create a new entity in which control is shared, whereas acquisitions tend to

result in the acquiring firm gains control over the target firm. According to Gauld (2016) mergers

results in mutual and two-way contribution by both the firms while in acquisitions there is only the

acquirer contributes. Table 2.1 provides a summary of transactions that Sedláček and Valouch

(2014) considered as M&A.

Table 2.1: Transactions that can be considered as Mergers and Acquisitions

Transaction Features

Merger The joining together of two or more firms into one successor firm

Joint Venture The joining together of two or more firms with equivalent proportion of voting rights

Tender Offer A direct offer to the shareholders of the target firm to present their shares for sale

Premium buy-back The buying of shares of a major stockholder at a price that is above the market price i.e. at a premium

Proxy Repurchase A technique used by some shareholders to gain representation in the board of the firm at the general assembly by way of proxy

Standstill agreement

A contractual agreement that restrains the bought-out shareholder from trying to take control over the business at a future date

Anti-takeover amendments The withdrawal or increase in price of a business takeover

Going private A small group of shareholders acquire the entire equity of the firm

Share repurchase The firm reacquires its outstanding shares by way of a tender offer

Leveraged buyouts This entails the buying of a firm by a small number of investors. The purchase is financed by way of leverage

Divesture This involves the sale of a portion of the firm to a third party. The aim of this transaction is to raise cash

10

Transaction Features

Spin-Off

This transaction results in the formation of a new legal entity. The shares of the new entity are divided with regard to the number of shares held by the shareholders of the parent firm.

Source: Sedláček and Valouch (2014)

Merger and Acquisitions can take place between firms in the same industry or those

operating in different industries. When the firms that are involved in the transaction are form the

same industry, this is referred to horizontal merger (Kumar & Bansal, 2008). These types of M&As

give rise to gains such as increased market share, reduction in costs, and new market opportunities

(Berman & Ddawson, 2013). Vertical M&As occur whereby firms in the same production process

combine (Bonnet & Schain, 2017). These transactions have the effect of reducing production and

operation costs and expanding the economies of scale. The third type of M&As are conglomerates

in which two distinctively different firms from different industries merge. For example, a textile

company can by a restaurant. The main objective of conglomerate mergers is to reduce

concentration risks and to diversify the firm’s activities. In this thesis, the term mergers and

acquisitions were used interchangeably.

2.2 Reasons for Mergers and Acquisitions Academics and scholars have indicated that there’s various factors that lead firms to participate

in M&As this section of the study reviews some of the most common factors.

2.2.1 Synergy Synergy is a concept mostly associated with physical sciences but not finance and economics

(Dertwinkel-Kalk & Wey, 2016). It refers to type of reaction that results when two items combine

to produce an effect which is often greater than the individual effect of the items operating

individually. Simply put, synergy refers to a phenomenon whereby 2+2= 5 (Dertwinkel-Kalk &

Wey, 2016). In mergers and acquisitions synergy results in the combination of firms which creates

entities that are more effective, efficient, and profitable when combined than when operating on

their own (Bearman & Dawson, 2013; Marks & Mirvis, 2015). In the theory of synergies, it is

postulated that firms utilise the different categories of resources and technical competencies in

order to create value (Göhlich, 2012).

11

Hinkir, Rauch, and Umber (2011) indicate that there are three types of synergies. Firstly, there

is the cost of production that creates operational synergy, the cost of capital that creates financial

synergy and the price-related which creates collusive synergy. According to Hinker et al., (2011),

synergy provides an explanation for M&As with the bidding firm aiming to realise the M&A

synergies so as to boost future cash flows and to increase the value of the firm. Operational

synergies are achieved by merging the operations and processes of the separate units and the

transfer of competencies (Hellgren, Löwstadt, & Werr, 2011). Göhlich (2012) indicates that the

synergies also arise from the possibilities of increase in revenue that occur due to cross and/or up

selling and cost reduction due to the gains of consolidation. Financial synergies arising from a

reduction in the cost of capital for example, the bidding firm is able to lower systematic risks by

investing in a firm that is unrelated to its core business or the firm can increase it size which result

in assets that lower the cost of capital. Hankir, et al (2011) indicated that the financial synergies

can arise from financial engineering, cash slacks, and tax savings.

2.2.2 Agency Theory This theory is associated with Jensen and Meckling (1976). The theory is based on the

separation of the interest of the firm’s shareholders and the managers. Jensen and Meckling (1976)

postulated that the shareholders (principals) and management (agents) are rational and aim to

maximise their utility. In neo-classical economic theory it is assumed that the only focus in the firm

is to maximise profits (Schmitz, 2013). However, behavioural economists have found that the

objectives of management are to satisfy their own interests and not to maximise the firm’s profits.

