chapter: 1 introduction

TRANSCRIPT

1

Chapter: 1

Introduction

1.1 Introduction

The rupee is posing a unique set of challenges for the Indian economy. The impact would

not be limited to macro economy alone but it will also affect down to the level of firms

under various sections of economy. This is conceptual study based on Rupee Dollar

relationship in terms of Rupee appreciation that is Dollar depreciation and Rupee

depreciation that is Dollar appreciation. It provides valuable insights into impact of

changes in currency relations on various sectors of economy keeping in focus economy in

general and Indian economy in particular. Pros and Cons of currency appreciation and

depreciation are studied as boon and bane for the economic growth. It also provides

suggestions or steps needed to control as well as to overcome ill-effects of excessive

fluctuations between rupee and dollar keeping in view current trends.

Global economy is much more interlinked than it was earlier due to lot of trade taking

place between different countries. It goes without saying that U.S. is major trading

partner for many nations and biggest trading importer of goods and services from across

the world. Change in any direction in U.S. economy is directly going to affect economy

of all related countries.

Democratic principle and human capital has given India unique position among world

community. Indian economic policies are flexible enough to get adjusted to the other

nations. India has always been major country when it comes to being trading partner of

U.S., which has always given economic and strategic support to country like India

occupying strategic importance among world community.

2

1.2 Importance of the study

The following are the importance of the study.

Ø To examine the reasons for the rapid variation in the home currency

Ø To analyze the impact of rupee variation on the economy.

Ø To critically analyze the role of the central bank in the foreign exchange market.

Ø To assess the possible future movement of the rupee vis-à-vis the US dollar.

Ø To understand the importance of exchange rate management.

1.3 Need for the Study

This study assesses the impact Indian Rupee Depreciation has on different sectors of the

Indian Economy. It mainly takes into account the imported goods as the main areas,

which have been impacted by the fall in the Indian Rupee against the US Dollar.

Indian Rupee Crisis mainly during the last quarter of 2013 & the impact it had on the

Indian Economy then & now. The study first summarizes the outlook of the Indian

Economy, its economical & financial history. It shows how the trend of the Indian rupee

has been from 1991 to 2013 & the main reasons behind the fluctuations in the Indian

Rupee.

1.4 Scope of the Study

The study is restricted to only momentum of Dollar V/s Rupee in particular. In other

words, this study has focused attention on How the Rupee movement affects different

stakeholders, actions initiated/taken by the Central Bank for controlling the variations,

external factors responsible for the Rupee movement.

This project tries to study the reasons for devaluation of pre liberalization era and post

liberalization that is of the year 2013. It also attempts to study the real implications of the

3

depreciation of the rupee on the Indian economy and shows that in the long run, the

Indian economy has more to lose and less to gain with weaker rupee.

This study gives its findings, suggestions/recommendations only on the basis of study

conducted on the available data/facts etc.

1.5 Objective

The following are the objectives of the study.

Ø This is conceptual study to understand Rupee Dollar relationship in terms of Rupee

appreciation and depreciation.

Ø To evaluate the relationship between various economic variables and value of Rupee.

Ø To explore the Pros and Cons of currency appreciation and depreciation as a boon and

bane for economic growth.

Ø To study the steps needed to control as well as to overcome ill-effects of excessive

fluctuations between rupee and dollar keeping in view current trends.

1.6 Methodology of the Study

1.6.1 Research Design

The research design is a Descriptive research which answers to a research question that

which is the thesis statement.

Research design can be defined as the plan and structure of inquiry, formulated in order

to obtain answer to research question on business aspects. It constitutes the overall

program of the business research process. Research design used in this research work is

both exploratory and causal research.

4

1.6.2 Sources of Data

For the accomplishment of this study the researcher has retrieved data from secondary

sources.

Secondary Data

The researcher has also extracted secondary data from sources such as textbooks,

reference books, journals, publications, magazines and websites.

1.6.4 Data Analysis and Interpretation

The following tools are used for statistical representation

Trend analysis or trend percentage

Comparison of past over a period of time with base year is known as trend analysis. So,

trend percentage or trend ratio analysis is a method of analysis under which the

percentage relationship that each financial statement item of each year bears to same item

in the base year is calculated. After the trend percentage of different items for various

years are calculated, the trend percentages or trend ratio are shown in comparative

financial statements.

Correlation

Degree and type of relationship between any two or more quantities (variables) in which

they vary together over a period; A positive correlation exists where the high values of

one variable are associated with the high values of the other variable(s). A 'negative

correlation' means association of high values of one with the low values of the other(s).

Correlation can vary from +1 to -1. Values close to +1 indicate a high-degree of positive

correlation, and values close to -1 indicate a high degree of negative correlation. Values

close to zero indicate poor correlation of either kind, and 0 indicates no correlation at all.

5

After the analysis, inferences were drawn and explained theoretically with the help of

exhibits

1.7 Limitations of the Study

The following are the limitations of the study

• The study is purely based on the facts and figures collected from the Central Bank,

SEBI or its other sources.

• The study is an academic effort; thus the findings cannot not be finalized.

• The study is mainly restricted to only momentum of Dollar V/s Rupee in particular

and other Currency variations are not studied

• Policies of Govt. of India and RBI might also contract the steps suggested in this

study.

• This research is subject to limitations of availability of data.

• Time constraints due to which limited data were included upon which conclusion can

be drawn

1.8 Concepts Used

1. RBI (Reserve Bank of India)

This organization is India's central banking institution, which controls the monetary

policy of the Indian rupee. It was established on 1 April 1935 during the British Raj in

accordance with the provisions of the Reserve Bank of India Act, 1934. The RBI plays an

important part in the development strategy of the Government of India.

2. GDP (Gross Domestic Product)

The monetary value of all the finished goods and services produced within a country's

borders in a specific time period, though GDP is usually calculated on an annual basis. It

includes all of private and public consumption, government outlays, investments and

exports less imports that occur within a defined territory.

6

3. FII (Foreign Institutional Investor)

Organizations that pool large sums of money and invest those sums in securities, real

property and other investment assets. The term is used most commonly in India to refer to

outside companies investing in the financial markets of India.

4. SEBI (Securities and Exchange Board of India)

The Securities and Exchange Board of India is the regulator for the securities market in

India. It was established in the year 1988 and given statutory powers on 12 April 1992

through the SEBI Act, 1992.

5. Secondary Data

Secondary data is the data that already exists which has been collected by some other

persons. Sources of secondary data include websites, trade association journals

6. Current Account Deficit

Occurs when a country's total imports of goods, services and transfers are greater than the

country's total export of goods, services and transfers. This situation makes a country a

net debtor to the rest of the world.

7. Fiscal Deficit

When a government's total expenditures exceed the revenue that it generates (excluding

money from borrowings). Deficit differs from debt, which is an accumulation of yearly

deficits.

7

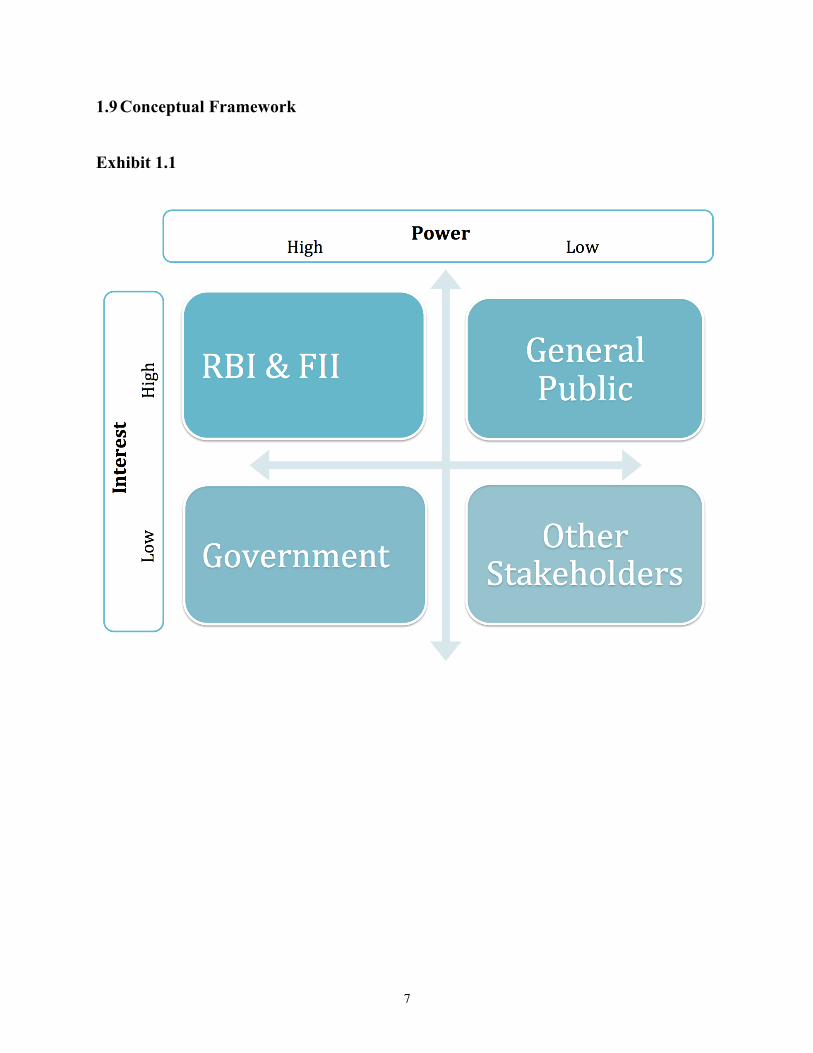

1.9 Conceptual Framework

Exhibit 1.1

8

1.10 List of Abbreviations BSE Bombay Stock Exchange Limited CAIIB Certified Associates by Indian Institute of Bankers ESOP Employee stock ownership plan ECB European Central Bank F&O Futures and Options. FCCB Foreign Currency Convertible Bond FFSIL Fortune Financial Services (India) Ltd FII Foreign Institutional Investor GDP Gross Domestic Product GDR Global depository receipt HPCL Hindustan Petroleum Corporation Limited IAS Indian Administrative Service IIT Indian Institutes of Technology INR Indian rupee IOC Indian Oil Corporation Ltd IPO Initial public offering IT Information technology IT Information technology MCX Multi Commodity Exchange MOSL Motilal Oswal Securities Ltd. NBFC Non-Banking Financial Company NCDEX National Commodity and Derivative Exchange NSE National Stock Exchange PMS Portfolio Management Services RBI Reserve Bank of India SBI State Bank of India

SEBI Securities and Exchange Board of India SWOT Strengths, Weaknesses, Opportunities, and Threats U.S United States USD United States dollar V/s, vs. Versus WTO World Trade Organization

9

1.11 Chapter Scheme

The following is the scheme of chapterisation found suitable for this study:

I Introduction

1.1 Introduction to the study

1.2 Importance of the study

1.3 Need for the Study

1.4 Scope of the Study

1.5 Objectives

1.6 Methodology of the study

1.7 Limitations of the Study

1.8 Concepts and Conventions

1.9 Chapter Scheme

II Review of Literature

2.1 Introduction

2.2 Review

2.3 Conclusion

III Profile of the Economy

3.1 Introduction

3.2 Effect of Depreciation

3.3 Reason for Depreciation

IV Profile of the Organization

3.1 Background and Inception

3.2 Subsidiaries of Fortune Financial services India Ltd

3.3 Nature of Business

10

3.4 Vision & Mission

3.5 Services of Fortune Financial services India Ltd

3.6 Areas of Operation

3.7 Shareholding Pattern

3.8 Board of Directors

3.9 Competitors of Fortune Financial Services India Ltd

3.10 Infrastructure Facilities

3.11 Work Flow Model

3.12 Future Plans and Prospects

3.13 Mckinsey’s 7S frame work

3.14 SWOT Analysis

V Data Analysis & Interpretation

VI Summary of Findings, Suggestions and Conclusion

Bibliography

Annexure(s)

11

Chapter: 2

Review of Literature

2.1. Introduction

It is essential for a researcher to review the literature related to the present study to have a

deep knowledge on the subject. It is only through this literature that the researcher takes

the initial step of fixing the problem of study. A thorough review of literature will

expose the researcher to the previous researchers conducted and their area of study etc.

A review of previous studies will also help the researcher to know about the limitations

of the study. The present chapter gives the reader, a broader outlook on the back ground

and situations under which the study has been undertaken. Following are a few of the

definitions and extracts from experts. A review of these studies enabled the researcher to

formulate the research problem.

2.2. Review

The following are some of the secondary data reviewed by the researcher.

Ø Singhal, Shelly (2011), “AN ANALYTICAL STUDY ON INDIAN CURRENCY

RUPEE DEPRECIATION AGAINST THE US DOLLAR AND ITS

ECONOMIC IMPACT”, Arth Prabhand: A Journal of Economics and Management,

Vol.1 Issue 1, April 2012, Pp. 73-83.

This paper mainly takes into account the Indian Rupee Crisis mainly during the last

quarter of 2012 & the impact it had on the Indian Economy then & now. The paper

first summarizes the outlook of the Indian Economy, its economical & financial

history. It shows how the trend of the Indian rupee has been from 1991 to 2011 & the

main reasons behind the fluctuations in the Indian Rupee.

12

After determining the reasons behind the fluctuations it talks about the depreciation in

the Rupee against the Dollar over the last financial year (2011-12). Basic reasons

identified in the paper are:

ü Persistent Inflation

ü Persistent Fiscal Deficits

ü Lack of Reforms

ü Global Economic Scenario

Ø Rupee Exchange Depreciation1

It mainly takes into account the imported goods as the main areas which have been

impacted by the fall in the Indian Rupee against the US Dollar. India is poor in oil

resources and is heavily dependent on coal and foreign oil imports for its energy

needs. Thus, oil imports & other imports form a major source for India when it comes

to its energy requirements. Other imported products are: machinery, gems, fertilizers

and chemicals. Main import partners are European Union, Saudi Arabia and United

States.

India being a major importer has various firms, which have huge imports on account

of the raw materials. With the depreciation in Indian rupee these firms have incurred

huge forex losses. Thus, in order to control their losses these firms are increasing

prices of the goods they sell which in turn has led to rise in inflation. Moreover, the

economic growth in India has slowed down with these factors playing a major role in

it. Thus, Indian Rupee depreciation has led to the slowing down of the economy as

whole.

1http://www.assocham.org/arb/general/Rupee_Exchange_Depreciation_Impact_Analysis- 2012.pdf

13

Ø Exchange Rate Slide2 –

This study also accounts for the impact that the Indian Rupee has had on the Indian

Economy. It has shown the fluctuations of the Indian Rupee with respect to various

major currencies like the USD, Pound Sterling, Japanese Yen & the Euro. The impact

of depreciation on the imports has also been considered in the paper. Moreover,

impact on the debt in the corporate sector has also been considered.

Falling Rupee: Understanding India’s financial statements like a company’s3

Ø International Monetary Fund (1998) "EXCHANGE RATE ARRANGEMENTS

AND ECONOMIC PERFORMANCE IN DEVELOPING COUNTRIES," by

Francesco Caramazza and Jahangir Aziz.

