corporate presentation - vistin pharma

TRANSCRIPT

Vistin Pharma – Corporate Presentation

October 2016

Content

Introduction to Vistin Pharma

Operational and financial update

Summary & outlook

Appendix

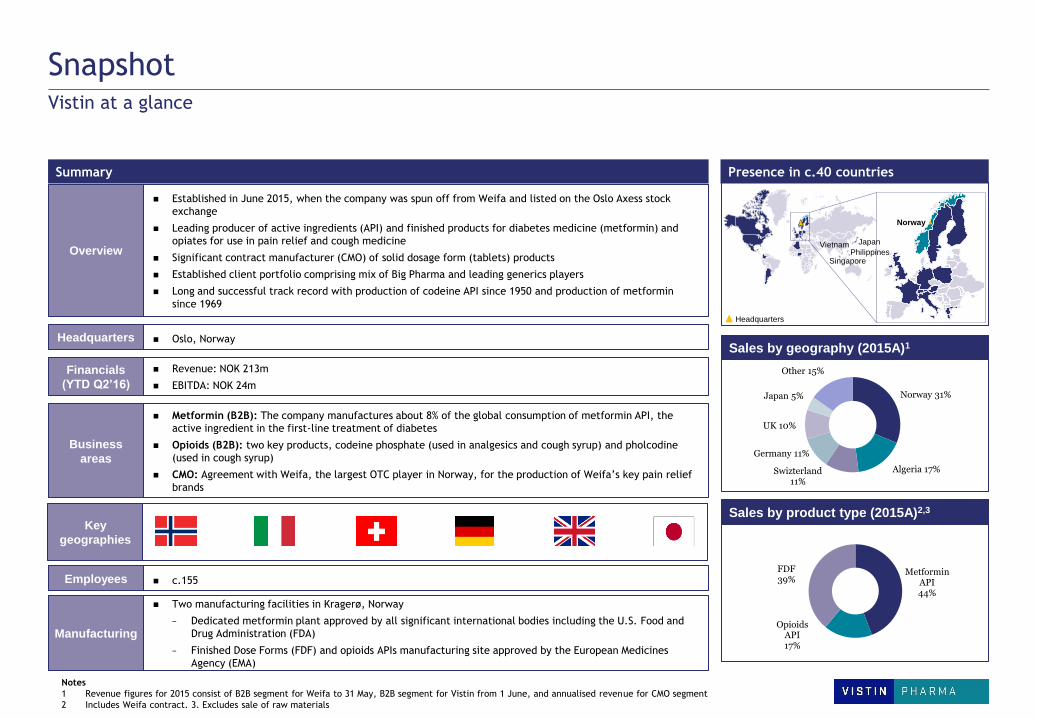

Snapshot

Summary Presence in c.40 countries

Vistin at a glance

Established in June 2015, when the company was spun off from Weifa and listed on the Oslo Axess stock

exchange

Leading producer of active ingredients (API) and finished products for diabetes medicine (metformin) and

opiates for use in pain relief and cough medicine

Significant contract manufacturer (CMO) of solid dosage form (tablets) products

Established client portfolio comprising mix of Big Pharma and leading generics players

Long and successful track record with production of codeine API since 1950 and production of metformin

since 1969

Overview

Business

areas

Metformin (B2B): The company manufactures about 8% of the global consumption of metformin API, the

active ingredient in the first-line treatment of diabetes

Opioids (B2B): two key products, codeine phosphate (used in analgesics and cough syrup) and pholcodine

(used in cough syrup)

CMO: Agreement with Weifa, the largest OTC player in Norway, for the production of Weifa’s key pain relief

brands

Manufacturing

Two manufacturing facilities in Kragerø, Norway

− Dedicated metformin plant approved by all significant international bodies including the U.S. Food and

Drug Administration (FDA)

− Finished Dose Forms (FDF) and opioids APIs manufacturing site approved by the European Medicines

Agency (EMA)

Employees c.155

Headquarters Oslo, Norway

Financials

(YTD Q2’16)

Revenue: NOK 213m

EBITDA: NOK 24m

Sales by product type (2015A)2,3

Sales by geography (2015A)1

Headquarters

Norway

Japan

Key

geographies

Notes

1 Revenue figures for 2015 consist of B2B segment for Weifa to 31 May, B2B segment for Vistin from 1 June, and annualised revenue for CMO segment

2 Includes Weifa contract. 3. Excludes sale of raw materials

Vietnam

Singapore Philippines

Norway 31%

Algeria 17%Swizterland 11%

Germany 11%

UK 10%

Japan 5%

Other 15%

Metformin API44%

Opioids API17%

FDF39%

Vistin’s key milestones Long and successful track record of producing high quality APIs and FDFs

Vistin’s evolution

2015 2016 1940 - 2014

1940:

Weiders

Farmasoytiske

A/S founded by

Olaf Weider

Weifa

1950:

Production

start of

codeine API

1952:

First

production

facility opened

in Kragerø

(Gruveveien)

1960:

Production

start of

Paralgin

Forte

1969:

Launch of

metformin API

2014:

Weifa AS

acquired by

Aqualis ASA

2014:

Codeine

tablets added

to the product

portfolio

2002:

New FDA-approved

metformin facility

opened in Kragero

(Fikkjebakke)

1977:

Production

start of

Paracet

1986:

Production

start of Ibux

2015:

Vistin Pharma

established as a

separate company

Vistin Pharma

2016:

Announcement of

significant expansion

in capacity at

metformin plant in

Kragerø

Content

Introduction to Vistin Pharma

Operational and financial update

Summary & outlook

Appendix

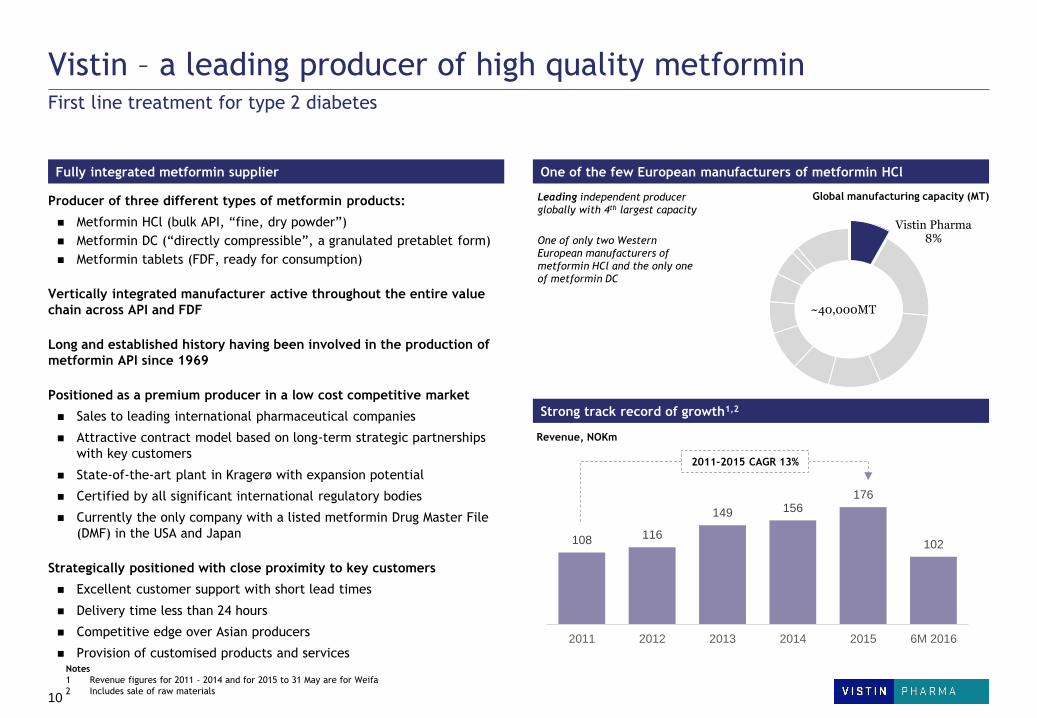

108 116

149 156 176

102

2011 2012 2013 2014 2015 6M 2016

Vistin – a leading producer of high quality metformin First line treatment for type 2 diabetes

Fully integrated metformin supplier One of the few European manufacturers of metformin HCl

Strong track record of growth1,2

Producer of three different types of metformin products:

Metformin HCl (bulk API, “fine, dry powder”)

Metformin DC (“directly compressible”, a granulated pretablet form)

Metformin tablets (FDF, ready for consumption)

Vertically integrated manufacturer active throughout the entire value

chain across API and FDF

Long and established history having been involved in the production of

metformin API since 1969

Positioned as a premium producer in a low cost competitive market

Sales to leading international pharmaceutical companies

Attractive contract model based on long-term strategic partnerships

with key customers

State-of-the-art plant in Kragerø with expansion potential

Certified by all significant international regulatory bodies

Currently the only company with a listed metformin Drug Master File

(DMF) in the USA and Japan

Strategically positioned with close proximity to key customers

Excellent customer support with short lead times

Delivery time less than 24 hours

Competitive edge over Asian producers

Provision of customised products and services

Revenue, NOKm

Global manufacturing capacity (MT)

2011-2015 CAGR 13%

Leading independent producer

globally with 4th largest capacity

One of only two Western

European manufacturers of

metformin HCl and the only one

of metformin DC

Vistin Pharma8%

~40,000MT

10

Notes

1 Revenue figures for 2011 – 2014 and for 2015 to 31 May are for Weifa

2 Includes sale of raw materials

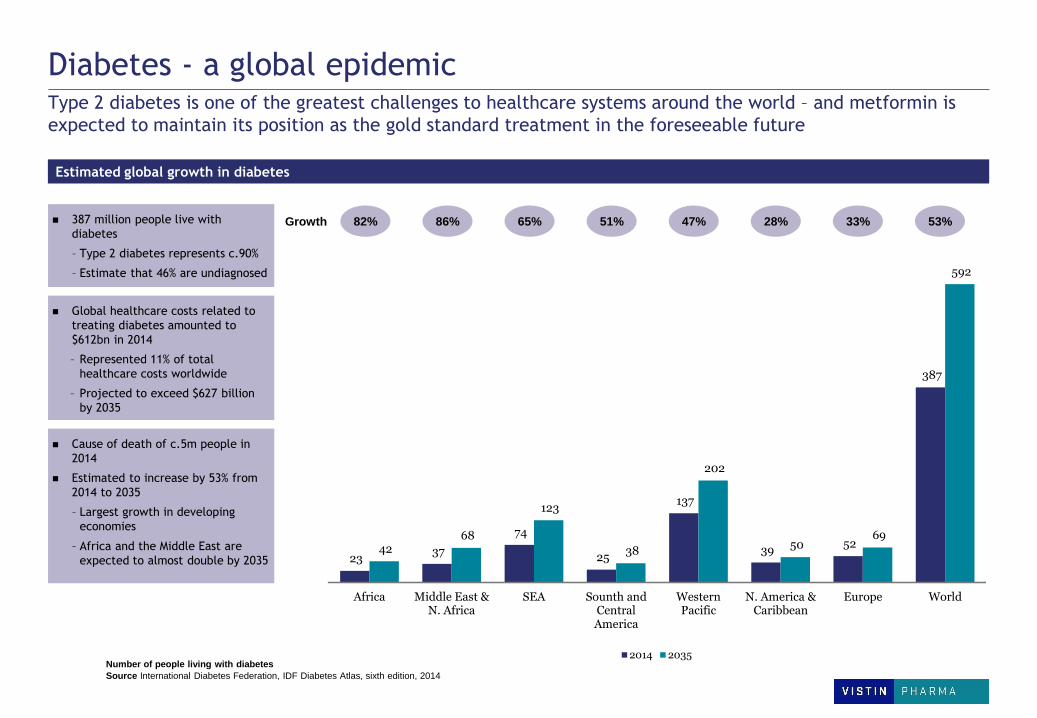

Diabetes - a global epidemic Type 2 diabetes is one of the greatest challenges to healthcare systems around the world – and metformin is

expected to maintain its position as the gold standard treatment in the foreseeable future

387 million people live with

diabetes

– Type 2 diabetes represents c.90%

– Estimate that 46% are undiagnosed

Estimated global growth in diabetes

Number of people living with diabetes

Source International Diabetes Federation, IDF Diabetes Atlas, sixth edition, 2014