In modern enterprises, the ownership is diversified and scattered, the management are often in-

charge. The management seek higher control, higher salaries, and better working conditions

(Hongxia, 2011). Gauld (2016) states that the modern organisation makes it very difficult and

costly to supervise the management effectively. A solution to the agency problem is to use incentive

schemes such as allocating fixed number of the firm’s shares at a pre-determined price at the

beginning of the period. The assumption is that the management will work hard to ensure that the

value of the shares increase so that they can sell them at a high price (Pink, 2009; Kräkel &

Schöttner, 2012). However, empirical research shows that this approach does not always work due

to information asymmetry (Garrone &Grilli, 2013). The managers can manipulate data and reports

in order to increase the value of the firm. This is referred to adverse selection and indicates

12

information asymmetry in markets. This problem is further enhanced by moral hazard (Peleg &

Raviv, 2019).

Another solution to the agency problem is a takeover through mergers and acquisitions.

Carpenter et al., (2009) indicate that resistance to the takeover is usually not in the interest of

shareholders and owners but it is in the interest of the managers as the transactions might result in

the loss of their jobs. Göhling (2012) asserts that management of the firm is reflected in the market

price of the firm, whereby firms with proper management are likely to have high share prices.

Poorly managed firms have lower share prices making them targets for takeovers as the bidders

see the potential gains from the improved management of the firm. The M&As are value enhancing

given that they instil discipline in otherwise corrupt managers.

2.2.3 Value Creation In the resource-based view (RBV) the resources and capabilities of the firms determine its

competitive advantage and overall performance (Barney, 1991). In the resource based theory, it is

argued that the amount of resources the firm owns or has control over, relative to the resources

available in the economy and the availability of the opportunities to use these resources, determine

the extent to which they create value (Krishnan, Krishnan, & Lefanowicz, 2009). The resources-

based theory forms the basis for synergistic M&As (Altunbas & Marques, 2008). In order to ensure

that their firm is competitive, the management of the firm continually restructure and reconfigure

their resources and capabilities. Mergers and acquisitions are thus venues of creating value by

transferring resources and capabilities between the firms which creates a new organisational with

new technical competencies (Graebner, Heimeriks, Huy, & Vaara, 2017). During the post M&A

period there is transfer of capabilities in either or both directions. Deng (2009) and Luo and Tung

(2018) established that gaining strategic capabilities was a key reason for firms in emerging

markets or less developed economies to merge with firms in more developed nations.

Grimpe and Hussinger (2007) conducted a comprehensive review of six hundred and fifty-two

European mergers and acquisitions that occurred during the period 1997-2003. They established

that the need for technological assets and innovations was a key motivation for the mergers and

acquisitions. Similarly, Grimpe (2007) in a study of pharmaceutical firms found that large

companies tend to acquire smaller firms for their technological innovations. Grimpe (2007)

concluded that smaller firms tend to exhibit a higher level of creativity and innovativeness. The

responses given by the respondents confirm the conclusions of Grimpe (2007).

13

In the Knowledge-based view (Grant, 1996; Kogut & Zander, 1992) argue that the tacit

knowledge is the most important strategic asset that firms which participate in cross border M&As

gain. The firms are able to gain access to new technologies and skills that are used by the indigenous

firms. The use of M&As solves the problems of technology, knowledge and skill deficiencies.

Anand and Delios (2002) found that M&As are driven by the desire of the firm to improve its assets

or to acquire specific assets. Similarly, Bertrand and Zuniga (2006) suggest that M&As serve as a

method for firms to restructure their research and redevelopment in order to reengineer their

operational actives and to enhance the overall productivity.

An emerging trend in M&A carried out by firms from emerging markets is the transfer of

knowledge and capabilities to the headquarters (Luo & Tung, 2007; Nair, Mehmut, & Kamal,

2015). Rabbiosi and Sangangelo (2013) refer to this type of transfer as reverse knowledge transfer

(RKT) whereby knowledge flows from the target firm to the parent firm. This transfer of

capabilities is important as it compensates for the latecomer disadvantages faced by firms operating

in less developed economies (Demirbag, Sahadev, & Mellahi, 2010; Mudambi, Piscitello, &

Rabbiosi, 2014; Rabbiosi & Santangelo, 2013). The acquisition of firms in more advanced

economies allows firms from emerging markets to catch up quickly which allows the firm to attain

competitive advantage and position in the global markets.

