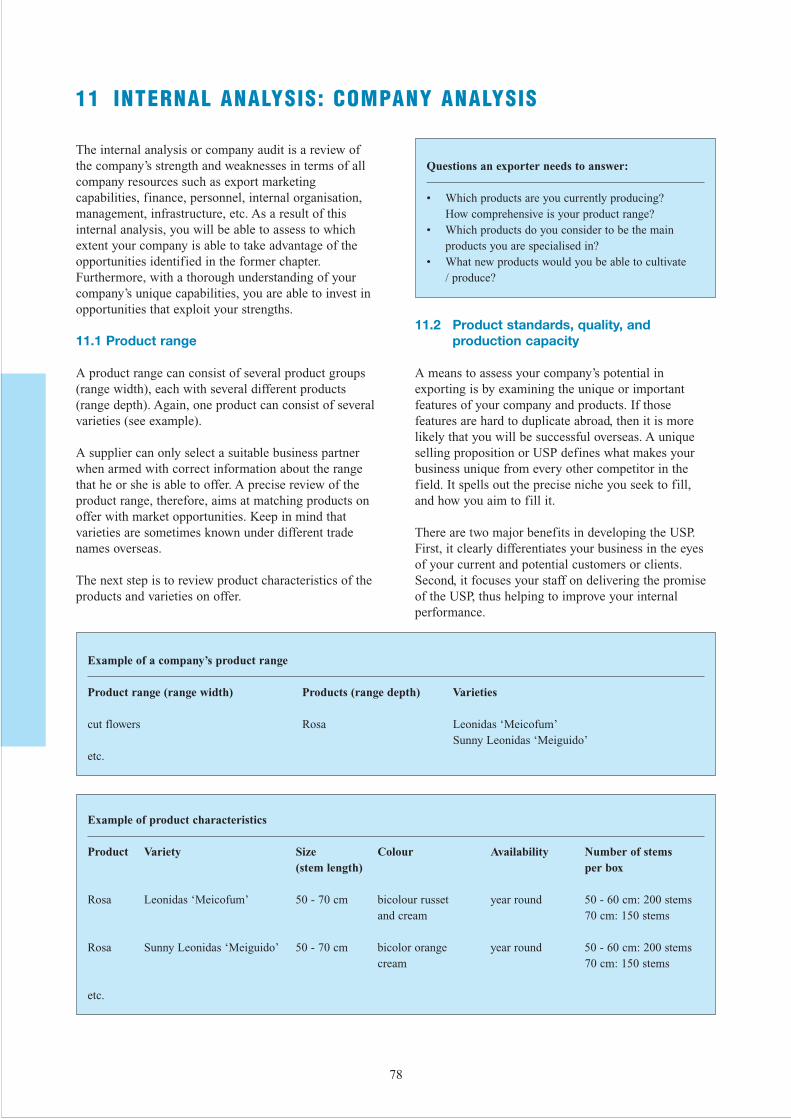

cut flowers

TRANSCRIPT

CENTRE FOR THE PROMOTION OF IMPORTS FROM DEVELOPING COUNTRIES

CUT FLOWERSAND FOLIAGE

EU MARKET SURVEY 2003

EU MARKET SURVEY

CUT FLOWERS AND FOLIAGE

Compiled for CBI by:

ProFoundAdvisers in Development

in collaboration withProVerde - Trade Strategies

and J. Lanning

October 2003

DISCLAIMERThe information provided in this market survey is believed to be accurate at the time of writing. It is, however, passedon to the reader without any responsibility on the part of CBI or the authors and it does not release the reader from theobligation to comply with all applicable legislation.

Neither CBI nor the authors of this publication make any warranty, expressed or implied, concerning the accuracy ofthe information presented, and will not be liable for injury or claims pertaining to the use of this publication or theinformation contained therein.

No obligation is assumed for updating or amending this publication for any reason, be it new or contrary informationor changes in legislation, regulations or jurisdiction.

Update of ‘EU Market Survey Cut Flowers and Foliage’ (2002) and ‘EU Strategic Marketing Guide Cut Flowers andFoliage’ (2000).

TABLE OF CONTENTSREPORT SUMMARY 7

INTRODUCTION 9

PART A: EU MARKET INFORMATION AND MARKET ACCESS REQUIREMENTS

1 PRODUCT CHARACTERISTICS 131.1 Product groups 131.2 Customs/Statistical Product Classification 13

2 INTRODUCTION TO THE EU MARKET 15

3 CONSUMPTION 173.1 Market size 173.2 Market segmentation 173.3 Consumption patterns and trends 18

4 PRODUCTION 21

5 IMPORTS 265.1 Total imports 265.2 Imports by product group 365.3 The role of the developing countries 42

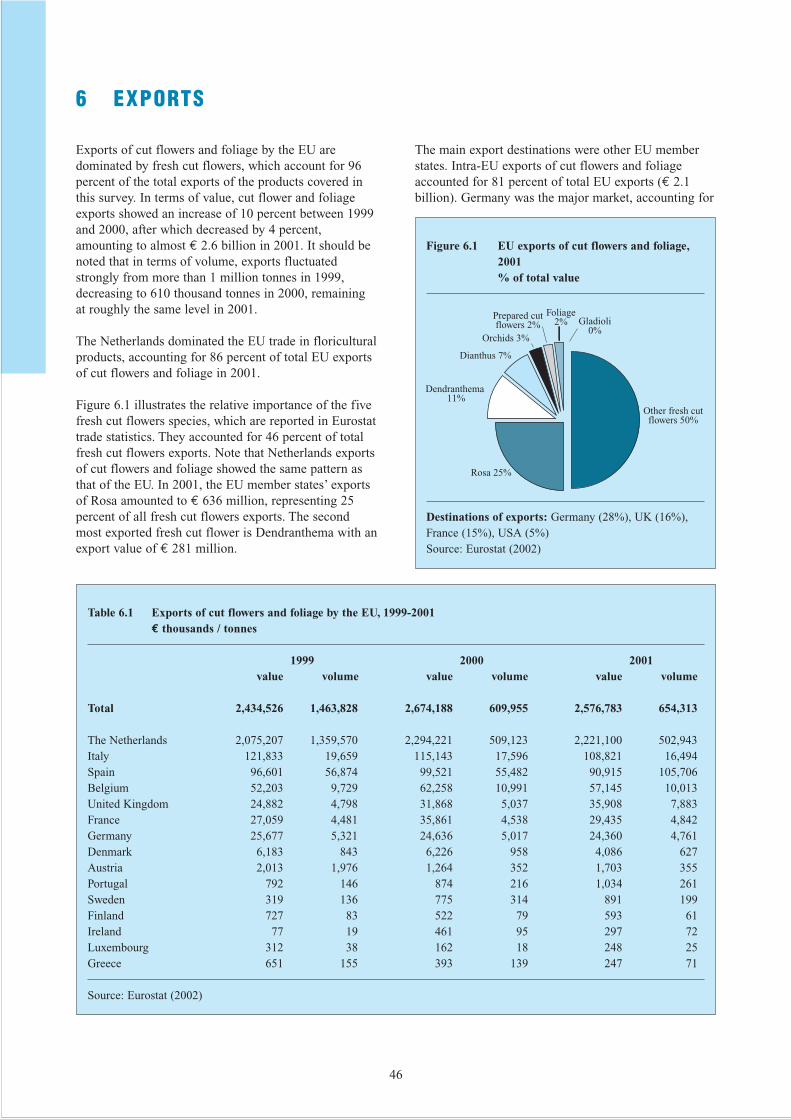

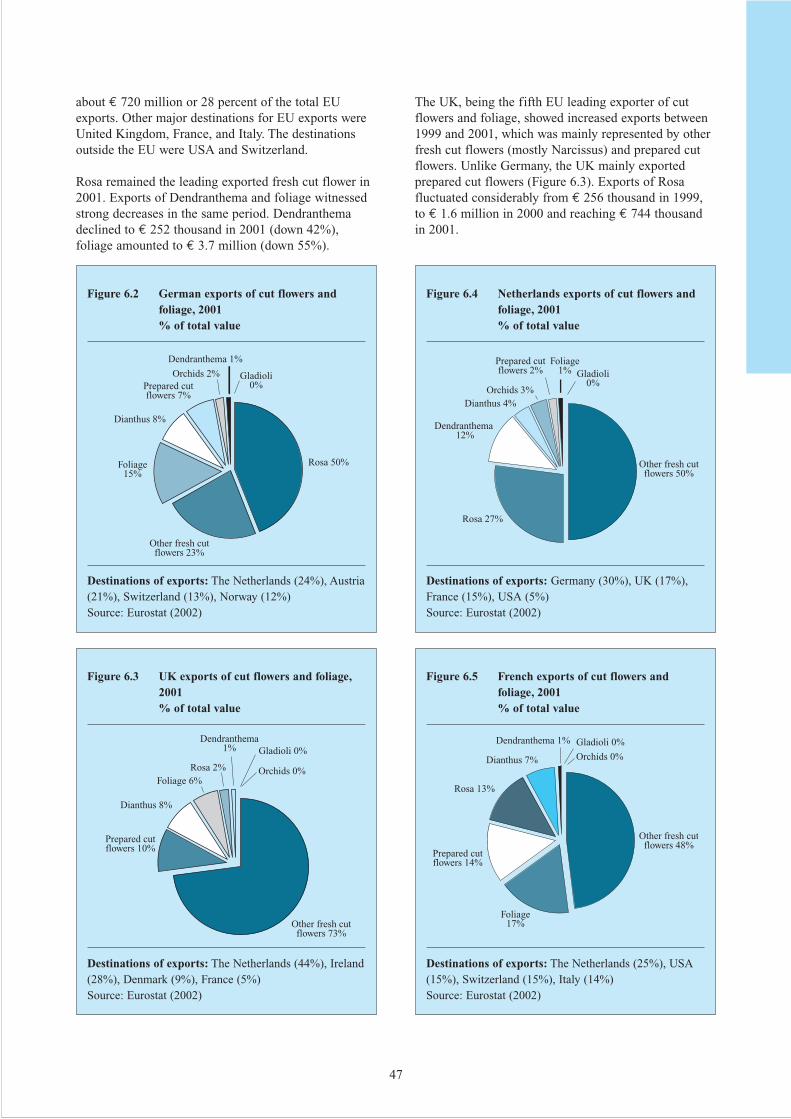

6 EXPORTS 46

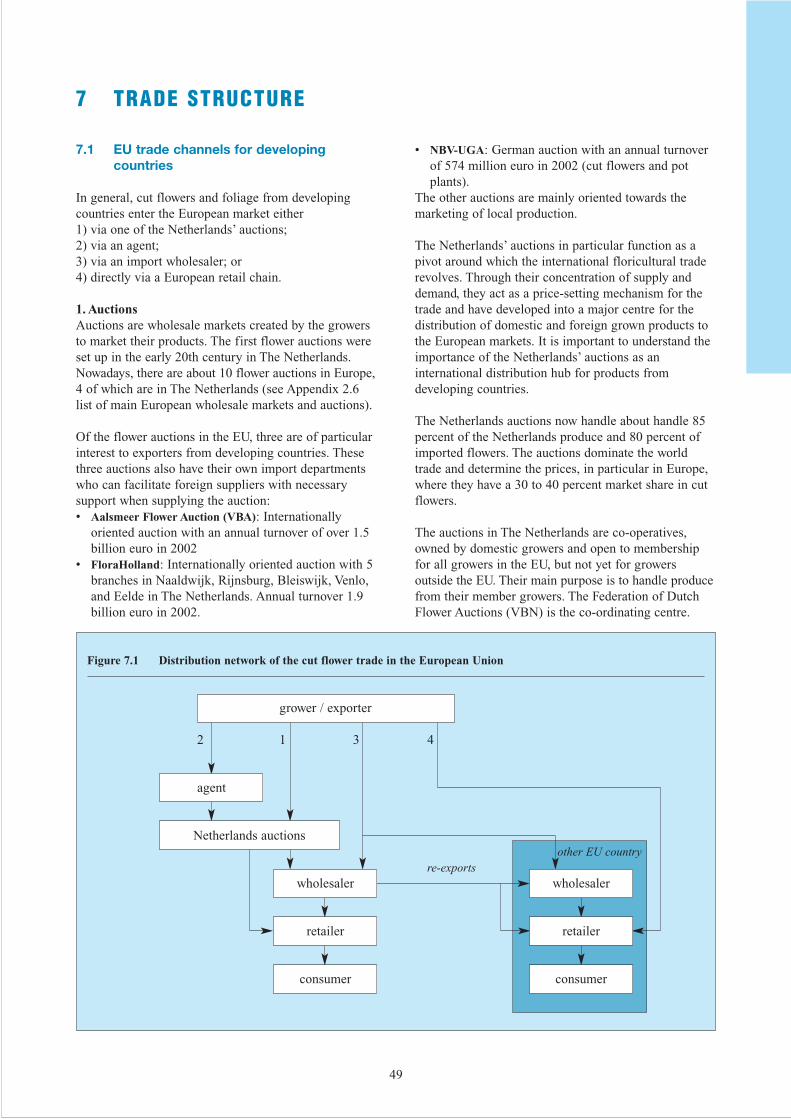

7 TRADE STRUCTURE 497.1 EU trade channels for developing countries 49 7.2 Wholesale level 51 7.3 Retail level 52

8 PRICES 558.1 Price developments 558.2 Sources of price information 55

9 EU MARKET ACCESS REQUIREMENTS 579.1 Non-tariff trade barriers 57

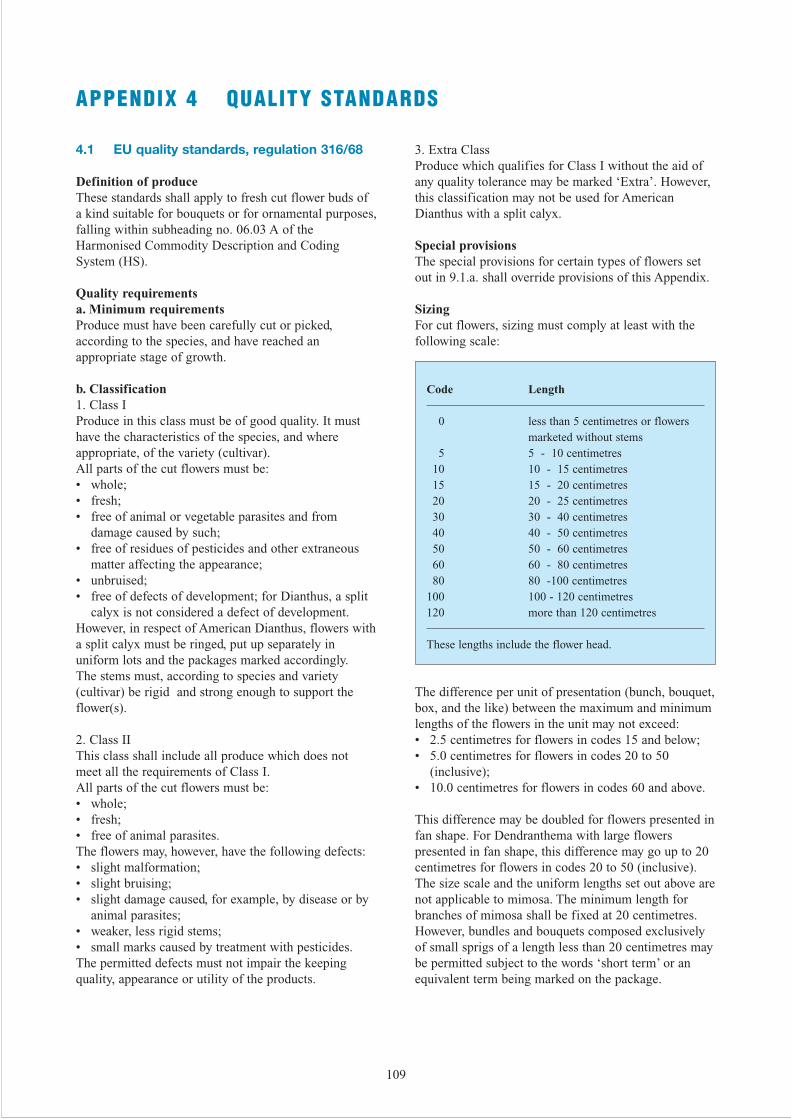

9.1.1 Relevant legislative requirements 579.1.2 Quality and grading standards 609.1.3 Trade related environmental, social and health & safety issues 619.1.4 Packaging and marking 63

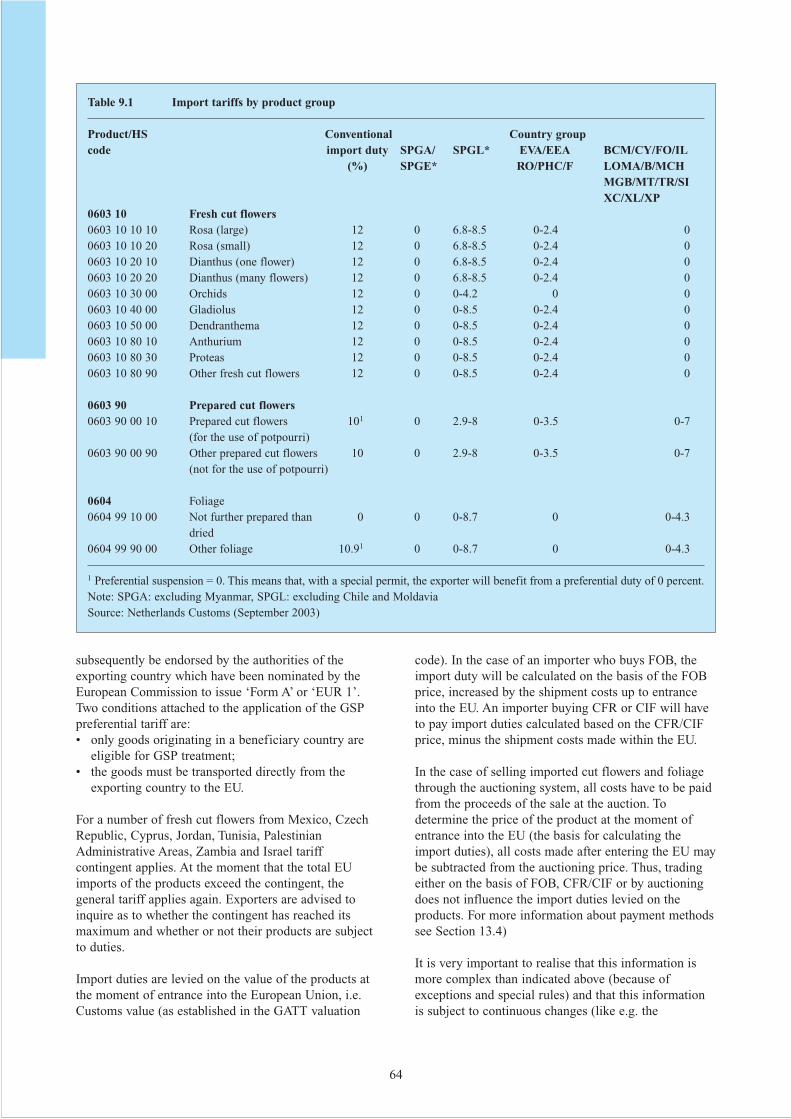

9.2 Tariffs and quotas 63

PART B: EXPORT MARKETING GUIDELINES: ANALYSIS AND STRATEGY

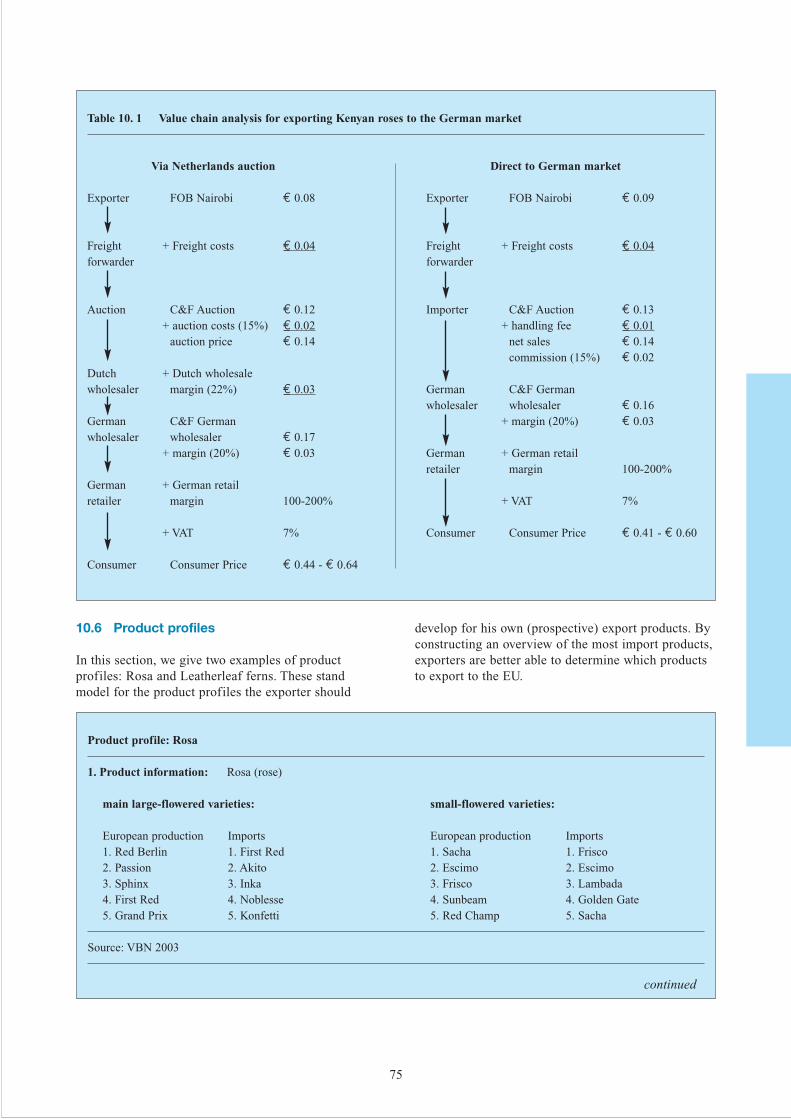

10 EXTERNAL ANALYSIS: MARKET AUDIT 7010.1 Market developments and opportunities 7010.2 Competitive analysis 7210.3 Sales channel assessment 7210.4 Logistics 7310.5 Price structure 7410.6 Product profiles 75

5

6

11 INTERNAL ANALYSIS: COMPANY AUDIT 7811.1 Product range 7811.2 Product standards, quality, and production capacity 7811.3 Logistics 8011.4 Marketing and sales 8111.5 Financing 8111.6 Capabilities 82

12 DECISION MAKING 8312.1 SWOT and situation analysis 8412.2 Strategic options and objectives 85

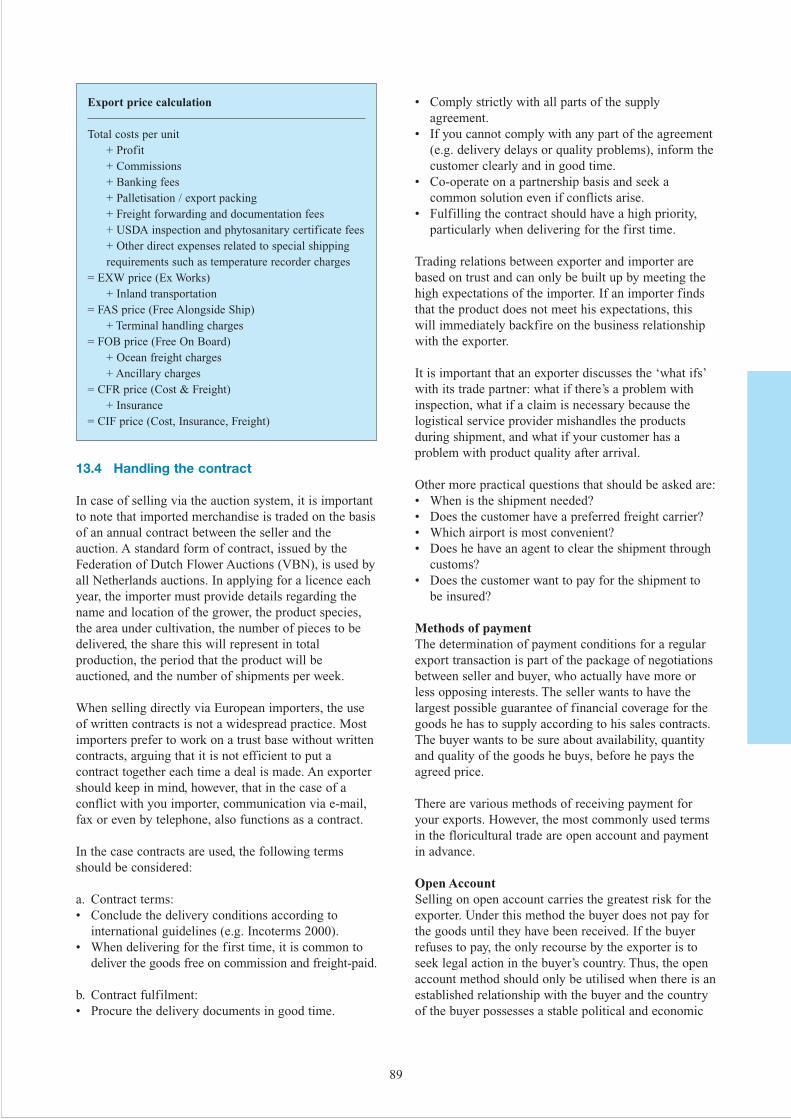

13 EXPORT MARKETING 8713.1 Matching products and the product range 8713.2 Building up a relationship with a suitable trade partner 8713.3 Drawing up an offer 8813.4 Handling the contract 8913.5 Sales promotion 91

APPENDICES 93

7

REPORT SUMMARY

This survey focuses on the market for cut flowers andfoliage in the European Union. The main reason for thisaggregation of the two product groups lies in the factthat the market and marketing channels for cut flowersand foliage for ornamental purposes are very similar.The primary usage of foliage is for bouquets, incombination with fresh or prepared cut flowers.