82% 86% 65% 51% 47% 28% 33% 53%

Global healthcare costs related to

treating diabetes amounted to

$612bn in 2014

– Represented 11% of total

healthcare costs worldwide

– Projected to exceed $627 billion

by 2035

Cause of death of c.5m people in

2014

Estimated to increase by 53% from

2014 to 2035

– Largest growth in developing

economies

– Africa and the Middle East are

expected to almost double by 2035

Growth

23 37

74

25

137

39 52

387

42 68

123

38

202

50 69

592

Africa Middle East &N. Africa

SEA Sounth andCentralAmerica

WesternPacific

N. America &Caribbean

Europe World

2014 2035

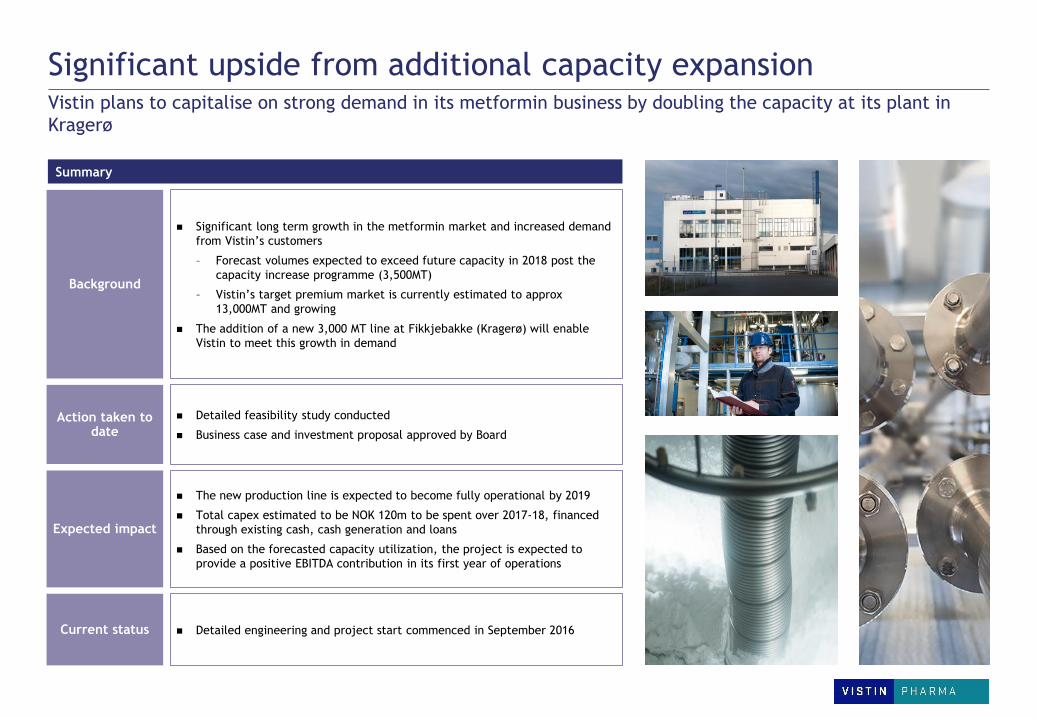

Significant upside from additional capacity expansion Vistin plans to capitalise on strong demand in its metformin business by doubling the capacity at its plant in

Kragerø

Background

Action taken to date

Expected impact

Current status

Significant long term growth in the metformin market and increased demand

from Vistin’s customers

– Forecast volumes expected to exceed future capacity in 2018 post the

capacity increase programme (3,500MT)

– Vistin’s target premium market is currently estimated to approx

13,000MT and growing

The addition of a new 3,000 MT line at Fikkjebakke (Kragerø) will enable

Vistin to meet this growth in demand

Detailed feasibility study conducted

Business case and investment proposal approved by Board

The new production line is expected to become fully operational by 2019

Total capex estimated to be NOK 120m to be spent over 2017-18, financed

through existing cash, cash generation and loans

Based on the forecasted capacity utilization, the project is expected to

provide a positive EBITDA contribution in its first year of operations

Detailed engineering and project start commenced in September 2016

Summary

58

75 71

82 81

50

2011 2012 2013 2014 2015 6M 2016

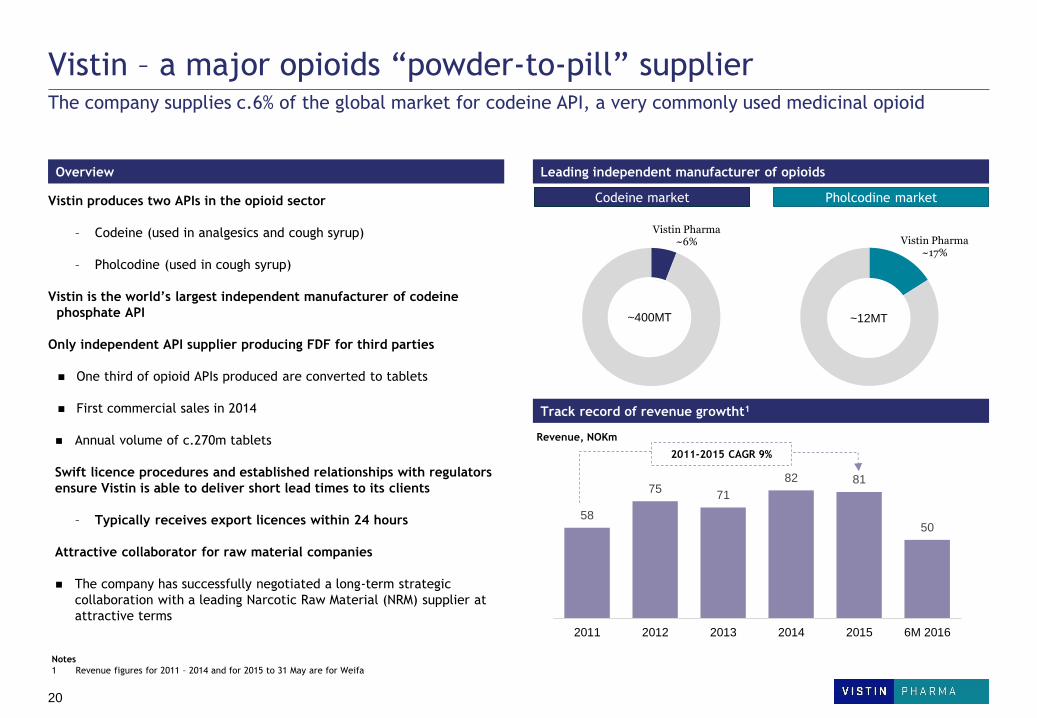

Vistin – a major opioids “powder-to-pill” supplier The company supplies c.6% of the global market for codeine API, a very commonly used medicinal opioid

Overview Leading independent manufacturer of opioids

Vistin produces two APIs in the opioid sector

– Codeine (used in analgesics and cough syrup)

– Pholcodine (used in cough syrup)