Ø Fixed or Flexible?

Getting the Exchange Rate Right in the 1990s4

Analysts agree that "getting the exchange rate right" is essential for economic stability

and growth in developing countries. Over the past two decades, many developing

countries have shifted away from fixed exchange rates and moved toward more

flexible exchange rates. During a period of rapid economic growth, driven by the twin

forces of globalization and liberalization of markets and trade, this shift seems to have

served a number of countries well. But as the currency market turmoil in Southeast

Asia has dramatically demonstrated, globalization can amplify the costs of

2 http://www.assocham.org/arb/general/Exchange_Rate_Study.pdf

3 http://sbr.sunstone.in/falling-rupee-understanding-indias-financial-statements-like-a-companys/ Published on August 19, 2013 By Aniket Khera

3 http://www.imf.org/external/pubs/ft/issues13/issue13.pdf Published on April, 1998

14

inappropriate policies. Moreover, the challenges facing countries may change over

time, suggesting a need to adapt exchange rate policy to changing circumstances.

This paper examines the recent evolution of exchange rate policies in the developing

world. It looks at why so many countries have made a transition from fixed or

"pegged" exchange rates to "managed floating" or "independently floating"

currencies. It discusses how economies perform under different exchange rate

arrangements, issues in the choice of regime, and the challenges posed by a world of

increasing capital mobility, especially when banking sectors are inadequately

regulated or supervised.

Ø Adjusting to Capital Inflows 5

In many fast-growing emerging market economies, upward pressure on the exchange

rate in recent years has stemmed largely from vastly increased private capital inflows.

When capital inflows accelerate, if the exchange rate is prevented from rising,

inflationary pressures build up and the real exchange rate will appreciate through

higher domestic inflation. To avoid such consequences, central banks have usually

attempted to "sterilize" the inflows–by using offsetting open market operations to try

and "mop up" the inflowing liquidity.

Ø Capital Account Convertibility6

In recent years, many emerging economies have gradually relaxed or removed

capitals controls and are now proceeding toward full capital account convertibility.

Remaining restrictions are nevertheless significant, and are mostly asymmetric–

5 http://www.imf.org/external/pubs/ft/issues13/issue13.pdf Published on April, 1998 6 http://www.imf.org/external/pubs/ft/issues13/issue13.pdf Published on April, 1998

15

placing more restrictions on capital flowing out than on capital flowing in. More

liberal rules in both directions would have the advantage of increasing economic

efficiency (allowing more capital to flow to where it gets the best returns).

Liberalization would also provide domestic investors with more opportunities to

diversify their portfolios and reduce the concentration of exposure to domestic market

risks.

2.3 Conclusion:

On understanding the reviews as extracted from secondary sources the researcher

came to know in any country, determining the currency rates fluctuations is a very

tough task. Thus, there are various factors, which can be considered in order to

determine the reasons behind such fluctuations of the home currency.

16

Chapter: 3

Profile of the Economy

3.1 Introduction

India got freedom from British rule on Aug 15, 1947. At that time the Indian rupee was

linked to the British pound and its value was at par with the American dollar. There was

no foreign borrowing on India's balance sheet. To finance welfare and development

activities, especially with the introduction of the Five-Year Plan in 1951, the government

started external borrowings. This required the devaluation of the rupee. After

independence, Indian chooses to adopt a fixed rate currency regime. The rupee was

pegged at 4.79 against a dollar between 1948 and 1966. India faced a serious balance of

payment crisis in 1991 and was forced to sharply devalue its currency. The country was

in the grip of high inflation, low growth and the foreign reserves were not even worth to

meet three weeks of imports. Under this situation, the currency was devalued to 17.90

against a dollar.

India being a developing economy with high inflation, depreciation of the currency is

quite natural. Depreciation of rupee is good, so long as it is not volatile. A random

depreciation that we have seen in the last few months is bad and it has hurt the economy.

Right from the beginning of year 2013, the value of rupee has been depreciating.

High growth coupled with a market driven exchange rate bears well for the economy.

However, when growth falters and macroeconomic parameters start appearing

vulnerable, one of the first casualties is the exchange rate. Currently, there is no clarity on

whether we have seen the worst of the storm or it is just the beginning. The problems are

manifold. Persistent high inflation and fiscal deficit, increasing subsidies, faltering

exports and slowing industrial production point towards an economy, which is

moderating in growth. Monetary policy has so far been ineffective in reversing the

inflation trajectory. Fiscal stimulus appears non-existent, especially when the government

17

has added to the subsidy bill by giving a go ahead to the food security bill. In this

weakened environment, the rupee has depreciated by close to 20% in the past few

months.

Secondly, the extent of volatility in the global economy hasn’t helped. Besides the

Eurozone crisis, the downgrade of the US economy has led to flight of capital in order to

boost the US home economy. The US dollar has become scarce and unlike its peers, India

needs to attract sufficient foreign funds to close the fiscal and current account gap. The

fact that a weakening of the Indian economy has happened at the same time as a global

debt crisis has elevated the exchange problem.

The appreciation in the US dollar has led to the decrease in the value of Indian rupee. The

value of US dollar has been rising ever since the US Federal Reserve has announced

quantitative easing. This has hit not only the emerging markets and assets of India but

also of other countries like Thailand, Brazil and Indonesia. Just as in other countries, the

foreign institutional investors (FIIs) have also started withdrawing their investments in

the Indian bond market. With growing concern for increasing risks in the global

environment, massive redemptions through the global exchange traded funds (ETFs) are

taking place. This has further initiated the selling by the FIIs in the equity market of India

leading to depreciation in the Indian rupee. The Reserve Bank of India does not wish to

intervene and control this depreciation as it is initiated by global factors that are beyond

the control of RBI. Moreover, the trade deficit of India has also not escalated further

decreasing any hope of appreciation in Indian rupee in close future.

Meanwhile the Indian economy, like any bank facing a run on its resources, is under

intense pressure. This is aggravated because our banking sector is both small and under-

capitalised and not well configured to take on rapid outflows of this nature. The rupee,

like the currency of any country nowadays, is underpinned by the working economy and

its fundamentals. And all parameters of these assessments are also very weak at present.

18

Indian officials and central bankers say their economy is only one of several emerging

markets that are suffering from the flight of investors back towards the US, where the

prospect of an end to the Federal Reserve’s ultra-easy monetary policies has made dollar

assets more attractive. The Historical Evolution of rupee can be traced from the chart

given below.

3.2 Effect of Depreciation

ü Trade deficit will widen because of costlier imports, worsening the current account

deficit.

ü Fuel price will keep petroleum subsidy in check, but fertilizer subsidy will rise.

ü Spending on any kind of foreign exchange denominated spending will increase.

ü Capital inflow will slow or reverse.

ü Spending on discretionary goods will increase.

ü Forex reserves could fall putting pressure on rupee.

ü In case of weak demand companies may not be able to pass on higher inputs costs.

ü The government and the RBI have issued a series of measures in recent days

designed to reduce the current account deficit and bolster the rupee, including

increases in the import duty on gold, the end of duty exemptions for flat screen

televisions brought in by airline passengers and restrictions on outward direct

investment by Indian companies and individuals.

ü Exports are unable to leverage the weak rupee fast enough given the speed of its

descent. In fact many exporters are caught out because of fixed price contracts in

rupees wherein they cannot get the benefits of its rapid fall. The balance of

payments is tilting sharply against us.

ü The Indian stock- market will take a hiding as opposed to a beating.

ü Global rating agencies will revise our rating downwards to “Junk” status, making

international borrowing difficult and even more expensive.

19

ü If the automated devaluation brought on by the rupee makes some asset classes

attractive, there may be slight recovery because of arbitrage opportunities and

bottom fishing.

Further, recent trends indicate a significant worsening of both trade and current accounts.

Both exports and imports actually declined in 2012-13 compared with the previous year,

but even so the trade deficit still increased by nearly 4 per cent, or more than $7 billion.

In April 2013, exports were 2 per cent higher than in April 2012—but imports were 11

per cent higher and non-oil imports were 15 per cent more. So the trade deficit increased

by more than 26 per cent in April 2013 compared with the previous year (Finance

Ministry, Monthly Economic Report for April 2013).

There are several ways in which the falling rupee immediately has an inflationary impact,

one of the most important of which is the price of energy. Since the misguided decontrol

of oil prices, it is not only the globally traded price of fuel but also the exchange rate that

determines domestic oil prices.

What is more, the increasing costs of imports can also affect exports, thereby wiping out

any global cost advantage accruing from the devaluation. For example, important export

sectors such as gems and jewellery, automobiles, machinery and chemicals are all very

import-dependent, and their rising costs could nullify the impact of the devaluation on

their ability to sell more cheaply in export markets. This is made worse by the fact that in

the current depressed global trade context, buyers are able to renegotiate contracts once

the exchange rate has changed. Indeed, many global buyers even in sectors such as

garments and leather goods now insist on contracts and invoicing in rupee terms. This

allows them to benefit completely from rupee depreciation, while the local producers are

forced to bear the rising domestic costs. This means that the falling rupee need not

generate any significant increase in exports as may be hoped.

20

3.3 Reason for Depreciation

ü One of the more obvious reasons why the current depreciation is not to be

welcomed is the effect on domestic living standards. There are several ways in

which the falling rupee immediately has an inflationary impact, one of the most

important of which is the price of energy. Since the misguided decontrol of oil

prices, it is not only the globally traded price of fuel but also the exchange rate that

determines domestic oil prices. Both durable consumer goods such as automobiles,

white goods and electronic items and non-durable goods such as soaps and

toiletries are all likely to become more expensive. And, of course, food inflation-

the most worrying aspect of recent price movements-is likely to go up as a well.

ü As per the data reported, FIIs (Foreign Institutional investors) are showing some

disinterest in Indian markets lately. Sluggish economy and recovery in stock

markets of developed economies like US and Japan are believed to be the key

reasons. Since FIIs inflows have played important role in keeping rupee at current

levels, an intense selling activity by them does not augur well for the near term

direction of the rupee.

ü Consistently high inflation has resulted into Indian goods becoming expensive in

the global markets, thus making it less competitive, especially when compared to

goods from China. Thus, rupee may have hardly any support by way of higher

exports. Lastly, gold imports, another key reason why the deficit is high and rupee

under pressure, may not slow down in a hurry.

ü The value of rupee follows the simple demand and supply rule of economics. If

the demand for the dollar in India is more than its supply, dollar appreciates and

21

rupee depreciates. Similarly, when the supply of dollars in India increases its

demand, the value of dollar decreases in terms of rupees.

ü The central banks of Eurozone and Japan are printing excessive money due to

which their currency is devalued. On the other hand, US Fed has shown signs to

end their stimulus. Hence, making the US dollar stronger against the other

currencies including the Indian rupee, at least in the short term.

ü Oil price is one of the most important factors that put stress on the Indian Rupee.

India is in the unhappy situation where it has to import a bulk of its oil

requirements to satisfy local demand, which is rising year-on-year. In International

markets, prices of oil are quoted in dollars. Therefore, as the domestic demand for

oil increases or the price of oil increases in the international market, the demand

for dollars also increases to pay our suppliers from whom we import oil. This,

increase in demand for dollar weakens the rupee further.

ü Our equity market has been volatile for some time now. So, the FII’s are in a

dilemma whether to invest in India or not. Even though they have brought in

record inflows to the country in this year chances are they may be thinking of

taking their money out of the equity market which might again results in less

inflow of dollars in India. Therefore, decrease in supply and increase in demand of

dollars results in the weakening of the rupee against the dollar.

On the investment front - steady decline in GDP growth, constant and continuing

contractions in industrial output, spiraling inflation, growing instance of financial

corruption, policy confusions etc. do not help in portraying India as a favoured

investment destination. It is here that the government has a very crucial role to play. In

22

reality the only role the government has played till date is to try and correct certain policy

nuances (FDI regulations etc.) but has done precious little to address the concerns of the

domestic economy.

The government would do better if it were to concentrate majorly on the domestic

economy. Foreign investment is a consequence of good domestic growth and not a

consequence of domestic fiscal and regulatory policy alone. The fiscal and domestic

policy regimes come secondary - primarily it is the fundamentals of the Indian economy,

which will attract foreign investment and thereby help the rupee in regaining some value.

23

Chapter: 4

Company Profile

Fortune Financial Services (India) Limited was incorporated in the year 1991 by Mr. J.

T. Poonja, Chairman and Mr.Nimish C Shah, Vice Chairman and Managing Director.

Fortune Group which comprises the holding company Fortune Financial Services (India)

Limited and its wholly-owned subsidiaries, is engaged in providing a range of Financial

Services right from Equities and Derivatives trading, Equity Research, Commodities

Trading, Portfolio Management Services, Distribution of Mutual Funds, IPO & Insurance

products and also Investment banking services.

4.1 Background and Inception of Fortune Financial Services India Ltd

In the year 1991 Mr. J.T. Poonja and Mr. Nimish C. Shah incorporated Fortune Financial

Services (India) Private Limited as a Non-Banking Financial Company (NBFC). Besides

core investment banking and corporate advisory services, Fortune's also focused on fund

based activities such as lease, hire purchase, bill discounting and inter-corporate loans. In

1993 Fortune became a SEBI registered Category - I Merchant Banker.

In the year 1994 in anticipation of a potential IPO, the name of the Company was

changed to Fortune Financial Services (India) Ltd. Opened an office in New Delhi to

increase the scope of activities. Fortune declared dividend @15%. Authorized Capital of

Fortune was increased to Rs.600 lacs.

Fortune Financial became the 1st Indian company to go in for a buyback of its shares,

subsequent to the guidelines for Buyback of shares coming into effect from Jan 1999.In

the year 2000 Acquired Corporate Membership of Bombay Stock Exchange Limited

(BSE). In 2005 commenced F&O operations on the National Stock Exchange (NSE).

Fortune was involved with varied domestic assignments - follow on issues, buyback

program, open offers and IPOs for Indian mid-sized corporate clients.

24

4.2 Subsidiaries of Fortune Financial Services India Ltd

M/s. Fortune Financial Services (India) Ltd

M/s. Fortune Financial Services (India) Ltd. is listed on the Bombay Stock Exchange Ltd

and is SEBI registered Category I Merchant Banker. It has recently got approval from

SEBI to launch its Portfolio Management Services (PMS). FFSIL has four business

verticals viz. Fortune Equity Brokers (India) Limited, Fortune Commodities &

Derivatives (India) Ltd., Fortune Credit Capital Ltd. and Fortune Financial India

Insurance Brokers Limited.

M/s. Fortune Equity Brokers (India) Ltd

M/s. Fortune Equity Brokers (India) Ltd. is 100% subsidiary company of M/s. Fortune

Financial Services (India) Ltd. It offers broking services in the Cash and Future & Option

Segments of the National Stock Exchange of India Ltd and the Bombay Stock Exchange

Limited. It is also a Depository Participant of Central Depository Services (India) Ltd.

M/s. Fortune Commodities & Derivatives (India) Ltd

M/s. Fortune Commodities & Derivatives (India) Ltd. is subsidiary company of M/s.

