doe - financial and operations procedures toolkit.pdf - saide

TRANSCRIPT

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 7

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 2

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 3

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 4

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 5

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 6

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 8

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 9

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 10

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 11

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 12

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 13

Composite

C M Y CM MY CY CMY K

TOOLKIT FOLDER COVER 19/11/03 1:53 pm Page 14

Composite

C M Y CM MY CY CMY K

Toolkit for Further Education and Training Colleges1

Toolkit for Further Education and Training Colleges 1

ContentsExecutive summary..................................................................................................................................................3

1 Statutory requirements ................................................................................................................................51.1 The Further Education and Training Act, no. 98 of 1998 ............................................................................................51.1.1 Interpretation ..........................................................................................................................................................51.1.2 Auditors....................................................................................................................................................................51.1.3 Financial year end ....................................................................................................................................................61.2 Companies Act, of 1973..............................................................................................................................................61.3 Statements of Generally Accepted Accounting Practice (GAAP) ..................................................................................61.3.1 Introduction ............................................................................................................................................................71.3.2 Deviations from GAAP ..............................................................................................................................................71.3.3 Financial statement components ..............................................................................................................................71.3.4 Preparation of financial statements ..........................................................................................................................81.3.5 Comparatives ..........................................................................................................................................................91.4 The Public Finance Management Act and its effect on FET Colleges (PFMA) ..............................................................9

2 Governance structures and requirements..................................................................................................132.1 Corporate governance ..............................................................................................................................................132.1.1 Governance structures ............................................................................................................................................132.1.2 Tone at the top ......................................................................................................................................................142.1.3 Strategy..................................................................................................................................................................142.1.4 Risk management ..................................................................................................................................................142.1.5 Managing management ........................................................................................................................................152.1.6 Communication......................................................................................................................................................152.1.7 Transaction approval ..............................................................................................................................................15

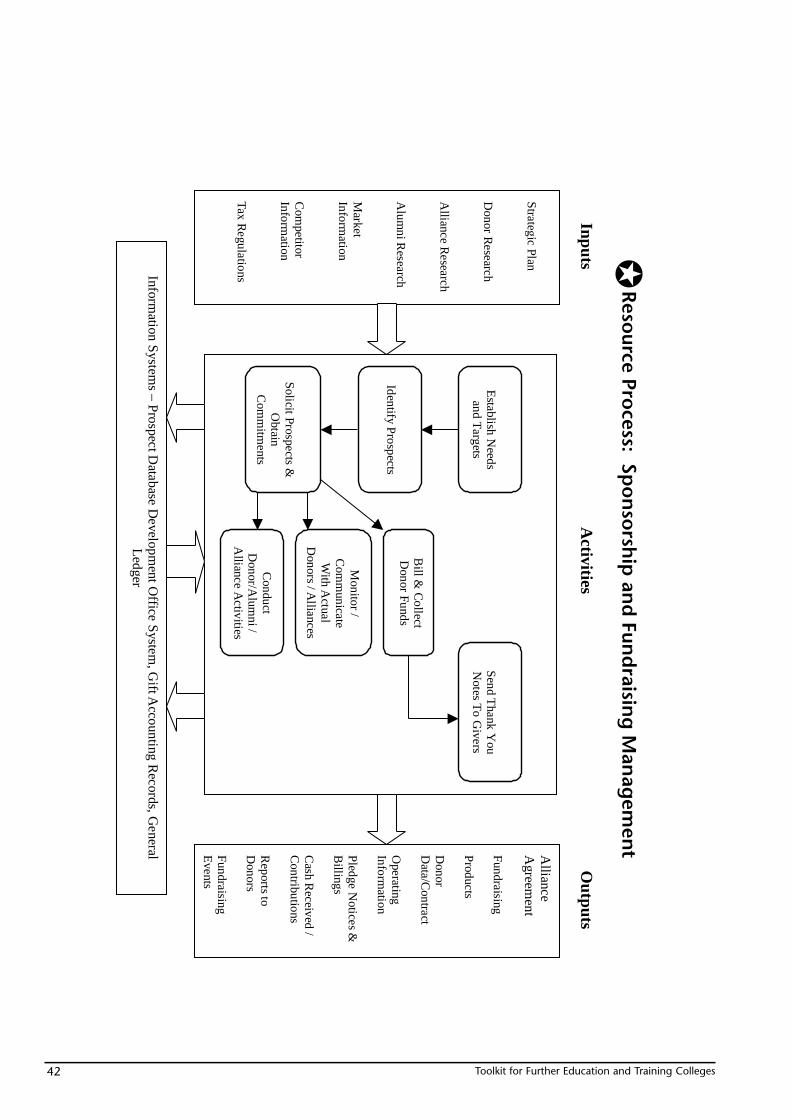

3 The FET business model..............................................................................................................................173.1 Introduction ..............................................................................................................................................................173.1.1 Co-ordinators of the business model development ................................................................................................173.1.2 How to use ............................................................................................................................................................173.1.3 Benchmarking – cautionary statements ..................................................................................................................173.2 FET business model ..................................................................................................................................................183.3 Process analysis template ..........................................................................................................................................213.4 Strategic management processes ..............................................................................................................................223.5 Core management processes ....................................................................................................................................243.5.1 Core process: enrolment ........................................................................................................................................243.6 Core business processes ............................................................................................................................................253.6.1 Core process: enrolment ........................................................................................................................................263.6.2 Core process: service delivery ................................................................................................................................313.6.3 Core process: curriculum management ..................................................................................................................353.7 Resource processes ....................................................................................................................................................363.7.1 Resource process: human resource management....................................................................................................373.7.2 Resource process: sponsorship and fundraising ......................................................................................................423.7.3 Resource process: materials management ..............................................................................................................473.7.4 Resource process: facilities management ................................................................................................................563.7.5 Resource process: financial management................................................................................................................553.7.6 Resource process: information management ..........................................................................................................58

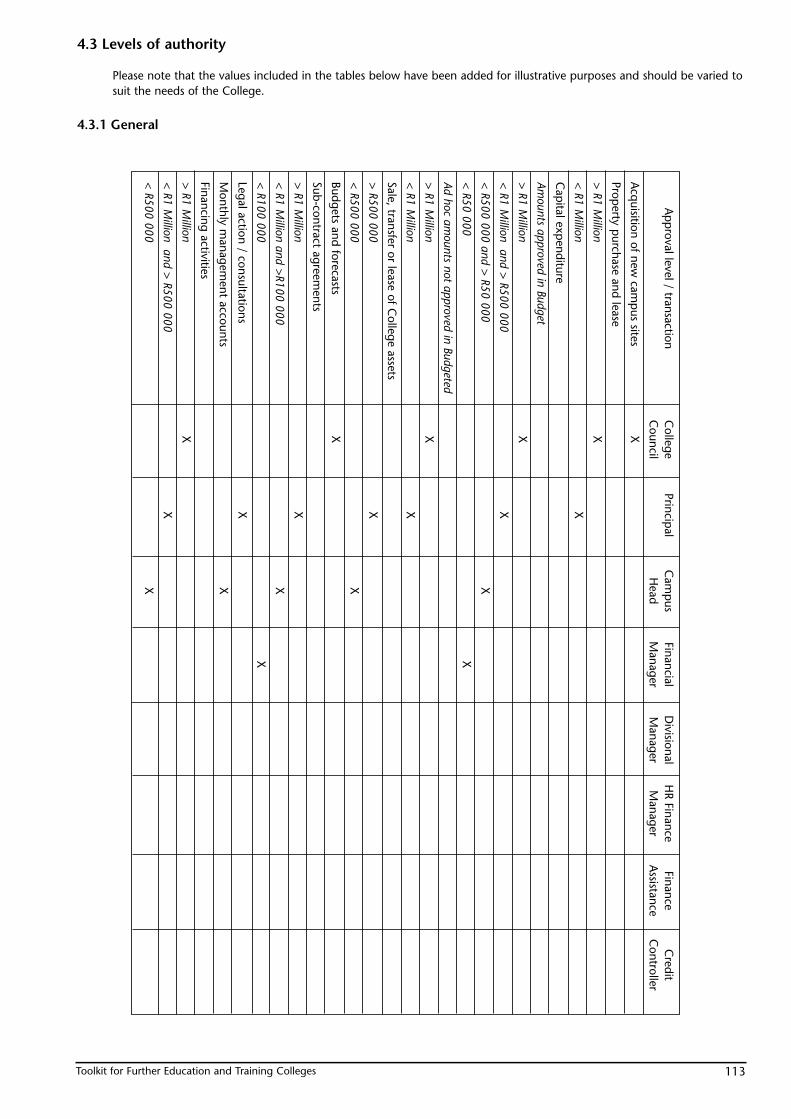

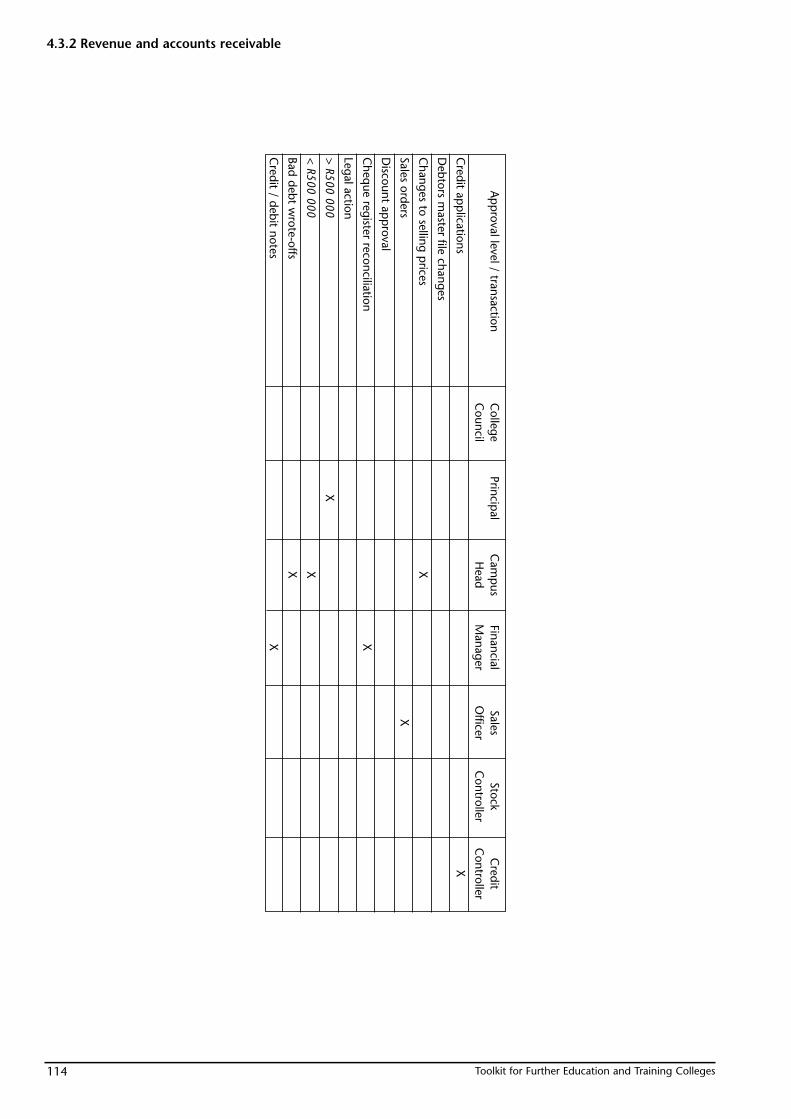

4 Policies and procedures manual ................................................................................................................614.1 Core processes ..........................................................................................................................................................614.1.1 Enrolment ..............................................................................................................................................................614.1.2 Service delivery ......................................................................................................................................................704.1.3 Curriculum management........................................................................................................................................744.2 Resource processes ....................................................................................................................................................754.2.1 Human resources management ..............................................................................................................................754.2.2 Sponsorship and fundraising management ............................................................................................................874.2.3 Materials management ..........................................................................................................................................894.2.4 Facilities management ............................................................................................................................................934.2.5 Financial management ..........................................................................................................................................984.2.6 Information management ....................................................................................................................................1094.3 Levels of authority ..................................................................................................................................................1134.3.1 General ................................................................................................................................................................1134.3.2 Revenue and accounts receivable ........................................................................................................................114

