employee buyouts: causes, structure, and consequences1

TRANSCRIPT

*Corresponding author: Tel.: 804/924-4810; fax: 804/243-7676; email: [email protected].

1The authors appreciate the helpful comments received from Edward Rice (the referee), CliffordSmith (the editor), Tom George, N.R. Prahbala, Greg Roth, Anil Shivdasani, Neil Sicherman, LuigiZingales, the seminar participants at Harvard University, Michigan State University, the Universi-ties of Georgia, Pittsburgh, and South Carolina, the 1994 Financial Management AssociationMeeting, the 1994 Western Finance Association Meeting, the research assistance of Rohan Christie-David, Andy Saporoschenko, Tom Smythe, and Cynthia McDonald.

Journal of Financial Economics 48 (1998) 283—332

Employee buyouts:causes, structure, and consequences1

Susan Chaplinsky!,*, Greg Niehaus", Linda Van de Gucht#! Colgate Darden Graduate School of Business Administration, University of Virginia, Charlottesville,

VA 22906, USA" The Darla Moore School of Business, The University of South Carolina, Columbia, SC 29208, USA

# Department of Applied Economics, Catholic University Leuven, 3000 Leuven, Belgium

Received 7 December 1994; received in revised form 25 August 1997

Abstract

This paper investigates the motivations for and consequences of including a broadgroup of employees in leveraged buyouts by comparing employee buyouts (EBOs) totransactions where only top level managers participate, or management buyouts(MBOs). We examine the implications of including employees in a buyout from a laborcontracting, financing, and management control point of view. A major finding is thatemployee participation helps to finance the buyout. The EBO allows firms to gain accessto excess pension assets by converting employees’ defined benefit pension capital intoequity claims, thus freeing the excess assets in the pension plan to help fund the buyout.Also, employee participation substitutes equity claims for cash labor compensation costsand therefore allows the firm to borrow more than otherwise would be possible. There isalso evidence consistent with managers including employees to maintain or enhanceincumbent management’s control. ( 1998 Elsevier Science S.A. All rights reserved.

JEL classification: G34

Keywords: ESOP; LBO; Employee ownership; Labor contracts

0304-405X/98/$19.00 ( 1998 Elsevier Science S.A. All rights reservedPII S 0 3 0 4 - 4 0 5 X ( 9 8 ) 0 0 0 1 3 - 0

2For literature on MBOs, see, DeAngelo et al. (1984), DeAngelo and DeAngelo (1987), Lehn andPoulsen (1989), Hite and Vetsuypens (1989), Kaplan (1989a,b), and Palepu (1990).

1. Introduction

During the 1980s, a small number of U.S. corporations went private by sellinga large part of the firm’s equity to a broad group of employees through anemployee stock ownership plan (ESOP). Because employee buyouts (EBOs)result in a large increase in employee ownership, these transactions present anopportunity to examine the implications of making employees residual claim-ants in their firm. Despite a number of studies examining going private transac-tions, systematic evidence on the factors that motivate employee participation inbuyouts remains unexplored.2 In this paper, we examine and provide evidenceon a number of hypotheses concerning the costs and benefits of employeeownership. We focus, in particular, on the circumstances that lead employees toparticipate in a buyout, and on the consequences of their participation for thestructure and decisions of the post-buyout firm.

One approach to investigating why a broad group of employees participate ina buyout is to examine the issue from the perspective of an optimal laborcontract. Cash flow rights can improve employee incentives (see, Alchian andDemsetz, 1972). These rights can also mitigate asymmetric information prob-lems when negotiating labor contracts (Ben-Ner and Jun, 1996; Kovenock andSparks, 1990). In addition, employee control rights can help protect employees’firm-specific capital (see, e.g., Klein et al., 1978; Williamson, 1979). However,a related cost of employee ownership is inefficient risk-sharing.

An alternative, but not mutually exclusive perspective, from which to examineemployee participation is that of corporate finance. For example, leveragedESOPs can provide a tax-advantaged source of funds (Beatty, 1995). Anotherfinancing benefit of including employees in buyout transactions occurs if theshares received by employees substitute for ongoing cash compensation com-mitments to pay wages or retirement plan contributions. In this case, part of thefirm’s existing operating commitments to labor costs are reduced in the post-buyout firm, and these funds become available to service the interest paymentson the buyout debt. This substitution lowers leverage-related costs and allowsEBO firms to borrow more than otherwise would be possible (Stewart, 1991).A potential cost of raising funds through an ESOP, however, is the presence ofa new claimant group — employees — whose interests can conflict with those ofother capital providers (Jensen and Meckling, 1979).

A third perspective from which we examine employee participation is that ofmanagerial control. In particular, we examine whether employees are includedbecause the ESOP helps incumbent management to maintain or enhance theircontrol (see, e.g., Stulz, 1988; Gordon and Pound, 1990; Chang, 1990; Chang and

284 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

Mayers, 1992; and Chaplinsky and Niehaus, 1994). This motivation does notexclude other perspectives. Indeed, if there are financing or labor contractadvantages to including employees in a buyout, then doing so will also helpmanagers maintain control. On the other hand, due to potential wealth trans-fers, the inclusion of employees in the buyout transaction could enhance mana-gerial control even when there are no net financing or labor contractingadvantages.

We compare EBOs to buyout transactions in which the only employeesparticipating are top-level managers, or management buyouts (MBOs). Thisapproach controls for the other organizational changes that are associated withemployee buyout transactions, such as the increase in leverage and managementownership, and the change to private ownership.

Our findings suggest that all three perspectives are relevant to understandingwhy employees participate in buyouts. Consistent with the optimal labor con-tract perspective, there is evidence suggesting that employee incentives, firm-specific capital, and risk-bearing are important considerations. For example, allof the consulting firms in our buyout sample include employees as equityparticipants, which is consistent with employee ownership being more likelywhen employee effort is difficult to monitor. EBO firms are more likely thanMBO firms to have excess pension assets, which is consistent with employees ofEBO firms having more firm-specific capital that is subject to appropriation.And consistent with risk-sharing considerations, employee participation is morelikely in firms where the ownership can be spread more diffusely across em-ployees, such as in firms with relatively low values of assets per employee.

Consistent with optimal financing policy, we find that tax avoidance isa strong motivation for including employees for a few firms, but not for themajority. Motivations related to financing considerations, nevertheless, appearimportant. As mentioned above, EBO firms are more likely to have excesspension assets in defined benefit pension plans than MBO firms. Almost always,EBO firms with excess pension assets undertake an excess asset reversion at thetime of the buyout. The excess pension assets materially reduce the amount ofoutside debt financing that is needed for the buyout. The existing literature oftenassociates the termination of pension plans with the appropriation of employees’firm-specific pension capital (see, e.g., Pontiff et al., 1990; Ippolito and James,1992). An alternative interpretation, which is consistent with the structure ofEBO transactions, is that the EBO converts employees’ defined benefit pensioncapital into equity claims, which frees the excess cash assets in the pension planto help finance the buyout.

Also consistent with the financing perspective is the evidence that EBO firmshave significantly lower pre-buyout stock price performance, indicating lowerfuture expected cash flows, and lower pre-buyout financial leverage, suggestinghigher leverage-related costs, than MBO firms. These findings suggest that EBOfirms are more likely to be constrained in their ability to raise outside capital. By

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 285

substituting equity claims for cash compensation, EBO firms increase theirability to support the debt needed to fund the buyout. In addition, a number ofEBOs take place in industries that are under competitive pressure to lower laborcosts, such as the textile, steel, and automobile industries. Consistent with theasymmetric information argument, employee ownership appears to be beneficialin obtaining concessions from employees. These concessions, in turn, enhancethe firm’s ability to borrow.

Some of the above findings, as well as additional results, are also consistentwith the hypothesis that EBOs are used by managers to maintain or enhancetheir control. Relative to MBO firms, EBO firms are more frequently undertakeover pressure, and their poorer prior performance suggests managers ofEBO firms would be concerned about losing their jobs. In addition, managers ofEBO firms tend to have lower pre-buyout ownership than managers of MBOfirms, suggesting that EBO managers have less ability to defend against a take-over bid. Finally, the evidence on post-buyout ownership indicates that EBOmanagers typically have greater control in the post-buyout firm than MBOmanagers, owing to the lack of third-party equity participation in EBOs and thefailure of employees to gain significant control rights early in the buyout.Typically employees do not control the voting of unallocated ESOP shares, andthey rarely receive board representation. While these findings are consistentwith EBOs being used to enhance managerial control, the general lack ofemployee control rights and the low level of third-party equity participation arealso consistent with EBOs being structured to minimize potential conflictsamong the providers of the buyout capital.

The paper proceeds as follows. In the next Section, we describe our sample ofEBOs and MBOs and describe the institutional features of employee buyouts. InSection 3, we discuss the hypotheses concerning the benefits and costs ofemployee participation in buyouts. The evidence presented in Section 4 isdivided into three parts: (1) evidence on the pre-buyout characteristics of firmsundertaking EBOs versus MBOs, (2) evidence on the financial and ownershipstructure of EBO firms, and (3) evidence on the post-buyout asset sales andemployment growth. We end with a short summary and our interpretation ofthe evidence.

