banking and finance in india post-independence

TRANSCRIPT

BANKING AND FINANCE IN INDIA

The Indian money market is classified in to : the organized

sector(comprising private, public and foreign owned

commercial banks and cooperative banks, together known as

scheduled banks); and the unorganized sector(comprising

individual or family owned indigenous bankers or money

lenders and non banking financial companies (NBFCs)).

The unorganized sector and micro credit and still preferred

over traditional banks in rural and sub-urban areas,

especially for non-productive purposes, like ceremonies and

short duration loans.

Early History

Banking in India originated in the first decade of 18th

century. The first banks were The General Bank of India,

which started in 1786, and Bank of Hindustan, both of which

are now defunct. The oldest bank in existence in India is

the State Bank of India, which originated in the "The Bank

of Bengal" in Calcutta in June 1806. This was one of the

three presidency banks, the other two being the Bank of

Bombay and the Bank of Madras. The presidency banks were

established under charters from the British East India

Company. They merged in 1925 to form the Imperial Bank of

India, which, upon India's independence, became the State

Bank of India. For many years the Presidency banks acted as

quasi-central banks, as did their successors. The Reserve

Bank of India formally took on the responsibility of

regulating the Indian banking sector from 1935. After

India's independence in 1947, the Reserve Bank was

nationalized and given broader powers.

Post-independence

The partition of India in 1947 adversely impacted the

economies of Punjab and West Bengal, paralyzing banking

activities for months. India's independence marked the end

of a regime of the Laissez-faire for the Indian banking. The

Government of India initiated measures to play an active

role in the economic life of the nation, and the Industrial

Policy Resolution adopted by the government in 1948

envisaged a mixed economy. This resulted into greater

involvement of the state in different segments of the

economy including banking and finance. The major steps to

regulate banking included:

In 1948, the Reserve Bank of India, India's central banking

authority, was nationalized, and it became an institution

owned by the Government of India.

In 1949, the Banking Regulation Act was enacted which

empowered the Reserve Bank of India (RBI) "to regulate,

control, and inspect the banks in India."

The Banking Regulation Act also provided that no new bank or

branch of an existing bank may be opened without a license

from the RBI, and no two banks could have common directors.

However, despite these provisions, control and regulations,

banks in India except the State Bank of India, continued to

be owned and operated by private persons. This changed with

the nationalization of major banks in India on 19th July,

1969.

Nationalization

By the 1960s, the Indian banking industry has become an

important tool to facilitate the development of the Indian

economy. At the same time, it has emerged as a large

employer, and a debate has ensued about the possibility to

nationalize the banking industry. Indira Gandhi, the-then

Prime Minister of India expressed the intention of the GOI

in the annual conference of the All India Congress Meeting

in a paper entitled "Stray thoughts on Bank Nationalization." The

paper was received with positive enthusiasm. Thereafter, her

move was swift and sudden, and the GOI issued an ordinance

and nationalized the 14 largest commercial banks with effect

from the midnight of July 19, 1969. Jayaprakash Narayan, a

national leader of India, described the step as a

"masterstroke of political sagacity." Within two weeks of the issue of

the ordinance, the Parliament passed the Banking Companies

(Acquisition and Transfer of Undertaking) Bill, and it

received the presidential approval on 9th August, 1969.

A second dose of nationalization of 6 more commercial banks

followed in 1980. The stated reason for the nationalization

was to give the government more control of credit delivery.

With the second dose of nationalization, the GOI controlled

around 91% of the banking business of India.

After this, until the 1990s, the nationalized banks grew at

a pace of around 4%, closer to the average growth rate of

the Indian economy.

Liberalisation

In the early 1990s the then Narsimha Rao government embarked

on a policy of liberalisation and gave licenses to a small

number of private banks, which came to be known as New

Generation tech-savvy banks, which included banks such as Global

Trust Bank (the first of such new generation banks to be set

up) which later amalgamated with Oriental Bank of Commerce,

UTI Bank (now re-named as Axis Bank), ICICI Bank and HDFC

Bank. This move, along with the rapid growth in the economy

of India, kick – started the banking sector in India, which

has seen rapid growth with strong contribution from all the

three sectors of banks, namely, government banks, private

banks and foreign banks.

