energ sector management assistance programme

TRANSCRIPT

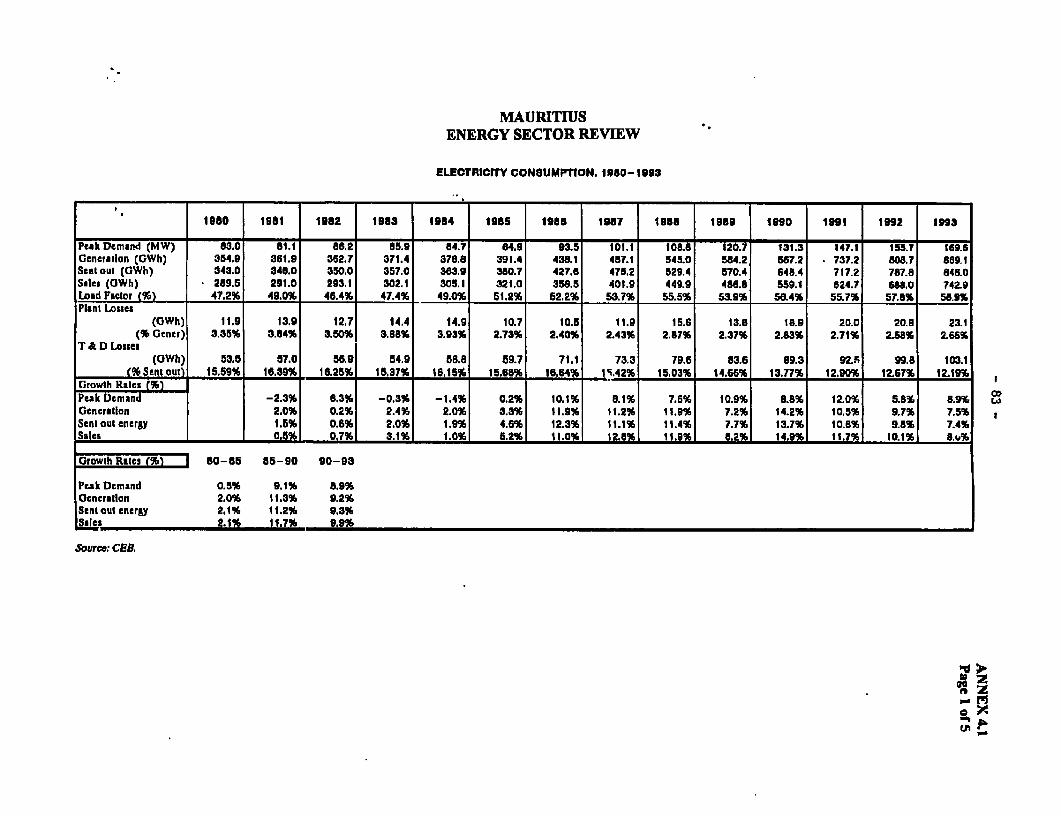

1 3(o4g

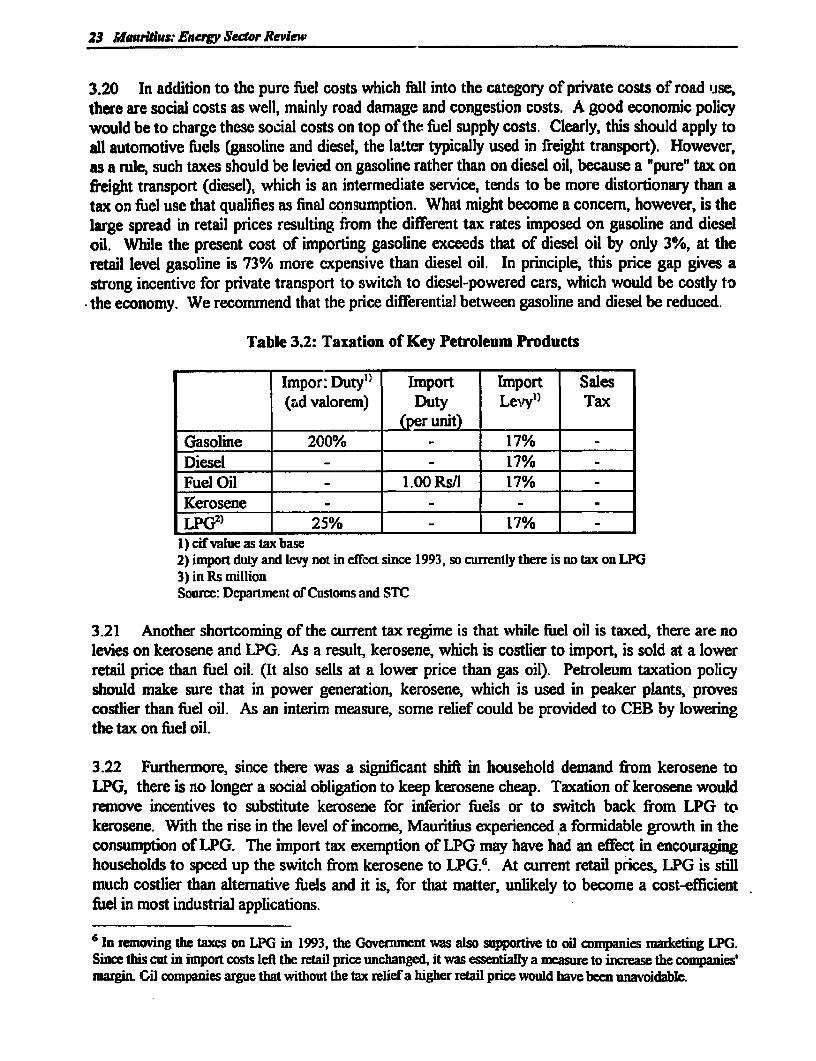

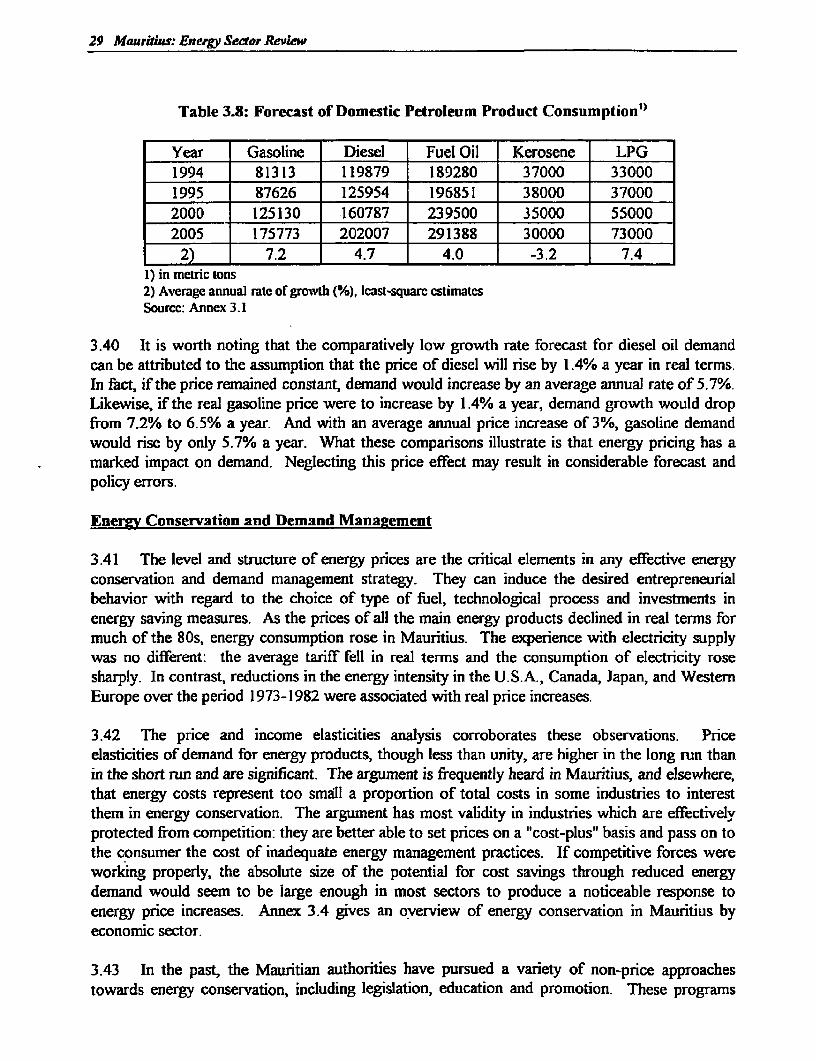

_Vf l- ; - - - Energ Sector Management Assistance Programme

>e2c. )'9T

MauritiusEnergy Sector Review

Report No. 3643-MAS

A joint report with the

Power Development, Efficiency and Household Fuels DivisionIndustry and Energy Department

&

Industry and Energy Operations DivisionCentral Africa and Indian Ocean Department

Africa Region

Pub

lic D

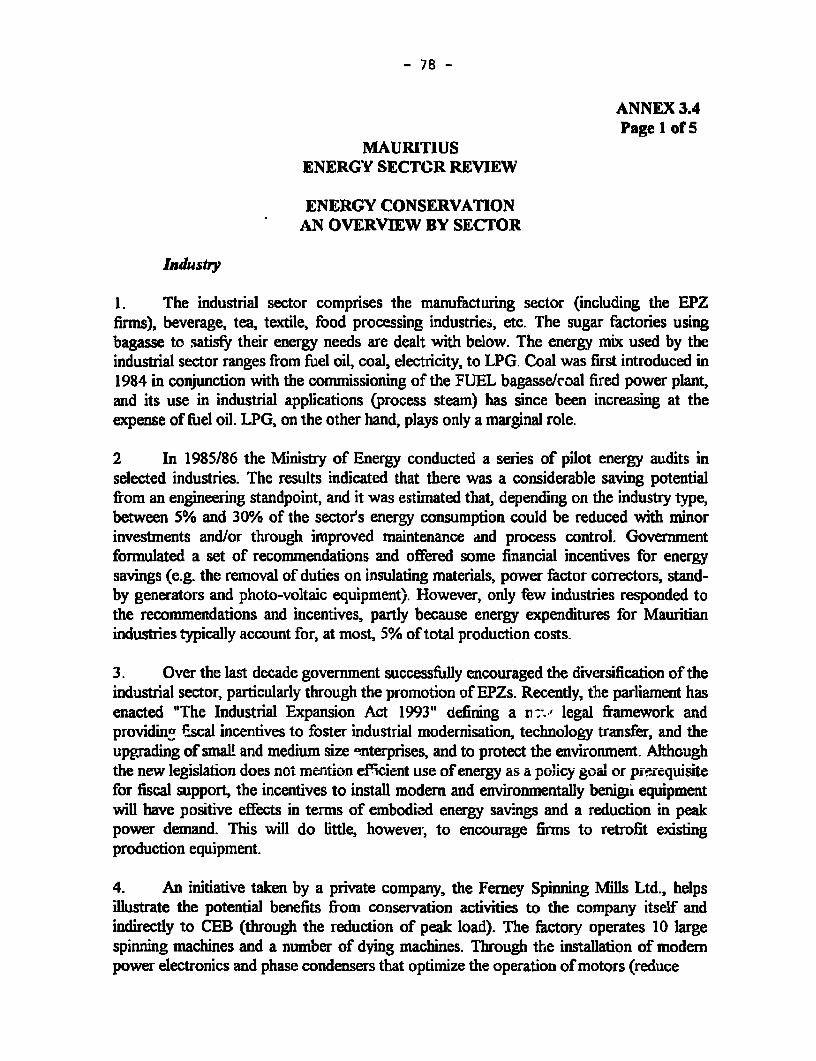

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JOINT UNDP / WORLD BANKENERGY SECTOR MANAGEMENT ASSISTANCE PROGRAMME (ESMAP)

PURPOSE

The Joint UNDP/World Bank Energy Sector Management Assistance Program me (ESMAP) waslaunched in 1983 to complement the Energy Assessment Programme, established three years earlier.ESMAP's original purpose was to implement key recommenidations of the Energy Assessmentreports and ensure that proposed investments in the energy sector represented the most efficient useof scarce domestic and external resources. In 1990, an international Commission addressedESMAP's role for the 1990s and, noting the vital role of adequate and affordable energy ineconomic growth, concluded that the Progran1 ne shoulld intensify its efforts to assist developingcountries to manage their energy sectors more effectively. The Commission also recommended thatESMAP concentrate on making long-term efforts in a smaller number of countries. TheComunission's report was endorsed at ESMAP's November 1990 Annual Meeting and prompted anextensive reorganization and reorientation of the Programme. Today, ESMAP is conducting EnergyAssessments, performing preinvestment and prefeasibility work, and providing institutional andpolicy advice in selected developing countries. Through these efforts, ESMAP aims to assistgovemrnments, donors, and potential investors in identfying, funding, and implementing economicallyand environmentally sound energy strategies.

GOVERNANCE AND OPERATIONS

ESMAP is governed by a Consultative Group (ESMAP CG), composed of representatives of theUNDP and World Bank, the governments and institutions providing financial support, andrepresentatives of the recipients of ESMAP's assistance. The ESMAP CG is chaired by the WorldBank's Vice President, Finance and Private Sector Development, and advised by a TechnicalAdvisory Group (TAG) of independent energy experts that reviews the Programme's strategicagenda, its work program, and other issues. ESMAP is staffed by a cadre of engineers, energyplanners and economists from the Industry and Energy Departnent of the World Bank. TheDirector of this Departnent is also the Manager of ESMAP, responsible for administering theProgramme.

FUNDING

ESMAP is a cooperative effort supported by the World Bank, UNDP and other United Na:ionsagencies, the European Conununity, Organization of American States (OAS), Latin AmericanEnergy Organization (OLADE), and countries including Australia, Belgium, Canada, Denmark,Germany, Finland, France, Iceland, Ireland, Italy, Japan, the Netherlands, Newr Zealand, Norway,Portugal, Sweden, Switzerland, the United Kingdom, and the United States.

FURTHER INFORMATION

For furdter information or copies of completed ESMAP reports, contact:

ESMAPc/o Industry and Energy Departmnent

The World Bank1818 H Street N.W.

Washington, D.C. 20433U.S.A.

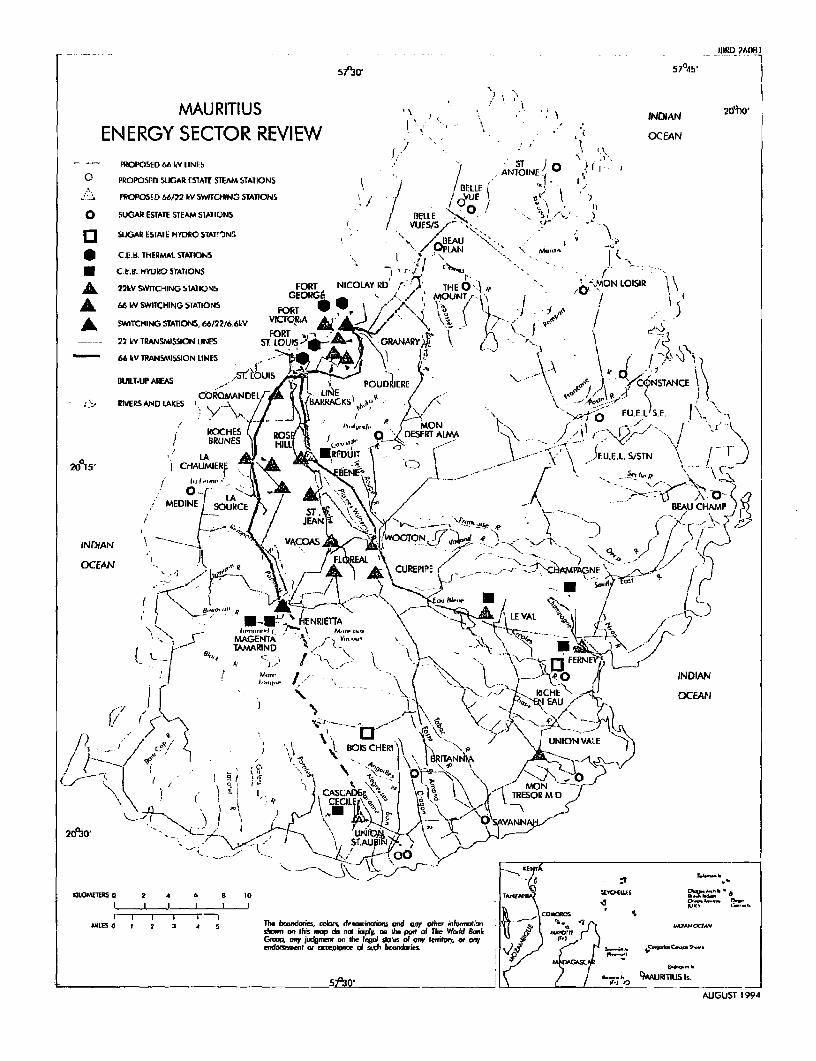

MAURITIUS

ENERGY SECTOR REVIEW

December 1994

A JOINT REPORT

Power Development, Efficiency Industry and Energy Operations Divisionand Household Fuels Division Cental Africa and Indian Ocean DepartmentIndustry and Energy Department Africa RegionThe World Bank1818 H Street, N.W.Washington, D.C. 20433

This document has restricted distribution and may be usedby recipients only in the performance of their officialdwties. Its c-ntent; may not otherwise be disclosed withoutWorld Bank authorizationi.

ABBREVIATIONS

BTU British Thermal UnitCST centistoke (viscosity unit)GWh gigawatt hour (one million of kilowatt-hours)ha hectareHFO heavy fuel oilHSFO high-sulfur fuel oilHV high voltagekcal kilocalorieskgoe kilogram of oil equivalentkm kilometerkV kilovolt (1,000 volts)kW kilowatt (1,000 watts)kWh kilowatt hourI literLPG liquified petroleum gasLSFO low-sulfur fuel oilIV low voltagem meterm3 cubic meterMJ megajouleMOGAS motor gasolineMIT metric tonMW megawatt (1,000 kW)MWh megawatt hour (1,000 kWh)RON research octane numbertoe ton of oil equivalenttpy metric ton per year

ACRONYMS

ESMAP Energy Sector Management and Assistance ProgramCEB Central Electricity BoardCSO Central Statistical OfficeDSM Demand Side ManagementEPZ Export Processing ZoneGEF Global Environmental FacilityGOM Government of MauritiusMEPD Ministry of Economic Planning and DevelopmentMEWRPS Ministry of Energy, Water Resources and Postal ServicesMF Ministry of FinanceMTS Minstry of Trade and ShippingOECD Organization for Economic Co-operation and DevelopmentSTC State Trading Corporation

FISCAL YEAR

July 1 - June 30

CURRENCY EQUIVALENTS

Currency Unit Mauritian Rupee (Rs.)US$1 = Rs 17.80 (March 1994)

= Rs 15.363 (1992 avcrage)= Rs 17.648 (1993 avcragc)= Rs 18.331 (1994 first six months)

ENERGY CONVERSION FACTORS

Energy Source Density (MT/m3) Oil Equivalent (toe/MT)

Liquid fuelsGasoline 0.75 1.08Kerosene 0.80 1.04Gas Oil 0.85 1.01Fuel Oil 1.00 0.96LPG 0.50 1.08

Coal 0.62Bagasse 0.16Electricity (1 kWh - 3.6 MJ = 860 kcal = 3,412 BTU 0.086 kgoe)

FOR OFFICIAL USE ONLY

PREFA CE

This report is based on the findings of an energy review mission which visitedMauritius in March 1994. The mission comprised Messrs. Nourredine Bouzaher (TaskManager), Witold Teplitz-Sembitsky (Economist, Consultant), Joao Baptista (PowerSector Specialist, Consultant), B. Wiese (Power Engineer, Consultant), 0. Dietrich(Energy Conservation and Demand Management Specialist, Consultant), and Ms. N. U.Tronstad (Petroleum Downstream Specialist, Consultant). Guidance and advice receivedfromn Robin Bates (IENPD), peer reviewer, and Ulrich Thumm, Lead Economist(AF3DR), are gratefully aknowledged. Ms. Liliane Yomekpe, Language Staff Assistant(AF3IE), provided secreterial support. Messrs. lain Christie (AF3IE) and FranciscoAguirre-Sacasa (AF3DR) are the managing Division Chief and Department Director,respectively.