2. Design of the study and sample descriptions

Because of the large increase in employee ownership occurring at the time ofthe transaction, employee buyouts provide an opportunity to examine the costsand benefits of employee ownership. To control for the other organizationalchanges occurring simultaneously with the increase in employee ownership (theincrease in managerial ownership and leverage associated with going-privatetransactions), we compare EBO transactions to management buyouts without

286 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

3As a result of our focus on publicly held companies, the sample does not contain somewell-known buyouts, including Avis, Inc., Simmons, Inc., and Burlington Industries. Buyouts werealso attempted by employees but did not ensue in a number of cases, including Alaska Airlines,Eastern Airlines, Frontier Airlines, Pan American Airlines, Peoples Express, and Scott and Fetzer.

broad employee participation or MBOs. Thus, the analysis focuses on theprimary distinction between EBOs and MBOs, which is the breadth of employeeownership.

Generally speaking EBOs involve more broad based employee participationthan MBOs, although the breadth of employee participation varies in bothtypes of transactions. Some MBOs can involve a very large management buyoutgroup. For example, the MBO of CS-First Boston included 290 managers in thebuyout group. Conversely, employee participation in EBOs may be limited toa subset of employees, such as those EBOs that include only salaried workers asequity participants.

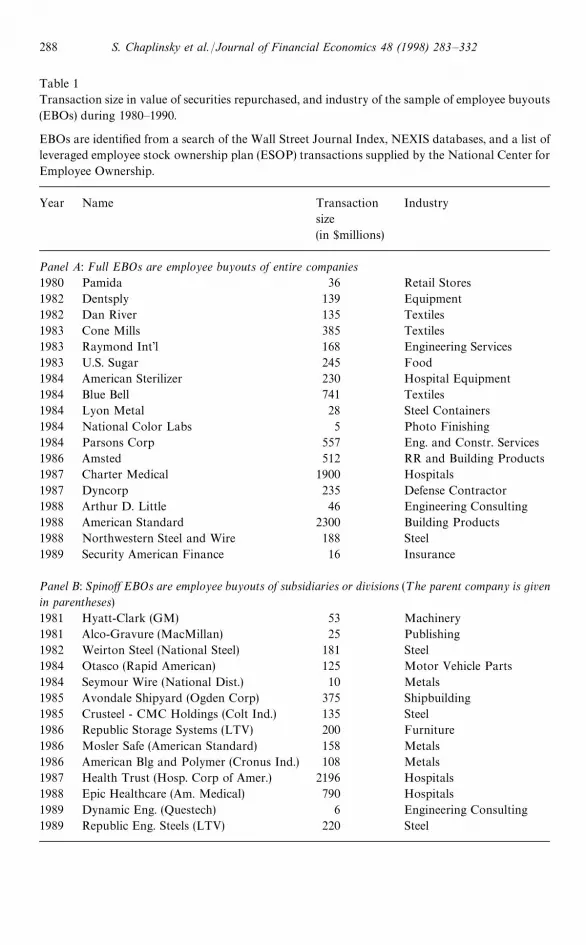

2.1. EBO sample

We search the Wall Street Journal Index, the NEXIS database, and a list ofleveraged ESOP transactions supplied by the National Center for EmployeeOwnership (NCEO) to identify publicly held firms during 1980—1990 that eithersuccessfully go private while giving non-managerial employees equity stakes inthe post-buyout firm through an ESOP, or divest assets to a newly formedprivate firm in which non-managerial employees have an equity stake throughan ESOP. The former type of transaction is referred to as a full EBO and thelatter as a spinoff EBO.

To be included in the sample, a transaction must satisfy each of the followingconditions. First, the post-buyout firm must not be publicly traded. Second, thebuyout announcement must appear in the Wall Street Journal Index or NEXIS.Third, we can obtain a Securities and Exchange Commission (SEC) filingdescribing the transaction, such as a proxy statement, a Schedule 13E-3, or 8-Kfiling.

We gather information on each EBO from SEC filings and collect pre- andpost-transaction information from the Wall Street Journal, NEXIS, and publi-cations included in ABI Proquest. Other financial data are taken from Compus-tat and the Center for Research in Security Prices (CRSP). There are 18 fullEBOs and 14 spinoff EBOs satisfying these conditions. The name, transactionsize, as measured by the market value of repurchased securities, and the generalindustry affiliation of each EBO is listed in Table 1. A brief case description ofeach full EBO appears in Appendix A.3

In all of the EBOs, employees receive their equity stakes through ESOPs,which are defined contribution pension plans with two unique features. First, at

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 287

Table 1Transaction size in value of securities repurchased, and industry of the sample of employee buyouts(EBOs) during 1980—1990.

EBOs are identified from a search of the Wall Street Journal Index, NEXIS databases, and a list ofleveraged employee stock ownership plan (ESOP) transactions supplied by the National Center forEmployee Ownership.

Year Name Transactionsize(in $millions)

Industry

Panel A: Full EBOs are employee buyouts of entire companies1980 Pamida 36 Retail Stores1982 Dentsply 139 Equipment1982 Dan River 135 Textiles1983 Cone Mills 385 Textiles1983 Raymond Int’l 168 Engineering Services1983 U.S. Sugar 245 Food1984 American Sterilizer 230 Hospital Equipment1984 Blue Bell 741 Textiles1984 Lyon Metal 28 Steel Containers1984 National Color Labs 5 Photo Finishing1984 Parsons Corp 557 Eng. and Constr. Services1986 Amsted 512 RR and Building Products1987 Charter Medical 1900 Hospitals1987 Dyncorp 235 Defense Contractor1988 Arthur D. Little 46 Engineering Consulting1988 American Standard 2300 Building Products1988 Northwestern Steel and Wire 188 Steel1989 Security American Finance 16 Insurance

Panel B: Spinoff EBOs are employee buyouts of subsidiaries or divisions (¹he parent company is givenin parentheses)1981 Hyatt-Clark (GM) 53 Machinery1981 Alco-Gravure (MacMillan) 25 Publishing1982 Weirton Steel (National Steel) 181 Steel1984 Otasco (Rapid American) 125 Motor Vehicle Parts1984 Seymour Wire (National Dist.) 10 Metals1985 Avondale Shipyard (Ogden Corp) 375 Shipbuilding1985 Crusteel - CMC Holdings (Colt Ind.) 135 Steel1986 Republic Storage Systems (LTV) 200 Furniture1986 Mosler Safe (American Standard) 158 Metals1986 American Blg and Polymer (Cronus Ind.) 108 Metals1987 Health Trust (Hosp. Corp of Amer.) 2196 Hospitals1988 Epic Healthcare (Am. Medical) 790 Hospitals1989 Dynamic Eng. (Questech) 6 Engineering Consulting1989 Republic Eng. Steels (LTV) 220 Steel

288 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

least 50% of an ESOP’s assets must be invested in the equity securities of thesponsoring plan. Second, the ESOP can borrow funds for the purpose ofpurchasing the employer’s securities. In our sample, all of the firms use leveragedESOPs, with the exception of Cone Mills.

In a typical EBO, the ESOP trust borrows funds that are then transferred tothe buyout firm in exchange for equity claims. The funds from the ESOP loan,along with other equity and debt funds, are then used to repurchase the firm’sexisting equity securities, converting all publicly held shares to privately heldshares. Contrary to what the term ‘employee buyout’ may suggest, in mostinstances the ESOP does not become the sole equity holder. Managers typicallyobtain ownership claims outside of the ESOP and in some cases, investmentbanks, and other institutional investors receive equity stakes.

The firm usually guarantees the ESOP loan by committing to make thecontributions to the ESOP necessary to service the loan. As the ESOP loan ispaid off, shares are allocated to employees’ individual accounts, usually inproportion to their compensation. Since the ESOP loan is nominally repaidfrom the firm’s cash flows, it may appear that employees receive shares withoutcontributing capital for the buyout. However, employees often contribute capi-tal indirectly, by foregoing some other form of compensation (Chaplinsky andNiehaus, 1990). We document the types of compensation changes that occur infull EBOs in Appendix A, and the types of compensation changes that occur inspinoff EBOs in Appendix B. As noted there, compensation changes occurringat the time of the EBO range from work-rule changes to large reductions in cashwages. For most firms in our sample, however, employees contribute capital byaccepting the elimination of, or reductions in, existing deferred compensationplans. From an economic perspective, employees pay a fair price for their ESOPshares if the present value of employee compensation concessions, which repres-ents the capital contributed by employees, is equal to the value of the ESOPshares. The complex nature of the compensation exchanges and the lack ofdetailed reporting often prevents assessment of whether the price paid byemployees is equal to the value of their ESOP shares.

Employees cannot remove the shares allocated to their ESOP accounts untiltheir service with the firm ends. Private firms, like EBO firms, must offer torepurchase retirees’ stock at a price determined by an independent valuation. Inthis way, retirees can cash out and diversify. In addition, employees who havereached the age of 55 or have achieved 10 years of service, whichever is later, canrequire that the assets in their ESOP account be diversified (Scholes andWolfson, 1990). However, assuming the inability of employees to use ESOPshares as collateral, the illiquidity of ESOP shares can impose costs on em-ployees without other resources or savings to cover expenses that may occurover time.