The next stage for the Indian banking has been setup with

the proposed relaxation in the norms for Foreign Direct

Investment, where all Foreign Investors in banks may be

given voting rights which could exceed the present cap of

10%at present it has gone up to 49% with some restrictions.

The new policy shook the Banking sector in India completely.

Bankers, till this time, were used to the 4-6-4 method

(Borrow at 4%; Lend at 6%;Go home at 4) of functioning. The

new wave ushered in a modern outlook and tech-savvy methods

of working for traditional banks. All this led to the retail

boom in India. People not just demanded more from their

banks but also received more.

Current situation

Currently (2007), banking in India is generally fairly

mature in terms of supply, product range and reach-even

though reach in rural India still remains a challenge for

the private sector and foreign banks. In terms of quality of

assets and capital adequacy, Indian banks are considered to

have clean, strong and transparent balance sheets relative

to other banks in comparable economies in its region. The

Reserve Bank of India is an autonomous body, with minimal

pressure from the government. The stated policy of the Bank

on the Indian Rupee is to manage volatility but without any

fixed exchange rate-and this has mostly been true.

With the growth in the Indian economy expected to be strong

for quite some time-especially in its services sector-the

demand for banking services, especially retail banking,

mortgages and investment services are expected to be strong.

One may also expect M&As, takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg

Pincus to increase its stake in Kotak Mahindra Bank (a

private sector bank) to 10%. This is the first time an

investor has been allowed to hold more than 5% in a private

sector bank since the RBI announced norms in 2005 that any

stake exceeding 5% in the private sector banks would need to

be vetted by them.

Currently, India has 88 scheduled commercial banks (SCBs) -

28 public sector banks (that is with the Government of India

holding a stake), 29 private banks (these do not have

government stake; they may be publicly listed and traded on

stock exchanges) and 31 foreign banks. They have a combined

network of over 53,000 branches and 17,000 ATMs. According

to a report by ICRA Limited, a rating agency, the public

sector banks hold over 75 percent of total assets of the

banking industry, with the private and foreign banks holding

18.2% and 6.5% respectively.

Since liberalization, the government has approved

significant banking reforms. While some of these relate to

nationalized banks (like encouraging mergers, reducing

government interference and increasing profitability and

competitiveness) other reforms have opened up the banking

and insurance sectors to private and foreign players.