Toolkit for Further Education and Training Colleges2

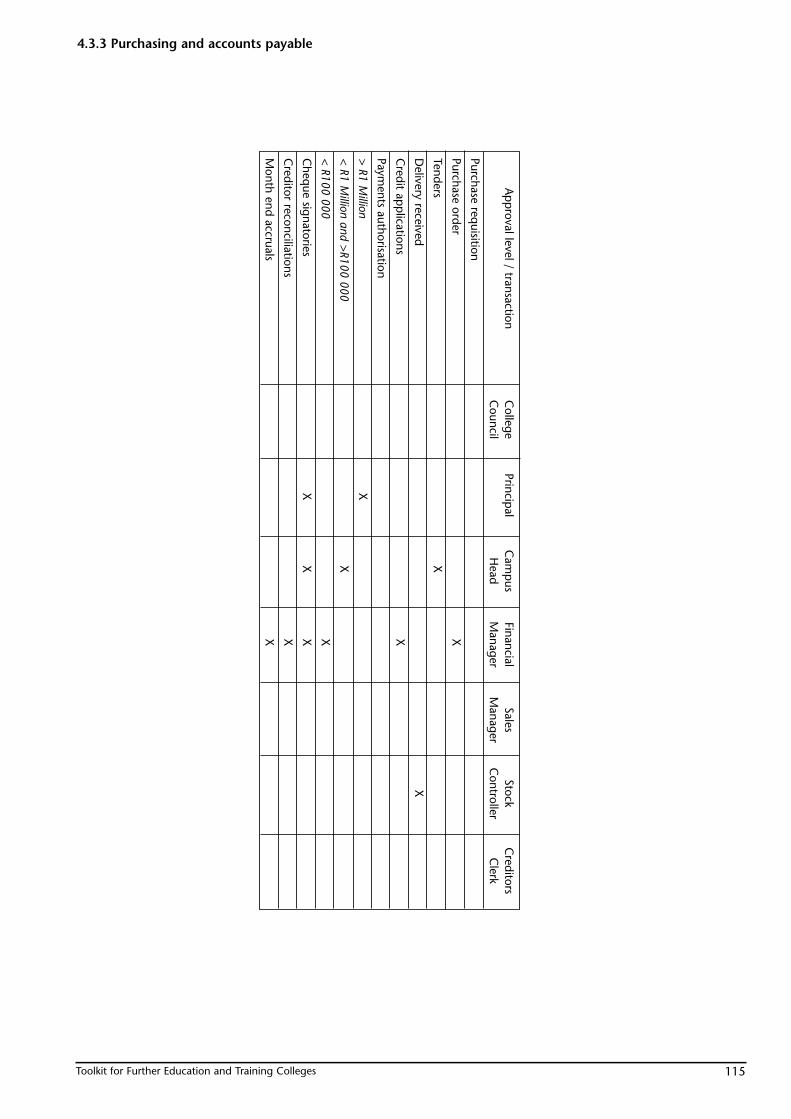

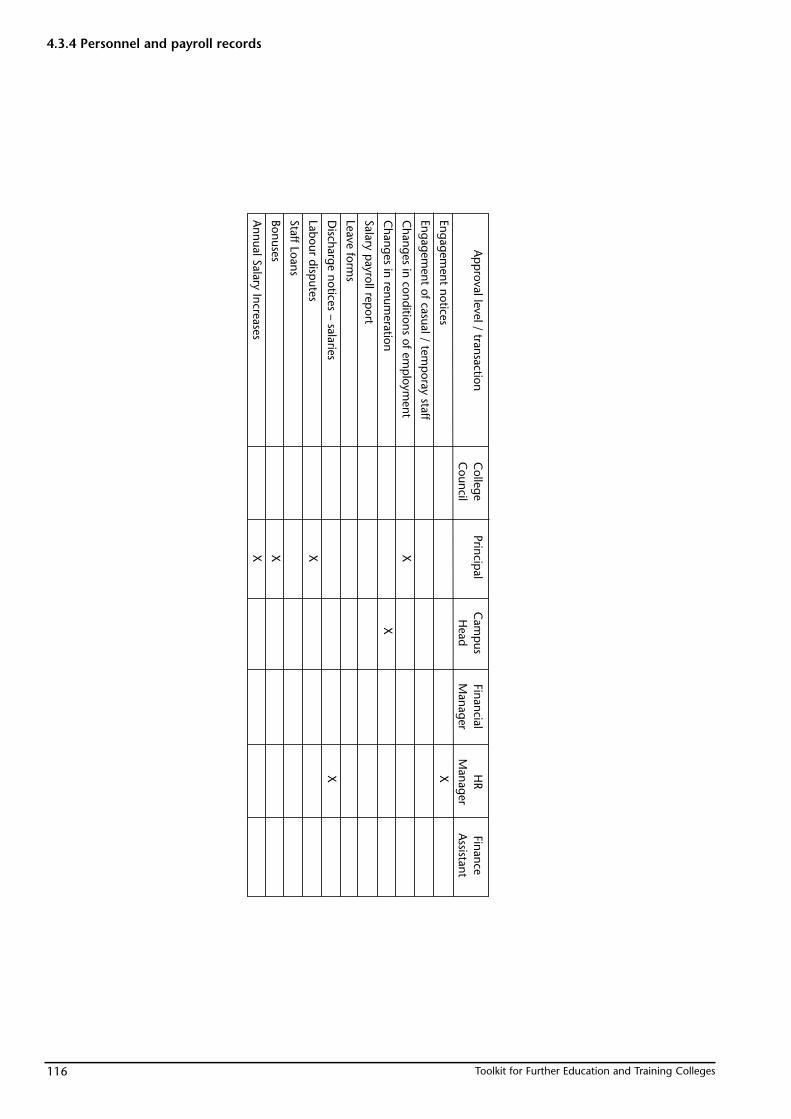

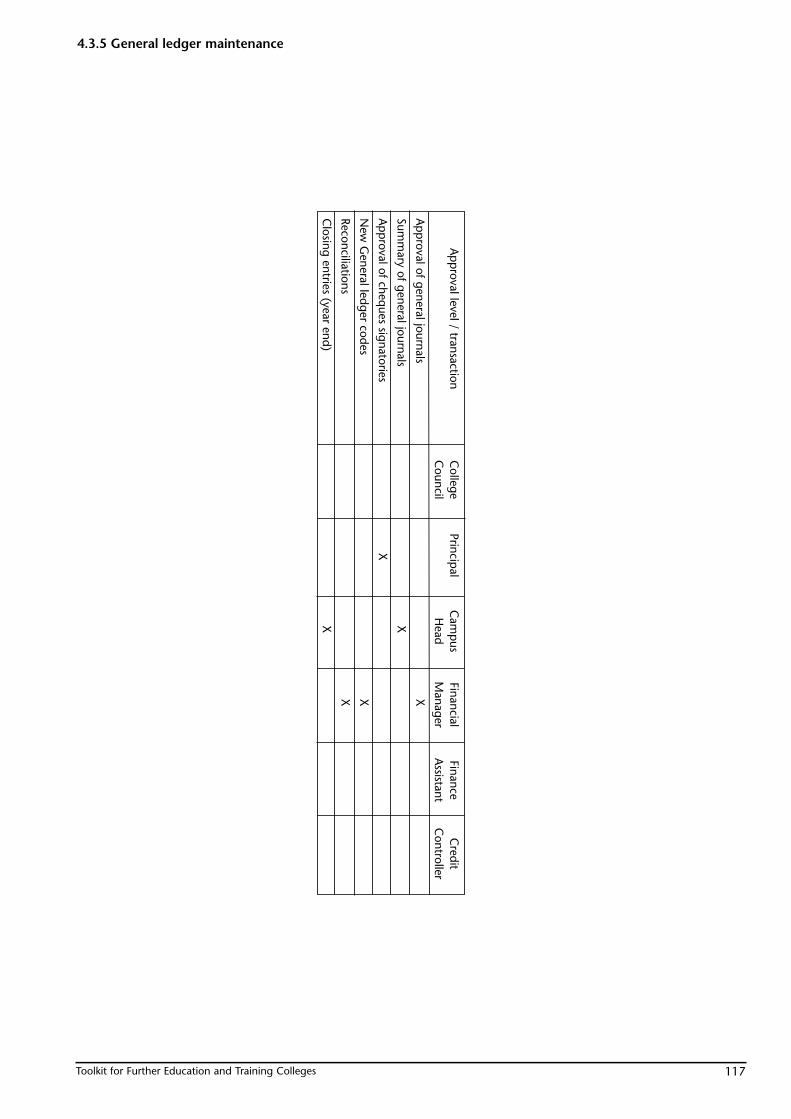

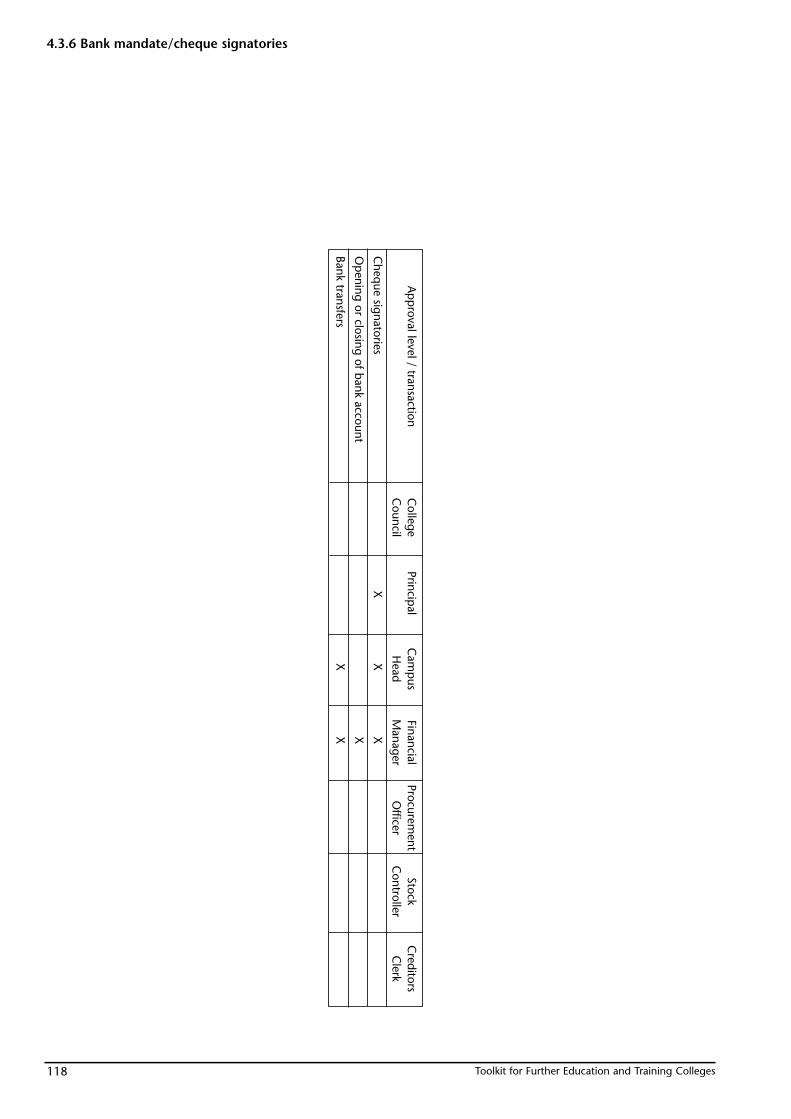

4.3.3 Purchasing and accounts payable ........................................................................................................................1154.3.4 Personnel and payroll records ..............................................................................................................................1164.3.5 General ledger maintenance ................................................................................................................................1174.3.6 Bank mandate/cheque signatories ........................................................................................................................118

5 Financial statements and disclosures ......................................................................................................119

6 Standardised chart of accounts ................................................................................................................153

7 Annexure 1: Fixed asset register ..............................................................................................................163

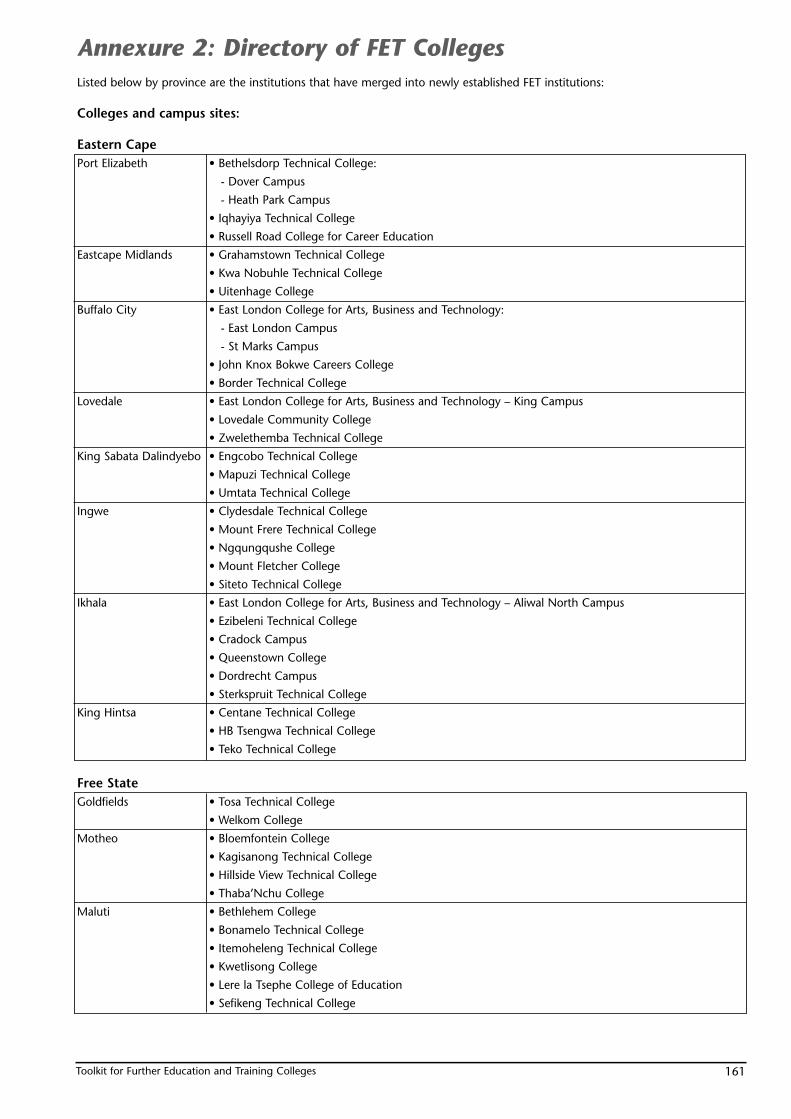

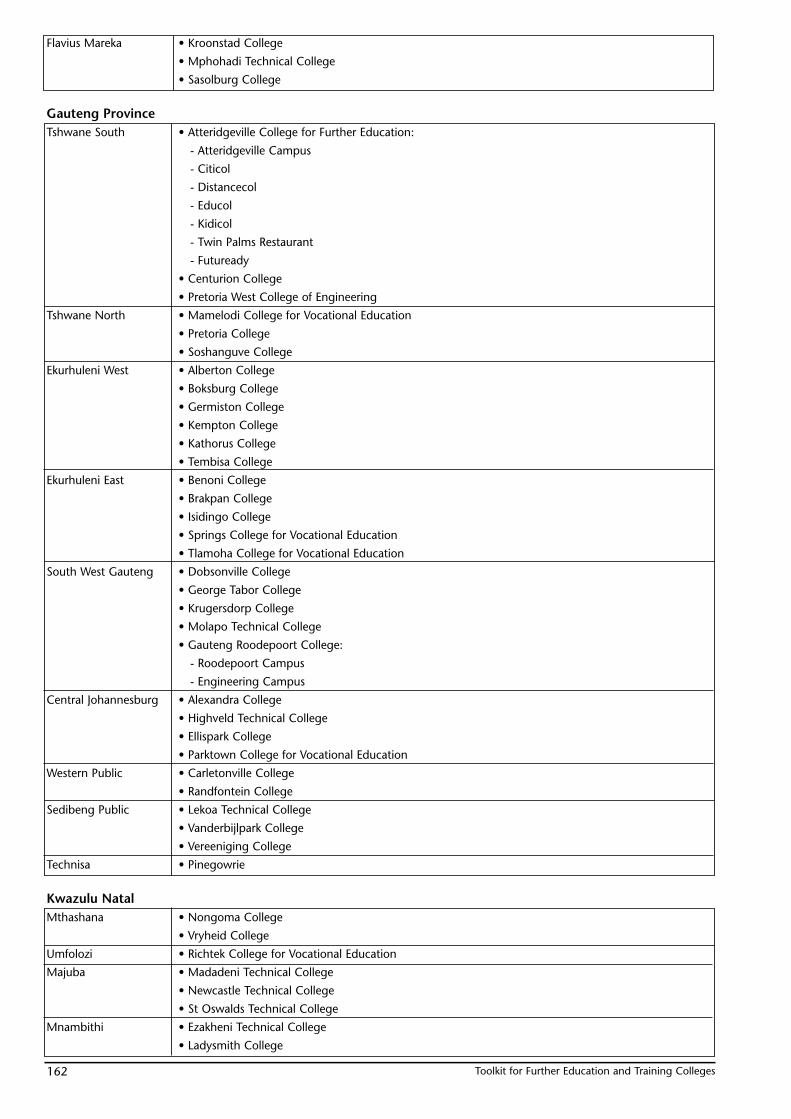

8 Annexure 2: Directory of FET Colleges ....................................................................................................165

9 Annexure 3: Contact details of Colleges and principals..........................................................................169

11 Annexure 4: List of Acts ............................................................................................................................173

12 Annexure 5: Useful websites ....................................................................................................................175

13 Annexure 6: Abbreviations and terminologies ........................................................................................177

Key of icons ..........................................................................................................................................................19

Toolkit for Further Education and Training Colleges 3

Executive summaryReform of the further education system is high on the priorities of the South African Government, not to effect change forchanges sake but to assist in the fundamental upskilling of the South African population and to assist in raisingcompetitiveness in the global economy. As such, there is a recognised need to address the future shape of furthereducation in South Africa. This important strategic analysis contributed towards the landscape for the future shape andconfiguration of further education across South Africa.

The Department of Education (DoE) has determined that a programme of reform over a relatively short period of timewould be appropriate. As result, the new institutional landscape for FET institutions has recently been established throughthe process of College mergers. All the Technical Colleges and a number of former Colleges of Education (some 160Colleges) are now consolidated into 51 merged institutions spread across the nine provinces, providing an infrastructureplatform to develop the intermediate labour skills of our country.

Through extensive research and scrutiny a need has become apparent that these Colleges require immediate guidanceand assistance in areas specific to financial statements, policies and procedures.

This toolkit has been devised in order to assist Colleges with multi-campus management by gaining an improvedunderstanding of the policies and procedures that are suggested to be in place for principals and campus managers and itis not intended to be prescriptive or rigid.

It is important to remember that ‘one size does not fit all’- indeed the issues within each province and within eachCollege will require variations from the model. Users of this toolkit are encouraged to provide commentary and furtherinput to the toolkit project manager (see below).

Extensive research has been carried out in the form of workshops whereby two Colleges were selected to provide inputfrom different provinces.

How to use this toolkit

This toolkit comprises of five different “sections” -

1 Statutory requirements2 The FET Business model3 The Policy and Procedures manual4 Standardised template for Annual Financial Statements5 Standardised template for a Chart of Accounts

Items one and two above will assist the reader in better understanding the legislative environment within which an FETCollege operates, as well as the generic processes in place at a College.

Items three, four and five are to assist Colleges in implementing best practise Policies and Procedures, and to improve thequality of the Annual Financial statements. The standardised Chart of accounts will allow more accurate benchmarkingand comparisons across campus sites in a multi-site College, as well as between Colleges and Provinces.

Who should use this toolkit?

Members of Council, College Principals, Campus Managers, Chief Financial Officers, Administrative assistants and anyoneinvolved in ensuring efficient and effective operations at a College.