2.2.4 Market Power In the market power theory, Feinberg (1985) argues that increased allocative synergies can

be obtained by a firm, when holding all other factors constant, the bigger the size of the firms, the

higher the market power. This market power allows the consolidated firms to charge higher prices

and to attain higher margins through the increase in number of customers. Eckbo and Wier (1985)

established that horizontal M&As create firms with greater market powers than other types of

M&As. This arises because the horizontal mergers reduce the number of producers of the given

goods and services in the market. With fewer suppliers in the market, the action of an individual

supplier is clearly discernible, and the probability of non-conformity is discovered. The easier it is

to discover non-conformity, the lower the monitoring costs; this results in enhanced stability,

profitability, and creates attractiveness of cartels.

2.2.5 Efficiency Gains These gains are associated with the production function. These gains include the

rationalisation of the production process which allows for cost savings and the reallocation of

14

resources and production throughout the new entity without increasing the joint technological

capabilities; there are savings which arise due to an increase in the level of total output;

technological advancements that may arise by transfer of competencies and know-how or increased

research and design; savings in factors prices such as the intermediate goods or cost of capital, and;

reduction in slack (Roller, Stennek, & Verboven, 2006). Al-Sharkas, Hassan, and Lawrence (2008)

established that M&As achieve efficiency gains through the new input-output matrix which often

minimises the costs and maximizes the revenues.

Esfahani (2019) identifies two types of efficiency gains that arise from mergers and

acquisitions. The first type is cost efficiency which results when the firms move toward the frontier-

efficient or best practice cost. This is achieved by producing the same level of goods and services

using the output bundles which minimise the costs of production. The second type is when the

firms achieve profit efficiency whereby the level of profits are at the optimal level or close to those

achieved by the best-practice firms. Esfahani (2019) argued that profit efficiency incorporates cost

efficiency, the effects of scale and scope, and product mix on both the costs and income streams.

2.2.6 Economies of Scale and Scope Economies of scale arise when the average costs of production fall as the level of output

increases. Economies of scope expand the definition of economies of scale by enhancing the

increase in output due to multiple products (Roller, Stennek, & Verboven, 2006). Economies of

scale are achieved through the combination of the firms though the coordination of the units of the

firms’ that were previously separate. This combination assists in the reduction of duplication of

indivisible tasks. Garzella and Fiorentino (2014) established that M&As create economies of scales

in manufacturing firms by sharing the fixed costs such as depreciation, amortization of capitalised

software, maintenance costs, interest expenses, lease payments, union, customer, and vendor

contracts, and taxes over an expanded level of production. When studying German firms

Schweinberger and Suedekum (2015) established that M&A create economies scope using a given

set of skills or assets currently employed in a producing a given product or service to produce other

goods or services.

2.2.7 Strategic Realignment According to Baker and Jones (2008) M&As are means for firms to adopt to their changing

external environments. For example, when a firm does not have sufficient room for internal growth

if it wants to grow it must turn to external partners. Additionally, external factors such as taxes,

15

technology, and new rules and regulations may necessitate firms in a given sector to consolidate in

order to be able to cope with such changes (Bange, 2017). Some examples of mergers and

acquisitions include: Tata Motors Ltd with Tata Finance Ltd which aimed at growing the auto-

financing business with the aim of have a one-stop process for buyers of Tata Motors, the

management felt that this would enable the company to hedge against the cyclicality of the motor

business (Leepse & Mishra, 2016). The merger between Gabriel India Ltd and Stallion Shox

limited was aimed to strategically realigning the operations of Gabriel India by upgrading the

technology using the research and development (R&D) and design capabilities of Stallion Shox

operations (Kumar & Rajib, 2007). Shinny Ltd acquired Apar Industries with the aim of increasing

the production capacity by enhancing the working capital position through the raw material

manufactured by Apar Industries (Deo & Shah, 2011). The management of EID Parry acquired

Nutraceuticals Velensa International in order to gain access to the science-based patents and

extractions technologies (Deo & Shah, 2011).