Messrs. lain Christie, Michel Del Buono (IENPD) and Nourredine Bouzaherdiscussed the main conclusions of this report with the Mauritian authorities in December1994.

The preparation of this energy sector review was cofinanced by the World Bank,the Norwegian Core Fund (ESMAP), and the Danish and Portuguese Trust Funds.

MAURITIUS: ENERGY SECTOR REVIEW

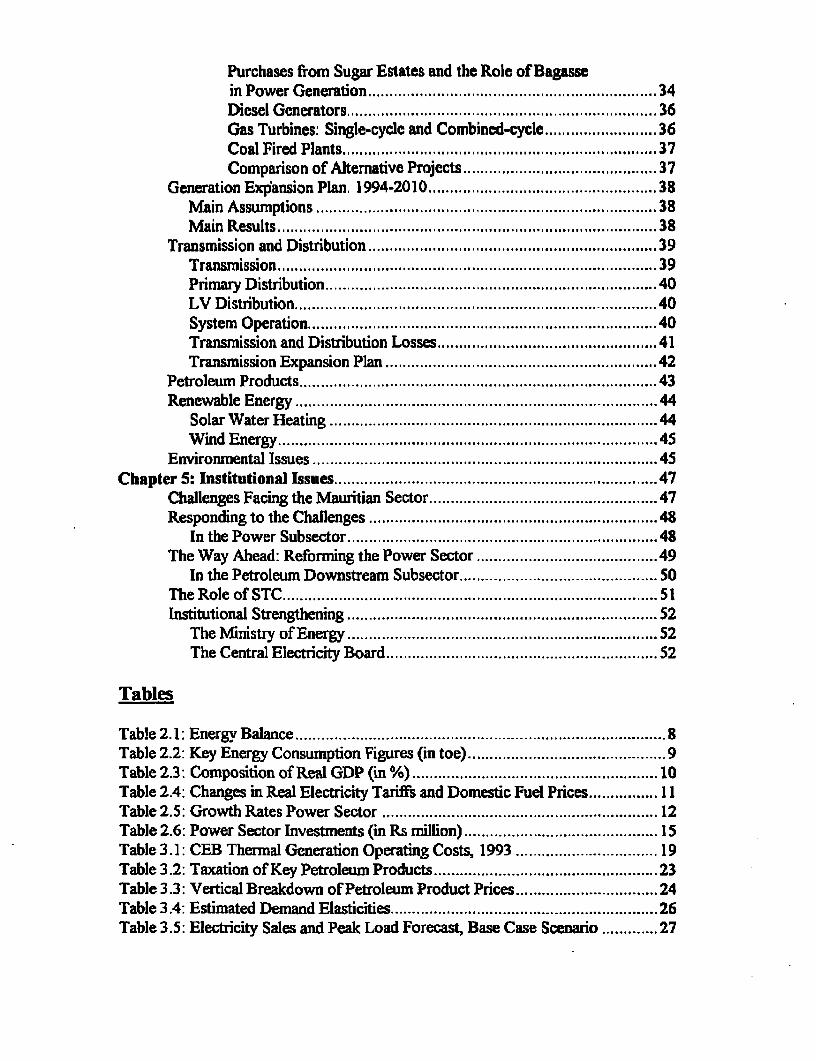

Table of Contents

EXECUTIVE SUMMARY ............................................... iChapter 1: Introduction ............................................... IChapter 2: Energy Sector Review ............................................... 4

Country Background ............................................... 4Energy and the Economy ............................................... 5

Energy Resources .............................................. S5Primary Energy Requirements ............................................... 7Final Energy ............................................... 8Energy Intensity .............................................. 10Real Price Developments .............................................. IIPast Demand and Supply Growth .............................................. 11The Energy Sector and Public Finances .............................................. 14

Overview of Sector Management Issues .............................................. 15Chapter 3: Future Demand for Energy and the Role of

Energy Pricing and Taxation .............................................. 18Pricing and Taxation .............................................. 18

Electricity Tariffs .............................................. 18Electricity Purchases .............................................. 20Bagasse Transfer Price and Other Incentives to Bagasse

Generated Electricity .............................................. 21Improvements in Power Purchasing Agreements ......................... ......... 22

Petroleum Products .............................................. 22Taxation .............................................. 22Pricing .............................................. 24

Income and Price Elasticities .............................................. 25Future Demand .............................................. 26

Electricity Demand .............................................. 26Demand for Petroleum Products ............................ .................. 28

Energy Conservation and Demand Management ........................................ 29Chapter 4: Planning Future Expansion .......................... .................... 31

The Power Sector .............................................. 31Generation .............................................. 31Capacity Balance .............................................. 32

Alternatives for Generation Expansion .......................................... .... 33Short-TermT .............................................. 33Medium-and Long-Term .............................................. 34

Plant Candidates .............................................. 34Hydro Plants .............................................. 34

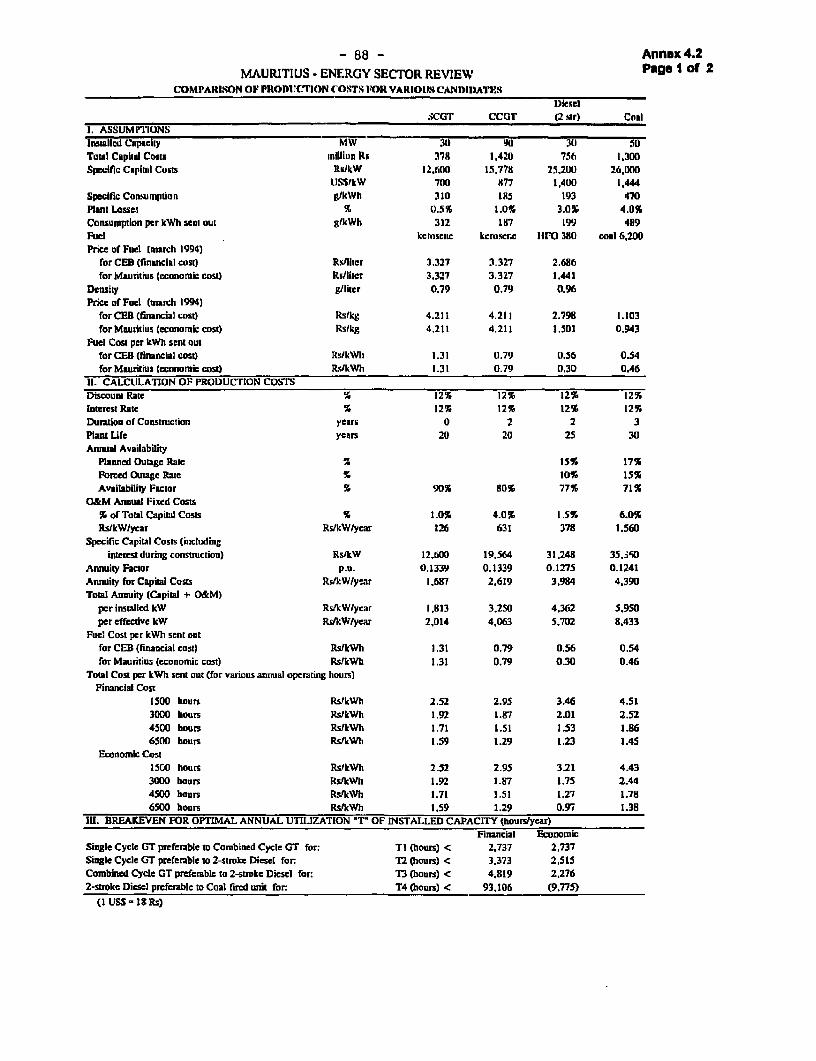

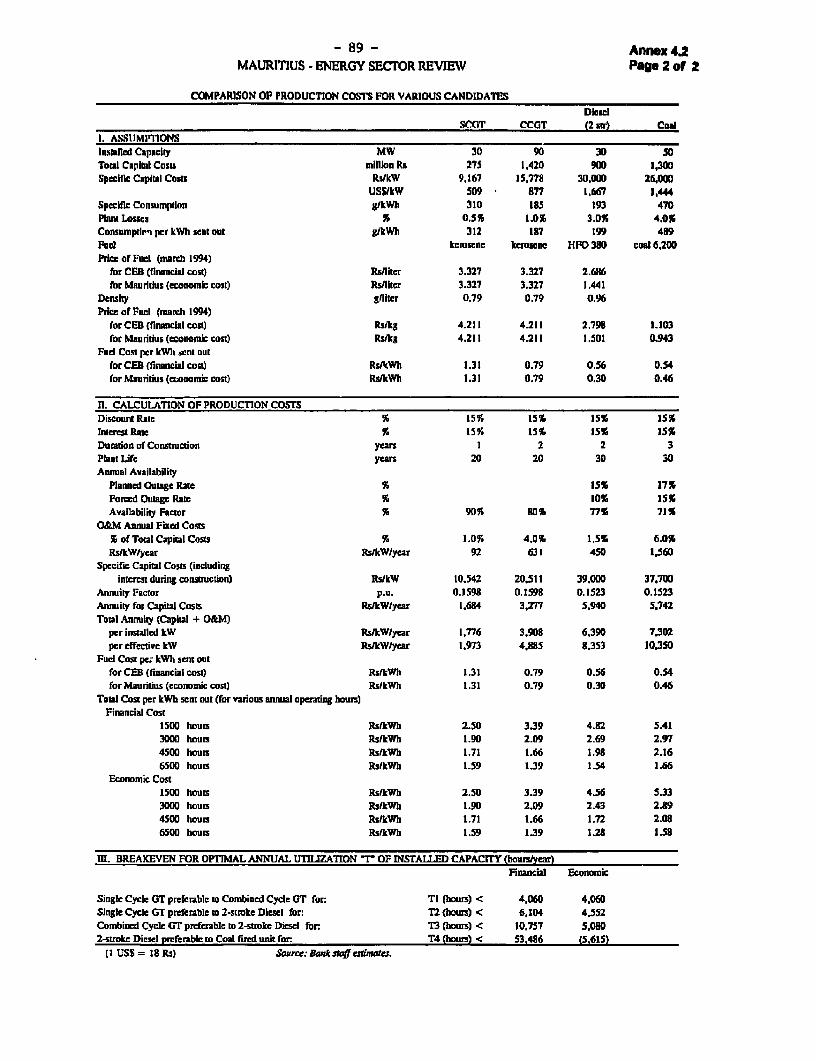

Purchases from Sugar Estates and the Role of Bagassein Power Generation ............ 34Diesel Generators .. .................,36Gas Turbines: Single-cycle and Combined-cycle .36Coal Fired Plants................ . 37Comparison of Alternative Projects ........................ ,.,...,.37

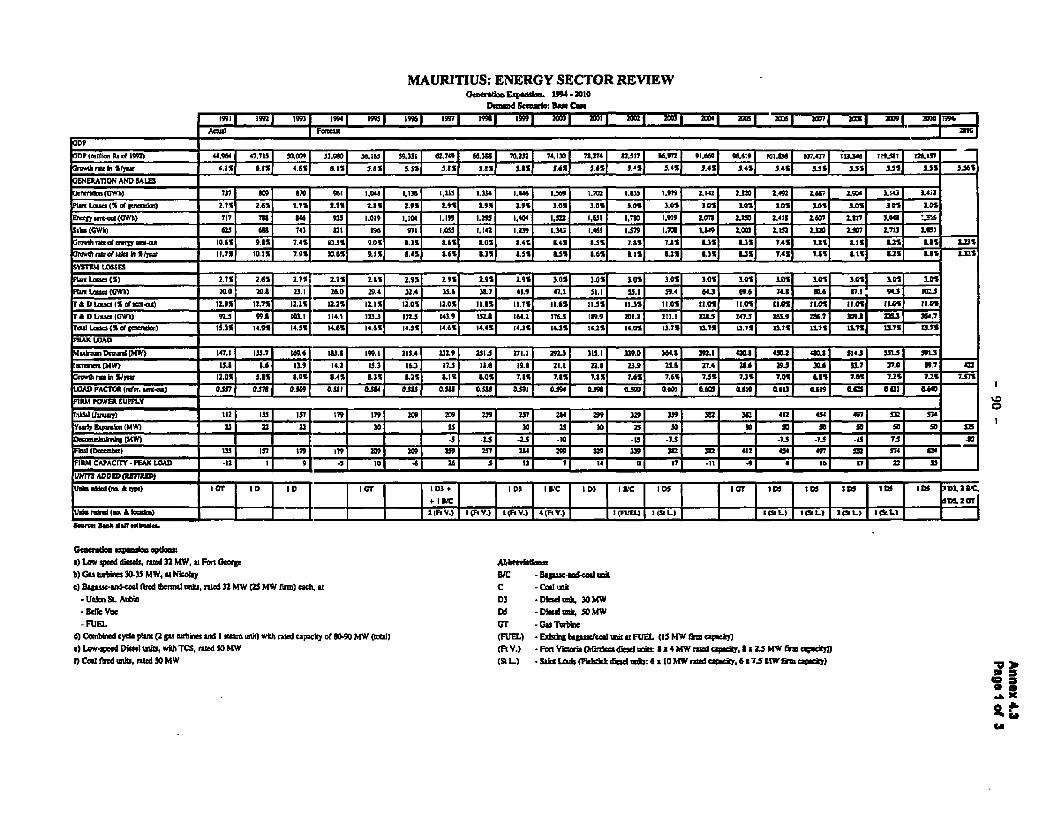

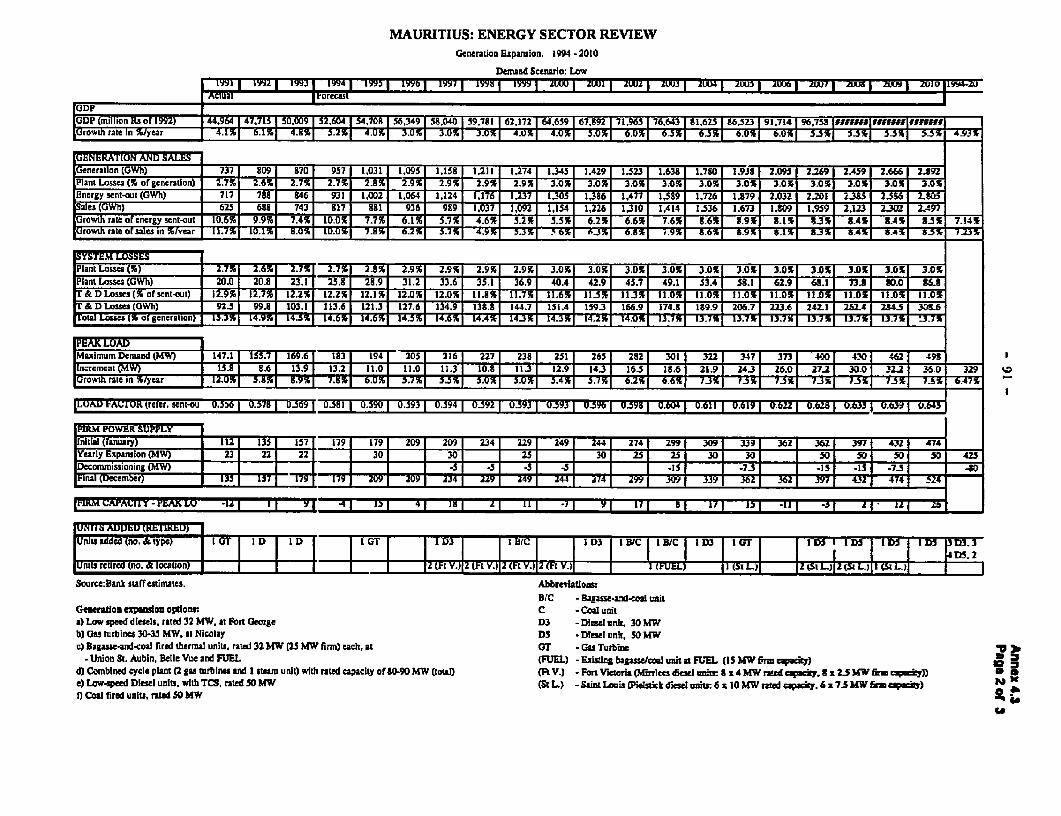

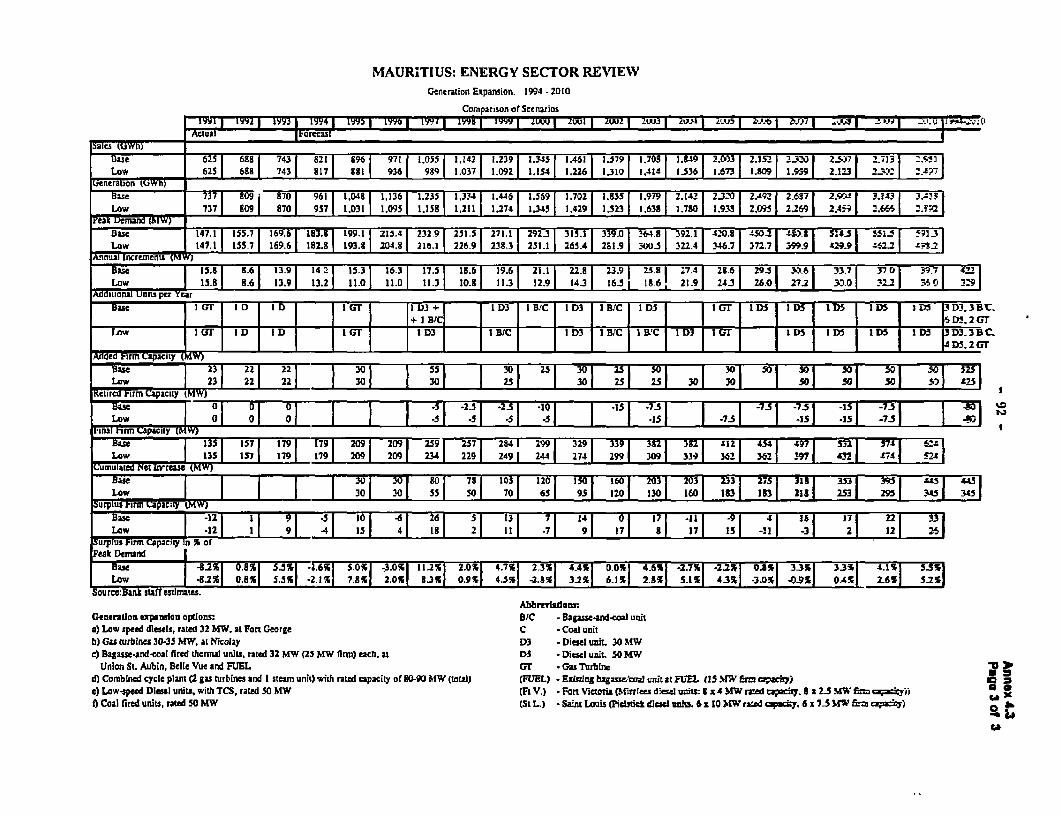

Generation Expansion Plan, 1994-2010 .......................... 38Main Assumptions ............ 38Main Results ......... .. ,. 38