Vistin is the world’s largest independent manufacturer of codeine

phosphate API

Only independent API supplier producing FDF for third parties

One third of opioid APIs produced are converted to tablets

First commercial sales in 2014

Annual volume of c.270m tablets

Swift licence procedures and established relationships with regulators

ensure Vistin is able to deliver short lead times to its clients

– Typically receives export licences within 24 hours

Attractive collaborator for raw material companies

The company has successfully negotiated a long-term strategic

collaboration with a leading Narcotic Raw Material (NRM) supplier at

attractive terms

Codeine market Pholcodine market

Revenue, NOKm

2011-2015 CAGR 9%

Vistin Pharma~17%

~12MT

Vistin Pharma~6%

~400MT

20

Notes

1 Revenue figures for 2011 – 2014 and for 2015 to 31 May are for Weifa

Track record of revenue growtht1

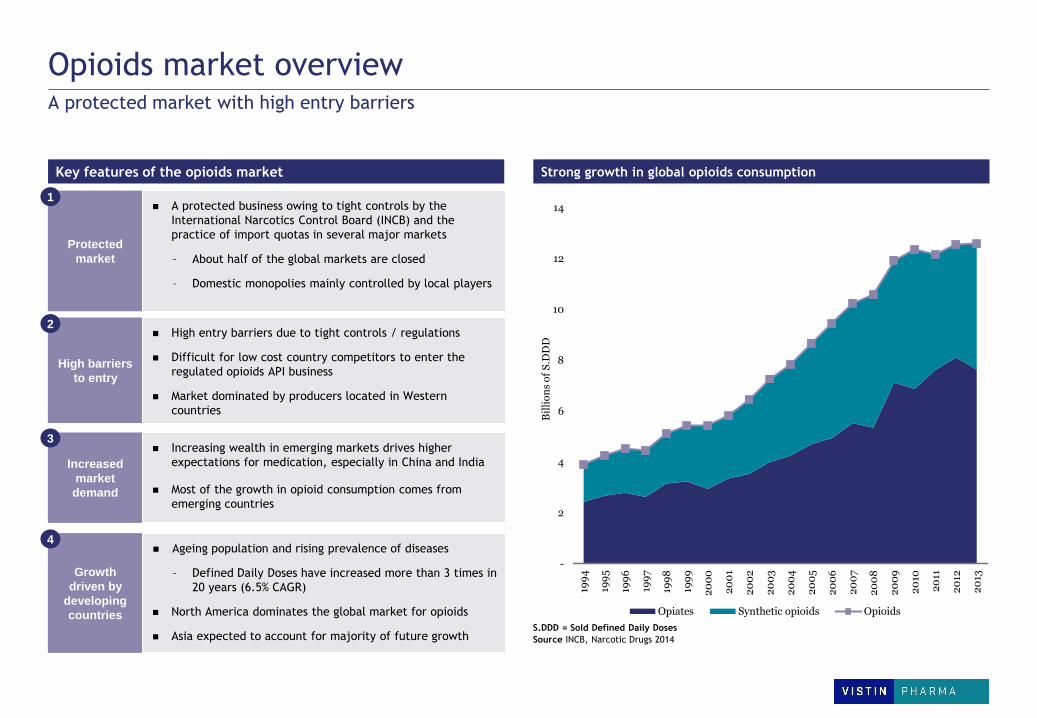

Opioids market overview

Key features of the opioids market Strong growth in global opioids consumption

Strong growth in global opioids consumption

A protected market with high entry barriers

S.DDD = Sold Defined Daily Doses

Source INCB, Narcotic Drugs 2014

Protected

market

A protected business owing to tight controls by the

International Narcotics Control Board (INCB) and the

practice of import quotas in several major markets

– About half of the global markets are closed

– Domestic monopolies mainly controlled by local players

Increased

market

demand

Increasing wealth in emerging markets drives higher

expectations for medication, especially in China and India

Most of the growth in opioid consumption comes from

emerging countries

Growth

driven by

developing

countries

Ageing population and rising prevalence of diseases

– Defined Daily Doses have increased more than 3 times in

20 years (6.5% CAGR)

North America dominates the global market for opioids

Asia expected to account for majority of future growth

-

2

4

6

8

10

12

14

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Bil

lio

ns

of

S.D

DD

Opiates Synthetic opioids Opioids

1

3

4

High barriers

to entry

High entry barriers due to tight controls / regulations

Difficult for low cost country competitors to enter the

regulated opioids API business

Market dominated by producers located in Western

countries

2

Vistin – A leading CMO tablet manufacturer Current annual production of c.750 million tablets with potential to expand capacity

Significant tablet manufacturer Summary of Weifa contract

Manufacture of tablets relating to opioids and metformin business and

reported as part of B2B segment

- Five-year supply agreement for codeine tablets for UK customer resulting in

volumes of approximately 270m tablets per annum

- Manufacture of metformin tablets

Tablet manufacturing plant at Kragerø, Norway

- GMP/GDP Certificate and Manufacturing License authorized by Norwegian

Medicines Agency with the latest inspection in August 2015

5 year agreement with Weifa for the production of its key pain relief brands

Overview

CMO agreement with Weifa for the production of:

- All tablets produced by Weifa’s Consumer segment

(including key pain relief brands)

- Certain 3rd party products to which Weifa has the

exclusive right to sell in certain territories

Duration

First term duration of five years

Option to extend for another two years at the discretion of

Weifa

Key products

Financials 2016B revenues: c.NOK 119m

Production 2016B: c.450m tablets

Production at the company’s plant in Gruveveien, Kragerø

Evolution of long-term customer partnership model in FDFs

2016 -

2017

2018 -

2020

2020 -

2025

Preferred CMO

Long term contract to manufacture the FDF

Fee-for-service CDMO

Preferred CMO with higher customer switching costs

Partnered CDMO

Exclusive CMO contract + profit share

Co-development alliance

Captures 50% of the value through fees and milestones

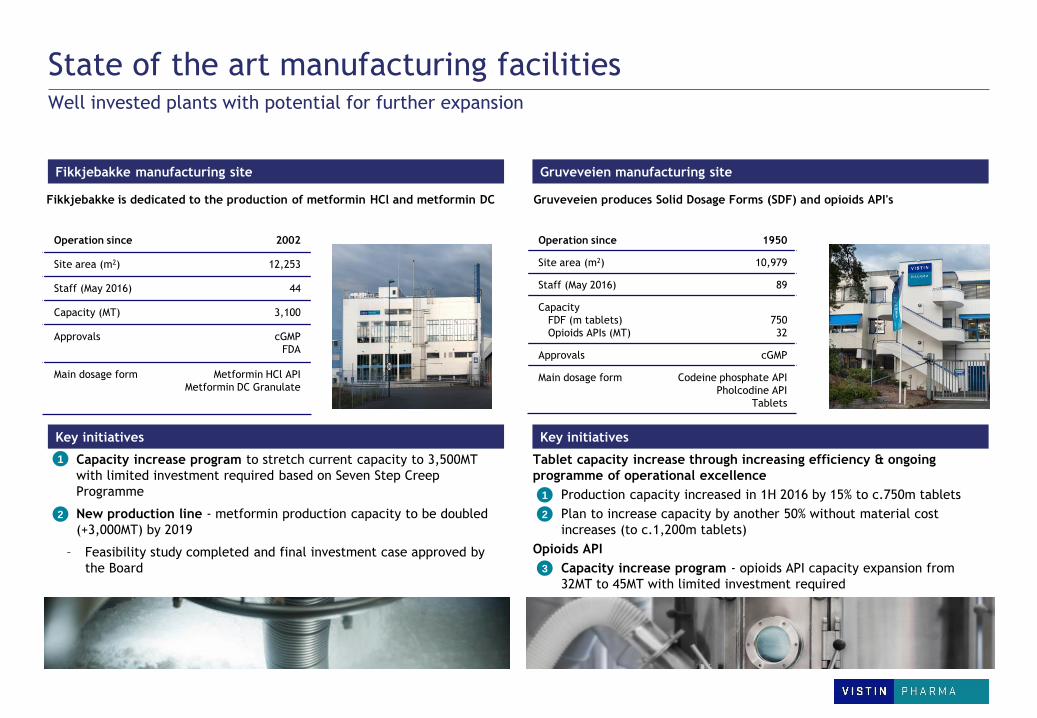

State of the art manufacturing facilities Well invested plants with potential for further expansion