2.2.8 Diversification Technology giant Microsoft merged with Nokia as a mean of entering into the highly

competitive and highly profitable smartphone market. Eventually, Microsoft acquired Nokia for $

7.2 billion. Similarly, the acquisition of Washington Post for $250 billion was a mean for Amazon

an e-commerce company to diversify its business operations (Tiwari, 2015). Facebook also

acquired Whatsapp as a mean of expanding its product offerings. Additionally, M&As have made

it possible for firms to grow beyond their borders. According to Dash (2010) geographical

expansion is important for many firms as the national borders often impose limits on the ability of

the firm to growth. In a study of firms in the United Kingdom, Berry-Stölzle, Liebenberg, Ruhland,

and Sommer (2012) established that M&As were used to expand the firm’s business. The

diversification strategies used by the firms were divided into several types including geographical,

international, vertical, and horizontal diversification. Dzhagityan (2012), established that firms in

the field of science and technology undertook international diversification so as to allow for

flexibility of operations. Ouimet (2013), found that firms used diversification as a mean of

managing cost of labour and of capital.

Ahern, Daminelli, and Fracassi (2012), found that firms undertake M&A transaction deals

as a mean to manage risk. The extent to which risks reduce is determined by the level of business

diversification. Further, Ahern et al. (2012), found that diversification and decision to enter into

16

M&A deals was stimulated by the firm’s desire to grow, increase profits, and profit stability. Wu

and Chiang (2019), found that diversification through M&As was through related and unrelated

firms. Wu and Chiang (2019) also established that firms often start with firms that are related to

the industry, and subsequently merger and/or acquire firms in unrelated industries. According to

related and unrelated diversifications are important considerations in M&A deals as they reduce or

help the firms to manage systematic risk.

2.2.9 Reduction of Tax Liabilities Devos, Kadapakkam, and Krishnamurthy (2012) established that M&As are motivated

by financial reasons. Firms are motivated by the chance to fully utilise the tax shields and possible

tax advantages. Fernandes (2014) in an evaluation of 640 M&As found that financial

considerations arising from tax optimisation such as the amortization of goodwill. The tax

advantages arise from the tax laws and use of past net operating losses. Profitable firms acquire

firms with accumulated losses in order to be able to reduce their tax burden (Ciobanu & Dobre,

2015).

Using a logit regression model, Devereux and Griffith (1998) established that the tax

consideration for M&A was stimulated by two considerations. Firstly, there was the simple investor

choice whereby the most important consideration was the effective average tax rate, this was found

to be significant because the effective average tax rate can easily be analysed at the beginning of

the transition. Secondly from the specialised investor’s perspective, the effective marginal tax rate

was considered important given that the tax considerations are relevant. Devereux and Griffith

(1998) concluded that investors and firm behaviour was driven by the desire to obtain lower and

favourable tax rates for their investments. The effects of taxation were established to also impact

the M&A processes. Martin, Wang, and Zou (2012) established that there the target firms tax

aggressiveness had a positive and significant impact on acquisition premiums. Chow, Klassen, and

Liu (2013), and Col (2012) found that the announcement returns of target firms and acquirers was

motivated by possible future tax avoidance which impacted the level of capital gain. The empirical

findings suggest that taxation indicators influence the decision on M&A. According to Ciobanu

and Dobre (2015) concluded that the possibility of tax avoidance on firms’ earnings and capital

gains significantly influence the decision by firms to undertake mergers and acquisitions.

17

2.3 Motives from the Sellers Perspectives Most of the motives for M&As discussed in this section give the perspective of the

bidding firm (the buyer) but do not fully take into consideration the factors that motivate the seller

(the target firm). Bonnet and Shchain (2017) and Benndort and Martinez-Martinez (2017) find that

the sellers motives include: the lack of resources needed to ensure growth; the perception within

the firm that they have maximised growth in the current market and the management do not think

the firm can expand into new markets alone; the perception that the firm has attained its historical

peak in valuation; lack of a suitable replacement of the founder; challenges in accessing capital;

demand by firms investors for cash out, and new competition.

Matt (2016) found that the decision to sell by the board of directors is determined by the

valuation of the firm, when the board of directors feel that the market is undervaluing the firms

shares and the shares are being traded in depressed multiples relatives to its peers, the board of

directors uses the strategic alternative which results in seeking a buyer for the firm. Financial

distress of the firm whereby the firm has too much debt on its books or macroeconomic factors

which make it difficult for the firm to meet its financial obligations, M&As offer a means to secure

the firm (Bearman& Dawson, 2013). Denison and Ko (2016) argue that mergers and acquisitions

are stimulated by the demands of the shareholders. Denison and Ko (2016) found that shareholder

activism particularly where the firm’s shares are held by hedge funds, often necessitates the firm

to engage in M&As. Additionally, when the main shareholder wants to divest, the most commonly

used exit strategy is M&As.

In comparison to the MNCs from developed countries (DMNCs), MNCS from developed

countries (EMNCs) have been found to have low technological competencies and resources due to

the latecomer disadvantages, and weak institutions at home (Hoskisson et al., 2013; Peng, 2012).