Fortune Financial Services (India) Ltd. and engaged in the business of commodities

broking. It is having memberships with the MCX and NCDEX, two leading Indian

Commodities Exchanges.

M/s. Fortune Credit Capital Ltd.

Fortune Credit Capital Ltd. is 100% subsidiary company of M/s. Fortune Financial

Services Ltd. It is formed for the purpose of financing, lending to the clients. The

Company has received license from RBI for NBFC operations.

25

M/s. Fortune Financial India Insurance Brokers Limited

M/s. Fortune Financial India Insurance Brokers Limited is 100% subsidiary company of

Fortune Financial India Insurance Brokers Limited and formed for the purpose of

providing insurance broking and related products and services.

4.3 Nature of Business

Fortune Financial Services is a broking company. The company offers a

complete range of trade service on the BSE (Bombay Stock Exchange) and the NSE

(National Stock Exchange). Whether the clients come in to the company’s

conventionally located offices and trade in a dedicated ambience or issue

instructions over the phone, our highly trained team and sophisticated equipment

ensure smooth transactions and prompt service.

• Investment Advisory Service

• Facilitation Services to Retail Investors, Corporate.

• Depository Services

• Investment options includes

i. Online trading (Includes equity, derivatives)

ii. Commodities trading

iii. Mutual Funds

iv. Portfolio management Services

4.4 Vision & Mission

Core Purpose of Fortune Financial Services is to be a well-respected and preferred global

financial services organization enabling wealth creation for all their customers. Values of

Fortune Financial Services core purpose are complemented by their organizational

values. Living these values, they believe, helps them to achieve their core purpose.

26

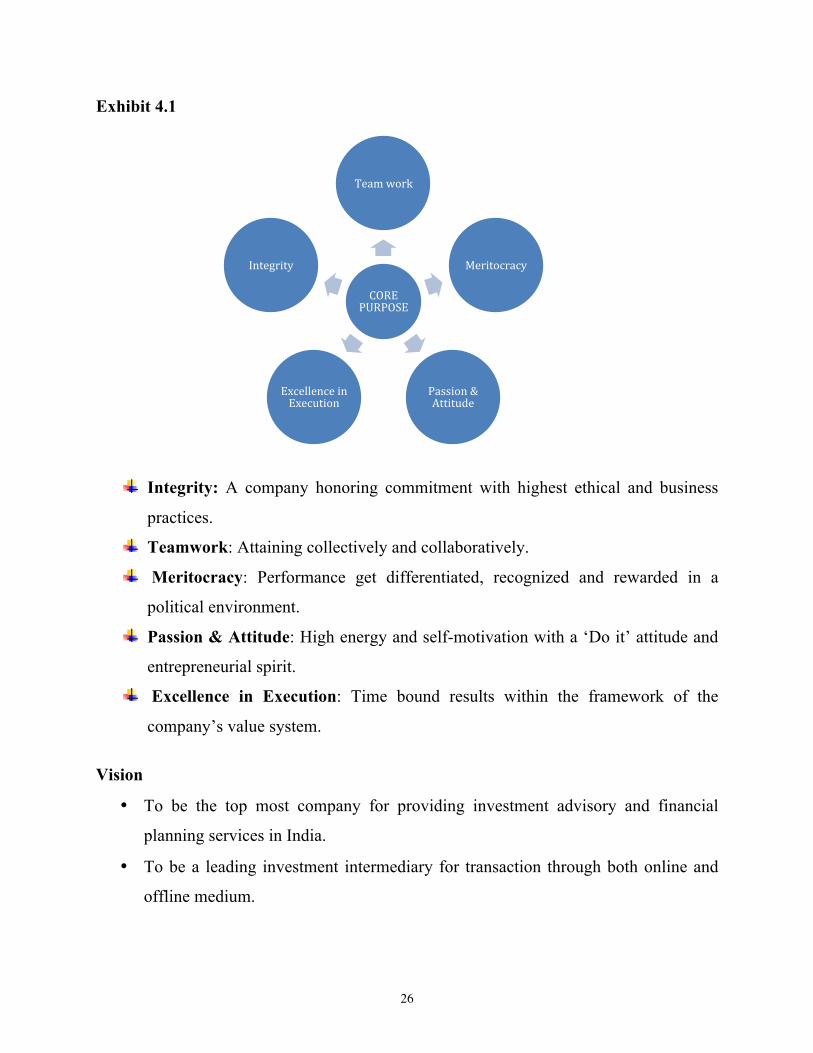

Exhibit 4.1

Integrity: A company honoring commitment with highest ethical and business

practices.

Teamwork: Attaining collectively and collaboratively.

Meritocracy: Performance get differentiated, recognized and rewarded in a

political environment.

Passion & Attitude: High energy and self-motivation with a ‘Do it’ attitude and

entrepreneurial spirit.

Excellence in Execution: Time bound results within the framework of the

company’s value system.

Vision

• To be the top most company for providing investment advisory and financial

planning services in India.

• To be a leading investment intermediary for transaction through both online and

offline medium.

CORE PURPOSE

Team work

Meritocracy

Passion & Attitude

Excellence in Execution

Integrity

27

Mission

• To educate and empower the individual investors to make investment decisions

through quality advice and superior service.

Superior service for

• Integrity

• Transference

• Professionalism

• Client driven approach

• Long term relationship

• Broad outlook

4.5 Services of Fortune Financial Services India Ltd

Fortune - Investment Banking, a Category I SEBI Registered Merchant Bank focuses on

providing corporate advisory services to Indian mid-sized corporate clients in both the

domestic and international capital markets.

Fortune retained its focus on mid-market corporate clients offering a variety of financial

solutions. Our Investment Banking services offered are:

Ø Equity / Debt Syndication

o Capital / Debt Restructuring

o Structured Financial Products

o Mezzanine Financing

Ø Issue Management

o Initial Public Offerings / Offer For Sale

o Rights Issues

o Preferential Issue / Private Placement

28

o Open Offer pursuant to Acquisition

o Buybacks / Delisting / ESOP

o Stock Option Schemes

Ø Mergers & Acquisitions and Corporate Advisory

o Buy-side / Sell-side Advisory

o Leveraged Acquisitions

o Cross-Border Transactions / Joint Ventures

Ø Fund Raising Advisory

o Offshore Fund Raising

o ECB/ FCCB / GDRs

By applying our knowledge capital, we believe in building lifetime client relationships by

providing unquestionable integrity, seamless execution and innovative solutions while

striving to assist our clients achieve their financial goals. We follow a client centric

approach to protect and enhance our client's wealth.

Our distinguished client base has evolved from our extensive experience and deep

understanding of the capital markets. We focus on identifying and understanding client

needs and persistently providing value-enhancing strategies that will benefit the client

over a sustained period of time.

With growing interest for Indian corporate clients from international investors, Fortune

pioneered grooming, advising and assisting mid-market companies to access international

capital markets. In the past two years, Fortune has been involved with:

Ø 10 Fund raising assignments in Indian capital markets of Rs.27.62 billion

Ø 2 corporate buyback program

Ø 2 management open offers

Ø 15 international issues where US$ 600 Million was raised

29

4.6 Area of Operation of Fortune Financial Services India Ltd

Maharashtra, Delhi, Karnataka, Tamil Nadu, Chandigarh, Andhra Pradesh, Goa

4.7 Shareholding Pattern of Fortune Financial Services India Ltd

Promoters having more than 50% holdings of Fortune financial Services India Ltd. There

are no government holdings and domestic institutions holding but FIIs having 42.5 % of

holdings. The public and other individuals having only 6.2 % of holdings in the company.

1.3% of holdings in the hands of non-promoter’s corporate holdings.

4.8 Board of Directors

Mr. J.T. Poonja

Co-Founder & Executive Chairman

Mr. J. T. Poonja is first generation entrepreneur and has over 43 years of experience in

Financial Service Sector ranging from Banking, Merchant Banking and Institutional

Broking Activities. He presently oversees the group operations, expansion and

extensively involved in strategic planning of Fortune's future growth plan.

Mr. Nimish C. Shah

Co-Founder, Vice Chairman & Managing Director

Nimish C Shah is first generation entrepreneur and has over 23 years of experience in

Indian Capital Market. His core acumen lies in Investment Banking, Institutional & HNI

Broking. He presently oversees assignments relating to structuring custom financial

solutions for clients, assisting companies in raising capital (private equity / venture

capital, debt and equity), mergers and acquisitions, strategic partnerships, valuations,

other merchant banking activity. He is also actively involved in pitching ideas and

30

concepts to prospective clients. He looks after the core business development and

contributes to evolving new growth strategies

Mr. Vishal Trehan

CEO-Broking & Distribution

Vishal Trehan, finance professional (Gold Medalist) has over 15 years of experience in

Indian Capital Markets. He has vast knowledge in all fields related to Equities and

Commodities Operations (both Front Office & Back Office), Surveillance & Risk

Management includes evolved real time tools for surveillance, and Chief Architect for

Technology initiatives includes developing CTCL & Internet software, DP Operations

(NSDL & CDSL), Compliance, Strategic Planning, Distribution with new innovative

initiatives. His role at Fortune includes expanding group presence geographically in Sales

- Direct & alternate channels and also looking after Operations, Technology and

Compliance.

Mr. B B Tantri

Chief Operating Officer

B. B. Tantri has over 38 years of total experience in Banking, Airlines, Financial Sectors

and Capital Market Industries. His varied and rich experience makes him a complete

team leader of the Company's operation and back office functions.

Mr. Muthu Kummar

Head - Corporate Affair

Muthu Kummar has over 26 years of experience in the areas of Finance, Accounting,

Taxation, EDP and Secretarial. He looks after planning, sourcing and disbursements of

financial resources of the Company, monitoring and managing the day-to-day working

capital requirements and ensures compliance to group policies and various statutes.

31

Mr. Pranav Kumar

National Head – Corporate Sales

Pranav Kumar has over 12 years of experience in the Financial Services Industry

including strategic planning and market analysis. He has worked with Kotak Securities

and KARVY group in similar roles prior to his joining Fortune. He also has hands on

experience in operational and legal nuances of the secondary markets. He has been a

front-runner in leveraging his relationships across big corporate and HNI clients to define

and drive mutually profitable partnerships. At Fortune he is responsible for originating

and managing corporate relationships across all product categories at a national level.

Mr. Sanjay Makhija

Head-Institutional Dealing

Sanjay Makhija has over a decade experience in the capital markets. He has experience in

setting up start-ups to taking charge of a large institutional desk. He has been successful

is advising and managing money of clients as a portfolio manager. He started his career

in the capital market as an equity analyst and moved through various positions in his

career and currently heads the Institutional Equities business at Fortune Group.

Mr. Naveen Sharma

EVP – Broking & Distribution

Mr. Naveen Sharma has over 22 years of experience in Indian Capital market and has a

vast knowledge in the field of Equity broking, Mutual Fund, Commodity market and

Insurance. Being a vast experienced person he has a great record of developing retail

network of branches in the Northern part of India. My role at Fortune includes

development of retail business such as creation of new franchisees and networking of

branches in the North.

32

Mr. Kalyansundaram

EVP – Funds & Settlement

Kalyanasundaram has done his Masters in Commerce and completed CAIIB (Part-I). He

is having good exposure in Industrial Financing and handling NBFCs with Credit

appraisal and credit proposal, having good contacts with Govt. organizations and IAS

officials. He is having experience of more than 35 years in similar field and he had also

managed recovery portfolio.

4.9 Competitors of Fortune Financial Services India Ltd

Indiabulls

Indiabull is an Indian company headquartered in Gurgaon (NCR Delhi), with its presence

in the Real Estate, Infrastructure, Financial Services, and Securities, Retail, Multiplex and

Power sectors. In middle of 1999, Sameer Gehlaut and his close IIT Delhi friend Rajiv

Rattan bought a defunct securities company with a NSE membership and started offering

brokerage services later joined by their friend Saurabh Mittal. In December 1999, the

company built one of the first online platforms in India for offering Internet brokerage

services. In mid 2000, Indiabulls Financial Services received venture capital funding

from Mr. Lakshmi Mittal & Mr. Harish Fabiani.

Indiabulls Group is one of India's large Business houses. The Group has several

businesses, which cover a wide spectrum of Real Estate, Financial Services, Securities,

Power and Chartered Aviation. Many of the companies are public entities and are listed

on Indian stock markets.

Edelweiss Capital

Edelweiss Capital is a financial services company based in Mumbai, India. Edelweiss

Capital Limited provides investment banking, institutional equities, private client

33

broking, asset management, wealth management, insurance broking and wholesale

financing services to corporate, institutional and high net worth individual clients. It

operates from 43 other offices in 19 Indian cities. Since its commencement of business in

1996, it has grown into a diversified Indian financial services company organized under

agency and capital business lines operated by the Company and its thirteen subsidiaries.

Edelweiss employs over 2900 professionals across 297 offices and branches spread

across 144 cities of India.

Future Capital

Future Capital is a provider of financial services across consumer and wholesale

businesses, with aspirations to grow into a significant financial conglomerate.

Conceptualized around a unique positioning of a financial services business, integrated

with a retail chain, Future Capital is establishing financial superstores within the Retail

stores of Future Group such as Big Bazaar, E-zone and Home Town to create India’s first

‘consumer-centric’ retailer of financial products and services.

Motilal Oswal

Motilal Oswal Securities Ltd. (MOSL) was founded in 1987 as a small sub-broking unit,

with just two people running the show. Focus on customer-first-attitude, ethical and

transparent business practices, respect for professionalism, research-based value investing

and implementation of cutting-edge technology have enabled us to blossom into an over

1600-member team.

Today Motilal is a well diversified financial services firm offering a range of financial

products and services such as Wealth Management, Broking & Distribution, Commodity,

Broking, Portfolio Management Services, Institutional Equities, Private

Equity, Investment Banking Services and Principal Strategies.

34

Eko India Financial Services

Eko India Financial Services Pvt. Ltd. is an Indian financial service company, which is a

business correspondent (BC) service for State Bank of India (SBI) and ICICI Bank,

India's top two largest banks, and provides no-frills bank accounts and deposit,

withdrawal and remittance services to customers (nearly 80% of whom are migrants or

the unbanked section of the population) through mobile banking. With Bharti AXA Life

Insurance Company, it provides Bharti AXA Life - Bachat Bima, micro-

insurance policies.

Brothers Abhishek and Abhinav Sinha in 2007 and two other founders who left after a

year, and allows low-wage immigrants workers in the Indian urban areas to remit money

to their homes using mobile phones established it. Sanjay Bhargava was the first

Chairman. He made important contributions to the business model of the company and

invented a security method that enabled a low-end mobile phone to be used to initiate

transactions securely.

Peerless Group

Peerless Group is an Indian business conglomerate with its head quarters located

at Kolkata, West Bengal. It was established in 1932 by industrialist Radhyashyam

Roy in Narayanganj, Bangladesh. Its major holding company is Peerless General Finance

& Investment Co Ltd, which is the India's largest Registered Residuary Non-banking

Company. It has subsidiaries like Peerless Hospital, Bengal Peerless (real estate), Kaizen

Holidays, Peerless Hotels, and Peerless Securities.