Gruveveien produces Solid Dosage Forms (SDF) and opioids API's

Fikkjebakke manufacturing site Gruveveien manufacturing site

Operation since 1950

Site area (m2) 10,979

Staff (May 2016) 89

Capacity

FDF (m tablets)

Opioids APIs (MT)

750

32

Approvals cGMP

Main dosage form Codeine phosphate API

Pholcodine API

Tablets

Operation since 2002

Site area (m2) 12,253

Staff (May 2016) 44

Capacity (MT) 3,100

Approvals cGMP

FDA

Main dosage form Metformin HCl API

Metformin DC Granulate

Key initiatives Key initiatives

Capacity increase program to stretch current capacity to 3,500MT

with limited investment required based on Seven Step Creep

Programme

New production line - metformin production capacity to be doubled

(+3,000MT) by 2019

– Feasibility study completed and final investment case approved by

the Board

Fikkjebakke is dedicated to the production of metformin HCl and metformin DC

Tablet capacity increase through increasing efficiency & ongoing

programme of operational excellence

Production capacity increased in 1H 2016 by 15% to c.750m tablets

Plan to increase capacity by another 50% without material cost

increases (to c.1,200m tablets)

Opioids API

Capacity increase program - opioids API capacity expansion from

32MT to 45MT with limited investment required

2

1

3

1

2

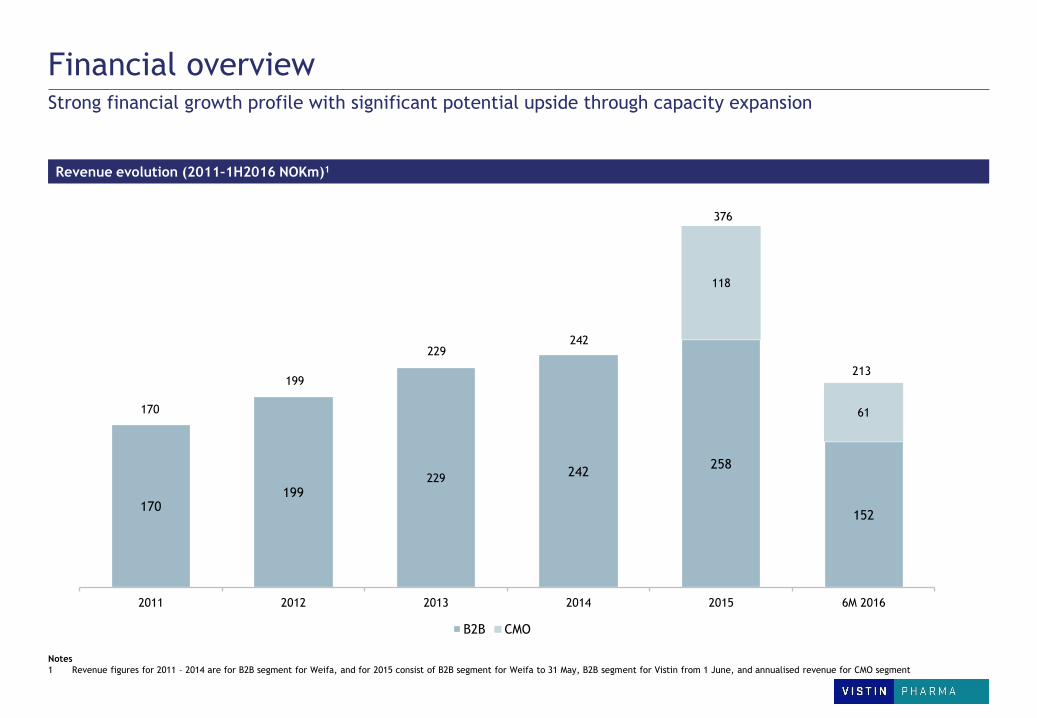

Financial overview Strong financial growth profile with significant potential upside through capacity expansion

Revenue evolution (2011–1H2016 NOKm)1

Notes

1 Revenue figures for 2011 – 2014 are for B2B segment for Weifa, and for 2015 consist of B2B segment for Weifa to 31 May, B2B segment for Vistin from 1 June, and annualised revenue for CMO segment

170 199

229 242

258

152

118

61

2011 2012 2013 2014 2015 6M 2016

B2B CMO

170

229 242

376

199 213

Content

Introduction to Vistin Pharma

Operational and financial update

Summary & outlook

Appendix

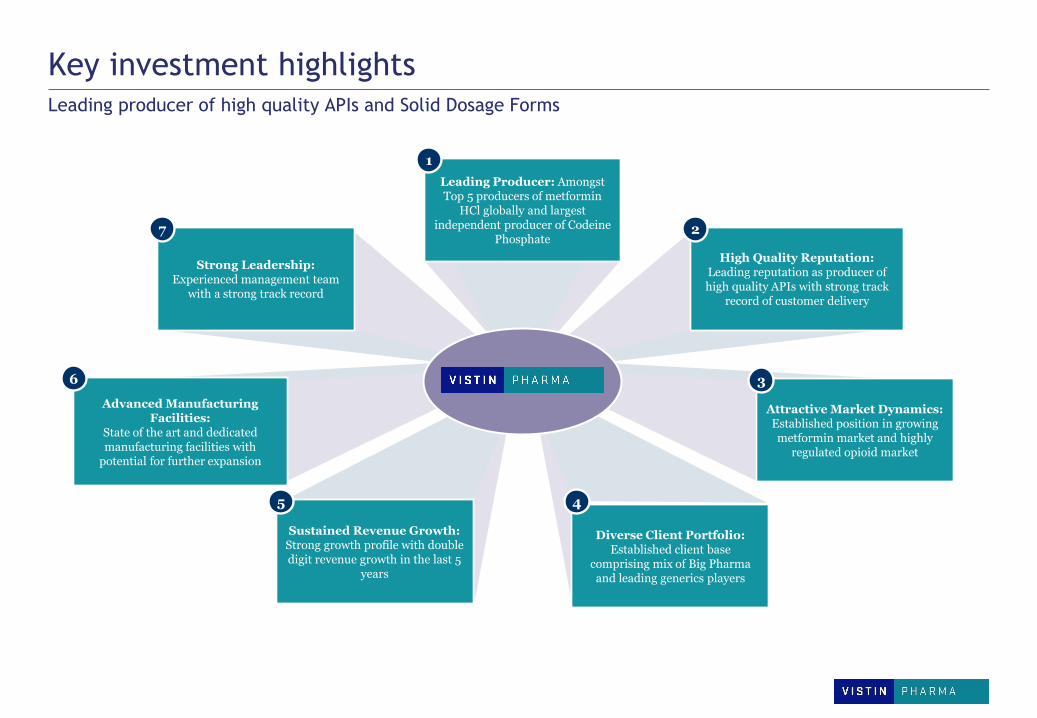

Key investment highlights Leading producer of high quality APIs and Solid Dosage Forms