Therefore, EMNCs seek strategic assets from developed economies and advanced companies

through M&As.

2.4 Cross Border Mergers and Acquisitions from firms in Emerging Markets Over the last three decades outward foreign direct investment (OFDI) from emerging

countries has grown exponentially and is now considered to be an important element of economic

growth across the globe. According to the United Nations Conference on Trade and Development

[(UNCTAD), 2018] emerging economies such as accounted for approximately 33% of all OFDI

flows in 2017. Further, a significant amount of OFDI from emerging economies is created through

cross-border M&As (UNCTAD, 2018). The aim of these M&As is to increase the pace of growth

18

through international avenues. Deng (2013), established that firms from emerging economies are

increasingly participating in M&As for strategic factors such as the acquisition of technology,

enhancing brand name, and to gain access to natural resources.

2.5 Summary Firms from emerging markets have over the years continued to undertake M&As both in

other emerging markets and in more advanced markets. Researchers (Ahern, Daminelli, &

Fracassi, 2012; Bearman& Dawson, 2013; Benndort & Martinez-Martinez, 2017; Denison & Ko,

2016; Roller, Stennek, & Verboven, 2006; Tiwari, 20150 have examined the factors that motivate

firms to undertake M&As. These reasons have been found to include synergy, agency theory, value

creation, market power, efficiency gains, diversification, economies of scope and scale, reduction

of tax liabilities, and strategic realignment. However, there are only few studies that evaluate the

cross-border M&As by firms from emerging markets. This thesis sought to establish the reasons

for M&As by a firm from an emerging market.

19

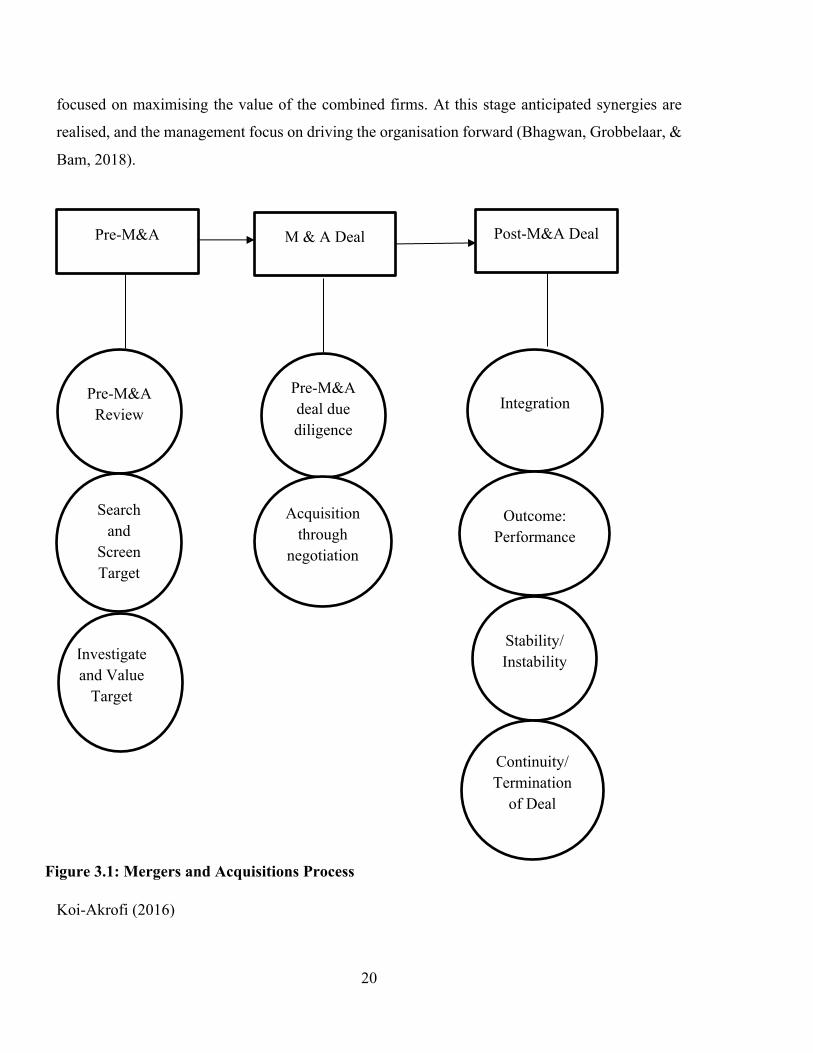

3 PHASES AND PROCESS OF MERGERS AND ACQUISITIONS Depending on the county or region, there are different phases of the M&A process. It is

important to distinguish the different phases of the M&A process as they influence the outcome of

the M&A. This section of the study reviews the phases and process of merger and acquisitions.