In this survey, the focus is on the assortment ofimported fresh cut flowers relevant to exporters indeveloping countries. Certain species of cut flowers andfoliage are highlighted (such as Rosa, Dianthus,Dendranthema, Orchids, etc.). However, not all cutflowers are sold as freshly picked products. A relativelysmall proportion of about 5 percent has in some waybeen prepared. Drying and dyeing, in particular, arepreparations that cut flowers can undergo. Other waysof preparing are bleaching or impregnating the flowers.

ConsumptionThe European Union is believed to consume over 50percent of the world’s flowers and includes manycountries with a relatively high per capita consumptionof cut flowers. Although some of the larger EU marketslike Germany, France and The Netherlands show signsof saturation, overall EU consumer sales of cut flowersare still increasing incessantly. Germany is the biggestconsumer of flowers, followed by the UK, France andItaly.

European consumers buy flowers for different purposes.The main purpose of purchase is to give them away as agift, representing about 40 to 50 percent of Europeanconsumer spending. Another 20 to 30 percent of theflowers is bought for special occasions like weddingsand funerals. The remaining 20 to 25 percent is spenton flowers for decoration of their own home.

By far the most important cut flower sold in Europe isRosa, followed at a distance by other flowers likeDendranthema, Dianthus, Tulipa, Lilium, Gerbera, etc.

ProductionThe Netherlands is the leading producer with an outputvalued at about € 2 billion. Germany and Francefollowed in order of importance.

In the production countries in North Europe (The Netherlands, Germany and Denmark), thefollowing main production trends can be recognised:• Production area is slowly declining;• Number of growers is decreasing; and • Total production is stable.This shows that the average cultivated area percompany and output per hectare is increasing.

Hence, scale-enlargement and an increase inproductivity have taken place.

In the main production regions around theMediterranean (Spain, Italy and Portugal), bothproduction area and output are slightly increasing.

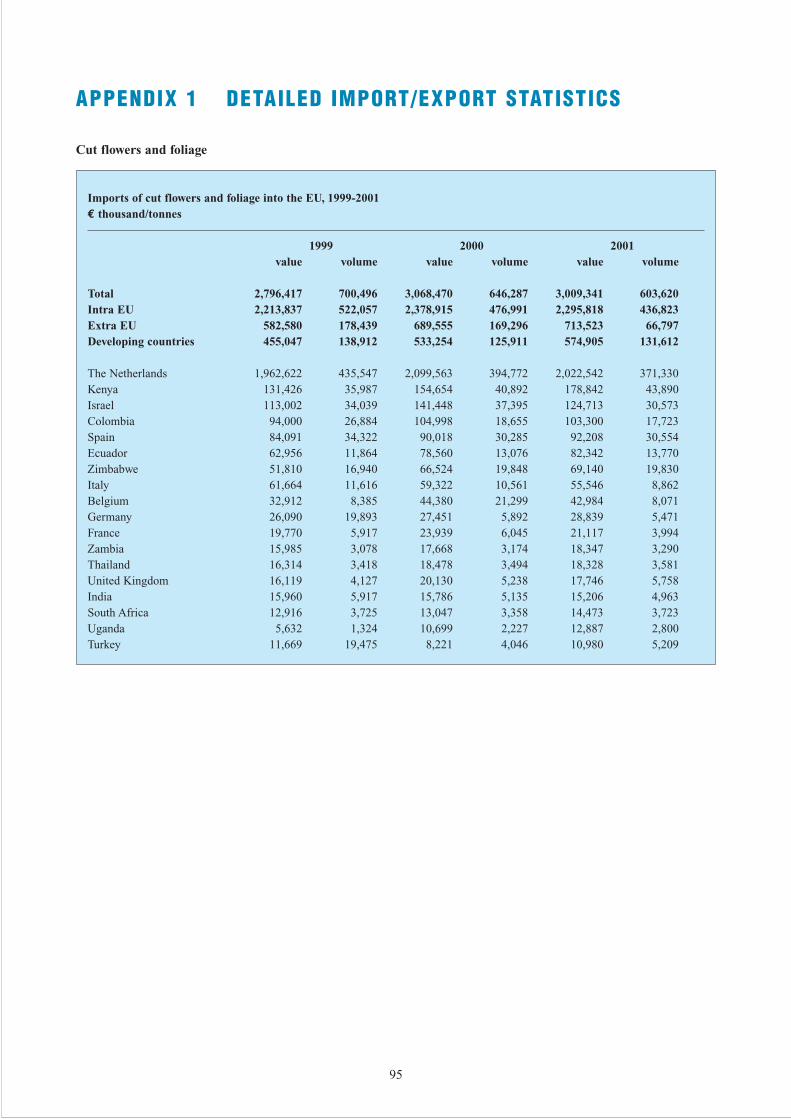

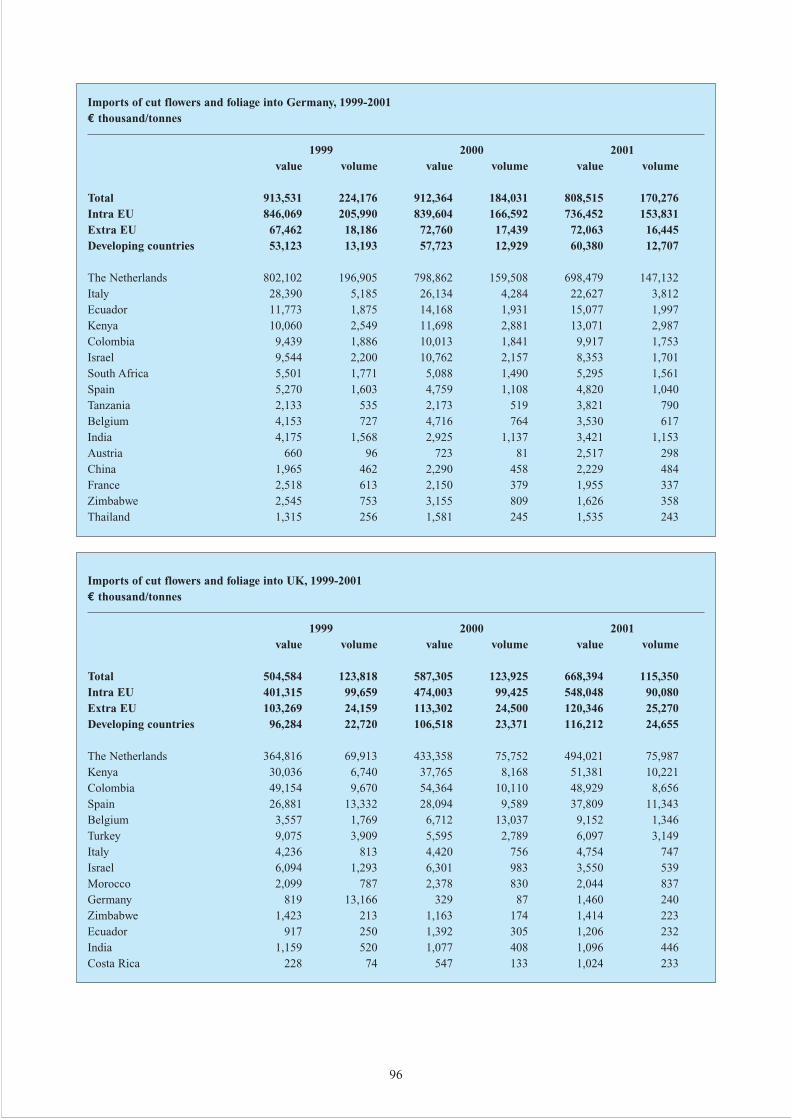

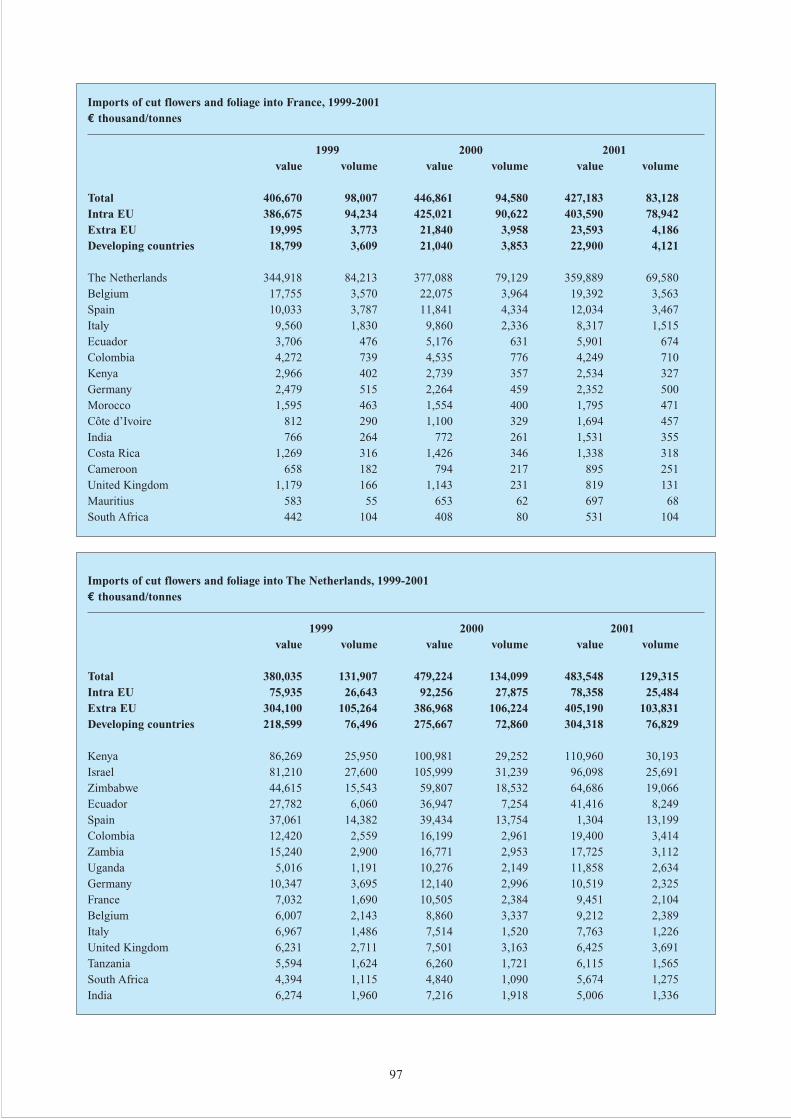

ImportsThe EU, is the world’s leading importer of cut flowersand foliage with total imports amounting to about € 3billion in 2001, which indicates a steady increase of 7percent compared to 1999. Germany was the largest EUimporter of cut flowers and foliage, mainly importingfrom The Netherlands. However, regarding extra-EUimports, The Netherlands was the leading importer,accounting for 57 percent of all cut flowers and foliageimported from outside the EU. In terms of volume, thatshare of The Netherlands is even larger, namely 63percent.

The Netherlands constitutes the major market fordeveloping countries because of its massive trading rolein distributing imported flowers throughout Europe. The importance of developing countries as suppliers tothe EU is demonstrated by the presence of Kenya,Colombia, Ecuador, Zimbabwe, Thailand, Zambia,India, South Africa, Turkey, Tanzania and Ugandaamong the top fifteen supplying countries.

Imports originating in developing countries have beenincreasing strongly over the past ten to fifteen years. In 2001, imports from developing countries amountedto € 575 million, accounting for 19 percent of the totalEU imports of cut flowers and foliage. Developing countries played a more important role inthe Netherlands imports than in the imports of other EU countries, illustrating The Netherlands’ gatewayfunction to the European market for imports fromdeveloping countries.

ExportsEuropean Union exports amounted to almost € 2.6billion in 2001, of which € 2.2 billion was exported andre-exported by The Netherlands alone.

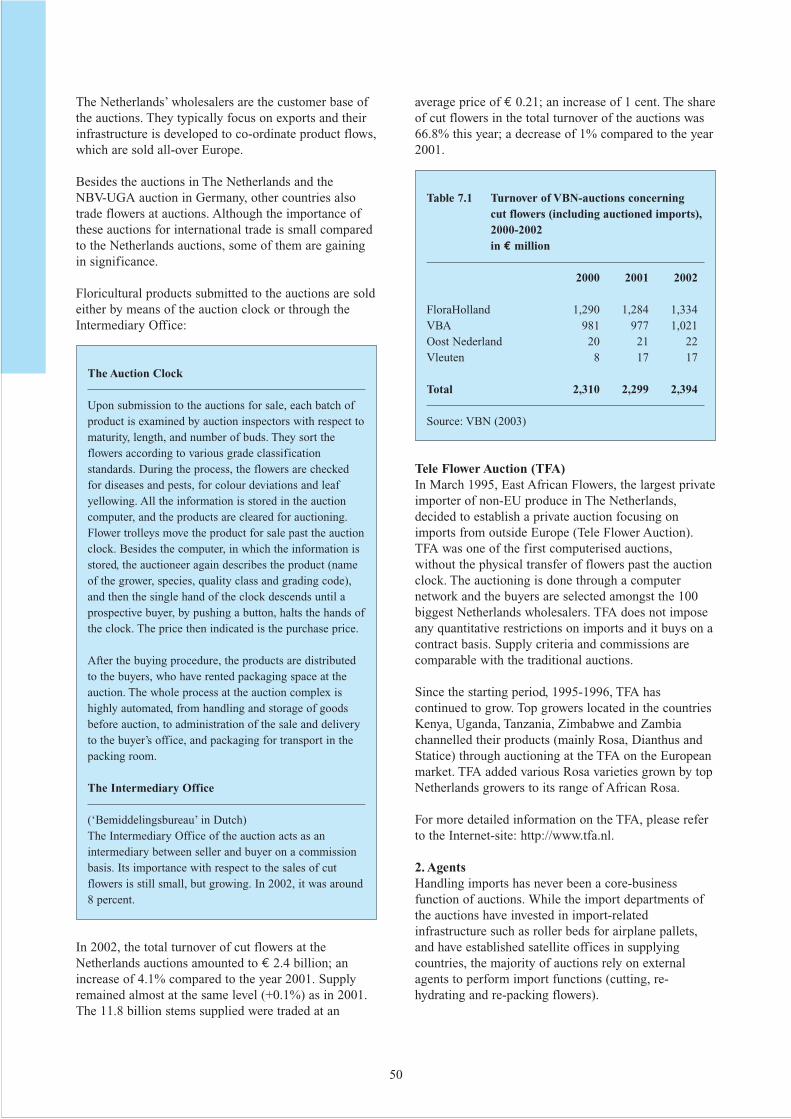

Trade channelsGrowers and traders exporting cut flowers and foliageto the EU send their merchandise either to a wholesaleror to an auction. In this respect, Netherlands auctionsplay a pivotal role in the trade of flowers destined forboth the domestic and other European markets.Products handled by agents and import wholesalers, areeither sold directly to a wholesale buyer or aresubmitted for auction. Export wholesalers re-export theproducts to other EU member countries, where the

flowers and foliage find their way to wholesalers andretailers.

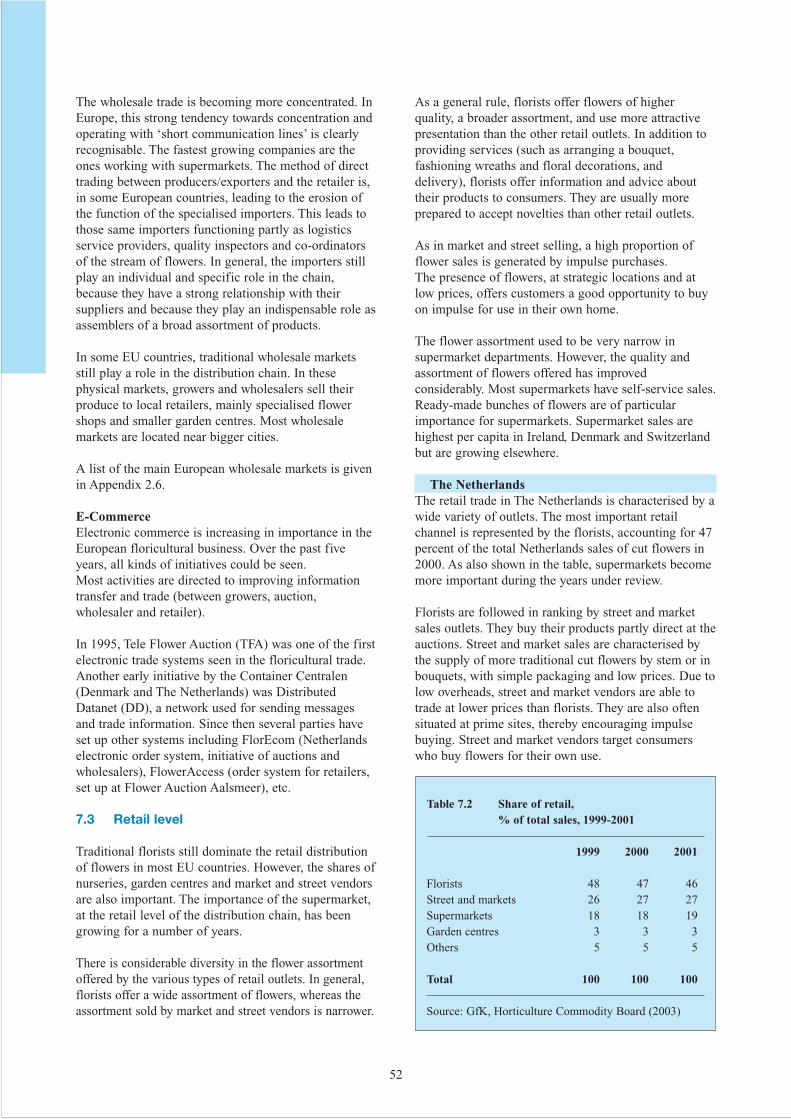

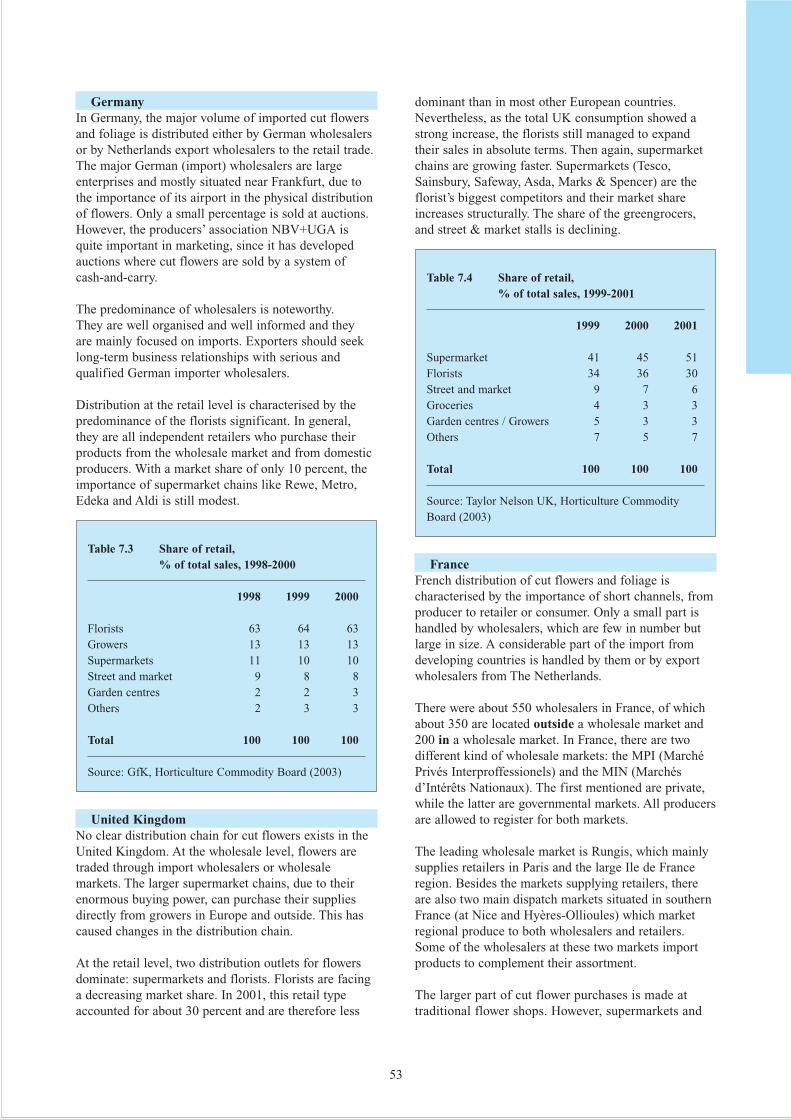

Developments at retail level show a slowly decreasingmarket share of traditional outlets like specialisedflower shops and street and market stalls. Nevertheless,although retail chains sell more and more flowers, about50-55 percent of flower purchases is still made atspecialised flower shops (florists). It is estimated thatretail chains have a market share of about 20 percent,the rest is bought at other places like street vendors andgas stations. Please note that shares of retail outletsvary strongly among different member states.

Opportunities for developing countriesThe market for cut flowers consists of a range ofproduct groups, which offer varying opportunities fordeveloping countries as potential suppliers. It is ahighly competitive market in which importers arecontinually seeking new, special and different products.They tend not to change easily from one rose supplierto another, but co-operation with a company supplyinga new product is considered attractive. The market isclearly searching for these kinds of novelties to takeover some of the market from the species preponderantat present. A new product also offers the prospect ofmaking higher profits than those gained from sellingconventional floricultural products.

Demand for different foliage varieties is still increasingin Europe, particularly for small-leafed foliage for usein cheap bouquets. Furthermore, European importers donot have any reticence about using tropical foliage.

Another opportunity exists in supplying products duringperiods when these products are scarce on the market.

In order to compete, developing country exporters mustbe able to supply products of consistent quality and ona regular basis. At times, this implies that they will haveto accept prices that are lower than those in TheNetherlands and other European markets. Unless exporters maintain a regular supply to the EUmarket, even during periods of low prices, they will notsucceed in developing a sustainable market in the EU.The new entrant to the EU market must recognise thatcompetition from the often long-established suppliers isintense.

CBI servicesFor information on current CBI programmes andtraining & seminars, and for downloading marketinformation and CBI News Bulletins, please refer towww.cbi.nl. Currently, CBI has an export promotionprogramme which seeks to support flower exporters inEast and Southern Africa by helping them to improvetheir export performance on the EU market in close co-operation and consultation with business support

8

organisations. For full details on the programme andapplication forms, please refer to the project documentwhich can be downloaded at the CBI Internet site:http://www.cbi.nl.

INTRODUCTION

This CBI survey consists of two parts: EU MarketInformation and EU Market Access Requirements (Part A), and Export Marketing Guidelines (Part B).

Chapters 1 to 8 of Part A profile the EU market for cutflowers and foliage. The emphasis of the survey lies onthose products, which are of importance to developingcountry suppliers. The major national markets withinthe EU for those products are highlighted. The surveyincludes contact details of trade associations and otherrelevant organisations. Furthermore statistical marketinformation on consumption, production and trade, and

9

information on trade structure and opportunities forexporters is provided.

Chapter 9 subsequently describes the requirementswhich have to be fulfilled in order to get market accessfor the product sector concerned. It is furthermore ofvital importance that exporters comply with therequirements of the EU market in terms of product

EU Market Information(Chapters 1-8)

Product characteristicsIntroduction to the EU marketConsumption and production

Imports and exportsTrade structure

Prices

EU Market Access Requirements(Chapter 9)

Quality and grading standardsEnvironmental, social and health & safety issues

Packaging, marking and labellingTariffs and quotas

Part BExport Marketing Guidelines: Analysis and Strategy

External Analysis (market audit)(Chapter 10)

Opportunities & Threats

Internal Analysis (company audit)(Chapter 11)

Strengths & Weaknesses

Decision Making(Chapter 12)

SWOT and situation analysis:Target markets and segments

Positioning and improving competitivenessSuitable trade channels and business partners

Critical conditions and success factors (other than mentioned)

Strategic options & objectives

Export Marketing(Chapter 13)

Matching products and product rangeBuilding up a trade relationship

Drawing up an offerHandling the contract

Sales promotion

Market Survey

Part AEU Market Information and Market Access Requirements

quality, packaging, labelling and social, health & safetyand environmental standards.

After having read Part A, it is important for an exporterto analyse target markets, sales channels and potentialcustomers in order to formulate export marketing andproduct strategies. Part B therefore aims to assist(potential) exporters from developing countries in theirexport-decision making process.

After having assessed the external (Chapter 10) andinternal environment (Chapter 11), the (potential)exporter should be able to determine whether there areinteresting export markets for his company. In fact, by matching external opportunities and internalcapabilities, the exporter should be able to identifysuitable target countries, market segments and targetproduct(s) within these countries, and possible tradechannels to export the selected products (Chapter 12).

The subjects and outcomes of the different paragraphsof Chapter 13 can be used as input for the Market EntryStrategy and Export Marketing Plan.

The survey is interesting for both starting exporters aswell as well as exporters already engaged in exporting(to the EU market). Part B is especially interesting formore experienced exporters starting to export to the EUand exporters looking for new EU markets, saleschannels or customers. Starting exporters are advised toread this publication together with the CBI’s Exportplanner, a guide that shows systematically how to set upexport activities.