Queries and Updates

The toolkit is designed as a dynamic document, and will be updates periodically. As it is intended to indicate “bestpractice”, readers are encouraged to comment and provide ideas. These should be routed to -

Name: Steve Mommen / Ros Jaff

Office: Department of Education: National / National Business Institute

E-mail address: [email protected] / [email protected]

Tel no: (012) 312 – 5 311 / (011) 482 5100

Fax no: (012) 328 – 5 911 / (011) 482 4638

Toolkit for Further Education and Training Colleges4

Toolkit for Further Education and Training Colleges 5

1 Statutory requirements1.1 The Further Education and Training Act, no. 98 of 1998

1.1.1 InterpretationThe FET Act, No. 98 of 1998 was passed to regulate further education and training; to provide for the establishment,governance and funding of public further education and training Colleges; to provide for the registration of private furthereducation and training Colleges; to provide for quality assurance and quality promotion in further education and training;to provide for transitional arrangements and the repeal of laws; and to provide for matters connected therewith.

The purpose of the Act is to establish a national co-ordinated further education and training system, which promotes co-operative governance and provides for programme-based further education training.

An FET institution has been defined by the Act (chapter 1(x)) as “any institution that provides further education and trainingon a full-time, part-time or distance basis and which is-

• Established or regarded as having been established as a public further education and training institution under this Act;• Declared as a public further education and training institution under this Act; or• Registered or conditionally registered as a private further education and training institution under this Act.”

A distinction is made in the Act between public (chapter 4) and private (chapter 5) FET Colleges.

Similarities in the Act for both Colleges:

1 Both have to keep books and records of income, expenditure, assets and liabilities;2 Both have to have their income and expenditure statements or records audited.

The distinctions from a financial perspective that can be deciphered from the FET Act are presented in the table below.Despite the fact that this is a broad overview, it is still very important to note as the Act prescribes the responsibilities ofthe College.

Public FET institution Private FET institution(Chapter 4 of FET Act, of 1998) (Chapter 5 of FET Act, of 1998)

GAAP (Generally Accepted Accounting Practices) is not “Every private further education and training institution must,

mentioned in the Act. Hence no referral is made it the in accordance with generally accepted accounting practice

financial statements being GAAP compliant. principles and procedures”.

The overall governance of the institution is required to The Act is silent in this regard.

be reported on.

• The Council must appoint an auditor. • The Act is silent in this regard (however see below).

• The statement of income and expenditure is only required • “Ensure that its books, records of account and financialto be audited. statements is carried out by an auditor...”

• The Act is silent in this regard. The auditor must conduct the audit in accordance withGenerally Accepted Auditing Standards (GAAS).

A balance sheet and cash flow statement is required to Not specifically mentioned.

be prepared.

The Act is silent in this regard. The Act indicates that financial statements have to be preparedwithin three months after the end of its financial year i.e.before the end of 31 March of the following year.

1.1.2 AuditorsIt is important to note that an auditor is defined in terms of the FET Act under chapter 1 as “any person registered interms of the Public Accountants’ and Auditors’ Act. 1991 (Act No. 80 of 1991)”

This has not been typically the case with certain Colleges and should be addressed when auditors are considered forreappointment.

Toolkit for Further Education and Training Colleges6

1.1.3 Financial year endThe Act also prescribes the “financial year” in respect to a public FET institution as being “a year commencing on the firstday of January and ending the last day of December of the same year.” This indicates that institutions should not preparetheir annual financial statements for a 31 March year-end, as to do so would be incorrect.

1.2 Companies Act, of 1973

If the company has been incorporated in terms of Section 21, the Companies Act will be applicable.

Specific sections in the Companies Act that relate to FET Colleges are Section 21, Section 286(3) and Section 284.

1.2.1 Section 21In certain instances, a College may decide to incorporate as a Section 21 company (that is an association not for gain).This section states the following:

Any association—

• formed or to be formed for any lawful purpose;• having the main object of promoting religion, arts, sciences, education, charity-, recreation, or any other cultural or

social activity or communal or group interests;• which intends to apply its profits (if any) or other income in promoting its said main object;• which prohibits the payment of any dividend to its members; and• which complies with the requirements of this section in respect to its formation and registration, may be incorporated

as a company limited by guarantee.

The memorandum of such association shall comply with the following provisions:

• The income and property of the association whencesoever derived shall be applied solely towards the promotion of itsmain object, and no portion thereof shall be paid or transferred, directly or indirectly, by way of dividend, bonus, orotherwise howsoever, to the members of the association or to its holding company or subsidiary: Provided that nothingherein contained shall prevent the payment in good faith of reasonable remuneration to any officer or servant of theassociation or to any member thereof in return for any services actually rendered to the association.

• Upon its winding-up, deregistration or dissolution the assets of the association remaining after the satisfaction of all itsliabilities shall be given or transferred to some other association or institution or associations or institutions havingobjects similar to its main object, to be determined by the members of the association at or before the time of itsdissolution or, failing such determination, by the Court.

If a company is not incorporated in terms of Section 21, the following sections will still apply to the College

1.2.2 Section 286(3)“The annual financial statements of a company shall, in conformity with generally accepted accounting practice, fairlypresent the state of affairs.... and the profit or loss....”.

1.2.3 Section 284: Duty of a company (or in this case the College) to keep accounting records• Every College shall keep in one of the official languages of the Republic such accounting records as are necessary fairly

to present the state of affairs and business of the College and to explain the transactions and financial position of thetrade or business of the College, including:

- records showing the assets and liabilities of the College1;- a register of fixed assets showing the respective dates of acquisition and the cost thereof, depreciation, if any, the date

of any revaluation and the revalued amount, the respective dates of any disposals and the consideration received inrespect thereof: Provided that in respect of fixed assets acquired before the commencement of this Act, a College may,as at the end of its first financial year after the said commencement, take an inventory of all fixed assets and make arealistic allocation of the total value of fixed assets as shown in the financial statements as at that date over the inventoryof assets;- records containing entries from day to day in sufficient detail of all cash received and paid out and of the matters in

respect of which receipts and payments take place;- where the business of the College has involved dealings in goods, records of all goods sold and purchased and records

showing the goods and the buyers and the sellers thereof in sufficient detail to enable the nature of those goods andthose buyers and sellers to be identified; and

- statements of the annual stocktaking.

• The accounting records referred to in subsection (1) may be kept either by making entries in bound books or by

1 Company has been replaced with College through this section.2 Directors have been replaced with principal

Toolkit for Further Education and Training Colleges 7

recording the matters in question in any other manner, and where such records are not kept by making entries inbound books, adequate precautions shall be taken for guarding against falsification and facilitating its discovery.

• The accounting records shall be kept at the registered office of the College or at such other place as the principal2 thinkfit and shall at all times be open to inspection by the principal and if such records are kept at a place outside theRepublic, there shall be sent to and kept at a place in the Republic, and be at all times open to inspection by theprincipal, such financial statements and returns with respect to the business dealt with in those records as will disclosewith reasonable accuracy the financial position of that business at intervals not exceeding twelve months, subject toSection 285, and will enable the Colleges annual financial statements to be prepared in accordance with this Act.

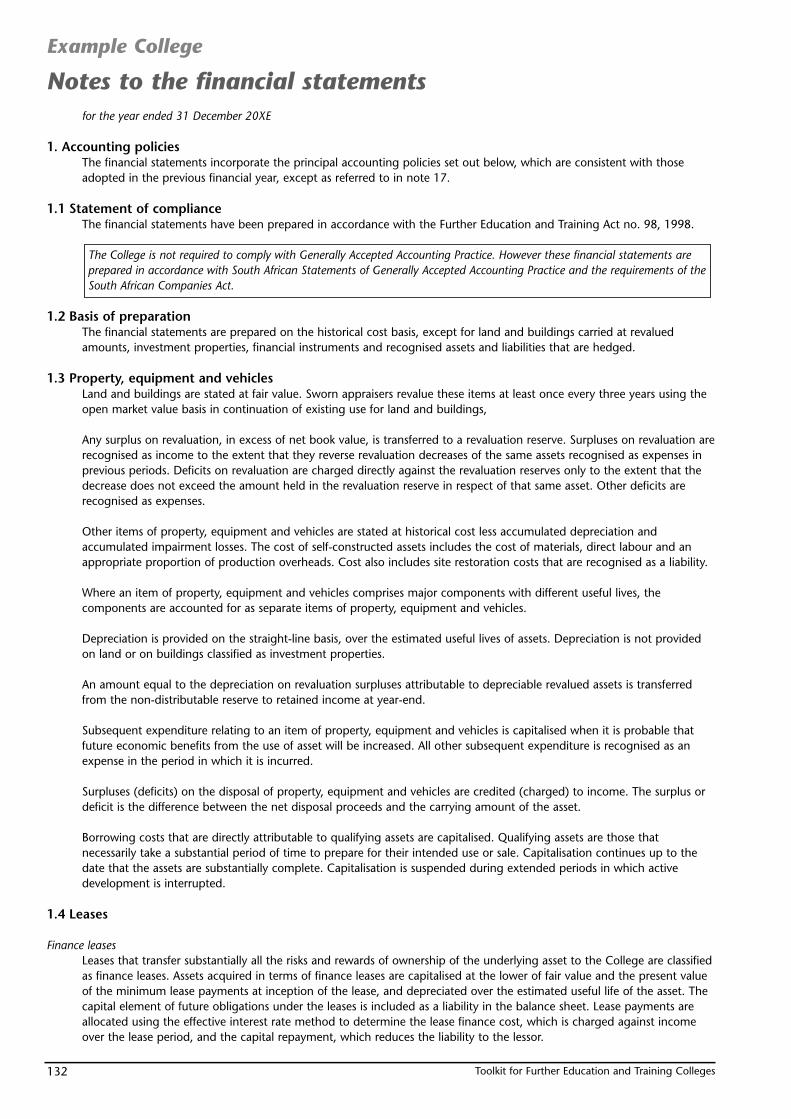

1.3 Statements of Generally Accepted Accounting Practice (GAAP)

1.3.1 IntroductionGenerally Accepted Accounting Practices is a set of accounting principles, standards and procedures used to standardisethe reporting of financial statements. Generally Accepted Accounting Practices is set by the Accounting Practices Board.

The objective of financial statements is to provide information about the financial position, performance and changes infinancial position of an enterprise or in this case a College that is useful to a wide range of users in making economicdecisions.

Financial statements form part of the process of financial reporting. A complete set of financial statements normallyincludes a balance sheet, an income statement, a statement of changes in financial position (which may be presented in avariety of ways, for example, as a statement of cash flows or a statement of funds flow), and those notes and otherstatements and explanatory material that are an integral part of the financial statements.

They may also include supplementary schedules and information based on or derived from, and expected to be readwith, such statements. Such schedules and supplementary information may deal, for example, with financial informationabout industrial and geographical segments and disclosures about the effects of changing prices. Financial statements donot, however, include such items as reports.

The management of the College has the primary responsibility for the preparation and presentation of the financialstatements of the College. Management is also interested in the information contained in the financial statements eventhough it has access to additional management and financial information that helps it carry out its planning, decision-making and control responsibilities.

Management has the ability to determine the form and content of such additional information in order to meet its ownneeds.

1.3.2 Deviations from GAAPIf a College’s financial statements comply with Statements of Generally Accepted Accounting Practice these shoulddisclose that fact. Financial statements should not be described as complying with Statements of Generally AcceptedAccounting Practice unless they comply with all the requirements of each applicable Statement and each applicableapproved interpretation.

Inappropriate accounting treatments are not rectified either by disclosure of the accounting policies used or by notes orexplanatory material.

In the extremely rare circumstances when management concludes that compliance with a requirement in a statementwould be misleading, and therefore that departure from a requirement is necessary to achieve a fair presentation, aCollege should disclose:

1 that management has concluded that the financial statements fairly present the College’s financial position, financialperformance and cash flows,

2 that it has complied in all material respects with applicable Statements of Generally Accepted Accounting Practiceexcept that it has departed from a statement in order to achieve a fair presentation,

3 the statement from which the College has departed, the nature of the departure, including the treatment that thestatement would require, the reason why that treatment would be misleading in the circumstances and the treatmentadopted, and

4 the financial impact of the departure on the College’s net surplus or loss, assets, liabilities, equity and cash flows foreach period presented.

1.3.3 Financial statement componentsA complete set of financial statements includes the following components:a) Balance sheet,b) Income statement,c) A statement showing either

Toolkit for Further Education and Training Colleges8

- All changes in equity, or- Changes in equity other than those arising from capital transactions with owners and distributions to owners

d) A cash flow statement, ande) Accounting policies and explanatory notes.

Each component of the financial statements should be clearly identified. In addition, the following information should beprominently displayed, and repeated when it is necessary for a proper understanding of the information presented:

a) The name of the reporting College or other means of identification.b) Whether the financial statements cover the individual College or a group of Colleges.c) The balance sheet date or the period covered by the financial statements, whichever is appropriate to the related

component of the financial statements.d) The reporting currency.e) The level of precision used in the presentation of figures in the financial statements.

1.3.4 Preparation of financial statements

Underlying assumptions

When preparing financial statements the following two underlying assumptions are relied upon:

Financial statements are prepared on the accrual basis of accounting. Under this basis, the effects of transactions andother events are recognised when they occur (and not as cash or its equivalent is received or paid) and they are recordedin the accounting records and reported in the financial statements of the periods to which they relate. Financialstatements prepared on the accrual basis inform users not only of past transactions involving the payment and receipt ofcash but also of obligations to pay cash in the future and of resources that represent cash to be received in the future.Hence, they provide the type of information about past transactions and other events that is most useful to users inmaking economic decisions.

The financial statements are normally prepared on the assumption that a College is a going concern and will continue inoperation for the foreseeable future. Hence, it is assumed that the College has neither the intention nor the need toliquidate or curtail materially the scale of its operations; if such an intention or need exists, the financial statements mayhave to be prepared on a different basis and, if so, the basis used is disclosed.

When management is aware, in making its assessment, of material uncertainties related to events or conditions that maycast significant doubt upon the College’s ability to continue as a going concern, those uncertainties should be disclosed.When the financial statements are not prepared on a going concern basis, that fact should be disclosed, together with thebasis on which the financial statements are prepared and the reason why the College is not considered to be a goingconcern.

Fair presentationThe overriding requirement of the Companies Act is fair presentation. The existence of a standard is an aid both tocomparability and to fair presentation. However, compliance with a standard is no guarantee that fair presentation will beachieved in the financial statements. Nevertheless, even though accounting standards are not conclusive as to fairpresentation they are highly influential and persuasive in that respect. Accordingly, it is necessary for departures to bedisclosed in an explanatory note to the financial statements.

It is recognised that there may be exceptional circumstances in which a statement of GAAP is not strictly applicablebecause, having regard to the circumstances, it would fail to yield fair presentation, i.e. to comply would be misleading.

Accounting policiesAccounting policies are the specific principles, bases, conventions, rules and practices adopted by a College in preparingand presenting financial statements.

Management should select and apply a College’s accounting policies so that the financial statements comply with all therequirements of each applicable Statement of Generally Accepted Accounting Practice and each applicable approvedinterpretation. Where there is no specific requirement, management should develop policies to ensure that the financialstatements provide information that is:

1 Relevant to the decision-making needs of users, and2 Reliable in that they:3 Present fairly the results and financial position of the College,4 Reflect the economic substance of events and transactions and not merely the legal form5 Are neutral, that is free from bias,6 Are prudent, and7 Are complete in all material respects.

Toolkit for Further Education and Training Colleges 9

1.3.5 ComparativesComparative information should be disclosed in respect of the previous period for all numerical information in thefinancial statements. Comparative information should be included in narrative and descriptive information when it isrelevant to an understanding of the current period’s financial statements.

When the presentation or classification of items in the financial statements is amended, comparative amounts should bereclassified, unless it is impracticable to do so, to ensure comparability with the current period, and the nature, amountof, and reason for, any reclassification should be disclosed. When it is impracticable to reclassify comparative amounts, aCollege should disclose the reason for not reclassifying, and the nature of the changes that would have been made ifamounts were reclassified.