3.1 Merger and Acquisition Process

In literature the M&A process and procedure are described differently by different authors.

Koi-Akrofi (2016) states that the M&A transactions involves three phases namely planning,

implementing, and integration. The planning process entails operational, managerial and legal

techniques, and optimization with regard to the next two phases. The implementation stage includes

the issuance of confidentiality or non-disclosure agreements, letters of intent and ends with the

signing of the M&A contract. The last phase is post-integration. Schweiger and Weber (1989)

indicate that the M&A process consist of two stages namely the pre-merger phase and the

implementation phase. Quah and Youg (2005) identify four stages in the M&A process to include

pre-acquisition, slow absorption, very active absorption, and totally absorbed. Marks and Mirvis

(2015) postulate that the M&A process involves three stages namely pre-combination,

combination, and post-combination

The Watson Wyatt Deal Flow Model breaks down the M&A process into five stages namely

formulation, location, investigation, negotiation, and integration (Ai & Tan, 2017). In the formulate

stage, the firm formulates its objectives and strategies, the management stipulate the characteristics

of a feasible target. The characteristics include the market share, the location and access to markets,

product and technology, and synergies. The locate stage entails the firm looking for a desirable

target firm. At this stage the management initiate conversation with the management of different

firms. The outcome of this stage is the issuing of the letter of intent that identifies the bidder firms

the initial deal parameters, terms, and conditions. The investigation and due diligence states

involves an extensive exploration of every facet of the target firm. The analysis covers areas such

as finance, operations, legal, and environmental factors. The outcome of this process results in a

summary of the key findings and identifies potential obstacles. The bidding firm uses the findings

of the due diligence process to negotiate the boundaries of the deal and establish the offer price.

The negotiation stage is managed by the deal team which develops the negotiating strategy and the

terms and conditions of the deal. The negotiation team considers the price, performance,

employees, legal factors and governance. The integration stage involves the combination of the

firm’s processes, employees, technology, and systems. The motivate stage is the final stage and is

20

focused on maximising the value of the combined firms. At this stage anticipated synergies are

realised, and the management focus on driving the organisation forward (Bhagwan, Grobbelaar, &

Bam, 2018).

Koi-Akrofi (2016)

Pre-M&A

Pre-M&A Review

Search and

Screen Target

Investigate and Value

Target

M & A Deal

Pre-M&A deal due diligence

Acquisition through

negotiation

Post-M&A Deal

Integration

Outcome: Performance

Stability/ Instability

Continuity/ Termination

of Deal

Figure 3.1: Mergers and Acquisitions Process

21

Ai and Tan (2018) describe the first three stages of the Watson Wyatt Deal Flow Model as the

planning stage, the negotiation stage is considered the implementation and the last stage is

considered the integration stage. Bauer and Matzler (2013) braked down the merger and acquisition

process into three phases represented in Figure 3.1. At the pre-merger phase the firm’s

management initiate the process; conduct feasibility studies where the financial and logistical

aspects of the deal are considered; commit to the process by allocating funding and necessary

resources; negotiate with the target firm in order to reach an agreements on the structure of the new

entity, and signing of the detailed merger contract (Sarrazin & West, 2011). The pre-merger phase

is managed by external consultants and specialists. Bauer and Matzler (2013) describe the post-

M&A stage as execution or implementation phase of the M&A process; it is the phase that

determines the outcome of the deal. Graebner et al., (2017) define the post-M&A stage as a gradual

process whereby the two entities learn to work together in order to achieve the set-out objectives

3.2 Effect of the Merger and Acquisition Process on Outcome of the Deal

The literature review suggests that the M&A process is divided into three phases: the

premerger, the actual deal, and the post-merger process. Each of the stages play a critical role in

the outcome of the transaction. The value creation and the combined firm’s ability to generate

returns and meet managements objectives is determined by the M&A process and the strategies put

in place to manage the process (Canina & Kim, 2010). Dertwinkel and Wey (2016) established that

the success of M&A deal was determined by the pre-merger decision making, plus the success of

the post-merger implementation.