10

Part AEU market information and market access requirements

A

12

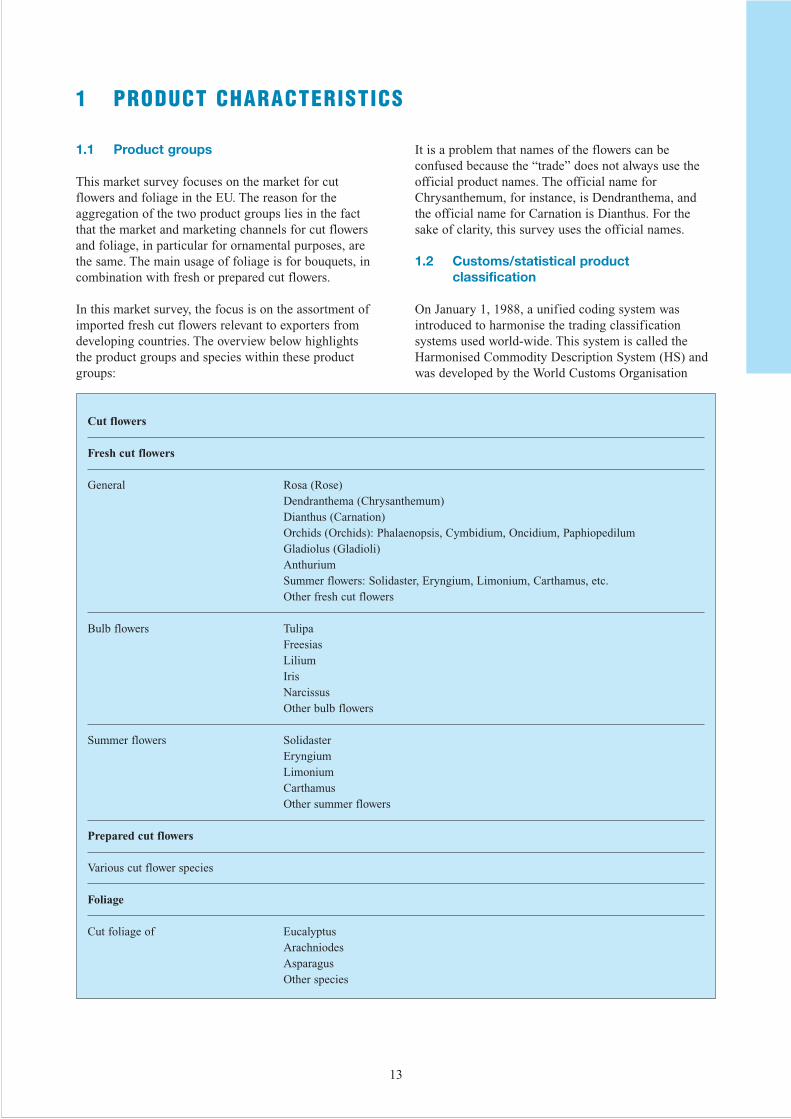

1.1 Product groups

This market survey focuses on the market for cutflowers and foliage in the EU. The reason for theaggregation of the two product groups lies in the factthat the market and marketing channels for cut flowersand foliage, in particular for ornamental purposes, arethe same. The main usage of foliage is for bouquets, incombination with fresh or prepared cut flowers.

In this market survey, the focus is on the assortment ofimported fresh cut flowers relevant to exporters fromdeveloping countries. The overview below highlightsthe product groups and species within these productgroups:

It is a problem that names of the flowers can beconfused because the “trade” does not always use theofficial product names. The official name forChrysanthemum, for instance, is Dendranthema, andthe official name for Carnation is Dianthus. For thesake of clarity, this survey uses the official names.

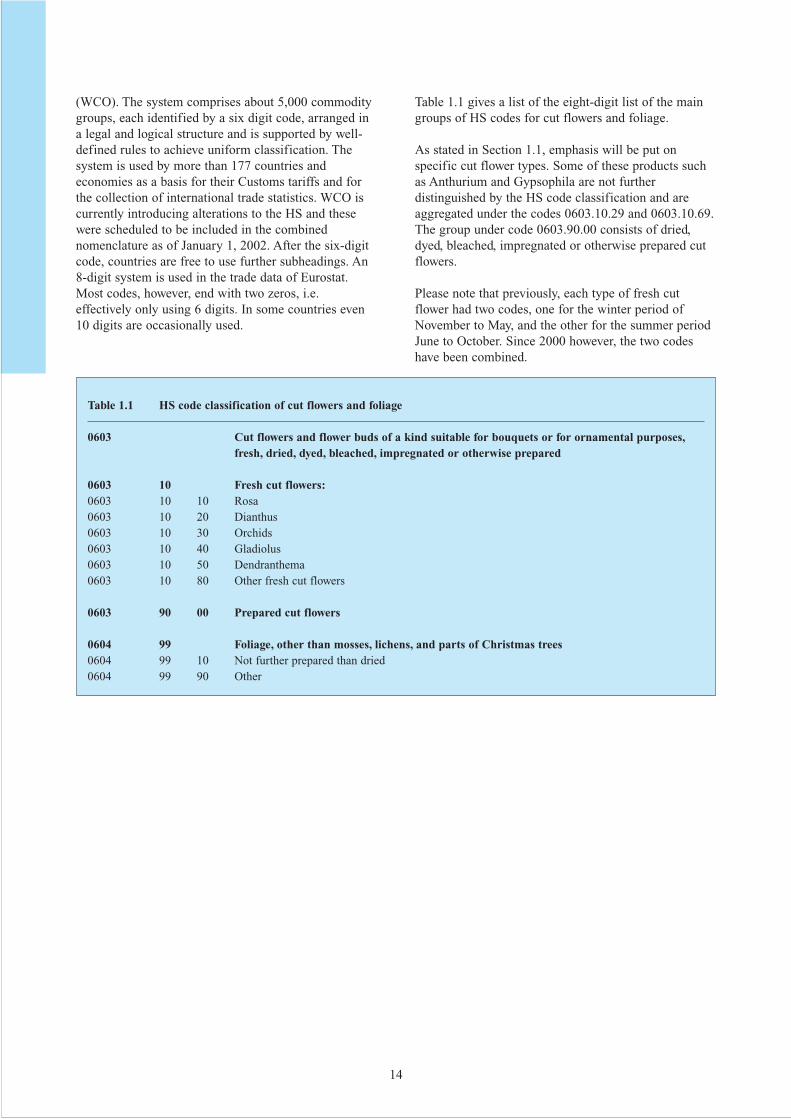

1.2 Customs/statistical product classification

On January 1, 1988, a unified coding system wasintroduced to harmonise the trading classificationsystems used world-wide. This system is called theHarmonised Commodity Description System (HS) andwas developed by the World Customs Organisation

13

1 PRODUCT CHARACTERISTICS

Cut flowers

Fresh cut flowers

General Rosa (Rose)Dendranthema (Chrysanthemum)Dianthus (Carnation)Orchids (Orchids): Phalaenopsis, Cymbidium, Oncidium, PaphiopedilumGladiolus (Gladioli)AnthuriumSummer flowers: Solidaster, Eryngium, Limonium, Carthamus, etc.Other fresh cut flowers

Bulb flowers Tulipa FreesiasLiliumIrisNarcissusOther bulb flowers

Summer flowers SolidasterEryngiumLimoniumCarthamusOther summer flowers

Prepared cut flowers

Various cut flower species

Foliage

Cut foliage of EucalyptusArachniodesAsparagusOther species

14

(WCO). The system comprises about 5,000 commoditygroups, each identified by a six digit code, arranged ina legal and logical structure and is supported by well-defined rules to achieve uniform classification. Thesystem is used by more than 177 countries andeconomies as a basis for their Customs tariffs and forthe collection of international trade statistics. WCO iscurrently introducing alterations to the HS and thesewere scheduled to be included in the combinednomenclature as of January 1, 2002. After the six-digitcode, countries are free to use further subheadings. An8-digit system is used in the trade data of Eurostat.Most codes, however, end with two zeros, i.e.effectively only using 6 digits. In some countries even10 digits are occasionally used.

Table 1.1 gives a list of the eight-digit list of the maingroups of HS codes for cut flowers and foliage.

As stated in Section 1.1, emphasis will be put onspecific cut flower types. Some of these products suchas Anthurium and Gypsophila are not furtherdistinguished by the HS code classification and areaggregated under the codes 0603.10.29 and 0603.10.69.The group under code 0603.90.00 consists of dried,dyed, bleached, impregnated or otherwise prepared cutflowers.

Please note that previously, each type of fresh cutflower had two codes, one for the winter period ofNovember to May, and the other for the summer periodJune to October. Since 2000 however, the two codeshave been combined.

Table 1.1 HS code classification of cut flowers and foliage

0603 Cut flowers and flower buds of a kind suitable for bouquets or for ornamental purposes,fresh, dried, dyed, bleached, impregnated or otherwise prepared

0603 10 Fresh cut flowers:0603 10 10 Rosa0603 10 20 Dianthus0603 10 30 Orchids0603 10 40 Gladiolus0603 10 50 Dendranthema0603 10 80 Other fresh cut flowers

0603 90 00 Prepared cut flowers

0604 99 Foliage, other than mosses, lichens, and parts of Christmas trees0604 99 10 Not further prepared than dried0604 99 90 Other

15

2 INTRODUCTION TO THE EU MARKET

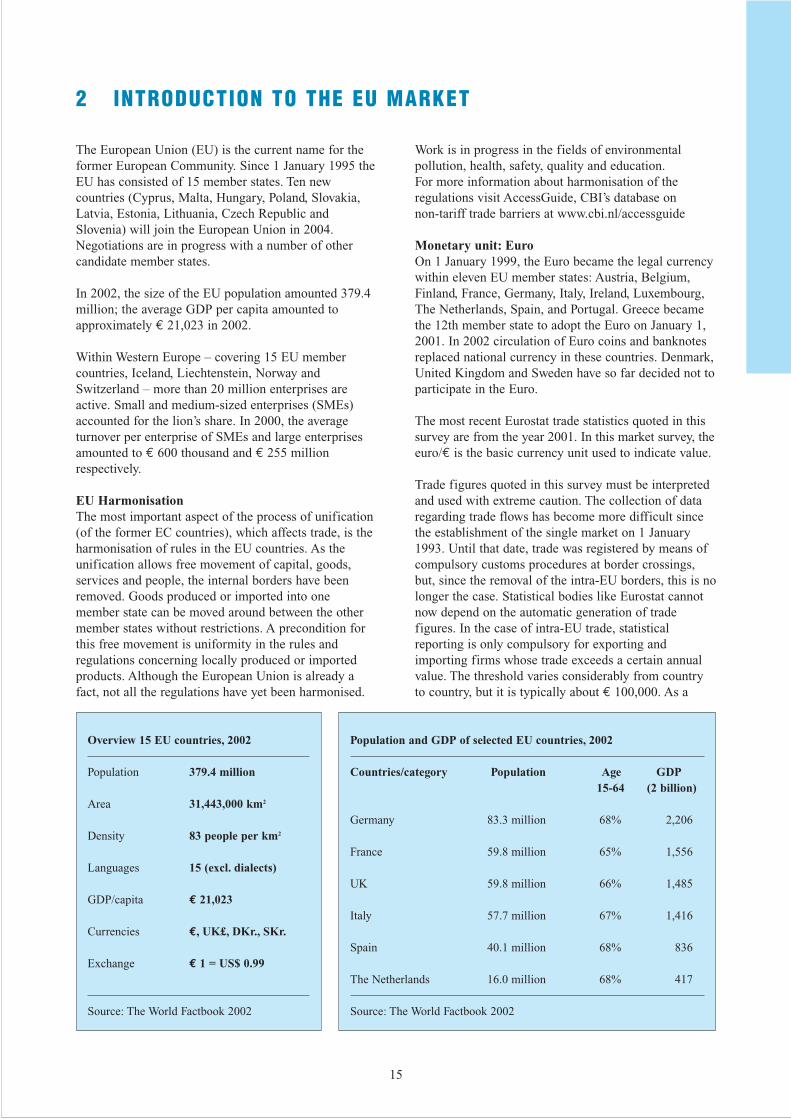

The European Union (EU) is the current name for theformer European Community. Since 1 January 1995 theEU has consisted of 15 member states. Ten newcountries (Cyprus, Malta, Hungary, Poland, Slovakia,Latvia, Estonia, Lithuania, Czech Republic andSlovenia) will join the European Union in 2004.Negotiations are in progress with a number of othercandidate member states.

In 2002, the size of the EU population amounted 379.4million; the average GDP per capita amounted toapproximately € 21,023 in 2002.

Within Western Europe – covering 15 EU membercountries, Iceland, Liechtenstein, Norway andSwitzerland – more than 20 million enterprises areactive. Small and medium-sized enterprises (SMEs)accounted for the lion’s share. In 2000, the averageturnover per enterprise of SMEs and large enterprisesamounted to € 600 thousand and € 255 millionrespectively.

EU Harmonisation The most important aspect of the process of unification(of the former EC countries), which affects trade, is theharmonisation of rules in the EU countries. As theunification allows free movement of capital, goods,services and people, the internal borders have beenremoved. Goods produced or imported into onemember state can be moved around between the othermember states without restrictions. A precondition forthis free movement is uniformity in the rules andregulations concerning locally produced or importedproducts. Although the European Union is already afact, not all the regulations have yet been harmonised.

Work is in progress in the fields of environmentalpollution, health, safety, quality and education. For more information about harmonisation of theregulations visit AccessGuide, CBI’s database on non-tariff trade barriers at www.cbi.nl/accessguide

Monetary unit: EuroOn 1 January 1999, the Euro became the legal currencywithin eleven EU member states: Austria, Belgium,Finland, France, Germany, Italy, Ireland, Luxembourg,The Netherlands, Spain, and Portugal. Greece becamethe 12th member state to adopt the Euro on January 1,2001. In 2002 circulation of Euro coins and banknotesreplaced national currency in these countries. Denmark,United Kingdom and Sweden have so far decided not toparticipate in the Euro.

The most recent Eurostat trade statistics quoted in thissurvey are from the year 2001. In this market survey, theeuro/€ is the basic currency unit used to indicate value.

Trade figures quoted in this survey must be interpretedand used with extreme caution. The collection of dataregarding trade flows has become more difficult sincethe establishment of the single market on 1 January1993. Until that date, trade was registered by means ofcompulsory customs procedures at border crossings,but, since the removal of the intra-EU borders, this is nolonger the case. Statistical bodies like Eurostat cannotnow depend on the automatic generation of tradefigures. In the case of intra-EU trade, statisticalreporting is only compulsory for exporting andimporting firms whose trade exceeds a certain annualvalue. The threshold varies considerably from countryto country, but it is typically about € 100,000. As a

Overview 15 EU countries, 2002

Population 379.4 million

Area 31,443,000 km2

Density 83 people per km2

Languages 15 (excl. dialects)

GDP/capita € 21,023

Currencies €, UK£, DKr., SKr.

Exchange € 1 = US$ 0.99

Source: The World Factbook 2002

Population and GDP of selected EU countries, 2002

Countries/category Population Age GDP15-64 (2 billion)

Germany 83.3 million 68% 2,206

France 59.8 million 65% 1,556

UK 59.8 million 66% 1,485

Italy 57.7 million 67% 1,416

Spain 40.1 million 68% 836

The Netherlands 16.0 million 68% 417

Source: The World Factbook 2002

consequence, although figures for trade between the EUand the rest of the world are accurately represented,trade within the EU is generally underestimated.Furthermore, the information used in this market surveyis obtained from a variety of different sources.Therefore, extreme care must be taken in the qualitativeuse and interpretation of quantitative data, both in thesummary and throughout the text, as well as incomparisons of different EU countries with regard tomarket approach, distribution structure, etc.

For more information on the EU market, please refer tothe CBI’s manual “Exporting to the European Union”.

The survey focuses on the 6 major EU markets for cutflowers and foliage. These are Germany, the UnitedKingdom, France, The Netherlands, Italy and Spain.These EU member countries will be highlighted,because of their relative importance in terms ofconsumption, production, imports and exports.

16

17

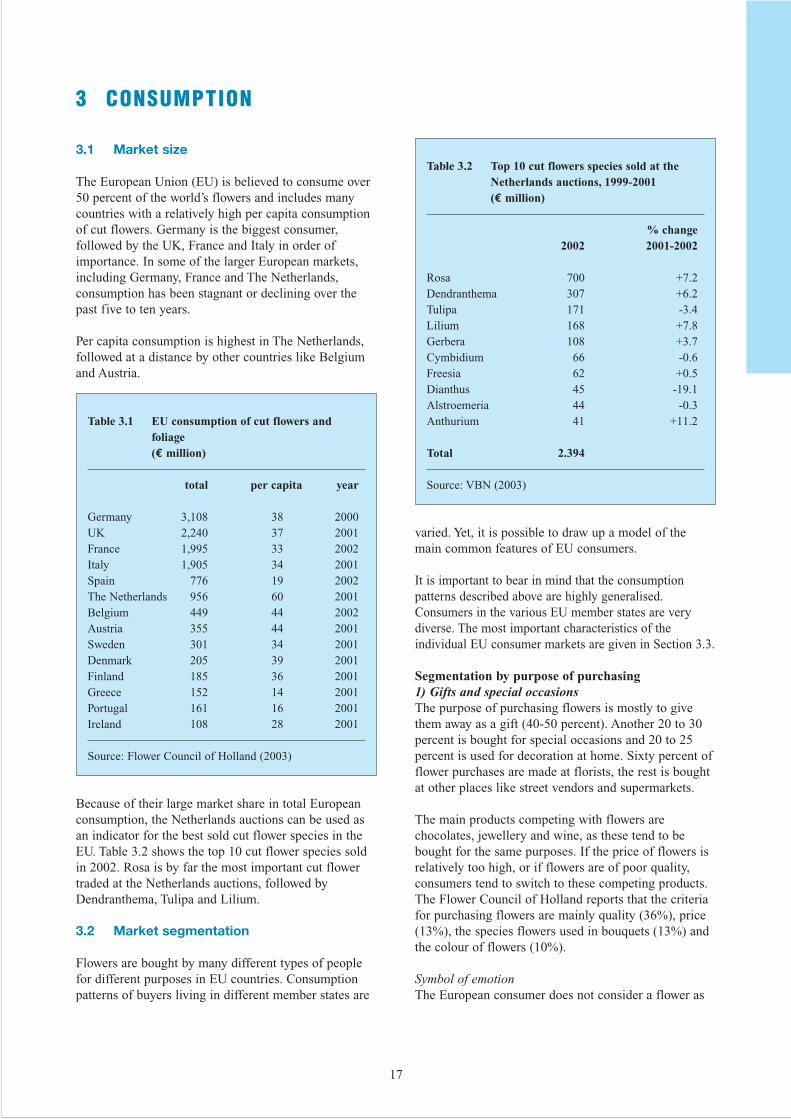

3 CONSUMPTION

3.1 Market size

The European Union (EU) is believed to consume over50 percent of the world’s flowers and includes manycountries with a relatively high per capita consumptionof cut flowers. Germany is the biggest consumer,followed by the UK, France and Italy in order ofimportance. In some of the larger European markets,including Germany, France and The Netherlands,consumption has been stagnant or declining over thepast five to ten years.

Per capita consumption is highest in The Netherlands,followed at a distance by other countries like Belgiumand Austria.

Because of their large market share in total Europeanconsumption, the Netherlands auctions can be used asan indicator for the best sold cut flower species in theEU. Table 3.2 shows the top 10 cut flower species soldin 2002. Rosa is by far the most important cut flowertraded at the Netherlands auctions, followed byDendranthema, Tulipa and Lilium.

3.2 Market segmentation

Flowers are bought by many different types of peoplefor different purposes in EU countries. Consumptionpatterns of buyers living in different member states are

varied. Yet, it is possible to draw up a model of themain common features of EU consumers.

It is important to bear in mind that the consumptionpatterns described above are highly generalised.Consumers in the various EU member states are verydiverse. The most important characteristics of theindividual EU consumer markets are given in Section 3.3.

Segmentation by purpose of purchasing1) Gifts and special occasionsThe purpose of purchasing flowers is mostly to givethem away as a gift (40-50 percent). Another 20 to 30percent is bought for special occasions and 20 to 25percent is used for decoration at home. Sixty percent offlower purchases are made at florists, the rest is boughtat other places like street vendors and supermarkets.

The main products competing with flowers arechocolates, jewellery and wine, as these tend to bebought for the same purposes. If the price of flowers isrelatively too high, or if flowers are of poor quality,consumers tend to switch to these competing products.The Flower Council of Holland reports that the criteriafor purchasing flowers are mainly quality (36%), price(13%), the species flowers used in bouquets (13%) andthe colour of flowers (10%).

Symbol of emotionThe European consumer does not consider a flower as

Table 3.1 EU consumption of cut flowers and foliage (€ million)

total per capita year

Germany 3,108 38 2000UK 2,240 37 2001France 1,995 33 2002Italy 1,905 34 2001Spain 776 19 2002The Netherlands 956 60 2001Belgium 449 44 2002Austria 355 44 2001Sweden 301 34 2001Denmark 205 39 2001Finland 185 36 2001Greece 152 14 2001Portugal 161 16 2001Ireland 108 28 2001

Source: Flower Council of Holland (2003)

Table 3.2 Top 10 cut flowers species sold at the Netherlands auctions, 1999-2001(€ million)

% change2002 2001-2002

Rosa 700 +7.2Dendranthema 307 +6.2Tulipa 171 -3.4Lilium 168 +7.8Gerbera 108 +3.7Cymbidium 66 -0.6Freesia 62 +0.5Dianthus 45 -19.1Alstroemeria 44 -0.3Anthurium 41 +11.2

Total 2.394

Source: VBN (2003)

18

just an ordinary gift; it also symbolises emotion andfeeling and flowers can deliver a message of emotion.The reason for a gift can be congratulations (birthday),an apology (argument, awkwardness), a commiserationwith someone’s grief (death, accident), or a sign of loveor affection for someone (Valentine’s Day).