Conceivably, EBOs could take place without an ESOP. Employees could allagree individually to borrow on their personal accounts the funds needed to

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 289

purchase a large stake in the firm. The leveraged ESOP, however, providesseveral advantages, one being tax benefits (see later sections and Beatty, 1995).In addition, the ESOP mechanism is likely to reduce transaction costs andexpected default costs. Finally, assuming there is an advantage to havingemployees as a group own a large stake, an ESOP enhances cooperativebehavior among employees by restricting their ability to sell shares to non-employee investors.

2.2. Comparison sample of MBOs

For comparison purposes, a sample of MBOs completed during the 1980sis collected from information obtained from Securities Data Corporationand the IDD Mergers and Acquisition database. To be included in the MBOsample, a buyout announcement must appear in the Wall Street JournalIndex or NEXIS, and top level management must take a stake in the post-buyout equity. The full MBO and parent firms of spinoff MBOs must beincluded in CRSP. The MBO sample consists of 118 full MBO and 64 spinoffMBOs.

The industry concentration of EBOs (see Table 1) indicates that three of the18 full EBO firms and one of the spinoff EBO firms are in the engineeringconsulting business, and have the Standard Industrial Classification (SIC) codeof 87. However, none of the MBOs is in the consulting business. On the otherhand, every two-digit SIC code with more than four full MBOs also has at leastone EBO. Both EBOs and MBOs occur with some frequency in the steel andtextile industries. Eight EBOs and seven full MBOs are in the steel industry (SICcodes "33, 34), and three EBOs and seven full MBOs are in the textile industry(SIC codes "22, 23, 24). The latter findings suggest that employee participationis not determined solely by industry factors.

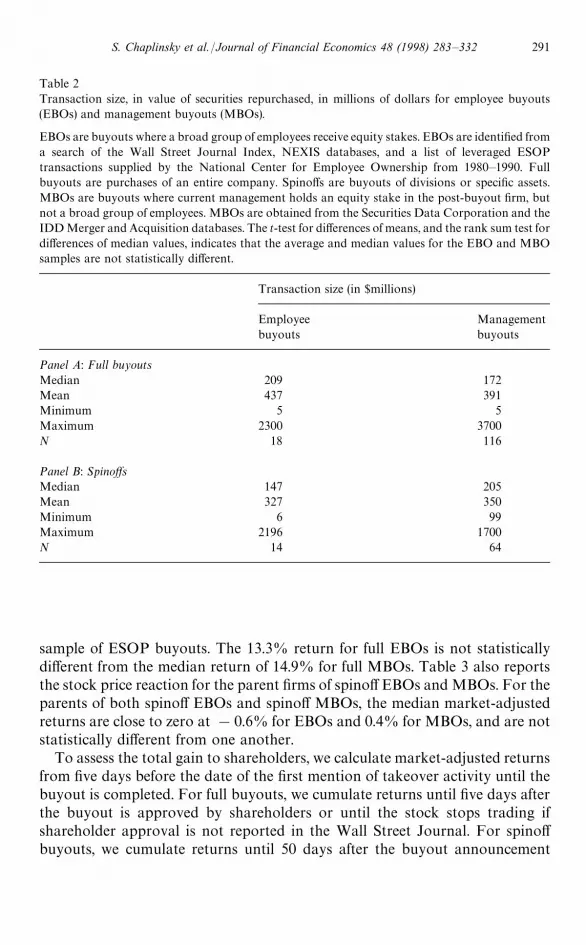

Table 2 provides summary statistics on the size of EBO and MBO transac-tions as measured by the market value of repurchased securities. Full EBOsrange in size from $5 million to $2.3 billion, and have a median value $209million. Full MBOs range in size from $5 million to $3.7 billion, and havea median value of $172 million. Although smaller, the median size of MBOtransactions is not statistically different from EBOs. Spinoff EBOs range from$6 million to $2.2 billion, with a median of $147 million. The median spinoffMBO transaction is $205 million, which is not statistically different from that ofspinoff EBOs.

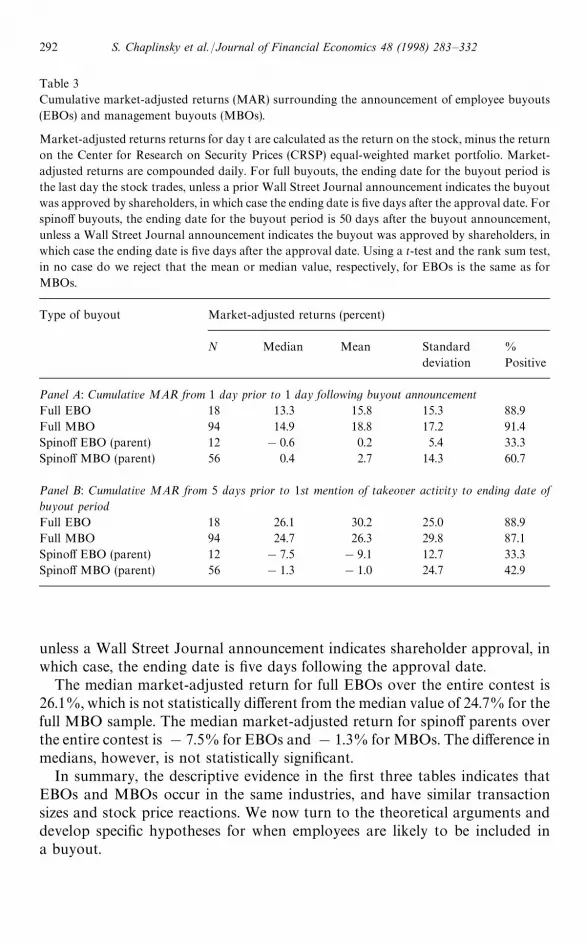

Table 3 investigates the market-adjusted returns surrounding the announce-ments of EBOs and MBOs. Market-adjusted returns are computed for each dayt as the firm’s stock return minus the return on the CRSP equal weighted index.The median three-day market-adjusted return from the day before the buyoutannouncement through day one following the announcement is 13.3% for fullEBOs. This is similar to the 11.5% return that Chang (1990) reports for his

290 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

Table 2Transaction size, in value of securities repurchased, in millions of dollars for employee buyouts(EBOs) and management buyouts (MBOs).

EBOs are buyouts where a broad group of employees receive equity stakes. EBOs are identified froma search of the Wall Street Journal Index, NEXIS databases, and a list of leveraged ESOPtransactions supplied by the National Center for Employee Ownership from 1980—1990. Fullbuyouts are purchases of an entire company. Spinoffs are buyouts of divisions or specific assets.MBOs are buyouts where current management holds an equity stake in the post-buyout firm, butnot a broad group of employees. MBOs are obtained from the Securities Data Corporation and theIDD Merger and Acquisition databases. The t-test for differences of means, and the rank sum test fordifferences of median values, indicates that the average and median values for the EBO and MBOsamples are not statistically different.

Transaction size (in $millions)

Employeebuyouts

Managementbuyouts

Panel A: Full buyoutsMedian 209 172Mean 437 391Minimum 5 5Maximum 2300 3700N 18 116

Panel B: SpinoffsMedian 147 205Mean 327 350Minimum 6 99Maximum 2196 1700N 14 64

sample of ESOP buyouts. The 13.3% return for full EBOs is not statisticallydifferent from the median return of 14.9% for full MBOs. Table 3 also reportsthe stock price reaction for the parent firms of spinoff EBOs and MBOs. For theparents of both spinoff EBOs and spinoff MBOs, the median market-adjustedreturns are close to zero at !0.6% for EBOs and 0.4% for MBOs, and are notstatistically different from one another.

To assess the total gain to shareholders, we calculate market-adjusted returnsfrom five days before the date of the first mention of takeover activity until thebuyout is completed. For full buyouts, we cumulate returns until five days afterthe buyout is approved by shareholders or until the stock stops trading ifshareholder approval is not reported in the Wall Street Journal. For spinoffbuyouts, we cumulate returns until 50 days after the buyout announcement

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 291

Table 3Cumulative market-adjusted returns (MAR) surrounding the announcement of employee buyouts(EBOs) and management buyouts (MBOs).

Market-adjusted returns returns for day t are calculated as the return on the stock, minus the returnon the Center for Research on Security Prices (CRSP) equal-weighted market portfolio. Market-adjusted returns are compounded daily. For full buyouts, the ending date for the buyout period isthe last day the stock trades, unless a prior Wall Street Journal announcement indicates the buyoutwas approved by shareholders, in which case the ending date is five days after the approval date. Forspinoff buyouts, the ending date for the buyout period is 50 days after the buyout announcement,unless a Wall Street Journal announcement indicates the buyout was approved by shareholders, inwhich case the ending date is five days after the approval date. Using a t-test and the rank sum test,in no case do we reject that the mean or median value, respectively, for EBOs is the same as forMBOs.