Central bank Reserve Bank of India

Nationalized Allahabad Bank · Andhra Bank · Bank of

banks

Baroda · Bank of India · Bank of

Maharashtra · Canara Bank · Central Bank

of India · Corporation Bank · Dena Bank ·

Indian Bank · Indian Overseas Bank ·

Oriental Bank of Commerce · Punjab & Sind

Bank · Punjab National Bank · Syndicate

Bank · Union Bank of India · United Bank

of India · UCO Bank · Vijaya Bank · IDBI

Bank

State Bank

Group

State Bank of India · State Bank of

Bikaner & Jaipur · State Bank of

Hyderabad · State Bank of Indore · State

Bank of Mysore · State Bank of Patiala ·

State Bank of Saurashtra · State Bank of

Travancore

Private banks

Axis Bank · Bank of Rajasthan · Bharat

Overseas Bank · Catholic Syrian Bank ·

Centurion Bank of Punjab · City Union

Bank · Development Credit Bank ·

Dhanalakshmi Bank · Federal Bank · Ganesh

Bank of Kurundwad · HDFC Bank · ICICI

Bank · IndusInd Bank · ING Vysya Bank ·

Jammu & Kashmir Bank · Karnataka Bank

Limited · Karur Vysya Bank · Kotak

Mahindra Bank · Lakshmi Vilas Bank ·

Nainital Bank · Ratnakar Bank · SBI

Commercial and International Bank · South

Indian Bank · Amazing Mercantile Bank ·

YES Bank

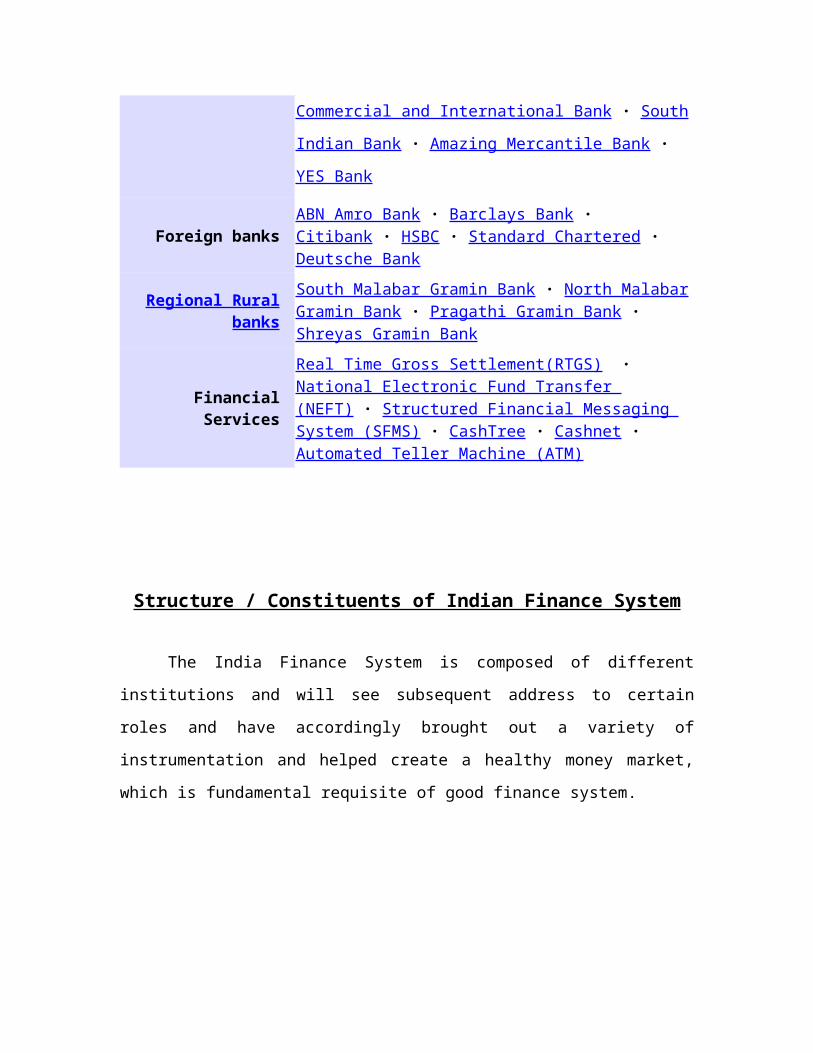

Foreign banksABN Amro Bank · Barclays Bank · Citibank · HSBC · Standard Chartered · Deutsche Bank

Regional Ruralbanks

South Malabar Gramin Bank · North MalabarGramin Bank · Pragathi Gramin Bank · Shreyas Gramin Bank

FinancialServices

Real Time Gross Settlement(RTGS) · National Electronic Fund Transfer (NEFT) · Structured Financial Messaging System (SFMS) · CashTree · Cashnet · Automated Teller Machine (ATM)

Structure / Constituents of Indian Finance System

The India Finance System is composed of different

institutions and will see subsequent address to certain

roles and have accordingly brought out a variety of

instrumentation and helped create a healthy money market,

which is fundamental requisite of good finance system.

Categories of Bank:

Banking in India falls mainly under two categories, viz.

Commercial banks and Co-operative banks, while commercial

banks cater to the needs of industry and trade largely; the

cooperative banks play a major role in financing agriculture

and allied activities in rural areas, and trade and services

in urban areas.

The commercial banks may be classified into four group in

terms of ownership: 1) Public Sector Banks 2) Regional Rural

3) Indian Private Sector Banks and 4) Banks incorporated

outside India.