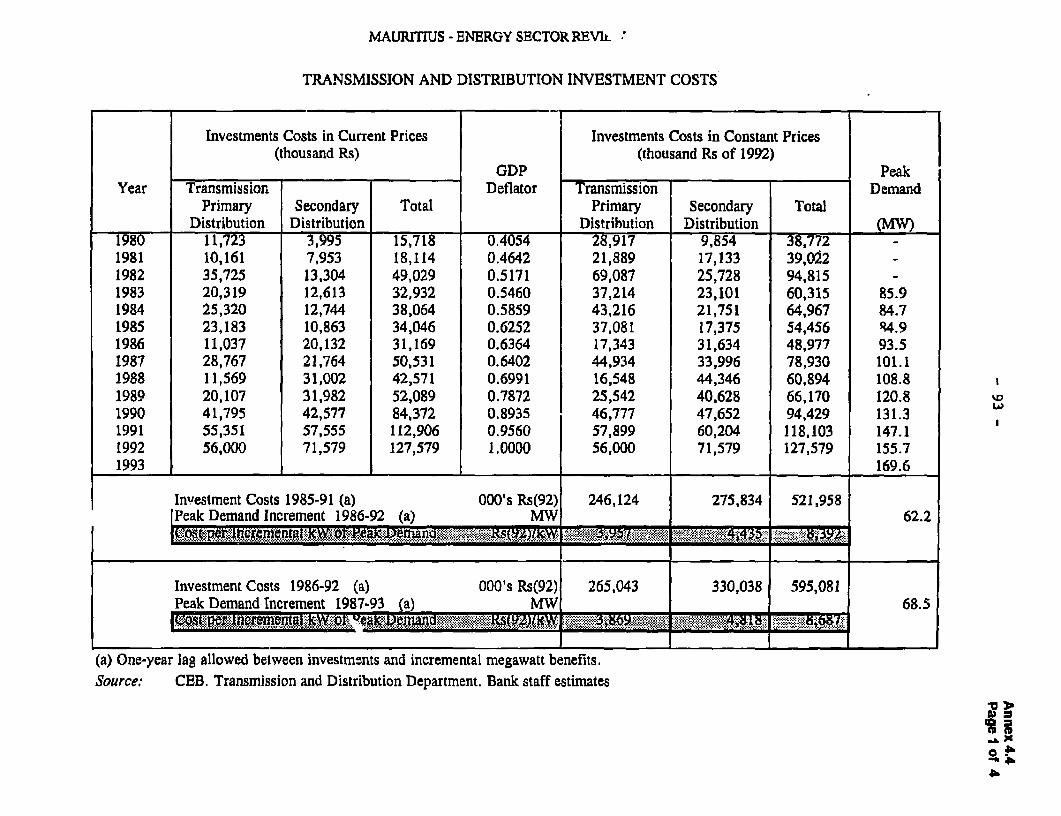

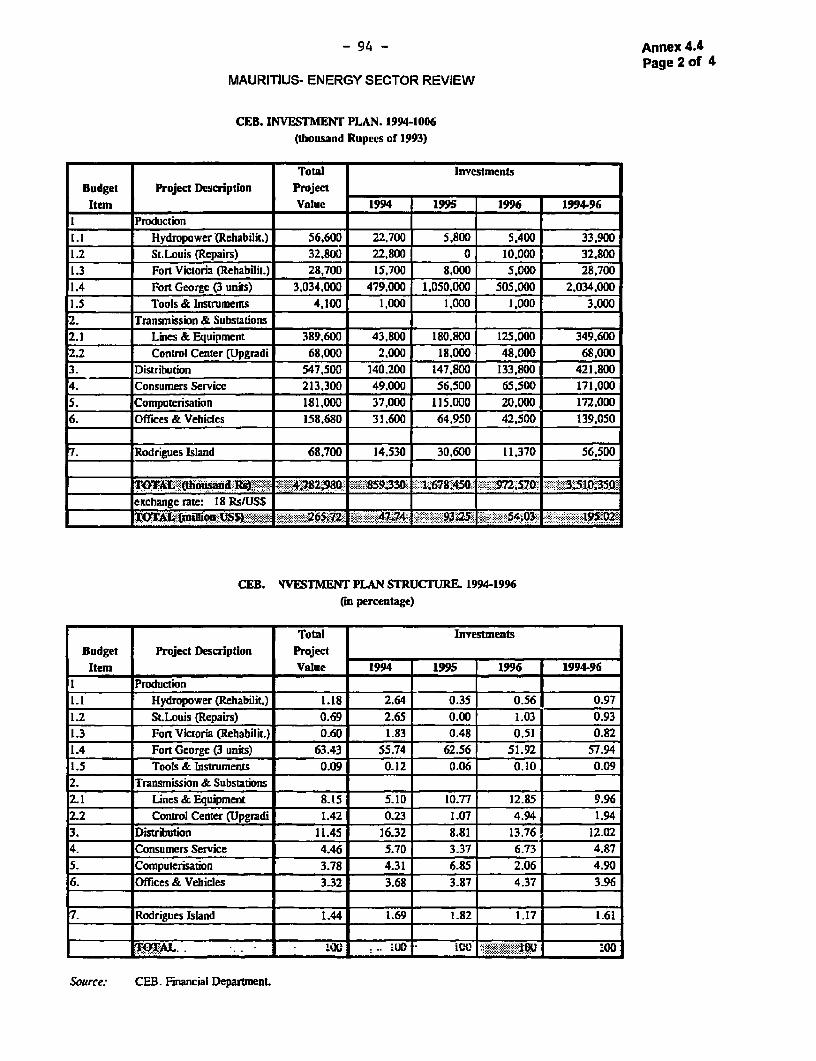

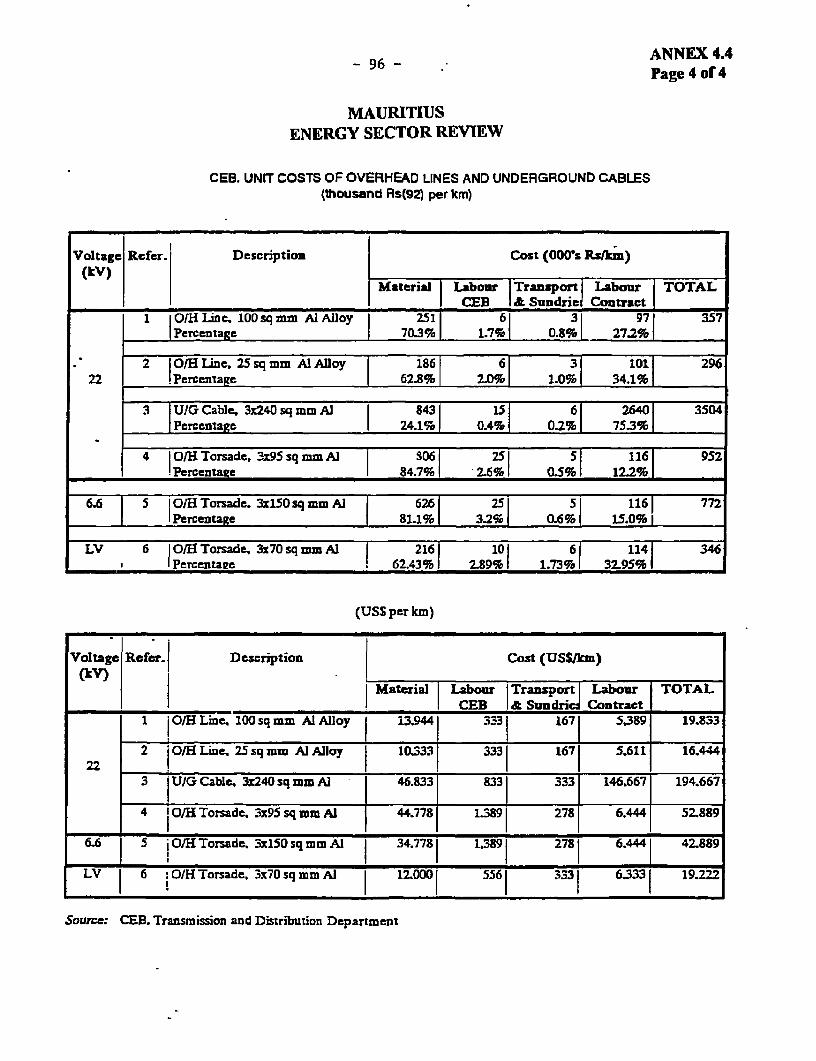

Transmission and Distribution ........................ 39Transmission.3.9............................. 39Primary Distribution . 40LV Distribution .......... 40System Operation ............. 40Transmission and Distribution Losses .41Transmission Expansion Plan .42

Petroleum Products ............... 43Renewable Energy .44

Solar Water Heating ............ 44Wind Energy ....... 45

Environmental Issues .45Chapter 5: Institutional Issues .47

Challenges Facing the Mauritian Sector .47Responding to the Challenges ................... 48

In the Power Subsector....................... 48The Way Ahead: Reforming the Power Sector .49

In the Petroleum Downstream Subsector .50The Role of STC ..................... 51Institutional Strengthening . 52

The Ministry of Energy .52The Central Electricity Board .52

Tables

Table 2.1: Energy Balance .8Table 2.2: Key Energy Consumption Figures (in toe) .9Table 2.3: Composition of Real GDP (in %) .10Table 2.4: Changes in Real Electricity Tariffs and Domestic Fuel Prices 11Table 2.5: Growth Rates Power Sector .12Table 2.6: Power Sector Investments (in Rs million) .15Table 3.1: CEB Thermal Generation Operating Costs, 1993 ................................. 19Table 3.2: Taxation of Key Petroleum Products .23Table 3.3: Vertical Breakdown of Petroleum Product Prices .24Table 3.4: Estimated Demand Elasticities .26Table 3.5: Electricity Sales and Peak Load Forecast, Base Case Scenario .27

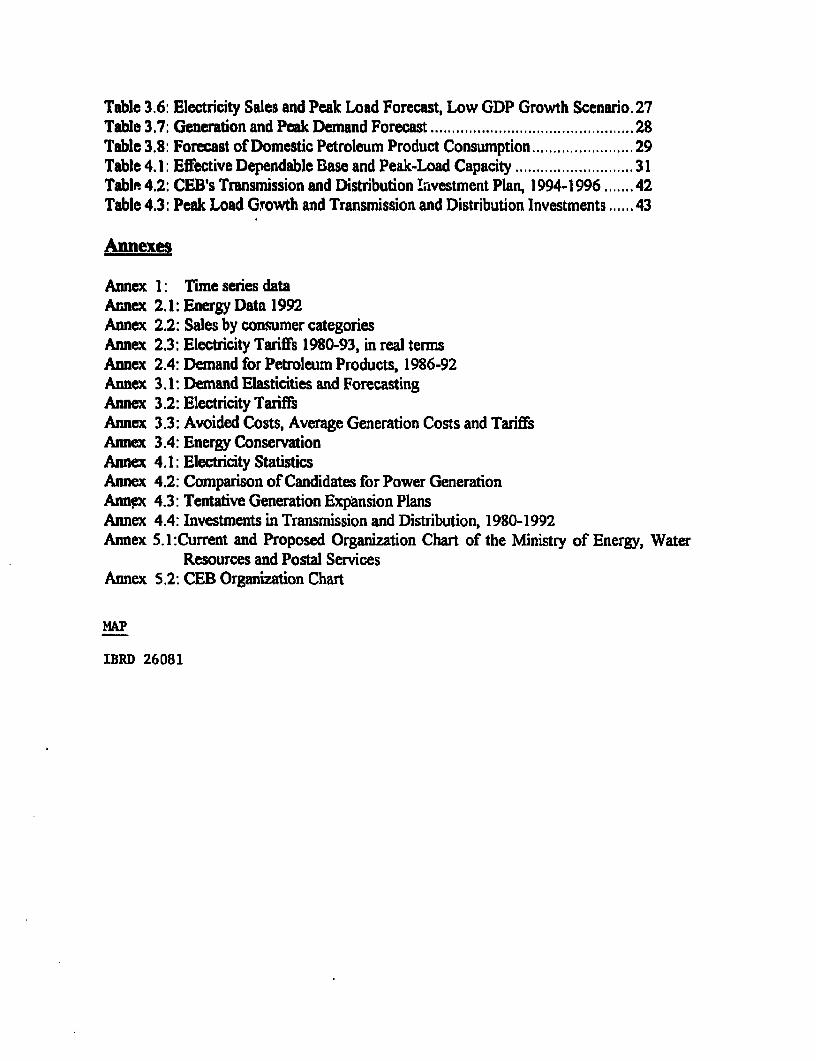

Table 3.6: Electricity Sales and Peak Load Forecast, Low GDP Growth Scenaro. 27Table 3.7: Generation and Peak Demand Forecast ................................................ 28Table 3.8: Forecast of Domestic Petroleum Product Consumption .29Table 4.1: Effective Dependable Base and Peak-Load Capacity .31Table 4.2: CEB's Transmission and Distribution iLvestment Plan, 1994-1996 . 42Table 4.3: Peak Load Growth and Transmission and Distribution Investments .43

Annexes

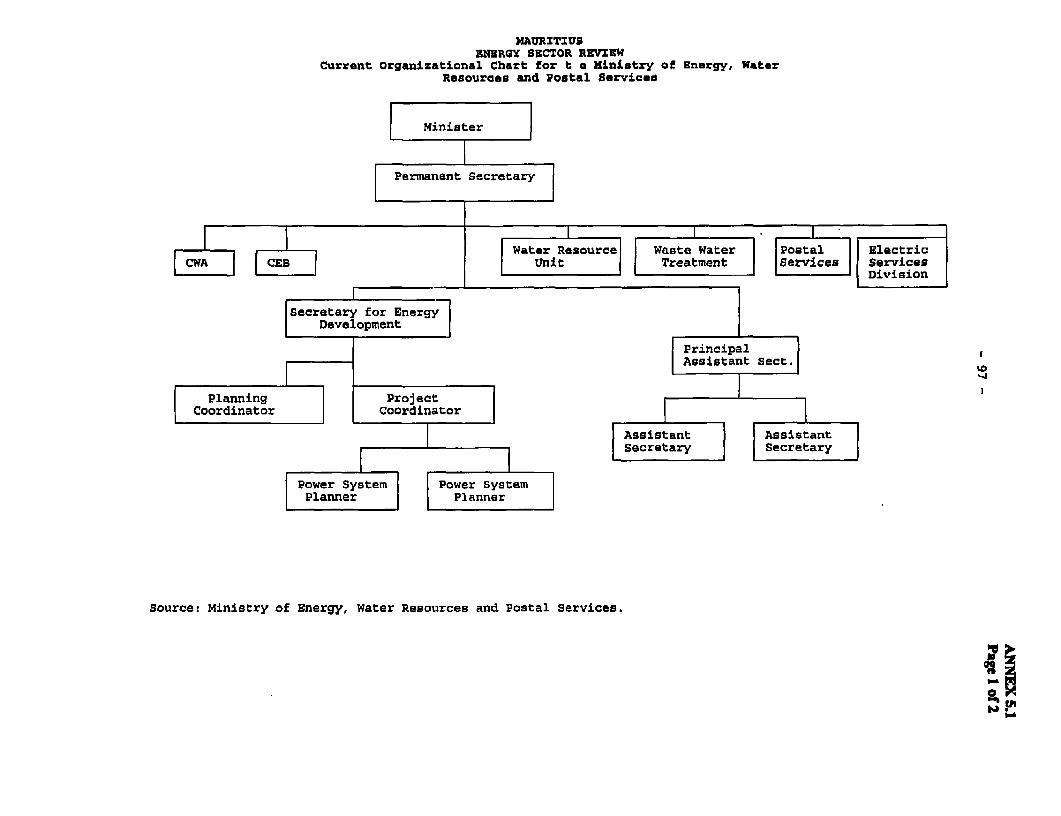

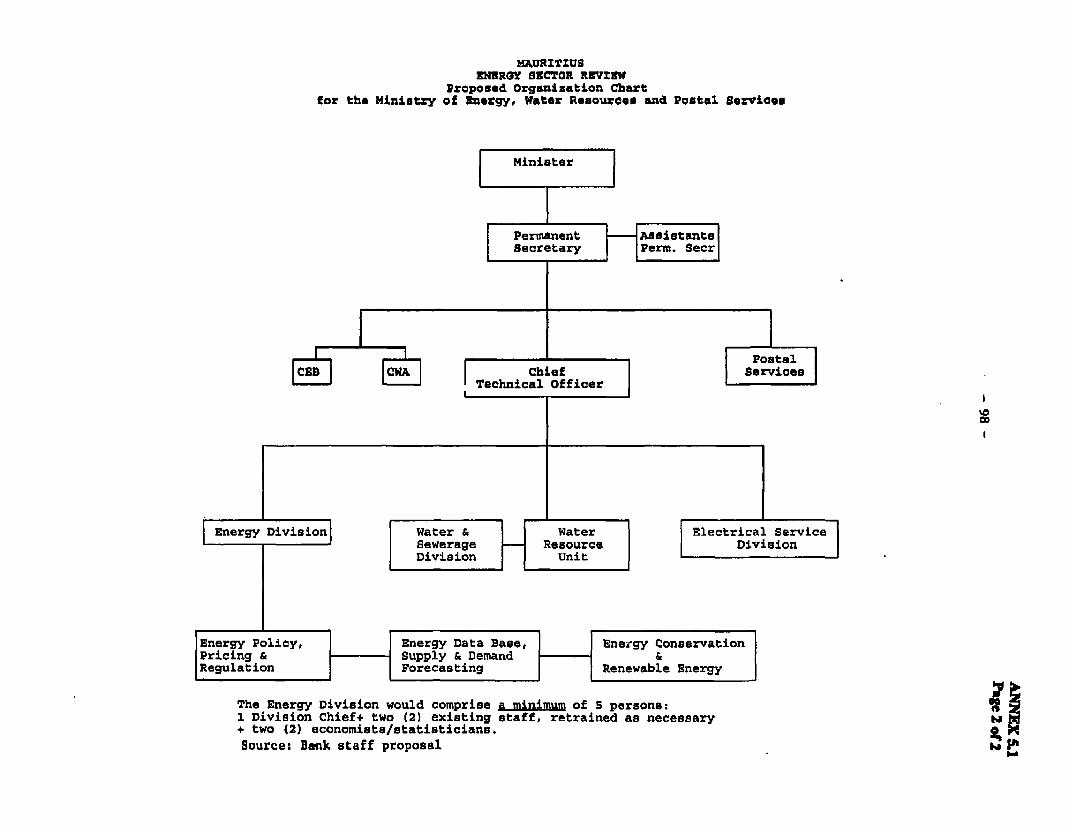

Annex 1: Time series dataAnnex 2.1: Energy Data 1992Annex 2.2: Sales by consumer categoriesAnnex 2.3: Electricity Tariffs 1980-93, in real termsAnnex 2.4: Demand for Petroleum Products, 1986-92Annex 3.1: Demand Elasticities and ForecastingAnnex 3.2: Electricity TariffsAnnex 3.3: Avoided Costs, Average Generation Costs and TariffsAnnex 3.4: Energy ConservationAnnex 4.1: Electricity StatisticsAnnex 4.2: Comparison of Candidates for Power GenerationAnn,x 4.3: Tentative Generation Expansion PlansAnnex 4.4: Investments in Transmission and Distribution, 1980-1992Annex 5.1:Current and Proposed Organization Chart of the Ministry of Energy, Water