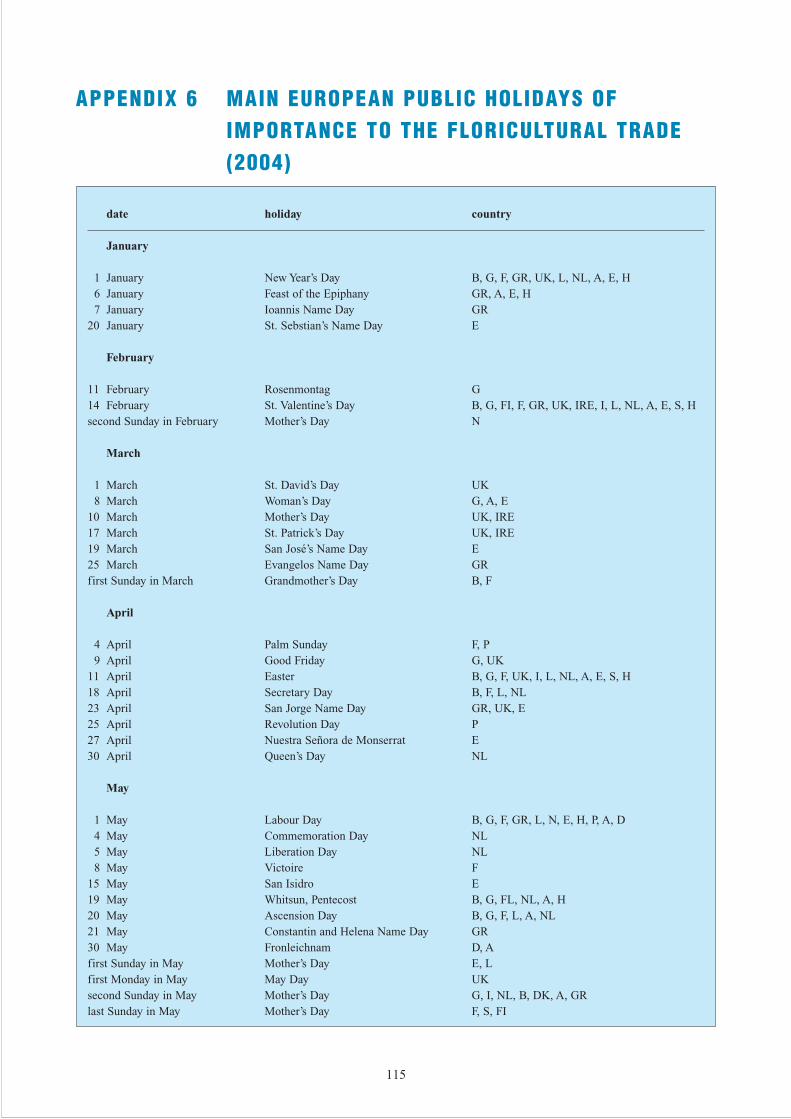

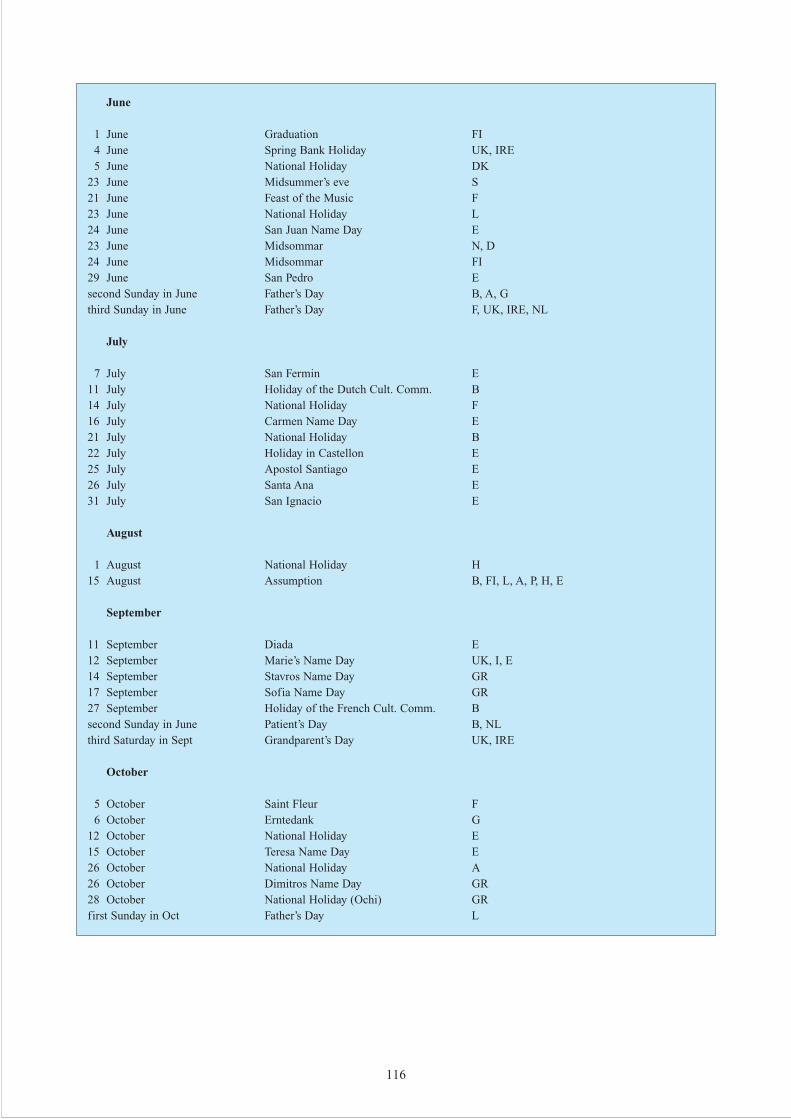

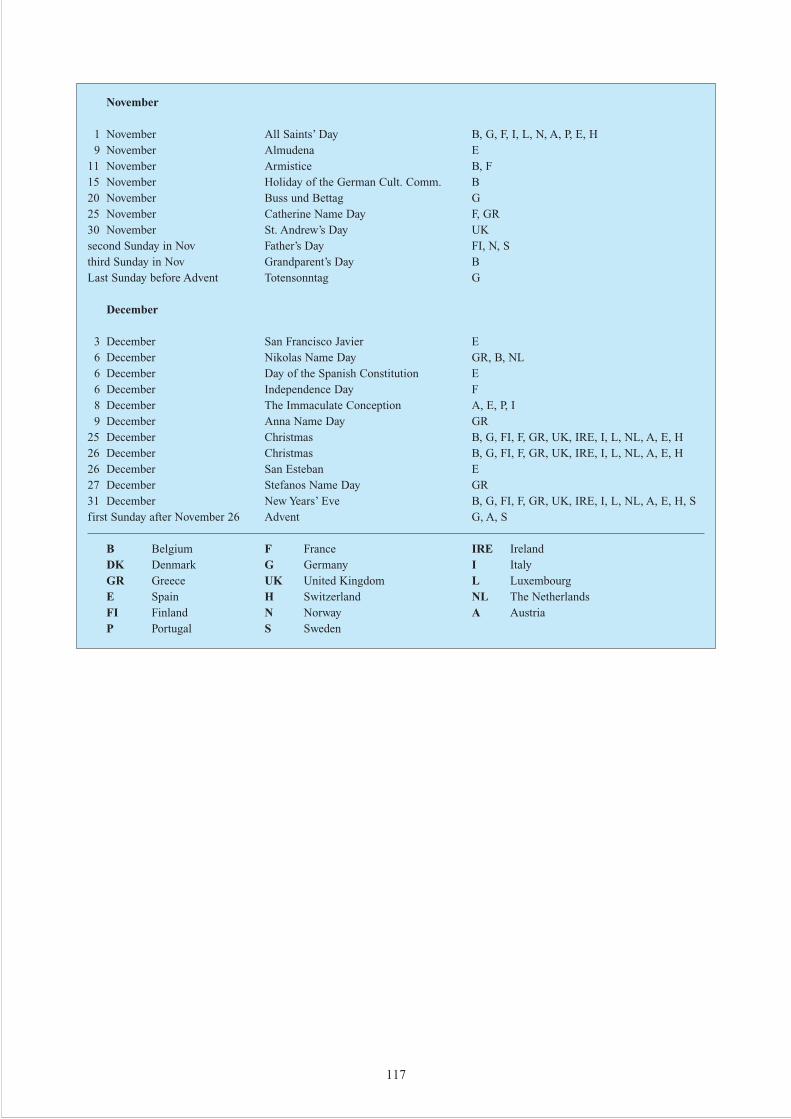

Public holidaysPublic holidays have an important influence on thedemand for cut flowers and foliage. At time ofValentine’s Day, Christmas, Mother’s Day, andSecretary’s Day there are substantial peaks in flowersales. Beside the internationally well-known holidays,most countries have their own special holidays.Appendix 6 lists the main European public holidays.

2) Own useThe second purpose why consumers buy flowers is forhis or her own use. This is often with the intention ofbrightening up the home and creating a pleasantenvironment. The same purpose applies for companies(businesses, restaurants, hotels, etc.) buying flowers todecorate and brighten up their offices, lobbies orrestaurants.

Segmentation by buyersWomen vs. menTypically the person who buys flowers will be a womanof older than 45 years of age, living in an urbanagglomeration where there are medium to high incomes.80 percent of flowers purchased in European countriesis bought by stem, the rest is in ready made bouquets.

Young people vs. older peopleThe sales of cut flowers to young people not older than30 years of age is decreasing. The reasons could befound in the following:• Young households are mainly couples both working

and therefore less at home. As a consequence, theyhave less opportunity and time to purchase flowers.Furthermore, they buy fewer flowers because theycannot enjoy the flowers since they are not homeoften.

• Households with young children due to practicalreasons (for example vases being knocked over) donot buy flowers often.

• Young people attach less emotional value to flowersthan older people.

Institutional market vs. consumer marketCompanies also purchase flowers to decorate andbrightening up offices. The non-profit sector and thecommercial services sector are major consumers offlowers, accounting for 50 percent of all flowers boughtby the small and medium-sized enterprises. About 89percent of the companies purchases flowers to givethem away as birthday and anniversary presents.

3.3 Consumption patterns and trends

Consumer preferences and patterns can differ stronglybetween countries. Purchasing patterns even differwithin countries by geographical region and incomestrata: affluent people buy more bouquets with“special” flowers; less affluent people buy simplebunches of flowers. Even colour preferences vary.Nevertheless, there are a few characteristics that areapplicable to most European consumers.

European consumers expect flowers to be colourful andbeautiful. The emotional element is important.Furthermore, the quality expected by consumers isgenerally very high. They expect not only freshness at themoment of purchase, but also a long vase life. The priceis not the main criterion, but is of course, of importance.Last, but not least, the scent of the flowers is valued.

For years, cut flowers in fashionable colours and flowerforms have been priced higher than the average crop.The traditional primary colours of red, yellow, white,and blue always enjoy a certain demand, but the ever-changing fashions in interior decor set the trends.30 percent to 70 percent of consumers demand thatcolour tones be combined in harmonious or contrastingarrangements, with decorative pots or wrappings.

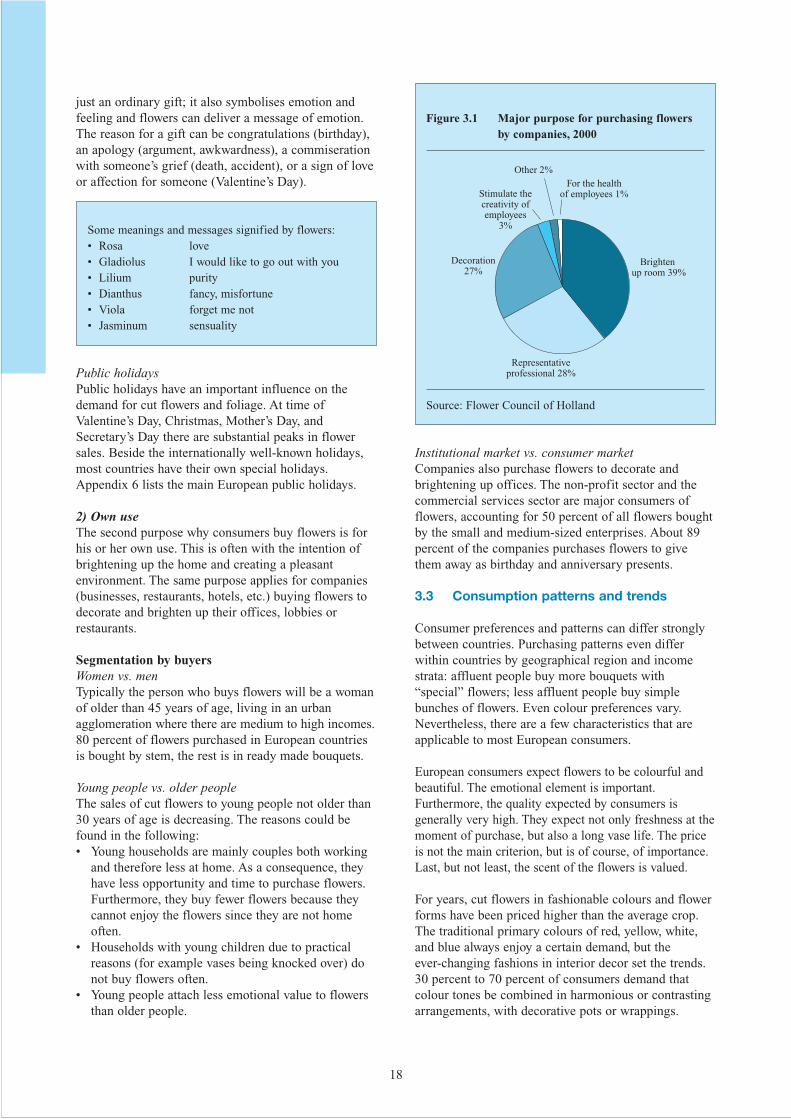

Representativeprofessional 28%

Brighten up room 39%

For the healthof employees 1%

Other 2%

Stimulate thecreativity ofemployees

3%

Decoration27%

Figure 3.1 Major purpose for purchasing flowersby companies, 2000

Source: Flower Council of Holland

Some meanings and messages signified by flowers:• Rosa love• Gladiolus I would like to go out with you• Lilium purity• Dianthus fancy, misfortune• Viola forget me not• Jasminum sensuality

19

The most important characteristics of the individual EUconsumer markets for flowers and foliage, according tothe Flower Council of Holland, are described below.

Germany• Sales in Europe’s largest market, Germany, have

been stabilising for a few years, and are now evenshowing signs of saturation.

• The average German consumer is very demandingand health-, environmental- and cost-conscious.

• About 63 percent of the German population buys cutflowers, of which 42 percent is accounted for bymono-bunches and 30 percent bouquets.

• Within mono-bunches, Rosa is the leading cut flowerpurchased. Dianthus, Tulipa, Orchids, andDendranthema follow in order of importance.

• 58 percent of the flowers bought is to give away aspresents, 23 percent for memorial and 18 percent forown use.

• Flowers are associated with special occasions, natureand a sign of affection and love.

• The decorative characteristics of flowers are mainlyappreciated by women. Young people and men relateflowers primarily to the giving of a present.

• Flowers and bouquets which are purchased to giveaway as present are mainly bought at florists.

UK• Since 1995, the UK consumption of cut flowers and

foliage has more than doubled. • The percentage of buyers of flowers showed increases

from 39 percent in 1999 to 46 percent in 2001.• About 43 percent of flowers bought is to give away

as a present, and 12 percent is for funerals.• Visits, birthdays and special holidays (Mother’s Day,

Christmas, Valentine’s Day) are major occasions tobuy flowers. Mono-bunches are mainly bought ashome decoration, and mixed bouquets as gifts.

• Mono-bunches are mainly purchased at supermarkets,while mixed bouquets are bought at florists.

• Regarding mono-bunches, Dianthus accounted for 34percent of flowers bought. Dendranthema (17%),Rosa (9%), Lilium (8%) and Freesia (5%) followedin order of importance. Other flowers are Tulipa,Daffodils, Gerbera, Iris and Gerbera.

• The market share of mixed bouquets decreasedslightly from 40 percent in 1998 to 37 percent in2001.

• Since British people prefer a classical and cosyinterior, they are most likely to choose bouquetsmixed with traditional flowers (such as Rosa, Freesia,Dendranthema) in “sweet” colours (pink and purple).

• Regarding mono-bunches, Dendranthema andDianthus are popular flowers bought, as these speciesare relatively cheap and have a longer vase lifecompared to other species of cut flowers.

• British consumers determine their purchasing choiceby focussing on the freshness, affordable price andthe scent.

The Netherlands• The Netherlands market for flowers and foliage is

showing signs of saturation.• The number of flower consumers has decreased in

the last few years, but consumers are spending moreon expensive flowers.

• Medium and large-sized enterprises, the so-calledinstitutional market, are becoming importantconsumers of flowers. About 80 percent of theseenterprises is spending on flowers.

• About 50 percent of the flowers is bought as presents(love, affection, weddings).

• Bouquets are the most popular product group,followed by Rosa.

• Of all coloured Dendranthema, the white and yelloware the most popular.

• Birthdays, visits and special holidays (Mother’s Day,Christmas, Valentine’s Day) are major occasions forbuying flowers.

Table 3.3 Occasions for buying flowers in the UK(% of sales), 1998-2001

1998 1999 2000 2001

Present 49 45 43 41Own use 32 37 39 43Funeral 15 13 14 12Other 5 5 4 4

Source: Flower Council of Holland

Top 10 cut flowers consumption in The Netherlands:

1 Mixed bouquets 2 Rosa3 Tulipa 4 Dendranthema5 Gerbera6 Lilium 7 Alstroemeria 8 Freesia9 Dianthus

10 Iris

20

France• Total French expenditure on flowers is stabilising.• French consumers are less satisfied with the

quality/price relationship.• Competition with other products increased (wine is

also frequently purchased as a gift).• French people are often away from home at the

weekend and therefore barely purchase flowers andfoliage to decorate their houses.

• Visits and birthdays are major occasions for buyingflowers. About 53 percent of flowers bought was togive as presents, while 31 percent was destined forfunerals and 17 percent for own use.

Italy• Italians buy flowers mainly to give away as gifts

(89%). Birthdays (31%) and funerals (13%) are theother two main occasions for buying flowers andfoliage.

• Mono-bunches accounted for 37 percent of flowerspurchased. Bouquets with a share of 30 percentfollowed in order of importance.

• Valentine’s day, Women’s day, Mother’s day andreligious (holi)days cause high sales. In the secondhalf of the year, All Saint’s Day and Christmas aremajor reasons to purchase flowers.

• Rosa, Gerbera, Lilium, Dianthus and Orchids are themost important flowers bought.

• Dendranthema are mainly bought on All Saint’s Day.Gladiolus are bought for funerals.

Spain• Spanish consumption of cut flowers has steadily been

steadily increasing for many years. In 2002, theaverage Spanish consumer spent € 19 euro onflowers. The coming years, cut flower consumption isexpected to increase by 6% per year.

• Special occasions (birthdays, funerals) are still themost important reason to purchase flowers.

Nevertheless, buying flowers for own use is slowlyincreasing in importance.

• Mixed bouquets are increasing in popularity inSpain, accounting for 32 percent of total cut flowersales. This increase is mainly at the expense of salesof flower arrangements (19 percent). About 48percent of the cut flowers is sold separately or in amono-bunch.

• The typical Spanish flower consumer lives in a city.The urban Catalunya region and Madrid togetheraccount for 36% of total Spanish flower sales.

Table 3.4 Occasions for buying flowers in Spain,1998-2002(% of sales)

1998 2002

Own use 8 14Special occasions 92 86

Source: Flower Council of Holland

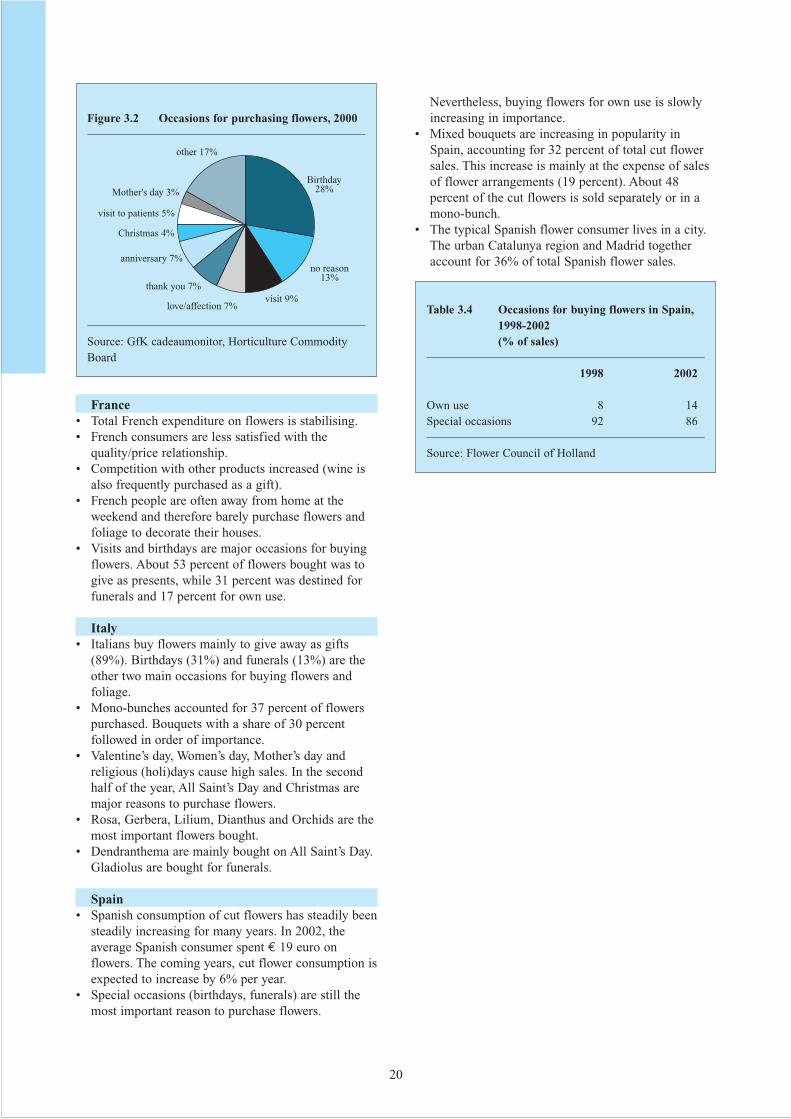

no reason13%

Birthday28%

other 17%

Mother's day 3%

visit 9%love/affection 7%

thank you 7%

anniversary 7%

Christmas 4%

visit to patients 5%

Figure 3.2 Occasions for purchasing flowers, 2000

Source: GfK cadeaumonitor, Horticulture CommodityBoard

21

4 PRODUCTION

In general, the following important production trendsare recognised in the main production countries inNorth Europe (The Netherlands, Germany andDenmark):\ Production area is slowly declining.\ Number of growers is decreasing.\ Total production is stable.

This means that the average cultivated area percompany and output per hectare is increasing. Hence, scale-enlargement and increased productivityhave taken place.

In most production regions around the Mediterranean,we can recognise a different trend with production areaand output slightly increasing.

Although there is often no (recent) data on productionof cut flowers in most EU countries, it is possible togive an indication of the main cut flower producingcountries in the EU, by looking at the figures availableand at the area under production.

In general, all EU countries described above reported alower production of cut flowers compared to the yearsbefore. AIPH (International Association of HorticulturalProducers) acknowledged this and even reported resultsas bad as in 1999 for cut flower production. Some East-European countries like Hungary and Czech Republic

reported a small increase in the production, in contrastto EU countries like Belgium, Germany, Finland,France, Luxembourg, The Netherlands and the UKwhere production decreased.

Over the last years, the number of producers in EUcountries has been decreasing steadily, reflecting theunfavourable situation in Europe. Only Hungaryreported an increased number of producers, in contrastto Luxembourg, Sweden and the Czech Republic, wherethe number of producers stagnated.

The development of the area used for flower productionin the EU differs strongly per country. Countriesshowing increases in area under production are mainlyMediterranean countries like Spain and Italy, whileNorthern European producing countries like TheNetherlands, Germany and Denmark show fairly stableto declining areas under cultivation.

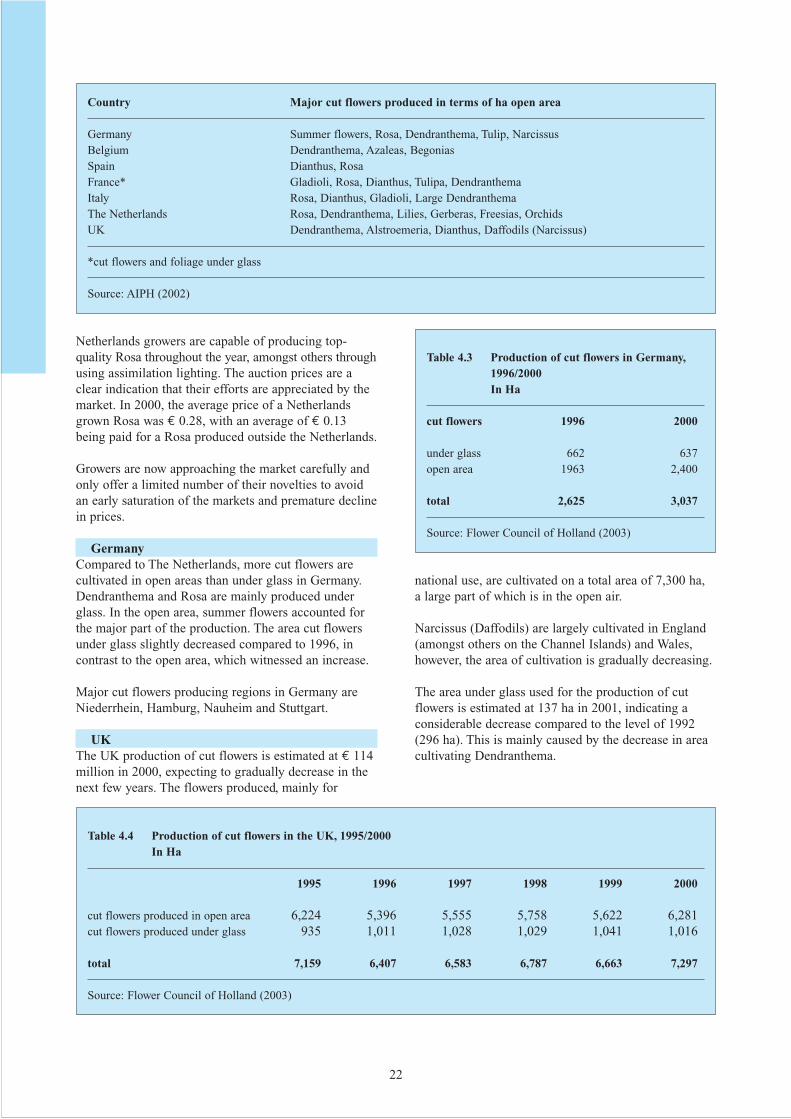

The following box provides the order of importance ofthe cut flower production in a number EU countries (interms of ha open area).

Table 4.2 Area under production for cut flowers and pot plantsIn Ha

Country Area Year

The Netherlands 8,479 2000Italy 8,463 1998Spain 7,617 1997Germany 7,056 2000UK 7,297 2000France 6,628 1999Belgium 1,721 1999Denmark 444 1999Finland 141 1999Sweden 63 1999

Source: AIPH Yearbook of the International HorticulturalStatistics (1999, 2002), Flower Council of Holland (2003)

Table 4.1 Production of cut flowers and pot plants in selected EU countriesIn € million

Country Production Year

The Netherlands 2,057 2002France 1,503 2000Germany 1,135 1997Italy 859 1999Denmark 354 1998Spain 345 1990Austria 240 1999Belgium 238 1999Sweden 199 1990UK 114 2000Finland 76 1999

Note: more recent data for Germany, Spain and Swedenare not available.

Source: AIPH Yearbook of the International HorticulturalStatistics (1999, 2000, 2001, 2002)

22

Netherlands growers are capable of producing top-quality Rosa throughout the year, amongst others throughusing assimilation lighting. The auction prices are aclear indication that their efforts are appreciated by themarket. In 2000, the average price of a Netherlandsgrown Rosa was € 0.28, with an average of € 0.13being paid for a Rosa produced outside the Netherlands.

Growers are now approaching the market carefully andonly offer a limited number of their novelties to avoidan early saturation of the markets and premature declinein prices.

GermanyCompared to The Netherlands, more cut flowers arecultivated in open areas than under glass in Germany. Dendranthema and Rosa are mainly produced underglass. In the open area, summer flowers accounted forthe major part of the production. The area cut flowersunder glass slightly decreased compared to 1996, incontrast to the open area, which witnessed an increase.

Major cut flowers producing regions in Germany areNiederrhein, Hamburg, Nauheim and Stuttgart.

UKThe UK production of cut flowers is estimated at € 114million in 2000, expecting to gradually decrease in thenext few years. The flowers produced, mainly for

national use, are cultivated on a total area of 7,300 ha, a large part of which is in the open air.

Narcissus (Daffodils) are largely cultivated in England(amongst others on the Channel Islands) and Wales,however, the area of cultivation is gradually decreasing.

The area under glass used for the production of cutflowers is estimated at 137 ha in 2001, indicating aconsiderable decrease compared to the level of 1992(296 ha). This is mainly caused by the decrease in areacultivating Dendranthema.