High Quality Reputation: Leading reputation as producer of high quality APIs with strong track

record of customer delivery

Attractive Market Dynamics: Established position in growing metformin market and highly

regulated opioid market

Sustained Revenue Growth: Strong growth profile with double digit revenue growth in the last 5

years

Strong Leadership: Experienced management team

with a strong track record

Diverse Client Portfolio: Established client base

comprising mix of Big Pharma and leading generics players

Advanced Manufacturing Facilities:

State of the art and dedicated manufacturing facilities with

potential for further expansion

2

3

5 4

6

7

Leading Producer: Amongst Top 5 producers of metformin

HCl globally and largest independent producer of Codeine

Phosphate

1

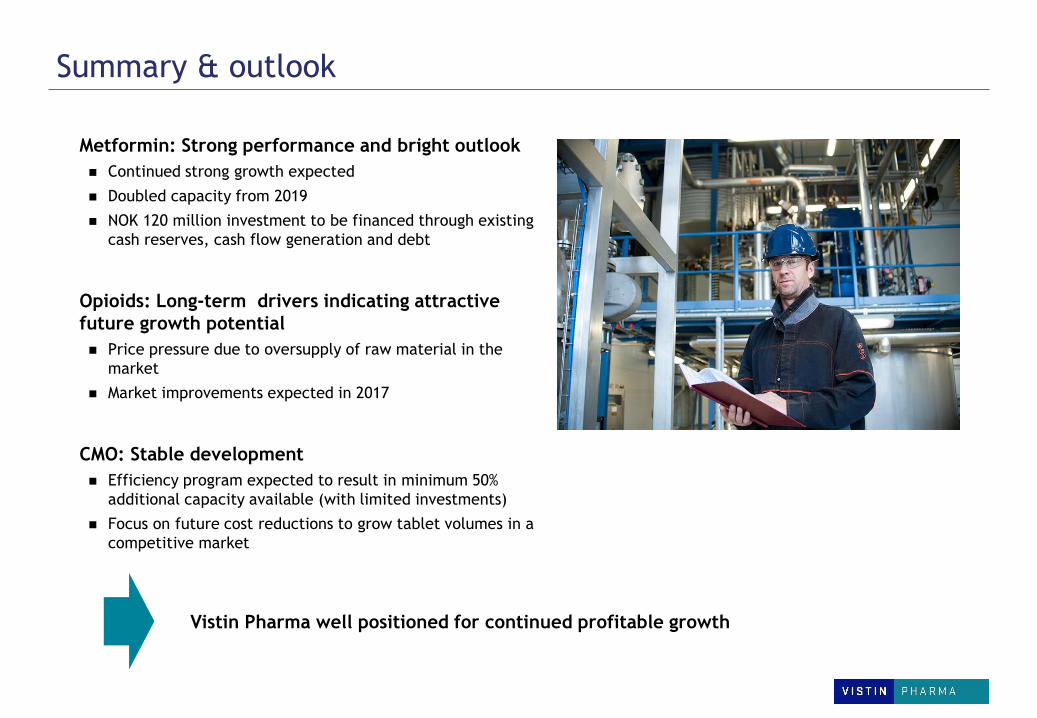

Metformin: Strong performance and bright outlook

Continued strong growth expected

Doubled capacity from 2019

NOK 120 million investment to be financed through existing

cash reserves, cash flow generation and debt

Opioids: Long-term drivers indicating attractive

future growth potential

Price pressure due to oversupply of raw material in the

market

Market improvements expected in 2017

CMO: Stable development

Efficiency program expected to result in minimum 50%

additional capacity available (with limited investments)

Focus on future cost reductions to grow tablet volumes in a

competitive market

Summary & outlook

Vistin Pharma well positioned for continued profitable growth

Content

Introduction to Vistin Pharma

Operational and financial update

Summary & outlook

Appendix

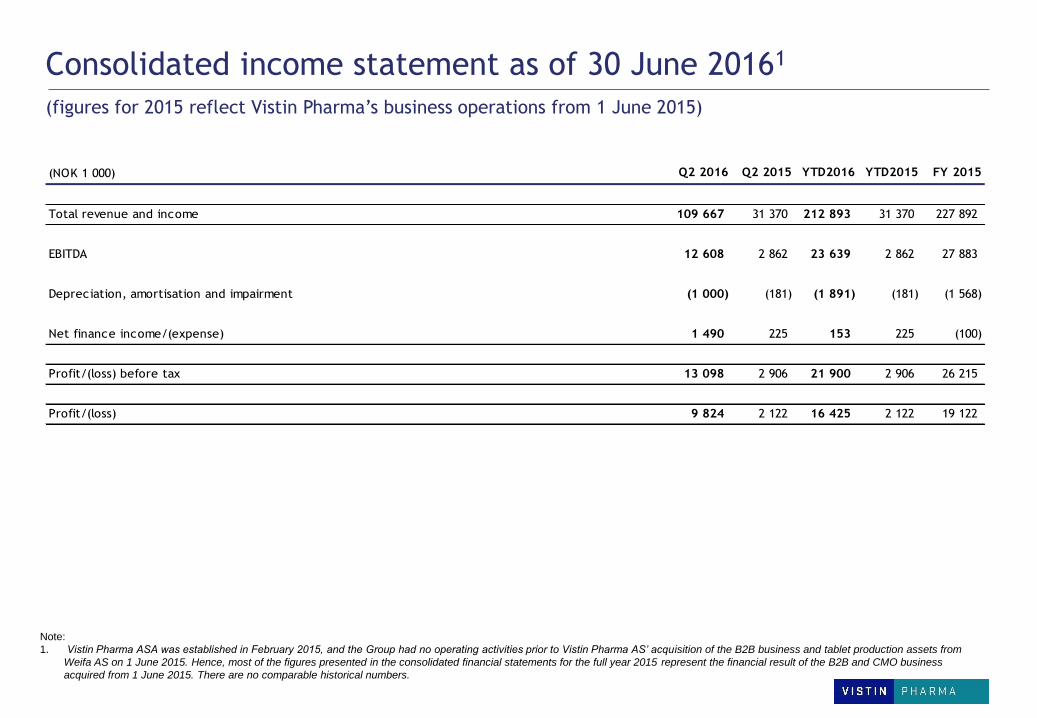

Consolidated income statement as of 30 June 20161

Note:

1. Vistin Pharma ASA was established in February 2015, and the Group had no operating activities prior to Vistin Pharma AS’ acquisition of the B2B business and tablet production assets from

Weifa AS on 1 June 2015. Hence, most of the figures presented in the consolidated financial statements for the full year 2015 represent the financial result of the B2B and CMO business

acquired from 1 June 2015. There are no comparable historical numbers.