1.4 The Public Finance Management Act and its effect on FET Colleges (PFMA)

The Public Finance Management Act, 1999, gives effect to Sections 213, 215, 216, 217, 218 and 219 of the Constitutionof the Republic of South Africa (Act 108 of 1996) for the national and provincial spheres of government. These Sectionsrequire national legislation to establish a national treasury, to introduce generally recognised accounting practices, tointroduce uniform treasury norms and standards, to prescribe measures to ensure transparency and expenditure control inall spheres of government, and to set the operational procedures for borrowing, guarantees, procurement and oversightover the various national and provincial revenue funds.

The Act adopts an approach to financial management, which focuses on outputs and responsibilities, rather than the rule-driven approach of the old Exchequer Acts. The Act is part of a broader strategy on improving financial management inthe public sector. The Act itself assumes a phased approach towards improving the quality towards improving thefinancial management in the public sector. Implementation in the first phase will focus on the basics of financialmanagement, like the introduction of proper financial management systems, appropriation control and the accountabilityarrangements for the management of budgets.

The Public Finance and Management Act (Act 1 of 1999) must be read together with the Public Finance ManagementAmendment Act (Act 29 of 1999). The Act stipulates the following:

“To regulate financial management in the national government and provincial governments; to ensure that all revenue,expenditure, assets and liabilities of those governments are managed efficiently and effectively; to provide for theresponsibilities of persons entrusted with financial management in those governments; and to provide for mattersconnected therewith.”

The aim of this Act is to modernise the system of financial management in the public sector and will lay the basis for amore effective corporate governance framework for the public sector.

As it currently stands FET Colleges are not required to comply with the PFMA. The explanation for this lies in Section 47and Section 3 of the Act.

In Section 47 (4) of the Act the Minister may not list the following institutions:

1) A constitutional institution, the South African Reserve Bank and the Auditor-General;2) Any public institution which functions outside the sphere of national or provincial government; and3) Any institution of higher education.

The Act contains an objective which is described as the following “ to secure, accountability and sound management ofthe revenue, expenditure, assets and liabilities of the institutions to which the Act applies”.

Section 3 of the Act lists the institutions, which currently have to comply, these are:

1) Departments;2) Public entities – national or provincial (higher education is precluded from being included)3) Constitutional entities and 4) Parliament and provincial legislatures.

However since the principal of a College is the accounting officer, the Department of Education has decided thatPFMA will be a future requirement for these Colleges. A policy decision will have to be made by the Department, ascurrently it is not a legislative requirement. This toolkit thus establishes the implementation framework for both thecurrent financial environment, as well as the imminent change to the PFMA policy framework.

The Annual Financial Statements requirements if PFMA is applicable, are as follows:The Accounting Authority is required in terms of Section 55(1)(b) of the PFMA to “prepare financial statements for eachfinancial year in accordance with generally accepted accounting practice.

Toolkit for Further Education and Training Colleges10

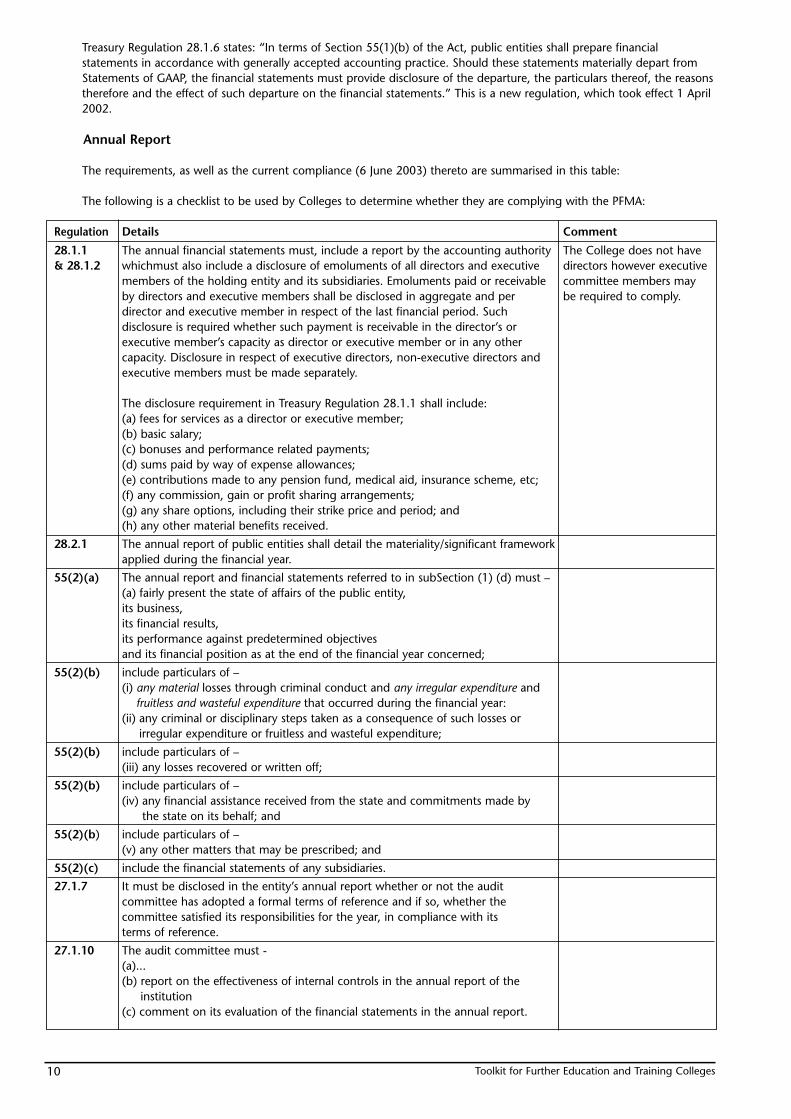

Treasury Regulation 28.1.6 states: “In terms of Section 55(1)(b) of the Act, public entities shall prepare financialstatements in accordance with generally accepted accounting practice. Should these statements materially depart fromStatements of GAAP, the financial statements must provide disclosure of the departure, the particulars thereof, the reasonstherefore and the effect of such departure on the financial statements.” This is a new regulation, which took effect 1 April2002.

Annual Report

The requirements, as well as the current compliance (6 June 2003) thereto are summarised in this table:

The following is a checklist to be used by Colleges to determine whether they are complying with the PFMA:

Regulation Details Comment

28.1.1 The annual financial statements must, include a report by the accounting authority The College does not have& 28.1.2 whichmust also include a disclosure of emoluments of all directors and executive directors however executive

members of the holding entity and its subsidiaries. Emoluments paid or receivable committee members mayby directors and executive members shall be disclosed in aggregate and per be required to comply.director and executive member in respect of the last financial period. Such disclosure is required whether such payment is receivable in the director’s or executive member’s capacity as director or executive member or in any othercapacity. Disclosure in respect of executive directors, non-executive directors and executive members must be made separately.

The disclosure requirement in Treasury Regulation 28.1.1 shall include:(a) fees for services as a director or executive member;(b) basic salary;(c) bonuses and performance related payments;(d) sums paid by way of expense allowances;(e) contributions made to any pension fund, medical aid, insurance scheme, etc;(f) any commission, gain or profit sharing arrangements;(g) any share options, including their strike price and period; and(h) any other material benefits received.

28.2.1 The annual report of public entities shall detail the materiality/significant framework applied during the financial year.

55(2)(a) The annual report and financial statements referred to in subSection (1) (d) must – (a) fairly present the state of affairs of the public entity,its business,its financial results,its performance against predetermined objectivesand its financial position as at the end of the financial year concerned;

55(2)(b) include particulars of – (i) any material losses through criminal conduct and any irregular expenditure and

fruitless and wasteful expenditure that occurred during the financial year: (ii) any criminal or disciplinary steps taken as a consequence of such losses or

irregular expenditure or fruitless and wasteful expenditure;

55(2)(b) include particulars of – (iii) any losses recovered or written off;

55(2)(b) include particulars of – (iv) any financial assistance received from the state and commitments made by

the state on its behalf; and

55(2)(b) include particulars of – (v) any other matters that may be prescribed; and

55(2)(c) include the financial statements of any subsidiaries.

27.1.7 It must be disclosed in the entity’s annual report whether or not the audit committee has adopted a formal terms of reference and if so, whether the committee satisfied its responsibilities for the year, in compliance with its terms of reference.

27.1.10 The audit committee must -(a)...(b) report on the effectiveness of internal controls in the annual report of the

institution(c) comment on its evaluation of the financial statements in the annual report.

Toolkit for Further Education and Training Colleges 11

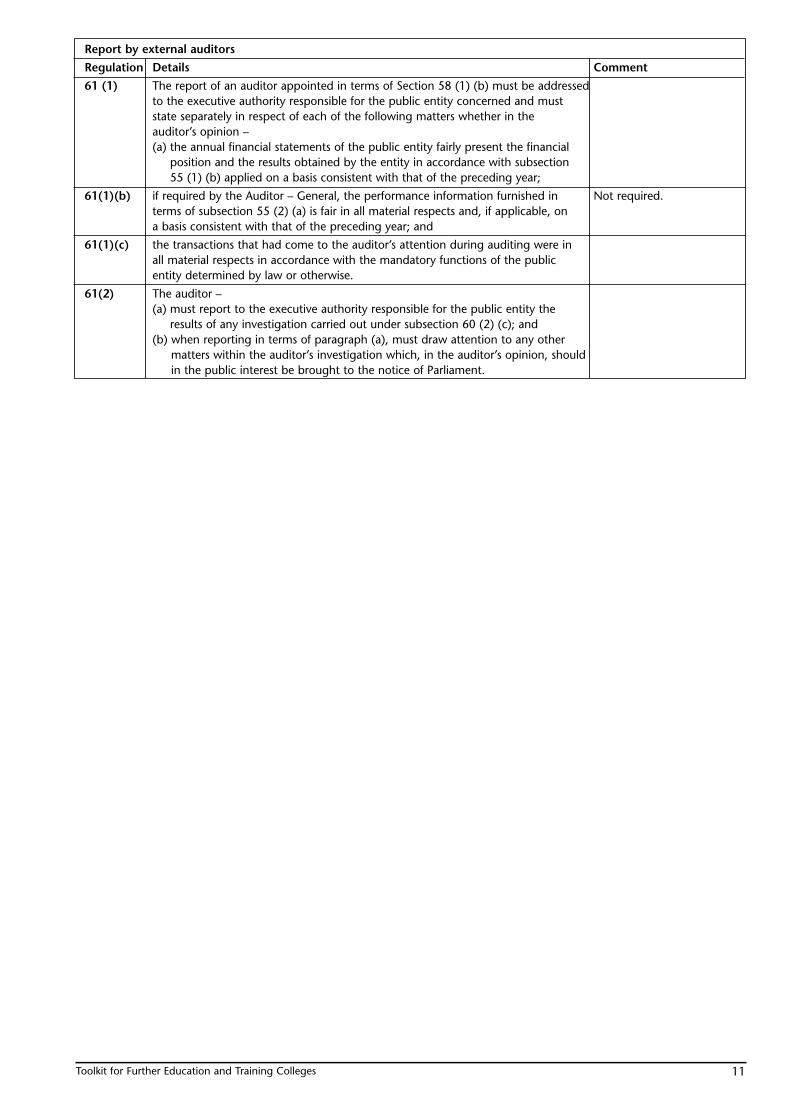

Report by external auditors

Regulation Details Comment

61 (1) The report of an auditor appointed in terms of Section 58 (1) (b) must be addressed to the executive authority responsible for the public entity concerned and must state separately in respect of each of the following matters whether in the auditor’s opinion – (a) the annual financial statements of the public entity fairly present the financial

position and the results obtained by the entity in accordance with subsection 55 (1) (b) applied on a basis consistent with that of the preceding year;

61(1)(b) if required by the Auditor – General, the performance information furnished in Not required.terms of subsection 55 (2) (a) is fair in all material respects and, if applicable, on a basis consistent with that of the preceding year; and

61(1)(c) the transactions that had come to the auditor’s attention during auditing were in all material respects in accordance with the mandatory functions of the public entity determined by law or otherwise.

61(2) The auditor – (a) must report to the executive authority responsible for the public entity the

results of any investigation carried out under subsection 60 (2) (c); and (b) when reporting in terms of paragraph (a), must draw attention to any other

matters within the auditor’s investigation which, in the auditor’s opinion, shouldin the public interest be brought to the notice of Parliament.

Toolkit for Further Education and Training Colleges12

Toolkit for Further Education and Training Colleges 13

2 Governance structures and requirements2.1 Corporate governance

Corporate governance embodies processes and systems by which Colleges are directed, controlled and held to account.Corporate governance in South Africa was institutionalised by the publication of the King Report on CorporateGovernance in November 1994, which report has subsequently been superseded by the King Code of 2002. The purposeof the King Report is to promote the highest standards of corporate governance in South Africa. The Code of CorporatePractices and Conduct contained in the King Report applies inter alia, to State-owned Enterprises and agencies that fallunder the PFMA. In this regard, it is applicable to FET Colleges. In addition, the FET Act (Act 90 of 1998) also includesprovisions relating to Governance, which have been summarised below.

2.1.1 Governance structures

2.1.1.1 Institutional governance structures1) Every further education and training institution must establish a Council, an academic board, a student representative

council and such other structures as may be determined by the council subject to the approval of the MEC.2) The structures referred to above must elect a chairperson, vice-chairperson and other, office bearers from among its

members in the manner determined by the MEC by notice in the Provincial Gazette or in terms of a provincial law.3) The chairperson, vice-chairperson or other office bearers of the Council may not be students or members of the staff of

the institution, but the secretary may be a member of staff.

2.1.1.2 Council1) The Council of a further education and training institution must perform all the functions, which are necessary to

govern the further education and training institution, subject to the FET Act – and any applicable provincial law.2) The Council of a public further education and training institution must consist of -

- a principal;- the vice-principal or vice-principals;- not more than five persons appointed by the MEC;- members of the academic board elected by the academic board;- members of the lecturer staff of the public further education and training institution elected by such staff;- students of the public further education and training institution, elected by its student representative Council;- staff other than lecturer staff elected by such staff of the public further education and training institution and- such additional persons as may be determined by the council in consultation with the MEC.

3) At least 60 per cent of the members of a council must be persons who are not employed by or who are not studentsof the public further education and training institution in question.

4) The members of the Council -a) must be persons with knowledge and experience relevant to the objects and governance of the public further

education and training institution in question; andb) must participate the deliberations of the Council in the best interest of the public further education and training

institution in question.5) Every further education and training institution must appoint a principal, a vice-principal or vice-principals and such

other officers as may be determined by the council subject to the approval of MEC.• The non-executive members should be of sufficient calibre that their views will carry significant weight within College

Council decisions. • The College Council should devise and regularly review criteria for membership.• An annual review of the required mix of skills, experience and other qualities, including core competencies of non-

executive members should be performed.• The College Council should establish performance criteria for itself and periodically review its performance against

those criteria.• A remuneration or management compensation committee could be established.• The College Council should establish an Audit Committee with written terms of reference confirmed by the College

Council.• Membership of the Audit Committee should include at least 2 non-executive members and should be chaired by a

non-executive member.• The Audit Committee should have the responsibility to ensure that management has instituted an effective system of

risk management and internal control. • Audit Committee meetings should be attended by the head of the internal audit department, the external audit

partner and the CFO.• The Audit Committee should periodically evaluate its performance against benchmarked criteria.

2.1.1.3 Academic BoardThe academic board of a further education and training institution is accountable to the council for – a) the academic functions of the further education and training institution and the promotion of the participation of

women and the disabled in the learning programmes;

Toolkit for Further Education and Training Colleges14

b) establishing internal academic monitoring and quality assurance procedures;c) ensuring that the requirements of accreditation to provide learning against standards and qualifications registered on

the National Qualifications Framework are met; andd) performing such other functions as maybe delegated or assigned to it by the Council.

Subject to the approval of the council and to the policy, the academic board must determine the learning programmesprovided by the further education and training institution.

The academic board of a further education and training institution must consist of – a) the principal;b) the vice-principal or vice-principals;c) members of the educator staff of the institution;d) members of the council;e) members of the student representative council; andf) such additional persons as may be determined by the council.

The majority of members of the academic board must be members of the educator staff of the public further educationand training institution in question.