The commercial banks can be further classified into

Scheduled banks and Non Scheduled Banks. Scheduled Banks are

Commercial Banks

Public Sector Private SectorState Bank of

India

Nationalized Banks

Non-Scheduled Banks

Regional Rural Banks

Other Banks in IndiaAssociate Banks

Foreign Banks in India

14 major banks nationalized on 19th

July 2, 1969

6 Banks nationalized on 15th April 1980

those listed in the second schedule to the Reserve Bank of

India Act 1934

These banks satisfy the criteria laid down under section 42

(6) of the RBI Act that they should have capital and reserve

of Rs. 5 lakhs and their activities should not be

detrimental to the interests of depositors. The scheduled

banks are required to maintain cash reserves equal to 5 % of

DTL which can go up to 15 % under section 42 (1). Those,

which are not included in the 2nd schedule, are called the

non-scheduled banks. The number of take- oven/liquidation as

also in some cases up gradation into scheduled banks

category.

Introduction to finance :

Finance is the handmaiden of economic growth Institutions

like banks, which command huge financial resources, can play

a crucial role in shaping the economy of a country by

judiciously deploying their funds over such important

activities as would lead to an overall economic growth. A

bank’s offer compared to a dam and the money lying scattered

with individuals and institutions in society to the water

running its own course without any direction. Money is

collected by banks by way of deposits, and from this fund

money is turned back to the community in the form of loans.

Thus, banks act as a vital link between the savers and the

needy.

India is striving to transform herself into an industrially

developed country based on a rural and agricultural economy

which should not only be able to feed the millions of her

populations but also to produce raw material for her mills.

This can be done by bringing about the necessary change from

an agrarian economy to a diversified one. Banks have crucial

role to play not only in the achievement of this objective

but more significantly in determining how speedily and

efficiently it is achieved. Since the nationalization of the

fourteen major banks, the banking industry has developed

adequately enough to meet the changing needs, both corporate

and personal. Banks now offer a wide range of financial

services in an extensively varied environment. The complex

task of managing these changes and their consequences

requires that banker should be more professional than ever

before.

The Business of Banking

Banking has been understood differently at different times

and indifferent countries. In India, the earliest

legislation that dealt with the business of banking was the

Indian Companies Act 1913. The Banking Regulations Act came

in 1936. Under this Act all companies having their principal

business, accepting deposits from the public were classified

as banks. Hence between 1936 and 1942 even trading and

industrial concerns accepting deposits were classified as

banks, if accepting such deposits was their principal

business. The Government of India passed a compressive

Banking Regulation Act in 1949. Accordingly a banking

company was defined as a company which carries on the

business of banking that is to say accepting for the purpose

of lending or investing deposits of money from the public,

repayable on demand of otherwise, and withdrawal cheque,

draft, order of otherwise. The study group reviewing

legislation affecting banking is of the opinion that

“banking should be abroad based.” The definition given by

the Banking Regulation Act 1949 is certainly not exhaustive,

and it needs certain alterations for the sake of

simplification. The purpose of accepting deposits is

strictly not relevant for the definition of banking, through

it is basic for banking regulation. There is no need to

distinguish between “loans” deposits” in the context of

banking regulation. The definition of banking should cover

all forms of deposits from the public, and banking

regulation should take into its ambit all the different

types of banking.

Functioning of a Bank:

Functioning of a Bank is among the more complicated of

corporate operations. Since Banking involves dealing

directly with money, governments in most countries regulate

this sector rather stringently. In India, the regulation

traditionally has been very strict and in the opinion of

certain quarters, responsible for the present condition of

banks, where NPAs are of a very high order. The process of

financial reforms, which started in 1991, has cleared the

cobwebs somewhat but a lot remains to be done. The

multiplicity of policy and regulations that a Bank has to

work with makes its operations even more complicated,

sometimes bordering on illogical. This section, which is

also intended for banking professional, attempts to give an

overview of the functions in as simple manner as possible.

Banking Regulation Act of India, 1949 defines Banking as

"accepting, for the purpose of lending or investment of

deposits of money from the public, repayable on demand or

otherwise and withdrawal by cheques, draft, order or

otherwise."