Type of buyout Market-adjusted returns (percent)

N Median Mean Standarddeviation

%Positive

Panel A: Cumulative MAR from 1 day prior to 1 day following buyout announcementFull EBO 18 13.3 15.8 15.3 88.9Full MBO 94 14.9 18.8 17.2 91.4Spinoff EBO (parent) 12 !0.6 0.2 5.4 33.3Spinoff MBO (parent) 56 0.4 2.7 14.3 60.7

Panel B: Cumulative MAR from 5 days prior to 1st mention of takeover activity to ending date ofbuyout periodFull EBO 18 26.1 30.2 25.0 88.9Full MBO 94 24.7 26.3 29.8 87.1Spinoff EBO (parent) 12 !7.5 !9.1 12.7 33.3Spinoff MBO (parent) 56 !1.3 !1.0 24.7 42.9

unless a Wall Street Journal announcement indicates shareholder approval, inwhich case, the ending date is five days following the approval date.

The median market-adjusted return for full EBOs over the entire contest is26.1%, which is not statistically different from the median value of 24.7% for thefull MBO sample. The median market-adjusted return for spinoff parents overthe entire contest is !7.5% for EBOs and !1.3% for MBOs. The difference inmedians, however, is not statistically significant.

In summary, the descriptive evidence in the first three tables indicates thatEBOs and MBOs occur in the same industries, and have similar transactionsizes and stock price reactions. We now turn to the theoretical arguments anddevelop specific hypotheses for when employees are likely to be included ina buyout.

292 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

4While some authors suggest unions are an effective mechanism for protecting firm-specificcapital from opportunism, Howse and Trebilcock (1993) argue that collective bargaining rules aregenerally insufficient for this purpose. Fruhan (1985) suggests that some EBOs occur because unioncontracts contain shutdown benefits that create a large liability that offsets the potential benefits ofliquidation. However, we are aware of only one instance of shutdown benefits in our sample, andthat involves Weirton Steel.

3. Benefits and costs of including employees in a buyout

In this section, we summarize the costs and benefits of employee ownershipthat have been proposed in the labor contracting and finance literatures.Traditionally, the role of employee ownership in labor contracts is studiedwithout consideration of the financing and managerial control implications tothe firm. Likewise, the finance literature often does not take into account thelabor contract motivations for establishing a leveraged ESOP, but insteadfocuses on tax and managerial control issues. We argue, however, that laborcontracting, financing, tax, and control considerations are important in deter-mining whether employees participate in a buyout.

3.1. Labor contract restructuring

We first hold financing fixed and focus on the impact of employee ownershipfrom an optimal labor contract perspective. The labor economics literature suggeststhat the desirability of employee ownership depends on four factors: employees’firm-specific capital, asymmetric information, incentives, and risk-sharing.

3.1.1. Protecting employees+ firm-specific capitalKlein et al. (1978) and Williamson (1979) suggest that employee control rights

can protect employees’ firm-specific capital. Specialized skills (Becker, 1975),monitoring costs (Lazear, 1981), and information asymmetries (Salop and Salop,1976) can result in employment contracts with the feature that the present valueof an employee’s expected future compensation from their current employmentexceeds the employee’s next best alternative. For example, contracts that payless than the value of marginal product early in an employee’s career, and morethan the value of marginal product late in the employee’s career, create a situ-ation where older employees earn more than they can earn in their next bestalternative. These contracts may be implicit. Informed employees will be con-cerned prior to entering such a contract that these quasi-rents will be appro-priated by opportunistic owners. Employees can protect themselves fromopportunism by obtaining control rights, either through board representation,also known as codetermination, or share ownership. Thus, employee ownershipcan be part of an efficient labor contract that induces employees to make firm-specific investments in the future (Furubotn, 1988; Chapman, 1993; Hyde, 1993).4

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 293

This argument implies that EBOs are more likely when other mechanisms forprotecting employees’ capital, such as implicit contracts, have become lesseffective and when firm-specific investments enhance productivity. Implicitcontracts prevent opportunism when the one-time gain from opportunisticbehavior is less than the present value of future rents foregone as a result ofemployees no longer trusting their employer (Klein and Leffler, 1981). Hence,implicit contracts are likely to become less effective when a firm is performingpoorly, because the firm’s expected life is shorter and future foregone rents willbe lower.

The previous discussion raises the issue of whether EBOs can be used toprotect employees’ existing firm-specific capital that has accumulated from pastinvestments as opposed to capital from future investments. In particular, sup-pose that as a result of past implicit contracts, employees have accumulatedfirm-specific capital, and that circumstances have changed so that the implicitcontract is more likely to be broken and the capital appropriated. Can em-ployees prevent the appropriation by purchasing control rights from existingshareholders? The problem this scenario presents to employees is that they haveto compensate shareholders for foregoing the gains from appropriation. Thus,shareholders would seem to extract the value of employees’ existing capitalthrough the buyout price. However, if employees place a higher value on theright to control whether their capital is appropriated than shareholders dobecause of risk aversion or a higher perceived likelihood of appropriation, or ifthe dissipative costs associated with shareholder appropriation are high, thena mutually beneficial trade between employees and existing shareholders couldtake place. The likelihood that the protection of existing capital would motivatean EBO increases as employees’ existing firm-specific capital increases, and asthe immediate threat of appropriation increases.

The protection of employees’ existing or future firm-specific capital ultimatelyis a concern about employees being compensated for the value of their marginalproduct. A related argument that does not rely on employees accruing firm-specific capital posits that because of asymmetric information employees areconcerned about the negotiated level of compensation. As we now discuss, thereis potentially a role for EBOs to improve labor contracting in this context,but employee cash flow rights play the key role in this argument, not controlrights.

3.1.2. Labor contract restructuring under asymmetric informationIf managers are better informed than employees about the value of the

marginal product of labor, or about rents that the firm is earning, employeesmay doubt managers’ claims when negotiating new labor contracts. Ben-Nerand Jun (1996) and Kovenock and Sparks (1990) present models where grantingemployees cash flow rights can reduce inefficiencies associated with this asym-metric information. To convey the intuition of these models, suppose that

294 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

employees are less informed about product market conditions than manage-ment. Then employees will be concerned that managers, acting on behalf ofowners, will seek a labor contract that gives employees less than the value oftheir marginal product. Employees, knowing that they have inferior informa-tion, interpret a fixed wage offer as indicating that the managers have goodinformation about product market conditions. In contrast, an offer with equityshares suggests managers want to share the bad results with employees. Anequilibrium is established where profitable firms pay fixed wages and poorlyperforming firms compensate employees with equity shares. The key predictionfrom these models is that poorly performing firms are more likely to engage inan EBO than an MBO.

Employees are more likely to distrust management’s motives when wageconcessions are sought or when employees’ firm-specific capital is threatened.Thus, the firm-specific capital arguments discussed above, and the asymmetricinformation arguments are complementary in the sense that both are likely to beimportant under similar circumstances. The importance of credibility in negotiat-ing wage concessions is emphasized in DeAngelo and DeAngelo’s analysis oflabor contract restructuring in the steel industry (DeAngelo and DeAngelo, 1991).They show that layoffs, reductions in management compensation and dividends,and lower reported earnings are often combined in a concerted effort to makecredible the need for union concessions. Granting employees cash flow rights isa potential substitute for these actions. The relatively large number of EBO firmsin industries, like steel and textiles, that faced increased competition during the1980s from foreign firms with lower labor costs is consistent with the argumentthat employee ownership helps these firms negotiate compensation concessions.

3.1.3. Improved incentivesA potential benefit of employees sharing in the firm’s residual cash flows is

greater employee effort and improved monitoring of employees and managers(Alchian and Demsetz, 1972). Accordingly, a large number of EBO firms citeimproved employee performance as a rationale for greater employee ownership.Free rider problems, however, are likely to reduce the magnitude of potentialproductivity gains, especially in firms with large workforces. Employee owner-ship is more likely to be used as an incentive mechanism when the productivityof a team member is difficult to assess, as in professional activities such asconsulting and law (Alchian and Demsetz, 1972). The fact that all four buyoutfirms in the consulting business include employees is consistent with the incen-tive hypothesis.

3.1.4. Inefficient risk-sharingBecause of their relatively large equity stakes, managers in both EBOs and

MBOs are likely to hold undiversified portfolios. With EBOs, however, generalemployees also are likely to hold undiversified portfolios. All things being equal,

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 295

5There is some evidence that firms structure the plans to reduce risk-sharing costs. For example,Amsted established additional defined benefit plans with an offset provision tied to the ESOP’sperformance that provided a floor on retirement income. Also, ESOPs hold preferred stock in six ofthe 18 full EBOs in our sample.

the resulting cost of employee risk-bearing increases with the proportion of eachemployee’s wealth invested in the firm, and with the variability of cash flows.5Thus, the greater the number of employees over which a given aggregateemployee ownership stake can be spread, the less risk that each individualemployee must bear in an EBO. Holding firm size and managerial ownershipfixed, risk-bearing costs for employees decline as the number of employeesincreases and as the variability of cash flows decreases, and thus we expect thelikelihood of employee participation to vary with these factors. However, if theabove ceteris paribus condition is not met, and managerial ownership inparticular is not held constant, then the prediction about the variability of cashflows does not necessarily follow. As the variability of cash flows increasesmanagers may be more likely to seek general employee participation in an effortto reduce their own risk-bearing costs without sacrificing control. This predic-tion is considered further in Section 3.4.