4.10 Infrastructural facilities:

Fortune Financial services outlets are designed to be places where retail investors can

come in touch with investment opportunities in an atmosphere of convenience and

35

comfort. The look and feel of the offices across India projects a consistent branch image

for the company. The features that enable a unique facility for retailing financial services

include among others: Easily visible branches set up in the commercial spaces of

potential investment zones ranging between 750 sft to 1000 sft.

Ø Most branches are located in the ground floor sporting huge glass frontage

promoting easy accessibility and reflecting our attitude of complete transparency.

Ø The major portion of the branch area dedicated for customer use. The furniture is

in CKD formats to add flexibility in using the branch for investor’s purposes.

Ø Connectivity to NSE for trading facilities.

Ø TV and other electronic mediums to facilitate real time update and dissemination

of information to our customers. Each branch comprises of trained and qualified

investment advisors to take care of the needs of the customers.

36

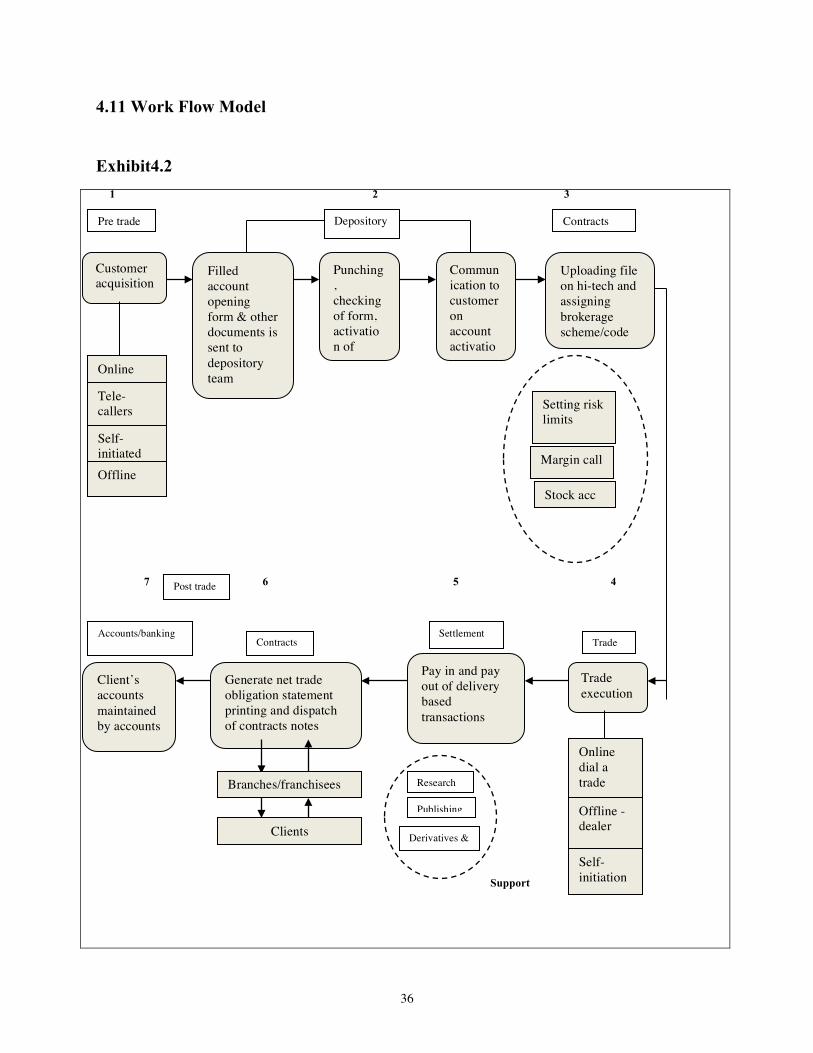

4.11 Work Flow Model

Exhibit4.2

1 2 3

7 6 5 4

Support

Pre trade Contracts Depository

Uploading file on hi-tech and assigning brokerage scheme/code

Communication to customer on account activatio

Punching, checking of form, activation of

Filled account opening form & other documents is sent to depository team

Customer acquisition

Online

Tele-callers Setting risk

limits Self-initiated Margin call Offline

Stock acc

Post trade

Accounts/banking

Client’s accounts maintained by accounts

Generate net trade obligation statement printing and dispatch of contracts notes

Pay in and pay out of delivery based transactions

Trade execution

Contracts Settlement

Trade

Online dial a trade

Offline - dealer Clients

Branches/franchisees Research

Publishing

Self-initiation

Derivatives & commodities

37

4.12 Future Plans and Prospectus

The Fortune Financial services India Ltd has following Future Plans and Prospectus

v Branches / Semi branches servicing affluent / aggressive traders through high skill

financial advisor.

v To become a market leader

v New initiatives Portfolio management Services and commodities trading

v The company has a good network of franchisee and offices in north India and is

planning open more offices in south India

4.13 Mckinsey’s 7S Frame Work

The McKinsey 7S Framework is a management model developed by well-known

business consultants Robert H. Waterman, Jr. and Tom Peters (who also developed the

MBWA-- "Management By Walking Around" motif, and authored In Search of

Excellence) in the 1980s. This was a strategic vision for groups, to include businesses,

business units, and teams. The 7S are structure, strategy, systems, skills, style, staff and

shared values.

The model is most often used as a tool to assess and monitor changes in the internal

situation of an organization. The model is based on the theory that, for an organization to

perform well, these seven elements need to be aligned and mutually reinforcing. So, the

model can be used to help identify what needs to be realigned to improve performance, or

to maintain alignment (and performance) during other types of change.

38

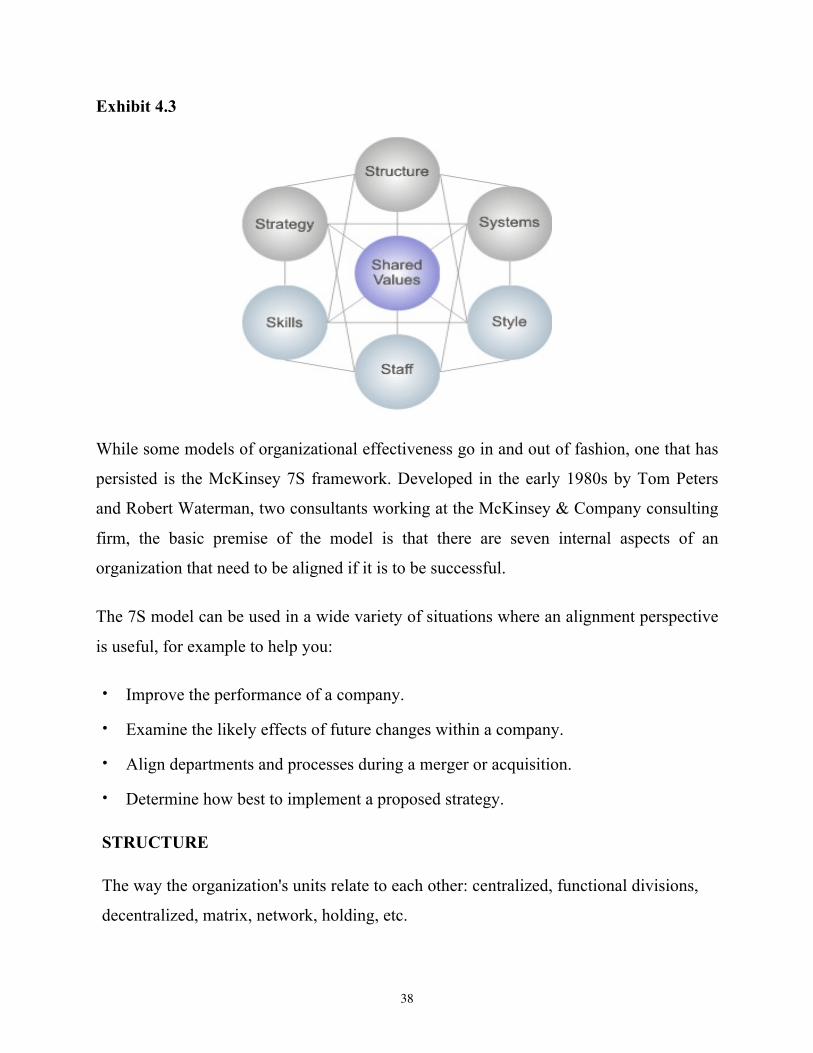

Exhibit 4.3

While some models of organizational effectiveness go in and out of fashion, one that has

persisted is the McKinsey 7S framework. Developed in the early 1980s by Tom Peters

and Robert Waterman, two consultants working at the McKinsey & Company consulting

firm, the basic premise of the model is that there are seven internal aspects of an

organization that need to be aligned if it is to be successful.

The 7S model can be used in a wide variety of situations where an alignment perspective

is useful, for example to help you:

• Improve the performance of a company.

• Examine the likely effects of future changes within a company.

• Align departments and processes during a merger or acquisition.

• Determine how best to implement a proposed strategy.

STRUCTURE

The way the organization's units relate to each other: centralized, functional divisions,

decentralized, matrix, network, holding, etc.

39

STRATEGY

Fortune aims at improving its customer base by providing integrated financial

services to all customers. Most prominent part of Fortune’s growth strategy is focus

on in house research to cater to deferent segments of client and meet their rising

expectation. Fortune believes in-house research is not only an essential part of

business requirement it also gives control over quality of input and relative advantage

in this intense business environment. Today fortune’s client base has increased to

73% n capital market and the branch and franchise network to 186 rom 49 in the

previous year.

SYSTEM

The systems are the routine processes and procedure followed within the

organization. In Fortune the core operation include

o Customer Acquisition: - the offline method of acquisition of customers through the

brokers is followed for this purpose.

o Research: -the research is done mainly at the head office in Mumbai. The

fundamental analysis of the deferent companies through balance sheet analysis of

the deferent companies through balance sheet analysis, profit and loss statement and

technical analysis with regards to various sectors, the volatility in these sectors is

also done at the head office.

o Dealing: - the dealing system refers to the actual trading activities that are done

through advice. The orders are placed according to the needs of the investors. The

volume generated through these activities forms the core revenue for the company.

o Back Office Operation: - this part of support operations handles the risk associated.

The software needed for these operations handles this and makes sure that all the

norms are met in any form of the transaction.

40

STYLE

The way in which key managers behave in achieving organizational goals is considered

to be the style variable; this variable is thought to encompass the cultural style of the

organization. Democratic style has been followed in fortune, which allows individual

department to take necessary decision. The style of operation that is followed towards

the customer is much focused and it is aimed to give utmost attention to the customer.

Personalized care is taken to satisfy with any of the problems faced by the clients.

SKILLS

The skill refers to the capitalized of the staff within the organization as a whole. The

company has the skill needed to carry out the company’s strategy like:

Ø Good and specialized knowledge about the products.

Ø High level of specialization in communication.

Ø Ability to convert people into customer.

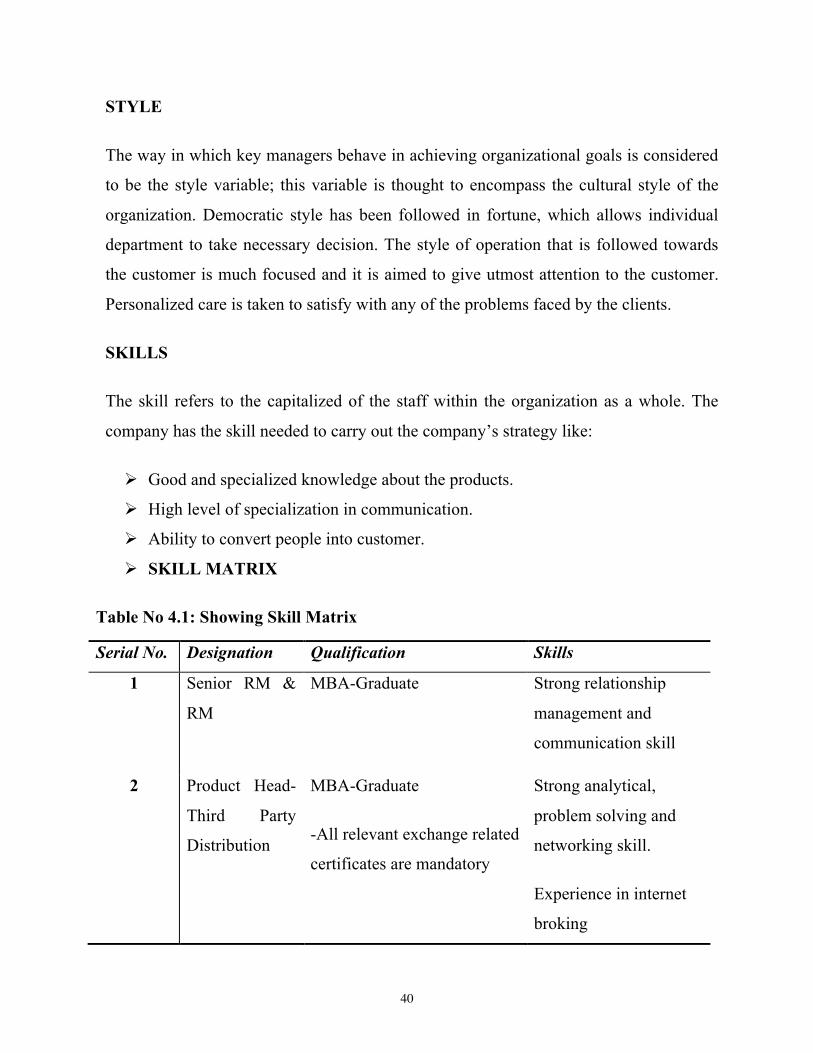

Ø SKILL MATRIX

Table No 4.1: Showing Skill Matrix

Serial No. Designation Qualification Skills

1 Senior RM &

RM

MBA-Graduate Strong relationship

management and

communication skill

2 Product Head-

Third Party

Distribution

MBA-Graduate

-All relevant exchange related

certificates are mandatory

Strong analytical,

problem solving and

networking skill.

Experience in internet

broking

41

STAFF

The term staff refers to the organization introduces young recruits into the main stream of

the activities and the manners in which they manage their careers in the new interns

develop employees and shape basic value.

The employees in all the departments are given training for 6months where they will be

given all the necessary skill that is needed for their respective job. The efficiency of the

existing employees is also measured to know the growth and their relative position in the

organization. There are 1600 employees all over the country.

SHARED VALUES

The shared values, originally termed as super ordinate goals, refer to the significant

meaning or guiding concepts that organizational members share. Shared values are

considered to be the foundation of ethics, community and culture. When people’s values

are met and matched, they feel a sense of satisfaction, harmony, or rapport. When their

values are not met or matched, people often feel dissatisfied, incongruent, or violated.

o Customer- personalized attention is the key.

o Integrity- highest ethical standards are used in all the transactions.

o Mutual Respect- trusts in working relationship.

o Quality Advice- scientific approach in quantifying the risk.