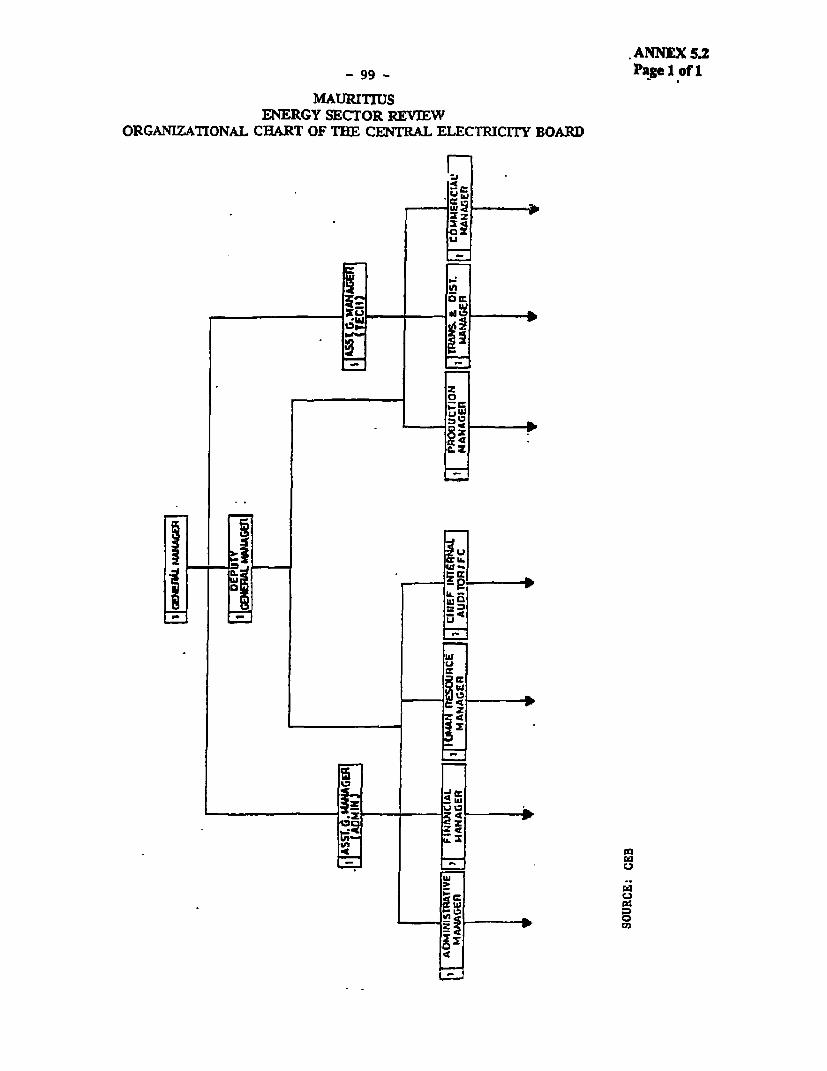

Resources and Postal ServicesAnnex 5.2: CEB Organization Chart

MAP

IBRD 26081

MAURITI US: ENERGY SECTOR REVIEW

EXECUTIVE SUMMARY

St9

1. The Mauritius Country FRconomic Memorandum' identified the need for greaterefficiency in the public sector, including a reduction in public expenditures as a keyelement in Mauritius' transition to a higher level of economic performance. The energysector, particularly the power subsector, has placed an increasing financial burder; on thegoverment budget, especially since the second half of the 1980s when CEB hunched asequence of investments financed through external borrowing in response to strongelectricity demand, which grew faster than GDP over most of the decade. Investmentprograms departed from least-cost principles to the extent that: (i) prices did not reflecteconomic costs; and (ii) delays in the implementation and procurement of generationequipment kept CEB off its least-cost expansion path. In the petroleum sector, price andmargin controls have been in effect for some time. This has distorted incentives, resourceallocation, and consumer choices.

2. This has had a negative effect on Mauritius' macroeconomic situation, throughhigher public irvestment and debt and a larger public deficit. The government should optfor a determined application of economic pricing and investment policies in the energysector. These policies should be coupled with institutional changes, in terms of a moreclearly defined and less interventionist government role, an adequate regulatoryfranework, and increased private sector participation.

3. The evolution of the final energy consumption by sector in Mauritius, over theperiod 1979-1992, reveals a moderate shift in the structure of final energy use away fromthe commercial and residential sectors towards industry and transport. This period is alsocharacterized by a decline in the relative importance of bagasse. While the sugar industrycontinued to use bagasse as a fuel at roughly the same level that prevailed in the late1970s, the rest of the economy (transport and power generation, in particular) met itsrapidly rising primary energy requirements with petroleum products.

Challensies in the Energy Sector:

4. There is a growing demand for electricity and petroleum products in the Mauritianeconomy. Given the precarious financial position of CEB and the constraints facing thepetroleum products industry on pricing (tightly controlled margins), demand will not bemet under the current envirornent and the sector will consequently be a drag on theeconomy. The challenge facing the government is to remove these botiltnecks to growththrough policies designed to support an appropriate fiamework in which a liberalizedsector would have the incentives to respond to market signals.

I Maufius: Comutr Economic Memondmn (The Worid Bank, lune 1994)

i Mauriftus: Energy Sector Review

Electric Power

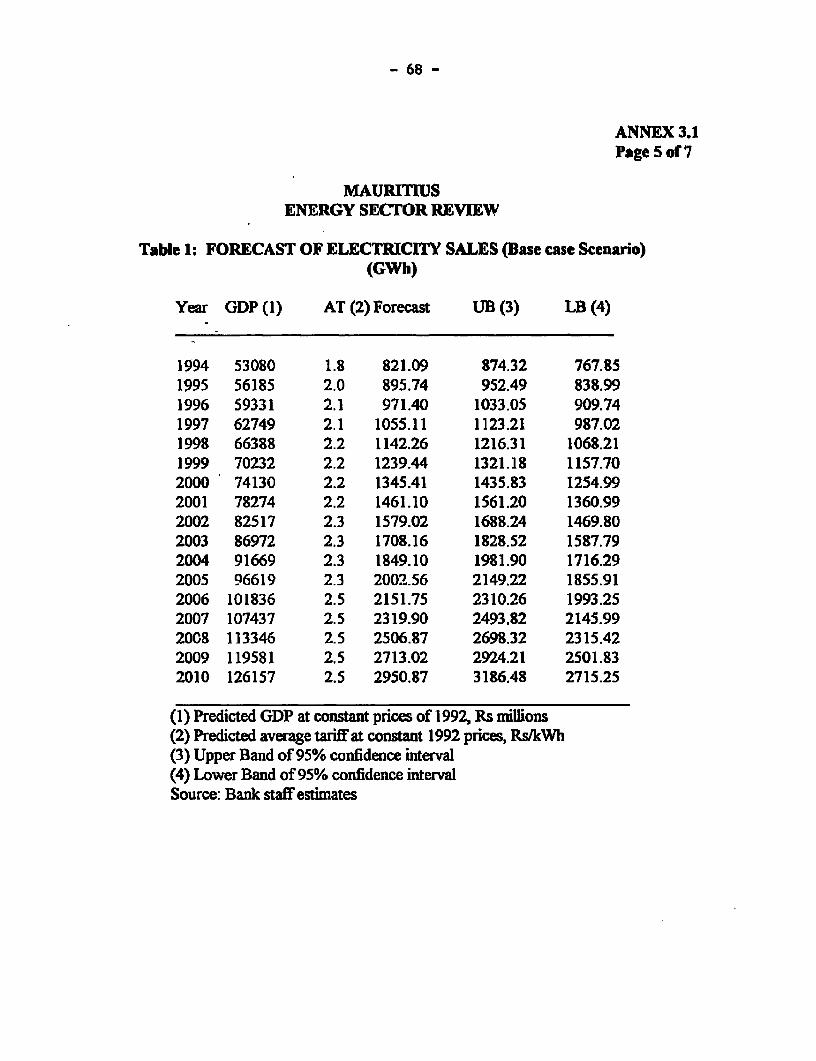

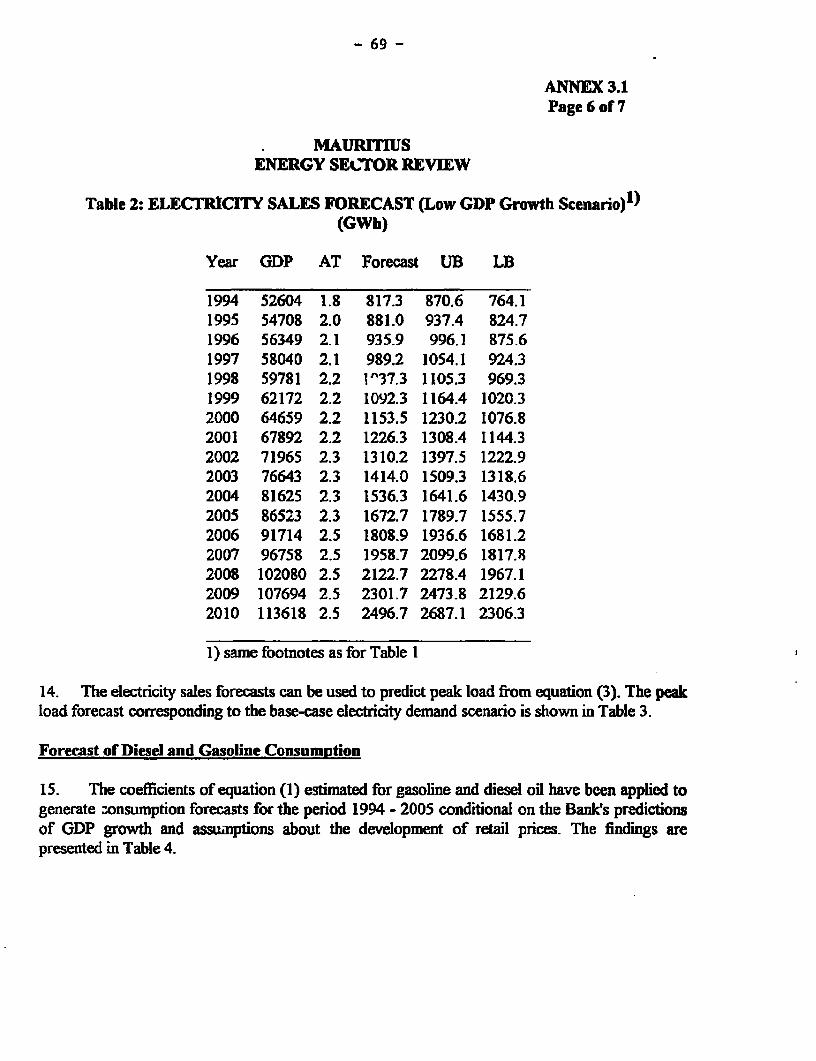

5. Power Demand. Two scenarios for clectricity demand were developed for theperiod 1994-2010 taking price adjustmcnts explicitly into account. Average tariffs (atconstant 1992 prices) were assumed to adjust to the level of average economic costs by1995, which is 2 Rs/kWh (US$0.13/kWh) in constant 1992 prices. and rise in discretesteps reflecting moderate increases in real operating costs. The base case scenarioassumed a GDP growth of about 6% per year, consistent with World Bank projections.The main assumption underlying this growth path is that the Mauritian economy willmaintain its competitive edge through export diversification and productivity gains. Thesecond scenario (termed low GDP growth) envisages a case where a period of adjustmentwould be needed for the economy to meet the challenges of the 1990s. For instance, thepolicy reforms are delayed or do not have the desired effects in the short-to medium-term.GDP growth has been forecast to reflect this until the year 2000, but to pick up at 6% peryear until 2007, and continue at 5.5% per year until the end of the forecast period. Underthe base case scenario, electricity demand is projected to increase at an average annualrate of 8 1% for the period 1994-2010, compared to 7.2% for the low growth scenario.The level and structure of electricity tariffs should be in line with economic costs, toensure an optimal level of investment, a sound financial situation of the sector and properdemand management ipractices. However, with a continuation of current practice and thuslagging price adjustments, the growth rate would jump to 9.2% under the base casescenario, hence the importance of implementing rational pricing policies.

6. The peak demand forecast is critical for detennining the size and timing of newgeneration units to be brought on stream. Annual peak demand was forecast assumingthat the load factor2 improves from 0.58 in 1994 to about 0.64 in 2010 as a consequenceof the increasing share of industrial consumption and the impact of tariffs. Under the basecase scenario, peak demand is expected to reach 292 MW in the year 2000, up from 184MW in 1994 at an average annual rate of about 8%. Under the low growth scenario, theannual rate of growth of peak demand will be 5.4% with a maximum demand of 251 MWin the year 2000. In determining generation requirements, it has been assumed that lossesin the transmission and distribution system will be reduced from the current 12.2% to11%. Under the base case scenano, generation requirements are expected to reach 1,569GWh in the year 2000, up from 961 GWh in 1994 at an average anual growth rate ofabout 8.5%. For the low growth scenario, generation requirements will increase at about5.8% annually to reach 1,345 GWh by the year 2000.

7. Generation Eixansion: Between 1994 and the year 2010, gross additions of finncapacity to the system, consistent with the demand projections, are 525 MW under thebase case scenario and 425 MW under the low growth scenario. The correspondingincrements in peak demand are 408 MW and 315 MW, respectively. If one accounts for

2 A measurement that compares a utiliWs average kilowatt-hour load to its peak. A high load factor meansgreater plant utilization.

ExeculJe Summry iII

the decommissioning of 80 MW c9 firm capacity (due to aging, breakdowns and othertechnical factors), the net additions are 445 MW and 345 MW respectively, which is closeto the peak demand increments.

8. In the short run, CEB may experience a shortage of capacity in 1994, but mostlikely in late 1995 or the beginning of 1996, duo to a conjunction of adverse factors, Acyclone in February 1994 caused damage to the cane fields and the output of bagasse isexpected to be below normal years. This event may combine with below average hydroconditions . The Flacq United Estates Limited (FUEL) power plant has been unreliablefor some time and the implementation of the bagasse-cum-coal Union St. Aubin (USA)project has been delayed to 1997. Finally, the contract award for a third 30-32 MW baseload unit at Fort George, is still pending. To meet short-term peak demand requirements,CEB opted for the urgent installation of a third gas turbine at the Nicolay power station.

9. Based on available informration, it is recommended to limit the rating of the newunit to a range of 30-32 MW. This would provide CEB with more flexibility in terms ofoptions for future use of the gas turbine in the framework of a least-cost expansion plan.In addition, the unit may be called upon to run as a semi-base load unit close to its optimalefficiency, if adverse conditions happen again.

10. In the medium-term, decisions already taken or in progress have by and largedefined the system. These decisions include: (i) the installation of one 32 MW diesel set(with the option for two more) at the Fort George Power Station where most of theinfrastructure is already in place; and (ii) the installation of three 32 MW bagasse-cum-coal units in three private sugar estates together with the signature of bulk supplycontracts with CEB. Therefore, until the year 2000, the issue is one of timing (date andsequence) to meet the projected demand rather than size or type. Since the Fort Georgediesel sets are to serve as base load units, typically for an operation of 5000 hours or moreper year, slow speed diesel units appear, excluding power purchases form sugar estates, asthe least-cost option. Furthermore, they have the advantage of sunk costs in theinfrastructure already in place. The bagasse-cum-coal power plants are also a competitiveoption for power generation, as the cost of producing electricity by private operatorscompares favorably with CEB's avoided costs3.

11. The diesel and bagasse-cum-coal power plants could both supply base load.However, the bagasse-cum-coal power plants seem to require a long lead time and thisrepresents importar.t risks for CEB. The major risk is related to the commissioning datesof the plants. This may result either in a low reserve margin or impose the urgentcommissioning of new generating units with a short delivery time such as gas turbines,causing over-investment and distorting CEB's optimal expansion path. Furthermore, themaintenance of the plants can only be undertaken during the inter-crop season. This is,however, the time when hydro generation is generally low and demand at its peak

3 Avoided costs are equal to the difference in costs that the utility incurs wfith and without an indepmendentgenerator (assumiir that the independent genemtor serves the part of the load thc utility would be obliged toscrve in its absence)-

iv Mauritius: Enery Sector Review

(December-January). As a normal part of its operations, CEB should therefore undertaketo simulate all these events on the system's ability to supply the load and take remedialaction, as necessary.

12 Depending on the scenario, bagasse-cum-coal power plants would be required in1997, 2000 and 2002 in the base case, and in 1999, 2002 and 2003 in the low growthscenario.

13 In the long-term, coal-fired power plants might be least-cost candidates when thepeak demand reaches 250 MW or more. Coal-fired power plants, however, should becarefully evaluated because of the lack of space for coal storage, ash disposal and for thepower plant itself. Fuithernore, the negative air quality impact might also be serious.