3.2. Tax advantages

One frequently cited motivation for EBOs is the tax benefits available to thesponsoring firm when employees participate in a buyout through an ESOP.These benefits include the following:

Interest exclusion. After 1984, financial institutions that make loans to ESOPscan exclude 50% of the interest received on the loans from taxable income. AfterJuly 1989, the interest exclusion only applies if the ESOP holds more than 50%of the sponsoring firm’s equity.

Dividend deduction. Dividends paid on ESOP stock are deductible expenses atthe corporate level if they are distributed directly to employees (effective post-1984) or used to pay off the ESOP loan (effective post-1986).

Avoid excise tax on excess pension assets. In 1986, Congress introduced anexcise tax on reversions of excess assets from a defined benefit plan. However, ifexcess pension assets are placed in an ESOP, the excise tax is reduced.

Ability to use loss carryforwards. The Tax Reform Act of 1986 restricts theability of corporations to carry losses forward following a change in control,unless an ESOP purchases at least 50% of the equity.

Owners of closely held firms can defer capital gains tax. After 1984, an owner ofa closely held company can defer capital gains taxes arising from a buyout byselling at least 30% of the outstanding shares to an ESOP.

Beatty (1995) finds that the interest exclusion and dividend deduction incen-tives provide measurable tax benefits to public firms using leveraged ESOPs.

296 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

However, since more than half of the EBOs occur prior to the enactment of theseESOP tax benefits, taxes cannot be the sole explanation for employee participa-tion in buyouts. The tax benefits associated with ESOPs do not yield a uniformprediction about the circumstances in which EBOs would arise. The dividenddeduction suggests that firms with a higher demand for tax shields would bemore likely to include employees in the buyout. The pension tax benefit impliesthat EBOs after 1986 would be more likely than MBOs to have overfundedpension plans, and the tax loss carryforward benefit implies that EBOs would bemore likely to have unused tax loss carryforwards.

3.3. Financing implications

We now discuss the effects of ESOP financing on leverage-related costs andincentive conflicts among capital providers.

3.3.1. Lowering leverage-related costsSubstituting equity claims for cash employee compensation costs, consisting

of wages and contributions to pension plans, can lower the leverage-relatedcosts arising from potential bankruptcy and agency costs for a given level ofdebt (Peterson, 1994; Stewart, 1991). To illustrate, suppose that fixed wages arereduced and employees receive equity claims of equal present value. Althoughthe present value of expected cash flows to employees is unchanged by thissubstitution, the substitution creates flexibility for the firm because cash flowsthat would have been allocated to employees can now be used for otherpurposes, such as paying off debt. In addition, to the extent that bankruptcycourts treat employee equity claims like other equity claims, the substitutionplaces creditor claims above part of employee compensation in the event ofdefault, which also could lower leverage-related costs.

In essence, the substitution lowers the priority of at least part of employeecompensation costs for an on-going firm. Further, if employee participation helpsto elicit compensation concessions, as suggested by Ben-Ner and Jun (1996) andKovenock and Sparks (1990), these savings are also available to service thebuyout debt. The implication of these arguments is that employee participationfacilitates financing for the buyout and, in the extreme, can relax a borrowingconstraint that prevents a buyout from occurring. Accordingly, firms with higherleverage-related costs are more likely to include employees in the buyout.

The capital structure literature suggests that leverage-related costs depend onexpected cash flows, the variability of cash flows, and the costs of redeployingassets. Myers (1977) and Williamson (1979) suggest that redeployment costs arehigher for firm-specific assets. Further, Shleifer and Vishny (1992) point out thatredeployment costs are likely to be high when secondary markets are illiquid,which might occur, for example, when there are few buyers for the assets becauseof depressed industry performance.

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 297

6There are additional costs of resolving conflicts among EBO stakeholders because of theill-defined nature of the laws concerning employee participation in buyouts. Both MBOs and EBOsare frequently subjected to lawsuits by pre-buyout shareholders. However, under the EmployeeRetirement Income Security Act (ERISA), the Department of Labor (DOL) has responsibility toensure that employees are treated ‘fairly’ when an ESOP is used in a buyout (Chaplinsky et al., 1994;Seelig, 1986). In our sample of full EBOs, four firms are subject to challenge under ERISA and thesesuits take an average of four years to settle.

3.3.2. Conflicts among claimantsMaking employees substantial equity holders can create additional conflicts

among capital providers. For example, conflicts can arise between employeesand outside investors over the level of wages and benefits, and over strategicdecisions like plant closings and layoffs that are difficult to anticipate andresolve contractually. The costs of resolving conflicts are further likely toincrease when employees are heterogeneous in their interests and skills(Hansmann, 1990, 1993).

One way to reduce conflicts between EBO debtholders and employees is tolimit employees’ control rights while the debt is outstanding. The institutionalfeatures of the ESOP loan are well suited for this purpose. ESOP shares areallocated to employees as the principal on the ESOP loan is repaid. Whileemployees must receive control rights on allocated shares, the control rights onunallocated shares can rest with the ESOP trustee. Thus, conflicts betweenemployees and ESOP lenders can be mitigated by having an ESOP trustee whocontrols unallocated shares and is appointed by non-employee capitalproviders.

Outside equity holders, on the other hand, cannot avoid potential conflictswith employees indefinitely because ESOP shares eventually are allocated toemployees. At this point, outside equity holders must contend with anothersizable blockholder group whose interests may conflict with their own. If agencycosts associated with outside equity are higher in EBOs than in MBOs, then lessoutside equity should be observed in EBOs.6

3.4. Management control

Finally, we examine whether employee participation in a buyout is motivatedby managers’ desire to enhance or retain control. Stulz (1988), Gordon andPound (1990), and Chang and Mayers (1992) argue that ESOPs can expandmanagers’ control rights beyond their percentage ownership if managers dir-ectly control unallocated shares, or if the parties controlling ESOP shares, eitherthe employees or the trustee, are more likely to be aligned with managers thanoutside investors. Accordingly, EBO managers can obtain greater control in thepost-buyout firm than MBO managers, holding constant managers’ percentageownership and the firm’s leverage. Moreover, to the extent that employee

298 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

7Greater managerial control can be wealth increasing or decreasing. We therefore do not use theterm ‘entrenchment’ which typically has a negative connotation. We do not attempt to estimate thewealth effects associated with greater management control in EBO transactions because it wouldrequire controlling for (1) all of the costs and benefits of employee ownership previously discussed,(2) all the determinants of value from going private transactions in general, and (3) all the potentialwealth transfers from employees and other stakeholder groups.

8See Chapman (1993) for a critical evaluation of the Shleifer and Summers (1988) hypothesis.Whether the breaching of implicit contracts with employees is the motivation for leveraged buyoutsis explored theoretically by Habib (1995) and empirically by Ippolito and James (1992).

ownership replaces equity ownership by third party investors, such as moretypically Kohlberg, Kravis, and Roberts, Inc. (KKR), who are likely to monitormanagement, managerial control can be further enhanced relative to MBOs.7

Managers would be more likely to include employees and enhance theircontrol if they are concerned about being replaced if the alternative in ouranalysis, an MBO took place. Managers’ concerns about being replaced arelikely to be related to several observable factors. First, prior takeover pressurecould suggest that at least some outsiders believe management should bereplaced. Second, poor pre-buyout performance could foster the perception thatincumbent management is part of the problem. Third, low pre-buyout manage-rial ownership suggests managers are more vulnerable to replacement. Inaddition, including employees in a buyout could help managers retain control ifemployees believed that an outsider is more likely to appropriate their firm-specific capital than incumbent management (Shleifer and Summers, 1988). Inthis case, employees could be willing to contribute part of their capital to helpincumbent management maintain control.8 Thus, the managerial controlhypothesis predicts that managers are more likely to pursue an EBO when thefirm is under takeover pressure, performs poorly, has low managerial ownership,or when employees have firm-specific capital that is subject to appropriation.

4. Evidence

The evidence compares EBOs and MBOs with respect to their: (1) pre-buyoutcharacteristics, (2) post-buyout financial structure, and (3) decisions and experi-ence after the buyout.

4.1. Pre-buyout characteristics

In this section we relate the pre-buyout characteristics of EBOs to thetheoretical motivations developed in the previous section. The pre-buyoutcharacteristics reviewed are financial performance, pension plans, takeoverpressure, the ownership by directors and officers, firm-specific assets, leverage,

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 299

9Market model abnormal returns generally indicate that the median EBO underperforms relativeto the median MBO, but the difference is not statistically significant. We place more emphasis on themarket-adjusted returns because of concerns about cumulating estimation errors in market modelparameters over long intervals and because the market model results are sensitive to the estimationperiod.