Deriving from this definition and viewed solely from the

point of view of the customers, Banks essentially perform

the following functions:

1. Accepting Deposits from public/others

(Deposits)

2. Lending Money to public (Loans)

3. Transferring money from one place to another.

4. Acting as trustees.

5. Keeping valuables in safe custody.

6. Government business.

But do these functions constitute banking? The answer must

be a no. There are so many intricacies involved in the

activities that a bank performs today, that the above list

must sound very simple to a seasoned banker. Please click on

the activity to see what a Bank has to do to give the above

services to its customers. These activities can also be

described as back office banking. Banks are organized in a

linear structure to perform these activities at the base of

which lies a Branch. The corporate office of a bank is

normally called Head Office

FORMS OF ADVANCES:

Advances by commercial banks are made in different forms

such as loans, cash credit, overdrafts, bills purchased,

bills discounted etc. These are generally short- term

advances. Commercial banks do not sanction advances on a

long-term basis beyond a small proportion of their demand

and time liabilities. They cannot afford to lock up their

funds for long period. Hence a considerable percentage of

their advances is repayable on demand.

Advances may be granted against tangible security or in

special deserving cases on an unsecured/clean basis.

1. Loans

1. Overdrafts

2. Cash credits

3. Temporary Overdrafts

4. Clean advances

5. Term loans

6. Bridge loan

7. Participation loan

8. Loans to small borrowers

10. Hire purchase and leasing finance

11. Bills purchased

12. Bills discounted

LOANS:

Bank loans are called indirect agents of production. For

achieving a sustained rate of economic growth over a long

period, greater efforts have to be made to increase

agricultural and industrial production, and in this

increased production, bank credit plays a significant role.

But banks in India are not free to employ their funds n an

arbitrary manner, while lending, they will have to keep in

mind factors like a desirable balance among liquidity,

safely and profitability, legal and statutory requirements,

socio-economic conditions of the country, priorities set by

economic planners, and so on. Banks try to achieve this

objective through maintaining a particular relationship

between their assets and deposits. As such, between advances

and deposits in the form of advances among as many different

types of securities and over as wide an areas as possible,

and they avoid granting too large a proportion of their

advances to one party or to a single industry. While the se

factors limit banks capability to lend, they are,

nevertheless expected to grant credit according to the

changing economic scene conditioned by the programs and

priorities of different Five Year Plans.

In a loan account the entire amount is paid to the debtor at

one time, either in cash or by transfer to his current

account. No subsequent debit ordinarily allowed except by

way of interest, incidental charges, insurance premiums,

expenses incurred is provided for by installment without

allowing the demand character of the loan to be affected in

any way. There is usually a stipulation that in the event of

installment remaining unpaid, the entire amount of the loan

will become due. Interest is charged on the debit balance,

usually with quarterly rests unless there is an arrangement

to the contrary. No cheque book is issued.

The security may be personal or in the form of shares,

debentures. Government paper, immovable property, fixed

deposit receipts, life insurance policies, goods etc.

Industry introduction

The Indian Banking industry, which is governed by the Banking Regulation

Act of India, 1949 can be broadly classified into two major categories,

non-scheduled banks and scheduled banks. Scheduled banks comprise

commercial banks and the co-operative banks. In terms of ownership,

commercial banks can be further grouped into nationalized banks, the

State Bank of India and its group banks, regional rural banks and

private sector banks (the old/ new domestic and foreign). These banks

have over 67,000 branches spread across the country in every city and

villages of all nook and corners of the land.

The first phase of financial reforms resulted in the nationalization of

14 major banks in 1969 and resulted in a shift from Class banking to

Mass banking. This in turn resulted in a significant growth in the

geographical coverage of banks. Every bank had to earmark a minimum

percentage of their loan portfolio to sectors identified as “priority

sectors”. The manufacturing sector also grew during the 1970s in

protected environs and the banking sector was a critical source. The

next wave of reforms saw the nationalization of 6 more commercial banks

in 1980. Since then the number of scheduled commercial banks increased

four-fold and the number of bank branches increased eight-fold. And that

was not the limit of growth.

After the second phase of financial sector reforms and liberalization of

the sector in the early nineties, the Public Sector Banks (PSB) s found

it extremely difficult to compete with the new private sector banks and

the foreign banks. The new private sector banks first made their

appearance after the guidelines permitting them were issued in January

1993. Eight new private sector banks are presently in operation. These

banks due to their late start have access to state-of-the-art

technology, which in turn helps them to save on manpower costs.