In their analysis of M&A deals Chanmugam, Shill, Mann, Ficery and Purche (2005) found that

managers viewed the premerger and post-merger phased as separate and unrelated process; the

managers often planned for the premerger stage but only began to plan for the post-merger

integration once the deal was announced or completed which was often too late to allow for a

successful outcome. Hu (2015), found that different groups and managers were tasked with

undertaking the pre-deal and the post-deal processes. This created disconnect between the

anticipated objectives of the deal and the achieved goals during the M&A process. Hu (2015),

concluded that in order for the deal to yield the desired outcome, the managers must incorporate

the plans and merge the pre-and post-deal processes.

22

4 CHALLENGES AND REASONS FOR FAILURE OF MERGERS AND ACQUISITIONS The main avenues for growth for MNE’s are through M&A. However, the expectations of the

managers sometimes are too high, and the difficulties associated with M&A’s are underestimated,

or not anticipated. This section evaluates the challenges and reasons for the failure of mergers and

acquisitions.

4.1 Indicators of Performance of the Merger and Acquisition Mergers and acquisitions are expected to create value through reduced costs, increased market

share, or both, and increased utilisation of tangible and intangible assets of the firms (Björkman,

Stahl, & Vaara, 2007; Gupta, Kumar, & Upa 2012). According to Rui, Zhang, and Shipman, the

success or failure of M&As is determined by the share value of the firms, increasing the share

prices implies positive performance while decrease implies failure. Zaheer, Castaner and Sounder

(2013) indicate that the most common indicators of the success or failure of M&As are accounting

and financial parameters. These parameters include profits, losses, return on assets, return on

investments, share price, earnings per share, and return on equity.

He, Khan, and Shenker (2018) and Lui and Woywode (2013) indicate that the success of an

M&A is the ability of the firm to protect its turf. They argue that M&A’s are not always undertaken

to enhance the monetary position of the firm but to ensure that the firm maintains its position in

the market and industry. Thus, if the firm is able to retain and/or improve its position then the M&A

can be considered to be successful. Similarly, Gomes, Angwin, Weber and Tarba (2013), indicate

that the success of M&As can be indicated by the attainment of the firm’s strategic objectives.

Rosenbush (2007) indicates that the performance of M&A can be indicated by the reaction of

the staff. Rosenbush (2007) in a study of firms in the United Kingdom established that firms

invested billions in the M&As but end up losing money and divesting because the M&As have

negative effects on the employees. According to Rosenbush (2007), the human capital of the firm

is the most important ingrediate to attaining the firm’s objectives of profit maximisation, growth,

cost reduction, growth in market share and increased customer satisfaction. The departure of

employees following the M&A is an indicator that the deal is likely to result in failure.

Wallace and Moles (2012) argued that establish that the success or failure of M&A can be

viewed from two extreme perspectives. Firstly, if the post-M&A deal results in the firm going into

liquidation then the result is considered to be a failure. Secondly, if the M&A deal was for the

purpose of short-term financial gain, then a significant increase in income, or return on capital

23

employed is considered a success. Barasa (2015) in a study of the impacts of M&As on the

performance of firms listed on the Nairobi Securities Exchange argues that the performance of the

M&A deal is determined by the prices of the shares of the target and bidder firm at the time of the

announcement. At the time of the announcement, if the price of the company shares increases, then

the M&A is considered a success but if the price falls, then it is considered a failure.

4.2 Reasons for Failures of Mergers and Acquisitions Empirical studies have shown that in some instances M&As fails and /or underperform the

expectations. The theory on M&A is divided into two broad categories that include value increasing

and value decreasing. This section reviews the value decreasing theories. The value decreasing

theories can be divided into two groups. In the first group it is assumed that the management of the

bidder firm due to overconfidence makes mistakes and that result reflects in losses. The intention

of the managers is to increase value, but this does not occur. The second group assumes that the

managers are rational, but act in their own self-serving interests, they maximise their utility at the

expense of the firm.

4.2.1 Hubris Hypothesis Over the years, research has empirically established that the bidder firms, on average, do not

gets as much profits from M&As as do the target firms (Campbell et al. 2011). In some instances,

the M&A diminishes the earnings or completely destroys the shareholders of the bidder firms’

wealth. Servae (1991) established that target firm had returns of 23.64% compared to 1.07% for

the bidder firm. Similarly, Andrade, Mitchell, and Stafford (2011) when evaluating data over a

three-day event window of the combined returns for the bidder and target firms, they found that on

average abnormal returns of 1.8% were realised after the M&A announcement. Andrade et al.

(2001) established that most if not all of the abnormal returns were attributed to increase in the

target firms. These effects were found to be more pronounced in transactions were the bidder firms

were larger (Billet & Qian, 2008; Bouwman, Fuller, & Nain, 2009). These destructive effects often

occur when the bidding firms are larger. Van de Waal (2013) attributed the dismal performance to

the hubris hypothesis.