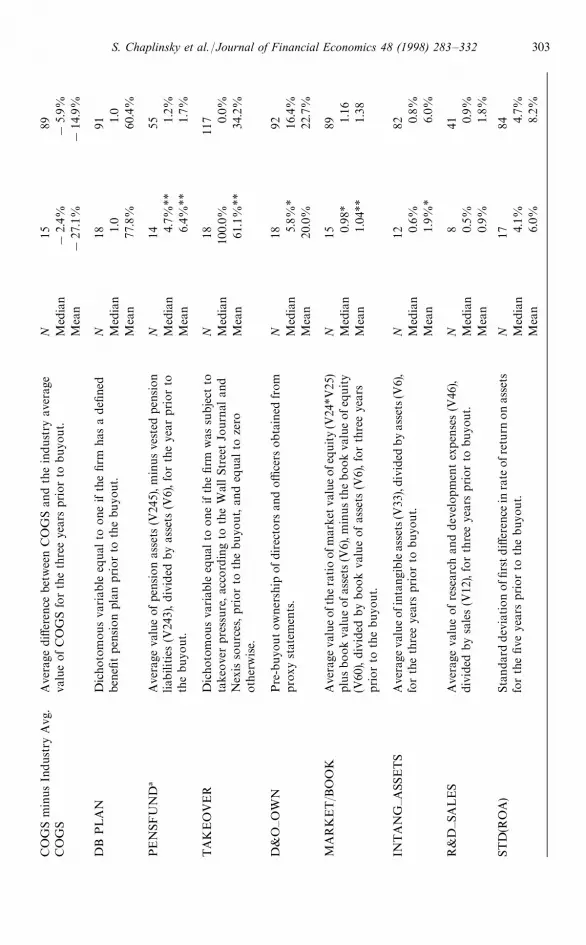

and assets per employee. We begin with univariate comparisons of the pre-buyout characteristics of EBO and MBO firms in Table 4. For the most part,the hypotheses are stated as predictions about a particular variable holdingother factors constant. Therefore, the univariate analysis should be viewed moreas data description than hypothesis testing.

4.1.1. Univariate analysisPre-buyout performance bears on a number of the motivations for EBOs. In

particular, the arguments about how employee ownership affects leverage-related costs, labor contracting under asymmetric information, the possibleappropriation of employees’ firm-specific capital, and managerial control allimply that employee participation is more likely when the firm is performingpoorly. Only the tax motivation implies the opposite. Stock price performanceevidence indicates that EBOs generally have poorer performance than MBOsprior to the buyout. For example, the median market-adjusted return from 550days before the buyout through 50 days before the first indication of a change incontrol (MAR[!550,!50]) is !23.3% for EBOs versus !3.6% for MBOs,a difference that is significant at the 1% level. Moreover, 16 of the 18 full EBOshave negative market-adjusted returns over this pre-buyout period. The twofirms with positive market-adjusted returns are consulting firms. To control fordifferences in risk, we also examine size-decile returns as calculated by Dimsonand Marsh (1986). The median value of size-decile returns for EBOs is !33.7%,significantly less than the 1.4% observed for MBOs.9

With respect to accounting-based performance measures, the median valuesof the pre-buyout return on assets (ROA) and sales growth (SALESGR)measures for EBOs are less than the medians for MBOs, but the differences arenot statistically significant. We find the same result after controlling for industryfactors by subtracting the industry averages from each firm’s value.

Additionally, we examine the production costs of EBOs and MBOs usinga variable that measures the average cost of goods sold, divided by sales(COGS). Cost of goods sold typically includes labor costs, raw materials, andoperating expenses depending on whether the firm is in the manufacturingor service sector. The results indicate that the value of COGS is signi-ficantly higher, and therefore the gross profit margin is lower in EBOs thanMBOs. However, we do not find significant differences after controlling forindustry.

300 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

The presence of a defined benefit pension plan is one factor that previousresearch associates with whether employees either have or will accrue firm-specific capital (see, Ippolito and James, 1992; Pontiff et al., 1990). Definedbenefit pension plans are typically structured so that legal pension liabilities toa particular employee increase at an increasing rate with the employee’s service.To the extent that employees pay for their pension benefits uniformly over theircareer through foregone wages, employees overpay, relative to their legal bene-fits, early in their careers. The accumulated value of these overpayments is thevalue of employees’ firm-specific pension capital. Since a plan termination cancause employees to lose their firm-specific pension capital, the willingness ofemployees to accumulate this firm-specific capital rests on an implicit agreementthat the firm will not opportunistically terminate the pension plan. Plan termi-nations do not necessarily impose losses on employees. A new pension plan, oran adjustment in other compensation, can compensate employees for lossesarising from a terminated plan.

While employee firm-specific capital exists in most defined benefit plans, itdoes not arise in defined contribution plans which is the other major type ofemployer-sponsored pension plan. Table 4 indicates that 77.8% of the EBOfirms have a defined benefit plan prior to the buyout (DB PLAN), compared to60.4% for MBO firms. However, a chi-square test of homogeneity fails to rejectthe hypothesis that the proportions are the same.

The amount of capital that employees have at stake in their defined benefitpension plans depends on a number of firm and labor force characteristics(Peterson, 1992). Ippolito and James (1992) and Pontiff et al. (1990) use thedifference between the value of pension assets and the legal pension liability asa measure of the amount of employees’ capital that can be appropriated througha plan termination. This measure is accurate if firms fund their pension plans sothat the value of pension assets equals the accumulated payments made byemployees.

Following the existing literature, we examine the extent to which pensionassets differ from legal pension liabilities for those firms that have defined benefitplans using the variable PENSFUND, which equals the value of pension assets,minus vested pension liabilities, divided by corporate assets. Positive values forPENSFUND indicate that there are excess pension assets relative to legalliabilities and thus employees have capital that is subject to appropriation. Themedian value of PENSFUND for EBO firms is 4.7%, compared to 1.2% forMBO firms. The difference in medians is statistically significant at the 5% level.The higher value of excess pension assets is consistent with employees havingmore capital at stake in EBO firms. If, contrary to the assumption underlyingthis analysis, the amount of overfunding is unrelated to the amount of employeecapital, the threat of opportunism related to plan termination still increases asoverfunding increases, because termination allows the firm to remove the excessassets and use them for other purposes.

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 301

Tab

le4

Pre

-buyo

utch

arac

terist

ics

ofem

plo

yee

buyo

uts

(EBO

s)an

dm

anag

emen

tbu

youts

(MBO

s)ofen

tire

com

pan

ies

com

ple

ted

during

1980

—199

0.

Com

pust

atva

riab

les

are

indi

cate

din

pare

nth

eses

with

the

desc

ript

ion

ofea

chan

alys

isva

riab

le.T

he

mea

nan

dm

edia

nva

lues

for

each

variab

lear

eco

mpa

red

for

the

EBO

sam

ple

and

the

MBO

sam

ple.

Stat

istica

lsign

ifica

nce

atth

e1%

,5%

,an

d10

%le

vels

are

note

d,re

spec

tive

ly,w

ith

*,**

,**

*.D

iffer

ence

inm

eans

isbas

edon

at-

test

,an

ddiff

eren

cein

med

ians

isba

sed

ona

rank

sum

test

.For

two

dic

hoto

mou

sva

riab

les,

DB

PLA

Nan

dTA

KEO

VER

,a

chi-sq

uar

ete

stis

used

tom

easu

reth

edi

ffere

nce

inpro

por

tions

.U

nle

ssoth

erw

ise

note

d,an

nua

lfinan

cial

stat

emen

tda

taar

efrom

Com

pust

at,M

oody’

s,or

Sec

uritie

san

dE

xcha

nge

Com

mission

discl

osu

redo

cum

ents

,and

stock

retu

rndat

aar

efrom

the

Cen

terfo

rR

esea

rch

on

Sec

urity

Price

s(C

RSP).

Var

iable

Des

crip

tion

Sta

tist

icEB

Os

MBO

s

MA

R[!

550,!

50]

Mar

ket

adju

sted

hold

ing

per

iod

retu

rnfrom

day!

550

today

!50

,wher

eday

0is

thefirs

tindi

cation

ofa

pos

sible

chan

gein

contr

ol.

N18

95M

edia

n!

23.3

%*

!3.

6%M

ean

!24

.3%

*6.

2%

Size

-Dec

ileA

dju

sted

Ret

urn

[!55

0,!

50]

Hold

ing

per

iod

retu

rnnet

ofsize

deci

leho

ldin

gpe

riod

retu

rnfrom

day

!55

0to

day!

50,w

her

eday

0is

the

first

indic

atio

nofa

poss

ible

chan

gein

contr

ol.

N18

95M

edia

n!

33.7

%**

*1.

4%M

ean

!32

.4%

**12

.2%

RO

AR

etur

non

asse

ts(R

OA

),ta

ken

asav

erag

ean

nua

loper

atin

gin

com

e(V

13),

divi

ded

by

tota

lass

ets(V

6),f

orth

ree

year

spr

ior

toth

ebuy

out

.

N17

89M

edia

n!

14.4

%**

*16

.0%

Mea

n!

11.8

%11

.9%

RO

Am

inus

Indus

try

Avg

.R

OA

Ave

rage

diff

eren

cebe

twee

nR

OA

and

indus

try

aver

age

valu

eofR

OA

for

thre

eye

ars

prior

toth

ebuyo

ut.

N17

89M

edia

n4.

5%6.