14. Transmission and Distribution. A transmission and distribution expansion plantied to generation developments and to the growth of demand should be prepared. Thetransmission plan should include a revision of the design assumptions and main linecharacteristics as well as costs (in the past, the cost of 66 kV lines was excessive). Plansto develop an extensive underground MV network should be postponed and theintroduction of a new voltage should be carefilly evaluated. In distribution, CEB seemsto be on the right track although a more detailed knowledge of consumers' chamcteristicsis necessary. Primary distribution at 6.6 kV should only be abandoned when the existingnevtwrks risk overloading or require frequent and extensive repairs. CEB's loss reductionprogram has been a success with losses averaging about 12%, down from 16% in 1986.Further improvements are possible but a better knowledge of how losses are split betweenthe MV and LV networks is necessary, which implies a campaign of measurementstogether with simulation (load flow) studies.

Petroleum Products

15. Domestic sales of petroleum products are expected to increase at about 5% a yearbetween 1994 andi 2005. Gasoline sales are expected to grow at 7.2% per year, diesel at4.7%, fuel oil at 4% and LPG at 7.4%. The demand for kerosene will continL't to bedominated by the fuel requirements of CEB's gas turbines. For the coming years, it isexpected that the existing units, probably supplemented by a third in 1995, will continue toserve peak and intermediate loads, resulting in a high level of kerosne consumption unfilnew diesel units come on stream. It is expected that both the coming on stream of newdiesel units and the removal of the kerosene tax exemption will reduce CEB's demand toabout 30,000 tons after the year 2000.

16. Given the expected growth of demand for petroleumn products, an expansion ofhandling and storage facilities will be needed in the near future. There is, however, strongdisagreement among different entities in Mauritius about relocating the existing facilitiesout of the port area and in particular about who is to bear the costs. On grounds of safety,the Mauritius Marine Authority (MMA) wants the oil companies to relocate their facilitiesout of the port area into a location close to CEB's Fort George power station and to the

ExecaFave Summary v

existing terminal. This would require substantial investments from the oil companies. Theoil companies, however, see these investments as impossible to carry out, given thepresent level of the marketers margin, Furthermore, the oil companies claim that thisrequest by MMA to relocate their facilities and their inability to do so is a pretext for StateTrading Corporation (STC) to intervene in the handling and storage of petroleumproducts by building a tank farm at the new location. There is no economic rationale forusing scarce public resources instead of involving the private sector, which is in a farbetter position to handle the whole chain of petroleum operations A compromise couldbe reached between the legitimate concern for the safety of oil operations in the port area(see para. 29) and the burden that investments in new facilities impose on oil companies.It is recommended that the government engage a dialogue with the private oil companiesdesigned to lead to a removal of these bottlenecks to growth. The issues of price controlsimposed on the petroleum industry and the monopoly of imports granted to STC areaddressed below (paras. 25, 33 and 34).

Pricing and Taxation

17. Given Mauritius' need to rely on productivity gains as a source of continued rapideconomic growth, there is a key role to be played by sound pricing and taxation policiesthat guide the allocation of both domestic and imported forms of energy.

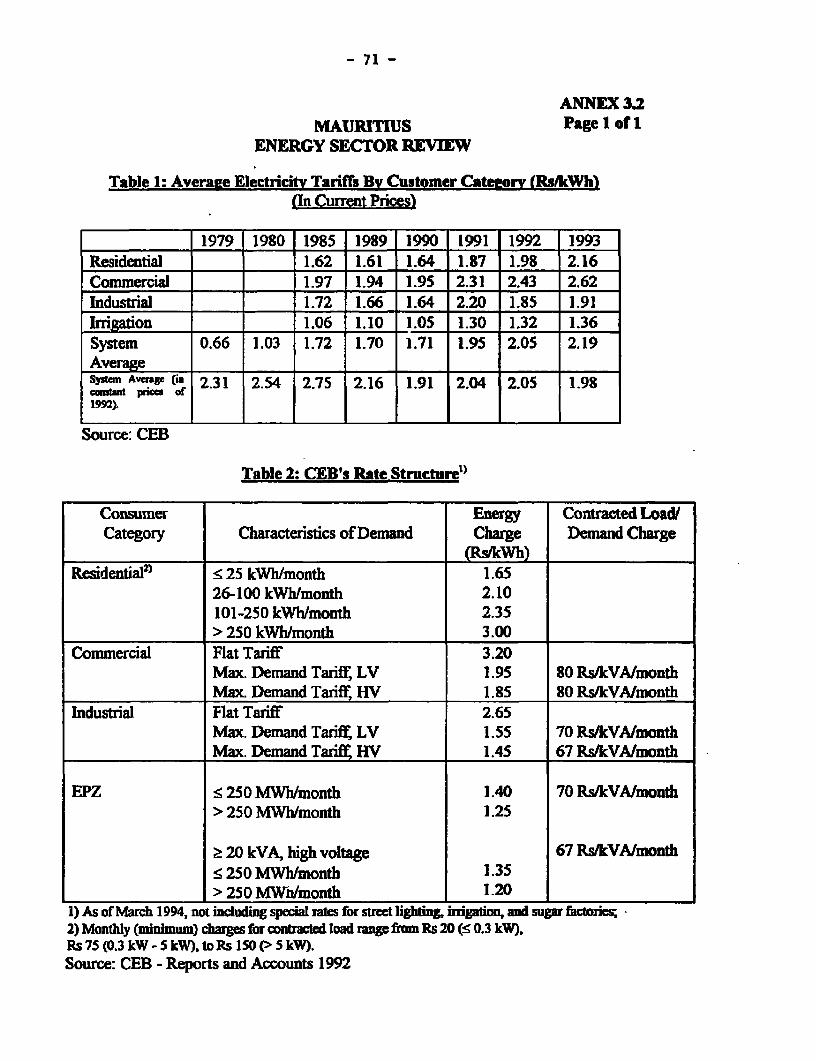

18. Electricity Tariffs: Since 1979, CEB's tariffs have been revised six times, thelast three adjustments took place in 1984, 1990 and 1992. Between 1985 and 1990,however, there was a steady erosion in real tariffs. This trend came to a halt in 1991/92,but continued in 1993. In earlv 1994, average tarifTs in real terms were about 30% belowtheir 1985 level, in spite of upward adjustments in 1990 and 1992. While CEB's revenuerequirements prompted these increases, the basic structure of the tariff system, save forminor refinements, has been kept unchanged for more than a decade. The rates in placedo not give electricity consumers the proper signals about scarcities and about the coststhey impose on the utility. They encourage wasteful consumption and provide little or norewards to those prepared to invest in energy conserv.ation.

19. To remedy these shortcomings, bold steps need to be taken to modernize CEB'stariff system applicable to both consumers and sellers of electricity. The main thrust of areformed tariff level and strdcture would be to charge electricity consumers the real coststhey impose upon the system. Tariffs that more accurately reflect economic costs andadjusted, as necessary, to meet CEB's financial requirements, will be more efficient andmore equitable. This will remove subsidies, give electricity users and autogeneratorseconomically correct incentives, and protect CEB, and therefore the govemment againstfinancial drains.

20. It is recommended that the government commnission a study leading to a new tariffsystem to reflect more closely the cost of generating, transmintting and distributingelectricity, depending on the consumer category served, its voltage level, the season andtime of use.

vi Mawitiuas: EnerV Sector Review

21. Petroleum Product Taxation: In the case of petroleum products, the pricelevel has been kept reasonably close to the international level over a long period of time,but now the structure has some serious shortcomings.

22. Domestic taxes levied on petroleum products are economicaly justified on thebasis of the negative externalities associated with their use such as pollution, wear and tearof the infrastructure, noise, etc. Taxation should be such that the internal price structureof petroleum products does not lead to inefficient interfuiel substitution. In Mauritius,taxes are also a major source of goveinment revenue, which lead to a number ofdistortions. In the future, a balance needs to be struck between pure fiscal revenue andother considerations (infrastructure use, environment, etc.). The best course of actionmay be to align taxation closely with Mauritius' main OECD trading partners and its maincompetitors.

23. Taxes on gasoline are the largest source of tax revenues from petroleum products.In 1993, the tax burden was UScents 28.1 per liter of gasoline, UScents 9.8 per liter forgas oil, and UScents 7.2 per liter of fuel-oil. On the other hand, no taxes are levied onkerosene and LPG. Of concern is the large spread in retail prices resulting from differenttax rates imposed on gasoline and diesel. While the present cost of importing gasolineexceeds that of diesel oil by only 3%, at the retail level, gasoline is 73% more expensivethan diesel oil. To avoid inefficient interfuel substitution between gasoline and diesel, thespread between the two fuels should be reduced.

24. Because fiLel oil is taxed, whereas kerosene and LPG are not, kerosene which iscostlier to import, is sold at a lower retail price than fuel-oil. This distorts CEB's fueloptions by making kerosene artificially cheaper than competing fuels. Petroleum producttaxation and pricing policy should ensure that in power generation, kerosene, which isused in peaker plants, proves costlier than fuel-oil (as an interim measure, some reliefcould be given to CEB by lowering the tax on fuel-oil). Furthermore, since there was asignificant shift of household kerosene demand to LPG, there is no longer a socialobligation to keep kerosene cheap. Taxation of kerosene would remove incentives tosubstitute kerosene for inferior fuels or to switch back from LPG to kerosene.

25. The retail prices and the margins of mark-eters and retailers have been fixed for along period of time. Price controls have been inposed in Mauritius to combat inflationand to protect consumers. However, price controls have never proved to be an efficienttool to contain inflation and healthy competition is a more effective way to protectconsumers. Furthermore, energy prices are not an appropriate vehicle for implementingthe government's income distribution policy. More efficient ways of helping thedisadvantaged include targeted support programs that meet both distributive and cost-saving objectives. The elimination of price controls would provide a great stimulus toincrease the efficiency with which resources are deployed in the petroleum sector.Furthermore, the actual level of profit margns, which have been frozen for about adecade, implying an erosion in real terni, makes it difficult for the private oil companies

Executive Summty vu

to mobilize the necessary capital for expanding the supply infrastructure to meet thegrowing demand for petroleum products. To meet this challenge, it is recommended thatprice controls in the petroleum sector be eliminated and that the import and marketing ofpetroleum products be completely liberalized. At the same time, the government shouldremove all barriers to entry into the petroleum sector and devise safeguards againstcollusion.

Enernr Conservation and Renewable Energy: The Importance of Pricing

26. The level and structure of energy prices are the critical elements in any effectiveenergy conservation strategy. It is recommended that the govemment rely to a greaterextent on economic pricing and competition to enhance energy conservation in Mauritius,especially in view of the expected continued strong growth of demand for energy in theyears to come. On the supply side, the role of the govemrnent should be limited toregulatory functions, including the provision of a credible and efficient institutional/legalframework that levels the playing field to encourage more private sector participation andprotects of the environment.

27. Savings of fossil fuels and electricity can also be accomplished through marketmechanisms that would lead to the economic expansion of the use of renewable energysources. Since Mauritius' hydro potential is almost exhausted, the scope for renewableenergy is limited to bagasse (which has already been discussed in the context of powergeneration), solar energy for water heating (photovoltaic power generation isuneconomic), and wind energy. The government could foster the use of renewable energyresources by making sure that the level and structure of electricity and petroleum productprices reflect economic costs.

28. Mauritius has favorable conditions for utilizing solar water heaters. There arepresently about 10,000 solar water heaters installed on the island, but the potential marketis estimated at five to ten times that number. This potential can be realized to a greatextent if the distortions that exist in electricity tariffs and petroleum product prices areremoved. The country also has a good wind regime. Although the experience with windgenerators has, so far, not been encouraging, the utilization of wind energy may proveattractive at selected sites.

Environmental Issues

29. It is recommended that the government adopt market based mechanisms,particularly taxation, as the main instrument for bringing about desired environmentaloutcomes, and ensure that its fiscal and environmental policies are compatible andmutually reinforcing. The goverrnent should also take steps to monitor theenviromnental impact of energy production and use and investigate the need for remedialactions, including taxation. Because there are potentially serious risks for the port and itssurrounding area, in the event of fire or other disaster, the provision of a contingency planfor the oil storage facilities should receive the highest priority. Should the use of coal in

viii Masuriius: Eiwrgy Sector Review

power generation and in other industrial applications continue to increase, closeenvironmental monitoring and the introduction of mitigation strategies will becomeimperative.

Institutional Issues

30. The actions recommended above on energy pricing should be complemented byinstitutional changes, notably private sector participation, to increase efficiency and tomobilize alternative sources to finance the expected expansion of power and petroleumsupply infrastructure. In the longer run, the energy sector could be transformed into adynamic part of the economy where the driving forces are the reliance on economic signalsand competition.

31. Electricitv. An enhanced role for the private sector in the development of thepower sector is important because of the potential it offers for contributing financial andmanagerial resources, as well as increasing efficiency through competition. To enablegreater private participation in all aspects of the provision of electric power, Mauritius hasseveral options to choose from, none of which, however, will work without some degreeof price efficiency. A competitive environment would be maintained so that privateenterprises could participate in any activity in the sector, with price as the main criterion ofchoice and efficiency would be stimulated through the pressure of actual or potentialcompetition

32. It is recommnended that the government appoint a working group to evaluate thedifferent options that are available for reforming the power sector, evaluate the options forsector regulation and set out a program for implementing the financial, legal andinstitutional reforms and propose measures for managing the transitione.

33. The Role of STC Under the recommended process of price deregulation andimport liberalization, there would be no role for STC to play in the petroleum sector However, since STC's levies on petroleum products are used to subsidize basiccommodities such as rice and flour, actions to improve efficiency may not be withoutundesirable equity and fiscal impacts, considerations at the center of Mauritian concerns.Fiscal neutrality should be respected. Income distribution has become more equal inMauritius during the last decade, which reduces the justification of some of thegovemment interventions of the 80s. More importantly, the time may have come toimprove the efficiency of income distribution policies. Proper targeting may be consistentwith both efficiency and fiscal considerations. In addition, international experience hasshown that efficient growth is the most powerful tool of income distribution.

34. STC's levies on petroleum products can be assimilated to a form of taxation and tothe extent that the govermment wishes to keep them, they can be collected as for other

4 lhere is some debatc in Mauritius surromunding these recommnedations.

Executive Sun,wy Lx

trade taxes and duties by the Ministry of Finance. If the government wishes to subsidizebasic commodities, such as rice and flour, in favor of groups it deems in need ofassistance, it can do so through appropriations ii' the general budget in a fully transparentmanner. This would help the government better iarget its interventions and eliminateacross-the-board subsidies.

1

INTRODUCTION

Obiectives of the Renort

1l1 The purpose of this report is to contribute to the discussion recently initiatedwithin the government of Mauritius on future energy sector developments in the short-,medium-, and long-term, through: (i) an assessment of the issues facing the energy sector;and (ii) the identification of the available options and the formulation of recommendationson the changes needed to stimulate sustainable energy sector development to better servethe country's overall development strategy of continued rapid economic growth throughgreater competitiveness of the economy and diversification.

The Enermv Sector and Country Stratear

1.2 Recent economic developments in Mauritius, particularly during the period 1989-1993, show that the economy has entered a period of slower growth in which inflation-induced macroeconomic instability and loss of international competitiveness are particulardangers. The govemment is devising a strategy to overcome internal and externalconstraints to firther rapid growth of the economy. During the transition, the governmentneeds to consolidate the macroeconomic and incentive framework in support of private-sector-led growth, and to reorient public sector activities to reduce their claims on thecountry's resources. In the energy sector, this has led to interest in redefining anddiminishing the role of government in the petroleum and power subsectors; introducingsound pricing policies and commercial principles, and where appropriate, competition intovarious elements of the sector; attracting private investors; and re-thinking the principlesof sector regulation and the administrative arrangements for making them work.

Survey of World Bank Involvement in the Sector

1.3 Under the joint UNDP/World Bank Energy Assessment Program (ESMAP), anenergy assessment of Mauritius was conducted in 1981. The Mauritius: Issues andOptions in the Energy Sector (Report No. 3510-MAS), identified: (i) the reduction ofelectricity losses, the rehabilitation of generating plants, and peak demand management;and (ii) the country's dependence in imported fuels as pinmary issues in the energy sector.These issues were addressed in two subsequent ESMAP reports. The first through thePower System Efficiency Study which was published in May 1987 (Report No. 070/87)

2 Mauritias: Energ Sedor Revww

and the second through the Bagasse Power Potential, 1987-2000 which was published inOctober 1987 (Report No.077/87).

1.4 The Power System Efficiency Study identified opportunities for operationalimprovements in hydroelectric plant rehabilitation; transmission and distribution powerloss reduction; and peak demand management. Notably, the report recommended theestablishment of a cobrporate planning unit to conduct market research and loadforecasting, investment planning in generation, transmission and distribution and tariffstudies. The implementation of the technical recommendations of the study led tosubstantial improvements in the reliability and cost of supply, particularly through thereduction of electricity losses. The recommendation concerning the corporate planningunit was not implemented.

1.5 On the second issue identified, the Bagasse Power Potential, 1987-2000 studyconcluded that the major option is to substitute indigenous bagasse for imported fuels inpower generation. This requires economizing on bagasse use in the sugar industry,handling and storing the resulting surplus, and transporting it to power generating stationsfor use as fuel. This was seen as an opportunity for the sugar industry to increase its valueadded and diversify revenue sources, reduce the countys dependence on imported fossilfiiels, meet a rapidly expanding demand for electricity at low cost, and reduce overall airemissions from the power sector by displacing fossil fuels.

1.6 In August 1991, a partnership was concluded between the government and thesugar industry through the adoption of the Bagasse Energy Development Program(BEDP). The BEDP envisaged investments in power generation and sugar millimprovements to effectively capture available bagasse for producing electricity, with coalserving as a supplementary off-season fuel. The purchase of electricity by the powerutility (CEB) was to be based on the avoided cost principle.

1.7 In 1991, the government requested assistance from the World Bank Group inlaunching the BEDP. In response, the Sugar Energy Development Project (Ln. 3458-MTS) of US$15.0 million and the Sugar Blo-Energy Technology Project (TF 028603), aGlobal Environmental Facility (GEF) grant of US$3.3 million were approved by the Boardof the World Bank in March 31, 1992. The main objective of the Sugar EnergyDevelopment Project is to expand electricity generation from bagasse from 70 to 120gigawatt hours (GWh) over a five year period by constructing a bagasse-cum-coal firedpower plant at the Union St. Aubin (USA) sugar factory in southern Mauritius andimproving the efficiency of sugar mills in the generation and use of steam. The GEF grantsupports the achievement of low carbon emission targets through the burning of bagassein replacement for fossil fuels. The institutional framework for enviromental protectionhas been developed by the government with the assistance of the World Bank whichsupported its implementation through the Environmental Monitoring and DevelopmentProject (Ln 3277-MA S) which was approved in 1990.