This hypothesis was put forward in 1986 by Roll. Roll (1986) postulated that the managers

overestimate their capacity to determine the potential of M&A. The result of the overestimation is

that the bidder pays too much for the target firm. The fundamental assumption for M&As is that

the financial markets are efficient, so firms are valued correctly. The hubris hypothesis does not

24

dispute the efficiency of the financial markets but focuses on the inefficiencies in managerial

behaviour. According to Brown and Sarma (2007), Doukas and Petzemas (2007), and Malmendier

and Tate (2008), the hubris effect is greater in larger firms.

Malmendier and Tate (2008) found that overconfident managers overestimate their abilities to

identify target firms that will maximize the earnings of their shareholders in M&A transactions.

Malmendier and Tate (2008) established that overconfident managers undertake more M&A

transactions and tend to overestimate the synergies that will accrue. The researchers concluded that

overconfident managers are more likely to undertake transactions that are destructive; they

estimated that on average the overconfident managers pay $ 7.7 million more than rational

managers. These findings confirmed the findings of Doukas and Petzemas (2007) who when

studying acquisitions of private firm established that there was a negative and significant

relationship between overconfident managers and performance. Doukas and Petzemas (2007)

found that the overconfident managers felt that they had superior skills; the overconfident CEOs

felt that the target firm could do significantly better under their management. Vagenos-Nanos

(2010) found that overconfident managers destroy more or generate less earnings than their more

rational counterparts. According to Nguyen (2015), one of the clearest signs of overconfidence was

the acquisition of WhatsApp for $19 billion by Facebook. Nguyen (2015) argued that the merger

was being driven by the pride and ego of the owner of Facebook, this is because the price of $ 19

billion was not justified.

4.2.2 Managerial Discretion Hypothesis This hypothesis is attributed to the works of Williamson (1963). Williamson hypothesised that

the objective of the management of joint stock firms is not the maximisation of shareholder’s

profits; the objective of the management was to maximise their own utility. The managers use their

discretion to develop and implement policies which would maximise their utilities without regard

for the effects on the shareholders (Trivedi, 2009). Essentially, the problem is that of the principal-

and-agent. Williamson (1964) assumed inefficient markets where there was imperfect competition;

separation of ownership and management; and few constraints on the firm’s ability to pay dividends

to its shareholders.

Management’s utility function consists of salary, job security, status, control, dominance, and

professional recognition. According to Nadar and Vijayan (2009) salary is the most important

variable; the other variables are non-monetary. Trivedi (2009), used the expenditure on staff

25

salaries, management slack, discretionary investments to develop the utility function given in

equation (3.1)

𝑈 = 𝑈(𝑆,𝑀, 𝐼() ...........................................................................................................(4.1)

Where 𝑈 denotes management’s utility; 𝑆 denotes expenditure on staff; 𝑀 denotes management

slack; and 𝐼( denotes discretionary investment.

The expenditure on staff includes the monetary payments given to the management and the

staff under the managers. Management slack includes items such as entertainment allowances,

lavish furniture and fittings, luxurious cars, the expense account, amongst others. These are benefits

given to the management that are above their salaries. These are perks that are meant to incentivise

the management to enhance their performance. The perks also increase the prestige and status of

management making them more likely to stay with the firm. These expenses are considered as part

of cost of production. Discretionary investments are the amount of residual income that are at the

manager’s disposal which they are allowed to spend at their own discretion. These investments are

those that go beyond those needed for the survival of the firm (Ahuja, 2009; Trivedi, 2009).

According to Chen, Li, & Pan (n.d.) the management of the firm uses their discretion to engage

in M&As in order to fulfil their personal interest. The management seek to maximise their benefits

at the expense of their shareholders. The managers are motivated by their private benefits. When

the managers engage in M&As they are able to enhance their welfare in a number of ways. In

situations where the firm has excessive cash flow, the management seek to enhance their welfare

by investing the free-cash flow on low-returns or value destroying M&As rather than distribute the

excess cash flow as dividend to the shareholders (Lang, Stulz & Walking, 1989, 1991).

Gondhalekar and Bhagwat (2003) when studying the motives for M&A of firms listed on the

NASDAQ during the 10 years before and after the 1987 financial markets crash. Established, that

the managerial self-interest was the driving motive for M&As that realised negative returns.

Hodgkinson and Partington (2008) found that there is still evidence of the managerial motives in

NASDAQ firms