4.14 SWOT Analysis

SWOT analysis is a strategic planning method used to evaluate the Strengths, Weakness,

Opportunities, and Threats involved in a project or in a business venture. It involves

specifying the objective of the business venture or project and identifying the internal and

external factors that are favorable and unfavorable to achieving that objective. A SWOT

analysis must first start with defining a desired end state or objective. Identification of

42

SWOT is essential because subsequent steps in the process of planning for achievement

of the selected objective may be derived from the SWOT.

First, the decision makers have to determine whether the objective is attainable, given

the SWOT. If the objective is NOT attainable a different objective must be selected and

the process repeated. The SWOT analysis is often used in academia to highlight and

identify strengths, weaknesses, opportunities and threats. It is particularly helpful in

identifying areas for development.

The usefulness of SWOT analysis is not limited to profit-seeking organizations. SWOT

analysis may be used in any decision-making situation when a desired end-state

(objective) has been defined. The aim of any SWOT analysis is to identify the key

internal and external factors that are important to achieving the objective. These come

from within the company's unique value chain. SWOT analysis groups key pieces of

information into two main categories:

The strengths and weaknesses internal to the organization, such as people (Human

Resources, Properties, process and procedures followed in the organization, products etc.

The opportunities and threats presented by the external environment to the organization

which affects its success or survival such as Social, Technological, Economic,

Environmental and Political factors.

Strengths

• Experience of more than decades of trust and creditability in the Indian stock

market

• Strong industry focus leading to innovative and informed strategic advisory

services

• Deep understanding of Indian mid market corporate client

• Debt free group

43

• Comprehensive range of financial services for HNI & retail investors

• Non exclusive working relationship with leading international investments banks

• Dedicated research team for technical and fundamental analysis

• A well equipped customer team, which will assist a new comer in the matters

relating to transaction billing, De-mat & other technical queries

Weakness

• Highly risk oriented business

• Slight entry level of investors

• The company does not conduct any promotion campaign, though the competitors

are aggressively doing the same.

• Concentrated much on HNIs and corporate clients which ignores small investors

Opportunities

• Booming financial market both country wide and worldwide

• Increase in varied domestic assignment – follow on issues. Buyback program,

open offers, IPOs

• Strong momentum In franchise in the last two year

• Overseas fund raising of approximately US$ 500 million in the last 18 months

• Critical mass and experience across the globe

• All factors, which aid to the well functioning of the capital market will pave the

way to the expansion of most of the brokerage firms

Threats

• Unexpected change in the capital market such as rules and regulation etc.

• Increasing competition in the industry

• Fast change in the technology

• Increasing number in the defaulters and threat of security in terminals

44

Chapter: 5

Data Analysis & Interpretation

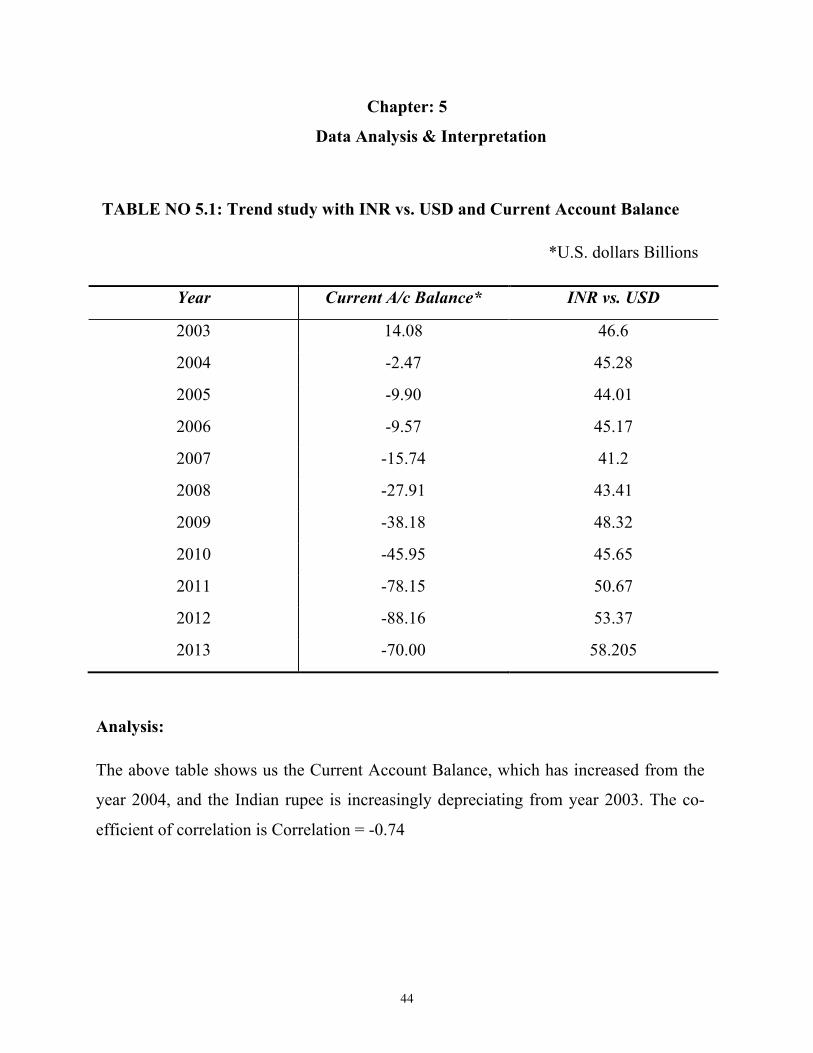

TABLE NO 5.1: Trend study with INR vs. USD and Current Account Balance

*U.S. dollars Billions

Year Current A/c Balance* INR vs. USD

2003 14.08 46.6

2004 -2.47 45.28

2005 -9.90 44.01

2006 -9.57 45.17

2007 -15.74 41.2

2008 -27.91 43.41

2009 -38.18 48.32

2010 -45.95 45.65

2011 -78.15 50.67

2012 -88.16 53.37

2013 -70.00 58.205

Analysis:

The above table shows us the Current Account Balance, which has increased from the

year 2004, and the Indian rupee is increasingly depreciating from year 2003. The co-

efficient of correlation is Correlation = -0.74

45

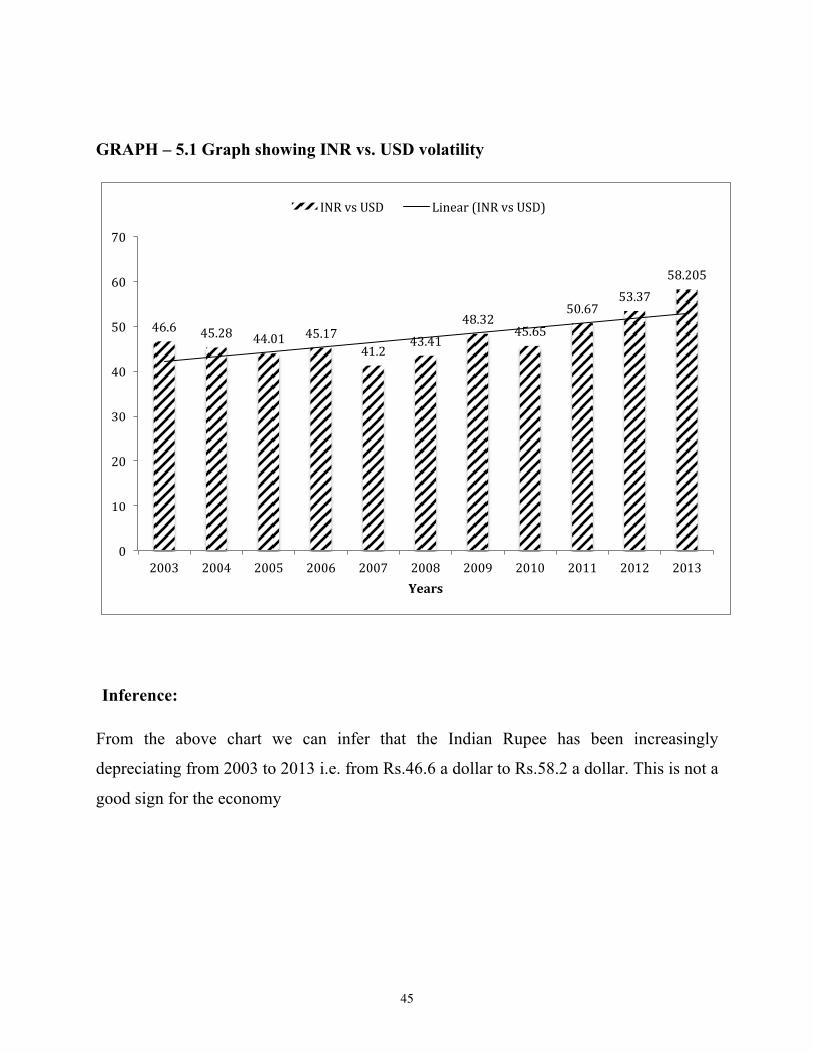

GRAPH – 5.1 Graph showing INR vs. USD volatility

Inference:

From the above chart we can infer that the Indian Rupee has been increasingly

depreciating from 2003 to 2013 i.e. from Rs.46.6 a dollar to Rs.58.2 a dollar. This is not a

good sign for the economy

46.6 45.28 44.01 45.17 41.2

43.41 48.32

45.65

50.67 53.37

58.205

0

10

20

30

40

50

60

70

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Years

INR vs USD Linear (INR vs USD)

46

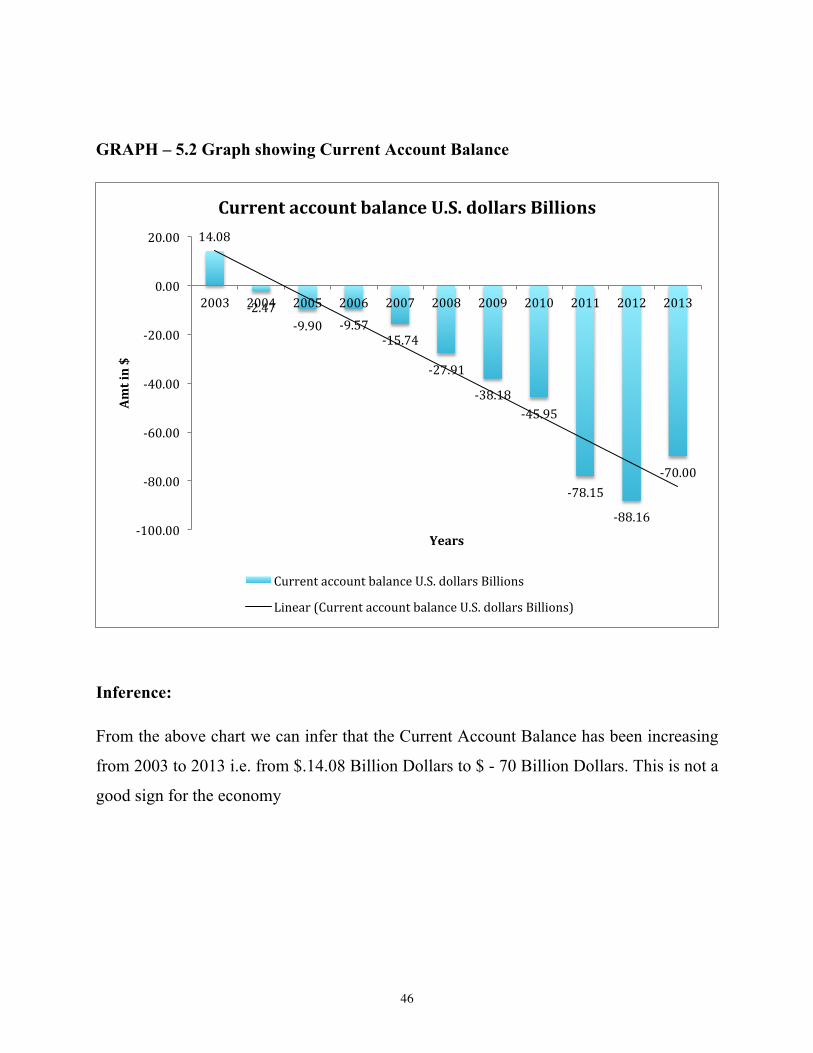

GRAPH – 5.2 Graph showing Current Account Balance

Inference:

From the above chart we can infer that the Current Account Balance has been increasing

from 2003 to 2013 i.e. from $.14.08 Billion Dollars to $ - 70 Billion Dollars. This is not a

good sign for the economy

14.08

-‐2.47 -‐9.90 -‐9.57

-‐15.74

-‐27.91

-‐38.18 -‐45.95

-‐78.15

-‐88.16

-‐70.00

-‐100.00

-‐80.00

-‐60.00

-‐40.00

-‐20.00

0.00

20.00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Amt in $

Years

Current account balance U.S. dollars Billions

Current account balance U.S. dollars Billions

Linear (Current account balance U.S. dollars Billions)

47

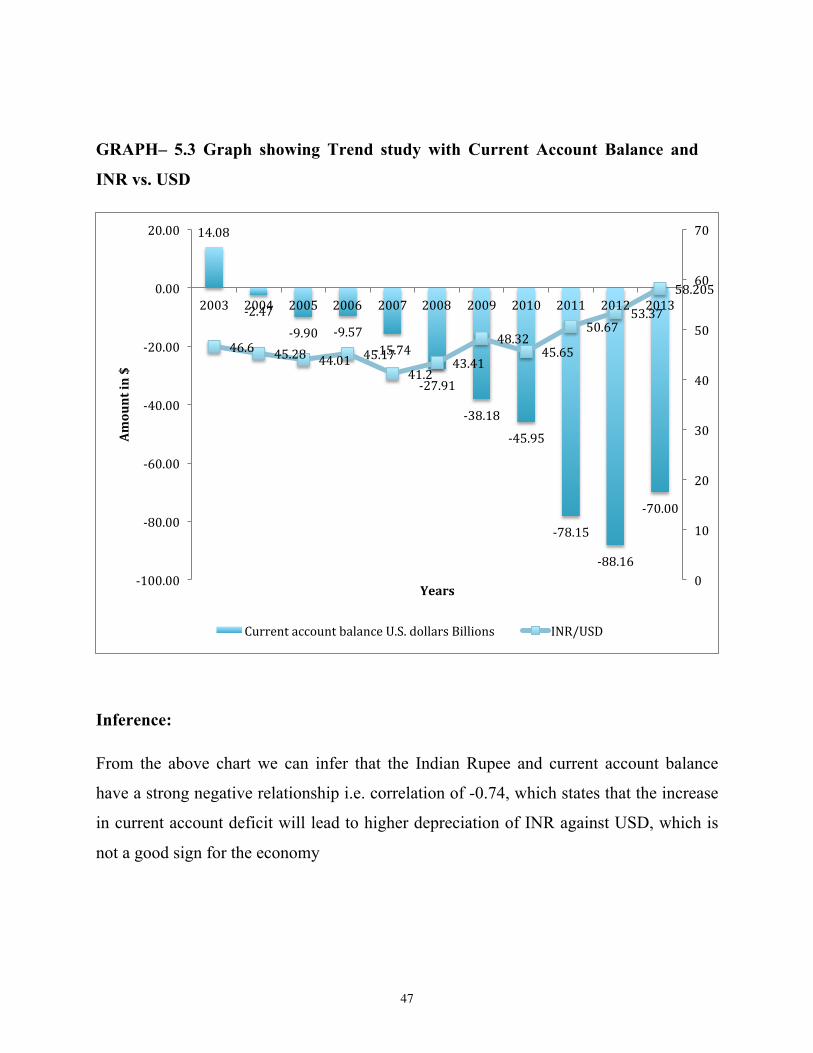

GRAPH– 5.3 Graph showing Trend study with Current Account Balance and

INR vs. USD

Inference:

From the above chart we can infer that the Indian Rupee and current account balance

have a strong negative relationship i.e. correlation of -0.74, which states that the increase

in current account deficit will lead to higher depreciation of INR against USD, which is

not a good sign for the economy

14.08

-‐2.47 -‐9.90 -‐9.57

-‐15.74

-‐27.91

-‐38.18

-‐45.95

-‐78.15

-‐88.16

-‐70.00

46.6 45.28 44.01 45.17 41.2

43.41

48.32 45.65

50.67 53.37

58.205

0

10

20

30

40

50

60

70

-‐100.00

-‐80.00

-‐60.00

-‐40.00

-‐20.00

0.00

20.00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Amount in $

Years

Current account balance U.S. dollars Billions INR/USD

48

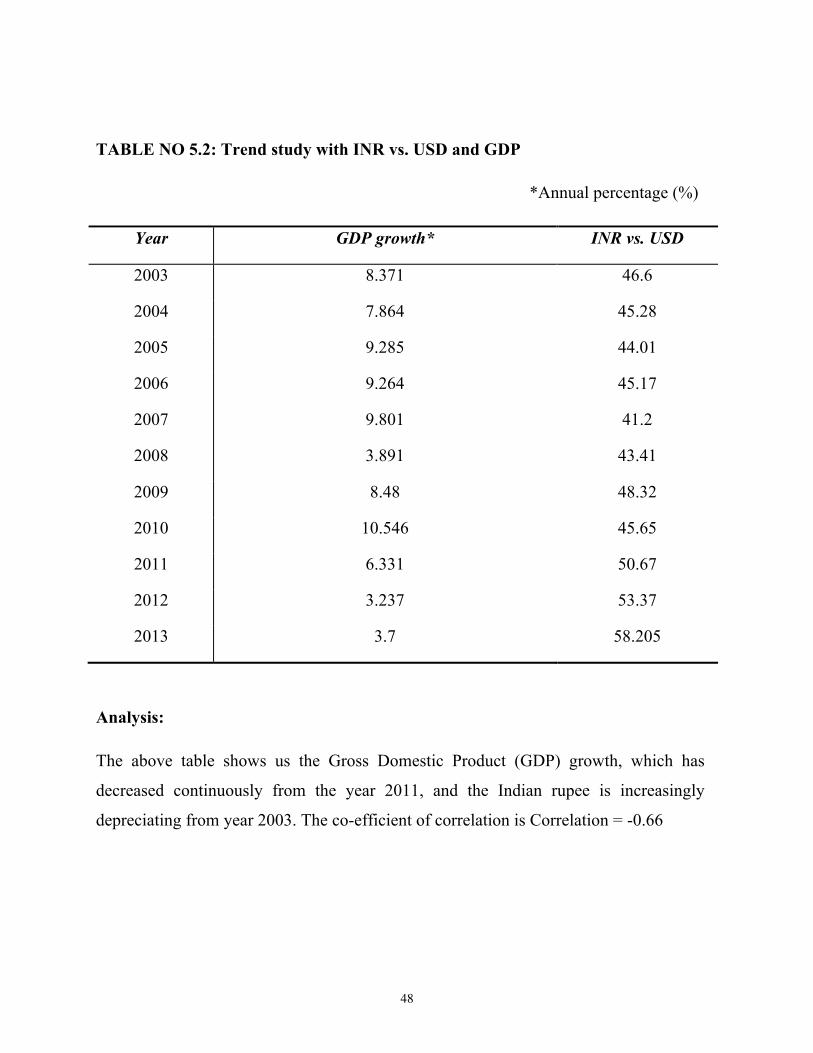

TABLE NO 5.2: Trend study with INR vs. USD and GDP

*Annual percentage (%)

Year GDP growth* INR vs. USD

2003 8.371 46.6

2004 7.864 45.28

2005 9.285 44.01

2006 9.264 45.17

2007 9.801 41.2

2008 3.891 43.41

2009 8.48 48.32

2010 10.546 45.65

2011 6.331 50.67

2012 3.237 53.37

2013 3.7 58.205

Analysis:

The above table shows us the Gross Domestic Product (GDP) growth, which has

decreased continuously from the year 2011, and the Indian rupee is increasingly

depreciating from year 2003. The co-efficient of correlation is Correlation = -0.66

49

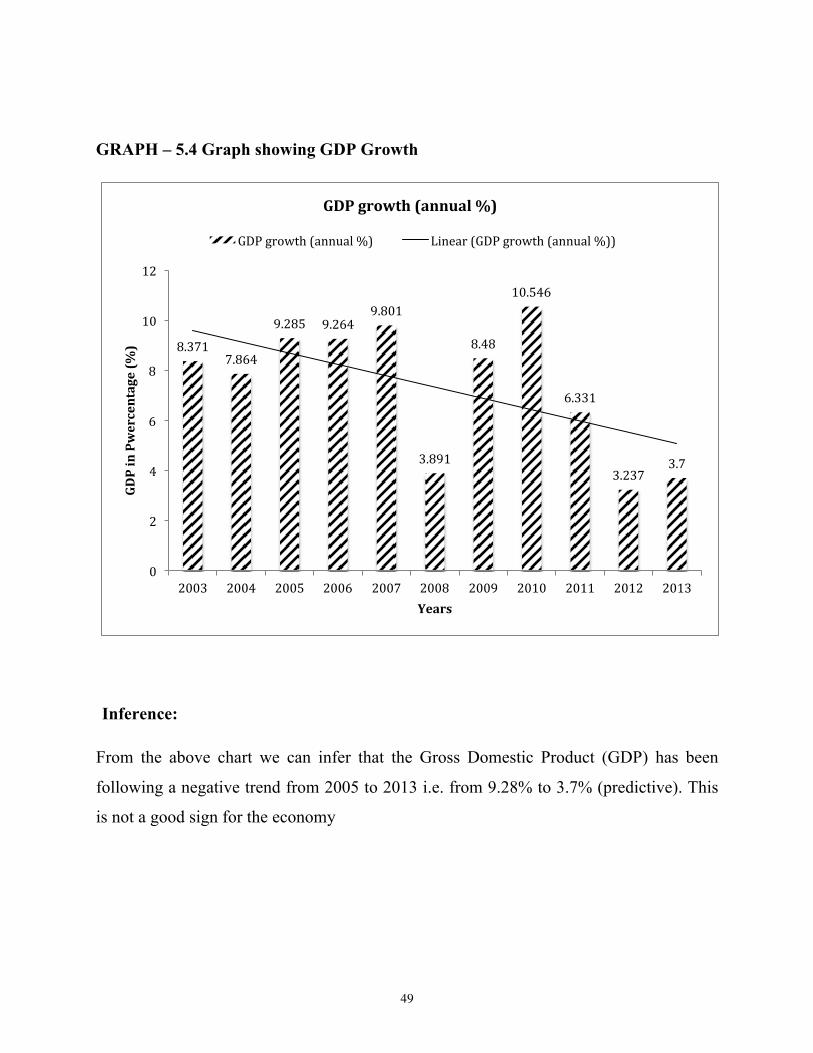

GRAPH – 5.4 Graph showing GDP Growth

Inference:

From the above chart we can infer that the Gross Domestic Product (GDP) has been

following a negative trend from 2005 to 2013 i.e. from 9.28% to 3.7% (predictive). This

is not a good sign for the economy

8.371 7.864

9.285 9.264 9.801

3.891

8.48

10.546

6.331

3.237 3.7

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

GDP in Pwercentage (%

)

Years

GDP growth (annual %)

GDP growth (annual %) Linear (GDP growth (annual %))

50

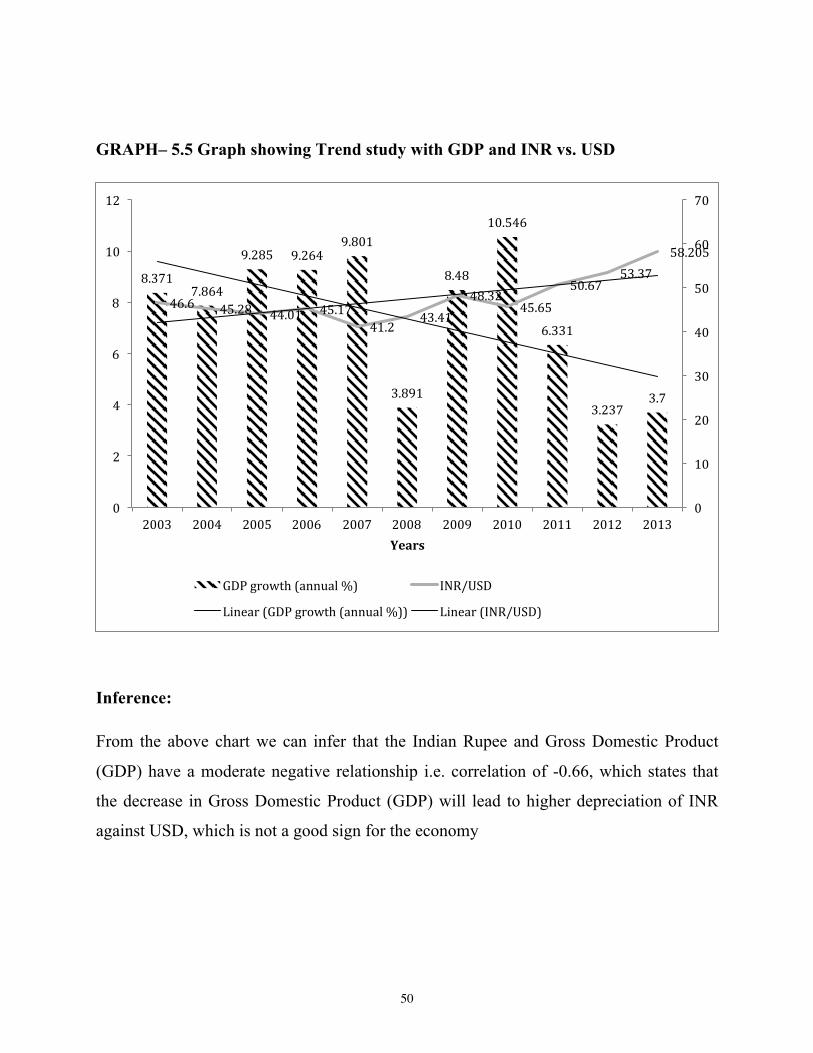

GRAPH– 5.5 Graph showing Trend study with GDP and INR vs. USD

Inference:

From the above chart we can infer that the Indian Rupee and Gross Domestic Product

(GDP) have a moderate negative relationship i.e. correlation of -0.66, which states that

the decrease in Gross Domestic Product (GDP) will lead to higher depreciation of INR

against USD, which is not a good sign for the economy

8.371 7.864

9.285 9.264 9.801

3.891

8.48

10.546

6.331

3.237 3.7

46.6 45.28 44.01 45.17 41.2

43.41 48.32

45.65 50.67

53.37 58.205

0

10

20

30

40

50

60

70

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Years

GDP growth (annual %) INR/USD

Linear (GDP growth (annual %)) Linear (INR/USD)