2.1.1.4 Funds of public further educations and training institutionsThe funds of the public further education and training institution consists of – - funds allocated by the State;- any donations or contributions received by the institution;- money raised by the institution;- money raised by means of loans subject to the approval of the MEC;- income derived from investments;- money received for services rendered to any other institution or person;- money payable by students for further education and training programmes provided by the institution;- money received from students or employees of the institution for accommodation or other services provided by the

institution and- other funds from any other source.• The non-executive members should be of sufficient calibre that their views will carry significant weight within College

Council decisions. • The College Council should devise and regularly review criteria for membership.• An annual review of the required mix of skills, experience and other qualities, including core competencies of non-

executive members should be performed.• The College Council should periodically review its size and composition to ensure it is appropriate for effective decision-

making.• The College Council should establish performance criteria for itself and periodically review its performance against those

criteria.• A remuneration or management compensation committee should be established.• The College Council should establish an Audit Committee with written terms of reference confirmed by the College

Council.• Membership of the Audit Committee should include at least 2 non-executive members and should be chaired by a non-

executive member.• The Audit Committee should have the responsibility to ensure that management has instituted an effective system of

risk management and internal control. • Audit Committee meetings should be attended by the head of the internal audit department, the external audit partner

and the CFO.• The Audit Committee should periodically evaluate its performance against benchmarked criteria.

2.1.2 Tone at the top• A Code of Ethics (incorporating stated values for the entity) should be developed and implemented by involving all

stakeholders.• The code should receive total commitment from the College Council and principal.• It should be sufficiently detailed to give a clear guide as to what is expected behaviour of all employees.• The College Council should establish and monitor policies to ensure the highest standards of ethics are maintained and

all relevant legislation is complied with.

2.1.3 Strategy• The College Council is responsible for the adoption of a strategic planning process. It should establish performance

criteria for itself and periodically review performance against those criteria.

2.1.4 Risk management• The College Council should identify the principle risks of the organisation and ensure the implementation of systems to

manage these risks.

Toolkit for Further Education and Training Colleges 15

• The Audit Committee should have the responsibility to ensure that management has instituted an effective system ofrisk management and internal control.

• The directors should conduct a review on the effectiveness of the organisation’s risk management and internal controlsystems and report to the shareholders that they have done so.

• The organisation should have an effective internal audit function. It should have the respect and co-operation of boththe College Council and senior management.

• The internal audit department should comply with the Standards for the Professional Practice of the Institute for InternalAuditing.

2.1.5 Managing management• The College Council should monitor the executive management and succession management. Performance related

elements of remuneration should form a significant portion of the management’s remuneration.

2.1.6 Communication• Any communication with stakeholders should be balanced, understandable, transparent and timeous.• The information provided should be based on the principles of openness, substance above form and should address

material matters of interest and concern to all stakeholders.• The College Council should report its approach to corporate governance in the annual financial statements detailing

the:- extent of compliance with the King Code of Corporate Governance recommendations- responsibility for the annual financial statements- functioning of the Audit Committee (where applicable)- functioning of the Remuneration Committee- role of internal audit- responsibility for risk management and control and how they have demonstrated their accountability- relevant commitment to ethical behaviour- adoption and maintenance of a code of ethics - going concern statement- relevant shareholder reporting, such as affirmative action, community commitment and environmental reporting.• The College Council should present a balanced and understandable assessment of the organization’s position in

reporting to stakeholders.• The College should report on performance against benchmarked criteria (refer to financial statement templates).

2.1.7 Transaction approval• The College Council should ensure that decisions on material matters are in their hands. They should have a formal

schedule of matters specifically reserved for decision-making and develop a definition of materiality. • The College Council should meet at least once a quarter. This should however be determined with reference to the

specific circumstances of each College.

Toolkit for Further Education and Training Colleges16

Toolkit for Further Education and Training Colleges 17

3 The FET business model3.1 Introduction

3.1.1 Co-ordinators of the business model developmentThe objective of this Further Education and Training (FET) business model is to assist in the continuing development andunderstanding of Further Education and Training sector through its availability and use by the FET Colleges. The modelalso attempts to set a standard or precedence amongst all Colleges within the FET sector. Deviations from the model arepossible based on the environment within which the College operates. This fact has been recognised and the model isnot intended to be rigid.

The information contained in this section of the policies and procedures toolkit has been based on information derivedfrom selected Colleges. These Colleges were selected based on the extent to which the merger process had been effectedand implemented.

The FET support manager at the Department of Education, will co-ordinate the update of the database and ensure that itis made available to all FET College members.

3.1.2 How to useIn principle, the model is intended to assist interested parties in order to obtain a better understanding of the keyprocesses/business drivers/risks within a Further Education and Training (FET) environment and draws on the model to actas an aid in that understanding. By the same token, the model is intended to be dynamic and be updated periodically asthe industry evolves.

It will be noted that the FET business model draws heavily on process analysis; many FET Colleges are wholly processmanaged, and many are almost wholly functionally managed. It is believed that large parts of the attached analysis willapply to all Colleges in the industry, even though in its totality it may not totally reflect the way the Colleges aremanaged and controlled.

It must be appreciated that this business model is essentially a generic FET business model based on best practiceprinciples. In other words, this business model is provided as a starting point for investigating and ultimatelyunderstanding your institution. Bear in mind that data analysis is the most important factor.

3.1.3 Benchmarking – cautionary statementsAlthough financial and non-financial benchmarks are very effective business analysis tools, there are several factors thatmay affect the reliability of ratios or the comparability of ratios among Colleges and industry average. The followingfactors highlight the importance of considering the underlying financial and non-financial data during benchmarkinganalysis.

The quality of a benchmarking analysis depends on the selection of the proper peer group. In order to avoid comparingapples and oranges and misinterpreting either financial or non-financial data, the structure of the peer group in terms ofthe industry, the segment, the products (i.e., Colleges with multiple campus sites), and the size of the College need to beconsidered carefully.

FinancialAccounting conventions and the choice of accounting methods may have a significant impact on financial statementsand, therefore on the ratios computed from those financial statements. Applying different accounting methods will impaircomparability of the ratios over time and across Colleges. Even the comparison of financial ratios between companieswithin the same country may be influenced by the selection of different accounting methods.

In addition, there are wide variations around the world when defining individual accounting items (e.g., ‘short/longterm’, ‘operating’, ‘extraordinary’), the format of accounts, and the depth of detail contained in the statementsthemselves and in the notes to the accounts. When cross-border companies are used in an analysis, the potential impactresulting from the currency conversion, inflation, and different costs of living have to be considered.

Obviously, linguistic and cultural diversity is reflected in financial accounts, but their form and content is influencedadditionally by less obvious factors (such as the legal system, the nature of corporate ownership), methods of corporatefinancing, customary business practices such as the maintenance of low-inventory levels, taxation, the prominence of theaccounting and auditing profession, and so on.

Although data providers try to make adjustments to unify financial data, it is important to understand the limitations ofratios as comparisons when different accounting methods are employed, in particular when cross-border comparisons arepart of the analysis.

Toolkit for Further Education and Training Colleges18

Non-financialIn contrast to financial data, the analysis of non-financial data is not affected by accounting methods or the influence ofdifferent currencies. Therefore, the validity of non-financial ratios depends on the exact definition of the information used.Because non-financial ratios are not yet generally standardised, it has to be ensured that the components of the ratio(measurement of time or process transactions) have been applied simultaneously by the Colleges within the analysis.Thus, non-financial data are not easily available through public domain; the methodology and the quality process of thedata provider as well as the population of the companies included in the computation of the data are critical with regardto the validity of non-financial information.

Picking the proper peer group (segment) when comparing Colleges is even more important for non-financial informationbecause processes vary greatly by segment and/or service provided or product.

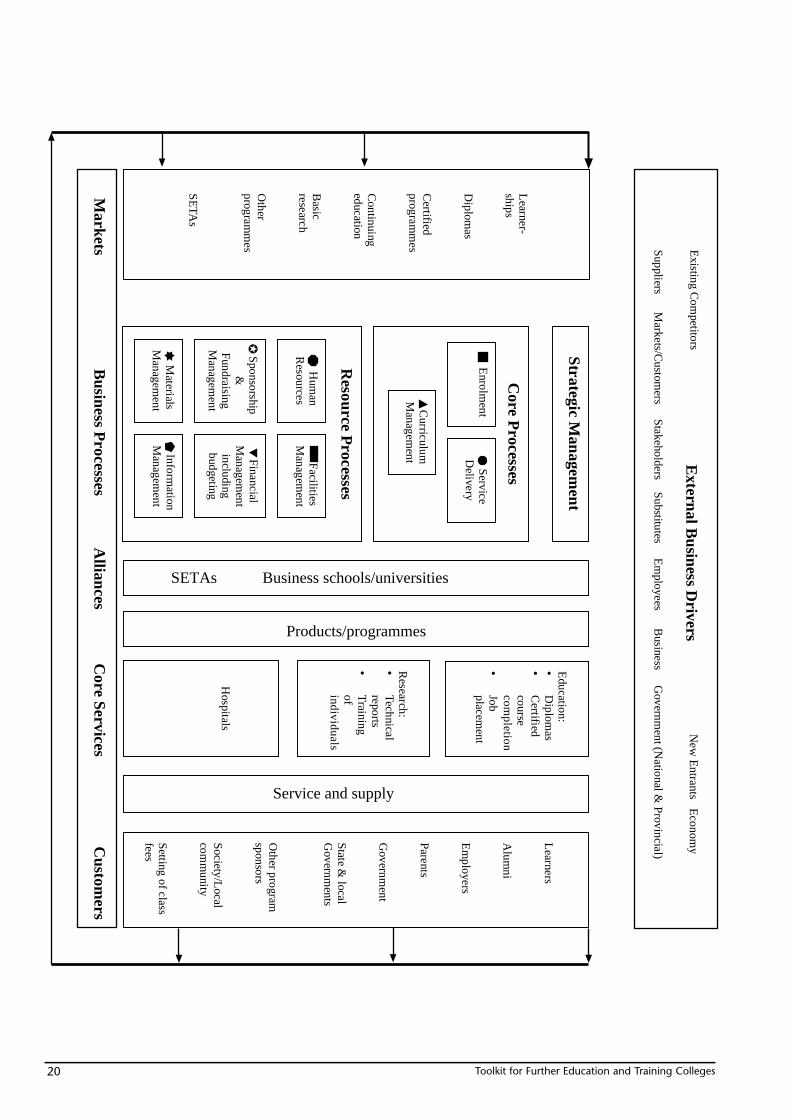

3.2 FET business model

The entity-level business model is used to describe the inter-linking activities carried out within a College, the externalbusiness drivers and stakeholders that bear upon the College, and the business relationships with persons outside theCollege. The items included in the entity-level business model include the following components:

3.2.1 External Business Drivers and Stakeholders

External Business Drives and Stakeholders are those outside factors, pressures etc that can prevent a College from attaining itsobjectives. One of the ways to classify such external forces follows:

General environment Competitive environment Operating environment

Political / legal Competitors Markets

Macroeconomics New entrants Customers

Technological Substitute products Competitiveness

Demographic Buyers Trade regulations

Socio-cultural Suppliers Economics

3.2.2 Markets

Markets are the segments of an industry that are applicable to the College.

When analysing markets we may:

• Identify the College’s significant market segments;

• Obtain an understanding of how the products and services are positioned within the market segments;

• Obtain an understanding of the relationship between a College’s market segments and its business objectives and strategies.

3.2.3 Business Processes

A business process is a structured set of activities within an College, designed to produce a specified output. A businessprocess emphasis how work is performed rather than what is done. It is also structuring of work activities across time andplace to transform inputs, such as information, materials and resources, to outputs, such as the products or services forcustomers or other users.

Processes are usually linked with the outputs of one process being the inputs of another process.

Strategic Management Process: the strategic management process is the process that:

• develops the College’s mission,

• defines the College’s business objectives,

• identifies the business risks that threaten attainment of the business objectives,

• manages the business risks by establishing business processes, and monitors progress toward meeting the business objectives.

When we analyse the Strategic Management Process we may include of how management (including the Board of directors,as appropriate):

• sets the overall direction for the College;

• monitor the external environment and asses the strategic implications of potential opportunities and threats;

• monitors the extent to which strategies have been implemented;

• understand the strategies and capabilities of the significant competitors;

• analyses the College’s strengths and weaknesses;

Toolkit for Further Education and Training Colleges 19

• appropriate resources to the other business processes.

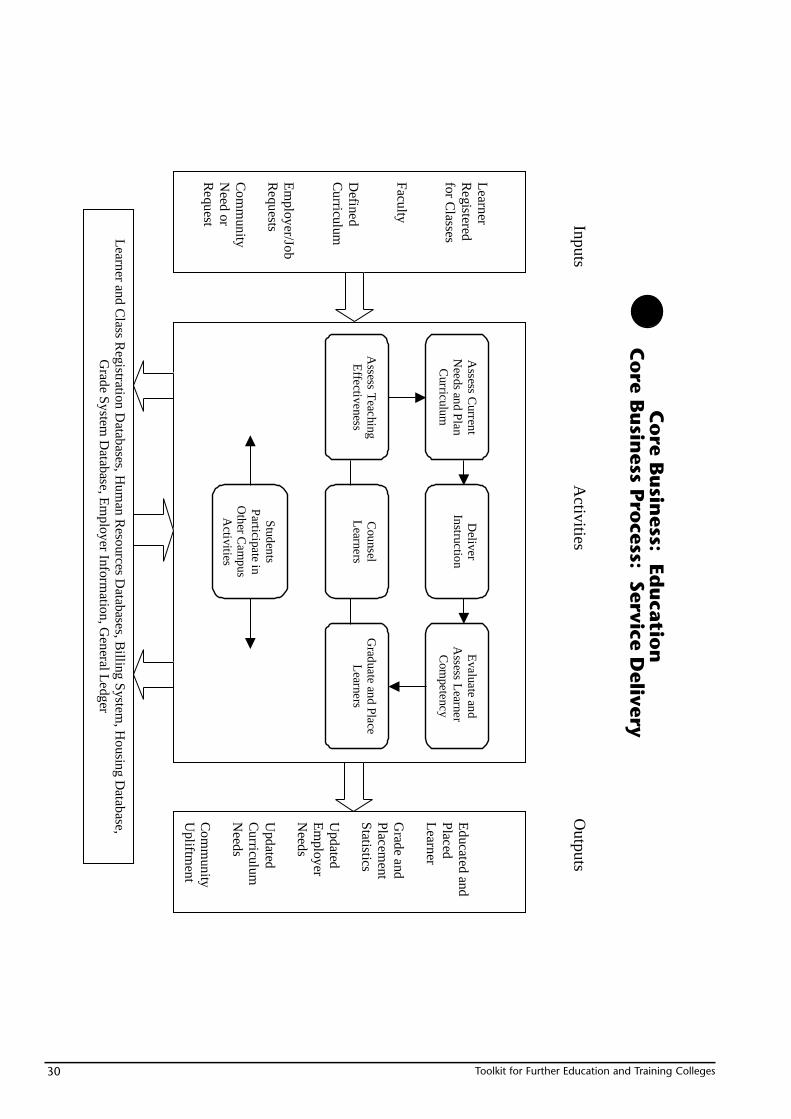

Core Business Processes

Core business processes are the processes that develop, produce, sell, and distribute a College’s products and services. Theseprocesses do not follow traditional organisational or functional lines, but reflect the grouping of related business activities.

3.2.4 Alliances / Relationships with Suppliers

Alliances are the types of relationships with third parties that entities in the industry may establish to:

attain business objectives,

• expand business opportunities

• reduce or transfer business risk.

When analysing Relationships with Suppliers we may

• identify a College’s significant suppliers;

• obtain an understanding of an College’s relationship with its suppliers;

• obtain an understanding of relationship between a College’s significant suppliers and its business objectives and strategies.

3.2.5 Products and Services

Products and Services are the significant products and services typically offered by entities within the industry. Whenanalysing Products and Services we may obtain

• an understanding of the College’s significant products and services;

• an understanding of the stage that significant products and services have reached in their life cycle;

• an understanding of the relationship between a College’s significant products and services and its business objectives andstrategies.

3.2.6 Customers

Customers are the significant types of consumers within the markets in the industry that entities may choose to focus on.When analysing customers we may

• identify a College’s significant customers;

• obtain an understanding of the relationship between a College’s significant customers and its business objectives andstrategies.