(NOK 1 000) Q2 2016 Q2 2015 YTD2016 YTD2015 FY 2015

Total revenue and income 109 667 31 370 212 893 31 370 227 892

EBITDA 12 608 2 862 23 639 2 862 27 883

Depreciation, amortisation and impairment (1 000) (181) (1 891) (181) (1 568)

Net finance income/(expense) 1 490 225 153 225 (100)

Profit/(loss) before tax 13 098 2 906 21 900 2 906 26 215

Profit/(loss) 9 824 2 122 16 425 2 122 19 122

(figures for 2015 reflect Vistin Pharma’s business operations from 1 June 2015)

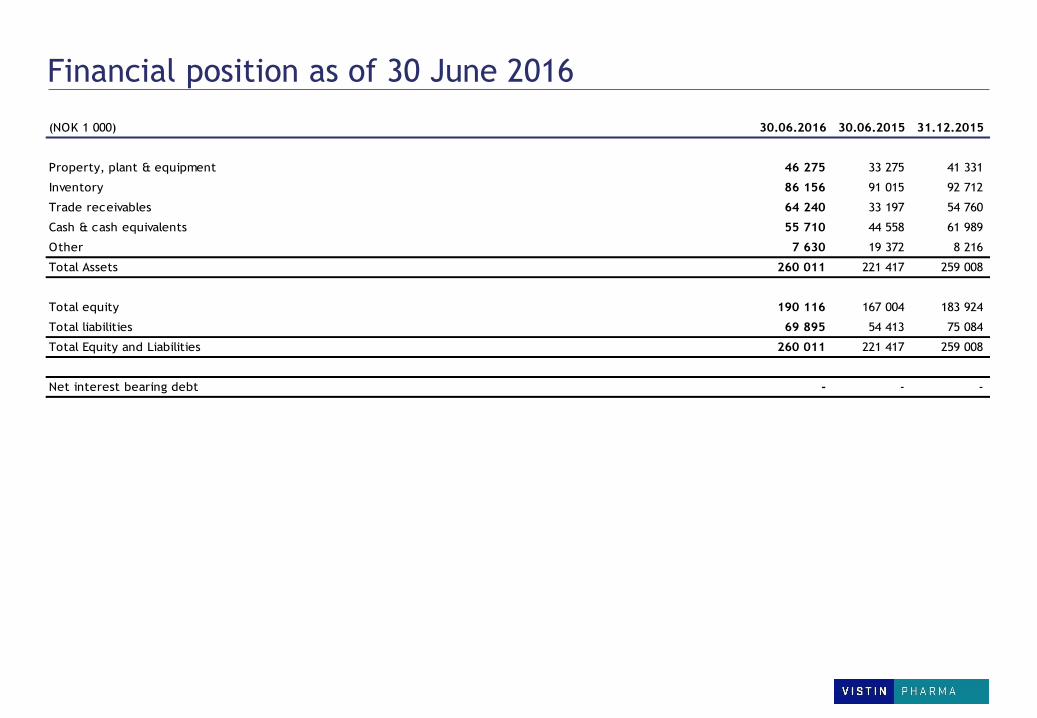

Financial position as of 30 June 2016

(NOK 1 000) 30.06.2016 30.06.2015 31.12.2015

Property, plant & equipment 46 275 33 275 41 331

Inventory 86 156 91 015 92 712

Trade receivables 64 240 33 197 54 760

Cash & cash equivalents 55 710 44 558 61 989

Other 7 630 19 372 8 216

Total Assets 260 011 221 417 259 008

Total equity 190 116 167 004 183 924

Total liabilities 69 895 54 413 75 084

Total Equity and Liabilities 260 011 221 417 259 008

Net interest bearing debt - - -

Experienced management team Highly experienced management team with a strong industry track record

Role Experience Name

Previous experience includes several years in top management positions at Alpharma,

a leading international generic pharmaceutical company

Holds a Master's degree in Pharmacy and Master's degree in Business Administration

Chief Executive

Officer Kjell-Erik Nordby

Previously SVP Operations, Tech. and Supply chain at REC Solar ASA and prior to that held

several senior management positions at Elkem, where he was employed for almost 20 years

Holds a Master of Management from BI Norwegian Business School

VP Operations Erik Løkke Øwre

Previously CFO at Aqualis for 7 years, and prior to that he worked 8 years as a

senior advisor at Handelsbanken Corporate Finance

Holds a MCom in Finance and Accounting from the University of New South Wales, Sydney

Chief Financial Officer Gunnar Manum

Previously spent 20 years at Pronova BioPharma, where she held several

management positions within Quality Assurance

Holds a Master of Science in Chemistry and a Master of Management

VP QA Hilde Merete Næss

Experienced executive manager within the biotechnology and pharmaceutical industry