During the year 2000, the State Bank Of India (SBI) and its 7 associates

accounted for a 25 percent share in deposits and 28.1 percent share in

credit. The 20 nationalized banks accounted for 53.2 percent of the

deposits and 47.5 percent of credit during the same period. The share of

foreign banks (numbering 42), regional rural banks and other scheduled

commercial banks accounted for 5.7 percent, 3.9 percent and 12.2 percent

respectively in deposits and 8.41 percent, 3.14 percent and 12.85

percent respectively in credit during the year 2000.about the detail of

the current scenario we will go through the trends in modern economy of

the country.

Current Scenario:

The industry is currently in a transition phase. On the one hand, the

PSBs, which are the mainstay of the Indian Banking system are in the

process of shedding their flab in terms of excessive manpower, excessive

non Performing Assets (Npas) and excessive governmental equity, while on

the other hand the private sector banks are consolidating themselves

through mergers and acquisitions.

PSBs, which currently account for more than 78 percent of total banking

industry assets are saddled with NPAs (a mind-boggling Rs 830 billion in

2000), falling revenues from traditional sources, lack of modern

technology and a massive workforce while the new private sector banks

are forging ahead and rewriting the traditional banking business model

by way of their

sheer innovation and service. The PSBs are of course currently working

out challenging strategies even as 20 percent of their massive employee

strength has dwindled in the wake of the successful Voluntary Retirement

Schemes (VRS) schemes.

The private players however cannot match the PSB’s great reach, great

size and access to low cost deposits. Therefore one of the means for

them to combat the PSBs has been through the merger and acquisition (M&

A) route. Over the last two years, the industry has witnessed several

such instances. For instance, HDFC Bank’s merger with Times Bank Icici

Bank’s acquisition of ITC Classic, Anagram Finance and Bank of Madurai.

Centurion Bank, Indusind Bank, Bank of Punjab, Vysya Bank are said to be

on the lookout. The UTI bank- Global Trust Bank merger however opened a

pandora’s box and brought about the realization that all was not well in

the functioning of many of the private sector banks.

Private sector Banks have pioneered internet banking, phone banking,

anywhere banking, mobile banking, debit cards, Automatic Teller Machines

(ATMs) and combined various other services and integrated them into the

mainstream banking arena, while the PSBs are still grappling with

disgruntled employees in the aftermath of successful VRS schemes. Also,

following India’s commitment to the W To agreement in respect of the

services sector, foreign banks, including both new and the existing

ones, have been permitted to open up to 12 branches a year with effect

from 1998-99 as against the earlier stipulation of 8 branches.

Tasks of government diluting their equity from 51 percent to 33 percent

in November 2000 has also opened up a new opportunity for the takeover

of even the PSBs. The FDI rules being more

rationalized in Q1FY02 may also pave the way for foreign banks taking

the M& A route to acquire willing Indian partners.

Meanwhile the economic and corporate sector slowdown has led to an

increasing number of banks focusing on the retail segment. Many of them

are also entering the new vistas of Insurance. Banks with their

phenomenal reach and a regular interface with the retail investor are

the best placed to enter into the insurance sector. Banks in India have

been allowed to provide fee-based insurance services without risk

participation, invest in an insurance company for providing

infrastructure and services support and set up of a separate joint-

venture insurance company with risk participation.

Aggregate Performance of the Banking Industry

Aggregate deposits of scheduled commercial banks increased at a

compounded annual average growth rate (Cagr) of 17.8 percent during

1969-99, while bank credit expanded at a Cagr of 16.3 percent per annum.

Banks’ investments in government and other approved securities recorded

a Cagr of 18.8 percent per annum during the same period.

In FY01 the economic slowdown resulted in a Gross Domestic Product (GDP)

growth of only 6.0 percent as against the previous year’s 6.4 percent.

The WPI Index (a measure of inflation) increased by 7.1 percent as

against 3.3 percent in FY00. Similarly, money supply (M3) grew by around

16.2 percent as against 14.6 percent a year ago.