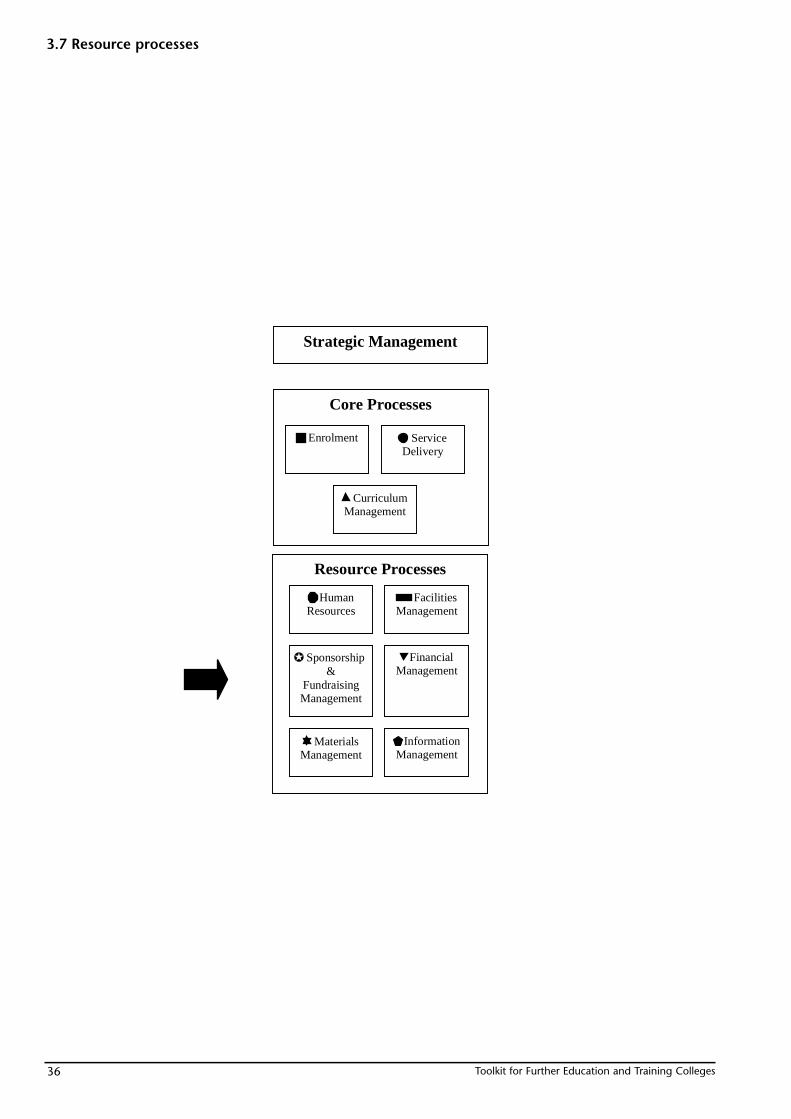

Enrolment

Service Delivery

Curriculum Management

Human Resources

Facilities Management

Sponsorship & Fundraising Management

Financial Management

Materials Management

Information Management

Key of iconsCross check icons in graphs along with theirrepresentation in the text

Toolkit for Further Education and Training Colleges20

External B

usiness Drivers

Suppliers M

arkets/Custom

ers Stakeholders S

ubstitutes Em

ployees Business G

overnment (N

ational & P

rovincial)

Existing C

ompetitors

New

Entrants E

conomy

Learner-

ships

Diplom

as

Certified

programm

es

Continuing

education

Basic

research

Other

programm

es

SE

TAs

Strategic Managem

ent

Core P

rocesses

Delivery

Managem

ent

Resource P

rocesses

Resources

Managem

ent

&F

undraisingM

anagement

Managem

entincludingbudgeting

Managem

entM

anagement

SETAs Business schools/universities

Products/programmes

Education:

• D

iplomas

• C

ertifiedcoursecom

pletion•

Jobplacem

ent

Research:

• Technicalreports

• T

rainingofindividuals

Hospitals

Service and supply

Learners

Alum

ni

Em

ployers

Parents

Governm

ent

State &

localG

overnments

Other program

sponsors

Society/L

ocalcom

munity

Setting of class

fees

Markets

Business P

rocesses Alliances

Core Services

Custom

ers

Enrolm

entS

ervice

Curriculum

Hum

anF

acilities

Sponsorship

Financial

Materials

Information

Toolkit for Further Education and Training Colleges 21

3.3 Process analysis template

A process analysis template is used throughout this business model to document the strategic management, corebusiness, and resource management processes. The following pages explain the components of the template.

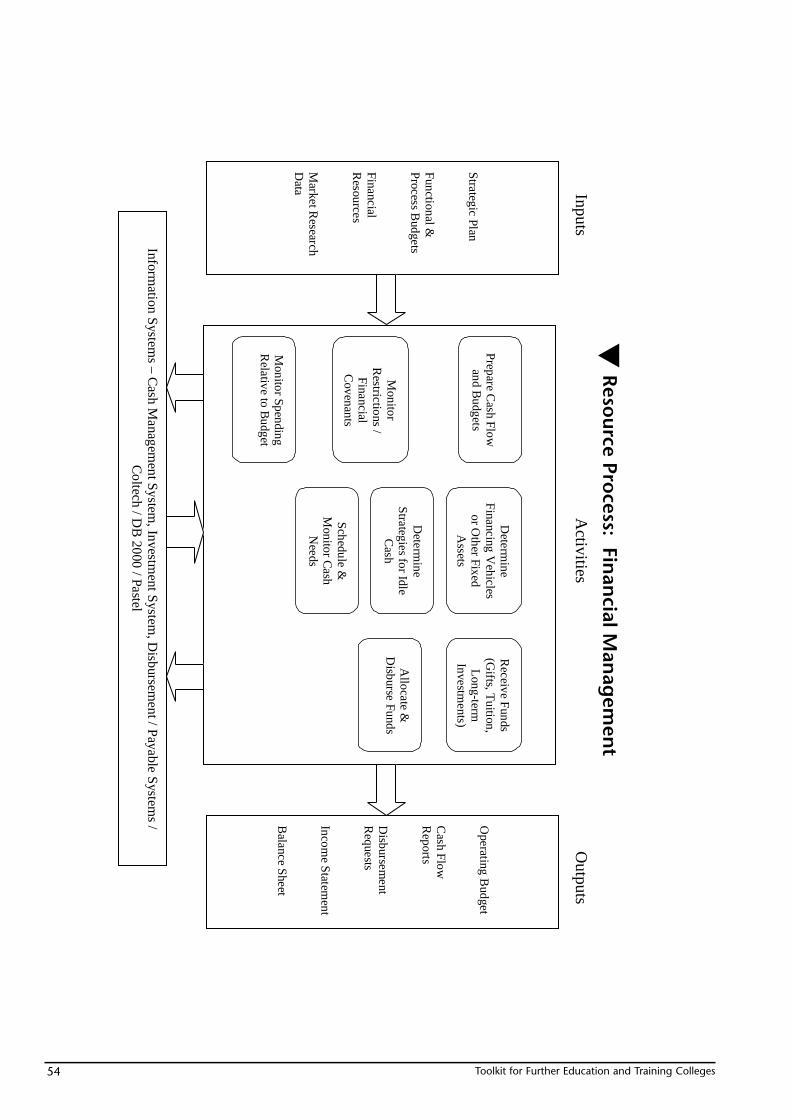

Process Objectives Processes are established to serve specific customer needs. The customers may be internalcustomers, such as another process, or external customers. The process objective defines whatvalue is going to be supplied to the customer. One can look at it as the whole purpose forwhich the organisation has put together this set of resources and activities.

Process objectives need to be specific, measurable, attainable, realistic, and have a sense oftime. Most organisations will have fairly similar strategic management processes. However,their core business and resource management processes may differ significantly, as they areshaped by the organisation’s strategic objectives and the related critical success factors.

Systems The systems are collections of resources designed to accomplish process objectives. Informationsystems produce reports containing operational-, financial-, and compliance-relatedinformation that make it possible to run and control the process.

Inputs The inputs to a process represent the elements, materials, resources, or information needed tocomplete the activities in the process.

Activities The activities are those actions or sub-processes that together produce the outputs of theprocess. For some processes, arrows are omitted due to the non-sequential nature of theactivities.

Outputs The outputs represent the end result of the process-the product, deliverable, information, orresource that is produced.

Critical Success Factors (CSFs) KPIs Linked to CSFs

Critical success factors (CSFs) are the prerequisites and areas Key performance indicators (KPIs) are quantitativeof dependency for a process to be successful. CSFs may be measurements, both financial and non-financial, of theinputs, parallel or supporting activities, or aspects of a process’s ability to meet its objectives and of the processbusiness’s philosophy or infrastructure necessary to ensure the performance. They are usually analysed through trend analysesproper delivery of the process. The CSFs relate directly to one within a College or through benchmarking against a peer of or more of the processes objectives. They are normally limited the College or its industry. The KPIs that should be listed must in number. be relevant to the CSFs and/or the process objectives. The KPIs

listed must have relevance to the organisation. Taken togetherthey should provide a key set of measures for measuringprocess performance-achieving process objectives.

Classes of Transactions The classes of transactions are data and information that are related to the process for use inone or more reports to management or third parties. The classes of transactions, which arebroken down into routine and non-routine transactions and accounting estimates, provide alink from the process to the financial statements of the College. Every process will have one ormore classes of transactions.

Toolkit for Further Education and Training Colleges22

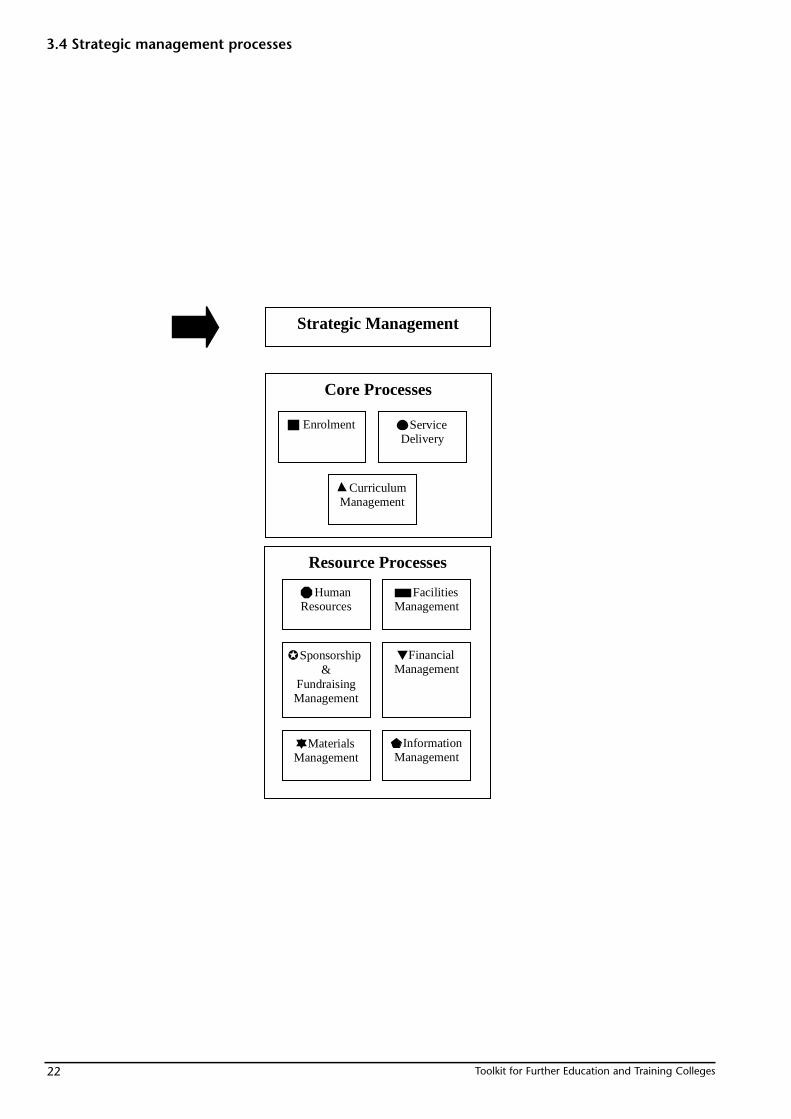

3.4 Strategic management processes

Strategic Management

Core Processes

Delivery

Management

Resources Management

&FundraisingManagement

Management

Management Management

Resource Processes

Enrolment Service

Curriculum

Human Facilities

Sponsorship Financial

Materials Information

Toolkit for Further Education and Training Colleges 23

Process Description Strategic Management is the process of defining the mission of the College and the community the College serves, formalising them into a mission statement and converting thestatement into a strategy that identifies market niches and programmes and services to beoffered. The mission may be singular (instruct students from a geographic area) or multiple(instruct students, carry out research). The community served may be local, regional, nationalor international and may be different for each mission. The strategy will then be codified into a long-range plan for the institution. The long-range plan is coordinated with shorter-termoperating plans (operating budgets, capital budgets, program reviews).

Process Objectives Promote College’s image through mailings, media and meetings with constituents

Maintain current accreditation status

Implement new programmes based upon market research or strategy/mission established