Chapter 1: Introdudion 3

1.8 Faced with the deterioration of the financial situation of the Central ElectricityBoard and requests by the utility for a tariff increase, the government felt thatinefficiencies that may exist in the utility should not be passed on to consumers andrequested the World Bank for assistance to carry out a study on Power SectorManagement and Restructuring. An Institutional Development Fund (IDF) grant ofUS$230,000 was approved in November 1993 to finance it. The study, which alsoincludes workshops to' familiarize decision makers with several aspects of power sectormanagement and restructuring, is underway.

1.9 In 1993, the World Bank was also requested by the government to review theenergy sector, identify issues and advise on possible options. The emphasis was placed ondevelopments in the power sector and World Bank advice was sought on the reasonablessof the power sector expansion program. Two World Bank missions were fielded for thispurpose. The first, in January 1994, worked closely with the government, particularly theMinistry of Energy, Water and Postal Services (MOE), the public and the private sector,to identify the issues in the energy sector to be covered in the energy sector review. Thesecond, in March 1994, covered the issues identified in some detail. These issues aresummarized in Chapter II of this report. Chapter I1 also presents an overview of theenergy sector in Mauritius. This sets the stage for a detailed discussion of pricing andtaxation and the role they play in affecting the future demandc for energy and energyconservation.in Chapter III. This leads naturally to a discussion on the planning of futureexpansion to meet the forecast demand growth in Chapter IV. Finally, Chapter Vconcludes with a review of the institutional issues confronting the energy sector and inparticular the role of the private sector.

2

ENERGY SECTOR OVERVIEW

Country Background

2.1 Mauritius, a small island nation of about 1.1 million inhabitants, comprises a groupof four islands in the Indian Ocean, with a total area of 1,870 square kilometers. The mainisland of Mauritius, located some 800 km east of Madagascar, accounts for 91 percent ofthe land area and 97 percent of the population. The other islands are Rodriguez(population: 38,000) and the two islands of Agalega (total population: 400).

2.2 In spite of severe macroeconomic imbalances in the early 1980s, the countrymanaged to grow at 6.7% a year between 1984 and 1993 (5.7% on a per capita basis).Solid growth was spearheaded by buoyant export industries (sugar, textile/garment,tourism) built on favorable external markets and use of low-cost labor. Benefits fromeconomic progress have been widely shared through broad-based social programs andhuman capital formation, thus transforming growth into stable and reasonably equitable

development.

2.3 With a GNP per capita of about US$ 3,000, and owing to the govemment's abilityto design and successfully implement flexible economic policies, Mauritius is in the processof becoming an upper-middle income country. New challenges, however, have beenunfolding since the late 1980s. Labor-intensive growth has reached the point of fiulemployment, placing an upward pressure on wages and unit costs. Other factors ofproduction, land and capital are also being heavily utilized. Export industries experienceincreased international competition, less favorable external market access, and stagnantforeign investment. The economic and regulatory system, created in the past to underpintwo distinct incentive environments for the export sector and the domestic sector, fostersmarket rigidities and hampers needed changes in industry structure, management and theperformance of markets.

2.4 The objective set by the medium-term (1992-94) National Development Plan is toattain a real GNP per capita of 5% growth annually through the year 1994 and 6%thereafter. This performance would double per capita income in just over a decade.

IThe trend fbr a more equitable development is confirmed by recent data collected by the 1991/92

housebold budget survey. The data show that the Gni coefficent fel from 0.445 in the early 1980s to0.379 in the early 1990s, i.e. the Lorenz curve became less convex and income is less concentrated andmore widely spread (Cemnal Statistical Offlc, 1992).

S Maurifis. Ener8y Secdor Review

Future growth of the magnitude envisaged is expected to come from greater efficiency inthe traditional growth sources and from new sources such as making Mauritius si IndianOcean hub for financial and maritime services. During the transition from ane ievel ofstrong performance to a higher plateau, good macroeconomic policy to hold aggregatedemand in line with the less vigorous supply is essential. One implication of thiS s a needfor greater efficiency in the public sector, including: (i) a reduction in current expendituregrowth; and (ii) a rationalization of the regulatory and incentive framework. The energysector is an area where efficiency gains could be realized and a process of rationalizationcould begin. Given the already high rate of utilization of the country's resource base,effbrts and incentives that channel productive factors to their best use are critical instimulating increased productivity and improved quality - the essential ingredients inachieving competitiveness at world standards.

Energy and the Economy

Energy Resources

2.5 Mauritius' indigenous energy resources are limited. Its hydroelectric potential haslargely been developed, and the remaining hydro resources are confined to non-energyuses (water supply and irrigation). While the installed hydro capacity is about 60 MW,output has been uneven. Over the last ten years, hydro generation varied between 64 GWhin 1984 and 147 GWh in 1989, with an average annual output of 104 GWh (equivalent to34,000 tons of oil). The medium-to-longer term prospects are that hydro generation willcontribute at most 130 GWh a year.

2.6 The most plentiful indigenous source of energy is bagasse, a by-product of sugarcane processing. Currently, sugarcane production anounts to 5.8 million tons a year,yielding about 1.7 million tons of bagasse. The bagasse is almost entirely used by sugarfctories for process heat and power generation, with excess power sold to the grid. In

21992, excess supply was 85 GWh generated frem 265,000 tons of bagasse. This leftabout 1.44 million tons of bagasse for internal consumption by the factories. Based on theenergy content that bagasse "commands" as a substitute for coal in power generation, theprimary energy equivalent of the power sales was 42,400 tons of oil (about 6%/o of totalprimary energy requirements), while the factories' own bagasse use made up for about229,000 tons of oil.

2.7 The potential availability of bagasse for power generation and other purposes isinexorably linked to the future of the sugar industry in Mauritius. Despite recentexpansion and diversification of the industrial sector, sugar production continues to be animportant economic activity in the country, accounting for 27.7% of total merchandiseexports and about 16% of employment in 1992. In the power sector, seasonality nd

2Bagasse conversion efficiencies vary significantly, rangig from 8 kg/Wh for 'tenntten' power to 227 kg/kWh

in the case of 'firm" power.

Chapter 2: Energy Sector Overview 6

variability in sugar production require power plants at sugar mills to use a dual fuel system(bagasse-cum-coal) to supply power to the grid at guaranteed levels all year ("firm"supply). The only plant that supplies firm power is the Flacq United Estates Limited(FUEL) sugar factory, which uses bagasse as fuel during the crop season (July-December)and coal the rest of the year. Two factories use bagasse to supply the grid during the cropseason only ("continuous" supply) and 12 other factories supply electricity intermnittently.There are no major etonomic uses for additional bagasse in Mauritius other than powergeneration. Its economic opportunity cost is therefore zero. Maximum economic benefitfrom bagasse use will be realized only if all the economically-competitive supply for powergeneration is so utilized. The role of bagasse in power generation is discussed in somedetail in Chapter 4. Planning Future Expansion.

2.8 Forest lands (plantations, nature reserves) cover 28,000 ha, and there are 28,000ha, mainly scrub and grazing land which is privately owned. In 1990, total supply ofindigenous forest products and wastewood was estimated at 140,000 m3 (roundwood), ofwhich 100,300 rm3 (about 65,000 tons, equivalent to 24,000 toe) qualify as woodfuels.Estimated woodfuel supply is roughly in line with figures on household woodfuel usewhich showed a downward trend during the 1980s. The Forestry Service estimates that by

31990 only 26% of the households relied on woodfuel . Based on an average consumptionof 100 kg per month and per household, the total woodfuel consumption was about

460,000 tons a year. Since 1990, the observed downward trend in woodfuel consumptionhas continued in line with the growth of per capita income as households substituted LPGfor woodfiiel.

2.9 At present, the impact of the other renewable sources of energy such as wind andsolar radiation is negligible. According to the Mauritius Meteorological Services,however, at many sites, particularly along the coasts, there is a favorable wind regime (upto an average annual speed of 8 mIs). Solar energy is plentiful, but has had only limitedapplications, for water heating in particular.

2.10 Mauritius has no (know-i) reserves of oil, gas, or coal and no refinery. Therefore,petroleum products as well as coal have to be imported. The size of these imports were amajor concern during the 1970s and in the early 1980s; yet the dependence onhydrocarbon imports has since become economically less precarious. While grosspetroleum product imports claimed about 23% of the country's (merchandise) exportearnings in 1982, the share came down to 9% in 1992, with net imports accounting for

3In 1985, one third of urban households and five out of seven households in rural areas were using

woodfuel.

4The figure of 100 kg/month/household was recorded by a household energy consumption surveyconducted in 1988 (Baguant, 1990). The same survey found that the average household size was 5.5members. With a population of 1.05 million in nid-1990, the total number of households was 191,000.

7 Mauritius: Eneqy Sector Review

little more than 6% of the export earnings. Nevertheless, between 1979 and 1992, grossimports of petroleum products almost tripled from 210,000 toe to about 600,000 toe, ofwhich 377,000 toe (about 63%) were used domestically, with the balance accounted forby re-exports and international bunkers. During the same period, coal imports climbedfrom 1,000 toe to 45,000 toe.

Primary Energy Requirements

2.11 Estimates of total primary energy use vary significantly depending on whether thesugar industry's auto consumption of bagasse is included or not. In fact, different energyaccounting rules were applied to bagasse in the past. Strictly speaking, however, theprimary energy equivalent of bagasse put into energy uses (heat and power) should beconsidered as part of the country's overall energy requirements. Since coal is the preferredalternative at the margin, coal in power generation qualifies as the benchmark for

calculating the energy content of bagasse used for cane processing.

2.12 In 1992, total primary energy requirements amounted to 718,000 toe (see Table2. 1), or 662 kgoe per capita. For comparison, per capita primuy energy consumption was570 kgoe in Costa Rica with per capita income of US$2,000, 858 kgoe in Jamaica withper capita income of US$1,500, and 1,066 kgoe in Malaysia with per capita income ofUS$2,600.

2.13 Between 1976 and 1992, total primary energy consumption rose by 239,500 toe,equivalent to 2.6% a year. If the sugar factorTies' internal bagasse consumption is excluded,primarv energy use increased by an impressive 289,000 toe, frozi about 198,000 toe in1976 to 487,000 in 1992, equivalent to an increase of 5.8% per year. Hence, the sugarindustry's primary energy requirements, which are a iunction of the volume of harvestedcane, were to a large extent stagnant; and the large increase in primary energy use ismainly attributable to the rest of the economy.

2.14 In 1992, oil products accounted for 52.5% of total primary energy consumption,followed by bagasse (37.8%) and hydro/coal (9.7%). Domestic consumption of oilproducts soared from 172,000 toe in 1976 to 377,000 toe in 1992, equivalent to anaverage annual growth rate of 5%. The only period where this strong upward trend in oilproduct consumption came to a halt was between 1979 and 1982 when the economy wasexposed to a sharp rise in oil prices. This temporary decline notwithstanding, petroleumproduct demand (derived mainly from transport and power generation) was the drivingforce behind the country's rapid growth of primary energy requirements.

The exact heating value of bagasse iepends on ;. moistur content. At 50% moisture contcnt, forinstance, estimates range between 7.5 and 10 GJIt. However, since in power generation one ton of bagassesubstitutes for 0.26 ton of coal, and given that one ton of coal is equivalent (on a heating value basis) to0.62 ton of oil, the adjusted energy content of a ton of bagasse matches that of 0.16 ton of oil (equivalentto about 6.6 GJ per ton of bagasse). The latter figure is used in this report.

Chapter 2: Energy Sedor Ovieaw 8

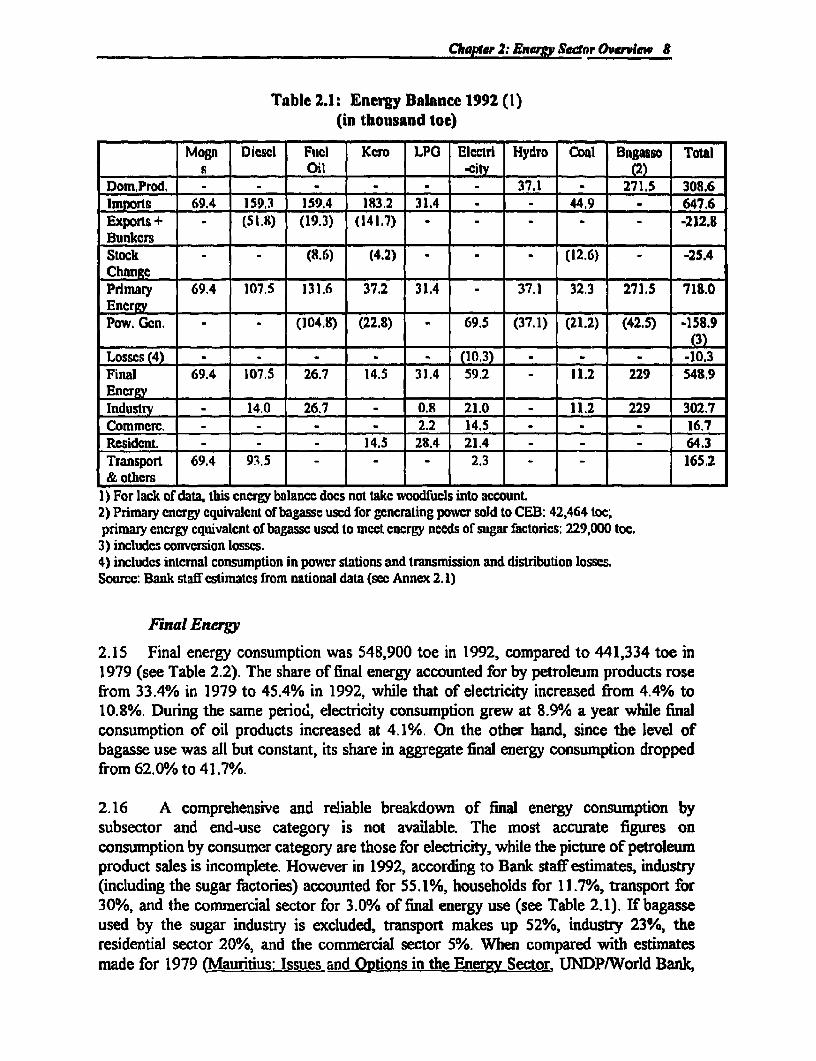

Table 2.1: Energy Balance 1992 (1)(in thousand toe)

Mogn Diesl Fucl Kcro LPG Electri Hydro Coal Bagalso Totals Oil _cily c2)

Dom,Prod. . . . . . 37.1 271.5 308.6Imports 69.4 159.3 159.4 183.2 31.4 . 44.9 - 647.6Exports+ - (51.8) (19.3) (141.7) - -212.5Bunkers ___Stock - - (8.6) (4.2) - - - (12.6) - -25.4Change - -- - - - - -

Primary 69.4 107.5 131.6 37.2 31.4 37.1 32.3 271.5 718.0EnergyPow. Gcn. (104.8) (22.8) - 69.5 (37.1) (21.2) (42.5) -158.9

- . . -~~~~~1(3)Losscs (4) - . - _ (10.3) - - -10.3Final 69.4 107.5 26.7 14.5 31.4 59.2 . 11.2 229 548.9

Industry - 14.0 26.7 - 0.8 21.0 . 11.2 229 302.7Commerc. - - 2.2 14.5 - - - 16.7Resident. - - 14.5 28.4 21.4 - - - 64.3Transport 69.4 93.5 -- - 2.3 = - 165.2& others - -- - - - --

l) For lack of data, this cnergy balance docs not takc woodfucls into accounL2) Primary cncrgy cquivalent of bagasse uscd for gncrating power sold to CEB: 42,464 toc;primary encrgy cquivalent of bagassc used to mcet energy needs of sugar factorics: 229,000 toc.3) includes conversion losses.4) includes intcrnal consumption in power stations and transmission and distribution losses.Source: Bank staff estimates from national data (see Annex 2.1)

Final Energy

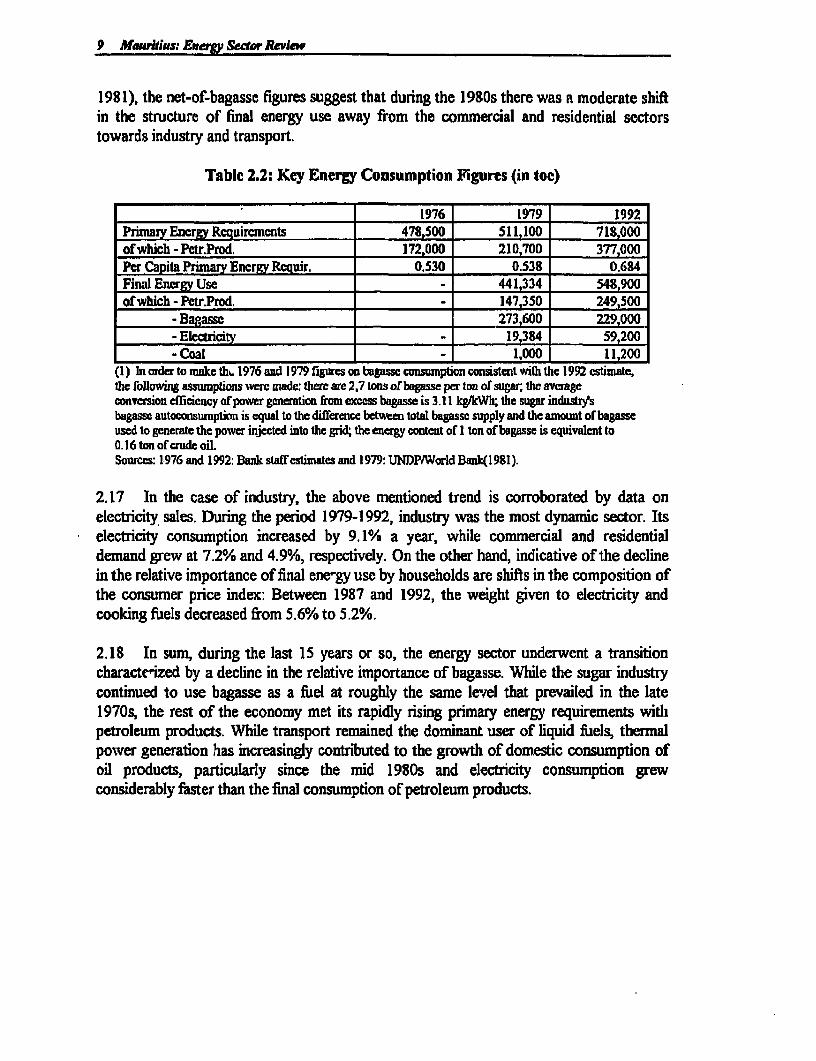

2.15 Final energy consumption was 548,900 toe in 1992, compared to 441,334 toe in1979 (see Table 2.2). The share of final energy accounted for by petroleum products rosefrom 33.4% in 1979 to 45.4% in 1992, while that of electricity increased from 4.4% to10.8%. During the same period, electricity consumption grew at 8.9% a year while finalconsumption of oil products increased at 4.1%. On the other hand, since the level ofbagasse use was all but constant, its share in aggregate final energy consumption droppedfrom 62.0% to 41.7%.