Country Major cut flowers produced in terms of ha open area

Germany Summer flowers, Rosa, Dendranthema, Tulip, NarcissusBelgium Dendranthema, Azaleas, BegoniasSpain Dianthus, RosaFrance* Gladioli, Rosa, Dianthus, Tulipa, DendranthemaItaly Rosa, Dianthus, Gladioli, Large Dendranthema The Netherlands Rosa, Dendranthema, Lilies, Gerberas, Freesias, OrchidsUK Dendranthema, Alstroemeria, Dianthus, Daffodils (Narcissus)

*cut flowers and foliage under glass

Source: AIPH (2002)

Table 4.3 Production of cut flowers in Germany,1996/2000In Ha

cut flowers 1996 2000

under glass 662 637open area 1963 2,400

total 2,625 3,037

Source: Flower Council of Holland (2003)

Table 4.4 Production of cut flowers in the UK, 1995/2000In Ha

1995 1996 1997 1998 1999 2000

cut flowers produced in open area 6,224 5,396 5,555 5,758 5,622 6,281cut flowers produced under glass 935 1,011 1,028 1,029 1,041 1,016

total 7,159 6,407 6,583 6,787 6,663 7,297

Source: Flower Council of Holland (2003)

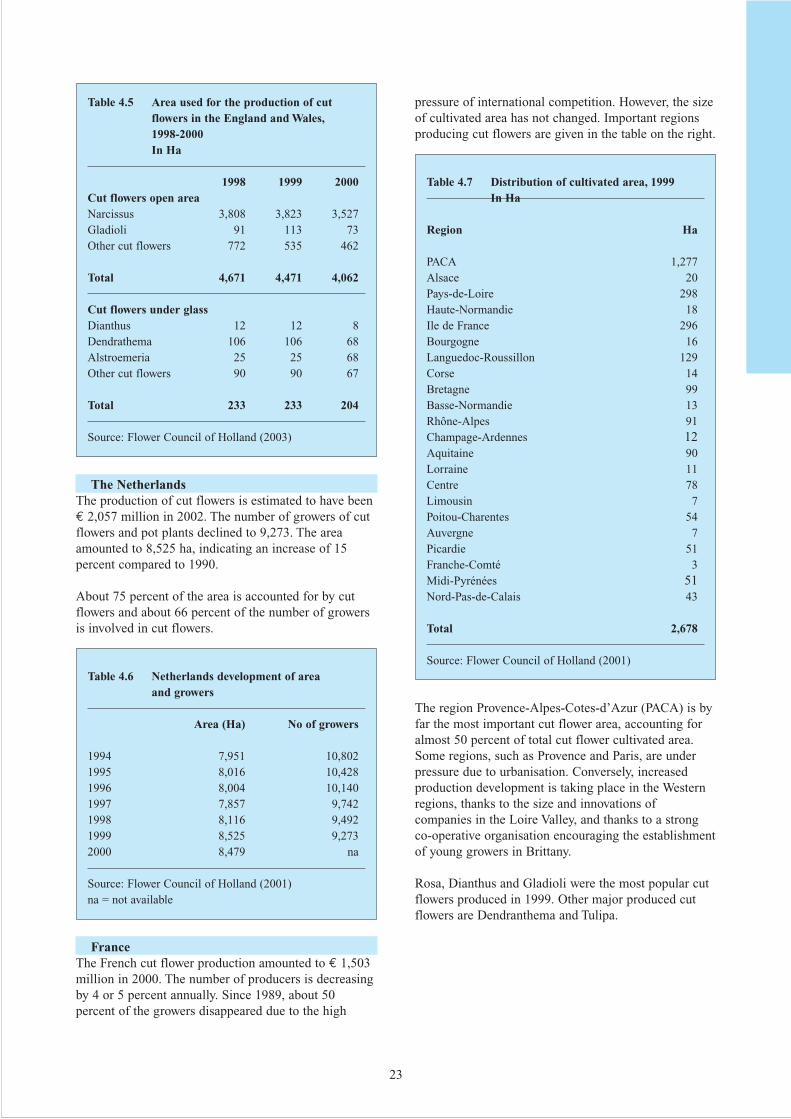

pressure of international competition. However, the sizeof cultivated area has not changed. Important regionsproducing cut flowers are given in the table on the right.

The region Provence-Alpes-Cotes-d’Azur (PACA) is byfar the most important cut flower area, accounting foralmost 50 percent of total cut flower cultivated area.Some regions, such as Provence and Paris, are underpressure due to urbanisation. Conversely, increasedproduction development is taking place in the Westernregions, thanks to the size and innovations ofcompanies in the Loire Valley, and thanks to a strongco-operative organisation encouraging the establishmentof young growers in Brittany.

Rosa, Dianthus and Gladioli were the most popular cutflowers produced in 1999. Other major produced cutflowers are Dendranthema and Tulipa.

23

The NetherlandsThe production of cut flowers is estimated to have been€ 2,057 million in 2002. The number of growers of cutflowers and pot plants declined to 9,273. The areaamounted to 8,525 ha, indicating an increase of 15percent compared to 1990.

About 75 percent of the area is accounted for by cutflowers and about 66 percent of the number of growersis involved in cut flowers.

FranceThe French cut flower production amounted to € 1,503million in 2000. The number of producers is decreasingby 4 or 5 percent annually. Since 1989, about 50percent of the growers disappeared due to the high

Table 4.6 Netherlands development of area and growers

Area (Ha) No of growers

1994 7,951 10,8021995 8,016 10,4281996 8,004 10,1401997 7,857 9,7421998 8,116 9,4921999 8,525 9,2732000 8,479 na

Source: Flower Council of Holland (2001)na = not available

Table 4.7 Distribution of cultivated area, 1999In Ha

Region Ha

PACA 1,277Alsace 20Pays-de-Loire 298Haute-Normandie 18Ile de France 296Bourgogne 16Languedoc-Roussillon 129Corse 14Bretagne 99Basse-Normandie 13Rhône-Alpes 91Champage-Ardennes 12Aquitaine 90Lorraine 11Centre 78Limousin 7Poitou-Charentes 54Auvergne 7Picardie 51Franche-Comté 3Midi-Pyrénées 51Nord-Pas-de-Calais 43

Total 2,678

Source: Flower Council of Holland (2001)

Table 4.5 Area used for the production of cutflowers in the England and Wales,1998-2000In Ha

1998 1999 2000Cut flowers open areaNarcissus 3,808 3,823 3,527Gladioli 91 113 73Other cut flowers 772 535 462

Total 4,671 4,471 4,062

Cut flowers under glassDianthus 12 12 8Dendrathema 106 106 68Alstroemeria 25 25 68Other cut flowers 90 90 67

Total 233 233 204

Source: Flower Council of Holland (2003)

24

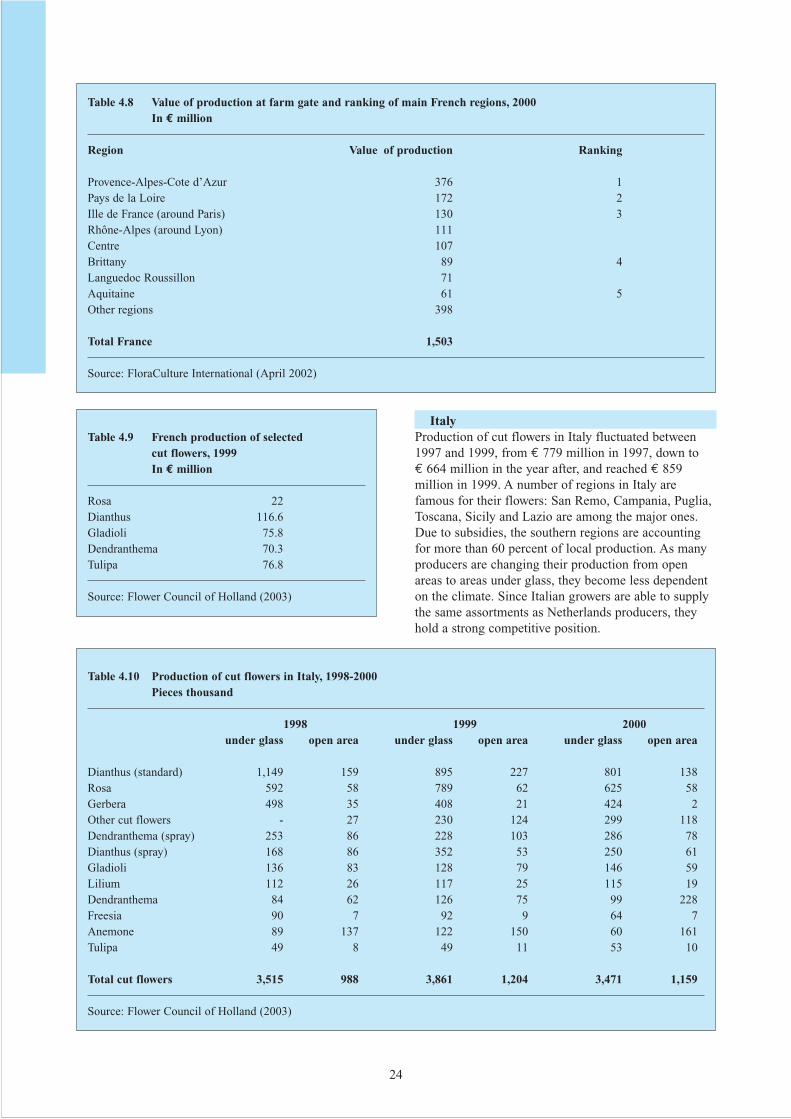

ItalyProduction of cut flowers in Italy fluctuated between1997 and 1999, from € 779 million in 1997, down to € 664 million in the year after, and reached € 859million in 1999. A number of regions in Italy arefamous for their flowers: San Remo, Campania, Puglia,Toscana, Sicily and Lazio are among the major ones.Due to subsidies, the southern regions are accountingfor more than 60 percent of local production. As manyproducers are changing their production from openareas to areas under glass, they become less dependenton the climate. Since Italian growers are able to supplythe same assortments as Netherlands producers, theyhold a strong competitive position.

Table 4.8 Value of production at farm gate and ranking of main French regions, 2000In € million

Region Value of production Ranking

Provence-Alpes-Cote d’Azur 376 1Pays de la Loire 172 2Ille de France (around Paris) 130 3Rhône-Alpes (around Lyon) 111Centre 107Brittany 89 4Languedoc Roussillon 71Aquitaine 61 5Other regions 398

Total France 1,503

Source: FloraCulture International (April 2002)

Table 4.9 French production of selected cut flowers, 1999In € million

Rosa 22Dianthus 116.6Gladioli 75.8Dendranthema 70.3Tulipa 76.8

Source: Flower Council of Holland (2003)

Table 4.10 Production of cut flowers in Italy, 1998-2000Pieces thousand

1998 1999 2000under glass open area under glass open area under glass open area

Dianthus (standard) 1,149 159 895 227 801 138Rosa 592 58 789 62 625 58Gerbera 498 35 408 21 424 2Other cut flowers - 27 230 124 299 118Dendranthema (spray) 253 86 228 103 286 78Dianthus (spray) 168 86 352 53 250 61Gladioli 136 83 128 79 146 59Lilium 112 26 117 25 115 19Dendranthema 84 62 126 75 99 228Freesia 90 7 92 9 64 7Anemone 89 137 122 150 60 161Tulipa 49 8 49 11 53 10

Total cut flowers 3,515 988 3,861 1,204 3,471 1,159

Source: Flower Council of Holland (2003)

25

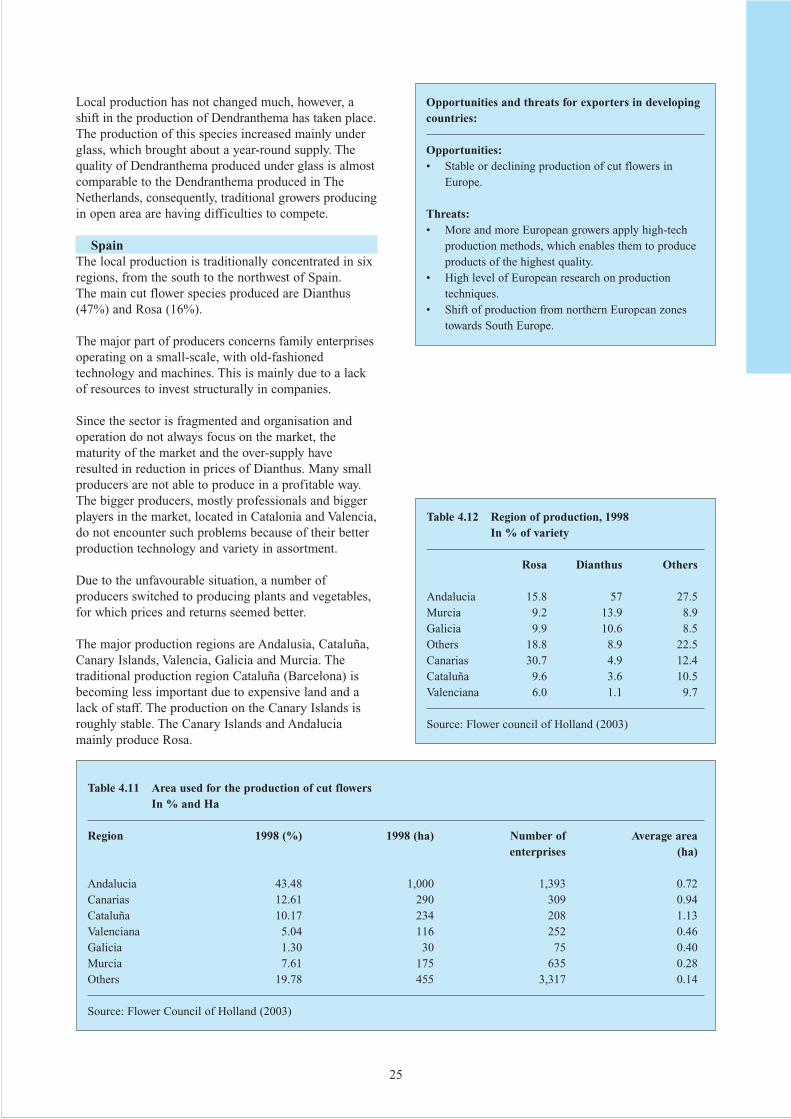

Local production has not changed much, however, ashift in the production of Dendranthema has taken place.The production of this species increased mainly underglass, which brought about a year-round supply. Thequality of Dendranthema produced under glass is almostcomparable to the Dendranthema produced in TheNetherlands, consequently, traditional growers producingin open area are having difficulties to compete.

SpainThe local production is traditionally concentrated in sixregions, from the south to the northwest of Spain. The main cut flower species produced are Dianthus(47%) and Rosa (16%).

The major part of producers concerns family enterprisesoperating on a small-scale, with old-fashionedtechnology and machines. This is mainly due to a lackof resources to invest structurally in companies.

Since the sector is fragmented and organisation andoperation do not always focus on the market, thematurity of the market and the over-supply haveresulted in reduction in prices of Dianthus. Many smallproducers are not able to produce in a profitable way.The bigger producers, mostly professionals and biggerplayers in the market, located in Catalonia and Valencia,do not encounter such problems because of their betterproduction technology and variety in assortment.

Due to the unfavourable situation, a number ofproducers switched to producing plants and vegetables,for which prices and returns seemed better.

The major production regions are Andalusia, Cataluña,Canary Islands, Valencia, Galicia and Murcia. Thetraditional production region Cataluña (Barcelona) isbecoming less important due to expensive land and alack of staff. The production on the Canary Islands isroughly stable. The Canary Islands and Andaluciamainly produce Rosa.

Opportunities and threats for exporters in developingcountries:

Opportunities:• Stable or declining production of cut flowers in

Europe.

Threats:• More and more European growers apply high-tech

production methods, which enables them to produceproducts of the highest quality.

• High level of European research on productiontechniques.

• Shift of production from northern European zonestowards South Europe.

Table 4.11 Area used for the production of cut flowersIn % and Ha

Region 1998 (%) 1998 (ha) Number of Average areaenterprises (ha)

Andalucia 43.48 1,000 1,393 0.72Canarias 12.61 290 309 0.94Cataluña 10.17 234 208 1.13Valenciana 5.04 116 252 0.46Galicia 1.30 30 75 0.40Murcia 7.61 175 635 0.28Others 19.78 455 3,317 0.14

Source: Flower Council of Holland (2003)

Table 4.12 Region of production, 1998In % of variety

Rosa Dianthus Others

Andalucia 15.8 57 27.5Murcia 9.2 13.9 8.9Galicia 9.9 10.6 8.5Others 18.8 8.9 22.5Canarias 30.7 4.9 12.4Cataluña 9.6 3.6 10.5Valenciana 6.0 1.1 9.7

Source: Flower council of Holland (2003)

26

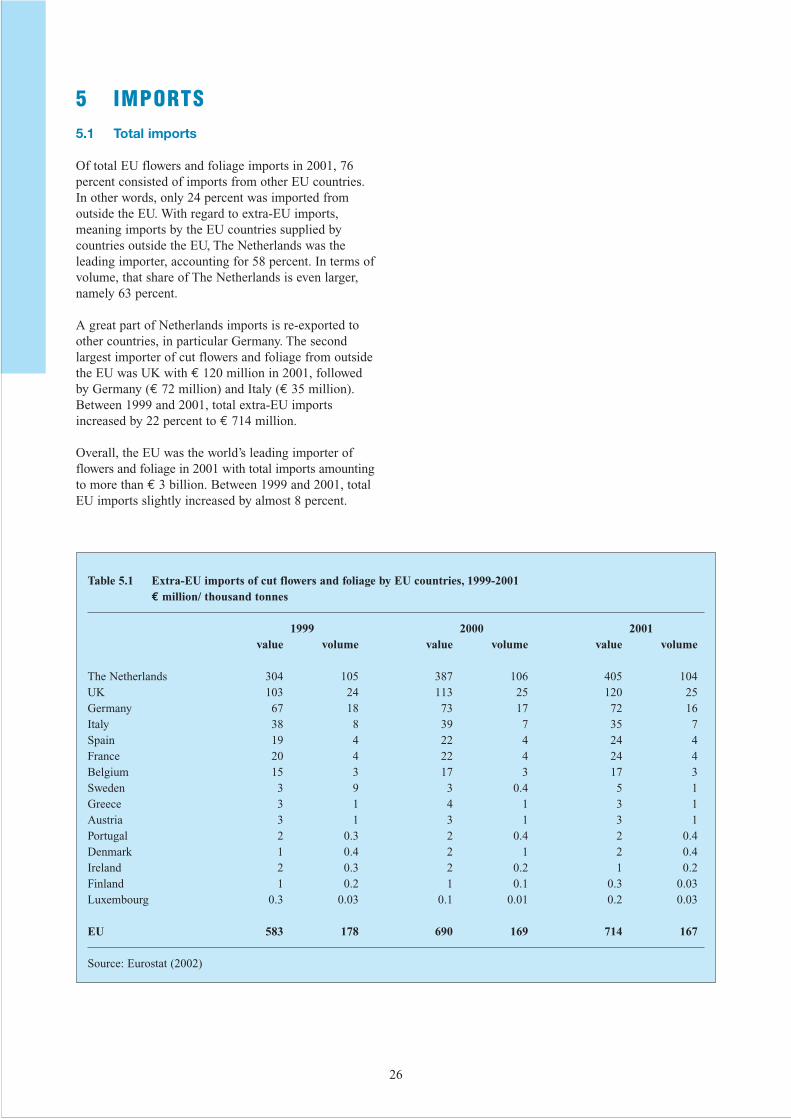

5 IMPORTS5.1 Total imports

Of total EU flowers and foliage imports in 2001, 76percent consisted of imports from other EU countries.In other words, only 24 percent was imported fromoutside the EU. With regard to extra-EU imports,meaning imports by the EU countries supplied bycountries outside the EU, The Netherlands was theleading importer, accounting for 58 percent. In terms ofvolume, that share of The Netherlands is even larger,namely 63 percent.

A great part of Netherlands imports is re-exported toother countries, in particular Germany. The secondlargest importer of cut flowers and foliage from outsidethe EU was UK with € 120 million in 2001, followedby Germany (€ 72 million) and Italy (€ 35 million).Between 1999 and 2001, total extra-EU importsincreased by 22 percent to € 714 million.

Overall, the EU was the world’s leading importer offlowers and foliage in 2001 with total imports amountingto more than € 3 billion. Between 1999 and 2001, totalEU imports slightly increased by almost 8 percent.

Table 5.1 Extra-EU imports of cut flowers and foliage by EU countries, 1999-2001€ million/ thousand tonnes

1999 2000 2001value volume value volume value volume

The Netherlands 304 105 387 106 405 104UK 103 24 113 25 120 25Germany 67 18 73 17 72 16Italy 38 8 39 7 35 7Spain 19 4 22 4 24 4France 20 4 22 4 24 4Belgium 15 3 17 3 17 3Sweden 3 9 3 0.4 5 1Greece 3 1 4 1 3 1Austria 3 1 3 1 3 1Portugal 2 0.3 2 0.4 2 0.4Denmark 1 0.4 2 1 2 0.4Ireland 2 0.3 2 0.2 1 0.2Finland 1 0.2 1 0.1 0.3 0.03Luxembourg 0.3 0.03 0.1 0.01 0.2 0.03

EU 583 178 690 169 714 167

Source: Eurostat (2002)

27

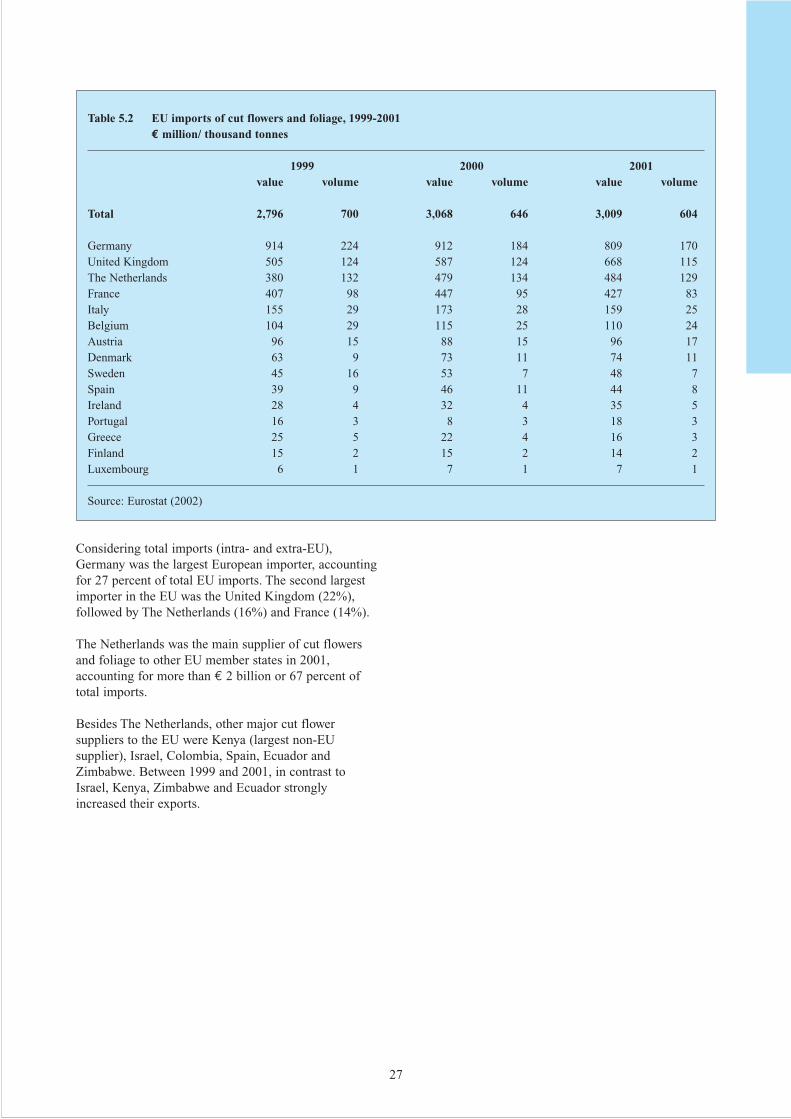

Considering total imports (intra- and extra-EU),Germany was the largest European importer, accountingfor 27 percent of total EU imports. The second largestimporter in the EU was the United Kingdom (22%),followed by The Netherlands (16%) and France (14%).

The Netherlands was the main supplier of cut flowersand foliage to other EU member states in 2001,accounting for more than € 2 billion or 67 percent oftotal imports.

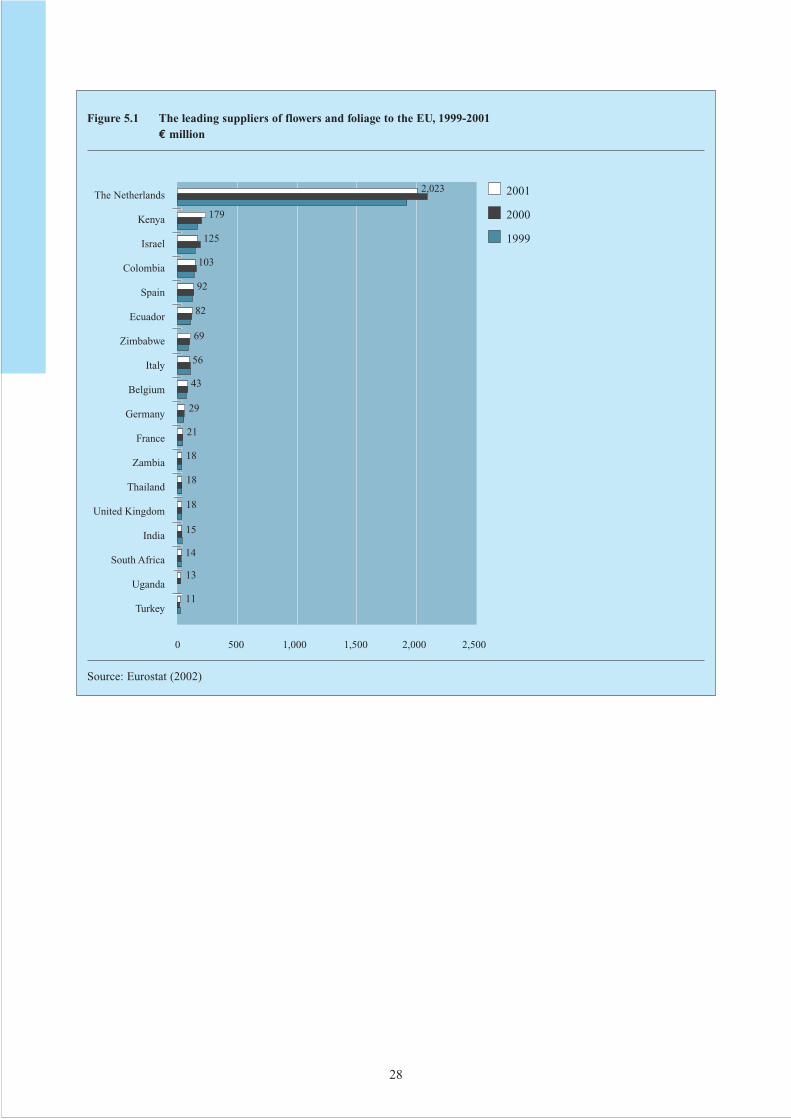

Besides The Netherlands, other major cut flowersuppliers to the EU were Kenya (largest non-EUsupplier), Israel, Colombia, Spain, Ecuador andZimbabwe. Between 1999 and 2001, in contrast toIsrael, Kenya, Zimbabwe and Ecuador stronglyincreased their exports.