Holds a BA in Biomedical Laboratory Science and an Executive Master in Business

& Administration

VP Sales & Marketing Valborg Godal Vold

Previous experience includes 5 years at Jordan, 9 years at Hydro and 4 years at

Volvo Car Corporation

Holds a BSc in Human Resource Development and Labour Relations

VP HR & Organisation Liesl Hellstrand

7

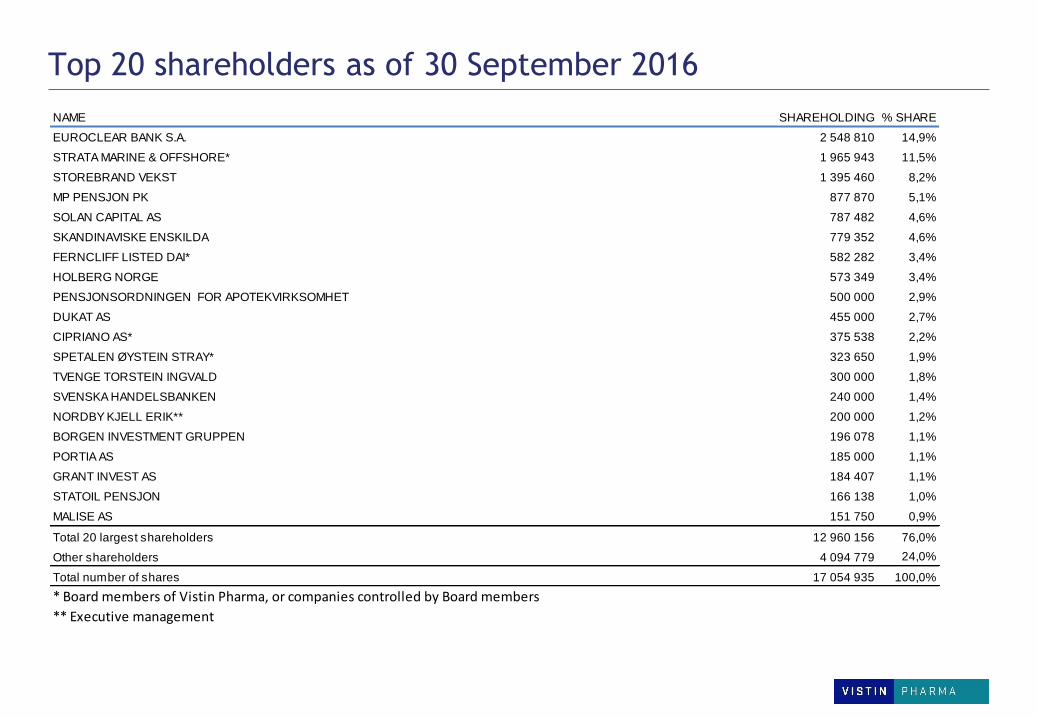

Top 20 shareholders as of 30 September 2016

NAME SHAREHOLDING % SHARE

EUROCLEAR BANK S.A. 2 548 810 14,9%

STRATA MARINE & OFFSHORE* 1 965 943 11,5%

STOREBRAND VEKST 1 395 460 8,2%

MP PENSJON PK 877 870 5,1%

SOLAN CAPITAL AS 787 482 4,6%

SKANDINAVISKE ENSKILDA 779 352 4,6%

FERNCLIFF LISTED DAI* 582 282 3,4%

HOLBERG NORGE 573 349 3,4%

PENSJONSORDNINGEN FOR APOTEKVIRKSOMHET 500 000 2,9%

DUKAT AS 455 000 2,7%

CIPRIANO AS* 375 538 2,2%

SPETALEN ØYSTEIN STRAY* 323 650 1,9%

TVENGE TORSTEIN INGVALD 300 000 1,8%

SVENSKA HANDELSBANKEN 240 000 1,4%

NORDBY KJELL ERIK** 200 000 1,2%

BORGEN INVESTMENT GRUPPEN 196 078 1,1%

PORTIA AS 185 000 1,1%

GRANT INVEST AS 184 407 1,1%

STATOIL PENSJON 166 138 1,0%

MALISE AS 151 750 0,9%

Total 20 largest shareholders 12 960 156 76,0%

Other shareholders 4 094 779 24,0%

Total number of shares 17 054 935 100,0%

* Board members of Vistin Pharma, or companies controlled by Board members

** Executive management

Disclaimer

This Presentation has been produced by Vistin Pharma ASA (the “Company” or “Vistin Pharma ”) solely for use at the presentation to investors and other stake holders and may not be reproduced or redistributed, in whole or in part, to any other person. This presentation has not been reviewed or registered with any public authority or stock exchange, and may not be reproduced or redistributed, in whole or in part, to any other person. To the best of the knowledge of the Company, the information contained in this Presentation is in all material respect in accordance with the facts as of the date hereof, and contains no material omissions likely to affect its importance. However, no representation or warranty (express or implied) is made as to, and no reliance should be placed on, any information, including projections, estimates, targets and opinions, contained herein, and no liability whatsoever is accepted as to any errors, omissions or misstatements contained herein, and, accordingly, neither the Company nor any of its subsidiary companies or any such person’s officers or employees accepts any liability whatsoever arising directly or indirectly from the use of this Presentation. This Presentation contains information obtained from third parties. Such information has been accurately reproduced and, as far as the Company is aware and able to ascertain from the information published by that third party, no facts have been omitted that would render the reproduced information to be inaccurate or misleading.

This Presentation contains certain forward-looking statements relating to the business, financial performance and results of the Company and/or the industry in which it operates. Forward-looking statements concern future circumstances and results and other statements that are not historical facts, sometimes identified by the words “believes”, expects”, “predicts”, “intends”, “projects”, “plans”, “estimates”, “aims”, “foresees”, “anticipates”, “targets”, and similar expressions. The forward-looking statements contained in this Presentation, including assumptions, opinions and views of the Company or cited from third party sources are solely opinions and forecasts which are subject to risks, uncertainties and other factors that may cause actual events to differ materially from any anticipated development. None of the Company or any of its parent or subsidiary undertakings or any such person’s officers or employees provides any assurance that the assumptions underlying such forward-looking statements are free from errors nor does any of them accept any responsibility for the future accuracy of the opinions expressed in this Presentation or the actual occurrence of the forecasted developments. The Company assumes no obligation, except as required by law, to update any forward-looking statements or to conform these forward-looking statements to our actual results.

AN INVESTMENT IN THE COMPANY INVOLVES RISK, AND SEVERAL FACTORS COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE COMPANY TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS THAT MAY BE EXPRESSED OR IMPLIED BY STATEMENTS AND INFORMATION IN THIS PRESENTATION, INCLUDING, AMONG OTHERS, RISKS OR UNCERTAINTIES ASSOCIATED WITH THE COMPANY’S BUSINESS, SEGMENTS, DEVELOPMENT, GROWTH MANAGEMENT, FINANCING, MARKET ACCEPTANCE AND RELATIONS WITH CUSTOMERS, AND, MORE GENERALLY, GENERAL ECONOMIC AND BUSINESS CONDITIONS, CHANGES IN DOMESTIC AND FOREIGN LAWS AND REGULATIONS, TAXES, CHANGES IN COMPETITION AND PRICING ENVIRONMENTS, FLUCTUATIONS IN CURRENCY EXCHANGE RATES AND INTEREST RATES AND OTHER FACTORS.

SHOULD ONE OR MORE OF THESE RISKS OR UNCERTAINTIES MATERIALISE, OR SHOULD UNDERLYING ASSUMPTIONS PROVE INCORRECT, ACTUAL RESULTS MAY VARY MATERIALLY FROM THOSE DESCRIBED IN THIS PRESENTATION. THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO UPDATE OR CORRECT THE INFORMATION INCLUDED IN THIS PRESENTATION.

By attending or receiving this Presentation you acknowledge that you will be solely responsible for your own assessment of the market and the market position of the Company and that you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the Company’s business. This Presentation does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make such an offer or solicitation in such jurisdiction.