51

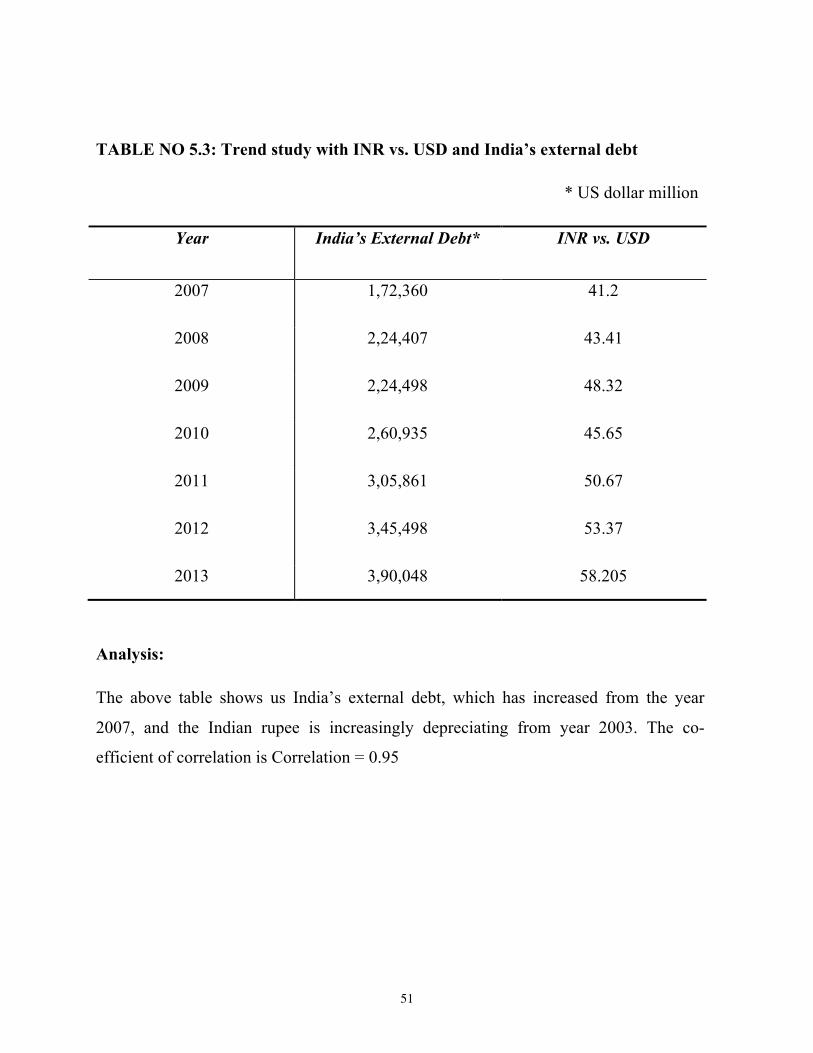

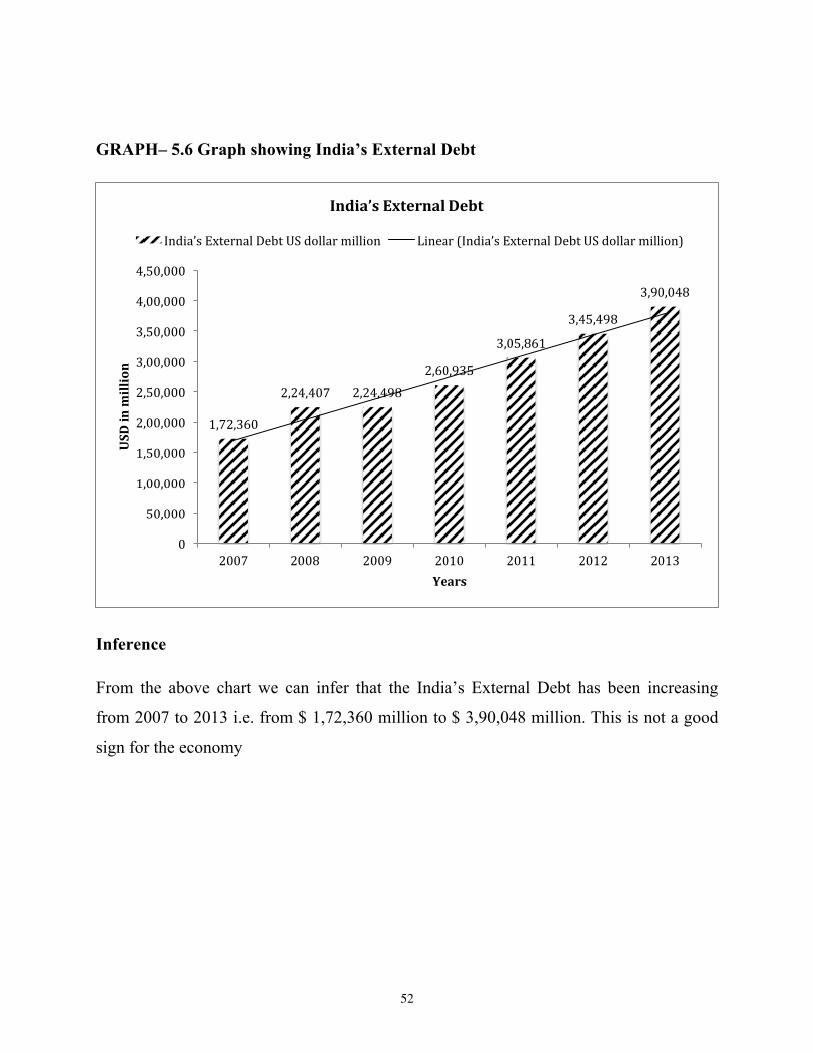

TABLE NO 5.3: Trend study with INR vs. USD and India’s external debt

* US dollar million

Year India’s External Debt* INR vs. USD

2007 1,72,360 41.2

2008 2,24,407 43.41

2009 2,24,498 48.32

2010 2,60,935 45.65

2011 3,05,861 50.67

2012 3,45,498 53.37

2013 3,90,048 58.205

Analysis:

The above table shows us India’s external debt, which has increased from the year

2007, and the Indian rupee is increasingly depreciating from year 2003. The co-

efficient of correlation is Correlation = 0.95

52

GRAPH– 5.6 Graph showing India’s External Debt

Inference

From the above chart we can infer that the India’s External Debt has been increasing

from 2007 to 2013 i.e. from $ 1,72,360 million to $ 3,90,048 million. This is not a good

sign for the economy

1,72,360

2,24,407 2,24,498 2,60,935

3,05,861

3,45,498

3,90,048

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

3,50,000

4,00,000

4,50,000

2007 2008 2009 2010 2011 2012 2013

USD in million

Years

India’s External Debt

India’s External Debt US dollar million Linear (India’s External Debt US dollar million)

53

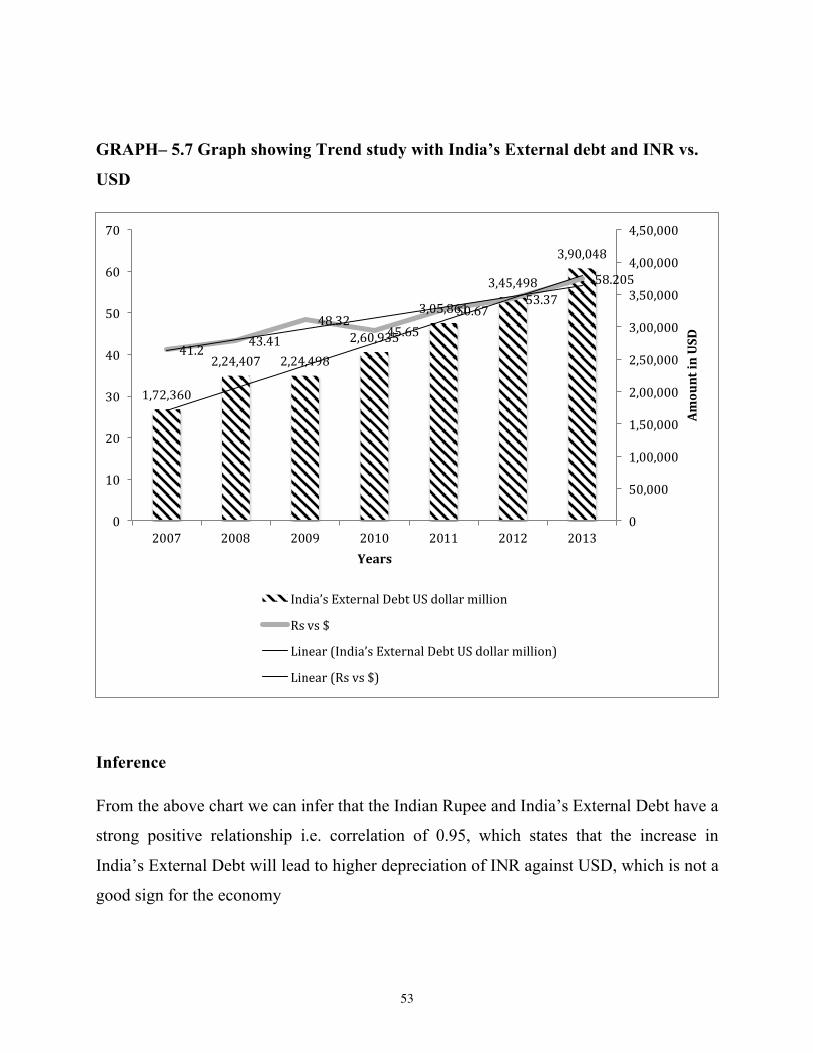

GRAPH– 5.7 Graph showing Trend study with India’s External debt and INR vs.

USD

Inference

From the above chart we can infer that the Indian Rupee and India’s External Debt have a

strong positive relationship i.e. correlation of 0.95, which states that the increase in

India’s External Debt will lead to higher depreciation of INR against USD, which is not a

good sign for the economy

1,72,360

2,24,407 2,24,498

2,60,935

3,05,861

3,45,498

3,90,048

41.2 43.41

48.32 45.65

50.67 53.37

58.205

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

3,50,000

4,00,000

4,50,000

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 2013

Amount in USD

Years

India’s External Debt US dollar million

Rs vs $

Linear (India’s External Debt US dollar million)

Linear (Rs vs $)

54

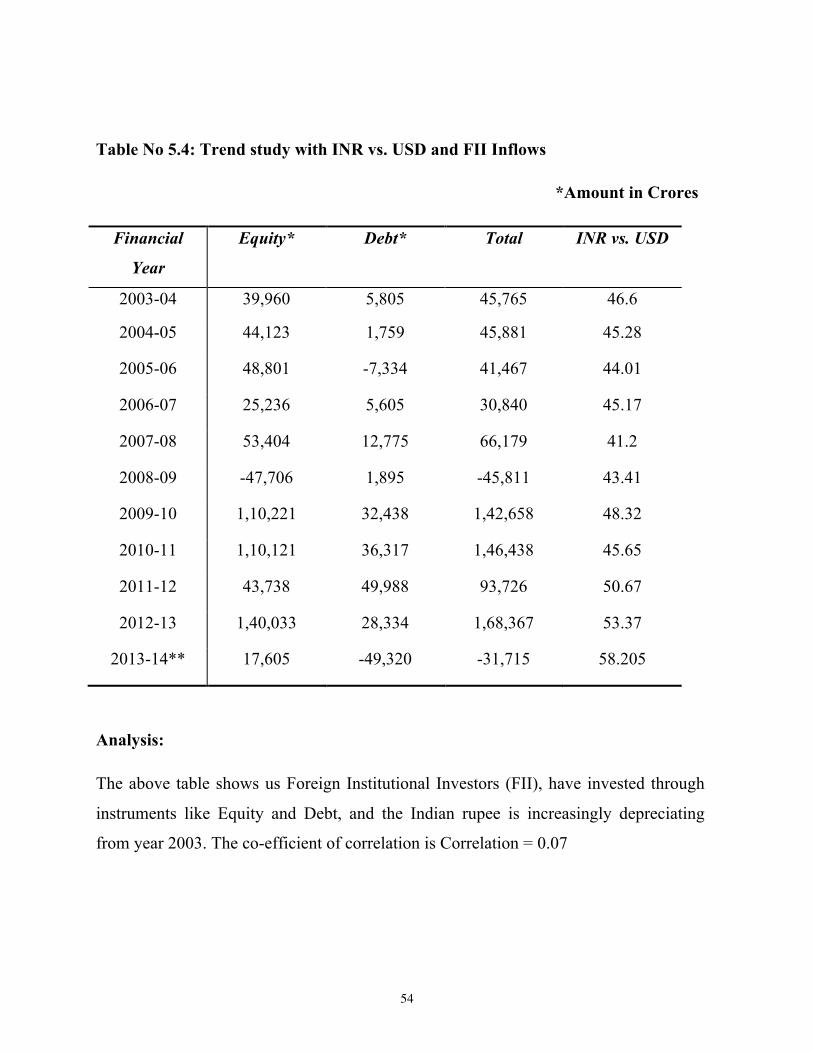

Table No 5.4: Trend study with INR vs. USD and FII Inflows

*Amount in Crores

Financial

Year

Equity* Debt* Total INR vs. USD

2003-04 39,960 5,805 45,765 46.6

2004-05 44,123 1,759 45,881 45.28

2005-06 48,801 -7,334 41,467 44.01

2006-07 25,236 5,605 30,840 45.17

2007-08 53,404 12,775 66,179 41.2

2008-09 -47,706 1,895 -45,811 43.41

2009-10 1,10,221 32,438 1,42,658 48.32

2010-11 1,10,121 36,317 1,46,438 45.65

2011-12 43,738 49,988 93,726 50.67

2012-13 1,40,033 28,334 1,68,367 53.37

2013-14** 17,605 -49,320 -31,715 58.205

Analysis:

The above table shows us Foreign Institutional Investors (FII), have invested through

instruments like Equity and Debt, and the Indian rupee is increasingly depreciating

from year 2003. The co-efficient of correlation is Correlation = 0.07

55

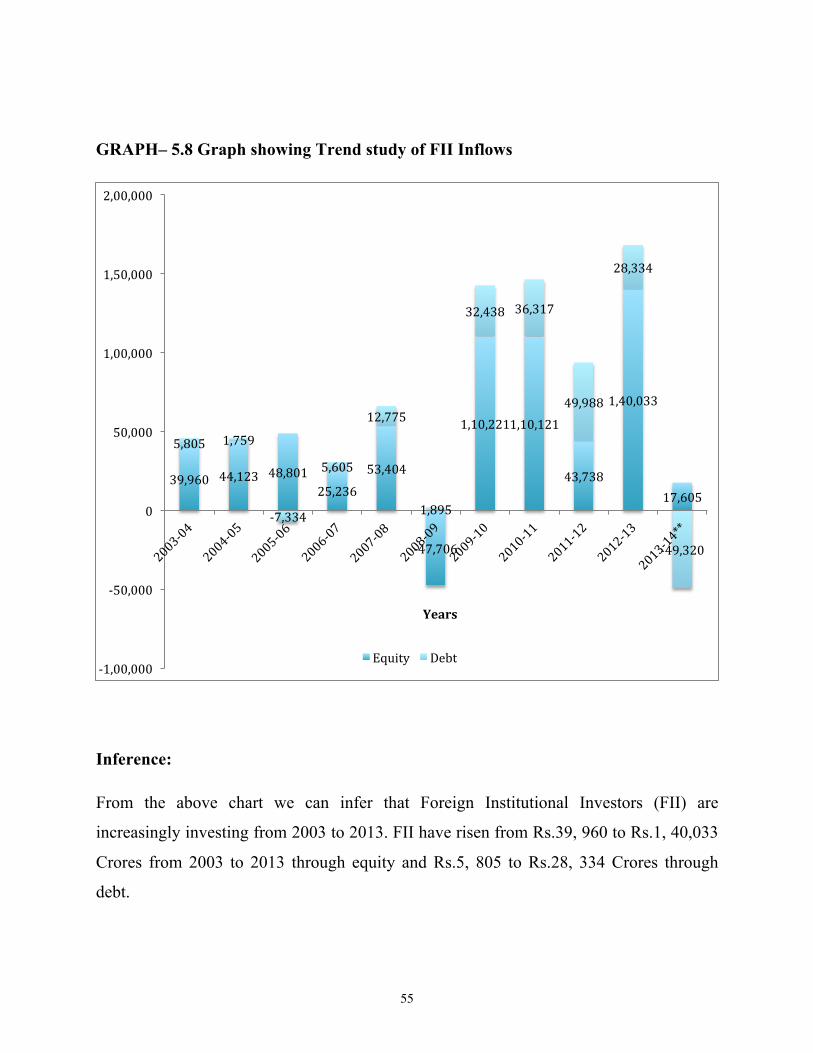

GRAPH– 5.8 Graph showing Trend study of FII Inflows

Inference:

From the above chart we can infer that Foreign Institutional Investors (FII) are

increasingly investing from 2003 to 2013. FII have risen from Rs.39, 960 to Rs.1, 40,033

Crores from 2003 to 2013 through equity and Rs.5, 805 to Rs.28, 334 Crores through

debt.