8%M

ean

6.8%

4.3%

SAL

ESG

RA

vera

gean

nual

grow

thin

sale

s(V

12)f

orth

eth

ree

year

sprior

toth

ebuy

out

.N

1786

Med

ian

8.3%

10.7

%M

ean

9.1%

13.3

%

SA

LESG

Rm

inus

Indus

try

Avg

.SA

LE

SGR

Ave

rage

diff

eren

cebe

twee

nSA

LE

SGR

and

the

indust

ryav

erag

eva

lue

ofSA

LESG

Rfo

rth

eth

ree

year

sprior

tobuy

out

.

N17

86M

edia

n!

11.6

%!

8.2%

Mea

n!

30.4

%!

38.5

%

CO

GS

Ave

rage

valu

eof

cost

ofg

ood

sso

ld(C

OG

S),(

V41

)di

vide

dby

sale

s(V

12),

for

the

thre

eye

ars

prio

rto

buyo

ut.

N15

89M

edia

n76

.1%

**68

.8%

Mea

n76

.7%

**66

.8%

302 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

CO

GS

min

us

Indust

ryA

vg.

CO

GS

Ave

rage

diff

eren

cebe

twee

nC

OG

San

dth

ein

dust

ryav

erag

eva

lue

ofC

OG

Sfo

rth

eth

ree

year

sprior

tobuy

out.

N15

89M

edia

n!

2.4%

!5.

9%M

ean

!27

.1%

!14

.9%

DB

PLA

ND

icho

tom

ous

variab

leeq

ual

toone

ifth

efir

mha

sa

defi

ned

ben

efitpen

sion

plan

prior

toth

ebu

yout.

N18

91M

edia

n1.

01.

0M

ean

77.8

%60

.4%

PEN

SFU

ND

!A

vera

geva

lue

ofpe

nsio

nas

sets

(V24

5),m

inus

vest

edpen

sion

liabili

ties

(V24

3),div

ided

by

asse

ts(V

6),fo

rth

eye

arprior

toth

ebuy

out.

N14

55M

edia

n4.

7%**

1.2%

Mea

n6.

4%**

1.7%

TA

KE

OV

ER

Dic

hoto

mou

sva

riab

leeq

ualto

one

ifth

efirm

was

subj

ectto

take

ove

rpre

ssure

,ac

cord

ing

toth

eW

allStr

eet

Jour

nal

and

Nex

isso

urc

es,pr

ior

toth

ebuyo

ut,

and

equa

lto

zero

oth

erw

ise.

N18

117

Med

ian

100.

0%0.

0%M

ean

61.1

%**

34.2

%

D&

O—O

WN

Pre

-buyo

utow

ner

ship

ofdi

rect

ors

and

offi

cers

obta

ined

from

pro

xyst

atem

ents

.N

1892

Med

ian

5.8%

*16

.4%

Mea

n20

.0%

22.7

%

MA

RK

ET

/BO

OK

Ave

rage

valu

eoft

hera

tio

ofm

arke

tva

lueofe

quity

(V24

*V25

)pl

usbo

okva

lue

ofa

sset

s(V

6),m

inusth

ebook

valu

eofe

quity

(V60

),div

ided

by

boo

kva

lue

ofas

sets

(V6)

,fo

rth

ree

year

sprior

toth

ebuy

out.

N15

89M

edia

n0.

98*

1.16

Mea

n1.

04**

1.38

INT

AN

G—A

SSETS

Ave

rage

valu

eof

inta

ngib

leas

sets

(V33

),div

ided

byas

sets

(V6)

,fo

rth

eth

ree

year

spr

ior

tobuyo

ut.

N12

82M

edia

n0.

6%0.

8%M

ean

1.9%

*6.

0%

R&

D—S

ALES

Ave

rage

valu

eof

rese

arch

and

dev

elop

men

tex

pen

ses

(V46

),di

vide

dby

sale

s(V

12),

for

thre

eye

ars

prior

tobuyo

ut.

N8

41M

edia

n0.

5%0.

9%M

ean

0.9%

1.8%

STD

(RO

A)

Sta

nda

rddev

iation

offi

rstdiff

eren

cein

rate

ofr

eturn

on

asse

tsfo

rth

efive

year

sprior

toth

ebuy

out.

N17

84M

edia

n4.

1%4.

7%M

ean

6.0%

8.2%

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 303

Tab

le4

(Con

tinued

)

Var

iable

Dec

ription

Sta

tist

icEBO

sM

BO

s

LTD

—VA

LU

EA

vera

geva

lue

ofl

ong

term

deb

t(V

9)ove

rth

em

arket

valu

eof

equity

(V24

*V25

)plu

slo

ng

term

deb

t(V

9)fo

rth

reeye

arspr

ior

toth

ebuy

out

.

N17

89M

edia

n12

.0%

*27

.0%

Mea

n15

.8%

*29

.5%

LTD

—ASS

ETS

Ave

rage

valu

eof

long

term

deb

tplu

sde

btin

curr

entliab

ility

(V34

)ove

ras

sets

(V6)

for

thre

eye

ars

prior

toth

ebuy

out.

N17

89M

edia

n9.

5%*

30.4

%M

ean

14.9

%*

39.4

%

UN

USE

DLO

SSC

AR

RY

-FO

RW

AR

DS

Ave

rage

valu

eofun

use

dlo

ssca

rryf

orw

ards

(V52

)div

ided

byto

talas

sets

(V6)

for

thre

eye

ars

prior

toth

ebuy

out

.N

1583

Med

ian

0.0%

0.0%

Mea

n2.

3%1.

1%

EM

PL

OY

EE

SA

vera

genum

berofe

mpl

oye

es(in

thousa

nds)

during

the

thre

eye

ars

prior

toth

ebuyo

ut.

N17

89M

edia

n7.

6*2.

4M

ean

10.3

***

5.0

ASS

ET

S—E

MP

Ave

rage

annu

alto

talas

sets

(V6)

per

empl

oye

e(V

30)fo

rth

eth

ree

year

sprior

toth

ebuy

out

."N

1788

Med

ian

44.9

*60

.5M

ean

46.0

212.

8

!Only

firm

sw

ith

defi

ned

ben

efit

plan

sar

ein

cluded

."A

few

finan

cial

inst

itut

ions

with

very

larg

eva

lues

ofa

sset

sre

lative

toem

ploye

esin

crea

seth

em

ean

sign

ifica

ntly

.Exc

ludi

ng

fina

nci

alin

stitutionsdoes

not

chan

geth

eco

nclu

sions

ofth

ean

alys

is.

304 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

Nine of the 13 full EBOs with excess pension assets terminate a pension planat the time of the EBO. In seven of the nine cases, it appears that the firm usesthe excess assets to finance the buyout without necessarily imposing losses onemployees. The mechanism by which this occurs is best illustrated with a simpleexample. Suppose that a firm with $50 million in excess pension assets estab-lishes an ESOP that borrows $50 million. The proceeds of the ESOP loan aregiven to the sponsoring firm to repurchase outstanding shares. In exchange, theESOP receives shares in the post-buyout firm, all of which are unallocated.Immediately following the buyout, the overfunded pension plan is terminatedand the excess assets are used to pay off the ESOP loan, which allocates sharesto employees. Provided employees do not pay for their ESOP shares byforegoing other compensation, the essential aspect of the transaction is thatemployees trade their defined benefit pension capital for equity capital. TheESOP loan serves simply as a bridge loan that gives the firm access to the cash inthe overfunded pension plan until the plan is terminated. This scenario effec-tively describes seven of the nine terminations, where the excess assets wererolled into the ESOP to repay the ESOP loan immediately following the buyout.

Management’s reluctance to impose losses on employees could suggest thatthey perceive the loss of future employee investments in the firm to be animportant source of value. Alternatively, as Shleifer and Summers (1988) sug-gest, incumbent managers may be more reluctant to appropriate employees’firm-specific capital even though it is in shareholders’ best interest to do so.Another potential interpretation is that the excess pension assets are rolled intothe ESOP to reduce excise taxes on pension reversions. However, only three ofthe nine pension plan reversions take place after the excise tax becomes effectivein 1986. Finally, the use of excess pension assets to reduce the level of debt couldreflect creditors’ desire to reduce quickly the post-buyout level of debt.

We also examine whether EBOs and MBOs are subject to prior takeoveractivity (TAKEOVER), which is defined as either a takeover bid or a Schedule13D filing in the year prior to the buyout announcement. We find that 61.1% ofthe full EBOs experience takeover pressure prior to the buyout, compared toonly 34.2% of the full MBOs, a difference which is statistically significant at the5% level. The higher incidence of takeover pressure for EBOs is consistent withEBOs being motivated as a means to protect employees’ firm-specific capital,and also with the managerial control hypothesis.

The ownership by directors and officers is examined to provide insight intohow capable management is of fending off a takeover threat. Pre-buyoutownership by directors and officers (D&O—OWN), as reported in the firm’sproxy statement during the year prior to the buyout, is 5.8% for the medianEBO and 16.4% for the median MBO, and this difference is statisticallysignificant. Among firms that are subject to takeover pressure, the median valueof director and officer ownership also is lower for EBOs at 3.0%, than for MBOsat 7.4%, however, the difference is not statistically significant. These findings are

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 305

consistent with the argument that managers with low ownership stakes are morelikely to include employees in a buyout when they have limited means ofdefending against a takeover attempt.