Table 5.2 EU imports of cut flowers and foliage, 1999-2001€ million/ thousand tonnes

1999 2000 2001value volume value volume value volume

Total 2,796 700 3,068 646 3,009 604

Germany 914 224 912 184 809 170United Kingdom 505 124 587 124 668 115The Netherlands 380 132 479 134 484 129France 407 98 447 95 427 83Italy 155 29 173 28 159 25Belgium 104 29 115 25 110 24Austria 96 15 88 15 96 17Denmark 63 9 73 11 74 11Sweden 45 16 53 7 48 7Spain 39 9 46 11 44 8Ireland 28 4 32 4 35 5Portugal 16 3 8 3 18 3Greece 25 5 22 4 16 3Finland 15 2 15 2 14 2Luxembourg 6 1 7 1 7 1

Source: Eurostat (2002)

28

The Netherlands

Kenya

Israel

Colombia

Spain

Ecuador

Zimbabwe

Italy

Belgium

Germany

France

Zambia

Thailand

United Kingdom

India

South Africa

Uganda

Turkey

2001

2000

1999

2,023

0 500 1,000 1,500 2,000 2,500

179

125

103

92

82

69

56

43

29

21

18

18

18

15

14

13

11

Figure 5.1 The leading suppliers of flowers and foliage to the EU, 1999-2001€ million

Source: Eurostat (2002)

29

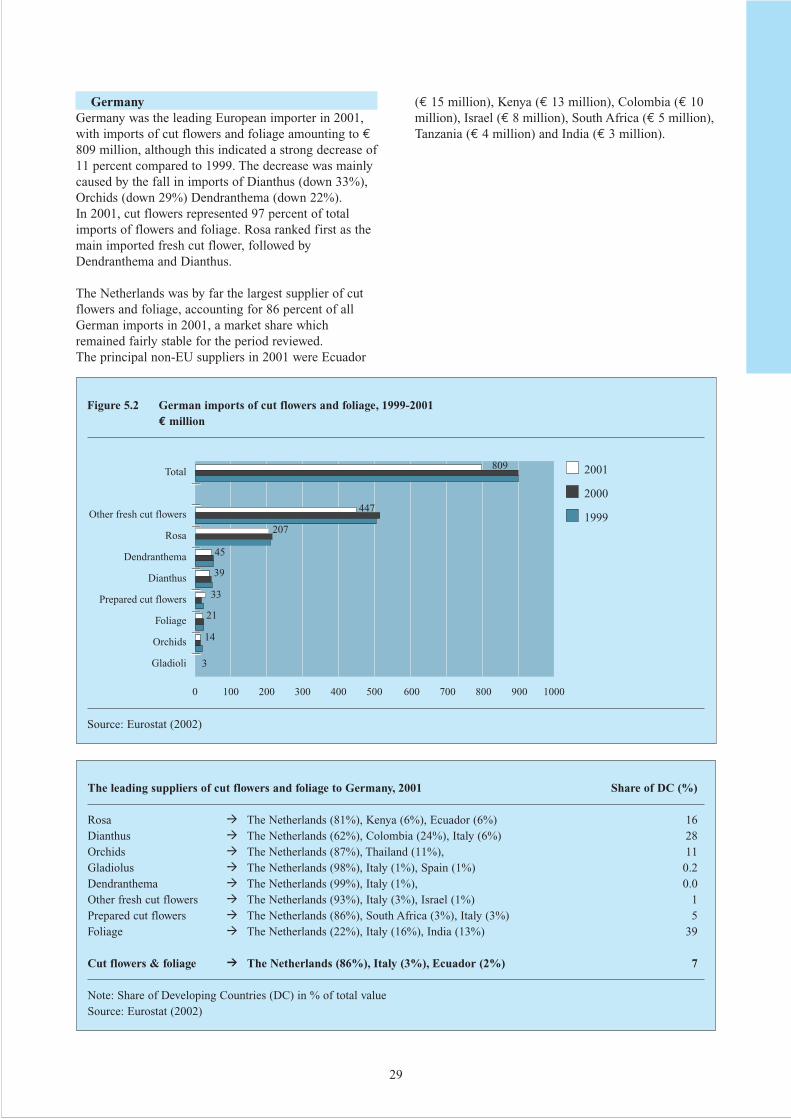

GermanyGermany was the leading European importer in 2001,with imports of cut flowers and foliage amounting to €809 million, although this indicated a strong decrease of11 percent compared to 1999. The decrease was mainlycaused by the fall in imports of Dianthus (down 33%),Orchids (down 29%) Dendranthema (down 22%). In 2001, cut flowers represented 97 percent of totalimports of flowers and foliage. Rosa ranked first as themain imported fresh cut flower, followed byDendranthema and Dianthus.

The Netherlands was by far the largest supplier of cutflowers and foliage, accounting for 86 percent of allGerman imports in 2001, a market share whichremained fairly stable for the period reviewed. The principal non-EU suppliers in 2001 were Ecuador

(€ 15 million), Kenya (€ 13 million), Colombia (€ 10million), Israel (€ 8 million), South Africa (€ 5 million),Tanzania (€ 4 million) and India (€ 3 million).

Total

Other fresh cut flowers

Rosa

Dendranthema

Dianthus

Prepared cut flowers

Foliage

Orchids

Gladioli

2001

2000

1999

809

207

45

447

0 100 200 300 400 500 600 700 800 900 1000

39

33

21

14

3

Figure 5.2 German imports of cut flowers and foliage, 1999-2001€ million

Source: Eurostat (2002)

The leading suppliers of cut flowers and foliage to Germany, 2001 Share of DC (%)

Rosa \ The Netherlands (81%), Kenya (6%), Ecuador (6%) 16Dianthus \ The Netherlands (62%), Colombia (24%), Italy (6%) 28Orchids \ The Netherlands (87%), Thailand (11%), 11Gladiolus \ The Netherlands (98%), Italy (1%), Spain (1%) 0.2Dendranthema \ The Netherlands (99%), Italy (1%), 0.0Other fresh cut flowers \ The Netherlands (93%), Italy (3%), Israel (1%) 1Prepared cut flowers \ The Netherlands (86%), South Africa (3%), Italy (3%) 5Foliage \ The Netherlands (22%), Italy (16%), India (13%) 39

Cut flowers & foliage _ The Netherlands (86%), Italy (3%), Ecuador (2%) 7

Note: Share of Developing Countries (DC) in % of total valueSource: Eurostat (2002)

30

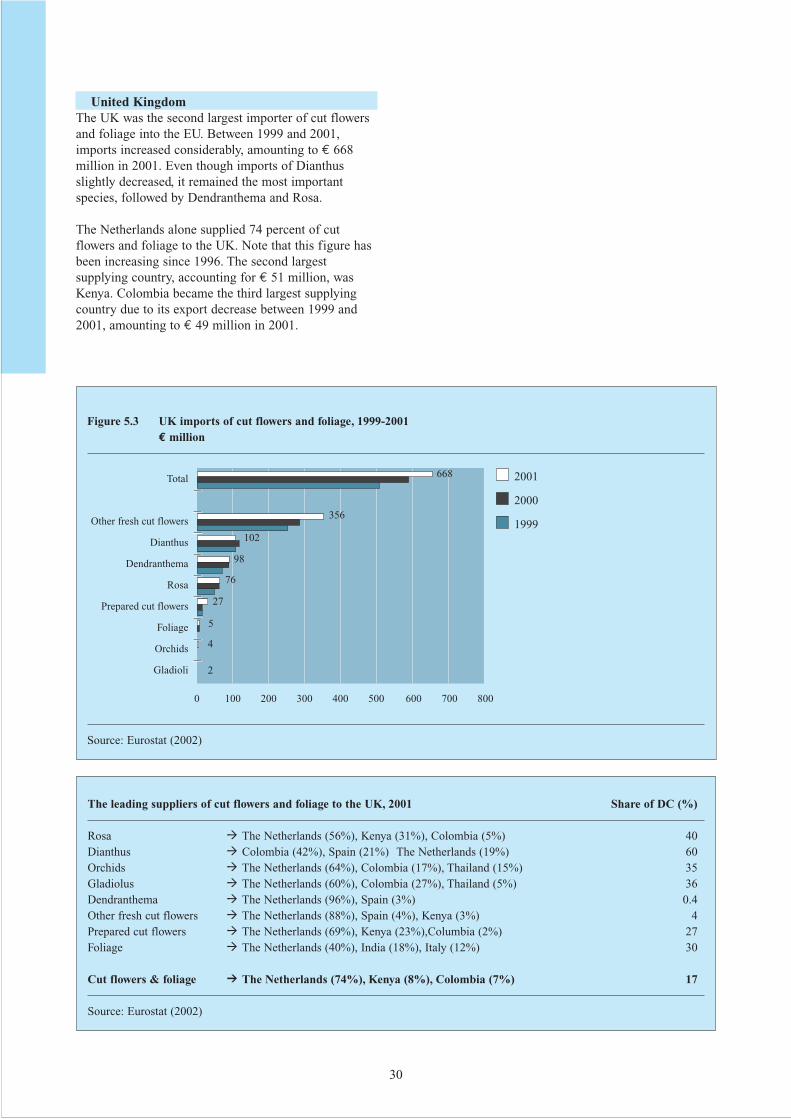

United KingdomThe UK was the second largest importer of cut flowersand foliage into the EU. Between 1999 and 2001,imports increased considerably, amounting to € 668million in 2001. Even though imports of Dianthusslightly decreased, it remained the most importantspecies, followed by Dendranthema and Rosa.

The Netherlands alone supplied 74 percent of cutflowers and foliage to the UK. Note that this figure hasbeen increasing since 1996. The second largestsupplying country, accounting for € 51 million, wasKenya. Colombia became the third largest supplyingcountry due to its export decrease between 1999 and2001, amounting to € 49 million in 2001.

The leading suppliers of cut flowers and foliage to the UK, 2001 Share of DC (%)

Rosa \ The Netherlands (56%), Kenya (31%), Colombia (5%) 40Dianthus \ Colombia (42%), Spain (21%) The Netherlands (19%) 60Orchids \ The Netherlands (64%), Colombia (17%), Thailand (15%) 35Gladiolus \ The Netherlands (60%), Colombia (27%), Thailand (5%) 36Dendranthema \ The Netherlands (96%), Spain (3%) 0.4Other fresh cut flowers \ The Netherlands (88%), Spain (4%), Kenya (3%) 4Prepared cut flowers \ The Netherlands (69%), Kenya (23%),Columbia (2%) 27Foliage \ The Netherlands (40%), India (18%), Italy (12%) 30

Cut flowers & foliage _ The Netherlands (74%), Kenya (8%), Colombia (7%) 17

Source: Eurostat (2002)

Total

Other fresh cut flowers

Dianthus

Dendranthema

Rosa

Prepared cut flowers

Foliage

Orchids

Gladioli

2001

2000

1999

668

102

98

356

0 100 200 300 400 500 600 700 800

76

27

5

4

2

Figure 5.3 UK imports of cut flowers and foliage, 1999-2001€ million

Source: Eurostat (2002)

31

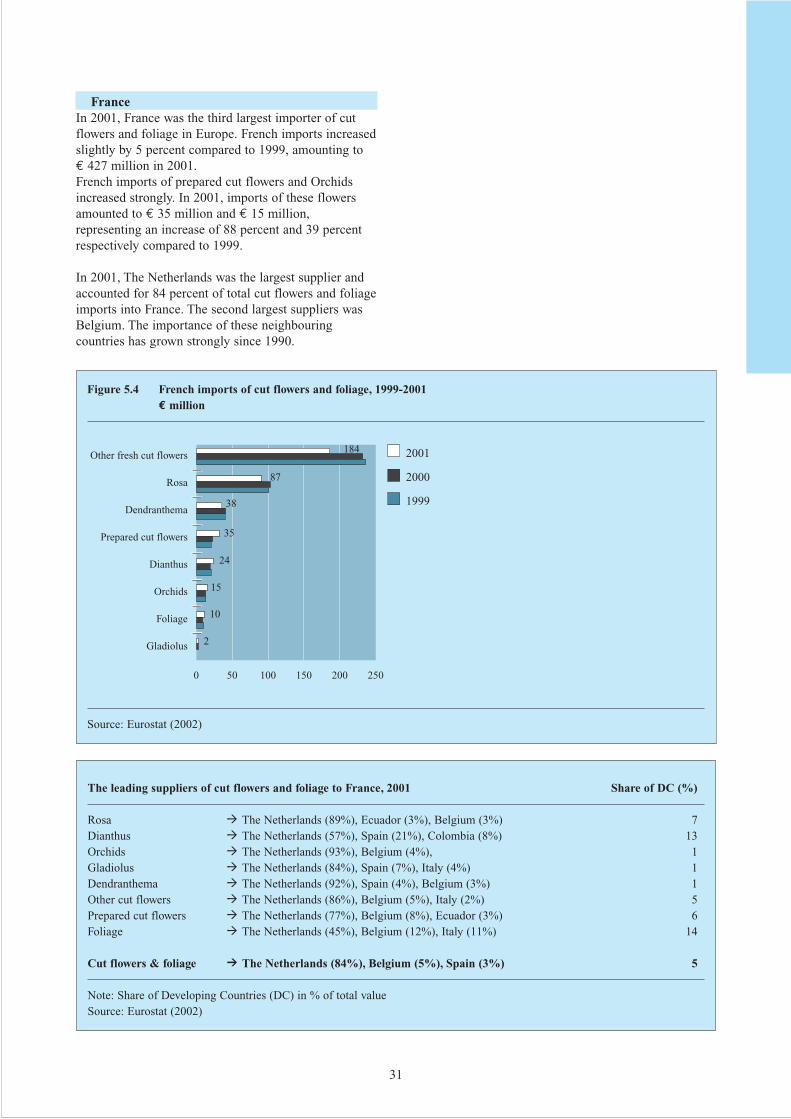

FranceIn 2001, France was the third largest importer of cutflowers and foliage in Europe. French imports increasedslightly by 5 percent compared to 1999, amounting to € 427 million in 2001.French imports of prepared cut flowers and Orchidsincreased strongly. In 2001, imports of these flowersamounted to € 35 million and € 15 million,representing an increase of 88 percent and 39 percentrespectively compared to 1999.

In 2001, The Netherlands was the largest supplier andaccounted for 84 percent of total cut flowers and foliageimports into France. The second largest suppliers wasBelgium. The importance of these neighbouringcountries has grown strongly since 1990.

The leading suppliers of cut flowers and foliage to France, 2001 Share of DC (%)

Rosa \ The Netherlands (89%), Ecuador (3%), Belgium (3%) 7Dianthus \ The Netherlands (57%), Spain (21%), Colombia (8%) 13Orchids \ The Netherlands (93%), Belgium (4%), 1Gladiolus \ The Netherlands (84%), Spain (7%), Italy (4%) 1Dendranthema \ The Netherlands (92%), Spain (4%), Belgium (3%) 1Other cut flowers \ The Netherlands (86%), Belgium (5%), Italy (2%) 5Prepared cut flowers \ The Netherlands (77%), Belgium (8%), Ecuador (3%) 6Foliage \ The Netherlands (45%), Belgium (12%), Italy (11%) 14

Cut flowers & foliage _ The Netherlands (84%), Belgium (5%), Spain (3%) 5

Note: Share of Developing Countries (DC) in % of total valueSource: Eurostat (2002)

Other fresh cut flowers

Rosa

Dendranthema

Prepared cut flowers

Dianthus

Orchids

Foliage

Gladiolus

2001

2000

1999

184

38

35

87

0 50 100 150 200 250

24

15

10

2

Figure 5.4 French imports of cut flowers and foliage, 1999-2001€ million

Source: Eurostat (2002)

32

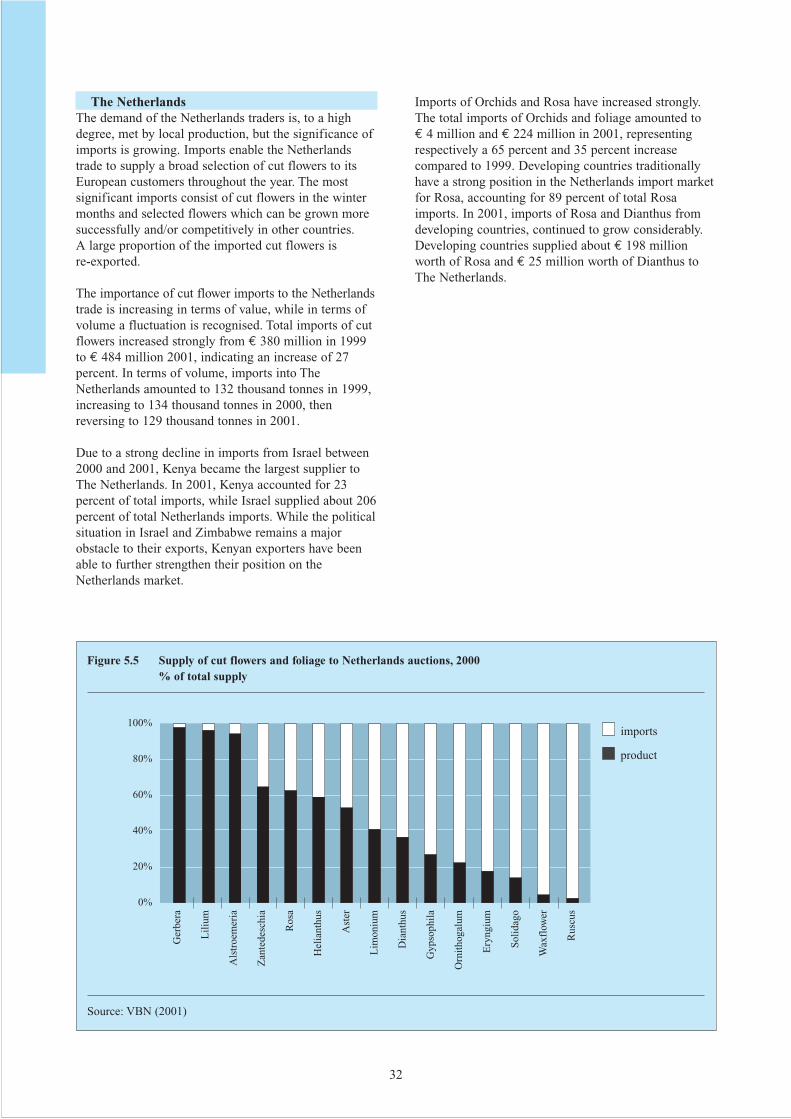

The NetherlandsThe demand of the Netherlands traders is, to a highdegree, met by local production, but the significance ofimports is growing. Imports enable the Netherlandstrade to supply a broad selection of cut flowers to itsEuropean customers throughout the year. The mostsignificant imports consist of cut flowers in the wintermonths and selected flowers which can be grown moresuccessfully and/or competitively in other countries. A large proportion of the imported cut flowers is re-exported.

The importance of cut flower imports to the Netherlandstrade is increasing in terms of value, while in terms ofvolume a fluctuation is recognised. Total imports of cutflowers increased strongly from € 380 million in 1999to € 484 million 2001, indicating an increase of 27percent. In terms of volume, imports into TheNetherlands amounted to 132 thousand tonnes in 1999,increasing to 134 thousand tonnes in 2000, thenreversing to 129 thousand tonnes in 2001.

Due to a strong decline in imports from Israel between2000 and 2001, Kenya became the largest supplier toThe Netherlands. In 2001, Kenya accounted for 23percent of total imports, while Israel supplied about 206percent of total Netherlands imports. While the politicalsituation in Israel and Zimbabwe remains a majorobstacle to their exports, Kenyan exporters have beenable to further strengthen their position on theNetherlands market.

Imports of Orchids and Rosa have increased strongly.The total imports of Orchids and foliage amounted to € 4 million and € 224 million in 2001, representingrespectively a 65 percent and 35 percent increasecompared to 1999. Developing countries traditionallyhave a strong position in the Netherlands import marketfor Rosa, accounting for 89 percent of total Rosaimports. In 2001, imports of Rosa and Dianthus fromdeveloping countries, continued to grow considerably.Developing countries supplied about € 198 millionworth of Rosa and € 25 million worth of Dianthus toThe Netherlands.

100%

80%

60%

40%

20%

0%

Ger

bera

Lil

ium

Als

troe

mer

ia

Zan

tede

schi

a

Ros

a

Hel

iant

hus

Ast

er

Lim

oniu

m

Dia

nthu

s

Gyp

soph

ila

Orn

itho

galu

m

Ery

ngiu

m

Sol

idag

o

Wax

flow

er

Rus

cus

imports

product

Figure 5.5 Supply of cut flowers and foliage to Netherlands auctions, 2000 % of total supply

Source: VBN (2001)

33

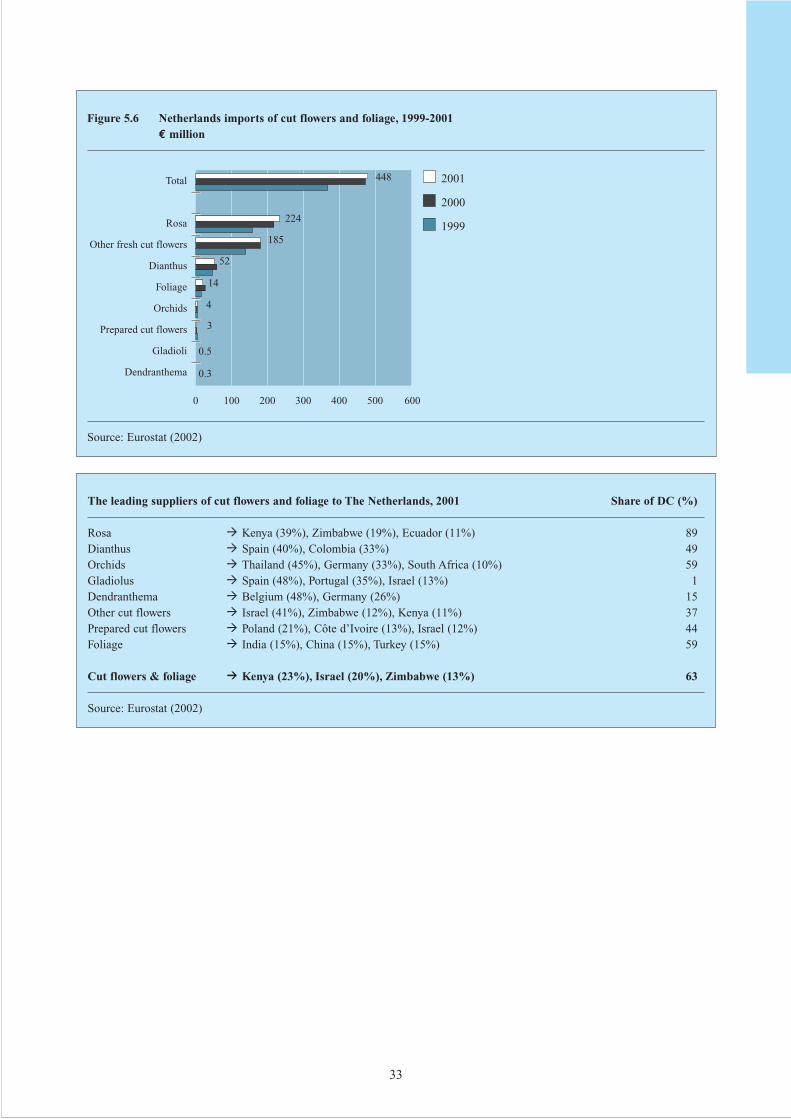

The leading suppliers of cut flowers and foliage to The Netherlands, 2001 Share of DC (%)

Rosa \ Kenya (39%), Zimbabwe (19%), Ecuador (11%) 89Dianthus \ Spain (40%), Colombia (33%) 49Orchids \ Thailand (45%), Germany (33%), South Africa (10%) 59Gladiolus \ Spain (48%), Portugal (35%), Israel (13%) 1Dendranthema \ Belgium (48%), Germany (26%) 15Other cut flowers \ Israel (41%), Zimbabwe (12%), Kenya (11%) 37Prepared cut flowers \ Poland (21%), Côte d’Ivoire (13%), Israel (12%) 44Foliage \ India (15%), China (15%), Turkey (15%) 59

Cut flowers & foliage _ Kenya (23%), Israel (20%), Zimbabwe (13%) 63

Source: Eurostat (2002)

Total

Rosa

Other fresh cut flowers

Dianthus

Foliage

Orchids

Prepared cut flowers

Gladioli

Dendranthema

2001

2000

1999

448

185

52

224

0 100 200 300 400 500 600

14

4

3

0.5

0.3

Figure 5.6 Netherlands imports of cut flowers and foliage, 1999-2001€ million

Source: Eurostat (2002)