Maintain balanced budget

Toolkit for Further Education and Training Colleges24

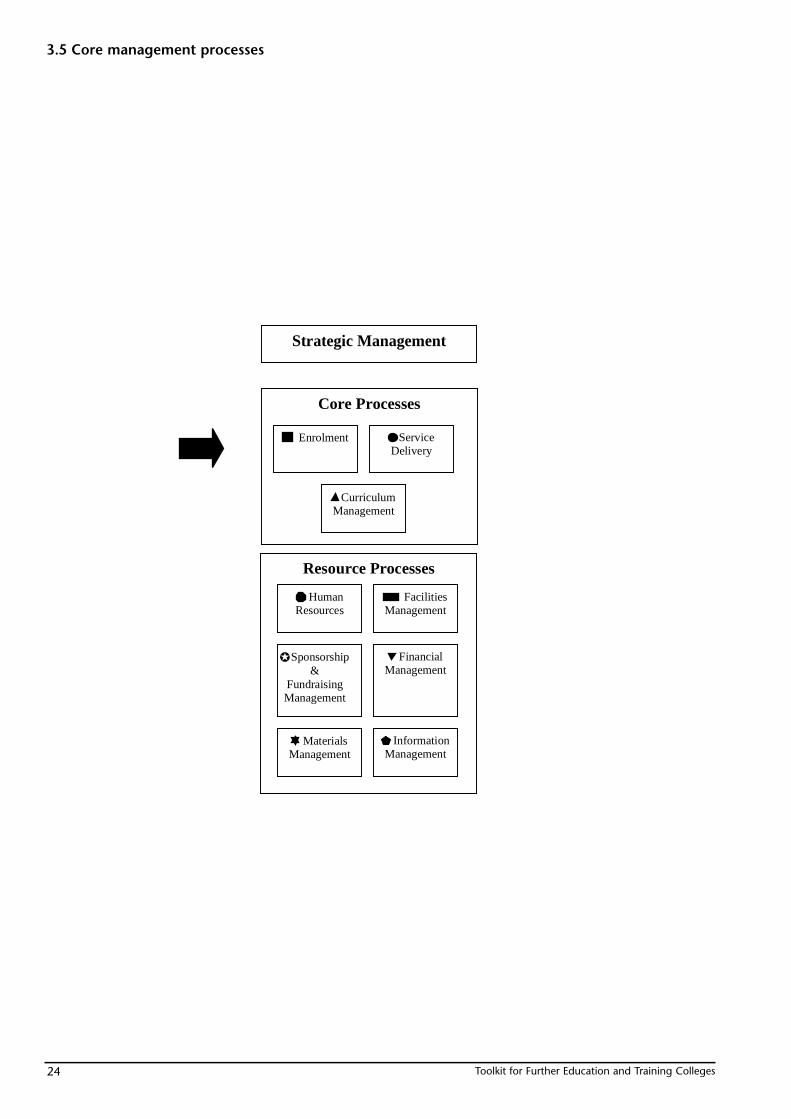

3.5 Core management processes

Strategic Management

Core Processes

Delivery

Management

Resources Management

&FundraisingManagement

Management

Management Management

Resource Processes

Enrolment Service

Curriculum

Human Facilities

FinancialSponsorship

Materials Information

Toolkit for Further Education and Training Colleges 25

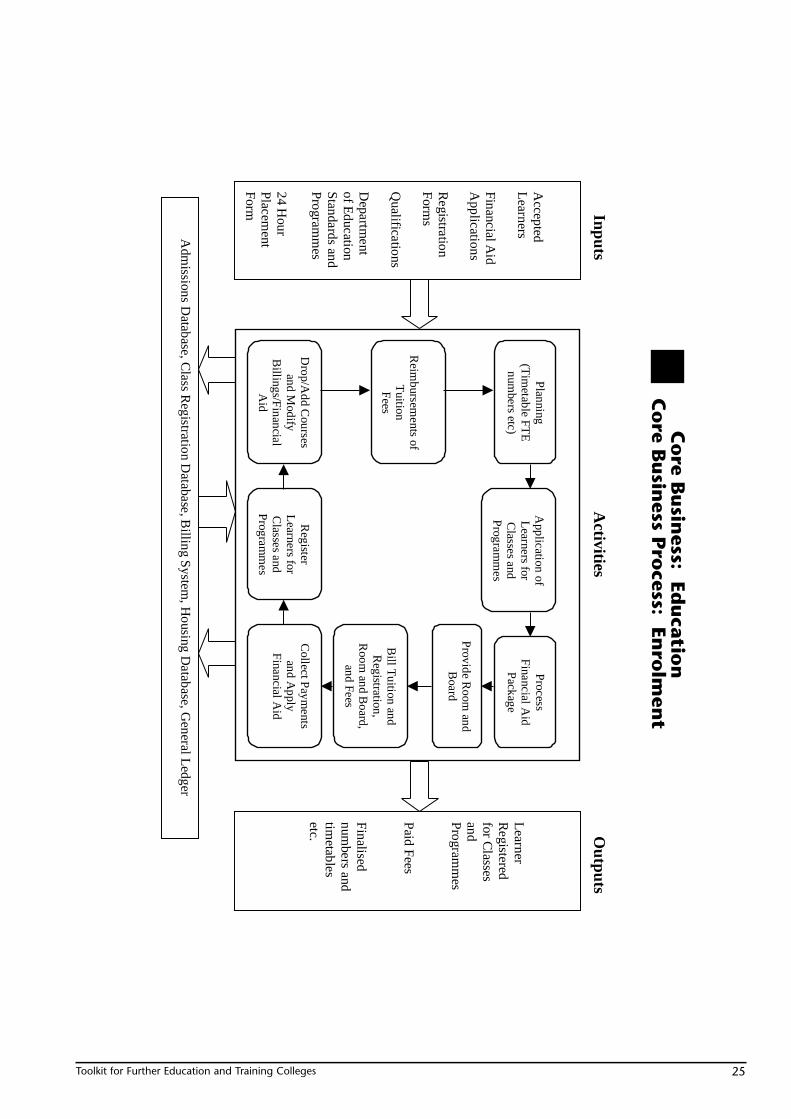

Co

re Bu

siness: Ed

ucatio

n C

ore B

usin

ess Pro

cess: Enro

lmen

t

Inputs A

ctivities Outputs

Adm

issions Database, C

lass Registration D

atabase, Billing S

ystem, H

ousing Database, G

eneral Ledger

Accepted

Learners

Financial A

idA

pplications

Registration

Form

s

Qualifications

Departm

entof E

ducationS

tandards andP

rogramm

es

24 Hour

Placem

entF

orm

Application of

Learners for

Classes and

Program

mes

Process

Financial A

idP

ackage

Provide R

oom and

Board

Bill T

uition andR

egistration,R

oom and B

oard,and Fees

Collect P

ayments

and Apply

Financial A

id

Drop/A

dd Courses

and Modify

Billings/F

inancialA

id

Planning

(Tim

etable FTE

numbers etc)

Register

Learners for

Classes and

Program

mes

Reim

bursements of

TuitionF

ees

Learner

Registered

for Classes

andProgram

mes

Paid Fees

Finalisednum

bers andtim

etablesetc.

Toolkit for Further Education and Training Colleges26

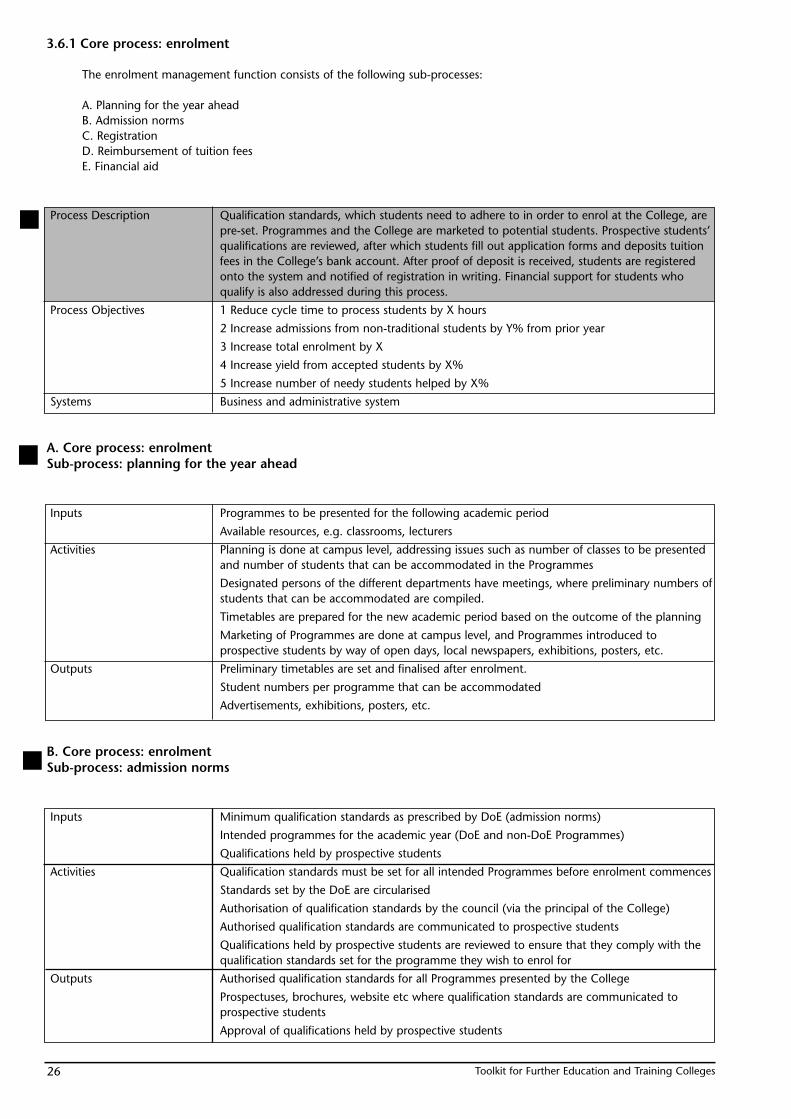

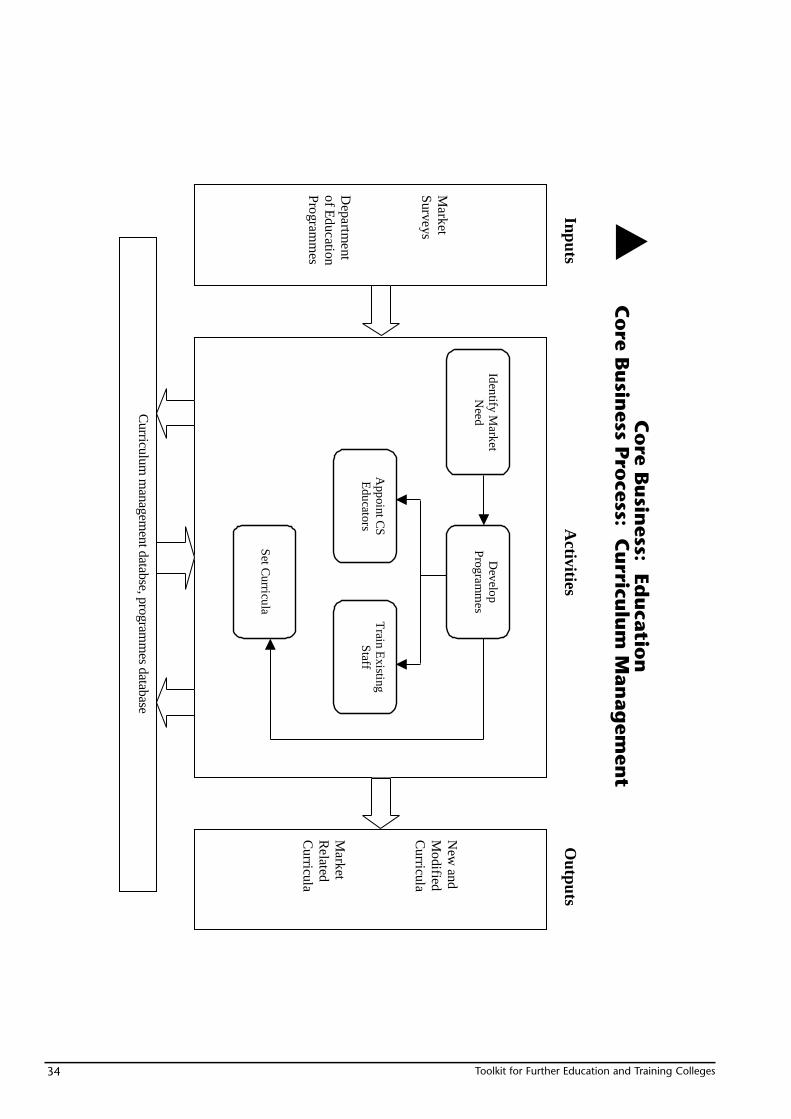

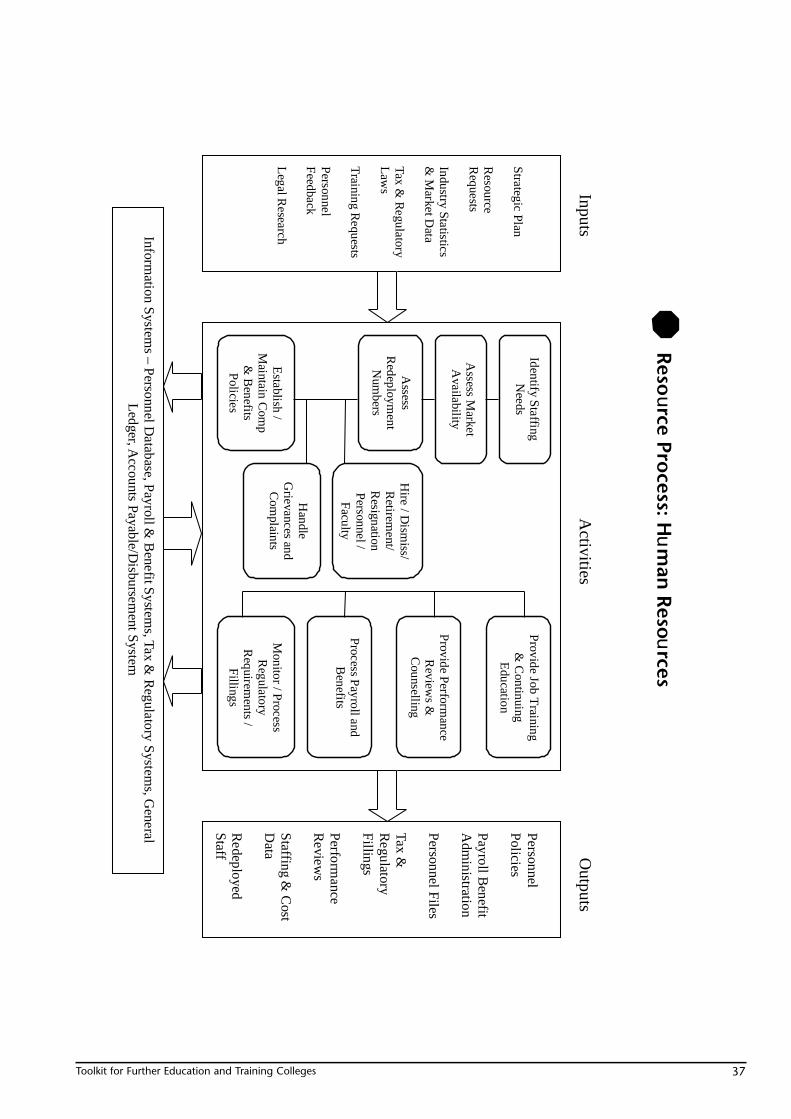

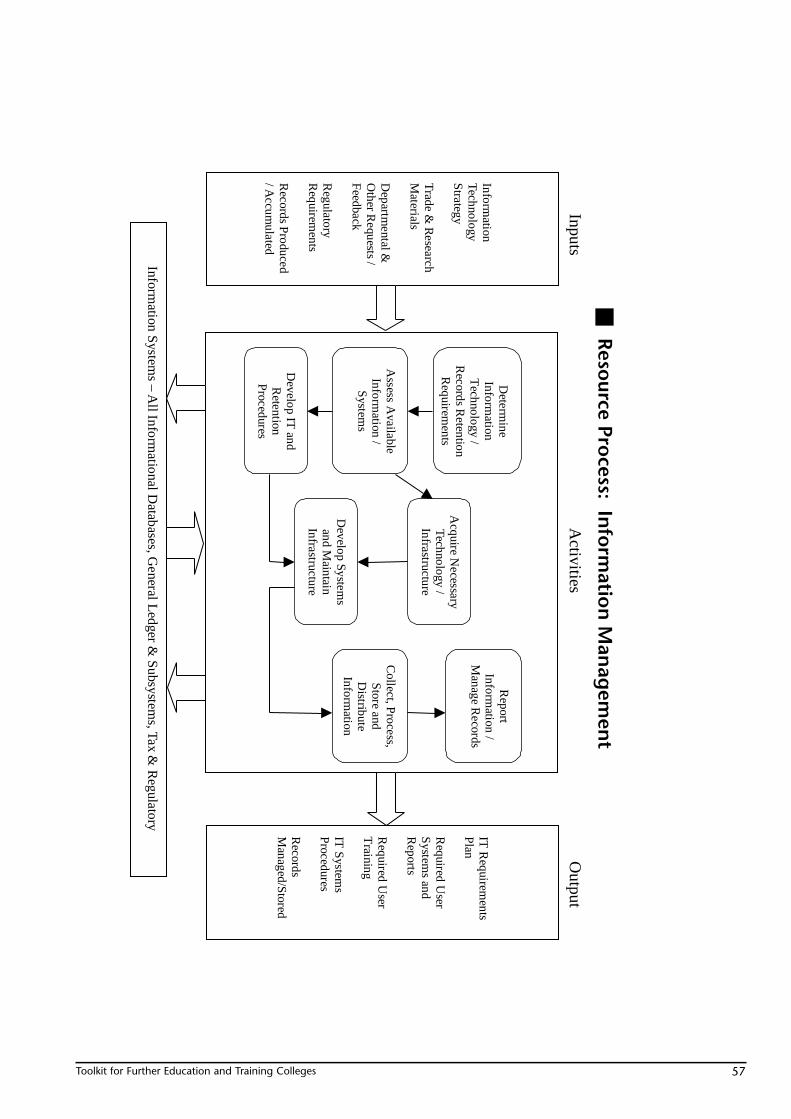

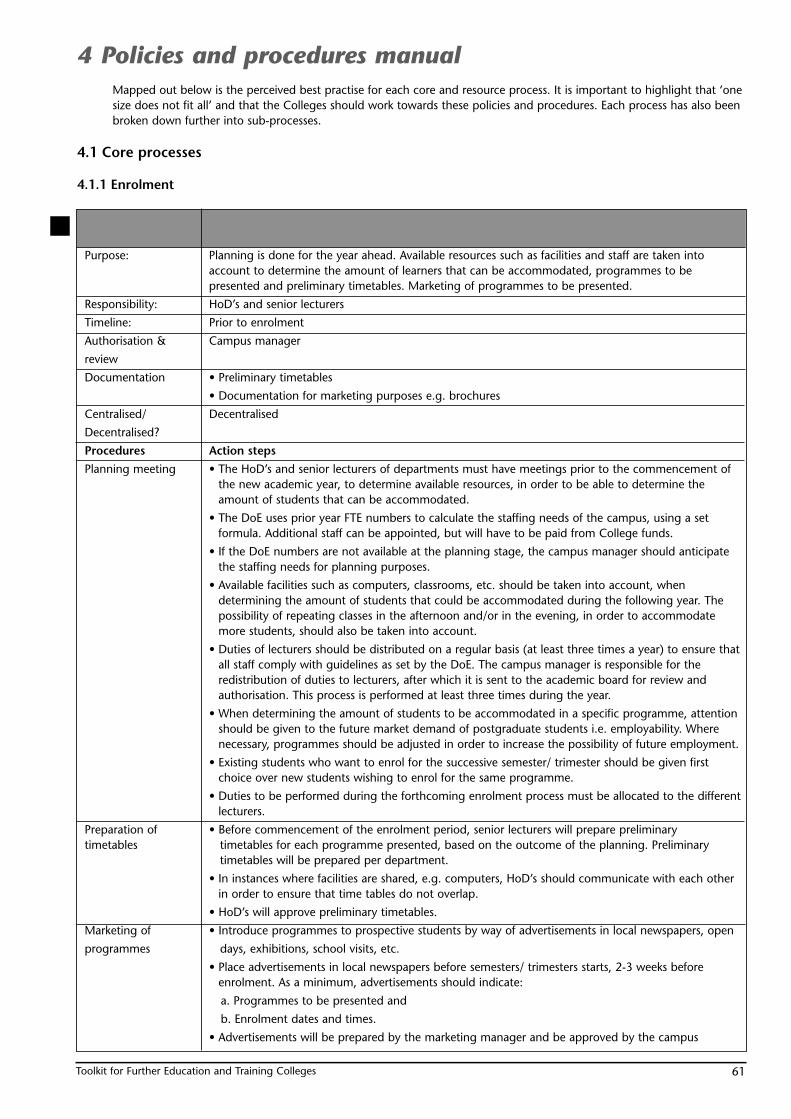

3.6.1 Core process: enrolment

The enrolment management function consists of the following sub-processes:

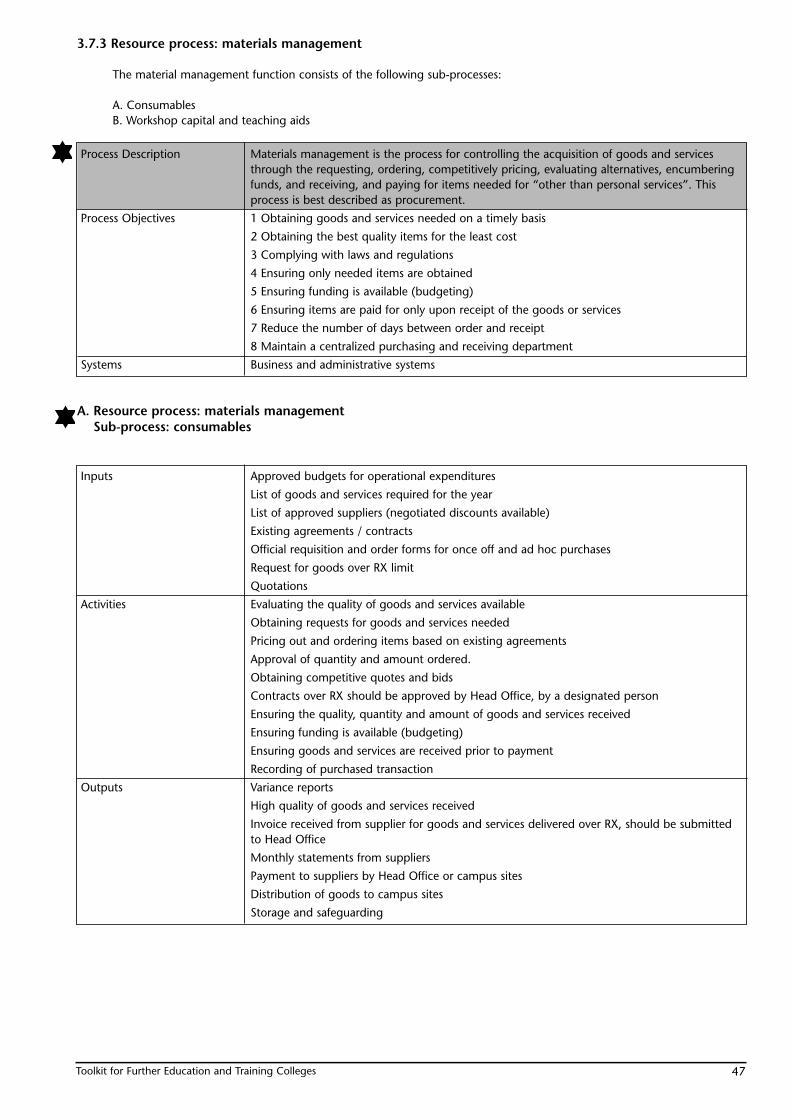

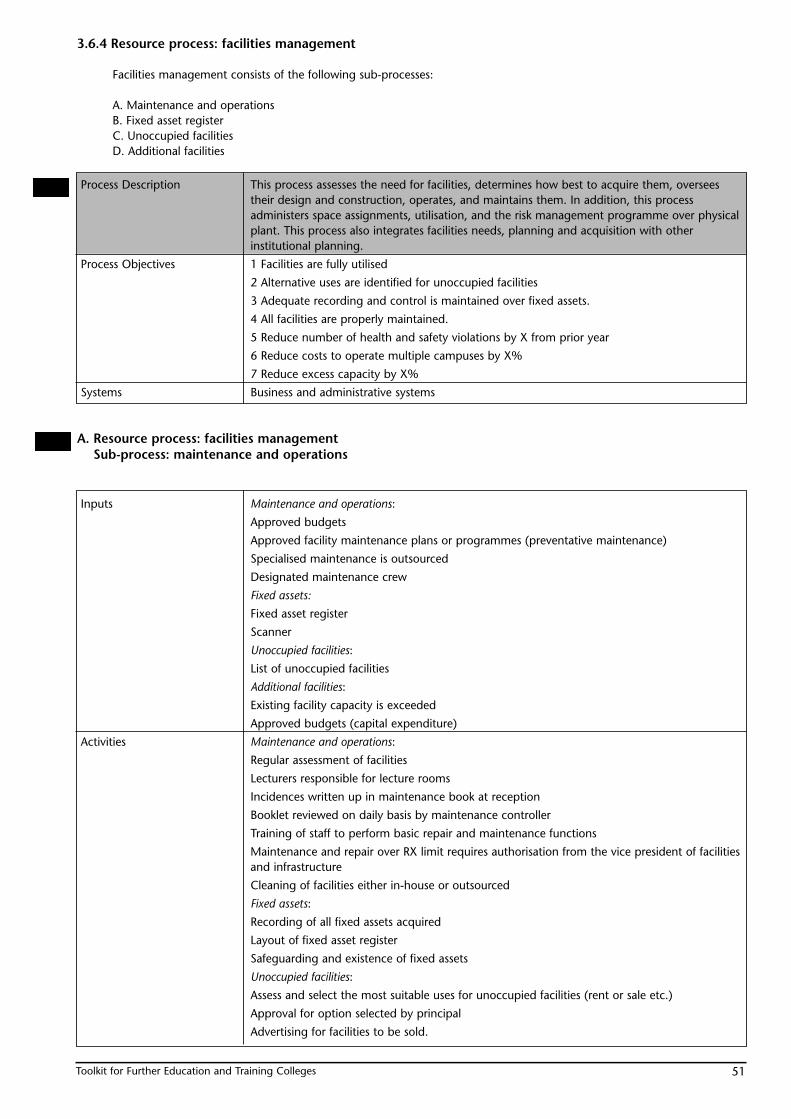

A. Planning for the year ahead B. Admission normsC. RegistrationD. Reimbursement of tuition feesE. Financial aid

Process Description Qualification standards, which students need to adhere to in order to enrol at the College, arepre-set. Programmes and the College are marketed to potential students. Prospective students’qualifications are reviewed, after which students fill out application forms and deposits tuitionfees in the College’s bank account. After proof of deposit is received, students are registeredonto the system and notified of registration in writing. Financial support for students whoqualify is also addressed during this process.

Process Objectives 1 Reduce cycle time to process students by X hours

2 Increase admissions from non-traditional students by Y% from prior year

3 Increase total enrolment by X

4 Increase yield from accepted students by X%

5 Increase number of needy students helped by X%

Systems Business and administrative system

A. Core process: enrolmentSub-process: planning for the year ahead

Inputs Programmes to be presented for the following academic period

Available resources, e.g. classrooms, lecturers

Activities Planning is done at campus level, addressing issues such as number of classes to be presentedand number of students that can be accommodated in the Programmes

Designated persons of the different departments have meetings, where preliminary numbers ofstudents that can be accommodated are compiled.

Timetables are prepared for the new academic period based on the outcome of the planning

Marketing of Programmes are done at campus level, and Programmes introduced toprospective students by way of open days, local newspapers, exhibitions, posters, etc.

Outputs Preliminary timetables are set and finalised after enrolment.

Student numbers per programme that can be accommodated

Advertisements, exhibitions, posters, etc.

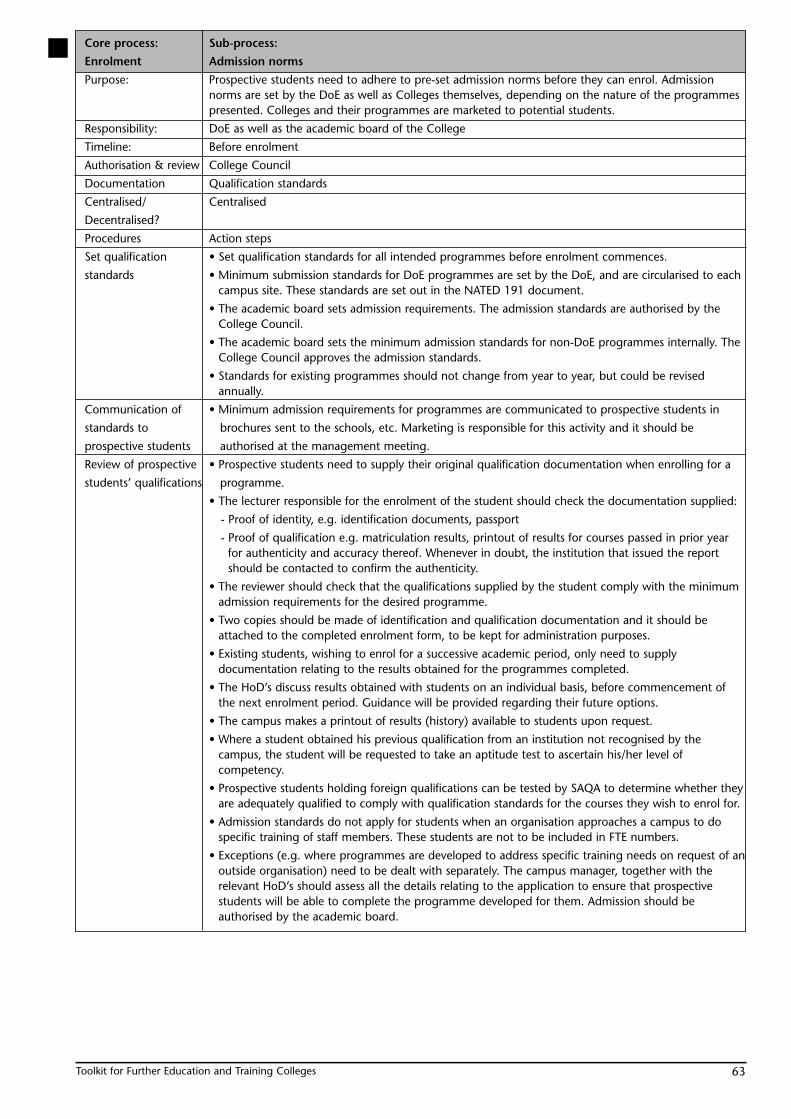

B. Core process: enrolment Sub-process: admission norms

Inputs Minimum qualification standards as prescribed by DoE (admission norms)

Intended programmes for the academic year (DoE and non-DoE Programmes)

Qualifications held by prospective students

Activities Qualification standards must be set for all intended Programmes before enrolment commences

Standards set by the DoE are circularised

Authorisation of qualification standards by the council (via the principal of the College)

Authorised qualification standards are communicated to prospective students

Qualifications held by prospective students are reviewed to ensure that they comply with thequalification standards set for the programme they wish to enrol for

Outputs Authorised qualification standards for all Programmes presented by the College

Prospectuses, brochures, website etc where qualification standards are communicated toprospective students

Approval of qualifications held by prospective students

Toolkit for Further Education and Training Colleges 27

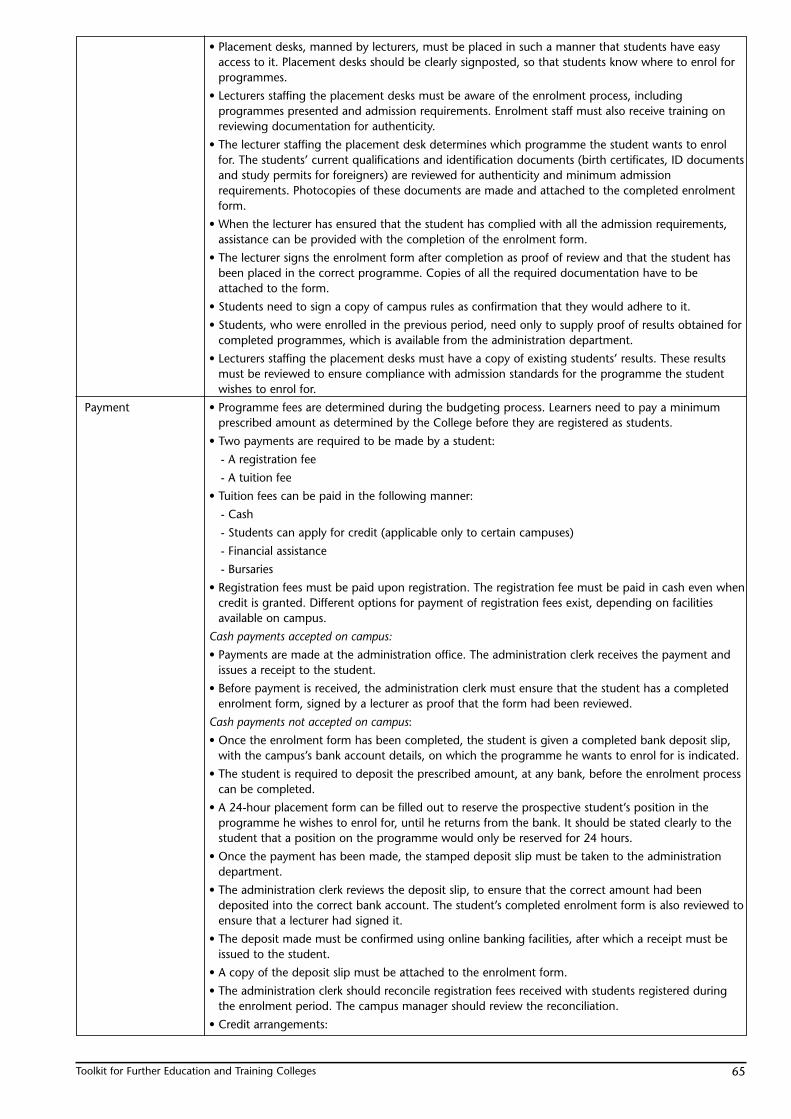

C. Core process: enrolment Sub-process: registration process

Inputs Programmes to be presented in the academic year

Cut-off dates for enrolment as prescribed by DoE

Prospective students

Information station and placement desks

Completed application forms

Deposit slips

Credit forms

Activities Application:

There are four enrolment periods during the year. Enrolment is done on a first come first servebasis and students need to apply personally.

Students must apply before cut-off dates as determined by the campus site.

An information station (information desk) is set up in the enrolment venue.

Prospective students go to the info desk, where all information needed by them is supplied andfrom where they are directed to the relevant placement desks

Existing students, who wish to enrol for a next course, can get a printout of results fromadministration. The printout should be stamped as proof of authenticity. Results can also beverified by lecturers