2.16 A comprehensive and reliable breakdown of final energy consumption bysubsector and end-use category is not available. The most accurate figures onconsumption by consumer category are those for electricity, while the picture of petroleumproduct sales is incomplete. However in 1992, according to Bank staff estimates, industry(including the sugar factories) accounted for 55.1%, households for 11.7%, transport for30%, and the commercial sector for 3.0% of final energy use (see Table 2.1). If bagasseused by the sugar industry is excluded, transport makes up 52%, industry 23%, theresidential sector 20%, and the commercial sector 5%. When compared with estimatesmade for 1979 (Mauritius: Issues and Options in the Energy Sector, LINDPIWorld Bank,

9 Mauriius: EMerwy Sector Reiew

1981), the net-of-bagasse figures suggest that during the 1980s there was n moderate shiftin the structure of final energy use away from the commercial and residential sectorstowards industry and transport.

Table 2.2: Key Energy Consumption Figures (in toe)

.___________ _____________________ $1976 1979 1992Primazy Encrgy Rcquircments 478,500 511,100 718,000of which - Petr.Prod. 172,000 210,700 377,000Per Capita Pimary Energy Requir. 0.530 0.53B 0.684Final Energy Use - 441,334 548,900of which - Pctr.Prod. 147,350 249,500

-Bagasse 273 600 229,000-Electricity 19,384 59,200-Coal 1,000 11,200

(1) In order to make th. 1976 and 1979 figmres on bagass consumption consistent with the 1992 cstimate,the following assunptions warc made: there are 2,7 tons of bagasse per ton of sugar, the averageconversion efliciency of pawer generation firm excess bagasse is 3.11 kg/kWh; the sugar indusrsbagasse autoconsumption is equal to the difference between total bagasse supply and the amount of bagasseused to generate the power injected into the grid; the energy content of I ton of bagasse is equivalent to0.16 ton of crude oil.Sources: 1976 and 1992: Bank staff estimates and 1979: UNDP/World Bank(l 981).

2.17 In the case of industry, the above mentioned trend is corroborated by data onelectricity sales. During the period 1979-1992, industry was the most dynamic sector. Itselectricity consumption increased by 9.1% a year, while commercial and residentialdemand grew at 7.2%/o and 4.9%, respectively. On the other hand, indicative of the declinein the relative importance of final ene-gy use by households are shifts in the composition ofthe consumer price index: Between 1987 and 1992, the weight given to electricity andcooking fuels decreased from 5.6% to 5.2%.

2.18 In sum, during the last 15 years or so, the energy sector underwent a transitioncharacte'ized by a decline in the relative importance of bagasse. While the sugar industrycontinued to use bagasse as a fuel at roughly the same level that prevailed in the late1970s, the rest of the economy met its rapidly rising primary energy requirements withlpetroleum products. While transport remained the dominant user of liquid fuels, thermalpoNver generation has increasingly contributed to the growth of domestic consumption ofoil products, particularly since the mid 1980s and electricity consumption grewconsiderably faster than the final consumption of petroleum products.

Chapter 2: &Eerg Setor Overview 10

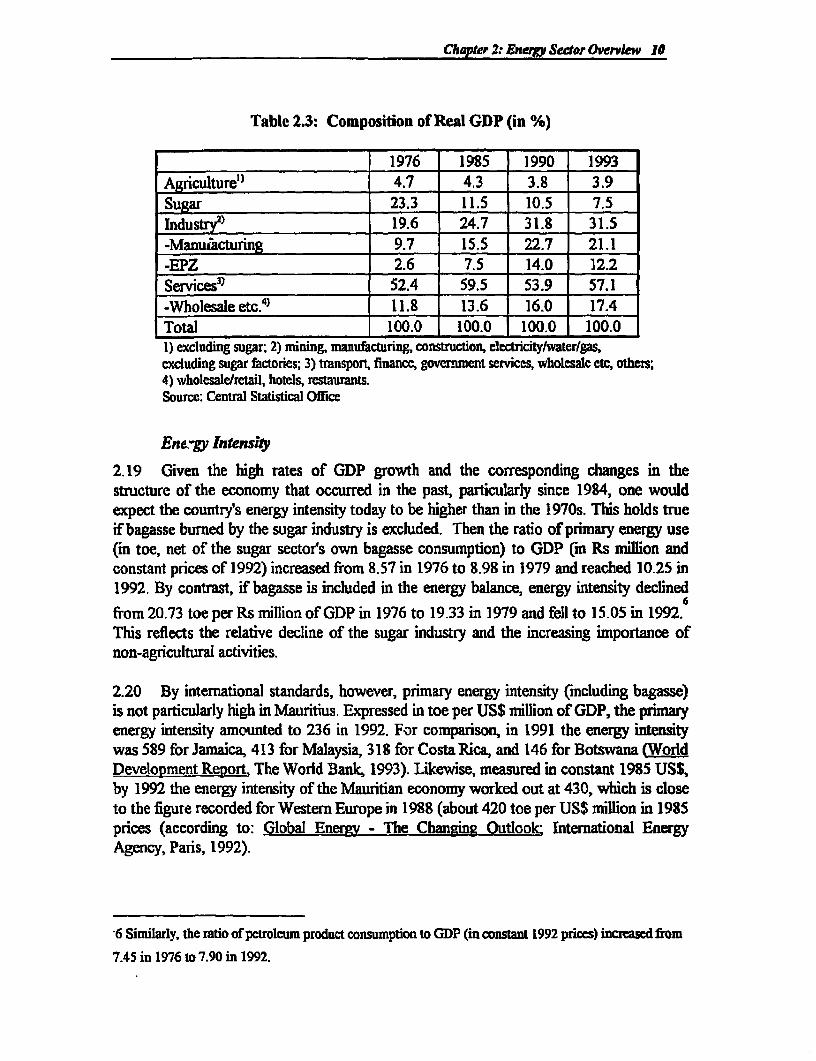

Table 2.3: Composition of Real GDP (in %)

1976 1985 1990 1993Agriculture" 4.7 4.3 3.8 3.9Sugar 23.3 11.5 10.5 7.5Industry2) 19.6 24.7 31.8 31.5-Manufacturing 9.7 15.5 22.7 21.1-EPZ 2.6 7.5 14.0 12.2Services3) 52.4 59.5 53.9 57.1-Wholesale etc.4) 11.8 13.6 16.0 17.4Total 100.0 100.0 100.0 100.01) excluding sugar; 2) mining, manufacturing, construction, electuicitytwatertgas,excluding sugar factories; 3) transpon, finance, government services, wholesale etc, others;4) wholesaletretail, hotels, restaurants.Source: Central Statistical Office

Energy Intensity

2.19 Given the high rates of GDP growth and the corresponding changes in thestructure of the economy that occurred in the past, particularly since 1984, one wouldexpect the country's energy intensity today to be higher than in the 1970s. This holds trueif bagasse burned by the sugar industry is excluded. Then the ratio of primary energy use(in toe, net of the sugar sector's own bagasse consumption) to GDP (in Rs milion andconstant prices of 1992) increased from 8.57 in 1976 to 8.98 in 1979 and reached 10.25 in1992. By contrast, if bagasse is included in the energy balance, energy intensity declined

6from 20.73 toe per Rs million of GDP in 1976 to 19.33 in 1979 and fell to 15.05 in 1992.This reflects the relative decline of the sugar industry and the increasing importance ofnon-agricultural activities.

2.20 By international standards, however, primary energy intensity (including bagasse)is not particularly high in Mauritius. Expressed in toe per US$ million of GDP, the primaryenergy intensity amounted to 236 in 1992. For comparison, in 1991 the energy intensitywas 589 for Jamaica, 413 for Malaysia, 318 for Costa Rica, and 146 for Botswana (orldDevelopment teport. The World Bank, 1993). Likewise, measured in constant 1985 US$,by 1992 the energy intensity of the Mauritian economy worked out at 430, which is closeto the figure recorded for Western Europe in 1988 (about 420 toe per US$ million in 1985prices (according to: Global Energy - The Changing Outlook' International EnergyAgency, Paris, 1992).

'6 Similarly, the ratio of petroleum product oDnsumption to GDP (in constant 1992 prices) incrcased frmm7.45 in 1976 to 7.90 in 1992.

11 Mauaritius: Energy Sector Review

Real Price Developments

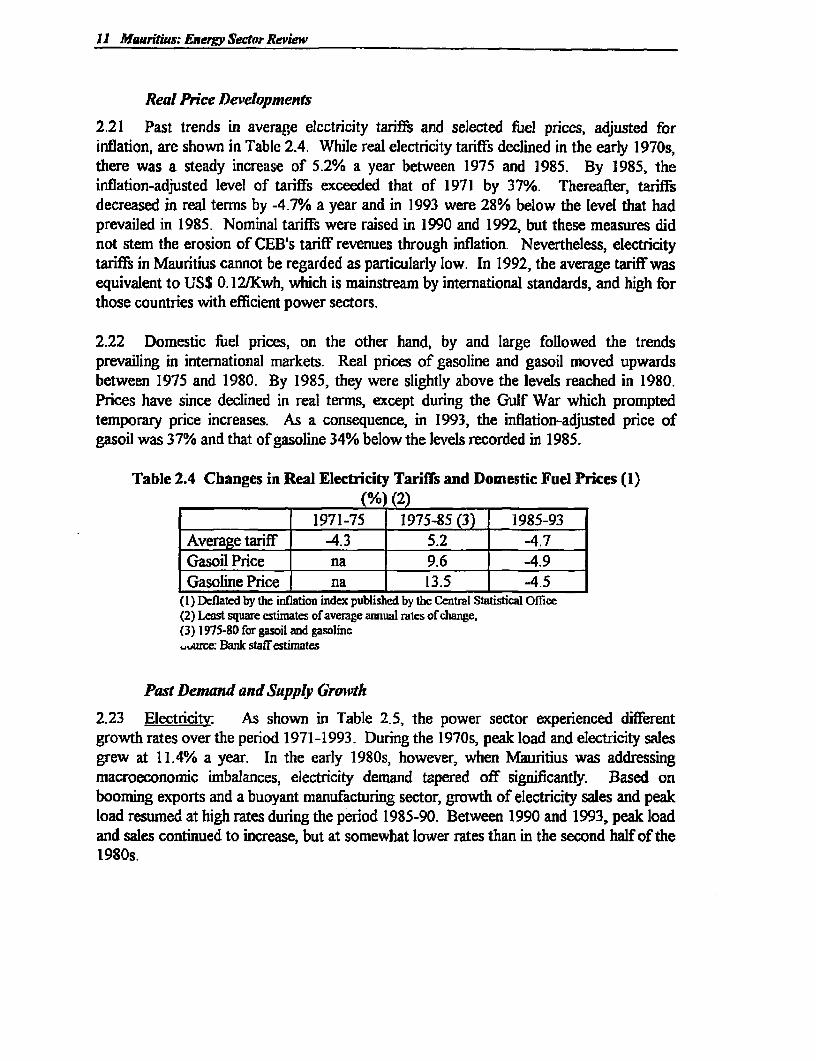

2.21 Past trends in average electricity tariffs and selected fUiel prices, adjusted forinflation, are shown in Table 2.4. While real electricity tariffs declined in the early 1970s,there was a steady increase of 5.2% a year between 1975 and 1985. By 1985, theinflation-adjusted level of tariffs exceeded that of 1971 by 37%. Thereafter, tariffsdecreased in real terms by -4.7% 0a year and in 1993 were 28% below the level that hadprevailed in 1985. Nominal tariffs were raised in 1990 and 1992, but these measures didnot stem the erosion of CEB's tariff revenues through inflation. Nevertheless, electricitytariffs in Mauritius cannot be regarded as particularly low. In 1992, the average tariff wasequivalent to US$ 0.12/Kwh, which is mainstream by international standards, and high forthose countries with efficient power sectors.

2.22 Domestic fuel prices, on the other hand, by and large followed the trendsprevailing in international markets. Real prices of gasoline and gasoil moved upwardsbetween 1975 and 1980. By 1985, they were slightly above the levels reached in 1980.Prices have since declined in real terms, except during the Gulf War which promptedtemporary price increases. As a consequence, in 1993, the inflation-adjusted price ofgasoil was 37% and that of gasoline 34% below the levels recorded in 1985.

Table 2.4 Changes in Real Electricity Tariffs and Domestic Fuel Prices (l).~(%Mo (2)1971-75 1975-85 (3) 1985-93

Average tariff -4.3 5.2 -4.7Gasoil Price na J 9.6 -4.9Gasoline Price na J 13.5 -4.5

(I) Deflated by the inflation index published by the Central Statistical Office(2) Least squarc estimates of average anual rates of change,(3) 1975-80 for gasoil and gasoline-urce: Bank staffestimates

Past Demand and Supply Growtk

2.23 Electrcity: As shown in Table 2.5, the power sector experienced differentgrowth rates over the period 1971-1993. During the 1970s, peak load and electricity salesgrew at 11.4% a year. In the early 1980s, however, when Mauritius was addressingmacroeconomic imbalances, electricity demand tapered off significantly. Based onbooming exports and a buoyant manufacturing sector, growth of electricity sales and peakload resumed at high rates during the period 1985-90. Between 1990 and 1993, peak loadand sales continued to increase, but at somewhat lower rates than in the second half of the1980s.

Chapter 2: Energy Sector Overview 12

Table 2.5: Power Sector Growth"'}( ).

1971-80 1980-90 1980-85 1985-90 1990-93Sales (GWh) 11.4 6.9 2.1 11.4 8.9Peak MD 11.4 4.7 0.7 8.9 8.0

(1) least square estimatesSource: Bank staff estirmates

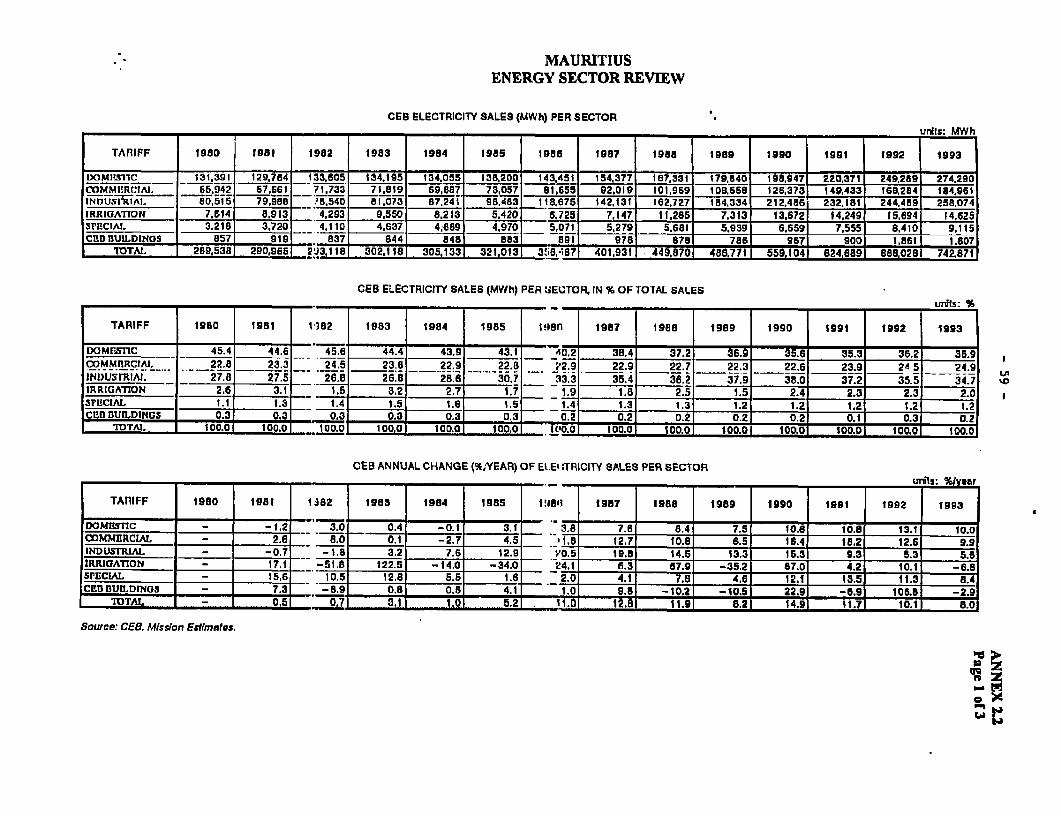

2.24 Between 1980 and 1990 the share of electricity sales accounted for by residentialconsumers fell from 45.4% to 35.6%; the industrial sector, especially the EPZ firms,increased its share from 27.8% to 38%; and the share of commercial users remainedconstant at 28.8%. This trend, however, came to a halt in the 1990s. By 1993, theindustrial share was down to 34.7%, while that of commercial customers went up to 25%and that of the residential sector rebounded to 37% (see Annex 2.2). These changes mirrorthe following developments:

(a) After 1988, the increase in demand by EPZ firms was driven mainly by thegrowing 'jutput of existing firms rather than by new entrants;

(b) Since 1990, demand per customer has grown fastest in the commercialsector (notably tourism and related activities), notwithstanding the relatively hightariffs charged to this customer group; and

(c) There was also a marked increase in sales per residential consumerreflecting a demand deepening enzouraged by declining real tariffs. In fact, manyhouseholds still use electricity to meet basic needs. In 1993, about 64% of theresidential consumers used 100 kWh or less per month. With the expected rapidgrowth of the Mauritian economy, there is a large potential for consumptiondeepening in the residential sector.