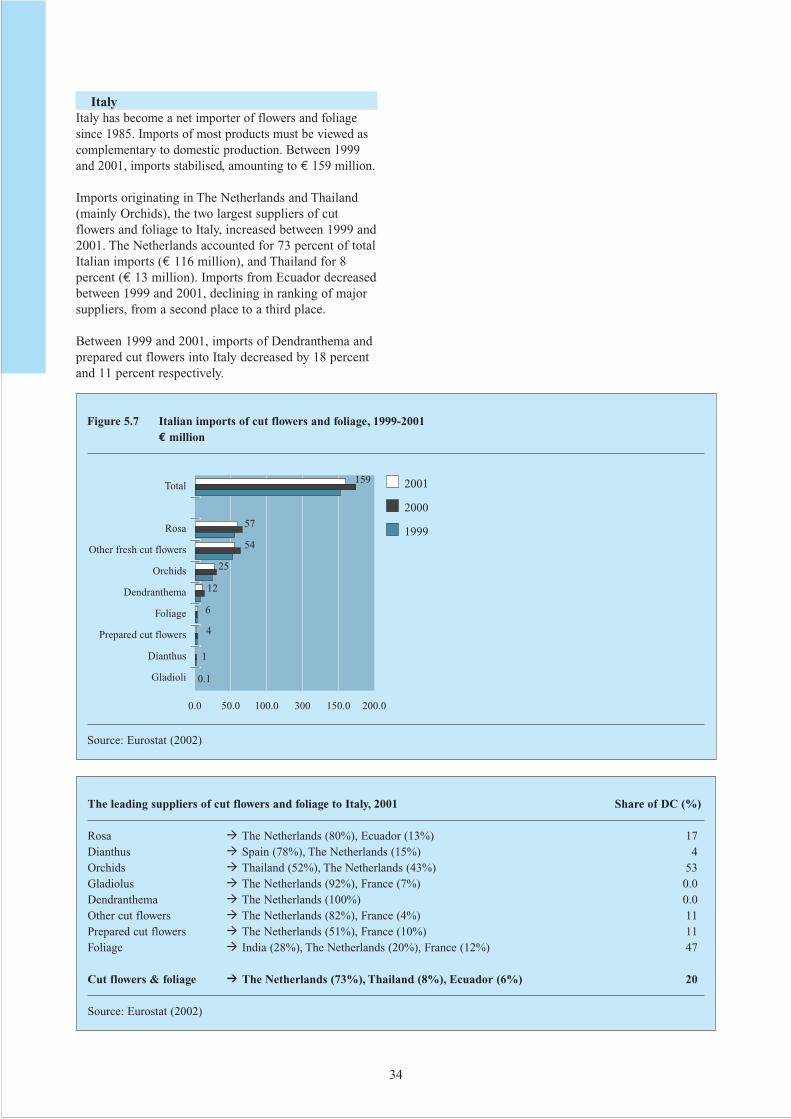

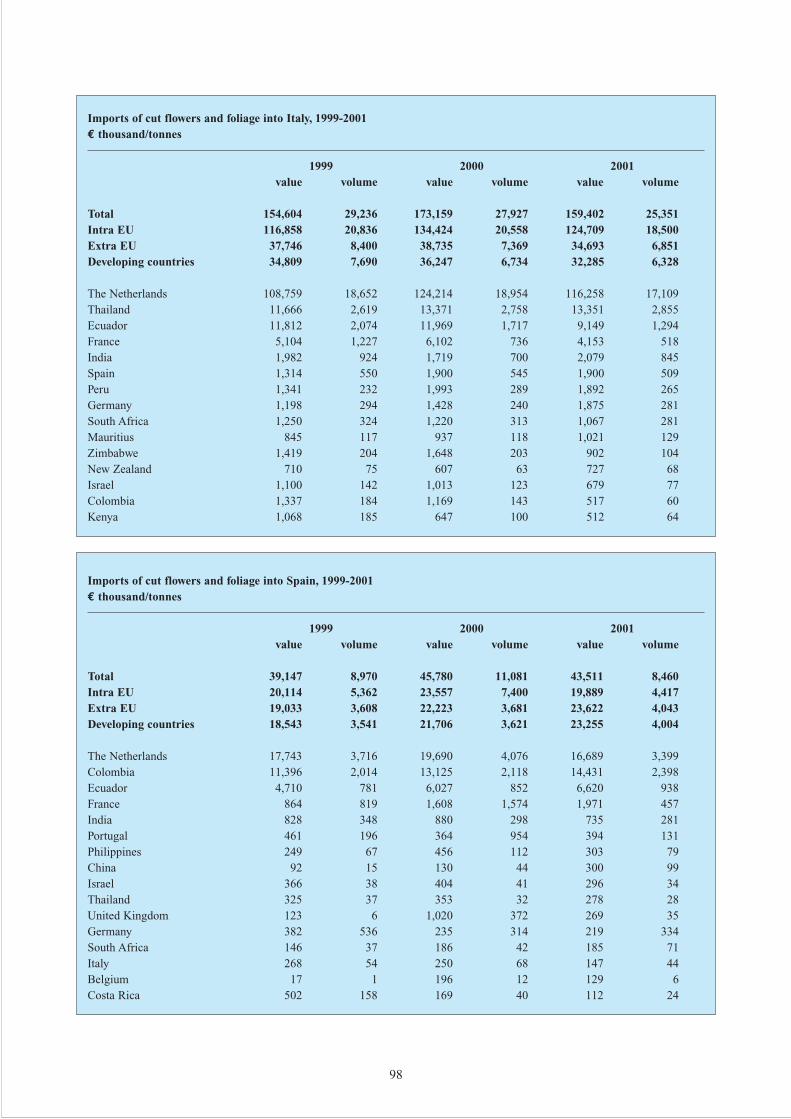

ItalyItaly has become a net importer of flowers and foliagesince 1985. Imports of most products must be viewed ascomplementary to domestic production. Between 1999and 2001, imports stabilised, amounting to € 159 million.

Imports originating in The Netherlands and Thailand(mainly Orchids), the two largest suppliers of cutflowers and foliage to Italy, increased between 1999 and2001. The Netherlands accounted for 73 percent of totalItalian imports (€ 116 million), and Thailand for 8percent (€ 13 million). Imports from Ecuador decreasedbetween 1999 and 2001, declining in ranking of majorsuppliers, from a second place to a third place.

Between 1999 and 2001, imports of Dendranthema andprepared cut flowers into Italy decreased by 18 percentand 11 percent respectively.

34

The leading suppliers of cut flowers and foliage to Italy, 2001 Share of DC (%)

Rosa \ The Netherlands (80%), Ecuador (13%) 17Dianthus \ Spain (78%), The Netherlands (15%) 4Orchids \ Thailand (52%), The Netherlands (43%) 53Gladiolus \ The Netherlands (92%), France (7%) 0.0Dendranthema \ The Netherlands (100%) 0.0Other cut flowers \ The Netherlands (82%), France (4%) 11Prepared cut flowers \ The Netherlands (51%), France (10%) 11Foliage \ India (28%), The Netherlands (20%), France (12%) 47

Cut flowers & foliage _ The Netherlands (73%), Thailand (8%), Ecuador (6%) 20

Source: Eurostat (2002)

Total

Rosa

Other fresh cut flowers

Orchids

Dendranthema

Foliage

Prepared cut flowers

Dianthus

Gladioli

2001

2000

1999

159

54

25

57

0.0 50.0 100.0 300 150.0 200.0

12

6

4

1

0.1

Figure 5.7 Italian imports of cut flowers and foliage, 1999-2001€ million

Source: Eurostat (2002)

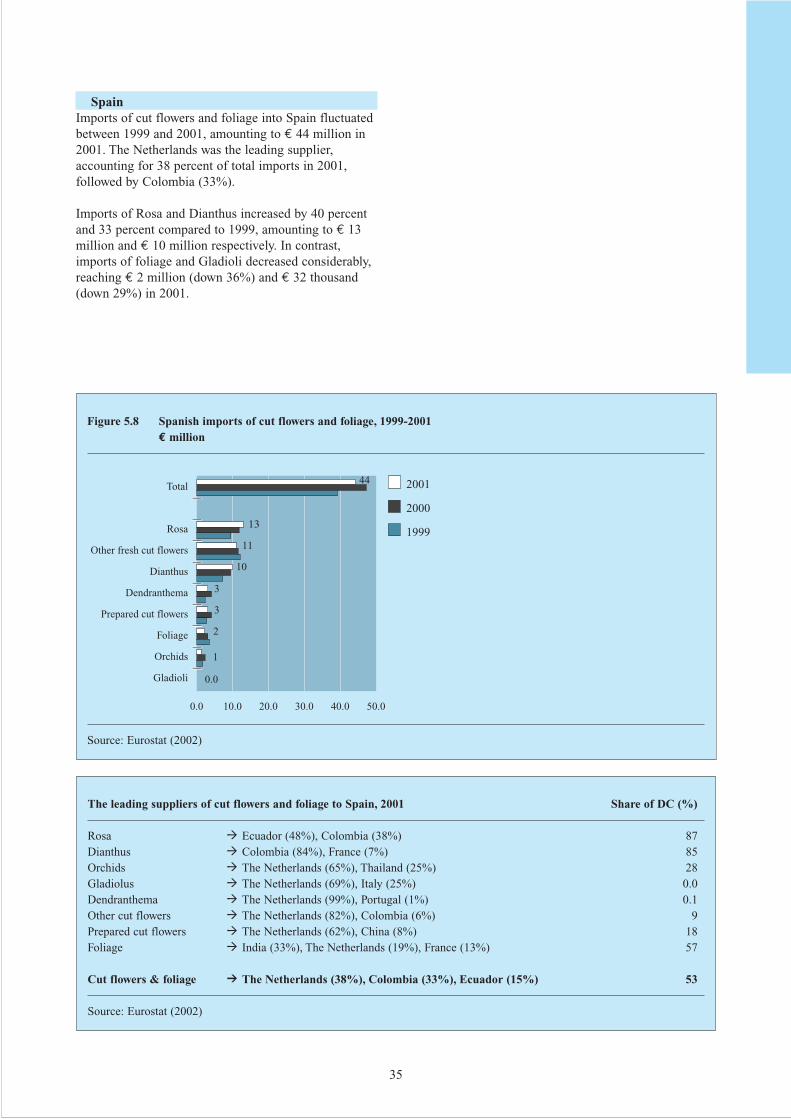

SpainImports of cut flowers and foliage into Spain fluctuatedbetween 1999 and 2001, amounting to € 44 million in2001. The Netherlands was the leading supplier,accounting for 38 percent of total imports in 2001,followed by Colombia (33%).

Imports of Rosa and Dianthus increased by 40 percentand 33 percent compared to 1999, amounting to € 13million and € 10 million respectively. In contrast,imports of foliage and Gladioli decreased considerably,reaching € 2 million (down 36%) and € 32 thousand(down 29%) in 2001.

35

Total

Rosa

Other fresh cut flowers

Dianthus

Dendranthema

Prepared cut flowers

Foliage

Orchids

Gladioli

2001

2000

1999

44

11

10

13

0.0 10.0 20.0 30.0 40.0 50.0

3

3

2

1

0.0

Figure 5.8 Spanish imports of cut flowers and foliage, 1999-2001€ million

Source: Eurostat (2002)

The leading suppliers of cut flowers and foliage to Spain, 2001 Share of DC (%)

Rosa \ Ecuador (48%), Colombia (38%) 87Dianthus \ Colombia (84%), France (7%) 85Orchids \ The Netherlands (65%), Thailand (25%) 28Gladiolus \ The Netherlands (69%), Italy (25%) 0.0Dendranthema \ The Netherlands (99%), Portugal (1%) 0.1Other cut flowers \ The Netherlands (82%), Colombia (6%) 9Prepared cut flowers \ The Netherlands (62%), China (8%) 18Foliage \ India (33%), The Netherlands (19%), France (13%) 57

Cut flowers & foliage _ The Netherlands (38%), Colombia (33%), Ecuador (15%) 53

Source: Eurostat (2002)

36

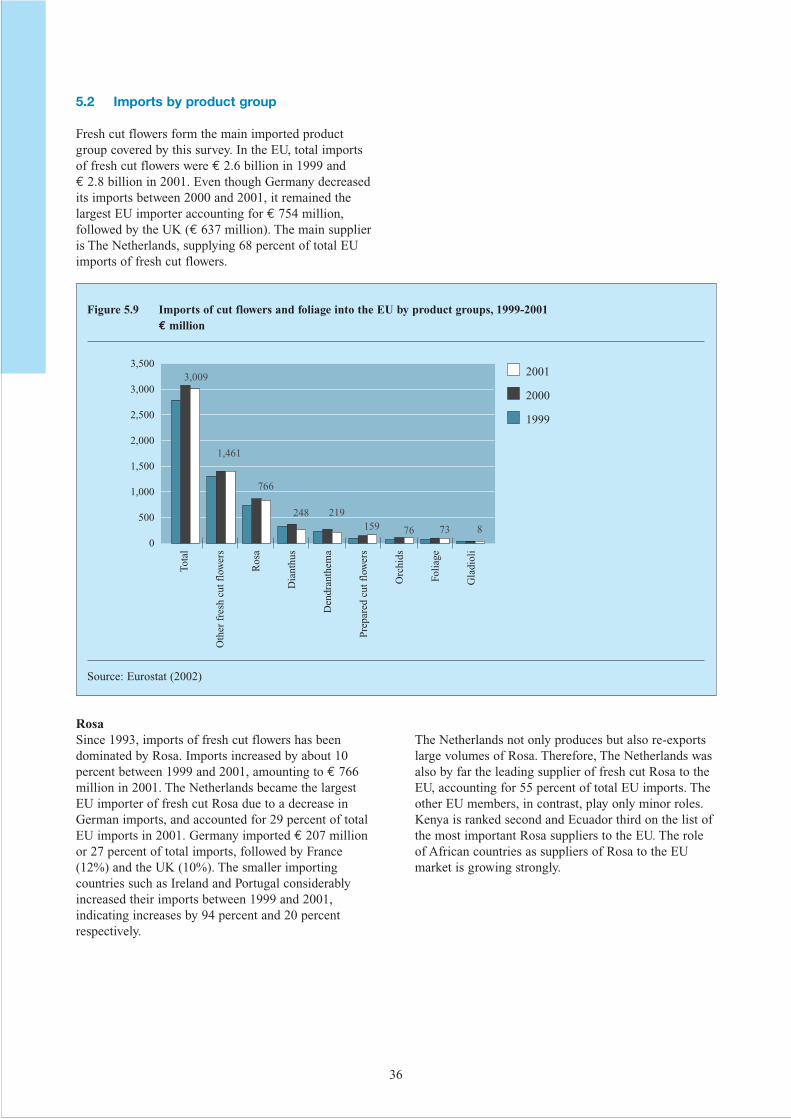

5.2 Imports by product group

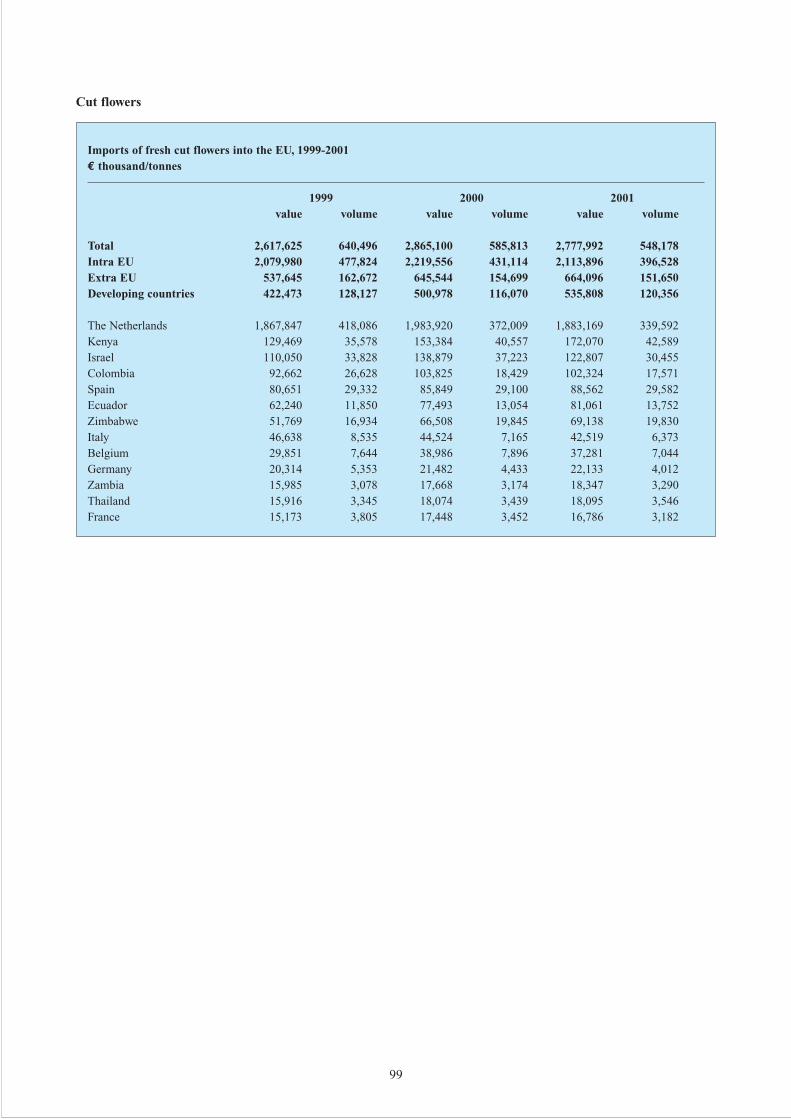

Fresh cut flowers form the main imported productgroup covered by this survey. In the EU, total importsof fresh cut flowers were € 2.6 billion in 1999 and€ 2.8 billion in 2001. Even though Germany decreasedits imports between 2000 and 2001, it remained thelargest EU importer accounting for € 754 million,followed by the UK (€ 637 million). The main supplieris The Netherlands, supplying 68 percent of total EUimports of fresh cut flowers.

RosaSince 1993, imports of fresh cut flowers has beendominated by Rosa. Imports increased by about 10percent between 1999 and 2001, amounting to € 766million in 2001. The Netherlands became the largestEU importer of fresh cut Rosa due to a decrease inGerman imports, and accounted for 29 percent of totalEU imports in 2001. Germany imported € 207 millionor 27 percent of total imports, followed by France(12%) and the UK (10%). The smaller importingcountries such as Ireland and Portugal considerablyincreased their imports between 1999 and 2001,indicating increases by 94 percent and 20 percentrespectively.

The Netherlands not only produces but also re-exportslarge volumes of Rosa. Therefore, The Netherlands wasalso by far the leading supplier of fresh cut Rosa to theEU, accounting for 55 percent of total EU imports. Theother EU members, in contrast, play only minor roles.Kenya is ranked second and Ecuador third on the list ofthe most important Rosa suppliers to the EU. The roleof African countries as suppliers of Rosa to the EUmarket is growing strongly.

Tota

l

Oth

er f

resh

cut

flo

wer

s

Ros

a

Dia

nthu

s

Den

dran

them

a

Pre

pare

d cu

t flo

wer

s

Orc

hids

Foli

age

Gla

diol

i

3,500

3,000

2,500

2,000

1,500

1,000

500

0

2001

2000

1999

3,009

1,461

766

248 219159 76 73 8

Figure 5.9 Imports of cut flowers and foliage into the EU by product groups, 1999-2001€ million

Source: Eurostat (2002)

37

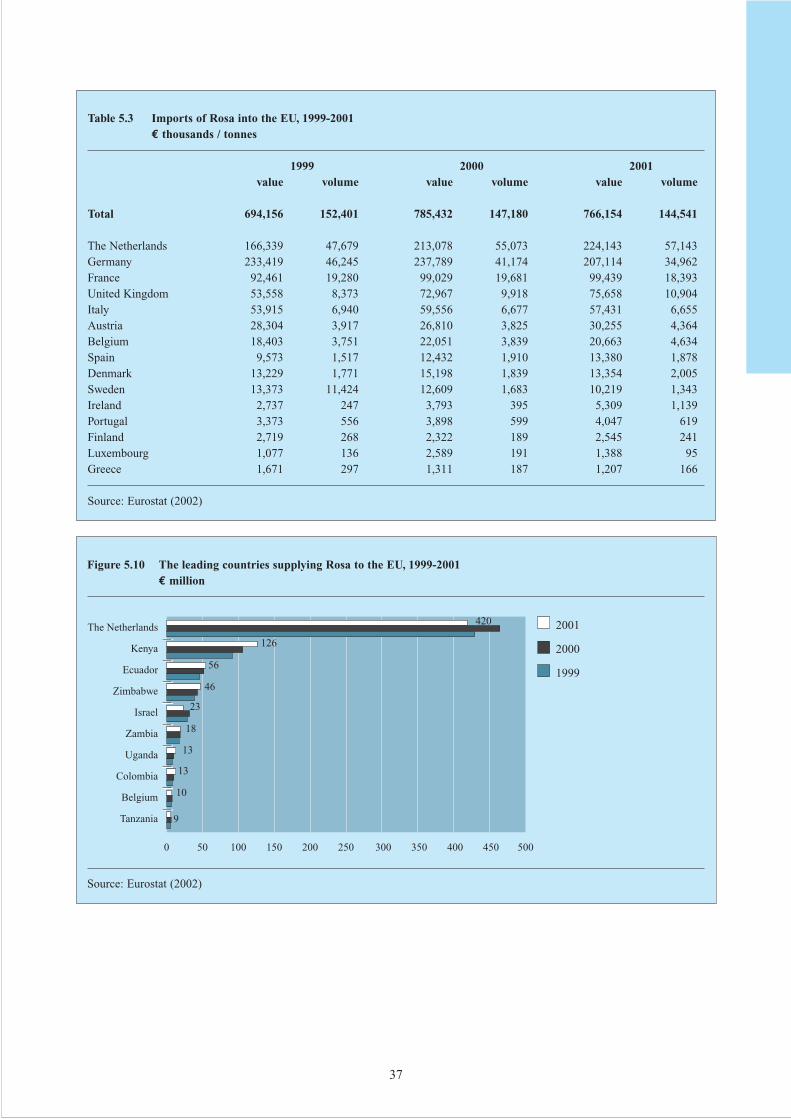

Table 5.3 Imports of Rosa into the EU, 1999-2001€ thousands / tonnes

1999 2000 2001value volume value volume value volume

Total 694,156 152,401 785,432 147,180 766,154 144,541

The Netherlands 166,339 47,679 213,078 55,073 224,143 57,143Germany 233,419 46,245 237,789 41,174 207,114 34,962France 92,461 19,280 99,029 19,681 99,439 18,393United Kingdom 53,558 8,373 72,967 9,918 75,658 10,904Italy 53,915 6,940 59,556 6,677 57,431 6,655Austria 28,304 3,917 26,810 3,825 30,255 4,364Belgium 18,403 3,751 22,051 3,839 20,663 4,634Spain 9,573 1,517 12,432 1,910 13,380 1,878Denmark 13,229 1,771 15,198 1,839 13,354 2,005Sweden 13,373 11,424 12,609 1,683 10,219 1,343Ireland 2,737 247 3,793 395 5,309 1,139Portugal 3,373 556 3,898 599 4,047 619Finland 2,719 268 2,322 189 2,545 241Luxembourg 1,077 136 2,589 191 1,388 95Greece 1,671 297 1,311 187 1,207 166

Source: Eurostat (2002)

The Netherlands

Kenya

Ecuador

Zimbabwe

Israel

Zambia

Uganda

Colombia

Belgium

Tanzania

2001

2000

1999

420

46

23

56

0 50 100 150 200 250 300 350 400 450 500

18

13

13

10

9

126

Figure 5.10 The leading countries supplying Rosa to the EU, 1999-2001€ million

Source: Eurostat (2002)

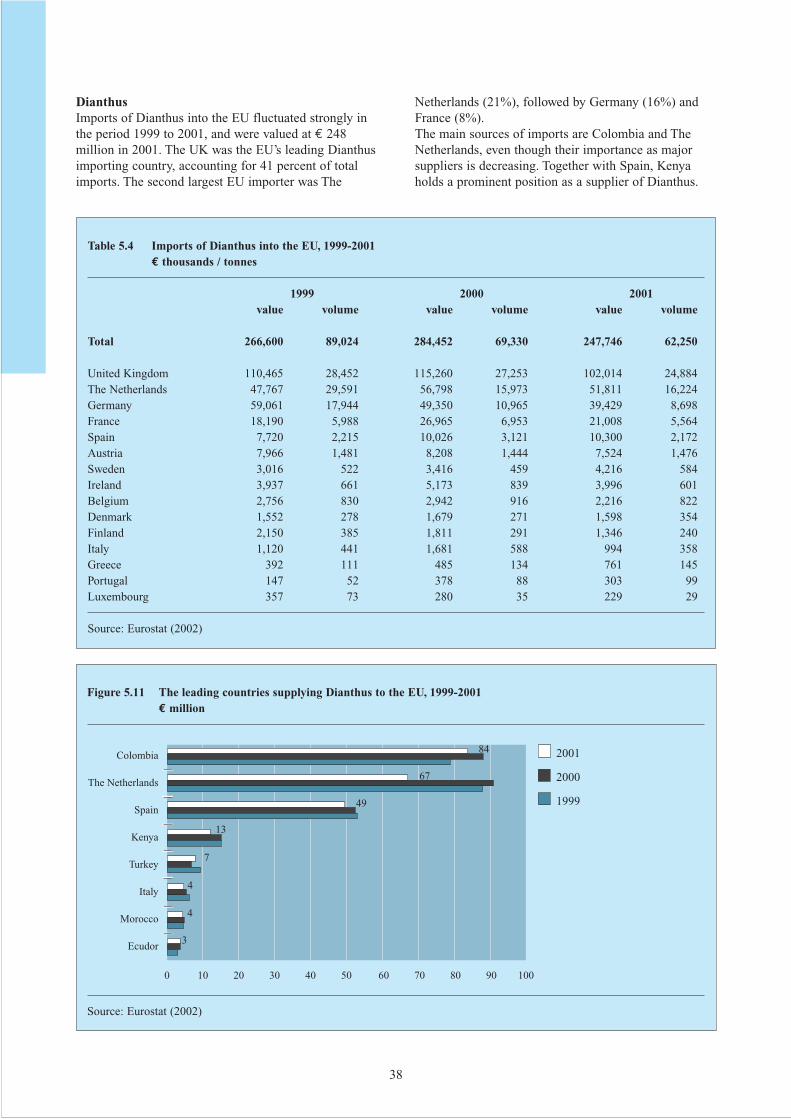

38

DianthusImports of Dianthus into the EU fluctuated strongly inthe period 1999 to 2001, and were valued at € 248million in 2001. The UK was the EU’s leading Dianthusimporting country, accounting for 41 percent of totalimports. The second largest EU importer was The

Netherlands (21%), followed by Germany (16%) andFrance (8%).The main sources of imports are Colombia and TheNetherlands, even though their importance as majorsuppliers is decreasing. Together with Spain, Kenyaholds a prominent position as a supplier of Dianthus.