The growth in aggregate deposits of the scheduled commercial banks at

15.4 percent in FY01 percent was lower than that of 19.3 percent in the

previous year, while the growth in credit by

SCBs slowed down to 15.6 percent in FY01 against 23 percent a year ago.

The industrial slowdown also affected the earnings of listed banks. The

net profits of 20 listed banks dropped by 34.43 percent in the quarter

ended March 2001. Net profits grew by 40.75 percent in the first quarter

of 2000-2001, but dropped to 4.56 percent in the fourth quarter of 2000-

2001.

On the Capital Adequacy Ratio (CAR) front while most banks managed to

fulfill the norms, it was a feat achieved with its own share of

difficulties. The CAR, which at present is 9.0 percent, is likely to be

hiked to 12.0 percent by the year 2004 based on the Basle Committee

recommendations. Any bank that wishes to grow its assets needs to also

shore up its capital at the same time so that its capital as a

percentage of the risk-weighted assets is maintained at the stipulated

rate. While the IPO route was a much-fancied one in the early ‘90s, the

current scenario doesn’t look too attractive for bank majors.

Consequently, banks have been forced to explore other avenues to shore

up their capital base. While some are wooing foreign partners to add to

the capital others are employing the M& A route. Many are also going in

for right issues at prices considerably lower than the market prices to

woo the investors.

Interest Rate Scene

The two years, post the East Asian crises in 1997-98 saw a climb in the

global interest rates. It was only in the later half of FY01 that the US

Fed cut interest rates. India has however

remained more or less insulated. The past 2 years in our country was

characterized by a mounting intention of the Reserve Bank Of India (RBI)

to steadily reduce interest rates resulting in a narrowing differential

between global and domestic rates.

The RBI has been affecting bank rate and CRR cuts at regular intervals

to improve liquidity and reduce rates. The only exception was in July

2000 when the RBI increased the Cash Reserve Ratio (CRR) to stem the

fall in the rupee against the dollar. The steady fall in the interest

rates resulted in squeezed margins for the banks in general.

Governmental Policy:

After the first phase and second phase of financial reforms, in the

1980s commercial banks began to function in a highly regulated

environment, with administered interest rate structure, quantitative

restrictions on credit flows, high reserve requirements and reservation

of a significant proportion of lendable resources for the priority and

the government sectors. The restrictive regulatory norms led to the

credit rationing for the private sector and the interest rate controls

led to the unproductive use of credit and low levels of investment and

growth. The resultant ‘financial repression’ led to decline in

productivity and efficiency and erosion of profitability of the banking

sector in general.

This was when the need to develop a sound commercial banking system was

felt. This was worked out mainly with the help of the recommendations of

the Committee on the Financial

System (Chairman: Shri M. Narasimham), 1991. The resultant financial

sector reforms called for interest rate flexibility for banks, reduction

in reserve requirements, and a number of structural measures. Interest

rates have thus been steadily deregulated in the past few years with

banks being free to fix their Prime Lending Rates(PLRs) and deposit

rates for most banking products. Credit market reforms included

introduction of new instruments of credit, changes in the credit

delivery system and integration of functional roles of diverse players,

such as, banks, financial institutions and non-banking financial

companies (Nbfcs). Domestic Private Sector Banks were allowed to be set

up, PSBs were allowed to access the markets to shore up their Cars.

Implications Of Some Recent Policy Measures:

The allowing of PSBs to shed manpower and dilution of equity are moves

that will lend greater autonomy to the industry. In order to lend more

depth to the capital markets the RBI had in November 2000 also changed

the capital market exposure norms from 5 percent of bank’s incremental

deposits of the previous year to 5 percent of the bank’s total domestic

credit in the previous year. But this move did not have the desired

effect, as in, while most banks kept away almost completely from the

capital markets, a few private sector banks went overboard and exceeded

limits and indulged in dubious stock market deals. The chances of seeing

banks making a comeback to the stock markets are therefore quite

unlikely in the near future.

The move to increase Foreign Direct Investment FDI limits to 49 percent

from 20 percent

during the first quarter of this fiscal came as a welcome announcement

to foreign players wanting to get a foot hold in the Indian Markets by

investing in willing Indian partners who are starved of net worth to

meet CAR norms. Ceiling for FII investment in companies was also

increased from 24.0 percent to 49.0 percent and have been included

within the ambit of FDI investment.