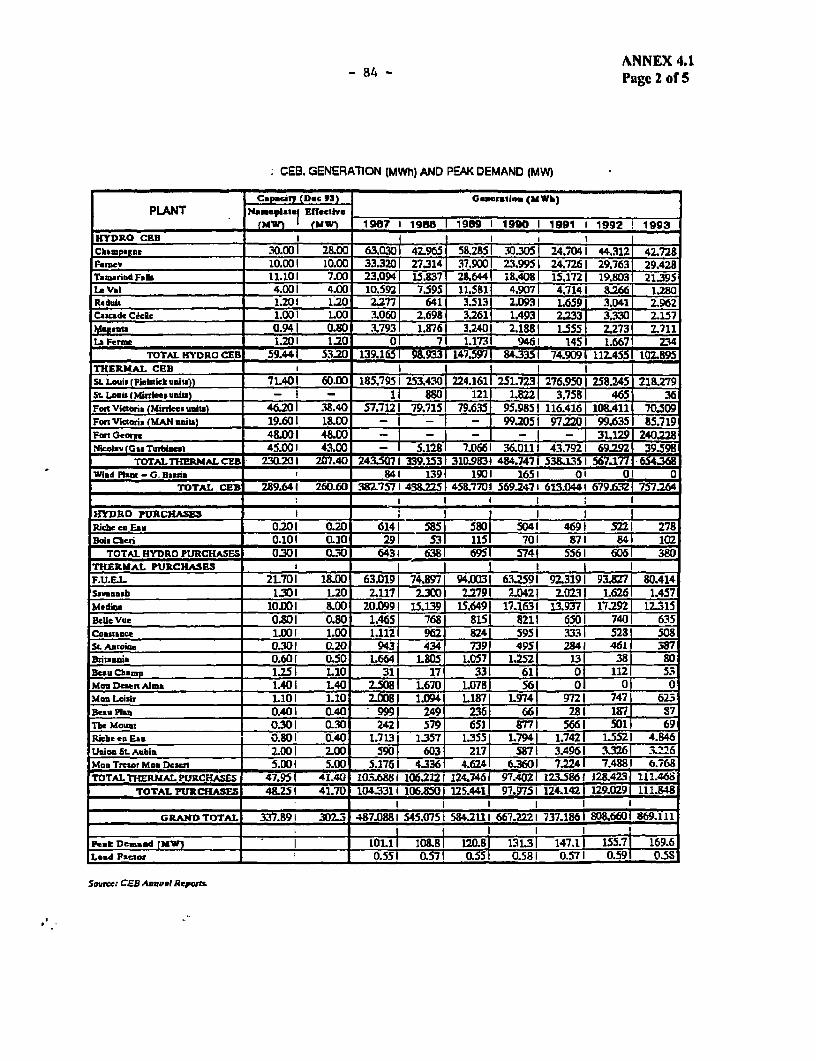

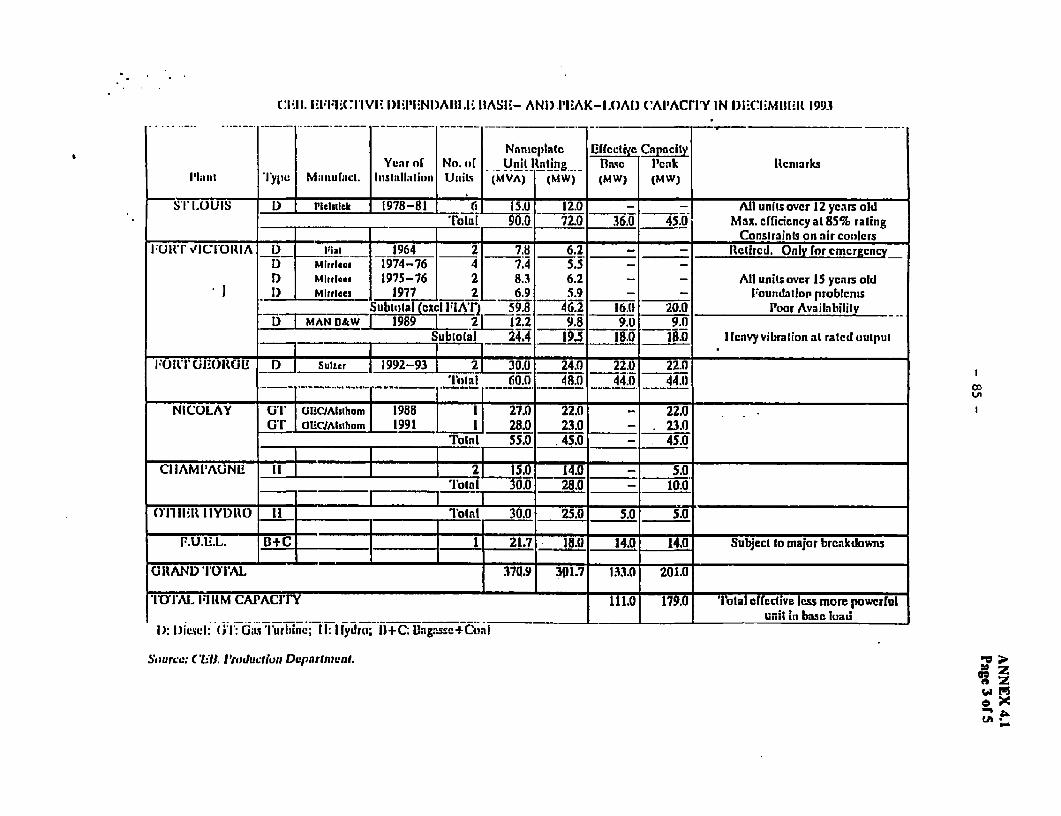

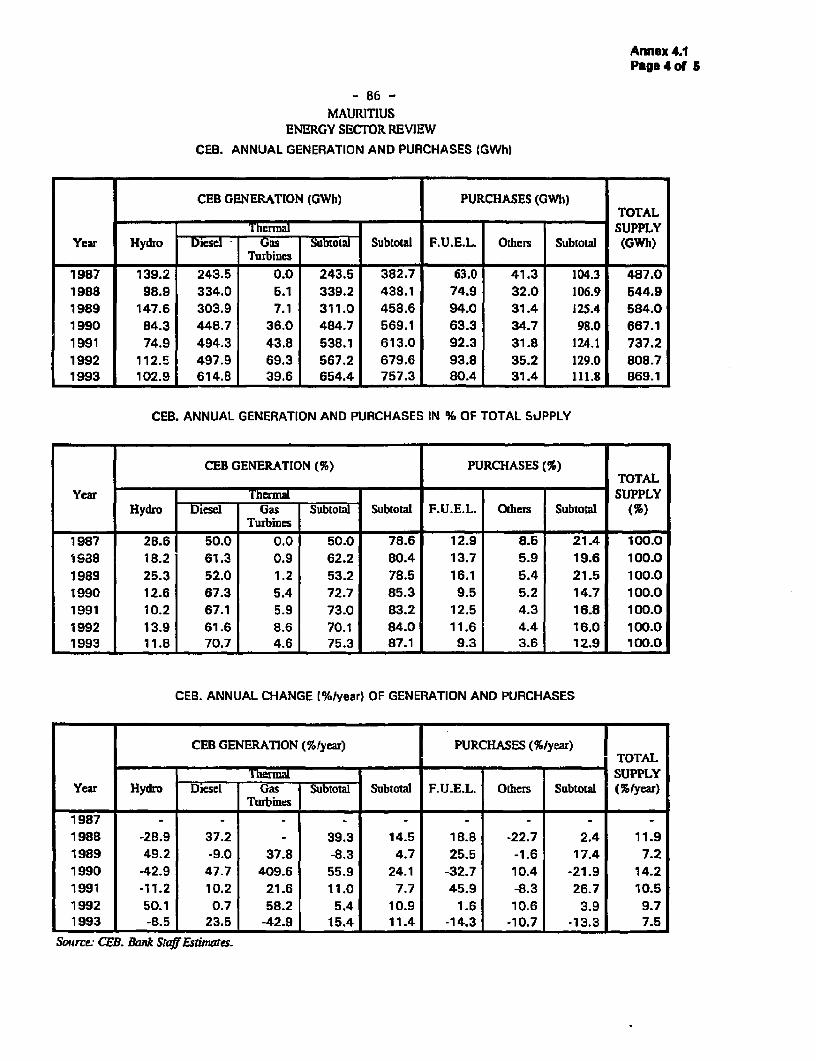

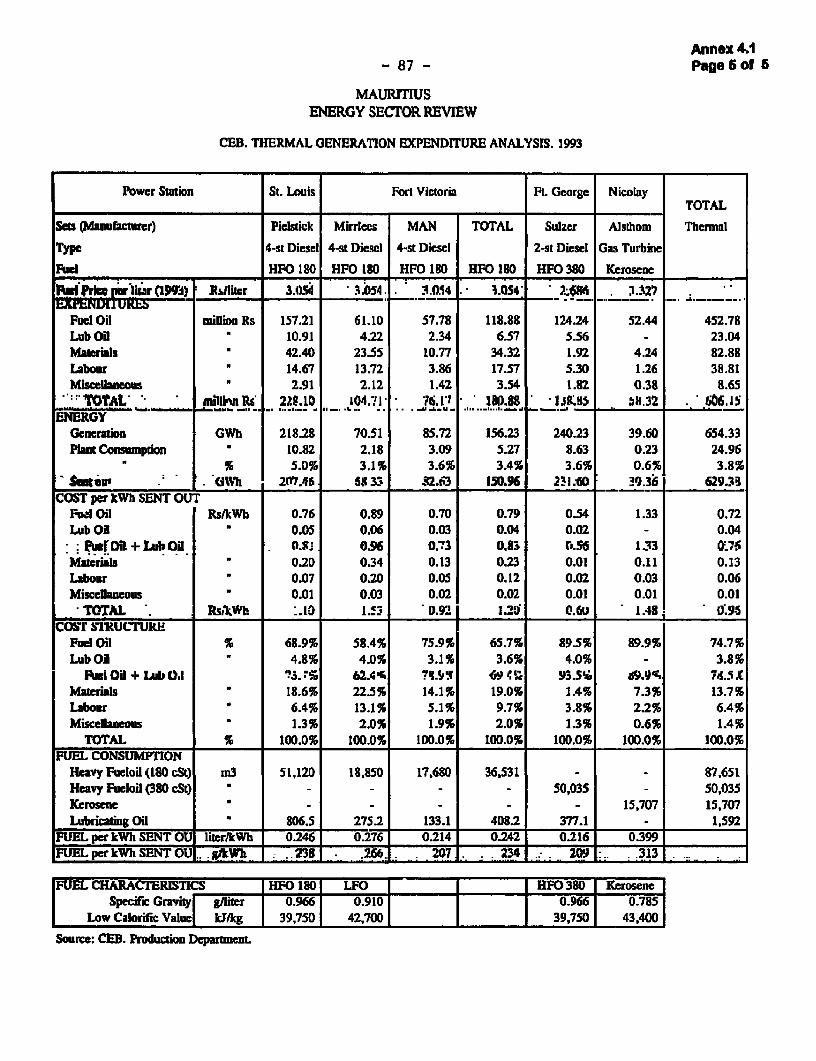

2.25 The existing power generation system is composed of hydroelectric and thermalplants. At the beginning of 1994, the installed capacity in CEB's plants, was 290 MW.However, available capacity was limited to 261 MW because of permanent deratings dueto aging and to thermal and other constraints. CEB operates nine hydroelectric plantswith a combined capacity of 60 MW, of which not more than 15 MW can be consideredfirm. The largest plant is Champagne with 30 MW installed capacity. In addition, CEBoperates three heavy fuel fired power plants with an installed capacity of 185 MW, and thekerosene fired gas turbine plant at Nicolay with an installed capacity of 45 MW. The mainthermal plants are St. Louis (71.4 MW), Fort Victoria (65.8 MW) and Fort George (48MW). CEB also buys energy generated from bagasse in 15 sugar factories. The mainsugar factories have an installed capacity of 37 MW out of a total of 48 MW. The largestis the Flack United Estates Limited (FUEL), with an installed capacity of 21.7 MW (seeAnnex 4.1 for details).

13 Mauritius: Enry Senor Review

2.26 The oil thermal power stations, all using imported fossil fuels, produced 654 GWh,or about 75% of the energy produced in 1993. The hydropower power plants accountedfor just under 12%, and the sugar factories 13%. Of the latter, 9.3% was generated byFUEL from bagasse and coal, and 3.7% from bagasse only and supplied by 14 other sugarfactories. Between 1987 and 1993, generation has increased at an average annual rate of10.8%. During the same period, peak demand increased by 69 MW, at 9% per year. Thedifference between these growth rates reflects an improvement in the system load factormainly due to the increasing share of industrial loads. As purchases from sugar factoriesremained relatively constant, the whole increase was met by new generating capacity.

2.27 Providing electricity with a high standard of reliability to meet the strong demandof an economy growing in complexity and sophistication is the main challenge of thepower sector in Mauritius. Delays in the implementation of major projects (e.g. anadditional diesel set at the Fort George Power Station and the in the commissioning of theUnion St. Aubin bagasse-cum-coal fired power plant) has put CEB off its optimal, ornormal, expansion path. The utility had to rely on gas turbines, designed principally forpeaking duty and acquired at great cost, to fill the gap. Unless action is taken to moveprojects forward more units with short lead time will probably be needed. An importantquestion that will continue to face power planners is the place and use to be made of thesegas turbines once CEB returns to a somewhat normal expansion path. However, while thethennal additions might not have been the optimal supply response if the shortfall had beencorrectly anticipated, this solution is nevertheless preferable to accepting the economiclosses associated with power shortages. The impact of these decisions on the medium-tern least-cost generation expansion plan needs to be studied.

2.28 Petroleum Products: Propelled by the high rates of economic growth Mauritiushas experienced since the mid-1980s, domestic petroleum product consumption increasedat an average annual rate of 14.9% between 1986 and 1992. Consequently, the share ofimports accounted for by sales on the domestic market climbed from 50.1% to 66.9%.Total imports, on the other hand, grew at a lower rate of 8.9% a year, from 340,000 tonsin 1986 to 601,000 tons in 1992. The most notable change in re-exports and intemationalbunkers, which grew at only 1.4% a year, was a shift away from diesel and fuel oiltowards jet fuel. By 1992, jet fuel made up 22% of total imports.

2.29 Annex 2.3 shows the demand for petroleum products between 1986-1992 for eachpetroleum product as well as the distribution of the consumption of these productsbetween domestic and international use. Of special note is:

(a) the dominance of three fuels in the petroleum market in 1992: fuel oil, dualpurpose kerosene (78% of which is jet fuel) and gasoil. Between 1986 and 1992, thedemand for fuel oil rose at 14.6%, increasing its share to 40.5% by 1992. gasoil andgasoline consumption rose at 8.9% a year and in 1992 accounted for 26.4% and 15.9% oftotal domestic petroleum product demand;

Chapter 2: Energy Sector Ouerview 14

(b) The most rapid growth was recorded for LPG (33% a year). In 1992 LPGmade up 8% of domestic petroleum product sales. It is used mainly by households (as asubstitute for kerosene in cooking) but also by commercial and industrial users. Householddemand for LPG was driven for the most part by rising income. In fact, during the period1986-1990 when per capita GDP grew at 6,4% year, LPG consumption soared by almost40% a year; and

(c) Despite the substitution of LPG for kerosene in the residential sector,domestic kerosene consumption rose by 11.9% a year between 1986 and 1992, mainlybecause of the increased use of kerosene in power generation (gas turbines) due to itsfavorable tax treatment.

The Energ Sector and Public Finances

2.30 The power sector has placed an increasing financial burden on the governmentbudget, especially since the second half of the 1980s when CEB staged a sequence ofinvestments financed tbrough external borrowing. CEB's debt rose from Rs 1.2 billion, (Rs1.9 billion in prices of 1992) or US$89 million in 1986 to almost Rs 3 billion, or US$176million, at the end of 1992. Furthermore, since 1987 the utility persistently ran into losses.By 1991, more than one third of the debt accrued from government (or government-mediated) loans, of which 44%/o were arrears. In order to ease CEB's financial difficulties,the government decided in 1992 to write off the arrears worth more than Rs 700 million(US$ 45 million), equivalent to almost 4% of total government debt in the same year. In1992, the cash-flow shortfall for the power sector was estimated at about Rs 63.4 million(US$ 3.6 million). CEB's losses are expected to reach Rs 62.9 million, or US$ 3.5 million,in 1994.

2.31 Reform is needed to increase the efficiency of the sector and to attract privateinvestment to respond to the challenge of rapidly growing demand and the need to expandcapacity. The financial situation of the power sector is likely to worsen with theimplementation of CEB's 1994-1996 investment program. The total cost of this programis estimated at Rs 4.5 billion (US$ 250 million). In addition to CEB's efforts to increasesupply, plans call for a US$ 50 million (Rs 900 million) investment in a 32 MW dual-fuelpower plant at the Union St. Aubin sugar factory to be jointly owned by the private sectorand CEB and to be completed before the turn of the century. In sum, public and privatepower sector investments during the 1990s can be expected to reach high levels.

2.32 In 1992, taxation of petroleum product imports raised about Rs 920 million, whichwas about 20% of government revenues from import tariffs and 8% of total governmentrevenues. Among petroleum products, the largest single source of tax revenues is gasolinewhich is charged a 200% ad valorem tax ("import duty") and a 17% o"import levy", bothon the cif-value. Fuel oil and gas oil are subject to a 17% import levy and a per-unit importduty of 1.00 Rs/l and 1.30 Rs/l, respectively. In 1993, the latter were equivalent to advalorem taxes of 50% on diesel and 70% on fuel oil. Unlike gasoline, however, taxation of

15 Maur;itus: Energy Sedor Review

fuel oil and gas oil is open to a number of exemptions. At any rate, in 1992, the average7

tariff paid on all petroleum products was about 52%.

Table 2.6: Power Sector Investments (in Rs million)

Year Power Sector Power Sector Public Sector Public SectorInvestments Investments Investments Investments

(in current Rs) (in Rs of 1992) (in current Rs) (in Rs of 1992)1990 402 450 4,365 4,8881991 1,081 1,131 3,515 3,6771992 755 755 4,650 4,6501993 _ 224 _ 203 4,900 4,434

Source: CEB, Central Statistical Office

2.33 While petroleum product imports give rise to government revenues, they absorbpart of the country's export earnings. The share of merchandise impon:s made up bypetroleum products, however, decreased from 18% in 1982 to 7.3% in ]992. What countsmore from a balance-of-payments point of view are the net imports whose share was downto 4.8% in 1992. In the same year, net energy imports of about Rs 1.2 billion (US$ 78million) were matched by 6.1% of the country's revenues from merchandise exports. Tenyears earlier, net energy imports were worth about 20O%/ of the export earnings. What canbe concluded from these figures is that the cost of importing oil products is sizeable, butno longer poses a vexing balance-of-payments problem.

2.34 Additional revenues are collected through levies on petroleum products by theState Trading Corporation (STC), the monopoly importer, to subsidize basic commodities.Staple rice and wheat flour have long been subsidized because of thcir significant weight inthe food basket of the population. STC is responsible for their import and sale at fixedprices in the domestic market. The subsidy has helped to stabilize the price of rice andwheat flour, but reform is needed. The well-to-do benefit forr. the subsidy more inabsolute value of subsidized consumption than do the poor, although it constitutes asmaller proportion of their expenditures. Also, the subsidy has lost much of its distributivejustification, with rapidly rising real wages and low unemployment contributing more toimproved income distribution and enhanced purchasing power of all income groups. Thesubsidy also takes a substantial bite out of the government budget, using resources thatmight be better put to alternative uses. It has been estimated that the elimination of the

subsidy would save 2.2% of government expenditures.

These taxes have been simplified in 1994 with yields broadly unchanged.

Mauritius: Toward th 21st Ce (UNDP/World Bank Trade Expansion Program), 1993

Chapter 2: Energy Sedor Overview 16

Overview of Sector Management Issues

2.35 There are five basic issues to be dealt with in formulating an energy strategy tosupport Mauritius in its drive to achieve a higher level of economic performance.