Colombia

The Netherlands

Spain

Kenya

Turkey

Italy

Morocco

Ecudor

2001

2000

1999

84

49

13

0 10 20 30 40 50 60 70 80 90 100

7

4

4

67

3

Figure 5.11 The leading countries supplying Dianthus to the EU, 1999-2001€ million

Source: Eurostat (2002)

Table 5.4 Imports of Dianthus into the EU, 1999-2001€ thousands / tonnes

1999 2000 2001value volume value volume value volume

Total 266,600 89,024 284,452 69,330 247,746 62,250

United Kingdom 110,465 28,452 115,260 27,253 102,014 24,884The Netherlands 47,767 29,591 56,798 15,973 51,811 16,224Germany 59,061 17,944 49,350 10,965 39,429 8,698France 18,190 5,988 26,965 6,953 21,008 5,564Spain 7,720 2,215 10,026 3,121 10,300 2,172Austria 7,966 1,481 8,208 1,444 7,524 1,476Sweden 3,016 522 3,416 459 4,216 584Ireland 3,937 661 5,173 839 3,996 601Belgium 2,756 830 2,942 916 2,216 822Denmark 1,552 278 1,679 271 1,598 354Finland 2,150 385 1,811 291 1,346 240Italy 1,120 441 1,681 588 994 358Greece 392 111 485 134 761 145Portugal 147 52 378 88 303 99Luxembourg 357 73 280 35 229 29

Source: Eurostat (2002)

39

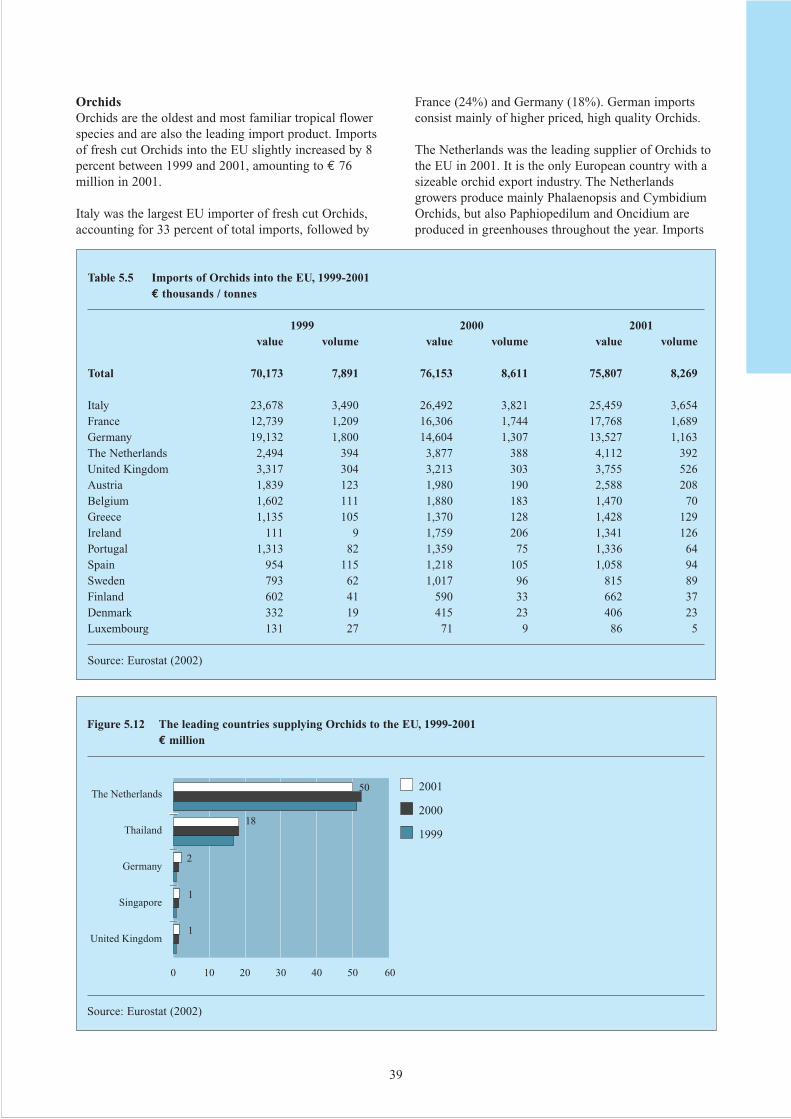

OrchidsOrchids are the oldest and most familiar tropical flowerspecies and are also the leading import product. Importsof fresh cut Orchids into the EU slightly increased by 8percent between 1999 and 2001, amounting to € 76million in 2001.

Italy was the largest EU importer of fresh cut Orchids,accounting for 33 percent of total imports, followed by

France (24%) and Germany (18%). German importsconsist mainly of higher priced, high quality Orchids.

The Netherlands was the leading supplier of Orchids tothe EU in 2001. It is the only European country with asizeable orchid export industry. The Netherlandsgrowers produce mainly Phalaenopsis and CymbidiumOrchids, but also Paphiopedilum and Oncidium areproduced in greenhouses throughout the year. Imports

Table 5.5 Imports of Orchids into the EU, 1999-2001€ thousands / tonnes

1999 2000 2001value volume value volume value volume

Total 70,173 7,891 76,153 8,611 75,807 8,269

Italy 23,678 3,490 26,492 3,821 25,459 3,654France 12,739 1,209 16,306 1,744 17,768 1,689Germany 19,132 1,800 14,604 1,307 13,527 1,163The Netherlands 2,494 394 3,877 388 4,112 392United Kingdom 3,317 304 3,213 303 3,755 526Austria 1,839 123 1,980 190 2,588 208Belgium 1,602 111 1,880 183 1,470 70Greece 1,135 105 1,370 128 1,428 129Ireland 111 9 1,759 206 1,341 126Portugal 1,313 82 1,359 75 1,336 64Spain 954 115 1,218 105 1,058 94Sweden 793 62 1,017 96 815 89Finland 602 41 590 33 662 37Denmark 332 19 415 23 406 23Luxembourg 131 27 71 9 86 5

Source: Eurostat (2002)

The Netherlands

Thailand

Germany

Singapore

United Kingdom

2001

2000

1999

50

0 10 20 30 40 50 60

18

2

1

1

Figure 5.12 The leading countries supplying Orchids to the EU, 1999-2001€ million

Source: Eurostat (2002)

40

from Thailand, the world’s largest exporter of tropicalcut Orchids and second largest supplier to the EU,amounted to € 18 million.

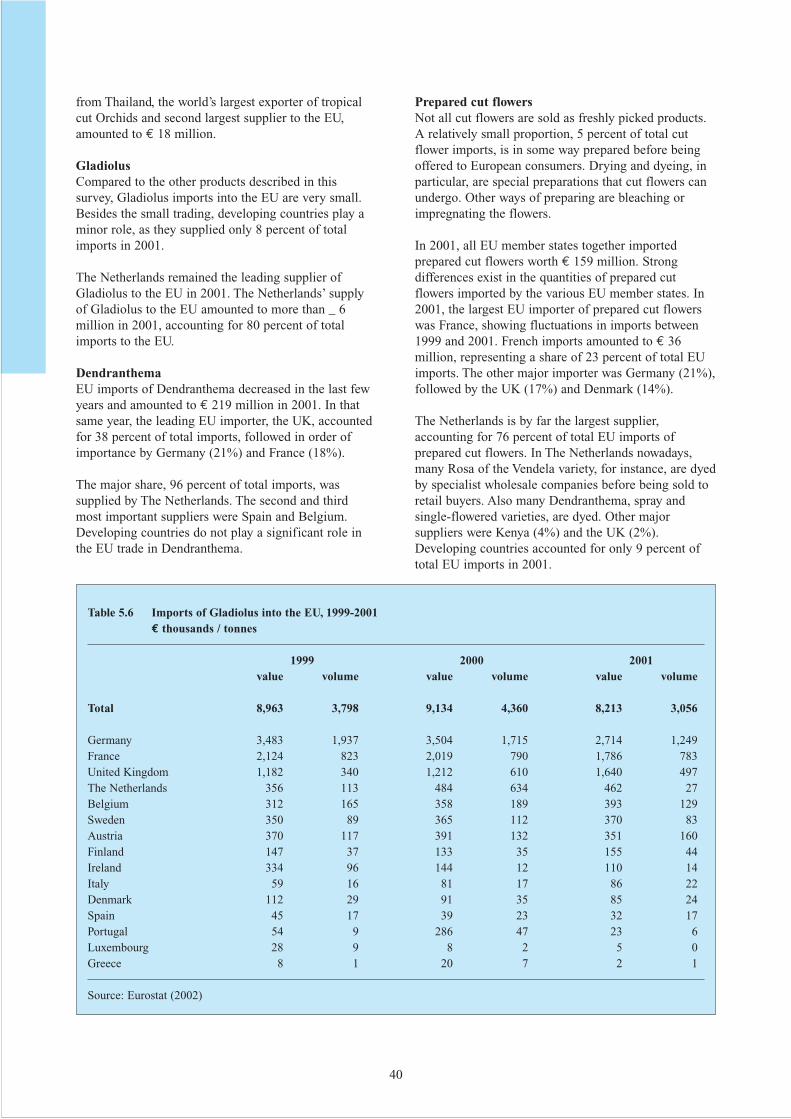

GladiolusCompared to the other products described in thissurvey, Gladiolus imports into the EU are very small.Besides the small trading, developing countries play aminor role, as they supplied only 8 percent of totalimports in 2001.

The Netherlands remained the leading supplier ofGladiolus to the EU in 2001. The Netherlands’ supplyof Gladiolus to the EU amounted to more than _ 6million in 2001, accounting for 80 percent of totalimports to the EU.

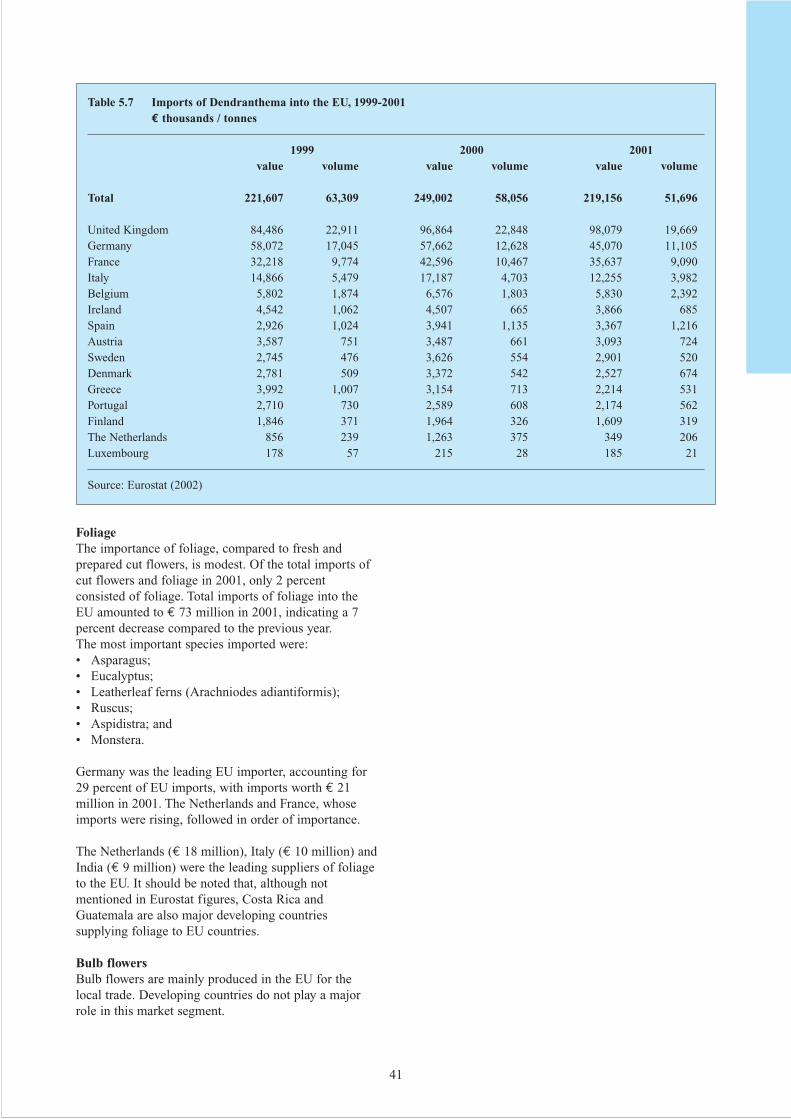

DendranthemaEU imports of Dendranthema decreased in the last fewyears and amounted to € 219 million in 2001. In thatsame year, the leading EU importer, the UK, accountedfor 38 percent of total imports, followed in order ofimportance by Germany (21%) and France (18%).

The major share, 96 percent of total imports, wassupplied by The Netherlands. The second and thirdmost important suppliers were Spain and Belgium.Developing countries do not play a significant role inthe EU trade in Dendranthema.

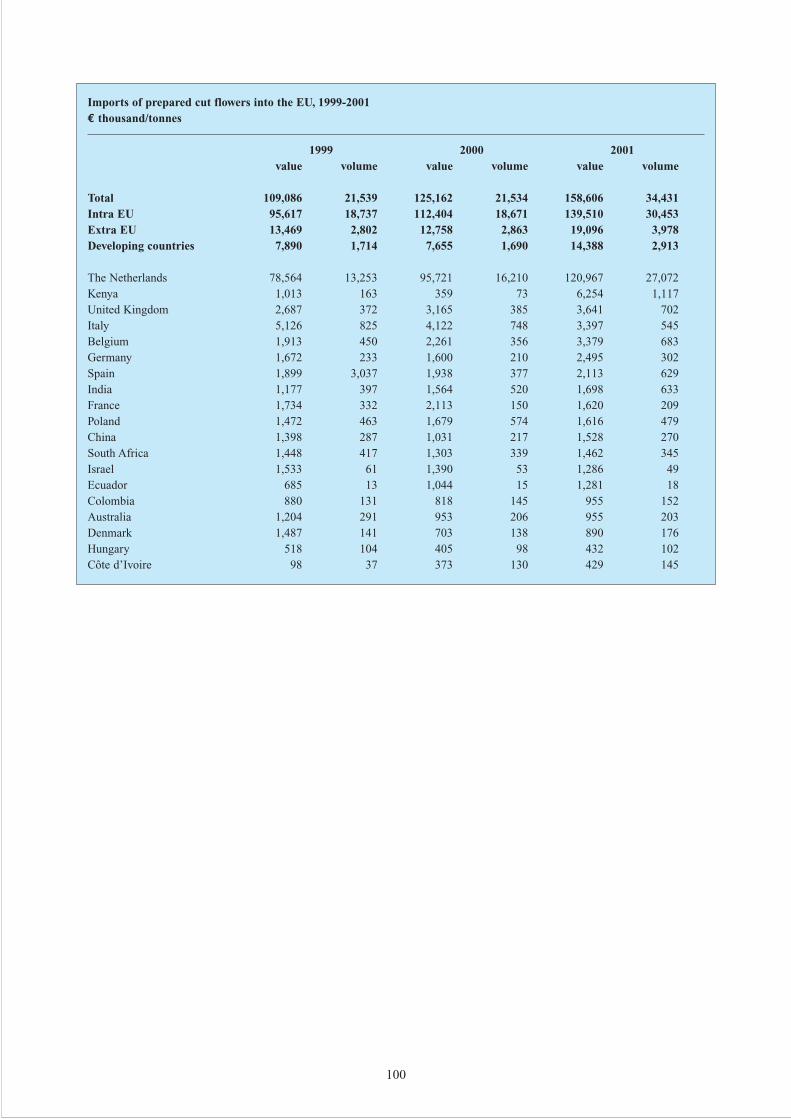

Prepared cut flowersNot all cut flowers are sold as freshly picked products.A relatively small proportion, 5 percent of total cutflower imports, is in some way prepared before beingoffered to European consumers. Drying and dyeing, inparticular, are special preparations that cut flowers canundergo. Other ways of preparing are bleaching orimpregnating the flowers.

In 2001, all EU member states together importedprepared cut flowers worth € 159 million. Strongdifferences exist in the quantities of prepared cutflowers imported by the various EU member states. In2001, the largest EU importer of prepared cut flowerswas France, showing fluctuations in imports between1999 and 2001. French imports amounted to € 36million, representing a share of 23 percent of total EUimports. The other major importer was Germany (21%),followed by the UK (17%) and Denmark (14%).

The Netherlands is by far the largest supplier,accounting for 76 percent of total EU imports ofprepared cut flowers. In The Netherlands nowadays,many Rosa of the Vendela variety, for instance, are dyedby specialist wholesale companies before being sold toretail buyers. Also many Dendranthema, spray andsingle-flowered varieties, are dyed. Other majorsuppliers were Kenya (4%) and the UK (2%).Developing countries accounted for only 9 percent oftotal EU imports in 2001.

Table 5.6 Imports of Gladiolus into the EU, 1999-2001€ thousands / tonnes

1999 2000 2001value volume value volume value volume

Total 8,963 3,798 9,134 4,360 8,213 3,056

Germany 3,483 1,937 3,504 1,715 2,714 1,249France 2,124 823 2,019 790 1,786 783United Kingdom 1,182 340 1,212 610 1,640 497The Netherlands 356 113 484 634 462 27Belgium 312 165 358 189 393 129Sweden 350 89 365 112 370 83Austria 370 117 391 132 351 160Finland 147 37 133 35 155 44Ireland 334 96 144 12 110 14Italy 59 16 81 17 86 22Denmark 112 29 91 35 85 24Spain 45 17 39 23 32 17Portugal 54 9 286 47 23 6Luxembourg 28 9 8 2 5 0Greece 8 1 20 7 2 1

Source: Eurostat (2002)

41

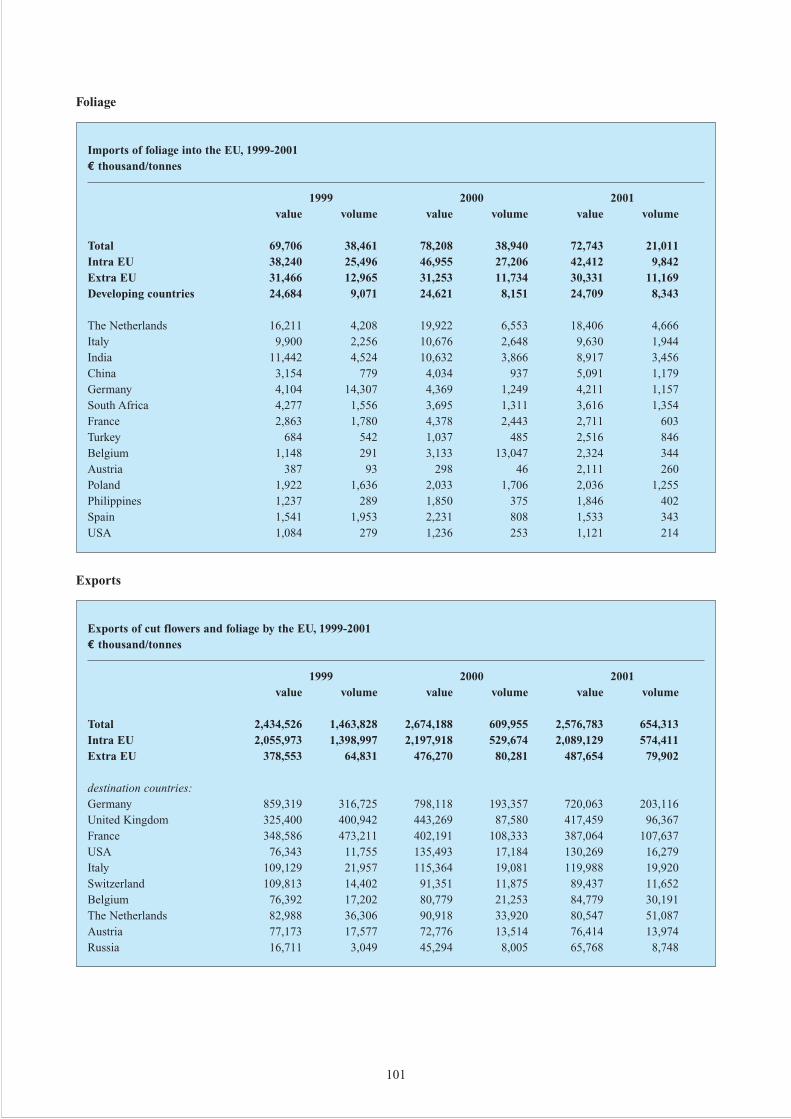

FoliageThe importance of foliage, compared to fresh andprepared cut flowers, is modest. Of the total imports ofcut flowers and foliage in 2001, only 2 percentconsisted of foliage. Total imports of foliage into theEU amounted to € 73 million in 2001, indicating a 7percent decrease compared to the previous year. The most important species imported were:• Asparagus;• Eucalyptus;• Leatherleaf ferns (Arachniodes adiantiformis);• Ruscus;• Aspidistra; and• Monstera.

Germany was the leading EU importer, accounting for29 percent of EU imports, with imports worth € 21million in 2001. The Netherlands and France, whoseimports were rising, followed in order of importance.

The Netherlands (€ 18 million), Italy (€ 10 million) andIndia (€ 9 million) were the leading suppliers of foliageto the EU. It should be noted that, although notmentioned in Eurostat figures, Costa Rica andGuatemala are also major developing countriessupplying foliage to EU countries.

Bulb flowersBulb flowers are mainly produced in the EU for thelocal trade. Developing countries do not play a majorrole in this market segment.

Table 5.7 Imports of Dendranthema into the EU, 1999-2001€ thousands / tonnes

1999 2000 2001value volume value volume value volume

Total 221,607 63,309 249,002 58,056 219,156 51,696

United Kingdom 84,486 22,911 96,864 22,848 98,079 19,669Germany 58,072 17,045 57,662 12,628 45,070 11,105France 32,218 9,774 42,596 10,467 35,637 9,090Italy 14,866 5,479 17,187 4,703 12,255 3,982Belgium 5,802 1,874 6,576 1,803 5,830 2,392Ireland 4,542 1,062 4,507 665 3,866 685Spain 2,926 1,024 3,941 1,135 3,367 1,216Austria 3,587 751 3,487 661 3,093 724Sweden 2,745 476 3,626 554 2,901 520Denmark 2,781 509 3,372 542 2,527 674Greece 3,992 1,007 3,154 713 2,214 531Portugal 2,710 730 2,589 608 2,174 562Finland 1,846 371 1,964 326 1,609 319The Netherlands 856 239 1,263 375 349 206Luxembourg 178 57 215 28 185 21

Source: Eurostat (2002)

42

5.3 The role of developing countries

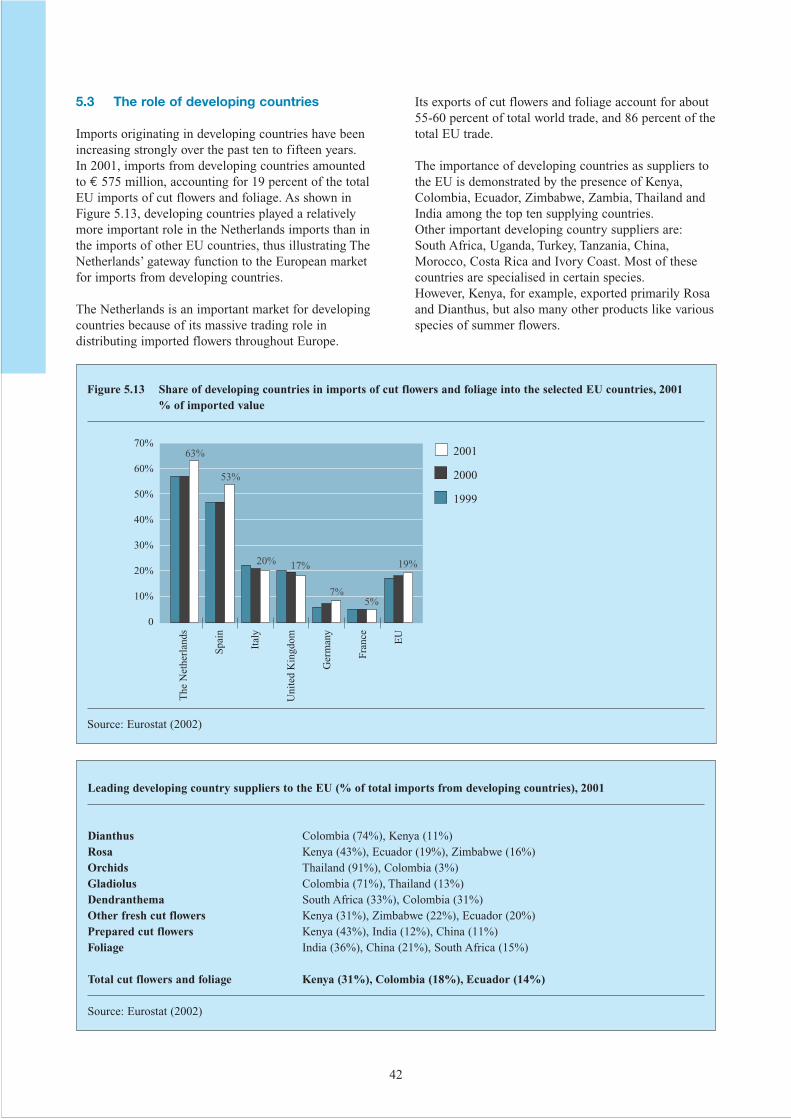

Imports originating in developing countries have beenincreasing strongly over the past ten to fifteen years. In 2001, imports from developing countries amountedto € 575 million, accounting for 19 percent of the totalEU imports of cut flowers and foliage. As shown inFigure 5.13, developing countries played a relativelymore important role in the Netherlands imports than inthe imports of other EU countries, thus illustrating TheNetherlands’ gateway function to the European marketfor imports from developing countries.

The Netherlands is an important market for developingcountries because of its massive trading role indistributing imported flowers throughout Europe.

Its exports of cut flowers and foliage account for about55-60 percent of total world trade, and 86 percent of thetotal EU trade.