INTRODUCTION OF INDUSTRY

ORIGI N OF BA NKI NG5

Banks are among the main participants of the financial system in India.Banking offers several facilities and opportunities.

Banks in India were started on the British pattern in the beginning ofthe 19th century. The first half of the 19th century, The East IndiaCompany established 3 banks The Bank of Bengal, The Bank of Bombay andThe Bank of Madras6.

These three banks were known as Presidency Banks. In 1920these three banks were amalgamated and The Imperial Bank of India wasformed. In those days, all the banks were joint stock banks and a largenumber of them were small and weak. At the time of the 2nd world warabout 1500 joint stock banks were operating in India out of which 1400were non- scheduled banks. Bad and dishonest management managed quiet aquiet a few of them and there were a number of bank failures. Hence thegovernment had to step in and the Banking Company’s Act (subsequentlynamed as the Banking Regulation Act) was enacted which led to theelimination of the weak banks that were not in a position to fulfil thevarious requirements of the Act. In order to strengthen their weakunits and review public confidence in the banking system, a new section45 was enacted in the Banking Regulation Act in the year 1960,empowering the Government of India to compulsory amalgamate weak unitswith the stronger ones on the recommendation of the RBI.

BUSINESS OF BANKINGBanking, in a traditional sense is the business of accepting deposits of

money from public for the purpose of lending and investment. These

deposits can have a distinct feature of being withdraw able by cheques,

which no other financial institution can offer.

In addition to this banks also offer various other financial services also

which include:-

Issuing Demand Drafts & Travelers Cheques

Collection of Cheques, Bills of exchange

Safe Deposit Lockers

Issuing Letters of Credit & Letters of Guarantee

Sale and Purchase of Foreign Exchange

Custodial Services

Investment services

The business of banking is highly regulated since banks deal with money

offered to them by the public and ensuring the safety of this public money

is one of the prime responsibilities of any bank. That is why banks are

expected to be prudent in their lending and investment activities. The

major regulations and acts that govern the banking business are:-

Banking Regulations Act

Reserve Bank of India Act

Foreign Exchange Regulation (Amendment) Act, 1993

Indian Contract Act

Negotiable Instruments Act

Banks lend money either for productive purposes to individuals, firms,

corporate etc. or for buying house property, cars and other consumer

durable and for investment purposes to individuals and others. However,

banks do not finance any speculative activity. Lending is risk taking. The

risk should be covered by having prudent norms for lending. The depositors

of banks are also assured of safety of their money by deploying some

percentage of deposits in statutory reserves like SLR & CRR.

NEW GENERATION BANKING

The liberalize policy of Government of India permitted entry to private

sector in the banking, the industry has witnessed the entry of nine new

generation private banks. The major differentiating parameter that

distinguishes these banks from all the other banks in the Indian banking

is the level of service that is offered to the customer. Verify the focus

has always been centered on the customer – understanding his needs,

preempting him and consequently delighting him with various configurations

of benefits and a wide portfolio of products and services. These banks

have generally been established by promoters of repute or by ‘high value’

domestic financial institutions. The popularity of these banks can be

gauged by the fact that in a short span of time, these banks have gained

considerable customer confidence and consequently have shown impressive

growth rates. Today, the private banks corner almost four per cent share

of the total share of deposits. Most of the banks in this category are

concentrated in the high-growth urban areas in metros (that account for

approximately 70% of the total banking business). With efficiency being

the major focus, these banks have leveraged on their strengths and

competencies viz. Management, operational efficiency and flexibility,

superior product positioning and higher employee productivity skills.

The private banks with their focused business and service portfolio have a

reputation of being niche players in the industry. A strategy that has

allowed these banks to concentrate on few reliable high net worth

companies and individuals rather than cater to the mass market. These

well-chalked out integrates strategy plans have allowed most of these

banks to deliver superlative levels of personalized services. With the

Reserve Bank of India allowing these banks to operate 70% of their

businesses in urban areas, this statutory requirement has translated into

lower deposit mobilization costs and higher margins relative to public

sector banks.