39,960 44,123 48,801 25,236

53,404

-‐47,706

1,10,221 1,10,121

43,738

1,40,033

17,605

5,805 1,759

-‐7,334

5,605

12,775

1,895

32,438 36,317

49,988

28,334

-‐49,320

-‐1,00,000

-‐50,000

0

50,000

1,00,000

1,50,000

2,00,000

Years

Equity Debt

56

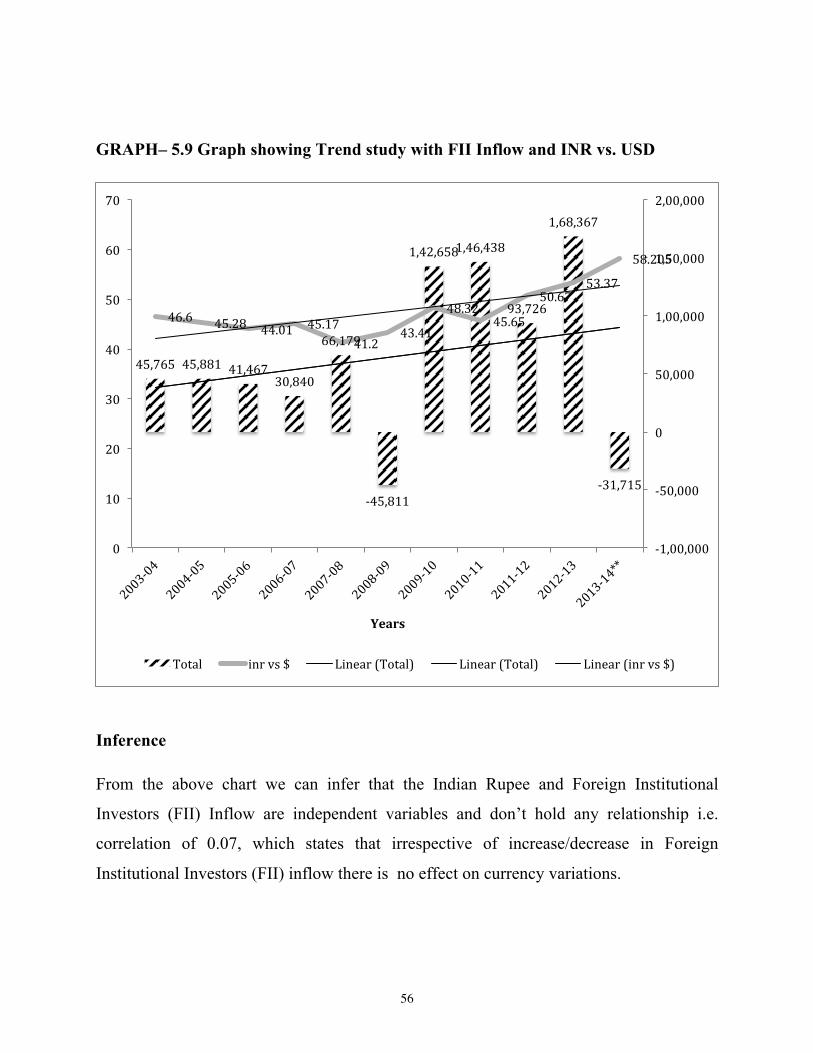

GRAPH– 5.9 Graph showing Trend study with FII Inflow and INR vs. USD

Inference

From the above chart we can infer that the Indian Rupee and Foreign Institutional

Investors (FII) Inflow are independent variables and don’t hold any relationship i.e.

correlation of 0.07, which states that irrespective of increase/decrease in Foreign

Institutional Investors (FII) inflow there is no effect on currency variations.

45,765 45,881 41,467 30,840

66,179

-‐45,811

1,42,658 1,46,438

93,726

1,68,367

-‐31,715

46.6 45.28 44.01 45.17 41.2

43.41

48.32 45.65

50.67 53.37

58.205

-‐1,00,000

-‐50,000

0

50,000

1,00,000

1,50,000

2,00,000

0

10

20

30

40

50

60

70

Years

Total inr vs $ Linear (Total) Linear (Total) Linear (inr vs $)

57

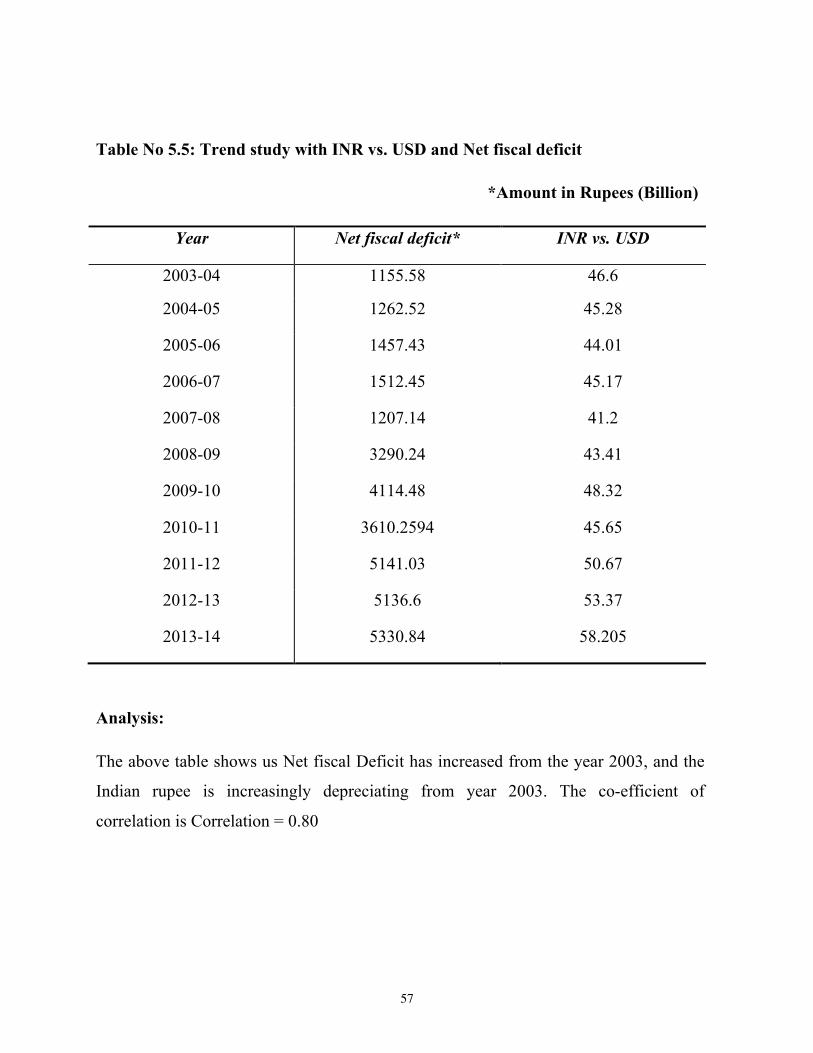

Table No 5.5: Trend study with INR vs. USD and Net fiscal deficit

*Amount in Rupees (Billion)

Year Net fiscal deficit* INR vs. USD

2003-04 1155.58 46.6

2004-05 1262.52 45.28

2005-06 1457.43 44.01

2006-07 1512.45 45.17

2007-08 1207.14 41.2

2008-09 3290.24 43.41

2009-10 4114.48 48.32

2010-11 3610.2594 45.65

2011-12 5141.03 50.67

2012-13 5136.6 53.37

2013-14 5330.84 58.205

Analysis:

The above table shows us Net fiscal Deficit has increased from the year 2003, and the

Indian rupee is increasingly depreciating from year 2003. The co-efficient of

correlation is Correlation = 0.80

58

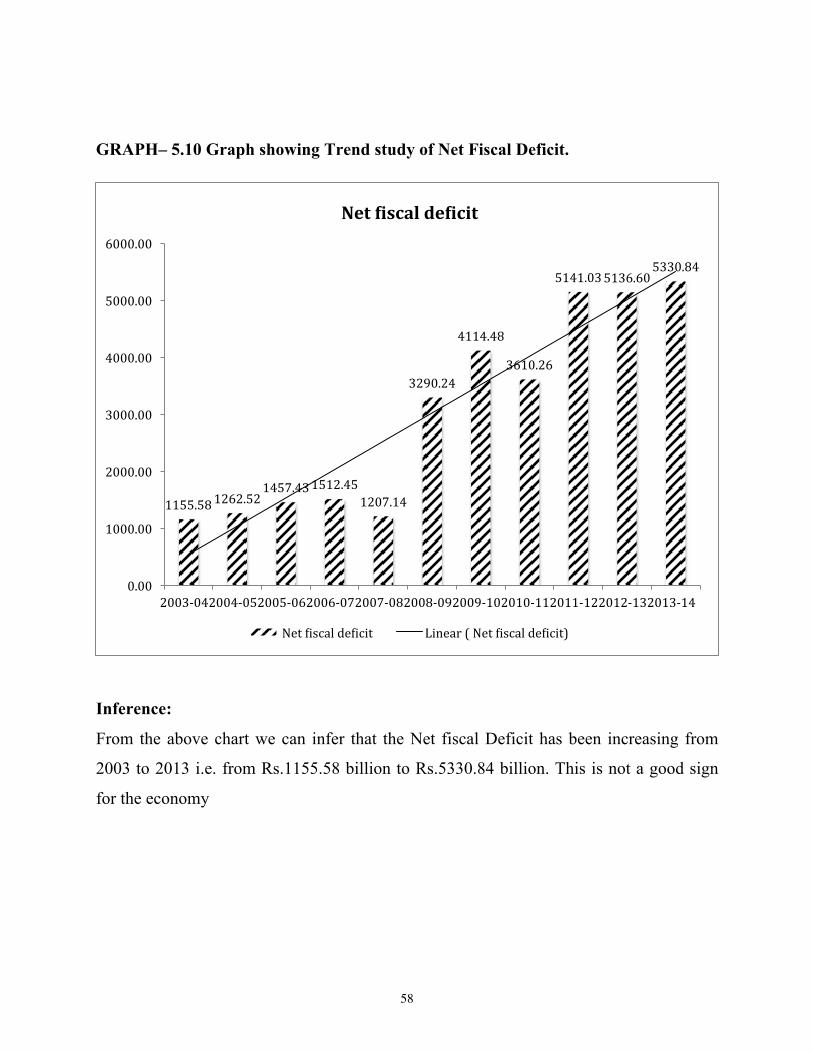

GRAPH– 5.10 Graph showing Trend study of Net Fiscal Deficit.

Inference:

From the above chart we can infer that the Net fiscal Deficit has been increasing from

2003 to 2013 i.e. from Rs.1155.58 billion to Rs.5330.84 billion. This is not a good sign

for the economy

1155.58 1262.52 1457.43 1512.45

1207.14

3290.24

4114.48

3610.26

5141.03 5136.60 5330.84

0.00

1000.00

2000.00

3000.00

4000.00

5000.00

6000.00

2003-‐04 2004-‐05 2005-‐06 2006-‐07 2007-‐08 2008-‐09 2009-‐10 2010-‐11 2011-‐12 2012-‐13 2013-‐14

Net Fiscal deFicit

Net \iscal de\icit Linear ( Net \iscal de\icit)

59

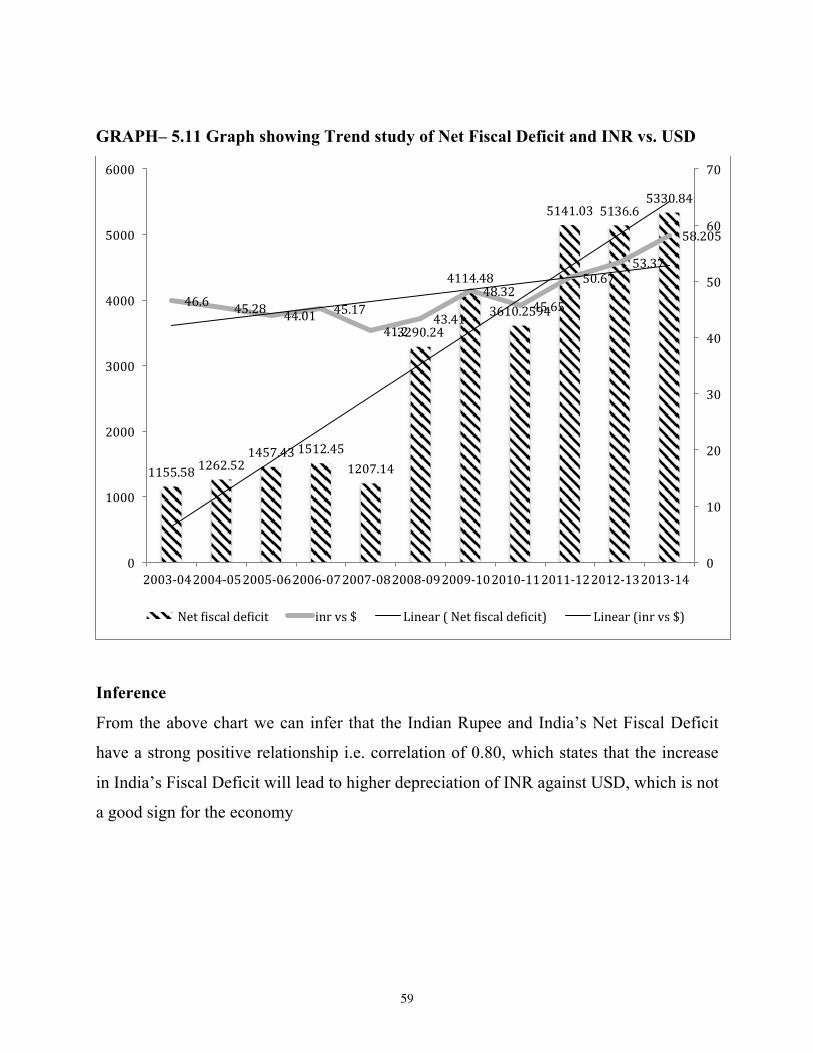

GRAPH– 5.11 Graph showing Trend study of Net Fiscal Deficit and INR vs. USD

Inference

From the above chart we can infer that the Indian Rupee and India’s Net Fiscal Deficit

have a strong positive relationship i.e. correlation of 0.80, which states that the increase

in India’s Fiscal Deficit will lead to higher depreciation of INR against USD, which is not

a good sign for the economy

1155.58 1262.52 1457.43 1512.45

1207.14

3290.24

4114.48

3610.2594

5141.03 5136.6 5330.84

46.6 45.28 44.01 45.17

41.2 43.41

48.32 45.65

50.67 53.37

58.205

0

10

20

30

40

50

60

70

0

1000

2000

3000

4000

5000

6000

2003-‐04 2004-‐05 2005-‐06 2006-‐07 2007-‐08 2008-‐09 2009-‐10 2010-‐11 2011-‐12 2012-‐13 2013-‐14

Net \iscal de\icit inr vs $ Linear ( Net \iscal de\icit) Linear (inr vs $)

60

Chapter: 6 Summary of Findings, Suggestions and Conclusion.

Findings:

ü The increase in current account deficit will lead to higher depreciation of INR

against USD, which is not a good sign for the economy

ü The increase in India’s Fiscal Deficit will lead to higher depreciation of INR

against USD, which is not a positive sign to the economy.

ü Irrespective of increase/decrease in Foreign Institutional Investors (FII) inflow

there is no effect on currency variations.

ü Decrease in Gross Domestic Product (GDP) will lead to higher depreciation of

INR against USD.

ü The increase in India’s External Debt will lead to higher depreciation of INR

against USD.

ü Rupee appreciation makes imports cheaper and exports more expensive.

ü The exchange rate is a significant tool that can be used to examine many key

industries; with fluctuations potentially having a serious impact on the economy,

industries, companies, and foreign investors. Rupee appreciation is generally

helpful for industries, which rely closely on imported inputs while depreciation of

the rupee is welcome news for industries, which are exporting a majority of their

products.

61

Suggestion/steps to control excessive fluctuations

ü The government should guarantee minimum exchange rate and if the market

moves sharply against the exporters then they should be compensated with

subsidy.

ü A range may be fixed around a particular rate say 4% around Rs.60 and the rupee

movement should be restricted around that range.

ü Hedging of currency is another option, which needs to be made popular in India.

It can be done in various ways like forward contracts or buying options. Forward

contract is the one in which future price is locked in. It can really provide

safeguard against risk and help to survive in foreign market. Small and medium

enterprises should be allowed to book forward contract without underlying

exposures or past records of export or import.

ü Incentives should be given to control cost and to remain competitive in the global

market.

ü Forecasting is required for floating currencies by planners of long run horizons. It

should take into account exchange rate system, forecast horizons [may be short,