Since EBOs are predicted to have greater leverage-related costs, we examinewhether EBOs have assets with greater firm-specific value (Myers, 1977; Will-iamson, 1979). While measuring the extent to which assets have firm-specificvalue is difficult, we follow the existing literature and use the following proxies:(1) the market-to-book ratio (MARKET/BOOK) which equals the market valueof equity, plus the book value of assets, minus the book value of equity, dividedby the book value of assets (Smith and Watts, 1992), (2) the ratio of intangibleassets to total assets (Titman and Wessels, 1988), and (3) the ratio of researchand development expenses to sales (Long and Malitz, 1985).

Contrary to the prediction that EBO firms have a higher proportion offirm-specific assets, the median values of all three measures indicate that EBOfirms typically have a lower proportion of firm-specific assets than MBO firms,although the difference is statistically significant only for the market-to-bookratio. One explanation for the lower market-to-book ratios observed for EBOsfollows from the earlier evidence that EBO firms typically have poor perfor-mance prior to the buyout which, in turn, suggests a higher likelihood ofdistress. All else being equal, a higher likelihood of distress would reduce themarket value of the firm and lower the market-to-book ratio.

Capital structure theory generally hypothesizes that leverage-related costs arepositively related to the variability of cash flows. Accordingly, firms with highervariability of cash flows may be more likely to include employees in a buyout,because their leverage-related costs make it more costly to borrow the fundsnecessary for the buyout without a change in operating commitments to em-ployees. The arguments concerning risk-bearing costs have conflicting predic-tions about the effect of cash flow variability on the likelihood of employeeparticipation. The risk-bearing costs associated with employee ownership implythat employee participation would be less likely the higher the variability of thefirm’s cash flows, holding managerial ownership fixed. However, managers, inan effort to maintain control, while at the same time reducing their ownrisk-bearing costs, may be more inclined to include employees in a buyout, thegreater the variability of cash flows. Consistent with conflicting effects, thestandard deviation of the first difference in the ratio of operating income toassets, shown in Table 4 as the variable STD(ROA), does not differ significantlyfor EBO firms and MBO firms.

An alternative approach to assessing leverage-related costs is to examine thefirm’s pre-buyout financial leverage ratios. A large body of theory proposes thata firm’s leverage ratio is endogenously chosen by management to take accountof all of the costs and benefits of debt. Since many of the costs and benefits areadmittedly hard to measure, the firm’s pre-buyout leverage provides a ‘reducedform’ measure of a firm’s leverage-related costs under the assumption that the

306 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332

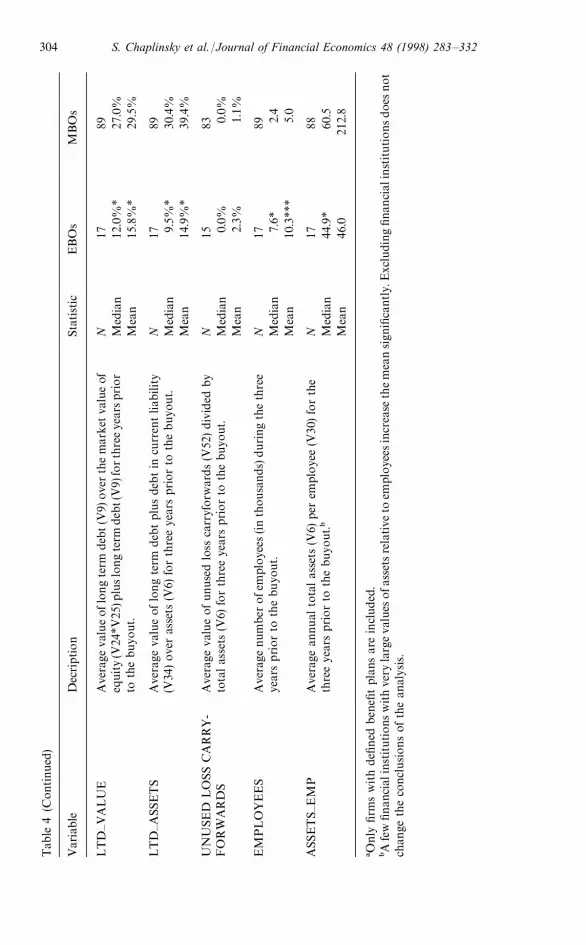

benefits of debt are constant across firms. The leverage ratios reported inTable 4, LTD—VALUE and LTD—ASSETS, indicate that EBOs experiencesignificantly lower median values of pre-buyout leverage than MBOs. Theseresults are consistent with EBOs having higher leverage-related costs thanMBOs prior to the buyout.

A tax based motivation for EBOs is explored with the variable unused losscarryforwards. EBOs could be motivated to preserve unused loss carryforwardsif the transaction results in more than 50% of employee equity being placed inan ESOP. However, the median value of unused loss carryforwards is zero forboth EBOs and MBOs, which is inconsistent with unused loss carryforwardsmotivating employee participation in most transactions.

The incentive alignment hypothesis suggests that employee participation isvaluable because it increases the productivity of workers. However, the magni-tude of potential productivity gains are likely to be reduced by free riderproblems, which increase, all else being equal, with the number of employees.The median level of employment is significantly greater in EBOs than in MBOs,and thus this finding is inconsistent with the incentive alignment hypothesis.

The final variable explored in Table 4, assets per employee (ASSETS—EMP),examines whether the risk-sharing costs of general employees are higher inEBOs or MBOs. EBO firms have a lower median value of assets per employeethan MBOs, and the difference is statistically significant at the 1% level. Thelower the value of the firm’s assets per employee, the less wealth that eachindividual employee must invest in order for employees as a group to obtaina given ownership stake. Since employee diversification opportunities increaseas the wealth invested decreases, the finding of lower assets per employee isconsistent with employees’ risk-bearing costs being lower in EBOs.

4.1.2. Multivariate analysisTo examine whether the findings from the univariate analysis also are valid in

a multivariate context, Table 5 summarizes the results of three logit models,where the dependent variable for each model is the probability that an EBO willoccur, divided by the probability that an MBO will occur. Given the smallnumber of observations and the potential for collinearity among variables, notall of the variables examined in the previous section are included in any singlemodel. Instead, each specification includes one measure for each of themain factors that are hypothesized to affect the choice to include employeesin the buyout. These hypothesized factors are firm performance, pension fund-ing, leverage-related costs, takeover pressure, employee risk-bearing costs, andthe level of ownership by officers and directors. To prevent omitting all firmswithout defined benefit plans from the models, the pension funding variable isassigned a zero value if the firm does not have a defined benefit plan. Since thechoice of variables to include in the models is conditioned on the univariateresults, the reported p-values should be interpreted with caution.

S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332 307

Table 5Logit analysis of the probability of an employee buyout (EBO) relative to a management buyout(MBO) of entire companies.

The dependent variable equals the probability that an EBO will occur, divided by the probabilitythat an MBO will occur. Coefficient estimates are reported with p-values below in parentheses.Independent variables are defined in Table 4.

Underlying factor Independent variable Model 1 Model 2 Model 3

Intercept Intercept !0.34 !0.03 0.77(0.74) (0.98) (0.43)

Firm performance MAR[!550,!50] !2.59 !2.62 !2.18(0.06) (0.05) (0.08)

Pension funding PENSFUND 11.64 16.85 15.17(0.14) (0.07) (0.06)

Leverage-related costs LTD—VALUE !5.41 !5.68(0.02) (0.02)

Leverage-related costs MARKET/BOOK !0.02(0.42)

Takeover pressure TAKEOVER 1.46 1.28 0.66(0.05) (0.11) (0.40)

Employee risk-bearing costs ASSETS—EMP !0.03 !0.03 !0.02(0.03) (0.03) (0.11)

Ownership of officers anddirectors

D&O—OWN 0.02(0.41)

Sample size d of EBOs 17 17 15d of MBOs 73 63 69

The logit models indicate that, after controlling for other factors, the likeli-hood of an EBO is (1) negatively related to pre-buyout stock market perfor-mance, (2) positively related to pension funding, (3) negatively related topre-buyout leverage, and (4) negatively related to the value of assets per em-ployee. In the last specification, the coefficient on the market-to-book ratio isnegative, but not statistically significant, which suggests that after controllingfor other factors, EBO firms do not have lower market-to-book ratios.

Two important conclusions emerge from the evidence on the pre-buyoutcharacteristics that help explain why employees participate in buyouts. First,EBO firms often have excess pension assets that can be used to help finance thebuyout. By rolling over the excess assets into an ESOP and allocating shares toemployees, managers gain access to the cash in the pension plan withoutnecessarily imposing losses on employees. Further, EBOs’ poorer performanceand lower pre-buyout financial leverage suggest that EBO firms havehigher leverage-related costs than MBO firms under their pre-buyout operating

308 S. Chaplinsky et al./Journal of Financial Economics 48 (1998) 283—332